Buku Peluang Investasi

25

MARINE AND FISHERIES INVESTMENT OPPORTUNITIES IN CENTRAL SULAWESI PELUANG INVESTASI KELAUTAN-PERIKANAN DI SULAWESI TENGAH Marine Affairs and Fisheries Service Province of Central Sulawesi Undata St. #7, Telp. +62 451 429379 Fax. +62 451 421560, Palu 94111 Indonesia Email: [email protected] Website: www.dkp.sulteng.go.id Dinas Kelautan dan Perikanan Daerah Provinsi Sulawesi Tengah Jl. Undata No. 7 Telp. (0451) 429379 Fax. (0451) 421560, Palu 94111 Email: [email protected] Website: www.dkp.sulteng.go.id

Transcript of Buku Peluang Investasi

MARINE AND FISHERIES INVESTMENT OPPORTUNITIES IN CENTRAL SULAWESI

PELUANG INVESTASI KELAUTAN-PERIKANAN DI SULAWESI TENGAH

Marine Affairs and Fisheries Service Province of Central Sulawesi

Undata St. #7, Telp. +62 451 429379 Fax. +62 451 421560, Palu 94111 IndonesiaEmail: [email protected] Website: www.dkp.sulteng.go.id

Dinas Kelautan dan Perikanan DaerahProvinsi Sulawesi Tengah

Jl. Undata No. 7 Telp. (0451) 429379 Fax. (0451) 421560, Palu 94111Email: [email protected] Website: www.dkp.sulteng.go.id

Pengantar

Provinsi Sulawesi Tengah mempunyai potensi yang

besar untuk sektor kelautan dan perikanan. Sejalan

dengan Visi Gubernur Sulawesi Tengah 2011-2016,

maka sektor kelautan dan perikanan merupakan

salah satu sektor unggulan yang akan

dikembangkan. Pemerintah Sulawesi Tengah

bersama dengan Pemerintah Kabupaten/Kota

akan berupaya memberikan kebijakan yang dapat

menciptakan iklim investasi yang baik, penyiapan

sarana prasarana dasar, kemudahan akses modal,

aspek perijinan, insentif pajak dan jaminan

berusaha yang kondusif bagi pelaku usaha.

Semoga buku kecil ini dapat memberikan

gambaran tentang arah pembangunan termasuk

peluang investasi kelautan dan perikanan di

Sulawesi Tengah.

Kepala Dinas Kelautan dan Perikanan Daerah

Provinsi Sulawesi Tengah

DR. Ir. Hasanuddin Atjo, MP

Central Sulawesi province has a great potential for Marine

and Fisheries Sector. In line with the vision of the Governor

of Central Sulawesi 2011-2016, the Marine and Fisheries

Sector is one of the leading sectors to be developed. The

government of Central Sulawesi, along with the the

government of District/City will seek to provide policies

that can create a favorable investment climate,

preparation of basic infrastructure, ease of access to

capital, aspects of licensing, tax incentives and sought

assurance that is conducive to business. Hopefully this

booklet can give you an idea of the policy of development

of marine and fisheries, including investment

opportunities in Central Sulawesi.

Head of the Regional Marine Affairs and Fisheries Service

Central Sulawesi Province

DR. Ir. Hasanuddin Atjo, MP

Preface

Gambaran Umum Provinsi

Sulawesi Tengah

Gambaran Umum Provinsi

Sulawesi Tengah

An Overview of

Central Sulawesi Province

An Overview of

Central Sulawesi Province

DAFTAR ISIDAFTAR ISI

OVERVIEWOVERVIEW

CONTENTSCONTENTS

INVESTMENT REGULATIONS IN CENTRAL SULAWESIINVESTMENT REGULATIONS IN CENTRAL SULAWESI

STRATEGIC COMMODITY DEVELOPMENT STRATEGYSTRATEGIC COMMODITY DEVELOPMENT STRATEGY

CONCLUSIONCONCLUSION

1

GAMBARAN UMUMGAMBARAN UMUM

STRATEGI PENGEMBANGAN KOMODITI UNGGULANSTRATEGI PENGEMBANGAN KOMODITI UNGGULAN

PENUTUPPENUTUP

REGULASI TERKAIT INVESTASI DI SULAWESI TENGAHREGULASI TERKAIT INVESTASI DI SULAWESI TENGAH

0101

1616

4444

1212

2525

DUKUNGAN INFRASTRUKTUR TERHADAP

KAWASAN INDUSTRI PALU (KIP)

DUKUNGAN INFRASTRUKTUR TERHADAP

KAWASAN INDUSTRI PALU (KIP)

3333

0101

1616

4444

1212

2525

3333

KAWASAN EKONOMI KHUSUS INDONESIA (KEKI)

DI KOTA PALU

KAWASAN EKONOMI KHUSUS INDONESIA (KEKI)

DI KOTA PALU

INDONESIAN SPECIAL ECONOMIC ZONE (KEKI)

IN PALU CITY

INDONESIAN SPECIAL ECONOMIC ZONE (KEKI)

IN PALU CITY

SUPPORTING INFRASTRUCTURE FOR THE

PALU INDUSTRIAL ZONE (KIP)

SUPPORTING INFRASTRUCTURE FOR THE

PALU INDUSTRIAL ZONE (KIP)

Kemiringan Lahan(Slope Of The Land)

Ketinggian dari Permukaan Laut(Plains From Sea Level)

0 - 3° ≈11,8%;

3 - 15° ≈ 8,9 %:

15 - 40 19,9 %;° ≈

> 40° ≈ 59,9 %

0 m - 100 m ≈ 20,2 % ;

101 m – 500 m ≈ 27,2 %;

501 m - 1.000 m ≈ 26,7%;

> 1.001 m ≈ 25,9%

Characteristics and Regional Economics

a. Luas dan Batas Wilayah Administrasi

Provinsi Sulawesi Tengah terletak di bagian tengah Pulau Sulawesi. Luas wilayah 63.305 Km2 atau 6.330.466,82 Ha. Luas wilayah daratan tersebut adalah 36,47 persen dari luas Pulau Sulawesi. Luas perairan laut Sulawesi Tengah mencapai 193.923,75 Km2 dengan jumlah pulau sebanyak 1.402 pulau. Batas-batas wilayah provinsi ini sebagai berikut:

- Sebelah Utara berbatasan dengan Laut Sulawesi dan Provinsi Gorontalo;

- Sebelah Timur berbatasan dengan Propinsi Maluku dan Maluku Utara;

- Sebelah Selatan berbatasan dengan Propinsi Sulawesi Selatan dan Propinsi Sulawesi Tenggara;

- Sebelah Barat berbatasan dengan Selat Makassar dan Propinsi Sulawesi Barat.

Berdasarkan administrasi, hingga tahun 2010 Provinsi Sulawesi Tengah terdiri atas 10 Kabupaten dan 1 Kota; meliputi Kabupaten Donggala, Poso, Tolitoli, Banggai, Buol, Morowali, Parigi Moutong, Banggai Kepulauan, Tojo Una-Una, Sigi dan Kota Palu; terdiri atas 155 Kecamatan, 159 Kelurahan dan 1.656 Desa. Jumlah Penduduk tahun 2010 sebanyak 2.635.009 jiwa.

Central Sulawesi Province is located in the central part of Sulawesi Island. The land area 6,330,466.82 hectares or 63,305 km2 or 36.47% of the broad ¬ island of Sulawesi. Waters areas of Central Sulawesi reached 193,923.75 km2 with a number of islands as much as 1402. The boundaries of this province as follows:

- North Side : The Celebes Sea and the Province of Gorontalo;

- East Side : Province of Maluku and North Maluku;

- South Side : Province of South Sulawesi and Southeast Sulawesi;

- West Side : The Strait of Makassar and West Sulawesi Province.

In the administration, until the year 2010 in Central Sulawesi Province comprises 10 districts and 1 city, those are the districts of Donggala, Poso, Tolitoli, Banggai, Buol, Morowali, Parigi Moutong, Banggai Islands, Tojo Una-Una, Sigi and Palu City; consisting of 155 municipality, 159 kelurahan (village level) and 1.656 village. Population in 2010 as much as 2.635.009 people.

(Area and Administrative Boundaries)

Karakteristik dan Ekonomi Wilayah b. Letak Geografis

2°22' Lintang Utara (North Latitude) dan 3°48' Lintang Selatan (South Latitude) serta 119°22' dan 124°22' Bujur Timur

(East Latitude).

(Geography)

d. Geologi

Struktur dan Karakteristik geologi wilayah Sulawesi Tengah didominasi oleh bentangan pegunungan dan dataran

tinggi. Pada wilayah Kabupaten Buol dan Tolitoli, terdapat deretan pegunungan yang berangkai ke jajaran

pegunungan di Provinsi Sulawesi Utara. Di tengah wilayah Sulawesi Tengah; yaitu Kabupaten Donggala dan Parigi

Moutong; terdapat tanah genting yang diapit oleh Selat Makassar dan Teluk Tomini. Sebagian besar merupakan

daerah pegunungan dan perbukitan. Di selatan dan timur yang mencakup wilayah Kabupaten Poso, Tojo Una Una,

Morowali dan Banggai, berjajar pegunungan seperti Pegunungan Tokolekayu, Verbeek, Tineba, Pampangeo,

Fennema, Balingara, dan Batui. Sebagian besar dari daerah pegunungan itu mempunyai lereng yang terjal dengan

kemiringan di atas 45 derajat.

c. Topografi (Topography)

