2009: Competitive Intelligence in Practice: Empirical Evidence from the UK Retail Banking Sector by...

24

INTRODUCTION It is difficult to ignore the increased significance of competitive threats which financial products and services companies face in today’s highly complex and dynamic environment. In order to create and maintain a market advantage, firms must monitor a vast array of elements about competitor activities, embracing all aspects of the business. In such an environment Competitive Intelligence (CI) has become a valuable tool in providing a framework for the gathering, analysis and dissemination of this effort. This study reports on the extent to which the major UK retail banks not only operate their competitive intelligence gathering activities, but also, the degree to which they “buy-in” to the information sharing attitude which is central to the achievement of effective CI practice. JOURNAL OF MARKETING MANAGEMENT, 2009, Vol. 25, No. 9-10, pp. 941-964 ISSN0267-257X print /ISSN1472-1376 online © Westburn Publishers Ltd. doi: 10.1362/026725709X479318 Competitive intelligence in practice: empirical evidence from the UK retail banking sector Sheila Wright, De Montfort University, UK * Elsayed R. Eid, Suez Canal University, Egypt Craig S. Fleisher, College of Costal Georgia, USA Abstract This paper presents the findings of an empirical study of the major UK retail banks, the purpose of which was to investigate, not only how they operate their competitive intelligence gathering activities, but the degree to which they “buy-in” to the information sharing attitude. The findings were applied to a best practice model which provides a clear picture of the current status of CI in these establishments and the attitudes of senior managers toward such activity. Recommendations are made on the improvements which would be required for the sector to be considered effective and efficient operators of CI practice. Keywords Retail banking, UK, Competitive intelligence, Empirical JOURNAL OF MARKETING MANAGEMENT *Correspondence details and biographies for the authors are located at the end of the article.

Transcript of 2009: Competitive Intelligence in Practice: Empirical Evidence from the UK Retail Banking Sector by...

INTRODUCTION

It is difficult to ignore the increased significance of competitive threats which financial products and services companies face in today’s highly complex and dynamic environment. In order to create and maintain a market advantage, firms must monitor a vast array of elements about competitor activities, embracing all aspects of the business. In such an environment Competitive Intelligence (CI) has become a valuable tool in providing a framework for the gathering, analysis and dissemination of this effort. This study reports on the extent to which the major UK retail banks not only operate their competitive intelligence gathering activities, but also, the degree to which they “buy-in” to the information sharing attitude which is central to the achievement of effective CI practice.

JOURNAL OF MARKETING MANAGEMENT, 2009, Vol. 25, No. 9-10, pp. 941-964ISSN0267-257X print /ISSN1472-1376 online © Westburn Publishers Ltd. doi: 10.1362/026725709X479318

Competitive intelligence in practice: empirical evidence from the UK retail banking sector

Sheila Wright, De Montfort University, UK*

Elsayed R. Eid, Suez Canal University, EgyptCraig S. Fleisher, College of Costal Georgia, USA

Abstract This paper presents the findings of an empirical study of the major UK retail banks, the purpose of which was to investigate, not only how they operate their competitive intelligence gathering activities, but the degree to which they “buy-in” to the information sharing attitude. The findings were applied to a best practice model which provides a clear picture of the current status of CI in these establishments and the attitudes of senior managers toward such activity. Recommendations are made on the improvements which would be required for the sector to be considered effective and efficient operators of CI practice.

Keywords Retail banking, UK, Competitive intelligence, Empirical

JOURNAL OF

MARKETINGMANAGEMENT

*Correspondence details and biographies for the authors are located at the end of the article.

Journal of Marketing Management, Volume 25

DEFINING THE SCOPE OF COMPETITIVE INTELLIGENCE

In a recent article, Brody (2008) explored and analysed the myriad of phrases which various authors, over time have proposed as their “definitive” version of a CI definition. These have come about, for the most part, by the tweaking of previous definitions, leaving out one word, adding another, but rarely anything more substantial. Fleisher and Bensoussan (2003) also commented on the problem of defining the still evolving field and practice of CI. They concluded that there was no single definition which was likely to be precise and/or universally accepted. Consequently, it is perhaps more useful to agree on identifying the scope of CI.

The importance of CI resides in the fact that it widens an organisation’s point of view and provides an integrated picture which can be used for informed decision-making, including predictive ability (Hussey and Jenster 1999; Fahey 1999; Gilad 2004).

For the purposes of this paper, CI is identified as

the process by which organisations gather information on competitors and the competitive environment, ideally using this in their decision-making and planning processes with the goal of adjusting activities to improve performance.

The overall goal of CI therefore is to identify and act upon signals, events and discernable patterns which can inform and enhance the organisation’s decision making activities.

THE CI PROCESS MODEL

There are a number of CI models currently utilised by companies in an effort to organise their CI activities (Kahaner 1996; Wright and Roy 1999; Fitzpatrick and Burke 2003). These range from a process driven approach, typically referred to as the “Intelligence Cycle” (Miller 2007) to an all encompassing, total firm, network type process as proposed by Bertacchini and Dou (2001), April (2002), Wright and Calof (2006).

McGonagle (2007) produced a thought provoking analysis of the various process models which have been offered since the 1980’s and concluded that the “classic CI cycle model” no longer serves practitioner needs, or pays attention to, the dynamic rapidly evolving environment within which most of them operate. In short, the notion of a CI cycle doesn’t work any more and there is sparse empirical evidence to show that it ever did.

There is however, agreement that the CI process is not just a function in the firm, rather it is an attitude towards organisational learning, information sharing, a co-operation driven management culture and a desire by decision makers to capitalise on gathered intelligence (Wright and Calof 2006). There is also agreement that CI is a widespread practice in competitive markets for firms of all sizes, strategies or cultures, regardless of whether it is formalised as a function or role (APQC 1998; APQC 2000; APQC 2003).

JMM942

Wright, Eid and Fleisher Competitive intelligence in practice 943

CI IN THE BANKING SECTOR

Journal articles which were published in the mid-late 80s were MacMillan et al. (1985) which focused on competitors’ responses to new products in the commercial banking sector, using the case study approach, Kenneth and Wong (1988) who produced competitive marketing profiles of differing financial services structures in the US, and Pottruck (1988) who reminded the banking community that they should be using their information as strategic weapons

In the 1990s, Kitchen and Dawes (1995) looked at MIS in small building societies, Sager (1988) assessed competitive information systems in Australian retail banking as the industry transitioned from oligopoly to competition and Ruiz (1998) presented a strategic group analysis of Spanish savings banks. Ruiz (1999) followed this with a dynamic analysis of competition in marketing, using strategic groups in Spanish banking. Virgoana and Purusitawati (1998) also presented a discursive paper which linked the terms “technology watch” and CI in the banking sector, but incorrectly termed this as “benchmarking”. In her analysis of competition in the US banking sector, Cetorelli (1999) recognised that banks were employing some aspects of CI practice in order to obtain relevant, information about their competitive environment and competitors. More recently Bernstel (2004) produced a white paper which looked at the more macro subject of sizing up competition in the banking sector, discussing the value of CI in the context of two short case studies.

In the past 10 years there has been a shift towards understanding what drives competition in the sector. At one end of the spectrum, Laeven and Claessens (2003) addressed what drives competition and Shaffer (2004) presented an analysis of patterns of competitive behaviour. At the other, Lymperopoulos and Chaniotakis (2005) published work on using the internet as an MIS tool in Greek bank branches and Ali and Ahmad (2006) offered a theoretical “Banking Knowledge Management Model” which was subsequently applied to case studies of two Malaysian banks, Tiger and Camel. More recently, DeSarbo et al. (2008) looked at the underlying dimensions for assessing an industry’s competitive structure, using public banks in the New York-New Jersey-Pennsylvania (NY-NJ-PA) tri-state area as their sample frame.

