Kerangka Konseptual & Pelaporan Keuangan, Manajemen Laba, Konsekuensi Ekonomis Laporan Keuangan

OVERVIEW FINANCIAL STATEMENT ANALYSIS

Agenda

2

Business Analysis1

Business Analysis Framework2

Analysis Preview

3

4

Business Activities & Reporting

3

Financial Statement Analysis = analisis yang dilakukan guna menguji keterkaitan angka-angka akuntansi dan trend angka tersebut dalam periode waktu tertentu.

Mengapa dilakukan?1. Menilai kondisi keuangan dan hasil usaha perusahaan

masa lalu, masa sekarang, dan prediksi yang akan datang2. Menilai kekuatan dan kelemahan keuangan perusahaan

Financial Statement Analysis

Business Analysis

Evaluate Prospects Evaluate Risks

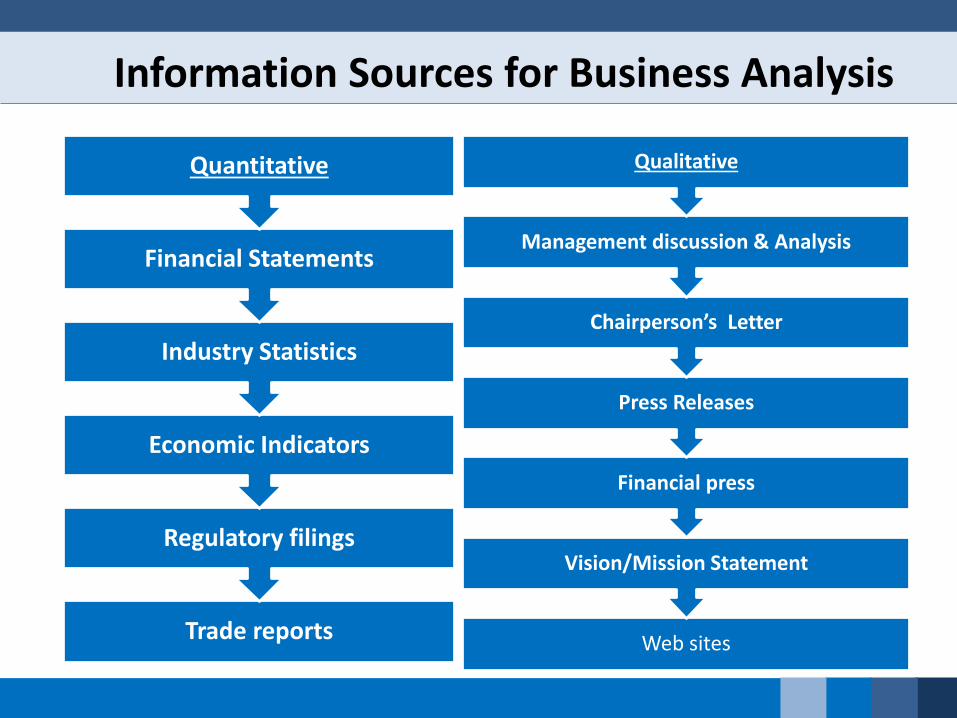

Information Sources for Business Analysis

Trade reports

Regulatory filings

Economic Indicators

Industry Statistics

Financial Statements

Quantitative

Web sites

Vision/Mission Statement

Financial press

Press Releases

Chairperson’s Letter

Management discussion & Analysis

Qualitative

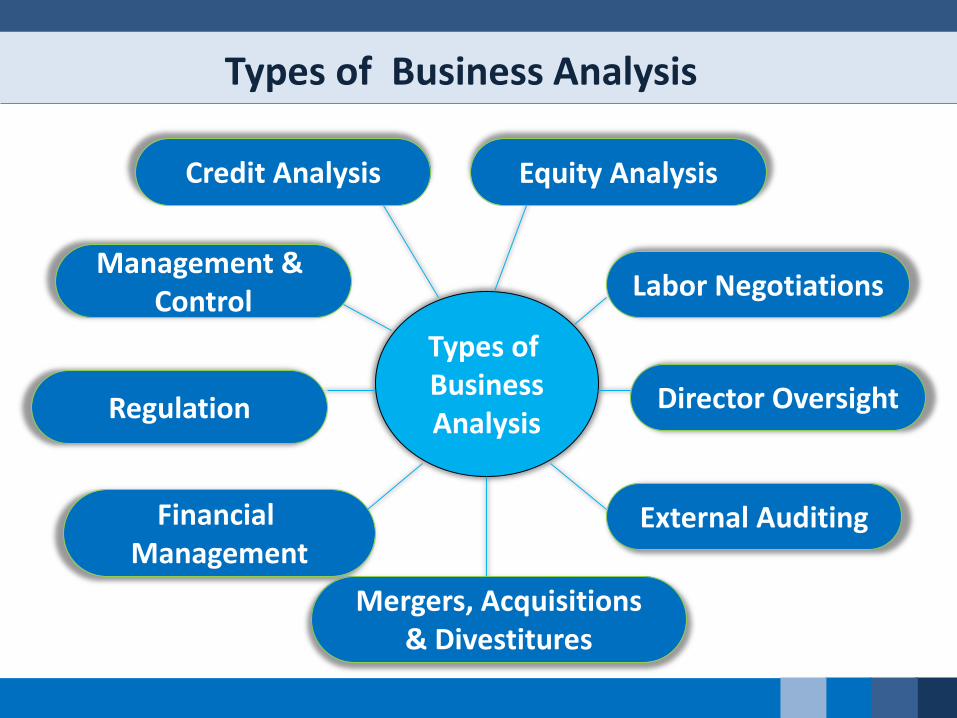

Types of BusinessAnalysis

Credit Analysis Equity Analysis

Management & Control

Mergers, Acquisitions& Divestitures

Director OversightRegulation

External Auditing

Labor Negotiations

Financial Management

Types of Business Analysis

Credit Analysis

Trade Creditors

Provide goods or services

Most short-term

Usually implicit interest

Bear risk of default

Non-trade Creditors

Provide major financing

Most long-term

Usually explicit interest

Bear risk of default

Credit Analysis

Liquidity

Ability to meet short-term obligationsFocus:

• Current cash flows• Make up of current

assets and liabilities• Liquidity of assets

Solvency

Ability to meet long-term obligations

Focus:• Long-term profitability• Capital structure

Credit worthiness: Ability to honor credit obligations

(downside risk)

