A GLOBAL / COUNTRY STUDY REPORT ON “PAKISTAN ...

175

1 A GLOBAL / COUNTRY STUDY REPORT ON “PAKISTAN” Submitted to Gujarat Technological University IN PARTIAL FULFILLMENT OF THE REQUIREMENT OF THE AWARD FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION S.R. LUTHRA INSTITUTE OF MANAGEMENT (Inst. Code: 805) MBA PROGRAMME Affiliated to Gujarat Technological University, Ahmedabad May 2012

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of A GLOBAL / COUNTRY STUDY REPORT ON “PAKISTAN ...

1

A

GLOBAL / COUNTRY STUDY REPORT

ON

“PAKISTAN”

Submitted to

Gujarat Technological University

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

S.R. LUTHRA INSTITUTE OF MANAGEMENT (Inst. Code: 805)

MBA PROGRAMME

Affiliated to Gujarat Technological University, Ahmedabad

May 2012

2

TABLE OF CONTENTS

Sr. NO. Particulars Page

NO.

PART I

1 History 2

2 Geography & Topology 8

3 Political & Legal Environment 13

4 Trade & Commerce 19

5 Macro Economic Environment 25

6 Capital Market 32

7 International Trade 39

8 Agriculture 45

9 Manufacturing 50

10 Services 55

PART II

1 Marine Industry 61

2 Iron & Steel Industry 71

3 Pharmaceutical Industry 80

4 Gems & Jewelry Industry 90

5 Leather, Meat & Poultry Industry 100

6 Chemical & Fertilizer Industry 110

7 Textile & Apparel Industry 122

8 Cereals & Pulses 130

9 Fruits & Vegetables 139

10 Dry – Fruits & Spices 143

Bibliography

Annexure

3

HISTORY

4

Pakistan contains the archeological remains of an urban civilization dating back 4,500 years.

Alexander the Great’s empire included the Indus Valley in 326 B.C. His successors founded

the Indo-Greek kingdom of Bactria based in what is today Afghanistan and extending to

Peshawar. Following the rise of the Central Asian Kushan Empire in later centuries, the

Buddhist culture of Afghanistan and Pakistan, centered on the city of Taxila, experienced a

cultural renaissance known as the Gandhara period.

Economy of Pakistan

Pakistan has a semi-industrialized economy and a rapidly developing country. The growth of

economy are situated along the Indus River. Diversified economies of Karachi and Punjab's

urban centers coexist with lesser developed areas in other parts of the country. Despite being

a very poor country in 1947, its economic growth rate has been better than the global average

during the subsequent four decades, but certain policies led to slowdown in the late 1990s.

Recently, wide-ranging economic reforms have resulted in a stronger economic outlook and

increased growth specifically in the manufacturing and financial sectors. Since the 1990s,

there has been an improvement in the foreign exchange position and rapid growth

in currency reserves. Pakistan's gross domestic product, as measured by purchasing power

parity, is estimated to be $475.4 billion while its per capita income is at $2,942. The poverty

rate in Pakistan is estimated to be between 23% and 28%.

GDP growth was steady during the mid-2000s at a rate of 7%; however, slowed down during

the Economic crisis of 2008 to 4.7%. A large inflation rate of 24.4% and a low savings rate,

and other economic factors, continue to make it difficult to sustain a high growth

rate. Pakistan's GDP is US$167 billions, which makes it the 48th-largest economy in the

world or 27th largest by purchasing power adjusted exchange rates. Today, it is regarded as

having the second largest economy in South Asia.

The structure of the economy has changed from a mainly agricultural base to a strong service

base. Agriculture now only accounts for 20% of the GDP, while the service sector accounts

for 53% of the GDP. Significant foreign investments have been made in several areas

including telecommunications, real estate and energy. Other important industries include

apparel and textiles, food processing, chemicals manufacture, and the iron and steel

industries. Pakistan's exports in 2008 amounted to $20.62 billion (USD).

5

Demographic view of Pakistan

The estimated population of Pakistan in 2010 was over 170 million making it the world's

sixth most-populous country, behind Brazil and ahead of Bangladesh. In 1951 Pakistan had a

population of 34 million. The population growth rate stands at 1.6%. It is expected that by

2030, Pakistan will overtake Indonesia as the largest Muslim country in the world.

Life expectancy at birth is 63 years for females and 62 years for males as of 2006 compared

to the healthy life expectancy at birth which was 54 years for males and 52 years for females

in 2003. Expenditure on health was at 2% of the GDP in 2006. It is a multilingual country

with more than sixty languages being spoken. English is the official language of Pakistan and

used in official business, government, and legal contracts, and Punjabi has a plurality of

native speakers. Urdu is the lingua franca and national language in Pakistan. Punjabi is the

regional language of Punjab. Saraiki is also spoken in the larger area of Punjab

province. Pashto is the provincial language of Khyber Pakhtunkhwa. Sindhi is the provincial

language of Sindh and Balochi is the provincial language of Balochistan.

The World Bank considers Pakistan a low-income country. GDP is around $166 billion at the

official exchange rate. The population numbered some 167 million in 2008 with a 1.81%

growth rate. No more than 55.0% of adults are literate, and life expectancy is about 64 years.

In FY 2008-2009, the GDP growth rate was 3.7%, and unemployment was estimated at 14%.

Year-over-year consumer price inflation averaged 13.6% in 2009. Main inflation drivers

include food and utility prices, the Pakistani rupee’s depreciation versus the U.S. dollar, and

higher international commodity prices. Low levels of spending in the social services and high

population growth have contributed to persistent poverty and unequal income distribution.

Pakistan's extreme poverty and underdevelopment are key concerns, specifically in rural

areas.

Religion in Pakistan

About 97 % of all Pakistanis are Muslims. Official documentation states that Sunni Muslims

constitute 77 % of the population and that adherents of Shia Islam make up an additional 20

%. Christians, Hindus, and members of other religions each account for about 1 % of the

population.

6

Literature

Pakistani literature originates from when Pakistan gained its nationhood as a sovereign state

in 1947. The common and shared tradition of Urdu literature and English literature of South

Asia was inherited by the new state. Over a period of time, a body of literature unique to

Pakistan has emerged all major Pakistani languages, including Pushto, Seraiki, Balochi,

Urdu, English, Punjabi and Sindhi.

Music

It ranges from traditional styles such as Qawwali and Ghazal to more modern forms that fuse

traditional Pakistani music with Western music. Pakistani music is represented by a wide

variety of forms.

Drama and theatre

These are very similar to stage plays in theatres. They are performed by well-known actors

and actresses in the Lollywood industry. The dramas and plays deal with many themes from

life events, often with a humorous touch. Pakistani poetry is the best.

Architecture

Mohenjo Daro, Harappa and Kot Diji belong to the pre-Islamic era settlements. The rise

of Buddhism and the Persian and Greek influence led to the development of the Greco-

Buddhist style, starting from the 1st century CE. The high point of this era was reached with

the culmination of the Gandhara style. An example of Buddhist architecture is the ruins of the

Buddhist monastery Takht-i-Bahi in Khyber-Pakhtunkhwa..

Recreation and sports

The official national sport of Pakistan is field hockey with squash and cricket also very

popular. The national cricket team has won the Cricket World Cup once (in 1992), were

runners-up once (in 1999), and co-hosted the games twice (in 1987 and 1996). Additionally,

they have also won the ICC World Twenty20 once (in 2009), and were runners-up (in 2007).

The team has also won the Australasia Cup in 1986, 1990, and 1994.

7

Cuisine

Urban centres of the country offer an amalgamation of recipes from all parts of the country,

while food with specific local ingredients and tastes is available in rural areas and villages.

Besides the main dishes of salan, with or without meat and cooked with vegetables or lentils,

there are a number of provincial specialties such as biryani, karahi, and tikka, in various

forms and flavours, eaten alongside a variety of breads such as naan,chapati and roti.

Ramadan

The holiest month of the Islamic Calendar, which is a month of fasting from sunrise to sunset

and self discipline, it is widely observed in Pakistan.

Eid celebrations

The two Eids, Eid ul-Fitr and Eid ul-Adha, commemorate the passing of the month of fasting,

Ramadan, and the willingness of Ibrahim to sacrifice his son Ishmael for God. On the night

before Eid, people search for the new moon to mark the end of Ramadan and arrival of Eid

ul-Fitr. On Eid ul-Fitr, money is given for charity and as gifts to young children. On Eid ul-

Adha, people may also distribute meat to relatives and neighbors and donate food for charity.

Muharram (Ashura)

In Pakistan, the first ten days of Muharram are observed officially. The 10th day of

Muharram is marked in the memory of Imam Hussain (Aliahsalam), the grandson of

Muhammad, who was a martyr, along with 72 family members, friends and followers during

the Battle of Karbala.

Independence Day

On August 14, the people of Pakistan celebrate the day Pakistan gained its independence

from British India and formed an independent state for Muslims.

8

National Dress

The national dress of Pakistan is Shalwar Qameez (for both men and women. It consists of a

long, loose fitting tunic with very baggy trousers. The men's version consists of solid,

masculine colours, and is almost always accompanied by a collar and buttons (similar to a

polo shirt). Men often wear an outer waistcoat over the shalwar kameez.

The sherwani or achkan with karakul hat is the recommended dress for male government

employees and officials, as it is not specifically associated with any of the provinces. Most

male government officials wear the formal black sherwani on state occasions.

The women's version almost never contains collar and buttons but is often embroidered and

consists of feminine colors and may feature lace or flower patterns.

Ethnic groups

Pakistanis are diverse, many possessing dark hair and eyes but light coloured eyes and light

coloured hair do occur in significant portions of the population as well. The

typical Pakistani can range from light to dark brown skin tones with a few exceptions in

mountainous regions of the north. Many of the people inhabiting Pakistan's western regions

share genetic affinities with ethnic groups in Iran, Afghanistan and Tajikistan. While the

racial features of each ethnic group in Pakistan are not uniform, Chitrali's and some of

the Dardic tribes in the north are the most Caucasoid phenotypically, followed by the

Pashtuns, Kashmiris, Balochis, Punjabis, and Sindhis, Muhajirs, and Seraikis. Pakistan's

genetic diversity is due to various factors including the numerous waves of migration from

other regions and include Aryans mainly in smaller amounts Greeks,

Iranians, Arabs, Turks, Scythians, Afghans to name a few and also because of its geopolitical

location straddling the Iranian Plateau, Central Asian, Tibetan and South Asian genetic

spheres and as a result, the phenotypic expression of its people is reflective of this diversity.

Large influxes of refugees from the surrounding nations have further exacerbated this change

(Muhajirs from India in 1947, Kashmiris refugees in 1948, Iranians in 1978, Afghans in th

1980s, Tajiks and Iraqis in 2001 etc..)

9

GEOGRAPHY &

TOPOLOGY

10

Pakistan is situated in South Asia. Pakistan’s southern boundary with 1,064 km of

coastline is The Arabian Sea.

The country is extended into a total area of 796,095 sq km and is nearly four times the size of

the United Kingdom. The country extends more than 1,800 km to the Khunjerab Pass on

China' border, From Gwadar Bay in its south-eastern corner. It is divided into four main

provinces: Sindh, Punjab, Khyber Pakhtun Khwa and Balochistan.

The country has a great agricultural economy including canals irrigating a major part of its

cultivated land. The major crops are Wheat, cotton, rice, millet and sugar cane. In abundance

in different parts of the country the fruits are grown like: mangos, oranges, bananas and

apples. The major natural resources are natural gas, coal, salt and iron. The country has a

growing industry. In its economy, Cotton, Textiles, sugar, cement, and chemicals play an

important role.

It is having such physical regions as a) the western offshoots of Himalayas which cover its

northern and north western parts of which the highest peak K-2 rises to 8611 meters above

sea level; b) the Balochistan plateau c) The Potohar Plateau and salt range and d) The Indus

plain, the most fertile and densely populated area of the country. It gets its sustenance from

the Indus River and its tributaries.

