10th ANNUAL REPORT 2019/2020 1 - Mega Bank Nepal

204

10 th ANNUAL REPORT 2019/2020 1 Mega Bank Nepal Limited

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 10th ANNUAL REPORT 2019/2020 1 - Mega Bank Nepal

10th ANNUAL REPORT 2019/2020

1Mega Bank Nepal Limited

10th ANNUAL REPORT 2019/2020

Key Financial Highlights

NET PROFIT

BALANCE SHEET

CAPITAL ADEQUACY RATIO

NON PERFORMING CREDIT

TOTAL LOANS

TOTAL DEPOSIT

BILLION

BILLION

BILLION

BILLION

155 132

114

1.58

13.24%

1.15

10th ANNUAL REPORT 2019/2020

3Mega Bank Nepal Limited

Contents

1. AGM Notice 12

2. Proxy Form 14

3. Chairman’s Speech 18

4. Message from CEO 22

5. Mega Bank Today 24

a. Our activities

b. What we are

c. Company’s performance

d. Key Figures

e. Mega Bank’s Presence

6. Business Model and Strategy 33

a. The Future of Banking

b. Business Model

c. What does a Mega Bank makes a difference

d. Management of Capital

e. Value Chain

f. Strategic Foundations for next 5 years

g. Capital & Business relationship

h. Comparative Results and Awards

7. Mega Bank’s Primary Business Activities 49

- Contents of Products and Services

8. A Framework of Trust 60

a. Corporate Governance Model

b. Lines of Management & Control

c. Risk Management

d. Ethics and Social Responsibility with

photos

9. Report of Board of Directors 74

10. Report under Section 109 86

Financial Report Part

11. Independent Auditor’s Report 89

12. Financial Statements 93

13. Notes to Accounts 102

14. Annexure 125

15. Additional Disclosure 163

Proposals and Approvals

16. Approval from NRB 198

17. Implementation Status of NRB Directions 199

18. MOA & AOA amendment 200

10th ANNUAL REPORT 2019/2020

4Mega Bank Nepal Limited

10th ANNUAL REPORT 2019/2020

5Mega Bank Nepal Limited

10th ANNUAL REPORT 2019/2020

6Mega Bank Nepal Limited

Branch Managers and Extension Counter In-Charge

S.N.Province 1 - Head Bibek Bandhu Neupane

Branch Branch Managers

1 Fungling Branch, Taplejung Sangam Deep Shrestha

2 Phidim Branch, Panchthar Prem Prasad Neupane

3 Kummayak Branch, Panchthar Chhtrapati Niraula

4 Rong Branch, Illam Prakash Bhattrai

5 Birtamod Branch, Jhapa Kuldip Bimoli

6 Birtamod Branch -2, Jhapa Prakash Giri

7 Damak Branch, Jhapa Samip Shrestha

8 Damak Branch -2, Jhapa Bishwo Raj Adhikari

9 Bhojpur Branch, Bhojpur Sumit Karmacharya

10 Dharan Branch, Sunsari Sabin Shrestha

11 Itahari Branch, Sunsari Sikkandar Thapa

12 Itahari Branch -2, Sunsari Devendra Khatri

13 Inaruwa Branch, Sunsari Dev Sharan Mehta

14 Biratnagar Branch, Morang Dipesh Jung Thapa

15 Biratnagar Branch -2, Morang Binod Raj Thapa

16 Biratnagar Branch -3, Morang Rajib Bikram Panta

17 Gramthang Branch, Morang Bishnu Prasad Ghimire

18 Khijidemba Branch, Okhaldhung Durga Bahadur Khatri

19 Okhaldhunga Branch, Okhaldhunga Shamnbhu Prasad Parajuli

20 Rautamai Branch, Udaypur Raisul Aajam

Incharge of Extension Counters

1 Shivasatakshi Extension Counter, Jhapa Pooja Adhikari

2 Dhanpalthan Extension Counter, Morang Siddhanta Shrestha

3 Ratuwamai Extension Counter, Morang Bikram Chauhan

4 Baraha Extension Counter, Sunsari Prashant Chaudhary

5 Koshi Extension Counter, Sunsari Rabin Upreti

S.N.Province 2 - Head Yashpal Kumar Tibrewal

Branch Branch Managers

1 Lahan Branch, Siraha Amrendra Shah

2 Lahan Branch -2, Siraha Prakash Sharma Ghimire

3 Bishnupur Branch, Siraha Bibek Raj Bhattrai

4 Laxminiya Branch, Dhanusha Dipak Kumar Mandal

5 Janakpur Branch, Dhanusha Galek Kumar Yadav

6 Janakpur Branch 2, Dhanusha Binay Kumar Shah

7 Bardibas Branch, Mahottari Yash Prasad Dahal

8 Hariwan Branch, Sarlahi Ishwor Timilsina

9 Ramnagar Branch, Sarlahi Ramesh Kumar Yadav

10 Birgunj Branch, Parsa Yashpal Kumar Tibrewal

11 Birgunj Branch -2, Parsa David Thapa

12 Birgunj Branch -3, Parsa Mukesh Adhikari

Incharge of Extension CountersIncharge of Extension Counters

1 Mithila Bihari Extension Counter, Dhanusha Santosh Kumar Mishra

2 Nagarain Extension Counter, Dhanusha Anil Kumar Joshi

10th ANNUAL REPORT 2019/2020

7Mega Bank Nepal Limited

S.N.

