1 3 samantha

23

MARKET INEFFICIENCY: “THE NEW FINANCE” INVESTMENT FINANCE UNIVERSITY OF KWAZULU- NATAL SCHOOL OF ECONOMICS AND MANAGEMENT DURBAN 4001 SAMANTHA BUSHELL (201501549) Date Submitted: 9 March 2004. Henry Mkhize Topic 1.3: “The New Finance” - 1 -

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of 1 3 samantha

MARKET INEFFICIENCY:“THE NEW FINANCE”

INVESTMENT FINANCE

UNIVERSITY OF KWAZULU- NATALSCHOOL OF ECONOMICS AND MANAGEMENT

DURBAN4001

SAMANTHA BUSHELL(201501549)

Date Submitted: 9 March 2004.Henry Mkhize

Topic 1.3: “The New Finance”

- 1 -

Abstract

The Efficient Market Hypothesis (EMH) claims that investors

purchasing securities should expect only to earn normal

profits. No opportunities for arbitrage should exist since all

stock prices fully mirror all publicly available information.

Investors holding stock portfolios along the efficient

frontier as assumed by the Capital Asset Pricing Model (CAPM)

should expect to earn a certain expected return given their

portfolio’s underlying risk.

“The New Finance”, arising from past research and other

studies finds evidence which is contradictory to Harry

Markowitz’s efficient market and provides proof of securities

producing returns which differ from their associated risk

levels.

This research paper explains how markets are found to be in

actuality, inefficient with respect to pricing as well as the

absorption of news by the market, due mainly to investor

behaviour. It will provide evidence in direct contradiction to

- 2 -

the EMH as well as the CAPM by giving details on the nature of

investor overreaction, the subsequent mispricing of securities

and the speed at which the stock market adjusts to news and

announcements. It will discuss the tendency of investors to

place great importance on the past earnings and performance of

certain stocks and the positive link which exists between this

past performance and future expectations by individuals. This

is an obvious violation of the EMH. I will also introduce

growth and value stocks and how their respective prices and

returns are affected by stock market expectations. Results

show value stocks, outperforming growth stocks, the supposed

“winner” stocks on more than one occasion.

Market Inefficiency: The New Finance

TABLE OF CONTENTS

Page Number

- 3 -

Abstract1. Introduction

22. The EMH and the CAPM – Realistic Models?

3 3. The CAPM’s Prediction in Terms of Growth and Value Shares

4 3.1Actual Performance of Growth and Value Shares

43.2 Implications for the Market

6 3.2.1 Mispricing6

3.2.2 A Contrarian Investment Strategy6 3.2.3 Reversals/Corrections7 4. Investor and Market Behaviour 7 4.1 Overreaction 7 5. Anomalies 10 5.1 Sluggish Markets10 5.2 The Size Effect/January Effect10 6. Conclusion 11 7. Appendix A 12 8. References 13

- 4 -

1. Introduction

An efficient market is described by Basu (1977) as one in

which “security prices fully reflect available information in

a rapid and unbiased fashion” (p.663). Share prices therefore

provide a true reflection of the intrinsic value of a firm,

providing shareholders and investors with an understanding of

their portfolio’s true worth. Since all publicly available

information is, according to the Efficient Market Hypothesis

(EMH) immediately embedded into share prices, there are no

exploitable opportunities for investors to take advantage of.

This is because all share prices are accurately priced and

arbitrage occurs only when there is a mispricing of

securities. The rule stating how assets should be priced is

known as the Capital Asset Pricing Model (CAPM) (Bodie, Z et al,

2002). The CAPM asserts a certain relationship to exist

between an assets’ level of expected return and its risk

(Bodie, Z et al, 2002). In other words an investor can expect to

earn a specific return, given the assets underlying level of

- 5 -

risk. The CAPM thus predicts value shares to earn relatively

lower returns since these shares contain relatively lower

levels of risk. The opposite is true for growth shares, where

high-risk levels associated with these shares command a

related high return. However, evidence has shown that this

positive relationship between risk and return does not

necessarily hold in the stock market. Research shows low-risk

shares (value shares) to be in fact, generating superior

returns. Correspondingly high-risk shares (growth shares) are

found to be earning relatively lower returns (Haugen, 1995).

