Bahasa

Halaman

Hukum

Electronic copy available at: http://ssrn.com/abstract=1603705

1

Liquidity Commonality in Commodities

Ben R. Marshall* Massey University

Nhut H. Nguyen University of Auckland

Nuttawat Visaltanachoti Massey University

Abstract We examine liquidity commonality in commodity futures markets. Using data from 16 agricultural, energy, industrial metal, precious metal, and livestock commodities, we show there is a strong systematic liquidity factor in commodities. Liquidity commonality was present in 1997 - 2003 when commodity prices were relatively stable and during the recent boom. There is some support for both “supply-side” and “demand-side” explanations for this commonality. We also find some evidence that changes in stock market liquidity positively influence changes in individual commodity liquidity.

JEL Classification: G11, G12, G13 Keywords: Commodity, Liquidity, Commonality

First Version: 8 April 2010 This Version: 27 July 2011

Acknowledgments: We thank conference participants at the 23rd Australasian Finance and Banking Conference, our discussant Phuong T. Pham, seminar participants at Auckland University, Massey University, and Waikato University and especially Andrea Bennett, Henk Berkman, Charles Corrado, Fei Wu, and Qian Sun for valuable comments.

Corresponding Author: School of Economics and Finance, Massey University, Private Bag 11-222, Palmerston North, New Zealand. Tel: +64 6 350 5799 Ext 5402, Fax: +64 6 350 5651.

Electronic copy available at: http://ssrn.com/abstract=1603705

2

1. Introduction

The liquidity of individual stocks is influenced by market-wide liquidity. This relation,

known as liquidity commonality, has also been documented in bond and foreign exchange

markets. We investigate whether liquidity commonality exists in commodity markets and

whether there is a link between commodity and stock market liquidity. Commodities have long

been used as hedging tools for commodity producers and consumers, and have more recently

become a popular asset class with investors. The dual hedging and speculative aspects of

commodity futures are unique features so liquidity commonality findings from other asset classes

may not necessarily apply in commodities.

Chordia, Roll and Subrahmanyam (2000) suggest both inventory risks and asymmetric

information affect commonality in liquidity. Commodity hedgers may have private information

in a few commodities but it is unlikely they will have this for all commodities so their trading

activities are unlikely to cause liquidity commonality. Hedgers are over twice as active as

investment funds in commodity markets in the period we study1 and their actions have an

important influence on commodity returns (e.g., de Roon, Nijman, and Veld, 2000; Acharya,

Lochstoer and Ramadorai, 2010). On the other hand, speculative demand for commodities,

which may lead to liquidity commonality has increased in recent times. Dunsby, Eckstein,

Gaspar, and Mulholland (2008) estimate that commodity index linked investment increased over

20-fold between 1997 and 2007, while Barclays Capital suggest commodity investment was in

excess of $US250 billion by the end of 2009 (see Jensen, 2010).2 Tang and Xiong (2010) find

1 This is based on cross-sectional time-series average of the share of hedger and fund open interest to total open interest over the 1997 – 2009 period according to US Commodity Futures Trading Commission (CFTC) data. 2 See Figure 21.1 in Dunsby, Eckstein, Gaspar, and Mulholland (2008).

Electronic copy available at: http://ssrn.com/abstract=1603705

3

the growth in commodity index investment over the last decade has resulted in an increase in the

return correlation of commodities in the major indices.

Part of the increase in popularity of commodities as an asset class is no doubt due to the

diversification benefits they bring to stock and bond portfolios (e.g., Gorton and Rouwenhorst,

2006). Bernanke (2008) suggests commodity price movements also have important policy

implications. He stresses that a greater understanding of the factors that drive commodity price

changes is required. A lack of understanding of, or disregard for, the liquidity of commodity

markets certainly contributed to the demise of the high-profile Amaranth hedge fund, which lost

$6.6 billion (e.g., Till, 2008).3 However, despite the popularity and diversification benefits of

commodity investment, relatively little is known about commodity liquidity as compared to

stocks and bonds. An exception is the recent work of Marshall, Nguyen, and Visaltanachoti

(2011) who document commodity transaction costs and show how effective various liquidity

proxies are at measuring the actual cost of trading commodities. These authors find that the

Amihud (2002) proxy is the best performer and that Amivest (e.g., Amihud, Mendelson, and

Lauterback, 1997) and Effective Tick (e.g., Holden, 2009) measures also work well.4

Chordia, Roll, and Subrahmanyam (2000), Hasbrouck and Seppi (2001), and Korajczyk

and Sadka (2008) all find that liquidity commonality exists in the US equity market. More

recently, Brockman, Chung, and Perignon (2009) show there is a systematic liquidity factor in

international stocks and there is evidence of a global liquidity factor, and Karolyi, Lee, and van

Dijk (2011) show liquidity commonality is stronger in countries with high market volatility and

3 Chincarini (2007) states, “Amaranth was close to the entire market in certain futures contracts. A simple analysis .... showed that the most excessive positions generated the greatest losses in September, indicating a liquidity penalty against Amaranth” (p. 102). 4 Other recent commodity papers include Chan, Treepongkaruna, Brooks, and Gray (2011) who document linkages between commodity and other asset classes in different regimes, Pukthuanthong and Roll (2011) who study the relation between the gold and various currencies, and Hong and Yogo (2010, p. 1) show growth in commodity open interest predicts “high commodity returns and low bond returns.”

4

more international investors. There has been less work on liquidity commonality in other asset

classes. Chordia, Sarkar, and Subrahmanyam (2005) document evidence of commonality in the

bond markets and find this is related to contemporaneous liquidity commonalities in the stock

market, while Mancini, Ranaldo, and Wrampelmeyer (2009) show there is a systematic liquidity

factor in the foreign exchange market, which is linked to equity market liquidity.

We find there is in fact a strong systematic liquidity factor in commodity markets.

