41116-023: MFF - Jammu and Kashmir Urban Sector ...

72

Completion Report Project Number: 41116-023 Loan Number: 2331 June 2021 India: Jammu and Kashmir Urban Sector Development Investment Program (Project 1) This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 41116-023: MFF - Jammu and Kashmir Urban Sector ...

Completion Report

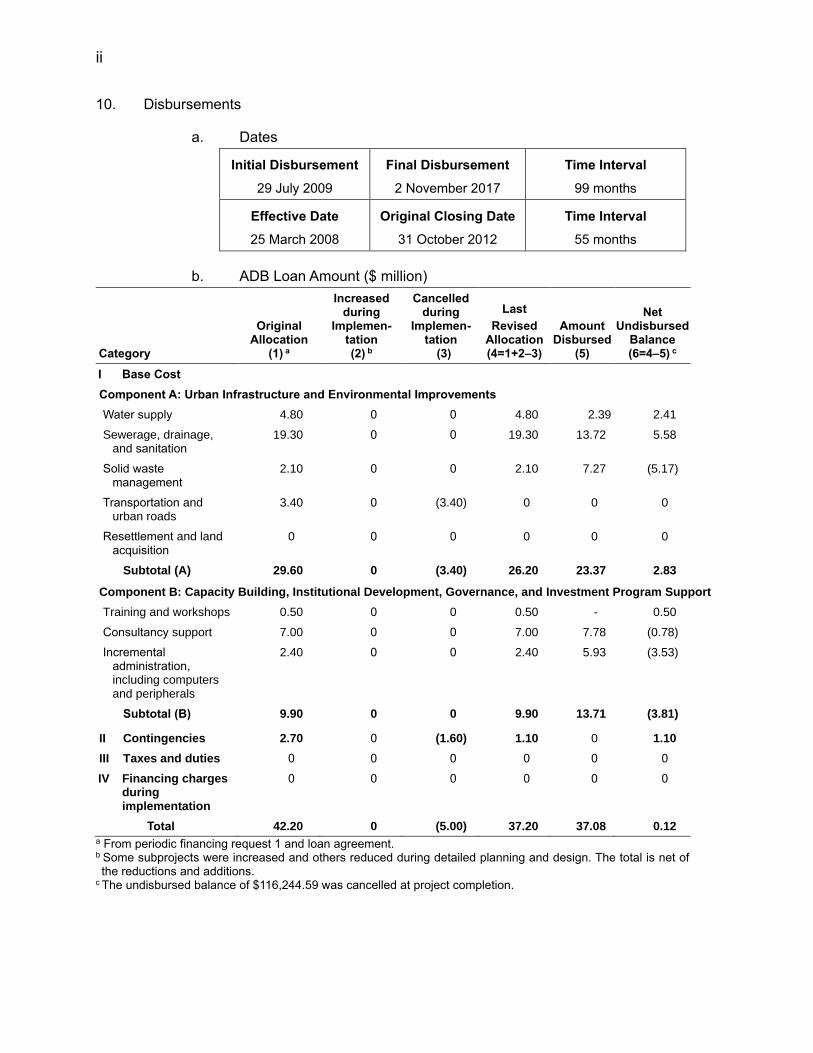

Project Number: 41116-023

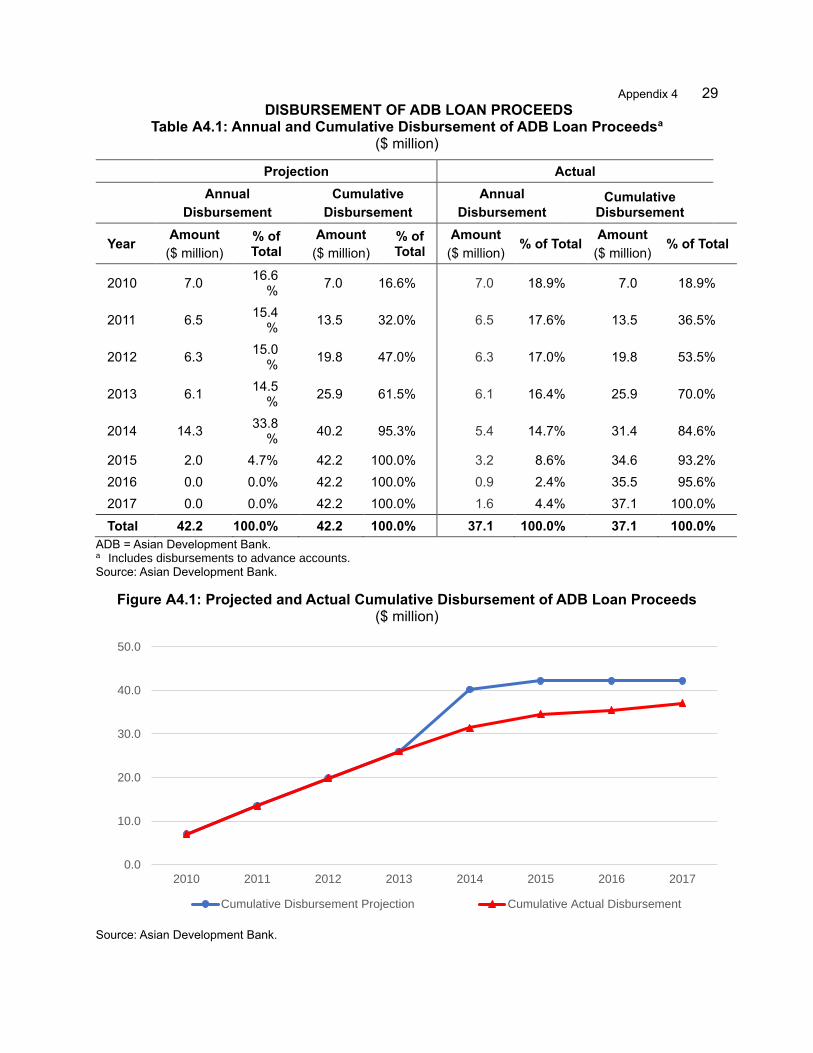

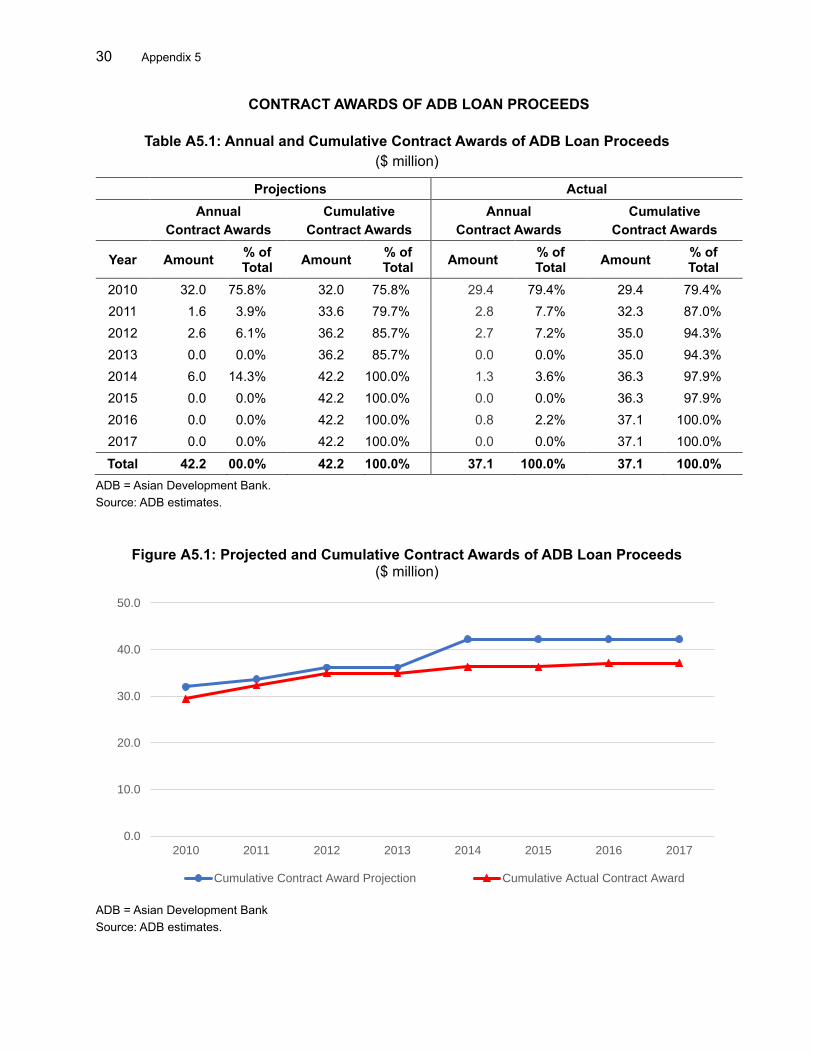

Loan Number: 2331

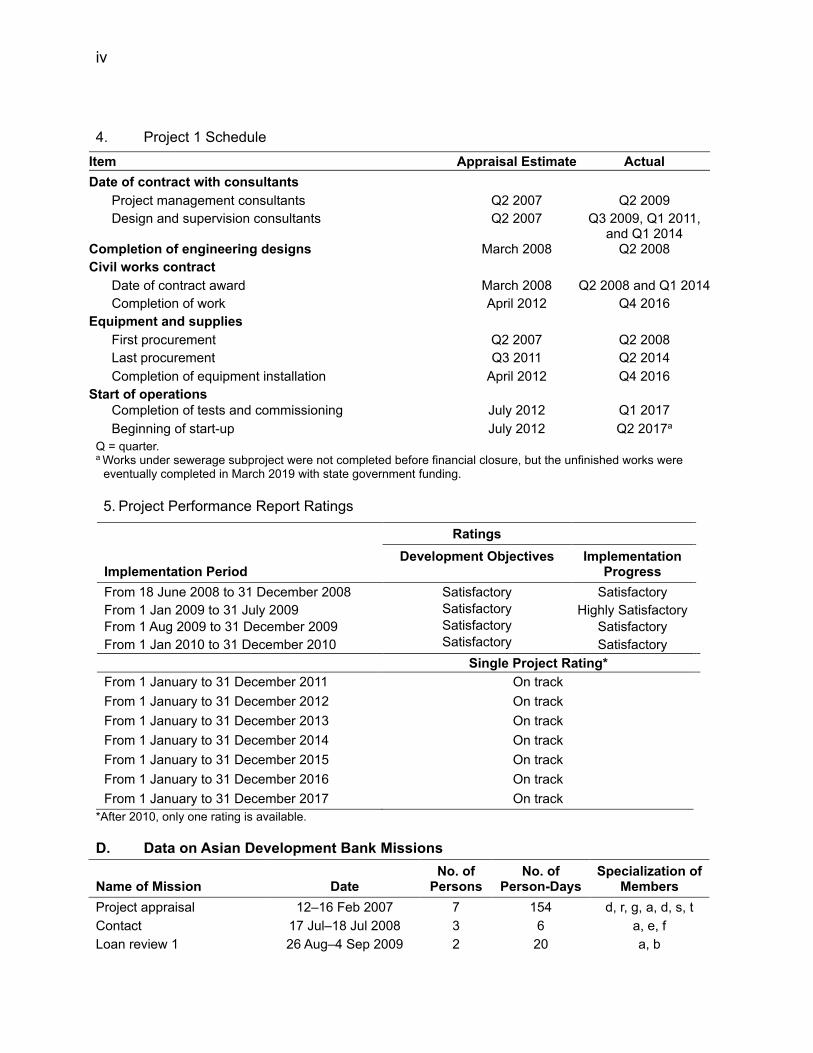

June 2021

India: Jammu and Kashmir Urban Sector Development Investment Program (Project 1)

