Aaa Stable - FMS Wertmanagement

6

SOVEREIGN AND SUPRANATIONAL CREDIT OPINION 1 August 2018 Update Analyst Contacts Heiko Peters +49.69.7073.0799 AVP-Analyst [email protected] Kathrin Muehlbronner +44.20.7772.1383 Senior Vice President [email protected] Polina Gotmann +49.69.7073.0725 Associate Analyst [email protected] Dietmar Hornung +49.69.7073.0790 Associate Managing Director [email protected] Yves Lemay +44.20.7772.5512 MD-Sovereign Risk [email protected] CLIENT SERVICES Americas 1-212-553-1653 Asia Pacific 852-3551-3077 Japan 81-3-5408-4100 EMEA 44-20-7772-5454 FMS Wertmanagement – Aaa Stable Regular update Summary Our credit view of FMS Wertmanagement (FMS-WM, Aaa stable) reflects its very close relationship and linkages with the German government (Aaa stable) and a consistent track record of financial support. FMS-WM, a public wind-up institution established in 2010, benefits from an explicit guarantee and loss compensation through the Financial Market Stabilisation Fund (SoFFin) whereby FMS-WM ultimately becomes an obligation of the German sovereign. Thus, FMS-WM is rated on a par with the Germany government. Exhibit 1 FMS-WM's wind-up portfolio is on a declining trajectory € billion, end-of-period Exhibit 2 Most of FMS-WM's portfolio doesn't mature until after 2028 € billion 0 20 40 60 80 100 120 140 160 180 2010* 2011 2012 2013 2014 2015 2016 2017 Public Sector Real Estate Structured Products Infrastructure Total wind-up portfolio *Refers to the transfer date (1 October 2010) Sources: FMS Wertmanagement, Moody's Investors Service 0 10 20 30 40 50 60 2018 2019-2022 2023-2027 After 2028 Public Sector Real Estate Structured Products Infrastructure Total wind-up portfolio Sources: FMS Wertmanagement, Moody's Investors Service Credit strengths » FMS-WM's loss compensation mechanism, with the German government as the ultimate obligor » Explicit guarantee from SoFFin Credit challenges » Very weak asset quality as a result of portfolio concentrations of long-maturity, complex and illiquid assets as well as low margins » The large maturity mismatch between assets and liabilities » Reliance on wholesale funding

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Aaa Stable - FMS Wertmanagement

SOVEREIGN AND SUPRANATIONAL

CREDIT OPINION1 August 2018

Update

Analyst Contacts

Heiko Peters [email protected]

KathrinMuehlbronner

+44.20.7772.1383

Senior Vice [email protected]

Polina Gotmann +49.69.7073.0725Associate [email protected]

Dietmar Hornung +49.69.7073.0790Associate Managing [email protected]

Yves Lemay +44.20.7772.5512MD-Sovereign [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

FMS Wertmanagement – Aaa StableRegular update

SummaryOur credit view of FMS Wertmanagement (FMS-WM, Aaa stable) reflects its very closerelationship and linkages with the German government (Aaa stable) and a consistent trackrecord of financial support. FMS-WM, a public wind-up institution established in 2010,benefits from an explicit guarantee and loss compensation through the Financial MarketStabilisation Fund (SoFFin) whereby FMS-WM ultimately becomes an obligation of theGerman sovereign. Thus, FMS-WM is rated on a par with the Germany government.

Exhibit 1

FMS-WM's wind-up portfolio is on a decliningtrajectory€ billion, end-of-period

Exhibit 2

Most of FMS-WM's portfolio doesn't matureuntil after 2028€ billion

0

20

40

60

80

100

120

140

160

180

2010* 2011 2012 2013 2014 2015 2016 2017

Public Sector Real Estate

Structured Products Infrastructure

Total wind-up portfolio

*Refers to the transfer date (1 October 2010)Sources: FMS Wertmanagement, Moody's Investors Service

0

10

20

30

40

50

60

2018 2019-2022 2023-2027 After 2028

Public Sector Real Estate

Structured Products Infrastructure

Total wind-up portfolio

Sources: FMS Wertmanagement, Moody's Investors Service

Credit strengths

» FMS-WM's loss compensation mechanism, with the German government as the ultimateobligor

» Explicit guarantee from SoFFin

Credit challenges

» Very weak asset quality as a result of portfolio concentrations of long-maturity, complexand illiquid assets as well as low margins

» The large maturity mismatch between assets and liabilities

» Reliance on wholesale funding

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Rating outlookThe rating outlook for FMS-WM is stable, reflecting the stable outlook on Germany's sovereign rating.

