accounting - principles - Ebooks | PapaCambridge

1295

TWELFTH EDITION ACCOUNTING PRINCIPLES

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of accounting - principles - Ebooks | PapaCambridge

T W E L F T H E D I T I O N

ACCOUNTINGPRINCIPLES

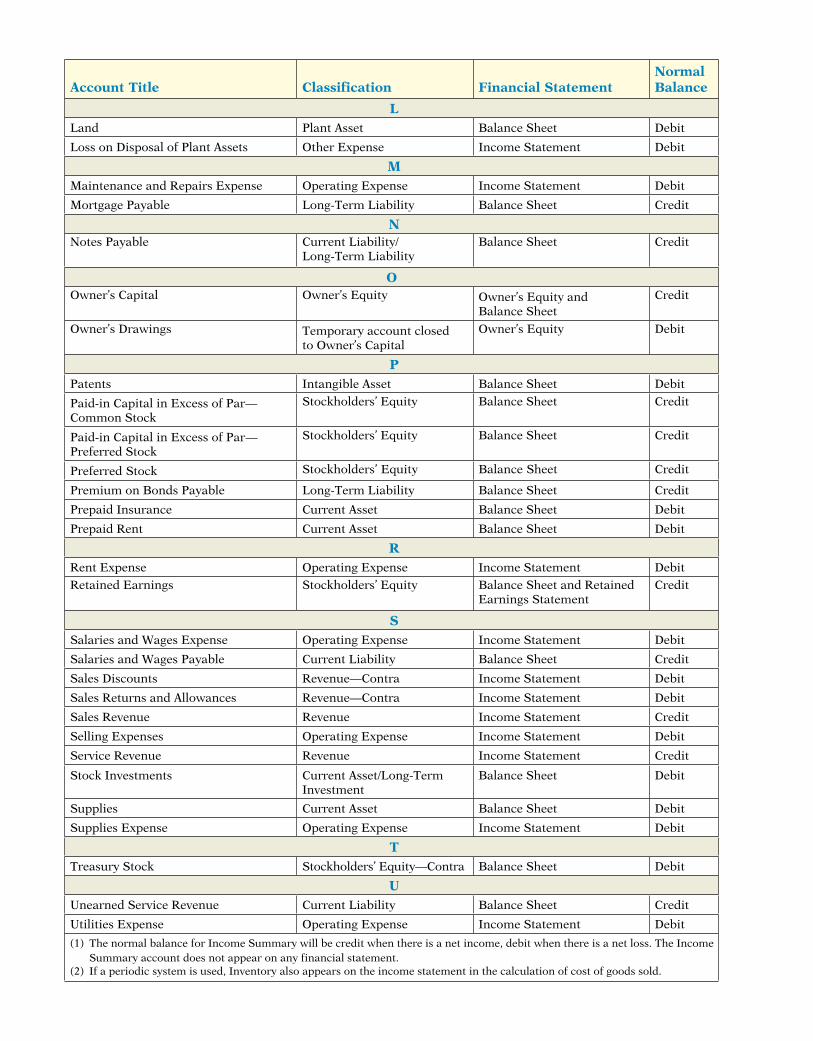

ACCOUNT CLASSIFICATION AND PRESENTATION

Account Title Classification Financial StatementNormalBalance

AAccounts Payable Current Liability Balance Sheet Credit

Accounts Receivable Current Asset Balance Sheet Debit

Accumulated Depreciation—Buildings Plant Asset—Contra Balance Sheet Credit

Accumulated Depreciation—Equipment Plant Asset—Contra Balance Sheet Credit

Advertising Expense Operating Expense Income Statement Debit

Allowance for Doubtful Accounts Current Asset—Contra Balance Sheet Credit

Amortization Expense Operating Expense Income Statement Debit

BBad Debt Expense Operating Expense Income Statement Debit

Bonds Payable Long-Term Liability Balance Sheet Credit

Buildings Plant Asset Balance Sheet Debit

CCash Current Asset Balance Sheet Debit

Common Stock Stockholders’ Equity Balance Sheet Credit

Copyrights Intangible Asset Balance Sheet Debit

Cost of Goods Sold Cost of Goods Sold Income Statement Debit

DDebt Investments Current Asset/Long-Term

InvestmentBalance Sheet Debit

Depreciation Expense Operating Expense Income Statement Debit

Discount on Bonds Payable Long-Term Liability—Contra Balance Sheet DebitDividends Temporary account closed

to Retained EarningsRetained Earnings Statement

Debit

Dividends Payable Current Liability Balance Sheet Credit

EEquipment Plant Asset Balance Sheet Debit

FFreight-Out Operating Expense Income Statement Debit

GGain on Disposal of Plant Assets Other Income Income Statement Credit

Goodwill Intangible Asset Balance Sheet Debit

IIncome Summary Temporary account closed

to Retained EarningsNot Applicable (1)

Income Tax Expense Income Tax Expense Income Statement Debit

Income Taxes Payable Current Liability Balance Sheet Credit

Insurance Expense Operating Expense Income Statement Debit

Interest Expense Other Expense Income Statement Debit

Interest Payable Current Liability Balance Sheet Credit

Interest Receivable Current Asset Balance Sheet Debit

Interest Revenue Other Income Income Statement Credit

Inventory Current Asset Balance Sheet (2) Debit

Account Title Classification Financial StatementNormalBalance

LLand Plant Asset Balance Sheet Debit

Loss on Disposal of Plant Assets Other Expense Income Statement Debit

MMaintenance and Repairs Expense Operating Expense Income Statement Debit

Mortgage Payable Long-Term Liability Balance Sheet Credit

NNotes Payable Current Liability/

Long-Term LiabilityBalance Sheet Credit

OOwner’s Capital Owner’s Equity Owner’s Equity and

Balance SheetCredit

Owner’s Drawings Temporary account closed to Owner’s Capital

Owner’s Equity Debit

PPatents Intangible Asset Balance Sheet Debit

Paid-in Capital in Excess of Par—Common Stock

Stockholders’ Equity Balance Sheet Credit

Paid-in Capital in Excess of Par—Preferred Stock

Stockholders’ Equity Balance Sheet Credit

Preferred Stock Stockholders’ Equity Balance Sheet Credit

Premium on Bonds Payable Long-Term Liability Balance Sheet Credit

Prepaid Insurance Current Asset Balance Sheet Debit

Prepaid Rent Current Asset Balance Sheet Debit

RRent Expense Operating Expense Income Statement DebitRetained Earnings Stockholders’ Equity Balance Sheet and Retained

Earnings StatementCredit

SSalaries and Wages Expense Operating Expense Income Statement Debit

Salaries and Wages Payable Current Liability Balance Sheet Credit

Sales Discounts Revenue—Contra Income Statement Debit

Sales Returns and Allowances Revenue—Contra Income Statement Debit

Sales Revenue Revenue Income Statement Credit

Selling Expenses Operating Expense Income Statement Debit

Service Revenue Revenue Income Statement Credit

Stock Investments Current Asset/Long-Term Investment

Balance Sheet Debit

Supplies Current Asset Balance Sheet Debit

Supplies Expense Operating Expense Income Statement Debit

TTreasury Stock Stockholders’ Equity—Contra Balance Sheet Debit

UUnearned Service Revenue Current Liability Balance Sheet Credit

Utilities Expense Operating Expense Income Statement Debit

(1) The normal balance for Income Summary will be credit when there is a net income, debit when there is a net loss. The Income Summary account does not appear on any financial statement.

(2) If a periodic system is used, Inventory also appears on the income statement in the calculation of cost of goods sold.

CHART OF ACCOUNTS

The following is a sample chart of accounts. It does not represent a comprehensive chart of all the accounts used in this textbook but rather those accounts that are commonly used. This sample chart of accounts is for a company that generates both service revenue as well as sales revenue. It uses the perpetual approach to inventory. If a periodic system was used, the following temporary accounts would be needed to record inventory purchases: Purchases, Freight-In, Purchase Returns and Allowances, and Purchase Discounts.

AssetsCash

Accounts Receivable

Allowance for Doubtful Accounts

Interest Receivable

Inventory

Supplies

Prepaid Insurance

Prepaid Rent

Land

Equipment

Accumulated Depreciation— Equipment

Buildings

Accumulated Depreciation— Buildings

Copyrights

Goodwill

Patents

LiabilitiesNotes Payable

Accounts Payable

Unearned Service Revenue

Salaries and Wages Payable

Unearned Rent Revenue

Interest Payable

Dividends Payable

Income Taxes Payable

Bonds Payable

Discount on Bonds Payable

Premium on Bonds Payable

Mortgage Payable

Owner’s and Stockholders’EquityOwner’s Capital

Owner’s Drawings

Common Stock

Paid-in Capital in Excess of Par— Common Stock

Preferred Stock

Paid-in Capital in Excess of Par— Preferred Stock

Treasury Stock

Retained Earnings

Dividends

Income Summary

RevenuesService Revenue

Sales Revenue

Sales Discounts

Sales Returns and Allowances

Interest Revenue

Gain on Disposal of Plant Assets

ExpensesAdvertising Expense

Amortization Expense

Bad Debt Expense

Cost of Goods Sold

Depreciation Expense

Freight-Out

Income Tax Expense

Insurance Expense

Interest Expense

Loss on Disposal of Plant Assets

Maintenance and Repairs Expense

Rent Expense

Salaries and Wages Expense

Supplies Expense

Utilities Expense

T W E L F T H E D I T I O N

ACCOUNTINGPRINCIPLES

Jerry J. Weygandt PhD, CPAUniversity of Wisconsin—Madison

Madison, Wisconsin

Paul D. Kimmel PhD, CPAUniversity of Wisconsin—Milwaukee

Milwaukee, Wisconsin

Donald E. Kieso PhD, CPANorthern Illinois University

DeKalb, Illinois

D E D I C A T E D T O

the Wiley sales representativeswho sell our books and service our adopters in a professional and ethical manner, and toEnid, Merlynn, and Donna

Vice President and Director George HoffmanExecutive Editor Michael McDonaldCustomer and Market Development Manager Christopher DeJohnDevelopment Editor Ed BrislinAssistant Development Editor Rebecca CostantiniEditorial Supervisor Terry Ann TatroEditorial Associate Margaret ThompsonSenior Content Manager Dorothy SinclairSenior Production Editor Valerie A. VargasSenior Director, Marketing Amy ScholzSenior Marketing Manager Karolina Zarychta HonsaProduct Design Manager Allison MorrisProduct Design Associate Matt OrigoniMedia Specialist Elena Santa MariaDesign Director Harry NolanCover Design Maureen EideInterior Design Maureen Eide/Kristine CarneySenior Photo Editor Mary Ann PriceMarket Solutions Assistant Elizabeth KearnsMarketing Assistant Anna WilhelmCover and title page Marina Grau/Shutterstock

This book was set in New Aster LT Std by Aptara®, Inc. and printed and bound by Courier Kendallville.The cover was printed by Courier Kendallville.

Founded in 1807, John Wiley & Sons, Inc. has been a valued source of knowledge and understanding for more than 200 years, helping people around the world meet their needs and fulfill their aspirations. Our company is built on a foundation of principles that include responsibility to the communities we serve and where we live and work. In 2008, we launched a Corporate Citizenship Initiative, a global effort to address the environmental, social, economic, and ethical challenges we face in our business. Among the issues we are addressing are carbon impact, paper specifications and procurement, ethical conduct within our business and among our vendors, and community and charitable support. For more information, please visit our website: www.wiley.com/go/citizenship.

Copyright © 2015, 2012, 2010, 2008, 2005, 2002, 2000 John Wiley & Sons, Inc. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning or otherwise, except as permitted under Sections 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc. 222 Rosewood Drive, Danvers, MA 01923, website www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030-5774, (201)748-6011, fax (201)748-6008, website http://www.wiley.com/go/permissions.

Evaluation copies are provided to qualified academics and professionals for review purposes only, for use in their courses during the next academic year. These copies are licensed and may not be sold or transferred to a third party. Upon completion of the review period, please return the evaluation copy to Wiley. Return instructions and a free of charge return shipping label are available at www.wiley.com/go/returnlabel. Outside of the United States, please contact your local representative.

ISBN-13 978-1-118-87505-6

Binder-Ready Version ISBN 978-1-118-96990-8

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

1 Accounting in Action 2 2 The Recording Process 48 3 Adjusting the Accounts 92 4 Completing the Accounting Cycle 148 5 Accounting for Merchandising Operations 206 6 Inventories 262 7 Accounting Information Systems 310 8 Fraud, Internal Control, and Cash 354 9 Accounting for Receivables 40410 Plant Assets, Natural Resources, and Intangible Assets 44211 Current Liabilities and Payroll Accounting 49012 Accounting for Partnerships 53213 Corporations: Organization and Capital Stock

Transactions 57014 Corporations: Dividends, Retained Earnings,

and Income Reporting 60815 Long-Term Liabilities 64416 Investments 69017 Statement of Cash Flows 72618 Financial Statement Analysis 78419 Managerial Accounting 83420 Job Order Costing 87621 Process Costing 91622 Cost-Volume-Profit 96023 Budgetary Planning 100424 Budgetary Control and Responsibility Accounting 105225 Standard Costs and Balanced Scorecard 110026 Incremental Analysis and Capital Budgeting 1146

APPENDICESA Specimen Financial Statements: Apple Inc.B Specimen Financial Statements: PepsiCo, Inc.C Specimen Financial Statements: The Coca-Cola Company D Specimen Financial Statements: Amazon.com, Inc.E Specimen Financial Statements: Wal-Mart Stores, Inc.F Specimen Financial Statements: Louis VuittonG Time Value of MoneyH Standards of Ethical Conduct for Managerial Accountants

Cases for Managerial Decision-Making*

*Available at the book’s companion website, www.wiley.com/college/weygandt.

iii

Brief Contents

Dear Student,

Why This Course? Remember your biology course in high school? Did you have one of those “invisible man” models (or maybe something more high-tech than that) that gave you the opportunity to look “inside” the human body? This accounting course offers something similar. To understand a business, you have to understand the finan-cial insides of a business organization. An accounting course will help you understand the essential financial components of businesses. Whether you are looking at a large multinational company like Apple or Starbucks or a single-owner software consulting business or coffee shop, knowing the fundamentals of accounting will help you understand what is happening. As an employee, a manager, an investor,a business owner, or a director of your own personal finances—any of which roles you will have at some point in your life—you will make better decisions for having taken this course.

Why This Book? Hundreds of thousands of stu-dents have used this textbook. Your instructor has chosen it for you because of its trusted reputation. The authors have worked hard to keep the book fresh, timely, and accurate.

How to Succeed? We’ve asked many students and many instructors whether there is a secret for success in this course. The nearly unanimous answer turns out to be not much of a secret: “Do the homework.” This is one course where doing is learning. The more time you spend on the homework assignments—using the various tools that this textbook provides—the more likely you are to learn the essential concepts, techniques, and methods of accounting. Besides the textbook itself, WileyPLUS and the book’s companion website also offers various support resources.

Good luck in this course. We hope you enjoy the experience and that you put to good use throughout a lifetime of success the knowledge you obtain in this course. We are sure you will not be disappointed.

Jerry J. WeygandtPaul D. KimmelDonald E. Kieso

“Whether you are looking at a large multinational company like Apple or Starbucks or a single-owner software consulting business or coffee shop, knowing the fundamentals of accounting will help you understand what is happening.”

From the Authors

iv

Jerry WeygandtJerry J. Weygandt, PhD, CPA, is Arthur Andersen Alumni Emeritus Professor of Accounting at the University of Wisconsin—Madison. He holds a Ph.D. in accounting from the University of Illinois. Articles by Professor Weygandt have appeared in the Accounting Review, Journal of Accounting Research, Accounting Horizons, Journal of Accountancy, and other academic and profes-sional journals. These articles have examined such financial reporting issues as accounting for price-level adjustments, pensions, convert-ible securities, stock option contracts, and interim reports. Professor Weygandt is author of other accounting and financial report-ing books and is a member of the American Accounting Association, the American Institute of Certified Public Accountants, and the Wisconsin Society of Certified Public Accountants. He has served on numerous committees of the American Accounting Association and as a member of the editorial board of the Accounting Review; he also has served as President and Secretary-Treasurer of the American Accounting Association. In addition, he has been actively involved with the American Institute of Certified Public Accountants and has been a member of the Accounting Standards Executive Committee (AcSEC) of that organization. He has served on the FASB task force that examined the report-ing issues related to accounting for income taxes and served as a trustee of the Financial Accounting Foundation. Professor Weygandt has received the Chancellor’s Award for Excellence in Teaching and the Beta Gamma Sigma Dean’s Teaching Award. He is on the board of directors of M & I Bank of Southern Wisconsin. He is the recipient of the Wisconsin Institute of CPA’s Outstanding Educator’s Award and the Lifetime Achievement Award. In 2001 he received the American Accounting Association’s Outstanding Educator Award.