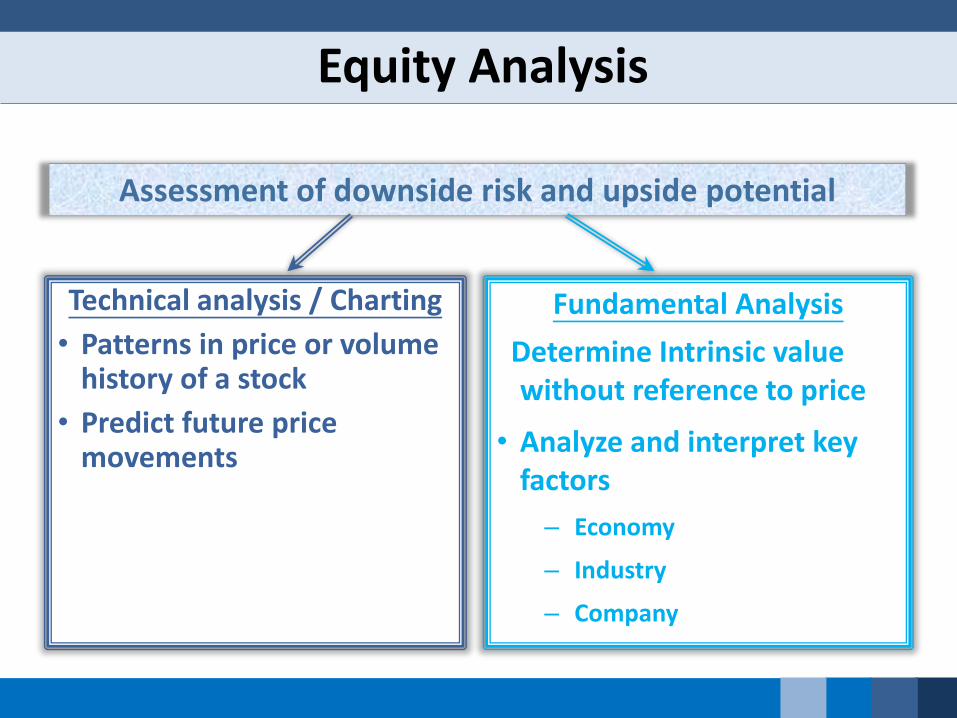

Equity Analysis

Technical analysis / Charting

• Patterns in price or volume history of a stock

• Predict future price movements

Fundamental Analysis

Determine Intrinsic value without reference to price

• Analyze and interpret key factors

– Economy

– Industry

– Company

Assessment of downside risk and upside potential

ProspectiveAnalysis

AccountingAnalysis

BusinessEnvironment &

Strategy Analysis

IndustryAnalysis

StrategyAnalysis

FinancialAnalysis

Analysisof cash flows

ProfitabilityAnalysis

RiskAnalysis

Cost of Capital Estimate Intrinsic Value

Component Processes of Business Analysis

11

FRAMEWORK ANALISIS LAPORAN KEUANGAN

Menilai lingkungan bisnis Membaca dan mempelajari laporan keuangan

& footnotes Menilai Kualitas Laba Analisis laporan keuangan Memprediksi laba atau cash flow masa

mendatang

12

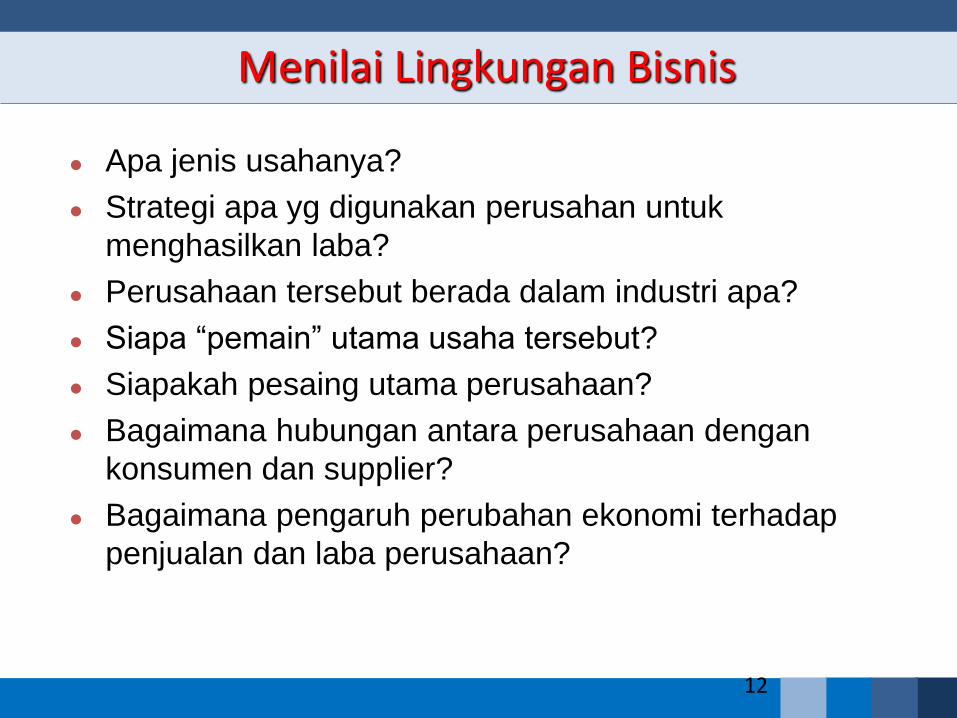

Menilai Lingkungan Bisnis

Apa jenis usahanya?

Strategi apa yg digunakan perusahan untuk

menghasilkan laba?

Perusahaan tersebut berada dalam industri apa?

Siapa “pemain” utama usaha tersebut?

Siapakah pesaing utama perusahaan?

Bagaimana hubungan antara perusahaan dengan

konsumen dan supplier?

Bagaimana pengaruh perubahan ekonomi terhadap

penjualan dan laba perusahaan?

13

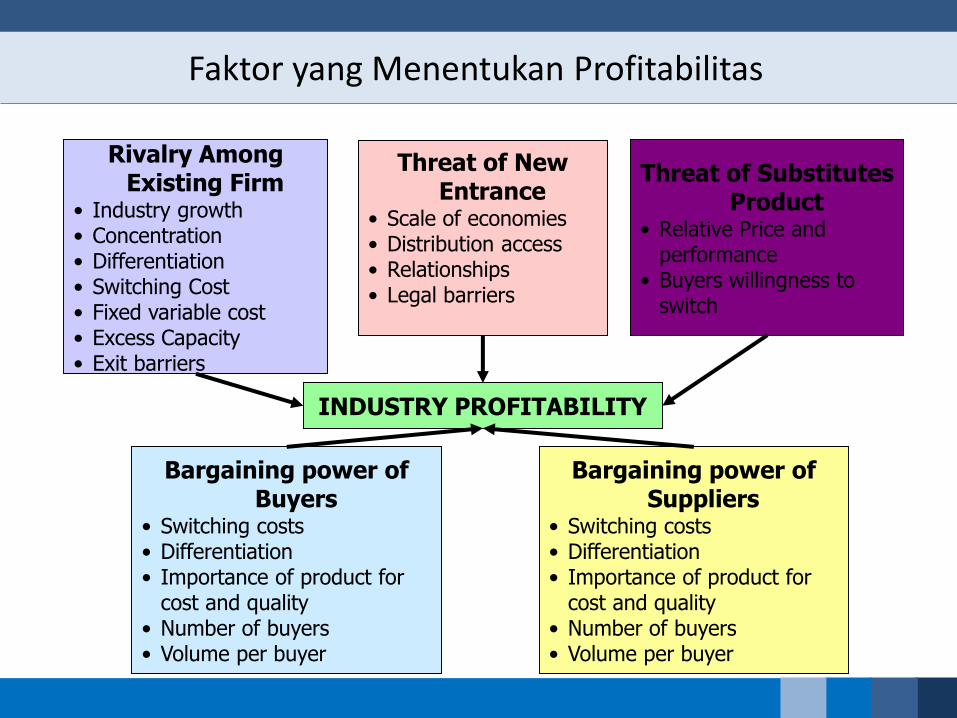

Analisis Industri

• Analisis potensi laba berdasarkan kondisi industri,

• Setiap industri memiliki profitabilitas yang berbeda tergantung dari keunggulan yang dimilikinya

• Kompetisi industri dengan industri lainnya akan mempengaruhi profitabiltas industri.