Liquidity changes in commodities have a highly statistically significant positive relation with

changes in market-wide liquidity. This relation existed during the 1997 – 2003 sub-period when

commodity prices were relatively flat and has strengthened during the more recent commodity

boom. We use high-frequency commodity futures data from the Thomson Reuters Tick History

(TRTH) database5 to calculate intraday proportional quoted and effective spreads. The TRTH

database contains pit and electronic trading data for all the major commodities. Thomson Reuters

Datastream daily data are used to calculate the Amihud liquidity measure. We include 16

commodities. These span the five major commodity families. The commodities are: Brent crude

oil, gasoil, natural gas, RBOB gas, heating oil, West Texas crude oil (energy), corn, red wheat,

soybeans, wheat (agricultural), feeder cattle, lean hogs, live cattle (livestock), gold, silver

(precious metals), and copper (industrial metal).

Two explanations have been put forward to explain liquidity commonality in stock

markets. Hameed, Kang, and Viswanathan (2010) show it is caused by liquidity providers

withdrawing liquidity in large market declines. This “supply-side” explanation is consistent with

the theoretical work of Brunnermeier and Pedersen (2008) which links asset liquidity and

5 We access these data via the Securities Industry Research Centre of Asia-Pacific (SIRCA) http://www.sirca.org.au/

5

traders’ funding liquidity.6 A “demand-side” explanation has been advanced by Kamara, Lou,

and Sadka (2008) who show that higher levels of institutional ownership lead to stronger

commonality due to coordinated buying and selling. Of course, these explanations are not

mutually exclusive. Both could play a role in liquidity commonality. We find there is evidence to

support both supply- and demand-side theories in commodities. Increases in fund ownership of

commodities result in an increase in liquidity commonality when the Amihud measure of

liquidity is used. There is also evidence of stronger liquidity commonality during large market

declines when the proportional quoted spread measure is adopted. However, these results carry a

couple of caveats. They are not consistent across all liquidity measures and we do not have data

on liquidity providers to verify the supply-side result.

We also find weak evidence that changes in stock market liquidity affect individual

commodity liquidity. An increase in stock market liquidity coincides with an increase in

commodity liquidity. There is evidence of this linkage based on changes in aggregate stock

market liquidity and changes in the liquidity of stocks in commodity-related industries. A

liquidity linkage between these two asset classes is consistent with the work of Chordia, Sarkar,

and Subrahmanyam (2005) who find that there is a link between stock and bond market liquidity

due to a connection in the money flows across these asset classes.

The rest of this paper is organized as follows: Section 2 contains a description of the data.

Methodology is discussed in Section 3. We present our results in Section 4, while Section 5

concludes the paper.

6 This explanation is also supported by the findings of Coughenour and Saad (2004). They show stock liquidity covaries with the liquidity of other stocks with the same NYSE specialist.

6

2. Data

We source the high-frequency commodity futures data from the Thomson Reuters Tick

History (TRTH) database, which we access via Securities Industry Research Centre of Asia-

Pacific (SIRCA). Fong, Holden, and Trzcinka (2011) use equity data from TRTH. These authors

note (p. 16) subscribers taking advantage of TRTH’s “millisecond-time-stamped tick data”7,

which are sourced directly from exchanges via the Reuters Integrated Data network, include

“central banks, investment banks, hedge funds, brokerages, and regulators”. More background on

TRTH is available one the Thomson Reuters website.8

We focus on commodities that are part of the S&P Goldman Sachs Commodity Index

(S&P GSCI) as these are the commodities that are determined to be the most important to the

global economy. 9 The TRTH database has history dating back to 1 January 1996. Some

commodities have data available from this date, data for others commences during 1996, while

data are not available for some commodities until more recent times. We chose a start point of 1

January 1997 so as to include as many commodities as possible and achieve a time-series of data

that is as long as possible. The end point is 31 August 2009. We include 16 commodities which

span the five major commodity families (energy, livestock, agricultural, precious metals, and

industrial metals). Many commodities trade on multiple exchanges so we source data from the

major exchange (based on S&P GSCI information and Dunsby, Eckstein, Gaspar, and

Mulholland (2008)). West Texas crude oil, RBOB gas, and heating oil data are from the New

York Mercantile Exchange (NYMEX), Brent crude oil and gasoil data comes from the

Intercontinental Exchange (ICE), the red wheat data are from the Kansas Board of Trade (KBT),

7 Recently, TRTH replaces a millisecond-time-stamp tick data with microsecond-time-stamp tick data. 8http://thomsonreuters.com/products_services/financial/financial_products/quantitave_research_trading/tick_history 9 http://www.standardandpoors.com/indices/sp-gsci/en/us/?indexId=spgscirg--usd----sp------

7

the wheat, corn, and soybeans data are from the Chicago Board of Trade (CBOT), live cattle,

feeder cattle, and lean hogs data are from the Chicago Mercantile Exchange (CME), copper, gold

and silver data are from COMEX.10

Following de Ville de Goyet, Dhaene, and Sercu (2008), we use data for individual

contracts to construct continuous series of the most actively traded contracts. A contract that

expires in a given month m is replaced with the next nearest-to-maturity contract on the last day

of the previous month m-1. We use futures rather than spot data because futures data are more

liquid, more prominent in the media, and more widely available.

We construct the Amihud liquidity measure using daily data from Thomson Reuters

Datastream (TRD). We obtain data for the identical contracts we used in the high-frequency data

analysis and form continuous series in an identical manner. Marshall, Nguyen, and

Visaltanachoti (2011) demonstrate the Amihud liquidity measure is a good proxy for the true

cost of transacting. The Amihud measure requires daily dollar value traded so we also use daily

data for the number of contracts. We convert this to a dollar volume variable by multiplying the

number of contracts traded by the contract size and then multiplying this by the settlement price

in USD. 11

Part of our analysis involves determining whether changes in stock market liquidity

influence individual commodity liquidity. We calculate systematic stock liquidity in accordance

with Kamara, Lou, and Sadka (2008). This involves using common stocks listed on the NYSE or

AMEX that are in the CRSP database. Risk-free rate data are obtained from Kenneth French’s

website for use in the regression analysis. We also investigate whether fund ownership of

10 The CME group now consists of CME, CBOT, COMEX, and NYMEX but they have retained their individual identities. http://www.cmegroup.com/company/history/timeline-of-achievements.html. Copper is also actively traded on the London Metals Exchange (LME) but we cannot source data for this contract back to 1997. 11 Thomson Reuters Datastream does not have daily data dating back to our start point of 1 January 1997 for four commodities so we do not calculate the Amihud measure for these.

