A different approach to information management by exceptions (toward the prevention of another Enron

13

This article appeared in a journal published by Elsevier. The attached copy is furnished to the author for internal non-commercial research and education use, including for instruction at the authors institution and sharing with colleagues. Other uses, including reproduction and distribution, or selling or licensing copies, or posting to personal, institutional or third party websites are prohibited. In most cases authors are permitted to post their version of the article (e.g. in Word or Tex form) to their personal website or institutional repository. Authors requiring further information regarding Elsevier’s archiving and manuscript policies are encouraged to visit: http://www.elsevier.com/authorsrights

Transcript of A different approach to information management by exceptions (toward the prevention of another Enron

This article appeared in a journal published by Elsevier. The attachedcopy is furnished to the author for internal non-commercial researchand education use, including for instruction at the authors institution

and sharing with colleagues.

Other uses, including reproduction and distribution, or selling orlicensing copies, or posting to personal, institutional or third party

websites are prohibited.

In most cases authors are permitted to post their version of thearticle (e.g. in Word or Tex form) to their personal website orinstitutional repository. Authors requiring further information

regarding Elsevier’s archiving and manuscript policies areencouraged to visit:

http://www.elsevier.com/authorsrights

Author's personal copy

A different approach to information management by exceptions(toward the prevention of another Enron)

Thang N. Nguyen *

College of Business Administration, Department of Information Systems, California State University, Long Beach, CA, United States

1. Motivation and literature review

Since the collapse of Enron in 2001 [28,31] and others [7,18,28]there have been issues identified [17,36,45,63,73,76], lessons

learned [6,11,15,43,50,54,60] and solutions and recommendations

[33,62,66,69] developed for the purpose of preventing anothersituation similar to that of Enron. However, a series of otherbankruptcies followed [26]: WorldCom in 2002 [46], Adelphia in2003 [59], Parmelat in 2003 [32], and one of the biggestbankruptcies of all time, Lehman Brothers, in 2008 [16].

Without going into the details of the above collapses, oneobvious and relevant observation is that they were all caused bythe wrongdoings of a group of managers (executives) [75]. Onemay ask: (1) Were the solutions and recommendations made toolate for those cases after Enron because they were rooted toodeeply before the recommended solutions? (2) Although thesolutions and recommendations were all valid, were theycollectively insufficient to prevent the collapses from happening?and (3) Did the institutions (i.e., management) just ignore them? Insearch of answers to these questions, we propose a differentapproach to bankruptcy prevention.

Our thinking is specifically related to how the wrongdoings

potentially leading to collapses can be exposed early enough to

exercise preventive measures. A possible answer is that an existing,

modified or newly built management by exception (MBE)application should be available to capture, discover, organize,analyze, and post the wrongdoings in terms of events or activitiesassociated with some severity level to draw management attentionto appropriate decision making.

Past experience has shown that by the time wrongdoingssurface, e.g., in the Barings bank case, when a margin call occurredthat was greater than the bank’s assets, or in the case of Enron,when the restatement of the 2001 Q3 financial report was faulted,leading to the consolidation of three consecutive years’ (1998–2000) financial statements, it was already too late, and collapsewas unavoidable. The nature of these cases is in some ways similarto that of cancer in humans. By the time the malignant tumor isdiagnosed, the cancer is often in an advanced stage, and death iscertain.

In this section, we will first review relevant bankruptcy casesfrom a perspective different than most: a ‘‘cancer’’ perspective.Cancer in humans is caused by abnormal cells that growuncontrollably to form malignant tumors, which spread to otherorgans and organ systems and eventually cause death to thehuman. Analogously, a group of abnormal employees can growuncontrollably within an institution, influence other organization-al units and eventually initiate bankruptcy.

The analogy to cancer requires us to re-examine the humanbody in terms of its anatomy (structure), physiology (functionali-ty), and behavior supported by lower-level processes and entitieswithin the guiding principles of its biological systems. Withinsights gained from such examinations, we propose a business

Information & Management 51 (2014) 165–176

A R T I C L E I N F O

Article history:

Received 10 January 2013

Received in revised form 3 November 2013

Accepted 18 November 2013

Available online 26 November 2013

Keywords:

Management by exceptions

Biologically inspired

Managerial cybernetics

Information management

A B S T R A C T

We review the fall of Enron and other bankruptcies from the perspective of information management by

exceptions (MBE) for insights into how to prevent another collapse. We entertain the idea that a group of

special employees in an institution such as Enron can be analogously equated to a malignant tumor in

human body, which can grow abnormally to bring the institution to collapse. Following this general

analogy, we examine the biological spectrum for insights into a business framework for an MBE in the

wrong doing detection. Such a model can be used to insure the institution’s stability, growth and

therefore profitability.

� 2013 Elsevier B.V. All rights reserved.

* Tel.: +1 7147280896; fax: +1 5629855478.

E-mail address: [email protected]

Contents lists available at ScienceDirect

Information & Management

jo u rn al h om ep ag e: ww w.els evier .c o m/lo c ate / im

0378-7206/$ – see front matter � 2013 Elsevier B.V. All rights reserved.

http://dx.doi.org/10.1016/j.im.2013.11.006

Author's personal copy

framework in which an MBE application is possible for bankruptcyprevention and potentially other applications.

Our contribution can be summarized as follows:

� We formulate a biologically inspired business stability-driven

framework that describes the institution’s structure, functionali-ty and behavior in terms of their elements: policy, project, task,account and traction to maintain stability. The framework issimilar to the biological homeostasis-driven framework in humans,in which human anatomy, physiology and behavior aresupported by genes (DNA), proteins, other macromolecules,chemical products and cellular exchanges between membranesto maintain homeostasis.� Within this framework, we use an analogy to human cancer to

gain insights into the development of an MBE application forbankruptcy prevention.� The purpose of the MBE is to expose symptoms of wrongdoing by

monitoring, analyzing and reporting them early enough toenable effective management decisions to be implemented.� The responsibility, accountability and authority of the MBE

application are in the hands of an oversight organizationchartered by the Board of Directors. This oversight organiza-tion might work alongside the Accounting Audit and LegalCounsel.

To our knowledge, there is no prior business framework basedon insights from the biological spectrum from particles to biosphere,and none of the previous investigations on preventing anotherEnron-like bankruptcy uses our proposed cancer analogy towardan MBE application for prevention.

1.1. An overview of the Enron collapse

Enron, the former Houston Natural Gas, was in debt after amerger with InterNorth, a gas pipeline company from Nebraska.Generally speaking, Ken Lay, who was Enron’s CEO, hired JeffSkilling in 1990 to serve as a McKinsey & Co. consultant to Enron todevelop a more competitive business strategy.

Skilling promoted his mark-to-market (MTM) strategy to KenLay with the concept of a gas bank. Note that MTM was not new toaccounting or financial markets [72]. It was a means to adjust fairmarket value that was recommended by the US GAAP (GenerallyAccepted Accounting Practice) and approved by the US SEC(Securities Exchange Commission). However, the use of MTM as atrading model, as suggested by Skilling, was novel in the sense thatit was an energy derivative in which Enron would act as anintermediary ‘‘bank.’’ As such, Enron assumed the risks to buy gasfrom suppliers and to sell it to consumers at contractually fixedprices and service fees [19]. MTM was used to achieve twosuccessful projects: the Cactus 3 project, with the GE CreditCorporation and other banks as partners, and the JEDI project, witha partnership with CalPERS [21]. All other projects following JEDIwere troublesome.

There were other strategies besides MTM that wereimplemented by Enron, e.g., the shift from asset-heavy toasset-light strategies [9]; strategies nicknamed the Death Star,Load Shift, Get Shorty, Fat Boy and Ricochet used in California’senergy market [30,57]; and a diversification strategy tobusinesses other than gas and electricity companies. Thesestrategies were realized in many subsequent projects: theDabhol electricity project in India, a gas project in Bolivia, awater project with the creation of the Azurix Corporation, and abroadband project with Blockbuster Video, among others. Theprojects were hedge funded from many SPE (Special PurposeEntities) created to minimize investment risk as off-balancesheet partnerships: Chewco LLC, JEDI II, LJM Cayman, LJM 2 and

LJM 3, Braveheart and Raptors from 1997 to 2000 [58]. Thesestrategies were questionable.