Paul KimmelPaul D. Kimmel, PhD, CPA, received his bachelor’s degree from the University of Minnesota and his doctorate in account-ing from the University of Wisconsin. He is an Associate Professor at the University of Wisconsin—Milwaukee, and has public accounting experience with Deloitte & Touche (Minneapolis). He was the recipient of the UWM School of Business Advisory Council Teaching Award, the Reggie Taite Excellence in Teaching Award and a three-time winner of the Outstanding Teaching Assistant Award at the University of Wisconsin. He is also a recipient of the Elijah Watts Sells Award for Honorary Distinction for his results on the CPA exam. He is a member of the American Accounting Association and the Institute of Management Accountants and has published articles in Accounting Review, Accounting Horizons, Advances in Management Accounting, Managerial Finance, Issues in Accounting Education, Journal of Accounting Education, as well as other journals. His research interests include accounting for finan-cial instruments and innovation in accounting education. He has published papers and given numerous talks on incorporating critical thinking into accounting education, and helped prepare a catalog of critical thinking resources for the Federated Schools of Accountancy.

Don KiesoDonald E. Kieso, PhD, CPA, received his bachelor’s degree from Aurora University and his doctorate in accounting from the University of Illinois. He has served as chairman of the Department of Accountancy and is currently the KPMG Emeritus Professor of Accountancy at Northern Illinois University. He has public accounting experience with Price Waterhouse & Co. (San Francisco and Chicago) and Arthur Andersen & Co. (Chicago) and research experience with the Research Division of the American Institute of Certified Public Accountants (New York). He has done post doctorate work as a Visiting Scholar at the University of California at Berkeley and is a recipient of NIU’s Teaching Excellence Award and four Golden Apple Teaching Awards. Professor Kieso is the author of other accounting and business books and is a member of the American Accounting Association, the American Institute of Certified Public Accountants, and the Illinois CPA Society. He has served as a member of the Board of Directors of the Illinois CPA Society, then AACSB’s Accounting Accreditation Committees, the State of Illinois Comptroller’s Commission, as Secretary-Treasurer of the Federation of Schools of Accountancy, and as Secretary-Treasurer of the American Accounting Association. Professor Kieso is currently serving on the Board of Trustees and Executive Committee of Aurora University, as a member of the Board of Directors of Kishwaukee Community Hospital, and as Treasurer and Director of Valley West Community Hospital. From 1989 to 1993 he served as a charter member of the national Accounting Education Change Commission. He is the recipient of the Outstanding Accounting Educator Award from the Illinois CPA Society, the FSA’s Joseph A. Silvoso Award of Merit, the NIU Foundation’s Humanitarian Award for Service to Higher Education, a Distinguished Service Award from the Illinois CPA Society, and in 2003 an honorary doctorate from Aurora University.

Author Commitment

Practice Made Simple

Personalized PracticeBased on cognitive science, WileyPLUS with ORION is a personalized, adaptive learning experience that gives students the practice they need to build profi ciency on topics while using their study time most effectively. The adaptive engine is powered by hundreds of unique questions per chapter, giving students endless opportunities for practice throughout the course.

The Team for Success is focused on helping students get the most out of their accounting course by making practice simple. Both in the printed text and the online environment of WileyPLUS, new opportunities for self-guided practice allow students to check their knowledge of accounting concepts, skills, and problem-solving techniques as they receive individual feedback at the question, learning objective, and course level.

Streamlined Learning ObjectivesNewly streamlined learning objectives help students make the best use of their time outside of class. Each learning objective is addressed by reading content, answering a variety of practice and assessment questions, and watching educational videos, so that no matter where students begin their work, the relevant resources and practice are readily accessible.

In WileyPLUS, the new practice assignments include several Do ITs, Brief Exercises, Exercises, and Problems, giving students the opportunity to check their work or see the answer and solution after their fi nal attempt.

In the text, the new Review and Practice section includes:

• Learning Objectives Review • Glossary Review • Practice Multiple-Choice Questions and Solutions • Practice Exercises and Solutions • Practice Problem and Solution

ReadingContent

EducationalVideos

Assessment

LearningObjective

Review and Practice A new section in the text and in WileyPLUS offers students more opportunities for self-guided practice.

WileyPLUS with ORIONOver 5,500 new questions are available for practice and review. WileyPLUS with Orion is an adaptive study and practice tool that helps students build proficiency in course topics.

Updated Content and DesignWe scrutinized all chapter material to find new ways to engage students and help them learn accounting concepts. Homework problems were updated in all chapters. A new learning objective structure helps students practice their understanding of concepts with DO IT! exercises before they move on to different topics in other learning objectives. Coupled with a new interior design and revised infographics, the new outcomes-oriented approach motivates students and helps them make the best use of their time.

WileyPLUS VideosOver 300 videos are available in WileyPLUS. More than 150 of the videos are new to the 12th Edition. The videos walk students through relevant homework problems and solutions, review important concepts, provide overviews of Excel skills, and explore topics in a real-world context.

Student Practice and SolutionsNew practice opportunities with solutions are integrated throughout the textbook and WileyPLUS course. Each textbook chapter now provides students with a Review and Practice section that includes learning objective summaries, multiple-choice questions with feedback for each answer choice, and both practice exercises and problems with solutions. Also, each learning objective module in the textbook is now followed by a DO IT! exercise with an accompanying solution. In WileyPLUS, two brief exercises, two DO IT! exercises, two exercises, and a new problem are available for practice with each chapter. These practice questions are algorithmic, providing students with multiple opportunities for advanced practice.

Real World ContextWe expanded our practice of using numerous examples of real companies throughout the textbook. For example, new feature stories highlight operations of Clif Bar, Groupon, and REI. Also, in WileyPLUS, real-world Insight boxes now have questions that can be assigned as homework.

ExcelNew Excel skill videos help students understand Excel features they can apply in their accounting studies. A new continuing Excel tutorial is also available at the end of each managerial accounting chapter.

More information about the 12th Edition is available on the book’s website at www.wiley.com/college/weygandt.

viii

What’s New?

1 Accounting in Action 2Knowing the Numbers: Clif Bar 2LO 1: Identify the activities and users associated

with accounting. 4Three Activities 4Who Uses Accounting Data 5

LO 2: Explain the building blocks of accounting: ethics, principles, and assumptions. 7

Ethics in Financial Reporting 7Generally Accepted Accounting Principles 8Measurement Principles 9Assumptions 9

LO 3: State the accounting equation, and defineits components. 12

Assets 12Liabilities 12Owner’s Equity 13

LO 4: Analyze the effects of business transactions on the accounting equation. 14

Transaction Analysis 15Summary of Transactions 19

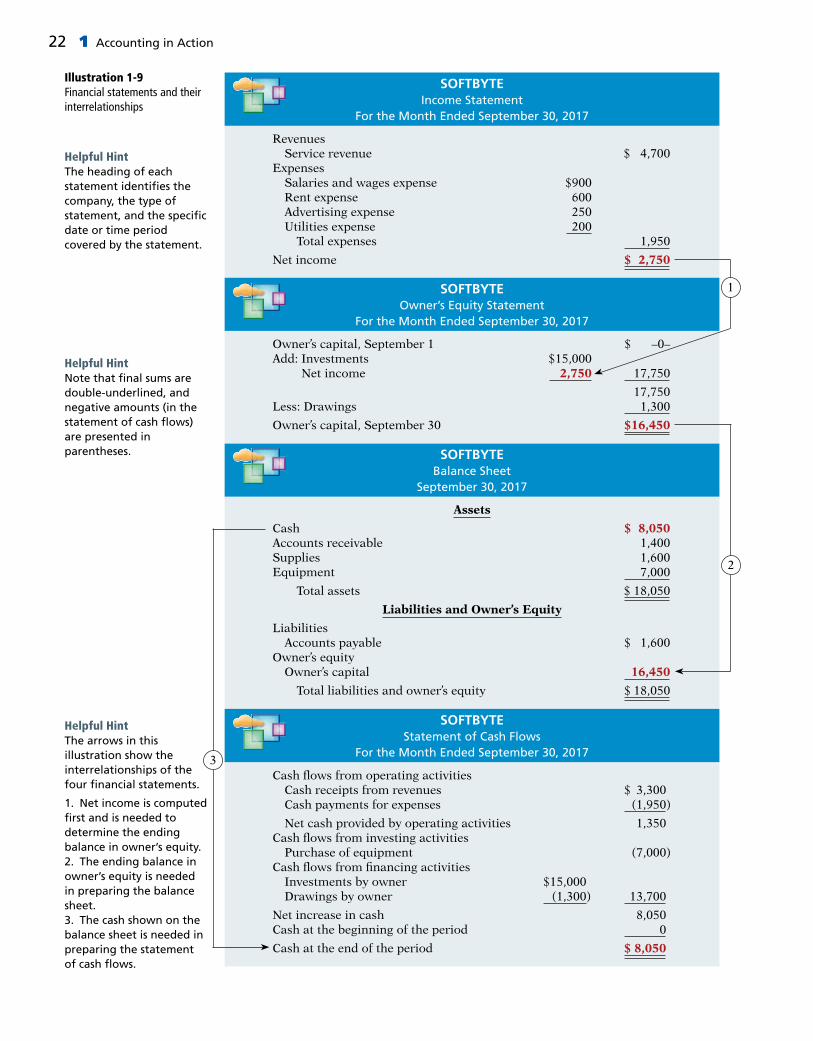

LO 5: Describe the four financial statements and how they are prepared. 21

Income Statement 21Owner’s Equity Statement 21Balance Sheet 23Statement of Cash Flows 23

LO *6: APPENDIX 1A: Explain the career opportunities in accounting. 25

Public Accounting 25Private Accounting 26Governmental Accounting 26Forensic Accounting 26“Show Me the Money” 26

A Look at IFRS 46

2 The Recording Process 48 Accidents Happen: MF Global Holdings 48LO 1: Describe how accounts, debits, and credits

are used to record business transactions. 50The Account 50Debits and Credits 50Summary of Debit/Credit Rules 53

LO 2: Indicate how a journal is used in the recording process. 54

Steps in the Recording Process 54The Journal 55

LO 3: Explain how a ledger and posting help in the recording process. 57

The Ledger 57Posting 59The Recording Process Illustrated 60Summary Illustration of Journalizing and

Posting 66LO 4: Prepare a trial balance. 68

Limitations of a Trial Balance 68Locating Errors 69Dollar Signs and Underlining 69

A Look at IFRS 90

3 Adjusting the Accounts 92Keeping Track of Groupons: Groupon 92LO 1: Explain the accrual basis of accounting

and the reasons for adjusting entries. 94Fiscal and Calendar Years 94Accrual-versus Cash-Basis Accounting 94Recognizing Revenues and Expenses 95The Need for Adjusting Entries 96Types of Adjusting Entries 96

LO 2: Prepare adjusting entries for deferrals. 97Prepaid Expenses 98Unearned Revenues 101

LO 3: Prepare adjusting entries for accruals. 104Accrued Revenues 104Accrued Expenses 106Summary of Basic Relationships 109

LO 4: Describe the nature and purpose of an adjusted trial balance. 111

Preparing the Adjusted Trial Balance 111Preparing Financial Statements 112

LO *5: APPENDIX 3A: Prepare adjusting entries for the alternative treatment of deferrals. 115

Prepaid Expenses 116Unearned Revenues 117Summary of Additional Adjustment

Relationships 118LO *6: APPENDIX 3B: Discuss financial reporting

concepts. 119Qualities of Useful Information 119Assumptions in Financial Reporting 119Principles in Financial Reporting 120Cost Constraint 121

A Look at IFRS 146

ix

Table of Contents

4Completing the Accounting Cycle 148

Everyone Likes to Win: Rhino Foods 148LO 1: Prepare a worksheet. 150

Steps in Preparing a Worksheet 150Preparing Financial Statements from a

Worksheet 157Preparing Adjusting Entries from a

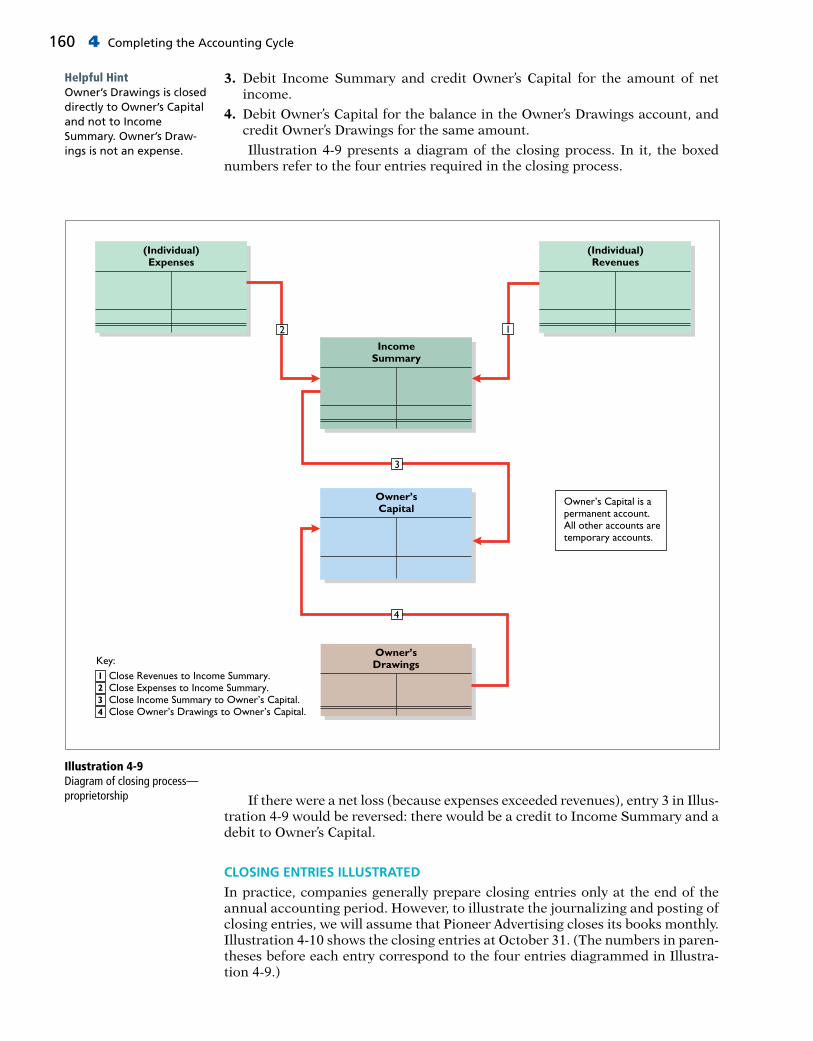

Worksheet 158LO 2: Prepare closing entries and a post-closing

trial balance. 158Preparing Closing Entries 159Posting Closing Entries 161Preparing a Post-Closing Trial Balance 163

LO 3: Explain the steps in the accounting cycle and how to prepare correcting entries. 166

Summary of the Accounting Cycle 166Reversing Entries—An Optional Step 166Correcting Entries—An Avoidable Step 167

LO 4: Identify the sections of a classified balancesheet. 169

Current Assets 170Long-Term Investments 171Property, Plant, and Equipment 171Intangible Assets 171Current Liabilities 172Long-Term Liabilities 173Owner’s Equity 174

LO *5: APPENDIX 4A: Prepare reversing entries. 175

Reversing Entries Example 175A Look at IFRS 202

5Accounting for Merchandising Operations 206

Buy Now, Vote Later: REI 206 LO 1: Describe merchandising operations and

inventory systems. 208Operating Cycles 208Flow of Costs 209

LO 2: Record purchases under a perpetual inventory system. 211

Freight Costs 213Purchase Returns and Allowances 214Purchase Discounts 214Summary of Purchasing Transactions 215

