2013 Outlook for Asia - The page cannot be found

140

See important disclosures, including any required research certifications, beginning on page 136 4 January 2013 All roads lead to China • We forecast Asia ex-Japan GDP growth of 6.8%, from 6.3% in 2012 • Backed by a rerating of deep cyclical sectors in early 2013 and the impact of QE3, we forecast about a 15% rise in the MSCI AeJ Index • Depending on the market, we favour cyclical high-beta stocks or structural recovery stories. Directly and indirectly, China is a recurring theme among Daiwa’s 10 regional stock picks for 2013 2013 Outlook for Asia Asia ex Japan

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of 2013 Outlook for Asia - The page cannot be found

See important disclosures, including any required research certifications, beginning on page 136

4 January 2013

All roads lead to China

• We forecast Asia ex-Japan GDP growth of 6.8%, from 6.3% in 2012 • Backed by a rerating of deep cyclical sectors in early 2013 and the

impact of QE3, we forecast about a 15% rise in the MSCI AeJ Index • Depending on the market, we favour cyclical high-beta stocks or

structural recovery stories. Directly and indirectly, China is a recurring theme among Daiwa’s 10 regional stock picks for 2013

2013 Outlook for Asia

Asia ex Japan

2013 Outlook for Asia 4 January 2013

Sector rating Analyst Page

Stock picks for 2013 Pranab Kumar Sarmah Daiwa Asia ex-Japan Research Team

3

Macroeconomic outlook for 2013 Mingchun Sun/Kevin Lai/Chi Sun/ Christie Chien

9

Market outlook for 2013 Pranab Kumar Sarmah/ Chang H. Lee/Mark Chang/ Alan Chan

20

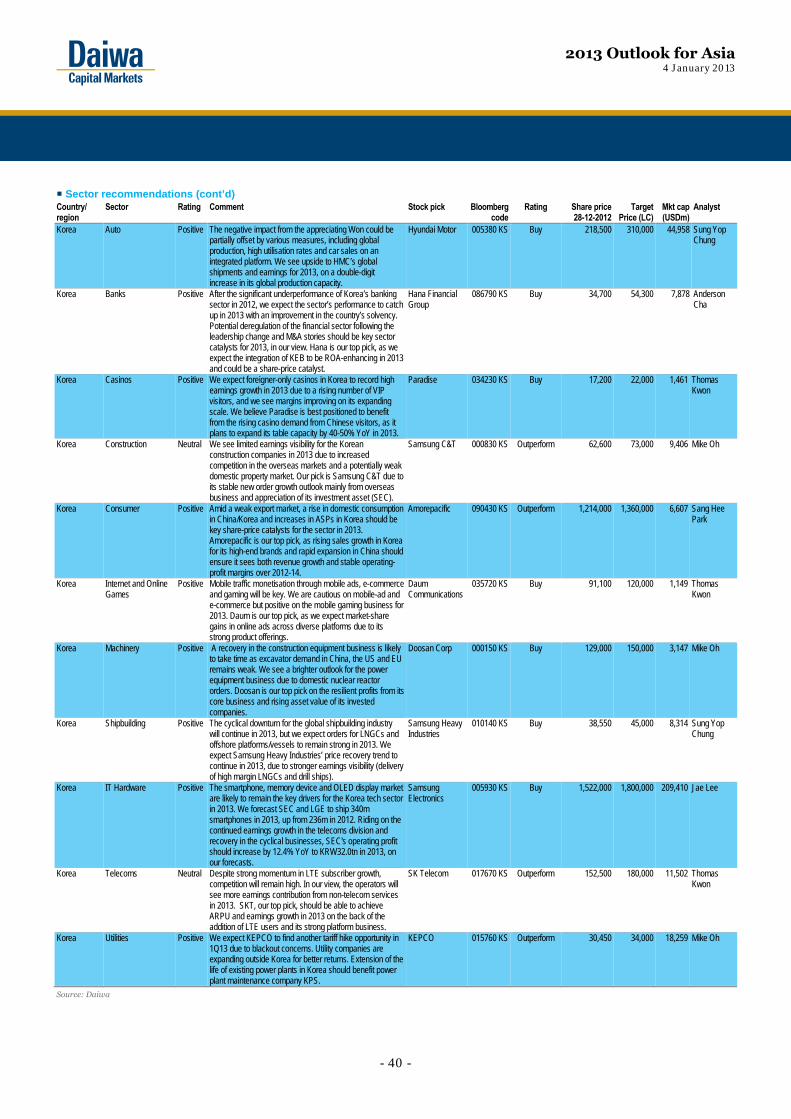

Sector outlooks Regional Oil & Gas Neutral Adrian Loh 42 Small/Mid-Caps Positive John Choi 44 Transportation Positive Kelvin Lau 46Greater China Semiconductors Neutral Eric Chen 48 Smartphones Positive Birdy Lu 50 PC Hardware Neutral Christine Wang 52Hong Kong/China Auto (China) Positive Jeff Chung 54 Banks (China) Positive Grace Wu/Leon Qi 56 City Gas (China) Positive Dave Dai 58 Construction Materials and

Building Products (China) Positive Felix Lam 60

Gaming (Macau) Neutral Bing Zhou 62 Infrastructure (China) Positive Joseph Ho/Winston Cao 64 Internet (China) Positive John Choi 66 Property (China) Positive Jonas Kan/Felix Lam/Maurine Wan 68 Property (Hong Kong) Positive Jonas Kan/Maurine Wan 70 Thermal Coal (China) Positive Dave Dai 72India Auto Positive Navin Matta 74 Financials Positive Punit Srivastava 76 Capital Goods Positive Saurabh Mehta 78 Consumer Neutral Mihir P. Shah 80 Materials Positive Deepak Poddar 82 Oil and Gas Positive Nirmal Raghavan 84Korea Auto Positive Sung Yop Chung 86 Banks Positive Anderson Cha 88 Casinos Positive Thomas Y. Kwon/Francis Kim 90 Construction Neutral Mike Oh 92 Consumer Positive Sang Hee Park 94 Internet and Online Games Positive Thomas Y. Kwon/Francis Kim 96 Machinery Positive Mike Oh 98 Shipbuilding Positive Sung Yop Chung 100 IT Hardware Positive Jae H. Lee 102 Telecoms Neutral Thomas Y. Kwon/Francis Kim 104 Utilities Positive Mike Oh 106Philippines Capital Goods Positive Rommel Rodrigo 108Singapore Capital Goods Positive Adrian Loh 110 REITs Neutral David Lum 112Taiwan Automation Positive Christine Wang 114 Financials Positive Jerry Yang 116 TFT-LCD Positive Chris Lin 118 Touch Panels Positive Chris Lin 120ASEAN Banks Positive Srikanth Vadlamani 122 Telecoms Positive Ramakrishna Maruvada/Jame Osman 124

Note: closing share prices as at 28 December 2012

Contents

2013 Outlook for Asia 4 January 2013

- 1 -

All roads lead to China Macro outlook • After the mixed bag of events we saw in 2012, the region’s economic hopes for 2013 are being

pinned on China once again, and its ability to stoke intra-Asian demand growth. We forecast Asia ex-Japan’s GDP to grow by 6.8% YoY for 2013, up from 6.3% YoY for 2012E.

• We expect a cyclical recovery in China until at least the middle of 2013, driven by restocking activity and the lagged effects of policy easing. Starting from 3Q13, we expect China to embark on mild policy tightening (two 25bp rate hikes) to ease renewed concerns about inflation.

• Asian currencies (excluding the Yen) should continue to appreciate on the back of QE3 and good regional economic fundamentals.

• We expect continued resilience among the ASEAN economies, on the back of strong domestic demand, their willingness to spend fiscally, and a cyclical recovery in China in 1H13.

• The Reserve Bank of India (RBI) is likely to depart from calibrated policy easing to more pervasive easing to protect growth; we forecast interest-rate cuts totalling 100bps in 2013.

• Risks: 1) more risk aversion during Spain’s and Italy’s large bond redemptions in the summer, 2) a potential increase in the risk premium for US treasuries, 3) a potential escalation of Sino-Japan political tensions, 4) higher-than-expected inflation in Asia due to a sharp rise in crude-oil prices and food prices, and 5) a meltdown in China’s shadow-banking system.

Market outlook • We forecast an increase of about 15% in the MSCI Asia ex-Japan Index over 2013, backed by

earnings growth and a moderate rerating of cyclical stocks. We forecast about 10% or more upside potential for the KOSPI, SENSEX, and Hang Seng Index over this year, while the TAIEX could end 2013 at the current level.

• We expect markets that host cyclical stocks, such as Hong Kong, China, and Taiwan, to see strong earnings recoveries in 2013. The Won’s strength over the Yen is an issue for Korea.

Stock picks • Most of our regional top picks have a connection with China, and four of our top picks from

China are directly linked to domestic demand.

• We prefer stocks from cyclical sectors in China and India, and companies that we believe offer structural recovery stories in Korea, Taiwan, and the ASEAN countries.

• Our preferred sectors are China property, Asia banks, shipping, China and India materials and infrastructure, consumer discretionary, and players in the smartphone chain.

• Our top-two non-consensus regional Sell ideas are Dongfeng Motor Group and AREIT.

Daiwa’s key regional stock calls for 2013 Company B’berg code Rating Share price (local) Target price Mkt. cap (USDm) Daiwa comment Guangzhou R&F Prop 2777 HK Buy 12.88 15.90 5,356 An undervalued regional play Orient Overseas Int’l 316 HK Buy 50.30 67.00 4,061 Upside potential from restocking demand ICBC 1398 HK Buy 5.53 6.70 249,029 Cyclical macro recovery should override any rise in

funding costs ENN Energy 2688 HK Buy 33.70 43.00 4,564 Structural earnings growth with a cyclical boost China Railway Const’n 1186 HK Buy 8.81 10.53 14,022 Policy-driven pick Samsung Electronics 005930 KS Buy 1,522,000 1,800,000 209,410 Cyclical earnings boost likely ahead Amorepacific 090430 KS Outperform 1,214,000 1,360,000 6,607 Increasing consumer demand from China and Korea MediaTek 2454 TT Buy 323.50 383.00 15,032 Beneficiary of China handset upgrade cycle Tata Steel TATA IN Buy 428.35 505.00 7,592 Well prepared to ride on a cyclical recovery Bank of Ayudhya BAY TB Buy 32.50 38.00 6,453 ASEAN consumer-demand pick Source: Daiwa. Note: prices in local currency as of close of 28 December 2012

2013 Outlook for Asia 4 January 2013

- 2 -

2013 Outlook for Asia 4 January 2013

- 3 -

Stock picks for 2013 Pranab Kumar Sarmah, CFA (852) 2848 4441 ([email protected]) Daiwa Asia ex-Japan Research Team