To further support the MTM strategy and other strategies,Skilling set out to hire the best and the brightest traders. Skillingdevised a new policy of performance review called the ‘‘360-degreereview’’ and a new mantra (RICE) for Respect, Integrity, Commu-nication and Excellence [22]. The policy appeared beneficial intheory, but its implementation departed from common humanresource practices (e.g., there were no defined job descriptions).The main goal was to initiate any deals that potentially generated agood return. This hiring was not limited to traders but alsoincluded auditors and lawyers. Even with an attrition rate of 15% orhigher, Skilling’s team was able to grow the set of special ‘‘revenue-driven’’ employees to act ‘‘Skilling-like.’’ One of these employeeswas Andrew Fastow, whom Skilling hired in 1990. The policy was asimilar to a mutation on typical HR standards.

Skilling successfully convinced the internal counsel, theAndersen accounting auditors and the SEC to approve the MTMchange to accounting practices. With increasing success and afterbecoming Enron COO in 1996, Skilling applied, with Ken Lay’sapproval, the mark-to-market trading model and accountingpractices not only to gas businesses but also to other energybusinesses (e.g., electricity, coal, etc.). Skilling then expanded thisapproach to even more businesses, e.g., paper, steel, water,weather, etc. He appointed Andrew Fastow as CFO to overseeEnron’s financing in 1998. The Enron Board of Directors alsoapproved a dual role for Fastow in 1999: Enron CFO and SPEmanager. Altogether, the MTM trading model, the group of toptraders, the expansion to other businesses, and the bull marketduring the 1990s that facilitated investment opportunitiesresulted in the incredible success of Enron. Nevertheless, therehad been violations of Enron’s business code of conduct.

After 1997, Enron’s profits were squeezed due to new entrantsand other smaller competitors: Dynegy, Duke Energy, El Paso andWilliams, etc. [19]. Enron began to lose its competitive advantage.To be financially stable and to maintain its high credit ratings,Enron began to devise the use of SPEs to access capital and hedgerisks as they entered into new mergers and acquisitions. Thecompany became more of a hedge fund than a trading company[74].

SPEs were shell partnerships sponsored by Enron that weresupposedly funded by independent financing. Two conditionswere satisfied in order to keep the SPEs separate from Enron: atleast 3% equity and 50% or more control of financial interest givento independent investors. SPEs were used to purchase forwardcontracts with producers and to sell to consumers under long-termcontracts [31]. However, the conditions of these terms were notalways clear. For example, in the Chewco partnership, 3% of JEDI IISPEs were owned and actually controlled by Enron executives. Thesituation was much more complex in the Raptors partnership [35].

As reported in the literature, Andrew Fastow, the mastermindbehind all of the SPEs, used some 3000 of them as a way to transferlosses from Enron’s books to book revenues as well as to maintainand/or increase the company’s credit ratings by reducing its debt-to-total-assets ratio in projects, notably through Chewco LLP, LJMClayman, and LJM 2 [27,74]. As later discovered and reported,starting from October 2001, $287 M for Azurix, $180 M for thebroadband project with Blockbuster, and $544 M for others, a totalof 22% of Enron’s expenditures from 1998 to 2000, were write-offs.In addition, Portland General Corp. was sold for $1.9B at a $1.1Bloss [31].

The first official wrongdoing that captured widespread atten-tion was Enron’s press release from Q3 2001 (October 16, 2001).There was no balance sheet disclosure, and it revealed a $1.2Bcharge against equity [19]. About one week later, the SEC inquiredabout Enron’s SPEs. Then, facing pressure from Wall Street in

T.N. Nguyen / Information & Management 51 (2014) 165–176166

Author's personal copy

November 2001, Enron admitted that it had hidden losses in theSPEs and posted re-statements with consolidations for 4 years(1997–2000) [35,38].

The re-statement of financial reports in the third quarter of2001 and financial consolidations resulted in a drop in Enron stockprices from $90 + per share to 26 cents per share within 2 months[15]. This steady and rapid decline led the company to collapse inNovember 2001.

1.2. Enron as a cancerous institution

One of the deadliest diseases to humans is cancer. Cancer isgenerally described as follows. The human body is made up ofmany types of cells. These cells grow and divide in a controlled wayto produce more cells, as the body needs to keep them working andhealthy. When cells become old, they die and are replaced withnew cells, with a possible exception in the case of brain cells [3]. Ahuman cell becomes abnormal when its DNA is mutated and/or itsgenes are damaged for one reason or another (internally orexternally).

The abnormal cell produces other cells by division or mitosis.The uncontrollable, growing collection of abnormal cells, calleda tumor, is classified as malignant when it invades nearbytissues. Malignant tumors eventually spread to other organsthroughout the body via the blood and/or lymph circulation, aprocess called metastasis. Malignant tumors cause seriousthreats to human health and may potentially cause death[39].

When an institution is considered analogous to a human, theinstitution’s employees can be considered analogous to biologi-cal cells. ‘‘Institutional tumors’’ in turn can be viewedanalogously to be groups of employees in organizational unitsthat grow uncontrollably and may become ‘‘malignant.’’ Theycan expand to other organizational units and become seriouslyharmful to the institution’s health, potentially leading tobankruptcy. The analogy to cancer is elaborated in the followingEnron case.

We equate Jeffrey Skilling, Andrew Fastow and other Enronexecutives to ‘‘special’’ or ‘‘abnormal cells’’ in the institutionalbody. Skilling used an accounting practice that he convinced theSEC to approve after he officially joined Enron. In a sense, Enron’sMTM approach to accounting was a mutation of commonaccounting practices similar to a DNA mutation in a gene of acell, therefore affecting the cell’s proliferation (cell division). The360-degree review is analogous to a mutation of human resources

hiring/firing policy. SPEs and accounting schemes can be viewed aschanges to or deviations (mutations) from commonly practiced SPEsand GAAP.

When Arthur Anderson, the auditing arm of Enron, wasinfluenced in the mishandling of accounting audits [70], theinstitutional ‘‘tumor’’ had in fact proliferated to other institu-tional ‘‘organs and organ systems’’ (the finance division,accounting, legal counsel, etc.). Cancerous symptoms began tosurface: Lay stepped down, Skilling replaced Lay as CEO, and thenSkilling resigned after only 6 months followed by the cancelationof deals with Blockbuster and later with Dynegy [31]. FollowingSEC inquiries and the change of the management, the revision offinancial statements from 1998 to 2000 was initiated [23–25].Discoveries of wrongdoing in SPEs required that Enron’sstatements include Chewco’s consolidations as well as those ofother projects. Enron’s stock prices slipped. The consolidationsshowed that Enron’s debts and liabilities were previously left offbalance sheets and caused additional stock price slips and cashshortfalls. Within just 60 days, the company’s stock went down to26 cents per share. Enron subsequently filed for bankruptcyprotection [74].

1.3. An approach to information management by exceptions for

detection and prevention

The general analogy between institutions and the human bodyappears enticing from a general cancer view, but the immediatequestion is ‘‘Why look to a complex disease such as cancer when

cancer is itself very much incurable?’’ In reality, our goal is not tolook to cancer for insights into treatment and/or cure, but onlyprevention. We can observe the following from the analogy tocancer:

� Every human body has cancer cells or abnormal cells. In mostcases, abnormal cells are contained and do not grow. We callthese benign tumors. Those that grow uncontrollably are termedmalignant. Similarly, every institution has employees who can begood or bad. In the scale of ‘‘good-bad,’’ success-failure, ‘‘right-wrong,’’ and/or similar dipole scales, one always finds the twoextreme groups of the dipole: some are extremely concernedwith the right ways to achieve success, some are just theopposite, i.e., cutting corners and/or deceiving their stakeholderswith the idea that ‘‘the end justifies the means.’’� Cancer is a deadly disease in humans. Early cancerous symptoms

are difficult to detect. By the time one finds them, the cancer isalready in its later phases, and death is most likely unavoidable.Similarly, the wrongdoings in institutions can be well-concealed,such as in the case of Enron. When the first symptoms ofwrongdoing surfaced in 3Q 2001, it was already too late to saveEnron from collapse.� The analogy of cancer to Enron, which analogizes the human–cell

relationship to the institution–employee relationship, motivatesus to further investigate the similarities and differences betweenthe human body and an institution in terms of structure,

functionality, organization and behavior for insights into preven-tion.

To explore the insights mentioned in the third bullet point,we begin in Section 2 with a biological spectrum that includescells, humans (as organisms) and institutions (as communities).We then need to explore their structure, functionality and

behavior within a larger context, the guiding principles in biologythat govern them, as well as in a more detailed context, theoperational level activities and events of the entities that supportthem.