2 3

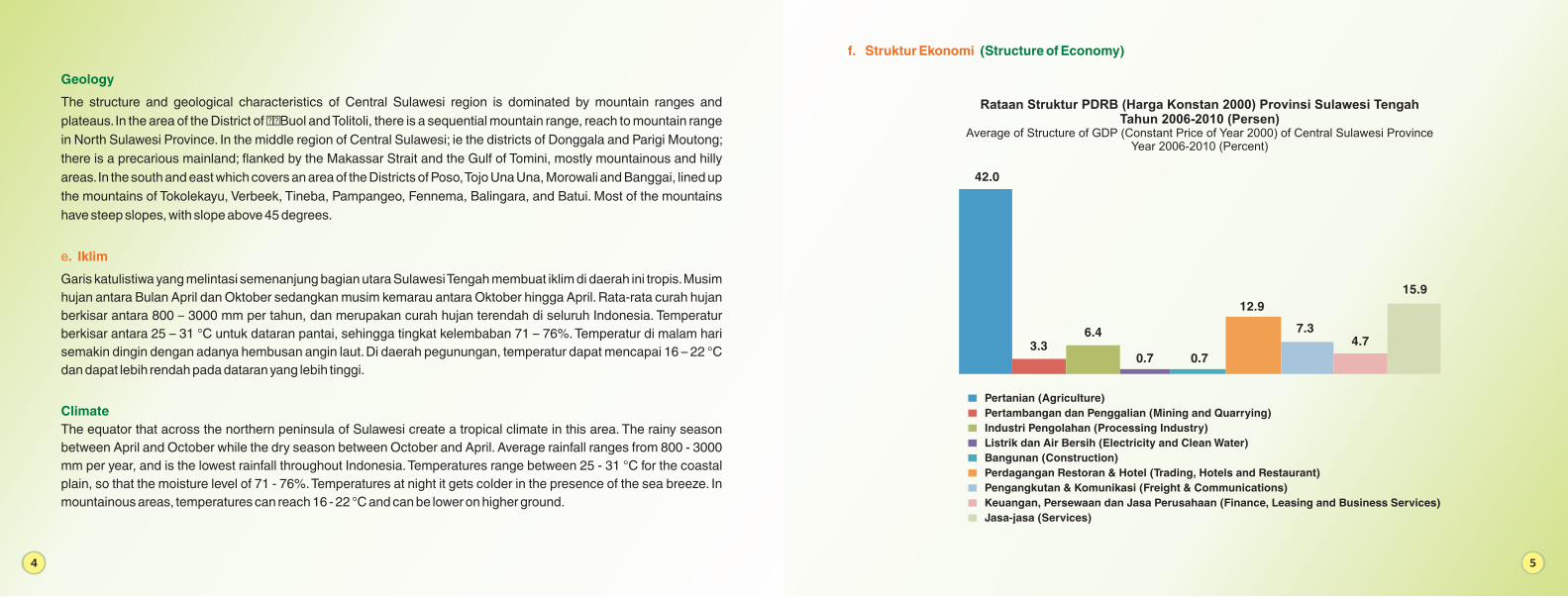

Rataan Struktur PDRB (Harga Konstan 2000) Provinsi Sulawesi Tengah Tahun 2006-2010 (Persen)

Average of Structure of GDP (Constant Price of Year 2000) of Central Sulawesi ProvinceYear 2006-2010 (Percent)

f. Struktur Ekonomi (Structure of Economy)

Geology

Climate

The structure and geological characteristics of Central Sulawesi region is dominated by mountain ranges and

plateaus. In the area of the District of ??Buol and Tolitoli, there is a sequential mountain range, reach to mountain range

in North Sulawesi Province. In the middle region of Central Sulawesi; ie the districts of Donggala and Parigi Moutong;

there is a precarious mainland; flanked by the Makassar Strait and the Gulf of Tomini, mostly mountainous and hilly

areas. In the south and east which covers an area of the Districts of Poso, Tojo Una Una, Morowali and Banggai, lined up

the mountains of Tokolekayu, Verbeek, Tineba, Pampangeo, Fennema, Balingara, and Batui. Most of the mountains

have steep slopes, with slope above 45 degrees.

Garis katulistiwa yang melintasi semenanjung bagian utara Sulawesi Tengah membuat iklim di daerah ini tropis. Musim

hujan antara Bulan April dan Oktober sedangkan musim kemarau antara Oktober hingga April. Rata-rata curah hujan

berkisar antara 800 – 3000 mm per tahun, dan merupakan curah hujan terendah di seluruh Indonesia. Temperatur

berkisar antara 25 – 31 °C untuk dataran pantai, sehingga tingkat kelembaban 71 – 76%. Temperatur di malam hari

semakin dingin dengan adanya hembusan angin laut. Di daerah pegunungan, temperatur dapat mencapai 16 – 22 °C

dan dapat lebih rendah pada dataran yang lebih tinggi.

The equator that across the northern peninsula of Sulawesi create a tropical climate in this area. The rainy season

between April and October while the dry season between October and April. Average rainfall ranges from 800 - 3000

mm per year, and is the lowest rainfall throughout Indonesia. Temperatures range between 25 - 31 °C for the coastal

plain, so that the moisture level of 71 - 76%. Temperatures at night it gets colder in the presence of the sea breeze. In

mountainous areas, temperatures can reach 16 - 22 °C and can be lower on higher ground.

e. Iklim

4 5

42.0

3.3 6.4

0.7

12.9

7.3 4.7

15.9

0.7

Pertanian (Agriculture)

Pertambangan dan Penggalian (Mining and Quarrying)

Industri Pengolahan (Processing Industry)

Listrik dan Air Bersih (Electricity and Clean Water)

Bangunan (Construction)

Perdagangan Restoran & Hotel (Trading, Hotels and Restaurant)

Pengangkutan & Komunikasi (Freight & Communications)

Keuangan, Persewaan dan Jasa Perusahaan (Finance, Leasing and Business Services)

Jasa-jasa (Services)

Grafik Trend Pertumbuhan Ekonomi Sulawesi Tengah Tahun 2006 - 2010

Trend Graph of Economic Growth in Central Sulawesi Year 2006 - 2010

Potensi Perikanan Tangkap

• Nelayan

• Selat Makassar Laut Sulawesi

• Teluk Tomini

• Teluk Tolo

TOTAL

&

: 444.954 jiwa

: 120.000 ton/tahun

: 174.000 ton/tahun

: 114.000 ton/tahun

: 408.000 ton/tahun

KOTA (PALU City)

PALU

KAB. BANGGAI (BANGGAI District)

KAB.(TOLITOLI District)

TOLITOLI

KAB. PARIMO (PARIMO District)

KAB. (DONGGALA District)

DONGGALA

KAB. POSO (POSO District)

KAB. BANGKEP (BANGKEP District)

KAB. TOUNA (TOUNA District)

KAB. MOROWALI(MOROWALI District)

KAB. BUOL (BUOL District)

KAB. SIGI (SIGI District)

TOGIANISLAND

• Tambak (Brackish-water ponds)• Mariculture • Seaweed Farming • Freshwater ponds • Freshwater bodies 1. Coast Line 2. Lakes 3. Rivers and Marshes

Aquaculture Resources

: 42.095 ha : 146.468 ha: 106.468 ha *: 11.740 ha : 4.013 km: 37.028 ha : 1.639.605 ha

: 444.954

: 120.000 tons/year

: 174.000 tons/year

: 114.000 tons/year

408.000 tons/year

• Fisherman

• Makassar Straits & Sulawesi Sea

• Tomini Bay

• Tolo Bay

TOTAL :

Capture Fisheries

POTENSI SUMBERDAYA ALAMNATURAL RESOURCES

Potensi Perikanan Budidaya

: 56.956 jiwa

: 42.095 ha

: 146.468 ha

: 106.468 ha *

: 11.740 ha

: 4.013 km

: 37.028 ha

: 1.639.605 ha

•

• Budidaya Tambak

• Budidaya Laut

Khusus Rumput Laut

• Budidaya Kolam

• Perairan Umum

1. Garis Pantai

2. Danau

3. Sungai dan Rawa

Pembudidaya

6 7

8.10

8.00

7.90

7.80

7.70

7.60

7.50

7.40

7.30

7.20

2006 2007 2008 2009 2010

7,82%

7,99%

7,78%

7,51%

7,79%

0

50

100

150

200

tropical

temperate

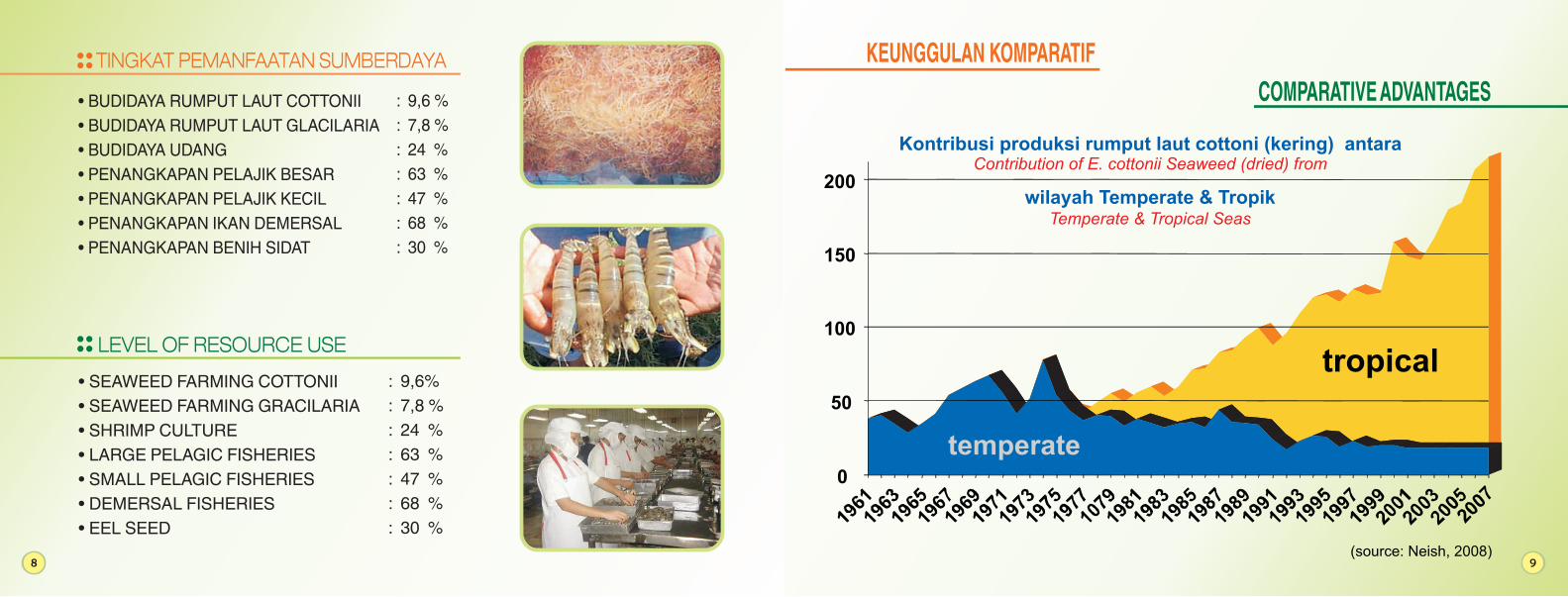

Kontribusi produksi rumput laut cottoni (kering) antara

wilayah Temperate & Tropik

(source: Neish, 2008)