This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

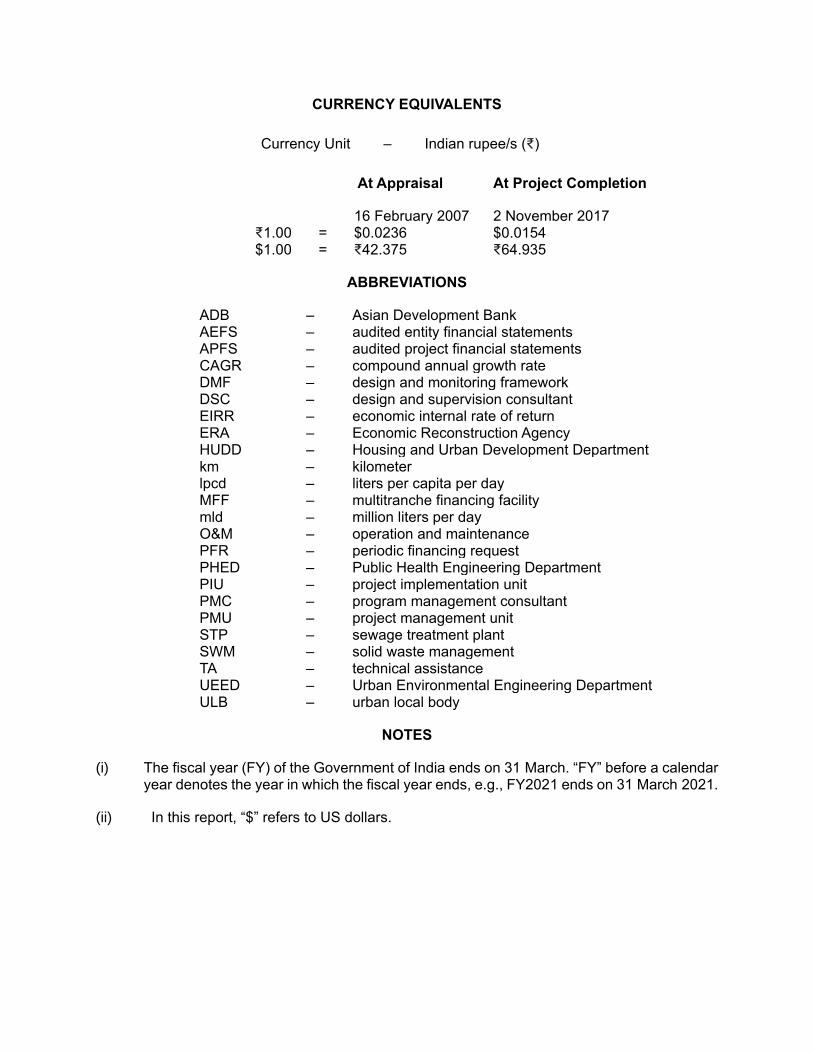

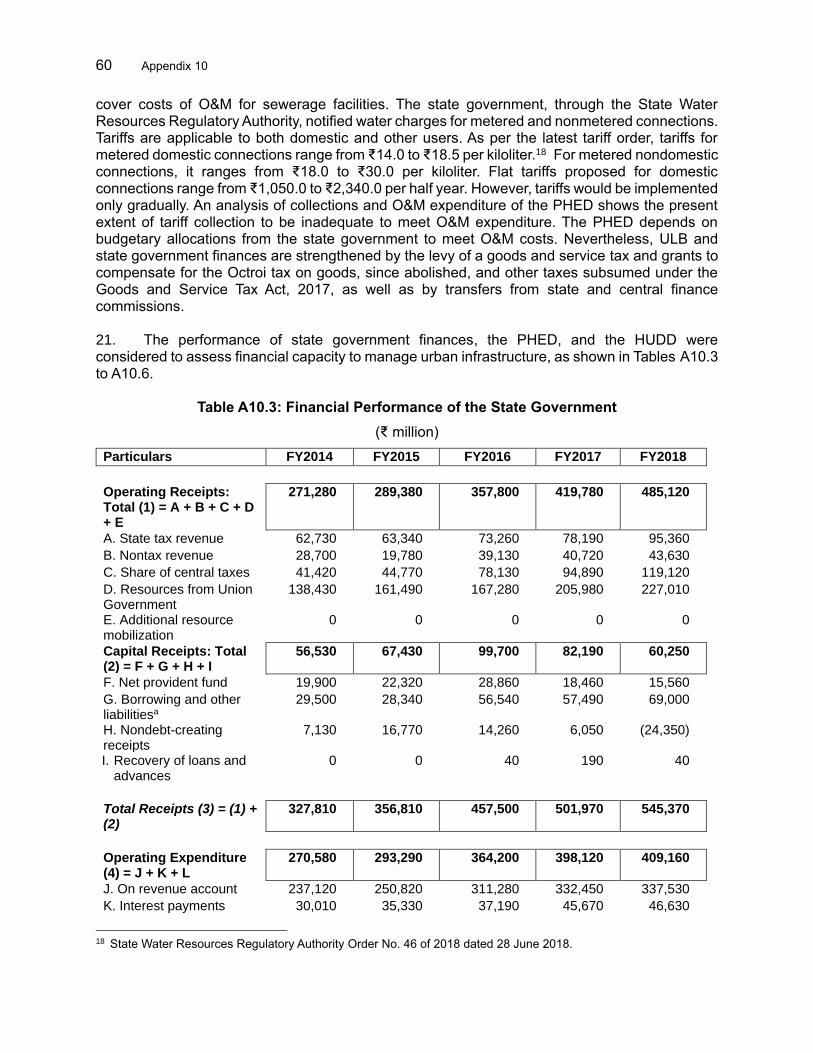

CURRENCY EQUIVALENTS

Currency Unit – Indian rupee/s (₹)