We then formulate a business stability-driven framework inSection 3 in which each and every concept (principles, organiza-tions and supporting entities) mentioned above is included. Wethen look at the institution in the context of an MBE for thedetection of wrongdoings and their symptoms with an illustrationof the model using the case of Enron. We provide a discussion,including lessons learned, in Section 4. Our concluding remarksand future work are highlighted in Section 5.

2. Formulating biologically inspired concepts towardprevention

The cancer analogy used in Section 1 suggests the followingquestion: ‘‘Is there a biological framework to which a businessframework can be analogously parallel and from which biologicalconstructs can suggest a solution to prevent institutions fromcollapse or bankruptcy?’’ In other words, ‘‘Can we identify frombiology some guiding principles on a larger scale and somebiological constructs on a smaller scale that would help formulatea business framework housing bankruptcy prevention in businessinstitutions?’’ In this section, we address the above questions.

Fig. 1 partially sketches the biological spectrum from particles-

protoplasms at the low end to the ecosystem-biosphere at the high

T.N. Nguyen / Information & Management 51 (2014) 165–176 167

Author's personal copy

end. From this spectrum, one can say that cells make up humans(organisms), humans as organisms make up institutions (commu-nities), and business institutions as communities make up businessecosystems.

Various authors have investigated this spectrum differently toarrive at different theories for different applications in differentdomains. Examples include but are not limited to the following:Maturala and Varela [49] theorized the self-organization ofcomponents such as cells and their emergent properties; Moore’sbusiness ecosystems [51–53] were modeled after the analogy ofecological systems for competitive marketing strategy; Moore’swork was followed by Cisco on partnership [10], Nguyen onsoftware [55], Iansiti and Levien on business strategy [40] andNguyen on e-business [80]; OO patterns in OO design were exploredafter Christopher Alexander’s the nature of order [2]; and theconcept of inheritance in an object-oriented paradigm wasdeveloped on the basis of Mendel’s inheritance. These exampleswere all inspired by the original biological spectrum as ananalogous and parallel concept with many different applications.

From the same spectrum sketched in Fig. 1, we propose adifferent view of cells to humans and humans to institutions. Ifhumans (as organisms) are considered analogous to institutions(as communities), the cells of a human body can be consideredanalogous to the employees of the institution (the red and bold boxin Fig. 1). From this analogy, a different perspective emerges(Fig. 2), i.e., the human body’s organization (cells, tissues, organs,organ systems) can be thought of as a structure in which allbiological processes operate (the middle part of the left side ofFig. 2) guided by biological principles (top-left) and supported bylower-level mechanisms (bottom-left).

In fact, on a larger scale, the first guiding principle is derivedfrom the powerful concept of the ‘‘milieu interieur’’ (or internalenvironment) of the body in which all cells exist, as stated byClaude Bernard [29]. Analogously, we observe that there exists aninformation environment in which all employees of an institutionlive and act.

Next is the principle of cybernetics, which deals with feedbackand control, a concept that was developed by Norbert Weiner [79]and was further exploited and applied to the business manage-ment discipline, termed managerial cybernetics by Stafford Beer [5].Cybernetics relate to maintaining homeostasis (equilibrium) in thehuman body. Homeostasis is a principle that was developed byWalter [8], originated from Ernest Starling [71] and was expanded

by others [56]. We can define stability in business as an analogousconcept to homeostasis.

At the lower scale, it appears that the biological processes fromthe molecular level up involve the basic constructs created by thecell’s organelles: protein synthesis. Analogously, the proteinscreated in cells are much like the tasks performed by theemployees in an institution. The cellular exchanges withinmembranes are much like the transactions created betweenemployees. Similarly, the relation of the proteins to all macro-

molecules and, in cell membranes, the relation of the cellular

exchanges to all chemical products in a human body are similar tothe relations of tasks to projects and transactions to accounts in aninstitution, respectively.

In other words, the human tissues, organs, organ systems thatmake up the structure, functionality and behavior of a human(middle level) are determined by the constituent cells governed bythe genes of the DNA in terms of proteins and chemical products(low level) to observe the biological principles of milieu interieur,cybernetics and homeostasis (top level). Fig. 2 summarizes thisanalogy. Admittedly, this analogy cannot be perfect, but it givesinsights into the formulation of a business framework withinwhich the structure, functionality and behavior of an institutioncan be investigated in terms of lower-level entities and higher-level guiding principles.

The analogy in Fig. 2, however, does not suggest how we canaddress prevention. Therefore, we rearrange the guiding principlesenumerated earlier (milieu interieur or internal environment,homeostasis and cybernetics) and the entities in the anatomy(structure), physiology (functionality and mechanisms) andbehavior in terms of activities, events and control mechanisms

(shown on the right side of Fig. 3).The dotted box (activities) in Fig. 3 indicates the making of

proteins by cells, which generate macro molecules, and which inturn are involved in chemical products by way of cellular exchangeduring biological processes. All constituent cells are bathed in theinterstitial fluid and plasma (milieu interior) to produce activities

in which events occur (e.g., results from diffusion due to differentlevels of concentration at cell membranes). The continuous bluearrows show the interconnections among the activities that causeevents.

Note that homeostasis comes into play when excessive orinsufficient nutrients or debris are detected by cells that play therole of chemical sensors, i.e., alpha cells and beta cells.

Fig. 1. Biological spectrum. (For interpretation of the references to color in text, the reader is referred to the web version of the article.)

T.N. Nguyen / Information & Management 51 (2014) 165–176168

Author's personal copy

Consider blood sugar as an example of homeostasis at work[8]. Either a low concentration or a high concentration of glucosein the blood will cause danger to the body. The control of bloodsugar is performed by the alpha and beta cells in the pancreas tomaintain a narrow range of blood sugar. A low concentrationwill be remedied by the amount of glucose released by the liverinto the blood. A high concentration will be neutralized bythe release of insulin to remove excess glucose to maintainhomeostasis.

Another example adapted from Walter Cannon [8] is presentedhere. In normal operations, the cardiovascular portion of thecirculation system provides oxygenated blood and nutrientsexiting the left ventricle to the aorta. The blood travels to thearteries and arterioles to arrive at all cells of the body bathing inClaude Bernard’s milieu interieur via the mesh of capillaries inevery tissue. It is from this milieu interieur that debris, dead cells,wastes, etc., including cancer cells, are picked up by the tiny lymphchannels (exchanges via the change in concentration and pressure,much like the capillaries). The latter deposit these cells to thelymph nodes, which then dump them into the veins to return them

to the filtering organs (liver, kidneys) and the heart. Thecardiovascular system and the lymphatic system work togetherwithin a global and local signaling system.

The signaling system involves the sensors (receptors of pressuredifferences and receptors of concentration differences), the brain,spinal cord, gland systems, etc., with hormones and impulses.Through these systems, information is integrated and transmittedamong all parts of the body to address external and internalchanges.

This process explains how, despite the change of temperature inthe environment, the human body is still generally able tomaintain a body temperature of 98.6 F in homeostasis. This is alsohow tumor suppressor genes in cells can destroy cancerous cells attheir first occurrences and how T cells and B cells in the blood(lymphocytes that produce antibodies) react to abnormal cells ofthe body in its defense system. This process also explains how allorgans and organ systems work together to keep the internalenvironment constant.

When events are out-of-bounds, as detected by the associatedsensors such as alpha or beta cells in the spleen, corrections based

Fig. 2. Possible human-institution analogy.

Fig. 3. Biological homeostasis-driven framework. (For interpretation of the references to color in text, the reader is referred to the web version of the article.)

T.N. Nguyen / Information & Management 51 (2014) 165–176 169

Author's personal copy

on regulations (e.g., gene regulations or the autonomic nervoussystem of the brain, at the bottom of Fig. 3) occur to maintainhomeostasis. The inability to make corrections will result inexceptions (or symptoms) that express some anomalies. The reddotted line in Fig. 3 indicates abnormal deviant behavior caused bycancerous cells and malignant tumors.

