Bahasa

Halaman

Hukum

Travel and tourism sector: Potential,

opportunities and enabling framework

for sustainable growth

December 2013

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

Theme Paper

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The Indian tourism and hospitality industry has emerged as one of the key drivers of growth among the services sector in India. Tourism in India is a potential game changer. It is a sun rise industry, an employment generator, a significant source of foreign exchange for the country and an economic activity that helps local and host communities.

India is a tourism product which is unparalleled in its beauty, uniqueness, rich culture and history has been aggressively pursuing the promotion of tourism both internationally as well as in the domestic market.

Indian tourism industry is thriving due to an increase in foreign tourist arrivals and greater number of Indians travelling to domestic destinations than before. In the past few years the real growth has come from within the domestic sector as around 30 million Indians travel within the country in a year.

India’s demographic dividend of a younger population compared to developed countries is leading to greater expenditure on leisure services. Travel and tourism sector’s contribution to capital investment is projected to grow at 6.5 per cent per annum during 2013-2023, above the global average of five per cent.

The Ministry of Tourism promotes the country’s various tourism products through its tactile campaigns under the Incredible India brand- both for international as well as domestic markets. The budget allocated for the Domestic Promotion & Publicity and Overseas Promotion & Publicity including Marketing Development stood at INR 1.1 billion (USD 17.73 million) and INR 3.5 billion (USD 56.41 million) for the financial year 2013-14.

The ministry has set up a Hospitality Development and Promotion Board, which will monitor and facilitate hotel project approvals. The allocation for Ministry of Tourism in the Union Budget 2013-14 has been increased by INR 876.6 million (USD 14.13 million) to INR 12,976.6 million (USD 209.30 million).

There is a need to take steps to improve the present scenario of tourism that includes extending facility of visa-on-arrival to tourists from more countries, simple tax rules and ensuring safety of tourists. There is a need for better marketing and brand strategies to promote the sector. The cost of obtaining an Indian visa is prohibitive and we need to take a relook at it. Creation of an enabling environment for the sector’s growth would lead to rise in foreign tourists’ inflows and foreign exchange earnings, thus, contributing to economic growth. This would also lead to creation of additional jobs in the sector, which would create opportunities for all sections of the society and in turn lead to attaining an all-inclusive development.

Set against this backdrop, CII is organising a mega event ‘CII Tourism Fest’ from 5 to 7 December 2013 in Chandigarh to bring all critical stakeholders like policy makers, officials of Ministry of Tourism, State Governments, International Tourism Boards, hoteliers, hospitals, tour operators and travel agents on one platform.

I hope that the deliberations not only reflect true voice of the industry, but also bring all stakeholders together to think alike to kick off a new campaign to create & establish roadmap for inclusive and seamless tourism.

Arjun Sharma

Chairman, CII Tourism Fest 2013

Co-Chairman, CII National Committee on Tourism and

Managing Director, Le Passage to India

Message

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The travel and tourism industry has emerged as one of the largest and fastest growing economic sectors globally. Its contribution to the global Gross Domestic Product (GDP) and employment has increased significantly. Increasingly, travel and tourism is emerging as an important category of services exports worldwide.

With increasing tourist inflows over the past few years, it is a significant contributor to Indian economy as well. As per forecasts by the World travel and tourism Council its total contribution to GDP is expected to witness a growth rate of 12 per cent per annum during 2013-2023. Rising income levels and changing lifestyles, development of diverse tourism offerings and policy and regulatory support by the government are playing a pivotal role in shaping the travel and tourism sector in India.

However, the sector is facing challenges such as lack of good quality tourism infrastructure, global concerns regarding health and safety of tourists, disparate passenger/road tax structures across various states and shortfall of adequately trained and skilled manpower. While several plans and programmes have already been devised for tackling these challenges, successful implementation would be critical to accelerate growth.

Concerted efforts by all stakeholders such as the central and state governments, private sector and the community at large are pertinent for sustainable development and maintenance of the travel and tourism sector in the country.

Jaideep Ghosh

Partner

Management Consulting

KPMG India

Foreword

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Table of contents

Executive summary 01

Introduction 03

1.1 Global tourism industry 04

1.2 Indian tourism industry 05

1.2.1 Growth in number of tourists 05

1.2.2 Impact of tourism sector on GDP 06

1.2.3 Impact of tourism sector on employment 07

1.2.4 Capital investment in tourism sector 07

1.2.5 Growth of tourism in India – Key drivers & trends 08

Performance of tourism sector in various states of India 09

2.1 Comparative assessment of major tourist states of India 10

2.2 Northern states in India 15

2.2.1 Growth of tourists in northern states 15

2.2.2 Profile of tourists in northern states 16

2.2.3 Role of government and private sector 18

2.2.4 Key tourism circuits in northern states 21

Seamless travel 23

3.1 Benefits of seamless travel 24

3.2 Case study: Seamless travel in European Union countries 24

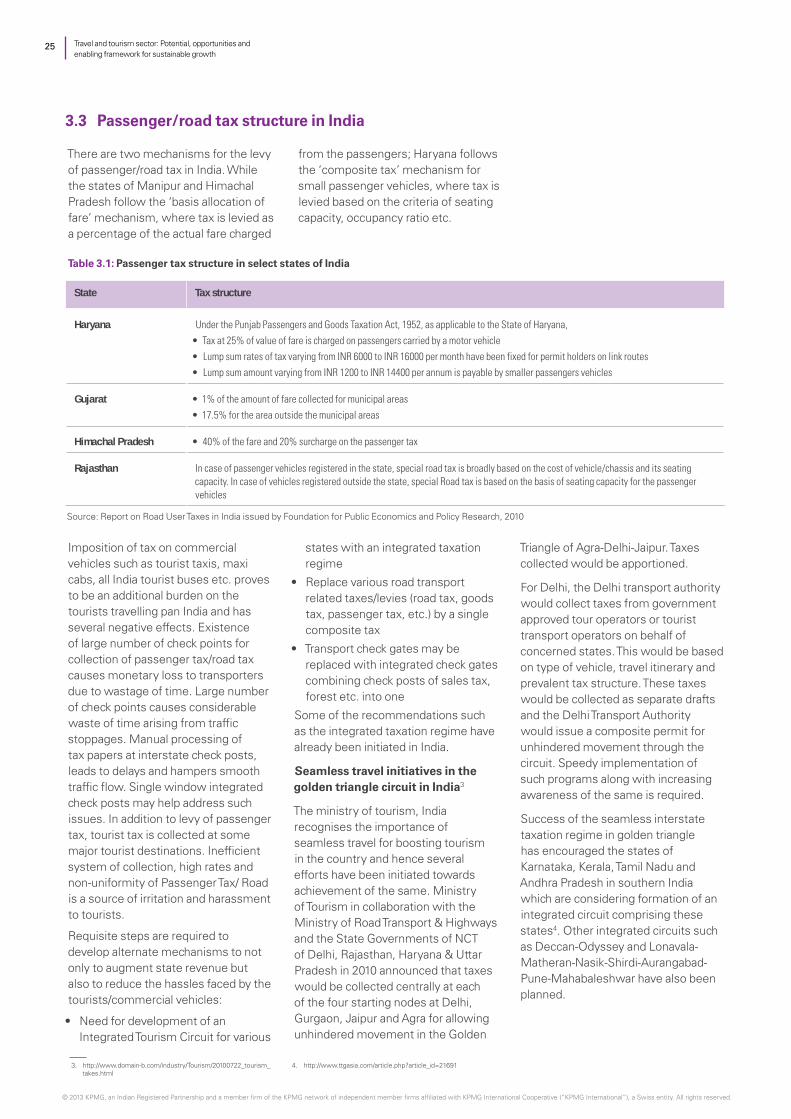

3.3 Passenger/road tax structure in India 25

Key issues in tourism sector in India 27

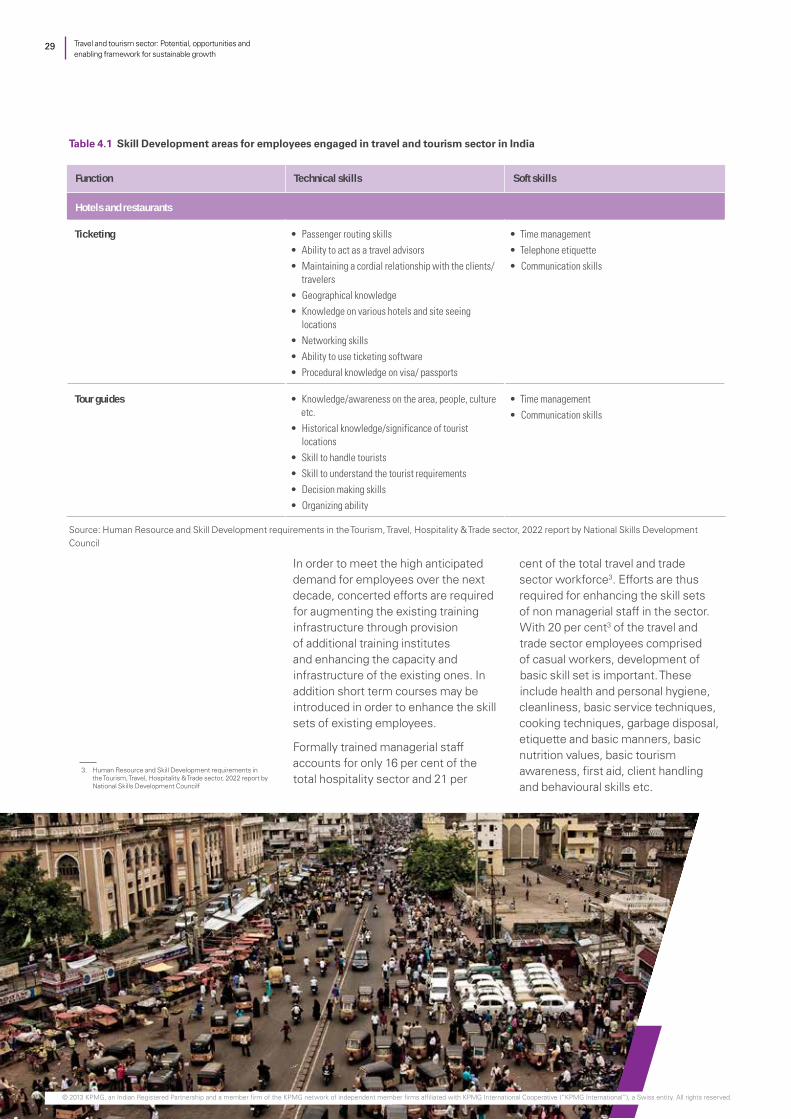

4.1 Training and skill development 28

4.2 Safety and security of tourists 30

4.3 Healthcare for tourists 31

4.4 Infrastructure 32

Recommendations 34

About KPMG in India 35

About CII 36

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The travel and tourism industry has emerged as one of the fastest growing sectors contributing significantly to global economic growth and development. While traditionally Europe and America have remained among the tourism markets, new emerging markets are expected to witness high growth in international tourist visits over the next decade.

India has significant potential to become a preferred tourist destination globally. Its rich and diverse cultural heritage, abundant natural resources and biodiversity provides numerous tourist attractions. The total tourist visits in India have been growing at a steady rate of about 16 per cent over the past five years. The travel and tourism sector in India provides significant socio economic benefits. While the direct contribution to GDP is estimated at INR 2222 billion in 2013, the total contribution is estimated at INR 7416 billion in the same year. These have further been forecasted to rise at a growth rate of 12 per cent over the next decade. While the sector supported 25 million direct and 40 million total jobs in 2012, these have been forecasted to increase at a growth rate of 2.1 per cent by 2023. Several industry drivers such as government initiatives, diverse product offerings, growing economy, increasing disposable income levels and marketing initiatives along with key trends such as increasing number of women and senior citizen travellers, multiple short trips and weekend holidays, introduction of innovative tourism concepts and customised tour packages are playing a pivotal role in shaping the Indian tourism sector.

Total tourist visits in various states of India over a five year period reveal that while states of Karnataka, Delhi, Punjab, Chhattisgarh, Tamil Nadu and Jammu & Kashmir have improved their positions in 2012 as compared to 2008, those of Uttar Pradesh, Rajasthan, Uttarakhand, West Bengal, Himachal Pradesh and Kerala have witnessed decline. Key attributable reason to the success of tourism in states is the increase in state investments towards the tourism sector. While the key commercial and leisure

destinations of Delhi and Maharashtra enjoy good quality transport and accommodation infrastructure, states of Jammu & Kashmir, Uttarakhand, Himachal Pradesh, Rajasthan and Jharkhand may need significant improvements in their rail, road and airport infrastructure.

