A STUDY ON CUSTOMERS' SATISFACTION TOWARDS E ...

536

A STUDY ON CUSTOMERS’ SATISFACTION TOWARDS E-BANKING WITH SPECIAL REFERENCE TO SBI AND ICICI BANKS IN THANJAVUR TOWN A thesis submitted to BHARATHIDASAN UNIVERSITY for the award of the degree of DOCTOR OF PHILOSOPHY IN COMMERCE By S.BELLARMIN DIANA [Ref.No.36049/PhD/Commerce/F.T/April 2007/Dated.04.04.2007 Under the Guidance of Dr.M.SWAMINATHAN, M.Com., M.Phil., M.B.A., B.G.L., Ph.D., Associate Professor P.G. AND RESEARCH DEPARTMENT OF COMMERCE, A.V.V.M. SRI PUSHPAM COLLEGE (AUTONOMOUS), POONDI – 613 503, THANJAVUR DISTRICT, TAMIL NADU, INDIA. MARCH 2014.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of A STUDY ON CUSTOMERS' SATISFACTION TOWARDS E ...

A STUDY ON CUSTOMERS’ SATISFACTION TOWARDS

E-BANKING WITH SPECIAL REFERENCE TO SBI AND ICICI

BANKS IN THANJAVUR TOWN

A thesis submitted to

BHARATHIDASAN UNIVERSITY

for the award of the degree of

DOCTOR OF PHILOSOPHY

IN

COMMERCE

By

S.BELLARMIN DIANA

[Ref.No.36049/PhD/Commerce/F.T/April 2007/Dated.04.04.2007

Under the Guidance of

Dr.M.SWAMINATHAN, M.Com., M.Phil., M.B.A., B.G.L., Ph.D.,

Associate Professor

P.G. AND RESEARCH DEPARTMENT OF COMMERCE,

A.V.V.M. SRI PUSHPAM COLLEGE (AUTONOMOUS),

POONDI – 613 503, THANJAVUR DISTRICT,

TAMIL NADU, INDIA.

MARCH 2014.

Dr.M.SWAMINATHAN, M.Com., M.Phil., M.B.A., B.G.L., Ph.D.,

Associate Professor,

Department of Commerce,

A.V.V.M. Sri Pushpam College (Autonomous),

Poondi – 613 503.

Thanjavur District.

CERTIFICATE

Date: /03/2014

This is to certify that the thesis entitled A STUDY ON CUSTOMERS’

SATISFACTION TOWARDS E-BANKING WITH SPECIAL REFERENCE TO

SBI AND ICICI BANKS IN THANJAVUR TOWN submitted by S.Bellarmin Diana

Full Time Research Scholar, Department of Commerce, A.V.V.M Sri Pushpam College

(Autonomous), Poondi, is a bonafide record of research work done by him under my

guidance as a full-time research scholar and that the thesis has not previously formed the

basis for the award to the candidate of any degree, Diploma, Associateship, Fellowship or

other similar titles. The thesis represents the independent work on the part of the

candidate.

(M.SWAMINATHAN)

ii

S.BELLARMIN DIANA,

Full – Time Research Scholar,

Department of Commerce,

A.V.V.M. Sri Pushpam College (Autonomous),

Poondi – 613 503.

Thanjavur District

Date: /03/2014

DECLARATION

I do hereby declare that this work has been originally carried out by me under the

supervision of Dr.M.SWAMINATHAN, Associate Professor, P.G. and Research

Department of Commerce, A.V.V.M. Sri Pushpam College (Autonomous), Poondi,

Thanjavur District, Tamil Nadu, affiliated to Bharathidasan University, Tiruchirappalli –

620 024 and this work has not been submitted elsewhere for any other degree.

(S.BELLARMIN DIANA)

Signature of the Candidate

iii

ACKNOWLEDGEMENT

Glory to The Almighty who bestowed the wisdom and health to prepare this

thesis.

I express my deep sense of gratitude to the college administration and staff

members who offered me an opportunity to carry out my research work in the

esteemed institution.

My sincere and heartfelt thanks to my Research Advisor

Dr.M.Swaminathan, Associate Professor in commerce, A.V.V.M. Sri Pushpam

College (Autonomous), Poondi, Thanjavur, whose encouragement and guidance

has been of immense help for me to complete this research.

I offer my gratitude to G.Vijaya Ramalingam, Associate Professor and

coordinator, Department of Commerce, A.V.V.M. Sri Pushpam College,

(Autonomous), Poondi,Thanjavur, for having taken steps to introduce me to the

full time reseach.

I would like to offer my profound regards to Dr.R.Rajendran, Principal,

A.V.V.M. Sri Pushpam College, (Autonomous), Poondi.

I am indebted to Bharathidasan University, Tiruchirapalli for giving

me an opportunity to do fulltime research and for all help.

iv

I cordially thank my beloved parents, sisters and each one of my

family members without whose effort and support the thesis would not have been

successfully submitted.

S.BELLARMIN DIANA

v

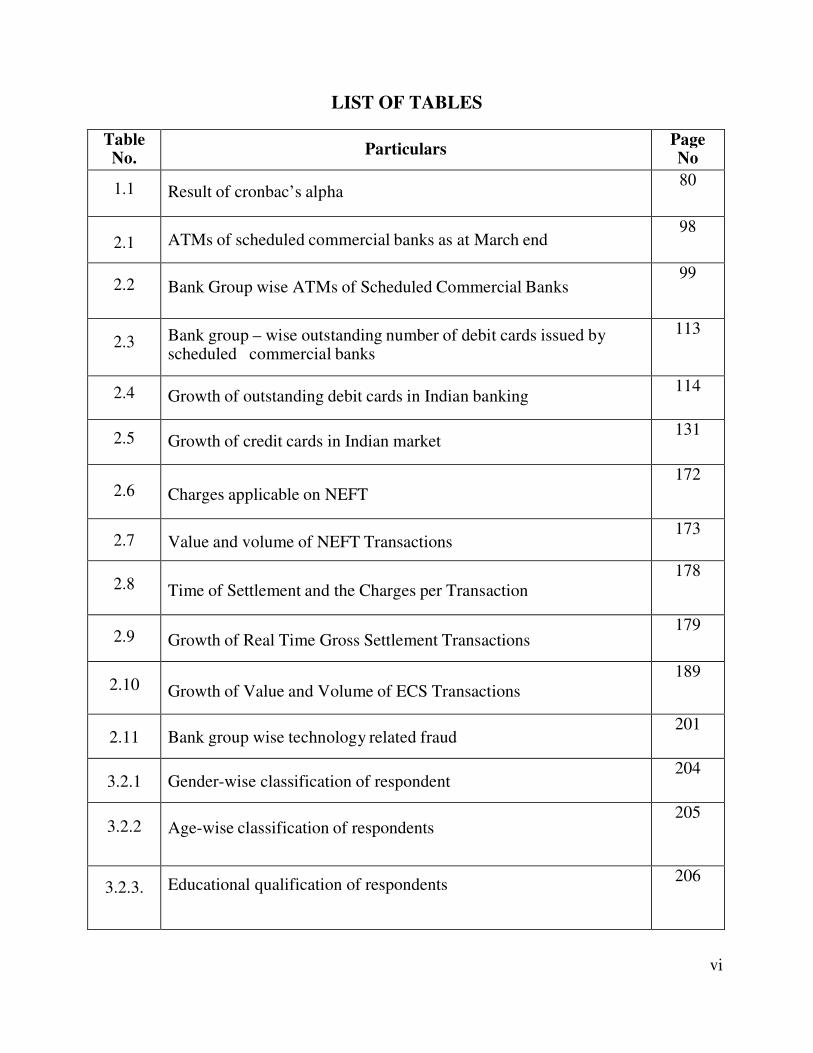

LIST OF TABLES

Table No.

Particulars Page No

1.1

Result of cronbac’s alpha 80

2.1

ATMs of scheduled commercial banks as at March end 98

2.2

Bank Group wise ATMs of Scheduled Commercial Banks

99

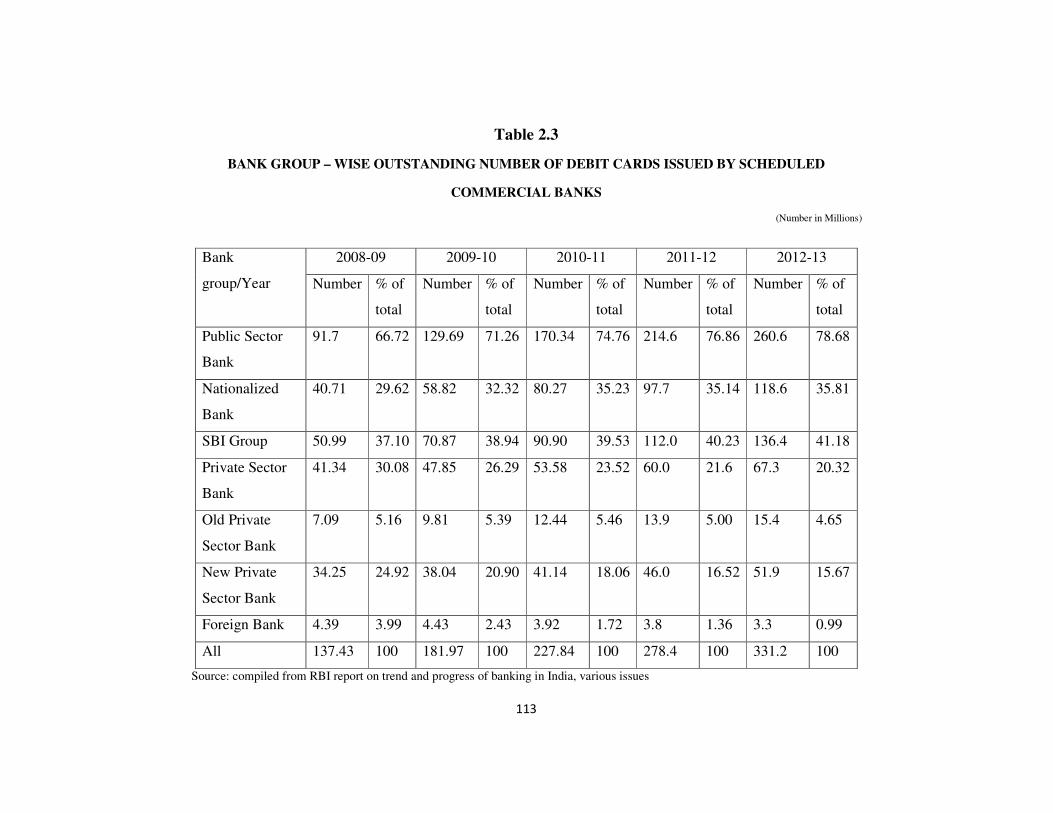

2.3

Bank group – wise outstanding number of debit cards issued by scheduled commercial banks

113

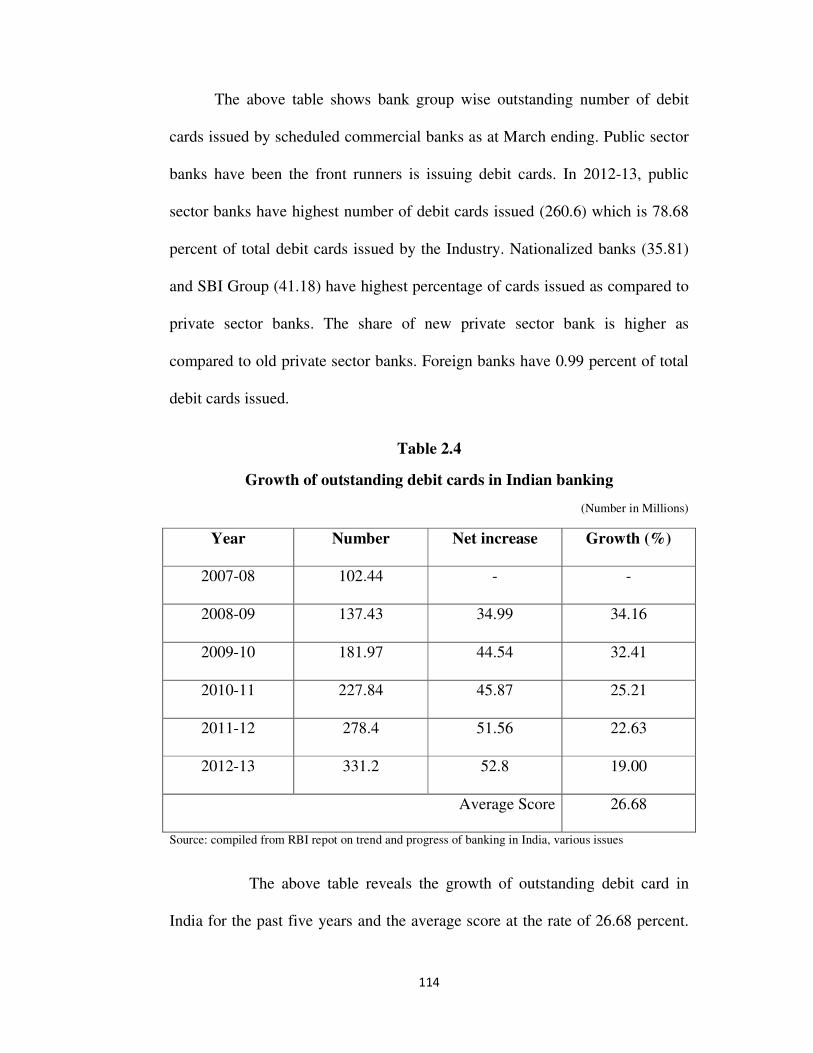

2.4

Growth of outstanding debit cards in Indian banking 114

2.5

Growth of credit cards in Indian market 131

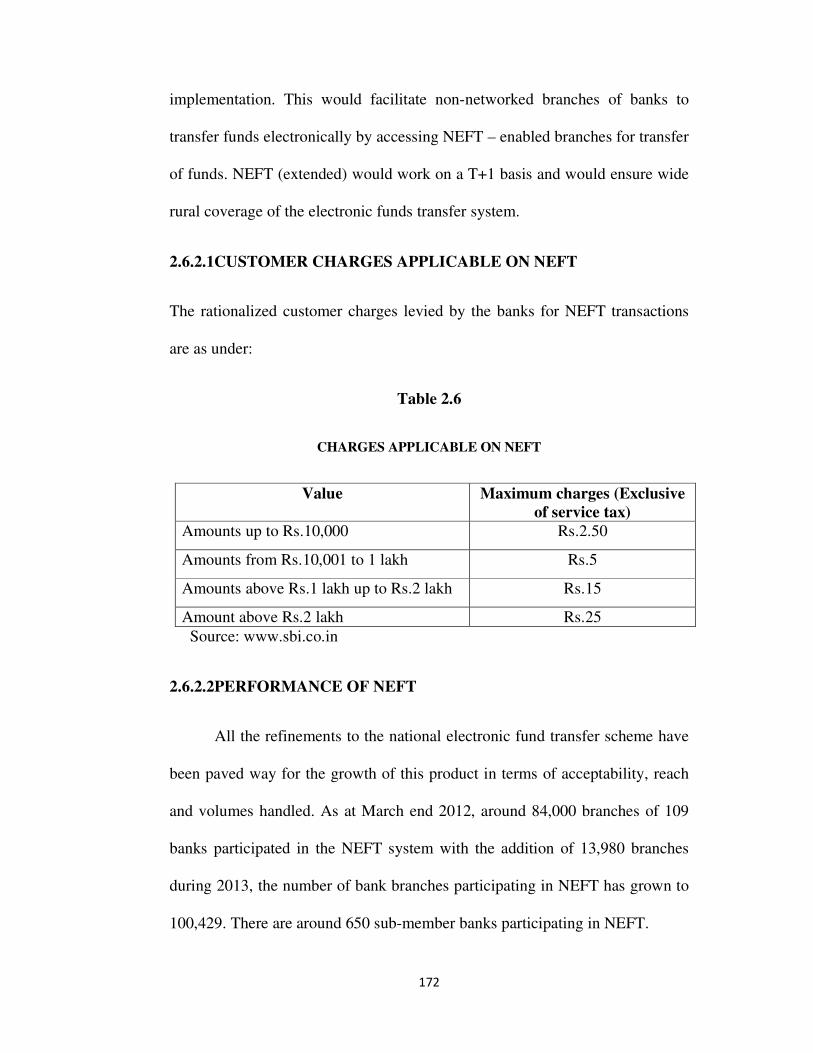

2.6 Charges applicable on NEFT

172

2.7

Value and volume of NEFT Transactions 173

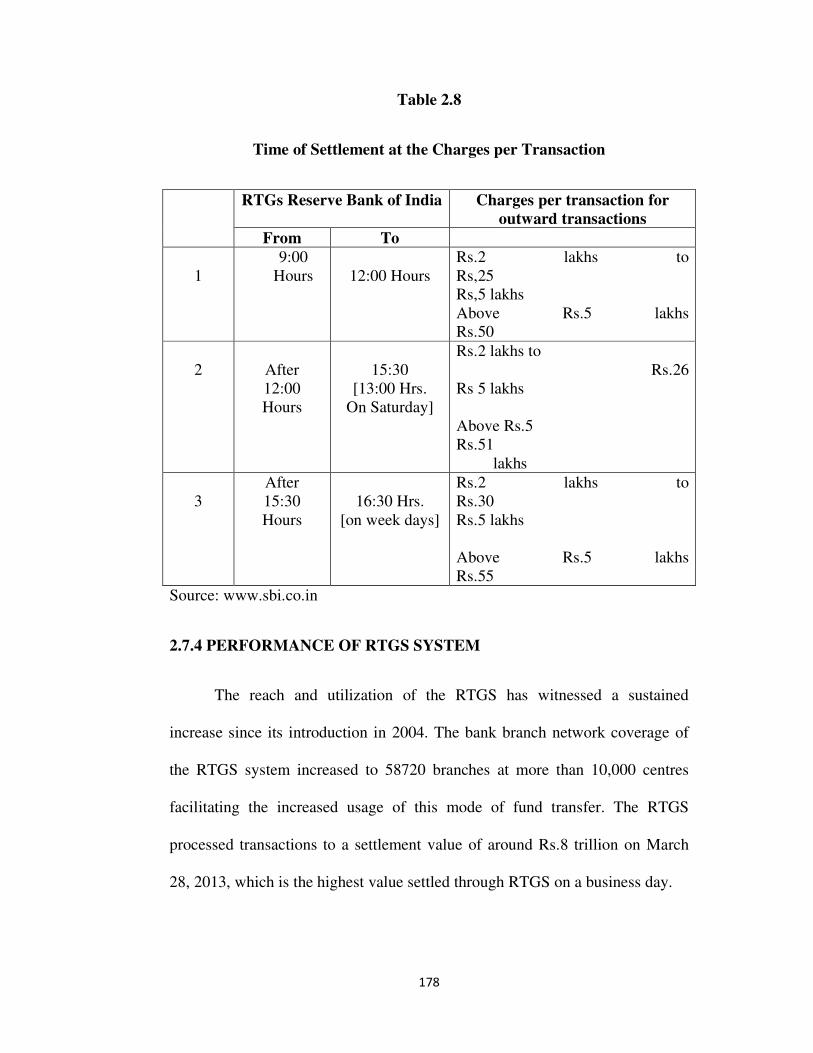

2.8 Time of Settlement and the Charges per Transaction

178

2.9

Growth of Real Time Gross Settlement Transactions 179

2.10 Growth of Value and Volume of ECS Transactions

189

2.11

Bank group wise technology related fraud 201

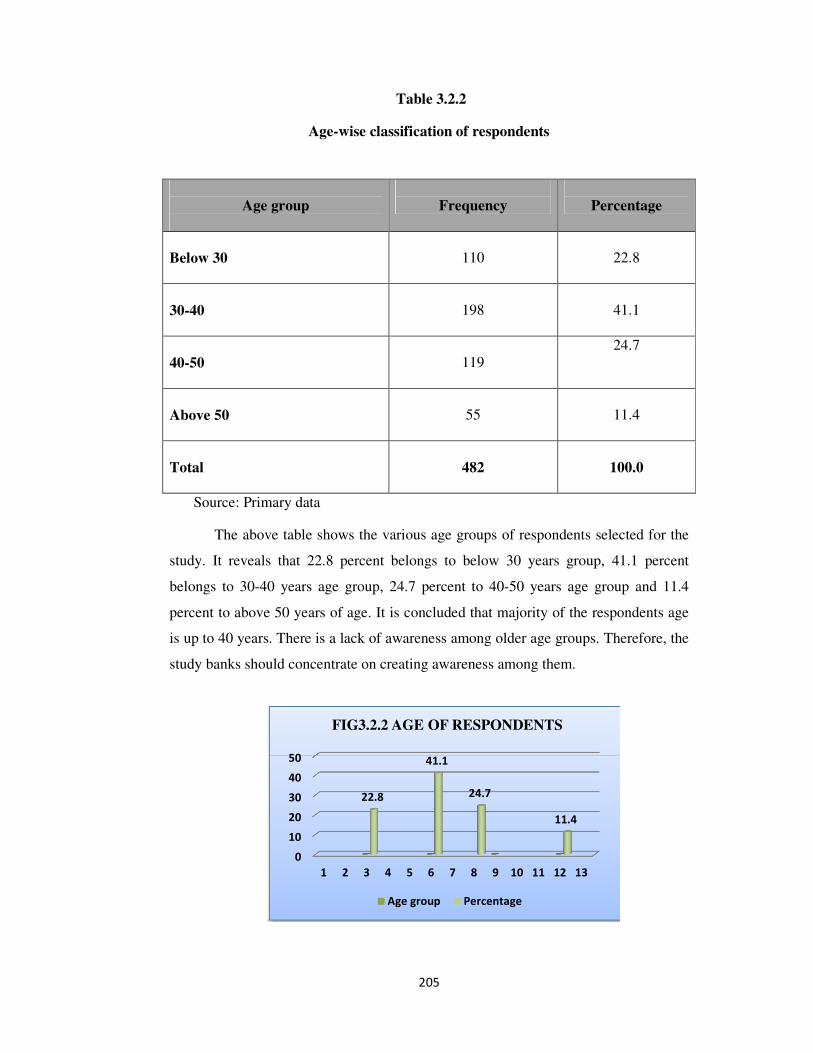

3.2.1

Gender-wise classification of respondent 204

3.2.2

Age-wise classification of respondents 205

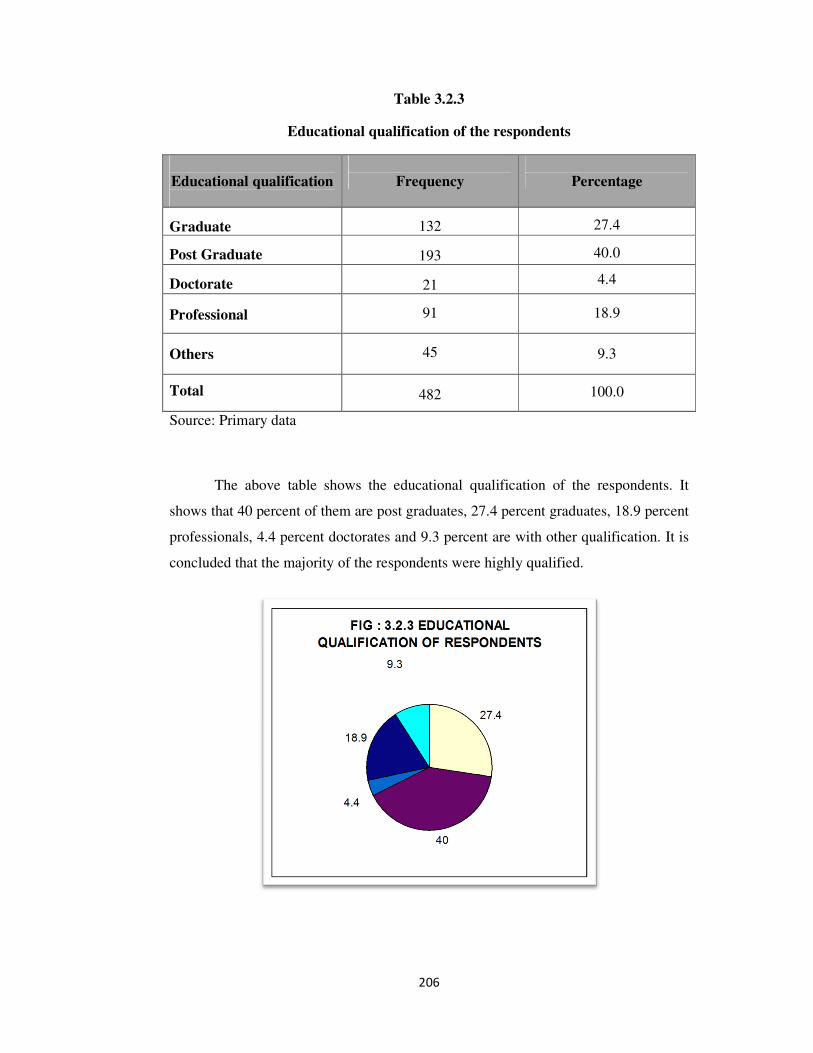

3.2.3.

