Bahasa

Halaman

Hukum

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa:JC, PY

Rocky Road, Take me home

Luxury residential and office subsectors to bottom

out ahead of other subsectors in 2017

Diversification remain a key strategy for most real

estate companies, cheap valuations could spark M&A

Deleveraging trend to kick in from 2017

Luxury residential and office are our sector picks in 2017. While the Singapore property market is expected to remain on a declining trend (suburban residential homes, industrial, retail and hospitality), we see green shoots in the office and luxury residential subsectors. This is mainly coming from expected higher transaction volumes and take-up rates for new buildings in 2017.

Continued focus on diversification while cheap valuations could spark M&A. We see continued interest from S-REITs and developers to invest overseas but see fewer completed deals given higher currency volatility. In Singapore, land-hungry developers are likely to turn towards the En-bloc market given limited sites in the public land tenders. S-REITs are likely to seek asset recycling in order to fund growth as cost of equity edge higher. Fueled by strong capital flows and attractive valuations of listed firms, we also see a sector consolidation as larger players look to gain access to land banks and income-producing properties at attractive prices.

Deleveraging trend in 2017 and beyond. With higher rates on the horizon, we expect selected developers and REITs to pare down debt over time when the opportunity arises. Of focus is close to c.S$6.3bn worth of bonds expiring in 2017-2018, where refinancingcould prove difficult for some given investor risk aversion post recent defaults in the oil & gas space.

Developers – too cheap to ignore. We see a myriad of catalysts for developers especially from M&A activities which will lift investor sentiment for the sector. Our picks are CDL and UOL. A wildcard could be a potential unwinding of government policies.

Singapore REITs – capital preservation is key. We prefer those with good earnings visibility and minimal downside to our/consensus estimates. Picks are K-REIT, A-REIT and MCT. Small cap picks are FLT, KDC REIT and Croesus.

STI : 2,880.76

Analyst Derek TAN +65 6682 3716 Mervin SONG CFA +65 6682 3715 [email protected] [email protected]

Rachel TAN +65 6682 3713 Singapore Research Team [email protected] [email protected]

Source: DBS Bank, Bloomberg Finance L.P.

Closing price as of 4 Jan 2017

DBS Group Research . Equity 6 Jan 2017

Singapore Industry Focus

Singapore Developers & REITs Refer to important disclosures at the end of this report

STOCKS

Price Mkt Cap Target Price Performance (%)

S$ US$m S$ 3 mth 12 mth Rating

Developers

City Developments 8.39 5,341 9.90 (8.5) 11.8 BUY UOL Group 6.12 3,448 7.20 7.5 1.2 BUY

REITs Ascendas REIT 2.31 4,597 2.65 (6.1) 3.1 BUY Keppel REIT 1.02 2,315 1.23 (8.0) 11.3 BUY Mapletree Commercial Trust 1.42 2,800 1.62 (8.0) 10.6 BUY

Frasers Logistics & Industrial Trust 0.94 925 1.10 (5.0) N.A BUY

Keppel DC REIT 1.20 938 1.33 2.5 20.4 BUY Croesus Retail Trust 0.85 452 0.99 (1.2) 3.9 BUY

Page 1

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 2

The DBS Asian Insights SparX report is a deep dive look into thematic angles impacting the longer-term investment thesis for a sector, country or the region. We view this as an ongoing conversation rather than a one-off treatise on the topic, and invite feedback from our readers, and in particular welcome follow-on questions worthy of closer examination.

Table of Contents

1. Investment Summary 3

2. Peer Comparisons 5

3. Key Charts 7

4. Developers – Catalysts abound to lift valuations from multi-year lows4.1 Attractive valuations with upcoming catalysts. 4.2 Diversification to remain a key strategy for developers. 4.3 Improved transactions in the luxury end of the market to continue. 4.4 Looming ABSD deadlines not a precursor for a significant price cuts.

4.5 Potential land-banking opportunities in Singapore. 4.6 More En-bloc transactions in 2017. 4.7 Merger and Acquisition (M&A) activities could pick up. 4.8 Will Developers need to deleverage?

10

5. Singapore REITs – Déjà vu 5.1 Impact of higher interest rates on prices and distributions 5.2 Modest DPU growth.

5.3 Potential risk to property values in the industrial and hospitality sectors.

5.4 Acquisitions may be difficult to execute with redevelopments an attractive option.

31

6. Residential Subsector Outlook: Luxury home prices to bottom out in 20176.1 Trends, demand and supply outlook

6.2 Scenarios where government could relax policy measures

47

7. Office Subsector Outlook: Grade A office space to bottom by end 20177.1 Trends, demand and supply outlook

55

8. Retail Subsector Outlook: Hampered by weakening retail sales8.1 Trends, demand and supply outlook

63

9. Industrial Subsector Outlook: Year of consolidation post supply spikes9.1 Trends, demand and supply outlook

67

10. Hospitality Subsector Outlook: No turnaround in sight yet10.1 Trends, demand and supply outlook

74

11. Charts: S-REIT yield and P/Bk NAV Charts: Developers P/Bk NAV

83

Stocks Profiles 102

Note: Prices used as of 04 Jan-2017

Page 2

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 3

Investment Summary

2017 remains a tenants' market as heightened supply completion poses a risk for most real estate sectors. It will be another year of moderation for the Singapore property market as we believe that most real estate subsectors will continue to see downside in rents and/or prices on the back of soft demand given the current economic slowdown. Meanwhile, heightened supply completion in 2017 means that it will remain a tenants' market.

Key Themes

1. Luxury-end of residential market and office sectors

bottoming out

Luxury residential and office sectors the brighter spot. However, among the real estate sectors, we see brighter prospects in the luxury end of the residential market and office subsectors. We believe that luxury residential prices in Singapore are attractive on a relative basis compared to home prices in the region which we expect higher investment transaction volumes in 2017. The office sector is projected to see slower rental declines of (5-10%) mainly due to better-than-projected take-up in upcoming new office buildings and see the sector bottoming out by end of 2017.

However, the retail, hospitality and industrial sectors are still expected to feel the pressure from projected negative net absorption, given excess supply outlook.

Singapore Property Clock

Source: DBS Bank

2. Developers and REITs to continue seeking overseas

opportunities; en-bloc deals to pick up in 2017

Diversification remains a key strategy but opportunities limited as currency volatility arises. We believe that property developers and REITs will continue their strategy to diversify overseas for growth but expect the acquisition momentum to taper on the back of increased currency volatility, coupled with higher cost of funds. Countries that we believe remain attractive on a currency-adjusted basis are London, Australia (Melbourne and Sydney) and selected Tier 1 cities of China like Shanghai.

Apart from acquisitions, REITs could also capitalize on the increased development limits (25% cap vs 10% previously subject to conditions) accorded by Monetary Authority of Singapore (MAS) to take on more asset enhancements to rejuvenate their portfolios and boost returns.

Developers are hungry for land in Singapore, more en-bloc deals in 2017. We expect continued increased participation from developers in the upcoming first half 2017 government land sales program (GLS) as developers look to replenish diminishing land banks which will mean that land prices are likely to remain firm. In addition, we expect to see more en-bloc deals for opportunities, especially in the luxury end of the market. These activities in our view, likely signal expectations that home prices should remain fairly stable in the coming years.

3. Privatisations, mergers and acquisitions to pick up

Privatizations, mergers and acquisitions (M&A) in the developer space to pick up. We believe that more listed property developers will take the delisting route along with the wave of privatizations that we saw in recent years. This puts valuations for property developers again in the spot light. Developers are trading at an attractive average 0.75x P/NAV, close to the -1SD of their historical trading range.

Reasons that drive this trend could be (i) sea of capital looking to deploy in Asian real estate, and (ii) strategic capital partners or major shareholders looking to recalibrate their strategies given the lacklustre capital markets and thus capturing the upside in the medium term.

We believe that such M&A activities highlight the attractive valuations of listed developers, namely City Developments, CapitaLand, Global Logistics Properties and UOL which are trading at close to -1 standard deviation (SD) to their 5-year historical trading range.

Page 3

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 4

4. Deleveraging a focus as interest rate risks loom

Balance sheet deleveraging a major wildcard; spike in bond expiry in 2017-2018 a key data-point to watch. In view of the uncertainty of the pace of interest rate hikes in 2017, we believe that the early refinancing and hedging of interest rates will be a key focus for developers and REITs going forward. Of noteworthy is close to S$6.3 worth of bonds (S$4.0bn among developers) expiring over 2017-2018 where issuers will need to source for refinancing or alternative means to repay the bonds. While we believe that refinancing for REITs are likely to be more straight forward given that credits are backed by consistent recurring cash flows, we believe that certain developers, especially those in the mid-cap space which have been more opportunistic in tapping the bond market in recent years could face more hurdles. The recent bond defaults in 2016 among the oil & gas firms have cooled investors’ interest in bonds and we believe that investors will be more selective on the credit for future bond issuances. As such, the inability to refinance these expiring bonds could mean that issuers (developers or REITs) might seek alternative financing sources such as banks or even issuance of equity. Strategies for:

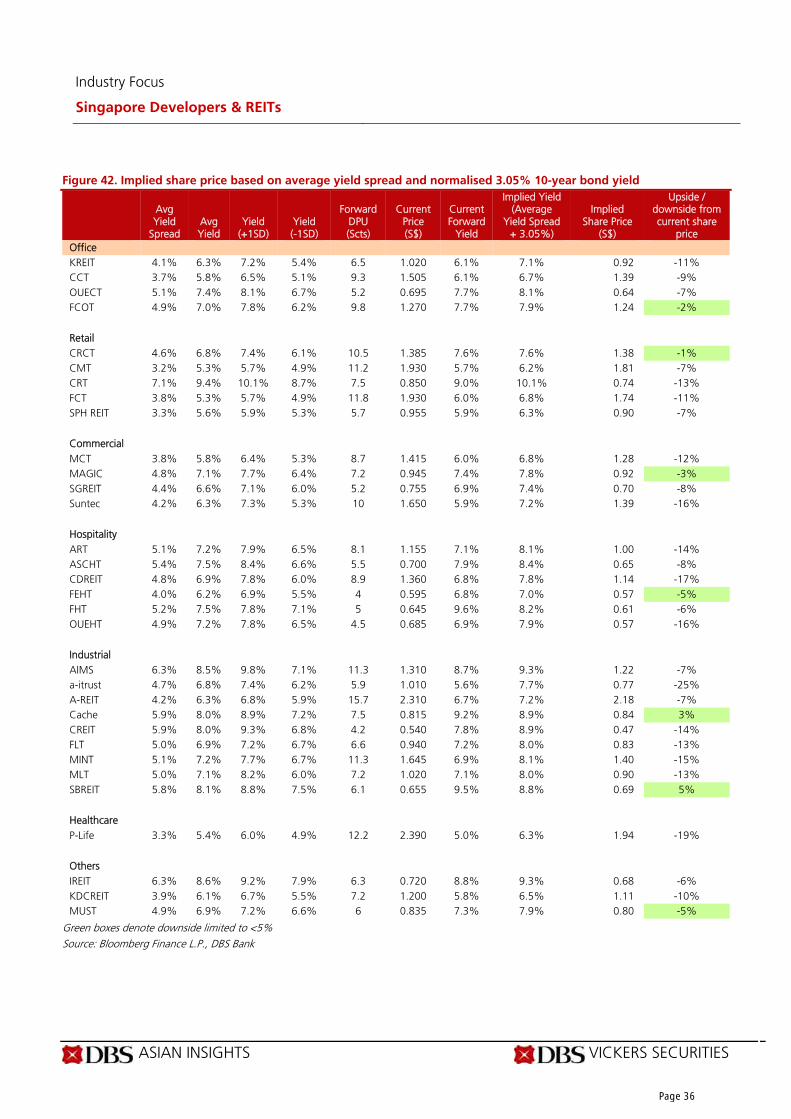

Singapore REITs – Capital preservation a key strategy Projected more hawkish four FED hikes to limit upside performance. We see increasing road-bumps to further outperformance for Singapore REITs (S-REITs) going into 2017, especially faced with a slowing DPU growth profile of 1.0% amidst a rising interest rate environment. DBS economist projects four FED rate hikes over the course of the year and as a result, the Singapore 10-year yield is expected to increase another 0.7% to a normalized c.3.0%. Forward FY17F yield spreads of 4.0% are already at historical mean levels which indicate that valuations for REITs are fair. Capital preservation is key. In an environment of low growth and rising interest rates, we believe that investors will look at stock-specific catalysts to maintain relative outperformance with the sector. These are S-REITs that provide (i) higher confidence in earnings sustainability and visibility, (ii) stronger relative growth, and (iii) lower gearing which limits impact of rising rates on distributions.

