A Ôtime–space odysseyÕ: management control systems in two multinational organisations

30

A Ôtime–space odysseyÕ: management control systems in two multinational organisations Paolo Quattrone a, * , Trevor Hopper b a Saı ¨ d Business School, The University of Oxford, Park End Street, OX1 1HP Oxford, UK b School of Accounting and Finance, The University of Manchester, Oxford Road, M13 9PL Manchester, UK Abstract This paper analyses the effects of implementing an Enterprise Resource Planning system (ERP) upon management control in two multinational organisations. How ERP was configured in each corporation created different forms of distance and relations between headquarters and the scattered subsidiaries. The construction of spatial and temporal separations (i.e. distance) and how they were understood and managed had profound effects on management control. In one organisation the ERP reproduced existing structures and distance which permitted conventional accounting con- trols based on action at a distance to be maintained. The second organisation used ERP to collapse distance through real-time information in a matrix structure. This did not increase centralisation but rather produced constantly chang- ing loci of control and managerial feelings of ÔminimalistÕ control. Ó 2004 Elsevier Ltd. All rights reserved. Introduction Information technology innovations, especially Enterprise Resource Planning systems (ERPs) are interesting sites for examining relations between distance and management control. ERPs have been defined as ‘‘enterprise wide packages that tightly integrate business functions into a single system with a shared database’’ (Newell, Huang, Galliers, & Pan, 2003, p. 26, drawing on Lee & Lee, 2000). The belief that integration improves visibility and control is often taken-for-granted in the ERP liter- ature (Dechow & Mouritsen, 2003). However, as Bloomfield and Vurdubakis note, information technologies and accounting should ‘‘be under- stood as [...] attempts to institute particular ver- sions of the organisation, its members, and their activities’’ (1997, p. 641). They are not neutral in defining what is seen. Analogously, how ERP implementations enact integration (Weick, 1979) influences how distances are created, managed, 0361-3682/$ - see front matter Ó 2004 Elsevier Ltd. All rights reserved. doi:10.1016/j.aos.2003.10.006 * Corresponding author. Tel.: +44 0 1865 278808; fax: +44 0 1865 278958. E-mail address: [email protected] (P. Quat- trone). Accounting, Organizations and Society 30 (2005) 735–764 www.elsevier.com/locate/aos Accounting, Organizations and Society 30 (2005) 735–764

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of A Ôtime–space odysseyÕ: management control systems in two multinational organisations

Accounting, Organizations and Society 30 (2005) 735–764

www.elsevier.com/locate/aos

Accounting, Organizations and Society 30 (2005) 735–764

A �time–space odyssey�: management control systems intwo multinational organisations

Paolo Quattrone a,*, Trevor Hopper b

a Saıd Business School, The University of Oxford, Park End Street, OX1 1HP Oxford, UKb School of Accounting and Finance, The University of Manchester, Oxford Road, M13 9PL Manchester, UK

Abstract

This paper analyses the effects of implementing an Enterprise Resource Planning system (ERP) upon management

control in two multinational organisations. How ERP was configured in each corporation created different forms of

distance and relations between headquarters and the scattered subsidiaries. The construction of spatial and temporal

separations (i.e. distance) and how they were understood and managed had profound effects on management control.

In one organisation the ERP reproduced existing structures and distance which permitted conventional accounting con-

trols based on action at a distance to be maintained. The second organisation used ERP to collapse distance through

real-time information in a matrix structure. This did not increase centralisation but rather produced constantly chang-

ing loci of control and managerial feelings of �minimalist� control.� 2004 Elsevier Ltd. All rights reserved.

Introduction

Information technology innovations, especially

Enterprise Resource Planning systems (ERPs) areinteresting sites for examining relations between

distance and management control. ERPs have been

defined as ‘‘enterprise wide packages that tightly

integrate business functions into a single system

0361-3682/$ - see front matter � 2004 Elsevier Ltd. All rights reserv

doi:10.1016/j.aos.2003.10.006

* Corresponding author. Tel.: +44 0 1865 278808; fax: +44 0

1865 278958.

E-mail address: [email protected] (P. Quat-

trone).

with a shared database’’ (Newell, Huang, Galliers,

& Pan, 2003, p. 26, drawing on Lee & Lee, 2000).

The belief that integration improves visibility and

control is often taken-for-granted in the ERP liter-ature (Dechow & Mouritsen, 2003). However, as

Bloomfield and Vurdubakis note, information

technologies and accounting should ‘‘be under-

stood as [. . .] attempts to institute particular ver-

sions of the organisation, its members, and their

activities’’ (1997, p. 641). They are not neutral in

defining what is seen. Analogously, how ERP

implementations enact integration (Weick, 1979)influences how distances are created, managed,

ed.

736 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

and reduced. ERP configurations can dramatically

affect accounting controls and how actions are

made visible (Quattrone & Hopper, 2001b).

Shared databases, simultaneously accessible

from many locations, fulfil the dream of manymanagement controllers––remote and instanta-

neous control by real-time performance informa-

tion. Some MNOs adopt ERPs believing that

they create a virtual vista of corporate activities

that eliminates distance between the controller

and controlled, and hence provide quicker, inte-

grated control (Granlund & Malmi, 2002; Quatt-

rone & Hopper, 2001b). This is linked tocentralisation vs. decentralisation debates: ‘‘When

computers first came into common use within

organizations there was an expectation shared

among many observers that they would centralise

organizational power. Information was equated

with power and the potent information processing

capacity of computers was seen as an extension of

managerial control’’ (Bloomfield & Combs, 1992,p. 459). On the other hand, Bloomfield and Combs

observe if: ‘‘having a computer was equated with

power then the proliferation of computers

throughout organizations could indicate a decen-

tralization of power’’ (p. 460). The effects of new

information technologies are contentious.

The centralisation vs. decentralisation debate

has preoccupied management accounting research.Two sets of research are pertinent. The first com-

menced with �behavioural� works by Argyris

(1953) and Simon, Guetzkow, Kozmetsky, and

Tyndall (1954), followed by studies such as Hop-

per (1980) and Sathe (1978). All examine where

the locus of control, especially for accounting,

should reside. Should accountants situated at

HQ, distant from operations, report to seniormanagers and reinforce central hierarchical con-

trol or be situated alongside and accountable to

line managers to service their accounting needs?

The second set of research, contingency theory,

matches control systems design to features of

organisations and their contexts. Perhaps the most

consistent and reliable results came from the Aston

studies. They found larger organisations were moredecentralised and had more formal administrative

controls (Child, 1977). This was corroborated by

accounting research. Large firms are more decen-

tralised and emphasise formal controls (Bruns &

Waterhouse, 1975), and large diverse decentralised

firms use more administrative controls (importance

of budgets, use of sophisticated budgets, formal

patterns of communications, and budget participa-tion, Chenhall, 2003; Merchant, 1981).

These results are consistent with Chandler�s ana-lysis (1966, 1977) of divisionalisation. He claimed

that management accounting was amajor twentieth

century innovation making commercial manage-

ment of conglomerates possible, something which

had eluded nineteenth century entrepreneurs (Pol-

lard, 1965). Divisional performance measurementsand delegated budgets enable senior management

to exercise �decentralised centralisation� (akin to

action at a distance discussed later). General man-

agers atHQ, assisted by staff specialists, can concen-

trate on strategy whilst retaining central control

through periodic accounting representations of

scattered units� performance and plans in budgets.

Segments are treated as black boxes: line managersmake operational decisions with little central inter-

vention providing financial targets are attained.

These studies examine centralisation vs. decen-

tralisation with respect to allocating authority,

information processing constraints, representing

and quickly making performance visible, and the

physical distance of personnel and segments from

HQ. However, centralisation and decentralisationis more complex than this.

The first issue is how discretion for tasks is as-

signed to hierarchical positions and organisational

order is created. The centralisation–decentralisa-

tion dichotomy implies this is a conscious design

decision taken prior to action. This can misrepre-

sent how hierarchies and order are achieved, for

power relations and their relation to authority arecomplex and fraught. As Bloomfield and Combs

note, power is not an objective, distributable re-

source: ‘‘We need to avoid the trap of falling into

the ascription of real interests, to avoid simple cause

and effect, and the idea that power is owned, while

seeking to understand the operation of power

through the constitution of the categories of organ-

isational life’’ (1992, p. 466). They argue that powershould be viewed as a ‘‘mechanism constituted by

the multiplicity of power/knowledge relationships

between agents’’ (1992, p. 467). Accounting

1 Latour defines translation as: ‘‘displacement, drift, inven-

tion, mediation, the creation of a link that did not exist before

and that to a degree modifies the original [design]’’ (1999, p.