Haugen (1995) attributes this violation of the CAPM to

inefficient stock market behaviour in which investors

overreact to earnings announcements. Consequently, growth and

value shares become mispriced as investors misinterpret good

or bad news. As a result growth and value shares become an

area of exploitation by profit-seeking investors. This is an

obvious contradiction of the EMH. However, not only is there

evidence of the CAPM’s failure, there is also confirmation of

a sluggish market in that there are found to be “lags and

frictions” [Basu, 1977 (p.681)] as the market attempts to

correct itself. Studies are showing increasing evidence that

markets may not be as efficient as previously thought. This

has a significant impact on expected returns for investors and

may, as a result change the mindsets of many individual and

institutional investors with respect to their portfolio

allocation decisions for the future.

- 6 -

2. The EMH and the CAPM – Realistic Models?

As discussed above, the EMH proposes the swift incorporation

of available information into share prices. It does not

allow for the possibility of abnormal profits to be

generated since prices are assumed to reflect a firm’s true

underlying value and there is therefore no room for excess

returns to be earned [Basu, 1977 (p.663)]. The instantaneous

adjustment of share prices to new information, in an

efficient market represents a neutral expectation for earnings

in the future (Bernard and Thomas, 1990). There is assumed

to be no relationship between past and future earnings

(Bernard and Thomas, 1990). The EMH dismisses the ability of

investors to earn excess returns based on past earnings

performance as this information has supposedly already been

included in the share’s price. Bernard and Thomas (1990)

however find evidence in direct contradiction to this. They

found that security prices to an extent represented a naïve

earnings expectation. In violation of the EMH, future

earnings were expected by investors to be the same as the

previous year’s earnings (Bernard and Thomas, 1990). This

has severe implications for the efficiency of the market.

The focus by investors on past earnings will be discussed at

a later stage in this paper.

Stout (2003) finds further discrepancies with respect to the

validity of the EMH. A market is described as efficient when

prices completely mirror publicly available information.

- 7 -

Stout (2003) argues that it is not always possible for every

investor to obtain and comprehend all publicly available

information. It can also be expensive to acquire and

administer. Therefore we can deduce that security prices may

not accurately reflect the market’s actual understanding of

the released news, which may further imply that share prices

are not a true reflection of their intrinsic value. Stout

(2003) goes on further to explain that even if the market

were efficient enough to adjust to new information

immediately, it wouldn’t necessarily mean that the market

would represent that information accurately.

Stout (2003) similarly doubts the reality of the CAPM’s

assumptions. The CAPM presumes that all investors have

homogenous expectations in terms of future returns and risk.

She disagrees with this supposition; arguing that investors

are not identical and do not always hold the same view

regarding the true value of a certain share. Investors are

found to disagree and have different opinions about shares

as well as their future outlook

(Stout, 2003). Her argument implies that not all investors

hold portfolios along the efficient frontier, as the CAPM

assumes everyone to do. This means that the market index

cannot be efficient, since it is the aggregation of every

investor’s portfolio along the efficient frontier that makes

up a market index, for example the S&P500 (Haugen, 1995).

Haugen (1995) concurs, finding the CAPM to be a “highly

inaccurate depiction of reality” (p.117).

- 8 -

3. The CAPM’s Prediction in Terms of Growth and Value Stocks

Growth shares have high market - book ratios, indicating a

relative high price in relation to their fundamental, book

value. The market expects these shares to grow at a faster

than average growth rate (Bodie, Z et al, 2002). Value shares

correspondingly are expected to grow at a below average rate

and have low market-book ratios. The CAPM prescribes growth

shares, with their high investor expectations to be risky

and therefore attaches a higher relative expected return to

them. The opposite is true for value shares with their low

market expectations and hence lower volatility. Value shares

have a lower expected return in line with the CAPM’s

prediction.

