Bahasa

Halaman

Hukum

JMC PROJECTS (INDIA) LIMITED(The Company was originally incorporated as "Civen Construction Private Limited" on June 5, 1986 under the Companies Act, 1956 withits registered office at Ahmedabad. Subsequently on December 10, 1987, the name was changed to Joshi & Modi Constructions PrivateLimited. The name was further changed to JMC Projects (India) Private Limited on January 21, 1994 and was subsequently convertedinto a Public Limited Company in the name of JMC Projects (India) Limited on February 4, 1994).

Registered & Corporate Office: A-104, Shapath-4, Opposite Karnavati Club, S.G.Road, Ahmedabad - 380 051, IndiaTel: +91-79-3001 1500 Fax: +91-79-3001 1600/1700 E-mail: [email protected]; Website: www.jmcprojects.com

(The Registered Office of the Company was shifted from People's Plaza Near Memnagar Fire Station, Navrangpura,Ahmedabad 380 009 to 4, Kuldip Society, Near Ishvar Bhuvan, Navrangpura, Ahmedabad - 380 009 w.e.f. May 9, 1988 and

subsequently to Level -11, JMC House, Ambawadi, Ahmedabad 380 006 w.e.f April 5, 2002 and to the present registeredoffice w.e.f .November 7, 2005).

LETTER OF OFFERISSUE OF 46,46,550 EQUITY SHARES OF RS. 10/- EACH AT A PREMIUM OF RS. 90/- PER EQUITY SHAREAGGREGATING RS. 4646.55 LAKHS TO THE EQUITY SHAREHOLDERS ON RIGHTS BASIS IN THE RATIO OFTWO (2) EQUITY SHARES FOR EVERY FIVE (5) EQUITY SHARES HELD ON THE RECORD DATE i.e.SEPTEMBER 21, 2006 ("ISSUE"). THE ISSUE PRICE IS 10 TIMES THE FACE VALUE OF THE EQUITY SHARE.

GENERAL RISKS

Investment in equity and equity related securities involve a degree of risk and investors should not invest any funds in thisIssue unless they can afford to take the risk of losing their investment. Investors are advised to read the Risk Factorscarefully before taking an investment decision in this Issue. For taking an investment decision, investors must rely on theirown examination of the Issuer and the Issue including the risks involved. The securities have not been recommended orapproved by Securities and Exchange Board of India ("SEBI") nor does SEBI guarantee the accuracy or adequacy of thisdocument. Investors are advised to refer to "Risk Factors" on page vi of this Letter of Offer before making aninvestment in this Issue.

ISSUER’S ABSOLUTE RESPONSIBILITY

The Issuer, having made all reasonable inquiries, accepts responsibility for, and confirms that this Letter of Offer containsall information with regard to the Issuer and the Issue, which is material in the context of this Issue, that the informationcontained in this Letter of Offer is true and correct in all material respects and is not misleading in any material respect,that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of whichmakes this document as a whole or any of such information or the expression of any such opinions or intentions misleadingin any material respect.

LISTING

The existing Equity Shares of the Company are listed on Bombay Stock Exchange Limited ("BSE"). The Company hasreceived the "in-principle" approval from BSE for listing the Equity Shares arising from this Issue vide letterno. DCS/SJK/SM/NS/JA/06 dated August 29, 2006.

Letter of Offer for Equity Shareholders of the Company only

ISSUE OPENS ON LAST DATE FOR RECEIVING ISSUE CLOSES ONREQUESTS FOR SPLIT FORMS

September 30, 2006 October 16, 2006 October 30, 2006

LEAD MANAGER TO THE ISSUE REGISTRAR TO THE ISSUE

Inga Advisors Private LimitedA-404, Neelam Centre,Hind Cycle Road, Worli,Mumbai - 400 030Tel: +91-22-2498 2937, 2498 2919, 2498 2954Fax: +91-22-2498 2956Email: [email protected]: www.ingaadvisors.com

Intime Spectrum Registry LimitedC-13, Pannalal Silk Mills Compound,LBS Marg, Bhandup (West)Mumbai - 400 078.Tel: +91-22-2596 0320Fax: +91-22-2596 0329E-mail: [email protected]: www.intimespectrum.com

C M Y B

TABLE OF CONTENTS

GLOSSARY OF TERMS AND ABBREVIATIONS ...................................................................................... ii

RISK FACTORS ........................................................................................................................................... vi

SELECTED FINANCIAL INFORMATION ................................................................................................... 1

GENERAL INFORMATION .......................................................................................................................... 2

CAPITAL STRUCTURE ............................................................................................................................... 5

OBJECTS OF THE ISSUE .......................................................................................................................... 11

BASIS FOR ISSUE PRICE ......................................................................................................................... 19

INDUSTRY OVERVIEW............................................................................................................................... 21

BUSINESS OVERVIEW ............................................................................................................................... 26

HISTORY AND CORPORATE STRUCTURE ............................................................................................ 28

PROMOTERS ............................................................................................................................................... 30

MANAGEMENT ............................................................................................................................................ 33

FINANCIAL STATEMENTS ......................................................................................................................... 46

MANAGEMENT DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION ANDRESULTS OF OPERATION ........................................................................................................................ 99

UNAUDITED WORKING RESULTS ........................................................................................................... 110

OUTSTANDING LITIGATIONS AND DEFAULTS ...................................................................................... 111

GOVERNMENT APPROVALS ..................................................................................................................... 178

STATUTORY AND OTHER INFORMATION .............................................................................................. 180

STOCK MARKET DATA .............................................................................................................................. 186

TERMS OF THE ISSUE .............................................................................................................................. 187

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ......................................................... 201

DECLARATION ............................................................................................................................................ 203

ii

GLOSSARY OF TERMS AND ABBREVIATIONS

Company 1JMC / Issuer JMC Projects (India) Limited

Issue related

Abridged Letter of Offer Abridged form of a Letter of Offer which discloses basic information laid down in Section IV of Chapter VI of the SEBI Guidelines which is sent to the Equity Shareholders along with CAF

Act The Companies Act, 1956 and amendments thereto

Articles Articles of Association of the Company

Board Board of Directors of JMC Projects (India) Limited

Board /Committee of Directors

Committee of the Board of Directors of JMC Projects (India) Limited authorized to take decisions on matters related to / incidental to this Issue

Depositories NSDL and CDSL

Designated Stock Exchange Bombay Stock Exchange Limited

DP Depository Participant

Director(s) Directors on Board of Directors of the Company

Equity share Equity shares of the company of Rs.10/- each

Equity Shareholders Means holder of Equity Shares

Issue or Rights Issue or Offer

Issue by the Company of 46,46,550 equity shares of Rs. 10/- each for cash at Rs. 100/- per equity share (including a premium of Rs. 90/- per equity share) on Rights basis to the existing Equity Shareholders of the Company in the ratio of Two (2) equity shares for every Five (5) equity shares held on September 21, 2006 i.e. Record Date aggregating to Rs. 4646.55 lakhs

Issue price Rs. 100/- per equity share

Issue Opening Date September 30, 2006

Issue Closing Date October 30, 2006

Lead Manager to the Issue Inga Advisors Private Limited

Letter of Offer / LOO/ Offer Document

The Letter of Offer which discloses information as laid down in Section III of Chapter VI of the SEBI Guidelines.The Equity Shareholders of the Company can request for a copy of Letter of Offer dated September 14, 2006 from the Registrar to the Issue

Memorandum Memorandum of Association of the Company

Record Date September 21, 2006

Registrars to the Issue Intime Spectrum Registry Limited

Rights Entitlement

The number of Equity Shares that an Equity Shareholder is entitled to under this Letter of Offer in proportion to his / her / its existing shareholding in the Company as on the Record Date

Security certificates Equity share certificates

SPA Share Purchase Agreement dated October 14, 2004 executed between the ‘Purchaser’ being ‘Kalpataru Power Transmission Limited, Kalpataru Energy Venture (Private) Limited and the ‘Sellers’ being Mr. I K Modi, Mr. Hemant Modi, Mr. Suhas Joshi, Mrs. Sonal Modi, Mrs. Suverna Modi, Mrs. Madhuri Joshi, Mrs. Maltiben Joshi, Ms Ami Modi, Ms Anar Modi, Minar Investments and Finance Private Limited and the Company

iii

Industry related

APDRP Accelerated Power Development and Reform Programme

BOT Build Operate and Transfer

BOOT Build Own Operate and Transfer

BRASS Measure of weight; one brass equals four tons

CAR Contractors All Risk

EPC Engineering, Procurement and Commissioning

MORTH Ministry of Road Transport and Highways

NH National Highway

NHAI National Highway Authority of India

NHDP National Highway Development Programme

Abbreviations

AGM Annual General Meeting

AS Accounting Standards issued by the Institute of Chartered Accountants of India

Anr. Another

BSE Bombay Stock Exchange Limited

BUTP Bombay Urban Transport Project

CDSL Central Depository Services (India) Limited

CAF Composite Application Form

CEO Chief Executive Officer

DD Demand Draft

GM General Meeting

EBIDTA Earnings before Interest, Depreciation, Tax and Amortisation

EGM Extra-ordinary General Meeting

EPS Earnings Per Share

EOU Export Oriented Unit

FCNR Foreign Currency Non-Resident account

FDI Foreign Direct Investment

FEMA

Foreign Exchange Management Act, 2000 read with rules and regulations there under and amendments thereto

FIFO First In First Out

FII(s) Foreign Institutional Investors registered with SEBI under applicable laws

FIPB Foreign Investment Promotion Board

FY

Financial year being a period commencing on April 1st and ending on March 31st of the following year