Tourist visits in the northern states of India witnessed a growth rate of 10.2 per cent during 2008-2012 compared to the national average growth rate of 16.3 per cent during the same period. U.S.A. and U.K. accounted for the maximum number of foreign tourist visits in the northern states of India in 2012. Fair share of tourists were received from non English speaking countries like Germany, Japan and UAE necessitating the availability of tourist information in multiple languages. While tourists visit states of Punjab, Haryana and Delhi for commercial and business related purposes, states of Himachal Pradesh, Uttarakhand, Jammu and Kashmir, Rajasthan and Punjab are preferred as leisure destinations. For religious tourism, they prefer states of Rajasthan, Uttar Pradesh, Uttarakhand and Jammu and Kashmir. While multiple tourism circuits based on diverse themes exist across northern states, low level of stay durations by both domestic and international tourists indicates the need for more entertainment and leisure activities.

Abundant natural and cultural resources in the northern states provide ample opportunities for development of diverse tourism products along with a single integrated tourism circuit. While an array of ancient and modern temples may provide an opportunity for developing states in northern India to emerge pilgrimage destinations, presence of palaces, forts and historical monuments help define their multi cultural heritage. Also, wildlife sanctuaries with a wide variety of flora and fauna, mighty Himalayas, rivers, deserts, climate and diverse landscape provide attractive opportunities for thrill and adventure activities.

Serene valleys of Himachal Pradesh provide an opportunity to promote medical, wellness and

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

01

Executive summary

Source:

India Tourism Statistics 2008, Ministry of Tourism and http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

WTTC travel and tourism economic impact 2013- India, Data taken at Nominal Prices

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

02Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

spiritual tourism in the state. Its topography provides innumerable opportunities to promote adventure tourism with sport activities like river rafting, para-gliding, trekking etc. Scenic landscape, castles, gardens and forts in the state of Jammu and Kashmir attract tourists worldwide. Presence of holy shrines, ancient temples and mosques also provide an opportunity for promoting spiritual tourism. Pilgrimage destinations in Haryana offer a wide range of sacred places with religious and historical significance. While Delhi is a major commercial and business destination, it offers tourism opportunities in form of political landmarks, national museums, Islamic shrines, Hindu temples, green parks, trendy malls etc. Punjab offers an opportunity for utilising its culture, ancient civilisation, spirituality and epic history for promoting tourism. Vast sand dunes of the Thar desert in Rajasthan along with the palaces and forts and rich cultural heritage attract tourists worldwide. While the glaciers, snow-clad mountains, valley of flowers, skiing slopes and dense forests in Uttarakhand are attractive tourist destinations, presence of shrines and pilgrimage destinations provides opportunity for promoting spiritual tourism. The tourism sector in India faces several issues which require immediate attention. Several recommendations may be suggested based on studies of successful domestic and international tourism case studies.

• India’s image needs to be projected as a safe and secure tourist destination

• Regulatory and policy changes may be introduced in order to increase international tourist inflow

• Private sector investments may be encouraged through provision of fiscal and non fiscal incentives for boosting infrastructure development

• New tourist destinations may be identified and further development of the same for offering innovative tourism products or experiences

• Integrated tourism circuits may be developed across states based on attributes, tourism potential, current and future connectivity and synergy within destinations

• Seamless travel may be facilitated across integrated circuits through introduction of integrated taxation regime, linkages between various public transportation modes and improvements in highway infrastructure such as petrol pumps, clean drinking water kiosks and sanitation facilities, road signages etc.

• Joint marketing programmes may be developed, usage of publicity material like brochures, print creative, audio video presentations, short films, radio jingles, online creatives and advertisements over media channels may be promoted and innovative marketing techniques over social media channels may be adopted along with increased involvement of local travel trade partners for promoting tourism in integrated circuits

• Participation in international events may be increased and customised tour packages with competitive pricing may be developed keeping in mind the profile of visitors, budget and travel requirements

• Training and skill development programmes may be introduced in order to not only meet the anticipated manpower shortfall but also develop an adequately skilled workforce

• Local community involvement may be encouraged through awareness programmes and workshops for sustainable development and maintenance of tourism in the country.

Successful implementation of such recommendations may be achieved through government ownership of development programmes and active participation and involvement of private sector.

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Introduction

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

03

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1.1 Global tourism industry

The travel and tourism industry has emerged as one of the largest and fastest growing economic sectors globally. According to the United Nations World Tourism Organization (UNWTO) Tourism Highlights 2013, tourism’s total contribution to worldwide GDP is estimated at 9 per cent. Tourism exports in 2012 amounted

to USD 1.3 trillion accounting for 6 per cent of the world’s exports. New tourist destinations, especially those in the emerging markets have started gaining prominence with traditional markets reaching maturity. Asia Pacific recorded the highest growth in the number of international tourist arrivals in 2012 at 7 per cent followed by Africa at 6 per cent.

Source: UNWTO Tourism Highlights, 2013

Figure 1.1: International tourist arrivals, million

International tourist arrivals are set to increase at a growth rate of 3.3 per cent per annum and amount to approximately 1.4 billion by 2020 and 1.8 billion by 2030 implying an increase of 43 million international tourist arrivals each year.

While international tourist arrivals in Europe and America are expected to witness modest growth rates of 2.5 per cent and 2.2 per cent respectively by 2030, Africa and Asia Pacific regions are expected to witness higher growth

rates at 5.7 per cent and 5.0 per cent per annum during the same period.

The global travel and tourism industry is expected to witness certain key trends:

• Increased inter region travel and hence increased air travel

• Arrivals for the purpose of visiting friends and relatives, health, religion etc. are expected to witness faster growth than those for business and professional purposes

04Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1.2.1 Growth in number of tourists

With the international tourist arrivals in India (pegged at 7.5 million in 2013) expected to witness an annual growth rate of 6.2 per cent over the next decade, visitor exports (expenditure generated by foreign tourists) are expected to amount to INR 2958 billion by 2023 growing at 9.6 per cent per annum3.

This growth can mainly be attributed to the rising income levels and changing lifestyles, diverse tourism offerings and policy & infrastructural support by the government such as simplification of visa procedures and tax holidays for hotels.

Source: India Tourism Statistics 2008, 2009, 2010, 2011, Ministry of Tourism

http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

Note: Domestic and foreign tourist visits to various states and union territories in India

Figure 1.2: Tourist visits in India, million

1. India Tourism Statistics 2008, Ministry of Tourism

2. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

3. WTTC travel and tourism Economic Impact 2013- India, Data taken at Nominal Prices

1.2 Indian tourism industry

The travel and tourism sector holds strategic importance in the Indian economy providing several socio economic benefits. Provision of employment, income and foreign exchange, development or expansion of other industries such as agriculture, construction, handicrafts etc. are some of the important economic benefits provided by the tourism sector. In addition, investments in infrastructural facilities such as transportation,

accommodation and other tourism related services lead to an overall development of infrastructure in the economy. According to the World Economic Forum’s Travel and Tourism Competitiveness Report 2013, India ranks 11th in the Asia pacific region and 65th globally out of 140 economies ranked on travel and tourism Competitiveness Index. India has been witnessing steady growth in its travel and tourism sector over the

past few years. Total tourist visits have increased at a rate of 16.3 per cent per annum from 577 million tourists in 20081 to 1057 million tourists in 20122.

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

05

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Source: WTTC Travel & Tourism Economic Impact 2013- India

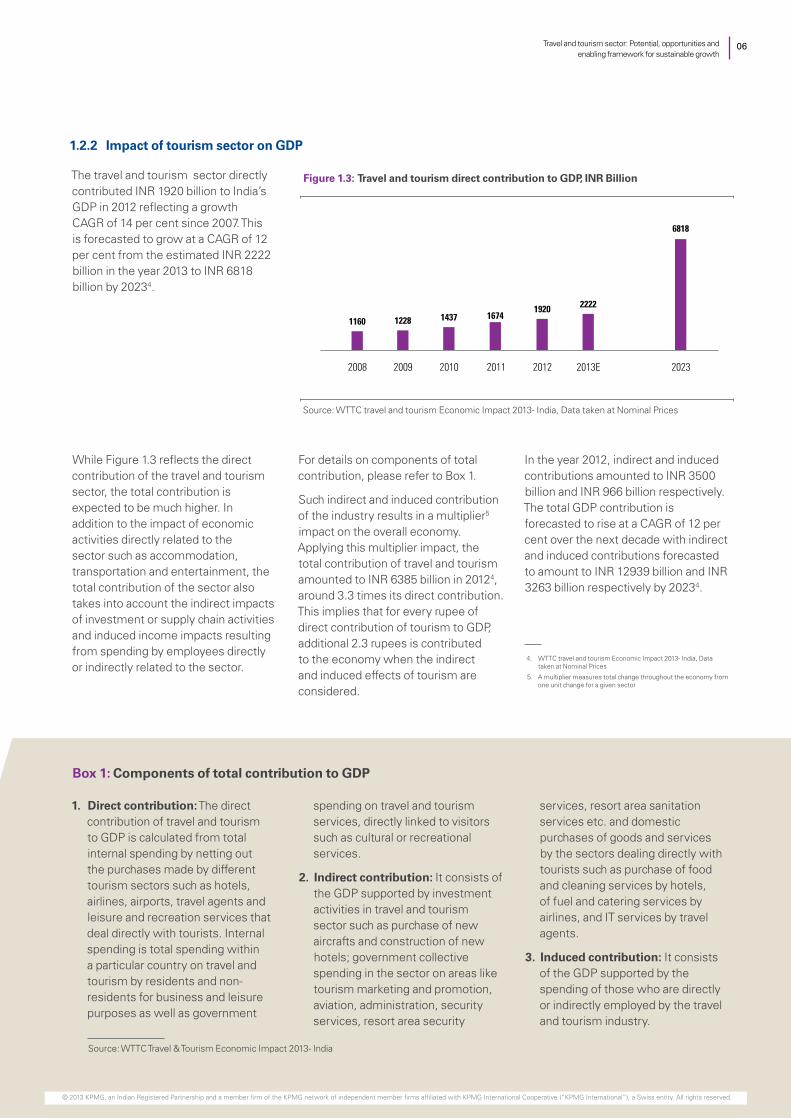

1.2.2 Impact of tourism sector on GDP

The travel and tourism sector directly contributed INR 1920 billion to India’s GDP in 2012 reflecting a growth CAGR of 14 per cent since 2007. This is forecasted to grow at a CAGR of 12 per cent from the estimated INR 2222 billion in the year 2013 to INR 6818 billion by 20234.

Box 1: Components of total contribution to GDP

1. Direct contribution: The direct contribution of travel and tourism to GDP is calculated from total internal spending by netting out the purchases made by different tourism sectors such as hotels, airlines, airports, travel agents and leisure and recreation services that deal directly with tourists. Internal spending is total spending within a particular country on travel and tourism by residents and non-residents for business and leisure purposes as well as government

spending on travel and tourism services, directly linked to visitors such as cultural or recreational services.

2. Indirect contribution: It consists of the GDP supported by investment activities in travel and tourism sector such as purchase of new aircrafts and construction of new hotels; government collective spending in the sector on areas like tourism marketing and promotion, aviation, administration, security services, resort area security

services, resort area sanitation services etc. and domestic purchases of goods and services by the sectors dealing directly with tourists such as purchase of food and cleaning services by hotels, of fuel and catering services by airlines, and IT services by travel agents.

3. Induced contribution: It consists of the GDP supported by the spending of those who are directly or indirectly employed by the travel and tourism industry.

Source: WTTC travel and tourism Economic Impact 2013- India, Data taken at Nominal Prices

Figure 1.3: Travel and tourism direct contribution to GDP, INR Billion

While Figure 1.3 reflects the direct contribution of the travel and tourism sector, the total contribution is expected to be much higher. In addition to the impact of economic activities directly related to the sector such as accommodation, transportation and entertainment, the total contribution of the sector also takes into account the indirect impacts of investment or supply chain activities and induced income impacts resulting from spending by employees directly or indirectly related to the sector.

For details on components of total contribution, please refer to Box 1.

Such indirect and induced contribution of the industry results in a multiplier5 impact on the overall economy. Applying this multiplier impact, the total contribution of travel and tourism amounted to INR 6385 billion in 20124, around 3.3 times its direct contribution. This implies that for every rupee of direct contribution of tourism to GDP, additional 2.3 rupees is contributed to the economy when the indirect and induced effects of tourism are considered.

