Bahasa

Halaman

Hukum

Electronic copy of this paper is available at: http://ssrn.com/abstract=964985

1

The Disposition Effect Demonstrated on IPO Trading Volume

Adam Szyszka

Poznan University of Economics, Poland Telephone number: +48 602 221152 Email: [email protected]

Piotr Zielonka

Department of Physics Warsaw Agricultural University

Telephone number: +48 660 222 999 Email: [email protected]

Abstract

The disposition effect is known as the reluctance of investors to realize losses and their

eagerness to realize gains. The aim of the present research was to examine the impact of the

disposition effect at the aggregate (market) level. In order to limit the number of factors

affecting the selling decision on the share exchange, the examination was done on Initial Public

Offerings. The main factor determining the volume of turnover on the first trading day should

be the initial rate of return. Our research shows that a higher turnover volume is associated with

a positive initial rate of return and a lower turnover volume associated with a negative initial rate

of return. This phenomenon can be explained by the disposition effect.

We conduct our research on the emerging market in Poland. The Warsaw Stock

Exchange has been recently the second largest IPO market in Europe, after London.

Keywords: disposition effect, behavioural finance, Initial Public Offering (IPO),

JEL classification: G11, G20,

Electronic copy of this paper is available at: http://ssrn.com/abstract=964985

2

Introduction

Investors constantly make decisions whether to buy, sell or hold. It turns out that they

do not always act as fully rational expected utility maximizers, as would be predicted by the neo-

classical theory of finance1. Over the last 40 years a large number of behavioural inclinations

affecting the process of financial decision-making have been documented. One of them is the

disposition effect.

The disposition effect was described as the “effect, whereby investors are anxious to sell

their winners, but reluctant to sell their losers” (Shefrin 2005, p. 419) or “the tendency to hold

losers too long and sell winners too soon” (Odean 1998, p. 1775). The disposition effect can be

considered as an implication of the prospect theory of Kahneman and Tversky (1979), which

