03-2016.pdf - icmai-wirc.in

36

1 WESTERN INDIA REGIONAL COUNCIL THE INSTITUTE OF COST ACCOUNTANTS OF INDIA (Statutory Body under an Act of Parliament) Rohit Chambers, Janmabhoomi Marg, Fort, Mumbai 400 001. Tel.: 2204 3406 / 2204 3416 / 2284 1138 • Fax : 2287 0763 E-mail : [email protected] • Website : www.icmai-wirc.in In this Issue .... EDITORIAL BOARD Chief Editor: CMA Harshad S. Deshpande Editorial Team: CMA Soumen Dutta CMA S. N. Mundra CMA Pradnya Y. Chandorkar Vol. 44 No. 3 March 2016 Price : Rs. 5/- For Members only Page • From the Desk of Chairman 3 • Analysis on Amendments Proposed in Draft CMA Harshad Deshpande 4 • Companies (Cost Records and Audit) • Amendment Rules 2016 • BUDGET ANALYSIS 2016-17 CMA Ashok B Nawal 9 • Returns under Goods and Service Tax CMA B F Modi 30 • Application of Cost Accounting Principles CMA Rajesh Kapadia 31 • Chapter News 33

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 03-2016.pdf - icmai-wirc.in

1

WESTERN INDIA REGIONAL COUNCILTHE INSTITUTE OF COST ACCOUNTANTS OF INDIA

(Statutory Body under an Act of Parliament)

Rohit Chambers, Janmabhoomi Marg, Fort, Mumbai 400 001.Tel.: 2204 3406 / 2204 3416 / 2284 1138 • Fax : 2287 0763 E-mail : [email protected] • Website : www.icmai-wirc.in

In this Issue....

EDITORIAL BOARD

Chief Editor:CMA Harshad S. Deshpande

Editorial Team:

CMA Soumen DuttaCMA S. N. Mundra

CMA Pradnya Y. Chandorkar

Vol. 44 No. 3 March 2016Price : Rs. 5/- For Members only

Page• From the Desk of Chairman 3

• Analysis on Amendments Proposed in Draft CMA Harshad Deshpande 4

• Companies (Cost Records and Audit)

• Amendment Rules 2016

• BUDGET ANALYSIS 2016-17 CMA Ashok B Nawal 9

• Returns under Goods and Service Tax CMA B F Modi 30

• Application of Cost Accounting Principles CMA Rajesh Kapadia 31

• Chapter News 33

WIRC BULLETIN – FEBRUARY 2016

2

Glimpses of Workshop on "How to conduct effective Cost Audit"conducted by WIRC on 6th February 2016 at WIRC Office, Mumbai

CMA Kailash Gandhi, Chairman P D Committee, WIRC CMA Debasish Mitra, Chairman WIRC

Mr. S.P. Kumar, Registrar of Companies, Mumbai lighting the lamp CMA Debasish Mitra, Chairman WIRC felicitating Mr. S.P. Kumar, Registrar of Companies, Mumbai

CMA Sukrut Mehta

CMA P.D. Modh interacting with the participants duringCEP organised by WIRC on 20th February 2016 at ThaneSMFC.

CMA Poonam Shah, Convener, North Mumbai CEP Study Circle

CMA Kishore Bhatia CMA R. Parvathy

CMA Kailash Gandhi, Chairman PD Committee, WIRCwelcoming CMA P.S. Guin, General Manager, InternalFinancial Control, L & T Ltd during CEP organised byWIRC on 27th February 2016 at Thane SMFC.

Institutes participated in Career Fest organised byNational HRD Network Mumbai Chapter on 19/2/2016at Nehru Centre, Worli, Mumbai

WIRC BULLETIN – MARCH 2016

3

Respected Colleagues,We congratulate Hon'ble Finance Minister for presentingthe Union Budget for the year 2016-17. This budget isone step forward for successful implementation of "Makein India", ease of doing business, generation ofemployment and boosting up of Infrastructure facilitiesin India.The Economic Survey forecasted that the Indian economywould grow in between 7.00 to 7.75 per cent in the 2016-17 fiscal year. Though there is no relief in the personaltaxation to the individuals but there are certain road mapswhich have been laid down in this budget towardscommitment to GST and Infrastructure development. Thegovernment proposes to spend Rs. 19,78,060 crore in 2016-17, which is 10.8% above the revised estimates of lastyear. The receipts (other than net borrowings) areexpected to increase by 15.5% to Rs. 14,44,156 crore,driven by disinvestment receipts, union excise duties andincome tax. Revenue deficit is targeted at 2.3% of GDP,and fiscal deficit is targeted at 3.5% of GDP.Railway Budget aims to achieve the long-felt desiresof the common man to be fulfilled by 2020, i.e., reservedaccommodation on trains available on demand, time tabledfreight trains, high end technology to improve safetyrecord, elimination of all unmanned level crossings,improved punctuality, higher average speed of freighttrains, semi high speed trains running along the goldenquadrilateral, zero direct discharge of human waste.

CEP ProgramsThis Council believes that the Continuing EducationProgram plays an important role to increase value basedknowledge for the members. Couple of good andinformative programs have been conducted by theProfessional Development Committee of the WIRC. Sameare as follows,• Practical Aspects on CAS 4 certification held on 13th

February 2016 at Borivli SMFC by CMA B.B.Prabhudesai.

• Emotional Intelligence at Thane & Borivli SMFC on20th Feb 2016 by CMA P. D. Modh.

• Internal Control - Regulatory Requirement &Relevance in Cost Accounting by CMA P. S. Guin,General Manager Internal Finance Control from L&TLtd., on 27th February, at Thane SMFC.

• Discussion on Draft Companies (Cost Records andAudit) Amendment Rules 2016 held on 1st March 2016lead by CMA S G Narsimhan.(I request all the members to send their comments /suggestions on the above matter to WIRC, as early aspossible).

• Discussion on Union Budget on 5th March 2016 byCMA V. S Datey , CMA A B Nawal and CMA Dr VishnuKanhere at WIRC and on 6th March, 2016 at Thane

From the Desk of ChairmanSMFC by CMA Amit Sarkar-Director IndirectTaxation - Deloitte and CA Anjana Singh - DirectorDirect Taxation, Deloitte. I request all the members tosend comments and suggestions on the Union Budget.

Pre-placement Orientation ProgramWe believe that our final passed members are equallycompetent with members of other professionalInstitutions, and are able to face and handle anychallenges of the corporate world. To sharpen their skilland knowledge, the Institute has organised Pre-placementOrientation Program form 1st March to 12th March 2016.This will ultimately help our new members to succeed infourth coming Campus Placement.Campus PlacementInstitute will organise Campus Placement on Friday the15th and Saturday, the 16th April 2016 at SGSJK ArunaManharlal Institute of Management& Research,Ghatkopar (West), Mumbai. This year also many notedorganisations from various parts of India will participatein the Campus Placement. WIRC has arranged a get-together (Alumni Meet) of the Members in the Industryon Saturday, the 19th March, 2016, at 5.30 p.m., at WIRCAuditorium. I appeal to our members from Industry toactively participate in the Institute's Campus Placementand contribute to the professional Development of theinstitute.

National Practitioners' ConventionNational Practitioners' Convention has been conductedat Kolkata on 21st February, 2016. Around 300 delegatesparticipated the event. The session "Horizons forpracticing CMA's in current and global environment", wasmoderated by CMA Sanjay Gupta and CMA B.B. Goyal,CMA Ashok Nawal and Chairman EIRC CMA Shiba PrasadPadhi. A nice presentation was made by CMA Padhi, on"CMA's role as Surveyors & Loss Assessors". Pleased toinform you that WIRC will organise similarprogram on CMAs as Surveyors & Loss Assessorson 11th March, 2016 at WIRC Auditorium.Career FestThe National HRD Network Mumbai Chapter hadorganised Career Fest at Nehru Centre on 19th February,2016. It was a good experience to be present at the festival.Around 10,000 students were participated to understandtheir career opportunities in diverse sectors. WIRC hadalso participated in that Fest. Lot of students from variouscolleges were visited our stall and enquired about ourprofession.Lastly, I appeal to our members to spend their valuabletime for career counselling program undertaken by theWIRC, for our prospective students. This will not onlyincrease the student strength of the Institute, at the sametime students will also avail proper and effective guidancefrom senior and experienced members of the Institute.Wishing you and your family a very bright, colourfuland joyful Holi!

