A brief overview of Australian water policy refroms and water markets

51

A brief overview of Australian water policy and water markets Jason Alexandra

Transcript of A brief overview of Australian water policy refroms and water markets

A brief overview of Australian water policy

and water markets

Jason Alexandra

CONTEXTAustralia is:• a federation - a country in a continent• highly urbanized• the driest inhabited continent with the highest per capita water resources• operating in a highly variable climate

Australia recent policies are focused on• natural resources sustainability• Pro –market economic reforms

Outline:1.Context and climate2.A brief history of water policy 3.Australian water markets4.Characteristics and lessons5.Related NRM policy challenges6. Some conclusions

Context - A country in a continent

Energy rich and water poor – learn to live like Australians

Accept the nature of the place, what it is, not what it is not.

Water is a strategic resource and lack of it a key limitation. Improving water policy and governance is a strategic opportunity.

Australian rainfall and the lie of averages. Less than 300mm/year in the west and centre to over 1000mm/year in the south, east and north

1.0%

1.7%

0.4%

20.3%23.3%

1.9%

0%6.1%

0.3%

21.1%

10.6%

13.3%

1.0%

1.7%

0.4%

20.3%23.3%

1.9%

0%6.1%

0.3%

21.1%

10.6%

13.3%

Average rainfall and runoff

Extreme variability in rainfall and runoff

June 20082,220 GL

2. A brief historyThe Murray - a nation’s changing

relationships with nature

1.Dreamtime and the next 60000 years2.Occupation and colonisation3.Navigation4.Federation5.Nation building6.Irrigation and economic development7.Integrated water resources policy8.Ecological restoration and care of

nature9.International Obligations

In 1836 Charles Darwin …. concluded that Australia could never become another America - its soil was too poor, its rains too unpredictable.

Instead it must depend on becoming "the centre of commerce for the southern hemisphere and perhaps on her future manufactories”

copy

headline“dreams of taming the rivers, greening the desert, and making land productive, run deep in the national psyche” (Lines

1994)

Successive Governments sponsored closer settlement and

intensive irrigation development, notwithstanding,

punishing droughts and misconceptions about the severity of the natural

constraints to settlement and production (Taylor 1940).

A brief history of Australian water policy

1890’s – 1980’s Water infrastructure development

– “drought, royal commission, new dam” then desal and water markets

1992 Industry Commission – TWE 1994 COAG reforms – environmental

flows, water markets, corporatisation and cost recovery

National Water Initiative 2004 – reaffirms commitments to reform, environmental flows and markets’ role in reallocating water

2008 – Water Act Reforms – Murray Darling Basin Authority – Basin Planning

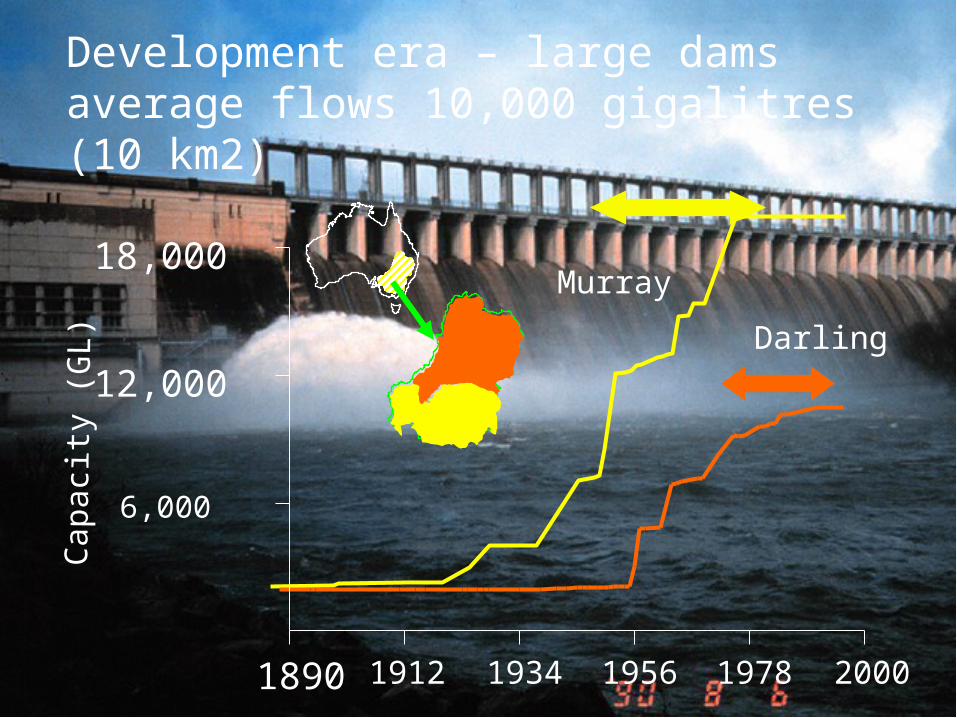

1890 1912 1934 1956 1978 2000

6,000

12,000

18,000

Capacity (GL)

