Accounting Itai Mbwende.pdf - Bindura University of Science ...

75

BINDURA UNIVERSITY OF SCIENCE EDUCATION FACULTY OF COMMERCE DEPARTMENT OF ACCOUNTANCY EVALUATION OF THE EFFECTIVENESS OF FORENSIC AUDIT TO RISK REDUCTION: A CASE OF ZESA NOTHERN REGION – BINDURA BY ITAI MBWENDE (B1646600) SUBMITTED TO BINDURA UNIVERSITY OF SCIENCE EDUCATION IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR BACHELOR OF ACCOUNTANCY DEGREE BINDURA, ZIMBABWE YEAR 2019

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Accounting Itai Mbwende.pdf - Bindura University of Science ...

BINDURA UNIVERSITY OF SCIENCE EDUCATION

FACULTY OF COMMERCE

DEPARTMENT OF ACCOUNTANCY

EVALUATION OF THE EFFECTIVENESS OF FORENSIC AUDIT TO RISK

REDUCTION: A CASE OF ZESA NOTHERN REGION – BINDURA

BY

ITAI MBWENDE

(B1646600)

SUBMITTED TO BINDURA UNIVERSITY OF SCIENCE EDUCATION IN PARTIAL

FULFILMENT OF THE REQUIREMENTS FOR BACHELOR OF ACCOUNTANCY

DEGREE

BINDURA, ZIMBABWE

YEAR 2019

ii

RELEASE FORM

Registration Number: B1646600

Dissertation Title:

Evaluation of the effectiveness of forensic audit to risk reduction: A case of ZESA Holdings

(Pvt) Ltd – Bindura

Year granted : 2019

Permission is granted to the Bindura University of Science Education Library and the

Department of Accounting to produce copies of this dissertation in an effort it deems necessary

for academic use only.

Signature of student …………………………………………………………

Date signed

Permanent Address:

3030 AERODROME, BINDURA

iii

APPROVAL FORM

TO BE COMPLETED BY THE STUDENT

I certify that the dissertation meets the preparation guidelines as presented in the faculty

guide and instruction for preparing dissertation.”

(Signature of student)……………… …………………Date…………………………………

TO BE COMPLETED BY THE SUPERVISOR

“This dissertation is suitable for presentation to the faculty .It has been checked for conformity

with the faculty guideline”.

(Signature of Supervisor ……………….Date ……………………………………………….

TO BE COMPLETED BY THE DEPARTMENTAL CHAIRPERSON

I certify to the best of my knowledge that the required procedures have been fulfilled and the

preparation criteria was met in this dissertation

(Signature of Chairperson ……Date ………………………………..……………………….

iv

DECLARATION

I, ITAI MBWENDE, declare that am a bonafide producer and owner of this research paper and

the work presented therein is my own. I do also affirm that it has not been submitted by any

other student to any academic institution. The contents of this paper have been submitted in

partial fulfillment of the Bachelor of Accountancy Degree.

Supervisor: ___________________Date: ___/___/___Signature: _______________

Student: ____________________Date: ___/___/____Signature: _______________

v

ACKNOWLEDGEMENTS

Firstly, l would like to praise and worship the Almighty God for His daily guidance, leadership

and providence. This piece of work has been made a success through the unfailing support and

assistance of a number of people whom I am heavily indebted to. My heartfelt gratitude and

appreciation goes to my supervisor Mr. ONIAS ZIVANAI for his untiring support, it has been

a pleasure working with you Sir. I would also like to extent my heartfelt appreciation to all

those who afforded me a helping hand be it in responding to my questionnaires or providing

all the relevant information essential for the victorious completion of this project.

To God, the Almighty I thank you for guiding me through up to this present day and affording

me a chance to be surrounded by caring people.

vi

DEDICATION

I would like to dedicate this project to my beloved family, thank you for seeing me succeed

before even I had started. I greatly appreciate your love and unwavering support throughout

my college life. You loved me when everybody else hated me, you stood by me when

everybody else stood out, you walked in when everybody else walked out and you listened

when everybody else shut me up. I want to thank you and nobody else will ever I compare with

you.

I am truly indebted to you, may God Richly bless you. I love you.

vii

ABSTRACT

Failure by financial audit to unearth financial crimes committed in many organisations both

private and public entities have called for more advanced methods to reduce these problems

and forensic audit is not an exception. This study sought to evaluate the effectiveness of

forensic audit in risk reduction using ZESA Holdings as a case study. The researcher employed

both quantitative and quantitative research methods. In order to carry out the research a sample

of 50 participants was drawn from a population of 60 employees from auditing department,

accounting, information systems and management departments using stratified random

sampling. Data was collected using both self-administered questionnaires and interviews.

Study findings indicated forensic audit can identify reversible insider transactions, can verify

unauthorised transfer of money and it is effective in assessing, monitoring and evaluation of

internal control systems. Since it was also found out that its application is still limited in

Zimbabwe the study recommended that there is need for providing a comprehensive framework

that involves the use of forensic audit methodology in areas like audit planning and execution

and there is need for an establishment of an independent forensic audit team in all government

owned entities

Key words: auditing, forensic audit, fraud, risk

viii

TABLE OF CONTENTS RELEASE FORM ...................................................................................................................... ii

APPROVAL FORM ................................................................................................................ iii

DECLARATION ...................................................................................................................... iv

ACKNOWLEDGEMENTS ....................................................................................................... v

DEDICATION .......................................................................................................................... vi

ABSTRACT ............................................................................................................................. vii

LIST OF TABLES ................................................................................................................. viii

CHAPTER 1 .............................................................................................................................. 1

1.0 Introduction .......................................................................................................................... 1

1.1 Background of the Study ..................................................................................................... 1

1.2 Statement of the Problem ..................................................................................................... 4

1.3 Purpose of the study ............................................................................................................. 5

1.4 Objectives of the study......................................................................................................... 5

1.4.1 Primary objective .............................................................................................................. 5

1.4.2 Secondary objectives ........................................................................................................ 6

1.5 Research questions ............................................................................................................... 6

1.6 Significance of the study .................................................................................................. 6

1.6.1 Benefits to the University ................................................................................................. 6

1.6.2 To the researcher ............................................................................................................... 6

1.6.3 To ZESA Holdings Pvt Ltd............................................................................................... 6

1.7 Delimitation of the study ..................................................................................................... 7

1.8 Assumptions ......................................................................................................................... 7

1.9 Limitations of the Study....................................................................................................... 7

1.10 Definition of terms and acronyms...................................................................................... 8

1.11 Project outline .................................................................................................................... 8

1.12 Chapter Summary .............................................................................................................. 8

CHAPTER II ............................................................................................................................ 10

LITERATURE REVIEW ........................................................................................................ 10

2.0 Introduction ........................................................................................................................ 10

2.1.1 What is Auditing ............................................................................................................. 10

2.1.2 Concept of Forensic audit ............................................................................................... 10

2.1.3 Fraud risks in organisations ............................................................................................ 12

2.1.4 Forensic Audit and Fraud risk......................................................................................... 13

2.1.5 Interrelationship between auditing, fraud investigation and forensic accounting .......... 14

2.1.6 Activities undertaken in forensic audit ........................................................................... 16

2.1.6.1 Investigations ............................................................................................................... 16

ix

2.1.6.2 Analysis of financial statements .................................................................................. 16

2.1.6.3 Reconstruction of incomplete accounting records ....................................................... 16

2.1.6.4 Embezzlement investigation ........................................................................................ 16

2.1.7 Role of a forensic auditor ................................................................................................ 17

2.1.8 Importance of forensic auditing ...................................................................................... 18

2.1.9 How forensic audit help in mitigating risk ..................................................................... 19

