Bahasa

Halaman

Hukum

REGULAR MEETING OF THE

BOARD OF COMMISSIONERS OF THE OKLAHOMA CITY HOUSING AUTHORITY

TELECONFERENCE 1700 Northeast Fourth Street

Oklahoma City, Oklahoma 73117 March 24, 2021

9:00 a.m.

AGENDA This meeting will be held by teleconference for the Board of Commissioners of the Oklahoma City Housing Authority (OCHA), as authorized by SB 1031 and the state of emergency declared by Gov. Kevin Stitt. If a member of the public wishes to participate, the meeting can be accessed online at:

https://zoom.us/j/95006293123?pwd=S2c1ZlgyZmpkd3MxMWdlb2UyQm1JZz09 (which allows the presentations to be viewed)

or by telephone at: (301) 715-8592 Meeting number: 950 0629 3123. The OCHA Commissioners will be appearing via teleconference, as follows: Dr. Jerry L. Steward (via teleconference) Ms. Alvah Boyd (via teleconference) Ms. Connie Mashburn (via teleconference) Ms. Lillie Swope (via teleconference)

Written materials for this meeting are available to the public at: https://cms7.revize.com/revize/ocha/BOC_Agenda_3-24-2021.pdf

If a member of the public wishes to speak under the agenda item “Citizens to be Heard,” please email [email protected] prior to the meeting time with your name, address, phone

number, and the topic on which you would like to speak. The meeting will be recorded.

1. Call to Order and Comments – Chair Jerry Steward.

A. Recognition of Leslie Batchelor

2. Announcement of Filing of Meeting Notice and Posting of the Agenda in Accordance with the Oklahoma Open Meeting Act.

3. Roll Call – Sherry Hearn, Executive Assistant

4. For Action: Approval of the Consent Docket A. Minutes of the Regular Meeting of the Board of Commissioners, February 24, 2021

5. For Action: Resolution No. 8-21 ratify Emergency Plumbing Repairs at AMP 106, Northeast Duplexes;

AMP 104, Scattered Sites; AMP 102, Oak Grove; and AMP 115, Reding Senior Center. Presented by Melanie Buckley.

6. For Action: Resolution No. 9-21 approving Revisions to the Admissions and Continued Occupancy Policy (ACOP) for Public Housing. Presented by Matt Mills.

go to TOC

7. For Action: Resolution No. 10-21 approving Revisions to the Administrative Plan for Section 8. Presented by Richard Marshall.

8. For Action: Resolution No. 11-21 approving Award of Contract to American Elevator for Five (5) Year Elevator Maintenance Service Contract. Presented by Mike Helms.

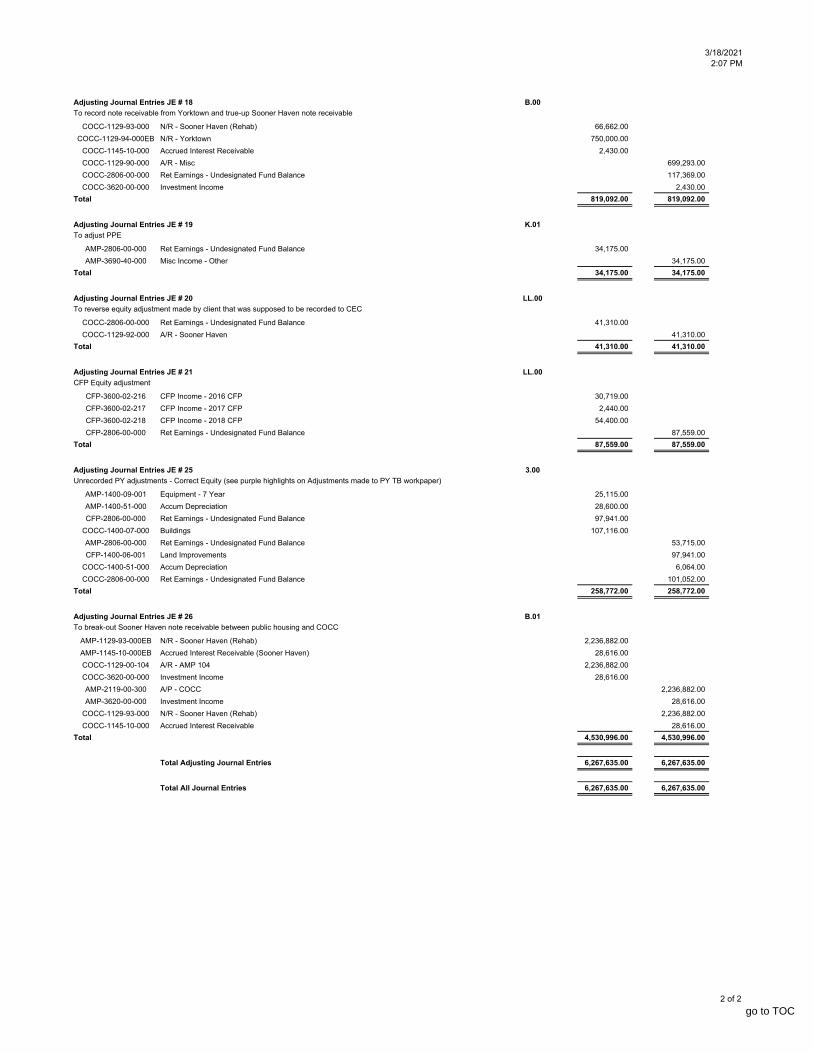

9. For Action: Resolution No. 12-21 approving Acceptance of Audited Financial Statements for year ended December 31, 2019. Presented by Thomas Henderson.