Development era – large dams average flows 10,000 gigalitres (10 km2)

MurrayDarling

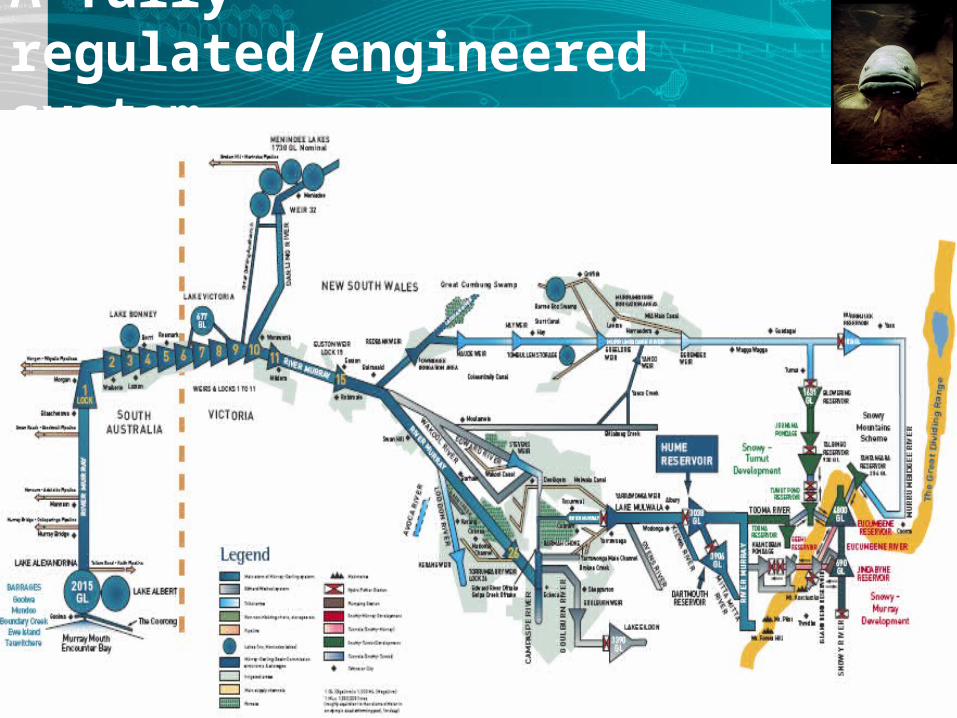

Major Water Storages on almost all tributaries in the MDB

A fully regulated/engineered system

Irrigation – 70% of water use - Irrigation – 70% of water use - most in MDBmost in MDB

Produces more than half the profit in Produces more than half the profit in Australian Agriculture & Horticulture, from Australian Agriculture & Horticulture, from 0.5% of land (NLWRA 2002)0.5% of land (NLWRA 2002)

0

200

400

600

800

1000

1920 1940 1960 1980 2000

Area (x

1000 ha

)

N SWVicQuSAW ATas

Large dams construction era 1950-1980’s –

nation building and response to climate variability

1990’s new policy directions –focus on improved management,

innovative water policy, integrated catchment management

and local landcare

3.Water market frameworkCap and trade system

Entitlement (notional permanent right to a share of a defined water resource)

Allocation (annual share – variable depends on supply)

Both allocation and entitlement can be traded

Depends on hydrological linkages

Rules continue to evolve

In times of scarcity - water moves from lower value to higher value uses

Markets assist communities & industry through drought

Enables water to move between uses and users

Recent seasons demonstrate that “market theory” works

Flexibility achieved due to pro-market policy reforms started in early 1990’s

Water markets experience

Over 5000 allocation transactions –total of 235GL

Interstate allocation transfers of over 40% of water used in Southern Connected Basin

More than 50% in 2008-09 Allocation water traded at average of

$650 ML – up to $1200 ML – much higher then gross margins of many crops

Assumed therefore that: - majority of water moved from pasture and annual crops to permanent crops

Entitlements (up to $2500) also bought Governments for environment and

corporates for new irrigation developments

2007-08 – a severe drought water market

Intra and inter-state trade

Water Productivity in MDB 2005/06 (ABS, 2008)

Water Use (%)

Pasture (hay & silage)Cereals (grain & seed)

Pasture (grazing)

Rice

Cotton

GrapevinesFruit, nuts &

berriesVegetables

0.3

0.2

0.6

0.91.51.8

$M/GL

Urban water trade

Inter-sectoral and inter-basin transfers

Water also moving to urban areas Eg Goldfields super pipe – 33 GL Australian Capital Territory

