Bahasa

Halaman

Hukum

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Structuring 1031 Like-Kind

Exchanges for Real Property Preserving Tax-Deferral Treatment for Transactions Involving Real Estate

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, APRIL 27, 2016

Joseph C. Mandarino, Partner, Smith Gambrell & Russell, Atlanta

Todd R. Pajonas, Esq., President, Legal 1031 Exchange Services, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

An exchange is no longer an actual “swap”.

It is sale and purchase with very little difference than a non-1031 transaction.

Exchange documents create the transaction.

The gain from the relinquished property is deferred into the replacement property.

OVERVIEW AND MYTHS OF AN IRC §1031 TAX

DEFERRED EXCHANGES

6

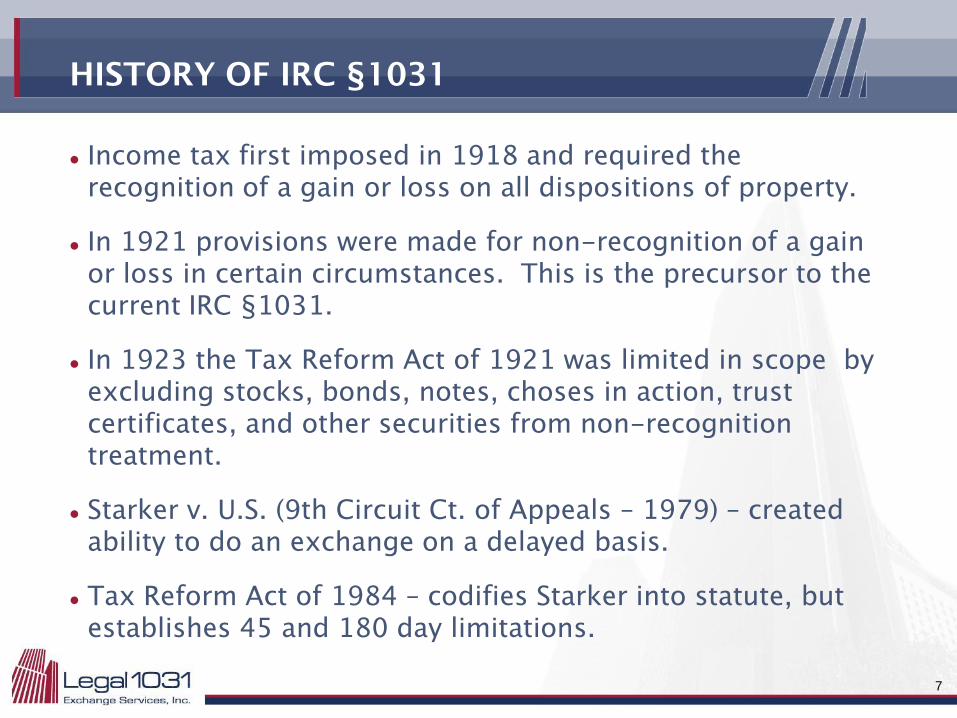

HISTORY OF IRC §1031

Income tax first imposed in 1918 and required the recognition of a gain or loss on all dispositions of property.

In 1921 provisions were made for non-recognition of a gain or loss in certain circumstances. This is the precursor to the current IRC §1031.

In 1923 the Tax Reform Act of 1921 was limited in scope by excluding stocks, bonds, notes, choses in action, trust certificates, and other securities from non-recognition treatment.

Starker v. U.S. (9th Circuit Ct. of Appeals – 1979) – created ability to do an exchange on a delayed basis.

Tax Reform Act of 1984 – codifies Starker into statute, but establishes 45 and 180 day limitations.

7

INVESTOR MOTIVES

Consolidation / Management Relief

Diversification

Restart / Increase Depreciation

Cash Flow

Retirement Planning

Estate Planning

8

IRC §1031 TAX DEFERRED EXCHANGES

No gain or loss shall be recognized on the exchange of property held for productive use in a trade or business or for investment if such property is exchanged solely for property of like-kind which is to be held either for productive use in a trade or business or for investment.

Deferral of tax, NOT a tax free transaction.

9

LIKE KIND – REAL PROPERTY

LIKE KIND PROPERTY

10

LIKE KIND – REAL PROPERTY

LIKE KIND

Held for productive use in a trade or business.

or

Held for investment purposes.

INTENT

Intent: actions over a period of time.

11

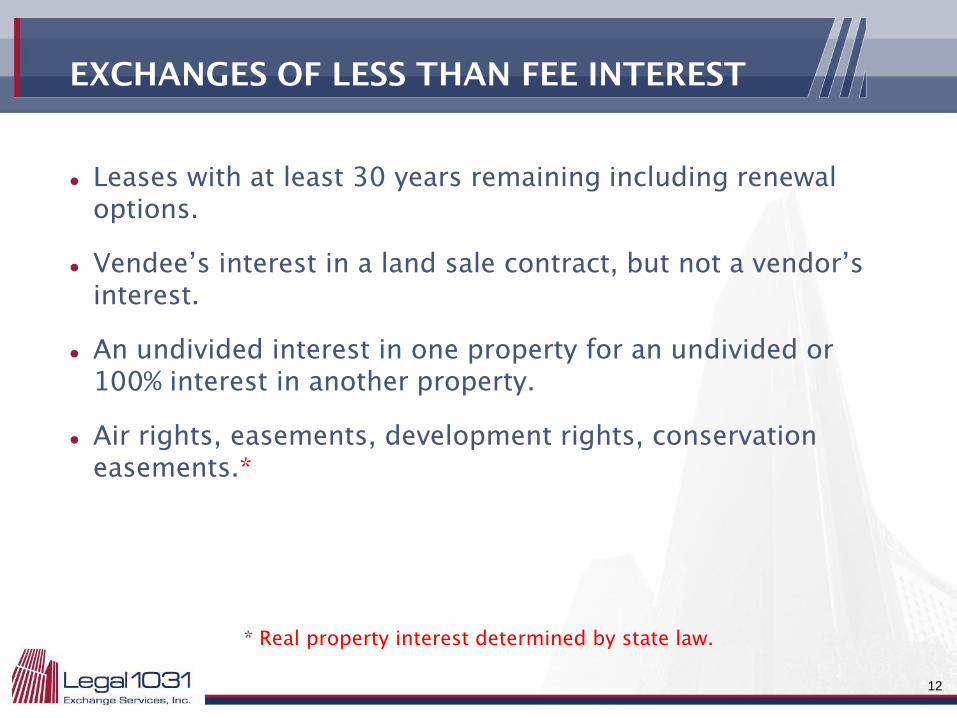

EXCHANGES OF LESS THAN FEE INTEREST

Leases with at least 30 years remaining including renewal options.

Vendee’s interest in a land sale contract, but not a vendor’s interest.

An undivided interest in one property for an undivided or 100% interest in another property.

Air rights, easements, development rights, conservation easements.*

* Real property interest determined by state law.

12

LIKE KIND

LIKE KIND – PERSONAL PROPERTY

NOT LIKE KIND

13

RULES TO OBTAIN A COMPLETE DEFERAL

Purchase replacement property of equal or greater value to the relinquished property.

Reinvest all of the net proceeds from the relinquished sale into the replacement property purchase.

Obtain equal or greater financing on the replacement property as was paid off on the relinquished property.

Receive nothing except like-kind property.

14

BOOT DEFINED

The term “BOOT” does not appear anywhere in the Internal Revenue Code or Regulations.

If the Exchanger does not use all of its net cash or have equal or greater liability on the replacement property, there is boot.

If the Exchanger receives non-like kind property or uses exchange funds to pay for non-exchange transactional costs, there is boot.

15

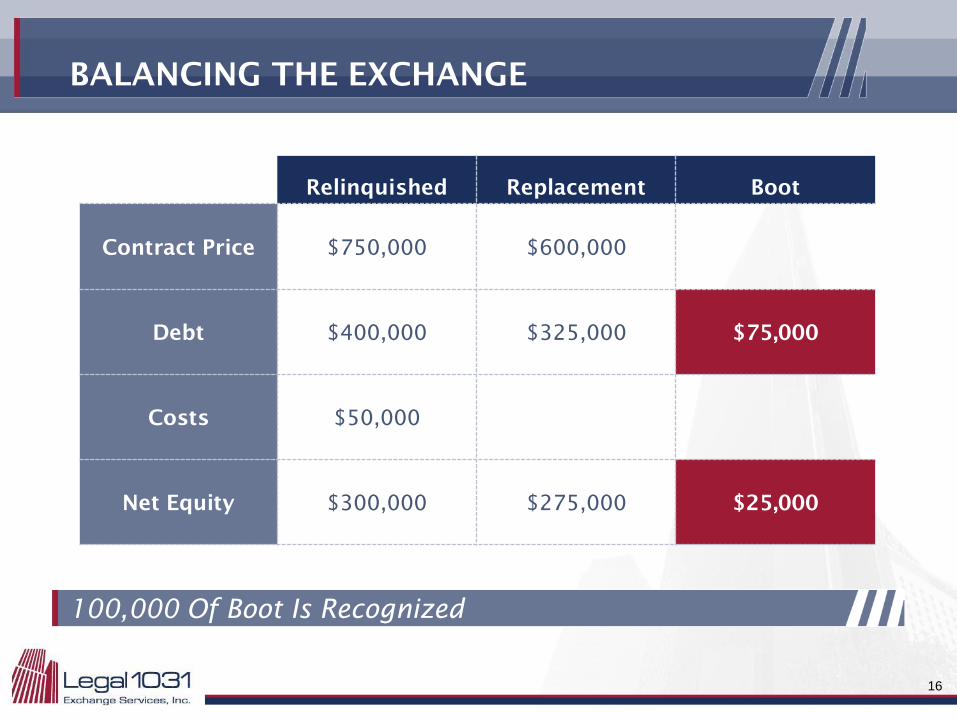

BALANCING THE EXCHANGE

Relinquished Replacement Boot

Contract Price $750,000 $600,000

Debt $400,000 $325,000 $75,000

Costs $50,000

Net Equity $300,000 $275,000 $25,000

100,000 Of Boot Is Recognized

16

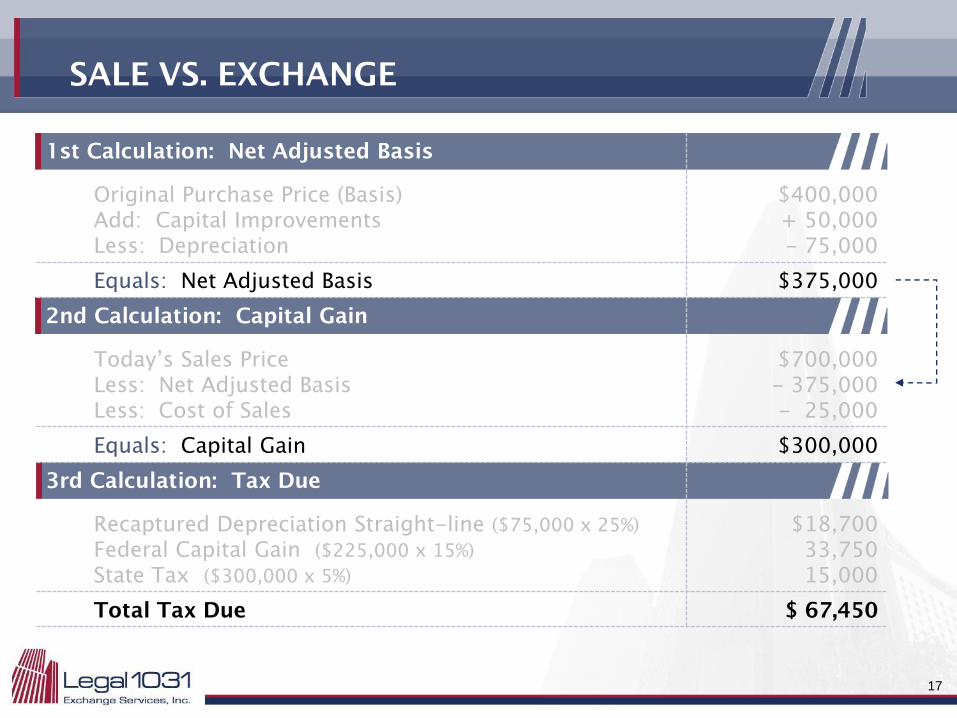

SALE VS. EXCHANGE

1st Calculation: Net Adjusted Basis

Original Purchase Price (Basis) Add: Capital Improvements Less: Depreciation

$400,000 + 50,000 - 75,000

Equals: Net Adjusted Basis $375,000

2nd Calculation: Capital Gain

Today’s Sales Price Less: Net Adjusted Basis Less: Cost of Sales

$700,000 - 375,000 - 25,000

Equals: Capital Gain $300,000

3rd Calculation: Tax Due

Recaptured Depreciation Straight-line ($75,000 x 25%)

Federal Capital Gain ($225,000 x 15%)

State Tax ($300,000 x 5%)

$18,700 33,750 15,000

Total Tax Due $ 67,450

17

SALE VS. EXCHANGE

4th Calculation: Net Equity

Today’s Sales Price Less: Cost of Sales Less: Loan Balance

$700,000 - 25,000 -220,000

Equals: Gross Equity (gross purchasing power) $455,000

Less: Taxes Due and Payable Equals: Net Equity

- 67,450 $ 387,550

5th Calculation: Sale vs. Exchange

Sale $387,550 x 4 =

$1,550,200 Purchase Price

Exchange $455,000 x 4 =

$1,820,000 Purchase Price

18

EXCEPTIONS TO IRC §1031

Stock in trade or other property held primarily for sale

Stocks, bonds, or notes

Other securities or evidences of indebtedness or interest

Interests in a partnership

Certificates of trust or beneficial interest

Choses in action

19

EXCHANGE SAFE HARBORS

Use of Qualified Intermediary to create exchange transaction.