10. Information:

A. COVID Update. Presented by Mark Gillett.

11. Report of Legal Counsel:

A. Lawsuits

B. Legal Request

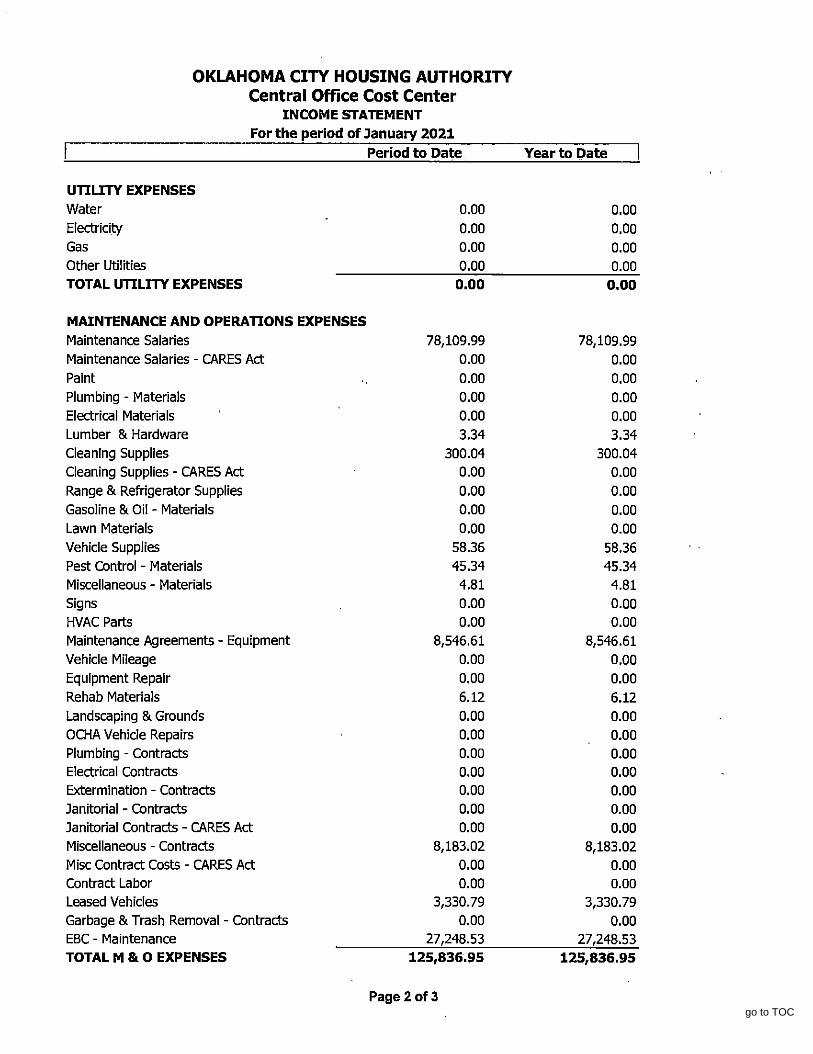

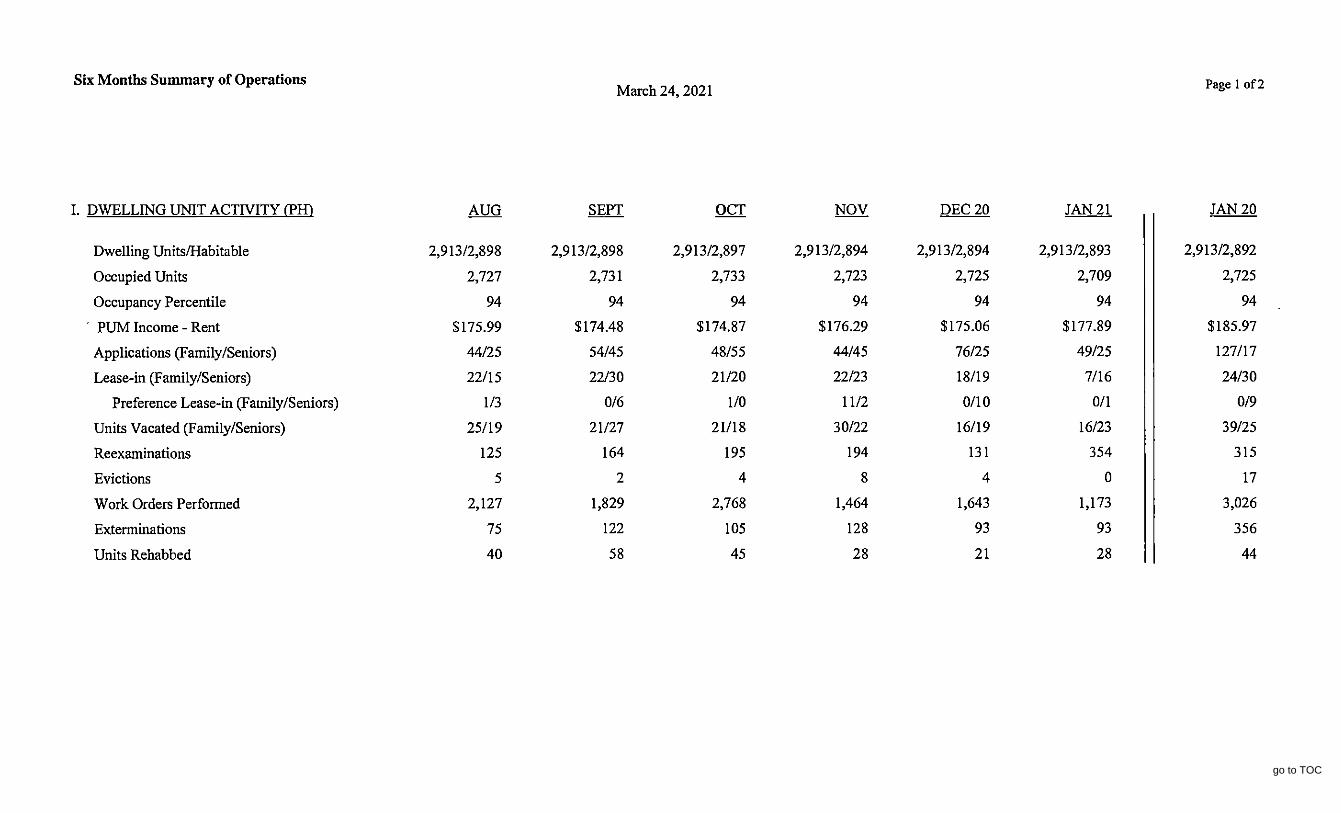

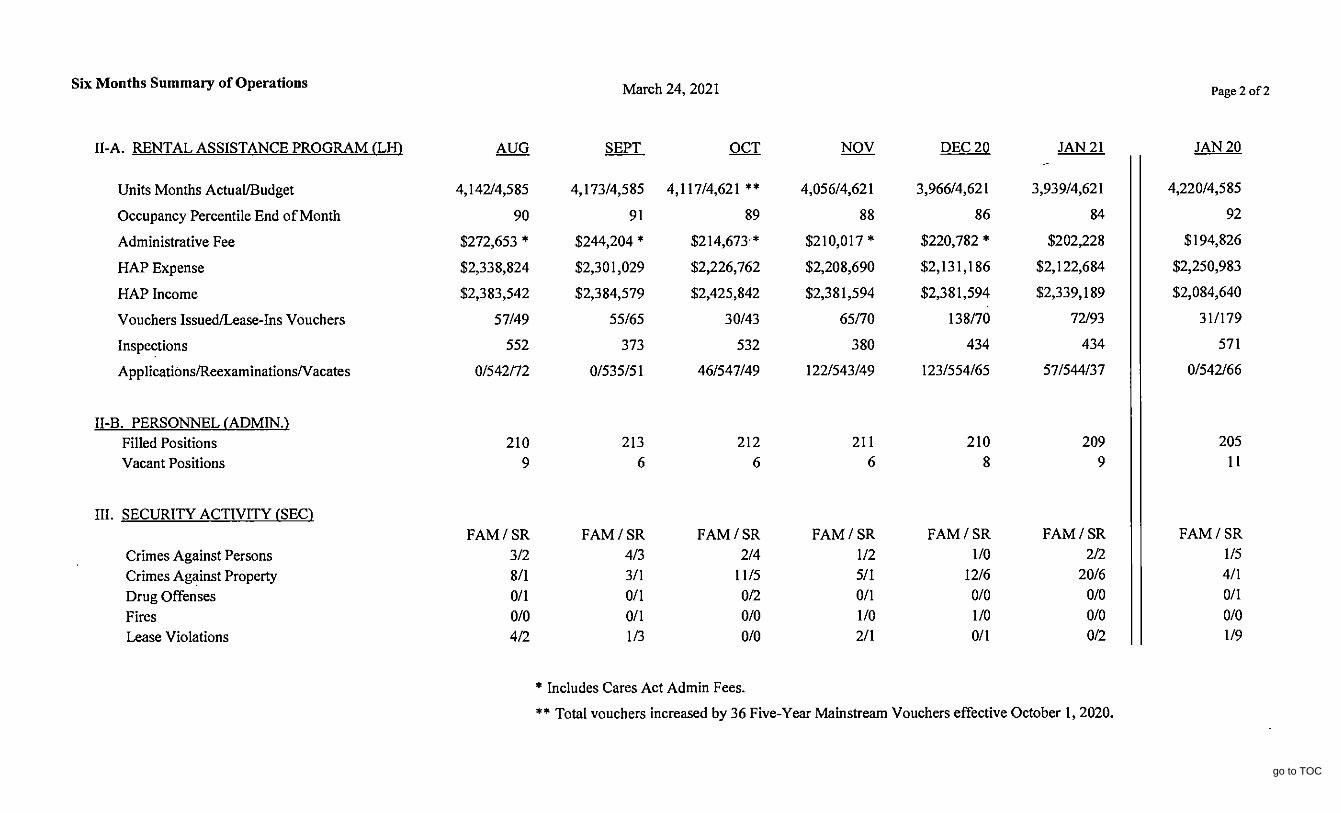

12. Reports of the Executive Director:

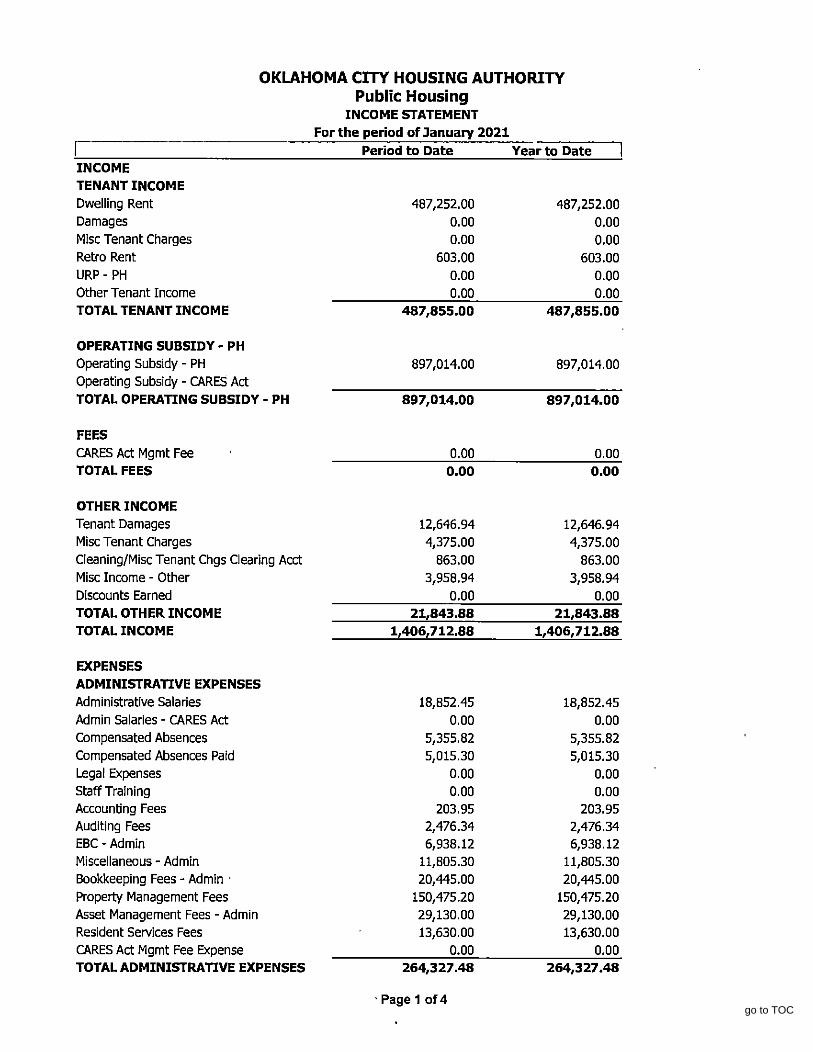

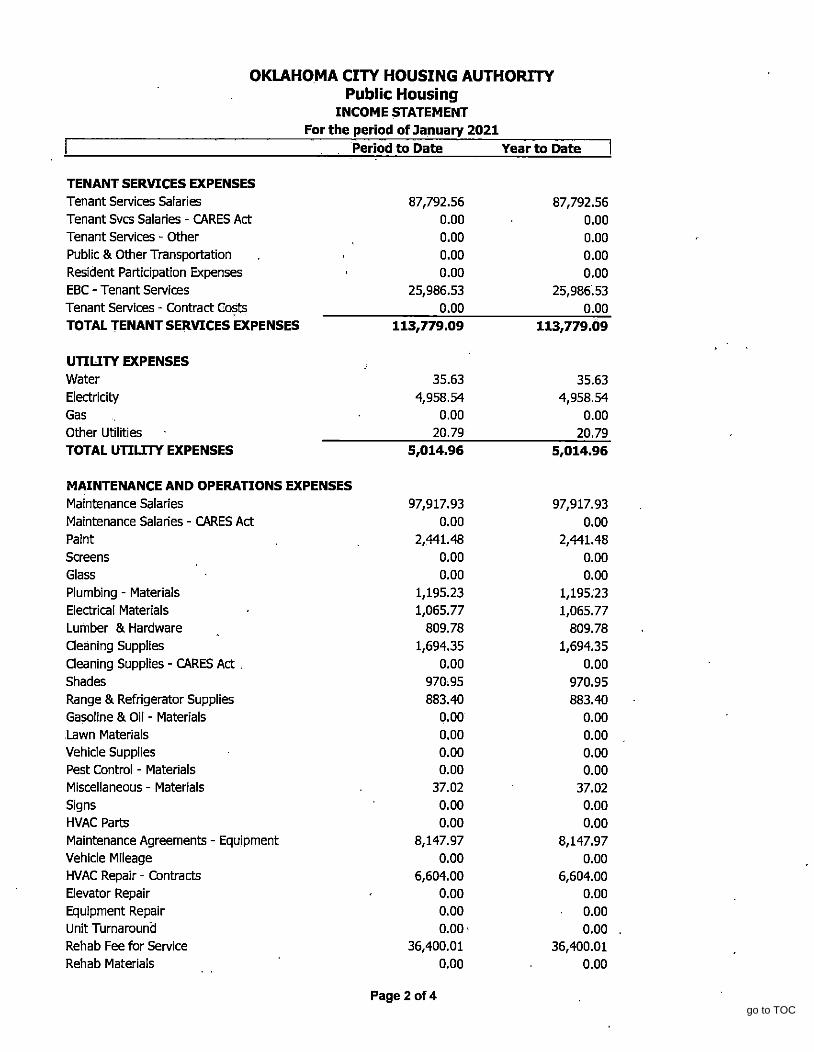

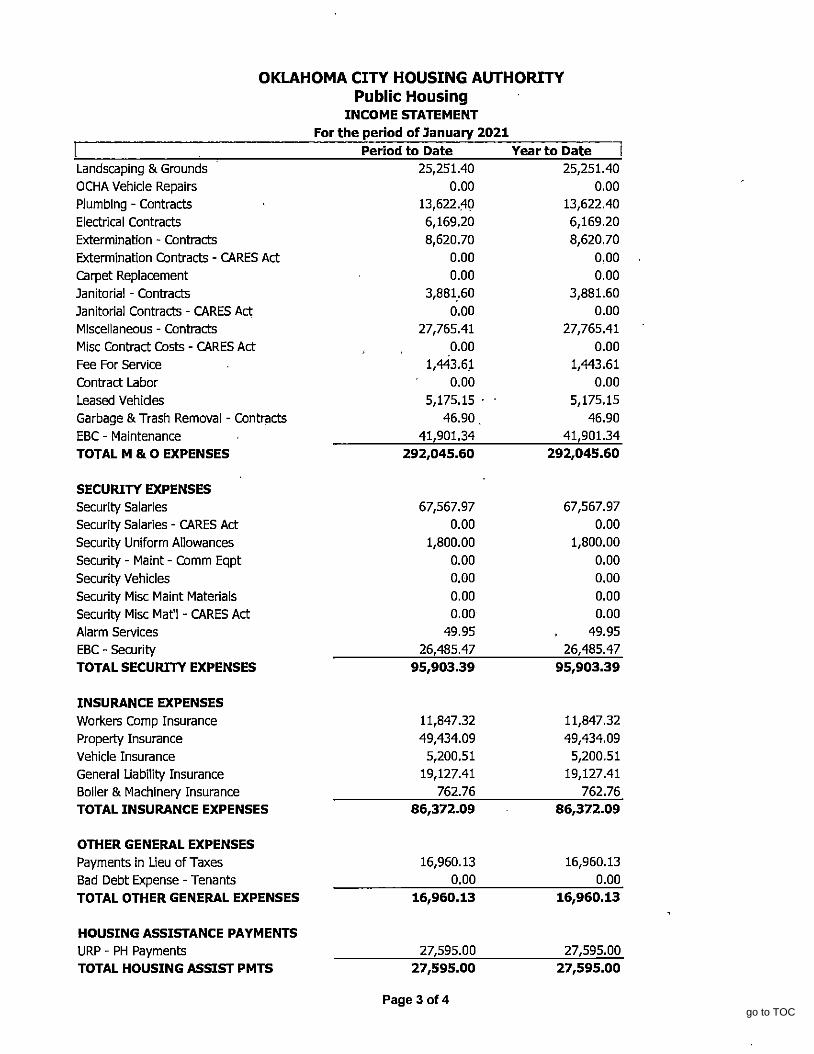

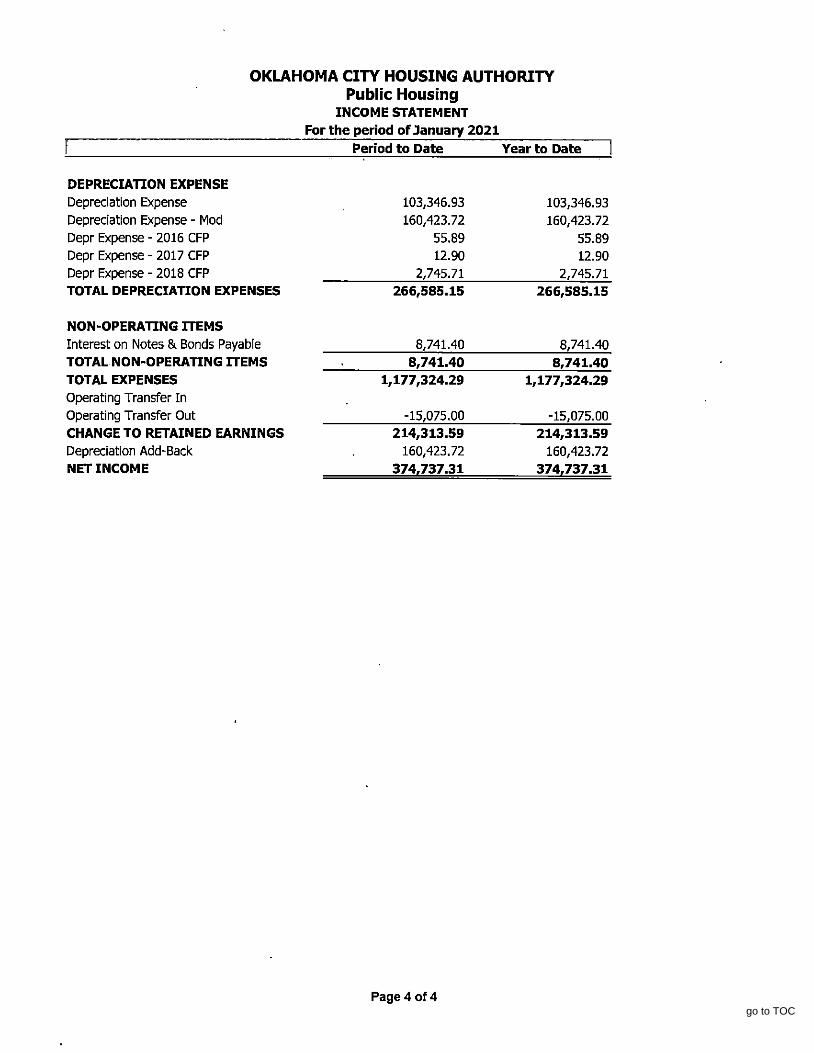

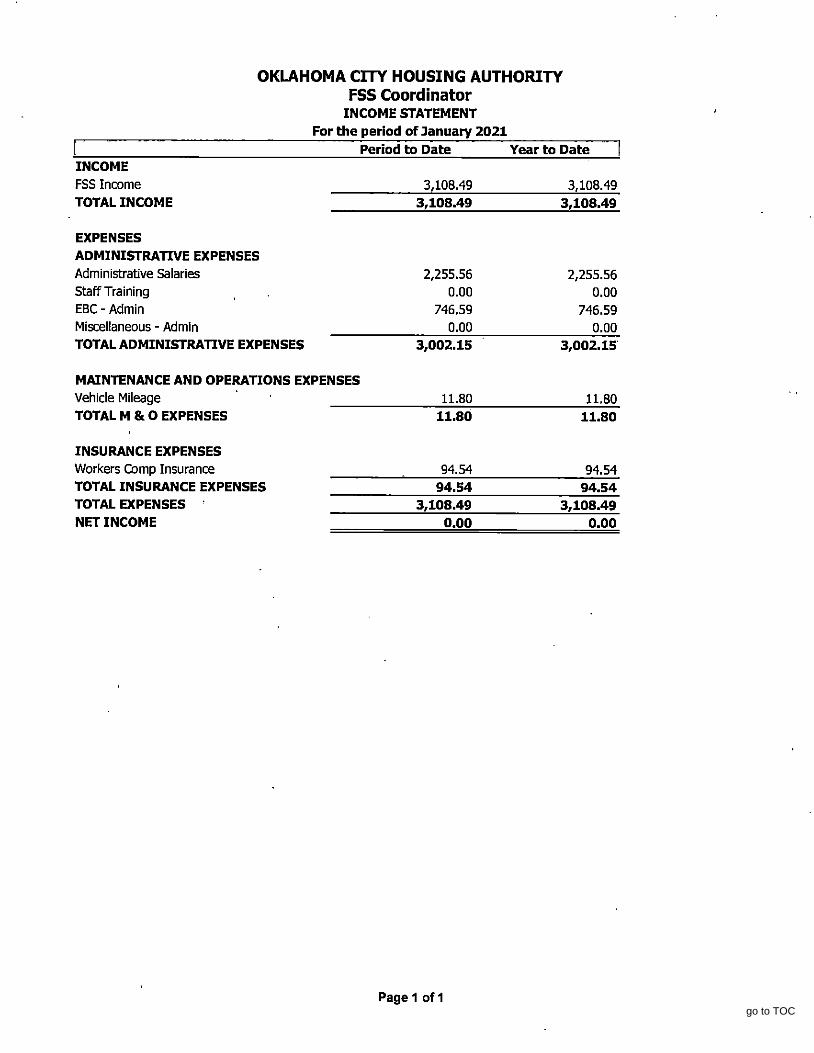

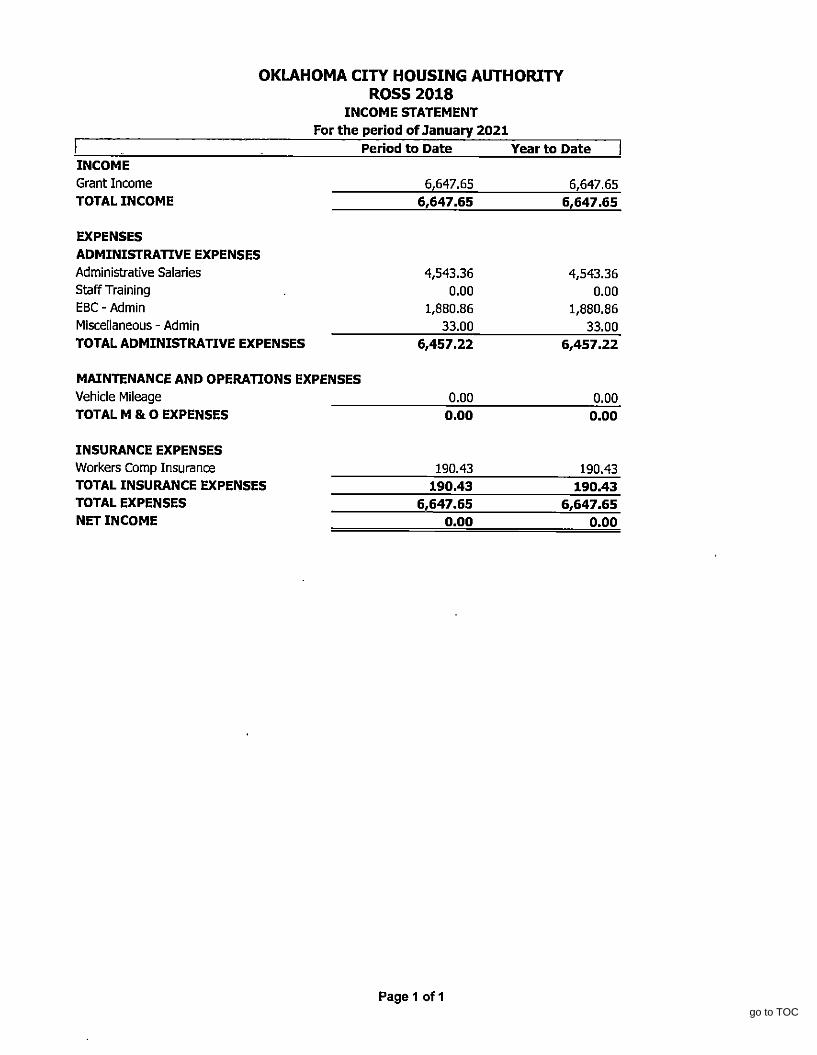

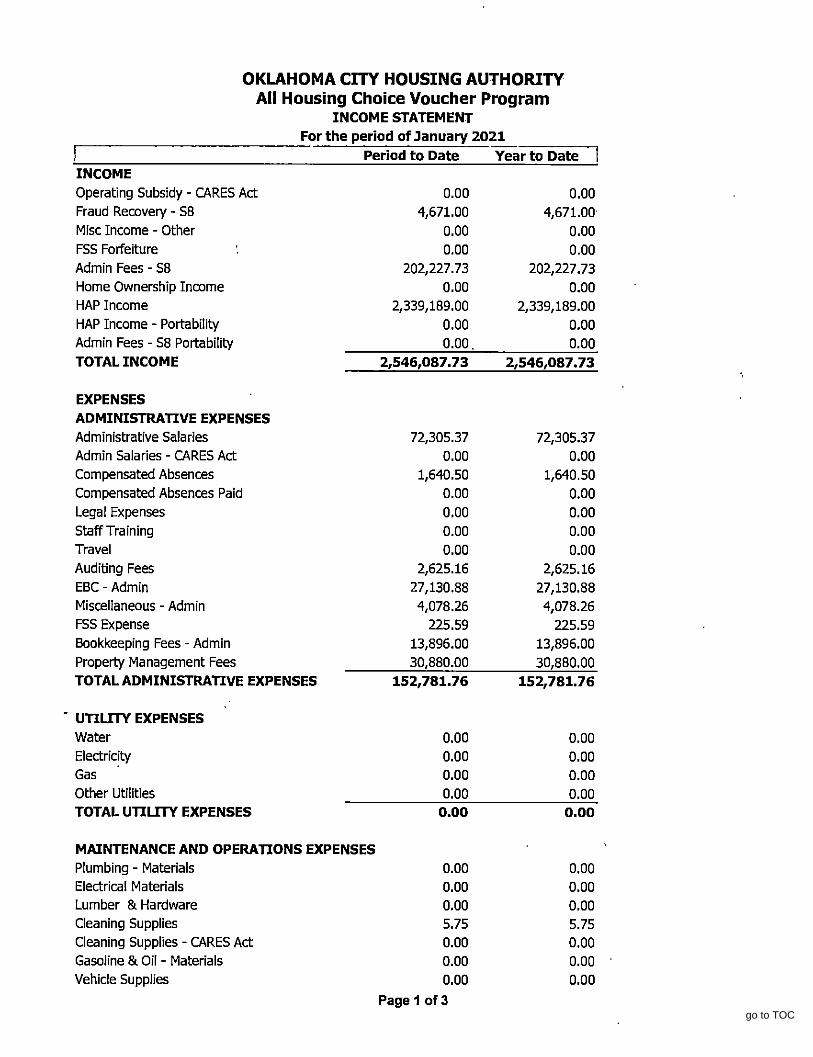

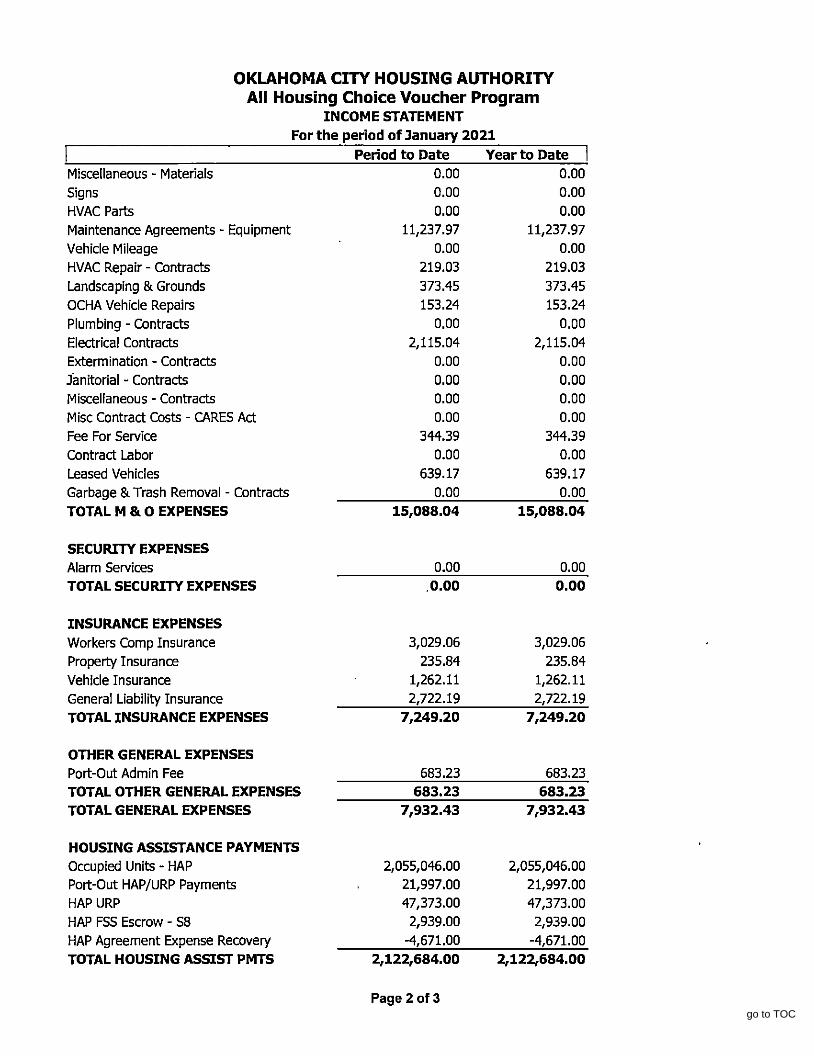

A. Income Statements – January 2021

B. Six Months Summary of Operations

13. Citizens to be heard

14. For Action: Adjournment

It is the policy of the Oklahoma City Housing Authority to ensure that communications with participants and members of the public with disabilities are as effective as communications with others. Anyone with a disability who requires an accommodation, a modification of policies or procedures, or an auxiliary aid or service in order to participate in this meeting should contact the ADA department coordinator at 605-3219 as soon as possible but not later than 48 hours (not including weekends or holidays) before the scheduled meeting. The department will give primary consideration to the choice of auxiliary aid or service requested by the individual with disability. If you need an alternate format of the agenda or any information provided at said meeting, please contact the ADA department coordinator listed above 48 hours prior to the scheduled meeting.

go to TOC

2/24/21 1.

MINUTES OF THE REGULAR MEETING OF THE BOARD OF COMMISSIONERS OF THE

OKLAHOMA CITY HOUSING AUTHORITY

February 24, 2021

The Board of Commissioners of the Oklahoma City Housing Authority met via Teleconference on Wednesday, February 24, 2021 at 9:02 a.m. Chair Steward thanked everyone for joining the teleconference meeting.

The Agenda for this meeting was filed with the Secretary of State and City Clerk for the 2021 meetings on

December 2, 2020, and amended on February 12, 2021, to advise of the change to a special meeting by

teleconference. A copy of this agenda was posted at 1700 and 1800 Northeast Fourth Street on February 19,

2021, at 4:15 p.m. in accordance with Oklahoma Open Meeting Statutes, posted on the Authority general

web site www.ochanet.org as required by Section 3106.2 of Oklahoma Statute Title 74, and written notice

via the Agenda was delivered to each Commissioner on February 19, 2021.

Item 1, meeting was called to order by Chair Jerry Steward, who presided.

Item 2, Announcement of Filing of Meeting Notice and Posting of the Agenda in Accordance with the Oklahoma Open Meeting Act, was announced by Sherry Hearn. Item 3, Sherry Hearn, Executive Assistant, performed roll call, those present were as follows:

PRESENT: Jerry Steward, Chair

Alvah Boyd Connie Mashburn Lillie Swope was absent.

Item 4, Consent Docket, was introduced by Chair Steward which included:

Item A. Minutes of the Regular Meeting of the Board of Commissioners dated January 27, 2021

Motion: Boyd. Second: Mashburn. AYES: Boyd, Mashburn, Steward. NAYES: None. The following Action items were introduced by Chair Steward: Item 5, Resolution No. 5-21 approving Section 8 Management Assessment Program (SEMAP) Certification with an anticipated High Performer rating and authorizing electronic submission to the U.S. Department of Housing and Urban Development by February 28, 2021. Motion: Mashburn. Second: Boyd. AYES: Boyd, Mashburn, Steward. NAYES: None. Item 6, Resolution No. 6-21 approving award of contract for Five (5) year on-call Design Professional Services with ADG beginning March 1, 2021. Motion: Boyd. Second: Mashburn. AYES: Boyd, Mashburn, Steward. NAYES: None. Item 7, Resolution No. 7-21 approving Agreement for General Counsel Legal Services with Phillips Murrah PC beginning March 1, 2021. Commissioner Boyd inquired what the total amount of this contract would be. Leslie Batchelor, legal counsel, stated that the contract does not have a cap but fees are based on an hourly rate, which is provided in the new contract. Chair Steward stated there is no cap the current general counsel contract and that the amount paid is in the financial information provided to the Board of Commissioners each month. It was further noted that legal fees fluctuate each month depending on claims and projects requiring legal review. Chair Steward notes the recommended law firm seems highly qualified and should serve the Board well. Motion: Mashburn. Second: Boyd. AYES: Boyd, Mashburn, Steward. NAYES: None.

go to TOC

2/24/21 2.

Item 8, Information:

Item A. Laura Gregory discussed the COVID Resident Support Grant received from Council of Large Public Housing Authority (CLPHA) in the amount of $10,000.00.

Item B. Mark Gillett discussed how OCHA continues to benefit from CARES Act funding. He