Top-10 regional picks

For 2013, our preference lies with stocks from cyclical sectors in China and India, and companies that we believe offer structural recovery stories in Korea, Taiwan and ASEAN countries. Our preferred sectors are China property, Asian banks, shipping, China/India infrastructure, consumer discretionary, and players in the smartphone chain. Our top picks are as follows. 1. Guangzhou R&F Properties (2777 HK) – an

undervalued regional play

2. Orient Overseas International (316 HK) – upside potential from restocking demand

3. ICBC (1398 HK) – cyclical macro recovery should override any rise in funding costs

4. ENN Energy (2688 HK) – structural earnings growth with a cyclical boost

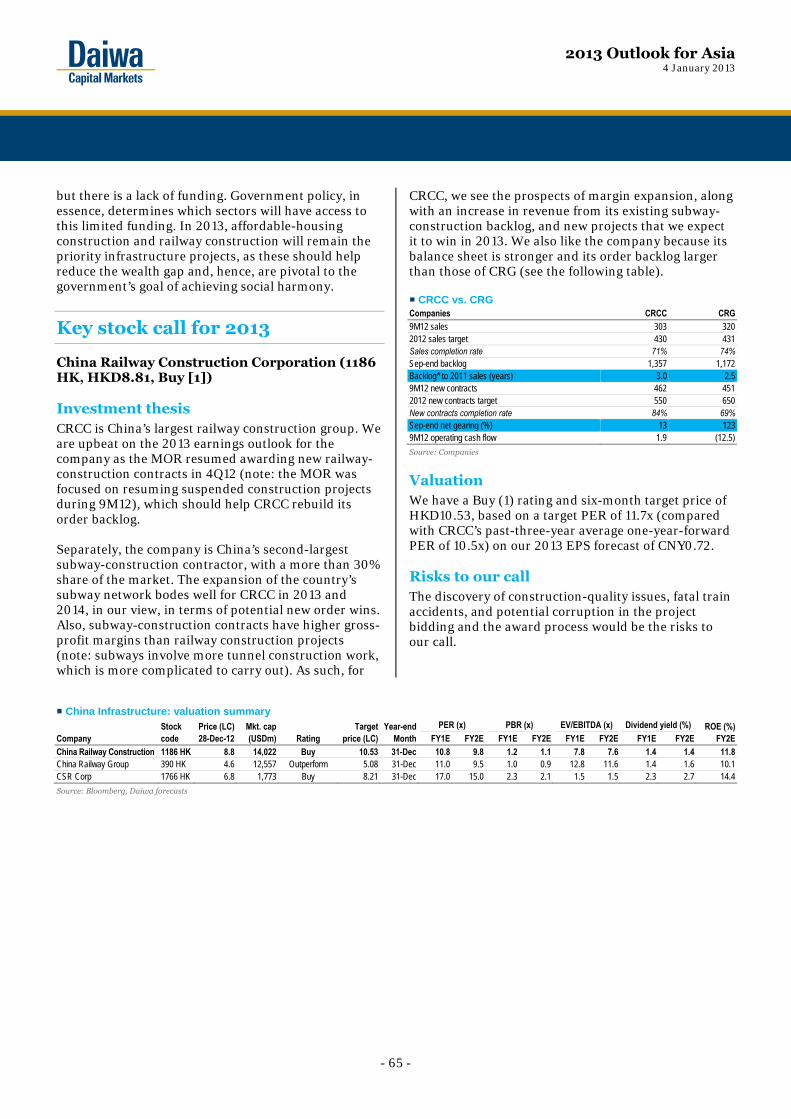

5. China Railway Construction Corporation (1186 HK) – policy-driven pick

6. Samsung Electronics (005930 KS) – cyclical earnings boost likely ahead

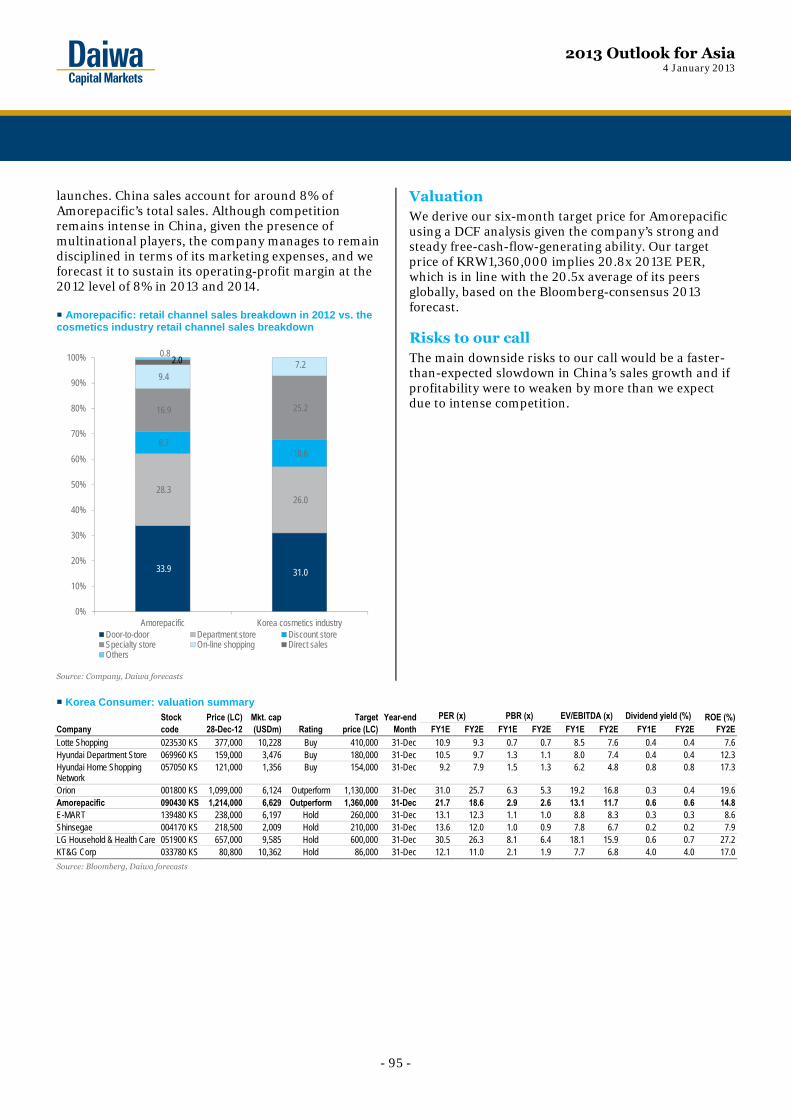

7. Amorepacific (090430 KS – should benefit from increasing consumer demand from China and Korea

8. MediaTek (2454 TT) –beneficiary of China handset upgrade cycle

9. Tata Steel (TATA IN) – well prepared to ride on a cyclical recovery.

10. Bank of Ayudhya (BAY TB) – ASEAN consumer-demand pick

Our top two non-consensus regional Sell ideas are Dongfeng Motor Group (489 HK) and Ascendas Real Estate Investment Trust (AREIT SP).

China exposure a blessing

In this report, our economics team presents its top-five macro themes for Asia ex Japan for 2013, and our regional analysts give their top Buy and Sell ideas within 42 sub-sectors. We have screened our top-10 Buy ideas based on the following metrics:

a) relevance to our macro themes,

b) structural stories, and

c) valuations. Most of our picks from the regions have a connection with China. For instance, one of our top picks in ASEAN is Bank of Ayudhya, which we believe stands to benefit from rising consumer demand as more manufacturing activities migrate from China to ASEAN countries. Another of our picks, Amorepacific in Korea, is selected for its exposure to rising consumer demand from China and high-end product demand in Korea. Four of our top picks from China are directly linked to domestic demand. For those stock markets that underperformed vs. the MSCI Asia ex-Japan Index in 2012 (mainly China), our picks are cyclical high-beta stocks. For markets that outperformed (such as ASEAN), or appear fairly valued now (such as Korea and Taiwan), our picks are mainly structural recovery stories.

2013 Outlook for Asia 4 January 2013

- 4 -

Our key macro themes and sector impact

Themes and sector impact for 2013 Theme Sector impact Theme 1. We expect a cyclical recovery in China to at least mid-2013, driven by restocking activity and the lagged effects of policy easing.

We expect to see a continuous improvement in sales volumes and profits of China demand-driven cyclical sectors such as property, transportation, building materials, etc. Indirect beneficiaries should be supporting industries such as banks, insurance and consumer discretionary. Among our stock picks, Guangzhou R&F Properties, Orient Overseas International, ICBC and China Railway Construction Corporation are beneficiaries of this macro theme.

Theme 2. Starting from 3Q13, we expect China to embark on mild policy tightening (two 25bp rate hikes) to ease potentially renewed concerns about inflation.

We believe such a move will prompt investors to park money in defensive sectors such as Telecoms, Utilities with low gearing, etc, in 2H13. However, banks should benefit during the early stage of an interest-rate-hike cycle due to improved NIMs. We think it is too early to park money in defensive sectors, thus we are not recommending any stocks in these except ENN Energy, which we believe has a structural growth story and policy-specific upside potential (possible gas-price hike).

Theme 3. Asian currencies (ex JPY) should continue to appreciate on QE3 and good economic fundamentals.

We expect the KRW’s strength against the JPY to impact negatively companies in Korea that compete directly with Japanese groups. These are in the auto, auto-components and electronics raw-material sectors. The health of Korea’s domestic consumption is likely to depend on the overall economy, which we expect to improve slightly in 2013. Appreciation of ASEAN currencies in 2013 should favour domestic-consumption, utilities, airlines, and telecoms names in those economies.

Theme 4. We expect continued resilience of ASEAN economies, on the back of strong domestic demand, their willingness to spend fiscally, and a cyclical recovery in China in 1H13.

QE3 should help drive a rerating of all Asian markets. The magnitude is difficult to quantify. However, we have seen increased fund flows from the US and Europe to Asian markets since late November 2012. In a strong economic recovery scenario, REITs are likely to underperform. We have a non-consensus Underperform rating on AREIT. Our pick for the ASEAN consumption theme are Bank of Ayudhya of Thailand. Amorepacific of Korea is a beneficiary of China/Korea discretionary consumer spending.

Theme 5. The Reserve Bank of India (RBI) is likely to depart from calibrated policy easing to more pervasive easing to protect economic growth; we forecast interest-rate cuts totalling 100bps in 2013.

Sectors with high financial leverage such as property and its derivatives such as infrastructure, construction, etc., should benefit from potential interest-rate cuts in India in 2H13. At this stage, we would favour quality cyclicals and our pick here is Tata Steel. Interestingly, in India interest cuts tend to have a limited impact on NIMs at private-sector banks but a high impact at public-sector banks.

Source: Daiwa

Structural recovery stories For most ASEAN markets and the Taiwan market that we believe are fairly valued now, we have focused on structural recovery stories and our two top picks here are Bank of Ayudhya (BAY) in Thailand and MediaTek in Taiwan. We forecast BAY’s ROE to improve by 2.6pp over the next two years, on the back of a change in its business mix. Samsung Electronics (SEC), our top pick in Korea, is also in a structural recovery phase. We forecast SEC to deliver operating-profit growth of 12.4% YoY for 2013, backed by its structural business growth in smartphones and a cyclical boost from the memory and TFT-LCD sectors. We expect strong revenue growth and profit-margin expansion for MediaTek in 2013 due to a favourable shift in its product mix.