3.1 Actual Performance of Growth and Value Stocks

Numerous studies, research papers and articles have shown

evidence of value shares outperforming growth shares (the

supposed “winners”), earning above average profits (Haugen,

1995). Growth shares have been found to often disappoint

investors by performing relatively worse compared to value

shares. American and South African evidence support these

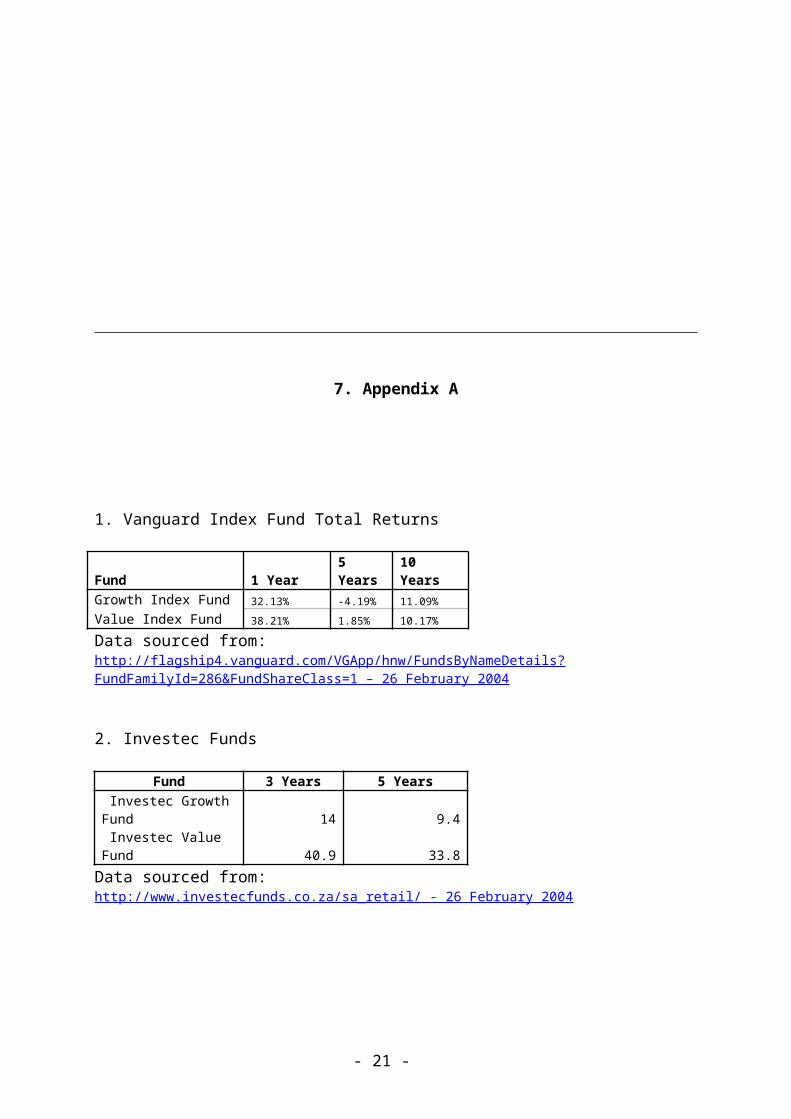

findings. Apppendix A provides the total returns of growth

and value shares in the Vanguard Index. The appendix also

shows local South African performance of Investec’s growth

and value funds. Featured on the following page are graphs