8

commodities drives the liquidity commonality. We source the open interest data from the US

Commodity Futures Trading Commission.12 All our analysis is based on the time-period 9.30am

to 4.00 pm Eastern Standard Time. This permits us to consider the link, if any, between stock

and commodity liquidity.

We plot the S&P Goldman Sachs Commodity Index (S&P GSCI) in Figure 1.

Commodity prices did not change much between 1997 and 2003. The GSCI increased just 27%.

Commodities then boomed, increasing some 172% between 2004 and 2009. We divide the data

into two sub-periods to show that our results are not specific to the recent “boom” sub-period.

[Insert Figure 1 Here]

3. Methodology

In this section we present and discuss the liquidity measures. We then explain the

approaches we use to measure liquidity commonality, the link, if any, with changes in stock

market liquidity, and document the techniques we apply to check for demand- and supply-side

liquidity commonality explanations.

3.1. Liquidity Measures

We use three different liquidity measures. The first two, which are based on Chordia,

Roll, and Subrahmanyam (2000) and Korajczyk and Sadka (2008), use intraday data.

Proportional effective spread is calculated as follows: 12 http://www.cftc.gov/MarketReports/CommitmentsofTraders/

9

Proportional Effective Spread = 2 ·| ln P - ln P | (1)

where Pt and PM are the trade price and the mid-point of the prevailing bid and ask quotes at the

time of the trade. Proportional quoted spread is calculated as follows:

Proportional Quoted Spread = (PA – PB) / PM (2)

where PA and PB are the ask price and bid price respectively and PM is the mid-point of these two

prices. Daily average proportional effective spread and proportional quoted spread are calculated

for each commodity.

We use a high-frequency data cleaning technique inspired by Brownlees and Gallo

(2006) to ensure data errors are not influencing our results. This involves estimating the α-

trimmed sample mean and standard deviation for the proportional effective spread and

proportional quoted spread liquidity measures. We use an α of 5%, which means the top and

bottom 2.5% of observations are ignored when calculating the trimmed mean and standard

deviation.13 The next step involves removing observations that are outside the trimmed mean +/-

three standard deviations.

The third liquidity proxy is the Amihud measure, which is given in equation 3. Kamara,

Lou, and Sadka (2008) and Korajczyk and Sadka (2008) use the Amihud liquidity measure in

their stock market liquidity commonality studies. Marshall, Nguyen, and Visaltanachoti (2011)

highlight that many low-frequency liquidity proxies do a poor job of capturing commodity

liquidity. However, they show that the Amihud measure performs well in commodities.

13 Brownlees and Gallo (2006) note that dirty data require a higher α. They set α at 10%, but we follow Mancini, Ranaldo, and Wrampelmeyer (2009) and use an α of 5%.

10

Amihud =|rt|

Volumet (3)

where rt is the return on day t and Volumet is dollar volume on day t.

3.2. Liquidity Commonality Measurement

We use two distinct approaches to determine if there is a systematic liquidity factor in

commodity markets. The first is based on Chordia, Roll, and Subrahmanyam (2000) and the

second follows Korajczyk and Sadka (2008). The Chordia, Roll, and Subrahmanyam (2000)

method uses market model time-series regressions of daily percentage changes in a liquidity

measure for a commodity regressed on the daily percentage change in the liquidity measure for

the market, as expressed in equation 4.

DLi,t= αi+ β1iDLM,t+ β2iDLM,t-1+ β3iDLM,t+1+ Controls+ εi,t (4)

where DLi,t represents the percentage change in liquidity measure L from day t-1 to day t for

commodity i, DLM,t is the concurrent change in commodity market liquidity L, and DLM,t-1 and

DLM,t+1 are the lag and lead changes in commodity market liquidity for L respectively. We

exclude the commodity that is the dependant variable from the measure of market liquidity.

Following Chordia, Roll, and Subrahmanyam (2000), the control variables include the individual

commodity squared return, and the contemporaneous, lead and lag market returns. We use the

GSCI as a proxy for the commodity market return. Changes in concurrent, lead and lag market

liquidity are measured as the cross-sectional average over all commodities (excluding the

11

commodity in question). We apply this method separately for the three different liquidity

measures.

The Korajczyk and Sadka (2008) approach to determining liquidity commonality is based

on principle component analysis. We calculate the cross-sectional average of the first liquidity

measure on a daily basis. We then compute the time-series mean and standard deviation of this

series. The next step involves standardizing each of the time-series observations by scaling the

difference between the observation and the time-series mean by the time-series standard

deviation. We then obtain the first three principle components across commodities and use these

as the liquidity commonality factors. This process is repeated for the proportional effective

spread, the proportional quoted spread, and the Amihud liquidity measure.