At Appraisal At Project Completion

16 February 2007 2 November 2017 ₹1.00 = $0.0236 $0.0154 $1.00 = ₹42.375 ₹64.935

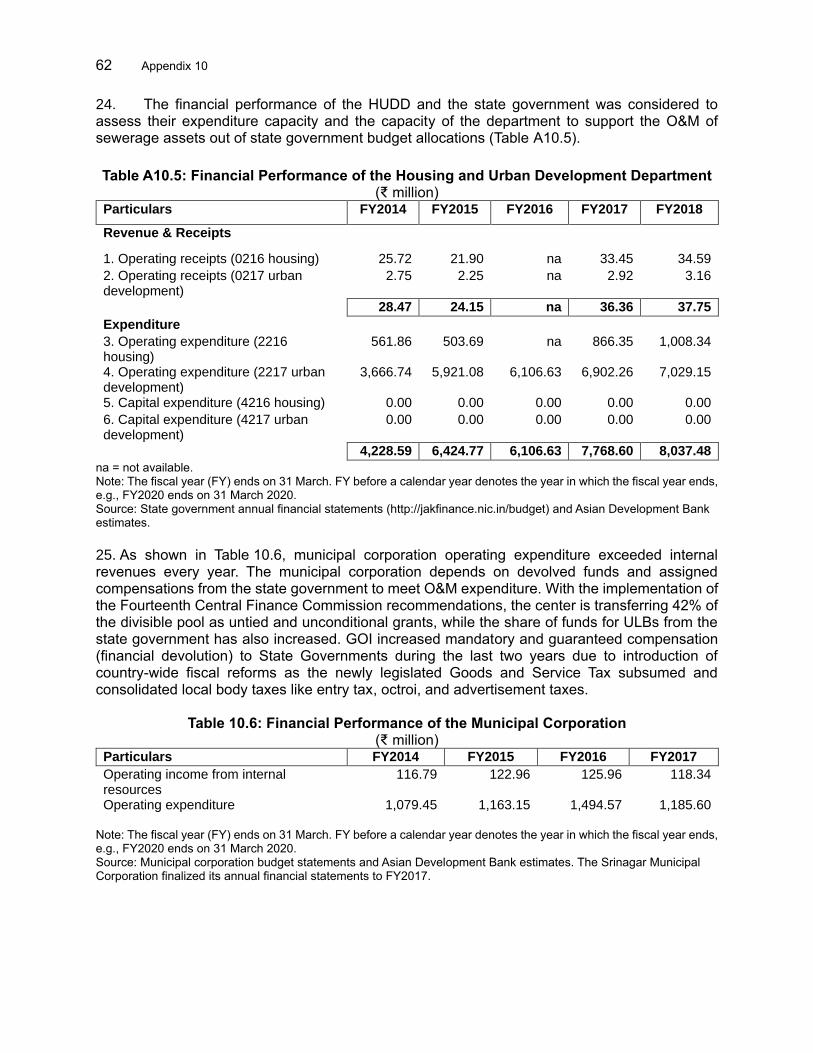

ABBREVIATIONS

ADB – Asian Development Bank AEFS APFS CAGR

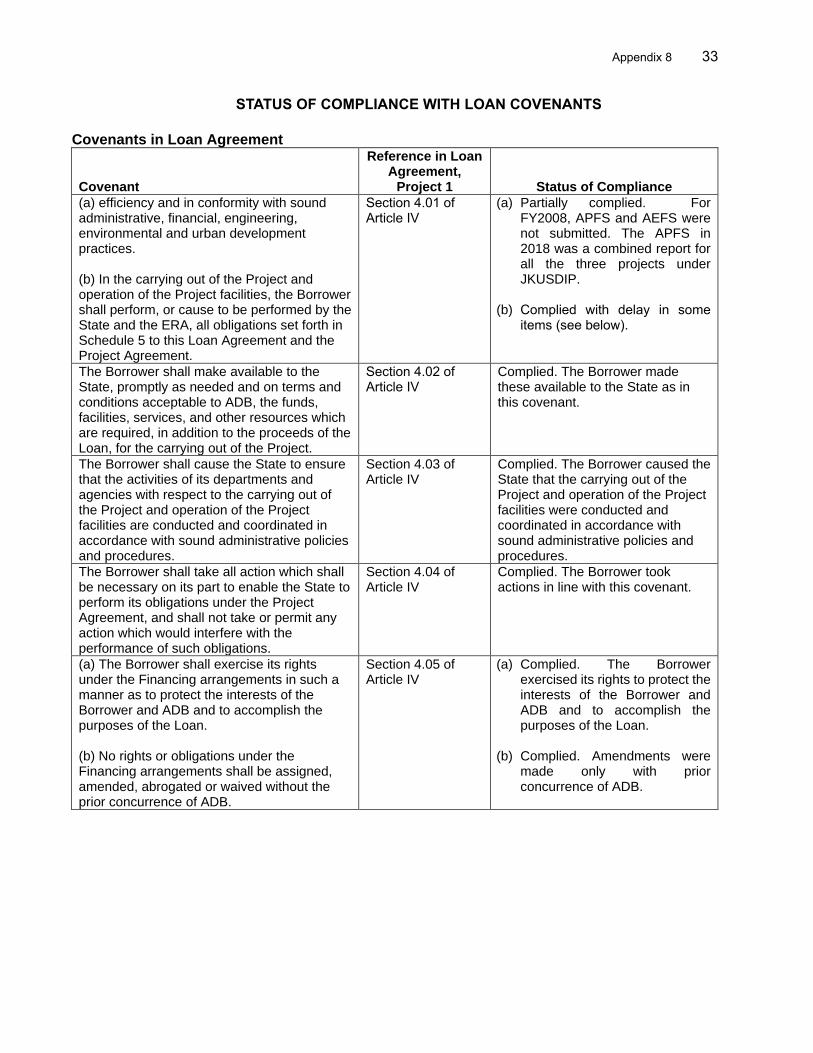

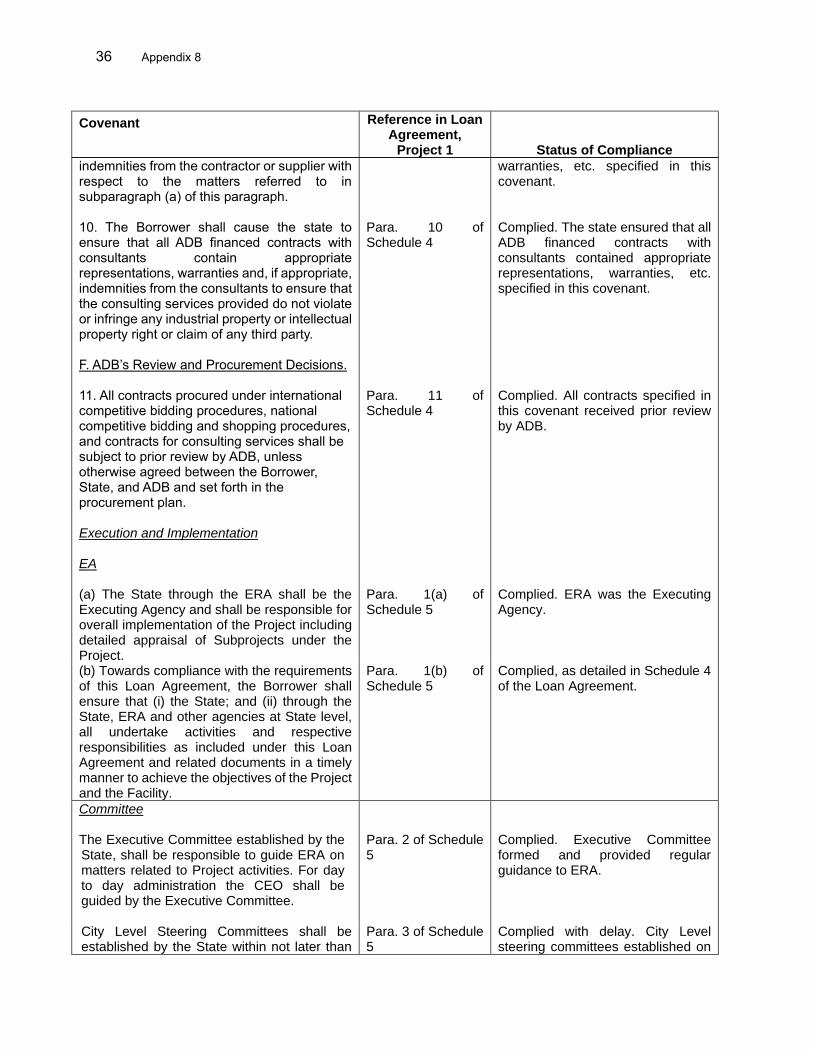

– – –

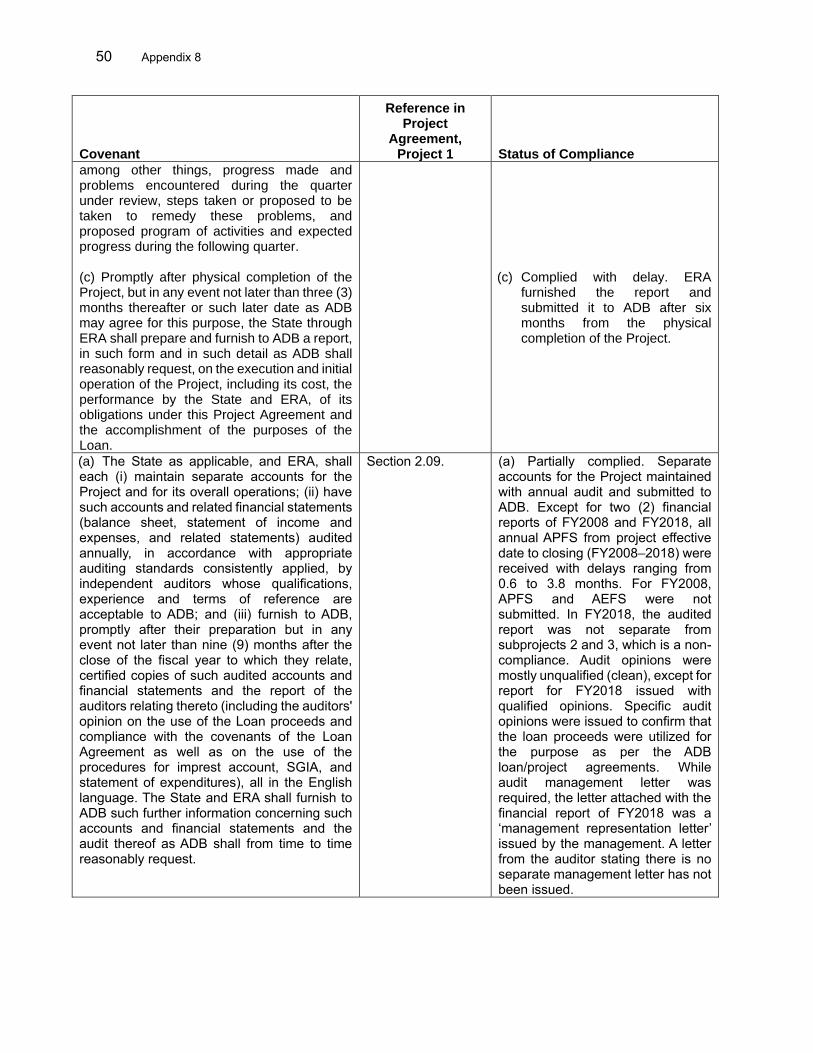

audited entity financial statements audited project financial statements compound annual growth rate

DMF – design and monitoring framework DSC – design and supervision consultant EIRR – economic internal rate of return

ERA – Economic Reconstruction Agency HUDD – Housing and Urban Development Department km – kilometer lpcd – liters per capita per day MFF – multitranche financing facility mld – million liters per day O&M – operation and maintenance PFR – periodic financing request PHED – Public Health Engineering Department PIU – project implementation unit PMC – program management consultant PMU – project management unit STP – sewage treatment plant SWM – solid waste management TA – technical assistance UEED – Urban Environmental Engineering Department ULB – urban local body

NOTES

(i) The fiscal year (FY) of the Government of India ends on 31 March. “FY” before a calendar year denotes the year in which the fiscal year ends, e.g., FY2021 ends on 31 March 2021.

(ii) In this report, “$” refers to US dollars.

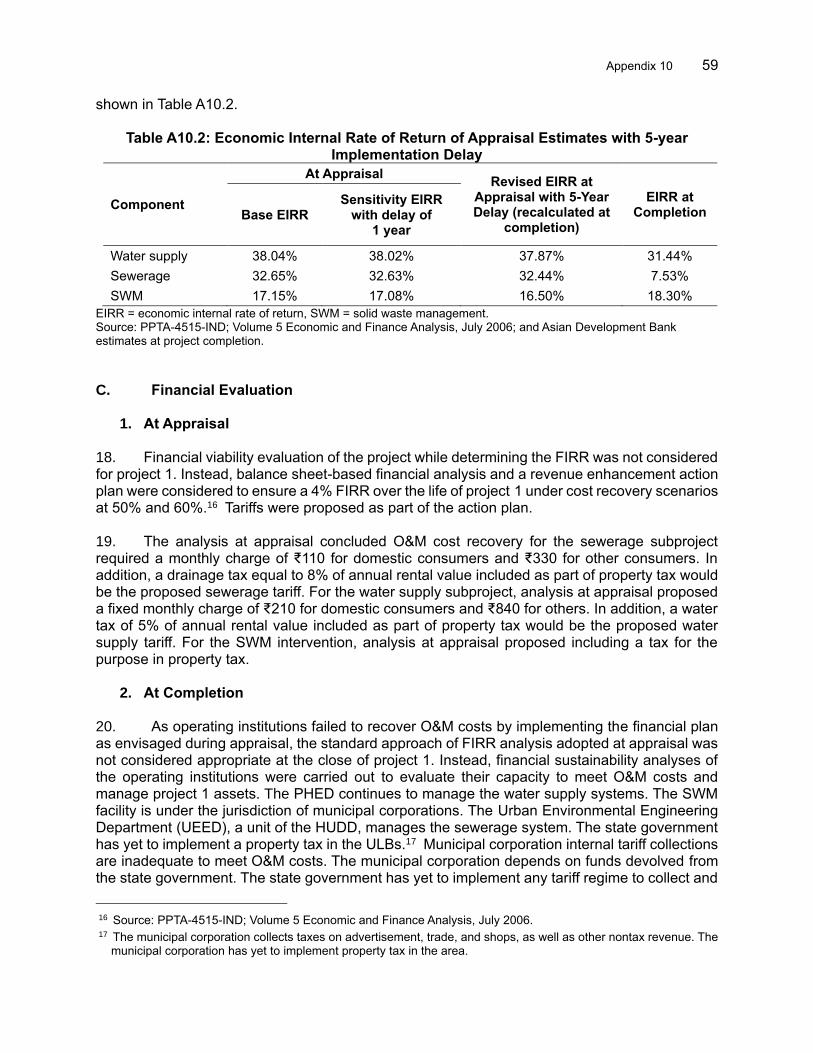

Vice-President Shixin Chen, Operations 1

Director General Kenichi Yokoyama, South Asia Department (SARD)

Director Norio Saito, Urban Development and Water Division (SAUW), SARD

Team leader Momoko Tada, Urban Development Specialist, SAUW, SARD

Team members Saswati Belliappa, Safeguards Specialist, SAUW, SARD Bhawna Kulshreshtha, Executive Assistant, India Resident Mission

(INRM), SARD Pradeep Kumar Pandey, Associate Operations Analyst, INRM, SARD Girish Mahajan, Senior Environment Officer, INRM, SARD Rodellyn Manalac, Operations Assistant, SAUW, SARD Suhail Mircha, Safeguard Officer, INRM, SARD

In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area.

CONTENTS Page

BASIC DATA i

I. PROJECT DESCRIPTION 1

II. DESIGN AND IMPLEMENTATION 2

A. Project Design and Formulation 2

B. Project Outputs 3

C. Project Costs and Financing 5

D. Disbursements 5

E. Project Schedule 6

F. Implementation Arrangements 6

G. Technical Assistance 6

H. Consultant Recruitment and Procurement 7

I. Gender Equity 8

J. Safeguards 8

K. Monitoring and Reporting 8

III. EVALUATION OF PERFORMANCE 9

A. Relevance 9

B. Effectiveness 10

C. Efficiency 11

D. Sustainability 11

E. Development Impact 12

F. Performance of the Borrower and the Executing Agency 12

G. Performance of the Asian Development Bank 13

H. Overall Assessment 13

IV. ISSUES, LESSONS, AND RECOMMENDATIONS 14

A. Issues and Lessons 14

B. Recommendations 15

APPENDIXES

1-1. Design and Monitoring Framework for Project 1 16

1-2. Details and Status of Outputs Originally Planned in the Periodic Financing Request 23

2. Project Cost at Appraisal and Actual 26

3. Project Cost at Appraisal and at Completion By Financier 27

4. Disbursement of ADB Loan Proceeds 29

5. Contract Awards of ADB Loan Proceeds 30

6. Chronology of Main Events 31

7. Summary of Contract Details 32

8. Status of Compliance with Loan Covenants 33

9. Safeguards Assessments 53

10. Economic and Financial Analysis 55

BASIC DATA A. Loan Identification 1. Country 2. Loan number and financing source 3. Project title 4. Borrower 5. Executing agency

6. Amount of loan 7. Financing modality

India 2331, ADB ordinary capital resources Jammu and Kashmir Urban Sector Development Investment Program (Project 1) India Economic Reconstruction Agency $42.2 million Multitranche financing facility

B. Loan Data 1. Appraisal – Date started – Date completed

2. Loan negotiations – Date started – Date completed

3. Date of Board approval

4. Date of loan agreement

5. Date of loan effectiveness – In loan agreement – Actual – Number of extensions

6. Project completion date – Loan agreement – Actual

7. Loan closing date – In loan agreement

– Actual – Number of extensions

8. Financial closing date – Actual 9. Terms of loan –Interest rate – Maturity (number of years) – Grace period (number of years)

12 February 2007 16 February 2007

16 April 2007 17 April 2007

31 May 2007

28 December 2007

27 March 2008 25 March 2008 0

30 April 2012 31 May 2017 31 Oct 2012 30 May 2017 4

2 November 2017a London interbank offered rate (LIBOR)-based (floating) + 0.60% 25 Years 5 Years

a Unfinished works were completed with state government funding in March 2019. March 2019 is the starting point for an 18-month period by the end of which this project completion report must be circulated.

ii

10. Disbursements

a. Dates

Initial Disbursement

29 July 2009

Final Disbursement

2 November 2017

Time Interval

99 months

Effective Date

25 March 2008

Original Closing Date

31 October 2012

Time Interval

55 months

b. ADB Loan Amount ($ million)

Category

Original Allocation

(1) a

Increased during

Implemen- tation (2) b

Cancelled during

Implemen- tation (3)

Last

Revised Allocation (4=1+2–3)

Amount Disbursed

(5)

Net Undisbursed

Balance (6=4–5) c

I Base Cost

Component A: Urban Infrastructure and Environmental Improvements

Water supply 4.80 0 0 4.80 2.39 2.41

Sewerage, drainage, and sanitation

19.30 0 0 19.30 13.72 5.58

Solid waste management

2.10 0 0 2.10 7.27 (5.17)

Transportation and urban roads

3.40 0 (3.40) 0 0 0

Resettlement and land acquisition

0 0 0 0 0 0

Subtotal (A) 29.60 0 (3.40) 26.20 23.37 2.83

Component B: Capacity Building, Institutional Development, Governance, and Investment Program Support

Training and workshops 0.50 0 0 0.50 - 0.50

Consultancy support 7.00 0 0 7.00 7.78 (0.78)

Incremental administration, including computers and peripherals

2.40 0 0 2.40 5.93 (3.53)

Subtotal (B) 9.90 0 0 9.90 13.71 (3.81)

II Contingencies 2.70 0 (1.60) 1.10 0 1.10

III Taxes and duties 0 0 0 0 0 0

IV Financing charges during implementation

0 0 0 0 0 0

Total 42.20 0 (5.00) 37.20 37.08 0.12 a From periodic financing request 1 and loan agreement. b Some subprojects were increased and others reduced during detailed planning and design. The total is net of the reductions and additions.

c The undisbursed balance of $116,244.59 was cancelled at project completion.

iii

C. Project Data 1. Project cost ($ million)

Cost Appraisal Estimate a Actual

Foreign exchange cost b … 2.48

Local currency cost … 57.85

Total 64.90 60.33

…= data not available. a No breakdown of foreign exchange cost and local currency cost was prepared at appraisal. b Includes interest and commitment charges.