Use of Qualified Escrow or Trust to hold the proceeds from the exchange.

Use of a Guarantee or Security Arrangement to secure exchange proceeds.

Interest paid on the exchange proceeds.

20

STEPS TO PREPARE SALE CONTRACT

Start with contract you would normally use.

Add exchange cooperation clause language to contract.

If, for some reason, you do not want to disclose that the transaction is being structured as a 1031 exchange, include a clause allowing seller to “direct the payment of the purchase price.”

If seller is unwilling to sign Notice of Assignment form it should be mailed by certified mail to give proper notice.

You may deposit the contract deposit in your escrow account so long as it is contingent on the transaction closing.

21

EXCHANGE COOPERATION CLAUSE

Buyer hereby acknowledges that it is the intent of the Seller to structure its sale as a tax deferred exchange under IRC §1031. Seller covenants that this will not delay the close of the subject transaction nor cause the Buyer any additional expenses. The Seller’s rights under the purchase and sale agreement may be assigned to Legal 1031 Exchange Services, Inc., a Qualified Intermediary for IRC §1031 Tax Deferred Exchanges. Buyer agrees to cooperate with the Seller and the Qualified Intermediary to complete the exchange.

22

SETTLEMENT STATEMENT

Settlement statement is not “required” for a 1031 exchange but it is good practice to prepare one.

Seller should be listed as “Legal 1031 Exchange Services, Inc. as Qualified Inc. for Exchanger Name.

List the exchange fee in the Settlement Charges section of the settlement statement if using a HUD.

If exchanger is cutting a separate check for the fee it should be listed as POC.

23

DELAYED EXCHANGE STRUCTURE

EXCHANGER

BUYER SELLER

IDENTIFICATION PERIOD TIME PERIOD TO ACQUIRE REPLACEMENT PROPERTY

0 45

DAYS

180

DAYS

$ $

Sale Purchase

24

DELAYED EXCHANGE TIME LIMITS

45 DAY IDENTIFICATION RULE Exchanger has 45 days from the date of the sale of the first property to identify potential replacement property.

180 DAY EXCHANGE PERIOD

Exchanger has 180 days from the date of the sale of the first property, or the date upon which Exchanger has to file its Federal tax return for the year in which the relinquished property was sold, to complete the acquisition of all replacement properties.

25

DELAYED EXCHANGE TIME LIMITS

There are no individual extensions.

45 and 180 days are calendar days, not business days.

Time limits begin to run on the earlier of the date the taxpayer transfers the benefits or burdens of ownership of the first relinquished property to a buyer, or recording a deed evidencing a transfer, whichever occurs first.

26

IDENTIFICATION RULES

THREE PROPERTY RULE

Exchanger may identify up to three properties regardless of value.

200% RULE

Exchanger can identify an unlimited number of properties, provided that the total value of the properties identified does not exceed 200% of the value of all relinquished properties.

95% EXCEPTION

If Exchanger identifies more than three properties which are worth more than 200% of the value of all relinquished properties than Exchanger must acquire 95% of the value of all properties identified.

27

PROCEDURE FOR PROPER IDENTIFICATION

Identification must be made in writing.

Unambiguously describe the property.

Signed and dated by the taxpayer.

Received by midnight of the 45th day or postmarked by the 45th day.

Delivered to Exchanger’s Qualified Intermediary or to a party related to the exchange who is not a disqualified person.

28

EXCHANGE VESTING ISSUES

With very limited exception, the person or entity who relinquishes property must be the same person or entity to buy the replacement property.

A good rule of thumb is that you must have the same tax identification number on both sides of the transaction.

29

EXCHANGE VESTING ISSUES

EXCHANGES INVOLVING ENTITIES

When a person or entity has an ownership interest in an entity (corporation, partnership, LLC, etc.) which owns real estate, that person or entity does not own real estate. They own an interest in an entity which owns real estate.

This creates issues when less than 50% of the ownership interest wants to do an exchange.

An existing entity will be deemed a “new” entity by the IRS is more than 50% of the ownership changes.

30

EXCHANGE VESTING ISSUES

STRUCTURING DISOLUTIONS FOR EXCHANGES INVOLVING ENTITIES

If you dissolve an entity and make each former member a tenant in common they will be holding property for resale purposes unless done with property planning a year or more in advance of the contemplated sale (a/k/a drop and swap).

If more than 50% of members/shareholders/partners wish to the exchange the most expedient solution is to make a distribution at the closing and let the surviving members do the exchange in the name of the entity.

Major issue when less than 50% of the ownership interest wants to do an exchange.

An existing entity will be deemed a “new” entity by the IRS if more than 50% of the ownership changes.

31

SAFE HARBOR RESTRICTIONS

A/K/A WHEN CAN MY CLIENT GET ITS MONEY BACK?

Treasury Regulations provides that an Exchange Agreement must restrict the

Exchanger’s right to receive, pledge, borrow, or otherwise receive the benefits of the

exchange funds, except:

After the end of the 45 day Identification Period where the Exchanger does not have identified replacement property

If the Exchanger has purchased all identified replacement property and is beyond the 45th day.

If the Exchanger has identified replacement property then upon or after the occurrence, after the end of the identification period, of a material and substantial contingency that, 1. related to the exchange; 2. is provided for in writing; and 3. is beyond the control of the Exchanger and of any disqualified party, other than the party obligated to transfer the replacement property to the Exchanger.

After the end of the 180 day Exchanger Period.

32

PRIMARY RESIDENCE AND 1031

Primary

Residence

§1031

§1031

§1031

Mixed Use Property

Vacation home, second home, retirement home as replacement property.

Conversion of replacement property to a primary residence.

33

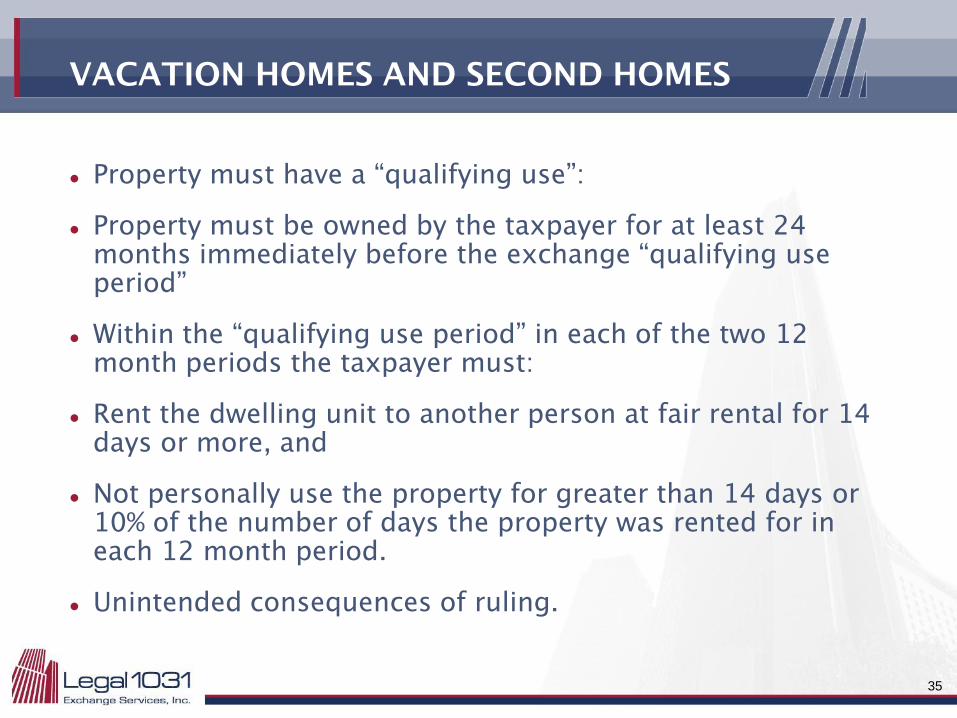

VACATION HOMES AND SECOND HOMES

Are vacation homes considered investment property or personal use property.

PLR 8103117 cited to structure vacation home sales and purchases as an exchange.

Moore v. Commissioner (T.C. Memo. 2007-134) made it clear that the property must be held for investment purposes, but did not clearly define of that standard might be applied.

Rev. Proc. 2008-16 limits its scope to “dwelling units” which are defined as “real property improved with a house, apartment, condominium, or similar improvement that provides basic living accommodations including sleeping space, bathroom and cooking facilities.

34

VACATION HOMES AND SECOND HOMES

Property must have a “qualifying use”:

Property must be owned by the taxpayer for at least 24 months immediately before the exchange “qualifying use period”

Within the “qualifying use period” in each of the two 12 month periods the taxpayer must:

Rent the dwelling unit to another person at fair rental for 14 days or more, and

Not personally use the property for greater than 14 days or 10% of the number of days the property was rented for in each 12 month period.

Unintended consequences of ruling.

35

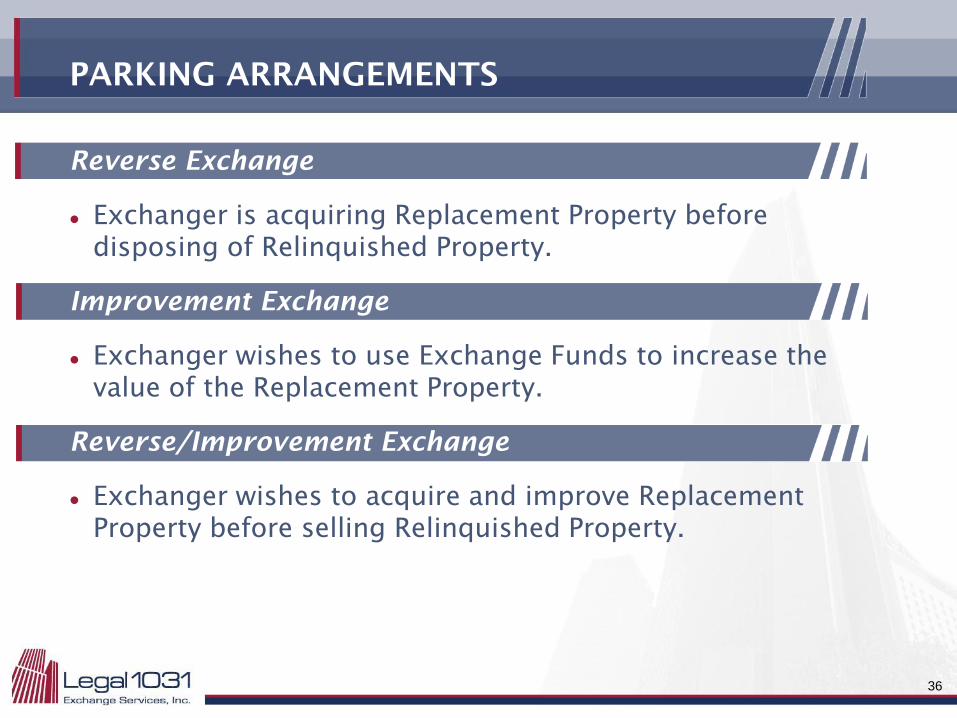

PARKING ARRANGEMENTS

Reverse Exchange

Exchanger is acquiring Replacement Property before disposing of Relinquished Property.

