2013 result presentation - Wärtsilä

39

© Wärtsilä BJÖRN ROSENGREN, PRESIDENT & CEO 29 JANUARY 2014 2013 RESULT PRESENTATION

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of 2013 result presentation - Wärtsilä

© Wärtsilä

BJÖRN ROSENGREN, PRESIDENT & CEO

29 JANUARY 2014

2013 RESULT PRESENTATION

• Order intake EUR 4,872 million, -1%

• Net sales EUR 4,654 million, -1%

• Book-to-bill 1.05

• EBITA EUR 552 million, 11.9% of net sales

• EBIT EUR 520 million, 11.2% of net sales

• EPS EUR 1.98 (1.72)

• Cash flow from operating activities

EUR 578 million (153)

• Group-wide efficiency programme initiated

EBITA is shown excluding non-recurring items and intangible asset amortisation related

to acquisitions.

EBIT is shown excluding non-recurring items.

Certain comparison figures in this presentation have been restated due to changes in

pension accounting.

Highlights 2013

NEW

PIC

© Wärtsilä

0

200

400

600

800

1000

1200

1400

Q4/2012 Q4/2013

0%

-13%

36%

-16%

1,357

MEUR

Fourth quarter development

MEUR

3

Order intake development

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

2009 2010 2011 2012 2013

1,351

Q1-Q3 Q4

Power Plants

Ship Power

Services

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

Q4/2012 Q4/2013

Net sales in line with our expectations

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

2009 2010 2011 2012 2013

-7.6%

-13%

12%

-8%

-5%

0%

-18%

1,533

MEUR

Fourth quarter development

MEUR

1,411

4

Net sales decreased due to unfavourable exchange rates

and delayed deliveries

Power Plants

Ship Power

Services

Q1-Q3 Q4

-1%

© Wärtsilä

Net sales by business 1-3/2012

Ship Power

28% (28)

Power Plants

31% (32)

Services

40% (40)

5

Net sales by business 2013

© Wärtsilä

0.63

0.88

1.07 1.05 1.05

0,0

0,2

0,4

0,6

0,8

1,0

1,2

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

6000

2009 2010 2011 2012 2013

Order intake Net sales Book-to-bill

MEUR

6

Book-to-bill ratio remains above one

© Wärtsilä

Order book distribution

0

1000

2000

3000

4000

Delivery next year Delivery after next year

31.12.2012 31.12.2013

MEUR

7

Order book distribution

© Wärtsilä

12.1%

10.7% 11.1% 10.9% 11.2%

12.8%

11.0% 11.5% 11.7% 11.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

50

100

150

200

250

2009 2010 2011 2012 2013

EBIT%

target:

10-14%

MEUR

Q2 Q1 Q3 Q4

Yearly EBIT% (operating result before non-recurring items)

Yearly EBITA% (operating result before non-recurring items

and intangible asset amortisation related to acquisitions)

8

Resilient profitability

Moderate activity in

power generation

markets

Power Plants – quoted MW per fuel type

10 © Wärtsilä

0

2000

4000

6000

8000

10000

12000

14000

16000

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2005 2006 2007 2008 2009 2010 2011 2012 2013

MW

Others

Natural gas

Heavy fuel oil

The share of natural gas is consistently increasing.

© Wärtsilä

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012 2013

MEUR

Q2 Q1 Q3 Q4

11

Power Plants quarterly order intake

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2009 2010 2011 2012 2013

MEUR Review period development

Total EUR 1,292 million (1,515)

IPP’s*

Utilities

Industrials

Oil

18%

Gas

82%

Review period order intake by fuel in MW

x%

12

Power Plants order intake by customer segment

46%

23%

31%

Q1-Q3 Q4

*IPP = Independent Power Producer

© Wärtsilä

• Turnkey order for 200 MW dual-fuel power plant

awarded by PT Indonesia Power

• The plant will be constructed by a consortium

with Wärtsilä as the lead partner

• The new power plant will ensure greater

reliability in the supply of electricity in Bali

• Key in the contract award was the ability to

deliver high quality, extremely efficient, and

flexible energy solutions on a fast-track basis

13

Wärtsilä to supply Indonesia’s largest ever engine

based power plant

NEW

PIC

© Wärtsilä

314

122

Order intake 2013: 2,401 MW (3,146)

18

268

131

Americas 418 (919)

Europe 320 (89)

Asia 1,083 (869)

Africa and Middle East 581 (1,269)

181

113 303

114

Utilities

IPP’s

Industrials

14

Power Plants global order intake Good demand in Asia

26

145

666

© Wärtsilä

Siemens

GE

MHI

Wärtsilä

Alstom

15

6.4%

H1 2013

34.6%

26.1%

5.9%

12.8%

Total market 18.8 GW (28.8)

5.9%

8.0%

Other GTs

Ansaldo

15

Market for gas and liquid based power plants

Includes all Wärtsilä power plants and other manufacturers’ gas and liquid fuelled power plants with prime

movers above 5 MW, as well as estimated output of steam turbines for combined cycles.