LO 3: Record sales under a perpetual inventory system. 216

Sales Returns and Allowances 217Sales Discounts 218

LO 4: Apply the steps in the accounting cycle to a merchandising company. 220

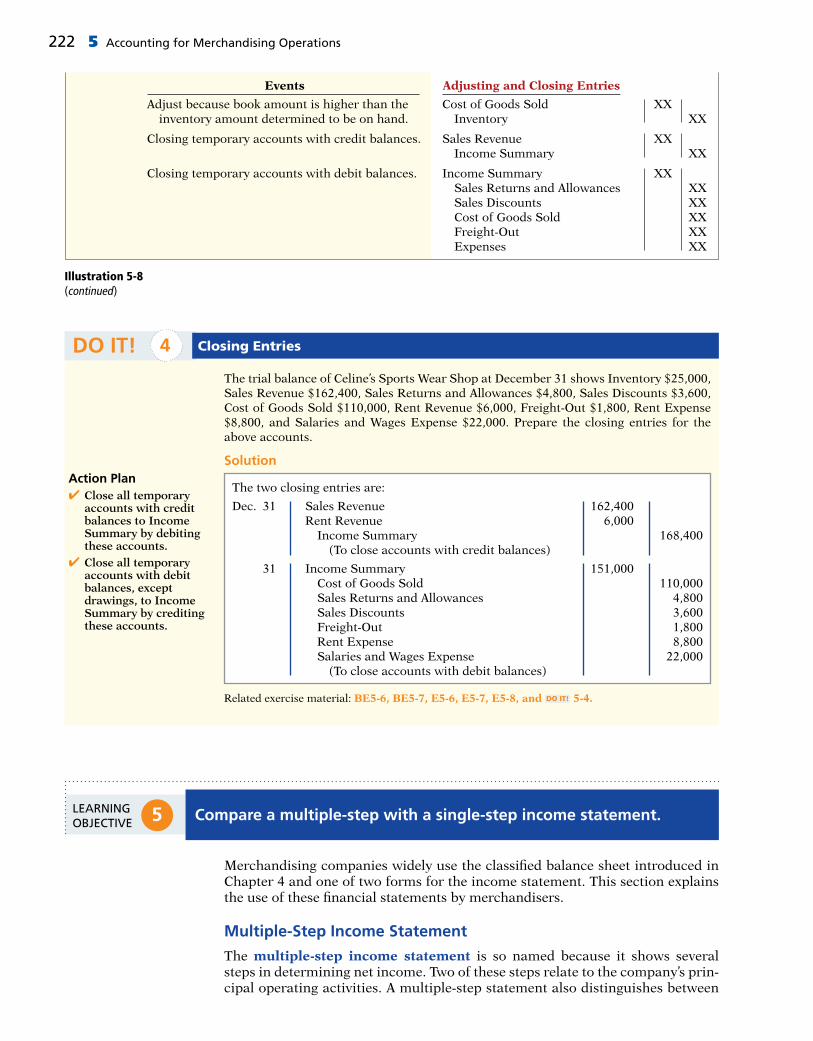

Adjusting Entries 220Closing Entries 220Summary of Merchandising Entries 221

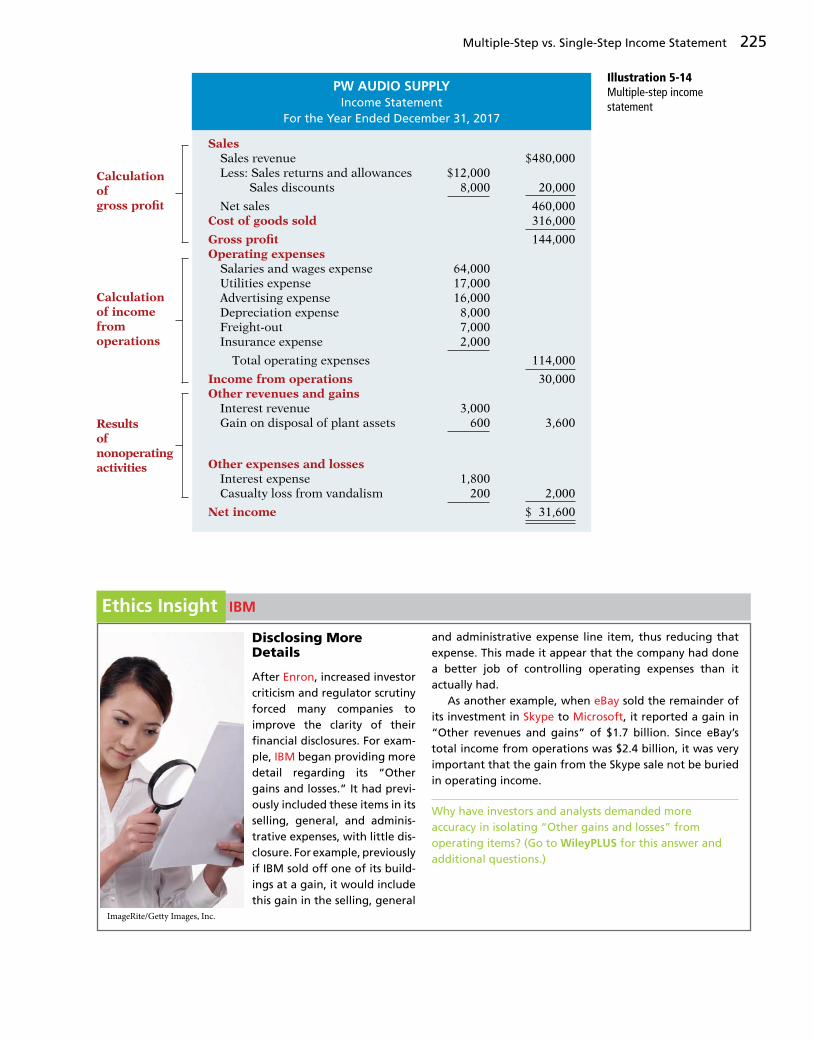

LO 5: Compare a multiple-step with a single-step income statement. 222

Multiple-Step Income Statement 222Single-Step Income Statement 226Classified Balance Sheet 226

LO *6: APPENDIX 5A: Prepare a worksheet for a merchandising company. 228

Using a Worksheet 228LO *7: APPENDIX 5B: Record purchases and sales

under a periodic inventory system. 229Determining Cost of Goods Sold Under a Periodic

System 230Recording Merchandise Transactions 230Recording Purchases of Merchandise 231Recording Sales of Merchandise 232Journalizing and Posting Closing Entries 233Using a Worksheet 234

A Look at IFRS 259

6 Inventories 262

“Where Is That Spare Bulldozer Blade?”: Caterpillar 262LO 1: Discuss how to classify and determine

inventory. 264Classifying Inventory 264Determining Inventory Quantities 265

LO 2: Apply inventory cost flow methods and discuss their financial effects. 268

Specific Identification 269Cost Flow Assumptions 269Financial Statement and Tax Effects of Cost Flow

Methods 274Using Inventory Cost Flow Methods

Consistently 275LO 3: Indicate the effects of inventory errors on

the financial statements. 277Income Statement Effects 277Balance Sheet Effects 278

LO 4: Explain the statement presentation and analysis of inventory. 279

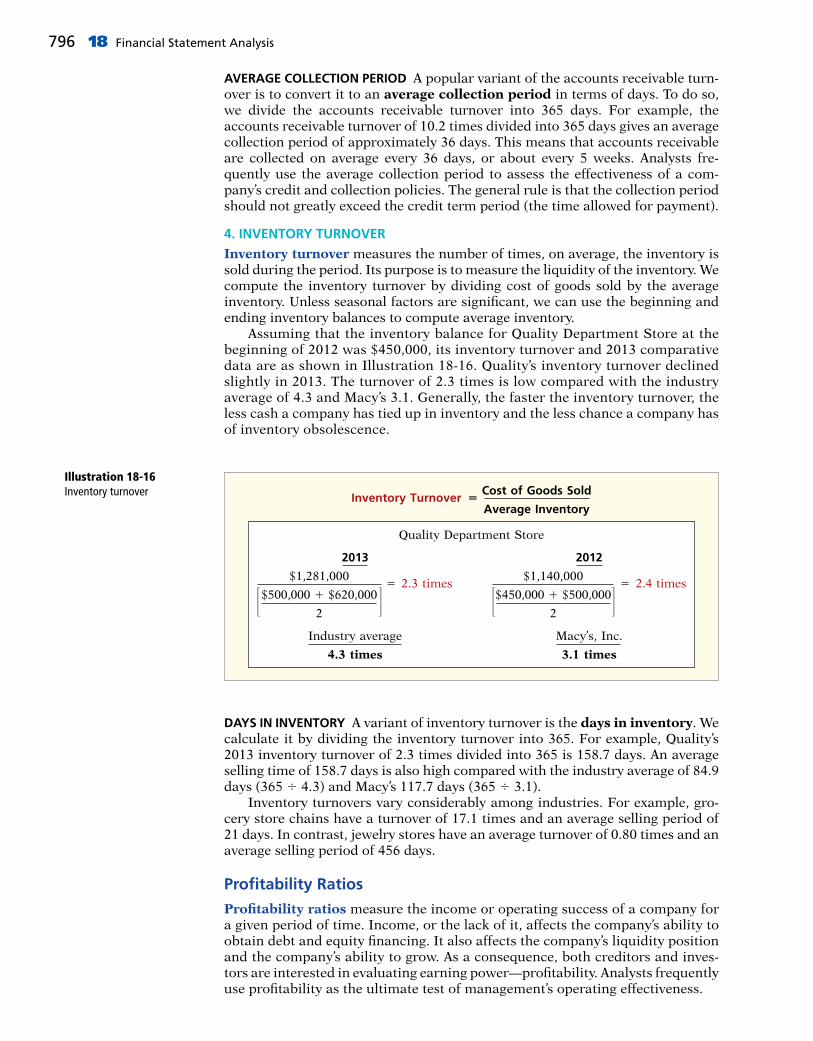

Presentation 279Lower-of-Cost-or-Net Realizable Value 279Analysis 280

LO *5: APPENDIX 6A: Apply the inventory cost flow methods to perpetual inventory records. 282

First-In, First-Out (FIFO) 282Last-In, First-Out (LIFO) 283Average-Cost 283

x

LO *6: APPENDIX 6B: Describe the two methods of estimating inventories. 284

Gross Profit Method 284Retail Inventory Method 285

A Look at IFRS 308

7Accounting Information Systems 310

QuickBooks® Helps This Retailer Sell Guitars 310LO 1: Explain the basic concepts of an accounting

information system. 312Computerized Accounting Systems 312Manual Accounting Systems 314

LO 2: Describe the nature and purpose of a subsidiary ledger. 315

Subsidiary Ledger Example 315Advantages of Subsidiary Ledgers 316

LO 3: Record transactions in special journals. 317Sales Journal 318Cash Receipts Journal 320Purchases Journal 324Cash Payments Journal 326Effects of Special Journals on the General

Journal 329Cyber Security: A Final Comment 330

A Look at IFRS 353

8Fraud, Internal Control, and Cash 354

Minding the Money in Madison: Barriques 354LO 1: Discuss fraud and the principles of internal

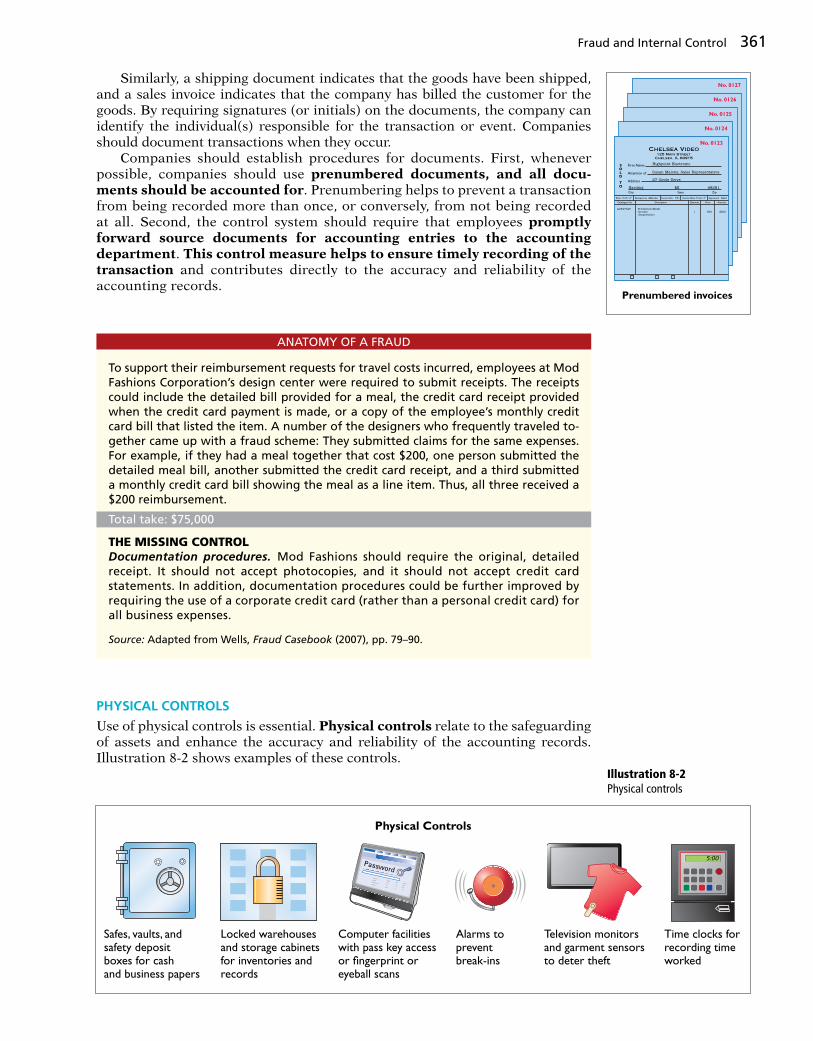

control. 356Fraud 356The Sarbanes-Oxley Act 356Internal Control 357Principles of Internal Control Activities 358Limitations of Internal Control 365

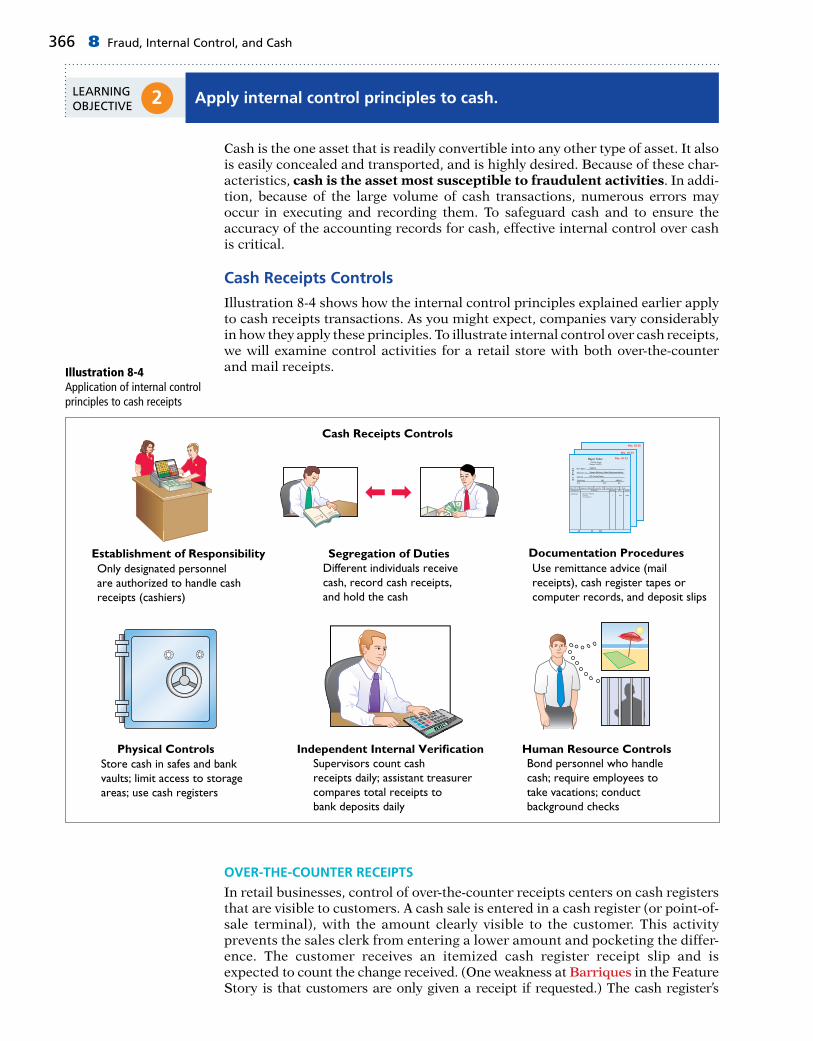

LO 2: Apply internal control principles to cash. 366

Cash Receipts Controls 366Cash Disbursements Controls 369Petty Cash Fund 370

LO 3: Identify the control features of a bank account. 373

Making Bank Deposits 373Writing Checks 374Bank Statements 375Reconciling the Bank Account 376Electronic Funds Transfer (EFT) System 380

LO 4: Explain the reporting of cash. 381Cash Equivalents 381Restricted Cash 382

A Look at IFRS 402

9 Accounting for Receivables 404A Dose of Careful Management Keeps Receivables Healthy: Whitehall-Robins 404LO 1: Explain how companies recognize accounts

receivable. 406Types of Receivables 406Recognizing Accounts Receivable 406

LO 2: Describe how companies value accounts receivable and record their disposition. 408

Valuing Accounts Receivable 408Disposing of Accounts Receivable 414

LO 3: Explain how companies recognize notes receivable. 417

Determining the Maturity Date 417Computing Interest 418Recognizing Notes Receivable 419

LO 4: Describe how companies value notes receivable, record their disposition, and present and analyze receivables. 420

Valuing Notes Receivable 420Disposing of Notes Receivable 420Statement Presentation and Analysis 422

A Look at IFRS 440

10Plant Assets, Natural Resources, and Intangible Assets

442

How Much for a Ride to the Beach?: Rent-A-Wreck 442LO 1: Explain the accounting for plant asset