Bagmati Province - Head Shreeram Giri

Branch Branch Managers

Valley Branches

1 Main Branch, Kamaladi, Kathmandu Ashish Kumar Shrestha

2 Kapan Branch, Kathmandu Rajesh Thapa

3 New Baneshwor Branch, Kathmandu Suhita Shrestha

4 New Baneshwor Branch -2, Kathmandu Saguna Shakya Bajracharya

5 Baneshwor Branch -3, Kathmandu Arjun Dhakal

6 Teku Branch, Kathmandu Preskshya Sapkota

7 Maharajgunj Branch, Kathmandu Abhasratna Tuladhar

8 Maharajgunj Branch -2, Kathmandu Manisha Manandhar

9 Maitidevi Branch, Kathmandu Ami Shrestha

10 Maitidevi Branch -2, Kathmandu Ami Shrestha

11 New Road Branch, Kathmandu Indira Paneru

12 New Road Branch -2, Kathmandu Ganesh Tamang

13 Kamalakshi Branch, Kathmandu Krishna Prasad Sharma

14 Khichhapokhari Branch, Kathmandu Rabin Shrestha

15 Thamel Branch, Kathmandu Ganesh Dhakal

16 Thamel Branch -2, Kathmandu Niraj Gautam

17 Boudhha Branch, Kathmandu Madhav Humagain

18 Kalanki Branch, Kathmandu Karna Bahadur Thapa

19 Kalanki Branch -2, Kathmandu Chhapendra Kunwar

20 Gyaneshwor Branch, Kathmandu Alina Shrestha

21 Chhabhil Branch, Kathmandu Manoj Raj Pathak

22 Gongabu Branch, Kathmandu Sunita Thapa

23 Khusibu Branch, Kathmandu Sushila Pandey

24 Hattigaunda Branch, Kathmandu Namrata Sharma

25 Baniyatar Branch, Kathmandu Shahdev Basnet

26 Jorankhu Branch, Kathmandu Ishwor Pandit

27 Baluwakhani Branch, Kathmandu Amit Kumar Khadka

28 Jorpati Branch, Kathmandu Krishna Shrestha

29 Samakhusi Branch, Kathmandu Naresh Lal Joshi

30 Jawalakhel Branch, Lalitpur Nitisha Giri

31 Imadol Branch, Lalitpur Sarina Karki

32 Imadol Branch -2, Lalitpur Pratima Malla

33 Kumaripati Branch, Lalitpur Heri Raj Maharjan

34 Thiaba Branch, Lalitpur Jyotsana Kunwar

35 Patan Branch, Lalitpur Shailesh Mulmi

36 Suryabinayak Branch, Bhaktapur Dipendra Chaulagain

37 Sukuldhoka Branch, Bhaktapur Ukesh Duwal

38 Balkot Branch, Bhaktapur Sumit Bhandari

39 Thimi Branch, Bhaktapur Manil Ratna Shahi

40 Thimi Branch -2, Bhaktapur Bikas Maharjan

Out of Valley BranchesOut of Valley Branches

41 Mainapokhari Branch, Dolakha Sushil Kumar Upreti

42 Charikot Branch, Dolakha Kapil Prasad Bhandari

43 Bagkhor Branch, Dolakha Manisha Shrestha

44 Manthali Branch, Ramechhap Pushkar Lamichhane

10th ANNUAL REPORT 2019/2020

8Mega Bank Nepal Limited

45 Khurkot Branch, Sindhuli Shailendra Sharma

46 Sindhuli Branch, Sindhuli Keshab Prasad Devkota

47 Bhiman Branch, Sindhuli Bijay Kumar Shah

48 Chautara Branch, Sindhupalchok Ram Krishna Parajuli

49 Indrawati Branch, Sindhupalchok Rajan Shrestha

50 Panchpokhari Branch, Sindhupalchok Chattur Prasad Bhattrai

51 Helambu Branch, Sindhupalchok Gopal Neupane

52 Banepa Branch, Kavrepalanchok Rajeshwor Shrestha

53 Syafrubeshi Branch, Rasuwa Chhokyal Dorje Lama

54 Malekhu Branch, Dhading Surya Kumar Tripathi

55 Malekhu Branch -2, Dhading Surya Kumar Tripathi

56 Dhading Branch, Dhading Santosh Khanal

57 Dhading -2 Branch, Dhading Rammani Neupane

58 Jwalamukhi Branch, Dhading Atma Ram Dawadi

59 Tripurasundari Branch, Dhading Devendra Giri

61 Hetauda Branch, Makwanpur Niranjan Devkota

62 Hetauda Branch -2, Makwanpur Madhavi Bose

63 Hetauda Branch -3, Makwanpur Sanam Lama

60 Mugling Branch, Chitwan Narhari Mishra

64 Tandi Branch, Chitwan Sushila Aryal

65 Tandi Branch 2, Chitwan Prem Ghimire

66 Narayangarh Branch, Chitwan Laxmi Thapaliya

69 Naryangarh Branch -2, Chitwan Suraj Sharma

67 Hakimchowk Branch, Chitwan Khadka Raj Parajuli

68 Bharatpur Branch, Chitwan Dipak Pathak

70 Chanauli Branch, Chitwan Gyanendra Prasad Mainali

71 Parsa Branch, Parsa Navaraj Aryal

72 Bhojad Branch, Chitwan Keshav Raj Acharya

73 Meghauli Branch, Chitwan Homnath Lamsal

Incharge of Extension Counters

1 Dahachowk Extension Counter, Kathmandu Sarswati Shrestha

2 Radhakirshan Mandi Extension Counter, Kathmandu Nirmala Barakoti

3 Balaju Extension Counter (DDC), Kathmandu Reshma Maharjan

4 Kavresthali Extension Counter, Kathmandu Madhav Prasad Pokhrel

5 Narayantar Extension Counter (Gokerneshwor), Kathmandu Anju Aryal

6 Harharmahadev Extension Counter, Kathmandu Karuna Upreti

7 Pasikot Extension Counter, Kathmandu Archana Bista

8 Jhor Extension Counter, Kathmandu Sama Aryal

9 Gandhimod Extension Counter, Kathmandu Lila Thapa

10 Thulo Bharayang Extension Counter, Kathmandu Sagin K.C.

11 Minbhawan Extension Counter, Kathmandu Suxmi Sthapit

12 Gamchha Extension Counter, Bhaktapur Rajju Heka

13 Kamalbinayak Extension Counter, Bhaktapur Iresh Baidya Shrestha

14 Gundu Extension Counter, Bhaktapur Rajiv Regmi

15 Dhapakhel Extension Counter, Lalitpur Sabina Shrestha

16 Sunakothi Extension Counter, Lalitpur Sailaja Neupane

17 Dhungrebas Extension Counter, Sindhuli Ganesh Mahato

10th ANNUAL REPORT 2019/2020

9Mega Bank Nepal Limited

S.N.Gandaki Provice - Head Gyanendra Pant

Branch Branch Managers

1 Bhimsen Branch, Gorkha Suman Bagale

2 Gorkha Branch, Gorkha Ajit Raman Khanal

3 Bhedabari Branch, Nawalpur Suman Khanal

4 Rajahar Branch, Nawalpur Janak Upadhaya

5 Kawasoti Branch, Nawalpur Gopal Khanal

6 Kawasoti Branch -2, Nawalpur Prakash Devkota

7 Chormara Branch, Nawalpur Dolraj Bhurtel

8 Chame Branch, Manang Keshar Thapa

9 Beshishahar Branch, Lamjung Sujan Poudel

10 Bhoteodar Branch, Lamjung Govinda Tiwari Chhetri

11 Bhanu Branch, Tanahun Sudip Joshi

12 Damuali Branch, Tanahun Arjun Prasad Subedi

13 Jamune Branch, Tanahun Pradip Adhikari

14 Bhimad Branch, Tanahun Kamal Thapa

15 Dulegaunda Branch, Tanahun Anand Subedi

16 Kagbeni Branch, Mustang Dinesh Poudel

17 Jomsom Branch, Mustang Sumita Sherpa

18 Jomsom Branch -2, Mustang Mahesh Thakali

19 Beni Branch, Myagdi Kumar Dhungana

20 Baglung Branch, Baglung Upendra Gautam

21 Kushma Branch, Parbat Thakur Prasad Gautam

22 Kushma Branch -2, Parbat Keshav Acharya

23 Huwas Branch, Parbat Bishnu Prasad Poudel

24 Hemja Branch, Kaski Rajan Bahadur Thapa

25 Lamachaur Branch, Surendra Basnet

26 Bagar Branch, Kaski Dinesh Kumar Shrestha

27 Chipledhunga Branch, Kaski Santosh Pokhrel

28 Pokhara New Road Branch, Kaski Prabindra Shrestha

29 Pokhara Branch, Kaski Sadip Dhakal

30 Pokhara Branch 2, Kaski Mohan Giri

31 Parsyang Branch, Kaski Pramod Ojha

32 Ratnachowk Branch, Kaski Laxman Baral

33 Lakeside Branch, Kaski Milan Pahari

34 Lakeside Branch -2, Kaski Milan Pahari

35 Birauta Branch, Kaski Shiva Bahadur Karki

36 Bajhpatan Branch, Kaski Laxman Acharya

37 Amarsingh Branch, Kaski Nabin Thapa

38 Chauthe Branch, Kaski Rabi Pradhan

39 Lekhnath Branch, Kaski Bishwa Raj Poudel

40 Lekhnath Branch -2, Kaski Prakash Sigdel

41 Talchowk Branch, Kaski Santosh Gurung

42 Gagangaunda Branch, Kaski Harishchandra Poduel

43 Syngja Branch, Syagnja Rabindra Nepal

44 Bhirkot Branch, Syangja Kamalkanta Adhikari

45 Waling Branch, Syangja Bhojraj Bhatta

46 Waling Branch -2, Syangja Chakrapani Bashyal

47 Bhumre Branch, Parbat Bishnu Prasad Bhattrai

10th ANNUAL REPORT 2019/2020

10Mega Bank Nepal Limited

S.N.Lumbini Province - Head Taranath Lamsal

Branch Branch Managers

1 Tamghas Branch, Gulmi Tejendra Karki

2 Gulmi Branch, Gulmi Kalidas Pande

3 Tansen Branch, Palpa Narayan Prasad Ghimire

4 Tansen Branch -2, Palpa Bishnu Prasad Bhandari

5 Rampur Branch, Palpa Tanka Prasad Neupane

6 Rampur Branch -2, Palpa Shukra Bikram Rana

7 Sunawal Branch, Nawalparasi Krishna Bhandari

8 Bardaghat Branch, Nawalparasi Dambar Bahadur Poudel

9 Butwal Branch, Rupandehi Milan Kuman Pun

10 Butwal Branch -2, Rupandehi Binita Shrestha

11 Butwal Branch -3, Rupandehi Dipak Neupane

12 B.P. Chowk Branch, Rupandehi Janendra Pokharel

13 Manigram Branch, Rupandehi Laxman Panthi

14 Thutipipal Branch, Rupandehi Subash Bhattrai

15 Kattaiya Branch, Rupandehi Dhiraj Dhakal

16 Bhairahawa Branch, Rupandehi Biplavi Tripathi

17 Bhairahawa Branch -2, Rupandehi Amrit Thapa

18 Nayagaun Branch, Rupandehi Ashok Rana

19 Sainamaina Branch, Rupandehi Santu Subedi

20 Sainamaina Branch -2, Rupandehi Santu Subedi

21 Semlar Branch, Rupandehi Ambika Lamichane

22 Amuwa Branch, Rupandehi Suraj Prasad Neupane

23 Kanchan Branch, Rupandehi Gopal Bhandari

24 Maanpakadi Branch, Rupandehi Gyan Prasad Subedi

25 Jitpur Branch, Kapilvastu Saroj Bhandari

26 Jitpur Branch -2, Kapilvastu Prakash Marasini

27 Taulihawa Branch, Kapilvastu Rajendra Prasad Sharma

28 Arghakhanchi Branch, Arghakhanchi Kiran Ghimire

29 Airawati Branch, Pyuthan Shreedhar Pokharel

30 Tulsipur Branch, Dang Rajan Bhandari

31 Tulsipur Branch -2, Dang Chhabilal Bhandari

32 Ghorai Branch, Dang Sharad Adhikari

33 Ghorai Branch -2, Dang Bibek Acharya

34 Kohalpur Branch, Banke Anil Rokaya

35 Kohalpur Branch -2, Banke Yadunath Khanal

36 Nepalgunj Branch, Banke Ashok Neupane

37 Nepalgunj Branch -2, Banke Mohan Chaudhary

38 Geruwa Branch, Bardia Ram Chandra Kadariya

39 Bansgadhi Branch, Bardiya Prem Chand

Incharge of Extension Counters

1 Ruru Extension Counter, Gulmi Bigyan Pant

2 Mathagadhi Extension Counter, Palpa Baburam Parajuli

3 Rupandehi District Court Extension Counter, Rupandehi Karishma Shrestha

4 Malarani Extension Counter, Arghakhanchi Suman Bashyal

5 Tulsipur Sub-Metropolitan City Extension Counter, Dang Shreedhar Pande

10th ANNUAL REPORT 2019/2020

11Mega Bank Nepal Limited

S.N.Karnali Province - Head Kamal Prasad Bhandari