The data is gathered from the McCoy Power Report.

Other combustion engines not included. In engine technology Wärtsilä has a leading position.

Improvement in

marine market

activity

© Wärtsilä 17

Vessel contracting continues strong

Source: Clarkson Research Services

* CGT= gross tonnage compensated with workload

*

*

© Wärtsilä

0

300

600

900

1200

1500

1800

2009 2010 2011 2012 2013

MEUR

Review period development Total EUR 1,662 million (1,453)

Offshore

42%

Merchant

34%

Special

vessels

7%

Cruise

& ferry

8% Navy

6%

18

Ship Power order intake by segment

Other

3%

Q1-Q3 Q4

© Wärtsilä

• Order for EPC delivery of 62 MW power module

solution for an FPSO vessel placed by Bumi

Armada

• Vessel to be deployed in the Kraken oil field in the

U.K. sector of the North Sea

• Scope of supply:

– 2 power generation modules, consisting of 16-

cylinder Wärtsilä 50DF engines with generators

– Waste heat recovery units

– Related fuel, oil and air and other utility systems

• Key in receiving the contract were the fuel

flexibility and the high levels of efficiency and

availability of Wärtsilä’s integrated power module

solutions

19

Wärtsilä power modules for North Sea FPSO

© Wärtsilä

• Order intake in Wärtsilä Hyundai

Engine Company Ltd in South

Korea, and Wärtsilä Qiyao

Diesel Company Ltd in China

totalled EUR 222 million (242)

during the review period January-

December 2013

• Wärtsilä’s share of ownership in

these companies is 50%, and the

results are reported as a share of

result of associates and joint

ventures

MEUR

Ship Power order intake

Joint venture order intake

20

Joint venture ordering activity

0

50

100

150

200

250

300

350

400

450

500

550

600

Q1/2

010

Q2/2

010

Q3/2

010

Q4/2

010

Q1/2

011

Q2/2

011

Q3/2

011

Q4/2

011

Q1/2

012

Q2/2

012

Q3/2

012

Q4/2

012

Q1/2

013

Q2/2

013

Q3/2

013

Q4/2

013

© Wärtsilä

Ship Power order book 31 December 2012

21

Cruise & Ferry

7%

Offshore

45%

Special

vessels

6%

Navy

7%

Bulkers

3%

Cargo

3%

Tankers

15%

Containers

4%

LNG*

5%

Merchant

32%

Others

1%

* Excluding order book from South Korean joint venture

Ship Power order book 31 December 2013

RoRo

1%

© Wärtsilä

Wärtsilä’s market shares are calculated on a 12 months rolling basis, numbers in brackets are from the end of the

previous quarter. The calculation is based on Wärtsilä’s own data portal.

Wärtsilä

52%(49)

Others

19%(18)

MAN D&T

25%(21)

Caterpillar

4%(12)

MAN D&T

88%(88)

Wärtsilä

10%(10)

Mitsubishi

2%(2)

Low-speed main engines

Total market volume last 12 months:

22,935 MW (20,540)

Total market volume last 12 months:

4,137 MW (4,438)

Medium-speed main engines

Wärtsilä

4%(5)

Auxiliary engines

Total market volume last 12 months:

5,966 MW (5,024)

Others

96%(95)

