KOtak Recommendation V2

6

Key Highlights Poised to witness above-average growth: We expect KMB to continue beating industry advance growth rates by a significant margin. Aided by robust (~29%) loan book growth and high NIMs (~5.2%) over the next two years, supported by the group’s asset mix (albeit some margin pressure in the medium term) we expect KMB to record healthy growth in NII going forward. Robust CAR presents soli d grou nd for loan book growth: KMB rep ort ed a robus t cap ita l adequacy ratio (CAR) of 19.5% and a Tier I capital ratio of 18.1% as at 31 March 2011 on a consolidated basis. This will support balance sheet growth going forward without the need for raising fresh capital in the foreseeable future and also allow the bank to grow its return on equity (RoE) going forward. ‘Financial supermarket’ model provides diversification: KMB’s ‘fina ncia l supermarket’ model gives it the advantage of exploiting the growth potential of various financial services verticals outside of traditional banking and opens up significant cross-selling opportunities. Further, as the bank generates a significant proportion of its income from non-balance sheet businesses it generates higher return on assets (RoA) compared to its peers. Company Description: Incorporated in 1985 as Kotak Capital Management Finance Ltd. and rechristened Kotak Mahindra Finance Ltd. a year later, the company started bill discounting activities in 1986. The company entered upon the lease and hire purchase bus ine ss in 1987 and in 1990 it commenced its car fin ance ope rat ion s. In 1991, the company’s investment banking division was started and in the same year it took over FICOM, one of India's largest financial retail marketing networks. In 2003, the company commenced full-fledged banking operations as Kotak Mahindra Bank Ltd. (KMB) after receiving a license from the Reserve Bank of India (RBI). Today KMB is a financial supermarket offering a wide range of services such as banking, car finance, life insurance, securities broking, investment banking and asset management. KMB operates the commercial banking business of the group and is also the holding company of 16 subsidiaries managing the other businesses of the company. KMB also holds a majority stake in its life insurance joint venture (JV) with Old Mutual Plc. As at 31 March 2011 the bank had 321 branches and 710 ATMs. KMB is the fourth largest private bank in India in terms of market capitalization. Hold - Kotak Mahindra Bank CMP: 453 Fiduciary Euromax Capital Markets Pvt. Ltd. 12 th Sept, 2011