GDP Gross Domestic Product

GIR Number General Index Registry Number

GoI Government of India

iv

HUF Hindu Undivided Family

IT/ITES Information Technology/ Information Technology Enabled Services

IT Act The Income Tax Act, 1961 and amendments thereto

JMQL/ JMC Mining JMC Mining and Quarries Limited

JV Joint Venture

Kms Kilometers

KPPL Kalpataru Properties Private Limited

KCPL Kalpataru Construction Private Limited

KPTL Kalpataru Power Transmission Limited

KV Kilo Volt

LC Letter of Credit

LIBOR London Interbank Offer Rate

LIC Life Insurance Corporation of India

MD Managing Director

MOU Memorandum of Understanding

MT Metric Ton

MUTP Mumbai Urban Transport Project

MW Mega Watt

NA Not Applicable

NAV Net Asset Value

NOC No Objection Certificate

NR Non-resident

NRI(s) Non-resident Indians

NRE Account Non Resident External account

NRO Account Non Resident Ordinary account

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

OCB(s) Overseas Corporate Body(ies)

Ors. Others

PAC Persons Acting in Concert

P/E or P/E ratio Price-Earnings Ratio

p.a. Per annum

PAN Permanent Account Number

PAT Profit After Tax

PBDIT Profit Before Depreciation Interest and Tax

PBT Profit Before Tax

PGCIL Power Grid Corporation of India Limited

PSU Public Sector Undertaking

PWD Public Works Department

v

R&D Research & Development

RBI The Reserve Bank of India

RONW Return on Networth

SEB State Electricity Board

SEBI Securities and Exchange Board of India

SEBI Guidelines/ SEBI (DIP)

SEBI (Disclosure & Investor Protection) Guidelines, 2000 as amended from time to time

SEBI (SAST) Securities and Exchange Board of India (Substantial Acquisitions of shares and Takeovers) Regulation, 1997 and subsequent amendments thereto

SPV Special Purpose Vehicle

Sq ft/ sq ft Square feet

SSI Small Scale Industry

TDS Tax Deducted at Source

UTI Unit Trust of India

vol Volume

w.e.f. With effect from

WPI Wholesale Price Index

In this Letter of Offer, all references to "Rs." refer to Rupees, the lawful currency of India. References to the singular also refer to the plural and one gender also refers to any other gender wherever applicable.

vi

RISK FACTORS

The investors should consider the following risk factors together with all other information included in this Letter

of Offer carefully, in evaluating the Company and its business before making any investment decision. Any

projections, forecasts and estimates contained herein are forward looking statements that involve risks and

uncertainties. Such statements use forward looking terminology like “may”, “believes”, “will”, “expect”,

“anticipate”, “estimate”, “plan” or other similar words. The Company’s actual results could differ from those

anticipated in these forward-looking statements as a result of certain factors including those, which are set forth

in the “Risk Factors”.

Market data used throughout this Letter of Offer was obtained from internal Company reports, data and industry

publications whose consents have not been sought. Industry publications database generally state that the

information contained in those publications has been obtained from sources believed to be reliable, but that their

accuracy and completeness and underlying assumptions are not guaranteed and their reliability cannot be

assured. Although, market data used in this Letter of Offer is reliable, it has not been independently verified.

Similarly, internal Company reports and data, while reliable, have not been verified by any independent source.

RISK FACTORS AND MANAGEMENT PERCEPTION

Note: Unless specified or quantified in the relevant risk factors below, the Issuer is not in a position to quantify financial or other implication of any risks mentioned herein under. The Issuer and the Lead Manager will keep the investors informed of any material changes till the listing and commencement of trading.

Litigations Against the Issuer Company: The Company/ its Directors/ Promoters / Group Companies /

Subsidiaries/ Ventures of the Promoters are defendants in certain legal proceedings, incidental to the

business and operations. These legal proceedings are pending at different levels of adjudication before

various courts and tribunals. Should any new development arise, such as a change in Indian law or rulings

by appellate courts or tribunals, the company would need to make provisions in its financial statements

which could adversely impact its business results. A brief of the outstanding litigations are as follows:

Litigations against JMC

I. Criminal Litigations

Against the Company

• A criminal litigation has been filed against the Issuer Company before the Judicial Magistrate, First Class,

Ahmedabad; vide Criminal Case No. 2678 of 1999 by the Government Labour Officer alleging violation of Section 3 of Child Labour (Prohibition and Regulation) Act, 1986 and rules framed there under at one of the JMC site. The Government Labour Officer has alleged that he found child workers on a JMC site. JMC has denied any violation of the said Act. An application has been filed on behalf of JMC dated 16.10.2003 seeking certain particulars, documents, on which the prosecution (complainant) seeks to rely, so that cross-examination could be done in respect thereof. The matter is pending at that stage as the said details are yet to be provided to JMC. The next hearing of the case is on 16/10/2006

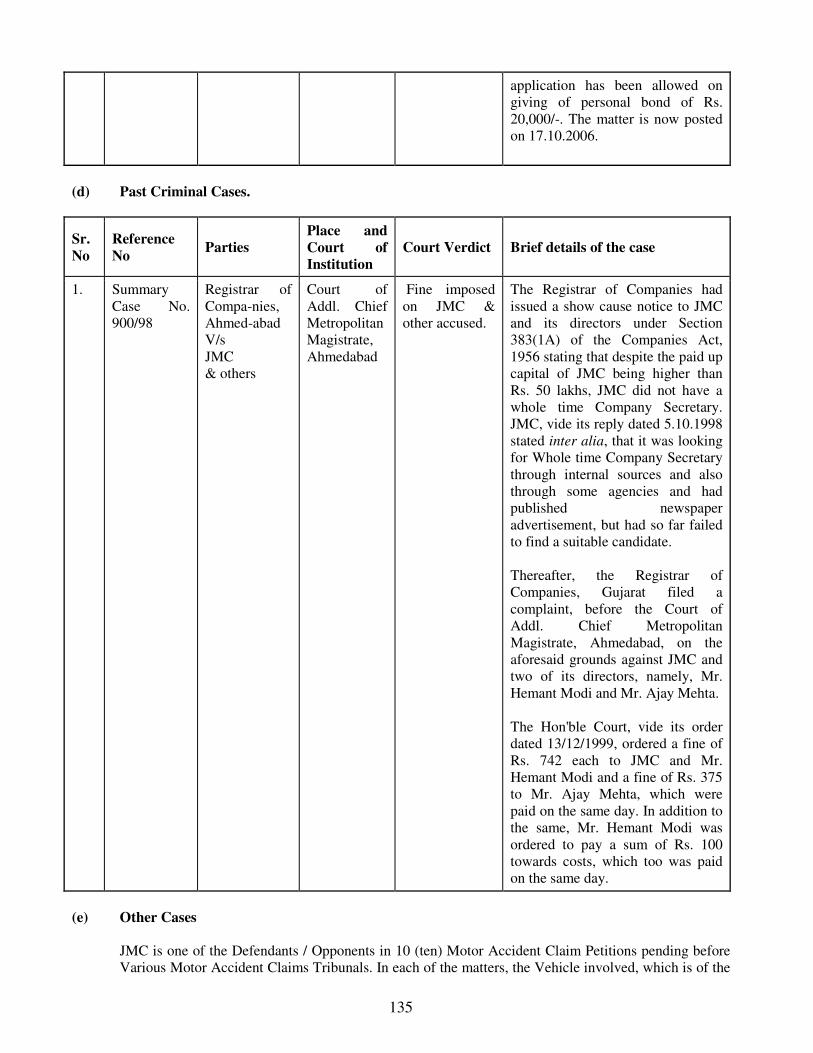

Past Criminal Cases

• A criminal litigation has been filed against the Issuer Company before the Court of Additional Chief Metropolitan Magistrate; vide Criminal Case No. 900/98 by the Registrar of Companies, Ahmedabad alleging violation of Section 383(1A) of the Companies Act, 1956. The case states that despite the paid up capital of JMC being higher than Rs. 50 lakhs, JMC did not have a whole time Company Secretary. The Hon'ble Court,

vii

vide its order dated 13/12/1999, ordered a fine of Rs. 742 /- to JMC which was paid on the same day. The case now stands discharged

Against Directors of the Company

Mr. Ajay Munot

• Case No. 379 of 2003 has been filed by the Senior Inspector of Factories and Boilers, Sri Ganganagar against Mr. Ajay Munot before Civil Judge (J. D.) and Judicial Magistrate, First Class, Padampur, District Sri Ganganagar, Rajasthan, for alleged violation of sections 21 and 61 of the Factories Act, 1948 in view of the death of a workman due to alleged non-fencing of the conveyor belt in the factory premises of KPTL at Padampur, The said case is pending.

Mr. Hemant Modi

• Criminal Case No. 2678 of 1999 has been filed by Government Labour Commissioner against Mr. Hemant Modi for alleged violation of the provision of Child Labour (Prohibition and Regulation) Act, 1986 The next hearing of the case is on 16/10/2006

• Criminal Complaint case no. 270/2002 has been filed by Mr. Mantu alleging that cheque no. 457936 dated 13/10/2001 for an amount of Rs. 4,19,327 issued by JMC, has returned unpaid. It has been alleged by Mr. Mantu that JMC, pursuant to alleged receipt of purported notice in terms of section 138 of Negotiable Instruments Act, 1881, did not make good the said amount and hence Mr. Mantu has filed the compliant..The case shall be listed on 19.09.2006.