2013 Outlook for Asia 4 January 2013

- 5 -

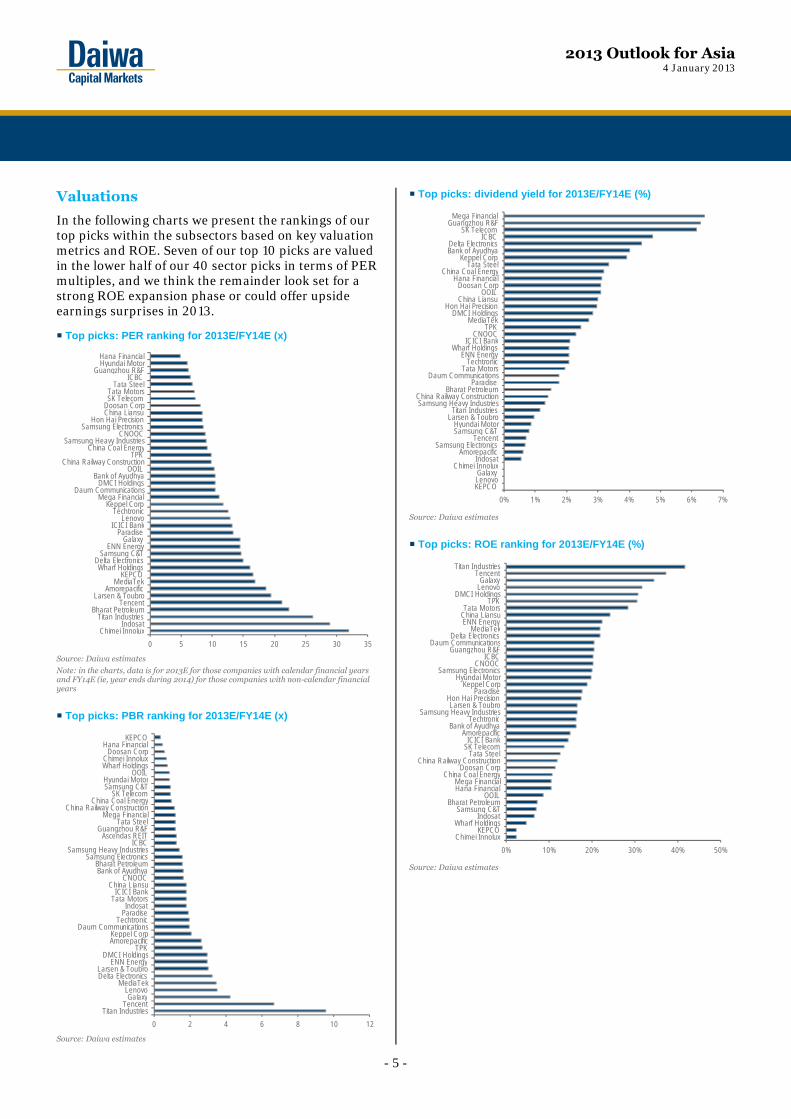

Valuations

In the following charts we present the rankings of our top picks within the subsectors based on key valuation metrics and ROE. Seven of our top 10 picks are valued in the lower half of our 40 sector picks in terms of PER multiples, and we think the remainder look set for a strong ROE expansion phase or could offer upside earnings surprises in 2013. Top picks: PER ranking for 2013E/FY14E (x)

Source: Daiwa estimates

Note: in the charts, data is for 2013E for those companies with calendar financial years and FY14E (ie, year ends during 2014) for those companies with non-calendar financial years

Top picks: PBR ranking for 2013E/FY14E (x)

Source: Daiwa estimates

Top picks: dividend yield for 2013E/FY14E (%)

Source: Daiwa estimates

Top picks: ROE ranking for 2013E/FY14E (%)

Source: Daiwa estimates

0 5 10 15 20 25 30 35Chimei Innolux

IndosatTitan Industries

Bharat PetroleumTencent

Larsen & ToubroAmorepacific

MediaTekKEPCO

Wharf HoldingsDelta Electronics

Samsung C&TENN Energy

GalaxyParadise

ICICI BankLenovo

TechtronicKeppel Corp

Mega FinancialDaum Communications

DMCI HoldingsBank of Ayudhya

OOILChina Railway Construction

TPKChina Coal Energy

Samsung Heavy IndustriesCNOOC

Samsung ElectronicsHon Hai Precision

China LiansuDoosan CorpSK TelecomTata Motors

Tata SteelICBC

Guangzhou R&FHyundai MotorHana Financial

0 2 4 6 8 10 12Titan Industries

TencentGalaxy

LenovoMediaTek

Delta ElectronicsLarsen & Toubro

ENN EnergyDMCI Holdings

TPKAmorepacificKeppel Corp

Daum CommunicationsTechtronic

ParadiseIndosat

Tata MotorsICICI Bank

China LiansuCNOOC

Bank of AyudhyaBharat Petroleum

Samsung ElectronicsSamsung Heavy Industries

ICBCAscendas REIT

Guangzhou R&FTata Steel

Mega FinancialChina Railway Construction

China Coal EnergySK Telecom

Samsung C&THyundai Motor

OOILWharf HoldingsChimei Innolux

Doosan CorpHana Financial

KEPCO

0% 1% 2% 3% 4% 5% 6% 7%KEPCOLenovoGalaxy

Chimei InnoluxIndosat

AmorepacificSamsung Electronics

TencentSamsung C&THyundai Motor

Larsen & ToubroTitan Industries

Samsung Heavy IndustriesChina Railway Construction

Bharat PetroleumParadise

Daum CommunicationsTata Motors

TechtronicENN Energy

Wharf HoldingsICICI Bank

CNOOCTPK

MediaTekDMCI Holdings

Hon Hai PrecisionChina Liansu

OOILDoosan Corp

Hana FinancialChina Coal Energy

Tata SteelKeppel Corp

Bank of AyudhyaDelta Electronics

ICBCSK Telecom

Guangzhou R&FMega Financial

0% 10% 20% 30% 40% 50%Chimei Innolux

KEPCOWharf Holdings

IndosatSamsung C&T

Bharat PetroleumOOIL

Hana FinancialMega Financial

China Coal EnergyDoosan Corp

China Railway ConstructionTata Steel

SK TelecomICICI Bank

AmorepacificBank of Ayudhya

TechtronicSamsung Heavy Industries

Larsen & ToubroHon Hai Precision

ParadiseKeppel Corp

Hyundai MotorSamsung Electronics

CNOOCICBC

Guangzhou R&FDaum Communications

Delta ElectronicsMediaTek

ENN EnergyChina LiansuTata Motors

TPKDMCI Holdings

LenovoGalaxy

TencentTitan Industries

2013 Outlook for Asia 4 January 2013

- 6 -

Top-10 Buy ideas

Guangzhou R&F Properties (2777 HK, HKD12.88, Buy [1]) An undervalued regional play. The share prices of leading China national property companies’ rallied substantially in 4Q12, and are now close to fair value, in our view. We believe it is now time for the valuations of quality regional players to catch up. Guangzhou R&F Properties (Guangzhou R&F) is a quality regional player, in our view, with a solid presence in Guangzhou, Beijing and Tianjin, is expanding to second-tier cities, and is trading at a significant discount to current NAV. With its strong balance sheet, we expect the company to become more active in replenishing its landbank in 2013. Its progress in securing urban-renewal projects in major cities should be another positive development this year. Our six-month target price of HKD15.9 is based on a 30% discount applied to our end-2013 NAV forecast. Orient Overseas International (316 HK, HKD50.3, Buy [1]) Upside potential from restocking demand. In the global shipping market, we expect capacity consolidation to remain intact and freight demand to recover by 6% YoY in 2013. Note that few major liners have announced capacity cuts for 2013. We believe liner Orient Overseas International (OOIL) stands to benefit from potential restocking demand in the near term due to low inventory levels in many industries in the US and better-than-expected US holiday-period sales. An increasing revenue contribution from inter-Asia routes would be a structural revenue-growth driver for the company. Also, we expect OOIL to be the most profitable liner globally at operating-profit level in 2013. Our six-month target price of HKD67 is based on a target PBR of 1.1x applied to our 2013E BVPS. ICBC (1398 HK, HK5.53, Buy [1]) Cyclical macro recovery should override any rise in funding costs. We expect NIM compression to become visible for the PRC Banks Sector from 1Q13 onwards and believe large banks such as ICBC will be less impacted than small ones. We expect ICBC to leverage on its low cost of funds stemming from its strong deposit franchise, steady asset quality and strong capital base. Also, the cyclical economic recovery that our economics team forecasts for China (GDP growth to accelerate to 8.7% YoY for 2Q13E) should ease concerns about asset quality for ICBC as it should help to offset any resultant rise in funding costs. Our six-month target price of HKD6.70 is based on the SOTP method and implies a blended PBR of 1.6x for 2013E.

ENN Energy (2688 HK, HKD33.7, Buy [1]) Structural earnings growth with a cyclical boost. Among the various utilities sub-sectors, China’s demand for gas has not slowed over the past decade and we expect full gas-price reform China in 2013, leading to a gas-price hike. ENN Energy (ENN) is our top pick for this theme, due to what we consider as its superior organic earnings growth, cheap valuation, and upside potential from the expansion of its refilling-station business. We forecast ENN’s organic growth to average around 23% per year over 2013-14 on strong natural-gas sales. Another earnings-growth driver is its investment in liquefied natural gas (LNG)-refilling stations. The company projects higher returns from LNG-refilling stations than from compressed-natural gas (CNG)-refilling stations. On valuation, the stock is trading at a below-sector-average 2013E PER based on our EPS forecast, while we forecast it to deliver the highest ROE in its sector this year. Our six-month target price of HKD43 is derived from our DCF valuation. China Railway Construction Corporation (1186 HK, HKD8.81, Buy [1]) Policy-driven pick. China Railway Construction Corporation (CRCC) is China’s largest railway construction group by revenue. We are upbeat about the company’s 2013 earnings outlook, as the Ministry of Railways (MOR) resumed awarding new railway-construction contracts in 4Q12. In addition, CRCC is China’s second-largest subway-construction contractor, with more than a 30% share of the market currently. The expansion of China’s subway network bodes well for CRCC in 2013 and 2014 in terms of potential new order wins, on our view. Also, subway-construction contracts generally have higher gross-profit margins than railway-construction ones, thus we see good prospects for profit-margin expansion for CRCC. Our six-month target price is HKD10.53, based on a target PER of 11.7x (compared with CRCC’s past-three-year average one-year-forward PER of 10.5x) applied to our 2013 EPS forecast. Samsung Electronics (005930 KS, KRW1,522,000, Buy [1]) Cyclical boost ahead. The smartphone, memory-device and OLED-display markets look set to remain key drivers for the Korea tech space in 2013, and SEC is among the market leaders in these product categories. We expect the company to upgrade its flagship products from its mobile division (65% of our 2012E operating profit), such as the Galaxy S and Note-series products, during 2013, with industry-leading specs, which are likely to drive market-share gains for the company in the high-end smartphone/tablet segment.