(ACT) NE Water

Water markets• Rely on Government systems and

regulations• Supports changes in irrigation

practices and location• Allows for “Green-fields” new

development• Allows for government buy backs -

purchases of environmental water• Used as risk management for both

drought and/or climate change• Suffers from administrative complexity

Markets support adoption of improved practice and technologyWater use efficiency through technology, and knowledge of crop demands

Markets supported new “greenfield” developments

New horticulture up to 14 kilometres from the rivers

Estimates of up 32000 hectares since trade started

Nearly all outside “historic irrigation districts”

Water for the environment

Commonwealth- $3 billion for purchases

Focused on entitlements Allocations bought “wet water” – eg

Narran lakes

Aim to– reduce barriers to trade– minimise transaction costs– protect environmental requirements

27

Basin plan water trading rules

Separation of bundled water rights:Entitlement (ownership}Allocation (renting type)Land Use rights (location and landuse constraints –eg salinity often has CMA involved) Channel capacity shareInfrastructure shares

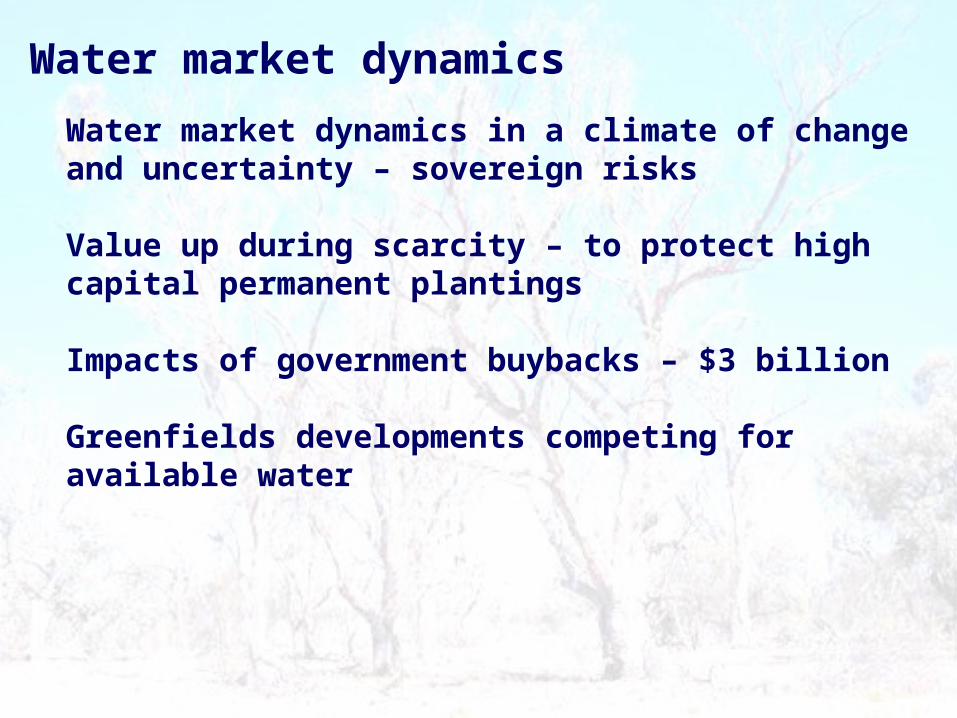

Water market dynamics in a climate of change and uncertainty – sovereign risks

Value up during scarcity – to protect high capital permanent plantings

Impacts of government buybacks – $3 billion

Greenfields developments competing for available water

Water market dynamics

Only one unreliable supplier – nature/rain gods – delivers too much or too little

Supply not responsive to demand increases

Always “local” geographically constrained – water can’t be traded internationally except as virtual water

Volatility due to multiple demand types – many markets

No alternatives or subsitutes

Water market characteristics

Water markets support:

Risk and drought responses – rural and urban

Irrigation technology and structural adjustment

New investments in horticultural and viticultural developments

A way of rebalancing extractions and environmental water

Australian experience

During periods of low water availability

Intense competition for waterAdaptation is paramount

Water trading – supports adaptation

Governance and admin of water markets will evolve

Range of policies required to support adjustment and adaptation

33

Water markets water trading allowed water to move between users and uses – important in droughts

Water markets sit as part of Australian water and natural resources reforms – complex governance and institutions

Why did Australia adopt NWI and Water Act reform:

• To optimise economic outcomes (economic reform)

• To implement ecologically sustainable development

• To overcome ecological degradation – e.g. water quality, species loss, wetlands conservation etc

• To achieve integrated catchment management• To reinforce emerging water markets 35

36

National river health assessments showed poor conditions in most rivers

Strategies for water quality management – diffuse source pollution, algal blooms etc

37

Modified catchments, nutrient and

suspended sediment loads and habitat

Very high nutrient and suspended sediment loads

Largely unmodified

River health and catchment Condition

Major erosion and sedimentation problems

4M tonnes of sediment pa and phosphorus exports - about 13,000 tonnes pa

Most agricultural lands have erosion 5-50 times greater than pre-European settlement.