• A criminal litigation has been filed against the Issuer Company before the Court of Additional Chief Metropolitan Magistrate; vide Criminal Case No. 900/98 by the Assistant Registrar of Companies, Ahmedabad alleging violation of Section 383(1A) of the Companies Act, 1956. The case states that despite the paid up capital of JMC being higher than Rs. 50 lakhs, JMC did not have a whole time Company Secretary. The Hon'ble Court, vide its order dated 13/12/1999, ordered a fine of Rs. 742 /- to JMC which was paid on the same day. The case now stands discharged

II. A summary of the litigations in which the Company is involved is set out below:

By the Company Against the Company

Sr. Particulars Number

of cases

Amount

involved, where

quantifiable

(Rs. lakhs)

Number

of cases

Amount

involved, where

quantifiable

(Rs. lakhs)

1. Income Tax / Sales Tax cases 2 Nil Nil

2. Civil cases including money suits.

7 852.31 7 21.71

3 Criminal Cases Nil

2 4.20

4. Labour Matters

Nil 14 58.18

5. Arbitration

5 2243.49 Nil

6. Misc. / Notices Nil 22 73.11

7. Other Cases (Motor Accident Claims)

Nil 10 74.60

viii

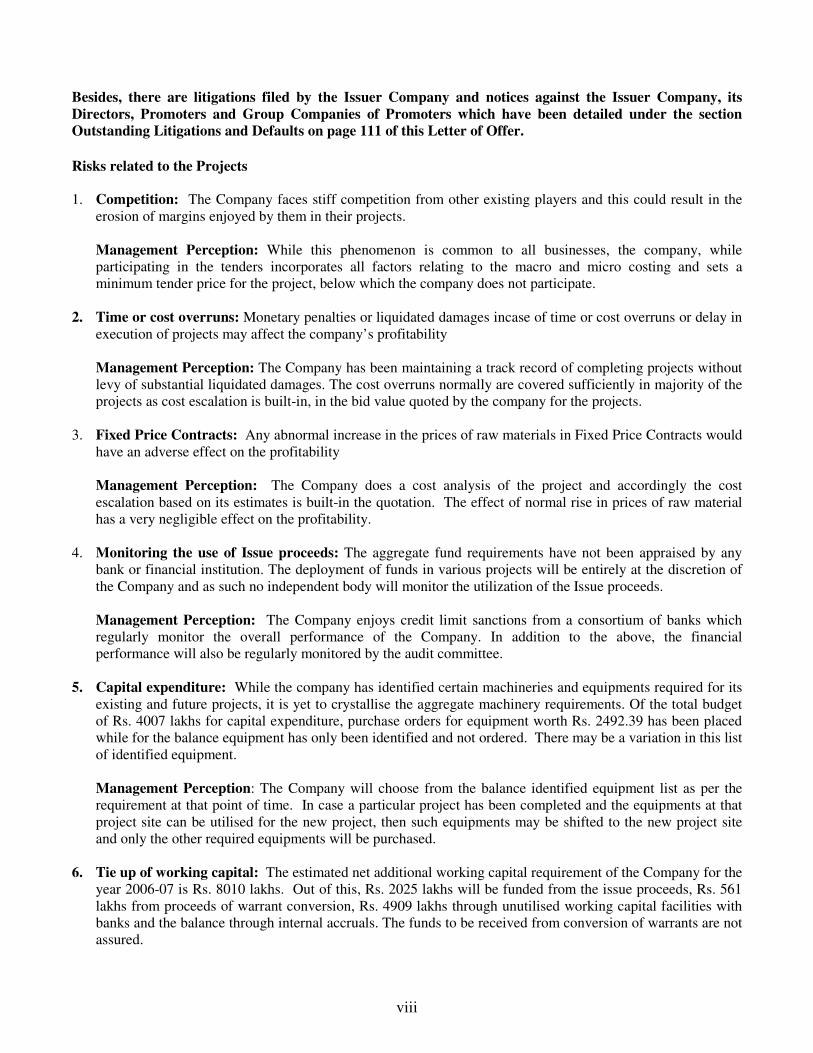

Besides, there are litigations filed by the Issuer Company and notices against the Issuer Company, its

Directors, Promoters and Group Companies of Promoters which have been detailed under the section

Outstanding Litigations and Defaults on page 111 of this Letter of Offer.

Risks related to the Projects 1. Competition: The Company faces stiff competition from other existing players and this could result in the

erosion of margins enjoyed by them in their projects.

Management Perception: While this phenomenon is common to all businesses, the company, while participating in the tenders incorporates all factors relating to the macro and micro costing and sets a minimum tender price for the project, below which the company does not participate.

2. Time or cost overruns: Monetary penalties or liquidated damages incase of time or cost overruns or delay in execution of projects may affect the company’s profitability

Management Perception: The Company has been maintaining a track record of completing projects without levy of substantial liquidated damages. The cost overruns normally are covered sufficiently in majority of the projects as cost escalation is built-in, in the bid value quoted by the company for the projects.

3. Fixed Price Contracts: Any abnormal increase in the prices of raw materials in Fixed Price Contracts would

have an adverse effect on the profitability

Management Perception: The Company does a cost analysis of the project and accordingly the cost escalation based on its estimates is built-in the quotation. The effect of normal rise in prices of raw material has a very negligible effect on the profitability.

4. Monitoring the use of Issue proceeds: The aggregate fund requirements have not been appraised by any

bank or financial institution. The deployment of funds in various projects will be entirely at the discretion of the Company and as such no independent body will monitor the utilization of the Issue proceeds.

Management Perception: The Company enjoys credit limit sanctions from a consortium of banks which regularly monitor the overall performance of the Company. In addition to the above, the financial performance will also be regularly monitored by the audit committee.

5. Capital expenditure: While the company has identified certain machineries and equipments required for its existing and future projects, it is yet to crystallise the aggregate machinery requirements. Of the total budget of Rs. 4007 lakhs for capital expenditure, purchase orders for equipment worth Rs. 2492.39 has been placed while for the balance equipment has only been identified and not ordered. There may be a variation in this list of identified equipment.

Management Perception: The Company will choose from the balance identified equipment list as per the requirement at that point of time. In case a particular project has been completed and the equipments at that project site can be utilised for the new project, then such equipments may be shifted to the new project site and only the other required equipments will be purchased.

6. Tie up of working capital: The estimated net additional working capital requirement of the Company for the year 2006-07 is Rs. 8010 lakhs. Out of this, Rs. 2025 lakhs will be funded from the issue proceeds, Rs. 561 lakhs from proceeds of warrant conversion, Rs. 4909 lakhs through unutilised working capital facilities with banks and the balance through internal accruals. The funds to be received from conversion of warrants are not assured.

ix

Management Perception: The Company already has a sanction of working capital limit of Rs. 5960 lakhs from a consortium of banks. The Company is in process of getting the sanctions from the remaining consortium banks which will increase its working capital limit to Rs. 6500 lakhs. It will approach the banks for enhancement of the credit limits, whenever required. Given the Group profile and their overall performance, the company is confident of sourcing these requirements in a cost effective manner. The balance requirement if any will be met through internal accruals and debt.

Risks Internal to the Company

1. Size deterrent in bidding for large projects: The Company’s moderate size could be a deterrent in bidding for large contracts.

Management Perception: Accepting their position in the industry, the management has initiated several steps to strengthen its financial and operational position which in the years to come will elevate the company to a level wherein they will qualify for large projects. The company will opt for a joint venture route for those projects where they are unable to qualify on a stand alone basis.

2. High fund requirement: High capital expenditure coupled with the large working capital needs may affect

the profit margins.

3. Promoters’ interest in similar ventures: Mr. Hemant Modi and Mr. Suhas Joshi, Promoters of the Company, (individually or jointly) together with their relatives have interest in the following ventures which are authorized by its main objects clause to carry on a similar line of activities. This may result in a conflict of business interests among these ventures and the Company. There are certain business transactions with the mentioned companies/firms. Their interest in the companies is given below:

Name of the venture Nature of interest

JMC Infrastructure Limited Shareholding (97.20%)

SAI Consulting Engineers Private Limited Shareholding (100.00%)

JMC Consultants and Developers Private Limited Shareholding (100.00%)

JM Construction Shareholding (100.00%)

Management Perception: The Companies mentioned above facilitate the project execution capabilities of the Company. JMC subcontracts the projects to its associate companies / seeks project consultancy services at market rates. In future, as agreed under the SPA, these associate companies / firms will not undertake any competing activities with the Company and shall carry out only those activities which are beneficial to the Company with the consent of the Board of the Company.

4. Loss by other ventures of the promoters and promoter group companies: The following ventures of the promoters have incurred losses: a. J. M. Construction incurred a loss of Rs. 0.20 lakhs and Rs. 12.03 lakhs for the year ended March 31,

2006 and March 31, 2005. b. Kalpataru Construction Private Limited incurred a loss of Rs. 123.60 lakhs for the year ended March

31, 2005 c. Kalpataru Properties Private Limited (formerly known as Kalpataru Constructions Overseas Private

Limited) incurred a loss of Rs. 587.50 lakhs for the year ended March 31, 2003. Management Perception: J.M. Construction incurred losses as there were no business activities in the last two years. Kalpataru Construction Private Limited incurred loss mainly on account of the valuation of stock of certain trading stock of premises at the market value which was lower than the cost of the same as on March 31, 2005. Subsequently there was a significant change in the market trend and the management is of the opinion that the said loss would be recoverable in the subsequent period. The losses incurred by Kalpataru Properties Private Limited were due to the reduction in net market realizable value of unsold stock

x

as compared to cost incurred on account of recessionary trend. Subsequently the Company has earned a profit of Rs. 375.81 lakhs in FY 2004 and Rs. 857.97 lakhs in FY 2005.

5. Shortfall in the promised performance: There has been a shortfall in the financial performance of the Company for the year 1995 vis-à-vis projections made in their prospectus dated September 2, 1994. The details are as under:

Rs. lakhs

Year ending

March 31

1995 1996

1997

Promised Actual Variation Promised Actual Variation Promised Actual Variation

A B ( B - A ) A B ( B - A ) A B ( B - A )

Income 1500.00 1372.63 -127.37 1750.00 3005.72 1255.72 2100.00 4910.07 2810.07

PBDIT 213.04 195.52 -17.52 285.01 485.61 200.60 344.86 738.34 393.48

Profit Before Tax 168.11 143.04 -25.07 232.63 308.84 76.21 292.9 403.74 110.84

Profit After Tax 159.84 140.41 -19.43 191.64 232.55 40.91 193.79 287.49 93.70

EPS (Rs.) 5.33 4.53 -0.80 6.39 7.51 1.12 6.46 9.28 2.82

Management Perception: The projected sales could not be achieved in the year 1995, due to heavy rains during the said period, which affected the commencement and progress of some of the projects. However steps are being initiated to minimize such aberrations in future.

