11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44 ...

1061

Jeffrey M. Swarts (Pro Se) 308 South Cedar Street Danville, OH 43014-0289 (740)-599-6516 [email protected] UNITED STATES BANKRUPCTY COURT SOUTHERN DISTRICT OF NEW YORK In re: ) ) ) Lead Case No. ) ) 11 CV 10613 (SHL) ) 10 CV 15466 (SHL) ) ) ) TERRE STAR CORPORATION, et al TERRESTAR NETWORKS, et al DEBTORS IN POSSESSION DERIVATIVE CLAIMS OF JEFFREY M. SWARTS BASED UPON: MATERIAL CONFLICTS-OF -INTEREST LEADING TO FRAUDULENT CONVEYANCES UNDER §3301 FROM OLD LORAL TO NEW LORAL AND TO THE TERRESTAR ESTATES INTRODUCTION I'm filing this derivative claim with regard to the impending court-sponsored §363 auction of Terrestar Corporation and Terrestar Networks, Inc in the jointly administered Terrestar bankruptcy proceedings. I have been an investor of Terrestar since before the launch ofTS-l in July of2009. I currently hold 30,000 common shares of Terrestar Corporation stock and assert herein derivative claims against the Loral Space & Communications' claims as creditors of these estates. In addition to Terrestar common stock, I have been an active investor in other satellite industry stocks since 1999 when I first bought a small position of Loral's common stock. In the past I have invested in and mostly lost money on Loral, Globalstar, ICO and now Terrestar. So, I have deep and longstanding knowledge of all four bankruptcies, their fiduciaries and professional advisors. I was also a member of the Official Loral Equity Committee during its bankruptcy. -1- 11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 1 of 15

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44 ...

Jeffrey M. Swarts (Pro Se)308 South Cedar StreetDanville, OH 43014-0289(740)[email protected]

UNITED STATES BANKRUPCTY COURTSOUTHERN DISTRICT OF NEW YORK

In re:

))) Lead Case No.)) 11 CV 10613 (SHL)) 10 CV 15466 (SHL))))

TERRE STAR CORPORATION, et alTERRESTAR NETWORKS, et alDEBTORS IN POSSESSION

DERIVATIVE CLAIMSOF JEFFREY M. SWARTS

BASED UPON:

MATERIAL CONFLICTS-OF -INTERESTLEADING TO FRAUDULENT CONVEYANCES UNDER §3301

FROM OLD LORAL TO NEW LORALAND TO THE TERRESTAR ESTATES

INTRODUCTION

I'm filing this derivative claim with regard to the impending court-sponsored §363 auction of

Terrestar Corporation and Terrestar Networks, Inc in the jointly administered Terrestar bankruptcy

proceedings. I have been an investor of Terrestar since before the launch ofTS-l in July of2009. I

currently hold 30,000 common shares of Terrestar Corporation stock and assert herein derivative

claims against the Loral Space & Communications' claims as creditors of these estates.

In addition to Terrestar common stock, I have been an active investor in other satellite

industry stocks since 1999 when I first bought a small position of Loral's common stock. In the past

I have invested in and mostly lost money on Loral, Globalstar, ICO and now Terrestar. So, I have

deep and longstanding knowledge of all four bankruptcies, their fiduciaries and professional

advisors. I was also a member of the Official Loral Equity Committee during its bankruptcy.

- 1 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 1 of 15

I hereby declare that I am a whistleblower and assert that I am afforded legal protections

under the Loral POR as an Official Equity Committee member and, in addition, under the SEC's

recently passed Dodd-Frank Wall Street Reform and Consumer Protection Act, HR 4173 Title IX

(B) sections 922, 923 & 924.

Furthermore, under HR 4173, section 919A, the Comptroller General of the United State has

been ordered to conduct a study - "to identify and examine potential conflicts of interest that exist

between the staffs of investment banking and equity and fixed income and fixed income securities

analyst functions within the same firm; and (2) to make recommendations to Congress to protect

investors in light of such conflicts." I believe that I was a victim of similar conflicts in the Loral

bankruptcy. I believe congruent conflicts with many of the same advisors exist in the Terrestar cases,

which I believe may lead to additional violations of §3301.

Conflicts among many of the same firms representing various parties in the Terrestar

bankruptcy also held key positions as advisors in the Loral bankruptcy. These conflicts negatively

distorted the valuation of the Loral debtors and led to the fraudulent conveyance of excess value to

creditors of the Loral estates, upon the emergence from bankruptcy on November 23, 2005. Loral's

emergence occurred within the statute oflimitations, as defined in §3301 (b) as "6 years after the

commission of the offense." I suggest that this statute of limitation should be tolled commencing

with the date of the filing of the Chapter 11 petition and stay of Terrestar Networks, Inc., et al

(TSN), Case No. 10-15446, from October 19,2010 forward until resolution of my claims.

Following Confirmation in the Loral bankruptcy, a group of ad hoc shareholders of the

company, the Loral Stockholders Protective Committee (LSPC), pursued an §1144 motion in the

bankruptcy court within statutory time limits. I include here an impassioned letter to the Loral

bankruptcy court, by Tony Christ, the spokesman of the LSPC seeking relief from threatened

sanctions. Weil Gotshal, the Terrestar Unsecured Creditors' attorneys and then Loral debtors'

attorneys, subsequently threatened all of us with sanction motions. 1

Despite providing the Loral bankruptcy court with direct documentary evidence and an

internal whistleblower letter questioning the concealment of Terrestar, ICO and Echostar satellite

orders, valued well in excess of $1 billion, Weil Gotshal stonewalled requests for authentication of

the documents as well as additional witnesses and depositions of company employees. Without this

discovery, it was impossible to prove fraud based upon asset concealment, as required by §1144.

1 Exhibit A-2836_LSPC Objection to Sanctions.pdf

-2-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 2 of 15

Judge Drain supported the debtors in this matter and did not investigate this well-documented

concealment despite the existence of an examiner in the case who could have readily performed

investigated this misconduct by fiduciaries and associated professionals. 2 3 4 5 6 7 8 Under threat of

blistering attacks from Weil Gotshal, and with the support of Akin Gump, Wilkie Farr, and the court,

John Plum and I withdrew from the §1144 motion and its legitimate claims by equity holders. 9

In response to the first sanction motion, I resigned as a member of the LSPC. By the time

Tony Christ signed a second Stipulation and Agreement with the debtors he was acting alone and

spoke only for himself. The sanction motions from the Loral debtors can only be described as

prejudicial and predatory, chilling legitimate claims in light of the substance of the Loral documents

presented. Furthermore, following an appeal by Mr. Christ to the district court, the bankruptcy court

again allowed Mr. Christ to be threatened by the debtors' attorneys. He was coerced to sign the

second Stipulation and Agreement in bad faith and under duress - even though terms in the

document stated that it was not signed under duress. 10

During the Loral bankruptcy and class action, I repeatedly stated that I was reserving all

rights. 11 This claim is an assertion of those rights. I declare that my wife and I are owed derivative

claims offset against the unsecured claims ofLoral Space & Communications in the Terrestar

bankruptcy proceedings, based upon the previously described fraudulent transfer of equity claims to

the former creditors of Old Loral. Loral has filed an unsecured claim against the debtors for three

unpaid invoices totaling 16,512,722.01 seeking payment for TS-2, the debtors' spare satellite. 12

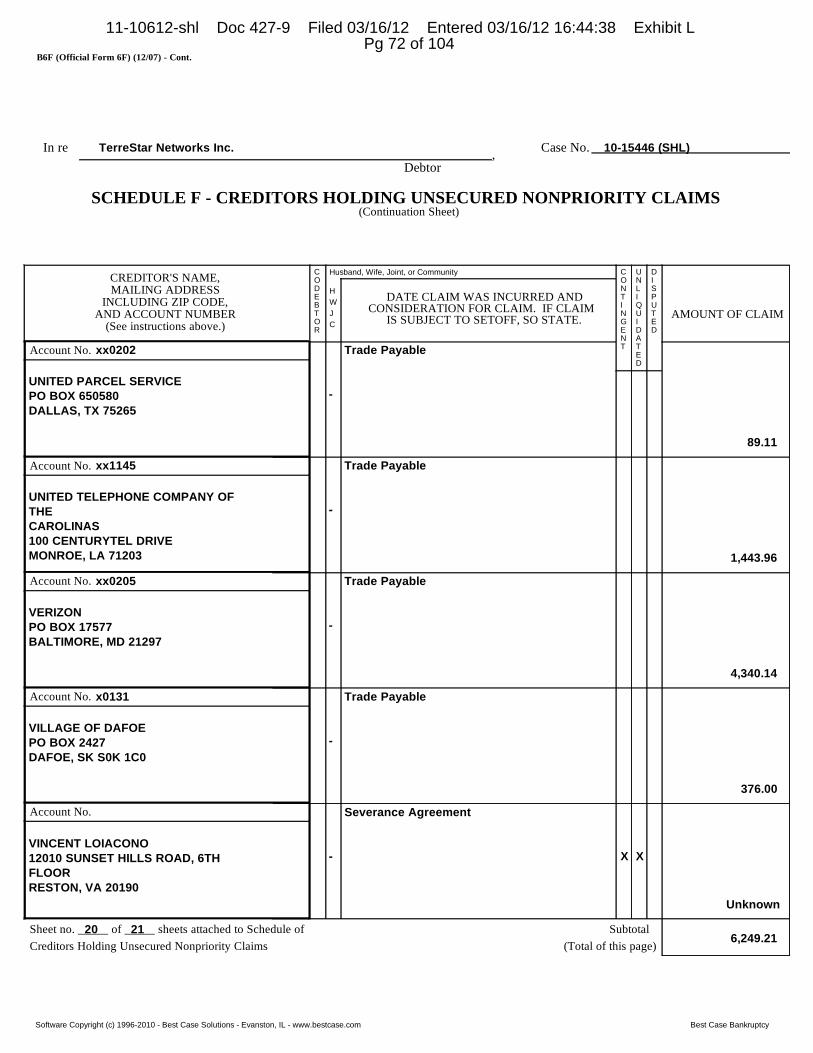

Another claim by Loral has been filed as an Unsecured Non-priority Claim against Terrestar's estate

in the amount of35,647,804.11. 13 I believe that portions of these claims are owed to as

compensation for the unjust losses we incurred in LORBQ (LORB) and LRLSQ (LOR) stocks.