In the year 2012, indirect and induced contributions amounted to INR 3500 billion and INR 966 billion respectively. The total GDP contribution is forecasted to rise at a CAGR of 12 per cent over the next decade with indirect and induced contributions forecasted to amount to INR 12939 billion and INR 3263 billion respectively by 20234.

4. WTTC travel and tourism Economic Impact 2013- India, Data taken at Nominal Prices

5. A multiplier measures total change throughout the economy from one unit change for a given sector

06Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1.2.3 Impact of tourism sector on employment

The travel and tourism sector supported 25 million jobs in 2012 directly related to the tourism sector. Constituting 4.9 per cent of the total employment in the country in 2012, this is expected to amount to 31 million jobs by 20237.

While these numbers indicate direct employment supported by the tourism sector reflecting employment by

hotels, travel agents, passenger transportation services or other restaurant and leisure employment, the total contribution including indirect and induced effects is expected to cause a multiplier impact on the economy resulting in greater employment generation.

Applying this multiplier impact, the travel and tourism sector supported

a total employment of 40 million jobs in 2012 constituting 7.7 per cent of the whole economy employment7. This implies that for every job directly supported by the tourism sector, an additional 0.6 job is supported in the economy when the indirect and induced effects of tourism is considered.

7. WTTC travel and tourism Economic Impact 2013- India, Data taken at Nominal Prices

1.2.4 Capital investment in tourism sector

Capital investments in the tourism sector include spending by all sectors directly involved in the travel and tourism industry. Spending by other industries on specific tourism assets such as new visitor accommodation and passenger transport equipment, as well as restaurants and leisure

facilities for specific tourism use also form part of capital investments. Such investments lead to social development of an economy as infrastructure created for tourism purposes in areas of transportation, accommodation etc. can also be utilised by the community in general.

Source: WTTC travel and tourism Economic Impact 2013- India, Data taken at Nominal Prices

Figure 1.4: Capital investment in travel & tourism sector, INR billion

Capital investment in the travel and tourism sector in 2012 was estimated at INR 1761.4 billion amounting to approximately 6.2 per cent of total investment in the Indian economy. It is

expected to increase by 14.2 per cent in 2013, and witness further annual growth rate of 10.5 per cent by 2023 amounting to INR 5459 billion7.

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

07

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

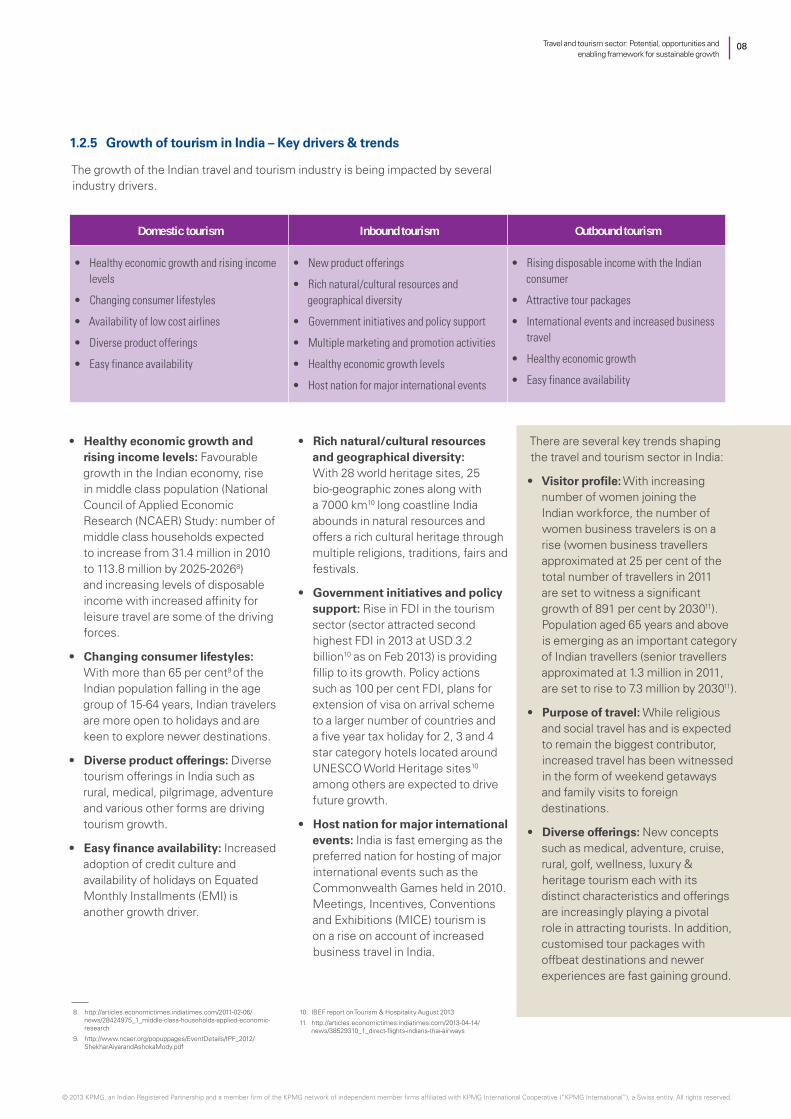

1.2.5 Growth of tourism in India – Key drivers & trends

The growth of the Indian travel and tourism industry is being impacted by several industry drivers.

Domestic tourism Inbound tourism Outbound tourism

• Healthy economic growth and rising income levels

• Changing consumer lifestyles

• Availability of low cost airlines

• Diverse product offerings

• Easy finance availability

• New product offerings

• Rich natural/cultural resources and geographical diversity

• Government initiatives and policy support

• Multiple marketing and promotion activities

• Healthy economic growth levels

• Host nation for major international events

• Rising disposable income with the Indian consumer

• Attractive tour packages

• International events and increased business travel

• Healthy economic growth

• Easy finance availability

• Healthy economic growth and rising income levels: Favourable growth in the Indian economy, rise in middle class population (National Council of Applied Economic Research (NCAER) Study: number of middle class households expected to increase from 31.4 million in 2010 to 113.8 million by 2025-20268) and increasing levels of disposable income with increased affinity for leisure travel are some of the driving forces.

• Changing consumer lifestyles: With more than 65 per cent9 of the Indian population falling in the age group of 15-64 years, Indian travelers are more open to holidays and are keen to explore newer destinations.

• Diverse product offerings: Diverse tourism offerings in India such as rural, medical, pilgrimage, adventure and various other forms are driving tourism growth.

• Easy finance availability: Increased adoption of credit culture and availability of holidays on Equated Monthly Installments (EMI) is another growth driver.

• Rich natural/cultural resources and geographical diversity: With 28 world heritage sites, 25 bio-geographic zones along with a 7000 km10 long coastline India abounds in natural resources and offers a rich cultural heritage through multiple religions, traditions, fairs and festivals.

• Government initiatives and policy support: Rise in FDI in the tourism sector (sector attracted second highest FDI in 2013 at USD 3.2 billion10 as on Feb 2013) is providing fillip to its growth. Policy actions such as 100 per cent FDI, plans for extension of visa on arrival scheme to a larger number of countries and a five year tax holiday for 2, 3 and 4 star category hotels located around UNESCO World Heritage sites10 among others are expected to drive future growth.

• Host nation for major international events: India is fast emerging as the preferred nation for hosting of major international events such as the Commonwealth Games held in 2010. Meetings, Incentives, Conventions and Exhibitions (MICE) tourism is on a rise on account of increased business travel in India.

There are several key trends shaping the travel and tourism sector in India:

• Visitor profile: With increasing number of women joining the Indian workforce, the number of women business travelers is on a rise (women business travellers approximated at 25 per cent of the total number of travellers in 2011 are set to witness a significant growth of 891 per cent by 203011). Population aged 65 years and above is emerging as an important category of Indian travellers (senior travellers approximated at 1.3 million in 2011, are set to rise to 7.3 million by 203011).

• Purpose of travel: While religious and social travel has and is expected to remain the biggest contributor, increased travel has been witnessed in the form of weekend getaways and family visits to foreign destinations.

• Diverse offerings: New concepts such as medical, adventure, cruise, rural, golf, wellness, luxury & heritage tourism each with its distinct characteristics and offerings are increasingly playing a pivotal role in attracting tourists. In addition, customised tour packages with offbeat destinations and newer experiences are fast gaining ground.

8. http://articles.economictimes.indiatimes.com/2011-02-06/news/28424975_1_middle-class-households-applied-economic-research

9. http://www.ncaer.org/popuppages/EventDetails/IPF_2012/ShekharAiyarandAshokaMody.pdf

10. IBEF report on Tourism & Hospitality August 2013

11. http://articles.economictimes.indiatimes.com/2013-04-14/news/38529310_1_direct-flights-indians-thai-airways

08Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Performance of tourism sector in various states of

India

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

09

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

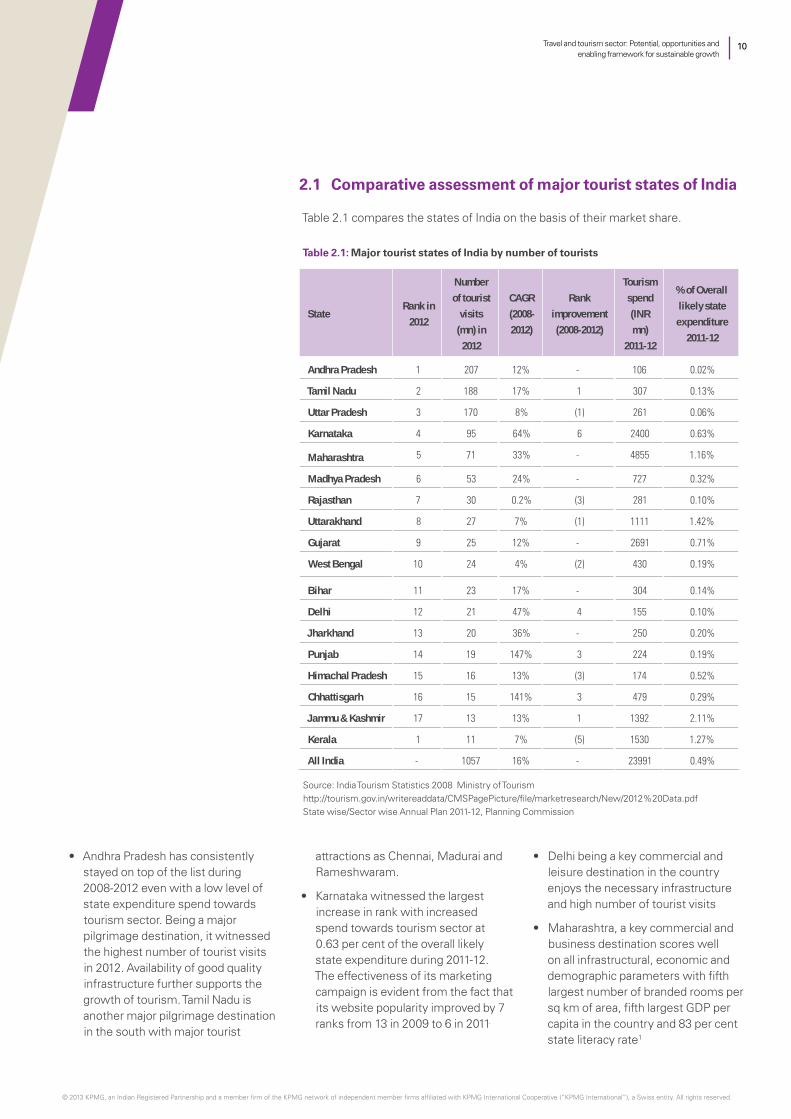

2.1 Comparative assessment of major tourist states of India

Table 2.1 compares the states of India on the basis of their market share.