Factors that could lead to a downgradeAny change to the rating of the German sovereign would have an impact on the rating of FMS-WM. Although not expected, anychanges to the current legal and contractual framework that would have a negative effect upon the strong link with the Germansovereign might also lead to a downgrade of the rating of FMS-WM.

Key indicators

Exhibit 3

FMS Wertmanagment 2010 2011 2012 2013 2014 2015 2016 2017

Total assets (EUR bn) 333.3 341.8 246.4 187.7 183.6 171.1 177.2 157.3

Wind-up portfolio (EUR bn) [1] 174.3 160.7 136.9 119.1 106.3 94.7 88.9 76.8

Amount of debt issued on capital market (EUR bn) 0.0 20.7 34.9 11.0 11.6 12.3 15.8 19.3

Own capital (EUR bn) 0.00 0.00 0.04 0.12 0.43 0.73 1.04 1.40

Operating result (EUR bn) -3.04 -9.96 0.04 0.15 0.37 0.41 0.39 0.43

Provisions & net income from investments (EUR bn) -2.97 -10.25 -0.43 -0.26 0.03 0.04 0.14 0.20

Note: Data refers to year-end.

[1] The initial wind-up portfolio transferred from HRE Group to FMS-WM amounted to EUR 175.7 billion in October 2010.

Sources: FMS Wertmanagement, Moody's Investors Service

Detailed credit considerationsFMS-WM is a German wind-up institution established in 2010 in order to wind up a €175.7 billion1 portfolio of risk exposures andnon-strategic assets from the Hypo Real Estate Group (HRE). Whilst FMS-WM may engage in those banking and financial servicetransactions that serve its purposes, FMS-WM does not hold a banking license and therefore has no access to ECB funding. At the sametime, FMS-WM is not subject to banking regulation and is free from regulatory requirements relating to capital and liquidity. FMS-WMis supervised by the Federal Agency for Financial Market Stabilisation (FMSA).

FMS-WM is rated on par with the German sovereign. This derives from a loss compensation obligation through SoFFin whereby FMS-WM ultimately becomes an obligation of the German sovereign. A loss compensation clause obliges SoFFin to pay promptly, and nolater than on the third business day following a request, any amount which the Executive Board of FMS-WM deems necessary to meetFMS-WM's liabilities in full and in a timely manner.

Since January 2014, SoFFin has provided an explicit guarantee for FMS-WM's liabilities (with a grandfathering of the outstanding debtof FMS-WM). This implies that SoFFin will be directly liable to third parties rather than indirectly liable via the loss compensationmechanism. It allows debt holders of FMS-WM to apply a 0% risk weight under Basel III rules for FMS-WM debt issues. Although theexplicit guarantee is stronger than the previous implicit guarantee, it did not alter our assessment, given that we already viewed theloss compensation mechanism as sufficiently strong to link FMS-WM's rating directly to that of the German sovereign.

The methodological approach for rating FMS-WM on par with the German sovereign is found in Moody's credit substitutionmethodology “Rating Transactions Based on the Credit Substitution Approach: Letter of Credit-backed, Insured and GuaranteedDebts”, whereby FMS-WM's credit rating is fully substituted by that of the German sovereign. As a consequence, FMS-WM'scredit metrics such as asset quality and capital adequacy do not have an impact on the credit rating of FMS-WM. Under the creditsubstitution approach, the credit rating of FMS-WM is driven solely by the German sovereign credit rating.

FMS-WM was established as a public law entity pursuant to Section 8a of the Financial Market Stabilisation Fund Act (FMStFG). Thelegal basis for the application of credit substitution to FMS-WM's rating is its charter and the FMStFG. SoFFin's loss compensationobligation is established by §7 of the FMS Charter, and the general liability for SoFFin's obligations by the German sovereign is set outin Section 5 of the FMStFG.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 1 August 2018 FMS Wertmanagement – Aaa Stable: Regular update

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

In May 2014, FMS-WM was mandated to wind-up DEPFA Bank plc (DEPFA), with total assets of €48.5 billion2 as of December 2014.DEPFA was a subsidiary of HRE Group, which transferred certain non-strategic assets to FMS-WM in 2010. Following a decision bythe European Commission in July 2011, DEPFA was not allowed to generate new business, subject to certain exceptions, unless thecompany was privatised. Since this privatisation did not occur in 2014, the inter-ministerial steering committee of FMSA decided totransfer the ownership of DEPFA from HRE Group to FMS-WM.