Our picks are Ascendas REIT (A-REIT), Keppel REIT (K-REIT), and Mapletree Commercial Trust (MCT). Among the mid-cap space, we like Croesus Retail Trust (CRT) , Keppel DC REIT (KDC REIT) and Frasers Logistics Trust (FLT). Singapore Developers – Catalysts abound to re-rate Potential policy relaxation and M&A could lift sentiment on developer stocks. Our call on the developers is mainly due to valuations supported by an improved outlook. Firstly, we view current trading levels of (P/Bk NAV of 0.75 and 0.65x P/RNAV) as attractive given that developers are trading at close to historical -1SD level. We believe that re-rating opportunities will come from the following data-points: (i) improved sell-through rates for existing developments on the back of improved transaction momentum, (ii) potential relaxation of selective government policy in 2017 driving higher demand for homes and investors’ sentiment, and (iii) potential privatization, M&A activities among developers or value-locking events like asset divestments which will provide a lift for NAVs and thus share prices for developers. Our picks are City Developments and UOL. Risks

1. Faster-than-projected rise in shorter-term interest rates which will negatively impact earnings and potentially capital values in the medium term.

2. External shocks impacting on GDP outlook and unemployment rates in Singapore which will have an overhang on demand/supply dynamics.

Page 4

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 5

2. Peer Comparison

Singapore REITs Peer Comparisons

REIT FYE Price Rec Target Price

Mkt Cap

Total Return

DPU (S Cts) CAGR Yield (%)

P/NAV

(S$) (S$) S$'Bn (%) FY16/ 17F

FY17/ 18F

FY18F/ 19F

FY16/ 17F

FY17/ 18F

FY18F/ 19F

(x)

Office CCT Dec 1.505 BUY 1.70 4.5 18% 9.0 9.3 9.2 1% 5.9% 6.1% 6.1% 0.87 FCOT Sep 1.270 BUY 1.49 1.0 25% 9.8 9.8 9.8 0% 7.8% 7.8% 7.8% 0.83 KREIT Dec 1.020 BUY 1.23 3.5 26% 6.5 6.5 6.5 0% 6.3% 6.3% 6.3% 0.74 OUECT Dec 0.695 HOLD 0.74 0.9 15% 5.3 5.2 5.0 -3% 7.7% 7.6% 7.3% 0.71 Suntec Dec 1.650 HOLD 1.71 4.3 9% 10.0 10.0 10.0 0% 6.0% 6.0% 6.0% 0.78 Retail - - - - 6.4% 6.3% 6.4% 0.80 CRCT Dec 1.385 BUY 1.60 1.2 22% 10.3 10.5 10.3 0% 7.4% 7.6% 7.4% 0.78 CMT Dec 1.930 BUY 2.25 6.9 21% 11.2 11.2 11.3 0% 5.8% 5.8% 5.8% 1.01 CRT Jun 0.850 BUY 0.99 0.6 26% 7.5 8.2 8.5 7% 8.8% 9.6% 10.0% 0.88 FCT Sep 1.930 BUY 2.29 1.8 23% 11.8 11.8 12.1 2% 6.0% 6.0% 6.2% 1.02 SPH REIT Aug 0.955 HOLD 1.00 2.4 9% 5.5 5.7 5.7 2% 5.8% 5.9% 5.9% 1.00 MCT Mar 1.415 BUY 1.62 4.1 19% 8.7 8.9 9.1 2% 6.0% 6.2% 6.3% 1.11 MAGIC Mar 0.945 BUY 1.11 2.7 24% 7.2 7.3 7.4 1% 7.5% 7.7% 7.8% 0.77 SGREIT Dec 0.755 BUY 0.87 1.6 21% 5.2 5.2 5.4 2% 6.8% 6.8% 7.1% 0.81 Industrial - - - - 6.3% 6.4% 6.5% 0.97 a-itrust Mar 1.010 BUY 1.13 1.0 18% 5.9 6.4 6.2 3% 5.8% 6.3% 6.1% 1.52 A-REIT Mar 2.310 BUY 2.65 6.7 19% 15.7 15.6 15.7 0% 6.7% 6.6% 6.7% 1.14 Cache Dec 0.815 HOLD 0.93 0.7 22% 7.9 7.5 7.5 -2% 9.6% 9.2% 9.2% 0.81 CREIT Dec 0.540 HOLD 0.54 0.7 6% 4.1 4.2 4.2 1% 7.5% 7.6% 7.6% 0.79 FLT Sep 0.940 BUY 1.10 1.3 23% 6.6 6.6 6.8 1% 7.0% 7.0% 7.2% 1.10 MINT Mar 1.645 BUY 1.90 2.9 23% 11.3 11.5 12.0 3% 6.9% 7.0% 7.3% 1.18 MLT Mar 1.020 BUY 1.15 2.5 19% 7.2 7.4 7.6 3% 7.0% 7.2% 7.3% 0.99 SBREIT Dec 0.655 BUY 0.75 0.7 22% 6.1 6.1 6.2 1% 9.2% 9.3% 9.4% 0.80 Hospitality - - - - 7.1% 7.1% 7.2% 1.07 ASCHT Mar 0.700 BUY 0.84 0.8 27% 5.5 5.4 5.6 1% 7.8% 7.6% 8.0% 0.81 ART Dec 1.155 BUY 1.32 1.9 21% 8.2 8.1 8.3 1% 7.1% 7.0% 7.2% 0.81 CDREIT Dec 1.360 BUY 1.59 1.3 23% 9.4 9.0 9.3 0% 6.9% 6.6% 6.8% 0.84 FEHT Dec 0.595 HOLD 0.62 1.1 10% 4.3 4.0 4.2 0% 7.1% 6.6% 7.0% 0.62 FHT Sep 0.645 BUY 0.75 1.2 15% 5.2 5.0 5.3 2% 8.0% 7.7% 8.2% 0.85 OUEHT Dec 0.685 BUY 0.72 1.2 13% 4.3 4.5 4.6 3% 6.4% 6.7% 6.8% 0.78 Healthcare - - - - 7.2% 7.1% 7.4% 0..80 P-Life Dec 2.390 BUY 2.75 1.5 20% 12.1 12.2 12.3 1% 5.1% 5.1% 5.1% 1.47 Others - - - - IREIT Dec 0.720 HOLD 0.75 0.4 1% 6.3 6.4 6.3 0% 8.7% 8.8% 8.7% 1.16 KDCREIT Dec 1.200 BUY 1.33 1.4 -3% 6.8 7.2 7.5 5% 5.6% 5.8% 6.1% 1.33 Manulife US REIT

Jan 0.835 BUY 0.93 0.7 19% 5.6 6.0 6.1 n/a 6.7% 7.2% 7.2% 1.06

Sector Average 6.8% 6.8% 6.9% 0.95

Note: Prices used as of 04 Jan-2017

Source: Bloomberg Finance L.P., DBS Bank

Page 5

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 6

Singapore Developers Peer Comparisons

Mkt Price 12-mth Company FYE Cap 4-Jan-17 RNAV *Assumed Target Price Upside P/RNAV Latest Qtr (S$m) (S$) (S$) Discount

(%) (S$) % Rcmd (x) P/NBV

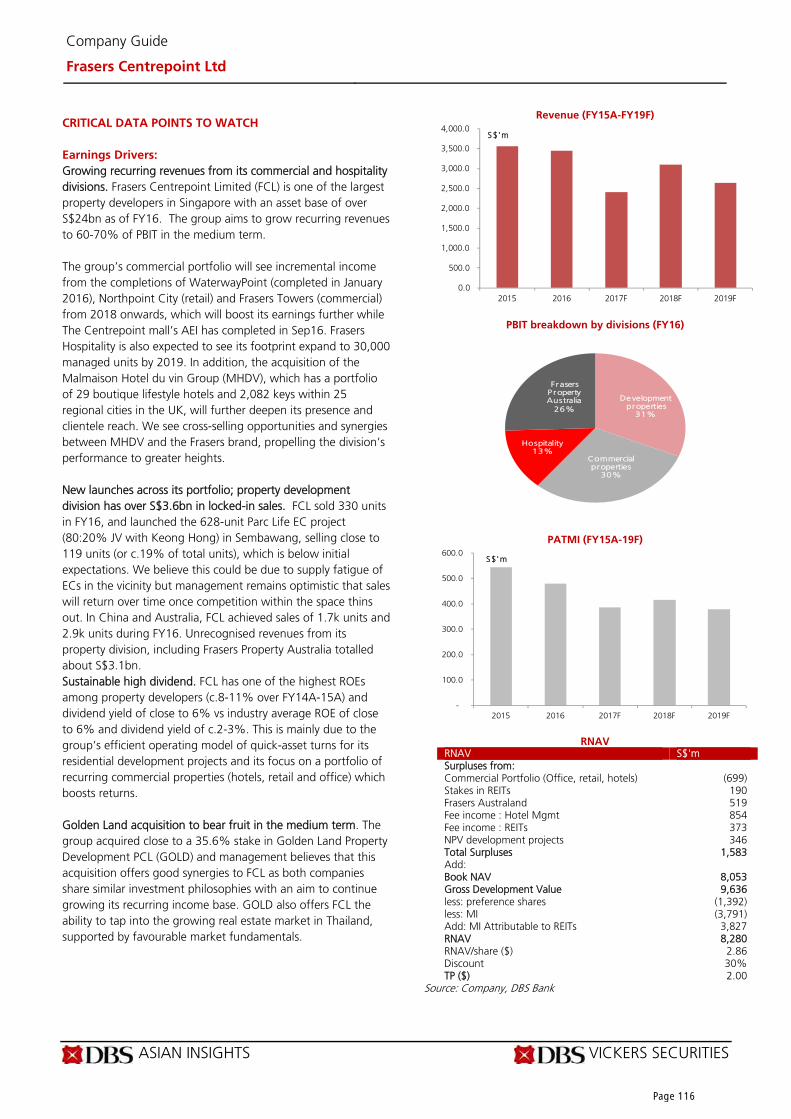

Developers Capitaland Dec 13.0 3.06 4.80 -25% 3.60 17% BUY 0.64 0.77 City Dev Dec 7.5 8.39 11.90 -17% 9.90 19% BUY 0.70 0.84 Frasers Centrepoint Ltd

Sep 4.4 1.60 2.86 -30% 2.00 31% BUY 0.53 0.67

Global Logistics Properties

Mar 10.1 2.24 3.53 -30% 2.47 14% BUY 0.61 0.83

UOL Dec 4.7 6.12 10.23 -30% 7.20 23% BUY 0.57 0.59 Average 0.57 0.75 Non-Covered Guocoland Dec 10.9 2.40 - - - - - na 0.90 UIC Dec 3.9 2.79 - - - - - na 0.66 Ho Bee Dec 1.4 2.04 - - - - - na 0.50 Wheelock Dec 1.8 1.49 - - - - - na 0.60 Wing Tai Jun 1.3 1.62 - - - - - na 0.40 Bukit Sembawang Dec 1.2 4.48 - - - - - na 0.90 United Engineers Dec 1.6 2.57 - - - - - na 0.90 Tuan Sing Dec 0.4 0.29 - - - - - na 0.39 Hiap Hoe Dec 0.3 0.72 - - - - - na 0.51 Heeton Holdings Dec 0.1 0.39 - - - - - na 0.41 Average na 0.63 Average sector 0.68

Note: Prices used as of 04 Jan-2017 Source: Bloomberg Finance L.P., DBS Bank

Page 6

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 7

2. Key Charts

Residential

Outlook – Positive (Luxury) Negative (Suburban)

Luxury end of the residential market bottoming out

Price differential across major cities (luxury hoe prices)

A tenants' market as vacancy rates spike

Home prices in the suburbs to see more downside

Key Assertions

DBS project prices for luxury residential homes (0% to +1%) to bottom out as transaction volumes and foreigner interests pick up within the Core Central region.