2. Financing plan ($ million)

Cost Appraisal Estimate Actual

Implementation cost

Borrower financed 18.30 21.21

ADB financed 42.20 37.08

Total implementation cost 60.50 58.30

Interest during implementation cost

Borrower financed ADB financed

4.40 0

2.03 0

Total 64.90 60.33 ADB = Asian Development Bank. Note: Numbers may not sum precisely because of rounding.

3. Cost breakdown by project component ($ million)

Component Appraisal Estimate Actual

I. Base Costs

A. Urban Infrastructure Improvements

Water supply augmentation 5.90 2.91

Rehabilitation of solid waste facilities 2.60 15.39

Rehabilitation of sewerage system 23.60 23.19

Rehabilitation of roads and bridge 4.10 0.00

Resettlement and land acquisition 1.00 0.46

B. Capacity Building and Institutional Development

Consultancy support 7.40 8.23

Incremental administration, including vehicles, computers, equipment, and laboratory

2.90 7.44

Training and workshops 1.00 0.00

II. Contingencies 5.80 0.00

III. Taxes and Duties 6.20 0.59

IV. Financing Charges During Implementation 4.40 2.03

Total 64.90 60.33

iv

4. Project 1 Schedule

Item Appraisal Estimate Actual

Date of contract with consultants

Project management consultants Q2 2007 Q2 2009

Design and supervision consultants Q2 2007 Q3 2009, Q1 2011, and Q1 2014

Completion of engineering designs March 2008 Q2 2008

Civil works contract

Date of contract award March 2008 Q2 2008 and Q1 2014

Completion of work April 2012 Q4 2016

Equipment and supplies

First procurement Q2 2007 Q2 2008

Last procurement Q3 2011 Q2 2014

Completion of equipment installation April 2012 Q4 2016

Start of operations

Completion of tests and commissioning July 2012 Q1 2017

Beginning of start-up July 2012 Q2 2017a

Q = quarter. a Works under sewerage subproject were not completed before financial closure, but the unfinished works were

eventually completed in March 2019 with state government funding. 5. Project Performance Report Ratings

Implementation Period

Ratings

Development Objectives Implementation Progress

From 18 June 2008 to 31 December 2008 Satisfactory

Satisfactory

Satisfactory

Satisfactory

Satisfactory

From 1 Jan 2009 to 31 July 2009

From 1 Aug 2009 to 31 December 2009

Highly Satisfactory

Satisfactory

From 1 Jan 2010 to 31 December 2010 Satisfactory

Single Project Rating*

From 1 January to 31 December 2011 On track

From 1 January to 31 December 2012 On track

From 1 January to 31 December 2013 On track

From 1 January to 31 December 2014 On track

From 1 January to 31 December 2015 On track

From 1 January to 31 December 2016 On track

From 1 January to 31 December 2017 On track *After 2010, only one rating is available.

D. Data on Asian Development Bank Missions

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of

Members

Project appraisal 12–16 Feb 2007 7 154 d, r, g, a, d, s, t

Contact 17 Jul–18 Jul 2008 3 6 a, e, f

Loan review 1 26 Aug–4 Sep 2009 2 20 a, b

v

Name of Mission Date No. of

Persons No. of

Person-Days Specialization of

Members

Special loan administration 4–12 Jan 2010 3 30 d, a, l

Loan review 2 28 Mar–2 Apr 2010 3 18 a, b, i

Contact 14–17 Jul 2010 2 8 a, e

Contact 24 Apr–7 May 2011 6 84 d, c, a, g, j, k

Loan review 3 23–28 Jan 2012 2 12 d, f

Loan review 4 / fact-finding 26 Mar–16 Apr 2012 7 154 d, r, g, a, d, s, t

Midterm review 1 22–26 Apr 2013 2 10 d, l

Special project administration

1–10 Jun 2013 3 30 d, a, l

Loan review 5 11–14 Jun 2013 2 8 e, u

Special loan administration 22–26 Oct 2013 2 10 a, l

Special loan administration 19–22 Nov, Apr 2013 2 8 l, g

Midterm review 2 10–17 Feb 2014 3 24 a, l, f

Loan review 6 21–25 Jul 2014 2 10 a, l

Loan review 7 17–24 Nov 2014 4 32 a, d, l, s

Special loan administration 15–17 Apr 2015 2 6 a, l

Loan review 8 7–9 Sep 2015 2 6 a, l

Midterm review 3

Loan review 9

Loan review 10

Loan review 11

16–21 Nov 2015

4–11 Apr 2016

21–22 Nov 2016

27 Feb–1 Mar 2017

7

5

3

3

42

40

6

9

d, b, a, l, t, j, f

d, l, s, t, s

d, a, c

d, a, s

Loan review 12 18–22 Jun 2018 2 10 d, v

Loan review 13 26–30 Nov 2018 4 20 d, s, w, x

a = project implementation officer, India Resident Mission, b = financial/administrative analyst, c = resettlement specialist, d = urban development specialist, South Asia Urban Development Division, e = urban economist, South Asia Urban Development Division, f = project analyst, India Resident Mission, g = safeguard specialist, j = environmental specialist, l = associate project analyst, r = project counsel, s = consultant project specialist, t = gender consultant, u = transport specialist, v = country director, India Resident Mission, w = principal portfolio management specialist, x = urban specialist, India Resident Mission. Source: Asian Development Bank.

I. PROJECT DESCRIPTION 1. The Jammu and Kashmir Urban Sector Development Investment Program was designed to expand and upgrade urban services in the major urban areas of the state to Indian national and state standards. The focus was on providing water and sanitation services to the poor and other low-income segments of the population. The program aimed to improve public health, the urban environment, and quality of life for more than 2.4 million people living in the state’s two main cities and other selected towns. It also aimed to modernize and streamline the planning, operation and maintenance (O&M), and administrative functions of the responsible city departments.1 Urban improvements were envisaged concurrently to promote commercial development, facilitate public–private partnership, and generally help to improve the economy of the state, in part by facilitating tourism. 2. The Asian Development Bank (ADB) approved the program as a multitranche financing facility (MFF) on 31 May 2007 at an estimated cost of $485 million. 2 The ADB loan was $300 million, and the state government contributed $185 million. The first loan under the MFF (Loan 2331-IND, project 1) was approved on 31 May 2007 for a project cost estimated at $64.9 million, the ADB loan being $42.2 million and the state government contribution $22.7 million. Project 1 aimed to achieve the expected impact and outcomes through the following outputs:3

(i) Part A: Urban infrastructure improved through investments in water supply, wastewater management, solid waste management (SWM), and urban transport and roads.

(ii) Part B: Capacity development and institutions developed 4 through (a) consultant services for project 1, (b) investment program administration assistance to the executing agency, (c) capacity building in the State Pollution Control Board, (d) developing an accrual-based accounting system in urban local bodies (ULBs), (e) preparing economic opportunity development plans for other towns and commercial centers in the state, (f) establishing e-governance systems in ULBs, and (g) training and institutional development to support the urban reform agenda.

3. The expected impact of project 1 (footnote 3) was sustainable economic growth through the provision of urban infrastructure and services and improved urban management. The anticipated outcomes were (i) improved living environments and employment opportunities for the 2.4 million people in Srinagar and Jammu (the target towns), and (ii) improved capacity in participating institutions to manage sector reform and service delivery.

1 Responsibility for basic urban services was shared as follows: capital works financed by external funding sources,

including ADB, were planned, designed, and implemented by the state Economic Reconstruction Agency (ERA) on behalf of ULBs. O&M responsibility was as follows: (i) water supply systems under the state’s Public Health Engineering Department (PHED), (ii) sewerage systems under the state Housing and Urban Development Department (HUDD); and (iii) solid waste facilities and transportation under ULBs. Billing and fee collection are operated by the respective entities, but revenues are passed to the state.

2 ADB. 2007. Report and Recommendation of the President to the Board of Directors for the Proposed Multitranche Financing Facility to India for the Jammu and Kashmir Urban Sector Development Investment Project. Manila.

3 A separate design and monitoring framework (DMF) for project 1 was not included when the MFF was approved. In 2011, a DMF for project 1 was formulated as part of the retrofitting of projects in eOps for all ongoing ADB projects. The indicators and targets were subsequently adopted by the government, and the DMF was monitored in progress review missions. The DMF did not, however, include all outputs listed in the report and recommendation of the President and the periodic financing report (PFR). A separate table in Appendix 1-1 contains the details and status of all originally planned outputs. Performance indicators and targets for impacts were also not established. In this PCR, the same MFF impact indicators and targets are applied to evaluate the impact of project 1.

4 Included subcomponents were continued through succeeding tranches and loans for the duration of the MFF.

2

4. Project 1 was expected to benefit 0.38 million people with improved water supply, 0.23 million people with improved municipal sewerage systems, and 1.10 million people with improved SWM facilities. It was further expected to advance sector reform, mainstream capacity building as part of the state’s urban development budget, and demonstrate the ability of agencies to perform effective O&M of assets using modern management techniques while reducing costs.

II. DESIGN AND IMPLEMENTATION A. Project Design and Formulation 5. Project 1 was designed in accordance with government and ADB sector strategies at appraisal in 2006–2007. The project was consistent with India’s Tenth and Eleventh Five-Year Plans (2002–2012), emphasizing improvement and augmentation of economic and social infrastructure and provision of improved municipal services in urban areas.5 It also was consistent with state government approaches and strategies in its Eleventh Five-Year Plan for achieving service standards in line with the national average with respect to critical indicators of quality of life by narrowing poverty and regional disparities, providing basic services, and developing infrastructure.6 Project 1 also aligned with the ADB country strategy and program for India, 2003–2006, which highlighted the need to address interregional disparities; the ADB Urban Sector Strategy, 1999; 7 and ADB Strategy 2020 and its focus on poverty reduction, environment protection, and institutional strengthening.8 Although the project predated ADB Strategy 2030,9 it aligns with the strategy’s operational priority 4 on livable cities and the provision of safe and effective water and sanitation services. 6. The program’s design reflected ADB’s learning from supporting urban projects in India and from an earlier urban sector loan to the state, which, as the first project in the sector in the state, was able to address only a small part of the large medium-term requirements.10 The program aimed to address the remaining priority development needs. Project 1, costing $64.9 million from a total program cost of $485.0 million, addressed the most urgent and basic infrastructure gaps and laid foundation for succeeding investments by building capacity in responsible agencies. ADB experience within India’s urban sector had shown project sustainability to depend on three main imperatives:11 (i) selecting subprojects through extensive consultation with a wide range of stakeholders and following a demand-driven approach, (ii) institutional development to ensure that adequate O&M funds are mobilized from internal resources and gradual transfers from the state to responsible institutions, and (iii) capacity building in service-delivery institutions to adopt corporatized or commercially oriented operations that include user fees and tariffs. These imperatives guided selection of subprojects for water

5 Government of India, Planning Commission. 2002. Tenth Five-Year Plan, 2002–2007. New Delhi; Government of

India, Planning Commission. 2007. Eleventh Five-Year Plan, 2007–2012. New Delhi. 6 State government, Planning and Development Department. 2007. Eleventh Five-Year Plan (2007–2012). New Delhi.

Project 1 was also consistent with the sector road map developed by the state government in conjunction with the Jawaharlal Nehru National Urban Renewal Mission, through which the Government of India fast-tracks reform-driven development planning to modernize 63 major towns of India.

7 ADB. 2003. Country Strategy and Program: India 2003–2006. Manila, ADB. 1999. Urban Sector Strategy. Manila. 8 ADB. 2008. Strategy 2020: The Long-Term Strategic Framework of the Asian Development Bank 2008–2020. Manila. 9 ADB. 2018. Strategy 2030: Achieving a Prosperous, Inclusive, Resilient, and Sustainable Asia and the Pacific.

Manila. 10 ADB. 2004. Report and Recommendation of the President to the Board of Directors on a Proposed Loan to India for

the Multisector Project for Infrastructure Rehabilitation in Jammu and Kashmir. Manila (Loan 2151-IND, for $250 million, approved on 22 December 2004). Loan 2151 addressed such urgent investment needs as rehabilitating water supply systems, and project 1 expanded these investments.

