Bahasa

Halaman

Hukum

Salt Lake City, Utah

December 13, 2019

2

Accounting Update

3

With You Today

WENDY HAMBLETONNational Assurance Partner

(312) [email protected]

TOMMY JENSENAssurance Partner

(801) [email protected]

MATT MCREYNOLDSAssurance Partner

(801) [email protected]

BRAD TOONEAudit director

(801) [email protected]

4

FASB Update

5

ASU 2019-10 amended the effective dates for several existing ASU’s as follows:Credit losses Public business entities that meet the definition of an SEC filer, excluding

entities eligible to be SRCs as defined by the SEC, for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years

All other entities for fiscal years beginning after December 15, 2022, including interim periods within those fiscal years.

Hedging Entities other than public business entities for fiscal years beginning after

December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021.

Effective Dates – ASU 2019-10

6

Leases: Public business entities; not-for-profit entities that have issued or are conduit

bond obligors for securities that are traded, listed, or quoted on an exchange or an over-the-counter market; and employee benefit plans that file or furnish financial statements with or to the SEC for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years (no change)

All other entities for fiscal years beginning after December 15, 2020, and interim periods within fiscal years beginning after December 15, 2021.

Effective Dates ASU 2019-10 (cont.)

7

A major update would first be effective for bucket-one entities, that is, public business entities that are Securities and Exchange Commission (SEC) filers, excluding entities eligible to be smaller reporting companies (SRCs) under the SEC’s definition. The Master Glossary of the Codification defines public business entities and SEC filers.

All other entities, including entities eligible to be SRCs, all other public business entities, and all nonpublic business entities (private companies, not-for-profit organizations, and employee benefit plans) would compose bucket two. For those entities, it is anticipated that the Board will consider requiring an effective date staggered at least two years after bucket one for major Updates.

Generally, it is expected that early application would continue to be allowed for all entities.

Effective Dates – General Approach for the Future:

8

Pronouncements Effective in 2020

9

ASU 2018-13, Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement Summary: Improves/clarifies disclosures related to fair value measurements required under ASC 820.

Modifications

1. Nonpublic entities: Replaces rollforward of Level 3 measurements with information about transfers into/out of Level 3 and purchases/issues of Level 3 assets and liabilities.

2. Requires disclosure of timing of liquidation of investee assets and date restrictions from redemption lapse related to investments in entities that calculation NAV only if investee has communicated timing.

3. Clarifies that measurement uncertainty disclosure relates to uncertainty in measurement as of the reporting date.

Additions (For public companies only)

1. Disclose changes in unrealized gains/losses included in OCI for recurring Level 3 measurements held at the end of the reporting period.

2. Disclose the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements. Certain alternatives apply.

10

ASU 2018-13, Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement Removals

1. Amount of and reasons for transfers between Level 1 and Level 2.

2. The policy for timing of transfers between levels.

3. The valuation processes for Level 3 fair value measurements.

4. Nonpublic entities: changes in unrealized gains and losses for the period included in earnings for recurring Level 3 fair value measurements held at the end of the reporting period.

Effective Date:

All entities* - FYs beginning after Dec. 15, 2019

* An entity is permitted to early adopt all disclosure requirements in the ASU or early adopt only the removed and modified disclosures and delay adoption of the additional disclosures until their effective date.

11

ASU 2018-15, Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract Summary: Requires a customer in a hosting arrangement (service contract) to apply the guidance on internal-use software to determine which implementation costs to recognize as an asset and which costs to expense.

Key Amendments: Customer must determine whether an implementation activity relates to the preliminary project

stage, the application development stage, or the post-implementation stage.

Costs for implementation activities in the application development stage will be capitalized depending on the nature of the costs, while costs incurred during the preliminary project and post-implementation stages will be expensed immediately.

Additional guidance on how to assess capitalized costs for impairment and appropriate presentation of capitalized costs and related amortization.

Effective Dates: Public business entities - FYs beginning after Dec. 15, 2019

All other entities – FYs beginning after Dec. 15, 2020

Early adoption is permitted

12

ASU 2018-17, Targeted Improvements to Related Party Guidance for Variable Interest Entities (VIEs)Summary: Improves application of the consolidation guidance for targeted areas.

Key Amendments:

Private company alternative – private companies may elect not to apply VIE guidance to legal entities under common control (including common control leasing arrangements) if both the parent and the legal entity being evaluated for consolidation are not public business entities.

Clarifies that indirect interests held through related parties in common control arrangements should be considered on a proportional basis for determining whether fees paid to decision makers and service providers are variable interests, consistent with how indirect interests held through related parties under common control are considered for determining whether a reporting entity must consolidate a VIE.

Effective Dates:

Public business entities - FYs beginning after Dec. 15, 2019

All other entities – FYs beginning after Dec. 15, 2020

13

Background

ASU 2016-13 – Measurement of Credit Losses on Financial InstrumentsASC 326 / ASU 2016-13

Issued June 2016

A Transition Resources Group

has issued nonauthoritative

guidance on practice and

implementation issues

4 Amendments

14

ASC 326 / ASU 2016-13In Scope

Financial assets measured at amortized cost: Trade Receivables Loans Contract Assets Reinsurance Receivables Held-to-maturity debt securities Financial Guarantees

Net Investment in leases recognized by a lessor

Off Balance Sheet loan commitments, standby letters of credit, Financial Guarantees

15

Out of Scope

Loans made to participants by

defined contribution employee benefit

plans (962)

Equity securities (321)

Pledge receivables of a not-for-profit

entity

Related party loans and receivables between entities under common

control

Policy loan receivables of an insurance entity

(944)

Equity method investments (323)

Derivatives (815)

Operating lease receivables (842,

ASU 2018-19 clarified)

Financial assets where Fair Value Option elected

(820)

16

The Current Expected Credit Loss (“CECL”) Model creates three significant shifts from the current incurred loss model:

Primary Changes in the New CECL Model

which requires the utilization of future information, and supportable forecasts to estimate ALLL levels

FORWARD LOOKING ANALYSIS

which requires you to forego worst-case and best-case scenario and evaluate the possibility that a loss exists or does not exist

REMOVES “PROBABLE” THRESHOLD

from the current 12 to 18 month horizon to the lifetime of the asset. This is broadly expected to expand the horizon used for estimating the ALLL.

LOSS HORIZON CHANGES

17

CECL –Objective

Reduce amortized cost to amount expected to be collected via valuation account. Off BS commitments will be a liability.

Expected credit losses shall be measured over: Contractual term, considering estimated payments Contractual term shall not be extended for

• Expected extensions and renewals unless they are in the original agreement and are not unconditionally cancelable (ASU – 2019-04)

• Expected modifications, unless TDR anticipated

No minimums or triggering events

Not required to record a loss when the risk of nonpayment is zero

18

CECL –Information to Consider

CECL requires estimates of expected credit losses based on internally and externally available information Past events Current conditions Reasonable and supportable forecasts- cannot solely rely on past events

• Qualitative and quantitative factors specific to borrowers and the economy Reversion – beyond reasonable and supportable period revert to historical loss

experience

CECL does not mandate specific approaches or policy decisions to determine expected credit losses

19

Key Steps to Consider for CECL Model

Historical Loss

Information

Reasonable, Supportable Forecasts

Reversion to History

Current Conditions

Expected Credit Loss

20

CECL –Zero Risk of Loss vs. Remote Risk of Loss

Zero risk of loss- No reserve required when no history of loss and no expectation of nonpayment US Treasury securities Cannot assume zero loss if asset is secured by collateral and collateral value exceeds

amortized cost basis. (Except for practical expedients)

An entity’s estimate of expected credit losses should include a measure of the expected risk of credit loss even if that risk is remote, regardless of the method applied to estimate credit losses.

The FASB concluded that a ‘bright-line’ approach would be inappropriate for all facts and circumstances and decided not to provide explicit guidance on what specific assets are appropriate for zero credit losses.

**It will be rare to have zero risk of loss.**

21

Trade Receivables

Companies typically apply an allowance

for doubtful accounts based on historical

losses by aging categories

Under CECL, companies will have to consider whether such historical data

requires adjustment, including upon

recognition of the receivable

Will likely result in recognition of

allowance for credit losses for receivables that are not yet past

due

Individually significant balances with

historical zero loss will most likely

require a loss factor.