Prices for homes in suburban region to fall further by as much as -3 to -5% as affordability remain curbed for upgraders given higher-than-average differential in prices between HDB resale prices and prices of suburban homes.

Potential policy relaxation in 2017 given macro uncertainties in 2017 coming on the back of the pace of interest rate increases and its impact on mortgages.

Risks

Looming from higher mortgage rates, diminishing rental spreads amidst higher market vacancy rates could worsen the holding power for households.

• External shocks causing a downturn in the Singapore economy and a loss of jobs, resulting in a significant decline in the property market.

Source: URA, CBRE, DBS Bank

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

160

180

1Q2004 3Q2005 1Q2007 3Q2008 1Q2010 3Q2011 1Q2013 3Q2014 1Q2016

(2010=100)

Property Price index (Outside Central Area) Spread vs HDB

High Demand From Upgraders

(P ublic to Private)

Af fordability Curbed but

spread is closing

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

20

11

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

Un its Units Sold in Core Central Region (LHS) Rolling 4 Quarters Growth (%)

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Monaco HongKong

London New York LosAngeles

Japan Singapore Toronto

US$ psf

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Jun-

04D

ec-0

4Ju

n-05

Dec

-05

Jun-

06D

ec-0

6Ju

n-07

Dec

-07

Jun-

08D

ec-0

8Ju

n-09

Dec

-09

Jun-

10D

ec-1

0Ju

n-11

Dec

-11

Jun-

12D

ec-1

2Ju

n-13

Dec

-13

Jun-

14D

ec-1

4Ju

n-15

Dec

-15

Jun-

164Q

16

Index Value(%)

Vacancy Rate (Non-Landed) (LHS) Rental Index (Non-Landed) (RHS)

Page 7

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 8

Retail Outlook - Neutral

Rental reversions to moderate as RSI declines

Upcoming supply are mainly in the fringe

Key Assertions

Muted retail sales outlook poses a risk to landlords’ occupancy costs and rental reversions.

• Consolidation among retailers to intensify in 2017 amid rising labour costs and labour shortage.

• Better-performing malls with sizeable operational scale, strong record of recurring traffic which will continue to attract retailers.

Risks

• Increased penetration of e-commerce causing decline in retail sales.

• Weaker-than-expected economic growth (GDP), affecting consumer sentiment and expenditure.

• Weaker-than-expected tourist arrivals which will have an impact on retail sales performance in Orchard Road malls.

Source: DBS Bank

Office Outlook - Positive

Supply to fall off from 2018 onwards

Two-tier Market with Premium Grade A office leading

Key Assertions

• Demand outlook remains uncertain with a merry-go-round of tenants gravitating towards Grade A office space.

• A two-tier market to emerge; with Grade A office space leading the pack and Grade B office space needing to drop rents or undergo refurbishments to attract tenants.

• Office rents could bottom by end of 2017 as pre-commitment rates for key office buildings remain strong.

Risks

• Earlier completion of new office supply. • Shadow space from further contraction in demand from

the financial services sector.

Source: DBS Bank

-

0.50

1.00

1.50

2.00

2.50

2016 2017 2018 2019 2020

m'sqft

Downtown Core Fringe Area Rest of Central Area

Orchard Outside Central Region

-4%-2%0%2%4%6%8%10%12%

7.00

8.00

9.00

10.00

11.00

12.00

13.00

Spread between Premium Grade vs Grade A (RHS)

Colliers Premium Grade Raffles Place/New Downtown (LHS)

CBRE Grade A Core CBD (LHS)

S$ psf / mth

‐

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

‐1,500

‐1,000

‐500

0

500

1,000

1,500

2,000

2,500

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

'000 sqft

Net supply: Downtown Core (LHS)

Net demand: Downtown Core (LHS)

CBRE Grade A office rents (RHS)

S$ psf pm

Post GFC2010‐2014 average:1.10m sqft

2015‐2019 average:1.15m sqft

Page 8

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 9

Industrial Outlook – Negative (Factory & Warehouse Space)

Positive (Business Parks)

Time to absorb supply that entered the market

Rental reversions remain negative

Key Assertions

Market rents to moderate 5% p.a. due to time needed to absorb supply completion in 2016-2017. Market vacancy rates to hit a high of 10%.

Business Park space to remain stable; given lack of new supply but downside risk persists if CBD office rents weaken further.

Industrial REITs' rental reversions to remain generally negative over 2017-2018.

Risks

Weaker than-expected Singapore economy resulting in further-than-expected declines in rents.

Shadow space in the single-user factory/warehouse sectors which result in increased competition for tenants.

Source: DBS Bank

Hospitality Outlook - Negative

Supply to continue outpace demand growth in 2017

RevPAR to remain under pressure in 2017

Key Assertions

We expect demand in 2017 to grow by 4% y-o-y. However, as corporate demand is expected to remain soft, projected demand for accommodation growth should remain modest.

Persistent supply pressures arising from a 6% increase in room stock will pressure room and occupancy rates. We project RevPAR to fall by 4% in 2017 before rebounding thereafter.

Risks

Slower-than-expected rebound in Chinese tourist arrivals and greater level of competition from regional markets would cause RevPAR to drop more than expected.

Upside risk would come from delays in opening of new hotels.

Source: DBS Bank

0%

2%

4%

6%

8%

10%

12%

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2,007 2,008 2,009 2,010 2,011 2,012 2,013 2,014 2,015 2016F 2017F 2018F 2019F 2020F

m' sqft

Demand Supply Vacancy Rate (RHS)-20%

-10%

0%

10%

20%

30%

40%

50%

2009 2010 2011 2012 2013 2014 2015 2016F 2017F 2018F

Business Park Warehouse Factory

7%

-3%

1%

9%

4%4%

6%

3%

-2%

3.4%

5%4%

7%

4%

7%

4%

6%

2%

-1% -1%

-5%-4% -4%

3%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2013 2014 2015 2016F 2017F 2018F

Visitor Arrivals Visitor Days Room supply RevPAR

y-o-y growth

61,287 2,520 3,857

1,355

45,000

50,000

55,000

60,000

65,000

70,000

75,000

2015 2016F 2017F 2018F

Rooms

Hotel rooms Expected net additions

4.1%

6.0%2.0%

Page 9

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 10

4. Developers – Catalysts abound to lift valuations from multi-year lows

Key Points

Developers to continue looking for opportunities overseas, high-end residential space

M&A and potential policy relaxation could lift sentiment for the sector

Top picks: City Developments Limited (CDL), UOL

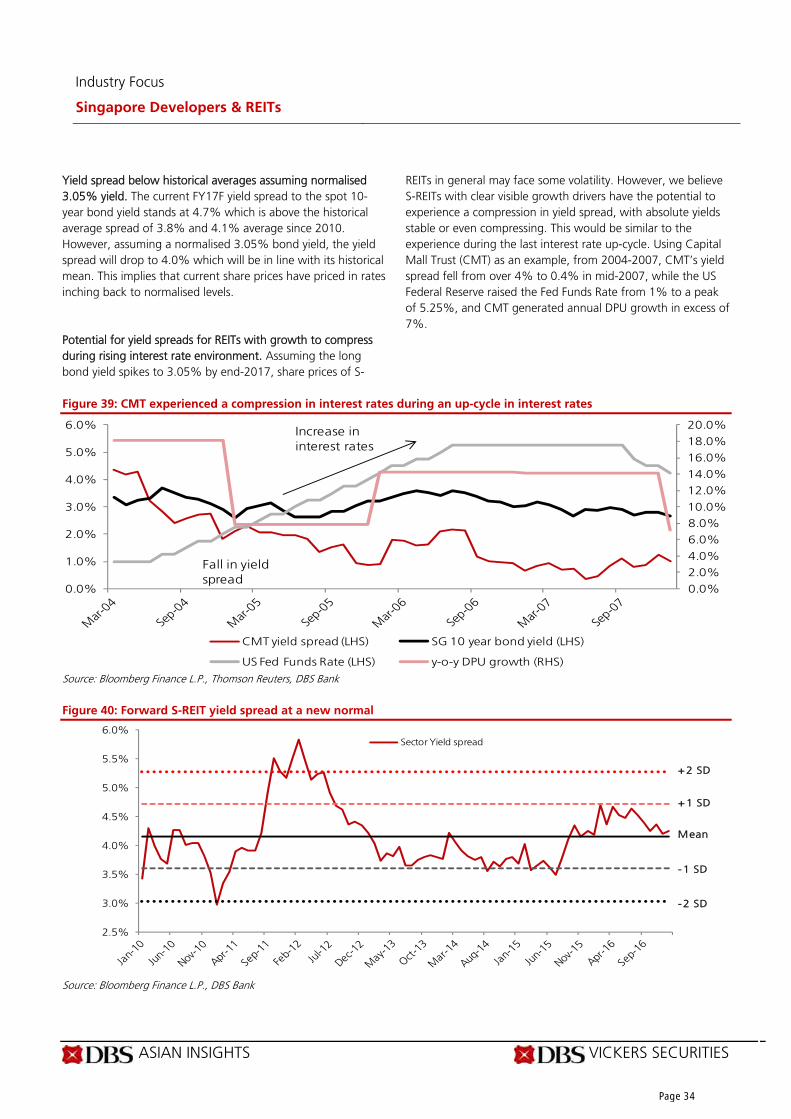

Range bound in 2016. The Singapore Property Developers (measured by the FSTREH index) has fallen by close to 5% since the start of 2016 and prices are generally c.9% below prices from the start of 2015. The FSTREH lagged the S-REITs for the most of 2016 but caught up after the recent spike in bond yields saw S-REIT prices weaken on the back of market expectations of a more hawkish FED rate hike momentum in 2017.

4.1 Attractive valuations with upcoming catalysts Looking forward, we believe that the Singapore developers (SG Developers) can outperform the S-REITs, especially with expected headwinds from the uncertainty in the number of

subsequent FED hikes over 2017 to mean limited re-rating opportunities for the S-REITs. We see re-rating catalysts for Singapore Developers come 2017 on the back of (i) improved investor sentiment on increasing expectations of a government policy easing in 2017 as property prices fall by as much as 12-15% from the peak (currently 11%) (ii) potential merger and acquisition (M&A) activities, and (iii) improved balance sheets on the back of expected asset recycling/deleveraging trend. The Singapore Developers, which are trading at an average P/NAV of 0.7x, close to its -1SD is attractive. Current P/NAV valuations are close to multi-year lows. At a 0.7x P/NAV, valuations for developers are similar during past periods of economic stress in 1997, 2003 and 2009, which we believe will not be the case going forward, especially with the Singapore GDP projected to grow by c.1.3% in 2017 according to our DBS economists. While we continue to expect Singapore residential prices to fall marginally in 2017, most negatives are priced in, in our view. We believe that we are closer to the trough, especially with expectations that the government will likely tweak policy measures to negate a further fall in prices.