11 Summarized in ADB. 2006. Special Evaluation Study on Urban Sector Strategy and Operations. Manila.

3

supply, sewerage, SWM, and transport based on public consultations and subsector masterplans. Also in line with these imperatives, priority investments under the first tranche of the program were linked with incremental reform and substantive support to build capacity and ensure sustainable financial operations. 7. The MFF modality was an appropriate and effective approach to facilitate a long-term relationship between the Economic Reconstruction Agency (ERA) and ADB.12 The modality suited the complex works in urban areas, requiring flexibility in scope and longer implementation periods to coordinate multiple stakeholders. Further, it allowed adjustments in ADB support given the severe winters and frequent monsoon flooding conditions in the project areas. During loan processing, the design and monitoring framework (DMF) for the facility was prepared and outcomes and outputs were defined (footnote 3). Achievements are detailed in Appendix 1-1. 8. Two minor changes in scope during implementation addressed realities on the ground. One scope change reduced a raw water pipeline in a water supply subproject from 10.0 kilometers (km) to 5.6 km, and the other shifted an urban transportation subproject to project 2 to better address congestion with larger scope. The need for these scope changes came to light only after detailed surveys and designs were conducted after approval of periodic financing request (PFR) 1 in 2007.13 Consequent loan savings were partly reallocated to expand the much-needed solid waste landfill site.14 Eventually, $5.0 million was cancelled from the ADB loan in 2014.15 While project 1’s design at appraisal was appropriate to achieve expected outcomes and outputs, it could have considered incorporating comprehensive end-to-end solutions, such as 24×7 water supply with well-defined O&M arrangements in construction contracts and integrated SWM with source segregation, collection, transportation, reuse, recycling, and disposal. Also, the assessment of state capacity at appraisal was rather optimistic, encouraging ambitious reform targets and delaying the start of some subprojects in part B, for capacity building and institutional development. 16 With these exceptions, the design remained relevant at completion as development needs for basic urban services remained unchanged in the targeted towns. B. Project Outputs 9. Project 1 outputs are summarized below. The targeted outputs are based on the DMF established in e-Operations (eOps) in 2011. The complete list of planned outputs of project 1 are in Appendix 1-2.

1. Part A: Urban Infrastructure Improvements 10. Water supply. The targeted output for this subproject was to lay 5.6 km of raw water pipeline. This was substantially achieved with a 4.8 km pipeline (86%). The original design was to lay a 10.0 km raw water pipeline from Sindh Canal to the Nishat water treatment plant, but detailed hydrological investigation discovered raw water of better quality from a nearer natural source. This alternative source would require only 5.6 km of new pipeline, including replacement

12 ADB recognized the benefits of longer-term relationships through its earlier long-term support to urban sectors in

Karnataka and Rajasthan. 13 During MFF preparation in 2007, only outline plans and designs were required to formulate the MFF and generate

cost estimates toward securing the proposed ADB financing. This program is the 12th MFF approved in ADB. 14 Savings were also used to cover incrementally higher administration costs, as project completion suffered a 5-year

delay, and to prepare subsequent projects under the MFF. 15 ADB. Loan 2331-IND: Jammu and Kashmir Urban Sector Development Infrastructure Development Investment

Program, Project 1-Partial Cancellation from the Loan Accounts. New Delhi (13 August 2014). 16 The state government’s capacity constraint was gradually mitigated by capacity building activities throughout the

program’s duration.

4

of existing pipes, and cost less to pump. The Public Health Engineering Department (PHED), state government, and ERA decided there was little benefit from the original Sindh Canal option, and ADB therefore approved a minor change in scope in 2010.17 With further refinement of the alignment, a 4.8 km pipeline was laid. The revised subproject provided an additional 533,000 people with water supply increased from 80 liters per capita per day (lpcd) to the national standard of 135 lpcd and extended service by 6 hours to 8 hours daily. The intended service improvement was in fact overachieved despite the reduced physical output (pipeline length).18 11. Sewerage. Targeted outputs for this subproject were to lay a 180 km sewerage network and construct a sewage treatment plant (STP) with capacity of 30 million liters per day (mld).19 Project 1 achieved these targets by laying a 190 km sewerage network, developing one STP with 30 mld capacity, and including 33,500 house connections to ensure expeditious realization of benefits. 20 By project completion in May 2017, ADB funding had completed 20,000 house connections, leaving 13,500 connections unfinished because implementation had been delayed by a misprocured contract and termination of other nonperforming contracts (paras. 22–23). The loan was not extended as extensive consultation and coordination with each household were necessary which required more time. The remaining connections were completed in March 2019 with funds provided by the state and by project 3 under the program,21 thus benefitting the original planned population of 230,000 with a centralized sewerage system. 12. Solid waste management. The targeted output for this subproject was to construct and improve sanitary landfill capacity by 250 metric tons per day.22 This was achieved by improving and expanding landfill capacity to 380 metric tons per day. Apart from meeting this output target, project 1 also expanded two other landfill sites with daily capacity increases of 243 and 335 metric tons. 23 This subproject also introduced weighing scales at entry and exit points, waste segregation equipment, cell liners, leachate collection and treatment, and additional collection bins and equipment. Biodegradable waste is collected and treated by composting at the landfill site. Facilities for drainage collection and treatment of runoff and leachate were also constructed, greatly reducing pollution loads in surrounding streams. The landfill site’s operations were improved to ensure daily cover of waste and fencing to avoid wind-blown trash, thereby reducing pest and disease vectors and odors. In addition, the two-lane access road to the landfill from the main highway benefited thousands of residents in surrounding areas. During the disastrous floods in 2014, the landfill site accommodated proper disposal of a large quantity of debris and municipal waste and thus facilitated the city’s early recovery and prevented disease outbreaks. 13. Urban transport. At appraisal, it was planned to include this subproject to expand an arterial road to six lanes and construct a flyover. During preparation of a mobility plan and detailed engineering design, however, it was found that the original scope would not effectively decongest

17 Approved by a memo for minor change in scope dated 22 June 2010. 18 Another positive outcome was reduced raw water extraction from Dal Lake. The lake has socioeconomic significance

for tourism, fisheries, and drinking water resources, but water quality has deteriorated with rapid urbanization and increased inflow of wastewater.

19 The plan in the 2007 PFR for project 1 was for a 200 km sewer network and a sewerage treatment plant with 30 mld capacity. In 2011, when the DMF was established, the target length of network was shortened to 180 km.

20 Past ADB-financed projects have experienced extensive delays in completing house connections because households had to pay for them.

21 ADB. 2014. Periodic Financing Request Report for Jammu and Kashmir Urban Sector Development Investment Program: Tranche 3. Manila (Loan 3132-IND)

22 The output in the 2007 PFR for project 1 included lined sanitary landfill cells with internal approach roads, a new two-lane access road to the main highway, and a weighbridge. In 2011, when the project 1 DMF was established, the target output was set at constructing and improving sanitary landfill capacity by 250 tons per day.

23 Loan savings from other subprojects, including shifting transport to subsequent projects, were reallocated to the SWM subproject to expand the scope than planned at appraisal.

5

arterial roads as intended. The updated cost was estimated at $20 million, substantially higher than the original cost of $4 million. This subproject was therefore cancelled from project 1 and shifted to project 2 through a minor change in scope.24

2. Part B. Capacity Building and Institutional Development 14. Although the DMF for project 1 set no targets, the planned outputs for part B in the PFR were mostly met and consequently contributed to the MFF targets.25 Targeted outputs achieved were (i) initiation of geographic information system mapping, 26 (ii) publication of municipal corporation balance sheets for fiscal year (FY) 2010 and 2011, and (iii) demonstration of staff capacities in management and service-delivery functions.27 Partly achieved outputs were the introduction of a computerized system for water billing and collection, updating of municipal database and introduction of a management information system. The system’s development was initiated under project 1, but completion was expected under succeeding projects. The same applied for updating a database on municipal corporation services, finances, staff, and assets, as well as the introduction of a municipal management information system for the Housing and Urban Development Department (HUDD). O&M costs of water supply were partly recovered and the remainder dependent on state budget allocation. Implementation made evident that reform targets were rather ambitious considering the state’s limited capacity and the local context, including frequent unrest, and required a longer implementation period than planned. It was decided to defer some reform to subsequent projects.28 C. Project Costs and Financing 15. The estimated project cost at appraisal was $64.9 million, with the ADB loan financing $42.2 million and the government contributing $22.7 million. Reallocation was made after minor changes in scope (para. 8), and $5.0 million was cancelled from the ADB loan. With this, project cost at completion was reduced to $60.3 million, with the ADB loan financing $37.1 million and the government contributing $23.2 million. The main reasons for the reduced ADB loan amount were rupee depreciation from the time of appraisal and lower actual disbursement, with no contingency disbursement required. Project costs at appraisal and completion are in Appendix 2 and summarized by financier in Appendix 3. D. Disbursements 16. In the early stages of implementation, disbursement was slow due to delayed procurement. After the first works contracts were awarded in 2010, annual disbursements were consistently more than $6 million from 2011 to 2013, reaching 77% of the revised loan amount, or 68% of the original loan amount, by the first revised loan closing date of 31 October 2014. After the severe flooding in September 2014, however, annual disbursement dropped to $5.4 million in 2014 and further to $3.2 million in 2015. In addition, poor performance by sewerage contractors

24 Memo for minor change in scope dated 26 August 2013. 25 The outputs expected in the PFR included administrative assistance through consultancy and the investment

program, capacity building in the state Pollution Control Board, and the development of an accrual-based accounting system. These outputs were not included when the DMF was established in 2011 in eOps. A separate table in Appendix 1-2 contains the details and status of all outputs originally planned in the PFR.

26 Subsequent projects used geographic information systems to develop property tax registers and billing and bill-collection systems.

27 Contractors provided institutional strengthening for better O&M of new and improved facilities through hands-on training. Specialists under the project management consultant (PMC) trained the State Pollution Control Board to apply state requirements more effectively for testing, monitoring, and reporting on effluent disposal.

28 Periodic Financing Request Reports for project 2 and 3.

6

(para. 23) brought annual disbursement to a low $0.9 million in 2016 and $1.6 million in 2017. By project completion, $37.08 million was disbursed, or 87.9% of the original loan amount of $42.2 million and 99.5% of the revised loan amount of $37.1 million. At financial closure in November 2017, the remaining $116,245 in unallocated loan funds were cancelled. All withdrawal applications were submitted to ADB through the Controller of Aid Accounts and Audit of the Ministry of Finance, Government of India. The project used the mechanism for disbursement through statements of expenditure and documented claims. 29 All disbursement-related qualifications raised by the auditors were duly addressed. Appendix 4 presents projected and actual loan disbursements. E. Project Schedule 17. The project was originally planned to be completed by April 2012 but was completed in May 2017. Major reasons were procurement delays caused by limited contractor interest and state capacity, which delayed disbursement; public unrest from time to time; and historic 100-year flooding in 2014. In subsequent years, project implementation was continually affected by local unrest which was external to the project and beyond ERA’s control. There were also issues with (i) initially weak staff capacity of project implementation units (PIUs), (ii) ERA and state staff being overloaded with multiple large projects, and (iii) an overlap period of project 1 with then-ongoing ADB Loan 2151 (footnote 11) and national programs, and concurrent appraisals of projects 2 and 3 of the MFF. By the time project 1 was fully implemented, it was already past the midpoint of the original implementation period for the whole program. This was exacerbated by weak contractor performance, termination of their contracts, and time required for rebidding. By loan closure in November 2017, 13 of the 14 contracts were completed. The contract for sewerage works was completed using funds from the state and project 3 in March 2019 (para. 11). The original loan closing date of 31 October 2012 was extended four times, and the loan account eventually closed on 30 May 2017.30 All extensions were required to (i) optimize loan utilization, (ii) enable the completion of ongoing works to maximize project outcomes, and (iii) complete retendered and slow-moving sewerage contracts. A chronology of main events is in Appendix 6.

F. Implementation Arrangements 18. Project implementation arrangements were as specified in the report and recommendation of the President, facility administration manual, and PFR 1. They were appropriate to achieve the envisaged outputs, albeit much later than estimated at appraisal. The executing agency was ERA, guided by state-level inter-ministerial and city committees and a works finalization committee chaired by the division commissioner. ERA established a dedicated project management unit (PMU) for project 1 and PIUs in the target cities. The PMU and PIUs were assisted by a project management consultant (PMC) and design and supervision consultants (DSCs). The DSCs supported preparation of detailed designs and bidding documents, the bidding process, and supervising construction. Safeguard consultants were mobilized for environmental and social aspects, including an external monitor for resettlement. G. Technical Assistance 19. The preceding ADB-funded project, Loan 2151, was accompanied by a $0.5 million project preparatory technical assistance (TA) grant to prepare a comprehensive investment

29 The project benefitted from a simplified process for statement of expenditure that did not require the submission of

supporting documents for individual payments up to $100,000. 30 Approved on (i) 23 May 2012, (ii) 14 April 2014, (iii) 27 April 2015, and (iv) 20 February 2017.