The standard applies to receivables that result from revenue

transactions, even if a non-customer party

will make the payment

22

ASU 2016-02 LeasesIntroduction

Lessees Right of use model – recognize ROU asset and lease liability at inception for all

leases• Optional exemption for leases with terms < 12 months

Classify all leases as finance or operating (5 criteria)• Finance lease – lessee effectively obtains control of underlying asset• Operating lease – lessee does not effectively obtain control of underlying

asset Similar balance sheet impact; different income statement and cash flow results

ACCOUNTING STANDARD

23

Introduction

Lessors Classify all leases as sales-type, direct finance, or operating (similar to existing

U.S. GAAP) based on same criteria as lessees, plus a few others• Sales-type lease - transfers all risks and rewards, plus control of underlying

asset, to lessee• Direct financing – transfers risks and rewards but not control• Operating – does not transfer risks and rewards or control

Subsequent accounting is consistent with existing U.S. GAAP* Control principle aligned with new revenue standard

* Leveraged lease treatment no longer available for new leases

SE ACCOUNTING STANDARD

24

Identifying a Lease

Lease: A contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an

identified asset) for a period of time in exchange for consideration

Determine at inception based upon: Whether contract fulfillment depends on use of an identified asset* Whether contract conveys right to control use of an identified asset and

obtain substantially all of the economic benefits for consideration for a time period

* Consider whether supplier has substantive right of substitution

25

Definition of a Lease

26

INITIALMEASUREMENT

Right-of-use asset

Present value (PV) of lease payments + lessee’s initial direct costs

Initial direct costs: Incremental costs directly attributable to negotiating and arranging a lease

Recognize lease incentives as a reduction in the right-of-use asset

Lease liability (LL)

PV of lease payments

Private company practical expedient - use risk-free rate to measure LL

SUBSEQUENTMEASUREMENT

Right-of-use asset

Amortized cost: Method of amortization depends on lease classification (finance or operating)

Impairment: Refer to existing standards (ASC 360)

Lease liability

Amortized cost: Use the effective interest method

Private company practical expedient - use risk-free rate to measure LL

Lessee Accounting

LEASE ACCOUNTING STANDARD

27

Lease Term and Payments

Lease Term Estimated as the non-cancellable period

of the lease

Include periods under option to extend IF lessee is reasonably certain to exercise option

Include periods under option to terminate IF lessee is reasonably certain NOT to exercise option

Same analysis for purchase options

Lease Payments (Rentals) Fixed lease payments (less incentives to

be paid by lessor)

Variable payments tied to an index

Variable payments which are in-substance fixed payments

Residual value guarantees (probable amount)

Exercise price of purchase option IF lessee is reasonably certain to exercise option

Termination penalties IF lease term reflects lessee exercising option

Fees paid to structure an SPE

Two elements form basis for PV of lease payments:

LASE ACCOUNTING STANDARD

28

Lease Payments

Variable payments:

• Day 1 - include index-based payments (e.g., CPI escalator) measurement based on the rate at commencement.

• Day 2 - only reassess when the lease liability is reassessed for other reasons (e.g., contract modification). Otherwise, changes in the index are period expenses.

• Guidance issued in July 2018 (ASU 2018-10) clarifies that a change to an index or rate on which some or all of the variable lease payments in a contract are based does not constitute the resolution of a contingency. As a result, a lessee does not re-measure the lease payments when there is solely a change to an index or rate on which variable lease payments are based.

In-substance fixed payments are included in Day 1 lease liability, consistent with current practice.

Discount rate - use the rate implicit in the lease if determinable, otherwise use incremental borrowing rate.

• Under guidance in ASC 2018-10 the rate cannot be less than zero

29

Lessee Accounting

Balance SheetAll leases:

Present separately* or within similar classes of assets and liabilities with proper disclosure

*No co-mingling of finance and operating leases

Income Statement Finance: Display interest on lease

liability and amortization of ROU asset consistently with other interest and amortization expenses (combine or separate)

Operating: Display interest on lease liability together with amortization of ROU asset, within income from continuing operations

Presentation for LESSEES:

EASE ACCOUNTING STANDARD

30

Lessee Accounting

Statement of Cash Flows Operating activities

• Interest on lease liability arising from finance leases*

• Payments arising from operating leases

• Variable lease payments and S/T lease payments not included in lease liability

Financing activities• Principal repayments on finance leases

*the requirement is to present consistent with Topic 230, which generally will result in operating classification

Presentation for LESSEES:

LEASE ACCOUNTING STANDARD

31

2019 Final ASUs Issued

ASU 2019- Title BDO Alert

01 Leases (Topic 842): Codification Improvements 2019-01 Alert

02Entertainment—Films—Other Assets—Film Costs (Subtopic 926-20) and Entertainment—Broadcasters—Intangibles—Goodwill and Other (Subtopic 920-350): Improvements to Accounting for Costs of Films and License Agreements for Program Materials

N/A

03 Not-for-Profit Entities (Topic 958): Updating the Definition of Collections N/A

04 Codification Improvements to Topic 326, Financial Instruments—Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments 2019-04 Alert

05 Financial Instruments—Credit Losses (Topic 326): Targeted Transition Relief 2019-05 Alert

06Intangibles—Goodwill and Other (Topic 350), Business Combinations (Topic 805), and Not-for-Profit Entities (Topic 958): Extending the Private Company Accounting Alternatives on Goodwill and Certain Identifiable Intangible Assets to Not-for-Profit Entities

2019-06 Alert

08Compensation—Stock Compensation (Topic 718) and Revenue from Contracts with Customers (Topic 606): Codification Improvements—Share-Based Consideration Payable to a Customer

Coming Soon

Current as of November 13, 2019

32

Clarifies certain aspects of new leases guidance• Allows non-manufacturer/dealer lessors to use cost, reflecting any volume or trade discounts, as

the fair value of the underlying asset

• Lessors that are depository/lending institutions will present all principal payments received under leases as investing cash flows. Other lessors will present all cash receipts from leases as operating cash flows.

• Provides an exception to the paragraph 250-10-50-3 interim disclosure requirements in the ASC 842 transition disclosure requirements (applies to lessees and lessors).

ASU 2019-01, Leases (Topic 842): Codification Improvements

Effective Dates Public Business Entities Other Entities

FYs beginning after 12/15/2019 FYs beginning after 12/15/2020

33

Aligns accounting for production costs of an episodic television series with accounting for production costs of films by removing the content distinction for capitalization

Provides guidance on reassessing estimates of the use of a film, assessing impairments, and relevant presentation and disclosures.

ASU 2019-02, Improvements to Accounting for Costs of Films and License Agreements for Program Materials

Effective Dates Public Business Entities Other Entities

FYs beginning after 12/15/2019 FYs beginning after 12/15/2020

34

Updates the definition of “collections” to align with commonly used code of ethics terminology:

Works of art, historical treasures, or similar assets that meet all of the following criteria:a. They are held for public exhibition, education, or research in furtherance of public service rather

than financial gain.

b. They are protected, kept unencumbered, cared for, and preserved.

c. They are subject to an organizational policy that requires the use of proceeds from items that are sold to be for the acquisitions of new collection items, the direct care of existing collections, or both.

Applies to all entities, including business entities, that maintain collections, but primarily affects not-for-profit entities such as museums, historic sites, art galleries, etc.

Certain incremental disclosures required.

ASU 2019-03, Updating the Definition of Collections

Effective Dates Public Business Entities Other Entities

FYs beginning after 12/15/2019 FYs beginning after 12/15/2019

35

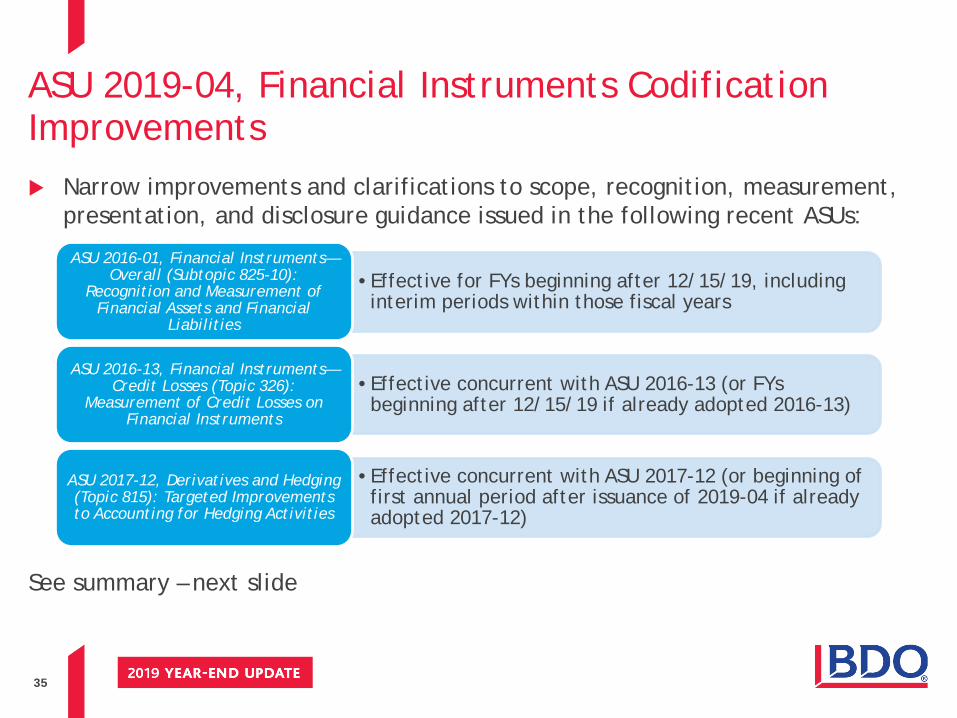

Narrow improvements and clarifications to scope, recognition, measurement, presentation, and disclosure guidance issued in the following recent ASUs:

See summary – next slide

ASU 2019-04, Financial Instruments Codification Improvements

•Effective for FYs beginning after 12/15/19, including interim periods within those fiscal years

ASU 2016-01, Financial Instruments—Overall (Subtopic 825-10):

Recognition and Measurement of Financial Assets and Financial

Liabilities

•Effective concurrent with ASU 2016-13 (or FYs beginning after 12/15/19 if already adopted 2016-13)

ASU 2016-13, Financial Instruments—Credit Losses (Topic 326):

Measurement of Credit Losses on Financial Instruments

•Effective concurrent with ASU 2017-12 (or beginning of first annual period after issuance of 2019-04 if already adopted 2017-12)

ASU 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities

36

Topic Issues addressedFinancial Instruments(ASU 2016-01)

HTM debt security FV disclosures; applying ASC 820 to the FV measurement alternative; and remeasuring equity securities at historical f/x rates.