The transfer of ownership from HRE Group to FMS-WM was completed in December 2014, when FMS-WM acquired all DEPFA equityat a purchase price of EUR 320 million. DEPFA is now a 100% subsidiary of FMS-WM, managed as an independent financial investment.DEPFA remains a regulated bank under Irish law and is, unlike FMS-WM, subject to the EU Bank Resolution and Recovery Directive(BRRD). FMS-WM is not obliged to publish consolidated IFRS accounts for DEPFA. Instead, FMS-WM reports according to GermanGAAP rules, whilst DEPFA reports its results according to IFRS rules.

We expect that FMS-WM will optimise DEPFA's liability management and funding costs with positive consequences for its financialresults. FMS-WM has no formal obligation to inject capital into DEPFA in cases of financial distress and it is as yet unclear how far FMS-WM might compensate any losses or funding shortfalls.

Recent developmentsFMS-WM reduced its wind-up portfolio further to €76.8 billion (or 2.3% of GDP) at year-end 2017, from €88.9 billion at year-end 2016.This was equivalent to a 13.6% year-on-year drop, larger than the 6.1% decline in 2016 (see Exhibit 1). The cumulative reduction sincethe FMS-WM's launch is now €99 billion (including currency effects), or 56.3% from the €175.7 billion nominal transferred value inOctober 2010 (or 6.8% of GDP). As the wind-up assets are included in our calculation of Germany's public debt level (64.1% of GDP in2017), almost 26% of the fall in Germany's debt-to-GDP ratio (roughly 17 percentage points) over 2010-17 was due to the fall in theFMS-WM's wind-up portfolio.

At year-end 2017, FMS-WM's wind-up portfolio contained 1,923 exposures (2,097 at year-end 2016 and 7,144 in October 2010) with915 counterparties, down from 986 (3,191 in October 2010). The wind-up portfolio contained assets in Commercial Real Estate (3%of total wind-up portfolio at year-end 2017), Infrastructure (13%), the Public Sector (53%) and Structured Products (31%). The largestcountry exposures recorded were in Italy (Baa2 on review for downgrade) (28%), the US (Aaa stable) (21%) and the UK (Aa2 stable)(22%). The portfolio was dominated by euro-denominated assets (45%), followed by US dollar-denominated assets (31%) and poundsterling-denominated assets (18%). In the €76.8 billion portfolio (as of year-end 2017), around 70% had a legal maturity extendingbeyond 2028.

The FMS-WM expects the portfolio to decline by €7.0 billion in 2018, driven by asset sales in Public Sector, Structured Products andCommercial Real Estate. We expect that the wind-up process will probably slow down significantly over the coming years as selling ofthe remaining assets will become progressively more challenging. The portfolio is to a large extent comprised of illiquid exposures withvery long maturities (Exhibit 2).

The bonds and securities held by FMS-WM are typically part of an asset swap package attached to derivatives which are mostly usedto hedge interest-rate risk. Selling those assets ahead of schedule would imply that the derivatives would have to be closed ahead ofthe original maturity and therefore with significant losses. As a consequence, a hold-to-maturity strategy promises better results in linewith the value maximization objective of FMS-WM in interest with the German taxpayer. Simultaneously to the asset reduction, FMS-WM will also reduce its operating costs (including reduction in number of employees, closure of IT platforms, synergies between FMS-WM Group).

FMS-WM has been profitable from its ordinary activities since 2012, posting profits of €429 million in 2017 and €391 million in 2016.This partially offsets a significant loss in 2011 mainly due to significant write-downs of €8.9 billion worth of Greek sovereign debtholdings. For the full year 2018, FMS-WM expects a break-even or a slightly positive result from ordinary activities. FMS-WM expectsinterest margins to decline in the coming years given that assets with higher margins, such as commercial real estate, will maturesooner than lower margin parts of the portfolio.