179). The implementation of SAP as a process of translation is

investigated in Quattrone and Hopper (2001b).

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 737

researchers have followed this advice and have iden-

tified how organisational categories such as space

and time (whether physical, or virtual) are crucial

to accounting control (Boland, 2001; Carmona,

Ezzamel, & Gutierrez, 2002; Ezzamel & Willmott,1998; Miller & O�Leary, 1994). They argue that

accounting creates distance, and accounting and

distance shape power and knowledge in organisa-

tions. All argue that technology––be it accounting

or ERP––power–knowledge relations, and dis-

tance, require scrutiny.

The second issue is how contingency studies

imply that distance between organisational units isa function of size: that is large organisations are

more complex or differentiated, hence the greater

the distance between their centre and peripheries,

decentralisation, and formalised controls. Control

is equated with structures and authority, and

authority and distance are collapsed into a single

exogenous variable––centralisation/decentrali-

sation. The �behavioural� studies recognise thatcentralisation/decentralisation has two indepen-

dent dimensions––authority relations, i.e. to whom

the accountant is responsible, and geographical or

spatial distances, i.e. where the accountant is physi-

cally located––but like contingency studies the

time dimension of distance is not studied explicitly.

The third issue concerns how both approaches

conceptualise space and time according to physicalattributes. They ignore virtual distance and how

distance is constructed by organisational practices

and accounting categories. In contrast, recent

accounting studies treat �distance� as socially cre-

ated. Chua and Briers (2001), Kirk and Mouritsen

(1996), Robson (1992), and Cooper (1992) trace

how recursive processes of constructing and accu-

mulating information creates a dichotomy betweencontrollers (the centre) and the controlled (the

periphery) (Latour, 1987, 1999) and thus establishes

distances between them. However, what becomes

real is fabricated: accounting does not reflect reality

but constructs it by providing particular forms of

organisational visibility and power–knowledge

relations. Accounting numbers, as say in budgets,

represent segments and foster �long distance con-trol� in organisations based on action at a distance

(Robson, 1992). Thus accounting categories create

organisational entities such as theHQand peripher-

ies, and then accounting numbers in reports make

performance visible and thence controllable (Quatt-

rone & Hopper, 2001a, 2001b). However, account-

ing data are numerical inscriptions: metaphorical

choices that rely on language. Their claims to repre-sent reality are problematical, as the �terms and con-

cepts of explanation do not unambiguously

‘‘correspond’’ to the real� (Robson, 1992, p. 690).

Moreover, accounting representations, as say in a

segment�s cost report, only emerge after a process

of translation1 involving mediations between vari-

ous interests and existing technologies that redefine

their attributes and why they were introduced.Thus accounting constructs distance and thence

control in organisations (Ezzamel & Willmott,

1998; Miller & O�Leary, 1994). Carmona et al.

(2002), for instance, viewed accounting as a time–

space ordering device linked to factory architecture,

observing that: ‘‘If space is configured in a ram-

shackle and haphazard way this may militate

against the possibility of its partitioning into . . .meaningful centres of calculation from an account-

ing perspective’’ (p. 268). Ezzamel and Willmott

(1998) observed how time recording compressed

time and space in accounting for teams. Ander-

son-Gough, Grey, and Robson (2001) observed

how: ‘‘individuals and organizations both con-

struct and are shaped by amultiplicity of time-reck-

oning modes, not all of which are reducible to thedominant conception of time as linear, uniform

and independent’’ (2001, p. 104). In summary, there

is a growing recognition that space and time are

subjectively created; accounting is integral to this;

and attributes of distance are not merely physical.

This paper�s affinity lies with the accounting re-

search above based on the sociology of translation

(Callon, 1981, 1986, 1991; Latour, 1987, 1999;Law & Hassard, 1999; Star & Greisemer, 1989).

However, accounting work of this ilk, contingency

and behavioural work, and linear depictions of

how ERPs shrink distance, share problems in their

treatment of control and distance. Constructs such

738 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

as ‘‘action-at-a-distance’’ and ‘‘inscription’’ (La-

tour, 1987, 1999) have been used in accounting

and organisational research to theorise manage-

ment control (e.g. Cooper, 1992; Robson, 1992).

They illustrate how dichotomies between control-lers (the centre) and the controlled (the periphery)

are created in recursive processes of constructing

and accumulating information (Latour, 1999).

However, these processes rely upon the very

dichotomy they intend to explain, for the ability

to accumulate inscriptions builds on �bringingthings back� to the centre (Latour, 1987, p. 220).

They too rest on a problematical linear notion ofspace and time (Hansen, 2001). Hence this paper

questions whether contemporary theories of con-

trol satisfactorily represent relations between enti-

ties in a MNO, especially when ERPs purporting

to eliminate distances through integrated real-time

information systems are implemented.

This is examined by studying ERP implementa-

tions, namely SAP/R3 (Systems, Applications, andProduct in data processing)2 in two multinational

organisations (MNOs).3 Different ERP configura-

2 SAP (Systeme Anwendungen und Programme in der Data-

enverarbeitung) is a German software package whose selling

point (likemany ERPs) is its ability to integrate operations across

business functions and geographical areas. The package, how-

ever, is not what a common software user might expect, i.e.

packages that work upon installation. SAP does not work that

way: the package is designed with an ideal company in mind (�AGerman company� as some managers interviewed stated). Al-

thoughmodified versions for specific industries have recently been

marketed, SAP still requires considerable customisation before

being operative. This is crucial for defining the functionality of the

system, the information it provides, and the format in which it is

presented. This aspect of SAP is the object of another study based

on the cases in this paper (see Quattrone & Hopper, 2001b).3 MNOs ‘‘account for over 40 percent of the world�s manufac-

turing output and almost a quarter of world trade’’ (Ghoshal &

Westney, 1993, p. 21). The global spread of MNOs has captured

the interest of many social scientists, including economic geogra-

phers (e.g. Clark, 1985; Taylor & Thrift, 1982), and scholars of

strategic management (Doz, 1986; Ghoshal & Barlett, 1990;

Gupta & Govirdarajan, 1991; Hedlund, 1986; Hennart, 1993;

Westney, 1993).Anencyclopaediadevoted toglobalisation reveals

the economic significance and variegation of MNOs (Buckley &

Casson, 1986; Dunning, 1993). Yet research on management

control systems in MNOs is slight and often not analytical (e.g.

Cunningham, 1978; Holzer & Schoenfeld, 1986; Salter &Niswan-

der, 1995): despite other disciplines paying increasing attention to

the MNO phenomenon accounting lags behind.

tions in each MNO defined distances between

headquarters (HQ) and scattered subsidiaries dif-

ferently, with consequences for how order, dis-

tance, accounting controls, and HQ–subsidiary

relations were constructed.The first case, a Japanese MNO (hereafter

anonymised as Sister Act) used ERP to maintain

spatio-temporal gaps between geographical and

functional areas, and the centre and the peri-

phery. Its reproduction of existing boundaries

permitted information delays between entities

and existing control methods to continue. Rather

than re-defining relations between hierarchicallevels, functional areas, and operational activities,

ERP reinforced the status quo. Its configuration

created a unitary notion of space and time en-

abling action at a distance (Latour, 1987) to

continue.4

The second case, in an American MNO (anon-

ymised as Think–Pink) demonstrates how the same

ERP (SAP) produced a different spatio-temporalframework. Think–Pink collapsed distances be-

tween segments to enact the ERP philosophy of

integration based on real-time control. Paradoxi-

cally, control suffered. The reorganisation of

processes and structures failed to match responsi-

bilities to accountability. The collapse of linear

assumptions of distance challenged managers� be-liefs about how control should be exercised, andproduced feelings of diminished control. The mul-

tiple and partial visibility afforded by ERP rein-

forced managers� perceptions that their

management control system (MCS) was incom-

plete and control was ‘‘minimalist’’, i.e. only effec-

tive in momentarily stable spaces (e.g. a factory)

and times (e.g. the monthly reporting deadline).