StateRank in

2012

Number of tourist

visits (mn) in

2012

CAGR (2008-2012)

Rank improvement (2008-2012)

Tourism spend (INR mn)

2011-12

% of Overall likely state

expenditure2011-12

Andhra Pradesh 1 207 12% - 106 0.02%

Tamil Nadu 2 188 17% 1 307 0.13%

Uttar Pradesh 3 170 8% (1) 261 0.06%

Karnataka 4 95 64% 6 2400 0.63%

Maharashtra 5 71 33% - 4855 1.16%

Madhya Pradesh 6 53 24% - 727 0.32%

Rajasthan 7 30 0.2% (3) 281 0.10%

Uttarakhand 8 27 7% (1) 1111 1.42%

Gujarat 9 25 12% - 2691 0.71%

West Bengal 10 24 4% (2) 430 0.19%

Bihar 11 23 17% - 304 0.14%

Delhi 12 21 47% 4 155 0.10%

Jharkhand 13 20 36% - 250 0.20%

Punjab 14 19 147% 3 224 0.19%

Himachal Pradesh 15 16 13% (3) 174 0.52%

Chhattisgarh 16 15 141% 3 479 0.29%

Jammu & Kashmir 17 13 13% 1 1392 2.11%

Kerala 1 11 7% (5) 1530 1.27%

All India - 1057 16% - 23991 0.49%

Table 2.1: Major tourist states of India by number of tourists

Source: India Tourism Statistics 2008 Ministry of Tourismhttp://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdfState wise/Sector wise Annual Plan 2011-12, Planning Commission

• Andhra Pradesh has consistently stayed on top of the list during 2008-2012 even with a low level of state expenditure spend towards tourism sector. Being a major pilgrimage destination, it witnessed the highest number of tourist visits in 2012. Availability of good quality infrastructure further supports the growth of tourism. Tamil Nadu is another major pilgrimage destination in the south with major tourist

attractions as Chennai, Madurai and Rameshwaram.

• Karnataka witnessed the largest increase in rank with increased spend towards tourism sector at 0.63 per cent of the overall likely state expenditure during 2011-12. The effectiveness of its marketing campaign is evident from the fact that its website popularity improved by 7 ranks from 13 in 2009 to 6 in 2011.

• Delhi being a key commercial and leisure destination in the country enjoys the necessary infrastructure and high number of tourist visits

• Maharashtra, a key commercial and business destination scores well on all infrastructural, economic and demographic parameters with fifth largest number of branded rooms per sq km of area, fifth largest GDP per capita in the country and 83 per cent state literacy rate1

10Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1. HVS State Ranking Survey 2011

2. http://www.exchange4media.com/50324_new-mp-tourism-ad-passes-with-flying-colours.html

• Gujarat with 0.71 per cent of state expenditure allocated for the tourism sector witnessed a considerable increase in its budgetary allocation proportion. With the success of the Gujarat tourism campaign with the brand ambassador as Amitabh Bachchan and other marketing and promotional activities, Gujarat has improved upon its tourism appeal many fold. For a detailed case study on Gujarat, please refer to Box 2

• Marketing and promotional campaigns such as ‘Bioscope : Hindustan Ka Dil Dekho’ in 2006, ‘Eyes Campaign’ and advertisements with hand shadowgraphy with the theme as ‘MP ajab hai, sabse gajab hai’ in 2010 helped Madhya Pradesh gain

position amongst the top 10 tourist states of India. New ad campaigns based on the idea of presenting the state through beautiful, vivid colours in 2013 are expected to further augment the tourism potential of the state2

• Rajasthan, West Bengal, Himachal Pradesh, Uttarakhand and Kerala are states that have witnessed decline in their positions as preferred tourist destinations. While an increase in funds allocated towards tourism sector in these states is required, effective implementation of the funds may require careful assessment of the impact of marketing and promotion activities in the state. Other areas requiring

consideration are improvements in overall state infrastructure

• While Kerala scores highest on literacy levels, low GDP per capita and low urbanisation levels have had a negative effect on the tourism appeal. However, adequate infrastructure in areas of accommodation and passenger transportation along with the government’s focused marketing and promotion activities are expected to help Kerala regain its lost position. For a detailed case study on Kerala please refer to Box 3.

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

11

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Box 2: Case study on tourism in Gujarat

The state government of Gujarat has taken multiple initiatives in order to enhance the tourism appeal of the state. Some of these are:

• Land bank scheme: Areas have been earmarked in the Gujarat Industrial Development Corporation estates and SEZs for development of hotels, resorts, restaurants and other tourist amenities. Concessions are provided either on lease and its tenure or on the rate to be charged for government land and on stamp duty and registration fee on land transaction for tourism projects.

• Tourism incentive package scheme: Special incentives are proposed to be provided over 2010-2015 including tax holidays on luxury tax on hotels, reduction in VAT charges on food and beverages and natural gas, reduction in entertainment tax, concessions such as interest subsidy, reduction of electricity duty and modifications in the lending criteria to cover wider tourism related projects like amusement parks, wayside facilities, service oriented projects like travel agencies, tour operators etc.

• Marketing & branding: Brand campaign ‘Khushboo Gujarat Ki’ was launched with Amitabh Bachchan as the brand ambassador to increase awareness of the state’s diverse tourism aspects. Several tourism information centres have been opened across India. The state website has been launched in seven different languages, especially to cater to both national and international tourists.

• Exhibitions, events & road shows: Gujarat tourism organises several exhibitions and road shows especially in the southern India for marketing diverse tourism aspects of Gujarat. Several road shows for 2013 have been planned in states of Kolkata, Hyderabad, Guwahati, Bangalore, Chennai, Ludhiana and Aurangabad. Events such as kite flying festivals are organised in order to attract tourists from various

countries. In addition events like Gujarat Tourism Summit and Gujarat Travel Mart help create tourism potential awareness across all stakeholders. Gujarat tourism has signed various MoUs with various states such as West Bengal, Tamil Nadu, Rajasthan, Kerala, Uttar Pradesh and Himachal Pradesh for collaborative tourism development.

• Infrastructure development: An outlay of INR 7.3 billion has been planned for development of tourism infrastructure in 22 districts across the state. PPP is being encouraged for the development of accommodation facilities, booking infrastructure, site operations and retail and development of eight tourism hubs. Government has entered into a tie up with IL&FS to develop 50 tourism sites and more than INR 20 billion of tourism related infra investments.

• Kids tourism, golf tourism and coastal tourism: Gujarat Tourism plans to introduce kids tourism during summer vacations in places that would be of interest to kids. Another new tourism concept on ‘Rama trail is planned to make tourists experience the journey that Lord Rama, Sita and Laxman undertook as part of their 14-year exile covering locations such as Sita Van, Ram Sarovar, Unai and Shabari Dham. For promotion of golf tourism in the state, private golf courses have been planned for development. There are plans to develop cruise terminals for dolphin sighting trips etc. for boosting coastal tourism in the state for which INR 1.6 billion have been allocated across 16 identified beaches.

• Training & skill development: Training and skill development for employees engaged in providing tourism services through 335 Kaushalya Vardhan Kendras providing vocational skills to rural youth in various sectors including tourism.

Source:

http://www.gujarattourism.com/downloads/tourism_sector_profile_new.pdf

http://www.india.diplo.de/contentblob/3839178/Daten/3075252/Economics_India_Figures_Gujarat_VDMA_Report_DD.pdf

http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Gujarat.pdf

http://www.vibrantgujarat.com/images/pdf/Service-Sector-Profile.pdf

12Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

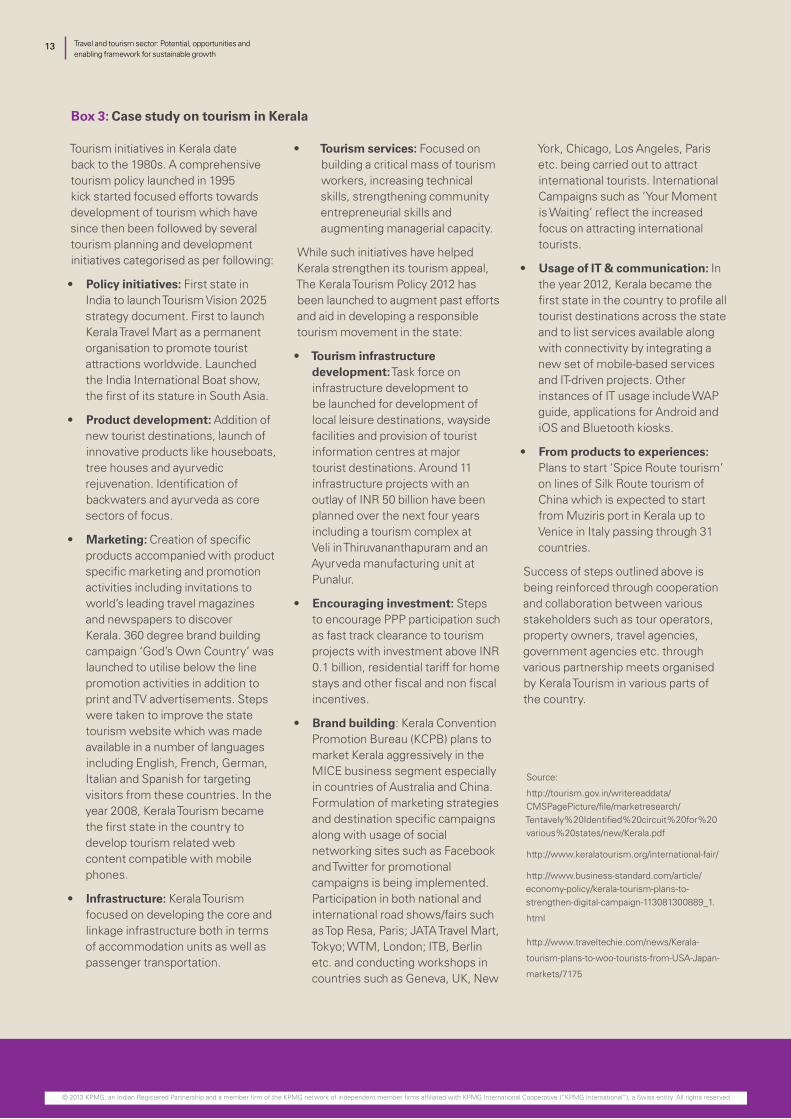

Box 3: Case study on tourism in Kerala

Tourism initiatives in Kerala date back to the 1980s. A comprehensive tourism policy launched in 1995 kick started focused efforts towards development of tourism which have since then been followed by several tourism planning and development initiatives categorised as per following:

• Policy initiatives: First state in India to launch Tourism Vision 2025 strategy document. First to launch Kerala Travel Mart as a permanent organisation to promote tourist attractions worldwide. Launched the India International Boat show, the first of its stature in South Asia.

• Product development: Addition of new tourist destinations, launch of innovative products like houseboats, tree houses and ayurvedic rejuvenation. Identification of backwaters and ayurveda as core sectors of focus.

• Marketing: Creation of specific products accompanied with product specific marketing and promotion activities including invitations to world’s leading travel magazines and newspapers to discover Kerala. 360 degree brand building campaign ‘God’s Own Country’ was launched to utilise below the line promotion activities in addition to print and TV advertisements. Steps were taken to improve the state tourism website which was made available in a number of languages including English, French, German, Italian and Spanish for targeting visitors from these countries. In the year 2008, Kerala Tourism became the first state in the country to develop tourism related web content compatible with mobile phones.

• Infrastructure: Kerala Tourism focused on developing the core and linkage infrastructure both in terms of accommodation units as well as passenger transportation.

• Tourism services: Focused on building a critical mass of tourism workers, increasing technical skills, strengthening community entrepreneurial skills and augmenting managerial capacity.

While such initiatives have helped Kerala strengthen its tourism appeal, The Kerala Tourism Policy 2012 has been launched to augment past efforts and aid in developing a responsible tourism movement in the state:

• Tourism infrastructure development: Task force on infrastructure development to be launched for development of local leisure destinations, wayside facilities and provision of tourist information centres at major tourist destinations. Around 11 infrastructure projects with an outlay of INR 50 billion have been planned over the next four years including a tourism complex at Veli in Thiruvananthapuram and an Ayurveda manufacturing unit at Punalur.

• Encouraging investment: Steps to encourage PPP participation such as fast track clearance to tourism projects with investment above INR 0.1 billion, residential tariff for home stays and other fiscal and non fiscal incentives.

• Brand building: Kerala Convention Promotion Bureau (KCPB) plans to market Kerala aggressively in the MICE business segment especially in countries of Australia and China. Formulation of marketing strategies and destination specific campaigns along with usage of social networking sites such as Facebook and Twitter for promotional campaigns is being implemented. Participation in both national and international road shows/fairs such as Top Resa, Paris; JATA Travel Mart, Tokyo; WTM, London; ITB, Berlin etc. and conducting workshops in countries such as Geneva, UK, New

York, Chicago, Los Angeles, Paris etc. being carried out to attract international tourists. International Campaigns such as ‘Your Moment is Waiting’ reflect the increased focus on attracting international tourists.

• Usage of IT & communication: In the year 2012, Kerala became the first state in the country to profile all tourist destinations across the state and to list services available along with connectivity by integrating a new set of mobile-based services and IT-driven projects. Other instances of IT usage include WAP guide, applications for Android and iOS and Bluetooth kiosks.

