10th Anniversary Annual Conference 2007 - Asian ...

212

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 10th Anniversary Annual Conference 2007 - Asian ...

A Decade of Developments10th Anniversary Annual Conference 2007

Edited by Masahiro Kawai and Susan F. Stone

Asian Development Bank Institute

Kasumigaseki Building, 8th Floor

3-2-5 Kasumigaseki, Chiyoda-ku

Tokyo 100-6008, Japan

www.adbi.org

©2008 Asian Development Bank Institute

ISBN: 978-4-89974-026-1

Freely available electronically at:

http://www.adbi.org/book/2008/11/20/2755.decade.dev.2007/.

The views expressed in this work are the views of the authors and do not necessarily reflect

the views or policies of the Asian Development Bank Institute (ADBI), the Asian Development

Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not

guarantee the accuracy of the data included in this work and accepts no responsibility for

any consequences of their use. Terminology used may not necessarily be consistent with ADB

official terms.

Foreword ivPreface viContributors viiAbbreviations xiii

I. Overview 1 Masahiro Kawai Susan F. Stone

II. Financing Asian Growth 23 Peter A. PetriIII. Asian Crisis Ten Years On: Policy Perspectives 45 Mohamed Ariff Azidin Wan Abdul KadirComments 70 Akira Ariyoshi Chia Siow Yue

IV. Poverty Reduction, Inclusive Growth, and Development Strategies 79 Justin Yifu Lin V. Rising Inequalities in Asia: An Imperative for Inclusive Growth 109 Ifzal Ali Comments 128 Iwan Azis Yasuyuki Sawada

VI. State of Integration in the Asia-Pacific Region: Current Patterns and Future Scenarios 135 Antoni Estevadeordal Kati SuominenVII. A Composite Index of Economic Integration in the Asia-Pacific Region 163 Chen Bo Yuen Pau WooComments 181 Shinji Takagi David Kruger VIII. Summary 185

The Asian Development Bank Institute (ADBI) was established in 1997 as a subsidiary of the Asian Development Bank to respond to two needs of developing member countries: identification of effective development strategies and improvement of capacity for sound management of agencies and organizations in those countries. As the chapters in this volume demonstrate, ADBI has indeed helped foster “A Decade of Developments.”

Asia has shown the way to regain economic buoyancy and vibrancy after the 1997/98 Asian financial crisis as demonstrated by its remarkable growth and development over the past decade. Reforms have put the previously affected countries in a good position to face any potential future turbulence. The lessons of the last crisis, and the need for reform to make economies competitive and resilient, are lessons that are just as relevant today. The spread across Asia of such reform more than 10 years ago raised the standard of performance across the region. However, as the current situation illustrates and is further shown in the chapters contained in this volume, much work still needs to be done—especially in the field of governance and institutional strengthening if the region, and indeed the world, are to face up to the challenges of globalization.

Asia’s rapid growth has contributed to a remarkable decline in the incidence of poverty throughout the region. Yet the chapters in this volume show that this growth has not been enjoyed equally among all Asia’s inhabitants. Indeed, a compelling case has been made that rising inequalities in Asia pose a “clear and present danger” to social and political stability. The work presented suggests that governments can help alleviate these concerns by ensuring broad access to economic opportunities, by providing a social safety net to those at most risk, and by equipping the poor with the tools necessary to become productive in the economy.

A by-product of the Asian financial crisis has been the increasing move by countries in the region toward enhanced economic cooperation and integration. Driven by the private sector, market-led regional economic integration has deepened as value and production networks have grown. Regional cooperation can nourish it further.

However, as the chapters on growth through regional cooperation and integration argue, increasing integration may have its downsides. One is the exposure of each country’s domestic sectors to greater regional competition and the possible dislocation of workers in such sectors. Another is the rising

number of regional agreements that may lead to an increasing complexity and a “noodle bowl” in the regional trading system, rather than the transparency such a system needs to maintain efficiency. It is important that governments in the region be given the support and tools, through research and capacity building such as those offered by ADBI, needed to meet these challenges.

It is somewhat ironic that as ADBI observed the anniversary of its founding in the wake of the Asian financial crisis, the seeds were being sown for another financial crisis. The current global financial crisis, starting in the US and having spread to Europe, is on a scale not seen in many decades. Indeed, in the wake of the collapse of some of the world’s leading investment banks there is growing concern over the specter of a deep and prolonged recession in the developed economies. While impact on the Asian economies has so far been relatively limited, deep and prolonged recession in the developed economies can eventually adversely affect Asian economies which for more than two decades have banked on export-oriented development strategies. Moreover, there is always concern that a decline in global growth may disproportionately affect the world’s most vulnerable, many of whom are in Asia.

As a development institution, ADB faces formidable challenges in the decades to come as Asia and the Pacific deals with the looming global economic slowdown and transforms itself rapidly. These challenges will test ADB’s ability to be more relevant at a time when a number of its traditional borrowers are developing quickly. ADB must rise to these challenges and adapt with the times to demonstrate that it is well equipped to effectively meet the emerging needs of its clients. In this regard, ADBI has an important role to play in providing the knowledge inputs to help strengthen the relevance of ADB.

So, on the occasion of its tenth anniversary, I congratulate ADBI on its achievements. I encourage the Institute to continue in its efforts to remain prescient and forward looking and hope to see the Institute become one of the leading knowledge centers in the region.

Haruhiko KurodaPresident, Asian Development Bank

This volume celebrates and revisits development issues in Asia and the Pacific highlighted by the Asian Development Bank Institute (ADBI) over the last ten years. A Decade of Developments covers a lot of ground, thanks to the distinguished scholars who addressed questions covering broad topics and the equally distinguished discussants who objectively commented on the key issues raised by the scholars. We are fortunate to have had honorable chairpersons with extensive knowledge who were able to guide us in an interesting set of intellectual debates on some specific issues. The conference did not dwell on the past but instead looked to the future regarding each of the topics, answering the key questions of:

(i) How the legacy of the Asian financial crisis of 1997–1998 impacts future economic and financial initiatives at the national and regional levels;

(ii) What analytical and policy implications are drawn by moving from the single objective of poverty reduction to including concerns about inclusive and sustainable growth; and

(iii) What will come as the region embarks on even greater regional cooperation and integration.

We are most grateful to these distinguished participants, as well as the attendees’ high-caliber questions and discussions, for providing an insightful and meaningful body of work.

Finally, I wish to acknowledge the talented and dedicated staff of ADBI, both past and present, without whose hard work and dedication ADBI could not fulfill its role.

Masahiro KawaiDean, Asian Development Bank Institute

Ifzal Ali is Chief Economist, Economics and Research Department, ADB. Over his career in ADB he has assumed various key positions including Senior Strategic Planning Officer, Assistant Treasurer, and Deputy Treasurer. Prior to ADB, he was Professor/Chairman of the Economics Area in the Indian Institute of Management Ahmedabad. His research interests include the role of macro and microeconomic policy reforms in the context of globalization and competitiveness for the developing countries of Asia. His research focus in the past two years has been on inclusive growth. He holds a PhD in economics from John Hopkins University.

Mohamed Ariff is the Executive Director of the Malaysian Institute of Economic Research (MIER). He was the Chair of Analytical Economics at the University of Malaya, where he also served as Dean of the Faculty of Economics and Administration. He was conferred emeritus professorship by the University of Malaya in 2004 and “Datukship” by His Majesty the King in 2007. He has authored, co-authored, and edited many books and monographs, in addition to publishing numerous articles in academic journals and mass media. His work deals with international trade, foreign direct investments, and regional economic integration. He obtained his PhD in 1970 at the University of Lancaster, England, as a Commonwealth Scholar.

Akira Ariyoshi is the Director of the International Monetary Fund (IMF) Regional Office for Asia and the Pacific, monitoring regional economic and financial developments in the region. He joined Japan’s Ministry of Finance as a career civil servant in 1976 and held a variety of positions, most recently Deputy Director-General of the International Bureau. He also has worked at the IMF in Washington, DC on two occasions, most recently from 1998 to 2000 as Assistant Director of the Monetary and Exchange Affairs Department (now Monetary and Financial Systems Department). He holds a PhD in economics from the University of Oxford.