2013 Outlook for Asia 4 January 2013

- 7 -

While it also plans to introduce low/mid-end smartphones to expand its share in emerging markets like China. We forecast SEC to ship 300m smartphones in 2013, up from 215m in 2012E. We believe there is significant scope for further earnings growth in 2013 as improvements are only just starting at its cyclical businesses (semiconductors and TFT-LCD). Riding on continuous growth of its telecoms division and a recovery in its cyclical business, we forecast the company’s operating profit to increase by 12.4% YoY to KRW32.0tn for 2013. Our SOTP-derived six month target price for SEC is KRW1.8m. Amorepacific (090430 KS, KRW1,214,000, Outperform [2]) Polarisation a positive. Amorepacific’s growing high-end brand business in Korea, a strong Won, and rapid business growth in China should benefit the company in 2013. The polarisation of consumer spending benefits the sales growth of high-end brands, and we forecast high-end brands (which also enjoy high margins) to account for 62% of Amorepacific’s total cosmetics sales for 2012. The China division should account for the highest sales growth for 2012-14E, as sales are rising by 25-30% a year on the back of its expanded distribution coverage, geographical expansion and new brand launches. China sales account for around 8% of Amorepacific’s total sales. We forecast the company to maintain its operating-profit margin for 2013 and 2014 at the 2012E level of 8%. Our six-month target price for KRW1,360,000 is based on a DCF methodology due to the company’s steady free cash flow-generating ability. Our target price implies a 2013E PER of 20.8x, which is in line with the 20.5x average of its peers globally based on the Bloomberg-consensus 2013 forecast. MediaTek (2454 TT, TWD323.5, Buy [1]) Beneficiary of China handset upgrade cycle. We project profit-margin expansion for MediaTek in 2013 on the back of a rebound in its blended ASP from rising smartphone-IC shipments and its shift to a more favourable product mix. One of the key growth drivers for semiconductors in 2013 is smartphone ICs for each of Apple, SEC and China (to which MediaTek has exposure), which we expect to outpace global semiconductor shipment growth in 2013. We forecast smartphone-IC shipments for MediaTek of 205m units for 2013, up from 108m for 2012E. We believe the Bloomberg consensus earnings forecasts for 2013 currently do not assume such strong shipment growth and are likely to be raised. Our six-month target price of TWD383 is based on PER of 20x (the stock’s average over the past year) applied to our 2013 EPS forecast.

Tata Steel (TATA IN, INR428.35, Buy [1]) Well prepared to ride on a cyclical recovery. Tata Steel is our pick from India. A reduction in material costs, recovery in China steel demand (FAI) and India demand (interest-rate cuts) would create a favourable environment for the steel players in 2013. The company commissioned a 2.9mtpa steel capacity expansion in India in 1H FY13 (increasing capacity by 43%), with the impact on output set to be felt in 2H FY13. We forecast a strong steel-sales CAGR of 15% for FY12-14. Further, the strong correction in the coking-coal price during July-December has benefited both the company’s India and its European divisions. Vertical integration to iron-ore mining for India operation makes it immune to the iron-ore shortages being faced by a peer. Our six-month target price of INR505 is based on our SOTP valuation. We value the Indian business at an FY14E EV/EBITDA multiple of 6.5x and the European business at 3.5x. Bank of Ayudhya (BAY TB, THB32.5, Buy [1])

ASEAN consumer demand looks set to pick up. Potentially rising funding costs would be the key issue for Asian banks in 2013, in our view. However, we would expect the impact on the Thai banks to be less severe than on other banks in the ASEAN region as we envisage strong growth in their high-yield consumer lending. Bank of Ayudhya (BAY) is our key call. We believe the bank’s high-yielding personal loans and credit-card businesses are growing rapidly due to rising consumer demand and the bank’s market-share gains, which should lead to 7bps YoY expansion of its NIM for 2013E, despite rising funding costs. Due to operating-expense and credit-cost leverage, we forecast the bank to record a 2pp decline in its cost-to-income ratio over the next two years. We project its ROE to expand to 16.3% for 2014, from 13.7% for 1H12. Our six-month target price of THB38 is based on our Gordon Growth Model.

2013 Outlook for Asia 4 January 2013

- 8 -

Top Sell ideas

Dongfeng Motor Group (489 HK, HKD11.98, Underperform [4]) Loser in the pack. While we have a positive view on China’s auto sector and forecast 10-12% YoY sales-volume growth for passenger vehicles in 2013 (backed by demand from inland areas), we would advise investors to be selective in their stock-picking following the sector’s strong performance in 2012. Dongfeng Motor (DFM) is our non-consensus Underperform call. We believe the company’s golden period of earnings growth has ended, and therefore expect its business momentum to lag peers in 2013 and the stock to continue to derate to the end of 2013. We forecast only a 6.7% EPS CAGR for 2012-14, down sharply from the 38.4% CAGR the company recorded for 2008-11. The company’s ageing passenger vehicle models and less-competitive products in the growing SUV market are likely to be key structural issues for DFM in 2013, in our view. Our six-month target price of HKD8.75 is based on a PER of 7x (which is 0.5SD lower than its past-five-year average) applied to our 2013 EPS forecast.

Ascendas Real Estate Investment Trust (AREIT SP, SGD2.39, Underperform [4]) For the sector, we believe the yield-gap theme is fully played out. We expect a deceleration in rental growth in 2013 due to sub-par GDP growth and a less hospitable operating environment. AREIT trades at a considerable premium (based on yield and NAV) to its industrial property S-REIT peers. AREIT is widely viewed as defensive, but we believe it is probably more vulnerable than its peers, due to its high exposure to multi-tenanted industrial properties. Moreover, we cannot rule out the possibility of a short-term share-price drag from another private placement in 2013, as occurred in early 2011 and 2012. Our six-month target price of SGD2.20 is pegged to parity with our 10-year DDM valuation.

2013 Outlook for Asia 4 January 2013

- 9 -

Macroeconomic outlook for 2013 Mingchun Sun (852) 2773 8751 ([email protected]) Kevin Lai (852) 2848 4926 ([email protected]) Chi Sun (852) 2848 4427 ([email protected]) Christie Chien (852) 2848 4482 ([email protected])

Top-5 macro themes

1. A cyclical recovery in China until mid-2013 (we forecast GDP growth of about 8.5% YoY for 1H13), driven by restocking activity and the lagged effects of policy easing.

2. Starting from 3Q13, China embarks on a round of mild policy tightening (eg, two 25bp rate hikes) to assuage renewed concern about inflation.

3. Asian currencies continue to appreciate on the back of QE3 and good economic fundamentals.

4. The continued resilience of the ASEAN economies, on the back of strong domestic demand, their willingness to spend fiscally, and China’s cyclical recovery in 1H13.

5. The Reserve Bank of India’s (RBI) departure from calibrated policy easing to more pervasive easing in order to protect economic growth – we forecast interest-rate cuts totalling 100bps over the course of 2013.

Top-5 risks

1. Another period of risk aversion globally during the summer, when Spain and Italy face large bond redemptions (in July and August, respectively).

2. A potential increase in the risk premium on US treasuries, reflecting investor concerns about the sustainability of the US debt level in the absence of a credible plan for medium-term consolidation.

3. A potential escalation of Sino-Japanese political tension stemming from territorial disputes.

4. A sharp rise in crude-oil prices stemming from geopolitical risks, or a sharp rise in food prices due to severe weather conditions or the outbreak of disease among livestock, leading to higher-than-expected inflation in Asia and stronger-than-expected policy tightening

5. A potential meltdown of China’s shadow banking system, which could spill over into the overall financial system and the economy at large.

Global outlook

2012: a year of disappointments and excitement In retrospect, 2012 was a year mixed with ‘growth scares’ and policy excitement. A year ago, the FocusEconomics consensus 2012 GDP growth forecast for Asia ex-Japan was 7.5% YoY. Throughout 2012, this forecast was cut progressively. The region is now on track to achieve somewhere close to 6.3% YoY growth, down from 7.3% YoY for 2011. The biggest disappointments were from Hong Kong, Singapore, Taiwan, Korea, and India. For the first three markets, the consensus cut its growth forecasts by more than half. Gap between the consensus forecasts and reality (2012 GDP)

Source: FocusEconomics, CEIC

However, stock markets in Asia performed fairly well, except for those in China. In 1Q12, the policy excitement from Operation Twist, Long-term Refinancing Operations, and numerous Asian central banks provided the reason for a change in sentiment. Then came the growth scare in 2Q12, on the back of Greece’s near Euro-exit, fear of a hard-landing in China, and consensus cuts to regional growth forecasts. In 3Q12, the introduction of Outright Monetary Transactions and QE3, and a cyclical recovery in China set the stage for another change in sentiment, sending markets higher.

0.01.02.03.04.05.06.07.08.09.0

China

Philip

pines

Indon

esia

India

Malay

sia

Thail

and

Korea

Sing

apore

Hong

Kon

g

Taiw

an

Overa

ll

GDP growth (9M12) Consensus forecast in Dec 2011

(% YoY)

2013 Outlook for Asia 4 January 2013

- 10 -

Stock-market performances (2012)

Source: CEIC, Daiwa

Note: last trading day in 2012 for China, Hong Kong, Singapore, Malaysia, and India is 31 December. Last trading day in 2012 for Taiwan, Korea, Thailand, Indonesia and the Philippines is 28 December.

2013: Asia should hold up better than G3 We believe the outlook for 2013 will again be highly dependent upon what extent there will be growth scares and the extent of policy excitement. We expect global demand growth to be slightly weaker. In particular, we find it hard to be upbeat about the G3 economies – Europe, the US, and Japan – which collectively continue to account for about half of all of Asia’s exports. We look for GDP growth for the G3 to be 1.0% YoY for 2013, down from 1.4% YoY for 2012. Global: GDP forecasts

2012E 2013E (% YoY) Daiwa Consensus Daiwa Consensus US 2.3 2.2 1.9 2.0 EU (0.5) (0.5) (0.2) 0.1 Japan 2.0 2.0 0.9 0.9 G3 1.4 1.4 1.0 1.2 Source: Bloomberg, Daiwa forecasts

Note: fiscal-year data for Japan

G3: GDP growth (1996-2013E)

Source: CEIC, Daiwa forecasts

The European crisis should continue to be the source of many problems. With governments compelled to undertake significant fiscal austerity, we expect deep recessions in the periphery countries. The possibility

that the crisis will escalate remains a major downside risk to our outlook, until the underlying issues are resolved. The degree of deleveraging stress is likely to continue. The largest burden of projected credit supply contraction falls on the periphery countries. Following on from a 0.5% YoY drop in euro-area GDP for 2012E, we forecast another 0.2% YoY decline for 2013. We believe the recession will be deeper and more prolonged than official forecasts currently suggest. Event risks concentrated in the summer In terms of event risks, we see them heavily concentrated in April and July-August. There will be general elections in Italy in April. Current polls in Italy predict no clear majority for any party, thus risking a Greek-style political gridlock. Spain faces large bond redemptions in July. Spain’s central government will have to keep funding its regions as their yields remain high. The highly front-loaded nature of the debt will put a large burden on the country’s finances. The risk is that Spain may need to request a bailout sometime in the summer. Italy faces similar large bond redemptions in August. The balance sheets of the country’s banks are already loaded with government bonds. US growth to remain anaemic Meanwhile, we expect the US to avoid excessive fiscal consolidation (fiscal cliff) in 2013, to raise the debt ceiling promptly, and to agree on a credible medium-term fiscal consolidation plan. We do not expect Congress to extend all the current tax breaks and to allow some scheduled spending cuts. In this regard, while economic growth is likely to remain low, we do not see a recession developing in the country. We forecast US GDP growth to fall slightly, from 2.3% YoY for 2012 to 1.9% YoY for 2013. Additional headwinds from Japan Given significant headwinds, both external and domestic, Japan’s economic growth peaked in March 2012 and has since slipped into recession. We believe the economy stagnated again in 4Q12, but expect some growth to return in 2013 and after, supported by: 1) earthquake-related reconstruction demand, 2) a recovery in China, and 3) further monetary easing by the BOJ. Meanwhile, the downside risks are: 1) any deterioration in Japan-China relations, 2) a sharp rise in crude-oil prices stemming from geopolitical risk, and 3) the current-account balance turning negative. We forecast Japan’s GDP growth to slow from 2.0% YoY for FY12 to 0.9% YoY for FY13.