There have been a small number of public presentations specifically looking at CI in banking, the more recent being Boland and Limacher (2005) who looked at actionable CI at Visa International, Basinger (2005) who focused on competitive insight at Barclays, Heppes (2006), who spoke of a maturing CI function in South American retail banks, and Armstrong (2007), who reported on the Royal Bank of Canada’s CI effort.

As can be seen from the above, empirical studies on the practice of CI in the banking sector, regardless of continent, are, at best, minimal. It is not surprising therefore, that the foundation for studying the practice of intelligence gathering in the UK retail banking sector was found in the CI literature rather than the banking literature.

RESEARCH METHODOLOGY

The main research questions were determined having due regard for the ‘best practice’ model developed from a study of CI active firms in the UK by Wright et al. (2002). The findings of that study revealed that UK firms operated at many different

Journal of Marketing Management, Volume 25

levels with regard to the four strands of study: Attitude, Gathering, Use and Location. Abridged descriptors for each strand are shown in Tables 1, 2, 3 and 4 in turn and in graphical format in Figure 1.

JMM944

TABLE 1 Attitude descriptors

Immune Attitude

Too busy thinking about today to worry about tomorrow. Thinks that CI is a waste of time. Minimal or no support from either top management or other departments.

Task Driven Attitude

Finding answers to specific questions and extending what the firm knows about its competitors, usually on an ad-hoc basis. Departments more excited about CI than top management who don’t see the benefits.

Operational Attitude

A process, revolving around the company as its centre, trying to understand, analyse and interpret markets. Management try to develop positive attitudes towards CI for short-term and personal bonus gain.

Strategic Attitude

Integrated procedure, competitors are identified, monitored, reaction strategies are planned and simulated. Gets top management support, co-operation from others, seen as essential for future success.

TABLE 2 Gathering descriptors

Easy Gathering Firms which use general publications and/or specific industry periodicals and think these constitute exhaustive information. Unlikely to commit resources to obtain difficult or costly information

Hunter Gathering

Firms which realise that CI needs extra, sustained effort than Easy Gathering. Resources are available to allow staff to act within reasonable cost parameters. Intellectual effort is supported.

TABLE 3 Use descriptors

Joneses User Firms trying to obtain answers to disparate questions with no organisational learning taking place. Has commissioned a CI report from a consultant because that is what everybody else has done.

Knee Jerk User Firms which obtain some CI data, fail to assess its quality or impact, yet act immediately. Can often lead to wasted and inappropriate effort, sometimes with damaging results.

Tactical User CI mostly used to inform tactical measures such as price changes, promotional effort, competitor activities in the market or segment, yet is acutely aware of its potential value to the business.

Strategic User CI is used to identify opportunities/threats in the industry and address “what if” questions. All levels of staff know the firm’s CSFs, open management culture which displays trust and encourages involvement.

Wright, Eid and Fleisher Competitive intelligence in practice 945

Whilst appreciating that not all firms can immediately go from a cold start to the ideal situation, nor would it make sense to recommend this as universally ideal, it was possible to conclude a structure for a utopian CI situation across the fours strands. This is indicated by the shaded boxes in Figure 1.

This framework was considered to be the most appropriate model to use, given that the empirical study and results which produced it, was conducted in the same country as that reported here. The state of understanding and sophistication regarding CI could safely be assumed to be similar, and there were no language or interpretation differences. This framework has also been used successfully by other researchers as a suitable basis to assess CI effectiveness, for example, Badr (2003); April and Bessa (2006); Lui and Wang (2008); Hudson and Smith (2008).

Whilst it was not intended to classify each individual bank against this typology, the framework provided guidance on the topic areas on which questions could be asked. Subsequent analysis of responses enabled a general allocation to be made within each category of enquiry. These were then aggregated and presented in the Conclusions and Recommendations section. The research study was designed as shown in Table 5 (overleaf).

TABLE 4 Location descriptors

Ad-Hoc Location No dedicated CI unit. Intelligence activities, where undertaken are on an ad-hoc basis, subsumed into other departments, with intermittent or non-existent sharing policies.

Designated Location

Firms with a specific intelligence unit, full time staff, dedicated roles, addressing agreed strategic issues. Staff have easy access to decision makers, status is not a barrier to effective communication.

ImmuneAttitude

Ad-HocLocation

JonesesUser

EasyGathering

Task DrivenAttitude

DesignatedLocation

Knee-JerkUser

HunterGathering

StrategicAttitude

StrategicUser

OperationalAttitude

TacticalUser

ATTITUDE TYPE GATHERING TYPE USER TYPE LOCATION TYPE

FIGURE 1 The Wright-Pickton best practice model for effective CI

Sample frame

It was not possible to identify, among the entire population of senior UK banking executives, those responsible for CI. Therefore this study selected the big seven UK banks and a series of interviews were conducted with senior UK banking executives which allowed discussion to be focussed on areas of particular interest, and permitted the selection of interviewees according to relevance as opposed to the degree to which they represented a status quo. “Snowballing”, in which interviewees were asked to identify other informants who they felt would be good sources of information, was used. This helped identify recognised experts within each bank: Abbey National, Alliance and Leicester, Barclays, Halifax/Bank of Scotland, HSBC, Lloyds TSB, and Nat West/Royal Bank of Scotland. A total of 23 executives were interviewed and each bank was randomly allocated a letter code for the purposes of analysis and reporting. When looking at the various features of case study research, Yin (1994) reminds us that the interviewing of informants who play a key role in the organisation is a critical element in determining a good result. This validated the choice of interview participants.

FINDINGS AND ANALYSIS

Longevity of intelligence use

Competitive intelligence in the UK banking sector is not new, as evidenced by Nathan Rothschild’s timely intelligence to make a fortune on the London Stock Exchange

Journal of Marketing Management, Volume 25JMM946

TABLE 5 Research design

Sample Frame Large UK Retail Banks

Research Strategy Case Study

Research Approach Qualitative, Exploratory, Descriptive

Data Collection Method

Interviews and document analysis

Data Analysis Within-Case Analysis, Cross-Case Analysis and the application of NVivo software to aid with classifying, sorting and identifying common threads and themes

Research Questions (as applied to the sample frame)

What is the longevity of intelligence use in your bank?What terminology is used for the intelligence gathering process?What is the process and/or procedures for acquiring intelligenceWhat are the reasons for intelligence gathering?What is the purpose of intelligence gathering in your bank?What is the attitude of senior executives towards CI activity?What types of intelligence is gathered?What sources of intelligence are used?What methods of analysis are used?What dissemination methods are employed?What accuracy mechanisms are employed?

