2000 Annual Report - AnnualReports.com

108

Annual Report and Accounts 2000

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2000 Annual Report - AnnualReports.com

Annual R

eport and Accounts 2000

Annual Report and Accounts 2000Advertising. Media Investment Management.Information & Consultancy. Public Relations & Public Affairs. Branding & Identity, Healthcare andSpecialist Communications.

27 Farm StreetLondon W1J 5RJTelephone 020 7408 2204Fax 020 7493 6819www.wpp.com

Who we areAbout WPP 3Our companies and associates 4

How we’re doing2000 financial summary 8Letter to share owners 10Operating and financial review 14

What we think The Clipboard and the Copywriterby Jeremy Bullmore 34Boom and Bust or Groundhog Day?by Martin Sorrell 40

The numbers in fullAccounting policies 56Consolidated profit and loss account 58Consolidated cash flow statement 60Consolidated statement of totalrecognised gains and losses 60Consolidated balance sheet 61Notes to the consolidated profit and loss account 62Notes to the consolidatedcash flow statement 64Notes to the consolidatedbalance sheet 65Company balance sheet 71Notes to the Company balance sheet 72Reconciliation to US AccountingPrinciples 73Notes to the Reconciliation to USAccounting Principles 73Five-year summary 75Consolidated profit and loss account:euro illustration 76Consolidated balance sheet:euro illustration 77Financial glossary 78Auditors’ report 79

Stewardship and remunerationBoard of directors 82Senior WPP executives andadvisors to the Board 84Directors’ responsibilities 85Directors’ remuneration and interests 87Other statutory information 90Corporate citizenship 91Compensation committee report 92

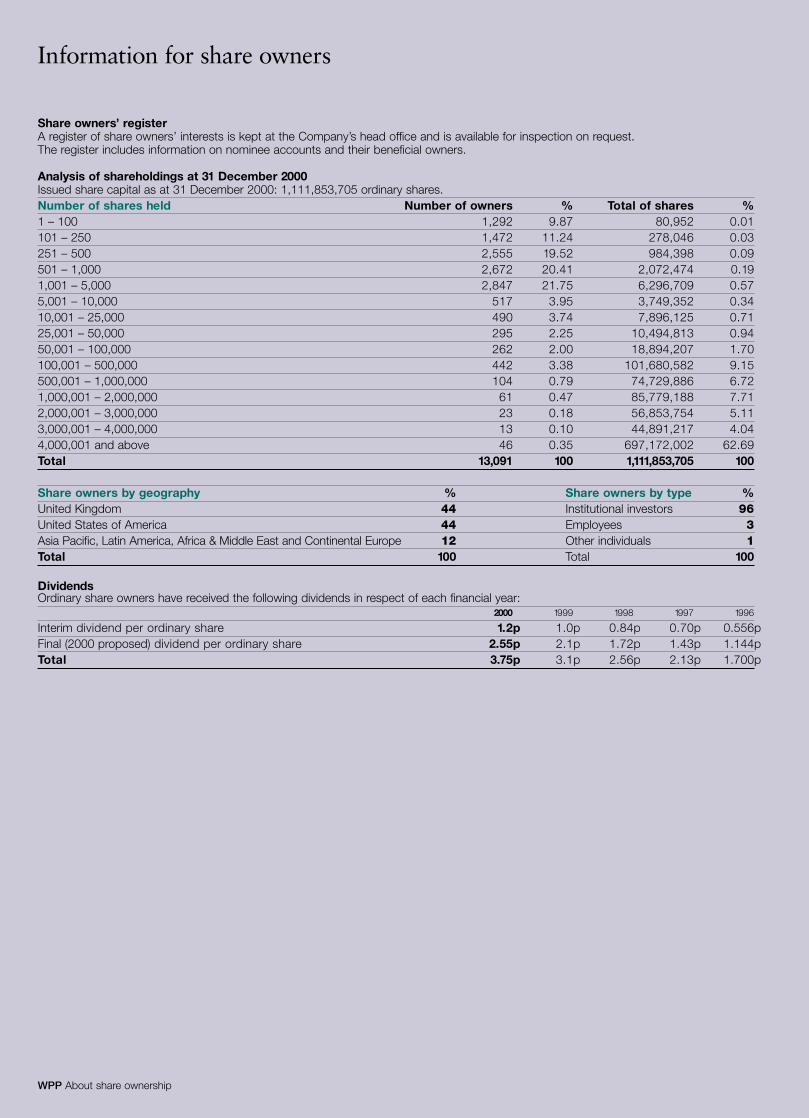

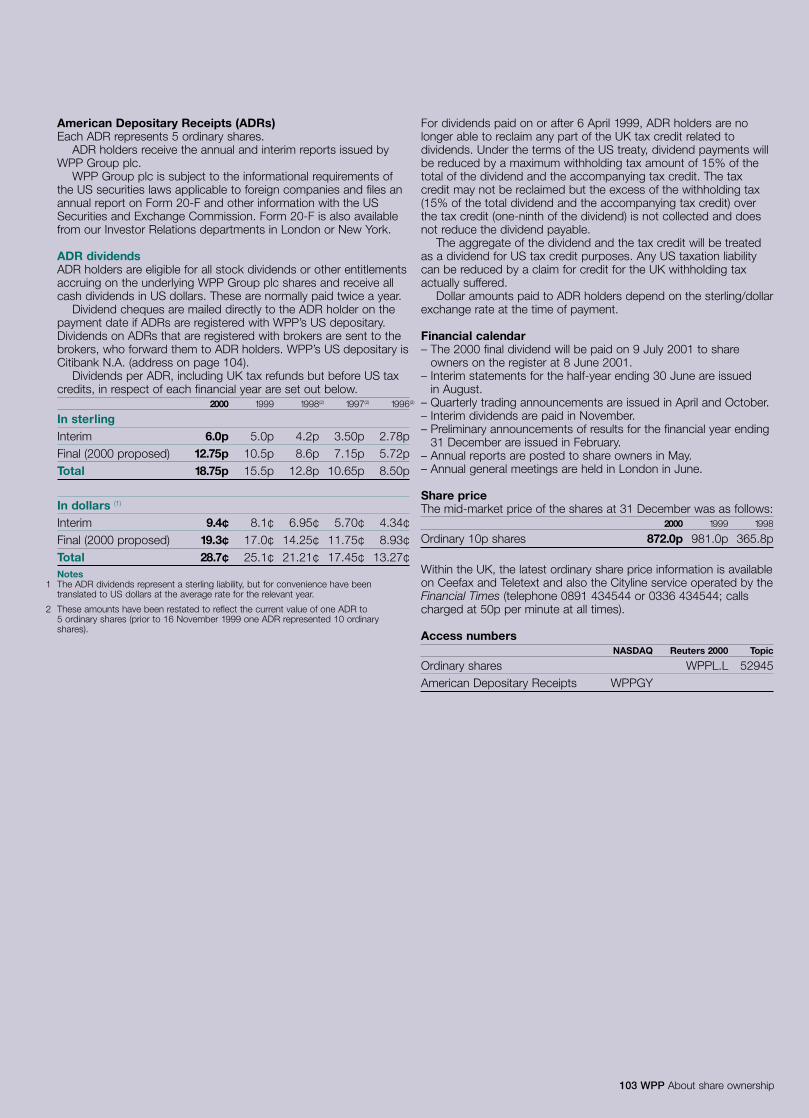

About share ownershipInformation for share owners 102

Where to find usContact points Inside back cover

WPP LondonWPP Group plc27 Farm StreetLondon W1J 5RJTel +44 (0)20 7408 2204Fax +44 (0)20 7493 6819

WPP New YorkWPP Group USA, Inc125 Park AvenueNew York NY 10017-5529Tel (212) 632 2200Fax (212) 632 2222

WPP Asia PacificStuart Neish, Hong KongTel (852) 2280 3801Fax (852) 2598 [email protected]

WPP Latin AmericaNick Read, São PauloTel +55 11 3888 [email protected]

Investor relationsPaul RichardsonGroup finance directorTel +44 (0)20 7408 2204Fax +44 (0)20 7493 [email protected]

Chris SweetlandDeputy Group finance directorTel +44 (0)20 7408 2204Fax +44 (0)20 7493 [email protected]

Media relationsFeona McEwanGroup communications directorTel +44 (0)20 7408 2204Fax +44 (0)20 7493 [email protected]

Group informationIf you would like further information about WPP, its companies or any of the programmes, publications orinitiatives mentioned in this report, please visit our website:www.wpp.com or contact:

Feona McEwan or Christian Andrewat WPP in LondonTel +44 (0)20 7408 2204Fax +44 (0)20 7493 [email protected]@wpp.com

Joan Einarsenat WPP in New YorkTel (212) 632 2200Fax (212) 632 [email protected]

Recognition for previous years’Annual Reports1999 Annual ReportSelected to appear in the D&AD 2001 Annual, ashowcase of the world’s best design work.

1999 ProShare Award for best Annual Reportand Accounts in a FTSE 100 Company, for thesecond year in a row.

1999 British Design and Art Direction Awards:Silver Award to WPP director Jeremy Bullmorefor his essay, Polishing the Apples.

1998 Stock Exchange and CharteredAccountants Annual Awards for PublishedAccounts: Highly Commended.

1998 ProShare Award for best Annual Reportand Accounts in a FTSE 100 Company.

Written and produced by WPP Group plcDesigned by Addison Corporate MarketingIllustrations by Richard BorgePortraits by Nick HigginsPrinted in the UK by Westerham Press, St Ives plc©WPPGroup plc 2001

Investor relations material andour financial statementsare available onlineat www.wppinvestor.com

Where to find us

WPP Who we are

To develop and manage talent;to apply that talent;throughout the world,for the benefit of clients;to do so in partnership;to do so with profit.

Our mission

WPP Who we are

WPP is one of the world’s leading communications services groups.Our companies provide communications services to clients aroundthe world, including more than 300 of the Fortune Global 500,over one-half of the Nasdaq 100 and over 30 of the Fortune e-50.Our 65,000 people work from 1,300 offices in 102 countries.

Every WPP company is a distinctive brand in its own right; all withtheir own identities and own areas of expertise. That is their strength.What they have in common is in harnessing intelligence, talent andexperience to bring competitive advantage to their clients.

WPP, as a parent, complements the professional activities of our individual operating companies through initiatives and programs thatprovide greater value to our clients, competitive advantage to ourcompanies, opportunities and rewards for our people.