4 The Sister Act case also illustrates how ERPs do not

necessarily overcome functional separations by bringing the

controller (the HQ) and the controlled (the subsidiary) closer,

and how the ideal of integration underpinning the ERP

philosophy depends on actors� enactment. However, this paper

focuses on control––not ERP technology. It is not concerned

for example with why ERP was implemented in the manner it

was in each case (although this is relevant). The focus is on how

each implementation related to management control and

distance.

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 739

The case questions taken-for-granted assumptions

of beneficial, linear relationships between integra-

tion, information, and control, i.e. that integration

reduces distance, increases visibility, and hence in-

creases control (Newell et al., 2003).The paper is organised as follows. The next sec-

tion theorises distance and accounting controls in

large, dispersed organisations such as MNOs.

The third section explains the methodology

adopted during the field studies. The fourth and

fifth sections analyse how ERP implementations

constructed different conceptions of distance and

controls in Sister Act and Think–Pink respectively.The conclusions outline areas requiring further re-

search if MCSs and MNOs are to be theorised as

complex, evolutionary systems.

A B

t1 t2

s2 s1

Fig. 1. A schematic interpretation of the conventional spatio/

temporal framework of �modern� control.

The ‘centre’ and the ‘periphery’: concepts of

distance, space, and time

Immanuel Kant describes the conceptualisation

of a project (the idea) and its realisation (the sche-

ma) as an architectonic project by humans to make

sense of an otherwise confused external reality. He

describes it thus:

By an architectonic I mean the art of sys-tems. [. . .] By a system, however, I meanthe unity of the manifold cognition underan idea. [. . .] For its execution the idearequires a schema, i.e., an essential manifold-ness as well as order of the parts that is deter-mined a priori from the principle of thepurpose. [. . .] A schema that arises only inconformity with an idea [. . .] is the basis forthe architectonic unity (Kant, 1874, p. 574;emphasis in original).

Kant is describing how people gain knowledge

by creating a priori ideas to put order in what

otherwise would be a confusion of phenomena.

Schemas, such as organisation structures––integral

to controls––put order into organisations. Sym-

metry between the idea and its means constitutes

an ‘‘architectonic’’ unity. This is consistent withLaw�s (1997) description of modernity and enlight-

enment as ordering projects that endorse a unitary

and unique view of the world, be it capitalist ideo-

logy or Roman Catholic doctrines (see Quattrone,

in press). In contrast, Law (1997) argues that every

�ordered order�, every ‘‘architecture’’, is incomplete

and destined to fail––all we can aspire to is a ‘‘min-

imalist attitude’’. Control and order are ‘‘always intension’’––feelings of being in control may occur

spasmodically but only on a small scale and never

from an enduring, unique centre. The paper illus-

trates this by demonstrating how relations between

ideas (the ERP project) and their schema (its

deployment) affected order, distance, and, ulti-

mately, control in both MNOs.

Prior to this, distance within MCSs needs defi-nition. A distance, say between the HQ of a

MNO and its subsidiaries, has two dimensions:

the �space� separating the centre from the periph-

ery, and the �time� between devising plans at HQ,

their execution in the subsidiary, and reports of

accomplishments by the subsidiary to HQ. Hoskin

and Macve (1986, p. 114) note that the etymology

of the word �control� draws upon an opposition be-tween two poles: a �role� (role-player) who acts to a

script, and a �contre-role� (counter-role) who mon-

itors the role player�s compliance (Lipari, 1984).

Thus the spatio-temporal framework between

poles can be depicted––as in Fig. 1––as a sequence

of fragmented but well-defined spaces (s1 and s2)

and times (t1 and t2) which rupture what otherwise

would be a seamless flow of organisational life.Quarterly reports, annual budgets, functions, pro-

cesses, cost centres, business divisions, for exam-

ple, are based on and reproduce this simple idea.

Constructing this dichotomy is crucial for hierar-

chical accountability (Quattrone, 2000, in press;

Roberts, 1991, 1996; Willmott, 1996) and Panopti-

cal control (Carmona et al., 2002; Carmona & Gu-

tierrez, 2003; Foucault, 1977).Economic geography, ‘‘the science of the spa-

tial’’ (Massey, 1985, p. 11), pays special attention

to large MNOs for:

Fig. 2. The ‘‘Incredible Shrinking World’’ (Harvey, 1989).

740 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

The hierarchy of managerial functions, andof managerial personnel, which stretches,say, from the headquarters in the metropoli-tan region, to a regional headquarters in asmaller city, to an outlying branch plant, isin part moulded in its form by the fact ofspatial separation (p. 15).

Information flows and technology alter percep-

tions of distances (Bingham, 1996; Clark, 1985;Schields, 1991; Soya, 1989; Taylor & Thrift, 1982).

However, assumptions that distances between �cen-tres� and �peripheries� are homogeneously and line-

arly reduced by more information, i.e. that the

world is �shrinking� through quicker transportation

and communications as depicted in Fig. 2, are ques-

tionable (see Kirsh�s critique (1995) of Harvey,

1989). Instead these writers adopt more complex,relative, and evolutionary models where distance

is not an objective measure of preordained features

but is defined by actors, and the instruments of con-

trol and knowledge used tomanage it (Thrift, 1996).

Moreover, intermediaries, information techno-

logies or people, continuously re-define what is

information (Bloomfield & Vurdubakis, 1997) and

hence perceptions of space and time (Brenner,1998; Lash & Urry, 1994; Thrift, 1996). Thus dis-

tance, information, and controls are integrally re-

lated and recursive.

Understanding how peripheries and centres

emerge and how distances between them are man-

aged requires attention to inscriptions. An inscrip-

tion, ‘‘refers to all the types of transformations

through which an entity becomes materialised intoa sign, an archive, a document, a piece of paper, a

trace’’ (Latour, 1999, p. 306). A double entry re-

cord in an account, for example, is an inscription.

However, representing distance by a sign is relative

as Urry explains:

Space and time only exist when there areentities in some sense in space and time.Hence, they do not exist without at leasttwo existent objects, which occupy a rela-tionship within time–space. [. . .] Thus spaceis a set of relations between entities and it isnot a substance. [. . .] There is no �arrow oftime� as though there were something con-

crete which could itself flow or fly or fall orpass us by (1985, pp. 24–25; emphasis inoriginal).

Researchers of distance face a paradox––a spa-

tio-temporal loop. Entities––be they HQs, subsidi-

aries, and departments of a MNO, or a town––are

defined by distance––yet they define distance. La-

tour argues this reciprocity requires making dis-

tance an object of inquiry. For example, he

argues with respect to time:

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 741

The obsession with calendar time makes his-torians sprinkle technologies with agricul-tural metaphors referring to maturation,slowness, obsolescence or germination, orelse mechanical metaphors. . . . In fact timedoes not count. Time is what is counted. Itis not an explanatory variable; it is a depen-dent variable that needs to be explained(1999, p. 88).

Latour illustrates this by showing how knowl-

edge of remote areas is gained through maps that

define spatial separations between centres and

peripheries. This gives rise to what he terms �actionat a distance�. He describes how Laperouse, cap-

tain of the Astrolabe on its trip to an unknown

part of the East Pacific in 1787, did not know

the small island he was about to discover (Latour,1987, p. 215ff). This would not be so for subse-

quent sailors armed with a map detailing the is-

land. They ‘‘will see [the] island, for the first

time, at leisure, in [their] own home, or in the

Admiralty office, while smoking [a] pipe. . .’’ (La-tour, 1987, p. 220). Thus:

[t]he first time we encounter some event, wedo not know it; we start knowing somethingwhen it is at least the second time we encoun-ter it, that is, when it is familiar to us(Latour, 1987, p. 219; emphasis in original).

He continues:

Knowledge cannot be defined without under-standing what gaining knowledge means. Inother words, �knowledge� is not somethingthat could be described by itself or by �oppo-sition� to �ignorance� or to �belief�, but only byconsidering a whole cycle of accumulation:how to bring things back to a place for some-one to see it for the first time so that othersmight be sent again to bring other thingsback (1987, p. 220, emphasis added).

This recursive cycle of accumulation constructs

divisions between a centre with abstract knowl-

edge, and the periphery without such knowledge.