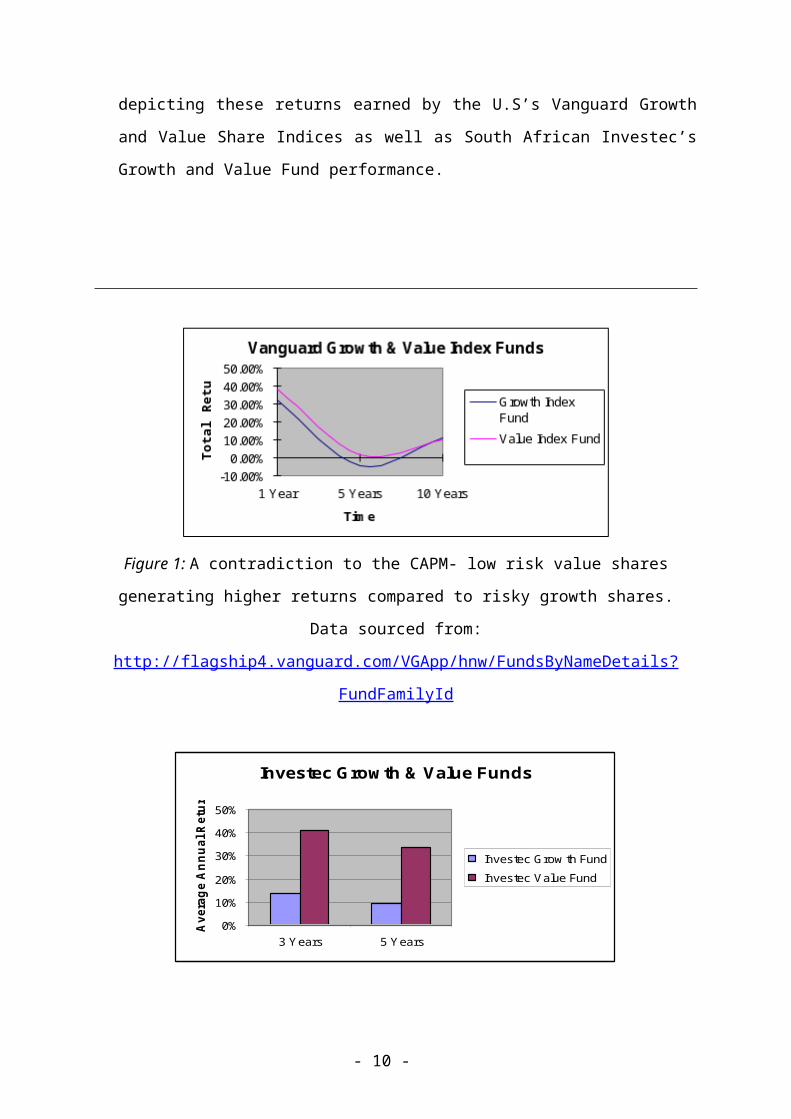

- 9 -

depicting these returns earned by the U.S’s Vanguard Growth

and Value Share Indices as well as South African Investec’s

Growth and Value Fund performance.

Figure 1: A contradiction to the CAPM- low risk value shares

generating higher returns compared to risky growth shares.

Data sourced from:

http://flagship4.vanguard.com/VGApp/hnw/FundsByNameDetails?

FundFamilyId

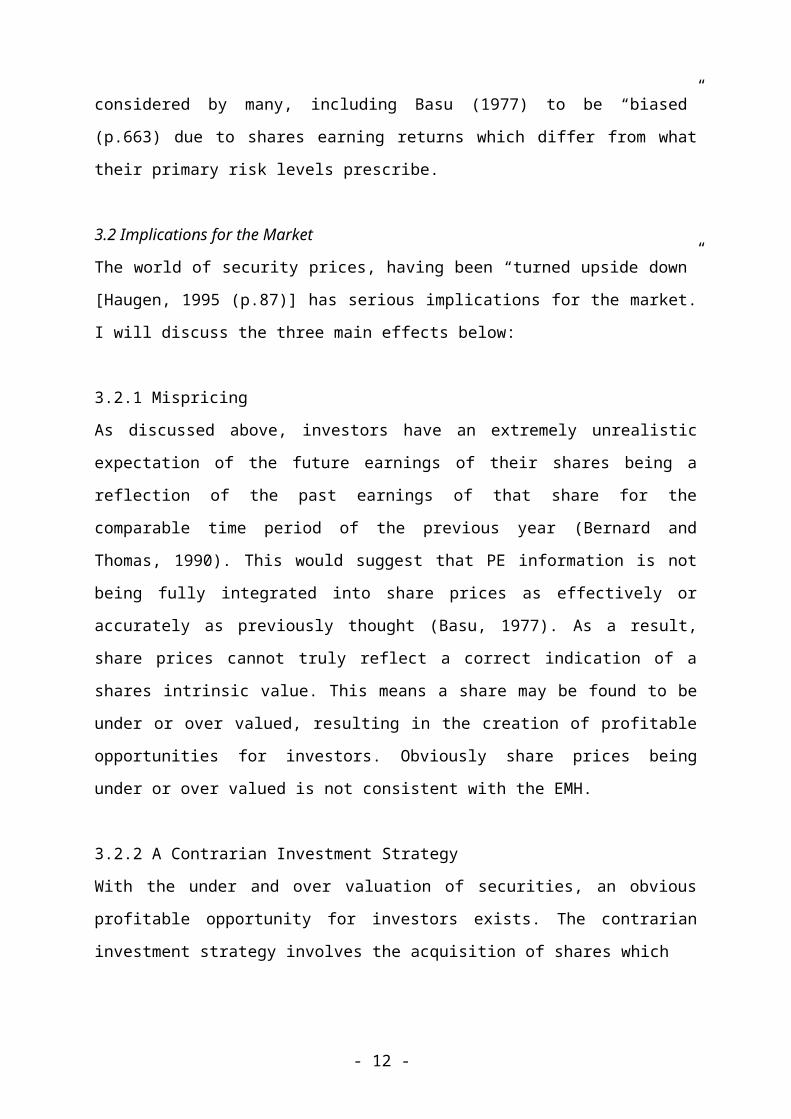

Investec Grow th & Value Funds

0%

10%

20%

30%

40%

50%

3 Years 5 Years

Averag

e An

nual Return

Investec Grow th Fund Investec Value Fund

- 10 -

Figure 2: South African evidence supports international

findings.