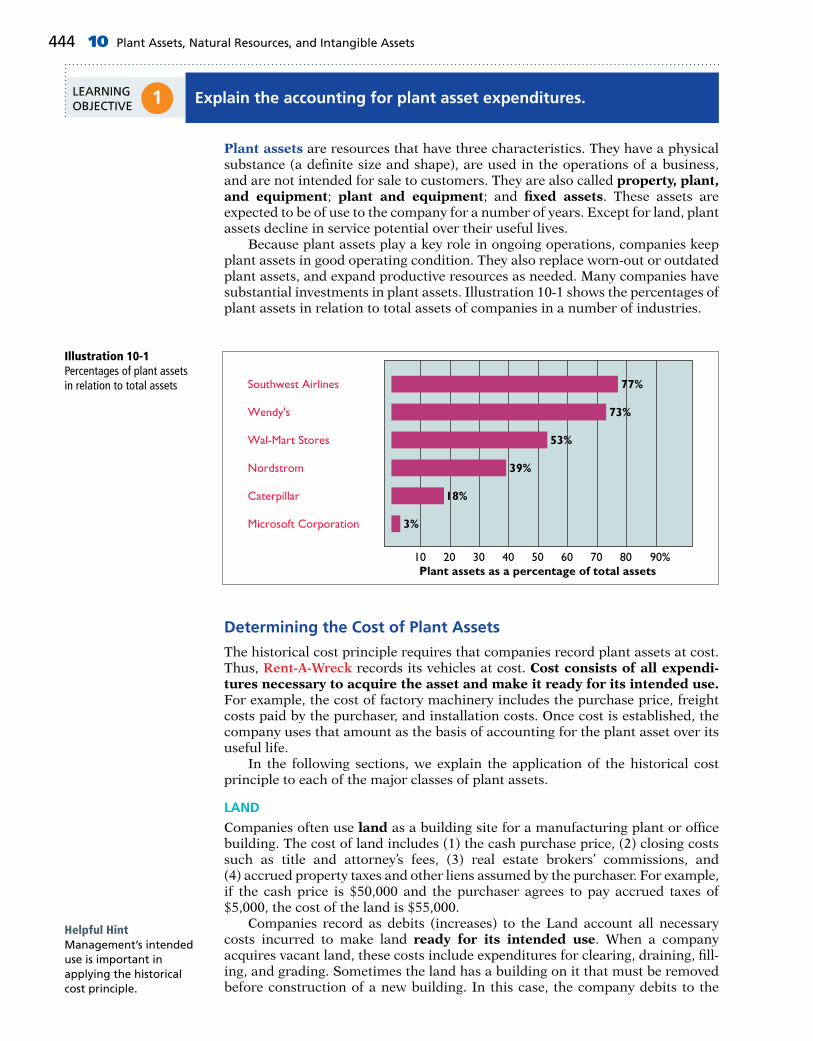

expenditures. 444Determining the Cost of Plant Assets 444Expenditures During Useful Life 446

LO 2: Apply depreciation methods to plant assets. 448

Factors in Computing Depreciation 449Depreciation Methods 449Depreciation and Income Taxes 454Revising Periodic Depreciation 454

LO 3: Explain how to account for the disposal of plant assets. 455

Retirement of Plant Assets 456Sale of Plant Assets 456

LO 4: Describe how to account for natural resources and intangible assets. 458

Natural Resources 458Depletion 458Intangible Assets 460Accounting for Intangible Assets 460Research and Development Costs 462

xi

LO 5: Discuss how plant assets, natural resources, and intangible assets are reported and analyzed. 463

Presentation 463Analysis 464

LO *6: APPENDIX 10A: Explain how to account for the exchange of plant assets. 465

Loss Treatment 465Gain Treatment 466

A Look at IFRS 487

11Current Liabilities and Payroll Accounting 490

Financing His Dreams: Wilbert Murdock 490LO 1: Explain how to account for current

liabilities. 492What Is a Current Liability? 492Notes Payable 492Sales Taxes Payable 493Unearned Revenues 494Current Maturities of Long-Term Debt 494

LO 2: Discuss how current liabilities are reported and analyzed. 495

Reporting Uncertainty 495Reporting of Current Liabilities 497Analysis of Current Liabilities 497

LO 3: Explain how to account for payroll. 499Determining the Payroll 499Recording the Payroll 503Employer Payroll Taxes 506Filing and Remitting Payroll Taxes 508Internal Control for Payroll 508

LO *4: APPENDIX 11A: Discuss additional fringe benefits associated with employee compensation. 510

Paid Absences 510Postretirement Benefits 511

A Look at IFRS 530

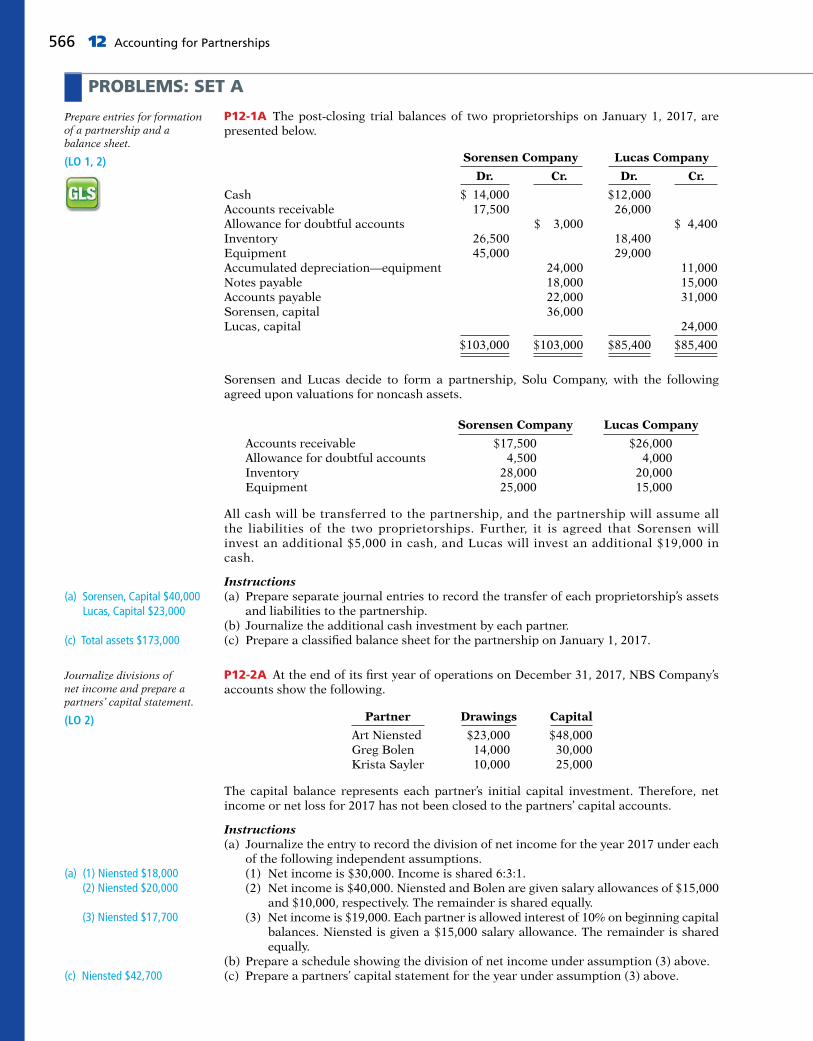

12Accounting for Partnerships 532

From Trials to the Top Ten: Razor & Tie 532LO 1: Discuss and account for the formation of a

partnership. 534Characteristics of Partnerships 534Organizations with Partnership

Characteristics 535Advantages and Disadvantages of

Partnerships 537The Partnership Agreement 537Accounting for a Partnership Formation 538

LO 2: Explain how to account for net income or net loss of a partnership. 539

Dividing Net Income or Net Loss 539Partnership Financial Statements 542

LO 3: Explain how to account for the liquidation of a partnership. 543

No Capital Deficiency 544Capital Deficiency 546

LO *4: APPENDIX 12A: Prepare journal entries when a partner is either admitted or withdraws. 549

Admission of a Partner 549Withdrawal of a Partner 552

13Corporations: Organization and Capital Stock Transactions 570

What’s Cooking?: Nike 570LO 1: Discuss the major characteristics of

a corporation. 572Characteristics of a Corporation 572Forming a Corporation 574Stockholder Rights 576Stock Issue Considerations 576Corporate Capital 579

LO 2: Explain how to account for the issuance of common and preferred stock. 581

Issuing Par Value Common Stock for Cash 581Issuing No-Par Common Stock for Cash 582Issuing Common Stock for Services or Noncash

Assets 582Accounting for Preferred Stock 583

LO 3: Explain how to account for treasury stock. 584

Purchase of Treasury Stock 584Disposal of Treasury Stock 585

LO 4: Prepare a stockholders’ equity section. 587A Look at IFRS 605

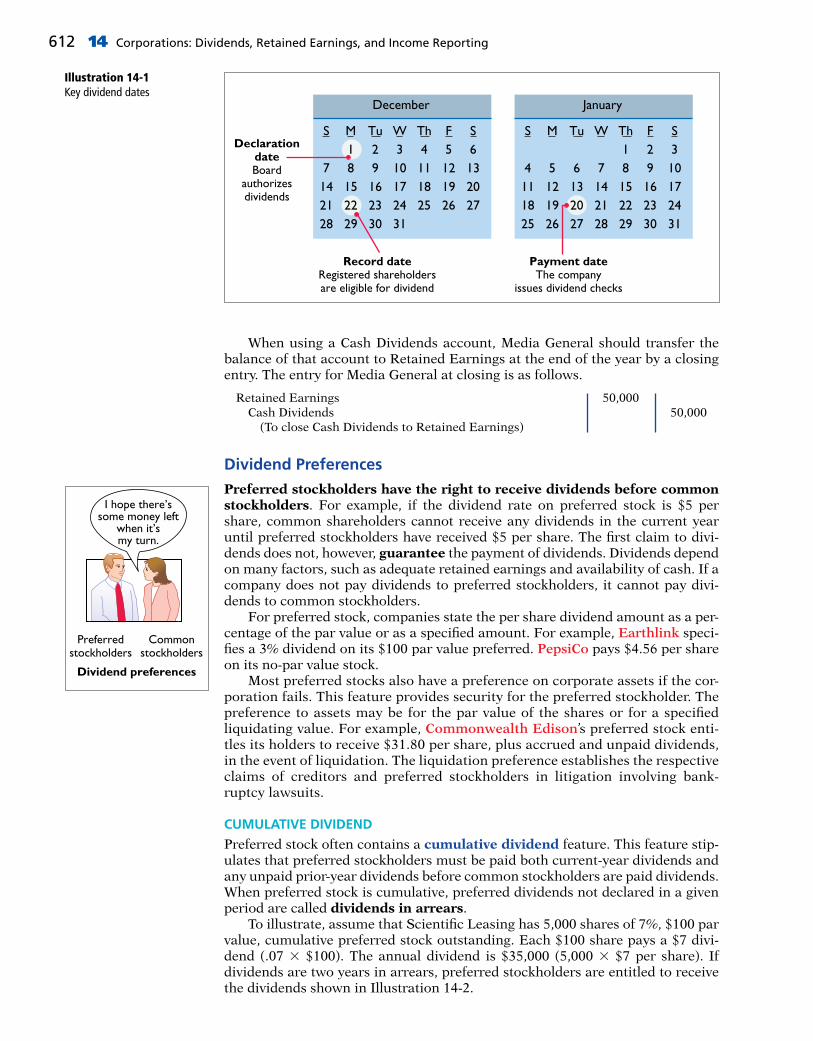

14Corporations: Dividends, Retained Earnings, andIncome Reporting

608

Owning a Piece of the Action: Van Meter Inc. 608LO 1: Explain how to account for cash

dividends. 610Cash Dividends 610Dividend Preferences 612

LO 2: Explain how to account for stock dividends and splits. 615

Stock Dividends 615Stock Splits 617

xii

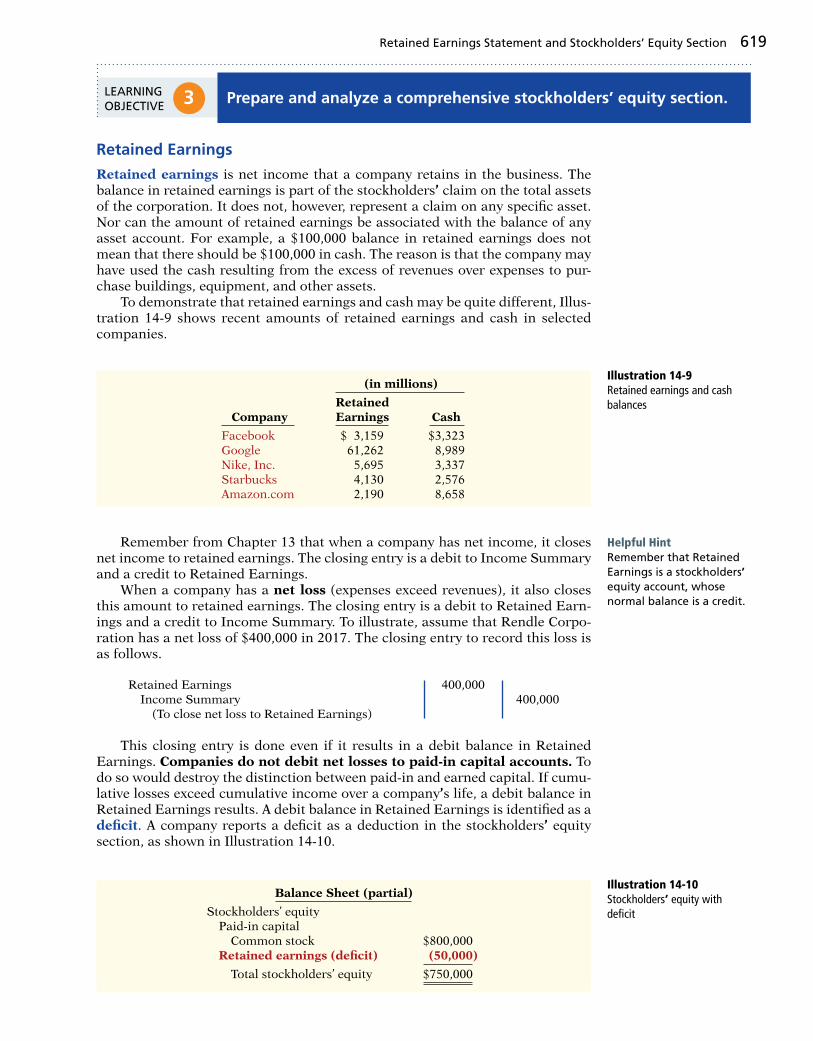

LO 3: Prepare and analyze a comprehensive stockholders’ equity section. 619

Retained Earnings 619Statement Presentation and Analysis 622

LO 4: Describe the form and content of corporation income statements. 623

Income Statement Presentation 623Income Statement Analysis 624

A Look at IFRS 642

15 Long-Term Liabilities 644And Then There Were Two 644LO 1: Describe the major characteristics of bonds. 646

Types of Bonds 646Issuing Procedures 646Determining the Market Price of a Bond 647

LO 2: Explain how to account for bond transactions. 649

Issuing Bonds at Face Value 649Discount or Premium on Bonds 650Issuing Bonds at a Discount 651Issuing Bonds at a Premium 652Redeeming and Converting Bonds 654

LO 3: Explain how to account for long-term notes payable. 656

Long-Term Notes Payable 656LO 4: Discuss how long-term liabilities are

reported and analyzed. 657Presentation 657Use of Ratios 658Debt and Equity Financing 658Lease Liabilities and Off-Balance-Sheet

Financing 659LO *5: APPENDIX 15A: Apply the straight-line

method of amortizing bond discount and bond premium. 662

Amortizing Bond Discount 662Amortizing Bond Premium 663

LO *6: APPENDIX 15B: Apply the effective-interest method of amortizing bond discount and bond premium. 664

Amortizing Bond Discount 665Amortizing Bond Premium 666

A Look at IFRS 686

16 Investments 690“Is There Anything Else We Can Buy?”: Time Warner 690LO 1: Explain how to account for debt

investments. 692Why Corporations Invest 692Accounting for Debt Investments 693

LO 2: Explain how to account for stock investments. 695

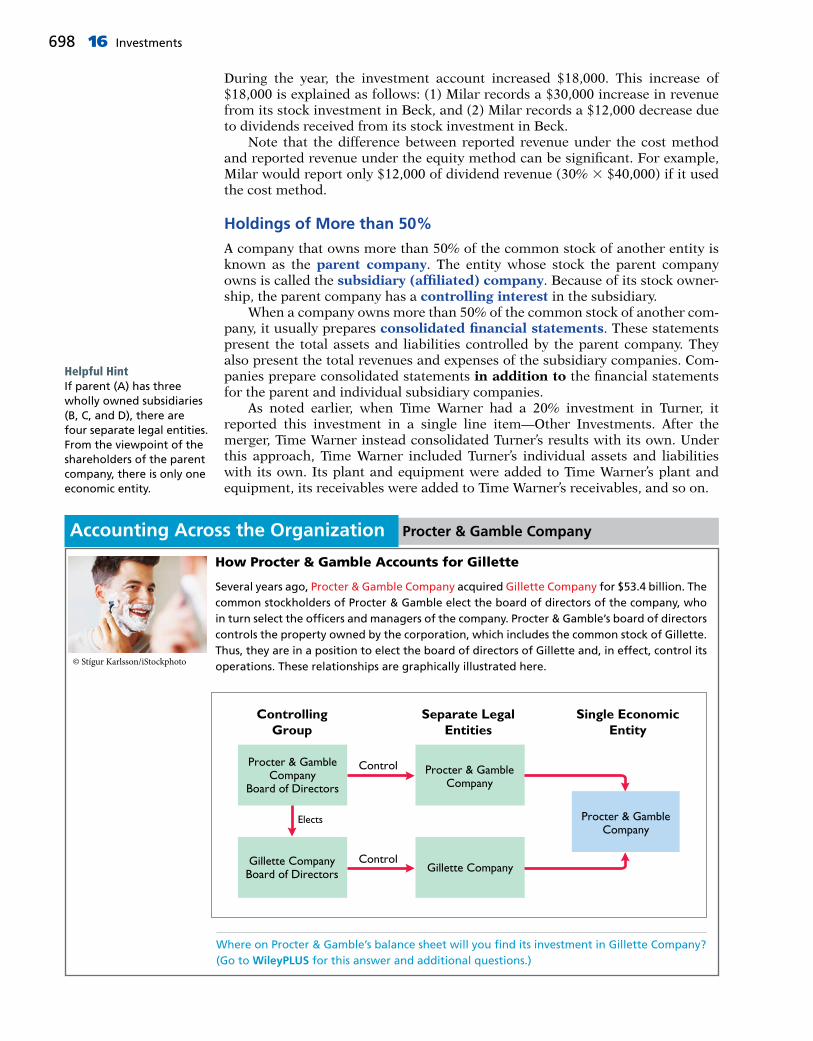

Holdings of Less than 20% 696Holdings Between 20% and 50% 696Holdings of More than 50% 698