Bordering Countries- Afghanistan, Iran, India and China

Land Area- 307,374 square miles (796,095 sq km)

Coastline- 650 miles (1,046 km)

Highest Point- K2 at 28,251 feet (8,611 m)

Major Cities- Pakistan has seven cities Karachi, Lahore, Faisalabad, Rawalpindi, Multan,

Hyderabad, and Gujranwala.

Principal Rivers- The main rivers are the Indus (2,749 kilometers within Pakistan) and its

tributaries: the Chenab (730.6 kilometers), Ravi (680.6 kilometers), Jhelum (611.3

kilometers), and Sutlej (530.6 kilometers). As a result of seasonal variations in water flows

11

and the presence of substantial irrigation structures, the navigable portions of these rivers are

generally small and unconnected

Land Boundaries- Pakistan is sharing borders with Afghanistan (2,430 kilometers), China

(523 kilometers), India (2,912 kilometers), and Iran (909 kilometers).

Natural Resources- The natural resources are the most important economic tool that

includes arable land, chromite, coal, copper, fireclay, gypsum, iron, limestone, oil, natural

gas, rock salt, and silica sand.

Land Use- Approximately 22 million hectares are used for cultivation, of which nearly 16

million hectares are actually sown, with the remainder left fallow. About 13.5 million

hectares of the sown area are irrigated, and 6.5 million hectares are sown more than once per

year. Pakistan has an extensive but inefficient canal system for irrigation, and much of the

crop area is rain fed, but precipitation tends to be unevenly distributed throughout the year.

Industries- 40% of working population is employed in agriculture. Industries includes

chemical, petro chemical, cement, dairy, fertilizers, leather, oil and Gas, paper, pulp and

sugar industries and so on. As 9.2 million hectares are unused but believed to be cultivable,

so this area can be used for cultivation for agro based industries such as fertilizer, sugar

industries, cotton industries etc. so as to increase the country’s total GDP.

Duration of Climate :-

Season Duration

Cold season Mid Nov to Mid April

Hot Season Mid April to Mid June

Warm Season Mid September to Mid Nov

Monsoon season Mid July to Mid September

Topography

Pakistan is an oblong stretch of land between the Arabian sea and Karakoram mountains,

lying diagonally between 24° N and 37° N latitudes and 61° E and 75° E longitudes, and

covering an area of 87.98 million hectares. Pakistan is located on a great landmass, north of

the Tropic of Cancer (between Latitudes 24 degree and 27 degree )

12

More than two-thirds of Pakistan is arid or semiarid. In the northern areas of Pakistan, the

forest-clad hills give way to lofty ranges, including 60 peaks over 6,700 m (22,000 ft) high.

K-2 (Godwin Austen), at 8,611 m (28,250 ft), is the second-highest mountain in the world.

The principal ranges, trending NW – SE , include several Himalayan ranges—notably the Pir

Panjal and Zaskar—leading into the Karakoram Mountains. The Indus is the principal river of

Pakistan. Its major tributaries are the Jhelum, Chenab, Ravi, and Sutlej.

Table of Irrigable Area and Area Covered by Forest

Forest Type NWFP Punjab Sindh Balochistan Northern

Areas

Azad

Kashmir

Total

Coniferous 1105 29 - 131 285 361 1911

Irr. Plantations - 142 82 - 2 - 226

Riverain

Forests

- 51 241 5 - - 297

Scrub Forests 115 340 10 163 658 1 1287

Coastal Forests - - 345 - - - 345

Mazri Lands 24 - - - - - 24

Linear Pltns. 2 4 - - - - 6

Private Pltns. 159 - - - - - 159

Range Lands 150 2683 490 787 2104 195 6409

TOTAL: 1555 3249 1168 1086 3049 557 10664

Pakistan: Breakdown of forest types, 2010

Primary forest (1000 ha | % of forest area) 0 0

Other naturally regenerated forest (1000 ha | % of forest area) 1347 80

Planted Forest (1000 ha | % of forest area) 340 20

13

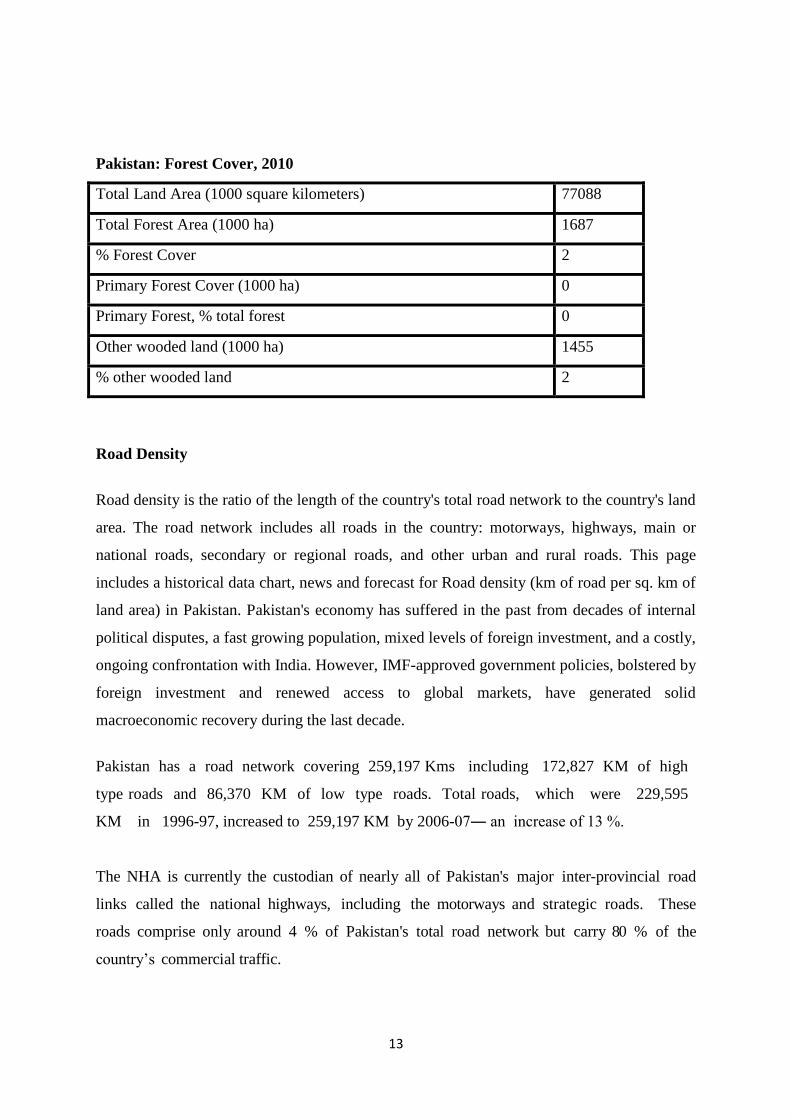

Pakistan: Forest Cover, 2010

Total Land Area (1000 square kilometers) 77088

Total Forest Area (1000 ha) 1687

% Forest Cover 2

Primary Forest Cover (1000 ha) 0

Primary Forest, % total forest 0

Other wooded land (1000 ha) 1455

% other wooded land 2

Road Density

Road density is the ratio of the length of the country's total road network to the country's land

area. The road network includes all roads in the country: motorways, highways, main or

national roads, secondary or regional roads, and other urban and rural roads. This page

includes a historical data chart, news and forecast for Road density (km of road per sq. km of

land area) in Pakistan. Pakistan's economy has suffered in the past from decades of internal

political disputes, a fast growing population, mixed levels of foreign investment, and a costly,

ongoing confrontation with India. However, IMF-approved government policies, bolstered by

foreign investment and renewed access to global markets, have generated solid

macroeconomic recovery during the last decade.

Pakistan has a road network covering 259,197 Kms including 172,827 KM of high

type roads and 86,370 KM of low type roads. Total roads, which were 229,595

KM in 1996-97, increased to 259,197 KM by 2006-07― an increase of 13 %.

The NHA is currently the custodian of nearly all of Pakistan's major inter-provincial road

links called the national highways, including the motorways and strategic roads. These

roads comprise only around 4 % of Pakistan's total road network but carry 80 % of the

country’s commercial traffic.

14

POLITICAL & LEGAL

ENVIRONMENT

15

situation of Pakistan

Executive Branch

Main office holders

Office Name Party Since

President Asif Ali Zardari PPP 9 September 2008

Prime Minister Yousaf Raza Gillani PPP March 25, 2008

Legislative Branch

The bicameral federal legislature consists of the Senate (upper house) and National Assembly

(lower house). According to Article 50 of the Constitution, the National Assembly, the Senate

and the President together make up a body known as the Majlis-i-Shoora (Council of

Advisers).

Senate

The chairman of the Senate, under the constitution, is next in line to act as president should

the office become vacant and until such time as a new president can be formally elected. Both

the Senate and the National Assembly can initiate and pass legislation except for finance

bills. Only the National Assembly can approve the federal budget and all finance bills.

National Assembly of Pakistan

Members of the National Assembly are elected by universal adult suffrage (formerly twenty-

one years of age and older but the seventeenth amendment changed it to eighteen years of

age.).

Judicial Branch

The judiciary includes the Supreme Court, provincial high courts, District & sessions Courts,

Civil and Magistrate courts exercising civil and criminal jurisdiction. Some federal and

provincial courts and tribunals such as Services court, Income tax & excise court, Banking

court and Boards of Revenue's Tribunals are as well established in all province

16

Political Parties and Elections

SOURCE: Election Commission Of Pakistan, Adam Carr's Electoral Archive

Supreme Court

The Supreme Court has original, appellate, and advisory jurisdiction. The Chief Justice of the

Supreme Court is appointed by the president; the other Supreme Court judges are appointed

by the president after consultation with the chief justice. The chief justice and judges of the

Supreme Court may remain in office until age sixty-five: now 68 years and this is also

another clause of seventeenth amendment.

Federal Shariat Court (FSC) of Pakistan

FSC is a court which has the power to examine and determine whether the laws of the

country comply with Shari'a law. It consists of 8 Muslim judges appointed by the President of

Pakistan after consulting the Chief Justice of this Court. Appeal against its decisions lie to the

Shariat Appellate Bench of the Supreme Court, consisting of 3 Muslim judges of the

Supreme Court and 2 Ulema, appointed by the President. If any part of the law is declared to

be against Islamic law, the government is required to take necessary steps to amend such law

appropriately.

17

Provincial & High Courts

In every province, there is one High Court. Currently all four provinces Punjab, Sindh,

Khyber Pakhtunkhwa and Balochistan have High courts, respectively called Lahore High

Court, Sindh High Court, Peshawar High Court, and Balochistan High Court.

Major laws governing Pakistan

The major laws governing Pakistan are

Labour Policy - Issued by the Government of Pakistan lays down the parameters for the

growth of trade unionism, the protection of workers’ rights, the settlement of industrial

disputes, and the redress of workers’ grievances.

Child Labour Policy - Child below the age of 14 shall not be engaged in any factory or mine

or in any other hazardous employment. All forms of forced labour and traffic in human

beings are prohibited.

