Abuja Journal ofBusiness and Management (AJBAM) is a ...

180

Ab1lja Joual ofBusiness and Managemenl Vo/.1, Issue I, March-2015 About the Journal Abuja Joual ofBusiness and Management (AJBAM) is a quarterly double-blind peer reviewed refereed open access online and print-journal that provides outlet for articles in al l fields of business and management. The J oual is a publication of the Department of Business Administration, Faculty ofManagement Sciences, University ofAbuja, Nigeria which welcomes high quality papers on theoretical developments and practical applications in business and management. Original research papers, sound reviews and high quality technical notes are invited for publications. Guidelines for Contributors All Research contributions should conform to high standards of scholarly research article by ensuring that the contents of al l manuscripts are original and has not been published e lsewhere in any language fully or partly, nor is it under review fo r publication elsewhere. Any article intended for publication inAJBAM should be in compliance with the following format: purpose/objective of the article, sound conceptualization/theoretical foundation, statement of the research problem or hypothesis, research methodology (where applicable), analysis/discussion of r e search findings (where appl icable) and conclusion. Guidelines for Manuscripts 1. Articles should preferably not exceed 5000 words including tables, figures and graphs, using the font Times New Roman ( 12 point) and 1 .5 line spacing. Authors should ensure that the contents ofvery short articles are substantial enough to warrant publication. 2. Al l tables, i l lustrations and figures should be incorporated in the body of the manuscript. The editor reserves the right to refuse publication of any submission for which the artwork is not ofan acceptable standard. 3. Since the AJ BAM fol lows a policy of blind peer review, the f irst page of the text proper should carry the title ofthe article, but not the name(s) ofthe author(s). 4. A separate page should carry the title of the article, its author(s) incl uding full name, academic title, current position and institution (where appropriate). Postal and e-mail addresses should also be provided. 5. The article should be preceded by a single paragraph abstract of the article, Italicized, not exceeding 200 words. The abstract should not form part ofthe text. A list of key words that is not fewer than four and not more than six should be submitted per article fo r cataloguing purposes. 6. The reference technique should be according to the Harvard Style. 7. Please remove al l page numbers. Submission and Review Process l. Manuscripts fo r the review process should be submitted by e-mail in MS Word to the address below. 2. Manuscripts will be submitted to independent reviewers. A policy of double blind peer review is fol lowed. The editor will make the final decision on whether to publish an article. 3. If approved subject to revision, the manuscript wil l be retued to the author(s) wh o wil l make the necessary alteations/corrections. The final copy of the manuscript will then be retued to the editors. This copy should be submitted in MS Word by e-mai l. 4. It is required that al l authors have their draft articles reviewed for language proficiency before submitting them to the editors. Sometimes excellent submissions have to be drastically amended or even rejected because oflinguistic ineptitude. The editors reserve the right to make minor editorial adjustments without consulting the author. The use of abbreviations should be avoided as far as possible. w.abuj ajournalofbusinessandmanagement.org.ng Page I

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Abuja Journal ofBusiness and Management (AJBAM) is a ...

Ab1lja Journal of Business and Managemenl Vo/.1, Issue I, March-2015

About the Journal Abuja Journal ofBusiness and Management (AJBAM) is a quarterly double-blind peer reviewed refereed open access online and print-journal that provides outlet for articles in all fields of business and management. The J ournal is a publication of the Department of Business Administration, Faculty ofManagement Sciences, University ofAbuja, Nigeria which welcomes high quality papers on theoretical developments and practical applications in business and management. Original research papers, sound reviews and high quality technical notes are invited for publications.

Guidelines for Contributors All Research contributions should conform to high standards of scholarly research article by ensuring that the contents of all manuscripts are original and has not been published elsewhere in any language fully or partly, nor is it under review for publication elsewhere. Any article intended for publication inAJBAM should be in compliance with the following format: purpose/objective of the article, sound conceptualization/theoretical foundation, statement of the research problem or hypothesis, research methodology (where applicable), analysis/discussion of research findings (where applicable) and conclusion.

Guidelines for Manuscripts 1. Articles should preferably not exceed 5000 words including tables, figures and graphs,

using the font Times New Roman ( 12 point) and 1 .5 line spacing. Authors should ensure that the contents of very short articles are substantial enough to warrant publication.

2. All tables, illustrations and figures should be incorporated in the body of the manuscript. The editor reserves the right to refuse publication of any submission for which the artwork is not of an acceptable standard.

3. Since the AJ BAM follows a policy of blind peer review, the first page of the text proper should carry the title ofthe article, but not the name(s) ofthe author(s).

4. A separate page should carry the title of the article, its author(s) including full name, academic title, current position and institution (where appropriate). Postal and e-mail addresses should also be provided.

5. The article should be preceded by a single paragraph abstract of the article, Italicized, not exceeding 200 words. The abstract should not form part of the text. A list of key words that is not fewer than four and not more than six should be submitted per article for cataloguing purposes.

6. The reference technique should be according to the Harvard Style. 7. Please remove all page numbers.

Submission and Review Process l. Manuscripts for the review process should be submitted by e-mail in MS Word to the

address below. 2. Manuscripts will be submitted to independent reviewers. A policy of double blind peer

review is followed. The editor will make the final decision on whether to publish an article.

3. If approved subject to revision, the manuscript will be returned to the author(s) who will make the necessary alternations/corrections. The final copy of the manuscript will then be returned to the editors. This copy should be submitted in MS Word by e-mail.

4. It is required that all authors have their draft articles reviewed for language proficiency before submitting them to the editors. Sometimes excellent submissions have to be drastically amended or even rejected because oflinguistic ineptitude. The editors reserve the right to make minor editorial adjustments without consulting the author. The use of abbreviations should be avoided as far as possible.

www.abujajournalofbusinessandmanagement.org.ng Page I

A buja Joumal ofBusiness and Management Vo/.1, issue I, March-201-

5. Footnotes should be avoided. Endnotes may be used, which should be consecutively numbered and listed at the end of the text, before the list of references.

6. Each document should be submitted through email: [email protected] or [email protected]

7. Since, AJBAM is a quarterly journal, manuscripts can be submitted up to 20th of each last month of the quarter of a year.

8 . The review process may take approximately l 0 to 14 days. As part of the submission process, authors are required to check off their submission's compliance with all of the above guidelines; submissions may be returned to authors that do not adhere to these guidelines.

Publication Fees The sum ofN5, 000 is paid as assessment fees to carter for the cost of editorial review report, while publication fees ofN20, 000 or US$ 1 00 for foreign authors (per article) is payable on the acceptance of the article to cover the cost of production of hard print copy, Internet-servicing, editing, handling, etc. The author(s) will receive written acknowledgement of acceptance payment accompanied by original receipt.

Account Payment Details: Account Name: Department ofBusiness Administration, University of Abuja, Gwagwalada. Banker: First Bank Nigeria PLC, Gwagwalada, Abuja. Account Number: 2005892921

Copyrights Agreements Authors relinquish the manuscript's copyright to theAbuja Journal of Business and Management, published by the Department of Business Administration, University of Abuja and must accept and adhere to the journal's publication policy. After acceptance, the copyright form will be mailed to the corresponding author; one of the authors must complete the copyright form.

Editorial Policy

All Correspondences to: The Editor-In-Chief, Abuja Journal ofBusiness and Management, Department ofBusiness Administration, Faculty ofManagement Sciences, University ofAbuja, P.M.B 1 1 7, Gwagwalada, Abuja, Federal Capital Territory, Nigeria. Email: [email protected] Website: www.abujajoumalofbusinessandmanagement.org.ng GSM: +2348036340963 or+2348 1 79275933

The editorial policy of the journal is to provide access not only to world class research materials, but through our professionals, hope to bring about a significant transformation in the realm of print and online open access journal in Nigeria. AJBAM is committed to ensuring a 'Paradigm Shift' in academic research which will result in major breakthroughs in the area of Scholarly Business and Management Research in Nigeria and the entire world.

Publication Ethics AJBAM publishes peer-reviewedjoumal in business and management discipline. This statement should guide the ethical behaviour of all parties involved in contributing articles for the journal, i .e. : the author, the Editor in Chief, the peer reviewer and the publisher. This statement is in line with the intemationally accepted Best Practice Guidelines for Joumal Editors.

www.abujajournalofbusinessandmanagement.org.ng Page I I

Abuja Joumal ofBw;iness and Manageme/11 Vol. I, Issue I, March-2015

Duties of Editors: Decision on the Publication of Articles The Editor in Chief of the Journal is responsible for deciding which of the articles submitted to the journal should be published. The Editor in Chief may be guided by the policies of the journal's editorial board and subjected to such legal requirements regarding libel, copyright infringement and plagiarism. The Editor in Chief may confer with other editors or reviewers in making this decision.

Fairplay Manuscripts shall be evaluated solely on their intellectual merit without regard to authors' race, gender, sexual orientation, religious belief, etlmic origin, citizenship, or political phi losophy.

Duties of Reviewers: Contribution of Peer Review Peer review assists the Editor in Chief and the editorial board in making editorial decisions while editorial communications with the author may also assist the author in improving the paper.

Acknowledgement ofSources Reviewers should identify relevant published work that has not been cited by the authors. Any statement that had been previously reported elsewhere should be accompanied by the relevant citation. A reviewer should also call to the Editor in Chiefs attention any substantial similarity or overlap between the manuscript under consideration and any other published paper of which they have personal knowledge.

Duties of Authors: Reporting standards Authors of reports of original research should present an accurate account of the work performed as well as an objective discussion of its significance. Underlying data should be represented accurately in the paper. A paper should contain sufficient detail and references to permit others to replicate the work. Fraudulent or knowingly inaccurate statements constitute unethical behaviour and are unacceptable.

Data Access and Retention Authors may be asked to provide the raw data in connection with a paper for editorial review, and should be prepared to provide public access to such, if practicable, and should in any event be prepared to retain such data for a reasonable time after publication.

Originality and Plagiarism Authors should ensure that they have written entirely original works, and if the authors have used the work and/or words of others this must be appropriately cited or quoted.

Multiple Publications An author should not in general publish manuscripts describing essentially the same research that was previously published in another journal. Submitting such manuscript to more than one journal constitutes unethical publishing behaviour and is unacceptable.

Acknowledgement of Sources Proper acknowledgment of the work of others must always be given. Authors should cite publications that have been influential in determining the nature of the reported work.

www.abujajournalofbusinessandmanagement.org.ng Page Ill

Abuja Joumal of Business and Management Vol. /, Issue I, March-2015

Authorship of the Paper Authorship should be limited to those who have made a significant contribution to the conception, design, execution, or interpretation of the reported study. All those who have made significant contributions should be listed as co-authors. Where there are others who have participated in certain substantive aspects of the research project, they should be acknowledged or listed as contributors.

Fundamental errors in published work When an author discovers a significant error or inaccuracy in his/her own published work, it is the author's obligation to promptly notify the journal editor or publisher and cooperate with the editor to retract or correct the paper.

www.abujajournalofbusinessandmanagement.org.ng Page IV

Ahuja Joumal of Business and Management Vol./, Issue /, Jv!arch-2015

Editorial Board Editor-In-Chief:

Dr. Bello Ayuba, Department of Business Administration, University of Abuja, Gwagwalada, Abuja, N igeria.

Editor: Associate Prof. N.C. Ozigbo, Department of Business Administration,

University of Abuja, Gwagwalada, Abuja, Nigeria.

Deputy Editor: Dr. U.D. Mohammed, Department of Business Administration,

University of Abuja, Gwagwalada, Abuja, Nigeria.

Editorial Advisory Board: Prof. G. C. Nzelibe,

Department of Business Administration, University of Abuja, Gwagwalada, Abuja, Nigeria.

Prof. A.B Akpan, Department of Business Administration,

Salem University, Lokoja, Kogi State, Nigeria.

Prof. Aminu A. Ayuba, Dean Faculty of Management Sciences,

University of Maiduguri, Borno State, Nigeria.

Prof. U. J. F. Ewurum, Department of Business Administration,

University of Nigeria Nsuka, Enugu State, Nigeria.

Prof. Sani Abdullahi, Department of Business Administration,

Ahmadu Bello University, Zaria.

Prof. A.K Kurfi, Department of Business Administration,

Bayero University Kano, Nigeria.

Prof. Victor E. Ekaetor, Dean, Faulty of Management Sciences,

University of Abuja, Gwagwalada, Abuja, Nigeria.

Prof. Ambrose. A. Okwoli, Dean, Faculty of Management Sciences,

University of Jos, Nigeria.

Dr. Munirat 0. Yusuf, Department of Business Administration,

University of Abuja, Gwagwalada, Abuja, Nigeria.

