UNIVERSITAS PADJADJARAN FAKULTAS EKONOMI DAN BISNIS...

33

131 17 APPENDIX KUESIONER PENELITIAN Assalamu'alaikum warahmatullahi wabarakatuh Kepada responden yang terhormat, perkenalkan sayar Muhammad Radian Suriaatmaja, mahasiswa S1 program studi Manajemen Universitas Padjadjaran yang tengah menyusun skripsi sebagai syarat utama meraih gelar sarjana strata satu atau (S1). Adapun judul dari penelitian yang tengah saya lakukan adalah “ The Influence of Religiosity and Corporate Reputation on Consumer Loyalty in (Survey on Consumers of An Islamic Bank in Bandung)” atau dalam Bahasa Indonesia “Pengaruh Religiusitas dan Reputasi Perusahaan terhadap Loyalitas Konsumen (Survey Pada Konsumen Sebuah Bank Syariah di Kota Bandung) Melalui kuesioner ini saya minta kesediaan dari Bapak/Ibu/Saudara/i yang merupakan 1. Beragama Islam 2. Berdomisili di Kota Bandung 3. Menggunakan tabungan BSM Bank Syariah Mandiri Agar dapat meluagkan waktunya untuk menjawab pertanyaan-pertanyaan yang ada pada penelitian ini. Seluruh jawaban yang telah dari Bapak/Ibu/Saudara/I berikan akan dipergunakan akan digunakan di ranah akademik Atas partisipasi dari Bapak/Ibu/Saudara/i, saya ucapkan terimakasih Hormat Saya, M. Radian Suriaatmaja UNIVERSITAS PADJADJARAN FAKULTAS EKONOMI DAN BISNIS PROGRAM STUDI MANAJEMEN

Transcript of UNIVERSITAS PADJADJARAN FAKULTAS EKONOMI DAN BISNIS...

131

17 APPENDIX

KUESIONER PENELITIAN

Assalamu'alaikum warahmatullahi wabarakatuh

Kepada responden yang terhormat, perkenalkan sayar Muhammad

Radian Suriaatmaja, mahasiswa S1 program studi Manajemen Universitas

Padjadjaran yang tengah menyusun skripsi sebagai syarat utama meraih gelar

sarjana strata satu atau (S1). Adapun judul dari penelitian yang tengah saya

lakukan adalah “ The Influence of Religiosity and Corporate Reputation on

Consumer Loyalty in (Survey on Consumers of An Islamic Bank in Bandung)”

atau dalam Bahasa Indonesia “Pengaruh Religiusitas dan Reputasi

Perusahaan terhadap Loyalitas Konsumen (Survey Pada Konsumen Sebuah

Bank Syariah di Kota Bandung)

Melalui kuesioner ini saya minta kesediaan dari Bapak/Ibu/Saudara/i yang

merupakan

1. Beragama Islam

2. Berdomisili di Kota Bandung

3. Menggunakan tabungan BSM Bank Syariah Mandiri

Agar dapat meluagkan waktunya untuk menjawab pertanyaan-pertanyaan yang

ada pada penelitian ini. Seluruh jawaban yang telah dari Bapak/Ibu/Saudara/I

berikan akan dipergunakan akan digunakan di ranah akademik

Atas partisipasi dari Bapak/Ibu/Saudara/i, saya ucapkan terimakasih

Hormat Saya,

M. Radian Suriaatmaja

UNIVERSITAS PADJADJARAN

FAKULTAS EKONOMI DAN BISNIS

PROGRAM STUDI MANAJEMEN

132

Petunjuk Pengisian

1. Bacalah dengan cermat setiap pernyataan pada kuesioner ini serta

pilihlah jawaban yang sesuai.

2. Berilah tanda checklist (√) pada kolom yang telah disediakan untuk

setiap jawaban yang sesuai dengan pendapat Anda.

3. Mohon kesediaan Bapak/Ibu/Saudara/i untuk dapat menjawab seluruh

pertanyaan yang ada pada kuesioner ini, karena kuesioner ini dapat

digunakan dengan optimal apabila seluruh pertanyaan/pernyataan telah

dijawab.

4. Jika terdapat pernyataan/pertanyaan yang tidak jelas dapat ditanyakan

kepada penulis.

133

BAGIAN 1-DATA DIRI RESPONDEN

1. Jenis Kelamin

Laki-laki Perempuan

2. Usia

– 35 tahun 36 – 45 tahun

– 55 tahun tahun

3. Pekerjaan Pelajar/Mahasiswa Ibu Rumah Tangga

Pegawai Negeri Tidak Bekerja

Pegawai Swasta Lainnya.....

Wirausaha

4. Pendapatan

(Apabila Anda merupakan seorang Ibu Rumah Tangga atau seseorang yang

belum berpenghasilan, maka kolom pendapatan dapat diisi dengan

penghasilan seseorang yang Anda andalkan dalam memenuhi kebutuhan

Anda. Bagi seseorang mahasiswa yang belum berpenghasilan dapat

mengisi kolom penghasilan dengan uang saku bulanannya)

Rp 500.000.000 0.000 – Rp 10.000.000

00.001 – Rp 15.000.000 .000.001 – Rp 20.000.000

– Rp 25.000.000 .000.001

134

BAGIAN 2 – Pengaruh Religiusitas dan Reputasi Perusahaan terhadap Loyalitas

Konsumen.

Berikanlah respon terhadap pernyataan-pernyataan berikut terkait religiusitas anda.

Berikanlah tanda silang (X) pada salah satu kotak pilihaan sebagai respon

anda dari masing-masing pernyataan berikut

Religiusitas Sangat

Tidak Setuju

Tidak

Setuju

Netral Setuju Sangat

Setuju

1

Saya sering membaca buku mengenai

Islam STS TS CS S SS

22

2

Saya bersemangat untuk memahami

ajaran-ajaran Islam STS TS CS S SS

3

3

Saya yakin Islam bisa memberikan

jawaban mengenai makna kehidupan STS TS CS S SS

4

4

Saya menjadikan Islam melatarbelakangi

seluruh pendekatan saya dalam hidup

terutama di bidang ekonomi

STS TS CS S SS

5

5

Saya menjadikan Islam mempegaruhi

seluruh urusan kehidupan saya terutama

dalam urusan keuangan

STS TS CS S SS

6

6

Saya sering meluangkan waktu untuk

merenung secaara mendalam mengenai

agama Islam

STS TS CS S SS

135

REPUTASI PERUSAHAAN (CORPORATE REPUTATION)