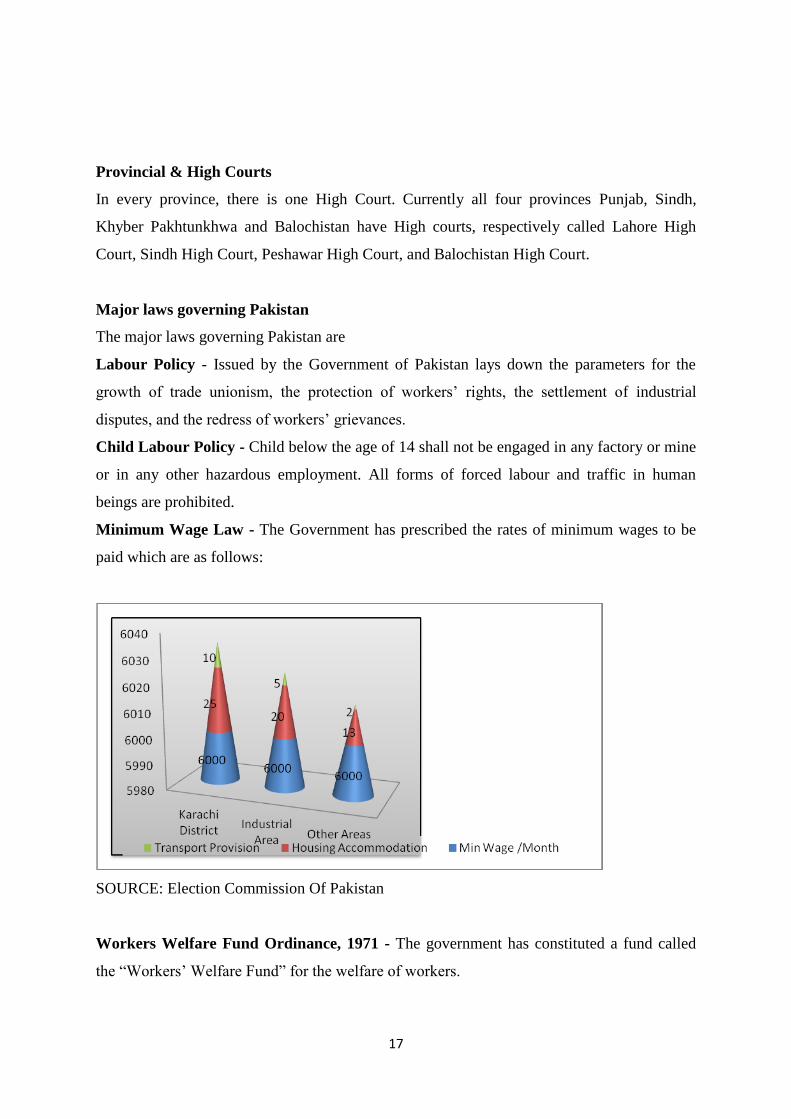

Minimum Wage Law - The Government has prescribed the rates of minimum wages to be

paid which are as follows:

SOURCE: Election Commission Of Pakistan

Workers Welfare Fund Ordinance, 1971 - The government has constituted a fund called

the “Workers’ Welfare Fund” for the welfare of workers.

18

Employees’ Old Age Benefits Act, 1976 - The 1976 Employees Old Age Benefits Act is

applicable to every industry or establishment where five or more persons are employed

directly or indirectly. The Employee Old Age Benefits Institute (the Institute) formed under it

collects and receives contributions, donations, bequests and all other payments. It deals with

pensions, invalidity pension, widow’s pensions, old age grants and other benefits, out of

contribution payable to the Institute by every employer of industry.

Employment—Legal Requirements - A typical work week is 48 hours for a full-time

employee, six days a week, eight hours a day. No employee can be required to work more

than nine hours a day without payment of overtime (double wages) and no more than 624

hours total during a one-year period. U.S. companies and government offices tend to follow a

shortened five-day work week of 42 to 45 hours. Seasonal (or outdoor) businesses serve as

the exception to this rule. There are no restrictions on hiring foreign employees, though prior

to doing so a company needs to obtain permission from the Board of Investment (BOI).

Legal and Registration of a Business

A business in Pakistan may be organized as a sole proprietorship, a partnership, or as a public

or private limited company. Foreign investors generally establish limited companies. They

must register with the Securities & Exchange Commission of Pakistan Company registration

offices are located in each of the provincial capitals and also in Islamabad and Multan.

Foreign and domestic investors are free to establish and own business enterprises in all

sectors of the economy with the exception of five restricted sectors: arms and munitions, high

explosives, currency/mint operations, nonindustrial alcohol, and radioactive substances.

Private entities are similarly free to acquire and dispose of their interests in business

enterprises.

Corporate and Employer Tax Obligations

Tax residency for a business: A company is considered resident for a tax year if it is

incorporated or formed by or under any law in force in Pakistan, the control and management

of its affairs is situated wholly in Pakistan at any time in the year, or if it is a provincial

government or a local authority in Pakistan.

Corporate taxes: Corporate income tax, social security tax, corporate pension contribution,

and value-added tax may all apply.

19

License requirements

Specialised Businesses

In Pakistan, certain businesses have been declared specialised and in addition to corporate

and tax requirements, a specific license is required to commence such businesses. Such

businesses are Banking Companies, Non‐ Banking Finance Companies, Security Service

Providing Companies, Corporate Brokerage Houses, Money Exchange Companies, a

Company which invests in Arms and Ammunition, Security Printing, Currency and Mint,

High Explosives and Radio Active Substances. Certain conditions e.g. as to minimum capital,

qualification of directors, corporate structure and area of operations etc. are required to be

complied with to obtain these licenses. However, the conditions for grant of license may vary

from business to business.

Foreign Investors in Pakistan

A foreign investor may establish an independent business with any of above mentioned

corporate structures. He can establish a sole proprietorship, can enter into partnership with

any local person or foreigner and even can establish a company with or without participation

of local shareholder(s) and director(s). If a foreign enterprise wishes to establish a business in

Pakistan as a part of its international operations, in addition to the said corporate structures it

can obtain registration with Board of Investment – Government of Pakistan, for opening of a

branch office, marketing office or liaison office. Companies Ordinance 1984 imposes certain

restrictions on the operations of the enterprise.

20

TRADE &

COMMERCE

21

TRADE, COMMERCE AND INDUSTRY

India Pakistan Trade Relations are facilitated by the Federation of Indian Chambers and

Commerce (FICCI) and the Federation of Pakistan Chambers of Commerce & Industry

(FPCCI). FICCI and FPCCI are the representatives of the trade and business community of

their respective countries. The main objective of these two chambers of commerce is to

facilitate trade and business opportunities between India and Pakistan. Further, their common

goal is to increase ethical business activities between each other and within all South Asian

nations. India Pakistan trade relations are focused on some policies.

Manufacturing Sector:

100% equity holding is allowed to the foreign investors on industrial projects,

which do not require any formal permission from the government of Pakistan.

No Objection Certificates (NOC) is not required for setting-up a business unit in

Pakistan except for areas that are marked as negative for business development.

Non-manufacturing sector:

Registration of the companies with Security Exchange Commission of Pakistan under the

Companies Ordinance, 1984 is a must. Further, the State Bank of Pakistan's relevant

provisions are to be met accordingly for making investments in Pakistan or setting up

a business in Pakistan. The government of Pakistan has further eased the investment norms

for the Pakistani repatriates to facilitate investment into Pakistan's domestic market.

Foreign investment in Pakistani market are now allowed in sectors like

Service

Infrastructure

Social and Agriculture

Export of Pakistan

Textile

Textile could be termed as the backbone of Pakistan's economy. It provides employment

to 38 % of overall labour force of the country and accounts for 27 % of value addition in

22

the manufacturing sector. The size of the cotton crop is not only higher (10.7 million

bales), but it exceeded the current year's target (9.7 million bales).

Carpets

The main buyers of carpets and rugs are Germany and USA. Pakistan's carpet and rug

industry is facing stiff competition in recent years. China, India and Iran have devalued

their currencies considerably and are giving us stiff competition.

Raw cotton

Cotton is the main cash crop and contributes significantly to the national economy. It

accounts for 11.5% of value added in agriculture and about 2.8% of GDP. In addition to

providing raw material is a major export item.

Rice

Rice is the second largest staple food crop in Pakistan and is also a major export item. It

accounts for 6.6% in value added in agriculture and 1.6% in GDP.

Leather

During the last 20 years, the industry has flourished by using trained and skilled

operations. The percentage share of leather in total export was 8.1% in 2000-01.The

industry has a potential to increase exports to 1 billion dollars in a span of ten years by

promotion of leather footwear.

Vegetable

Production of Mung and Mash has increased by 10.2 % and 8.0 %; respectively while the

production of Masoor declined by 5.9 % during 2000-01.

Production or potato and onion are estimated to have decreased by 7.6 and 9.2 %,

respectively while production of chillies is estimated to increase by 42.0 % in 2000-01

over the last year.

Fruits

Fruit’s is one of Pakistan's major exports. There are many units working in the Fruits

fields. They are producing good Fruits. Pakistan Fruits is famous around the world. Many

Fruits shows are arranged in Expo center Karachi to show the quality Fruits of Pakistan.

Fish

23

Pakistan also exports a reasonable quantity of shrimp and fish and earns a substantial

amount of foreign exchange. Thus, during the calendar year 2000, 84693 m. tons of

fishery products were exported to Japan, USA, UK, Germany, Middle East and other

countries.

The total number of persons engaged in fisheries sector is estimated at 360,000. Out of

which, 135,000 persons (37.5 %) were engaged in marine sector and 225,000 (62.5 %) in

inland fisheries.

Sports goods

Pakistan Sports Goods is famous around the world. Many Sports Goods shows are

arranged in Expo Center Karachi to show the quality Sports Goods of Pakistan.

Sugar

Its shares in value added in agriculture and GDP are 6.4 % and 1.5 %, respectively.

Sugarcane was cultivated on an area of 961 thousand hectares during the current fiscal

year, showing a decline of 4.9 % over the last estimated at 43608 thousand tonnes which

is lower by almost 5.9 %, as compared with last year.

Import of Pakistan

Textile machinery

The trade volume of supply of Textile Machinery, which showed an increase of 20 %

during the year, is set to register a further 25-30 % increase during the year 2005.

Electrical machinery

The total imports of Electrical Machinery in this year $12.85 billion as against the total

imports of $10.33 billion. Pakistan has imported 8,442,611 MT (metric tons) of Electrical

products in this year at the cost of $1.694 billion and 6,792,071 MT at the cost of $1.3

billion, while the country imported 9,228,545 MT Electrical Products at the cost of $1.57

billion and 7,140,384

Silk yarn

The imports, of Silk Yarn remained at $524 million as against the imports of $406 million

in the previous year. The country imported $97.9 million construction and mining

machinery, which was in 2001-02 imported at the cost of $118 million. Pakistan imported

Silk Yarn worth $211 million.

24

Plastic

The provincial government is said to have ordered purchase of 20 million woven

polypropylene (WPP) bags for storage of wheat this year. The government was buying

20,000 bales of 1,000 bags each. About 7,000 bales are bought at the rate of Rs12.79 per

bag against last year's Rs12.25 per bag and the remaining 13,000 bales at the rate of

Rs13.15 per bag.

Medical product

The government has reduced the customs duty from 10% to 5% on import of medical

equipment and apparatus based on the use of X-rays or other radiation which were used

for diagnostic purposes in the hospitals and medical institutions.

Iron, Steel and Aluminum

Pakistan Steel is one of the important ventures in public sector industries, which is aimed

at providing basic raw material to local high-tech industries in the country. The installed

capacity of 1.1 million tonnes of raw steel is extendable up to 3 million tonnes. The main

products of Pakistan Steel are coke, pig iron, billets, hot rolled coils / sheets, galvanized

sheets etc.

Pakistan's Import and Export Indicators and Statistics at a Glance (2010)

IMPORTS

25

EXPORTS

Leading from world bank (year by year chart)

26

MACRO ECONOMIC

ENVIRONMENT

27

The macro environment will influence performance, and the amount of the influence will

depend on how much of the company's business is dependent on the overall

economy. Cyclical industries, for example, are heavily influenced by the macro environment.

Macro environment is basically a combination of a number of factors. Macro environment

is beyond the control of an individual of a firm. Macro environment is formed by

the policies of the rule as well as the general conditions in the world. The Macro environment

of Pakistan constitutes of the following:

Technological: Pakistan man a developing country is much behind the developed countries

in technology. However, the previous government be very supportive of technology due to

which a dramatic change in the telecommunications and other mechanical industries were

seen.

Political/Legal: Pakistan is a politically unstable country these days. The government is new

and faces a number of problems such as corrupt individuals, internal terrorism, external

pressure etc. The legal condition is also very serious as the Chief Justice of Pakistan himself

is aggression a war against the government for getting his rightful status.