Transcript of KOtak Recommendation V2

8/3/2019 KOtak Recommendation V2

http://slidepdf.com/reader/full/kotak-recommendation-v2 1/6

8/3/2019 KOtak Recommendation V2

http://slidepdf.com/reader/full/kotak-recommendation-v2 2/6

Fiduciary – Euromax Capital Markets Pvt. Ltd. Kotak Mahindra

Bank

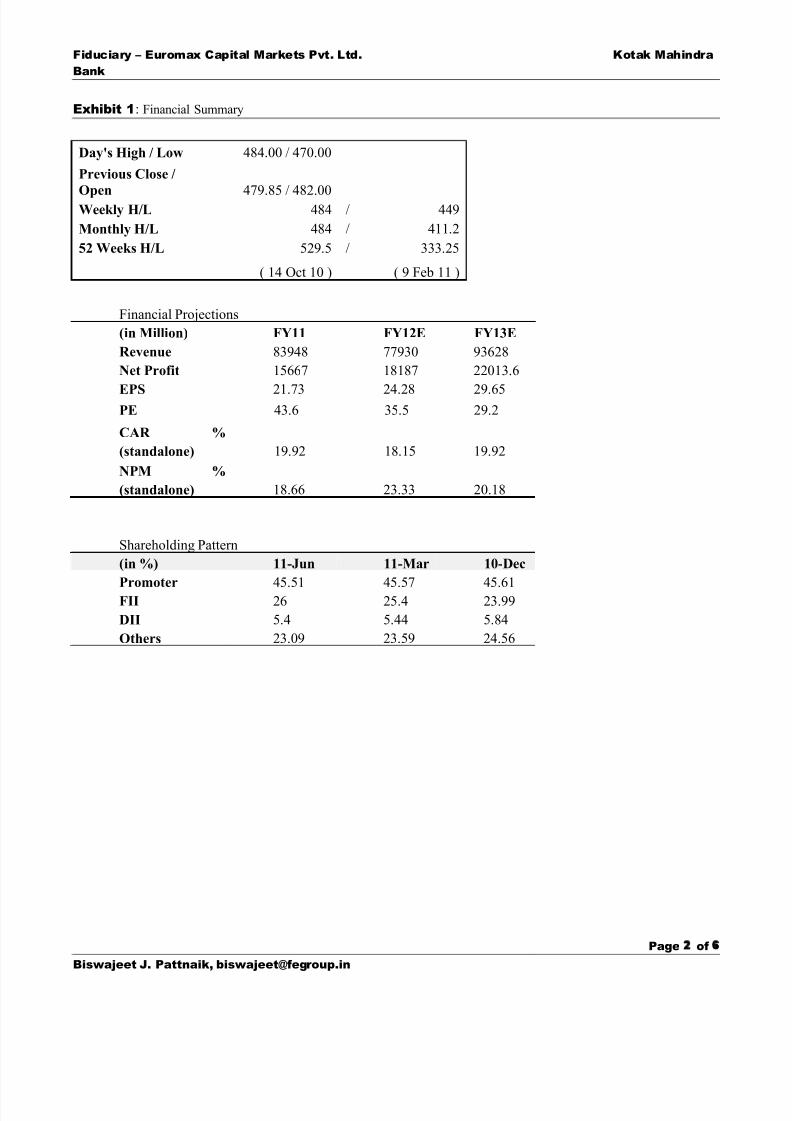

Exhibit 1: Financial Summary

Day's High / Low 484.00 / 470.00

Previous Close /

Open 479.85 / 482.00Weekly H/L 484 / 449

Monthly H/L 484 / 411.2

52 Weeks H/L 529.5 / 333.25

( 14 Oct 10 ) ( 9 Feb 11 )

Financial Projections

(in Million) FY11 FY12E FY13E

Revenue 83948 77930 93628

Net Profit 15667 18187 22013.6

EPS 21.73 24.28 29.65PE 43.6 35.5 29.2

CAR %

(standalone) 19.92 18.15 19.92

NPM %

(standalone) 18.66 23.33 20.18

Shareholding Pattern

(in %) 11-Jun 11-Mar 10-Dec

Promoter 45.51 45.57 45.61FII 26 25.4 23.99

DII 5.4 5.44 5.84

Others 23.09 23.59 24.56

Page 2 of 6

Biswajeet J. Pattnaik, [email protected]

8/3/2019 KOtak Recommendation V2

http://slidepdf.com/reader/full/kotak-recommendation-v2 3/6

Fiduciary – Euromax Capital Markets Pvt. Ltd. Kotak Mahindra

Bank

Exhibit 2: Shareholding pattern (exceeding 1%)

Sl. No.

Na

ShaSumit

Key Strengths

Poised to witness above-average growth

KMB’s loan book grew by a robust CAGR of 32% compared with an industry average of 21% between 2006 and

2011. The bank’s deposit base grew at a CAGR of 37% during the same period compared to an industry average

of 20%. KMB’s NIMs have always been higher than most of its peers, attributable to its asset mix with significant

presence in high yielding segments such as car finance, and commercial vehicle (CV) and commercial equipment

(CE) finance (car finance: 21%; CVs & CEs: 15% as at the end of FY 2011). The bank, historically, had a

Page 3 of 6

Biswajeet J. Pattnaik, [email protected]

8/3/2019 KOtak Recommendation V2

http://slidepdf.com/reader/full/kotak-recommendation-v2 4/6

Fiduciary – Euromax Capital Markets Pvt. Ltd. Kotak Mahindra

Bank

relatively high exposure to retail loans, which over the past few years has reduced (FY 2011: 3% vs. FY 2008:

14%). For FY 2011, KMB reported an NIM of 5.8% on a consolidated basis. We expect NIM to be pressured a bit

during FY 2012 due to higher cost of funds. In general, too, we expect NIMs to trend lower than the high

historical levels (FY 2010: 6.1%) as the bank increases exposure to lower yielding asset classes such as corporate

and mortgage loans; nonetheless, we expect consolidated NIM to remain above 5% over the next couple of years.

Robust CAR presents solid ground for loan book growth

KMB reported a robust capital adequacy ratio (CAR) of 19.5% and a Tier I capital ratio of 18.1% as at 31 March

2011 on a consolidated basis. This will support balance sheet growth going forward without the need for raising

fresh capital in the foreseeable future. We expect the advances to grow by an average of ~29% annually over the

next couple of years, a rate substantially higher than the expected rate of growth for industry advances. The

bank’s strong capital position will also allow it to grow its return on equity (RoE) going forward.

‘Financial supermarket’ model provides diversification

KMB’s ‘financial supermarket’ model gives it the advantage of exploiting the growth potential of various

financial services verticals outside of traditional banking. This model also opens up significant cross-selling

opportunities with the group having presence in a gamut of services in both the retail as well as corporate markets.