For example, in Latour�s example it is the source

of differences between the island�s natives and for-

eign sailors:

. . .at every run [of accumulation] the asym-metry . . . between the foreigners and thenatives grows, ending today in somethingthat indeed looks like a Great Divide, or atleast like a disproportioned relation betweenthose equipped with satellites who localisethe �locals� on their computer maps withouteven leaving their air-conditioned room inHouston, and the helpless natives who donot even see the satellites passing over theirheads (1987, p. 221).

Distances separating controllers from the con-

trolled stem from knowledge fabrication, including

that of accounting. Accounting knowledge too is a

recursive phenomena as it implies (and relies on)

similar divisions.Latour�s insights on how maps orientate hu-

mans have inspired accounting scholars. Kirk

and Mouritsen (1996), for example, argue that

accounting and control systems are maps that

guide managers in the vast ocean of their MNO.

The financial controller of a large American

MNO may not have visited a remote subsidiary

but, thanks to inscriptions, recursively recordedin accounting reports, it becomes familiar. Indeed:

An accounting system creates and presentscertain financial and economic relations fora firm. It portrays headquarters and subsidi-aries as a set of relationships that are pro-duced to facilitate interaction and control(Kirk & Mouritsen, 1996, p. 244).

The remote and unfamiliar is rendered close

and recognisable, and thence controllable, through

action at a distance. However, as Robson remarks,

�translations� modify and displace organisational

actors� intents and worldviews (Latour, 1999, p.

311). Moreover:

The more remote . . . the actor is from the set-ting he or she wishes to act upon, the moretranslations or forms of the setting (‘‘informa-tion’’) need to be mobilised in order to over-come the problem of distance. . . . Action at a

distance implies not merely physical spacebetween two points, but the capacity,through ‘‘strong’’ explanations, to influence

742 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

many contexts at the same time (Robson,1991, p. 691, emphasis in original).

Thus, the greater the distance, the more

translations are required. Action at a distance pro-

vided by accounting systems mollifies this by prof-

fering a ubiquitous system. Like cartographers

who make local knowledge of indigenous people

universal and accessible, accounting systems accu-mulate inscriptions, such as records in accounting

books, for those with access. They provide manag-

ers with a simplified and manageable view of what

�happens� across an MNO�s dispersed operations.

Accounting inscriptions render distant segments

homogenous, visible, and simultaneously control-

lable by a centre. Without accounting inscriptions

and translations (Robson, 1991, 1992), managers�ideas of distance would be a vague concept in a

vacuum––an uneasy feeling which cannot be quan-

tified, represented, and ultimately managed. They

offer a neat, generalised model to guide actions.

However, spatial and temporal demarcations

have ideological and practical consequences:

As a fundamental system of spatial division(e.g. subject–object, inclusion–exclusion)and distinctions (near–far, present–absent,civilised–natural), spatialisation [and tempo-ralisation] [provide]s part of the necessarysocial co-ordination of perceptions toground hegemonic systems of ideology andpractice (Schields, 1991, p. 46).

Kirk and Mouritsen (1996) explore this with re-

spect to how accounting helps MNOs conceive

control, space, and time.

The distinction between headquarters andsubsidiary echoes the distinction betweencentre and periphery and illustrates that allspaces do not count equally. [. . .] In MNOs,headquarters often render subsidiaries visiblevia accounting systems measuring their activ-ities and reporting their consequences asbudget performance, profitability, and pro-ductivity. [. . .] Accounting shapes whatcounts and produces an optic by whichevents produced at the subsidiary can betranslated (into profits) and transported

(via information systems) to headquarters(p. 247).

This re-emphasises the immateriality of dis-

tance: it is influenced by the intensity of informa-

tion flows. Indeed, Lash and Urry (1994) argue

that shortfalls––not physical separation––make

places �distant� from each other. Hence corporate

HQs develop surveillance activities such asaccounting to monitor subsidiaries and reduce

distance.

However, assuming a linear relationship be-

tween information volume and distance is simplis-

tic (Mouritsen, 1993, 1995; Mouritsen & Bekke,

1999). What constitutes information, how this

information flows, and from where and whence,

are crucial for establishing centres, subsidiaries,and action at a distance, and how they change.

MCS research cannot be limited to static analyses

of structures and how controls operate, for this ne-

glects how the �periphery� and �centre� are defined

initially (Quattrone, 2004; Quattrone & Hopper,

2001a). This goes to the heart of the problem of ac-

tion at a distance and accounting control––how the

separation between �role� (role) and �contre-role�(counter-role) is constructed and managed. This

is germane for the eruption of real-time informa-

tion technologies and shared databases challenge

the spatio-temporal framework that is the basis

of this dichotomy (see Fig. 1). The issue is theoret-

ical as action-at-a-distance requires a spatio-tem-

poral framework which recognises the possibility

of �bringing things back� (e.g. information on a sub-sidiary) (Latour, 1987, p. 220) from somewhere

(e.g. a subsidiary) to somewhere else (e.g. the HQ

of an MNO). The dichotomy it creates constitutes

the background of its own explanation.

Defining spatial distinctions between the �centre�and �periphery�; �here� and �there�; and temporal cat-

egories of �before� and �after� is not exclusive to

accounting––it is the terrain of ERPs (Newellet al., 2003). ERP�s potential to quicken information

flows and collapse distance is whymanyMNOman-

agers adopt real-time systems (Mouritsen, 1999).

Moreover, ERPs and accounting are not mutually

exclusive: ERPs rely upon inscriptions, often from

accounting systems, to make faraway events famil-

iar and to define �roles� and �contre-roles�.

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 743

ERP implementations are a continuous process

of translating visions of the organisation into a

working technology (Bloomfield & Vurdubakis,

1997; Dechow & Mouritsen, 2003; Quattrone &

Hopper, 2001b). They must mediate between tech-nological problems, e.g. programming issues, and

human interests, especially those of employees.

Mediations continually define the ERP project�sobjectives, the ERP, organisational order, and

eventually habitual work routines. However,

‘‘one never travels directly from objects to words,

from the referent to the sign, but always through

a risky intermediary pathway’’ (Latour, 1999, p.40). This can render identical ERP packages very

different after implementation.

However, the focus of the paper is on control––

not ERP technology. It investigates how transla-

tions of ERPs� principles produced contrasting

ways of conceiving and managing distance, and af-

fected control as defined in Fig. 1. Like the Odys-

sey, the journey of a project from an idea to anorganisational schema is perilous and beset by al-

lies, enemies, technologies of destruction and

enablement, competing interests, and natural

forces. Introducing ERP into the MNOs led organ-

isational actors into a �space-time odyssey�––a jour-ney marked by struggles, and changing perceptions

of distance. This paper describes these journeys

and their repercussions for management control.

Research methods

Case study research methodology: its role in

theorising 5

Arguments derived from empirical studies can-not be divorced from the theory underpinning

them.6 Theories can be viewed as, ‘‘an ordered

set of assertions about a generic behaviour or

5 This section largely draws on Quattrone (2002, 2004).6 It is beyond the scope of this paper to review theories in

accounting, organisation studies, and elsewhere, which are

linked to philosophical and epistemological issues. The special

issues of the Academy of Management Review (1989), Admin-

istrative Science Quarterly (1995), Chua (1986), and Hopper

and Powell (1987) are useful sources for organisation studies

and accounting.

structure assumed to hold throughout a signifi-

cantly broad range of specific instances’’ (Suther-

land, 1975, quoted in Weick, 1989, p. 517). This

emphasises generalisation and abstraction: a state-

ment is a theory when it establishes a frameworkto order and represent �instances�.

Latour (1988) argues that scientific methods are

crucial for establishing theories but are not neutral

representational tools. When science is the object

of study, and scientific methods become the,

‘‘means of regulating the connection between our

object and its representations, we then draw upon

a concept which is part of the object we wish torepresent. [. . .] The character of our object (sci-

ence) shapes the character of our investigation

(our method) and hence the nature of our repre-

sentation (portrayal of science)’’ (Woolgar, 1988,

p. 21). Thus in social studies of science (SSS), sci-

entific methods become the problem rather than

the means for investigation.