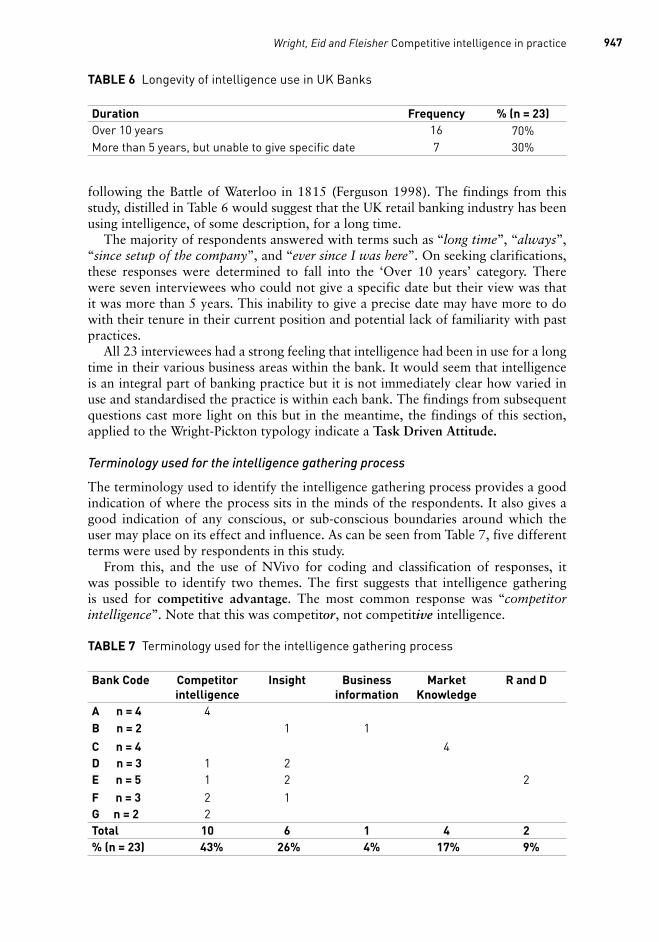

following the Battle of Waterloo in 1815 (Ferguson 1998). The findings from this study, distilled in Table 6 would suggest that the UK retail banking industry has been using intelligence, of some description, for a long time.

The majority of respondents answered with terms such as “long time”, “always”, “since setup of the company”, and “ever since I was here”. On seeking clarifications, these responses were determined to fall into the ‘Over 10 years’ category. There were seven interviewees who could not give a specific date but their view was that it was more than 5 years. This inability to give a precise date may have more to do with their tenure in their current position and potential lack of familiarity with past practices.

All 23 interviewees had a strong feeling that intelligence had been in use for a long time in their various business areas within the bank. It would seem that intelligence is an integral part of banking practice but it is not immediately clear how varied in use and standardised the practice is within each bank. The findings from subsequent questions cast more light on this but in the meantime, the findings of this section, applied to the Wright-Pickton typology indicate a Task Driven Attitude.

Terminology used for the intelligence gathering process

The terminology used to identify the intelligence gathering process provides a good indication of where the process sits in the minds of the respondents. It also gives a good indication of any conscious, or sub-conscious boundaries around which the user may place on its effect and influence. As can be seen from Table 7, five different terms were used by respondents in this study.

From this, and the use of NVivo for coding and classification of responses, it was possible to identify two themes. The first suggests that intelligence gathering is used for competitive advantage. The most common response was “competitor intelligence”. Note that this was competitor, not competitive intelligence.

947Wright, Eid and Fleisher Competitive intelligence in practice

TABLE 6 Longevity of intelligence use in UK Banks

Duration Frequency % (n = 23)Over 10 years 16 70%More than 5 years, but unable to give specific date 7 30%

TABLE 7 Terminology used for the intelligence gathering process

Bank Code Competitor intelligence

Insight Business information

Market Knowledge

R and D

A n = 4 4B n = 2 1 1

C n = 4 4D n = 3 1 2E n = 5 1 2 2F n = 3 2 1G n = 2 2Total 10 6 1 4 2% (n = 23) 43% 26% 4% 17% 9%

Wright et al. (2002) drew attention to the difference between the two terms and lamented that some commentators still used these terms interchangeably to mean the same thing. Almost 20 years ago, Lendrevie and Lindon (1990) noted that competitor intelligence comprised those activities by which a company assessed its industry, identified and understood its competitors, evaluated their strengths and weaknesses, and anticipated their moves. Shortly afterwards, Lauginie et al. (1994) made a more descriptive and succinct distinction and pointed out that competitor intelligence was not competitive intelligence but only one part of a much broader intelligence effort. Respondents who regarded competitor intelligence as the same as competitive intelligence were realising only one very small portion of what should be a much larger, overall, collaborative, intelligence effort. It is difficult to see how such a narrow activity delivers the second most common response of “insight”, but the respondents clearly thought that that was the case.

The third most common term was “market knowledge”. It is interesting to see that all four interviewees from Bank A thought that the main purpose was to obtain competitor intelligence. A similar situation emerged with Bank C where all four interviewees were in strong agreement, but this time thought that the main purpose of intelligence gathering was to gain market knowledge. This may be a revelation in the UK banking sector as some banks’ business strategies take a reactive form, preferring to find out what competitors are doing first, then formulating their response strategy accordingly (Hanssens et al. 2005). The fact that 14 interviewees within this theme came from the largest UK retail banks suggests there is a significant agreement that intelligence gathering is primarily applied for competitive advantage, particularly over other banks.

The second theme evident from the data was centred upon enhancing business understanding and insight. This was derived from the combination of six interviewees who mentioned “insight”, two who likened it to “RandD” and one who said “business information”. This would indicate that for some banks, intelligence gathering is viewed as a business wide activity which promotes, sustains and delivers business critical information. There is obviously a perceived need to be aware of what is happening in the industry (insight), the wider environment (business information), and the need to remain innovative and creative in product development and service delivery (RandD). From a marketing perspective, banks engage in RandD to perfect their existing products or to develop new products with the ultimate aim of making the business responsive to the needs of customers.

It is possible to place these two themes at opposite ends of a continuum of competitive behaviour, yet recognising that banks need to be pragmatic in their adoption of reactive and proactive business strategies at all times. Reactive behaviour would emanate from competitor intelligence, while proactive behaviour is more likely to result from RandD activities. Within the limits of these two extremes, the bank would be able to generate intelligence that would bring insight into the manner in which the business should be conducted for both shareholder and stakeholder benefit.

Overall, these findings show that UK banks have a common understanding of intelligence despite the fact that they describe it in various ways. This confirms the classification of a Task Driven Attitude.

Process and/or procedure for acquiring intelligence

From the analysis provided in Table 8, it can be seen that the majority of interviewees

Journal of Marketing Management, Volume 25JMM948

(61 %) felt their banks did not have specific procedures or a process for acquiring intelligence information. Typical comments were: “No real formalised process or procedure, but there are specific outputs disseminated”, “Really depends on what data is being gathered and the context” and “We don’t really have a process. It is really routinely collating information into intelligence.”

This may mean that although intelligence has been established in the UK retail banking sector for some time, no standard systems or processes exist to gather the various data required. Similarly, those interviewees who said there were no specific procedures for acquiring intelligence information may have been influenced by the wide range of data sources that exist. As a consequence, the bank may not have direct control of the generation and distribution of such data since it is in the hands of other stakeholders. Another variable would be the market dynamics due to local and international socio-political and economic factors. These findings, when applied to the descriptors of the Wright-Pickton typology reveal an Ad-Hoc Location.

Reasons for intelligence gathering

Table 9 shows that 61% of interviewees strongly believed that intelligence was being used for the purpose of understanding the market and its trends. Some of the issues mentioned included “industry regulations”, “product development”, “understanding competitors” and “strategies to gain market share”.

Responses from four interviewees revealed the following views regarding the main role intelligence played in understanding market and its trends:

1. “...diagnoses opportunities to improve the business”

2. “…monitors our competitors”

3. “…(helps us) to offer good products and services that make us different”

4. “…so we increase market share”

Wright, Eid and Fleisher Competitive intelligence in practice 949

TABLE 8 Process and/or procedure for acquiring intelligence

Procedure Frequency % (n = 23)No particular procedure 14 61%Designated teams 5 22%Through agencies 3 13%Database management 1 4%

TABLE 9 Reasons for intelligence gathering

Reason Frequency % (n = 23)Understanding market and its

trends14 61%

Understanding customer 9 39%Essential 2 9%To enable pro-activity 1 4%

NB: More than one response per interviewee permitted

Journal of Marketing Management, Volume 25

Nine interviewees (39%) argued that the critical role intelligence played in their banks was in understanding customers. Two pertinent comments were:

1. “…know your customers fi rst, then competitors”

2. “We want to maximise the amount of business they do with us”

It us noted that three interviewees provided more than one reason in response to this question stating that both customers and the market were the essential reasons for gathering intelligence. One of these believed that their business operations always needed intelligence, saying, somewhat enigmatically: “It’s obvious why we do it, but no specific reason.”