6. Status of deployment of funds of previous rights issue proceeds The main objects for the previous Rights Issue are given below along with the actual utilization

As on March 31, 2006, there was an unutilized balance of Rs. 278.27 lakhs held in cash credit account with banks. The funds were fully utilized by June 2006.

7. Contingent liabilities: As per the last audited accounts, the contingent liabilities are as follows:

Rs. lakhs

Particulars As at March

31, 2006

As at

September 30,

2005

A. Bank Guarantees* 3.20 3.20

Rs. lakhs

Particulars Proposed Actual

April 05 -

Sept 05

Oct 05 –

March 06

Total Upto June

30, 2006

Purchase of premises for new Registered office

165.00 - 165.00 164.32

Purchase of capital equipment

600.00 300.00 900.00 912.42

Repayment of debt 1035.00 1035.00 1038.54

Working capital margin 695.00 290.00 985.00 981.46

Issue expenses 51.42 - 51.42 39.68

Total 2546.42 590.00 3136.42 3136.42

xi

B. Counter Guarantees given in respect of cash credit and loans advanced to the Subsidiary Company (Outstanding balance of Cash credit as on 31/03/2006 is Rs. 62.66 lakhs.)

79.10 79.10

C. Letters of Credit 241.26 573.03

D. Claims against the Company not acknowledged as debts** 536.29 536.57

E Estimated amount of orders remaining to be executed on capital account and not provided for (net of advances)

486.90 41.43

No provision has been made for these contingent liabilities

*As per opinion by the expert advisory committee of the Institute of Chartered Accountants of India, Bank Guarantee furnished in respect of performance, retention and mobilization advance, etc. are not in the nature of contingent liabilities, hence same are excluded from the bank guarantee outstanding as on as on as on March 31, 2006 and September 30, 2005.

**The figures shown in “D” above does not include amount of claims raised by way of counter claims by clients against the claims raised by the Company in terms of provisions of Accounting Standard 29.

8. Accidents and consequent liabilities: Improper handling of materials and machines used in the projects can

result in accidents and the Company could face significant liabilities.

Management Perception: The Company has been executing a variety of projects using modern techniques and state-of-the-art plant & equipment. The Company has taken requisite insurance policies to mitigate financial risk. The Company has a prescribed safety policy implemented and the workers are also given training for proper handling of the machines thereby minimising accident related risks.

9. Restrictive covenants in Loan Agreements: The loan agreements entered into by the Company contain certain restrictive covenants. These covenants primarily relate to:

• Declaration and payment of dividend

• Raising further capital

• Effecting any change in the Company’s capital structure

• Formulating any scheme of amalgamation or reconstruction

• Obtaining financial resources from any other source

Management Perception: No Objection Certificates have been obtained from the bankers for raising capital under the current issue and similar approvals will be taken whenever required.

10. Restrictive covenants in the Share Purchase Agreement:

A MOU was entered into between Mr. I.K. Modi, Mr. Hemant Modi, Mr. Suhas Joshi and their relatives and Minar Investments and Finance Pvt. Ltd. (“Sellers”) and Kalpataru Power Transmission Limited and Kalpataru Energy Venture Pvt. Ltd. (“Purchaser”) on October 1, 2004.Subsequently a Share Purchase Agreement was entered into between the aforesaid parties on October 14, 2004 for purchase of 15,00,000 Equity Shares at Rs. 40/- each representing 32.28% of the share capital of JMC. There are certain restrictive covenants in the Share Purchase Agreement. These covenants require certain key decisions to be taken up for consideration at a Board meeting after they have been approved by the Purchaser (KPTL, Kalpataru Energy Venture Private Limited) in writing.

11. Mr. Vijay Choraria, Chairman of the Company is associated with SEBI registered entities wherein routine

enquiries have been made by SEBI which pertain to trades concluded as also the bank details for payments made/received and demat details like delivery instructions with respect to purchase/sale of shares on behalf of its clients. SEBI has issued warning letters dated August 22, 2006 to A.K Equities Ltd. and V. J. Finsecurities

xii

Pvt. Ltd. in relation to the transaction of purchase/sale of shares of a company carried out on behalf of its clients who were related / connected/ associated to that company. These entities have been advised to exercise caution on compliance of SEBI Act, 1992 and all rules and regulations in future transactions.

External Risk Factors

The following factors which are beyond the control of the Company could have a negative impact on its performance. 1. Project delays: There could be project delays due to unfavourable climatic conditions or transportation

delays, which may affect the overheads and increase financing costs, on account of material, machinery and workforce that is employed at the construction site. Unlike in a manufacturing enterprise, the inventory and manpower cannot be re-shuffled between the projects, as it is difficult to move the resources quickly across the country.

2. Availability of raw materials: Inadequate supply of raw materials can adversely affect the performance of

the Company. 3. Government Policies: Adverse changes if any in the Government Policies in the Infrastructure Sector and

particularly the Road Sector could affect business prospects. 4. Other factors: Political, economic, social developments, natural calamity, acts of violence or war could

adversely affect the industrial and commercial operations in the country thereby affecting the business of the Company. Such events could also create a perception that investments in Indian companies involve a higher degree of risk, which could have an adverse effect on the market for securities of Indian companies.

5. Changes in technology: Changes in technology may render Company’s current Plant & Machineries

obsolete and require it to make substantial capital investments. 6. Change in political and regulatory environment: Global, economic and political factors that are beyond the

Company’s control influence the forecasts and directly affect performance. These factors include interest rates, rates of economic growth, fiscal and monetary policies of governments, inflation, deflation, consumer credit availability, consumer debt levels, tax rates and policy, unemployment trends, terrorist threats and activities, worldwide military and domestic disturbances and conflicts, and other matters that influence consumer confidence, spending and tourism. Increasing volatility in financial markets may cause these factors to change with a greater degree of frequency and magnitude. Increases in interest rates may increase the Company’s financing costs. The taxation system within the country still remains complex. Any change in the regulatory environment may have an impact on the business of the Company.

Notes to Risk Factors

1. Investors are advised to refer to “Basis for Issue Price” on page 19 of this Letter of Offer. 2. Net worth of the Company as on March 31, 2006 is Rs.3722.48 lakhs. The size of the Issue is Rs. 4646.55

lakhs. The net asset value per share (book value) as on March 31, 2006 is Rs.32.05 per share. 3. Cost of acquisition per share by the promoters :

Mr. Suhas Joshi Rs. 32.46 per share

Mr. Hemant Modi Rs. 42.08 per share

Kalpataru Power Transmission Limited Rs. 50.63 per share

4. Details of transactions of shares of the Company by the promoter during the last six months from the date of

filing the document with the Stock Exchange are:

xiii

a. Purchase

Name of Promoter /

PAC

No. of

shares

Date of

Purchase

Price per

share Rs.

Amount Rs.

115867 29/03/2006 231.45* 26816871.48 Kalpataru Power Transmission Ltd. (Promoter)

34133 31/03/2006 247.24 8439202.13

* KPTL has purchased 115867 equity shares on 29/03/2006 in different lots and at various rates between Rs. 228.14 to Rs. 233.16. The average rate has been considered.

b. Market Sale

There were no sale transactions by any Promoters or PAC during last six months.

5. The Company had entered into certain related party transactions for the financial years ending March 31, 2006, September 30, 2005 and March 31, 2004. The same has been disclosed in the Financial Statements- Related Party Transaction

6. The Lead Manager and the Company are obliged to keep this Letter of Offer updated and inform the public of

any material change/development.

1

SELECTED FINANCIAL INFORMATION

SUMMARY STATEMENT OF ASSETS AND LIABILITIES (AS RESTATED)

Rs. lakhs

As at March 31 Description As at March

31, 2006

As at

September

30, 2005 2004 2003 2002

Net Fixed Assets 5938.14 5108.81 4343.50 4003.54 4121.22

Investments 51.15 51.61 51.61 51.85 51.86

Deferred Tax Assets 20.60 95.74 - - -

Current Assets, Loans and Advances 11932.37 10454.69 9660.38 8770.40 8848.91

Less: Liabilities and Provisions 14219.77 12119.86 12404.25 10774.63 10601.80

Net Worth 3722.48 3590.99 1651.24 2051.16 2420.19

Represented by :

Shareholder’s Funds

Share Capital 1161.64 1161.64 464.66 464.66 464.66

Reserves 2560.85 2468.54 1186.58 1592.87 1966.63

3722.48 3630.18 1651.24 2057.53 2431.29

Less: Profit & Loss Account ( Debit Balance )

-

39.19 - - -

Less: Miscellaneous Expenditure (to the extent not written off or adjusted)

-

- - 6.36 11.09

Net Worth 3722.48 3590.99 1651.24 2051.16 2420.19

STATEMENT OF PROFITS AND LOSSES AS RESTATED

Rs. lakhs

For the year ended March 31, Particulars For the six

months

period ended

March 31,

2006

For the eighteen

months period

ended September

30, 2005

2004 2003 2002

Total Income 14331.06 35311.27 18573.38 21082.42 24473.46

Expenditure 13412.11 34106.72 17816.07 19357.39 22691.32

Profit/ (Loss) before interest, depreciation, tax & extra-ordinary items

918.95 1204.55 757.31 1725.03 1782.14

Interest 493.10 1689.09 1075.33 1091.05 1095.01

Depreciation 201.04 531.64 315.84 305.05 293.37

Profit/ (Loss) before Tax & Extra-ordinary Items

224.81 (1016.18) (633.86) 328.93 393.76

Less : Extra ordinary expense - 966.70 - - -

Add: Extra ordinary income - 209.00 - - -

Profit/ (Loss) before tax 224.81 (1733.88) (633.86) 328.93 393.76

Taxation (Previous Year) - - - 16.97 -

Taxation (Current Year) - - - 36.00 30.11

Deferred Tax Provision 75.14 (627.46) (229.89) 71.46 24.69

Fringe Benefit Tax 18.18 10.55 - - -

Net Profit/ (Loss) after tax 131.49 (1156.97) (403.97) 204.50 338.96

2

GENERAL INFORMATION

Dear Shareholder(s), Pursuant to the resolutions passed by the Board of Directors of the Company at its meeting held on May 2, 2006 and by the Shareholders at the Annual General Meeting held on June 17, 2006, it has been decided to make the following offer to the Equity Shareholders of the Company:

ISSUE OF 46,46,550 EQUITY SHARES OF Rs. 10/- EACH AT A PREMIUM OF Rs. 90/- PER EQUITY

SHARE AGGREGATING RS. 4646.55 LAKHS TO THE EQUITY SHAREHOLDERS ON RIGHTS

BASIS IN THE RATIO OF TWO (2) EQUITY SHARES FOR EVERY FIVE (5) EQUITY SHARES

HELD ON THE RECORD DATE i.e. SEPTEMBER 21, 2006 (“ISSUE”). THE ISSUE PRICE IS 10

TIMES THE FACE VALUE OF THE EQUITY SHARE.