KEUNGGULAN KOMPARATIF

Contribution of E. cottonii Seaweed (dried) from

Temperate & Tropical Seas

COMPARATIVE ADVANTAGES• BUDIDAYA RUMPUT LAUT COTTONII

• BUDIDAYA RUMPUT LAUT GLACILARIA

• BUDIDAYA UDANG

• PENANGKAPAN PELAJIK BESAR

• PENANGKAPAN PELAJIK KECIL

• PENANGKAPAN IKAN DEMERSAL

• PENANGKAPAN BENIH SIDAT

TINGKAT PEMANFAATAN SUMBERDAYA

• SEAWEED FARMING COTTONII

• SEAWEED FARMING GRACILARIA

• SHRIMP CULTURE

• LARGE PELAGIC FISHERIES

• SMALL PELAGIC FISHERIES

• DEMERSAL FISHERIES

• EEL SEED

: 9,6%

: 7,8 %

: 24 %

: 63 %

: 47 %

: 68 %

: 30 %

: 9,6 %

: 7,8 %

: 24 %

: 63 %

: 47 %

: 68 %

: 30 %

LEVEL OF RESOURCE USE

8 9

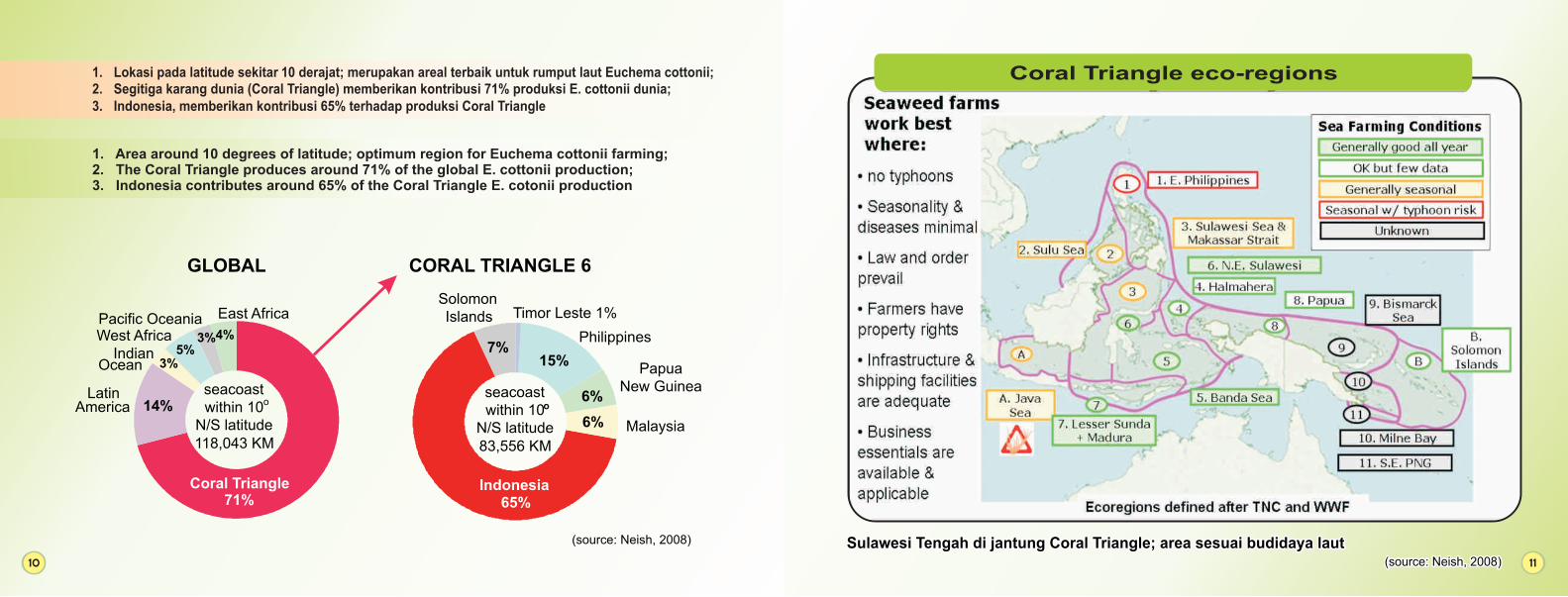

1. Lokasi pada latitude sekitar 10 derajat; merupakan areal terbaik untuk rumput laut Euchema cottonii;2. Segitiga karang dunia (Coral Triangle) memberikan kontribusi 71% produksi E. cottonii dunia;3. Indonesia, memberikan kontribusi 65% terhadap produksi Coral Triangle

Coral Triangle71%

LatinAmerica 14%

IndianOcean

West AfricaPacific Oceania East Africa

seacoastwithin 10o

N/S latitude118,043 KM

SolomonIslands

7%

Indonesia65%

Malaysia6%

PapuaNew Guinea

6%

Philippines

15%

Timor Leste 1%

seacoastwithin 10o

N/S latitude83,556 KM

5%3%

4%

GLOBAL CORAL TRIANGLE 6

(source: Neish, 2008)

1. Area around 10 degrees of latitude; optimum region for Euchema cottonii farming;2. The Coral Triangle produces around 71% of the global E. cottonii production;3. Indonesia contributes around 65% of the Coral Triangle E. cotonii production

3%

(source: Neish, 2008)(source: Neish, 2008)

Sulawesi Tengah di jantung Coral Triangle; area sesuai budidaya laut Sulawesi Tengah di jantung Coral Triangle; area sesuai budidaya laut

Coral Triangle eco-regions

10 11

1

2

3

4

5

6

KORIDOR SUMATRA

KORIDOR JAWA

KORIDOR KALIMANTAN

KORIDOR SULAWESI

KORIDOR BALI-NUSATENGGARA

SULAWESI PUSAT PRODUKSI DAN PENGOLAHAN

HASIL PERTANIAN, PERKEBUNAN, PERIKANAN,

NIKEL DAN PERTAMBANGAN NASIONAL

2011 - 2025

KORIDOR EKONOMI INDONESIA Master Plan Percepatan dan Perluasan Ekonomi Indonesia

INDONESIAN ECONOMIC CORRIDORS Master Plan for the Acceleration and Extension of Indonesian Economic Growth

1

2

3

4

5

6

SUMATRAN CORRIDOR

JAVANESE CORRIDOR

KALIMANTAN CORRIDOR

SULAWESI CORRIDOR

BALI-NUSATENGGARA CORRIDOR

FOKUS PENGEMBANGAN

SULAWESI AS A NATIONAL PRODUCTION

AND PROCESSING CENTRE

FOR AGRICULTURAL AND PLANTATION COMMODITIES,

FISHERIES, NICKEL AND OTHER MINING COMMODITIES

2011 - 2025

DEVELOPMENT FOCUS

Regulasi Terkait Investasi

di Sulawesi Tengah

Regulasi Terkait Investasi

di Sulawesi Tengah

Investment Regulations

in Central Sulawesi

Investment Regulations

in Central Sulawesi

12 13

KORIDOR PAPUA-MALUKU

PAPUA-MALUKU CORRIDOR

MISI1

2

3

4

5

SULAWESI TENGAH

DENGAN PROVINSI MAJU DI

KAWASAN TIMUR DALAM

PENGEMBANGAN

MELALUI PENINGKATAN

KUALITAS SUMBERDAYA

MANUSIA YANG

2020

SEJAJAR

AGRIBISNIS

DAN KELAUTAN

BERDAYA SAING

PADA TAHUN

VISIPeningkatan Kualitas SDM yang Berdaya Saing

Brdasarkan Keimanan Dan Ketaqwaan

Peningkatan Pertumbuhan Ekonomi Melalui

Pemberdayaan Ekonomi Kerakyatan

Peningkatan Pembangunan Infrastruktur

Percepatan Reformasi Reformasi Birokrasi,

Penegakan Supremasi Hukum dan HAM

Pengelolaan SDA Secara Optimal dan Berkelanjutan

VISI-MISI PROVINSI 2011-2016

MISION1

2

3

4

5

VISION

Central Sulawesi WITH DEVELOPED PROVINCES

IN EASTERN INDONESIA IN THE

THROUGH THE DEVELOPMENT OF

HUMAN RESOURCES

2020

ON A PAR

AGRIBUSINIS AND MARINE(FISHERIES) SECTORS

COMPETITIVE

by the year

Capacity building to develop competitive human resources based on integrity and (religious) moral standards

Accelerated Economic Growth through Empowerment of Grass-Roots Economy

Increased Infrastructure Development

Accelerated Administrative Reform, Enforcement of Legal Supremacy and Human Rights,

Optimal and Sustainable Management of Natural Resources

PROVINCIAL VISION-MISSION 2011-2016

1. Jaminan keamanan dan kepastian hukum dari pemerintah daerah

2. Lokasi usaha tersedia

3. Pelayanan Perizinan Sistem Satu Pintu (One roof service)

4. Biaya perizinan murah dan mudah

5. Pajak usaha dipungut setelah perusahaan berproduksi komersial

6. Jaminan hak guna usaha 30 tahun diupayakan menjadi 90 tahun oleh Pemerintah Daerah

7. Tersedia Tenaga kerja lokal yang produktif.

8. Mengupayakan berkoordinasi dengan Pemerintah Pusat bebas biaya impor mesin-mesin guna keperluan pabrik

9. Pemerintah Daerah berupaya menyiapkan jaminan adanya fasilitas listrik dan fasilitas lainnya ke lokasi perusahaan

10. Tersedianya Kawasan Industri Palu, Kawasan Pengembangan Ekonomi Terpadu (Kapet) Palapas dan Kawasan Ekonomi Khusus (KEK) Kota Palu.