CMA Debasish Mitra

WIRC BULLETIN – MARCH 2016

4

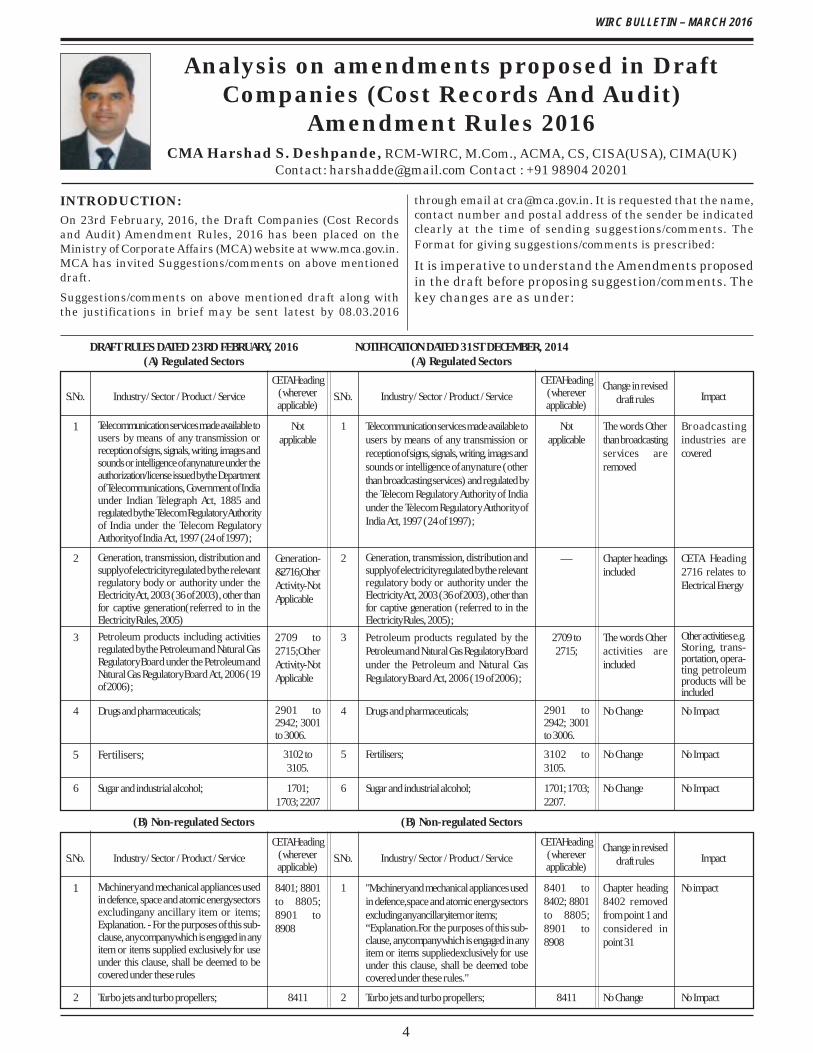

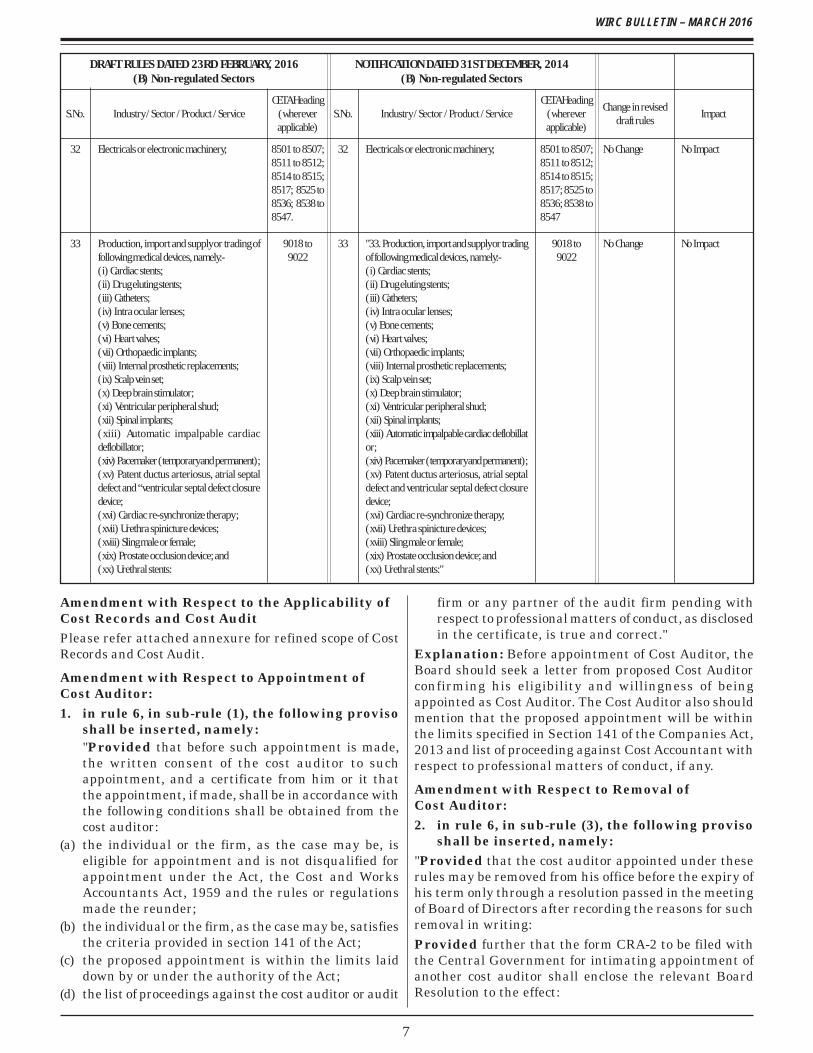

S.No. Industry / Sector / Product / Service Industry / Sector / Product / Service

CETA Heading(whereverapplicable)

Change in reviseddraft rules ImpactS.No.

CETA Heading(whereverapplicable)

DRAFT RULES DATED 23RD FEBRUARY, 2016(A) Regulated Sectors

NOTIFICATION DATED 31ST DECEMBER, 2014(A) Regulated Sectors

1 Telecommunication services made available tousers by means of any transmission orreception of signs, signals, writing, images andsounds or intelligence of any nature under theauthorization/license issued by the Departmentof Telecommunications, Government of Indiaunder Indian Telegraph Act, 1885 andregulated by the Telecom Regulatory Authorityof India under the Telecom RegulatoryAuthority of India Act, 1997 (24 of 1997);

Telecommunication services made available tousers by means of any transmission orreception of signs, signals, writing, images andsounds or intelligence of any nature (otherthan broadcasting services) and regulated bythe Telecom Regulatory Authority of Indiaunder the Telecom Regulatory Authority ofIndia Act, 1997 (24 of 1997);

Notapplicable

The words Otherthan broadcastingservices areremoved

Broadcas t i ngindustries arecovered

1Notapplicable

2 Generation, transmission, distribution andsupply of electricity regulated by the relevantregulatory body or authority under theElectricity Act, 2003 (36 of 2003), other thanfor captive generation(referred to in theElectricity Rules, 2005)

Generation, transmission, distribution andsupply of electricity regulated by the relevantregulatory body or authority under theElectricity Act, 2003 (36 of 2003), other thanfor captive generation (referred to in theElectricity Rules, 2005);

–– Chapter headingsincluded

CETA Heading2716 relates toElectrical Energy

2Generation-&2716;OtherActivity-NotApplicable

3 Petroleum products including activitiesregulated by the Petroleum and Natural GasRegulatory Board under the Petroleum andNatural Gas Regulatory Board Act, 2006 (19of 2006);

Petroleum products regulated by thePetroleum and Natural Gas Regulatory Boardunder the Petroleum and Natural GasRegulatory Board Act, 2006 (19 of 2006);

2709 to2715;

The words Otheractivities areincluded

Other activities e.g.Storing, trans-portation, opera-ting petroleumproducts will beincluded

32709 to2715;OtherActivity-NotApplicable

4 Drugs and pharmaceuticals; Drugs and pharmaceuticals; 2901 to2942; 3001to 3006.

No Change No Impact42901 to2942; 3001to 3006.

5 Fertilisers; Fertilisers; 3102 to3105.

No Change No Impact53102 to3105.

6 Sugar and industrial alcohol; Sugar and industrial alcohol; 1701; 1703;2207.

No Change No Impact61701;1703; 2207

S.No. Industry / Sector / Product / Service Industry / Sector / Product / Service

CETA Heading(whereverapplicable)

Change in reviseddraft rules ImpactS.No.

CETA Heading(whereverapplicable)

(B) Non-regulated Sectors (B) Non-regulated Sectors

1 Machinery and mechanical appliances usedin defence, space and atomic energy sectorsexcludingany ancillary item or items;Explanation. - For the purposes of this sub-clause, any company which is engaged in anyitem or items supplied exclusively for useunder this clause, shall be deemed to becovered under these rules

"Machinery and mechanical appliances usedin defence,space and atomic energy sectorsexcluding any ancillaryitem or items;“Explanation.For the purposes of this sub-clause, anycompany which is engaged in anyitem or items suppliedexclusively for useunder this clause, shall be deemed tobecovered under these rules."

8401 to8402; 8801to 8805;8901 to8908

Chapter heading8402 removedfrom point 1 andconsidered inpoint 31

No impact18401; 8801to 8805;8901 to8908

2 Turbo jets and turbo propellers; Turbo jets and turbo propellers; 8411 No Change No Impact28411

INTRODUCTION:On 23rd February, 2016, the Draft Companies (Cost Recordsand Audit) Amendment Rules, 2016 has been placed on theMinistry of Corporate Affairs (MCA) website at www.mca.gov.in.MCA has invited Suggestions/comments on above mentioneddraft.

Suggestions/comments on above mentioned draft along withthe justifications in brief may be sent latest by 08.03.2016

through email at [email protected]. It is requested that the name,contact number and postal address of the sender be indicatedclearly at the time of sending suggestions/comments. TheFormat for giving suggestions/comments is prescribed:

It is imperative to understand the Amendments proposedin the draft before proposing suggestion/comments. Thekey changes are as under:

Analysis on amendments proposed in DraftCompanies (Cost Records And Audit)

Amendment Rules 2016CMA Harshad S. Deshpande, RCM-WIRC, M.Com., ACMA, CS, CISA(USA), CIMA(UK)

Contact: [email protected] Contact : +91 98904 20201

WIRC BULLETIN – MARCH 2016

5

S.No. Industry / Sector / Product / Service Industry / Sector / Product / ServiceCETA Heading

(whereverapplicable)

Change in reviseddraft rules

ImpactS.No.CETA Heading

(whereverapplicable)

DRAFT RULES DATED 23RD FEBRUARY, 2016(B) Non-regulated Sectors

NOTIFICATION DATED 31ST DECEMBER, 2014(B) Non-regulated Sectors

3 Arms, ammunitions and Explosives; Arms and ammunitions; 3601 to3603; 9301to 9306.

Word "Explosive"is added

E x p l o s i v eproducts will becovered

33601 to3603; 9301to 9306.