Bacalah pernyataan-pernyataan di bawah ini dan berikan respon anda terhadap

Reputasi Bank Mandiri Syariah

Berikanlah tanda silang (X) pada salah satu kotak pilihaan sebagai respon

anda dari masing-masing pernyataan berikut

Reputasi Perusahaan Sangat

Tidak

Setuju

Tidak

Setuju

Netral Setuju Sangat

Setuju

1

1

Saya memiliki rasa suka terhadap Bank

Syariah Mandiri STS TS CS S SS

2

Saya memiliki rasa kagum terhadap

Bank Syariah Mandiri STS TS CS S SS

3

Saya memiliki rasa percaya kepada Bank

Syariah Mandiri STS TS CS S SS

4

Menurut saya Bank Syariah Mandiri

memberikan pelayanan tabungan yang

sesuai dengan yang dijanjikan

STS TS CS S SS

5

Menurut saya pelayanan tabungan BSM

Bank Syariah Mandiri memiliki kualitas

yang tinggi

STS TS CS S SS

6

Menurut saya tabungan BSM Bank

Syariah Mandiri memberikan

keuntungan berupa bagi hasil yang tinggi

STS TS CS S SS

7

Menurut saya Bank Syariah Mandiri

selalu melakukan inovasi dalam

memperbaiki pelayanan tabungan BSM

STS TS CS S SS

8

Bank Syariah Mandiri mendukung hal

positif di masyarakat dengan mendukung

pertumbuhan Usaha Mikro Kecil dan

Menengah (UMKM)

STS TS CS S SS

9

Bank Syariah Mandiri menunjukan

kepedulian terhadap lingkunan dengan

melakukan penghijauan lingkungan

melalui program CSR

STS TS CS S SS

10

Bank Syariah Mandiri mempelakukan

umat dengan baik dengan menyalurkan

bantuan CSR kepada masjid-masjid

STS TS CS S SS

136

LOYALITAS KONSUMEN (CONSUMER LOYALTY)

Bacalah pernyataan-pernyataan di bawah ini dan berikanlah respon anda terhadap

loyalitas (kesetiaan) anda sebagai konsumen Bank Mandiri Syariah

Berikanlah tanda silang (X) pada salah satu kotak pilihaan sebagai respon

anda dari masing-masing pernyataan berikut

Loyalitas Konsumen Sangat

Tidak

Setuju

Tidak

Setuju

Netral Setuju Sangat

Setuju

1

1

Menurut saya tingkat pelayanan tabungan BSM

Bank Syariah Mandiri lebih baik dibandingkan bank

lain

STS TS CS S SS

2

2

Menurut saya tingkat bagi hasil yang saya terima

dari tabungan BSM Bank Syariah Mandiri lebih

besar dibandingkan tabungan bank lain

STS TS CS S SS

3

3

Menurut saya tabungan BSM Bank Syariah Mandiri

lebih baik dibandingkan tabungan bank lain STS TS CS S SS

4

Saya memiliki rasa ketertarikan pada tabungan

BSM Bank Syariah Mandiri karena pelayanan yang

diberikan Bank Syariah Mandiri kepada saya baik

STS TS CS S SS

5

Saya merasa senang menggunakan tabungan BSM

Bank Syariah Mandiri karena pelayanan yang

diberikan Bank Syariah Mandiri kepada saya baik

STS TS CS S SS

6

Saya merasa tertarik pada tabungan BSM Bank

Syariah karena pelayanan yang diberikan Bank

Syariah Mandiri kepada saya baik

STS TS CS S SS

7

Saya berniat untuk tetap menggunakan tabungan

BSM bank Syariah Mandiri di masa yang akan

datang

STS TS CS S SS

8

Saya berniat menggunakan produk-produk lain

selain tabungan yang disediakan oleh Bank Syariah

Mandiri

STS TS CS S SS

9

9

Saya berniat merekomendasikan tabungan BSM

Bank Syariah Mandiri kepada orang lain STS TS CS S SS

10

Saya tetap menggunakan tabungan BSM Bank

Syariah Mandiri walaupun biaya administrasi

tabungan mengalami kenaikan

STS TS CS S SS

11

Saya memberitahukan hal positif

mengenaikeunggulan tabungan BSM Bank Mandiri

Syariah kepada orang lain meskipun adanya isu

negative mengenai Bank Syariah Mandiri

STS TS CS S SS

12

Saya menjadikan tabungan Bank Syariah Mandiri

sebagai pilihan utama meskipun adanya tawaran-

tawaran menarik dari bank lain

STS TS CS S SS

137

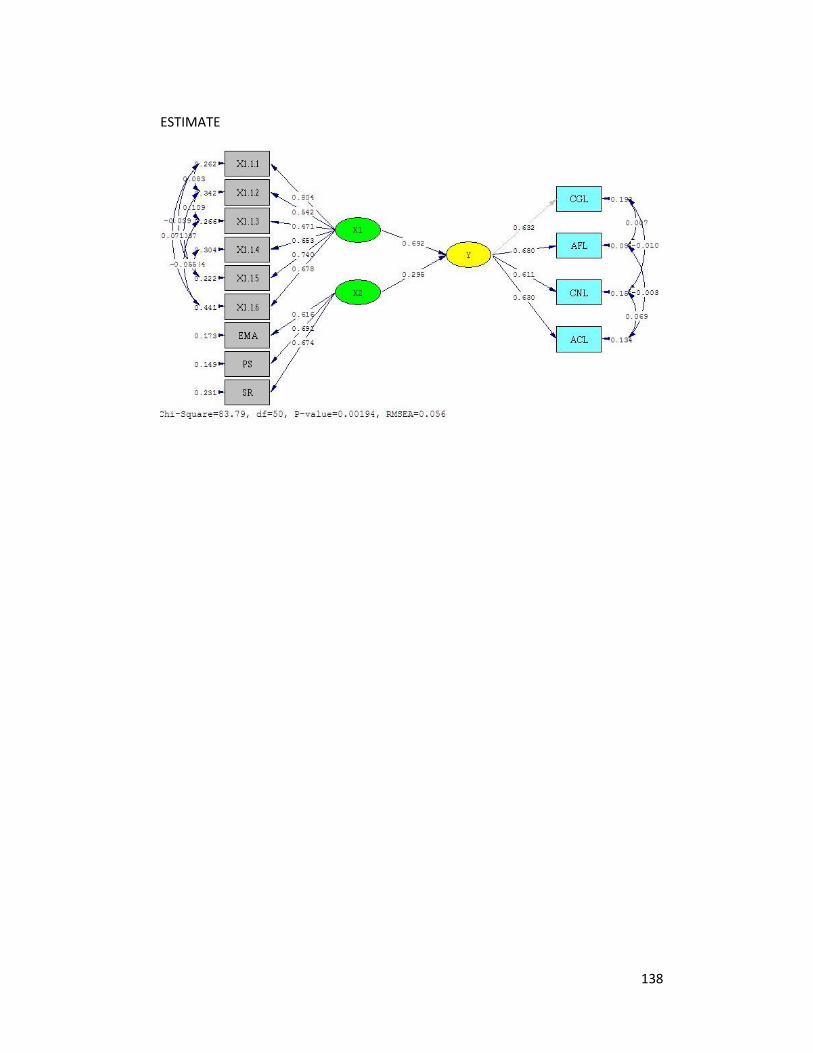

LAMPIRAN OUTPUT MODEL STRUKTURAL

T-valueS

STANDARDIZED

138

ESTIMATE

139

DATE: 8/21/2018

TIME: 14:28

L I S R E L 8.80

BY

Karl G. Jöreskog & Dag Sörbom

This program is published exclusively by

Scientific Software International, Inc.