2.1.10 Application of forensic auditing in developing countries ............................................. 19

2.2 Theoretical framework ....................................................................................................... 20

2.2.1 Fraud Triangle theory ..................................................................................................... 20

2.2.1.1 Opportunity .................................................................................................................. 21

2.21.2 Pressure/Incentive ......................................................................................................... 21

2.2.1.3 Rationalization ............................................................................................................. 22

2.2.2 White collar crime theory ............................................................................................... 22

2.3 Conceptual framework ....................................................................................................... 23

2.4 Empirical Review............................................................................................................... 24

2.4 Summary ............................................................................................................................ 25

CHAPTER IV .......................................................................................................................... 26

RESEARCH METHODOLOGY............................................................................................. 26

3.0 Introduction ................................................................................................................... 26

3.1 Research Design............................................................................................................ 26

3.1.1 Qualitative research design ............................................................................................. 26

3.1.2 Quantitative research ...................................................................................................... 27

3.2 Target Population ............................................................................................................... 27

3.3 Population sample ......................................................................................................... 28

3.4 Sampling techniques .......................................................................................................... 28

3.4.1 Probability sampling ................................................................................................. 29

3.4.1.1 Stratified random sampling method ............................................................................. 29

3.5 Data collection sources ...................................................................................................... 29

3.5.1 Secondary sources of data ............................................................................................... 29

3.5.2 Primary sources of data ............................................................................................. 30

3.6 Research Instruments ......................................................................................................... 30

3.6.1 Questionnaires................................................................................................................. 31

3.6.1.1 Questionnaire Pre-testing or Pilot testing .................................................................... 31

3.6.1.2 Designing the Questionnaire ........................................................................................ 32

3.6.2 Interviews ........................................................................................................................ 32

3.6.2.1 Structured Interviews ................................................................................................... 33

3.6.2.2 Interview administration .............................................................................................. 33

x

3.7 Data collection procedures ................................................................................................. 33

3.8 Data presentation ............................................................................................................... 33

3.9 Data analysis ...................................................................................................................... 34

3.10 Reliability and validity ..................................................................................................... 34

3.11 Ethical considerations ................................................................................................... 35

3.12 Chapter summary .......................................................................................................... 35

CHAPTER IV .......................................................................................................................... 36

DATA PRESENTATION, ANALYSIS AND DISCUSSION ................................................ 36

4.1 Data Presentation and Analysis ......................................................................................... 36

4.2 Response rate ..................................................................................................................... 36

4.3 Demographic information .................................................................................................. 37

4.3.1 Gender distribution ......................................................................................................... 37

4.3.2 Educational qualifications ............................................................................................... 39

4.3.3 Working experience ........................................................................................................ 40

4.3.4 Department worked ......................................................................................................... 41

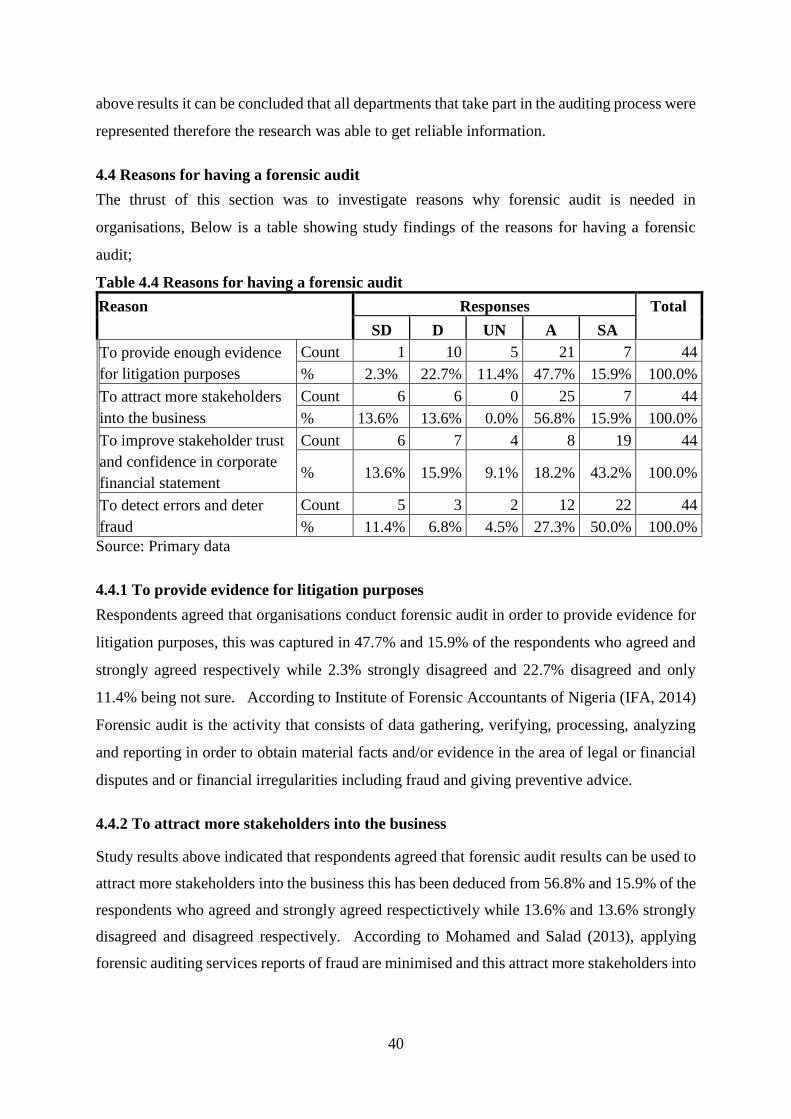

4.4 Reasons for having a forensic audit ................................................................................... 42

4.4.1 To provide evidence for litigation purposes ................................................................... 42

4.4.2 To attract more stakeholders into the business ............................................................... 42

4.4.3 To improve stakeholder trust and confidence in corporate financial statement ............. 43

4.4.4 To detect errors and deter fraud ...................................................................................... 43

4.5 Awareness of the use forensic audit................................................................................... 43

4.5.1 Forensic auditing is more advanced than financial auditing ........................................... 43

4.5.2 In forensic auditing investigative activities are undertaken ............................................ 44

4.5.3 Application of forensic auditing is still limited in many government entities in

Zimbabwe ................................................................................................................................ 45