• Kompetisi dalam industri akan mempengaruhi profitabilitas masing-masing perusahaan dalam industri

• Struktur pasar dalam suatu industri menentukan apakah perusahaan dalam industri tersebut dapat memperoleh laba yang abnormal

• Kondisi perekonomian mempengaruhi profitabilitas industri dan perusahaan

Faktor yang Menentukan Profitabilitas

INDUSTRY PROFITABILITY

Rivalry Among Existing Firm

• Industry growth• Concentration• Differentiation• Switching Cost• Fixed variable cost• Excess Capacity• Exit barriers

Threat of New Entrance

• Scale of economies• Distribution access• Relationships• Legal barriers

Threat of Substitutes Product

• Relative Price and performance

• Buyers willingness to switch

Bargaining power of Buyers

• Switching costs• Differentiation• Importance of product for

cost and quality• Number of buyers• Volume per buyer

Bargaining power of Suppliers

• Switching costs• Differentiation• Importance of product for

cost and quality• Number of buyers• Volume per buyer

15

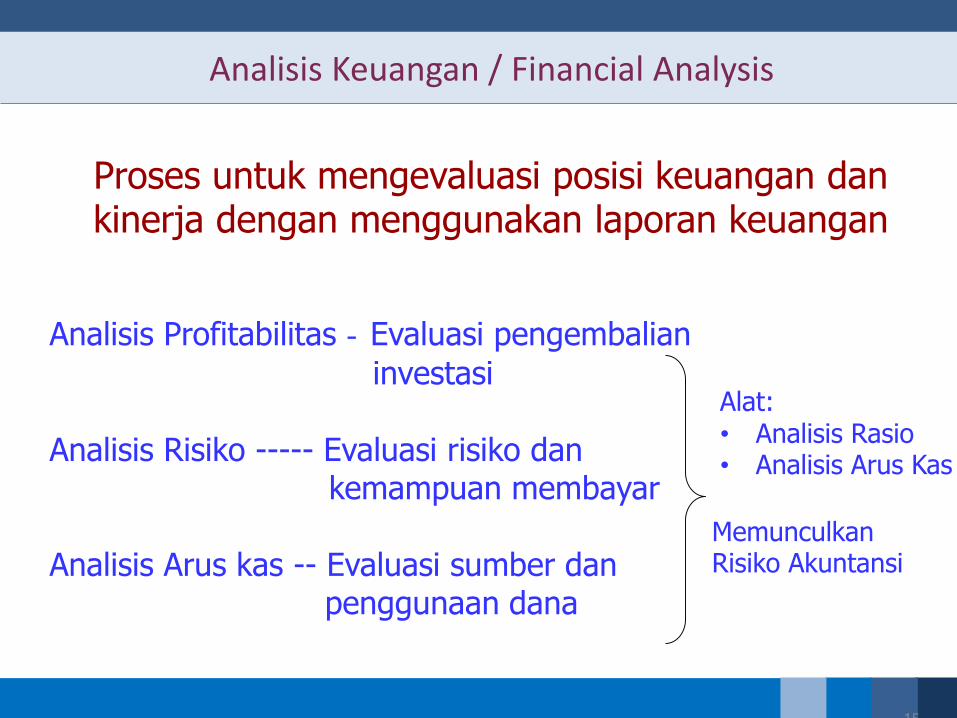

Analisis Keuangan / Financial Analysis

Analisis Profitabilitas - Evaluasi pengembalian

investasi

Analisis Risiko ----- Evaluasi risiko dankemampuan membayar

Analisis Arus kas -- Evaluasi sumber danpenggunaan dana

Alat:• Analisis Rasio• Analisis Arus Kas

MemunculkanRisiko Akuntansi

Proses untuk mengevaluasi posisi keuangan dan kinerja dengan menggunakan laporan keuangan

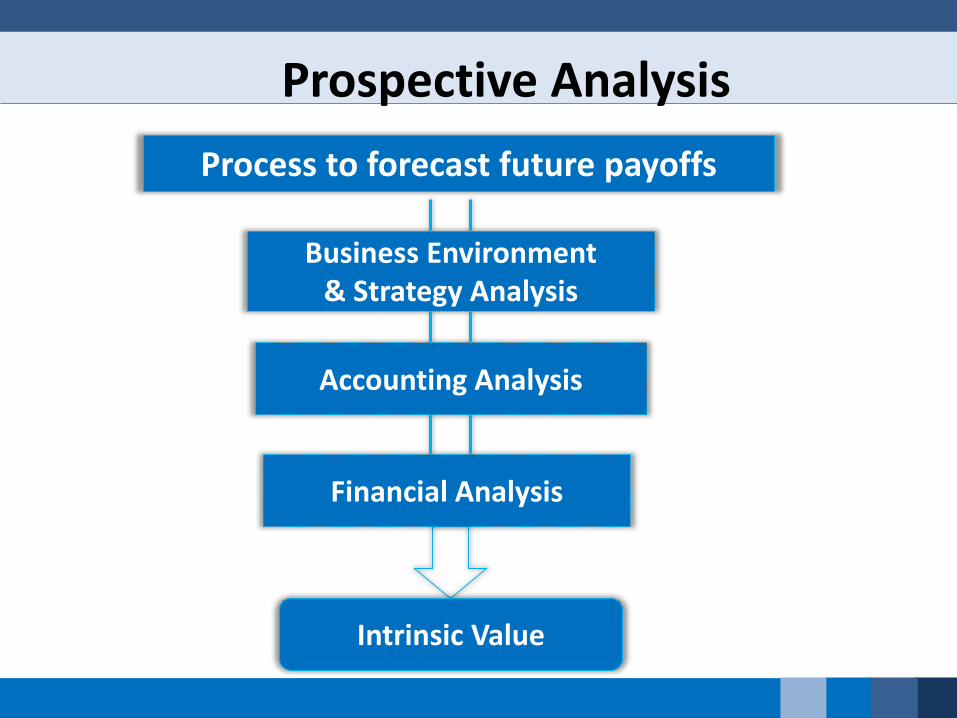

Prospective Analysis

Intrinsic Value

Business Environment& Strategy Analysis

Accounting Analysis

Financial Analysis

Process to forecast future payoffs

Dynamics of Business Activities

End of period

Beginning of period

Business Activities Time

Investing

Operating

FinancingPlanning

Planning

FinancingInvesting

Business Activities

Planning Activities:

Goals& Objectives

Competition Pricing

Market demands Tactics

Promotion

Managerial performance

Opportunities

Projections

Distribution

Obstacles

Business Activities

Financing

Financing activities

• Owner (equity)

• Nonowner (liabilities)