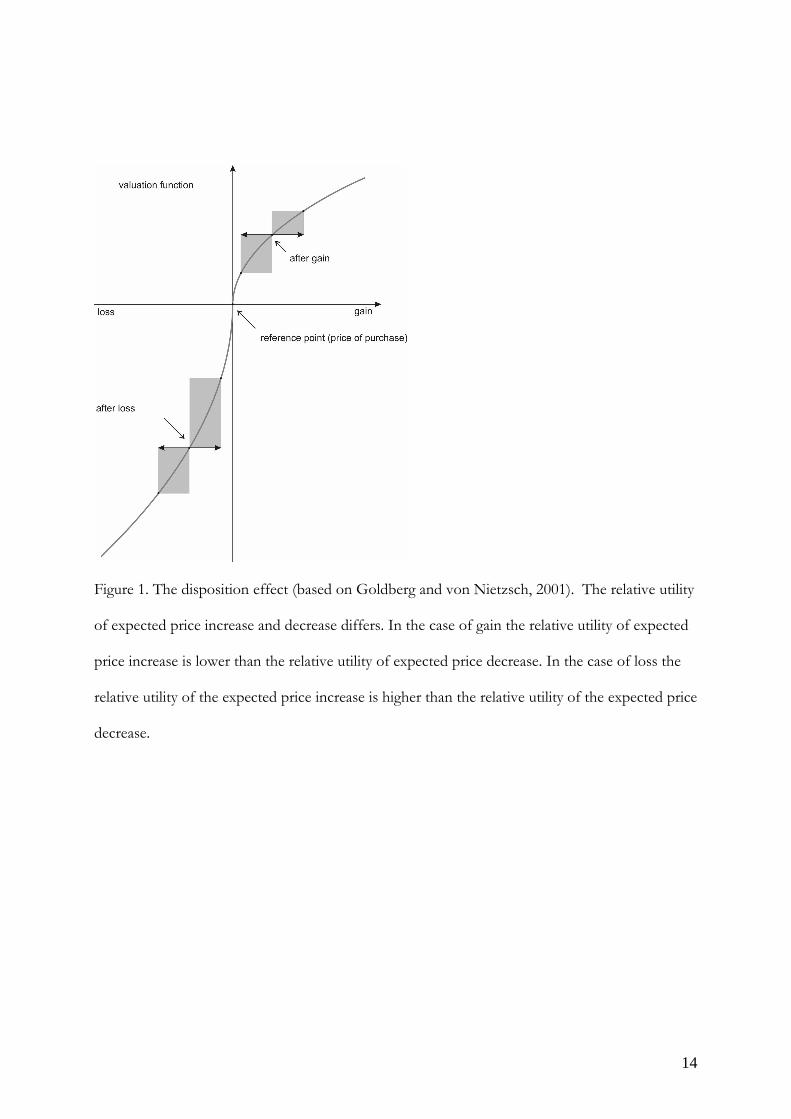

says that investors exhibit an S-shaped valuation function (Figure 1). Investors avoid risk in the

case of potential gains and seek risk in the case of potential losses.

{Figure 1 here}

Figure 1 presents attempts at explaining the disposition effect. A share being sold faster

after gain than after loss was explained by the S-shaped utility function. After a gain the

diminishing curvature of the utility function makes an investor tend to sell a share because the

utility of further share price growth is smaller than the utility of a further share price drop of the

same value.

The disposition effect can be analysed from various perspectives: individual, group and

aggregate.

1 For surveys of behavioural finance see Shefrin (2000), Hirshleifer (2001). Shapira & Venezia (2001), Barberis & Thaler (2002)

3

The individual perspective concerns the decision making process itself. Weber and

Camerer (1998) made an experimental analysis showing that, contrary to Bayesian optimization,

subjects were selling winners and keeping losers. Dacey and Zielonka (forthcoming) offered a

time-independent explanation of the disposition effect implementing a probability of the future

price change.

The group level of the disposition effect refers to the characteristics of particular groups

of investors. Dhar and Zhu (2002), using the demographic and socio-economic data as proxies

for investors’ sophistication, found wealthier investors and investors in professional occupations

to be less prone to the disposition effect. Shapira and Venezia (2001) compared investors

making independent decisions to those whose accounts were managed by brokerage

professionals. They found that both individual investors and professionals exhibit the disposition

effect, but that the effect is weaker for professionals. Locke and Mann (2005) examined the

discipline of professional traders versus their tendency to exhibit the disposition effect.

Discipline was defined according to two factors: the adherence to trade exit strategies, measured

by the general speed of trading, and the avoidance of riding losses, determined by the magnitude

of paper losses per contract held for a long time. More disciplined traders were more immune to

the disposition effect. Feng and Seasholes (2005) tested what impact the level of an investor’s

sophistication has on his exhibition of the disposition effect. The proxies for an investor’s

sophistication were the following: the number of trading rights, the initial portfolio diversification

and two demographic variables (gender and age). The research proved that neither sophistication

nor trading experience alone eliminated the disposition effect. Both of them together were able

to eliminate investors’ reluctance to realize losses, however they did not fully eliminate the

propensity to realize gains. Men were more likely to realize losses than women. Younger

investors (under 35) were more likely to realize losses than older ones. The group level research

shows that the disposition effect is common in all investors but expresses itself stronger in less

4

experienced individuals rather than among professionals. This indicates a possible influence on

pricing

The aggregate level of the disposition effect is defined as that exhibited on the market.

Behavioural finance researchers have discovered a number of cognitive and motivational

inclinations but the main question still unanswered is what impact the individual biases have at

the aggregate market level. Some researchers suggest that individual biases are eliminated at the

market level (heterogeneous investors, learning). The market can be thus unbiased if all investors

behave rationally (Oehler et al, 2003). However, we take a different position and argue that

individual mistakes, human misjudgements and behavioural inclinations do not always cancel out

and may demonstrate themselves also at the aggregate market level.

In this paper we focus on the disposition effect and look at whether it can be found at the

market level. We propose a hypothesis that the disposition effect influences turnover volume.