Dr. A. Y. Dutse, School of Management Technology,

Abubakar Tafawa Balewa University, Bauchi, Bauchi State, Nigeria.

www.abujajournalofbusinessandmanagement.org.ng Page V

A huja Journal of Business and Management Vo/.1, issue 1 March-2015

Associate Editot·s

Prof Siyan Peter, Department of Economics.

University of Ahuja, Gwagwalada, Ahuja, Nigeria.

Associate Prof Y. M. Damagum, Department of Accounting,

University of Ahuja, Gwagwalada, Abuja, Nigeria.

Associate Prof Sule Magaji, Department of Economics,

University of Ahuja, Gwagwalada, Ahuja, Nigeria.

Dr. Musa L Fodio, Department of Accounting,

University of Ahuja, Gwagwalada, Ahuja, Nigeria.

Dr. Hamid Ozohu-Suleiman, Department of Public Administration,

University of Ahuja, Gwagwalada, Ahuja, Nigeria.

Dt: U.G. Moti, Department of Public Administration,

University of Ahuja, Gwagwalada, Ahuja, Nige1ia.

Consulting Editor Waziri Garba

Department of Public Administration, Head of lnfonnation and Publications Unit

University of Abuja, Gwagwalada, Ahuja, Nigeria.

Technical Advisor: Mr. Osagie Samauel E.

Legal Advisor: A.M. Kontagora Faculty ofLaw

University of Ahuja, Gwagwalada, Ahuja, Nigeria.

Administrative Secretary: Mrs. Gloria Samari

Department of Business Administration, University of Ahuja

www.abujajournalofbusinessandmanagement.org.ng Page VI

Ahuja Joumal of Business and Management Vol. I, Issue I, March-2015

Table of Contents: Articles; Vol. 1, Issue 1, March 2015: Investigating the Relationship between Employee Motivation and Job Satisfaction: A Study of Patterson Zochonis (PZ) Nigeria Limited Dr. Ezekiel Adeleye, Yekini Lawai, Omolara Olatunde

The Influence of Investors Sentiment on Stock Market Reforms in Nigeria Mohammed Zubairu

Effect of Basic Planning Factors on Performance of Manufacturing Firms in Nigeria Prof Ayuba A. Aminu, Prof S.K. Msheliza, I.M.B. Chekene

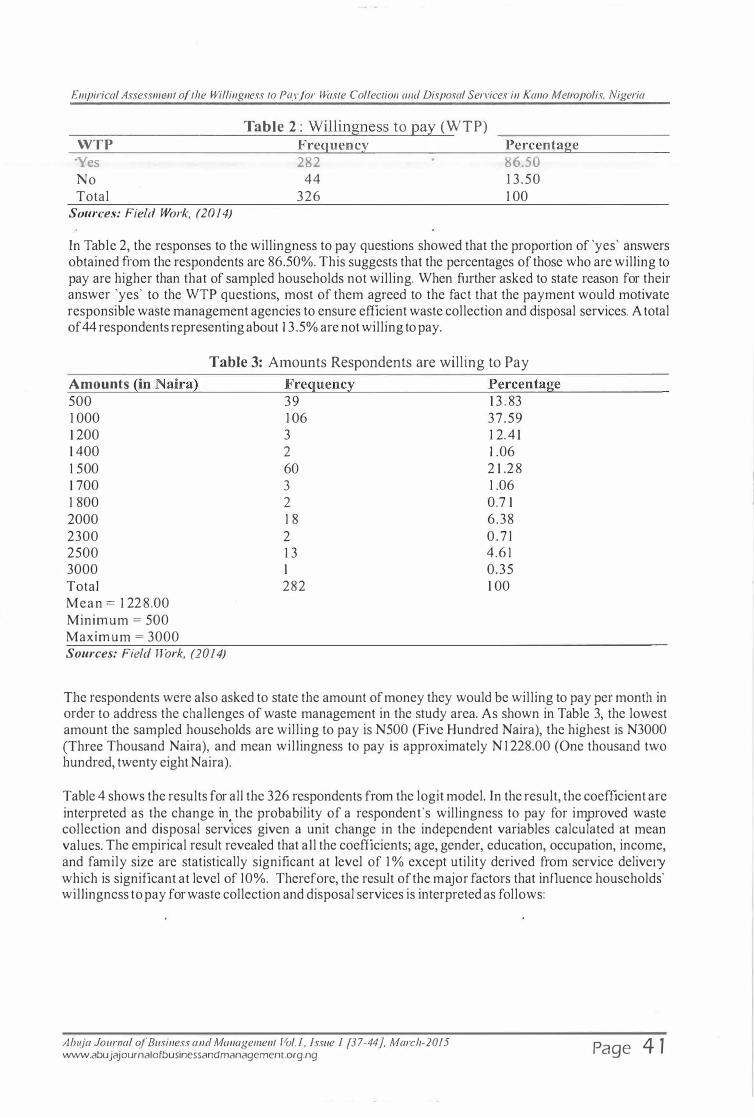

Empirical Assessment of the Willingness to Pay for Waste Collection and Disposal Services in Kano Metropolis, Nigeria Mustapha Mukhtar, PhD, Nura Aliyu Kabuga.

The Impact of Public Expenditure on Economic Growth in Nigeria:1982-2012 D1� Mohammed Yelwa, Prof S.A.J Obansa, Alfa Mohammed Danlami

Small and Medium Enterprises Development in Nigeria: A sustainable Approach to Employment Generation Dr. Umaru Danladi Mohammed, Abdullahi Ndaman, Kaka Abdullahi, Theresa Ndulue, Roko Lumi Peter

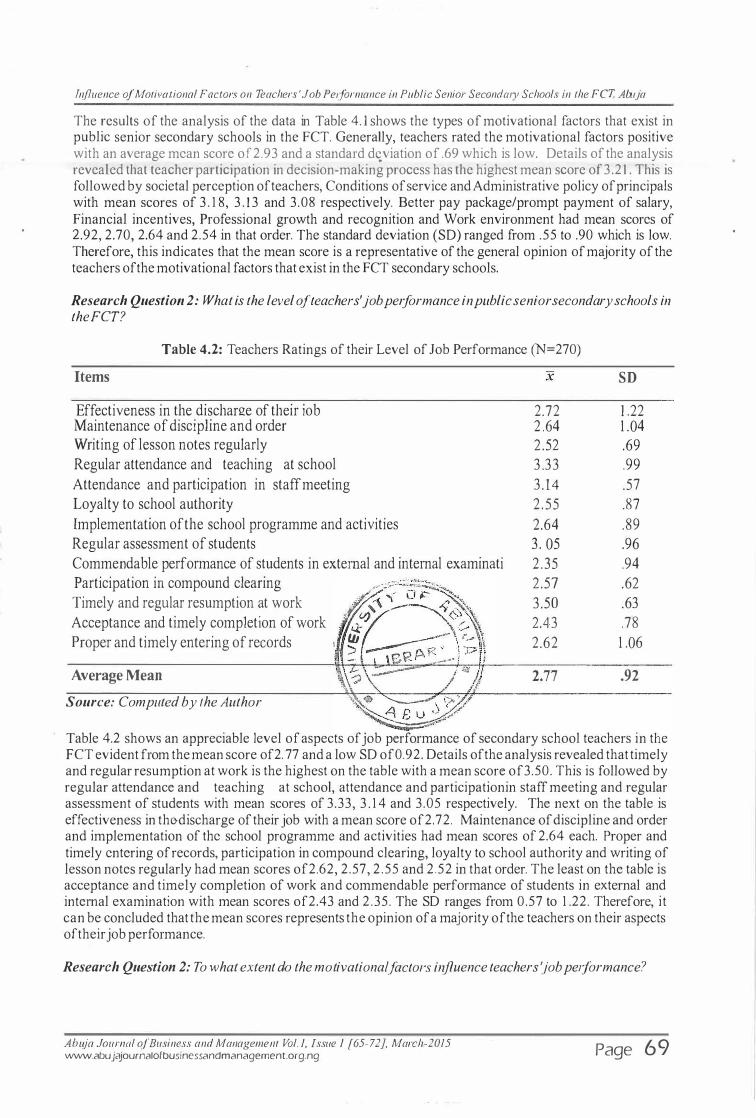

Influence of Motivational Factors on Teachers Job Performance in Public Senior Secondary Schools in the FCT, Abuja Hauwa Mohammed, PhD

Effect of Electronic- Customer Relationship Management (e-CRM) On Business Organizations Idris Bashir Bugaje

Principals' Transformational Leadership Behaivour and Teachers Commitment to Duty in public Schools in Borno State, Nigeria Dr. Zaifada B.l, Dr. Hauwa Mohammed, Dr. Garbadeen WO

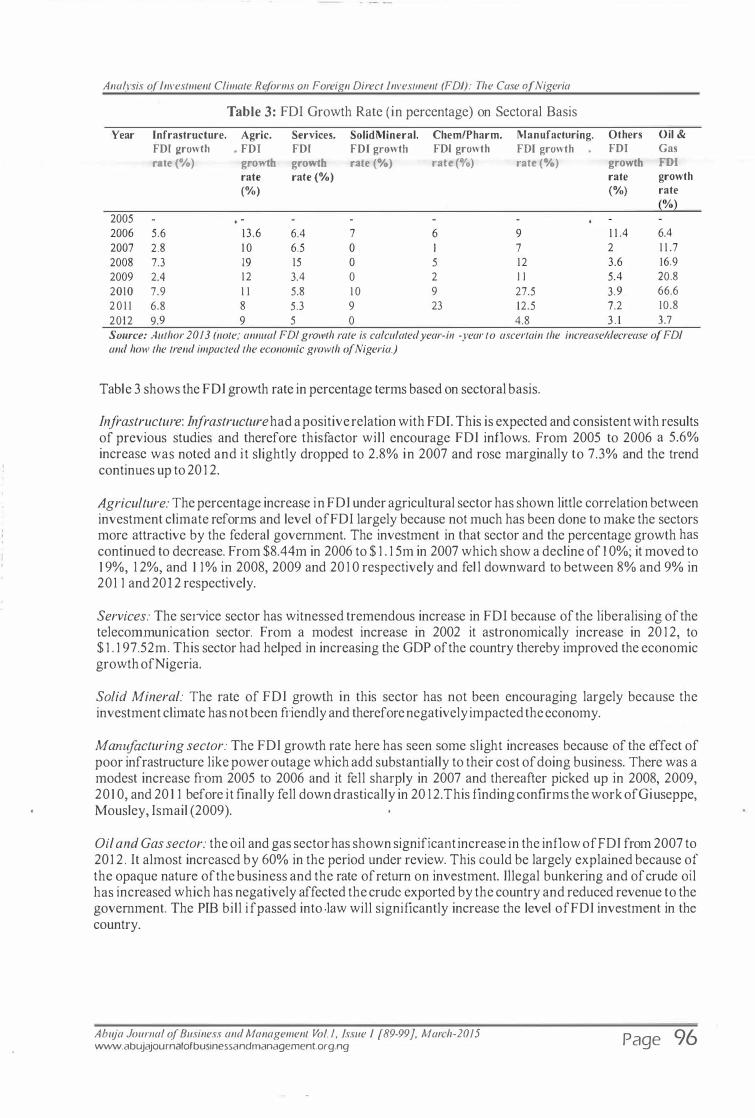

Analysis of Investment Climate Reforms on Foreign Direct Investment (FDI):

The Case of Nigeria Hamza Zubairu Kofarbai

Customer Relationship Management as a Strategic Marketing Tool in the

Nigerian Banking Sector Ibrahim Fari Okeji

www.abujajournalofbusinessandmanagement.org.ng

1-10

11-29

37-44

45-55

65-72

73-80

81-88

100-109

Page VI I

Abu} a .Journal of Business and Management Vo/.1, Issue /, Marclt-20 15

The Impact of Electricity on the Growth of Small and Medium Enterprises (SMEs) in Nigeria Dr. Nuhu Dogara Gada, Ezie Obumneke

Takaful (Islamic Insurance) in Nigeria: Hopes, Hurdles and Harmonization Abdul-Maliq, 0. Yekeen, Dr. Salaudeen M. Yinka.