• From products to experiences: Plans to start ‘Spice Route tourism’ on lines of Silk Route tourism of China which is expected to start from Muziris port in Kerala up to Venice in Italy passing through 31 countries.

Success of steps outlined above is being reinforced through cooperation and collaboration between various stakeholders such as tour operators, property owners, travel agencies, government agencies etc. through various partnership meets organised by Kerala Tourism in various parts of the country.

Source:

http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Kerala.pdf

http://www.keralatourism.org/international-fair/

http://www.business-standard.com/article/economy-policy/kerala-tourism-plans-to-strengthen-digital-campaign-113081300889_1.

html

http://www.traveltechie.com/news/Kerala-

tourism-plans-to-woo-tourists-from-USA-Japan-

markets/7175

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

13

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

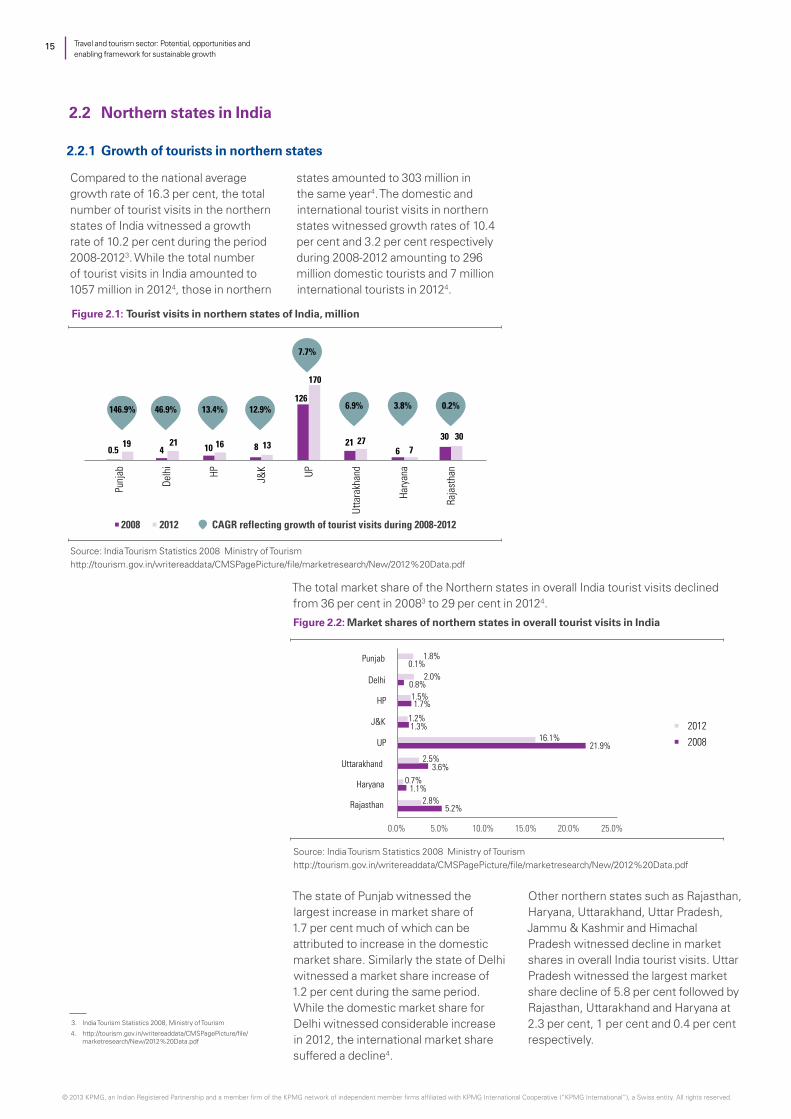

2.2.1 Growth of tourists in northern states

Compared to the national average growth rate of 16.3 per cent, the total number of tourist visits in the northern states of India witnessed a growth rate of 10.2 per cent during the period 2008-20123. While the total number of tourist visits in India amounted to 1057 million in 20124, those in northern

states amounted to 303 million in the same year4. The domestic and international tourist visits in northern states witnessed growth rates of 10.4 per cent and 3.2 per cent respectively during 2008-2012 amounting to 296 million domestic tourists and 7 million international tourists in 20124.

0.5 4 10 8

126

216

3019 21 16 13

170

277

30

Punj

ab

Del

hi HP

J&K

UP

Utt

arak

hand

Har

yana

Raj

asth

an

146.9% 46.9% 13.4% 12.9%

7.7%

6.9% 3.8% 0.2%

2008 2012 CAGR reflecting growth of tourist visits during 2008-2012

Source: India Tourism Statistics 2008 Ministry of Tourismhttp://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

Figure 2.1: Tourist visits in northern states of India, million

3. India Tourism Statistics 2008, Ministry of Tourism

4. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

2.2 Northern states in India

The total market share of the Northern states in overall India tourist visits declined from 36 per cent in 20083 to 29 per cent in 20124.

Source: India Tourism Statistics 2008 Ministry of Tourismhttp://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

Figure 2.2: Market shares of northern states in overall tourist visits in India

The state of Punjab witnessed the largest increase in market share of 1.7 per cent much of which can be attributed to increase in the domestic market share. Similarly the state of Delhi witnessed a market share increase of 1.2 per cent during the same period. While the domestic market share for Delhi witnessed considerable increase in 2012, the international market share suffered a decline4.

Other northern states such as Rajasthan, Haryana, Uttarakhand, Uttar Pradesh, Jammu & Kashmir and Himachal Pradesh witnessed decline in market shares in overall India tourist visits. Uttar Pradesh witnessed the largest market share decline of 5.8 per cent followed by Rajasthan, Uttarakhand and Haryana at 2.3 per cent, 1 per cent and 0.4 per cent respectively.

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

15

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

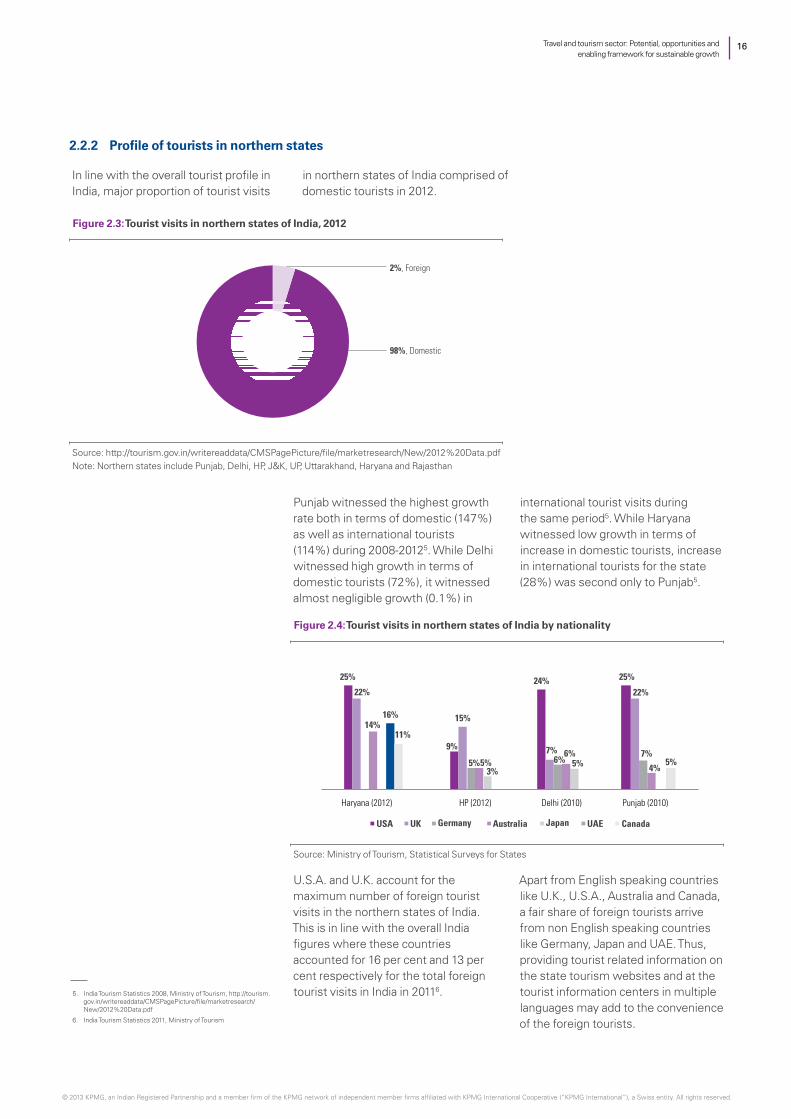

2.2.2 Profile of tourists in northern states

In line with the overall tourist profile in India, major proportion of tourist visits

in northern states of India comprised of domestic tourists in 2012.

Source: http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdfNote: Northern states include Punjab, Delhi, HP, J&K, UP, Uttarakhand, Haryana and Rajasthan

Figure 2.3: Tourist visits in northern states of India, 2012

Punjab witnessed the highest growth rate both in terms of domestic (147%) as well as international tourists (114%) during 2008-20125. While Delhi witnessed high growth in terms of domestic tourists (72%), it witnessed almost negligible growth (0.1%) in

international tourist visits during the same period5. While Haryana witnessed low growth in terms of increase in domestic tourists, increase in international tourists for the state (28%) was second only to Punjab5.

Source: Ministry of Tourism, Statistical Surveys for States

Figure 2.4: Tourist visits in northern states of India by nationality

U.S.A. and U.K. account for the maximum number of foreign tourist visits in the northern states of India. This is in line with the overall India figures where these countries accounted for 16 per cent and 13 per cent respectively for the total foreign tourist visits in India in 20116.

Apart from English speaking countries like U.K., U.S.A., Australia and Canada, a fair share of foreign tourists arrive from non English speaking countries like Germany, Japan and UAE. Thus, providing tourist related information on the state tourism websites and at the tourist information centers in multiple languages may add to the convenience of the foreign tourists.

5. India Tourism Statistics 2008, Ministry of Tourism, http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/New/2012%20Data.pdf

6. India Tourism Statistics 2011, Ministry of Tourism

16Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

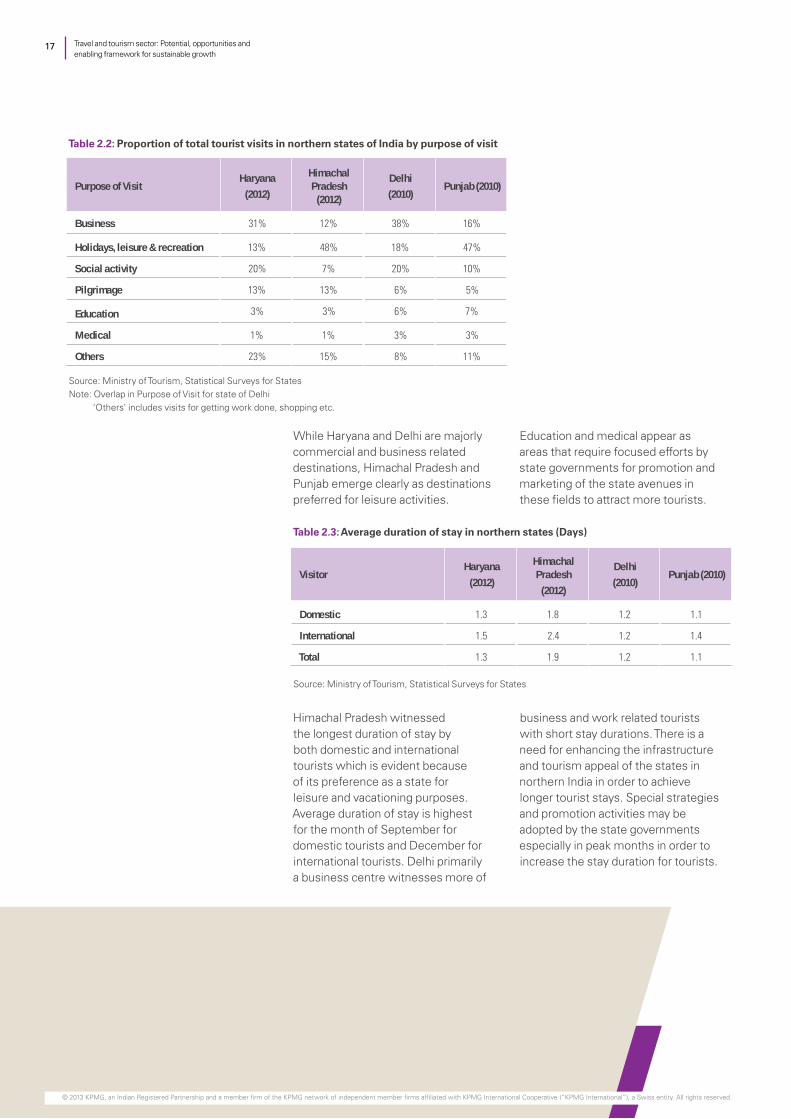

While Haryana and Delhi are majorly commercial and business related destinations, Himachal Pradesh and Punjab emerge clearly as destinations preferred for leisure activities.