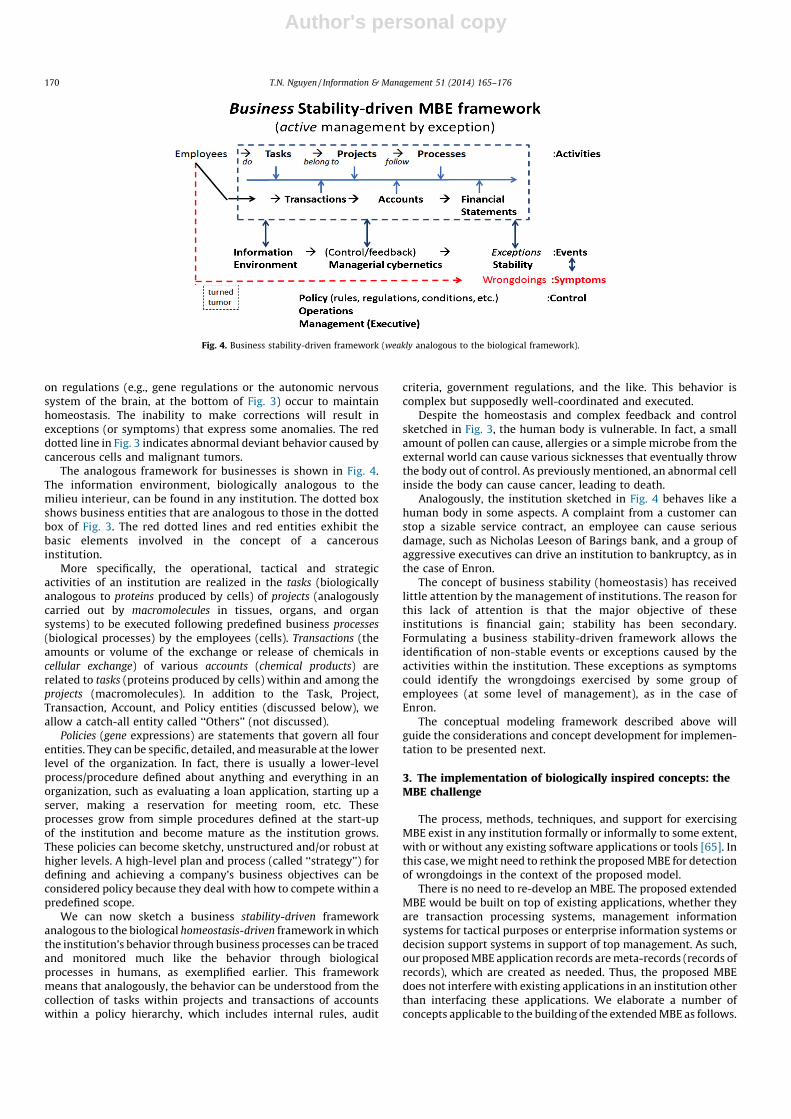

The analogous framework for businesses is shown in Fig. 4.The information environment, biologically analogous to themilieu interieur, can be found in any institution. The dotted boxshows business entities that are analogous to those in the dottedbox of Fig. 3. The red dotted lines and red entities exhibit thebasic elements involved in the concept of a cancerousinstitution.

More specifically, the operational, tactical and strategicactivities of an institution are realized in the tasks (biologicallyanalogous to proteins produced by cells) of projects (analogouslycarried out by macromolecules in tissues, organs, and organsystems) to be executed following predefined business processes

(biological processes) by the employees (cells). Transactions (theamounts or volume of the exchange or release of chemicals incellular exchange) of various accounts (chemical products) arerelated to tasks (proteins produced by cells) within and among theprojects (macromolecules). In addition to the Task, Project,Transaction, Account, and Policy entities (discussed below), weallow a catch-all entity called ‘‘Others’’ (not discussed).

Policies (gene expressions) are statements that govern all fourentities. They can be specific, detailed, and measurable at the lowerlevel of the organization. In fact, there is usually a lower-levelprocess/procedure defined about anything and everything in anorganization, such as evaluating a loan application, starting up aserver, making a reservation for meeting room, etc. Theseprocesses grow from simple procedures defined at the start-upof the institution and become mature as the institution grows.These policies can become sketchy, unstructured and/or robust athigher levels. A high-level plan and process (called ‘‘strategy’’) fordefining and achieving a company’s business objectives can beconsidered policy because they deal with how to compete within apredefined scope.

We can now sketch a business stability-driven frameworkanalogous to the biological homeostasis-driven framework in whichthe institution’s behavior through business processes can be tracedand monitored much like the behavior through biologicalprocesses in humans, as exemplified earlier. This frameworkmeans that analogously, the behavior can be understood from thecollection of tasks within projects and transactions of accountswithin a policy hierarchy, which includes internal rules, audit

criteria, government regulations, and the like. This behavior iscomplex but supposedly well-coordinated and executed.

Despite the homeostasis and complex feedback and controlsketched in Fig. 3, the human body is vulnerable. In fact, a smallamount of pollen can cause, allergies or a simple microbe from theexternal world can cause various sicknesses that eventually throwthe body out of control. As previously mentioned, an abnormal cellinside the body can cause cancer, leading to death.

Analogously, the institution sketched in Fig. 4 behaves like ahuman body in some aspects. A complaint from a customer canstop a sizable service contract, an employee can cause seriousdamage, such as Nicholas Leeson of Barings bank, and a group ofaggressive executives can drive an institution to bankruptcy, as inthe case of Enron.

The concept of business stability (homeostasis) has receivedlittle attention by the management of institutions. The reason forthis lack of attention is that the major objective of theseinstitutions is financial gain; stability has been secondary.Formulating a business stability-driven framework allows theidentification of non-stable events or exceptions caused by theactivities within the institution. These exceptions as symptomscould identify the wrongdoings exercised by some group ofemployees (at some level of management), as in the case ofEnron.

The conceptual modeling framework described above willguide the considerations and concept development for implemen-tation to be presented next.

3. The implementation of biologically inspired concepts: theMBE challenge

The process, methods, techniques, and support for exercisingMBE exist in any institution formally or informally to some extent,with or without any existing software applications or tools [65]. Inthis case, we might need to rethink the proposed MBE for detectionof wrongdoings in the context of the proposed model.

There is no need to re-develop an MBE. The proposed extendedMBE would be built on top of existing applications, whether theyare transaction processing systems, management informationsystems for tactical purposes or enterprise information systems ordecision support systems in support of top management. As such,our proposed MBE application records are meta-records (records ofrecords), which are created as needed. Thus, the proposed MBEdoes not interfere with existing applications in an institution otherthan interfacing these applications. We elaborate a number ofconcepts applicable to the building of the extended MBE as follows.

Fig. 4. Business stability-driven framework (weakly analogous to the biological framework).

T.N. Nguyen / Information & Management 51 (2014) 165–176170

Author's personal copy

3.1. Governance with completeness in the information environment:management by exception (MBE) revisited

We establish in previous sections that the information

environment is the analogous counterpart to the milieu interieur

concept. As we have said previously, the information is derivedfrom data obtained from the business entities performed by theemployees (tasks, projects, transactions, accounts and others)similarly to how proteins, macromolecules, and exchanges acrosscell membranes and chemical products are produced by the cells.

We make the assumption that all data obtained would be onlineand able to be accounted for. If current MBE systems do not havedata available, the MBE will create these records. The data can beabout a hiring/firing process, a particular job application, aschedule for work, an office supply purchase, an accountreceivable, a travel expense reimbursement, a plan formanufacturing, the strategic minutes of a meeting, a documentfrom a legal counsel, a product design, financial reports, or anegotiation contract, among others. The information environmentis therefore the complete collection of data. If there are anyintended wrongdoings or anomalies, the information environmentwill capture them in one way or another.

The complexity of this situation is that we have data from allpossible formats. For an existing institution, all data are availableunder some format and storage medium. Most of them areavailable for the operational, tactical or strategic planning of theinstitution, and most are already connected logically by the natureof their topics, content, or otherwise existing applications. Ifneeded, some special document or artifact will be newly created,collected, reviewed, worked on, etc. This raises the need for apossible middle entity to incorporate data for the proposed MBE.

If anything causes any concerns among the responsibleemployees, the employee can tag a value to a field in the onlinemetarecord of the MBE. This is an exception field with a severity (orcriticality) level attached: ‘‘normal, warning or severe.’’ A notifica-tion is sent to the appropriate channel in the case of a warning orsevere notification. The severity marked on the record is date/timestamped and can contain or link to the information on theresponsibility, accountability and authority of the employeesresponsible. The next time the record is called upon (by itself oras part of a chain of linked records), the exception flag will appearalong with other data or information. The chain of records isobtained either via integrated (hierarchical) or aggregated (acrosshierarchies) schemes.

