Accounting for Merchandising Businesses - Universitas ...

107

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Accounting for Merchandising Businesses - Universitas ...

1

Adeng Pustikaningsih, M.Si.

Dosen Jurusan Pendidikan Akuntansi

Fakultas Ekonomi

Universitas Negeri Yogyakarta

CP: 08 222 180 1695

Email : [email protected]

2

2

6

Accounting for Merchandising

Businesses

3

3

1. Distinguish between the activities and

financial statements of service and

merchandising businesses.

2. Describe and illustrate the financial

statements of a merchandising

business.

After studying this chapter, you should

be able to:

4

4

3. Describe and illustrate the accounting for

merchandise transactions including:

sale of merchandise

purchase of merchandise

transportation costs, sales taxes, trade discounts

dual nature of merchandising transactions.

After studying this chapter, you should

be able to:

4. Describe the adjusting and closing process

for a merchandising business.

5

5

Distinguish between the

activities and financial

statements of service and

merchandising businesses.

Objective 1

6-1

6

6

Service Business

Fees earned $XXX

Operating expenses –XXX

Net income $XXX

6-1

7

7

Merchandising Business

Sales $XXX

Cost of Merchandise Sold –XXX

Gross Profit $XXX

Operating Expenses –XXX

Net Income $XXX

6-1

8

8

When merchandise is sold, the

revenue is reported as sales, and

its cost is recognized as an

expense called cost of

merchandise sold.

6-1

9

9

The cost of merchandise sold is

subtracted from sales to arrive at

gross profit. This amount is

called gross profit because it is

the profit before deducting the

operating expenses.

6-1

10

10

Merchandise on hand (not

sold) at the end of an

accounting period is called

merchandise inventory.

6-1

11

11

On August 25, Gallatin Repair Service extended an offer of

$125,000 for land that had been priced for sale at $150,000. On

September 3, Gallatin Repair Service accepted the seller’s

counteroffer of $137,000. On October 20, the land was assessed

at a value of $98,000 for property tax purposes. On December 4,

Gallatin Repair Service was offered $160,000 for the land by a

national retail chain. At what value should the land be recorded

in Gallatin Repair Service’s records?

Follow My Example 1-1

$137,000. Under the cost concept, the land should be recorded at

the cost to Gallatin Repair Service. 31

1-2

During the current year, merchandise is sold for

Rp250,000,000 cash and for Rp975,000,000 on account.

The cost of the merchandise sold is Rp735,000,000. What

is the amount of the gross profit?

Follow My Example 6-1

The gross profit is Rp490,000,000 (Rp250,000,000 +

Rp975,000,000 –Rp735,000,000).

6-1

Example Exercise 6-1

10 For Practice: PE 6-1A, PE 6-1B

12

12

11

6-1

13

13

Describe and illustrate the

financial statements of a

merchandising business.

Objective 2

6-2

14

14

The multiple-step

income statement

contains several sections,

subsections, and

subtotals.

6-2 Multiple-Step Income Statement

15

15

The Sales account

provides the total amount

charged to customers for

merchandise sold,

including cash sales and

sales on account.

6-2

16

16

Sales returns and

allowances are granted by

the seller to customers for

damaged or defective

merchandise.

6-2

17

17

Sales discounts are granted

by the seller to customers

for early payment of

amounts owed.

6-2

18

18

Net sales is determined by

subtracting sales returns

and allowances and sales

discounts from sales.

6-2

19

19

18 (Continued)

Revenue from sales:

Sales Rp720,185

Less: Sales returns and allowances Rp 6,140

Sales discounts 5,790 11,930

Net sales Rp708,255

Cost of merchandise sold 525,305

Gross profit Rp182,950

SolusiNet

Income Statement

For the Year Ended December 31, 2009 (in Rp000)

6-2 Multiple-Step Income Statement

20

20

Operating expenses:

Selling expenses:

Sales salaries expense Rp53,430

Advertising expense 10,860

Depr. Expense–store equipment 3,100

Delivery Expense 2,800

Miscellaneous selling expense 630

Total selling expenses Rp 70,820

Administrative expenses:

Office salaries expense Rp21,020

Rent expense 8,100

Depr. expense–office equipment 2,490

Insurance expense 1,910

Office supplies expense 610

Misc. administrative expense 760

Total admin. expenses 34,890

Total operating expenses 105,710

Income from operations Rp 77,240

19 (Continued)

(In Rp000)

21

21

(Concluded)

Other income and expenses:

Rent revenue Rp 600

Interest expense (2,440) (1,840)

Net income Rp75,400

6-2

20

(In Rp000)

22

22

Cost of merchandise sold

was discussed earlier. It is

the cost of the merchandise

sold to customers.

6-2

23

23

As we discussed in Slide 16,

sellers may offer customers

sales discounts for early

payment of their bills. From

the buyer’s perspective, such

discounts are referred to as

purchase discounts.

6-2

24

24

The buyer may return merchandise

to the seller (a purchase return),

or the buyer may receive a

reduction in the initial price at

which the merchandise was

purchased (a purchase allowance).

6-2

25

25

Merchandise Inventory, January 1,2009............ Rp 59,700 Purchases Rp521,980 Less: Purchases returns and allowances ......... Rp9,100 Purchase discounts ................................ 2,525 11,625 Net purchases ................................................... Rp510,355 Add transportation in.......................................... 17,400 Cost of merchandise purchased .................. 527,755 Merchandise available for sale .......................... Rp587,455 Less merchandise inventory, December 31, 2009 62,150 Cost of merchandise sold .................................. Rp525,305

Cost of Merchandise

Sold

6-2

26

26

6-2 Single-Step Income Statement

An alternative form of income

statement is the single-step

income statement. As shown in

the next slide, the income

statement for SolusiNet deducts

the total of all expenses in one

step from the total of all

revenues.