Education and medical appear as areas that require focused efforts by state governments for promotion and marketing of the state avenues in these fields to attract more tourists.

Purpose of Visit Haryana

(2012)

Himachal Pradesh

(2012)

Delhi (2010)

Punjab (2010)

Business 31% 12% 38% 16%

Holidays, leisure & recreation 13% 48% 18% 47%

Social activity 20% 7% 20% 10%

Pilgrimage 13% 13% 6% 5%

Education 3% 3% 6% 7%

Medical 1% 1% 3% 3%

Others 23% 15% 8% 11%

Table 2.2: Proportion of total tourist visits in northern states of India by purpose of visit

Source: Ministry of Tourism, Statistical Surveys for StatesNote: Overlap in Purpose of Visit for state of Delhi

‘Others’ includes visits for getting work done, shopping etc.

Visitor Haryana

(2012)

Himachal Pradesh

(2012)

Delhi (2010)

Punjab (2010)

Domestic 1.3 1.8 1.2 1.1

International 1.5 2.4 1.2 1.4

Total 1.3 1.9 1.2 1.1

Table 2.3: Average duration of stay in northern states (Days)

Source: Ministry of Tourism, Statistical Surveys for States

Himachal Pradesh witnessed the longest duration of stay by both domestic and international tourists which is evident because of its preference as a state for leisure and vacationing purposes. Average duration of stay is highest for the month of September for domestic tourists and December for international tourists. Delhi primarily a business centre witnesses more of

business and work related tourists with short stay durations. There is a need for enhancing the infrastructure and tourism appeal of the states in northern India in order to achieve longer tourist stays. Special strategies and promotion activities may be adopted by the state governments especially in peak months in order to increase the stay duration for tourists.

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

17

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

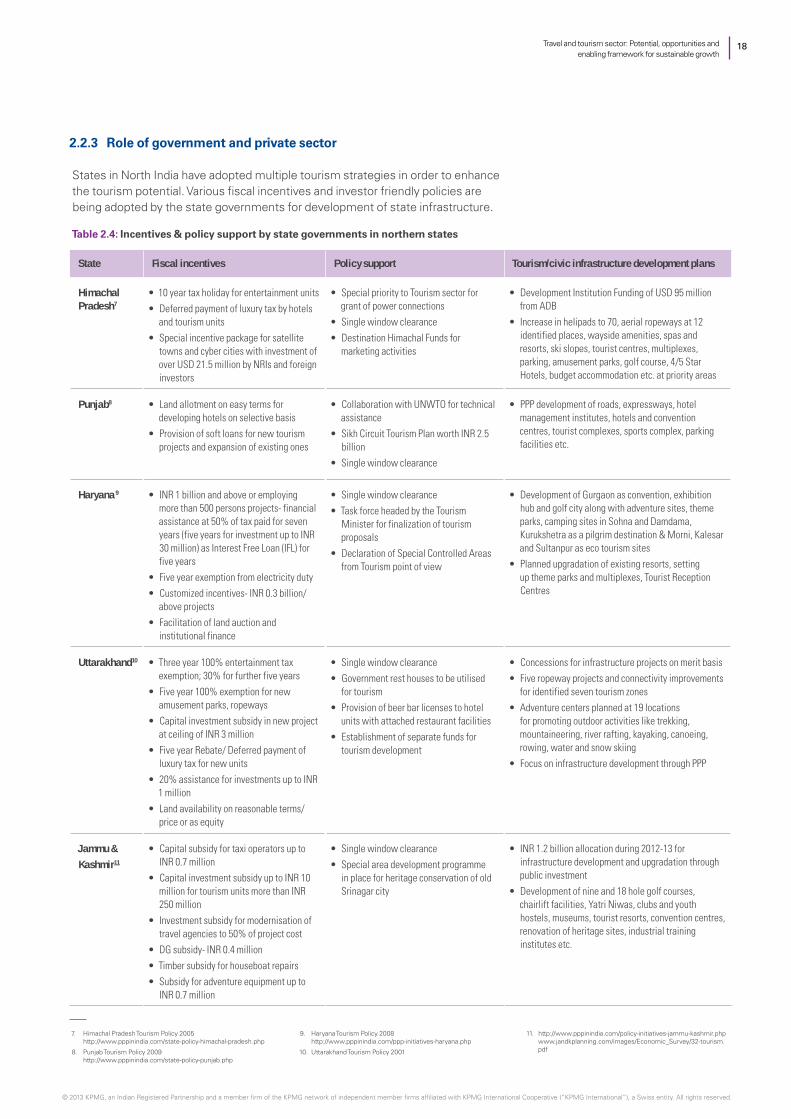

2.2.3 Role of government and private sector

States in North India have adopted multiple tourism strategies in order to enhance the tourism potential. Various fiscal incentives and investor friendly policies are being adopted by the state governments for development of state infrastructure.

7. Himachal Pradesh Tourism Policy 2005 http://www.pppinindia.com/state-policy-himachal-pradesh.php

8. Punjab Tourism Policy 2009 http://www.pppinindia.com/state-policy-punjab.php

State Fiscal incentives Policy support Tourism/civic infrastructure development plans

Himachal Pradesh7

• 10 year tax holiday for entertainment units • Deferred payment of luxury tax by hotels

and tourism units• Special incentive package for satellite

towns and cyber cities with investment of over USD 21.5 million by NRIs and foreign investors

• Special priority to Tourism sector for grant of power connections

• Single window clearance • Destination Himachal Funds for

marketing activities

• Development Institution Funding of USD 95 million from ADB

• Increase in helipads to 70, aerial ropeways at 12 identified places, wayside amenities, spas and resorts, ski slopes, tourist centres, multiplexes, parking, amusement parks, golf course, 4/5 Star Hotels, budget accommodation etc. at priority areas

Punjab8 • Land allotment on easy terms for developing hotels on selective basis

• Provision of soft loans for new tourism projects and expansion of existing ones

• Collaboration with UNWTO for technical assistance

• Sikh Circuit Tourism Plan worth INR 2.5 billion

• Single window clearance

• PPP development of roads, expressways, hotel management institutes, hotels and convention centres, tourist complexes, sports complex, parking facilities etc.

Haryana 9 • INR 1 billion and above or employing more than 500 persons projects- financial assistance at 50% of tax paid for seven years (five years for investment up to INR 30 million) as Interest Free Loan (IFL) for five years

• Five year exemption from electricity duty • Customized incentives- INR 0.3 billion/

above projects• Facilitation of land auction and

institutional finance

• Single window clearance • Task force headed by the Tourism

Minister for finalization of tourism proposals

• Declaration of Special Controlled Areas from Tourism point of view

• Development of Gurgaon as convention, exhibition hub and golf city along with adventure sites, theme parks, camping sites in Sohna and Damdama, Kurukshetra as a pilgrim destination & Morni, Kalesar and Sultanpur as eco tourism sites

• Planned upgradation of existing resorts, setting up theme parks and multiplexes, Tourist Reception Centres

Uttarakhand10 • Three year 100% entertainment tax exemption; 30% for further five years

• Five year 100% exemption for new amusement parks, ropeways

• Capital investment subsidy in new project at ceiling of INR 3 million

• Five year Rebate/ Deferred payment of luxury tax for new units

• 20% assistance for investments up to INR 1 million

• Land availability on reasonable terms/price or as equity

• Single window clearance • Government rest houses to be utilised

for tourism • Provision of beer bar licenses to hotel

units with attached restaurant facilities• Establishment of separate funds for

tourism development

• Concessions for infrastructure projects on merit basis• Five ropeway projects and connectivity improvements

for identified seven tourism zones • Adventure centers planned at 19 locations

for promoting outdoor activities like trekking, mountaineering, river rafting, kayaking, canoeing, rowing, water and snow skiing

• Focus on infrastructure development through PPP

Jammu & Kashmir11

• Capital subsidy for taxi operators up to INR 0.7 million

• Capital investment subsidy up to INR 10 million for tourism units more than INR 250 million

• Investment subsidy for modernisation of travel agencies to 50% of project cost

• DG subsidy- INR 0.4 million • Timber subsidy for houseboat repairs• Subsidy for adventure equipment up to

INR 0.7 million

• Single window clearance • Special area development programme

in place for heritage conservation of old Srinagar city

• INR 1.2 billion allocation during 2012-13 for infrastructure development and upgradation through public investment

• Development of nine and 18 hole golf courses, chairlift facilities, Yatri Niwas, clubs and youth hostels, museums, tourist resorts, convention centres, renovation of heritage sites, industrial training institutes etc.

Table 2.4: Incentives & policy support by state governments in northern states

9. Haryana Tourism Policy 2008 http://www.pppinindia.com/ppp-initiatives-haryana.php

10. Uttarakhand Tourism Policy 2001

11. http://www.pppinindia.com/policy-initiatives-jammu-kashmir.php www.jandkplanning.com/images/Economic_Survey/32-tourism.pdf

18Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

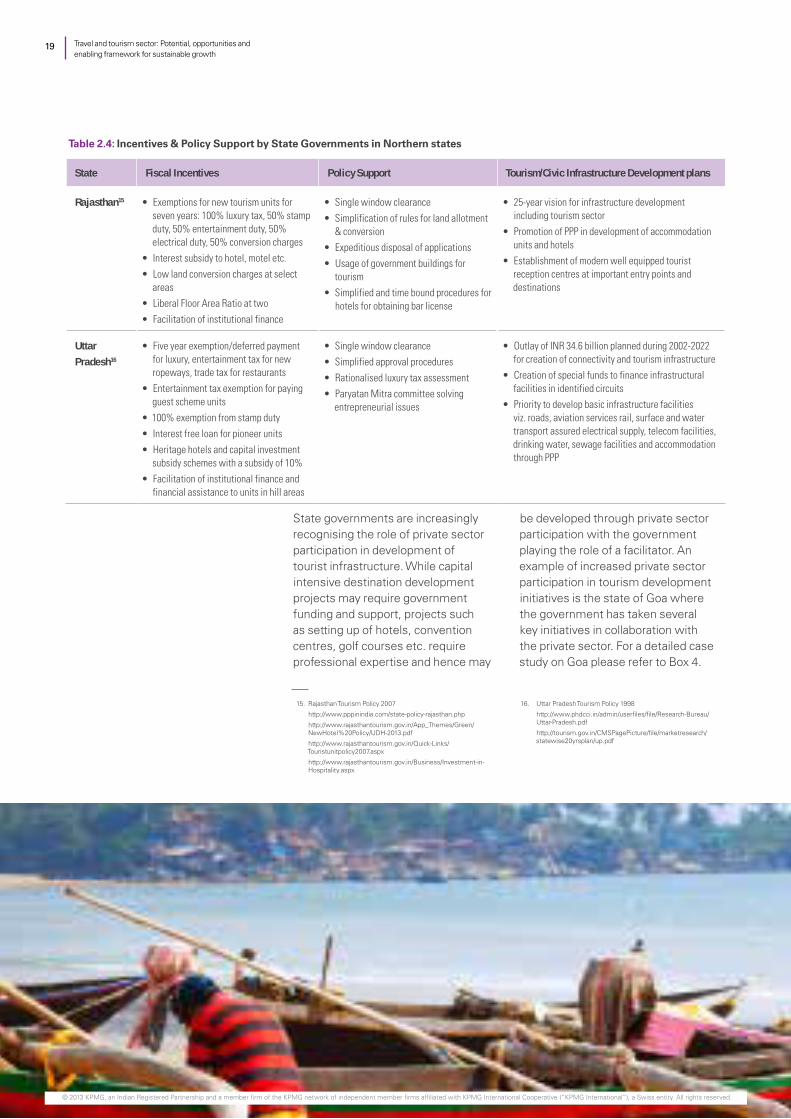

15. Rajasthan Tourism Policy 2007

http://www.pppinindia.com/state-policy-rajasthan.php

http://www.rajasthantourism.gov.in/App_Themes/Green/NewHotel%20Policy/UDH-2013.pdf

http://www.rajasthantourism.gov.in/Quick-Links/Touristunitpolicy2007.aspx

http://www.rajasthantourism.gov.in/Business/Investment-in-Hospitality.aspx

State Fiscal Incentives Policy Support Tourism/Civic Infrastructure Development plans

