A discussion on the regulation and deregulation of the home loan industry in Australia

58

DEPARTMENT OF MANAGEMENT James Cook University of North Queensland A DISCUSSION ON THE REGULATION & DEREGULATION OF THE HOME LOAN INDUSTRY IN AUSTRALIA MBA RESEARCH REPORT submitted by Darren Charles Lelliott B.Com in January 1997 1996 in partial fulfillment of the requirements for the Degree of Master of Business Administration in the Faculty of Commerce and Economics

Transcript of A discussion on the regulation and deregulation of the home loan industry in Australia

DEPARTMENT OF MANAGEMENT James Cook

University of

North

Queensland

A DISCUSSION ON THE REGULATION & DEREGULATION

OF THE HOME LOAN INDUSTRY IN AUSTRALIA

MBA RESEARCH REPORT

submitted by

Darren Charles Lelliott B.Com

in January 1997

1996 in partial fulfillment of the requirements for the Degree of Master of Business Administration in the Faculty of Commerce and Economics

A DISCUSSION ON THE REGULATION & DEREGULATION

OF THE HOME LOAN INDUSTRY IN AUSTRALIA

Dissertation Submitted By

Darren Charles Lelliott B.Com

in January 1997

in partial fulfilment of the requirements for the

Degree of Master of Business Administration

in the Department of Management of

James Cook University of North Queensland

I

II

DECLARATION

I declare that this dissertation is my own work and has not been submitted in any

form for another degree or diploma at any university or other institution of

tertiary education. Information derived from the published or unpublished work

of others has been acknowledged in the text and a list of reference is given.

Darren Charles Lelliott

January 18th, 1997

II III

I, the undersigned, the author of this dissertation, understand that James Cook

University of North Queensland will make it available for use within the

Department of Management and, be microfilm or other photographic means,

allow access to users in other approved libraries. All users consulting this

thesis will have to sign the following statement:

"In consulting this thesis I agree not to copy or closely paraphrase it in

whole or in part without the written consent of the author; and to make

proper written acknowledgment for any assistance which I have

obtained from it."

Darren Charles LELLIOTT

18

th January 1997

III

Iv

ABSTRACT

This discussion is made up of several elements. The first is background on the

periods of Regulation and Deregulation. It attempts to concisely cover the

period giving key dates for important development, legislation, and

implementations. A background knowledge is necessary before being able to

discuss the implications of deregulation on the industry.

Chapter two opens up the discussion on Post-deregulation competition. It is

this competition that was seen as one of the main benefits sought from the

deregulation of the finance industry. Post-deregulation competition breaks

down the effects as they have been felt by sectors within the industry. It is

divided into Banks, Credit Unions, Securitisers, and Other Finance providers.

A full discussion on the benefits sought and those gained thus far is made.

Part of the competition benefits to the consumer include the differentiation of

products that banks have undertaken to give themselves some market advantage.

Banks have lost some market share in the last two years of intense competition

and have been utilising marketing strategies to avoid further losses. Chapter 3

discusses these marketing strategies and how they have been effective, and how

some have just been negated through further government regulation.

Of course to the consumer it is the bottom line benefit that they want to see. To

IV

V

measure these benefits or disadvantages to deregulation measures of Spread and

Fees have been taken. There is then a comparison of those Spreads and fees for

banks and other financiers against comparable foreign banks, this is a Reserve

Bank research piece that has found. Australian banks are well ranked on both

measures.

As stated in the marketing strategies segment there has recently been a degree of

Re-regulation over the industry. Much of the new regulation and controls affects

all consumer loan providers, however, some of it only applies to the banks.

Chapter 5 discusses these new regulations and how they have already started to

reshape the face of competition by avoiding the 'honeymoon' loan strategy of the

banks.

My conclusion is a discussion of where I foresee the future of the home loan

industry. It is sometimes difficult to separate the home loan industry and the

finance industry as a whole and in chapter 6 I have largely incorporated a

discussion on the two as being synonymous. In the future I expect the industry

will see integrations, mergers, and more rapid technology adoptions. For the

customer it seems apparent that some benefits will be gained in mid-term through

competition and further contractions in margins, fees or both. We will also see a

change to the banking industry fee structures for other products, such as

transaction accounts. In the near future they will have to become self funding and

profit making or else they will become extinct. In the face of current and

V

predicted future competition cross-product subsidies will not be acceptable.

VI

VI

TABLE OF CONTENTS

Chapter No. Page No.

INTRODUCTION

1 REGULATION AND DEREGULATION - AN OUTLINE OF THE EVENTS

Regulation Deregulation

1

1

2

2

2

2

4

4

4

6

6

6

6

- 1

- 3

- 1

- 4

- 5

- 6

-1

- 6

- 7

- 4

- 4

- 5

- 6

2 POST-DEREGULATION COMPETITION

Banks

Credit Unions Securitisers

Other Finance Providers

3 A MARKETING DIFFERENTIATION

4 QUANTITATIVE MEASURES OF COMPETITION

Spread

Fees

International Comparison

5 RE-REGULATING THE MARKET

6 CONCLUSION - FUTURE DEVELOPMENTS FOR THE INDUSTRY

Integration

Mergers

Future of Non-Bank Lenders

Future Developments for Customers

APPENDICES

BIBLIOGRAPHY

VII

VII

TABLES

Table No. Page No.

4.1 - Breakup of Deposit Funds 4 - 3

VIII

VIII

APPENDICES

Appendix No.

1 Timeline of the Banking & Finance Sector in Australia:

Since 1911

2 Timeline of Non-Bank Financial Intermediaries in Australia:

Since 1920

3 Table 1: Assets of Financial Intermediaries:

1929 - 91

Table 2: Assets of Financial Intermediaries:

1992 - 96

4 Table 1: Bank Market Share of Owner-Occupied Home Loans

5 Table 1: Simple Bank Spread:

Variable Rate & 90 day bill rate

Table 2: Simple Bank Spread:

Variable Rate & 6 month fixed rate deposit

Table 3: Simple Spread:

Mortgage Managers & 90 day bill rate

6 Gross Interest Spreads:

Major Banks, average for year

1

INTRODUCTION

A DISCUSSION ON THE REGULATION & DEREGULATION

OF THE HOME LOAN INDUSTRY IN AUSTRALIA

The following chapters comprise a discussion that has transpired as a result of researching the

current environment of the home loan industry.

My original research was to have been centred around creating a knowledge base from which I

could make educated guesses for the future of home lending, in particular to increase my

ability to better service my own customers in my occupation as lending officer.

When I commenced this generalised investigation of the industry I found that there was no

single concise source for references. So it was decided that a more expanded investigation was

necessary.

To really understand the present industry environment, and hopefully the expectations for the near

future, it was necessary to understand the industry history. I have been fortunate and have found a

combination of references that followed a chronological order of developments in Australian