Registered Office of the Company:

JMC Projects (India) Limited Registration No.: 04-8717 Registered Office: A-104, Shapath-4, Opposite Karnavati Club, S. G. Road, Ahmedabad – 380 051, India Tel: 91-79- 3001 1500 Fax: 91-79-3001 1600/1700 E-mail: [email protected] Website: www.jmcprojects.com Address of Registrar of Companies, Gujarat Dadra & Nagar Haveli: ROC Bhavan, Opp. Rupal Park Society, Near Ankur Bus Stand, Naranpura, Ahmedabad – 380013.

Board of Directors

Name of Director Designation

Vijay Choraria Chairman

Hemant Modi Vice Chairman

Suhas Joshi Managing Director

M.D. Khattar Managing Director

Ajay Munot Director

Kamal Jain Director

Narsinhbhai Patel Director

Mahendra G Punatar Director

For more details regarding the Directors please refer to “Management” on page 33 of this Letter of Offer. Company Secretary & Compliance Officer Ashish Shah A-104, Shapath –4 Opposite Karnavati Club, S.G. Road Ahmedabad -380051 Tel: 91-79- 3001 1500 Fax: 91-79-3001 1600/1700 Email: [email protected] Investors may contact the Compliance Officer for any pre-Issue/post Issue related matter.

3

Legal Advisors to the Company

Singhi & Co. Advocates, Solicitor & Notary 7-8, Premchand House Annexe, Ashram Road, Ahmedabad – 380 009 Tel:91-79-26588336; Fax:91-79-26587536 Email:[email protected]

Bankers of the Company

Oriental Bank of Commerce “Neel Kamal”, Opp: Sales India Ashram Road Ahmedabad – 380 009 Tel: 91- 79-27542029 Fax: 91-79-27541113 The Karur Vysya Bank Limited Motilal Centre, Ashram Road Ahmedabad – 380 009 Tel: 91-79-27546247 Fax: 91-79-27546087 State Bank of India “Paramsiddhi Complex” Opp: V S Hospital, Ellisbridge Ahmedabad – 380 006 Tel: 91-79-2658 5623 Fax: 91-79- 26581512

Andhra Bank 41, Parimal Society, CG Road Ahmedabad – 380 006 Tel: 91-79-2646 0945 Fax: 91-79-26460947 Lead Manager to the Issue

Inga Advisors Private Limited

A-404, Neelam Centre,Hind Cycle Road,Worli, Mumbai – 400 030. Tel: 91-22-24982937, 24982919, 24982954 Fax No.:91-22-24982956 Contact Person: Ms. Roopa Parameswaran Email: [email protected] Website: www.ingaadvisors.com

4

Bankers to the Issue

Industrial Development Bank of India

IDBI Complex, Off C.G.Road Ellisbridge Ahmedabad -380006 Tel: +91-79-26431902/1909 Fax: +91-79-26565105 Email: [email protected] Registrar to the Issue

Intime Spectrum Registry Limited C-13, Pannalal Silk Mills Compound L.B.S. Marg, Bhandup (West) Mumbai 400 078 Tel: 91-22-2596 0320 Fax: 91-22-2596 0329 Contact Person: Ms. Awani Punjani Email:[email protected] Auditor of the Company

Sudhir N Doshi & Co.

Chartered Accountants 22, Empire Tower, 2nd Floor, Adjoining Associated Petrol Pump, C. G. Road, Ellisbridge, Ahmedabad – 3800 006 Tel: 91-79-2644 9403

Credit Rating

This being an issue of Equity Shares, no credit rating is required.

5

CAPITAL STRUCTURE

Capital Structure as on September 5, 2006

* Warrants were allotted on September 9 2005 vide Letter of Offer dated June 20 2005. The conversion ratio of these warrants is 1:2 i.e. two (2) warrants will get converted into one (1) Equity Share. The warrant conversion period commenced from September 9, 2006 and will close on March 8, 2007. ** The share premium account post conversion of warrants cannot be determined as the warrant conversion shall be at a discount of 10% to the average daily closing market price of the shares during the three calendar months immediately preceding the month in which the warrant conversion is exercised or the floor price of Rs. 50/- per share whichever is higher. # As on March 31, 2006, as per the audited Balance Sheet.

Description Aggregate

Nominal Value

(Rs.)

Aggregate Value

at Issue Price

(Rs.)

A Authorised Share Capital

2,00,00,000 Equity Shares of Rs. 10/- each

20,00,00,000

B Issued, Subscribed and Paid up Share Capital 1,16,16,375 Equity Shares of Rs. 10/- each

11,61,63,750

C Present Issue being offered to the existing

shareholders through this LOO

46,46,550 Equity shares of Rs. 10/- each at a premium of Rs. 90/- i.e. at a price of Rs. 100/- each

4,64,65,500

46,46,55,000

D Paid up Capital after the present issue 1,62,62,925 Equity Shares of Rs. 10/- each Upon conversion of warrants * 1,85,86,172 Equity Shares of Rs. 10/- each (assuming full conversion)

16,26,29,250

18,58,61,720

**

E Share Premium Account

♦ Existing Share Premium Account #

♦ On Issue of Equity Shares

♦ On conversion of warrants

24,68,54,194 41,81,89,500

**

6

Notes to Capital Structure

1. Shareholding pattern as on September 8, 2006 (Pre and Post Issue)

Pre Issue Rights Issue Post Issue* Category

No. of shares % to total No. of shares No. of

shares*

% to total

PROMOTER GROUP

Promoters

KPTL 5795999 49.90 2318400 8114399 49.90

Hemant Modi 172804 1.49 69122 241926 1.49

Suhas Joshi 56654 0.49 22662 79316 0.49

Sub- Total (a) 6025457 51.87 2410183 8435640 51.87

PAC

Nina Shishir Modi 67500 0.58 27000 94500 0.58

Sonal Hemant Modi 2500 0.02 1000 3500 0.02

Ami Hemant Modi 5000 0.04 2000 7000 0.04

Rasilaben Vinodchandra Modi 3199 0.03 1280 4479 0.03

Varsha Hiren Gandhi 1875 0.02 750 2625 0.02

Sub- Total (b) 80074 0.69 32030 112104 0.69

Total Promoters (a+b) 6105531 52.56 2442212 8547743 52.56

Non- Promoter Holding

Mutual Funds and UTI 4244 0.04 1698 5942 0.04

Pvt. Corporate Bodies 898278 7.73. 359311 1257589 7.73

Indian Public 4261157 36.68 1704463 5965620 36.68

NRIs and OCBs 290211 2.50 116084 406295 2.50

Others 56954 0.49 22782 79736 0.49

Sub-total (c) 5510844 47.44 2204338 7715182 47.44

Grand Total (a+b+c) 11616375 100.00 4646550 16262925 100.00

* Warrants were allotted on September 9 2005 and warrant conversion period commenced on September 9, 2006 and will close on March 8, 2007. Equity Shares that would be allotted pursuant to conversion of the said warrants are not considered in the Post Issue shareholding as the conversion of warrants is optional.

7

2. None of the Promoters and persons forming part of the Promoter Group have been restrained from

accessing the capital market for any reasons by SEBI or any other authorities.

3. Details of Promoters’ shares pledged with Banks/Financial Institutions

No shares have been pledged.

4. The promoters have confirmed vide their letter of intent dated July 12, 2006 that they intend to subscribe to the full extent of their entitlement in the issue.

In case of undersubscription the promoters either jointly or severally undertake to subscribe to such undersubscribed portion of the Issue. As a result of this subscription and consequent allotment, the promoters may acquire equity shares over and above their entitlement in the issue, which may result in their shareholding in the Company being above their current shareholding. This subscription and acquisition of such undersubscribed shares by the promoters, if any, will not result in change of control of the management of the Company and shall be exempt in terms of proviso to Regulations 3(1) (b) (ii) of the SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 1997. As such, other than meeting the requirements indicated in Objects of the issue (refer “Particulars of the Issue”), there is no other intention / purpose for this issue, including any intention to delist the Company, even if, as a result of allotments to the Promoters through this Issue, the Promoter shareholding in the Company exceeds their current shareholding.

5. The Promoters have given an undertaking that in case the Rights Issue of the Company is completed with

their subscribing to Equity Shares over and above their entitlement and as a result, if the public shareholding in the Company after the Rights Issue falls below the “permissible minimum level” on the basis of which the securities of the Company continue to be listed, they will either individually or jointly with other Promoters make an offer for sale of their holdings so that the public shareholding is raised to the “permissible minimum level” within a period of 3 months from the date of allotment in the proposed Issue, as per the requirements of sub-clause 17.1 and 17.2 of SEBI (Delisting of Securities) Guidelines, 2003 or as per any amendment thereto or any other period as may be directed by SEBI or any appropriate authority.