CECL(ASU 2016-13)

Accrued interest; transfers between classifications or categories of loans and securities; asset recoveries; reinsurance recoverables; projecting variable interest rates; effect of prepayments on effective interest rate; costs to sell when foreclosure is probable; vintage disclosures for LOC arrangements converted to term loans; and contract renewals.

Hedging(ASU 2017-12)

Partial-term FV hedges of interest rate risk; amortization and disclosure of FV hedge basis adjustments; consideration of hedged contractually specified interest rate in the hypothetical derivative method; scope of NFP entities; hedge documentation for private companies; first-payments-received cash flow hedging technique; and transition.

ASU 2019-04, Financial Instruments Codification Improvements

37

Provides alternative to irrevocably elect the fair value option for eligible financial assets measured at amortized cost upon adoption of ASU 2016-13 (credit losses standard)

For an instrument to be eligible:• Asset must be within the scope of the new credit losses standard, and • Asset must be eligible for applying the fair value option in ASC 825-10

Apply on instrument-by-instrument basis Not available for available-for-sale or held-to-maturity debt securities Effective concurrent with ASU 2016-13, or FYs beginning after 12/15/19 if

already adopted 2016-13

ASU 2019-05, Credit Losses: Targeted Transition Relief

38

Allows NFPs to elect private company accounting alternatives:

Goodwill (ASC 350)

• Option to amortize goodwill on a straight line basis over a period of 10 years (or less if appropriate)

• If elected, entity must test goodwill when a triggering even occurs at either the entity level or reporting level.

Certain identifiable intangible assets in a bizcom (ASC 805)

• Option to subsume the following into goodwill:

- Customer-related intangible assets that are incapable of being sold or licensed independently from other assets acquired, and

- All non-complete agreements

• If elected, must also elect ASC 350 goodwill alternative

Effective immediately with same open-ended one-time election available to private companies

ASU 2019-06, Extending Private Company Alternatives on Goodwill and Certain Identifiable Intangible Assets to Not-for-Profit Entities

39

Effective Dates Public Business Entities Other Entities

FYs beginning after 12/15/2019 FYs beginning after 12/15/20191

1 And interim periods beginning after 12/15/2020, unless entity adopted ASU 2018-07, in which case it would be for interim periods beginning after 12/15/2019.

ASU 2018-07 on Improvements to Nonemployee Share-Based Payment Accounting require that share-based payment awards granted to a customer in conjunction with selling goods or services be accounted for under ASC 606

Lack of guidance on measuring share-based payment awards granted to a customer could result in diversity, because entities may apply: • ASC 606 noncash consideration guidance (measure at contract inception), or• ASC 718 guidance (measure at grant date)

ASU 2019-08 requires measurement and classification of share-based payment awards granted to a customer by applying ASC 718

ASU 2019-08, Codification Improvements—Share-Based Consideration Payable to a Customer

40

2019 Select Proposals

Title Comment Deadline

Invitation to Comment, Identifiable Intangible Assets and Subsequent Accounting for Goodwill

October 7, 2019BDO comment letter

Proposed ASU, Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting

October 7, 2019BDO comment letter

Proposed ASU, Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity

October 14, 2019BDO comment letter

Proposed ASU, Debt (Topic 470): Simplifying the Classification of Debt in a Classified Balance Sheet (Current versus Noncurrent)

October 28, 2019BDO comment letter

41

Solicits feedback on: Whether to change the subsequent accounting for goodwill

• Explores possibilities of amortizing goodwill, modifying the impairment test, costs and benefits of recent simplifications to goodwill model

Whether to modify the recognition of intangible assets in a business combination • Explores whether to subsume all or some intangible assets into goodwill,

principles-based approach, or status quo Whether to add or change disclosures about goodwill and intangible assets Comparability and scope Other topics for consideration

Invitation to Comment, Identifiable Intangible Assets and Subsequent Accounting for Goodwill

42

Reduce the number of models in ASC

470-20 (convertible instruments)

Revise the guidance in ASC 815-40

(derivatives scope exception)

Update diluted EPS models (ASC 260)

Expand related disclosures

Overview of Proposed ASU – Convertible Instruments and Contracts in an Entity’s Own Equity

43

Convertible Instruments* - Existing GAAP Proposed GAAPEmbedded derivative model (ASC 815-15) to account for convertible debt instruments with embedded conversion features that are not clearly and closely related to the host contract, meet the definition of a derivative, and do not meet the criteria for the derivatives scope exception. Conversion features are bifurcated as derivatives from the host contract and measured at fair value.

Model retained

Cash conversion model (ASC 470-20) to account for convertible debt instruments that may be settled entirely or partially in cash upon conversion. Host contract is measured at the fair value of a similar debt without conversion features, and conversion features are recorded as equity components at the residual amount.

Model eliminated

Beneficial conversion feature model (ASC 470-20) to account for convertible debt instruments with conversion features that are in the money at the commitment date or that become in the money at a later date after the occurrence of a contingent event. Conversion features are recorded as equity components at intrinsic value, and the host contract is recorded at the residual amount.

Model eliminated

Substantial premium model (ASC 470-20) to account for convertible debt instruments issued at substantial premiums. Conversion features are recorded as equity components.

Model eliminated

Traditional convertible debt model (ASC 470-20) to account for other convertible debt instruments as a single debt instrument measured at amortized cost.

Model retained

Proposed ASU – Convertible Instruments and Contracts in an Entity’s Own Equity

* Proposed amendments have a similar effect on convertible debt and convertible preferred stock guidance

44

Revise the guidance in ASC 815-40 (derivatives scope exception), as follows: Layer a likelihood threshold to existing indexation guidance

• Evaluating any potential adjustments that have a remote likelihood of occurring no longer would be required

• Will create new requirement for companies and auditors to analyze and document whether a triggering event is probable, involving time, effort, and judgment.

Remove the following from the settlement guidance:• Requirement to evaluate provisions that could require net cash settlement

but have a remote likelihood or occurring • Condition regarding settlement in unregistered shares• Condition regarding collateral• Condition regarding shareholder rights

Proposed ASU – Convertible Instruments and Contracts in an Entity’s Own Equity

45

Update EPS guidance to align with amendments to convertible debt and derivatives scope exception, as follows: Require the if-converted method for convertible instruments (versus treasury

stock method); should not change practice in most cases Require share settlement presumption for calculating diluted EPS when an

instrument may be settled in cash or shares (i.e., remove current guidance allowing a rebuttable presumption)

Include equity-classified convertible preferred stock that includes a down round feature in the scope of the recognition and measurement guidance for down-rounds in EPS guidance.

Require average market price to calculate diluted EPS denominator when the exercise price or number of shares to be issued varies based on share price.