3.3. Commodity Market Liquidity Links with Stock Market Liquidity

We investigate the link between changes in commodity liquidity and stock market

liquidity. Stock market liquidity is measured as the value-weighted average of the Amihud

measures for all NYSE and AMEX stocks. We then include the systematic stock market liquidity

factor as an additional variable in equation 4 to determine if changes in systematic stock market

liquidity influence changes in individual commodity liquidity. We then repeat this analysis for

the sub-set of stocks that are in commodity-related industries

12

3.4. Supply-Side and Demand-Side Explanations

Hameed, Wang, and Viswanathan (2010) show liquidity commonality in stocks is caused

by liquidity providers withdrawing market liquidity following market declines. This is consistent

with the theoretical model of Brunnermeier and Pedersen (2009) which proposes a link between

asset liquidity and traders’ funding liquidity. We investigate whether this supply-side effect is

responsible for liquidity commonality in commodities. Following Hameed, Wang, and

Viswanathan (2010) we run the regression:

DLi,t= αi+ βLIQ,iDLM,t+ βLIQ,DOWN,iDLM,t DDOWN,M,t + βi,k

4

k=1

RM,t-k

+ βDOWNi,k

4

k=1RM,t-kDDOWN,M,t-k + γi,k

4

k=1Ri,t-k (5)

+ γDOWNi,k

4

k=1

Ri,t-kDDOWN,i,t-k + γiVOLAi,t

+ εi,t

Daily changes in individual commodity liquidity (DLi,t) are regressed on the change in

average commodity liquidity (DLM,t), lagged market returns (RM,t‐k), and commodity returns

(Ri,t‐k) . DDOWN,M,t is a dummy variable that equals one if RM,t‐k is more than 1.5 standard

deviations below its conditional mean. VOLAi,t is volatility.

Kamara, Lou, and Sadka (2008) show liquidity commonality is influenced by the level of

institutional ownership. Those participating in the commodity futures market can be broadly

13

termed “hedgers”, “funds”, and “small speculators” (e.g., Sanders, Boris, and Manfredo, 2004).14

We measure the proportion of a commodity owned by funds as fund open interest divided by the

total open interest on a weekly basis. We then follow the method of Kamara, Lou, and Sadka

(2008) and estimate the liquidity beta for each commodity on a weekly basis (in a similar fashion

to equation 4) and then conduct the following regression, where FOI is fund open interest:

βi,t= + FOIi,t-1+ εi,t (6)

4. Results

In section 4 we present the core liquidity commonality results and by sub-period. We

then present results relating the link (if any) between changes in stock market liquidity and

commodity liquidity. These are generated for the aggregate stock market and just those stocks

that are closely related to commodities. The final section contains results for supply-side and

demand-side commonality explanations.

4.1. Overall Liquidity Commonality

We present market-wide results based on the market model approach of Chordia, Roll,

and Subrahmanyam (2000) and the principle component method of Korajczyk and Sadka (2008)

14 We assume hedger positions consist of commercial long and short positions, fund positions consist of non-commercial long, short, and spreading positions, and small speculator positions consist of non-reported long and short positions.

14

in Table 1.15 The results generated using both methods indicate there is strong evidence of

liquidity commonality in the commodity market. Based on the market model results, a 1%

change in commodity market liquidity induces a contemporaneous average percentage change in

individual commodity liquidity ranging from 0.12 to 0.18, depending on the liquidity proxy. All

three market model t-statistics are statistically significant at the 1% level.16 The commodity

market average concurrent coefficient results are less than those reported for the US stock market

by Chordia, Roll, and Subrahmanyam (2000). Their average concurrent coefficient ranges from

0.28 to 1.37. However, they are of a similar size to those for European equity markets as reported

by Brockman, Chung, and Perignon (2009). These authors show the majority of European

markets have coefficients in the 0.10 – 0.25 range.17

The pattern of commonality is relatively consistent across individual commodities.

Changes in the liquidity of 81% of the commodities have a positive statistically significant

relation with changes in systematic liquidity based on the proportional effective, and this

increases to 88% and 100% respectively when quoted spread and Amihud measures are used.

The commonality effect appears to be more pervasive in commodities than in stocks despite the

prevalence of hedgers in the commodity market. Chordia, Roll, and Subrahmanyam (2000)

report the proportion of stocks with a positive, statistically significant relation ranges from 14%

to 35% for U.S. stocks, depending on the liquidity proxy used.

[Insert Table 1 Here]

15 Following Chordia, Roll, and Subrahmanyam (2000), we do not report the coefficients and t-statistics of the control variables. 16 As Chordia, Roll, and Subrahmanyam (2000) report in their footnote 8, the ratio of the true standard error to the typical standard error is [1+2(N-1)ρ]1/2, where N is the number of repressors. Like, Chordia, Roll, and Subrahmanyam (2000) we find that ρ is negative for some liquidity proxies which means the adjustment reduces the size of the standard error and increases the t-statistic. 17 See their Table 2.

15

The principle component results are very similar to their market model equivalents. The

results we present relate to regressions which include the first factor only, as this is the one that

is most likely to capture systematic liquidity. However, results based on all three factors are

qualitatively identical as Appendix 1 shows. There is a strong positive relation between the first

factor derived from all three liquidity measures. The average concurrent coefficient ranges from

0.21 to 0.50 and this relation is highly statistically significant. The consistency of the liquidity

commonality results across individual commodities also remains high when the principle

component method is used. Some 94% of the individual commodities have a positive statistically

significant relation with systematic liquidity based on the proportional quoted spread measure

and this increases to 100% when either the proportional effective spread or Amihud measures are

used.

4.2. Commonality in Sub-Periods

We now turn our attention to the question of whether commodity liquidity commonality

is unique to the recent period of surging commodity prices. As Figure 1 shows, commodity

prices increased just 27% between 1997 and 2003 and then surged 172% between 2004 and

2009. We calculate results by year and then present time-series averages for sub-period 1 (1997 –

2003) and sub-period 2 (2004 – 2009) in Table 3. These results allow us to form two

conclusions. Firstly, liquidity commonality was present in the early sub-period when commodity

prices and investment flows into commodities were relatively flat and in the more recent sub-

period. Secondly, there is evidence that the strength of the liquidity commonality increased

between sub-periods. Five of the six adjusted R2 are higher in sub-period 2 than sub-period 1 and

some of these increases are dramatic. For instance, the principle component analysis proportional

16

quoted spread adjusted R2 increases from 12.9% to 47.3%. Five of the six slope coefficients are

also larger in sub-period 2. Some increases are quite pronounced, such as those of proportional

quoted and effective spread with the market model. However, other increases, such as those

relating to principle component analysis (proportional effective spread and Amihud) are smaller.