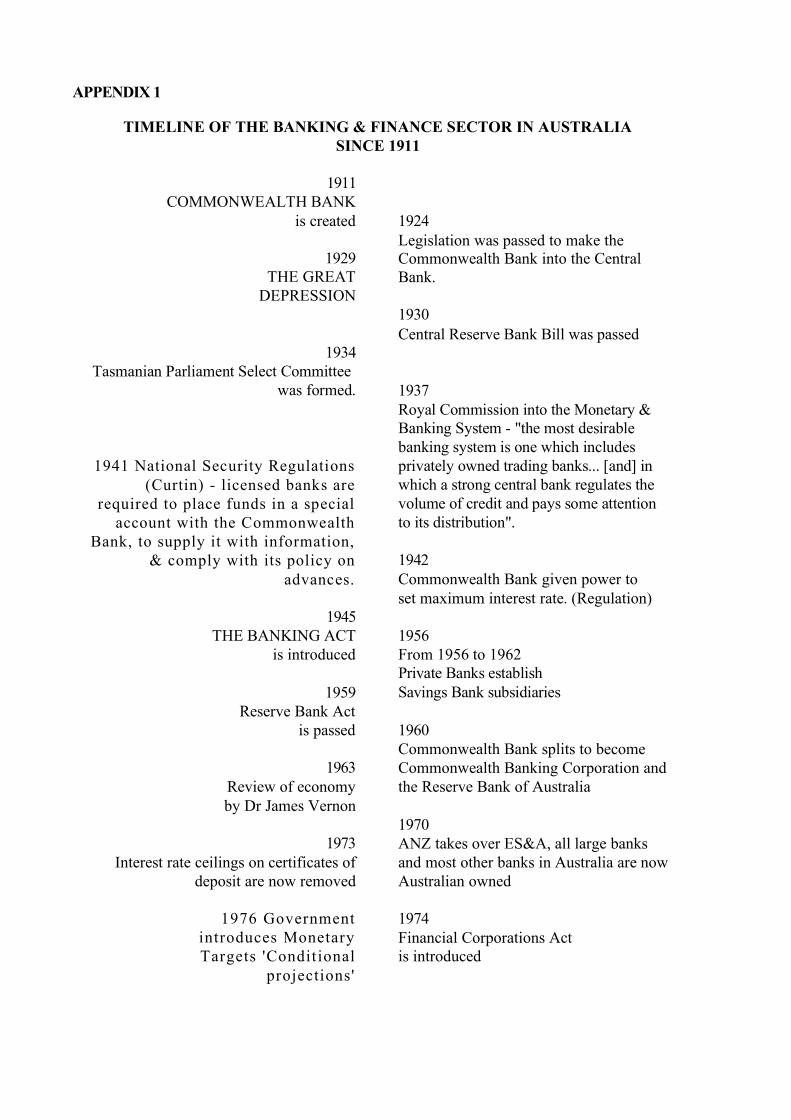

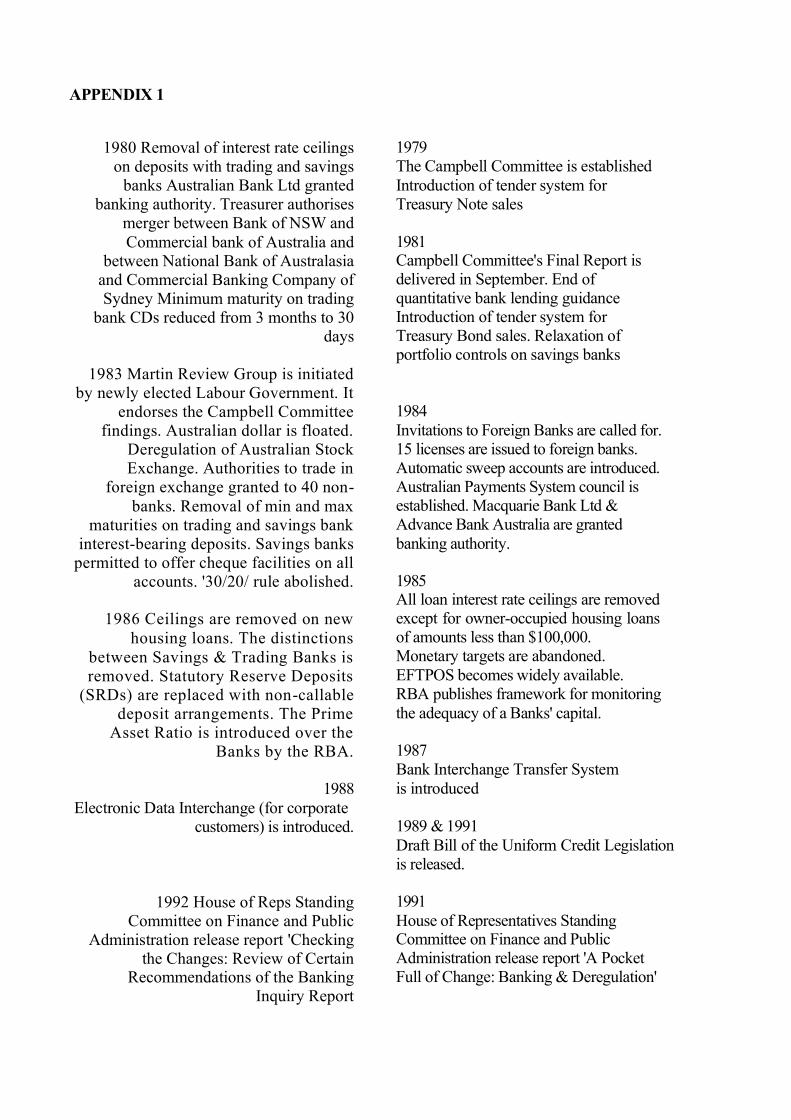

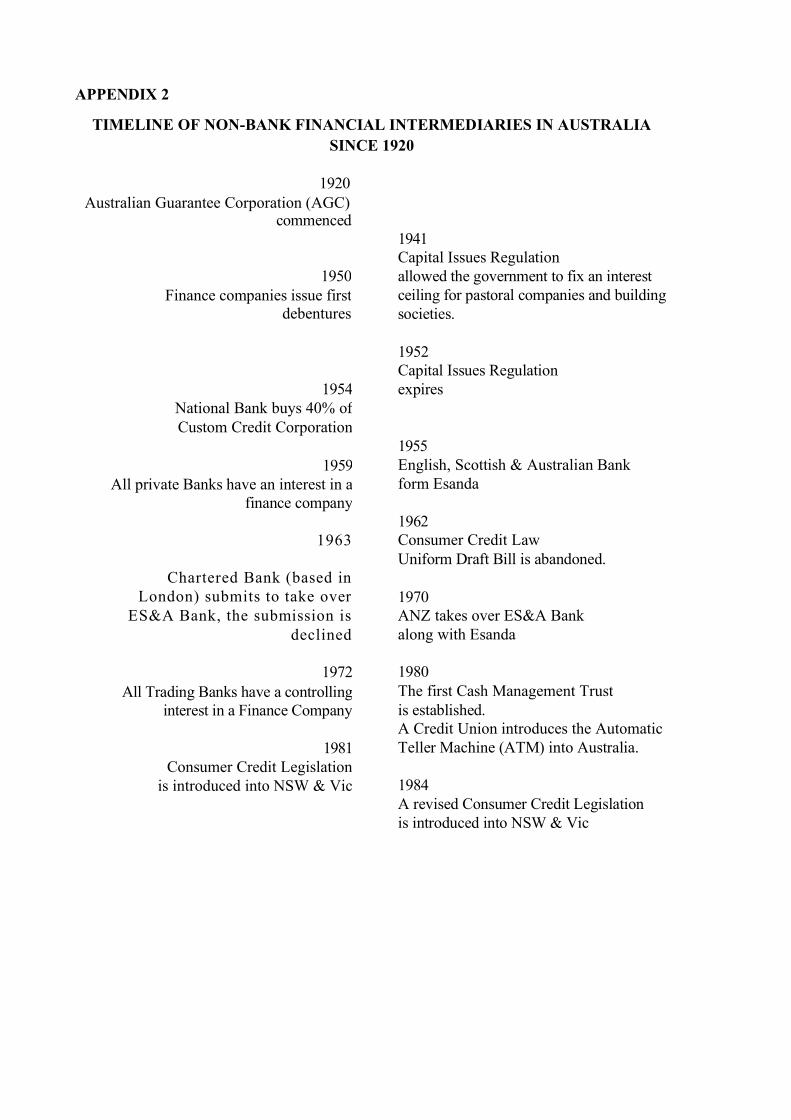

financial industry history. The Timelines at Appendix 1 & 2 were originally compiled to allow me

quick reference while writing report. I have found these appendices quite helpful and thought it

advantageous for the reader if they were included.

The investigation of the industry history led me to the sources of information I needed to

formulate my understanding and expectations as outlined in the report.

2

I have drawn heavily on the Print Media, for up-to-the-moment reporting, and the Reserve

Bank Bulletins for statistical data and analytical frameworks. Working in the industry and

being a member of an industry body, the Australian Institute of Banking and Finance, has

certainly been of benefit.

Chapter 1 Regulation & Deregulation

3

1 - 1

1 - 2

CHAPTER 1

REGULATION & DEREGULATION

REGULATION

In 1937 the Royal Commission into the Monetary & Banking System, instigated as a result of the

Great Depression, tabled a report that would mould Australian Banking for the next generation and

a half. The commission recommended that "the most desirable banking system is one which

includes privately owned trading banks... [and] in which a strong central bank regulates the

volume of credit and pays some attention to its distribution". The Royal Commission's findings are

acknowledged as the beginning of the Regulation phase.

Economists throughout Australia and other Western Nations were desperate to ensure that

there could never again be another Great Depression. To do so it was widely believed that

government regulation would allow for greater control of factors causing a depression and

could therefore avoid another repeat of the Great Depression.

Of course with the Commonwealth Government having previously created the Commonwealth

Bank in 1911 and used it in a Central Reserve Bank role, after the 1930 passing of the Reserve

Bank Bill, it was immediately recognised as the obvious candidate to implement any further

central banking regulations and would do so for some time, much to the dismay of many of the

privately owned competition.

Chapter 1 Regulation & Deregulation

In 1941 the Prime Minister John Curtin introduced the National Security Regulations, requiring

Chapter 1 Regulation & Deregulation

4

all licensed banks to place funds in a special account with the Commonwealth Bank and

supply it with specified information and to comply with its policy on advances. The deposited

funds were seen as protecting the depositors in a bank. If it became necessary they would be

available to make refunds back to depositors. During the Second World War these deposited

funds were given an interest rate as set by the Commonwealth Bank, interest rates were

carefully chosen, ensuring they did not exceed the interest rate received prior to the war.

In 1942 the Commonwealth Bank, in the role of Central Bank, was given the power to set

maximum interest rates, this applied to all deposit and loan funds and for the Home Loan Industry

can be seen as the true start of Regulation. 1945 The Banking Act was passed limiting a trading

bank's ability to offer certain product types to consumer business. From 1956 to 1962 existing

retail banks established Savings Bank subsidiaries to counter this effect.

After much political lobbying by the privately owned banks 1959 saw the passing of the

Reserve Bank Act. The Act provided for the splitting of the Commonwealth Bank into the

Commonwealth Banking Corporation and the Reserve Bank of Australia. It was felt that as

both the central bank and a trading bank the Commonwealth Bank had unfair trading

advantages over competitors.

In 1963 Dr James Vernon, of the Committee of Economic Inquiry, stated "Non-bank financial

intermediaries..reduced the effect of monetary policy decisions and accordingly a means of

formal regulation should be devised" (House of Reps 1991). Although the Non-Bank Financial

Chapter 1 Regulation & Deregulation

5

Intermediaries (NBFIs) had been regulated under the Capital Issues Regulation of 1941 this

regulation was only intended to control the setting of maximum interest rates during the years of

the Second World War. It subsequently expired in 1952 and was not reviewed or a replacement

ever implemented. Therefore the NBFIs, in particular pastoral companies and finance companies,

have not had to comply with the same level of regulation as the banks.

DEREGULATION

For the banking segment of the Home Loan Industry deregulation became effective in 1985

and 1986, however, for the finance industry deregulation started in 1973 with interest rate

ceilings being removed from certain deposit products.

In January 1979 The Campbell Committee was established to inquire into the Australian financial

system. In September 1981 the Committee's final report was submitted. The Campbell Committee

found that 'the community, while recognising a government responsibility to ensure stability and

confidence, was nevertheless receptive to the prospect of a more open and flexible financial

system, substantially free of intrusive government controls and regulations' (House of Reps 1991).

This finding, which had been hinted at in the initial brief to the Committee, was to open the way

for Australia's finance industry deregulation and the current financial environment.

The election of a new Labor government 1983 saw the creation and quick resolution of the Martin

Review Group. This group reviewed the Campbell Committee findings and found in favour of their

recommendations for deregulation. In late 1983 the Australian dollar was floated in a

Chapter 1 Regulation & Deregulation

6

1 - 4

spectacular display of deregulation initiatives, including the deregulation of the Australian Stock

Exchange.

1985 provided the removal of interest rate ceilings on home loans, except for owner-occupied

housing loans of amounts less than $100,000, and 1986 removed all other home loan interest rate

ceilings, while also removing all distinctions between Trading and Savings banks. These

moves in 1985 and 1986 are arguably the most important new development for the Home Loan

industry since the 1942 setting of maximum interest rates.

It was expected that the deregulation of the industry would allow for greater competition and the

result would be for greater benefits to flow on to the consumer. It was envisaged that these benefits

would come primarily from the lowering of interest margins (discussed in a later section) and

therefore a reduction of real interest costs to the consumer. What was also expected was an increase

in service and product options, but the rate of option increase was probably not equal to that seen

today.