Figure 1: Developers underperformed S-REITs in 2016 but caught up in 4Q16

Source: Bloomberg Finance L.P., DBS Bank

600.00

650.00

700.00

750.00

800.00

850.00

900.00

‐10%

‐8%

‐6%

‐4%

‐2%

0%

2%

4%

6%

1/1/15 1/4/15 1/7/15 1/10/15 1/1/16 1/4/16 1/7/16 1/10/16

Index Value Relative Performance (%)

Relative Performance Developers

Page 10

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 11

Figure 2: Valuations attractive as developers still trade at close to past 3 market down-cycle troughs

Source: Bloomberg Finance L.P., DBS Bank

Figure 3: Historical developers Price-to-Bk NAV vs

PPI

Figure 4: Developers trading at 45% discount to

RNAVs (-1.0 standard deviation)

Source: URA, DBS Bank

-

0.50

1.00

1.50

2.00

2.50

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0 (x )Index Value

Property Price Index Developer P/Bk NAV

1997-98 Asian Financial Crisis

2008-2009 Global Financial Crisis

2002-2003 Dot Com Crash

2011 Euro Crisis

Mean: 0.95x

-1 SD: 0.60x

+1 SD: 1.30x

-

0.50

1.00

1.50

2.00

2.50

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17

P/NAV (x)

P/NAV (w/o GLP) Mean - 1 SD +1 SD P/NAV (with GLP)

-60%

-50%

-40%

-30%

-20%

-10%

0%2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Discount to RNAV Mean +1 SD - 1 SD

Page 11

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 12

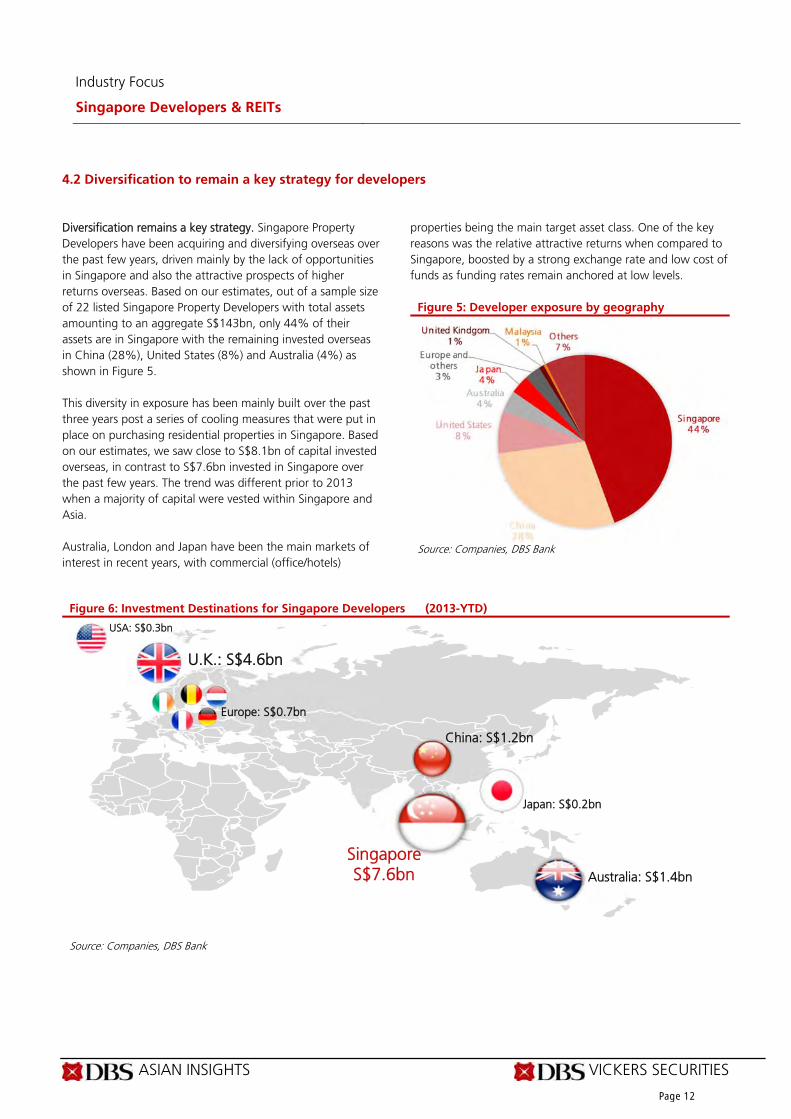

4.2 Diversification to remain a key strategy for developers Diversification remains a key strategy. Singapore Property Developers have been acquiring and diversifying overseas over the past few years, driven mainly by the lack of opportunities in Singapore and also the attractive prospects of higher returns overseas. Based on our estimates, out of a sample size of 22 listed Singapore Property Developers with total assets amounting to an aggregate S$143bn, only 44% of their assets are in Singapore with the remaining invested overseas in China (28%), United States (8%) and Australia (4%) as shown in Figure 5. This diversity in exposure has been mainly built over the past three years post a series of cooling measures that were put in place on purchasing residential properties in Singapore. Based on our estimates, we saw close to S$8.1bn of capital invested overseas, in contrast to S$7.6bn invested in Singapore over the past few years. The trend was different prior to 2013 when a majority of capital were vested within Singapore and Asia. Australia, London and Japan have been the main markets of interest in recent years, with commercial (office/hotels)

properties being the main target asset class. One of the key reasons was the relative attractive returns when compared to Singapore, boosted by a strong exchange rate and low cost of funds as funding rates remain anchored at low levels.

Figure 5: Developer exposure by geography

Source: Companies, DBS Bank

Figure 6: Investment Destinations for Singapore Developers (2013-YTD)

Source: Companies, DBS Bank

Australia: S$1.4bn

Singapore S$7.6bn

U.K.: S$4.6bn

Europe: S$0.7bn

USA: S$0.3bn

Japan: S$0.2bn

China: S$1.2bn

Page 12

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 13

Overseas capital deployment to continue but opportunities limited as currency volatility impact returns. While we believe that developers will continue to seek higher returns overseas, the yield compression seen for prime assets over the past few years will mean that market focus will likely change. According to JLL, an SGD investor total foreign currency (FX) adjusted total return will diminish over 2016-2018 and is forecasted to yield in the -3% to 10% range with Shanghai, Sydney and Melbourne offering the highest returns which will continue to feature regularly on developers’ horizon over time. We believe that London will remain one of the key investment markets, despite Brexit going forward and JLL expecting returns to moderate, mainly due to weak GBP in the medium term. Developers are likely to be still keen on the UK if it maintains its financial hub status in Europe. As developers are expected to continue targeting to grow their recurring income base, we believe that core assets in the commercial space which offer stable cash flows will be key acquisition targets.

DBS economist believes that most major currencies will depreciate against the US dollar over 2017, as the normalization of the US monetary policy and hawkish policies from new President Trump might lead to flows from emerging markets back to the US. Looking forward, currency volatility will continue to have a big impact on total returns for investors diversifying into real estate outside their home markets, and it is important to closely monitor currency movements.

In Singapore, developers could turn to M&A and en-bloc opportunities to land bank. Developers who are looking to replenish their property land banks in Singapore have turned up in force in the government land sales program (GLS) in 2016 and have also ventured into the En-bloc market to gain access to land banks. Looking ahead, we believe that another avenue will be in the listed space, especially with listed developers trading at 0.7x P/NAV and certain mid-cap developers trading below that. As pressure from additional buyer stamp duties (ABSD) on land purchase and Qualifying Charges (QC) increase from 2017 onwards, we believe this could spark merger and acquisition (M&A) activities going forward.

Figure 7: FX adjusted returns over time

Source: JLL, DBS Bank

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Sing

apor

e

Mel

bour

ne

Sydn

ey

Hon

g Ko

ng

Seou

l

Toky

o

Lond

on

New

Yor

k

Beiji

ng

Shan

ghai

Del

hi

Mum

bai

Kual

a Lu

mpu

r

Sing

apor

e

Mel

bour

ne

Sydn

ey

Hon

g Ko

ng

Seou

l

Toky

o

Lond

on

New

Yor

k

Beiji

ng

Shan

ghai

Del

hi

Mum

bai

Kual

a Lu

mpu

r

Sing

apor

e

Mel

bour

ne

Sydn

ey

Hon

g Ko

ng

Seou

l

Toky

o

Lond

on

New

Yor

k

Beiji

ng

Shan

ghai

Del

hi

Mum

bai

Kual

a Lu

mpu

r

FX gain/loss Property Return FX adjusted total return

2016 2017 2018

Page 13

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 14

Figure 8: Prime Yields for commercial real estate

Source: JLL, DBS Bank

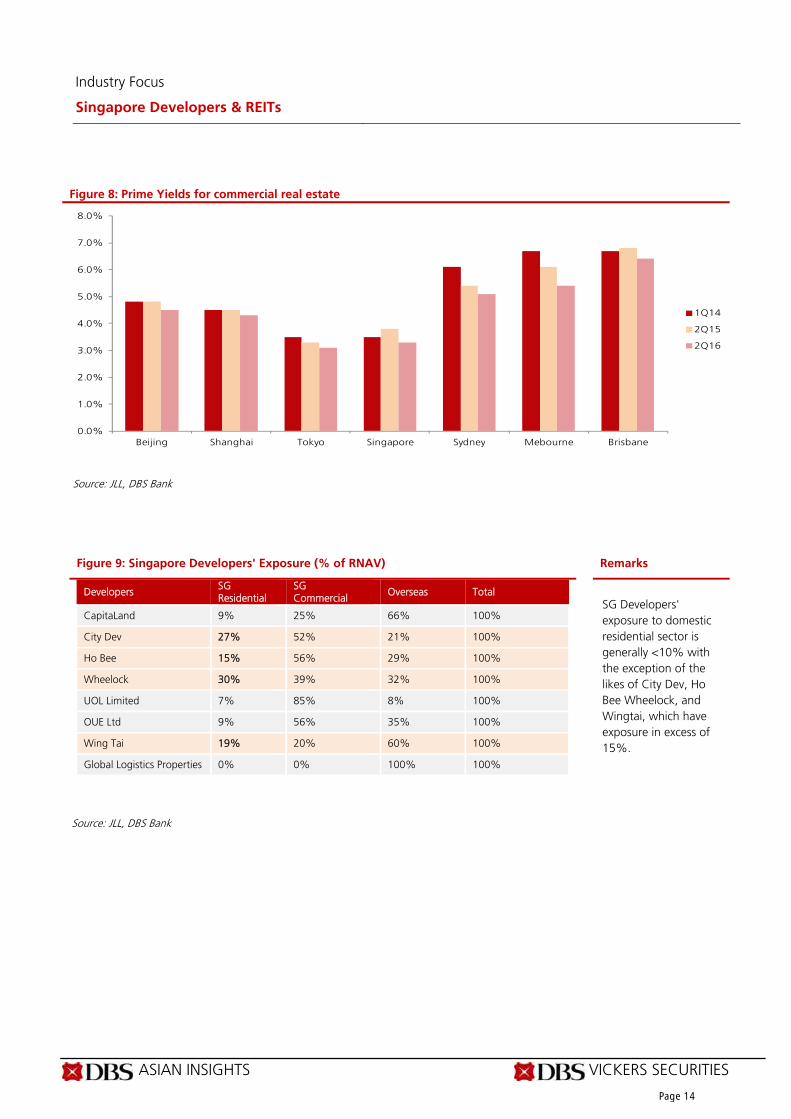

Figure 9: Singapore Developers' Exposure (% of RNAV) Remarks

Developers SG Residential

SG Commercial

Overseas Total

CapitaLand 9% 25% 66% 100%

City Dev 27% 52% 21% 100%

Ho Bee 15% 56% 29% 100%

Wheelock 30% 39% 32% 100%

UOL Limited 7% 85% 8% 100%

OUE Ltd 9% 56% 35% 100%

Wing Tai 19% 20% 60% 100%

Global Logistics Properties 0% 0% 100% 100%

SG Developers' exposure to domestic residential sector is generally <10% with the exception of the likes of City Dev, Ho Bee Wheelock, and Wingtai, which have exposure in excess of 15%.