4 Propellant powders; prepared explosives(other than propellant powders); safety fuses;detonating fuses; percussion or detonatingcaps; igniters; electric detonators;

Propellant powders; prepared explosives(other than propellant powders); safety fuses;detonating fuses; percussion or detonatingcaps; igniters; electric detonators;

3601 to3603

No Change No Impact43601 to3603

5 Radar apparatus, radio navigational aidapparatus and radio remote controlapparatus;

Radar apparatus, radio navigational aidapparatus and radio remote controlapparatus;

8526 No Change No Impact58526

6 Tanks and other armoured fightingvehicles,motorised, whether or not fitted withweapons andparts of such vehicles, that arefunded (investment made in the company) tothe extent of ninety per centor more by theGovernment or Government agencies;

Tanks and other armoured fighting vehicles,motorised, whether or not fitted with weaponsand parts of such vehicles, that are funded(investment made in the company) to the extentof ninety per cent or more by the Governmentor Government agencies;

8710 No Change No Impact68710

7 Port services of stevedoring, pilotage, hauling,mooring, re-mooring, hooking, measuring,loadingand unloading services rendered by aPort in relation to a vessel or goods regulatedby the Tariff Authority for Major Ports undersection 47A of the Major Port Trusts Act, 1963(38 of 1963);

Port services of stevedoring, pilotage, hauling,mooring,re-mooring, hooking, measuring,loading and unloading services rendered by aPort in relation to a vessel or goods regulatedby the Tariff Authority for Major Portsundersection 111 of the Major Port Trusts Act,1963 (38 of1963);

Notapplicable.

Section forFormation of TariffA u t h o r i t ycorrected toSection 47A fromSection 111.

No Impact7Notapplicable.

8 Aeronautical services of air traffic management,aircraft operations, ground safety services,groundhandling, cargo facilities and supplyingfuel renderedby airports and regulated by theAirports Economic Regulatory Authorityunder the Airports Economic RegulatoryAuthority of India Act, 2008 (27 of 2008);

Aeronautical services of air traffic management,aircraft operations, ground safety services,ground handling, cargo facilities and supplyingfuel rendered by airports and regulated by theAirports Economic Regulatory Authorityunder the Airports Economic RegulatoryAuthority of India Act, 2008 (27 of 2008);

Notapplicable.

No Change No Impact8Notapplicable.

9 Iron and Steel; Steel; 7201 to7229; 7301to 7326

Word "Iron" isinserted

Iron industry willbe covered

97201 to7229; 7301

to 7326

10 Roads and other infrastructure projectscorresponding to para No. (1) (a) as specifiedin Schedule VI of the Companies Act, 2013;

Roads and other infrastructure projectscorresponding to para No. (1) (a) as specifiedin Schedule VI of the Companies Act, 2013;

Notapplicable.

No Change No Impact10Notapplicable.

11 Rubber and allied products includingproducts regulated by the Rubber Boardconstituted under the Rubber Act, 1947 (XXIVof 1947).

Rubber and allied products being regulatedby the Rubber Board constituted under theRubber Act, 1947 (XXIV of 1947).

4001 to4017

Words "BeingRegulated" isreplaced with"including pro-ducts regulated"

All productsunder mentionedchapter headingwill be coveredirrespective ofregulated or not.

114001 to4017

12 Coffee and tea; Coffee and tea; 0901 to0902

No Change No Impact120901 to0902

13 Railway or tramway locomotives, rolling stock,railway or tramway fixtures and fittings,mechanical (including electro mechanical)traffic signalling equipment’s of all kind;

Railway or tramway locomotives, rolling stock,railway or tramway fixtures and fittings,mechanical (including electro mechanical)traffic signalling equipment’s of all kind;

8601 to8608.

No Change No Impact138601 to8608

14 Cement; Cement; 2523; 6811to 6812

No Change No Impact142523; 6811to 6812

15 Ores and Mineral products; Ores and Mineral products; 2502 to2522; 2524 to2526; 2528 to2530; 2601 to2617

No Change No Impact152502 to2522; 2524 to2526; 2528 to2530; 2601 to2617

WIRC BULLETIN – MARCH 2016

6

S.No. Industry / Sector / Product / Service Industry / Sector / Product / ServiceCETA Heading

(whereverapplicable)

Change in reviseddraft rules

ImpactS.No.CETA Heading

(whereverapplicable)

DRAFT RULES DATED 23RD FEBRUARY, 2016(B) Non-regulated Sectors

NOTIFICATION DATED 31ST DECEMBER, 2014(B) Non-regulated Sectors

16 Mineral fuels (other than Petroleum), mineraloils etc.;

Mineral fuels (other than Petroleum), mineraloils etc.;

2701 to2708

No Change No Impact162701 to2708

17 Base metals; Base metals; 7401 to 7403;7405 to 7413;7419;7501 to7508; 7601 to7614; 7801 to7614; 7804;7806; 7901 to7905;7907;8001; 8003;8007; 8101 to8113

No Change No Impact177401 to 7403;7405 to 7413;7419; 7501 to7508; 7601 to7614; 7801 to7802; 7804;7806; 7901 to7905; 7907;8001; 8003;8007; 8101 to8113

18 Inorganic chemicals, organic or inorganiccompounds of precious metals, rare-earthmetals of radio achievements or isotopes, andOrganic Chemicals;

Inorganic chemicals, organic or inorganiccompounds of precious metals, rare-earthmetals of radioactive elements or isotopes, andOrganic Chemicals;

2801 to 2853;2901 to 2942;3801 to 3807;3402 to 3403;3809 to 3824.

No Change No Impact182801 to 2853;2901 to 2942;3801 to 3807;3402 to 3403;3809 to 3824.

19 Jute and Jute Products; Jute and Jute Products; 5303, 5310 No Change No Impact195303, 5310

20 Edible Oil; Edible Oil; 1507 to1518

No Change No Impact201507 to1518

21 Construction Industry as per para No. (5) (a)as specified in Schedule VI of the CompaniesAct, 2013(18 of 2013)

Construction Industry as per para No. (5) (a)as specified in Schedule VI of the CompaniesAct, 2013 (18 of 2013)

Notapplicable.

No Change No Impact21Notapplicable.

22 Health services, namely functioning as orrunning hospitals, diagnostic centres, clinicalcentres or test laboratories;

Health services, namely functioning as orrunning hospitals, diagnostic centres, clinicalcentres or test laboratories;

Notapplicable.

No Change No Impact22Notapplicable.

23 Education services, other than such similarservices falling under philanthropy or as partof social spend which do not form part of anybusiness.

Education services, other than such similarservices falling under philanthropy or as partof social spend which do not form part of anybusiness.

Notapplicable.

No Change No Impact23Notapplicable.

24 Milk powder; Milk powder; 0402 No Change No Impact240402

25 Insecticides; Insecticides; N No Change No Impact253808

26 Plastics and polymers; Plastics and polymers; 3901 to3914; 3916 to3921; 3925

No Change No Impact263901 to3914; 3916 to3921; 3925

27 Tyres and tubes; Tyres and tubes; 4011 to4013

No Change No Impact274011 to4013

28 Paper; Paper; 4801 to4802

No Change No Impact284801 to4802

29 Textiles; Textiles; 5004 to 5007;5106 to 5113;5205 to 5212;5303; 5310;5401 to 5408;5501 to 5516

No Change No Impact295004 to 5007;5106 to 5113;5205 to 5212;5303; 5310;5401 to 5408;5501 to 5516

30 Glass; Glass; 7003 to 7008;7011; 7016

No Change No Impact307003 to 7008;7011; 7016

31 Other machinery and Mechanical Appliances; Other machinery; 8403 to8487

The words "AndM e c h a n i c a lAppliances" areadded andChapter heading8402 added

Other mechanicalappliances will getspecifically covered.All products undermentioned chapterheading will becovered.

318402 to8487

WIRC BULLETIN – MARCH 2016

7

S.No. Industry / Sector / Product / Service Industry / Sector / Product / ServiceCETA Heading

(whereverapplicable)

Change in reviseddraft rules

ImpactS.No.CETA Heading

(whereverapplicable)

DRAFT RULES DATED 23RD FEBRUARY, 2016(B) Non-regulated Sectors

NOTIFICATION DATED 31ST DECEMBER, 2014(B) Non-regulated Sectors

32 Electricals or electronic machinery; Electricals or electronic machinery; 8501 to 8507;8511 to 8512;8514 to 8515;8517; 8525 to8536; 8538 to8547

No Change No Impact328501 to 8507;8511 to 8512;8514 to 8515;8517; 8525 to8536; 8538 to8547.