4.6 Forensic audit in detecting and preventing risk ................................................................. 46

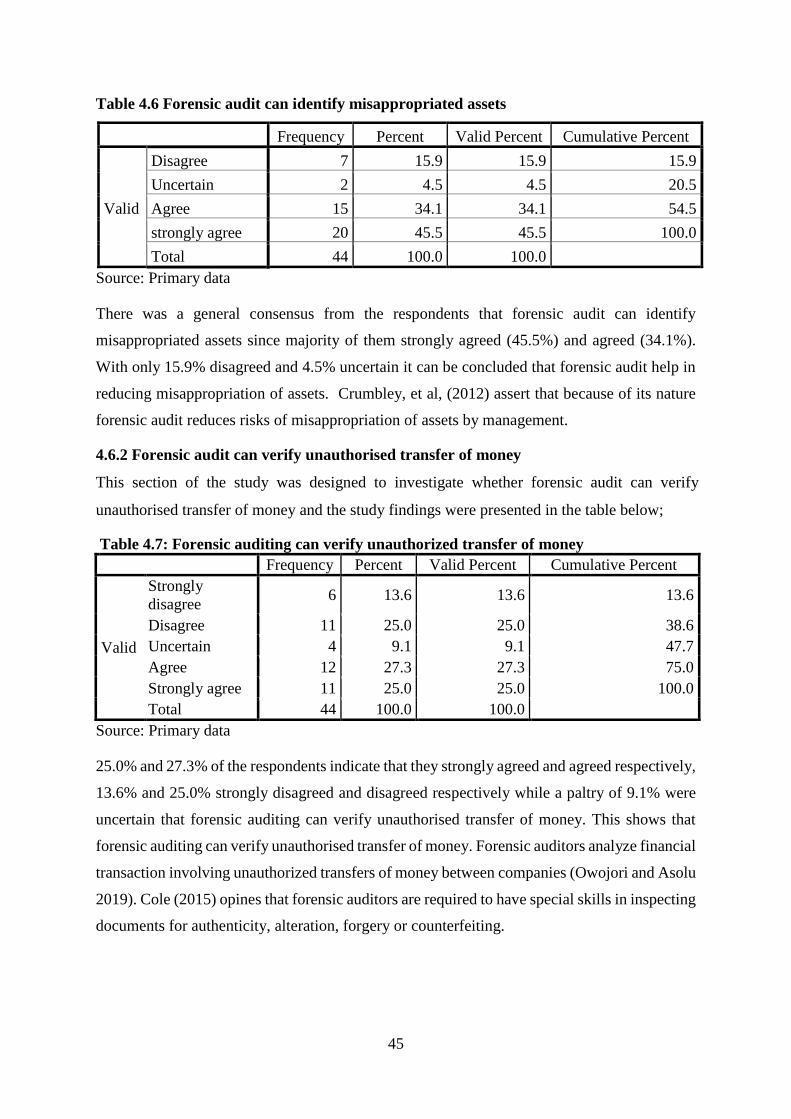

4.6.1 Forensic audit can identify misappropriated assets ........................................................ 46

4.6.2 Forensic audit can verify unauthorised transfer of money .............................................. 46

4.6.3 Forensic auditing can identify reversible insider transaction ......................................... 47

4.6.4 Forensic auditing can enhance disclosure of forward looting information..................... 47

4.7 Ability of forensic auditing to reduce risks........................................................................ 48

4.7.1 Forensic auditing is solely enough as a tool to prevent suspicious or fraudulent

transactions .............................................................................................................................. 48

4.7.2 Forensic auditing is effective in assessing, monitoring and evaluation of internal control

systems ..................................................................................................................................... 48

4.7.3 Forensic investigations deals directly with fraud investigation and this reduces financial

reporting expectations gap ....................................................................................................... 49

4.7.4 Forensic auditing can help avert corporate failures ........................................................ 49

xi

4.7.5 Forensic auditing is an effective tool to reduce management theft ................................ 50

4.8 Interviews ........................................................................................................................... 51

4.8.0 Data analysis of the interview ......................................................................................... 51

4.8.1 Causes of fraud in organisations ..................................................................................... 51

4.8.2 Reasons for carrying out forensic audit .......................................................................... 52

4.8.3 Challenges of forensic auditing application .................................................................... 52

4.8.4 The importance of carrying out forensic audit ................................................................ 52

4.8.5 What do you think are the benefits accrued to organisations that employ forensic

auditing .................................................................................................................................... 53

4.9 Summary ............................................................................................................................ 53

CHAPTER V ........................................................................................................................... 54

SUMMARY, CONCLUSION AND RECOMMENDATIONS .............................................. 54

5.0 Introduction ........................................................................................................................ 54

5.1 Summary of the study ........................................................................................................ 54

5.2 Summary of major findings ............................................................................................. 54

5.3 Conclusion ......................................................................................................................... 55

5.4 Recommendations .............................................................................................................. 56

5.5 Suggestions for further research ........................................................................................ 57

5.6 Summary ............................................................................................................................ 57

REFERENCES ........................................................................................................................ 58

QUESTIONNAIRE ................................................................................................................. 62

INTERVIEW GUIDE .............................................................................................................. 64

xii

LIST OF FIGURES

FIGURE PAGE

Figure 1.1: Project Outline 8

Fig 2.2 Interrelationship between auditing, fraud investigation and forensic accounting 15

Fig 2.1: Fraud triangle 21

Figure 1.1: Conceptual framework 23

Figure 4.1: Gender distribution 39

Figure 4.2 Educational qualification 41

Figure 4.3: Forensic auditing is more advanced than financial auditing 45

Figure 4.4 Application of forensic audit in Zimbabwe 46

Figure 4.4: Forensic auditing can identify reversible insider transactions 48

Figure 4.5: Forensic auditors can help averting corporate failures 51

Figure 4.6: Forensic auditing is an effective tool to reduce management theft 52

xiii

LIST OF TABLES

TABLE PAGE

Table 4.1 Response rate 38

Table 4.2 Working experience 42

Table 4.3 Department worked 42

Table 4.4 Reasons for having a forensic audit 43

Table 4:5: In forensic auditing investigative activities are undertaken 45

Table 4.6 Forensic audit can identify misappropriated assets 47

Table 4.7: Forensic auditing can verify unauthorized transfer of money 47

Table 4.8: Forensic auditing can enhance disclosure for forward looting information 49

Table 4.9 Forensic auditing is tool to prevent suspicious or fraudulent transactions 49

Table 4.10: Forensic auditing is effective in monitoring of internal control systems 50

Table 4.11: Forensic investigations deals directly with fraud investigation 50

1

CHAPTER 1

1.0 Introduction

The level of fraud in Zimbabwean public entities has assumed an epidemic dimension ((Auditor

General Report, 2016). Fraud is the number one enemy of the business world, no company is

immune to it and it is in all works of life. The fear is now rife that the increasing wave of fraud in

the public sector in recent years, if not arrested might pose certain threats to stability and the

survival of individual financial institution and the performance of the industry as a whole and no

area of the economy is immune from fraudsters. The purpose of this study was to evaluate the

extent to which forensic audit can effectively reduce fraud risk in Zimbabwe’s public sector.

The study used ZESA Holdings Pvt Ltd as a case study. This chapter begins by giving the

background of the study; it then gives the statement of the problem, the purpose of the study,

research objectives, research questions, and significance of the study, definition of terms,

assumptions, delimitations and limitations of the study.

1.1 Background of the Study

Fraud and financial crimes are global phenomena. They run across all human race irrespective

of their social and economic status. Financial crime includes money laundering, bribery,

looting, embezzlement, fraud; tax evasion, foreign exchange malpractice and oil bunkering

(Mukoro, Yamusa & Faboyede, 2014). Rise in financial scandals at the beginning of the

twenty-first century was associated with increased fraud incidence and awareness, thereby

questioning the role of auditor in fraud prevention and detection (Bhalla Mohit 2018). Onuorah

and Appah (2016) also affirmed that the widespread frauds in modern organizations have made

traditional auditing and investigation inefficient and ineffective in the detection and prevention

of the various types of frauds confronting businesses world-wide especially in financial

institutions. Fraud is an endemic that are gradually becoming a normal way of life in both

public and private sectors, from the presidential cabinets, down to the political officer, to the

ward councillors, from managing directors of companies, through middle management cadre

and to lower managers (Gbegi and Adebisi, 2014). In order to counter, stop and prevent the

perpetration of such risks comes forensic auditing or accounting.

Forensic auditing is perceived to have evolved to tackle fraud related cases and financial

crimes. According to Zaden and Ramazani (2015), forensic auditing is a specialized field of

accounting which deals with legal claims and complaints. Adegbie and Fakiel (2017) posited

2

that forensic auditing is the practice of utilizing accounting, auditing and investigative skill to

assist in legal matter. Forensic auditing is generally acclaimed to be capable of preventing,

detecting and controlling fraud. Forensic auditing is a specialization within the field of

accounting, and forensic auditors often provide expert testimony during trial proceedings

(Strayer, 2015). Forensic tools, techniques and procedures conducted aid auditors in detecting

abnormalities such as misstatement of financial facts, prevention and detection of fraud.