27

27

26

Revenues:

Net sales Rp708,255

Rent revenue 600

Total revenues Rp708,855

Expenses:

Cost of merchandise sold Rp525,305

Selling expenses 70,820

Administrative expenses 34,890

Interest expense 2,440

Total expenses 633,455

Net income Rp 75,400

SolusiNet

Income Statement

For the Year Ended December 31, 2009 (in Rp000)

6-2 Exhibit 3: Single-Step Income Statement

28

28

27

6-2 Exhibit 4: Statement of Owner’s Equity

Chris Clark, capital, 1/1/09 Rp153,800

Net income for year Rp75,400

Less withdrawals 18,000

Increase in owner’s equity 57,400

Chris Clark, capital, 12/31/09 Rp211,200

SolusiNet

Statement of Owner’s Equity

For the Year Ended December 31, 2009 (in Rp000)

29

29

SolusiNet

Balance Sheet

December 31, 2009 (in Rp000)

28

Assets

Current assets:

Cash Rp52,950

Accounts receivable 91,080

Merchandise inventory 62,150

Office supplies 480

Prepaid insurance 2,650

Total current assets Rp209,310

(Continued)

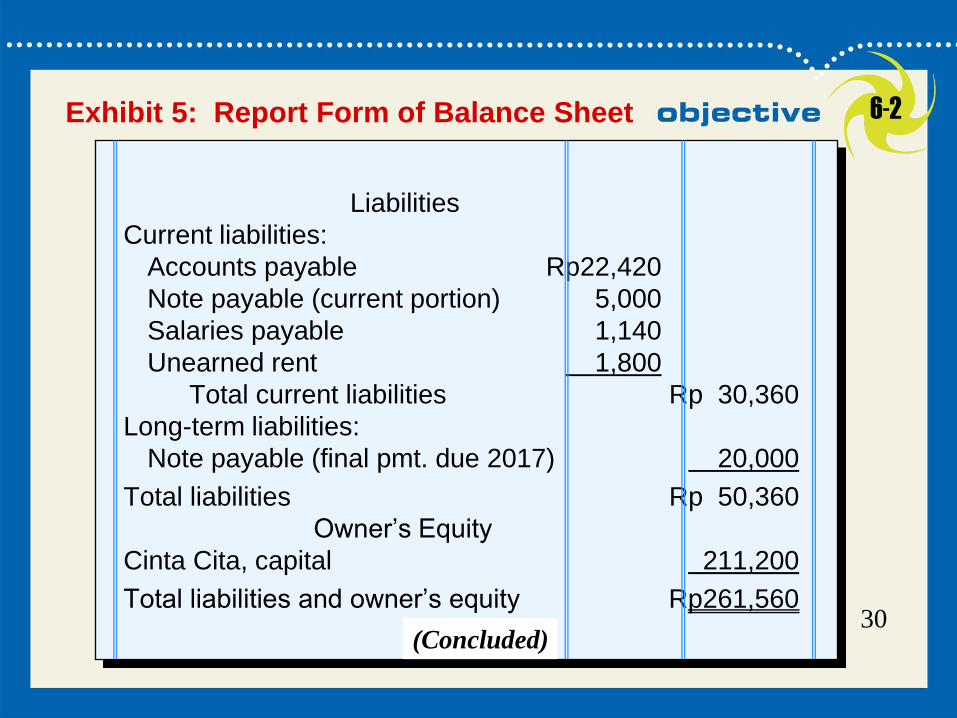

6-2 Exhibit 5: Report Form of Balance Sheet

30

30

Property, plant, and equip.: Land Rp20,000 Store equipment Rp27,100 Less accumulated

depreciation 5,700 21,400

Office equipment Rp15,570 Less accumulated depreciation 4,720 10,850 Total property, plant, and equipment 52,250

Total assets Rp261,560

29

6-2

(Continued)

Exhibit 5: Report Form of Balance Sheet

(In Rp000)

31

31

30

Liabilities

Current liabilities:

Accounts payable Rp22,420

Note payable (current portion) 5,000

Salaries payable 1,140

Unearned rent 1,800

Total current liabilities Rp 30,360

Long-term liabilities:

Note payable (final pmt. due 2017) 20,000

Total liabilities Rp 50,360

Owner’s Equity

Cinta Cita, capital 211,200

Total liabilities and owner’s equity Rp261,560

6-2

(Concluded)

Exhibit 5: Report Form of Balance Sheet

32

32

6-2

Example Exercise 6-2

Based upon the following data, determine the cost of

merchandise sold for May. Use the format seen in

Exhibit 2.

Merchandise Inventory, May 1 Rp121,200,000

Merchandise Inventory, May 31 142,000,000

Purchases 985,000,000

Purchases Returns and Allowances 23,500,000

Purchases Discounts 21,000,000

Transportation In 11,300,000 31

33

33

Follow My Example 6-2

32

Merchandise Inventory, May 1 Rp 121,200

Purchases Rp985,000

Less: Purchases returns and allowances Rp23,500

Purchases discounts 21,000 44,500

Net purchases Rp940,500

Add transportation in 11,300

Cost of merchandise purchased 951,800

Merchandise available for sale Rp1,073,000

Less merchandise inventory, May 31 142,000

Cost of merchandise sold Rp 931,000

6-2

For Practice: PE 6-2A, PE 6-2B

34

34

Describe and illustrate the accounting

for merchandise transactions including:

sale of merchandise; purchase of

merchandise; transportation costs, sales

taxes, trade discounts; dual nature of

merchandise transactions.