33 Production, import and supply or trading offollowing medical devices, namely:-(i) Cardiac stents;(ii) Drug eluting stents;(iii) Catheters;(iv) Intra ocular lenses;(v) Bone cements;(vi) Heart valves;(vii) Orthopaedic implants;(viii) Internal prosthetic replacements;(ix) Scalp vein set;(x) Deep brain stimulator;(xi) Ventricular peripheral shud;(xii) Spinal implants;(xiii) Automatic impalpable cardiacdeflobillator;(xiv) Pacemaker (temporary and permanent);(xv) Patent ductus arteriosus, atrial septaldefect and “ventricular septal defect closuredevice;(xvi) Cardiac re-synchronize therapy ;(xvii) Urethra spinicture devices;(xviii) Sling male or female;(xix) Prostate occlusion device; and(xx) Urethral stents:

"33. Production, import and supply or tradingof following medical devices, namely:-(i) Cardiac stents;(ii) Drug eluting stents;(iii) Catheters;(iv) Intra ocular lenses;(v) Bone cements;(vi) Heart valves;(vii) Orthopaedic implants;(viii) Internal prosthetic replacements;(ix) Scalp vein set;(x) Deep brain stimulator;(xi) Ventricular peripheral shud;(xii) Spinal implants;(xiii) Automatic impalpable cardiac deflobillator;(xiv) Pacemaker (temporary and permanent);(xv) Patent ductus arteriosus, atrial septaldefect and ventricular septal defect closuredevice;(xvi) Cardiac re-synchronize therapy;(xvii) Urethra spinicture devices;(xviii) Sling male or female;(xix) Prostate occlusion device; and(xx) Urethral stents:"

9018 to9022

No Change No Impact339018 to9022

Amendment with Respect to the Applicability ofCost Records and Cost AuditPlease refer attached annexure for refined scope of CostRecords and Cost Audit.

Amendment with Respect to Appointment ofCost Auditor:1. in rule 6, in sub-rule (1), the following proviso

shall be inserted, namely:"Provided that before such appointment is made,the written consent of the cost auditor to suchappointment, and a certificate from him or it thatthe appointment, if made, shall be in accordance withthe following conditions shall be obtained from thecost auditor:

(a) the individual or the firm, as the case may be, iseligible for appointment and is not disqualified forappointment under the Act, the Cost and WorksAccountants Act, 1959 and the rules or regulationsmade the reunder;

(b) the individual or the firm, as the case may be, satisfiesthe criteria provided in section 141 of the Act;

(c) the proposed appointment is within the limits laiddown by or under the authority of the Act;

(d) the list of proceedings against the cost auditor or audit

firm or any partner of the audit firm pending withrespect to professional matters of conduct, as disclosedin the certificate, is true and correct."

Explanation: Before appointment of Cost Auditor, theBoard should seek a letter from proposed Cost Auditorconfirming his eligibility and willingness of beingappointed as Cost Auditor. The Cost Auditor also shouldmention that the proposed appointment will be withinthe limits specified in Section 141 of the Companies Act,2013 and list of proceeding against Cost Accountant withrespect to professional matters of conduct, if any.

Amendment with Respect to Removal ofCost Auditor:2. in rule 6, in sub-rule (3), the following proviso

shall be inserted, namely:"Provided that the cost auditor appointed under theserules may be removed from his office before the expiry ofhis term only through a resolution passed in the meetingof Board of Directors after recording the reasons for suchremoval in writing:Provided further that the form CRA-2 to be filed withthe Central Government for intimating appointment ofanother cost auditor shall enclose the relevant BoardResolution to the effect:

WIRC BULLETIN – MARCH 2016

8

Provided also that nothing contained in this sub-rule shallprejudice the right of the cost auditor to resign from suchoffice of the company."

Explanation: Cost Auditor may be removed before endof term by passing a Board Resolution. On such removal,Form CRA-2 should be re-filed mentioning details ofparticulars of new Cost Auditor along with a copy of suchBoard Resolution. Further, Cost Auditor can tender hisresignation at any time before end of his tenure.

Approval of Cost Statements:3. in rule 6, after sub-rule (3A), following sub-rule

shall be inserted, namely:"(3B) The cost statements, including other statements tobe annexed to the cost audit report, shall be approved bythe Board of Directors before they are signed on behalfof the Board by any of the director authorized by theBoard, for submission to the cost auditor to reportthereon"

Explanation: Board should approve the cost statementsalong with annexure to cost audit report beforesubmission of the same to the Cost Auditor. After receiptof such approved cost statement along with the annexure,Cost Auditor will prepare his Cost Audit Report.

Submission of Report by Cost Auditor:4. in rule 6, for sub-rule (5), the following sub-rule

shall be substituted, namely:-"Every cost auditor shall forward his duly signed reportto the Board of Directors of the company within a periodof one hundred and eighty days from the closure of thefinancial year to which the report relates and the Board

of Directors shall consider and examine such report,particularly any reservation or qualification containedtherein."Explanation: Cost Auditor shall submit his duly signedreport with a period of one hundred and eighty days fromclosure of Financial Year to which it relates to the Boardof Directors of the Company. Board of Directors shallreceive, consider and examine the reservations andqualifications stated in the Cost Audit Report.

Filing of Cost Audit Report by the Company:5. in rule 6, for sub-rule (6), th following sub-rule

shall be substituted, namely:"Every company covered under these rules shall, withina period of thirty days from the date of receipt of a copyof the cost audit report, furnish the Central Governmentwith such report along with full information andexplanation on every reservation or qualificationcontained therein, in form CRA-4 in Extensible BusinessReporting Language (XBRL) format in the manner asspecified in the Companies (Filing of Documents andForms in Extensible Business Reporting language) Rules,2015 along with fees specified in the Companies(Registration Offices and Fees) Rules 2014."Explanation: The Board of Directors shall prepare a noteproviding necessary information and explanation on thereservation and qualifications stated in the Cost AuditReport. Thereafter the Company shall submit Cost AuditReport along with such note containing information andexplanation in Form CRA-4 in XBRL Format within aperiod of thirty days of receipt of the Report from CostAuditor.

WIRC organised followingCEPs during the month

1. CEP on "Practical Aspects on CAS 4 certification"- 13th February 2016 at Borivli SMFC. CMA V. B.Prabhudesai was the speaker.

2. CEP on Emotional Intelligence - at Thane & BorivliSMFC - 20th February 2016. CMA P.D. Modh wasthe speaker.

3. CEP on "Internal Controls - RegulatoryRequirements & relevance in Cost Accounting" -CMA P. S. Guin, General Manager, InternalFinancial Control, Larsen & Toubro Limited on27th Feb at Thane SMFC

4. Discussion on "Draft Companies (Cost Records andAudit) Amendment Rules, 2016" - 1st March 2016at WIRC. CMA S. G. Narasimhan, lead thediscussion.

5. Discussion on Union Budget was organised on 5thMarch at WIRC office. CMA V. S. Datey, CMA A. B.Nawal & CMA & CA Dr. Vishnu Kanhere were thespeakers and on 6th March at Thane SMFC - CMAAmit Sarker & CA Anjana Singh, from Deloittewere the speakers.

Pune Central CEP Study Circle‘Pune Central CEP Study Circle formedunder the guidelines of the Institute of CostAccountants of India organized its eighthfunction on 20th February 2016. Mr. SagarKanade, Expert on Transfer Pricing gave thelecture on this occasion. Topic of the lecturewas ‘Transfer pricing and the role of CostAccountants’. Speaker elaborated about theconcept of Transfer pricing and also toldabout the areas wherein Cost Accountantscan play a decisive role. CMA Prashant Vaze,Convener of the Study Circle along withCMA Rajendra Pardeshi (Members of theAdvisory committee of the Study Circle)arranged the Program. CMA HarshadDeshpande, RCM was also present at thisevent.

WIRC BULLETIN – MARCH 2016

9

Sec.No.

AmendmentEffective Date Provision Existing Provision

Amendment in Existing /New Provision Analysis

5A(5 & 6)

From the date ofAscent of Presidentof India

Power to grantexemption fromduty of excise

(5) Every notification issued under sub-section (1) or sub-section 2(A) shall,(a) unless otherwise provided, come intoforce on the date of its issue by the CentralGovernment for publication in the OfficialGazette;(b) also be published and offered for saleon the date of its issue by the Directorate ofPublicity and Public Relations, Customs andCentral Excise, New Delhi, under the CentralBoard of Excise and Customs constitutedunder the Central Boards of Revenue Act,1963 (54 of 1963).(6) Notwithstanding anything contained insub-section (5), where a notification comesinto force on a date later than the date of itsissue, the same shall be published andoffered for sale by the said Directorate ofPublicity and Public Relations on a date onor before the date on which the saidnotification comes into force.

(5) Every notification issued under sub-section (1) or sub-section 2(A) shall, -

(a) unless otherwise provided, come intoforce on the date of its issue by the CentralGovernment for publication in the OfficialGazette;

Now there is no requirement ofpublishing and offering for sale anynotification issued, by the Directorateof Publicity and Public Relations ofCBEC.

11A From the date ofAscent of Presidentof India

Recovery of dutiesnot levied or notpaid or short-leviedor short-paid ore r r o n e o u s l yrefunded.

(1) Where any duty of excise has not beenlevied or paid or has been short-levied orshort-paid or erroneously refunded, for anyreason, other than the reason of fraud orcollusion or any wilful misstatement orsuppression of facts or contravention of anyof the provisions of this Act or of the rulesmade thereunder with intent to evadepayment of duty,-

(a) the Central Excise Officer shall, withinone year from the relevant date, serve noticeon the person chargeable with the dutywhich has not been so levied or paid or whichhas been so short-levied or short-paid or towhom the refund has erroneously beenmade, requiring him to show cause why heshould not pay the amount specified in thenotice;

(b) the person chargeable with duty may,before service of notice under clause (a),pay on the basis of,-

(i) his own ascertainment of such duty; or

(ii) duty ascertained by the Central ExciseOfficer, the amount of duty along with interestpayable thereon under section 11AA.

(2) The person who has paid the duty underclause (b) of sub-section (1), shall informthe Central Excise Officer of such payment inwriting, who, on receipt of such information,shall not serve any notice under clause (a)of that sub-section in respect of the duty sopaid or any penalty leviable under theprovisions of this Act or the rules madethereunder.