Proposed ASU – Convertible Instruments and Contracts in an Entity’s Own Equity

46

Expand convertible debt (instrument) disclosures to compensate for reduction in accounting models: Add disclosure objective Add information about events or conditions that occur during the reporting

period that significantly affect the conversion conditions Add information on which party controls the conversion rights Align disclosure requirements for contingently convertible instruments with

other convertible instruments Require that existing fair value disclosures in ASC 825, Financial Instruments, be

provided at the individual instrument level rather than in the aggregate

Proposed ASU – Convertible Instruments and Contracts in an Entity’s Own Equity

47

Proposes a principles-based model for determining classification: An entity would classify an instrument as noncurrent if either of the following

criteria is met as of the balance sheet date: 1. Liability is contractually due to be settled more than one year (or operating

cycle, if longer) after B/S date2. Entity has a contractual right to defer settlement of the liability for a period

greater than one year (or operating cycle, if longer) after B/S date Continue to classify debt as noncurrent (separate from other noncurrent) if

waiver received for covenant violation Additional disclosures proposed Would apply to all debt arrangements, including convertible debt instruments,

liability-classified mandatorily redeemable financial instruments, and lease liabilities

Proposed ASU, Simplifying the Classification of Debt (Current versus Noncurrent)

48

Reference rate reforms under way may affect accounting for existing contracts referring to LIBOR Regulators have undertaken reference

rate reform initiatives

Significant volume of contracts will need to be modified such as debt agreements, lease agreements, derivative instruments

Challenges likely to arise in accounting for:

1. Contract modifications (e.g., debt modification, lease modification accounting)

2. Hedge accounting.

Proposal would provide optional expedients and exceptions in applying US GAAP to contracts affected by reference rate reform if certain criteria are met. Applies only to contracts referring to

LIBOR, or other rate expected to be discontinued due to reference rate reform

Changes must be related to replacement of reference rate

Would not apply to contract modifications entered after December 31, 2022

Proposed ASU, Reference Rate Reform

49

PCC and EITF Update

50

The PCC met on April 1-2 to discuss the following: An update on plans for the next PCC Town Hall meeting

Implementation—leases

Implementation—revenue recognition

Distinguishing liabilities from equity (including convertible debt)

Disclosures by business entities about government assistance

Financial performance reporting—disaggregation of performance information

Simplifying the balance sheet classification of debt

Disclosure framework: disclosure review—income taxes

Disclosure improvements in response to the SEC’s release on disclosure update and simplification

PCC Issue No. 2018-01, “Practical Expedient to Measure Grant Date Fair Value of Equity-Classified Share-Based Awards”

Other PCC issuesAccess the meeting recap

Private Company Council (PCC) APRIL 2019 MEETING

51

The PCC met on June 25 to discuss the following: Share-based payments: expedient to measure FV

Leases: implementation readiness

Pending ITC: goodwill and intangibles

Effective dates for private companies

Reference rate reform

CECL implementation

Income tax simplification

EITF revenue recognition issue

Access the meeting recap

Private Company Council (PCC) JUNE 2019 MEETING

52

The PCC met on September 11 to discuss the following: Practical expedient to measure grant-date fair value of equity-classified share-based

awards

Implementation of ASU 2016-02, Leases (Topic 842)

Identifiable intangible assets and subsequent accounting for goodwill

Simplifying the balance sheet classification of debt

Distinguishing liabilities from equity (including convertible debt)

Reference rate reform: facilitation of the effects of the interbank offered rate transition on financial reporting

Effective date philosophy

Access the meeting recapNext meeting: December 16-17, 2019

Private Company Council (PCC) SEPTEMBER 2019 MEETING

53

Issue 18-A: Recognition under Topic 805 for an Assumed Liability in a Revenue ContractStatus: Completed (subsumed on 7/31/19 into research project on Recognition and Measurement of Revenue Contracts with Customers under Topic 805) Discussed comment letters on proposed ASU and invitation to comment Recommended the FASB add a project on measuring assumed contract liabilities in a

revenue contract acquired in a business combination Postponed decision on recognition until measurement & related issues are addressed

Issue 19-A: Financial Instruments—Clarifying the Interactions between Topic 321 and Topic 323Status: Final Consensus Under the ASC 321 measurement alternative, consider observable transactions requiring

application or discontinuation of equity method Apply ASC 321 instead of ASC 323 to certain forward contracts and purchased options on

equity securities that are not derivatives and not deemed in-substance common stock

Emerging Issues Task Force (EITF)

54

Issue 19-B: Revenue Recognition—Contract Modifications of Licenses of Intellectual PropertyStatus: Initial Deliberations Task force members discussed the issues; no tentative decisions reached Issues:

• Accounting for contract modifications in which another right is added to the existingrights, and situations in which licensing rights are revoked, including options toconvethe contract term is extended (i.e., whether to apply ASC 606 guidance onlicense renewals or guidance on modifications)

• Accounting for rt from software license to hosted (service) arrangement

Issue 19-C: Warrant Modifications: Issuers’ Accounting for Modifications of Equity ClassifiedFreestanding Call Options That Are Not within the Scope of Topic 718 or Topic 815Status: Added to EITF agenda on September 18, 2019. No deliberations yet.

Next meeting: tentatively March 12, 2020

Emerging Issues Task Force (EITF)

55

SEC Matters Update

56

SEC Update and Reporting Reminders - Agenda

2019 SEC Activities and Rulemaking

•Revenue Recognition (Topic 606)•Non-GAAP Measures•Management Discussion and Analysis (“MD&A”)•Other

Comment Letter Topics

• Internal Control over Financial Reporting•SAB 74 Disclosures – Current and Expected Credit Losses •Reference Rate Reform – LIBOR Transition Disclosures•Contractual Obligations Table Reporting•Form 10-K Process Reminders

SEC Reporting Reminders

57

2019 SEC ACTIVITIES AND RULEMAKING

58

Commission Developments• New Commissioner

- Allison Lee (D) - July

• Robert Jackson Jr. (term expired in 2019)

Staff Developments• Chief Accountant, Wes Bricker, departs

• Sagar Teotia (former Deputy Chief Accountant in OCA) named Chief Accountant

People Developments

59

SEC Rulemaking – Focus Areas

59

Capital Formation

Disclosure Effectiveness

Investor Protection

60

SEC FINAL RULEMAKING

61

Streamline and simplify disclosure requirements, discourage repetition and disclosure of immaterial information

Include changes to:

• MD&A• Confidential treatment requests• Cross-referencing• Property Disclosures• Risk Factors• XBRL and hyperlinks

Refer to BDO SEC Alert

SEC Rulemaking – FAST Act Modernization & Simplification of Regulation S-K (Final Rules)

62

Amendments to MD&A:• Omit reference to year-to-year comparisons and allow registrants to use any

presentation that enhances an investors understanding of the registrant’s financialcondition and results

• Option to generally omit MD&A discussion of the earliest of the three years presentedin the financial statements if the discussion is included in any of prior filings

• Disclose location in prior filing where discussion can be found

Ability to omit confidential information from exhibits without first asking the staff for confidential treatment

Effective Dates:- Confidential treatment requests – April 2, 2019

- Use of XBRL tags on the cover pages of certain filings - phased in over a three years

- All other amendments – May 2, 2019

SEC Rulemaking – FAST Act Modernization & Simplification of Regulation S-K (Final Rules)

63

Extends the “test-the-waters” accommodation currently only available to emerging growth companies to ALL issuers

Enables issuers to gauge market interest in possible offering with certain institutional investors prior to, or following, the filing of a registration statement

Final Rule is effective December 3, 2019

Refer to Press Release for more information

SEC Rulemaking – Solicitations of Interest Prior to a Registered Public Offering (Final Rules)

63

64

SEC PROPOSED RULEMAKING

65

Proposal would change the definitions of an accelerated and large accelerated filer to exclude issuers that otherwise qualify as a smaller reporting company and have annual revenues of less than $100 million in their most recently completed fiscal year.

SEC Rulemaking – Proposed Amendments to Accelerated and Large Accelerated Filer Definitions

65

These proposed changes would reduce the number of issuers

that qualify as accelerated filers and

are intended to reduce compliance costs for smaller

reporting companies

If adopted, certain low-revenue issuers

would not be subject to SOX 404(b) auditor

attestation requirements regarding ICFR

These low-revenue issuers would not need

to comply with the shorter SEC reporting

deadlines that apply to accelerated and large

accelerated filers

66

Maintain the existing initial qualification thresholds for accelerated and large accelerated filer status based on public float

Add a conforming revenue test to the transition thresholds for exiting both accelerated and large accelerated filer status

Increase the public float transition thresholds for exiting accelerated and large accelerated filer status to 80% of the initial qualification thresholds

Refer to BDO SEC Alert

SEC Rulemaking – Proposed Amendments to Accelerated and Large Accelerated Filer Definitions

66

67

Proposed significant changes to: The calculations for measuring the significance of acquired and disposed

businesses under S-X Rule 1-02(w) The financial statement requirements for a significant acquired business under

S-X Rule 3-05 The financial statement requirements for a significant acquired real estate

operation under S-X Rule 3-14 Article 11, Pro Forma Financial Information

Investment company acquisitions

Refer to BDO SEC Alert

SEC Rulemaking – Proposed Amendments to Financial Disclosures About Acquired and Disposed Businesses

68

Proposed amendments to S-X Rule 1-02(w): Investment test – compare investment to aggregate worldwide market

capitalization Income test – add a revenue component to the test and require the use of after-

tax income from continuing operation

Proposed amendments to S-X Rule 3-05: Reduce maximum period of audited annual financial statements to two years Eliminate the requirement to present acquired business financial statements in

registration and proxy statements in certain circumstances Permit registrants to use abbreviated financial statements to satisfy S-X Rule 3-

05 requirements when certain criteria are met Permit the use of financial statements prepared under IFRS as issued by the

IASB in certain circumstances

SEC Rulemaking – Proposed Amendments to Financial Disclosures About Acquired and Disposed Businesses

69

Proposed amendments to Article 11 would permit additional pro forma adjustments which are prohibited under today’s rules Two categories of pro forma adjustments under the proposal:

• “Transaction adjustments” (to reflect the accounting for the transaction) • “Management adjustments” to reflect certain synergies and other

transaction effects of the acquired business)

SEC Rulemaking – Proposed Amendments to Financial Disclosures About Acquired and Disposed Businesses

70

Proposed changes to the Description of Business, Legal Proceedings, and Risk Factor disclosure requirements

Description of Business• Emphasize a principles-based approach to disclosure• Provide a non-exclusive list of types of information that may need to be

disclosed• Permit registrants to provide an update of general development of business

that focuses on material developments in the reporting period with a hyperlink to previous filing where full discussion can be found

SEC Rulemaking – Proposed Amendments to Regulation S-K Items 101, 103, and 105

71

Legal Proceedings• May be provided using hyperlinks or cross-references to legal proceedings

disclosure included elsewhere in the filing to avoid duplication Risk Factors

• Require a summary risk factor disclosure if the section exceeds 15 pages• Change the disclosure standard from the “most significant” factors to the

“material” factors required to be disclosed• Require risk factors to be organized under relevant headings

Refer to BDO SEC Alert

SEC Rulemaking – Proposed Amendments to Regulation S-K Items 101, 103, and 105

72

Add new subpart 1400 of Regulation S-K and replace Guide 3 Codify certain Guide 3 disclosures and eliminate overlapping or redundant

disclosures Require some new disclosures

Refer to BDO SEC Alert

SEC Rulemaking – Proposed Amendments to UpdateDisclosure Requirements for Banking Registrants

73

COMMENT LETTER TOPICS

74

Comment Letter Topics HIGH FOCUS AREAS

74

Revenue Recognition (“Topic 606”)

Non-GAAP Financial Measures

MD&A

75

Comment letters seek clarity on Topic 606 accounting and disclosures, including: The identification of performance obligations The type and nature of variable consideration, including whether any variable

consideration is constrained Information regarding the method used to recognize revenue for performance

obligations and why the method is appropriate The analysis for presenting revenue on a gross vs. net basis (i.e., principal vs.

agent considerations) Disaggregation of revenue that reflect how economic factors affect the nature,

amount, timing and uncertainty of revenue and cash flows

Revenue Recognition (“Topic 606”)

76

Revenue Recognition (example)

With respect to your ABC and XYZ licensing agreements, please address the following: Identify for us the promised goods and/or services under the agreement. Tell us how you determined which promised goods and services were material

and distinct, and thus performance obligations, as well as which promises may have been combined.

Quantify for us the total transaction price, how it was determined as well as the items (i.e. milestones, royalties, etc.) included/excluded and the reasons therefore, the amounts allocated to the various performance obligations, and the amounts recognized during the year ended December 31, 2018 and the three months ended March 31, 2019.

Provide us a breakout of the regulatory milestones you may be eligible to receive by type and amount.

77

Revenue Recognition (example)

Your disclosure on page F-26 related to your ABC Innovation Platform indicates that license revenue is recorded at a point-in-time given your determination that delivery of the intellectual property to the licensee is a distinct performance obligation. You also disclose that you record the associated milestone payment portions of transaction prices as revenue at a point-in-time. Please address the following as it specifically relates to your License and Development Agreement with XYZ, Inc.:

Identify for us the promised goods and/or services under the agreement;

Explain to us how you considered the development services you are required to perform in determining that the license was a distinct performance obligation;

Quantify for us the total transaction price, how you determined it, and the amounts allocated to the various performance obligations;

Tell us the method (ASC 606-10-32-8) you use to estimate variable consideration for reaching development and regulatory milestone events and the nature, amount and trigger for each constrained milestone; and

Provide us your accounting analysis supporting your accounting policy of recognizing milestones at a point-in-time.

78

Comments focus on measures that appear to: • Modify GAAP recognition and measurement principles (i.e., constitute an

individually tailored accounting principle)• Exclude normal cash operating expenses from performance measures• Be applied inconsistently period to period (i.e., changing measures over

time) Expense associated with the reduction of the right-of-use asset for operating

leases over time is a component of rent expense and should not be reflected as “amortization” in EBITDA or Adjusted EBITDA performance measures.

Non-GAAP Financial Measures

79

The staff frequently commented on MD&A disclosures. The nature of these comments:• Increasing specificity in describing “why” changes have occurred period over

period.• Seeking more information about the underlying causes and effects of known

trends, events, and uncertainties.• Focusing the discussion of critical accounting estimates on the significant

judgements and estimates that, if changed or varied, will significant impact their results.

• Providing more detail about performance indicators, financial or nonfinancial that are used to manage the business.

MD&A

80

Other perennial favorites• Fair value measurements• Intangible assets and goodwill • Income taxes• Segment reporting

Other Comment Letter Topics

81

SEC REPORTING REMINDERS

82

Takeaways from recent SEC enforcement actions against companies with long-outstanding material weaknesses in internal control over financial reporting • Disclosure of material weaknesses isn’t enough without meaningful

remediation• Refer to press release for more information

Internal Control over Financial Reporting

83

ASU 2016-13 Financial Instruments – Credit Losses (Topic 326) will be effective for SEC filers excluding Smaller Reporting Companies for periods beginning after December 15, 2019 (December 15, 2022 for all other entities). • Final ASU deferring effective dates for certain companies pending as of

November 12 Standard will require companies to measure all expected credit losses for

financial assets (including trade receivables) based on historical experience, current conditions and reasonable supportable forecasts about collectability.

SAB 74 disclosures are to provide investors with information about the impact that recently issued accounting standard will have on the financial statements.

SAB 74 Disclosures - Current and Expected Credit Losses (CECL)

84

The London Interbank Offered Rate (LIBOR) is expected to be replaced by an alternative rate after 2021.

The staff encourages registrants to disclose (in MD&A):• Status of Company’s efforts and significant matters to be addressed related

to the expected discontinuation of LIBOR.• When the Company does not yet know or cannot yet reasonably estimate the

impact.• Information used by management and the board in assessing and monitoring

how transitioning from LIBOR may affect the Company.

Reference Rate Reform – LIBOR Transition Disclosures

85

Disclosure of the future maturities of operating lease obligations is required in the financial statement footnotes.

ASC Topic 842 defines what should be included in the future minimum lease payments disclosure. For example, Topic 842 requires lessees to include renewal options that are reasonably certain of being exercised. This is a change from Topic 840 which did not provide such guidance.

The payment obligations included in the contractual obligations table in MD&A should be consistent with the future minimum lease payments schedule.

Contractual Obligations Table Reporting

86

Completion of the financial reporting process requires careful attention to detail. Processes should ensure that:• The EDGARized version of the 10-K is complete and accurate (i.e., no

missing paragraphs or columns from tables, no truncation of information in tables, etc.)

• All relevant dates appear within the audit reports, consents, and signatures • The form and content of registrants’ annual certifications are accurate• All material contracts are included within the exhibits to the filing• New cover page regarding market/trading symbol and delinquent section 16

reports• New Item 601(b)(4)(vi) requires an exhibit with Item 202 information

(description of securities)

Form 10-K Process Reminders

87

PCAOB Update

88

Project Current Stage TimingAuditing Accounting Estimates, Including Fair Value Measurements, and Amendments to PCAOB Auditing Standards

Final Standard issued on 12/20/2018 – approved by SEC on 7/1/2019

Effective for audits of fiscal years ending on or after December 15, 2020.

Amendments to Auditing Standards for Auditor’s Use of the Work of Specialists

Final Standard issued on 12/20/2018 – approved by SEC on 7/1/2019

Effective for audits of fiscal years ending on or after December 15, 2020.

PCAOB Recently Completed Standard-Setting

Refer to: https://pcaobus.org/Standards/Pages/recently-completed-standard-setting-activities.aspx

89

Project Current StageQuality Control Standards, Including Assignment and Documentation of Firm Supervisory Responsibilities

Developing a concept release for public comment for the Board’s consideration in Q4 2019.

Supervision of Audits Involving Other Auditors

Analyzing comments to determine next steps.

Going Concern Monitoring effect on audits of the changes to the relevant accounting standards. Reminder: AS 2415, Consideration of an Entity's Ability to Continue as a Going Concern, and Staff Audit Practice Alert No. 13 continue to provide the applicable requirements and guidance.

PCAOB Current Projects – Standard Setting

Refer to: https://pcaobus.org/Standards/research-standard-setting-projects/Pages/default.aspx

90

PROJECT STATUS

Changes in the Use of Data and Technology in the Conduct of Audits

Researching whether impediments exist in PCAOB audit standards.

Auditor’s Role Regarding Other Information and Company Performance Measures, Including Non-GAAP Measures

Summarizing research findings and developing recommendations for next steps.

Auditor’s Consideration of Noncompliance with Laws and Regulations

Summarizing research findings and developing recommendations for next steps.

PCAOB Research Agenda

Refer to: https://pcaobus.org/Standards/research-standard-setting-projects/Pages/default.aspx

91

Featured Videos on CAMs

CAM often relate to matters identified as significant risks; however, there is not a 1:1 relationship.