Economic: There is a lot of inflation and the country is dependent on IMF for all its desires.

Socio-cultural: The society is modernizing day by day. People are getting away from their

old culture, especially within the modern and urban areas.

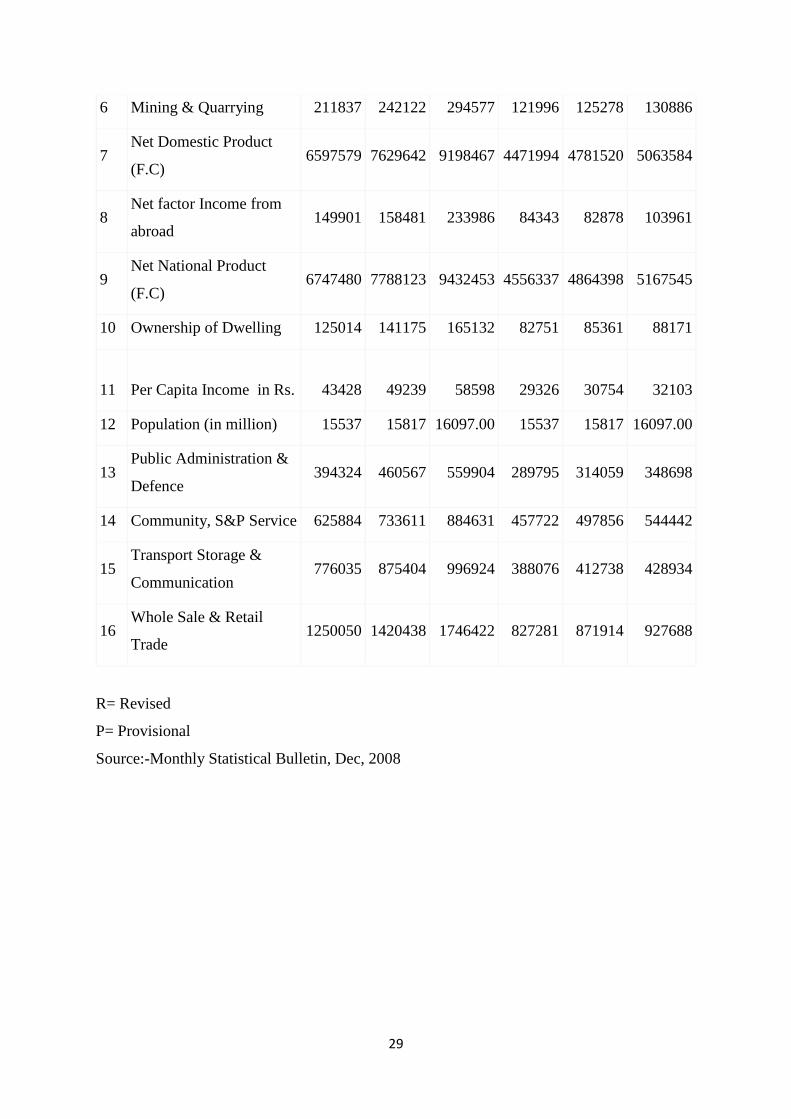

Gross Domestic Product

28

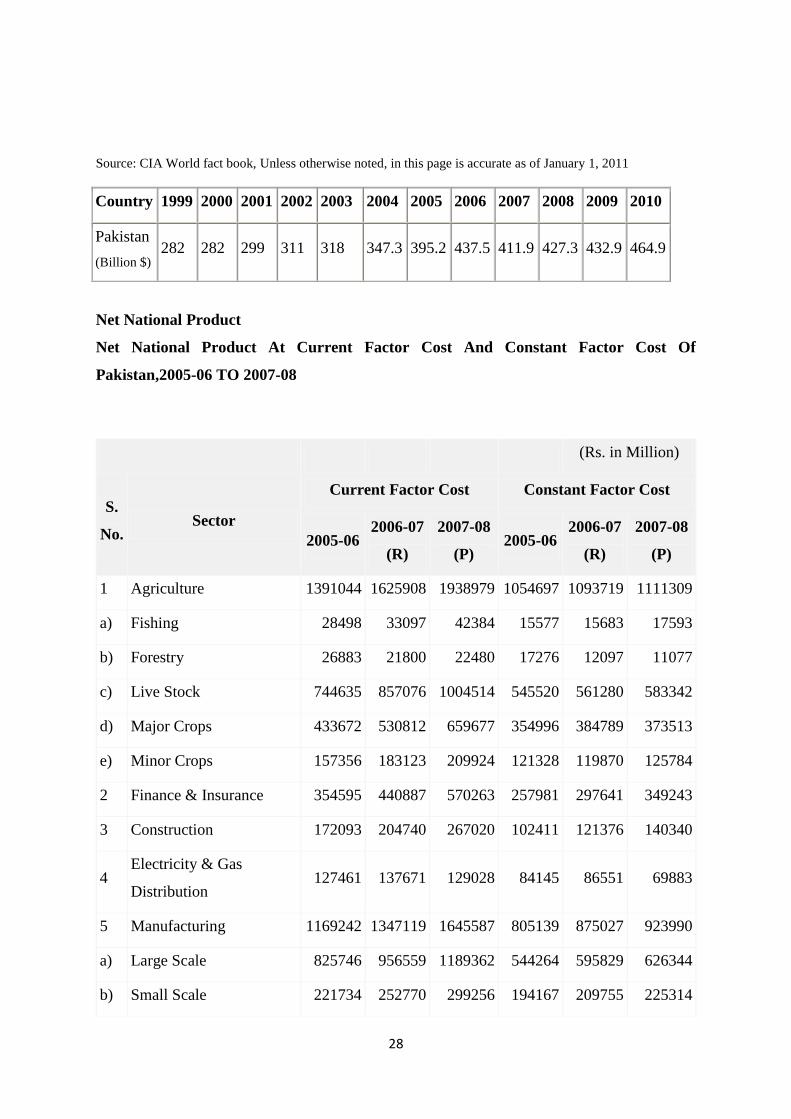

Source: CIA World fact book, Unless otherwise noted, in this page is accurate as of January 1, 2011

Net National Product

Net National Product At Current Factor Cost And Constant Factor Cost Of

Pakistan,2005-06 TO 2007-08

(Rs. in Million)

S.

No. Sector

Current Factor Cost Constant Factor Cost

2005-06 2006-07

(R)

2007-08

(P) 2005-06

2006-07

(R)

2007-08

(P)

1 Agriculture 1391044 1625908 1938979 1054697 1093719 1111309

a) Fishing 28498 33097 42384 15577 15683 17593

b) Forestry 26883 21800 22480 17276 12097 11077

c) Live Stock 744635 857076 1004514 545520 561280 583342

d) Major Crops 433672 530812 659677 354996 384789 373513

e) Minor Crops 157356 183123 209924 121328 119870 125784

2 Finance & Insurance 354595 440887 570263 257981 297641 349243

3 Construction 172093 204740 267020 102411 121376 140340

4 Electricity & Gas

Distribution 127461 137671 129028 84145 86551 69883

5 Manufacturing 1169242 1347119 1645587 805139 875027 923990

a) Large Scale 825746 956559 1189362 544264 595829 626344

b) Small Scale 221734 252770 299256 194167 209755 225314

Country 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Pakistan

(Billion $) 282 282 299 311 318 347.3 395.2 437.5 411.9 427.3 432.9 464.9

29

6 Mining & Quarrying 211837 242122 294577 121996 125278 130886

7 Net Domestic Product

(F.C) 6597579 7629642 9198467 4471994 4781520 5063584

8 Net factor Income from

abroad 149901 158481 233986 84343 82878 103961

9 Net National Product

(F.C) 6747480 7788123 9432453 4556337 4864398 5167545

10 Ownership of Dwelling 125014 141175 165132 82751 85361 88171

11

Per Capita Income in Rs.

43428

49239

58598

29326

30754

32103

12 Population (in million) 15537 15817 16097.00 15537 15817 16097.00

13 Public Administration &

Defence 394324 460567 559904 289795 314059 348698

14 Community, S&P Service 625884 733611 884631 457722 497856 544442

15 Transport Storage &

Communication 776035 875404 996924 388076 412738 428934

16 Whole Sale & Retail

Trade 1250050 1420438 1746422 827281 871914 927688

R= Revised

P= Provisional

Source:-Monthly Statistical Bulletin, Dec, 2008

30

0

1000

2000

3000

4000

5000

6000

7000

1 3 5 7 9 11

India

Pakistan

Year

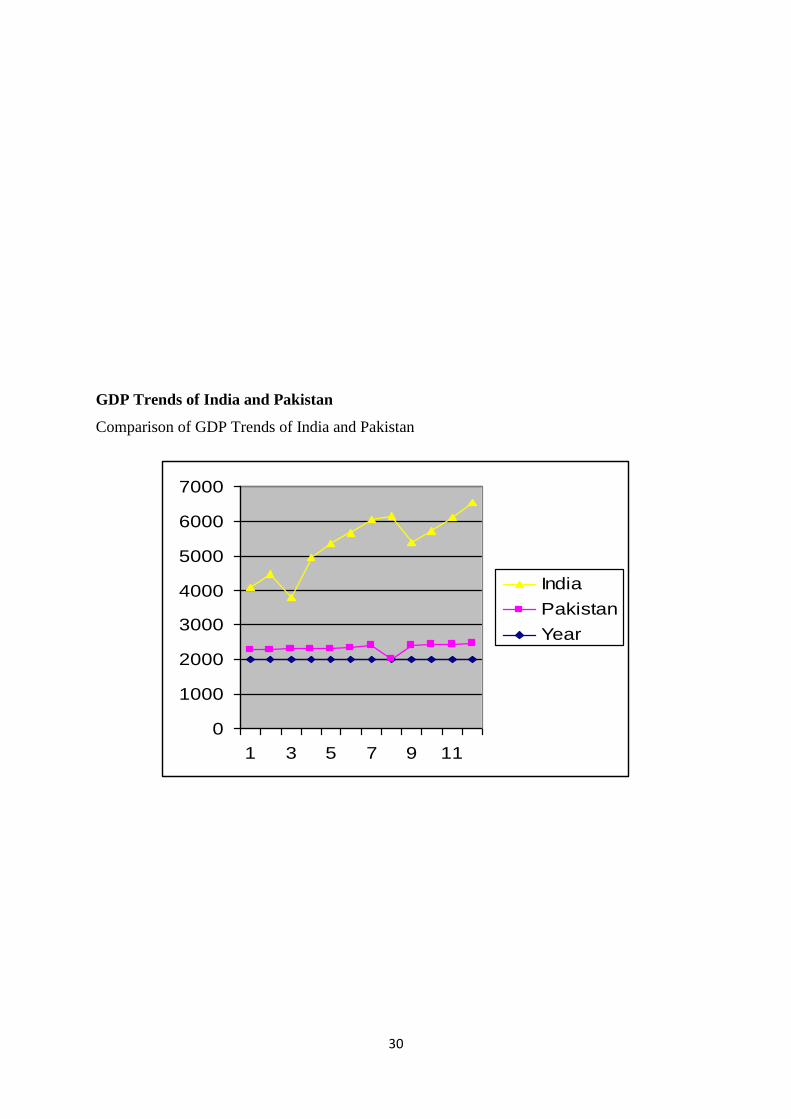

GDP Trends of India and Pakistan

Comparison of GDP Trends of India and Pakistan

31

Per Capita Income

Comparison of per capital income of India Pakistan

comparisition of per capital

income

0

1000

2000

3000

4000

1 3 5 7 9 11

Year

pe

r c

ap

ita

l in

co

me

Year

India (Us $)

Pakistan (Us

$)

Economy today

Due to inflation and economic crisis worldwide, Pakistan's economy reached a state

of Balance of Payment crisis. "The International Monetary Fund bailed out Pakistan in

November 2008 to avert a balance of payments crisis and in July last year increased the loan

to $11.3 billion from an

By October 2007, Pakistan raised back its Foreign Reserves to $16.4 billion. Exceptional

policies kept Pakistan's trade deficit controlled at $13 billion, exports boomed to $18 billion,

revenue generation increased to become $13 billion and attracted foreign investment of $8.4

billion.