Data sourced from:

http://www.investecfunds.co.za/sa_retail

Similarly, Basu’s (1977) empirical evidence gives results

contradictory to the CAPM. He found that higher levels of

return are not linked with a correspondingly higher level of

systematic risk for a portfolio. This conclusion was reached

after discovering the higher returns generated by low PE

(Price-Earnings) ratio portfolios (value shares) were not

linked with higher levels of risk (Basu, 1977). The Jensen

measure – a measure of excess return in comparison to the rate

of return as predicted by the CAPM (Bodie, Z et al, 2002) shows

two

value share portfolios to have produced returns of 4,5% and 2%

per annum respectively. These rates of return are higher than

what is inferred by the underlying levels of risk inherent in

these portfolios [Basu, 1977 (p.667)]. Similarly, growth share

portfolios generated a 2,5-3% per annum return – less than what

they should have been given their underlying levels of risk

[Basu, 1977 (p.667)]. These results are in obvious violation

of the CAPM. Haugen (1995) echoes this when he states the CAPM

relationship between risk and return to have been “turned

upside down” (p.87) with the less volatile value shares

earning the highest return. As a result, share prices are

- 11 -

considered by many, including Basu (1977) to be “biased”

(p.663) due to shares earning returns which differ from what

their primary risk levels prescribe.

3.2 Implications for the Market

The world of security prices, having been “turned upside down”

[Haugen, 1995 (p.87)] has serious implications for the market.

I will discuss the three main effects below:

3.2.1 Mispricing

As discussed above, investors have an extremely unrealistic

expectation of the future earnings of their shares being a

reflection of the past earnings of that share for the

comparable time period of the previous year (Bernard and

Thomas, 1990). This would suggest that PE information is not

being fully integrated into share prices as effectively or

accurately as previously thought (Basu, 1977). As a result,

share prices cannot truly reflect a correct indication of a

shares intrinsic value. This means a share may be found to be

under or over valued, resulting in the creation of profitable

opportunities for investors. Obviously share prices being

under or over valued is not consistent with the EMH.

3.2.2 A Contrarian Investment Strategy

With the under and over valuation of securities, an obvious

profitable opportunity for investors exists. The contrarian

investment strategy involves the acquisition of shares which

- 12 -

have performed poorly in the past (value shares) and selling

growth shares, having performed well in the past (Chan, 1988).

According to Chan (1988) profitable opportunities exist since

undervalued shares (value shares) represent a “bargain” to

investors and recent market evidence has suggested that these

shares outperform overvalued growth shares, providing

investors

with a gainful profit margin. Profits are obtained when share

prices are corrected and revert back to their true worth

(Chan, 1988). A contrarian investor, having acquired value

shares at

their undervalued prices can expect to receive an excess

return and it is this clear success of the contrarian

investment strategy that has led many researchers to believe

that the stock market does in fact, overreact (Chan, 1988) and

that the certain securities studied are inappropriately

priced.

3.2.3 Reversals/Corrections

The success of the contrarian investment strategy depends the

market recognising investor overreaction and revising share

prices to their true intrinsic value. The exploitation of

under and over valued shares and the subsequent profits that

are earned implies that the stock market has acknowledged its

prior overreaction and has now corrected prices back to their

original values. As Lo (1997) states, “what goes up must come

down” (p.xvii) and this is precisely how contrarian profits

- 13 -

are generated. Once again, we see the real world workings of

the stock market and how it does not correlate with capital

market theory.

4. Investor and Market Behaviour

4.1 Overreaction

As we have already seen, stock markets do not always behave in

the way they are meant to in terms of the EMH and CAPM. Stout

(2003) attributes this to “human emotion” (p.31) and discusses

this impact on investment decisions. As previously mentioned,

investors differ with respect to their perceptions regarding

the future (Stout, 2003). Their inconsistent perspectives of

the actual worth of a share (Stout, 2003) means that share

prices are not as accurate a depiction of actual value as the

EMH pertains. Overreaction by investors and the market stems

from the overemphasis that is placed on past performance

(Haugen, 1995).