Objective 3

6-3

35

35

Post

RefJan 2009 3 Cash 1 800 000

Sales 1 800 000

To record cash sales

JOURNAL Page 25

Date Description Debit Credit

On January 3, SolusiNet sold

Rp1,800,000 of merchandise for cash.

@solusinet

Cash Sales 6-3

36

36

Jan 3 Cost of Merchandise Sold 1 200 000

Merchandise Inventory 1 200 000

To record the cost of merch. sold

Using a perpetual inventory, the

Rp1,200,000 cost of the inventory must be

recorded.

Cash Sales (continued) 6-3

37

37

36

6-3

At the end of the month, Rp48,000

was sent to pay the service charge on

credit card sales.

Credit Card Sales

Jan 3 Credit Card Expense 48 000

Cash 48 000

To record service charges on credit

card sales for the month

38

38

37

6-3 Sales on Account Using a Perpetual

Inventory

Jan. 12 Accounts Receivable—CV Agung Surya 510 000

Sales 510 000

Invoice No. 7172

On January 12, SolusiNet sold CV Agung Surya

merchandise on account, Rp510,000. The cost of

the merchandise to the seller was Rp280,000.

12 Cost of Merchandise Sold 280 000

Merchandise Inventory 280 000

Cost of merchandise sold on

Invoice No. 7172.

39

39

The terms for when payments for

merchandise are to be made, agreed

on by the buyer and the seller, are

called credit terms. If buyer is

allowed an amount of time to pay, it

is known as the credit period.

6-3 Sales Discounts

40

40

39

If invoice is

paid within

10 days of

invoice date

Invoice for

Rp1,500,000

Terms:

2/10, n/30

Rp1,470,000 paid

(Rp1,500,000 less a

2% discount)

6-3 Credit Terms

41

41

40

If invoice is

NOT paid

within 10

days of

invoice date

Invoice for

Rp1,500,000

Terms:

2/10, n/30

Full amount

(Rp1,500,000) is due

within 30 days of

invoice date

6-3

42

42

41

Sales Discounts 6-3

On January 22, SolusiNet receives the

amount due, less the 2 percent discount.

Jan. 22 Cash 1 470 000

Accounts Receivable–Omega Tech. 1 500 000

Sales Discounts 30 000

Collection of Invoice No.

106-8, less 2% discount.

43

43

Jan. 13 Sales Returns and Allowances 225 000

Accounts Receivable-PT Krisna 225 000

Credit Memo No. 32

13 Merchandise Inventory 140 000

Cost of Goods Sold 140 000

Cost of merchandise returned.

Credit Memo No. 32.

6-3

42

On January 13, issued Credit Memo 32 to PT

Krisna for merchandise returned to SolusiNet.

Selling price, Rp225,000; cost to SolusiNet,

Rp140,000.

44

44

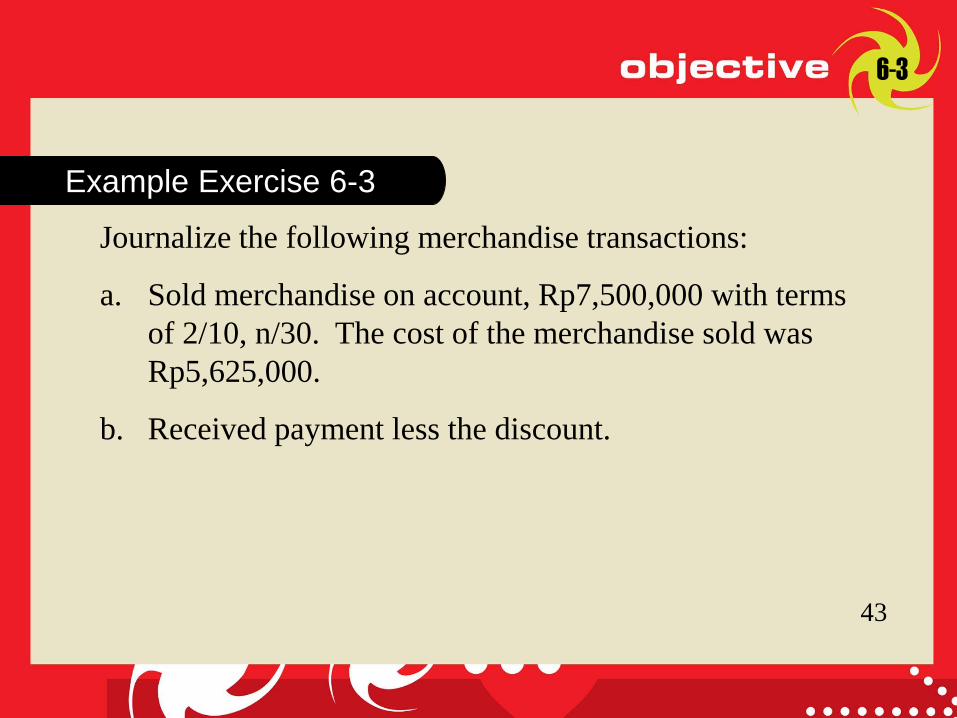

1-2

Journalize the following merchandise transactions:

a. Sold merchandise on account, Rp7,500,000 with terms

of 2/10, n/30. The cost of the merchandise sold was

Rp5,625,000.

b. Received payment less the discount.