Who we are

4 WPP Who we are

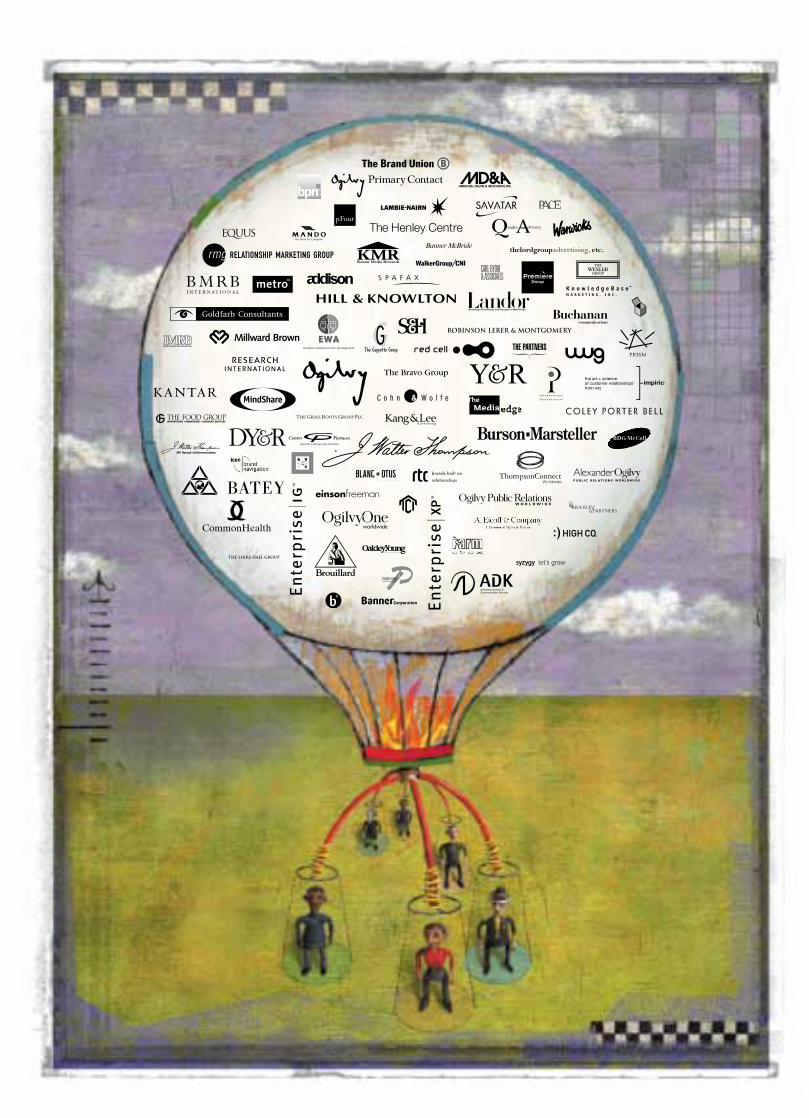

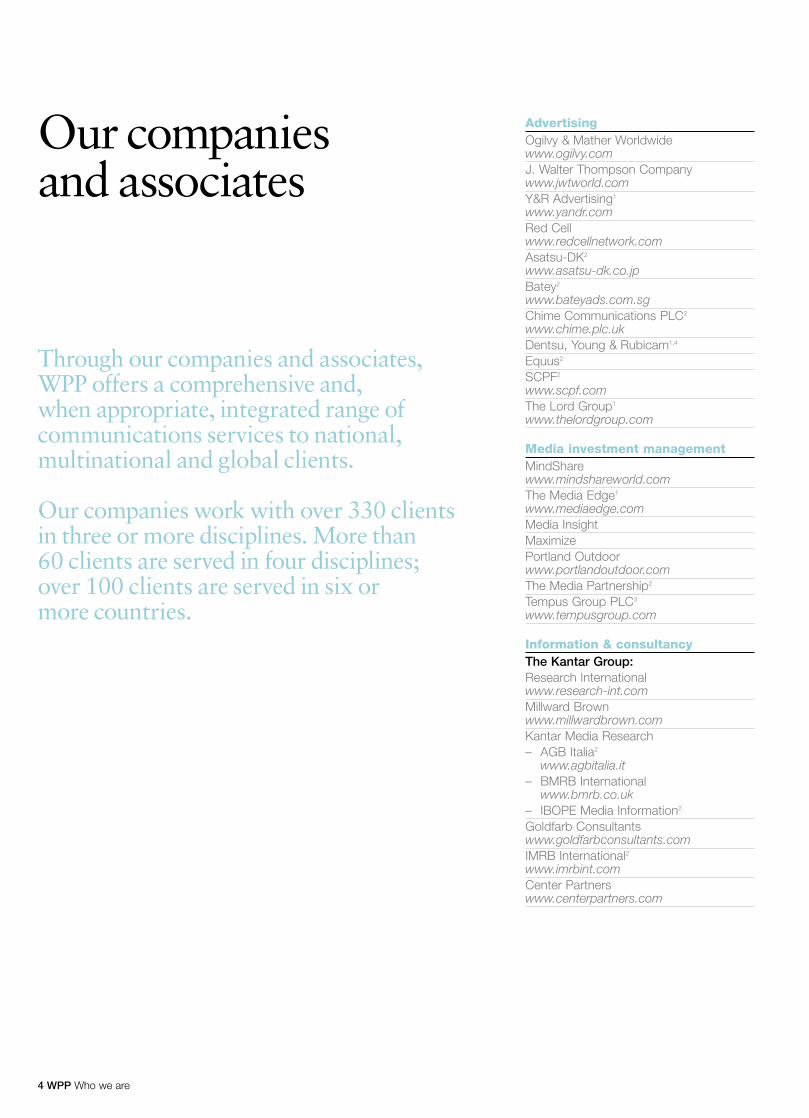

Through our companies and associates, WPP offers a comprehensive and, when appropriate, integrated range of communications services to national, multinational and global clients.

Our companies work with over 330 clientsin three or more disciplines. More than60 clients are served in four disciplines; over 100 clients are served in six or more countries.

AdvertisingOgilvy & Mather Worldwidewww.ogilvy.comJ. Walter Thompson Companywww.jwtworld.comY&R Advertising1

www.yandr.comRed Cellwww.redcellnetwork.comAsatsu-DK2

www.asatsu-dk.co.jpBatey2

www.bateyads.com.sgChime Communications PLC2

www.chime.plc.ukDentsu, Young & Rubicam1,4

Equus2

SCPF2

www.scpf.comThe Lord Group1

www.thelordgroup.com

Media investment managementMindSharewww.mindshareworld.comThe Media Edge1

www.mediaedge.comMedia InsightMaximizePortland Outdoorwww.portlandoutdoor.comThe Media Partnership2

Tempus Group PLC3

www.tempusgroup.com

Information & consultancyThe Kantar Group:Research Internationalwww.research-int.comMillward Brownwww.millwardbrown.comKantar Media Research– AGB Italia2

www.agbitalia.it– BMRB International

www.bmrb.co.uk– IBOPE Media Information2

Goldfarb Consultantswww.goldfarbconsultants.comIMRB International2www.imrbint.comCenter Partnerswww.centerpartners.com

Our companies and associates

WPP Who we are

Public relations & public affairsBuchanan Communicationswww.buchanan.uk.comBurson-Marsteller1

www.bm.comCarl Byoir & AssociatesCohn & Wolfe1

www.cohnwolfe.comHill and Knowltonwww.hillandknowlton.comOgilvy Public Relations Worldwidewww.ogilvypr.comRobinson Lerer & Montgomery1

Timmons and CompanyThe Wexler Groupwww.wexlergroup.comChime Communications PLC2

www.chime.plc.uk

Branding & identityThe Brand Union:

Addison Corporate Marketing*

www.addison.co.ukBDG McColl*www.bdgmccoll.com BPRI*www.bpri.co.ukColey Porter Bell*www.cpb.co.ukDovetail*www.dovetaillondon.comEnterprise IG*

www.enterpriseig.comEnterprise XP*

www.enterprisexp.com– Banner McBride*

www.bannermcbride.com– Clever Media*

www.clever.co.uk– Eurosem*

www.eurosem.com– The Clinic*

www.planetpoint.com/clinicLambie-Nairn*

www.lambie-nairn.comOakley Young*

www.oakley-young.co.uk Walker Group/CNI*www.wgcni.comWarwicks*

www.warwicks-uk.comCB’awww.cba.tm.fr icon brand navigationwww.icon-brand-navigation.com Landor Associates1

www.landor.comThe Partners1

www.thepartners.co.uk

HealthcareCommonHealthwww.commonhealth.comOgilvy HealthcareShire Hall Groupwww.shirehall.comSudler & Hennessey1

www.sudler.com

Direct, promotion & relationship marketingA. Eicoff & Cowww.eicoff.comBrierley & Partners2

www.brierley.comEinson Freemanwww.einsonfreeman.comEWAwww.ewa.ltd.uk The Grass Roots Group2

www.grg.co.ukHigh Co2

www.highco.fr Impiric1

www.impiric.comKnowledgeBase Marketing1

www.knowledgebasemarketing.comMando Marketingwww.mando.co.ukOgilvyOne Worldwidewww.ogilvyone.comRMG International RTCwww.rtcdc.comSavatarwww.savatar.comThompsonConnect Worldwide

Specialist communicationsStrategic marketing consultingGlendinningwww.glendinning.comThe Henley Centre*

www.henleycentre.comManagement Ventureswww.mventures.compFour Consultancywww.pfour.co.ukQuadra Advisory2

www.quadraadvisory.com

Sector marketingCorporate/B2BBrouillardwww.brouillard.comOgilvy Primary Contactwww.primary.co.ukDemographic marketingThe Bravo Group1

www.thebravogroupyr.comThe Geppetto Groupwww.geppettogroup.comKang & Lee1

www.kanglee.comThe Market Segment Group2

www.marketsegment.comMendoza Dillon & Asociadoswww.mendozadillon.comUniWorld2

www.uniworldgroup.comFoodserviceThe Food Groupwww.thefoodgroup.comInvestor relationsInternational Presentations2

www.intpres.com PR & sports marketingPremière Groupwww.premieregroup.co.uk PRISM Groupwww.prismteam.com Real estatePacewww.paceadv.comTechnologyBanner Corporation1

www.b1.comMedia & technology servicesClockwork Capital2www.clockworkcapital.comDigiReelswww.digireels.co.ukThe Farm2