Psychologists find that people tend to base their future

prospects on the past performance of shares held in their

portfolio (Stout, 2003). The market, observing excess returns

generated on growth shares in the past, develop high

expectations of these shares believing growth will be above

average once again in the future (Haugen, 1995). The market,

however, is incorrect in believing excess returns will continue

to be earned long into the future (Haugen, 1995). This

- 14 -

confidence places an upward pressure on growth share prices,

resulting in growth shares becoming over-priced (Haugen,

1995). Haugen (1995) describes of “inertia” (p.27) occurring

in the market over the short run. The market extends positive

earnings results, for example, far into the future, instead of

correctly recognising that the positive news may only be a

forerunner to a few more good earnings results (Haugen, 1995).

This “inertia” [Haugen, 1995 (p.27)] characterised by an

inaccurate inflation of the share price (in the case of growth

shares) is projected well into the future by the market.

Haugen (1995) then found that once growth shares started

displaying unsatisfactory rates of return, the past increase

in growth share prices began to turn around as the market

corrected this overpricing of the growth share (Haugen, 1995).

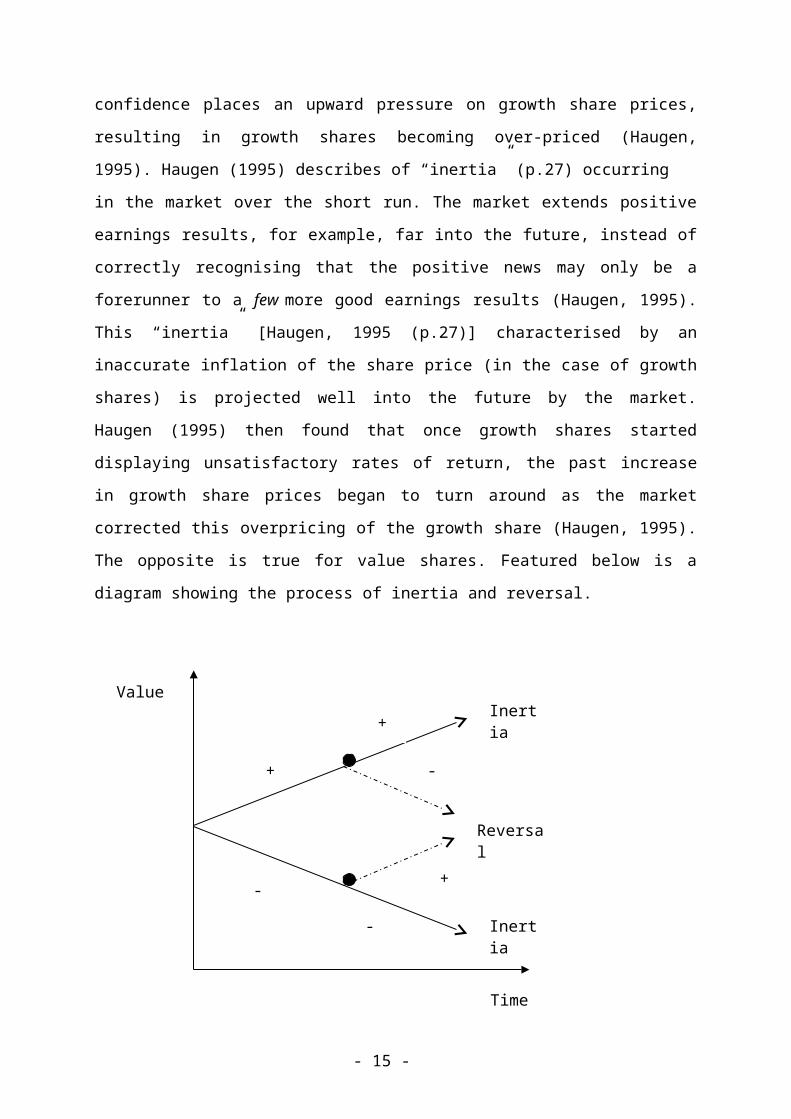

The opposite is true for value shares. Featured below is a

diagram showing the process of inertia and reversal.

- 15 -

Value

+

+ Inertia

Inertia

Reversal

-

-

-

+

Time

FFF

Where: “+” denotes an upward pressure on prices

“-“denotes a downward trend on prices.