Forensic audit techniques, tools and procedures are used to identify and to gather evidence to

prove a case at a court of law.

United States and Canada were the pioneers in the development and implementation of forensic

auditing. Countries that are utilizing the forensic accounting expertise to address the

different financial fraud cases they are experiencing, have managed to reduce fraud risk.

Owojori and Asoula (2019) states that the failure of statutory audit to prevent and reduce

misappropriation of corporate fraud and increase in corporate crime has put pressure on

the professional accountant and legal practitioner to find a better way of exposing fraud in

business world. The failure by some formerly prominent public companies such as Enron

and Tyco in the late 1990s fuelled the prominence of forensic auditing, creating a new,

important and lucrative specialty (Mandeya, 2019). Forensic auditing procedures target

financial and operational fraud, discovery of hidden assets and adherence to statutory

provisions.

Forensic auditing has proven to be an effective weapon in the fight against financial crimes in

developed countries. Statements recently released by the Director of the Department of

Income and Sales during the dialogue session held by the Transparency International have

shown that the value of tax evasion for 2016 amounted to about 1.5 JD billion while the

value of collected tax revenues reached 3.828 billion dinars for the same year

(http://assabeel.net/news/4947/2017/3/19)). According to Ifath Shaheen et al (2014) Forensic

auditing in India has come to limelight only recently due to rapid increase in white collar

crimes. It helps companies in accomplishing their organization’s objectives, with a systematic,

disciplined approach to evaluate and improve the effectiveness of risk management, control

and governance processes.

Both in US common law or in French codified law, Forensic Accountants aim to serve justice,

by illuminating technical, financial facts in the context of a dispute or a trial (Crumbley, 2016).

According to the American Institute of Certified Public Accountants (AICPA), Forensic

3

accounting services “generally involve the application of specialized knowledge and

investigative skills possessed by CPAs to collect, analyze, and evaluate evidential matter and

to interpret and communicate findings in the courtroom, boardroom, or other legal or

administrative venue. In Africa the use forensic auditing in Nigeria proves that it is an effective

tool for fraud detection and prevention. According to Okafar and agbiogwu (2016) possession

of basic forensic skills significantly reduce the occurrence of fraud cases in the banking sector

in Nigeria and there is a significant difference between services of forensic accountants and

external auditors. They further argued that the presence of forensic accountants in Banks can

aid in reducing fraud cases. Akhidime and Uagbala-Ekatah (2014), in their exploration of the

growing relevance of forensic accounting in Nigeria, found that though forensic accounting in

Nigeria have helped fraud detection, it is lacking statutory back up.

Although forensic audit has been around for a long time now its use in Zimbabwe is still

limited however the rate at which financial irregularities is spreading especially in parastatals

has put the focus on the need for forensic audit techniques to be utilized. Fraud in many

government owned enterprises in Zimbabwe have resulted in government losing millions of

dollars. Regardless of internal auditing as well as external auditing carried out in each and

every publicly owned company in Zimbabwe cases of fraud continues to rise on daily basis.

Findings of the forensic audit by Grant Thornton at the Zimbabwe National Roads Authority

(ZNARA) concluded in 2017 reveals that the parastatal failed to account for expenditure

vouchers amounting to US$2,4 million and other massive financial abuse including payment

of $71 million and R31 million to contractors cherry-picked without going to

tender, among many other irregularities (www.zimferrets.com). In another case a forensic audit

on the operations of the Zimbabwe Revenue Authority (ZIMRA) that covers the period January

2014 to August 2016 has revealed endemic corruption, violation of Government laws and poor

corporate governance among other shenanigans. The audit has unearthed irregularities

regarding the revenue collector’s vehicle loan scheme and the importation of cars by the five

executives, executive perquisites, salaries, loans to senior management, staff secondment and

the procurement of goods and services, among others. Findings of the audit are coming at a

time the government’s revenue collector is losing (www.zimferrets.com).

Zimbabwe Electricity Power Supply Holdings (Zesa) has been rocked by massive tender

scandals. According to the Zimbabwe Independent energy tenders were inflated to over

US$500 million. At one point three solar plants which were initially pegged at US$549 million

4

were inflated to around US$720 million after tenders were awarded and this create a variance

of US$171 million. In addition the Gairezi Project which was initially pegged at US$90 million

was also heavily inflated to US$248 million, creating a variance of US$158 million according

Elton Mangoma former Energy Minister. Further to that the Kariba South Power Extension

project was initially pegged at US$355 million, but shot up to US$533 million. The cost

escalation was US$178 million (www.zimferrets.com). The inflated costs totalled US$507

million.

However the use of forensic auditing in Zimbabwe is still limited as well as its awareness

therefore it is against this background that this study will be undertaken to evaluate the

effectiveness of forensic auditing to risk reduction. This study will use Zimbabwe electricity

Supply Authority Holdings (Private) Limited (ZESA) as a case study since it is among some

of the parastatals that have been affected by financial irregularities and fraud. ZESA Holdings

(Private) Limited is incorporated under the Companies Act [Chapter 24:03]. ZESA Holdings

(Pvt) LTD is a state-owned company whose task is to generate, transmit, and distribute

electricity in Zimbabwe. The Company is governed by the Electricity Act [Chapter 13:19].

1.2 Statement of the Problem

Financial irregularities, frauds and corruptions are a severe problem of concern globally. It is

the major concern to developing nations and as well as Zimbabwe. Serious problems have

emerged in the state enterprises in Zimbabwe from the period 2014 to 2019 (Godana and

Hlatshwayo 2019). It is of key insight to note that the major source of problems encountered

by state owned enterprises is derived from failure of both internal and external audit to detect

and deter risks of fraud and corruptions. Fraud has become one of the major risks that has

entrenched itself in state owned enterprises especially at ZESA holdings PVT LTD. This shows

that internal controls are either non-existent or if they do, they are not serving the intended

purpose. Massive tender scandals at ZESA have resulted in the parastatal losing over US$507

million (Auditor General Report, 2019). Apart from being engulfed in tender scandals

surrounding the controversial energy deals, Zesa is also hamstrung by a giant debt overhang

estimated at US$1 billion in arrears owed to international and domestic suppliers (Auditor

General Report, 2019). This has negatively affected service delivery by the parastatal since one

of the South African power utility Eskom has persistently threatened to switch off its northern

neighbour for non-payment of electricity imports through Zesa. Among the number of

fraudulent deals the Auditors General’s 2018 report revealed that ZESA entered into contracts

5

in 2010 for supply of transformers worth USD 4 962 722 and USD 561 935 in 2016 with Pito

Investments which are not delivered to date (2019) according to AG’s Report. In addition the

company’s subsidiary ZPC paid ZAR 196 064 in 2014 for gas to York International not yet

supplied again. The company’s current liabilities exceeded its current assets by US$65,321,490

(2013: US$67,367,127), by $67 998 471 (2015: $66 178 819), by USD 92 118 178 (2017: USD

84 167 798) and by US$92 118 178 (2018) (Auditor General’s Report on paras tatals,

2015, 2017 and 2019). In addition the company is failing to service its foreign loans

amounting to $29 878 40. ZESA owes its local and international suppliers close to US$1

billion and is only managing to service interest accrued on loans without settling

premiums (Zimbabwe Independent, November 2018). This also has been worsened by

corruption and incompetence at the state entity which resulted in the company reporting loss

before tax of $111 474 084 (2014: $118 312 961) for the year ended December 31, 2015

and as of that date its current liabilities exceeded its current assets by $771 383 372

(2014: $958 567 146) (Audit Report, 2016). According to the Auditor General Chiri

these conditions along with other matters indicate the existence of a material uncertainty

that may cast significant doubt about the ability of the company to continue operating as

a going concern. The financial statements indicate that some of the institutions' debts have

gone for nearly two decades without being repaid and are long overdue (The Independent,

November 2018).