Educational qualification of respondents 206

vi

[

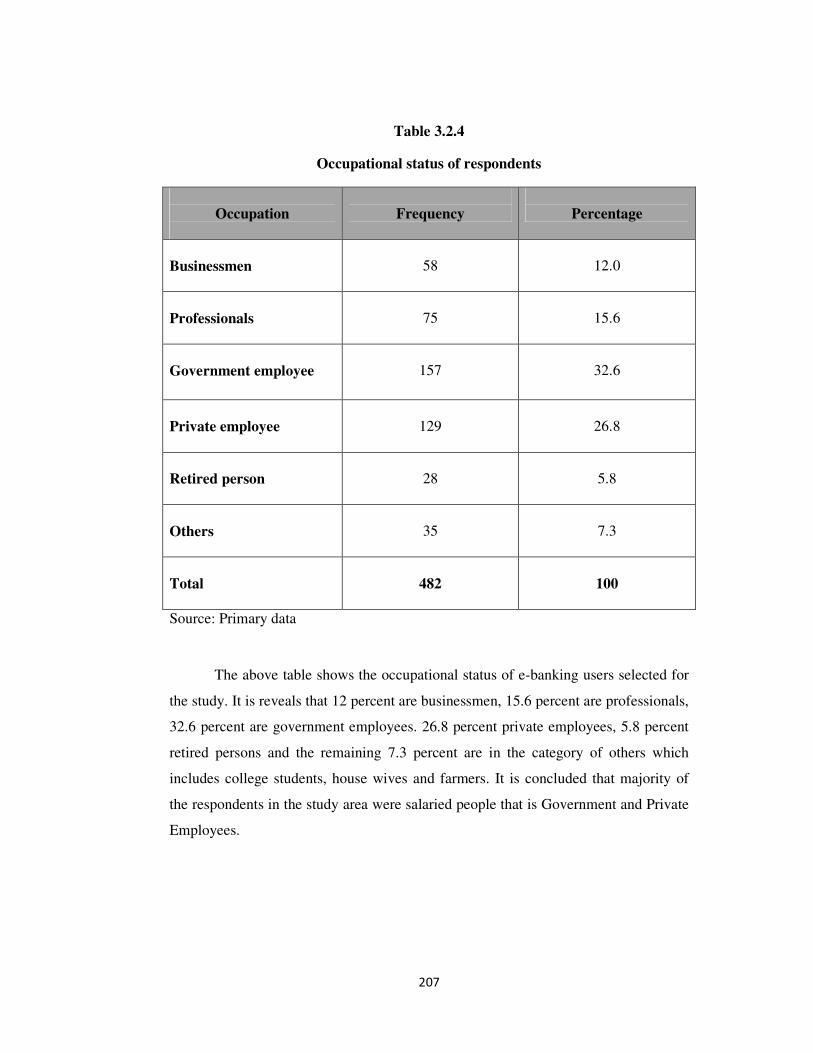

3.2.4

Occupational status of respondents 207

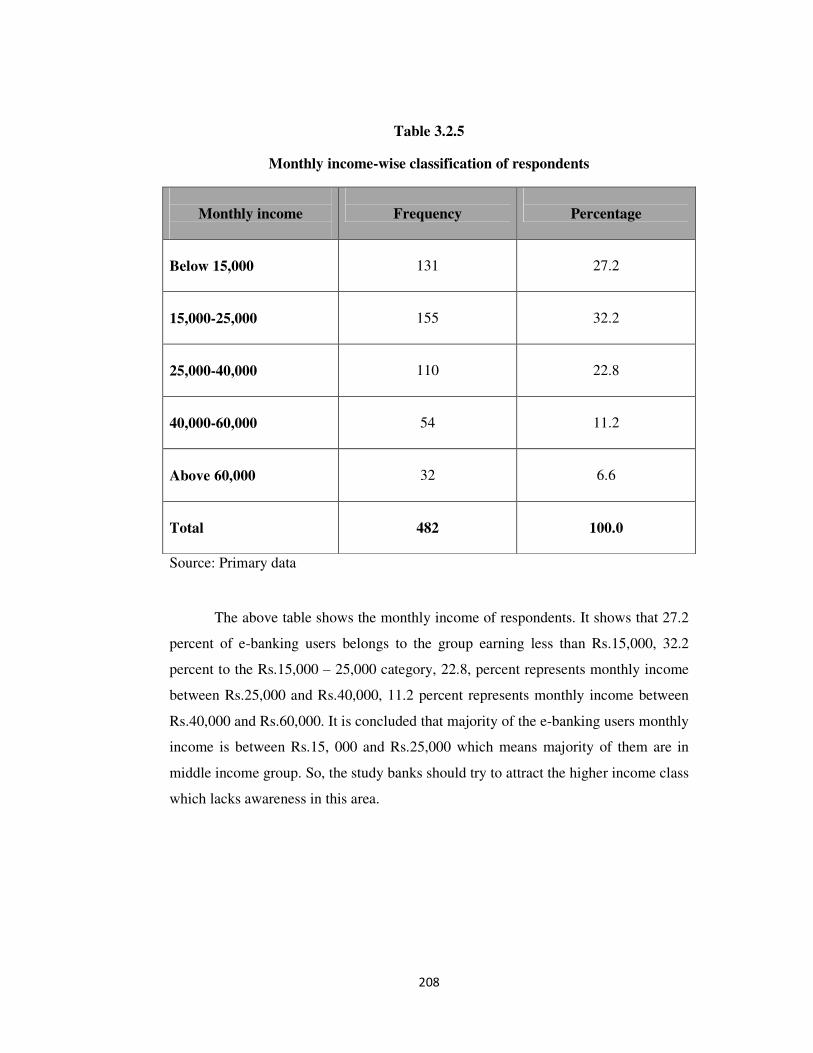

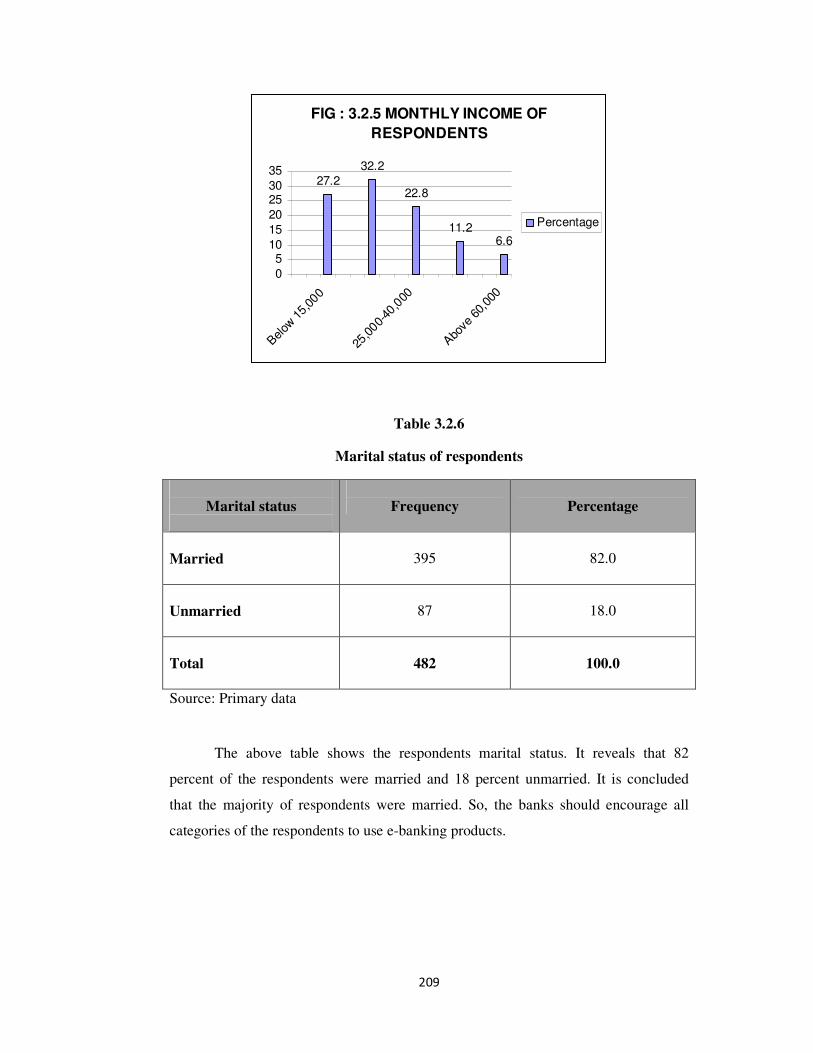

3.2.5

Monthly income-wise classification of respondents 208

3.2.6

Marital status of respondents 209

3.2.7

Classification of Respondents on the basis of e-banking facilities 210

3.2.8

Motivational factor to avail e-banking products 211

3.2.9

Number of years of utilization 212

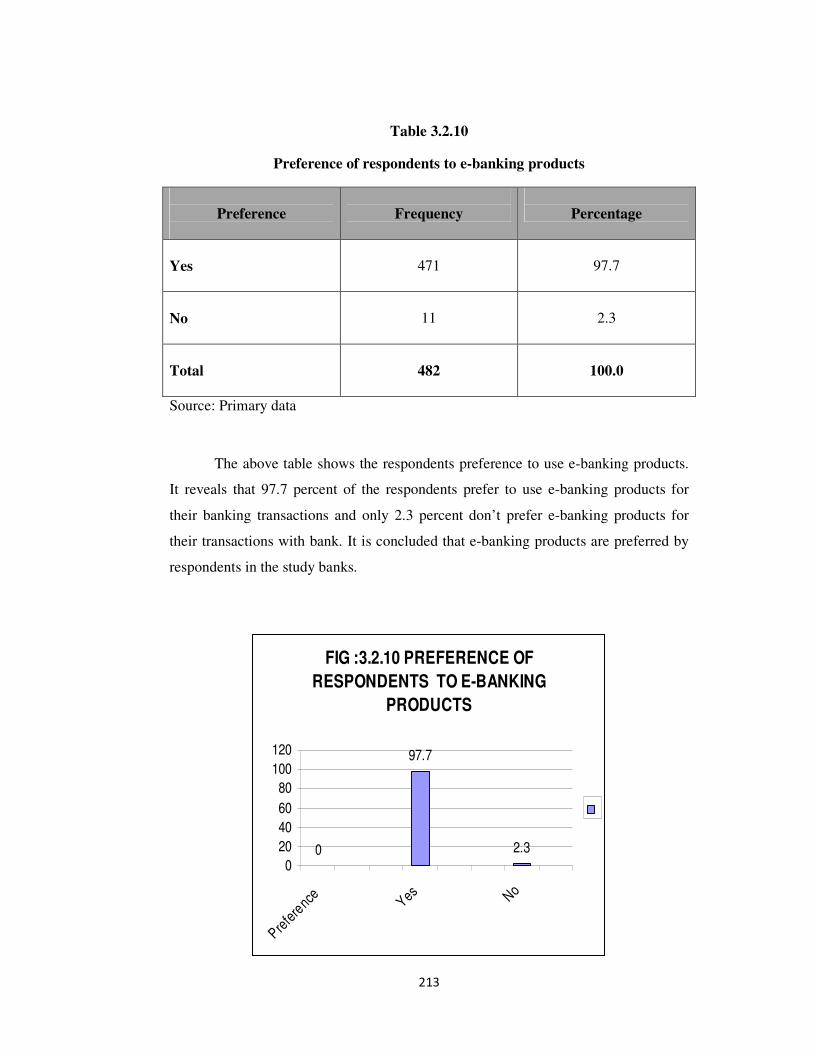

3.2.10 Preference of respondents to e-banking products

213

3.2.11

Reason for preference to e-banking products 214

3.2.12

Frequency of usage in the past three months 215

3.2.13

Occupational status of Internet banking users 216

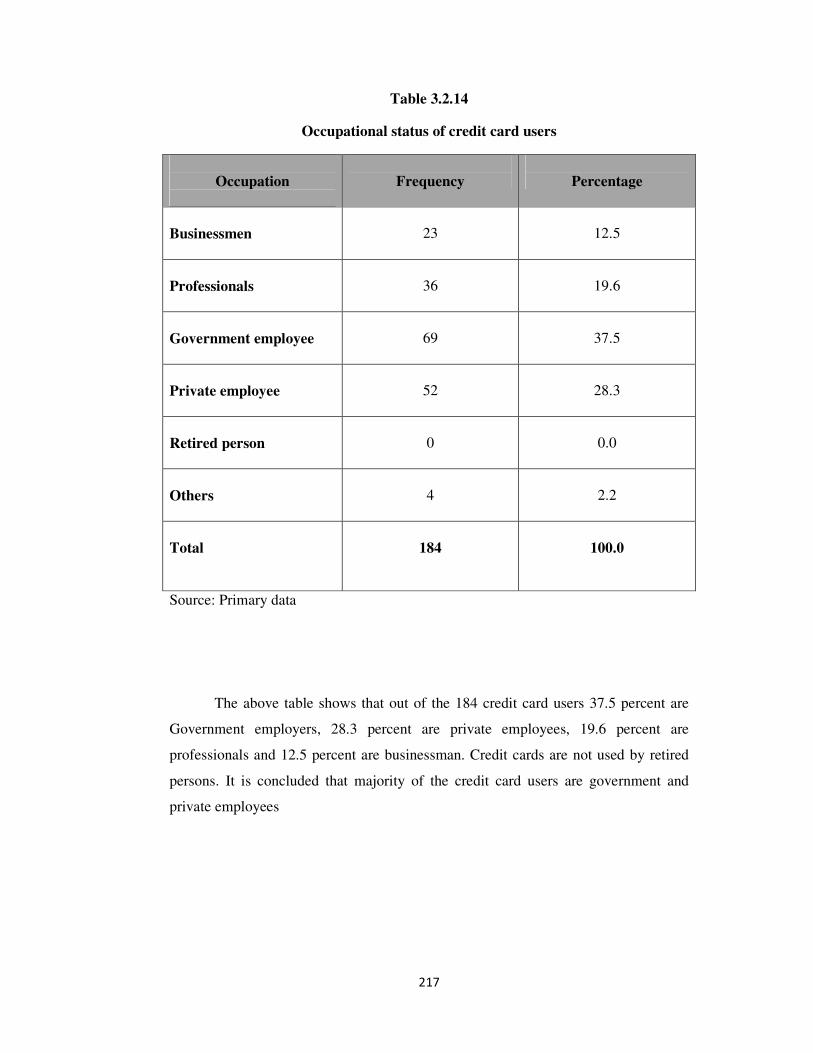

3.2.14

Occupational status of Credit card users 217

3.2.15

Occupational status of mobile banking users 218

3.2.16

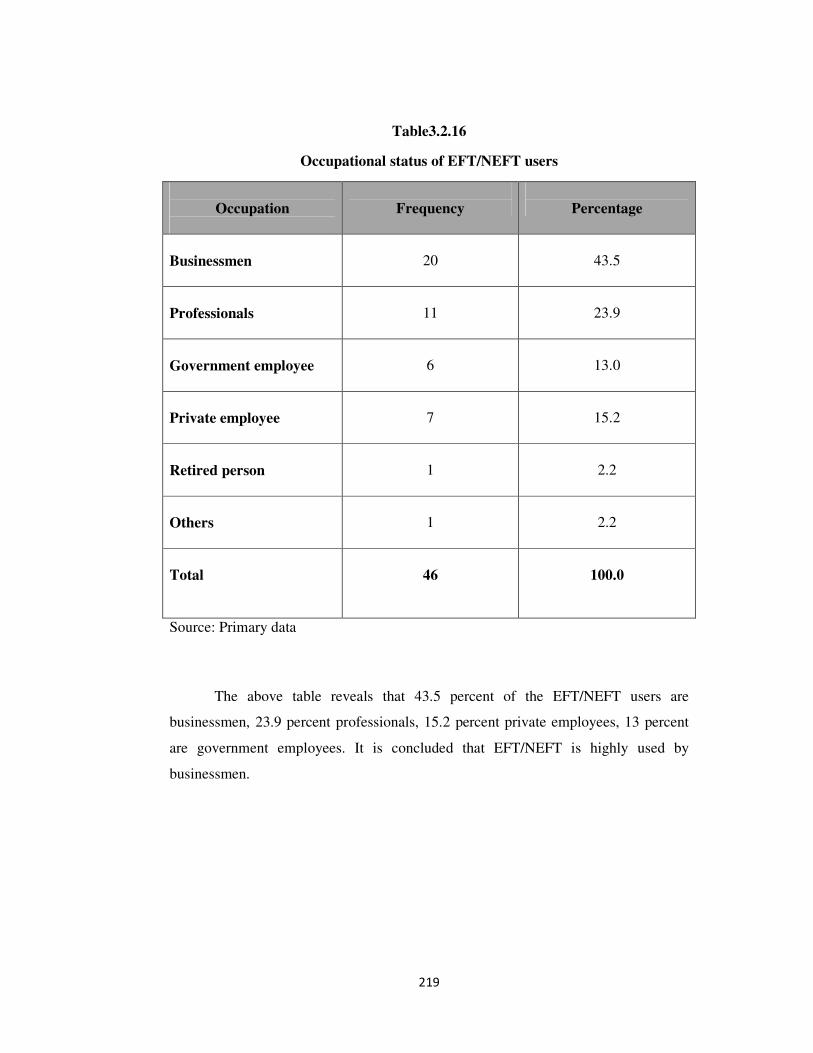

Occupational status of EFT/NEFT users 219

3.2.17 Occupational status of RTGS users

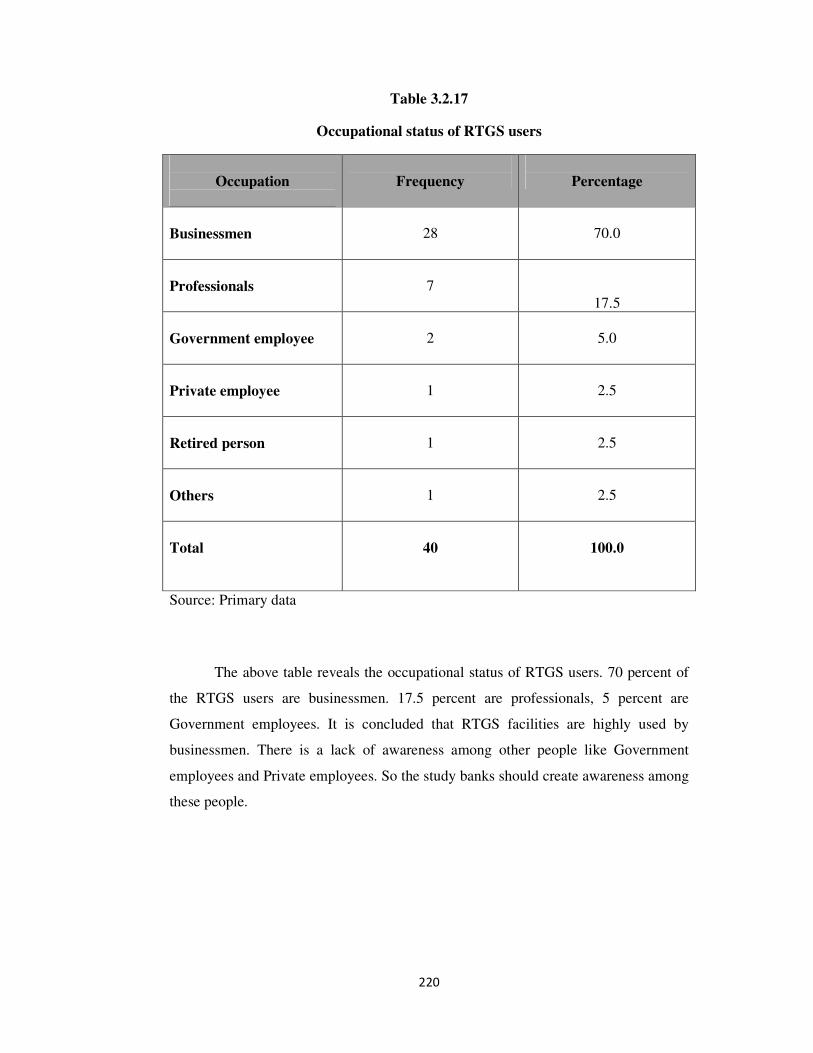

220

3.2.18 Occupational status of ECS users

221

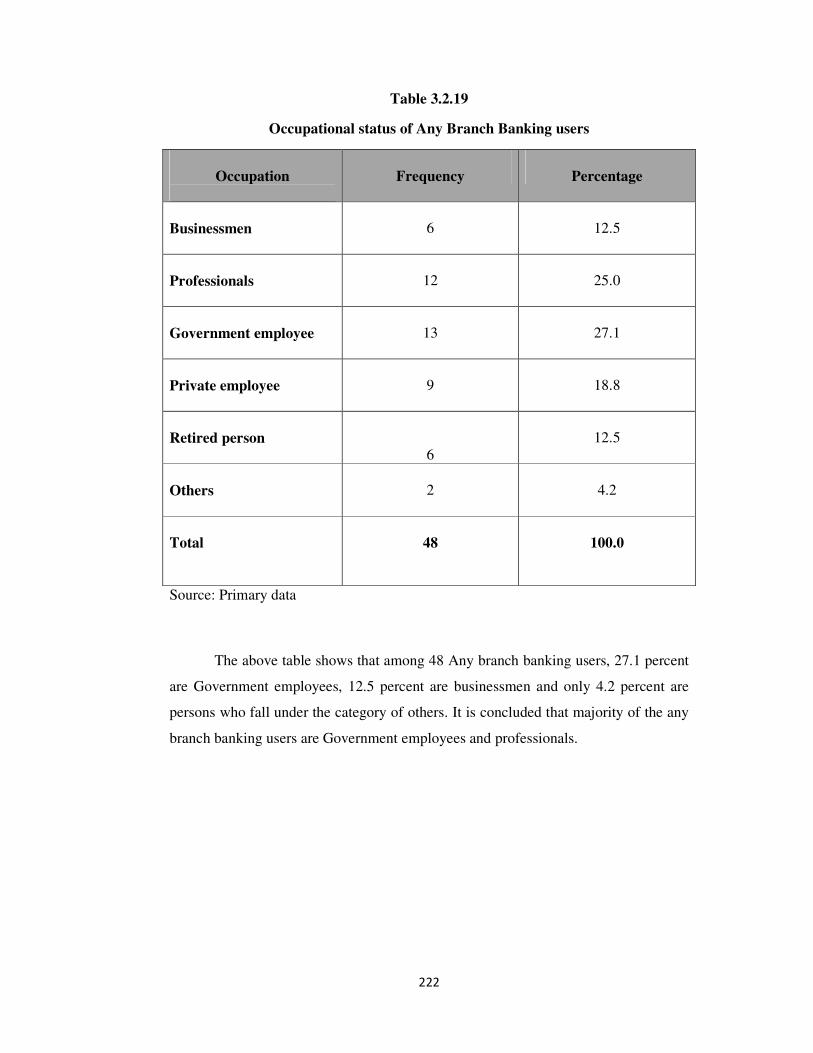

3.2.19

Occupational status of Any Branch Banking 222

3.2.20

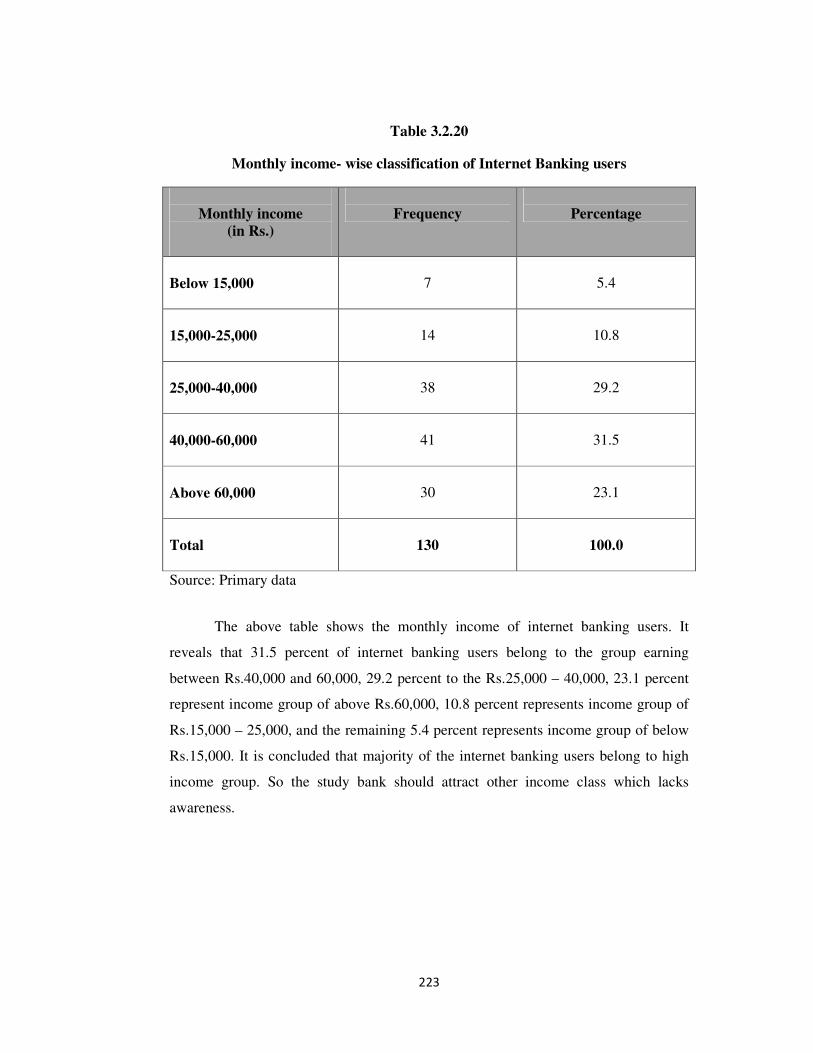

Monthly income-wise classification of Internet Banking users 223

vii

3.2.21

Monthly income-wise classification of Credit card users 224

3.2.22

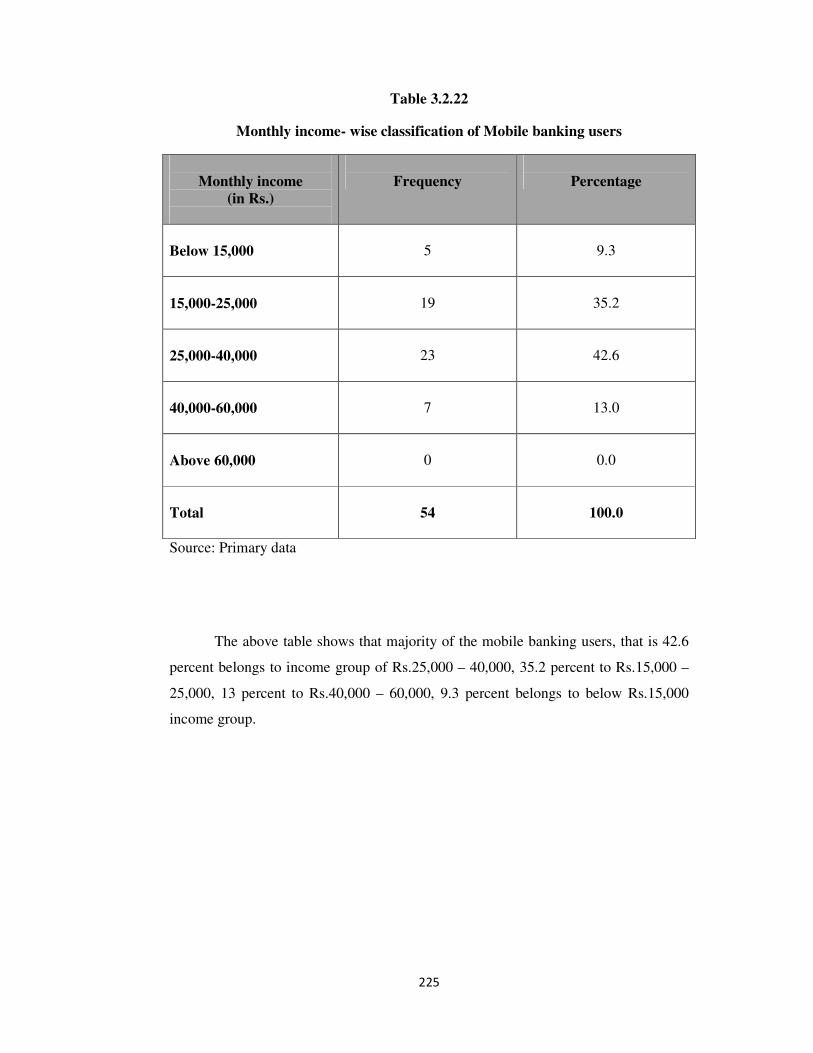

Monthly income-wise classification of Mobile banking users 225

3.2.23

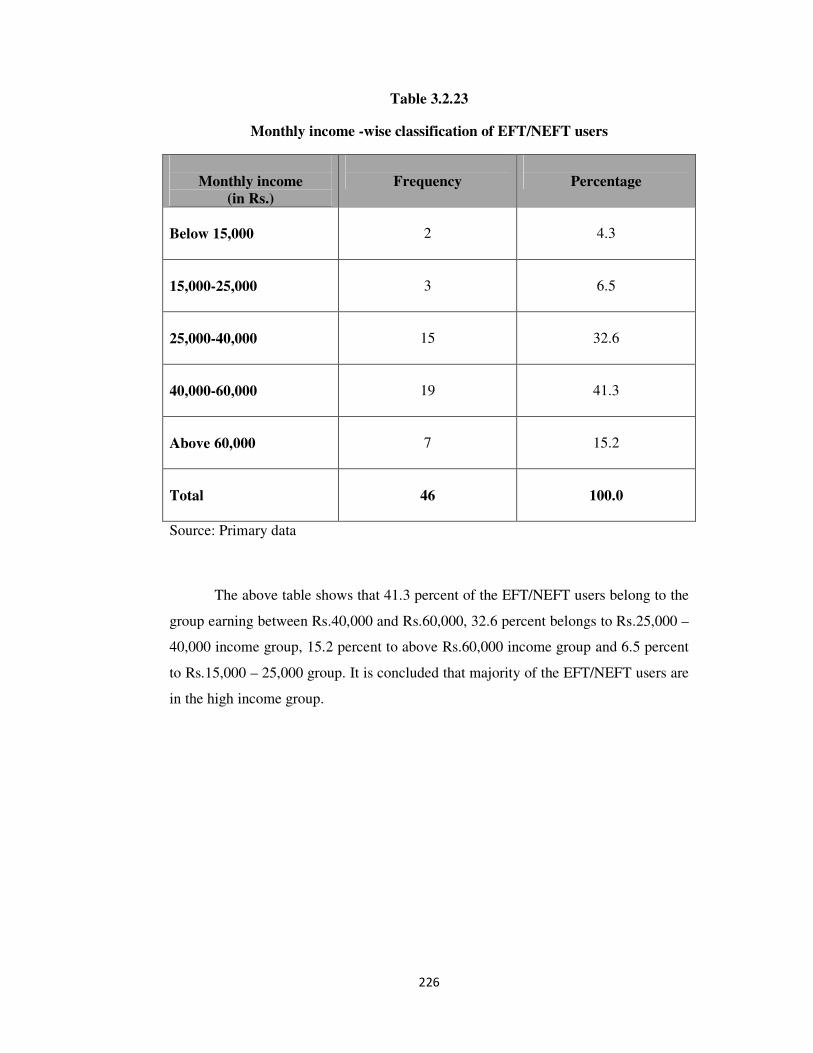

Monthly income-wise classification of EFT/NEFT users 226

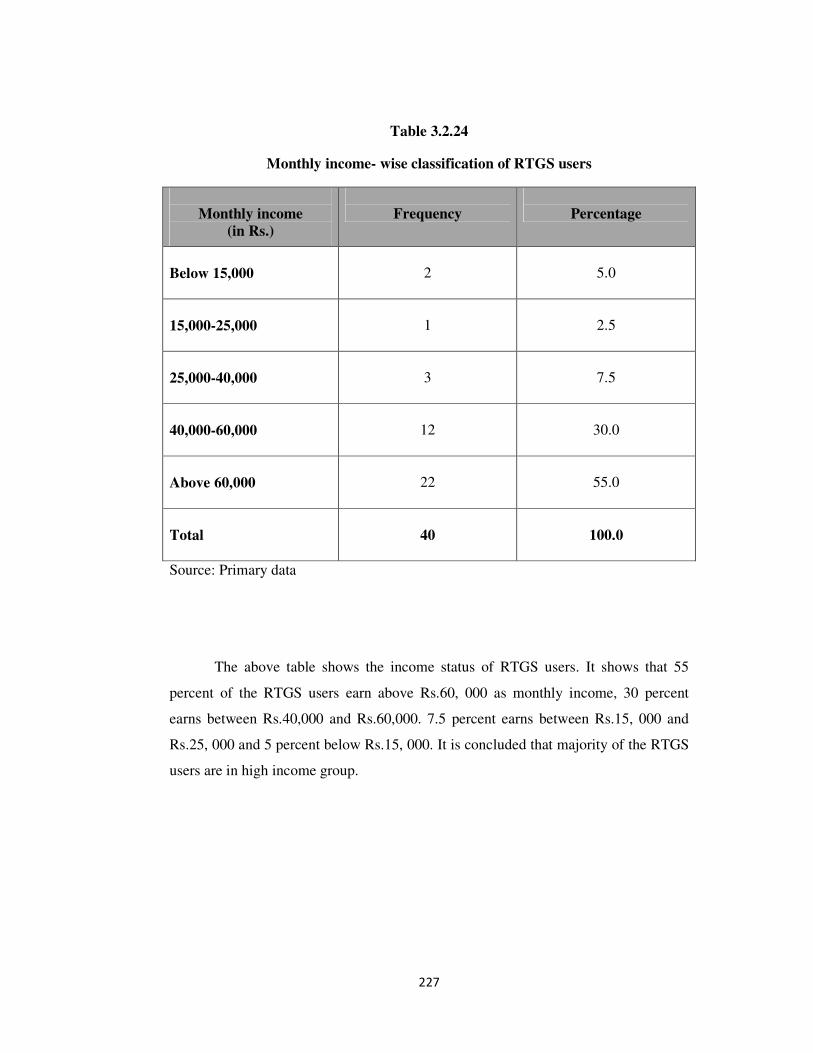

3.2.24 Monthly income-wise classification of RTGS users

227

3.2.25 Monthly income-wise classification of ECS users

228

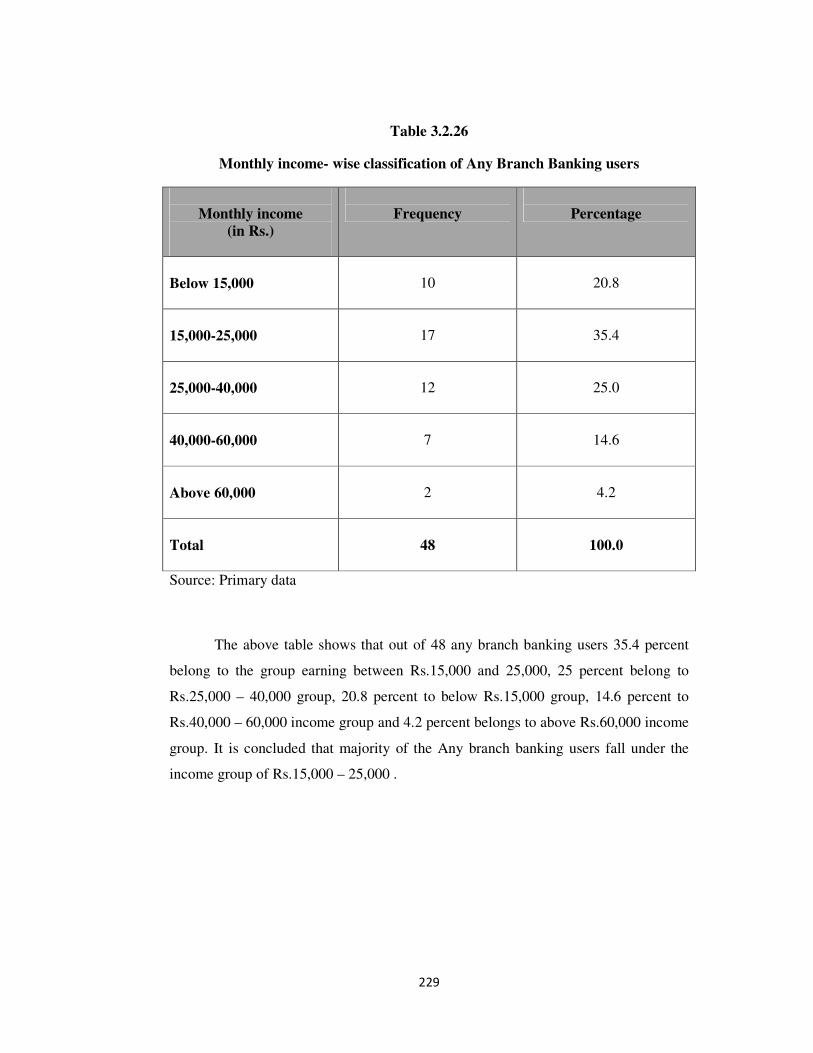

3.2.26

Monthly income-wise classification of Any Branch Banking 229

3.2.27 Respondents’ view on security of electronic delivery channels

230

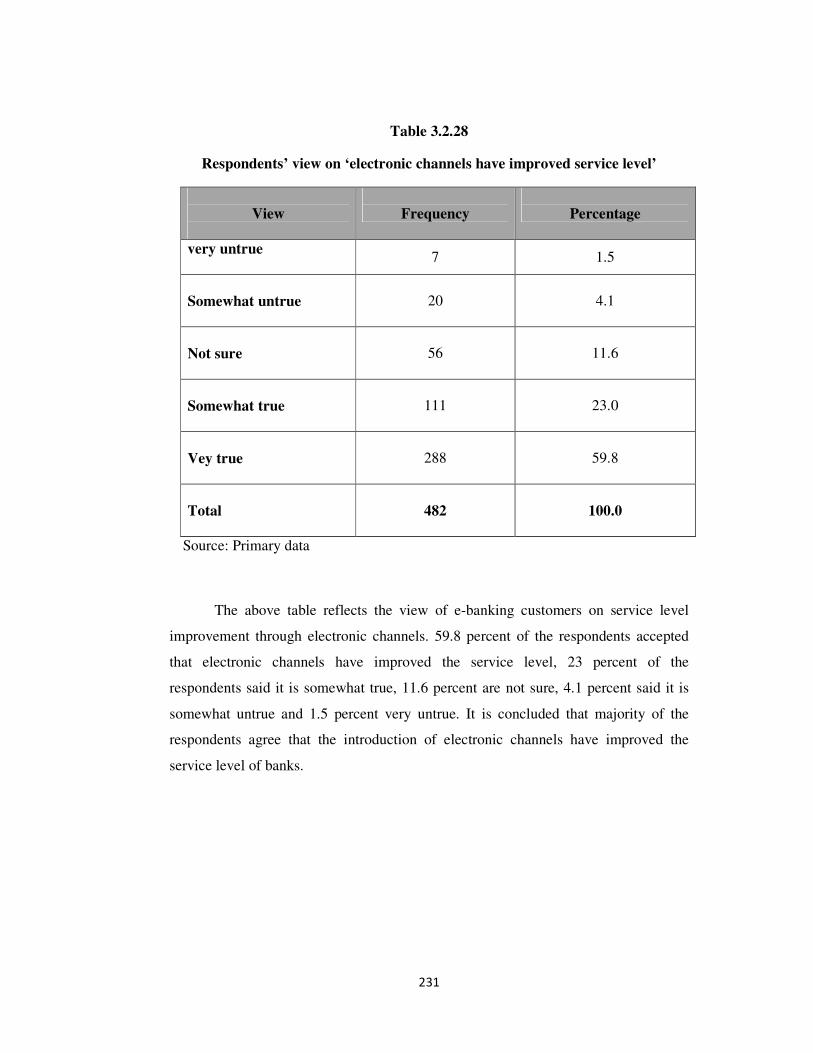

3.2.28 Respondents’ view on service level improvement

231

3.3.1

Association between age group and number of years of availing e-

banking services

232

3.3.2

Association between occupation and number of years of availing e- banking services

233

3.3.3

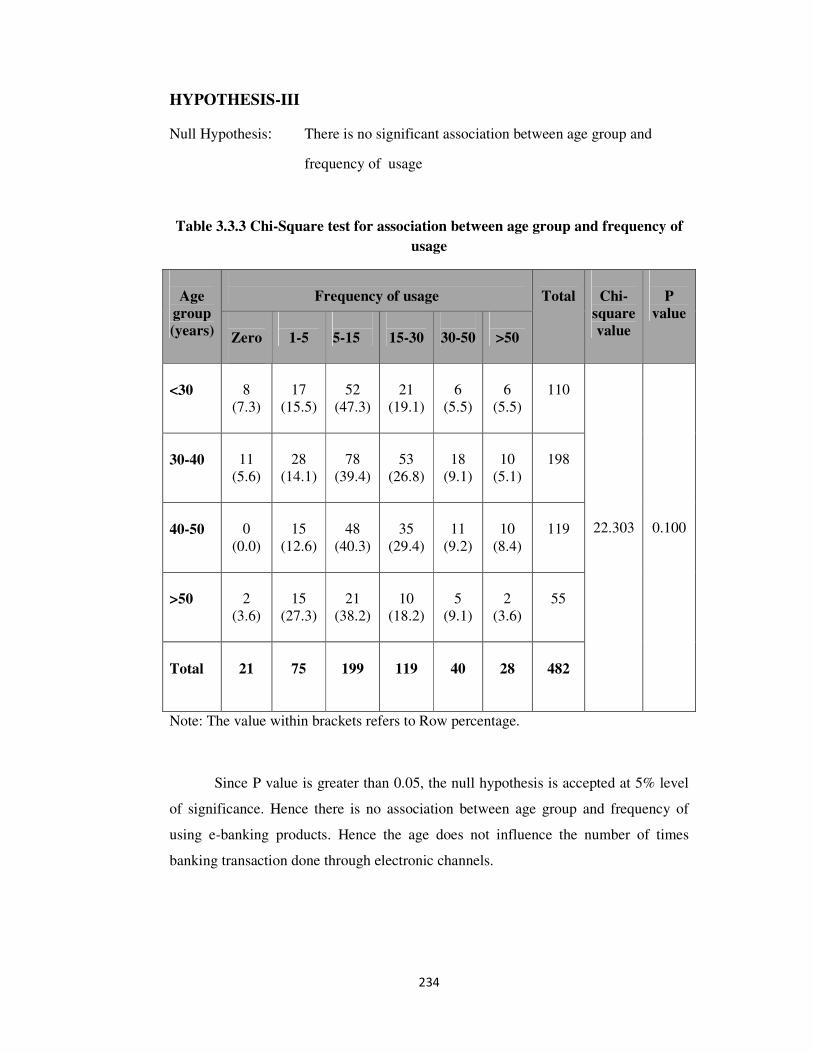

Association between age group and frequency of usage 234

3.3.4

Association between occupation and frequency of usage

235

3.3.5

Association between monthly income and frequency of usage 236

4.2.1

Multiple Response Analysis of Awareness towards convenience

services at ATM

244

4.2.2.

Multiple Response Analysis of Awareness towards value added

services at ATM

246

viii

4.2.3

Multiple Response Analysis of Awareness towards Debit card services at POS

248

4.2.4

Multiple Response Analysis of Awareness towards other services of Debit card

249

4.2.5