Overall, this demonstrates that their primary focus for competitive intelligence is on understanding customers and market trends. Although the issue of RandD was not explicitly stated, it is implied in that once information becomes available, which might suggest changes in the range of products and the distribution systems; new ways are sought and implemented. These characteristics fit very well with the descriptors for Joneses Users.

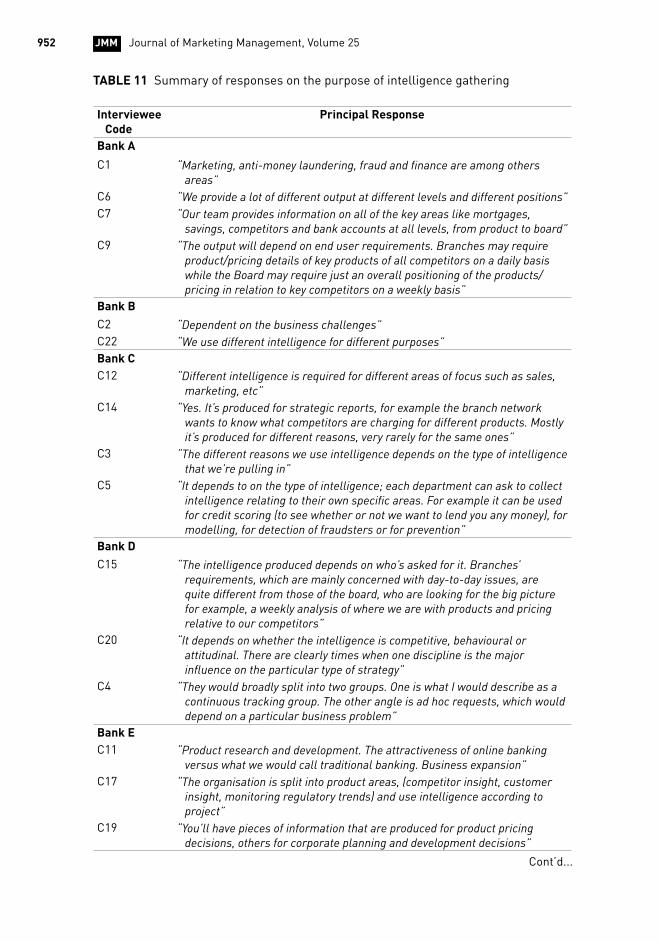

Purpose of intelligence gathering

By examining the responses and analysing these with the aid of NVivo, three themes emerged in relation to this question. Some interviewees gave more than one answer and are thus represented in more than one theme. Table 10 below itemises the responses:

The first theme, and the one most commonly cited was that intelligence was used for Strategic planning. This is where the bank uses actionable intelligence to map out its business plans. Respondents mentioned “strategy”, “strategic planning”, “merger and acquisition”, and “product and service development” in this category.

The second theme, revealed by the data and just less frequently cited, was Marketing. For a significant number of respondents, intelligence was seen as an important tool to help understand customers and markets. This would also assist the bank to directly meet the challenge and needs of customers. Descriptors used in this category were: “sales department”, “meeting customer needs”, “customer…information sharing”, “pricing”, “promotion”, and “self-serve channels”.

The final theme to emerge, somewhat surprisingly less frequently cited was Understanding Competitors and Markets. Terms used by respondents which related to this category were: “monitoring competitors”, “awareness of financial environment” and “online capability and online network”.

All interviewees responded positively to this question, being able to provide at least one valid reason for intelligence gathering in their bank. Due to the interesting nature of their comments, and the insight gleaned, a summary of all 23 interviewee

JMM950

TABLE 10 Purpose of intelligence gathering

Intelligence Purpose Frequency % (n = 23)Strategy and planning 22 96%Marketing 19 83%Understanding competitors and markets 9 39%

NB: More than one response per interviewee permitted

Wright, Eid and Fleisher Competitive intelligence in practice 951

responses to this question is given in Table 11 (overleaf).All respondents felt that intelligence took different forms depending on the area

of focus, be it customers, competitors, information management, product launch or strategic corporate planning, to mention just a few. While it is not immediately clear how it could be done, the data seems to reveal that intelligence is as good as the extent to which the bank can prioritise business needs and competently process the intelligence data. On the whole, respondents felt strongly that intelligence had to be taken as a business culture rather than an optional task. Put differently, intelligence was the banking business, not just a part of it. The analysis suggests that UK banks see intelligence as an umbrella term to describe specific strategic information and as such, has a multi-faceted use in the sector.

It also emerges from Table 11, that intelligence is used for various purposes, ranging from supporting the overall business strategy or direction, through to the functions of individual business units. Despite suggestions to the contrary, the responses clearly indicate that the intelligence is more likely to be specific and tailored to its prospective use such as product improvements, monitoring and evaluation, marketing, sales and understanding consumer behaviour. As all of these elements most definitely sit at the tactical level, this produces the inevitable designation of Tactical Users.

Attitude of senior executives toward CI Activity

High support was demonstrated by senior executives, which may explain the long history of intelligence existence which, for all banks involved in this study, and itemised in Table 12 (overleaf), had been in place for more than 5 years. Senior managers were also reported to see relevance in the use of intelligence in the business life of the bank. Table 12 itemises the responses.

With the exception of three interviewees who were not able to provide an opinion, senior executives overwhelmingly exhibited positive attitudes towards the intelligence concept in general and the CI effort in particular.

None viewed it negatively, and the most enthusiastic category, “highly supportive”, included more than half of the responses. In fact, they treated intelligence as a key asset in conducting the tasks of the business. The 12 respondents who rated the senior executives as highly supportive were heads of departments in marketing and strategy in all the banks. The 8, who felt that their senior executives appreciated (4), supported (3), or gave good support (1) represented the following departments in their respective banks: marketing, finance, research and development, competitor analysis, and information management. Whilst these findings suggest that senior executives have confidence, and trust, in intelligence output produced within the organisation, it is largely at the task level, typically addressing particular questions and producing largely template style answers. This view was reinforced in the responses provided to subsequent questions and compared sufficiently with the Wright-Pickton typology descriptor of a Task Driven Attitude.

Types of intelligence gathered

Eleven types of intelligence gathered were identified. Table 13 (overleaf) itemises the responses and it can be seen that these are indicative of a fairly fluid approach.

The fact that such a wide range of intelligence is gathered by the various banks would suggest that the subsequent intelligence information has a multi-purpose use. With post-analysis evaluation, it is possible to group the intelligence types into three major foci.