6-3

Example Exercise 6-3

43

45

45

Follow My Example 6-3

44

a. Accounts Receivable 7,500,000

Sales 7,500,000

Cost of Merchandise Sold 5,625,000

Merchandise Inventory 5,625,000

b. Cash 7,350,000

Sales Discounts 150,000

Accounts Receivable 7,500,000

For Practice: PE 6-3A, PE 6-3B

6-3

46

46

45

On January 3, SolusiNet purchased merchandise

for cash from Alden Company, Rp2,510,000.

Purchase Transactions (Perpetual

Inventory)

6-3

JOURNAL

Date Description Post.

Ref. Dr Cr.

PAGE 24

Jan. 3 Merchandise Inventory 2 510 000 2009

Cash 2 510 000

Purchased inventory from

CV Budi.

47

47

46

6-3

Jan. 4 Merchandise Inventory 9 250 000

Accounts Payable—CV Thomas 9 250 000

Purchased inventory on

account.

On January 4, SolusiNet purchased

merchandise on account from CV Thomas,

Rp9,250,000.

48

48

PT Alpha Technologies

issues an invoice for

Rp3,000,000 to SolusiNet

dated March 12, with terms

2/10, n/30.

Purchases Discounts 6-3

49

49

SolusiNet borrows cash at an annual interest rate

of 6%. Should the firm borrow cash to pay the

invoice within the discount period?

6-3

Discount of 2% on Rp3,000,000 Rp60,000

Interest for 20 days at the rate

of 6% on Rp2,940,000 – 9,800

Savings from borrowing Rp50,200

YES

50

50

49

Mar. 12 Merchandise Inventory 3 000 000

Accounts Payable— PT Alpha Tech. 3 000 000

Purchased inventory on

account.

6-3

On March 12, SolusiNet purchased

merchandise on account from PT Alpha

Technologies, Rp3,000,000.

Purchase Transactions (Perpetual

Inventory)

51

51

Mar. 22 Accounts Payable— PT Alpha Technol. 3 000 000

Cash 2 940 000

Merchandise Inventory 60 000

Paid PT Alpha Technologies

for March 12 purchase.

6-3

If payment is made by March 22, SolusiNet

records the discount as a reduction in cost. Notice

that Merchandise Inventory is credited because

NetSolutions maintains a perpetual inventory. 50

52

52

Apr. 11 Accounts Payable— PT Alpha Technol. 3 000 000

Cash 3 000 000

Paid PT Alpha Technologies

for March 12 purchase.

6-3

51

If SolusiNet does not pay the invoice until

April 11, it would pay the full amount.

53

53

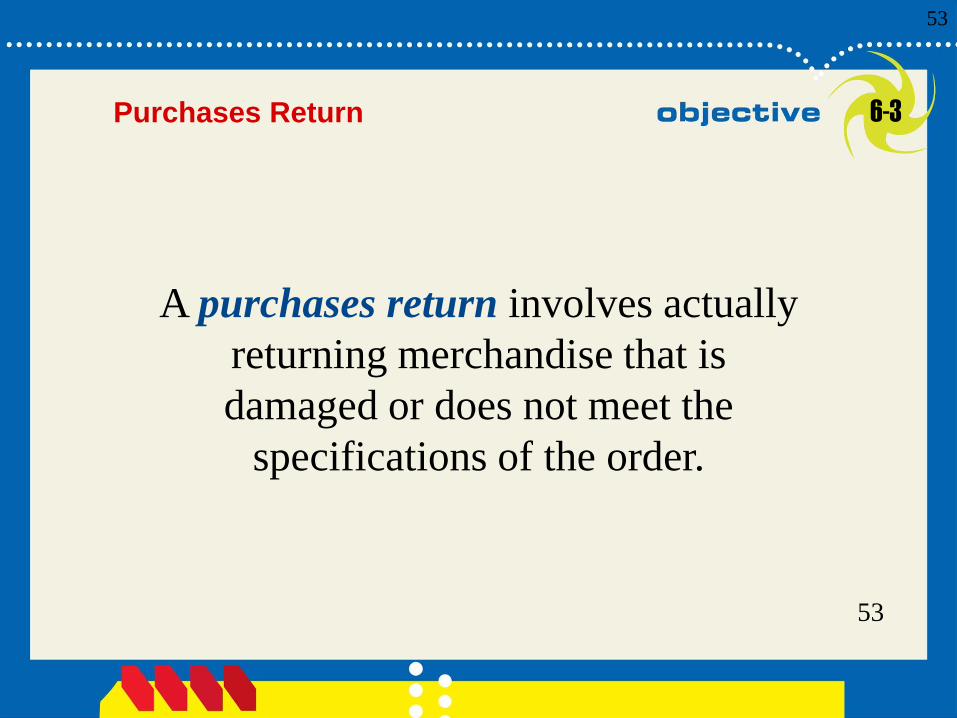

A purchases return involves actually

returning merchandise that is

damaged or does not meet the

specifications of the order.

Purchases Return 6-3

54

54

When the defective or incorrect

merchandise is kept by the

buyer and the vendor makes a

price adjustment, this is a

purchases allowance.

6-3 Purchases Allowance

55

55

SolusiNet receives the delivery

from PT Malang Komputer and

determines that Rp900,000 of the

items are not the merchandise

ordered. Debit memorandum #18

(also called a debit memo) is

issued to Maxim Systems.