Investing activities

• Buying resources

• Selling resources

Investing = Financing

Investing

PlanningActivitiesInvesting

Activities

FinancialActivities

Operating ActivitiesRevenues and expenses from providing

goods and services

Business Activities

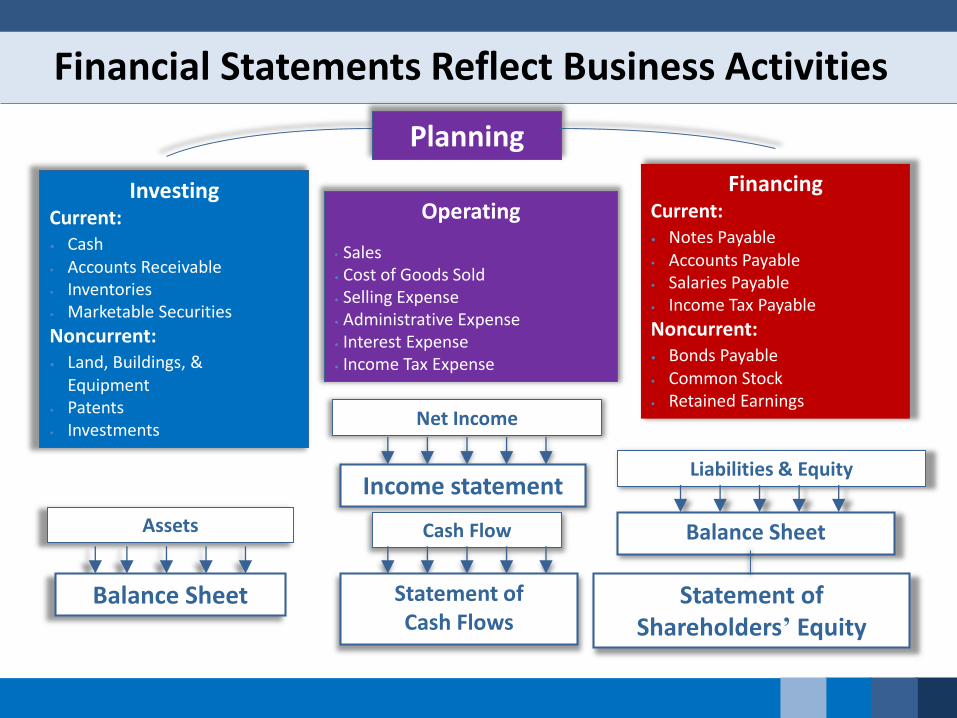

Financial Statements Reflect Business Activities

Planning

InvestingCurrent:• Cash• Accounts Receivable• Inventories• Marketable Securities

Noncurrent:• Land, Buildings, &

Equipment• Patents• Investments

Assets

Balance Sheet

FinancingCurrent:• Notes Payable• Accounts Payable• Salaries Payable• Income Tax Payable

Noncurrent:• Bonds Payable• Common Stock• Retained Earnings

Liabilities & Equity

Balance Sheet

Statement of Shareholders’ Equity

Operating

• Sales• Cost of Goods Sold• Selling Expense• Administrative Expense• Interest Expense• Income Tax Expense

Net Income

Income statement

Cash Flow

Statement of Cash Flows

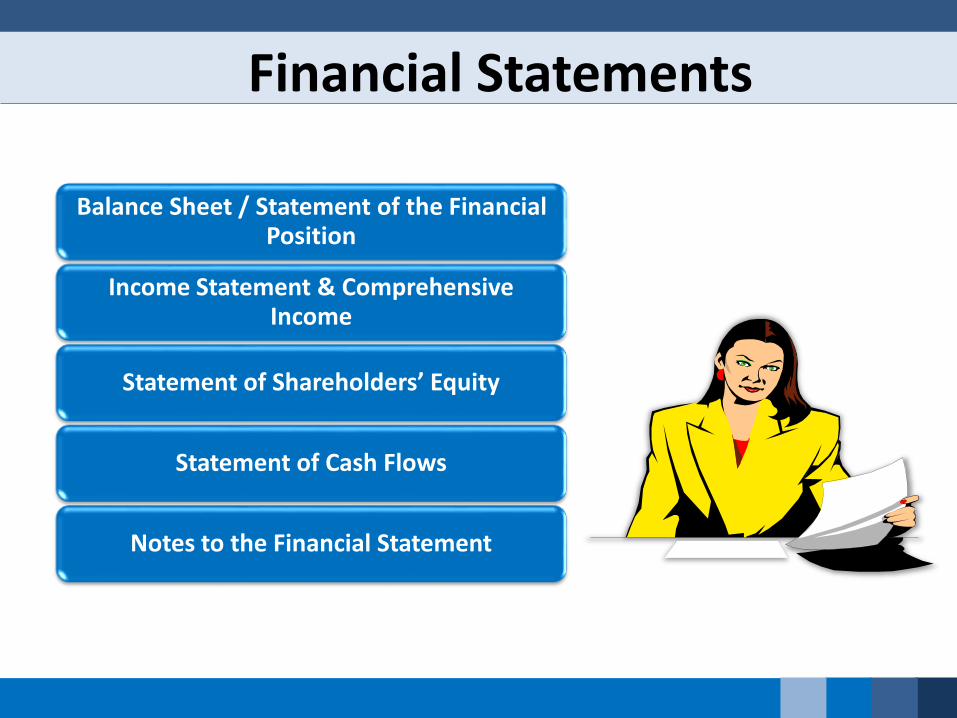

Financial Statements

Balance Sheet / Statement of the Financial Position

Income Statement & Comprehensive Income

Statement of Shareholders’ Equity

Statement of Cash Flows

Notes to the Financial Statement

1-23

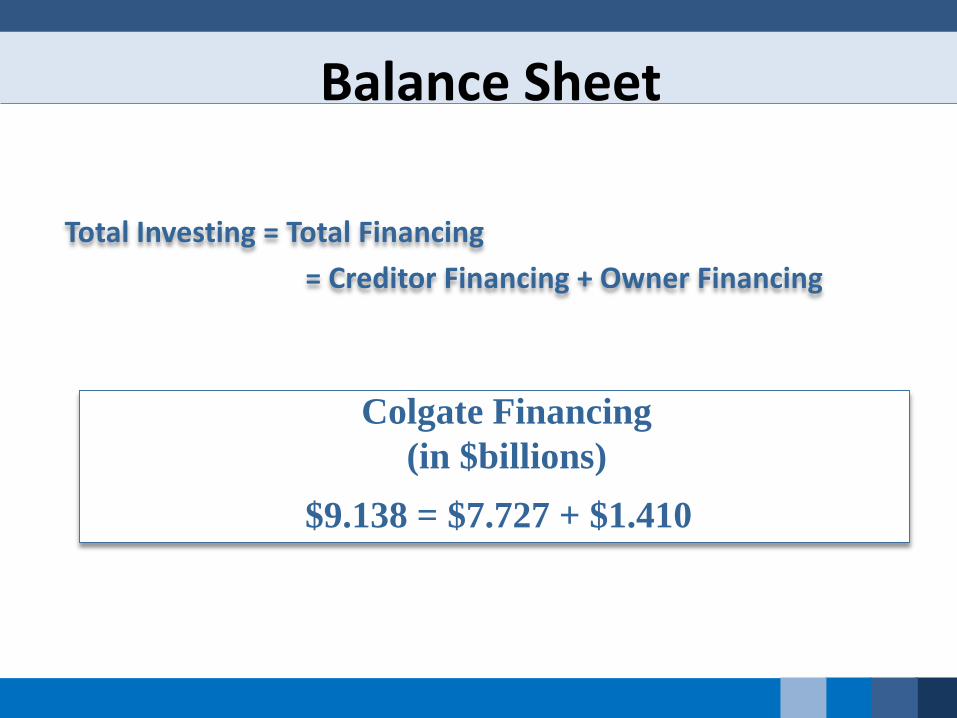

Balance Sheet

Total Investing = Total Financing

= Creditor Financing + Owner Financing

Colgate Financing

(in $billions)