22

Ship Power market Market position of Wärtsilä’s marine engines

Stable

development in

the service

markets

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2009 2010 2011 2012 2013

-3%

0

100

200

300

400

500

600

Q4/2012 Q4/2013

MEUR

Fourth quarter development

MEUR

531 -5% 507

0% 0%

24

Services net sales development

5%

Q1-Q3 Q4

© Wärtsilä

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012 2013

Q1 Q2 Q3 Q4

MEUR

25

Services net sales by quarter

© Wärtsilä

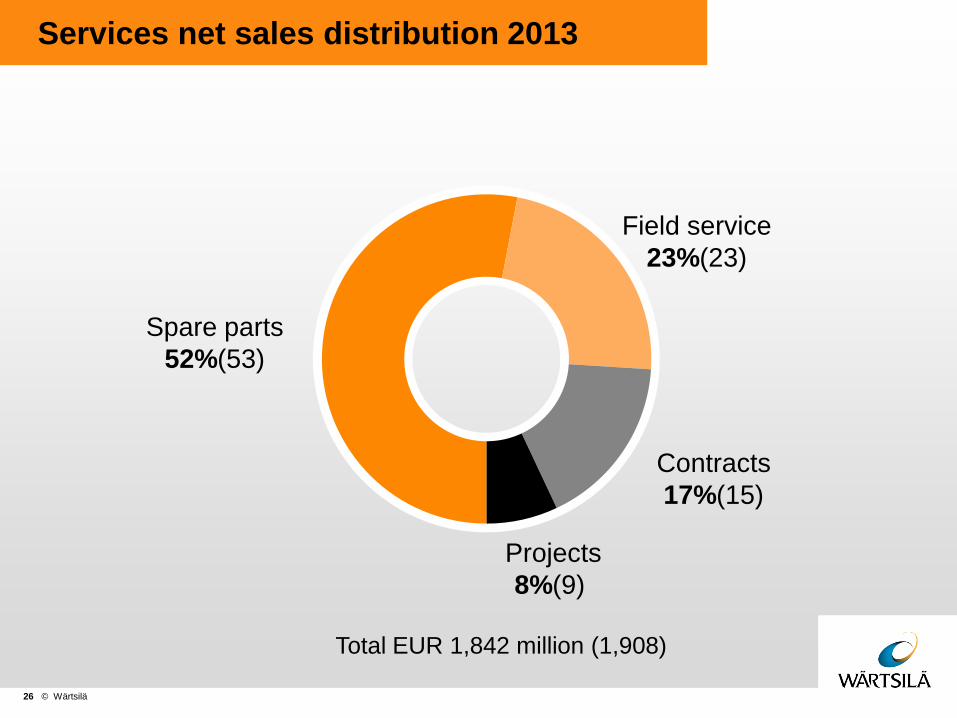

Spare parts

52%(53)

Field service

23%(23)

Contracts

17%(15)

Projects

8%(9)

26

Total EUR 1,842 million (1,908)

Services net sales distribution 2013

© Wärtsilä

Services distribution per business 2013

27

Net sales Total EUR 1,842 million

Installed base Total 182,000 MW

Ship

Power Power

Plants

Ship

Power

Power

Plants

© Wärtsilä

• Serveral services agreements signed with marine and power plant customers in 2013:

– 10-year agreement with Portland General Electric Company in the USA

– 10-year maintenance agreement with Energy Developments Ltd of Australia

– 10-year Operations & Maintenance agreement with Ndola Energy Company Ltd in Zambia

– 5-year maintenance agreement for world’s largest LNG fuelled passenger ferry Viking Grace with Finnish Viking Line

• Agreements guarantee full performance and operational accountability, enabling customers to reduce operating expenses and focus on their core business

• Over 17 GW of generating capacity in marine and land based installations covered by service agreements