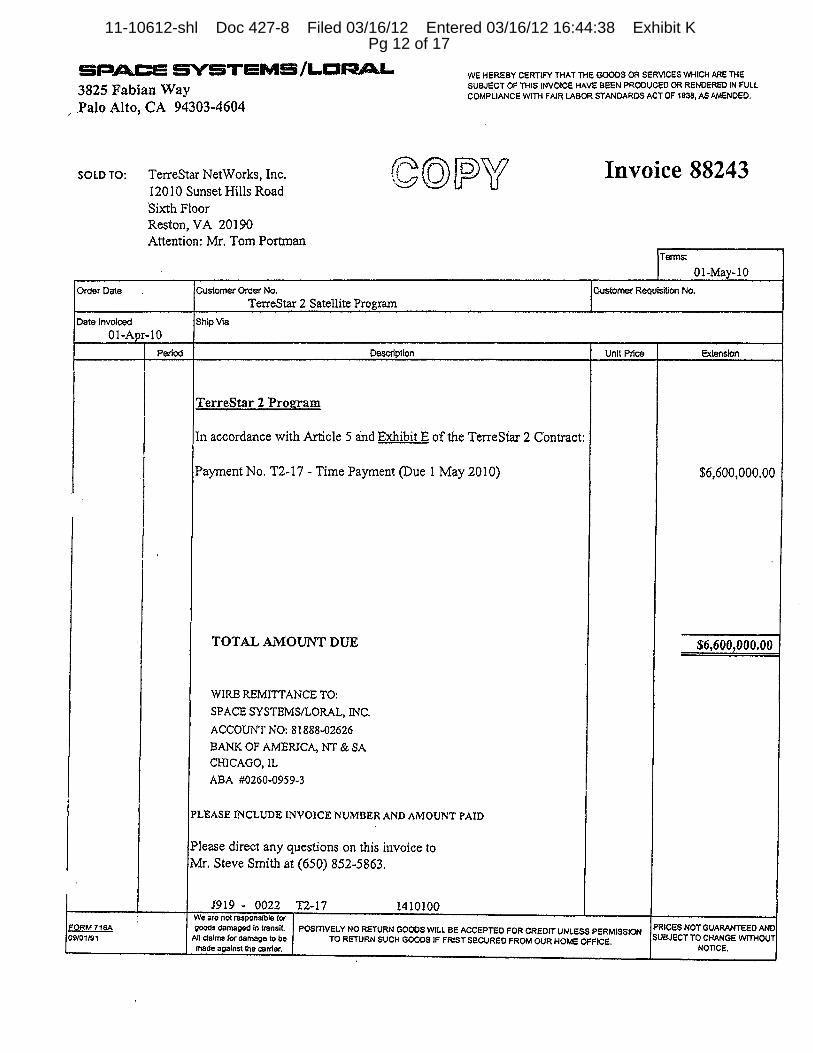

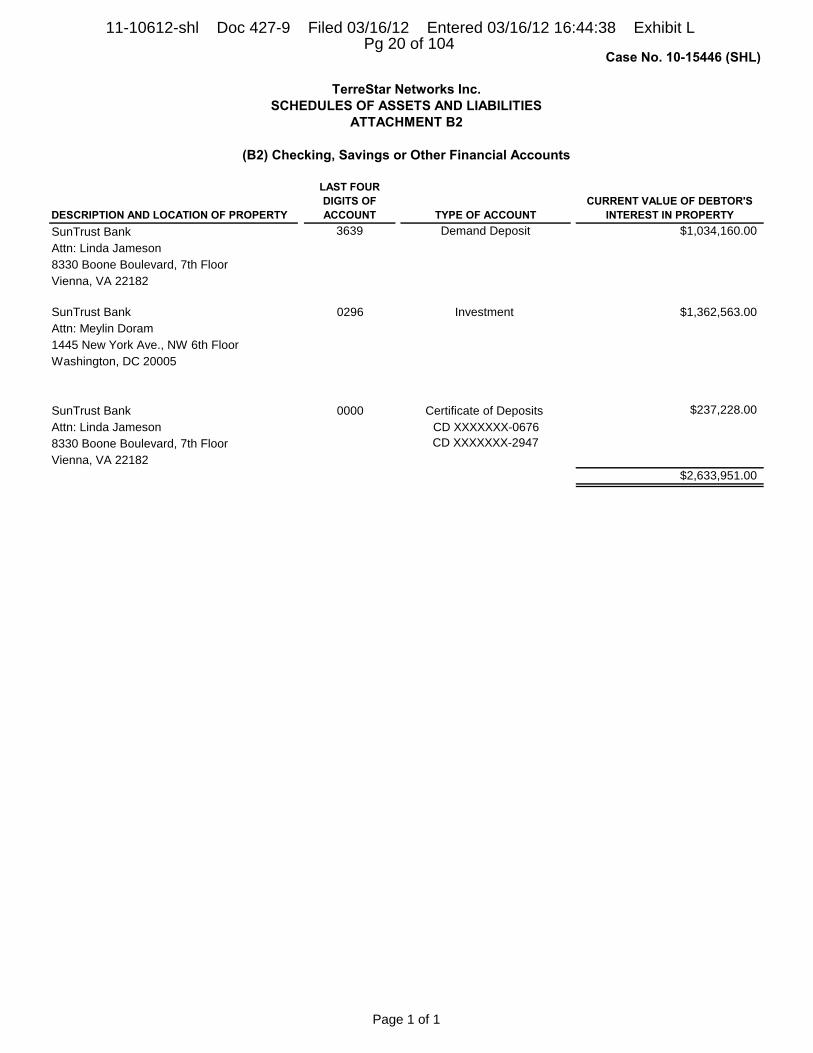

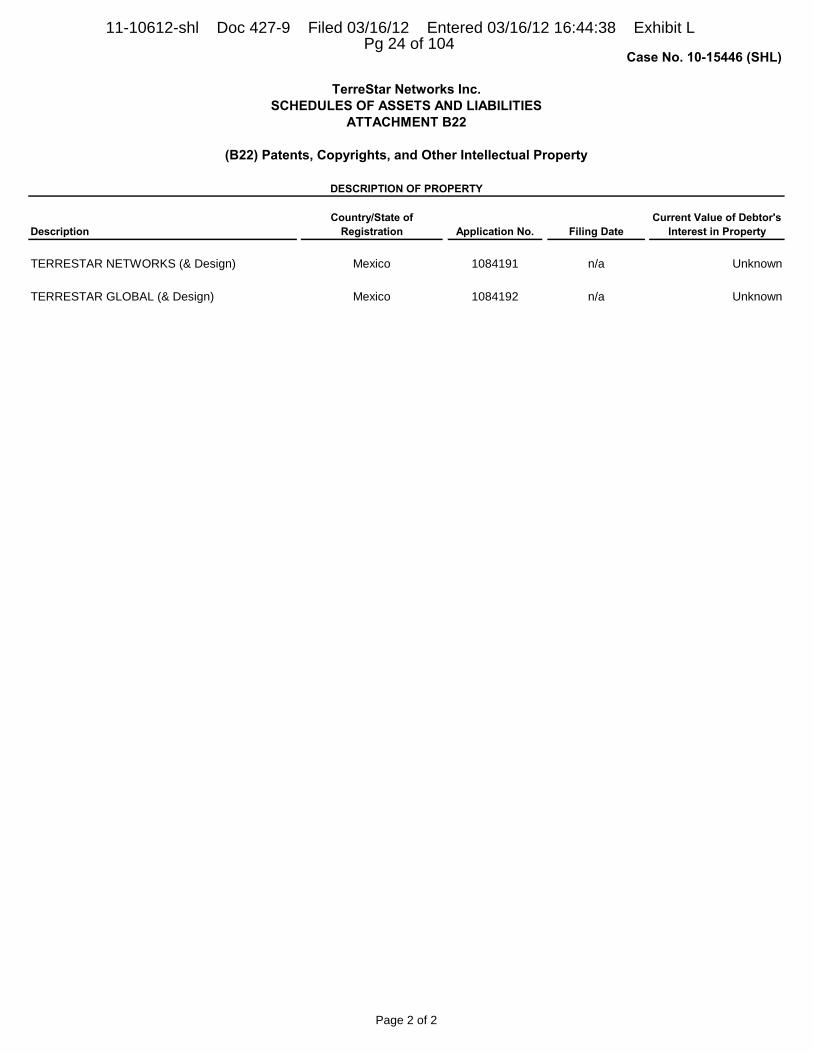

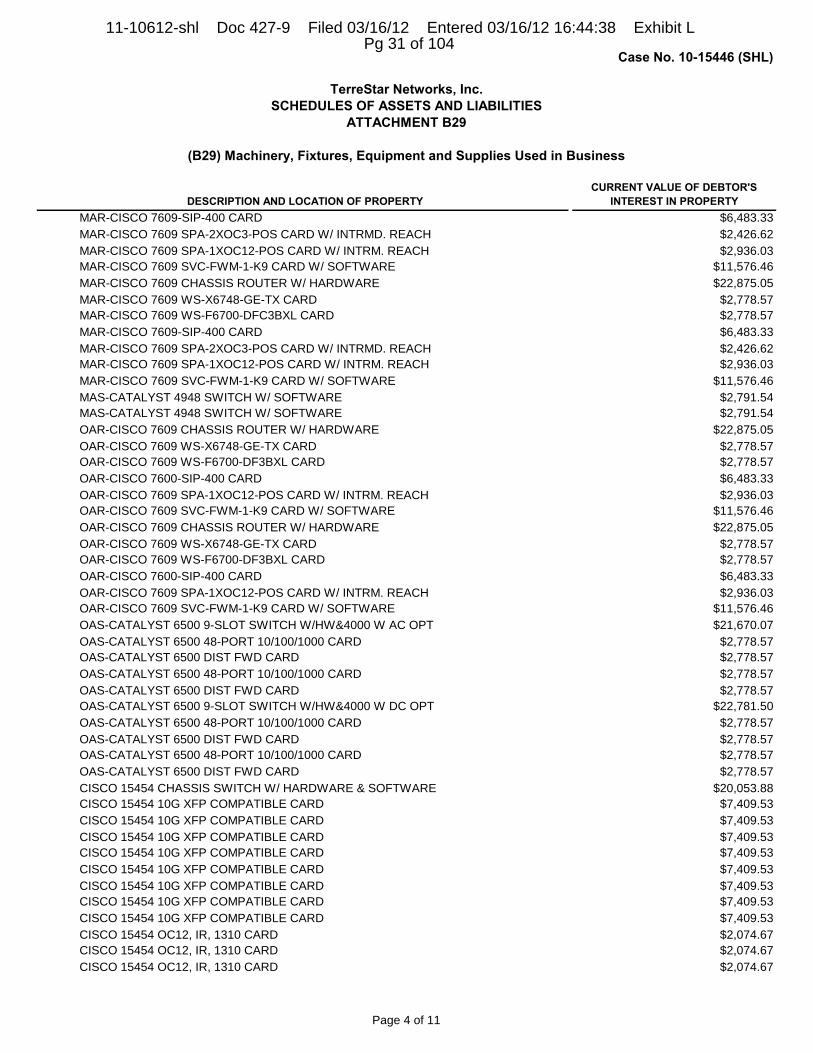

2 Exhibit B-Weil Gotshal Letter with Whistle Blower Letter.pdf3 Exhibit C-LORL News 2005 4 11 Terrestar.pdf4 Exhibit D-LoraI2280-T~rrest;-Unr~dacted Contract.pdf5 Exhibit El- TerreStar-Statement ofWork-l.jpg, Exhibit E2- TerreStar-Statement ofWork-2.jpg6 Exhibit F-LORLyews_2005_ 4_26_ICO.pdf7 Exhibit G l-ICO-I-Master Schedule.jpg, Exhibit G2-ICO-Statement ofWork-l.jpg, Exhibit G3-ICO-Statement ofWork-2.jpg8 Exhibit H-Echostar 117W - Factory Loading - l.jpg9 Exhibit 1-2834-Jeffrey M Swarts Declaration & Objection.pdf10 Mr. Christ sued Bernard L. Schwartz in a Richmond, VA court, after opting out of the class action settlement. Hereportedly settled for an undisclosed amount in six figures.II Exhibit J-Jeffrey M Swarts - Request for Exclusion from Loral Class Action.pdf12 Exhibit K-532_Loral TS2 Contract.pdf, pg. 313 Exhibit L-97_15446-Assets & Liabilities of Terrestar Networks.pdf, pg. 69

- 3 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 3 of 15

Although we are hopeful that Terrestar's estate will bring sufficient value in the §363 auction

to provide a distribution to common shareholders, I believe that our derivative claims against Loral

are a separate matter. I believe, based upon the actual current value of Loral, that Loral's claim

against Terrestar is yet another example of the company's former creditors seeking additional value

that rightfully belongs to the equity holders of Old Loral. Following is an analysis, which is not

comprehensive, itemizing my claims. I expect to provide further evidence to this court and to the

SEC, in a whistleblower filing, which will perfect our claims.