Forex Rates Pakistan

Forex is short for foreign exchange also known as FX. Forex is to assist international trade

and investment and Forex market is one of the largest and most liquid financial markets in the

32

world with an average traded value that exceeds $1.9 trillion per day and includes all of the

currencies in the world. Forex Rates Pakistan updated multiple times during the day.

Interest Rates

The benchmark interest rate in Pakistan was last reported at 13.5 %. In Pakistan, interest rates

decisions are taken by the State Bank of Pakistan. The official interest rate is the discount

rate. From 1992 till 2010, its average interest rate was 12.78 % reaching an historical high of

20% in October of 1996 and a record low of 7.50 % in November of 2002.

33

CAPITAL MARKET

34

Trading at FY12 Price Earning Ratio (PER), Pakistan equities reflect 26 % discount to

historical mean of over 50 % discount to regional comparable markets. Conversely put,

Pakistan equities currently reflect forward earning yield of 14% compared to 6 % for the

region and 5% for India and China. Moreover, excluding very few scripts, which are

currently trading at premium valuations, the rest of the market is actually as cheap as forward

PER and 20 % in terms of forward earning yield.

Foreign Investment and KSE Index

Source:- Ministry of Finance, Government of Pakistan

Reserve Requirements Ratio

35

Global Equity Markets The leading stock markets of the world observed high growth

during the fiscal year 2010-11 ranging from 8.1 % in Japan to the highest market return up to

66.8 % as peace dividend in Sri Lanka.

Global Index

Source:-Invisor securities

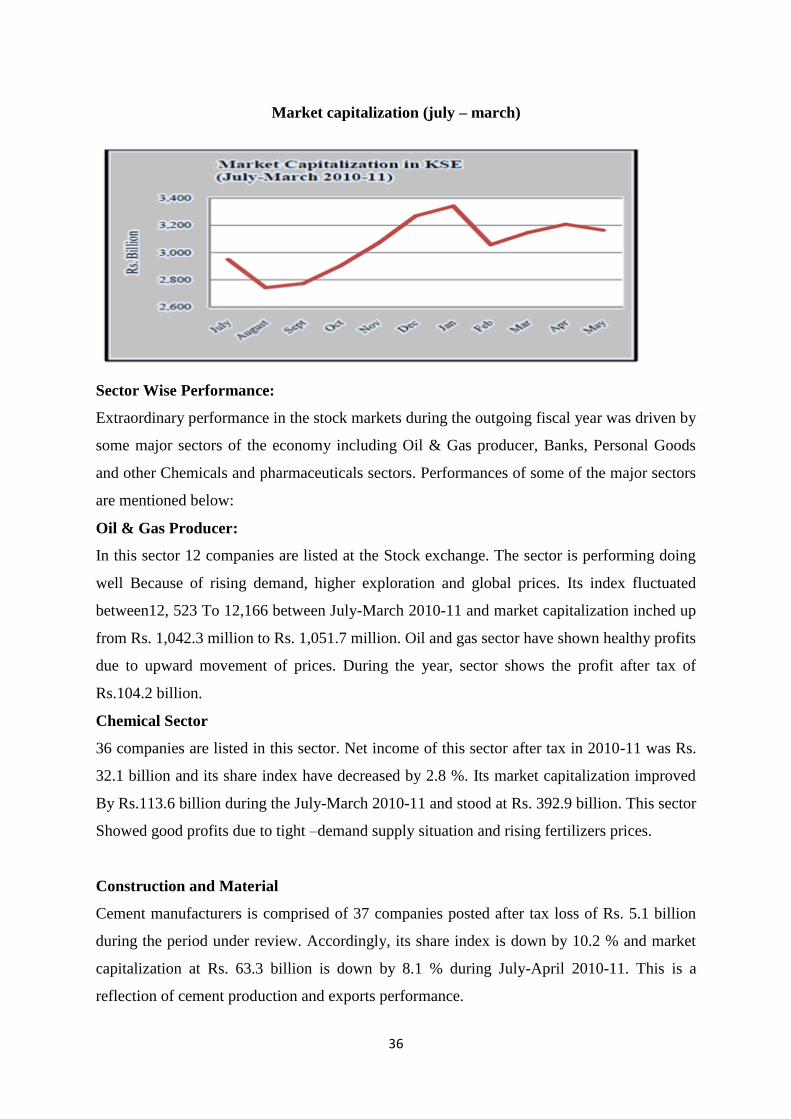

Market capitalization (july – may)

Source :- Ministry of Finance, Government of Pakista

36

Market capitalization (july – march)

Sector Wise Performance:

Extraordinary performance in the stock markets during the outgoing fiscal year was driven by

some major sectors of the economy including Oil & Gas producer, Banks, Personal Goods

and other Chemicals and pharmaceuticals sectors. Performances of some of the major sectors

are mentioned below:

Oil & Gas Producer:

In this sector 12 companies are listed at the Stock exchange. The sector is performing doing

well Because of rising demand, higher exploration and global prices. Its index fluctuated

between12, 523 To 12,166 between July-March 2010-11 and market capitalization inched up

from Rs. 1,042.3 million to Rs. 1,051.7 million. Oil and gas sector have shown healthy profits

due to upward movement of prices. During the year, sector shows the profit after tax of

Rs.104.2 billion.

Chemical Sector

36 companies are listed in this sector. Net income of this sector after tax in 2010-11 was Rs.

32.1 billion and its share index have decreased by 2.8 %. Its market capitalization improved

By Rs.113.6 billion during the July-March 2010-11 and stood at Rs. 392.9 billion. This sector

Showed good profits due to tight –demand supply situation and rising fertilizers prices.

Construction and Material

Cement manufacturers is comprised of 37 companies posted after tax loss of Rs. 5.1 billion

during the period under review. Accordingly, its share index is down by 10.2 % and market

capitalization at Rs. 63.3 billion is down by 8.1 % during July-April 2010-11. This is a

reflection of cement production and exports performance.

37

Fixed Line Communication

The sector of 5 companies is affected by saturation of mobile communication in the country

and the total after tax profit was Rs.7 billion. Market capitalization of the sector decreased

from Rs. 83.8 billion to 69 billion during July-March 2010-11. Its share index also decreased

to 8392 points from 10191 points at the end of March 2011.

Food Producers.

The sector having 61 sugar dominated companies posted total after tax profit of Rs.11.9

billion. The Share index moved up from 12,625 to 19,824 during July-March 2010-11. Its

market capitalization increased by 58.2 % to 282.9 billion.

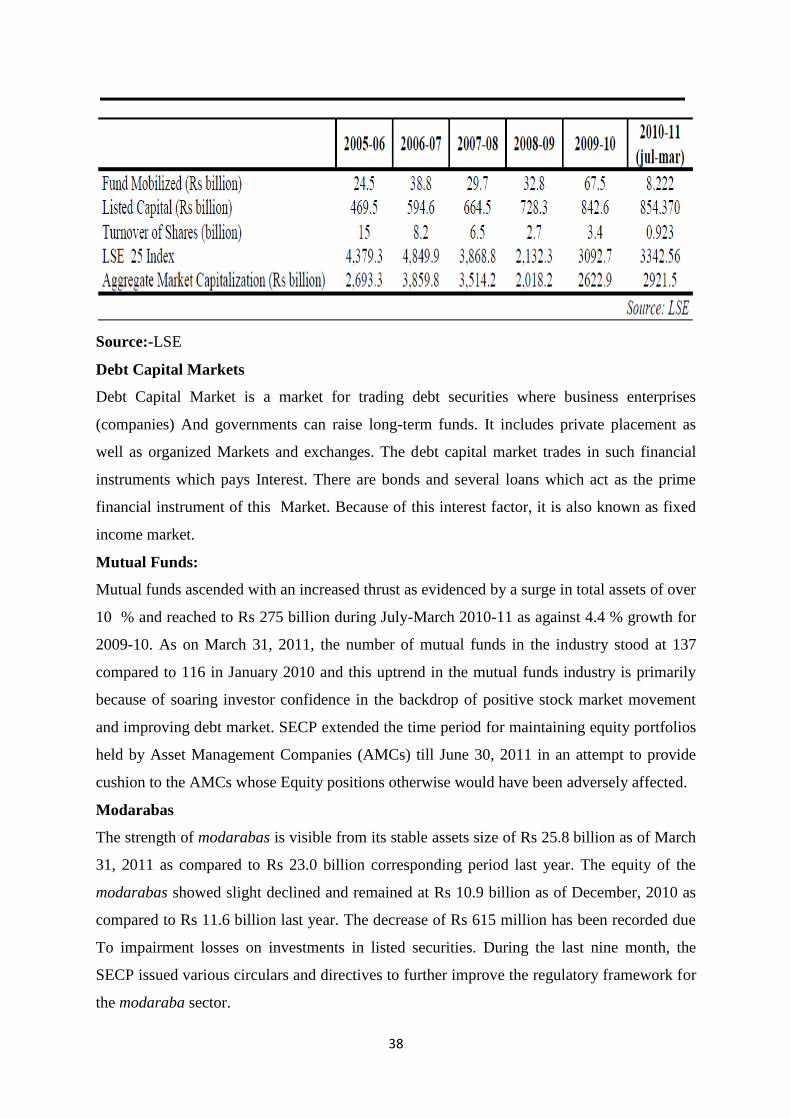

Lahore Stock Exchange

The market indicators witnessed mixed trends in Lahore Stock Exchange. The LSE -

25Index, which was 3093 on 30 June 2010, increased to 3343 points as on March 31,

2011with total paid up capital increased from Rs 842.6 billion to Rs 854.4 billion. Total

turnover of the shares on LSE during July-March 2010-11 is 0.9 billion shares as compared to

3.4 billion shares in the corresponding last

Period, with Fund mobilization of Rs 8.2 billion and market capitalization is Rs.2921.5

billion During July-March 2010-11.Only six new companies were listed in the period under

consideration as compared to 25 companies in the fiscal year 2009-10.

Capital contribution of Industry

38

Source:-LSE

Debt Capital Markets

Debt Capital Market is a market for trading debt securities where business enterprises

(companies) And governments can raise long-term funds. It includes private placement as

well as organized Markets and exchanges. The debt capital market trades in such financial

instruments which pays Interest. There are bonds and several loans which act as the prime

financial instrument of this Market. Because of this interest factor, it is also known as fixed

income market.

Mutual Funds:

Mutual funds ascended with an increased thrust as evidenced by a surge in total assets of over

10 % and reached to Rs 275 billion during July-March 2010-11 as against 4.4 % growth for

2009-10. As on March 31, 2011, the number of mutual funds in the industry stood at 137

compared to 116 in January 2010 and this uptrend in the mutual funds industry is primarily

because of soaring investor confidence in the backdrop of positive stock market movement

and improving debt market. SECP extended the time period for maintaining equity portfolios

held by Asset Management Companies (AMCs) till June 30, 2011 in an attempt to provide

cushion to the AMCs whose Equity positions otherwise would have been adversely affected.

Modarabas

The strength of modarabas is visible from its stable assets size of Rs 25.8 billion as of March

31, 2011 as compared to Rs 23.0 billion corresponding period last year. The equity of the

modarabas showed slight declined and remained at Rs 10.9 billion as of December, 2010 as

compared to Rs 11.6 billion last year. The decrease of Rs 615 million has been recorded due

To impairment losses on investments in listed securities. During the last nine month, the

SECP issued various circulars and directives to further improve the regulatory framework for

the modaraba sector.

