Bahasa

Halaman

Hukum

Electronic copy available at: http://ssrn.com/abstract=2384594

1

BAFFI Center on International Markets, Money and Regulation

BAFFI Center Research Paper Series No. 2014-149

Governance of the Single Supervisory Mechanism: Some Reflections

By Donato Masciandaro

and Maria J.Nieto

This Paper can be downloaded without charge from The Social Science Research Network Electronic Paper Collection:

http://ssrn.com/abstract=2384594

Electronic copy available at: http://ssrn.com/abstract=2384594

2

Governance of the Single Supervisory Mechanism: Some Reflections

Donato Masciandaro (Bocconi University and SUERF)

María J. Nieto1 (Bank of Spain)

1- Introduction:

Since the inception of the Euro, European policy makers have been increasingly

recognizing the ‘efficiency’ gaps in EU financial supervision against a background of a

decentralized institutional architecture for regulation, supervision and financial stability.

Recognition of this gap had led to tangible efforts to capture some of the potential

efficiency gains through legally binding mechanisms and policy coordination mechanisms

(i.e. European System of Financial Supervisors –ESFS-). That ongoing iterative process of

cooperation and coordination can be interpreted as having already internalized some of the

EU´s potential negative externalities of cross border banking (Nieto and Schinasi, 2007).

Nonetheless, the first global financial crisis since the Euro´s inception has highlighted the

limitations of the decentralized approach not only for prudential supervision but also for

bank resolution and its financing. In the face of the twin banking and sovereign crisis in

some Euro area countries, heads of state government representatives agreed on the Single

Supervisory Mechanism (SSM) involving the European Central Bank (ECB) for banks in

1 Donato Masciandaro ([email protected]); Maria J. Nieto ([email protected]). The views in this article do not

necessarily represent those of Banco de España or the Eurosystem. Any errors are our own. The original version of this article was published in 112 Revue D´economie Financiere, 51‐70 (4‐2013).

Electronic copy available at: http://ssrn.com/abstract=2384594

3

the euro area. The centralization of bank supervision is the first step in the banking union,

which should also encompass a single resolution regime, a deposit guarantee scheme and

liquidity assistance from the central bank (Huertas and Nieto, 2012). Banking union

heavily relies on the effectiveness of the centralized bank supervision in order to better

control safety net subsidies.

Our article reflects on the involvement of the ECB in bank supervision and the governance

arrangements of the new centralized supervisor that still rely on coordination along

different dimensions. The integration of bank prudential supervision in the ECB is in line

with the observed national developments in Europe after the inception of the crisis, which

highlighted the complementarities of information on banks´ liquidity and solvency. Also, it

aims to solve the problem of the lack of incentives to share information on the true financial

condition of banks among national supervisors, and strengthens the supervisory powers at

the center. Secondly, our article reviews the national bank supervisors’ governance

arrangements, highlighting critical individual criteria on which there has been lack of

convergence that would have helped to smooth coordination among bank supervisors in the

context of the crisis. Going forward, harmonization of governance arrangements would

align incentives between the ECB and national supervisors, which together form the SSM.

Both the ECB and the national supervisors are bound by the principle of cooperation

(Article 5).2 The ECB will be ultimate responsible for the effective and consistent

functioning of the SSM. Against this background, we analyze the governance

arrangements of the ECB as defined in the Council Regulation. We focus on the operational

2 At the time of writing, there is a final compromise text for the Council Regulation conferring specific tasks on the ECB concerning policies relating to the prudential supervision of credit institutions (16 April, 2013).

4

content of the independence and accountability arrangements as well as the implications of

those governance arrangements for more effective bank supervision.

In addition to this introduction, our article starts with a general review of the architecture of

bank supervision and the role of central banks as well as changes triggered by the current

financial crisis, describing also the trends in Europe (Section 2). We then proceed in

Section 3 with a discussion of the literature on governance of bank supervision with

particular emphasis on Europe. Section 4 presents and reflects on the governance

arrangements of the ECB as bank supervisor and ultimate responsible for the effective and

consistent functioning of the SSM. Section 5 concludes and makes some policy

considerations.

2- Architecture of financial supervision and the role of the central bank: Has the

financial crisis triggered changes?

Should central banks be in charge of pursuing financial stability through the

prudential oversight of individual banks (micro supervision)? The question is a long-

standing one. The abundant literature dealing with the central banks´ involvement in

prudential supervision does not seem to provide a unique response. Hence, it is not

surprising to observe that over time and across countries, the involvement of central banks

in prudential supervision (CBS) has varied. Therefore, in order to analyze the evolution of

the CBS, it is necessary to complete the economic analysis with a political economic one

that looks closely at the cost and benefit analysis of the policymaker, who ultimately

decides on the CBS.

5

On the one hand, micro prudential supervision is a task that historically has not

always been assigned to central bankers.3 Furthermore, the CBS had decreased over the

last two decades (the age of Great Moderation)4 On the other hand, during the decades

before the Great Moderation, several central banks were actively and deeply involved in

tightly pursuing structural policies,5 which were considered to be integrated in the overall

responsibility of the central bank liquidity management.

But going beyond historical patterns and focusing on the economic rationale of the

relationship between monetary and prudential supervision policies, it is possible to

disentangle the pros (“integration view”) and cons (“separation view”) of having monetary

and supervisory functions in the central bank?6

The central bank’s high involvement in supervision (“integration view”) is usually

supported by arguments related to the informational advantages and economies of scale that

derive from bringing all functions under the umbrella of the authority in charge of

managing liquidity.7 Having access to all the information on the banks´ financial situation

would help central bankers to be also more effective prudential supervisors i.e. greater CBS

brings potential efficiency gains.