Since CAM are defined as matters that involve especially challenging, subjective, or complex auditor judgment, not every significant risk identified by an engagement team would necessarily meet that definition and accordingly would not result in a CAM communication. Conversely, matters other than significant risks may also rise to the level of a CAM. One such example may be a nonrecurring transaction.

Number of identified CAM vary and are unique to the nature of each audit. Since CAM are unique to a particular audit and are based on the facts and circumstances of each audit, there may be CAM even in an audit of a company with limited operations or activities.

PCAOB Resources: https://pcaobus.org/Standards/Implementation-PCAOB-Standards-rules/Pages/new-auditors-report.aspx#resources

Critical Audit Matters

In May 2019, Erin Dwyer joined the PCAOB as a direct point of contact for liaison to investors, audit committees, and preparers. Erin shares some additional information about her role and these CAMs-related resources in this short video.

Megan Zietsman, the PCAOB’s Chief Auditor, describes some of the latest resources available on CAMs ahead of the effective dates.

92

Of the large accelerated filer survey respondents that participated in dry runs: 62% reported 3–6 meetings with their auditors 76% indicated that the process lasted 0–6 months 43% of ACs identified additional controls that required implementation, while an additional

19% are still considering such changes

Intelligize Survey Findings:CAM Lessons Learned from Dry Runs

For additional information see the Intelligize report, Critical Audit Matters: Public Company Adaptation to Enhanced Auditor Reporting

93

Intelligize Survey Findings

94

Average of 1.8 CAMs per company No reports where no CAMs were

identified Includes:

• First 44 LAF reports filed• 10 of the S&P 500• 1 Foreign Private Issuer

Observations from June 30, 2019 Large Accelerated Filers

95

Observations from June 30, 2019 Large Accelerated Filers

96

Corporate Governance: Audit Committee Tools and Resources

97

Click here for Top 5 Takeaways publication

2019 BDO Board Survey

98

https://www.thecaq.org/archive-audit-committee-

transparency-barometer/

Key findings from 2019 Audit Committee Barometer:

The CAQ concludes that year over year finding trends indicate that while progress is encouraging, AC can do more to increase transparency and, as a result, investor confidence in voluntarily providing robust disclosures to inform investors.

CAQ 2019 Audit Committee Barometer

Positive Trends Concerns

Increases in discussion of • non-audit services and

independence

Many disclosure levels are stagnant or slowing for all size companies

• auditor tenure Low disclosure continues around:

• Criteria for evaluating the auditor

• Significant areas addressed w/ auditor

• Involvement in audit partner selection

• Auditor compensation

• Cybersecurity • Audit fees and audit quality

99

This edition of Profession in Focus features Christopher Tower, National Assurance Managing Partner for Audit Quality and Professional Practice at BDO USA LLP. Tower provides an overview of the many ways that BDO communicates the firm’s strong commitment to audit quality, both externally and internally. He also provides insights into how BDO developed its 2019 Audit Quality Report, including its use of the CAQ’s Audit Quality Disclosure Framework to help inform the report’s structure and content.

CAQ Profession in Focus: Communicating the Commitment to Audit Quality

100

Delivering Sustained Audit Quality

Source: BDO 2019 Audit Quality Report

101

April 2019 – The Center for Audit Quality (CAQ) issued an updated tool with sample questions for ACs to consider in assessing the external auditor on a “1-5 satisfaction” scale: Quality of services & sufficiency of resources provided

within the audit engagement team Quality of services & sufficiency of resources provided by

the audit firm Communication & interaction with the external auditor Auditor independence, objectivity, & professional

skepticismLearn more by reading BDO’s flash report

CAQ Updated External Auditor Assessment Tool

102

In addition to educating stakeholders on ICFR, this publication includes the

addition of significant research demonstrating the importance

and impact of ICFR and integrated audits on the quality

of financial reporting.

Access BDO’s Alert here.

After the SEC recently fined a number of companies for failing to remedy material weaknesses in ICFR, the PCAOB released a Staff Preview of its 2018 Inspection Observations, highlighting the testing of ICFR remains a common audit deficiency.

ICFR remains an important component to fostering confidence in a company’s financial reporting, and ultimately, trust in our capital markets. To assist in these concerns, the Center for Audit Quality (CAQ) has updated and re-released its popular Guide to Internal Control over Financial Reporting as an overview to assist stakeholders in understanding key ICFR concepts, roles and responsibilities, and what ICFR means for companies, investors, and the markets.

CAQ Guide: Internal Control over Financial Reporting

103

Learn more by reading BDO’s release discussing the CAQ’s publication

The CAQ has released Emerging Technologies, Risk and the Auditor’s Focus: A Resource for Auditors, Audit Committees, and Managementto highlight the financial reporting implications of the evolving use of technology together with the benefits, risks, and associated auditor considerations. Building on the previously released 2018 CAQ Emerging Technologies: An Oversight for Audit Committees, the CAQ provides insight to key stakeholders in the following areas:

CAQ: Digital Transformation & Audit

EMERGING TECHNOLOGIES –RISK ASSESSMENT

AND THE AUDIT

TECHNOLOGY IMPACT –

POTENTIAL AREAS OF AUDITOR FOCUS

KEY TECHNOLOGY DEVELOPMENTS –THE BASICS AND

AUDITOR IMPLICATIONS

104

Resources

105

The roles and responsibilities of the

Audit Committee continue to evolve adding to the

continuing need to stay on top of accounting and audit regulations and

mandatory and voluntary disclosures.

BDO continues to compile tools and resources to

assist Audit Committees in fulfilling their obligations

and documenting their activities, designed so

that members may focus on the risks at hand.

Stay tuned for more tools being released this summer and fall!

BDO Audit Committee Resources

Recommended Resources Intended Use

BDO Audit Committee Self Assessment

Tool to assist in evaluating how the Audit Committee is executing governance responsibilities.

BDO Audit Committee Requirements Practice Aid

Tool to assist Audit Committees in fulfilling their oversight responsibilities and documenting their activities.

BDO Audit Committee Illustrative Charter

Tool with example to assist Audit Committees in constructing their own company-specific charter to be used as a working document or practical roadmap of responsibilities and duties.

BDO Professional Judgment Framework

Tool to assist professionals in their capacity to logically assess situations or circumstances and to draw sound, objective conclusions that are not influenced by cognitive traps and biases or by emotion.

106

A resource center with the continual education needs of those charged with governance andfinancial reporting in mind!

The BDO Center for Corporate Governance and Financial Reporting

AN INCREDIBLE RESOURCE AT YOUR FINGERTIPSThe BDO Center for Corporate Governance and Financial Reporting was born from the need to have a comprehensive, online, and easy-to-use resource for topics relevant to boards of directors and financial executives. We encourage you to visit the Center often for up-to-date information and insights you can rely on.

What you will find includes:

Thought leadership, practice aids, tools, and newsletters

Technical updates and insights on emerging business issues

Three-pronged evolving curriculum consisting of upcoming webinars and archived self-study content

Opportunities to engage with BDO thought leaders

External governance community resources

For more information about BDO’s Center for Corporate Governance and Financial Reporting,please go to: www.bdo.com/resource-centers/governance

To begin receiving email notifications regarding BDO publications and event invitations (live and web-based), visit www.bdo.com/member/registration and create a user profile.

If you already have an account on BDO’s website, visit the My Profile page to login and manage your account preferences www.bdo.com/member/my-profile.

A dynamic and searchable on-line resource for board of directors and financial executives

107

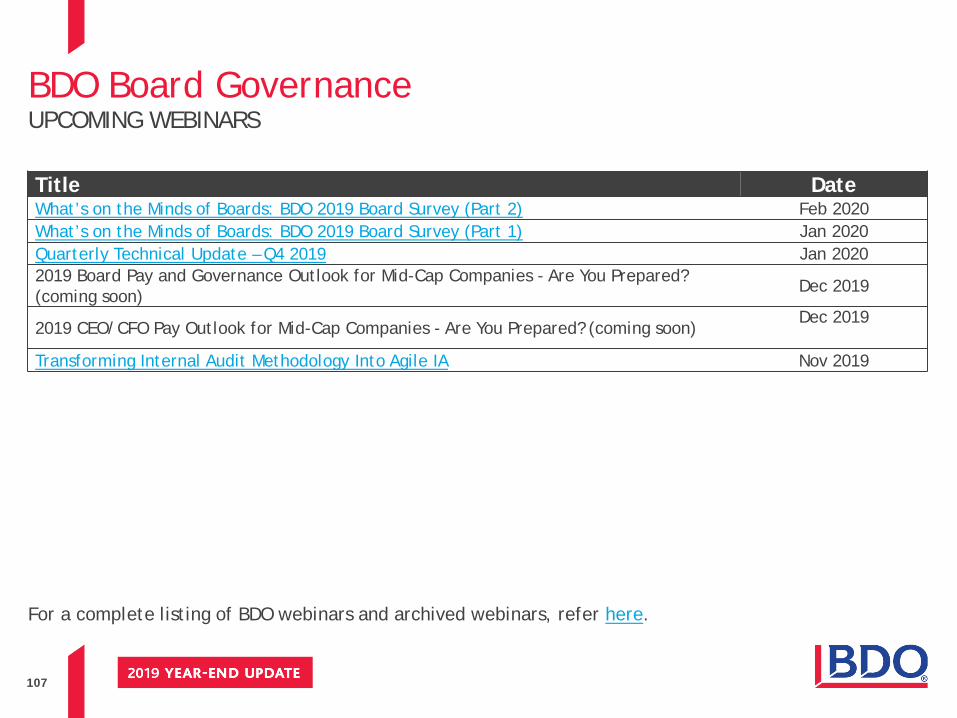

Title DateWhat’s on the Minds of Boards: BDO 2019 Board Survey (Part 2) Feb 2020What’s on the Minds of Boards: BDO 2019 Board Survey (Part 1) Jan 2020Quarterly Technical Update – Q4 2019 Jan 20202019 Board Pay and Governance Outlook for Mid-Cap Companies - Are You Prepared? (coming soon) Dec 2019