www.farmpost.co.uk Metro Groupwww.metrobroadcast.co.ukSpafaxwww.spafax.com

1 Member of Y&R Group2 Associate 3 Minority investment4 Joint venture* Member of The Brand Union

How we’re doing

WPP How we’re doing

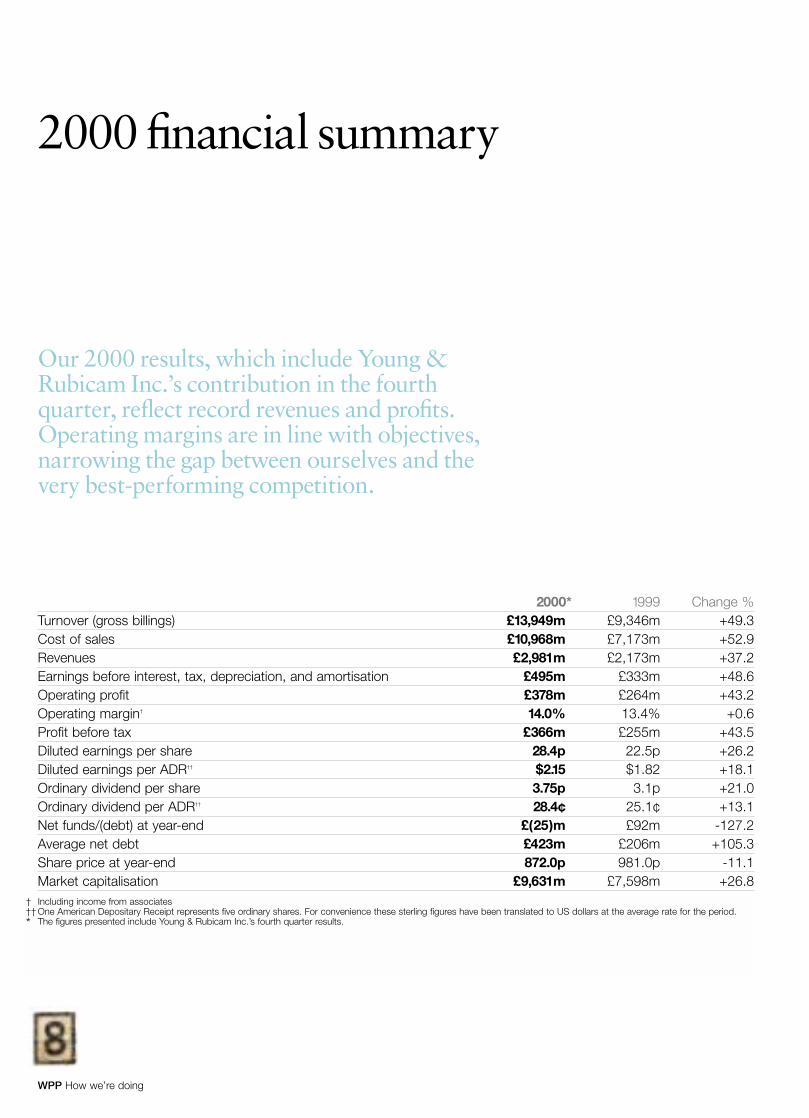

2000 financial summary

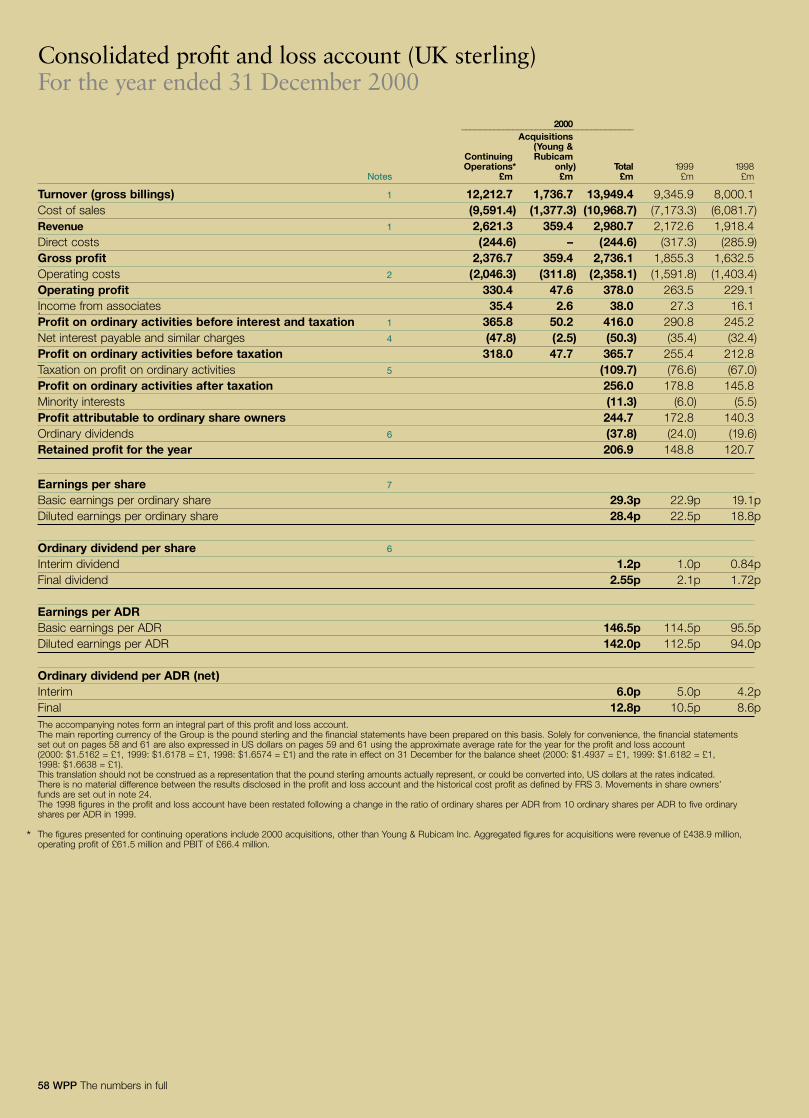

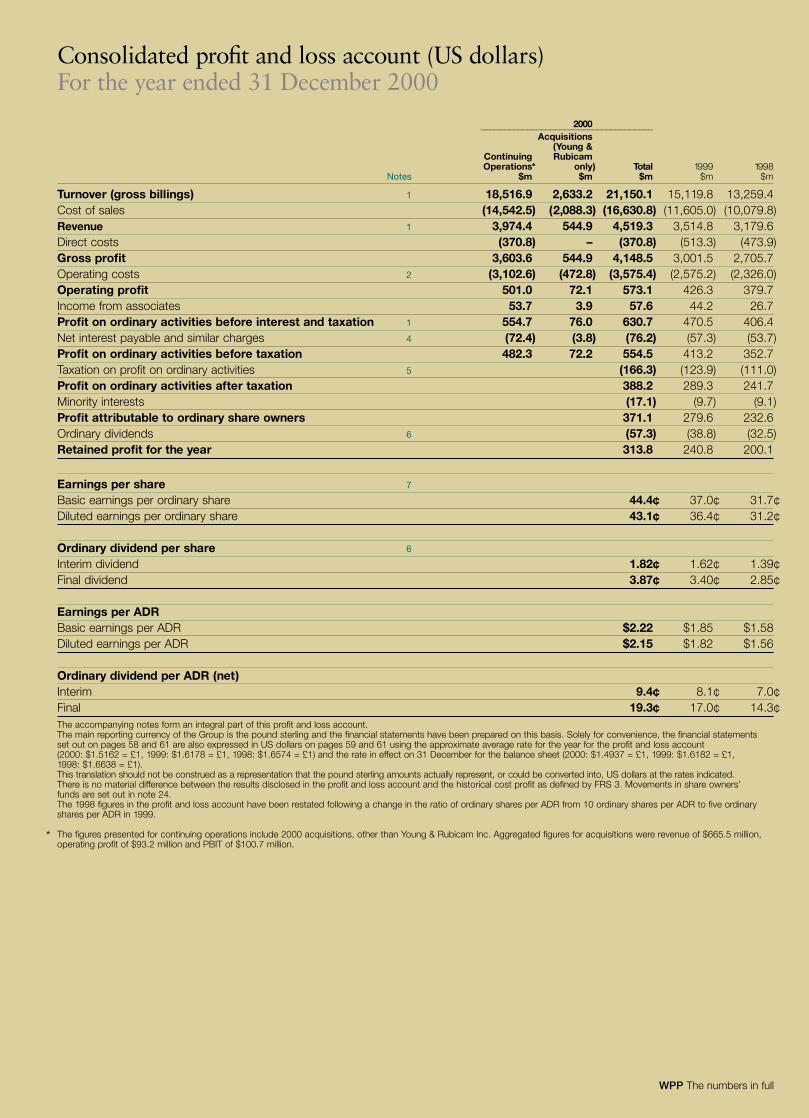

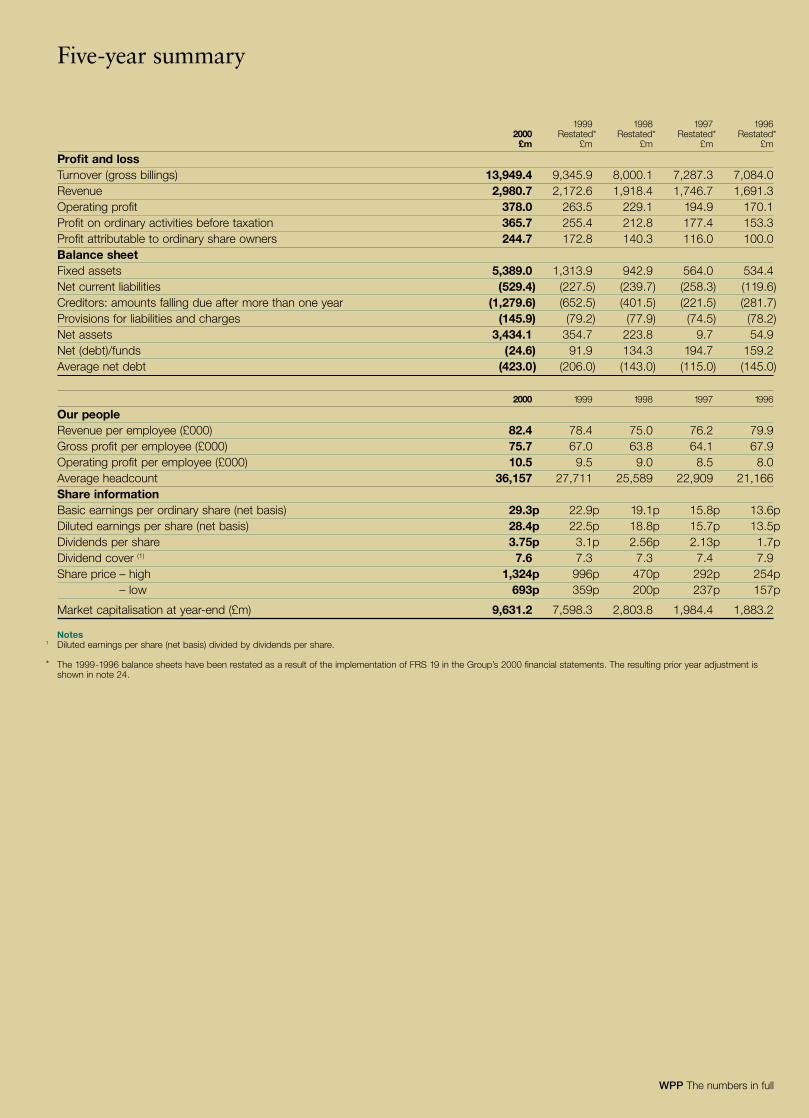

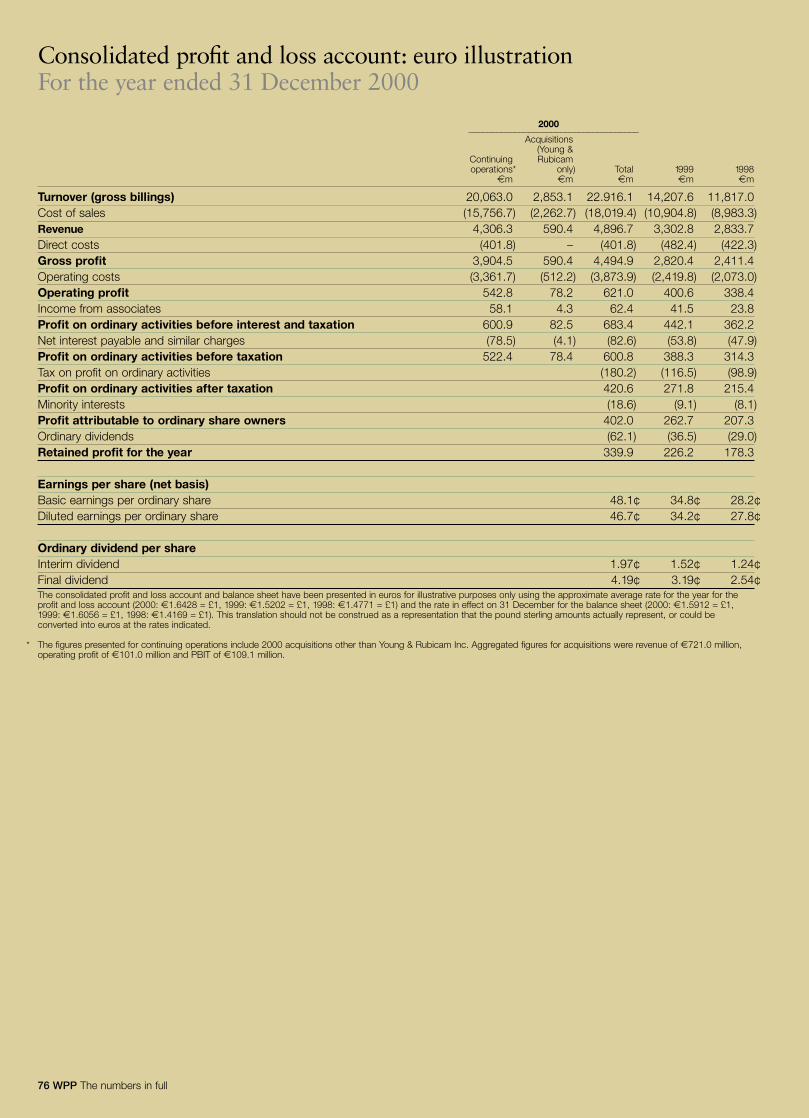

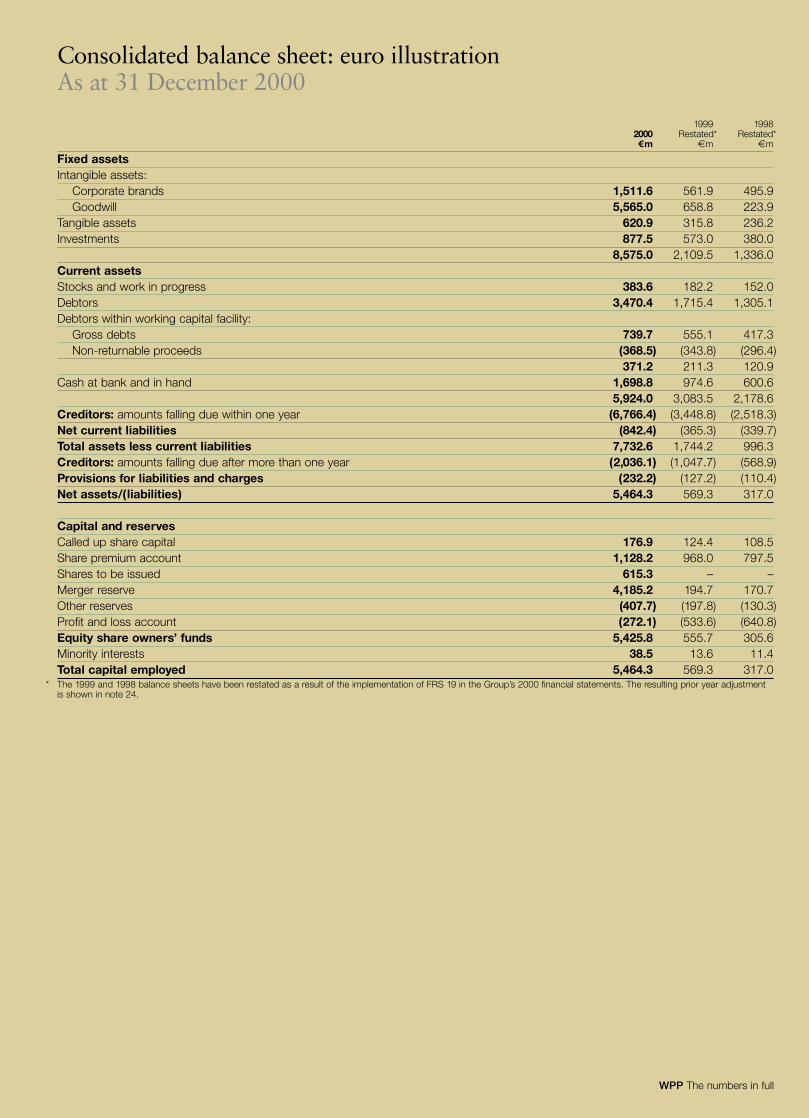

2000* 1999 Change %Turnover (gross billings) £13,949m £9,346m +49.3Cost of sales £10,968m £7,173m +52.9Revenues £2,981m £2,173m +37.2Earnings before interest, tax, depreciation, and amortisation £495m £333m +48.6Operating profit £378m £264m +43.2Operating margin† 14.0% 13.4% +0.6Profit before tax £366m £255m +43.5Diluted earnings per share 28.4p 22.5p +26.2Diluted earnings per ADR†† $2.15 $1.82 +18.1Ordinary dividend per share 3.75p 3.1p +21.0Ordinary dividend per ADR†† 28.4¢ 25.1¢ +13.1Net funds/(debt) at year-end £(25)m £92m -127.2Average net debt £423m £206m +105.3Share price at year-end 872.0p 981.0p -11.1Market capitalisation £9,631m £7,598m +26.8

Our 2000 results, which include Young &Rubicam Inc.’s contribution in the fourthquarter, reflect record revenues and profits.Operating margins are in line with objectives,narrowing the gap between ourselves and thevery best-performing competition.

† Including income from associates†† One American Depositary Receipt represents five ordinary shares. For convenience these sterling figures have been translated to US dollars at the average rate for the period.* The figures presented include Young & Rubicam Inc.’s fourth quarter results.

9 WPP How we’re doing

1691Revenue £m

96

1747 1918 2173 2981

97 98 99 00

211Earnings beforeinterest, tax,depreciation andamortisation £m

96

235 279 333 495

97 98 99 00

182PBIT £m

96

206 245 291 416

97 98 99 00

10.8PBIT margins %

96

11.8 12.8 13.4 14.0

97 98 99 00

13.5Diluted earnings per share p

96

15.7 18.8 22.5 28.4

97 98 99 00

10.1After tax return on average capital employed† %and weighted average cost of capital (WACC) %

96

11.0 11.9 12.8 13.1

97 98 99 00

WACC

†Calculated gross ofgoodwill, revaluationreserve and usingprofit after tax. The1996-1999 balanceshave been restatedas a result of theimplementation of FRS 19 in theGroup’s 2000financial statements.

12

11

10

9

8

7

6

5

4

3

2

1

0

WPP total returnto share ownersrelative to peergrouprebased to 1996

96 97 98 99 00 01

WPPPeer groupS&P 500FTSE 100

1000

0

200

400

600

800

145Average net debt£m & interest cover multiples

96

115 143 206 423

97 98 99 00

Net interest cover

9

1

2

3

4

5

6

7

8

0

2000 revenue bygeography %

44

18

20

18

North America

United Kingdom

Continental Europe

Asia Pacific, Latin America,Africa & Middle East

2000 PBIT bygeography %

48

15

20

17

North America

United Kingdom

Continental Europe

Asia Pacific, Latin America,Africa & Middle East

2000 revenue bysector %

47

17

11

25

Advertising, mediainvestment management

Public relations & public affairs

Information & consultancy

Branding & identity,healthcare and specialistcommunications

2000 PBIT by sector %

56

12

10

22

Advertising, mediainvestment management

Public relations & public affairs

Information & consultancy

Branding & identity,healthcare and specialistcommunications

WPP How we’re doing

Dear share owner

2000, our fifteenth year, was another record year.

Turnover was up over 49% to almost £14 billionreflecting strong organic growth, the first timefourth quarter inclusion of Young&Rubicam Inc.and continued rapid growth in our mediainvestment management activities.

Revenues grew over 37% to almost £3 billion for the first time. Pre-tax profits rose by over 43% to £366 million, earnings per share by over26% to 28.4p and dividends by 21% to 3.75p.

The only disappointment was that the share price,the real measure of your wealth, fell by 11.1%during 2000. However, your Company’s shareprice performance ranks third in terms of shareprice appreciation against a comparator group of 14 global competitors since 1 January 1999.

11 WPP How we’re doing

The rest of this letter is based onconstant currency comparisons, which are more meaningful given thecontinued strength of sterling in 2000.On a like-for-like basis, revenues wereup by almost 15% and gross profitsup 16%, very strong growth, albeit ina quadrennial Olympic and Presidentialyear; particularly with global inflationat 3-4%. However, growth at suchstrong pro forma levels is probablyunsustainable in the medium to longterm. If WPP were to grow consistentlyat these levels, it would be equivalent toa significant proportion of the current US GDP within 10 years. Double-digitlike-for-like revenue growth remainsyour Company’s growth objective.

All our disciplines – advertising;media investment management;information and consultancy; publicrelations and public affairs; andbranding and identity, healthcare andspecialist communications – grewstrongly. However, with advertisingand media investment managementgrowing more strongly than in 1999,the balance between advertising andmarketing services remained the sameat 47%-53%.

The same strength was seengeographically, but with ContinentalEurope and Asia Pacific, LatinAmerica, Africa and the Middle Eastsurpassing the US and the UK, asthese countries benefited from eurocurrency weakness and fully-fledgedrecovery from the 1997 Asian andLatin American recessions.

Operating margins were up by0.7%, in excess of our objective of0.6%. Productivity and efficiencyagain increased significantly as like-for-like revenues grew by almostdouble the like-for-like increase instaff numbers of 8.0%.

As a result, profit before interest andtax grew by almost 40% to £366 million.Pre-tax profits were up even more atover 40%. We generated £291 millionof free cash flow, up over 70% overlast year and which was more thanabsorbed by acquisition payments andinvestments of £247 million, sharerepurchases and cancellations of £94million and dividends of £26 million.Partly as a result, average net debt roseto £423 million, compared to £225