7

plan.31 With TA support, the state designed and prepared the program as an MFF including project 1. Sector plans and policies to promote cost recovery through tariff reform were also prepared under preparatory TA, which became part of institutional strengthening under the program. To further support ERA implementation of projects, ADB approved a $0.4 million grant for advisory TA in December 2006.32 The advisory TA supported ERA—especially at early stages of the MFF until TA closure in March 2009—to (i) improve its functionality, (ii) build its project management and implementation capacity, (iii) expedite contract award and execution by providing guidance to ERA on procurement-related issues, and (iv) assist in setting and achieving yearly targets for contract award and disbursement. H. Consultant Recruitment and Procurement 20. Consultants were recruited in accordance with ADB Guidelines on the Use of Consultants (2006, as amended from time to time). ERA followed the quality- and cost-based selection procedure to select the PMC and two DSCs (one for each target city). No local engineering firms could qualify for the large consulting contracts. As ERA had a functioning PMU for Loan 2151, consultant recruitment for project 1 should have proceeded immediately upon ADB approval of project 1 in December 2007, but ERA did not proceed until after the loan became effective in March 2008 for lack of staff and overload from multiple large projects. As a result, it took 15 months to recruit the PMC and one of the DSCs, delaying project 1 start-up. 21. Overall consultant performance is rated less than satisfactory. The original PMC and one of the DSCs were weak and had difficulty fielding and maintaining experienced staff in the planned positions. Absence was frequent, and several senior engineers were replaced. This resulted in delayed output delivery. Upon contract completion for the original PMC and one of the DSCs, new consultants were hired and performed substantially better. However, implementation delays continued caused by various factors such as site constraints, design changes, and consequent delay in finalizing and issuing technical and as-built drawings. The performance of the second DSC was generally satisfactory, and its services were retained in succeeding loan extensions. As a result of necessary changes, there were four consulting contracts in total. 22. Procurement was generally carried out as planned although there were delays due to limited contractor interest and state capacity. Except for misprocurement in one sewerage-laying package,33 procurement of all civil works contracts followed ADB Procurement Guidelines (2006, as amended from time to time). All works contracts were estimated to cost $10 million or less and therefore procured through national competitive bidding, using single-stage, two-envelope bidding procedures. The 30 mld STP contract was turnkey and with successful O&M for 12 months.34 The other nine contracts were bills of quantity based on item rates. Preparation of standard bidding documents, bids evaluation, and contracts award were per ADB guidelines. Review of all stages as under the Procurement Guidelines was conducted by ADB prior to contract award. Other than the transport subproject being shifted to a subsequent project, the original contract award projections were realistic and reflected in actual awards (Appendix 5).

31 ADB. 2004. Technical Assistance for Preparation of the Jammu and Kashmir Urban Infrastructure Development

Project. Manila (TA 4515-IND, approved on 21 December 2004). 32 ADB. 2006. Technical Assistance to India for Strengthening Urban Project Management in Jammu and Kashmir.

Manila (TA 4888-IND, approved on 2 December 2006). 33 Confidentiality during bid evaluation was not adequately managed by ERA. Upon ADB’s decision to cancel its

financing of the package, the state government executed the works with its own funds. 34 Concurrently, the contractor trained Urban Environmental Engineering Department staff under HUDD in O&M of the

new STP.

8

23. The performance of the water supply contractor and four solid waste contractors was satisfactory. Except for the STP contractor, however, performance of the other four contractors for laying sewers was unsatisfactory. The PMU and PIUs, assisted by the PMC and DSC, held regular meetings with contractors to resolve hindrances and execution issues and clarify relevant contractual issues. Despite this support, the four contracts proceeded slowly, as many instances of unacceptable workmanship had to be corrected. As a result, three sewerage-laying contracts had to be terminated by ERA, with ADB approval, in 2014 and 2016, leaving works unfinished. ERA subsequently hired new contractors with state funds and partly under a subsequent project to complete the original scope of the sewage collection network. The contracts and amounts of ADB loan disbursements are detailed in Appendix 7. I. Gender Equity 24. Although project 1 was categorized no gender elements, improved water supply by 1–2 hours per day to a minimum of 8 hours daily has reduced the time women must spend collecting water. Further, the waste management system and replacement of open drains by sanitary piped sewers has improved neighborhood conditions, benefitting women as household’s primary caregivers. The project also involved women in awareness campaigns conducted by local nongovernment organizations and consultants. It indirectly built awareness in local governments of public health benefits gained by including women in planning and implementing projects. J. Safeguards

25. Project 1 was classified category B sensitive for the environment, and category A for involuntary resettlement and indigenous peoples, as per ADB safeguard policies. 35 An environmental assessment review framework, a resettlement framework, and an indigenous peoples development framework were prepared during loan processing. A summary initial environmental examination report was prepared for the four subprojects, two in each target town. A full resettlement plan was prepared for the urban transport subproject and a short resettlement plan for the SWM subproject. As mentioned in para. 8, the urban transport subproject was transferred to project 2. Environmental impacts associated with the works were limited to the worksites, temporary and reversible in nature, and addressed through the environmental management plans. The project acquired 0.47 hectares of land belonging to two households and common property for constructing the approach road to the sanitary landfill. Negotiations with landowners failed, and the land was acquired under provisions of the State Land Acquisition Act, 1990. The landowners asked the High Court to revise rates, and their petition is pending. ERA had deposited compensation in an escrow account and confirmed it would be disbursed to the landowners in line with the decision. 36 During implementation, no indigenous people were affected. Safeguard compliance management—including institutional arrangements, information disclosure, consultations, grievance redressal, project staff capacity building, and regular submission of semiannual safeguard monitoring reports—was rated generally satisfactory.37 K. Monitoring and Reporting 26. Of 66 loan covenants, 56 were complied with, 9 were partially complied with, and 1 was

35 ADB. 2002. Environmental Policy of the Asian Development Bank. Manila; ADB. 1995. Involuntary Resettlement.

Manila; and ADB. 1998. The Bank’s Policy on Indigenous Peoples. Manila. 36 The land compensation budgeted in the approved short resettlement plan for the subproject is ₹8.51 million, and

ERA has deposited ₹21.08 million in the escrow account. 37 Adequate safeguard monitoring and management was ensured by executing agency safeguards experts supported

by PMC and DSC safeguard experts.

9

inapplicable. The covenants related to financial empowerment of the target towns were only partially complied with under project 1. Although initiated under project 1 with some delay, they were more fully achieved under succeeding projects. The covenant on the levy of sustainable user tariffs was partially complied with. Infrastructure development or urban development taxes are being levied, albeit at low levels. SWM charges are yet to be levied, and door-to-door collection is outsourced to private agencies. Safeguard covenants were complied with, but compensation directed by the court is still being challenged by three landowners at the SWM site (para. 25). The covenants related to contractor procurement were partially complied with due to poor contractor performance, one misprocurement, and implementation delay in a sewerage subproject. Covenants on financial statements were partially complied with (para. 27). 27. Financial management arrangements of the borrower and executing agency were robust and counterpart funding timely. Separate project financial accounts were maintained and audited by statutory auditors. Except for FY2008 and FY2018, audited project financial statements (APFS) were received, albeit with delays of 0.6 to 3.8 months from due dates, within the grace period of 6 months.38 For FY2008, no APFS or audited entity financial statements (AEFS) were submitted. The APFS for FY2018 were rejected as they included a combined audit report for all three projects despite separate reports and opinions being required. This constituted noncompliance. Appendix 8 details the status of compliance with loan covenants.

III. EVALUATION OF PERFORMANCE A. Relevance 28. The project is relevant to government development objectives and ADB country and sector strategies, both at appraisal and completion (para. 5).39 Though the project predated ADB Strategy 2030, it aligns with the strategy, especially its operational priority 4 to build livable cities and provide safe and effective water and sanitation services (footnote 10). At completion, the project remains aligned with the ADB policy focus for India on inclusive growth, infrastructure, and environmental sustainability. The project aligns with the government’s successive 5-year plans, the National Institution for Transforming India (NITI) Aayog’s 3-year action agenda, FY2018–FY 2020,40 and the state’s Eleventh and Twelfth Five-Year Plans, FY2007–FY2018, which prioritized potable water supply in urban areas, wastewater management, and urban poverty alleviation.41 It aligns with state priorities on poverty reduction through improved access to potable water and sanitation, good governance, and private enterprise participation.

29. The MFF modality was appropriate considering the complexity of the design, the flexibility of moving outputs to other tranches without affecting the facility outcome, and the advantage of longer engagement with the executing and implementing agencies (para. 7). Weaknesses were noted in the DMF for project 1, such as incomplete outputs and inconsistent targets based on the PFR (footnote 3). Also, inclusion of improved employment opportunities in the outcome statement would have been more appropriate under impact. Nevertheless, output

38 Reports were late by 0.8 months for FY2010, 0.7 months for FY2011, 3.8 months for FY2012, and 0.6 months for

FY2015. 39 Government of India, NITI Aayog. 2012. Twelfth Five-Year Plan, 2012–2017. Delhi. ADB. 2013. India: Country

Partnership Strategy (2013–2017). Manila. 40 NITI Aayog is a policy think tank of the Government of India that provides directional and policy inputs, designs

strategic and long-term policies and programs, and provides technical advice to the central and state governments. 41 Government of India, NITI Aayog. 2017. India Three-Year Action Agenda, 2017–2018 to 2019–2020. Delhi; State

government, Planning Department. 2012. Eleventh and Twelfth Five-Year Plans, 2007–2018. Delhi.

10

indicators and the subprojects developed were appropriate to achieve intended outcomes.42 Project implementation also adhered to the planned outputs based on the PFR even if they were not captured in the DMF (Appendix 1-2). 30. Changes in scope were timely and appropriate to better address emerging realities, and thus enhanced project relevance. In particular, the water supply subproject was adjusted to accommodate a source offering better-quality raw water that yielded enhanced outcomes. The urban transport subproject was shifted to project 2 to better address congestion.43 Loan savings resulting from these changes in scope were reallocated to the SWM subproject to further expand the landfill site. Further, the funds were used to finance the substantial rise in incremental administration cost as unanticipated external factors, particularly elevated local unrest and the historic 100-year flooding in 2014, required loan extension up to 5 years. The state also demonstrated strong ownership and commitment by completing the remaining works of the sewerage subproject with its own funding. B. Effectiveness

31. The project is rated effective in achieving the outcome and output targets. In line with ADB’s evaluation guidelines, project effectiveness is assessed against the three outcome and four output targets indicated in the DMF for project 1 as established in 2011. A separate table in Appendix 1-2 shows details and the status of all originally planned outputs based on the PFR to supplement the assessment.44 Of the three outcome targets for urban infrastructure (part A of the DMF), two were achieved and one was achieved with delay. Though the physical scope of the water supply subproject was reduced, its outcome target was overachieved because it increased the beneficiaries to 533,000 people against a target of 380,000 people. This was a major contribution to the MFF target of 2.4 million beneficiaries. Water supply quantity also increased from 80 lpcd to 135 lpcd, meeting the Government of India’s national target. 45 Further, it lengthened water supply service by 1–2 hours per day to 8 hours. The outcome target for SWM was also achieved. The Achan landfill site was expanded to benefit an additional 1.1 million people. The outcome of the sewerage subproject was achieved with delay, serving the target of 230,000 (para. 11). The new STP with 30 mld capacity will serve beneficiaries until 2036. These outcome achievements were directly attributable to the subprojects’ achieved outputs. Safeguards were implemented effectively, and no adverse effect from the project was observed (para. 25 and Appendix 9). 32. Output and outcome targets were not specified for capacity building and institutional development (part B) in project 1’s DMF, but output targets based on the PFR were mostly achieved (para. 14, footnote 26, Appendix 1-2) and have contributed to applicable MFF outcome targets (Appendix 1-1). These include (i) strengthened capacity in the government entities through a structured institutional development plan prepared under the MFF; and (ii) sector reforms, including economic opportunity development plans and introduction of e-procurement for e-submission. In addition, action was taken to outsource some municipal functions regarding SWM and water billing, including an assessment for sewerage that freed up human resources for improved urban governance and management of municipal service delivery. Related training programs, including those under the state budget, effectively reoriented government agency staff toward a professional approach to municipal services and better urban governance.