Iwan Azis is a Professor and Director of Graduate Study in Regional Science at Cornell University. He was the Chair of the economics department at the University of Indonesia and Director of the Inter-University Center for Economics. He has conducted research and consulting work for various international organizations, universities, and governments. He has addressed topics of financial economics, regional economic modeling, and linkages

between macro-financial policy and social issues. During the last five years, he has published numerous articles, and is currently working on two books. In 2006, he received a “Distinguished Scholar in Regional Science, Financial Economics, and Economic Modeling” award (in Lisbon, Portugal). He is a regular Visiting Fellow at ADBI.

Thanong Bidaya is a Visiting Fellow at ADBI. He served as Associate Researcher at the World Bank, and later as Assistant Professor at the National Institute of Development Administration (NIDA) in Thailand. His private sector experience includes the Thai Military Bank (TMB) and the Shinnawatra group developing project finance for telecommunications systems. In 1993, he became President of TMB. In 1997, he was appointed Finance Minister to manage Thailand’s economic crisis. He was appointed Chairman of the National Economic and Social Development Board as well as Thai Airways International before joining the Thai cabinet as Commerce Minister. He later served again as Finance Minister from 2005 to 2006. He received a PhD in management and a master’s degree in economics from Northwestern University.

Siow Yue Chia is a Senior Research Fellow at Singapore Institute of International Affairs. She was previously a professor of economics at the National University of Singapore and retired as Director of the Institute of Southeast Asian Studies in 2002. She was the Regional Coordinator of the East Asian Development Network and has also been a consultant to several international and regional organizations. She has published extensively, with over 150 books and journal and professional articles. Her research interests include the Singaporean economy; economic integration and regional trading agreements in the Association of Southeast Asian Nations (ASEAN) and Asia-Pacific Economic Cooperation (APEC); international trade and foreign direct investment in Asia and the Pacific region; and poverty, economic development, and labor migration in East Asia. She has a PhD in economics from McGill University.

Antoni Estevadeordal is Manager of the Integration and Trade Sector at the Inter-American Development Bank (IADB). He has expertise in trade policy, economic integration, and regional cooperation in Latin America and the Caribbean, Asia, and Europe. He is responsible for IADB operational support, technical assistance, and the policy research program on trade development issues and regional integration initiatives. He coordinates several joint initiatives with partner agencies. Before joining IADB, he taught at the University of Barcelona and Harvard University.

He has published in major journals and contributed to several books. He has coordinated several IADB reports and is currently preparing a report on Latin America and India. He has a PhD in economics from Harvard University.

Azidin Wan Abdul Kadir is a fellow in the macroeconomic trends and forecasting section of the Malaysian Institute of Economic Research (MIER). His section produces the quarterly outlook report for the Malaysian economy and the quarterly survey reports on consumer and business confidence. He has been involved in projects for the public and private sectors, such as studies for the national industrial master plans, the auto industry, and the wood industry. He holds a MSc in statistics from the University of Iowa, United States.

Masahiro Kawai became Dean of ADBI in 2007 after serving as Head of ADB’s Office of Regional Economic Integration. Previously, he was a professor of economics at the University of Tokyo’s Institute of Social Science. He also served as Deputy Vice Minister of Finance for International Affairs of Japan’s Ministry of Finance and Chief Economist for the World Bank’s East Asia and the Pacific region. He has published numerous books and academic articles on economic globalization and regionalization, and regional financial integration and cooperation in East Asia. He earned his PhD in economics from Stanford University.

Justin Yifu Lin is Professor and Founding Director of the China Center for Economic Research (CCER) at Peking University and a professor of economics at Hong Kong University of Science and Technology. He is also a Senior Advisor to the Drafting Committee of China’s Tenth Five-year Plan, the State Leading Group of IT Development, and the mayors of Beijing, Shanghai, Tianjin, and Liaoning Provinces. He is a member of the National Committee, China People’s Political Consultation Conference. He is the author of eight books, including The China Miracle: Development Strategy and Economic Reform and State-owned Enterprise Reform. He has published over 100 articles in refereed international journals and other publications on history, development, and transition. He received his PhD in economics from the University of Chicago.

Peter McCawley is a former Dean of ADBI and Visiting Fellow at the Australian National University. He has worked as an adviser to the Australian Government, Indonesian Ministry of Finance, and various international agencies on foreign aid and international economic issues. He is a former Deputy Director General of AusAID, where he served on

the Executive Committee until 2002, and was a member of ADB’s Board of Directors from 1992 to 1996. He has regularly been involved in the negotiations for the replenishment of ADB’s Asian Development Fund. He has published numerous articles in academic journals and the media. He graduated from the Australian National University with a PhD in economics.

Peter A. Petri is Dean of the International Business School and the Carl J. Shapiro Professor of International Finance at Brandeis University. He has served as Visiting Scholar at the Organisation for Economic Co-operation and Development (OECD) Development Centre, as a Fulbright Research Scholar at Keio University, and as a Brookings Policy Fellow. He has consulted for the World Bank, OECD, and United Nations. He is a member of the Board of the United States Asia Pacific Council, the International Advisory Group of the Pacific Economic Cooperation Council’s Trade Policy Forum, and the Pacific Trade and Development Forum (PAFTAD) International Steering Committee, and is a former Chair of the US APEC Study Center Consortium. He received his PhD in economics from Harvard University.

Yasuyuki Sawada is an Associate Professor of Economics at the Graduate School of Economics, Tokyo University. His field of expertise includes development economics, applied micro-econometrics, and field surveys. He has worked on both micro-econometric studies of household poverty and community participation and on macroeconomic analyses of debt and currency crises of middle- and low-income countries. His current interests include natural and manmade disasters, official development assistance, economic analysis of suicide, dualistic development, and intra-household resource allocation in Japan. He has a PhD in economics from Stanford University.

Aftab Seth is Chairman of the International Advisory Committee and a professor of the Global Security Research Institute, Keio University. He is a former Ambassador of India to Japan, Greece, Viet Nam, and Federated States of Micronesia. He is a member of the Advisory Board of the Global Indian International School of Tokyo and the Board of Management of the Indian Institute of Foreign Trade. He is also Chairman of the International Advisory Board of the World Peace and Development Association, People’s Republic of China, and Director to the Japan–India Association. He was a Rhodes Scholar at Oxford and received his law degree from the American College of Greece.

Kati Suominen has served since 2003 as International Trade Specialist at the Inter-American Development Bank in Washington, where she leads team research projects on global trade issues and coordinates several inter-institutional initiatives. She has spoken at such venues as the World Bank, World Trade Organization, US International Trade Commission, United Nations, Organization of American States, European Commission, and Asia-Pacific Economic Cooperation conferences. She is currently co-authoring and editing six books, among them Regional Rules in the Global Trading System Trade Agreements (IDB-WTO book to be published by the Cambridge University Press, 2009) and Sovereign Remedy? Leveraging Trade Agreements in Globalization (Oxford University Press, 2008). She is a candidate at the Wharton School’s MBA Program for Executives Class of 2009. She holds a PhD in political economy from the University of California, San Diego (2004).

Shinji Takagi is a Visiting Fellow at ADBI and professor of economics at the Graduate School of Economics, Osaka University. His numerous professional appointments have included Economist, IMF; Senior Economist, Japanese Ministry of Finance; Visiting Professor of Economics, Yale University; and Advisor, IMF Independent Evaluation Office. He is a specialist in international monetary economics and is the author of over 70 publications, including four books. His recent work has dealt with exchange rate policy, emerging market crises, capital market development, and regional policy cooperation. His textbook on international monetary economics is currently in its third edition. He holds a PhD in economics from the University of Rochester.

Hiroshi Watanabe is Special Advisor to the President of the Japan Center for International Finance (JCIF), and is Japan’s former Vice Minister of Finance for International Affairs. He joined the Ministry of Finance in 1972 and served in many areas, including taxation policy formulation. From 1998 to 2001, he served as the personal secretary to then Finance Minister Kiichi Miyazawa and took the leadership in the discussion on the New Miyazawa Initiative to assist crisis-affected Asian countries. In addition, as a senior official of the International Bureau of Japan’s Ministry of Finance from 2001 to 2003, he focused on promoting Asian monetary cooperation and bilateral assistance. He graduated with a law degree from the University of Tokyo and holds a master’s degree in economics from Brown University.