Multiple Response Analysis of Awareness towards convenience services of internet banking

251

4.2.6

Multiple Response Analysis of Awareness towards value added

services of internet banking

253

4.2.7

Multiple Response Analysis of Awareness towards information based services of mobile banking

255

4.2.8

Multiple Response Analysis of Awareness towards Financial

transaction based services of mobile banking

257

4.2.9

Multiple Response Analysis of Awareness towards convenience

services of credit card

258

4.2.10

Multiple Response Analysis of Awareness towards value added services of credit card

260

4.2.11

Multiple Response Analysis of Awareness towards Benefit services

of credit card

261

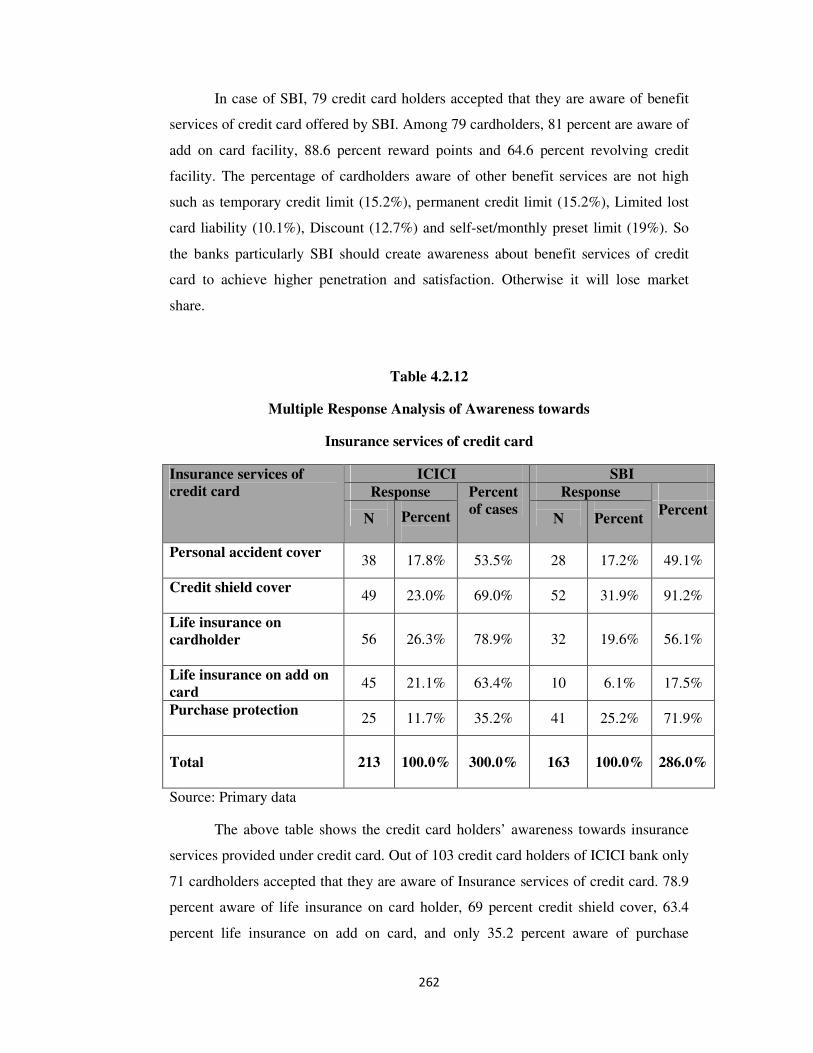

4.2.12

Multiple Response Analysis of Awareness towards insurance services of credit card

262

4.2.13

Multiple Response Analysis of Awareness towards Any Branch

Banking services

264

4.3.1

Association between age group and ICICI bank customers’

awareness with respect to dimensions of ATM –cum-Debit card

services

265

4.3.2 Association between age group and SBI bank customers’ awareness

with respect to dimensions of ATM –cum-Debit card services

267

ix

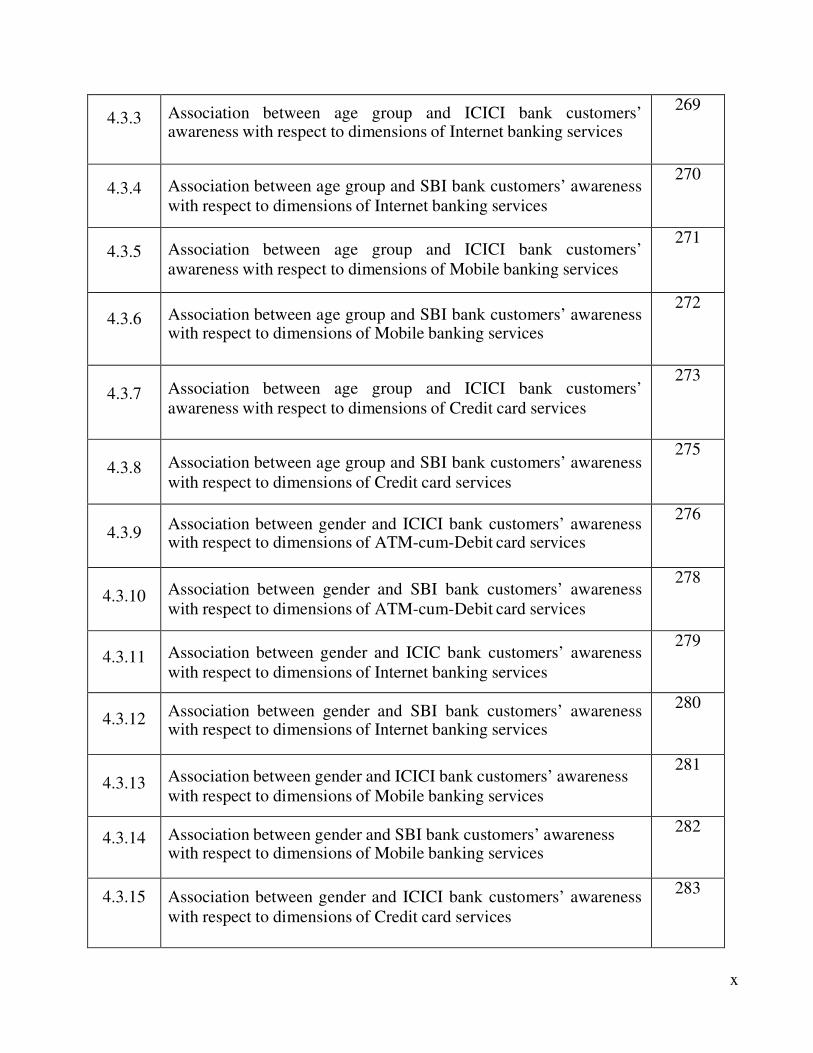

4.3.3

Association between age group and ICICI bank customers’ awareness with respect to dimensions of Internet banking services

269

4.3.4

Association between age group and SBI bank customers’ awareness

with respect to dimensions of Internet banking services

270

4.3.5

Association between age group and ICICI bank customers’

awareness with respect to dimensions of Mobile banking services

271

4.3.6

Association between age group and SBI bank customers’ awareness with respect to dimensions of Mobile banking services

272

4.3.7

Association between age group and ICICI bank customers’

awareness with respect to dimensions of Credit card services

273

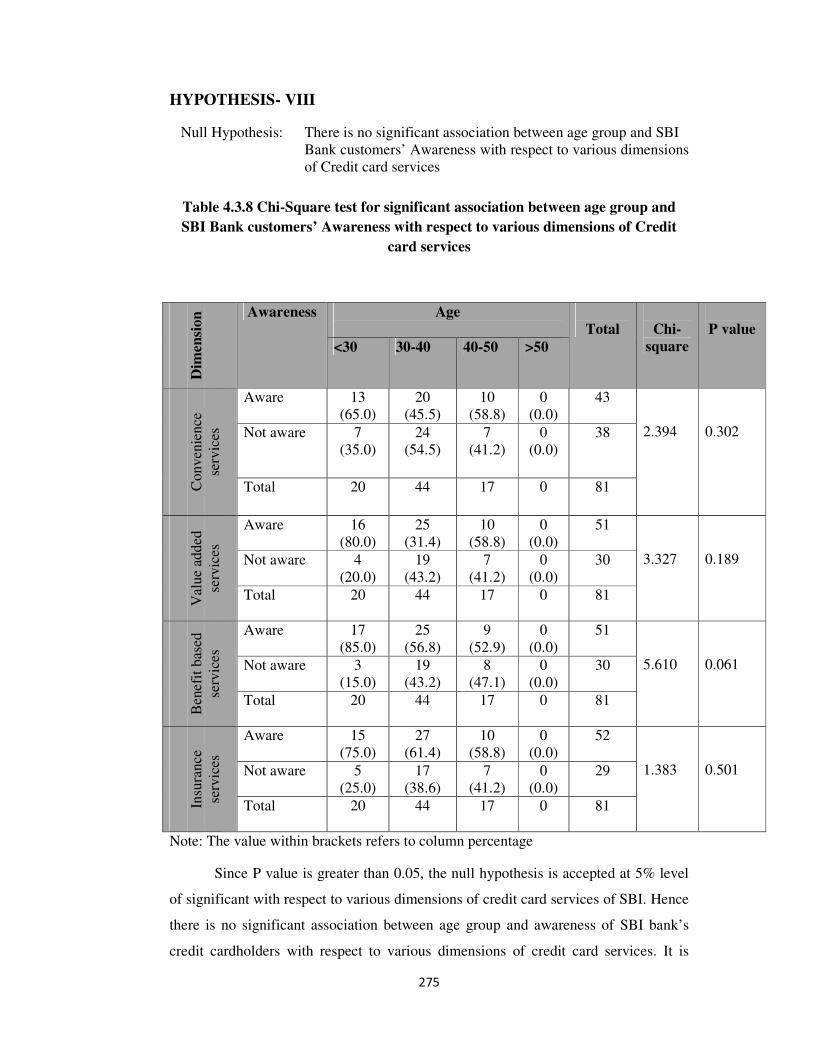

4.3.8

Association between age group and SBI bank customers’ awareness

with respect to dimensions of Credit card services

275

4.3.9

Association between gender and ICICI bank customers’ awareness with respect to dimensions of ATM-cum-Debit card services

276

4.3.10

Association between gender and SBI bank customers’ awareness

with respect to dimensions of ATM-cum-Debit card services

278

4.3.11

Association between gender and ICIC bank customers’ awareness

with respect to dimensions of Internet banking services

279

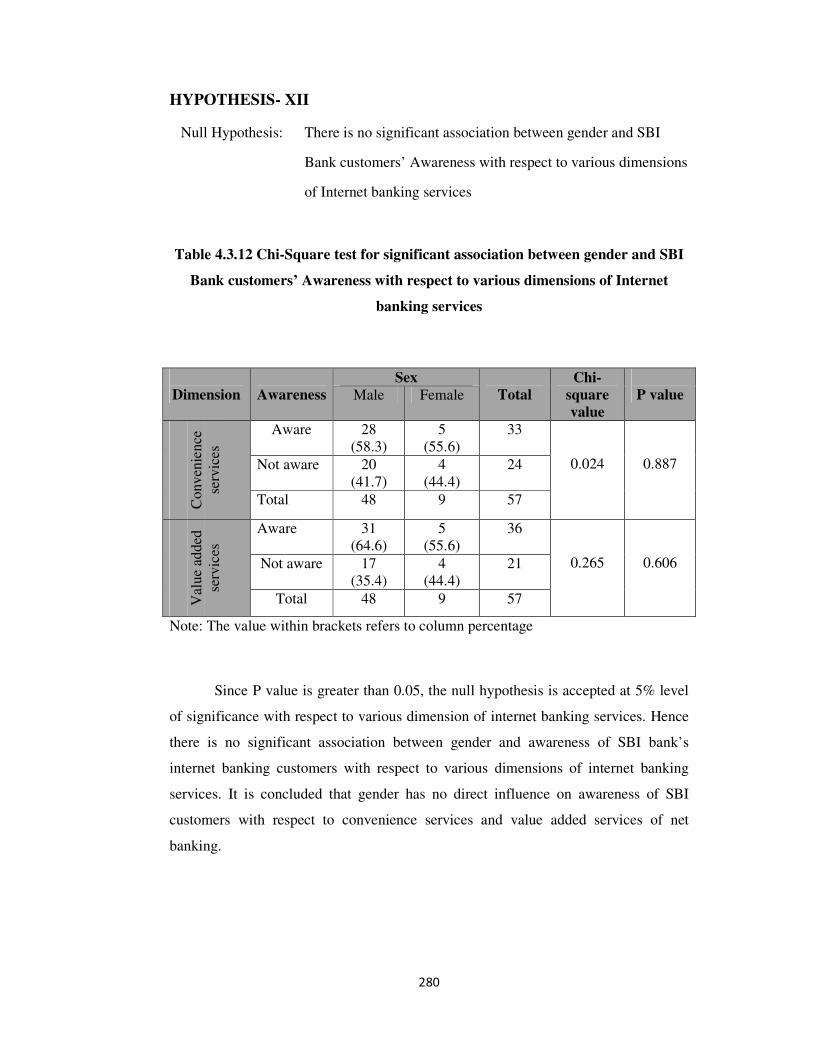

4.3.12

Association between gender and SBI bank customers’ awareness with respect to dimensions of Internet banking services

280

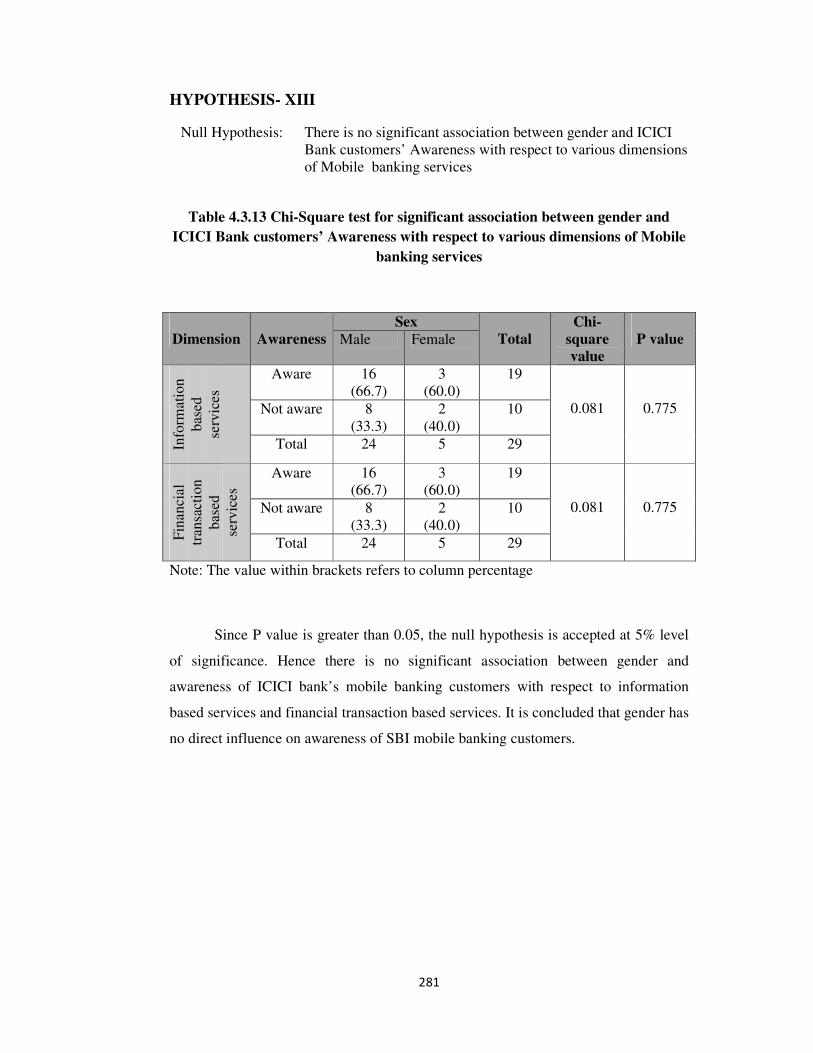

4.3.13

Association between gender and ICICI bank customers’ awareness

with respect to dimensions of Mobile banking services

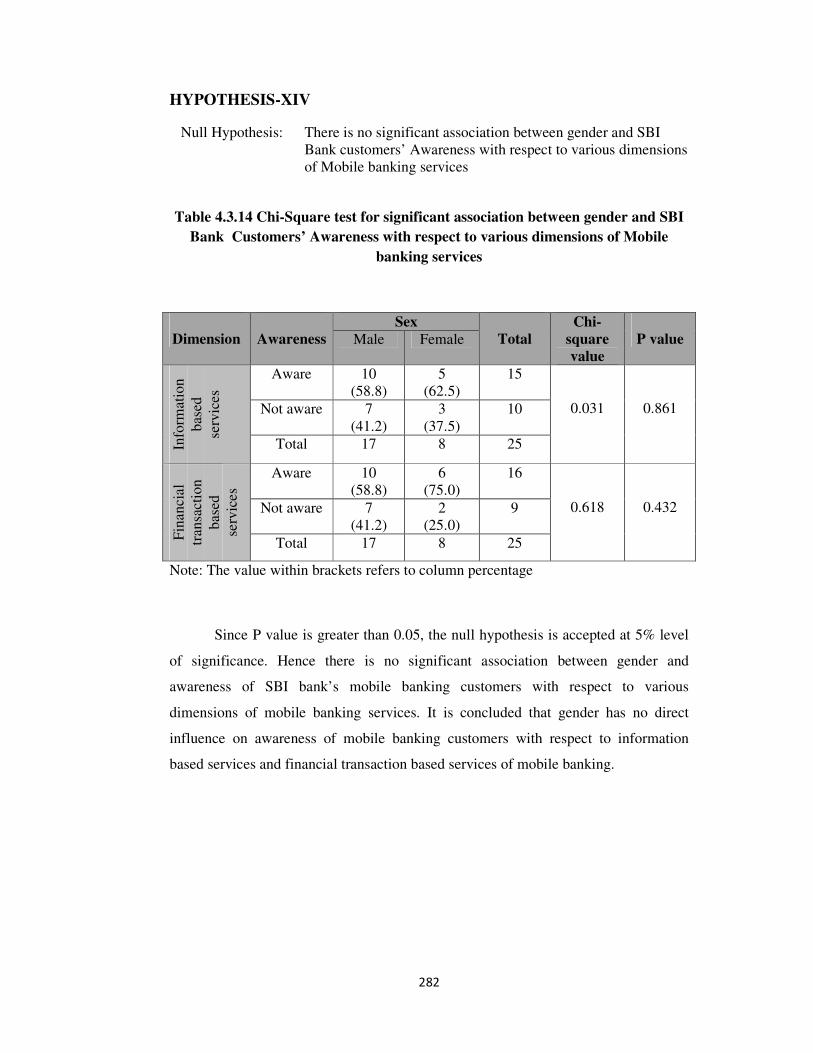

281

4.3.14

Association between gender and SBI bank customers’ awareness with respect to dimensions of Mobile banking services