28

Strategic focus on long-term service agreements

continues

NEW

PIC

© Wärtsilä

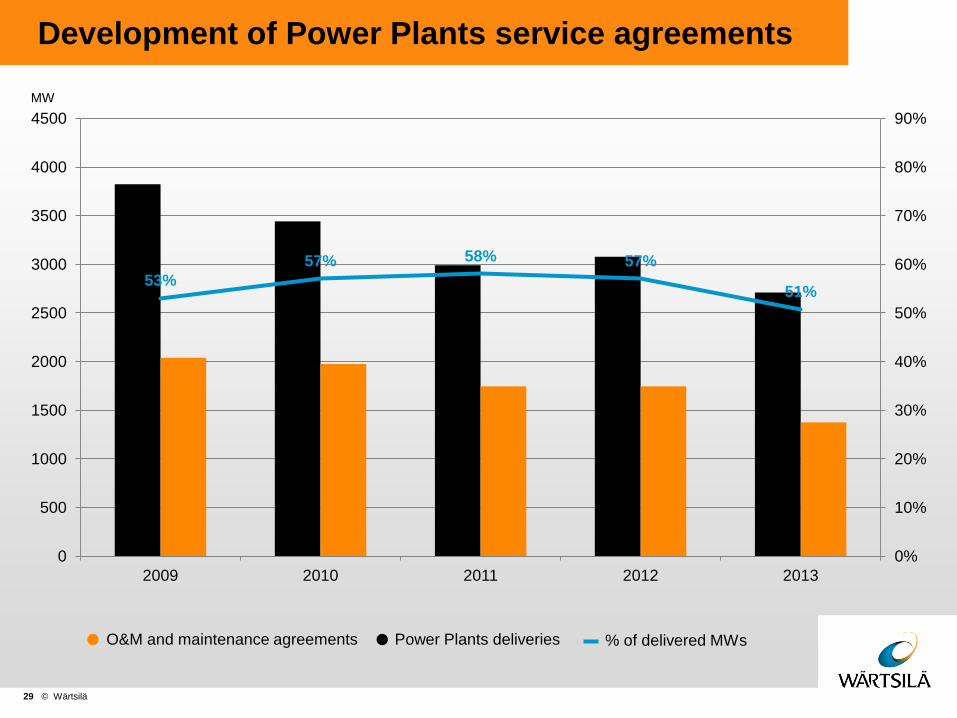

O&M and maintenance agreements Power Plants deliveries % of delivered MWs

MW

29

Development of Power Plants service agreements

53%

57% 58% 57%

51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2009 2010 2011 2012 2013

© Wärtsilä

Fleet utilisation

* Source Bloomberg. Sample of more than 25 000 vessels (>299 GT) covered by IHS AIS Live.

** Source Bloomberg

30

Fleet utilisation

Fleet Average Speed, knots**

Anchored Vessels & Fleet Development*

20000

20500

21000

21500

22000

22500

15%

20%

25%

30%

35%

06.1

1

09.1

1

12.1

1

03.1

2

06.1

2

09.1

2

12.1

2

03.1

3

06.1

3

09.1

3

12.1

3

Nr

of

Active V

essels

Perc

ent A

nchore

d

Anchored Active Fleet

8,0

8,5

9,0

9,5

10,0

10,5

07.1

1

10.1

1

01.1

2

04.1

2

07.1

2

10.1

2

01.1

3

04.1

3

07.1

3

10.1

3

01.1

4

Solid financial

standing

© Wärtsilä

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013

MEUR

32

Strong development in cash flow from operating activities

© Wärtsilä

Working capital Total inventories Advances received Working capital / Net sales

MEUR

33

Working capital Good development in advances received

267

486

118

235

465

313

5.8%

9.2%

3.7%

6.8%

9.8%

6.7%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2008 2009 2010 2011 2012 2013

© Wärtsilä

Solvency Gearing

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009 2010 2011 2012 2013 -0,10

0,00

0,10

0,20

0,30

0,40

0,50

2009 2010 2011 2012 2013

34

Financial position

© Wärtsilä

EPS and

35

0,00

0,50

1,00

1,50

2,00

2,50

EPS Dividend Extra dividend

EUR

2009 2010 2011

*Dividend 2013 - Proposal of the Board

2012 2013*

1.98

1.05

EPS and dividend per share

© Wärtsilä

• Power Plants: Based on the forecasted GDP

growth in 2014, the overall market for liquid and

gas fuelled power generation is expected improve

slightly. Ordering activity remains focused on

emerging markets, which continue to invest in

new power generation capacity.

• Ship Power: The main drivers supporting activity

in shipping and offshore are in place. Overall

contracting is expected to remain on improved

levels, keeping in mind the prevailing

overcapacity and the market’s limited capacity to

absorb new tonnage.

• Services: The overall service market outlook

remains stable.

36

Market outlook

NEW

PIC

© Wärtsilä

• Process started to realign organisation to secure

future profitability and competitiveness in a

challenging business environment

• Planned reductions of approx. 1,000 jobs globally,

impacting all businesses and support functions

• Expected annual savings of EUR 60 million are

estimated to materialise fully by the end of 2014

• The non-recurring costs related to the

restructuring measures are EUR 50 million, of

which EUR 11 million was recognised in 2013

Group-wide efficiency programme initiated

37

Wärtsilä expects its net sales

for 2014 to grow by 0-10% and

its operational profitability

(EBIT% before non-recurring

items) to be around 11%.

Prospects for 2014

IR Contact:

Natalia Valtasaari

Director, Investor Relations

Tel. +358 (0) 40 187 7809

E-mail: [email protected]