$9.138 = $7.727 + $1.410

1-25

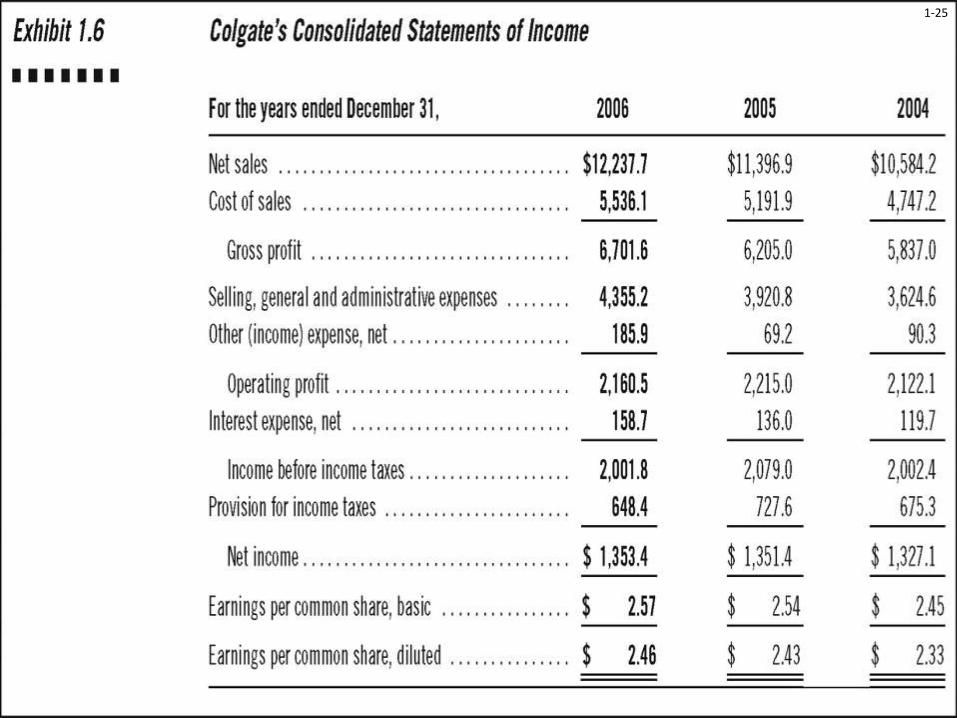

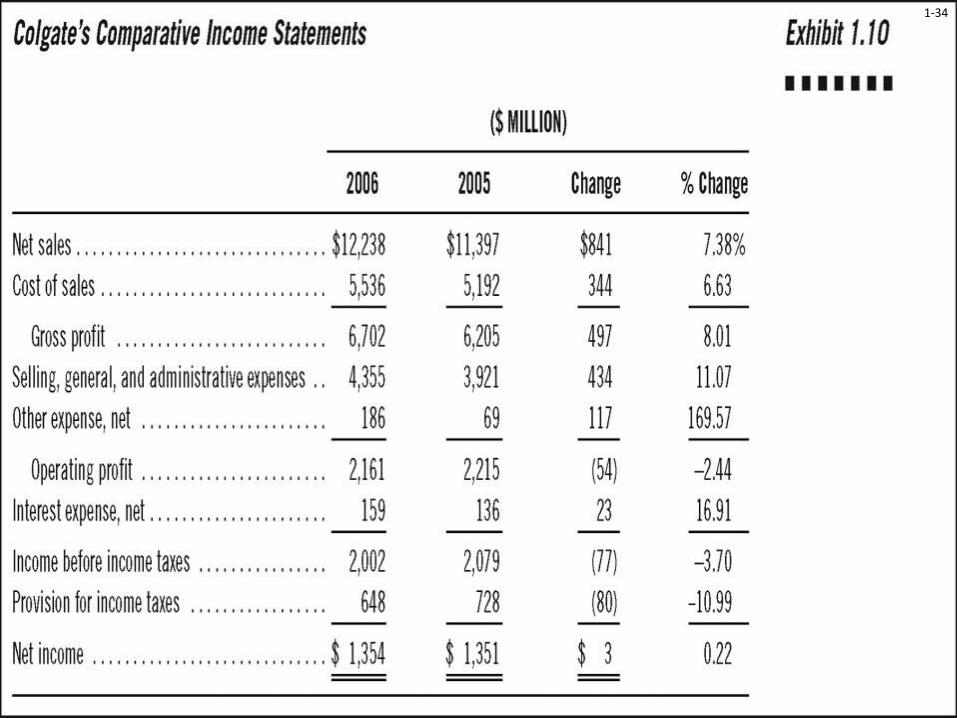

Income Statement

Revenues – Cost of goods sold = Gross Profit

Gross profit – Operating expenses = Operating Profit

Colgate’s Profitability

(in $billions)

