2018 PROXY SEASON REVIEW & OTHER TOPICS

34

2018 PROXY SEASON REVIEW & OTHER TOPICS Hugessen Breakfast Seminar | June 13, 14 & 20 2018

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2018 PROXY SEASON REVIEW & OTHER TOPICS

2018 PROXY SEASON REVIEW & OTHER TOPICSHugessen Breakfast Seminar | June 13, 14 & 20 2018

2

Agenda for Today’s Event

Welcome

Highlights from 2017 Proxy Season

Comments from Guests

Open Discussion

Closing Remarks

Highlights from 2018 Proxy Season

3

4

Highlights from 2018 Proxy Season

Performance and Pay

Pay Mix and Plan Design

Say on Pay Results

Emerging Topics and U.S.

Scope of study:

▪ Companies in the TSX 60 Index

▪ 2018 proxies commenting on Fiscal 2017 (n = 59)

▪ Say on Pay results among the TSX Composite as of June 11, 2018 (n = 155)

5

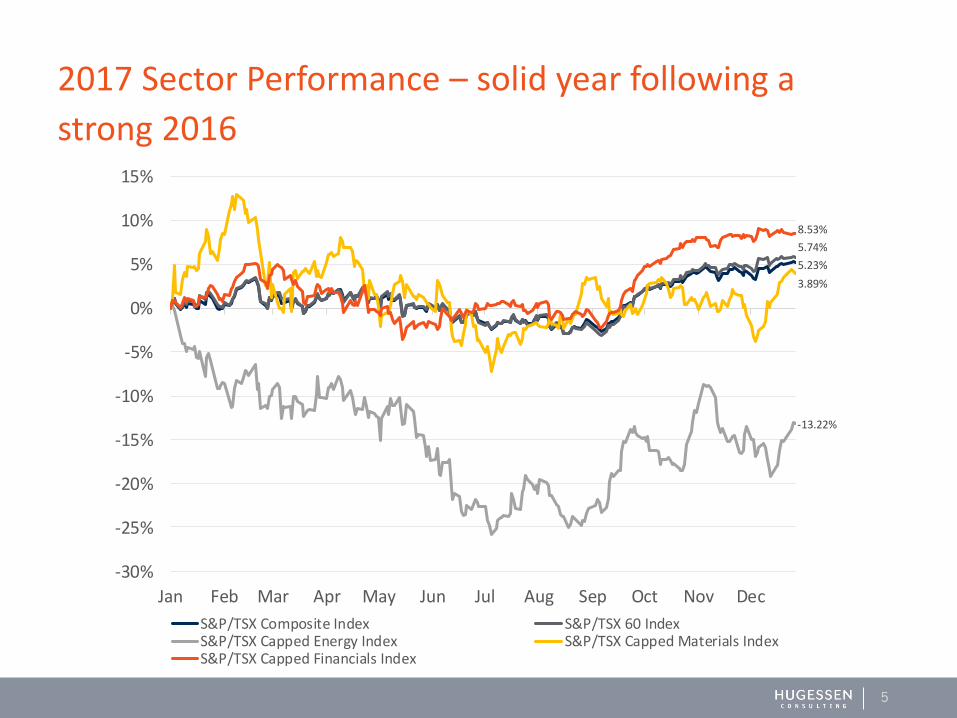

2017 Sector Performance – solid year following a

strong 2016

5.23%

5.74%

-13.22%

3.89%

8.53%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

S&P/TSX Composite Index S&P/TSX 60 IndexS&P/TSX Capped Energy Index S&P/TSX Capped Materials IndexS&P/TSX Capped Financials Index