282

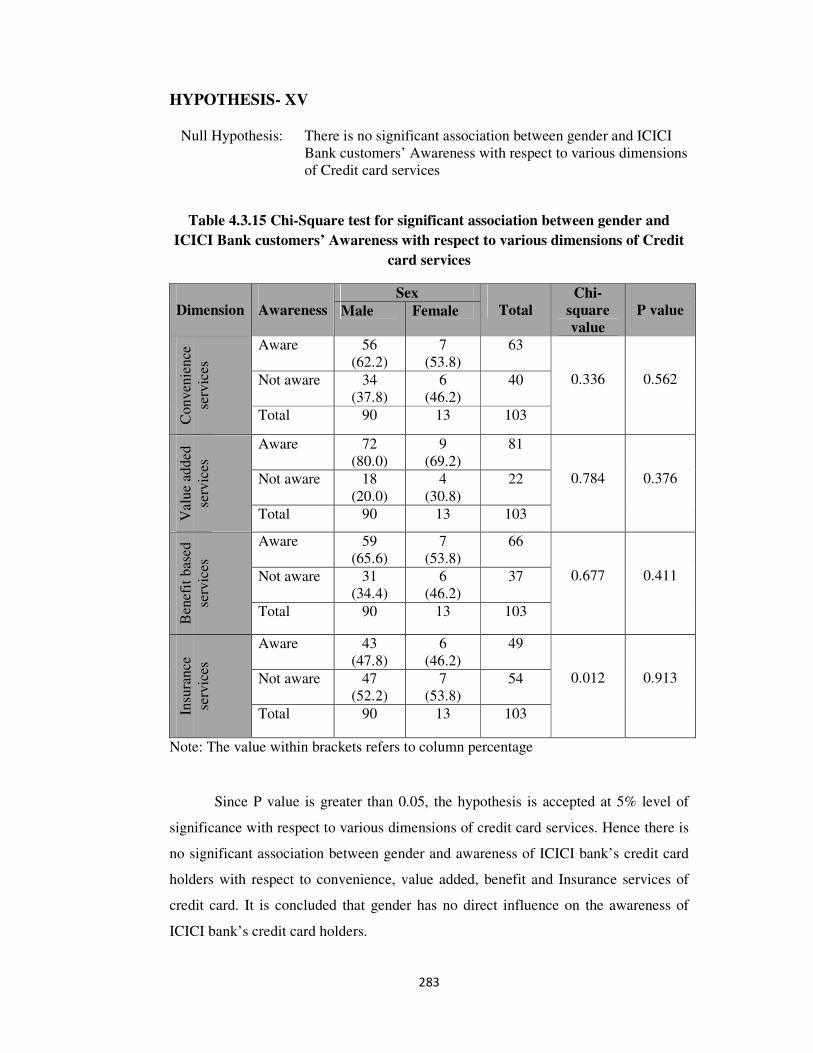

4.3.15

Association between gender and ICICI bank customers’ awareness

with respect to dimensions of Credit card services

283

x

4.3.16

Association between gender and SBI bank customers’ awareness with respect to dimensions of Credit card services

284

4.3.17

Association between educational qualification and ICICI bank

customers’ awareness with respect to dimensions of ATM-cum-

Debit card services

286

4.3.18

Association between educational qualification and SBI bank

customers’ awareness with respect to dimensions of ATM-cum-

Debit card services

288

4.3.19

Association between educational qualification and ICICI bank

customers’ awareness with respect to dimensions of Internet

banking services

290

4.3.20

Association between educational qualification and SBI bank

customers’ awareness with respect to dimensions of Internet

banking services

291

4.3.21

Association between educational qualification and ICICI bank

customers’ awareness with respect to dimensions of Mobile banking

services

292

4.3.22

Association between educational qualification and SBI bank

customers’ awareness with respect to dimensions of Mobile banking

services

293

4.3.23

Association between educational qualification and ICICI bank

customers’ awareness with respect to dimensions of Credit card

services

294

4.3.24

Association between educational qualification and SBI bank

customers’ awareness with respect to dimensions of Credit card

services

296

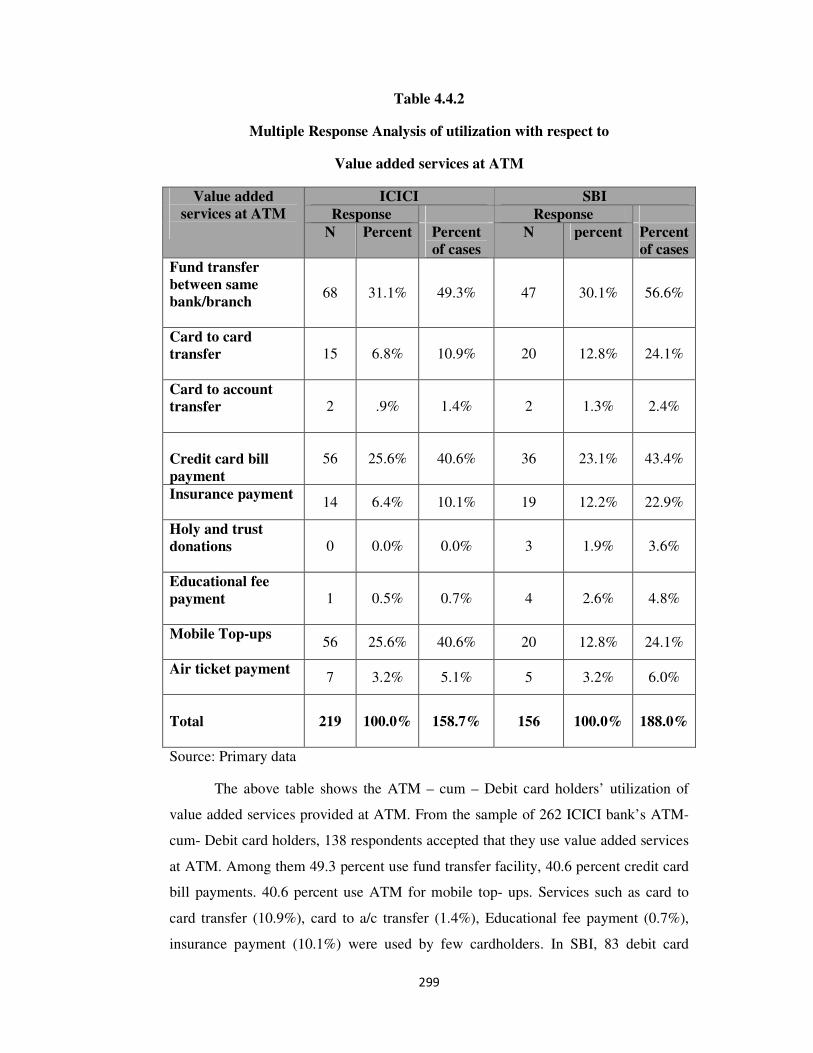

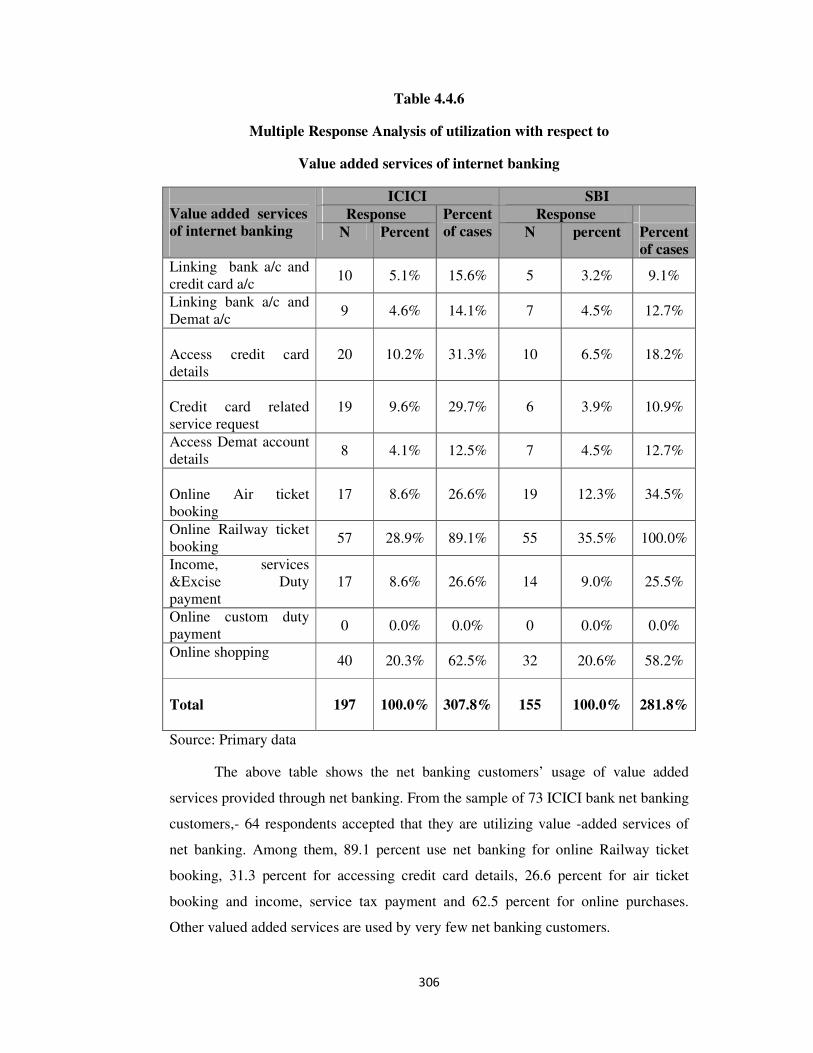

4.4.1

Multiple Response Analysis of utilization with respect to convenience services at ATM

297

xi

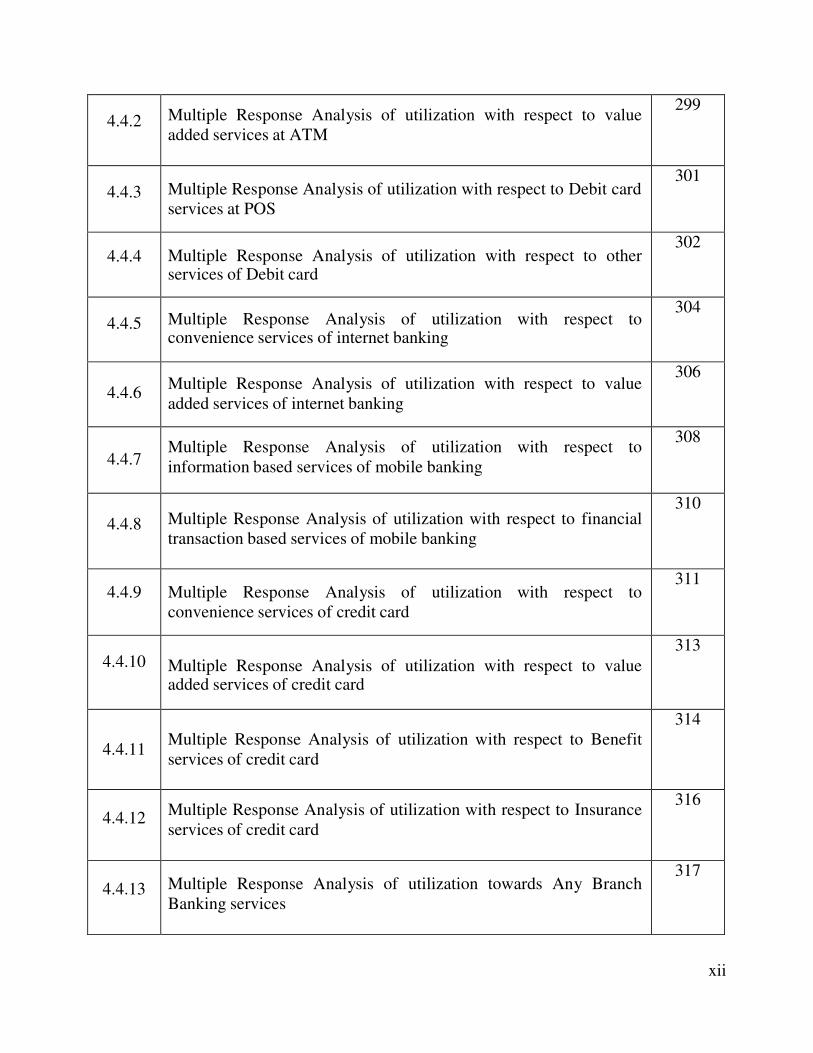

4.4.2

Multiple Response Analysis of utilization with respect to value

added services at ATM

299

4.4.3

Multiple Response Analysis of utilization with respect to Debit card

services at POS

301

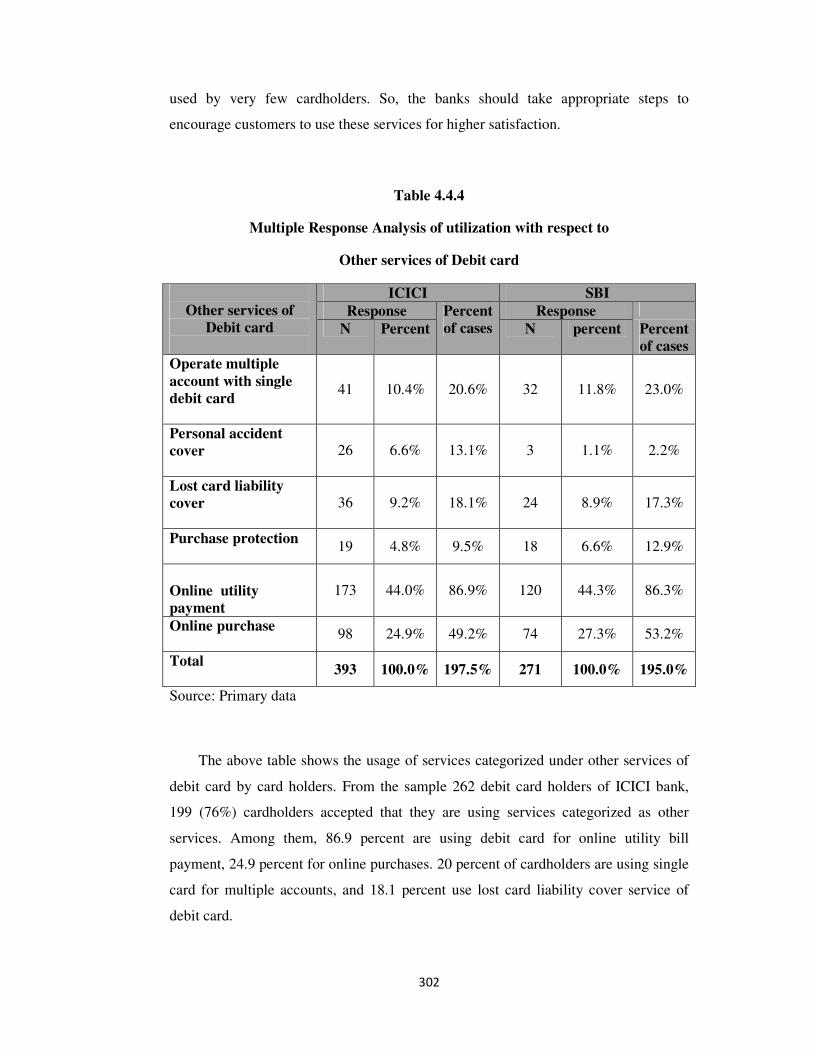

4.4.4

Multiple Response Analysis of utilization with respect to other services of Debit card

302

4.4.5

Multiple Response Analysis of utilization with respect to convenience services of internet banking

304

4.4.6

Multiple Response Analysis of utilization with respect to value

added services of internet banking

306

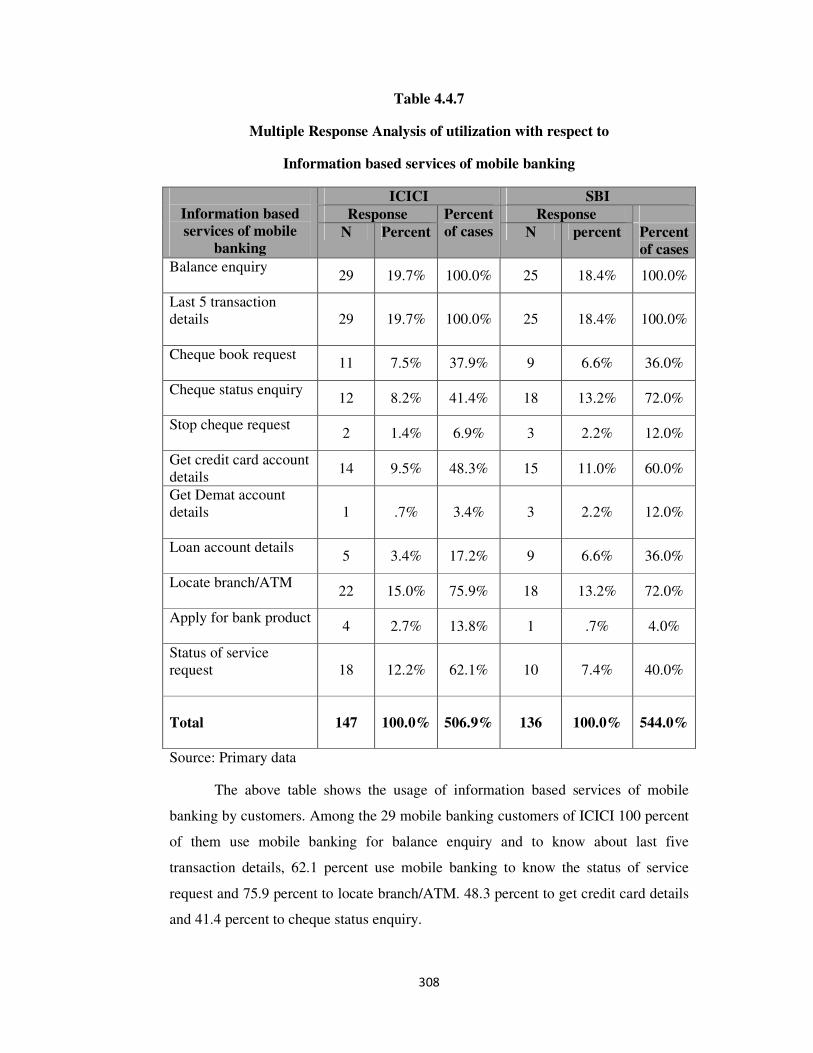

4.4.7

Multiple Response Analysis of utilization with respect to

information based services of mobile banking

308

4.4.8

Multiple Response Analysis of utilization with respect to financial

transaction based services of mobile banking

310

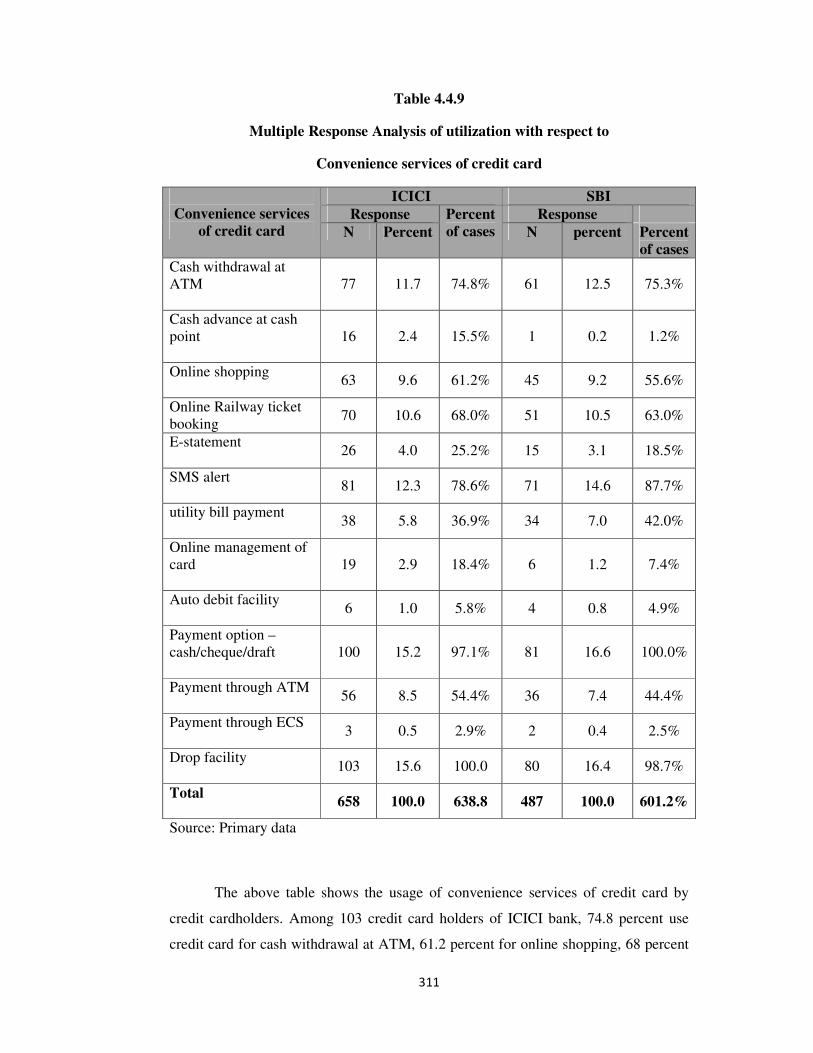

4.4.9

Multiple Response Analysis of utilization with respect to

convenience services of credit card

311

4.4.10

Multiple Response Analysis of utilization with respect to value added services of credit card

313

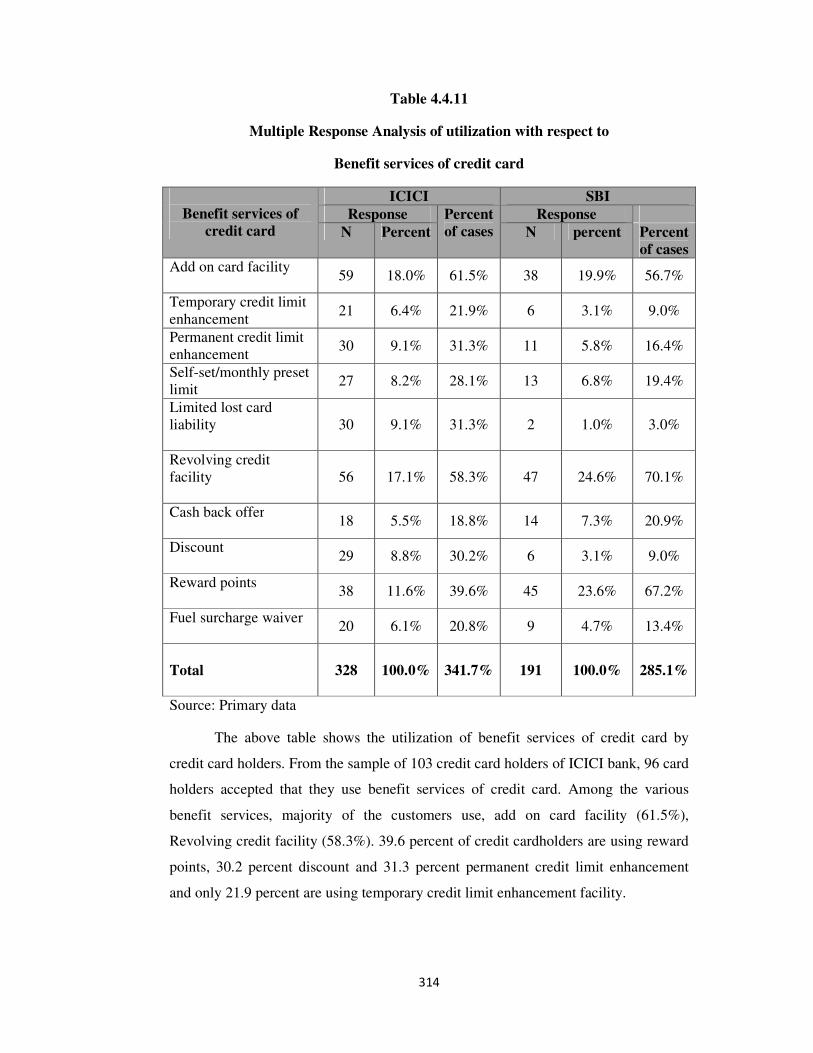

4.4.11

Multiple Response Analysis of utilization with respect to Benefit

services of credit card

314

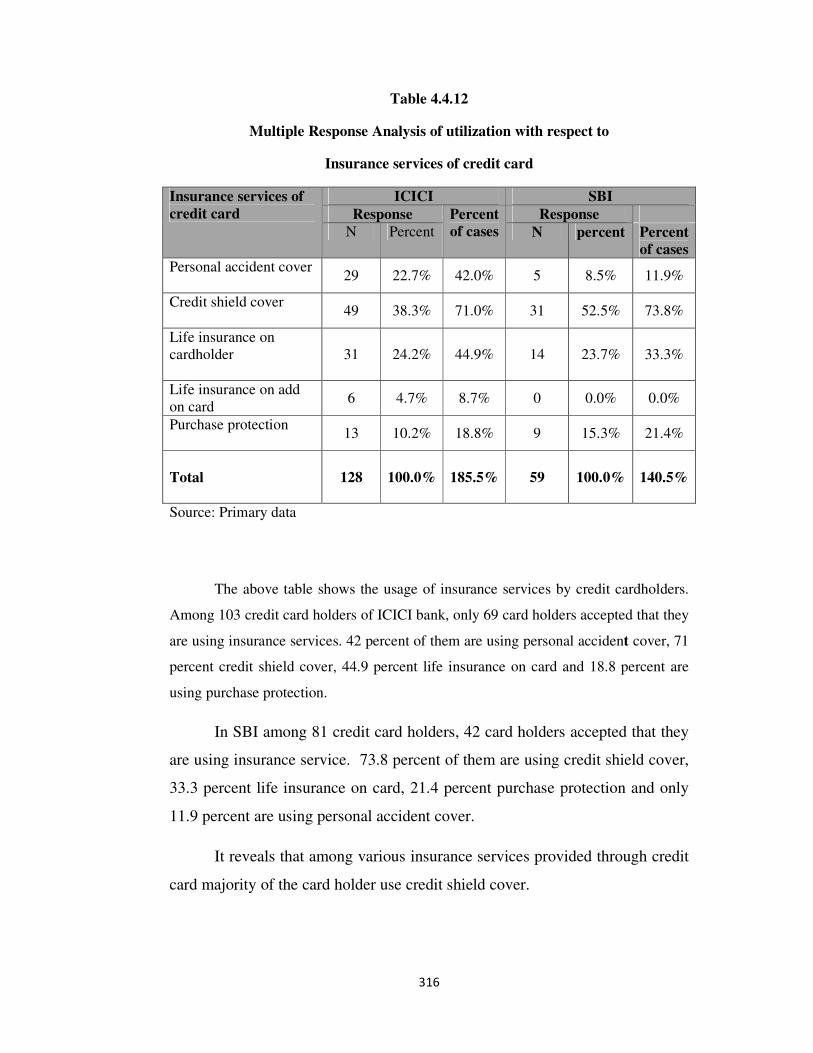

4.4.12

Multiple Response Analysis of utilization with respect to Insurance

services of credit card

316

4.4.13

Multiple Response Analysis of utilization towards Any Branch

Banking services

317

xii

4.5.1

Association between occupation and ICICI bank customers’

utilization with respect to dimensions of ATM-cum-Debit card

services

318

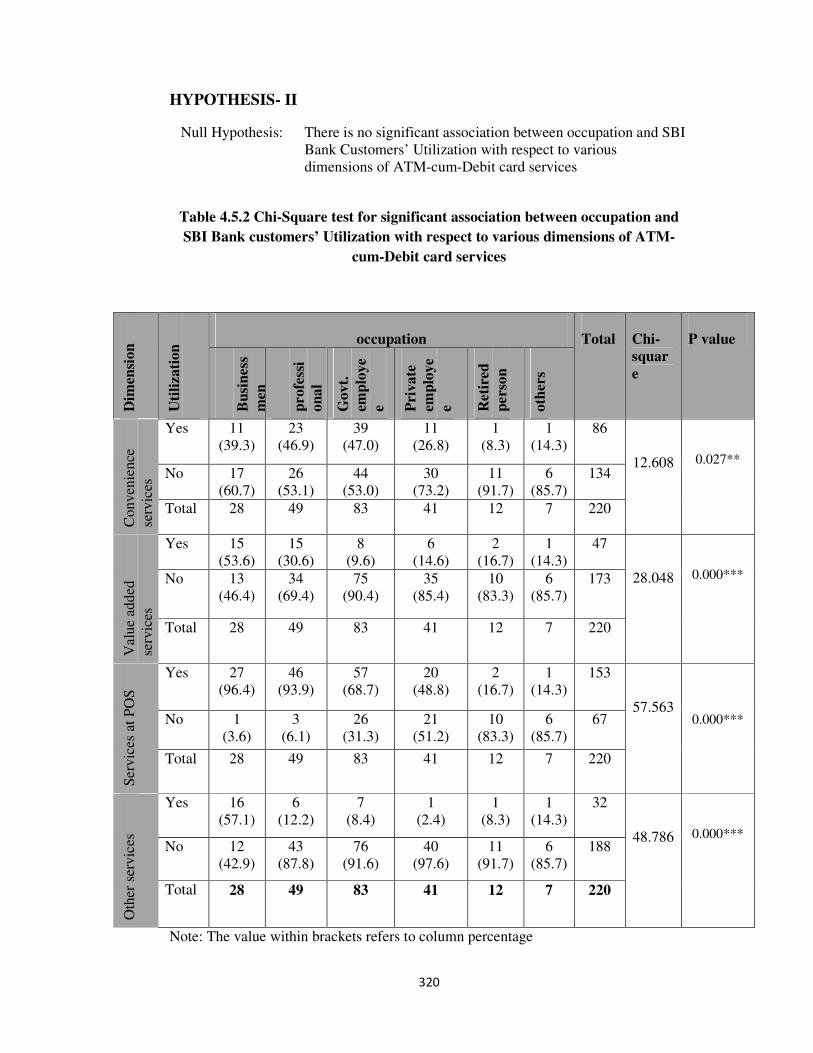

4.5.2

Association between occupation and SBI bank customers’

utilization with respect to dimensions of ATM-cum-Debit card

services

320

4.5.3

Association between occupation and ICICI bank customers’ utilization with respect to dimensions of Internet banking services