To fund its operations, FMS-WM issued €19.3 billion in capital market instruments in 2017, higher than €15.8 billion issued in 2016and the €11-€12 billion originally forecast for 2017. The largest share of the 2017 issuance was euro denominated (45%), followed

3 1 August 2018 FMS Wertmanagement – Aaa Stable: Regular update

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

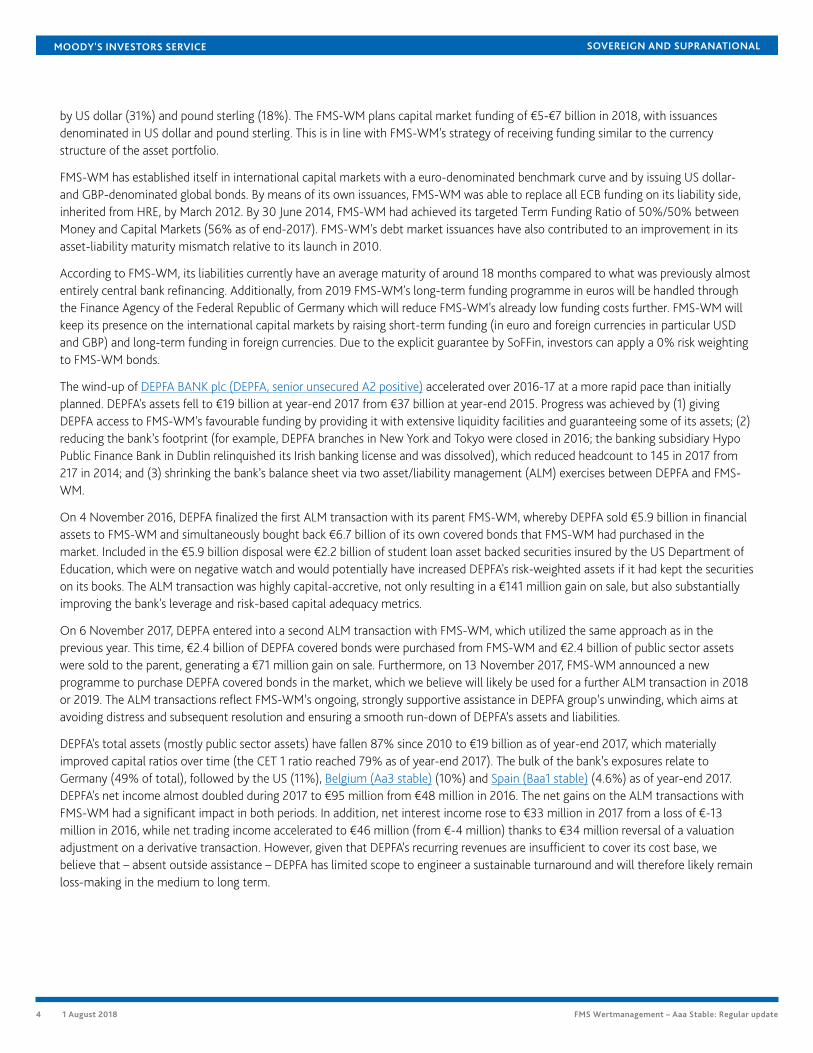

by US dollar (31%) and pound sterling (18%). The FMS-WM plans capital market funding of €5-€7 billion in 2018, with issuancesdenominated in US dollar and pound sterling. This is in line with FMS-WM's strategy of receiving funding similar to the currencystructure of the asset portfolio.

FMS-WM has established itself in international capital markets with a euro-denominated benchmark curve and by issuing US dollar-and GBP-denominated global bonds. By means of its own issuances, FMS-WM was able to replace all ECB funding on its liability side,inherited from HRE, by March 2012. By 30 June 2014, FMS-WM had achieved its targeted Term Funding Ratio of 50%/50% betweenMoney and Capital Markets (56% as of end-2017). FMS-WM's debt market issuances have also contributed to an improvement in itsasset-liability maturity mismatch relative to its launch in 2010.

According to FMS-WM, its liabilities currently have an average maturity of around 18 months compared to what was previously almostentirely central bank refinancing. Additionally, from 2019 FMS-WM's long-term funding programme in euros will be handled throughthe Finance Agency of the Federal Republic of Germany which will reduce FMS-WM's already low funding costs further. FMS-WM willkeep its presence on the international capital markets by raising short-term funding (in euro and foreign currencies in particular USDand GBP) and long-term funding in foreign currencies. Due to the explicit guarantee by SoFFin, investors can apply a 0% risk weightingto FMS-WM bonds.