At the same time, the economic literature acknowledges that central bankers as

liquidity managers also involved in prudential supervision can incur larger policy failure

costs (“separation view”). The risk of policy failure is endogenous with respect to the

3 Ugolini 2011. 4 See among others Bean 2011. 5 Cagliarini et al. 2010, Goodhart 2010, Bordo 2011, Toniolo 2011. 6 The integration versus separation approach was introduced in Masciandaro 2012. 7 See, among others, Bernanke 2011, Herrings and Carmassi, 2008, Klomp and de Haan 2009, Blanchard et al., 2010,

Blinder 2010, Lamfalussy 2010, Papademos 2010.

6

distribution of power: it exists only if the supervisor is the central bank acting as liquidity

manager. However, this risk could be differently motivated, shedding light on its various

sources.

First, moral hazard risk may increase if the supervisor can discretionally manage

banks’ liquidity.8

Secondly, in those cases in which the action of the central bank is discretionary, it

can increase the uncertainty in the markets.9 If the supervisor is the liquidity manager,

greater moral hazard and greater uncertainty may occur.

Thirdly, the central bank as prudential supervisor may incur reputational risks that

would negatively affect monetary policy.10 Also, it may incur distorted incentives for risk

taking as potential conflicts of interest between monetary policy and prudential supervision

emerge.11

Fourthly, the central banker as liquidity manager may be captured by the constituent

banks, instead of pursuing social welfare. The capture risk is highest when the central bank

is also the prudential supervisor,12 since the banking industry may be more willing to

capture supervisors which are powerful.13

8 Masciandaro 2007, Lamfalussy 2010. 9 Taylor 2010. 10 Papademos 2010 and Ioannidou 2005. 11 Goodhart and Shoenmaker 1995, Blinder 2010, Gerlach et al. 2009, Masciandaro et al. 2011. 12 Barth et al. 2004, Djankov et al. 2002, Quintyn and Taylor 2002, Boyer and Ponce 2011a and 2011b. 13 Boyer and Ponce 2011a and 2011b.

7

Finally, the centralization of banking supervision and monetary policy in the central

bank can create an overly powerful bureaucracy.14

The empirical studies are similarly inconclusive, although we should acknowledge

that there is a dearth of studies and those available are very recent. The integration view

finds empirical support in Arnone and Gambini (2007) who study the degree of compliance

with Basel standards to analyze the role of the central bank as main banking supervisor in

different countries. In turn, the separation view seems to find support in Eichengreen and

Dincer (2011), whose conclusions indicate that the performance of financial markets is

better when the supervision is delegated to an independent agency different from the central

bank. But results also show some evidence in favor of supervisory consolidation being

established within the central bank. Finally, Čihák and Podpiera (2007) show that the

location of the unified supervisor (bank, insurance and securities) whether inside or outside

the central bank does not have a significant impact on the quality of supervision.

In sum, the economic literature comparing the integration and separation views is

inconclusive regarding the optimal involvement of central banks in prudential supervision

(CBS). Hence, it is not possible to conclude that the integration view is superior to the

separation view, or vice versa.

Against this background, in order to explain the changing patterns of central banks

involvement in supervision, we focus on the political economy approach.15 The

policymaker’s actual choices related to the assignment of supervisory tasks are conditional

14 Padoa Schioppa, 2003; Masciandaro, 2007; Blinder 2010; Oritani ,2010; Goodhart, 2010; Eichengreen and Dencer

2011. 15 Masciandaro 2006, 2007 and 2009; Masciandaro and Quintyn, 2008.

8

on the economic and institutional environment existing at a given time, which in turn,

determine the political weights put on the pros and cons of the policy choices.

This theoretical framework is based on two hypotheses. First, gains and losses of a

given central bank institutional setting are variables computed by the incumbent

policymaker, who maintains or reforms the supervisory regime following his/her own

preferences. Secondly, policymakers are politicians, and as such, they are held accountable

at elections for how they have managed to please voters. The main difference among

politicians is their different concern on which constituents they wish to please in the first

place. Therefore the CBS is likely to change over time following the political preferences

favoring a stronger (or weaker) supervisory power delegation to the monetary authority.

Moving from the theoretical to the institutional analysis and reviewing whether the

role of central banks as supervisor has changed in the last two decades, towards integration

rather than separation, a question arises: How can the CBS be evaluated? Is it possible to

track the CBS evolution in a measurable way, using the qualitative narrative of the actual

central bank regimes to build up quantitative analyses? Masciandaro (2006, 2007 and

2008), and Masciandaro and Quintyn (2009 and 2011) have built quantitative indicators on

the level of central bank involvement in supervision: Central Bank as Financial Supervisor

(CBFS index).16 The authors show that the CBS has changed before and after the financial

crisis. Before the inception of the crisis, the “separation view” between central banking and

prudential supervision was dominant. Against the background of the political economy

model, the authors argue that on average policymakers gave more weight to the expected

16 We refer to these authors for a detailed description of the index methodology and scope.

9

gains of specializing the central bank as monetary authority and giving prudential

supervision powers to a different agent, as compared to the benefits of delegating both

functions to the central bank and facing the potential costs derived from the risk of policy