Improvement Exchange

Exchanger wishes to use Exchange Funds to increase the value of the Replacement Property.

Reverse/Improvement Exchange

Exchanger wishes to acquire and improve Replacement Property before selling Relinquished Property.

36

Structuring 1031 Like-Kind Exchanges for Real Property

April 27, 2016

Joseph C. Mandarino Partner

Smith, Gambrell & Russell, LLP Atlanta, Georgia

• Reverse Exchanges

• Tenancy-in-Common (“TIC”) interests

• Delaware Statutory Trusts (“DSTs”)

• Related Party Exchanges

38

Reverse Exchanges

39

Overview

• In a simultaneous exchange, a taxpayer (the “exchangor”) sells property (the “relinquished property”) at the same time as he/she acquires new property (the “replacement property”).

• In a forward exchange, the exchangor sells the relinquished property and at a later time acquires replacement property.

• In a reverse exchange, the exchangor acquires the replacement property before selling the relinquished property.

40

Reverse Exchanges

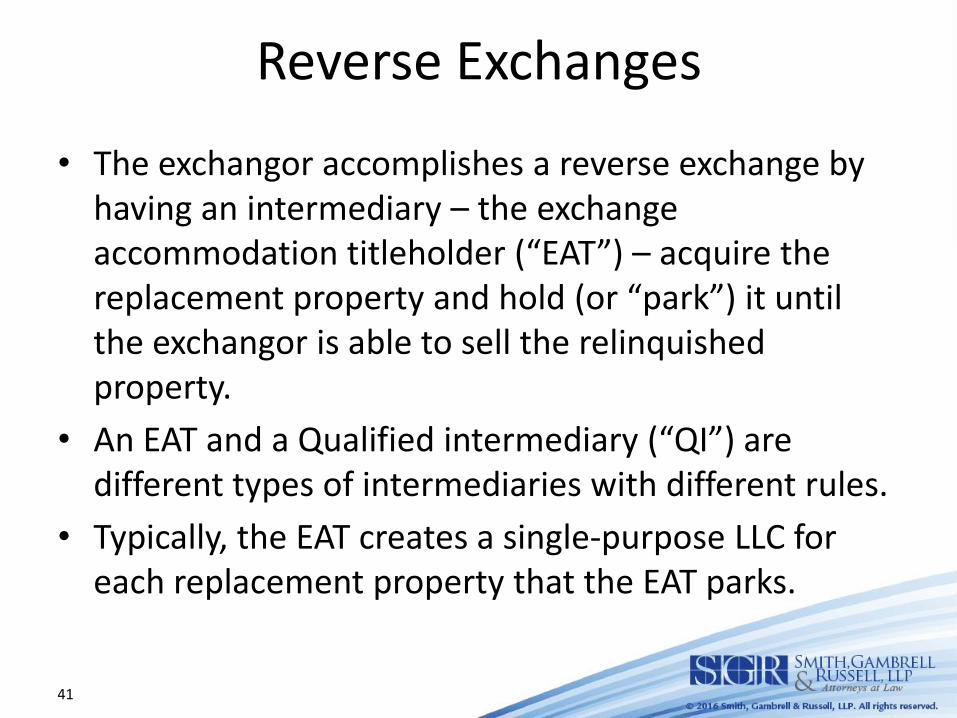

• The exchangor accomplishes a reverse exchange by having an intermediary – the exchange accommodation titleholder (“EAT”) – acquire the replacement property and hold (or “park”) it until the exchangor is able to sell the relinquished property.

• An EAT and a Qualified intermediary (“QI”) are different types of intermediaries with different rules.

• Typically, the EAT creates a single-purpose LLC for each replacement property that the EAT parks.

41

Reverse Exchanges

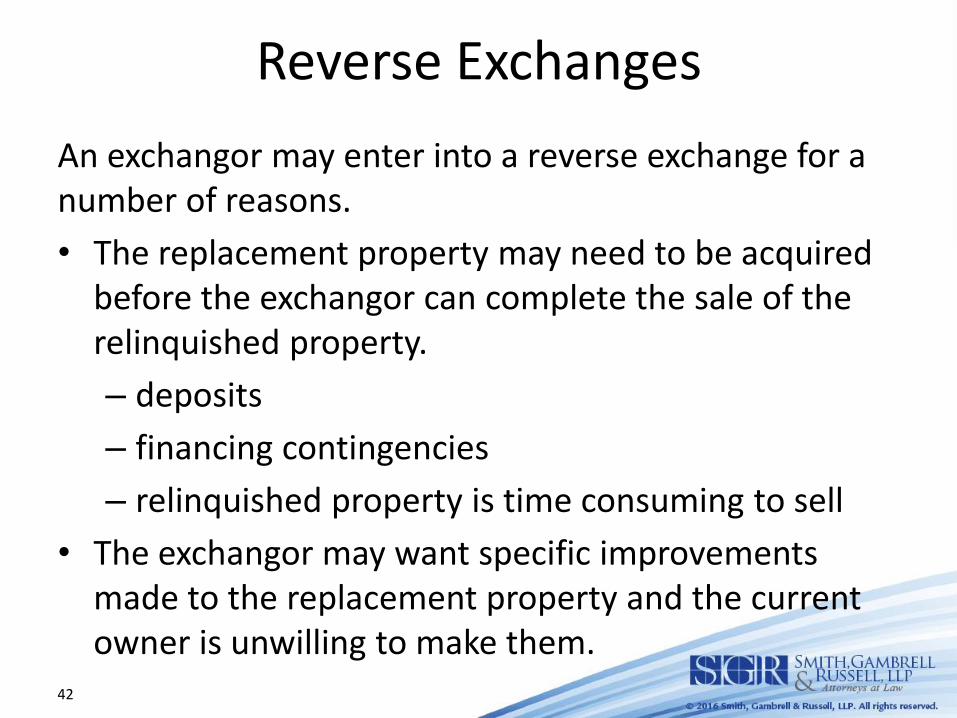

An exchangor may enter into a reverse exchange for a number of reasons.

• The replacement property may need to be acquired before the exchangor can complete the sale of the relinquished property.

– deposits

– financing contingencies

– relinquished property is time consuming to sell

• The exchangor may want specific improvements made to the replacement property and the current owner is unwilling to make them.

42

Reverse Exchanges – Parking

• Reverse exchanges are also referred to as “parking” arrangements.

• In the most common variant, the exchangor parks the replacement property with the EAT prior to the 1031 exchange.

• Later, the exchangor enters into a simultaneous exchange of the relinquished property for the replacement property.

43

Reverse Exchanges – Net Lease

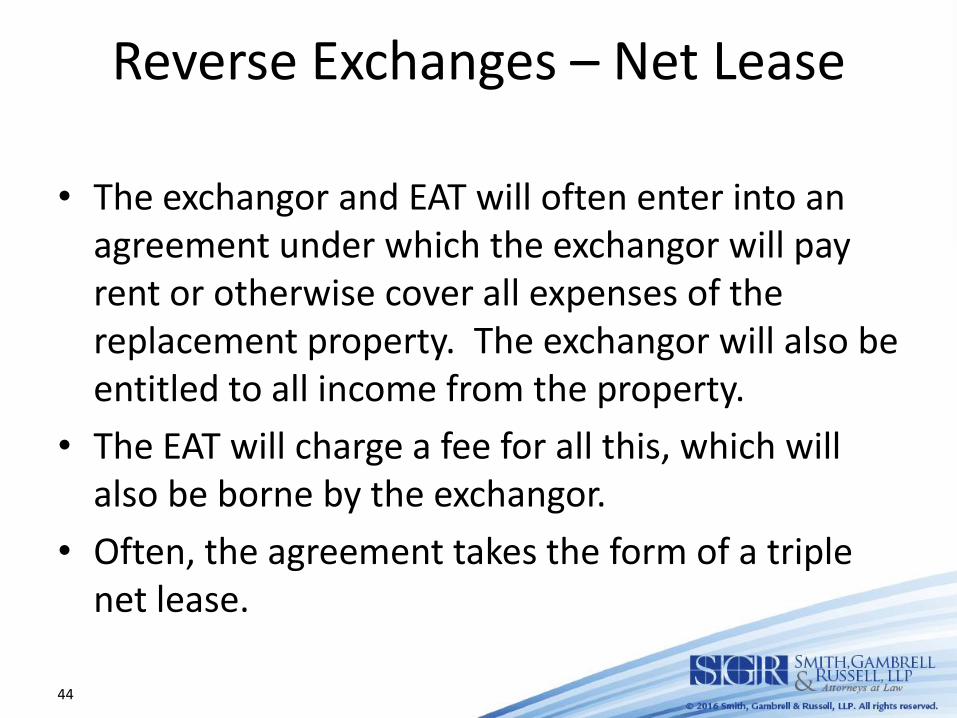

• The exchangor and EAT will often enter into an agreement under which the exchangor will pay rent or otherwise cover all expenses of the replacement property. The exchangor will also be entitled to all income from the property.

• The EAT will charge a fee for all this, which will also be borne by the exchangor.

• Often, the agreement takes the form of a triple net lease.

44

Reverse Exchanges – Improvements

• If the exchangor desires improvements to be constructed on the replacement property an additional agreement is usually set up between the exchangor and the EAT.

• In its simplest form, the exchangor agrees to act as the general contractor for the EAT, with the EAT passing along the cost of the improvements to the exchangor.

45

Reverse Exchanges – Financing

• The exchangor will also need to provide funds to the EAT to allow it to purchase the replacement property.

• Generally, either the exchangor loans funds to the EAT, or a third party lender loans funds to the EAT. In the latter case, the parties may contemplate that the exchangor will assume the loan after the replacement property is transferred.

• Sometimes the replacement property is subject to an existing loan the EAT will assume or take subject to.

• While a loan from the exchangor is relatively straightforward, any attempt to use third party funding creates many difficult security and banking issues.

46

Reverse Exchanges – Closing Steps

• When the exchangor is ready to complete the transaction, the regular steps of a simultaneous 1031 exchange occur – the “trick” is that EAT is treated as a third party.

• Thus, the exchangor uses a QI to transfer the relinquished property to a buyer. The QI holds the sales proceeds.

• The QI then uses the sales proceeds to purchase the replacement property from the EAT, and transfers this property to the exchangor.

• The EAT uses the sales proceeds it receives from the QI to close out any funding arrangements that are not assumed or taken subject to.

47

Reverse Exchanges – EAT Rules

• Reverse exchanges rely on a finding that the EAT “holds” the replacement property.

• In Rev. Proc. 2000-37, the IRS set out a reverse exchange safe harbor and listed several conditions that mush be met in order to meet the EAT-holds-property requirement.

48

Reverse Exchanges – EAT Rules • The EAT must be unrelated to the exchangor. • The EAT must hold qualified indicia of ownership in the

replacement property. • Within 5 days of acquiring the replacement property, the

EAT and the exchangor must enter into an accommodation agreement which specifies that the EAT will be treated as the owner of the replacement property for tax purposes.

• The relinquished property must be identified within 45 days after the replacement property is acquired by the EAT.

• Within 180 days after the EAT acquires the property, it is transferred to the exchangor as replacement property. (Alternatively, it is transferred as relinquished property to a third party.)

• The combined period for holding the acquired property by the EAT cannot exceed 180 days.

49

Reverse Exchanges – Variations

• Rev. Proc. 2000-37 sets out safe harbor requirements – it does not purport to describe or define the limits of the law.

• Transactions occur outside the safe harbor.

• These non-conforming arrangements usually follow all but one of the requirements. For example, the most common difference is a holding period that exceeds the 180-day limit.