Yuen Pau Woo is President and Co-CEO of the Asia Pacific Foundation of Canada. He is Canada’s representative on the Standing Committee of

the Pacific Economic Cooperation Council (PECC), chairing the Pacific Economic Outlook forecasting panel, and he coordinates the annual State of the Region report. He is Director of the APEC Study Centre in Canada and is on the management boards of the National Centres of Excellence in Immigration (University of British Columbia and Simon Fraser University) and Emerging Markets (University of Ottawa). He is also an advisor to the Centre for Asia-Pacific Initiatives at the University of Victoria, the Shanghai WTO Affairs Consultation Centre, and the Asian Development Bank. He was educated at the University of Cambridge and the University of London.

ADB Asian Development Bank

ADBI Asian Development Bank Institute

AFTA Association of Southeast Asian Nations Free Trade Agreement

AKFTA Association of Southeast Asian Nations–Republic of Korea Free Trade Agreement

AP Asia-Pacific

APEC Asia-Pacific Economic Cooperation

ASA Association of Southeast Asian Nations Swap Arrangement

ASEAN Association of Southeast Asian Nations

BIT bilateral investment treaty

CAD comparative advantage-defying

CAF comparative advantage-following

CAFTA Central America Free Trade Agreement

CER closer economic relations

CF common factor

CFA common factor analysis

CI convergence index

CMI Chiang Mai Initiative

ECAFE Economic Commission for Asia and the Far East

EPA economic partnership agreement

ESCAP Economic and Social Commission for Asia and the Pacific

EU European Union

FDI foreign direct investment

FTA free trade agreement

FTAAP Free Trade Area of the Asia-Pacific

GDP gross domestic product

HDI Human Development Index

IADB Inter-American Development Bank

ICOR incremental capital-output ratio

IMF International Monetary Fund

KORUS Republic of Korea–United States Free Trade Agreement

LSI Lisbon Strategy Indices

M&A merger and acquisition

MFN Most Favored Nation

NAFTA North American Free Trade Agreement

NEER nominal effective exchange rate

NIE newly industrializing economy

NPL non-performing loan

OECD Organisation for Economic Co-operation and Development

OLS ordinary least squares

PC principal component

PCA principal component analysis

PRC People’s Republic of China

PTA preferential trade agreement

R&D research and development

REER real effective exchange rate

ROOs rules of origin

RTA regional trade agreement

SWF sovereign wealth funds

TCI technology choice index

UNCTAD United Nations Conference on Trade and Development

UNDP United Nations Development Programme

US United States

WCO World Customs Organization

WTO World Trade Organization

Masahiro Kawai

Susan F. Stone

This volume represents the first in a series of publications of the Asian Development Bank Institute (ADBI) Annual Conference. The 2007 conference, entitled “A Decade of Developments,” marked the tenth anniversary of ADBI and, as such, attempted to combine a retrospection of its history along with an anticipatory look at potential issues for its future. Asia and the Pacific region has seen many developments since the Institute’s inception in 1997 and the diversity of chapters contained herein reflects this.

When ADBI was founded, several East Asian economies were in the midst of a financial crisis. Over the ten years since that time, Asia has seen not only a remarkable economic renewal, but also substantial growth based on a solid foundation of financial and governance reforms. East Asia has re-emerged as the most dynamic region of the world economy, demonstrating its resilience and robustness. ADBI’s own growth has mirrored this dynamism and robustness.

Since the 1997–1998 crisis, there have been numerous studies identifying its causes and effects. Now, ten years later, it is time to take stock of the region’s progress in post-crisis reform and assess its adaptation to the new global and regional landscapes. The first session of the conference dealt with these issues. Specifically, the session asked: What are the lessons from the crisis? How can Asian policymakers strengthen their economic and financial conditions to sustain growth and stability? How will this growth be financed?

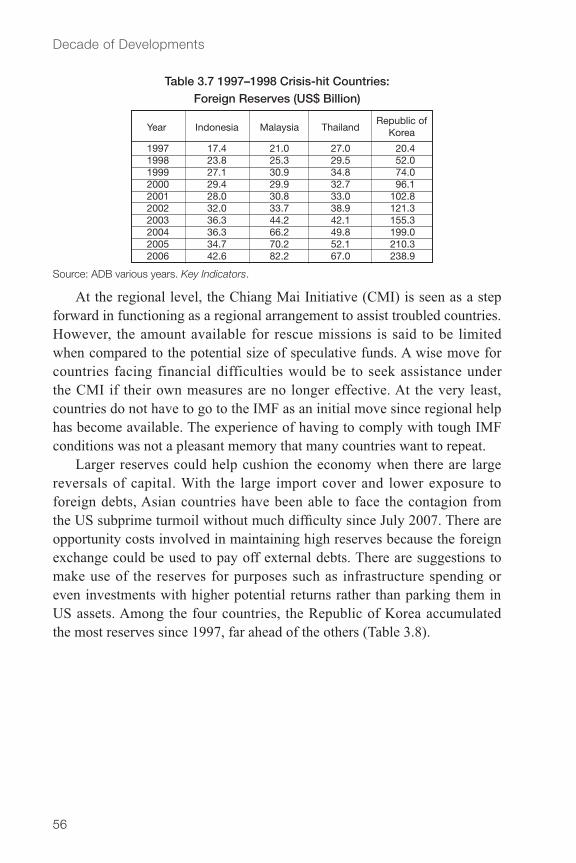

Ariff and Kadir, in Chapter III, “Asian Crisis Ten Years On: Policy Perspectives,” argue that crisis-hit countries have recovered, but not to the level of their past performance. On the positive side, significant reforms have been carried out in the banking and corporate sectors. However, the crisis has precipitated a precautionary move by many governments to self-insure by amassing large amounts of foreign reserves as protection against another precipitous outflow of funds. This strategy highlights continued weakness in the area of capital flow management and the fragility of financial institutions. Asian countries should adopt a flexible exchange

rate regime that is in line with clearly stated monetary policy objectives. A stronger regulatory and supervisory framework for financial institutions, sound risk management tools, and greater competition in the financial markets are needed. Regulations have been improved and lending practices made more prudent, but more work needs to be done.

The rigidity of exchange rates has been identified as a key cause of the crisis. Today, there is little evidence that the level of flexibility has changed much, measured in terms of volatility. The “fear of floating,” or the fear of volatility, is still present in Asian countries, as is the fear of overvalued currencies, which could potentially undermine the export competitiveness that was a key engine for the rapid emergence from the crisis. Thus, there is little incentive for crisis-hit countries to adopt fully flexible exchange rate regimes despite the strong evidence to the contrary (see, for example, Shatz and Tarr 2006; Yu 2007).

The large stocks of foreign exchange reserves accumulated to guard against adverse capital movements are not optimal and involve costs. This is especially true when the returns on these stocks are less than debt servicing, which is the case for a number of Asian economies. In addition, it is not even clear whether such large stocks would alleviate or exacerbate another crisis, depending on the source of the crisis.

The case for a regionally cooperative approach to these matters is strengthened by the rise in intra-Asian trade as well as growing integration of the financial sector. While such regional economic cooperation would provide support during bad times, it can also mean that countries are more exposed to external shocks and destabilizing capital movements. Balancing these two opposing forces requires consistent policy frameworks across the region. While there are no policies that can totally insulate a country from the threat of destabilizing capital movements, consistently prudent and transparent macroeconomic policies can reduce the chances of reversals in capital flows.

These foreign exchange reserves have traditionally been channeled almost exclusively to Western nations such as the United States (US) in the form of Treasury bonds. The wisdom of this approach is being questioned, especially given Asia’s continued growth, the emergence of the People’s Republic of China (PRC) and India as large economic agents, and the fact that the need for investment within the region is at an all-time high. The estimated need for investment in infrastructure alone is expected to exceed US$250 billion annually for the next ten years (Sharan et al. 2007). Part of Asia’s foreign exchange reserves could be invested abroad in such

infrastructure projects through newly established Sovereign Wealth Funds. In Chapter II, “Financing Asian Growth,” Petri examines the micro and macro aspects of funding a region that is expected to grow faster than the rest of the world over the next decade.