6. Details of transactions in Equity Shares by the Promoter and Promoter Group during the last six

months

a. Purchase

Name of Promoter /

PAC

No. of

shares

Date of

Purchase

Price per

share Rs.

Amount Rs.

115867 29/03/2006 231.45* 26816871.48 Kalpataru Power Transmission Ltd. (Promoter)

34133 31/03/2006 247.24 8439202.13

* KPTL has purchased 115867 equity shares on 29/03/2006 in different lots and at various rates between Rs. 228.14 to Rs. 233.16. The average rate has been considered.

b. Market Sale

There were no sale transactions by any Promoters or PAC during last six months.

8

Highest and Lowest price details for above market purchases and sales transactions

Rs. per share

Purchases Sales Name of Promoter / PAC

High Low High Low

Kalpataru Power Transmission Ltd. (Promoter)

247.24 228.14 Not Applicable

7. Top Ten shareholders

a. Top ten Shareholders as on date of filing the Letter of Offer

b. Top ten Shareholders as on ten days prior to filing the Letter of Offer

S.No. Name of the Shareholder No. of Shares % of total capital

1 Kalpataru Power Transmission Limited 5795999 49.90 2 Hemant Modi 172804 1.49 3 Mukul Agrawal 150757 1.30 4 Dr Sanjeev Arora 135300 1.16 5 Bishwanath Prasad Agrawal 78876 0.68 6 Nina Modi 67500 0.58 7 Suvarna Commercial Private Limited 66325 0.57 8 Suhas Joshi 56654 0.49 9 Ashish Choudhary 55000 0.47

10 Pinkky Shah 54000 0.46

c. Top ten Shareholders two year prior to filing the Letter of Offer

S.No. Name of The Shareholder No. of Shares % of total capital

1 Suhas Joshi 553775 11.92

2 Hemant Modi 472696 10.17

3 Anubhav Aggarwal 426104 9.17

4 Sonal Hemant Modi 188866 4.06

5 Ishverlal K. Modi 187125 4.03

6 Madhuri Suhas Joshi 173197 3.73

7 Maltiben Vasantrao Joshi 128613 2.77

8 Minar Investments And Finance Pvt. Ltd. 76317 1.64

9 Nina Modi 67500 1.45

10 Arun Sarabhai Sheth 45000 0.97

S.No. Name of the Shareholder No. of Shares % of total capital

1 Kalpataru Power Transmission Limited 5795999 49.90

2 Hemant Modi 172804 1.49

3 Mukul Agrawal 150757 1.30

4 Dr Sanjeev Arora 134300 1.16

5 Bishwanath Prasad Agrawal 78876 0.68

6 Nina Modi 67500 0.58

7 Suvarna Commercial Private Limited 66325 0.57

8 Suhas Joshi 56654 0.49

9 Ashish Choudhary 55000 0.47

10 Pinkky Shah 54000 0.46

9

8. The total number of shareholders as on September 8, 2006 is 8929. 9. The present Issue being a Rights Issue, as per clause 4.10.1(c) of extant SEBI guidelines, the requirement of

Promoters’ contribution and lock-in are not applicable. 10. The Company has received a sanction for a bridge loan of Rs. 1000 lakhs from Karur Vysya Bank for

purchase of capital goods. As on September 6, 2006, the Company has availed Rs. 575.53 lakhs of the sanctioned bridge loan. It has been utilized for purchase of capital equipment. The Company proposes to repay the bridge loan from the proceeds of the present Rights Issue. The tenure of the loan is six months and the applicable interest rate is 10.00% p.a (BPLR-2.50) which is to be serviced on monthly basis. The loan is to be repaid within four months from the date of the first disbursement. During the period between the date of filing of the Letter of Offer and Issue closing date, the Company may avail the balance bridge loan of Rs. 424.47 lakhs which will also be repaid out of the proceeds of the Rights Issue.

11. The Promoters and Directors of the Company and Lead Managers of the Issue have not entered into any

buy-back, standby or similar arrangements for any of the securities being issued through this Letter of Offer.

12. The terms of issue to Non-Resident Equity Shareholders/Applicants have been presented under the section

“Terms of the Issue” on page 187 of this Letter of Offer. 13. At any given time, there shall be only one denomination of the Equity Shares of the Company. 14. The Company has 46,46,493 outstanding warrants which are convertible into 23,23,247 equity shares at the

option of the warrant holder during the conversion period (September 9, 2006 and March 8, 2007). The Company also has a one time call option during the conversion period. As per the terms of the warrant conversion, allotment of these shares would commence only in October 2006. The rights entitlement has been computed on 116,16,375 equity shares, the outstanding share capital as on the record date (September 21, 2006).

15. The Company does not have any partly paid Equity Shares 16. The Company has not issued any shares out of the revaluation reserves. 17. The Company has complied with the provisions of chapter XV of the SEBI guidelines. In terms of

provisions 15.1.10, a certificate duly signed by the issuer company and counter signed by the Company Secretary in practice has been submitted to SEBI on February 26, 2000 certifying compliance of all terms and conditions (as provided in the guidelines) for issue of 15,48,850 bonus shares.

18. There has been no issue of shares for consideration other than cash except to the extent of Bonus Shares

issued to the existing shareholders by capitalisation of free reserves. 19. The Company as well as major shareholders have duly complied with the provisions of Chapter II of SEBI

(SAST) Regulations, 1997 but with a delay for the years 1997-2002. The Company has filed necessary disclosures on March 31, 2003 under the SEBI Regularisation Scheme, 2002. The filings for the subsequent years i.e. March 31, 2003, 2004, 2005 and 2006 were done on April 8, 2003 and September 23, 2003 (for dividend), April 12, 2004 and April 14, 2005 and April 12, 2006 respectively.

20. No further issue of capital by way of issue of bonus Equity Shares, preferential allotment, rights issue or

public issue or in any other manner which will affect the capital of the Company, except on account of conversion of warrants upto a maximum of 23,23,247 Equity Shares, shall be made during the period commencing from the filing of the Letter of Offer with the SEBI till the Equity Shares issued under this Letter of Offer have been listed or application moneys are refunded on account of the failure of the Issue.

10

Further, presently the Company does not have any proposal, intention, negotiation or consideration to alter the capital structure by way of split / consolidation of the denomination of the shares / issue of shares on a preferential basis or issue of bonus or rights or public issue of Equity Shares or any other securities within a period of six months from the date of opening of the present Issue.

However, if the business needs of the Company so require, the Company may alter the capital structure by way of split / consolidation of the denomination of the shares / issue of shares on a preferential basis or issue of bonus or rights or public issue of shares or any other securities during the period of six months from the date of listing of the Equity Shares issued under this LOO or from the date the application moneys are refunded on account of failure of the Issue, after seeking and obtaining all the approvals which may be required for such alteration.

11

OBJECTS OF THE ISSUE The main objects clause and objects incidental or ancillary to the main objects of the Memorandum of Association of the Company enable the Company to undertake its existing activities and the activities for which the funds are being raised through this Issue. The total fund requirements of the Company are given below:

Particulars Rs lakhs

Purchase of Capital Equipment* 3257

Repayment of short term loan from UTI Bank Ltd. 750

Working Capital Margin 2025

Issue Expenses 50

Total 6082

* The Company has availed a bridge loan of Rs. 575.53 lakhs from Karur Vysya Bank Ltd. and has utilized the same to purchase capital equipments. The said bridge loan will be recouped from the proceeds of the present Issue. The requirement of funds for the purposes described above and use of the proceeds from this Issue in the manner detailed above are based on internal management estimates and have not been appraised by any bank or financial institution. In view of the competitive and dynamic nature of the industry in which the company operates, the company may have to revise its business plan from time to time and consequently its fund requirement may also change. This may include rescheduling of capital expenditure programs, starting unplanned new projects and increase or decrease in the capital expenditure for a particular business unit vis-à-vis current plans at the discretion of the Board. In case of any variations in the actual utilization of funds earmarked for the above activities, increased fund deployment for a particular activity will be met from internal accruals of the Company and by raising additional resources as may be decided by the Board of Directors.

Means of Finance

Particulars Rs. lakhs

Proceeds from the present Rights Issue 4646.55

Internal Accruals 36.11

Equipment Advance 1399.34

Total 6082.00

The internal accrual of Rs. 36.11 lakhs has been fully utilized towards capital expenditure and issue expenses.

Details of Utilisation of Funds

1. Purchase of capital equipment The projects undertaken by the Company fall under three main categories namely: Industrial projects, Building projects and Infrastructure projects. These projects require huge investments in capital equipment at regular intervals. However these expenses are in the normal course of the business. The Company intends to expand its presence in infrastructure projects like roads, railways, etc. The work on hand including Joint Venture contracts as on July 31, 2006 is Rs. 80638 lakhs. The Company has bid for various projects to the tune of approximately Rs. 134636 lakhs. The Company has budgeted a sum of Rs. 4007 lakhs towards capital expenditure. This includes equipments and machineries worth Rs. 700 lakhs which have not been identified. Depending upon the requirements/ bids awarded, the Company will place orders for the machineries.

12

List of Equipments for which purchase orders have been placed and part payment has been made.

List of Equipments Details of Purchase Order Raised for Equipments

Payments

made

Sr.

No. Equipment No. Rs lakhs PO No. Name of Supplier No. Rs lakhs

Rs

lakhs

1 JCB 4 71.19 17/2006-07 & 20/2006-07

L&T Case Equi. / JCB India Ltd.