LORAL'S ESTIMATED VALUATION IN BANKRUPTCY

The impact of individual GEO orders on the financial viability of Space Systems/Loral

(SSIL) was and is substantial and was understood as such by all the financial advisors in Loral's

bankruptcy proceedings. Under examination, company fiduciaries, including CFO Richard

Townsend and SS/L President Patrick DeWitt, indicated that SSIL required 4-satellites/year to break

even. Any more than that exceeded the overhead of the company and contributed substantially to

EBITDA, and the company's valuation. However, an analysis of the Loral debtors' valuation in the

First Amended Plan of Reorganization submitted to the bankruptcy court on October 22, 2004, when

compared to the Fourth Amended Plan of Reorganization, submitted on June 3, 2005 does not make

any sense. A simple comparison does not indicate that an additional $750-$900 million in satellite

orders was taken in the interim. 1415

The 1st POR stated:

"For purposes of the Plan, the reorganization value (the "Reorganization Value") isestimated to range from approximately $650,000,000 to $800,000,000. (For purposes ofdetermining the estimated recoveries for creditors in Classes 4, 5 and 5A under thePlan, a compromise Reorganization Value of $777,475,000 has been used, which iswithin this range.) The Reorganization Value assumes an Effective Date of December31,2004 and reflects the going concern value of the Reorganized Debtors after givingeffect to the implementation of the Plan.

14 Exhibit M-1516-Lorall st POR-Disclosures-Main Document.pdf, pg. 7415 Exhibit N-2074-LoraI4Ih POR-Disclosures Main Document.pdf, pg. 93

-4-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 4 of 15

"The equity value (the "Equity Value") of the Reorganized Debtors is estimated torange from approximately $420,000,000 to $570,000,000 or from approximately$21.00 per share to $28.50 per share of New Loral Common Stock assuming a total of20,000,000 shares of common stock are issued and outstanding on the Effective Date.(For purposes of determining the estimated recoveries for creditors in Classes 4,5 and5A under the Plan, a compromise Equity Value of $547,475,000 has been used, whichis within this range.) The Equity Value reflects the difference between theReorganization Value and the total amount oflong-term net debt that is estimated to beoutstanding after giving effect to the Plan."

The 4thAmended paR stated:

"For purposes of the Plan, the reorganization value (the "Reorganization Value") isestimated to range from approximately $708,000,000 to $939,000,000. (For purposesof determining the estimated recoveries for creditors in Ltd. Class 4 and Orion Class4 under the Plan, a compromise Reorganization Value of $875,300,000 has beenused, which is within this range.) The Reorganization Value assumes an EffectiveDate of June 30, 2005 and reflects the going concern value of the ReorganizedDebtors after giving effect to the implementation of the Plan.

"The common equity value (the "Equity Value") of the Reorganized Debtors isestimated to range from approximately $388,000,000 to $619,000,000 or fromapproximately $19.40 per share to $30.95 per share of New Loral Common Stockassuming a total of20,000,000 shares of common stock are issued and outstanding onthe Effective Date. 13 (For purposes of determining the estimated recoveries forcreditors in Ltd. Class 4 and Orion Class 4 under the Plan, a compromise EquityValue of approximately $555,000,000 has been used, which is within this range.) TheEquity Value reflects the difference between the Reorganization Value and the totalamount of long-term net debt and preferred stock that is estimated to be outstandingafter giving effect to the Plan.

To summarize, the 1st paR compromise Reorganization Value, dated October 22,2004,

without the benefit of the ICO and Terrestar orders "taken" in the spring of2005, was $777,475,000.

It also did not include spare satellites for these programs, which were required by the FCC spectrum

licenses to be built and in storage within l-year of the launch and commencement of ATC

commercial service. Despite these FCC requirements, during pre-confirmation depositions, Loral

fiduciaries, citing technical and funding issues, described the ICO-2 and TS-2 spares as uncertain

and as "options". They were making these statements, under oath, despite a contemporaneous ICO

debt offering, sponsored by Jefferies and UBS, which indicated that the spares were not optional to

- 5 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 5 of 15

capture the full value of the spectrum. 1617 The ICO debt solicitation valued ICO's spectrum at $9.8

billion. ICO's 2GHz spectrum is adjacent to Terrestar's and virtually identical.

The Loral4th POR compromise Reorganization Value was $875,300,000, with the benefit of

the ICO and TerreStar orders. In the 1st POR those orders had not yet been "taken". In other words,

about $750-$900 million in additional forecast revenues for the ICO and Terrestar orders, "taken"

between the 1st and 4th POR's only added $97,825,000 to the Reorganization Value. Judge Drain

found the Reorganization Value to be $970,000,000, without substantial values for intangible assets,

like substantial orbital slots, real estate and intellectual property assets. Judge Drain did not state a

common equity value figure that I am aware of.

The discrepancy in the Equity Value between the two plans was even more revealing. The 1st

POR Equity value was $547,475,000 versus the 4th POR Equity value, presumably with the benefit

ofthe additional GEO orders was $555,000,000, or only about $7,525,000 more - perhaps meaning

that substantial vendor financing was provided by Loral to Terrestar, ICO and Echostar. The Loral

claims exceeding $52 million against the Terrestar estate, and congruently in the DBSD bankruptcy,

indicates that Loral provided vendor financing to Terrestar and ICO, while still in bankruptcy - a

complete abdication of fiduciary duty at the time. It served an agenda of asset conversion in the

Loral bankruptcy and serves similar agendas today in the DBSD and Terrestar bankruptcies.

Avi Katz, Loral's long-time counsel throughout the late 90's, and throughout Loral's

bankruptcy, now sits on the Terrestar Networks, Inc. unsecured creditors committee. He is the

current Senior Vice President and Secretary ofLoral. Mr. Targoff, a former fiduciary of Loral and

Globalstar until the late 90's left in 1998 to form Michael B. Targoff and Company. After acting as

an agent in the Leap Wireless bankruptcy, for Dr. Rachesky and MHR Fund, Mr. Targoffreturned to

Loral in 2004 as Vice-CEO at Loral in a similar role. He is the current CEO ofLoral. Dr. Rachesky,

a former Managing Director for Carl Icahn, is the Chairman of the BOD.

Loral's Terrestar satellite program was originally contracted on July 14,2002, I-year and 1-

day prior to Loral entering Chapter 11 protection on July 15,2003. 18 The Terrestar order was not

16 Exhibit O-ICO Debt Offering, pg. 2917 Jefferies was concurrently representing the unsecured creditors committee in the Loral bankruptcy proceedings.Michael Henkin, former Vice President of Business Development at Loral was a contact in the offering and was alsoan advisor to the creditors committee, via the Jefferies representation. Loral CEO, Michael B. Targoff also has a son,Joshua, who was then employed as an attorney by Jefferies as well.18 Exhibit D-Loral2280- Terrestar-Unredacted Contract.pdf, pg. 14 of the fax: Note that the transmittal ofthisdocument from Weil Gotshal to Sonnenschein is dated August 15, 2005, post-dating the confirmation hearing by 3-weeks.

-6-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 6 of 15

recognized by Loral in any known news release, or other SEC filing until April 1, 2005, nearly 3

years after the original contract was signed. During the pre-petition period, prior to July 15,2003,

CEO Bernard L. Schwartz stated repeatedly that Loral had not received any orders and was seeking

asset sales to enhance shareholder value. The original rationale provided by fiduciaries for Loral' s

bankruptcy was that Intelsat demanded a Chapter 11 filing as a precondition of purchasing the North

American Telstar fleet. Management then set about using the bankruptcy to pursue its own agenda,

including using the court to launder prior asset sales to company fiduciaries at K&F Industries and

L3 Communications. The asset "sales" were facilitated and capitalized upon by the ever-present

Lehman Brothers - now disgraced and bankrupted itself, following the fmancial meltdown in 2008.

Loral concealed the Terrestar contracts, among others. Had these contracts been disclosed in

a timely manner, it would have led to much higher Discounted Cash Flow (DCF) valuations of the

company in bankruptcy. DCF's were the methodology used by all the financial advisors in the Loral

proceedings to promulgate minimal valuations to the Court. 19 Higher DCF valuations would have

led to much stronger arguments for larger and/or make-whole distributions to junior creditors and

shareholders in the case. Despite the elimination of equity in Loral's flawed plan of reorganization, I

did not sell 1170 shares of common stock or 11,250 shares of Preferred Series C stock, prior to their

elimination by the bankruptcy court. My derivative claim is based upon these facts. The current

market value of Loral proves that using DCF models for valuing a high-technology company like

Loral was deeply flawed. It represents an excessive and fraudulent transfer of value from the estate

of Old Loral to prior creditors, the Orion and Loral LTD bondholders -the majority owners of New

Loral. I believe that this transfer was fraudulent in nature and was a violation of §330 1.