provided an update on vaccinations of staff and residents, positivity rate, and changes by the Administration to the CARES Act Emergency Rental Assistance Fund.

Item C. 2019 Write Offs. Thomas Henderson discussed the write offs and stated next year’s will be

larger due to the Eviction Moratorium during COVID pandemic. Item D. Thomas Henderson introduced the Utilities charts information item by noting that the

agenda sheet stated 2019 Utilities but the information is for 2020 Utilities. Chair Steward asked Leslie Batchelor, legal counsel, if the item could be discussed. Leslie Batchelor stated it was perfectly fine because the agenda provided reasonable notice of what was to be discussed, and Chair Steward added that it was an information item only. The utilities charts were then presented by Thomas Henderson.

Item 9, Report of Legal Counsel, Leslie Batchelor:

Item A. There were no new lawsuits. Still monitoring two that have been pending for some time.

Item B. Legal Requests. There were no formal legal requests. Leslie Batchelor stated a couple of the attorneys from the Phillips Murrah law firm were joining the

meeting. Item 10, Reports of the Executive Director. Mark Gillett stated the December 2020 Financial Statements and Six Months Summary of Operation slides were emailed to them and shown on the screen. Item 11, Citizens to be heard. Item 12, Adjournment. Motion: Boyd. Second: Mashburn. AYES: Boyd, Mashburn, Steward. NAYES: None. This meeting adjourned at 9:43 a.m. The next meeting of this Board will convene at 9:00 a.m. CDST March 24, 2021 at the Oklahoma City Housing Authority Central Office, 1700 Northeast Fourth Street, Oklahoma City, Oklahoma. ______________________________ Mark W. Gillett, Secretary ATTEST: ____________________________________ Jerry L. Steward, Chair

go to TOC

go to TOC

go to TOC

1

RESOLUTION NO. 8-21

RESOLUTION TO RATIFY EMERGENCY PLUMBING REPAIR AT AMP 106, NORTHEAST DUPLEXES, AMP 104, SCATTERED SITES, AMP 102, OAK GROVE, AND

AMP 115, REDING SENIOR CENTER

WHEREAS, during February 2021, Oklahoma's historic freezing temperatures and snow

resulted in burst water and sewer lines throughout Oklahoma City Housing Authority ("OCHA")

property, namely, AMP 106, Northeast Duplexes, AMP 104, Scattered Sites, AMP 102, Oak

Grove, and AMP 115, Reding Senior Center; and

WHEREAS, it was quickly determined that OCHA staff did not have the in-house

capability to make the repair in a timely manner; and

WHEREAS, the notice requirements of the Oklahoma Housing Authority Act make it

difficult for the Commissioners of OCHA to meet in a timely manner in the event of an emergency;

and

WHEREAS, the OCHA Procurement Policy allows noncompetitive proposals "where an

emergency exists due to a sudden, unexpected happening or unforeseen occurrence or condition

whereby the public health or safety is endangered, the provisions of the Oklahoma Public

Competitive Bidding Act of 197, 61 O.S. § 101, et seq., with reference to notice and bids shall not

apply, provided that the conditions of 61 O.S. § 130 have been met;" and

go to TOC

2

WHEREAS, OCHA staff declared the necessary plumbing repairs an emergency that

existed due to a sudden, unexpected happening or unforeseen occurrence or condition whereby the

public health or safety was endangered, and that there was an immediate and serious need to repair

the plumbing system, such that that the conditions of 61 O.S. § 130 had been met; and

WHEREAS, OCHA staff began contacting local vendors for bids to perform the repairs,

and All Day Plumbing was the only one to respond; and

WHEREAS, All Day Plumbing was tasked with repairing water lines, replacing hot water

tanks and repairing sewer lines to 46 units at AMPs 106, Northeast Duplexes, and 104, Scattered

Sites; and

WHEREAS, All Day Plumbing submitted a price of $32,150 for repairing water lines,

replacing hot water tanks and repairing sewer lines to 46 units at AMPs 106, Northeast Duplexes,

and 104, Scattered Sites; and

WHEREAS, All Day Plumbing was tasked with repairing a 4” water main and replacing a

pressure tee on a water main at AMP 102, Oak Grove; and

WHEREAS, All Day Plumbing submitted a price of $8,500 for repairing a 4” water main

and replacing a pressure tee on a water main at AMP 102, Oak Grove; and

WHEREAS, All Day Plumbing was tasked with cutting out and repairing the 8" ductal iron

water main at AMP 115, Reding Senior Center; and

go to TOC

3

WHEREAS, All Day Plumbing submitted a price of $10,000 for cutting out and repairing

the 8" ductal iron water main at AMP 115, Reding Senior Center; and

WHEREAS, OCHA staff authorized All Day Plumbing to perform the work to perform the

repairs at a total cost of $50,650; and

WHEREAS, the Commissioners of OCHA find it appropriate and desirable to affirm the

plumbing repairs as an emergency situation, and to ratify and approve the actions taken in

procuring and accepting the bid to perform the plumbing repairs and in awarding and executing

the emergency repair contract with All Day Plumbing in the total amount of $50,650.