Journal of Marketing Management, Volume 25JMM952

TABLE 11 Summary of responses on the purpose of intelligence gathering Interviewee

CodePrincipal Response

Bank A

C1 “Marketing, anti-money laundering, fraud and fi nance are among others areas”

C6 “We provide a lot of different output at different levels and different positions”C7 “Our team provides information on all of the key areas like mortgages,

savings, competitors and bank accounts at all levels, from product to board”C9 “The output will depend on end user requirements. Branches may require

product/pricing details of key products of all competitors on a daily basis while the Board may require just an overall positioning of the products/pricing in relation to key competitors on a weekly basis”

Bank BC2 “Dependent on the business challenges”C22 “We use different intelligence for different purposes”Bank CC12 “Different intelligence is required for different areas of focus such as sales,

marketing, etc”C14 “Yes. It’s produced for strategic reports, for example the branch network

wants to know what competitors are charging for different products. Mostly it’s produced for different reasons, very rarely for the same ones”

C3 “The different reasons we use intelligence depends on the type of intelligence that we’re pulling in”

C5 “It depends to on the type of intelligence; each department can ask to collect intelligence relating to their own specifi c areas. For example it can be used for credit scoring (to see whether or not we want to lend you any money), for modelling, for detection of fraudsters or for prevention”

Bank DC15 “The intelligence produced depends on who’s asked for it. Branches’

requirements, which are mainly concerned with day-to-day issues, are quite different from those of the board, who are looking for the big picture for example, a weekly analysis of where we are with products and pricing relative to our competitors”

C20 “It depends on whether the intelligence is competitive, behavioural or attitudinal. There are clearly times when one discipline is the major infl uence on the particular type of strategy”

C4 “They would broadly split into two groups. One is what I would describe as a continuous tracking group. The other angle is ad hoc requests, which would depend on a particular business problem”

Bank EC11 “Product research and development. The attractiveness of online banking

versus what we would call traditional banking. Business expansion”C17 “The organisation is split into product areas, (competitor insight, customer

insight, monitoring regulatory trends) and use intelligence according to project”

C19 “You’ll have pieces of information that are produced for product pricing decisions, others for corporate planning and development decisions”

Cont’d...

Wright, Eid and Fleisher Competitive intelligence in practice 953

Interviewee Code

Principal Response

C21 “There would of course be different items produced depending on the context e.g. a marketing report or a strategy paper etc”

C8 “The organisations split in to product areas, each of which collate information relating to their own product and use according to project”

Bank FC10 “Depending on the importance, as when a competitor is about to launch a

new product”C16 -C23 “Customer intelligence, Branch intelligence, and competitor intelligence”Bank GC13 “It’s produced for ongoing monitoring, to keep aware what’s going on in the

marketplace, where our relative position lies”C18 “Intelligence would be required for different reasons. For example marketing,

customer information, database management, etc”

TABLE 12 Attitude of senior executives towards CI activity

Option Selected Frequency % (n = 23)Highly supportive of CI effort 12 52%Appreciates the CI effort 4 17%Supports the CI effort 3 13%Gives good supportive to the CI effort 1 4%Not Supportive of CI effort 0 0%Unknown 3 13%

TABLE 13 Types of intelligence gathered

Intelligence Type Frequency % (n = 23)Market and market share 15 65%Competitors 13 57%Customer and consumer behaviour 11 48%Product and sales 9 39%Economic 6 26%Government data (rules and regulations) 3 13%Financial 2 9%Political 2 9%Technological 2 9%Unknown 2 9%Crime and fraud 1 4%

NB: More than one response per interviewee permitted

Journal of Marketing Management, Volume 25

Competitor focus

• Competitor: The issue here is that the more a bank knows or understands its competitors and their actions, the more strategically positioned it becomes. The 13 interviewees who said that their banks gathered competitor intelligence affirm this. However, when assessing the contents of Table 14, it can be seen that the sources of intelligence employed are heavily biased towards public domain and the internet. This does not suggest a dynamic or innovative approach to understanding competitors or their behavioural predisposition.

Industry focus

• Marketing and market share: The 15 interviewees who said that their banks gathered this kind of intelligence may be an indication that intelligence in the banking industry is confined to this function and little else.

• Customers and consumer behaviour: The 11 interviewees said that their banks collect intelligence that assists them to understand their customers. This has an obvious relationship to those 15 interviewees who mentioned marketing and market share.

• Product and sales: The intelligence gathered by these respondents was specifically for providing the bank with information about products and sales trends, both specifically for their organisation and for the industry as a whole.

Macro environment focus

• Economic: Intelligence gathered to provide information with which to understand economic trends in the banking industry in particular and nationally, which would enable the bank to better position itself strategically.

• Government: The intelligence gathered focuses on understanding rules and regulations that need to be observed and practiced in the banking industry. Such intelligence is said to help the banks to trade within a given legal framework.

• Financial: This intelligence helped the bank understand the financial patterns and trends in the banking industry. Information such as investment portfolios, interest rates, and lending and borrowing information assist a particular bank to strategically tailor its financial products to individual customer segments.

• Political: Intelligence gathered to gain insight, appreciation and understanding of the prevailing political environment within and outside the UK.

• Technological: This type of intelligence provides a view of the various technological resources in use by other banks inside and outside UK in such areas as ATMs and security systems.

• Crime and fraud: One interviewee mentioned crime and fraud as the type of intelligence the bank gathered, notably, money laundering.

• Unknown: Two interviewees could not say what type of intelligence their banks gathered. This may indicate that the intelligence which is gathered in these banks is general in nature, which calls into question the use to which it can be put.

For an intelligence effort to be effective it would be essential for the bank to encourage cross fertilisation across these themes as one clearly has the potential to inform and

JMM954

Wright, Eid and Fleisher Competitive intelligence in practice 955

support another. The type of intelligence gathered is superficial in content, pedestrian in nature and largely backward facing. In other words, banks seem to be very good at commenting on what has happened, but quite ill-prepared to assess the future. The information generated is used for different areas of focus within a bank and this may explain why no one bank indicated a single source, each source bringing disparate data to produce certain information. In applying this element to the Wright-Pickton typology, the most appropriate match with the findings was that of Easy Gathering.

Sources of intelligence

Table 14 shows that the sources of intelligence used by respondents are varied and wide.

The spread across several items indicates a fairly eclectic approach to data sourcing which is subsequently formulated into intelligence to meet specific needs.

A number of interviewees indicated that their use of sources would change depending on the problem being addressed. This was not unexpected, and typical comments received were:

1. “Diffi cult to say, depends on what the information is used for.”

2. “Depends on what kind of intelligence we’re looking for.”

3. “Banks have lots of different sources of intelligence but are not very good at collating them and benefi ting from them.”

The final comment is indicative of a “scatter gun” approach towards data collection and that can lead to duplication of effort and lack of co-ordination on the gathering process.

The wide range of sources suggests that UK banks tend to rely heavily on information on their day-to-day business activities. Conversely, the low frequencies shown in different sources is also indicative that there is no specific source a given bank relies upon to find intelligence, but rather a combination of sources depending on the intelligence need of the moment. Again, this further reveals the multiple uses to which intelligence information can potentially be put. For instance, if the focus is to understand customers and their needs, customer feedback will be a logical but not

TABLE 14 Sources of intelligence

Sources of Intelligence Frequency % (n = 23)Money facts 8 35%Public domain 8 35%Internet 7 30%All sources 6 26%Customer feedback 5 22%Trade bodies 5 22%External consultants 4 17%Customer database 4 17%Company reports 3 13%Customer application forms 2 9%

NB: More than one response per interviewee permitted

Journal of Marketing Management, Volume 25

exclusive source. One can see that for intelligence to thrive, the bank almost has to have a culture of being exposed to various data sources and develop and sustain the ability to process such data. The strongly held notion stated earlier in this research that intelligence is used for competitive advantage and insight cannot be supported. This later analysis confirms the classification of Easy Gathering.

Methods of analysis employed

In common with the findings of other studies (Gib and Gooding 1998; Rigby 2001; Rigby 2003, 2009) and the work of other subject matter experts (Self 2003; Marteniuk 2003; Morecroft 2006; Swanson 2007; Fleisher and Bensoussan 2007), a distinct lack of familiarity with, and employment of, even some basic analytics, and certainly the more advanced tools was evident. The responses are given in Table 15.