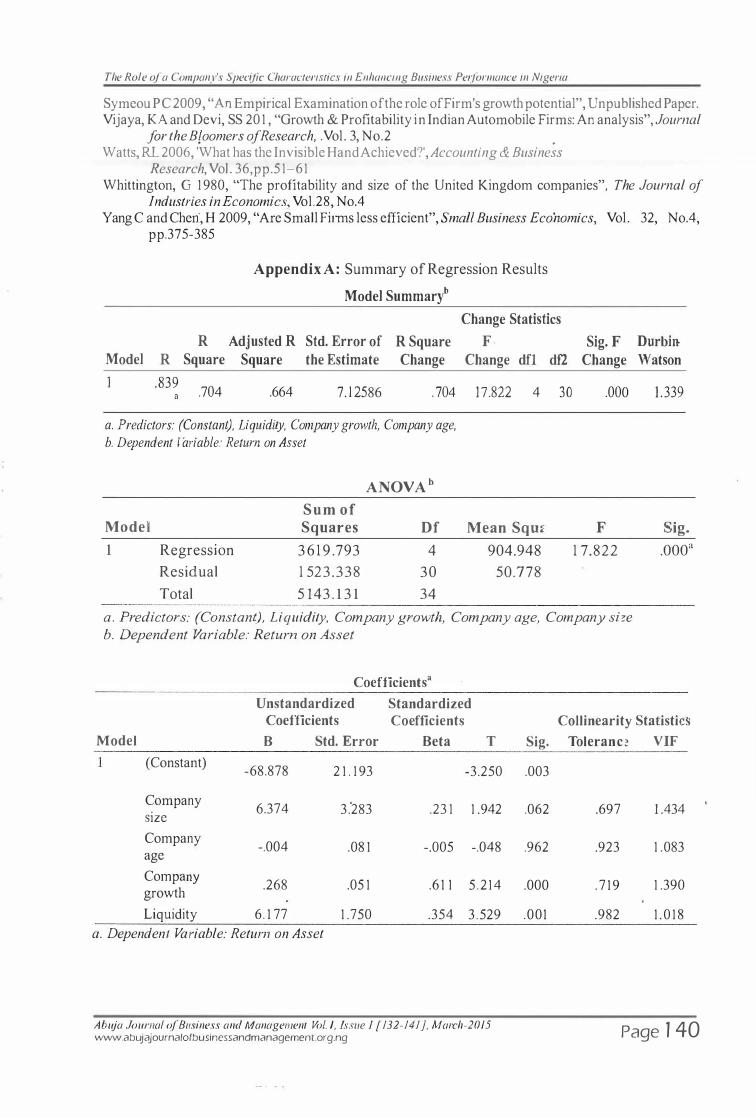

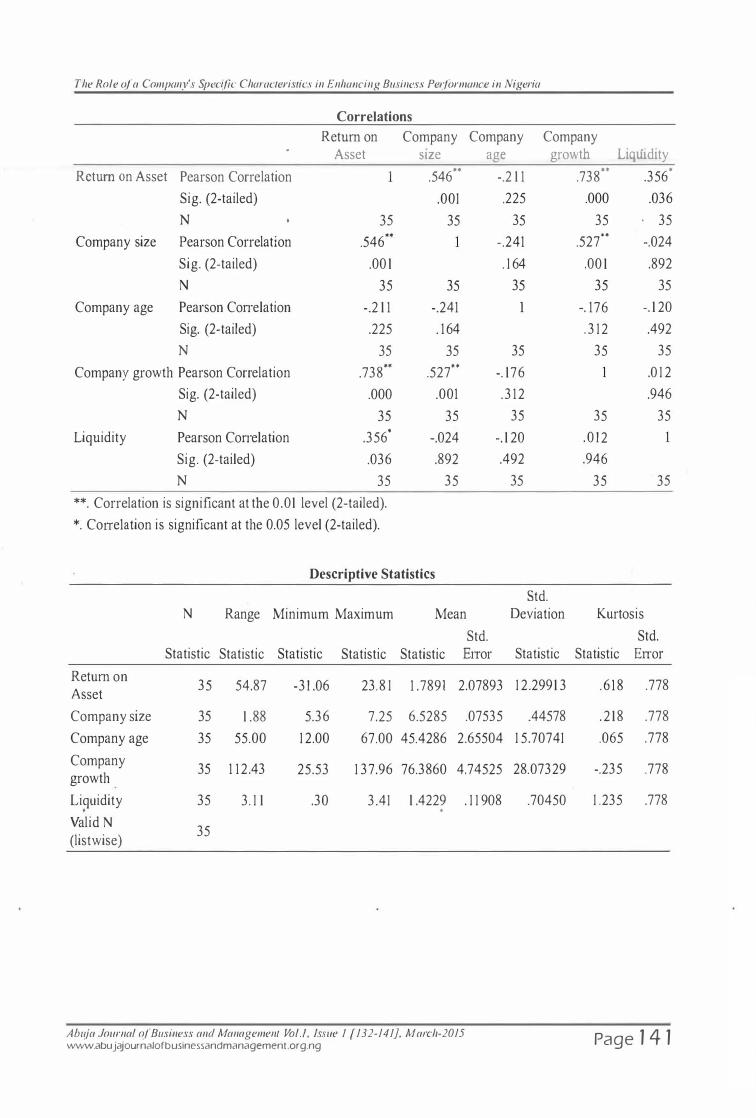

The Role of a Company's Specific Characteristics in Enhancing Business Performance in Nigeria Musa Adeiza Faruk, Lawai Bawa Maru Muhammad

Appraising Corporate Finance Application in the Nigerian Banking Industry Ibrahim Fari Okeji

Influence of Micro - Credit on Asset Accumulation: A Study of Selected Local Government Areas (LGA's) In Bauchi State Mohammed Sani lsyaka, Dr. Sule, Magaji

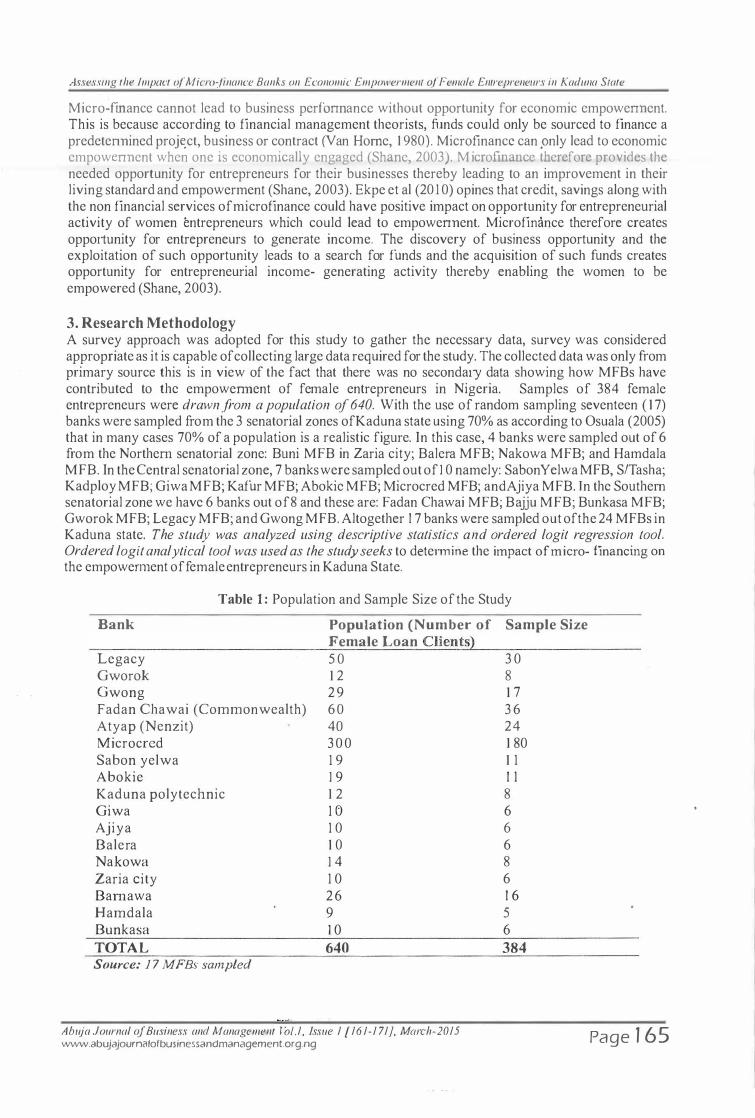

Assessing the Impact of Micro-finance Banks on Economic Empowerment of Female Entrepreneurs in Kaduna State Anietie Charles Dikld

www.abujajournalofbusinessandmanagement.org.ng

110-123

124- 131

132-141

142-152

153-160

161-171

Page VIII

Investigating the Relationship Between Employee Motivation and Job Satisfactio.n: A Study of Paterson Zochonis (PZ) �ig. Limited

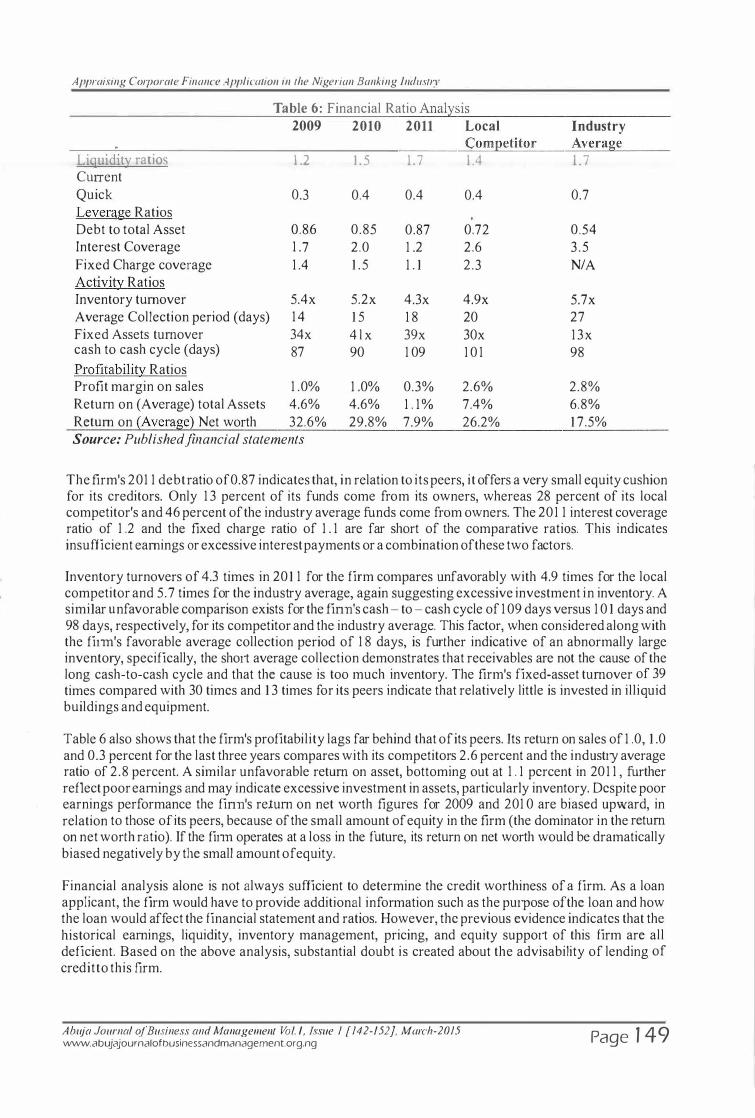

Dr. Ezekiel Adeleye\ Yekini Lawaf, Omolara Olatunde3 1 (Department of Business Administration, E/izade University, Jlara-Mokin. Ondo State)

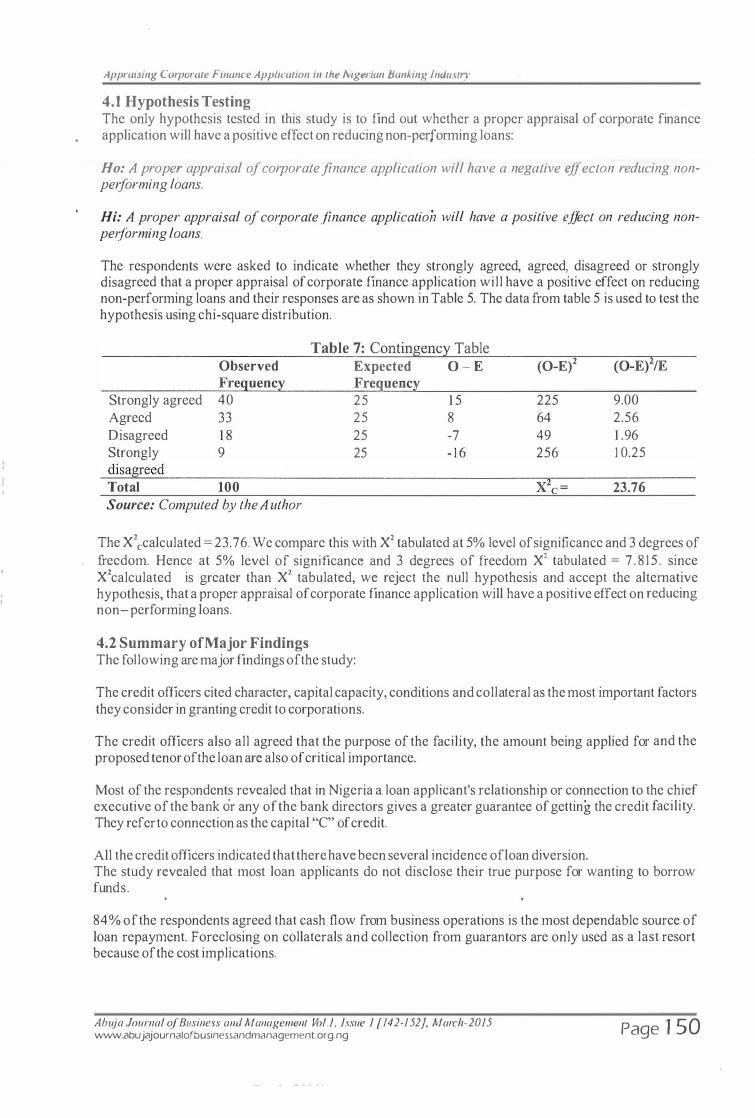

1 'Department of Business Administration, Afe Babalola University, Ado Eldti) �'Department of Busin:ess-Administration, Afe Babalola University, Ado Ekiti)