NOW, THEREFORE, BE IT RESOLVED by the Commissioners of the Oklahoma City

Housing Authority that the plumbing repairs at AMP 106, Northeast Duplexes, AMP 104,

Scattered Sites, AMP 102, Oak Grove, and AMP 115, Reding Senior Center, constituted an

emergency that existed due to a sudden, unexpected happening or unforeseen occurrence or

condition whereby the public health or safety was endangered, and that there was an immediate

and serious need to perform the repairs.

BE IT FURTHER RESOLVED that the actions of the OCHA staff in declaring an

emergency and procuring bids for the plumbing repairs, and in awarding and executing the contract

with All Day Plumbing for the emergency plumbing repairs, in the total amount of $50,650, are

hereby ratified and approved.

ADOPTED this 24th day of March, 2021.

go to TOC

4

OKLAHOMA CITY HOUSING AUTHORITY

By Jerry L. Steward, Chair

I, Mark W. Gillett, Secretary of the Board of Commissioners of the Oklahoma City Housing Authority, certify that the foregoing Resolution No. 8-21 was duly adopted at a regular meeting of the Board of Commissioners of the Oklahoma City Housing Authority, held by teleconference and accessible by phone (301) 715-8592 Meeting number: 950 0629 3123 Password: 563905 or online at https://zoom.us/j/95006293123?pwd=S2c1ZlgyZmpkd3MxMWdlb2UyQm1JZz09 on the 24th day of March, 2021; that said meeting was held in accordance with the By-Laws of the Oklahoma City Housing Authority and the Oklahoma Open Meeting Act; that a quorum was present at all times during said meeting; and that the resolution was duly adopted by a majority of those Commissioners present.

Secretary

AYE NAYJERRY L. STEWARD LILLIE SWOPE ALVAH L. BOYD CONNIE MASHBURN

go to TOC

go to TOC

1

RESOLUTION NO. 9-21

RESOLUTION APPROVING REVISIONS TO THE ADMISSIONS AND CONTINUED OCCUPANCY POLICY (ACOP) FOR PUBLIC HOUSING

WHEREAS, the Oklahoma City Housing Authority ("OCHA") staff has prepared revisions

to several sections of OCHA's Admissions and Continued Occupancy Policy ("ACOP") for Public

Housing in order to incorporate temporary waivers and procedures related to the COVID-19 Public

Health Emergency and additional clarifications and modifications to bring content current with

Department of Housing and Urban Development ("HUD") regulations and guidelines; and

WHEREAS, OCHA staff recommends approval of the proposed revisions to the

ACOP as shown on the attached document and that the proposed revisions will become effective

March 24, 2021.

NOW, THEREFORE, BE IT RESOLVED by the Board of Commissioners of the

Oklahoma City Housing Authority that the proposed revisions to the ACOP, as shown in the

attached document with a revision date of March 24, 2021, are hereby approved.

BE IT FURTHER RESOLVED that the proposed revisions to the ACOP shall take

effect as of March 24, 2021.

ADOPTED this 24th day of March, 2021.

go to TOC

2

OKLAHOMA CITY HOUSING AUTHORITY

By Jerry L. Steward, Chair

I, Mark W. Gillett, Secretary of the Board of Commissioners of the Oklahoma City Housing Authority, certify that the foregoing Resolution No. 9-21 was duly adopted at a regular meeting of the Board of Commissioners of the Oklahoma City Housing Authority, held by teleconference and accessible by phone (301) 715-8592 Meeting number: 950 0629 3123 Password: 563905 or online at https://zoom.us/j/95006293123?pwd=S2c1ZlgyZmpkd3MxMWdlb2UyQm1JZz09 on the 24th day of March, 2021; that said meeting was held in accordance with the By-Laws of the Oklahoma City Housing Authority and the Oklahoma Open Meeting Act; that a quorum was present at all times during said meeting; and that the resolution was duly adopted by a majority of those Commissioners present.

Secretary

AYE NAY

JERRY L. STEWARD

LILLIE SWOPE

ALVAH L. BOYD

CONNIE MASHBURN

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

1

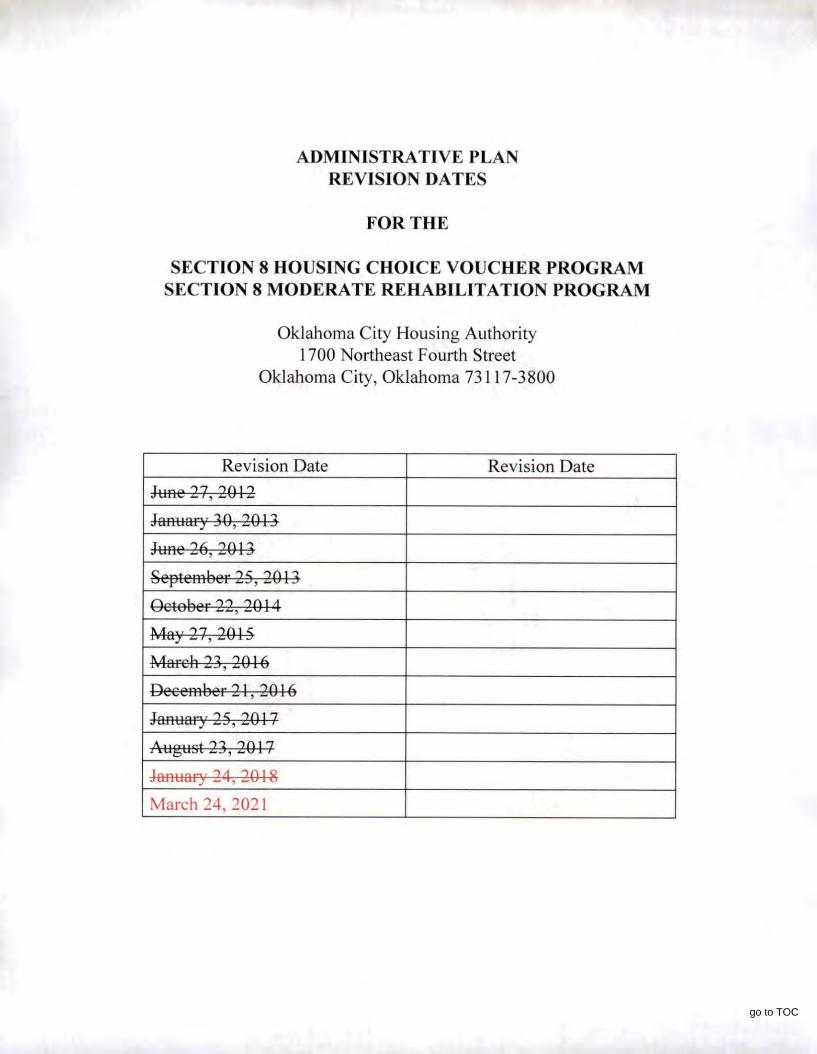

RESOLUTION NO. 10-21

RESOLUTION APPROVING REVISIONS TO THE ADMINISTRATIVE PLAN - HOUSING CHOICE VOUCHER PROGRAM FOR SECTION 8

WHEREAS, the United States Department of Housing and Urban Development

("HUD") requires the Oklahoma City Housing Authority ("OCHA") to adopt, and OCHA has so

adopted, a written administrative plan that establishes its policies for administering the Section 8

Housing Choice Voucher program ("Administrative Plan"); and

WHEREAS, the Administrative Plan states OCHA’s policies on matters for which

it has discretion, but the Administrative Plan must be in accordance with all HUD regulations and

requirements; and

WHEREAS, OCHA staff has determined that it has become necessary to revise

certain sections of the OCHA documents governing its Section 8 program; and

WHEREAS, OCHA must revise the Administrative Plan to comply with HUD

requirements, and to add the COVID-19 pandemic operations and HUD statutory regulations, as

well as other minor modifications and clarifications to bring content current with HUD regulations

and guidelines; and

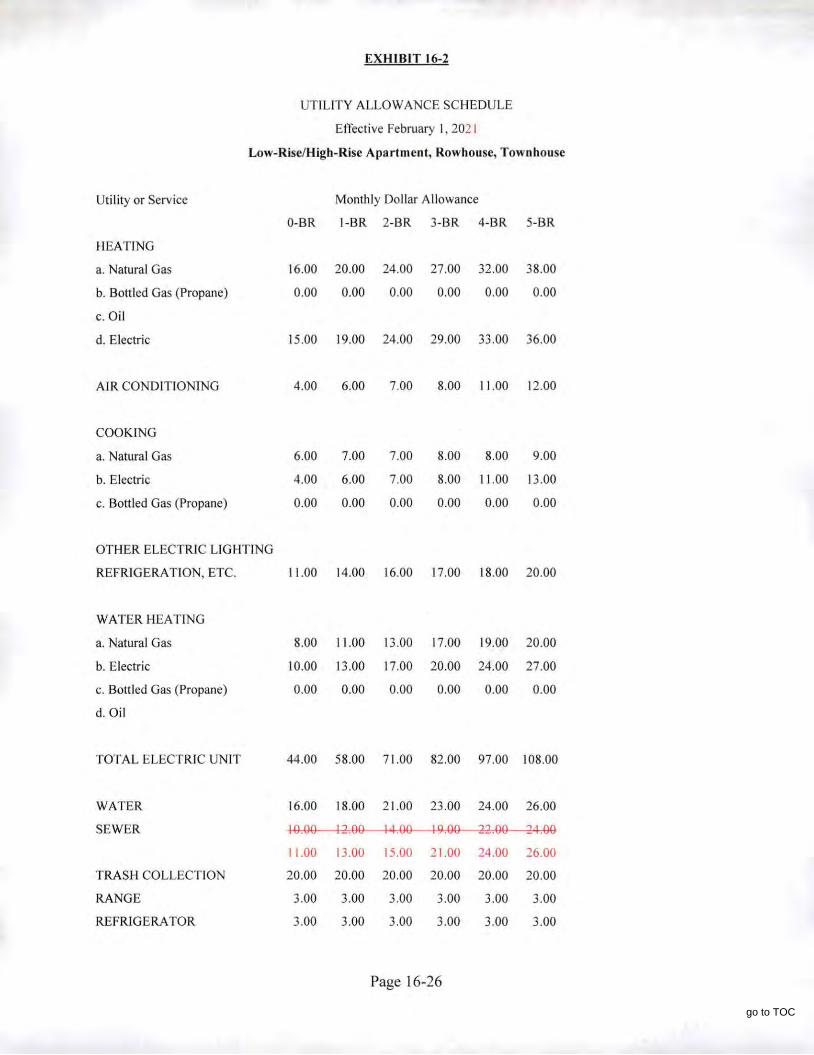

WHEREAS, additional revisions are necessary in order to update the

Administrative Plan with current Utility Allowances effective February 1, 2021; and

go to TOC

2

WHEREAS, additional revisions are necessary in order to add remote Informal

Hearing procedures; and

WHEREAS, additional revisions are necessary in order to be in compliance with

the CARES Act waivers requirements; and

WHEREAS, other minor modifications and clarifications are required to bring

content current with HUD regulations and guidance; and

WHEREAS, to accomplish these aims, OCHA staff recommends revising the

Administrative Plan as shown on the attached "Administrative Plan Amendments."

NOW, THEREFORE, BE IT RESOLVED by the Board of Commissioners of the

Oklahoma City Housing Authority that the revisions to the Administrative Plan, as shown in the

attached "Administrative Plan Amendments," are hereby approved and adopted.

BE IT FURTHER RESOLVED that the Executive Director is authorized and

directed to prepare and execute such documents as may be appropriate to carry out the approval

and adoption contained in this Resolution.

ADOPTED this 24th day of March, 2021.

go to TOC

3

OKLAHOMA CITY HOUSING AUTHORITY By

Jerry L. Steward, Chair

I, Mark W. Gillett, Secretary of the Board of Commissioners of the Oklahoma City Housing Authority, certify that the foregoing Resolution No. 10-21 was duly adopted at a regular meeting of the Board of Commissioners of the Oklahoma City Housing Authority, held by teleconference and accessible by phone (301) 715-8592 Meeting number: 950 0629 3123 Password: 563905 or online at https://zoom.us/j/95006293123?pwd=S2c1ZlgyZmpkd3MxMWdlb2UyQm1JZz09 on the 24th day of March, 2021; that said meeting was held in accordance with the By-Laws of the Oklahoma City Housing Authority and the Oklahoma Open Meeting Act; that a quorum was present at all times during said meeting; and that the resolution was duly adopted by a majority of those Commissioners present.

Secretary

AYE NAYJERRY L. STEWARD LILLIE SWOPE ALVAH L. BOYD CONNIE MASHBURN

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

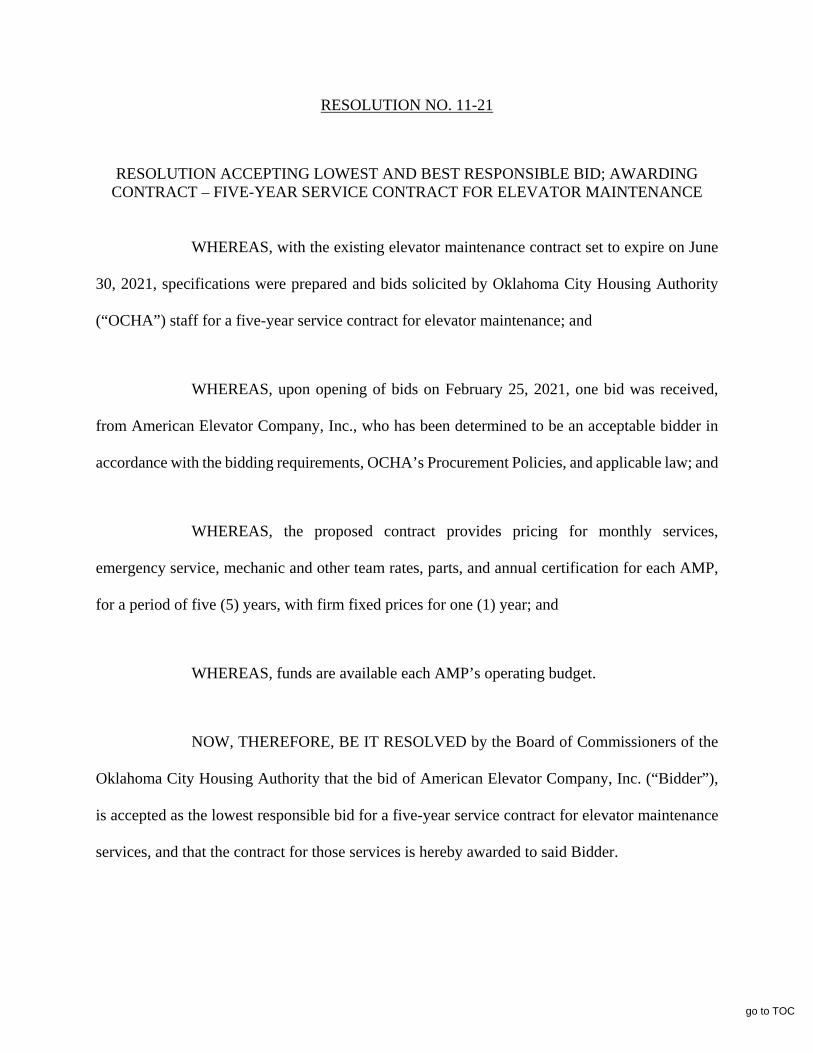

RESOLUTION NO. 11-21

RESOLUTION ACCEPTING LOWEST AND BEST RESPONSIBLE BID; AWARDING CONTRACT – FIVE-YEAR SERVICE CONTRACT FOR ELEVATOR MAINTENANCE

WHEREAS, with the existing elevator maintenance contract set to expire on June

30, 2021, specifications were prepared and bids solicited by Oklahoma City Housing Authority

(“OCHA”) staff for a five-year service contract for elevator maintenance; and

WHEREAS, upon opening of bids on February 25, 2021, one bid was received,

from American Elevator Company, Inc., who has been determined to be an acceptable bidder in

accordance with the bidding requirements, OCHA’s Procurement Policies, and applicable law; and

WHEREAS, the proposed contract provides pricing for monthly services,

emergency service, mechanic and other team rates, parts, and annual certification for each AMP,

for a period of five (5) years, with firm fixed prices for one (1) year; and

WHEREAS, funds are available each AMP’s operating budget.