322

4.5.4

Association between occupation and SBI bank customers’

utilization with respect to dimensions of Internet banking services

323

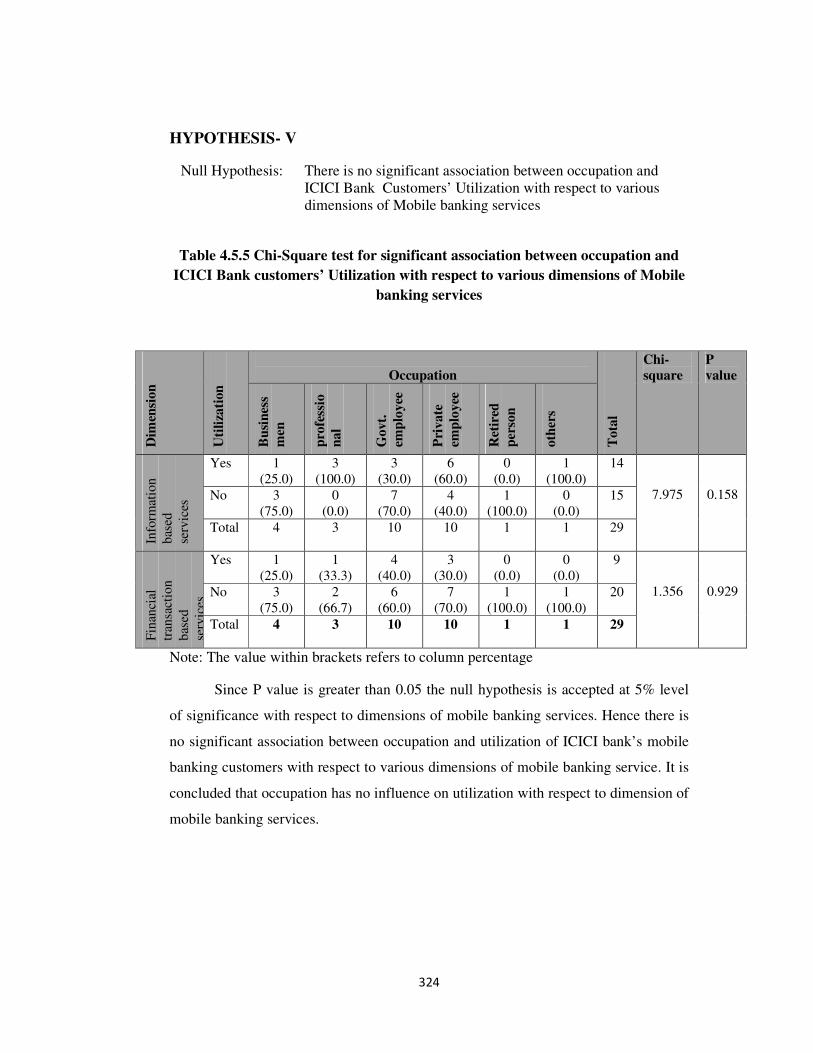

4.5.5

Association between occupation and ICICI bank customers’ utilization with respect to dimensions of Mobile banking services

324

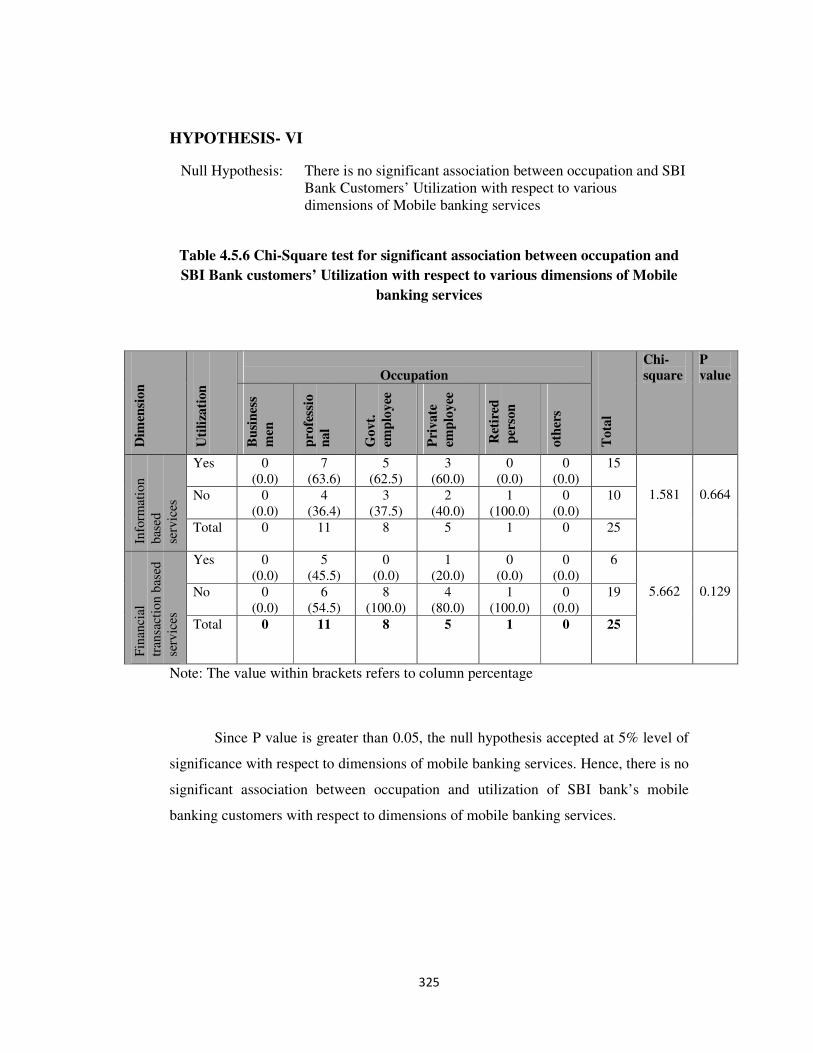

4.5.6

Association between occupation and SBI bank customers’

utilization with respect to dimensions of Mobile banking services

325

4.5.7

Association between occupation and ICICI bank customers’ utilization with respect to dimensions of Credit card services

326

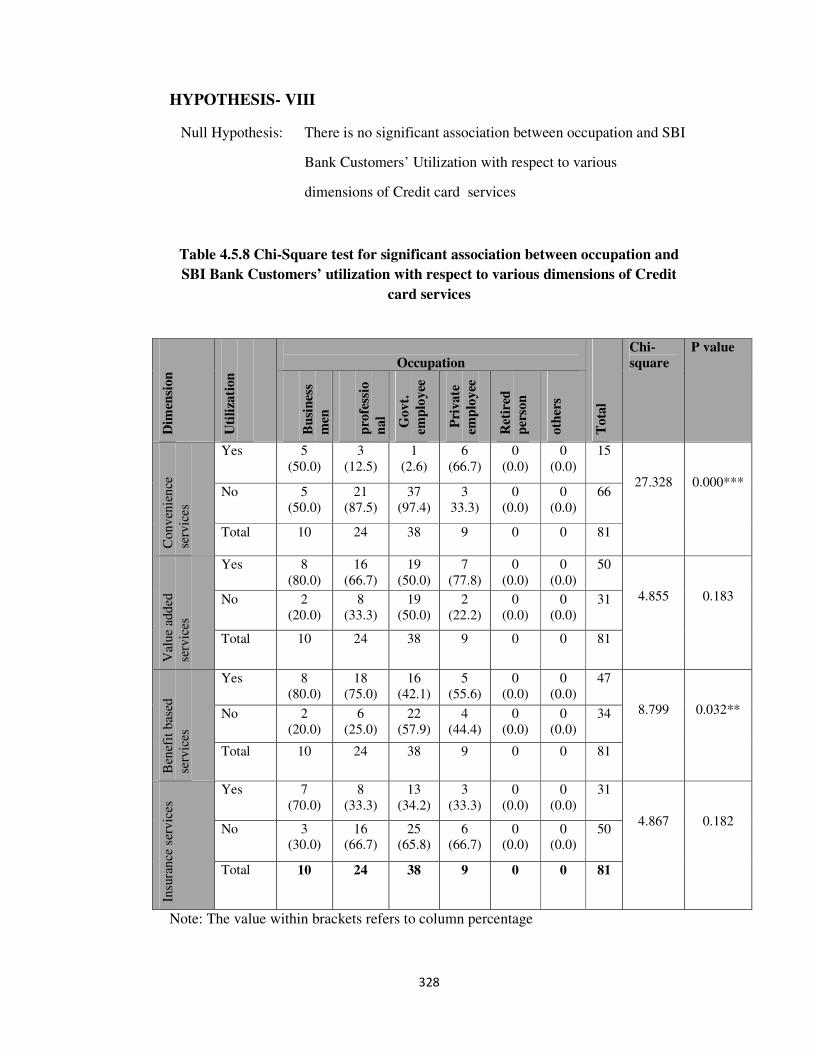

4.5.8

Association between occupation and SBI bank customers’

utilization with respect to dimensions of Credit card services

328

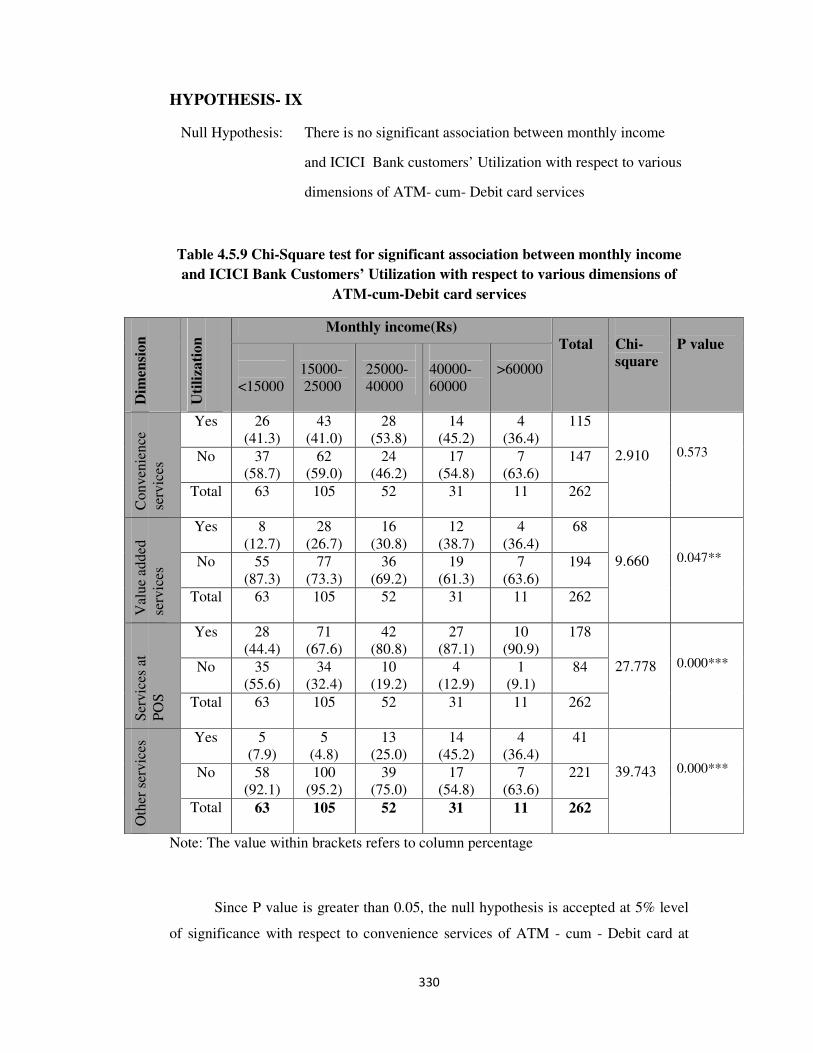

4.5.9

Association between monthly income and ICICI bank customers’

utilization with respect to dimensions of ATM-cum-Debit card

services

330

4.5.10

Association between monthly income and SBI bank customers’

utilization with respect to dimensions of ATM-cum-Debit card

services

332

4.5.11

Association between monthly income and ICICI bank customers’

utilization with respect to dimensions of Internet banking services

334

4.5.12 Association between monthly income and SBI bank customers’ utilization with respect to dimensions of Internet banking services

335

xiii

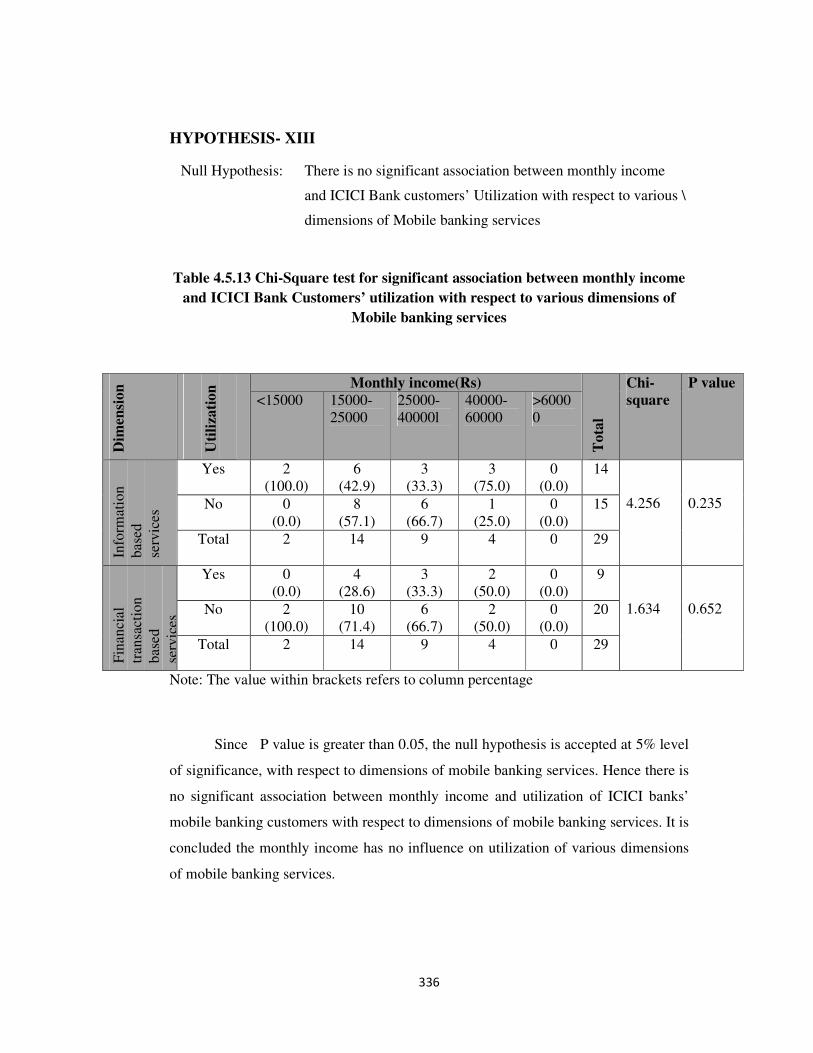

4.5.13

Association between monthly income and ICICI bank customers’

utilization with respect to dimensions of Mobile banking services

336

4.5.14

Association between monthly income and SBI bank customers’

utilization with respect to dimensions of Mobile banking services

337

4.5.15

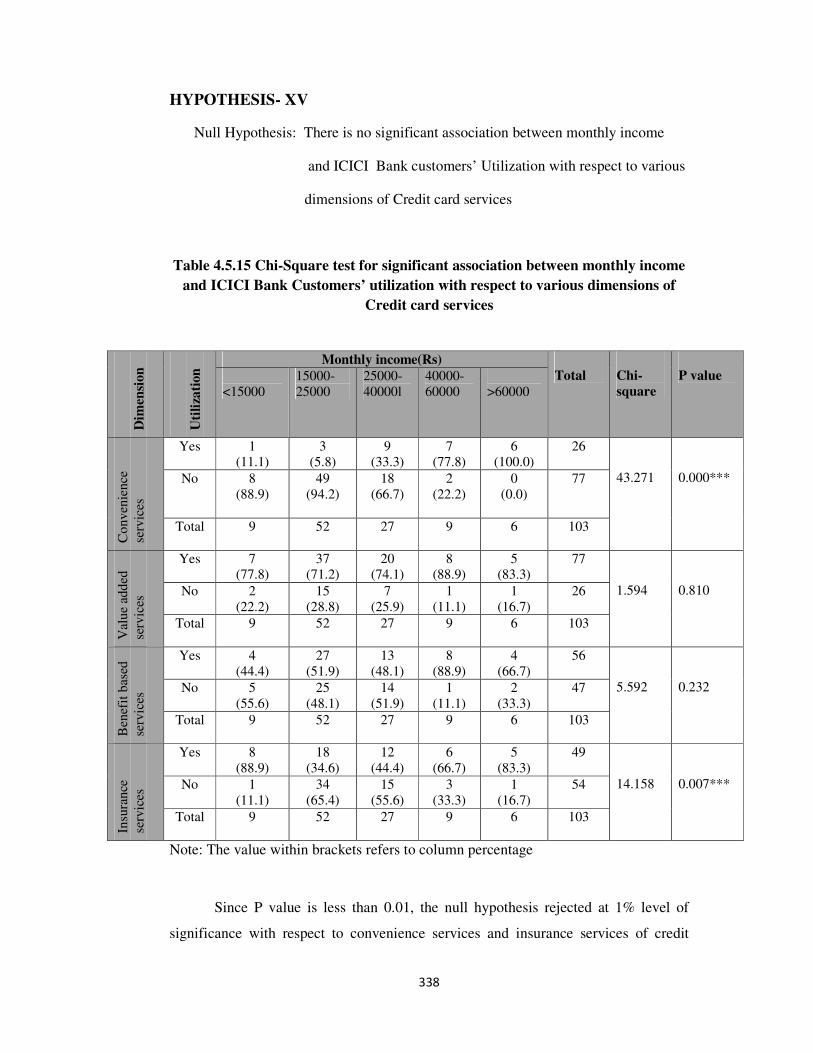

Association between monthly income and ICICI bank customers’

utilization with respect to dimensions of Credit card services

338

4.5.16

Association between monthly income and SBI bank customers’