From a SSS� perspective, Weick�s depiction oftheory typifies modern science�s separation of the

investigator (who creates order through sets of

assertions) from the investigated object (specific in-

stances). Once this separation is constructed, and

if legitimate investigative methods are used (La-

tour, 1987, 1991), �instances� are framed within a

theory that excludes other interpretations. Thus

modern science seeks to dominate �instances� byelevating �theory� over �empirics� using recursive

cycles of knowledge accumulation. However,

creating a dichotomy between investigators and

subjects replicates problems of action at a dis-

tance––the topic of this paper. If this research were

to use case studies to generate theories by abstract-

ing and generalising organisational phenomena,

then the case studies would likewise be both themeans and object of inquiry. To avoid this what

is meant by case studies and theory needs to be

rethought.

With regard to doing case study research, Calas

and Smircich (1999) note that Actor-Network

Theory (ANT)7 gained prominence through case

study research despite an apparent contradiction:

7 For a literature review see Law and Hassard (1999).

744 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

ANT is reflexive, because it both constitutes

8 This neologism origins from the fusion of the etymology of

the words �description� (from Latin �de-�, to be about, and

�scribere�, to write) and �explanation� (from Greek �ex-�, out of,from, and Latin �planus�, plane. Literally it means �to make

level�, Merriam-Webster English On-Line Dictionary).9 Theory comes from the Greek teorein, a way of seeing

(Merriam-Webster English On-Line Dictionary). Each way is

partial for it is a form of not seeing something else.10 Latour comments on the term actant as follows: ‘‘ACTOR,

ACTANT: The great interest of science studies that is offers,

through the study of laboratory practice, many cases of the

emergence of an actor. Instead of starting with entities that are

already components of the world, science studies focuses on the

complex and controversial nature of what it is for an actor to

come into existence. The key is to define the actor by what it

does––its performances––under laboratory trials. Later its

competence is deducted and made part of an institution. Since

in English the word ‘‘actor’’ is often limited to humans, the

word ‘‘actant’’, borrowed by semiotics, is sometimes used to

include nonhumans in the definition.

and describes its object of interest. The stud-ies may be conducted through ethnographicresearch in a laboratory, for instance, butboth the way ‘‘things out there’’ are lookedat and the way they are reported back con-tribute to the constitution of those samethings ‘‘in here’’. There is irony behind this.Critics of positivism, many social construc-tionist, and all post-structuralist would saythat [this] is exactly what any other empiricalstudy does. [. . .] ANT scholars [insteadmake this contradiction as] their point ofdeparture, as well as their end. ANT pro-vides a very good way of telling stories about‘‘what happens out there’’ that defamiliarizeswhat we may otherwise take for granted (p.663).

Calas and Smircich argue that ANT case re-

search avoids the object of investigation being

the means of its own investigation by not purport-

ing to empirically test whether relations between

established categories of behaviour hold ‘‘through-

out a broad set of instances’’. Instead it challenges

taken-for-granted explanations with interpreta-

tions drawn from cases. The aim of fieldwork isto gain insights into problematic issues––in this

paper how ERP technologies frame distance and

its relation to management control.

With regard to theory, if there is no distinction

between how an object is investigated (the

method) and the object itself, then dichotomies

between description (i.e. the listing of phenom-

ena�s features) and explanation (i.e. the abstrac-tion of general and common features of these

phenomena) disappear along with oppositions

such as:

The empirical and the theoretical, between�how� and �why�, between stamp collecting––acontemptible occupation––and the search forcausality––the only activity worthy of atten-tion. Yet, nothing proves that this kind of dis-tinction is necessary (Latour, 1991, p. 129).

Each description is an explanation because

observers cannot be detached from their

observations. Thus we term our case study as a

�deplation�8––a description and explanation simul-

taneously––a way of seeing.9 The issue is whether

a �deplation� is interesting and whether other

researchers are persuaded that it sheds fresh light

on issues (see Quattrone, 2002; Weick, 1989, 1999).Having clarified relations between case studies

and theorisation in this paper, the field research

can be described. This is not done to prove that

the researchers collected enough material to repre-

sent the reality observed (an absolute and relative

impossibility given the vastness of MNOs). Rather

the aim is to clarify how the researchers� interpre-tations of events and attributions of significance tokey actants10 were derived to create a story perti-

nent to the research problems under scrutiny.

Details on the two case studies

The mantra of ANT is �follow the actants� (bethey people, technologies, or documents). It is a

‘‘laisser faire sociology’’ (Latour, 1999, p. 170) thatstudies how science and technologies are recogni-

sed as such. To understand how a technology such

as ERP acquires particular characteristics requires

a fluid, adaptive mode of investigation that follows

trails revealed in the field. However, this is time

consuming and expensive, especially in an MNO.

It requires a travel budget beyond most research

grants, including that for this project. Thus the

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 745

spirit rather than the letter of ANT was followed.

Personnel in different locations were inter-

viewed and relevant documentation collected. As

far as possible key actors identified in previous

interviews were contacted but interviews oftenhad to be predetermined when arranging overseas

visits. Some return visits were made but e-mails

or correspondence were normally used to follow

up new trails.

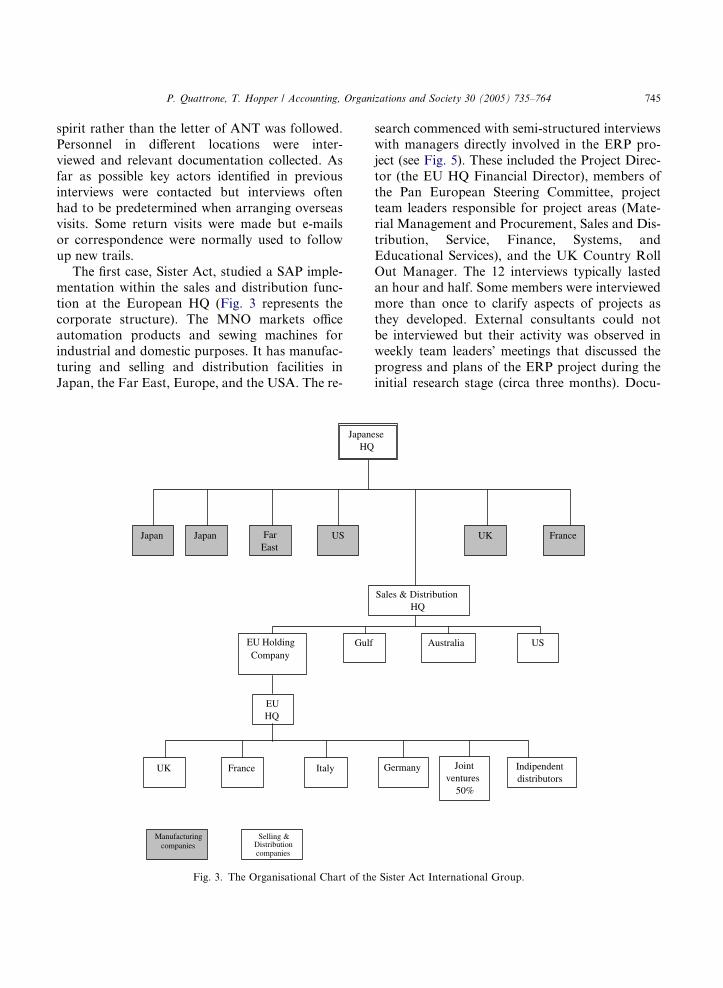

The first case, Sister Act, studied a SAP imple-

mentation within the sales and distribution func-

tion at the European HQ (Fig. 3 represents the

corporate structure). The MNO markets officeautomation products and sewing machines for

industrial and domestic purposes. It has manufac-

turing and selling and distribution facilities in

Japan, the Far East, Europe, and the USA. The re-

Japan Japan Far East

US

EU Holding Company

Gulf

EU HQ

UK France Italy

Manufacturing companies

Selling & Distribution companies

JapanHQ

Fig. 3. The Organisational Chart of th

search commenced with semi-structured interviews

with managers directly involved in the ERP pro-

ject (see Fig. 5). These included the Project Direc-

tor (the EU HQ Financial Director), members of

the Pan European Steering Committee, projectteam leaders responsible for project areas (Mate-

rial Management and Procurement, Sales and Dis-

tribution, Service, Finance, Systems, and

Educational Services), and the UK Country Roll

Out Manager. The 12 interviews typically lasted

an hour and half. Some members were interviewed

more than once to clarify aspects of projects as

they developed. External consultants could notbe interviewed but their activity was observed in

weekly team leaders� meetings that discussed the

progress and plans of the ERP project during the

initial research stage (circa three months). Docu-

UK France

Sales & Distribution HQ

Australia US

Germany

Joint ventures

50%

Indipendentdistributors

ese

e Sister Act International Group.