1.3 Purpose of the study

The main purpose of this research study is to find out whether using forensic can be an effective

way of reducing risk.

1.4 Objectives of the study

The objectives of the study are what the researcher aims to achieve at the end of the research.

According to Malhotra (2015) an objective is the short frame goal which is specific,

measurable, achievable, result oriented and time framed (SMART). This study was be guided

by the following objectives.

1.4.1 Primary objective

The primary objective of this study is to assess the effectiveness of forensic audit to risk

reduction.

6

1.4.2 Secondary objectives

1. To determine the reasons for having forensic audits in an organization

2. To ascertain the level of awareness of the use of forensic auditing for risk reduction

3. To establish how well fraud investigation help in detecting and preventing risk.

4. To ascertain whether forensic audit is able to reduce risks.

1.5 Research questions

1. What are the reasons for having forensic auditing in an organisation?

2. What awareness effort has been created on the use of forensic accounting in risk

reduction?

3. What fraud investigation does which can help in detecting and preventing risk?

4. What level of depth can forensic audit go in reducing risks?

1.6 Significance of the study

The significance of the study is its importance to various stakeholders; this study is useful to

the student (researcher), the organization (ZESA Holdings Pvt Ltd) as well as the university.

1.6.1 Benefits to the University

The research will provide valuable literature on forensic auditing and its impact risk reduction.

The research will enrich the University library by adding value and contributing to the existing

body of knowledge as well as providing scope for further research on areas that this research

did not cover in the field of forensic accounting.

1.6.2 To the researcher

The study assisted the researcher in enhancing her researching skills and practical aspects

forensic audit. It enabled her to have a deeper understanding of how forensic audit can be used

to reduce risk in organisations.

1.6.3 To ZESA Holdings Pvt Ltd

This study will be of great importance as it will give a clear picture to the company on the

concept of forensic audit, its importance, and advantages and when it can be used. In addition

to that the findings of the study will shed light on how risks faced by the parastatal can be

reduced through use of forensic audit. Finally management will be able to understand the extent

to which the use of forensic audit can reduce fraud and all sorts of irregularities it faces.

7

1.7 Delimitation of the study

Delimitation of the study is the area to be covered by the study. Suanders (2016) defines

delimitations as the research precise limit of the issues he/she wants to cover. This study was

limited to a geographical entity known as Zimbabwe and specifically ZESA Holdings Pvt Ltd

Particular consideration was ZESA offices in Mashonaland West Region. The study was

limited to investigate the effectiveness of forensic audit to risk reduction. The research covered

the financial period 2014-2019 for ZESA Holdings Pvt ltd and it was undertaken for a period

of one year January 2019 to December 2019.

1.8 Assumptions

Saunders et tal (2015) views an assumption as a condition which is taken without which the

research effort would be impossible. The study was undertaken under the following

assumptions.

Enough information for carrying out the research can be gathered

Internal and external audit fails to uncover some of the irregularities and fraud

committed

Respondents responded wholly and truthfully and were willing to give full information

Sufficient time was available to carry out the research in a stipulated time

1.9 Limitations of the Study

Burker et al (2014) defines limitations as hindrances which block the researcher to go further

than the expected borders or boundaries. The researcher expected to face a time constraint since

this was an academic paper and needs to be completed according to the academic almanac;

hence it was a short period of time for the compilation, review and analysis of the research,

however the researcher effectively managed the available time so as to meet the required

deadlines. Limited financial resources were another hindrance, however cost effective

strategies were employed and concentration was given to important areas of the study so as to

minimize costs. Access to confidential information was also a limiting factor. The researcher

guaranteed confidentiality of volunteered data as this would be used for academic purposes.

1.10 Definition of terms and acronyms

Auditing- is an independent systematic examination, evaluation-and investigation of an

entity’s business transactions, procedures, operations and performance results (Borthakur

Shristi, 2017).

8

Risk- It is a chance of loss or any other negative occurrence that is caused by external or

internal vulnerabilities and that may be avoided through pre-emptive action.

Fraud- means an intentional and dishonest act involving deception or misrepresentation by a

person, to obtain or potentially obtain an advantage for themselves or any other person (CPA

Australia Ltd, 2015). The term “fraud” commonly includes activities such as theft, corruption,

conspiracy, embezzlement, money laundering, bribery and extortion.

Forensic audit- is a technique to legally determine whether accounting transactions are in

consonance with various accounting, auditing and legal requirements and eventually determine

whether any fraud has taken place.

Risk reduction – is the process of reducing the likelihood of occurrence of loss and severity

of loss should it occur.

ZESA - Zimbabwe Electricity Supply Authority

1.11 Project outline

The project outline has been organised as shown in the diagram below, foundation of the entire

study has been constructed in chapter I followed by chapter II, chapter III, chapter IV and

finally chapter V.

CHAPTER V

CHAPTER IV

CHAPTER III

CHAPTER II

CHAPTER I

Source: Researcher

Figure 1.1: Project Outline

1.12 Chapter Summary

This introductory chapter looked at the background of the study, including statement of the

problem, research objectives and questions, research hypothesis, justification of the study,

limitations as well as the assumptions upon which the study is based. The following chapter

(Chapter II) reviews literature on the effectiveness of forensic audit in risk reduction.

Research

problem and its

background

Literature

review

Research

methodology

Data

presentation

and analysis

Summary and

conclusions and

recommendations

9

CHAPTER II

LITERATURE REVIEW

2.0 Introduction

This chapter prompts answers to the sub research questions by taking a comprehensive review

on the literature propounded by various authors and reputable authorities in prior studies on the

effectiveness of forensic audit to risk reduction. Conceptual, theoretical as well as empirical

studies have been reviewed in this chapter

2.1.1 What is Auditing

The word ‘audit’ is usually used to refer to the process of providing an opinion on the accuracy

or validity of some subject matter specifically in this matter, financial information (Chandler

2014). Auditing is also explained as an independent systematic examination, evaluation-and

investigation of an entity’s business transactions, procedures, operations and performance

results (Anichebe, 2015). The international Auditing and Assurance Standard Board defined

an audit as precise examination and coming up with an independent opinion concerning

financial performance of a business by a selected evaluator as stated by those state of the

arrangement and appropriate statutory and execution procurements. In support literature

reviewed by Salome and Rotim (2016) contends that the motivation behind an audit is to

provide sensible certification on whether the financial statement of an entity present fairly in

all material aspects the financial position, performance and cash flows of an entity in

accordance with the generally accepted accounting principles, and also to evaluate internal

control system put in place by management of the entity in question. The auditor is actually an

independent third party who is there to establish a degree of correspondence between the

assertions made and presented by management and user criteria (Soltani, 2017).

2.1.2 Concept of Forensic audit

The term forensic means “relating to the application of scientific knowledge to legal problems

or usable in a court of law” (Chandra Shekhar, 2017). Webster dictionary defines forensic as

belonging to, used in, or suitable to courts of judicature or to public discussions and debate.

Forensic auditing and forensic accounting can be used interchangeably. According to AICPA

(2018) forensic auditing services generally involve application of special skills in auditing,

accounting, quantitative methods, finance, specific areas of the law, information and computer

technologies research and investigative skills to collate, analyze, and evaluate evidential

matter which in the forensic area is called the evidence. Crumbley (2015) defined forensic

10

auditing as an accounting analysis that can uncover possible fraud that is suitable for

presentation in court. Also known as investigative accounting, forensic accounting is a detailed

examination and analysis of financial documents and records for use as evidence in a court of

law. Dalal and Bhakti (2017), described forensic auditing as the utilization of specialized

investigative skills in carrying out an enquiry conducted in such a manner that the outcome

will have application to the court of law. They further stated that the primary aim of forensic

auditing is fraud detection, unlike the traditional auditing that focuses on review of internal

control system, error identification and prevention.