The black dots represent market correction of past

over/underpricing.

Studies undertaken, investigating whether or not there is in

fact a link between past and future growth, provide evidence

to the satisfaction of the EMH: that there is no correlation

with respect to growth of earnings between a future period and

the period preceding it (Haugen, 1995). Investors would well

be taken advice of this – recent achievements are not

equivalent to prolonged success in the future (Haugen, 1995).

However, while researchers are aware of this academic fact, it

is another aspect altogether what the market base their

investment decisions on.

As previously discussed, the mispricing of shares and the

ultimate performance of growth and value shares can be

ascribed to investor emotion and perception. The high

expectations placed on growth shares to outperform in the

future drives up their prices, resulting in them becoming

overpriced. Investors purchasing growth shares pay an

extremely inflated price and when returns turn out to be

disappointing and the market corrects itself, adjusting price

downward so that price is equivalent to intrinsic value,

- 16 -

Time

Figure 3: Extracted andadapted from Haugen (1995)

investors realise a loss. Much research verifies this

“overreaction hypothesis” as described by Chopra, N et al (1992)

(p.804) where value share portfolios are found time and again

to outperform growth share portfolios. Chopra, N et al (1992)

discovered prior “losers” (p.804) to have generated a return

of 25% more than the prior “winners” (p.804). Haugen (1995)

found in a study that value shares outperformed growth shares

as well as the S&P500, a well-known market benchmark (p.60).

Studies of the long-term behaviour of share returns provide

evidence of something called the “fads hypothesis” [Bodie, Z et

al, 2002 (p.358)]. This hypothesis finds that overreaction

often occurs to certain significant news. This overreaction,

according to Bodie, Z et al (2002) results in “positive serial

correlation” (p.358) - meaning positive returns on a share are

inclined to be repeated and negative returns are also

recurring. The “fads hypothesis” asserts that this occurs over

the short term; however the hypothesis finds that over the long

run, negative serial correlation prevails. This means that

negative returns or below average returns follow on from

positive returns (Bodie, Z et al, 2002). The “fads hypothesis”

concurs with empirical evidence in that past abnormal profits

generated by growth shares do not continue into the future, as

expected by investors. Instead, below average returns are

earned and investors realise losses, as they sell their growth

shares assisting the market in correcting itself. Value

shares, on the other hand, enjoy excess returns as high

returns follow on from low returns and value stock investors

find themselves outperforming their growth stock counterparts.

- 17 -

5. Anomalies

Anomalies are described by Lo (1997) as a “regular pattern in

assets returns which (are) reliable, widely known and

inexplicable” (p.xviii). These anomalies serve as a direct

contradiction to the EMH’s principals, yet they continue to

play a part in today’s capital markets. Discussed below are

two observed market anomalies:

5.1 Sluggish Markets

Market efficiency hinges on the rapid adjustment of new

information into share prices. It is this speed of adjustment

that ensures that no arbitrage opportunities come into

existence. However, research has uncovered this anomaly

whereby prices, in fact react slowly to earnings announcements

(Bodie, Z et al, 2002). It has been found that following a good

earnings announcement, the particular share’s excess return

remains on its upward growth trend. The continued increase in

growth of these abnormal returns highlights the markets gradual

adjustment of price in response to the earnings announcement

(Bodie, Z et al, 2002). The implication of the sluggish nature

of price adjustment in the market is obviously that profitable

opportunities exist: Bodie, Z et al (2002) point out – one could

earn positive profits simply by purchasing the said portfolio

of shares once the earnings have been announced. Such an

investment strategy would earn abnormal returns due to the

market’s slow reaction and the continued period of high

- 18 -

returns that subsequently ensues. This should not be possible

in an efficient market (Bodie, Z et al, 2002).

5.2 The Size Effect/January Effect

This phenomenon as described by Lo (1997) is whereby small

firm portfolios are observed to outperform large firm

portfolios significantly over the new year (Lo, 1997). It is

believed that small cap shares are relatively riskier than

larger cap shares. However, Bodie, Z et al (2002) found that

even with these small cap shares being adjusted for risk,

there was still a considerable profit being earned by small

cap shares compared to the larger cap shares (Bodie, Z et al,

2002). A theory behind this odd occurrence is that a lot of

selling occurs during this period, with investors getting rid

of poor performing shares in an attempt to reduce their

realised losses before the tax year-end. These investors do

not transfer their

profits back into the market by acquiring other shares until

January. There subsequently ensues a surge of demand for

shares, driving prices upward (Bodie, Z et al, 2002).