2019 CEO/CFO Pay Outlook for Mid-Cap Companies - Are You Prepared? (coming soon)Dec 2019

Transforming Internal Audit Methodology Into Agile IA Nov 2019

BDO Board GovernanceUPCOMING WEBINARS

For a complete listing of BDO webinars and archived webinars, refer here.

108

Title DateDemystifying Critical Audit Matter (CAM) Reporting Oct 2019Quarterly Technical Update – Q3 2019 Oct 2019How Audit Committees Manage Difficult Moments Sep 2019Top IT Audit Risks Sep 2019Quarterly Technical Update – Q2 2019 July 2019Audit Speed – Opportunities for Enhancement Jun 2019Building Tomorrow’s Business: What Does Digital Transformation Mean for Middle-Market Companies in 2019 Jun 2019

California Consumer Privacy Act: 6 Mont Countdown for Retailers Jun 2019Power Growth: Complexities of Accounting in a Global World May 2019Getting to the Point – Effective Audit Ratings Apr 2019Corporate Governance – Spotlight on Evolving Diversity on the Board Apr 20192019 Shareholder Meetings – What’s On Deck? Part 1 Apr 20192019 Shareholder Meetings – What’s On Deck? Part 2 Apr 2019Quarterly Technical Update – Q1 2019 Apr 2019Innovative Use of Robotics in Internal Audit Feb 2019BDO’s 2019 IPO Outlook Survey and Key Takeaways from a Successful IPO Feb 2019

BDO Board GovernanceARCHIVED WEBINARS

For a complete listing of BDO webinars and archived webinars, refer here.

109

Title DateQuarterly Technical Update – Q4 2018 Jan 20192018 Executive and Board Pay Outlook for Mid-Cap Companies – Are Your Prepared? Dec 2018Adding Value Via Internal Audit Transformation: Finding the Right Balance Nov 2018What’s on the Minds of Boards – BDO 2018 Cyber Governance Survey Nov 2018What’s on the Minds of Boards - BDO 2018 Board Survey Nov 2018New SOC 2 Guidance and What It Means for Your Company Nov 2018The New GILTI Proposed Regulations: What Have We Learned Nov 2018Quarterly Technical Update – Q3 2018 Oct 2018Cybersecurity: Protecting Your Organizations from Today’s Everchanging Threats Oct 2018GDPR: What U.S. Boards of Directors Need to Know Sep 2018Cybersecurity - Resources Boards Want to Know About Sep 2018How To Deal With the Impacts of Wayfair Aug 2018Quarterly Technical Update – Q2 2018 July 2018

BDO Board GovernanceARCHIVED WEBINARS

For a complete listing of BDO webinars and archived webinars, refer here.

110

Title DateImpact of Tax Reform on Corporate Strategic M&A Transactions Jun 2018From Scandals to Serious Setbacks: How a Poor Company Culture Can Impact… Jun 2018Impact of U.S. Income Changes on Cross Board Mobility May 2018The New Leasing Standard – Are Your Ready? May 20182018 Shareholder Meetings – What’s on Deck? Apr 2018Quarterly Technical Update – Q1 2018 Apr 2018Compensation Committee: Tax Reform Impacts & Other Trends… Feb 2018Understanding the New Hedging Standard Feb 2018Tax Reform and the Board’s Role Jan 2018

BDO Board GovernanceARCHIVED WEBINARS

For a complete listing of BDO webinars and archived webinars, refer here.

111

Title DateInternal Audit’s Role in Monitoring and Controlling International Exposure Nov 2017Building an Effective Compensation Committee Oct 2017Harnessing the Power of Data and Data Analytics and Continuous Monitoring Sep 2017Applying the New Revenue Standard (Part 2) Aug 2017Applying the New Revenue Standard (Part 1) Aug 2017ASC 606, Revenue from Contracts with Customers Aug 2017Internal Audit’s Role in Highly Acquisitive Organizations Jun 2017AICPA SOC for Cybersecurity - What You Need to Know Now Jun 2017Director Diversity – Striking the Right Balance in the Boardroom Jun 2017Board Leadership – How to Onboard Your Board May 2017Reducing the Burden of Sox Compliance Apr 2017What Boards Need to Know About Cybersecurity (But May Be Afraid to Ask) Mar 2017

BDO Board GovernanceARCHIVED WEBINARS

For a complete listing of BDO webinars and archived webinars, refer here.

112

Title DateBoards as Catalysts for Intrapreneurship and Innovation Feb 2017Small Cap Boards – Realities and Strategies for Capital Structuring Jan 2017Board Collaboration: Leveraging Communication Tools and Technology Oct 2016Navigating the Rising Tide of Cybersecurity Regulation – How Is Your Board Preparing? July 2016M&A Execution: Planning with Post-Integration in Mind May 2016How Is Your Board Positioned to Respond to Illegal Acts? May 2016When and Why Should a Board Require an Independent Fairness Opinion May 2016Executive Performance Goals Which Do Not Create Enterprise Risk Apr 2016

BDO Board GovernanceARCHIVED WEBINARS

For a complete listing of BDO webinars and archived webinars, refer here.

113

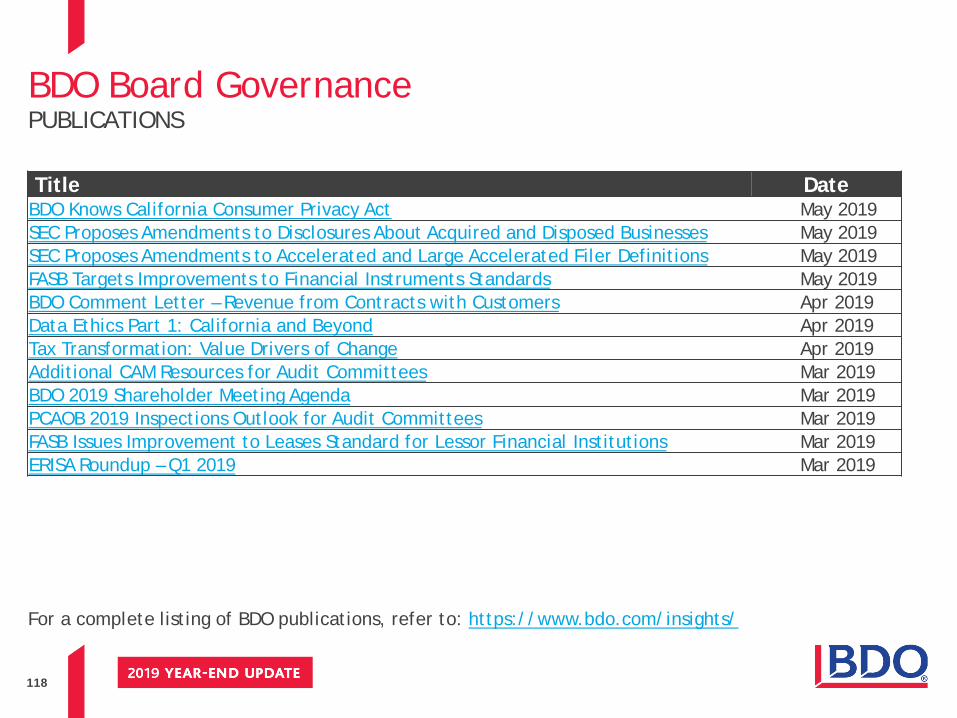

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title Date3 Reasons Why You Need to Forge Ahead with Lease Accounting Implementation Nov 20192019 SEC Reporting Insights Nov 2019BDO Knows Lease Accounting Nov 2019BDO Knows Lease Accounting: Road to Compliance Checklist Nov 2019BDO Comment Letter – Simplifying the Classification of Debt in a Classified Balance Sheet Nov 2019