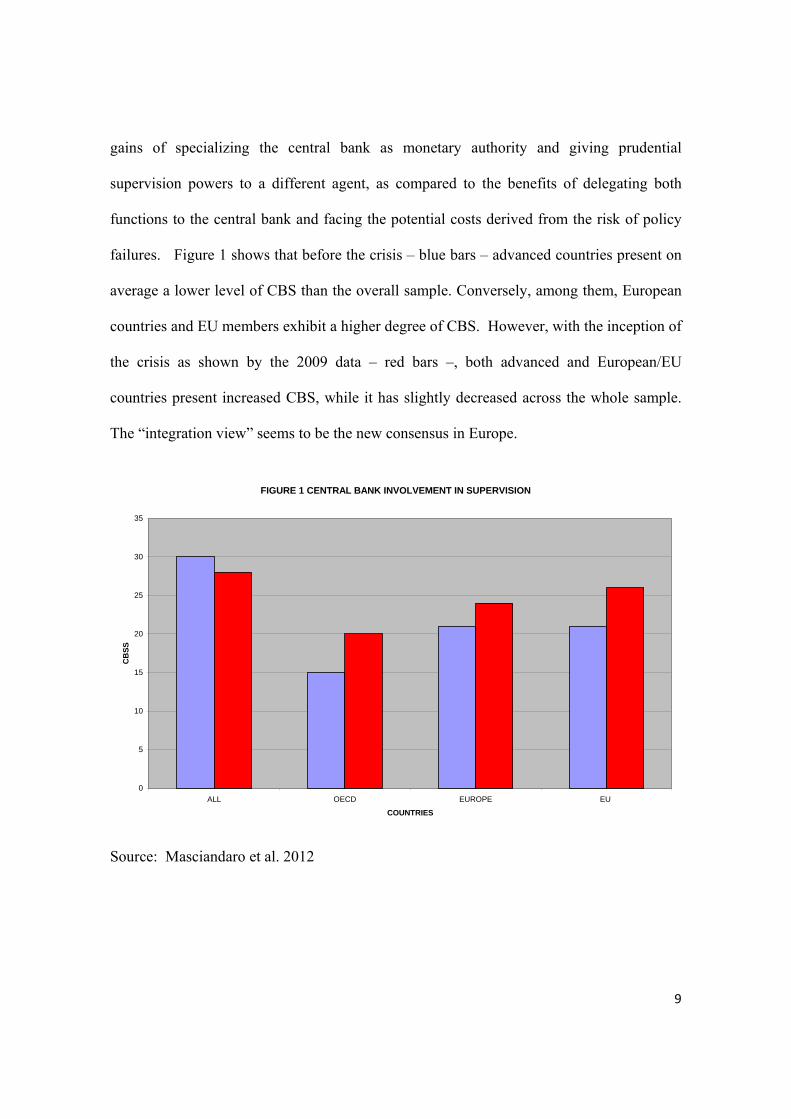

failures. Figure 1 shows that before the crisis – blue bars – advanced countries present on

average a lower level of CBS than the overall sample. Conversely, among them, European

countries and EU members exhibit a higher degree of CBS. However, with the inception of

the crisis as shown by the 2009 data – red bars –, both advanced and European/EU

countries present increased CBS, while it has slightly decreased across the whole sample.

The “integration view” seems to be the new consensus in Europe.

FIGURE 1 CENTRAL BANK INVOLVEMENT IN SUPERVISION

0

5

10

15

20

25

30

35

ALL OECD EUROPE EU

COUNTRIES

CB

SS

Source: Masciandaro et al. 2012

10

3- A review of the architecture of financial supervision and governance

In their quest for an effective financial supervision, policy makers have focused not only on

the revision of the national supervisory architecture but also on the governance of

supervision. This section focuses on the latter.

At the international level, the first international initiative on governance of supervision was

the Basel Core Principles for Effective Banking Supervision (BCP) issued in 1997. The

objective of the BCPs was to promote best practices of bank´s prudential regulation and

supervision. The BCPs were complemented a few years later by similar codes for the

supervision of securities operations (IOSCO) and insurance supervision (IAIS).

Best practices of supervision were paving the way for good supervisory governance in

order to withstand various sources of supervisory capture: political, industry and self-

capture. 17 Das and Quintyn (2002) and Quintyn (2007) proposed a governance framework

consisting of four reinforcing pillars (independence, accountability, transparency and

integrity), while Rochet (2004) used a theoretical model to argue in favor of establishing

independent and accountable banking supervisors. Additional work on supervisory

independence (Quintyn and Taylor, 2003) and accountability (Hüpkes et al., 2005) spelled

out necessary operational components of these governance pillars. These authors conclude

that independent supervisors need a detailed set of accountability arrangements to offset the

fact that it is not possible to define a very specific contract for financial supervision, given

the broad range of contingencies that can occur in supervision (see also Schuler, 2003, and

17 The work on supervisory governance complemented the BCPs which contain some of these elements, but are mainly focused on the necessary components of the regulatory and supervisory frameworks. The 2006 BCP revision took on board more elements of operational independence, accountability and transparency as best practices. On these issues see Masciandaro et al. 2012.

11

Dijkstra, 2010). A wide consensus exists that the accountability of financial supervision is

more complex than for monetary policy because supervisors have multiple and harder to

measure objectives; they operate in a multiple principals environment (in the principal-

agent sense) and supervisors have extensive legal powers that should go hand in hand with

their legal immunity.

Quintyn, Ramirez and Taylor (2007) made a first attempt to rate supervisors´ independence

and accountability based on their legal frameworks.18 Their work is particularly interesting

because it spells out the different dimensions of those two components of supervisory

governance that are emerging as best practices in the literature. Supervisors´ independence

has three dimensions that deal with its institutional setting (i.e. legal basis that explicitly

spells out that the supervisor is independent; the political independence of the chairman and

senior executives as well as the members of the board, which should be a collective

decision-making body; the legal immunity of the staff for actions taken in good faith and

the clear criteria for dismissal of the President); its independence in regulating and

supervising financial institutions (i.e. issuance of legally binding prudential regulations

free from political independence; sole right to issue and withdraw licenses as well as to

impose sanctions and enforce supervisory actions) and its budgetary independence (i.e.

budget process and staff salary structure that is independently set from the government as

it should be the supervisor hiring policy; supervisor funding based on fees from the

supervised entities).