Loral never defaulted on a single loan and never required debtor-in-possession financing. It

displayed few signs of insolvency other than the distressed prices of its securities, caused by an

incestuous, self-serving management. The company's liquidity position was always sufficient to

operate the businesses at SSIL and Skynet. The Loral debtors argued in the 4thpaR, before Judge

Drain, that the company was worth $708-$939 million - with a mid-point of $875.3 million. The

debtors argued, pursuant to the paR, that the new company equity value would be only $388-$619

million - with a midpoint of $555 million. In per share prices on 20,000,000 shares, the forward-

looking equity value promoted by the debtors to the Court was $19.40-$30.95. 20

19 Exhibit P-1764-Loral Examiner's Report20 Exhibit N-2074-LoraI4th POR-Disclosures Main Document, pg. 93

-7-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 7 of 15

LORAL'S ACTUAL REORGANIZED VALUATION

Loral emerged from bankruptcy protection on November 23,2005.21 Since then, Loral's

common stock, LORL, has traded as high as $85.16, representing a market capitalization high of

$2.61 billion. Loral is currently trading at about $70 per share and has a current market cap of about

$2.2 billion. To correct for the value of additional post-bankruptcy preferred equity investment of

$337 million, one must subtract it from the current market cap, leaving an adjusted market cap of

$1.863 billion as the actual Loral estate value in bankruptcy. This does not include direct valuation

for Skynet, which was spun-off post-emergence to the Canadian company, Telesat. 22 This market-

based valuation, when contrasted against the Loral equity deficit of$I.044 billion, published in the

Loral2004 10-K, demonstrates that the Loral debtors' estate value was fictitious -- designed to serve

a creditor and management agenda of self-enrichment.

Subtracting the Old Loral equity deficit of $1.044 billion from the current adjusted market

cap of $1.863 billion, leaves $819 million that should have been available for distribution to Old

Loral equity. The Loral preferred liquidation preference was $237 million, which subtracted from

$819 million, leaves $582 million. This remainder, attributable to the pre-petition 44 million shares

of common stock, would have provided a distribution of as much as $13.23 per common share,

minus the per share administrative costs of the bankruptcy.

Why did the debtors fabricate their estimated values? How could they have been so wrong?

The answer is quite simple. Loral's management received 6.5% in bankruptcy, with the assent of its

long-time crony creditors, represented by Akin Gump and Jefferies. The valuation differential of

$819 million, between the Loral debtors' equity deficit in the 2004 10-K and the true value shown by

the current market cap, minus the post-emergent preferred investment of $337 million, quantifies

this fraudulent transfer of significant wealth to the creditors of the Loral estate in violation of §3301.

These values go way beyond the statutory requirement of "adequate protection" for creditors in

Chapter 11 bankruptcy. At the current market valuation of the estate, all Loral claimants, including

bondholders, trade creditors, employees, ERISA claimants and preferred shareholders would have

been made whole, with a substantial distribution of as much as $13.23 per share going to common

shareholders. My derivative claims against Loral are based upon these numbers.

21 This event started the clock on the statute oflimitations defined as 6 years in §3301(b).22 Loral retains a significant equity interest in Telesat.

-8-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 8 of 15

LORAL'S CHAPTER 11 VALUATION HISTORY & CONFLICTS

In July of 2004 the Loral Stockholders Protective Committee filed a motion request for an

official equity committee. 23 The debtors in July of 2004 claimed that there was an equity deficit of

$937 million. The LSPC claimed an equity surplus of $879 million with a per share value of$19.92,

including make whole values for all creditors and preferred shareholders. This equity surplus

calculation is much closer to the $13.23 actual per share value, calculated using the current market

cap, than that calculated by the "professionals" at Greenhill and Jefferies, the financial advisors for

the Loral debtors and the unsecured creditors committee, respectively. Weil Gotshal and Akin Gump

both claimed that Loral was hopelessly insolvent. They beat back shareholder requests for an official

equity committee a third time in the summer of 2004, with Judge Drain again denying the motion.

The LSPC then filed a motion for an examiner. Judge Drain again denied the motion, despite

the plain reading ofthe statute. His decision was appealed to the US District Court. I made the

argument for the examiner in the bankruptcy court and before the appeals court. 24 I successfully

argued for an examiner before Judge Patterson in the US District Court and Judge Drain was

reversed. However, he did not follow the direction of Judge Patterson, limiting the examiner to

"confirmatory due diligence", which did not include intangible assets. Judge Patterson's order

specifically included provisions for valuation of the company's intangible assets, including the

orbital slots. 25 The examiner, Harrison Goldin was appointed by the US Trustee. Notwithstanding

Judge Drain's restrictions, the examiner found "that certain assumptions and the application or

weighting of the various valuation approaches resulted in a not insignificant understatement in value,

amounting in the aggregate to $281 - $463 million." 26

The examiner's valuation was not a "full-blown" valuation per Judge Drain's order, and did

not include significant "intangible" assets like orbital slots, real estate, intellectual property or

numerous concealed satellite orders. 27 On March 14,2005, before the release of the lCO and

TerreStar orders, or subsequent Echostar orders, the examiner found an estate value of$931,000,000

to $1,263,000,000, with a mid-range value of $1,072,000,000. This "understatement" of 36-60% was

23 Exhibit Q-1293-Loral-Motion for Equity Committee, pg. 69-7424 Exhibit R-Loral Examiner Appeal Hearing Transcript-12170425 Exhibit S-Examiner-US Court Order, pg. 2 & 426 Exhibit P-1764-Loral Examiner's Report, pg. 727 Exhibit T-Loral1661-Examiner Order

- 9-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 9 of 15

extreme in a company that had originally been valued at about $770 million by the Debtors' financial

advisors, Greenhill & Company and its lead advisor, former Weil Gotshal attorney Harvey Miller. 28

The results of the examiner's valuation led directly to the appointment of an Official Equity

Committee by the US Trustee. A few weeks later, after a letter from John Bicks complaining ofthe

committee's choice oflegal advisors, she reconstituted the committee by adding two additional

preferred members. This action precipitated the resignations of Mr. Christ and his long-time

associate, Vadim Mostovoy. The new membership was largely populated by preferred investors with

extreme conflicts-of-interest vis-a-vis Loral's debtor and creditor cronies. They dictated the selection

of professionals who also had extreme conflicts, including Mr. Bicks and Sonnenschein. Neither the

US Trustee's office nor Judge Drain questioned the lack of disinterest of most of the remaining

equity committee members or the committee's professionals, nor did the US Trustee replace the

common equity committee members who had resigned, despite repeated requests from me and other

common shareholders. Once one knows the extent of these conflicts, it is clear that the outcome of

confirmation was a foregone conclusion. Not a single decision or order by Judge Drain was ever

questioned or appealed by the equity committee or its conflicted "professionals", despite the court's

demonstrable bias against equity.

Chanin, Loral's Official Equity Committee fmancial advisor, selectively disclosed prior and

current relationships with numerous interested creditors and associated corporate parties in Docket

#1949, otherwise referred to as the Belinsky Affidavit. 29 Neither the Chairman of the official equity

committee, David Kilcoyne nor I were served with the affidavit at the time. I discovered it post-

confirmation in the docket. In it Mr. Belinsky acknowledged ongoing and prior relationships with

Michael B. Targoff, CEO of Loral, and Mark H. Rachesky, Chairman of Loral, by way of his MHR

Fund Management LLC and Highland Capital - all principals of the Leap Wireless Chapter 11.

Former Loral VP and Controller, Robert V. LaPenta also was and is a Leap Wireless fiduciary. In

addition, Mr. Belinsky and Chanin had ongoing business relationships with former Loral Director

Gershon Kekst and his public relations company, Kekst and Company; and Loral Equity Committee

members, Alan Cohen, principal of York Capital Management, Neil Subin, Managing Director of

Aspen Advisors, Aspen Capital and Trendex Capital.

28 Exhibit U-Greenhill Retention Letter - Exhibit A, pgs. 8-23 of the PDF29 Exhibit V-Loral 1949-Belinsky Affidavit

- 10-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 10 of 15

Mr. Belinsky also disclosed an ongoing relationship with Lehman Brothers, a constant

investor in Bernard Schwartz ventures over the years, including but not limited to Globalstar, K&F

and L3. Belinsky disclosed that Chanin was representing an ad hoc group of bondholders in the

Satmex insolvency proceedings. The Loral debtors were an equity holder of Satmex, reporting losses

of$51.7 million in 2003 and $25.1 in 2002. In his affidavit, Mr. Belinsky did not disclose that the

Satmex bondholders had an adversary relationship to Loral and its investors.

In his affidavit, Mr. Belinsky did not disclose that Chanin, Kekst and Company, Greenhill

and Robert D. Drain, all key parties in the Loral Chapter 11, had previously advised an investment

group led by Onex Corporation and Oaktree Capital Management in the bankruptcy buyout of

Loews Cineplex. Mr. Belinsky did not disclose that William Q. Derrough, lead financial advisor of

Jefferies for the Unsecured Creditors Committee and chaired by Mr. Rachesky, had been a prior

employee of Chanin throughout most of the 90's. There was no disclosure by Mr. Belinsky or any

other party that Mr. Derrough continued to be a principal partner of Chanin until at least mid-2004,

post-dating the sale of Loral's North American Telstar fleet in a court-sponsored sale.

There is no doubt that Mr. Belinsky's prior representation of debtor and creditor parties

should have disqualified him from representing Loral's Official Equity Committee. Neil Subin, the

defacto chairman of the equity committee insisted on Chanin's retention, with the strong support of

other Subin-dependent equity committee members and Sonnenschein attorneys, Bicks and Wolfson.

30 There is no doubt that Judge Drain, the US Trustee's Office and SEC's New York office knew of

Chanin's conflicted prior representations. However, more importantly, no government agency or

employee ever publicly questioned or objected to Chanin's retention as the financial advisor for the

Loral Official Equity Committee.

Why didn't Mr. Belinsky go to SSIL and research the company's satellite order status and

current RFP's as instructed by the equity committee? Why didn't the other equity committee

members take a more active role in overseeing the committee's professionals? Why did the equity

committee professionals latch onto "Government Orders" as equity's Holy Grail, when the company

had no recent experience providing GEO satellites to the federal government? And, even when

Sonnenschein did prosecute the government orders issue, why did the equity committee

30 Peter Wolfson, the head of Sonnenschein's bankruptcy group was and is Carl Icahn's personal attorney. Carl Icahnis the former employer of Mark Rachesky, the current Chairman ofthe BOD of Loral. John Bicks is a former attorneyand associate of Raymond L Steele, a former Director and interim CEO ofMotient, Terrestar's predecessorcorporation.

- 11 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 11 of 15

professionals fail to discover the US DOD-Homeland Security "anchor tenant" contract on the

Terrestar satellite program, disclosed by Bernard Schwartz under oath? That would have validated

their "government contracts" arguments, but they never presented this information to the court. 31

Why didn't Sonnenschein seek an audit at SS/L to inquire about specific satellite programs

and/or RFP's that would have provided the evidence needed to convince the Court of additional

estate value? Who stood to gain when the value ofthe company was understated and what was the

mechanism by which that understatement was discovered, massaged and promoted to the bankruptcy

court during confirmation?