Further, as the bank generates a significant proportion of its income from non-balance sheet businesses (non-

interest income contributed 58% of total income in FY 2011) it generates higher return on assets (RoA) compared

to its peers. KMB also has a well established agricultural lending business (~10% of loan book at the end of FY

2011) which is profitable and has witnessed robust growth. Its agri portfolio has also enabled the bank to

consistently meet its priority sector lending (PSL) targets which in turn has resulted in the bank not requiring

putting significant amounts of money into the low-yielding Rural Infrastructure Development Fund (RIDF).

Subsequently, this has contributed positively to the high NIMs of the bank. Further, this has also enabled the bank

to restrict its microfinance institution (MFI) exposure to ~0.2% of total advances.

Key Risks

Any deterioration of the overall economic environment may lead to slower credit off take an increase in

slippages compared to what have been modeled into our forecasts, thereby negatively impacting profits. As

KMB’s asset mix consists of a high proportion of high-yield assets, a worsening of the economic environment

is likely to impact KMB more than the banks having a greater proportion of low-yield, and thereby less risky,

assets on its books.

Kotak is heavily exposed to capital markets, via retail and institutional brokering, investment banking, and

third-party funds distribution. We believe, however, that it may not be able to exploit these opportunities as

well as it had in the past because:

Brokering—Yields and market share are declining: Market share and yields in the online

brokering business are trending down, with increased competition and further geographical

penetration decelerating.

Investment banking: Activity is picking up but float income could be lower: The investment

banking business is likely to see tighter margins this time around, especially with float

Page 4 of 6

Biswajeet J. Pattnaik, [email protected]

8/3/2019 KOtak Recommendation V2

http://slidepdf.com/reader/full/kotak-recommendation-v2 5/6

Fiduciary – Euromax Capital Markets Pvt. Ltd. Kotak Mahindra

Bank

income being capped by tighter regulation. Also, the number of days of float income is also

being capped and this would further put pressure on revenue from IB.

Distribution fees under pressure: Third-party distribution income is also under pressure, with

front-end fees restricted on mutual funds and overall fees capped on life insurance.