LO 3: Discuss how debt and stock investments are reported in financial statements. 700

Categories of Securities 700Balance Sheet Presentation 703Presentation of Realized and Unrealized Gain or

Loss 704Classified Balance Sheet 705

A Look at IFRS 723

17 Statement of Cash Flows 726Got Cash?: Microsoft 726LO 1: Discuss the usefulness and format of the

statement of cash flows. 728Usefulness of the Statement of Cash Flows 728Classification of Cash Flows 728Significant Noncash Activities 729Format of the Statement of Cash Flows 730

LO 2: Prepare a statement of cash flows using the indirect method. 731

Indirect and Direct Methods 732Indirect Method—Computer Services

Company 732Step 1: Operating Activities 734Summary of Conversion to Net Cash Provided

by Operating Activities—Indirect Method 737Step 2: Investing and Financing Activities 738Step 3: Net Change in Cash 739

LO 3: Analyze the statement of cash flows. 742Free Cash Flow 742

LO *4: APPENDIX 17A: Prepare a statement of cash flows using the direct method. 743

Step 1: Operating Activities 745Step 2: Investing and Financing Activities 749Step 3: Net Change in Cash 751

LO *5: APPENDIX 17B: Use a worksheet to prepare the statement of cash flows using the indirect method. 751

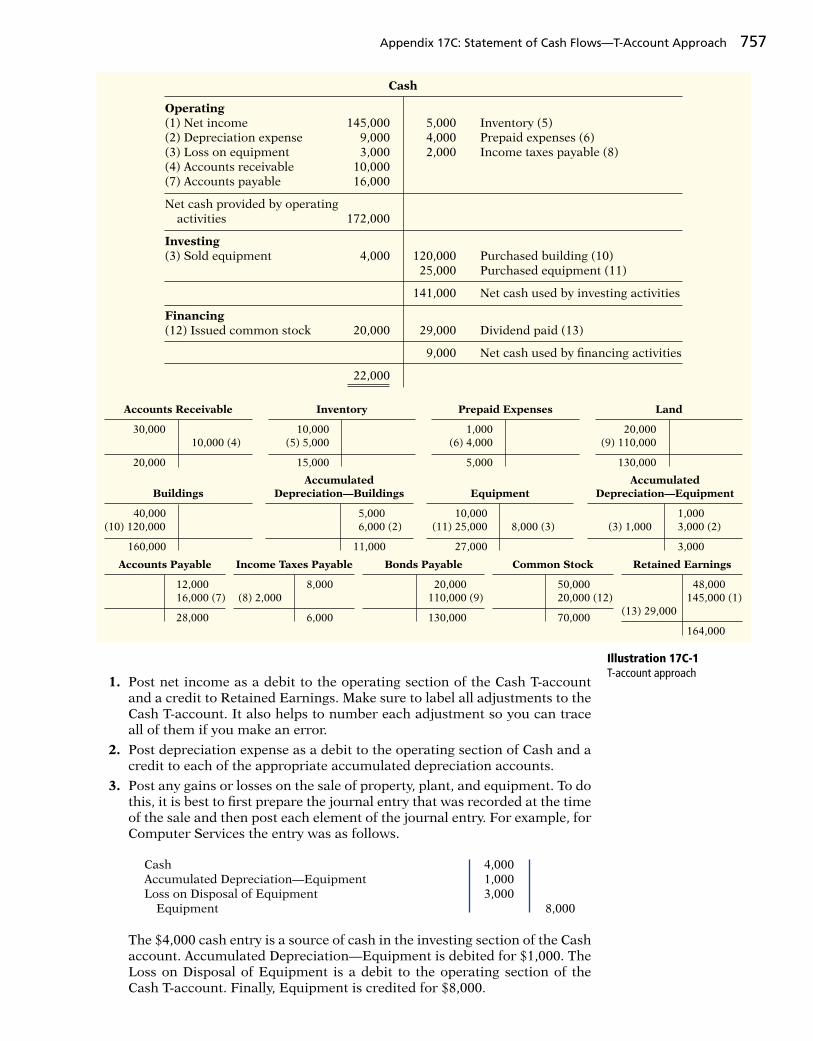

Preparing the Worksheet 752LO *6: APPENDIX 17C: Use the T-account approach

to prepare a statement of cash flows. 755A Look at IFRS 782

18Financial Statement Analysis 784

It Pays to Be Patient: Warren Buffett 784LO 1: Apply horizontal and vertical analysis to

financial statements. 786Need for Comparative Analysis 786Tools of Analysis 786

xiii

Horizontal Analysis 787Vertical Analysis 790

LO 2: Analyze a company’s performance using ratio analysis. 792

Liquidity Ratios 793Profitability Ratios 796Solvency Ratios 800Summary of Ratios 802

LO 3: Apply the concept of sustainable income. 804Discontinued Operations 805Other Comprehensive Income 805

A Look at IFRS 832

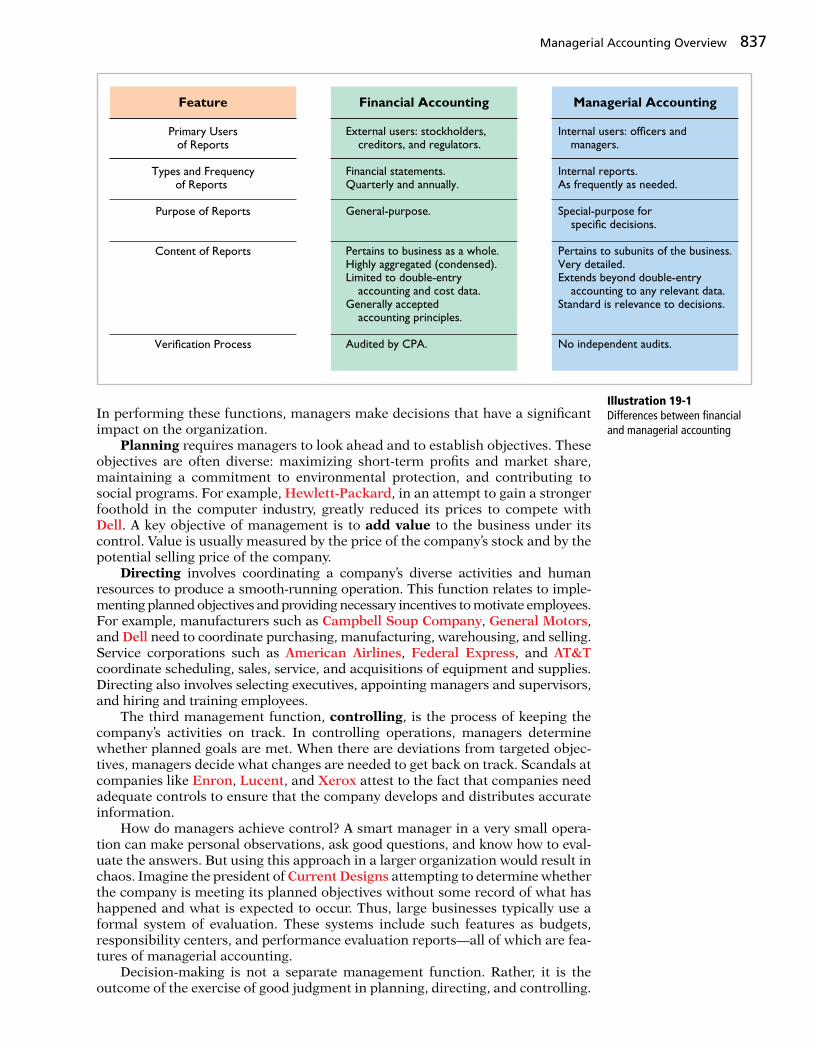

19 Managerial Accounting 834Just Add Water . . . and Paddle: Current Designs 834 LO 1: Identify the features of managerial

accounting and the functions of management. 836

Comparing Managerial and Financial Accounting 836

Management Functions 836Organizational Structure 838

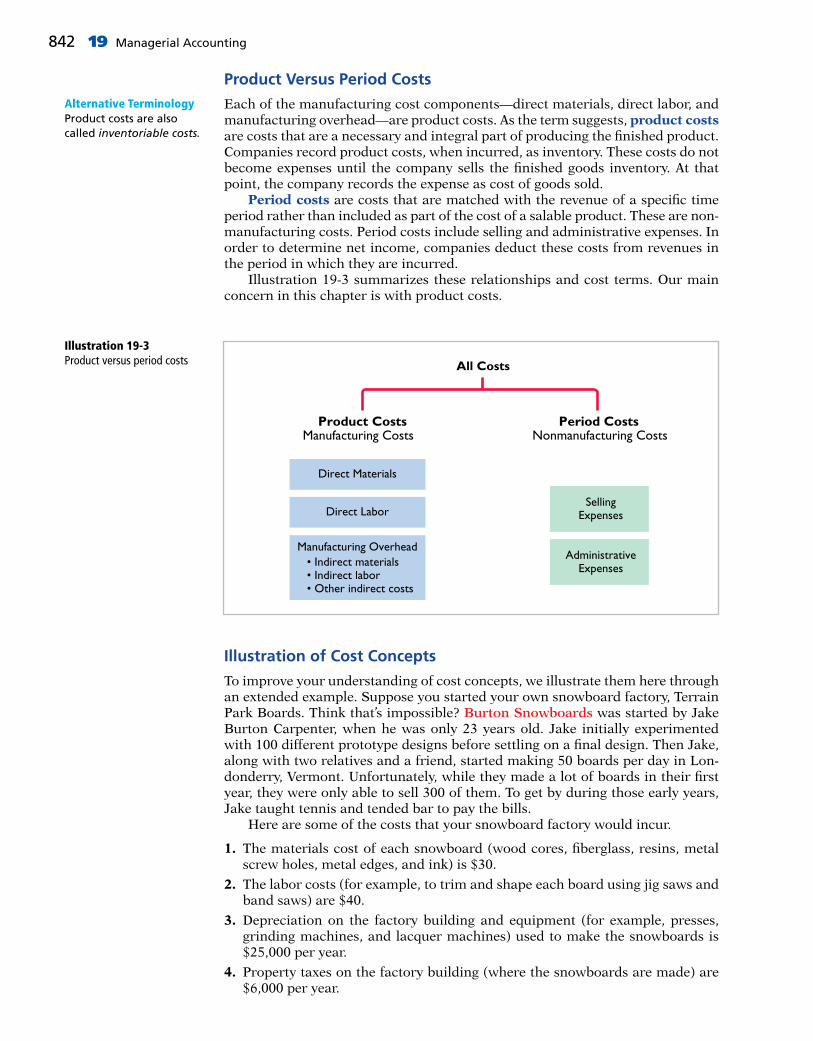

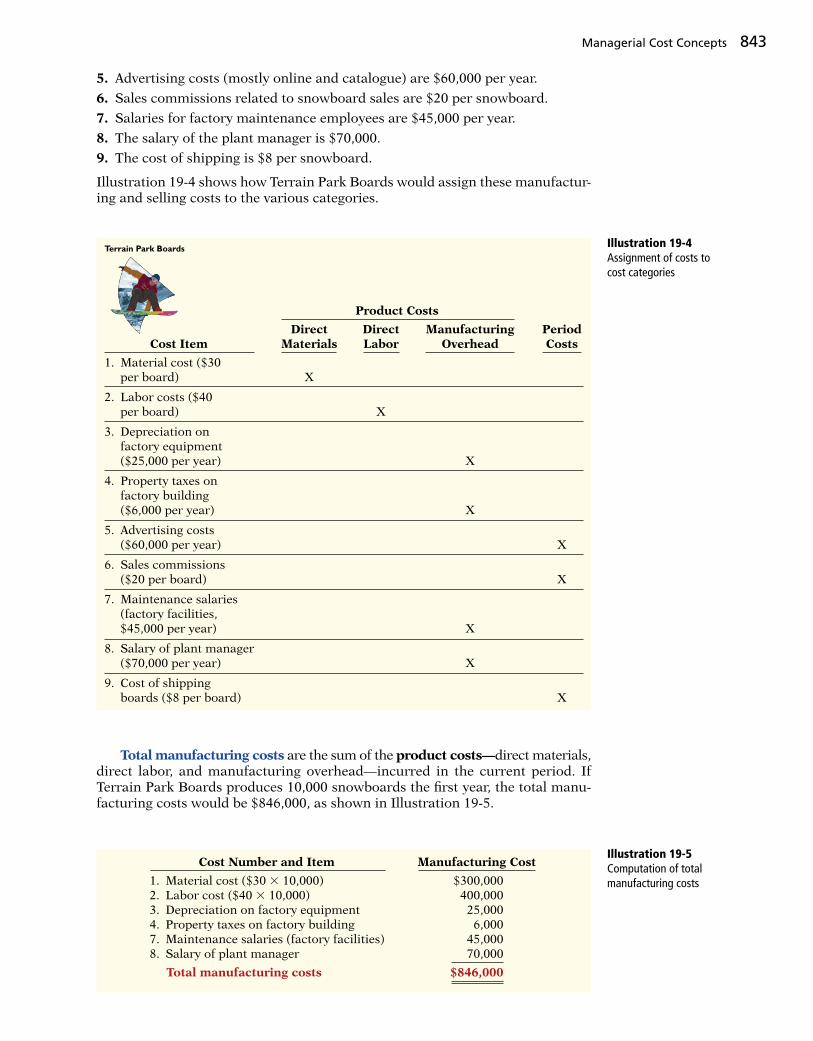

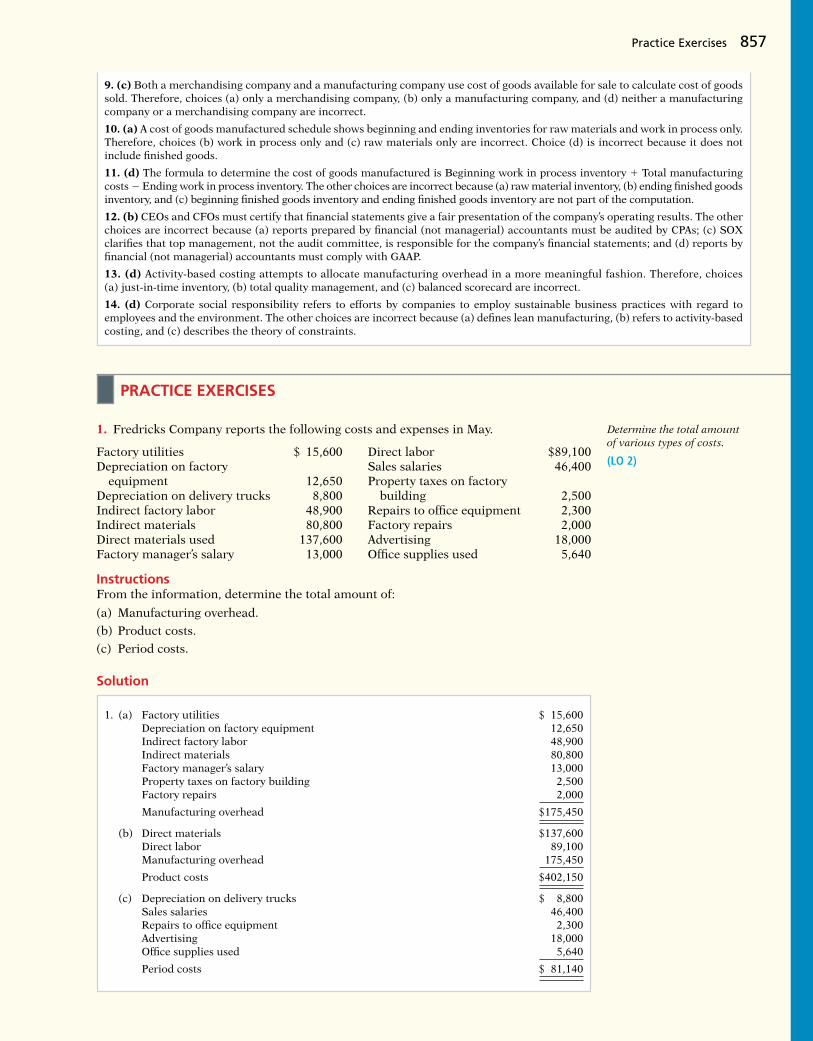

LO 2: Describe the classes of manufacturing costs and the differences between product and period costs. 840

Manufacturing Costs 840Product versus Period Costs 842Illustration of Cost Concepts 842

LO 3: Demonstrate how to compute cost of goods manufactured and prepare financial statements for a manufacturer. 844

Income Statement 844Cost of Goods Manufactured 845Cost of Goods Manufactured Schedule 846Balance Sheet 846