There is no doubt that once the equity committee was appointed that its inner workings were

almost immediately sabotaged by members who were creditor and debtor cronies. Repeated

procedural and legal errors by its professionals obfuscated their true agenda which was to undermine

equity's last remaining hope - the official equity committee. The procedural missteps were many,

but just a few examples will suffice. 1) Belinsky attempted to provide testimony for Roger Rusch,

the orbital slot expert, who was never allowed by the court to testify. 2) Belinsky cherry-picked the

valuations of the debtors' and the creditors' valuations and when caught in act of doing derivative

work, Sonnenschein did not object or provide further supporting evidence. 3) During the

Confirmation Hearing, John Bicks focused on minutia related to a relatively insignificant

government marketing budget until the court silenced him. 4) Wolfson admitted that he had never

tried a confirmation hearing before. 5) All of these "professionals" allowed Tony Christ, a pro se

litigant, to take over equity's agenda and dominate not only the depositions of fiduciaries and

creditors, but also the confirmation hearing itself, with Judge Drain's assent. 6) They never went to

SSIL to investigate its satellite order book or the company's RFP's.

The LSPC was right and the debtors and the court were wrong about the value of the estate,

as evidenced by the current Loral2010 lO-K. The current annual report lists an equity surplus of

$1.02 billion. The same "Loral professionals" at Akin Gump, Weil Gotshal and Wilkie Farr are

again running a sophisticated shell game designed to separate the legitimate owners of Terrestar, its

shareholders, including myself, from legitimate claims on the estate.

31 This "anchor tenant contracf' between Terrestar and the Federal government, referenced by Bernard L Schwartz,under oath, has yet to be disclosed in the financial press by fiduciaries of Terre star, including its President and CEO,

- 12 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 12 of 15

TERRESTAR'S UPCOMING §363 SALE

The current §363 sale, scheduled for June, should be overseen by the court with great care. A

similar "§363 auction" for the North American Telstar fleet in the Loral bankruptcy, successfully

excluded all suitors except Intelsat and Echostar. At the time, common shareholders were excluded

by Judge Drain's confidentiality rulings from any meaningful transparency into the process. Then,

once the auction terms were set, Echostar not only did not bid, but Intelsat won a one-party

"auction" for $975 million after making a single bid. I've been to quite a few auctions in my life, but

I've never attended one where there was only one bidder and only one bid. The result was well

below the $1.5 billion contemporaneous appraisal by W.L Prichard, quoted by Bernard L. Schwartz

under oath. 32 One hopes that the Terrestar §363 auction and sale will not be similarly managed,

without any 3rd party or on-site governmental verification.

So enamored was Echostar's management in late 2003, with Loral and its technology, that

Mr. Ergen attempted to buy the entire assets of Loral for $1.85 billion, prior to the auction. The

LSPC made extensive overtures to Echostar in an effort to get them to buy the post-auction assets of

Loral. In fact, for 12-months Echostar declined to buy additional satellites from Loral, despite their

stated intent to do so. An excerpt from Echostar's 2004 lO-K follows:

"During 2004, we entered into a contract for the construction of Echo Star XI, a SpaceSystems Loral FS 1300 class DBS satellite. In connection with this agreement, weobtained an option for the construction of other additional satellites. Construction isexpected to be completed during 2007 ... " 33

On December 9, 2005, two weeks after the effective date of the Loral paR, Echostar and its

CEO, Charles Ergen, in a 13G SEC filing, declared themselves as beneficial owners of New Loral

common stock. As a percentage of class, EchoStar and Mr. Ergen received distributions of 6.8% and

7.0%, respectively. So, Echostar GEO order recognition was apparently delayed for good reason, to

the benefit of Mr. Ergen and Echostar and to the detriment of Old Loral's equity holders. I believe

that this was one piece of a complex strategy used to purposefully understate Loral' s financial

condition in bankruptcy.

Jeffrey Epstein or Chairman of the BOD, William Freeman, the former CEO of Leap Wireless from 2004-2005.32 Exhibit W-1125-Loral Transcript-102203.pdf, pg. 174.

- 13 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 13 of 15

In EchoStar's 2005 lO-K (F-37) the Company stated:

"During 2005 and 2004, we entered into contracts for the construction of fiveadditional SSL Ka and/or Ku expanded band satellites which are expected to becompleted during 2008."

If this is true, then why had Loral only announced three by then? It takes 2-112 years to

design, build and launch a GEO satellite. What this statement clearly shows, is that the Echostar

GEO awards predated the Loral Confirmation hearing. Subtracting 2-1/2 years from the end of 2008,

shows that the orders were taken no later at the end of June, 2005, one month prior to Confirmation,

and contemporaneous with the depositions during Confirmation of Loral's fiduciaries, Schwartz,

Townsend, Dewitt and creditor representatives, Rachesky and Derrough. The total value of those

contracts was estimated at more than $800 million on a truncated 4-year Loral 4thAmended POR

forecast of $2.2 billion. Clearly, Loral' s estimates of future revenues, including conceal ed values for

satellite construction in the Terrestar, ICO and Echostar satellite programs, upon which the entire

POR was premised, were grossly understated.

Judge Drain's oversight of these shenanigans was negligent at best. Why was he so intent

upon preserving maximum recoveries for creditors? I have previously stated that I believe he had

serious undisclosed conflicts-of-interest. While still in private practice he represented a creditor in

the first ICO bankruptcy with a claim junior to Akin Gump's client, the unsecured creditors

committee. He also represented the now bankrupt and disgraced Lehman Brothers while in private

practice, which should have, ethically, precluded him from adjudicating the Loral bankruptcy.

Lehman Brothers was the recipient of substantial assets of profitable divisions of Loral, spun off in

the late '90's. Lehman Brothers partnered with Loral fiduciaries and former fiduciaries to form K&F

Industries and L3 Communications. These conflicts have continued to muddy the waters of

subsequent bankruptcies including DBSD and here in the Terrestar proceedings. Judge Drain's

former firm, Paul, Weiss, Rifkind, Wharton & Garrison, has also represented Harbinger many times.

Harbinger and its Managing Director, Philip Falcone, are key participants in these cases and holders

of all of the debtors' securities. Lightsquared, Harbinger's privately held Satellite Company, is

expected to compete directly with the Terrestar system and yet Harbinger controls the "lease" for

one ofTSC's most valuable assets, its 1.4GHz spectrum.

33 Exhibit X-Echostar-lOK-2004-Construction.pdf

- 14-

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 14 of 15

THE VALUATION OF MY DERIVATIVE CLAIMS

I believe that the facts described above, so long in coming to light, cry out for further judicial

review of my derivative claims against Loral's claims in the Terrestar case. The Preferred Series C

shares (LORBQ) of Loral, pre-petition, had a face value of $50 per share accruing at 6% per year.

According to the 2003 Loral 10-K, dividend payments were suspended by Loral in August of 2002.

That's 8-years and 8 months ago, or 104 months. Our 11,250 shares of LORBQ had a face value of

$562,500 plus interest, which, at the contract rate of 6% simple interest, paid in arrears and

compounded annually, is currently valued at $944,863.03. My 1170 LRLSQ common shares,

calculated at the above midpoint value of $13.23 are worth $15,479.10.

I value my and my wife's total derivative claim against Loral's unsecured debt claim,

including preferred and common shares plus interest at $960,342.13. We also request additional

damages that the Court finds just and proper in punitive damages for lost investment opportunity

dating to 1999 and emotional distress to me and my wife, including the near ruin of a successful full-

time commercial art business dating to 1991.

As proof of my claims I attach contemporaneous statements from my and my wife's brokers

at the time of the erroneous elimination of our interest in the Loral estate by Judge Drain. I have

previously stated these claims in general terms in a pleading before this Court in re: TerreStar

Networks Inc., et al. Case No. 10-15446 (SHL), docket #200, captioned as "Order Denying Requests

of Jeffrey M. Swarts Signed On 11/23/2010. (Ebanks, Liza) (Entered: 11/23/2010)". Please read it

for a supplemental summary of the functional basis for my claims, reserving all rights as a defrauded

investor, and as a whistleblower with protection under the Dodd-Frank Wall Street Reform and

Consumer Protection Act. Additional detail in support of these claims will be forthcoming as

required by the Court.

~ 1;7.~rtZtvIsl Jlf.f~SwartsMay 7, 2011

Mr. Jeffrey M. Swarts (pro se)308 South Cedar StreetDanville, OH [email protected]

- 15 -

11-10612-shl Doc 427 Filed 03/16/12 Entered 03/16/12 16:44:38 Main Document Pg 15 of 15

11111111111111111111111111111111111111111111111111111111111111111UNITED STATES BANKRUPTCY COURfFOR THE SOUTHERN DISTRICT OFNEWYORK

Your Claim is Scheduled As Follows:

If an amount is identified above, you have a claim,AloV' 9i .::t IJ i b scheduled by one of the Debtors as shown. (This

r scheduled amount of your claim may be anTelephone number: 7~ 0- S7<9- ~,' S" / f.:, amendment to a previously scheduled amount.) IfEmail Address: -:5".' 1'''~ r-rs So"ec", n eC you agreewith the amount and priority of your claim~--"""7"""7-;---;-....:...-...:·v:...-.;..r..;"'--:--;--7~7-;----:-~"~;-:-;:;:----:--;:--7"-:----I-----------------135 scheduled by the Debtor and you have no other

_ Name andaddresswherepayment should be sent (if differentfrom above): _. ._ 0 claim against the Debtor, you do not-need-to-file-this. ----_. Check this box if youareaware" that - proof of claim form,EXCEPTASFOLLOWS: If the

anyone else has filed a proof of claim amount shown is listed as any of DISPUTED,relating to your claim. Attach copy UNLIQUIDATED, or CONTINGENT, a proof ofof statement giving particulars. claim MUST be filed in order to receive any

distribution in respect of your claim. If you havealready filed a proof of claim in accordance with theattached instructions you need not file again.

Name of Debtor (Check Only One): Case No.~ TerreStar Corporation 11-10612o TerreStarHoldings Inc. 11-10613

'.t IO,.CI/·~f!Jif(';'C:-I ~i/cd/I/"'~ &~ V.r SS /i-

NOTE: This form should not be used to make a claim Jor an administrative expense arising after the commencement oj the case, but may be used(or purposes of asserting a claim under 11 US.c. §503(b)(9) (see Item # 6). All other requests for payment oj an administrative expense may befiled pursuant to 1J Us. C. §503.

£)cr;vt'i ft've. (J. Lq, t' I')JA-C-t:.T /Jt;. )( )(:0 I bb

o

Name of Creditor(th:person or other ep.ti~ to whom the debtor o~es money 0:property): /?:E;=r;<£~ 11Ft"A7t2iCIA 13 SWART)

Check this box to indicate that thisclaim amends a previously filedclaim. TStv P,X/L.::.--f

Court Claim Number: 20 0(Ifknown)

Name and address where notices should be sent:

•.T£Fr-I<..G:!;1' H, J;-vA-J2../:530 8" ~-c)t(TtI C:c;::.ZJ;4)2 SI;OA II.) r.LLE. '-'If .Lt'3CJ /.Ll- (,72 t''1,

Filed on:

Telephone number:o Check this box if you are the debtor

or trustee in this case.

1. Amount of Claim as ofDate Case Filed: $ . 11 tf btJ i 3 if 2 I /3 iltftu ft~ 7/ ').{)l/If all or part of your claim is secured, complete item 4 below; however, if all of your claim is unsecured, do not complete item # 4.