6-3

@solusinet

56

56

Mar. 7 Accounts Payable—PT Malang Komp. 900 000

Debit Memo No. 18

Merchandise Inventory 900 000

6-3

55

On March 7, SolusiNet records the return

of the merchandise indicated in Debit

Memorandum No. 18.

57

57

56

On May 2, SolusiNet purchased

Rp5,000,000 of merchandise from Delta

Data Link, subject to terms 2/10, n/30.

May 2 Merchandise Inventory 5 000 000

Purchased merchandise.

Accounts Payable—Delta Data 5 000 000

6-3

58

58

57

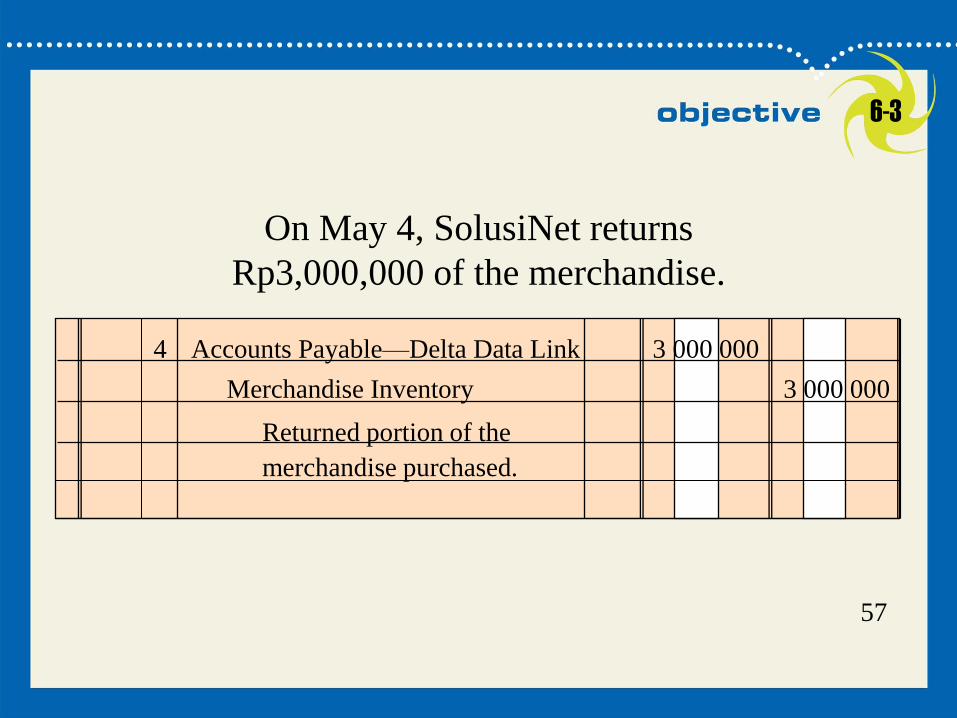

On May 4, SolusiNet returns

Rp3,000,000 of the merchandise.

6-3

4 Accounts Payable—Delta Data Link 3 000 000

Returned portion of the

merchandise purchased.

Merchandise Inventory 3 000 000

59

59

58

On May 12, SolusiNet pays the amount due,

Rp1,960,000 [Rp2,000,000 – (Rp5,000,000 –

Rp3,000,000) x 2%)].

12 Accounts Payable—Delta Data Links 2 000 000

Paid invoice [(Rp5,000,000 –

Rp3,000,000) x 2% = Rp40,000;

Rp2,000,000 – Rp40,000 =Rp1,960,000]

Cash 1 960 000

Merchandise Inventory 40 000

6-3

60

60

6-3

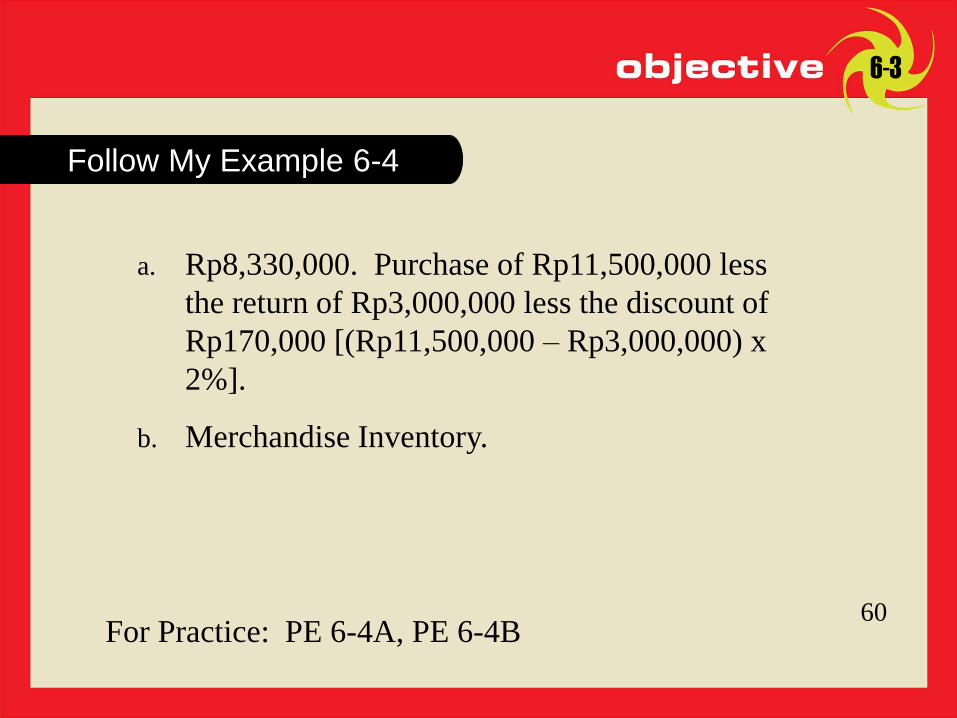

Ramli Company purchased merchandise on account from a

supplier for Rp11,500,000, terms 2/10, n/30. Rofles Company

returned Rp3,000,000 of the merchandise and received full

credit.