Some interviewees found this a difficult question to respond to, being unable to give a specific answer. A typical response was that it depended on the needs of the department which had requested the information and the use to which the intelligence was to be put. This state of affairs is supported by the high incidence of “various mechanisms” (10). Another interviewee concurred: “…marketing a point of view we use marketing tools…if we are trying to understand a competitor…we probably use Porter Five Forces.” Overall, the analysis mechanisms provided revealed a paucity of techniques used and on far too many occasions, as in the example above, the wrong tool cited for the purpose given.

It is somewhat surprising that given the technologically driven nature of the banking industry and the pivotal role which banks play in any countries’ economy, it would appear from these finding that its participants are far from being analytically astute and have yet to develop an intelligence analysis system that meets the needs, or demands of its markets. The most appropriate descriptor to apply to this element is that of Joneses Users.

Dissemination methods employed

Eight different modes of sharing and dissemination were cited by the interviewees. It is apparent from Table 16 that the mode most used briefings/face to face meetings.

It seems that in the banking industry, the intelligence message is better communicated and understood within an interpersonal interaction mode. Coming in very close behind was a high incidence of interviewees citing electronic communication (e-mail and intranet) as a leading form of sharing and disseminating intelligence in their bank. This could be a realisation that intelligence is as good as the speed with which it is transmitted to the user. With post analysis evaluation, it is possible to group these responses into three main categories: interpersonal, electronic and print.

JMM956

TABLE 15 Analytical tools applied Analysis Methods Frequency % (n = 23)Various mechanisms 10 43%Spreadsheets and filtering databases 7 30%PEST and SWOT 5 22%Team working and brainstorming 3 13%Valuation techniques 2 9%Financial ratios 1 4%Statistical programmes 1 4%

NB: More than one response per interviewee permitted

Wright, Eid and Fleisher Competitive intelligence in practice 957

From the responses, it can be seen that:

• interpersonal mode is the preferred way, is quick, allows for dialogue/feedback and is, consequently, likely to be the most effective

• electronic mode is quick in delivery, so likely to be efficient but with little opportunity for dialogue/feedback

• print mode is likely to be the least effective as there is no dialogue as well as being the least efficient in terms of time take to prepare a document

It is clear that the challenge for UK banks is to make each one of these modes both efficient and effective if they are to fully capitalise on their competitive intelligence efforts. Until such time, in this element, they have to be classified as Knee-Jerk Users.

Accuracy mechanisms

The responses provided demonstrate that the majority felt accuracy to be a relative term. They strongly argued that accurate information depended on where one used the information gathered. Table 17 itemises the elements mentioned.

These findings would suggest that information is inherently valuable. One interviewee said, “Every piece of information is potentially valuable; it’s just how and where you use it.” The other aspect that was evident from the table above centres on comparability as a plausible mechanism to check for information accuracy. Interviewees mentioned triangulation and credibility checks on data suppliers. This suggests that for a piece of information to be deemed accurate, the data used to produce that information must have come from more than one credible source. This is a situation one would expect to find in a sector such as banking, but more surprising, and potentially alarming was that the responses revealed the absence of a

TABLE 17 Accuracy mechanisms employedMechanisms Employed Frequency % (n = 23)Triangulation using different data sources 13 57%Competent and experienced staff 5 22%Credibility check of (data) information

providers4 17%

Maintaining sound relationship with suppliers 3 13%Using existing data analysis tools 3 13%Unknown 2 9%

TABLE 16 Methods of sharing and disseminationMethods Used Frequency % (n = 23)Briefings and face to face meetings 14 61%E-mail 12 52%Intranet 11 48%Written reports 11 48%Daily flash 3 13%Newsletter 2 9%As per request 2 9%Conference 1 4%

NB: More than one response per interviewee permitted

Journal of Marketing Management, Volume 25JMM958

“gold standard” for checking the accuracy of information. This may have arisen due to the multi-use nature of intelligence in these UK banks, or the range of sources. In any event, the accuracy mechanisms employed were neither exhaustive, rigorous, scientific nor innovative. When applied to the Wright-Pickton typology, these findings were seen to straddle the two categories of both Joneses Users and Knee-Jerk Users.

CONCLUSIONS AND RECOMMENDATIONS

On looking back to the research questions posed at the start of this study, it is possible to produce the following summary which gives the most common responses from the UK retail banking sector as a whole and also apply the interpretation of these to the Wright-Pickton Best Practice Model. This is shown in Table 18.

To elaborate, the major findings of this research were:

1. There was no common term used for CI

2. There was common agreement on what CI information is used for in the various banks and specific business functions

TABLE 18 Summary of findings

Research Questions Most Common Response Wright-Pickton Best Practice Verdict

What is the longevity of intelligence use in your bank?

Over 10 years Task Driven Attitude

What terminology is used for the intelligence gathering process?

Competitor Intelligence Task Driven Attitude

What is the process and/or procedures for acquiring intelligence

No particular procedure Ad-Hoc Location

What are the reasons for intelligence gathering?

Understanding markets and trends

Joneses Users

What is the purpose of intelligence gathering in

your bank?

Strategic Planning(but this was inaccurately

identified)

Tactical Users

What is the attitude of senior executives towards CI activity?

Management attempting to develop positive attitudes

Task Driven Attitude

What types of intelligence is gathered?

Market intelligence and market share

Easy Gathering

What sources of intelligence are used?

Public domains, internet Easy Gathering

What methods of analysis are used?

Elementary Joneses Users

What dissemination methods are employed?

Interpersonal Knee-Jerk Users

What accuracy mechanisms are employed?

Triangulation Jones/Knee Jerk Users

Wright, Eid and Fleisher Competitive intelligence in practice 959

3. It was apparent in the findings that the way CI is gathered might differ depending on the area of focus

4. CI in UK banks uses a diversity of sources and a wide range for multiple uses

5. Senior executives in UK banks actively support the CI system and processes yet there are no standard mechanisms in place for the CI process

6. No specific mechanisms are used to evaluate CI information

7. There was plausible agreement that CI is a critical component of strategic planning and decision making and strategy formulation but little evidence that this is what actually happens

8. There was general agreement that CI is primarily about understanding competitive environment, competitors and customers

9. UK banks have some understanding of CI despite the fact that they describe it various ways

It is possible to overlay the findings against the Wright-Pickton Best Practice Model and suggest what actions are now required for the sector to improve its performance. This is shown in Table 19.

TABLE 19 Performance of UK retail banks versus Wright-Pickton best practice model

Typology Element

Sector Verdict Desired Best

Practice State

Commentary

Attitude Type Task Driven Attitude

Strategic Attitude

A task driven attitude is very comfortable. Questions are asked, and answered with little value added. The supportive attitude needs to embrace all strategic issues and be seen as essential for future success, otherwise the CI effort will never mature beyond a “stick-fetching” activity

Gathering Type

Easy Gathering

Hunter Gathering

Too much effort being spent on easy tasks producing volume not value. More focus on “need to know” rather than “like to know” will produce more intelligent intelligence

User Type Joneses UserKnee-Jerk

UserTactical User

Strategic User

The sector is confused about what intelligence is used for. Although the respondents think they are inputting to strategic decision, their understanding of a strategic issue is misplaced and there is no evidence to support heir claims. It the sector really does want to embrace CI at the strategic level, then it has to include all levels of staff, the critical success factors (CSFs) have to be articulated and shared, and a management culture of trust and openness has to be maintained

Location Type Ad-Hoc Location

Designated Location

The firms in this sector need to define roles, responsibilities and establish a defined location for the collection, interpretation and dissemination of all competitive intelligence elements. Only then can economies of scale be achieved, duplication of effort eliminated and the technical and cognitive skills of full time staff be developed

Journal of Marketing Management, Volume 25JMM960

Data analysis convincingly shows that banks regard CI as one of the underpinning factors of their business operations, especially in the degree to which they can make competitive offerings to customers. There was a clear recognition that a good CI system leads to increased revenues and profitability, and consequently to increased share value. However, there was little evidence of high-level commitment to fund the establishment of the right processes, procedures and training for this to be accomplished.