If all or part of your claim is entitled to priority, complete item # 5. ~% ,:nb..e..4 tsmet A-itf.< ;'1Jt,~1-)If' Check this box if claim includes interest or other charges in addition to the principal amount of claim. Attach

itemized statement of interest or charges. fJ..~Cj'p.b:l 5 Ga./5tJo 'r-51/ S; if 79, 101-=--::---:--:----::::-:--"T7-~-::-:---:-"7"--,.:m-:----*-=-- -~:-L----l":""7"'-:r;:<-----------fSpecifY the priority of the claim.2. Basis for Claim: / / 'AC,;".:; J .• N '1/' {'f/.'./.oAA / Di!/vf V4-i j'..4!-- r: S.s/ "-

(See instruction #2 on reverse side.) 0 Domestic support obligations under'"'3,.-.":'L:-a-s-t""fo-u-r-'di"'-'g""'i-ts-o""f-a-ny-nu-m-"';b-er-'b"-y-,-",:-hi:-c:-h-c-re""'d"'-it-o-r:-id:-e-ntifi""~e-s-d:-e:-b-to-r-:=================----------1 11 U.S.C. § 507( a)(I )(A) or (a)( I)(B).

o .Wages, salaries, or commissions (up3a. Debtor may have scheduled account as: to $11,725*) earned within 180 days

(See instruction #3a on reverse side.)before filing of the bankruptcy

4. Secured Claim (See instruction #4 on reverse side.) petition or cessation of the debtor'sCheck the appropriate box if your claim is secured by a lien on property or a right of setoff and provide the requested business, whichever is earlier _ 11information. U.S.C. § 507(a)(4).

o Contributions to an employee benefitplan - 11 U.S.C. § 507(a)(5).

o Up to $2,600* of deposits towardpurchase, lease, or rental of property

-- _._or..sen.tices..for..personal,...fami4r,..or --t---household use-ll U.s.C. § 507(a)(7).

o Taxes or penalties owed togovernmental units - II U.S.C. § 507(a)(8).

o Other - Specify applicable paragraphof 11 U.S.C. § 507(a)U.

o Real Estate o Motor Vehicle o Equipment o OtherNature of property or right of setoff:Describe:

Value of Property:$. Annual Interest Rate_%

.:---Amount-of arrearage-amt'uttrercharges as-of tinre-cas-efil-ed-irrclude-din--se-cured c:lalllr,-

ifany: $, _ Bas~forperfection: ~

:l96~3r:211'3Amount of Secured Claim: $ Amount Unsecured: $

6. Claim Pursuant to 11 U.S.C. § 503(b)(9): .Indicate the amount of your claim arising from the value of any goods received by the Debtor within 20 days beforeFebruary 16,2011, the date of commencement of the above cases, in which the goods have been sold to tlie Debtor in the ordi-nary course of such Debtor's business. Attach documentation supporting such claim, $

7. Credits: The amount of al1 payments on this claim has been credited for the purpose of making this proof of claim.

8. Documents: Attach redacted copies of any documents that support the claim, such as promissory notes, purchaseorders, invoices, itemized statements or running accounts, contracts, judgments, mortgages, and security a,greements.You may also attach a summary. Attach redacted copies of documents providing evidence of perfection ora security interest You may also attach a summary. (See instruction # 8 and de]inition of "redacted" on reverse side.)

DO NOT SEND ORIGINAL DOCUMENTS. ATTACHED DOCUMENTS MAY BE DESTROYED AFTERSCANNING.

If the documents are not available, please explain in an attachment.

PROOF OF CLAIM

5. Amount of Claim Entitled toPriority under 11 U.S.C. § 507(a).If any portion of your claim fallsin one of the following categories;check the box and state theamount.

Amount entitled to priority:

$._----

*Amounts are subject to adjustment on4/1/13 and every 3years thereafter withrespect to cases commenced On or afterthe date of adjustment.

Signature: The person filing this claim must sign it. Sign and print name and title, if any, of the creditor orother person authorized to file this claim and state address and telephone number if different from the noticeaddress above. Attach copy of power of attorney, if any.

FOR COURT USE ONLY5'/9Date;.w II

11-10612-shl Doc 427-1 Filed 03/16/12 Entered 03/16/12 16:44:38 Proof of Claim Pg 1 of 5

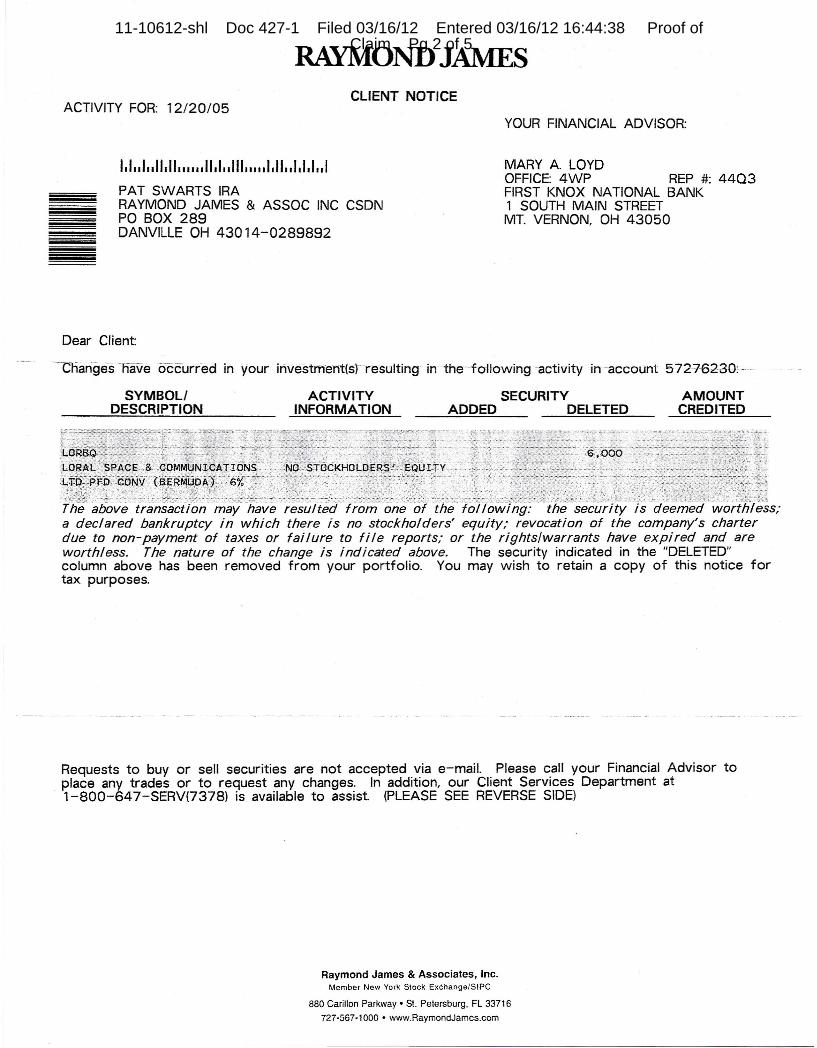

RAYMOND JAMESCLIENT NOTICE

ACTIVITY FOR: 12/20105YOUR FINANCIAL ADVISOR:

1.1 •• 1•• 11.11 •••••• 11.1 •• 111••••• 1,11.,1,1.1 •• 1PAT SWARTS IRARAYMOND JAMES & ASSOC INC CSDNPO BOX 289DANVILLE OH 43014-0289892

MARY A. LOYDOFFICE: 4WP REP #: 44Q3FIRST KNOX NATIONAL BANK1 SOUTH MAIN STREETMT. VERNON, OH 43050

Dear Client:

-Tnangesnaveoccurfed in your investrnerrttsrresuttirrq tn the--foll-owing-activity in-accoLint 572-=7-62-30:---

SYMBOl!DESCRIPTION

ACTIVITYINFORMATION

SECURITYADDED DELETED

AMOUNTCREDITED

above transaction may security is deemed worthless;a declared bankruptcy in which there is no stockholders' equity; revocation of the company's charterdue to non-payment of taxes or failure to file reports; or the rights/warrants have expired and areworthless. The nature of the change is indicated above. The security indicated in the "DELETED"column above has been removed from your portfolio. You may wish to retain a copy of this notice fortax purposes.

Requests to buy or sell securities are not accepted via e-mail. Please call your Financial Advisor toplace any trades or to request any changes. In addition, our Client Services Department at1-800-647-SERV(7378) is available to assist. (PLEASE SEE REVERSE SIDE)

Raymond James & Associates, Inc.Member New York Stock Exchange/Slpe

880 Carillon Parkway· SI. Petersburg. FL 33716

727-567-1000· www.RaymondJames.com

11-10612-shl Doc 427-1 Filed 03/16/12 Entered 03/16/12 16:44:38 Proof of Claim Pg 2 of 5

Account StatementRetain for Your Records

Statement Period: January 1, 2006 to January 31,2006Last Statement: December 31,2005

Rollover IRAAccount Number: 5032-4935

Going paperless is easy. Log on to:www.schwab.com/estatementsQuestions? CaI/1-800-435-4000

Banking Inquiries: Call 1-800-435-4000

Account Opened in: 2001Page 1

31/01-CN1B1902·002747·MED·43014028900997232 ·2JEFFREY M SWARTSCHARLES SCHWAB & CO INC CUSTIRA ROLLOVER308 CEDAR STPO BOX 289DANVILLE OH 43014-0289

I Total Account Value $ 0.31\

---IrC~hra-n-g-e~ln~Va~lru-e~S-u-m-m-a-ry--------------------I

Change in Value Since December 31, 2005: $ 0.01 ==Change in Value Since January 1,2006: $ 0.01 ;;;;;;;;;;;;;;;===-

;;;;;;;;;;;;;;;===

'-;:A::-c_c:-o,-::u~n-,-"t_V--,a-:-lu-::-e=-;-=s....::u:.:..:m:.:..:m..:..:-=:a:...lry,----:-:--ICash, Money Market, and Deposit Accounts $ 0.31Investments $ 0.00

'-.:R..:..:a=te=-s.=..:u=m.:..;..:mc.:..:.a=r-Ly 1

Deposit Accounts: Interest rate as of 01/31 (Z) 0.50% --;;;;;;;;;;;;;;;===--;;;;;;;;;;;;;;;~~--~--~--~----------------------------------------------------------------------I Investment Detail

Cash, Money Market, and Deposit AccountsDEPOSIT ACCOUNTS (X,Z)

Description SvmbolQuantity

loag/Sbort Price

Settle TradeDate Date Transaction Description Quantitv Price

Market Value ,.G')0

$ 0.31 000I\)

$0.311-...j~-...j0~0-...j~,.

Total

$ 0.01

ITotal Account Value

I Transaction Detail

Cash, Money Market, and Deposit Accounts Activity01/17 01/15 Bank Interest ()(,Z) BANK INT 121605-011506

Investments Activity01/18 01/18 Deemed Worthless LORAL SPAC & COMMUN NXXX

WORTHLESS EFF 11/21/05(1,170 )

Please see "Footnotes for Your Account" section for an explanation of the footnote codes and symbols on this statement.