$12.238 - $5.536 = $6.701 Gross Profit

$6.701 - $4.5411 = $2.160 Operating profit

Ilustrasi Penerapan PSAK 1 R2013

27Referensi : Laporan Tahunan BP 2014

Ilustrasi Penerapan PSAK 1 R2013

28

Referensi : Laporan Tahunan BP 2014

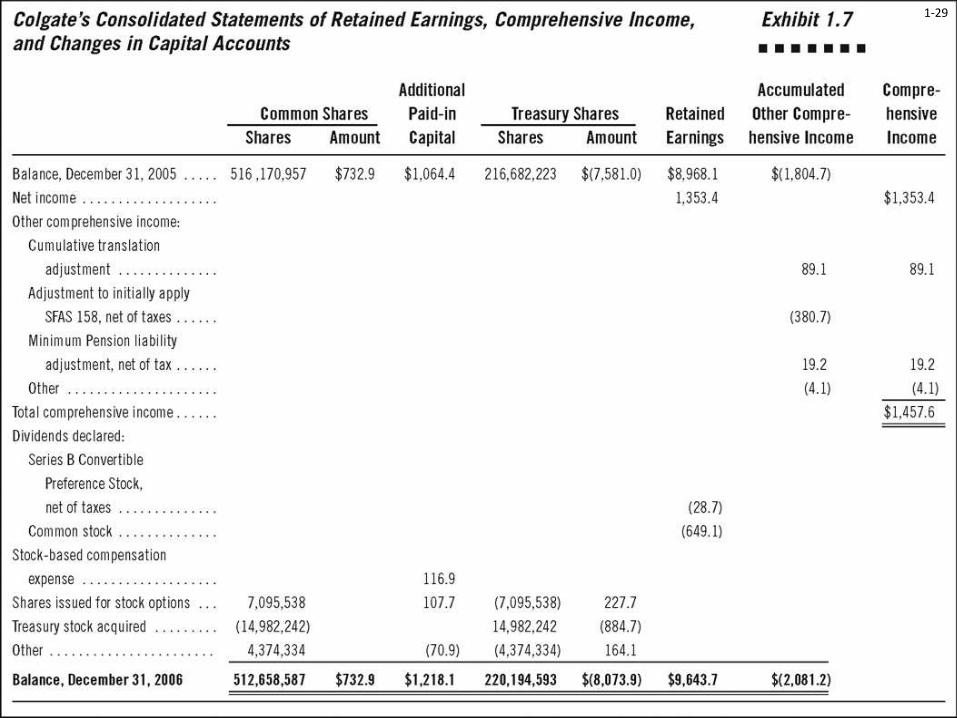

1-29

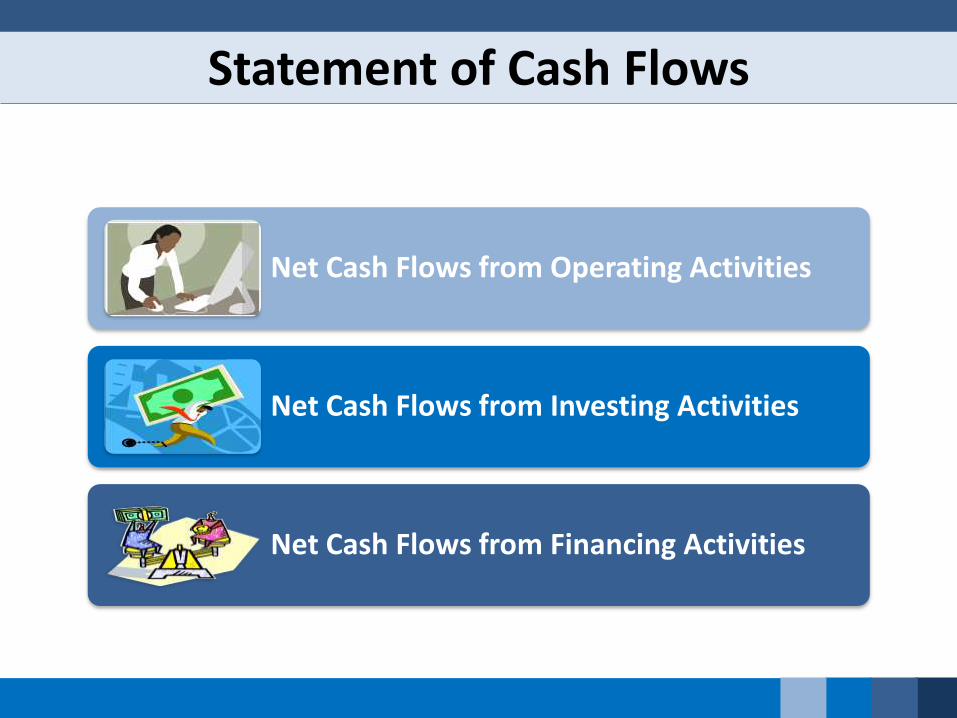

Statement of Cash Flows

Net Cash Flows from Operating Activities

Net Cash Flows from Investing Activities

Net Cash Flows from Financing Activities

1-31

Additional Information (Beyond Financial Statements)

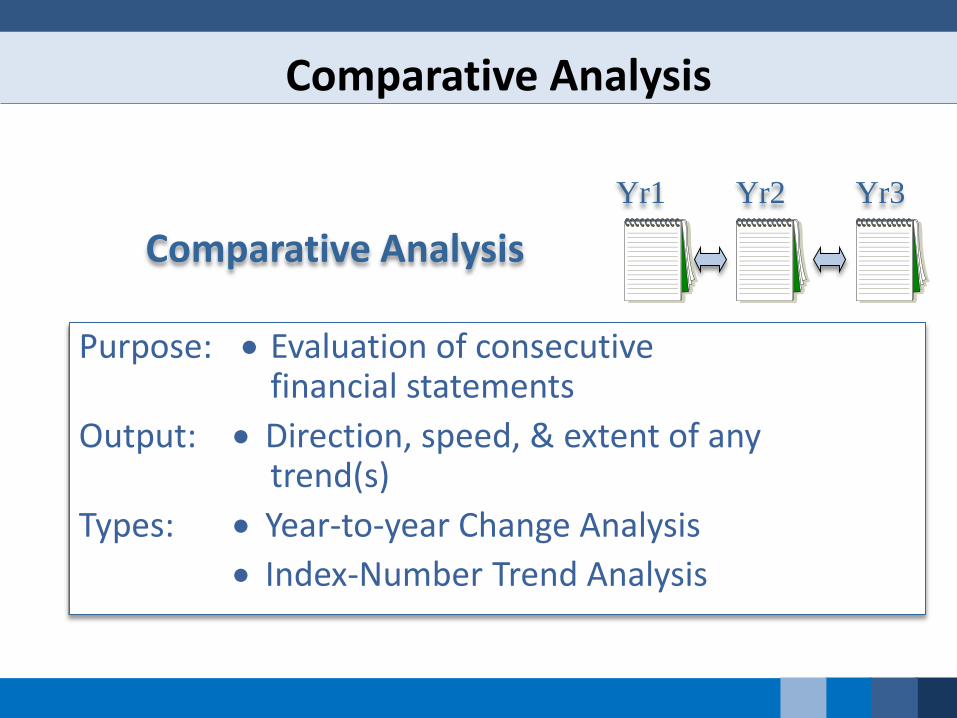

Comparative Analysis

Purpose: Evaluation of consecutive financial statements

Output: Direction, speed, & extent of any trend(s)