NOW, THEREFORE, BE IT RESOLVED by the Board of Commissioners of the

Oklahoma City Housing Authority that the bid of American Elevator Company, Inc. (“Bidder”),

is accepted as the lowest responsible bid for a five-year service contract for elevator maintenance

services, and that the contract for those services is hereby awarded to said Bidder.

go to TOC

2

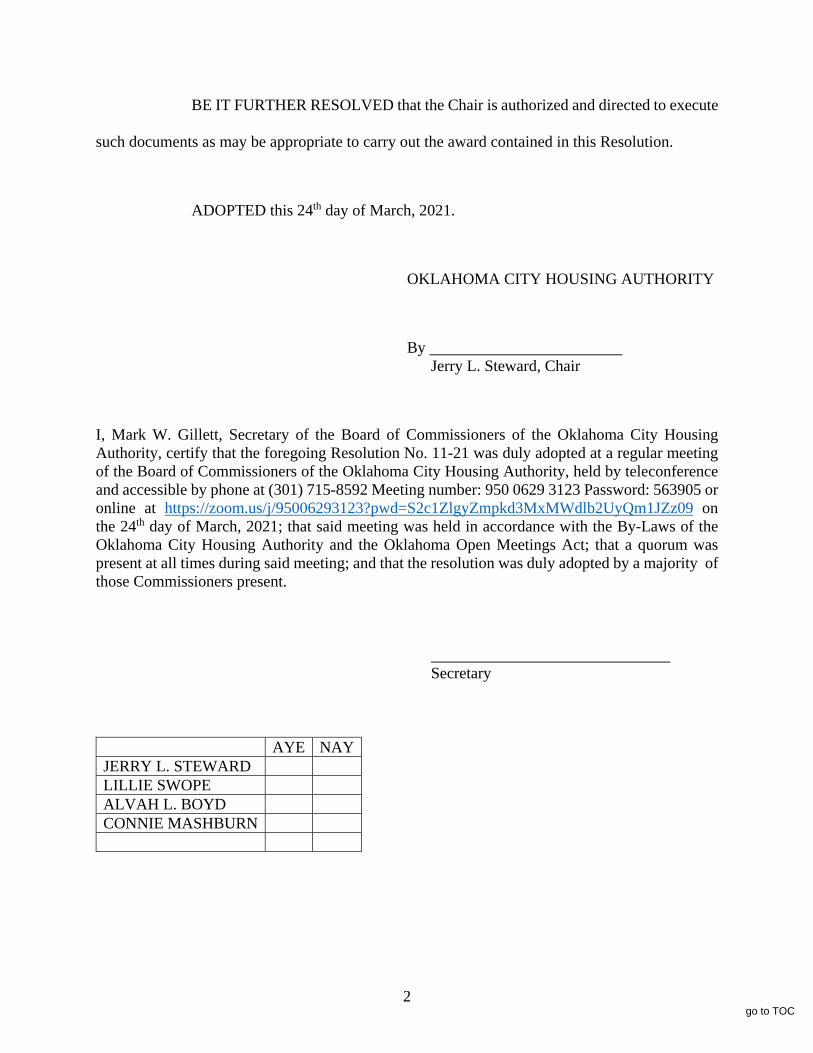

BE IT FURTHER RESOLVED that the Chair is authorized and directed to execute

such documents as may be appropriate to carry out the award contained in this Resolution.

ADOPTED this 24th day of March, 2021.

OKLAHOMA CITY HOUSING AUTHORITY

By Jerry L. Steward, Chair

I, Mark W. Gillett, Secretary of the Board of Commissioners of the Oklahoma City Housing Authority, certify that the foregoing Resolution No. 11-21 was duly adopted at a regular meeting of the Board of Commissioners of the Oklahoma City Housing Authority, held by teleconference and accessible by phone at (301) 715-8592 Meeting number: 950 0629 3123 Password: 563905 or online at https://zoom.us/j/95006293123?pwd=S2c1ZlgyZmpkd3MxMWdlb2UyQm1JZz09 on the 24th day of March, 2021; that said meeting was held in accordance with the By-Laws of the Oklahoma City Housing Authority and the Oklahoma Open Meetings Act; that a quorum was present at all times during said meeting; and that the resolution was duly adopted by a majority of those Commissioners present.

Secretary

AYE NAYJERRY L. STEWARD LILLIE SWOPE ALVAH L. BOYD CONNIE MASHBURN

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

go to TOC

RESOLUTION NO. 12-21

RESOLUTION ACCEPTING AUDITED FINANCIAL STATEMENTS FOR YEAR ENDED DECEMBER 31, 2019

WHEREAS, the books and records of the Oklahoma City Housing Authority

(“OCHA”) are audited on an annual basis, as required by the United States Department of Housing

and Urban Development; and

WHEREAS, Eide Bailly LLP is the contracted auditing firm that performed the

audit of the OCHA financial statements for the year ended December 31, 2019; and

WHEREAS, the auditors proposed material adjustments to the financial statements,

a deficiency to internal control over financial reporting, and a deficiency in internal control over

compliance resulting in findings; and

WHEREAS, OCHA management has prepared the required responses and

corrective action plans.

NOW, THEREFORE, BE IT RESOLVED by the Board of Commissioners of the

Oklahoma City Housing Authority that the Audited Financial Statements for the Year Ended

December 31, 2019 are accepted.

ADOPTED this 24th day of March 2021.

go to TOC

OKLAHOMA CITY HOUSING AUTHORITY

By Jerry L. Steward, Chair

I, Mark W. Gillett, Secretary of the Board of Commissioners of the Oklahoma City Housing Authority, certify that the foregoing Resolution No. 12-21 was duly adopted at a regular meeting of the Board of Commissioners of the Oklahoma City Housing Authority, held by teleconference and accessible by phone (301) 715-8592 Meeting number: 950 0629 3123 Password: 563905 or online at https://zoom.us/j/95006293123?pwd=S2c1ZlgyZmpkd3MxMWdlb2UyQm1JZz09 on the 24th day of March, 2021; that said meeting was held in accordance with the By-Laws of the Oklahoma City Housing Authority and the Oklahoma Open Meeting Act; that a quorum was present at all times during said meeting; and that the resolution was duly adopted by a majority of those Commissioners present.

Secretary

AYE NAYJERRY L. STEWARD LILLIE SWOPE ALVAH L. BOYD CONNIE MASHBURN

go to TOC

Financial Statements December 31, 2019 and 2018

Oklahoma City Housing Authority

eidebailly.comgo to TOC

Oklahoma City Housing Authority Table of Contents

December 31, 2019 and 2018

Independent Auditor’s Report ................................................................................................................................... 1

Management’s Discussion and Analysis ................................................................................................................ 4

Financial Statements

Statement of Net Position ................................................................................................................................... 11 Statement of Revenues, Expenses and Changes in Net Position ......................................................................... 15 Statements of Cash Flows .................................................................................................................................... 17 Notes to Financial Statements ............................................................................................................................. 19