-50%

-25%

0%

25%

50%

75%

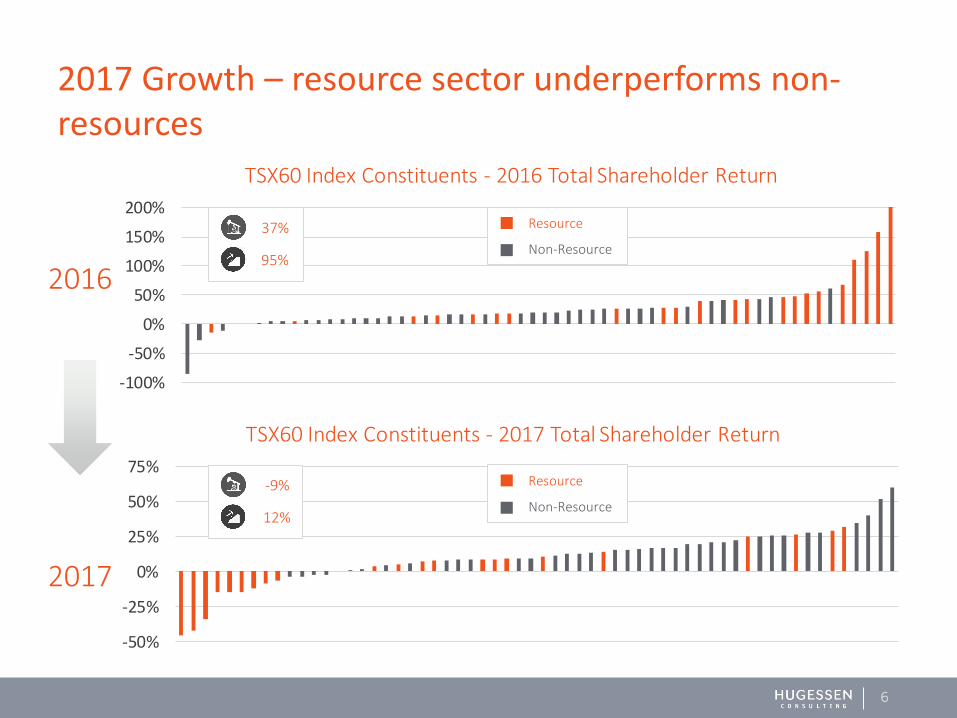

TSX60 Index Constituents - 2017 Total Shareholder Return

-100%

-50%

0%

50%

100%

150%

200%

TSX60 Index Constituents - 2016 Total Shareholder Return

6

2017 Growth – resource sector underperforms non-resources

2016

2017

-9%

12%

Resource

Non-Resource

Resource

Non-Resource

37%

95%

7

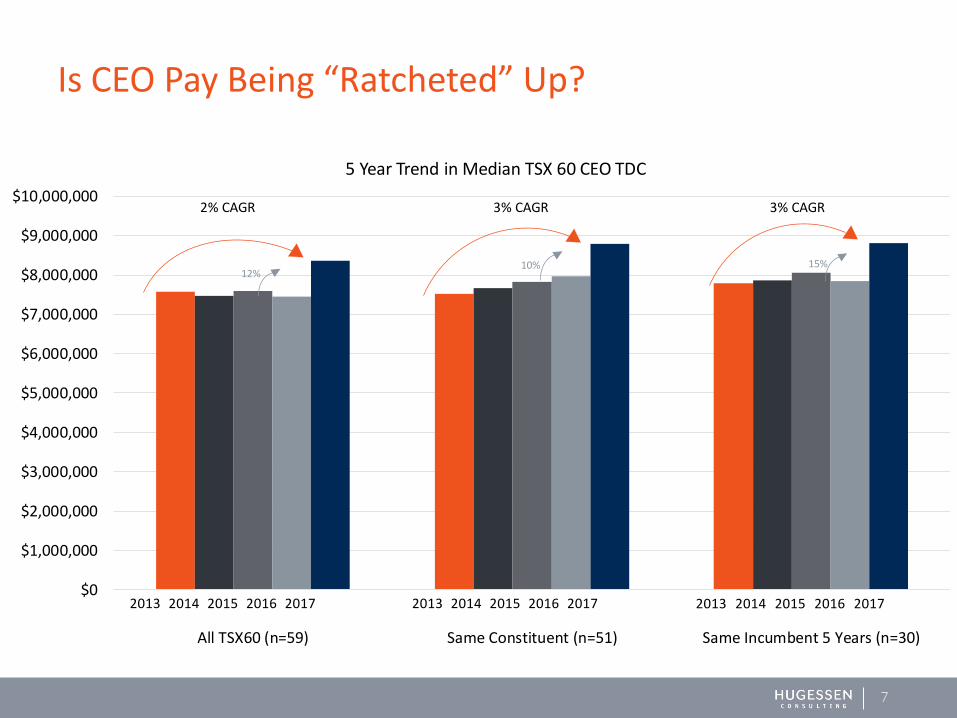

Is CEO Pay Being “Ratcheted” Up?

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

$9,000,000

$10,000,000

All TSX60 (n=59) Same Constituent (n=51) Same Incumbent 5 Years (n=30)

5 Year Trend in Median TSX 60 CEO TDC

2% CAGR 3% CAGR 3% CAGR

2013 2014 2015 2016 2017

12%10% 15%

2013 2014 2015 2016 20172013 2014 2015 2016 2017

$7,447

$2,680

$1,116

$8,368

$3,257

$1,200

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000

TDC

TCC

Salary

CAD '000s

TSX60: Year-Over-Year Changes in Actual Compensation 2016 & 2017

2017 2016

8

2017 CEO Pay Trends – material increase in STIP

8%

22%

12%

9

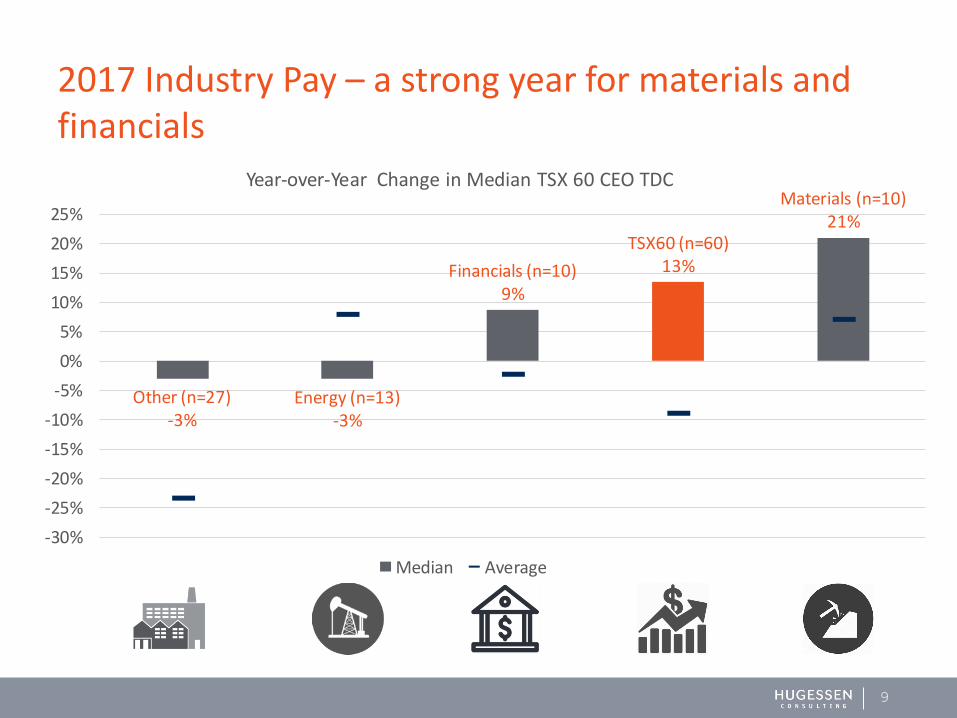

2017 Industry Pay – a strong year for materials and financials

Other (n=27)-3%

Energy (n=13)-3%

Financials (n=10)9%

TSX60 (n=60)13%

Materials (n=10)21%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Year-over-Year Change in Median TSX 60 CEO TDC

Median Average

10

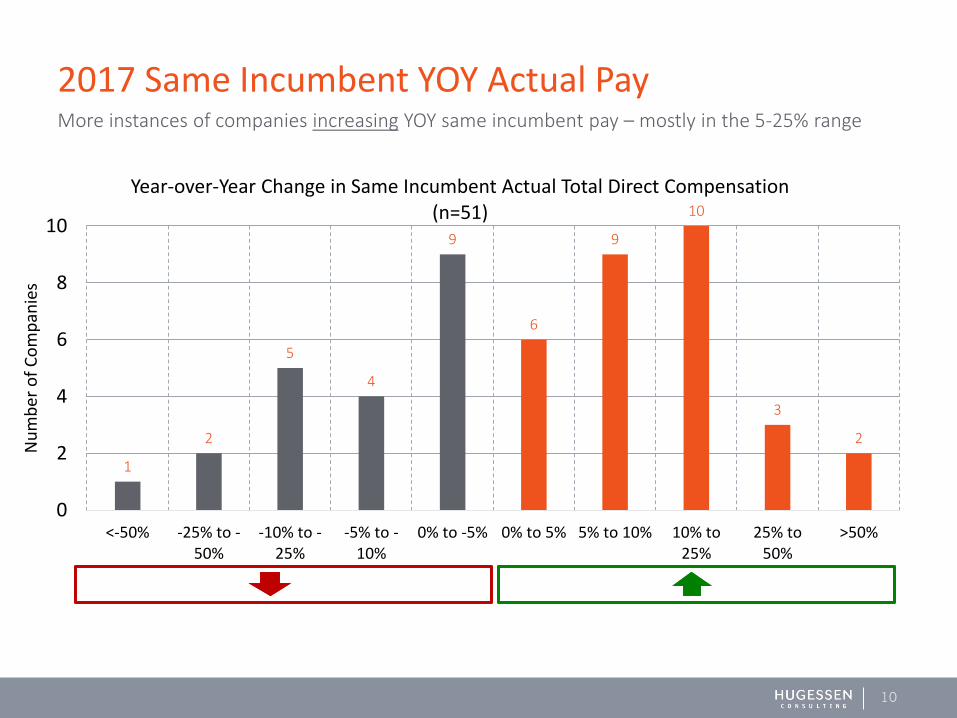

2017 Same Incumbent YOY Actual Pay

1

2

5

4

9

6

9

10

3

2

0

2

4

6

8

10

<-50% -25% to -50%

-10% to -25%

-5% to -10%

0% to -5% 0% to 5% 5% to 10% 10% to25%

25% to50%

>50%

Nu

mb

er o

f C

om

pan

ies

Year-over-Year Change in Same Incumbent Actual Total Direct Compensation (n=51)