Increasing commonality in the second sub-period could be due to demand- or supply-side

factors. Tang and Xiong (2010) note there has been a strong increase in commodity index

investing in the last decade and this has led to an increase in the return correlations of the major

commodities which are part of these indices. This financialization of commodities is a demand-

side explanation for the stronger commonality. The most recent sub-period also includes the

global financial crises, which saw sharp declines in the price of many commodities. This would

explain the stronger commonality from a supply-side perspective.

[Insert Table 2 Here]

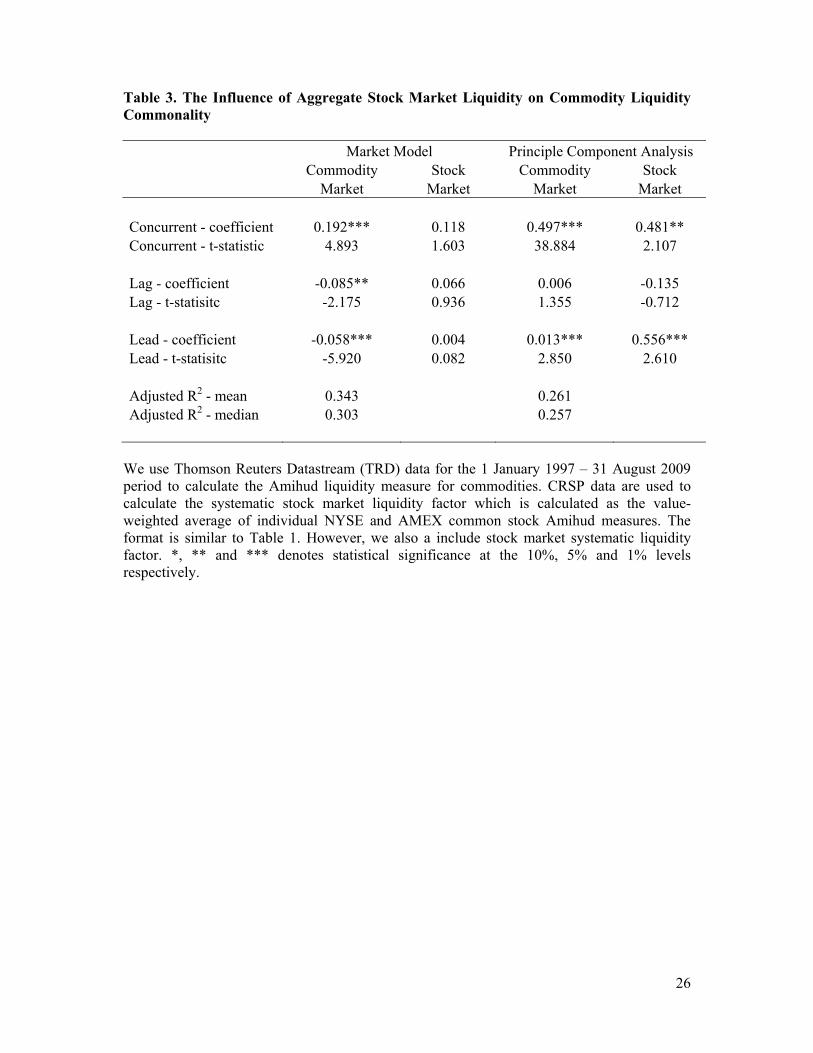

4.3. Stock Market Liquidity and Commodity Liquidity

The next issue we investigate is the influence, if any, that changes in stock market

systematic liquidity have on individual commodity liquidity. Chordia, Sarkar, and

Subrahmanyam (2005) find there is a link between stock market liquidity and bond market

liquidity due a relation between money flows across these asset classes. If investors view

commodities as a complementary risk asset to stocks then one would expect a positive relation

driven by investors exiting individual commodities and the equity market in times of heightened

risk aversion. Alternatively, if investors view commodities as an alternative asset class to stocks

then a decline in stock market liquidity might correspond with an increase in commodity

17

liquidity as investors sell stocks and buy commodities. Of course, it is possible that there is no

clear relation between stock and commodity liquidity due to the above effects being true for

some investors and not others and therefore cancelling each other out in aggregate. To ensure

consistency in liquidity measurement we use the Amihud measure to represent both commodity

and stock market liquidity. This liquidity proxy is popular in the equity literature (e.g., Kamara,

Lou, and Sadka (2008)) and has been shown by Goyenko, Holden, and Trzcinka (2009) to

correlate well with high-frequency stock liquidity benchmarks. We follow Kamara, Lou, and

Sadka (2008) and use the value-weighted average of individual NYSE and AMEX common

stock Amihud measures. More recently, Marshall, Nguyen, and Visaltanachoti (2011) show the

Amihud proxy is the best low-frequency measure of the actual cost of transacting in

commodities.

The market model results are generated by including changes in contemporaneous, lead,

and lag systematic stock liquidity as explanatory variables in the individual commodity liquidity

market-model regressions (equation 4). We produce the principle component results by

extracting the systematic stock liquidity factor using principle component analysis and including

this in our analysis. Changes in stock market liquidity have a positive relation with changes in

individual commodity liquidity when both the market model and principle component

approaches are used. However, the relation is only statistically significant when principle

component analysis is used. We conclude there is some evidence of a link between changes in

stock market and commodity liquidity. This is consistent with investors viewing commodities as

complementary assets to stocks and purchasing (selling) both in times of lower (higher) risk

aversion.

18

[Insert Table 3 Here]

We next investigate the relation between changes in the liquidity of commodities and the

subset of stocks that are most closely related to commodities. We match commodities to stocks

based on four-digit SIC codes as per Gorton and Rouwenhorst (2006) and calculate the value-

weighted average of Amihud measures for common stocks in the same SIC code. The related

industry stock liquidity for each commodity is the simple average of the SIC-based Amihud

measures. The Table 4 results suggest that changes in related-industry stock liquidity are related

to changes in commodity liquidity. However, this relation appears weaker than the link between

changes in individual commodity liquidity and changes in aggregate stock liquidity does. The

concurrent coefficient for the related stock industries is less than half that for the aggregate stock

market in both the market model and principle component analysis settings. The coefficient

related-stock industry coefficient is (not) statistically significant when the market model

(principle component) approach is used.