Deregulation has been reviewed by the House of Representatives Standing Committee on Finance

and Public Administration in 1991 and 1992, and its benefits and disadvantages are cause for many

debates between Economists or lay-persons throughout Australia. When assessing the effects of

deregulation I feel the presiding Governor of the RBA, Mr Fraser, summed it up as such "In

assessing its effects, we should remember that deregulation has existed for less than a decade [at

the time of the speech], after several decades of regulation." (Reserve Bank Bulletin 1991).

Chapter 2 Post-deregulation Competition

7

2 - 1

CHAPTER 2

POST-DEREGULATION COMPETITION

As previously stated one of the motivations for deregulation was to open the financial services

markets to the effects of market competition, but has this happened?

BANKS

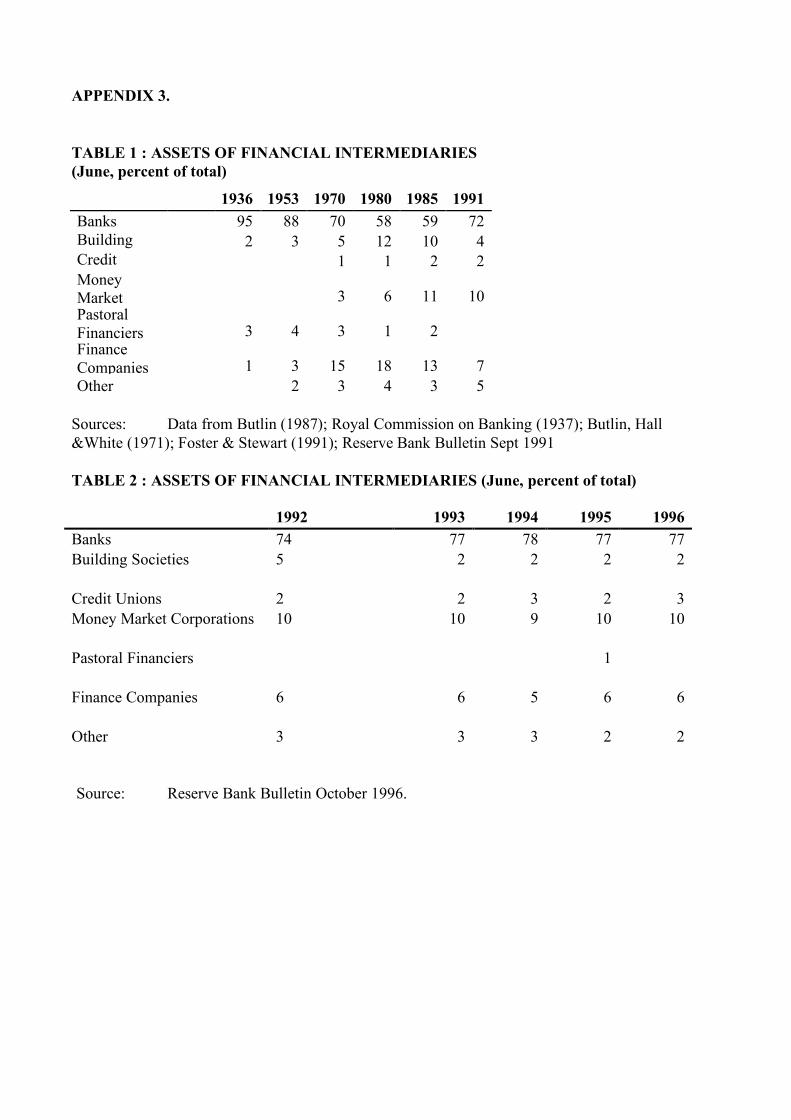

Appendix 2 provides a breakdown of the Assets of Financial Intermediaries from 1929 to the

present. In the context of competition we must assume that measuring the sector's Assets

provides a strong indication of the percentage of business being performed in the financial

industry. It is also acknowledged that this gauge does not break down the figures for product

types, e.g. Home Loans, deposit accounts, Bank Bills. However, we can assume that the

percentage of Asset ownership is indicative of percentages of dominance in the common

product areas. This assumption will not always work as for example it is unlikely that Money

Market Corporations will have a large market share of Consumer Home Lending products.

If we first examine the Banking industry we can follow a trend that has taken the banks from

almost complete dominance of the financial industry in the 1920s, to the period following 1936

where we see the Banking sector loose Asset dominance to the NBFIs, particularly the finance

companies. This loss of Asset shares can be closely traced along the period of regulation where

the banks had to conform to the regulations placed upon them while the finance companies were

unregulated after the expiry of the Capital Issues Regulation in 1952. As of 1959 all Australian

Chapter 2 Post-deregulation Competition

8

2 - 2

Chapter 2 Post-deregulation Competition

Banks had an interest in a finance company in an effort to circumvent the banking regulations.

The lowest period of banking sector percentage ownership of industry assets occurs between

1970 and 1991. After the deregulation measures of the early 80s the banking sector gains market

asset percentages, however, the sector has never again climbed above 80% industry asset

ownership.

Finance companies and building societies enjoyed the most growth during the late stages of

regulation and both have subsequently lost asset percentages in the wake of deregulation. Over

the changing financial and societal environment of the last 20 years pastoral companies have

gone into decline and credit unions have sprung up in their place.

The area of most interest in the face of increased competition through deregulation is the

category of 'Other' which steadily grew in asset position and then declined again.

For the purposes of a discussion on Home Loan market share the Assets measure may also fail

when we take into account the rise of Mortgage Securitisers. Mortgage Securitisers (Mortgage

Managers) will be discussed in the next section.

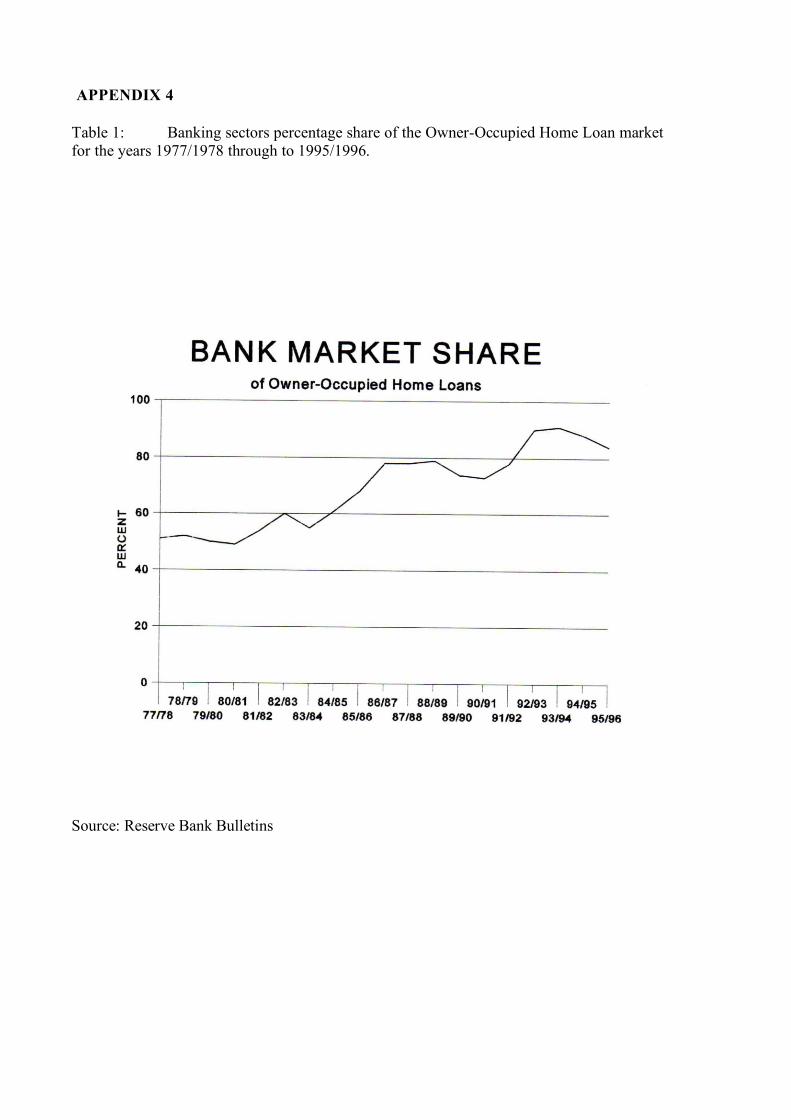

Mother indicator of the trends in the market is appendix 4. This shows the 'Bank Market Share -

of owner-occupied Home Loans' for the industry. This data was collected from several issues of

the RBA Bulletin and only breaks down the information into total figures and the dollar value

financed by the banking sector.

Banks have been following a steady trend, increasing total market share since the early 1980s.

Chapter 2 Post-deregulation Competition

9

2 - 3

2 - 4

The low of 50% during the 70s would have been at a time when the banks were regulated and

had Savings and Trading Bank distinctions. During the 70s the building societies held around

30% of the market, and insurance companies, which played a major role then but slipped out of

the market until recently, held between 10 - 15%.

At this time it is not possible to deter crone if the 94 - 96 decrease is the turning point for market

share or Wit is another cycle. These figures and the growth trend for banks is significant in that

although there has been much discussion on the margins and overall profitability of the banks

the percentage of market share continues to grow. The House of Reps Standing Committee (A

Pocket Full of Change, 1991) had this to say about the level of competition and margins.

'The main influence on margins is the degree of competition for providing deposits and

loans in a given market. However, as the scope of the banking market has broadened

over the 1980s, a finding that interest margins have increased somewhat would not

necessarily imply that borrowers are being exploited It may be a reflection of banks

lending for riskier proposals now that they are no longer rationers of credit. These

riskier proposals may previously have been funded by finance companies or money

market corporations.' (House of Reps 1991).

For a full discussion on margins refer to the section 'Spread'.

There has been some movement in the industry with strong competition being waged by the

mortgage managers, insurance companies, and other bodies we have seen particularly active in the

industry. But does this mean that there is significant movement away from the banks. An article in

Chapter 2 Post-deregulation Competition

10

2 - 5

the Townsville Bulletin (17/4/96) would have us believe that 'Home buyers desert banks in droves.

This article reported that 'housing finance approvals rose by 2.9 per cent in February

[1996]...finance approvals by banks grew by only 0.3 per cent in February compared with a 17.8

per cent increase for other lending institutions - a 49.3 per cent improvement since January last

year'. If we look at appendix 4 again these figures can be substantiated for early 1996, however, are

they signs of a long term swing away from the banks or merely the downside of a cycle?