Example Exercise 6-4

a. If Rofles Company pays the invoice within the

discount period, what is the amount of cash required

for the payment?

b. Under a perpetual inventory system, what account is

credited by Rofles Company to record the return?

59

61

61

Follow My Example 6-4

60

a. Rp8,330,000. Purchase of Rp11,500,000 less

the return of Rp3,000,000 less the discount of

Rp170,000 [(Rp11,500,000 – Rp3,000,000) x

2%].

b. Merchandise Inventory.

For Practice: PE 6-4A, PE 6-4B

6-3

62

62

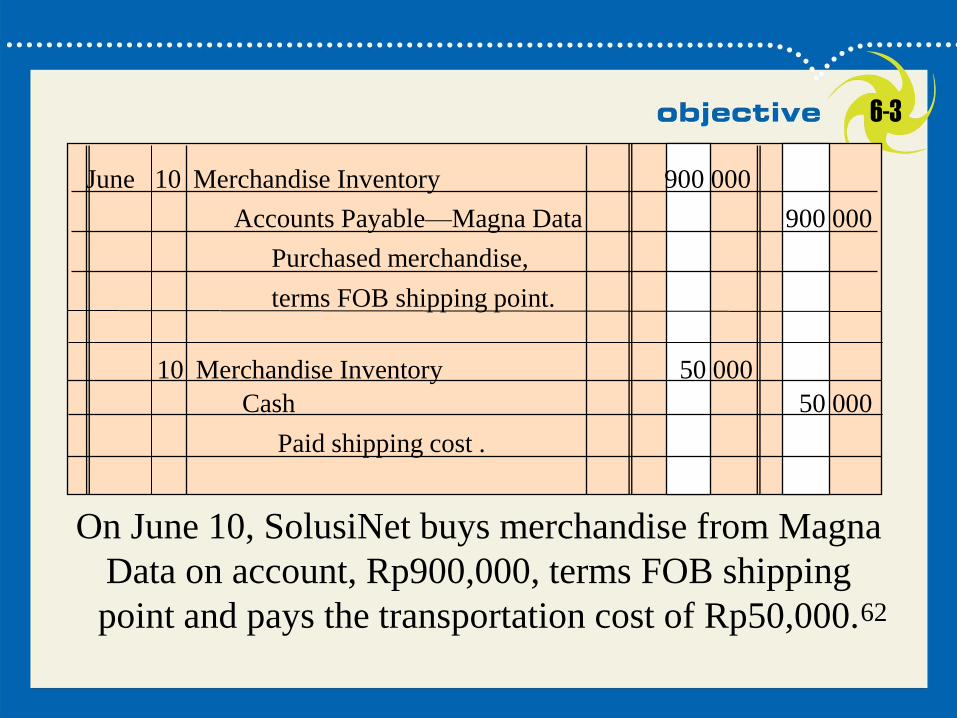

If ownership of the merchandise

passes to the buyer when the seller

delivers the merchandise to the

freight carrier, it is said to be FOB

(free on board) shipping point.

6-3 Transportation Costs

63

63

62

On June 10, SolusiNet buys merchandise from Magna

Data on account, Rp900,000, terms FOB shipping

point and pays the transportation cost of Rp50,000.

June 10 Merchandise Inventory 900 000

Purchased merchandise,

terms FOB shipping point.

Accounts Payable—Magna Data 900 000

10 Merchandise Inventory 50 000

Cash 50 000

Paid shipping cost .

6-3

64

64

If ownership of the merchandise

passes to the buyer when the

buyer receives the merchandise,

the terms are said to be FOB

(free on board) destination.

6-3 Transportation Costs

65

65

On June 15, SolusiNet sells

merchandise to PT Kiki on account,

Rp700,000, terms FOB destination.

The cost of the merchandise sold is

Rp480,000.

6-3 FOB Destination

@solusinet

66

66

65

6-3

June 15 Accounts Receivable—PT Kiki 700 000

Sold merchandise, terms

FOB destination.

Sales 700 000

15 Cost of Merchandise Sold 480 000

Merchandise Inventory 480 000

Record cost of merchandise

sold to PT Kiki

67

67

66

6-3

On June 15, SolusiNet pays the

transportation cost of Rp40,000.

June 15 Delivery Expense 40 000

Cash 40 000

Paid shipping cost on

merchandise sold.

68

68

On June 20, SolusiNet sells

merchandise to CV Permadi on

account, Rp800,000, terms FOB

shipping point. The cost of the

merchandise sold is Rp360,000.

6-3 FOB Shipping Point

69

69

68

6-3

June 20 Accounts Receivable—CV Permadi 800 000

Sold merchandise, terms

FOB shipping point.

Sales 800 000

20 Cost of Merchandise Sold 360 000

Merchandise Inventory 360 000

Record cost of merchandise

sold to CV Permadi

70

70

69

6-3

SolusiNet pays the transportation cost

of Rp45,000 and adds it to the invoice.

June 20 Accounts Receivable—CV Permadi 45 000

Cash 45 000

Prepaid shipping cost on

merchandise sold.