Source: JLL, DBS Bank

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Beijing Shanghai Tokyo Singapore Sydney Mebourne Brisbane

1Q14

2Q15

2Q16

Page 14

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 15

4.3 Improved transactions in the luxury end of the market to continue Pick-up in transactions in the luxury residential market. We believe that the luxury end of the market is approaching a near-term bottom, judging by the increased number of transactions seen in the core central region. According to URA-lodged caveats, YTD 9M16 transactions by Foreigners (excluding Singapore permanent residents) rose by close to 12% compared to the same period a year ago. We note that the increase in transactions mainly come from buyers in China, Malaysia and Indonesia, up more than 15% y-o-y respectively. If transaction volumes sustain, it will imply investors’ confidence in Singapore’s fundamentals and prospects of long-term capital gains from current levels. Attractive relative pricing compared to other popular investment destinations. According to JLL, Singapore remains an attractive investment destination, especially with additional

stamp duties recently levied on foreign purchases by other popular residential investment destinations such as London, Melbourne, Sydney which somewhat makes Singapore attractive again for international investors looking for real estate purchases. In addition, we note that (figure 1212) Singapore luxury home prices have corrected 11% over the past few years and the gap has widened over time, when compared to other residential investment destinations such as Hong Kong, London and New York, where prices have continued to increase over the past few years (figure 13). Therefore, we believe that Singapore luxury home is attractive from a relative pricing across countries with potential capital upside in the medium term once the current over-supply situation normalizes.

Figure 10: Transactions in Core Central region growing Figure 11: Core Central Region transactions

outpacing overall total Singapore market

Source: Companies, DBS Bank Figure 12: % Growth in prices Figure 13: Prices of luxury residential homes

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

20

11

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

Un its Units Sold in Core Central Region (LHS) Rolling 4 Quarters Growth (%)

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

20

11

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

14

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

15

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

16

Q1

20

16

Q2

20

16

Q3

% Change (Rolling 4 Quarters)

Overall Transactions Core Central Region

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Monaco HongKong

London New York LosAngeles

Japan Singapore Toronto

US$ psf

90.0

110.0

130.0

150.0

170.0

190.0

210.0

230.0

Q1

201

0

Q2

201

0

Q3

201

0

Q4

201

0

Q1

201

1

Q2

201

1

Q3

201

1

Q4

201

1

Q1

201

2

Q2

201

2

Q3

201

2

Q4

201

2

Q1

201

3

Q2

201

3

Q3

201

3

Q4

201

3

Q1

201

4

Q2

201

4

Q3

201

4

Q4

201

4

Q1

201

5

Q2

201

5

Q3

201

5

Q1

201

6

Q2

201

6

Q3

201

6

Index Value

Hong Kong Korea Malaysia Singapore Taiwan Thailand

Source: URA, MAS, Christie Real Estate, JLL, Knight Frank, DBS Bank

Page 15

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 16

4.4 Looming ABSD deadlines not a precursor for a significant price cuts for all developments. Strong sales in the core central region could mean firmer prices going forward. There were close to 22,502 unsold units (both completed and uncompleted) as of 3Q16 of which 24% of 5,464 units were located in the Core Central region as of 3Q16. The strong sales seen in recent quarters (especially for recently re-launched completed projects – Gramercy Park, OUE Twin Peaks near downtown Orchard) have brought the number of available units for sale down by 6% q-o-q, which is one of the fastest fall compared to homes in other regions. Based on the current run-rate for residential transactions, we estimate that total transactions in 2016 will likely come in at close to 15,500 (c.8,000 primary sales and 7,500 secondary sales), which implies close to 10% growth y-o-y. The increase is mainly driven from a marked increase in both the primary and secondary transactions. The former is mainly due to generally more aggressive marketing activities and price discounts. The improvement seen in the secondary market mainly came from i) higher transactions in the Core Central region and ii) innovative financing schemes and price discounts offered by developers for selected de-licensed projects which resulted in fairly good response from buyers (see figure 14).

Selected impact of ABSD deadlines as most projects continue to enjoy healthy margins. Developers with projects that are subjected to deadlines on the ABSD remission on residential sites in 2017-2018 have also done well, in our view. Based on our analysis of selected projects with significant unsold inventories at the start of 2016 and are likely to be under pressure to clear stock due to looming ABSD deadlines in 2017-2018, most have cleared a substantial portion of their inventory. This is mainly coming from more aggressive marketing activities while prices dipped slightly by 4-12%, with some staying steady as shown in Figure 15. This is against investors’ initial concern that developers might have to suffer deep cuts in prices in order to move unsold inventories. The pick-up in sales momentum, in our view, will likely give developers more optimism to continue marketing existing projects while upcoming property launches in the Central region could also increase in order to capture the current improved sentiment in that space. We believe that developers are likely to pay the ABSD for most projects come 2017 as margins are expected to remain healthy (figure 16).

Figure 14. Pipeline supply of unsold private homes (excluding executive condominiums) as of end of 3rd quarter 2016

Total Units Core Central Region

Rest of Central Region

Outside Central Region

Remarks

(units) (units) (units) (units) Units Available for sale (3Q16): Unsold uncompleted units 20,577 4,711 7,130 8,736 Unsold completed units 1,925 753 543 629 Total unsold units 22,502 5,464 7,673 9,365 % Chg Q-o-Q -3% -6% 1% -5% Demand : Primary Sales (YTD 9M16) 5,253 444 1,715 3,094 Secondary Sales 6,337 1568 1792 2977 Total Sales 11,590 2,012 3,507 6,071

Ratio (Supply/ annualised primary sales) 3.2 9.2 3.4 2.3 Ratios for CCR and RCR regions improved while OCR ratios declined.

Primary Sales (2015) 7,440 407 1,884 5,147 Secondary Sales (2015) 6,677 1,452 1,944 3,281 14,117 1,859 3,828 8,428 Ratio of Supply/Demand 3.0 13.4 4.1 1.8 Ratios for CCR highest due to

low number of primary sales. Average Primary Sales (2013-2016) 7,030 530 4,400 2,100 Average Secondary Sales (2013-2016) 7,475 1,572 2,071 3,464 14,505 2,102 6,471 5,564

Source: URA, DBS Bank

Page 16

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 17

Figure 15: ABSD payable for selected projects with high unsold inventory in 2017 / 2018

ABSD liability

Region Project Developer Total Units

Unsold (Jan’16)

Unsold Unsold (Nov’16)

Unsold Units Sold in

2016

Land Cost

Estimated ABSD

(%) (%) (S$’m) (S$’m)

ABSD Payable for projects from government land sites

Jan’17 OCR The Trilinq IOI Properties 755 528 70% 303 40% 225 408 52.1

Feb’17 RCR Mon Jervois Singapore Land 140 61 44% 45 32% 16 118.9 15.2

Mar’17 OCR Kingsford Hillview Peak

Kingsford 512 249 49% 22 4% 227 243.2 31

Jun’17 OCR Vue 8 Residences

Capital Devt. 463 172 37% 84 18% 88 211 26.9

Jul’17 CCR Pollen & Bleu Singapore Land 106 94 89% 93 88% 1 113.2 14.4

Jul’17 RCR Sant Ritz Santarli Corp 214 24 11% 10 5% 14 114.8 14.7

Sep’17 CCR The Siena Far East Org. 54 22 41% 12 22% 10 45.8 5.8

Sep’17 RCR The Crest Wingtai,Metro,UE

469 366 78% 325 69% 41 516 65.9

Oct’17 OCR The Glades Keppel Land 726 343 47% 134 18% 209 434.6 55.5

Dec’17 RCR Alex Residences

Singapore Land 429 173 40% 152 35% 21 332.7 41.6

Jan’18 OCR The Panorama Wheelock 698 126 18% 28 4% 98 550 70.2

Apr’18 OCR Riverbank @ Fernvale

UOL Group 555 188 34% 64 12% 124 262.1 50.2

Jun’18 RCR Highline Residences

Keppel Land 500 320 64% 215 43% 105 550.3 105.3

Apr’18 OCR The Santorini MCC Land 597 390 65% 328 55% 62 289.7 55.5

Sep’18 CCR Sophia Hills Hoi Hup 493 437 89% 346 70% 91 442.3 84.7

ABSD Payable for projects from private land sites

Mar’17 CCR Meyer Melodia Cang Properties

16 15 94% 15 94% 0 9.4 1.2

Mar’17 CCR Robin Suites Robin25 Pte Ltd

92 26 28% 6 7% 20 54 6.8

Jan’17 RCR Ascent @ 456 Quest Homes 28 13 46% 10 36% 3 24 3.1

Apr’17 OCR The Bently Residences

Goodland Group

48 15 31% 5 10% 10 27 3.4

Jun’17 RCR Neem Tree Aylesbury Pte Ltd

84 67 80% 64 76% 3 46 5.9

Sep’17 OCR The Creek @ Bukit

Chiu Teng Group

260 144 55% 107 41% 37 190 24.5

Sep’17 OCR Rezi3Two Tee, KSH and Heeton

65 22 34% 7 11% 15 22.6 2.8

Oct’17 OCR Lotus Ville JVA Venture 11 8 72% 7 64% 1 18 2.3

Nov’17 CCR The Rise @ Oxley

Hao Yuan 120 51 43% 25 21% 26 130 16.6

Source: URA, DBS Bank

Page 17

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 18

Figure 16: Selling prices indicate that most projects will still earn good margins after payment of ABSD

Project Est. Breakeven

Est. Breakeven with ABSD

Selling Prices

< 2016

Selling prices in

2016 % Chg Average

Prices Margins

(q/o ABSD) Margins

(with ABSD)

(S$’psf) (S$’psf) (S$’psf) (S$’psf) (%) (S$’psf) (%) (%)