[Insert Table 4 Here]

4.5. Supply-Side and Demand-Side Commonality Results

Hameed, Wang, and Viswanathan (2010) show that liquidity commonality in equity

markets is caused by liquidity providers withdrawing liquidity following large market declines.

We follow the approach of Hameed, Wang, and Viswanathan (2010) and investigate this in

Table 5 Panel A. Changes in individual commodity liquidity are regressed on changes in average

commodity market liquidity ( , and on an interaction term , , , ) that equals

19

average commodity market liquidity when the commodity market return is more than 1.5

standard deviations below its conditional mean and zero otherwise. Control variables (see

equation 5) are also included but we do not report these. The results provide some evidence that

liquidity commonality is stronger following market declines. , , , is positive and

statistically significant when proportional quoted spread is used to measure liquidity. This lends

support to the Hameed, Wang, and Viswanathan (2010) supply-side explanation.

Liquidity commonality may also be caused by demand-side factors. Kamara, Lou, and

Sadka (2008) find liquidity commonality driven by the level of institutional ownership. We

calculate commodity futures market “fund” open interest and then calculate the proportion of

each commodity that is owned by funds each week as fund open interest divided by the total

open interest. We then calculate the beta for each commodity and then regress this beta on the

fund ownership proxy. The Table 5 Panel B results indicate the relationship between changes in

the fund ownership proxy and liquidity commonality is positive for each liquidity measure. The

coefficient is strongly statistically significant when the Amihud measure is used. In summary, we

conclude there is weak evidence to support both the supply-side and demand-side commonality

explanations.

[Insert Table 5 Here]

5. Conclusions

Commodities have increased in popularity with investors in the last decade. However,

there has been relatively little attention given to commodities in the academic literature, as

20

compared to that given to stocks and bonds. We address this deficit by considering whether there

is liquidity commonality in commodity markets. Previous authors have shown there is a

systematic stock market liquidity factor that influences the liquidity of individual stocks. It has

also been shown that there is a systematic liquidity factor in bond markets and foreign exchange

markets. However, it is not clear whether these findings are transferable to commodities as many

commodity market participants are hedgers who trade for risk management purposes.

We consider liquidity commonality in 16 major commodities which span the five major

commodity families of energy, industrial metals, precious metals, agriculture, and livestock.

There is strong evidence of liquidity commonality in all 16 commodities. This existed when

commodity prices were relatively flat and in the more recent period of the commodity boom.

There is some evidence that liquidity commonality in commodities is driven by supply-side

factors, which would imply liquidity providers withdraw liquidity at the same time in different

commodities and this is especially pronounced following large price declines. There is also

evidence of demand-side factors affecting commodity liquidity commonality. The commonality

is stronger when fund ownership is higher.

We also find evidence of a positive relation between changes in stock market liquidity

and individual commodity liquidity. This result is consistent with the notion that investors

viewing commodities as complementary assets to stocks. This results in them purchasing

(selling) both in times of lower (higher) risk aversion.

21

References

Acharya, Viral, Lochstoer, Lars, and Tarun Ramadorai (2010). Does hedging affect commodity prices? The role of producer default risk. SSRN Working Paper: http://ssrn.com/abstract=1105546 Amihud, Yakov. (2002). Illiquidity and stock returns: Cross-section and time-series effects, Journal of Financial Markets, 5, 31-56. Amihud, Yakov, Haim Mendelson, and Beni Lauterbach (1997). Market microstructure and securities values: Evidence from the Tel Aviv Stock Exchange, Journal of Financial Economics, 45(3), 365–390. Bernanke, Ben. (2008). Outstanding Issues in the Analysis of Inflation. Speech at the Federal Reserve Bank of Boston’s 53rd Annual Economic Conference, Chatham, Massachusetts June 9, 2008 Brockman, Paul., Chung, Dennis., and Christophe Perignon. (2009). Commonality in liquidity: A global perspective. Journal of Financial and Quantitative Analysis, 44(4), 851-882. Brownlees, Christian T. and Giampiero M. Gallo (2006). Financial econometric analysis at ultra-high frequency: Data handling concerns. Computational Statistics and Data Analysis, 51, 2232-2245. Brunnermeier, Markus., and Lasse Pedersen. (2009). Market liquidity and funding liquidity. Review of Financial Studies, 22, 2201–2238. Chan, Kam Fong., Treepongkaruna, Sirimon., Brooks, Robert., and Stephen Gray. (2011). Asset market linkages: Evidence from financial, commodity and real estate assets. Journal of Banking and Finance, 1415-1426. Chincarini, Ludwig (2007). The Amaranth debacle: A failure of risk measures or a failure of risk management? Journal of Alternative Investments, Winter, 91–104. Chordia, Tarun, Roll, Richard., and Avanidhar Subrahmanyam. (2000). Commonality in liquidity. Journal of Financial Economics, 56, 3-28. Chordia, Tarun, Roll, Richard., and Avanidhar Subrahmanyam. (2005). Evidence on the speed of convergence to market efficiency. Journal of Financial Economics, 76, 271-292. Chordia, Tarun, Sarkar, Asani., and Avanidhar Subrahmanyam. (2005). An empirical analysis of stock and bond market liquidity. Review of Financial Studies, 18(1), 85-129. Coughenour, Jay., and Mohsen Saad. (2004). Common market makers and commonality in liquidity. Journal of Financial Economics, 73, 37–69.