©2004 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. CRS 22640 (0001-0386) STP10479R1-03 (12/04)

eN1 B1902·002747 97232

11-10612-shl Doc 427-1 Filed 03/16/12 Entered 03/16/12 16:44:38 Proof of Claim Pg 3 of 5

Account StatementRetain for Your Records

Statement Period: December 1, 2005 to December 31, 2005Last Statement: November 30, 2005

Roth Contributory IRAA.ccount Number: 1288-3560

Going paperless is easy. Log on to:www.schwab.comJestatementsQuestions? CaI/1-800-435-4000

Banking Inquiries: Call 1-800-4354000

Account Opened in: 1999Page 1

30/12·PNC02007-003211-SML-430140289009941746 '1-2JEFFREY M SWARTSCHARLES SCHWAB & CO INC CUSTROTH CONTRIBUTORY IRA308 CEDAR STPO BOX 289DANVILLE OH 43014-0289 ------

Total Account Value $22.751

I_C-'-h-Oa-'-Cn:>iL9-=-e..::.;;ln..:..v..:..a:.:.:I..=ue-=-=S.=u:;cm:.:;:m..:..;:a:;cryL.- IChange in Value Since November 30, 2005: $ (17.27) ~Change in Value Since January 1, 2005: $ (1,287.40)

--=-A_C-:-c_o-:-:un:-t;;...v_a;;...l..:..u-=-e-'S;..;:.u~mc:.:m.:.:.=a'-"ry _'_ 1Cash, Money Market, and Deposit Accounts $ 22.15Investments $ 0.60

--I_R_a_te'-S-"-u'-m_m_a;;....ry.L- 1

Deposit Accounts: Interest rate as of 12/30 (Z) 0.50% _-

Investment Detail

Cash, Money Market, and Deposit AccountsDEPOSIT ACCOUNTS (X,Z)

Description SymbolQuantity

Long/Short Price Market Value .•G)0

$ 22.15 000INI\)...•.

$ 0.60 -'-0

N/A I\)0en<.•

$ 22.751

InvestmentsSYQUEST TECH INC NEWLORAL SPACE &COMM 6%PXXX

WORTHLESS EFF 11/21/05

SYQTQ 2,0002,250

LL

$ 0.0003NIA

I Total Account Value (excludes unpriced securities)

Transaction DetailSettle TradeDate Date Transaction Description Quantity Price TotalCash, Money Market, and Deposit Accounts Activity12/1612/15 Bank Interest (X,Z) BANKINT111605-121505 $ 0.01

Please see "Footnotes for Your Account" section for an explanation of the footnote codes and symbols on this statement.

©2004 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. CRS 22640 (0001-0386) STP10479R2-03 (12/04)

PNC02007·003211 941746

11-10612-shl Doc 427-1 Filed 03/16/12 Entered 03/16/12 16:44:38 Proof of Claim Pg 4 of 5

Account StatementRetain for Your Records

._-------------Statement Period: January 1, 2006 to January 31,2006

Last Statement: December31, 2005

Brokerage AccountAccount Number: 8650-0742

Going paper/ess is easy. Log on to:www.schwab.com/estatementsQuestions? Callt-800-435-4000

Account Opened in: 1999Page 1

31101-CN181902-002747-MEO-43014028900997235 "1

JEFFREY M SWARTS &PATRICIA E SWARTS JT TEN308 CEDAR STPO BOX 289DANVILLE OH 43014-0289 -=--

Cash & Sweep Money Market FundsInvestments

$ 42.41$ 0.00

---I-C~h-a-n-ge~ln~v~a~lu-e-S~u-m-m-a-r-y---------1

Change in Value Since December 31, 2005: $ 45.00 -Change in Value Since January 1,2006: $ 45.00 _=--

I Account Value Summary

I Total Account Value $ 42_411

I Investment Detail

Cash and Money Market Funds (Sweep)CASH

Description SvmbolQuantity

Long/Shod Price

InvestmentsLORAL SPACE &COMM 6%PXXX

WORTHLESS EFF 11/21/053,000 L N/A

Market Value ,.G')0

$ 42.41 000N-..j~

N/A-..j0(1)0-..j(1)

$ 42.411,.I Total Account Value (excludes unpriced securities)

I Transaction DetailSettle TradeDate Date Transaction Description Quantitv Price TotalCash Activity01/06 09/28 Misc Credits CUST SERVICE GEST $ 45.00

.~

©2004 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. CRS 22640 (0001-0386) STP1 0479R1-03 (12/04)

CN1 81902-00274797235

11-10612-shl Doc 427-1 Filed 03/16/12 Entered 03/16/12 16:44:38 Proof of Claim Pg 5 of 5

1

Tony Christ (Pro Se) 6635 Kennedy Lane Falls Church, Virginia 22042 Telephone (703) 533-3077 UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK ) In re: ) Chapter 11 Case Nos. ) LORAL SPACE & COMMUNICATIONS LTD., et al. ) Lead Case 03-41710(RDD) ) 03-41709 (RDD) through ) 03-41728 (RDD) ) ) Debtors ) (Jointly Administered) _______________________________________________ )_____________________________

THE LSPC’S OBJECTION TO DEBTOR’S MOTION FOR SANCTIONS

The LSPC takes issue with Debtor’s portrayal at p. 2, no. 1, “that (i) this Court repeatedly has rejected the LSPC’s baseless allegations regarding Debtor misconduct and “asset minimization.” For three years up to and including the February 7, 2006 hearing the Court supported the LSPC. Recently is a better word then repeatedly.

Yet the quandary of the components of the ‘projections’ remained an unanswered enigma to the LSPC at Confirmation. Notwithstanding our dissatisfaction with the confirmation decision at year-end, the LSPC had not planned to introduce new litigation to revisit the Confirmation decision. However, during the first six months of 2006 there were a number of disclosures that refuted the projections relied upon to determine value at SS/L. I felt a duty to bring this new information to bankruptcy court since its availability at Confirmation was unknown outside of the Debtor.

Mr. Karotkin’s lawyering prevented the LSPC first in its request for limited discovery

then from supplementing the 1144 Motion with the new disclosures. The LSPC had talked to Mr. Karotkin, Debtor’s lead Counsel, encouraging him to look into the new information and his response was to successfully move the court to repress any supplementation of the 1144. His response might be in violation of his disinterestedness requirement.

When the LSPC attempted to appeal the 1144 it had withdrawn at the April 10, 2006

hearing, we did not know that you could not appeal to a higher court a matter you had withdrawn with prejudice in the bankruptcy court. Shortly thereafter the LSPC was presented with two choices: either sign the stipulation, or be brought before the Court on Mr. Karotkin’s sanctions

11-10612-shl Doc 427-2 Filed 03/16/12 Entered 03/16/12 16:44:38 Exhibit A Pg 1 of 7

2

charge. I chose to sign the stipulation that Mr. Karotkin wrote. However I had a slightly different understanding of the stipulation agreement than Mr. Karotkin. My different understanding relates to my insistence before signing the agreement that Debtor also agree to withdraw the sanctions that related to the 1144 charge with prejudice. When he agreed to do this I signed the stipulation.

The Stipulation Agreement states on page 4 at No. 1: “the 1144 Appeal and the Fee Appeal each shall be and hereby is deemed withdrawn by the LSPC, with prejudice.” When the LSPC filed its appeal based on new information, we argued it was not the 1144 deemed withdrawn with prejudice. We argued that the District Court Appeal was based on new information as well as a new focus that made it different than either the 1144 or the Disgorgement with an 1144 component. The District Court has not yet answered this question.

However, if the Court views it as an appeal, subject to the above restriction, then the Debtor is also in violation because they have agreed not to bring sanctions that relate to that specific Appeal. On page 4 at no. 3, “On the Stipulation date, (i) the Motion to Dismiss shall be withdrawn and (ii) the Sanctions Motion shall be deemed withdrawn with prejudice;”

This raises the question if the District Court views it as the same motion withdrawn with prejudice, which the LSPC is confident it will not, then how can Debtor, who also promised to withdraw the sanctions with prejudice that relate to that motion, be any less guilty of violating the stipulation that they constructed. Although the LSPC has argued it is a different charge based on new information, if not, then how can Debtor bring a sanction motion it has agreed to “withdraw with prejudice” against the same motion? The LSPC does not dispute Debtors right to bring a Sanction Motion in general, however the LSPC does dispute Debtor’s right to bring sanctions specifically against what it is has previously agreed to withdraw with prejudice.

Admittedly, there is nothing that prevents Debtor from seeking sanctions for anything it might choose at no. 3: “that nothing herein shall preclude the Reorganized Debtors from seeking sanctions against the LSPC and/or Mr. Tony Christ in respect of any future conduct, . . .”. This right exists without this affirmation in the stipulation for Debtor as well as the LSPC.

The LSPC, in light of specific dangling participles at Confirmation, when applying strict logic, felt it was their duty to file a motion that brought the new information withheld, but available in the Confirmation time frame, to further the truth and better explain an erroneous finding at Confirmation. From this frame of reference the sanction motion sought can be viewed as a further endeavor to repress information hence to darken or obfuscate the Court’s effort to establish value. The LSPC took the Court’s admonition into consideration and “thought long and hard” before filing the Motion. However the disclosure documents filed by Loral and EchoStar in 2005 revealed both significant reductions in costs and significant increases in sales that were not disclosed at Confirmation and were key to the SS/L valuation. The March depositions confirmed that the experts had not reviewed the individual Satellite contracts. I would remind the Court that in its decision it relied on the experts that ‘the experts thoroughly vetted the projections’. Apparently not. Also the Quarterly disclosures from debtor disclosed that sales were at a run rate

11-10612-shl Doc 427-2 Filed 03/16/12 Entered 03/16/12 16:44:38 Exhibit A Pg 2 of 7

3

approximately 10% above projections during 2006 and increasing while audited cost at year end 2005 for SS/L were substantially less on actual 2005 sales that matched the projections. The court in valuing SS/L had to rely on the Discounted Cash Flow models because at the time there were no comparable sales therefore the evaluation was dependant overly reliant on debtors projections. In April 2006 Elana, a comparable Satellite manufacturer owned by Alcatel was sold or $2.14 billion. This sale does not compare well with the courts $230 million valuation of SS/L at Confirmation based solely on the projections and DCF evaluations of he experts. For these reasons and more the LSPC believed it had a duty and an obligation to further the truth and decided that the new information was wrongly withheld from Confirmation and would further the truth in these cases. The LSPC believed as a matter of conscious tat the new information required Judicial Review and a stipulation obtained through duress is not proper. There was other supporting information that came from disclosures and depositions in addition to the disclosure statements.