Supplementary Information

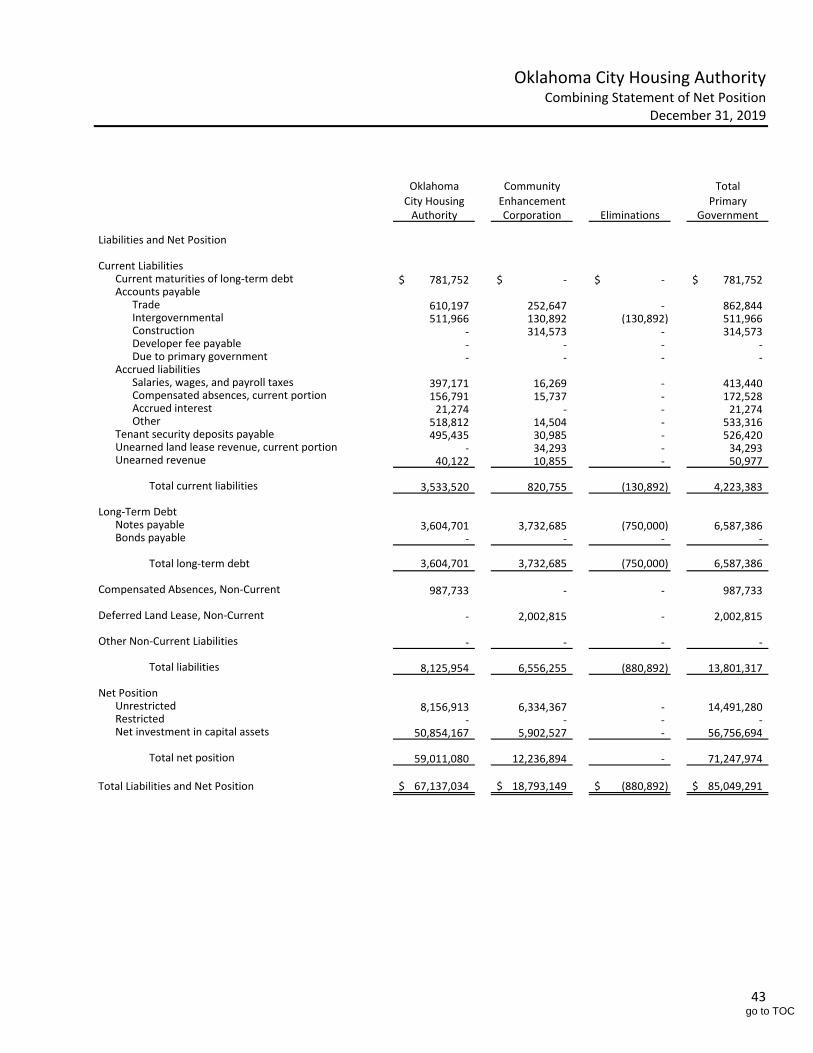

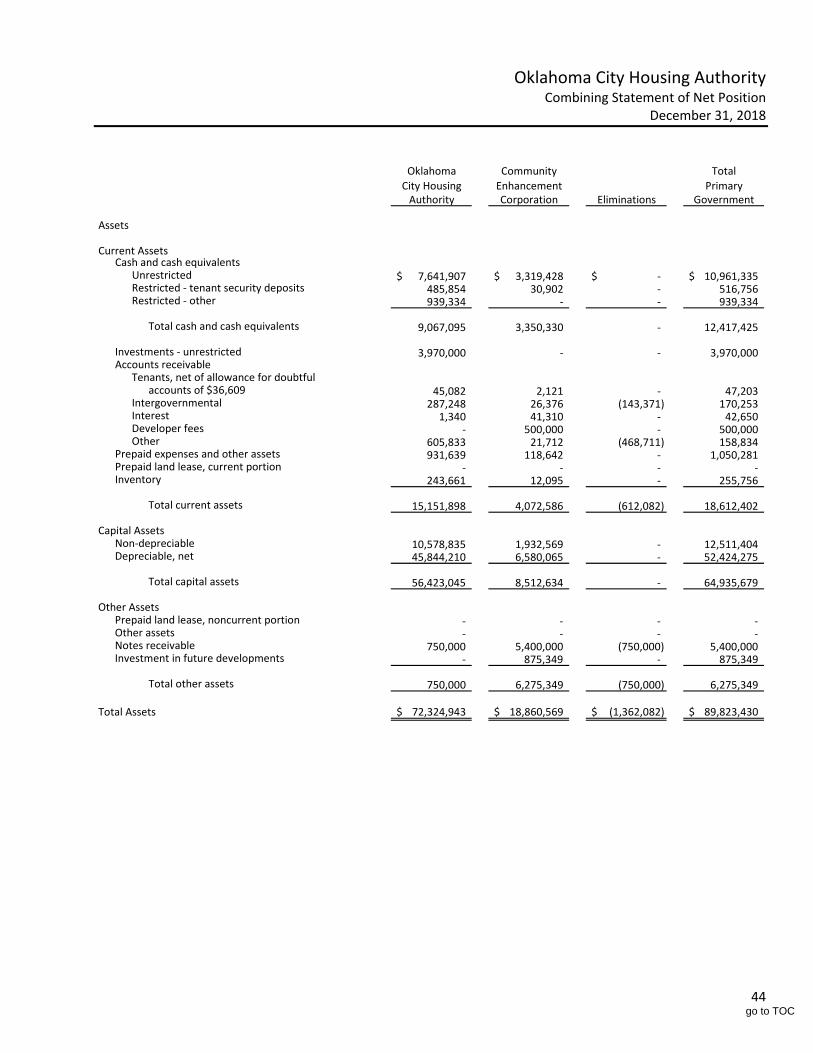

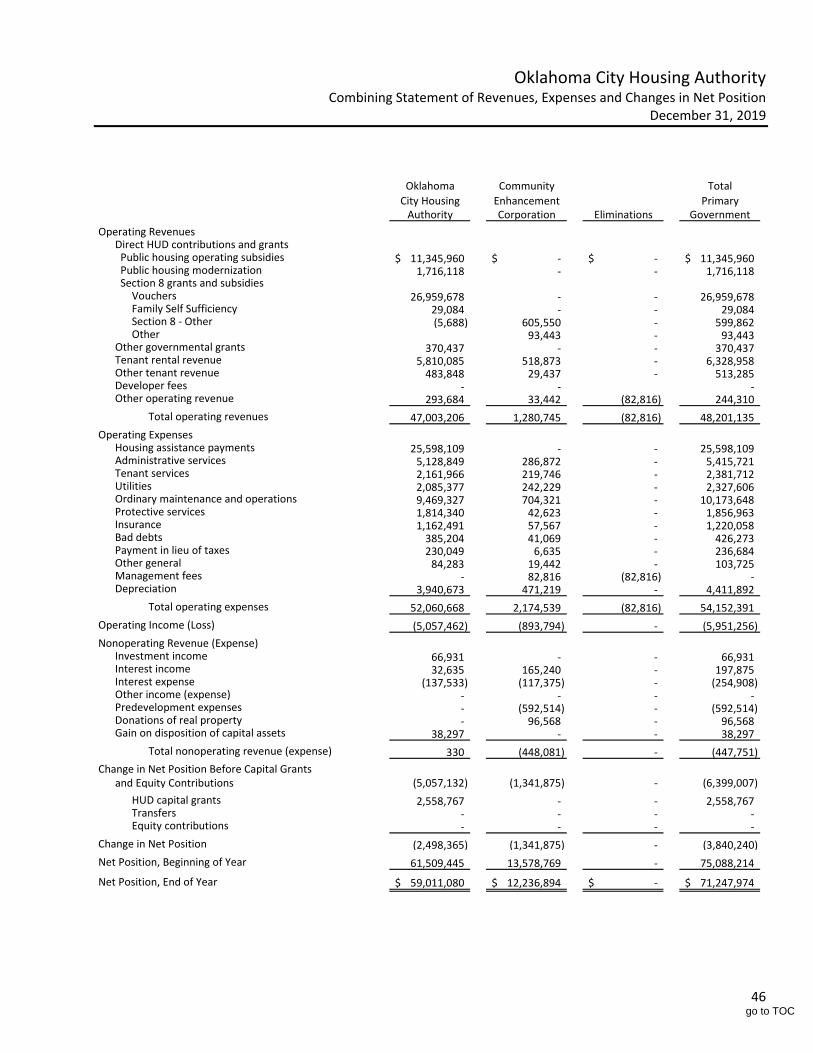

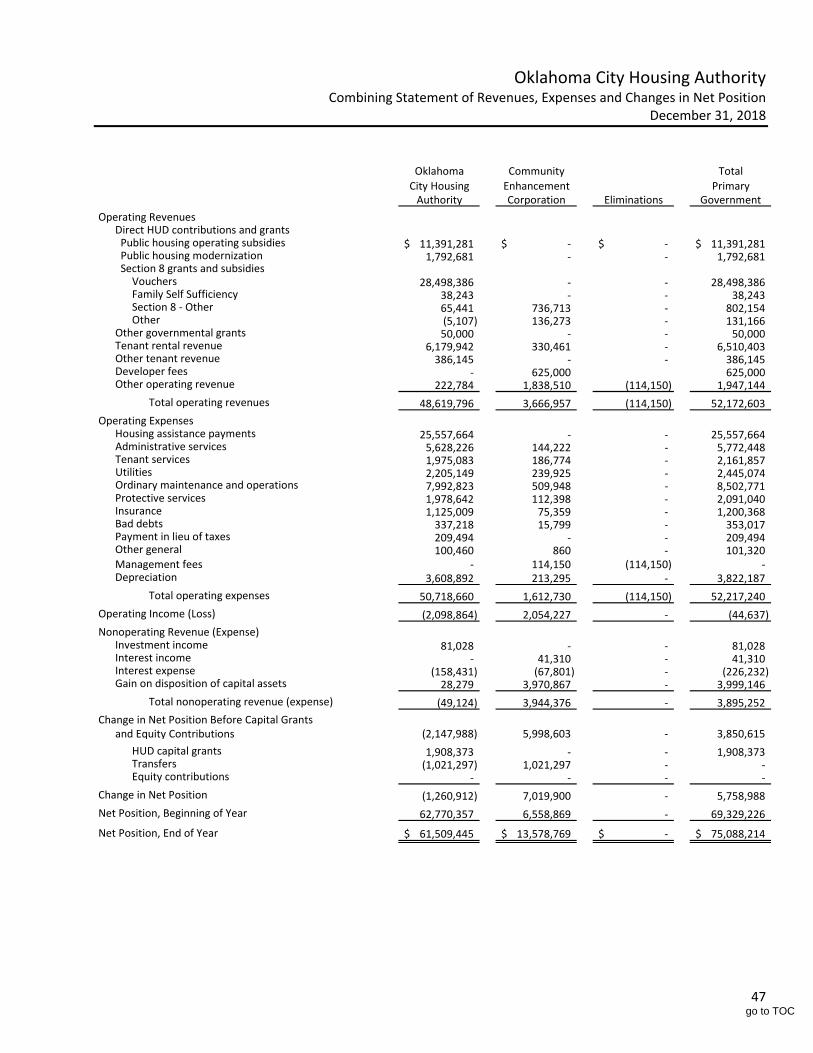

Schedule of Expenditures of Federal Awards ...................................................................................................... 40 Notes to Schedule of Expenditures of Federal Awards ....................................................................................... 41 Combining Statement of Net Position ................................................................................................................. 42 Combining Statement of Revenues, Expenses and Changes in Net Position ...................................................... 46

Other Information

Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ................................................................................................................................................................. 48

Independent Auditor’s Report on Compliance for Each Major Federal Program; Report on Internal Control Over Compliance Required by the Uniform Guidance ..................................................................................................... 50

Schedule of Findings and Questioned Costs ............................................................................................................ 53

go to TOC

1

Independent Auditor’s Report To the Board of Commissioners Oklahoma City Housing Authority Oklahoma City, Oklahoma Report on the Financial Statements We have audited the accompanying financial statements of the business‐type activities and the aggregate discretely presented component units of the Oklahoma City Housing Authority (the Authority) as of and for the years ended December 31, 2019 and 2018, which collectively comprise the Authority’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express opinions on the financial statements based on our audits. We did not audit the financial statements of Sooner Haven, LLC, a discretely presented component unit, which represents 52% of the assets, 56% of the net position, and 100% of the revenues of the discretely presented component units as of and for the year ended December 31, 2019 and 52% of the assets, 56% of the net position, and 100% of the revenues of the discretely presented component units as of and for the year ended December 31, 2018. Those statements were audited by other auditors whose report has been furnished to us, and our opinion, insofar as it relates to the amounts included for Sooner Haven, LLC is based solely on the report of the other auditors. We conducted our audits in accordance with auditing standards generally accepted in the United States of America, and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risk of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Authority’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Authority’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

What inspires you, inspires us. | eidebailly.com

1730 Burnt Boat Loop, Ste. 100 | P.O. Box 1914 | Bismarck, ND 58502-1914 | T 701.255.1091 | F 701.224.1582 | EOE

go to TOC

2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the business‐type activities and the aggregate discretely presented component units of the Authority as of December 31, 2019 and 2018, and the respective changes in its financial position and, where applicable, cash flows thereof for the years then ended, in accordance with accounting principles generally accepted in the United States of America. Correction of Error As discussed in Note 13 to the financial statements, a certain error resulting in understatement of amounts previously reported for capital assets and accounts payable as of December 31, 2018 were discovered during the current year. Accordingly, amounts reported for capital assets and accounts payable have been restated in the 2018 financial statements now presented. Our opinion is not modified with respect to that matter. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 4 through 10 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the management discussion and analysis in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Oklahoma City Housing Authority’s financial statements. The accompanying supplementary schedules on pages 42 ‐ 47 are presented for purposes of additional analysis and are not a required part of the basic financial statements. The accompanying Schedule of Expenditures of Federal Awards is presented for purposes of additional analysis, as required by the Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance) and are not a required part of the financial statements.

go to TOC

3

The supplementary schedules on pages 42 ‐ 47 and the Schedule of Expenditures of Federal Awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the supplementary schedules on pages 39 – 44 and the Schedule of Expenditures of Federal Awards is fairly stated, in all material respects, in relation to the financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated March 17, 2021 on our consideration of the Authority’s internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is solely to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the Authority’s internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Authority’s internal control over financial reporting and compliance.

Bismarck, North Dakota March 17, 2021

go to TOC

4

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

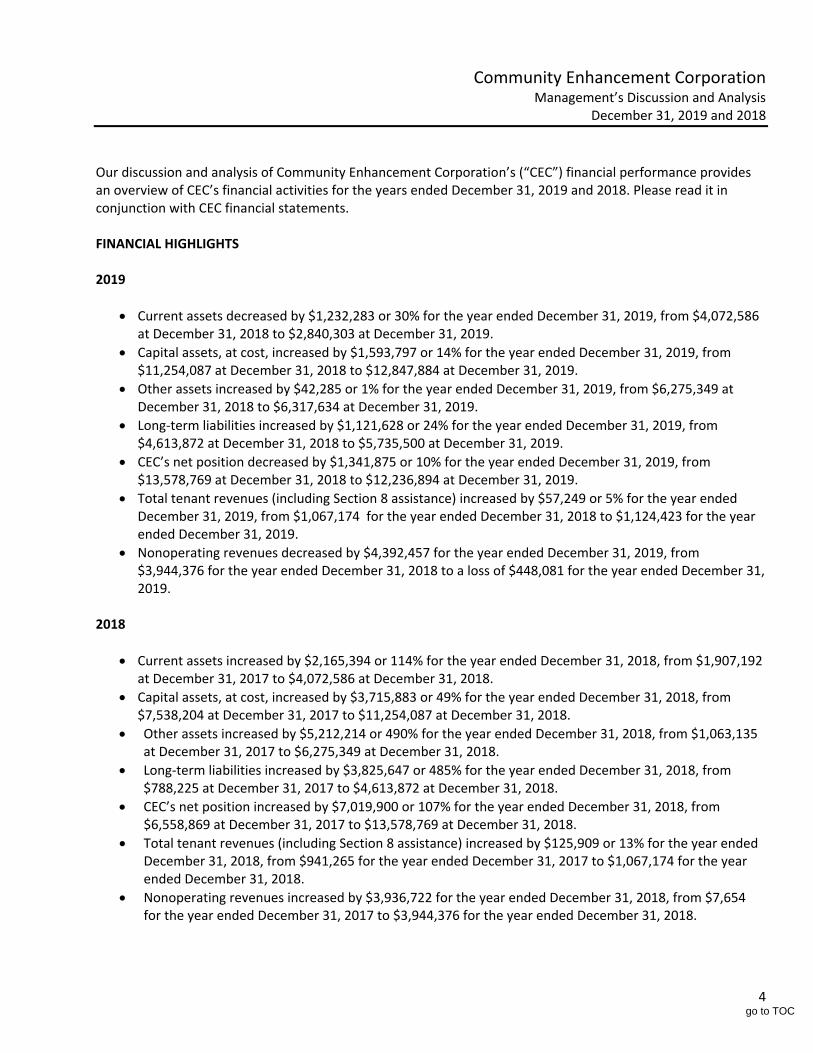

The discussion and analysis of the Authority’s financial performance provides an overview of the Authority’s financial activities for the years ended December 31, 2019 and 2018. Please read it in conjunction with the Authority’s financial statements. Financial Highlights 2019

The Authority added approximately $4,352,000 in capital assets relating to land, building improvements and renovations during 2019.

The Authority’s net position decreased by $3,840,240 or 5% during the year ended December 31, 2019, from $75,088,214 at December 31, 2018 to $71,247,974 at December 31, 2019.

Total operating revenues of the Authority decreased by $3,971,468 or 8% for the year ended December 31, 2019, from $52,172,603 for the year ended December 31, 2018 to $48,201,135 for the year ended December 31, 2019.

Total operating expenses of the Authority increased by $1,935,151 or 4% for the year ended December 31, 2019, from $52,217,240 for the year ended December 31, 2018 to $54,152,240 for the year ended December 31, 2019.

Total nonoperating revenue (expense), including capital grants, decreased by $3,692,609 for the year ended December 31, 2019, from $5,803,625 for the year ended December 31, 2018 to $2,111,016 for the year ended December 31, 2019.

2018

The Authority added approximately $12,951,000 in capital assets relating to land, building improvements and renovations during 2018.

The Authority’s net position increased by $5,758,988 or 8% during the year ended December 31, 2018, from $69,329,226 at December 31, 2017 to $75,088,214 at December 31, 2018.

Total operating revenues of the Authority increased by $5,425,070 or 12% for the year ended December 31, 2018, from $46,747,533 for the year ended December 31, 2017 to $52,172,603 for the year ended December 31, 2018.

Total operating expenses of the Authority increased by $518,750 or 1% for the year ended December 31, 2018, from $51,698,490 for the year ended December 31, 2017 to $52,217,240 for the year ended December 31, 2018.

Total nonoperating revenue (expense), including capital grants, increased by $3,514,750 for the year ended December 31, 2018, from $2,288,875 for the year ended December 31, 2017 to $5,803,625 for the year ended December 31, 2018.

go to TOC

5

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

Overview of Financial Statements The following summarizes the content of the Authority’s financial statements, which include its blended component unit, Community Enhancement Corporation ("CEC"). Separate financial statements for CEC may be obtained at the Authority's administrative offices.

1. Management Discussion and Analysis 2. Financial Statements, including the Statements of Net Position on page ten, the Statements of

Revenues, Expenses and Changes in Net Position on page fourteen, and the Statements of Cash Flows on page sixteen.

3. Statements of Net Position which presents information on all of the Authority's assets and liabilities,

with the difference between the two reported as net position. Over time, increases or decreases in net position usually serve as a useful indicator of whether the change in the financial position of the Authority is improving or deteriorating.

4. Statements of Revenues, Expenses, and Changes in Net Position which presents information showing how the Authority's net position changed during the most recent period. This statement shows the total revenues and total expenses of the Authority and the difference between them is the Authority's net income.

5. Statements of Cash Flows which presents changes in cash and cash equivalents resulting from operations, capital and noncapital financing activities, and investing activities.

6. Notes to Financial Statements, which provide additional information essential to the understanding of the Authority's financial statements.

The primary focus of the Authority’s financial statements is on the Authority as a whole. This perspective allows the user to address relevant questions, broaden a basis for comparison and enhance the Authority’s accountability. Entity Wide Financial Statements The Authority engages in only business‐type activities. The financial statements are designed to be corporate‐like in that all business‐type activities are consolidated to a total for the entire entity. The Authority’s major business activities include the following:

Rental of real estate under a low‐rent public housing contract. Provide rental assistance and Family Self Sufficiency counseling under Section 8 voucher contracts, and also through CEC’s Section 8 housing.

Provision of tenant services funded from both low‐rent public housing contracts and grant funding.

Through CEC, the acquisition and rehabilitation of rental units to provide Section 8 housing funded by federal grant programs.

go to TOC

6

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

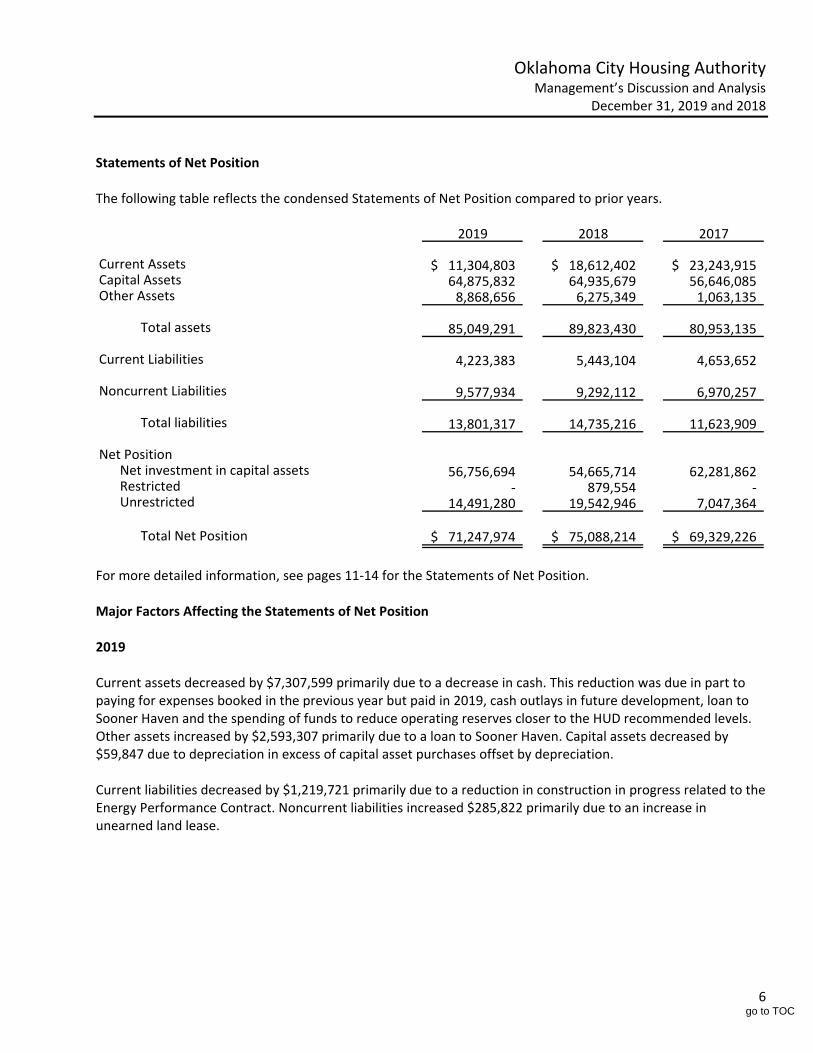

Statements of Net Position The following table reflects the condensed Statements of Net Position compared to prior years.