CREDIT 'UNIONS

As previously stated the credit unions were the second largest market shareholder in the owner-

occupied home loan market during the seventies, with market share fluctuating between 28 and

33%. During the 80s, with the deregulation of the banks, credit unions rapidly lost ground to

other institutions particularly the banks. In 1994 the banks were holding almost 91% of the

market share leaving 9% to be divided between credit unions, finance companies, and others.

Since the 94 peak the banks have dropped back to 84% in 1996 and we know that the mortgage

managers now hold 9% of the difference leaving 7% to the rest (these figures are the

interpolation of data provided by the Reserve Bank over the period 1970 to 1996).

In April 1996 the Credit Union Services Corp of Australia Ltd attempted to raise funds in the

bond market to enable its member credit unions to offer cheap home-loans. Unfortunately this

failed and the credit unions do not seem to have recovered. They cite the banks and mortgage

managers as being the main cause of their market share erosion. There is some indication that

Chapter 2 Post-deregulation Competition

11

credit unions will move to establish themselves as mortgage securitisers in order to continue

operating in the home loan market.

SECURITISERS

Mortgage Securitisers (Mortgage Managers) take parcels of Home loans and offer them to

wholesale investors secured by mortgage securities. In recent years these securitisers have risen

to take on the Banks in competition for Home Loans. Mortgage managers are the exciting

development in the home loan industry. They have made rapid inroads into the market shares of

many of Australia's traditional home lending sources. The banks appear to have been caught

unprepared for them, as do the credit unions and finance companies. They could be compared to

a Scottish terrier gnawing at the leg of a Stegosaur. They are small, able to adapt quickly due to

their size, operate at very little cost and do not bear any of the liability associated with the home

loan.

For example a Securitiser will seek the business of home buyers until they have parcelled together

the borrowing requirements for $1 million of home lending. The securitiser then offers this $1

million worth of debt, secured by mortgages and mortgage insurance policies (home lending where

the borrower has less than 20% equity in the loan securities is secured by mortgage insurance) on

the wholesale investors markets. Although the spread, in this case being the difference between the

interest rates paid by the home buyer and the rate at which the wholesale investor purchases the

parcel, will be less than that of the banks, difference between interest rates given to depositors and

that payed by borrowers, the securitisers are able to benefit through low operating costs.

Chapter 2 Post-deregulation Competition

12

2 - 7

Securitisers are able to maintain low operating costs, compared to banks and other NBFIs,

because of the branch networks and high levels of staffing these other institutions have.

Furthermore as the Securitiser is not the direct provider of funds, nor the holder of the

security, they do not maintain the debt burden on their balance sheets, this is borne by the

wholesale investor.

In effect the Securitiser is no more than the middleman between the home lender and the

wholesale investor. They conveniently package together parcels and are paid a managers fee.

This simple strategy, that works so well in an environment where wholesale funding can be

raised at relatively inexpensive rates, has seen the mortgage managers move from a market

share of 1% four years ago, to their current 9% market share in 1996. Aussie Home Loans,

a mortgage securitiser, is ranked in the top 5 home lenders in Australia writing $250

million worth of business per month.

OTHER FINANCE PROVIDERS

The home loan market has long been regarded as an attractive area for financiers because of the

high margins obtainable compared with other finance products. This attraction has seen many

sources of finance come and go. In today's environment of post-deregulation competition we are

seeing new operators and the return of some that had otherwise almost dropped out of the

market completely. We can now obtain housing finance from domestic or foreign banks, from

mortgage securitisers, from life offices, unions, and solicitors.

Chapter 2 Post-deregulation Competition

13

Life Insurance offices used to operate at up to 25% of market share during the 60s decreasing

in the 70s to 5%. During the 1980s they virtually left the market but they are now making a

comeback. They have been attracted back to the industry because of the high margins, the

inexpensive and readily available funds they can tap into and the because of the changes that

have occurred in their industry resulting from competition. Life offices are now waiting for the

outcome of the Wallis Inquiry and the implications for their being able to operate in the finance

markets. If they are given the all clear then we may see mergers, take-overs, or simply the

existing operations expanding to perform more of the traditional banking operations.

Many of the 'Other' category of home loan financiers operate at margins allowing them to

undercut the banks so why are banks still able to maintain their market share, or at least not

lose it in the volumes that would be expected? To answer this we must consider what is really

on offer, that is a home loan is not simply a home loan and a lot of the decision comes down to

what I classify as the Marketing.

3 - 1

Chapter 3 A Marketing Differentiation

14

3 - 2

CHAPTER 3

A MARKETING DIFFERENTIATION

As noted under 'Competition' the mortgage managers, unions, solicitors and other market share

takers are able to operate at lower costs than the larger and higher operating cost banks and

credit unions. So why do these latter sectors still maintain such a large share of the market

when the others outperform them on costs?

Historically the simple answer has been for the banks to outperform the NBFIs on services and

product range. Banks are able to 'Tailor' a package of products to the home buyer from their

stables of other banking facilities. They can offer discounts on these other products to new

customers and entice them into the market.

The RBA found that, in an effort to maintain the banks market share, they were offering three

product benefits that mortgage managers had not been able to meet.

1. 'Honeymoon' loans. These loans operate on a discounted initial interest rate, designed to

attract the home lender. At the end of the term of discounted rate the interest would return

to normal customer rates. For example a customer may go onto a 12 month fixed interest

rate of 7.5% while the normal fixed interest rate was 9.50%. A honeymoon loan normally

tied borrowers into the deal in an effort to ensure some customer stability. These conditions

varied between banks, but normally worked on a five year term. This way the customer

would take the 7.50% for 12 months and then convert to the standard variable interest

3 - 1

Chapter 3 A Marketing Differentiation

15

3 - 3

rate for the remaining four years of the term. If they sought to refinance during this

term they would be required to pay a fee for breaking the terms of the contract, a

prepayment fee. This product variant has now changed and will be discussed further in

'Reregulation'.

2. Fixed-rate loans. As mortgage lenders have been unable to offer fixed rate loans this

product is a further benefit to the banks. Using a fixed rate, customers are able to ensure

that their repayments will not increase during the term of fixed rate. This gives them the

benefit of being able to budget for the fixed term. For the banks it means providing a

guarantee that the customer finance will be held for the fixed rate term, allowing greater

planning of funds and providing the bank greater scope to compete at the margin for new

customers.

3. 'Basic' variable-rate loans. These 'no-frills' options allow the banks to attract new

customers with rates below the standard variable-rate. The banks can afford to do this

in an effort to attract customers for some categories, as they can cross-subsidise this

product group with other products. This is seen more as an aggressive marketing tool

designed to gain back market share from other finance providers than it is as a revenue

gaining source. These products are as the name claims 'basic' and often come with none

of the associated benefits of discounted banking products such as redraw facility,

savings accounts, credit cards, etc.

To a lesser extent the regional banks have been offering special deals based on geographical

area. These offer discounted rates in a new area compared to the rate offered in the banks home

3 - 1

Chapter 3 A Marketing Differentiation

16

3 - 4

area. This is another aggressive marketing tool that aims to gain quick market share in a

geographic location.

It may be noted that a lot of the focus for these products has been the maintaining of customer

loyalty. The reason, (RBA Bulletin June 1996) is that 'in mid 1991, 8 per cent of loans for

established houses were refinancing, but this figure is now around 28 per cent'. A customer

migration rate of 28% for established dwellings is a further indicator of the level of post-

deregulation competition. It is also a warning to industry players that they can gain and lose

market share extremely quickly in the current competitive environment.

It has already been said that the product differentiation has been the level of service and associated

products banks can offer, over those offered by non-bank lenders. The non-bank lenders are now

taking steps to overcome these limitations and, with recent developments, may have come a long

way in doing so. The Weekend Australian (Kavanagh, J 1996) reported that 'non-bank home loan

providers are shedding their no-frills image. after Sydney-based Financial Directions Australia

launched a home loan package that includes redraw facilities, a line of credit and a facility for

switching between variable and fixed'. If all mortgage lenders are soon able to do similar loan

packaging then the bank advantage, already held, will reduced.

Along with the marketing aspects of post-deregulation competition comes another new player

for the industry: the referral partner.

With competition heating up and competitive advantage being depleted all industry players will

3 - 1

Chapter 3 A Marketing Differentiation

17

be looking for new advantages to keep them ahead. Realtors are now standing up and pointing

out to industry players that they are integral to the majority of home purchases. So what does it

mean? Home lenders will need to reinforce their positions with these referral sources in order to

get a competitive advantage. Unfortunately for the banks, the realtors have realised the

competitive advantage they have and the relatively inexpensive cost of originating the finance

themselves. If this trend of realtors acting as originators continues, it will add to the competition

faced by banks, and further reduce the competitive advantage they currently enjoy.

3 - 1

Chapter 4 Quantitative Measures of Competition

18

4 - 1

CHAPTER 4

QUANTITATIVE MEASURES OF COMPETITION

It is very good to be able to say that competition has been encouraged into the Australian

finance industry, or that qualitative measures might indicate a level of competition that has not

before been seen in Australia. But it is always the quantitative measures of any benefits from

competition that must prove or disprove the benefits of deregulation. In this chapter, two

quantitative measures of competitive benefit are discussed. Of course to the consumer there are

two benefits sought from competition and they are cheaper housing loans, and a greater choice

of product. The issues concerning the product are covered under the title of Marketing this

section talks about the bottom line differences for the consumers home loan cost. To measure

these costs to the consumer, spread and fees must both be considered.

SPREAD

'Despite considerable publicity suggesting that increases in customer margins have been large

and widespread, evidence available to the Reserve Bank suggest that they have been minimal

and have had little effect on banks' average interest spreads' RBA Bulletin 1992.