Branch Branch Managers

1 Khalanga Branch, Salyan Shiv Dev Gautam

2 Jumla Branch, Jumla Ashok Shah

3 Kalikot Branch, Kalikot Rohan Kumar Bista

4 Dailekh Branch, Dailekh Padam Prasad Adhikari

5 Birendranagar Branch, Surkhet Bikram Thapa

6 Birendranagar Branch -2, Surkhet Prakash Shrestha

Incharge of Extension Counters

1 Kapoorkot Extension Counter, Salyan Umesh Shrestha

S.N.Sudurpachim Province - Head Sagar Ojha

Branch Branch Managers

1 Sanfebagar Branch, Accham Chetraj Pant

2 Attariya Branch, Kailali Padam Bahadur Chand

3 Dhangadhi Branch, Kailali Homendra Upadhaya

4 Dhangadhi Branch -2, Kailali Yogendra Raj Awasthi

5 Khalanga Branch, Darchula Lok Raj Bhatta

6 Baitadi Branch, Baitadi Jaya Raj Bhatta

7 Jogbudha Branch, Dadeldhura Rabindra Karki

8 Mahendranagar Branch, Kanchanpur Bishnu Raj Bhatta

9 Mahendranagar Branch -2, Kanchanpur Prakash Phullara

Incharge of Extension Counters

1 Pahalmanpur Extension Counter, Kailali Durga Dutta Bhatta

2 Shailyashikhar Extension Counter, Darchula Surendra Bhatta

3 Mahendranagar Yatayat Karyala Extension Counter, Kanchanpur Krishna Singh Bhaat

4 Mahendranagar Malpot Extension Counter, Kanchanpur Yokesh Chandra Bhatta

10th ANNUAL REPORT 2019/2020

12Mega Bank Nepal Limited

Notice of Tenth Annual General Meeting

Dear Shareholders,As per the decision of the Board of Directors of Mega Bank Nepal Limited dated 22nd December 2020 (2077/09/07), meeting number 308th, the Tenth Annual General Meeting of this Bank is going to be held in following date, time and place and for the purpose of discussion and decision of below mentioned agendas this notice has been published as per section 67 of the Companies Act 2063 to all the shareholders for their information and their valuable presence.

1. Date, Time and Place of Meeting Date : 13th January 2021 (Poush 29, 2077) Time : 11:30 AM Place : Head Office of the Bank, Kamaladi, Kathmandu

2. Resolution A) Ordinary Resolution

1. Discussion and approval of Chairman’s Speech and report of Board of Director for FY 2019/20 (FY 2076/77).

2. Discussion and approval of Consolidated Statement of Financial Position as of Mid-July 2020, Consolidated Profit or Loss Account for the period from 17th July 2019 to 15th July 2020, Consolidated Other Comprehensive Income, Consolidated Cash Flow Statement, Consolidated Statement of Changes in Equity, Significant Accounting Policies and Notes to Accounts, Annexure of Financial Statements and Disclosure & Additional Information including Audited Financial Statements (including its Subsidiary Mega Capital Markets Limited).

3. Approval of cash dividend of Rs. 406,342,210.19 (Four hundred six million, three hundred forty two thousands, two hundred ten rupees and nineteen paisa only) as proposed by Board of Directors which is 3.05 percent of current paid up share capital Rs. 13,322,695,416 (Thirteen billions, three hundred twenty two millions, six hundred ninety five thousands, four hundred sixteen rupees only).

4. Appointment of Statutory auditor of the Bank for the FY 2020/21 as per section 111 of the Companies Act 2063 and concluding his/her remuneration (Current auditor C.S.C. & Co. is eligible for reappointment).

B) Special Resolution1. Approval for issue of Bonus Share of Rs. 1,332,269,541.60 (One billion, three hundred thirty two million,

two hundred sixty nine thousands, five hundred forty one rupees and sixty paisa only) as proposed by Board of Directors which is 10 percent of current paid up share capital Rs. 13,322,695,416 (Thirteen billions, three hundred twenty two millions, six hundred ninety five thousands, four hundred sixteen rupees only) and after issue of bonus shares retaining the resultant fraction shares to be adjusted in future.

2. As a result of issue of bonus shares out of profits from FY 2019/20, the capital of the Bank will increase and capital structure of the Bank require amendment therefore amending para. (a), (b) and (c) of section 6 of Memorandum of Association.

3. Delegating authority for necessary changes in Memorandum of Association proposed for amendments if any changes are directed by regulating authorities.

4. Delegation of authority in relation to mergers or acquisitions with/to other banks or financial institutions with regard to all the activities relating to mergers or acquisition including formation of merger/acquisition committee, signing Memorandum of Understanding (MOU), appointing approved valuator (national and international) for conducting due diligence audit, prescribing remuneration of valuator, assessing share swap ratio, concluding final agreement for merger/acquisition and all other activities related with mergers and acquisition.

5. For the purpose of bringing foreign strategic partner as per prevailing laws and regulations, delegating authority to Board of Director for conducting necessary activities relating to identifying foreign strategic partner.

C) Miscellaneous

.........................….……………………………..By order of Board of Director

Company Secretary

10th ANNUAL REPORT 2019/2020

13Mega Bank Nepal Limited

1. For the purpose of Annual General Meeting, the record of share registrar of Mega Bank Nepal Limited shall be closed for one day on 2077/09/17. The shareholders transacted in Nepal Stock Exchange Limited till 2077/09/16 and included in record of share registrar of Mega Capital Markets Limited shall be allowed to attend general meeting.

2. To participate in the meeting on the date of General Meeting, shareholders attendance register will be opened from 9:00 A.M. to time until the completion of Annual General Meeting. To participate in the AGM Shareholders must present compulsorily, the original share certificate or documents proving their identity and shareholders who have dematerialized their shares must present DEMAT account number and original authorized identity card.

3. In order to prevent and control corona virus pandemic (Covid-19) that has been spread all over the world, considering the protection of the health of our valued shareholders and as per the Directions and Guidelines relating to health issues issued by Nepal Government and also as per the practice followed by peer banks and financial institutions, arrangement has been done for online virtual (Zoom) medium for attending meeting, presenting their views and voting. Therefore, in order to prevent or prevented from Corona Virus infection it is requested to attend through online (virtual) medium and shareholders attending physically are requested to bring their PCR report with them.

4. Shareholders attending meeting, presenting their views and voting at the General Meeting through online (virtual) (Zoom) medium must send, 48 hours before the commencement of AGM, a scanned copy of share certificate/Demat account at email [email protected] or viber/whatsapp at mobile number 985708413 or 9840073295 or SMS typing AGM then Meeting ID and Password shall be made available. The shareholders desiring to present their views in AGM can send their written views in mentioned email address.

5. The proxy form as prescribed by the Bank and containing Bank’s seal and signature of company secretary shall only be accepted.

6. Either public or promoter shareholders interested in appointing a proxy for attending the AGM shall fill the proxy form appointing all of their one category of shares to single shareholders and shall submit the form at least 48 hours before the AGM commencement to the office of Company Secretary of the Bank, Rising Mall, Kamaladi, Kathmandu. Shareholders who want to appoint a proxy for attending the AGM can appoint only to Bank’s shareholders as a proxy.

7. In case, if any shareholder appoints more than one proxy than he should apply attending himself/herself stating that “validate my current proxy by cancelling all other earlier appointed proxy” then only his/her earlier proxy shall be cancelled and proxy submitted with application shall only be valid. If any shareholder appoints more than one proxy, by way of division or not, but without any application, his/her all proxy will be cancelled.

8. If any shareholder present himself or herself in the AGM after appointing a proxy for attending the AGM then his/her proxy shall be automatically cancelled.

9. If any corporate entity or company who has purchased shares nominates representative, such representative can attend general meeting in a capacity of shareholder.

10. If any shareholder is minor or incapable, then the person who is registered as his guardian in the shareholders’ register shall be entitled to take part, vote, or appoint a proxy in the AGM.

11. The shareholders from domestic or foreign country unable to attend general meeting by himself/herself can download the proxy form from Bank’s authorized website www.megabank.com.np and signing in it can send scan copy to the Bank.

12. For more information about general meeting of the Bank, it is requested to contact at Bank’s phone numbers 4169216, 4169217 and extension numbers 108, 300, 306 and 193 at Bank’s Head Office or can be contacted to phone numbers 4262772 and 4262775 of our share registrar Mega Capital Markets Limited at Sanket Complex, Tripureshwor Kathmandu.