7383 N. Lincoln Avenue, Suite 100

Lincolnwood, IL 60712, U.S.A.

Phone: (800)247-6113, (847)675-0720, Fax: (847)675-2140

Copyright by Scientific Software International, Inc., 1981-2006

Use of this program is subject to the terms specified in the

Universal Copyright Convention.

Website: www.ssicentral.com

The following lines were read from file C:\Users\User\Documents\Data

Statistik\LISREL\MODEL STRUKTURAL.SPJ:

Raw Data from file 'C:\Users\User\Documents\Data Statistik\LISREL\MODEL

STRUKTURAL.psf'

Sample Size = 218

Latent Variables Y X1 X2

Relationships

CGL = 0.373*Y

AFL = Y

CNL = Y

ACL = Y

X1.1.1 = X1

X1.1.2 = X1

X1.1.3 = X1

X1.1.4 = X1

X1.1.5 = X1

X1.1.6 = X1

EMA = X2

PS = X2

SR = X2

Y = X1 X2

Set the Variance of X1 to 1.000

Set the Variance of X2 to 1.000

Set the Error Covariance of ACL and CNL Free

Set the Error Covariance of X1.1.2 and X1.1.1 Free

Set the Error Covariance of X1.1.3 and X1.1.2 Free

Set the Error Covariance of X1.1.5 and X1.1.1 Free

Set the Error Covariance of X1.1.5 and X1.1.2 Free

140

Set the Error Covariance of X1.1.5 and X1.1.4 Free

Set the Error Covariance of X1.1.6 and X1.1.1 Free

Set the Error Covariance of X1.1.6 and X1.1.3 Free

Path Diagram

Number of Decimals = 3

Admissibility Check = Off

End of Problem

Sample Size = 218

Covariance Matrix

CGL AFL CNL ACL X1.1.1 X1.1.2

-------- -------- -------- -------- -------- --------

CGL 0.327

AFL 0.265 0.589

CNL 0.225 0.444 0.552

ACL 0.227 0.460 0.454 0.627

X1.1.1 0.286 0.481 0.410 0.449 0.906

X1.1.2 0.191 0.338 0.286 0.299 0.506 0.629

X1.1.3 0.123 0.251 0.264 0.231 0.351 0.357

X1.1.4 0.229 0.348 0.306 0.352 0.515 0.353

X1.1.5 0.230 0.383 0.339 0.375 0.555 0.368

X1.1.6 0.263 0.384 0.326 0.355 0.614 0.347

EMA 0.139 0.259 0.271 0.256 0.216 0.286

PS 0.116 0.265 0.246 0.254 0.202 0.277

SR 0.146 0.284 0.273 0.296 0.247 0.275

Covariance Matrix

X1.1.3 X1.1.4 X1.1.5 X1.1.6 EMA PS

-------- -------- -------- -------- -------- --------

X1.1.3 0.486

X1.1.4 0.338 0.731

X1.1.5 0.365 0.589 0.770

X1.1.6 0.249 0.430 0.512 0.904

EMA 0.203 0.227 0.191 0.164 0.552

PS 0.159 0.190 0.213 0.162 0.428 0.626

SR 0.193 0.215 0.222 0.218 0.406 0.470

Covariance Matrix

SR

--------

SR 0.685

141

Number of Iterations = 13

LISREL Estimates (Maximum Likelihood)

Measurement Equations

CGL = 0.373*Y, Errorvar.= 0.189 , R² = 0.423

(0.0194)

9.733

AFL = 0.705*Y, Errorvar.= 0.0950 , R² = 0.839

(0.0637) (0.0184)

11.061 5.168

CNL = 0.630*Y, Errorvar.= 0.156 , R² = 0.716

(0.0602) (0.0210)

10.481 7.456

ACL = 0.654*Y, Errorvar.= 0.201 , R² = 0.679

(0.0638) (0.0256)

10.256 7.864

X1.1.1 = 0.800*X1, Errorvar.= 0.269 , R² = 0.704

(0.0562) (0.0421)

14.246 6.387

X1.1.2 = 0.546*X1, Errorvar.= 0.338 , R² = 0.468

(0.0514) (0.0384)

10.614 8.807

X1.1.3 = 0.469*X1, Errorvar.= 0.265 , R² = 0.454

(0.0439) (0.0286)

10.688 9.237

X1.1.4 = 0.653*X1, Errorvar.= 0.304 , R² = 0.583

(0.0520) (0.0375)

12.546 8.123

X1.1.5 = 0.735*X1, Errorvar.= 0.228 , R² = 0.703

(0.0518) (0.0368)

14.180 6.210

X1.1.6 = 0.678*X1, Errorvar.= 0.442 , R² = 0.509

(0.0597) (0.0516)

11.356 8.574

EMA = 0.617*X2, Errorvar.= 0.172 , R² = 0.689

(0.0432) (0.0240)

142

14.270 7.167

PS = 0.689*X2, Errorvar.= 0.151 , R² = 0.758

(0.0451) (0.0258)

15.289 5.877

SR = 0.675*X2, Errorvar.= 0.230 , R² = 0.665

(0.0485) (0.0305)

13.918 7.536

Error Covariance for ACL and CNL = 0.0445

(0.0183)

2.427

Error Covariance for X1.1.2 and X1.1.1 = 0.0830

(0.0260)

3.189

Error Covariance for X1.1.3 and X1.1.2 = 0.107

(0.0243)

4.401

Error Covariance for X1.1.5 and X1.1.1 = -0.034

(0.0220)

-1.536

Error Covariance for X1.1.5 and X1.1.2 = -0.036

(0.0199)

-1.824

Error Covariance for X1.1.5 and X1.1.4 = 0.107

(0.0304)

3.519

Error Covariance for X1.1.6 and X1.1.1 = 0.0749

(0.0336)

2.231

Error Covariance for X1.1.6 and X1.1.3 = -0.057

(0.0236)

-2.407

143

Structural Equations

Y = 0.673*X1 + 0.280*X2, Errorvar.= 0.289 , R² = 0.709

(0.0838) (0.0629) (0.0650)