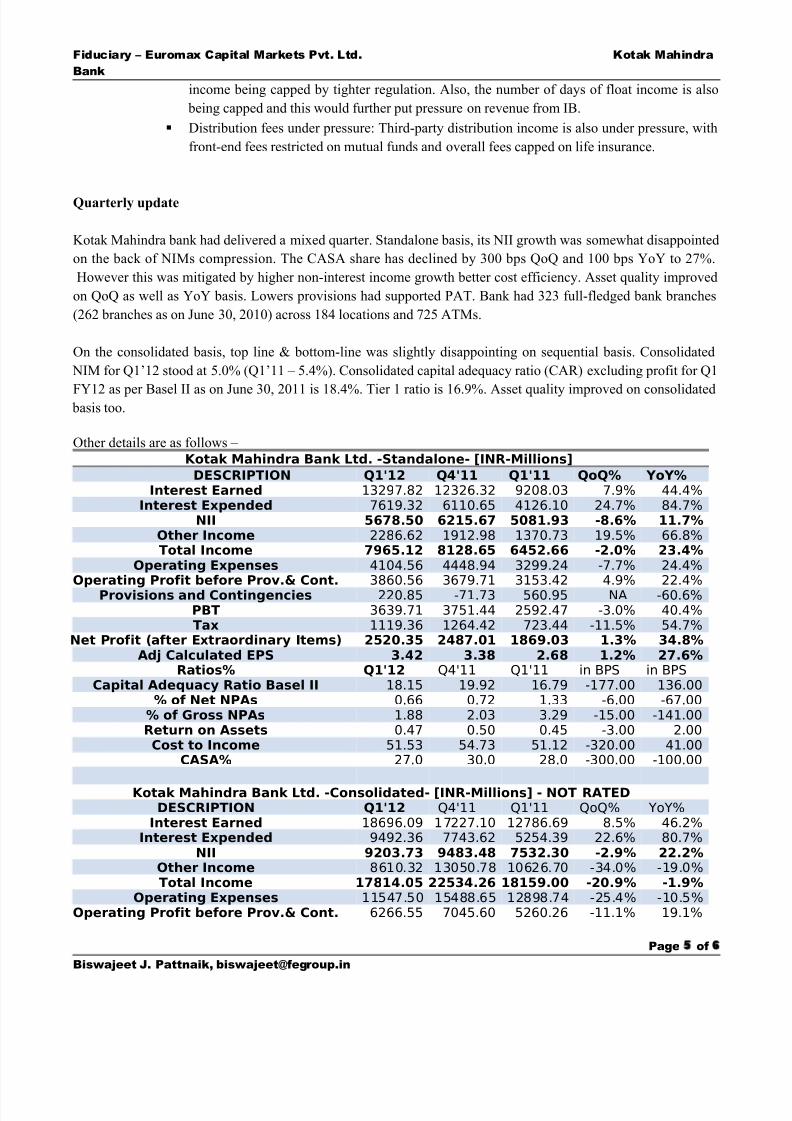

Quarterly update

Kotak Mahindra bank had delivered a mixed quarter. Standalone basis, its NII growth was somewhat disappointed

on the back of NIMs compression. The CASA share has declined by 300 bps QoQ and 100 bps YoY to 27%.

However this was mitigated by higher non-interest income growth better cost efficiency. Asset quality improved

on QoQ as well as YoY basis. Lowers provisions had supported PAT. Bank had 323 full-fledged bank branches

(262 branches as on June 30, 2010) across 184 locations and 725 ATMs.

On the consolidated basis, top line & bottom-line was slightly disappointing on sequential basis. Consolidated

NIM for Q1’12 stood at 5.0% (Q1’11 – 5.4%). Consolidated capital adequacy ratio (CAR) excluding profit for Q1

FY12 as per Basel II as on June 30, 2011 is 18.4%. Tier 1 ratio is 16.9%. Asset quality improved on consolidated basis too.

Other details are as follows –

Kotak Mahindra Bank Ltd. -Standalone- [INR-Millions]

DESCRIPTION Q1'12 Q4'11 Q1'11 QoQ% YoY%Interest Earned 13297.82 12326.32 9208.03 7.9% 44.4%

Interest Expended 7619.32 6110.65 4126.10 24.7% 84.7%

NII 5678.50 6215.67 5081.93 -8.6% 11.7%Other Income 2286.62 1912.98 1370.73 19.5% 66.8%

Total Income 7965.12 8128.65 6452.66 -2.0% 23.4%Operating Expenses 4104.56 4448.94 3299.24 -7.7% 24.4%

Operating Profit before Prov.& Cont. 3860.56 3679.71 3153.42 4.9% 22.4%

Provisions and Contingencies 220.85 -71.73 560.95 NA -60.6%

PBT 3639.71 3751.44 2592.47 -3.0% 40.4%

Tax 1119.36 1264.42 723.44 -11.5% 54.7%

Net Profit (after Extraordinary Items) 2520.35 2487.01 1869.03 1.3% 34.8%Adj Calculated EPS 3.42 3.38 2.68 1.2% 27.6%

Ratios% Q1'12 Q4'11 Q1'11 in BPS in BPS

Capital Adequacy Ratio Basel II 18.15 19.92 16.79 -177.00 136.00

% of Net NPAs 0.66 0.72 1.33 -6.00 -67.00

% of Gross NPAs 1.88 2.03 3.29 -15.00 -141.00

Return on Assets 0.47 0.50 0.45 -3.00 2.00

Cost to Income 51.53 54.73 51.12 -320.00 41.00

CASA% 27.0 30.0 28.0 -300.00 -100.00

Kotak Mahindra Bank Ltd. -Consolidated- [INR-Millions] - NOT RATEDDESCRIPTION Q1'12 Q4'11 Q1'11 QoQ% YoY%

Interest Earned 18696.09 17227.10 12786.69 8.5% 46.2%

Interest Expended 9492.36 7743.62 5254.39 22.6% 80.7%

NII 9203.73 9483.48 7532.30 -2.9% 22.2%Other Income 8610.32 13050.78 10626.70 -34.0% -19.0%

Total Income 17814.05 22534.26 18159.00 -20.9% -1.9%Operating Expenses 11547.50 15488.65 12898.74 -25.4% -10.5%

Operating Profit before Prov.& Cont. 6266.55 7045.60 5260.26 -11.1% 19.1%

Page 5 of 6

Biswajeet J. Pattnaik, [email protected]