22

de Roon, Frans, Nijman, Theo., and Chris Veld. (2000). Hedging pressure effects in futures markets. Journal of Finance, 55(3), 1437-1456. de Ville de Goyet, Cedric., Dhaene, Geert., and Piet Sercu (2008). Testing the martingale hypothesis for futures prices: Implications for hedgers. Journal of Futures Markets, 28(11), 1040–1065. Dunsby, Adam., Eckstein, John., Gaspar, Jess., and Sarah Mulholland. (2008). Commodity investing: Maximizing returns through fundamental analysis. John Wiley and Sons Inc. New York. Fong, Kingsley., Holden, Craig., and Charles Trzcinka. (2011). What are the best liquidity proxies for global research? SSRN Working Paper: http://ssrn.com/abstract=1558447 Gorton, Gary., and K. Geert Rouwenhorst. (2006). Facts and fantasies about commodity futures. Financial Analysts Journal. 62(2), 47-68. Goyenko, Ruslan, Craig Holden, and Charles Trzcinka. (2009). Do liquidity measures measure liquidity? Journal of Financial Economics, 92, 153-181. Hameed, Allaudeen., Kang, Wenjin, and S. Viswanathan. (2010). Stock market declines and liquidity. Journal of Finance, 65(1), 257-293. Hasbrouck, Joel., and Duane Seppi. (2001). Common factors in prices, order flows, and liquidity. Journal of Financial Economics, 383-411. Holden, Craig (2009). New low-frequency spread measures. Journal of Financial Markets, 12, 778–813. Hong, Harrison., and Motohiro Yogo. (2010). Commodity market interest and asset return predictability. SSRN Working Paper. http://ssrn.com/abstract=1364674 Jensen, Niels. (2010). The commodities con. The Absolute Return Letter, May, 1-9. Kamara, Avraham., Lou, Xiaoxia, and Ronnie Sadka. (2008). The divergence of liquidity commonality in the cross-section of stocks. Journal of Financial Economics, 89, 444-466. Karolyi, G. Andrew., Lee, Kuan-Hui, and Mathijs van Dijk. (2011). Understanding commonality in liquidity around the world. Journal of Financial Economics – forthcoming. Korajczyk, Robert., and Ronnie Sadka. (2008). Pricing the commonality across alternative measures of liquidity. Journal of Financial Economics, 87, 45-72. Mancini, Loriano, Ranaldo, Angelo, and Jan. Wrampelmeyer. (2009). Liquidity in the foreign exchange market: Measurement, commonality and risk premiums. SSRN Working Paper: http://ssrn.com/abstract=1447869

23

Marshall, Ben., Nguyen, Nhut., and Nuttawat Visaltanachoti. (2011). Commodity liquidity measurement and transaction costs. Review of Financial Studies – Forthcoming. Pukthuanthong, Kuntara and Richard Roll. (2011). Gold and the Dollar (and the Euro, Pound, and Yen). Journal of Banking and Finance, 35, 2070-2083. Sanders, Dwight, Boris, Keith., and Mark Manfredo. (2004). Hedgers, funds, and small speculators in the energy futures markets: an analysis of the CFTC’s Commitments of Traders reports. Energy Economics, 26, 425-445. Tang, Ke and Wei Xiong. (2010). Index investment and financialization of commodities. NBER Working Paper No. 16385 http://www.nber.org/papers/w16385. Till, Hilary (2008). Amaranth lessons thus far. Journal of Alternative Investments, Spring, 82–98.

24

Table 1. Overall Results

Market Model Principle Component Analysis Prop.

Effective Spread

Prop. Quoted Spread Amihud

Prop. Effective Spread

Prop. Quoted Spread Amihud

Concurrent - coefficient 0.118*** 0.138*** 0.176*** 0.210*** 0.317*** 0.496*** Concurrent - t-statistic 3.381 3.763 3.820 8.432 3.841 38.020 % positive 81% 88% 100% 100% 94% 100% % p significant 63% 38% 100% 100% 88% 100%

Lag - coefficient 0.028** 0.036** -0.085** 0.002 -0.013 0.006 Lag - t-statistic 1.970 2.235 -2.119 0.388 -0.471 1.364 % positive 63% 75% 0% 63% 44% 50% % p significant 0% 0% 0% 50% 25% 25%

Lead - coefficient 0.059 0.009 -0.055*** 0.012** -0.014 0.013** Lead - t-statistic 1.594 0.274 -4.848 2.301 -0.526 2.984 % positive 63% 50% 0% 94% 50% 42% % p significant 31% 6% 0% 50% 25% 25%

Adjusted R2 - mean 0.027 0.015 0.321 0.401 0.464 0.261 Adjusted R2 - median 0.011 0.008 0.292 0.386 0.542 0.256

We use Thomson Reuters Tick History (TRTH) and Thomson Reuters Datastream (TRD) data for the 1 January 1997 – 31 August 2009 period. TRTH data are used to calculate proportional effective spreads and proportional quoted spreads. TRD are used for Amihud. Following Chordia, Roll, and Subrahmanyam (2000) we use a market model regression approach. The daily change in each liquidity measure is regressed on the cross-sectional market average for that liquidity measure. Following Korajczyk and Sadka (2008) we use principle component analysis to extract three factors from the data. We then regress each liquidity measure on the first factor. We report cross-sectional averages of the time-series coefficients and the overall t-statistic. “Concurrent”, “Lag”, and “Lead” results are based the same, previous, and prior day’s market liquidity respectively. % positive and % pos significant refer to the proportion of commodities that have positive and positive and statistically significant coefficients respectively. *, ** and *** denotes statistical significance at the 10%, 5% and 1% levels respectively.

25

Table 2. Sub-Period Results

Market Model Principle Component Analysis Mean t-statistic Adjusted R2 Mean t-statistic Adjusted R2

Panel A: Proportional Effective Spread

1997 - 2003 0.087** 2.286 -0.019 0.219*** 7.119 0.230 2004 - 2009 0.252** 2.610 0.034 0.242*** 5.996 0.372

Panel B: Proportional Quoted Spread

1997 - 2003 0.003 0.021 0.027 0.346*** 6.396 0.129 2004 - 2009 0.176*** 5.166 0.019 0.328*** 2.976 0.473

Panel C: Amihud

1997 - 2003 0.151*** 3.640 0.281 0.481*** 30.388 0.145 2004 - 2009 0.258*** 5.067 0.541 0.515*** 59.378 0.189

We use Thomson Reuters Tick History (TRTH) and Thomson Reuters Datastream (TRD) data for the 1 January 1997 – 31 December 2003 and 1 January 2004 - 31 August 2009 sub-periods. TRTH data are used to calculate proportional effective spreads and proportional quoted spreads. TRD are used for Amihud. Following Chordia, Roll, and Subrahmanyam (2000) we use a market model regression approach. The daily change in each liquidity measure is regressed on the cross-sectional market average for that liquidity measure. Following Korajczyk and Sadka (2008) we use principle component analysis to extract three factors from the data. We then regress each liquidity measure on the first factor. We report cross-sectional averages of the time-series coefficients and the overall t-statistic. *, ** and *** denotes statistical significance at the 10%, 5% and 1% levels respectively.