SEPULUH KEMUDAHAN INVESTASI DI SULAWESI TENGAH

TEN WAYS OF MAKING INVESTMENT EASIER IN CENTRAL SULAWESI

1. Local Government guarantee of security and the rule of law

2. Site availability

3. One roof service for permits and licensing

4. Simple and inexpensive permit and licensing system

5. Business taxes levied after the company begins commercial production

6. Local Government initiative to extend 30 year commercial rights guarantees to 90 years

7. Availability of a productive local workforce

8. Assistance in coordinating with Central Government for the tax-free import of production machinery

9. Local Government efforts to ensure the supply of electriicity and other services to business sites

10. The Palu Industrial Zone, the Palapas Integrated Economic development Zone (Kapet) and the Palu City Special Economic Zone (KEK).

14 15

Strategi Pengembangan Komoditi Unggulan

Sulteng di Koridor Sulawesi 4

Strategi Pengembangan Komoditi Unggulan

Sulteng di Koridor 4 Sulawesi

Strategic Commodity Development Strategy

For Central Sulawesi in Corridor 4 - Sulawesi

Strategic Commodity Development Strategy

For Central Sulawesi in Corridor 4 - Sulawesi

1

2

3

4

5

PERIKANAN BUDIDAYARUMPUT LAUT (E. COTTONII dan GRACILARIA Sp)

UDANG (WINDU dan VANNAME)

SIDAT (ANGUILLA CELEBENSIS dan MARMORATA)

PERIKANAN BUDIDAYA

PERIKANAN TANGKAP

PELAJIK BESAR (TUNA DAN CAKALANG)

DEMERSAL (KERAPU dan Ikan Karang lainnya)

1

2

3

4

5

PERIKANAN BUDIDAYA

SEAWEED (E. COTTONII and GRACILARIA Sp)

SHRIMP (TIGER PRAWN and VANNAMEI)

EELS (ANGUILLA CELEBESENSIS and MARMORATA)

AQUACULTURE

CAPTURE FISHERIES

LARGE PELAGICS (YELLOWFIN and SKIPJACK TUNA)

DEMERSAL (GROUPERS and other Reef fish)

KOMODITI UNGGULAN

STRATEGIC COMMODITIES

16 17

1.RUMPUT LAUT a. Penyediaan bibit Generatif (kultur jaringan &

sejenisnya) b. Produksi Massal dengan metoda Generatif c. Pabrikasi untuk Industri Karaginan dan Agar 2. UDANG a. Pembibitan (Hatchery) Udang Vanname dan Windu b. Tambak Udang Intensif seluas 3000 – 5000 Ha c. Industri Pembekuan (Cold Storage) dan industri pengolahan bernilai tambah (Added Value)

3. SIDAT (Fresh Water Ells) a. Penangkaran benih sidat (Glass Ell dan Elver) b. Produksi Massal di Tambak & Kolam Secara Intensif c. Industri Pengolahan (Unagi, Sidat asap) 4. TUNA-CAKALANG a. Pembibitan Ikan Tuna b. Produksi Massal melalui Karamba Jaring Apung

Modern c. Industri Pembekuan (Cold Storage) dan industri pengolahan bernilai tambah (Added Value)

5. IKAN DEMERSAL (Kerapu, Kakap dan lain-lain) a. Pembibitan (Hatchery) Ikan Demersal b. Budidaya Massal melalui Karamba dan Rumah Ikan c. Industri Pembekuan (Cold Storage) dan industri pengolahan bernilai tambah (Added Value)

6. INDUSTRI PENUNJANG a. Pabrik Tali dan Pelampung (Floating buoy) b. Pabrik Pakan Udang & Ikan c. Pabrik Es d. Industri Pengolahan Limbah & Komoditi Unggulan e. Industri Fiber (untuk galangan kapal, coolbox, dll)

1. SEAWEED a. Provision of seed from vegetative propagation (ring culture and

similar) b. Mass production with Generative propagation methods c. Factories for the Carrageenan and Agar Industries 2. SHRIMP a. Hatcheries for Vannamei shrimp and Tiger Prawns b. Intensive shrimp Tambak brackish-water ponds 3000 – 5000 Ha c. Frozen food industry (Cold Storage) and Added Value industries 3. FRESH WATER EELS a. Husbandry of Eel Seed (Glass Eels and Elvers) b. Intensive Mass Production in Tambak & Freshwater ponds c. Processing Industry (Unagi, Smoked Eels) 4. YELLOW-FIN & SKIPJACK TUNA a. Tuna seed production b. Mass production in modern floating net cages c. Frozen fish industry (Cold Storage) and other Added Value

industries

5. DEMERSAL FISH (Grouper, Snapper and others) a. Hatchery for Demersal Fish b. Mass culture in Cages and Fish Homes c. Frozen fish industry (Cold Storage) and other Added Value

industries

6. SUPPORT INDUSTRIES a. Rope and Buoy making factories b. Fish and Shrimp feed factories c. Ice-making factories d. Waste Processing and Strategic Commodity Processing

Industries e. Fibre-glass Construction Industry (ship/boat building,

coolboxes, etcetera)

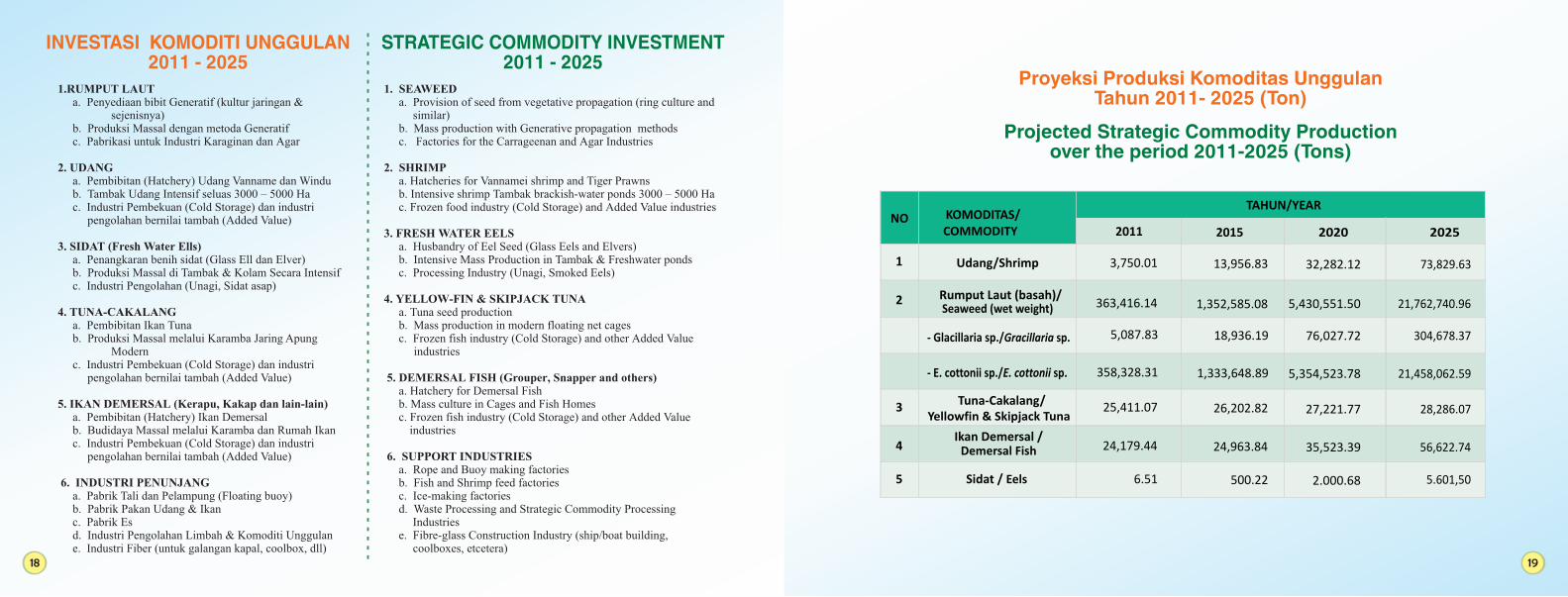

INVESTASI KOMODITI UNGGULAN2011 - 2025

STRATEGIC COMMODITY INVESTMENT 2011 - 2025

NO KOMODITAS/TAHUN/YEAR

2011 2015

1 Udang/Shrimp 3,750.01 13,956.83

2 Rumput Laut (basah)/363,416.14 1,352,585.08

- Glacillaria sp./Gracillaria sp. 5,087.83 18,936.19

- E. cottonii sp./E. cottonii sp. 358,328.31 1,333,648.89

3 Tuna-Cakalang/ 25,411.07 26,202.82

4Ikan Demersal /

Demersal Fish 24,179.44 24,963.84

5 Sidat / Eels 6.51 500.22

2020

32,282.12

5,430,551.50

76,027.72

5,354,523.78

27,221.77

35,523.39

2.000.68

2025

73,829.63

21,762,740.96

304,678.37

21,458,062.59

28,286.07

56,622.74

5.601,50

Projected Strategic Commodity Production over the period 2011-2025 (Tons)

COMMODITY

Seaweed (wet weight)

Yellowfin & Skipjack Tuna

Proyeksi Produksi Komoditas UnggulanTahun 2011- 2025 (Ton)

18 19

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2011 (M)/(B) 2012 (M)/(B) 2013 (M)/(B) 2014 (M)/(B) 2015 (M)/(B)

1 UDANG/SHRIMP

- Tambak Intensif/Intensive Tambak ponds

- Hatchery/Hatcheries - -

- ColdStorage /Cold Storage/Frozen Shrimp - -- Pabrik Pakan/Feed Factory - - - - -