746 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

mentary material such as company histories, bro-

chures, and the project newsletter were collected

and compared with interview material. The re-

search continued with a visit to the corporate

HQ in Japan (see Fig. 3) where the board memberresponsible for the corporation�s information tech-

nology strategy and the former Managing Director

of the European HQ were interviewed for three

hours.

The second case, Think–Pink, was in a large

American MNO manufacturing and supplying

products for home buildings and composite mate-

rials world-wide. The case concentrated on linksbetween the UK subsidiary making insulation

products and the HQ in the USA, which operated

via a regional HQ for its European businesses. The

research commenced with a pilot study of an ERP

implementation in the UK subsidiary. This phase

consisted of six semi-structured interviews includ-

ing the Director of Finance of the UK Subsidiary,

the Director of the Shared Service Centre, and theCustomer Service Centre who were directly in-

volved in configuring SAP in the UK subsidiary.

The interviews focussed on accounting and con-

trol, and subsidiary–HQ relations. Interviews

lasted an hour and half on average. The second

phase involved a visit to the European regional

HQ in Belgium to interview the European Director

of Accounting and Finance, the European Con-troller involved in the first ERP deployment in

the UK, and the manager responsible for Informa-

tion Systems (IS) throughout the corporation. The

three managers were interviewed for two hours on

average. A second round of interviews was con-

ducted later to corroborate and explore issues that

emerged during the previous visit. The case culmi-

nated with a visit to the USA HQ. Fourteen man-agers, members of the accounting, budgeting and

planning team, and those responsible for IS strat-

egy and SAP implementation throughout the

MNO were interviewed for one hour each. The

company provided reports produced by the ERP

and material on the corporation. These were ana-

lysed and compared with interviews.

All interviews (except one) were tape-recordedand transcribed. After each interview, the re-

searcher�s first impressions were noted and later

compared with the transcriptions. As the cases

evolved, the researchers iterated theoretical issues

with empirical material and discussed them fort-

nightly. Drafts of papers were fed back to manag-

ers in both MNOs, who were forthcoming in theircomments.

‘Does distance matter?’ Stretching modernity to

its limits in a Japanese MNO

GLOBAL, GROUP, GROWTH, The 3Gs have

entered upon a new phase (front cover of SisterAct�s 1999 annual report).

Sister Act has always been a manufacturing led

company: ‘‘They produce everything they can and

then we have to sell it’’ (ERP team leader). Its orga-

nisation structure, detailed in Fig. 3, separates

manufacturing, and sales and distribution into dif-

ferent companies, with manufacturing directly con-

trolled by HQ in Japan, which is typical of manyJapanese MNOs. The Japanese HQ (the �centre�)integrates the functional and spatial divisions be-

tween manufacturing and sales companies hierar-

chically. Accounting records that trace flows of

goods, bills, and physical products define each

company within the MNO. How these are co-ordi-

nated and ordered is illustrated in Fig. 4. The Euro-

pean selling and distribution (S & D) HQ collectsorders from the European S & D companies. It

then communicates the orders to manufacturing

facilities across the world. The manufacturing

subsidiaries produce the goods and ship them

directly to the S & D subsidiaries. The Japanese

HQ, which owns the manufacturing subsidiaries,

bills the European S & D HQ, which in turn bills

the European S & D subsidiaries for productsreceived from manufacturing. Thus the physical

passage of goods from manufacturing plants

dispersed across three continents to S & D compa-

nies is controlled hierarchically by each S &D com-

pany in the relevant area (in this instance Europe)

and the global operations centre in the Japanese

HQ.

Transactions and accounting inscriptionswithin Sister Act define its organisation structure

and reproduce distinct geographical, hierarchical,

Bills European HQ

Sister act EU HQ

S&D Subsidiary

Receives orders

S&D Subsidiary

S&D Subsidiary

S&D Subsidiary

Communicates orders to

Manufacturing sites

Manufacturing sites

Manufacturing sites

Bills

Send finished products to

Japanese HQ

Fig. 4. The relationships between manufacturing and sales and distribution within Sister Act group. (� � �� � �) Flows of bills; (– -–-) flowsof products; (––) flows of orders to EUHQ; (– - -– - -) communication of orders.

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 747

and functional responsibilities. These complicated

transactions, for example between the HQ in Ja-

pan and the regional HQ in Europe, define the

European HQ�s existence. Without this intricate

web of relations the organisation structure of Sis-

ter Act in Fig. 4 would be different. For example,the distinction between manufacturing and selling,

and the hierarchical separation between Japan,

Europe, and individual subsidiaries might be re-

placed by a matrix structure. Sister Act�s organisa-tion structure is characterised by complexity,

distance, and hierarchical accounting controls. If

the �incredibly shrinking world� prophets are cor-

rect, then Sister Act�s decision to implement ERPshould dramatically change its controls and

structure.

The origin of SAP as a strategic act

The ERP project did not mark a discontinuity

in information systems development in Sister Act

but extended a project on group integrated ac-

counts started in the early 1990s. Prompted bychanged legal regulations for reporting overseas

subsidiaries, Sister Act started to homogenise

group consolidation. The Financial Director of

the European HQ explained:

1994, I think it was, Japanese fiscal law chan-ged to allow dividends from subsidiaries topass through a second layer of corporatestructure and still carry the tax credit. Thatenabled us to move from a situation where

748 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

we were all directly owned by [the HQ] tobeing owned by a European holding com-pany. . . . That gave us the need to have a. . . different type of emphasis on our report-ing structure. . . . We started to do statutoryconsolidations within Europe and not justwithin Japan and the whole thing startedthen to evolve.

A Microsoft Excel template was created calledJ-consoly (short for Japanese consolidation pack-

age) for all subsidiaries. It offered a simple but

effective way of consolidating consistent with ac-

cepted accounting principles. Each subsidiary used

the same template, shaped by accounting catego-

ries within Profit and Loss accounts, and Balance

Sheets. The Financial Director of the European

HQ explained how the new ERP (SAP) wouldnot replace J-consoly but would provide a com-

mon database for filling it in. This was needed

urgently because in the eighteen European

subsidiaries:

There are 18 different systems out there . . .all operating their own semi-automated orautomated systems . . . they all had to . . . findways of creating information to go intospreadsheet packages that form the consoli-dation exercise.

He explained how:

Over the past 18 months . . . there has been afaster move towards creating a global infor-mation system. Now, how does that mani-fest itself? Globally this spreadsheetpackage, reporting budgeting system isalready in place. But they wanted to gobeyond just the management informationprocess. . . . They wanted to embrace all ofthe supply chain management, the logisticscontrol, and working capital reduction pos-sibilities in inventories in receivables andso on, and so we are embarking on anERP project.

As the project unrolled it was gradually trans-

formed from facilitating consolidation for external

reporting to the global provision of an integrated

database for management information. It became

an important element of the 3G�s strategy extolled

in company reports, i.e. Global, Group and

Growth.

The ERP implementation in European sales,

marketing and distribution subsidiaries attractedconsiderable attention, as the project had a novel

structure (see Fig. 5) and a budget of £16 million

(£17m. by 2000). Managers from the European

HQ of Sister Act based in the UK led the project

(see Fig. 5). The steering committee comprising

of the executive directors from the European HQ

gave the project exceptional legitimacy. The ERP

System Team Leader described his project as oneof the �biggest projects that certainly the European

organisation has ever done [and] is also [its] first

properly organised project. . . . We have never had

an organisational structure like that before�.The ERP project could have been a vehicle for

large, dramatic (and often painful) re-organisa-

tions (see Jazayeri & Scapens, 1999). Newell et al.

(2003) argue that integration means overcomingfunctional barriers. If so, then SAP�s potential con-tribution to the �3Gs� strategy might have been

consolidating the Group by introducing standard,

real-time, integrated systems to collapse distance

and simplify the complex, differentiated organisa-

tion structure. This would enable HQ to substitute

hierarchical control with an integratedGlobal strat-

egy of increased efficiency, greater responsivenessto customers and markets, and ultimately Growth.

This was not to be. The ERP implementation

proved more complicated than the linear journey

inferred by the rhetoric of Sister Act�s 1999 annual

report. As SAP�s implementation began, discrepan-

cies emerged between its abstract philosophy of

integration and its enactment as a working practice

(Hines, 1988; Quattrone & Hopper, 2001a).