Abstract: Workers' expectations are endless even as the practice of motivation as a means of ensuringjob satisfaction and maximum performance may be hard to realise. It is therefore important to understand the factors that arouse and sustain the interest of employees in their work and measure the impact of motivation on employee job satisfaction. Most work in this area either studied the individual impact of motivation and job satisfaction on business performance or discussed job satisfaction as a means of achieving motivation. In contrast, this paper proposes a reversal of the relationship and argued that motivation is a means of enhancing job satisfaction. It discusses the nature of motivation and job satisfaction, and investigates the relationship between them. Data were collected from the staff of the Ikorodufactory ofPZ Cussons (Nigeria) PLC via a survey by questionnaire. The hypotheses were tested using Chi-square, Regression and Analysis of Variance (ANOVA) tests. Although many studies have established a relationship between motivational practices and organizational performance, the intervening process through job satisfaction remained largely unexplored. The research explored this missing link and discovered a strong relationship between motivation and job satisfaction. In addition, it was found out that intrinsic and_g�trimJk..mo#-vation dfffers in their impacts on business performance. The main implication of the study is that businesses need to motivate employees as a means of eliciting higher job satisfaction. In addition, businesses need to focus more on aspects of motivation with greater impact on job satisfaction. Keywords: Chi-square, Job satisfaction, Motivation, PZNigeria Limited

1 . Introduction The management of people at work has become an important aspect of the employers' duty if organisational performance objectives are to be achieved. An employee that is adequately motivated would have a higher level of job satisfaction and would likely put in more effort and commitment. For many years, motivation and job satisfaction have been studied in isolation as drivers of organizational effectiveness. A few studies that have explored the business performance impact of both concepts expressed motivation as the intervening variable between job satisfaction and business performance. The position taken in this.. paper is that motivation would cause a positive change in business performance only if it impacts positi�y on job satisfaction. However, empirical studies of this link between motivation and business performance through job sat-tifaeti-on-are rare.

In other words, low achievement of organizational objectives arises from poor motivational effort caused by low levels of job satisfaction. The problem remains that most organizations failed to consider employees' needs or get them involved in initiatives that can adequately motivate and keep them servicefocused. Given that each employee has a motive for working, once these desires are not fully met; there are negative consequences on effort, commitment and petfotmance. Hence, this work explores the empirical link between employee motivation and job satisfaction which is crucial to the attainment of business objectives.

Given that each employee has a motive for joining a given organization and once these desires or goals arc not fully met, it has negative effect on employees' performance at work. For this reason, in most organizations today, job satisfaction appears rather low. However, by rethinking our approach to employee motivation as a determinant to job satisfaction, business performance could improve.

1.1 Objectives of the Study The main objective of the study is to investigate motivation as a determinant of job satisfaction with special focus on employees ofPZ Cussons Nigeria PLC. The specific objectives are:

Ahuja Joumal of Business and Management Vol. /, issue I [1-10}, March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 1

Investigating the Relationship Beflveen Employee Motivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

1. To study current practices of employee motivation at PZ Cussons PLC Ikorodu. 2 . To identify the relative effect o f extrinsic and intrinsic motivation on business perfonnance. 3 . To explore the relationship between motivation and job satisfaction.

1.2 Hypotheses of the Study In order to answer the questions that emerge directly from these objectives, the following Null hypotheses were formulated, which shall be tested and discussed:

•

H01 PZ Cussons PLC does not motivate their employees.

H02 There is no difference i n performance induced by extrinsic and intrinsic motivation.

H03 There is no significant relationship between motivation and job satisfaction in PZ PLC.

The study reviewed the literature on need-based theories of motivation and job satisfaction. This was followed by a survey of motivation and job satisfaction in PZ Cussons Nigeria PLC. The goal is to understand motivational practices in companies gauge the level of employee's job satisfaction and identify the link between employee motivation and job satisfaction.

2. Literature Review This section reviews some prior theoretical and empirical work on motivation and job satisfaction, and presents the theoretical basis for the study.

2.1 Concept ofMotivation _ _ ..

Motivation is the psycho-social process of arousing the interest of employees in their work. In work organisations, it consists of management efforts to stimulate the desire, energy, interest and commitment of employees towards the attainment of organisational goals (Sansone and Harackiewicz, 2000; TeckHong and Waheed, 20 1 1 ) . Such efforts can be extrinsic or intrinsic (Schmidt and Scholl, 2014; Akanbi, 2014). Extrinsically motivated bchavioms are actions that result in the attainment of externally administered rewards, including pay, material possessions, prestige, and positive evaluations from others. It is a drive to action that springs from outside influences instead of own inner feelings. This seems quite unlike motivation in learning which mostly comes from within, through self-applied positive behaviour and attitude displayed for its own sake or prestige rather than for material or social rewards. The latter is intrinsic motivation, which even if also available at work, may wane sooner than later if not appropriately supported by extrinsic motivation. Nevertheless, if both intrinsic and extrinsic motivation are combined, employees would experience a tremendous degree of job satisfaction and work place commitment which stimulates performance (Ajila and Awonusi, 2004; Ojokuku, 2007; Akanbi, 20 14). In order to maximize job satisfaction as a means of achieving performance objectives, organizations need to continuously motivate their employees from both the intrinsic and extrinsic dimensions. . ... -·--·

Work is inevitable and in whatever form it is done, people desire satisfaction in what they do and managers need to understand and find the ways and means of helping employees reasonable aspirations. This is because an adequately motivated worker performs even above the level expected of their intelligence and ability (Paul and Anantharaman, 2003; Pratheepkanth, 201 1). When conscientious efforts are made to fulfill employees motivational needs, they derive job satisfaction and tend to contribute maximally.

Motivational needs have been discussed extensively within the need-based and the process-based theories (Ryan and Deci, 2000; Schmidt and Scholl, 20 14). The Need- based theories focus on the specific needs within the person that energize, direct and sustain behaviour. In contrast, the process-based theories accm.mt for factors external to the person tpat affect how behaviour is energized, directed, sustained and. stopped. The process-based theories often focus on complex psychological processes relating to behaviour, and are often not pursued in mainstream business research.

Maslow ( 1 943; 1 954) for instance, proposed five levels of hierarchical needs ananged in an ascending order of importance. The first is the physiological needs for food, water, sex, rest, clothing and other existential needs required for body chemistry and biology that must be satisfied in order to live. Following

Ahuja Journal of Business and Management Vol.!, Issue I [1- 10]. March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 2

Investigating the Relationship Between Employee Motivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

next is safety needs in terms of prevention from physical and psychological harm at work. The third is social needs including love, care, belonging and affection. The fourth is esteem needs including job enrichment, enhanced status, le�ser supervision, more holistic jobs, reputation and rccognition.within and outside the munedtate work environment. The fifth IS self-actualization in terms of achieving the maximum possible in one's lifetime relative to one's ability, competences and talents.

Alderfer ( 1 972) also developed a hierarchy of three needs namely- existence, relatedness and growth needs. The first is similar to the ·physiological needs while the second is similar to the safety !belonging needs of the Maslow model. The third is also close-knit with Maslow's esteem and actualization categories combined. David McClelland ( 1 96 1 ) also articulated three classes of human needs namely: achievement, affiliation and power. These three theories captured the same elemental details of hwnan needs ranging from food to esteem to power and to a sense of personal accomplishment in that order.

Alderfer and Maslow differ on how people move through the different sets of needs. Maslow proposed that a lower level need must be significantly met before attempts on a higher level need. Although Alderfer agreed with the progression process proposed by Maslow, he identified a frustration-regression process at work. If a person is continually frustrated in meeting an esteem need for instance, a relatedness need may re-emerge as a major motivating force, causing the individual to redirect efforts toward exploring new ways to satisfy this lower-order category of need. David McClelland ( 1 961) also introduced a cultural dimension to the effect that managers should recognize cultural differences- that human needs and their order of importance vary across cultures.

Some other need-based theories are David McGregor's Theory XY, WiJJiam Ouchi's Theory Z and the 2-factor theory by Frederick Herzberg. They all opined that motivation accounts for high levels of commitment, loyalty and productivity (Olagunju, 20 I I; Reece and Brandt, 1 996; Ogungbamila, 2006). By and large, the 2-factor theory has received the greatest research interest because it is practical and grounded in rounds of empirical studies of two hundred engineers and accountants from over nine companies in the United States (Herzberg et. al., 1959; Jibowo, 1 997).

The Herzberg approach has the additional benefit of departing from other need-based theories which perceived job satisfaction as the opposite of job dissatisfaction (Herzberg, 1 966). Hygiene factors of motivation were identified, which prevent bad feeling and job dissatisfaction but are not the real motivators that lead to job satisfaction. The theory argues that a satisfied need ceases to motivate. AJJ these theories provide the pointer that motivation is a dynamic process- a journey not a destination. It requires evetyday preparation, improvement, sustenance and testofimpactonjob satisfaction.

2.2 Extrinsic and Intrinsic Motivation Organisations deploy a wide range of tools and techniques to motivate employees, the most popular being money by way of higher salaries and wages as well as several other financial perquisites (Deci, 1 975; Jibowo, 1997; Pinder, 1 998; Selden and Facer, 2000; Tyilana, 2005; Teck-Hong and Waheed, 20 11) . Classical theories of motivation are grounded in the use of financial incentives and other external rewards to motivate workers. Some other extemal I extrinsic tools which deal with behaviours motivated by factors external to the individual include leadership, supervision; group solidarity and company policy.

Financial and the other extrinsic rewards sometime provide the carrot that people want because they symbolize many goals. In their study of the affluent worker, Goldthorpe et al ( 1 969) found that considerations over wages and other financial rewards seem the most powerful factor in holding people to their present jobs. Employees who disliked their repetitive jobs in their Coventry car assembly plant were found to hold on to the jobs rather than move on to more interesting jobs with lower financial rewards in nearby plants. Financial rewards have the benefitofmeasmability and constitute the most direct means of rewarding employees for their contributions towards the achievements of organizational goals ( TcckHongand Wahced, 20 1 1 ) .

Neo-classical theory and research evidence was less supportive of money and the other extrinsic tools but stressed the need to motivate employees from within via intrinsic means such as job enrichment and

Ahuja Journal of Business and Management Vol./, Issue I [1-10]. March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 3

Investigating the Relationship Between Employee Motivation and Job Satisfaction: A Study of Paterson Zoclzonis (PZ) Nig. Limited

challenging work, whose impacts are less transient and more permanent (Herzberg et a!, 1 966; Goldthorpe et.al., 1 969; Deci, 1975; Jibowo, 1997; Kirkman and Shapiro, 200 1 ; Ogungbamila, 2006). Such tools harp on competence, indepcl')dencc, self-determination and job-orientation irrespective of<}ny external rewards. Nevertheless, there are conflicting results on the relative impact o!' extrinsic and intnnsic motivation even as the former tend to have greater impact in industrial sectors characterized by rapid change (Teck-Hong and Waheed, 201 1 ).

2.3 Job Satisfaction Job satisfaction is an expression of personal attitude and well-being associated with performing an assigned job or role (Tella et. al., 2007; Aziri, 201 1 ) . Simply, it is a measure of how people feel generally about their job- the like or dislike. It is an attitude of commitment arising from positive or negative feeling about the work. This commitment is the willingness to exert high levels of effort for the organization (Bailey, 1993). Higher job satisfaction implies a generally positive attitude whilst lower job satisfaction entails a negative attitude (Teck-Hong and Waheed, 20 1 1 ; Kian, et. al., 20 1 4) . The strength of the feeling of responsibility towards higher job performance, which is achievable via job satisfaction, is cmcial to business survival.