The main problem in verifying this hypothesis in a standard market situation is that investors buy

the same shares at different points of time and for a different price. When making a decision on a

day t to sell or hold a particular share various investors have different perspectives. Some of them

may have their reference point below and others above the reference point, this being their

purchase price. An Initial Public Offering is a unique non-standard market situation that offers a

remedy for this issue and enables us to search for the disposition effect at the aggregate level. All,

or at least most, investors participating in a public offering buy shares at the same purchase price.

Therefore on the first trading day those investors have the same reference point. If the return is

positive they will be more eager to sell than if they suffer a loss. Changes in supply resulting from

the disposition effect at the individual level should be observable at the aggregate level as

differences in turnover volume on the first trading day depending on a negative or positive value

of the IPO return.

Kaustia (2004) found that the turnover is significantly lower for a negative initial return of

IPOs when the share is traded below the offering price and increases on the day the price

5

surpasses the offering price for the first time. His research concerns US IPOs between 1980 and

1996. We conduct our research on a vibrant emerging market in Poland. The Warsaw Stock

Exchange was the second most active IPO market in Europe in 2006 (after London). Our

hypothesis was that similarly to mature markets (Kausta, 2004) the first trading day volume on

the emerging markets would be higher on price levels above the offer price than below the offer

price. This will confirm an observation that strong behavioural biases such as the disposition

effect are common both for experienced mature market investors and novice emerging markets

ones.

Data Description and Methodology

The sample we used consisted of 32 IPOs that occurred on the Warsaw Stock Exchange

(WSE) from the beginning of 2000 till the end of 2005. From the total number of 36 IPOs that

happened during that period on the WSE we excluded cases in which so called allotment

certificates (PDA) were traded before the first listing of shares 2.

For each IPO in our sample we calculated two types of returns:

- a nominal initial rate of return calculated as:

=

IPOabsolute P

PR 1ln [1]

- a market-adjusted initial rate of return calculated as:

−

=

IPOIPOadj WIG

WIG

P

PR 11

. lnln [2]

2 Allotment certificates are financial instruments that were introduced to enable investors who have already been allotted rights to new shares but have not yet received the shares to trade these rights on the exchange through the allotment certificates prior to the shares first quotation date. Trading of allotment certificates is governed by the same rules as equity trading on the Warsaw Stock Exchange. However, allotment certificates do not give full shareholder’s rights before they are converted into true shares, and usually they are traded with a small discount compared to the value of equivalent shares. Allotment certificates offer the possibility of cashing out before the first formal listing of the equity and therefore they could blur the picture of disposition effect in IPOs.

6

where:

1P is the closing price at the first day of listing,

IPOP is the IPO’s offer price. If the issuer used market segmentation and prices offered to

professional and individual investors were different, we employed for calculation the price

available to individual investors;

IPOWIG is the closing level of the WIG index3 on the last day of the IPO. If the IPO was

organized on different dates for individual and professional investors, we took the date of the last

day when the offer was available for small investors.

1WIG is the closing level of WIG index at the date of the first listing.

Employing both nominal and market-adjusted initial rates of return allows us to verify if

investors pay more attention to pure profits and losses or if they put the returns in the context of

market performance in the period of time between the IPO and the first listing.

We calculated three measures of the relative volume:

totalV

VRV 1

1 = , [3]

IPOV

VRV 1

2 = , [4]

averageV

VRV 1

1 = , [5]

where:

1V is the number of share traded on the first day of listing,

totalV is the total number of shares admitted for public trading on the market,

IPOV is the number of shares offered in a public offer,

3 WIG is the main market-wide index of the Warsaw Stock Exchange.

7

averageV is the average number of shares per trading day traded between 31st and 270th trading day

after the first listing.

1RV measures what percentage of all shares admitted to the market, including those

offered publicly and those distributed privately, was traded on the first trading day. The purchase

price in the IPO and through private distribution may vary substantially. Furthermore, acquisition

of shares in these two different ways might not have occurred at the same time. Hence depending

solely on 1RV for the purpose of detecting the disposition effect seems not to be sufficient. We

decided to adopt two additional measures of the relative volume.