ABSD Payable for projects from government land sites

The Trilinq 920 990 1,405 1,404 0% 1,404 53% 42%

Mon Jervois 1,265 1,400 1,981 1,832 -8% 1,907 51% 36%

Kingsford Hillview Peak 1,010 1,090 1,367 1,286 -6% 1,326 31% 22%

Vue 8 Residences 780 830 983 992 1% 988 27% 19%

Pollen & Bleu 1,450 1,575 1,922 1,801 -6% 1,862 28% 18%

Sant Ritz 1,000 1,080 1,419 1,358 -4% 1,388 39% 29%

The Siena 1,500 1,650 2,067 1,826 -12% 1,947 30% 18%

The Crest 1,350 1,470 1,698 1,718 1% 1,708 27% 16%

The Glades 1,530 1,675 1,454 1,412 -3% 1,433 -6% -14%

Alex Residences 1,350 1,500 1,705 1,943 14% 1,824 35% 22%

The Panorama 1,180 1,300 1,243 1,220 -2% 1,232 4% -5%

Riverbank @ Fernvale 850 940 976 992 2% 984 16% 5%

Highline Residences 1,600 1,800 1,879 1,735 -8% 1,807 13% 0%

The Santorini 950 1,035 1,131 1,082 -4% 1,106 16% 7%

Sophia Hills 1,450 1,650 1,995 1,916 -4% 1,955 35% 19%

ABSD Payable for projects from private land sites

Mayer Melodia 510 530 2,226 - 0% 1,113 >100% >100%

Robin Suites 1,450 1,600 2,496 2,276 -9% 2,386 65% 49%

Ascent @ 456 1,400 1,580 1,506 1,527 1% 1,516 8% -4%

The Bently Residences 1,000 1,050 1,408 1,229 -13% 1,319 32% 26%

Neem Tree 1,180 1,285 1,616 1,756 9% 1,686 43% 31%

The Creek @ Bukit 1,180 1,400 1,589 1,656 4% 1,622 37% 16%

Rezi3Two 1,000 1,050 1,507 1,533 2% 1,520 52% 45%

Lotus Ville 775 830 803 754 -6% 779 0% -6%

The Rise @ Oxley 1,525 1,685 2,335 2,283 -2% 2,309 51% 37%

Source: URA, DBS Bank

Page 18

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 19

4.5 Potential land-banking opportunities in Singapore

Developers could turn towards the en-bloc sites or even M&A to grow. The government residential land tenders have remained competitive, driving land bid prices high, following the dearth of land supply since the property market peaked in 2013, coupled by developers having pre-sold most of their inventory on their balance sheets on hand. Looking ahead, as the government continues to maintain a low supply in the upcoming 1H17 land tenders, we believe that developers could turn towards the en-bloc market or even look to M&A to continue land banking and to seek growth.

Apart from government land sales, developers have turned to opportunities in the private market as evidenced by the recent pick-up in en-bloc transactions.

Smaller developers, some of which on average trade at a 50% discount to book values, could be attractive acquisition or privatisation candidates.

Limited government land sales (GLS) to result in sticky

land bid prices

Government residential land sales at its lowest level since GFC. Since the property market peaked in 2013, the government has been moderating the land supply into the market. Total GFA of government residential land sales

tendered out in 2016 has reached its lowest level at approximately 4.4m sqft, 75% below the peak in 2012.

Unsold inventory at the lowest since 2001. With the government moderating the land supply for a few years now, unsold inventory of residential properties has reached its lowest levels since 2001. As at 3Q2016, unsold inventory had almost halved since its peak in 2011.

Land prices have remained sticky. While land prices from the government land tenders have moderated marginally in 2014 to 2015 (highest land prices within the respective year fell c.27% to close to S$900psf ppr levels from a high of S$1,163psf ppr in 2013), we saw land prices in 2016 achieve a record high of S$1,239 psf ppr.

Land bids are increasingly more competitive as spreads thin. The spreads between the winning bid compared to the 2nd and median bids have also narrowed from 15% back in 2013 (peak of 62% in 2009) to 3% in 2016. The number of bids has increased to an average of 12 in 2016, above the historical average of eight bids.

Figure 17: Shortage of land supply from the government

Figure 18: Land prices remain steady as competition remains high

Source: Realis, DBS Bank Source: Realis, DBS Bank

197 245 350 318 228 203 280 320 291

418 489 438 483 481

285 268 350

507

639

460 533

607

869

1,108 1,163

849 871

1,239

241 256 350

413 436 310

463 404

463

681 724650 695

809

-

200

400

600

800

1,000

1,200

1,400

2002

2003

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Pri

ce (S$psf

)

Min Average Max

-

100

200

300

400

500

600

700

800

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Aver

age

Land P

rices

(S$'p

sf)

Govern

men

t La

nd S

ale

s by

GFA

(sq

ft)

GLS by GFA (sqft) Average Land Price (S$'psf)

Page 19

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 20

Figure 19: Winning margin and average range of bid have narrowed

Figure 20: Number of bidders has increased

Source: Realis, DBS Bank Source: Realis, DBS Bank

Figure 21: GLS Sites awarded in 2016 Date of Award Location Type of

Development Lease (yrs)

No. of Bids

Name of Successful Tenderer Developer Successful Tender

Price (S$'m)

$S$ psf per plot

ratio

Units

6-Dec-16 (tender closed)

Margaret Drive Residential 99 14 MCL Land (Regency) Pte Ltd SG Listed 238.4 997.8 275

1-Oct-16 Fernvale Road Residential 99 14 Sing Development (Pte) Ltd and Wee Hur Development Pte Ltd

SG Listed 287.1 517.2 575

5-Sep-16 Anchorvale Lane

Executive Condominium

99 16 Hoi Hup Realty Pte Ltd and Sunway Developments Pte Ltd

Foreign 240.9 355.2 635

1-Jul-16 Martin Place Residential 99 13 First Bedok Land Pte Ltd (Guocoland)

SG Listed 595.1 1,239.4 450

30-May-16 Bukit Batok West Avenue 6

Commercial & Residential

99 11 Qingjian Realty (BBR) Pte Ltd. And Qingjian Realty (BBC) Pte Ltd

Foreign 301.2 634.8 425

13-Apr-16 Jalan Kandis Residential 99 9 Dillenia Land Pte Ltd Foreign 51.1 481.2 110

29-Feb-16 Yio Chu Kang Road

Executive Condominium

99 10 Hoi Hup Realty Pte Ltd Foreign 183.8 331.1 520

26-Feb-16 New Upper Changi Road (Parcel B)

Residential 99 8 CEL Residential Development Pte Ltd

SG Listed 419.4 760.8 570

18-Jan-16 Siglap Road Residential 99 8 FCL Topaz Pte Ltd, Sekisui House Ltd and KH Capital Pte Ltd

SG Listed 624.2 858.3 800

Total 2,702.8 4,085

Source: Companies, DBS Bank

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Ave

rage

aver

age

range

of bid

(%

)

Highest vs Lowest Highest vs Median Highest vs 2nd

winning bid margin and average range of bid has narrowed

12

6

8

6

16

8 8 8

10

8

10

12

-

2

4

6

8

10

12

14

16

18

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Aver

age

no. of

bid

s

A verage no. of bids = 8

Page 20Page 20

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 21

Figure 22: 1H17 Government Land Sales Program

S/N Location

Site area (ha)

Proposed GPR

Est. No. of Housing

Units

Est, No. of hotel

rooms

Estimated commercial

space (sqm)

Estimated launch

date

Sales agent

CONFIRMED LIST 2H15

Residential Sites

1 Toh Tuck Road 1.87 1.4 325 - - Feb-17 URA 2 Tampines Avenue 10 (Parcel C) 2.17 2.8 715 - - Mar-17 URA 3 Lorong 1 Realty Park 1.31 Landed 50 - - Apr-17 URA 4 Serangoon North Avenue 1 1.72 2.5 505 - - May-17 URA 4 Woodleigh Lane 1.96 3 735 - - May-17 URA

Total (Confirmed List) 2,330 - -

RESERVE LIST Residential sites 1 Stirling Road 2.11 4.2 1110 - - Available URA 2 Bartley Road / Jalan Bunga Rampai 0.47 2.1 115 - - Available URA 3 Sumang Walk (EC) 2.71 3 775 - - Available HDB 4 Yishun Avenue 9 2.17 2.8 715 - - May-17 URA 5 Owen Road 1.38 3.5 605 - - Jun-17 URA 6 Jiak Kim Street 1.33 3.8 515 - 1,500 Jun-17 URA 7 Fourth Avenue 2.02 1.8 455 - - Jun-17 URA 8 1.72 3 575 - - Jun-16 URA Commercial & Residential Sites 9 Holland Road 2.3 2.6 570 - 13,500 Available URA Commercial Sites 10 Beach Road 2.1 4.2 - - 88,200 Available URA 11 Woodlands Square 2.24 3.5 260 - 60,030 Available URA

Total (Reserve List) 5,135 - 158,080 Total (Confirmed List and Reserve List) 7,465 - 158,080

Source: URA, DBS Bank

Page 21

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 22

4.6 More En-bloc transactions in 2017

Increase in en-bloc transactions in 2016. From 2005-2007, we saw a pick-up in en-bloc transactions when there was a shortage of government land supply. Following the implementation of property cooling measures, en-bloc transactions have dwindled down since 2011 to no transactions in 2014. In 2015, only one successful transaction (the sale of Thong Sia building) was recorded. Nevertheless, we have seen a pick-up of en-bloc transactions in 2016 with Harbour View Gardens being successfully transacted in August 2016 at an average price of S$1.3k psf, five en-bloc deals announced, and increasing media / news on property owners engaging property consultants (such as JLL and CBRE) to set up collective sales committee. The five en-bloc deals announced (excluding en-bloc sales for asset recycling purposes or specifically to be exempted from ABSD or QC charges) were i) Shunfu Ville, Bishan which was the first en-bloc sale of privatised former HUDC estate in nine years at

S$639m (S$557 psf ppr), ii) Raintree Gardens, Potong Pasir second en-bloc sale of privatised former HUDC estate at S$334m (S$593psf ppr) to UOL / UIC JV, iii) No.3 Cuscaden Walk, Orchard at S$103.8m (S$1,826 psf ppr) to SL Capital, a consortium led by Sustained Land, iv) No. 120 Grange Road, Orchard at S$48.5m (S$1,841 psf ppr) to Roxy-Pacific Holdings, and v) No. 8 Hullet Road, Orchard at S$38.2m (S$2,073 psf ppr) to a consortium led by Patrick Kho of Lian Huat Group. Media / news reported properties for sale including two apartments at The Claymore, Lakeside Towers in Jurong, Villa D’Este on Dalvey Road and Cairnhill Mansion on Orchard Road. Despite the tighter rules on en-bloc sales and more tedious process to complete an en-bloc transaction, developers are now willing to undertake these properties, implying that i) developers are hungry for land bank, and ii) developers are taking a more positive outlook in the medium term.