(3) Where the Central Excise Officer is of theopinion that the amount paid under clause(b) of sub-section (1) falls short of theamount actually payable, then, he shall

(1) Where any duty of excise has not beenlevied or paid or has been short-levied orshort-paid or erroneously refunded, for anyreason, other than the reason of fraud orcollusion or any wilful misstatement orsuppression of facts or contravention of anyof the provisions of this Act or of the rulesmade thereunder with intent to evadepayment of duty,-(a) the Central Excise Officer shall, withinTwo years from the relevant date, serve noticeon the person chargeable with the dutywhich has not been so levied or paid or whichhas been so short-levied or short-paid or towhom the refund has erroneously beenmade, requiring him to show cause why heshould not pay the amount specified in thenotice;(b) the person chargeable with duty may,before service of notice under clause (a),pay on the basis of,-(i) his own ascertainment of such duty; or(ii) duty ascertained by the Central ExciseOfficer, the amount of duty along with interestpayable thereon under section 11AA.(2) The person who has paid the duty underclause (b) of sub-section (1), shall informthe Central Excise Officer of such payment inwriting, who, on receipt of such information,shall not serve any notice under clause (a)of that sub-section in respect of the duty sopaid or any penalty leviable underthe provisions of this Act or the rules madethereunder.(3) Where the Central Excise Officer is of theopinion that the amount paid under clause(b) of sub-section (1) falls short of theamount actually payable, then, he shallproceed to issue the notice as provided for in

Period of limitation has beenincreased from one year to two yearsfor issuing SCN & Demand Notices, incase not involving fraud, suppressionof facts, willful mis-statement, etc

However, period of limitation has notbeen extended in the matter of refundin Section 11B.

BUDGET ANALYSIS 2016 - 17CENTRAL EXCISE ACT 1944Complied by CMA Ashok B. Nawal

Contact: +91 9890165001 • Email: [email protected]

WIRC BULLETIN – MARCH 2016

10

CENTRAL EXCISE ACT 1944Sec.No.

AmendmentEffective Date Provision Existing Provision

Amendment in Existing /New Provision Analysis

proceed to issue the notice as provided forin clause (a) of that sub-section in respect ofsuch amount which falls short of the amountactually payable in the manner specifiedunder that sub-section and the period of oneyear shall be computed from the date ofreceipt of information under sub-section(2).(4) Where any duty of excise has not beenlevied or paid or has been shortlevied orshort-paid or erroneously refunded, by thereason of-

(a) fraud; or(b) collusion; or(c) any willful mis-statement; or(d) suppression of facts; or(e) contravention of any of the provisions ofthis Act or of the rules made thereunder withintent to evade payment of duty,

by any person chargeable with the duty, theCentral Excise Officer shall, within five yearsfrom the relevant date, serve notice on suchperson requiring him to show cause why heshould not pay the amount specified in thenotice along with interest payable thereonunder section 11AA and a penalty equivalentto the duty specified in the notice.(5) Where, during the course of any audit,investigation or verification, it is found thatany duty has not been levied or paid or short-levied or short-paid or erroneouslyrefunded for the reason mentioned in clause(a) or clause (b) or clause (c) or clause (d)or clause (e) of sub-section (4) but thedetails relating to the transactions areavailable in the specified record, then in suchcases, the Central Excise Officer shall withina period of five years from the relevant date,serve a notice on the person chargeable withthe duty requiring him to show cause whyhe should not pay the amount specified inthe notice along with interest under section11AA and penalty equivalent to fifty per centof such duty.

(6) Any person chargeable with duty undersub-section (5), may, before service of showcause notice on him, pay the duty in full or inpart, as may be accepted by him along withthe interest payable thereon under section11AA and penalty equal to one per cent ofsuch duty per month to be calculated fromthe month following the month in which suchduty was payable, but not exceeding amaximum of twenty-five per cent of the duty,and inform the Central Excise Officer of suchpayment in writing.

7) The Central Excise Officer, on receipt ofinformation under sub-section (6) shall-(i) not serve any notice in respect of theamount so paid and all proceedings inrespect of the said duty shall be deemed tobe concluded where it is found by the CentralExcise Officer that the amount of duty, interestand penalty as provided under sub-section

clause (a) of that sub-section in respect ofsuch amount which falls short of the amountactually payable in the manner specified underthat sub-section and the period of Two yearsshall be computed from the date of receipt ofinformation under sub-section (2).

(4) Where any duty of excise has not beenlevied or paid or has been shortlevied orshort-paid or erroneously refunded, by thereason of-

(a) fraud; or

(b) collusion; or

(c) any wilful mis-statement; or

(d) suppression of facts; or

(e) contravention of any of the provisions ofthis Act or of the rules made thereunder withintent to evade payment of duty,

by any person chargeable with the duty, theCentral Excise Officer shall, within five yearsfrom the relevant date, serve notice on suchperson requiring him to show cause why heshould not pay the amount specified in thenotice along with interest payable thereonunder section 11AA and a penalty equivalentto the duty specified in the notice.

(5) Where, during the course of any audit,investigation or verification, it is found thatany duty has not been levied or paid or short-levied or short-paid or erroneously refundedfor the reason mentioned in clause (a) orclause (b) or clause (c) or clause (d) orclause (e) of sub-section (4) but the detailsrelating to the transactions are available in thespecified record, then in such cases, theCentral Excise Officer shall within a period offive years from the relevant date, serve a noticeon the person chargeable with the dutyrequiring him to show cause why he shouldnot pay the amount specified in the notice alongwith interest under section 11AA and penaltyequivalent to fifty per cent of such duty.

(6) Any person chargeable with duty undersub-section (5), may, before service of showcause notice on him, pay the duty in full or inpart, as may be accepted by him along withthe interest payable thereon under section11AA and penalty equal to one per cent ofsuch duty per month to be calculated fromthe month following the month in which suchduty was payable, but not exceeding amaximum of twenty-five per cent of the duty,and inform the Central Excise Officer of suchpayment in writing.

7) The Central Excise Officer, on receipt ofinformation under sub-section (6) shall-

(i) not serve any notice in respect of theamount so paid and all proceedings inrespect of the said duty shall be deemed to beconcluded where it is found by the CentralExcise Officer that the amount of duty, interestand penalty as provided under sub-section(6) has been fully paid;

(ii) proceed for recovery of such amount iffound to be short-paid in the manner specified

WIRC BULLETIN – MARCH 2016

11

CENTRAL EXCISE ACT 1944Sec.No.

AmendmentEffective Date Provision Existing Provision

Amendment in Existing /New Provision Analysis

(6) has been fully paid;(ii) proceed for recovery of such amount iffound to be short-paid in the mannerspecified under sub-section (1) and theperiod of one year shall be computed fromthe date of receipt of such information.(8) In computing the period of one yearreferred to in clause (a) of subsection (1)or five years referred to in sub-section (4)or sub-section (5), the period during whichthere was any stay by an order of the courtor Tribunal in respect of payment of suchduty shall be excluded.(9) Where any appellate authority orTribunal or court concludes that the noticeissued under sub-section (4) is notsustainable for the reason that the chargesof fraud or collusion or any wilful mis-statement or suppression of facts orcontravention of any of the provisions of thisAct or of the rulesmade thereunder with intent to evadepayment of duty has not been establishedagainst the person to whom the notice wasissued, the Central Excise Officer shalldetermine the duty of excise payable by suchperson for the period of one year, deemingas if the notice were issued under clause (a)of sub-section (1).(10) The Central Excise Officer shall, afterallowing the concerned person anopportunity of being heard, and afterconsidering the representation, if any, madeby such person, determine the amount ofduty of excise due from such person notbeing in excess of the amount specified in thenotice.(11) The Central Excise Officer shalldetermine the amount of duty of excise undersub-section (10)-(a) within six months from the date of noticein respect of cases falling under subsection(1);(b) withinone year from the date of notice inrespect of cases falling under subsection (4)or sub-section (5).(12) Where the appellate authority modifiesthe amount of duty of excise determined bythe Central Excise Officer under sub-section(10), then the amount of penalties andinterest under this section shall standmodified accordingly, taking into account theamount of duty of excise so modified.(13) Where the amount as modified by theappellate authority is more than the amountdetermined under sub-section (10) by theCentral Excise Officer, the time within whichthe interest or penalty is payable under thisAct shall be counted from the date of the orderof the appellate authority in respect of suchincreased amount.(14) Where an order determining the dutyof excise is passed by the Central ExciseOfficer under this section, the person liable

under sub-section (1) and the period of Twoyears shall be computed from the date ofreceipt of such information.

(8) In computing the period of Two yearsreferred to in clause (a) of subsection (1) orfive years referred to in sub-section (4) orsub-section (5), the period during whichthere was any stay by an order of the court orTribunal in respect of payment of such dutyshall be excluded.

(9) Where any appellate authority or Tribunalor court concludes that the notice issuedunder sub-section (4) is not sustainable forthe reason that the charges of fraud orcollusion or any wilful mis-statement orsuppression of facts or contravention of anyof the provisions of this Act or of the rules

made thereunder with intent to evade paymentof duty has not been established against theperson to whom the notice was issued, theCentral Excise Officer shall determine the dutyof excise payable by such person for theperiod of two years, deeming as if the noticewere issued under clause (a) of sub-section(1).

(10) The Central Excise Officer shall, afterallowing the concerned person anopportunity of being heard, and afterconsidering the representation, if any, madeby such person, determine the amount of dutyof excise due from such person not being inexcess of the amount specified in the notice.

(11) The Central Excise Officer shalldetermine the amount of duty of excise undersub-section (10)-

(a) within six months from the date of noticein respect of cases falling under subsection(1);

(b) withinTwo years from the date of notice inrespect of cases falling under subsection (4)or sub-section (5).