million in 1999 at 2000 exchange ratesand the historical target range of £200-250 million. Your Board is prepared toincrease net debt further to the rangeof £400-450 million, if there aresufficient small- to medium-sized cashacquisition opportunities available andthere are attractive opportunities forshare repurchases. Finally, earnings pershare rose by 23%.

2001 will be a more difficult year.The world’s stock markets aresignalling a recession with no oneable to determine whether there willbe a hard or soft landing, or whetherthe recession will be U-shaped orV-shaped or, worst of all, Japanese L-shaped. Softness is also notconfined to the technology, media andtelecommunications sectors. The ‘old’economy, although less affected, isstill suffering.

At WPP, reported revenues are upover 73% in the first three months of2001, reflecting organic growth, thefirst time contribution of Young &Rubicam Inc., other acquisitions andthe strength of the dollar and majorContinental European currenciesagainst sterling. On a like-for-like basis,revenues are up 6%. Operating marginsare still forecast to grow by one margin point to 15% this year in line with our objectives. Our ability to achieve this will in part depend on our ability to control variable staff costs.

We continue to seek ways ofunlocking added value for both clientsand our people and proving that thereis real value in WPP’s strategy. Ourgoal remains to become the world’smost successful, and preferred providerof communications services to bothmultinational and national companies.

Our six objectives remain as follows:● First, to continue to raise operatingmargins to the level of the bestperforming competition, from 14%last year to 15% this year and to15.5% by 2002.

We have also indicated that there islife after 15.5%, setting an objective of 20% in due course. Some agencies,such as Dentsu, have achieved this and mini-holding companies, such asMcCann, have too – so there should be scope.

● Second, to increase the flexibilityin our cost structure to cope withrecessions as they develop. Thisflexibility should act as a ‘shockabsorber’ to protect our marginswhen revenues are squeezed by aneconomic slowdown.

Our investment in people andproperty accounts for approximately60% of revenues. Variable staff costs,including incentive compensation,freelancers and consultants, nowaccount for 6.6% of revenues and weaim for 7-8%.● Third, we have achieved ourobjective of de-leveraging the Companyand interest cover of over seven times.Now we have to continue to focus onhow we can improve share owner valueby maximising the return on alternativeinvestments in capital expenditures,acquisitions and investments, dividendsor share buy-backs.

Although capital expenditures haverisen recently primarily reflectingYear 2000 issues and propertyrationalisation, they are unlikely toabsorb more than 100-150% of thedepreciation charge in the mediumand long term.

We continue to trawl carefullyfor acquisition and investmentopportunities and have addedresources to our central acquisitionteam. However, we remain concernedabout value in certain markets. We willtherefore probably remain primarilyactive in acquiring strategicallyimportant, small- to medium-sizedbusinesses of up to $300 million invalue unless exceptional strategic andfinancial opportunities, such as Young& Rubicam Inc., arise.

Increasing dividends tend to raisethe fixed charges in the business andas a result we will continue to favourshare repurchases and cancellations asa use of our free cash flow. In 2000we invested £94 million here, butcontinue to be committed to a rollingannual buy-back program of arecently increased amount of £150-200 million, equivalent toapproximately 1-2% of our sharecapital. Historical data seems toindicate that programs on this scalehave the most significant impact onshare owner returns.

Letter to share owners continued

12 WPP How we’re doing

● Fourth, to advance further the roleof the Company from that of afinancial holding or investmentcompany (concentrating solely onfinancial matters such as planning,budgeting, reporting, control, treasury,tax, mergers and acquisitions andinvestor relations) to that of a parentcompany that adds value to ourclients and our people.

We are focused on the key added-value areas that we have identified– human resources, propertymanagement, procurement,information technology and practicedevelopment. This work is done by alimited number of 150 or so parentcompany people in London and NewYork, with some support in HongKong and São Paulo, and includingthose who joined us from the Young& Rubicam Inc. holding companyfollowing the merger.

In the human resources area wecontinue to develop our short-termand long-term incentive plans, ourrenamed WPP Leaders, WPP Partnersand WPP High Potential groups, ourWorldwide Ownership Plan, ourWorldwide Partnership Program andAtticus Awards – our literary Oscars;our training and knowledge-sharingprograms and specialised seminars oncreativity, retailing and interactive;our Marketing Fellowship Program;our Group directory, Navigator, ourglobal newspaper, The WIRE and ourmonthly online news bulletin, e.wire.

In property management, wecontinue to implement the WPP SpaceProgram which seeks to improve thereturn on our annual investment of$600 million in our property, byimproving communications, speed ofresponse and efficiency, through newdesign and layout of our premises.

In procurement, we continue totake initiatives in various regions ofthe world to improve the way wepurchase goods and services andco-ordinate their buying.

In information technology, we are increasingly co-ordinating our$350 million annual investment inhardware, software and informationtechnology salaries.

Finally, in practice development wecontinue our ‘horizontal’ initiatives in

10 identified high growth areas acrossour ‘vertical’ operating brands – inmedia investment management; inhealthcare; in privatisation; in newtechnologies; in new geographicmarkets; in retailing; in internalcommunications; in entertainmentand media; in financial services; andin telecommunications and hi-tech.In addition, we are developing ourdirect investments in new media andour start-ups and internal strategicalliances, which reinforce our practicedevelopment initiatives.