50

Tenancy-in-Common Exchanges

51

“TIC” Exchanges

• Recall that in order to qualify as a 1031 exchange, the replacement and relinquished properties must be of like kind.

• Generally, an interest in a partnership or other entity cannot serve as replacement or relinquished property.

• However, most types of real property interests are treated as of like kind to other real property.

• A tenancy-in-common (“TIC”) interest presents a problem under the tax rules.

• For example, in Bergford v. Commissioner, 12 F.3d 166 (9th Cir. 1993), the court held that a TIC ownership arrangement was a partnership.

52

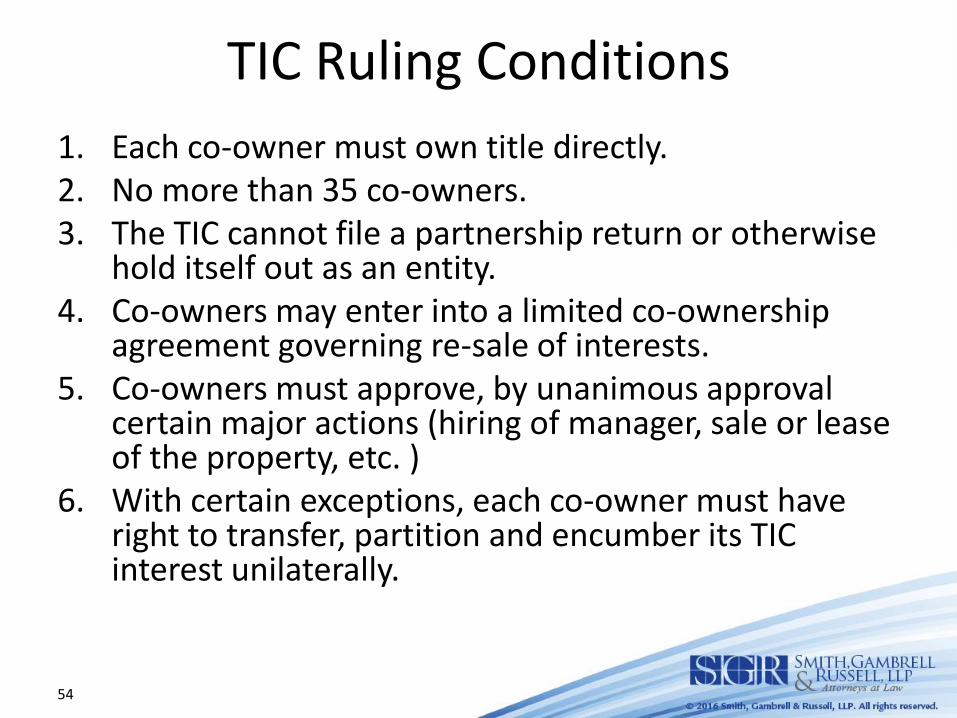

TIC Relief

• The risk, then, is that an otherwise routine exchange of real estate for a TIC interest could fail if the TIC is treated as a partnership.

• To help resolve this problem, the IRS issued Rev. Proc. 2002-22 which listed the requirements under which it would find that a TIC arrangement was not a partnership.

• The following slides set out these 15 requirements.

53

TIC Ruling Conditions

1. Each co-owner must own title directly. 2. No more than 35 co-owners. 3. The TIC cannot file a partnership return or otherwise

hold itself out as an entity. 4. Co-owners may enter into a limited co-ownership

agreement governing re-sale of interests. 5. Co-owners must approve, by unanimous approval

certain major actions (hiring of manager, sale or lease of the property, etc. )

6. With certain exceptions, each co-owner must have right to transfer, partition and encumber its TIC interest unilaterally.

54

TIC Ruling Conditions

7. Upon sale of the property, the net proceeds must be distributed to the co-owners.

8. Generally, each co-owner must share in all revenues and all costs associated with the property pro rata based on its respective percentage TIC interest.

9. Each co-owner must share in all debt secured by blanket liens on the property pro rata based on its respective TIC interest.

10. A co-owner may issue an option to purchase its TIC interest provided the exercise price reflects the fair market value of the property as of the time the option is exercised.

11. Activities of co-owners are limited to those customarily performed in connection with the maintenance and repair of rental real property (“qualifying rents” test).

12. The co-owners may enter into management or brokerage agreements with a manager and/or agent which are subject to specific limitations.

55

TIC Ruling Conditions

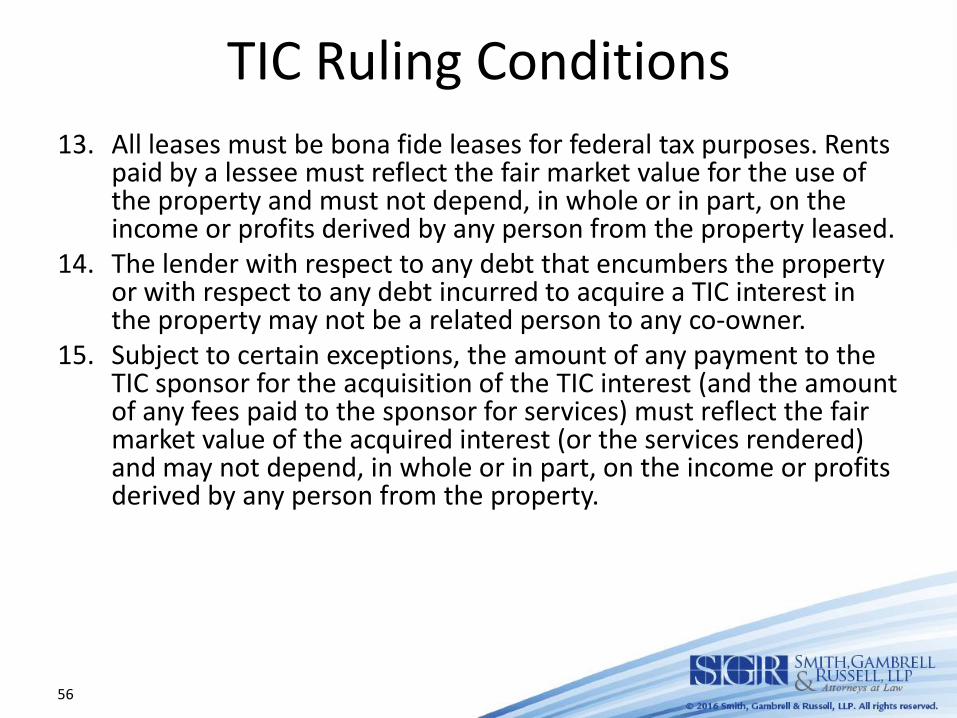

13. All leases must be bona fide leases for federal tax purposes. Rents paid by a lessee must reflect the fair market value for the use of the property and must not depend, in whole or in part, on the income or profits derived by any person from the property leased.

14. The lender with respect to any debt that encumbers the property or with respect to any debt incurred to acquire a TIC interest in the property may not be a related person to any co-owner.

15. Subject to certain exceptions, the amount of any payment to the TIC sponsor for the acquisition of the TIC interest (and the amount of any fees paid to the sponsor for services) must reflect the fair market value of the acquired interest (or the services rendered) and may not depend, in whole or in part, on the income or profits derived by any person from the property.

56

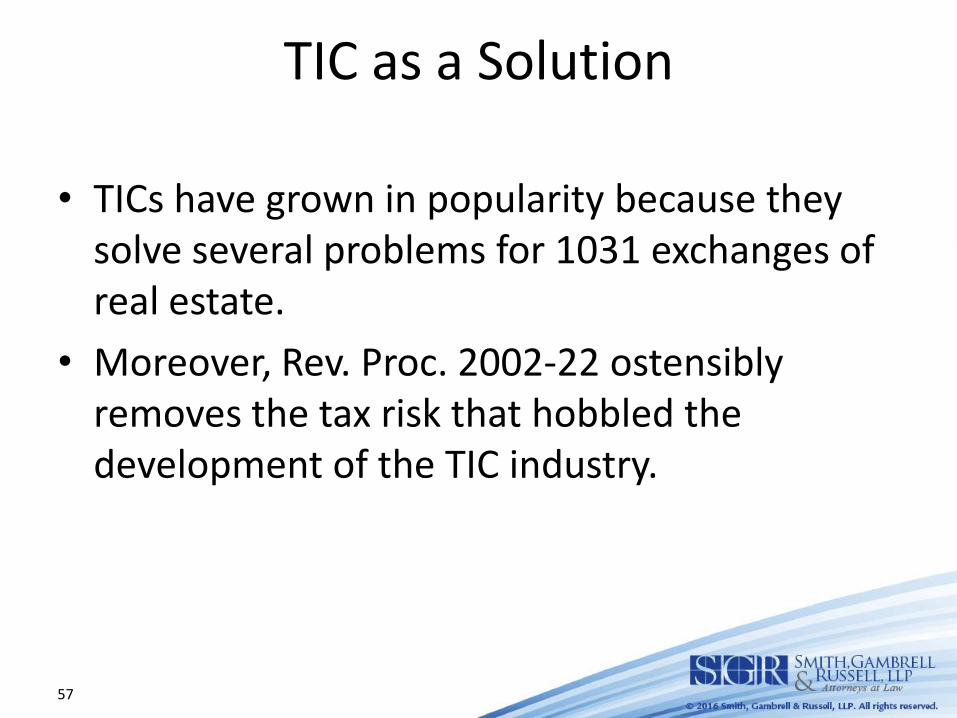

TIC as a Solution

• TICs have grown in popularity because they solve several problems for 1031 exchanges of real estate.

• Moreover, Rev. Proc. 2002-22 ostensibly removes the tax risk that hobbled the development of the TIC industry.

57

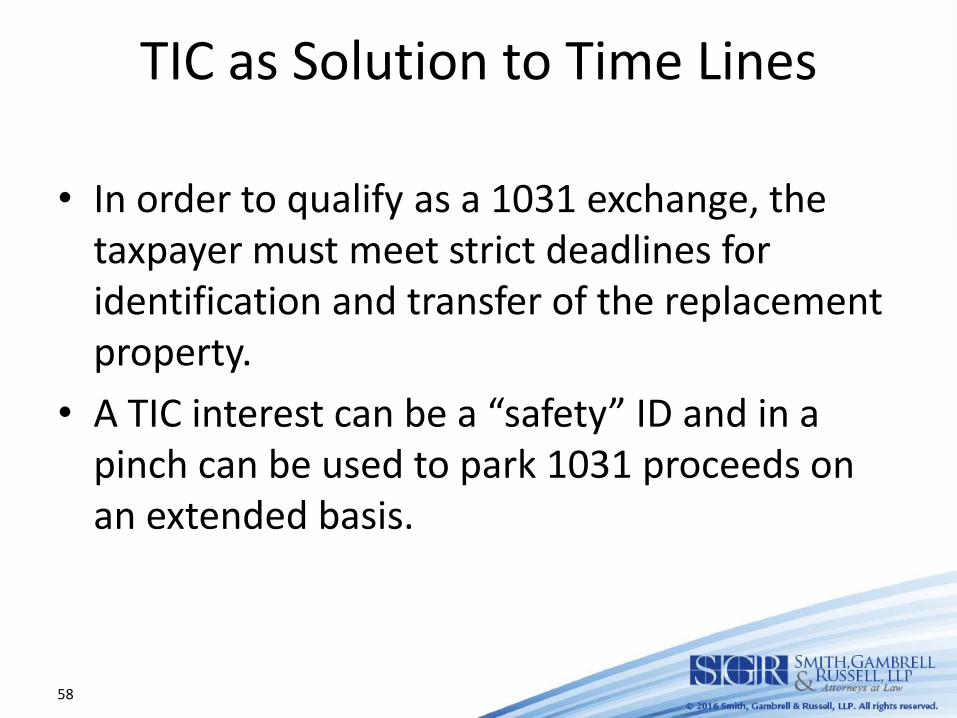

TIC as Solution to Time Lines

• In order to qualify as a 1031 exchange, the taxpayer must meet strict deadlines for identification and transfer of the replacement property.

• A TIC interest can be a “safety” ID and in a pinch can be used to park 1031 proceeds on an extended basis.