(12) Where the appellate authority modifiesthe amount of duty of excise determined bythe Central Excise Officer under sub-section(10), then the amount of penalties andinterest under this section shall standmodified accordingly, taking into account theamount of duty of excise so modified.

(13) Where the amount as modified by theappellate authority is more than the amountdetermined under sub-section (10) by theCentral Excise Officer, the time within whichthe interest or penalty is payable under thisAct shall be counted from the date of the orderof the appellate authority in respect of suchincreased amount.

(14) Where an order determining the duty ofexcise is passed by the Central Excise Officerunder this section, the person liable to paythe said duty of excise shall pay the amount sodetermined along with the interest due onsuch amount whether or not the amount ofinterest is specified separately.

Explanation.-For the purposes of this sectionand section 11AC,-

WIRC BULLETIN – MARCH 2016

12

CENTRAL EXCISE ACT 1944Sec.No.

AmendmentEffective Date Provision Existing Provision

Amendment in Existing /New Provision Analysis

to pay the said duty of excise shall pay theamount so determined along with the interestdue on such amount whether or not theamount of interest is specified separately.Explanation.-For the purposes of this sectionand section 11AC,-(a) "refund" includes rebate of duty of exciseon excisable goods exported out of India oron excisable materials used in themanufacture of goods which are exportedout of India;(b) "relevant date" means,-(i) in the case of excisable goods on whichduty of excise has not been levied or paid orhas been short-levied or short-paid, and noperiodical return as required by theprovisions of this Act has been filed, the lastdate on which such return is required to befiled under this Act and the rules madethereunder;(ii) in the case of excisable goods on whichduty of excise has not been levied or paid orhas been short-levied or short-paid and thereturn has been filed on due date, the dateon which such return has been filed;(iii) in any other case, the date on which dutyof excise is required to be paid under thisAct or the rules made thereunder;(iv) in a case where duty of excise isprovisionally assessed under this Act or therules made thereunder, the date ofadjustment of duty after the final assessmentthereof;(v) in the case of excisable goods on whichduty of excise has been erroneouslyrefunded, the date of such refund;(c) "specified records" means recordsincluding computerised records maintainedby the person chargeable with the duty inaccordance with any law for the time being inforce.'.

(a) "refund" includes rebate of duty of exciseon excisable goods exported out of India oron excisable materials used in themanufacture of goods which are exportedout of India;

(b) "relevant date" means,-

(i) in the case of excisable goods on whichduty of excise has not been levied or paid orhas been short-levied or short-paid, and noperiodical return as required by theprovisions of this Act has been filed, the lastdate on which such return is required to befiled under this Act and the rules madethereunder;

(ii) in the case of excisable goods on whichduty of excise has not been levied or paid orhas been short-levied or short-paid and thereturn has been filed on due date, the dateon which such return has been filed;

(iii) in any other case, the date on which dutyof excise is required to be paid under thisAct or the rules made thereunder;

(iv) in a case where duty of excise isprovisionally assessed under this Act or therules made thereunder, the date ofadjustment of duty after the final assessmentthereof;

(v) in the case of excisable goods on whichduty of excise has been erroneouslyrefunded, the date of such refund;

(c) "specified records" means recordsincluding computerised records maintainedby the person chargeable with the duty inaccordance with any law for the time being inforce.'

37B From the date ofAscent of Presidentof India

Instructions toCentral ExciseOfficers.

The Central Board of Excise and Customsconstituted under the Central Boards ofRevenue Act, 1963 (54 of 1963), may, if itconsiders it necessary or expedient so to dofor the purpose of uniformity in theclassification of excisable goods or withrespect to levy of duties of excise on suchgoods, issue such orders, instructions anddirections to the Central Excise Officers as itmay deem fit, and such officers and all otherpersons employed in the execution of thisAct shall observe and follow such orders,instructions and directions of the saidBoard:

Provided that no such orders, instructionsor directions shall be issued-

a) so as to require any Central Excise Officerto make a particular assessment or todispose of a particular case in a particularmanner; or

b) so as to interfere with the discretion of theCommissioner of Central Excise (Appeals)in the exercise of his appellate functions.

The Central Board of Excise and Customsconstituted under the Central Boards ofRevenue Act, 1963 (54 of 1963), may, if itconsiders it necessary or expedient so to dofor the purpose of uniformity in theclassification of excisable goods or withrespect to levy of duties of excise on suchgoods OR for the implementation of any otherprovisions of this Act, issue such orders,instructions and directions to the CentralExcise Officers as it may deem fit, and suchofficers and all other persons employed inthe execution of this Act shall observe andfollow such orders, instructions anddirections of the said Board :Provided that no such orders, instructionsor directions shall be issued-a) so as to require any Central Excise Officerto make a particular assessment or todispose of a particular case in a particularmanner; orb) so as to interfere with the discretion of theCommissioner of Central Excise (Appeals)in the exercise of his appellate functions.

Section 37B is being amended so asto empower the Board forimplementation of any otherprovision of the said Act in addition tothe power to issue orders,instructions and directions

Earlier clarifications issued u/s 37Bwas only applicable for goods andthose are binding on Assessee as wellas Department. Now, powers has beengiven to the Central Excise Departmenteven to issue the clarifications u/s 37Bfor any provisions under the Act.

It means Department may issue thecirculars u/s 37B for each provisionunder this Act and that will be bindingon Department as well as Assessee.

This is absolutely wrong provisionand needs to be represented by Trade& Industries.

WIRC BULLETIN – MARCH 2016

13

CENTRAL EXCISE ACT 1944Sec.No.

AmendmentEffective Date Provision Existing Provision

Amendment in Existing /New Provision Analysis

ThirdSche-dule

1st March 2016 Deemed Manufac-turing

Schedule provides the process which isdeemed to be manufactured in accordancewith Sec 2(f)(iii).

Tariff No. 3401 :

Soaps in any form other than the following

(i) soap, other than for toilet use, whetheror not containing medicament ordisinfectant;

(ii) soap, in or in relation to the manufactureof which no process has been carried onwith the aid of power or of steam; and

(iii) laundry soaps produced by a factoryowned by the Khadi and Village IndustriesCommission or any organisation approvedby the said Commission for the purpose ofmanufacture of such soaps

Tariff No. 3402 :

All goods other than sulphonated castor oil,fish oil or sperm oil

All Goods

All Goods

It means, packing, repacking, labeling,relabeling etc for the purpose of retailsale of the following products also willamounts to manufacture:

(i) soap, other than for toilet use,whether or not containingmedicament or disinfectant;

(ii) soap, in or in relation to themanufacture of which no process hasbeen carried on with the aid of poweror of steam; and

(iii) laundry soaps produced by afactory owned by the Khadi and VillageIndustries Commission or anyorganisation approved by the saidCommission for the purpose ofmanufacture of such soaps

sulphonated castor oil, fish oil orsperm oil (Tariff No. 3402)

All Goods falling under ChapterHeading 7607 related to AluminumFoil

Wrist wearable devices commonlyknown as Smart Watches falling underChapter Heading 8517 62

Parts, Components and Accessoriesand Assemblies falling under ChapterHeading 87 excluding vehicle fallingunder 8712, 8713, 8715, 8716

Parts, Components and Accessoriesand Assemblies falling under ChapterHeading 84 excluding vehicle fallingunder 8426 4100, 8427, 8429,8430 10

CENTRAL EXCISE RULES 2002Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

Rule 9 ofCentral

Excise Rules,2002

1st Mar2016

05/2016-CE(NT)dated 1stMar 2016

Exempts from the separate registration to everymanufacturing factory or premises engagedin the manufacture or production of articles ofjewellery other than articles of silver jewellerybut inclusive of articles of silver jewellerystudded with diamond, ruby, emerald orsapphire, falling under chapter heading 7113(herein after referred to as the specifiedgoods), where the manufacturer of suchgoods has a centralized billing or accountingsystem in respect of such specified goodsmanufactured or produced by differentfactories or premises and opts for registeringonly the factory or premises or office, fromwhere such centralized billing or accountingis done and where the accounts/recordsshowing receipts of raw materials and finishedexcisable goods manufactured or receivedback from job workers are kept.

Centralized registration system is providedto Manufacturer of articles of jewellery(including articles of studded jewellery tariffheading 7113) subject to centralized billingor accounting is done and where the accounts/records are kept. Provided saidmanufacturer shall give details of all premises.

However this at the option at the manufacturer

–

WIRC BULLETIN – MARCH 2016

14

CENTRAL EXCISE RULES 2002Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

Rule 9 ofCentral

Excise Rules,2002

1st Mar2016

06/2016-CE(NT)dated 1stMar 2016

35/2001 CE(NT) dated 26th June 2001as amended by 7/2015 CE (NT) dated 1stMar 15

Insertion of sub-clause (iii) to Clause 8 ofNotification 3/2001 CE (NT) dated 1st June2001 as under:"(iii) Every manufacturing factory or premisesengaged in the manufacture or production ofarticles of jewellery other than articles of silverjewellery but inclusive of articles of silverjewellery studded with diamond, ruby, emeraldor sapphire, falling under chapter heading7113 of the First Schedule to the Central ExciseTariff Act, 1985 (5 of 1986), shall be exemptedfrom sub-clauses (i) and (ii) above."

Physical verification of the premises is notrequired for manufacture or production ofarticles of jewellery other than articles of silverjewellery but inclusive of articles of silverjewellery studded with diamond, ruby,emerald or sapphire, falling under chapterheading 7113.

1st Mar2016

07/2016CE(NT)dated 1st

March 2016

9/2012 CE(NT) dated 17th Mar 2012 Existing Notification No. 9/2012 CE (NT) dated17th Mar 2012 rescinded.