Other additional Information:The Book containing the annual report of Board of Director to be discussed at the meeting, Report of Auditors including Balance Sheet, Profit or Loss Account and schedules related thereto shall be made available at Head Office of the Bank and at Bank’s share registrar Mega Capital Markets Limited, Tripureshwor, Kathmandu and also at venue of general meeting on the date of general meeting. In addition, such reports shall be made available to shareholders’ emails available at Bank’s record and also in Bank’s website www.megabank.com.np. Abridged annual financial information has been published in national daily newspaper as per sub-section 4 and 5 of section 84 of the Companies Act 2063. Also, the annual report of Board of Director and proxy form can be downloaded from Bank’s website www.megabank.com.np.

Common Information relating to General Meeting

10th ANNUAL REPORT 2019/2020

14Mega Bank Nepal Limited

Proxy Form

Entrance

To Board of DirectorMega Bank Nepal LimitedRising Mall, Kamaladi, Kathmandu

Subject: Appointment of Proxy.

Sir,

I/we ………....................................................................… residing at …………..................................….. District ……….......................................……….

Municipality/ Rural Municipality ward number …………, in a capacity of shareholder of the Bank and being

unable to attend for the discussion and decision at Tenth Annual General Meeting being held on 13th January 2021

(2077/09/29), want to appoint representative to ………............................………. (Shareholder number/DEMAT number)

residing at ….......................................…………….. District ……….................................................…….. Municipality/ Rural Municipality ward

number ………........… to attend and vote at general meeting.

Representative Applicant

Signature: Signature:

Name: Name:

Address: Address:

Shareholder No: Shareholder No:

DEMAT No. DEMAT No.

Number of Shares Number of Shares

Date: Date:

Signature of Company Secretary

Bank’s Seal

Note: This application must be submitted to Bank’s Head Office before 48 hours of commencement of the

general meeting.

Shareholder’s Name: M/s ………………................................................……………. Shareholder Identity/DEMAT No: …………....………………

Number of Shares: ………………………….. Issued for attendance at Mega Bank Nepal Limited’s Tenth Annual General

Meeting.

………………….......................……… ……..…................……………..

Shareholder’s Signature Company Secretary

ljZjf; lhTb}=== cl3 a9\b}===

10th ANNUAL REPORT 2019/2020

16Mega Bank Nepal Limited

Mr. Bhoj Bahadur ShahChairman

An academician by profession, Mr. Bhoj Bahadur Shah is the former President of Private and Boarding School’s Organization of Nepal (PABSON) and Vice President of All Nepal School's Sports Association. He brings along great experiences of being the Founder / Chairman of Ananda Bhumi High School, Founder/ Chairman of National Integrated College and Director of Sahas Urja Hydro Power Company.

Mr. Mukti Ram Pandey Director

Mr. Mukti Ram Pandey holds a Bachelor Degree in Economics and has been the Chairperson of Samrat Group of Company (Tours /Travels/adventure/Hotel/Resort /Helicopter) for over two decades. He has previously held the prestigious appointment as the Board of Director of Nepal Tourism Board (NTB) and has also been a Board of Director of Nepal Airlines Corporation (NAC), the national flag carrier airlines, since 2014. He was amongst the founder Board of Directors of Mega Bank Nepal Ltd. and was also a Board of Director of Tourism Development Bank Ltd from 2012.

Ms. Shiba Devi Kafle Independent Director

Ms. Shiba Devi Kafle holds M.Phil. degree in Monetary Economics with optional International Economics from the University of Glasgow, UK after completing MA in Economics from Tribhuwan University, Nepal. Started her career as an Assistant Lecturer with Mahendra Ratna Campus in 1980, Ms. Kafle joined Nepal Rastra Bank and served various important departments in various capacities such as Public Debt Officer in Public Debt Department, Deputy Director of Research Department, Director of Research Department, Balance of Payment Division, between 1990 to 2010. After serving for several years with the Central Bank of Nepal, Ms. Kafle was briefly appointed as the CEO of Rastriya Banijya Bank (RBB) in 2011 before being appointed as the member of the Board of Directors of RBB from 2011-14. She has also served as the SAARC Finance Coordinator between 2004-2010 and was the Vice Chairperson of Nepal Rastra Bank’s ex-Employees’ Association from 2011-14.

Mr. Bal Krishna SiwakotiDirector

Mr. Bal Krishna Siwakoti holds a Bachelor’s degree in Management and is a successful businessman. He is a Board Member of Investment Board Nepal, Board Director of Kalinchowk Cable Car and the Managing Director of Dibya Saw Mill and KasthaUdhyog. He is the Chairman of Kalinaag Multiple College, Jiri Tea Udhyog Ltd. and Nirman Mediya Camp Pvt. Ltd. He was the former Chairman of Then Kalinchowk Development Bank Ltd., Secretary of AFRO Asia Peoples Solidarity Organization (AAPSO), Member of Bank, Finance & Insurance Committee (FNCCI) and former Central Committee Member of Nepal-Bharat Friendship Association.

Board of Directors

10th ANNUAL REPORT 2019/2020

17Mega Bank Nepal Limited

Mr. Gopal KhanalDirector

A Successful Businessman, a well-known Publisher and an Educational Entrepreneur, Mr. Gopal Khanal is the Chief Executive Director of Nepal Mega College and President of Asia Publication, Universal Printing Press and Pariskrit Carpet Industry. He is a member of the Executive Committee of the Federation of Nepalese Chambers of Commerce & Industry. Mr. Khanal is also a Council member of Sopan Multiple Company Limited.

Mr. Madan Kumar AcharyaDirector

Mr. Madan Kumar Acharya is a well-known social worker and a successful businessman with over two decades of rich experiences and contribution in the tourism sector of Nepal. He is the Managing Director of one of Nepal's leading Travel Company, Loyal Travels and Tours Pvt. Ltd. He is also a Central Member of the Canoeing & Rafting Association under Nepal National Sports Council and a member of the Airlines Program Joint Council (APJC) of Nepal.

Dr. Indra Bahadur Malla ThakuriDirector

Mr. Indra Bahadur Malla Thakuri holds Ph. D in Contribution of Tourism in Rural Economy of Nepal from Mewar University, Rajasthan India and is a successful academician. He is a Lecturer of Economics for 25 years and is the Principal in National Integrated College and NIC Secondary School. He was Board Director in Mega Bank Nepal Ltd. during Jan-Dec 2011. He has participated in various workshops, seminars and training programs.

10th ANNUAL REPORT 2019/2020

Respected shareholders,On the auspicious occasion of Tenth Annual General Meeting, I would like to express warm welcome to all the respected promoters and shareholders of this reputed institution from the entire mega family.Due to the hazardous impact of covid-19 pandemic, we have to forcefully organize and conduct meetings through electronic media. Despite of the fact that we were unable to conduct meetings through physical presence of all the members, I feel glad in a sense that we got the valuable opportunity to get connected with each other through the optimum use of emerging technologies.

Impact of covid-19Even though, the first 8 months of review period was in good condition in terms of Nepalese economy, the remaining period was devastating. You all are well familiar with the harshening and degrading economic conditions of Nepal as well as the entire world due to the tremendous and rocket speeding spread of Covid-19. The pandemic exerted the adverse effect on the entire industrial and business sector. The banking sector was also directly influenced. As the developed economy of the world are facing complexities in facing a war with covid-19, Nepal is no exception to it. As a result, the current financial year will also be directly influenced by the Covid-19.

Bhoj Bahadur ShahChairman

MEGA BANK NEPAL LIMITED

Chairman’s Speech

10th ANNUAL REPORT 2019/2020

19Mega Bank Nepal Limited

The role of remittance in the Nepalese economy is fundamental. The fund generated through remittance has been contributing to deposit mobilization, loan disbursement, and foreign currency management & commission income in banking sector. As the job loss seems to have been practiced largely in the global markets, and we expect decreasing inflow of remittance in future which would have profound impact on Nepalese economy. As various sectors of the economy such as export, import, construction, transportation, education has been influenced by Covid-19, it has negatively impacted income from foreign currency transaction, and fees income from non-funded services like letter of credit and bank guarantees.

Human resourceDespite the risk and fear of Covid-19 transmission, employees of Mega Bank were dedicated towards rendering quality customer services. I would like to thank all of them from the bottom of my heart. I am grateful to the dedication shown by Bank’s employees towards fulfillment of their roles and responsibilities by working in alternate working days and as per the security measures prescribed by regulatory authority. Thus, we consider our staffs not as resources but as assets for the organization. For the overall development and skill of employee, I want to memorize you that we have established Mega Learning & Development Center and have conducted various trainings and seminars.

Future StrategiesIn order to uplift the economic condition of the nation, we are providing the various rebates and facilities directed by regulatory authority, flowing subsidized loans, rescheduling and restructuring of the loans and installment, exempting penal amount and providing rebates in interest amount from the Bank’s side. Where the banking services which directly affects the daily life of the people, are categorized as basic services by Nepal Government, Mega Bank, under various additional policies and direction of government and regulatory authority, will carry on its day to day banking operation more efficiently and effectively making it more strong and stable.