Proyeksi Investasi Komoditas Unggulan 2011-2025 (Milyar Rupiah)Proyeksi Investasi Komoditas Unggulan 2011-2025 (Milyar Rupiah)Projected Strategic Commodity Investment 2011-2025 (Billion Rupiah)Projected Strategic Commodity Investment 2011-2025 (Billion Rupiah)

NO. KOMODITAS/COMMODITYTAHUN/YEAR

1 UDANG/SHRIMP

- Tambak Intensif/Intensive Tambak ponds

- Hatchery/Hatcheries

- ColdStorage /Cold Storage/Frozen Shrimp - Pabrik Pakan/Feed Factory

2016 (M)/(B) 2017 (M)/(B) 2018 (M)/(B) 2019 (M)/(B) 2020 (M)/(B)

20.00 - 40.00- - -

NO. KOMODITAS/COMMODITYTAHUN/YEAR

1 UDANG/SHRIMP

- Tambak Intensif/Intensive Tambak ponds

- Hatchery/Hatcheries

- ColdStorage /Cold Storage/Frozen Shrimp - Pabrik Pakan/Feed Factory

Sub Total

2021 (M)/(B) 2022 (M)/(B) 2023 (M)/(B) 2024 (M)/(B) 2025 (M)/(B)

231.00

455.00- 40.00 - 200.00

- - - 85.00969.00

TOTAL (M)/(B)

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2011 (M)/(B) 2012 (M)/(B) 2013 (M)/(B) 2014 (M)/(B) 2015 (M)/(B)

2 RUMPUT LAUT/SEAWEED- Kebun Bibit / Nurseries- Perbaikan/ dan Saluran Irigasi- Repair/Construction of Tambak Ponds/Irrigation Channels

Pencetakan Tambak

- Pergudangan (Depo)/Warehousing- Pabrik - Carageenan/Agar Factories

Karaginan/agar

10.00 15.00 15.00 20.00 25.00

10.00 15.00 15.00 20.00 25.00

10 15 20 25 25

10 20 30 40 25

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2016 (M)/(B) 2017 (M)/(B) 2018 (M)/(B) 2019 (M)/(B) 2020 (M)/(B)

2 RUMPUT LAUT/SEAWEED- Kebun Bibit / Nurseries- Perbaikan/ dan Saluran Irigasi- Repair/Construction of Tambak Ponds/Irrigation Channels

Pencetakan Tambak

- Pergudangan (Depo)/Warehousing- Pabrik - Carageenan/Agar Factories

Karaginan/agar

25.00 30.00 35.00 40.00 45.00

25.00 30.00 35.00 40.00 45.00

25.00 27.00 - - 30.00

25.00 - - - 30.00

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2021 (M)/(B) 2022 (M)/(B) 2023 (M)/(B) 2024 (M)/(B) 2025 (M)/(B)

2 RUMPUT LAUT/SEAWEED- Kebun Bibit / Nurseries- Perbaikan/ dan Saluran Irigasi- Repair/Construction of Tambak Ponds/Irrigation Channels

Pencetakan Tambak

- Pergudangan (Depo)/Warehousing- Pabrik - Carageenan/Agar Factories

Karaginan/agar

TOTAL (M)/(B)

50.00 60.00 70.00 80.00 85.00 605.00

50.00 60.00 70.00 80.00 85.00 605.00

- - - - 45.00 222.00

- - 40.00 - 45.00 265.00

1.697.00Sub Total

20 21

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2011 (M)/(B) 2012 (M)/(B) 2013 (M)/(B) 2014 (M)/(B) 2015 (M)/(B)3 TUNA- YELLOWFIN & SKIPJACK TUNACAKALANG/

Revitalisasi Revitalisation (P3)*P3/ 0.45 0.55 1.00 1.50 2.50

Karamba Tuna/Tuna Net Cages 0.00 0.00 0.00 0.00 0.00Hatchery Tuna/Tuna Hatchery - - - - -

Industri Processing IndustryPengolahan/ 2.00 3.00 5.00 7.00 9.00

Sub Total 839.00

-

--

-

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2016 (M)/(B) 2017 (M)/(B) 2018 (M)/(B) 2019 (M)/(B) 2020 (M)/(B)3 TUNA- YELLOWFIN & SKIPJACK TUNACAKALANG/

Revitalisasi PPI dan Revitalisation (PPI and P3)*P3/

Karamba Tuna/Tuna Net CagesHatchery Tuna/Tuna Hatchery

Industri Processing IndustryPengolahan/

-

--

-

4.00 5.00 7.00 8.00 8.00

20.00 24.00 28.00 32.00 45.00- 10.00 14.00 17.00 22.00

11.00 11.00 11.00 12.00 12.00

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2021 (M)/(B) 2022 (M)/(B) 2023 (M)/(B) 2024 (M)/(B) 2025 (M)/(B)3 TUNA- YELLOWFIN & SKIPJACK TUNACAKALANG/

Revitalisasi PPI dan Revitalisation (PPI and P3)*P3/

Karamba Tuna/Tuna Net CagesHatchery Tuna/Tuna Hatchery

Industri Processing IndustryPengolahan/

-

---

TOTAL (M)/(B)

10.00 12.00 15.00 17.00 20.00 112.0050.00 56.00 45.00 45.00 45.00 390.00

27.00 30.00 15.00 13.00 10.00 158.00

15.00 17.00 19.00 21.00 24.00 179.00

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2011 (M)/(B) 2012 (M)/(B) 2013 (M)/(B) 2014 (M)/(B) 2015 (M)/(B)

4 IKAN DEMERSAL/DEMERSAL FISH- Kapal 10-15 GT/Fishing Vessels 10-15 GT 2.50 3.75 6.00 6.25 7.50- Revitalisasi PPI dan P3/Revitalisation (PPI and P3)* - 3.00 3.00 3.00 3.00

- Pembuatan Fish Home/Fish Home Construction - 5.00 10.00 15.00 20.00

- Hatchery Ikan Demersal/Demersal Fish Hatchery - - 10.00 - 10.00

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2016 (M)/(B) 2017 (M)/(B) 2018 (M)/(B) 2019 (M)/(B) 2020 (M)/(B)

4 IKAN DEMERSAL/DEMERSAL FISH- Kapal 10-15 GT/Fishing Vessels 10-15 GT- Revitalisasi PPI dan P3/Revitalisation (PPI and P3)* - Pembuatan Fish Home/Fish Home Construction

- Hatchery Ikan Demersal/Demersal Fish Hatchery

9.00 11.00 13.00 15.00 18.003.00 3.00 3.00 3.00 5.00

25.00 27.00 30.00 33.00 35.00

- 15.00 - 15.00

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2021 (M)/(B) 2022 (M)/(B) 2023 (M)/(B) 2024 (M)/(B) 2025 (M)/(B)

4 IKAN DEMERSAL/DEMERSAL FISH- Kapal 10-15 GT/Fishing Vessels 10-15 GT- Revitalisasi PPI dan P3/Revitalisation (PPI and P3)* - Pembuatan Fish Home/Fish Home Construction

- Hatchery Ikan Demersal/Demersal Fish Hatchery

TOTAL (M)/(B)

Sub Total

21.00 24.00 27.00 30.00 33.00 227.00

5.00 7.00 7.00 7.00 8.00 63.0038.00 40.00 43.00 47.00 50.00 418.00

- 25.00 - - 35.00 110.00

818.00

22 23

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2011 (M)/(B) 2012 (M)/(B) 2013 (M)/(B) 2014 (M)/(B) 2015 (M)/(B)

5 SIDAT/Eels- Sarana penangkap benih/Seed collection gear 0.25 0.25 0.25 0.50 0.75- penangkar benih/Glass eel/elver husbandry 0.50 0.50 0.50 0.75 1.00

- Karamba dan tambak/Net Cages and Ponds 1.00 1.50 3.00 3.50 4.00

- Industri pengolahan Sidat/Eel Processing Industry 0.25 0.25 0.75 1.00 1.25

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2016 (M)/(B) 2017 (M)/(B) 2018 (M)/(B) 2019 (M)/(B) 2020 (M)/(B)

5 SIDAT/Eels- Sarana penangkap benih/Seed collection gear- penangkar benih/Glass eel/elver husbandry

- Karamba dan tambak/Net Cages and Ponds

- Industri pengolahan Sidat/Eel Processing Industry

1.00 1.50 1.50 1.50 1.50

1.25 2.00 2.50 3.00 3.00

4.50 5.00 6.50 7.00 7.50

1.50 2.00 3.00 4.00 5.00

NO. KOMODITAS/COMMODITYTAHUN/YEAR

2021 (M)/(B) 2022 (M)/(B) 2023 (M)/(B) 2024 (M)/(B) 2025 (M)/(B)

5 SIDAT/Eels- Sarana penangkap benih/Seed collection gear- penangkar benih/Glass eel/elver husbandry

- Karamba dan tambak/Net Cages and Ponds

- Industri pengolahan Sidat/Eel Processing Industry

1.50 1.50 2.50 3.00 3.25 20.753.00 3.50 3.50 4.00 4.50 33.50

8.00 8.50 9.00 9.50 10.00 88.506.00 7.00 8.00 9.00 10.00 59.00

201.75

4.526.75

TOTAL (M)/(B)

Sub Total

GRAND TOTAL

KAWASAN EKONOMI KHUSUS INDONESIA (KEKI)

DI KOTA PALU

INDONESIAN SPECIAL ECONOMIC ZONE (KEKI)