Now articles of jewellery falling under chapterheading 7113 of the First Schedule to theCentral Excise Tariff Act, 1985 (5 of 1986)will be valued at 'Transaction Value' instead offixed tariff value.

Rule 7 (4) ofCentral

Excise Rules,2002

1st Mar2016

08/2016 CE(NT) dated1st March

2016

The assessee shall be liable to pay interest onany amount payable to Central Government,consequent to order for final assessmentunder sub-rule (3), at the rate specified bythe Central Government by notification issuedunder section 11AA of the Act from the firstday of the month succeeding the month forwhich such amount is determined, till the dateof payment thereof.

Rule 7 sub-rule (4) substituted as under:"(4) The assessee shall be liable to pay intereston any amount paid or payable on the goodsunder provisional assessment, but not paidon the due date specified under sub-rule (1)of rule 8 and the first proviso thereto, as thecase may be, at the rate specified by the CentralGovernment, vide, notification under section11AA of the Act, for the period starting with thefirst day after the due date till the date of actualpayment, whether such amount is paid beforeor after the issue of order for final assessment.

In case of provisional assessment Interest willbe payable from the due date till date of actualpayment instead of first day of succeedingmonth.

e.g. 1. Date of payment of goods underprovisional assessment on 29th Feb 16& dateof payment of duty is 6th March 2016, date ofreceipt of order is 1st June 16 and differentialliability is Rs. 5,000/-

Interest will be applicable from 7th Mar 16 toactual date of payment.

Rule 11 sub-rule (8)

1st April2016

08/2016 CE(NT) dated1st March

2016

Provided that where the duplicate copy of theinvoice meant for transporter is digitallysigned, a hard copy of the duplicate copy ofthe invoice meant for transporter and self-attested by the manufacturer shall be usedfor transport of goods.

Provided that where the duplicate copy of theinvoice meant for transporter is digitally signed,a hard copy of the duplicate copy of the invoicemeant for transporter shall be used fortransport of goods.

Now no need to self-attest by manufacturerthe duplicate copy of digitally signed invoicefor transporter.

Rule 8 ofCentral

Excise Rules,2002

1st April2016

08/2016 CE(NT) dated1st March

2016

Explanation.1. - For the purposes of thisproviso, it is hereby clarified that an assesseeshall be eligible, if his aggregate value ofclearances of all excisable goods for homeconsumption in the preceding financial year,computed in the manner specified in the saidnotification, did not exceed rupees fourhundred lakhs.

Amendment in Explanation 1 of 2nd provisoto Rule 8 as under:

Explanation 1:

(a) an assessee, engaged in the manufactureor production of articles of jewellery, other thanarticles of silver jewellery but inclusive of articlesof silver jewellery studded with diamond, ruby,emerald or sapphire, falling under chapterheading 7113 of the First Schedule of the TariffAct shall be eligible, if his aggregate value ofclearances of all excisable goods for homeconsumption in the preceding financial year,computed in the manner specified in the saidnotification, did not exceed rupees twelve crore;

(b) an assessee, other than (a) above, shall beeligible, if his aggregate value of clearances ofall excisable goods for home consumption inthe preceding financial year, computed in themanner specified in the said notification, didnot exceed rupees four hundred lakhs.".

Manufacturers engaged in the manufactureor production of articles of jewellery, otherthan articles of silver jewellery but inclusiveof articles of silver jewellery studded withdiamond, ruby, emerald or sapphire, fallingunder chapter heading 7113 of the FirstSchedule of the Tariff Act, having aggregatevalue of clearances below 12 crores inpreceding FY may discharge their liability onquarterly basis.

Rule 12 sub-rule (2) (a)

& (b)

1st April2016

08/2016 CE(NT) dated1st March

2016

(2) (a) Notwithstanding anything containingin sub-rule (1), every assessee shall submitto the Superintendent of Central Excise, anAnnual Financial Information Statement forthe preceding financial year to which thestatement relates in the form specified bynotification by the Board by 30th day ofNovember of the succeeding year.

Substitution of the word 'Annual FinancialInformation Statement' by the word 'AnnualReturn'

The word 'Annual Financial InformationStatement' (i.e. for ER-4 Return) substitutedby the word 'Annual Return'

WIRC BULLETIN – MARCH 2016

15

CENTRAL EXCISE RULES 2002Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

(b) The Central Government may, bynotification, and subject to such conditionsor limitations as may be specified in suchnotification, specify assessee or class ofassessees who may not require to submitsuch an Annual Financial InformationStatement.

Rule 12 sub-rule 2A

1st April2016

08/2016 CE(NT) dated1st March

2016

(2A) (a) Every assessee shall submit to theSuperintendent of Central Excise, an AnnualInstalled Capacity Statement declaring theannual production capacity of the factory forthe financial year to which the statement relatesin the form specified by notification by theBoard by 30th day of April of the succeedingfinancial year :

Provided that for the year 2007-08, the saidstatement shall be furnished by 31st day ofOctober, 2008.

(iii) sub-rule (2A) shall be omitted; Henceforth ER-7 Return i.e. for filing of'Annual Installed Capacity Statement' is notrequired to file from FY 2016-17.

Any way no one was serious on filing &checking the same.

Rule 12 sub-rule 2 (c)

1st April2016

08/2016 CE(NT) dated1st March

2016

– Newly inserted (c ) provisions of this sub-ruleand clause (b) of sub-rule (8) shall mutatismutandis apply to a hundred per cent. Export-Oriented.

This provision is also applicable to EOUincluding that of revised return as specifiedunder sub-rule 8.

Rule 17 1st April2016

08/2016 CE(NT) dated1st March

2016

– "(7) An assessee, who has filed a return in theform referred to in sub-rule (3) within the datespecified under that sub-rule, may submit arevised return by the end of the calendar monthin which the original return is filed.

Explanation.- Where an assessee submits arevised return under this sub-rule, the"relevant date" for the purpose of recovery ofCentral Excise duty, if any, under section 11Aof the Act shall be the date of submission ofsuch revised return";

Above mentioned provisions w.r.t RevisedReturn, Relevant date and monthly return incase of EOU will be same.

Rule 12 1st April2016

08/2016 CE(NT) dated1st March

2016

– after sub-rule (7), the following sub-rule shallbe inserted, namely:-" (8)(a) An assessee, who has filed a return inthe form referred to in sub-rule(1) within thedate specified under that sub-rule or thesecond proviso thereto, may submit a revisedreturn by the end of the calendar month inwhich the original return is filed.Explanation.- Where an assessee submits arevised return under clause (a), the "relevantdate" for the purpose of recovery of CentralExcise duty, if any, under section 11A of the Actshall be the date of submission of such revisedreturn.(b) An assessee who has filed Annual Returnreferred to in clause (a) of sub-rule (2) by thedue date mentioned in clause (a) of that sub-rule, may submit a revised return within aperiod of one month from the date ofsubmission of the said Annual Return.

Welcome move allowing filing of revisedreturn by the end of the calendar month inwhich the original return is filed.

Relevant date for the purpose of recovery ofCE duty under Section 11A shall be the date ofsubmission of said revised return.

However in care of revised 'Annual Return'(ER-4) it may be submitted in month fromthe date of filing of original return.

Rule 12 sub-rule 6

1st April2016

08/2016 CE(NT) dated1st March

2016

(6) Where any return or Annual FinancialInformation Statement or Annual InstalledCapacity Statement referred to in this rule issubmitted by the assessee after due date asspecified for every return or statements, theassessee shall pay to the credit of the CentralGovernment, an amount calculated at the rateof one hundred rupees per day subject to amaximum of twenty thousand rupees for theperiod of delay in submission of each suchreturn or statement.

In sub-rule 6 the words Annual FinancialInformation Statement or Annual InstalledCapacity Statement shall be omitted.

WIRC BULLETIN – MARCH 2016

16

CENTRAL EXCISE RULES 2002Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

Rule 26 sub-rule (1)

1st April2016

08/2016 CE(NT) dated1st March

2016

– "Provided that where any proceeding for theperson liable to pay duty have been concludedunder clause (a) or clause (d) of sub-section(1) of section 11AC of the Act in respect ofduty, interest and penalty, all proceedings inrespect of penalty against other persons, if any,in the said proceedings shall also be deemedto be concluded.

This is welcome provision, no personalpenalty on any other person can be imposedif assessee pays the duty with interest andpenalty under section 11AC is paid then

CENVAT CREDIT RULES 2004Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

Rule 2 (a) 1st April2016

13/2016- CE(NT) dated

1st Mar2016

– Definition of Capital Goods added wagons ofsub-heading 860692

Cenvat Credit of wagons brought by serviceproviders will be available.

Rule 2 (a) 1st April2016

13/2016- CE(NT) dated

1st Mar2016

Capital goods …

(1) in the factory of the manufacturer of thefinal products, but does not include anyequipment or appliance used in an office; or

Definition of Capital Goods:

(1) in the factory of the manufacturer of thefinal products

The wording equipments or appliances usedin an office have been removed. Henceforwards, Cenvat credit will be allowed on thegoods / equipment which are used in the officewithin the factory.No of litigations will be reduced.

Rule 2 (a) 1st April2016

13/2016- CE(NT) dated

1st Mar2016

Capital goods …

Used (1A) outside the factory of themanufacturer of the final products forgeneration of electricity for captive use withinthe factory; or;

Definition of Capital Goods:

(1A) outside the factory of the manufacturerof the final products for generation of electricityor for pumping of water for captive use withinthe factory; or;

Goods used for pumping of water for captiveuse will be entitled for Cenvat credit as CapitalGoods.

Rule 2 ( e) 1st March2016

13/2016- CE(NT) dated

1st Mar2016

Exempted Service….(3) taxable service whose part of value isexempted on the condition that no credit ofinputs and input services, used for providingsuch taxable service, shall be taken;but shall not include a service which isexported in terms of rule 6A of the Service TaxRules, 1994

Exempted Service (3)….