Information TechnologyIn order to lessen the effect of COVID-19 through social distancing and securing financial transactions, cash transactions are discouraged and emphasis has been provided to Digital platform for performing banking transactions. At the time of pandemic, most of the banking transactions have been performed through the use of Digital platform, thus, we consider it as the opportunity created by COVID-19 pandemic. To tackle the challenges created by COVID-19, the Bank has also established Digital Product Department. We have also formed and implemented high level Digital Transformation Steering Committee. We have launched the system wherein the Customer can open their account conveniently and safely at home through the use of Video Account Opening System developed by the Bank.

Risk Management and AchievementThe Bank has been more cautious on operational risk exposed to when regular banking operation were conducted during the country lockdown because of COVID-19 pandemic, as Bank has continued its day to day operation through rotation and alternation of staffs, working from home with the use of digital platform, emphasis put on digital transaction and so on. Due to excessive liquidity in the market, interest rate on deposits and interest rate on loans has been decreasing as a result of which base rate has also been decreasing which has resulted tough competition in interest rate in the market. Decreasing interest rate on loans has acted as ointment for various business institution but on the other hand has also increased interest rate risk in banking system. From Ashad 2077, the regulatory authority has directed banks to reduce the differential average interest rate to 4.4 percent. This ensures the profound effect on the bank’s profit. The bank has been performing analysis regarding various internal and external activities related to risks.

International AwardsBank has increased investment by prioritizing the micro, small, cottage and medium industries as per its objectives. Considering the initiatives taken by the Bank, the Bank has been awarded with awards on two different discipline, Best bank for micro-finance and Best Bank for SMEs from International Journal “The Asiamoney Publication”. Adding another milestone in our journey, we have been awarded with the prestigious “BANK OF THE YEAR 2019” award from UK based reputed Financial Publication through publication in famous magazine “The Banker”.

Merger and Network ExpansionIn order to boost the corporate objectives of establishing as a leading bank in terms of capital and business volumes, the Bank by using the authority provided by its eighth Annual General Meeting, had signed Memorandum of Understanding (MOU) on 25th September 2019 with national level “B” class licensed institution “Gandaki Bikas Bank Limited”, head office situated at Pokhara Metropolitan city of Gandaki Province for its due acquisition. After receiving final approval from Nepal Rastra Bank, both Banks commenced their joint transactions effective from 4th July 2020 (21st Ashad 2077). After acquisition of Gandaki Bikas Bank Limited, the Bank has been leading strong institution in Gandaki Province and its position in Kathmandu Valley including Bagmati Province and Lumbini Province has be strengthen. In addition, the branch network of the Bank all over Nepal has been extended to 206 in numbers. After acquisition, the branches of the Bank has been extended to 58 districts from previous 51 districts. In the review period, the Bank has increased its volume (deposits and loans) by around 60 percent establishing itself amongst top 11 commercial banks that existed now in terms of business volume. In recent times, with continuous practices of mergers and acquisitions, voice has been raised for the need of big mergers. Thus, I assure that we have developed strategic foundation for prioritizing such initiation. I assume that mergers and acquisitions materialized until now have given us that experiences and knowledge as well. Current year, we are planning to adjust appropriately the duplicating branches occurred in same place due to acquisition of erstwhile Gandaki Bikas Bank Limited after which the activities for further branch expansion will get a pace.

Land Purchase and BuildingThe provincial building constructed in its own land situated in Butwal has been completed and is in use. Also, the Bank is inquisitive for appropriate land or building for its central office.

Corporate Social ResponsibilityWith an effort to ensure bright future of girl children, Mega Bank has started a campaign named as “Education is Enlightenment” where each branch has provided financial support and education materials to one girl student from economically deprived family from the previous year. Through this program, the Bank supports these selected girl children from Grade 1 to Grade 12. In continuation of that program and expanding the support, the Bank has provided support for 2 girl students from each branch effective from session commencing for 2077. In the panic situation of Covid-19 in the review period, the Bank provided financial support of Rs. 10 million to the fund established by Central Government and Rs. 5 hundred thousand each to the funds established by all State Governments, total funding being Rs. 13.5 million (Including contribution from staffs and member of Board of Director). We believe that these types of social activities are building positive perception among people towards the Bank.

At last, on behalf of Board of Directors and myself, I want to present heartfelt thanks to the promoters, shareholders, customers, Nepal Rastra Bank, Nepal Government, Securities Board Nepal, Nepal Stock Exchange Limited, Company Registrar’s Office, CDS and Clearing Limited and other regulators, Chief Executive Officer Mrs. Anupama Khunjeli her management team, Senior Deputy General Manager cum Company Secretary Mr. Tulsi Ram Pokharel, staffs, media and all those who directly or indirectly have contributed in business growth and development of the Bank.

10th ANNUAL REPORT 2019/2020

20Mega Bank Nepal Limited

JENU THAPAChief Liability Officer

MANOJ KHADKAChief Marketing Officer (CMO)

RAVEENA DESRAJ SHRESTHADeputy Chief Executive Officer

CHHABINDRA NATH SHARMABusiness Development Officer (BDO)

AMIT SHRESTHAChief Credit Officer (CCO)

Senior Management

10th ANNUAL REPORT 2019/2020

21Mega Bank Nepal Limited

RAJESH SHARMAChief Operating Officer (COO)

DENY SHRESTHAChief Global Market

ANUPAMA KHUNJELIChief Executive Officer

TULSI RAM POKHARELSenior Deputy General Manager

PRAGYA PANDEYChief Risk Officer (CRO)

10th ANNUAL REPORT 2019/2020

22Mega Bank Nepal Limited

2020 - A year to remember!

10 years is a milestone. It is an occasion to celebrate, an opportunity to momentarily look back and also a golden ticket to chart the path forward. With the completion of a decade long journey, this year it was marred by the unsurprising event CORORNA VIRUS.

With the worldwide spread of the virus, Nepal was affected equally with an uncertainty of business, jobs and even our life. This toughest period taught us to combat together; since the initial state of COVID-19 crisis, Mega Bank Nepal Limited (MBNL) have put its Customers at its ‘First Priority’ above and beyond all the scenario.

Yet, despite the odd stumbling blocks along the way - we have completed a decade - together, supportive, encouraging and enduring like a family. We, ‘Mega Bank’ not only saw the drawbacks of crisis but we took it as an opportunity to respond and give best facilities as possible to our Customers and communities equally.

Being one of the standing milestones of the economy, Bank has taken some corporate and non-corporate stand to help customers who were impacted by the coronavirus by deferring payments on their mortgages, personal loans, auto loans, and business loans which in-turn helped to realize that Bank act an important financial shock absorber for individuals, households, small businesses, and corporations by providing important liquidity when it is needed most and we ‘Mega Bank’ were able to stand by our customers going forward.

To our customers I would like to say: Thank you for your patience and enormous belief towards our Bank. We do not take it for granted.

Paradigm Shift of Business: The acquisition of erstwhile Gandaki Bikas Bank Limited with the huge increase on customer base in a considerable way is like paradigm Shift over our business module. The acquisition of Gandaki Bikas Bank Limited is a step forward for continuous growth, the cooperation of the Board of director and their tireless efforts in making our Bank function smoothly in such a contingent situation in the right direction is acknowledgeable.

Technology is the future!Technology has been creating a revolution in the world. Digitalization in banking does not only mean online

banking, internet banking, mobile banking or paperless banking rather it is the application of new technologies to transform the existing banking business model into a new banking business model.

A model which will itself produce new customer base, unveil new financial services, ensure faster and seamless services to clients with reduced operational cost, zero error, ease of use and apparently, maximum security. Therefore, it’s not only a new channel; rather it’s a whole new way of transforming existing transaction-based banking into the experience-based banking.

So that, banking can be accessed by customers anytime and from anywhere. Keeping this in mind, we have set up a MIS department where we gather the innovative ideas and put those ideas into the real time execution.

Being in the service industry, we are always looking forward to provide our customers the top most service.

In the coming years, our vision is to create the value creation to our customers where they can tap from anywhere in Nepal and get the desired service from our Bank without being able to visit any branch.

For example; we have introduced the account opening through video call which rightly gives path to our vision. Similarly, our internal control mechanism has been strengthen on year to year basis and ever improving towards mitigating and minimizing various risks. The Bank is committed to adopt and implement good governance system and has included corporate culture and ethics in its core values for its sustainable growth.

I would like to thank all of our stakeholders including our customers for their continued support and confidence they have put in the Bank. I would also like to express my appreciation to our dedicated Board of Directors, Management and Staffs for their invaluable contribution and hard work which brought the Bank at today’s position.

Not to forget, I am very grateful to Nepal Rastra Bank and other regulating bodies for their continuous guidance, framework and support.

Chief Executive OfficerAnupama Khunjeli

Message from CEO

10th ANNUAL REPORT 2019/2020

23Mega Bank Nepal Limited

10th ANNUAL REPORT 2019/2020

5. Mega Bank Today

a. Our Activities Our activities are concentrated over

two segments Retail Banking and Corporate Banking.

Retail Banking Mega Bank’s Retail Banking segment

offers various banking solutions to our retail customers through multiple channels offering various products and services featured with latest technologies.