It is estimated that between 2005 and 2025, PRC, Viet Nam, India, and Bangladesh will experience some of the highest economic growth rates in the region, as measured by per capita gross domestic product (GDP). This growth is projected to be matched by the highest population growth. Figure 1.1 shows the effect of population growth on per capita GDP. Population growth follows the GDP per capita projections.

The key macro question is whether world savings will be large enough to finance global growth, let alone Asia’s rapid expansion. The figures in Table 1.1 show that the rapid productivity improvements and capital accumulation are driving forces of future Asian growth (Roland-Holst, Verbiest, and Zhai 2005). Some of the highest growth due to capital growth can be seen in developing Asia. These have important implications for Asia’s investment environment and its large pool of savings.

-1% 0% 1% 2% 3% 4% 5% 6% 7% 8%

Japan

Rest of the world

Europe 17

Hong Kong, China

Singapore

Latin America

United States

Australia, NZ

Taipei,China

Republic of Korea

Philippines

Sri Lanka

Malaysia

Indonesia

Thailand

Bangladesh

India

Viet Nam

PRC

Per capita GDP

Population

In his estimation of future savings rates for Asia, Petri uses growth rates that are slightly higher than those reported in Roland-Holst, Verbiest, and Zhai (2005). However, Petri argues that the numbers reported in Roland-Holst et al. were prepared some time ago and appear “... to have underestimated what appears to be the accelerating dynamism of Asian economies” (35).

While the current high level of optimism cannot be expected to continue for another 15 years, Asian economies appear to be creating enough independent regional engines of growth to sustain significant expansion. Deepening regional ties should reinforce this dynamism and lead to faster growth than appeared possible even a few years ago. Several scenarios are built on three basic components: savings rates, capital/output ratios, and growth rates.

Petri uses incremental capital output ratios at levels consistent with, or slightly below, the 1999–2005 average for the region. Historically, these levels change little and, indeed, do not vary much across countries. Thus, the assumptions have limited impact on the overall results and play only a modest role in distinguishing scenarios in Petri’s work.

All countries in the region are shown to be major capital exporters in the next 15 years, with the exceptions of Japan and Singapore. These two countries will experience declining savings rates in the face of expected demographic changes and will converge toward developed-country norms. The overall range of outcomes, however, shows that Asian savings are very likely to remain positive and that the region will be an exporter of capital.

The chapter goes on to deal with issues of risk sharing and allocational efficiency. How does the difference between Asia’s deepening intra-regional trade and its much less regionalized pattern of asset holdings affect its ability to fund future growth? Asia generates over 30% of world savings and yet absorbs about 20% of world investment and produces only 22% of world output. How does such a pattern affect Asia’s ability to fund its growth?

According to Petri’s forecasts, based in part on the distribution of current portfolio holdings and taking into account differentials in projected growth and savings rates, real global portfolio assets are expected to grow by 4.5%. However, the structure of these investments is shown to change less dramatically. While the most rapidly growing cross-border investment occurs for Asia’s investment in Asian assets, these holdings total only about 2% of global assets. Thus, while Asia is expected to produce more than a quarter of world output by 2020, Asian assets will comprise only 13% of the global portfolio. This implies the risks of Asian economic fluctuations will remain disproportionately held by Asians and the region will not benefit from the diversification that full participation in capital markets would bring.

This finding points to a generally accepted axiom: the key to financing Asia’s future is in the efficient handling of the region’s savings and investment. Inefficiencies may arise in the form of excess savings but equally important is an insufficient stock of internally traded assets and thus an inadequate sharing of investment risk. Petri suggests an answer could come in the form of increased consumption, which would develop regional demand and help offset potential declines in international demand for investment opportunities. He argues that measures needed to combat these potential pitfalls would be to reduce uncertainty faced by individuals (suggesting social insurance); relax constraints of inconsistent income and consumption streams by reforming financial markets, allowing for greater latitude in investment instruments; and keep inflation rates low through exchange rate and other policies.

These policies would need to consider not only the impact of aggregate flows of savings and investment, but the distribution of those flows. The next

session of the conference turns to this question: how can Asians share in the tremendous growth of the region? How do policymakers maintain diligence in poverty reduction efforts while assuring equitable growth opportunities for all?

The same substantial growth that has led to financial market dilemmas has also helped achieve significant and dramatic poverty reduction in the region (see Table 1.2). Each of the subregions shown has experienced large declines in extreme poverty while overall Asia has gone from 35% of the population living on US$1 per day to 18%: an almost 50% decline. However, poverty incidence measured at the US$2 per day level remains high. Between 1990 and 2005, this measure fell only 30%, from 75% to 52%. While this is not an insubstantial amount, it means that over half of the population of developing Asia is still living in very poor conditions.

At the same time, the report of ADB’s Eminent Persons Group pointed out that only four of the ten developing economies in the region—accounting for the vast majority of the region’s population, GDP, trade, and savings—are estimated to have per capita incomes close to the internationally accepted threshold for low-income countries (ADB 2007). In addition, the World Bank projects that by 2020, 95% of East Asians will live in middle-income countries and fewer than 25 million of the two billion East Asians will live below the poverty line (World Bank 2007).

So, while Asia continues to be home to low-income and small economies where development challenges persist, a significant number of economies are dealing with the issues of strong growth and rapid expansion. The support needs and policy responses to these two distinct trends are quite different. The Asian Development Bank, and ADBI as a key provider of a long-term strategic perspective, needs to grapple with the challenge of remaining relevant and serving the needs of the fast growing members of the region without forgetting about those still mired in poverty and stuck in a pattern of underperformance.

While rising disparities in income are not unusual during periods of rapid growth, structural changes need to ensure that the majority of people benefit from the growth. Unless the rising disparities between and within countries are addressed immediately, they could ultimately threaten the social cohesion and political stability of many countries. This, in turn, could lead to a political backlash bringing to power political leaders opposed to economic liberalization. Were this to happen, economic growth and private capital flows to Asia and the Pacific region would suffer major setbacks. In Chapter IV, “Poverty Reduction, Inclusive Growth, and Development Strategies,” Lin asks what the appropriate development strategy should be to lead a nation out of poverty in an equitable way. In Chapter V, “Rising Inequalities in Asia: An Imperative for Inclusive Growth,” Ali argues that growth strategies have to be broadened beyond simply “pro-poor” to encompass increased opportunities for all economic agents.

Development strategy is a key determinant of a developing country’s ability to achieve sustainable, dynamic, inclusive, and equitable growth, according to Lin. Distortions in a developing country are endogenous to the degree that policies are adopted that protect and subsidize nonviable firms. He refers to this as the comparative advantage-defying (CAD) strategy. Under this approach, governments implement industrial policies based on “catching up” with developed countries through the rapid adoption of technologies used in these economies.

On the other side is the comparative advantage-following (CAF) strategy. Under this approach, governments encourage firms to enter industries for which the country has a comparative advantage and to adopt production technologies based on this comparative advantage. Lin argues that this strategy leads to the development of viable firms. A developing country that adopts this strategy has no need to provide subsidies or protections to firms, thus reducing a firm’s potential rent seeking activities and the drain on government finances.

Much has been written on the ability of a developing country to “catch up” with the developed world by importing technology and therefore effectively skipping a stage of development. However, as has been shown elsewhere (Rodrik 1998; Acemoglu, Johnson, and Robinson 2001; Acemoglu and Robinson 2002, for example), developing countries often fail to catch up due to bad institutions and inappropriate government intervention. This stems from a basic conflict between the government’s development strategy and the country’s endowment structure. By promoting the development of modern, capital-intensive industries to the exclusion of other industries that may be more conducive to the country’s natural resource endowment, a country sets itself on an untenable path.

Governments that believe that supporting capital-intensive heavy industries will lead to greater growth, in the face of an incompatible factor endowment structure, will find themselves with unsustainable industries requiring constant subsidies. This will then lead to a lack of resources available to develop more “endowment-consistent” industries.