utilization with respect to dimensions of Credit card services

340

5.2.1

Respondents interest in complaining about the problem 355

5.2.2 Reason for not making complaints

356

5.2.3

Methods of complaining 357

5.2.4

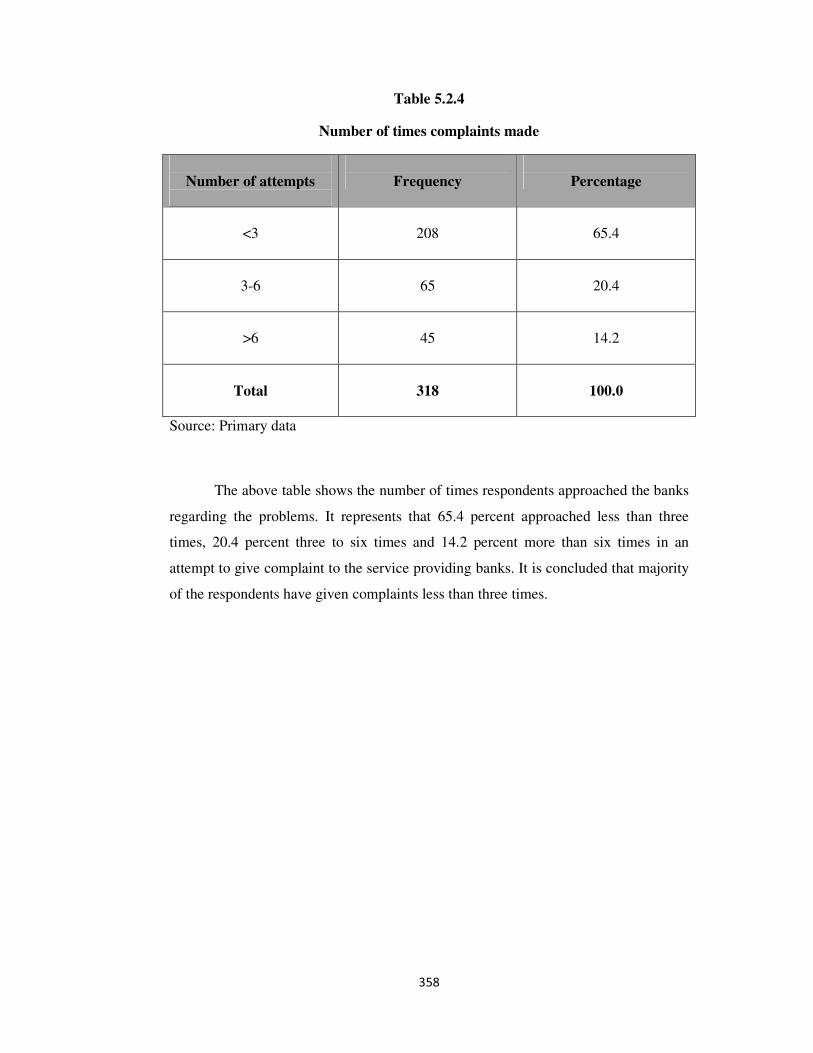

Number of times complaints made 358

5.2.5

Problems solved by banks 359

5.2.6

Duration of time required for the bank to solve the problem 360

5.2.7

Overall problems of e-banking customers 361

5.2.8

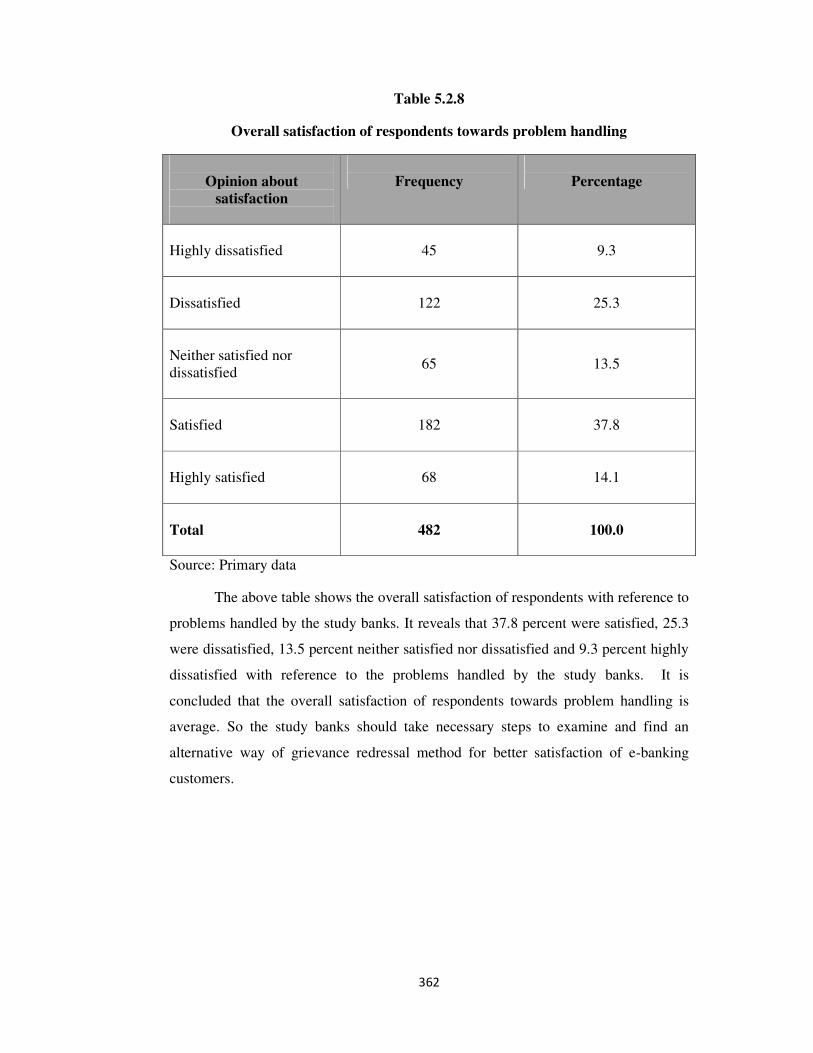

Overall satisfaction of respondents towards problem handling 362

5.3.1

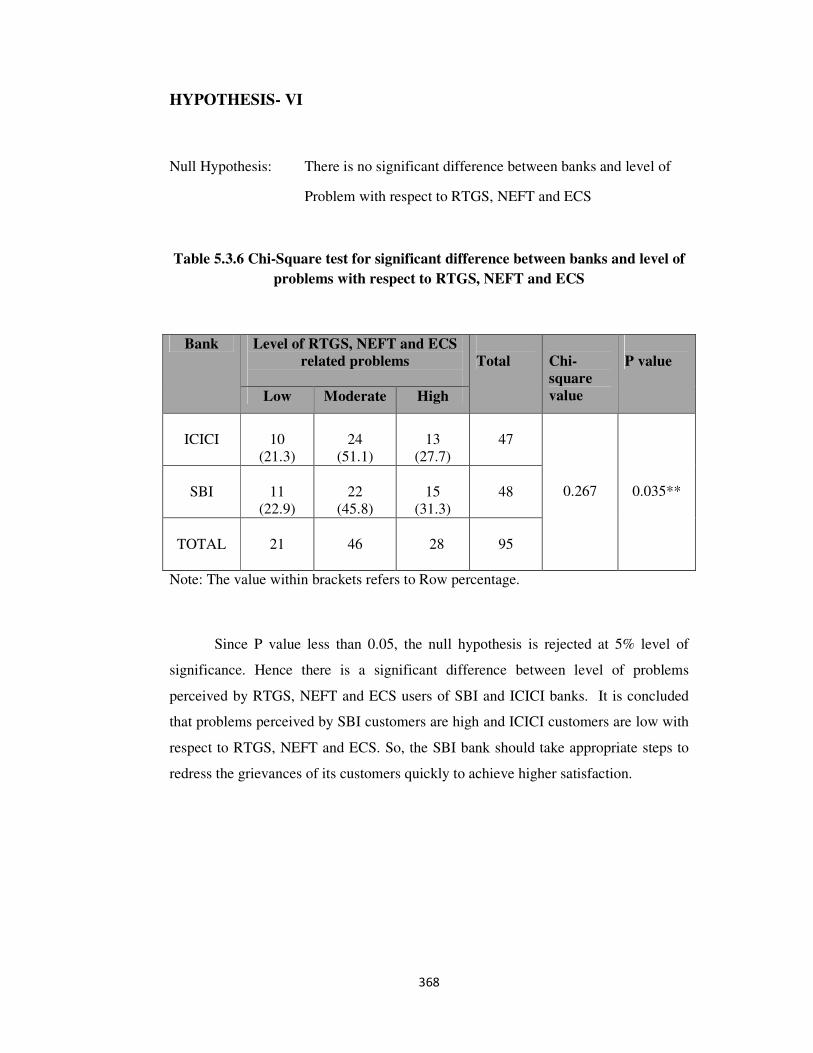

Difference between banks and level of problems with respect to ATM

363

5.3.2

Difference between banks and level of problems with respect to credit card

364

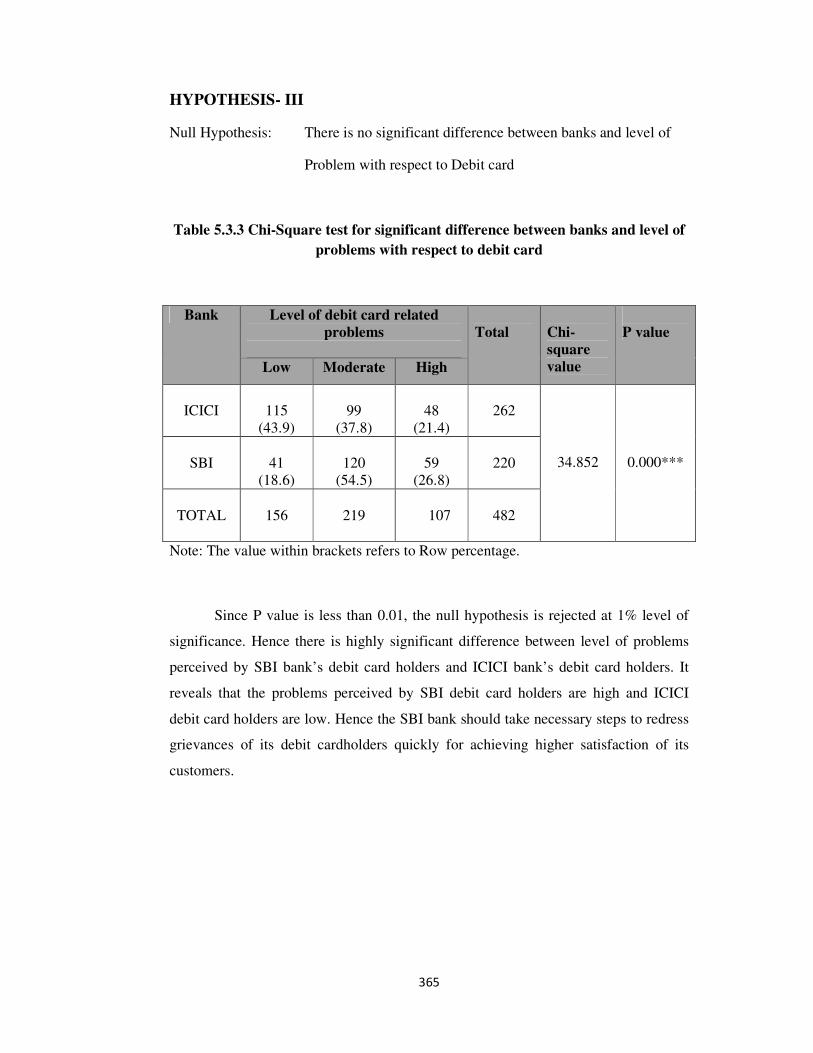

5.3.3 Difference between banks and level of problems with respect to

debit card

365

5.3.4 Difference between banks and level of problems with respect to internet banking

366

xiv

5.3.5

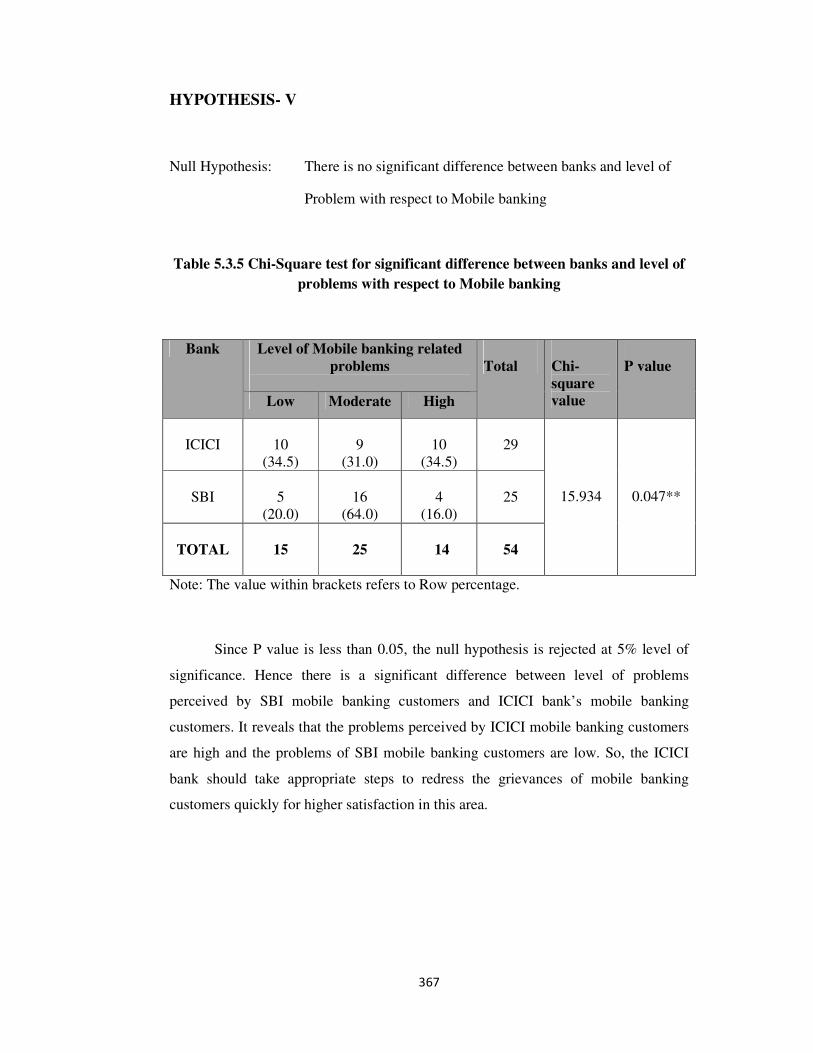

Difference between banks and level of problems with respect to

mobile banking

367

5.3.6

Difference between banks and level of problems with respect to RTGS, NEFT, and ECS

368

5.3.7

Difference between banks and level of problems with respect to Any

branch banking

369

5.3.8

Difference between banks and level of problems with respect to fraud

370

5.3.9

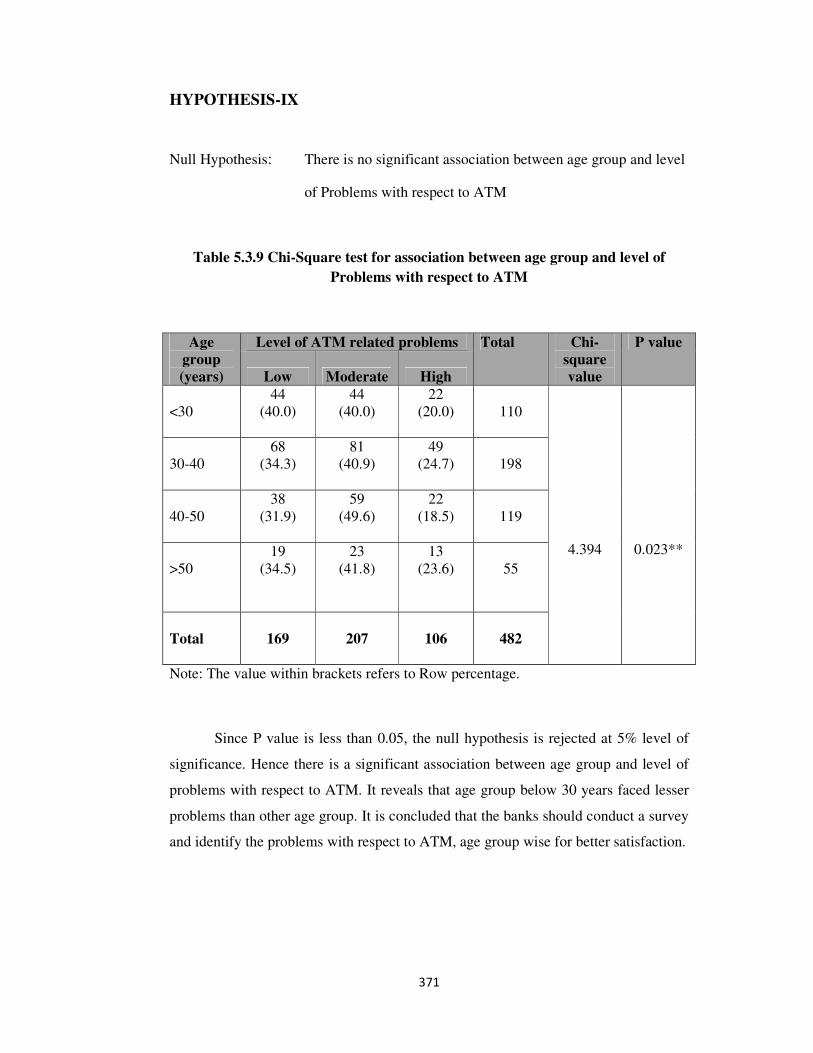

Association between age group and level of Problems with respect

to ATM

371

5.3.10

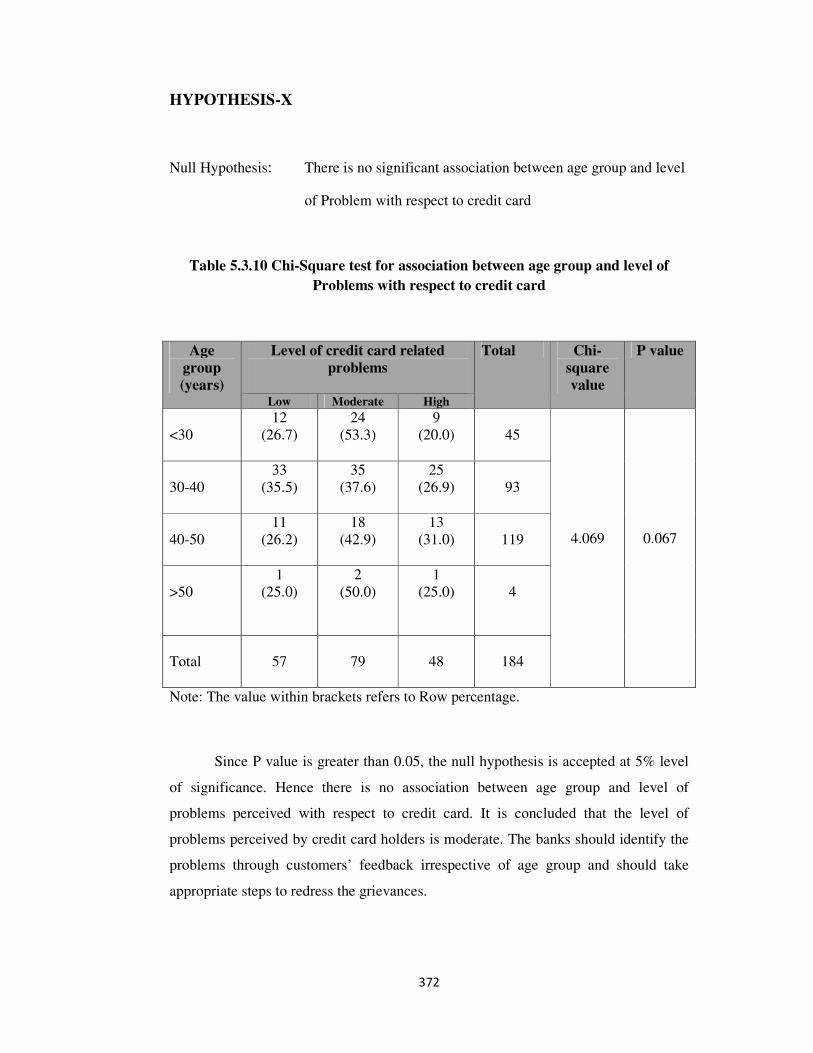

Association between age group and level of Problems with respect to Credit card

372

5.3.11

Association between age group and level of Problems with respect to DEBIT card

373

5.3.12

Association between age group and level of Problems with respect to Internet banking

374

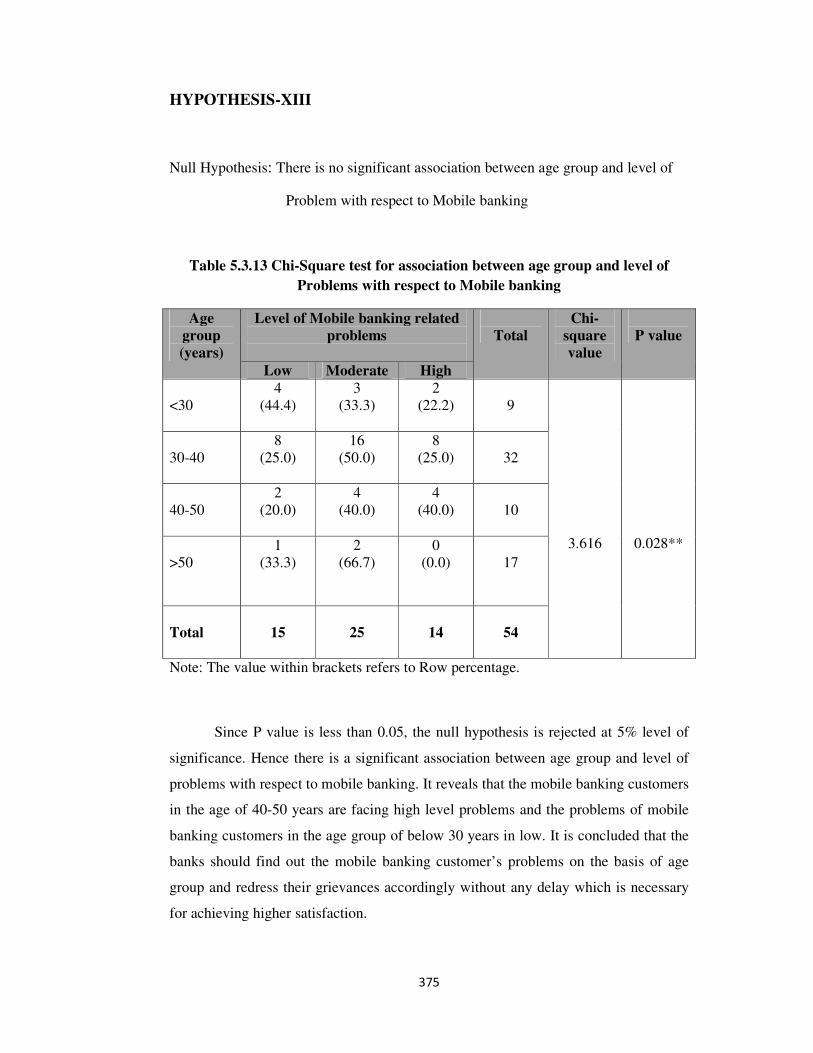

5.3.13

Association between age group and level of Problems with respect to Mobile banking