Types: Year-to-year Change Analysis

Index-Number Trend Analysis

Comparative Analysis

Yr2Yr1 Yr3

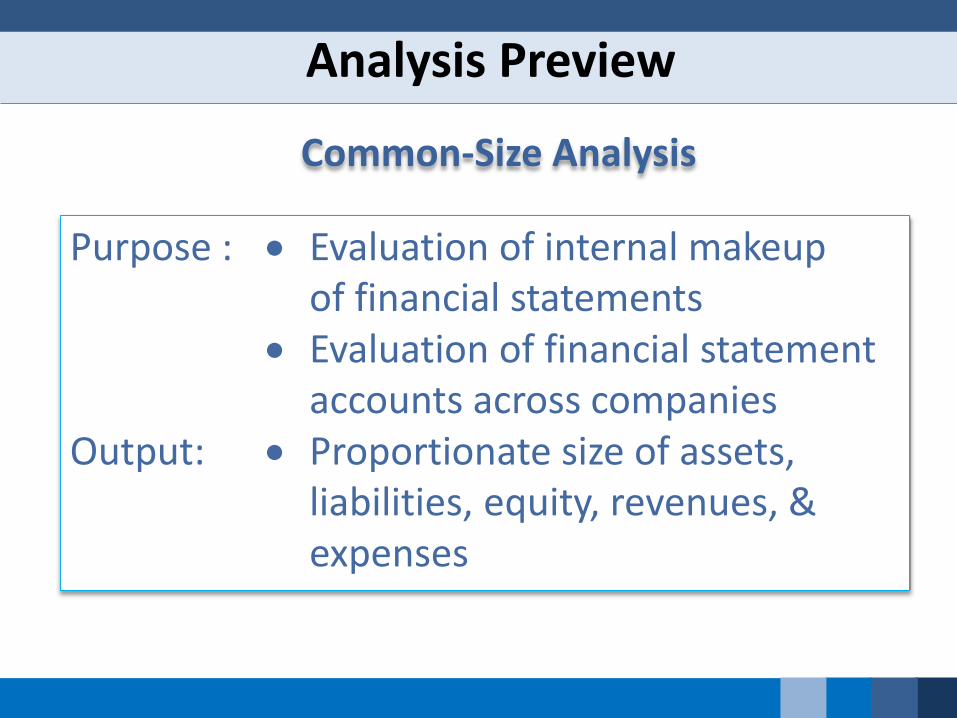

Analysis Preview

1-34

Analysis Preview

Purpose : Evaluation of internal makeupof financial statements

Evaluation of financial statement accounts across companies

Output: Proportionate size of assets, liabilities, equity, revenues, & expenses

Common-Size Analysis

Analysis Preview

Analysis Preview

Ratio Analysis

Purpose : Evaluate relation between two or more economically important items (one starting point for further analysis)

Output: Mathematical expression of relation between two or more items

Cautions: Prior Accounting analysis is important

Interpretation is key - long vs short term & benchmarking

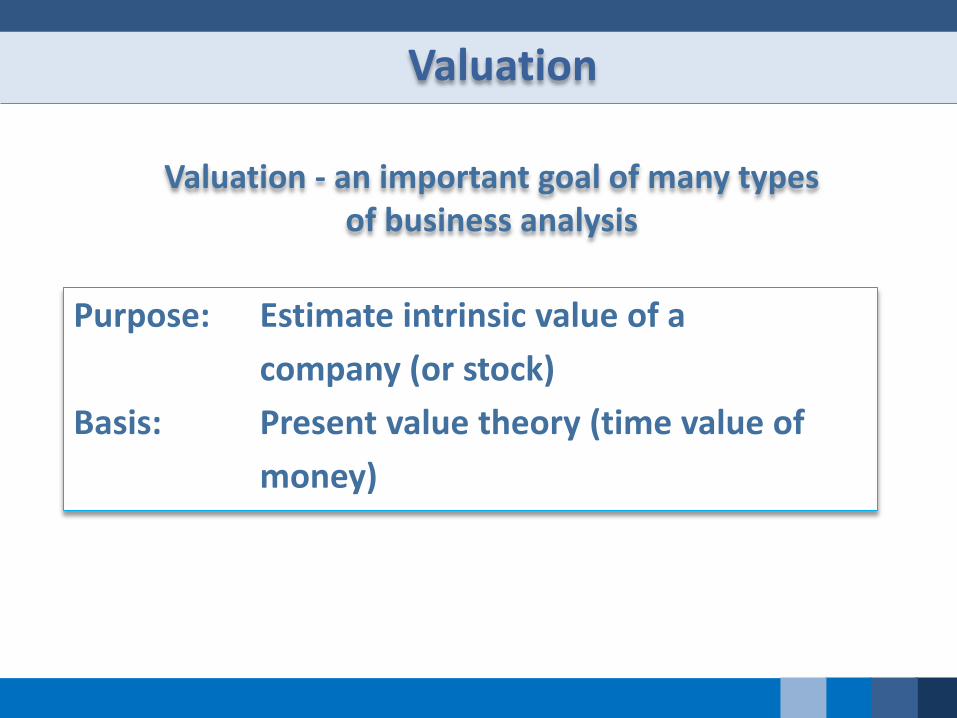

Purpose: Estimate intrinsic value of a

company (or stock)

Basis: Present value theory (time value of

money)

Valuation

Valuation - an important goal of many types of business analysis

Debt (Bond) Valuation

Bt is the value of the bond at time tIt +n is the interest payment in period t+nF is the principal payment (usually the debt’s face value)r is the investor’s required interest rate (yield to maturity)

Equity Valuation

Vt is the value of an equity security at time tDt +n is the dividend in period t+nk is the cost of capitalE refers to expected dividends

Equity Valuation - Free Cash Flow to Equity Model

FCFt+n is the free cash flow in the period t + n [often defined as cash flow from operations less capital expenditures]

k is the cost of capitalE refers to an expectation

Equity Valuation - Residual Income Model

BVt is the book value at the end of period tRit+n is the residual income in period t + n [defined as

net income, NI, minus a charge on beginning book value, BV, or RIt = NIt - (k x BVt-1)]

k is the cost of capitalE refers to an expectation

Analysis in an Efficient Market

Tiga asumsi bentuk pasar efisien

Weak Form - prices reflect information in past prices

Semi-strong Form - prices reflect all public

Form information

Strong Form - prices reflect all public and private information

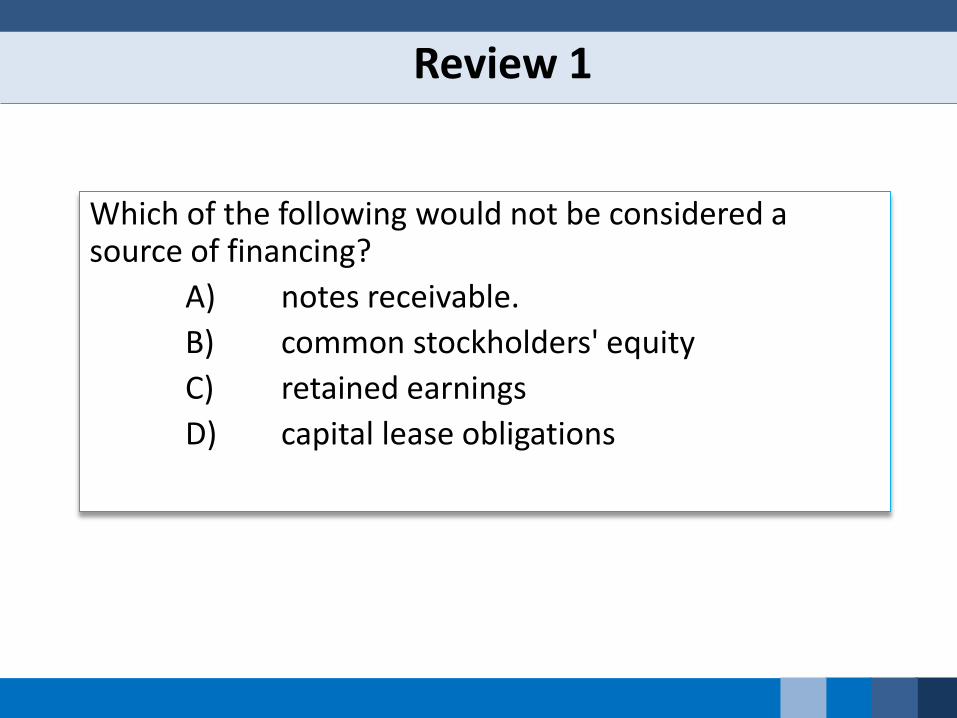

Review 1

Which of the following would not be considered a source of financing?

A) notes receivable.