Spread or Margin (the terms are used interchangeably in the literature) is the difference taken

3 - 1

Chapter 4 Quantitative Measures of Competition

19

4 - 2

4 - 3

between the rate of interest paid by the lender for funds and the rate of interest received on those

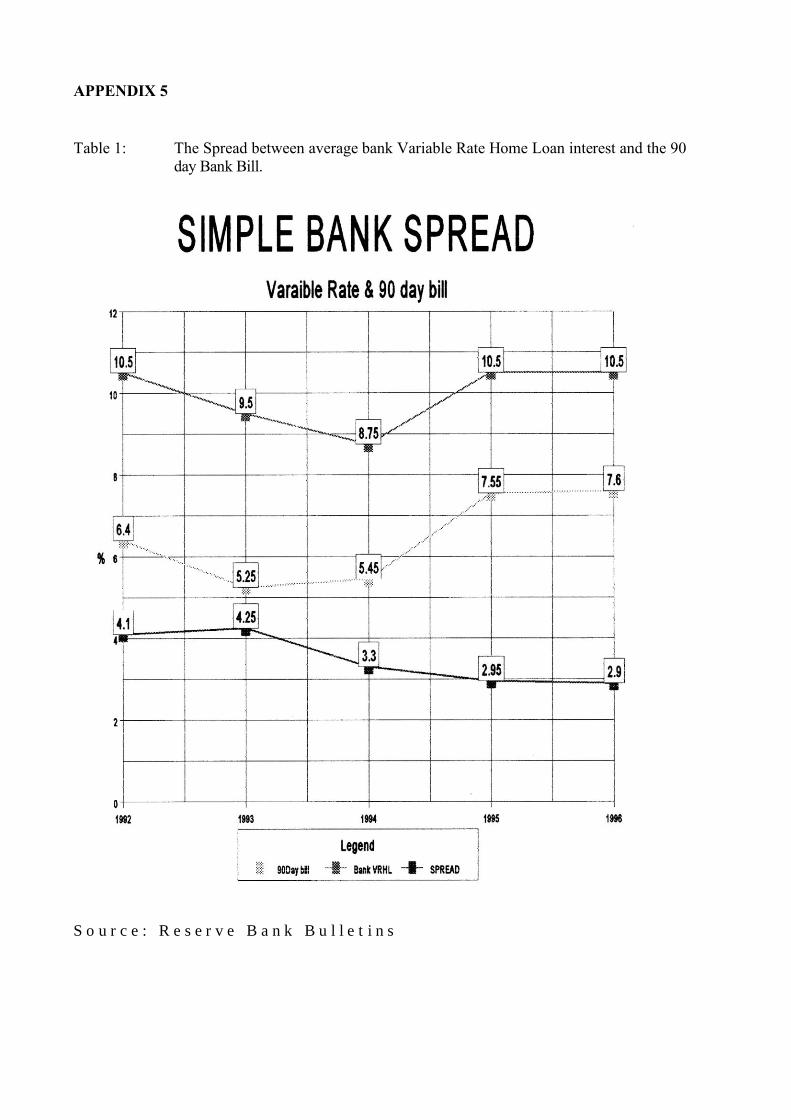

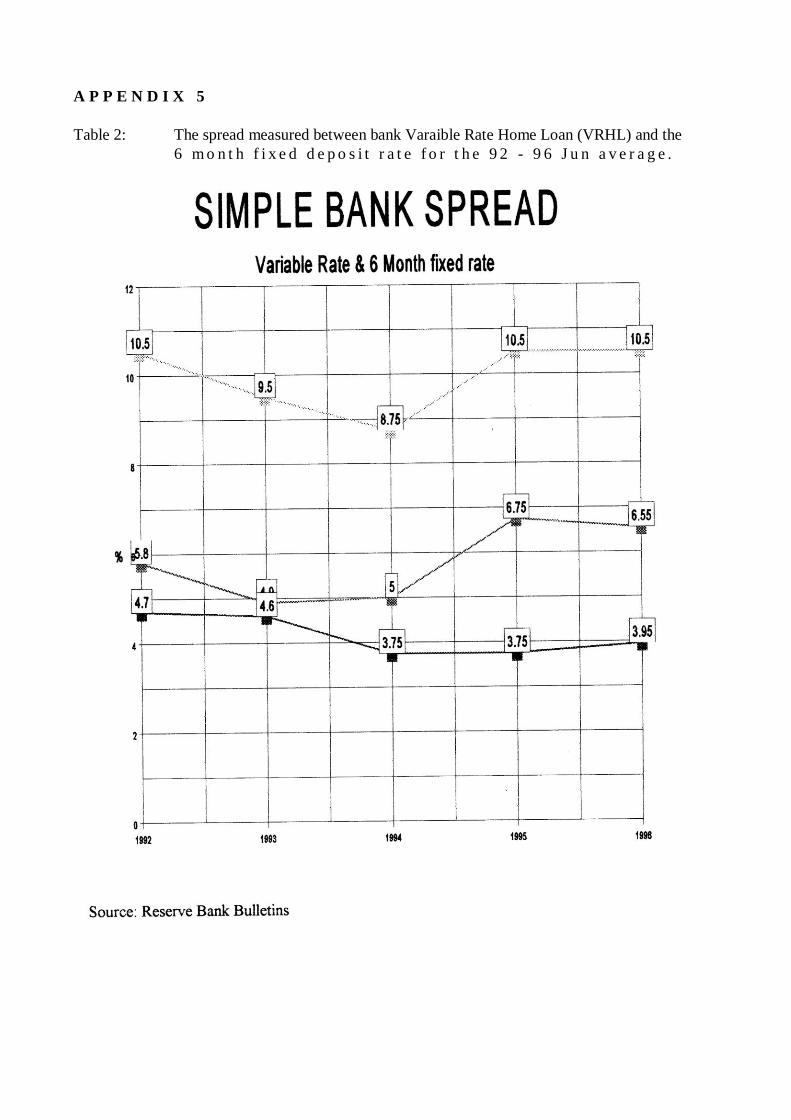

funds. This may seem like a simple discussion and is commonly misinterpreted as being such. For

example many journalists quote spread on Variable Rate Home Loans(VRHLs) as simply being

the difference between the Variable loan rate of the day and the 90 day bank bill rate, as is shown

in appendix 5. or the difference between VRHL and a chosen statement or deposit account. Again

appendix 5 gives an example of 'VR and the 6 month fixed deposit rate. Dr David Clark of the

University of NSW provides an example of 'The Interest Rate Margin Which Interests most

Australians - Difference between average home loan rates and 3 month, fixed-deposit rates' in his

Economic Briefing (AFR 19/6/96). Surprisingly, although this measure is overly simplistic and

may have been thought to be a matter of scare tactics, the graph provides a margin starting at less

than 2% in 1960, peaking at just over 4% in 1992 and dropping back to about 2.5% in June 1996.

This simplistic view of Margin is actually better than the measure of Average Gross and Net

Margins as preferred by the Reserve Bank.

The problem with taking a simplistic view on margins is how do we know which product and

term to choose?

It is not as simple as saying that all of the money used to provide Home Loans by banks is gained

only from the 3 month fixed-deposit market. These funds are in fact gained by a combination of

all of the revenue raising sources a bank utilises. From simple statement accounts, to fixed-

deposit products, through to treasury raised capital.

In 1991 the Reserve Bank of Australia(RBA) was requested to provide an update on the effects

of deregulation to the House of Representatives Standing Committee on Finance and Public

Administration. To do so the RBA investigated simple measures of spread and found them

inadequate, for the reason previously given. Instead the RBA had to ascertain the Gross and

Net Average Margin for the banking industry.

3 - 1

Chapter 4 Quantitative Measures of Competition

20

4 - 4

This pie graph shows that for the deposit funds sources from the Australian banking sector

there is no simple source from which to base a measure of spread.

Table 4.1: Breakup of Deposit Funds

Source: Reserve Bank Bulletin June 1996.

It was found that the pattern was the same for the data up until 1996. If we further consider

that, within each of the above deposit sources, there will be several products, it exacerbates the

case against such a simple measure of spread.

What is the Gross or Net Interest Spread? The Net Average Interest Spread is measured by the

difference between the average interest rate received on all loans and investments (including non-

3 - 1

Chapter 4 Quantitative Measures of Competition

21

4 - 5

accrual loans) and the average interest rate paid on deposits (including zero-interest deposit

accounts) and other interest-bearing liabilities. Gross Average Interest Spread differs from the

Net Average Interest Spread as non-accrual loans and zero-interest deposit accounts are not used

in the calculation. The difference in real terms can be quite significant, dependent on the level of

debt write-offs an institution maintains. For example, the difference between Gross and Net

Spread during the early 1990's would have been more pronounced than that of today.

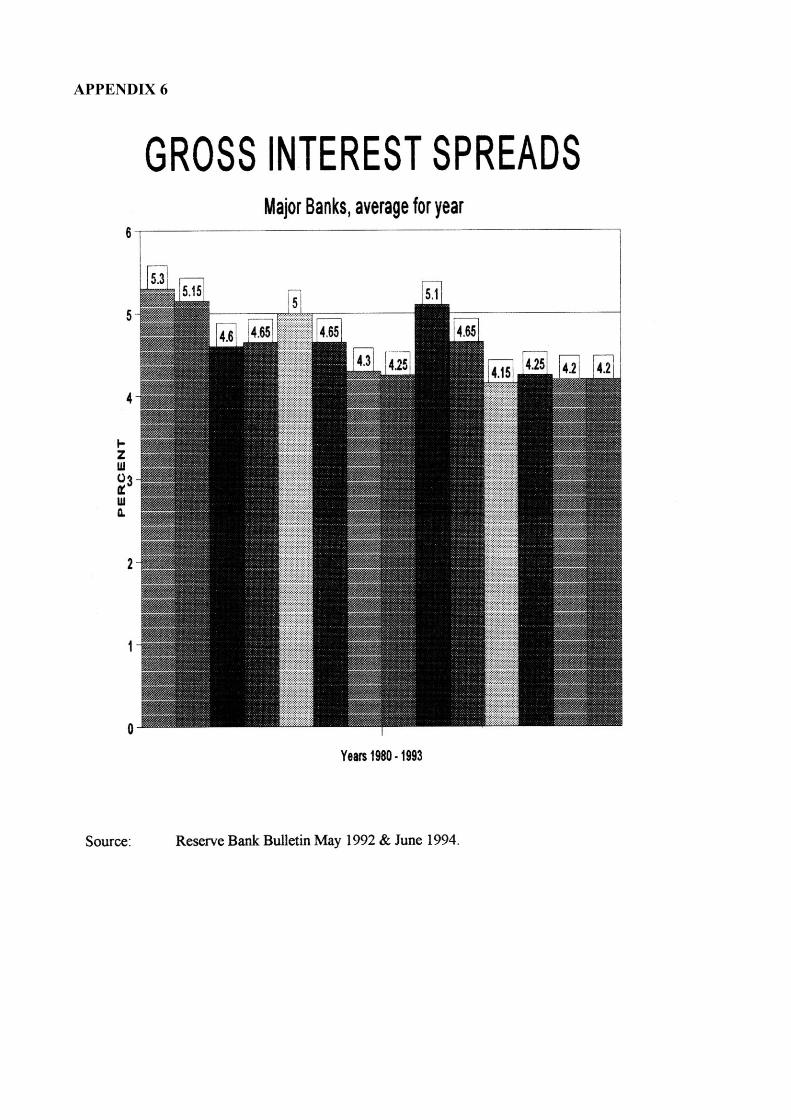

Appendix 6 shows the calculations for the Gross Average Margin from 1980 through to 1993.