8.033 4.441 4.450

Correlation Matrix of Independent Variables

X1 X2

-------- --------

X1 1.000

X2 0.460 1.000

(0.063)

7.301

Covariance Matrix of Latent Variables

Y X1 X2

-------- -------- --------

Y 0.994

X1 0.802 1.000

X2 0.590 0.460 1.000

Goodness of Fit Statistics

Degrees of Freedom = 54

Minimum Fit Function Chi-Square = 107.382 (P = 0.000)

Normal Theory Weighted Least Squares Chi-Square = 101.674 (P = 0.000)

Estimated Non-centrality Parameter (NCP) = 47.674

90 Percent Confidence Interval for NCP = (23.077 ; 80.084)

Minimum Fit Function Value = 0.495

Population Discrepancy Function Value (F0) = 0.220

90 Percent Confidence Interval for F0 = (0.106 ; 0.369)

Root Mean Square Error of Approximation (RMSEA) = 0.0638

90 Percent Confidence Interval for RMSEA = (0.0444 ; 0.0827)

P-Value for Test of Close Fit (RMSEA < 0.05) = 0.114

Expected Cross-Validation Index (ECVI) = 0.810

90 Percent Confidence Interval for ECVI = (0.696 ; 0.959)

ECVI for Saturated Model = 0.839

ECVI for Independence Model = 19.727

Chi-Square for Independence Model with 78 Degrees of Freedom = 4254.840

Independence AIC = 4280.840

Model AIC = 175.674

Saturated AIC = 182.000

Independence CAIC = 4337.838

144

Model CAIC = 337.900

Saturated CAIC = 580.989

Normed Fit Index (NFI) = 0.975

Non-Normed Fit Index (NNFI) = 0.982

Parsimony Normed Fit Index (PNFI) = 0.675

Comparative Fit Index (CFI) = 0.987

Incremental Fit Index (IFI) = 0.987

Relative Fit Index (RFI) = 0.964

Critical N (CN) = 164.827

Root Mean Square Residual (RMR) = 0.0299

Standardized RMR = 0.0496

Goodness of Fit Index (GFI) = 0.933

Adjusted Goodness of Fit Index (AGFI) = 0.887

Parsimony Goodness of Fit Index (PGFI) = 0.554

The Modification Indices Suggest to Add the

Path to from Decrease in Chi-Square New Estimate

X1.1.2 X2 22.9 0.22

The Modification Indices Suggest to Add an Error Covariance

Between and Decrease in Chi-Square New Estimate

X1.1.3 CNL 11.1 0.05

Time used: 0.031 Seconds

145

LAMPIRAN OUTPUT CFA VARIABEL X1

STANDARDIZED

T-valueS

146

DATE: 8/19/2018

TIME: 3:09

L I S R E L 8.80

BY

Karl G. Jöreskog & Dag Sörbom

This program is published exclusively by

Scientific Software International, Inc.

7383 N. Lincoln Avenue, Suite 100

Lincolnwood, IL 60712, U.S.A.

Phone: (800)247-6113, (847)675-0720, Fax: (847)675-2140

Copyright by Scientific Software International, Inc., 1981-2006

Use of this program is subject to the terms specified in the

Universal Copyright Convention.

Website: www.ssicentral.com

The following lines were read from file C:\Users\User\Documents\Data

Statistik\LISREL\RELIGIOSITY.SPJ:

Raw Data from file 'C:\Users\User\Documents\Data Statistik\LISREL\Religiosity.psf'

Latent Variables X1

Relationships

X1.1.1-X1.1.6=X1

Path Diagram

Number of Decimals = 3

Admissibility Check = Off

End of Problem

Sample Size = 218

147

Covariance Matrix

X1.1.1 X1.1.2 X1.1.3 X1.1.4 X1.1.5 X1.1.6

-------- -------- -------- -------- -------- --------

X1.1.1 0.906

X1.1.2 0.506 0.629

X1.1.3 0.351 0.357 0.486

X1.1.4 0.515 0.353 0.338 0.731

X1.1.5 0.555 0.368 0.365 0.589 0.770

X1.1.6 0.614 0.347 0.249 0.430 0.512 0.904

Number of Iterations = 8

LISREL Estimates (Maximum Likelihood)

Measurement Equations

X1.1.1 = 0.776*X1, Errorvar.= 0.303 , R² = 0.665

(0.0547) (0.0367)

14.188 8.257

X1.1.2 = 0.556*X1, Errorvar.= 0.320 , R² = 0.491

(0.0486) (0.0341)

11.431 9.384

X1.1.3 = 0.480*X1, Errorvar.= 0.256 , R² = 0.474

(0.0430) (0.0270)

11.167 9.453

148

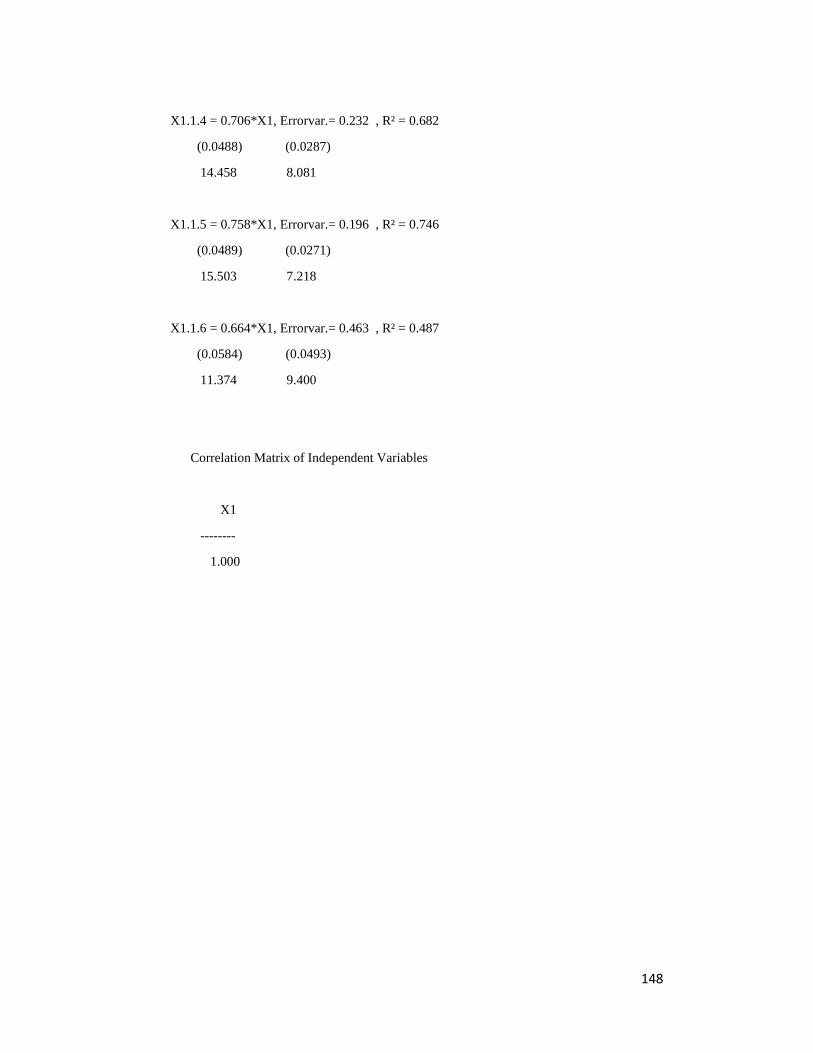

X1.1.4 = 0.706*X1, Errorvar.= 0.232 , R² = 0.682

(0.0488) (0.0287)