The American institute of certified public accountants defines forensic accounting as “the

ability to identify, collect, analyse, and interpret financial and accounting data and information;

apply the relevant data and information to a legal dispute or issue; and render an opinion”

(AICPA, 2018). Dalal and Bhakti (2017), agree with AICPA definition and buttresses that

forensic accounting is not “accounting for dead people”, rather it is the use of a wide range of

accounting, auditing, and investigative skills to measure and verify economic damages and

resolve financial disputes. Forensic auditing arises from the integration of accounting,

investigative auditing, criminology, and litigation services (Gbegi, D.O and Adebisi, J.F.

2014). Singleton et al (2016) and Levi (2015) concluded that a forensic accountant is part cop,

part lawyer, part auditor and part psychologist and a skeptic. Hence forensic auditing is the

application of accounting, investigative, criminology, and litigation services skills for the

purpose of identifying, analyzing, and communication of evidence of underlying reporting

event. According to Institute of Forensic Accountants of Nigeria (IFA, 2014) Forensic audit

is the activity that consists of data gathering, verifying, processing, analyzing and reporting in

order to obtain material facts and/or evidence in the area of legal or financial disputes and or

financial irregularities including fraud and giving preventive advice.

Forensic auditing is regarded as a comprehensive auditing tool which stakeholders should

capitalize by implementing controls to reduce the risk associated with the event identified as

having material and significant ratings and being most likely to occur. In so doing the strength

of either current preventive or detective controls should be taken into consideration (Gupta and

Gupta, 2015). Forensic auditing combines legalities alongside the techniques of propriety

(VFM audit), regularly, investigate and financial audits (Iyer Sriram, 2018). The main aim is

to find out whether or not true business value has been reflected in the financial statements and

whether any fraud has taken place.

11

2.1.3 Fraud risks in organisations

According to Oxford Advanced Learner`s Dictionary, fraud can be defined as the crime

of deceiving somebody in order to get money or goods illegally. EFCC Act (2014)

defines fraud as illegal act that violates existing legislation and these include any form of

frauds, narcotic drug, trafficking, money laundering, embezzlement, bribery, looting and any

form of corrupt malpractices and child labour, illegal oil bunkering and illegal mining, tax

evasion, foreign exchange malpractice including counterfeiting, currency, theft of intellectual

property and piracy, open market abuse, dumping of toxic waste and prohibited good etc.

This definition is all-embracing and conceivably includes financial crimes in corporate

organization (Joshi Apporva (2017).

Naik Devesh (2015), highlighted the types of fraud in occurrence to include tax fraud,

bankruptcy fraud, theft of intellectual property and proprietary information, embezzlement,

fraudulent substitution, unauthorized lending, tempering with reserves, insider abuses and

forgeries, defalcation, suppression, unofficial borrowing, impersonation, teeming and lading,

fraudulent use of the company’s documents, use of fictitious accounts, manipulation of

vouchers, over invoicing, dry posting, inflation of statistical data, ledger accounts manipulation

or falsified account information, duplication of cheque books, fictitious contracts

award/execution, lending to ghost workers, kite flying and cross firing, misuse of suspense

accounts, computer fraud and false declaration of cash shortage.

According to Joshi Apporva (2017), it is seen that fraud committed in businesses are of two

types and these are; personal use of business resources and the drawing up of false financial

statement for the business. The latter is to give the business a robust look in order to boost

investors’ confidence on the business. There are classical examples such as embezzlement of

company’s cash during its collection before it is recorded in the book of accounts. Another

example is when the bank records are tampered with so as to gain advantage of the system in

monetary terms. Added to this is gaining advantage through forgery of documents, making

payments which ordinarily should not be made or payment that has been previously been made

(Olanike, B. & Adebola, J. 2014). The creation of fictitious debt, inventory and scrap theft,

office supplies and fixed assets theft or creating fictitious expenses are avenues through which

fraud is perpetrated.

12

2.1.4 Forensic Audit and Fraud risk

Forensic audit’s focus is on the detection, analysis, and communication of evidence of

underlying financial and reporting events. Unlike the traditional audit which is rule-base and

single-event based, forensic audit is not conducted for the purpose of rendering audit opinion.

Hence, forensic audit operates in a principle-based environment (Public Company Accounting

Oversight Board, 2007; Simth and Crumbley, 2014). Basically, forensic accounting aims at

using accounting report in a form suitable for legal purposes (Dhar and Sarkar, 2010). Bhasin

(2017) notes that the objectives of forensic accounting include:

assessment of damages caused by an auditor`s negligence,

fact finding to see whether an embezzlement has taken place, in what amount, and

whether criminal proceedings are to be initiated;

collection of evidence in a criminal proceedings;

Computation of asset values in a divorce proceedings.

Forensic audit is one of the most effective and efficient approach to reduce and prevent

fraudulent activities as it is concerned with the evidentiary nature of accounting data, and as a

practical field concerned with accounting fraud and forensic auditing; compliance, due

diligence and risk assessment; detection of financial misrepresentation and financial statement

fraud (Rasey, 2011)

Fraud is rarely seen, but what is observed or noticed are the symptoms, hence forensic audit

services provide firms with the necessary tools to detect and deter fraudulent practices (Godiwn

2015). Thus forensic audit can be adapted as internal audit strategy to prevent fraudulent

activities. According to Olanike, B. & Adebola, J. (2014) forensic accounting services offer

banks with the necessary tools to deter fraudulent activities. Similarly, Onodi, B. E., Okafor,

T. G. & Onyali, C. I. (2015) agreed that forensic accounting is a critical tool in the fight against

corruption, detection and prevention of fraud. Concurring, Njanike, Dube, and Mashayanye

(2016) recognized forensic accounting as administrative function in Zimbabwe whilst they

identified forensic auditor’s duties to include detection and prevention of fraud as well as

detection of potential red flag. Centre for Forensic Studies (2010) report that forensic

accounting could be used to reverse the leakages that cause corporate failures. Shah Bhavesh

(2014), noted that forensic accounting has to do with the comprehensive fraud investigation

consisting of preventing frauds and analyzing antifraud control, the audit of accounting records

in search of evidence of fraud and fraud audit.

13

Many cases against corrupt officers could not be established in the court of law partly as a

result of improper investigation and on the other hand due to the absence of combined skills of

accounting/auditing and legal/litigation services by the investigator (Lokanan, 2014).

However, with the advent of forensic accounting a sigh of relief is expected (Silverstone and

Pedneault, 2013) and that forensic accounting marks the beginning of a new era and with its

investigative techniques perpetrators of corruption can easily be brought to justice. Curtis

(2018) noted that one of the grey areas where forensic accounting is needed most and more

frequently is in the area of investigation and subsequently the prosecution of corrupt

officers. Forensic accounting approach specifically encompasses all other forms of

investigation that have bearing with the discovery of fraud and corruption. The ever increasing

as well as the sophistication of corrupt practices (Tapang, A.T., Bessong, P.K. & Ujah, P.I.

2015) require the use of forensic accounting as the necessary means for successful corruption

investigation and prosecution of fraudsters.