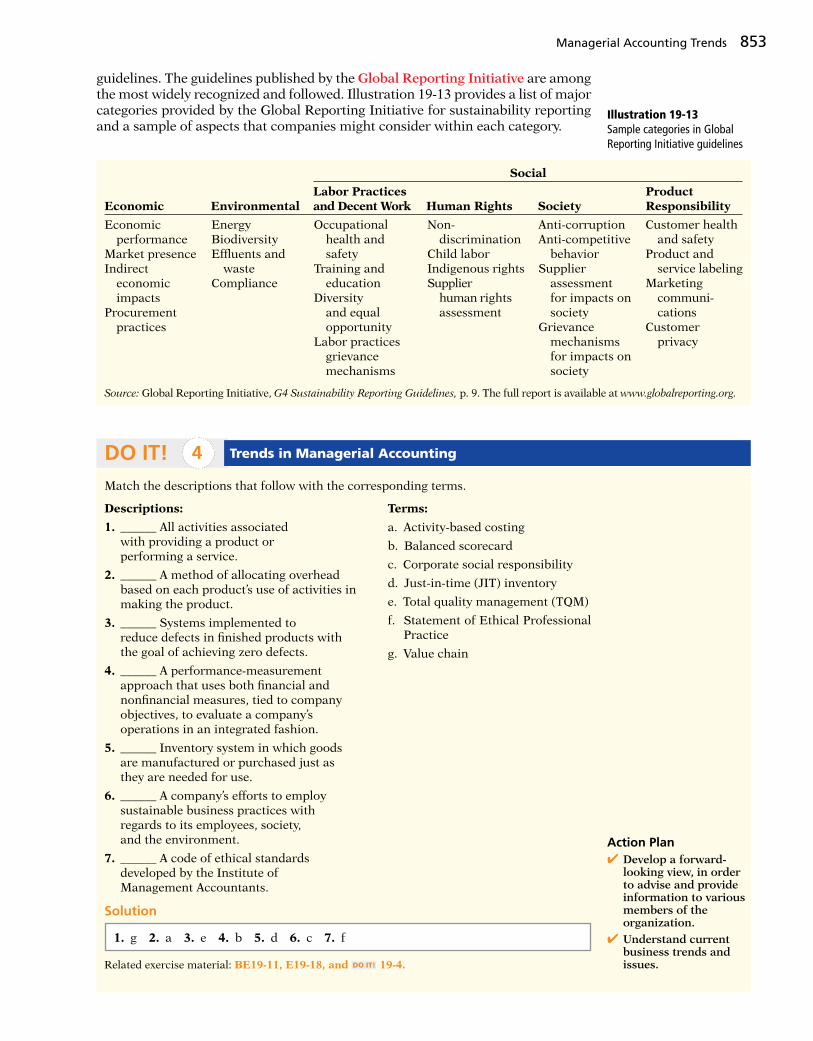

LO 4: Discuss trends in managerial accounting. 848Service Industries 848Focus on the Value Chain 849Balanced Scorecard 850Business Ethics 851Corporate Social Responsibility 852

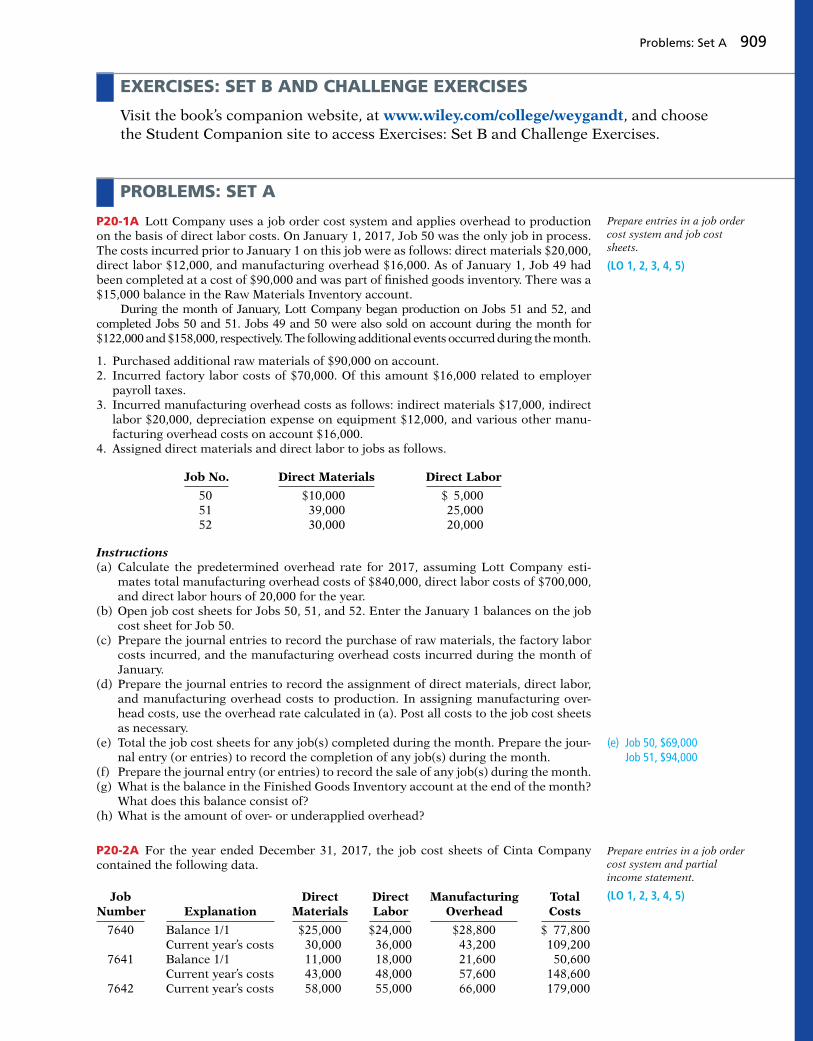

20 Job Order Costing 876Profiting from the Silver Screen: Disney 876LO 1: Describe cost systems and the flow of costs

in a job order system. 878Process Cost System 878Job Order Cost System 878Job Order Cost Flow 879Accumulating Manufacturing Costs 880

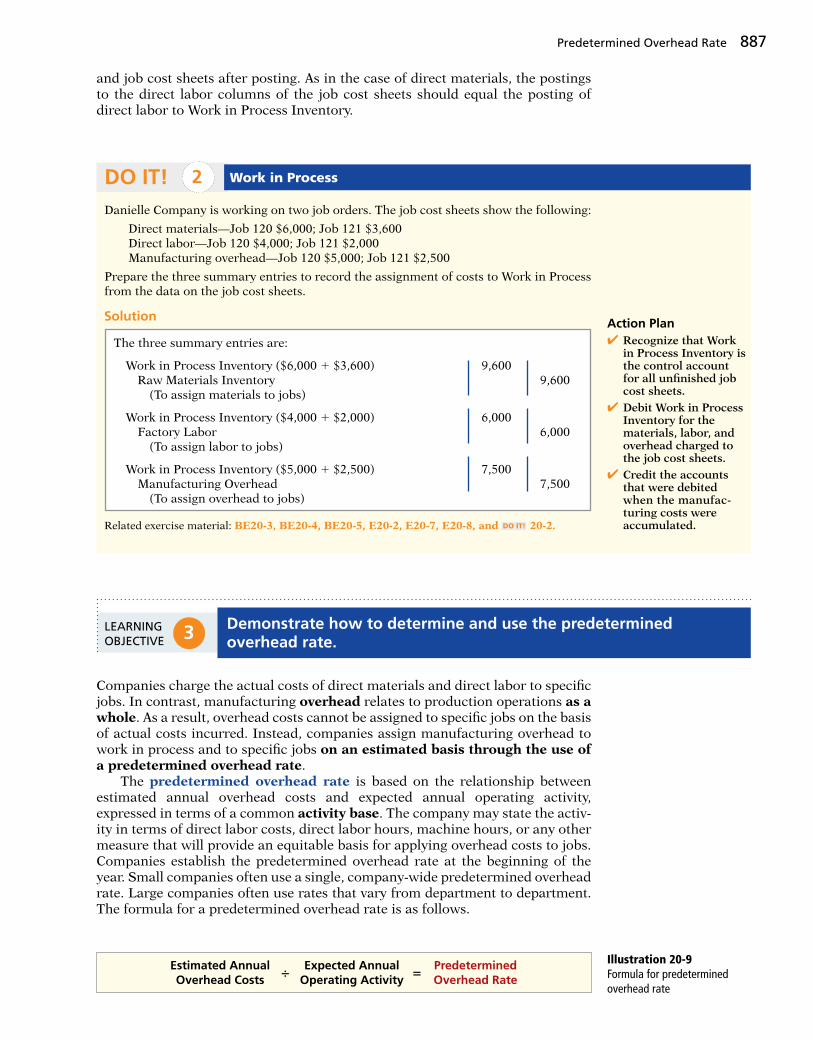

LO 2: Use a job cost sheet to assign costs to work in process. 882

Raw Materials Costs 883Factory Labor Costs 885

LO 3: Demonstrate how to determine and use the predetermined overhead rate. 887

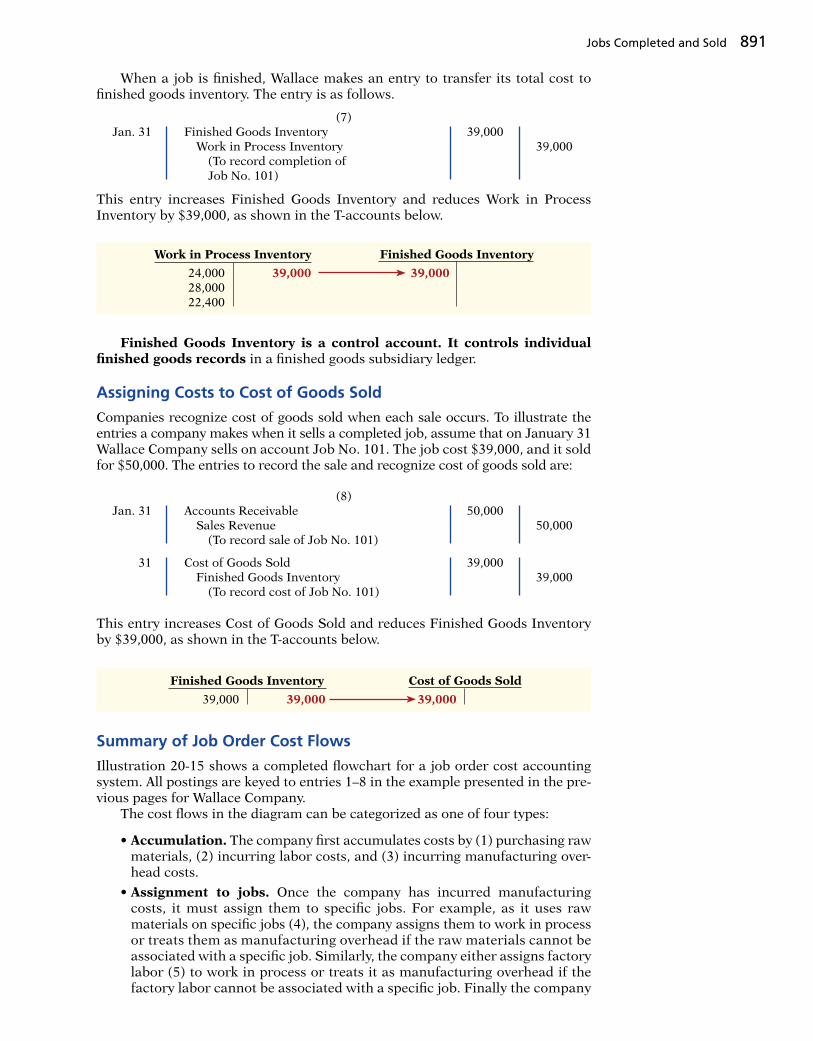

LO 4: Prepare entries for manufacturing and service jobs completed and sold. 890

Assigning Costs to Finished Goods 890Assigning Costs to Cost of Goods Sold 891Summary of Job Order Cost Flows 891Job Order Costing for Service Companies 893Advantages and Disadvantages of Job Order

Costing 894LO 5: Distinguish between under- and overapplied

manufacturing overhead. 895Under- or Overapplied Manufacturing

Overhead 896

21 Process Costing 916The Little Guy Who Could: Jones Soda Co. 916LO 1: Discuss the uses of a process cost

system and how it compares to a job order system. 918

Uses of Process Cost Systems 918Process Costing for Service Companies 919Similarities and Differences Between Job Order

Cost and Process Cost Systems 919LO 2: Explain the flow of costs in a process

cost system and the journal entries to assign manufacturing costs. 921

Process Cost Flow 921Assigning Manufacturing Costs—Journal

Entries 921LO 3: Compute equivalent units. 924

Weighted-Average Method 924Refinements on the Weighted-Average

Method 925LO 4: Complete the four steps to prepare a

production cost report. 927Compute the Physical Unit Flow (Step 1) 928Compute the Equivalent Units of Production

(Step 2) 928Compute Unit Production Costs (Step 3) 929Prepare a Cost Reconciliation Schedule

(Step 4) 930Preparing the Production Cost Report 930Costing Systems—Final Comments 931

LO 5: Explain just-in-time (JIT) processing and activity-based costing (ABC). 932

Just-in-Time Processing 932Activity-Based Costing 934

xiv

LO *6: APPENDIX 21A: Apply activity-based costing to a manufacturer. 936

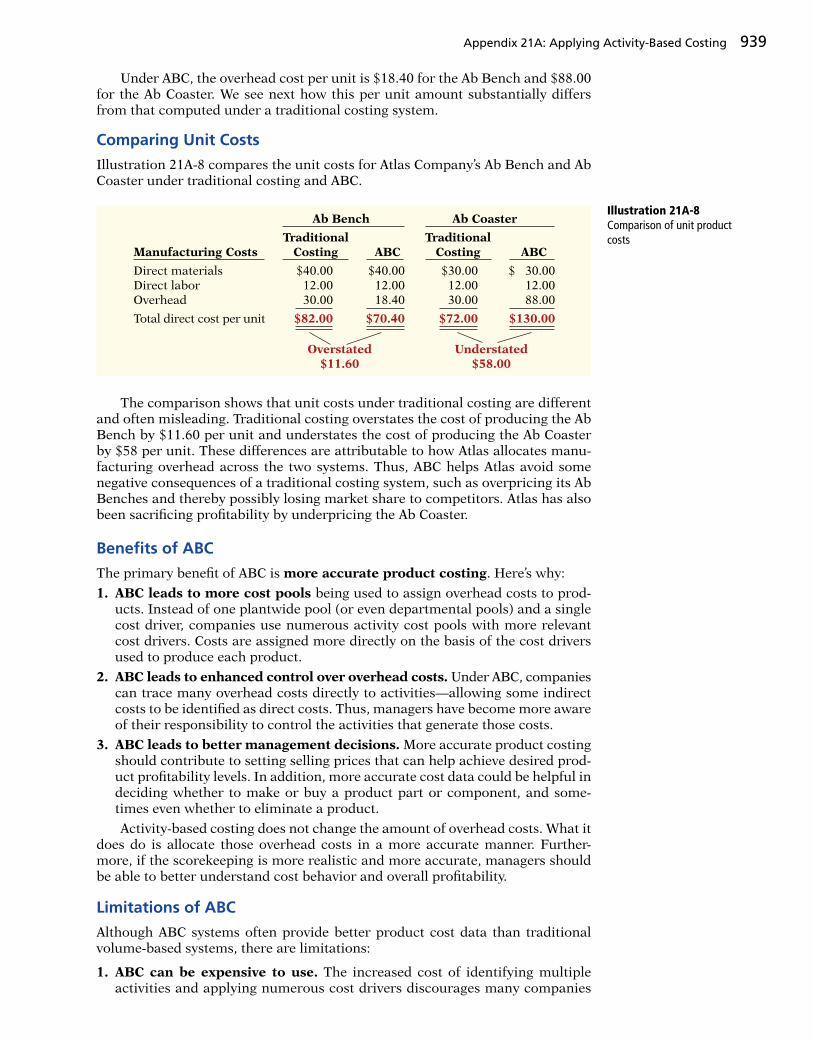

Identify and Classify Activities and Assign Overhead to Cost Pools (Step 1) 936

Identify Cost Drivers (Step 2) 937Compute Activity-Based Overhead Rates

(Step 3) 937Allocate Overhead Costs to Products (Step 4) 938Comparing Unit Costs 939Benefits of ABC 939Limitations of ABC 939