More instances of companies increasing YOY same incumbent pay – mostly in the 5-25% range

11

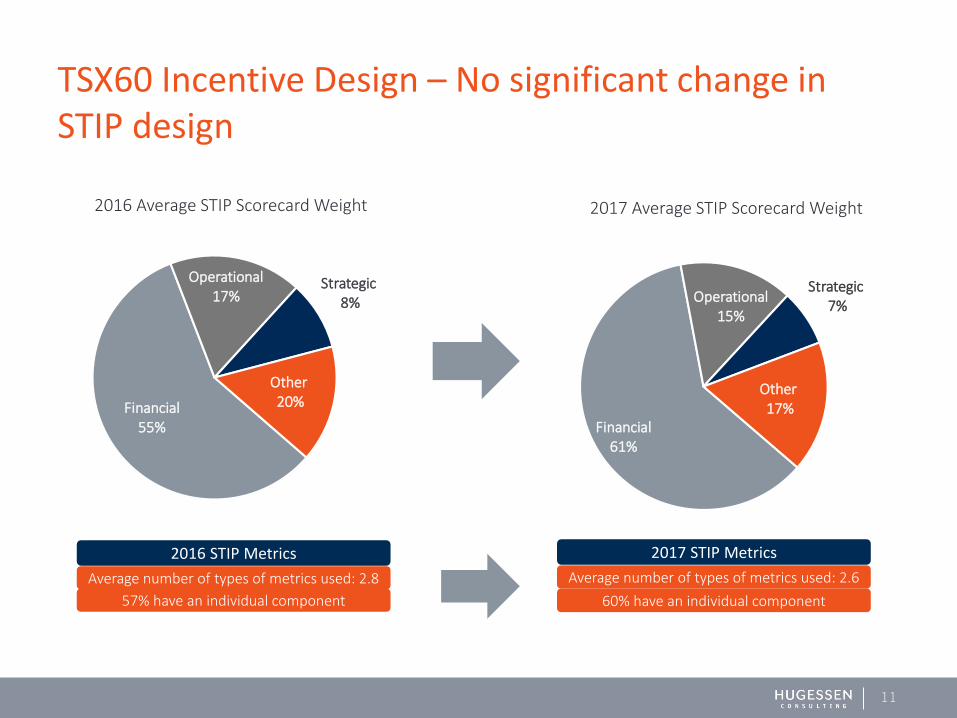

TSX60 Incentive Design – No significant change in STIP design

57% have an individual component

Average number of types of metrics used: 2.8

2016 STIP Metrics

60% have an individual component

Average number of types of metrics used: 2.6

2017 STIP Metrics

Financial55%

Operational17%

Strategic8%

Other20%

2016 Average STIP Scorecard Weight

Financial61%

Operational15%

Strategic7%

Other17%

2017 Average STIP Scorecard Weight

12

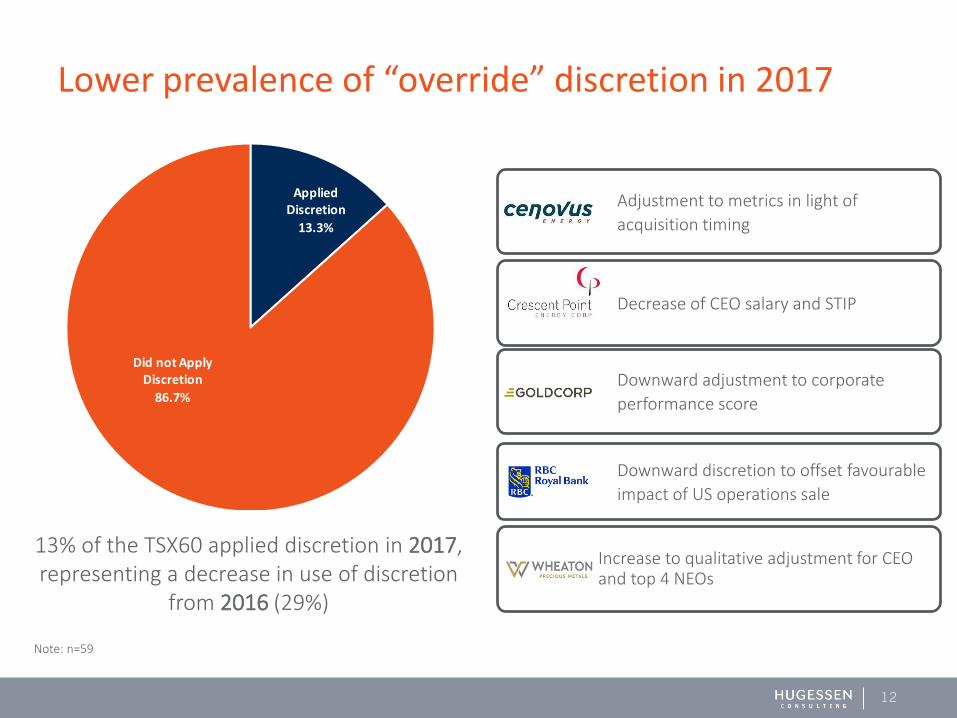

Lower prevalence of “override” discretion in 2017

Adjustment to metrics in light of

acquisition timing

Decrease of CEO salary and STIP

Downward adjustment to corporate

performance score

Downward discretion to offset favourable

impact of US operations sale

Increase to qualitative adjustment for CEO and top 4 NEOs

Note: n=59

13% of the TSX60 applied discretion in 2017, representing a decrease in use of discretion

from 2016 (29%)