18 We refer to these authors for details on the quantitative assessment of the criteria of independence and accountability.

12

Supervisors´ accountability also has three dimensions towards the two branches of State as

well as to the general public, particularly to markets. More specifically, supervisors are

accountable towards the political/executive branch (i.e. its mandate and objectives are

defined in the enabling legislation); the law envisages regular and ad hoc hearings before

the relevant Parliament committee, which are not delegated to the ministry of finance; and

the agency presents the annual report to the executive branch); towards the judicial branch

(i.e. supervised entities have the right to appeal supervisory decisions to courts and distinct

judicial processes are in place to handle these appeals, the law provides for penalties for

faulty supervision) and towards the public –transparency- (i.e. public disclosure of the

supervisor´s mission statement as well as policies and decisions; regular public reports and

the possibility for inquiries from the general public; ex ante consultation process before

consumers, supervised entities and the public at large; external and internal audit of the

supervisor).

European supervisors have, on average, the highest governance ratings by worldwide

standards. Moreover, Quintyn, Ramirez and Taylor (2007) show that Europeans have on

average improved their governance arrangements more than the rest of the world.

Masciandaro, Nieto and Quintyn (2009) analyze the convergence of governance of

supervision among EU countries and conclude that there is a fair convergence on

independence towards the highest standards, while there is clearly a lesser degree of

compliance and convergence on accountability in line with developments in other non-EU

countries. Furthermore, the levels of independence and accountability seem to be only

weakly correlated, which seems to be explained by the fact that both are determined by

different explanatory variables: independence is related to the level and quality of

13

democracy as well as demonstration effects, while accountability is driven by the quality of

the public sector and the level of supervisory unification. Hence, differences in

independence and accountability scores are observed according to the location of

supervision. Supervisors located in central banks have the highest level of independence,

particularly political and budgetary independence, but the least developed accountability

arrangements particularly towards the judicial branch. Also, supervisors in central banks

are in general more likely to be publicly funded, and European bank supervisors are more

oriented towards the public funding regime (Masciandaro, Nieto and Prast, 2007). In turn,

supervisors located outside the central banks show lower overall degrees of independence

(although they score high on their autonomy to issue prudential regulation and impose

sanctions) and do have more sophisticated accountability arrangements. Also, they are

more likely to be funded via a levy on the regulated banks.

The launching of the euro and years later the financial crisis acted as a catalyst to enhanced

coordination among national supervisors and across financial supervisors (banking,

insurance and securities). In 2010, the European System of Financial Supervision (ESFS)

was set up to fulfill those objectives and to develop a single rule book.

The ESFS mechanism of supervisory coordination has coexisted with national supervisors

that have retained full powers with respect to the oversight of their domestic financial

system. This complex structure of multiple agents and principals has implicitly demanded

certain governance convergence. However, upward harmonization of governance criteria

has not been a consideration for European policy makers. As of 2009, the most critical

individual criteria for independence and accountability on which there was lack of

convergence, were the inexistent or insufficient legal protection for supervisors, the

14

presence of politicians on their decision-making bodies, the shared responsibilities with the

government or courts regarding the right to license and withdraw licenses (independence)

as well as the weak judicial accountability. High convergence on these criteria would have

helped to smooth European supervisory coordination at the time of the crisis. As

Masciandaro, Nieto and Quintyn (2009) conclude, weakness and divergence of governance

potentially undermine national and European supervisors trust on their financial reporting,

sanctioning and ultimately intervention powers. Weak governance and lack of convergence

towards the highest standards could have increased forbearance of national supervisors,

making them prone to industry or government capture and resulting in difficulties in

pursuing a level playing field among supervisors.

4- Single Supervisory Mechanism: architecture, coordination and governance

arrangements

4.1 SSM and the “integration view” of bank supervision in the ECB

The launching of the SSM is in line with the recent developments in member states in the

present crisis, when the “integration view” of central banking and bank supervision seems

to be the new consensus. Such integration is envisaged in the TFEU (Article 127.6), which

contemplates that the ECB could take “specific powers in the area of banking supervision”

for the euro area countries. The political agreement on the SSM distinguishes between

significant and non significant institutions. With regard to the first, the ECB is vested with

ample tasks (Article 4), which include issuance of regulations, guidelines or general

instructions to national competent authorities that perform day to day supervision and adopt

decisions (Article 5.5). When necessary, the ECB may on its own initiative, exercise

15

directly all the relevant powers over one or more banks in order to ensure consistent

application of high supervisory standards.

National supervisors participating in the SSM may or may not be within their respective

central banks since the degree of unification within the central bank varies in the euro area.

While integration will happen from the institutional point of view, the separation of

monetary policy and bank supervision functions is materialized in the principle of no

interference and organizational separation between both functions and the need to regulate

the exchange of information between them. Also, the responsible bodies are different and

there is an organizational separation of the staff working on monetary policy and prudential

supervision. The Supervisory Board where all participating national supervisors are

represented is responsible for the “planning and execution of the tasks conferred upon the

ECB” in the realm of bank supervision. According to the TFEU (Art. 129), the ultimate

power of decision rests on the Governing Council of the ECB. As a consequence, the

Supervisory Board proposes to the Governing Council complete draft decisions that would

be considered adopted unless the Governing Council objects within a predefined time

period that varies in line with the urgency of the required decision. Such objection shall be

reasoned and monetary concerns deserve particular attention. Ex post, a mediation panel in

which ECB representatives participate without vote aims at resolving differences of views

in any objection of the Governing Council to a draft decision by the Supervisory Board.