Retail Deposits Retail deposits include saving

accounts, fixed deposits, high net-worth individuals, senior citizens, students, newly married couples, salaried employees, retired officials, remittance income earners, etc.

Retail Lending The Bank offers various ranges

of retail asset products including home loans, auto loans, consumer products loans, loan against gold/gilt securities/FD Receipts, education loans, personal loans, etc.

Payment Solutions The Bank’s payment products and

services are debit cards, credit cards, travel cards, Point of Sale (POS), QR Scan to Pay, etc. Other alternatives payments products and services are ATMs, Mobile Banking, Remittances and Online Internet Banking.

Corporate Banking Mega Bank’s Corporate Banking

segment offers various banking solutions to our corporate customers through various products and services like Credit, Treasury, Transaction Banking and Investment Banking.

Credits The Bank’s loan products and

fee-based products and services are targeted to meet the financial requirements of large corporate houses, medium-sized corporate clients and SMEs. Our products and services include corporate credits, mid-corporate credits, SMEs, demand loans, short-term loans, project financing, export credit, bills discounting, documentary credits, guarantees, and foreign exchange and derivative products. Our products and services on the liability side include current accounts, call accounts and time deposits.

Treasury The Treasury function in Bank

manages our non-credit funds by investing them in debt instruments including bonds and T-bills, and also engages in trading of equity

instruments of listed companies in Nepal Stock Exchange. The Treasury also manages regulatory reserve requirement of the Bank including Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). In addition, the Treasury division governs investment in mutual funds and manages foreign exchanges. It does private placements in domestic and foreign nostro balances and offers a wide range of treasury products and services to the Bank’s corporate clients including forward contracts deals and bullion trading.

Transaction Banking The Bank’s Transaction Banking

units offers varieties of inter-related and integrated products and services like current accounts, cash management services, capital market services (via. Subsidiary Company), foreign exchange and derivatives, correspondent banking services, revenue collection and dissemination on behalf of local governments, etc.

Investment Banking We provide investment banking

services and trusteeship services to our individual and corporate clients through our wholly-owned subsidiary Mega Capital Markets Limited. The wide range of services provided include investment management, share management, corporate advisory solutions, issue management, underwriting and services of securities registrars.

b. What We Are In addition to performing

contemporary banking, we are committed to set up business models that creates values by transforming various capital inputs (financial, social, intellectual, human) into value outputs (people, planet and prosperity).

We aim to do banking on financial realm of fair interest rates to savers, reasonable long-term return to investors, credit disbursements to sustainable entrepreneurs delivering real impact in the economy. For that purpose, we aim to use deposits rather than long term debt instruments and borrowings from other banks and we endeavor to deliver a healthy balance between loans and deposits so that we could mobilize as much of our deposits as possible.

We also maintain healthy levels of

financial capital, well above regulatory requirements. This will help us to do sustainable banking and makes us more resilient over the long-term.

10th ANNUAL REPORT 2019/2020

10th ANNUAL REPORT 2019/2020

26Mega Bank Nepal Limited

Call

Saving

Fixed

c. Key Figures

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

8,472

19,678

28,90336,375

73,082

Rs.

In M

illio

n

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

10,3718,446

15,452

20,821

33,409

Rs.

In M

illio

n

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

9,933

8,796

13,973

17,476

12,834

Rs.

In M

illio

n

10th ANNUAL REPORT 2019/2020

27Mega Bank Nepal Limited

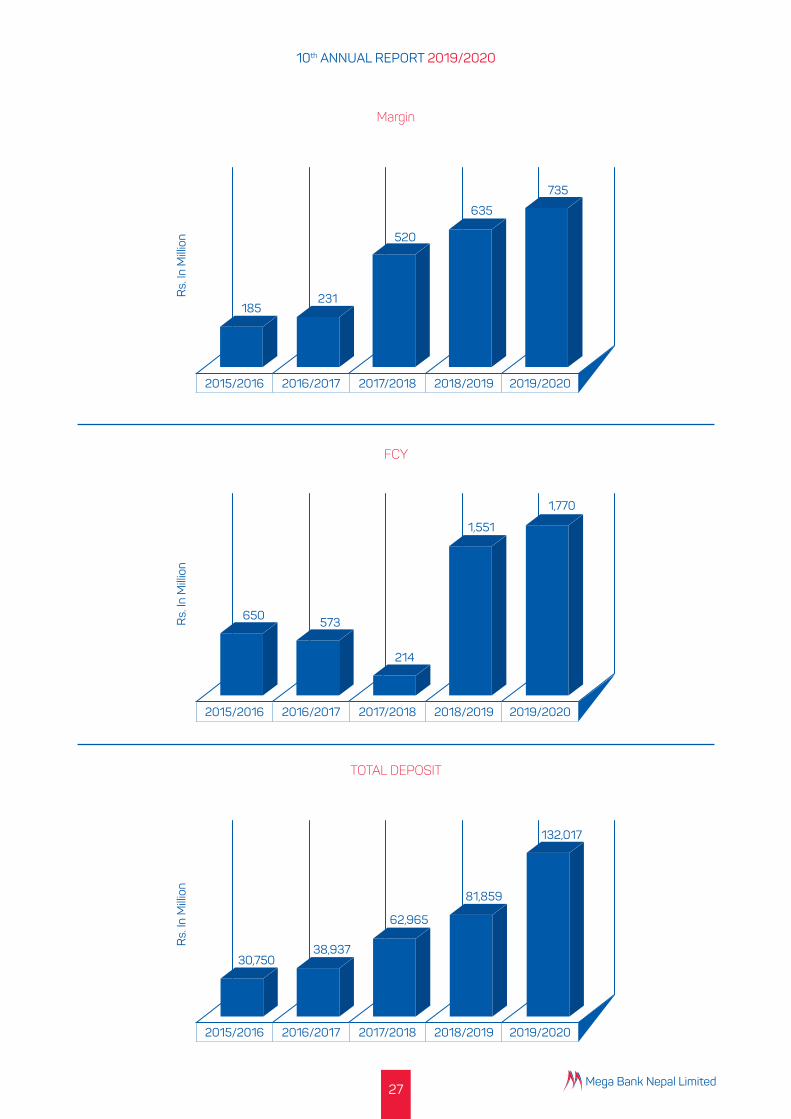

Margin

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

185231

520

635

735R

s. In

Mill

ion

FCY

TOTAL DEPOSIT

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

30,75038,937

62,965

81,859

132,017

Rs.

In M

illio

n

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

650 573

214

1,551

1,770

Rs.

In M

illio

n

10th ANNUAL REPORT 2019/2020

28Mega Bank Nepal Limited

CORPORATE

MID-CORPORATE

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

6,0547,673

12,108

19,372

30,044R

s. In

Mill

ion

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

7,930

10,898

13,96214,749

14,012

Rs.

In M

illio

n

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

6,045 6,526

10,78812,381

23,289

Rs.

In M

illio

n

SME

10th ANNUAL REPORT 2019/2020

29Mega Bank Nepal Limited

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

5,878 7,488

16,62819,720

38,687R

s. In

Mill

ion

RETAIL

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

27,82735,191

57,264

72,744

113,809

Rs.

In M

illio

n

TOTAL LOANS

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

1,5052,214

3,506

4,881

6,814

Rs.

In M

illio

n

MICRO

10th ANNUAL REPORT 2019/2020

30Mega Bank Nepal Limited

d. Mega Bank’s Presence Networks of Branches and Extension Counters

Bagmati ProvinceProvince 1

Province 2

Branches -20

Branches -12

Branches -73

Extension Counters -5

Extension Counters -2

Extension Counters -17

10th ANNUAL REPORT 2019/2020

31Mega Bank Nepal Limited

Gandaki Province Lumbini Province

Karnali Province Sudurpachim Province

Branches -47 Branches -39

Branches -9Branches -6

Extension Counters -5

Extension Counters -4Extension Counters -1

10th ANNUAL REPORT 2019/2020

32Mega Bank Nepal Limited

Other forms of NetworksBranchless Banking 89

Point of Sale 666

ATMs 142

QR Merchant Point 5600

Domestic 3200+International 23

Subsidiaries of Mega Bank Nepal LimitedMega Capital Markets Limited is in operation from 1st April 2019

Mega Stock Market Limited is incorporated and license under process.

Subsidiaries ofMega Bank

Nepal Limited

Subsidiaries

PartiallyFully

MegaCapital

MarketsLimited

10th ANNUAL REPORT 2019/2020

33Mega Bank Nepal Limited

6. Business Model and Strategy

a. The Future of Banking The three areas i.e. intangibility of the Bank’s service,

customer integration and heterogeneity in quality of service (caused by different individuals serving differently) will continue to pose opportunities and challenges for the Bank towards in future. In addition, the growing technologies and its dynamism is posing different challenges in pursuing the business model and our banking landscape.