Rajasthan15 • Exemptions for new tourism units for seven years: 100% luxury tax, 50% stamp duty, 50% entertainment duty, 50% electrical duty, 50% conversion charges

• Interest subsidy to hotel, motel etc.• Low land conversion charges at select

areas• Liberal Floor Area Ratio at two • Facilitation of institutional finance

• Single window clearance • Simplification of rules for land allotment

& conversion• Expeditious disposal of applications • Usage of government buildings for

tourism • Simplified and time bound procedures for

hotels for obtaining bar license

• 25-year vision for infrastructure development including tourism sector

• Promotion of PPP in development of accommodation units and hotels

• Establishment of modern well equipped tourist reception centres at important entry points and destinations

Uttar Pradesh16

• Five year exemption/deferred payment for luxury, entertainment tax for new ropeways, trade tax for restaurants

• Entertainment tax exemption for paying guest scheme units

• 100% exemption from stamp duty• Interest free loan for pioneer units• Heritage hotels and capital investment

subsidy schemes with a subsidy of 10%• Facilitation of institutional finance and

financial assistance to units in hill areas

• Single window clearance • Simplified approval procedures • Rationalised luxury tax assessment • Paryatan Mitra committee solving

entrepreneurial issues

• Outlay of INR 34.6 billion planned during 2002-2022 for creation of connectivity and tourism infrastructure

• Creation of special funds to finance infrastructural facilities in identified circuits

• Priority to develop basic infrastructure facilities viz. roads, aviation services rail, surface and water transport assured electrical supply, telecom facilities, drinking water, sewage facilities and accommodation through PPP

16. Uttar Pradesh Tourism Policy 1998

http://www.phdcci.in/admin/userfiles/file/Research-Bureau/Uttar-Pradesh.pdf

http://tourism.gov.in/CMSPagePicture/file/marketresearch/statewise20yrsplan/up.pdf

State governments are increasingly recognising the role of private sector participation in development of tourist infrastructure. While capital intensive destination development projects may require government funding and support, projects such as setting up of hotels, convention centres, golf courses etc. require professional expertise and hence may

be developed through private sector participation with the government playing the role of a facilitator. An example of increased private sector participation in tourism development initiatives is the state of Goa where the government has taken several key initiatives in collaboration with the private sector. For a detailed case study on Goa please refer to Box 4.

Table 2.4: Incentives & Policy Support by State Governments in Northern states

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

19

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Source: http://www.hotelierindia.com/article-10093-investing_in_goa/

http://articles.timesofindia.indiatimes.com/2013-05-31/goa/39654732_1_goa-tourism-marketing-strategies-promotion-committee

http://www.business-standard.com/article/pti-stories/brand-consultant-for-goa-tourism-industry-soon-minister-113040800226_1.html

http://articles.timesofindia.indiatimes.com/2013-09-25/goa/42392405_1_cctv-cameras-goa-tourism-development-corporation-gtdc

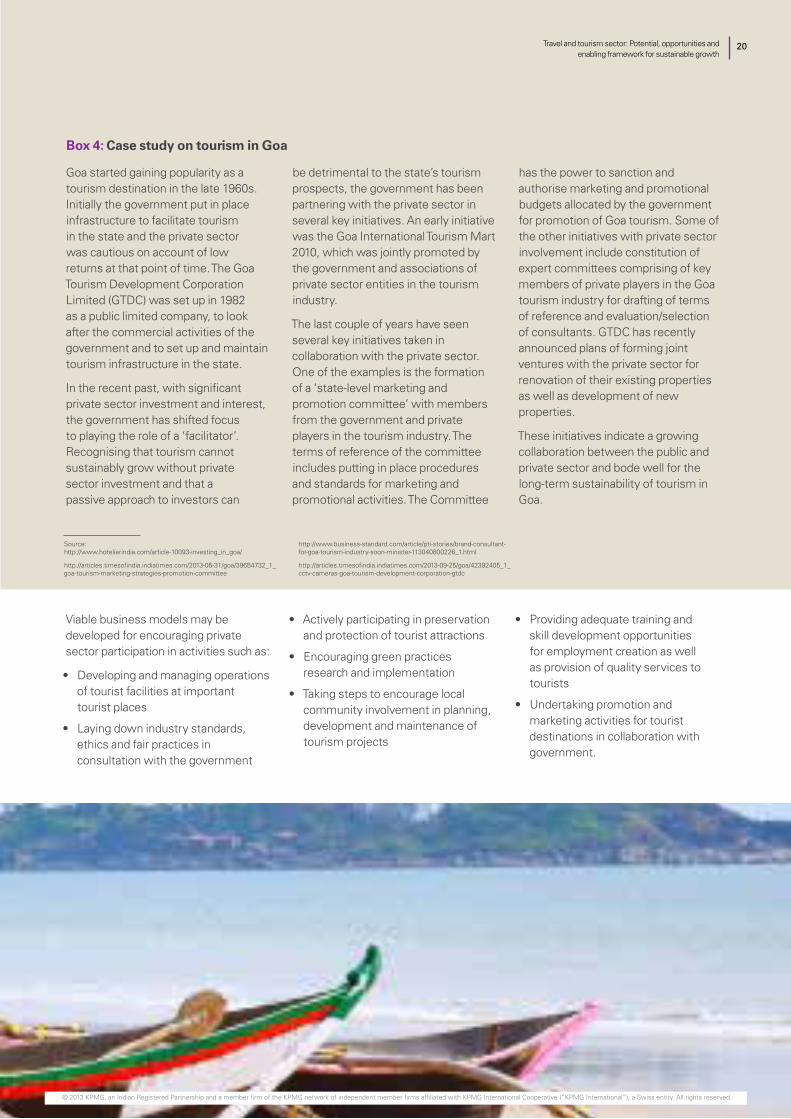

Box 4: Case study on tourism in Goa

Goa started gaining popularity as a tourism destination in the late 1960s. Initially the government put in place infrastructure to facilitate tourism in the state and the private sector was cautious on account of low returns at that point of time. The Goa Tourism Development Corporation Limited (GTDC) was set up in 1982 as a public limited company, to look after the commercial activities of the government and to set up and maintain tourism infrastructure in the state.

In the recent past, with significant private sector investment and interest, the government has shifted focus to playing the role of a ‘facilitator’. Recognising that tourism cannot sustainably grow without private sector investment and that a passive approach to investors can

be detrimental to the state’s tourism prospects, the government has been partnering with the private sector in several key initiatives. An early initiative was the Goa International Tourism Mart 2010, which was jointly promoted by the government and associations of private sector entities in the tourism industry.

The last couple of years have seen several key initiatives taken in collaboration with the private sector. One of the examples is the formation of a ‘state-level marketing and promotion committee’ with members from the government and private players in the tourism industry. The terms of reference of the committee includes putting in place procedures and standards for marketing and promotional activities. The Committee

has the power to sanction and authorise marketing and promotional budgets allocated by the government for promotion of Goa tourism. Some of the other initiatives with private sector involvement include constitution of expert committees comprising of key members of private players in the Goa tourism industry for drafting of terms of reference and evaluation/selection of consultants. GTDC has recently announced plans of forming joint ventures with the private sector for renovation of their existing properties as well as development of new properties.

These initiatives indicate a growing collaboration between the public and private sector and bode well for the long-term sustainability of tourism in Goa.

Viable business models may be developed for encouraging private sector participation in activities such as:

• Developing and managing operations of tourist facilities at important tourist places

• Laying down industry standards, ethics and fair practices in consultation with the government

• Actively participating in preservation and protection of tourist attractions

• Encouraging green practices research and implementation

• Taking steps to encourage local community involvement in planning, development and maintenance of tourism projects

• Providing adequate training and skill development opportunities for employment creation as well as provision of quality services to tourists

• Undertaking promotion and marketing activities for tourist destinations in collaboration with government.

20Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

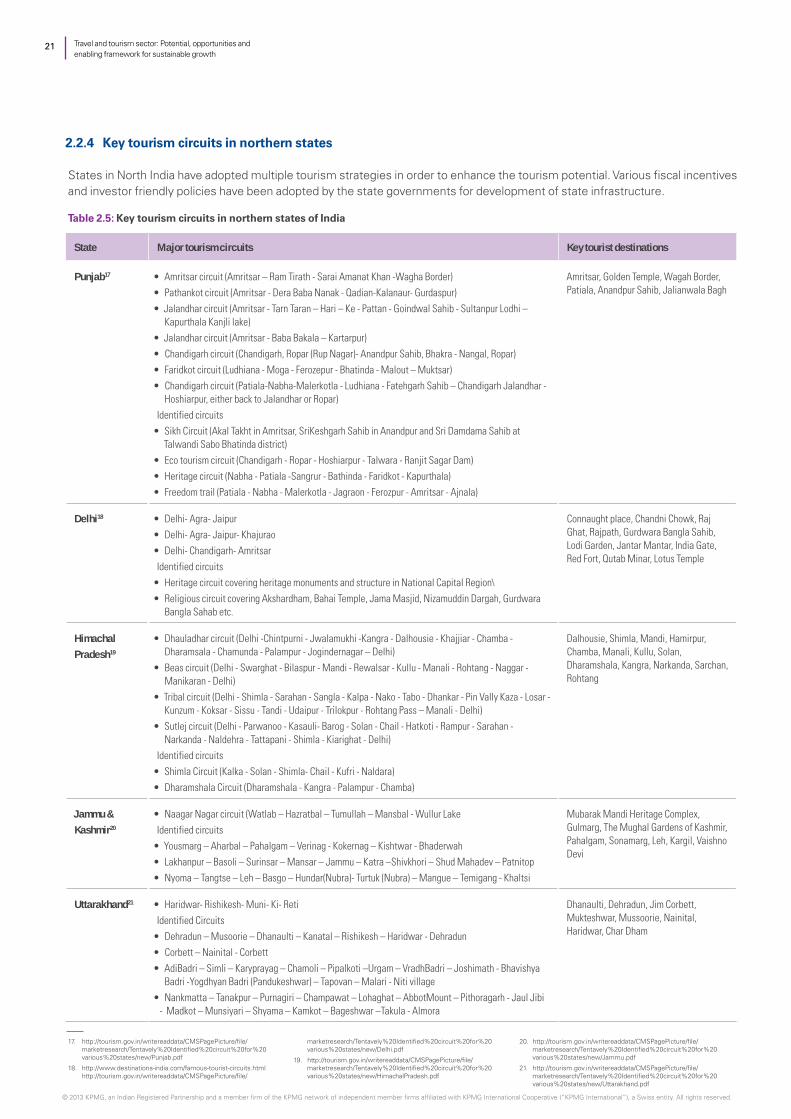

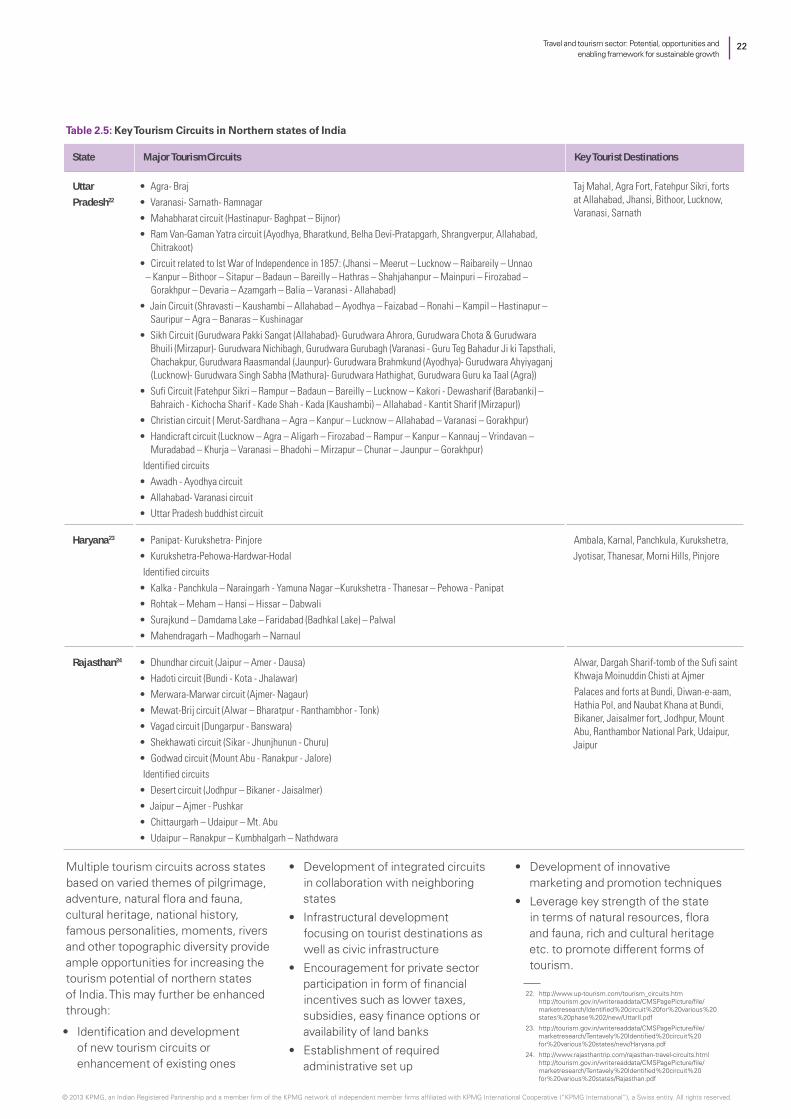

2.2.4 Key tourism circuits in northern states

States in North India have adopted multiple tourism strategies in order to enhance the tourism potential. Various fiscal incentives and investor friendly policies have been adopted by the state governments for development of state infrastructure.