35.833.0

25.722.9

19.7

12.99.5 9.4 8.9

3.1

0

5

10

15

20

25

30

35

40

Thai

land

Phili

ppin

es

Indi

a

Hong

Kon

g

Sing

apor

e

Indo

nesi

a

Mal

aysi

a

Kore

a

Taiw

an

Chin

a A

-sh

are

(%)

-5

-4

-3

-2

-1

0

1

2

3

4

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

E

2013

E

G3 Real GDP growth(% ,YoY)

2013 Outlook for Asia 4 January 2013

- 11 -

Regional macro outlook

Hopes are being pinned on China again As demand from the G3 is unlikely to be inspiring for 2013, the region cannot rely on a demand recovery from those economies. Asia consumes about 30% of its exports itself. Intra-Asia demand is probably the only area that might offset G3 weakness. Therefore, our overall outlook for regional growth depends to a large extent on Asia’s ability to boost its internal demand. China will continue to be the major source of intra-Asian demand growth. We expect the country’s cyclical rebound to last into 1H13, as destocking ends and restocking starts. A low base of comparison (1H12) and the lagged impact of stimulus programmes should also push GDP growth higher in 1H13, possibly to almost 9.0% YoY for 2Q13. This level of GDP growth, however, is likely to invite another round of (mild) policy tightening in 3Q13, which should bring GDP growth back to a downtrend. China: GDP and final demand

Source: CEIC, Daiwa forecasts

At the same time, we see inflation becoming a fresh concern again in China in 3Q13, on the back of a food-price rise and a weak base of comparison (3Q12). We expect CPI inflation to rise above 3.0% YoY for 3Q13 and 4.0% YoY for 4Q13, triggering two 25bp rate hikes in 2H13 as the People’s bank of China (PBOC) tries to narrow the magnitude of negative real rates. In this regard, China would provide a cyclical boost to intra-Asia demand but this would only last for about 6-9 months from now.

CPI inflation and one-year deposit rate

Source: CEIC, Daiwa forecasts

As this cyclical bounce is driven mostly by inventory adjustments and the ‘mini stimulus programme’ that focuses on infrastructure investment (see our report Mini stimulus under way, published on 26 June 2012), the extra demand should come mainly from commodities rather than capital goods. The benefits would be mostly felt by the ASEAN economies. Some of the policy space has been used up Elsewhere in Asia, the space for further policy easing is likely to be more limited this year, and depends highly on the US Dollar trend. Numerous rate cuts in Asia have used up the space available – output gaps are still positive and real policy rates remain well below their pre-crisis averages. Nominal policy rates are either close to or barely above CPI inflation levels. Moreover, in view of QE3 and its potential inflation challenges (including inflation expectations), the room for more easing should be much less in 2013 than in 2012. Besides China, we expect Malaysia, Indonesia, Thailand, and the Philippines to reverse some of the easing they undertook in 2012, mostly in 2H13, but any rate hikes are likely to be moderate because of the need to protect economic growth at the same time. For the same reason, the space for currency depreciation to boost exports should be equally limited. QE3-driven inflation challenges mean that Asian central banks are still required to allow currency appreciation to mitigate import inflation pressures. With the exception of the Rupee, we expect Asian currencies to be 1.4-5.2% stronger throughout 2013. There is still room for fiscal expansion but it should be more limited in 2013. Most of the Asian countries are likely to continue to run fiscal deficits. Lingering inflation concerns should also limit the space for further fiscal spending. For example, despite a very sharp economic slowdown, Singapore has resisted the temptation to launch major fiscal measures. Instead, it believes in policies to boost productivity over the long run.

6

9

12

15

Mar-0

1

Mar-0

2

Mar-0

3

Mar-0

4

Mar-0

5

Mar-0

6

Mar-0

7

Mar-0

8

Mar-0

9

Mar-1

0

Mar-1

1

Mar-1

2

Mar-1

3

Final demand Aggregate demand (GDP)

(% YoY)

ForecastInventory accumulation

Destocking

(2)02468

10

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

(%) Estimate

1-year deposit rate, % p.a. CPI inflation, % YoY

2013 Outlook for Asia 4 January 2013

- 12 -

Keep an eye on the US Dollar However, if the US Dollar continues to strengthen, it would help reduce the inflation pressure on Asian economies, especially in the more industrialised northeast part of the region, and thus provide more space for easing in terms of both rate cuts and currency depreciation. Under such a scenario, the chance of a domestic-demand recovery would be higher. In our base case, however, we expect the US Dollar to be relatively flat compared with the current level throughout the whole year, as we do not see any strong catalysts to drive it either higher or lower. ASEAN: an oasis in the desert In our base-case scenario, we continue to favour ASEAN economies in 2013. They were resilient in 2012. The clear advantage is their ability to provide policy support to boost domestic demand at times when external demand tumbles. While Asia as a whole should see limited room for policy manoeuvre, the ASEAN countries are in a better position to maintain domestic demand because of their willingness and commitment to invest in infrastructure and development projects. The fortunes they have amassed (in many ways at the expense of the more industrialised Asian economies) could allow them to spend their way out of the difficult times for a few more years. Moreover, if the US Dollar were to weaken against the other major currencies, the ASEAN economies would continue to enjoy a terms-of-trade advantage over the industrialised economies. US Dollar index

Source: CEIC, Daiwa In the event that the US Dollar strengthened against the other major currencies in 2013, we would favour the more industrialised and more Dollar-centric Asian countries, including China, Korea, Taiwan, Hong Kong and Singapore. In this scenario, we would expect these economies to experience terms-of-trade improvements, lower import inflation pressure, and see more space for monetary easing and currency depreciation. All these factors might facilitate a domestic-demand recovery.

India’s sharp rate cuts to protect demand India’s economy has been quite problematic because of the country’s need to control inflation and deficits simultaneously. As growth slowed rapidly in 2012, the RBI was no longer under pressure to act aggressively to suppress inflation. We expect the RBI to be increasingly dovish over the course of 2013, and forecast the policy rate to be cut by 100bps over the year. A slowdown in GDP growth from 8.6% YoY for 1H11 to just 5.4% YoY for 9M12 can be seen almost as a hard-landing, in our view. The balance of risk between inflation and growth has started to tilt. The task for the RBI in 2013 is likely to be to protect growth rather than fight inflation. Regional growth should be mildly better YoY for 2013 Overall, we forecast Asia ex-Japan GDP growth to be mildly better, at 6.3% YoY for 2012 and 6.8% YoY for 2013. This compares with a FocusEconomics consensus forecast of 6.8% YoY for 2013. In this regard, we believe the consensus forecast is more or less in line with the fundamentals. While the space for policy excitement is likely to be less in 2013 than in 2012, the room for further growth scares should also be more limited. Barring any major negative developments globally, we forecast Asia ex-Japan economic growth to be 6.6% YoY for 2014, on the back of a slowdown in China from a long-term perspective. Asia ex-Japan: real GDP growth

Source: IMF, Daiwa forecasts

90

95

100

105

110

115

120

125

130

Nov-0

2Ma

r-03

Jul-0

3No

v-03

Mar-0

4Ju

l-04

Nov-0

4Ma

r-05

Jul-0

5No

v-05

Mar-0

6Ju

l-06

Nov-0

6Ma

r-07

Jul-0

7No

v-07

Mar-0

8Ju

l-08

Nov-0

8Ma

r-09

Jul-0

9No

v-09

Mar-1

0Ju

l-10

Nov-1

0Ma

r-11

Jul-1

1No

v-11

Mar-1

2Ju

l-12

Nov-1

2

(1997=100)

QE1+QE2

(4)(2)

02468

10121416

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

E

2013

E

2014

E

Forecasts(% YoY)

2013 Outlook for Asia 4 January 2013

- 13 -

Regional: GDP forecasts 2012E 2013E

(% YoY) Daiwa Consensus Daiwa Consensus Asia ex-Japan 6.3 6.3 6.8 6.8 China 7.8 7.7 8.4 8.1 Hong Kong 0.9 1.6 2.3 3.4 Taiwan 1.2 1.4 3.0 3.4 Korea 2.2 2.4 3.3 3.3 India 5.6 5.7 6.0 6.3 Singapore 1.3 2.0 3.0 2.9 Indonesia 6.2 6.2 6.2 6.2 Malaysia 5.2 4.8 5.3 4.9 Philippines 6.4 5.4 5.8 5.3 Thailand 6.0 5.3 4.8 4.5 Source: FocusEconomics, Daiwa forecasts

Note: Fiscal year for India

Region: CPI forecasts

2012E 2013E (% YoY) Daiwa Consensus Daiwa Consensus Asia ex-Japan 3.4 3.5 3.8 3.8 China 2.6 2.7 3.3 3.3 Hong Kong 4.1 4.0 3.5 3.9 Taiwan 2.0 1.9 1.5 1.8 Korea 2.2 2.3 2.8 2.8 India 7.5 7.6 6.5 6.5 Singapore 4.6 4.5 3.8 3.7 Indonesia 4.3 4.5 6.0 5.3 Malaysia 1.7 1.8 2.8 2.5 Philippines 3.3 3.3 4.0 3.9 Thailand 3.0 3.1 3.5 3.3 Source: FocusEconomics, Daiwa forecasts

Note: WPI data and fiscal year for India

Market-by-market macro outlook

China: a cyclical upturn As China’s economic recovery was likely to have started in 4Q12 and should last into 2Q13, we now boost our real GDP growth forecast for 2013 to 8.4% YoY (versus 8.0% YoY previously), from 7.8% YoY for 2012. We also expect the country’s new leaders to embark on a broad range of economic reforms in 2013, aiming to put the economy on a more sustainable path. However, we do not believe reforms will change the long-term downtrend in China’s GDP growth. China: annual real GDP growth (1981-2015)

Source: CEIC, Daiwa forecasts

Investment should be the key driver of economic growth again. The impact of the mini stimulus programme introduced in the summer of 2012 should become more obvious in 2013, underpinning infrastructure investment growth. Improved liquidity conditions for developers, due to strong sales and a loosened credit policy, should support a recovery in property investment growth. Meanwhile, consumption growth should remain solid and stable, as we expect income growth to maintain a high single-digit pace throughout this year. On the other hand, we expect net exports to make a small negative contribution to GDP growth, due to weakness in external demand from the EU and Japan. Contribution to real GDP growth

Source: CEIC, Daiwa forecasts

CPI inflation should rise steadily in 2013. Pork prices have stayed below/at the breakeven level since April 2012, and so we expect them to rise in 2013. Combined with a low base effect, the rises in pork prices and other food prices should push CPI inflation to 3.3% YoY for 2013E from 2.6% YoY for 2012E. Property prices should remain stable in 2013, with a bias towards the upside. However, prices are unlikely to rise sharply as long as the current purchase-restriction policy remains in place. Given our forecasts for GDP, CPI, and property prices, we expect mild policy tightening in 2H13. In particular, we expect two 25bp interest-rate hikes in the period, but the PBOC should keep the reserve requirement ratio unchanged. Meanwhile, fiscal policy should remain supportive of the economy. We now forecast the fiscal deficit to widen to 1.8% of GDP for 2013 from 1.5% for 2012. The government is likely to spend more on social welfare (such as education, healthcare, and pensions) as it focuses on improving the quality of life for people.