It would appear that the concept of CI is an area that is increasingly being recognised in the financial services industry in general and banking in particular. Even though the basic foundations of CI have existed for a long time, the management and implementation framework still needs improvement. CI provides banks with actionable intelligence that can help them strategise and make effective decisions in the face of constant challenges thrown up by a dynamic, challenging and competitive market, shrinking global boundaries and increasingly customer-centred markets. This would also have the added benefit of not only encouraging, but actually requiring decision makers to think through the consequences of their actions, before, rather than after, the event.

LIMITATIONS, POTENTIAL FOR EXTENSION AND FURTHER WORK

The most obvious limitation is sample size. It would be unwise to extrapolate the views from 23 respondents, albeit knowledgeable representatives of the major UK retail banks, and state that this is representative of the entire sector either within the UK or outside. Qualitative research conducted by individual interview is by its very nature, small scale. The research instrument developed for this study proved to be robust. Being non country specific there is scope for this to be employed with similarly placed retail banks in other countries, not necessarily just English speaking ones. There is also considerable scope for country comparisons to be undertaken in the banking sector, especially by researchers with language skills appropriate to the country being studied. The research instrument would also work well in other industry sectors which could facilitate cross sectoral analysis. There is much that is still unknown about the ability, or otherwise, of organisations to learn from, and interpret, the competitive intelligence it receives. As the evidence from this study shows, recognising when CI is available and understanding what to do with it would be a good place to start.

REFERENCES

Ali, H. M. and Ahmad, N. H. (2006), “Knowledge Management in Malaysian Banks: A New Paradigm”, Journal of Knowledge Management Practice, Vol. 7, No. 3, September. E-Journal. Available at: http://www.tlainc.com/jkmp.htm [Accessed 5th February 2008].

April, K. (2002), “Guidelines for Developing a K-Strategy”, Journal of Knowledge Management, Vol. 6, No. 5, pp. 445-456.

April, K. and Bessa, J. (2006), “A Critique of the Strategic Competitive Intelligence Process within a Global Energy Multinational”, Problems and Perspectives in Management, Vol. 4, No. 2, pp. 86-99.

APQC International Benchmarking Clearinghouse (1998), Managing Competitive Intelligence Knowledge in a Global Economy, Houston, TX: American Productivity and Quality Center.

Wright, Eid and Fleisher Competitive intelligence in practice 961

APQC International Benchmarking Clearinghouse (2000), Developing a Successful Competitive Intelligence Program: Enabling Action, Realizing Results, Houston, TX: American Productivity and Quality Center.

APQC International Benchmarking Clearinghouse (2003), User-Driven Competitive Intelligence: Crafting the Value Proposition, Houston, TX: American Productivity and Quality Center.

Armstrong, S. (2007), “The intelligence behind CI: the Royal Bank of Canada’s CI efforts”, Proceedings of CALL Conference, Toronto, Canada.

Badr, A. (2003), The Role of Competitive Intelligence in Formulating Marketing Strategy, Doctor of Philosophy Thesis, Leicester Business School, De Montfort University, UK.

Basinger R. (2005), “Barclays competitive insight: A case study,” Society of Competitive Intelligence Professionals Conference, Chicago, USA.

Bernstel, J. B. (2004), “Sizing Up the Competition,” Bank Marketing, Vol. 36, No. 6, pp. 6-21.

Bertacchini, Y. and Dou, H. (2001), “The Territorial Competitive Intelligence: A Network Concept”, Actes du Colloque VSST 2001: Barcelona, Universite Politecnica de Catalunya, pp. 101-111.

Boland, J and Limacher, M. (2005), “Actionable CI at Visa International: A real-life case study”, Society of Competitive Intelligence Professionals Conference, Chicago, USA.

Brody, R. (2008) “Issues in Defining Competitive Intelligence: An Exploration”, Journal of Competitive Intelligence and Management, Vol. 4, No. 3, pp. 3-16.

Cetorelli, N. (1999), “Competitive Analysis in Banking: Appraisal of the Methodologies”, Economic Perspectives, Vol. 23, No. 1, pp. 2-15.

DeSarbo, W. S., Grewal, R., Hwang, H. and Wang, Q. (2008), “The Simultaneous Identification of Strategic/Performance Groups and Underlying Dimensions for Assessing an Industry’s Competitive Structure”, Journal of Modelling in Management, Vol. 3, No. 3, pp. 220-248.

Fahey, L. (1999), Competitors: Outwitting, Outmaneuvering, and Outperforming, New York, NY: John Wiley and Sons.

Ferguson, N. (1998), The House of Rothschild Extract in Who’s Who in British History (2000), London, UK: Collins and Brown Limited/Cico Books.

Fitzpatrick, W. M. and Burke, D. R. (2003), “Competitive Intelligence, Corporate Security and the Virtual Organisation”, Advances in Competitiveness Research, Vol. 11, pp. 20-30.

Fleisher, C. S. and Bensoussan, B. E. (2007), Business and Competitive Analysis: Effective Application of New and Classic Methods. Upper Saddle River, NJ: FT Press.

Fleisher, C. S. and Bensoussan, B. E. (2003), Strategic and Competitive Analysis: Methods and Techniques for Analysing Business Competition, Upper Saddle River, NJ: Prentice Hall.

Gib, A. and Gooding, R. (1998), “CI Tool Time: What’s Missing From Your Toolbag?”, In: Proceedings of the 1998 international conference of the Society of Competitive Intelligence Professionals, Chicago, IL, pp. 25-39.

Gilad, B. (2004), Early Warning: Using Competitive Intelligence to Anticipate Market Shifts, Control Risk and Create Powerful Strategies, New York, NY: AMACOM.

Hanssens, D. M., Leeflang, P. S. H. and Wittink, D. R. (2005), “Market Response Models and Marketing Practice”, Applied Stochastic Models in Business and Industry, Vol. 21, No. 4/5, pp. 423-434.

Heppes, D. W. (2006), “An Assessment Of The Level Of Maturity Of The Competitive Intelligence Function Within A South African Retail Bank”, Magister Commercii in Business Management Dissertation, University of Johannesburg, South Africa. Available at: http://hdl.handle.net/10210/260 [Accessed 12th January 2008].

Hudson, S. and Smith, J. R. (2008), “Assessing Competitive Intelligence Practices in a Non-profit Organization”. Proceedings of 2nd European Competitive Intelligence Symposium 27th and 28th March, Lisbon, Portugal.

Hussey, D. and Jenster, P. (1999), Competitor Intelligence: Turning Analysis into Success. Chichester, UK: John Wiley and Sons.

Kahaner, L. (1996), Competitive Intelligence: How to Gather, Analyse, and Use Information to

Journal of Marketing Management, Volume 25JMM962

Move Your Business to the Top, Carmichael, CA: Touchstone Books. Kitchen, P. J. and Dawes, J. F. (1995), “Marketing Information Systems in Smaller Building

Societies,” International Journal of Bank Marketing, Vol. 13, No. 8, pp. 3-9.Kenneth, T. R. and Wong, J. P. (1988), “The Competitive Marketing Profile of Banks, Savings

and Loans, and Credit Unions,” Journal of Professional Services Marketing, Vol. 3, No. 3/4, pp. 107-121.

Laeven, L. A. and Claessens, S. (2003), “What Drives Bank Competition? Some International Evidence”, World Bank Policy Research Working Paper No. 3113.