The direction and magnitude of these attitudes originate significantly from the motivational climate made up of variables such as pay, working conditions, leadership, recognition and achievement (Aziri, 201 1 ; Schmidt and Scholl, 20 1 4). Equity, fairness and the processes used to meet employees' motivational needs are also crucial to feelings of job satisfaction or dissatisfaction. A positive motivational climate is cmcial to job satisfaction and consequently the effectiveness and optimal functioning of work organizations (Tell a et. al, 2007). Hence, motivation may be everything and a happy worker would be surely productive (Bailey, 1 993; Paul andAnantharaman, 2003; Dawson, 2005; Aziri, 20 1 1 ) .

2.4 Theoretical Bases for the Study Several studies have highlighted the importance of motivation to work performance, the relative merit of intrinsic and extrinsic motivation as well as the impact of job satisfaction on the attainment of business objectives (Herzberg, 1 966; Ajila and Awonusi, 2004; Tella et. al., 2007; Ajayi, 20 1 1 ). However, the literature on motivation and job satisfaction has two major weaknesses.

First, empirical studies on the relative performance impact of intrinsic and extrinsic motivation as the two major dimensions of motivation generate conflicting results (Jibowo, 1 997; Fuller et. al., 2008; Robbins and Judge, 20 1 0; Pratheepkanth, 20 1 1 ; Teck-Hong and Waheed, 201 1 ) . As a consequence, many researchers prefer to study the effect of individual motivators such as pay, supervision and recognition. Secondly, there are specification and modeling problems as regards which of motivation and job satisfaction is the dependent or intervening variable in their relationship with business performance. This study proposes that job satisfaction is dependent on motivation and that the two dimensions of motivationextrinsic and intrinsic- would have different levels of impact on performance outcomes (Herzberg et. a!., 1 959; Herzberg, 1 966; Jibowo, 1 997; Tella et. al., 2007; Teck-Hong and Wabeed, 20 1 1 ; Kian et. a!., 201 4) .

The study also adopts the notion of "locus of causality"- a cyclical and positive relationship between extrinsic and intrinsic motivation, to the effect that both could be deployed jointly (Deci, 1 975; Ryan and Deci,' 2000). However, they wamed that the joint effect of intrinsic and extrinsic rewards may be quite complex, not be additive in their overall effects and that their interaction may be negative under some conditions. Nevertheless, in spite of the debate on their relative merit, it has been argued that organisations that motivate from both dimensions of motivation would get the best out of employees (Tella et. al, 2007; Ajayi, 20 1 1 ; Teck-Hong and Waheed, 201 1 ; Akanbi, 20 1 4; Kian et. al., 20 1 4) . Yet, managers may need to strengthen the dimension that adds greater value to job satisfaction.

3. Methodology This is a single case study of Paterson Zochonis (PZ), a company founded in 1 879 as a trading post in Sierra Leone. A branch office in Nigeria was opened in 1 899, followed by its first soap factory via acquisition in 1 9 48 . PZ has grown into an international and highly diversified business conglomerate. The PZ vision states in part: We shall profitably grow our business, strengthen our products portfolio, and

Ahuja Joumal of Business and Management Vol. I, Issue I [/-10], March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 4

Investigating the Relationship Between Employee Motivation and Job Satisfaction: A Study of Paterson Zoclzonis (PZ) Nig. Limited

enhance the lives of om employees, consumers and all other stakeholders by living and breathing our shared values. PZ Nigeria manufactures a wide range of consumer products and home appliances- the leading brand names being Robb, Elephant, Jet, Thermocool and Cussons soap. It is a large pub)ic company with immense contributions to the Nigerian economy over its long existence. The survey research method was used for the study. A close-ended questionnaire consisting of twenty questions was administered on the employees of PZ Nigeria PLC at the lkorodu Plant. This method is often used in exploratory studies where it is important to capture the opinion of a large number of people on a real-life issue within a relatively tight budget of money and time. •

It was a census survey of all two hundred direct production employees including middle level managers and supervisors but excluding cleaners, security and casual staff. Most of the excluded staff was not literate enough to answer the questions even as the shop floor workers were the main target. The twenty-five item questionnaire included ten questions on motivation and nine on job satisfaction, all of which were categorized using the five-point Likert Scale. Two hundred questionnaires were administered out of which ninety-nine usable questionnaires ( 49.5 percent) were returned. Due to paucity of funds and restriction of access, no formal interviews were conducted. The study applied popular procedures and processes in questionnaire design and administration (Adeleye, 2002; Teck-Hong and Waheed, 20 1 1 ;Adeleye and Oni, 2013).

Data was analysed using Percentages, Frequencies; Chi-square (X2) and Regression tests. The Chi-square was used to explore the relationship between intrinsic and extrinsic motivation as specified in Hypothesis 2. With the Chi-square model of the form: X2 == �(0-E/ IE (Equation 1 ), the decision rule is to reject H0 if the calculated value ofX2 is greater than the critical value. Lastly, regression test was applied to explore the dependency ofjob satisfaction on motivation (Hypothesis 3). Given the linear regression model: Y== Bo+ B ,x (Equation 2), the decision rule is to reject the null hypothesis if the p- value is less than the significant value.

4. Results and Discussions This section reports the findings which were interpreted and discussed. The respondents' demographic characteristics were: Sex distribution- 23.2 and 76.8 percent of female and male; age structure- 22.2, 74.8 and 3.0 percent below 30 years, 30-55 years and above 55 years respectively. The much higher percentage of male workers appears normal for a manufacturing concern whilst the very high proportion of workers aged between 30- 55 appears normal for a successful manufacturing conglomerate expected to select the highly matured, who would sit in for a career. Sixty eight percent of the employees had spent a minimum of six years with the company. Forty nine percent were classified as senior staff, 6 4 percent had a first degree with another 26.3 percent having a diploma. With this level of education, maturity, ripeness on the job, and an almost equal divide between junior and senior staff, the respondents were expected to be honest and mature with their responses.

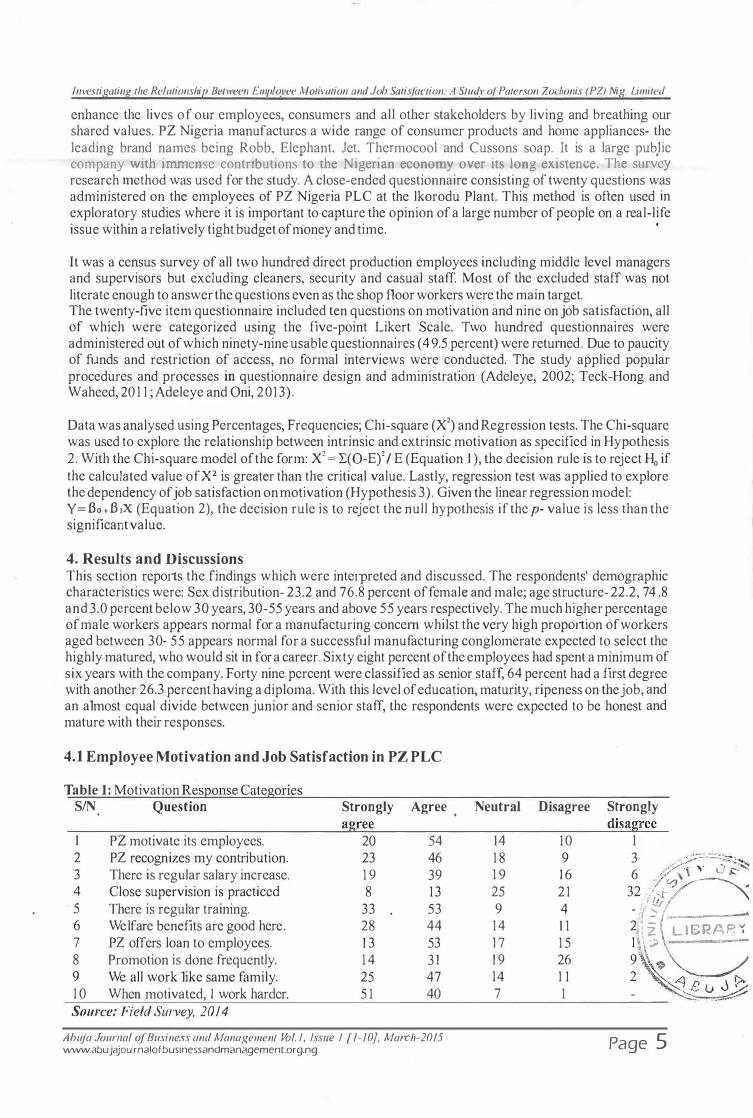

4.1 Employee Motivation and Job Satisfaction in PZ PLC

Table 1: Motivation ResQonse Categories SIN Question Strongly Agree Neutral Disagree Strongly

agree disagree 1 PZ motivate its employees. 20 5 4 1 4 10 1 2 PZ recognizes my contribution. 23 46 1 8 9 3 . . ' �:-.=...:::..:.;,:::-:- · ....

6 ��1 y lJ'i� 3 There is regular salaty increase. 1 9 39 4 Close supervision is practiced 8 13 5 There is regular training. 33 53 6 Welfare benefits are good here. 28 44 7 PZ offers loan to employees. 1 3 53 8 Promotion is done frequently. 1 4 3 1 9 We all work like same family. 25 47 1 0 When motivated, I work harder. 5 1 40 Source: Field Survey, 2014

Abu} a Journal of Business and Management Vol. I, Issue I [1-10}, March-2015 www.abujajournalofbusinessandmanagement.org.ng

1 9 1 6 25 2 1 9 4 1 4 1 1 17 1 5 1 9 26 1 4 1 1 7 1

32 ./ . ,y- � - :1 !.1/j �I -2'- v ,. z LIE;RAR I 1 \\;) -

� �

�'� -.:. ��

Page 5

Investigating the Relationship Between Employee Motivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

Table 1 shows the research instruments on motivation and the response categories. The response categories in Table 1 provide the evidence that PZ motivate their workers. They agreed strongly that salary increase is regular, that thejr contribution is being recognized by the company, and tha_t the company scored highly on training and welfare provisions However, the employees rated close supervision very poorly as a motivator.

Table 2 reports the job satisfaction measures and the response categories. It shows that the company fared well on most of the measures. In particular, over 80 percent of the employees are generally satisfied with the company's working rate culture, job security as well as working relationships with supervisors and subordinates. It is noteworthy however that about twenty-five percent of the employees are dissatisfied with salaries, benefits offered and payment for vacation/sick leave.

Table 2: Job Satisfaction Response Categories

SIN Question Highly Satisfied Average Dissatisfied Highly

satisfied dissatisfied

1 Working rate culture 7 46 42 4 2 Rate your job security 20 40 24 1 3 2

3 Satisfaction with salary 3 24 48 20 4 4 The reward system 8 2 1 43 23 4 5 Relationships with juniors 1 7 55 25 1 1 6 Supervisor relationship 23 44 26 6 7 Benefits offered. 1 0 33 32 20 4 8 Location of work. 20 5 4 1 8 6 1 9 Pay for vacation/sick leave 8 25 39 2 1 6