71

71

6-3

Determine the amount to be paid in full settlement of each

of invoices (a) and (b), assuming that credit for returns and

allowances was received prior to payment and that all

invoices were paid within the discount period.

Example Exercise 6-5

70

Transportation Returns and

Merchandise Paid by Seller Transportation Terms Allowances

a. Rp4,500,000 Rp200,000 FOB shipping point, Rp800,000

1/10, n/30

b. Rp5,000,000 60,000 FOB destination, Rp2,500,000

2/10, n/30

72

72

Follow My Example 6-5

71

a. Rp3,863,000. Purchase of Rp4,500,000 less

return of Rp800,000 less the discount of

Rp37,000 [(Rp4,500,000 – Rp800,000) x 1%]

plus Rp200,000 of shipping.

b. Rp2,450,000. Purchase of Rp5,000,000 less

return of Rp2,500,000 less the discount of

Rp50,000 [(Rp5,000,000 – Rp2,500,000) x 2%].

For Practice: PE 6-5A, PE 6-5B

6-3

73

73

18 72

6-3

74

74

18 73

On August 12, merchandise is sold

on account to Lemon Company,

Rp100,000. The state has a 6% sales

tax.

Aug. 12 Accounts Receivable—CV Lemon 106 000

Sales 100 000

Sales Taxes Payable 6 000

Invoice No. 339

Sales Taxes 6-3

75

75

18 74

On September 15, the seller sends in a

payment of Rp2,900,000 to the taxing unit

for the August taxes collected.

Sept. 15 Sales Tax Payable 2 900 000

Cash 2 900 000

Payment for sales taxes

collected during August.

6-3

76

76

When wholesalers offer special

discounts to certain classes of buyers

that order large quantities, these

discounts are called trade discounts.

Trade Discounts 6-3

77

77

Dual Nature of Merchandise

Transactions 6-3

Each merchandising transaction affects a buyer

and a seller. In the following illustrations, we

show how the same transactions would be

recorded by both the seller and the buyer.

July 1. CV Santi sold merchandise on account

to CV Budiman, Rp7,500,000, terms

FOB shipping point, n/45. The cost of

the merchandise sold was Rp4,500,000.

78

78

18 77

CV Santi (Seller)

Accounts Receivable—CV Budiman 7,500,000 Sales 7,500,000 Cost of Merchandise Sold 4,500,000 Merchandise Inventory 4,500,000

CV Budiman (Buyer)

Merchandise Inventory. 7,500,000 Accounts Payable—CV Santi 7,500,000

6-3

79

79

July 2 CV Budiman paid transportation

charges of Rp150,000 on July 1

purchase from CV Santi.

6-3

80

80

18 79

CV Santi (Seller)

No entry.

CV Budiman (Buyer)

Merchandise Inventory 150,000 Cash 150,000

6-3

81

81

July 5 CV Santi sold merchandise on

account to CV Budiman,

Rp5,000,000, terms FOB

destination, n/30. The cost of the

merchandise sold was

Rp3,500,000.

6-3

82

82

18 81

CV Santi (Seller)

Accounts Receivable—CV Budiman 5,000,000 Sales 5,000,000 Cost of Merchandise Sold 3,500,000 Merchandise Inventory 3,500,000

CV Budiman (Buyer)

Merchandise Inventory. 5,000,000 Accounts Payable—CV Santi 5,000,000

6-3

83

83

July 7. CV Santi paid transportation

costs of Rp250,000 for delivery

of merchandise sold to CV

Budiman on July 5.

6-3

84

84

18 83

CV Santi (Seller)

Delivery Expense 250,000 Cash 250,000

CV Budiman(Buyer)

No entry.

6-3

85

85

July 13. CV Santi issued CV Budiman a

credit memorandum for

Rp1,000,000 of merchandise

returned from a July 5 purchase

on account. The cost of the

merchandise was Rp700,000.

6-3

86

86

18 85

CV Santi (Seller)

Sales Returns and Allowances 1,000,000 Accounts Receivable—CV Budiman 1,000,000 Merchandise Inventory 700,000 Cost of Merchandise Sold 700,000

CV Budiman (Buyer)

Accounts Payable—CV Santi 1,000,000 Merchandise Inventory 1,000,000

6-3

87

87

July 15. CV Santi received payment

from CV Budiman for purchase

of July 5.

6-3

88

88

18 87

CV Santi (Seller)

Cash 4,000,000 Accounts Receivable—CV Budiman 4,000,000

CV Budiman (Buyer)

Accounts Payable—CV Santi 4,000,000 Cash 4,000,000

6-3

89

89

July 18. CV Santi sold merchandise on

account to CV Budiman,

Rp12,000,000, terms FOB

shipping point, 2/10, n/eom.

Santi prepaid transportation costs

of Rp500,000, which were added

to the invoice. The cost of the

merchandise sold was

Rp7,200,000.

6-3

90

90

18 89

CV Santi (Seller)

Accounts Receivable—CV Budiman 12,000,000 Sales 12,000,000

Accounts Receivable—CV Budiman 500,000 Cash 500,000

Cost of Merchandise Sold 7,200,000 Merchandise Inventory 7,200,000

6-3

CV Budiman (Buyer)

Merchandise Inventory 12,500,000 Accounts Payable—CV Santi 12,500,000

91

91

July 28. CV Santi received payment from CV

Budiman for purchase of July 18,

less discount (2% x Rp12,000,000).