All these initiatives are designed toensure that we, the parent company,really do (and are perceived to)inspire, motivate, coach, encourage,support and incentivise our operatingcompanies to achieve their strategicand operational goals.● Fifth, as we move up the margincurve we are placing greater emphasison revenue growth. A legitimatecriticism of our performance againstthe best performers in the industry isthat our internal organic growth ratehas been lower. For the four years upuntil 1999, we grew organically byapproximately 8% per annum, againstapproximately 10% for the very bestof the best-performing competition(although their definition of organicgrowth is more flattering than ours).

Our objective is to move up to thislevel by better positioning our revenueportfolio in faster-growing functionalareas. Perhaps the results for 2000 areindicative of some success, althoughone swallow does not make a summer.In 2000 we achieved the highest rate of organic growth for any groupat over 15%. If the more liberaldefinition of organic growth were used,this would have been closer to 19%.

Our practice developmentinitiatives are aimed at helping withthis, and acquisitions so far in 2001– in advertising and media investmentmanagement in the US, the UK, SouthKorea and Brazil; in information &consultancy in Germany; in publicrelations & public affairs in the US,France and South Korea; and inbranding & identity, healthcare andspecialist communications in the US,the UK, France, Japan and HongKong – are also key.

Information and consultancy, publicrelations and public affairs andspecialist communications currentlyaccount for just 53% of our revenues.We would like to see them at 662/3%in five years.

Similarly, our geographic expansionis aimed at improving our organicrevenue growth rate. Despite recentdifficulties we still believe that the keygrowth areas will be in Asia Pacific,Latin America, Central and EasternEurope, Africa and the Middle East.Currently these areas account for over18% of our revenues, versus 13% afew years ago. We would like to seethem at one-third within five years,equally balanced with North Americaand Europe.

To achieve this we will expand our strong institutional networks –Ogilvy & Mather Worldwide,J. Walter Thompson Company,Young & Rubicam Advertising,Red Cell, MindShare, The MediaEdge, Research International,Millward Brown, Kantar MediaResearch, Hill and Knowlton,Ogilvy Public Relations Worldwide,Burson-Marsteller, Cohn & Wolfe,OgilvyOne, Impiric, CommonHealth,Sudler & Hennessey, Enterprise IGand Landor in high growth markets or where their market share isinsufficient. In 2000, we tackledAustralia, Belgium, Canada, China,Denmark, France, Ireland, Israel,Italy, Mexico, the Middle East,the Netherlands, Pakistan, Poland,Portugal, Puerto Rico, Singapore,Spain, Sweden, Switzerland, Turkeyand the US. In 2001 there is morework to do in the heartland ofContinental Europe – France, Germany,Italy and Spain, for example.

We will also enhance ourleadership position in informationand consultancy by continuing todevelop our key brands withparticular emphasis on NorthAmerica, Latin America and AsiaPacific. We will also reinforce ourgrowing position in media researchthrough Kantar Media Research.This includes our investments intelevision audience research throughIBOPE and AGB Italia, whichfollowing even greater success in

WPP How we’re doing

the UK and Australia, now havestrong representation in 27 countriesin Europe, Latin America andAsia Pacific.

In addition, we will reinforce ourworldwide strength in direct andinteractive marketing and researchthrough our traditional channels suchas OgilvyOne, Impiric, digital@jwt,Alexander Ogilvy, Blanc & Otus andMB Interactive. Where the recentcompressions in financial valuationsmay offer significant opportunities,we will also invest directly in thenew channels.

Lastly, we will continue to developour specialist expertise in areas suchas healthcare, retail and interactiveand to identify new high growth areas.● Sixth, and you will be pleased toknow our final objective, is to improvestill further the quality of our creativeoutput. Of the three things we do,strategic thinking, creative executionand co-ordination, creative executionis probably the most important – butwe use the phrase in its broadest sense.Clients look for creative thinking andoutput not just from advertisingagencies, public relations and designcompanies, but also from our mediainvestment management companies,MindShare and The Media Edge andour research companies. MillwardBrown is already arguably one of ourmost creative brands.

We will do this by stepping up ourtraining and development programs;by recruiting the finest talent fromoutside; by celebrating and rewarding,both tangibly and intangibly, out-standing creative success; by acquiringstrong creative companies; and byencouraging, monitoring andpromoting our companies’ achieve-ments in winning creative awards.

A colossal amount remains to bedone – and given the pace of changethat our clients face and thereforechallenge us with, it seems certainthat once these objectives are achieved they will be replaced by new ones.

As companies grow in size, mostchairmen and CEOs becomeconcerned that their organizationsmay become flabby, slow to respond,bureaucratic and sclerotic.

Any sensible chairman or CEO wouldnot want this to be the case. Theywould want both the benefits of sizeand scale with the responsiveness andenergy of a smaller firm. For the firsttime new technologies enable this tobe achieved more effectively and easily.

WPP is no different. We want thescale and resources of the largest firmtogether with the heart and soul of asmall one.

As a parent company, we aredeveloping practical principles andpolicies for charitable giving, theenvironment and support forcommunities and the arts, based onbest practice guidelines. Our activitiesrun in parallel with our operatingcompanies’ initiatives and programs in each of these areas. A summary of the Group’s initiatives to date canbe found on page 91.

Numbers alone – which of necessitymake up the essence of an annualreport – can only poorly express thecreativity, the applied discipline andthe infinite diversity that make upyour Company. It is, of course, anintensely personal and intenselycreative business. Our many clientscome to us for the brains andinventiveness of our people. Acrossthe disciplines, around the world,project by project, each assignment is individually undertaken and eachsolution painstakingly made-to-measure. And when all the hundredsof assignments are totalled up, andexpressed as they must be in monetaryterms, they deliver the numbersreported here.

So we would ask you now, as shareowners, to look behind those numbers,to remember their origin, to recognisethe 65,000 people who work for WPP companies around the world: andto join us in respect and admirationfor their talent and gratitude for theirdedication. We hope they enjoyedthemselves.

It was an outstanding year: and inmore ways than can be measured.

2001, although a more difficultyear, should be an even better one.

WPP is delighted that AmbassadorPhilip Lader has agreed to become chairman of your Company.Businessman, government executiveand diplomat, with a wide knowledgeof the world, Philip Lader brings with him an unparallelled range of skills and contacts which will be of immeasurable benefit to us and all our operating companies.

At the same time, it is with regret,gratitude and affection that we saygoodbye to Hamish Maxwell, ourchairman for the past four years.Formerly chairman and CEO of oneof the world’s largest and mostsuccessful companies, he was anoutstanding source of wisdom, counseland kindness. We shall miss himsorely and wish him well.

Philip LaderChairman

Sir Martin SorrellGroup chief executive

14 WPP How we’re doing

Operating and financial review

Competitive performanceThere is still a significant profitopportunity in matching the operatingmargins of the best-performingcompetition. The best-performingcompetitive listed holding companies,The Interpublic Group of CompaniesInc. (‘IPG’) and Omnicom Group Inc.(‘Omnicom’), achieve 16-18%operating margins, whilst their best-performing individual agencies suchas McCann-Erickson Worldwide andBBDO Worldwide are estimated toachieve operating margins of as muchas 20%. This compares to a WPPparent company margin of 14.0% andreported combined margins of theOgilvy & Mather Worldwide,J. Walter Thompson Company andY&R Advertising brands of 18%.

Historically, listed public relationscompanies showed operating marginsof more than 10% which have nowbeen more than matched by our ownoperations. Operating managementhas indicated that margin performancecan be improved further.

The Group is targeting animprovement in operating margin of1% in 2001 to 15% and 15.5% by2002, to bring us in line with the bestperforming of these competitors.

One of the Group’s most importantobjectives is to increase its rate oforganic revenue growth which is a keymeasure of the success of its value-added strategy. Excluding acquisitions,this was approximately 15% in 2000,a rate of growth that, althoughdelightful, is clearly unsustainable inthe long term.

Comparison with our competitorsis difficult given that, to the best ofour knowledge, they define organic

growth rates differently absorbingacquisition revenues into organicgrowth rates more quickly. If we wereto use their method of calculation,our organic growth rate would havebeen closer to 19%. Clients in thehigh revenue growth areas ofinformation and technology,telecommunications, healthcare,financial services and entertainmentand media now account for almost28% of Group revenues. As abenchmark at the end of 2000 thesesectors (excluding healthcare)accounted for approximately the samepercentage of the FTSE 100 bymarket capitalisation.

Geographic performanceEconomic conditions in NorthAmerica are now, to say the least,more challenging. The UK andContinental Europe, however,particularly France, Germany, Italyand Spain are currently stronger, alongwith Asia Pacific and Latin America.Our fourth quarter performance in2000 reflected this pattern with theUS and UK performing in line withexpectations and Continental Europe,Asia Pacific and Latin Americaperforming more strongly than forecast.Recent relaxation in monetary policyon both sides of the Atlantic maystimulate those economies in thesecond half of the year.

However, it may well be that the realeconomic challenge may come not in2001 but in 2002, if lower interest ratesand US tax cuts overheat the economyand general inflation and wages risebeyond the rates of 3-4% that we havebecome used to in the 1990s. YourBoard continues to believe that Asia

Pacific, Latin America, Africa, theMiddle East and Central and EasternEurope will offer superior opportunitiesfor growth in the medium to long term.These markets now account for morethan 18% of the Group’s revenue asopposed to 13% in 1992, and morethan 20% if our share of associates’revenues are included. These marketsare still forecast to continue to grow at significantly faster rates than those of North America and Western Europein the long term.

WPP, according to the AdvertisingAge Agency Report, ranks in the topthree in all of the 10 fastest-growingmarkets of the world.

Sector performanceOn the following pages the heads ofour nine operating brands summarisetheir operational activities andhighlights for 2000.

15 WPP How we’re doing

Competitive performanceRevenue per head $000

WPP

O&M/JWT/Y&R/MindShare

Omnicom

IPG

99 †

99 †

99

99

00 †

00 †

00

00

126.0

112.9

130.5

122.0

128.4

120.6

124.3

129.6† Constant currency

Geographic performanceConstant currencyrevenue growth %

North America

United Kingdom

Continental Europe

Asia Pacific, Latin America,Africa & Middle East

99

99

99

99

00

00

00

00

16.8

10.5

11.0

4.0

29.8

22.5

47.2

38.2

Sector performanceConstant currency revenue growth %

Advertising, media investmentmanagement

Information & consultancy

Public relations & public affairs

Branding & identity, healthcareand specialist communications

99

99

99

99

00

00

00

00

5.2

13.9

30.5

19.2

33.8

19.8

75.6

27.6

Operating marginsby geography % North America

United Kingdom

Continental Europe

Asia Pacific, Latin America,Africa & Middle East

99

99

99

99

00 4

00 4

00

00

14.8

11.8

13.1

11.7

14.9

11.8

14.0

13.8

PBIT margins %

WPP

O&M/JWT/Y&R/MindShare

Omnicom

IPG 3

99

99 †

99

99 2

99

00

00 †

00 1

00

13.4

16.4

16.0

16.6

16.6

14.0

17.4

15.9

17.9† Constant currency

Staff cost to gross margin ratio %

WPP

O&M/JWT/Y&R/MindShare

Omnicom

IPG

99

99 †

99

99 2

00

00 †

00

00

58.8

56.4

55.2

99 56.5

59.5

59.1

56.5

59.0

55.5† Constant currency

Operating marginsby sector %Advertising, media investmentmanagement

Information & consultancy

Public relations & public affairs

Branding & identity, healthcareand specialist communications

99

99

99

99

00

00 4

00 4

00

15.4

10.0

13.3

12.3

16.5

10.1

13.1

12.1

Revenue by geography £m

96 97 98 99 00

3000

0

1000

500

1500

2000

2500

Continental Europe

Asia Pacific, Latin America,Africa & Middle East

United Kingdom

North America

Revenue by sector £m

96 97 98 99 00

3000

0

1000

500

1500

2000

2500

Advertising, media investmentmanagement

Information & consultancy

Public relations & public affairs

Branding & identity, healthcareand specialist communications

1PBIT margin for Omnicom as presented for 2000 is stated excluding the gain on disposal of an investment in Razorfish Inc. of $110m. Including the gain, PBIT margin was 17.7%.2Based on profit and loss restated for pooling of interests.3PBIT margin for 2000 as presented above excludes restructuring and merger costs of $116.1m and Deutsch transaction costs of $44.7m, and for 1999 excludes restructuringand merger costs of $84.2m. After these charges PBIT margin for 2000 was 15.1%, and for 1999 was 14.7% (14.9% as restated for pooling of interests).