2

4

6

8

10

12

14

16

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

E

2015

E

(% YoY) 6 years 7 years 8 years

(3)

0

3

6

9

12

1520

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

E

2013

E

2014

E

(pp)

Consumption Investment Net exports

2013 Outlook for Asia 4 January 2013

- 14 -

We expect the Renminbi to appreciate against the US Dollar in 2013, forecasting it to reach USD1:CNY6.10 by the end of the year. This is likely to be driven by trade and current-account surpluses, as well as net foreign direct investment inflows. CNY exchange rate against the US Dollar

Source: CEIC, Daiwa forecasts

We expect a lot of reforms to be introduced this year, judging by the recent encouraging comments from the new leaders. In our view, time is running out for China to embark on major economic reforms (eg, financial-market liberalisation, deregulation of the service sector, and the privatisation of state-controlled sectors), and the new leaders are aware of the urgency and complexity of the reforms. If such reforms are implemented successfully and in a timely manner, it would be very positive for China’s economy and the financial markets, in our view. Risks. Inflation and the shadow banking system are the key issues to watch. If there is unexpectedly bad weather or outbreaks of disease among livestock, CPI inflation could rise sharply, forcing policymakers to tighten more aggressively than we expect. In the financial sector, if some of the trust loans or wealth-management products were to default, the risks to the country’s shadow banking system could be exposed and spill over into the rest of the financial system and the economy.

China: key forecasts 1Q12 2Q12 3Q12 4Q12E 1Q13E 2Q13E 3Q13E 4Q13E 2012E 2013E 2014EReal GDP YoY % 8.1 7.6 7.4 8.1 8.5 8.7 8.5 7.9 7.8 8.4 7.5CPI YoY % 3.8 2.8 1.9 2.1 2.2 2.8 3.7 4.3 2.6 3.3 3.5PPI YoY % 0.1 (1.4) (3.3) (2.0) (0.2) (0.2) 2.1 2.7 (1.6) 1.1 3.6Fixed assets investment (nominal, YTD) YoY % 20.9 20.4 20.5 20.5 20.4 20.5 20.0 18.0 20.5 18.0 16.0Retail sales (nominal) YoY % 15.8 13.9 13.5 14.1 14.6 15.3 15.4 14.9 14.3 15.0 14.8Industrial production YoY % 11.5 9.5 9.1 9.7 9.9 10.3 10.1 9.8 9.9 10.0 9.0Exports YoY % 7.6 10.5 4.5 10.4 7.2 9.3 10.7 8.4 8.2 9.0 11.0Imports YoY % 6.9 6.4 1.4 1.8 9.0 12.0 13.0 12.0 4.0 11.0 13.0Trade balance USDbn 0.3 68.6 79.4 92.8 (2.5) 70.6 77.0 80.5 241 226 210 Exchange rate CNY/USD 6.29 6.32 6.28 6.23 6.20 6.15 6.12 6.10 6.23 6.10 6.00M2 YoY % 13.4 13.6 14.8 14.0 13.7 13.2 12.6 12.0 14.0 12.0 10.01-year base lending rate % pa 6.56 6.31 6.00 6.00 6.00 6.00 6.25 6.50 6.00 6.50 6.501-year deposit rate % pa 3.50 3.25 3.00 3.00 3.00 3.00 3.25 3.50 3.00 3.50 3.50Required reserve ratio % 20.0 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5 19.5Current account balance % of GDP 2.6 2.2 1.9Foreign reserves USDtn 3.3 3.2 3.3 3.4 3.4 3.5 3.5 3.5 3.5 3.5 3.5Fiscal balance % of GDP (1.5) (1.8) (2.0)Source: CEIC, Daiwa forecasts

Hong Kong: market exuberance versus economic fundamentals A year ago, the FocusEconomics consensus forecast 2012 GDP growth of 4.5%. For 9M12, the result was just 1.0%, easily the biggest disappointment in the region. We expect the economy to end the year with just 0.9% growth (full year), implying another dip to 0.6% YoY for 4Q12E, on the back of weaker exports and retail sales. In our view, the consensus has significantly underestimated the impact of the three external shocks on a small open economy like Hong Kong, ie, the European debt crisis, China’s economic slowdown and QE-driven inflation. These three factors have hit

where it hurts – service exports (financial services, tourism, etc) and domestic consumption. Both were considered to be resilient. We expect exports (of goods and services) to benefit mildly from a cyclical recovery in China in 1H13, although the pain from G3 demand softness and European deleveraging is here to stay for now. Market sentiment in Hong Kong has been more positive. There is a clear disconnect with the fundamentals. The onset of QE3 and the Fed’s willingness to keep rates low seem to be keeping sentiment running high. This will probably continue in 2013. But this disconnect could spell problems in the longer term. Interest rates have been too low for too long. Households and companies have taken low rates

6.05

6.15

6.25

6.35

6.45

6.55

6.65

Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

Reference rate (set by PBoC) Closing spot rate

Appreciation

Daily trading spread: from 0.5% to 1.0%

(CNY/USD)

Forecasts

2013 Outlook for Asia 4 January 2013

- 15 -

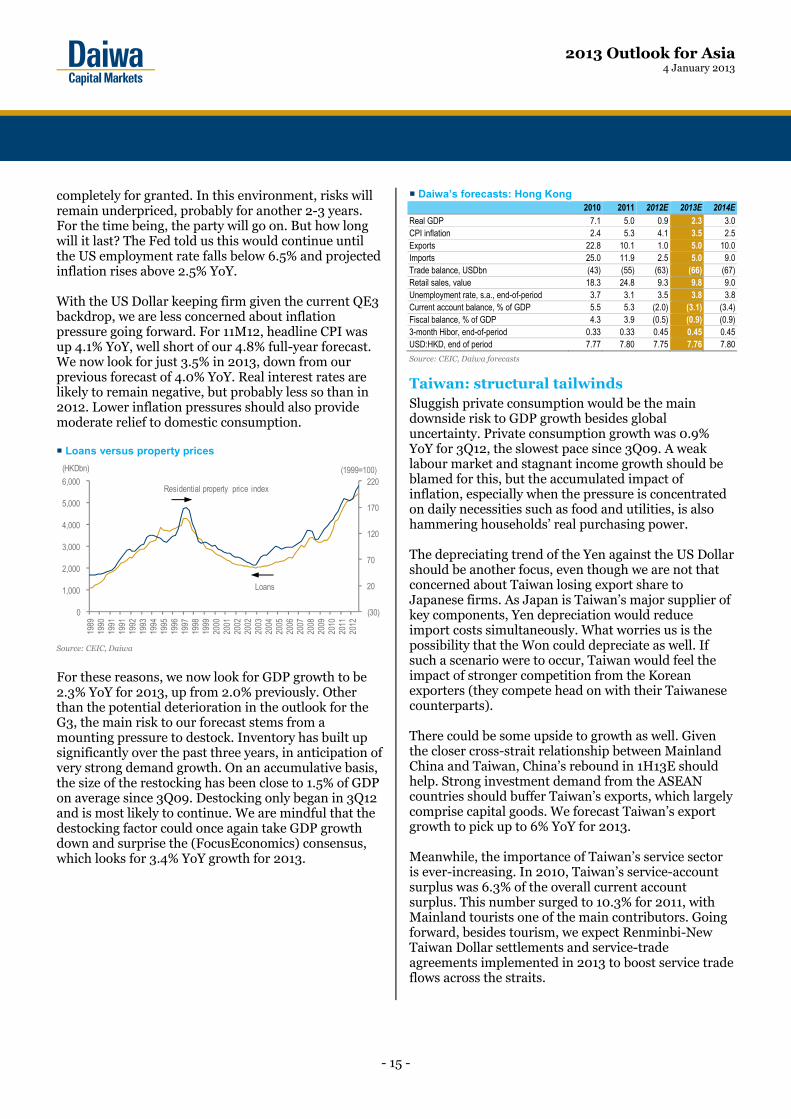

completely for granted. In this environment, risks will remain underpriced, probably for another 2-3 years. For the time being, the party will go on. But how long will it last? The Fed told us this would continue until the US employment rate falls below 6.5% and projected inflation rises above 2.5% YoY. With the US Dollar keeping firm given the current QE3 backdrop, we are less concerned about inflation pressure going forward. For 11M12, headline CPI was up 4.1% YoY, well short of our 4.8% full-year forecast. We now look for just 3.5% in 2013, down from our previous forecast of 4.0% YoY. Real interest rates are likely to remain negative, but probably less so than in 2012. Lower inflation pressures should also provide moderate relief to domestic consumption. Loans versus property prices

Source: CEIC, Daiwa

For these reasons, we now look for GDP growth to be 2.3% YoY for 2013, up from 2.0% previously. Other than the potential deterioration in the outlook for the G3, the main risk to our forecast stems from a mounting pressure to destock. Inventory has built up significantly over the past three years, in anticipation of very strong demand growth. On an accumulative basis, the size of the restocking has been close to 1.5% of GDP on average since 3Q09. Destocking only began in 3Q12 and is most likely to continue. We are mindful that the destocking factor could once again take GDP growth down and surprise the (FocusEconomics) consensus, which looks for 3.4% YoY growth for 2013.

Daiwa’s forecasts: Hong Kong 2010 2011 2012E 2013E 2014EReal GDP 7.1 5.0 0.9 2.3 3.0 CPI inflation 2.4 5.3 4.1 3.5 2.5 Exports 22.8 10.1 1.0 5.0 10.0 Imports 25.0 11.9 2.5 5.0 9.0 Trade balance, USDbn (43) (55) (63) (66) (67)Retail sales, value 18.3 24.8 9.3 9.8 9.0 Unemployment rate, s.a., end-of-period 3.7 3.1 3.5 3.8 3.8Current account balance, % of GDP 5.5 5.3 (2.0) (3.1) (3.4)Fiscal balance, % of GDP 4.3 3.9 (0.5) (0.9) (0.9)3-month Hibor, end-of-period 0.33 0.33 0.45 0.45 0.45 USD:HKD, end of period 7.77 7.80 7.75 7.76 7.80

Source: CEIC, Daiwa forecasts

Taiwan: structural tailwinds Sluggish private consumption would be the main downside risk to GDP growth besides global uncertainty. Private consumption growth was 0.9% YoY for 3Q12, the slowest pace since 3Q09. A weak labour market and stagnant income growth should be blamed for this, but the accumulated impact of inflation, especially when the pressure is concentrated on daily necessities such as food and utilities, is also hammering households’ real purchasing power. The depreciating trend of the Yen against the US Dollar should be another focus, even though we are not that concerned about Taiwan losing export share to Japanese firms. As Japan is Taiwan’s major supplier of key components, Yen depreciation would reduce import costs simultaneously. What worries us is the possibility that the Won could depreciate as well. If such a scenario were to occur, Taiwan would feel the impact of stronger competition from the Korean exporters (they compete head on with their Taiwanese counterparts). There could be some upside to growth as well. Given the closer cross-strait relationship between Mainland China and Taiwan, China’s rebound in 1H13E should help. Strong investment demand from the ASEAN countries should buffer Taiwan’s exports, which largely comprise capital goods. We forecast Taiwan’s export growth to pick up to 6% YoY for 2013. Meanwhile, the importance of Taiwan’s service sector is ever-increasing. In 2010, Taiwan’s service-account surplus was 6.3% of the overall current account surplus. This number surged to 10.3% for 2011, with Mainland tourists one of the main contributors. Going forward, besides tourism, we expect Renminbi-New Taiwan Dollar settlements and service-trade agreements implemented in 2013 to boost service trade flows across the straits.