Biodiversity conservation Responsibility for 60 million years of separate evolution

International obligations to protect biodiversity

Increased protection of wetlands and aquatic ecosystems

- National and international obligations

41

•MDB – •16 RAMSAR •28,000 wetlands • 6 million ha• 98% floodplains• ~3% protected

Chowillafloodplain Barmah-Millewa

Forest

Macquarie Marshes

Gwydir wetlands

Lowbidgee floodplain

Narran Lakes

Coorong

Kulkyne Lakes

Challenges ahead - The approaching storm? climate chaos!!! And its impacts!!! Adaptation imperative

Climate Change Climate change is likely to be the greatest yet most uncertain threat to the shared water resources of the MDB

Up to 4400 GL/yr reduction in flows in 20 years

“Most of the effects of climate change operate

through water”Sir Nicholas Stern, 2007

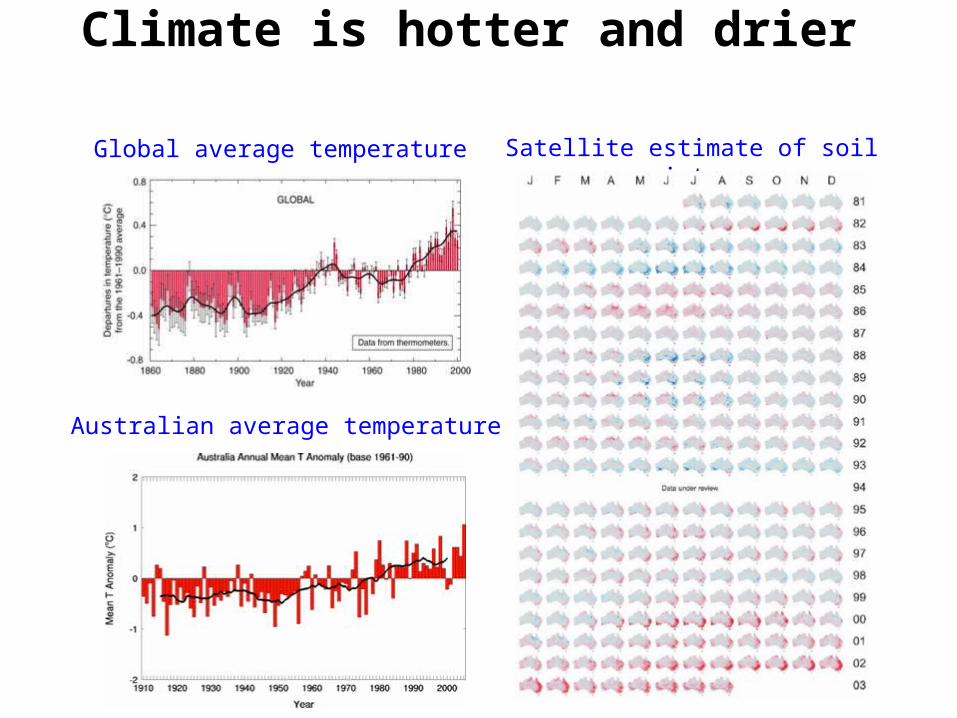

Climate is hotter and drier

Global average temperature

Australian average temperature

Satellite estimate of soil moisture

Modeled Projections• Majority of models project predict reduced runoff for SE Australia, including Murray system headwaters

• Up to 40% reduction in runoff and stream flow

Projected changes in run-off at 2030 under scenario A1B, showing the number of climate models (out of 15) yielding an increase or decease in run-off; from F. Chiew.

Actual Decreases in Runoff

ChallengesWater policy and planning under uncertainty – “stationarity is dead”.

Climate impact and risk management

Directions 1: Develop capacity for robust water policy under uncertainty Use scenarios - plan for extremes - low water availability and deeper drought/unseasonal rains, climate change impacts

Accept a future of intense competition for water

Institutional and policy innovation required Build diverse, local adaptive capacity - use

markets for risk management and allocation

Directions 2: institutions and capacity for adaptive governance:

Adaptive governance systemsPolicy and institutional design – evolution

Build robust adaptive institutionsPolicy reform as experimentMarkets sit within planning and regulatory frameworks

50

CONCLUSION - POLICY EVOLUTION

1.Institutional and policy innovation by design

2.Policies to support adjustment and adaptation eg water market reforms supports risk management and local adaptation

3.Community involvement in integrated catchment management

4.Basin scale water planning5.Steering with rigorous monitoring and

evaluation