Applied Discretion

13.3%

Did not Apply Discretion

86.7%

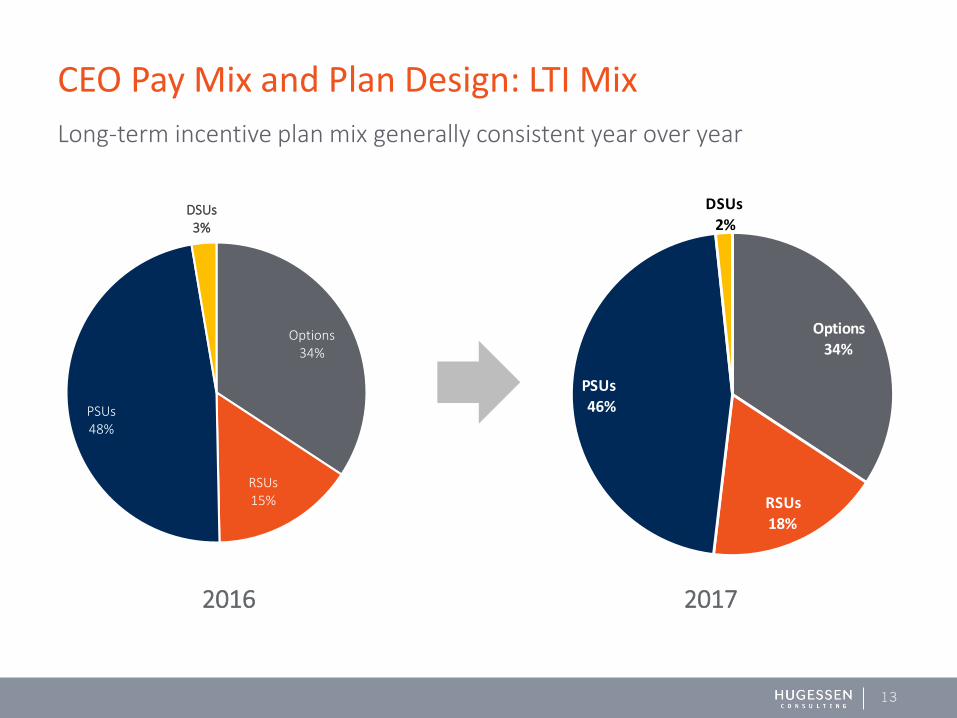

Options34%

RSUs15%

PSUs 48%

DSUs3%

Options34%

RSUs18%

PSUs46%

DSUs2%

13

Long-term incentive plan mix generally consistent year over year

CEO Pay Mix and Plan Design: LTI Mix

2016 2017

14

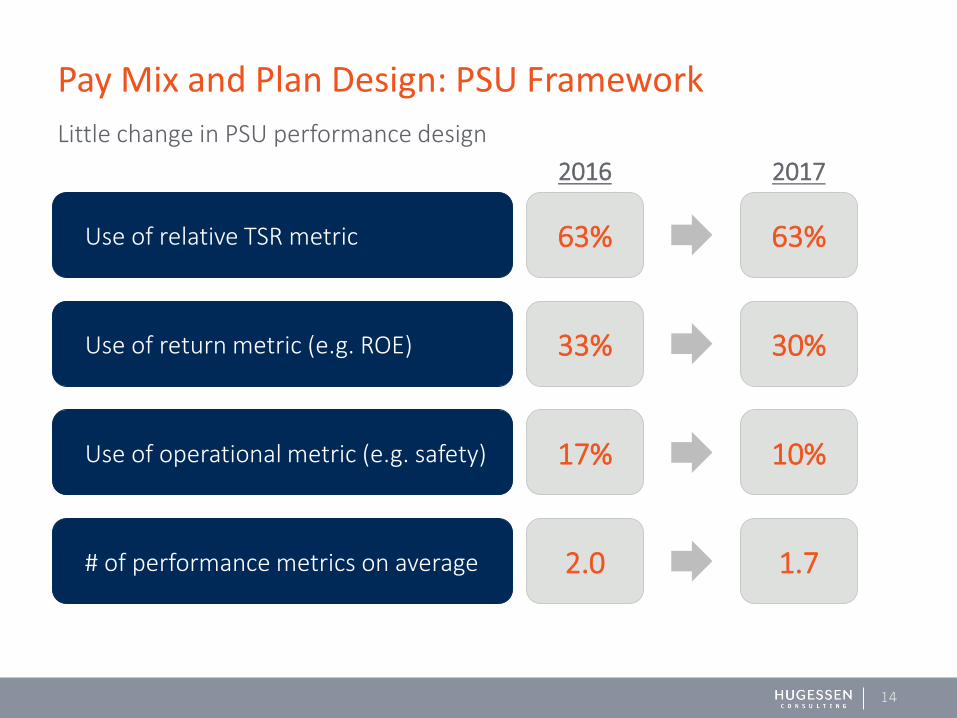

Pay Mix and Plan Design: PSU Framework

2016 2017

Use of relative TSR metric

Use of return metric (e.g. ROE)

Use of operational metric (e.g. safety)

# of performance metrics on average

63%

33%

17%

2.0

63%

30%

10%

1.7

Little change in PSU performance design

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

>90% 80-90% 70-80% 60-70% 50-60% <50%

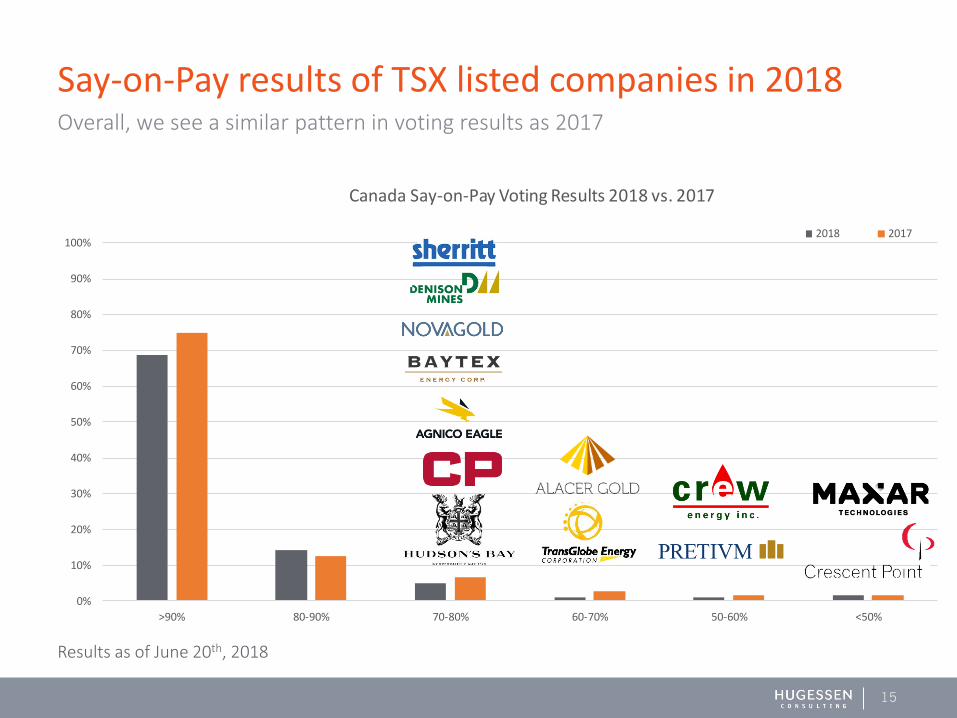

Canada Say-on-Pay Voting Results 2018 vs. 2017

2018 2017

15

Say-on-Pay results of TSX listed companies in 2018Overall, we see a similar pattern in voting results as 2017