22 Cost-Volume-Profit 960Don’t Worry—Just Get Big: Amazon.com 960LO 1: Explain variable, fixed, and mixed costs

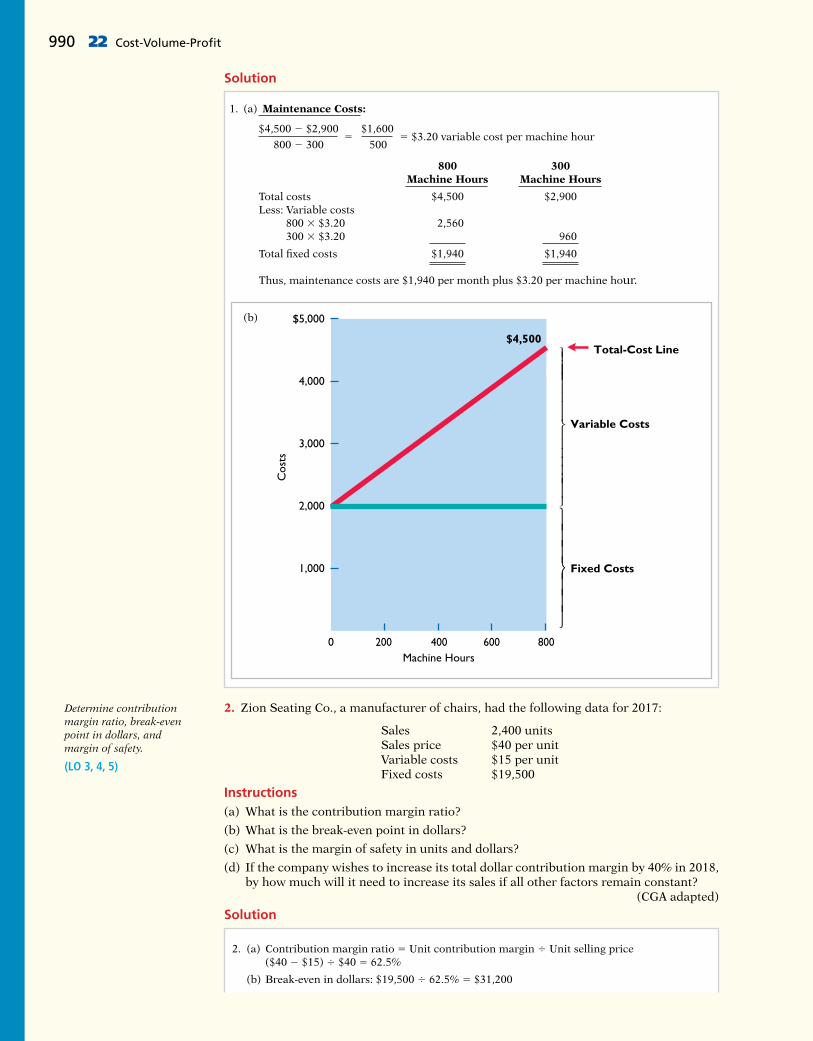

and the relevant range. 962Variable Costs 962Fixed Costs 963Relevant Range 964Mixed Costs 965

LO 2: Apply the high-low method to determine the components of mixed costs. 966

High-Low Method 967Importance of Identifying Variable and Fixed

Costs 969LO 3: Prepare a CVP income statement to

determine contribution margin. 970Basic Components 970CVP Income Statement 970

LO 4: Compute the break-even point using three approaches. 974

Mathematical Equation 974Contribution Margin Technique 975Graphic Presentation 976

LO 5: Determine the sales required to earn target net income and determine margin of safety. 977

Target Net Income 977Margin of Safety 979

LO 6: Use CVP analysis to respond to changes in the business environment. 980

Case I: Offering a Discount 980Case II: Investing in New Equipment 981Case III: Determining Required Sales 981CVP Income Statement Revisited 982

LO *7: APPENDIX 22A: Explain the differences between absorption costing and variable costing. 983

Example Comparing Absorption Costing with Variable Costing 984

Rationale for Variable Costing 986

23 Budgetary Planning 1004What’s in Your Cupcake?: BabyCakes NYC 1004LO 1: State the essentials of effective budgeting

and the components of the master budget. 1006Budgeting and Accounting 1006The Benefits of Budgeting 1006Essentials of Effective Budgeting 1006The Master Budget 1009

LO 2: Prepare budgets for sales, production, and direct materials. 1011

Sales Budget 1011Production Budget 1012Direct Materials Budget 1013

LO 3: Prepare budgets for direct labor, manufacturing overhead, and selling and administrative expenses, and a budgeted income statement. 1016

Direct Labor Budget 1016Manufacturing Overhead Budget 1017Selling and Administrative Expense Budget 1018Budgeted Income Statement 1018

LO 4: Prepare a cash budget and a budgeted balance sheet. 1020

Cash Budget 1020Budgeted Balance Sheet 1023

LO 5: Apply budgeting principles to nonmanufacturing companies. 1025

Merchandisers 1025Service Companies 1026Not-for-Profit Organizations 1027

24Budgetary Control and Responsibility Accounting 1052

Pumpkin Madeleines and a Movie: Tribeca Grand Hotel 1052LO 1: Describe budgetary control and static budget

reports. 1054Budgetary Control 1054Static Budget Reports 1055

LO 2: Prepare flexible budget reports. 1057Why Flexible Budgets? 1057Developing the Flexible Budget 1060Flexible Budget—A Case Study 1060Flexible Budget Reports 1062

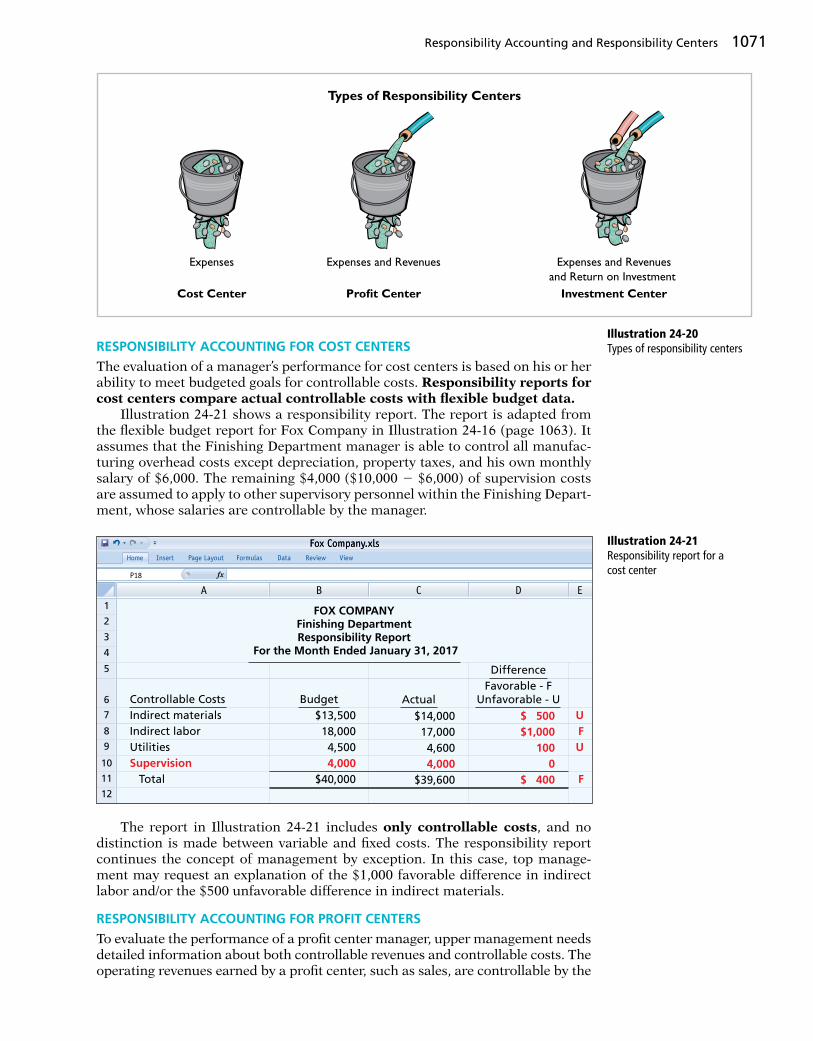

LO 3: Apply responsibility accounting to cost and profit centers. 1064

Controllable versus Noncontrollable Revenues and Costs 1066

Principles of Performance Evaluation 1066Responsibility Reporting System 1068Types of Responsibility Centers 1070

xv

LO 4: Evaluate performance in investment centers. 1073

Return on Investment (ROI) 1073Responsibility Report 1074Judgmental Factors in ROI 1075Improving ROI 1075

25Standard Costs and Balanced Scorecard 1100

80,000 Different Caffeinated Combinations: Starbucks 1100LO 1: Describe standard costs. 1102

Distinguishing Between Standards and Budgets 1103

Setting Standard Costs 1103LO 2: Determine direct materials variances. 1107

Analyzing and Reporting Variances 1107Direct Materials Variances 1108

LO 3: Determine direct labor and total manufacturing overhead variances. 1111

Direct Labor Variances 1111Manufacturing Overhead Variances 1113

LO 4: Prepare variance reports and balanced scorecards. 1115

Reporting Variances 1115Income Statement Presentation of

Variances 1116Balanced Scorecard 1117

LO *5: APPENDIX 25A: Identify the features of a standard cost accounting system. 1120

Journal Entries 1120Ledger Accounts 1122

LO *6: APPENDIX 25B: Compute overhead controllable and volume variances. 1123

Overhead Controllable Variance 1123Overhead Volume Variance 1124

26Incremental Analysis and Capital Budgeting 1146

Keeping It Clean: Method Products 1146LO 1: Describe management’s decision-making

process and incremental analysis. 1148Incremental Analysis Approach 1148How Incremental Analysis Works 1149Types of Incremental Analysis 1150

LO 2: Analyze the relevant costs in various decisions involving incremental analysis. 1151

Special Price Order 1151Make or Buy 1152Sell or Process Further 1155

Repair, Retain, or Replace Equipment 1156Eliminate an Unprofitable Segment or

Product 1157LO 3: Contrast annual rate of return and cash

payback in capital budgeting. 1159Capital Budgeting 1159Evaluation Process of Capital Budgeting 1159Annual Rate of Return 1160Cash Payback 1162

LO 4: Distinguish between the net present value and internal rate of return methods. 1164

Net Present Value Method 1164Internal Rate of Return Method 1166Comparing Discounted Cash Flow

Methods 1168

ASpecimen Financial Statements: Apple Inc. A-1

BSpecimen Financial Statements: PepsiCo, Inc. B-1

CSpecimen Financial Statements: The Coca-Cola Company

C-1

DSpecimen Financial Statements: Amazon.com, Inc.

D-1

ESpecimen Financial Statements: Wal-Mart Stores, Inc.

E-1

FSpecimen Financial Statements: Louis Vuitton F-1

G Time Value of Money G-1LO 1: Compute interest and future values. G-1

Nature of Interest G-1Future Value of a Single Amount G-3Future Value of an Annuity G-4

xvi

LO 2: Compute present values. G-7Present Value Variables G-7Present Value of a Single Amount G-7Present Value of an Annuity G-9Time Periods and Discounting G-11Present Value of a Long-Term Note or

Bond G-11LO 3: Compute the present value in capital

budgeting situations. G-14LO 4: Use a financial calculator to solve time value

of money problems. G-15Present Value of a Single Sum G-16Present Value of an Annuity G-17Useful Applications of the Financial

Calculator G-17

HStandards of Ethical Conduct for Management Accountants

H-1

IMA Statement of Ethical Professional Practice H-1

Principles H-1Standards H-1Resolution of Ethical Conflict H-2

Cases for Managerial Decision-Making*Company Index I-1Subject Index I-3

*Available online at www.wiley.com/college/weygandt.

xvii

Accounting Principles has benefited greatly from the input of focus group participants, manuscript reviewers, those who have sent comments by letter or e-mail, ancillary authors, and proofers. We greatly appreciate the constructive suggestions and innovative ideas of reviewers and the creativity and accuracy of the ancillary authors and checkers.

Twelfth EditionKaren AndrewsLewis-Clark State CollegeSandra BaileyOregon Institute of TechnologyShele BannonQueensborough Community CollegeRobert BartaSuffolk County Community CollegeQuent BelowRoane State Community CollegeLila BergmanHunter CollegeGlen BrauchleDowling CollegeDouglas BrownForsyth Technical Community CollegeRonald CampbellNorth Carolina A&T State UniversityElizabeth CapenerDominican University of CaliforniaBeth CarrawayHorry-Georgetown Technical CollegeJackie CaseuCape Fear Community CollegeKim CharlandKansas State UniversitySuzanne CorySt. Mary’s UniversityPaul CoxMedgar Evers CollegeJoseph CunninghamHarford Community CollegeKate DemarestCarroll Community CollegeRichard DuggerKilgore CollegeBill ElliottOral Roberts UniversityCole EngelFort Hays State UniversityGary FordTompkins Cortland Community CollegeAlan FosterJ.S. Reynolds Community CollegeDale FowlerOhio Christian UniversityGeorge GardnerBemidji State University

Willard GarmanUniversity of California, Los AngelesJospeh JurkowskiD’youville CollegeRandy KiddMetropolitan Community CollegeCindy KillianWilkes Community CollegeShirly KleinerJohnson County Community CollegeDavid KrugJohnson County Community CollegeChristy LandCatawba Valley Community CollegeAnita LeslieYork Technical CollegeLori MajorLuzerne County Community CollegeCharles MaloneNorth Carolina A&T State UniversityKen MarkKansas City Kansas Community CollegeBarbara MichalUniversity of Rio GrandeAllison MooreLos Angeles Southwest CollegeBrandis PhillipsNorth Carolina A&T State UniversityMary PhillipsNorth Carolina Central UniversityLa Vonda RameySchoolcraft CollegeJ. Ramos-AlexanderNew Jersey City UniversityMichelle RandallSchoolcraft CollegeRuthie ReynoldsTennessee State UniversityKathie RogersSuffolk Community CollegeKent SchneiderEast Tennessee State UniversityNadia SchwartzAugustana CollegeMehdi SheikholeslamiBemidji State UniversityBradley SmithDes Moines Area Community CollegeEmil SorianoContra Costa College

John StancilFlorida Southern CollegeLinda SummeyCentral Carolina Community CollegeJoan Van HiseFairfi eld UniversityPat WrightLong Island UniversityJudith ZanderGrossmont College

WileyPLUS Developers and Reviewers

Carole Brandt-FinkLaura McNallyMelanie Yon

Ancillary Authors, Contributors, Proofers, and Accuracy Checkers

Bridget AnakweDelaware State UniversityMichael BarnesLansing Community CollegeEllen BartleySt. Joseph’s CollegeLuAnn BeanFlorida Institute of TechnologyJack BorkeUniversity of Wisconsin—PlattevilleSandee CohenColumbia College ChicagoTerry ElliottMorehead State UniversityJames EmigVillanova UniversityLarry FalcettoEmporia State UniversityHeidi HanselKirkwood Community CollegeCoby HarmonUniversity of California—Santa BarbaraKaren HernGrossmont CollegeDerek JacksonSt. Mary’s University of MinnesotaLaurie LarsonValencia College

xviii

Acknowledgments

xix

Jeanette MiliusIowa Western Community College

Jill MisuracaUniversity of Tampa

Barbara MullerArizona State University

Yvonne PhangBorough of Manhattan Community College

Laura ProsserBlack Hills State University

Alice SineathUniversity of Maryland University College

Lakshmy SivaratnamKansas City Kansas Community College

Teresa SpeckSt. Mary’s University of Minnesota

Lynn StallworthAppalachian State UniversityCalvin TanKapiolani Community CollegeMike TrebeshLansing Community CollegeDick WassonSouthwestern CollegeLori Grady ZaherBucks County Community College

Advisory Board

Janice AkaoButler Community CollegeMichael BarnesLansing Community College

Jackie CaseyCape Fear Community CollegeLisa ColeJohnson County Community CollegeSusan CordesJohnson County Community CollegeKim GatzkeDelgado Community CollegeDrew GoodsonCentral Carolina Community CollegeThomas KamHawaii Pacifi c UniversityAlfonso MaldonadoLaredo Community CollegeLakshmy SivaratnamKansas City Kansas Community CollegePatricia WalczakLansing Community College

We appreciate the considerable support provided to us by the following people at Current Designs: Mike Cichanowski, Jim Brown, Diane Buswell, and Jake Greseth. We also ben-efited from the assistance and suggestions provided to us by Joan Van Hise in the preparation of materials related to sustainability. We appreciate the exemplary support and commitment given to us by executive editor Michael McDonald, senior mar-keting manager Karolina Zarychta Honsa, customer and prod-uct development manager Christopher DeJohn, development editor Ed Brislin, assistant development editor Rebecca Costantini, market solutions assistant Elizabeth Kearns, marketing assistant Anna Wilhelm, editorial supervisor Terry Ann Tatro, editorial associate Margaret Thompson, productdesign manager Allie Morris, product design associate Matt

Origoni, designers Maureen Eide and Kristine Carney, photo editor Mary Ann Price, indexer Steve Ingle, and Denise Showers at Aptara. All of these professionals provided innu-merable services that helped the textbook take shape. Finally, our thanks to Amy Scholz, Susan Elbe, George Hoffman, Tim Stookesberry, Douglas Reiner, Brent Gordon, Joe Heider, and Steve Smith for their support and leadership in Wiley’s Global Education. We will appreciate suggestions and comments from users—instructors and students alike. You can send your thoughts and ideas about the textbook to us via email at: [email protected].

Jerry J. Weygandt Paul D. Kimmel Donald E. Kieso Madison, Wisconsin Milwaukee, Wisconsin DeKalb, Illinois

Many students who take this course do not plan to be

accountants. If you are in that group, you might be thinking,

“If I’m not going to be an accountant, why do I need to know

accounting?” Well, consider this quote from Harold Geneen,

the former chairman of IT&T: “To be good at your business,

you have to know the numbers—cold.” In business,

accounting and fi nancial statements are the means for

communicating the numbers. If you don’t know how to read

fi nancial statements, you can’t really know your business.

Many businesses agree with this view. They see the value of

their employees being able to read fi nancial statements and

understand how their actions affect the company’s fi nancial

results. For example, consider Clif Bar & Company. The

original Clif Bar® energy bar was created in 1990 by Gary

Erickson and his mother in her kitchen. Today, the company

has almost 300 employees.