Figure 23: Shortage of land supply from the government Figure 24: Land prices remain high due to competitive bids

Source: URA, DBS Bank Source: URA, DBS Bank

Figure 25: Pick-up in en-bloc sales during shortage of government land supply

Figure 26: Total land transactions has fallen from 2013 onwards, post the implementation of cooling measures

Source: URA, DBS Bank Source: URA, DBS Bank

Page 22

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 23

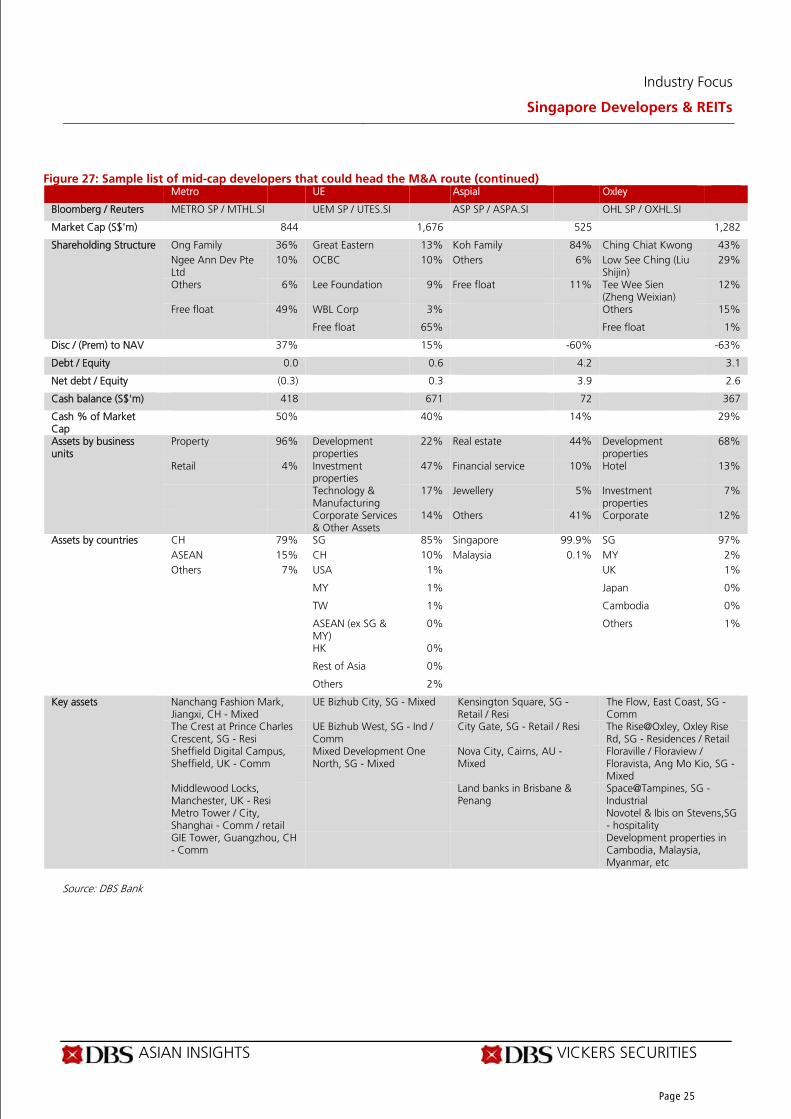

4.7 Merger and Acquisition (M&A) activities could pick up With the recent proposed privatisation of various property-related companies and news reports on potential takeovers of United Engineers (UE) (please refer to our report: Another Centenarian for Sale) and Global Logistic Properties (GLP), we believe that some of the smaller-cap developers which are trading at deep discounts to NAV could look attractive for potential M&A as an alternative to acquire assets / land

banking. We reviewed a list of smaller-cap developers with the key summary of each of the developers below. The smaller-cap developers are trading at an average discount to NAV of 29% with most trading at a range of 40-93% discount to NAV. Companies that are in deep discounts with attractive assets includes Bukit Sembawang (93% discount), Wing Tai (60%), Hiap Hoe (51%), and Hobee (50%).

Figure 27: Sample list of mid-cap developers that could head the M&A route

Bukit Sembawang Wing Tai Hiap Hoe Bloomberg / Reuters BS SP / BSES.SI WINGT SP / WTHS.SI HIAP SP / HIAP.SI Market Cap (S$'m) 1,177 1,298 335

Shareholding Structure Lee Family 44% Cheng Family 50% Teo Family 70%Aberdeen 11% Others 2% Others 1%Asia Fountain Inv (Guoco Grp)

5% Free Float 48% Free float 29%

Free float 39% Disc / (Prem) to NAV 93% 60% 51%

Debt / Equity no debt 0.4 0.7

Net debt / Equity no debt 0.1 0.6

Cash balance (S$'m) 401 966 23

Cash % of Market Cap 34% 74% 7%

Assets by business units Development properties 99.6% Development properties 57.0% Investment properties 45%Investment properties 0.4% Investment properties 39.0% Hotel 11%

Retail 2.0% Development properties 8%

Others 2.0% Construction 4%

Leisure 0%

Others 31%

Assets by countries n/a SG 47% SG 82%

HK 29% AU 18%

CH 11% MY 13%

Key assets Paterson Collection, Orchard, SG - Resi

The Crest, SG - Resi Signature At Lewis, SG - Resi

St Thomas Walk, River Valley, SG - Resi

Le Nouvel KLCC, MY - Resi HH @ Kallang, SG - Industrial

Luxus Hill, Seletar, SG - Landed resi Winsland House, SG - comm Zhongshan Park Integrated, Novena, SG - Mixed

Watercove, Sembawang, SG - Landed resi

Development in Suzhou Industrial Park - Comm

Lanson Place, Shanghai - hospitality Source: DBS Bank

Page 23

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 24

Figure 27: Sample list of mid-cap developers that could head the M&A route (continued) Hobee Roxy Wheelock Bloomberg / Reuters HOBEE SP / HBEE.SI ROXY SP / RXYP.SI WP SP / WPSL.SI Market Cap (S$'m) 1,477 501 1,789

Shareholding Structure Chua Family 76% Teo Family 72% Wheelock and Company Limited

76%

Others 1% Others 6% Aberdeen 6%Free float 23% Free float 22% Free Float 18%

Disc / (Prem) to NAV 50% 45% 40%

Debt / Equity 0.5 1.9 0.0

Net debt / Equity 0.5 1.2 (0.4)

Cash balance (S$'m) 77 327 1,319

Cash % of Market Cap 5% 65% 74%

Assets by business units Commercial 63% Development properties 57% Development properties 58%Residential 35% Hotel 11% Investment properties 35%Industrial 1% Investment properties 16% Investments 7%

Others 17% Assets by countries SG 55% SG 42% SG 80%

UK 29% AU 36% Other 20%CH 12% JP 8% AU 4% TH 4% MY 4% HK 5% ID 1%

Key assets Turquoise, Seascape & Cape Royale, Sentosa Cove, SG

Hotel properties in SG, JP, AU, TH & Maldives

Ardmore Three, Orchard, SG - Resi

Residential projects in Shanghai, Tangshan, Zhuhai

Sunnyvale Residences, SG - Resi Scotts Square, Orchard, SG - Resi

6 commercial buildings in London Trilive, SG - Resi / Retail Fuyang project, Hangzhou, CHThe Metropolis, Buona Vista, SG - Comm / Retail

New World Towers, South Brisbane, AU - Resi

Wheelock Place, SG - Comm / Retail

HB Centre 1 & 2, SG - Ind Land banks in SG, AU, ID Source: DBS Bank

Page 24

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 25

Figure 27: Sample list of mid-cap developers that could head the M&A route (continued)

Metro UE Aspial Oxley Bloomberg / Reuters METRO SP / MTHL.SI UEM SP / UTES.SI ASP SP / ASPA.SI OHL SP / OXHL.SI Market Cap (S$'m) 844 1,676 525 1,282

Shareholding Structure Ong Family 36% Great Eastern 13% Koh Family 84% Ching Chiat Kwong 43%Ngee Ann Dev Pte Ltd

10% OCBC 10% Others 6% Low See Ching (Liu Shijin)

29%

Others 6% Lee Foundation 9% Free float 11% Tee Wee Sien (Zheng Weixian)

12%

Free float 49% WBL Corp 3% Others 15%

Free float 65% Free float 1%

Disc / (Prem) to NAV 37% 15% -60% -63%

Debt / Equity 0.0 0.6 4.2 3.1

Net debt / Equity (0.3) 0.3 3.9 2.6

Cash balance (S$'m) 418 671 72 367

Cash % of Market Cap

50% 40% 14% 29%

Assets by business units

Property 96% Development properties

22% Real estate 44% Development properties

68%

Retail 4% Investment properties

47% Financial service 10% Hotel 13%

Technology & Manufacturing

17% Jewellery 5% Investment properties

7%

Corporate Services & Other Assets

14% Others 41% Corporate 12%

Assets by countries CH 79% SG 85% Singapore 99.9% SG 97%ASEAN 15% CH 10% Malaysia 0.1% MY 2%Others 7% USA 1% UK 1%

MY 1% Japan 0%

TW 1% Cambodia 0%

ASEAN (ex SG & MY)

0% Others 1%

HK 0% Rest of Asia 0% Others 2%

Key assets Nanchang Fashion Mark, Jiangxi, CH - Mixed

UE Bizhub City, SG - Mixed Kensington Square, SG - Retail / Resi

The Flow, East Coast, SG - Comm

The Crest at Prince Charles Crescent, SG - Resi

UE Bizhub West, SG - Ind / Comm

City Gate, SG - Retail / Resi The Rise@Oxley, Oxley Rise Rd, SG - Residences / Retail

Sheffield Digital Campus, Sheffield, UK - Comm

Mixed Development One North, SG - Mixed

Nova City, Cairns, AU - Mixed

Floraville / Floraview / Floravista, Ang Mo Kio, SG - Mixed

Middlewood Locks, Manchester, UK - Resi

Land banks in Brisbane & Penang

Space@Tampines, SG - Industrial

Metro Tower / City, Shanghai - Comm / retail

Novotel & Ibis on Stevens,SG - hospitality

GIE Tower, Guangzhou, CH - Comm

Development properties in Cambodia, Malaysia, Myanmar, etc

Source: DBS Bank

Page 25

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 26

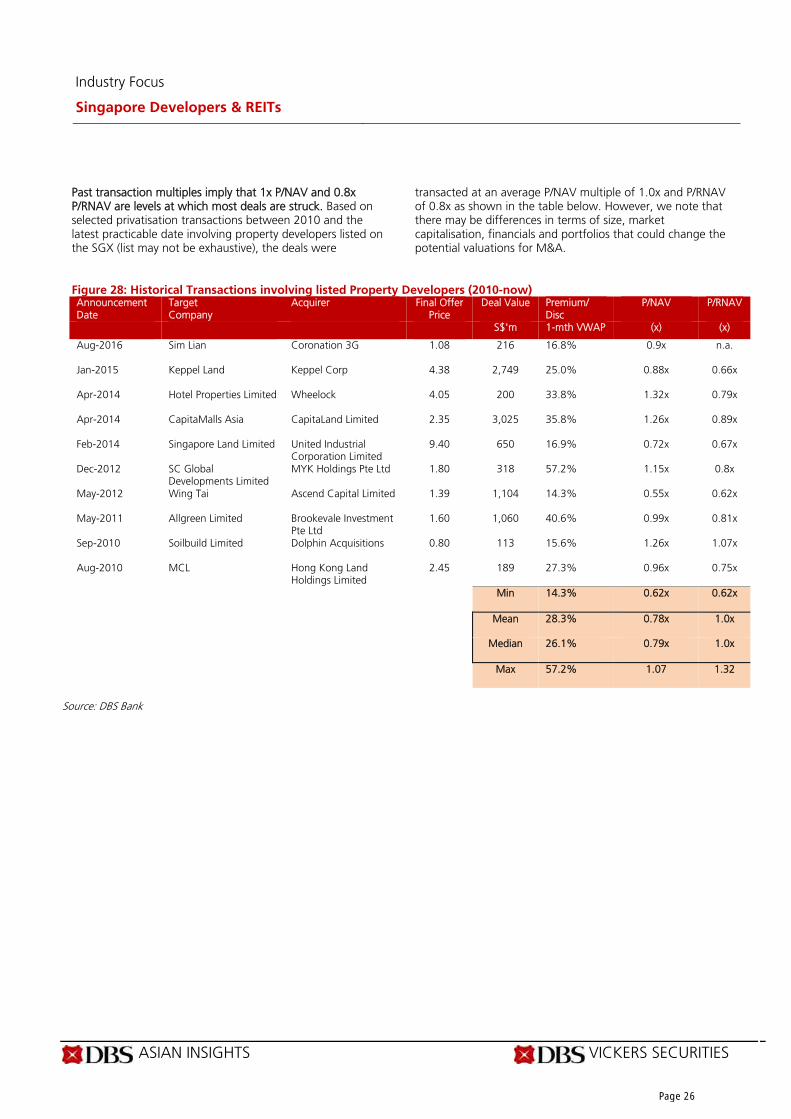

Past transaction multiples imply that 1x P/NAV and 0.8x P/RNAV are levels at which most deals are struck. Based on selected privatisation transactions between 2010 and the latest practicable date involving property developers listed on the SGX (list may not be exhaustive), the deals were

transacted at an average P/NAV multiple of 1.0x and P/RNAV of 0.8x as shown in the table below. However, we note that there may be differences in terms of size, market capitalisation, financials and portfolios that could change the potential valuations for M&A.