These figures have been calculated by the RBA. Unfortunately, due to the difficulty in

obtaining and interpolating the Gross Average Margin, there is no indication for the period

subsequent to 1993. A period which may reveal, in Margin terms, the most intense period of

competition and possibly a significant decrease in margins.

The House of Reps Standing Committee (A Pocket Full of Change, 1991) found that 'the

aggregate interest spread has been on a downward trend during the 1980s, interrupted only by

the rush of funds into the banks after the 1987 sharemarket crash". If we compare this trend

against the simple spread analysis in Appendix 5, of the VRHL against the 6 month fixed rate,

then we can find comparable downward trend over the last four years, with a margin wavering

around the 4% level.

The Standing Committee of 1991 also noted the following 'in the early years.. [the regulated

period].. the housing loan rate was subject to a ceiling and while loans were cheaper they were

harder to obtain. Many borrowers had to top up housing loans with expensive personal loan

3 - 1

Chapter 4 Quantitative Measures of Competition

22

4 - 6

rates or loans from finance companies and so the average rate paid exceeded the advertised

housing loan rate'. Taking this increase in spread into consideration it would indicate an even

greater benefit having been gained from deregulation. To the consumer these trends provide

quantitative evidence that there has been some benefit gained through deregulation and the level

of competition achieved.

A procedure we have witnessed in recent history has been the reduction in home loan rates for

new borrowers while there is a lag in the time until this change will be felt by existing borrowers.

In 'A Pocket Full of Change' the Standing Committee investigated these occurrences and reported

that such lags were carried out for the following reasons:

1. Stability of interest rate. For the customers benefit the banks decide that they will wait

to ensure that the interest rate decrease is sustainable before amending existing

customer rates.

2. The margin rate will move much more slowly than the home loan rate, as banks raise

much of the funds from long-dated fixed rate deposits.

3. Banks, attempting to recover from bad and doubtful debts, will lag adjustments

downwards. This lag will result in some financial margin benefit to the bank, helping to

recoup such debts.

FEES

3 - 1

Chapter 4 Quantitative Measures of Competition

23

The other quantitative measure to the consumer is the costs they must incur in fees.

There are a number of perspective on the fees issue to the Home Loan industry. One claims

that banks will have to increase the fees paid on home lending to make up for the margin

shortfall that will result from the increased competition of a deregulated market. The other

perspective counters this argument by stating that competition will result in the abandonment

of fees, both upfront and ongoing, in an effort to increase or maintain market share.

It was recently reported that when the ANZ increased the monthly service fee on one of its home

loan products, the customer backlash was such that the bank quickly had to backtrack on the

decision, and wear the extra cost. Other reports almost go so far as to claim there is no alternative

but for the banks to increase fees. The Australian Financial Review (Gray & Rogers 17/6/96)

reported that the Chairman of the Australian Competition and Consumer Commission (ACCC),

Prof Allan Fels, would 'come under pressure...to allow higher fees and charges to preserve the

industry's profits'. A Westpac spokesman claimed in the same article that 'interest margins would

continue to be squeezed and banks would have to focus on revenue growth from

3 - 1

Chapter 4 Quantitative Measures of Competition

24

fee income'.

'In the UK, banks offer home loan rates at the official market rate, and make their profits from

follow-on fees.' The Weekend Australian (J. Kirby 3/8/96).

The RBA Bulletin also had this to say about fees 'Fees are also relevant. Some, such as

application fees or establishment charges, are once-only payments, levied when a loan is first

arranged Other fees, such as line service fees, are charged continuously over the life of the

loan and are, in effect, an additional interest margin'.

INTERNATIONAL COMPARISON

By reviewing the available international comparisons, of banking spreads and fees, it was found

that overly simplistic data has been used, and is therefore of limited application to Australia.

This data prepared by Salomon Brothers and the OECD either made comparisons between banks

that were so different in the markets in which they dealt as to be unusable, or else the data was so

surrounded by disclaimers as to be considered unworkable. The RBA, in a commitment to the

House of Reps Standing Committee, conducted its own research, and, after much frustration,

provided a statement in the RBA Bulletin of October 1994. The statement, in short, claimed that a

workable comparison could only be made between Australian retail banks and their counterparts in

the United States, the United Kingdom, Canada, and New Zealand.

3 - 1

Chapter 4 Quantitative Measures of Competition

25

The international comparison found:

I. Australian banks' margins were slightly higher than most, ranking second highest

behind

the US.

2. Australian banks ranked the lowest for fees and charges.

In conclusion as to whether customers are seeing quantitative benefits from deregulation, my

research has found the same outcome as that of the RBA researchers and they have expressed

these findings as 'some [customers] are better off, some are worse off and some are, like the

average, neither one or the other' the RBA further justifies this conclusion with 'on average,

borrowers are paying more for their loans than they did a decade or so ago but they are

paying not the banks but those people who lend money to or deposit money with the banks'.

3 - 1 5 - 2

Chapter 5 Re-regulating the Market

26

CHAPTER 5

RE-REGULATING THE MARKET

At no time has the home loan market really been without regulations of some sort. Private

banks must abide by prudential supervision measures. These measures in turn affect home

loans. In fact at no time has it been suggested that banks should operate without a degree of

government supervision.

Deregulation was the removal of regulations that limited certain bank operations. We have

seen that when one sector is regulated while another is not, for example the bank sector against

finance companies, then one sector will prosper at the expense of another. Deregulation was

supposed to be about the consumer prospering as a result of competition.

Now we discuss the issue of re-regulation over certain sectors and customer types. This set of

regulations can be said to be ethical regulations. The regulations to which I refer are the Code

of Banking Practice and the new Uniform Consumer Credit Code.

The Banking Code of Practice came into effect in 1995. It was a banking industry wide set of

guidelines that ensured customers were being treated fair and equitably. The code is not an

official regulation as such, more an industry standard. For home lending the code has had little

implications nor effect, other than to attempt to provide some conformity between the banks.

3 - 1 5 - 2

Chapter 5 Re-regulating the Market

27

Uniform Consumer Credit Code is a set of government legislation that act to ensure that all

consumer customers are treated in a fair and ethical manner. It aims to ensure that all consumers

of financial products are aware of all obligations before obtaining finance. The Credit Code has

meant significant alterations for the finance industry. Finance contracts have been rewritten in

plain English, the method of presenting finance information has had to change and the customer is

now required, by some institutions, to seek independent legal and financial advice before being

able to settle finance. This move has been taken to ensure that customers are fully aware of their

obligations, rights, and that the finance decision is the correct one for them.

On the home loan industry the effect is most dramatic where the banks have offered 'honeymoon'

loans to get new customers. Under the new Credit Code no penalties will apply to consumer

finance. This means that 'honeymoon' loans will not be possible for the banks and the competitive

advantage they maintained over mortgage lenders will be greatly reduced. Rogers (AFR 1996) put

it this way 'Banks may face another round of margin pressure on their home loan business ....

when new consumer credit laws invalidate the shackles banks place on borrowers who take up

cheap loan offers'. This could also see the percentage of mortgage defections going up in the short

run as customers use the high levels of competition and the credit code to shop around for their

home loan refinance.

3 - 1 5 - 2

Chapter 5 Re-regulating the Market

28

5 - 3

Despite these restrictions to early payout penalties under the credit code, National Australia Bank

went ahead and announced a 'honeymoon' loan of 6.99% for 12 months, on 31/10/96, the day

before the credit code became effective. Rogers (AFR 1996) reported that 'NAB ...surprised its

rivals by choosing to rely on a product line which many regard as uneconomic with the

introduction...of a national consumer credit law.' It would appear that even though the

'honeymoon' loan may not prove profitable it will continue to be used in an effort to attract

customers into the banks.

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

29

CHAPTER 6

CONCLUSION

FUTURE DEVELOPMENTS FOR THE INDUSTRY

So far the discussion has taken a course from the history of the Home Loan market, through the

period of regulation and then deregulation, and up to the present. An analysis was shown for

the present environment. This analysis attempted to measure the effects, positive or negative,

of deregulation. Now in conclusion I attempt to outline trends and predictions for the future of

the Australian Home Loan market.

TECHNOLOGY

The largest influence on this market over the past 15 years has been deregulation, however, the

second largest influence has been technology.

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

30

6 - 2

Although, the technological revolution has largely coincided with the period of deregulation in

Australian financial markets, the level of technological adoption in Australia is arguably due

more to deregulation than the availability of new technologies. It is suggested that new levels of

competition in the finance sector, resulting from deregulation, was the necessary motivation to

improve processes through technological developments, these improvements aim to reduce

operating costs and increase benefits to customers, giving the organisation a competitive

advantage. Without the increased competition, of a deregulated industry, there would have

been little advantage in adopting expensive technological changes.

In the future, with entrenched levels of competition between all financial institutions, the level

of technological adoption will continue to grow as each institution strives to find, marketing, or

operational cost, advantages over their competitors.

For the banks technological develop will include the continuing centralisation of services. For the

banks to regain some competitive advantage they must unite the benefits from both their own and

the originators business. That will mean that banks will have to reduce the costs of operations.

The major operating costs to banks is the extensive branch networks. Therefore banks will have to

rationalise this network by shedding less efficient and less needed branches. Already there have

been moves my banks to open Supermarket kiosk facilities. These kiosks operate on small staff

numbers offering only the basic product service range. They are small and inexpensive while still

being able to reach the major population centres. The US already has kiosk networks from which

Australian banks may be taking an overall framework.

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

31

Supporting this kiosk structure will be more mobile bankers operating from a vehicle or home.