Alternative voices and organisational choice

The ERP project was not the only information

systems project in Sister Act––other initiatives

apparently pursuing the �3Gs� strategy were under-

way. For example, the �Warehouse project� soughtto centralise warehousing for European operationsin Belgium, Holland, and France. However, de-

spite being a major initiative for European S &

EU HQ Managing Director

PAN EUROPEAN STEERING GROUP

• EU HQ Managing Director • EU HQ Financial director • Japanese Manager • EU ERP project Leader

EU ERP Project Leader

Project Management Group • ERP Project leader • Systems Team leader • Lead external consultant

Project co-ordinator Country Roll out Managers

Sister Act Europe Sister Act UK Sister Act Germany Sister Act France

Change Management Sister Act Europe Sister Act UK

Educational services

Team leader EU HQ

Systems

Team leader EU HQ

Finance

Team leader EU HQ

Service

Team leader EU HQ

Sales & Distribution

Team leader EU HQ

Material Management

& Procurement

Team leader EU HQ

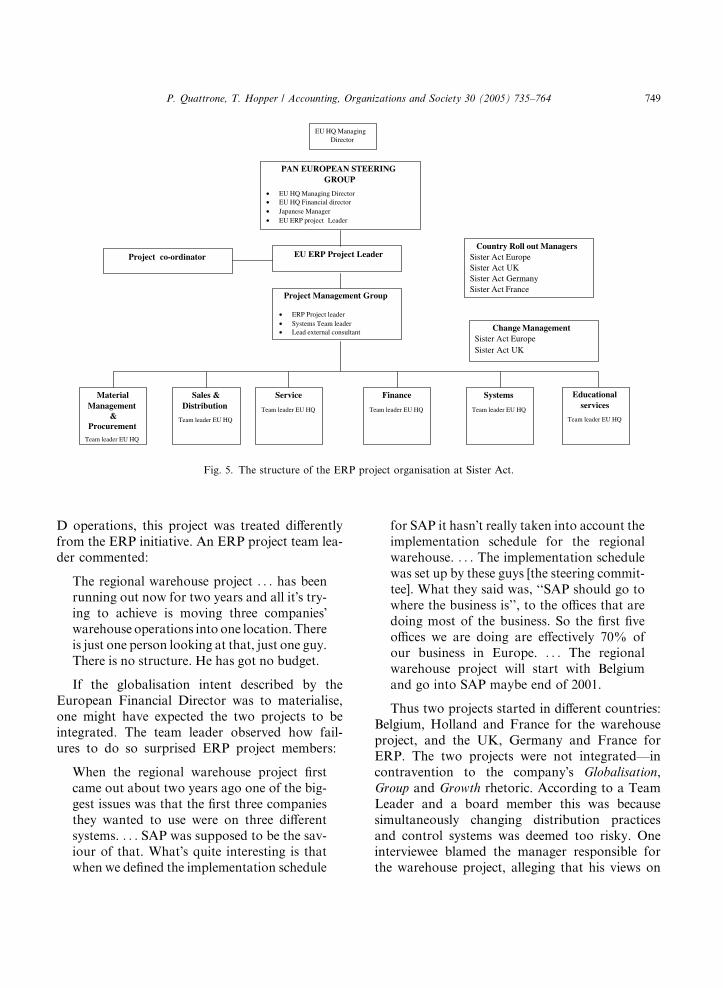

Fig. 5. The structure of the ERP project organisation at Sister Act.

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 749

D operations, this project was treated differently

from the ERP initiative. An ERP project team lea-

der commented:

The regional warehouse project . . . has beenrunning out now for two years and all it�s try-ing to achieve is moving three companies�warehouse operations into one location. Thereis just one person looking at that, just one guy.There is no structure. He has got no budget.

If the globalisation intent described by the

European Financial Director was to materialise,

one might have expected the two projects to be

integrated. The team leader observed how fail-

ures to do so surprised ERP project members:

When the regional warehouse project firstcame out about two years ago one of the big-gest issues was that the first three companiesthey wanted to use were on three differentsystems. . . . SAP was supposed to be the sav-iour of that. What�s quite interesting is thatwhen we defined the implementation schedule

for SAP it hasn�t really taken into account theimplementation schedule for the regionalwarehouse. . . . The implementation schedulewas set up by these guys [the steering commit-tee]. What they said was, ‘‘SAP should go towhere the business is’’, to the offices that aredoing most of the business. So the first fiveoffices we are doing are effectively 70% ofour business in Europe. . . . The regionalwarehouse project will start with Belgiumand go into SAP maybe end of 2001.

Thus two projects started in different countries:Belgium, Holland and France for the warehouse

project, and the UK, Germany and France for

ERP. The two projects were not integrated––in

contravention to the company�s Globalisation,

Group and Growth rhetoric. According to a Team

Leader and a board member this was because

simultaneously changing distribution practices

and control systems was deemed too risky. Oneinterviewee blamed the manager responsible for

the warehouse project, alleging that his views on

11 The researcher was called to an urgent meeting with the EU

Financial Director to discuss issues of privacy when interview

questions gradually but increasingly shifted to this issue. It was

made evident that this incongruity was not to become manifest.

750 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

what it should deliver changed daily. Nevertheless,

responsibility for the project could have been

changed or integrated into the bigger, richer, more

officially favoured ERP project. But this was not

done, despite joint meetings of the two projectgroups to identify �best practices� to yield savings

and release resources for growth.

It transpired that Sister Act�s ideal of globalisa-tion and integration was different from the taken-

for-granted meaning purveyed in the company�sannual report. Believers in greater integration

were disappointed to find many colleagues did

not share their ideal. For example, a team leaderstated:

Japan will have the UK manufacturing facil-ity on their system and all the production willbe on their system. They will be able to seethat. They should be able to derive the salesand stock information from our system.

However, this was not as envisaged:

I thought that we were all going to be on thesame server, Japan and Europe because thatto me is the big strategic advantage of goingto a common platform and linking the manu-facturing base. . . . With the end user on acommon platform the computer�s ability ofstocking information is the advantage. . . .We are getting two servers––one in Japanand one in Europe. So our template becomesthe European template and then we have tofind a way of interfacing. Now, in five yearstime we will all be wishing: ‘‘Oh slow down,let�s get a global template’’. . . . We will say,‘‘Wait a minute! It is now time for the twoservers to join. AHA!! But Wait a minute . . .you have got a different standard there, youhave got a different material number . . . whydidn�t we think about that five years ago?’’!

Another team leader, wanting more time to de-velop a common template for Europe, Asia, and

America complained about tight time schedules

for �going live�:

What extra benefit would you get for thatextra cost? . . . It will cost us more in the nextfive years to revisit an urgently needed pro-

ject than it would to have an extra sixmonths of consultants and live time. . . . Ido not think anybody understands, and Idon�t, the full scope of the project.

He illustrated his worries:

The placing of orders is done in differentdepartments, so �fax� do their own ordersand �spare parts� do theirs and so on and soforth. From a SAP point of view the orderprocess entry is the same, so it would be . . .more efficient to have one small departmentprocessing orders. [The European HQ] said,‘‘No, No, No, we don�t do that’’. But [wesaid] ‘‘This is the most efficient way . . . andnow the system allows you to do that’’. [Theysaid], ‘‘No, we have always been that wayand we want to remain that way’’. . . .Nobody is really checking on the businessbenefits. . . . We are going to spend a lot ofmoney and we had some great ideals aboutwhat to do . . . but ‘‘Is anybody really check-ing to make sure we get that?’’

These worries were practical, for SAP is not

easy to re-configure once installed as the ERP Sys-tem Team Leader confirmed: When we looked at

[the different ERPs] we found that SAP is the most

difficult to change once it is implemented.

Managers responsible for introducing SAP

soon found that enacting global in the 3Gs strategy

was different from their anticipations. Integrating

manufacturing, logistics, and finance, predicated

as a feature of globalisation of MNOs, did not cor-respond with the meaning of global within Sister

Act. The ERP Project Steering Committee�s idea

of integration did not embrace changing organisa-

tion structures, combining MIS projects, or even

common servers.11 Instead SAP�s ideology of inte-

gration was translated into an exercise to speed up

communication between functions and divisions.