The CAD approach engenders a reinforcing cycle as these capital-intensive sectors’ incentives are to use their viability problem as an excuse, increasing the resources used to lobby government officials for preferential loans, tax credits, etc. The more the government follows this misguided policy and succumbs to these lobbying efforts, the more hampered is its ability to spend on programs in areas such as health and education. Further, this strategy leads a country to become more inward-looking as it attempts to substitute imports of capital-intensive manufactured goods for domestic production.

These CAD strategies are most detrimental to the poor, most of whom are living on agricultural incomes in rural areas not supported by any consistent government policies. The most important asset of the poor is their labor, which is helped little by the promotion of capital-intensive industries. In addition, the farm products they produce, such as grains, have low income and price elasticities. Because of the low elasticity of income,

overall economic growth will have minimum effects on the demand for farm produce. Because of the low price elasticity, production increases of an individual rural household may increase its income. However, when most households increase their production, the resulting downturn in prices will have a detrimental effect on farm income.

To study the effect empirically, Lin developed a technology choice index (TCI), which is a proxy for the development strategy followed by a country. The TCI measures the relative relationship between manufacturer and labor value added in total value added. Each of a group of developing countries was then assigned a TCI. If a country adopted a CAD strategy, the TCI was expected to be larger than if it did not. Lin then examined the relationship of the index with various income distribution measures, including Gini coefficients.

The results strongly support the hypothesis that the more a country pursues a CAD strategy the more severe will be the income disparity in that country. Lin argues that his results hold regardless of the initial income distribution. From these findings, the development strategy is an important determinant of income distribution in a country. When a country follows a CAF strategy, income distribution tends to become more equal over time even if the country’s initial income distribution is unequal.

When a country follows a CAD strategy, the existing distortions become endogenous to the needs of protecting and subsidizing the nonviable firms. To achieve inclusive and equitable growth, the government should stop investing in these industries and invest in education so that the labor in the rural and traditional sectors will have the ability to adapt to the job requirements in the modern, urban sectors.

In his chapter, Ali echoes Lin’s argument that governments have neglected the agricultural sector. He argues that while economic development entails a move away from the farm to industry and services, deficiencies in public investments in agriculture and the rural economy more generally have been problematic precisely because the productivity of agriculture determines the living standards of many people in Asia. Thus, a major factor affecting poverty alleviation efforts—agriculture—remains underexploited.

The 2006 World Development Report (World Bank 2005) also argued for the importance of the pursuit of equal opportunity while avoiding extreme deprivation. Achieving inclusive growth hinges on the ability to create economic opportunities through sustainable growth and to make those opportunities available to all, including the poor.

The chapter’s key message is that rising inequalities and the persistence of unacceptably high levels of non-income inequalities pose a serious challenge to Asia’s sustained progress. Inclusive growth that focuses on creating opportunities rapidly and making them accessible to all, including the disadvantaged, is a necessary but not sufficient condition for reducing inequality. Broader measures need to be taken.

Uneven growth in Asia has occurred over three dimensions. Growth has been uneven geographically, between rural and urban sectors, and across households, such that incomes at the top of the distribution have grown faster than those in the middle or bottom.

While there has been significant post-crisis improvement in some areas, a broad deterioration of public ethics, public institutions, and public administration has resulted in significant leakages in public expenditures, preventing them from reaching the target groups. Not only is there unequal access to the opportunities brought about by strong economic growth, there is a basic inequality in access to public services, which perpetuates this unequal access and undermines the potential of the region’s poor. The lack, or misspecification, of public expenditures contributes to social pressures, as indicated by higher poverty rates or lower literacy rates, and has been found to be significantly associated with a higher intensity of violent crime.

Both chapters explore the validity of the Kuznets curve in the Asian context. Lin rejects the inverted-U hypothesis of income distribution. Ali also finds problems with this theory, noting weak empirical evidence. The examples of the Republic of Korea and Taipei,China, where Gini coefficients actually declined over some periods of rapid growth, go some way to substantiate this skepticism. Ali’s chapter argues that the causality may even run in the opposite direction, meaning that great inequality can actually hinder future growth.

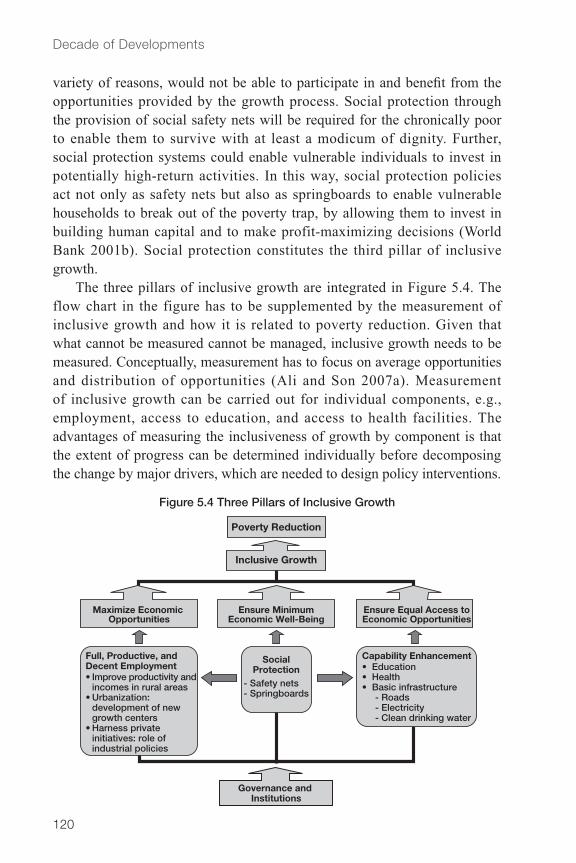

If inclusive growth has to do with opportunities and the distribution of opportunities throughout the population, policymakers need to look beyond traditional income redistribution schemes to correct the problem. Ali argues that inclusive growth needs to be built around three pillars: maximizing economic opportunities; ensuring a minimum economic well-being with social protections; and ensuring equal access to economic opportunities through education and health programs as well as basic infrastructure, keeping in mind the distinction between the equality of opportunities and the equality of outcomes. The equality of opportunities is a necessary but not sufficient condition to ensure equality of outcomes.

When taking a regional perspective, however, is equality of outcomes a practical goal? The region needs to strive for equal opportunities and this can be achieved through a transparent and integrated economic community in which opportunities can be accessed region-wide. Regional integration in Asia has been underway for some time through market-driven trade, foreign direct investment and finance, and the formation of regional production clusters and supply chains. However, it is only since the 1997–1998 crisis that Asian policymakers have begun to join forces in a more systematic way to strengthen regional economic and financial cooperation.

East Asian economies have grown rapidly over the last four decades. This growth has been driven by the expansion of production networks and supply chains, formed initially by global multinational corporations and later by East Asian business firms. More recently, East Asian governments have embarked on policy initiatives for formal economic integration through a series of bilateral and plurilateral free trade agreements (FTAs). The Association of Southeast Asian Nations (ASEAN) is emerging as the integration hub for FTA activities in East Asia, with PRC, Japan, and Republic of Korea all making formal economic ties with ASEAN. More recently, India and Australia have joined the rush to be part of the FTAs with East Asia.

There is a view, however, that the proliferation of multiple, overlapping FTAs and regional trade agreements (RTAs) may work against the World Trade Organization (WTO) Doha round. As Estevadeordal and Suominen point out in Chapter VI, “State of Integration in the Asia-Pacific Region: Current Patterns and Future Scenarios,” the number of RTAs has grown to such an extent that today some 200 agreements have been notified to the WTO. That number is expected to double by 2010. While Asia has been a relative newcomer to this trend, it has caught up fast (see Table 1.3). The Asian financial crisis has been a significant force in propelling Asia toward RTAs in recent years. This event increased awareness of the importance of regional economic policy coordination.

As the region deepens its economic and financial interdependence, an increasing acknowledgement has emerged among the region’s national authorities that they cannot achieve financial stability by acting independently—that they need to work together (Baldwin 2006). Along these lines, the region has developed several cooperative initiatives other

than RTAs, including the Chiang Mai Initiative and the Asian Bond Markets Initiative.