Results as of June 20th, 2018

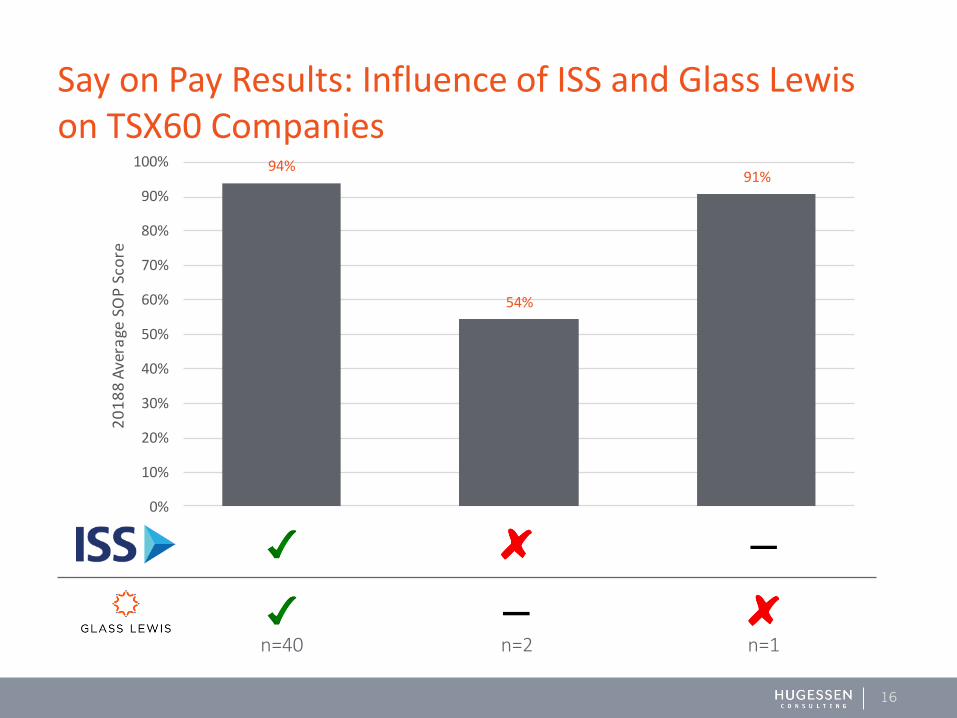

94%

54%

91%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

18

8 A

vera

ge S

OP

Sco

re

16

Say on Pay Results: Influence of ISS and Glass Lewis on TSX60 Companies

n=2n=40 n=1

17

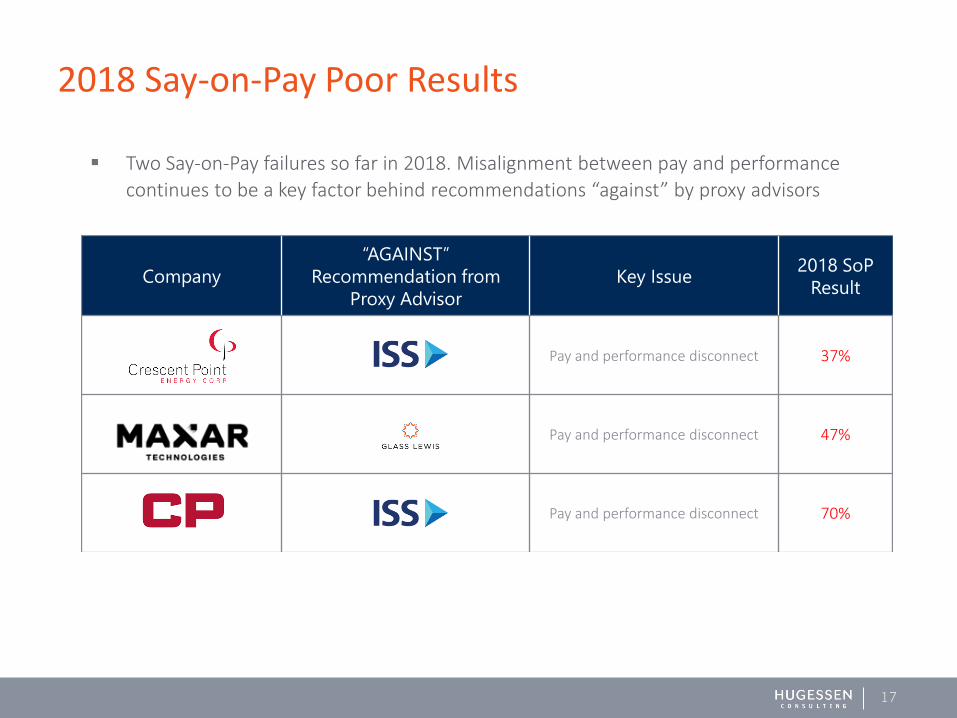

2018 Say-on-Pay Poor Results

▪ Two Say-on-Pay failures so far in 2018. Misalignment between pay and performance

continues to be a key factor behind recommendations “against” by proxy advisors

Company

“AGAINST”

Recommendation from

Proxy Advisor

Key Issue2018 SoP

Result

Pay and performance disconnect 37%

Pay and performance disconnect 47%

Pay and performance disconnect 70%

18

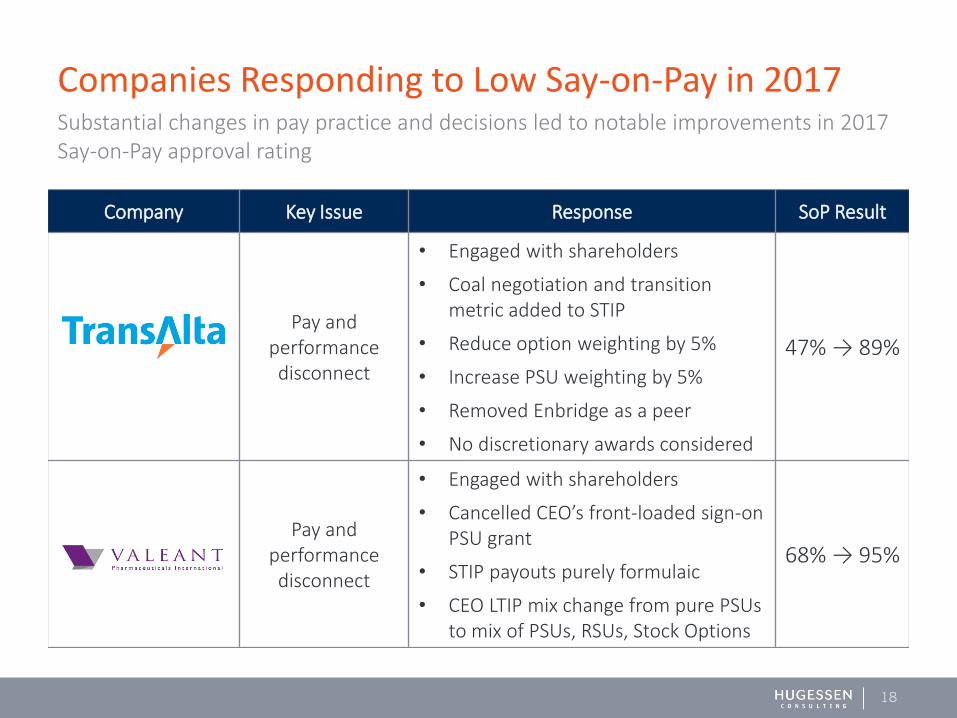

Companies Responding to Low Say-on-Pay in 2017

Company Key Issue Response SoP Result

Pay and performance disconnect

• Engaged with shareholders

• Coal negotiation and transition metric added to STIP

• Reduce option weighting by 5%

• Increase PSU weighting by 5%

• Removed Enbridge as a peer

• No discretionary awards considered

47% → 89%

Pay and performance disconnect

• Engaged with shareholders

• Cancelled CEO’s front-loaded sign-on PSU grant

• STIP payouts purely formulaic

• CEO LTIP mix change from pure PSUs to mix of PSUs, RSUs, Stock Options

68% → 95%

Substantial changes in pay practice and decisions led to notable improvements in 2017 Say-on-Pay approval rating