To be successful and for sustainable banking, the

Bank of the future will need to embrace emerging technology, remain flexible to adopt evolving business models, and put customers at the center of every strategy. The future of banking will look very different from today. Faced with changing consumer expectations, emerging technologies, and new business models, banks will need to start putting strategies in place now to help them prepare for banking in future. As per Deloitte, the Bank needs to explore following eight key trends that are changing the banking landscape in future:

Enterprise Agility: The accelerated pace of technology innovation is

giving rise to new business model at an even faster speed. Today, competitive advantage doesn’t come from being big, but from being fast and nimble in adhering to latest technology.

Future of Work:

Banks are embracing new technologies and investing heavily in digital transformation initiatives in a ways to change the future work and workforce. Automation and artificial intelligence are replacing human thinking and urging Banks to revisit their talent landscape and knowledge management process.

Leveraging Platforms and monetizing data: Banks Today must offer customers the desirable

service in a way they want to receive it. Bank must use data to optimize their products and services to decide how they want to utilize platforms and the data, in order to grow.

Orchestrating across the ecosystem: The financial services ecosystem is growing.

Regulators, fintechs, banks, businesses and all others need to work together. The importance of deliberate ecosystem strategy and the effective orchestration will be vital in a days to come.

Cyber Risk and Financial Crime: The financial crime ecosystem is evolving as

criminals are adopting new and innovative ways

to commit crime. The Bank needs to embrace advanced technologies such as analytics and artificial intelligence to improve threat visibility and detect fraud effectively.

Data Integrity and Analytics: Data is power and it is plentiful in current context but

is not easily accessible, clean enough or integrated. Integrity of data will have profound impact over business intelligence.

Digital and Emerging Technologies: New technologies are drastically changing the

banking industry and financial markets. Artificial Intelligence and automation are proving to be valuable in ways we never thought possible. Blockchain and cloud computing are changing the industry outside Nepal and has implications as companies are trying to understand these technologies.

Embracing and becoming Digital:

Technology will continue to be the driver of the business growth and central to delivering a wide range of services through strong customer experiences. For Banks, it can be a vital to succeed through digital business model in a changing business environment.

Digitization, meanwhile, is driving down costs and causing commoditization. Intangibles enable a business to differentiate from its competitors. They are already the main drivers of the value that a business can create. The quality of its decision making enables a business to adapt more swiftly than its competitors to the opportunities and threats presented by the digital age and the developments in its markets. It is also the key intangible that unlocks the potential to develop other intangibles within the business, such as its competitive position, its brand’s reputation, the qualities of its people, its intellectual capital and how well it implements its decisions.

Customers are also changing the way they buy financial services. That means we can’t afford to sit on the sidelines when it comes to our digital capabilities. In order to enhance our digital capabilities, we have already established digital banking department.

Till Today, the Bank has already started various digital services like Smart Banking, Internet Banking, Online Account Opening and QR merchant payment system for our digital-savvy customer through which customer can perform both financial and non-financial transactions. Further to this, Bank is also launching Online Loan & Credit Card eligibility

10th ANNUAL REPORT 2019/2020

34Mega Bank Nepal Limited

module, Missed Call Based Banking Services & Chabot to electrify the consumers’ experiences.

Digital Banking Department’s preliminary focus is on the digital transformation of the Bank through research & design of digital products by analyzing the value proposition. Moreover, Digital Banking Department is also doing rigorous study of current business processes and automating the processes to enhance the efficiency as well as easing the control functions.

Banking is getting branch-less, contemporary and digital at a very fast pace. As Banks compete to gain competitive advantage, the need for managing big data and data analytics becomes more relevant. Data Analytics has transformed the way traditional banks worked in the past and has been very helpful

in informed decision-making. Banks are using predictive analytics software for studying customer behavior, fraud analysis, data processing and validation, use analytics to manage credit lines and collections.

Through associated data analytics tools, the Bank is trying to gain greater visibility into customers’ behaviors, assess the probability of risk and help small businesses. MIS & Automation unit of the Bank is combining various data sources like Core Banking Data & Transactional Data including other various alternate channels and analyzing those data to generate analytical MIS which is helping all the level of management for the effective decision making purpose.

b. Mission, Vision, Values

“Bank’s Mission is to serve the entire Economic Pyramid by enhancing inclusiveness amongst all strata of Nepalese Society while providing complete financial solutions. Delivering ‘Service Excellence to Create Mutually Beneficial Relationships' with all our stakeholders i.e. Shareholders, Customers, Regulators, Staff & Society to create, build and strengthen relationship of mutual benefit.

Service CentricProviding the best services in the industry

TransformationalAdopting latest knowledge and skills

Action OrientedBelieving in work ratherthan words

Result Focused & ResponsivenessDelivering consistent results

SynergisticWorking as a team to meet the needs

‘Banker of every Nepali from Plough to Power - Halo to Hydro’.

10th ANNUAL REPORT 2019/2020

35Mega Bank Nepal Limited

C. What does a Mega Bank makes a difference Mega Bank’s presence in the society is impacting

our various stakeholders in different ways. Its contribution to the environment in which it is operating includes human development, social relationship, financial return, nature preservation, cultural development, nation’s growth, social security development, etc. Following are the Bank’s key business models including products, services and approaches that signposts that the Bank has been playing pivotal role in shaping society and the country:

Inclusive business models including vision and

mission directs the Bank to contribute towards every strata of population.

Provincial specific CSR activities.

Focused products and services.

Typical rural presence over various parts of the country.

Tab banking and BLBs services aligned with our mission statement.

Adequate and standardized policies.

Flexible and effective organizational structure.

Adherences to corporate ethics and culture.

Country-wide branches and other networks like BLBs, ATMs, remittance agents, etc.

Embracing to latest technologies and services for customers like QR Payments, VISA & Master cards, Online banking, Mobile Banking, etc.

Committed and qualified workforce.

Priority over risk assessment, risk management and compliance issues.

Enhanced customers’ services because of our skilled and trained manpower.

In-house dedicated training centre - Mega Learning & Development Centre.

Knowledge management through knowledge portal (Mega Learning Portal) and frequent personal development programs like mock exams to each of the staff.

Dedicated functions in organizational structure like R&D unit, Product Optimization Unit, New Product Development Unit, Digitization Unit, etc.

Continuous development in Mega ERP software.

Diversified business operations via its subsidiaries

d. Management of Assets (Capital) The Bank holds valuable assets for the development

of its business model. The strategy defined by the Bank transforms these assets (capital) to create value for all its Stakeholders. Generally there are six different types of assets (capital) that company deploys to create value viz. Financial, Manufactured, Intellectual, Human, Social & Relationship and Natural. For the Bank, being wholly a service industry and investment concentrated over financial assets, manufactured capital is not much significant and natural assets deployment are not direct therefore not much material. However, Bank uses other major four types of assets in creating value for its stakeholders.

Assets (Capital) What is it? Significant

AreasManagement

Approach

Financial

Financial resources the company already has or obtains through financing.

However, the description of financial capital focuses on the source of funds (e.g., debt or equity) rather than its application, which may be in the form of intellectual property, or in other forms of capital.

Debt, Equity& Deposits

Balanced growth

Sound financial structure

Operational efficiency

Sustainable results and dividends

The financial resilience of this

model is built on fair interest rates

to savers to attract loyal, values-aligned customers

Reasonable long-term

returns for investors

Deposits deployment to sustainable entrepreneurship

Use of deposits rather than

borrow from other banks.

Use equity above regulatory requirements

10th ANNUAL REPORT 2019/2020

36Mega Bank Nepal Limited

Human

Employee knowledge, skills, experience and motivation.

Human resources management

Knowledge Management

Secured workplace

Talent management

Diversity

Equal opportunity

We focus on following three aspects:

Competencies: tacit and implicit knowledge and attitudes,

including skills acquired through formal

education and on the job

training

Capabilities: the sum of

expertise and ability to carry out an organizational activity.

Organizational culture: Indeed included in social

and relationship capital, but plays

an important role

in the ability of an organization to add value through human capital

development

Intellectual

Intangible, knowledge-based assets. Intellectual capital as a composite of other capitals

Promotion of R&D

Efficiency and new products and services

Disruptive technology and business models

Software, rights and licenses

Development of organizational capital such as tacit knowledge, system,

procedures and protocols

Developments of brands and reputation

Social & Relationship

Ability to share, relate, and collaborate with its Stakeholders, promoting community development and well-being

Stakeholder relations

CSR activities

Group foundations

Corporate reputation

Brand management

Informational transparency

Promote and maintain relations of trust with stakeholders

Improving quality of life of people

Creation of an organization’s social license to operate

e. Value Chain

Value Creation Value activities are the means by which a firm

creates value in its products and services.

Porter (in Competitive Advantage) grouped the various activities of an organization into a value chain. He has distinguished activities as primary activities and support activities. The excess the customer is prepared to pay over the cost to the Bank of obtaining resource inputs and providing value activities is the profit margin. It represents the value created by the value activities themselves and by the management of the linkages between them.

The activities of the Bank can be linked over to the Porter’s Value Chain Model as Business Functions (i.e. primary activities) like Deposit Business, Credit Business, Remittance, Global Business, Cards & Alternate Channel, etc. and Support Functions (i.e. support activities) like Finance & Planning, Credit Administration, Information Technology, Human Resource Management, etc.