6-3

92

92

18 91

CV Santi (Seller)

Cash 12,260,000 Sales Discounts 240,000 Accounts Receivable—CV Budiman 12,500,000

CV Budiman (Buyer)

Accounts Payable—CV Santi 12,500,000 Merchandise Inventory 240,000 Cash 12,260,000

6-3

93

93

1-2

Santi Co. sold merchandise to Butet Co. on account,

Rp11,500,000, terms 2/15, n/30. The cost of the

merchandise sold is Rp6,900,000. Santi Co. issued a credit

memorandum for Rp900,000 for merchandise returned and

later received the amount due within the discount period.

The cost of the merchandise returned was Rp540,000.

Journalize Santi Co.’s and Butet Co.’s entries for the receipt

of the check for the amount due from Butet Co.

6-3

Example Exercise 6-6

92

94

94

Follow My Example 6-6

93

6-3

For Practice: PE 6-6A, PE 6-6B

Santi Company Journal Entries:

Cash (Rp11,500,000 – Rp900,000 – Rp212,000) 10,388,000 Sales Discounts [(Rp11,500,000 – Rp900,000) x 2%] 212,000 Accounts Receivable—Butet Co. (Rp11,500,000 – Rp900,000) 10,600,000

Butet Company Journal Entries:

Accounts Payable—Santi Co. (Rp11,500,000 –Rp900,000) 10,600,000 Merchandise Inventory [(Rp11,500,000 – Rp900,000)x 2%] 212,000 Cash (Rp11,500,000 – Rp900,000 – Rp212,000) 10,388,000

95

95

Describe the adjusting and

closing process for a

merchandising business.

Objective 4

6-4

96

96

6-4

Merchandising businesses may experience

some loss of inventory due to shoplifting,

employee theft, or errors in recording or

counting inventory. If the balance of the

Merchandise Inventory account is larger than

the total amount of merchandise count, the

difference is often called inventory shrinkage

or inventory shortage.

Inventory Shrinkage

97

97

SolusiNet inventory records

indicate that Rp63,950,000 of

merchandise should be

available for sale on December

31, 2009. The physical count

reveals that only Rp62,150,000

is actually available.

6-4

@solusinet

98

98

18 97

Inventory records Rp63,950,000

Inventory count 62,150,000

Inventory shortage Rp 1,800,000

Dec. 31 Cost of Merchandise Sold 1 800 000

Merchandise Inventory 1 800 000

Adjusting Entry

Inventory shrinkage

(Rp63,950,000 – Rp62,150,000).

6-4

99

99

6-4 Step 1: Closing Entries

Close the temporary accounts with credit

balances to Income Summary.

2009

Date Item PR Debit Credit

Closing Entries

Dec. 31 Sales 410 720 185 000

Rent Revenue 610 600 000

Income Summary 312 720 785 000

98

100

100

6-4

99

Close the temporary accounts

with debit balances to

Income Summary.

6-4 Step 2: Closing Entries

101

101

6-4 6-4 Step 2: Closing Entries

100

31 Income Summary 312 645 385 000 Sales Returns and Allow. 411 6 140 000 Sales Discounts 412 5 790 000 Cost of Merchandise Sold 510 525 305 000 Sales Salaries Expense 520 53 430 000 Advertising Expense 521 10 860 000 Depr. Exp.—Store Equip. 522 3 100 000 Delivery Expense 523 2 800 000 Misc. Selling Expense 529 630 000 Office Salaries Expense 530 21 020 000 Rent Expense 531 8 100 000 Depr. Exp.—Office Equip. 532 2 490 000 Insurance Expense 533 1 910 000 Office Supplies Expense 534 610 000 Misc. Administrative Exp. 539 760 000 Interest Expense 710 2 440 000

102

102

6-4 Step 3: Closing Entries

101

Close Income Summary (the balance represents

a Rp75,400,000 profit for SolusiNet in 2009) to

Cinta Cita, Capital.

31 Income Summary 312 75 400 000

Cinta Cita, Capital 310 75 400 000

103

103

6-4

Close Cinta Cita, Drawing to Cinta Cita,

Capital.

Step 4: Closing Entries

102

31 Cinta Cita, Capital 310 18 000 000

Cinta Cita, Drawing 311 18 000 000

104

104

1-2

Parulian Company’s perpetual inventory records indicate that

Rp382,800,000 of merchandise should be on hand on March

31, 2008. The physical inventory indicates that Rp371,250,000

of merchandise is actually on hand. Journalize the adjusting

entry for the inventory shrinkage for Parulian Company for the

year ended March 31, 2008.

6-4

Example Exercise 6-7

103

Follow My Example 6-7

For Practice: PE 6-7A, PE 6-7B

Mar. 31 Cost of Merchandise Sold

(Rp382,800,000 –(Rp371,250,000) 11,550,000

Merchandise Inventory 11,550,000

105

105

The ratio of net sales to assets

measures how effectively a business is

using its assets to generate sales.

Financial Analysis 6-4

Net sales

Average total assets

Ratio of Net

Sales to Assets =

106

106

PT Hero

Supermarket

PT Matahari

Prima Putra

Total revenues (net sales) Rp5,147,229 Rp9,768,075

Total assets:

Beginning of year 1,615,240 6,048,441

End of year 1,753,298 8,403,470

Average Total asset 1,684,269 7,225,956

Ratio of net sales to assets 3.06 1.35

Ratio of Net Sales to Assets 6-4

107

107

6-4 Interpretation

Based on these ratios, Sears

appears better than J. C.

Penney in utilizing its assets to

generate sales.