3.2. Governance by automated policy hierarchy and processes:

management by exception (MBE) revisited

As the backbone of the MBE, a policy system of the institutionhas to be in place to account for all policies and regulations. Policiesin the institution act similarly to genes in the human body. Mosttasks by employees are fairly well understood for day-to-dayoperations. The related policy (regulations, rules, etc.) andprocesses are guided by the most well-thought out and well-defined policy in the institution.

More complex is a new policy of a strategic nature (orcorporate strategy). It is difficult to detect flawed policy,especially when the policy or strategy shows some initial success.In fact, a new policy is commonly unstructured and unclear, andits effects are not known until the execution of the policy (orstrategy). An example of this phenomenon is Jeff Skilling’s mark-to-market strategy, which was a modified strategy for the gasbusiness. The strategy generated two initially successful projects(Cactus 3 and JEDI).

Deviations from the current policy or strategy, if detected,would be flagged. These deviations in the case of Enron included

Enron’s ‘‘360-degree review’’ policy, which departed from commonhuman resources practices, the MTM strategy that was adapted tocreate a gas bank and expanded to other businesses, the form ofMTM accounting that was ‘‘mutated’’ from the US GAAP, the SPEsfor which the 3% condition stipulated by SEC regulations wasviolated, and the dual role of Andrew Fastow, which was allowedby the Board of Directors, as stated earlier.

3.3. Complementarity property: management by exception (MBE)

revisited

Both the human body and institutions exhibit some hierarchicalorganization. However, the human body’s hierarchy is slightlydifferent from an institutional hierarchy. In the human body’sorganization, there are multiple paths, from a lower level oforganization to higher levels.

In fact, atoms, molecules, and macromolecules are notnecessarily connected only to the next higher level. They canconnect to other higher levels and directly to the human organism.This type of hierarchy enjoys the complementarity conceptaccording to Looijen [47], which indicates that the whole is

complemented by all of its parts. As noted by Looijen, thisorganization is subject to increased complexity but promotesthe excellent functioning of the ten organ systems of the body insupport of the biological processes. Institutional organizations,either strictly hierarchical (such as common business) orcommittee-typed (such as the US Congress or universities)organizations, do not entertain this type of hierarchy withcomplementarity.

We allow the complementarity feature in our implementationmodel. Entities such as tasks, projects, transactions, and accountsare linked to express the complementarity property. The feature isachieved by allowing lower-level institutional entities to be linkedto all higher-level entities and by allowing sideways linkagesbetween entities of the same level of organization (or level ofabstraction). This linkage is implemented as links with roll-up anddrill-down capability, which exhibit the inheritance property(integration), and/or sideway links, which exhibit the aggregationof different entities.

Higher-level entities (for example, projects of projects ortransactions of transactions of projects as parent or sibling entitieswould include all exceptions that occurred on lower levels.Integration is performed for each hierarchy of relevant nodes.Aggregation is performed for nodes that are parts of differenthierarchies. Thus, the links are the nodes of a network ofconnections from which their severity is aggregated and integrat-ed. We can therefore ‘‘drill down’’ or ‘‘roll up’’ within the hierarchyand offer links among different hierarchies.

3.4. Overall corporate governance

It is generally recognized that the business market is extremelycomplex, as is its corporate governance. From Barings Bank withNicholas Leeson to the Lehman Brothers case involving a group oftop executives, corporate governance was identified as one of thekey reasons contributing to the institutions’ failure. The MBE mustobserve the overall corporate governance, which includes recom-mendations from the Higgs report and Powers report as well asthose recommended in US congressional reports captured aspolicy. This notion also means that exceptions are allowed to beoverridden by the management-executive team with statedreasons. However, the responsibility of monitoring and reportingmust be assigned to an organizational unit that is outside of themanagement-executive team. We call this unit an Oversightorganization (or Task force) chartered by the institution’s Board ofDirectors.

T.N. Nguyen / Information & Management 51 (2014) 165–176 171

Author's personal copy

3.5. The Enron case in the proposed MBE context for bankruptcy

prevention

The first and main strategy introduced to Enron by Skilling wasthe mark-to-market strategy and accounting practice approved bythe Board of Directors. This strategy and accounting practice,however, raised the concerns of some Enron employees. The firstemployee to express concern was David Woytek. In 1992, Woytekquestioned the MTM when it was first introduced internally bySkilling’s team. The concerns or objections were overridden by KenLay and were ignored.

When the 1992 annual report was published, the Mark-to-Market scheme in the footnotes caught the attention of Toni Mackof Forbes. She voiced her concern about the footnotes of the 1992financial statement in her ‘‘Hidden Risks’’ article in 1993 [48].Again, Ken Lay replied to Mack personally and overrode theexception by ignoring it. In 1999, Carl Bass also objected to theMTM accounting scheme, but his objections were not given seriousattention [12]. The warning from Sherron Watkins did not produceany changes either [78].

If the concerns and objections above were properly registered,as dictated in our model, all responsible employees would beaware of what was going on from the day the policy wasimplemented. The transparency of the entities would be preservedamong the responsible parties.

More specifically, the objections by David Woytek and Carl Bassto the MTM Policy and the doubt raised by Toni Mack in her articleare of the Others entity type. These activities and events would bemarked with warning (Yellow) severity. The objections and doubts(Others) overridden by Ken Lay would be recorded as ‘‘Override.’’

Other examples would include the approval of the Board of the

dual role of Fastow and partnership as a policy, the $30 M paid as

management fees to Fastow for LJM and Raptors to appear intransactions and accounts, and the off-balance sheet amounts in thefinancial statements of Enron and in and across SPE accounts(although legally, the assets and losses are off the balance sheets).These items should be marked with a severe (Red) level of severity(or criticality). These indicate potential wrongdoings subject tocorrelation in analyses and other means of aggregating records andthe vertical and horizontal integration of information. If aggregat-ed records across all entities, tasks, projects, transactions, accountsand others can be shown, it will be harder to hide any of the above,and in the case of Enron, the 3% investment of Michael Kopper (Enronemployee) in the Chewco project might have drawn significantattention.

A similar scenario occurred with the use of SPEs when Duncanwas approached by Fastow to set up a SPE for LJM to be managed byFastow himself. Although advised against this action by BenjaminNeuhausen of the Andersen Professional Standard Group [64] dueto a conflict of interest, Duncan said he would go along with thesetup if Skilling and Enron’s Board approved. In the end, thismeasure was approved by both Skilling and the Board. Had thesesymptoms been recorded officially via the records in MBE, thechance for them to be ignored or approved by the Board would bemuch less likely. Had an integrated record been shown, theattrition rate (15% in Skilling’s division) should have raisedconcerns about the effectiveness of the ‘‘360-degree-review’’policy. The huge number of SPEs (in the thousands) should haveraised concerns.

Note that detecting wrongdoings that would potentially lead tocatastrophic results in anything at any level is not an overnighttask, especially when the seeds for later failure are initiated at thetop level of the institution, such as in the case of Enron. Note alsothat at higher levels of management, most entities are unstruc-tured, especially policy and strategy. The effectiveness of a newpolicy or strategy, e.g., MTM, virtual integration, diversification,

etc., on a new market, as in the case of Enron, e.g., energy ‘‘banks,’’energy trading, commodities trading, etc., cannot be seen until thepolicy is at least partially implemented. It is also more difficult tofind out the wrongdoings when the said policy or strategy, such asMTM, initially worked successfully.

4. Discussion and lessons learned

As previously indicated, we are not mainly interested in why

Enron collapsed (e.g., conspiracy, greed, corruption, abuse, ethics,and the like), but focus more on how Enron’s wrongdoings wereperformed to trace the symptoms in documents and artifacts basedon what we now know. We may want to know, however, why thewrongdoings were not caught until October 2001 [1,20,61] despitesome early and sporadic warnings and explicit objections, e.g.,fuzzy accounting, clear conflicts of interest, etc., from 1992 to thefall of 2001 [13,14,67–69]. This type of knowledge will help theimplementation of future policies.

The idea is related to mechanisms to make symptomstransparent through MBE. The symptoms of wrongdoing areburied somewhere in the business’ entities: tasks, projects,transactions, accounts and financial reports. They are notdiscovered, ignored or forced to be ignored by the responsiblepeople, e.g., the board, auditors and legal counsel, despite all rulesand regulations [77].