4Reflects restructuring costs incurred following the acquisition of Young & Rubicam Inc.

Operating and financial reviewReports from operating brands

WPP How we’re doing

Advertising and media investmentmanagementOn a reported basis, combined advertisingand media investment managementrevenues at Ogilvy & Mather Worldwide(which was named by Adweek the United States Agency of the Year in 2000),J. Walter Thompson Company, Y&RAdvertising, Red Cell (formerly Conquest),MindShare and The Media Edge rose byalmost 34%. The combined operatingmargin of this group of companies was16.5%. Combined operating costs rose by32% and the combined staff costs torevenue ratio excluding incentive paymentsfell to 52.6% from 53.7%.

In 2000, Ogilvy & Mather Worldwidegenerated net new billings of £515 million,J. Walter Thompson Company £373million and Y&R Advertising (fourth quarteronly) £28 million.

Also in 2000, MindShare generated netnew billings of £1.5 billion. Plans are beingdeveloped to create a ‘WPP media’ parentcompany which, like Kantar in informationand consultancy, will seek to add value toour clients and our people through ‘tribal’co-operation.

Red Cell’s revenues rose almost 11%and operating profits and margins were up significantly. Net new billings were £13 million.

Ogilvy & Mather WorldwideSimply put, Ogilvy had another greatyear. In a world exploding with newtechnologies, new media and newglobal markets, clients are tending totheir brands as never before, makingOgilvy more relevant than ever.

We have long been advocates ofbranding – a principle that goes backto David Ogilvy. Our revival of thisphilosophy as Brand Stewardshipseven years ago both linked us to ourpast and positioned us for our future.We have since expanded that focusbeyond traditional media to encom-pass every point of contact with theconsumer. This has become ourguiding star: creating integrated,multi-disciplined, brand-based andconsumer-focused communications.That makes 360 Degree BrandStewardship Ogilvy’s core businessstrategy and one that fits well withtoday’s marketplace.

What makes our claim solid on thisstrategy is its pedigree. For decades wehave had a multi-disciplined approachwith robust direct marketing andpublic relations divisions, and even aveteran interactive unit. We brokeground in this discipline 16 years ago,and today we are the leadinginteractive agency in terms of globalreach, financial strength, growth (50%in 2000), creativity and innovation.(Adweek named OgilvyInteractive its2000 Integrated Agency of the Year.)These units are the growth engines ofour company.

The greatest benefit of our 360Degree strategy is that it gives us aunifying point of view – one thattakes full advantage of our range oftalent and capabilities. For this

reason, we continue to expand ourservices beyond our core strengths to such growing areas as brandconsultancy, design, healthcare,mobile communications, loyaltymarketing and CRM initiatives.Through the start-up of new units,strategic acquisitions and jointventures, and our relationships withthe WPP family of companies, we are building a 360 Degree networkthat is unparalleled.

As a result, I believe the agency isin the strongest position it has been inyears. Once again, all regions areperforming well, with many key markets– the US, France, India, Philippines,Brazil, Mexico and Guatemala amongthem – being singled out for local topagency accolades.

Our continued focus on our workhas made it better. Certainly we have more offices in more countriescontributing to our creative reputation,as attested by another strong year interms of awards. Importantly, manyof these awards came from beyondadvertising, and that reflects ourgrowing weight as a creative force inmulti-discipline and integratedmarketing. All told, our people, ouroperations and our work netted wellover 250 different honours from allindustry sectors.

Our client roster continues to bethe envy of the industry, includingsuch clients as IBM, American Express,Unilever, Kraft, Kodak, Ford, Nestlé,BP, Telefonica and Terra Networks.Our share across the board with theseand other clients has been growingwith assignments that are broad andincreasingly multi-disciplined.

While growth with existing clientsis paramount, last year we addedseveral important new brands, led bythe assignment of Motorola’s globalaccount. In total, we added close to$1 billion in new billings.

I am very optimistic about thiscoming year. We have a superbstrategy, and we are committed todelivering it – everywhere it counts, ineach office, for each client, every day.That’s where the promise of 360Degree Brand Stewardship translatesinto success for our clients and for us.Shelly Lazarus

17 WPP How we’re doing

J. Walter Thompson CompanyJ. Walter Thompson continued itsstrong forward momentum in 2000.We posted one of the best newbusiness, revenue and profitperformances in our 137-year history. In addition, we acceleratedour transformation to a totalcommunications company bydeepening our roster of superior talent and capabilities in everymarketing discipline.

Net new billings (in constantcurrency) won worldwide totalled$615 million. We welcomed a host ofnew blue-chip clients including SunMicrosystems, KPMG, iPlanet,Spencer Stuart, Foster’s Beer, Avonand Telecom Italia. In addition, wewere entrusted with significant newassignments from valued currentglobal clients including Ford, Unilever,Nestlé, Diageo/UDV, Qwest, PhilipMorris and Pfizer.

Our company generated dynamicgrowth across the board in everyregion, led by the United States andEurope. Latin America reboundedstrongly after a difficult 1999 andAsia Pacific continued its sustainedimprovement.

We broadened JWT’s global reachand invested in premier resources toextend our service offering in specialisedcommunications. Our networkexpanded to 311 offices in 155 citiesin 90 countries, serving leadingmarketeers in virtually every categoryof goods and services.

Our solid financial and creativefoundation enabled us to completemore than 20 strategic acquisitionsworldwide. Top-flight companiesjoined our ranks in every disciplinewith particular emphasis on digitalbranding, direct response, databaseand promotional marketing.

JWT now holds majority stakes in:TMI, a full-service agency operatingin eight Middle East countries andAPCU Thompson Asociados, ageneral agency operating in sixCentral American countries. We alsoincreased our stake in one of Israel’spacesetting agencies, Tamir Cohen.

In addition, our line-up of digitaland technology communicationscompanies was enhanced with theaddition of Tonic 360, San Francisco;

Imagio/JWT, Seattle; Coolfire, New York; Interactive MarketingConcepts, Toronto; and ThompsonDigital Korea; as well as Go DirectMarketing, a database firm in Toronto and Vancouver.

Our diversified communicationsand marketing services companiesachieved significant growth:● ThompsonConnect, our global direct marketing subsidiary, with 600 professionals in 15 countries, grew to $76 million in revenue.● JWT Specialized Communications,our recruitment and employeecommunications firm, with a globalreach of 600 professionals in 34offices, rose to $75 million in revenue.The group continued to diversify intohigh-growth areas such as technologyadvertising and mature marketcommunications.● digital@jwt, our full-serviceinteractive and digital brandmarketing arm, made progress inforging its worldwide network anddelivered award-winning work. It isbecoming a recognised force in newmedia, with 450 professionals andnearly $50 million in revenue.

We launched several researchinitiatives to understand more deeply how people consumecommunications, extending JWT’srenowned heritage of brand learning.These efforts are driving the creationof new tools aimed at providingleading-edge brand communicationsplanning in the year ahead.

In sum, we became a strongermarketing partner better able todeliver integrated solutions for our clients, using our proprietaryapproach called Thompson TotalBranding.

The entrepreneurial spirit of ourpeople is our most valuable competitiveadvantage. Their single-minded focuson great ideas that build relationshipsbetween brands and consumers – ideaswith the power to resonate across theentire communications spectrum – willensure our leadership in a marketinglandscape whose only constant is warpspeed change.Peter Schweitzer

Peter SchweitzerPresident and chief executive officerJ. Walter Thompson Company

Shelly LazarusChairman and chief executive officerOgilvy & Mather Worldwide

Operating and financial review continued

18 WPP How we’re doing

Young & Rubicam Inc.The year 2000 was a year of greattransformation for Young & RubicamInc. – a year in which we defined ourstrategy for the future by joining theWPP Group of companies.

We share a number of key clientswith WPP. That makes the transitionsimpler. But even more important,we share common philosophy andvalues. Joining WPP will help usdeliver the most powerfulcommunications programs to ourclients. At the same time, we areconfident that our singular 30-yearhistory of building brands throughintegrated communications will addvalue to the entire WPP network.

Philosophically, Young & Rubicamfits easily into the Group: Young &Rubicam is a global group of people,disciplines and companies dedicatedto bringing our clients the best incommercial persuasion. Our goal is tobuild powerful, sustainable brands...to move minds, move products andhelp drive marketplace results.

We often say that our currency isideas. Ideas that are founded on anexhaustive knowledge of our audiences,executed through the industry’sbroadest range of communicationsdisciplines. That the essence of Young& Rubicam is knowing when andhow to integrate these disciplines tocreate persuasive messages that cantravel the world.

We do it by organising ourselvesaround our clients – across alldisciplines and geography. Ourdedicated brand teams give our clientsthe best of both worlds: the size andmuscle of a world leader in marketingand the nimbleness and flexibility ofan entrepreneurial enterprise.

In 2000 we reaffirmed thiscommitment to client focus throughseveral key initiatives. We namedSatish Korde president, ClientSolutions, in charge of our keycorporate accounts, and designatedtop-management accountability foreach of our major clients. Lessonslearned at this level resound with allof our clients everywhere.

Some time ago, we coined thephrase, Best Alone, Better Together.It’s still the best description of whatdrives our success. Our strength

together is predicated on theindividual strengths of our partnercompanies, each a top-ranking leaderin its field. Each lending particularexpertise to a client problem. Eachcompany profitable in its own right,with its own core group of clients,accomplishments and credentials.

At Y&R Advertising, Ed Vickreturned as chairman and CEO, after serving as chief creative officerfor Y&R Inc. In this year of change,the agency suffered some difficult andhigh profile account losses – US Kraftbusiness, United Airlines, Ericsson,KFC, USPS, Ford Europe, among them.

These were counterbalanced by astrong new business momentum.Wins included Computer Associates,Xenical, Pennzoil, Marks & Spencer,Scotts Co., Ford’s Land Rover,NASCAR, additional business fromSony, as well as Chanel’s global mediabusiness. The agency launched a newintegrated unit, Brand Buzz, that grewto be a $60 million agency in its firstyear of operation. In London, Y&Racquired The Partners, a premierbrand design firm.

At Y&R’s media planning, buyingand placement services operation, TheMedia Edge, important new globalproduct offerings gained momentum in2000, including The Digital Edge andTME 360, a total communicationsoffering that is acting as a culturalchange agent within TME. TME’sMedia Convergence was created tohelp clients wade through the dizzyingarray of interactive media options thatare available now, as well as thosesoon to come. Industry recognitionwas high: Advertising Age namedTME the Media Agency of the Year inthe US. ‘Agency of the Year’ honourswere also bestowed upon TMECanada and Australia, and numerousawards for people and work markeda strong performance.

At Impiric, new capabilities inconsulting, interactive services andcustomer dialogue were added in2000. With these forward-lookingchanges also came the recognitionthat the company must also be true to its direct marketing roots. Newregional leadership at our flagshipNew York agency and in Europehas already had a positive impact.

Mike DolanChief executive officerYoung & Rubicam Inc.

WPP How we’re doing

At the start of 2001, the appointmentof Daniel Morel as the new chairmanand CEO strongly positions Impiricfor the future.

Under the leadership of Ron Bess, theDiversified Communications Groupdelivered a strong performance last year.

In 2000, Burson-Marstellerstrengthened its commitment to thedistinguishing features and initiativesthat position Burson-Marsteller as anindustry leader. Global capabilities,groundbreaking research, technologyfocus, and client service have positionedthe company for continued growthand innovation.

Notable achievements included ane-fluentials study that identified, forthe first time ever, a group of opinionmakers who have an exponentialinfluence shaping and driving publicopinion through the internet. Threenew investments in technology wereBM3W, FastForward – both of whichreturned a profit in their first monthof operation – and Speed Branding.