8/3/2019 KOtak Recommendation V2

http://slidepdf.com/reader/full/kotak-recommendation-v2 6/6

Fiduciary – Euromax Capital Markets Pvt. Ltd. Kotak Mahindra

Bank

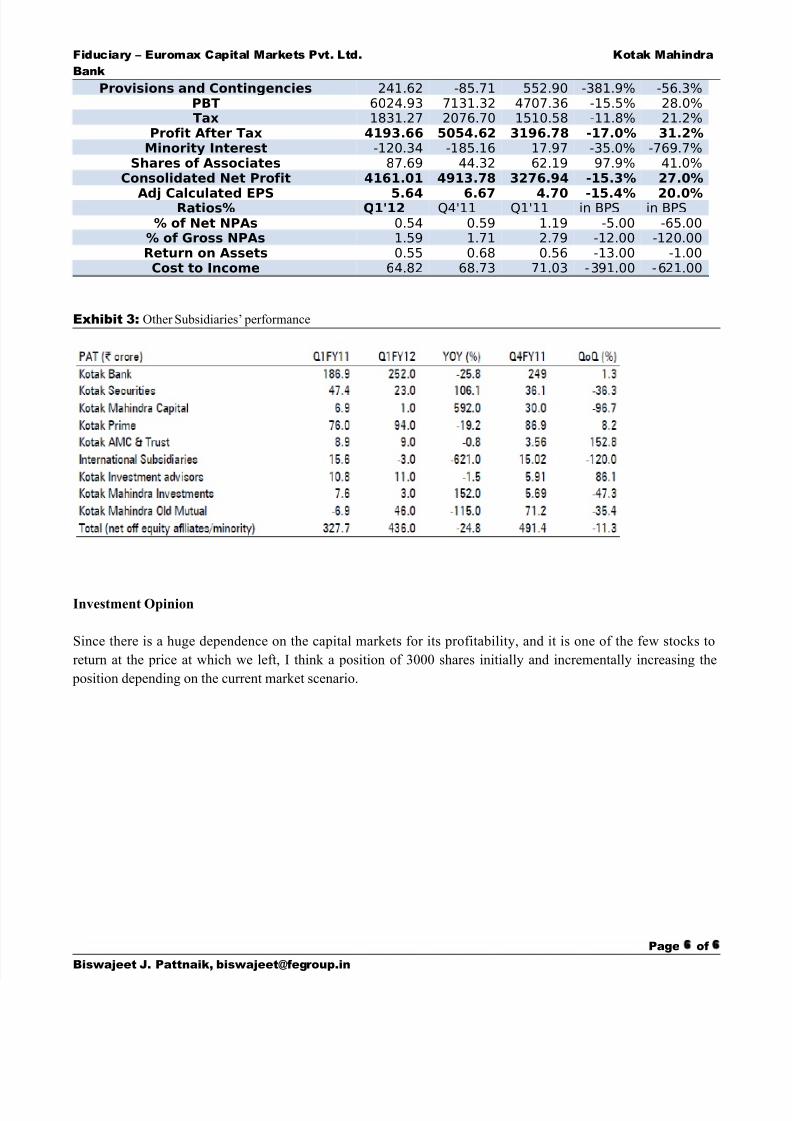

Provisions and Contingencies 241.62 -85.71 552.90 -381.9% -56.3%

PBT 6024.93 7131.32 4707.36 -15.5% 28.0%

Tax 1831.27 2076.70 1510.58 -11.8% 21.2%

Profit After Tax 4193.66 5054.62 3196.78 -17.0% 31.2%Minority Interest -120.34 -185.16 17.97 -35.0% -769.7%

Shares of Associates 87.69 44.32 62.19 97.9% 41.0%

Consolidated Net Profit 4161.01 4913.78 3276.94 -15.3% 27.0%

Adj Calculated EPS 5.64 6.67 4.70 -15.4% 20.0%Ratios% Q1'12 Q4'11 Q1'11 in BPS in BPS

% of Net NPAs 0.54 0.59 1.19 -5.00 -65.00

% of Gross NPAs 1.59 1.71 2.79 -12.00 -120.00

Return on Assets 0.55 0.68 0.56 -13.00 -1.00

Cost to Income 64.82 68.73 71.03 -391.00 -621.00

Exhibit 3: Other Subsidiaries’ performance

Investment Opinion

Since there is a huge dependence on the capital markets for its profitability, and it is one of the few stocks to

return at the price at which we left, I think a position of 3000 shares initially and incrementally increasing the

position depending on the current market scenario.

Page 6 of 6

Biswajeet J. Pattnaik, [email protected]

![201009 Recommendation[Selatan 2011]](https://static.fdokumen.com/doc/165x107/577d23561a28ab4e1e9988b4/201009-recommendationselatan-2011.jpg)