14.458 8.081

X1.1.5 = 0.758*X1, Errorvar.= 0.196 , R² = 0.746

(0.0489) (0.0271)

15.503 7.218

X1.1.6 = 0.664*X1, Errorvar.= 0.463 , R² = 0.487

(0.0584) (0.0493)

11.374 9.400

Correlation Matrix of Independent Variables

X1

--------

1.000

149

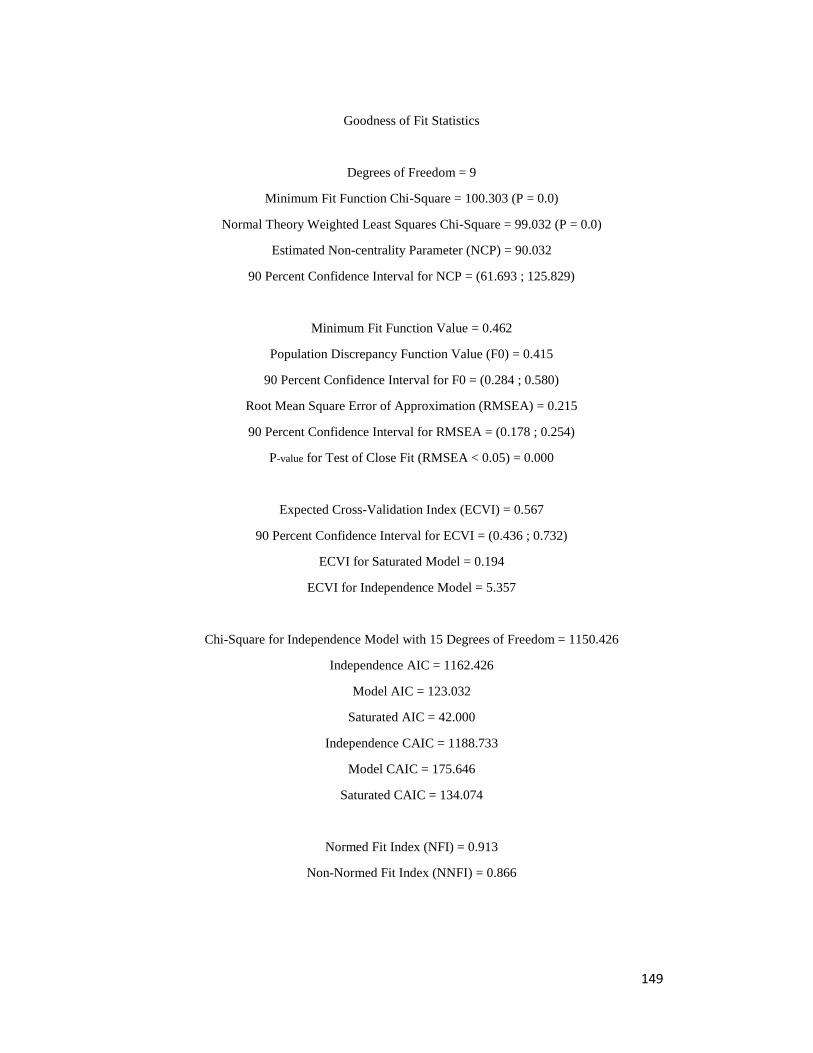

Goodness of Fit Statistics

Degrees of Freedom = 9

Minimum Fit Function Chi-Square = 100.303 (P = 0.0)

Normal Theory Weighted Least Squares Chi-Square = 99.032 (P = 0.0)