(30)

20

70

120

170

220

0

1,000

2,000

3,000

4,000

5,000

6,000

1989

1990

1991

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(HKDbn) (1999=100)

Loans

Residential property price index

2013 Outlook for Asia 4 January 2013

- 16 -

Current account: services

Source: CEIC, Daiwa

Finally, policy support could help. Despite limited room for fiscal and monetary expansion, deregulation could lure investment. For example, we expect a free economic demonstration zone, with more relaxed laws on hiring, land acquisition and Mainland capital inflows, to be set up in 2013. This is more of a long-term project; however, we are still pinning hopes on its ability to attract investment in the near term. Although some buffers do exist, as a highly open economy with a lack of product-line diversity, any deterioration in global prospects could drag the island back to a recession. We forecast real GDP to grow by 1.2% YoY for 2012 and 3.0% YoY for 2013. Meanwhile, inflation should be tame, as the one-off utility-price adjustment effect dissipates and the high base effect kicks in. The Central Bank of China (CBC) is likely to resume its rate normalisation schedule as it sees more solid growth in 2013. And we expect the CBC to raise rates from 1.875% to 2.25% by the end of 2013.

Daiwa’s forecasts: Taiwan 2010 2011 2012E 2013E 2014EReal GDP 10.7 4.0 1.2 3.0 4.0 CPI inflation 1.0 1.4 1.9 1.5 1.9 Exports 34.8 12.3 (2.0) 6.0 7.0 Imports 44.1 12.0 (2.5) 6.5 8.5 Trade balance, USDbn 23.4 26.8 27.7 28.0 25.6 Current-account balance, % of GDP 9.3 8.9 9.2 8.7 7.8 Fiscal balance, % of GDP (3.3) (2.2) (2.1) (2.0) (1.8)Benchmark interest rate, end of period 1.625 1.875 1.875 2.25 2.75 USD:TWD, end of period 30.5 30.3 29.0 28.6 28.3Source: CIEC, Daiwa forecasts

Korea: some cyclical improvements Last year was not a good one for Korea. In our 2012 outlook, we highlighted that troubles from the G3 and China’s slowdown would present significant problems for the country. The consensus GDP forecast has been consistently cut from 3.9% to 2.4%. And the consensus is now looking for 3.3% YoY growth in 2013, which is broadly in line with our forecasts.

The key impediments for a recovery in Korea remain: 1) G3 and intra-Asia demand weaknesses, 2) a lack of policy stimulus, and 3) the negative impact of inflation pressures on domestic demand. These impediments have been dominant in 2012. However, we expect some cyclical improvements at least from: 1) a demand recovery in China, 2) lower inflation pressures helped by lower import prices, and 3) the accumulated impact of monetary-policy easing. We now expect the BOK to deliver one more 25bp interest-rate cut in January or February before keeping rates on hold for the rest of the year. On top of this, the current Yen depreciation against the US Dollar and other currencies could also present challenges for the Korean manufacturers. Yen strength has been a major cyclical force in the region for the past two years, and the Korean companies seem to have benefited from it. We project the Won to keep appreciating to 1,020 against the US Dollar until the end of 2013, representing about 5.2% appreciation over 2013. Nevertheless, the US Dollar trend itself is also important. If the US Dollar continues to slide against other currencies, we think it would still make sense for the Won to keep appreciating to protect its terms-of-trade position and vice versa if the US Dollar strengthens going forward.

Korea: Won strength can help protect purchasing power

Source: CEIC, Daiwa

As our base case is for the US Dollar to remain flat on a trade-weighted basis, we believe that any potential Yen depreciation would only reduce some of the pressure on the Won’s appreciation. For the time being, we are leaving our Won forecasts unchanged, as a relatively strong Won is still needed to reduce import inflation pressures, especially when crude-oil prices remain too high for the Koreans.

-3

-2

-1

0

1

2

3

Sep-9

8Ma

r-99

Sep-9

9Ma

r-00

Sep-0

0Ma

r-01

Sep-0

1Ma

r-02

Sep-0

2Ma

r-03

Sep-0

3Ma

r-04

Sep-0

4Ma

r-05

Sep-0

5Ma

r-06

Sep-0

6Ma

r-07

Sep-0

7Ma

r-08

Sep-0

8Ma

r-09

Sep-0

9Ma

r-10

Sep-1

0Ma

r-11

Sep-1

1Ma

r-12

Sep-1

2

(USDm) Open for Chinese tourism

Signature of ECFA

50

60

70

80

90

100

Mar-0

2Se

p-02

Mar-0

3Se

p-03

Mar-0

4Se

p-04

Mar-0

5Se

p-05

Mar-0

6Se

p-06

Mar-0

7Se

p-07

Mar-0

8Se

p-08

Mar-0

9Se

p-09

Mar-1

0Se

p-10

Mar-1

1Se

p-11

Mar-1

2Se

p-12

(Jan 02 = 100) Ter ms of tr ade index

Weak USD

Strong USD

Weak USD

2013 Outlook for Asia 4 January 2013

- 17 -

We now look for GDP growth to be 3.3% YoY for 2013, a tad lower than our previous 3.5% forecast. Compared with our forecast of 2.2% for 2012, our forecast still points to a modest cyclical improvement for 2013 on the back of China’s demand recovery and a better inflation profile for the economy. We are cutting our CPI inflation forecast from 3.8% to 2.8% for 2013.

Daiwa’s forecasts: Korea

2010 2011 2012E 2013E 2014EReal GDP 6.3 3.6 2.2 3.3 4.0 CPI inflation 2.9 4.0 2.2 2.8 2.5 Exports 28.3 19.0 (0.9) 6.0 12.0 Imports 31.6 23.3 (0.5) 5.9 11.0 Trade balance, USDbn 41.2 30.8 28.4 30.7 39.9 Current account balance, % of GDP 2.9 2.3 2.2 2.1 2.6 Fiscal balance, % of GDP 1.4 1.5 (0.5) (0.6) 0.0 Policy rate, end of period 2.50 3.25 2.75 2.50 3.00USD:Won, end of period 1,135 1,152 1,064 1,020 1,000 Source: CEIC, Daiwa forecasts

India: when doves fly For FY12/13, the consensus GDP forecast has been cut from 7.8% YoY a year ago to just 5.7% now. In our view, India’s growth-inflation dynamic has started to change, with rising downside risks to growth. GDP growth decelerated from 9.2% YoY for 1Q11 to 5.4% YoY for 9M12, which could arguably be described as a hard-landing. The slowdown in investment demand has been acute. Poor external demand and crude oil-price rises have adversely affected net exports. Industrial growth has been more or less stagnant for four quarters. The economy seems to be operating significantly below its potential. The Reserve Bank of India’s (RBI) baseline GDP projection was recently cut from 6.5% YoY to 5.8% YoY for FY12/13, just above our 5.6% YoY forecast. For 1H FY12/13, GDP growth reached just 5.4%, undershooting this projection. To satisfy this assumption, growth needs to be 6.2% YoY for 2H FY12/13, which should be very difficult to achieve without any policy support. In its latest policy assessment, the RBI attributed the slowdown to several factors, including ‘monetary tightening’. This kind of assessment has been rare in the past, because the RBI seemed to believe that aggregate demand was too strong, to which tightening was a necessary policy response. Since April 2012, the RBI has shifted its policy stance to more ‘calibrated easing’, through a 50bp cut in the policy rate (repo) and two 25bp reductions in the cash reserve ratio (CRR). It has not been prepared for more pervasive easing, mainly due to lingering concerns about inflation.

Inflation pressure should be about to ease. The headline Wholesale Price Index (WPI) moderated from its peak of 10.9% YoY in April 2010, to an average of 7.6% YoY for January-November 2012 (and 7.2% YoY for November). In the short term, the RBI is still under the pressure to manage the effects from energy price increases, poor harvests, wage rises, and household inflation expectations. However, it believes inflation should start easing in 1Q13, amid slower growth, capacity underutilisation in some sectors, and stability in global commodity prices. We look for headline WPI to fall further to 7.0% YoY over the next 3 months and to 6.5% YoY on average for FY13/14. On top of this, the RBI can also take comfort from a mild improvement in the current-account deficit in 2Q12 and some improvement in the projected fiscal deficit.

India: policy interest rate (repo)

Source: CEIC, Daiwa

We forecast a 25bp rate cut in 1Q13, followed by three more 25bp cuts over 2013. We now forecast the policy rate to drop from 8.0% to 7.0% over 2013. We believe a progressively dovish RBI could help arrest some of the growth slowdown, giving investment demand, in particular, much-needed relief. As such, while our FY12/13 GDP forecast remains 5.6% YoY, we recently raised our FY13/14 forecast to 6.0% from 5.8%.

Daiwa’s forecasts: India 10/11 11/12 12/13E 13/14E 14/15EReal GDP 8.4 6.5 5.6 6.0 6.5WPI inflation 9.6 9.0 7.5 6.5 6.0Exports 42.3 21.4 (4.0) 9.0 14.0Imports 22.3 32.2 (3.0) 4.0 8.0Trade balance, USDbn (119) (184) (182) (174) (169)Current account balance, % of GDP (2.7) (4.2) (4.9) (3.8) (2.8)General fiscal balance, % of GDP (4.9) (5.8) (5.8) (5.3) (4.8)Policy rate, end of period 6.75 8.50 7.75 7.00 6.75INR:USD, end of period 44.9 50.4 54.7 58.0 58.0Source: CEIC, Daiwa forecasts

0123456789

10

Apr-0

5Au

g-05

Dec-0

5A p

r-06

Aug-0

6De

c-06

A pr-0

7Au

g-07

Dec-0

7A p

r-08

Aug-0

8De

c-08

A pr-0

9Au

g-09

Dec-0

9A p

r-10

Aug-1

0De

c-10

A pr-1

1Au

g-11

Dec-1

1A p

r-12

Aug-1

2De

c-12

Apr-1

3Au

g-13

Dec-1

3

(% )Daiwa's forecast

2013 Outlook for Asia 4 January 2013

- 18 -

ASEAN: in the midst of a long-term upturn Robust domestic demand has shielded most of the ASEAN economies from the global downturn in 2012. For 2013, we still see plenty of cushions. Private consumption has been resilient, thanks to stable growth in real income and on-going urbanisation. Low-income members of ASEAN have become another ideal production base for labour-intensive manufacturing, which has triggered acceleration in public investment in infrastructure and attracted private and foreign investment in manufacturing. Most ASEAN economies still have plenty of room for fiscal expansion, as their fiscal deficits are well within control (mostly below 2% of GDP), and their debt-to-GDP ratios remain below 60%. ASEAN: fiscal balance as a % of GDP (2011)

Source: CEIC, Daiwa

China’s restocking cycle in the coming quarters is likely to bolster ASEAN members that are more exposed to commodity exports (such as Malaysia and Indonesia). Moreover, if the US Dollar weakens and if the weakness drives up commodity prices, these ASEAN economies will benefit from better terms of trade. Nevertheless, Japan’s lethargic demand for commodities, exacerbated by the depreciation of the Yen against the US Dollar if the trend continues, could be a downside risk, as Japan still consumes more than 10% of ASEAN’s exports. Although China’s recovery is likely to mitigate the shock, the uncertainties should increase in 2H13 when China starts to tighten its policy. Overall, economic growth in most ASEAN countries should remain robust in 2013. Inflation pressure is likely to increase across the region on the back of strong credit growth and rising wages. We expect most of the ASEAN central banks to turn hawkish and hike interest rates by 25-50bps in 2013.