19

Companies Responding to Low Say-on-Pay in 2017

Company Key Issue Response SoP Result

Misalignment of value distribution

between shareholders and

executives

• Engaged with shareholders

• Removal of Working Capital and Cost/Oz metrics, addition of Strategic Initiatives metric

• 2-Year relative TSR replaced with 50/50 split between 1-Year and 3-Year relative TSR

• Clarified equity award metrics

68% → 95%

Poor overall design

• Adoption of clawback

• Improved disclosure of STIP metrics and discretionary bonuses

• STIP scorecard reweighting (50% discretionary to 25% discretionary)

• Introduction of PSU plan

73% → 96%

Substantial changes in pay practice and decisions led to notable improvements in 2018 Say-on-Pay approval rating

20

Best Practices in Proxy Disclosure (CCGG)

Shareholder

Engagement

Executive

Succession

Use of Visual Aid

Executive

Compensation and

Risk Management

Director Nominee

Profiles

Diversity Policy

21

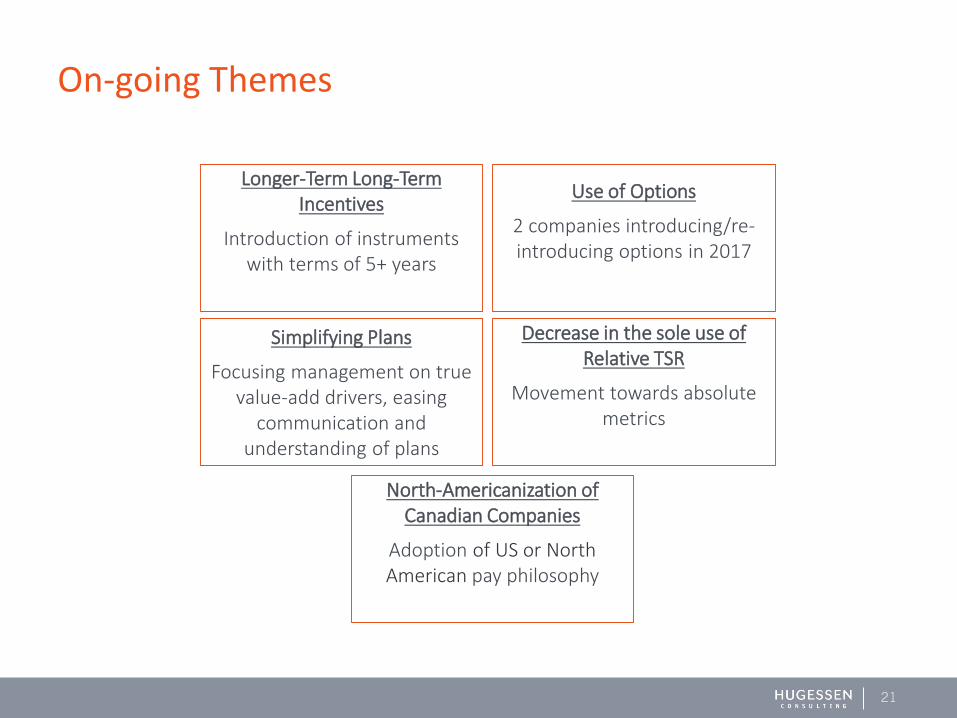

On-going Themes

Longer-Term Long-Term Incentives

Introduction of instruments with terms of 5+ years

Use of Options

2 companies introducing/re-introducing options in 2017

Decrease in the sole use of Relative TSR

Movement towards absolute metrics

Simplifying Plans

Focusing management on true value-add drivers, easing

communication and understanding of plans

North-Americanization of Canadian Companies

Adoption of US or North American pay philosophy

22

Case Studies – Crescent Point and Hydro One

• Minority shareholder, Cation Capital, launches a proxy contest in April 2018

• Cation puts forward 4 nominees, of which ISS supported two

• Shareholders voted down the proposal and voted to re-elect all Crescent Point directors

• Key Takeaways: Board quickly engaged shareholders in response to the dissident proposal

• Average Management Nominee director support: 83%

• 2018 Say-on-Pay support: 38.5%

• Hydro One’s executive and director compensation and related governance provisions drew criticism from Ontario politicians

• Province of Ontario (47% owner) abstained from voting on Say-on-Pay. Balance of shareholders voted 92% in favor on SoP

• Key Takeaways: importance of effectively communicating the rationale for pay framework (Canadian growth, expansion to the US, financial performance)

• Yet not immune from politicization

23

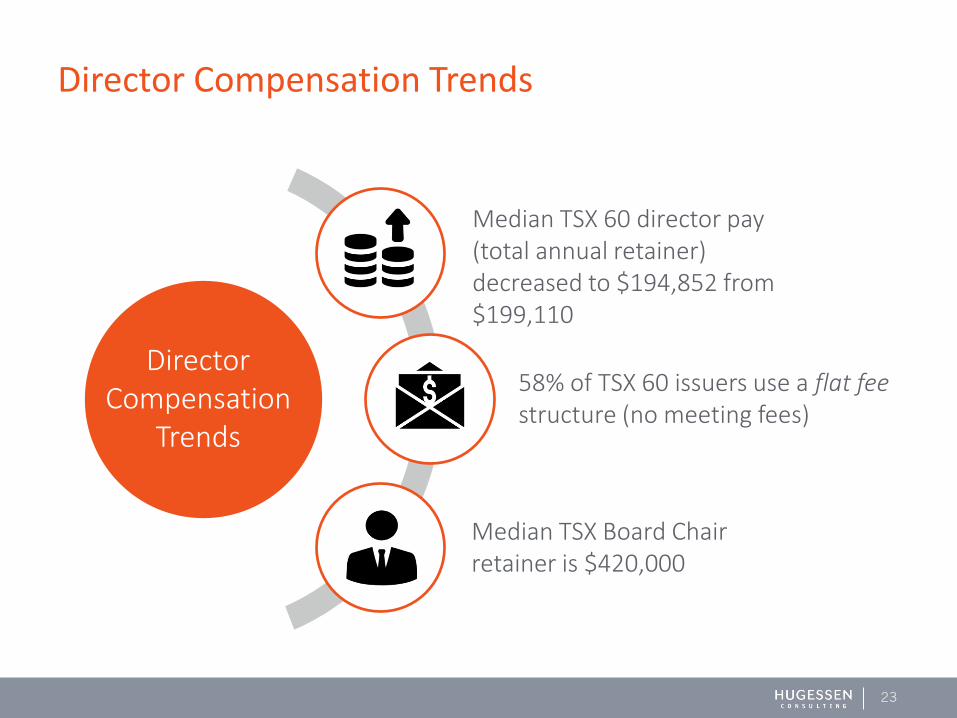

Director Compensation Trends

Median TSX 60 director pay (total annual retainer) decreased to $194,852 from $199,110