2.1.5 Interrelationship between auditing, fraud investigation and forensic accounting

14

Fig 2.2 Interrelationship between auditing, fraud investigation and forensic accounting

Source: National Institute of Justice Special Report 2017

The diagram above shows the knowledge and skills of traditional accounting, auditing, fraud,

and forensic accounting interrelationship is articulated. Traditional auditing procedures address

fraud to the extent as prescribed by Statement on Auditing Standards; however, auditors have

no responsibility to plan and perform auditing procedures to detect misstatements that are not

judged to be material (including those caused by error as well as fraud) (Tapang, A.T., Bessong,

P.K. & Ujah, P.I. 2015). Where fraud issue is reported, the required action is investigation into

the subject matter. This is because it is a more in-depth fact finding in specific area of concern

than the regular audit. Fraud detection and prevention is a specific search to ascertain whether

fraud took place or not to determine the extent of fraud perpetuated. Even though, allegations

of fraud are often resolved through court action that may include calculated estimates of losses

(damages), it suggests that fraud investigation and forensic accounting often overlap. However,

both encompasses activities unrelated to the other: fraud professionals often assist in fraud

prevention and deterrence efforts that do not directly interface with the legal system, and

forensic accountants work with damage claims, valuations, and legal issues that do not involve

allegations of fraud (Soni Bhagwan Lal (2016).

2.1.6 Activities undertaken in forensic audit

2.1.6.1 Investigations

In combating fraudulent activities forensic auditors conduct investigations. The forensic

auditor does not carry out procedural audit, but carries an audit which conducts investigation

as to detect fraud or crime using computer programs or scientific knowledge (Soni Bhagwan

Lal, 2016). Thus by using the computer forensic tools in carrying out his responsibilities,

sophisticated fraudulent activities can be combated.

2.1.6.2 Analysis of financial statements

Forensic auditors analyze financial transaction involving unauthorized transfers of money

between companies (Owojori and Asolu 2016). Cole (2017) opines that forensic auditors are

required to have special skills in inspecting documents for authenticity, alteration, forgery or

counterfeiting. Hence, by possessing such skills, the forensic auditor in carrying out his/her

duties can easily detect errors, fraudulent activities and omissions thereby preventing and

reducing fraudulent activities (Prakash et al (2018). Prakash et al (2018), states that the forensic

15

auditor is responsible for analyzing, identifying the kinds of fraud that could occur and their

symptoms.

2.1.6.3 Reconstruction of incomplete accounting records

In addition forensic auditors reconstruct incomplete accounting records. In carrying out his

function an auditor reconstructs incomplete accounting records as to settle insurance claims,

over inventory valuation, proving money laundering activities by reconstructing cash

transactions (Owojori and Asaolu 2016). With both technological and communication skills an

auditor can combat fraudulent activities by reconstructing incomplete accounting records,

hence helping to detect and prevent fraud and ensuring good internal control system and good

corporate governance.

2.1.6.4 Embezzlement investigation

Forensic auditors also carry out embezzlement investigation in order to detect the culprit and

amount embezzled. According to Cabole (2016) forensic auditors calculate economic damages;

trace income and assets, often in an attempt to find hidden assets or income. The auditor also

reconstructs financial statement that may have been destroyed or manipulated.

2.1.7 Role of a forensic auditor

Basing on several definitions of forensic auditing it could be said that a forensic auditor is an

expert in financial matters who can detect, investigate and deter fraud and white collar crimes

which are to be presented to court for legal action or to public discussion and debate. An

understanding of effective fraud and forensic accounting techniques can assist Professional

Forensic Accountants in identifying illegal activity and discovering and preserving evidence

(Houck et al 2016). Hence, it is important to understand that the role of a forensic accountant is

different from that of regular auditor.

Forensic auditors are experienced auditors, accountants, and investigators of legal and financial

documents that are hired to look into possible suspicion of fraudulent activity within a company

or are hired by a company who may just want to prevent fraudulent activities from occurring

(Crumbley, 2014). It demands reporting, where accountability of the fraud is established and

the report is considered as evidence in the court of law or in administrative proceedings. A

forensic accountant uses his knowledge of accounting, law, investigative auditing,

criminology, and psychology to uncover fraud, find evidence and present such evidence in

court if required (Carnes & Gierlasinski, 2014).

16

The forensic auditor draw conclusions, calculate values and identify irregular patterns or

suspicious transactions by critically analyzing the financial data. This auditor provides an

accounting analysis to the court for dispute resolution in certain cases and also provides the

courts with explanation the fraud that has been committed (Naik Devesh, 2015). Forensic

auditors investigate beyond the figures, make him different traditional accountants and

auditors, in fact, while the traditional accountants look at the numbers, Forensic auditors look

behind the numbers and the mind of the culprits. Forensic audit is a concept that link accounting

system to legal system. Thus, we can say that forensic auditing is an accounting that is used to

help the court to arrive at the truth about a particular case in a court of law.

Krell (2012) says forensic accounting often involves an exhaustive, detailed effort to penetrate

concealment tactics. Seliskar (2013) says, “in terms of the Sheer labor, the magnitude of effort,

time and expense required to do a single, very focused (forensic) investigation –as contrasted

to auditing a set of the financial statements-the difference is incredible. As an investigator a

Professional Forensic Accountant can be seen as those who are specialist in fraud detection,

and particularly in documenting exactly the kind of evidence required for successful criminal

prosecution; able to work in complex regulatory and litigation environments; and with

reasonable accuracy, can reconstruct missing, destroyed, or deceptive accounting records

(Ibrahim Kabir, 2016). In regard to the above arguments, forensic accounting should play an

important role as expert witnesses and fraud investigators. Accordingly, forensic accountant

should possess a specific skills and training that enable them to play their roles as expert

witnesses and fraud investigators. The area of forensic accounting, as Houck et al (2006) argue,

consists of a rather unique skill set that ordinarily requires additional expertise and training

beyond an academic degree in accounting, and beyond being a CPA (Certified Public

Accountant), a CFE (Certified Fraud Examiner) or CIRA (Certified Insolvency and

Restructuring Advisor).

2.1.8 Importance of forensic auditing

Zimbabwe is a country which has a well constituted statutory instruments and national accounting

standards. Despite all these measures still there are financial scams and financial losses due to

company’s practicing creative accounting techniques and able to take advantages of the loopholes

of International Accounting Standards (IAS’s) and Generally Accepted Accounting Principles

(GAAP’s). because of failure by both internal and external audits to unearth some of the scams, it

is better to have a forensic cell and as external audit is mandatory to make such forensic audit also

17

mandatory for the publicly listed companies so that financial scams may be minimized and have a

healthy financial and sound environment of investment and accounting practices.

A basic use of forensic auditing skills can enable an organization to take the proper steps in the

event of a suspected fraud. The point about proactive forensic auditing is worth reinforcing

(Gbegi, D.O and Adebisi, J.F. (2014). Keating further on added that, a forensic audit will

always take the uncovering of misconduct as its primary theme. This is the reason why there

is need for forensic audit in organizations. Stephen (2012), states that a standard accounting

audit is not a true forensic audit designed to uncover wrong doing but rather only a sampling

audit that may entirely miss the problem, this showing that the existence of forensic audit is

really of great help in today's commercial world. There is also need for forensic auditing

because according to, Crumbley and Hitger (2017), forensic auditors are often asked to provide

litigation support where they are called on to give expert testimony about financial data and

accounting activities forensic audit also give a measure of comfort to the shareholders.

According to Smith et al (2012), forensic auditors help is needed in price fixations, stock

market manipulations and at times even manipulation of the financial figures by the

managements to window dress the balance sheet and profit and loss account figures to hide real

facts from the stake holders and general public, for the funds misused or misappropriated by

the top management. Statutory audit is an audit required by law to ensure that proper and

adequate financial records have been maintained as required by statutes an GAAP and also to

lay credence to financial statements (Eyisi and Ezuwsore, 2014).

2.1.9 How forensic audit help in mitigating risk

Forensic auditing plays an important role in detecting, reducing and eliminating risks

(Al-Shami, S. S. A., Majid, A., Bin, I., Rashid, N. A., Hamid, B. A., & Rizal, M. S. 2014).