42 The DMF could have included outcomes and outputs for capacity building. 43 Project 1 remained relevant after the scope change as savings were used for a much-needed waste landfill site. 44 Of 26 outputs in the PFR, excluding the transport subproject, 21 were achieved (81%) and 5 were partly achieved. 45 Government of India. 2010. A Handbook on Service Level Benchmarking. New Delhi.

11

C. Efficiency 33. Project 1 is rated efficient. The overall economic internal rate of return (EIRR), while not assessed at appraisal, was recalculated at completion at 12.27%. Subproject EIRRs at completion were also recalculated against their appraisal estimates. The EIRR at completion for the water supply subproject was recalculated as 31.44%, lower than the appraisal estimate of 38.04%.46 For the SWM subproject, the EIRR at completion was recalculated as 18.30%, higher than the appraisal estimate of 17.15%. Thus, for these two subprojects, the recalculated EIRRs were above ADB’s 12% threshold for economic viability. For the sewerage subproject, the EIRR at completion was recalculated as 7.53%, much lower than the appraisal estimate of 32.65% and below the threshold because the interventions were reduced by poor contractor performance and termination of three contract packages. 47 The originally planned scope of works, including household connections, was nevertheless completed under state government funding. The EIRR of the urban transport subproject was not reassessed at completion, as it was shifted to project 2.48 The economic net present value of all completed subprojects except sewerage was positive when applying the 12% discount rate. Costs were $5.1 million less than the original ADB loan amount after scope changes and reallocation of funds (para. 30). Time extension of 5 years was necessitated due to issues on contractor and staff capacity, but also significantly because of local unrest and the major floods which were beyond project’s control. Institutional efficiencies and grievance redress mechanisms developed by ERA reduced transaction costs in terms of process and time and improved transparency and governance accountability while significantly augmenting the administrative capacity of ERA. Details are in Appendix 10. D. Sustainability 34. Project 1 is rated likely sustainable. The Constitution of India mandates that the state allocate to ULBs the funds required to maintain their functions and sustain service delivery.49 PHED is responsible for technical O&M of water supply systems, HUDD for sewerage systems, and municipal corporations for solid waste facilities. Their responsibilities include billing and fee collection for these services, but the revenue is remitted to the state government, which is responsible for financial management of these assets and services. For municipal corporations, finances are structured through fiscal transfers from the state as compensation grants and transfers from central and state finance commissions.50 The project was not designed to recover capital costs, so state government operating ratios were calculated to assess sustainability.51 They averaged 0.96, meaning that operating revenues are enough to meet O&M expenses.52 Similar reviews at PHED, HUDD, and municipal corporations indicate they are able to meet O&M

46 The EIRR for the water supply subproject at appraisal included incremental water supply at expected tariffs based

on a survey of willingness to pay. At project completion, the EIRR was based on incremental water supply at willingness-to-pay tariff determined during project preparatory TA and adjusted for inflation, as field missions to update the survey on willingness to pay were rendered impossible by local unrest and travel restrictions due to the coronavirus disease (COVID-19) pandemic. The subproject realized most projected benefits despite reduced costs.

47 The contract for the sewage treatment plant was the only one completed with ADB loan funds. 48 The estimate at appraisal was 16.70%. 49 Article 243 X and schedule XII. 50 The Central Finance Commission transfers accounts for 30%–40% of ULB finances, of which up to 90% may be

used for the O&M of municipal assets. 51 The operating ratio is operating receipts against operating expenditures. The cost-recovery calculation does not

include asset depreciation. 52 The state finance commission allocates a percentage of net tax proceeds to local governments to support financially

weaker local bodies (categories II–IV). The Central Finance Commission offers in addition the provision of 5% toward a performance incentive and is in the process of expanding the pool and criteria.

12

costs of water supply, sewerage, and SWM assets through the state budgetary allocations.53 The analysis assumed consistency in state government’s timely release of requisite O&M funds to PHED, HUDD, and municipal corporation, as providing these urban services is a fundamental responsibility of the state government. Details of the financial reevaluation are in Appendix 10. 35. Institutional capacity was strengthened as part of ongoing reform and under the facility. A result was improved operational functions, such as door-to-door collection of municipal solid waste by the municipal corporation and O&M of water treatment plants by PHED and of STPs by HUDD.54 Water billing and collection with the sewerage surcharge were improved. While PHED and HUDD have sufficient human resources and technical capacity for O&M of water supply and sewerage assets, municipal corporations in targeted towns need to continue augmenting human resources and institutional capacity to achieve better asset management and governance. E. Development Impact 36. The development impact of project 1 is rated satisfactory. Based on the DMF impact indicators, real income per capita in the state rose by 162.46% from 2007 to 2017, for a compound annual growth rate (CAGR) of 10.13%. Also, income outside the primary sector in districts encompassing project cities grew by 225.06% (CAGR 13.85%), with investment in industry and trade increasing by 100.45% (CAGR 7.20%). Tourist inflow grew by 22.60% (CAGR 2.06%). Data obtained from aide memoires, consultations during missions and EA PCR suggest that overall, people feel that their quality of life has improved due to the construction of facilities under the project, resulting in better service delivery. Project 1 is the MMF’s first phase, comprising only 18% of the whole investment. These impact indicators are too high-level to establish the contributions of project 1. Nonetheless, project 1 interventions contributed to other development impacts such as increased access to economic opportunities with improved quality of life and public health. The project contributed substantially to the MFF’s outcome targets of improved water supply (benefitted 0.53 million of the MFF target’s 2.2 million people); sewerage system improvement (benefitted 0.13 million of the MFF target of 1.0 million people);55 and improved SWM (benefitted 1.1 million of the targeted 2.0 million people).56 There are also long-term impacts of sanitation and SWM toward reducing high morbidity and mortality among the poor, as well as environment quality.57 Project environmental impacts are as assessed in para. 25 and Appendix 9. F. Performance of the Borrower and the Executing Agency 37. The performance of the borrower and executing agency is rated satisfactory. The borrower, represented by the Indian Department of Economic Affairs, provided timely guidance

53 For water supply, O&M costs are not fully recovered without dependence on state support for operating expenses.

Meanwhile, the tariff increased by 10% annually from 2011 to 2019. The state government is developing a computerized billing and collection system, the software application for which is not yet complete.

54 The construction contract for the STP included 1 year of O&M in addition to a 6-month trial run. After a year, O&M of the STP was handed over to the Urban Environmental Engineering Department.

55 As an environmental impact, the sewerage system reduced pollution loads into storm drains, which improved water quality in local streams.

56 Infrastructure improvements for water supply and SWM benefitted many of the same beneficiaries, as did sewage collection and sewage treatment.

57 Contributions to the ADB Strategy 2030 are (i) OP 4.1: People benefiting from improved services in urban areas (1.76 million people); (ii) OP4.1.1: Service providers with improved performance (HUDD, PHED, and the two municipal corporations); (iii) OP 4.1.2: Urban infrastructure assets established or improved (4.8 km of raw water pipeline, 190 km of sewerage network, 1 sewage treatment facility, 3 landfill sites); and (iv) OP 4.3: Zones with improved urban environment, climate resilience and disaster risk management of cities improved (three landfill sites with reduced pollution loads on nearby streams and accommodating a large quantity of debris from the 2014 flood).

13

and decisions to the state government and undertook regular tripartite review meetings with ADB, the state government, and ERA. This helped identify bottlenecks, resolve issues, and monitor progress. The state government provided ERA strong support, including timely counterpart funding, not least to complete sewerage works after loan closure. Early in the project, however, the cities had difficulty assigning experienced staff, as most were still dedicated to Loan 2151. 38. After initial delay, the PMU improved its project management and implementation. It established implementation procedures in the project cycle, as well as effective monitoring and implementing mechanisms through PIUs. These arrangements facilitated interagency coordination, monitoring, and progress reporting from the field, as well as information flow to ERA and ADB. The major flood in 2014 hampered project implementation, but ERA and PMU efficiently worked to restore and repair the ongoing works. The PMU handled safeguard compliance and monitoring requirements well and submitted timely environmental reports to ADB. Other than the pending compensation payment to landowners at the landfill site, now in court, no major issues arose through complaint mechanisms, and minor concerns related to construction were handled in a timely manner. APFS and AEFS for FY2008 were not submitted. APFS for FY2018 were rejected for their having a combined audit report for all three projects. This was noncompliant with loan covenants and indicates that ERA financial management was less than satisfactory. All loan covenants were complied with except for institutional empowerment, and resettlement for the landfill site, which is in court. G. Performance of the Asian Development Bank 39. ADB’s performance is rated satisfactory. ADB missions for regular review, midterm review, and special project administration were undertaken to assess progress, provide advice for resolving outstanding issues, and facilitate minor changes in scope and reallocation of loan proceeds. ADB monitoring, capacity building, and guidance through 22 missions and 10 tripartite reviews throughout the project cycle helped define processes, address issues through time-bound actions and targets, and expedite project implementation. ADB provided training to support adherence to procurement guidelines, proper disbursement, and safeguards. On the other hand, the project implementation schedule at MFF appraisal proved to be overly ambitious and should have more realistically considered the time required to implement ADB-financed projects.58 ADB financial management was less than satisfactory since it could have closely monitored and followed up with ERA on compliance with APFS and AEFS requirements. H. Overall Assessment 40. Project 1 is rated successful. It was relevant to government development objectives and ADB policies at appraisal and continued to be relevant upon completion. Changes in scope were timely and appropriate. The project is assessed effective as two outcome targets were achieved and one was achieved with delay. The project is rated efficient, as the EIRRs for project 1 and for the water supply and SWM subprojects were estimated to be above ADB’s discount rate of 12%. The project is rated likely sustainable, as O&M costs for project assets are met through statutory transfers from state and central finance commissions, municipal taxes, and user charges.

Table 1: Overall Ratings

Criteria Rating

Relevance Relevant

58 This will be evaluated in the facility completion report of the program.

14

Criteria Rating

Effectiveness Effective

Efficiency Efficient

Sustainability Likely sustainable

Overall assessment Successful

Development impacts Satisfactory

Borrower and executing agency Satisfactory

Performance of ADB Satisfactory

Source: ADB estimates.

IV. ISSUES, LESSONS, AND RECOMMENDATIONS A. Issues and Lessons 41. The following important lessons emerged from the project:

(i) Greater readiness at the time of MFF approval, including advance action for detailed designs and coordination for utility shifting prior to contract award, would help deliver projects in a timely, responsive, and efficient manner. Proper identification of land requirements helps avoid or minimize resettlement impacts.59

(ii) MFFs impose a heavy burden on executing and implementing agencies in the initial years as they prepare for subsequent tranches while also being responsible for implementing the first project. This requires sufficient implementation support, particularly for preparing subsequent tranches.

(iii) To ensure timely realization of benefits from wastewater management systems, property connections should be provided in conjunction with the laying of the sewerage network.60

(iv) To improve ownership for the new facilities, it would be beneficial to ensure more input from the state agencies during planning, design, and implementation.

(v) Continued payment of O&M fees for water treatment plants and STPs by municipal corporations to PHED and the Urban Environmental Engineering Department is necessary for optimal maintenance and sustainability.

(vi) Water supply and sewerage works contracts should include a reasonable O&M period until local organizations are properly trained and have sufficient budget to take over. House connection should adhere to an annual implementation and financing plan and be considered part of contract performance.

(vii) Consultant performance needs to be closely monitored for optimal utilization of consulting services and timely delivery of outputs.

(viii) ERA has been headed by senior officers of the state government, to the benefit of decision making and interdepartmental coordination. A senior official with strong government support is essential.

(ix) A realistic schedule for consultant recruitment, detailed design development, and contract periods should be incorporated into the project schedule at appraisal.

(x) Close assessment of state agency capacity is needed at appraisal to inform realistic reform targets.

(xi) Subproject’s scope should be oriented toward outcomes and provide

59 The process may be expedited by considering alternative measures to obtain land, such as land pooling or early identification of alternative sites for negotiated settlement.

60 For the low-income group, the government may consider additional subsidies for the cost of connection.

15

comprehensive end-to-end solutions for the entire target area, such as 24×7 water supply with 5–10 years of O&M, subject to capacity of the asset operator.

(xii) ADB should follow up more closely on compliance with submission requirements for APFS and AEFS.

(xiii) Categorization for involuntary resettlement and indigenous people should be revised in case the impacts are reduced during project implementation.