58

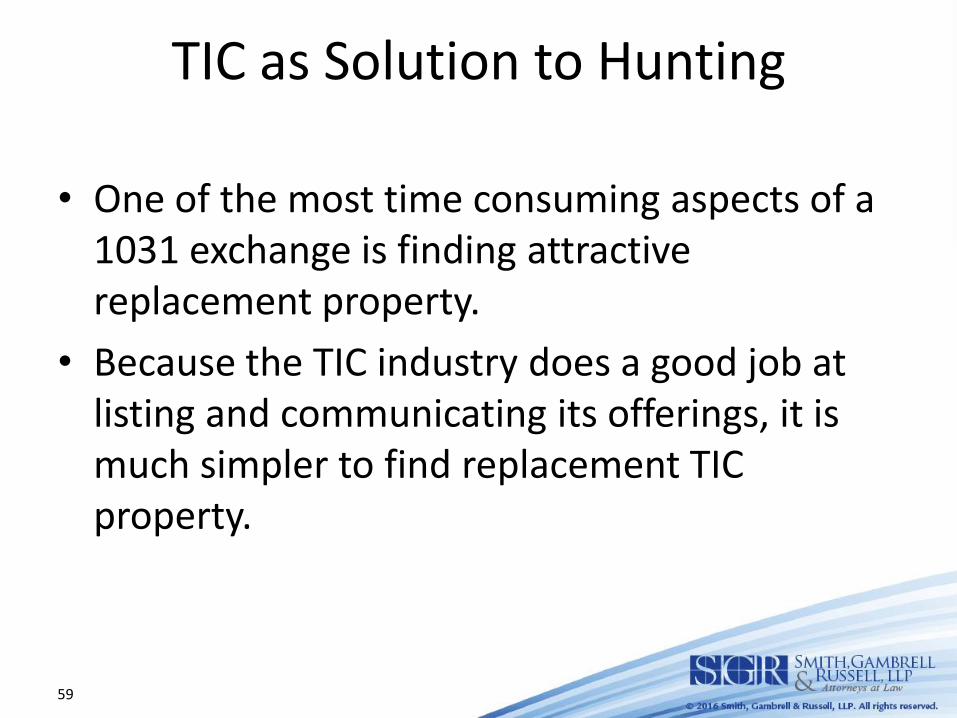

TIC as Solution to Hunting

• One of the most time consuming aspects of a 1031 exchange is finding attractive replacement property.

• Because the TIC industry does a good job at listing and communicating its offerings, it is much simpler to find replacement TIC property.

59

TIC as Solution to Scaling

• To qualify for 1031 treatment, the taxpayer has to roll over into a specific amount of investment to cover all his/her gain.

• TIC investments are often easy to scale. As a result, it is generally the case that a TIC investment can be structured to cover all gain.

• Even if a taxpayer has identified a non-TIC interest to roll over into, a TIC interest can be used to bridge the gap if the main investment is not large enough.

60

TIC as Solution to Diversification

• TIC industry takes stable, income producing properties (i.e., fully-rented office buildings) and packages them for use as replacement property.

• Thus, a taxpayer holding investment property that does not produce income (i.e., raw land that is sold to a developer), can diversify into a different type of investment without triggering any tax.

61

Delaware Statutory Trusts (“DSTs”)

62

DSTs – Basics • DST is a statutory creation – the Delaware Statutory

Trust Act. Do not confuse with common law trusts. • The owners of a DST are shielded from liability from

the debts and obligations of the DEST. • Each owner has an undivided interest in the DST’s

assets. • The DST is managed by a trustee. • The rights and obligations of the DST owners are set

out in a trust document (sometimes called an indenture).

• Historically, DSTs have been used as securitization vehicles for finance transactions.

63

DSTs – Tax Classification

• DST looks a lot like an LLC.

• If a DST were classified as a business entity, then it could never be utilized as replacement or relinquished property.

• However, if a DST is classified as an investment trust, then the owners are treated as owning an indivisible portion of the underlying assets of the DST.

64

DSTs – Rev. Rul. 2004-86

• The IRS issued Rev. Rul. 2004-86 to address many of these issues.

• If properly structured, a DST will be treated as an investment trust.

• The IRS further determined that if a DST is classified as an investment trust, then an interest in a DST would be looked through.

• In essence, a interest in a DST owning only real estate will be treated as an interest in that real estate and can qualify as replacement or relinquished property.

65

DSTs – Key Facts • The key facts on investment trust classification relate to the limited

powers of the trustee. Generally, the trustee’s powers should be limited to the collection and distribution of income.

• In addition, certain powers will cause the DST to be treated as a business entity and interests in the DST will fail as replacement property:

– The power to dispose of all or parts of the DST’s assets and acquire new assets;

– The power to renegotiate the leases on the DST’s assets or enter into new leases

– The power to renegotiate or refinance the debt used to purchase the DST’s assets;

– The power to invest cash from operations in certain ways; or

– The power to make more than minor non-structural modifications to the DST’s assets (unless required by law).

66

DSTs – Advantages • A properly structured DST may present several advantages over a TIC.

• Number of owners. TICs are capped at 35 owners under the relevant IRS safe harbor. In contrast, a DST has potentially no limit (although most DSTs have a limit of 99 to 499 owners).

• Financing. Tic investors typically arrange their own financing. A DST can arrange its own financing on the underlying assets.

• Voting rights. DST owners have no voting rights; TIC owners have voting rights (unanimous approval means TIC owners often have veto rights).

• Owner liability. DST owners have no personal liability, while TIC owners do.

• Prevalence. TICs are a more developed industry, but that is changing.

67

Related Party Exchanges

68

Related Party Rules

• General Rule

• Basis Shifting

• Guidance

69

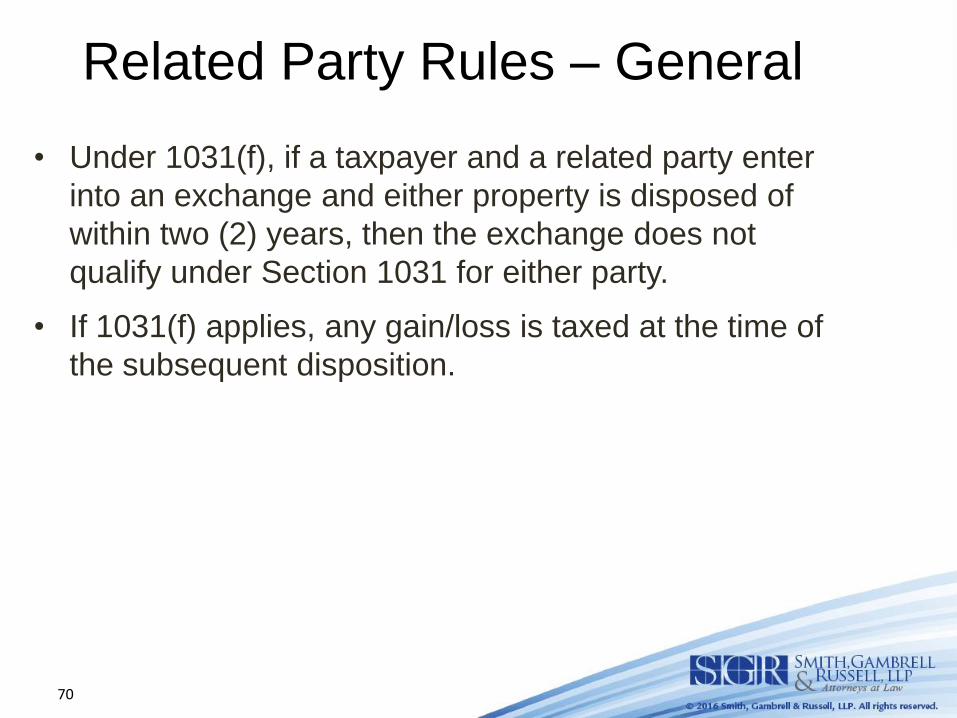

Related Party Rules – General

• Under 1031(f), if a taxpayer and a related party enter

into an exchange and either property is disposed of

within two (2) years, then the exchange does not

qualify under Section 1031 for either party.

• If 1031(f) applies, any gain/loss is taxed at the time of

the subsequent disposition.

70

Who Are Related Parties

• A related person is any person bearing a relationship

to the taxpayer described in section 267(b) or

707(b)(1).

• Section 707(b)(1) relationships:

• a partnership and a person owning, directly or

indirectly, more than 50% of the capital interest, or

the profits interest, in such partnership, or

• two partnerships in which the same persons own,

directly or indirectly, more than 50% of the capital

interests or profits interests.

71

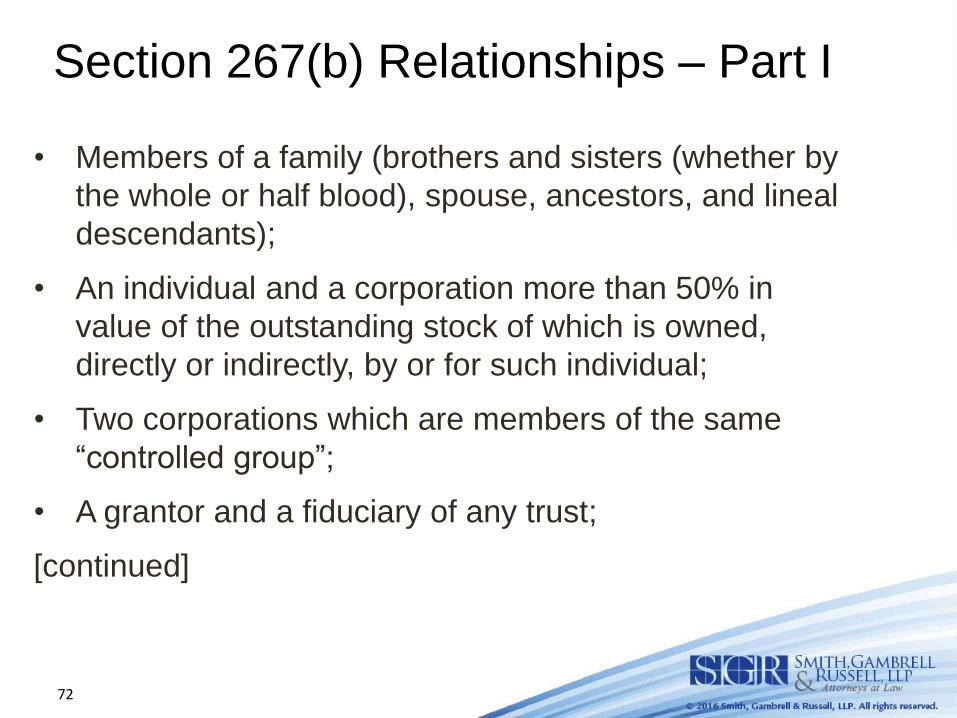

Section 267(b) Relationships – Part I

• Members of a family (brothers and sisters (whether by

the whole or half blood), spouse, ancestors, and lineal

descendants);

• An individual and a corporation more than 50% in

value of the outstanding stock of which is owned,

directly or indirectly, by or for such individual;

• Two corporations which are members of the same

“controlled group”;

• A grantor and a fiduciary of any trust;

[continued]