Figure 28: Historical Transactions involving listed Property Developers (2010-now) Announcement Date

Target Company

Acquirer Final Offer Price

Deal Value Premium/ Disc

P/NAV P/RNAV

S$'m 1-mth VWAP (x) (x)

Aug-2016 Sim Lian Coronation 3G 1.08 216 16.8% 0.9x n.a.

Jan-2015 Keppel Land Keppel Corp 4.38 2,749 25.0% 0.88x 0.66x

Apr-2014 Hotel Properties Limited Wheelock 4.05 200 33.8% 1.32x 0.79x

Apr-2014 CapitaMalls Asia CapitaLand Limited 2.35 3,025 35.8% 1.26x 0.89x

Feb-2014 Singapore Land Limited United Industrial Corporation Limited

9.40 650 16.9% 0.72x 0.67x

Dec-2012 SC Global Developments Limited

MYK Holdings Pte Ltd 1.80 318 57.2% 1.15x 0.8x

May-2012 Wing Tai Ascend Capital Limited 1.39 1,104 14.3% 0.55x 0.62x

May-2011 Allgreen Limited Brookevale Investment Pte Ltd

1.60 1,060 40.6% 0.99x 0.81x

Sep-2010 Soilbuild Limited Dolphin Acquisitions 0.80 113 15.6% 1.26x 1.07x

Aug-2010 MCL Hong Kong Land Holdings Limited

2.45 189 27.3% 0.96x 0.75x

Min 14.3% 0.62x 0.62x

Mean 28.3% 0.78x 1.0x

Median 26.1% 0.79x 1.0x

Max 57.2% 1.07 1.32

Source: DBS Bank

Page 26

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 27

4.8 Will Developers need to deleverage? Average indebtedness across developers over time remain stable; larger-cap developers have been generally more conservative. Property developers have generally been conservative in their approach towards capital management and over the past few years, kept net gearing in the range of 0.4-0.6x. Tracking the average indebtedness across developers over time, we found that mid-sized developers (defined as those with market capitalisation of up to S$2bn) have generally taken more debt in recent years and thus average gearing of c.0.8x in the last four years, higher than the sector’s average of c.0.7x over the same period. On average, over the same period, the large-cap developers have an average net gearing ratio of c.0.5x. Developers that stand out in terms of higher gearing than their peers as of the latest reported quarter are the likes of Guocoland (large-sized developer) at 1.2x and in the mid-sized developer space - Oxley, Tee Land and Roxy-Pacific which all have net gearing in excess of 1.0x (Fig. 30). Chip Eng Seng and Tuan Sing also have high net gearing of above 0.9x. Developers to deleverage as outlook remains subdued. 2017 will turn out to be a tough year for developers to deploy

capital. Firstly, we expect the land-banking climate to remain competitive in Singapore given limited land sites available for tender from the government, which means that most mid-sized developers could be crowded out by their larger competitors or foreign developers. Secondly, increased currency volatility going forward is expected to be a drag on returns when deploying more capital overseas. As such, given limited avenues to deploy capital and fairly strong balance sheets, we believe that a possible avenue where developers could look to deleverage their balance sheet or if not pay higher dividends going forward. The recent spike in swap-offer rates (SOR) could imply higher refinancing costs going forward. As such, faced with a slowing top-line growth and increasing prospects of higher interest obligations, we believe that a viable strategy will be to utilise proceeds that are recognised from subsequent years’ pre-sales to pare down on debt obligations when they come due in 2017-2018. In our interest rate analysis, we estimate impact on PATMI for the developers from a 1% increase in interest rates result in a 4-40% impact on PATMI.

Figure 29: Gearing levels of Property Developers over

time have remained fairly stable Figure 30: Net gearing of Selected Mid-Cap

Developers (Latest Quarter)

Source: Bloomberg Finance L.P., DBS Bank

Source: Bloomberg Finance L.P., DBS Bank

0.47 0.50 0.54 0.71

0.85 0.94 0.98 1.07 1.16

2.15

0.00

0.50

1.00

1.50

2.00

2.50

Hobee

Hia

p H

oe

OU

E

Fragra

nce

Heeto

n

Chip

Eng S

eng

Tuan S

ing

TEE L

and

Roxy

-Paci

fic

Oxl

ey

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Ne

t D

eb

t/Equit

y (x

)

Large cap Mid cap Average

Page 27

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 28

Figure 31: Summary of Developers Financial position (As of latest quarter ended Sept-2016)

Developer Type* Market Cap

Total Assets

Total Debt

Total Equity

Cash Total Debt/

Equity

Net Debt/

Equity

Total Debt/

EBITDA (TTM)

Net Debt/

EBITDA

EBITDA/Interest

expense (TTM)

(S$'bn) (S$'bn) (S$'bn) (S$'bn) (S$'bn) (x) (x) (x) (x) (x)

Capitaland Large 13.56 46.21 15.58 23.88 4.24 0.7 0.5 11 8 3.0

GLP Large 8.77 27.73 6.21 18.30 2.47 0.3 0.2 10 6 3.0

Citydev Large 7.40 19.93 6.35 11.02 3.29 0.6 0.3 5 3 11.8

UOL Large 4.52 11.60 2.57 8.51 0.27 0.3 0.3 8 7 9.8

FCL Large 4.32 24.20 9.80 11.84 2.17 0.8 0.6 12 9 5.1

UIC Large 3.86 8.62 1.31 6.98 0.08 0.2 0.2 4 4 28.9

Guocoland Large 2.21 8.15 4.05 3.47 1.13 1.2 0.8 22 16 3.9

Wheelock Mid 1.78 3.28 0.02 3.02 0.40 0.0 (0.1) 0l0 (7) 55

OUE Mid 1.57 8.09 2.97 4.59 0.21 0.6 0.6 17 14 1.5

Perennial RE Mid 1.49 6.71 2.52 3.64 0.19 0.7 0.6 221 1 1.2

Ho Bee Mid 1.44 4.29 1.39 2.79 0.08 0.5 0.5 9 8 21

Wingtai Mid 1.31 4.71 1.13 3.34 0.97 0.3 0.0 89 13 0.3

Oxley Mid 1.23 4.48 2.43 0.96 0.37 2.5 2.1 8 7 8.4

Bukit Sembawang Mid 1.16 1.42 - 1.27 0.40 - (0.3) 0.0 (4) 0.0

Fragrance Mid 1.09 2.00 0.82 1.06 0.06 0.8 0.7 93 85 1.6

Roxy-Pacific Mid 0.53 1.50 0.89 0.48 0.33 1.8 1.2 12 8 4.8

Chip Eng Seng Small 0.39 2.18 1.17 0.75 0.46 1.6 0.9 12 7 5

Tuan Sing Small 0.35 2.09 1.04 0.89 0.16 1.2 1.0 16 14 2.4

Hiap Hoe Small 0.33 1.30 0.45 0.69 0.02 0.7 0.6 8 6 4.4

SingHaiyi Small 0.30 0.95 0.30 0.47 0.12 0.6 0.4 -29 -17 -1.3

Heeton Small 0.14 0.72 0.31 0.33 0.03 0.9 0.9 -85 -77 -0.2

TEE Land Small 0.09 0.42 0.21 0.17 0.03 1.2 1.1 153 135 0.3

Total Debt/

Equity

Net Debt/

Equity

(x) (x)

Average Sector 0.6 0.4

Average Large Cap 0.6 0.4

Average Mid Cap 0.7 0.5

Average Small Cap 1.1 0.9

*Large Cap denotes Market Cap > S$2.0bn, Mid-Cap Developers refer to those with market cap > S$0.5bn to less than S$2.0bn, Small Cap <S$0.5bn in market cap Source: Bloomberg Finance L.P., DBS Bank

Page 28

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 29

Bond markets issuances have increased in recent years. With strong investor demand for yields in recent years amidst the low interest rate environment, we have seen an increase in new bond issuances in Singapore. In the real estate space, we saw close to S$34bn of new issues over the past five years, which is more than 20% of the total amount of new bond issuances over the preceding five years. In the real estate sector, bond issuances peaked in 2011, and again reached new highs in 2012 and 2015. In 2015, bond issuances totalled S$8.7bn across the real estate sector. We also note that mid-sized developers have also been tapping the bond markets in recent years. A total of S$3.5bn worth of bonds will be due in 2017. Average cost of funds has also been falling over time, hovering at about 3% since 2008.

S$3.4bn worth of bonds from developers due in 2017 that need to be refinanced. Continued access to funding is a key enabler to a healthy real estate development and investment market. However, recent bond defaults in the oil & gas space has resulted in heightened risk aversion among investors in bonds. In addition, the market for future bond issues appears to be shut for most aspiring issuers for now. If the current risk-off sentiment remains in the medium term, it might be a headwind for issuers in the real estate sector who need to refinance upcoming bond expires in 2017-2018 which total S$6.3bn, out of which S$4.0bn will be from real estate developers. We note that among the bonds due in 2017, developers like Guocoland and OUE will need to refinance expiring bonds. Developers such as OUE and Heeton’s existing cash balances and receivables may not be sufficient for repayment of bonds. Additional financing may be required in due time for bond repayments.

Figure 32: Bond issuances by developers peaked in

2015 Figure 33: Bonds Expiry profile

Source: Bloomberg Finance L.P., DBS Bank

Source: Bloomberg Finance L.P., DBS Bank

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

S$'m

Total amount issued (S$m) Average cost of debt

2.9

1.1 1.2

3.6

0.7

2.6

1.40.9

6.00.8

1.5 1.3

1.3

2.1

1.2

1

0.9

3.2

2 0 1 7 2 0 1 8 2 0 1 9 2 0 2 0 2 0 2 1 2 0 2 2 2 0 2 3 2 0 2 4 > 2 0 2 4

S$'BN Developers REITs

Page 29

Industry Focus

Singapore Developers & REITs

ASIAN INSIGHTS VICKERS SECURITIES Page 30

Figure 34. Selected property developers’ outstanding bonds, 2017-2018 (S$m)

Issuer Maturity Amount Outstanding (S$'m)

SingHaiyi Group Ltd Jan-17 100

Fragrance Group Ltd Jan-17 85

OUE Ltd Feb-17 300

City Developments Ltd Feb-17 250

GLL IHT Pte Ltd (Guocoland) Feb-17 160

UOL Group Ltd May-17 75

Oxley Holdings Ltd May-17 150

Heeton Holdings Ltd Jun-17 60

CapitaLand Treasury Ltd Jul-17 50

GLL IHT Pte Ltd (Guocoland) Aug-17 170

Keppel Land Ltd Aug-17 100

GLL IHT Pte Ltd (Guocoland) Sep-17 105

Chip Eng Seng Corp Ltd Oct-17 150

TEE Land Ltd Oct-17 30

Hongkong Land Dec-17 50

City Developments Ltd Mar-18 100

Perennial Treasury Pte Ltd (Perennial) Mar-18 100

UOL Treasury Services Pte Ltd (UOL) Apr-18 175

Global Logistic Properties Ltd May-18 67

Centurion Corp Ltd Jul-18 65