In addition to primary and support activities, other few functions are streamlined with their operational strategy in order to have control and overlook into actions of both primary and support functions known as Control Functions like Internal Audit, Compliance, Risk, etc.

The Bank’s value creation process of the Bank is driven by transforming capital inputs. These inputs include the skills and entrepreneurship of the people within our organisation and money from shareholders, debt holders and customers, via our core products and services.

Bank transforms these inputs into value outputs so that they make a valuable contribution to the development of an environment around us.

10th ANNUAL REPORT 2019/2020

37Mega Bank Nepal Limited

Capital Input for Value Creation Value Created

Financial Capital:Bank uses capital effectively so as to maximize the value to be created. Our dynamically managed and deposit driven funding modality together with well diversified deposit mix and opportunistic utilization of alternative funding drives our disciplined, sustainable and financial growth. With a 6 times growth of paid up equity capital since 2010, challenges lies in sustaining business growth in order to cope with growing equity capital. Thus, it is our goal to constantly improve our business model and processes with an operational and environmental efficiency point of view and seek cost and revenue synergies in creating value to the providers of financial capital.

We contribute to the economy and the society by paying dividends to our shareholders, salaries to our employees, invoices to our suppliers and tax revenues to governments.

Total value addition to the economy by the Bank is NPR. 9.717 billion.

Return on equity 14.65%

Return on Assets 1.64%

Capital Adequacy Ratio 13.241%

We make a significant contribution to public finances not only through our own tax payments, but also, through third party tax collection (TDS) due to our economic activity.

Intellectual Capital:We constantly invest in digital platforms so as to provide transaction convenience, unrivaled customer experience and pioneering solution suggestions to our around 1.09 million banking customers. We are expanding our digital customer base and increasing the share of digital channels in our sales. Our efforts are directed towards employees’ skill development, creativity, problem solving techniques, enhancing customers’ loyalty and brand development of the Bank. We use various channels and advertising media to create our intellectual assets. However, we take precautions against all types risks which comfort us in providing secure and uninterrupted service ensuring information security.

Our investment in digital channels resulted in increase in revenue of:

Mobile banking fee 109%

Credit Card related fee 36%

Other Cards fee 38%

We have been able to increase our:

Mobile banking user by 92.91%

Internet banking user by 11.22%

Credit card user by 31.46%

Other card customer by 44.17%

Four number of new saving deposits products were developed and issued with varied features and facilities

Human skills development though not measurable with rigidity, but impacting our performance due to increase in confidence and enhancement of skills in our employee.

ERP software integrating all HR functionality and comprehensive platform for knowledge and information sharing

We have been capable of disseminating good footprint over various media i.e. newspaper, online news, radio, televisions, hoarding boards, banners, programs, etc.

10th ANNUAL REPORT 2019/2020

38Mega Bank Nepal Limited

Human Capital:We invest in our employees by focusing on their development, satisfaction and well-being through training and well-being programs. We strive to form teams possessing team spirit, acting with shared wisdom, social responsibility and delivering results. We embrace a fair and transparent management policy based on performance, focused on equal opportunities and diversity.

Our relationship with our customers is built on trust by exceeding their expectations and enhancing their satisfaction.

Customer experience focus is at the core of our business model.

Our efforts in supporting financial literacy, CSR activities have contributed to thousands of people and millions of customers.

We have had partnership with various projects, INGOs/NGOs like Sakchhyam, DFID, Helvetas, etc.

We are supporting to government development plans by flowing the government funds at local level through our dedicated branches and other networks.

Bank creates value by transforming capital inputs viz. financial capital, intellectual capital, human capital and relationship capital. Normally, these inputs include the skills and entrepreneurship of the people within our organisation and money from customers, via our core products and services. Bank transforms these inputs into value outputs posing positive contribution to people and planet and compels for prosperity in future. The financially measured value addition by the Bank in past five years have been depicted in following figure:

Value Addition by Bank Rs. in millions

Value NetworksSince our stakeholders, all internal, connected and external, are of great importance to us, regular communication with our stakeholders gives us the opportunity to be an inclusive Bank. The feedback from our stakeholders allows us to determine risk and opportunity areas more comprehensively as well as understand stakeholder expectations and meet their needs more sensitively. In addition to maintaining the dialogue with our stakeholders through various channels all year round we have separate various units/departments and assigned functional roles to individual staffs:

Promoter Networking Management:To coordinate, communicate and support large base of the Bank’s promoters

Corporate Affairs Department:Tackle and manage media and publication

Grievance Handling Unit:Listening to the grievances and complaints of customers

Relationship Managers/Officers:Maintaining cordial relationship with loan clients

Deposit Relationship Managers/Officers:Maintaining cordial relationship with deposit clients

Bank has defined following stakeholders as the key stakeholders in the Bank’s value network:

Board

Regulating Bodies/Government

Shareholders/Investors

Customers

Suppliers & Vendors

SeniorManagement (BOD)

Employees2,131

4,016

6,191

9,0569,717

2015/2016 2016/2017 2017/2018 2018/2019 2019/2020

10th ANNUAL REPORT 2019/2020

39Mega Bank Nepal Limited

Bank manages the various stakeholders in order to create value as below:

Stakeholder Issue What do we do about it?

Customers

Networks over country

Appropriate return to depositors

Flexible products

Customer satisfaction

Financial health of the Bank assuring security of their deposits

Customer privacy and information security

Digital transformation and technological advancement

Business model captures the benefits of the emerging digital world with the aim of offering an excellent banking experience

QR code based transaction options

Online banking

Mobile banking & SMS alert

Knowing all the information needed to resolve customer issues in a practical way through dedicated units and people

Services to customers from customer care line.

Customer focused loan and deposit products

Branch expansion is our continuous process

ShareholdersandInvestors

Financial performance

Good corporate governance

Transparent disclosure of information for stakeholders

Risk and crisis management

Stakeholder dialogue

Financial capital always kept above regulatory requirement

Good corporate governance is our commitment

Work culture and ethics is injected in blood of each employee through our corporate values

Increased engagement of the CEO visibility with the investors and the media

Healthy flow of the funding received to the commercial market and to the investment community

Transparency in accounting, reporting and disclosures

Employees

Transparent disclosure of information for stakeholders

Compliance

Risk & crisis Management

Governance issue

Social contribution

Value addition to government exchequer

Contribution to national sustainable goals

Listed in stock exchange

Reliable CBS for database and its security

Close supervision and timely inspection by regulator (NRB)

Quick response and follow up of regulatory ] directions

Contributed largely in capital formation through enhancement of lending in productive sector

Supported government’s financial inclusion programs by opening branches at rural municipalities and routed government budget at local level

Supported prime minister’s slogan of every Nepali’s bank account

Contributed to various government approx. NPR. 709 million as direct tax and millions of rupees in the form of tax collection at source

10th ANNUAL REPORT 2019/2020

40Mega Bank Nepal Limited

GovernmentAgenciesandRegulatoryBodies

Transparent disclosure of information for stakeholders

Compliance

Risk & crisis Management

Governance issue

Social contribution

Value addition to government exchequer

Contribution to national sustainable goals

Listed in stock exchange

Reliable CBS for database and its security

Close supervision and timely inspection by regulator (NRB)

Quick response and follow up of regulatory directions

Contributed largely in capital formation through enhancement of lending in productive sector

Supported government’s financial inclusion programs by opening branches at rural municipalities and routed government budget at local level

Supported prime minister’s slogan of every Nepali’s bank account

Contributed to various government approx. NPR. 669.78 million as direct tax and millions of rupees in the form of tax collection at source

TopManagement

Management of risks

Financial sustainability

Digital transformation and technological advancement

Financial performance

Increasing customer satisfaction

Investing in human capital

Customer privacy and information security

Mitigating various risks and managing adequate capital internally for credit risk, liquidity risk, market risk, strategic risk, operational risk, etc.

Business models are designed based on Digital Banking products

Separate team is dedicated for data mining and analysis and developing platforms for creating value from existing data

Strategies are developed to increase the return every year by expanding business and bringing efficiency in cost

Re-structuring the organogram with market dynamism and business complexity

Structure developed with provincial framework

Value DistributionBank’s value distribution is spread over triple Ps i.e. People, Planet and Prosperity.

Planet Credit lending for sustainable and inclusive enterprise Financial inclusiveness in our strategy and action Funding to environmental protectionist via our CSR programs

Prosperity Fair Return on Equity above 10% in average in last 7 years High capital adequacy ration ensuring capital resilience Developing inclusive visions for the future Thought process of digitalization in future of banking

People A positive contribution to the healthy development of society’s people Brought about social change through employment creation, credit creation, social initiatives, etc. Enabling values-driven entrepreneurs to fulfil societal needs through productivity and services Transparency in finance and investment activities

Distribution of value created by the Bank to its various major stakeholders are as below:

9%14%

21%

56%

FY 2014/15

EmployeeDepositors/LendersGovernment Shareholders

10th ANNUAL REPORT 2019/2020

41Mega Bank Nepal Limited

Employee

Employee

Depositors/Lenders