72

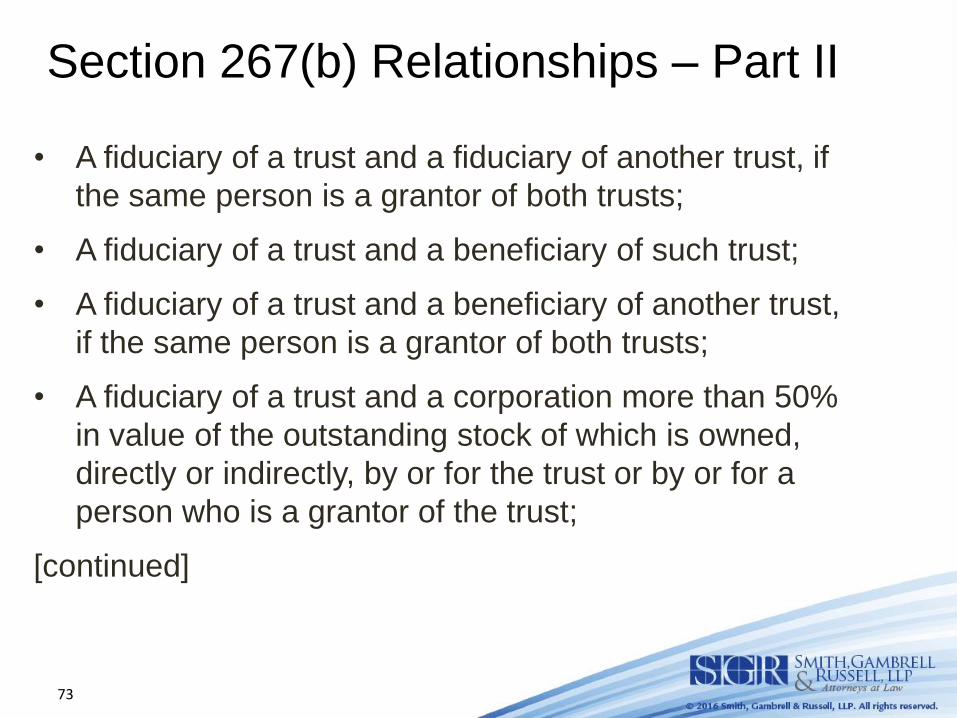

Section 267(b) Relationships – Part II

• A fiduciary of a trust and a fiduciary of another trust, if

the same person is a grantor of both trusts;

• A fiduciary of a trust and a beneficiary of such trust;

• A fiduciary of a trust and a beneficiary of another trust,

if the same person is a grantor of both trusts;

• A fiduciary of a trust and a corporation more than 50%

in value of the outstanding stock of which is owned,

directly or indirectly, by or for the trust or by or for a

person who is a grantor of the trust;

[continued]

73

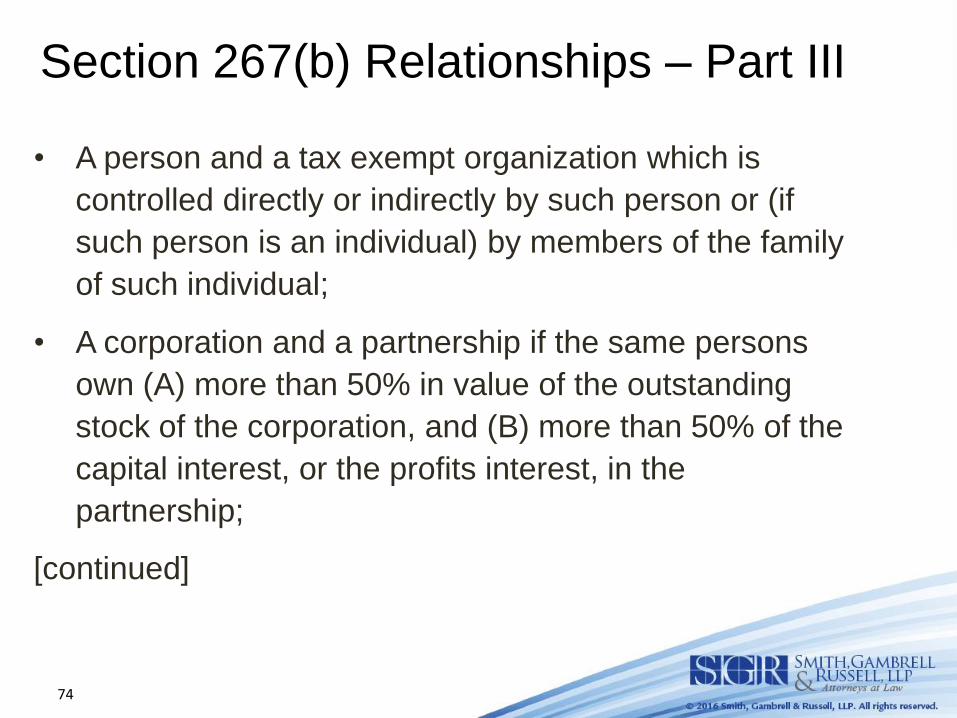

Section 267(b) Relationships – Part III

• A person and a tax exempt organization which is

controlled directly or indirectly by such person or (if

such person is an individual) by members of the family

of such individual;

• A corporation and a partnership if the same persons

own (A) more than 50% in value of the outstanding

stock of the corporation, and (B) more than 50% of the

capital interest, or the profits interest, in the

partnership;

[continued]

74

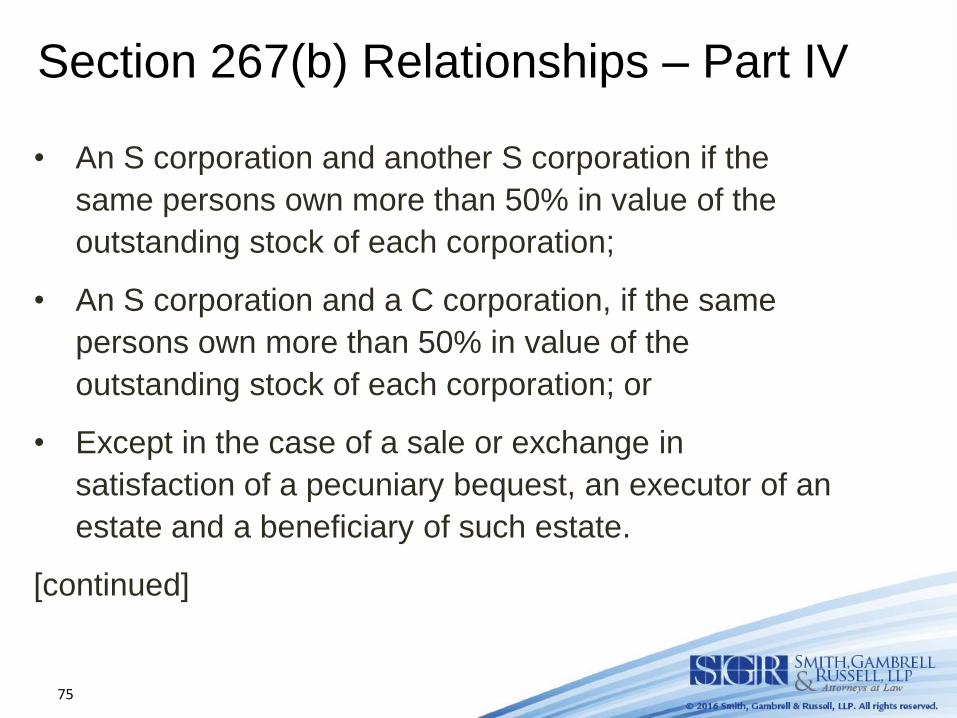

Section 267(b) Relationships – Part IV

• An S corporation and another S corporation if the

same persons own more than 50% in value of the

outstanding stock of each corporation;

• An S corporation and a C corporation, if the same

persons own more than 50% in value of the

outstanding stock of each corporation; or

• Except in the case of a sale or exchange in

satisfaction of a pecuniary bequest, an executor of an

estate and a beneficiary of such estate.

[continued]

75

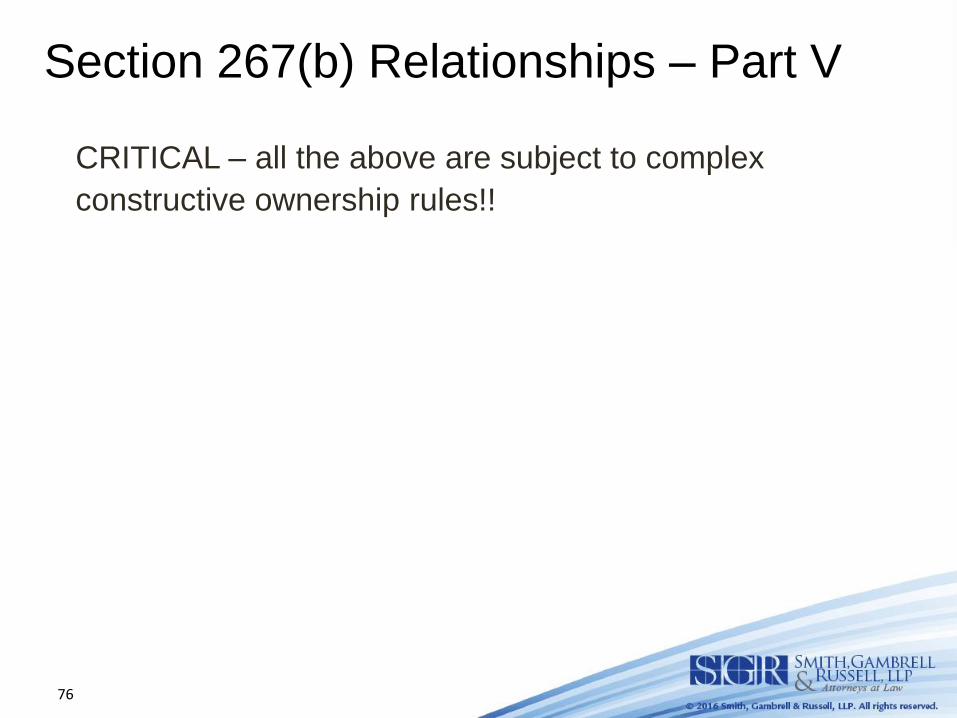

Section 267(b) Relationships – Part V

CRITICAL – all the above are subject to complex

constructive ownership rules!!

76

Basis Shifting

• Adam and Eve are spouses.

• Adam owns Blackacre with FMV of $100 and basis of $100.

• Eve owns Whiteacre with FMV of $100 and basis of $25.

• Eve would like to sell Whiteacre. If Eve sells Whiteacre,

she will have $75 gain.

• If Adam and Eve enter into a like-kind exchange and swap

properties, Eve will take Blackacre with a tax basis of $25

and Adam will take Whiteacre with a tax basis of $100.

• If Adam sells Whiteacre, but for Section 1031(f), he would

have no gain on the sale.

77

Holding Period

• If a related party exchange occurs, both parties must

hold the received properties for two (2) years.

• BUT – the holding period is extended for any time

during which either party’s “risk of loss” with respect to

its property is substantially diminished by:

• the holding of a put with respect to such property,

• the holding by another person of a right to acquire

such property, or

• a short sale or any other transaction

78

Permitted Dispositions -- I Certain dispositions are permitted during the holding

period:

• a disposition after the earlier of the death of the

taxpayer or the death of the related person,

• a disposition that occurs in a compulsory or involuntary

conversion if the exchange occurred before the threat

or imminence of such conversion, or

• a disposition with respect to which it is established to

the satisfaction of the IRS that neither the exchange

nor such disposition had as one of its principal

purposes the avoidance of federal income tax.

79

Permitted Dispositions -- II • The third “out” has given rise to considerable

commentary.

• Because basis shifting is the stated rationale for

Section 1031(f), a transaction that does not implicate

basis shifting should be approved by the IRS.

80

Anti-Abuse Rule

• There is very little guidance on this rule.

• If a taxpayer overtly enters into a related party

exchange, the burden or “cost” is compliance with the

holding period rules.

• If a taxpayer attempts to avoid the related party rules in

form, but not in substance, then this anti-avoidance rule

prohibits any part of Section 1031 from applying.

• For example, the IRS takes the position that using a QI

to mask a direct exchange with a related party triggers

the anti-avoidance rule.