They will seek the home loan applications and then sign the customers up. All other back office

work will be conducted from a central area, such as the home loan centre operated by ANZ in

Chapter 6 Conclusion - Future Developments for the Industry Melbourne. The customer's home

loan will then be maintained and administered between the bank and the customer through non-

branch contacts such as correspondence, telephone, or computers.

Tele operations, any service that can be provided over the telephone, have been identified as a

relatively inexpensive means of reducing costs and increasing customer service. Today more and

more banks offer "over-the-phone" service. This allows the banks to centralise a single facility

for either a state or national operations. Centralisation reduces duplication and therefore the

associated costs. Many banks have made use of telephone servicing of customers for some

years, and now we see all banks offering more of their product lines over the phone.

Computer based services will be utilised more and more as they become both more readily

accessible and offer greater customer confidentiality. At present some services are offered to

differing customer segments via either the internet or dedicated computer systems. On the future

of Internet services, computer and software giants, such as Oracle, predict that PCs will be

replaced by simple home terminals that draw all processing power from a centralised computer

source. This will allow applications to be uniform throughout all homes, and therefore offer

uniformity of banking operations via the service. In the computer industry this home terminal

alternative to PCs is expected to be the next revolution in affordable computing, and could well

be the computing generation banks have waited for, before implementing nationwide computer

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

32

6 - 4

services.

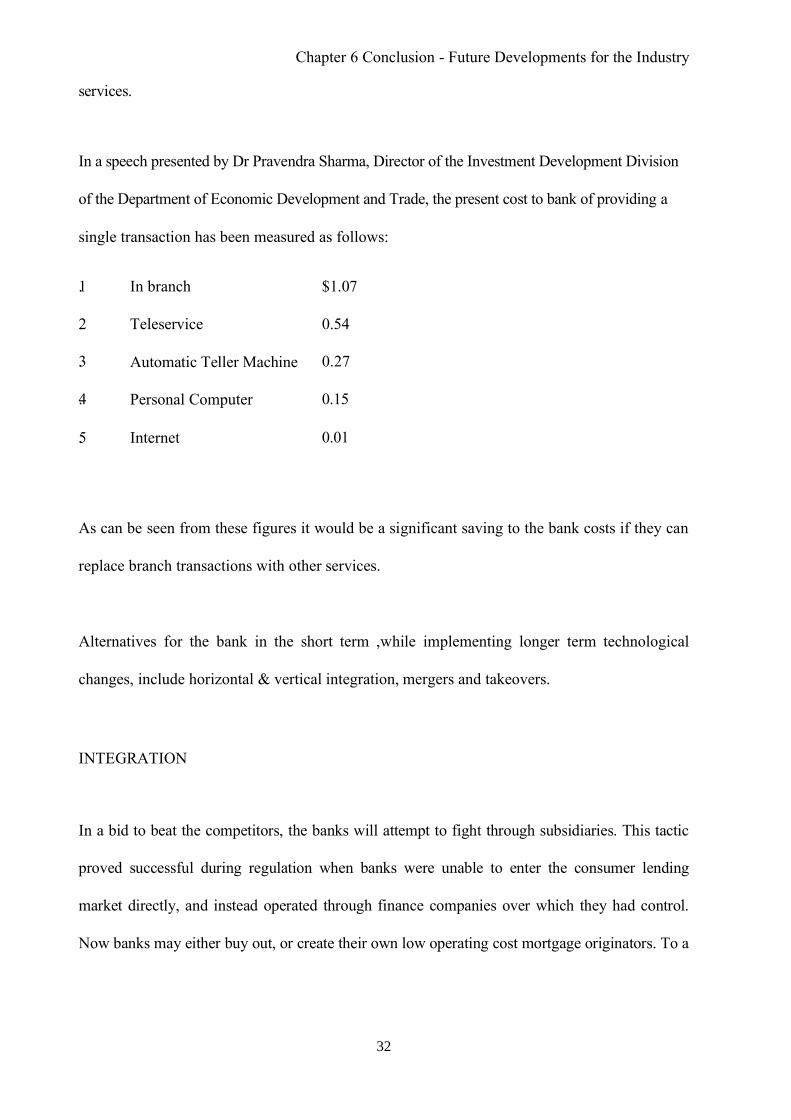

In a speech presented by Dr Pravendra Sharma, Director of the Investment Development Division

of the Department of Economic Development and Trade, the present cost to bank of providing a

single transaction has been measured as follows:

1. In branch $1.07

2. Teleservice 0.54

3. Automatic Teller Machine 0.27

4. Personal Computer 0.15

5. Internet 0.01

As can be seen from these figures it would be a significant saving to the bank costs if they can

replace branch transactions with other services.

Alternatives for the bank in the short term ,while implementing longer term technological

changes, include horizontal & vertical integration, mergers and takeovers.

INTEGRATION

In a bid to beat the competitors, the banks will attempt to fight through subsidiaries. This tactic

proved successful during regulation when banks were unable to enter the consumer lending

market directly, and instead operated through finance companies over which they had control.

Now banks may either buy out, or create their own low operating cost mortgage originators. To a

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

33

6 - 5

degree we have already seen this through the offering of 'basic' home loans either directly or

indirectly (NAB operates basic home loans through the wholly owned Bank of New Zealand).

Alternatively banks may diversify into real estate offering both realtor services and home loan

origination.

MERGERS

At present the Wallis Inquiry is 'charged with providing a stocktake of the results arising from

the financial deregulation of the Australian financial system' [Terms of reference]. A major

outcome that is eagerly being awaited from the inquiry, is the recommendation to allow major

Australian banks to merge without substantially decreasing competition. It is thought that Mr

Wallis, Chairman of the inquiry, is pro-merger and will recommend that they be allowed to go

ahead. The possibility of major banks and insurance companies being able to perform mergers

could speed the rationalisation of the industry and reductions in the cost of providing services.

With or without mergers the banking industry seems set to see a significant number of job

losses. Recently Westpac sought the early retirement or redeployment of 300 branch managers.

This is suspected to be only one of many waves of job loss that will affect the industry over the

next five years. ANZ is currently planning staff reductions of between six and seven thousand

over the next 12 months.

In a bank merger, such as Westpac and NAB, there would be the opportunity to effectively reduce

total operating costs through the closure of branches in all localities that presently site both a NAB

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

34

6 - 6

and a Westpac branch. Other services such as teleservices, and documentation services can also be

centralised for both operations. Management will not need to be duplicated, and the bank could use

the opportunity to thin out the ranks of both banks' staff during the reshuffle. Prof Fels, head of the

ACCC, is quoted as having said that "Branch reduction of the magnitude required to deliver a

highly efficient banking sector in this country will require a reduction in the number of banks"

(RBA June 1996) it is thought a reduction of branches of up to 40 percent would still allow branch

access equivalent to that in the United States.

FUTURE OF NON-BANK LENDERS

The last five years of relatively low interest rates and low inflation have served to give the

mortgage managers a niche entry into the home loan market, but will it last?

At the present moment the future still looks bright for mortgage managers. The banks' marketing

advantages have all but disappeared, with either the credit code reducing the benefits of

'honeymoon' loans, or mortgage managers being able to offer greater varieties in the home loan

packaging. Interest rates decreased again in early November, and the RBA is not expecting an

increase in inflation in the foreseeable future. The Mortgage managers do not have any

immediate concerns about technology changes, as their services are not technology dependent.

Are there gloomy days ahead for mortgage managers? I think if the banks have their way then

mortgage managers will only be a short lived phenomenon. Banks will do everything they can

to price mortgage managers out of the market if they lose too great a percentage of the market

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

35

6- ?

share, and they can do so through cross-subsidising the home loan product through other

products. They have the size, and could sustain a price war for longer than most mortgage

managers. They will also look for ways of closing the niche to future mortgage managers. The

best way for banks to do so is through long term cost reductions in their own operations. This

will keep the banks playing on the same playing field and give them room to operate margins on

a product by product basis. It is possible that the margin squeeze on mortgage managers is

already being felt. In August one mortgage manager was accused of only providing a 'half-

measure' when it failed to pass on an interest rate decrease from the Reserve Bank, an accusation

that is more familiar to banks than mortgage managers. Yet another securitiser has had to close

three of its sales offices in August, while it claimed to still be recruiting it was not explained why

the closure had to occur, given the expansion it had enjoyed recently.

FUTURE DEVELOPMENTS FOR CUSTOMERS

The consumer, it has been said, is the one that is supposed to get the benefits from

deregulation. How have they fared over the period of deregulation in the home loan market?

From a pricing perspective it can be said that the customer has only received marginal benefit from

deregulation. The average gross margin for banks has only trended downwards slightly over the

period and possibly the difference could be made up in fees. Non-bank financial intermediaries

appear to be offering the consumer some greater price benefit when we consider that they are

operating on margins around 2%, again some of this benefit may be consumed through fees.

3 - 1 5 - 2

6 - 1

Chapter 6 Conclusion - Future Developments for the Industry

36

6 - 8

But what about the other benefits consumers have gained from the increase in competition. The

product choice now seen in home lending is tenfold in comparison to that offered during

regulation. Not all consumers will have the same needs and therefore some will require the

different options they are now offered. This benefit should not be forgotten in the pre and post-

deregulation comparison. Technology adaptations encouraged by the increased competition have

also added to the convenience offered to many borrowers and can be considered a benefit.

Mr B. Fraser, the past Governor of the Reserve Bank, is a supporter of the deregulation process,

and had the following to say about it 'Everyone would like to see lower costs and margins, but not

everyone is as keen to see the service fees, branch closures, staff reductions and other changes

necessary to bring them about. Those changes must, however, be part of the process. There is no

doubt in my view that deregulation has been - and will continue to be - of substantial net benefit to

the community. This benefit comes mainly through the increased choice available to both lenders

and depositors (if anything, there is too much choice), and through the greater access which

consumers now have to financial services from banks on more competitive terms than existed

under regulation' (RBA March 1991).

APPENDIX 1

TIMELINE OF THE BANKING & FINANCE SECTOR IN AUSTRALIA

SINCE 1911

1911

COMMONWEALTH BANK

is created

1929

THE GREAT

DEPRESSION

1934

Tasmanian Parliament Select Committee

was formed.

1941 National Security Regulations

(Curtin) - licensed banks are

required to place funds in a special

account with the Commonwealth

Bank, to supply it with information,

& comply with its policy on

advances.