At Cohn & Wolfe, new businesscame from Orange, Microsoft, Pfizer,DuPont and Sony. The networkexpanded to include Kendo in Parisand new offices in Madrid and SanFrancisco, and Cohn & Wolfe wasnamed Best Healthcare Agency inthe UK.

At Landor Associates, new brandidentities were launched for numerousmajor clients, including BP, FranceTelecom, NYSE (the New York StockExchange), Delta, Corning, 7UP andbmi british midland. In 2000, Landoralso strengthened its network, both inthe US, where the company acquiredthe brand strategy consulting firm ofSt. James, and globally, with theaddition of new offices in Vienna,Dubai and Singapore.

Sudler & Hennessey added Rochebusiness in the US and Europe, as wellas a global campaign for professionalsfor Roche Tamiflu. The network wasstrengthened by the addition of S&Hconsumer groups in New York, Londonand Milan; digital health strategies –Avenue-e – in Milan, Melbourne andFrankfurt; Sentrix global healthcommunications in Short Hills, Paris,Milan and Munich, as well as a Precepteducation service in Short Hills.

The Bravo Group continued toprovide critical marketing services toclients targeting Hispanic audiencesin the US. New units of the agencyincluded BravoMed, a healthcarespecialty unit; Bravo 2.1, seamlesslyintegrating on-line and off-linecommunications, as well asBravoLateeno, which helps clientsreach the bi-cultural, bilingual Latinoyouth segment.

In its 15th year of operation, Kang & Lee went to market with thelargest single campaign done by theagency: integrated advertisingprograms for the US Census Bureauthat targeted 13 ethnic groups in 14languages. Research for the campaignearned the agency the prestigiousOgilvy Research award.

Finally, Young & Rubicam acquiredRobinson Lerer & Montgomery, one of the world’s premier strategiccommunications firms.

In joining WPP, Young & Rubicamhas made important changes,restructuring the organisation tomake us leaner, more focused andbetter directed. We are a bettercompany than we were a year ago.There is a wonderful depth of talentand commitment that resides in all ofour companies across the world.

Raymond Rubicam liked to say thatevery generation of Y&R would haveto reinvent itself for its own time. We have done so in 2000. We enterthe 21st century with tremendousconfidence about our future, and a real eagerness to demonstrate the power of Young & Rubicam’sintegrated communications.Michael Dolan

WPP How we’re doing

Red Cell 2000 has been a great year for eachof the four founding companies ofRed Cell: European-based Conquest,US agency Cole & Weber, UKmarketing communications groupPerspectives and Asia Pacific alliancepartner, Batey.

Together, they have created a newglobal communications networkfocused on the needs of ‘challengerbrands.’ Individually, each companygrew in terms of revenues, awardsand client wins, including OCBCBank and TNT Air Express in Asia,Freight Traders in the UK, AtkinsNutritionals and Nike ACG in theUS, Celanese in Germany and GrapesTelecom across Europe.

To deliver global brand buildingcommunication solutions, Red Cellemploys fundamentally new rules ofengagement, consciously seeking deepand broad creative talent and having atits core the capability to react quicklyand effectively to shifting marketopportunities. A thousand talentedpeople in Düsseldorf, London, Milan,Paris, Seattle, Singapore and 16 otherkey business centres, work locally orglobally for brands such as Alfa Romeoand Ermenegildo Zegna.

Most agencies have the fundamentalskills to work for a variety of clients and established agencies have proven to be highly successful forestablished brands.

Our business focus is different.Challenger opportunities – people,brands, or companies in need of rapidchange – are seeking a new breed of agency. Red Cell’s singular focus is to deliver global communicationstrategies for these challengeropportunities.

A challenger brand can be a fastgrowing private company in theluxury business or financial servicemarket, or a group of managerswithin a large multinational fmcgcorporation with a need to revitalisean existing brand. It is not about size, but rather the brand attitude and life cycle condition that defineschallenger brands.

At Red Cell we use BrandStormto provide clients with fresh andchallenging solutions to theirbusiness opportunities.

Luca LindnerChief executive officerRed Cell (formerly Conquest)

Operating and financial review continued

BrandStorm is an inclusive forumwhich empowers clients, account andcreative managers and planners towork collaboratively from the outsetof a project. This ‘collectivepartnership’ mentality delivers resultsin half the time typically experiencedwith conventional agencies.

Finally, at Red Cell we believe that in a globalised and internet-connected world there is a fantasticopportunity to work with the besttalent in the world. The location and employment status of talent isincreasingly irrelevant. We arebuilding a community, The EclecticNetwork, of exceptional creatives,financial analysts, brand architects,and individuals from the movieindustry, all with provencommunication and brand buildingskills – Sir Bob Geldof being anexcellent example. Every Red Cellpartner in charge of a client’s brandwill have the ability to leverage thegold mine of talent represented byThe Eclectic Network.Luca Lindner

21 WPP How we’re doing

MindShareIn 2000, MindShare continued todominate the media marketplace asthe world’s largest media investmentmanagement company with annualbillings growing to $20 billion,and global new business wins of$2.6 billion.

As MindShare Worldwide enters itsfourth year as a stand-alone mediainvestment management company,we are distinguished by our depth oftalent around the world, thesophistication of our research andsystems, our strategic capabilities andthe power of our media investmentclout in almost every market in whichwe operate.

Because of our global size, we areable to invest efficiently in researchand systems initiatives that benefit theentire organisation and provide us andour clients with proprietary insightsto the ever-changing media landscapeand how consumers everywhereinteract with media. As mediaconvergence becomes a reality,MindShare is taking a leadership rolein bringing to our clients all thattechnology offers.

MindShare’s position as the largestglobal media network was solidifiedin 2000 with the launch of MindShareNorth America. In the US, MindSharequickly established its leadership inthe market with several significantnew business wins that truly unitedour operation. These wins include theconsolidated media accounts of majorclients Unilever and Sears.

By bringing together a managementteam that represents the best andbrightest in all aspects of mediainvestment management, MindShareUS earned the moniker ‘LionsShare’by trade publication Advertising Agein 2000. The US operation has officesin nine cities and first-in-class localand national broadcast capabilities, inaddition to research, strategic, non-traditional, promotion, and newmedia offerings.

In addition to our success in theUS, MindShare experiencedsignificant growth in Europe, Asia andthe growing Latin American market.Dominic Proctor, our chief operatingofficer, has been integral to the roll-out worldwide. We have attracted

several top media executives from ourmajor competitors in Europe, Asiaand Latin America, and had anequally impressive new business runin these regions. Major new regionalclients include Nike and Volvosigning on with MindShare Europe,Terra giving us assignments inMexico and Hang Seng Bankawarding MindShare Hong Kong itsbusiness. We’ve also had importantlocal wins such as Allianz inGermany, Bass in the UK, NationalLotteries in Sweden and Belgium, and Kraft in Italy, Greece and theCzech Republic.

Media consolidation continues to bethe trend that drives much of ourregional and global growth. Numerousnew clients awarded MindShare theirglobal media business, including Boots,easyEverything, KPMG and Lufthansa.

As we look forward, key growthwill come from additional mediaconsolidations as well as thedevelopment of our unique specialistofferings that set us apart in key regionsof the world. Our ATG researchsystems represent a truly globalproprietary initiative. Our revolutionaryMindCast operation creates televisioncontent for clients in China, and soonin Japan and Thailand. M-Digitalprovides interactive competency andcapabilities that will be critical as weevolve to a converged environment,and already accounts for more onlinebillings than any other agency inthe world.

We see the next year as one inwhich we continue to break newground in bringing new mediasolutions to our clients around theworld and to lead the industry in thedevelopment of innovative researchand systems. With the professionalswe have in place around the world,MindShare is poised to continue itsleadership position in all areas ofmedia investment management.Irwin Gotlieb

Irwin GotliebChairman and chief executive officerMindShare

WPP How we’re doing

Information & consultancyThe Group’s information and consultancybusinesses continued their strong revenuegrowth with gross profit rising by almost20% and operating margins up slightlyover the previous year. Particularly strongperformances were recorded by MillwardBrown in the United States, UnitedKingdom, Germany, Hungary, the CzechRepublic, Singapore, Japan and Australia;by Research International in the UnitedStates, Germany, Greece, Japan, South Africa and Brazil; by Kantar MediaResearch at BMRB in the UnitedKingdom; by IMRB in India; and byGoldfarb Consultants in Canada, Italy and the United Kingdom.

The Kantar GroupLast year I talked of 1999 being a yearof laying foundations to better serveour clients’ needs and to seize theopportunities presented to ourindustry by e-commerce and theinternet. I am pleased to report that in 2000 we saw payoff for much ofthat preparatory work with organicrevenue growth ahead of the marketand strong operating marginimprovement. This organic growthwas supplemented by the successfulintegration and development of ourmajor 1999 acquisitions. During 2000,we acquired SIFO, the largest researchcompany in Scandinavia, as part ofResearch International, and Ergo, thelargest qualitative research company inSpain, as part of Millward Brown.

Research International’s majorinitiative last year was its Project 100program. Designed to improve service levels to major global andimportant local clients, Project 100’swatchword is focus… focus on keyclients, where Key Account Directorshave been appointed for the top 40clients, and focus on core areas ofresearch expertise.

Operationally, RI’s critical mass inthe US market was improved by itsmerger with the Winona Group, astrong but previously self-standingbusiness within Kantar. This mergerhas successfully produced one companywith the resources to compete moreeffectively than either could separately.

Center Partners, acquired in 1999 asour entry into out-sourced call handlingfor technology and telecommunicationcompanies, won major contracts duringthe year and is now the fastest-growingpart of our business.

Millward Brown had an outstandingyear in its two major units in the USand UK. In the US, the integration ofIntelliQuest, acquired in 1999, wasachieved successfully and goingforward IntelliQuest will form thecore of MB’s technology researchexpertise. In the UK, the focus onbranding knowledge based on theBrandDynamics system successfullyrepositioned the company higher upthe client value chain.

Kantar Media Research continuedto expand the geographic reach of itsTarget Group Index media-planningtool, which is now available in 30countries. AGB, in which WPP holds a significant minority interest,won the UK Television AudienceMeasurement contract, a tremendousvictory over the long-term incumbent.

BMRB, in the UK, was awardedprestigious contracts by the UKgovernment for major social policystudies in areas such as health, citizenshipand the criminal justice system.

Goldfarb Consultants strengthenedits presence geographically, bringingon stream a West Coast office in theUS, and functionally through gains inpharmaceutical and financial researchin Canada.

Sadly, our business success wasmarred at a personal level by theunexpected and untimely death ofRamesh Thadani, the head of IMRB,our Indian company. Ramesh was asuccessful business leader, but an evenfiner man. As his legacy, he leavesbehind a strong, intellectually vibrantorganisation in IMRB.

2000 was an interesting year forinternet research. Along witheveryone else, we observed thedotcom bust, but in fact our internetrevenues doubled as our traditionalblue-chip clients turned to us forinternet-based research, and we areforecasting a continuation of this trend.

This, I believe, is and will be theongoing competitive strength of Kantarversus internet start-ups. Our operatingcompanies are valued by our clients notas data collectors, but as trusted advisorsto turn to as the nature of their industriesand ours change. We will ensure thatKantar continues to provide the skillsneeded to meet these changing needs. David Jenkins

David JenkinsChief executive officerThe Kantar Group

Operating and financial review continued

WPP How we’re doing

Public relations & public affairsThe Group’s public relations and publicaffairs activities continued to advancestrongly.

Hill and Knowlton’s revenues rose bymore than 31% and operating costs by more than 29%. As a result, marginsincreased to almost 13%, ahead ofpreviously established targets.

Revenues at Ogilvy Public RelationsWorldwide (which was named both byPR Week and The Holmes Group as‘Agency of the Year’) rose by almost 61%and operating costs by approximately 59%.For the fourth year in a row following thechange in leadership, profitability improvedsignificantly over the previous year.

In the final quarter of 2000, Burson-Marsteller’s revenues rose by more than8% and Cohn & Wolfe’s by more than31%. Robinson Lerer & Montgomery,which was acquired by Young & RubicamInc. in the first quarter of 2000, made astrong first time contribution to the Group.