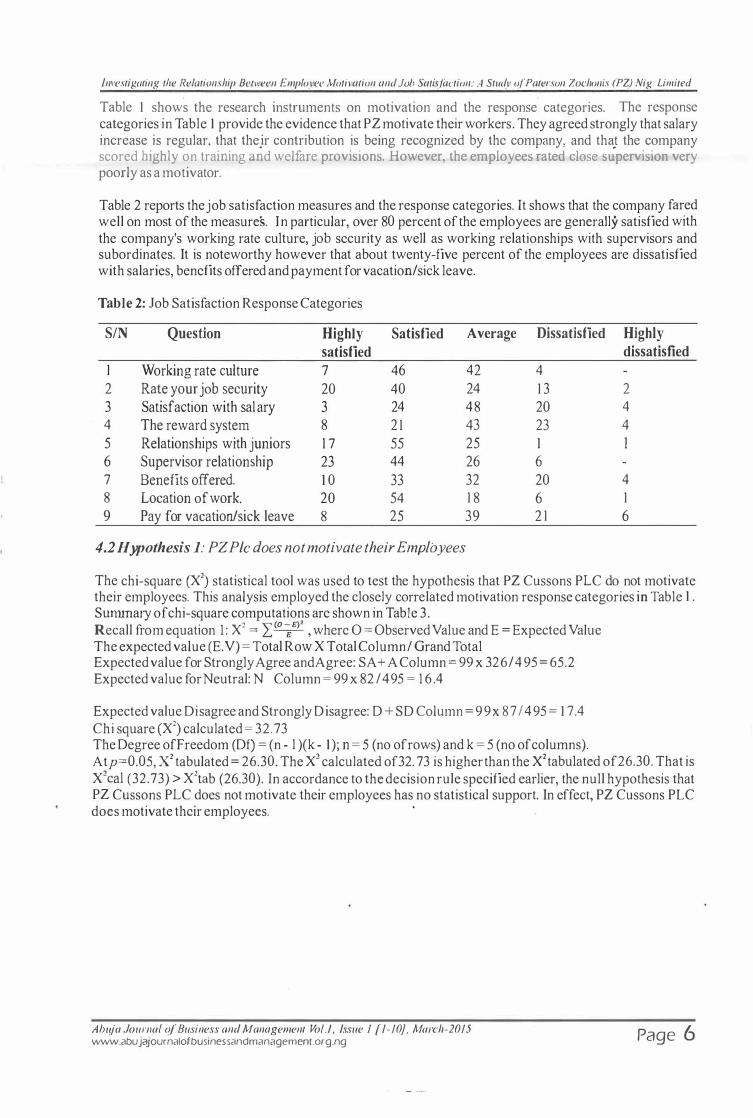

4.2 Hypothesis 1: PZ Pic does not motivate their Employees

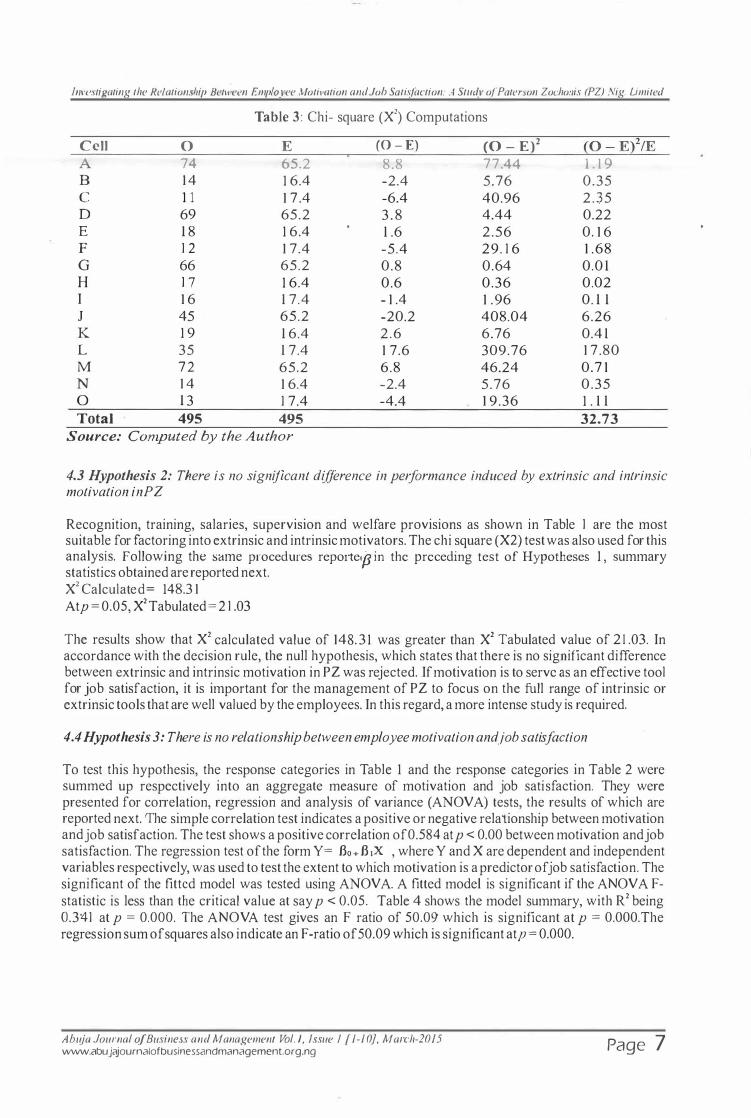

The chi-square (X2) statistical tool was used to test the hypothesis that PZ Cussons PLC do not motivate their employees. This analysis employed the closely correlated motivation response categories in Table 1 . Summary of chi-square computations are shown in Table 3 . Recall from equation 1 : X2 = I(O�E)' ' where O = Observed Value and E = Expected Value The expected value (E. V) = Total Row X Total Column I Grand Total Expected value for Strongly Agree and Agree: SA+ A Column = 99 x 326/ 495 = 65.2 Expected value for Neutral: N Column = 99 x 82 I 495 = 1 6 .4

Expected value Disagree and Strongly Disagree: D + SD Column = 99 x 87 I 495 = 1 7. 4 Chi square (X2) calculated= 32.73 The Degree ofFreedom (Df) = (n - l )(k - 1 ); n = 5 (no of rows) and k = 5 (no of columns). Atp=0.05, X2 tabulated = 26.30. The X2 calculated of32. 73 is higher than the X2tabulated of26.30. That is X2cal (32.73) > X2tab (26.30). In accordance to the decision rule specified earlier, the null hypothesis that PZ Cussons PLC does not motivate their employees has no statistical support. In effect, PZ Cussons PLC does motivate their employees. ·

Abu) a Jouma/ of Business and Management Vol./, Issue I [1-10]. March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 6

Investigating the Relationship Between Employee Motivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

Table 3 : Chi- square (X2) Computations

Cell 0 E (0 - E) (0 - E)2 {0 - E}2/E A 74 65.2 8.8 77.44 1 . 1 9 B 1 4 1 6.4 -2.4 5.76 0.35 c 1 1 1 7 .4 -6.4 40.96 2 . 3 5 D 69 65.2 3 . 8 4.44 0.22 E 1 8 1 6.4 1 .6 2.56 0. 1 6 F 1 2 1 7.4 -5.4 29. 1 6 1 . 68 G 66 65.2 0.8 0.64 0.0 1 H 1 7 1 6.4 0.6 0.36 0.02 I 1 6 1 7.4 - 1 .4 1 . 96 0. 1 1 J 45 65.2 -20.2 408.04 6.26 K 1 9 1 6.4 2 . 6 6.76 0.4 1 L 35 1 7.4 1 7.6 309.76 1 7 .80 M 7 2 65.2 6.8 46.24 0.7 1 N 1 4 1 6.4 -2.4 5.76 0.35 0 1 3 1 7.4 -4.4 1 9 .36 1 . 1 1 Total 495 495 32.73

Source: Computed by the Author

4.3 Hypothesis 2: There is no significant difference in performance induced by extrinsic and intrinsic motivation inPZ

Recognition, training, salaries, supervision and welfare provisions as shown in Table 1 are the most suitable for factoring into extrinsic and intrinsic motivators. The chi square (X2) test was also used for this analysis. Following the same procedures repo1te•,B in the preceding test of Hypotheses 1 , summary statistics obtained are reported next. X2 Calculated= 148.3 1 Atp = 0.05, X2Tabulated = 2 1 .03

The results show that X2 calculated value of 148. 3 1 was greater than X2 Tabulated value of 2 1 .03. In accordance with the decision rule, the null hypothesis, which states that there is no significant difference between extrinsic and intrinsic motivation in PZ was rejected. If motivation is to serve as an effective tool for job satisfaction, it is important for the management of PZ to focus on the full range of intrinsic or extrinsic tools that are well valued by the employees. In this regard, a more intense study is required.

4.4 Hypothesis 3: There is no relationship between employee motivation and job satisfaction

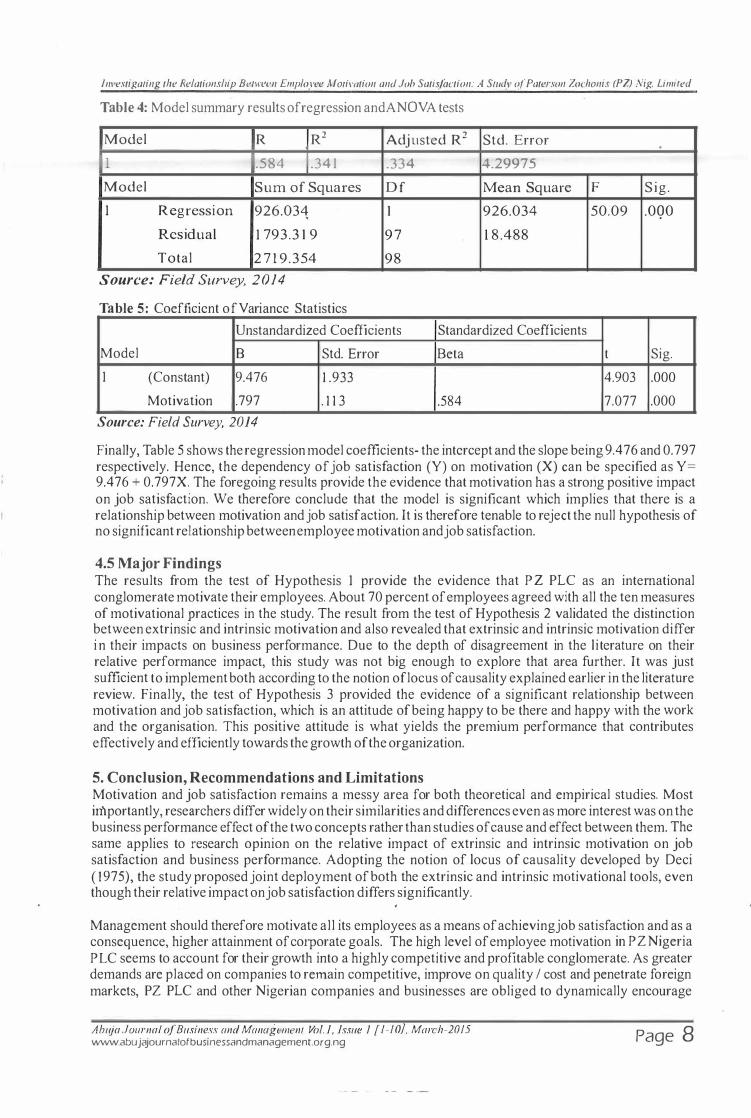

To test this hypothesis, the response categories in Table 1 and the response categories in Table 2 were summed up respectively into an aggregate measure of motivation and job satisfaction. They were presented for conelation, regression and analysis of variance (ANOVA) tests, the results of which are reported next. The simple correlation test indicates a positive or negative relationship between motivation and job satisfaction. The test shows a positive correlation of0.584 atp < 0.00 between motivation and job satisfaction. The regression test of the form Y= Bo+ B ix , where Y and X are dependent and independent variables respectively, was used to test the extent to which motivation is a predictor of job satisfaction. The significant of the fitted model was tested using ANOVA. A fitted model is significant if the ANOVA Fstatistic is less than the critical value at say p < 0.05. Table 4 shows the model summary, with R2 being 0.341 at p = 0.000. The ANOVA test gives an F ratio of 50.09 which is significant at p = O.OOO.The regression sum of squares also indicate an F-ratio of50.09 which is significant atp = 0.000.

Ahuja Journal of Business and Management Vol. /, Issue 1 [ 1-1 OJ, March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 7

Investigating the Relationsllip Bellreen Employee Motivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

Table 4: Model summary results of regression andANOVA tests

Model R Rz Adjusted R2 Std. Error .

1 .584 .34 1 .334 4.29975 Model Sum of Squares Df Mean Square F Sig.

1 Regression 926.034 < 1 926.034 50.09 .OQO Residual 1 793.3 1 9 9 7 1 8 .488

Total 2 7 1 9.354 98

Source: Field Survey, 2014 Table 5 : Coefficient of Variance Statistics

Unstandardized Coefficients Standardized Coefficients

Model B Std. Error Beta t Sig.

1 (Constant) 9.476 1 .933 4.903 .000

Motivation .797 . 1 1 3 .584 7.077 .000

Source: Field Survey, 2014 Finally, Table 5 shows the regression model coefficients- the intercept and the slope being 9.476 and 0. 797 respectively. Hence, the dependency of job satisfaction (Y) on motivation (X) can be specified as Y= 9.476 + 0.797X. The foregoing results provide the evidence that motivation has a strorig positive impact on job satisfaction. We therefore conclude that the model is significant which implies that there is a relationship between motivation and job satisfaction. It is therefore tenable to reject the null hypothesis of no significant relationship between employee motivation and job satisfaction.