Thus, in brief, for the detection of wrongdoings as well as theirsymptoms, the MBE have two basic features:

(1) The ability to capture data on five entities as metarecords:policy, tasks, projects, transactions, accounts and everything else(others) with marked severity levels. Data must be treated as awhole, integrated and aggregated across all functional areas ina transparent and ‘‘autonomic-like’’ system. Data with‘‘warning’’ or ‘‘severe’’ severity levels must be disseminatedto responsible people for timely decision making: employeesand management, external auditors, counsels, regulators andinvestors/partners.

(2) The ability to perform an analysis when needed to allow fordeeper investigation. This also means that the results of theanalyses will be disseminated to the proper authorities and theability to allow analysts to voice their findings of discrepanciesor wrongdoings must be ensured. Again, the analysis must betransparent to all responsible people, and therefore, if anoverriding action by some authority is performed, it will beaccounted for.

Feature (1) results from the principle of the information

environment while feature (2) supports the principle of managerial

cybernetics for business stability.In the example illustration below, captured in Fig. 5, we

showcase the exceptions of Enron by an MBE revealing thesymptoms leading to wrongdoings as proof of the concept.

The first row (P-003) shows SPE as a policy (or strategy) devisedby Andrew Fastow to enter into partnerships with investors. Thesecond row records as a project the decision that Jeff Skilling madeto invest in Rhythms NetConnections, a high risk business(therefore originally marked Yellow). He approved the investmentnevertheless (and turned it to Green). When asked by Skilling,Vince Kaminski performed the task of financial analysis andconcluded that it was severely risky (third row, Red).

The severity shown by the collection of Yellow and Red markswould have triggered some management and/or professionalattention even though some indicators were overridden.

As part of the scenario, LJM Cayman was summoned to hedgeRhythms NetConnections (fourth row, Yellow). Fastow used Enronstock and his own investment to go into partnership with the

T.N. Nguyen / Information & Management 51 (2014) 165–176172

Author's personal copy

Cayman Islands and overrode the warning (fifth row, Yellow). Bothwere high risk decisions, however, and were overridden by Fastowto turn them to Green. The project and its transactions were carriedout anyway to hide the losses in this investment in the 1999financial statement (sixth row, turning Red to Green).

Other projects, accounts, transactions and financial statementsfollowed (not shown) until the financial statement of the 3rdquarter 2001 (eighth row, Red). When the SEC inquired (ninth row,Red) about the obscure 2001 financial statement from the thirdquarter, other financial statements from 1997 to 2001 wererestated with losses (not shown). This eventually led to Enron’scollapse.

The list of exceptions in Fig. 5 was compiled from the availablesources (policy, project, task, transaction, account and others) ofthe MBE (implementing the concept of information environment)with detailed information on who did what, where, when and how(through supporting documents), as partially captured in Figs. 6and 7.

SPE creation (the first row in the Exception report in Fig. 5) wasamong three strategies listed under the Policy entity report in thetop part of Fig. 6. The Financial Analysis task was assigned to aprofessional (Kaminski) who raised concerns (‘‘Yellow’’). The Taskentity report included other tasks performed by an Enron manager(Woytek), an accountant (Bass), and an outsider (Mack), whoraised concerns (all ‘‘Yellow’’) about the MTM scheme in the 1990s.The Project entity report shows an example of a good project(Cactus III, marked ‘‘Green’’) and two projects (Chewco andRhythms NetConnections) with warning indicators due to SPEpartnerships (‘‘Yellow’’); however, both of them were overriddenby Lay and Skilling.

Fig. 7 shows the corresponding reports on Accounts, Transac-tions and Others from which the symptoms of wrongdoings were

compiled. Every transaction is aggregated in Accounts, and everytask is aggregated in Projects (details not shown). Every accountlinks to one or more projects as siblings, and vice versa. The markedseverity level was rolled up from tasks, transactions and others toprojects and accounts. The reason for the severity of any entity canbe found by drilling down to its constituents. Communications orartifacts are expressed as ‘‘Others’’ if they are not the result of a taskor transaction. In the Enron case illustration, the entities markedwith Yellow and/or Red involved the LJM Cayman and Chewcoprojects with the SPE accounts.

4.1. Lessons learned and extension to cases of other businesses

The next issue is: ‘‘Can we prevent another Enron with the MBEsystem discussed in the previous sections?’’

Recall that our proposed model is employee-centered in the waythat an organism is cell-centered. Everything in the institution isconsidered as product of the employee’s tasks in the way thateverything in the human body is the product of a cell’s organellesas proteins. The product is described not only in terms of tasks butalso in terms of projects, transactions or accounts and is not limitedto other entities that the institution might use.

Secondly, the system is policy-driven across all levels oforganizations, much like the system of the human body is gene-

driven, to measure results against faulty strategy, managerialmishandlings, intended wrongdoings, diverted tasks withinprojects, out-of-the-ordinary transactions hidden in financialaccounts and underreporting statements. These are eithersupported by existing policy and/or regulations or are question-ably violated, as we mentioned in Section 1.

Thirdly, the system is geared toward evaluating and labelingexceptions in terms of severity levels as a complete set of relevant

Fig. 5. Enron rhythms NetConnections project. (For interpretation of the references to color in text, the reader is referred to the web version of the article.)

Fig. 6. Business entities. (For interpretation of the references to color in text, the reader is referred to the web version of the article.)

T.N. Nguyen / Information & Management 51 (2014) 165–176 173

Author's personal copy

symptoms for diagnosing wrongdoings. All records have drill-down and roll-up capabilities and sideway links. Thus, the MBEsystem is capable of displaying the set of information on aparticular issue as completely as possible, including all analysessubstantiating it and all actions/decisions for or against it.

The lessons learned from Enron as a result of this MBE can bepotentially applied to other Enron-like institutions such asWorldCom, Tyco International, Adelphia, and Lehman Brothers.For example, for WorldCom, we now know that the two mainfigures that constituted ‘‘the institution malignant tumor’’ wereBernie Ebbers, CEO, and Scott Sullivan, CFO. They were involved inmega-deals with over 60 acquisitions during the 1990s (complex,potentially uncontrollable growth). The main fraud in this case wasaccounting, in which they involved staff to list operating expensesas assets, whereby huge losses turned into enormous profits ofsome $1.38 billion in net income in the company’s 2001 financialstatement [46]. They also misused reserve funds. Meanwhile,Ebbers netted some $140 M and Sullivan some $45 M from stocksales. The detection of wrongdoing by the MBE would be easierthan detecting the Enron cancer in terms of transactions andaccounts concerning different projects transparently recorded inMBE.

The case of Lehman Brothers’ collapse is of a different scale andcomplexity. The effect of its bankruptcy rippled throughout themarket. It caused a large decline in the Dow Jones index. It involvedthe subprime market and the market of Credit Default Swaps(CDOs), the misuse of Repo 105 and obscure financial statements,the FED, its complex structure, and many others. The finding wasdescribed in a 9-volume, 2200 + page report [4]. The investigationregarding its prevention [42] confirmed that the symptoms ofwrongdoings were detectable from cash flow reports, which wereignored by analysts. Investors and auditors either did notunderstand the statements or, blinded by superficial performance,did not see the items hidden by top management and executives.There were many warning signs. This case is worth an in-depthinvestigation from the MBE approach, which will be a subject ofour continuing research.

There is another specific type of problem: the collapse causedby one single person in the organization. The typical examples ofthis phenomenon are Bernard Madoff with his Ponzi scheme orNicholas Leeson of Barings Bank [44]. The wrongdoings would havebeen discovered had the entities been recorded and analyzedproperly with complete transparency to the proper authority. Inthe former case, warning signs were also indicated by HarryMarkopolos, who had investigated Madoff since 1999 [41].Similarly, in the case of Nick Leeson, the head of Barings SecurityOperations had warned top management since 1992 about thedual role of Leeson in trading and settlement [34]. These warnings

were ignored or forgotten because they were not part of an MBEscheme or equivalent.

We believe that the above cases, from Barings Bank to LehmanBrothers, can be examined as cases for the proposed MBE indeveloping different exception-detection algorithms capable ofconsistently exposing symptoms to all responsible people acrossall system boundaries.