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 751

Managers would not countenance changed rela-

tions between manufacturing sites, S & D compa-

nies, and HQ in Japan. The dynamics of this

change are investigated below.

Translating the idea of global and integration into

SAP: issues of order, distance, and control

The lack of integration between manufacturing

and sales, and the ERP and warehouse projects,

made the 3Gs strategic ambitions questionable.

Why was there an apparent incoherence between

the ambition of becoming a globally integratedcorporation and the ERP design? Was it a matter

of culture? The Financial Director of the Euro-

pean HQ argued that Japanese companies differ

from American and European ones.

Japanese culture is very . . . conservative. . . .Lots of fantastic things have come out ofJapan but . . . decision-making in Japanseems to be a difficult thing. . . . It�s a com-mittee process.

He illustrated this with comments about a

phone call from the Managing Director:

What [the Managing Director] said to me onthe phone, ‘‘When we come over here we aregoing to do this, and we are going to do that’’but [. . .] he would come back . . . from Japanand I would say:

‘‘How was your trip?’’[then the MD would say] (respondent imitating

a Japanese accent)

‘‘Very good, very busy, very busy meeting sche-

dule, meetings all the time’’

‘‘Anything decided’’?

‘‘Of course not!’’

And this is very frustrating!!!

However, this paper is not on how cultural differ-

ences affect change processes, important though

this may be at Sister Act. The focus is on controland distance. Nevertheless, the conservatism of Sis-

ter Act affected how the ideal of being a globally

integrated firm was translated into an operational

technology, namely SAP. Managers at the Japanese

HQ responsible for information technology world-

wide confirmed that Sister Act always pursued

change incrementally, preserved employment, and

maintained hierarchical controls. When Sister Act�smanagers were asked to comment on differences be-

tween SAP implementations in Sister Act and

Think–Pink, they argued that implementing SAP

according to the manuals would flatten hierarchies

and cut jobs, it could take two years for people to

understand SAP�s potential, and changing the spa-

tio-temporal framework people were used to would

create chaos in operations. A metaphor from theEuropean Financial Director is informative:

What are the three things that are most likelyto cause you stress in your personal life?Usually it would be financially related, itwould be divorce related, or it would bemoving house related and very often thosethree all come together and that�s when theindividual can�t cope! . . . If you can takeaway key elements of the stress then youmay have more success in the way you goabout doing the most important thing, whichis implementing a new system.

Sister Act enacted ERP integration through

processes of translation involving less disruptiveoptions, consistent with Sister-Act�s culture of con-servatism and incremental change.

Enacting the ERP philosophy began with the

organisation of the ERP project, which replicated

spatial and functional differentiations between

the European HQ and European subsidiaries with

respect to Material Management and Procure-

ment, S & D, Services, Finance, Systems, andEducational Services (see Fig. 5). It mirrored pre-

vailing organisational relationships akin to the

spatio-temporal framework of Figs. 3 and 4. The

role of managers from the European HQ on pro-

ject teams was to homogenise attitudes and create

a single notion of space and time underpinning

governance. They were expected to filter out and

mediate with other interests (especially Europeansubsidiaries). ERP project teams (see Fig. 5) with

equal numbers of managers from the three biggest

subsidiaries gave the appearance of pluralism but

752 P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764

each member was expected to return to their sub-

sidiary and convince colleagues of the ERP pro-

ject�s effectiveness. Thus, team members became

allies for preserving the status quo of manufactur-

ing and selling relationships rather than agents ofstructural reform. The ERP project�s hierarchical

organisation constrained the unknown (in this case

SAP) and protected centralised power and control

via the European HQ.

The ERP project structure reproduced the di-

vide between the centre (EU HQ) and the periph-

ery (EU subsidiaries): between those in control

and those controlled. This was apparent when ateam leader described the physical space around

the ERP project leader�s desk as an �oasis of tran-quillity’’ in a chaotic open-plan ERP office. The

interviewer assumed the team leader�s boss, the

project leader, was twenty meters away in a silent

and remote corner making important decisions

about the £16 million budget, while others worked

in turmoil. When the interviewer saw the office, thedistance between the project leader and the team

leader was only a meter and a half. The researcher

realised that distance (like power and control) is

not physical but a social artefact. Given the repro-

duction of existing distances within the ERP pro-

ject organisation, it is unsurprising that the SAP

implementation reproduced and reinforced exist-

ing distances and kept the organisation structureof Sister Act intact.

When the ERP project leader discussed the po-

tential benefits of SAP for Sister-Act, he stated

that it was not just:

. . .a replacement for the existing [IT] systemsbut we aimed to change the process itself. . . .Changing the way the cash management ishandled––changing the stock inventory pro-cesses and going through the people changes.. . . What SAP can do is provide the solutionfor the best practice for the business . . . not toreplace the existing processes but to look toimprove the way we do things. The ideawas to look at best business practices.

Thus initial grandiose expectations that SAP

would facilitate global integration changed to find-

ing the �best� ways of conducting operations. How-

ever, defining a �best practice� was as difficult as

defining integration. The Director of Finance re-

called how consultants hired as advisors on SAP

implementation got, �Headaches in how to deal with

some issues but we didn�t promise them an easy life�.For example, the �best� stock valuation method

was an issue:

Moving averages . . . is theway that [SAP] doesit and therefore they say that that is the bestpractice. I maintain that that may be the waythat you do it but it is not best practice. . . .FIFO is best practice in the warehouse.

Bloomfield and Danieli (1995) claim consul-

tants sell their products to, ‘‘not so much target

themselves at a particular niche, as seek to create

a niche and persuade the client that they are within

it’’ (p. 29). Consultants must convince clients that

they have a problem that the consultant�s tool-kitcan mend. That is, consultants create a space

and a time within which the client�s problems can

be framed. In Sister Act, however, the consultants

did not achieve this: instead a power struggle to

reassert Sister Act�s notion of time and space en-

sued as the European Financial Director recalled:

We are saying, ‘‘Let�s do it [Sister Act�s] way and

that is a good efficient way and SAP will work.’’Gradually the project emphasised making existing

practices more efficient to release resources for

growth: revolutionary change was rejected.

The European HQ was central to this. Collaps-

ing distances between Europe and Japan, and Sales

and Manufacturing, could eliminate or downsize

the European HQ. Mediations between systems

designers and managers facing this threat wroughta translation of ERP different from that originally

sought. SAP was not allowed to challenge existing

organisation structures (illustrated in Fig. 3), or

financial and physical systems tracking orders

(flow-charted in Fig. 4). Senior managers sponsor-

ing SAP ensured accounting inscriptions (albeit

more efficiently) continued to record the compli-

cated intra-company transactions that maintaineddistances (Quattrone & Hopper, 2001b). Before

and after (represented by the discontinuous stages

over time between placing an order and receiving

it), and here and there, (represented by spatially

P. Quattrone, T. Hopper / Accounting, Organizations and Society 30 (2005) 735–764 753

separated segments) continued to exist. Thus the

ERP project regulated and reproduced existing dis-

tances between the entities. The poles A and B and

the spatio-temporal distance entailed by the mod-

ern conception of control (t1–t2 and s1–s2) were pre-served: participants in Sister Act did not wish to

abandon them. SAPmay have speeded up informa-

tion flows, and audited and diffused best practices,

but it became an exercise in stretching modern con-

trol, illustrated in Fig. 1, to its limits. Paradoxi-

cally, ERP commonly considered as state-of-the-

art technology for integrated controls came to pre-

serve hierarchical controls using well understoodbut �re-designed� business practices. When the

Material Management and Procurement Team

Leader was asked when the three ERPs would

share a common platform he jokingly replied

‘‘Not at least until 2017!’’

So what did this project do? A paraphrased pas-

sage from Law is pertinent:

[The ERP project] makes a hierarchy. It cre-ates a �larger context� for itself––yes, a con-text which is singular. It creates a flat space:a larger homogeneous world, or container.And then it locates itself, along with the enti-ties which do not belong to it, within the flatspace: within the container. Which is, ofcourse, a description of pluralism. . . . Themaking of a pluralist space in which variousactors, endowed with more or less the sameattributes, work within a larger, topographi-cally homogeneous, context. Which is, to besure, an abstract way of talking of . . . themodern world (1997, p. 9).

Law�s comments capture what the translation of

the ERP project came to represent in Sister Act. As

in a disciplinary regime (Foucault, 1977), it created