State Major tourism circuits Key tourist destinations

Punjab17 • Amritsar circuit (Amritsar – Ram Tirath - Sarai Amanat Khan -Wagha Border)• Pathankot circuit (Amritsar - Dera Baba Nanak - Qadian-Kalanaur- Gurdaspur)• Jalandhar circuit (Amritsar - Tarn Taran – Hari – Ke - Pattan - Goindwal Sahib - Sultanpur Lodhi –

Kapurthala Kanjli lake)• Jalandhar circuit (Amritsar - Baba Bakala – Kartarpur)• Chandigarh circuit (Chandigarh, Ropar (Rup Nagar)- Anandpur Sahib, Bhakra - Nangal, Ropar)• Faridkot circuit (Ludhiana - Moga - Ferozepur - Bhatinda - Malout – Muktsar)• Chandigarh circuit (Patiala-Nabha-Malerkotla - Ludhiana - Fatehgarh Sahib – Chandigarh Jalandhar -

Hoshiarpur, either back to Jalandhar or Ropar)Identified circuits

• Sikh Circuit (Akal Takht in Amritsar, SriKeshgarh Sahib in Anandpur and Sri Damdama Sahib at Talwandi Sabo Bhatinda district)

• Eco tourism circuit (Chandigarh - Ropar - Hoshiarpur - Talwara - Ranjit Sagar Dam)• Heritage circuit (Nabha - Patiala -Sangrur - Bathinda - Faridkot - Kapurthala)• Freedom trail (Patiala - Nabha - Malerkotla - Jagraon - Ferozpur - Amritsar - Ajnala)

Amritsar, Golden Temple, Wagah Border, Patiala, Anandpur Sahib, Jalianwala Bagh

Delhi18 • Delhi- Agra- Jaipur• Delhi- Agra- Jaipur- Khajurao• Delhi- Chandigarh- AmritsarIdentified circuits

• Heritage circuit covering heritage monuments and structure in National Capital Region\• Religious circuit covering Akshardham, Bahai Temple, Jama Masjid, Nizamuddin Dargah, Gurdwara

Bangla Sahab etc.

Connaught place, Chandni Chowk, Raj Ghat, Rajpath, Gurdwara Bangla Sahib, Lodi Garden, Jantar Mantar, India Gate, Red Fort, Qutab Minar, Lotus Temple

Himachal Pradesh19

• Dhauladhar circuit (Delhi -Chintpurni - Jwalamukhi -Kangra - Dalhousie - Khajjiar - Chamba - Dharamsala - Chamunda - Palampur - Jogindernagar – Delhi)

• Beas circuit (Delhi - Swarghat - Bilaspur - Mandi - Rewalsar - Kullu - Manali - Rohtang - Naggar - Manikaran - Delhi)

• Tribal circuit (Delhi - Shimla - Sarahan - Sangla - Kalpa - Nako - Tabo - Dhankar - Pin Vally Kaza - Losar - Kunzum - Koksar - Sissu - Tandi - Udaipur - Trilokpur - Rohtang Pass – Manali - Delhi)

• Sutlej circuit (Delhi - Parwanoo - Kasauli- Barog - Solan - Chail - Hatkoti - Rampur - Sarahan - Narkanda - Naldehra - Tattapani - Shimla - Kiarighat - Delhi)

Identified circuits• Shimla Circuit (Kalka - Solan - Shimla- Chail - Kufri - Naldara)• Dharamshala Circuit (Dharamshala - Kangra - Palampur - Chamba)

Dalhousie, Shimla, Mandi, Hamirpur, Chamba, Manali, Kullu, Solan, Dharamshala, Kangra, Narkanda, Sarchan, Rohtang

Jammu & Kashmir20

• Naagar Nagar circuit (Watlab – Hazratbal – Tumullah – Mansbal - Wullur LakeIdentified circuits

• Yousmarg – Aharbal – Pahalgam – Verinag - Kokernag – Kishtwar - Bhaderwah • Lakhanpur – Basoli – Surinsar – Mansar – Jammu – Katra –Shivkhori – Shud Mahadev – Patnitop• Nyoma – Tangtse – Leh – Basgo – Hundar(Nubra)- Turtuk (Nubra) – Mangue – Temigang - Khaltsi

Mubarak Mandi Heritage Complex, Gulmarg, The Mughal Gardens of Kashmir, Pahalgam, Sonamarg, Leh, Kargil, Vaishno Devi

Uttarakhand21 • Haridwar- Rishikesh- Muni- Ki- RetiIdentified Circuits

• Dehradun – Musoorie – Dhanaulti – Kanatal – Rishikesh – Haridwar - Dehradun• Corbett – Nainital - Corbett• AdiBadri – Simli – Karyprayag – Chamoli – Pipalkoti –Urgam – VradhBadri – Joshimath - Bhavishya

Badri -Yogdhyan Badri (Pandukeshwar) – Tapovan – Malari - Niti village• Nankmatta – Tanakpur – Purnagiri – Champawat – Lohaghat – AbbotMount – Pithoragarh - Jaul Jibi

- Madkot – Munsiyari – Shyama – Kamkot – Bageshwar –Takula - Almora

Dhanaulti, Dehradun, Jim Corbett, Mukteshwar, Mussoorie, Nainital, Haridwar, Char Dham

Table 2.5: Key tourism circuits in northern states of India

Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

21

17. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Punjab.pdf

18. http://www.destinations-india.com/famous-tourist-circuits.html http://tourism.gov.in/writereaddata/CMSPagePicture/file/

marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Delhi.pdf

19. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/HimachalPradesh.pdf

20. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Jammu.pdf

21. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Uttarakhand.pdf

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

State Major Tourism Circuits Key Tourist Destinations

Uttar Pradesh22

• Agra- Braj• Varanasi- Sarnath- Ramnagar• Mahabharat circuit (Hastinapur- Baghpat – Bijnor)• Ram Van-Gaman Yatra circuit (Ayodhya, Bharatkund, Belha Devi-Pratapgarh, Shrangverpur, Allahabad,

Chitrakoot)• Circuit related to Ist War of Independence in 1857: (Jhansi – Meerut – Lucknow – Raibareily – Unnao

– Kanpur – Bithoor – Sitapur – Badaun – Bareilly – Hathras – Shahjahanpur – Mainpuri – Firozabad – Gorakhpur – Devaria – Azamgarh – Balia – Varanasi - Allahabad)

• Jain Circuit (Shravasti – Kaushambi – Allahabad – Ayodhya – Faizabad – Ronahi – Kampil – Hastinapur – Sauripur – Agra – Banaras – Kushinagar

• Sikh Circuit (Gurudwara Pakki Sangat (Allahabad)- Gurudwara Ahrora, Gurudwara Chota & Gurudwara Bhuili (Mirzapur)- Gurudwara Nichibagh, Gurudwara Gurubagh (Varanasi - Guru Teg Bahadur Ji ki Tapsthali, Chachakpur, Gurudwara Raasmandal (Jaunpur)- Gurudwara Brahmkund (Ayodhya)- Gurudwara Ahyiyaganj (Lucknow)- Gurudwara Singh Sabha (Mathura)- Gurudwara Hathighat, Gurudwara Guru ka Taal (Agra))

• Sufi Circuit (Fatehpur Sikri – Rampur – Badaun – Bareilly – Lucknow – Kakori - Dewasharif (Barabanki) – Bahraich - Kichocha Sharif - Kade Shah - Kada (Kaushambi) – Allahabad - Kantit Sharif (Mirzapur))

• Christian circuit ( Merut-Sardhana – Agra – Kanpur – Lucknow – Allahabad – Varanasi – Gorakhpur)• Handicraft circuit (Lucknow – Agra – Aligarh – Firozabad – Rampur – Kanpur – Kannauj – Vrindavan –

Muradabad – Khurja – Varanasi – Bhadohi – Mirzapur – Chunar – Jaunpur – Gorakhpur)Identified circuits

• Awadh - Ayodhya circuit• Allahabad- Varanasi circuit• Uttar Pradesh buddhist circuit

Taj Mahal, Agra Fort, Fatehpur Sikri, forts at Allahabad, Jhansi, Bithoor, Lucknow, Varanasi, Sarnath

Haryana23 • Panipat- Kurukshetra- Pinjore• Kurukshetra-Pehowa-Hardwar-HodalIdentified circuits

• Kalka - Panchkula – Naraingarh - Yamuna Nagar –Kurukshetra - Thanesar – Pehowa - Panipat• Rohtak – Meham – Hansi – Hissar – Dabwali• Surajkund – Damdama Lake – Faridabad (Badhkal Lake) – Palwal• Mahendragarh – Madhogarh – Narnaul

Ambala, Karnal, Panchkula, Kurukshetra, Jyotisar, Thanesar, Morni Hills, Pinjore

Rajasthan24 • Dhundhar circuit (Jaipur – Amer - Dausa)• Hadoti circuit (Bundi - Kota - Jhalawar)• Merwara-Marwar circuit (Ajmer- Nagaur)• Mewat-Brij circuit (Alwar – Bharatpur - Ranthambhor - Tonk)• Vagad circuit (Dungarpur - Banswara)• Shekhawati circuit (Sikar - Jhunjhunun - Churu)• Godwad circuit (Mount Abu - Ranakpur - Jalore)Identified circuits

• Desert circuit (Jodhpur – Bikaner - Jaisalmer)• Jaipur – Ajmer - Pushkar• Chittaurgarh – Udaipur – Mt. Abu• Udaipur – Ranakpur – Kumbhalgarh – Nathdwara

Alwar, Dargah Sharif-tomb of the Sufi saint Khwaja Moinuddin Chisti at AjmerPalaces and forts at Bundi, Diwan-e-aam, Hathia Pol, and Naubat Khana at Bundi, Bikaner, Jaisalmer fort, Jodhpur, Mount Abu, Ranthambor National Park, Udaipur, Jaipur

Multiple tourism circuits across states based on varied themes of pilgrimage, adventure, natural flora and fauna, cultural heritage, national history, famous personalities, moments, rivers and other topographic diversity provide ample opportunities for increasing the tourism potential of northern states of India. This may further be enhanced through:

• Identification and development of new tourism circuits or enhancement of existing ones

• Development of integrated circuits in collaboration with neighboring states

• Infrastructural development focusing on tourist destinations as well as civic infrastructure

• Encouragement for private sector participation in form of financial incentives such as lower taxes, subsidies, easy finance options or availability of land banks

• Establishment of required administrative set up

• Development of innovative marketing and promotion techniques

• Leverage key strength of the state in terms of natural resources, flora and fauna, rich and cultural heritage etc. to promote different forms of tourism.

Table 2.5: Key Tourism Circuits in Northern states of India

22Travel and tourism sector: Potential, opportunities and enabling framework for sustainable growth

22. http://www.up-tourism.com/tourism_circuits.htm http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Identified%20circuit%20for%20various%20states%20phase%202/new/UttarII.pdf

23. http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/new/Haryana.pdf

24. http://www.rajasthantrip.com/rajasthan-travel-circuits.html http://tourism.gov.in/writereaddata/CMSPagePicture/file/marketresearch/Tentavely%20Identified%20circuit%20for%20various%20states/Rajasthan.pdf

© 2013 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.