4.2 Coordination within the SSM, with non-euro area supervisors and among

sectoral supervisors

16

The effective and consistent functioning of the SSM requires close cooperation in those

three dimensions. The framework of coordination between the ECB and national bank

supervisors participating in the SSM varies depending on whether the banks are considered

significant or less significant. This is, whether the ECB is exclusively competent for

supervision or the national supervisors are responsible for adopting decisions. Under both

circumstances, the ECB is exclusively responsible for licensing (also withdrawal of

banking licenses) and authorization of mergers and acquisitions. Very close cooperation

will be particularly needed on sanctioning; exchange of banks´ financial information and

methodologies of on-site and off-site supervision. Such cooperation would be facilitated by

a common accounting framework for the valuation of assets, liabilities and off site balance

sheet items in line with the international financial standards; a single set of supervisory call

reports; a common set of supervisors´ remedial powers as the situation deteriorates and a

single closure rule for banks. Even if these conditions are met, incentives for cooperation

will not be fully aligned to the extent that safety nets remain national. This is, until the

Banking union is completed.

Moreover, the ECB will closely coordinate with bank supervisors in EU countries whose

currency is not the euro if both the national bank supervisors and the ECB so agree under

two conditions (Article 6): National supervisors will abide by the guidelines or requests

issued by the ECB including the exchange of information and will adopt relevant national

legislation to ensure that national supervisors will be obligated by any measure requested

by the ECB. Such close cooperation ensures that supervised entities in all participating

countries (although not directly supervised by the ECB) in the SSM, whether they belong to

the euro area or not, are treated the same. Furthermore, it brings closer the perimeter of the

17

Single Rule Book and the SSM. The agreement of close cooperation is reversible and it

can be terminated at the request of either party.

Last but not least, the ECB will need to coordinate with the ESFS19 (Article 3). This is, the

three sectoral supervisory authorities: the European Banking Authority (EBA), the

European Insurance and Occupational Pension Authority (EIOPA), and the European

Securities Authority (ESA). The launching of the SSM crystallizes the sectoral approach of

financial supervision in Europe, with separate supervisory systems for the banking,

securities and insurance industries as enshrined in the framework of the ESFS.

Particularly close coordination between the SSM and the banking regulators will be needed

in developing a true single rule book, which is fundamental to the success of the SSM. The

Council Regulation envisages ex ante coordination of the SSM with the EU Commission

participating as observer on the Supervisory Board.

The SSM is limited to the banks of the participating member states. The functional

separation of supervision for securities and insurance, which will remain under national

authorities, may result in regulatory arbitrage in spite of the SSM, given the fungibility of

modern finance. Improved financial stability may demand further centralization of

securities and insurance supervision as well as single rule books for these sectors.

4.3 Governance

This section focuses on the two main dimensions of supervisory governance. This is

independence and accountability of the SSM.

19 As proposed in the Larosière Report to the European Commission in early spring of 2009. The SSM will also coordinate with the European Systemic Risk Board.

18

Independence

Institutional independence

The ECB central role in the SSM has the backing of the TFEU. The Proposed Council

Regulation confers the ECB specific tasks relating to the prudential supervision of credit

institutions. Its objective is to contribute to the safety and soundness of credit institutions

and the stability of the financial sector within the EU and each member. As it is generally

the case for supervisors, the objectives are multiple and difficult to measure and this goes to

the most important difference between the objective of monetary policy and financial

supervision. An additional dimension of complexity rises from the fact that the objective

is also multiple in geographic scope and that may, at certain point in time, potentially create

conflicts. Nonetheless, this possibility is limited by the strong European mandate of the

Supervisory Board and particularly the Chair and Vice-Chair. Furthermore, the Council

Regulation (Article 16) states that the ECB shall act independently from the influence of

national interest and market participants, when carrying out its supervisory tasks and

meeting those objectives. It also refers specifically to the independence of the Supervisory

Board in its decision making. Hence, the importance of having national supervisors free

from the interference of politicians that could favor national interests, for example,

applying forbearance.

The TFEU (Article 340) envisages that the ECB should make good any damage caused by

its staff in the performance of their duties. However, neither the TFEU nor the Council

Regulation refer to the ECB staff legal immunity or the supervisors’ legal immunity when

exercising their job in good faith. Also, the Council Regulation does not make it a

19

requirement for the national supervisors in the SSM. Legal immunity is a conditio sine qua

non for effective supervision that limits the possibility of forbearance. In the SSM,

however, national supervisors´ forbearance is much limited to the extent that the ECB can

take responsibility of the direct supervision of any particular bank at any time.

The political independence of the supervisory process could be hindered by the process of

appointment of the Chair and Vice Chair of the Supervisory Board because it requires the

approval of the European Parliament, which is a political body. In turn, the requirement of

an implementing decision of the Council by qualified majority20 strengthens the European

mandate of the Chair and Vice Chair of the Supervisory Board. Limitations of the term of

office of the Chair as well as the provision for his/her removal as a result of serious

misconduct could serve as a mechanism of ex post accountability. However, the value of

this arrangement is limited considering that, first, misconduct cannot be interpreted as

including bad performance of his/her statutory functions, and second, the dismissal would

require the European Parliament approval.

Regulatory and Supervisory independence

In line with the European tradition,21 the ECB tasks are concentrated on bank supervision.