5. Concluding remarks and future work

In summary, in this initially proposed MIS-driven solution, theinformation environment is biologically inspired from the conceptof the internal environment described by Claude Bernard. It offersthe availability and the transparency of information to theresponsible employees. The responsible employees would beaware of the situation at any time, and they would detectirregularities or anomalies and report them in the system asconcerns or warnings (Yellow) or severe issues (Red) at theappropriate level of severity.

These exceptions are aggregates of lower-level exceptions as acontrol echelon in the sense described by Beer [5]. They areescalated upwards to higher levels to the proper authority fordecision making. Furthermore, they report the accountability toresponsible employees at any level of the structural or functionalorganization, including those authorities who may override thewarnings or red flags.

When the number of exceptions is numerous, more attentionfrom management will be given. These exceptions exercise thenotion of keeping the performance within the defined norms. Thisis biologically inspired from the homeostasis concept introduced byWalter Cannon and Sherwin Nuland.

The system allows management at all levels to exercise controlin driving the performance back to normal when exceptions clearlyindicate out-of-bounds situations that could lead to more seriousor catastrophic events.

The prevention of institutional cancer by management byexceptions (MBE) illustrated in this paper is just a scratch on thesurface of an application system that could truly preventinstitutional diseases. It sets the stage for further horizontalcontrol (via the association or relevancy between tasks andtransactions, projects and accounts) and vertical control (via rollup and drill down) of activities and associated events.

At this point, one might say that there is no need for the canceranalogy because the solution as we have proposed can bereached without the analogy. Truthfully speaking, had no canceranalogy been drawn, this human-centered business model (asopposed to a business-centered, profit-centered, or process-centered model, etc.) would not make sense, the structural

Fig. 7. Business entities (cont.). (For interpretation of the references to color in text, the reader is referred to the web version of the article.)

T.N. Nguyen / Information & Management 51 (2014) 165–176174

Author's personal copy

property of complementarity and information environmentwould have been difficult to conceive, the biological mechanismswould be too far-reaching, or other concepts such as homeostasisor cybernetics would not give rise to stability with managerialcybernetics.

One might question that the proposed solution model in whichbusiness stability is one of the strategic goals might make sense butmight take all business innovation away. We argue that if stabilityis one of the goals, detection and prevention of wrongdoings wouldnot only be found, but they would be a solid approach to growthand profitability.

As part of this conclusion, there are two other considerations:(1) technological innovation and advances, and (2) the humanfactor. We have seen the first consideration in a plethora ofenterprise software. Examples include sophisticated ERP systemsfor internal controls; application systems, such as Enron EOL fortrading; and transaction processing systems, such as that of ChaseManhattan bank in Bournemouth, UK, which interlocks everytransaction from around the globe.

Therefore, what has motivated all the collapses that followedEnron and will surely motivate future collapses in spite of newlaws, rules and regulations, such as Sarbanes-Oxley? The answer isembedded in the second consideration. Human nature spans bothends of the dipole concept: conservative and liberal, low-risk andhigh-risk takers, right and wrong, restrained and greedy, whichdefine the situation that the business environment is in. No matterhow brilliantly a remedy or prevention may be devised, there willbe someone or some group to break the rules for any reason at all,one of which is high levels of risk taking. The issue resides in carefulhiring, leadership and ethics, and others that go beyond the scopeof this article. The general approach to the issue is to improve thehuman factor, much like when we teach a class, we would want toimprove students’ mean scores and reduce the standard deviationvia effective learning and teaching.

On the other hand, our framework and MBE model do notguarantee that it will work absolutely, but it could embrace othersolutions for the simple reason that it is a shell with metadata onexisting data (task, projects, transactions, accounts, policy, and

others). It can grow as fast and/or as wide as our means can afford.Philosophically, it seems like a natural way to solve problemscaused by humans that are part of the nature of the problem.

Another important point involves the institution’s manage-ment-leadership team. Despite all discoveries of wrongdoing,executives can choose to ignore them, override them or hide them,and so on. How can we make sure that these executives seriouslyconsider the warnings in order to make proper decisions? This is atopic of our future work. We will make sure that each executiveseriously considers any warnings by eliciting their input on eachand every warning in order to build a set of personal constructs inthe sense described by George Kelly [37]. The constructs will thenbe analyzed and evaluated in a fashion similar to Valerie Stewart’sRepertory Grid [72]. The combined measure can be expressed on afailure-success scale that measures the management-leadershipteam’s performance.

Acknowledgements

The author wishes to thank Richie Nguyen of Wharton School ofManagement, University of Pennsylvania, and the I&M JournalCopy Editor for language help and proof reading the article.

References

[1] D. Ackman, Enron’s Lawyers: Eyes Wide Shut? Forbes 2002.[2] C. Alexander, The Nature of Order, The Center for Environmental Structure,

Oxford University Press, New York, 2002.

[3] B. Alberts, D. Bray, A. Johnson, J. Lewis, M. Raff, K. Roberts, P. Walter, Essential CellBiology, Garland Publishing, New York, 1998.

[4] A. Azadinamin, The Bankruptcy of Lehman Brothers: Causes of Failures & Recom-mendations Going Forwards, Swiss Management Center, 2012.

[5] A.S. Beer, Brain of the Firm: Managerial Cybernetics of Organization, The PenguinPress, London, 1972.

[6] H. Bierman Jr., Accounting/Finance Lessons on Enron – A Case Study, WorldScientific Publishing Co. Pte. Ltd., Singapore, 2008.

[7] K.F. Brickey, From Enron to WorldCom and beyond: life and crime after Sarbanes-Oxley, Washington University Law Quarterly 81, 2003, pp. 357–382.

[8] W. Cannon, The Wisdom of the Body, The Penguin Press, London, 1963.[9] S. Chatterjee, B. Fellow, Enron’s Asset-Light Strategy: Why It went Astray, 2002.

[10] Cisco, The Internet Ecosystem: The Business Model for the Internet Economy,1999.

[11] R.J. Clayton, W. Scroggins, C. Westley, Enron: market exploitation and correction,Journal of Financial Decisions 14 (1), 2002, pp. 1–15.

[12] CNNMoney, Andersen Auditor Questioned Enron, 2002 http://money.cnn.com/2002/04/02/news/companies/andersen_bass/.

[13] Congressional Testimony – Sherron Watkins, 2002 http://www.sherronwatkin-s.com/sherronwatkins/Congressional_Testimony.html.

[14] Congressional Testimony. CEO Jeffrey Skilling’s Testimony to Congress, February7, 2002.

[15] S. Deakin, J.K. Suzanne, Learning from Enron, ESRC Centre for Business Research,University of Cambridge, 2003.

[16] M.R. Desmond, Lehman’s Brothers, Forbes, 2008 http://www. forbes. com/2008/09/16/lehman-layoffs-biz-wall-cx_mrd_0916lehmanbar.html (16.09.08).

[17] B.G. Dharan, R.B. William, Red Flags in Enron’s Reporting of Revenues and KeyFinancial Measures, 2002 www.ruf.rice.edu/�bala/files/dharan-bufkins_enron_-red_flags.pdf.

[18] B. Dharan, N. Rapoport (Eds.), Enron and Other Corporate Fiascos, The FoundationPress, Wet Academic, MN, 2009.

[19] B.G. Dharan, Enron’s Accounting Issues – What We Can Learn to Prevent FuturePrepared Testimony, US House Energy and Commerce Committee’s Hearing onEnron Accounting, 2002.

[20] F.R. Edwards, US Corporate Governance: What Went Wrong and Can It Be Fixed?BIS and Federal Reserve Bank of Chicago Conference, October 2003, 2003.

[21] K. Eichenwald, M. Brick, Enron Collapse: The Strategy, NY Times, 2002.[22] K. Eichenwald, Conspiracy of Fools: A True Story, Broadway Books, New York,

2005.[23] Enron Annual Report 1998, 1998. www.picker.uchicago.edu/Enron/EnronAn-

nualReport1998.pdf.[24] Enron Annual Report 1999, 1999. www.picker.uchicago.edu/Enron/EnronAn-

nualReport1999.pdf.[25] Enron Annual Report 2000, 2000. www.picker.uchicago.edu/Enron/EnronAnnual-

Report2000.pdf.[26] Foster School of Business, Washington, A decade’s worst financial scandals, 2010,

April.[27] T. Fowler, LJM2 partnership files for bankruptcy, Unit created to hide debt in

Enron deals. Houston Chronicle, 2002.[28] L. Fox, Enron: The Rise and Fall, John Wiley & Sons, New Jersey, 2003.[29] C.G. Gross, Claude Bernard and the constancy of the internal environment,

Neuroscientist 4 (1), 1998, pp. 380–385.[30] A. Haglund, Failed Strategies of Enron, 2011 http://mg312.wordpress.com/2011/

09/02/failed-strategies-of-enron/.[31] P.M. Heally, K.G. Palepu, The fall of Enron, Journal of Economic Perspectives 17

(Spring (2)), 2003.[32] R. Heller, Parmalat: A Particularly Italian Scandal, Forbes, 2003 http://www.

forbes.com/2003/12/30/cz_rh_1230parmalat.html (30.12.03).[33] D. Higgs, Review of the role and effectiveness of non-executive directors, Depart-

ment for Business, Enterprise and Regulatory Reform, 2003 http://www.berr.gov.uk/files/file23012.pdf.