4.5 Major Findings The results from the test of Hypothesis 1 provide the evidence that PZ PLC as an international conglomerate motivate their employees. About 70 percent of employees agreed with all the ten measures of motivational practices in the study. The result from the test of Hypothesis 2 validated the distinction between extrinsic and intrinsic motivation and also revealed that extrinsic and intrinsic motivation differ i n their impacts on business performance. Due to the depth of disagreement in the literature on their relative perfotmance impact, this study was not big enough to explore that area further. It was just sufficient to implement both according to the notion oflocus of causality explained earlier in the literature review. Finally, the test of Hypothesis 3 provided the evidence of a significant relationship between motivation and job satisfaction, which is an attitude of being happy to be there and happy with the work and the organisation. This positive attitude is what yields the premium performance that contributes effectively and efficiently towards the growth of the organization.

5. Conclusion, Recommendations and Limitations Motivation and job satisfaction remains a messy area for both theoretical and empirical studies. Most importantly, researchers differ widely on their similarities and differences even as more interest was on the business performance effect of the two concepts rather than studies of cause and effect between them. The same applies to research opinion on the relative impact of extrinsic and intrinsic motivation on job satisfaction and business performance. Adopting the notion of locus of causality developed by Deci ( 1975), the study proposed joint deployment of both the extrinsic and intrinsic motivational tools, even though their relative impact on job satisfaction differs significantly.

Management should therefore motivate all its employees as a means of achievingjob satisfaction and as a consequence, higher attainment of corporate goals. The high level of employee motivation in PZ Nigeria PLC seems to account for their growth into a highly competitive and profitable conglomerate. As greater demands are placed on companies to remain competitive, improve on quality I cost and penetrate foreign markets, PZ PLC and other Nigerian companies and businesses are obliged to dynamically encourage

Abuja Journal of Business and Management Vol. I, Issue I [1-10}, March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 8

Investigating the Relationship Between Employee Motivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

their employees from both dimensions of extrinsic and intrinsic motivation. The need arises however to identify and strengthen the dimension that are of greater value to employees. Unless this is done, most spending and programmes of motivation may be money .down the drain. One powerful motivational tool which however is hard to position between extnnsic and intrinsic motivation is share ownerships scheme. Over a long working l ife, an employee may become a major shareholder in a company to which he has committed his life and career.

This study has some limitations- time and money. Als6, the permission to conduct this kind of study appears rather hard to secme. The regular excuse was no time and that operations would get disrupted. Accordingly, only one company was studied even as the researcher was made to scale down the investigation. Further studies are required to gauge the relative effectiveness of the two dimensions of motivation. This is in addition to modeling studies which could clarify the direction of cause and effect between motivation and job satisfaction.

References Adeleye, E.O. 2002, "An Investigation into Agile Manufacturing Design", Nottingham UK: The

Nottingham Trent University Press, Unpublished PhD Thesis Adeleye, E.O. and Oni, M.O. 2014, "A Study of the Impact of Organisational Structure on the

Performance of Mobile Telecoms Network (MTN) Nig. Ltd., African Journal of Stability and Development, 8 ( 1 ) : 38- 50.

Ajayi, A.B. 201 1 , " Motivation and Job Satisfaction as a Basis for Productivity". University of Ilorin, Nigeria, UnpublishedMSc. Dissertation

Ajila, C. and Awonusi, A. 2004, "Influence of Rewards on Workers Performance in an Organization", Journal ofSocial Science, 8( 1 ) : 7- 1 2

Akanbi, P.A. 20 1 4, " Influence o f Extrinsic and Intrinsic Motivation o n Employees' Performance" ,Accessed 1 3/8/ 14 : http://www. indabook. org/previewlarlotrtdbRb Y5XdW

Alderfer, C. P. 1 972, "Existence, Relatedness and Growth: Human Needs in Analysis of the Factors that Affect Job Satisfaction: A Case Study on Private Companies Employees of Bangladesh", Retrieved 1 9/3/ 1 3 www.iiste.org

Aziri, B . 20 1 1 , "Job Satisfaction: A LiteratW'e Review", ManagementResearch andPractice, 3(4):77-86 Bailey, T. 1 993, "Discretionary Effort and the Organization ofWork: Employee Participation and Work

Reform since Hawthorne", Columbia University, New York, Working Paper David, M. S . and DavenpOJi, M. A. 200 1 , Using SPSS to Solve Statistical Problems: A Self-Instruction

Guide, USA: Merrill Prentice Hall Dawson, B. 2005, "Motivation Leads to Better Results", Journal of Rubber and Plastics, 3 7:11-15 Deci, E.L. 1 975, Intrinsic Motivation, New York: Plenum Fuller, M.A, Valacich, J.S. and George, J.F. 2008, "Information Systems Project Management: A Process

and Team Approach ", New Jersey: Prentice Hall Inc. Goldthorpe, J.H., Lockwood, D., Bechhofer F. and Platt J . 1 969, "The Affluent Worker: Industrial

A ttitudes and Behaviour, " Cambridge Studies in Sociology, 1:167- 1 69 Herzberg, F., Manser, J. and Synde1man, B.B. 1 959, "The Motivation ofWork'. New York: John Wiley and

Sons Inc. Herzberg, F. 1 966, "Work and the Nature of Man ", Cleveland: World Publishing Company

Jibowo, A.A. 1 997, "Effect of Motivators and Hygiene Factors on Job Performance among Extension Workers in the Former Western State ofNigeria", The Quarterly Journal of Administration, 1 2 ( 1 ) : 45-54

Kian T.S., Yusoff, W.F. and Rajah S. 2014, "Job Satisfaction and Motivation: What are the Difference among these Two?" European Journal ojBusiness and Social Sciences, 3(2): 94- 1 02

Kirkman, B. L. and Shapiro, D. L. 200 1 , "The Impact of Cultmal Values on Job Satisfaction and Organizational Commitment in Self-Managing Work Teams: The Mediating Role of Employee Resistance", Academy ofManagementJournal, 44(3):557-570.

Maslow, A. 1 943, "ATheoiy ofHuman Motivation", Psychologica/Review,July: 370-396. Maslow, A. 1 954, "Motivation and Personality ", New York: Harper and Row McClelland, D. C. 1 96 1 , "The Achieving Society ", New York : Van Nostrand Reinhold

Abuja Journal of Business and Management Vol. /, Issue I [ 1-1 OJ, March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 9

Investigating the Relationship Between Employee 1\1/otivation and Job Satisfaction: A Study of Paterson Zochonis (PZ) Nig. Limited

Ogungbamila, B . 2006, "Psychological Needs and Workplace Commitment of Selected Local Government Workers", Aji·ican Journal for the Psychological Study ofSocialissues, 9(2): 1 52- 1 6 1

Ojokuku, R . M . 2007, "Impact of Rewards Ol) Motivation ofWorkcrs: A Study of the Civil Service ofOsun State, Nigeria",lnternational Business Management, 1 (4):99-103

Olagunju, O.A. 201 1 , "Impact ofMotivation on Productivity in the Service Industry", University ofllorin, Nigeria, Unpublished B.Sc. Dissertation

Paul, A.K. and Anantharaman, R.N. 2003, "Impact of People Management Practices on Organizational Perfom1ance: Analysis of a Causal Model", International Journal of Human Resource Management, 1 4(7): 1 246-1266

Pinder, C. C. 1 998, "WorkMotivation in Organizational Behavior". N.J. : Prentice Hall Pratheepkanth, P. 20 1 1 , "Reward System and its Impact on Employee Motivation in Commercial Bank of

Sri Lanka Plc in Jaffna District", Global Journal of Management and Business Research, 1 1 ( 4 ): 84-92

Reece, L. B. and Brandt, R. 1 996, "Effective human Relations in Organizations ". 6th Edition. Boston

Toronto: Houghton Mifflin Company Ryan, R.M. and Deci, E.L. 2000, "Self -determination Theory and the Facilitation oflntrinsic Motivation,

Social Development and Well-being", American Psychologist, 55 : 68-78 . Robbins, S.P. and Judge, T.A. 20 10, "Essentials of Organisational Behaviour". 1 Oth Edition. New Jersey:

Pearson Educational Publishers. Sansone C. and Harackiewicz, J. M. 2000, Intrinsic and Extrinsic Motivation - the Search for Optimal

Motivation andPe1jormance, California: Academy Press Schmidt, C.T and Scholl, R.W 20 14, "Sources of Motivation", Accessed 1 2/08/2014 :

http :1 lwww. uri. edu/researchllrclscholllwebnotes/Motivation _Sources. htm Selden, A. and Facer, Q. 2000, "Introduction to Human Resource Management". Theory and Practice,

New York: Palgrave. Teck-Hong, T. and Waheed, Amna 201 1 , "Herzberg's Motivation-Hygiene and Job Satisfaction in the

Malaysian Retail Sector: Mediating Effect of Love of Money", Asian Academy of management Journal, 16 ( 1 ):73-94

Tella, A., Ayeni, C.O. and Popoola, S.O. 2007, "Work motivation, Job satisfaction and Organisational Commitment of L ibrary personnel in Academic and Research Libraries in Oyo State, Nigeria", Library Philosophy and Practice, April : 1 - 1 6

Tyi1ana, G . 2005, "The Relationship of Extrinsic, Intrinsic and Demographic Predictors to Various Types ofWithdrawal Behaviours", Journal of Applied Psychology, 70:442-450

Abu) a Journal of Business and Management Vol. !, Issue 1 [ 1-1 OJ, March-20 15 www.abujajournalofbusinessandmanagement.org.ng Page 1 0

The Influence of Investors Sentiment on Stock Market Returns in Nigeria

Mohammed Zubairu Department of Business Administration, Ahmadu Bello University, Zaria - Nigeria

Abstract: The study investigates how investors ' sentiment index (Non- market fundamental), equity market fundamentals (long term interest rate and excess demand for equity) and economic fundamentals (expected inflation) impact on equity prices. In the estimation of collected data, an econometric technique known as the ordinary least square regression (OLS), error-correction models (ECM), unit root and cointegration test were adopted. Results show that investors' sentiment had a statistically significantly relationship with equity prices in Nigeria for both in the short and long run. In the case of long term interest rate and excess demand for equity, in the short run the impact of excess demand for equities was statistically significant but both of them became statistically insignificant in the long run. This means that investors in Nigerian often consider short run equity marketfundamentals than long run. The expected inflation rate was statistically insignificant both in the short and long run. This shows that investors in Nigeria's equity market are likely to ignore economic news but focus more on sentiment when investing in shares. The study recommended that investors would be better off when they know and avoid the potential psychology bias that is detrimental to their investment policy guideline or objectives. · Keywords: Investor Sentiment, Stock Returns, Consumer Confidence Index, and Economic Sentiment Indicator.