But these agreements, as some may worry, are not part of a drive to isolate Asia from the rest of the world. If designed properly, economic regionalism can lead to deeper global integration (Kawai 2007). A particularly strong motivation for those signing up to RTAs, argue Estevadeordal and Suominen, is the concern about remaining outside the proliferating network of RTAs around the world as well as in the region. Asian countries do not want to be excluded from potential markets and growth opportunities. But there continue to be concerns that the proliferation of agreements will lead to a “noodle bowl” effect, reducing efficiency, creating trade diversion, and unnecessarily complicating regional business dealings.

On the other hand, Estevadeordal and Suominen point out that the rise of RTAs can also act as a catalyst for greater regional cooperation as countries work together against potential negative externalities or the possible transmission of “crises” across borders. Positive externalities from RTAs can engender trust and institutionalization of cooperation, stimulating further cooperation.

In Estevadeordal and Suominen’s view, Asian agreements have some of the least restrictive concessions, including rules of origin (ROO) regimes. Unlike the “straitjacket” ROO model that the European Union (EU) uses, agreements in Asia and the Americas are marked by diversity, allowing for the accommodation of RTA-specific idiosyncrasies. The regional agreements have also employed such measures as short supply clauses to help producers adjust to shocks in availability of interregional inputs.

Estevadeordal and Suominen go on to compare customs procedures, investment service provisions, and other aspects of RTAs. They conclude that Asian agreements are somewhat less encompassing in some of the major trade-related provisions explored. These types of agreements imply that the region may be better placed than other RTAs in allowing participants to take advantage of changing global trends. History teaches us that it is important to embed regional groupings in a broader geographic context to avoid the risk of becoming closed blocs (Bergsten 2007). By taking this approach, Asia could sweep under one umbrella the exploding proliferation of bilateral and subregional preferential trade agreements throughout the region. It would eliminate, in whole or in part, the increasing discrimination that such pacts are introducing to the region.

The pulling together of agreements in Asia could follow a precedent set by other megaregional trade negotiations that have proceeded in an area with a number of preexisting RTAs. In these cases, the new agreement builds on those already in existence, the EU being the most obvious example. While Asia’s “noodle bowl” of agreements can be quite messy, the reality is that regionalism is here to stay and policymakers must work within its confines. Indeed, in Chapter VII by Bo and Woo, “A Composite Index of Economic Integration in the Asia-Pacific Region,” the authors show that regionalism and economic integration over and above that driven by RTAs have steadily strengthened in the region over the past 15 years. Indeed, they argue, this steady integration has created a need for consistent and reliable measures of integration.

A useful approach to resolve this proliferation of regionalism is to multilateralize regionalism and make the process as multilateral-friendly

as possible (Bergsten 2007). One direction along this line is the creation of an East Asia-wide FTA based on ASEAN+3 countries (East Asian FTA) or ASEAN+6 countries (Comprehensive Economic Partnership in East Asia) by consolidating bilateral and plurilateral FTAs in the region (Kawai and Wignaraja 2008).1 Another direction is the formation of an FTA among Asia-Pacific Economic Cooperation (APEC) members, i.e., an FTA of the Asia-Pacific (Bergsten 2007). Under the latter direction, the need for such transpacific institutions as APEC is only strengthened, according to Bo and Woo. The challenge for such institutions is not so much the complications that arise from the proliferation of East Asian RTAs but rather, as Bo and Woo state, from the lack of institutional commitment to the regional approach these organizations have at times displayed.

Thus, the main challenge for the region in the near term is to define a future integration strategy that leverages the wave of reforms and RTAs while retaining Asia’s already important gains from liberal global trade and investment regimes. To build on this regionalism, it is important to determine the exact nature of the integration Asia has been undergoing and whether this level is sufficient to move into a multilaterization of regionalism such as that called for above. Bo and Woo attempt to go beyond conventional measures of integration by taking a spectrum of indicators to arrive at a composite index. They point out that although there are many single variable measures of regional economic integration, relatively little work has been done on a composite index. To derive an index of integration, Bo and Woo apply a method similar to that used by the United Nations Conference on Trade and Development in determining their Trade and Development Index.

To include as much information as possible, Bo and Woo use a multi-dimensional dataset. Given the diversity of the dataset, determining the weights becomes a key element in the process. A good index carries the essential information of the underlying data without bias toward one or a handful of indicators. The authors argue that by using a two-stage principle components analysis (PCA) to obtain the weights, such bias is minimized. The first stage measures the dispersion of the sample countries’ main macroeconomic indicators while the second stage applies indicators of trade,

1 ASEAN countries consist of Brunei Darussalam, Cambodia, Indonesia, Lao People’s Democratic Republic, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Viet Nam. The “plus six” includes Japan, People’s Republic of China, Rep. of Korea, India, Australia, and New Zealand.

foreign direct investment, and tourism, as well as the convergence index to compute the final composite index.

Seven measures are collected for a range of countries covering East Asia, North America, Southeast Asia, and Oceania from the period 1990 through 2005. An important variation in this index is the exclusion of flows between Asia-Pacific economies that are already part of a subregional unit. Bo and Woo argue that the shortcoming of previous integration measures is that they ignore the effects of such agreements and, as such, are an overstatement of the level of integration in the region. Since most of the studies measuring integration ignore the effects of these regional agreements on an economy’s broader integration with the world, the chapter argues that they provide an inaccurate reading of globalization.

Using their composite index, Bo and Woo find results consistent with the anecdotal evidence that the level of economic integration in the region is growing. From a broad view, the relative ranking of the level of economic integration in the Asia-Pacific region has remained remarkably steady over the time period examined. Individual economies like Singapore and Hong Kong, China are shown to be most integrated with the region, while the US and Canada are the least integrated with Asia and the Pacific.

The ASEAN economies are the most integrated in the Asia-Pacific region (that is, they rely most heavily on the Asia-Pacific regional market), followed by Australia, whose level of integration is close to the regional average. The PRC is next but its level has been declining in the past five years as it increases its links with Hong Kong, China; Macau; and Taipei,China as well as expands its markets in the EU.

The authors point out that while there may be some issues with the PCA measure, such as the overreliance on sample-dependent weights, the problems can be overcome using different permutations such as a “chained index.” In the end, the importance of accurately measuring the state of integration in the Asia and Pacific region is too important not to try.

So it would appear that several metrics show the Asia and Pacific region to be highly integrated. It remains a challenge to find a clear path through the proliferating approaches to this integration—whether it be through RTAs or subregional “cooperatives”—to join together under a transparent and effective policy framework in promoting an inclusive, equitable, sustainable future.

The final session of the conference was a lively panel discussion on the future directions for the Asia and Pacific region as well as the identification of the most pressing issues that will confront the region in the next decade. Seven panelists—Mohamed Ariff, Iwan Azis, Thanong Bidaya, Siow Yue Chia, Justin Yifu Lin, Aftab Seth, and Hiroshi Watanabe—were asked to identify challenges and issues that should be the focus for research, in-depth study, and capacity building for the public sector.

The major issues can be loosely grouped into four areas of concern (although there is considerable overlap):

(i) Needs for improved management, such as the serious challenges of exchange rate management and managing domestic debt in a region whose experience is mostly with foreign debt.

(ii) Needs related to institutional structures, such as the need for financial restructuring through the development of a bond market and the need to identify the best institutional framework to deal with the twin concerns of poverty reduction and economic competitiveness.

(iii) The importance of understanding interactions between issues and the special challenges they pose, such as the link between macro policies and poverty; the invasive economic implications of high levels of liquidity and excess savings, requiring a study on flows of funds; and the interaction between environmental sustainability and demographic change and their profound impacts on economic productivity.

(iv) The changing dynamics of the region, including the impact of the rise of India and PRC in comparative advantage and labor markets; the need to generate and then retain intellectual capacity in the region; and the impact of the rise of capital-intensive industries, especially in PRC and India, and its implications for social and economic policy.

Having recovered from the 1997–1998 financial crisis, Asia and the Pacific region is again the most dynamic growth center of the world economy. This growth has led to significant poverty reduction throughout the region. It has also stemmed from and benefited from the strong economic interdependence through market-driven integration the region has achieved.