58% of TSX 60 issuers use a flat feestructure (no meeting fees)

Median TSX Board Chair retainer is $420,000

Director Compensation

Trends

Emerging Topics

24

25

Rewarding Growth vs Returns

ISS Updates – Return Metrics

• Updated pay-for-performance methodology in 2017 to include ROE, ROA and ROIC relative to peers

Board Considerations

OTPP recommendations:• STIP metrics per share and debt adjusted• Focus management on ROE and ROCE• Supplement Relative TSR with Absolute

Addition of Return Metrics

• Crescent Point

• Magna

• TD

Shareholder Community Concern

• Shareholders have become increasingly vocal on over-emphasis of growth (v. returns) in compensation design, particularly in extractive industries

• Ontario Teachers’ Pension Plan article, Sailing Stone, Paulson & Co have all commented on lack of management and shareholder alignment

26

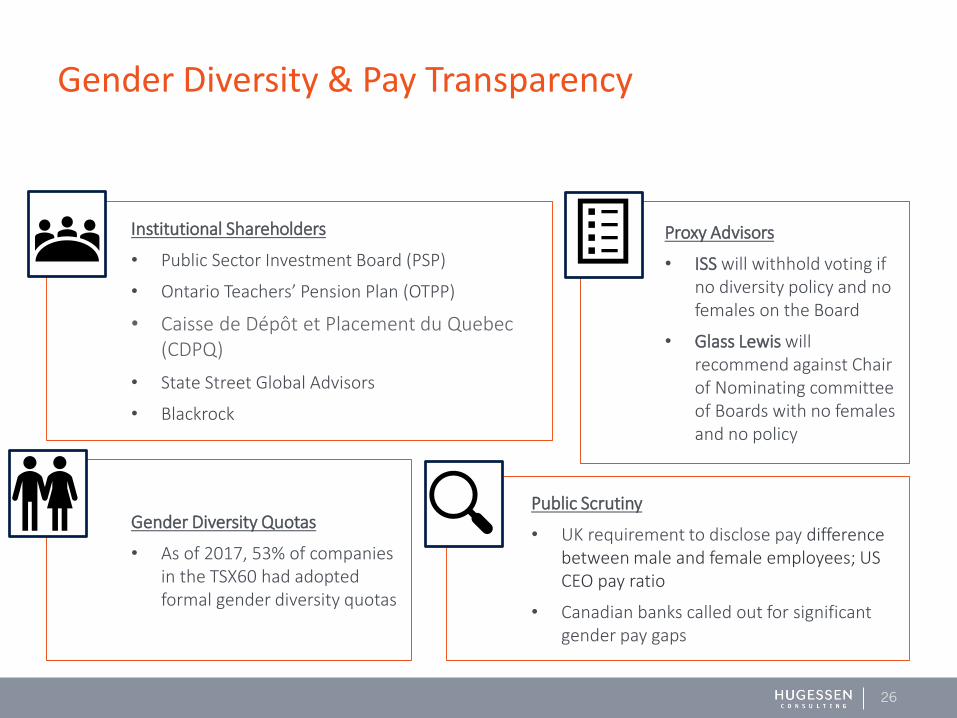

Gender Diversity & Pay Transparency

Proxy Advisors

• ISS will withhold voting if no diversity policy and no females on the Board

• Glass Lewis will recommend against Chair of Nominating committee of Boards with no females and no policy

Public Scrutiny

• UK requirement to disclose pay difference between male and female employees; US CEO pay ratio

• Canadian banks called out for significant gender pay gaps

Gender Diversity Quotas

• As of 2017, 53% of companies in the TSX60 had adopted formal gender diversity quotas

Institutional Shareholders

• Public Sector Investment Board (PSP)

• Ontario Teachers’ Pension Plan (OTPP)

• Caisse de Dépôt et Placement du Quebec (CDPQ)

• State Street Global Advisors

• Blackrock

27

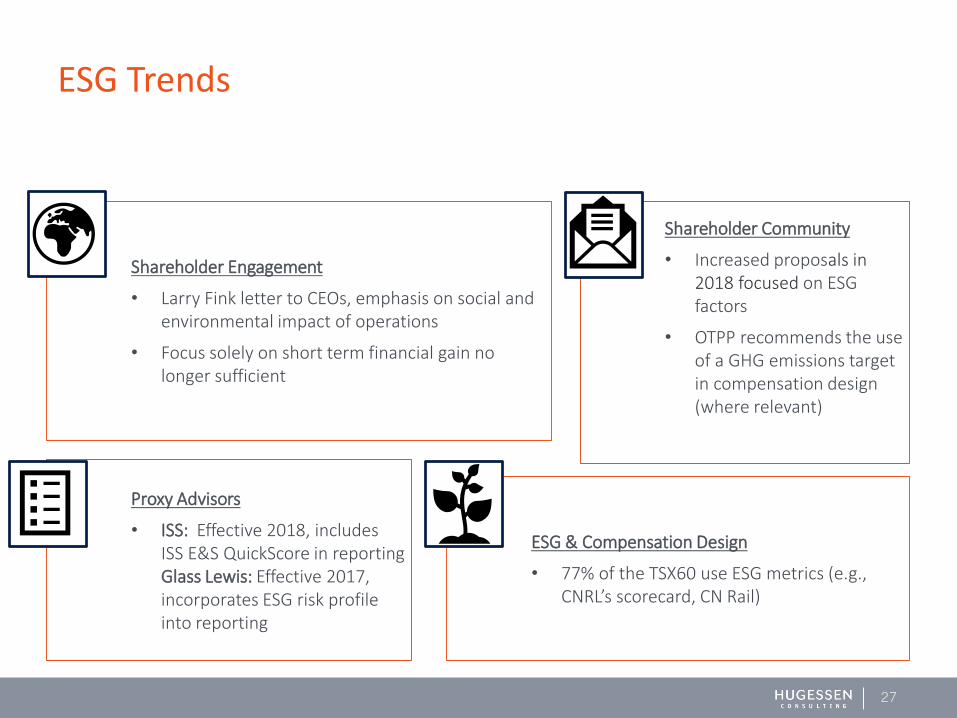

ESG Trends

Shareholder Community

• Increased proposals in 2018 focused on ESG factors

• OTPP recommends the use of a GHG emissions target in compensation design (where relevant)

ESG & Compensation Design

• 77% of the TSX60 use ESG metrics (e.g., CNRL’s scorecard, CN Rail)