The LSPC is not filing any new motions against the Debtor, nor does it intend to, other than filings in connection with requirements and actions underway. In this context, the sanctions will accomplish nothing but pure punishment and are ineffective as a tool to repress litigation that was the intent of the Debtor. The LSPC believes that, if fully vetted, the new information would show the projections relied upon by the experts and the Court at Confirmation were clearly erroneous and significantly understated the assets of the estates. The District Court will decide whether to hear or not to hear that information. A District Court decision may moot any sanctions. Therefore to avoid conflicting decisions between courts and prevent additional litigations, if the Court is of the mind that it wants to impose sanctions it should adjourn the motion till the other litigation is completed.

Consequently, this is a personal and punitive sanction against Tony Christ. The LSPC only has such assets that its members contribute to fund its expenses. The strategy of these sanctions is to unfairly intimidate Mr. Christ, create hardship, and inhibit certain litigation from advancing to Appeal. The previous threats of sanctions similarly intimidated Mr. Swarts and Mr. Plum who upon being threatened resigned the LSPC. Hence treats have been successful in debtor’s restriction of courtroom information. Imposing an agreement that was signed in duress is not the duty of the bankruptcy court, a court of equity.

Furthermore, the scope of the fee responsibility the sanctions seek to date is for a 19-

page response signed by Mr. Karotkin and cumbersomely titled “Appellees’ Memorandum of Law In Support of Motion To Dismiss The Loral Stockholders Protective Committee’s Appeal As It Relates To A Request For Relief Under 11 U.S.C. Sec. 1144” to certain aspects of the Appeal that the Debtor alleges is subject to the stipulation. However their have been other documents submitted in connection with the Greenhill Disgorgement, in connection with the election Appeal and the Substantial Contribution Appeal and two additional documents that rehash the response to repress the new information as well as two Affidavits by Ted Tsekerides that frankly I don’t know what they relate two and if any of these are improperly billed it would wrongly go beyond the relief sought in the Sanctions Motion. It would wrongly inflate their bill and would represent punishment in excess of the alleged violation.

11-10612-shl Doc 427-2 Filed 03/16/12 Entered 03/16/12 16:44:38 Exhibit A Pg 3 of 7

4

Also of import the LSPC is seeking sanctions against Weil Gotshal on grounds that they violated their disinterestedness requirement They have responded and I understand they will be submitting a Sir Reply in addition. It would be completely improper to sign the Debtor’s open-ended order allowing Weil Gotshal to bill for future matters they undertake at their order or upon other filings granting discretion in billing that could be abused. The Court has already cited debtors’ counsel for over billing and partially disgorged them on February 7, 2006.

The issue of admitting the new information to the Appeal has been briefed at District

Court and awaits a decision. It would be patently unfair to give Weil Gotshal a card de blanche to bill my family in other pleadings intended to answer other briefs before the United States District Court that have no bearing on the narrow area of the relief requested. Hence the order as written is subject to the same abuses for which the Court has already debited this Counsel in the amount of <$800,000> at final fee hearing on February 7, 2006. Furthermore the Court is a Court of equity and it is not the intent of the court to leave an open-ended order on a narrow issue that has been fully briefed. Such punishment could ruin my family financially in addition to the considerable expense and loss my family has already sustained while acting on our duty to bring forward these important issues for Judicial review. Therefore although opposed on grounds of punishing the victims if imposed they should be determined in accord with the effort to have heard the new information which is completed and not open-ended

The allegations against the Debtor of erroneous projections is a part of the Disgorgement

brief that is connected to the ‘new information,’ If the District Court determines that the evidence requires a hearing and that this aspect of the Appellant Brief is substantially different and of adequate merit wouldn’t the District Court be denying the stipulation? For the stipulation to hold doesn’t the United States District Court have to rule to not hear those aspects of the Appeal that deal with the erroneous projections charge?

To the degree that the order sought by Weil Gotshal is intended to generally inhibit or

restrict litigation it presumes on the one hand to preempt the District Court review and, fails to prevent or restrict future litigation. A broader interpretation of the sanctions agreement would wrongly presume to know in advance that such future litigation is ‘frivolous,’ ‘vexatious,’ or ‘blunder buss’ prior to its filing or even its conception and is not sought in the sanction motion. Therefore any sanction might be premature and is certainly unfair, and should be withdrawn without prejudice or denied without prejudice until such time that the District Court determines whether to hear the subject. This would prevent cross-decisions in the event that, after the review of the United States District Court, the litigation is found to have merit.

This deflection of litigation costs mocks the process of pro se Appeal that has a proud and

longstanding tradition in the United States District Court and endeavors to gain court sanctification of Debtor’s ongoing efforts to repress information. Placing this added financial burden on my family very well may accomplish Debtor’s agenda of restriction and obfuscation. The LSPC would note that any pressure on the Court to finish these cases within two years, which to the degree it exists, may have biased the court regarding reopening the case on the basis of new information withheld from Confirmation. The LSPC believes it is the duty if the Court as a Court of Equity to hear this information. The new information was not planned by the LSPC but released by the debtor and a major customer in required disclosures for 2005 and withheld

11-10612-shl Doc 427-2 Filed 03/16/12 Entered 03/16/12 16:44:38 Exhibit A Pg 4 of 7

5

from Confirmation. The LSPC acted out of a duty to disclose the truth on the record even if painful to the Loral insiders or inconvenient to the bankruptcy court. Therefore we respectfully request and pray from relief from this debtor and its allegations.

RELIEF REQUESTED Given the present context that no new actions are to be filed against the Debtor, THE OBJECTIVE OF THE SANCTIONS MOTION HAS BEEN ACOMPLISHED WITH OUT ENFORCING THE HARDSHIP OF A MONETARY PUNISHMENT OF MY FAMILY. The LSPC is awaiting decisions from the District Court regarding this very matter, any sanction would be entirely punitive, imposing costs on my family, which has born the cost of a total loss of our investment, as well as the costs of self-representation throughout these cases. The Bankruptcy Court is a court of equity, and it is inequitable to punish the victims given these facts. Therefore we respectfully pray for denial of the motion.

1) I respectfully request that the relief requested be denied because the matter is before the District Court, and if the District Court should decide that the Appeal is not the same and may go forward, the bankruptcy court will have penalized the LSPC for a pleading that the District Court will hear. Furthermore if found it was the same as was withdrawn with prejudice debtor is equally in violation for bringing the same sanctions they withdrew with prejudice.

2) A decision by the United States District Court to hear the disputed parts of the subject

appeal. If for any reason the Court decides not to hear it, there will be no more costs accruing from it. Presently, there should be no more costs associated with it. If the court decides it can hear the appeal, it will mean that the Court believes it is not bound by Debtors’ claims, including the Stipulation, therefore, there should not be any future liability to me for litigating the appeal based on the new information. The Order, as written, is open-ended and allows Weil Gotshal to bill in the future on this narrow matter of the 1144. Therefore, if it is determined at this time by this Court that the LSPC should be sanctioned, the sanction should relate to the 19-page response incurred, and not other pleadings submitted on other matters. Therefore we respectfully object to a finding in support of sanctions and an open-ended order. Would request that the sanction fit the specific response in opposition to the new information and be a fixed amount the cost of that response and not other pleadings.

3) Alternatively, the LSPC respectfully requests a proper adjournment of the sanctions

motion until the outstanding matters are resolved in the District Court in that such resolution cold mute the charge that we have brought the same information and are therefore in violation with the Stipulation. The LSPC has argued that it is not the same information.

11-10612-shl Doc 427-2 Filed 03/16/12 Entered 03/16/12 16:44:38 Exhibit A Pg 5 of 7

6

CONCLUSION

Mr. Karotkin’s persuasive and repetitive attacks against the LSPC should be directly contrasted to his admitted lack of personal investigation, intentional or otherwise, of the issues that underlie Mr. Karotkin’s unending attacks based on allegations against the LSPC:

THE COURT: Let me though ask you a different 22 question. I don't know, I -- when I was practicing, I worked 23 on a lot of disclosure statements, including, you know, 24 representing the Debtor and it depends sometimes how active 25 attorney is in preparing disclosure statements. What you're 1 telling me though, Mr. Karotkin, is that you all did not like 2 examine that your client about all their assets and that you 3 basically took what they gave you; is that what you're saying? 4 As far as the description of their assets? 5 MR. KAROTKIN: That's a fairly opened ended question. 6 I mean, you know, they had a lot of assets. If you're asking 7 me would I question them if they told me about the status of 8 construction of a satellite contract -- 9 THE COURT: Right. 10 MR. KAROTKIN: -- or would I take their word for it? 11 THE COURT: Right. 12 MR. KAROTKIN: I can't imagine that I would question 13 them about a status of a satellite contract.

These abusive attacks, without foundation, have gone on for three years against the pro se LSPC, which has undergone significant sacrifice and expense to attend and participate in the hearings. Mr. Karotkin’s prejudicial attitude toward equity may be a violation of his disinterestedness requirement, and is a subject in the LSPC Sanctions Motion before the United States District Court.

It should be further noted that before each and every filing by the LSPC the Court

admonished the LSPC to talk with the debtor and we did and were in every instance rebuked and resorted to filing a pleading to request the court intervention which the court was mostly reluctant to grant.

It would be inequitable in light of the fact that the LSPC intends to initiate no more

pleadings against the Debtor, and that the portions of the filing in dispute regarding the new information to be decided by the District Court have not been determined.

We include one case submitted by the debtor in their response in district court and remind the Court that we have respectfully attended over thirty hearings and any experience we have obtained has come from that experience we are still pro se and should not suffer for our dutiful response to bring forth new information for judicial review. Information that was in large part withheld from Confirmation.

11-10612-shl Doc 427-2 Filed 03/16/12 Entered 03/16/12 16:44:38 Exhibit A Pg 6 of 7

7

As authority for our request for NO monetary sanctions we submit a case debtor submitted to the district court. In re Mauakolam v. Columbia Univ., 866 F.2d 53, 56 (2d Cir. 1989) a Nigerian Engineering student failed an exam question in 1979. Then in 1982 sought monetary and injunctive relief for his failure. The action was dismissed for want of prosecution by the district court in April 21, 1983. Then on April 21, 1987, four years to the day from the order dismissing the case in U.S. District Court the Nigerian submitted a motion in U.S. District Court to reopen the case. The Court found no reason to exclude the four-year delay took note of a separate civil court action on the same grievance and awarded attorney’s fees of $3,243.50 to Columbia University. On Appeal to the second circuit concluded “Plaintiffs appellent’s motion for relief from judgment was filed out of time, four years latter. We therefore find no abuse of the courts discretion to deny the motion under 60(b)(1). However we do not believe that sanctions are warranted on the facts of the case.” “Accordingly the judgment of the district court is affirmed in part and reversed in part, . . . vacate judgment as awards defendants –appellee’s fees in amount of $3,243.50.”

On its face the plaintiff seeks to involve the courts in collecting what he believes to be damages owing to his failed exam grade. Notwithstanding the baseless predicate for the complaint and the filing in circuit court and the four-year lag the second circuit did “not believe that sanctions are warranted on the fact of the case.”

Finally we remind the court that through numerous pleadings and attendances at Court