B) common stockholders' equity

C) retained earnings

D) capital lease obligations

Review 2

Which of the following would not be considered a source of financing?

A) notes receivable

B) common stockholders' equity

C) retained earnings

D) capital lease obligations

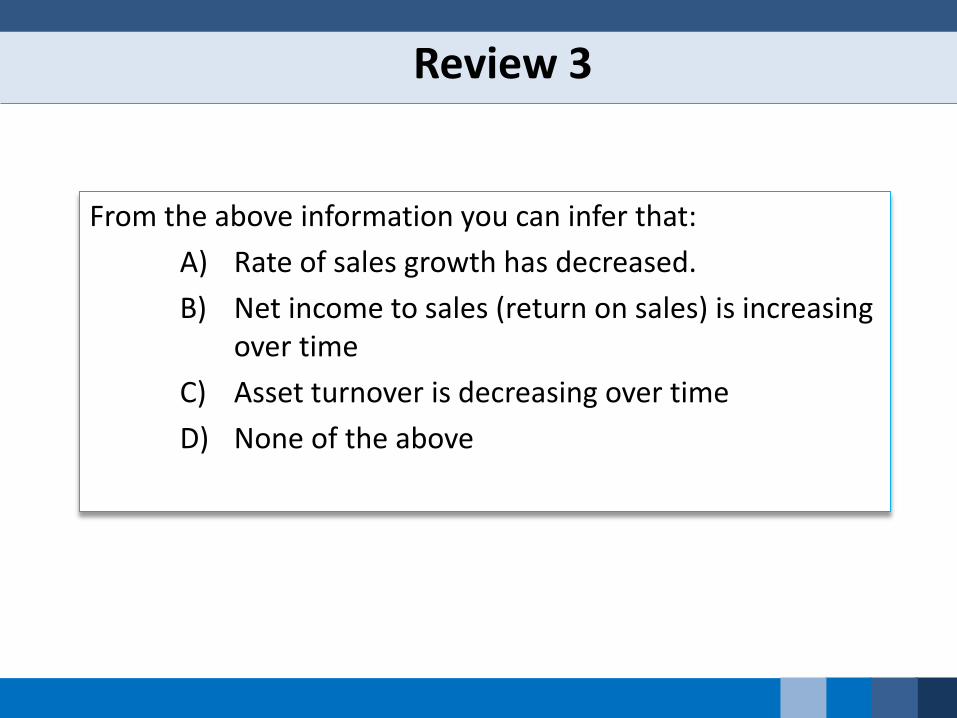

Review 3

From the above information you can infer that:

A) Rate of sales growth has decreased.

B) Net income to sales (return on sales) is increasing over time

C) Asset turnover is decreasing over time

D) None of the above

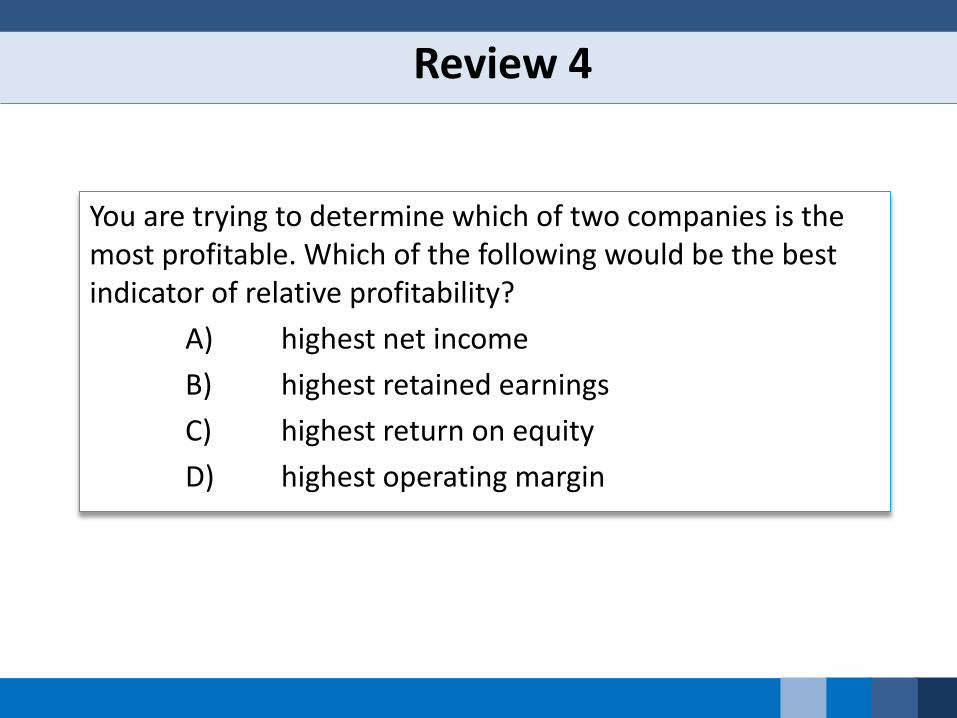

Review 4

You are trying to determine which of two companies is the most profitable. Which of the following would be the best indicator of relative profitability?

A) highest net income

B) highest retained earnings

C) highest return on equity

D) highest operating margin

Review 5

Wilco Company reports the following:

2005 2004

Retained Earnings $2,000,000 $ 1,300,000

Common Stock $ 500,000 $ 500,000

Paid-in Capital $3,000,000 $ 3,000,000

Net Income for year $ 900,000 $ 400,000

Dividend payout ratio for 2005 was:

A) 27%

B) 12%

C) 22.2%.

D) Not determinable

Review 6

Which of the following statements concerning financial ratios is incorrect?

A) accounting principles and methods used by a company will not affect financial ratios.

B) the informational value of a ratio in isolation is limited

C) a ratio is one number expressed as a percentage or fraction of another number

D) calculation of financial ratios is not sufficient for a complete financial analysis of a company

Review 7

Liquidity of a company is generally defined as a measure of:

A) the ability of a company to pay its employees in a timely manner

B) the ability to pay interest and principal on all debt

C) the ability to pay dividends

D) the ability to pay current liabilities.

Review 8

Which of the following statistics would be the most useful in determining the efficiency of a car rental company?

A) inventory turnover

B) number of employees per car rental

C) average length of car rental

D) number of days cars rented as percentage of number of days available for rent.

Review 9

Fluno Corporation has 1M shares outstanding at the end offiscal 2005. Its stock is trading at $15 per share. It issued$0.6M in dividends, and had net income of $1M in fiscal 2005.At the end of 2000 its total assets, liabilities and retainedearnings were $25M, $15M and $7.5M, respectively. Fluno'sprice to book ratio and dividend yield ratios for 2005 are:

Price to Book Dividend Yield

A) 2 60%

B) 1.5 60%

C). 1.5 4%

D) 2 4%

Review 10

Urban Company has 5M shares outstanding and issueddividends of $1 per share in fiscal 2005. Dividends areexpected to grow at a rate of 6% per annum in perpetuity.Urban's cost of equity is 10%. What is the implicit value ofUrban Company at the end of 2005?

A) $50M

B) $53M

C) $125M

D) $132.5M.

TERIMA KASIH

Tempat kamiMengabdi untuk

Negeri

Copyright © 2022 FDOKUMEN