They added on to say that forensic auditing reduces both overall business risk and information

risks. Some even see forensic accounting as practiced by skilled accounting specialists

becoming part and parcel of most financial audits an extra quality control step in the auditing

process that will help reduce financial statement fraud. Crumbley, et al, (2012) assert that

because of its nature forensic audit reduces risks of misappropriation of assets by management.

Many researchers have attempted to examine the effect of forensic auditing on fraud detection,

for example, Madumere and Onumah, (2013) revealed that corporate fraud is on the increase

because most managers want to be independent at the expense of their employers. Aduwo,

18

(2016) further explained that forensic auditing can go a long way to influence financial

scandals in corporate organization. Modugu and Anyaduba (2013) found that there is

significance agreement amongst stakeholder on the effectiveness of forensic auditors in fraud

control, financial reporting and internal control quality.

2.1.10 Application of forensic auditing in developing countries

Though financial fraud in Zimbabwe has witnessed highly publicized cases especially in the public

sector, Kosmas (2017) suggests that the application of forensic accounting applies to all scenes

where fraud is a possibility. Okoye and Akenbor (2013) commenting on the application of forensic

auditing in developing economies and Zimbabwe is not an exception, notes that forensic accounting

is faced with so many bottlenecks. These includes inability to operate more independently and

effectively, lack of technical capabilities and inability of gathering information that is admissible

in a court of law, less focus on offering service quality, conflicting regulatory codes and standards,

lack of harmonization and unification of all the existing sectoral corporate governance codes

applicable (Okoye, 2017).

Crumbly et al (2014) revealed the following challenges confronting the application of forensic

accounting/ in developing countries.

A significant challenge that faces a forensic accountant is the task of gathering

information that is admissible in a court of law.

The admissibility, of evidence in compliance with the laws of evidence is crucial

to successful prosecutions of criminal and civil claims.

Globalization of the economy and the fact that a fraudster can be based anywhere in the

world has led to the problem of inter-jurisdiction.

The law is not always up to date with the latest advancements in technology. Therefore,

lawyers and forensic accountants have to rely on outdated acts, laws that are of

general nature, or on acts that have not yet proven their effectiveness in prosecuting

fraudsters.

Forensic investigations often wind up as evidence in legal proceedings, including full-

fledged trails.

2.2 Theoretical framework

2.2.1 Fraud Triangle theory

Forensic auditing relies on the fraud triangle to identify weak points in the business systems

and find possible suspects in cases of fraud. It consists of three core concepts which together

create a situation ripe for fraud: incentive, opportunity, and rationalization. People must have

19

the incentive and opportunity to commit financial fraud, as well as the ability to justify it

(Rasey, 2015). Recent analysis has suggested adding a fourth concept to make a diamond

capability.

Fig 2.1: Fraud triangle

Source: Kassem and Higson, (2012)

2.2.1.1 Opportunity

Employees use their position to commit fraud when internal controls are weak, or where there

is poor management oversight on internal control implementation. Rae and Subramaniam

(2018) suggested that, if a susceptible individual perceives opportunities due to a lack of or

inefficient internal controls and has the ability or power to exploit these opportunities, that

individual may perpetrate a fraud. Most Employees who commit fraud do so, because they

have the opportunity to access assets and information that allows them obscure their fraudulent

deeds (Hill et al, 2016). It is true that employees need access to certain platform to perform

their jobs. The same access can provide the employee with opportunity to commit fraud.

20

2.21.2 Pressure/Incentive

Pressure can be defined as the motivation that leads the perpetrator to engage in unethical

behaviours. Perceived pressures can happen for different reasons and also that it can happen to

employees at any level in companies. Pressure does not only mean financial pressure. Lister

(2017), state that there are three types of motivation or pressure: Personal pressure to pay for

lifestyle, employment pressure from continuous compensation structures, or management’s

financial interest, and external pressure such as threats to the business financial stability,

financier covenants, and market expectations. Akhidime, E. A & Uagbale-Ekatah, R. E. (2014)

argued that although an individual may demonstrate different motives, research has shown that

fraud often occurs as a response to economic pressures, and most pressures involve a financial

need such as greed, living beyond one’s means, large expenses or personal debt, poor credit,

personal financial losses, and an inability to meet a financial. The identified matters are the

motivation that can influence fraud.

2.2.1.3 Rationalization

Rationalization is an attempt by an employee to justify why they commit fraud. Rationalization

is an act of employee who commits fraud to give reasons for his action (Bhalla Mohit, 2018).

It is a way of covering up for the wrong done to the employer. In other words, rationalization

allows the fraudster to view his or her illegal actions as acceptable. Das Sandeep (2016)

concluded that, if a person cannot justify unethical actions, it is unlikely that he or she will

engage in fraud. That person, however, may rationalize those actions in different ways using

various justifications.

2.2.2 White collar crime theory

This theory result from the work by Sutherland in 1949 as cited in Michael (2014). The term

white-collar crime dates back to 1939. Sutherland as cited in Michael (2014) was the first to

coin the term, and hypothesis white-collar criminals, attributed different characteristics and

motives than typical street criminals. According to Sutherland white collar crime is crime

committed by a person respectability and high social status in the course of his occupation

(Sutherland 1949, cited in Michael 2014). Federal Bureau of Investigation (FBI) defines white-

collar crime as those illegal acts which are characterized by deceit, concealment, or violation

of trust and which are not dependent upon the application or threat of physical force or violence.

Sutherland’s goal was to prove a relation between money, social status, and likelihood of going

to jail for a white-collar crime, compared to more visible, typical crimes. According to him

21

white-collar criminals are opportunists, who over time learn they can take advantage of their

circumstances to accumulated financial gain. They are educated, intelligent, affluent,

individuals who are qualified enough to get a job which allows them the unmonitored access

to often large sum of money. Compared to blue collar crime, white collar crimes have gone a

long way undetected since it requires more skills to unearth it. According to this theory it is

estimated that a great deal of white-collar crimes is undetected or if detected, it is not reported

(Gangully Jagdish (2015). Because of the high status of the perpetrators of these crimes, a

highly trained and experienced examiner or investigator like the Professional Forensic

Accountant is needed to forestall the occurrence of such high profile fraud (Freidrihs, 2016).

2.3 Conceptual framework

The Conceptual framework was designed to show the relationship between utilisation of

forensic audit and risk reduction. The term forensic means “relating to the application of

scientific knowledge to legal problems or usable in a court of law” (Bolgana and Robert

2015).

Figure 1.1: Conceptual framework

Source: Researcher

Gangully Jagdish (2015) described forensic auditing involves utilization of specialized

investigative skills in carrying out an enquiry conducted in such a manner that the outcome

will have application to the court of law. Forensic auditing is fraud detection, unlike the

traditional auditing that focuses on review of internal control system, error identification and

prevention. Forensic audit’s focus is on the detection, analysis, and communication of evidence

of underlying financial and reporting events. Where fraud issue is reported, the required action

22

is investigation into the subject matter. This is because it is a more in-depth fact finding in

specific area of concern than the regular audit. Fraud detection and prevention is a specific

search to ascertain whether fraud took place or not to determine the extent of fraud perpetuated.

Even though, allegations of fraud are often resolved through court action that may include

calculated estimates of losses (damages), it suggests that fraud investigation and forensic

accounting often overlap. However, both encompasses activities unrelated to the other: fraud

professionals often assist in fraud prevention and deterrence efforts that do not directly

interface with the legal system, and forensic accountants work with damage claims, valuations,

and legal issues that do not involve allegations of fraud (Ibrahim Kabir (2016). When forensic

accounting practices are incorporated into a separate forensic audit, they have the potential to

overcome problems associated with identifying financial malfeasance within the traditional

audit-reporting model.

2.4 Empirical Review