2019 2018 2017

Current Assets 11,304,803$ 18,612,402$ 23,243,915$ Capital Assets 64,875,832 64,935,679 56,646,085 Other Assets 8,868,656 6,275,349 1,063,135

Total assets 85,049,291 89,823,430 80,953,135

Current Liabilities 4,223,383 5,443,104 4,653,652

Noncurrent Liabilities 9,577,934 9,292,112 6,970,257

Total liabilities 13,801,317 14,735,216 11,623,909

Net PositionNet investment in capital assets 56,756,694 54,665,714 62,281,862 Restricted ‐ 879,554 ‐ Unrestricted 14,491,280 19,542,946 7,047,364

Total Net Position 71,247,974$ 75,088,214$ 69,329,226$

For more detailed information, see pages 11‐14 for the Statements of Net Position. Major Factors Affecting the Statements of Net Position 2019 Current assets decreased by $7,307,599 primarily due to a decrease in cash. This reduction was due in part to paying for expenses booked in the previous year but paid in 2019, cash outlays in future development, loan to Sooner Haven and the spending of funds to reduce operating reserves closer to the HUD recommended levels. Other assets increased by $2,593,307 primarily due to a loan to Sooner Haven. Capital assets decreased by $59,847 due to depreciation in excess of capital asset purchases offset by depreciation. Current liabilities decreased by $1,219,721 primarily due to a reduction in construction in progress related to the Energy Performance Contract. Noncurrent liabilities increased $285,822 primarily due to an increase in unearned land lease.

go to TOC

7

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

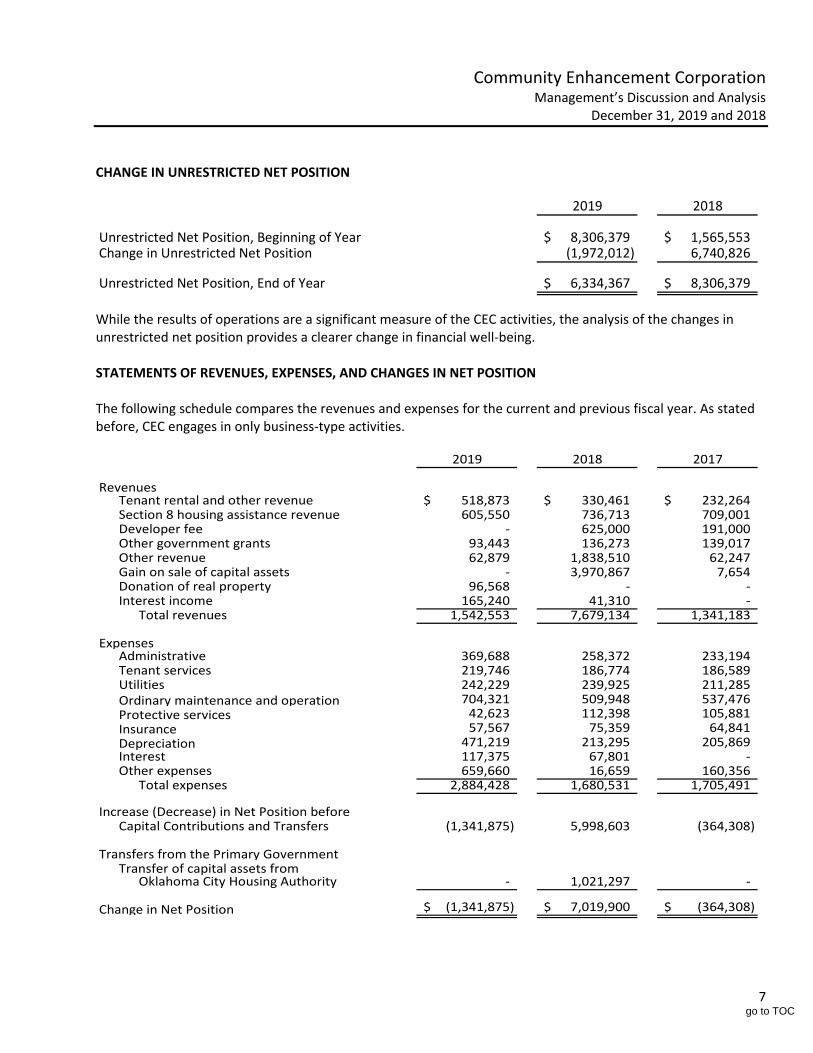

2018 Current assets decreased by $4,631,513 primarily due to a decrease in cash that was used to pay for energy efficiency improvements. Other assets increased by $5,212,214 primarily due to the note receivable from Sooner Haven, LLC. Capital assets increased by $6,905,043 due to capital asset purchases offset by depreciation. Current liabilities decreased by $595,000 primarily to a decrease in accounts payable. Noncurrent liabilities increased $2,321,855 primarily due to the long‐term debt related to the acquisition and renovation of Yorktown Apartments. Change in Unrestricted Net Position

2019 2018

Unrestricted Net Position, Beginning of Year 19,542,946$ 7,047,364$

Change in Unrestricted Net Position (5,051,666) 12,495,582

Unrestricted Net Position, End of Year 14,491,280$ 19,542,946$

While the results of operations are a significant measure of the Authority's activities, the analysis of the changes in unrestricted net position provides a clearer change in financial well‐being.

go to TOC

8

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

Statements of Revenues, Expenses and Changes in Net Assets The following schedule compares the revenues and expenses for the current and previous fiscal years. As stated before, the Authority engages in only business‐type activities.

2019 2018 2017

RevenuesOperating grants and subsidies 41,114,582$ 42,703,911$ 39,049,033$ Capital grants 2,558,767 1,908,373 2,303,205 Tenant rental and other revenue 6,842,243 6,896,548 7,152,591 Investment income 66,931 81,028 85,863 Interest income 197,875 41,310 ‐ Other 379,175 6,571,290 568,076

Total revenues 51,159,573 58,202,460 49,158,768

ExpensesAdministrative services 5,841,994 6,125,465 6,381,746 Tenant services 2,381,712 2,161,857 2,181,405 Utilities 2,327,606 2,445,074 2,530,687 Maintenance 10,173,648 8,502,771 8,939,983 Protective services 1,856,963 2,091,040 2,047,699 Section 8 Housing assistance payments 25,598,109 25,557,664 24,602,198 Depreciation 4,411,892 3,822,187 3,698,378 Insurance 1,220,058 1,200,368 1,035,388 Interest 254,908 226,232 122,360 Other 932,923 310,814 281,006

Total expenses 54,999,813 52,443,472 51,820,850

Change in Net Position (3,840,240)$ 5,758,988$ (2,662,082)$

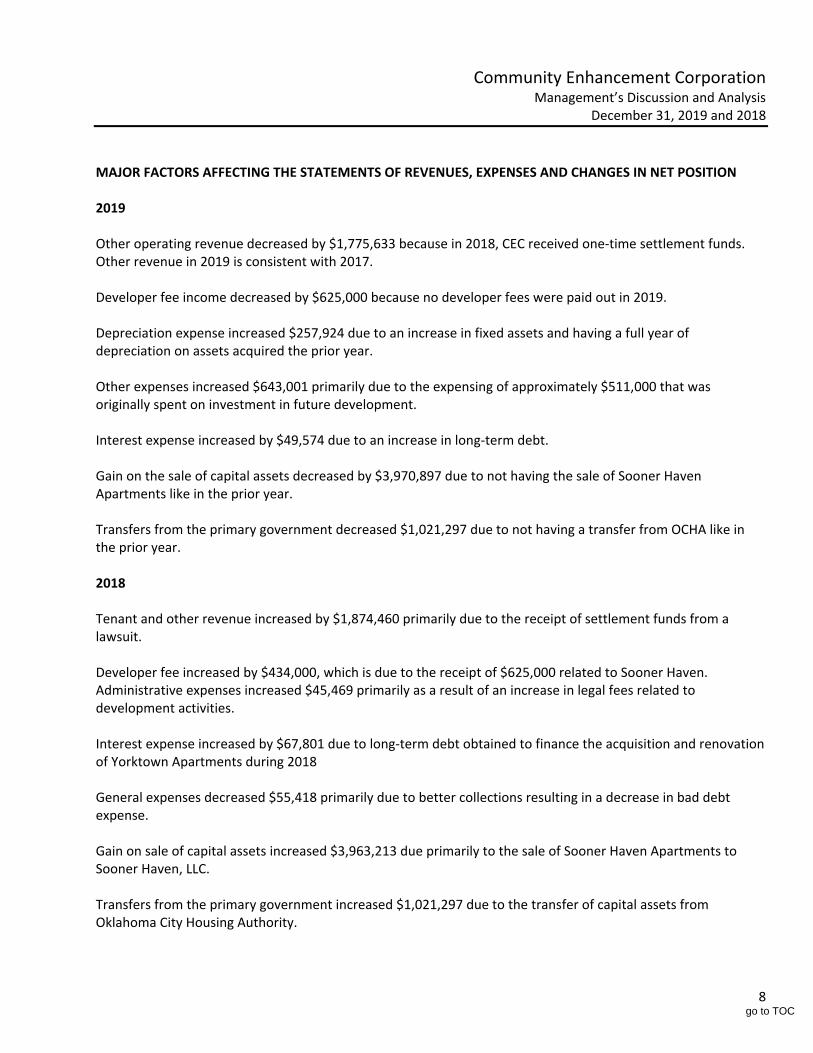

Major Factors Affecting the Statement of Revenues, Expenses and Changes in Net Position 2019 Operating grants and subsidies, including HUD capital grants decreased by $939,935 primarily due to a reduction in Section 8 funds. Other revenue decreased by $6,192,115 primarily due to receiving one time settlement funds, proceeds from the sale of Sooner Haven and developer fees in 2018 that did not occur in 2019. Total expenses increased by $2,474,976 primarily due to increases in Maintenance and Operations costs from various contract work as well as increases in depreciation expenses due to a full year of depreciation on assets acquired the previous year and the addition of assets acquired under the Energy Performance Contract.

go to TOC

9

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

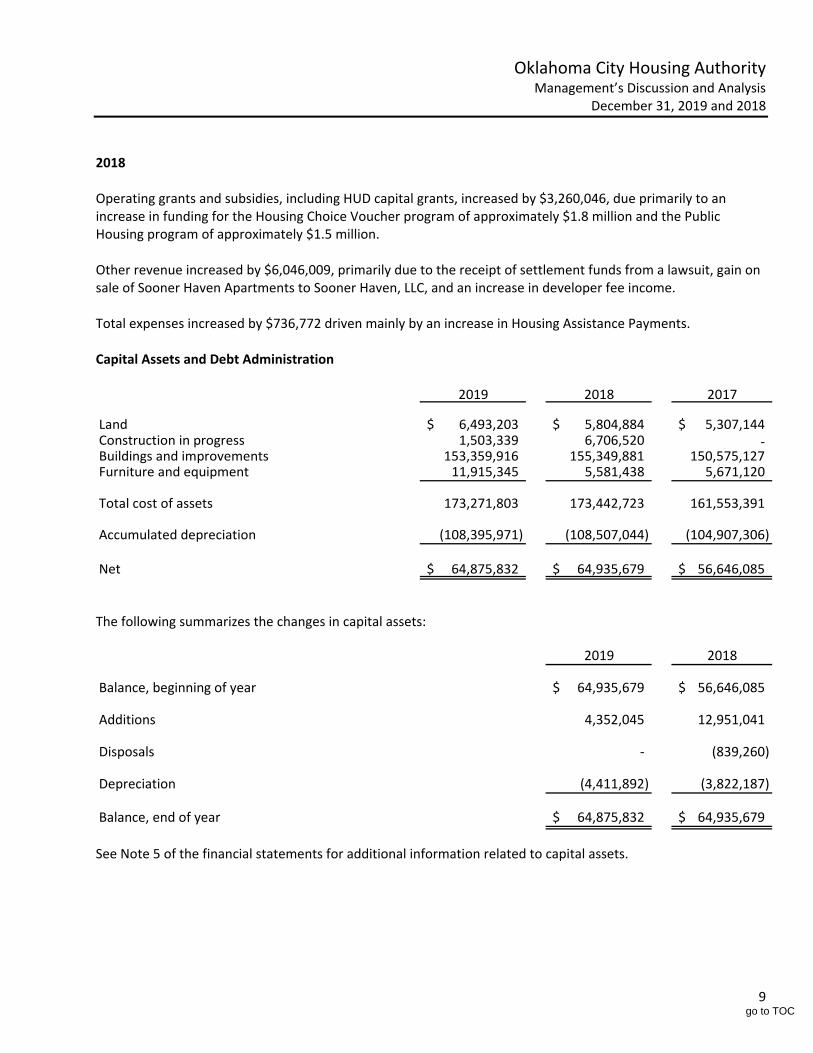

2018 Operating grants and subsidies, including HUD capital grants, increased by $3,260,046, due primarily to an increase in funding for the Housing Choice Voucher program of approximately $1.8 million and the Public Housing program of approximately $1.5 million. Other revenue increased by $6,046,009, primarily due to the receipt of settlement funds from a lawsuit, gain on sale of Sooner Haven Apartments to Sooner Haven, LLC, and an increase in developer fee income. Total expenses increased by $736,772 driven mainly by an increase in Housing Assistance Payments. Capital Assets and Debt Administration

2019 2018 2017

Land 6,493,203$ 5,804,884$ 5,307,144$ Construction in progress 1,503,339 6,706,520 ‐ Buildings and improvements 153,359,916 155,349,881 150,575,127Furniture and equipment 11,915,345 5,581,438 5,671,120

Total cost of assets 173,271,803 173,442,723 161,553,391

Accumulated depreciation (108,395,971) (108,507,044) (104,907,306)

Net 64,875,832$ 64,935,679$ 56,646,085$

The following summarizes the changes in capital assets:

2019 2018

Balance, beginning of year 64,935,679$ 56,646,085$

Additions 4,352,045 12,951,041

Disposals ‐ (839,260)

Depreciation (4,411,892) (3,822,187)

Balance, end of year 64,875,832$ 64,935,679$

See Note 5 of the financial statements for additional information related to capital assets.