1945

THE BANKING ACT

is introduced

1959

Reserve Bank Act

is passed

1963

Review of economy

by Dr James Vernon

1973

Interest rate ceilings on certificates of

deposit are now removed

1976 Government

introduces Monetary

Targets 'Condit ional

projections'

1924

Legislation was passed to make the

Commonwealth Bank into the Central

Bank.

1930

Central Reserve Bank Bill was passed

1937

Royal Commission into the Monetary &

Banking System - "the most desirable

banking system is one which includes

privately owned trading banks... [and] in

which a strong central bank regulates the

volume of credit and pays some attention

to its distribution".

1942

Commonwealth Bank given power to

set maximum interest rate. (Regulation)

1956

From 1956 to 1962

Private Banks establish

Savings Bank subsidiaries

1960

Commonwealth Bank splits to become

Commonwealth Banking Corporation and

the Reserve Bank of Australia

1970

ANZ takes over ES&A, all large banks

and most other banks in Australia are now

Australian owned

1974

Financial Corporations Act

is introduced

APPENDIX 1

1980 Removal of interest rate ceilings

on deposits with trading and savings banks Australian Bank Ltd granted

banking authority. Treasurer authorises merger between Bank of NSW and

Commercial bank of Australia and between National Bank of Australasia

and Commercial Banking Company of Sydney Minimum maturity on trading

bank CDs reduced from 3 months to 30 days

1983 Martin Review Group is initiated by newly elected Labour Government. It

endorses the Campbell Committee findings. Australian dollar is floated.

Deregulation of Australian Stock Exchange. Authorities to trade in

foreign exchange granted to 40 non-

banks. Removal of min and max maturities on trading and savings bank

interest-bearing deposits. Savings banks permitted to offer cheque facilities on all

accounts. '30/20/ rule abolished.

1986 Ceilings are removed on new

housing loans. The distinctions

between Savings & Trading Banks is removed. Statutory Reserve Deposits

(SRDs) are replaced with non-callable deposit arrangements. The Prime

Asset Ratio is introduced over the

Banks by the RBA.

1988

Electronic Data Interchange (for corporate customers) is introduced.

1992 House of Reps Standing Committee on Finance and Public

Administration release report 'Checking the Changes: Review of Certain

Recommendations of the Banking Inquiry Report

1979 The Campbell Committee is established

Introduction of tender system for Treasury Note sales

1981 Campbell Committee's Final Report is delivered in September. End of quantitative bank lending guidance Introduction of tender system for Treasury Bond sales. Relaxation of portfolio controls on savings banks

1984

Invitations to Foreign Banks are called for. 15 licenses are issued to foreign banks. Automatic sweep accounts are introduced. Australian Payments System council is established. Macquarie Bank Ltd & Advance Bank Australia are granted

banking authority.

1985 All loan interest rate ceilings are removed except for owner-occupied housing loans of amounts less than $100,000. Monetary targets are abandoned.

EFTPOS becomes widely available. RBA publishes framework for monitoring

the adequacy of a Banks' capital.

1987 Bank Interchange Transfer System

is introduced

1989 & 1991

Draft Bill of the Uniform Credit Legislation is released.

1991

House of Representatives Standing Committee on Finance and Public Administration release report 'A Pocket

Full of Change: Banking & Deregulation'

APPENDIX 1

1993

'Clarification of Risk Weighting for

Mortgage Secured loans' is released by

RBA 1996

Wallis Inquiry (The Daughter of Campbell

Inquiry) is established

Code of Banking Practice is introduced

Uniform Consumer Credit Code becomes

effective in November

1950

Finance companies issue first

debentures

1954

National Bank buys 40% of

Custom Credit Corporation

1959

All private Banks have an interest in a

finance company

1963

Chartered Bank (based in

London) submits to take over

ES&A Bank, the submission is

declined

1972

All Trading Banks have a controlling

interest in a Finance Company

1981

Consumer Credit Legislation

is introduced into NSW & Vic

APPENDIX 2

TIMELINE OF NON-BANK FINANCIAL INTERMEDIARIES IN AUSTRALIA

SINCE 1920

1920

Australian Guarantee Corporation (AGC) commenced

1941

Capital Issues Regulation

allowed the government to fix an interest

ceiling for pastoral companies and building

societies.

1952

Capital Issues Regulation

expires

1955

English, Scottish & Australian Bank

form Esanda

1962

Consumer Credit Law

Uniform Draft Bill is abandoned.

1970

ANZ takes over ES&A Bank

along with Esanda

1980

The first Cash Management Trust

is established.

A Credit Union introduces the Automatic

Teller Machine (ATM) into Australia.

1984

A revised Consumer Credit Legislation

is introduced into NSW & Vic

APPENDIX 3.

TABLE 1 : ASSETS OF FINANCIAL INTERMEDIARIES

(June, percent of total)

1

929

1936 1953 1970 1980 1985 1991

Banks 9

4

95 88 70 58 59 72

Building

Societies 2 2 3 5 12 10 4

Credit

Unions

1 1 2 2

Money

Market

Corporations

3 6 11 10

Pastoral

Financiers 4 3 4 3 1 2

Finance

Companies

1 3 15 18 13 7

Other 2 3 4 3 5

Sources: Data from Butlin (1987); Royal Commission on Banking (1937); Butlin, Hall

&White (1971); Foster & Stewart (1991); Reserve Bank Bulletin Sept 1991

TABLE 2 : ASSETS OF FINANCIAL INTERMEDIARIES (June, percent of total)

1992 1993 1994 1995 1996

Banks 74 77 78 77 77

Building Societies 5 2 2 2 2

Credit Unions 2 2 3 2 3

Money Market Corporations 10 10 9 10 10

Pastoral Financiers 1

Finance Companies 6 6 5 6 6

Other 3 3 3 2 2

Source: Reserve Bank Bulletin October 1996.

APPENDIX 4

Table 1: Banking sectors percentage share of the Owner-Occupied Home Loan market

for the years 1977/1978 through to 1995/1996.

Source: Reserve Bank Bulletins

Source: Reserve Bank Bulletins

APPENDIX 5

Table 1: The Spread between average bank Variable Rate Home Loan interest and the 90

day Bank Bill.

S o u r c e : R e s e r v e B a n k B u l l e t i n s

A P P E N D I X 5

Table 2: The spread measured between bank Varaible Rate Home Loan (VRHL) and the

6 m o n t h f i x e d d e p o s i t r a t e f o r t h e 9 2 - 9 6 J u n a v e r a g e .

APPENDIX 5

Table 3: The spread measured between Mortgage Manager (Securitiser) Variable Rate

Home Loan (VRHL) and the 90 day bill rate for the 92 - 96 Jun average.

APPENDIX 6

BIBLIOGRAPHY

Reserve Bank of Australia, Reserve Bank of Australia Bulletin June 1996: The Evolution of the Housing Loan Market in Australia, AGPS, Canberra.

Reserve Bank of Australia, Reserve Bank of Australia Bulletin March 1991: Some Comments on the Economy, Deregulation and Housing (Governor B.W. Fraser), AGPS, Canberra.

Reserve Bank of Australia, Reserve Bank of Australia Bulletin May 1992: Bank Interest Rate Margins, AGPS, Canberra.

Reserve Bank of Australia, Reserve Bank of Australia Bulletin September 1995: Trends in the Housing Sector, AGPS, Canberra.

Reserve Bank of Australia, Reserve Bank of Australia Bulletin October 1994: Some Recent Banking Developments (Deputy Governor I.J. MacFarlane), AGPS, Canberra.

Reserve Bank of Australia, Reserve Bank of Australia Bulletin June 1994: Some Current Issues in Banking (Governor B.W. Fraser), AGPS, Canberra.

Reserve Bank of Australia, Reserve Bank of Australia Bulletin October 1996: Current Banking Issues (Deputy Governor G.J. Thompson), AGPS, Canberra.

Ullmer, M. 1996, 'The Wallis Inquiry - A challenging nine months', The Australian Banker,

Vol. 110, No. 4 August 1996, pp. 122 - 126 & p. 143.

House of Representatives Standing Committee on Finance and Public Administration

November 1991, A Pocket full of Change: Banking and Deregulation, AGPS, Canberra.

House of Representatives Standing Committee on Finance and Public Administration October

1992, Checking the Changes: Review of Certain Recommendations of the Banking Inquiry Report, AGPS, Canberra.

Perkins, J.O.N. 1989, The Deregulation of the Australian Financial System: the experience of the 1980s, Melbourne University Press, Melbourne.

Kirby, J. 1996, 'Prepare for fees squeeze by banks' Weekend Australian, 3 - 4 Aug.

Gray, J., Rogers, I. 1996, 'Banks look to higher fees' Australian Financial Review 17 Jun.

Clark, D 1996,Banking in age of Technology Power' Australian Financial Review, 19 Jun., p. 40.

Huyland, A 1996,'Aussie on track to be top home lender' The Courier-Mail, 7 May.

'Solicitors become lenders' Townsville Bulletin, 30 Mar.

Brown, B 1996,'Home buyers bank on realtors, Weekend Australian, 17 - 18 Aug.

'Home buyers desert banks in droves, Townsville Bulletin, 17 Apr., p. 15.

Gray, J 1996,'ANZ products target home loan market, Australian Financial Review, 4 Jul.

Kavanagh, J 1996, 'Non-bank lenders moving upmarket', Weekend Australian, 26 - 27 Oct.

Rogers, I 1996,'New consumer law's open door on lower loans, Australian Financial Review,

23 Oct.

Rogers, I 1996,'NAB unveils 6.99% 'honeymoon' loan rate despite risks, Australian Financial

Review, 1 Nov.

Rogers, I 1996,'Credit unions cancel cheap loans, Australian Financial Review, 22 Apr., p. 34.

'Rams shuts three of its sales offices; Australian Financial Review, 5 Aug.

Rogers, I 1996,'Aussie's interest cut a half-measure', The Australian Financial Review, 2 Aug.,

p. 33.

Kirby, J 1996,'ANZ opens home-loan war bunker, Weekend Australian, 17 - 18 Aug.

Gray, J 1996,'Schroders urges more mergers, The Australian Financial Review, 28 Mar.

Gray, J 1996, Managers' jobs on line in Westpac shake-up, The Australian Financial Review,

23 Oct.