375

5.3.14

Association between age group and level of Problems with respect

to fraud

376

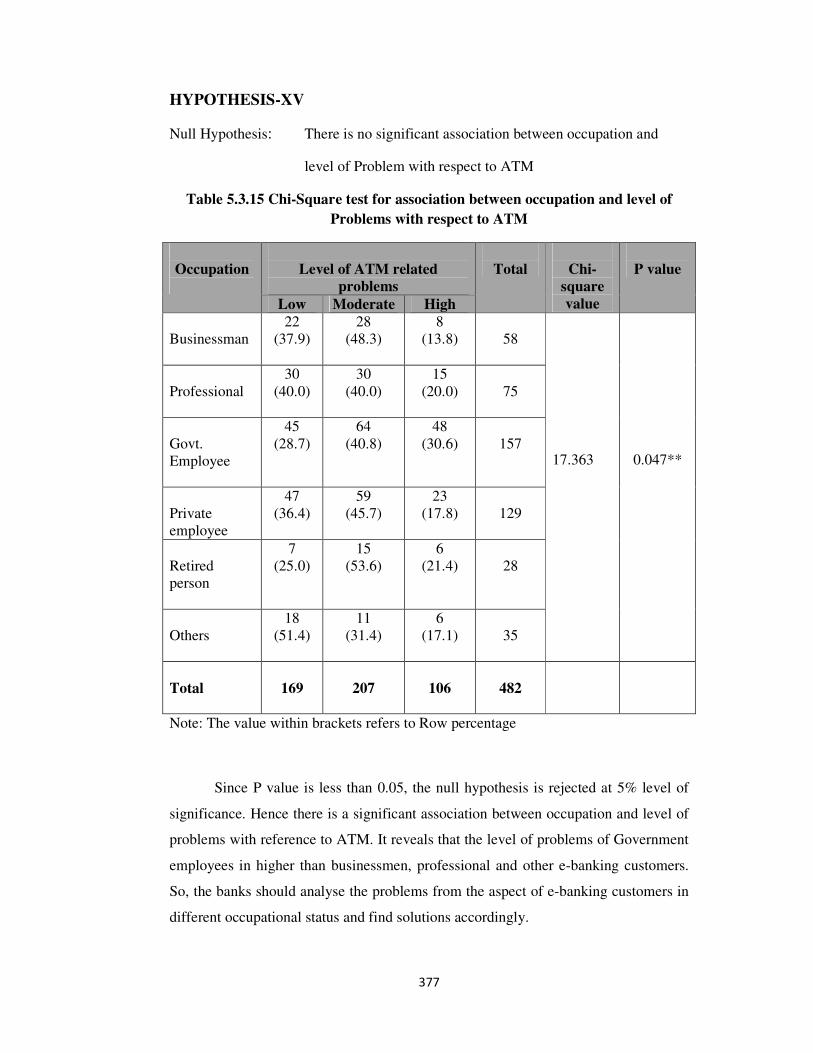

5.3.15

Association between occupation and level of Problems with respect to ATM

377

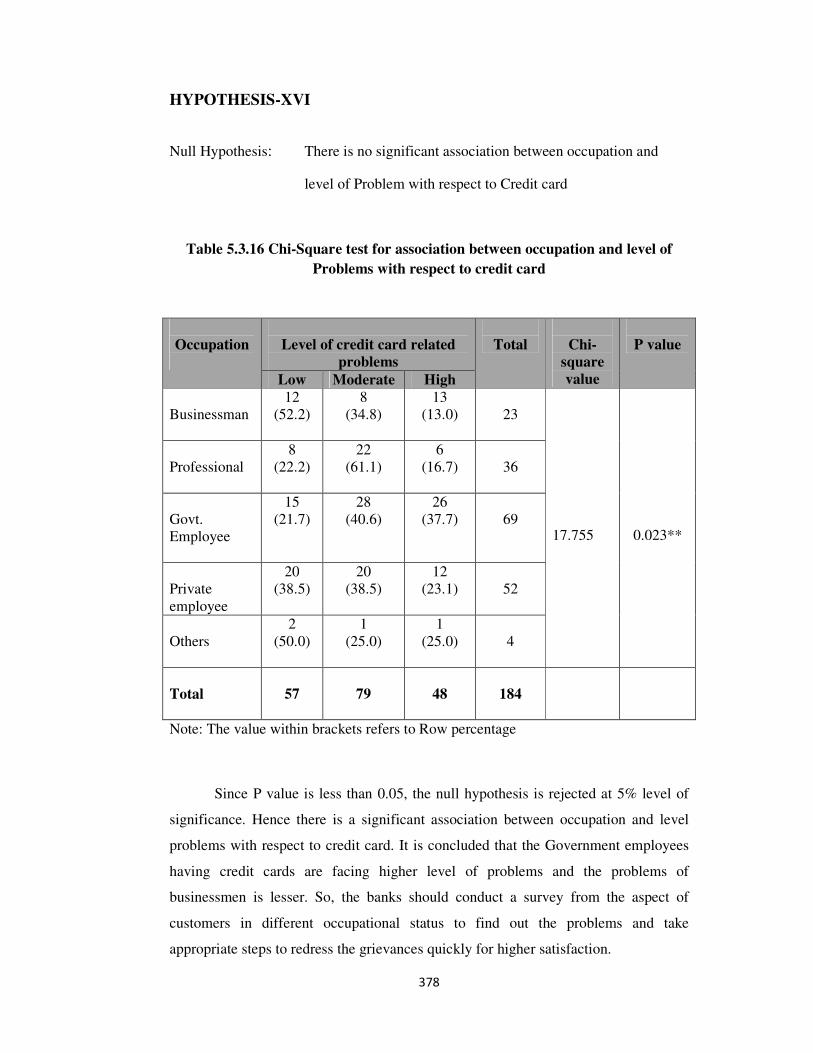

5.3.16

Association between occupation and level of Problems with respect to Credit card

378

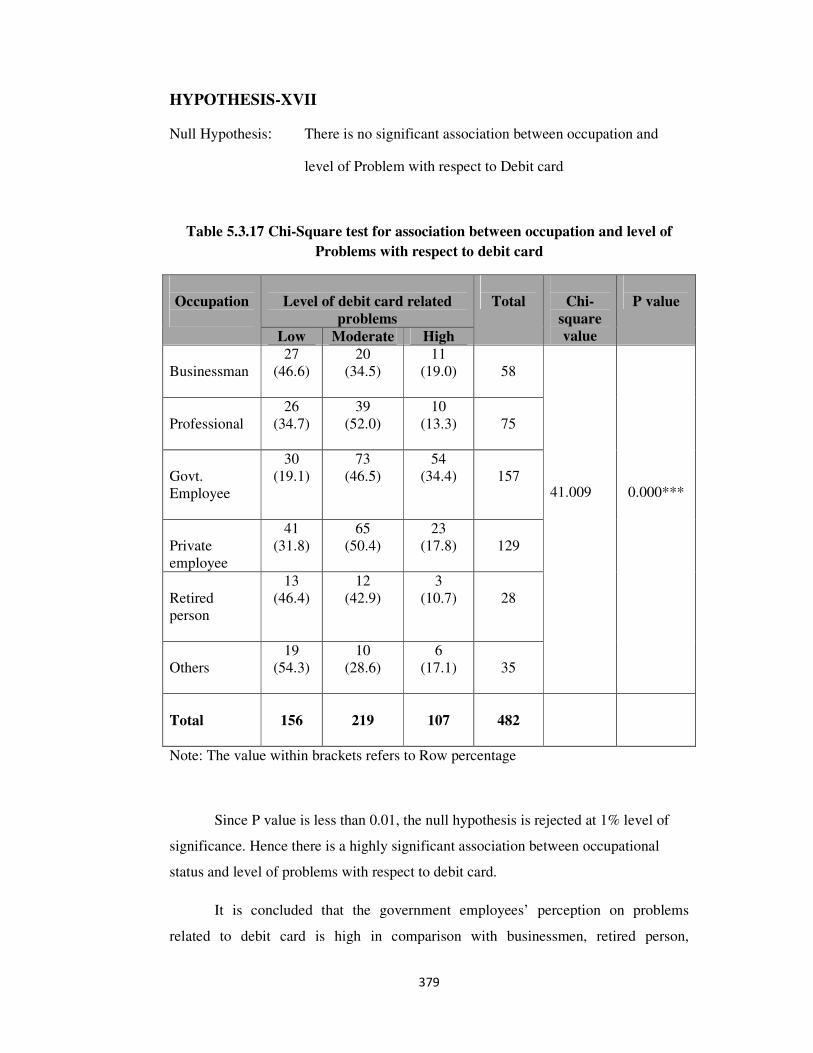

5.3.17

Association between occupation and level of Problems with respect to DEBIT card

379

5.3.18 Association between occupation and level of Problems with respect

to Internet banking

380

xv

5.3.19

Association between occupation and level of Problems with respect

to Mobile banking

382

5.3.20

Association between occupation and level of Problems with respect

to RTGS, NEFT and ECS

384

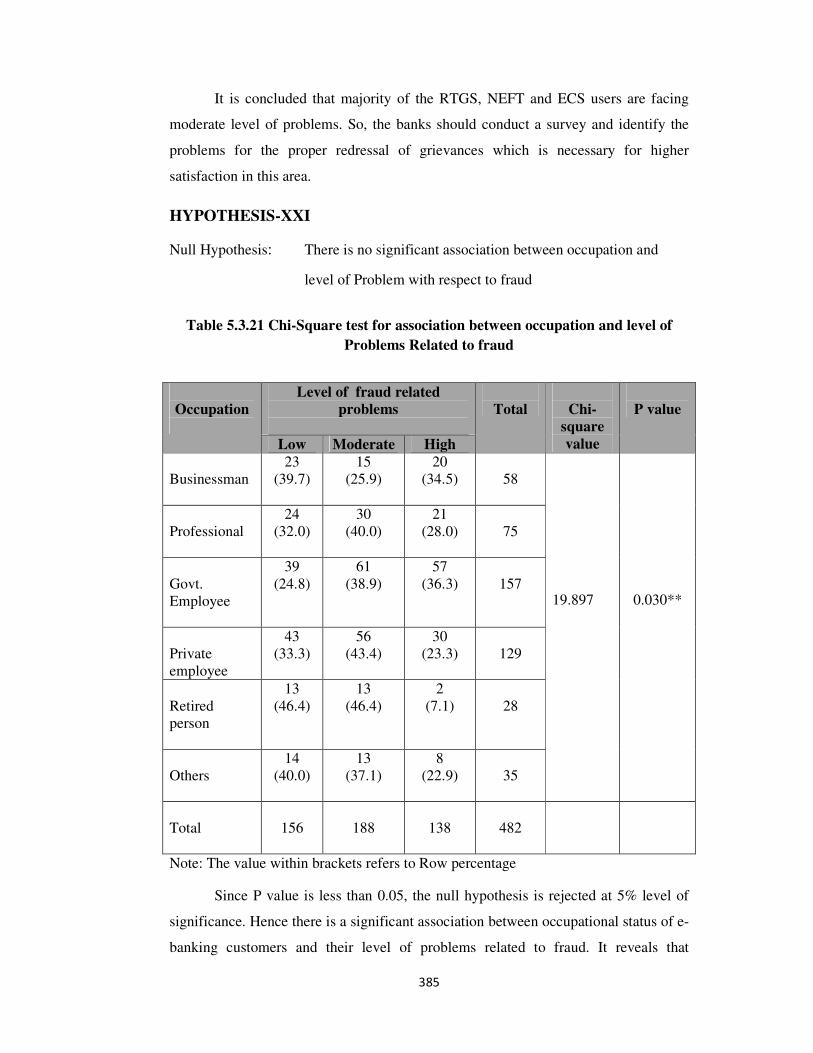

5.3.21

Association between occupation and level of Problems with respect

to fraud

385

6.2.1

Overall level of satisfaction of E-Banking customers 392

6.2.2

Level of satisfaction of ATM-cum-Debit card users 393

6.2.3

Level of satisfaction of credit card users 394

6.2.4

Level of satisfaction of Internet banking users 395

6.2.5

Level of satisfaction of Mobile banking users 396

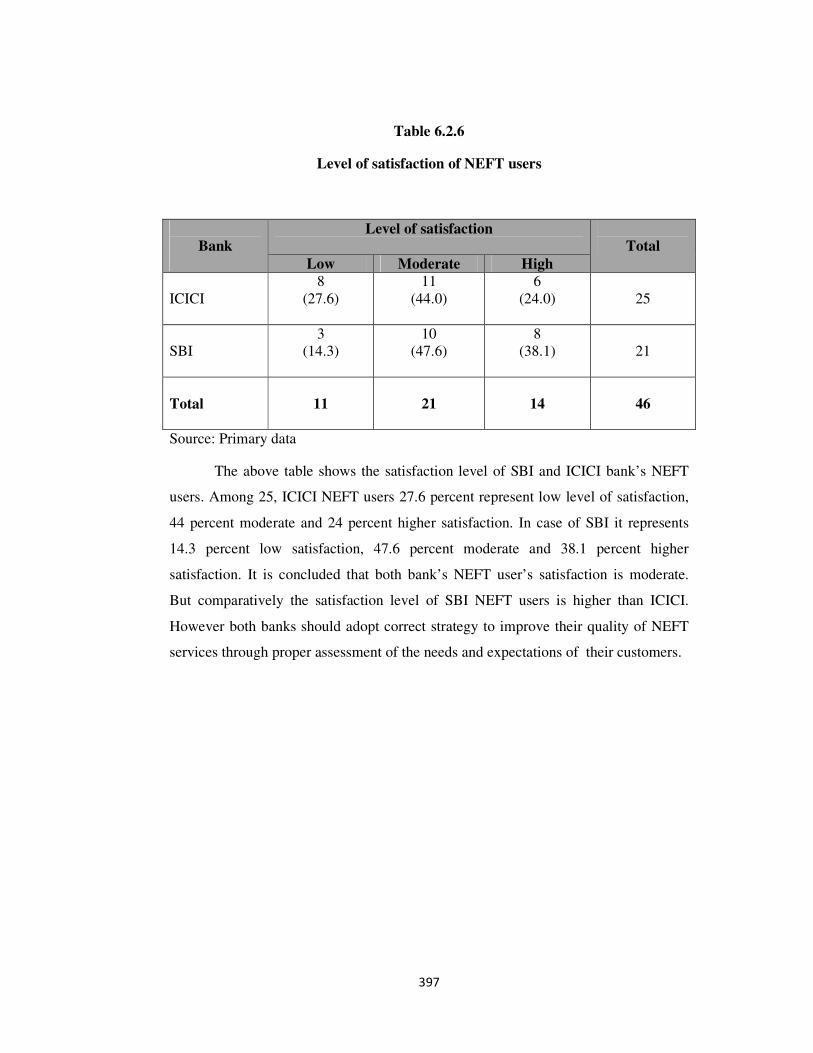

6.2.6 Level of satisfaction of NEFT users 397

6.2.7

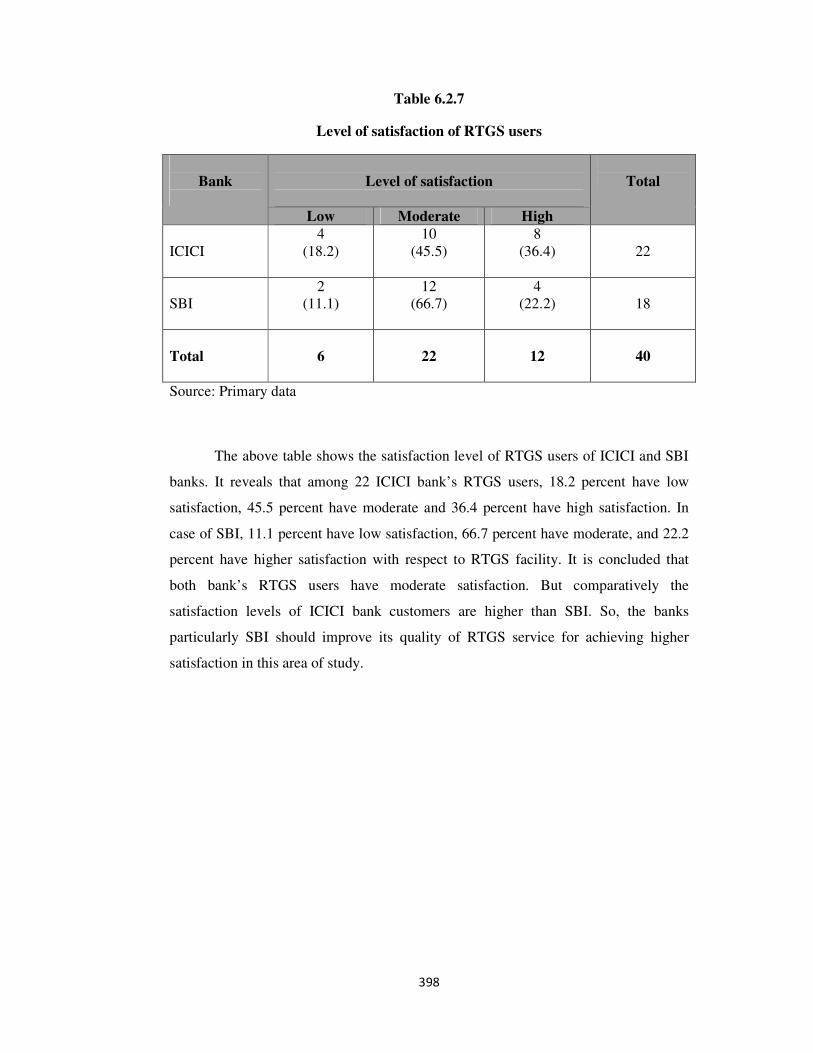

Level of satisfaction of RTGS users 398

6.2.8

Level of satisfaction of ECS users 399

6.2.9

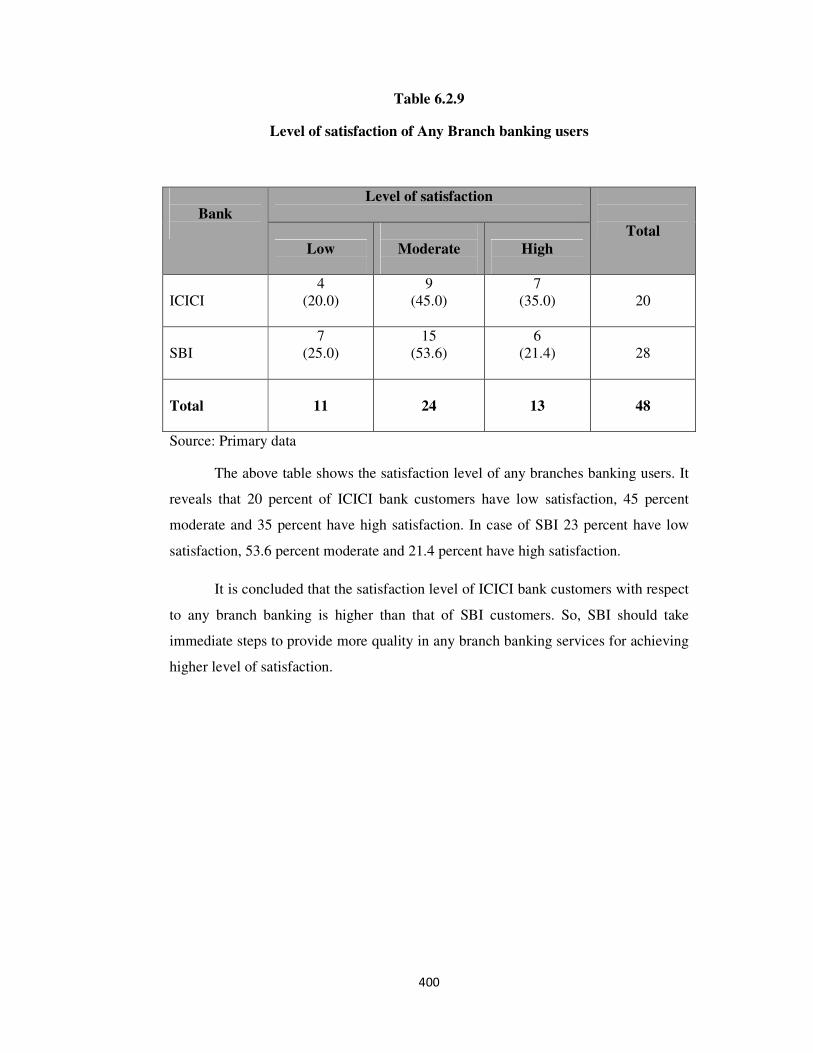

Level of satisfaction of Any Branch banking users 400

6.3.1

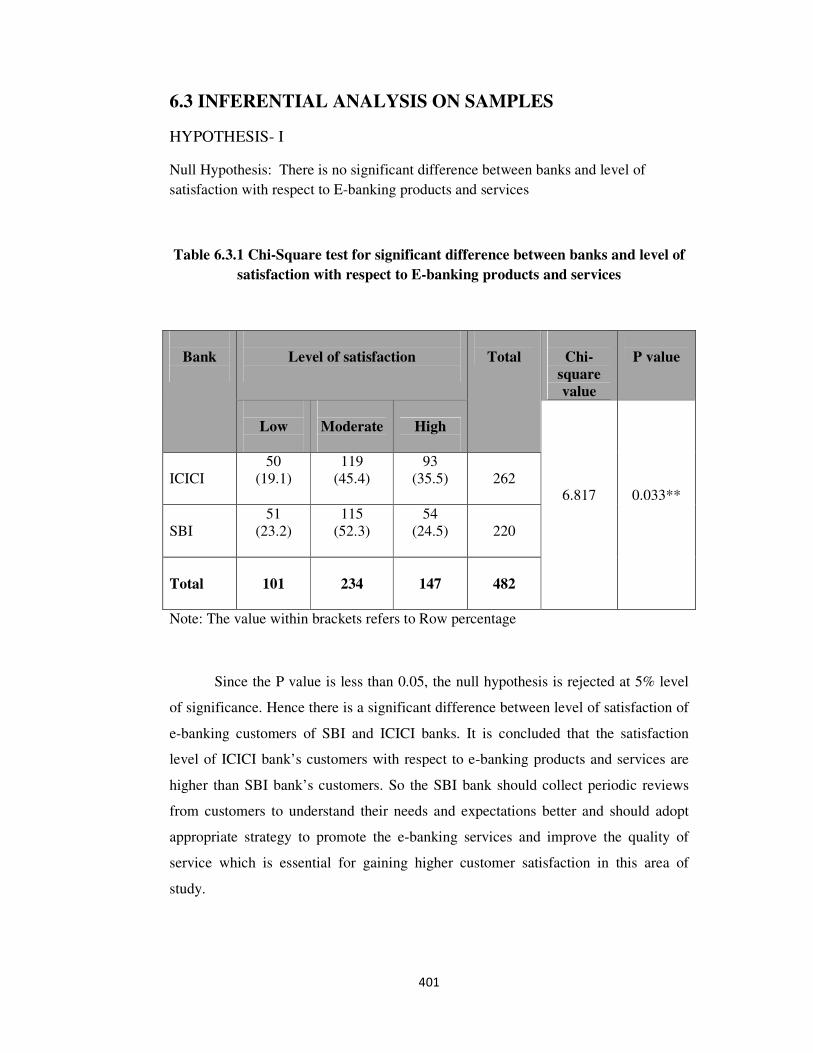

Difference between banks and level of satisfaction With respect to E-banking products and Services

401

6.3.2

Difference between male and female e-banking customers With

respect to satisfaction level

402

6.3.3

Difference between married and unmarried e- banking Customers

with respect to satisfaction level

403

6.3.4

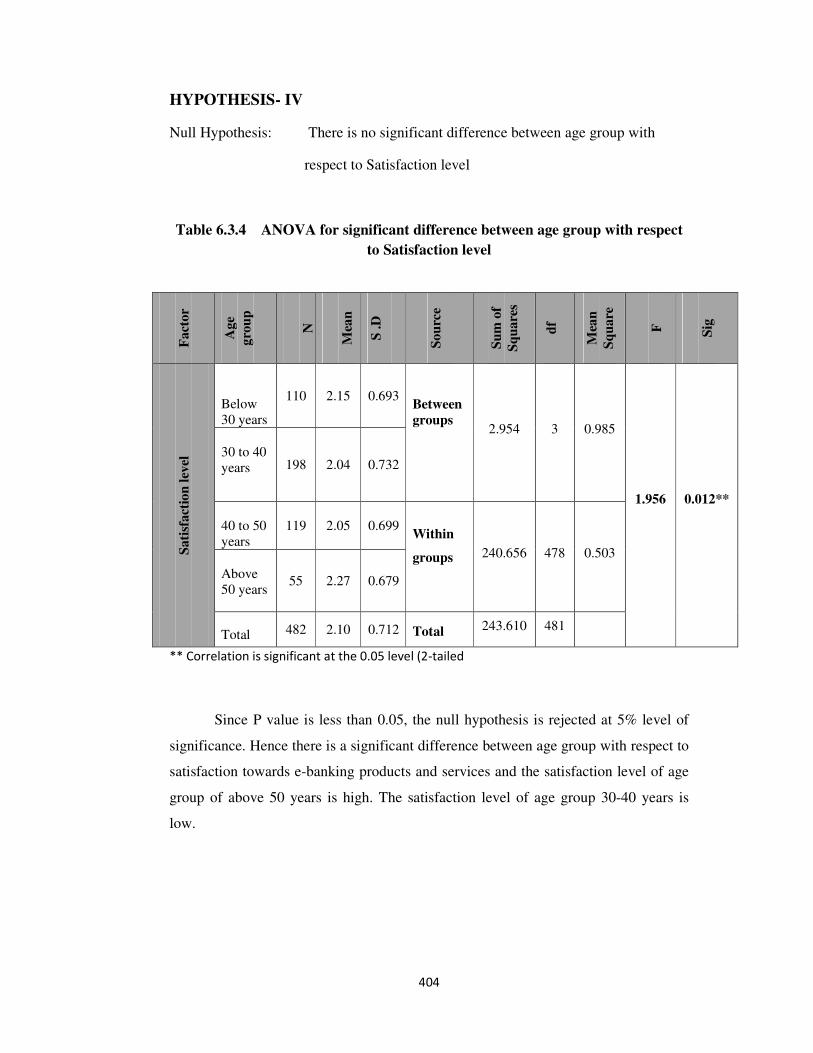

Difference between age group with respect to Satisfaction level 404

6.3.5

Difference in satisfaction level of e-banking customers with

different educational qualification

405

xvi

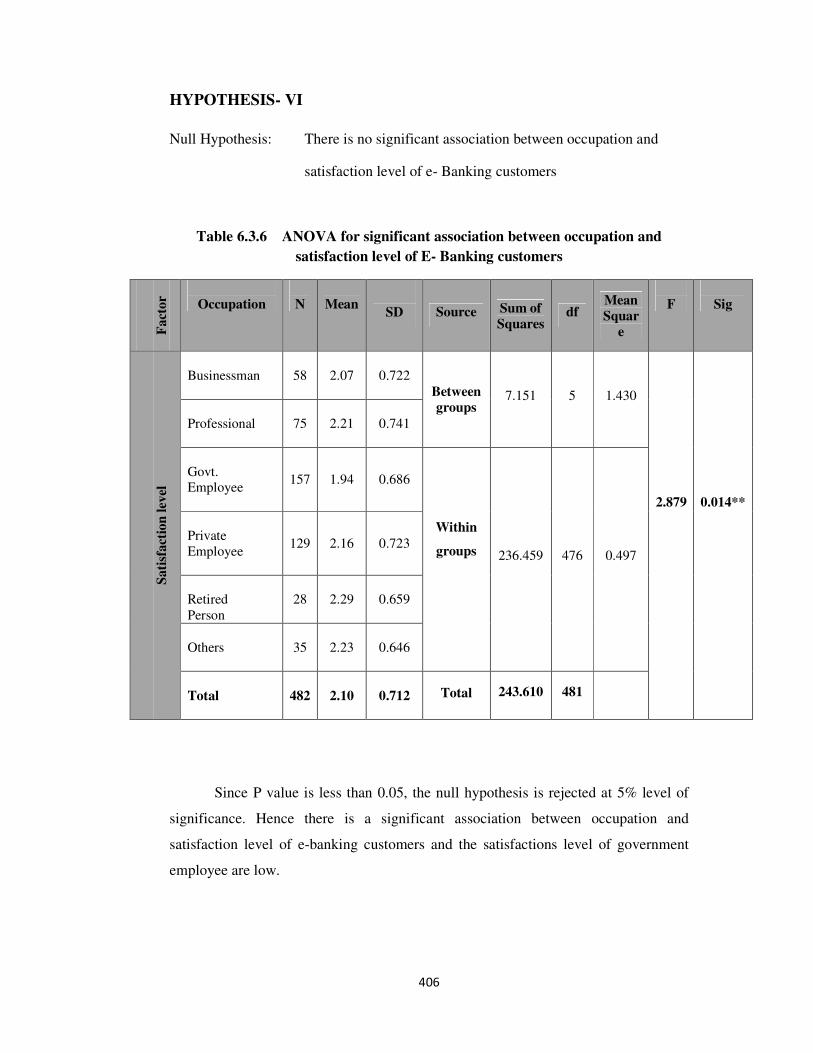

6.3.6 Association between occupation and satisfaction level of E- Banking

customers

406

6.3.7

Association between monthly income and satisfaction level of e-

Banking customers

407

6.3.8

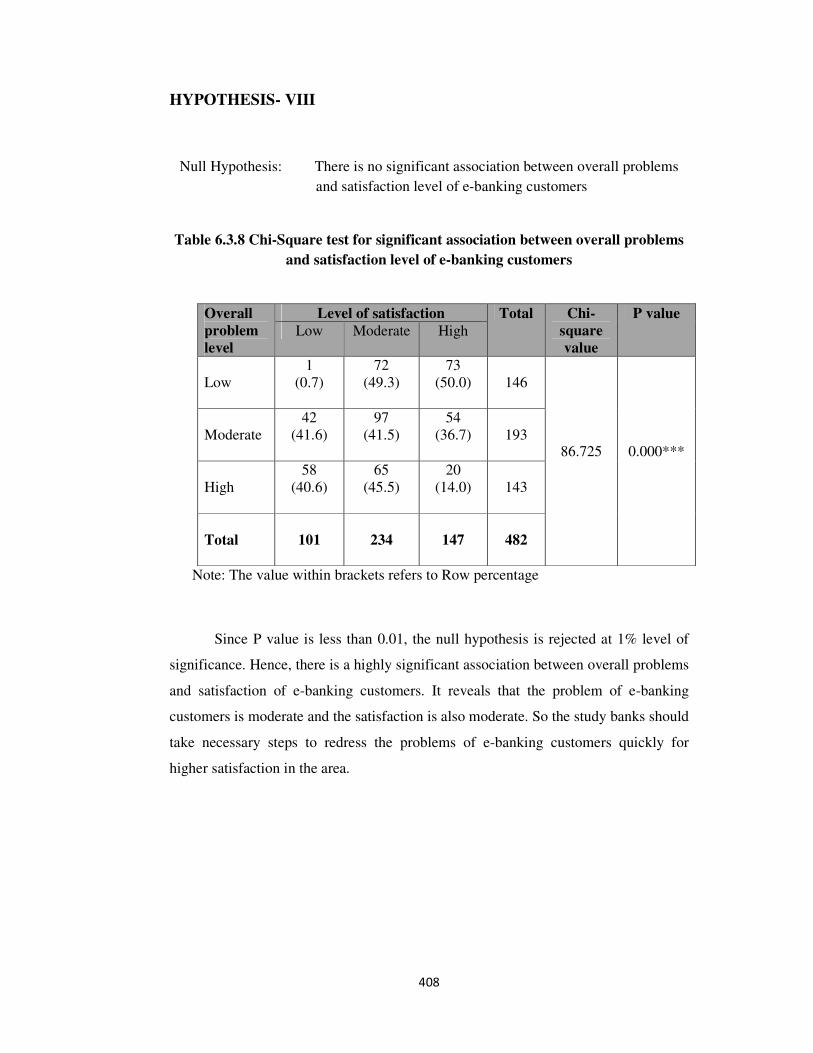

Association between overall problems and satisfaction level of e-

banking customers

408

xvii

LIST OF CHARTS

Chart No.

Particulars Page No

3.2.1

Gender of respondents

204

3.2.2

Age-wise classification of respondents

205

3.2.3.

Educational qualification of respondents

206

3.2.5

Monthly income-wise classification of respondents

209

3.2.9

Number of years of utilization

212

3.2.10

Preference of respondents to e-banking products

213

5.2.7

Overall problems of e-banking customers

361

6.2.1 Overall level of satisfaction of E-Banking customers

392

xviii

LIST OF ABBREVIATIONS

ALPM - Advanced Ledger Posting

ATM - Automated Teller Machine

BIS - Bank for International Settlement

CBS - Core Banking Solutions

CDSL - Central Depository Service Ltd

CMR - Cyber Media Research

DP - Depository Participant

DVSS - Digital Video Surveillance System

EBT - Electronic Benefit Transfer

ECS - Electronic Clearing Service

EDI - Electronic Data Interchange

EFT - Electronic Fund Transfer

FTC - Federal Trade Commission

FY - Financial Year

GPRS - General Packet Radio Service

IBA - Indian Bank’s Association

IDRBT - Institute for Development and Research in Banking

Technology

IAMAI - Internet and Mobile Association of India

IMPS - Inter-bank Mobile Payment System

IP - Internet Protocol

KYC - Know Your Customer

MDR - Merchant Discount Rate

MICR - Magnetic Ink Character Recognition

MMID - Mobile Money Identifier

NECS - National Electronic Clearing Service

NEFT - National Electronic Fund Transfer

NFS - National Financial Switch

NPCI - National Payment Corporation of India

xix

NSDL - National Securities Depository Ltd

PDA - Personal Digital Assistant

PI - Participant Interface

PKI - Public Key Infrastructure

POS - Point Of Sales

RBI - Reserve Bank of India

RECS - Regional Electronic Clearing Service

RTGS - Real Time Gross Settlement

SBI - State Bank of India

SEFT - Special Electronic Fund Transfer

SFMS - Structured Financial Messaging Solutions

SPNS - Shared Payment System

STP - Straight Through Processing

TBA - Total Bank Automation

TRAI - Telecom Regulatory Authority of India

USSD - Unstructured Supplementary Service Data

VSAT - Very Small Aperture Terminal

WAP - Wireless Application Protocol

WI - Web Interface

xx

CHAPTERS

PARTICULARS

PAGE.

NO

Acknowledgement

iv

List of Tables

vi

List of Charts

xviii

List of Abbreviations

xix

I

Introduction

1

II

Electronic banking products and services

86

III

Socio – Economic profiles of E-Banking

customers

203

IV

Awareness and Utility of E-Banking services

240

V

Problems perceived by E-Banking customers

252

VI

Customers’ satisfaction towards E-banking products and services

389

VII

Summary of Findings, Suggestions and

Conclusion

412

Bibliography

xxi

Appendix

xxviii

xxi

CONTENTS

d

1

CHAPTER - I

INTRODUCTION

Banking is an indispensable constituent of the financial system and the

economy of a country. Its development is being reflected by the economic

development of the nation. It is like a backbone for the country, inevitable for

prosperity.

Indian banks are on sound footing. They have become strong, healthy,

dynamic and resilient a necessary condition for sustained economic growth and

financial stability. Banks in the country have provided stability in the wake of

international fiscal problems and meltdown was a credit to the functioning of the

banks here.

Indian banking is fairly mature in terms of services, product range and

reach. There has been a phenomenal expansion in the geographical coverage and

functional reach of the banking system in India. Indian banks have come out of

their traditional business of banking into various other fields of operation such as

merchant banking, venture capital, mutual funds, housing finance, factoring and

other financial services. They have transformed themselves and are offering

services through electronic delivery channels. From computerization to networking

and to e-banking, banks have moved up in the value chain. The adoption of

technology has heralded a transformational development in the banking sector.

2

1.1 HISTORY OF BANKING IN INDIA

In India, the business of banking and credit was in practice even in very

early times. The modern type of banking however was developed by the agency

house of Calcutta and Bombay after the establishment of rule by the East India

Company in 18th

and 19th

centuries. The General Bank of India was the first bank

in India established in 1786.

The beginning of Occidental banking started with the establishment of the

Bank of Hindustan in Bengal as a joint-stock bank under control of Britishers for

undertaking the banking operations for the benefit of their constituent which failed

in 1832 due to the failure of its parent firm.

The first bank of Indian origin was started in 1809, called Presidency Bank

of Bengal followed by the setting up of presidency Bank of Bombay in 1840 and

Presidency Bank of Madras in 1843. In between many banks had sprung up like

mushrooms and failed mostly due to speculation, mismanagement and failure of

their parent companies. Due to large scale failure of the banks, the development of

banking went on at a slower pace and only two important banks viz., Allahabad

bank ltd (1865) and The Punjab National Bank (1894) were established by the end

of the nineteenth century.

At the beginning of twentieth century under the influence of Swadeshi

movement, a number of joint stock banks were established by Indians, but the

outbreak of First World War disrupted this process. The conditions during world

War period (1914-1918) emphasized the need for a unified banking institution to

3

run the accounts of the Government efficiently, as a result of which Imperial Bank

of India was setup in 1921 by amalgamating all three presidency banks.1

Reserve Bank of India was established in 1935 with a view to manage the

currency and credit of the country by acting as a bank of the Government and the

commercial banks. India like other developing countries followed the path of

planned development after independence in 1947. In 1948 Banking Regulation Act

was passed which came into force in March 1949.2

It imposed certain discipline on the joint stock companies doing banking

business in India. During that period banks were largely urban oriented and

remained beyond the reach of the rural population. The RBI was nationalized in

the year 1948 and vested with the extensive power for the supervision and

regulation of banking in India as a Central Banking Authority.

With the introduction of economic planning in 1951, the need was felt for

aligning monetary and banking activity with the requirements of planning. On the

basis of recommendations of the All India Rural Credit Survey committee, the

Imperial Bank of India was nationalized and renamed as SBI from July 1955. The

main objective behind the establishment of SBI was to extend banking facilities on

a large scale more particularly in the rural & semi-urban areas.3

1en.wikipedia.org/wiki/banking_in_India.

2.http://banknetindia.com

3.Dr.T.K.Velayudham “Developments in Indian Banking; past present and Future”, The Journal of the Indian Institute

of Barkers, Bank Quest, 2002, Vol:73, No.4, pages.23-37

4

As part of the process of geographic expansion of banking facilities to meet

the credit needs of co-operatives, certain banking companies functioning in

formerly princely states were converted in 1959 in to subsidiaries of SBI later,

came to be known as associate banks of SBI.

In order to turnout the mere business of money lending in to the major force

controlling the economy of a nation, banks were nationalized which is considered

as a historic beginning to the vast development. It is an important mile stone in the

history of Indian banking. Banks were nationalized in two stages. On 19th

July

1969, 14 major commercial banks with deposit of over 50 crores were

nationalized. Again on 15th

April 1980, 6 more banks with deposits of not less than

200 crores were nationalized. As a result, 91 percent of the banking system in

India was brought under the public sector.4

The banks were nationalized only after the failure of social control

measures adopted by the Government in 1968. Until1969, the Indian banks did not

play a proper role in the planned development of the nation. They were

concentrated on individuals benefit than social benefits.

The nationalization of major commercial banks ushered in big changes in

the style, approach and functioning of banks. Since nationalization, the banking

industry has been progressing in a significant manner. There has been a six fold

increase in the number of bank offices. One of the significant results has been the

setting up of branches in rural and semi-urban area.

4.http://www.ftkm.com/banking

5

The mobilized resources have been properly utilized for rural & semi-urban

areas representing agriculture, small and tiny industrial units. The saving habit of

the public developed to commendable level. Common people got priority over the

elite. The emphasis moved from profit to service.

The euphoric experience of nationalization was so encouraging that the

Government of India based on the recommendations of Narasimham committee

decided to setup Regional Rural Bank in 1975 for developing rural economy by

meeting the credit needs of the weaker sections of the society. The RRBs were

established at selected regions where the co-operative system was weak and where

commercial banks were not very active.

During late eighties and early nineties of the twentieth century, social

considerations were dominant over commercial judgment, which led to

compromise on the quality of the credit leading to poor profitability of the banks

resulting in to booking of losses by the nationalized banks. Revamping the

structure of the banking industry was of extreme importance, as the health of the

financial sector in particular and the economy as a whole would be reflected by its

performance.

India embarked upon a massive programme of stabilization and structural

reforms in the midst of the unprecedented balance of payment and financial crisis

in mid – 1991. When the reform process started in the Indian economy following

the crisis, policy makers in India took a much more holistic view, and the reform

programme embraced various sectors of the macro economy.

6

The reforms have enhanced the opportunities and challenges for the real

sector making them operate in a borderless global market place. However to

harness the benefit of globalization, there should be an efficient financial sector to

support the structural reforms taking place in the real economy.

Hence Government of India and the RBI thought it was necessary to

introduce reforms in the financial sector also to promote rapid economic growth

and development with stability through the process of globalization, liberalization,

and privatization in the financial system, so that the financial system becomes

more competitive and gets integrated with the world economy through

internationalization of financial markets in the world.

Accordingly, the process of financial sector reforms initiated based on the

recommendations of Narasimham committee in 1992. This committee report made

radical recommendations for the banking sector by emphasizing the need for

deregulation and liberalization. According to this report, banks are permitted to

raise capital from the public, New Private sector banks were allowed to operate,

nationalization of banks were stopped, and no distinction was made between

private and public sector banks. More importantly to complete the global economic

integration process, foreign banks were allowed to operate in India.

The Narasimham committee suggested that there should be functional

autonomy, flexibility in operations, dilution of banking strangulations, reduction in

reserve requirements and adequate financial infrastructure in terms of supervision,

audit and technology. The committee further advocated introduction of prudential

7

norms, transparency in operations and improvement in productivity, not only

aimed at liberalizing the regulatory frame work but also to keep them in time with

international standards. The emphasis shifted to efficient and prudential banking

linked to better customer care and customer service.5

Banking scenario since 1991 has been a process of transformation and

consolidation. There has been paradigm shift in operational, functional,

environmental and technological spheres. Almost all insulation to commercial

banking has been peeled off and it has been susceptible to all types of exposures

now.

As part of reform, Indian banking was opened for private sector by which

old and new private sector banks came to limelight. They gave a big boost to

technology and created a platform to use it for backside and front side operations.

When they started adopting it this put a tremendous pressure on the nationalized

and public sector banks. With the result of such healthy competitive environment,

overall banking system became more work prone, efficient, and technology savvy.

With the development of telecom sector, communication infrastructure,

BPOs, the entire country became a single hub of transmitting the information

which helped in the reduction of total cost. This had directly helped banks. During

the same period, banks were busy in connecting their branches with centralized

data base and core banking solution for offering anywhere, anytime services.

5Rakesh Mohan “ Financial Sector Reforms in India”, Economic & Political Weekly, Vol-XL No.12, March 19, 2005.

8

RBI made several changes in the basic structure of banking sector and laid

down numerous guidelines on electronic banking, fund transfer, core banking

solutions, payment system, clearing services and internet banking. With the

advancement and adoption of technology a lot of changes have been made in

payment system and banking system as a whole. Now banks can reach their

customers anywhere, anytime and customers are able to get instant access to their

accounts from any corner of the globe anytime.

1.2 ELECTRONIC BANKING

Financial sector is metamorphosing in the impact of competitive regulatory

and technological forces. Technology is emerging as a key driver of business in the

financial service industry. The transition of business operations by banks using

electronic forces created new modes of operations called e-banking.

E-banking is defined as an automated delivery of new and traditional

products and services directly to customers through electronic, interactive

communication channels. E-banking includes the systems that enable financial

institution customers, individuals or businesses to access accounts, transact

business or obtain information on financial products and services through a public

or private network including the internet.

9

According to a survey of electronic cash and electronic banking report by

FINCEN “electronic banking is an umbrella term for the process by which a

customer may perform banking transactions electronically without visiting a brick

and mortar institution.”6.

E-banking is a generic term encompassing internet banking, telephone

banking and mobile banking. In other words, it is a process of delivery of banking

services and products through electronic channels such as telephone, internet and

cell phone.

Electronic banking allows banks to expand their market for traditional

deposit – taking and credit extension activities and to offer new products and

services or strengthen their competitive position in the market. It has given an

opportunity for banks to find solutions to manage problems like saving time,

money and energy of customers by reducing or minimizing, paper works, waiting

in queues, lack of communication and lack of efficiency. E-banking has provided

ease and flexibility in banking operations.

The major driving force behind the rapid speed of E-banking is its

acceptance as an extremely cost effective delivery channel. But it is associated

with risks such as reputational risk, security risk, cross-border risk and strategic

risk, which are unique to e-banking.

6.www.bankersonline.com

10

1.3 CONCEPT OF E-BANKING

The concept and scope of e-banking is still evolving. Electronic banking is

the new trend significantly adopted by banking sector worldwide due to its wider

scope for the customers as well as banks at large. E-banking facilitates an effective

payment and accounting system thereby enhancing the speed of delivery of

banking services considerably. While e-banking has improved efficiency and

convenience, it has also posed several challenges to the regulators and supervisors.