Clif Bar is guided by what it calls its Five Aspirations—

Sustaining Our Business, Our Brands, Our People, Our

Community, and the Planet. Its website documents its efforts

and accomplishments in these fi ve areas. Just a few examples

include the company’s use of organic products to protect soil,

water, and biodiversity; the “smart” solar array (the largest in

North America), which provides nearly all the electrical needs

for its 115,000-square foot building; and the incentives Clif

Bar provides to employees to reduce their personal

environmental impact, such as $6,500 toward the purchase

of an effi cient car or $1,000 per year for eco-friendly

improvements toward their homes.

One of the company’s proudest moments was the creation of

an employee stock ownership plan (ESOP) in 2010. This plan

gives its employees 20% ownership of the company (Gary and

his wife Kit own the other 80%). The ESOP also resulted in

Clif Bar enacting an open-book management program,

including the commitment to educate all employee-owners

about its fi nances. Armed with this basic fi nancial knowledge,

employees are more aware of the fi nancial impact of their

actions, which leads to better decisions.

Many other companies have adopted this open-book

management approach. Even in companies that do not practice

open-book management, employers generally assume that

managers in all areas of the company are “fi nancially literate.”

Taking this course will go a long way to making you fi nancially

literate. In this textbook, you will learn how to read and

prepare fi nancial statements, and how to use basic tools to

evaluate fi nancial results. Throughout this textbook, we

attempt to increase your familiarity with fi nancial reporting

by providing numerous references, questions, and exercises

that encourage you to explore the fi nancial statements of

well-known companies.

Knowing the Numbers

The Feature Story below about Clif Bar & Company highlights the importance of having good fi nancial information and knowing how to use it to make effective business decisions. Whatever your pursuits or occupation, the need for fi nancial information is inescapable. You cannot earn a living, spend money, buy on credit, make an investment, or pay taxes without receiving, using, or dispensing fi nancial information. Good decision-making depends on good information.

CHAPTER PREVIEW

1

FEATURE STORY

Accounting in Action

The Feature Story helps you picture how the chapter topic relates to the real world of accounting and business.

The Chapter Preview describes the purpose of the chapter and highlights major topics.

2

Analyze the effects of business transactions on the accounting equation.

Describe the four fi nancial statements and how they are prepared.

Explain the building blocks of accounting: ethics, principles, and assumptions.

State the accounting equation, and defi ne its components.

2

3

4

5

Identify the activities and users associated with accounting.1

CHAPTER OUTLINE

Basic ConceptsDO IT! 1• Three activities• Accounting data users

Building Blocks of Accounting

DO IT! 2

• Ethics• GAAP• Measurement principles• Assumptions

Learning Objectives

Owner’s Equity EffectsDO IT! 3• Assets• Liabilities• Owner’s equity

Tabular AnalysisDO IT! 4

Financial Statement ItemsDO IT! 5

• Transaction analysis• Summary of transactions

• Income statement• Owner’s equity statement• Balance sheet• Statement of cash fl ows

© Dan Moore/iStockphotoThe Chapter Outline presents the chapter’s topics and subtopics, as well as practice opportunities.

Go to the REVIEW AND PRACTICE section at the end of the chapter for a review of key concepts and practice applications with solutions.

Visit WileyPLUS with ORION for additional tutorials and practice opportunities.

Analyze the effects of business t ti th ti

Explain the building blocks of accounting: ethics, principles, and assumptions.

State the accounting equation, and defi ne its components.

2

3

4

Building Blocks of Accounting

DO IT! 2

• Ethics• GAAP• Measurement principles• Assumptions

Owner’s Equity Effects DO IT! 3• Assets• Liabilities• Owner’s equity

T b l A l iDO IT! 4• Transaction analysis

Identify the activities and usersassociated with accounting.1

CHAPTER OUTLINE

Basic Concepts DO IT! 1• Three activities• Accounting data users

Learning Objectives

© D© D© DDD© D© D© Dananananan MoMMooMMooMooMooMooMoooo /re/re//re/re/re/rre/re/re/iStSiStStiStiStiStiStiSt kkkkckocockocockoock hhphohhphoohophohophottttototototoThThe ChChapter Outline presents the chapter’s topics and subtopics, as well as practice opportunities.

4 1 Accounting in Action

1 Identify the activities and users associated with accounting.LEARNING OBJECTIVE

What consistently ranks as one of the top career opportunities in business? What frequently rates among the most popular majors on campus? What was the undergraduate degree chosen by Nike founder Phil Knight, Home Depot co-founder Arthur Blank, former acting director of the Federal Bureau of Inves-tigation (FBI) Thomas Pickard, and numerous members of Congress? Account-ing.1 Why did these people choose accounting? They wanted to understand what was happening fi nancially to their organizations. Accounting is the fi nancial information system that provides these insights. In short, to understand your organization, you have to know the numbers. Accounting consists of three basic activities—it identifi es, records, and communicates the economic events of an organization to interested users. Let’s take a closer look at these three activities.

Three Activities

As a starting point to the accounting process, a company identifi es the economic events relevant to its business. Examples of economic events are the sale of snack chips by PepsiCo, the provision of cell phone services by AT&T, and the payment of wages by Facebook. Once a company like PepsiCo identifi es economic events, it records those events in order to provide a history of its fi nancial activities. Recording consists of keeping a systematic, chronological diary of events, measured in dollars and cents. In recording, PepsiCo also classifi es and summarizes economic events. Finally, PepsiCo communicates the collected information to interested users by means of accounting reports. The most common of these reports are called fi nancial statements. To make the reported fi nancial information meaningful, PepsiCo reports the recorded data in a standardized way. It accumulates infor-mation resulting from similar transactions. For example, PepsiCo accumulates all sales transactions over a certain period of time and reports the data as one amount in the company’s fi nancial statements. Such data are said to be reported in the aggregate. By presenting the recorded data in the aggregate, the account-ing process simplifi es a multitude of transactions and makes a series of activities understandable and meaningful. A vital element in communicating economic events is the accountant’s ability to analyze and interpret the reported information. Analysis involves use of ratios, percentages, graphs, and charts to highlight signifi cant fi nancial trends and relationships. Interpretation involves explaining the uses, meaning, and limitations of reported data. Appendices A–E show the fi nancial statements of Apple Inc., PepsiCo Inc., The Coca-Cola Company, Amazon.com, Inc., and Wal-Mart Stores, Inc., respectively. (In addition, in the A Look at IFRS section at the end of each chapter, the French company Louis Vuitton Moët Hennessy is analyzed.) We refer to these statements at various places throughout the text-book. At this point, these fi nancial statements probably strike you as complex and confusing. By the end of this course, you’ll be surprised at your ability to under-stand, analyze, and interpret them. Illustration 1-1 summarizes the activities of the accounting process.

1The appendix to this chapter describes job opportunities for accounting majors and explains why accounting is such a popular major.

Essential terms are printed in blue when they fi rst appear, and are defi ned in the end-of-chapter Glossary Review.

Accounting Activities and Users 5

You should understand that the accounting process includes the bookkeeping function. Bookkeeping usually involves only the recording of economic events. It is therefore just one part of the accounting process. In total, accounting involves the entire process of identifying, recording, and communicating economic events.2

Who Uses Accounting Data

The fi nancial information that users need depends upon the kinds of decisions they make. There are two broad groups of users of fi nancial information: internal users and external users.

INTERNAL USERS

Internal users of accounting information are managers who plan, organize, and run the business. These include marketing managers, production supervisors, fi nance directors, and company offi cers. In running a business, internal users must answer many important questions, as shown in Illustration 1-2.

Illustration 1-1The activities of the accounting process

Identification Recording

Communication

Select economic events (transactions) Record, classify, and summarize

Prepare accounting reports

Analyze and interpret for users

CHIP CITY

DELL

. . . .

.........

2The origins of accounting are generally attributed to the work of Luca Pacioli, an Italian Renaissance mathematician. Pacioli was a close friend and tutor to Leonardo da Vinci and a contemporary of Christopher Columbus. In his 1494 text Summa de Arithmetica, Geometria, Proportione et Proportionalite, Pacioli described a system to ensure that fi nancial information was recorded effi ciently and accurately.

To answer these and other questions, internal users need detailed information on a timely basis. Managerial accounting provides internal reports to help users make decisions about their companies. Examples are fi nancial comparisons of operating alternatives, projections of income from new sales campaigns, and forecasts of cash needs for the next year.

Illustration 1-2Questions that internal users ask

STOCK

ONSTRIKEON

STRIKE

ONSTRIKE

Snack chips Beverages

CO

LA

Questions Asked by Internal Users

Is cash sufficient to paydividends to

Microsoft stockholders?

Finance

Can General Motors afford to give its employees pay

raises this year?

Human Resources

Which PepsiCo product line is the most profitable? Should any

product lines be eliminated?

Management

What price should Apple chargefor an iPod to maximize the

company's net income?

Marketing

6 1 Accounting in Action

EXTERNAL USERS

External users are individuals and organizations outside a company who want fi nancial information about the company. The two most common types of exter-nal users are investors and creditors. Investors (owners) use accounting infor-mation to decide whether to buy, hold, or sell ownership shares of a company. Creditors (such as suppliers and bankers) use accounting information to evalu-ate the risks of granting credit or lending money. Illustration 1-3 shows some questions that investors and creditors may ask.

The Scoop on Accounting

Accounting can serve as a useful recruiting tool even for the human resources department. Rhino Foods, located in Burlington, Ver-mont, is a manufacturer of specialty ice cream. Its cor-porate website includes the following:

“Wouldn’t it be great to work where you were part of a team? Where your input and hard work made a difference?

Where you weren’t kept in the dark about what management was thinking? . . . Well—it’s not a dream! It’s the way we do business . . . Rhino Foods believes in family, honesty and open communication—we really care about and appreciate our employees—and it shows. Operating results are posted and monthly group meetings inform all employees about what’s happening in the Company. Employees also share in the Company’s profi ts, in addition to having an excellent comprehensive benefi ts package.”

Source: www.rhinofoods.com/workforus/workforus.html.

What are the benefi ts to the company and its employees of making the fi nancial statements available to all employees? (Go to WileyPLUS for this answer and additional questions.)© Agnieszka Pastuszak-Maksim/

iStockphoto

Rhino FoodsAccounting Across the Organization

Accounting Across the Organization boxes demonstrate applications of accounting infor-mation in various business functions.

Illustration 1-3Questions that external users ask

What do we doif they catch us?

BILLCOLLECTOR

Yeah!

Questions Asked by External Users

Is General Electric earningsatisfactory income?

Investors

How does Disney compare in size and profitability with Time Warner?

Investors

Will United Airlines be ableto pay its debts as they come due?

Creditors

Financial accounting answers these questions. It provides economic and fi nancial information for investors, creditors, and other external users. The infor-mation needs of external users vary considerably. Taxing authorities, such as the Internal Revenue Service, want to know whether the company complies with tax laws. Regulatory agencies, such as the Securities and Exchange Commission or the Federal Trade Commission, want to know whether the company is operating within prescribed rules. Customers are interested in whether a company like Telsa will continue to honor product warranties and support its product lines. Labor unions such as the Major League Baseball Players Association want to know whether the owners have the ability to pay increased wages and benefi ts.

Building Blocks of Accounting 7

Indicate whether each of the fi ve statements presented below is true or false.

1. The three steps in the accounting process are identifi cation, recording, and communi-cation.

2. Bookkeeping encompasses all steps in the accounting process.

3. Accountants prepare, but do not interpret, fi nancial reports.

4. The two most common types of external users are investors and company offi cers.

5. Managerial accounting activities focus on reports for internal users.

DO IT! 1 Basic Concepts

1. True 2. False. Bookkeeping involves only the recording step. 3. False. Accoun-tants analyze and interpret information in reports as part of the communication step. 4. False. The two most common types of external users are investors and creditors. 5. True.

Related exercise material: E1-1, E1-2, and DO IT! 1-1.

Solution

2 Explain the building blocks of accounting: ethics, principles, and assumptions.

LEARNING OBJECTIVE

A doctor follows certain protocols in treating a patient’s illness. An architect follows certain structural guidelines in designing a building. Similarly, an accoun-tant follows certain standards in reporting fi nancial information. These standards are based on specifi c principles and assumptions. For these standards to work, however, a fundamental business concept must be present—ethical behavior.

Ethics in Financial Reporting

People won’t gamble in a casino if they think it is “rigged.” Similarly, people won’t play the stock market if they think stock prices are rigged. In recent years, the fi nancial press has been full of articles about fi nancial scandals at Enron, World-Com, HealthSouth, AIG, and other companies. As the scandals came to light, mistrust of fi nancial reporting in general grew. One article in the Wall Street Jour-nal noted that “repeated disclosures about questionable accounting practices have bruised investors’ faith in the reliability of earnings reports, which in turn has sent stock prices tumbling.” Imagine trying to carry on a business or invest money if you could not depend on the fi nancial statements to be honestly prepared. Infor-mation would have no credibility. There is no doubt that a sound, well-functioning economy depends on accurate and dependable fi nancial reporting. United States regulators and lawmakers were very concerned that the econ-omy would suffer if investors lost confi dence in corporate accounting because of unethical fi nancial reporting. In response, Congress passed the Sarbanes-Oxley Act (SOX). Its intent is to reduce unethical corporate behavior and decrease the likelihood of future corporate scandals. As a result of SOX, top management must now certify the accuracy of fi nancial information. In addition, penalties for fraudulent fi nancial activity are much more severe. Also, SOX increased the independence requirements of the outside auditors who review the accuracy of corporate fi nancial statements and increased the oversight role of boards of directors. The standards of conduct by which actions are judged as right or wrong, hon-est or dishonest, fair or not fair, are ethics. Effective fi nancial reporting depends on sound ethical behavior. To sensitize you to ethical situations in business and

ETHICS NOTE

Circus-founder P.T. Barnum is alleged to have said, “Trust everyone, but cut the deck.” What Sarbanes-Oxley does is to provide measures that (like cutting the deck of playing cards) help ensure that fraud will not occur.

Ethics Notes help sensitize you to some of the ethical issues in accounting.

The DO IT! exercises ask you to put newly acquired knowledge to work. They outline the Action Plan necessary to complete the exercise, and they show a Solution.

Action Plan✔ Review the basic

concepts discussed.✔ Develop an under-

standing of the key terms used.

8 1 Accounting in Action

to give you practice at solving ethical dilemmas, we address ethics in a number of ways in this textbook:

1. A number of the Feature Stories and other parts of the textbook discuss the central importance of ethical behavior to fi nancial reporting.

2. Ethics Insight boxes and marginal Ethics Notes highlight ethics situations and issues in actual business settings.

3. Many of the People, Planet, and Profi t Insight boxes focus on ethical issues that companies face in measuring and reporting social and environmental issues.

4. At the end of the chapter, an Ethics Case simulates a business situation and asks you to put yourself in the position of a decision-maker in that case.

When analyzing these various ethics cases, as well as experiences in your own life, it is useful to apply the three steps outlined in Illustration 1-4.

Illustration 1-4Steps in analyzing ethics cases and situations

#1ALT

#2ALT

2. Identify and analyzethe principal elementsin the situation.

Identify the stakeholders—persons or groups who maybe harmed or benefited. Askthe question: What are theresponsibilities and obligationsof the parties involved?

3. Identify the alternatives,and weigh the impact ofeach alternative on variousstakeholders.

Select the most ethicalalternative, considering all theconsequences. Sometimes therewill be one right answer. Othersituations involve more thanone right solution; thesesituations require an evaluationof each and a selection of thebest alternative.

1. Recognize an ethicalsituation and the ethicalissues involved.

Use your personal ethics toidentify ethical situations andissues. Some businesses andprofessional organizationsprovide written codes ofethics for guidance in somebusiness situations.

Insight boxes provide examples of business situations from various perspectives—ethics, investor, international, and corporate social responsibility. Guideline answers to the critical thinking questions are available in WileyPLUS and at www.wiley.com/college/weygandt. Additional questions are offered in WileyPLUS.

Generally Accepted Accounting Principles

The accounting profession has developed standards that are generally accepted and universally practiced. This common set of standards is called generally accepted accounting principles (GAAP). These standards indicate how to report economic events.

I Felt the Pressure —Would You?

“I felt the pressure.” That’s what some of the employees of the now-defunct law fi rm of Dewey & LeBoeuf LLP indicated when they helped to overstate revenue and use accounting tricks to hide losses and cover up cash shortages. These employees worked for the former fi nance director and former chief fi nancial offi cer (CFO) of the fi rm.

Here are some of their comments:

• “I was instructed by the CFO to create invoices, knowing they would not be sent to clients. When I created these invoices, I knew that it was inappropriate.”

• “I intentionally gave the auditors incorrect information in the course of the audit.”

What happened here is that a small group of lower-level employees over a period of years carried out the instructions of their bosses. Their bosses, however, seemed to have no concern as evidenced by various e-mails with one another in which they referred to their fi nancial manipulations as accounting tricks, cooking the books, and fake income.

Source: Ashby Jones, “Guilty Pleas of Dewey Staff Detail the Alleged Fraud,” Wall Street Journal (March 28, 2014).

Why did these employees lie, and what do you believe should be their penalty for these lies? (Go to WileyPLUS for this answer and additional questions.)

Dewey & LeBoeuf LLPEthics Insight

© Alliance/Shutterstock

Building Blocks of Accounting 9