39

Leasing

The leasing sector in It faces multitude problems like liquidity issues, low capitalization,

limited sources for resource mobilization, high cost of funds, level of non-performing assets

and Limited outreach. SECP enhanced the validity of licenses issued to Non-Banking

Financial Companies (NBFCs) from one year to three years for providing operational

flexibility to them. system would gain grip and substance. So far, nine pension funds have

been launched under the VPS.

Derivative Markets

In order to provide investors with basic hedging instruments, financing options and increased

nvestment alternatives, deliverable futures contracts and cash-settled futures contracts are

available for trading at the three stock exchanges. Additionally stock index Futures Contract

based on the KSE 30 Index and Sectoral Indices for oil and gas sector and banking sector are

available at the Karachi Stock Exchange (KSE).

The success of FDI policies can be judged by the size of the inflows of foreign capital. If we

critically analyse the pattern of foreign direct investment inflows over the last two decade, it

is found that It performed poorly in this field. Lack of political stability has been the hallmark

of It during the last fifty years. It has never had an elected government to survive long enough

to be voted out of office. The importance of infrastructure can be realized from the fact, that

it plays the same role in generating investment as soil plays in cropping. The inadequacy of

physical infrastructure creates a bottleneck in the investment process and will negative impact

the decisions of the prospective investors.

40

INTERNATIONAL

TRADE

41

International trade allows us to expand our markets for both goods and services that

otherwise may not have been available to us. Owing to competition, a country can obtain

optimum advantage from its buying and selling in the world only through having adequate

knowledge of trade data.

Pakistan's Import and Export Indicators and Statistics at a Glance (2010)

GRAPH NO: 1 Pakistan Trade

Source: www.pakgov.pk

Exports

Manufacturing still works with relatively basic technologies, generates few value-added products,

and has a narrow production base, i.e., it does not diversify into many different product groups.

Textiles are Pakistan's primary industry, and in 1999 accounted for 8.5 % of the gross domestic

product, 31 % of total investment, 38 % of industrial employment, and almost 60 % of total exports.

It is Asia's eighth-biggest textiles exporter, with export revenues of US$5.7 billion in the first half of

2000. Export growth has been declining since a recent peak of 6.1 % in 1996. The trend is reversing,

encouraged by large cotton crops in the past 2 years which have lifted output to about 11 million

bales (each bale weighing 170 kilograms), the bulk of which is consumed at home, and large-scale

capital investment to modernize plants. However, progress is still expected to fall short of targets,

notably to be among Asia's top 5 exporters with sales of US$14 billion by 2005.

42

Cumulative exports by various countries

Imports

It imports were worth 3806 Million USD in August of 2011. It imports mainly petroleum,

petroleum products, machinery, plastics, transportation equipment, edible oils, paper and

paperboard, iron and steel and tea. Its major import partners are: European Union, China,

Saudi Arabia, United Arab Emirates and United States.

Countries July-2011 to Aug. 2011 July-2010 to Aug. 2010

Value %Shares Value %Shares

Total 354096.65 100 296417.15 100

USA 63000.05 17.79 58289.42 19.66

Afganistan 38366.12 10.83 24558.16 8.28

UAE 33218.89 9.38 26831.13 9.05

UK 19925.68 5.63 15914.10 5.37

China 19904.71 5.63 16040.83 5.41

Germany 19553.18 5.52 14613.08 4.93

Belgium 9916.45 2.80 7787.15 2.63

Itlay 9724.63 2.75 8188.21 2.76

Netherlands 8653.71 2.44 5506.02 1.86

Bangladesh 8483.64 2.40 8861.19 2.99

Spain 8305.16 2.35 6593.80 2.22

Turkey 6855.74 1.94 8650.19 2.92

France 6037.09 1.7 4665.34 1.57

Saudi Arabia 5827.17 1.65 6409.33 2.16

Kenya 4842.42 1.37 1390.29 .47

Hong kong 4501.38 1.27 6805.25 2.30

India 4422.08 1.25 3586.72 1.21

South Africa 4343.49 1.23 3070.76 1.04

Korea 4230.36 1.19 2939.29 .99

43

Countries shares in international trade with Pakistan

IMPORT BY ECONOMIC category

Exports Imports

Countries Share % Countries Share %

US 15.87 US 4.81

UAE 12.85 UAE 9.8

Afghanistan 8.48 Saudi Arabia 10.54

UK 4.7 India 4.02

China 4.4 Kuwait 4.73

- - Malaysia 4.43

- - China 15.37

44

Export by Economic category

(Source:www.ministryoffinance.pk)

statistic data on imports and exports

45

VALUE BY FOREIGN TRADE

46

AGRICULTURE

47

Pakistan's total land area is about 803,940 square kilometers. About 48 million hectares, or 60

%, is often classified as unusable for forestry or agriculture consists mostly of deserts,

mountain slopes, and urban settlements. Some authorities, however, include part of this area

as agricultural land on the basis that it would support some livestock activity even though it is

poor rangeland. Thus, estimates of grazing land vary widely--between 10 % and 70 % of the

total area.

The Agriculture Sector continues to play central role in Pakistan’s economy. It is the 2nd

largest sector, accounting for over 21% of GDP , and remains by far the largest employer,

absorbing 45% of the country’s total labor force. Nearly 62% of the country’s population

resides in rural areas, and directly or in directly linked with agriculture for livelihood.

Despite its critical importance to growth, exports, incomes and food security, the agriculture

sector has been suffering from secular decline.

48

Agriculture Growth

Agriculture Growth (%)

Year Agriculture Major Crops Minor Crops Livestock

2003‐04 2.4 1.7 3.9 2.9

2004‐05 6.5 17.7 1.5 2.3

2005‐06 6.3 ‐3.9 0.4 15.8

2006‐07 4.1 7.7 ‐ 1.0 2.8

2007‐08 1 ‐6.4 10.9 4.2

2008‐09 4 7.3 ‐1.7 3.5

2009‐10(P) 2 ‐0.2 ‐1.2 4.1

(P): Provisional Source: Federal Bureau of Statistics

Comparative Agriculture Growth Rate

Country Name 2006 2007 2008 2009 2010

India 4.2 5.8 -0.1 0.4 5

Pakistan 6.3 4.1 1 4 2

China 5 3.7 5.4 4.2 4.5

Thailand 5 1.2 4.2 1.3 -2.2

Malaysia 5.2 1.3 4.3 0.4 ..

Source: World Bank Data

Agriculture Growth Rate of Pakistan

No. Year Growth Rate Target Difference

1. 2009-10 2.0% 3.8% -1.8%

2. 2008-09 4.7% 3.5% +1.2%

3. 2007-08 1.5% 4.8% -3.3%

4. 2006-07 5.0% – –

5. 2005-06 2.5% 4.2% -1.7%

6. 2004-05 7.9% 4.0% +3.9%

49

Contribution of Agriculture in the Economy

More specifically; the agricultural sector plays an important part in Pakistan's economy by:

Contributing 24 % towards GDP;

Providing food to about 130 million people;

Earning about 60 % of the country's total export earnings;

Providing employment to 47 % of the total work force;

Providing the main source of livelihood for the rural population of Pakistan;

Providing raw materials for many industries and a market for many locally produced

industrial products.

Private Sector Institutions

As mentioned, agriculture remain to be an important economic contributor as in fact It is

the largest producers and suppliers of agricultural products according to the 2005 Food

and Agriculture Organization. It likewise ranks high with respect to farm output. It is the

fifth in the Muslim world and worldwide it ranks within the two twenty farm output

contributors.

Major crops, accounting for 31.1 % of agricultural value added, registered a negative

growth of 4.0 % for second year in a row mainly because of decrease in production of rice

and cotton by 29.9 and 11.3 %, respectively. Major crops, such as, wheat, rice, cotton and

sugarcane account for 90 % of the value added in the major crops. The value added in

major crops accounts for 31 % of the value added in the agriculture. Thus, four major

crops (wheat, rice, cotton, and sugarcane) on average, contribute 28 % to the value

added in overall agriculture and 5.9 % to GDP.

Production Of major crops

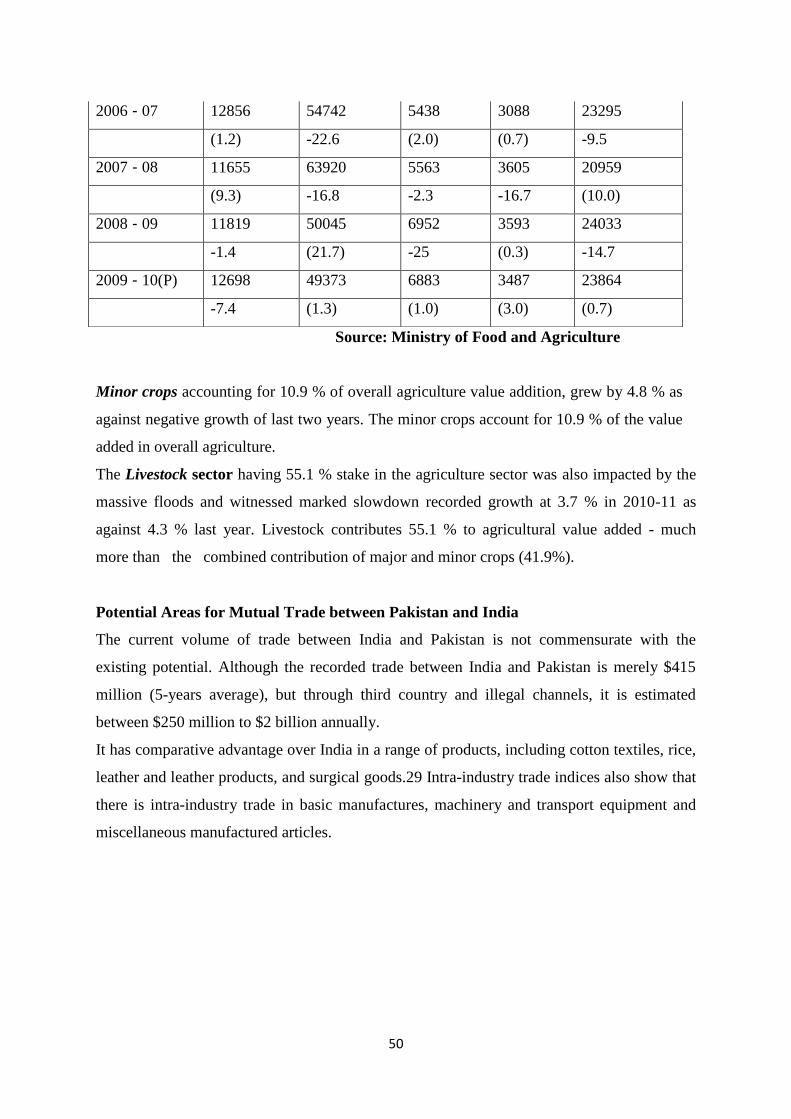

Production of Major Crops (’000 Tons)

Year Cotton

(000 bales) Sugarcane Rice Maize Wheat

2004 - 05 14265 47244 5025 2797 21612

-42 (11.6) -3.6 -47.4 -10.8

2005 - 06 13019 44666 5547 3110 21277

(8.7) (5.5) -10.4 -11.2 (1.6)

50

Source: Ministry of Food and Agriculture

Minor crops accounting for 10.9 % of overall agriculture value addition, grew by 4.8 % as

against negative growth of last two years. The minor crops account for 10.9 % of the value

added in overall agriculture.

The Livestock sector having 55.1 % stake in the agriculture sector was also impacted by the

massive floods and witnessed marked slowdown recorded growth at 3.7 % in 2010-11 as

against 4.3 % last year. Livestock contributes 55.1 % to agricultural value added - much

more than the combined contribution of major and minor crops (41.9%).