Estimated Non-centrality Parameter (NCP) = 90.032

90 Percent Confidence Interval for NCP = (61.693 ; 125.829)

Minimum Fit Function Value = 0.462

Population Discrepancy Function Value (F0) = 0.415

90 Percent Confidence Interval for F0 = (0.284 ; 0.580)

Root Mean Square Error of Approximation (RMSEA) = 0.215

90 Percent Confidence Interval for RMSEA = (0.178 ; 0.254)

P-value for Test of Close Fit (RMSEA < 0.05) = 0.000

Expected Cross-Validation Index (ECVI) = 0.567

90 Percent Confidence Interval for ECVI = (0.436 ; 0.732)

ECVI for Saturated Model = 0.194

ECVI for Independence Model = 5.357

Chi-Square for Independence Model with 15 Degrees of Freedom = 1150.426

Independence AIC = 1162.426

Model AIC = 123.032

Saturated AIC = 42.000

Independence CAIC = 1188.733

Model CAIC = 175.646

Saturated CAIC = 134.074

Normed Fit Index (NFI) = 0.913

Non-Normed Fit Index (NNFI) = 0.866

150

Parsimony Normed Fit Index (PNFI) = 0.548

Comparative Fit Index (CFI) = 0.920

Incremental Fit Index (IFI) = 0.920

Relative Fit Index (RFI) = 0.855

Critical N (CN) = 47.874

Root Mean Square Residual (RMR) = 0.0439

Standardized RMR = 0.0622

Goodness of Fit Index (GFI) = 0.868

Adjusted Goodness of Fit Index (AGFI) = 0.692

Parsimony Goodness of Fit Index (PGFI) = 0.372

The Modification Indices Suggest to Add an Error Covariance

Between and Decrease in Chi-Square New Estimate

X1.1.2 X1.1.1 19.1 0.11

X1.1.3 X1.1.2 27.3 0.11

X1.1.5 X1.1.1 10.9 -0.09

X1.1.5 X1.1.2 18.6 -0.10

X1.1.5 X1.1.4 39.7 0.15

X1.1.6 X1.1.1 23.3 0.15

X1.1.6 X1.1.3 11.4 -0.09

Time used: 0.031 Seconds

151

LAMPIRAN OUTPUT CFA VARIABEL X2

STANDARDIZED

T-valueS

152

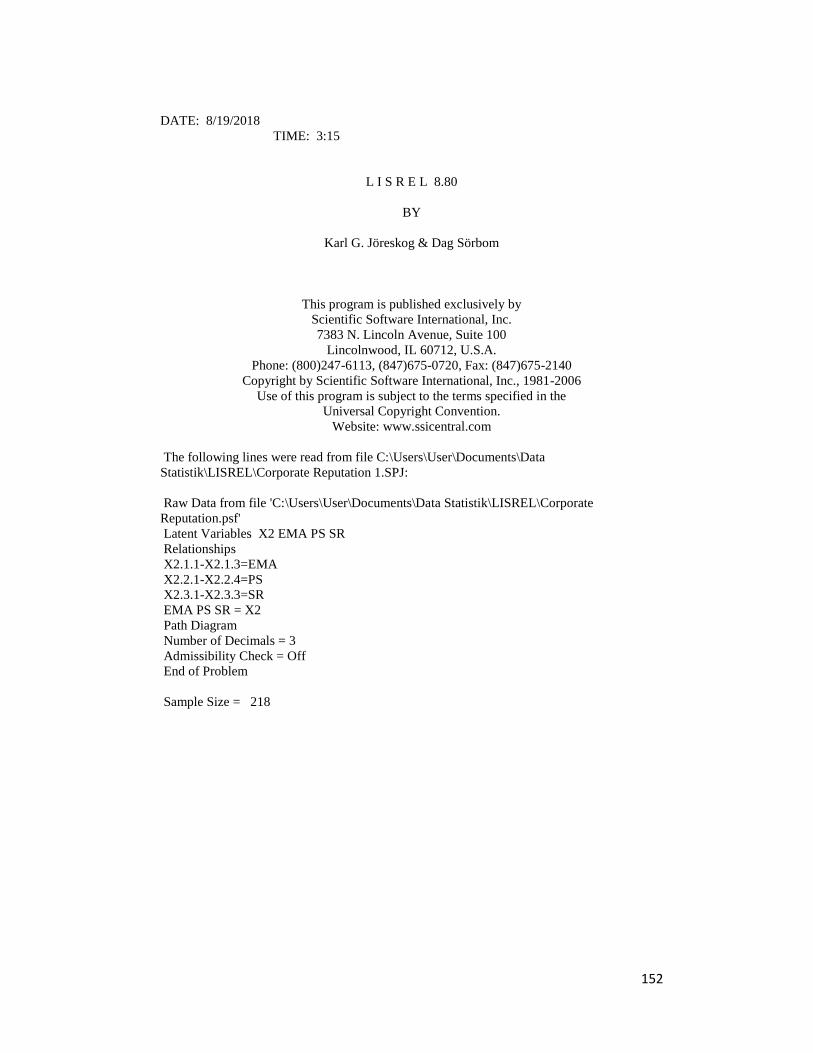

DATE: 8/19/2018

TIME: 3:15

L I S R E L 8.80

BY

Karl G. Jöreskog & Dag Sörbom

This program is published exclusively by

Scientific Software International, Inc.

7383 N. Lincoln Avenue, Suite 100

Lincolnwood, IL 60712, U.S.A.

Phone: (800)247-6113, (847)675-0720, Fax: (847)675-2140

Copyright by Scientific Software International, Inc., 1981-2006

Use of this program is subject to the terms specified in the

Universal Copyright Convention.

Website: www.ssicentral.com

The following lines were read from file C:\Users\User\Documents\Data

Statistik\LISREL\Corporate Reputation 1.SPJ:

Raw Data from file 'C:\Users\User\Documents\Data Statistik\LISREL\Corporate

Reputation.psf'

Latent Variables X2 EMA PS SR

Relationships

X2.1.1-X2.1.3=EMA

X2.2.1-X2.2.4=PS

X2.3.1-X2.3.3=SR

EMA PS SR = X2

Path Diagram

Number of Decimals = 3

Admissibility Check = Off

End of Problem

Sample Size = 218

153

Covariance Matrix

X2.1.1 X2.1.2 X2.1.3 X2.2.1 X2.2.2 X2.2.3

-------- -------- -------- -------- -------- --------

X2.1.1 0.675

X2.1.2 0.521 0.763

X2.1.3 0.443 0.492 0.617

X2.2.1 0.408 0.437 0.476 0.799

X2.2.2 0.395 0.496 0.458 0.636 0.762

X2.2.3 0.319 0.430 0.347 0.474 0.495 0.757

X2.2.4 0.393 0.526 0.446 0.641 0.650 0.583

X2.3.1 0.403 0.488 0.417 0.518 0.508 0.427

X2.3.2 0.324 0.423 0.358 0.454 0.440 0.441

X2.3.3 0.360 0.484 0.393 0.454 0.456 0.414

Covariance Matrix

X2.2.4 X2.3.1 X2.3.2 X2.3.3

-------- -------- -------- --------

X2.2.4 0.741

X2.3.1 0.527 0.818

X2.3.2 0.491 0.584 0.794

X2.3.3 0.504 0.628 0.621 0.888

Number of Iterations = 18

LISREL Estimates (Maximum Likelihood)

Measurement Equations

X2.1.1 = 0.658*EMA, Errorvar.= 0.242 , R² = 0.642

(0.0289)

8.387

X2.1.2 = 0.772*EMA, Errorvar.= 0.167 , R² = 0.781

(0.0531) (0.0264)

14.532 6.338

X2.1.3 = 0.658*EMA, Errorvar.= 0.185 , R² = 0.700

(0.0482) (0.0239)

13.649 7.729

X2.2.1 = 0.773*PS, Errorvar.= 0.201 , R² = 0.748

(0.0222)

9.064

154

X2.2.2 = 0.783*PS, Errorvar.= 0.149 , R² = 0.805

(0.0415) (0.0176)

18.863 8.433

X2.2.3 = 0.676*PS, Errorvar.= 0.301 , R² = 0.603

(0.0468) (0.0308)

14.444 9.769

X2.2.4 = 0.835*PS, Errorvar.= 0.0448 , R² = 0.940

(0.0378) (0.0114)

22.106 3.939

X2.3.1 = 0.792*SR, Errorvar.= 0.191 , R² = 0.767

(0.0280)

6.816

X2.3.2 = 0.750*SR, Errorvar.= 0.231 , R² = 0.710

(0.0477) (0.0298)

15.719 7.746

X2.3.3 = 0.800*SR, Errorvar.= 0.248 , R² = 0.721

(0.0503) (0.0327)

15.914 7.588

Structural Equations

EMA = 0.879*X2, Errorvar.= 0.227 , R² = 0.773

(0.0754) (0.0553)

11.665 4.096

PS = 0.910*X2, Errorvar.= 0.172 , R² = 0.828

(0.0677) (0.0465)