Our public relations and public affairsbusinesses as a whole showed operatingmargins of more than 13%, in excess ofthe Group’s objective for 2000 and in linewith the best-performing publicly listedcomparables. Operating management hasdeveloped new three year plans thatindicate further significant improvement inoperating margins.

Hill and KnowltonIn a record year for the firm, Hill andKnowlton reaffirmed its commitmentto a tradition of quality client service,industry leadership, and breadth anddepth of resources. Significant organicgrowth and targeted acquisitionscombined to help H&K exceed itsgoals for the year. Accommodatingclient growth needs and marketdemand, worldwide additions includedGaia (Italy), SocketPR (US), TheRockey Company (US), H&K Berlin,Hiller Wüst (Munich), RPCA (Paris)and Vox Consulting (Argentina).

H&K continued to be the agency ofchoice particularly with organisationsseeking global reach and expertisesuch as Motorola, Compaq, Ernst &Young and the International OlympicCommittee. The firm’s worldwidereputation in crisis and issuesmanagement was best summed up inOlympic newsletter Around the Rings,which named Hill and Knowlton asamong the most influential groupswithin the Olympic movement.

Ford Motor Company stepped up its PR business throughout thesystem as well as expanded its workwith H&K’s exclusive television and movie product placement firm,Showcase International. Asia Pacificcontinued to dominate the M&Awork in that region.

Indicative of its public affairs andenergy specialisations, H&K Canada,augmenting WPP’s privatisationexpertise, developed a fully integratedgovernment, media and communityrelations program on behalf of clientBritish Energy assisting in theprivatisation of the Bruce Nuclearfacility of Ontario Hydro.

Hill and Knowlton’s technologypractice, led by Blanc & Otus PublicRelations, represents industry leaders around the world, fromcommunications giant BT, to internetexpert Ariba, and on to digitalentertainment pioneers TiVo andLivePlanet. Each has turned to H&Kfor powerful public relations servicesthat change market behaviour oropinion, redefine existing markets orcreate new ones, or simply establishlasting leadership positions.

Similarly, as part of the wpp.cominitiative to improve Group company

Howard PasterChairman and chief executive officerHill and Knowlton Worldwide

24 WPP How we’re doing

Ogilvy Public Relations Worldwide2000 was a year of strong growth,award-winning programs andunprecedented change in themarketplace. During 2000, we:● Were named ‘Agency of the Year’ by both PR Week andThe Holmes Group.● Grew organically by 35%.● Tripled in size in three years, going from $55 million in 1997 to $169 million, and codified ourposition as one of the industry’sfastest-growing firms.● Expanded geographically to51 offices by opening Ogilvy PRlocations in Bucharest, Colombo,Düsseldorf, Frankfurt, Hyderabad,Istanbul and Sydney.● As a result of our integrationefforts and synergy, all three specialtyunits grew significantly faster asintegrated units than they did asindependents – Feinstein KeanHealthcare (acquired in November1999) grew 48.6%, B|W|R (acquiredin October 1999) grew 22.2% andAlexander Ogilvy (acquired inOctober 1998) grew 43.2%.● Ranked third in size globally in thehealthcare, consumer and technologyarenas, according to the Council ofPR Firms.● Won nine PR Week Awards and six CIPRAs in 2000 (the most of any firm).

We continued to have one of thelowest client turnover rates in theindustry and added key brand namesto our roster, such as BP, Kodak,Tricon, Boehringer Ingelheim,Kimberly-Clark, Microsoft andMerrill Lynch.

Growth happened across each ofour five practices, with the technologypractice leading the way with a 44.2%growth rate in 2000.

In a marketplace bolstered byopportunity, and the talent to fulfillthose opportunities difficult to find,we launched a critical initiative in2000 to Attract, Grow and Keep theBest People (affectionately known asAGK), which helped us reduceturnover by 30% and attract 400 newstaff members. AGK componentsincluded the introduction of anemployee work-visit program;professional development fund;

Bob SeltzerChairman and chief executive officerOgilvy Public Relations Worldwide

Operating and financial review continued

interactive communicationscapabilities, Hill and Knowltonformalised the global Netcomspractice, providing clients withcutting edge internet, extranet andintranet services and strategies. The practice has created onlinecommunications programs for clientssuch as the BT Global Challengeyacht race, the California oliveindustry, and Roche treatments forAIDS and Hepatitis C.

The year was marked by bellwetherinitiatives specifically engineered toenhance quality client service. Suchofferings included the launch of theMedical Knowledge Groupthroughout Europe, Canada and theUS, and the development ofPRecision™, a toolbox that deliversagainst the age-old conundrum ofmeasuring and evaluating PR, as well as targeting and benchmarking.A Group collaboration, developersincluded a working group of H&K,and WPP partners Millward Brown,Millward Brown Precis and MindShare’sAdvanced Techniques Group.

Benchmarking internal and externalperceptions, the firm again participatedin two major transnational studies: theThomas L. Harris/Impulse ResearchEmployee Satisfaction survey and theCorporate Reputation Watch surveyconducted by Yankelovich and ChiefExecutive Magazine, targeting the chiefexecutive officer to raise the visibilityof corporate reputation among seniormanagers and boards of directors.

In recognition of its achievements,H&K scooped the PR Week Awardsfor Best Business Campaign 2000 forits work for Europe’s leading B2Bprovider of ‘e-construction’ services,BuildOnline. As well, H&K HongKong’s technology practice won‘Technology Campaign of the Year’for its work on launching internetcurrency – beenz – into the GreaterChina market.Howard Paster

WPP How we’re doing

O-village (our newly launchedcompany-wide intranet); internal jobposting database and enhancedtraining and knowledge sharingthrough Client Service College, TechBoot Camp, our Core Curriculum and mandatory Management SkillsTraining. Our anniversary celebrationon 3 September 2000 also helped usbuild a deeper appreciation of ourOgilvy heritage.

Our efforts to provide full globalcapabilities to clients progressedsignificantly, aided in large part by O-village. Its state-of-the-art searchfunction allows any employee anywherein the network to access knowledge andresources within seconds.

Ogilvy PR is well positioned tomeet the challenges of 2001, whichwill be driven by an economy verydifferent to that of the past severalyears. Nonetheless, we will continueto grow by expanding geographically,positioning ourselves as leaders in thefastest-growing industries, expandingclient relationships, broadening ourofferings, fostering employee develop-ment and enhancing our approach toclient service.

We enter 2001 ready to face thechallenges and opportunities clearlyahead of us. Bob Seltzer

Branding & identity, healthcareand specialist communicationsBranding and identity, healthcare andspecialist communications revenues roseby more than 27%. Although gross profitrose even more strongly, operating costsrose faster, resulting in overall operatingmargins declining by 0.2 margin points,chiefly due to margin erosion at ourhealthcare operations. Several of ourcompanies in this sector performedparticularly well including in promotion anddirect marketing – Einson Freeman,OgilvyOne, A Eicoff & Company; in identityand branding – Addison CorporateMarketing, Brouillard, Banner McBride,BPRI, Coley Porter Bell, Lambie-Nairn,Scott Stern and Enterprise IG Group; inhealthcare – The Shire Hall Group; and inother specialist marketing resources – The Henley Centre, pFour Consultancy,Management Ventures, Metro, The Farm,The Geppetto Group, JWT SpecializedCommunications and Perspectives Red Cell.

In 2001 this communications servicessector will be split into three parts forstrategic (but not share owner reporting)purposes – first, branding and identity,secondly, healthcare and finally specialistcommunications.

Since its formation and before it wasin vogue, WPP recognised thepotential of marketing specialists toplay a highly valued role and toproduce a concentrated impact on ourclients’ businesses. Over recent years,our strategy has evolved beyond thesimple acquisition of new specialistcapabilities, which for the most partstill characterises the approach of ourcompetitors. With ventures likeCommonHealth, first, Enterprise IGmore recently, and now the BrandUnion in 2001, we have demonstratedhow co-operative ventures can createscale and industry leadership accessibleto even the smallest of our specialistunits. These ‘focused clusters’ ofcomplementary companies are provingmore attractive to clients, creating amore sustainable competitive advantage,and proving the membership benefitsof WPP.

Some of the specific accomplishmentsin our two most sizeable sectors, aswell as a few key events among our other specialist companies, aresummarised below.

The Brand UnionThe goal of the Brand Union is to builda group of leading consulting brandscapable of meeting all the brand,identity and design needs of the world’smost demanding brand owners.

It comprises Enterprise IG; the newlyformed ‘brand experience’ offeringEnterprise XP, which brings together ina single network Banner McBride,Clever Media, Eurosem and The Clinic.Also within The Brand Union are someof the strongest independent brands in our industry – Addison CorporateMarketing, BDG McColl, BPRI, ColeyPorter Bell, Dovetail, The Henley Centre,Lambie-Nairn, Oakley Young,WalkerGroup and newly acquiredWarwicks.

John ZweigChief executive officerBranding & identity, healthcare and specialist communications

26 WPP How we’re doing

Some highlights:● Enterprise IG grew from eightoffices to 17 worldwide and set inmotion plans to open several newoffices in 2001.● Client assignments include themerger of Qwest and US West,programs for Ford Motor Company,Guardian Media Group, Holderbank,Merck’s Vaccine Division, MerrillLynch Investment Managers andWestvaco; many of these clientassignments are serviced throughGroup partnerships with ourworldwide advertising networks,J. Walter Thompson and Ogilvy & Mather.● Addison continued to build itsreputation as WPP’s corporatemarketing arm through stakeholderengagement programs for Novartisand Syngenta together with thenaming and rebranding of Caradon to Novar.● Tutssels, the award-winningLondon-based consumer brand designconsultancy, joined the Enterprise IGnetwork late in 2000.● Banner McBride launched its BrandEngagement offering which led toprograms with Gala Bingo, Getronicsand One 2 One.● BDG McColl’s environmentaldesign projects included work forAmerican Express, Argos and KPMG.● Coley Porter Bell more thandoubled its profitability, and manyof the business wins came fromnon-packaging projects including Fordand Jersey Tourism.● Lambie-Nairn continued todominate the broadcast design sectorand moved into telecommunications,securing clients like ntl and eircom.

Among the awards won were goldin Creativity 30 (Enterprise IG),silvers in the D&AD andPromax/BDG (Lambie-Nairn for BBCidentity and design work); and goldand a silver at the New York Festivals(Clever Media for Getronics video).

CommonHealthIn a year dominated by consolidationamong many of the global pharma-ceutical companies, the world’s leadinghealthcare communications network,CommonHealth, further expanded its

range of capabilities and reach intothe marketplace.

CommonHealth’s core platformsspan the spectrum from professionalto consumer advertising, relationshipmarketing, market research and medicaleducation. Beyond that, the networkoffers clients specialised expertise inbrand identity and design, experientialmarketing and ethnic marketing throughjoint ventures with sister WPPcompanies. In 2000 CommonHealthannounced four such partnerships and launched two new operatingcompanies – noesis, a full servicemedical advertising agency; and anagency uniquely focused on patient-physician communications, MBS/Vox,that was created as an alternative tothe reconstructed reality of focusgroups. A US joint venture was alsoformed with Shire Hall Group, aleading UK-based healthcare publicrelations agency within WPP.

CommonHealth’s philosophy ofnurturing discipline-specificcompanies served the organisationwell in 2000 as newly merged pharmacompanies increasingly sought toconsolidate accounts with a singleresource. We also took advantage ofthe outsourced-marketing trend,forming an alliance with a leadingcontract sales organisation to take onthe marketing of brands that otherwisewould not be significantly promoted.

In 2000, CommonHealth companiescontinued to build blockbuster brandslike Procrit (Ortho Biotech division ofJ&J), Avandia (GlaxoSmithKline) andSchering-Plough with the introductionof its new antihistamine, Clarinex. The organisation picked up major new business assignments – BectonDickinson, Knoll Pharmaceutical,Ortho Dermatological, Ortho-McNeilPharmaceutical, Inc., Novartis,Parkstone Medical InformationSystems, Inc., Ross Laboratories,Sanofi-Synthelabo and Schering-Plough– and saw a major introduction,Bristol-Myers Squibb’s Glucovance.

Technology was a focal point asWPP made minority investments inMedical Broadcasting Company(MBC) and CommonHealth formedstrategic alliances with PedagogueSolutions and SoftWatch.