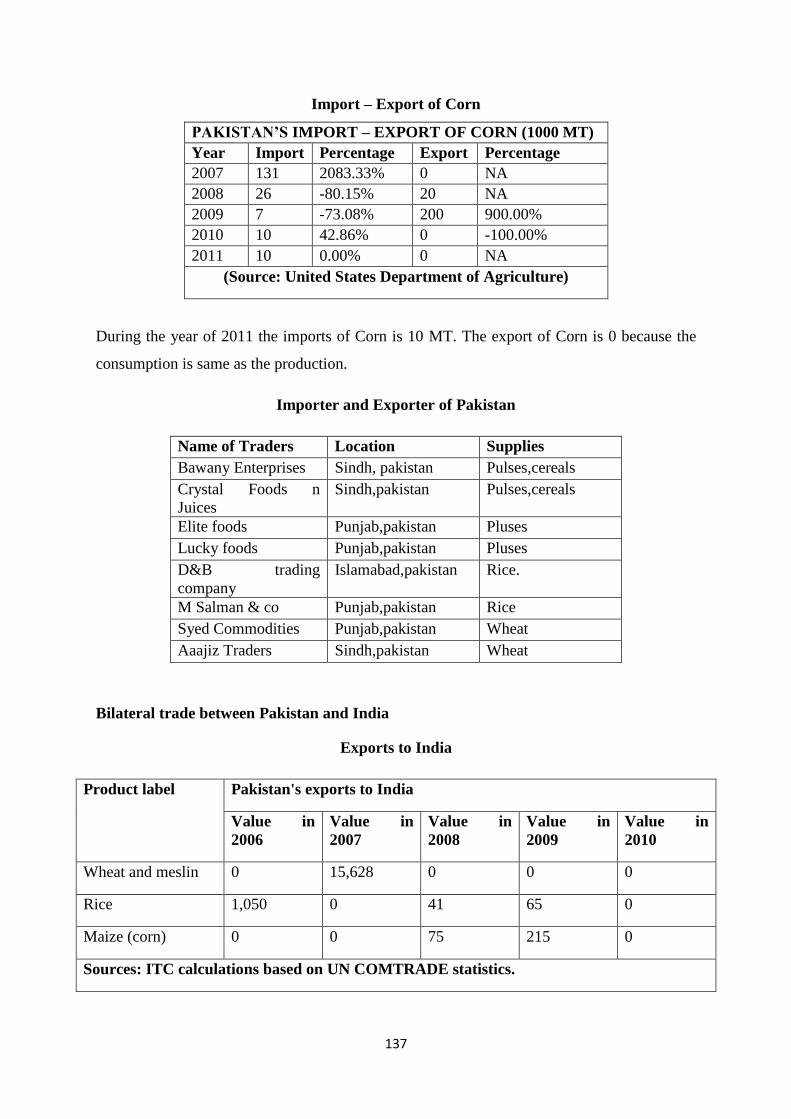

Potential Areas for Mutual Trade between Pakistan and India

The current volume of trade between India and Pakistan is not commensurate with the

existing potential. Although the recorded trade between India and Pakistan is merely $415

million (5-years average), but through third country and illegal channels, it is estimated

between $250 million to $2 billion annually.

It has comparative advantage over India in a range of products, including cotton textiles, rice,

leather and leather products, and surgical goods.29 Intra-industry trade indices also show that

there is intra-industry trade in basic manufactures, machinery and transport equipment and

miscellaneous manufactured articles.

2006 - 07 12856 54742 5438 3088 23295

(1.2) -22.6 (2.0) (0.7) -9.5

2007 - 08 11655 63920 5563 3605 20959

(9.3) -16.8 -2.3 -16.7 (10.0)

2008 - 09 11819 50045 6952 3593 24033

-1.4 (21.7) -25 (0.3) -14.7

2009 - 10(P) 12698 49373 6883 3487 23864

-7.4 (1.3) (1.0) (3.0) (0.7)

51

MANUFACTURING

52

Pakistan's manufacturing sector accounts for about 25% of GDP. Cotton textile production

and apparel manufacturing are Pakistan's largest industries, accounting for about 51.4% of

total exports. Other major industries include food processing, beverages, construction

materials, clothing, and paper products. Manufacturing sector growth has slowed in the last 2

years due to energy shortages and capacity constraints. However, the sector is forecast to

grow 5.5% for FY 2010. Despite government efforts to privatize large-scale parastatal units,

the public sector continues to account for a significant proportion of industry. The

government seeks to diversify the country's industrial base and bolster export industries. Net

foreign investment in Pakistani industries is only 0.5% of GDP. Pakistan's search for

additional foreign direct investment has been hampered by concerns about the security

situation, domestic and regional political uncertainties, and questions about judicial

transparency.

Cost of production of manufacturing sector of Pakistan

53

Composition to the Manufacturing Sector

SOUR

CE: India Reporting Country from Monthly Statistics of Foreign Trade

Manufacturing Sector Of Pakistan

Year 2006 2007 2008 2009 2010

Industry 26.9 26.9 26.8 24.3 23.6

i. Mining & Quarrying 3.1 3.1 3.0 2.9 2.5

ii. Manufacturing 19.1 19.0 19.7 17.1 17.1

a) Large-Scale 14.0 14.0 14.8 12.4 12.4

b) Small-Scale 3.4 3.4 3.4 3.3 3.2

c) Slaughtering 1.7 1.7 1.5 1.4 1.5

iii. Construction 2.5 2.7 2.6 2.4 2.2

iv. Electricity and Gas

Distribution

2.1 2.1 1.5 1.8 1.8

Source: Federal Bureau of Statistics

Note: S & P = Social & Public P = Provisional

54

PRODUCTION DATA OF SELECTED LARGE SCALE MANUFACTURING

ITEMS (July-March-2010-11)

Sr.

No.

ITEM NAME

NO.

OF

UNITS

2010-11

JUL-MARCH

(in tons)

%

CHANGES

1 Sugar 84 3,892,141 26.46%

2 Cigarettes 07 47,458 (04.14)%

3 Cotton yarn 215 220,041 01.91%

4 Cotton cloth 439 6,736,130 01.32%

5 Jute goods 10 66,686 (14.44)%

6 Paper & board 55 345,283 02.86%

7 Soda ash $ caustic 04 405,245 (05.01)%

8 Fertilizer total 14 4,471,287 (16.61%)

9 Sheet/float glass 07 10,150 (16.61)%

10 Cement ® 31 20,781 (09.67)%

11 Bicycles ® 04 267,800 (19.31)%

12 Steel sector 168 891,318 (15.09)%

13 Steel melters 300 1,213,046 (03.08)%

14 Auto sector 24 1,364,388 17.52%

15 Motor cycle ® 76 1,194,567 18.73%

Total weightage= 44.5101%

TEXTILES AND CLOTHING

Pakistan’s total imports of textile and clothing in FY09 stood at $65.3 million (of which 85.6

% was raw cotton imports).

IRON& STEEL

Steel with a production capacity of 1.1 million tons of raw steel per annum, with a built-in

potential to expand capacity to over 3 million tons per annum.

CHEMICALS AND PHARMACEUTICALS

55

During FY09, the total imports of chemicals (fertilizers, insecticides, plastic materials,

medicinal products, and other organic and inorganic chemicals) stood at $2.8 billion, an

increase of 29.5 % over the last year. During the FY08-09 the automotive industry

contributed over Rs 30 billion to the government exchequer in the form of duties and taxes,

with a contribution of Rs 17 billion from the top four manufacturers alone.

AUTOMOBILES

The vehicle manufacturers alone employ around 10,000 workers with more than 100,000

people working in the vendor industry. Presently, the automobile Industry mainly comprises.

SMALL AND MEDIUM ENTERPRISES (SMES)

Two million small and medium enterprises (SMEs) spread across the country contribute 30 %

to GDP and generate around 25 % of the manufacturing sector’s export earnings. The SMEs

constitute 90 % of the business and are responsible for 80 % of non- farm based employment.

Over 90 % SMEs are very small in size, both in terms of investment and workforce.

56

SERVICE

57

The services sector has risen to 53.3 % in 2010-11 which is the highest share in last two

decades. The services sector grown by 4.1 % against the target of 4.7 % and actual outcome

of 2.9 % the services sector had made a contribution of 90 % to the GDP growth.

The sector consists of the following sub-sectors are as: Transport, storage and

communication; wholesale & retail trade; finance and insurance, ownership of dwellings;

public administration and defense, and social services. The current year’s performance is

dominated by public administration and defense and social services where the value addition

grown by 13.2 % and 7.1 % respectively. The former reason of 50 % pay rise for government

servants and higher defense spending, and the later because of logistics support and flood

generated social activities.

Finance and insurance sector has displayed a contraction in value addition for the last three

years as its value addition decreased on average by 8.4 %. Finance and insurance sector was

recorded negative growth of 6.3 % in 2010-11 as against contraction of 11.3 % last year.

Transport, Storage and Communication sub sector had depicted to a sharp deceleration in

growth during the last three years as it grown on average 2.5 % in as compared to 3.8 % has

witnessed in the last eight years preceding three years. And mechanized road transport has

been depicted a growth of 2.8 %, followed by storage (3.8 %). The value addition of It

Railways has been declined substantially. Other sectors also showed that declines are;

communication (12.1 %) and pipeline transport (15.9 %).

Wholesale and retail trade sector is mainly based on the margins taken by traders on the

transaction of commodities that traded in the wholesale and retail market. In 2010-11, this

sector grown at 3.9 % as compared to 4.6 % of last year and the target for the year of 5.1 %.

Public administration and defense posted a stellar growth of 13.2 % as compared to 2.5 %

in last year. The estimates of this sector are mainly based on budgeted figures of federal,

provincial, district and local governments. The performance of this sector far outstripped the

target of 5.0 % mainly because of a positive change in the wage component of public sector

employees, and an increase in defense and security related expenditures also.

Ownership of Dwellings had remained constant at 3.5 % for the past 5 years but it was badly

impacted by other factors. Social Services Sector grown by 7.1 % which is slightly more than

the target of 5.0 % but lower than last year’s actual growth of 7.8 %.

58

Education In Educational Sector, there is 0.5% increase in the fiscal year (2010-2011). And

spending of government on education is Rs.95.442 million. According to year of 2009-10 the

literacy rate is 57.7%. Public sector has an enrollment of 25,213,894 (67%) in various

categories of educational institutions, where as 12,248,990 (33%) enrollment is in the private

sector. There is the total teaching staff is 1,363,501, out of which 0.756 million (56%) is in

the public sector and 0.606 million (44%) in the private sector. And out of the total 1.363

million teachers, 0.617 million (47%) are male teachers and 0.695 million (53%) are female

teachers.

Health In case of the Ministry of Health of It is a government agency is responsible for

Pakistan's health system. The specific health projects as under:

National Programme for Family Planning & Primary Health Care

National Maternal, Neonatal and Child Health (MNCH) Programme

National Programme for Prevention and Control of Hepatitis

National AIDS Control Programme

National Tuberculosis Control Programme

Tourism is governed through the Board of Directors headed by the Minister for Tourism. It

received more than 500,000 tourists per annual. However, this number has now come down to

near zero figures since 2008 due to the instability in the country and many countries declaring

It as unsafe and dangerous to visit. An amount of Rs. 1.28 billion is planned to be spent

during MTDF 2005-10 for the promotion of tourism, in promoting infrastructure and its

improvement.

The Services sector contributes 53.8% to Pakistan’s GDP. Its major sub sectors are under such

as Finance and Insurance, Transport and Storage, Wholesale and Retail Trade, Public

Administration and Defense. Services contribution to our GDP is gradually increases. During

the current period of financial downturn, the services sector has been a major contributor to

growth. The services sector grown at the rate of 4.1% as against 2.9% last year. The main

contributors to this growth are as public admin and defense (13.2%) and social services sector.