ADBI looks forward to addressing the next decade of challenges that lie ahead for Asia and the Pacific to help the region reach its full potential.

Many of the major themes identified fit in well with ADB’s new Long-Term Strategic Framework, which was being formulated at the time of the conference. This document, which outlines ADB’s strategic priorities until 2020, states that in pursuing a vision of a poverty-free Asia and Pacific, ADB must achieve inclusive economic growth, environmentally sustainable growth, and regional integration. And it can achieve these objectives through five key drivers of change: the private sector, good governance and capacity development, gender equity, knowledge, and partnerships. Each of these drivers is covered in the pressing issues identified above.

This volume consists of the chapters outlined above as well as comments provided by chapter discussants and the panel discussion.

Acemoglu, D., S. Johnson, and J. Robinson. 2001. The Colonial Origins of Comparative Development: An Empirical Investigation. American Economic Review 91 (5): 1,369–1,401.

Acemoglu, D., and J. Robinson. 2002. Economic Backwardness in Political Perspective. Massachusetts Institute of Technology Department of Economics Working Paper No. 02-13.

Asian Development Bank (ADB). 2007. Toward a New Asian Development Bank in a New Asia: Report of the Eminent Persons Group to the President of the Asian Development Bank. Manila: ADB.

Ali, I., and J. Zhuang. 2007. Inclusive Growth toward a Prosperous Asia: Policy Implications. ERD Working Paper No. 97. Manila: ADB.

Baldwin, R. 2006. Multilateralising Regionalism: Spaghetti Bowls as Building Blocs on the Path to Global Free Trade. Centre for Economic Policy Research Discussion Paper No. 5,775. London: Centre for Economic Policy Research. Retrieved from http://www.cepr.org/pubs/dps/DP5775.asp.

Bergsten, C.F. 2007. Toward a Free Trade Area of the Asia Pacific. Presented at the Japan Economic Foundation and Peterson Institute for International Economics New Asia-Pacific Trade Initiatives, Washington, DC.

Kawai, M. 2007. Evolving Economic Architecture in East Asia. Kyoto Economic Review 76 (1, June): 9–52.

Kawai, M., and G. Wignaraja. 2008. Regionalism as an Engine of Multilateralism: A Case for a Single East Asian FTA. Working Paper Series on Regional Economic Integration, No. 14 (February). Manila: ADB.

Rodrik, D. 1998. Where did all the Growth Go? External Shocks, Social Conflict and Growth Collapse. NBER Working Paper W6350.

Roland-Holst, D., J.P. Verbiest, and F. Zhai. 2005. Growth and Trade Horizons for Asia: Long-term Forecasts for Regional Integration. Asian Development Review 22 (2): 76–107.

Sharan, D., B.N. Lohani, M. Kawai, and R. Nag. 2007. ADB’s Infrastructure Operations: Responding to the Client Needs. Manila: ADB.

Shatz, H.J., and D. Tarr. 2006. Exchange Rate Overvaluation and Trade Protection: Lessons from Experience. In Trade Policy and WTO Accession for Economic Development in Russia and the CIS: A Handbook, edited by David Tarr. Washington, DC: World Bank Institute.

Yu, Y.D. 2007. PRC’s Macroeconomic Management: Issues and Solutions. Presentation as part of ADBI Distinguished Seminar Series, post-event statement retrieved from http://www.adbi.org/event/2252.yu.distinguished.speaker/.

World Bank. 2005. World Development Report 2006. Washington, DC: World Bank.

World Bank. 2007. East Asia Update. Washington, DC: World Bank.

Peter A. Petri

Asia already produces more than one fifth of world output, and is likely to grow much faster than the rest of the world over the next decade or so. How will its growth be financed?

More specifically, we examine whether world savings will be large enough—at roughly constant cost—to finance global growth including Asia’s continued expansion. If savings turn out to be insufficient, Asia’s—and the world’s—investment or consumption trajectory would have to adjust downward, under the pressure of rising capital costs. If savings turn out to be excessive, world demand could turn sluggish, and would need to adjust (or be adjusted through policy measures) upward under the pressure of falling capital costs. Even relatively small variations in world savings could lead to significant adjustment pressures; at times the world is thought to be short on savings, and at times to be awash in liquidity. In the early 1990s, for example, the global savings rate dropped to 21.6% and a substantial economic literature emerged concerning the global “capital shortage.” In 2006, with world savings up to 23.6% (the highest in a decade), discussion turned to a world “savings glut.” In fact, world savings rates have remained within a two percent range for two decades.

This chapter explores the financing requirements of Asian economies,1

looking ahead to 2020. Because the global financial environment more than a decade from now will be shaped by economic and political developments that cannot be foreseen, this kind of analysis is inherently speculative. We therefore use a scenario approach, rather than specific projections, to explore potential growth trajectories and their associated capital requirements. The purpose of the exercise is to shed light on the evolution of the components of the world’s savings balance, and in the process, to form some judgment about what pressures are likely to build on financial markets and policies.

To look ahead, our principal conclusions are that Asia’s robust propensity for savings and its growing weight in the world economy will tend to generate high global savings. When added to tighter budget constraints in the United States and potentially high savings from primary-goods exporters, global capital markets are likely to face conditions usually associated with a “savings glut.” In other words, the challenge will be to sustain demand, rather than to finance investment. From a policy 1 The study deals with 12 Asian economies that produce 97% of total Asian gross domestic

product (GDP). The economies are identified in subsequent tables.

perspective, these pressures argue for vigorous initiatives to build demand in Asia—for example, in consumption in the People’s Republic of China (PRC), and in investment in Southeast Asia.

Section 1 introduces the chapter’s scenario methodology. Section 2 develops scenario estimates of Asian savings and investment. Section 3 places these in a global context, developing scenario estimates of the evolution of global net savings. Section 4 offers brief conclusions.

Asia is important in global savings and investment and will become more so by 2020. In 2005, Asia generated one third of world savings and absorbed 29% of world investment, yet produced only 22% of world output. In other words, Asia used more than its share of capital, but saved still more—in effect financing significant investment elsewhere. We will examine the evolution of this equation by breaking it into parts and analyzing its components. Specifically, global net savings will be “dissected” by country and by analytical component. We will then project these pieces forward under several different assumptions (or scenarios).

In 2005, world capital flowed “uphill” in the sense that it moved from low- to high-income economies (Figure 2.1). The advanced economies of the world (especially the United States) imported about US$0.7 trillion in capital, with US$0.4 trillion coming from Asia, and another US$0.3 trillion from emerging markets outside Asia (principally the Middle East).

While Asian savings were generally high, there was considerable dispersion in savings performance across the region (Table 2.1), with Japan and PRC contributing approximately two thirds of the region’s overall net savings. Singapore; Malaysia; and Hong Kong, China were the region’s biggest net savers relative to income. India, Thailand, and Viet Nam were net borrowers, but borrowed relatively little. Asia overall had net savings equal to nearly 4% of income. Nearly all Asian economies (except for the Philippines) had savings rates above the world average. PRC’s and Singapore’s savings rates were no less than twice as high.

Savings, investment, and growth are linked by accounting identities and the equations of growth for the world as a whole; they are not so constrained for any country or region in the modern global economy. High savings rates can coexist with low investment rates, and vice versa. For example, in 2005, Singapore’s national savings rate was 49% while its domestic investment rate was 19%—so a full 30% of Singaporean national income was invested abroad. The relationship between investment and growth is tighter, but evidence provided below suggests that it, too, is variable when evaluated over short time periods.

We use scenarios to identify plausible future outcomes rather than attempting a specific projection. We build these scenarios for each Asian

economy from three components: savings rates, capital/output ratios, and growth rates (and specifically low, medium, and high assumptions for each). The potential number of alternatives (324 = 3 × 3 × 3 × 12 countries) is large, so we will analyze only the “all-medium” scenario and some extreme outcomes, such as the aggregate scenario (over all countries and factors) that leads to the highest net savings for Asia. Ranges constructed this way are generously wide. For example, if scenarios were combined randomly instead of selected to produce extreme outcomes, factors favorable to net savings would be paired with others that are not, and countries with positive savings outcomes would be combined with others that have negative ones. If factors and countries do not move in parallel, the aggregates fall well within the extreme range, as opposing effects offset each other.