6. Conclusion

Years of research and articles still haven’t concluded whether

or not the market is indeed efficient (Lo, 1997). The “upside

down” [Haugen, 1995 (p.87)] world of security pricing has led

- 19 -

many economists and researchers to question the validity of

the CAPM. Vibrant, risky, growth shares are seen to generate

below average returns and unexciting value shares high returns

(Haugen, 1995). This is in direct opposition to what should be

occurring. The CAPM predicts that a share’s expected return is

in direct correlation to its underlying risk, namely that

risky shares should enjoy relatively higher returns and the

opposite should be true for value shares. Haugen (1995) cites

the CAPM as being a “highly inaccurate depiction of reality”

(p.117). He believes that the foundation of the CAPM’s demise

is the failure of an efficient market. The sluggishness of

price adjustments to new information; mispricing of shares as

a result of investor overreaction and behaviour as well as the

evident profitability of a contrarian investment strategy has

led many to doubt the efficiency of the stock market. Stout

(2003) finds room for further research into the workings of

the market and highlights three areas of further study: a

“heterogenous pricing model” (p.40), which explains actual

market behaviour; arbitrage opportunities; and a detailed

investigation into the speed with which the market integrates

news into prices. She asserts that research into these three

areas may help us understand some market anomalies. The

efficiency of the market is liable to be a subject of great

discussion and research for a while to come. There is still

great debate amongst economists as to the reasons behind

certain anomalies and this only serves to provide a further

incentive for additional study into this area of finance

economics.

- 20 -

7. Appendix A

1. Vanguard Index Fund Total Returns

Fund 1 Year5 Years

10 Years

Growth Index Fund 32.13% -4.19% 11.09%Value Index Fund 38.21% 1.85% 10.17%

Data sourced from:http://flagship4.vanguard.com/VGApp/hnw/FundsByNameDetails?FundFamilyId=286&FundShareClass=1 – 26 February 2004

2. Investec Funds

Fund 3 Years 5 Years Investec GrowthFund 14 9.4 Investec Value Fund 40.9 33.8Data sourced from:http://www.investecfunds.co.za/sa_retail/ - 26 February 2004

- 21 -

8. References

Basu, S. (1977) Investment Performance of Common Stocks in Relation to Their Price – Earnings Ratios: A Test of the Efficient Market Hypothesis. Journal of Finance, XXXII (3), June, 663-82.

Bernard, V and Thomas, J. (1990) Evidence that Stock Prices donot fully reflect the Implications of Current Earnings for Future Earnings. Journal of Accounting and Economics, 13, 305 – 40.

Bodie, Z et al. (2002) Investments. New York, McGraw – Hill Irwin.

Chan, K. (1988) On the Contrarian Investment Strategy. Journal of Business, 61(2), 147-63.

Chopra, N et al. (1992) Measuring Abnormal Performance: Do StocksOverreact? Journal of Financial Economics, 31, 235-68.

- 22 -

Haugen, R. (1995) The New Finance: The Case Against Efficient Markets. Prentice – Hall Inc.

Lo, A (ed) (1997) Market Efficiency: Stock Market Behaviour in Theory and Practice. Volume II, The International Library of Critical Writings in Financial Economics. Edward Elgar Publishing Limited.

Stout, L. (2003) The Mechanisms of Market Inefficiency: An Introduction to the New Finance. UCLA School of Law and Economics. Research Paper No. 03-23. Social Science Research Network Electronic Library. Available from: http://ssrn.com/abstract=470161 (Accessed 24 February 2004).

Websites:Vanguard Index Fund Performance. Available from: http://flagship4.vanguard.com/VGApp/hnw/FundsByNameDetails?FundFamilyId=286&FundShareClass=1 (Accessed 26 February 2004).

Investec Growth and Value Performance. Available from:http://www.investecfunds.co.za/sa_retail/ (Accessed 26 February 2004).

- 23 -

![1-{( E )-[3-(1 H -Imidazol-1-yl)-1-phenylpropylidene]amino}-3-(2-methylphenyl)urea](https://static.fdokumen.com/doc/165x107/6324d53685efe380f30663d5/1-e-3-1-h-imidazol-1-yl-1-phenylpropylideneamino-3-2-methylphenylurea.jpg)