IN PALU CITY

24 25

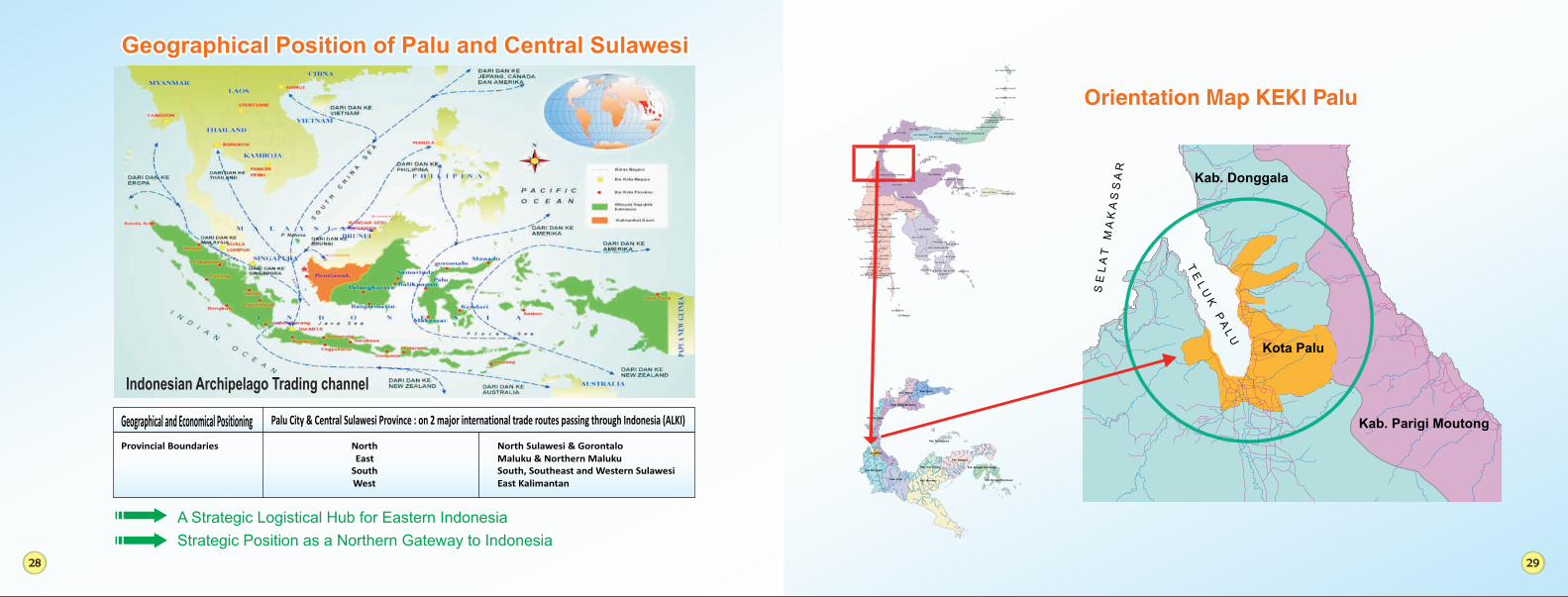

Geoposisi & Geoekonomi Kota Palu & Provinsi Sulawesi Tengah terletak di 2 Jalur Perdagangan Dunia (ALKI)

Batas Wilayah Propinsi UtaraTimur

SelatanBarat

Sulut & GorontaloMaluku & Maluku UtaraSulsel, Sultra & SulbarKalimantan Timur

GEOPOSISI Palu dan Sulawesi TengahGEOPOSISI Palu dan Sulawesi Tengah

Indonesian Archipelago Trading channel

Strategis sebagai Pusat Logistik Nasional Indonesia Timur

Strategis sebagai Northern Gate Indonesia

1. Pemberian KEKI kepada suatu wilayah bertujuan• Membangun daya saing wilayah;• Mendorong pertumbuhan ekonomi wilayah;• Menyerap tenaga kerja

2. Terdapat 12 kandidat KEKI di Indonesia, salah satunya Kota Palu; Sulawesi Tengah3. KEKI Kota Palu bersinergi dengan Kapet Palapas, terdiri dari:

• Kota Palu;• Kabupaten Donggala;• Kabupaten Parigi Moutong, dan • Kabupaten Sigi

KAWASAN EKONOMI KHUSUS INDONESIA (KEKI) UU 39 TAHUN 2009KAWASAN EKONOMI KHUSUS INDONESIA (KEKI) UU 39 TAHUN 2009

INDONESIAN SPECIAL ECONOMIC ZONE (KEKI) UU No. 39 of the year 2009INDONESIAN SPECIAL ECONOMIC ZONE (KEKI) UU No. 39 of the year 2009

1. The aims of designating an area as a KEKI are to:• Improve the competiveness of the area;• Drive regional economic development;• Provide Employment

2. There are 12 KEKI candidate areas in Indonesia, including Palu City in Central Sulawesi3. The Palu City KEKI will synergise with the Palapas Kapet (integrated economic

development zone), which comprises :• Palu City;• Donggala District;• Parigi Moutong District, and • Sigi District

26 27

Geographical Position of Palu and Central SulawesiGeographical Position of Palu and Central Sulawesi

Geographical and Economical Positioning Palu City & Central Sulawesi Province : on 2 major international trade routes passing through Indonesia (ALKI)

Provincial Boundaries NorthEast

SouthWest

North Sulawesi & GorontaloMaluku & Northern Maluku South, Southeast and Western Sulawesi East Kalimantan

A Strategic Logistical Hub for Eastern Indonesia

Strategic Position as a Northern Gateway to Indonesia

Indonesian Archipelago Trading channelT E

L U K

P A

L U

Kab. Parigi Moutong

Kab. Donggala

Kota Palu

Orientation Map KEKI Palu

S E

L A

T M

A K

A S

S A

R

Kab. MorowaliKab. Poso

Kab. Banggai

Kab. Donggala

Kab. Buol

Kab. Parigi Moutong

Kab. Tolitoli

Kab. Tojo Unauna

Kab. Donggala

Kab. Banggai Kepulauan

Kota Palu

Kab. Tojo Unauna

Kab. Banggai Kepulauan

Kab. POSO

Kab. KENDARI

Kab. MOROWALI

Kab. KOLAKA

Kab. BANGGAI

Kab. MAMUJU Kab. LUWU UTARA

Kab. BONE

Kab. BUOL

Kab. POHUWATOKab. BOLAANG MONGONDOW

Kab. BUTON

Kab. KEP. SULA

Kab. BUTON

Kab. DONGGALA

Kab. LUWU TIMUR

Kab. TOLI-TOLI Kab. GORONTALO

Kab. LUWU

Kab. W A J O

Kab. PARIGI MOUTONG (PARIMO)

Kab. TANATORAJA

Kab. DONGGALA

Kab. M U N A

Kab. M U N A

Kab. KONAWE SELATAN

Kab. GOWA

Kab. MAMUJU UTARA

Kab. MAMASA

Kab. MINAHASA

Kab. PINRANG

Kab. MAROS

Kab. POLEWALI MAMASA

Kab. ENREKANG

Kab. BOALEMO

KAb. BARRU

Kab. BONE BOLANGO

Kab. SOPPENG

Kab. MINAHASA SELATAN

Kab. BANGGAI KEPULAUAN

Kab. LUWU

Kab. MAJENE

Kab. SINJAIKab. BUTON

Kab. SIDENRENG RAPANG

PALU

Kab. BULUKUMBA

Kab. BUTON

Kab. KENDARI

Kab. SELAYAR

Kab. KEP. SULA

Kab. TAKALAR

Kab. JENEPONTO

Kota BAU BAU

KOTA KENDARI

Kab. PANGKAJENE KEPULAUAN

Kab. SANGIHE TALAUD

Kab. BANTAENG

Kota BITUNG

Kota PALOPO

Kota MANADO

Kab. BUTON

Kab. SELAYAR

Kab. BANGGAI KEPULAUAN

KOTA TOMOHON

Kab. SELAYAR

Kota UJUNGPANDANG

Kota PARE PARE

Kab. SANGIHE TALAUD

Kota BITUNG

Kab. TAKALAR

Kab. SANGIHE TALAUD

Kab. GORONTALO

Kab. LUWU UTARA

28 29

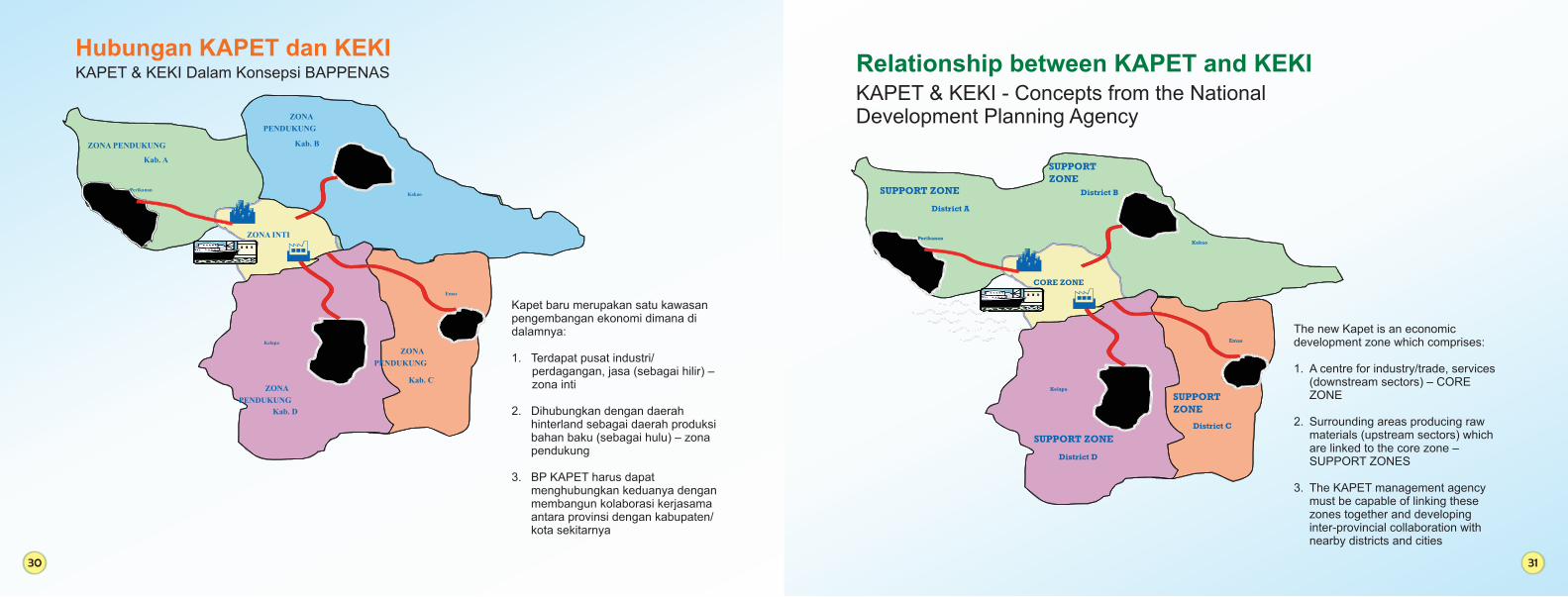

Hubungan KAPET dan KEKIKAPET & KEKI Dalam Konsepsi BAPPENAS

F

CZONA INTI

Kab. A

Kab. B

Kab. D

Kab. C

PerikananKakao

Kelapa

Emas

ZONA PENDUKUNG

ZONA

PENDUKUNG

ZONA

PENDUKUNG

ZONA

PENDUKUNG

Kapet baru merupakan satu kawasan pengembangan ekonomi dimana di dalamnya:

1. Terdapat pusat industri/ perdagangan, jasa (sebagai hilir) – zona inti

2. Dihubungkan dengan daerah hinterland sebagai daerah produksi bahan baku (sebagai hulu) – zona pendukung

3. BP KAPET harus dapat menghubungkan keduanya dengan membangun kolaborasi kerjasama antara provinsi dengan kabupaten/ kota sekitarnya

Relationship between KAPET and KEKIKAPET & KEKI - Concepts from the National Development Planning Agency

F

CCORE ZONE

District A

District B

District D

District C

PerikananKakao

Kelapa

Emas

SUPPORT

ZONESUPPORT ZONE

SUPPORT ZONE

SUPPORT

ZONE

The new Kapet is an economic development zone which comprises:

1. A centre for industry/trade, services (downstream sectors) – CORE ZONE

2. Surrounding areas producing raw materials (upstream sectors) which are linked to the core zone – SUPPORT ZONES

3. The KAPET management agency must be capable of linking these zones together and developing inter-provincial collaboration with nearby districts and cities

30 31

INSENTIF FISKAL DAN NONFISKAL

INSENTIF FISKAL

Keputusan Menteri Keuangan No.200/KMK.04/2000 jo. Keputusan Menteri Keuangan No.11/KMK.04/2001 tentang Insentif Pajak:

• Bea masuk impor 5% untuk mesin• 30% pengurangan penghasilan neto selama 6

tahun (5% per tahun)• Depresiasi dan atau amortisasi yang

dipercepat• Kompensasi kerugian fiskal untuk 10 tahun• Pengenaan pajak penghasilan pasal 26 atas

deviden sebesar 10%

INSENTIF NONFISKAL

• Pelayanan Satu Atap untuk Provinsi dan Kota• Aftercare Service dan Investor Desks• Pusat Pengembangan Bisnis• Area Industri

FISCAL and NON-FISCAL INCENTIVES

FISCAL INCENTIVES

Decree by the Minister of Finance No.200/KMK.04/2000. Decree by the Minister of Finance No.11/KMK.04/2001 regarding Tax Incentives:

• Import duty of 5% for machinery• 30% reduction of net income over a period of 6

years (5% per year)• Acceleration of Depreciation and/or

amortisation• Fiscal compensation for losses over 10 years• Applicable income tax on dividend under article

26 is set at 10%

NON-FISCAL INCENTIVES

• "One roof service" for the Province and City• Aftercare Service and Investor Desks• Business Development Centre• Industrial Estates

DUKUNGAN INFRASTRUKTUR TERHADAP KAWASAN INDUSTRI PALU (KIP)

SUPPORTING INFRASTRUCTURE FOR THE PALU INDUSTRIAL ZONE (KIP)

32 33

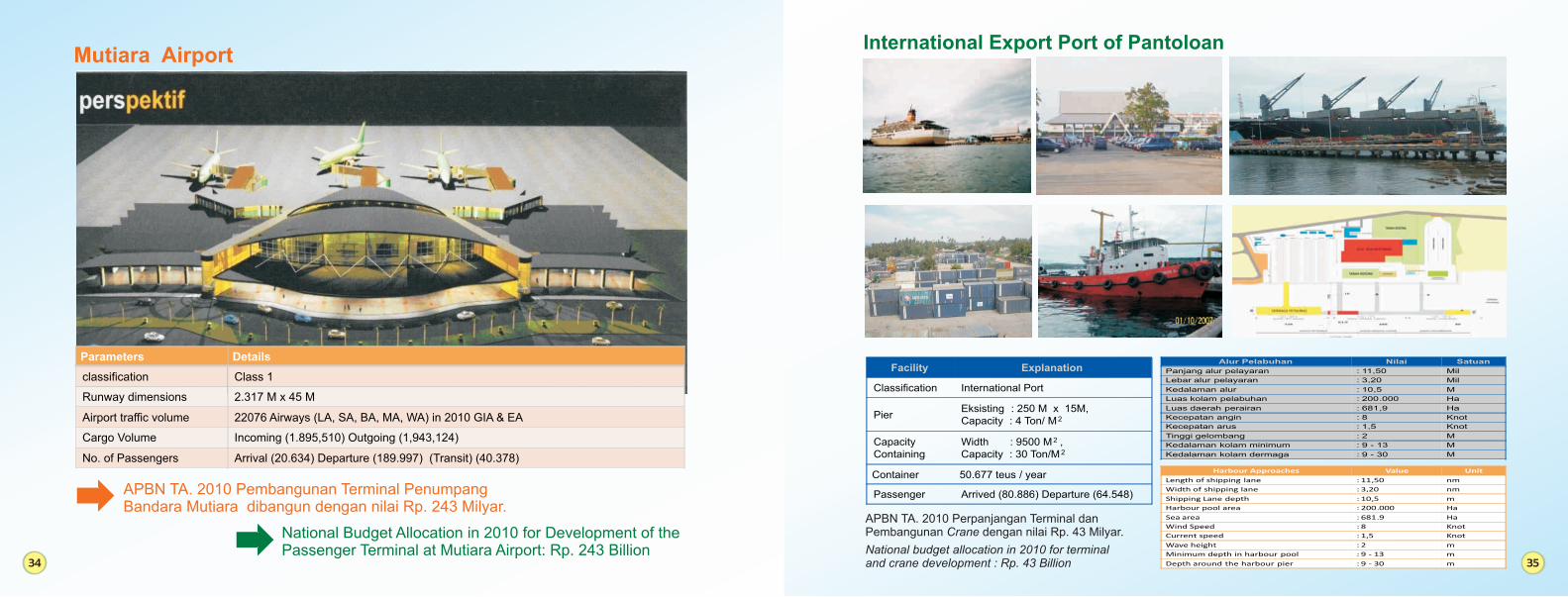

Mutiara Airport

Parameters Details

classification Class 1

Runway dimensions 2.317 M x 45 M

Airport traffic volume 22076 Airways (LA, SA, BA, MA, WA) in 2010 GIA & EA

Cargo Volume Incoming (1.895,510) Outgoing (1,943,124)

No. of Passengers Arrival (20.634) Departure (189.997) (Transit) (40.378)

APBN TA. 2010 Pembangunan Terminal Penumpang Bandara Mutiara dibangun dengan nilai Rp. 243 Milyar.

National Budget Allocation in 2010 for Development of the Passenger Terminal at Mutiara Airport: Rp. 243 Billion

International Export Port of Pantoloan

Facility Explanation

Classification International Port

PierEksisting : 250 M x 15M, Capacity : 4 Ton/ M2

Capacity Containing

Width : 9500 M2 , Capacity : 30 Ton/M 2

Container 50.677 teus / year

Passenger Arrived (80.886) Departure (64.548)

Alur Pelabuhan Nilai Satuan

Panjang alur pelayaran : 11,50 Mil

Lebar alur pelayaran : 3,20 Mil

Kedalaman alur : 10,5 M

Luas kolam pelabuhan : 200.000 Ha

Luas daerah perairan : 681,9 Ha

Kecepatan angin : 8 Knot

Kecepatan arus : 1,5 Knot

Tinggi gelombang : 2 M

Kedalaman kolam minimum : 9 - 13 M

Kedalaman kolam dermaga : 9 - 30 M

APBN TA. 2010 Perpanjangan Terminal dan Pembangunan Crane dengan nilai Rp. 43 Milyar.

Harbour Approaches Value Unit

Length of shipping lane : 11,50 nm

Width of shipping lane : 3,20 nm

Shipping Lane depth : 10,5 m

Harbour pool area : 200.000 Ha

Sea area : 681.9 Ha

Wind Speed : 8 Knot

Current speed : 1,5 Knot

Wave height : 2 m

Minimum depth in harbour pool : 9 - 13 m

Depth around the harbour pier : 9 - 30 m

National budget allocation in 2010 for terminal and crane development : Rp. 43 Billion34 35