After projecting net savings for Asian countries, we turn to explore their viability in the global context (Section 2). Whether Asian projections are feasible depends on the balances in the rest of the world. Even in 2020, Asia will represent only one quarter of world output, so it could run a significant net surplus or deficit—if the rest of the world is willing. But if Asia’s projected net savings are inconsistent with rest-of-the-world borrowings, then the scenarios will not be realized—some combination of market and policy adjustments will have to “restore” the global savings and investment balance.

More formally, we construct net savings projections for Asia using the equation:

NS = (s−i)Y0(1+g)15, (1) where: NS = net national (regional) savings, s = savings rate, i = investment rate, g = growth rate, Y = national (regional) income, and subscript 0 indicates initial level (no subscript indicates 2020 level).

The variables of this equation are the building blocks of the analysis that follows. Considerable theoretical and empirical literature exists on the determinants of these variables. That, in turn, provides a strategy for “pushing back” the level of explanation to a deeper layer of (hopefully) exogenous determinants, and thus for developing forecasts. This task is taken up in Section 2.

We now implement the scenario approach by computing alternative values for the three major components of Equation 1—namely savings rates, investment rates, and growth rates—for the 12 Asian economies examined in this chapter. Our strategy is to review the theoretical determinants of each component and collect information on the likely evolution of these deeper factors. At the end of this section, the results of the analysis are then combined using Equation 1 to develop scenarios of net savings.

Savings rates are predictable and well researched. Extensive applied work in this area was recently reviewed in a World Bank “meta study” (Loayza, Schmidt-Hebbel, and Servén 2000), which also filled gaps with new research. That study identified the following factors as critical determinants of savings rates:

• Persistence. Savings rates stay put over time. The inertial component may reflect cultural or institutional factors. For example, in our Asian dataset, the standard deviation of savings rates among economies was approximately nine percentage points, while the standard deviation of changes in the savings rate over a decade was only two percentage points.

• Income. Higher incomes lead to higher savings for low-income economies. The relationship appears to plateau at higher incomes, and is generally stronger for lower-income economies than for those at middle incomes. In developing countries, a doubling of per capita income generally leads to a 10-percentage-point increase in savings from disposable income.

• Growth. More rapid growth increases savings. This is not predicted by theory; consumption smoothing, for example, suggests higher consumption from income (and hence lower savings rates) if incomes are rising rapidly. The observed result more likely reflects consumption inertia—people take time to regard higher incomes as permanent and to adopt higher consumption levels. The World Bank survey concluded that, on average, a one-percentage-point increase in the growth rate leads to a one-percentage-point increase in the national savings rate.

• Demographics. Several channels connect the population structure with savings, including lifecycle effects and changes in productivity and dependency ratios. The effects also depend on how society supports the

aged, and on other behavioral characteristics, such as the desire to leave bequests. The World Bank survey concluded that a one-percentage-point increase in the young-dependency ratio reduces savings by 0.3 percentage points, and a one-percentage-point increase in the aged-dependency ratio reduces savings by 0.6 percentage points.

• Uncertainty. General economic uncertainty, including income volatility and inflation, contributes to higher savings rates. Uncertainty at the individual level, due a lack of health or social insurance and other safety nets, does so as well.

In addition to private savings (as discussed above), national savings also include public savings. However, the latter may be offset by opposite changes in private savings, to the extent that the population anticipates the collective cost of servicing public debt. But this “Ricardian equivalence” holds strictly only if individuals have infinite planning horizons, that is, value the welfare of their children as much as their own. Empirical studies find that public savings are offset partially, at rates varying from 30% to 80%.

These theoretical determinants of savings rates can be summarized in the equation:

s = so0+ α (y − y0 ) /y0 + β (g − g0 ) + γ (d − d0 ) + δ (s0* − s0 ), (2)where: s = savings rate,y = per capita income,g = growth rate,d = dependency ratio,α , β , γ , δ = constants,subscript 0 indicates initial level (no subscript indicates 2020 level), andsuperscript * indicates a convergence target.

The terms of the equation account for (i) persistence, through the effect of the initial savings rate for 1999–2005, (ii) income changes, (iii) growth changes, and (iv) changes in the dependency ratio. In addition, we include a term that assumes some gradual “regression to the mean” of international norms, as reflected in the region’s average savings rate. (We do not include government savings because we know how to project them, and because they may be offset by changes in private savings.)

Values for the parameters of Equation 2 can be derived from the World Bank’s meta estimates. We assume: α = 0.1 for y < US$3,000, 0.05 for

US$3,000 < y < US$6,000, and 0 for y > US$6,000; β = 1; γ = -0.5; and δ = 0.5. The value of δ is arbitrary, and assumes that half of the difference between the nation’s initial savings rate and the target will disappear by 2020.

Values for independent variables are based on the following assumptions:

• Income levels (y). Assumptions about income growth rates are described below. In each projection scenario, savings rates are used in conjunction with a particular income growth assumption, which is then used to calculate the term (y – y0 )/y0.

• Growth rates (g). As above, this term reflects the growth assumption incorporated into a particular scenario.

• Dependency ratios (d). Asian demographic change is explored in detail by Mason, Lee, and Lee (2007). They calculate an “economic support ratio” (Figure 2.2) as the effective labor power of a population divided by its effective consumption requirements. Both the labor power and consumption requirements constructs are weighted averages of the age distribution; labor power uses incomes as weights and consumption requirements use consumption by age as weights. A rising index means that labor power is increasing relative to consumption requirements.

Most of Asia’s demographic drama will unfold beyond the time horizon of this study, sometime between 2020 and 2050 (Figure 2.2). Japan is an exception: its economic support ratio peaked early in the 1980s and will fall by a further 7% by 2020. The support ratios for Republic of Korea and PRC are near their peak, but will not change significantly between 2005 and 2020. The support ratios for Association of Southeast Asian Nations (ASEAN) members and India are still rising, and will increase by about 10% by 2020.

Total dependency ratios (as used in the World Bank estimates) move inversely with the support ratios calculated by Mason, Lee, and Lee and are typically around 40%. For purposes of scenario analysis, we thus calculate that over the next 15 years, demographic factors will (i) reduce Japan’s average savings rate by 1.4 percentage points (=0.07*0.40/2), (ii) increase ASEAN and Indian savings rates by 2 percentage points (=0.10*0.40/2), and (iii) leave other Asian savings rates unaffected.

• Target savings rates (s*) National savings rates are assumed to converge to international norms, defined in terms of the savings rates of peer countries. We specify low, medium, and high convergence targets in terms of the distributions of peer savings rates, as follows:

slow* = 25th percentile of peer countries = 15% for Japan, 26% for others

smedium* = 50th percentile of peer countries = 19% for Japan, 30% for others

shigh* = 75th percentile of peer countries = 23% for Japan, 38% for others

Japan’s peer group is the G7 countries, while the 11 other Asian economies comprise each other’s peer group. By these scenarios, savings rates will fall to the lower quartile of the peer distribution, regress to its mean, or rise to its upper quartile. Convergence to these different targets provides a range of possible future rates.

These values for the parameters and independent variables of Equation 2 are then used to calculate three alternative savings rate scenarios, as reported in Table 2.2.

The scenarios suggest that Asian savings rates will change relatively little, overall, between now and 2020. But this constancy is the result of substantial offsetting changes in the savings of different economies; there will be substantial change in the composition of Asian savings (Table 2.2). Japan’s savings rates, and to a lesser extent those of the PRC, are likely to fall, while those of India and ASEAN are likely to rise. The assumptions that lead to these results will be further discussed when overall regional net savings are derived in Table 2.5.

The other side of the net savings “scissor” consists of the investment rate, which is in turn related to the productivity of capital and the country’s growth rate. A simple accounting identity defines this relationship: the investment rate (capital formation divided by gross domestic product [GDP]) is equal to a country’s expected growth rate multiplied by its incremental capital-output ratio (ICOR, or capital per unit of additional output):