81

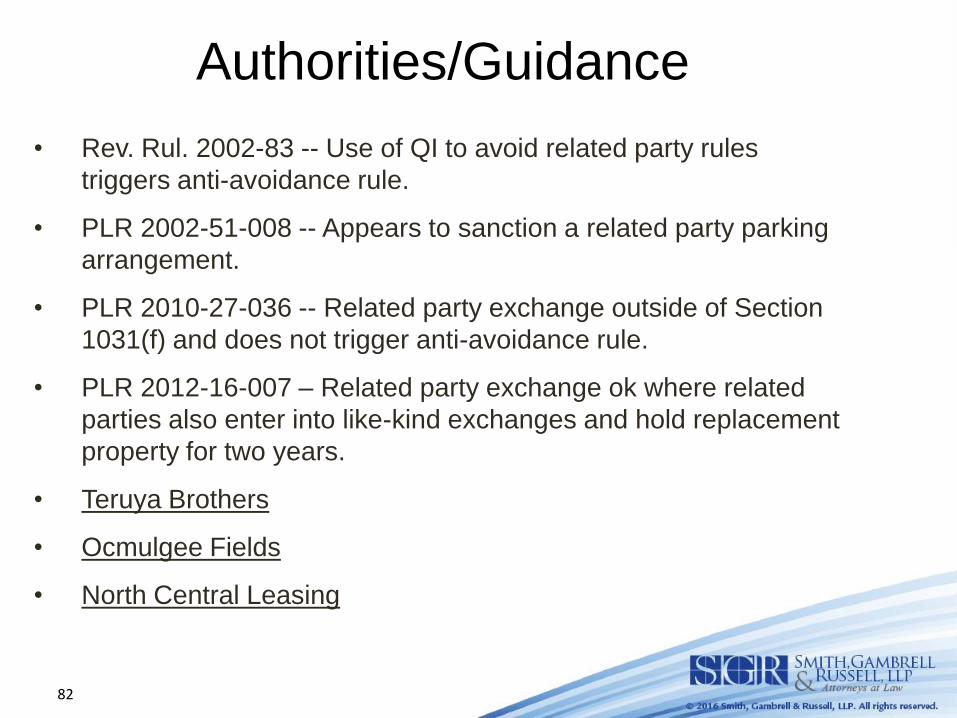

Authorities/Guidance

• Rev. Rul. 2002-83 -- Use of QI to avoid related party rules

triggers anti-avoidance rule.

• PLR 2002-51-008 -- Appears to sanction a related party parking

arrangement.

• PLR 2010-27-036 -- Related party exchange outside of Section

1031(f) and does not trigger anti-avoidance rule.

• PLR 2012-16-007 – Related party exchange ok where related

parties also enter into like-kind exchanges and hold replacement

property for two years.

• Teruya Brothers

• Ocmulgee Fields

• North Central Leasing

82

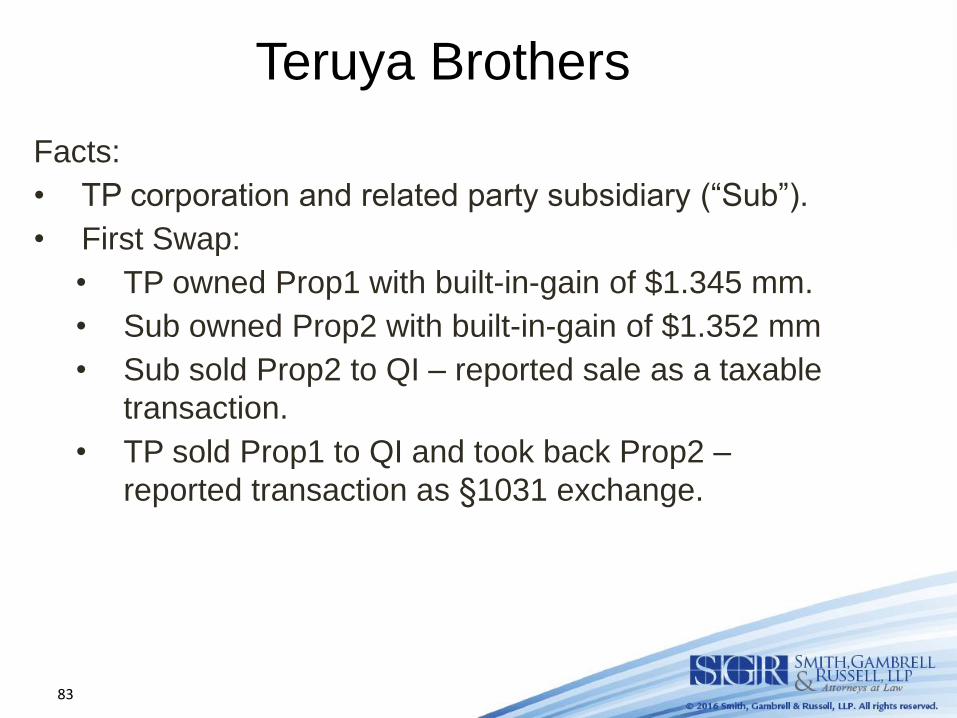

Teruya Brothers

Facts:

• TP corporation and related party subsidiary (“Sub”).

• First Swap:

• TP owned Prop1 with built-in-gain of $1.345 mm.

• Sub owned Prop2 with built-in-gain of $1.352 mm

• Sub sold Prop2 to QI – reported sale as a taxable

transaction.

• TP sold Prop1 to QI and took back Prop2 –

reported transaction as §1031 exchange.

83

Teruya Brothers

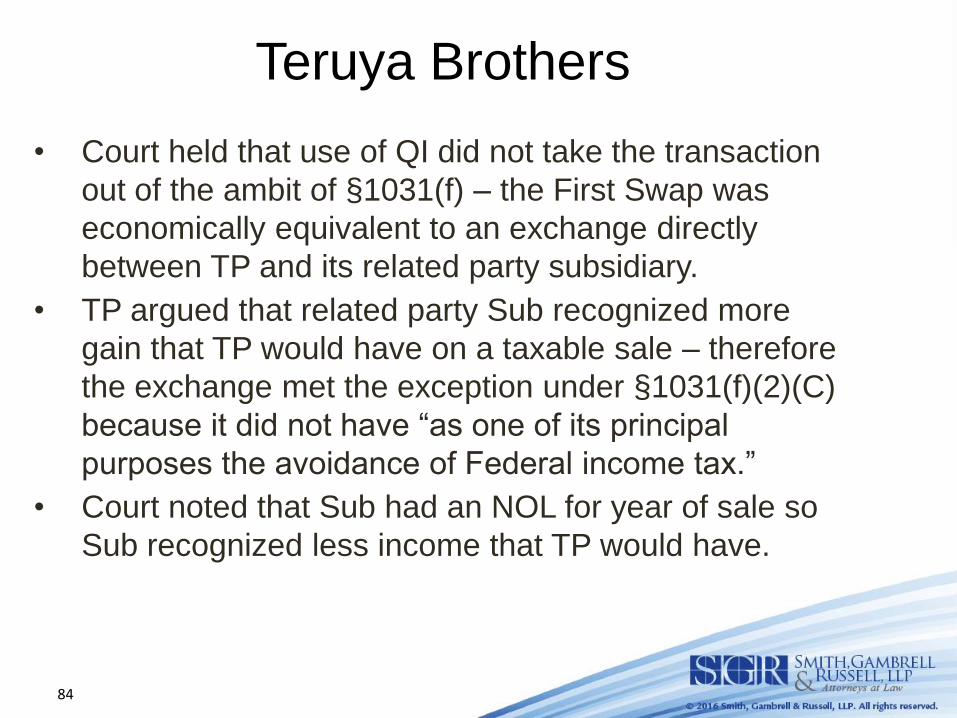

• Court held that use of QI did not take the transaction

out of the ambit of §1031(f) – the First Swap was

economically equivalent to an exchange directly

between TP and its related party subsidiary.

• TP argued that related party Sub recognized more

gain that TP would have on a taxable sale – therefore

the exchange met the exception under §1031(f)(2)(C)

because it did not have “as one of its principal

purposes the avoidance of Federal income tax.”

• Court noted that Sub had an NOL for year of sale so

Sub recognized less income that TP would have.

84

Teruya Brothers

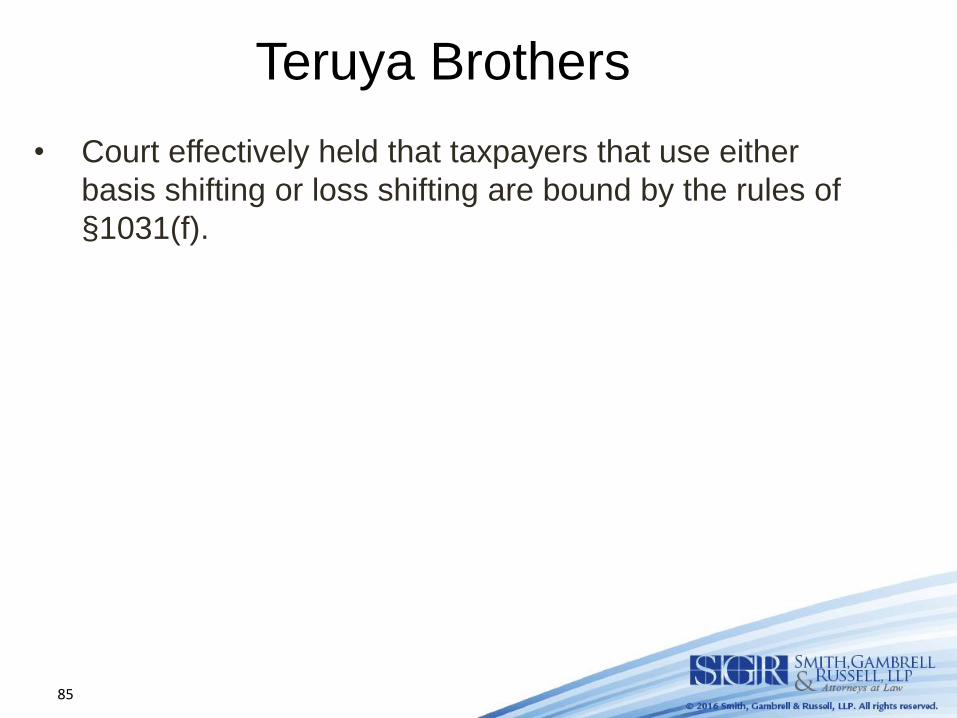

• Court effectively held that taxpayers that use either

basis shifting or loss shifting are bound by the rules of

§1031(f).

85

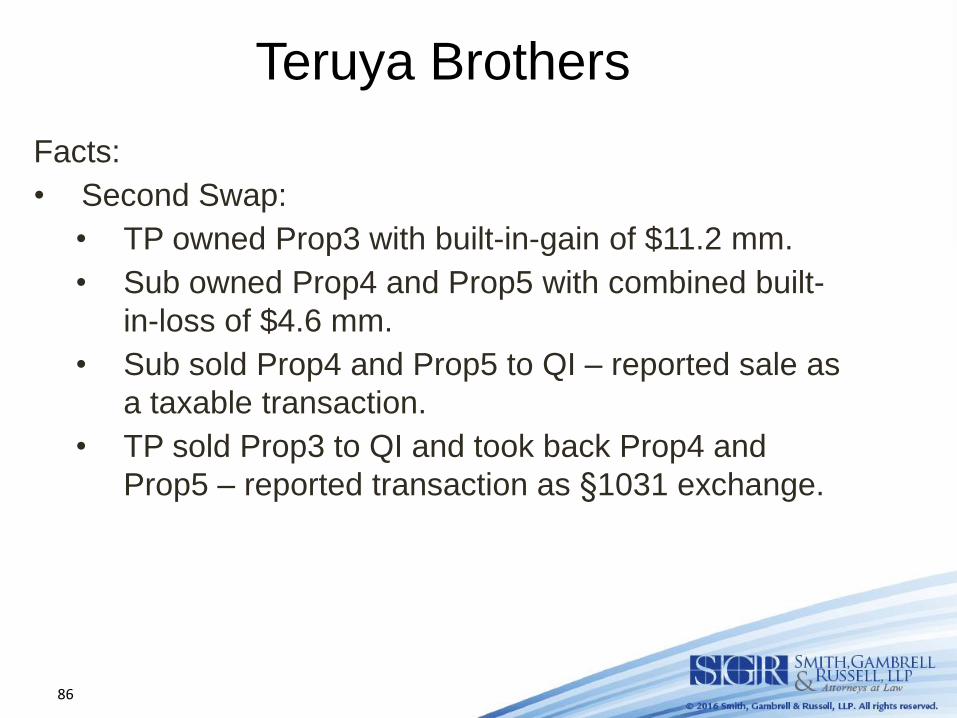

Teruya Brothers

Facts:

• Second Swap:

• TP owned Prop3 with built-in-gain of $11.2 mm.

• Sub owned Prop4 and Prop5 with combined built-

in-loss of $4.6 mm.

• Sub sold Prop4 and Prop5 to QI – reported sale as

a taxable transaction.