2RV shows what part of the shares offered in the IPO changed owners on the first

trading day. It is a good measure for the purpose of the study when the size of the IPO is large

compared to the number of shares admitted to the market that were distributed privately.

However this measure might be weaker if most of the shares sold on the first trading day come

from “old” shareholders. Their transactions during the first trading days might be a part of an

exit strategy from their long-term investment, in contrast to short-term speculators that had

acquired shares a few weeks earlier through the IPO. The perspective and preferences of “old”

shareholders might be completely different from the new buyers from the IPO.

3RV measures volume on the first trading day in comparison to the normal volume,

defined as the number of shares of a particular company traded on average between 31st and 270th

trading day after the first listing. This measure is immune to the difference between the number

of shares in free float and the number of shares in the IPO. However it is sensitive to any

extraordinary events that might have occurred during the observation window of 240 trading

days and might have influenced the volume of shares over time.

Despite the fact that each of the above measures of volume has some limitations, we

expect that the combined use of all three of them will be sufficient to test the hypothesis that the

disposition effect is present among investors acquiring shares in public offers.

8

We divided the sample of IPOs into two groups: “winners” – shares that generated

positive return between the first listing and the IPO’s offer, and “losers” – shares that made

negative return on their debut. We excluded cases with zero return. For each group we calculated

average values of 1RV , 2RV , 3RV . We tested the significance of the difference between averages

for “winners” and “losers”. Distributions of volume measures do not fit the Gaussian

distribution (Shapiro-Wilk test). Thus U Mann-Whitney tests were employed. We did the same

exercise twice: once using the nominal rate of return [1] and another time using the market-

adjusted return [2] as the criteria for separation into two groups.

Results

The range of the positive rates of IPO return was from 0% to 57.7%. The range of the

negative rates of IPO return was from -10% to 0%.

We tested the difference between the turnover volume for positive vs. negative initial rate

of return IPO (see: [1]). U Mann-Whitney tests showed a statistically significant positive

difference between the turnover volume of positive initial rate of return shares and negative

initial rate of return shares for all turnover measures (Table 1): RV1 (p<0.001, U=11, Z=-3.51),

RV2 (p<0.01, U=17, Z=-3.20), RV3 (p<0.001, U=15, Z=-3.31).

{Table 1 here}

In the second step the nominal initial rate of return of IPO was replaced by a market-

adjusted one (see: [2]).The results also indicated that the turnover volume of positive initial

market-adjusted rate of return shares is significantly higher than of the negative initial market-

9

adjusted rate of return shares (Table 2): RV1 (p<0.05, U=43, Z=-2.54), RV2 (p<0.01, U=35, Z=-

2.88), RV3 (p<0.01, U=37, Z=-2.88)

{Table 2 here}

Discussion and Conclusions

Our research shows that for both the nominal and market-adjusted rates of return the

turnover volume turns out to be significantly higher for winners than for losers. What is more,

regardless of the type of measure of relative turnover utilized for calculations the results gave

similar picture. This is also in accordance with the previous research by Kaustia (2004).

We presume that this observation is due to the disposition effect exhibited by individual

investors. Analysis of IPO cases offers a unique opportunity to identify the effect in the

aggregated market data. Contrary to other market conditions, in the case of IPO the purchase

price (i.e. the price in the public offering) is the same for a large number of investors and

therefore may be regarded as a common benchmark and anchor, particularly for those investors

participating in the IPO.