Lauginie, J. M., Mansillon, G. and Dubouin, J. (1994), Action Commerciale Mercatique, Paris: Foucher.

Liu, C-H. and Wang, C-C. (2008), “Forecast Competitor Service Strategy with Service Taxonomy and CI Data”, European Journal of Marketing, Vol. 42, No 7/8, pp. 746-765

Lendrevie, J. and Lindon, D. (1990), Mercator: Theorie et pratique du marketing, Paris: Dalloz.

Lymperopoulos, C. and Chaniotakis, I. E. (2005), “Factors Affecting Acceptance of the Internet as a Marketing Intelligence Tool Among Employees of Greek Bank Branches”, International Journal of Bank Marketing, Vol. 23, No. 6, pp. 484-505.

MacMillan, I., McCaffery, M. L. and Van Wyck, G. (1985), “Competitors’ Responses to Easily Imitated New Products: Exploring Commercial Banking Product Introduction,” Strategic Management Journal, Vol. 6, No. 1, pp. 75-86.

Marteniuk, J. (2003), “How do Companies find the Best Balance between the Technical and Personal in Effective Competitive Intelligence Systems”. In: Fleisher, C. S. and Blenkhorn, D. L. (eds.), Controversies in Competitive Intelligence: The Enduring Issues, Westport, CT: Praeger Publishers, pp. 176-189

McGonagle, J. J. (2007), “An Examination of the ‘Classic’ CI Model”, Journal of Competitive Intelligence and Management, Vol. 4, No. 2, pp. 71-86.

Miller, S. H. (2007), Competitive Intelligence – An Overview. Available at: http://www.docstoc.com/docs/11157/Competitive-Intelligence-An-Overview [Accessed 12th March 2008].

Morecroft, J. D. (2006), “The Feedback View of Business Policy and Strategy”, Systems Dynamics Review, Vol. 1, No. 1, pp. 4-19.

Pottruck, D. S. (1988), “Turning Information into Strategic Marketing Weapons”, International Journal of Bank Marketing, Vol. 6, No. 5, pp. 49-56.

Rigby, D. K. (2001), “Putting the Tools to the Test: Senior Executives Rate 25 top Management Tools”, Strategy and Leadership, Vol. 29, No. 3, pp. 4-12.

Rigby, D. K. (2003), Management Tools 2003, White Paper. Boston, MA: Bain and Company.Rigby, D. K. (2009), Management Tools 2009: An Executive’s Guide, White Paper, Boston,

MA: Bain and Company.Ruiz, F. J. M. (1998), “Strategic Group Analysis in Strategic Marketing: An Application to

Spanish Savings Banks”, Marketing Intelligence and Planning, Vol. 16, No. 4, pp 277-286.Ruíz, F. J. M. (1999), “Dynamic Analysis of Competition in Marketing: Strategic Groups in

Spanish Banking”, International Journal of Bank Marketing, Vol. 17, No. 5, pp. 233-250Sager, M. T. (1988), “Competitive Information Sys-tems in Australian Retail Banking”,

Information and Management, Vol. 15, No 1, pp. 59-67.Self, K. (2003), “Why Do So Many Firms Fail at Competitive Intelligence?”, In: Fleisher, C. S.

and Blenkhorn, D. L. (eds.), Controversies in Competitive Intelligence: The Enduring Issues, Westport, CT: Praeger Publishers, pp. 190-202

Shaffer, S. (2004), “Patterns of Competition in Banking”, Journal of Economics and Business, Vol. 56, No. 4, pp. 287–313.

Swanson, R. A. (2007), Analysis for Improving Performance: Tools for Diagnosing Organizations and Documenting Workplace Expertise, San Francisco, CA: Berrett-Koehler Publishers.

Virgoana, M. and Purusitawati, P. D. (1998), “Application and Utilization of Technology Watch and Competitive Intelligence on Banking Sector,” International Journal of Information Sciences for Decision Making, Vol. 2, April, pp. 1-10.

Wright, P. C. and Roy, G. (1999), “Industrial Espionage and Competitive Intelligence: One You

963

Do; One You Do Not”, Journal of Workplace Learning, Vol. 11, No. 2, pp. 53-59.Wright, S. and Calof, J. L. (2006), “The Quest for Competitive, Business and Marketing

Intelligence: A Country Comparison of Current Practice” European Journal of Marketing, Vol. 40, No. 5/6, pp. 453-465.

Wright, S., Pickton, D. W. and Callow, J. (2002), “Competitive Intelligence in UK firms: A Typology”, Marketing Intelligence and Planning, Vol. 20, No. 6, pp. 349-360.

Yin, R. K. (1994) Case Study Research, Design and Methods, 2/E, London: Sage Publications.

ABOUT THE AUTHORS AND CORRESPONDENCE

Sheila Wright is a Reader in Competitive Intelligence and Marketing Strategy, Leicester Business School, De Montfort University, UK and a Fellow of the Chartered Institute of Marketing. As well as supervising PhD students, she teaches Strategic and Competitive Analysis, Competitive Intelligence and Marketing Strategy on selected MSc, executive and corporate programmes. She is the author of dozens of articles on CI, analysis and strategy, has been the guest editor for a ground-breaking Special Issue on CI for the European Journal of Marketing, is the former co-editor of the Journal of Competitive Intelligence and Management, and leads the Competitive Intelligence and Marketing Teaching and Research Initiative (CIMITRI) at De Montfort University. Her research interests are competitive intelligence, analysis, positioning, strategy formulation and decision making.

Corresponding author: Sheila Wright, Reader - Competitive Intelligence & Marketing Strategy, Leicester Business School, De Montfort University, Leicester, LE1 9BH, UK

T +44 (0)116 207 8205 F +44 (0)116 251 7648 E [email protected] Elsayed R. Eid is a Lecturer in the Business Administration Department, Faculty of Commerce, Suez Branch, Suez Canal University, Egypt. He received his PhD in Competitive Intelligence and Strategy from Leicester Business School, De Montfort University, UK. As well as acting as a Vice President of the Internal Quality Assurance and Accreditation Project for the Faculty of Commerce, Suez Branch, Suez Canal University, his key areas of responsibility are supervising postgraduate students, teaching at postgraduate and undergraduate level for his own Faculty and others in Egypt. He has contributed to the design and implementation of several training programs in Egypt and other Arab countries in the field of Business Administration. His research interests lie in the fields of Competitive Intelligence and Strategy.

Dr Elsayed R. Eid, Lecturer - Business Administration Department, Faculty of Commerce, Suez Branch, Suez Canal University, Egypt.

T +2 010 732 8890 E [email protected]

Craig S. Fleisher is Chair of Business and Public Affairs, Professor of Management at the College of Coastal Georgia in Brunswick, USA. He received his PhD in Business Administration from the Katz Graduate School, University of Pittsburgh. A Fellow and former President of the Society of Competitive Intelligence Professionals, he was the recipient of the Society’s Meritorious Award in 2009. He originated, and was

Wright, Eid and Fleisher Competitive intelligence in practice

Journal of Marketing Management, Volume 25JMM964

inaugural chair of, the Competitive Intelligence Foundation (Washington, DC), and executive co-editor of the Journal of Competitive Intelligence and Management. He has authored or edited ten books, and more than a hundred articles in the areas of business intelligence, competitive analysis, and public affairs. He is also Docent in Business Information Management at the Tampere University of Technology, Finland, and is associated with faculties in Australia, South Africa, Switzerland, and the UK.

Dr Craig S. Fleisher, Chair of Business and Public Affairs, Professor of Management, College of Coastal Georgia, 3700 Altama Avenue, Brunswick, Georgia 31520-3644, United States of America.

T +1 912 279 5705 E [email protected]