B. Recommendations 42. Specific recommendations for project implementation are as follow: First, the PMU should be strengthened with a combined technical and legal team and/or specialist to handle any contract arbitration. Second, ADB should communicate frequently with executing agencies and monitor them closely when they prepare audited financial reports to ensure compliance with ADB requirements. Including a financial management specialist—to monitor and support the project team and the executing and implementing agencies, including with missions as necessary—is key to improving financial management performance and ensuring that reports are properly prepared.

43. General recommendations for MFF and project preparation are as follow: First, greater readiness at MFF approval—including advance action for detailed planning, designs, and coordination for utility shifting prior to contract award—would help deliver projects in a timely, responsive, and efficient manner.61 Second, more support from ADB is needed during the early years of MFF implementation for executing and implementing agencies less experienced with ADB projects. Such agencies may need TA for preparation of succeeding tranches. Third, the project scope and implementation period should be realistic in light of executing agency capacity to work on projects involving multiple stakeholders. Fourth, hybrid payment structures that permit payments based on deliverables for designs, reports, and other documents would improve accountability and consultant performance, as would payments for supervision based on inputs. Fifth, robust procurement and contract management should be established by extending e-procurement beyond e-submission, establishing a database for contract performance, and e-registration of contractors, as well as an e-project accounting system for billing and progress payments under works contracts. 44. Items for further follow-up include the following: First, ERA is expected to provide details of O&M fee payments from ULBs to PHED and the Urban Environmental Engineering Department by completion of the facility completion report for the MFF. Second, he municipal corporations of the target towns need to continue augmenting human resources and institutional capacity to achieve better asset management and governance. Third, ERA is expected to ensure disbursement of compensation from the escrow account to landowners of the sanitary landfill site as per the court decision. Fourth, ERA was expected to provide answers by completion of the facility completion report for the MFF to questions and requests from ADB concerning the points raised in an ADB letter dated 21 November 2019. 45. Compliance with covenants relating to levy of SWM charges by ULBs should be ensured.

61 ADB now requires a high degree of readiness in many projects prior to loan approval, including completion of contract

awards for 20% or more of the first project loan.

16 Appendix 1-1

DESIGN AND MONITORING FRAMEWORK FOR PROJECT 1 Design

Summary of MFF

Performance Indicators/Targets of MFF

Performance Indicators/Targets of Project 1a

Project Achievements of Project 1 b,c

Impacts

Sustainable economic growth through the provision of urban infrastructure and services and the promotion of urban management in the state, and selected towns with tourism potential in the state d

• Increase in per capita real income in Jammu and Srinagar

• Increase in per capita real income in Jammu and Srinagar

• Per capita real income in the State increased by 162.46% from 2007 to 2017, for a CAGR of 10.13%.e

• Growth in non-primary sector income in districts encompassing project cities.

• Growth in non-primary sector income in districts encompassing project cities.

• Non-primary sector income in districts encompassing project cities grew by 225.06% from 2007 to 2016, for a CAGR of 13.85%.f

• Increase in investment in industry and trade

• Increase in investment in industry and trade

• Investments in industries and trades increased by 100.45% from 2007 to 2017, for a CAGR of 7.20%.g

• Increase in tourist inflow • Increase in tourist inflow • Tourist inflow increased by 22.6% from 2007 to 2017, for a CAGR of 2.06%.h

• People’s perception of their quality of life improved

• People’s perception of their quality of life improved

• Exact analysis is possible only after completion of all tranches as all tranches were overlapping within the entire project.

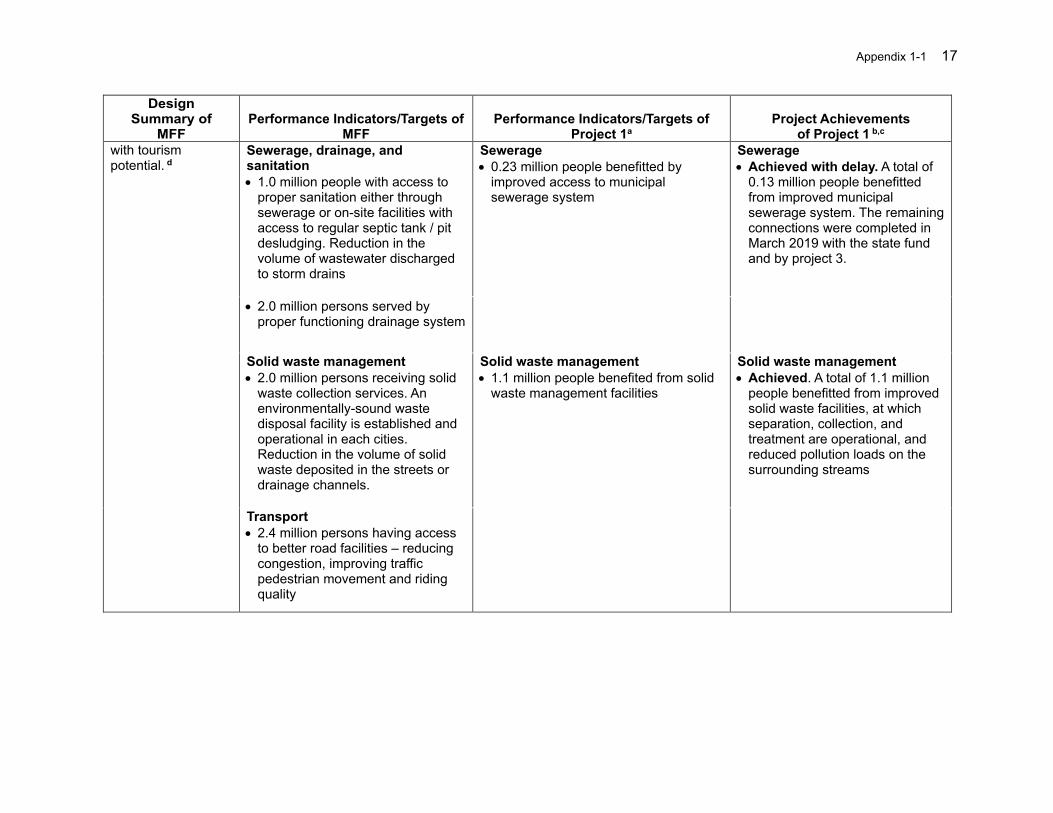

Outcomes By the end of Investment Program: By end of Project 1: By end of Project 1:i

Improved the living environment and employment opportunities for the 2.4 million people in Srinagar and Jammu, and other participating towns

Increased population coverage of infrastructure services:

Increased population coverage of infrastructure services:

Water supply

• 2.2 million people with access to municipal water supply system

Water supply

• 0.38 million people benefitted by improved access to water supply

Water supply

• Achieved. A total of 0.53 million people benefitted from improved access to water supply

Appendix 1-1 17

Design Summary of

MFF Performance Indicators/Targets of

MFF Performance Indicators/Targets of

Project 1a Project Achievements

of Project 1 b,c

with tourism potential. d

Sewerage, drainage, and sanitation

• 1.0 million people with access to proper sanitation either through sewerage or on-site facilities with access to regular septic tank / pit desludging. Reduction in the volume of wastewater discharged to storm drains

Sewerage

• 0.23 million people benefitted by improved access to municipal sewerage system

Sewerage

• Achieved with delay. A total of 0.13 million people benefitted from improved municipal sewerage system. The remaining connections were completed in March 2019 with the state fund and by project 3.

• 2.0 million persons served by proper functioning drainage system

Solid waste management

• 2.0 million persons receiving solid waste collection services. An environmentally-sound waste disposal facility is established and operational in each cities. Reduction in the volume of solid waste deposited in the streets or drainage channels.

Solid waste management

• 1.1 million people benefited from solid waste management facilities

Solid waste management

• Achieved. A total of 1.1 million people benefitted from improved solid waste facilities, at which separation, collection, and treatment are operational, and reduced pollution loads on the surrounding streams

Transport

• 2.4 million persons having access to better road facilities – reducing congestion, improving traffic pedestrian movement and riding quality

18 Appendix 1-1

Design Summary of

MFF Performance Indicators/Targets of

MFF Performance Indicators/Targets of

Project 1a Project Achievements

of Project 1 b,c

Improved capacities of participating institutions in managing sector reforms and service delivery

• Sector Reforms in place

• Mainstreaming of capacity building as part of State urban development budget

• Demonstrated capacities of agencies in effective O&M performance of assets including through cost reduction and management measures.

• Increased public private partnership in service delivery.

Note: The DMF did not include indicators/targets for Part B. Detailed output targets and actual achievements are found in Appendix 2-1; thus related outcome achievements are also reported.

Economic opportunity development plans, e-procurement were established. Capacity building of relevant agencies has been ongoing using State budget. Agencies’ capacity for better O&M was developed through hands-on training by the contractors and consultants.

Outputs

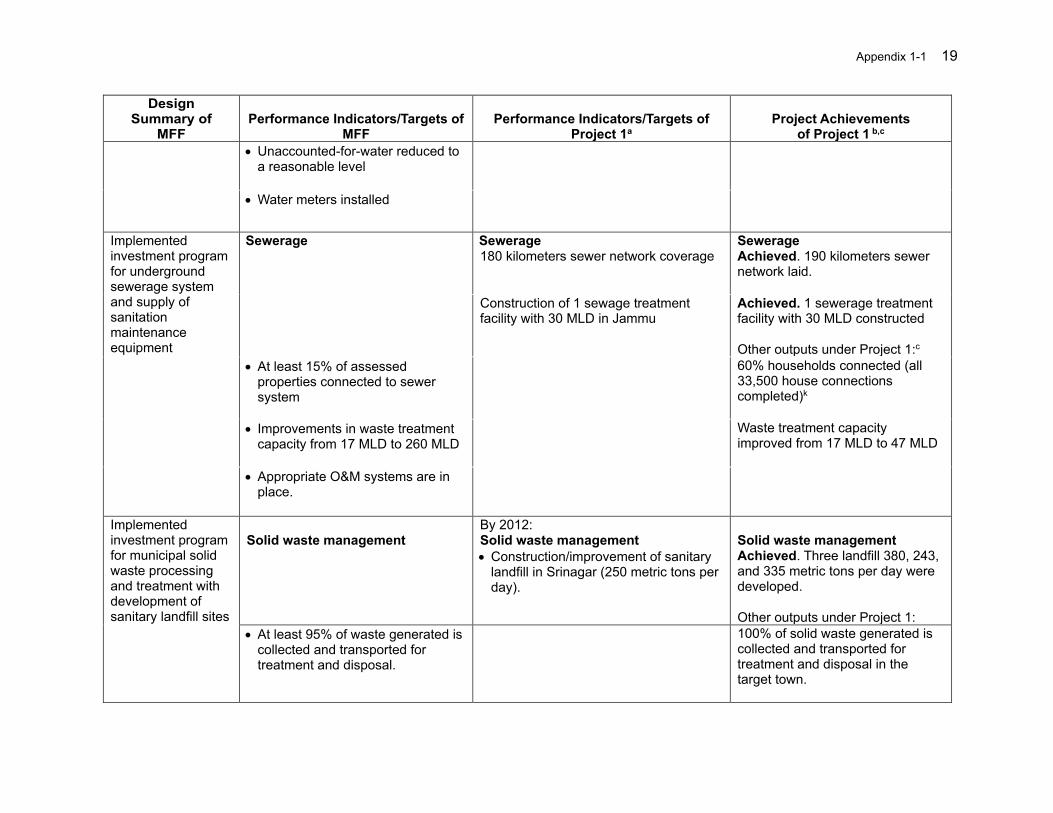

Part A: Urban Infrastructure Improvement

By End of Investment Program: By 2012:

Implemented investment program for water supply

Water supply

• Average supply increased from 80 to 135 lpcd

Water supply 5.6 km raw water pipeline laid.j

Water supply Substantially achieved. 4.8 km raw water pipeline laid Other outputs under Project 1:c Water supply raised from 80 lpcd to 135 lpcd

• Increase in minimum supply hours from 2 to 8 hours

Period of service increased from 2 hours to 8 hours a day

• At least 80% of assessed properties connected to water supply system

Appendix 1-1 19

Design Summary of

MFF Performance Indicators/Targets of

MFF Performance Indicators/Targets of

Project 1a Project Achievements

of Project 1 b,c

• Unaccounted-for-water reduced to a reasonable level

• Water meters installed

Implemented investment program for underground sewerage system and supply of sanitation maintenance equipment

Sewerage

Sewerage 180 kilometers sewer network coverage

Sewerage Achieved. 190 kilometers sewer network laid.

Construction of 1 sewage treatment facility with 30 MLD in Jammu