Indonesia Robust domestic demand should support our GDP growth forecast at 6.2% YoY in 2013 (largely unchanged), the same as in 2012. But an indicator to watch is the 2012 current-account balance, which is likely to have ended up in a deficit, at 2.4% of GDP. We expect the deficit to remain and to narrow, as rising commodity exports (possibly at higher prices) should more than offset increased imports for domestic consumption and investment. However, given that 16.6% of its exports were shipped to Japan in 2011, a higher exposure than its ASEAN neighbours (around 10%), weaker-than-expected demand from Japan could pose a downside risk to our forecast. Due to its high short-term external debt to FX reserves ratio (38.1% as at the end of 3Q12), if Indonesia’s current-account deficit were to widen, this could increase the volatility of the IDR and hurt investor confidence. Malaysia An expansive fiscal policy and acceleration in infrastructure investment should provide considerable support to the economy in 2013. A 4% fiscal deficit, set in ‘Budget 2013 Malaysia’, should create a spill-over effect not only for consumption but also for investment activities. For example, a one-off RM250 cash hand-out to low income households and some tax relief could boost private consumption. Tax incentives for private corporates in the oil and gas industry and more support on financing to SMEs should encourage private investment. The projects under the Economic Transformation Programme (ETP) announced in November 2012, with investment totalling RM26.1bn, should underpin public investment. Therefore, we expect strong domestic demand to push up our real GDP growth forecast to 5.3% YoY in 2013 (versus 4.8% YoY previously), from 5.2% in 2012. The Philippines Due to its export structure, the Philippines is less exposed to commodity exports. As such, the economy moves more closely with the global electronics cycle, which makes it more vulnerable to demand shocks from the US and Europe, and means it will benefit less from China’s recovery in 2013. Due to a high base for 1Q13, YoY real GDP growth is likely drop below 6% YoY as the new year starts. That said, due to the fact that the services sector accounts for a large share of GDP (56.4% in 2011), the economy should maintain robust growth as long as the service industries (such as business-process outsourcing) continue to do well. Meanwhile, overseas-worker remittances have been holding up well despite the global economic slowdown. With strong private consumption growth and aggressive

1.3

-1.1 -1.4-2.0

-5.0-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

Singapore Indonesia Thailand Philippines Malaysia

(% of GDP)

2013 Outlook for Asia 4 January 2013

- 19 -

fiscal expansion, we now forecast the economy to grow by 5.8% YoY in 2013 (versus 4.5% YoY previously), which compares with 6.4% YoY in 2012. Thailand Despite a high base (due to a surge in post-flood reconstruction activities in 1H12), we now forecast Thailand’s real GDP to grow by 4.8% YoY in 2013 (up from 4.2% YoY previously), thanks to continued efforts in post-flood reconstruction, an export recovery and aggressive fiscal policy aimed at pushing up investment. Similar to the Philippines, Thailand is also more exposed to weaknesses in developed economies as it relies more on exports of manufacturing products than commodities. Hence, it is likely to benefit less from an economic recovery in China in 2013 than Malaysia or Indonesia will do. In addition, political risk is something that investors need to watch out for in 2013, as was the case in the past few years.

Singapore As an international financial and trade centre, Singapore’s economy is more open and more exposed to global demand shocks and financial turmoil. Being the most export-dependent economy in the region (228% of GDP in 2011) and with high exposure to the EU banks, Singapore is set to face another challenging year as the EU enters another year of recession, and Japan and the US continue to deliver sluggish growth. The good news is that the recovery in China and resilient growth in its ASEAN neighbours should help offset the downward pressure from the developed economies. Therefore, we now forecast a rebound in real GDP growth to 3.0% YoY in 2013 (versus 2.5% YoY previously), from 1.3% YoY in 2012.

Daiwa forecasts: ASEAN

GDP (% YoY) CPI (% YoY) Fiscal balance % of GDP 2011 2012E 2013E 2014E 2011 2012E 2013E 2014E 2011 2012E 2013E 2014E

Singapore 4.9 1.3 3.0 4.5 5.3 4.6 3.8 3.0 1.3 1.0 1.2 1.3Indonesia 6.5 6.2 6.2 6.4 5.4 4.3 6.0 5.0 (1.1) (2.0) (1.5) (1.2)Malaysia 5.1 5.2 5.3 5.5 3.2 1.7 2.8 3.5 (5.0) (5.0) (4.2) (4.0)Philippines 3.9 6.4 5.8 6.5 4.7 3.3 4.0 4.5 (2.0) (2.6) (2.2) (2.0)Thailand 0.1 6.0 4.8 5.0 3.8 3.0 3.5 4.0 (1.4) (3.0) (3.0) (2.5)Source: CEIC, Daiwa forecasts

Daiwa forecasts: ASEAN

Current account balance % of GDP Policy rate (%, end of period) Exchange rate (end of period) 2011 2012E 2013E 2014E 2011 2012 2013E 2014E 2011 2012 2013E 2014E

Singapore 21.9 16.0 15.0 18.0 - - - - 1.30 1.20 1.18 1.15Indonesia 0.2 (2.4) (1.8) (0.7) 6.00 5.75 6.25 7.00 9,068 9,637 9,200 9,000Malaysia 11.0 5.3 6.8 9.5 3.00 3.00 3.25 3.75 3.18 3.06 2.90 2.80Philippines 3.2 2.6 2.5 2.4 4.50 3.50 4.00 4.50 43.9 41.1 39.0 38.0Thailand 1.7 0.7 0.5 1.0 3.25 2.75 3.25 3.75 31.7 30.6 29.5 29.0Source: CEIC, Daiwa forecasts

2013 Outlook for Asia 4 January 2013

- 20 -

Market outlook for 2013 Pranab Kumar Sarmah, CFA (852) 2848 4441 ([email protected]) Alan Chan, CFA (852) 2848 4970 ([email protected]) Daiwa’s end-2013E index targets and valuations Index target

Index Daiwa's Range Upside (%) EPS growth (%) PER (x) PBR (x) Based on historical PER Based on historical PBR (31/12/2012) End-2013E target 2012E 2013E 2013E 2013E Average +1SD -1SD Average +1SD -1SDMSCI Asia ex-Japan 466 530 425-580 14 8.6 13.8 10.9 1.50 517 589 445 526 638 415Hang Seng 22,656 24,800 22,000-28,000 9 -1.9 7.2 11.0 1.36 26,852 31,896 21,809 28,709 35,129 22,290KOSPI 1,997 2,300 1,870-2,400 15 27.2 20.2 9.5 1.01 1,880 2,170 1,591 2,117 2,476 1,759TAIEX 7,699 7,800 7,000-8,600 1 3.5 29.0 14.7 1.52 7,009 8,423 5,594 8,255 9,244 7,266SENSEX 19,435 21,800 18,000-24,800 12 10.2 14.4 14.0 2.30 21,325 24,807 17,844 23,699 29,103 18,294

Source: Thomson Reuters, Daiwa forecasts

We expect a rally of about 15% from current levels We forecast an increase of about 15% in the MSCI Asia ex-Japan Index in 2013 after its 18% rally in 2012. Our economics team forecasts GDP growth for Asia ex-Japan of 6.8% YoY for 2013 (up from 6.3% YoY for 2012), which is in line with the consensus forecast, and therefore, we believe the consensus index earnings growth forecast of 13.8% YoY for 2013 is achievable. We also expect a rerating in the index to at least its mid-cycle PER valuation of 12.1x, due mainly to our expectation of a rerating of deep cyclical sectors in early 2013 and the impact of QE3. MSCI Asia markets: real GDP growth (2010-13E) Year to 31-Dec 2010 2011 2012E 2013EAsia ex-Japan 9.3 7.3 6.3 6.8China 10.4 9.2 7.8 8.4Hong Kong 7.1 5.0 0.9 2.3India* 8.4 6.5 5.6 6.0Korea 6.3 3.6 2.2 3.3Singapore 14.8 4.9 1.3 3.0Taiwan 10.7 4.0 1.2 3.0

Source: CEIC, Daiwa estimates and forecasts Note: fiscal year to end-March for India

Our economists’ GDP growth forecasts for 2013 are higher than those of the consensus for China and most ASEAN countries, but lower for Hong Kong, India, and Taiwan. By country, China, Korea, Singapore, Hong Kong and India are trading at a discount while the Indonesia, Philippines, and Thailand are trading at a premium to the historical PER valuations of the respective indices. We expect a rerating of the China

market to continue to early 2013 before slowing down by mid-2013. MSCI Asia markets: premium/(discount) to historical PER (by country)

Source: Thomson Reuters

The MSCI Asia ex-Japan Index rose by 18% in 2012, the fifth-highest yearly gain over the past 10 years. Among the larger markets, the outperformers in 2012 were India, Hong Kong and Singapore, while the underperformers were Korea, Taiwan and China. The smaller ASEAN markets experiencing a structural recovery, such as Thailand and the Philippines, also outperformed the index substantially, while the markets that rely on commodity prices, such as Indonesia and Malaysia, underperformed the MSCI Asia ex Japan Index.

(30%)(25%)(20%)(15%)(10%)(5%)

0%5%

10%15%20%

MSC

I Phi

lippi

nes

MSC

I Ind

ones

ia

MSC

I Tha

iland

MSC

I Tai

wan

MSC

I Mal

aysi

a

MSC

I Hon

g Ko

ng

MSC

I Sin

gapo

re

MSC

I Asi

a x

Japa

n

MSC

I Ind

ia

MSC

I Kor

ea

MSC

I Chi

na

2013 Outlook for Asia 4 January 2013

- 21 -

MSCI Asia x Japan, China, Korea, Taiwan, India - 2012 Performance (Rebased to 100)

MSCI Asia x Japan, Singapore, Philippines, Indonesia, Thailand - 2012 Performance (Rebased to 100)

Source: Bloomberg Source: Bloomberg