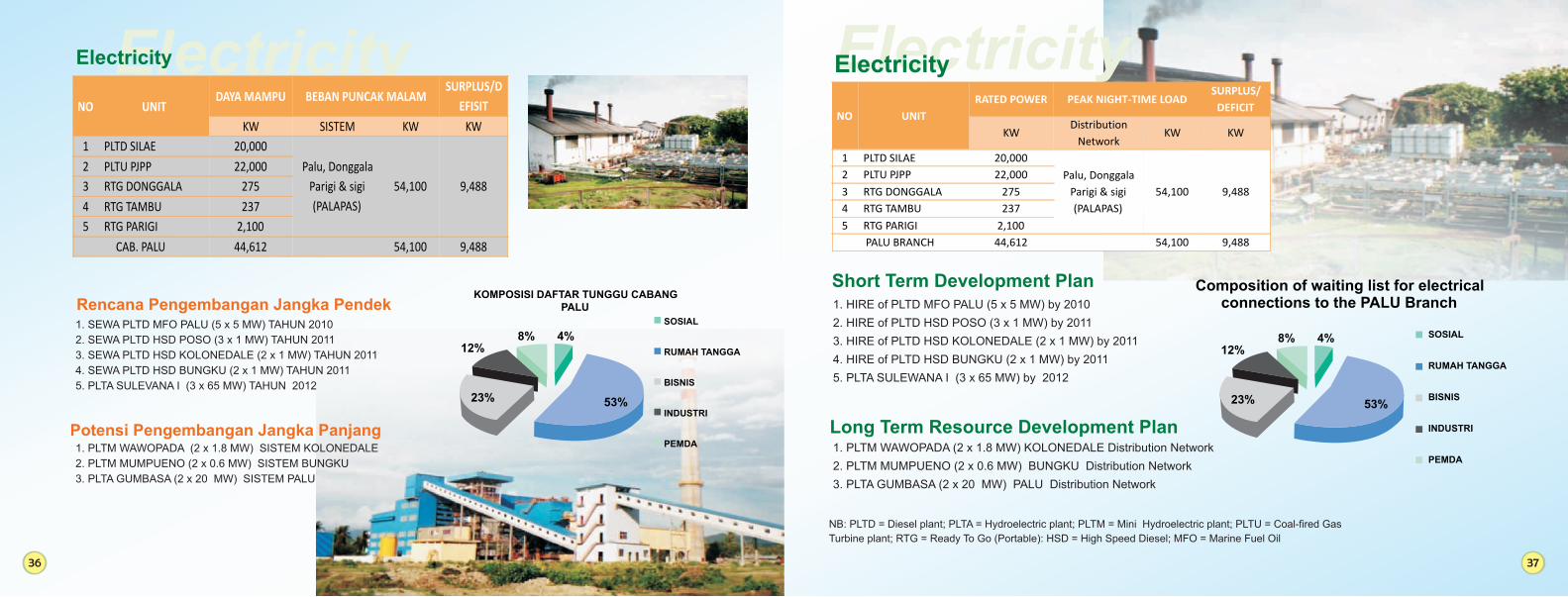

ElectricityElectricity

NO UNITDAYA MAMPU BEBAN PUNCAK MALAM

SURPLUS/D

EFISIT

KW SISTEM KW KW

1 PLTD SILAE 20,000

Palu, Donggala

Parigi & sigi

(PALAPAS)

54,100 9,488

2 PLTU PJPP 22,000

3 RTG DONGGALA 275

4 RTG TAMBU 237

5 RTG PARIGI 2,100

CAB. PALU 44,612 54,100 9,488

Rencana Pengembangan Jangka Pendek1. SEWA PLTD MFO PALU (5 x 5 MW) TAHUN 2010

2. SEWA PLTD HSD POSO (3 x 1 MW) TAHUN 2011

3. SEWA PLTD HSD KOLONEDALE (2 x 1 MW) TAHUN 2011

4. SEWA PLTD HSD BUNGKU (2 x 1 MW) TAHUN 2011

5. PLTA SULEVANA I (3 x 65 MW) TAHUN 2012

Potensi Pengembangan Jangka Panjang1. PLTM WAWOPADA (2 x 1.8 MW) SISTEM KOLONEDALE

2. PLTM MUMPUENO (2 x 0.6 MW) SISTEM BUNGKU

3. PLTA GUMBASA (2 x 20 MW) SISTEM PALU

KOMPOSISI DAFTAR TUNGGU CABANG PALU

4%12%

8%

23% 53%

SOSIAL

RUMAH TANGGA

BISNIS

INDUSTRI

PEMDA

ElectricityNO UNIT

RATED POWER PEAK NIGHT-TIME LOADSURPLUS/

DEFICIT

KWDistribution

NetworkKW KW

1 PLTD SILAE 20,000

Palu, Donggala

Parigi & sigi

(PALAPAS)

54,100 9,488

2 PLTU PJPP 22,000

3 RTG DONGGALA 275

4 RTG TAMBU 237

5 RTG PARIGI 2,100

PALU BRANCH 44,612 54,100 9,488

Short Term Development Plan1. HIRE of PLTD MFO PALU (5 x 5 MW) by 2010

2. HIRE of PLTD HSD POSO (3 x 1 MW) by 2011

3. HIRE of PLTD HSD KOLONEDALE (2 x 1 MW) by 2011

4. HIRE of PLTD HSD BUNGKU (2 x 1 MW) by 2011

5. PLTA SULEWANA I (3 x 65 MW) by 2012

Long Term Resource Development Plan1. PLTM WAWOPADA (2 x 1.8 MW) KOLONEDALE Distribution Network

2. PLTM MUMPUENO (2 x 0.6 MW) BUNGKU Distribution Network

3. PLTA GUMBASA (2 x 20 MW) PALU Distribution Network

Electricity

Composition of waiting list for electrical connections to the PALU Branch

SOSIAL

RUMAH TANGGA

BISNIS

INDUSTRI

PEMDA

NB: PLTD = Diesel plant; PLTA = Hydroelectric plant; PLTM = Mini Hydroelectric plant; PLTU = Coal-fired Gas

Turbine plant; RTG = Ready To Go (Portable): HSD = High Speed Diesel; MFO = Marine Fuel Oil

4%12%

8%

23% 53%

36 37

Water SupplyWater SupplyWater supply Explanation

Water Source Gumbasa River

Reservoar Location Ngata Baru Village in Sigi -Biromaru Regency

Tapped Building Elevation 500 M

Water Terminal Elevation 300 M

Distance between water source to Reservoar

35 Km

Water Source Potency 20 M3/Second

Water stream 5.000 L/Second

Water Terminal Capacity 4.500 L/Second

Pipe Transmission Material needed Corougated Steel Pipe (CSP)/High Dencity Pilyethylene Pipe

Pipe Irrigation Diameter 1.200 mm x 2 line

Used for

a. Clean waterb. Agriculturec. Green City Programd. Power Plant of Water

Diajukan melalui APBN-Perubahan TA. 2010 untuk Kota Palu dan Distribusi Kawasan Industri dengan nilai Rp. 50 Milyar.

Submitted via the National Budget Adjustment for 2010 to supply Palu City and the Industrial Zone with a budget of Rp. 50 Billion.

HotelsHotel Guess Rooms

Swissbel Hotel 9557 81

Rama Garden Hotel 3437 20

Palu Golden Hotel 8913 55

Merry glow Hotel 311 10

Fahmil Hotel 567 17

Pondok Indah Hotel 570

20

Sentral Hotel 15817 50

Formosa Hotel 159 19

Dely Baru Hotel 1544 13

Wisata Hotel 909 25

Buana Hotel 2023 34

Alam Raya Hotel 805 27

Pembangunan Hotel dalam tahun

2009-2010 mencapai 5 buah

sebagai dampak meningkatnya

tingkat hunian hotel

During the period of 2009-2010 there

were 5 Hotels built in Palu as a result

of increased hotel occupancy rates

38 39

Infrastructure investment (Opportunity investment)

Coconut Industry & Tree

Cold Storage and Ice Factory Real Estate Low Cost Housing Clean Water Distribution International Hub Port of Pantoloan

Power Plant of Condence

Hotels Tourism Object of Palu Bay Entertainment Park RestaurantRecycling Iron Factory Shopping Center

Mutiara Airport Expansion Road Access Office Rent Hospital & Clinic

Airlines & Aircargo

Education Infrastructure International Banking

Shipping & Cargo Passenger

Entertainment & Sport Center

Infrastructure Of Road, Bridge, And Drainage

Road Type Length (km)

National Road 125,45

Provincial Road 16,83

City Road 648,38

Number of Bridge Length (km)

39 bridges 1646.7

Drainage Length (km)

Palu Barat District 6,241.4

Palu Timur District 6,146.6

Palu Selatan District 25,498

Palu Utara District 900

Total Number 38,786

40 41

Going to be SEZ Candidate- Palu Industrial EstateAccessibity From Distance (Km) Time Taking Road

Mutiara Airport 20 ½ jam Reguler

Pantoloan Seaport 1 5 menit Reguler

Economics Center 15 ½ jam Reguler

Palu Industrial Estate AccessibilityLet’s make it realLet’s make it real

PALU INDUSTRIAL ESTATEPALU INDUSTRIAL ESTATE42 43

PENUTUP / CONCLUSION

DENGAN MENGACU KEPADA REGULASI MP3EI

Visi Pemerintah Sulawesi Tengah 2011 -2016

MAKA

: bahwa koridor 4 Sulawesi sebagai pusat Produksi dan Pengolahan PANGAN di Indonesia, yang sejalan dengan

bahwa : Sulawesi Tengah Sejajar dengan Provinsi Maju di kawasan timur Indonesia di bidang agribisnis dan kelautan melalui pengembangan sumberdaya manusia yang berdaya saing 2010. ;Berkaitan dengan itu Provinsi Sulawesi Tenga bersama 11 kabupaten Kota akan memberikan dukungan antara lain berupa 10 Kemudahan berinvestasi bagi setiap calon Investor

IN ACCORDANCE WITH REGULATION NUMBER MP3EI 2011 -2016 Vision of the Central Sulawesi Government

THEREFORE;

: which designates corridor 4 - Sulawesi as a national centre for FOOD Production and Processing, which is in line with the that : Central Sulawesi should be ON A PAR with Developed Provinces in Eastern Indonesia in the agribusiness and marine sectors through the development of competitive human resources,In connection with these goals, the Province of Central Sulawesi in cooperation with the 11 Districts/Cities will provide support to all potential investors. including the "ten ways of making investment easier"

KOTA (PALU City)

PALU

KAB. BANGGAI (BANGGAI District)

KAB.(TOLITOLI District)

TOLITOLI

KAB. PARIMO (PARIMO District)

KAB. (DONGGALA District)

DONGGALA

KAB. POSO (POSO District)

KAB. BANGKEP (BANGKEP District)

KAB. TOUNA (TOUNA District)

KAB. MOROWALI(MOROWALI District)

KAB. BUOL (BUOL District)

KAB. SIGI (SIGI District)

TOGIANISLAND

44