26

Table 3. The Influence of Aggregate Stock Market Liquidity on Commodity Liquidity Commonality

Market Model Principle Component Analysis Commodity Stock Commodity Stock

Market Market Market Market

Concurrent - coefficient 0.192*** 0.118 0.497*** 0.481** Concurrent - t-statistic 4.893 1.603 38.884 2.107

Lag - coefficient -0.085** 0.066 0.006 -0.135 Lag - t-statisitc -2.175 0.936 1.355 -0.712

Lead - coefficient -0.058*** 0.004 0.013*** 0.556*** Lead - t-statisitc -5.920 0.082 2.850 2.610

Adjusted R2 - mean 0.343 0.261 Adjusted R2 - median 0.303 0.257

We use Thomson Reuters Datastream (TRD) data for the 1 January 1997 – 31 August 2009 period to calculate the Amihud liquidity measure for commodities. CRSP data are used to calculate the systematic stock market liquidity factor which is calculated as the value-weighted average of individual NYSE and AMEX common stock Amihud measures. The format is similar to Table 1. However, we also a include stock market systematic liquidity factor. *, ** and *** denotes statistical significance at the 10%, 5% and 1% levels respectively.

27

Table 4. The Influence of Commodity-Related Stock Market Liquidity on Commodity Liquidity Commonality

Market Model Principle Component Analysis Commodity Stock Commodity Stock

Market Industry Market Industry

Concurrent - coefficient 0.199*** 0.055** 0.516*** 0.151 Concurrent - t-statistic 5.156 2.000 29.613 1.479

Lag - coefficient -0.124*** 0.028 0.030*** 0.906*** Lag - t-statisitc -3.078 1.455 5.857 6.036

Lead - coefficient -0.051*** 0.032 0.056*** 0.134** Lead - t-statisitc -4.081 1.564 9.707 1.912

Adjusted R2 - mean 0.404 0.250 Adjusted R2 - median 0.371 0.232

We use Thomson Reuters Datastream (TRD) data for the 1 January 1997 – 31 August 2009 period to calculate the Amihud liquidity measure for commodities. CRSP data are used to calculate the systematic stock market liquidity factor for stocks in commodity industries. The format is similar to Table 1. However, we also a include stock market systematic liquidity factor. *, ** and *** denotes statistical significance at the 10%, 5% and 1% levels respectively.

28

Table 5. Supply-Side and Demand-Side Liquidity Commonality Explanations Prop. Effective Spread Prop. Quoted Spread Amihud

Panel A: Supply Side

DLM, 0.083** 0.082*** 0.070*** t-statistic 2.916 3.392 4.757 DLM, DDOWN,M, 0.052 0.262** 0.001 t-statistic 0.554 2.585 0.654

Panel B: Demand Side

FOI 0.566 0.990 0.351*** t-statistic 0.819 1.350 6.376

We use Thomson Reuters Tick History (TRTH) data for the 1 January 1997 – 31 August 2009 period to calculate proportional effective spreads and proportional quoted spreads. In Panel A individual commodity liquidity changes are regressed on changes in average commodity market liquidity and control variables. , is the coefficient of average commodity market liquidity. , , , is the coefficient of an interaction term. , , is a dummy variable that equals one if , is more than 1.5 standard deviations below its conditional mean. The Panel B results are generated by regressing the slope (commonality) coefficient for each commodity on the level of fund ownership for that commodity. FOI, which represents the sensitivity of changes in liquidity commonality to fund open interest, is reported. *, ** and *** denotes statistical significance at the 10%, 5% and 1% levels respectively.

29

Figure 1. S&P Goldman Sachs Commodity Index (S&P GSCI)

The S&P Goldman Sachs Commodity Index. Data are sourced from Thomson Reuters Datastream (TRD)

0

100

200

300

400

500

600

700

800

900

1000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Period 1 Period 2

30

Appendix 1. Principle Component Analysis Results for Three Components

Prop. Effective Spread Prop. Quoted Spread Amihud

Factor 1 - coefficient 0.216*** 0.277** 0.531*** Factor 1 - t-statistic 5.502 2.428 9.191 % positive 100% 88% 100% % p significant 94% 88% 100%

Factor 2 - coefficient -0.046 0.268* 0.068 Factor 2 - t-statistic -0.709 1.685 0.394 % positive 44% 56% 42% % p significant 31% 56% 42%

Factor 3 - coefficient -0.036 -0.001 0.149 Factor 3 - t-statistic -0.234 -0.006 0.443 % positive 31% 69% 42% % p significant 25% 56% 42%

Adjusted R2 - mean 0.424 0.670 0.506 Adjusted R2 - median 0.377 0.687 0.463

We use Thomson Reuters Tick History (TRTH) and Thomson Reuters Datastream (TRD) data for the 1 January 1997 – 31 August 2009 period. TRTH data are used to calculate proportional effective spreads and proportional quoted spreads. TRD are used for Amihud. Following Korajczyk and Sadka (2008) we use principle component analysis to extract three factors from the data. We then regress each liquidity measure on each of the three factors. We report cross-sectional averages of the time-series coefficients and the overall t-statistic. *, ** and *** denotes statistical significance at the 10%, 5% and 1% levels respectively.

Top Related

Copyright © 2022 FDOKUMEN