The ECB´s enforcement is envisaged to be proactive. It can take action on its own

initiative in accordance with its mandate. In order to enable the ECB to effectively enforce

bank´ prudential supervision, the ECB and national supervisors in the SSM will coordinate

an extensive supervisory tool kit. A high degree of coordination, if not full centralization,

is expected for licensing, sanctioning and approval of M&As.

20 Without taking into account the vote of the member states that are not participating in the SSM. 21 Only a minority of EU countries do have the autonomy to define their prudential regulations.

20

The ECB can directly impose administrative (pecuniary) sanctions in case of breach of

Union law (including directives and regulations on prudential regulation) or EC regulations

and decisions. The ECB could not only require national supervisors to use certain early

intervention and precautionary powers but also require them to impose sanctions for

breaches of national legislation, which confers specific powers that are currently not

required by Union Law to ensure prompt corrective action and effective supervision within

the SSM.

Budgetary independence

Consistent with the trend toward more private funding, the ECB bank supervision function

will be funded through annual fees from the supervised banks in the euro area, including

branches of banks outside the euro. The ECB enjoys a high level of independence to set the

resources needed for effective bank supervision, protecting itself from political interference

including from national authorities. However, funding structures based on fees are

vulnerable, particularly if risk based, to the possibility that the supervisor´s income will be

most limited when the banks are under strain (prociclicality). Also, there is no

harmonization of funding of supervision throughout the countries participating in the SSM

and this is recognized in the Council Regulation. Coordination with national supervisors

(i.e. high quality staff with competitive salaries) may be impaired by large discrepancies in

funding fee structures.

Accountability

Political accountability

21

The ECB as bank supervisor is accountable ex post to the political authorities (European

Council) and the legislature (Parliament) for the appropriateness of its actions and

execution of the stated objectives in its mandate (Article 17). The EU Parliament and

Council influence on the supervisory activities ought to be exerted primarily through its law

making powers. Accountability towards the executive branch (Council) also aims at having

them informed about developments in the banking sector and not to influence the

supervisory decision process. Moreover, such accountability towards the executive branch

should be understood in light of the arrangements to appoint the Chair and Vice Chair of

the Supervisory Board, which strengthen their position in relation to the supervised banks.

The formal channels of communication include a regular report on the execution of the

ECB supervisory tasks and its funding based on fees charged to the banks. The Council

Regulation (Article 17) envisages the right of inquiry of the EU Parliament (legislative

branch) as well the Eurogroup (executive branch).

The accountability is also towards the national parliaments of the countries participating in

the SSM. The rationale is justified by the fact that bank resolution and the safety net are

still national responsibilities. National tax payers can be called upon financially to support

their banks. All of this provides ground for the harmonization of accountability

arrangements of bank supervisors integrated in the SSM.

Judicial accountability

The need for judicial accountability mechanisms must be understood as a counterweight

against the sanctioning and enforcement powers conferred to the ECB.

22

The ECB as bank supervisor is accountable ex post to the Court of Justice of the European

Union for the legality of its actions (TFEU Article 263). The ultimate objective of the

judicial review is to ensure that the bank supervisor acts within its powers as established in

the Regulation. Judicial accountability applies to the process (procedural) and, in some

cases, to outcome (substantive). Substantive accountability is often limited to review of

legality, ensuring that discretion is not exercised in bad faith or for incorrect purposes.

From the view point of the recipients of the ECB decisions, due process for adopting

supervisory decisions demands that the ECB, before taking decisions, should give the

opportunity of being heard by those that are the subject of the decision. Procedural

accountability, for example, requires that the parties be given access to the documents on

which the ECB relies in taking the decision. Such right to access is envisaged in the

accountability of the ECB as a supervisor (Article 17). The observance of due process is

not applicable if financial stability is at risk. In this case, the due process should be ex post

taking the decision.

In addition to the judicial review, the Council Regulation (Article 17) also envisages an

Administrative Board of Review within the ECB and composed of individuals with proven

track record of relevant knowledge and experience in supervision matters. This panel will

address the requests regarding the review of decisions taken by the supervisor such as

licensing; sanctioning and approval of M&As. The review procedure provides for the

Supervisory Board to reconsider former draft decisions suspending its application. It is

time bound and it does not have a suspensive effect of the Board decisions,22 both

22 Decisions are considered “provisional” in the Council Regulation.

23

characteristics are consistent with prudential supervisory efficiency. Moreover, this review

process is without prejudice to the right to bring proceedings before the Court of Justice of

the EU.

An additional accountability arrangement aims to supervisory liability by a failure in the

exercise of the ECB supervisory responsibilities. Yet, the liability for faulty supervision is

limited by the need to ensure the ECB independence so that there are limitations on this

liability in line with the damage compensation envisaged in the TFEU (Article 340).

Only a few EU countries have well developed mechanism of supervisors´ judicial

accountability. Masciandaro, Nieto and Quintyn (2009) link weak judicial accountability

practices to forms of industry capture.

Accountability towards the banks and the general public

The ECB´s function as ultimate body responsible for the effective and consistent

functioning of the single supervisory system heavily relies on cooperation with national

supervisors within the SSM. Hence, the importance of making public the framework of

cooperation as envisaged in the Council Regulation (Article 5), which is a form of

accountability before banks, national supervisors and the general public. The nature of the

prudential supervisory process as compared to the regulatory one does not lend itself to

consultation with the stakeholders and the public at large. Consultation with supervised

entities focuses on the definition of the annual supervisory fees and it aims at making a

better assessment of costs and benefits of the proposed fee structures.