[34] W.P. Hogen, The Barings Collapse: Explanations and Implications, IDEAS, 1996http://ideas.repec.org/p/syd/wpaper/2123-6743.html.

[35] M.P. Holtzman, E. Venuti, R. Fonfeder, Enron and the Raptors, The CPA Journal,2003 http://www.nysscpa.org/cpajournal/2003/0403/features/f042403.htm.

[36] M. Jickling, The Enron Collapse: An Overview of Financial Issues, RS21135,Updated January 30, 2003, CRS Report for Congress, 2003.

[37] G. Kelly, A Theory of Personality: The Psychology of Personal Constructs, W.W.Norton & Company, New York, 1963.

[38] J.E. Ketz, Hidden Financial Risk: Understanding Off-Balance Sheet Accounting,Wiley, New Jersey, 2003.

[39] King G R.J.B., Cancer Biology, Addison Wesley, England, 1996.[40] M. Iansiti, R. Levien, The new operational dynamics of business ecosystems:

implications for policy, operations and technology strategy, Harvard BusinessSchool, Working paper 03-030, 2003.

[41] J. La Roche, And Now We Know Why Nobody Took Madoff Whistleblower HarryMarkopolos Seriously, 2011 http://articles.businessinsider.com/2011-10-07/wall_street/30253397_1_trial-dates-bny-mellon-bank.

[42] J. Le Maux, D. Morin, Black and white and red all over: Lehman Brothers’inevitable bankruptcy splashed across its financial statements, InternationalJournal of Business and Social Sciences 2 (20), 2011, pp. 39–65.

[43] J. Leber, How to Spot the Next Big Banking Scandal. MIT Technology Review, 2012,August.

[44] N. Leeson, Rogue Trader, Little Brown Book Group, 2012.[45] Y. Li, The case analysis of the scandal of Enron, International Journal of Business

and Management 5 (October (10)), 2010 in: www.ccsenet.org/ijbm.

T.N. Nguyen / Information & Management 51 (2014) 165–176 175

Author's personal copy

[46] B. Lyke, M. Jicking, WorldCom: The Accounting Scandal. CRS Report for Congress,RS21253, 2002, August.

[47] R.C. Looijen, Ecosystem management: a management view, 2009.[48] T. Mack, Hidden Risks, Forbes, 1993.[49] H.R. Maturana, F.J. Varela, Autopoesis and Cognition: The Realization of the Living,

D. Reidal Publishing Company, Holland, 1980.[50] MIT Sloan Newsroom, Can we stop another Enron? Kothari says new laws won’t –

MIT Sloan Newsroom 2002 http://mitsloan.mit.edu/newsroom/2002-kothari.php.

[51] J.F. Moore, The rise of a new corporate form, Washington Quarterly 21 (Winter(1)), 1998, pp. 167–181.

[52] J.F. Moore, The Death of Competition – Leadership and Strategy in the Age ofBusiness Ecosystems, Harper Business, Wiley, New York, 1996 p. 297.

[53] J.F. Moore, Predators and prey: a new ecology of competition, Harvard BusinessReview (May–June), 1993, pp. 75–86.

[54] A. Nakayama, Lessons from the Enron Scandal, 2002 http://www.scu.edu/ethics/publications/ethicalperspectives/enronlessons.html.

[55] T.N. Nguyen, The ecology of software: a framework for the investigation ofbusiness IT integration, Journal of American Academy of Business 2 (1), 2002,pp. 7–11.

[56] S. Nuland, The Wisdom of the Body, Alfred A. Knoff, 1997.[57] R.A. Oppel Jr., Enron’s Many Strands: The Strategies, NY Times, 2002, May.[58] D.B. Patten, Summary of the Enron Trading Strategies in California, 2002, June.[59] P. Patsuris, The Corporate Scandal Sheet, Forbes, 2002 http://www.forbes.com/

2002/07/25/accountingtracker.html (26.08.02).[60] K.V. Peursem, M. Zhou, T. Flood, J. Buttimore, Three Cases of Corporate Fraud: An

Audit Perspective, Number 94, University of Waikato, 2007, June.[61] E.J. Pollock, Enron’s Lawyers Faulted Deals But Failed to Blow the Whistle, The

Wall Street Journal, 2002 http://faculty.msb.edu/.ching/ENRON/Enron’s%20Lawyers%20Faulted%20Deals%20But%20Failed%20to%20Blow%20the%20Whistle.htm.

[62] W. Powers Jr., Report of Investigation, 2002.[63] D. Puscas, A Guide to the Enron Collapse: A Few Points for a Clearer

Understanding, Polaris Institute, 2002 in: www.polarisinstitute.org.[64] A. Raghavan, How a Bright Star at Andersen Burned Out along with Enron, Wall

Street Journal, 2002, May.[65] J.A. Ricketts, R.R. Nelson, Management-by-exception reporting: an empirical

investigation, Information & Management 12 (May (5)), 1987, pp. 235–246.[66] Sarbanes-Oxley Act, 2002. http://www.soxlaw.com.

[67] SEC versus Richard A. Causey, 2004. http://www.sec.gov/litigation/complaints/comp18551.htm.

[68] SEC versus Jeffrey K. Skilling and Richard A. Causey, 2004. http://www.sec.gov/litigation/complaints/comp18582.htm.

[69] Senate Committee on Governmental Affairs, The Role of the Board of Directors inEnron’s Collapse, 2002.

[70] N.C. Smith, M. Quirk, From grace to disgrace: the rise and fall of Arthur Andersen,Journal of Business Ethics Education 1 (1), 2004, pp. 91–130.

[71] E. Starling, The wisdom of the body, Br. Med. J. 2 (October (3277)), 1923, pp. 685–690.

[72] V. Stewart, 2010. http://valeriestewart-repertorygrid.blogspot.com/.[73] The Enron Blog, Jonathan Weil’s Six Business Lessons, 2008 http://caraellison.

wordpress. com/2008/06/12/jonathan-weils-six-business-lessons/.[74] C.W. Thomas, The rise and fall of Enron, Journal of Accountancy (April), 2002,

http://journalofaccountancy.com/Issues/2002/Apr/TheRiseAndFallofEnron.htm.[75] H. Touryabal, 10 biggest banking scandals of 2012, Forbes, 2012.[76] US versus Andrew Fastow, 2003. www.dindloa.com.[77] US GAAP, The Enron Fraud Why didn’t anyone see it? 2002 http://www.thegaap.

net/articles/The_Enron_Fraud.html.[78] S. Watkins, Letter to Ken Lay, 2001 www.findlaw.com,news.findlaw.com/hdocs/

docs/enron/empltr2lay82001.pdf.[79] N. Weiner, Cybernetics or Control and Communication in the Animal and the

Machine, The MIT Press, MA, 1948.[80] T.N. Nguyen, in: Appa Rao Korukonda (Ed.), The ecology of e-business in Readings

in Business and Administrative Sciences, Lambert Academic Publishing, 2012.

Dr. Thang N. Nguyen received his BS in electricalengineering from Universite Laval, Quebec, PQ, Canada,his MS in information and computer science fromGeorgia Institute of Technology, GA and his PhD fromGeorge Mason University, VA. He previously publishedin Information & Management, Communications of TheAssociation for Information Systems (CAIS), IBM Journalof Research and Development, and other journals. Hisresearch interest has been in robotics and automation,decision science, software engineering, business-ITintegration and biologically-inspired computing. Heauthored a textbook ‘‘Essentials of Statistics forBusiness and Economics: An Effective Approach’’published by Great River Technologies.

T.N. Nguyen / Information & Management 51 (2014) 165–176176