Export and Import of Services

Year 2009 -10 2010 -11

Imports of services ( million $) 6911 7590

Exorts of services ( million $ ) 5229 5455

59

Export and Import of Services

Source:http://www.commerce.gov.pk/.../Services_%20Export_Web_%20Page.pdf

IMPORTS AND EXPORTS OF PAKISTAN SERVICES

Table 2: Export Receipts by Major Groups of Services (Amount in Million)

Services October July- October % Change

2011 2011 2010 2011-12 2010-11

Pak Rs. US $

services

Transportation 11,230 128 119 513 477 7.7

Travel 2,353 27 26 112 102 9.6

Communication

Services 1,417 16 17 62 65 -4.2

Construction

Services 51 1 1 8 7 2.5

Insurance

Services 443 5 3 39 9 350.0

Financial

Services 543 6 2 23 27 -13.0

Computer &

Information

Services

1,414 16 15 77 61 25.5

Royalties & 59 1 1 2 1 58.6

60

License fees

Other Business

Services 4,251 49 61 248 245 1.1

Personal,cultural

&ecreational

Services

6 0 0 0 0 -14.3

Government

services 18,933 218 175 565 497 13.7

Export of

Services 40,698 467 420 1,649 1,491 10.6

Major MNC’s in Pakistan

The multinational companies have been invested Rs. 60 million in It. Initially, the British and

European trading and business houses had taken the lead as they had been present in this area for a

long time period. However, today USA leads with 25% investment, followed by UK (13%),

International lending institutions (11%), Germany (6%), Japan (3.25%). Also recently, Japan's

investment in the automobile industry has increased substantially, thereby increasing its share

List of multinational corporations working in Pakistan

SECTOR WISE BREAKUP

BANKING Engineering

• Citibank Siemens

• HSBC Medicines

• Al-Falah Bank Novartis

• Royal Bank Of Scotland Aventis

• Standard Charter Bank

• Pak al Saudi Bank

• Crescent Commercial Bank

• Dubai Islamic Bank

61

Telecommunication and IT

• Mobilink

• Warid Telecom

• Telenor

• Wateen Telecom

• China Mobile

62

MARINE INDUSTRY

63

Introduction

In past, It has faced many difficulties in mercantile scenario. Due to nationalization there was

a change in shipping industry. So, because of that there was a healthy competition in shipping

between public and private sector. A new policy was introduced to boost private investment

in shipping sector.

Mostly, the international trade is carried out through the sea and it is noticed that 36.3% GDP

was due to this. There are many dispute like heavy dependence, continental mindset of the

ruling elite which result to negligence of maritime sector. This resulted to problem such as

deteriorated the existing infrastructure, non performing shipping industry, declining merchant

marine and unexploited offshore natural resources. The Pakistan navy receives the list

priority in the armed force.

Seaborne trade is the backbone of Pakistani economy; the domestic shipping industry has

remained neglected in the past. The number of ships in the national flag carrier, the Pakistan

National Shipping Corporation, has steadily shrunk. At present, the Pakistani merchant fleet

transports only 5% of the total seaborne trade as against the 40% outlined by the United

Nations Commission on Trade and Development (UNCTAD) for national carriers. $1.5

billion in foreign exchange annually on freight charges, which is approximately 2.2% of the

GDP which the country uses. Uninterrupted flow of seaborne trade is important not only for

economic growth but also for national security of the country simply because of the reason

that the economy and national security are interdependent. It is heavily dependent on

importing energy resources.

The two main elements of maritime strategy for Pakistan are seaborne trade and shipping

industry. The main factor that affects the marine sector of Pakistan is declining merchant

marine growth. The decline stage of marine industry is due to ill advised economic policies,

capital intensive shipping nature, unabated public corruption and the prevalent geo political

situation. There are two main reason of neglecting marine industry i.e. there was no ability to

generate the revenue from shipping industry and there was a negative impression to spend

hard and earned resources.

The maritime fisheries industry was started by It when it has no partition of the resources, no

fish harbour just fish processing plant was available. The new fish harbour was constructed at

64

Karachi port in 1958. The fishing fleet grew and become mechanized. Total fish production

was 522 200 metric tons out of which 26 000 metric tons are of shrimps.

In the Pakistan Economy, the fishery plays an important role. The total employment in

fishery industry is around 379 000 employees. Moreover, 400 000 employees are employed

in ancillary industries. Fishery is the main source of export earnings. It has enough fishery

resources through the coastline of about 814 km. The livelihood of population of costal area

around Sindh and Balochistan was depended on fisheries.

It is endowed with rich fishery potential. It is located in the northern part of the Arabian Sea

and has a coastline of about 1120 km with a broad continental shelf and its Exclusive

Economic Zone extends upto 200 miles from the coast. In Pakistan, there are many marine

and inland fishery resources which has potential upto 1 million tones. It majorly include 250

demersal fish species, 50 small pelagic fish species, 15 medium sized pelagic species and 20

large pelagic fish species.

Mechanized docked boats: There are over 4,000 boats of this kind registered. it constitute

shrimp trawlers and as well as gillnetters. Both are also locally made of wood, according to

traditional design and fitted with 80-220 hp diesel engines. The average length of a trawler is

10–25 m while that of a gillnetter is 15–35 m. For transportation, many trawlers have

a transom stern.

Mechanized sailboats: This boat is made of wood and equipped with two or more outboard

engines, but generally smaller than docked vessels, they are locally called 'hora' boats. Most

of these sailboats now operate in freshwater bodies. 'Doonda' boats are

fiber scrapped lifeboats, with an average length of 7–10 m and 22–33 hp engines.

Role of marine industry in economy

The Pakistani marine sector has the potential to contribute significantly in the overall

economic growth in many ways. A prosperous shipping industry can help in saving foreign

exchange, reduce freight cost and thus promote country’s foreign trade. It can also earn

revenues from profitable shipping operation, create added employment opportunities, and

assure adequate and reliable shipping services. Ports are providing the link between the sea

and land transports and are a great source of revenue generation.

65

The Pakistani shipbuilding industry is facing severe financial difficulties in the absence of

work and continuously burdening government resources for its existence. Since a strategic

capability, the country cannot afford to permanently lose; immediate attention is required to

make it financially self-sustaining. At present, the activity is restricted to living resources in

terms of marine fisheries which are a major source of employment in coastal areas. The

Pakistani fishermen activities are largely confined to territorial waters, and a vast expanse of

the Exclusive Economic Zone (EEZ) remains unexploited. Fish is exported in raw form as

against a value-added product in the absence of modern processing plants, which would

provide a greater margin of profit.

Structure of marine industry

This sector offers employment to over one million people and most of which work as

fishermen. There are 38 processing units out of which 27 are used for freezing. Their total

capacity is about 450 tons per day. Their average capacity utilization is 25%. However, only

21 out of the 27 freezing plants are functioning. The other 11 are used for canning. The total

installed capacity for these canning plants is 106 MT/day. However, only one is functioning.

Areas where marine fishing is carried out are Karachi, Gwadar and Pasni.

The biggest and most important harbour for fishing in Pakistan is Karachi harbour.

Infrastructure facilities are available include 10 floating piers with a berthing capacity of 32

vessels on both sides. There is also an ice/oil supply bunker available for future

accommodation of 300 tons/day flake ice plant and an oil dispensing station. This harbour is

handling over 2000 vessels.

Other harbours in Pakistan do not have the relevant infrastructure for transport such as roads

and utilities of fisheries. The Korangi fish harbour was constructed to divert congestion from

the Karachi harbour and to promote deep-sea fishing. And It has a 709-meter long jetty.

However, though recently a few deep-sea vessels have begun to use the harbour facilities, it

is still not operational. The Gwadar harbour is the third important harbour in It and has a 416

meter long and 65 meter wide jetty.

66

Fisheries sector is a source of livelihood for the coastal population. A part from marine

fisheries, inland fisheries (based in rivers, lakes, ponds, dams etc.) is also very important

activity throughout the country. During the year 2010-11, a total of 86,680 MT of fish and

fishery products were exported to earn $ 197.3 million. China, Thailand, Malaysia, Middle

East, Sri Lanka, Japan, etc. are buyer of Pakistan’s fishery product.

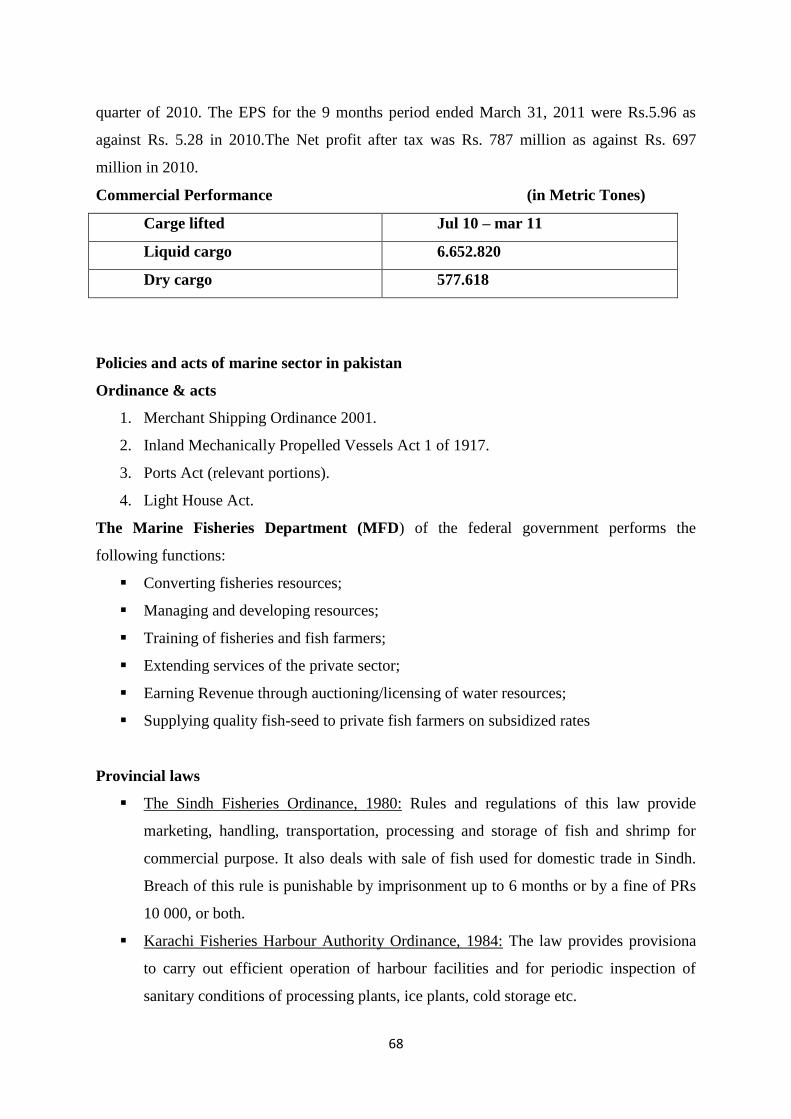

PORTS AND SHIPPING

a) Karachi Port Trust (KPT)

The Karachi Port Trust (KPT) has established an annual cargo handling record of over 41.4

million tons during 2010-11, indicating an increase of 6.9% over 2009-2010. There has also

been remarkable increase in all types of cargo handling.

Cargo Handled at Karachi Port (000 Ton)

Year import % change Export % change total % change

2007 -08 25,518 9.4 11,675 55.3 37,193 20.6

2008 -09 255,368 -0.6 13,364 14.5 38,732 4.1

2009 -10 27,892 9.9 13,528 1.23 41,420 6.9

Source: KPT

67

b) Gwadar Port

In March 2008, The Gwadar Port started operations with biggest ship of any port of Pakistan

namely 76000 DWT Panamax Bulker POS Glory which discharged a total of 63000 M. Tons

of wheat. In 31st January 2011, Gwadar port carrying a total cargo of 2,286,781 M.Tons.

Cargo Handled at Gwadar Port (000 Ton)

Year Import % change Export % change total % change

2007 -08 231.639 - - - 231.639 -

2008– 09 2055.142 787.22 - - 2055.142 -

2009 - 10 705.969 191.11 - - 705.969 -

Source: Gwadar Port Trust

c) Port Qasim Authority

Port Qasim is first industrial and commercial Port of It and it is handling 40% shipping of the

country. Qasim Authority (PQA) handled a volume of 13.019 million tones cargo during