The BDO 600 – 2019 Study of Board Compensation Practices Oct 20192019 Board Survey Oct 2019Tax Reform Impact Continues Oct 2019FASB Affirms Decisions to Defer Effective Dates of Major New Accounting Standards Oct 2019BDO Comment Letter – Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity Oct 2019

BDO Comment Letter – Identifiable Intangible Assets and Subsequent Accounting for Goodwill Oct 2019

BDO Comment Letter – Reference Rate Reform (Topic 848) (File Reference No. 2019-770) Oct 2019

114

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title Date2019 Board Survey – Top 5 Takeaways Sep 2019SEC Proposes to Update Disclosures Requirements for Banking Registrants Sep 20192019 Tax Planning Timeline Sep 2019CECL for Non-Financial Institutions Sep 20192020 Cybersecurty Guidelines for C-Suite Executives Sep 2019BDO Comment Letter – Financial Instruments—Credit Losses (Topic 326) Sep 2019BDO Comment Letter – Clarifying the Interactions Between Topic 321, Topic 323, and Topic 815 Aug 2019

Delivering Sustained Audit Quality Aug 2019FASB Proposes to Defer Effective Dates of Major New Accounting Standards Aug 2019SEC Proposes More Changes to Modernize Regulation S-K Disclosure Aug 2019

115

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title DateBDO Comment Letter – Codification Improvements to Topic 326, Financial Instruments – Credit Losses July 2019

The Future of Auditor Reporting is Here July 2019BDO Cyber Threat Insights - 2019 2nd Quarter Report July 2019Significant Accounting & Reporting Matters Q2 2019 July 2019PCAOB Issues CAM Resources For Non-Auditors July 2019Illustrative Audit Committee Charter July 2019CAQ Issues External Auditor Assessment Tool: A Reference For U.S. Audit Committees July 2019PCAOB Preview of 2018 Inspection Observations July 2019CAQ Issues External Auditor Assessment Tool: A Reference for U.S. Audit Committees July 2019Illustrated Audit Committee Charter July 2019

116

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title DateBDO Comment Letter - Disclosure Improvements Jun 2019CAQ Issues Emerging Technologies, Risk, and the Auditor's Focus Jun 2019ASC 842 Implementation for Private Companies: Lessons Learned from Public Companies Jun 2019

Six Month Countdown to CCPA: The 10 Information Governance Steps Needed for Compliance Jun 2019

FASB Simplifies Accounting for Goodwill & Certain Identifiable Intangible Assets for NFPs Jun 2019

Benefits of Independent Analysis of Lease Portfolios Jun 2019CAQ Issues a Tool For Audit Committees: Preparing for the New Credit Losses Standard Jun 2019Understanding ICFR Jun 2019Three Ways to Reduce Income Tax Reporting Risk Jun 2019FASB Issues Transition Relief for Credit Losses Standard Jun 2019Understanding Complex Financial Instruments Jun 2019Understanding Internal Control over Financial Reporting Jun 2019BDO Professional Judgment Framework Jun 2019

117

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title DateBDO Comment Letter - Disclosure Framework Changes to the Disclosure Requirements for Income Taxes May 2019

Audit Committee Self Assessment May 2019GDPR One Year Later: A Data Privacy Retrospective May 2019FASB Issues Targeted Improvements to Financial Instruments Standards May 2019BDO Knows California Consumer Privacy Act May 2019SEC Proposes Amendments to Disclosures About Acquired and Disposed Businesses May 2019SEC Proposes Amendments to Accelerated and Large Accelerated Filer Definitions May 2019FASB Targets Improvements to Financial Instruments Standards May 2019

118

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title DateBDO Knows California Consumer Privacy Act May 2019SEC Proposes Amendments to Disclosures About Acquired and Disposed Businesses May 2019SEC Proposes Amendments to Accelerated and Large Accelerated Filer Definitions May 2019FASB Targets Improvements to Financial Instruments Standards May 2019BDO Comment Letter – Revenue from Contracts with Customers Apr 2019Data Ethics Part 1: California and Beyond Apr 2019Tax Transformation: Value Drivers of Change Apr 2019Additional CAM Resources for Audit Committees Mar 2019BDO 2019 Shareholder Meeting Agenda Mar 2019PCAOB 2019 Inspections Outlook for Audit Committees Mar 2019FASB Issues Improvement to Leases Standard for Lessor Financial Institutions Mar 2019ERISA Roundup – Q1 2019 Mar 2019

119

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title DateMuch Ado About Tariffs: Preparing for March 1 and Beyond Feb 2019BDO Comment Letter: Extending Private Company Accounting Alternative on GW and Certain Intangible Assets Feb 2019

For a Smoother Landing into the New Leases Standard Feb 20192019 BDO IPO Outlook Feb 2019Significant Accounting & Reporting Matters – Q4 2018 Feb 2019Tax Transformation Guide Feb 2019De-Mystifying Cyber Threat Intelligence Feb 2019Getting ‘On Board’ with Gender Diversity Jan 2019Eight Key Tax Planning Opportunities for 2019 Jan 20192018 Audit Committee Round Up Jan 20192018 Accounting Year in Review Jan 2019

120

BDO Board GovernancePUBLICATIONS

For a complete listing of BDO publications, refer to: https://www.bdo.com/insights/

Title DateBDO’s Integrated Thinking and Reporting Journey Guide Jan 2019FASB Issues Narrow-Scope Improvements of Lessors Jan 2019Cryptocurrency: The Top Things You Need to Know Jan 20192019: The Year of Legal Digital Transformation Jan 2019SEC 2018 Year in Review Jan 2019Embracing Digital Transformation Jan 2019BDO’s 2019 Middle Market Digital Transformation Survey Jan 2019CECL Update Jan 2019SEC Examination Priorities for 2019 Jan 2019Auditor Communications: CAQ Issues Audit Quality Disclosure Framework Jan 2019BDO Cyber Threat Insights – 2018 Q4 Report Jan 2019SEC Releases Request for Comment on Quarterly Reporting Jan 2019CAQ CAM Implementation Tool: Early Lessons Being Learned Jan 2019

121

Questions?

122

Domestic and InternationalTax Update

123

With You Today

STEVE CULLIMORETransfer Pricing Principal

(206) [email protected]

JERRY BREGGTax Office Managing Partner

(619) [email protected]

CHIP MORGANInternational Tax Partner

(310) [email protected]

124

Today’s Discussion Topics

Three Stages of Tax Reform Domestic Tax International Tax

125

The Three Stages of Tax Reform

126

Anticipating Tax Reform

127

Digesting Tax Reform

128

Reflections on Tax Reform

129

Domestic Tax Landscape

130

Reduced Tax Rates

ReflectionsThe rate cut was a cornerstone provision of the TCJA but was coupled with various, less favorable provisions which offset some of that benefit including impacting many unsuspecting taxpayers:

• Interest Deduction Limitations

• Repeal of DPAD

• GILTI

• BEAT

• Modified Ownership Attribution Rules

35%

21%

Tax Law ChangeCorporate tax rate was reduced from 35% to 21% effective January 1, 2018.

131

State Income Tax Conformity = Windfall

ReflectionsSignificant added complexity in complying with the varied conformity around the new federal provisions.

For those states which conformed, in most cases, the new provisions had an unfavorable impact on the income base without a corresponding reduction to their own tax rates creating windfalls for state governments.

Tax Law ChangeMany of the state jurisdictions conformed their rules to the federal rules while others decoupled.

132

State Income Tax Conformity (cont’d)

133

Net Operating Loss Carryovers

Reflections

Scheduling of deferred tax assets has become noticeably more complex.

The ability of an organization to “smooth out” its income over time has some significant limitations now and will require companies to be more cautious in planning out taxable income/loss from one year to the next.

Secondary tax incentives such as tax credits will now be of greater utility to companies with NOL carryovers.

Some taxpayers should consider opting out of bonus depreciation or other capitalization provisions.

Impact of Code Sec. 382 has changed given the indefinite carryforward period.

Tax Law Change

Tax loss carryovers are limited to 80% of taxable income for losses arising in tax years beginning after December 31, 2017.

The carryback provisions have been repealed for tax years ending after December 31, 2017.

Carryforward period is indefinite for NOL’s generated in post-2017 tax years.

134

Limitation on Deduction for Interest

Tax Law ChangeInterest deduction is limited to 30% of a business’ adjusted taxable income

Adjusted taxable income is computed without regard to deductions for business interest expense or business interest income, net operating losses, 20% deduction for certain pass throughs and, in the case of tax years beginning before January 1, 2022, depreciation, amortization, and depletion.

Complicated rules relating to partnership interests included.

135

Limitation on Deduction for Interest

ReflectionsSignificant lost deduction for many companies,in particular, private equity owned portfolio companies.

While initially recorded as a deferred tax benefit due to indefinite carryforward period, for many this will become a “permanently” lost deduction absent significantly improved operating performance.

Beginning in tax year 2022 and beyond, the lost deduction will affect a large number of additional taxpayers and further limit the benefit for those already impacted.