Investors who bought shares in the public offer and later see them going down on the

first trading day are very reluctant to admit that they might have made an investment mistake and

rather prefer to hold the asset than sell with a loss. In this case neo-classical risk aversion is

replaced by behavioural loss-aversion, as predicted by the perspective theory of Kahneman and

Tversky (1979). Investors who face a possibility of realizing the loss are prepared to take even

more risk hoping for another chance and willing to postpone the definite loss. On the contrary,

investors who see their shares going up are eager to sell and to realize the profit. Their degree of

risk aversion increases as the potential profit waiting to cash out becomes greater. Such changes

10

in investors’ preferences and in their degree of risk aversion result in shifts in supply function at

the aggregated market level. Limited (increased) supply when the IPO return is negative (positive)

causes the relative overpricing (underpricing) of the asset on the first trading day. The limited

supply of the overpriced asset meets a smaller demand. On the other hand, the increased supply

of the underpriced asset comes across a higher demand. This results in lower (higher) volume

turnover for the negative (positive) return on the first trading day after the IPO, as documented

by this paper.

Behavioural finance usually is criticized for the lack of the empirical link between the

numerous biases described at the individual level of an investor’s decision-making process and

their implications on the market. The present research offers such a link between the individuals’

disposition effect and the aggregated volume turnover in the specific conditions of IPO. We

hope this paper may also give some stimulus towards next seeking behavioural phenomena at the

aggregate level.

11

References

Dacey, Raymond and Piotr Zielonka (forthcoming). A Detailed Time Independent

Explanation of The Disposition Effect, Journal of behavioral Finance.

Dhar, Ravi and Ning Zhu (2002). Up Close and Personal: An Individual Level Analysis of the

Disposition Effect. Yale ICF Working Paper No. 02-20.

Feng, Lei and Mark S. Seasholes (2005). Do Investor Sophistication and Trading Experience

Eliminate Behavioral Biases in Financial Markets? Review of Finance (2005) 9: 305–351.

Goldberg, Joachim and Rüdiger von Nietzsch (1999). Behavioral Finance, New York: John

Wiley & Sons, Inc.

Hirshleifer, Daniel (2001). Investor Psychology and Asset Pricing, Journal of Finance, Vol.

56, 5, 1533-1597.

Kahneman, Daniel and Amos Tversky (1979). “Prospect Theory: An Analysis of Decisions

Under Risk,” Econometrica 47: 263-291.

Kaustia, Markku (2004). Market-Wide Impact of the Disposition Effect: Evidence from IPO

Trading Volume, Journal of Financial Markets 7, 207–235.

Locke, Peter and Steven Mann (2005). “Professional trader discipline and trade disposition”.

Journal of Financial Economics 76: 401–444.

Oehler, Andeas, Heilmann, Klaus, Läger, Volker and Michael Oberländer (2003).

“Coexistence of Disposition Investors and Momentum Traders in Stock Markets:

Experimental Evidence”, Journal of International Financial Markets, Institutions &

Money 13: 503-524.

Shapira, Zur and Itzhak Venezia (2001). “Patterns of Behavior of Professionally Managed and

Independent Investors”, Journal of Banking and Finance, Vol. 25 (8): 1573-87.

Shefrin, Hersh (2000). Beyond Greed and Fear. Understanding Behavioral Finance and the

Psychology of Investing, Boston, MA, Harvard Business School Press

Weber, Martin and Colin Camerer (1998). “The Disposition Effect in Securities Trading: An

Experimental Analysis”, Journal of Economic Behavior and Organization. Vol. 33: 167-

184.

12

turnover measures

RV1 RV2 RV3

turnover for

positive rate

of return

7.0% 17.4% 5047%

turnover for

negative rate

of return

0.9% 3.0% 817%

Table 1. The three measures turnover volume for positive and negative initial nominale rate of

return.

13

turnover measures

RV1 RV2 RV3

turnover for

positive rate

of return 6,4% 16,6% 4774%

turnover for

negative rate

of return 1,7% 3,5% 1044%

Table 2. The three measures turnover volume for positive and negative initial market adjusted

rate of return.

14

Figure 1. The disposition effect (based on Goldberg and von Nietzsch, 2001). The relative utility

of expected price increase and decrease differs. In the case of gain the relative utility of expected

price increase is lower than the relative utility of expected price decrease. In the case of loss the

relative utility of the expected price increase is higher than the relative utility of the expected price

decrease.

Top Related

Copyright © 2022 FDOKUMEN