The wind-up of DEPFA BANK plc (DEPFA, senior unsecured A2 positive) accelerated over 2016-17 at a more rapid pace than initiallyplanned. DEPFA's assets fell to €19 billion at year-end 2017 from €37 billion at year-end 2015. Progress was achieved by (1) givingDEPFA access to FMS-WM's favourable funding by providing it with extensive liquidity facilities and guaranteeing some of its assets; (2)reducing the bank’s footprint (for example, DEPFA branches in New York and Tokyo were closed in 2016; the banking subsidiary HypoPublic Finance Bank in Dublin relinquished its Irish banking license and was dissolved), which reduced headcount to 145 in 2017 from217 in 2014; and (3) shrinking the bank’s balance sheet via two asset/liability management (ALM) exercises between DEPFA and FMS-WM.

On 4 November 2016, DEPFA finalized the first ALM transaction with its parent FMS-WM, whereby DEPFA sold €5.9 billion in financialassets to FMS-WM and simultaneously bought back €6.7 billion of its own covered bonds that FMS-WM had purchased in themarket. Included in the €5.9 billion disposal were €2.2 billion of student loan asset backed securities insured by the US Department ofEducation, which were on negative watch and would potentially have increased DEPFA's risk-weighted assets if it had kept the securitieson its books. The ALM transaction was highly capital-accretive, not only resulting in a €141 million gain on sale, but also substantiallyimproving the bank's leverage and risk-based capital adequacy metrics.

On 6 November 2017, DEPFA entered into a second ALM transaction with FMS-WM, which utilized the same approach as in theprevious year. This time, €2.4 billion of DEPFA covered bonds were purchased from FMS-WM and €2.4 billion of public sector assetswere sold to the parent, generating a €71 million gain on sale. Furthermore, on 13 November 2017, FMS-WM announced a newprogramme to purchase DEPFA covered bonds in the market, which we believe will likely be used for a further ALM transaction in 2018or 2019. The ALM transactions reflect FMS-WM’s ongoing, strongly supportive assistance in DEPFA group’s unwinding, which aims atavoiding distress and subsequent resolution and ensuring a smooth run-down of DEPFA’s assets and liabilities.

DEPFA's total assets (mostly public sector assets) have fallen 87% since 2010 to €19 billion as of year-end 2017, which materiallyimproved capital ratios over time (the CET 1 ratio reached 79% as of year-end 2017). The bulk of the bank’s exposures relate toGermany (49% of total), followed by the US (11%), Belgium (Aa3 stable) (10%) and Spain (Baa1 stable) (4.6%) as of year-end 2017.DEPFA's net income almost doubled during 2017 to €95 million from €48 million in 2016. The net gains on the ALM transactions withFMS-WM had a significant impact in both periods. In addition, net interest income rose to €33 million in 2017 from a loss of €-13million in 2016, while net trading income accelerated to €46 million (from €-4 million) thanks to €34 million reversal of a valuationadjustment on a derivative transaction. However, given that DEPFA's recurring revenues are insufficient to cover its cost base, webelieve that – absent outside assistance – DEPFA has limited scope to engineer a sustainable turnaround and will therefore likely remainloss-making in the medium to long term.

4 1 August 2018 FMS Wertmanagement – Aaa Stable: Regular update

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Moody's related publications

» Rating Action: Moody's affirms Germany's Aaa government bond rating; maintains stable outlook, 24 February 2017

» Credit Opinion: Government of Germany – Aaa Stable: Regular update, 18 July 2018

» Credit Analysis: Government of Germany – Aaa stable: Annual credit analysis , 23 January 2018

» Rating Action: Moody's upgrades DEPFA's debt and deposit ratings to A2; changes outlook to Positive, 27 June 2018

» Rating Methodology: Rating Transactions Based on the Credit Substitution Approach: Letter of Credit-backed, Insured andGuaranteed Debts, 25 May 2017, Sovereign Bond Ratings, 22 December 2016

Authors

Heiko PetersAVP – Analyst

Polina GotmannAssociate Analyst

Endnotes1 According to German GAAP accounting standards.

2 According to IFRS accounting standards.

5 1 August 2018 FMS Wertmanagement – Aaa Stable: Regular update

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

© 2018 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1131837

6 1 August 2018 FMS Wertmanagement – Aaa Stable: Regular update

![Phenomenology in Contact Archaeology [AAA 2013]](https://static.fdokumen.com/doc/165x107/6319d63f77252cbc1a0ee287/phenomenology-in-contact-archaeology-aaa-2013.jpg)