• TP sold Prop3 to QI and took back Prop4 and

Prop5 – reported transaction as §1031 exchange.

86

Teruya Brothers

• Court again found that use of QI did not take the

transaction out of the ambit of §1031(f) – the First

Swap was economically equivalent to an exchange

directly between TP and its related party subsidiary.

• Here, appeared to fit within the basis shifting concern

that underlies §1031(f).

87

Teruya Brothers

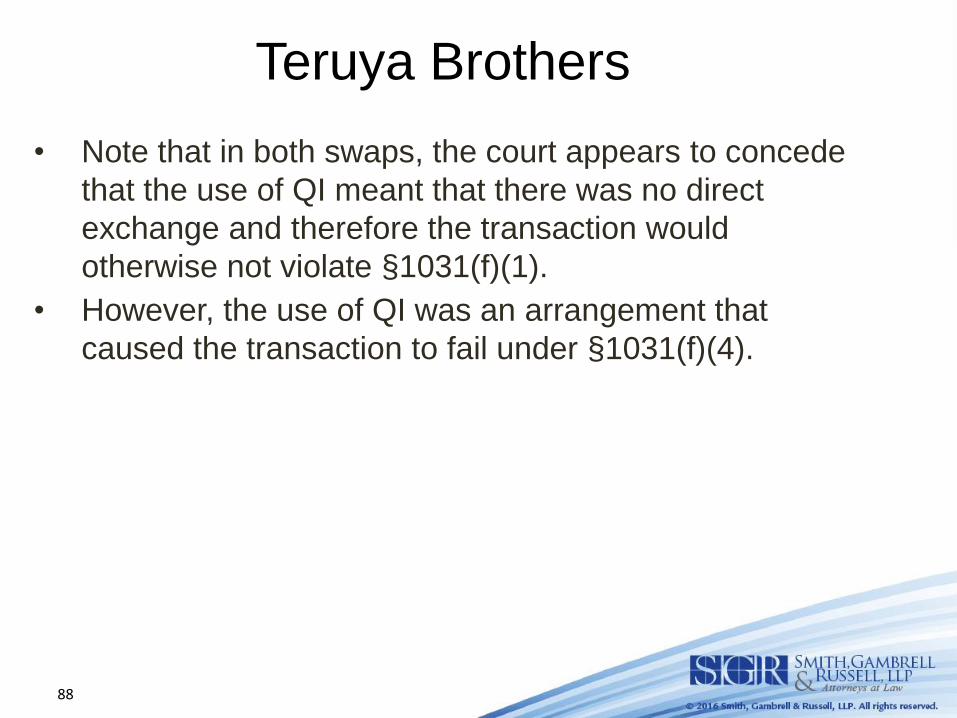

• Note that in both swaps, the court appears to concede

that the use of QI meant that there was no direct

exchange and therefore the transaction would

otherwise not violate §1031(f)(1).

• However, the use of QI was an arrangement that

caused the transaction to fail under §1031(f)(4).

88

Ocmulgee

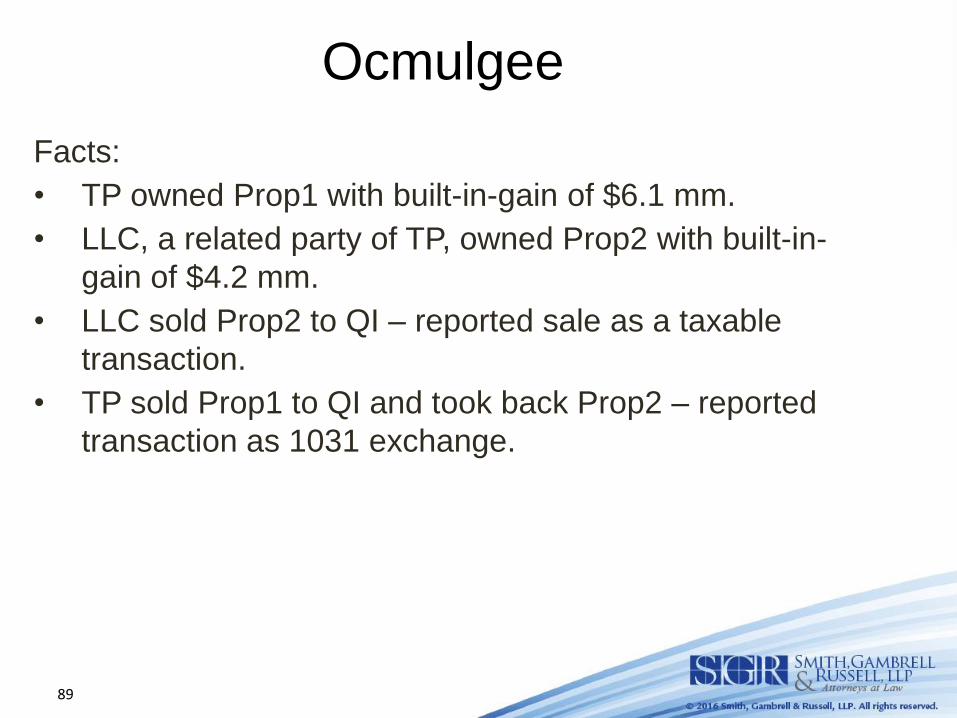

Facts:

• TP owned Prop1 with built-in-gain of $6.1 mm.

• LLC, a related party of TP, owned Prop2 with built-in-

gain of $4.2 mm.

• LLC sold Prop2 to QI – reported sale as a taxable

transaction.

• TP sold Prop1 to QI and took back Prop2 – reported

transaction as 1031 exchange.

89

Ocmulgee

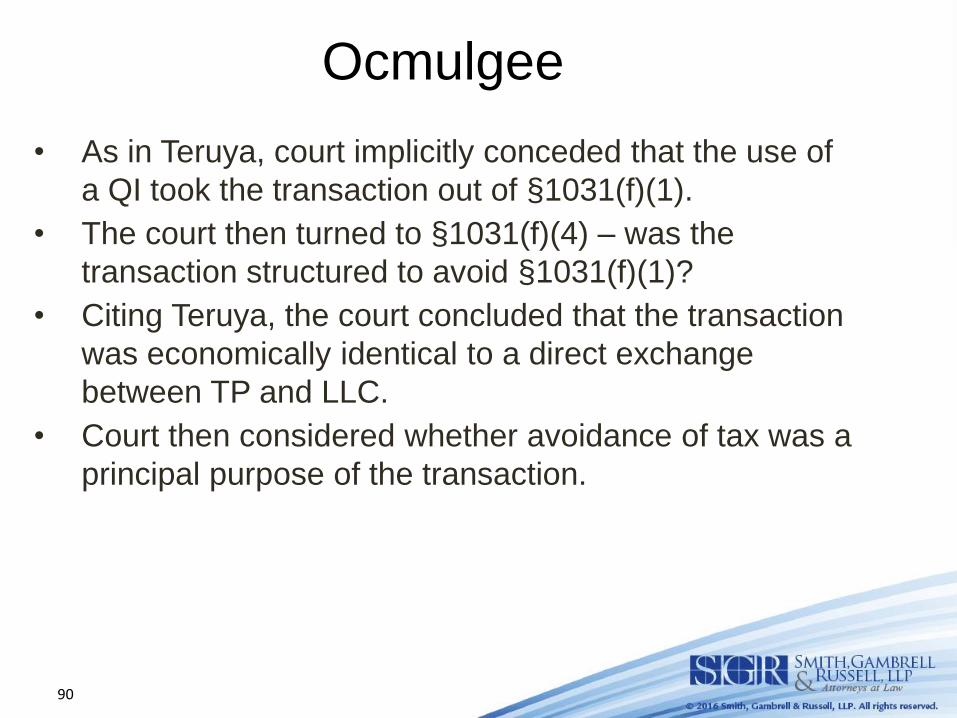

• As in Teruya, court implicitly conceded that the use of

a QI took the transaction out of §1031(f)(1).

• The court then turned to §1031(f)(4) – was the

transaction structured to avoid §1031(f)(1)?

• Citing Teruya, the court concluded that the transaction

was economically identical to a direct exchange

between TP and LLC.

• Court then considered whether avoidance of tax was a

principal purpose of the transaction.

90

Ocmulgee

• The court noted that TP would have paid tax on an

additional $1.8 mm in gain, and that by triggering gain

in LLC, a pass-through entity, what tax was triggered

was also subject to a lower tax rate.

• The court cautioned that it was possible that what

otherwise appeared to be a basis-shifting transaction

could, because of countervailing facts, lack a tax avoid

purpose.

• Finally, the court noted that it did not matter in the

analysis whether the use of a related party was pre-

arranged or not.

91

North Central

Facts:

• TP was the 99% subsidiary of Owner, a related party.

• TP operated an equipment leasing business.

Because it often disposed of used equipment and

acquired new equipment in replacement, it set up a

like-kind exchange program.

• During the period before the court, TP entered into

about 400 transactions that is reported as §1031

exchanges

92

North Central

Representative Transaction (1 of 2):

• TP owns Prop1 with FMV of $750 and built-in-gain of

$630.

• TP wants to Prop 2 from the equipment manufacturer

(unrelated party).

• TP sells Prop1 through QI to true third party.

• Third party pays $750 and acquires Prop1 through QI.

• Owner, the 99% owner of TP, buys Prop2 from the

equipment manufacturer (unrelated party) for $750.

• Under equipment manufacturer incentives, Owner

does not need to pay the $750 for six months.

93

North Central

Representative Transaction (2 of 2):

• Owner sells Prop2 to TP through QI and QI transfers

$750 to Owner.

• Owner pays equipment manufacturer $750 six months

later.

• TP reports the sale of Prop1 and acquisition of Prop2

as a §1031 exchange.

• Owner reports the acquisition and re-sale of Prop2 as

a taxable exchange.

94

North Central

• Court found the various steps in the exchanges

unnecessarily complex. In particular, the court could

not find reasonable ground for the involvement of

Owner.

• Court suggests that involvement of Owner was an

instance of overreaching.

• Specifically, the court suggests that the only purpose

for involving Owner was to take advantage of the six-

month payment delay: “In sum, [Owner] was not

necessary to the transactions at issue yet possessed

significant, unearmarked cash proceeds as a result of

the transactions.”

95

North Central

• Court found the unnecessary interposition of a party

(Owner) and the retention of cash proceeds by a

related party was sufficient to demonstrate that the

exchange program was structured to avoid

§1031(f)(1).

• Court also found that the use of a QI was

unnecessary. Although TP argued that the use of QI

permitted TP to come with the identification and

receipt safe harbors, the court upheld the factual

finding of the lower court that the intent of TP was to

use a QI to avoid §1031(f)(1).

96

North Central

• Note that if TP purchased the replacement property

directly from the equipment manufacturer the

transactions arguably would have qualified under

§1031.

• Moreover, as re-structured, such an exchange

program that utilized a QI would likely also have

passed muster.

• Given that, the court may have been correct that the

involvement of Owner suggests that the parties simply

wanted the free use of sale proceeds, even if only for

a short period.

97

Observations

• Related party exchanges are common.

• Diligence – are related parties present?

• Consider/weigh cost of holding period requirement.

• Use of QI will not defeat related party rules.

• But often the benefits of a QI are significant.

• Consider obtaining a PLR.

98

Observations

Lessons from case law:

• Basis shifting triggers §1031(f)(4) anti-avoidance

analysis – this was mentioned in legislative history.

• So does NOL shifting and tax rate shifting – this does

not appear to be mentioned in legislative history.

• Unfettered use of proceeds (even if only for short-

term) also appears to trigger anti-avoidance analysis.

• Courts will scrutinize structures that are overly

complex – interposition of unnecessary parties can

trigger anti-avoidance analysis.

99

Observations

Lessons from North Central:

• If you could have structured the transaction to fit within

§1031, courts will scrutinize the rationale for the

structure you ended up using.

• If that structure facilitates (1) basis shifting, (2) NOL

shifting, (3) tax rate shifting, or (4) access to sales

proceeds, then court will likely apply §1031(f)(4) anti-

avoidance analysis and often that will be fatal.

100

Top Related

Copyright © 2022 FDOKUMEN