4 71.19 70.18

2 Bitumen Bowser / Distributor

2 12.48 Agreement copy Dodsal Private Ltd 2 12.48 12.48

3 WMM Senser Paver

3 107.24 7/2006-07 & 10/2006-07

Gujarat Apollo Equipments

3 107.24 97.94

4 WMM Plant 1 24.11 6/2006-07 Gujarat Apollo Equipments

1 24.11 22.18

5 Asphalt Senser Paver (HM paver)

2 71.24 Agreement copy Dodsal Private Ltd. 2 71.24 67.68

6 Pneumatic Tyre Roller

2 23.40 Agreement copy Dodsal Private Ltd. 2 23.40 22.23

7 Concrete Batching Plant - Mobile (20 Cum & 15 Cum )

2 45.85 36/2006-07 & 37/2006-07

Maxocrete equipments

2 45.85 45.85

8 Transit Mixer 9 203.87 28/2006, 29/2006, 62/2006

& 6/3/2006

Greaves Cotton Ltd./Ashok Leyland

6 90.61 71.09

9 DG Set - 40 KVA 6 20.32 32/2006 Powerica Ltd. 2 6.77 6.77

10 DG Set- 125 KVA

6 36.29 24/2006 & 25/2006

Powerica Ltd. 4 24.19 12.10

11 DG Set - 725 KVA

1 39.41 76/2006 GMMCO Ltd. 1 39.41 35.68

12 Crusher - 200 TPH

2 489.74 PUZZ / 2005-06 & MECH / 2005-

06

Puzzolana Machinery Fabricators / Mechtech Engg.

2 489.74 313.79

13 Weigh Bridge - 100 Tons

1 8.95 66/2006 Essae Digitronics Pvt. Ltd.

1 8.95 7.16

14 Weigh Bridge - 50 Tons

1 4.50 67/2006 Essae Digitronics Pvt. Ltd.

1 4.50 3.60

15 Kerb Casting Machine

1 7.86 8/2006-07 Apollo Construction Equip.pvt.Ltd.

1 7.86 7.21

13

List of Equipments Details of Purchase Order Raised for Equipments

Payments

made

Sr.

No. Equipment No. Rs lakhs PO No. Name of Supplier No.

Rs

lakhs

Rs

lakhs

16 Shuttering / Scaffolding

Lot 551.00 44/2006-07 , 42/2006-07, 43/2006-07 ,

82/2006, 90/2006, 72/2006, 74/2006,

NH7/shut/06/097 & 028, 45/2006-07, 46/2006-07,

47/2006-07, 48/2006-07 49/2006-07 50/2006-07 54/2006-07 55/2006-07 56/2006-07 57/2006-07

MOR-BDMC00027,

MOR-BDMC00026,

MOR-CHAR00013

Tata Steel Ltd. / Max International / Hi Reach Construction / Scaff India / Kacharu Panchal (labour) / N Mohamed Kasim (Labour) / S M S Trading / Economic Traders, Devam Enterprises/Reliance Steel Traders/Jaygauri Fabricators/United Scaffolding Pvt. Ltd./Polytech Industries/Hi-reach construction Equipment Pvt. Ltd./Furquan Steel Works/I S Steels/New Age Scaffolds Pvt. Ltd./Saff India/Shah Steel & Tubes/amar Tubes (P) Ltd./grace Castings Pvt. Ltd./N R Steel Corporation/Ambica Iron and Steel Re-rolling Mill

Lot 379.02 157.00

17 Surveying Equipment Set

Lot 6.00 MOR-DRGL00003

MOR-GLFH00008

K K Sales, Lawrence & Mayo (I) Pvt. Ltd.

Lot 1.04 1.04

18 Bar Cutting M/c. 7 10.81 TMRP / KI/871, 34-A/2006

Modern Equipments, Ispat Infrastructure India Pvt. Ltd.

3 4.79 3.25

19 Tough Rider 11 28.60 9-A/2006-07 Universal Sales Corporation

8 20.80 5.20

20 Vibratory Compactor - 850 Kg.

2 4.16 1/2006 Surelia Engg. Works 2 4.16 4.16

21 FO Heating system for Batch mix plant

1 10.00 84/2006 Gujarat Apollo Equipments

1 10.00 9.78

22 Misc. Machinery & Tools

Lot 33.00 Lot

6.81 6.81

23 Loader 3 107.06 68/2006 & 16/2006-07

Gunangxi Liugong / Caterpillar India Pvt. Ltd.

3 107.06 88.41

14

List of Equipments Details of Purchase Order Raised for Equipments

Payments

made

Sr.

No. Equipment No. Rs lakhs PO No. Name of Supplier No.

Rs

lakhs

Rs

lakhs

24 Motor Grader 8 332.02 JMC/ SANY/2005-06

SANY Heavy Indust.India Pvt.Ltd.

8 332.02 109.39

25 Reversible Drum Mixer

5 21.35 87/2006 Universal Sales Corporation

1 4.27 4.27

26 Concrete Pump 5 83.75 26/2006 SANY Heavy Indust.India Pvt.Ltd.

1 16.75 16.75

27 Hydra Crane 4 40.59 23/2006-07 & 13/2006-07 &

12/2006-07

Action Construction Equip. Ltd.

4 40.59 40.59

28 Vibratory Compactor - 2 MT

2 22.92 27/2006 Greaves Cotton Ltd. 2 22.92 22.92

29 DG Set- 25 KVA 5 11.78 19/2006-07 Supernova Engg. Ltd.

1 2.36 2.36

38/2006-07 & 39/2006-07

Xiangtan jianglu imp & exp co.ltd. / SA Syncon Infrastructure India Pvt. Ltd.

1 51.01 30 Tower crane 1

51.01

59/2006-07 Jiangsu Zhengxing Construction Machine Co. Ltd.

2 58.25

4.80

31 Mobile Tower Crane

2 47.91 14/2006-07 Action Construction Equip. Ltd.

1 23.95 23.95

32 Computers-HW/SW/Connectivity

Lot 30.00 IT/064/2006, IT/065/2006, IT/066/2006, IT/067/2006, IT/068/2006 IT/069/2006 IT/070/2006, IT/071/2006, IT/072/2006, IT/073/2006, IT/075/2006, IT/076/2006, IT/077/2006,

TMRP/PO/B/126/06-07,

TMRP/PO/A/240/06-07

Silvertouch Technologies Ltd. Compulink Systems, Trident Infotech Services, Mascom Electronics Pvt. Ltd., Dixit Infotech Services, Kavish Engieer, Tulip IT Services Ltd., HV Computers, MU_Tech Computers

Lot 13.99 3.15

Total (A) 2558.41

2127.34 1343.01

15

List of Equipments for which purchase orders have been placed but no payment have been made.

List of Equipments Details of Purchase Order raised for Equipments

Sr.

No. Equipment No. Rs. lakhs PO No. Name of Supplier No.

Rs.

lakhs

1 Hot Mix Plant 2 316.01 4-A/2006-07 & 5/2006-07

Gujarat Apollo Equipments 2 316.01

2 Tandom Roller 1 19.97 15/2006-07 L&T Case Equi. 1 19.97

3 DG Set- 380 KVA

1 16.20 18/2006-07 Supernova Engg. Ltd. 1 16.20

4 Total Station 1 3.68 83/2006 Topcon South Asia Pte Ltd. 1 3.68

5 Laboratory Equipment

Lot 9.18 58/2006-07 EIE Instruments Pvt. Ltd. Lot 0.74

Total (B) 365.05

356.60

Equipments identified by the Company for which Purchase orders have not yet been placed

Sr. No. Equipment No. Rs lakhs

1 Batching Plant 3 105.00

2 Tipper- 20 MT 15 240.00

3 Welding M/c. 1 2.00

4 Compressor 1 1.00

5 Site Conveyance - Four Wheelers 6 30.00

6 Site Conveyance - Two wheelers 13 5.20

7 Equipments to be finalised based on present/bids awarded 700.00

Total (C) 1083.20

The Company has budgeted a capital expenditure of Rs. 4007 lakhs. The Company has placed orders for equipments worth Rs. 2483.94 lakhs and payment to extent of Rs. 1343.01 lakhs has been made. The Company has utilized internal accruals to the extent of Rs. 17.48 lakhs as well as the short term loan of Rs. 750 lakhs from UTI Bank Ltd. and the bridge loan of Rs. 575.53 lakhs towards this payment.

2. Repayment of Short Term Loan from UTI Bank.

The Company has availed a short term loan of Rs. 750 lakhs from UTI Bank Ltd. The Company proposes to repay this loan from the proceeds of the Issue which has been utilized towards purchase of capital equipment. Terms of the Loan are:

• Tenor: 6 months

• Date of Disbursement: June 15, 2006

• Interest Rate: PLR-4.00% p.a i.e. 9.00%. Interest to be serviced on monthly basis

• Repayment: Repayment in one bullet payment at the end of six months from date of disbursement

• Security: (1) Residual charge on the assets of the Company (2) Post dated cheque for the amount of Loan (3) Comfort letter for the loan extended from Kalpataru Power Transmission Limited

16

3. Working Capital Margin The work on hand as on July 31, 2006 was Rs. 80638 lakhs (includes Rs. 40119 lakhs through joint venture). With the large value addition to the contracts on hand and the Company’s plan to expand further, the requirement of long term working capital has been estimated as under:

Working Capital Calculations

Rs. lakhs

Particulars

2006-07

(Estimated)

2005-06

(Actual)

Raw Materials Inventory 2683 1467

Sundry Debtors 12267 8105

Loans & Advances 1606 1482

Cash & Bank Balances 933 879

Sub Total 17489 11933

Less :

Sundry Creditors 4780 7221

Other Current Liabilities 940 952

Sub Total 5720 8173

Net Working Capital Requirement 11769 3759

Working capital as on 31/03/2006 3759

Additional Working Capital Requirement 8010

Less: Balance fund based working capital limit available *4909

Financed by proceeds of this Rights Issue 2025

Financed by proceeds of Outstanding Warrant Conversion 561

Balance from Internal Accruals 515

* calculated based on the to-be enhanced limit of Rs. 6500 lakhs.