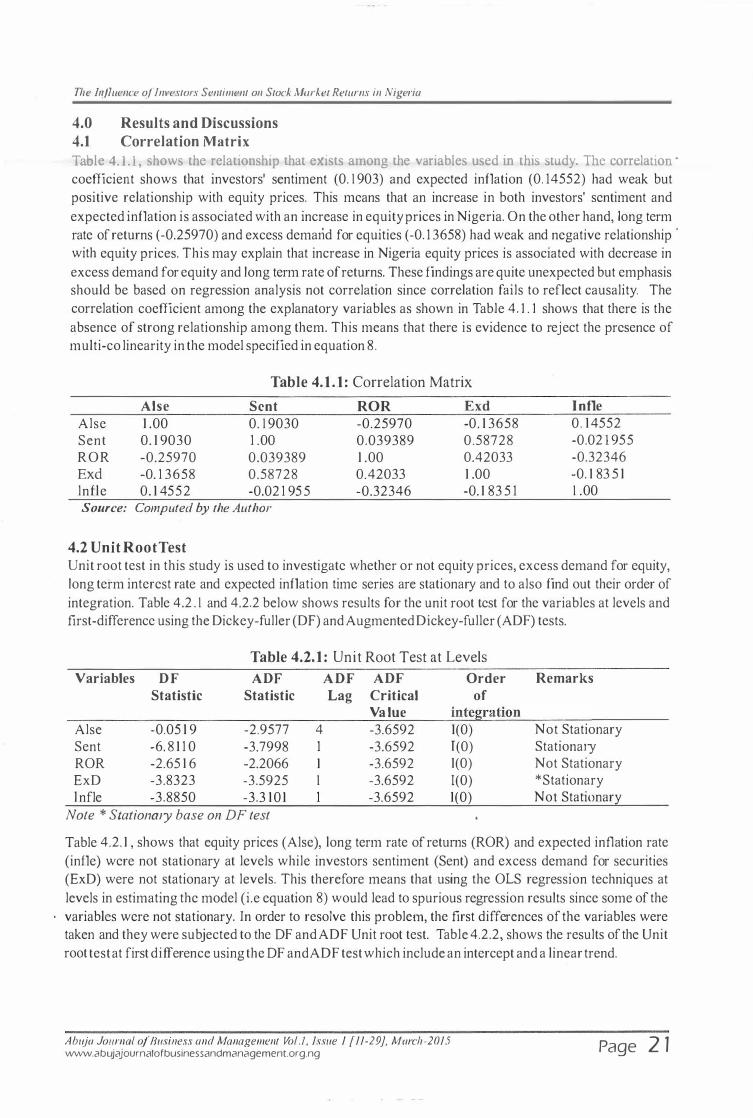

1.0 Introduction There have been controversies among scholars, researchers and finance professionals with regards to what triggers movement in equity prices in emerging equity markets. This disagreement among financial experts has taken a new dimension since the coming of indices for measuring investors' sentiment. The introduction of investor's sentiment as an explanatmy variable in predicting equity price moves is now being considered. The disagreement has created different perspective on the issue of investors' sentiment. The classical finance theorists leave no role for investors' sentiment in explaining equity price movement rather they consider competition among rational investors to be the ultimate. Fama ( 1 98 1 ) in his efficient market hypothesis (EMH) argued that available information in the market is all that matters and this information can be either market, economic or non-market driven. This therefore implies that he suppmts the idea of investors' sentiment (non-market) as a determinant of financial asset prices. Technical analysts are another group that have also provided explanations for stock price movement. They used historical financial data, chart and price pattern index to predict equity price movement. In the case of the Capital asset pricing model (CAPM) and the Arbitrager pricing Theory (APT), the CAPM focused only on stock market risk factor in explaining changes in stock prices while the APT related stock prices to unspecified risk factors which may likely include investor's bias. The fusion theory which is a holistic approach uses market, economic and non-factors (investors' sentiment) in explaining the systematic variations in equity prices but the fusion theory lack empirical evidence in Nigeria. In explaining stock market price dynamics in Nigeria, there has been quiet a large volume of literature and these literatures tend to use firm specific factors, CAPM and APT models without given consideration to investors sentiments.( see Osaze, 2000; Alilc and Anao, l 986; Udcgbunam and Oaikhenan, l 999; Omole and Falokun, l 999; Emenuga 1989; Yohannes 1999; !nanga and Emcnuga, 1 997; Edo, l 996 among others). This study therefore seeks to fill this gap.

This study seeks to provide answers to the following research questions; Does investors' sentiment cause significant movement in equity prices in emerging stock market? And to what extent do market and economic fundamentals explain variations in stock market prices?

Abu) a Journal of Business and Management Vol. /, Issue 1 [ 11-29], March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 1 1

The fnjluence of Investors Sentiment on Stock Market Retums in Nigeria

The objectives of this study are to evaluate the impact of investor's sentiment on equity price movement in an emerging stock market like that of Nigeria and also to evaluate the extent to which economic and market fundamentals contribute to equity price movement in Nigeria. In order to realize the objectives of this research, the following hypothesis have been formulated and tested:

H01: Investors sentiment has no significant relationship with equity prices. H01: Mai·ket rate ofreturns (long term interest rate) has no significant relationship with equity prices. H03: Inflation exerts a non significant impact on equity prices. H04: Equity market demand and supply imbalance (excess demand for securities) is not related to equity prices movement.

1.0 Review of Literature 2.1 Concept and Evidence of investors Sentiment The need to integrate investors' sentiment as a factor responsible for equity price movement has recently being debated in behavioural finance. In describing the concept of investors' sentiment, there have been arguments among financial economists and finance experts. Barker and Stein (2004) described investors' sentiment as the misevaluation that is created by a group of investors. Lee, Shleifer and Thaler ( 1 99 1 ) viewed investors' sentiment as investors' beliefs that are not justified by market and economic fundamentals. In Zwerg ( 1973), Brown and Cliff (2005), it was revealed that investors' sentiment is the discrepancy that exist between rational and irrational investors. This therefore means that investors' heterogeneity can also be called investors sentiment. Prior empirical studies on investors' sentiment and how the concept can be measured have generated the issue of whether investors' sentiment is directly observable or not. This is why investors' sentiment i s viewed by some researchers from a normative perspective. The definition of Baker and Wurgler (2007) confirms the subjective nature of investors' sentiment. They described investors' sentiment as what asset prices should be and not what it is.

There are quite a numbers of ways investors' sentiment can be developed and these investors sentiment formation process are rooted in behavioural finance. Traditional finance theory centered on market and economic fundamentals in explaining equity price movement but recent market situations all over the world have shown that behavioural factors have a strong influence on the valuation process of financial assets. The major forms of investor's' sentiment are drawn from heuristic-driven bias, noise trading, limits to arbitrage, frame dependence, emotions and social influence and others. The heuristic-driven bias centred on overconfidence, anchoring, representatives, innumeracy and aversion to ambiguity. Overconfidence manifests itself in excessive trading in equity markets. Solt and Statman(l 989) and Shefrin and Statman(1 996) relate investor's bias in pricing assets to overconfidence and this tends to occur when the investor's overestimate the accuracy of asset prices forecasts. Overconfidence to investor's is like a stimulant that is based on the use of special information or knowledge. This means that investor's trade excessively when they are overconfident. Anchoring bias results when after forming an investment opinion, investor's are unwilling to change their opinions even when market and economic fundamentals are changing. The anchoring bias is a major attack on the efficient market hypothesis (EMH).

Representativeness, as another form of heuristic-driven bias is the tendenc1' of investor's to form investment judgements based on stereotypes. Equity investors may beliefthat a stable growth of corporate earnings in the past may be representative of high growth rate in future. This is why investor's would continue to buy stock even when economic and market fundamentals arc weak. Innumeracy as a form of investor's sentiment affects investors' asset pricing process and it simply describes the investors experience in calculating and estimating data for stock market price determination. The innumeracy bias is a potential explanation of why investors ignore market and economic mathematics in pricing equity. Aversion to ambiguity bias as a type of investors' sentiment that is heuristic-driven refers to the investors fear for ambiguous information and uncertainty. This aspect of investor's biases creates a situation where investors trade irrationally when there is rum om or unclear information.

Frame dependence is an aspect of investor's sentiment formation that is derived from emotional and cognitive factors. The emotional aspects of frame dependence focuses on how investors feel when they

Abu) a Journal of Business and Management Vo/. 1, Issue 1 [11-29], March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 1 2

The Influence of Investors Sentiment 011 Stock Market Returns in Nigeria

receive and digest stock market information while the cognitive aspect refers to how investors organise information mentally, in particular how investors react to gains and loss outcomes. Kahneman and Tversky ( 1.982) in their prospect the01y followed the frame dependence approach in explaining investors' decision making under uncertainty. They stated that investors frame and values plays a vital role in their actions under uncertainty, and that investors feel more strongly about the pains from loss than the pleasure from an equal gain. Thaler ( 1985) used the concept of mental accounting to explain frame dependence. In mental accounting, investors tend to mentally operate two accounts, one of the accounts is managed rationally and the other is managed itTationally. This means that investoi·s are conservative about losing capital invested while the dividend income stream can be spent irrationally. Narrow framing as a form of frame dependence often leads to myopic risk aversions which captured how investors evaluate their asset returns separately rather than as a whole p01tfolio. Market inefficiency and investment mistakes are often common because investors focus on changes in wealth that are narrow in scope both across investment class and over time. Shefrin and Statman ( 1996) in explaining frame dependence they used behavioural portfolio which follows a pyramid pattern and helped on diversifications that result from investors' diversification goals, not from their purposeful asset diversification. This means that most investors do not have efficient portfolio. They often ignore economic and market fundamentals in planning their asset portfolio and take too much risk for the returns expected from their asset portfolio. In explaining frame dependence, the snake bite effect or house-money effect or shadow of the past biases refers to a situation where investors are less inclined to take risk after incurring a huge financial loss.

Herd instincts, overreaction and emotional time line are some of the emotional and social influence that can also affect investors' rationality. Among these emotional and social influence, herd instinct and overreaction has taken center stage. There is a natural propensity for investors to follow market sentiment or follow group investors' investment strategy rather than using market and economic fundamentals. The existence of herd behaviour in most fmancial markets has been greatly discussed by scholars. Scharfstern and Stem ( 1 990) provide evidence that herd instincts, characterised the behaviour of fund managers. The fact that a significant changes in equity prices in most stock market in the world are not necessarily related to the use of markel information or to the fundamental change in economic and corporate performance indexes may lead to the conclusion that certain investors crowd effect exist (Count and Bouchaud,2000). Overreaction as a form of investor bias tend to occur when investors ignore new economic and market information and follow imitated behaviour of certain large group of investors which often overreact to both good and bad news. The overreaction of investors to news is today suspected to be the major cause of stock market bubbles and crashes. This therefore means herd behaviour and overreaction are non-market fundamental factors that cause upward or downward trend in stock price. This in other words means that investors' sentiment is a potential factor to consider when predicting stock market price crashes or bubbles.

Noise trading and limits of arbitrage are also accepted causes of market inefficiency. Noise traders are group of investors that are not rational. They trade equity base on their beliefs or sentiment and not by stock fundamentals. De Long and Shleifer ( I 989) found out that prices can actually diverge significantly from fundamental values even in the absence of fundamental risk and that noise traders strategy is becoming more attractive due to high chance of the noise trader earning higher than the rational investors. The continued practice of noise trading has generated the arbitrage profit opportunities. Arbitragers operations are also a cause of price v·ariations as they try to take advantage of mood swings of noise traders. Shleifer and Summers (1 990) identify arbitrage practices as a stimulant which interest other rational investors to contribute to further deviation between asset prices and their fundamental values. This means that arbitrageurs in the short-rw1 create market prices jw11ps and at the same time help to return asset prices to their fundamentals. Brown ( 1999) explain the effect of noise traders, he described noise traders as non-professional traders with no special information. He found out that when there is shifts in investors' market sentiment, noise traders move together and take similar actions thereby increase the prices ofthei r targeted securities.

2.2 Measurement oflnvestors Sentiment Fmihcnnorc, recognizing the fact that investors sentiment exist is no longer an issue in finance, what matters is how the concept can be quantified and how it triggers movement in equity prices in the stock

Abu) a Journal of Business and Management Vol. /, Issue I [11-29], March-2015 www.abujajournalofbusinessandmanagement.org.ng Page 1 3

The Influence of Investors Sentiment on Stock Market Retums in Nigeria

market. Many investors sentiment index have been identified in the academic literature, for instance Fisher and Statman (2003) used the ratio of investors optimism to pessimism from a survey to proxy

. investors sentiment. Investors and consumer confidence ind.ex was adopted by Charocnrock (2003) and Fisher and Statman (2003) while Lashgair (2003) used a specific confidence index called Barron's confidence index to measure investors sentiment/confidence in the market. Dennis and Mayhow (2002) use the ratio of put to call. This index is highly limited in emerging stock markets due to the non-existence of a recognised options market. Whaley (2000) usc VIX investors fear Gauge which is popularly known · as implied option volatility. This index i s also limited due to the absence ofunorganised options market in emerging countries. Branch ( 1 976), Randhall, Suk and Tully (2003), Neal and Wheatley ( 1 998) measured investors sentiment using mutual fund cash reserve. They stressed that low cash holding of mutual fund managers is an indicator of aggressive buying (investors' optimism) while large cash balance is as a result of investors pessimism or uncertainty in the market. Kein and Madhavan (2000) use bid-ask spread of quoted traded stock in New York stock exchange (NYSE) to explaining investor's sentiment. To them, a wide deviation between the bid and ask seat prices indicates high level of investors sentiment. The closedend fund discount was also heavily use by researchers in capturing investors sentiment, see Lee, Schleifer and Thaler ( 1 99 1 ), Neal and Wheatley ( 1 998), Baker and Wurgler (2006) and Chopra, Lee, Schleifer and Thaler ( 1993 ).

The problem of finding a best proxy for investors' sentiment was also tackled by some researchers through the use of composite/group index. The most respected and popular composite index for investors' sentiment is found in the work of Baker and Stein (2004) and Baker and Wurgler (2004). In their composite sentiment index they used measures like investors survey, retail investors trades, investors mood proxies (weather, seasonal and periodical factors which affects investors attitude to invest), mutual fund flows, dividend premium, closed end fund discounts, option implied volatility, first day retums on initial public offerings, volume of initial public offering (IPO), new equity issues and trading volume. Guohua (2008), uses four sentiment measures and these are short sell volume, turnover ratio (average turnover for 10 days divided by averaged turnover for 250 days), Relative strength index, money flow index, insider trading and the level of institutional ownership. The relative strength index which is popular known as RSI index is used to determine the level of oversold and overbought attitude of investors while the insider trading and institutional ownership was seen as a good proxy for investors' sentiment because owners and executives of companies have material information. This therefore means that insider trading patterns may indicate sentiment. Seyhun ( 1 998) gives evidence that users of insider trading information can predict stock returns.