Several initiatives taken by the Government of India as well as Reserve Bank of

India have facilitated the development of E-banking in India.7 Daniel (1999)

defines electronic banking as the delivery of bank’s information and services by

banks to customers via different delivery platforms that can be used with different

terminal devices such as a personal computers and a mobile phone with browser or

desktop software, telephone or digital television8.

According to Karjaluoto (2002) Electronic Banking is a construct that

consists of several distribution channels. It should be noted that e-banking is a

larger concept than banking via Internet.9 E-banking is a brew of services that

embody internet banking, Mobile banking, ATM Kiosks, Fund Transfer system,

Real Time Gross Settlement (payment and allotment system), credit/debit/smart/

7 www.rbi.org.in

8Daniel, E(1999), “Provision of electronic banking in the UK and the Republic of Ireland”, International Journal of

Bank Marketing, Vol, 17,No.2, Pages.72-82.

9Karjaluoto, H, (2002), “Electronic banking in Finland; Commercial belief, Attitude, Intentions and Behaviours,

Doctoral Dissertation, University of Jyvaskyla, Jyuvaskyla.

11

kisan cards, cash government services, as well as data warehousing, operational

interpretation for MIS as well as customer relationship management (E tools 4

all).10

Electronic distribution channels provide alternatives for faster delivery of

banking services to a wider range of customers (Kaleem and Ahmad, 2008).11

The

definition of e-banking varies amongst researchers partially because e-banking

refers to several types of services through which a bank’s customers can request

information and carryout most retail banking services via computer, television or

mobile phone (Mols, 1998, Sathye 1999).12

A perusal of the concept of e-banking as described in the literature reveals

that the term e-banking is an upper construct that encompasses an array of banking

services delivered through electronic media, be it through phone, PC, or internet.

Thus the term e-banking includes ATM, Credit Card, Debit Card, Internet banking,

Mobile banking, RTGS, NEFT & ECS.

10E tools 4911, E-banking? Recent trends in India, http://etools4all.org/e-banking-reunttrends.in.india. html accessed on

16 August 2013.

11 Kaleem A and Ahmad.S. (2008) “Bankers perceptions of electronic banking in Pakistan”, Journal of Internet banking

and Commerce, Vol.13, No.1, pages.23-36.

12Mols.S.N. (1998), “Behavioral consequence of PC banking’ International, Journal of Bank Marketing, Vol.16, No.5,

pages.195-201.

12

1.4 ADOPTION OF TECHNOLOGY AND EVOLUTION OF E-BANKING

IN INDIA

Technology adoption has changed the face of banking in India. What started

as a mere automation of some routine work process in banks in the mid-80s has

moved on to become business process re-engineering which has resulted in making

banking services branchless, anytime and anywhere, facilitated new product

development and enabled near real time service delivery. It has helped banks to

reach the door steps of the customer by overcoming the limitations on

geographical/physical reach in branch banking and easing the resource and volume

constraints posed by the brick and mortar model.

The introduction of mechanization and particularly computerization has laid

foundation, for the evolution of e-banking. The use of computers has led to the

introduction of online banking. In 1967-71 about 100 computers were installed in

different enterprises. But only two of them were located in banking industry. The

first bipartite settlement on mechanization and computerization was made in 1966

between Indian Bank’s Association and the All India Bank Employees Association

which accounted for the use of IBM and ICT accounting machine for inter branch

reconciliation etc.13

13http://www.preservearticles.com

13

The first serious effort and blue print, for computerization in banking

industry was drawn up in 1983 under the aegis of Dr.C.Rangarajan committee. The

committee recommended that computerization and installation of Advanced

Ledger Posting Machine (ALPM) at branch, regional and head offices of the bank

will bring around new era in bank. In 1986 the RBI decided to use MICR

technology in cheque collection and clearance which is the basic function of the

banking industry.

The second committee constituted in 1988 drew up a detailed perspective

plan for computerization in banks and for extension of automation to other areas

like fund transfer. The branch automation enabled setting up of single window

service facilities which were focused on customers. Then banks started exploring

the idea of total Banks Automation. Although titled Total Bank Automation, TBA

was in most cases confined to branch automation. It was only in early 1990s that

banks started thinking about tying up disparate branches together to facilitate

information sharing. Saraf committee was constituted by RBI in 1994 that

recommended the use of electronic fund Transfer System (EFT), introduction of

electronic clearing service and extension of magnetic ink character recognition

(MICR) beyond metropolitan cities and branches14

. Meanwhile the networking of

the already computerized branches also assumed urgency and some of the banks

have started inter connecting their computerized branches using leased telephone

lines or very small Aperture terminal (VSATs).

14http://www.rbi.org.in/scripts/publications.

14

This is meant to provide more comprehensive service to customers and at

the same time give banks better centralized control over the branch operations.

An important stage in the evolution of the user friendly technology or e-

banking arrived with the deployment of ATMs. This was the first stage of

empowerment of the customer for his own transactions. The liberalization in 1991

marked the entry of foreign and new private sector banks. They brought new

technology with them and banking products became more and more competitive.

Hence, a need for differentiation of products and services was felt. The ICICI bank

had started online banking in 1997 under the brand name infinity.

The development and use of communication network have also helped the

banking industry to improve the quality of its services. Beginning modestly with

leased terrestrial technology i.e. BANK NET and its communication software the

RBINET, a milestone was passed in February 1997 with the operationalization of

the Shared Payment Network System (SPNS) of ATMs of the Indian Bank

Association in Mumbai.

With the setting up of IDRBI, three most important technology

infrastructures were created and these were INFINIT in 1999, the implementation

of public key infrastructure (PKI) based data transfer and structured Financial

Messaging System (SFMS) which facilitated the development of secured payment

system practice in India. INFINIT is the back bone for a safe, reliable and effective

communication network and messaging system. It has now incorporated low cost

15

yet reliable technologies in the form of Multi-pocket – label switch (MPLS)

technology in an effort to offer state – of – the art – network.15

A slew of innovations in newer delivery channels like internet banking,

mobile banking and prepaid cards issued by non-banking entities emerged. The

rapid shift towards electronic transactions in the form of automated teller

machine, debit cards, internet, banking etc. has made real time core banking

system a requirement to support for the up to the minute balance reporting

requirement, that the older system cannot support. According to RBI report, the

percentage of branches under core banking solutions increased by 79.4 percent as

at end March 2009 to 90 percent at the end of March 2010.16

Among the path breaking initiatives in the area of payment and settlement

systems of the country, electrification of payment system has become the hall

mark of the decade that has gone by. Electronic based payments are superior to

paper based system in terms of traceability, efficiency speed and safety. The

introduction of RTGS in 2004 has resulted in not only compliance with

international standards but also paved the way for risk free fund transfers settled

on a real time basis. The facility for inter-bank fund settlement through RTGS is

available across more than 88,000 branches of banks spanning more than 5000

centres of the country, a coverage that has perhaps, not witnessed anywhere else in

the world.17

15www.idrbt.ac.in

16RBI report on trend and progress of banking in India 2009-10, Page.55 http://rbi.org.in/scripts/publications.

17http://en.wikipedia.org.wiki.real-Time-Gross-settlement.

16

The facility for inter-bank fund settlement through RTGS is available across

more than 88,000 branches of banks spanning more than 5000 centres of the

country, a coverage that has perhaps, not witnessed anywhere else in the world.17

Thus, the introduction of various electronic delivery channels has had a

beneficial impact on both banks and customers. For banks, electronic channels

have emerged as a strategic resource for achieving higher efficiency, control of

operation, productivity and profitability. For customers, it is the realization of their

anywhere anytime and any way banking dream.

1.5 IMPACT OF E-BANKING

Electronic banking has turned the world of personal finance upside down by

completely changing what consumers expect from a bank. Whereas, formerly

banks would distinguish themselves through the quality of their direct interaction

with consumers. Today, providing them with a convenient, safe and fail – proof

banking interface has instead turned in to the main focus.

The impact of e-banking is not limited to industrial and the most advanced

economies. Even for countries with underdeveloped banking system, E-banking

offers an opportunity to leapfrog. Because e-banking is much cheaper since its

lower processing cost for providers and search and switching costs for consumers.

Providers can market banking services involving smaller transactions to

lower income borrowers even in remote areas. According to industry experts, a

bank spends an average of Rs.40 for each transaction conducted at a branch. If a

customer uses the ATM facility, the cost drops to Rs.18 – 20 per transaction, but it

17

is still much higher than the cost involved in online banking. For net banking, the

cost is Rs.4 for transaction. As per the reason survey by IBM Global Services

Consulting Groups, Traditional Banks spend 60 percent of the revenue generated

to run a branch, whereas the cost of providing the same services via, internet

comes out to be only 15 percent. Thus there is a huge savings for banks and

consumers.18

The advent and proliferation of e-banking enable broader and inclusive e-

banking sector and in the process is a key driver for sustained and inclusive growth

of the economy. Branch customers are now bank customers as they can access

their account from anywhere. It has become well recognized that the use of e-

banking helps in increasing the transparency of the banking system. This has

become essentially important due to the latest international initiatives in relation to

anti-money laundering. The movement from paper based payment to electronic

means of payment that the funds being transferred are easily track able. This also

adds to the accountability of funds in an economy.

In a developing economy like India, e-banking has helped in modernizing

the financial systems, creating economic transparency and contributing to greater

predictability, liquidity and stability. One of main advantage and main reason for

migration to electronic banking from paper based banking is that of the improved

operational efficiency brought about by its use. Reduction in transaction time and

18http://articles.economictimes.indiatimes

18

transaction cost has helped companies and government and other end users of e-

banking products to improve their operational efficiency.

1.6 ISSUES AND CHALLENGES OF E-BANKING

Electronic channels have brought fundamental shift in the functioning

banks. It is not only helping them bring improvements in their internal functioning

but also enable them to provide better customer service. It provides the opportunity

of breaking all boundaries and encouraging cross border banking business.

There are several benefits associated with the introduction of e-banking.

Benefits may vary depending upon various perspectives. From the banks

perspective provision of e-banking delivery channel to consumers would enhance

the opportunity to maximize their profit. The chief goal of many businesses in

monetary terms is associated with profit maximization (Nathan 1999). Moreover,

from the banker’s point of view, proliferation of the e-banking is an essential

requisite not only in terms of cost saving by reducing the human interaction,

improving competitiveness by way of differentiation and retaining existing

customer base as well as attractive potential consumers.

Banks throughout the world, face an increasingly tough challenge of

boosting their revenues while controlling their cost (Durkin 2004).Therefore the

common trend followed by many banks globally is stream lining their branch

networks and redirecting their consumers to alternative service delivery channels

19

and encouraging consumers to adopt self- service technologies.19

Thus banks are

reducing the cost incurred in maintaining the branch staff (pyumetal 2002). Also,

banks often build better brand image by way of responding to the rapid market

changes and would therefore be perceived as leaders in adoption of innovative

technologies.

From consumers point of view automation of banking services by

introducing electronic delivery channels provides 24 hours accessibility, reduces

costs in accessing and using of banking products and services, proper cash

management, reduced time demands, increased comfort as well as quick and

continuous access to the information (Aladwani, 2001).

Existing studies report that consumers by way of utilizing electronic

channels can manage funds in a better manner. Majority of the consumers are

happy with the speed and convenience associated with the e-banking (Gurau,

2001).

Besides the various opportunities, there are certain concerns and challenges

exerted by the banks and well as consumers with regard to the uptake and use of e-

banking. Banks initially promoted their core capabilities through the internet. Due

to the relative newness of the technology associated with e-banking banks as well

as consumers often concerned about the security of internet access to client

account (stamoulis, 2000).20

19Sujance Adapa, “Global E-banking Trends: Evolution, Challenges and opportunities”, University of New

England Australia.

20Stamoulis. DS (2000) “How Banks Fit in an Internet Commerce Business Activities Model”, Journal of Internet

Banking and Commerce, June 5 available online at http://www.arraydev.com/commerce/J1BC/articles

20

Several studies indicated that the acceptance of e-banking by consumers’ is

affected by perceived security (Dourish&Redmiles, 2001).21

Several banks in

order to maintain their competitive advantages mimic new channel approaches

quickly, as product differentiation is very difficult for banks (Nemzow, 1999).22

Moreover, the threat of substitutes to banking in terms of competition from

non-banking, financial and micro credit sectors is increasing rapidly (Mia etal.,

2007). The competition is fierce in the banking and financial sector environment as

every entrant is participating to some extent of e-banking which raises the issues of

security, privacy and risk (Constantine 2000).23

In e-banking system, information is considered as an asset and so worthy of

protection. According to online Banking Association, member institutions rated

security as the most important issue of online banking. There is a dual requirement

to protect customers’ privacy and protection against fraud. As most banks urge

customers to shift to the virtual space, their ability to create fortresses against

cyber aggression has come in to the spotlight.24

From just a few stray cases of identity theft a few years ago, internet frauds

have not only risen in scale but also gone high-tech, so much so that it has become

difficult to identify the origin of crime and nail the culprits. Cyber heist is an issue

21Dourish. Pand D.Redmiles (2002), “An approach to usable security based on event monitoring and visualization”, in

proceedings of the 2002 workshop on New Security paradigms (New York, ACM press)pages. 5-81.

22Nemzaw.M (1999), “E-commerce stickiness for customer retention”, Journal or internet banking and commerce,

October 4 (1).

23ConstantineG (2000) “Banks Provide Internet on-ramp” Hoosier Banker, Indianapolis, March, USA.

24www.banknetindia.com

21

that not just Indian banks are faced with. Cyber-attacks ranked fourth among top

global risks, in terms of likelihood, according to the World Economic Forum

Report ‘Global Risks 2012’. Two Indian payment processors Electric Card, and

Enstage, were in the spot light recently for their alleged role in a $45 million credit

card fraud impacting Indian and International cards. The total amount involved in

frauds relating to credit card, debit card, internet banking rise 74 percent to Rs.38.4

crores in 2012.25

Experts suggest that simple rules such as not sharing login ID and

passwords with anyone, would keep customers safe.

1.7 GROWTH AND DEVELOPMENT OF E-BANKING

E-banking is one of the emerging trends in the Indian banking and is

playing a unique role in strengthening the banking sector and improving service

quality. It has enabled the banks to handle the payments electronically, inter- bank

settlement faster and in large volumes. Availability of ATMs, plastic cards, EFT,

electronic clearing services, internet banking and mobile banking to a large extent

avoid customers going to branch premises and has provided wider range of

services to customers. According to the ICICI bank statement more and more

people are shifting to alternative delivery channels, which accounted for nearly 30-

40 percent of customers at present. Over the next few years this is likely to go up

to 70-80 percent.26

25www.weforum.org/report/global-risks-2012-seventh edition.

26businesstoday.intoday.in/story/India.

22

ATM is the oldest of the alternative banking channels and enjoys the

highest level of acceptance among customers. The number of ATMs in India has

doubled in the past three years. By 2013, there are more than 1,00,000 ATMs

around 70 percent of them in urban locations. Global research firm Celent expects

that the number of ATMs to double by 2016, with more than 50 percent being set

up in small towns.

Banking has also been seeing a change due to the efforts of the RBI to

include a habit of paperless payments such as credit card, debit cards, electronic

transfer and mobile banking. During 2011-12, the volume of online fund transfer

through NEFT and RTGS grew by 71 percent and 11.7 percent respectively,

according to RBI report27

. According to a report by IAMAI, penetration of

cashless transaction stands at measly 0.43 percent. It has been said that only about

3.6 percent of households in India make cash less transactions. About 11 percent

households in urban area undertake cashless transactions while, in rural India only

0.43 percent of the households make cashless transaction.28

.

Today, consumer’s usage of internet banking is growing at a rapid pace

across geographies. Internet banking usage in India increased to seven percent

from one percent five years ago. The use of internet for banking has seen a

massive rise in the 2010-11, taking the overall number of bank consumers who use

the net to close seven percent of total bank account holders.29

It is a seven-fold

27www.rbi.org.in/database

28www.iamai.in/Press lease-details 29 www.infosys.com/industries/white paper.

23

jump since 2007, even as for the first time in the past 13 years. Branch banking has

come down by a full 15 percentage point during the same period. As of 2013, India

has the third largest number of Internet users. It is next to United States and China.

India is expected to have in excess of 125 million users by 2013 end.30

Mobile phones are seen as an enabler of electronic payments as the costs

are low. Mobile transactions have increased in the past few years, but the use of

mobile banking services is quite low. Most of the transactions carried out using

mobile phones are non-financial in nature. Notwithstanding this the growth in

mobile transactions has shown increasing trend. For example, in the month of June

2012, 3.43 million transactions amounting to Rs.3067.10 million were processed

as compared to 1.41 million transactions amounting toRs.984.66 million processed

in June 2011 an increase of about 143 percent in volume and approximately 211

percent in value terms.31

Modern electronic payment systems are still concentrated in metros and

large towns. A large chunk of the Indian population still does not have access to

formal banking channels. According to RBI, there were around 147,000 bank

outlets for more than 6,00,000 villages in India. Some banks though are using the

business correspondent model to expand their reach and bring more people under

formal banking using technologies such as hand held devices and micro ATMs32

.

30www.thehindu.com

31R.Srividya “India awaits boom in mobile banking, www.mydigitalfc.com/banking/India.

32 articles.economictimes.indiatimes.com

24

With mobility and customer convenience seen as keys to growth, banks are busy in

exploring new technologies. Experiments with near field communication

technology have failed to provide mass-scale payment solution, but the industry is

buzzing with terms cloud computing and mobile solutions.

1.8 REVIEW OF LITERATURE

A review has been primarily to identify appropriate methodology. It is a

subject of the articles/reports which has been received. A few available literatures

on e-banking products such as internet banking Mobile banking, ATMs debit cards

and credit cards in India and internationally reflect the current status of E-banking.

There are numerous research and papers that study the evolution and growth of

electronic banking in India and outside India. A review of some of them is given

below, the description has been organized under the heads: E-banking, Mobile

banking, Electronic payment and E-cheque, ATM and Credit Card, Technology

and Customer Service.

E-BANKING

The Research paper, “ Internet banking in India- consumer concern and bank

strategies” of P.K.Gupta and Jamai Millai Islamia33

presents the data drawn from a

survey of internet banking consumers and service providers (banks) that offer

internet banking and also on the products and services they offer. This research has

developed a functional model for maximizing value to the consumers, which the

33P.K.Gupta and Jamia Millia Islamia, ‘ Internet banking in India- Consumer concerns and Bank strategies.” Global

conference of business and finance proceedings, Vol.2, No.2, 2007

25

banks may choose to adopt internet banking strategically. An attempt has been

made to identify the weakness in the present conventional banking and to explore

the consumer awareness, use patterns, satisfaction and preferences for internet

banking vis-a-vis conventional form of banking. The factors that may affect the

strategy of the bank to adopt internet banking have been characterized. The paper

also addresses the regulatory and supervisory concerns of internet banking.

Richard Nayangosi, J.S.Arora and Sumanjeet34

Singh have conducted a

research on e-banking. The title of their research paper is “The evolution of e-

banking: a study of India and Kenyan technology awareness”. In this study they

collected customers’ opinions regarding the importance of e-banking and the

adoption level of various e-banking technologies in India and Kenya. This study

collected the trends of e-banking indicators in India and Kenya. Further the

researchers segregated the data collected in to an Indian and a Kenyan customer

basis to identify differences in their attitudes towards the emergence of e-banking.

The overall result of this study indicates that customers in both countries have

developed positive attitudes and they give much importance to the emergence of e-

banking.

34Richard Nayangosi, J.S.Arora and Sumanjeet “The evolution of e-banking: a study of India and Kenyan technology

awareness”, International Journal of El; electronic finance 2009, volume.3 No.2pages.149-165.

26

An article has been published by R.K.Mishra and J.Kiranmani35

on the topic

“E. banking: A case of India” This article presents an overview of e-banking, its

evolution and comparison of the internet banking facilities in Indian banks. The

case study approach has been used to compare various banks rendering different

internet banking services to its customers. It also explains that the shift towards the

involvement of the customers in the financial service with the help of technology,

especially internet, has helped in reducing cost of financial institutions as well as

clients/ customers who use the service at any time and from virtually anywhere

with access to an internet connection.

Pooja Malhotra and Balwinder singh36

have undertaken a research on

“Determinants of internet banking adoption by banks in India”. In this exploratory

study they have attempted to discover the factors affecting a bank’s decision to

adopt internet banking in India. The data for this study consists of panel data of 88

banks in India covering financial year 1997-98 to 2004-05.

The results show that the larger banks, banks with younger age, private

ownership, higher expenses for fixed assets, higher deposits and lower branch

intensity evidence a higher probability of adoption of this new technology. Banks

with lower market share also see the internet banking technology as a means to

increase the market share by attracting more and more customers through this new

channel of delivery. Further, adoption of internet banking by other banks es

35R.K.Mishra and J.Kiranmani, “ e-banking: a case of India”. The ICFAI University Journal of Public administration,

Vol. Year 2009 Issue month, January Pages 55-65

36Pooja Malhotra and Balwinder Singh, “ Determinants of Internet banking adoption by banks in India.” Journal of

Internet Research, Vol.17, Issue.3, 2007, Pages 323-339, emerald group publishing ltd.

27

of delivery. Further, adoption of internet banking by other banks increases the

probability that a decision to adopt will be made.

The Research paper “Technologies for ecommerce:: India Initiatives” of

Saxena. A and Dani.A.R37

, discusses various payment instruments and present one

of them namely e-cheque protocol and development activities along with its usage

and advantages over other. It also discusses about the integrated product suite for

conducting end-to-end commerce transaction using credit card and e-cheque with

PK1 technology for payment purpose, and to address the perimeter security

firewall and intruder detection system which was developed by the research

activities of IDRBT.

N.Krishna Veni38

in her article “Introduction to e-commerce, e-business and

e-banking” explains the meaning of e-banking, different forms of e-banking, its

common and support services, components and risk issues related to certain e-

banking services. This article gives various valid suggestions for bankers. It is

stated that the banks should have a clear and widely disseminated strategy that is

driven from the top and should take into account the effects of e-banking, together

with an effective process for measuring performance against it. It should take into

account the effect that e-provision will have upon their business risk exposure and

manage these accordingly.

37Saxena A.andDani.A.R. “Technologies for E-commerce: India Initiatives”, TENCON2003, conference on convergent

Technologies for Asia-pacific Region, vol.4, Oct 2003, pages 1434-1438.

38N.Krishnaveni, “Introduction to E-Commerce, E-business and E-banking http:/www.Indian,mba.com, March 2007.

28

A research paper has been published by Sarkar Partha De, Yadav

Surendra.S.Banwet D.K.39

on the topic “Emergence of flexible distribution

channels for financial products: Electronic banking a competitive strategy for

banks in India”. In this paper, the four major categories of players, in the Indian

banking sector, i.e, public sector banks, private sector banks, financial institutions

like ICICI and IDBI and foreign banks have been studied to identify competitive

strategies followed by each to get in to the non-branch delivery business.

Developmental banks, rural banks, co-operative banks have been left out of the

scope of this study, since this is not their area of focus. In this paper, it is

emphasized that all players in this market should gear up their supply chain

management processes for better customer acquisition and retention.

N.Kamakodi and Basheer Ahmed Khan40

have conducted a research on “e-

banking channel acceptance by Indian Customers”. In this research, survey result

has been obtained from 292 respondents about their view on electronic banking

channels. The result has indicated that the majority of the customers are very

comfortable and willing to use e-banking channels. At the same time, over 80%

feel that human contact is necessary. It has also revealed that the technology alone

can’t give a sustainable competitive advantage for the banks. When all banks

39Sarkar Partha De, Yadav Surender.S. and Banwet .D.K “Emergence of flexible distribution channels for financial

products: Electronic banking as competitive strategy for banks in India,’ Global Journal of flexible systems

management, vol.2 issue 3, 2001.

40N.Kamakodi and Basheer Ahmed Khan, “Looking beyond technology: A study of e-banking channel acceptance by

Indian Customers”, International Journal of Electronic Banking, Vol.1, No.1, 2008, pages 73-94.

29

introduce IT in their technology, IT would lose its position as a differentiator. The

conclusion derived from the research is that, beyond point IT along with ‘personal

touch’ will be necessary for the banks to retain the existing clients and attract new

clients.

The research article “Deploying Internet banking and e-commerce-case

study of a private sector bank in India” of G.Kannabiran and P.C. Narayan41

discusses the experience of a private sector bank in deploying internet banking and

e-commerce in India. Strategic alignment of business and IT strategies, planning

and implementation of e-banking initiatives and management of benefits are

captured along with key contributions to development.

Avinandan Mukherjee and Prithviraj Nath42

in their study on “A model of

trust in online relationship banking” tested five hypotheses with a sample of 510

internet users of various profiles in India. It is observed from the study that shared

value is most critical to develop trust as well as relationship commitment.

Communication has a moderate influence on trust. While opportunistic behaviour

has significant negative effect. It is found that higher perceived trust would

significantly enhance customer’s commitment in online banking transaction. It is

added that future commitment of the customer to online banking depends on

perceived trust.

41G.Kannabiran and P.C.Narayan, “ Deploying Internet banking and E-commerce- case study of a Private Sector Bank

in India”, Journal : Information Technology for Development, Vol.11, Issue 4, Sept 2005, pages: 363-379, published on

line on 23rd Sept 2005.

42Avinandan Mukherjee and Prithwiraj Natha, “ A model of Trust in online relationship banking, “ International journal

of bank marketing Vol.21 issue.1, 2003, pages 5-15

30

Serkan Akinci, Safak Aksey and Eda Atilgan43

conducted a research on the

topic” Adoption of internet banking among sophisticated consumer segments in an

advanced developing country”. This descriptive study was conducted to develop

an understanding of consumers’ attitudes and adoption of internet banking among

sophisticated consumers. Based on a random sample of academicians,

demographic, attitudinal, and behavioural characteristics of internet banking users

and non-users were examined. The analyses revealed significant differences

between the demographic profiles and attitudes of users and non-users. IB users

were further investigated and there-sub-segment were defined according to a set of

bank selection criteria. Finally, based on the similarities between various web-

based bank services, four homogeneous categories of services were defined.

Sylvie Laforet and Xiaoyan Li44

in their study on “Consumers attitude

towards online and mobile banking in China” investigated the market status for

online/mobile banking in china. The demographic, attitudinal and behavioural

characteristics of online and mobile banking users were examined. Respondents

from six major Chinese cities participated in the consumer survey. The results

showed that Chinese online and mobile bank users were predominantly males, not

necessarily young and highly educated, in contrast with electronic bank users in

west. The issue of security was found to be the most important factor that

motivated Chinese consumer adoption of online banking. Main Barriers to online

43Serkan Akinci, Safak Aksoy, and Eda Atilgan, “ Adoption of Internet banking among Sophisticated consumer

segments in an advance developing country,” international journal of Bank marketing, vol.22, issue –3, 2004, pages

212-232.

44Sylive Laforet and Xiaoyon Li, “consumers’ attitude towards online and mobile banking in China”. International

journal of bank marketing, 2005, Vol.23, issue.5 pages 362-380.

31

banking were the perception of risks, computer and technological skills and

Chinese traditional cash-carrying banking culture. The barriers to mobile banking

adoption were lack of awareness and understanding of the benefits provided by

mobile banking. Distinct differences and common trends between Chinese and

other countries were observed with clear indication of marketing strategy to be

deployed by the service providers.

Petrus Guriting and Nelson oly Ndubis45

, in their research work on “Borneo

online banking: evaluating customer perceptions and behavioural intention”

examined the factors that determined intention to use online banking in Malaysia

Borneo. The results indicated that perceived usefulness and perceived ease of use

were strong determinants of behavioural intention to adopt online banking. There

was also an indirect effect of computer self-efficacy and prior general computing

experience on behavioural intention through perceived usefulness and perceived

ease of use.

Shumaila Y.Yousaf zai, John G.Pallister and Gordon R.Foxal46

in their

study on “strategies for building and communicating trust in electronic banking”

have examined the effectiveness of potential trust-building strategies for e-banking

and their impact on on-line customer perceptions of trust worthiness of the bank,

by specially focusing on the information clues presented on the banks website.

45Petrus Guriting and Nelson only Ndubisi, “ Borneo online banking: evaluating customer perceptions and

Behavioural intention”. Management Research News, 2006, Vol.29, issue1/2, pages 6-15

46Shumaila Y.Yousafzai, John.G.Pallister, and Gordon.R.Foxall, Cardiff University strategies for building and

communicating trust in electronic banking: A field experiment’, journal: information technology for development,

2005, wiley periodicals inc.

32

Structural assurance and situational normality mechanism both had an impact on

customers’ trustworthiness perceptions, suggesting that banks need to use a

portfolio of strategies to build the customer’s trust. The results further suggest that

the communication of meaningful and timely information has the potential to

influence customer’s trusting intentions.

A study has been undertaken by Hsin-Ginn Hwang, Rai-Fuchen and Jai-min

Lee47

on “measuring customer satisfaction with internet banking”. A web survey

was used with the subject being internet banking user of Taiwanese banks. A total

of 226 valid questionnaires were obtained with an 85% response rate. For the