– but shall not include a service –

(a) which is exported in terms of rule 6A of theService Tax Rules, 1994; or

(b) by way of transportation of goods by avessel from customs station of clearance inIndia to a place outside India;

Transportation of goods by a vessel fromcustoms station of clearance in India to a placeoutside India is also excluded from Definitionof Exempted services.

Rule 2 (k) 1st April2016

13/2016- CE(NT) dated

1st Mar2016

(k) "input" means----(iii) all goods used for generation of electricityor steam for captive use; or

(iii) all goods used for generation of electricityor steam or pumping of water for captive use;or

Goods (other than capital goods) used forpumping of water for captive use will beentitled for Cenvat Credit as Inputs.

Rule 2 (k) 1st April2016

13/2016-CE (NT)dated 1stMar 2016

NA (v) all capital goods which have a value uptoten thousand rupees per piece

Capital Goods having value Rs 10,000 or lesswill be treated as Inputs Goods. In otherwords, full cenvat credit will be allowed onthose goods.

Rule 2 (m) 1st April2016

13/2016-CE (NT)dated 1stMar 2016

(m) "input service distributor" means anoffice of the manufacturer or producer of finalproducts or provider of output service, whichreceives invoices issued under rule 4A of theService Tax Rules, 1994 towards purchasesof input services and issues invoice, bill or, asthe case may be, challan for the purposes ofdistributing the credit of service tax paid onthe said services to such manufacturer orproducer or provider, as the case may be;

(m) "input service distributor" means an officeof the manufacturer or producer of finalproducts or provider of output serviceor anoutsourced manufacturing unit, whichreceives invoices issued under rule 4A of theService Tax Rules, 1994 towards purchasesof input services and issues invoice, bill or, asthe case may be, challan for the purposes ofdistributing the credit of service tax paid on thesaid services to such manufacturer orproducer or provider, as the case may be;

The definition of ISD has been amended toinclude the "outsource manufacturing unit"(i.e. Job Worker). The subsequentprovisions are made w.r.t distribution of creditto the outsourced manufacturing unit who isdischarging the duty under Rule 10 ofValuation Rules

Rule 3 Subrule (4)

1st March2016

13/2016-CE (NT)dated 1stMar 2016

Provided also that the CENVAT credit of anyduty specified in sub-rule (1), except theNational Calamity Contingent duty in item (v)thereof, shall not be utilized for payment ofthe said National Calamity Contingent duty ongoods falling under tariff items 85171210 and85171290 respectively of the First Scheduleof the Central Excise Tariff:

Provided also that the CENVAT credit of anyduty specified in sub-rule (1), except theNational Calamity Contingent duty in item (v)thereof, shall not be utilized for payment of theNational Calamity Contingent duty leviableundersection 136 of the Finance Act, 2001 (14of 2001)

Utilization of other duties (other than NCCD)in cenvat credit was restricted only forpayment of NCCD on Push button styleTelephone Sets and Wireless Cellphone(8517 12 10) and other Telephone Sets andWireless Cellphone (8517 12 90). For NCCDon other goods, the basic Cenvat duties wereallowed to be utilized.With this amendment basic duties cannot beutilized for payment of NCCD on any goods.

WIRC BULLETIN – MARCH 2016

17

CENVAT CREDIT RULES 2004Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

Rule 3 Subrule (4)

1st March2016

13/2016-CE (NT)dated 1stMar 2016

NA Provided also that CENVAT credit shall not beutilised for paymentof Infrastructure Cessleviable under sub-clause (1) of clause 159 oftheFinance Bill, 2016

The Cenvat credit cannot be utilized forInfrastructure Cess levied on the specifiedautomobiles under chapter 87

Rule 4 - Sub-rule 2

(Clause a)

1st March2016

13/2016-CE (NT)dated 1stMar 2016

– Explanation. - For the removal of doubts, itis hereby clarified that an assessee, shall beeligible, if his aggregatevalue of clearances ofall excisable goods for home consumption inthepreceding financial year, computed in themanner specified in the saidnotification, didnot exceed rupees four hundred lakhs.

– Explanation. - For the removal of doubts, itis hereby clarified that-

(i) an assessee engaged in the manufacture ofarticles of jewellery, other than articles of silverjewellery but inclusive of articles of silverjewellery studded with diamond, ruby, emeraldor sapphire, falling under chapter heading7113 of the First Schedule of the Excise TariffAct, shall be eligible, if his aggregate value ofclearances of all excisable goods for homeconsumption in the preceding financial year,computed in the manner specified in the saidnotification, did not exceed rupees twelve crore;

(ii) an assessee, other than (a) above, shall beeligible, if his aggregate value of clearances ofall excisable goods for home consumption inthe preceding financial year, computed in themanner specified in the said notification, didnot exceed rupees four hundred lakhs

The articles of jewellery, otherthan articles ofsilver jewellery but inclusive of articles ofsilverjewellery studded with diamond, ruby,emerald or sapphire, fallingunder chapterheading 7113 having turnover below 12 crwill be entitled for full credit of capital goodsin the same year in which it has received.

Rule 4 sub-rule 5 clause

(b)

1st April2016

13/2016-CE (NT)dated 1stMar 2016

– (b) The CENVAT credit shall also be allowedto a manufacturer of final products in respectof jigs, fixtures, moulds and dies or tools sentby such manufacturer to, -

(i) another manufacturer for the productionof goods; or

(ii) a job worker for the production of goodson his behalf,according to his specifications:

– (b) The CENVAT credit shall also be allowedto a manufacturer of final products in respectof jigs, fixtures, moulds and dies or tools fallingunder Chapter 82 of the First Schedule to theExcise Tariff Act, sent by such manufacturer to,

(i) another manufacturer for the productionof goods; or

(ii) a job worker for the production of goodson his behalf,according to his specifications:

Provided that such credit shall also be allowedwhere jigs, fixtures, moulds and dies or toolsfalling under Chapter 82 of the First Scheduleto the Excise Tariff Act, are sent by themanufacturer of final products to the premisesof another manufacturer or job workerwithout bringing these to his own premises

The jigs, fixtures falling under ITCHS 82 nowcan be sent directly to the job workers withoutbringing the same in the factory of themanufacturer. In other words, themanufacturer will be entitled for cenvat crediton the jigs which are sent directly to jobworker.

Rule 4 sub-rule 6

1st April2016

13/2016-CE (NT)dated 1stMar 2016

(6) The Deputy Commissioner of CentralExcise or the Assistant Commissioner ofCentral Excise, as the case may be, havingjurisdiction over the factory of themanufacturer of the final products who hassent the input or partially processed inputsoutside his factory to a job-worker may, byan order, which shall be valid for a financialyear, in respect of removal of such input orpartially processed input, and subject to suchconditions as he may impose in the interest ofrevenue including the manner in which duty,if leviable, is to be paid, allow final products tobe cleared from the premises of the job-worker.

(6) The Deputy Commissioner of CentralExcise or the Assistant Commissioner ofCentral Excise, as the case may be, havingjurisdiction over the factory of themanufacturer of the final products who hassent the input or partially processed inputsoutside his factory to a job-worker may, by anorder, which shall be valid for three financialyear, in respect of removal of such input orpartially processed input, and subject to suchconditions as he may impose in the interest ofrevenue including the manner in which duty, ifleviable, is to be paid, allow final products to becleared from the premises of the job-worker.

The permission can be given by the DeputyCommissioner / Assistant Commissionerupto period 3 years for clearance of finalproducts from the job worker premises.

Rule 4 sub-rule 6

1st April2016

13/2016-CE (NT)dated 1stMar 2016

NA Provided also that CENVAT Credit of ServiceTax paid on the charges paid or payable for theservice provided by way of assignment, by theGovernment or any other person, of the rightto use any natural resource, shall be spreadover such period of time as the period forwhich the right to use has been assigned.CENVAT Credit in the financial year in which

The cenvat credit on the service tax paid onpayment on right of natural resources willavailable as Cenvat Credit proportionatelyover the period of assignment of such right.

WIRC BULLETIN – MARCH 2016

18

CENVAT CREDIT RULES 2004Rule No.

AmendmentEffective Date

NotificationNo. Existing Provision

Amendment in Existing /New Provision Analysis

the right to use is acquired and in thesubsequent years during which such right isretained by the manufacturer of goods orprovider of output service as the case may be,shall be taken of an amount determined as perthe following formula:

Amount of CENVAT Credit that shall be taken ina financial year = Service Tax paid on thecharges payable for the assignment of the rightto use / No. of Years for which the rights havebeen assigned

Provided also that where the manufacturer ofgoods or provider of output service, as thecase may be, further assigns such right to useassigned to him by the Government or anyother person, in any financial year, to anotherperson against a consideration, such amountof balance CENVAT credit as does not exceedthe service tax payable on the considerationcharged by him for such further assignment,shall be allowed in the same financial year

Provided also that CENVAT credit of annual ormonthly user charges payable in respect ofany service by way of assignment of right touse natural resources shall be allowed in thesame financial year in which they are paid.

Rule 6 Sub-rule (1)

1st April2016

1 3 / 2 0 1 6CE (NT)dated 1stMar 2016

6. Obligation of a manufacturer or producerof final products and a provider of outputservice

(1) The CENVAT credit shall not be allowedon such quantity of input used in or in relationto the manufacture of exempted goods or forprovision of exempted services, or inputservice used in or in relation to themanufacture of exempted goods and theirclearance upto the place of removal or forprovision of exempted services, except in thecircumstances mentioned in sub-rule (2).