13.445 3.709

SR = 0.859*X2, Errorvar.= 0.261 , R² = 0.739

(0.0683) (0.0544)

12.588 4.802

Correlation Matrix of Independent Variables

X2

--------

1.000

155

Covariance Matrix of Latent Variables

EMA PS SR X2

-------- -------- -------- --------

EMA 1.000

PS 0.800 1.000

SR 0.756 0.782 1.000

X2 0.879 0.910 0.859 1.000

Goodness of Fit Statistics

Degrees of Freedom = 32

Minimum Fit Function Chi-Square = 98.580 (P = 0.000)

Normal Theory Weighted Least Squares Chi-Square = 107.556 (P = 0.00)

Estimated Non-centrality Parameter (NCP) = 75.556

90 Percent Confidence Interval for NCP = (47.802 ; 110.913)

Minimum Fit Function Value = 0.454

Population Discrepancy Function Value (F0) = 0.348

90 Percent Confidence Interval for F0 = (0.220 ; 0.511)

Root Mean Square Error of Approximation (RMSEA) = 0.104

90 Percent Confidence Interval for RMSEA = (0.0830 ; 0.126)

P-value for Test of Close Fit (RMSEA < 0.05) = 0.000

Expected Cross-Validation Index (ECVI) = 0.708

90 Percent Confidence Interval for ECVI = (0.580 ; 0.871)

ECVI for Saturated Model = 0.507

ECVI for Independence Model = 17.802

Chi-Square for Independence Model with 45 Degrees of Freedom = 3843.060

Independence AIC = 3863.060

Model AIC = 153.556

Saturated AIC = 110.000

Independence CAIC = 3906.905

Model CAIC = 254.399

Saturated CAIC = 351.147

Normed Fit Index (NFI) = 0.974

Non-Normed Fit Index (NNFI) = 0.975

Parsimony Normed Fit Index (PNFI) = 0.693

Comparative Fit Index (CFI) = 0.982

Incremental Fit Index (IFI) = 0.983

Relative Fit Index (RFI) = 0.964

Critical N (CN) = 118.745

Root Mean Square Residual (RMR) = 0.0241

Standardized RMR = 0.0323

Goodness of Fit Index (GFI) = 0.910

156

Adjusted Goodness of Fit Index (AGFI) = 0.845

Parsimony Goodness of Fit Index (PGFI) = 0.529

The Modification Indices Suggest to Add the

Path to from Decrease in Chi-Square New Estimate

X2.1.1 PS 8.2 -0.23

The Modification Indices Suggest to Add an Error Covariance

Between and Decrease in Chi-Square New Estimate

X2.1.3 X2.1.2 8.7 -0.08

X2.2.1 X2.1.2 27.4 -0.09

X2.2.1 X2.1.3 19.3 0.07

X2.2.2 X2.2.1 12.6 0.06

X2.2.3 X2.2.1 11.0 -0.06

X2.2.3 X2.2.2 8.1 -0.05

X2.2.4 X2.1.2 11.0 0.04

X2.2.4 X2.2.3 22.4 0.07

Time used: 0.016 Seconds

157

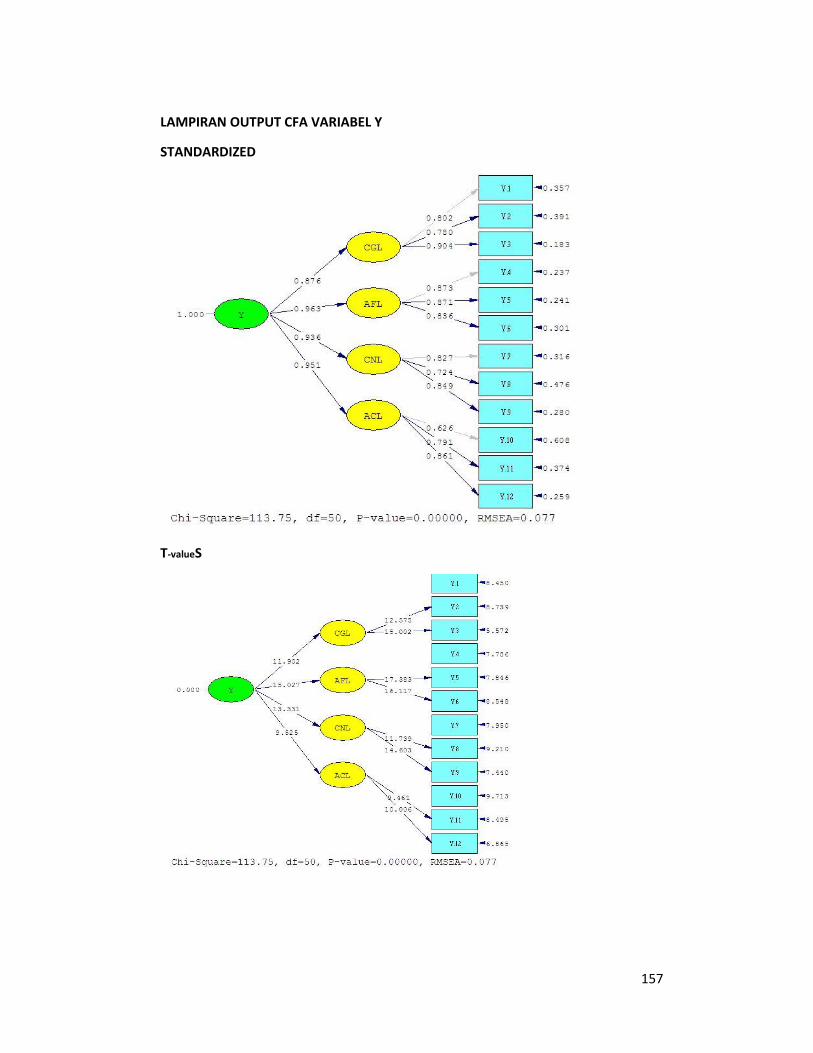

LAMPIRAN OUTPUT CFA VARIABEL Y

STANDARDIZED

T-valueS

158

DATE: 8/19/2018

TIME: 3:26

L I S R E L 8.80

BY

Karl G. Jöreskog & Dag Sörbom

This program is published exclusively by

Scientific Software International, Inc.

7383 N. Lincoln Avenue, Suite 100

Lincolnwood, IL 60712, U.S.A.

Phone: (800)247-6113, (847)675-0720, Fax: (847)675-2140

Copyright by Scientific Software International, Inc., 1981-2006

Use of this program is subject to the terms specified in the

Universal Copyright Convention.