Accountability of the budgeting process is one of the most relevant dimensions of

transparency. Bank supervision should be financially independent. The ECB will have a

24

separate budget of income and expenditures for its supervisory tasks, which will be clearly

segregated from the budget corresponding to its monetary policy function (Article 23).

This accountability arrangement is consistent with good supervisory governance because

supervision will be financially independent and self-supporting. It also strengthens the

separation between monetary policy and bank supervision. Furthermore, it is an

improvement from the existing practices among supervisors housed in central banks that

present a single financial statement whether the supervisory tasks are financed by

segniorage or by supervised institutions. In this regard, there is no harmonization in the

EU.

The accounts will have annual periodicity and they will be subject to ex post financial audit

before the European Court of Auditors that will also examine the operational efficiency of

the management of the ECB supervisory tasks and whether the financial reports represent a

true and fair view.

5- Conclusions and policy reflections

In sum, the ECB enjoys a sufficient level of independence as bank supervisor seemingly to

“piggy back” on the arrangements ensuring monetary policy independence. However,

such independence would be further enhanced by:

- The exercise of self-restraint by the European Parliament in its responsibilities

of appointment and dismissal of the Chair and Vice Chair of the Supervisory

Board so that political considerations derived of their supervisory decisions do

not interfere with their European mandate;

25

- The necessary addition of supervisors’ legal immunity when exercising their job

in good faith.

At the same time, the ECB enjoys strong arrangements for accountability providing public

oversight, maintaining legitimacy and enhancing integrity and performance. The ECB

accountability arrangements show better governance than the average of the EU supervisors

located in central banks, which fall behind on judicial accountability and transparency.

Nonetheless, accountability would be strengthened by clear rules of dismissal of the Chair

and Vice Chair of the Supervisory Board that specify ex ante the terms of bad performance

of his/her statutory functions that would not necessarily be subject to the European

Parliament approval.

Also, the ECB funding based on annual fees from supervised banks is quite distinctive

from the bank supervisors located in the central banks, further strengthening separation

from monetary policy.

Further harmonization of governance arrangements among the national supervisors in the

euro area and, more generally, in the EU, would facilitate the coordination of the SSM

within and with other national bank supervisors that are not euro area participating

members, particularly at the inception when the safety nets are national and banking union

is not completed yet.

26

6- References

* Arnone, M. and A. Gambini (2007), Architecture of Supervisory Authorities and Banking Supervision. In: Masciandaro D. and Quintyn M. (Eds.), Designing Financial Supervision Institutions: Independence, Accountability and Governance, Edward Elgar, Cheltenham, 262-308.

* Barth, J.R., G. Caprio, and R. Levine (2004), ‘Bank regulation and supervision: What works best?’, Journal of Financial Intermediation, 117(13), 205–248.

* Bean C. (2011), Central Banking Then and Now, Sir Leslie Melville Lecture, Australian National University, Canberra, mimeo.

* Bernanke, B. (2011), The Effect of the Great Recession on Central Bank Doctrine and Practice, Board of Governors of the Federal Reserve System, mimeo.

* Blanchard O., Dell’Ariccia, G. & Mauro, P. (2010), Rethinking Macroeconomic Policy, IMF Working Paper Series, WP 10.

* Blinder, A. (2010), ‘How central should the central bank be’, Journal of Economic Literature, 48(1), 123–133.

* Bordo M. (2011), Long Term Perspectives on Central Banking, in A.Berg et al. (eds.), What is a Useful Central Bank?, Norges Banks Occasional Papers, n.42.

* Boyer, P.C. and J. Ponce (2011a), ‘Central banks and banking supervision reform’, in S. Eijffinger and D. Masciandaro (eds.), The Handbook of Central Banking, Financial Regulation and Supervision after the Crisis, (ed.), Edward Elgar, Cheltenham.

* Boyer, P.C. and J. Ponce (2011b), Regulatory Capture and Banking Supervision Reform, Journal of Financial Stability, vol.8, 206-217.

* Cagliarini A., Kent C. and Stevens G. (2010), Fifty Years of Monetary Policy: What Have We Learned?, in C. Kent and M. Robson (eds), 50th Anniversary Symposium, Conference Volume, Reserve Bank of Australia.

* Čihák, M. and Podpiera, R. (2007), Experience with Integrated Supervisors: Governance and Quality of Supervision. In Masciandaro D. and Quintyn M. (eds.), Designing Financial Supervision Institutions: Independence, Accountability and Governance, Edward Elgar, Cheltenham, 309-341.

* Das, U.S., Quintyn, M., 2002. Financial Crisis Prevention and Crisis Management—The Role of Regulatory Governance. In Litan, R., Pomerleano, M., Sundararajan, V. (Eds.), Financial Sector Governance: The Roles of the Public and Private Sectors. Brookings Institution Press, Washington, DC.

27

* Dijkstra, R., 2010. Accountability of financial supervisory agencies: An Incentive Approach. Journal of Banking Regulation, 11 (2), 115-128.

* Djankov, S., R. La Porta, F. Lopez-de Silanes, and A. Shleifer (2002), The regulation of Entry, Quarterly Journal of Economics, 117(1), 1–37.

* Eichengreen B. and Dincer N. (2011), Who Should Supervise? The Structure of Bank Supervision and the Performance of the Financial System, NBER Working Paper Series, National Bureau of Economic Research, n.17401.

* Gerlach S. (2010), Are the Golden Years of Central Banking Over? Monetary Policy after the Crisis”, 38th Economic Conference, Austrian National Bank, Vienna, mimeo.

* Goodhart C. (2010), The Changing Role of Central Banks, BIS Working Papers, n.326.