Assumptions for the Calculation of Working Capital Requirement

Assumptions 2006-07

(Estimated)

2005-06

(Actual)

Inventory Days 45 39

Debtor Days 100 106

Creditor Days for Materials 36 37

Creditor Days for Labour 30 51

Creditor Days for Expenses 17 32

Sources of finance for the working capital as at March 31, 2006

Particulars Rs lakhs

Fund Based Limits from Banks 1591

Unsecured loan from promoters and fixed deposit 1522

Project specific working capital loan from Banks in lieu of mobilization advance.

468

Internal accruals 179

Total Working Capital 3759

17

Details of existing working capital limits: Sanctioned Working Capital facilities as on August 31, 2006

Particulars Rs lakhs

Fund Based Limits from Banks Total

Oriental Bank of Commerce

Cash Credit 624

WCDL Foreign Currency & Rupee 2496 3120

The Karur Vysya Bank Ltd

Cash Credit 325

WCDL Foreign Currency & Rupee 1300 1625

State Bank of India*

Cash Credit 140

WCDL Foreign Currency & Rupee 700 840

Andhra Bank*

Cash Credit 75

WCDL Foreign Currency & Rupee 300 375

Total of Fund Based Limits 5960

Sanctioned Non- Fund Based Limits

Oriental Bank of Commerce

Bank Guarantee 15000

Sub Limit for Letter of Credit (1200) 15000

The Karur Vysya Bank Ltd

Bank Guarantee 10625

Sub Limit for Letter of Credit (1000) 10625

State Bank of India

Bank Guarantee 2400

Sub Limit for Letter of Credit (500) 2400

Andhra Bank

Bank Guarantee 800

Sub Limit for Letter of Credit (300) 800

Total Non Fund Based Limits 28825

* The credit limits from these banks are expected to be increased thereby taking the total fund based

limit upto Rs. 6500 lakhs

4. Issue Expenses The Issue expenses are estimated at Rs. 50 lakhs, comprising of fees and expenses payable to the Lead Manager to the Issue, Banker to the Issue, Registrar to the Issue, Auditor, Legal Advisor, printing and stationery expenses, advertising expenses and other statutory expenses like SEBI/ Stock Exchange fees and all other incidental and miscellaneous expenses for listing the Equity Shares on the Stock Exchange. The Company has already deployed Rs. 18.63 lakhs towards the issue expenses. The components of the Issue expenses are:

Particulars Rs. lakhs

Fees to Lead Manager, Legal Advisors & Auditors 23.53

Registrar’s Fee 1.10

Regulatory and Statutory expenses 5.43

Printing, stationery, postage and advertising 10.93

Miscellaneous & Contingencies 9.01

Total 50.00

18

The Company does not propose to utilize any part of the rights issue proceeds to repay loans taken from

the promoters/ relatives of the promoters/directors or their associate companies. No part of the Issue

proceeds will be paid as consideration to promoter, directors, key management personnel, associate or

group companies.

Schedule of Implementation/Deployment of Issue Proceeds

The details of funds utilized and proposed deployment of Issue proceeds are as follows: Rs. lakhs

Utilisation of funds Funds

utilized as on

Sept 6, 2006

Oct 06-Mar

07 April 07-

Sept 07 Oct 07-

Mar 08 Total

Purchase of Capital Equipments 593.01 1906.99* 457.00 300.00 3257.00

Working Capital Margin - 2025.00 - - 2025.00

Repayment of short term loan from UTI Bank Ltd. - 750.00 - - 750.00

Issue Expenses 18.63 31.37 - - 50.00

Total from rights issue proceeds 611.64 4713.36 457.00 300.00 6082.00

* Includes repayment of bridge loan from Karur Vysya Bank Ltd.

Sources & Deployment of Funds as on September 6, 2006

Particulars Rs. lakhs

A Deployment of Funds

Rights Issue Expenses 18.63

Purchase of Capital Equipment 1343.01

Total 1361.64

B Sources of Funds

Internal Accruals:

Rights Issue Expenses 18.63

Purchase of Capital Equipment 17.48 36.11

Short Term Loan from UTI Bank Ltd. 750.00

Bridge Loan from Karur Vysya Bank Ltd.

575.53

Total 1361.64

The above statement of sources of financing and deployment of funds have been certified by Sudhir N. Doshi & Co., Chartered Accountants, 22, Empire Tower, 2nd floor, Sheth C G Road, Ellisbridge, Ahmedabad – 380006, Membership No. 030539, vide their letter dated September 6, 2006.

Monitoring the use of funds There is no external monitoring agency appointed for the purpose of monitoring the use of funds. On a quarterly basis the audit committee and the board will review the use of funds. Interim Use of Funds Pending any use as described above, proceeds of the Issue shall be used by the Company for reduction of cash credit limits and invest the funds in high quality, interest/dividend bearing short term/long term liquid instruments including deposits with banks for the necessary duration. The Company may also deploy the proceeds of this Issue in temporarily reducing its exposure to working capital borrowings from banks and financial institutions. Such investments would be in accordance with the directives of the Board of Directors.

19

BASIS FOR ISSUE PRICE Qualitative Factors

• JMC has execution capabilities across a variety of construction segments including industrial, institutional, infrastructural, residential and commercial complexes.

• JMC has 20 years track record of project execution. It has executed major institutional buildings and projects on a turnkey basis, demonstrating an adequate integrating and project management capacity

• The Company is one of the leading companies in the Industrial and Factory building segment.

• The maximum bid capacity as on date of the Company for NHAI projects is Rs. 671.20 crore and the Company can execute individual NHAI projects upto Rs. 204.55 crore. Presently the Company is pre-qualified to bid for some of the road projects to be invited by NHAI & PWD of various states.

• Emerged as a player with autonomous offices at the following strategic locations: Mumbai, Chennai, Bangalore, Hyderabad and New Delhi.

• Repeat orders from prestigious customers like Asian Paints, Nirma, Cadila Healthcare, Bajaj Auto, IIM, Videocon, Prestige Group, Raheja Group, Mantri Group, etc.

• The company follows standard practices uniformly at all sites in accordance with the quality plans as laid down under ISO where each method statement is standardised. Records of all results are maintained and approved by the client.

Quantitative Factors

1. Adjusted Earnings Per Share (EPS)

Basic EPS Rs. Weight

12 months ended March 31, 2004 (8.70) 1

18 months ended September 30, 2005 (6.64)* 2

6 months ended March 31, 2006 2.26* 3

Weighted Average EPS --

*Annualised

2. Price/Earning Ratio (P/E) in relation to Issue Price at Rs. 100/- per share.

(a) Based on annualized EPS for the year ended March 31, 2006 – 44.25 (b) Industry P/E (i) Highest 229.30 (ii) Lowest 2.30 (iii) Average 34.10 Source: Capital Market Aug 28-Sept 10, 2006; Category: Construction 3. Return on Net Worth (RONW)

RONW (%) Weight

12 months ended March 31, 2004

(24.46) 1

18 months ended September 30, 2005

(21.48)* 2

6 months ended March 31, 2006 7.06* 3

Weighted Average RONW (7.70)

* Annualised

20

4. Minimum Return on Total Net Worth after Issue Needed to maintain EPS :4.39% 5. Net Asset Value (NAV) per Equity Share (a) As on March 31, 2006: Rs. 32.05 (b) After Issue: Rs. 51.46 (c) Rights Issue price: Rs. 100.00 6. Comparison with Financial Ratios of Peer Group

Accounting Ratios for the FY 2005-06 Name of the Peer Group

Company Book Value

Rs.

RONW % EPS Rs. P/E Ratio

(price as on

August 21,

2006)

JMC Projects (India) Limited* 32.00 7.06 2.26 38.40

BL Kashyap & Sons Ltd. 237.80 21.60 26.30 38.98

Era Constructions (India) Limited 124.00 20.20 14.60 14.10

Hindustan Construction Co. Ltd. 34.70 12.40 3.20 32.40

MSK Projects Limited 34.50 13.30 5.00 13.40

Nargarjuna Construction Co. Ltd. 91.10 16.40 9.90 24.50

Subhash Projects 26.10 4.60 6.80 14.50

Unitech Limited 2.80 35.00 0.80 138.60

Valecha Engineering Company Limited

170.40 11.60 12.20 13.30

Source: Capital Market Aug 28-Sept 10, 2006 * Information for JMC Project (India) Ltd. is based on six months period ended March 31, 2006 and RONW and EPS have been annualized.

7. Issue Price

In view of the reasons mentioned above, the Company and the Lead Managers to the Issue, in consultation with whom the premium has been decided, are of the opinion that the premium is reasonable and justified.

The face value of each Equity Share is Rs. 10 per Equity Share and the Issue Price of Rs. 100/- per Equity Share is 10 times the face value.

21

INDUSTRY OVERVIEW

Data in this section has been sourced from the following:

The ET Knowledge Series, Economic Times- Infrastructure & Construction Report, Press Information Bureau

and Midterm Appraisal of Tenth Five Year Plan, www.ibef.org and CMIE April’06, May’06 and June’06 and

other publicly available documents.

Overview

Construction activity is an integral part of a country’s infrastructure and industrial development and can be termed as the basic input for socio-economic development. It includes urban infrastructure, hospitals, schools, townships, offices, houses, commercial buildings, highways, roads, ports, railways, airports, power system, etc. The size of the construction industry in India is over $25 billion and accounts for more than 6% of the GDP. It is also the largest employer in the country after the agriculture sector, employing almost 18 million people. The Indian construction industry is riding on a growth wave and this wave is powered by the large spends on the ongoing infrastructure programs. The sectors contributing to high growth rates are power, transport, petroleum and urban infrastructure. The construction industry has linkages with several other sectors such as steel, cement, etc.

Sector wise break up of the industry