Proxy Advisors

• ISS: Effective 2018, includes ISS E&S QuickScore in reporting Glass Lewis: Effective 2017, incorporates ESG risk profile into reporting

Shareholder Engagement

• Larry Fink letter to CEOs, emphasis on social and environmental impact of operations

• Focus solely on short term financial gain no longer sufficient

U.S. Compensation

28

Pay packages increased 8.5% to $11.7 million in 2017

29

2018 early proxy filer data – median 1 year change in CEO total compensation

7.9%

2.5%

5.7%

14.1%

5.9%

7.6%6.7%

11.0%

27.5%

9.8%

Total Sample(n=100)

ConsumerDiscretionary

(n=14)

ConsumerStaples(n=5)

Energy(n=5)

Financials(n=12)

Health Care(n=10)

Industrials(n=26)

InformationTechnology

(n=16)

Materials(n=8)

Utilities(n=4)

30

2018 US Say-on-Pay Votes reveals 2% of companies falling below 50%

76%

16%

6%

2%

2018 SAY-ON-PAY ‘FOR’ VOTES

>90% 70% - 90% 50% - 70% <50%

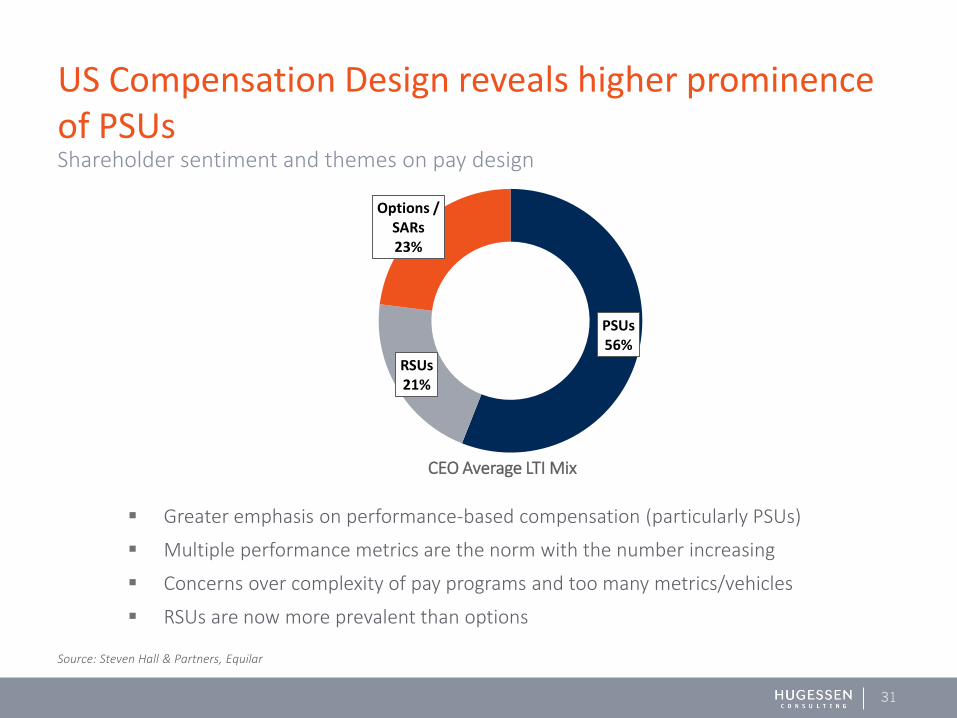

PSUs56%

RSUs21%

Options / SARs23%

CEO Average LTI Mix

▪ Greater emphasis on performance-based compensation (particularly PSUs)

▪ Multiple performance metrics are the norm with the number increasing

▪ Concerns over complexity of pay programs and too many metrics/vehicles

▪ RSUs are now more prevalent than options

31

US Compensation Design reveals higher prominence of PSUs

Source: Steven Hall & Partners, Equilar

Shareholder sentiment and themes on pay design

32

➢ Tax Cuts and Job Act of 2017

➢ Corporate Governance Reform and Transparency Act of 2017

➢Dodd-Frank Rollback

➢Wells Fargo – Federal Reserve Restrictions

➢ Continued Trends in Shareholder Engagement

➢ Pay ratio Findings

US Snapshot: Regulatory & Related Governance

33

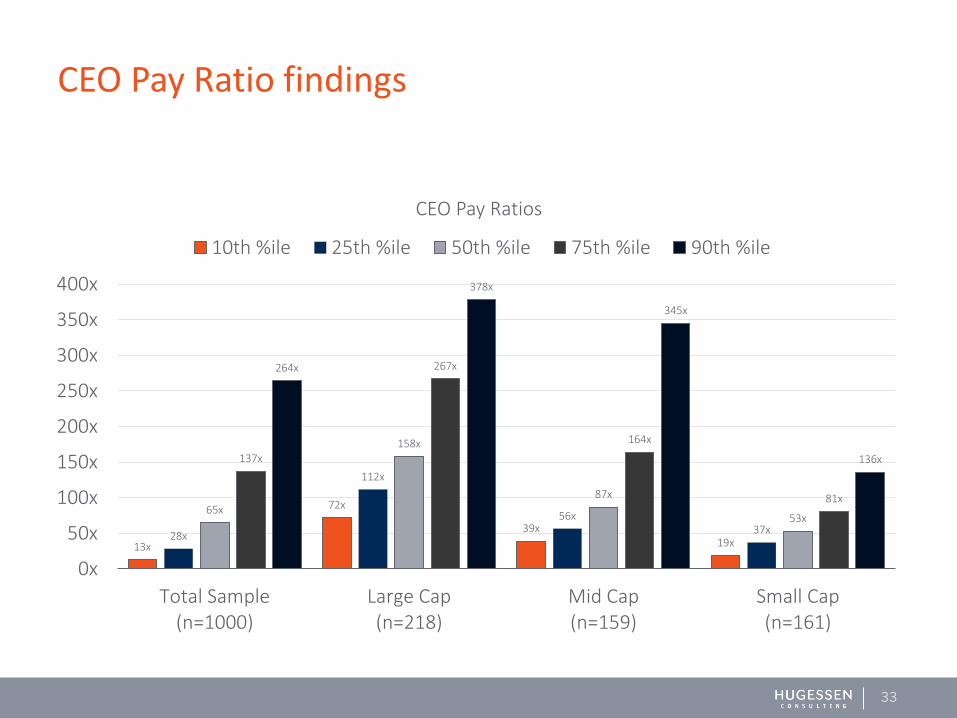

CEO Pay Ratio findings

13x

72x

39x19x

28x

112x

56x37x

65x

158x

87x

53x

137x

267x

164x

81x

264x

378x

345x

136x

0x

50x

100x

150x

200x

250x

300x

350x

400x

Total Sample(n=1000)

Large Cap(n=218)

Mid Cap(n=159)

Small Cap(n=161)

CEO Pay Ratios

10th %ile 25th %ile 50th %ile 75th %ile 90th %ile

Discussion

34