* Goodhart, C. and D. Schoenmaker (1995), ‘Should the functions of monetary policy and banking supervision be separated?’, Oxford Economic Papers, 47, 539–560.

* Hermings, R. J. & Carmassi, J. (2008). The Structure of Cross – Sector Financial Supervision, Financial Markets, Institutions and Instruments, vol.17, n.1.51-76.

*Huertas, T. and María J. Nieto (2012). Banking Union and Bank Resolution: How should the two meet? EU Vox (http://www.voxeu.org/article/banking-union-and-bank-resolution-how-should-two-meet)

* Hüpkes, E., Quintyn M., Taylor, M., 2005. The Accountability of Financial Sector Supervisors: Principles and Practice. European Business Law Review 16 (6), 1575-1620.

* Klomp J. and J. De Haan (2009), Central Bank Independence and Financial Stability, Journal of Financial Stability, 5, 321-338.

* Ioannidou V.P. (2005), Does Monetary Policy affect the Central Bank’s Role in Bank Supervision?, Journal of Financial Intermediation, 14, 58-85.

* Lamfalussy A. (2010), The Future of Central Banking under Post – Crisis Mandates, BIS Papers, n.55.

* Masciandaro, D. (2007). Divide et Impera: Financial Supervision Unification and Central Bank Fragmentation Effect, European Journal of Political Economy, 23, No.2, June, 285-315.

* Masciandaro, D., Pansini R.V. and Quintyn M. (2011), The Economic Crisis: Did Financial Supervision Matter?, IMF Working Paper Series, n.261, Washington, International Monetary Fund.

* Masciandaro, D. (2006). E Pluribus Unum? Authorities Design in Financial Supervision: Trends and Determinants, Open Economies Review, 17 (1), 73-102.

28

* Masciandaro, D. (2007). Divide et Impera: Financial Supervision Unification and Central Bank Fragmentation Effect, European Journal of Political Economy, 23, No.2, June, 285-315.

* Masciandaro (2009), Politicians and Financial Supervision outside the Central Bank: Why Do They Do it?, Journal of Financial Stability, 5, n.2, 124-147.

* Masciandaro (2012), Back to the Future? Central Banks as Prudential Supervisors in the Aftermath of the Crisis, European Company and Financial Law Review, 12, No.2, 112-130.

* Masciandaro D., Nieto M. and Quintyn (2011), Exploring Governance of the New European Banking Authority: a Case for Harmonization?, Journal of Financial Stability, .Vol. 7, n.4. 204-214.

* Masciandaro D., Nieto M. and Prast H. (2007), Who Pays for Banking Supervision? Principles and Trends, Journal of Financial Regulation and Compliance, 2007, Vol. 15, n.3.

* Masciandaro, D. and Quintyn, M. (2008). Helping Hand or Grabbing Hand? Politicians, Supervisory Regime, Financial Structure and Market View, North American Journal of Economics and Finance, 153-174.

* Masciandaro, D. and Quintyn, M. (2009), Reforming Financial Supervision and the Role of the Central Banks: A Review of Global Trends, Causes and Effects (1998-2008), CEPR Policy Insight, Centre for Economic Policy Research, n.30.

* Masciandaro, D. and Quintyn, M. (2011), Who and How: Measuring the Financial Supervision Architectures and the Role of the Central Banks. The Financial Supervision Herfindahl Hirschman Index, Journal of Financial Transformation, n.32, 9-14.

* Nieto, Maria J. and Garry J. Schinasi (2007), EU Framework for Safeguarding Financial Stability: Towards an Analytical Benchmark for Assessing its Effectiveness. IMF Working Papers, 07/260

* Oritani, Y. (2010). Public Governance of Central Banks: An Approach from New Institutional Economics, BIS Working Papers, Bank for International Settlements, n. 299.

* Padoa Schioppa, T. (2003). Financial Supervision: Inside or Outside the Central Banks?, In: Kremers J., Schoenmaker D., Wierts P., Financial Supervision in Europe, Edward Elgar, Cheltenham, 160-175

* Papademos L. (2010), Central Bank Mandates and Governance Arrangements, BIS Papers, n.55.

* Quintyn, M. and M. Taylor (2002), Regulatory and Supervisory Independence and Financial Stability, IMF Working Paper Series, n.46, Washington, International Monetary Fund.

29

* Quintyn, M., Taylor, M., 2003. Regulatory and Supervisory Independence and Financial Stability. CESifo, Economic Studies 49 (2), 259-294.

* Quintyn M., Ramirez, S., Taylor M.W., 2007. The Fear of Freedom. Politicians and the Independence and Accountability of Financial Supervisors. In Masciandaro, D., Quintyn M. (Eds.), Designing Financial Supervision Institutions: Independence, Accountability and Governance. Cheltenham/Edward Elgar, United Kingdom/Northampton, Massachusetts.

* Rochet, J.C., (2004), Macroeconomic Shocks and Banking Supervision, Journal of Financial Stability, 1(1), 93-110.

Schuler, M., 2003. Incentive Problems in Banking Supervision–The European Case. Centre for European Economic Research, ZEW Discussion Paper 03-62.

Taylor J. (2010), Macroeconomic Lessons from the Great Deviation, 25th NBER Macro Annual Meeting, mimeo.

* Toniolo G. (2011), What is a Useful Central Bank? Lessons from Interwar Years, in A.Berg et al. (eds.), What is a Useful Central Bank?, Norges Banks Occasional Papers, n.42.

* Ugolini S. (2011), What Do We Really Know About the Long Term Evolution of Central Banking?, Working Paper Series, n.15, Norges Bank.

Top Related

Copyright © 2022 FDOKUMEN