Website: www.ssicentral.com

The following lines were read from file C:\Users\User\Documents\Data

Statistik\LISREL\Consumer Loyalty.SPJ:

Raw Data from file 'C:\Users\User\Documents\Data

Statistik\LISREL\Consumer Loyalty 1.psf'

Latent Variables Y CGL AFL CNL ACL

Relationships

Y.1-Y.3=CGL

Y.4-Y.6=AFL

Y.7-Y.9=CNL

Y.10-Y.12=ACL

CGL AFL CNL ACL = Y

Path Diagram

Number of Decimals = 3

Admissibility Check = Off

End of Problem

Sample Size = 218

159

Covariance Matrix

Y.1 Y.2 Y.3 Y.4 Y.5 Y.6

-------- -------- -------- -------- -------- --------

Y.1 0.772

Y.2 0.487 0.833

Y.3 0.548 0.574 0.757

Y.4 0.444 0.438 0.492 0.672

Y.5 0.405 0.386 0.448 0.536 0.652

Y.6 0.545 0.472 0.569 0.526 0.509 0.832

Y.7 0.389 0.365 0.407 0.428 0.424 0.435

Y.8 0.350 0.357 0.362 0.407 0.408 0.402

Y.9 0.459 0.439 0.456 0.455 0.484 0.553

Y.10 0.310 0.351 0.383 0.363 0.302 0.396

Y.11 0.420 0.402 0.434 0.425 0.459 0.532

Y.12 0.515 0.472 0.543 0.516 0.522 0.622

Covariance Matrix

Y.7 Y.8 Y.9 Y.10 Y.11 Y.12

-------- -------- -------- -------- -------- --------

Y.7 0.636

Y.8 0.433 0.755

Y.9 0.494 0.464 0.791

Y.10 0.383 0.434 0.438 0.905

Y.11 0.410 0.437 0.508 0.459 0.803

Y.12 0.478 0.431 0.571 0.484 0.571 0.905

Number of Iterations = 21

160

LISREL Estimates (Maximum Likelihood)

Measurement Equations

Y.1 = 0.705*CGL, Errorvar.= 0.275 , R² = 0.643

(0.0326)

8.450

Y.2 = 0.712*CGL, Errorvar.= 0.326 , R² = 0.609

(0.0566) (0.0373)

12.575 8.739

Y.3 = 0.786*CGL, Errorvar.= 0.138 , R² = 0.817

(0.0524) (0.0248)

15.002 5.572

Y.4 = 0.716*AFL, Errorvar.= 0.160 , R² = 0.763

(0.0205)

7.786

Y.5 = 0.703*AFL, Errorvar.= 0.157 , R² = 0.759

(0.0405) (0.0201)

17.383 7.846

Y.6 = 0.762*AFL, Errorvar.= 0.251 , R² = 0.699

(0.0473) (0.0293)

16.117 8.548

Y.7 = 0.660*CNL, Errorvar.= 0.201 , R² = 0.684

(0.0253)

7.950

Y.8 = 0.629*CNL, Errorvar.= 0.360 , R² = 0.524

(0.0536) (0.0391)

11.739 9.210

Y.9 = 0.755*CNL, Errorvar.= 0.221 , R² = 0.720

(0.0517) (0.0297)

14.603 7.440

161

Y.10 = 0.596*ACL, Errorvar.= 0.550 , R² = 0.392

(0.0567)

9.713

Y.11 = 0.709*ACL, Errorvar.= 0.301 , R² = 0.626

(0.0749) (0.0354)

9.461 8.495

Y.12 = 0.819*ACL, Errorvar.= 0.235 , R² = 0.741

(0.0818) (0.0342)

10.006 6.865

Structural Equations

CGL = 0.876*Y, Errorvar.= 0.232 , R² = 0.768

(0.0736) (0.0480)

11.902 4.843

AFL = 0.963*Y, Errorvar.= 0.0724 , R² = 0.928

(0.0641) (0.0313)

15.027 2.313

CNL = 0.936*Y, Errorvar.= 0.123 , R² = 0.877

(0.0702) (0.0405)

13.331 3.038

ACL = 0.951*Y, Errorvar.= 0.0951 , R² = 0.905

(0.0999) (0.0433)

9.525 2.195

Correlation Matrix of Independent Variables

Y

--------

1.000

162

Covariance Matrix of Latent Variables

CGL AFL CNL ACL Y

-------- -------- -------- -------- --------

CGL 1.000

AFL 0.844 1.000

CNL 0.820 0.902 1.000

ACL 0.833 0.916 0.891 1.000

Y 0.876 0.963 0.936 0.951 1.000

Goodness of Fit Statistics

Degrees of Freedom = 50

Minimum Fit Function Chi-Square = 116.159 (P = 0.000)

Normal Theory Weighted Least Squares Chi-Square = 113.751 (P = 0.000)

Estimated Non-centrality Parameter (NCP) = 63.751

90 Percent Confidence Interval for NCP = (36.547 ; 98.678)

Minimum Fit Function Value = 0.535

Population Discrepancy Function Value (F0) = 0.294

90 Percent Confidence Interval for F0 = (0.168 ; 0.455)

Root Mean Square Error of Approximation (RMSEA) = 0.0767

90 Percent Confidence Interval for RMSEA = (0.0580 ; 0.0954)

P-value for Test of Close Fit (RMSEA < 0.05) = 0.0109

Expected Cross-Validation Index (ECVI) = 0.782

90 Percent Confidence Interval for ECVI = (0.657 ; 0.943)

ECVI for Saturated Model = 0.719

ECVI for Independence Model = 23.467

Chi-Square for Independence Model with 66 Degrees of Freedom = 5068.246

Independence AIC = 5092.246

Model AIC = 169.751

Saturated AIC = 156.000

Independence CAIC = 5144.860

Model CAIC = 292.516

Saturated CAIC = 497.991

Normed Fit Index (NFI) = 0.977

Non-Normed Fit Index (NNFI) = 0.983

Parsimony Normed Fit Index (PNFI) = 0.740

Comparative Fit Index (CFI) = 0.987

163

Incremental Fit Index (IFI) = 0.987

Relative Fit Index (RFI) = 0.970

Critical N (CN) = 143.273

Root Mean Square Residual (RMR) = 0.0283

Standardized RMR = 0.0358

Goodness of Fit Index (GFI) = 0.920

Adjusted Goodness of Fit Index (AGFI) = 0.875

Parsimony Goodness of Fit Index (PGFI) = 0.590

The Modification Indices Suggest to Add the

Path to from Decrease in Chi-Square New Estimate

Y.4 ACL 12.2 -0.58

Y.6 CGL 19.9 0.44

Y.6 ACL 18.4 0.80

The Modification Indices Suggest to Add an Error Covariance

Between and Decrease in Chi-Square New Estimate

Y.5 Y.4 25.7 0.09

Y.6 Y.5 8.5 -0.06

Y.10 Y.5 11.3 -0.08

Y.10 Y.8 9.0 0.10

Time used: 0.031 Seconds