go to TOC

10

Oklahoma City Housing Authority Management’s Discussion and Analysis

December 31, 2019 and 2018

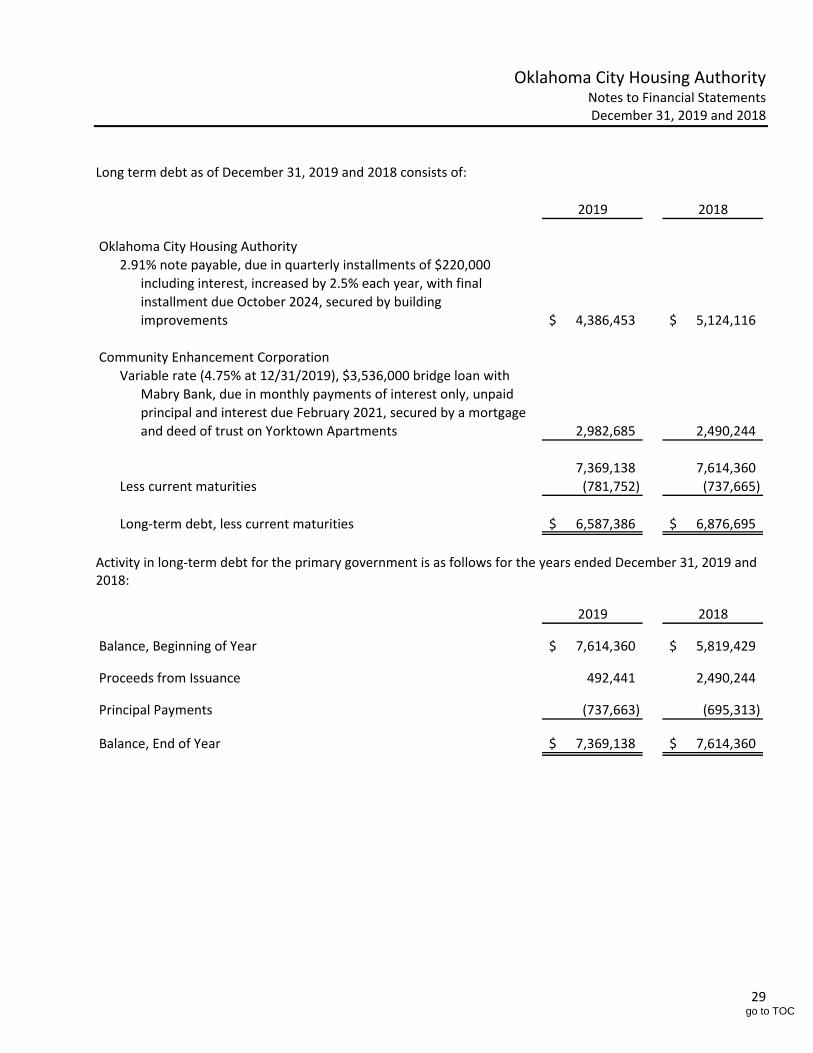

Debt Outstanding During 2019, the Authority made principal payments of $737,663 and incurred additional debt of $492,441. The proceeds of the debt were used to finance the renovation of Yorktown Apartments. During 2018, the Authority made principal payments of $695,31 and incurred additional debt of $2,490,244. The proceeds of the debt were used to finance the acquisition and renovation of Yorktown Apartments. See Note 6 of the financial statements for additional information relating to long‐term debt. Economic Factors Significant economic factors affecting the entity are as follows:

Federal funding from the Department of Housing and Urban Development (or applicable agency)

Local labor supply and demand, which can affect salary and wage rates

Local inflationary, recessionary, and employment trends, which can affect resident incomes, and therefore the amount of rental income

Inflationary pressure on utility rates, supplies, and other costs

Financial Contact The individual to be contacted regarding this report is Thomas Henderson, Chief Financial Officer of the Oklahoma City Housing Authority, at (405) 239‐7551. Specific requests may also be submitted to Thomas Henderson, at 1700 Northeast Fourth Street, Oklahoma City, Oklahoma, 73117‐3800.

go to TOC

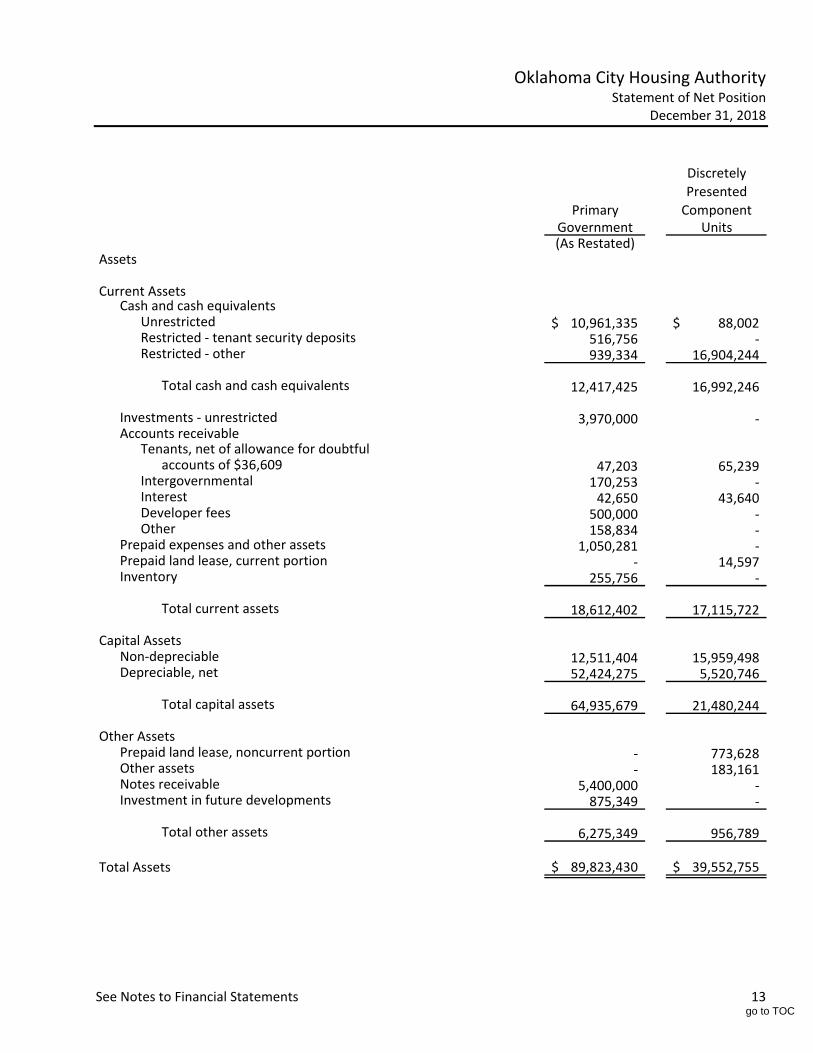

See Notes to Financial Statements 11

Oklahoma City Housing Authority Statement of Net Position

December 31, 2019

Discretely

Presented

Primary ComponentGovernment Units

Assets

Current AssetsCash and cash equivalents

Unrestricted 5,536,551$ 825,392$ Restricted ‐ tenant security deposits 526,420 14,775 Restricted ‐ other 90,948 12,954,117

Total cash and cash equivalents 6,153,919 13,794,284

Investments ‐ unrestricted 2,500,000 ‐ Accounts receivable

Tenants, net of allowance fordoubtful accounts of $88,762 40,367 14,095

Intergovernmental 398,392 26,841 Interest 239,185 42,204 Developer fees 500,000 ‐ Other 317,604 ‐

Prepaid expenses and other assets 1,007,273 39,521 Prepaid land lease, current portion ‐ 14,597 Inventory 148,063 5,775

Total current assets 11,304,803 13,937,317

Capital AssetsNon‐depreciable 7,996,542 24,438,560 Depreciable, net 56,879,290 9,787,258

Total capital assets 64,875,832 34,225,818

Other AssetsPrepaid land lease, noncurrent portion ‐ 759,031 Other assets ‐ 170,797 Notes receivable 7,951,022 ‐ Investment in future developments 917,634 ‐

Total other assets 8,868,656 929,828

Total Assets 85,049,291$ 49,092,963$

go to TOC

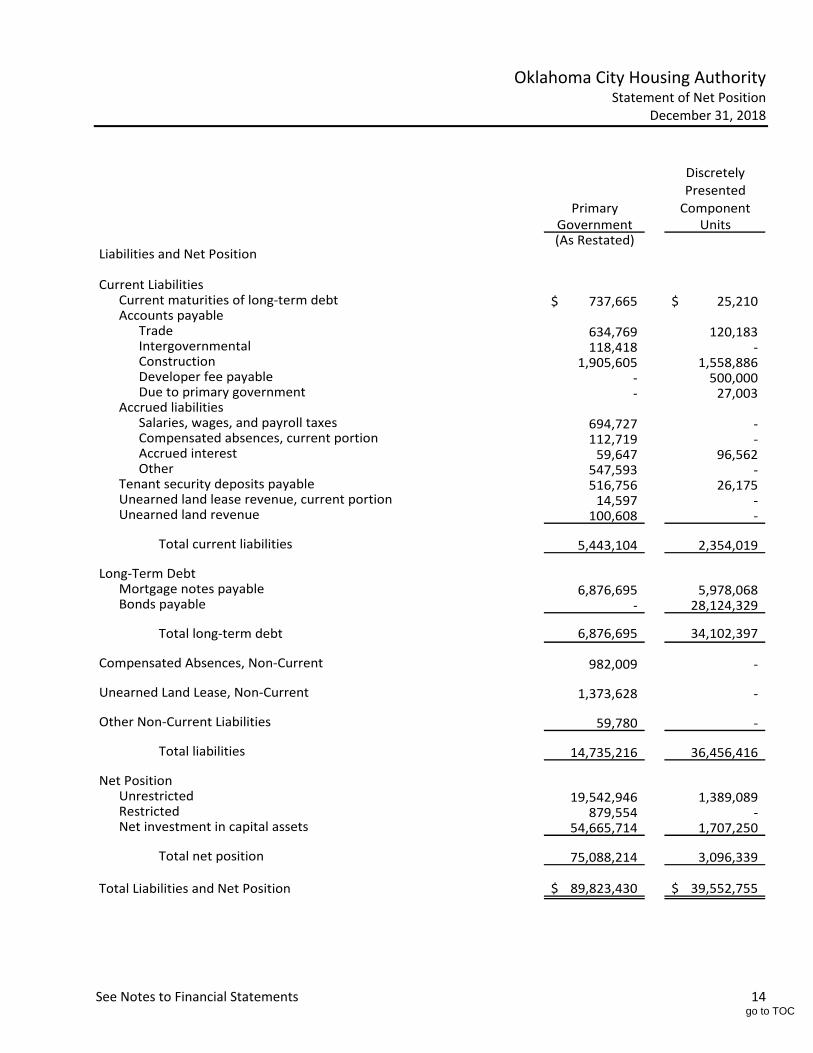

See Notes to Financial Statements 12

Oklahoma City Housing Authority Statement of Net Position

December 31, 2019

Discretely

Presented

Primary ComponentGovernment Units

Liabilities and Net Position

Current LiabilitiesCurrent maturities of long‐term debt 781,752$ 133,233$ Accounts payable

Trade 862,844 131,635 Intergovernmental 511,966 ‐ Construction 314,573 4,852,945 Developer fee payable ‐ 500,000 Due to primary government ‐ 25,157

Accrued liabilitiesSalaries, wages, and payroll taxes 413,440 39,727 Compensated absences, current portion 172,528 ‐ Accrued interest 21,274 413,184 Other 533,316 6,083

Tenant security deposits payable 526,420 14,775 Unearned land lease revenue, current portion 34,293 ‐ Unearned revenue 50,977 14,737

Total current liabilities 4,223,383 6,131,476

Long‐Term DebtMortgage notes payable 6,587,386 10,980,068 Bonds payable ‐ 28,150,966

Total long‐term debt 6,587,386 39,131,034

Compensated Absences, Non‐Current 987,733 ‐

Unearned Land Lease, Non‐Current 2,002,815 ‐

Other Non‐Current Liabilities ‐ ‐

Total liabilities 13,801,317 45,262,510

Net PositionUnrestricted 14,491,280 1,268,444 Restricted ‐ ‐ Net investment in capital assets 56,756,694 2,562,009

Total net position 71,247,974 3,830,453

Total Liabilities and Net Position 85,049,291$ 49,092,963$

go to TOC

See Notes to Financial Statements 13

Oklahoma City Housing Authority Statement of Net Position

December 31, 2018

Discretely

Presented

Primary ComponentGovernment Units(As Restated)

Assets

Current AssetsCash and cash equivalents

Unrestricted 10,961,335$ 88,002$ Restricted ‐ tenant security deposits 516,756 ‐ Restricted ‐ other 939,334 16,904,244

Total cash and cash equivalents 12,417,425 16,992,246

Investments ‐ unrestricted 3,970,000 ‐ Accounts receivable

Tenants, net of allowance for doubtfulaccounts of $36,609 47,203 65,239

Intergovernmental 170,253 ‐ Interest 42,650 43,640 Developer fees 500,000 ‐ Other 158,834 ‐

Prepaid expenses and other assets 1,050,281 ‐ Prepaid land lease, current portion ‐ 14,597 Inventory 255,756 ‐

Total current assets 18,612,402 17,115,722

Capital AssetsNon‐depreciable 12,511,404 15,959,498 Depreciable, net 52,424,275 5,520,746

Total capital assets 64,935,679 21,480,244

Other AssetsPrepaid land lease, noncurrent portion ‐ 773,628 Other assets ‐ 183,161 Notes receivable 5,400,000 ‐ Investment in future developments 875,349 ‐

Total other assets 6,275,349 956,789

Total Assets 89,823,430$ 39,552,755$

go to TOC

See Notes to Financial Statements 14

Oklahoma City Housing Authority Statement of Net Position

December 31, 2018

Discretely

Presented

Primary ComponentGovernment Units(As Restated)

Liabilities and Net Position

Current LiabilitiesCurrent maturities of long‐term debt 737,665$ 25,210$ Accounts payable

Trade 634,769 120,183 Intergovernmental 118,418 ‐ Construction 1,905,605 1,558,886 Developer fee payable ‐ 500,000 Due to primary government ‐ 27,003

Accrued liabilitiesSalaries, wages, and payroll taxes 694,727 ‐ Compensated absences, current portion 112,719 ‐ Accrued interest 59,647 96,562 Other 547,593 ‐

Tenant security deposits payable 516,756 26,175 Unearned land lease revenue, current portion 14,597 ‐ Unearned land revenue 100,608 ‐

Total current liabilities 5,443,104 2,354,019

Long‐Term DebtMortgage notes payable 6,876,695 5,978,068 Bonds payable ‐ 28,124,329

Total long‐term debt 6,876,695 34,102,397

Compensated Absences, Non‐Current 982,009 ‐

Unearned Land Lease, Non‐Current 1,373,628 ‐

Other Non‐Current Liabilities 59,780 ‐

Total liabilities 14,735,216 36,456,416

Net PositionUnrestricted 19,542,946 1,389,089 Restricted 879,554 ‐ Net investment in capital assets 54,665,714 1,707,250

Total net position 75,088,214 3,096,339

Total Liabilities and Net Position 89,823,430$ 39,552,755$

go to TOC

See Notes to Financial Statements 15

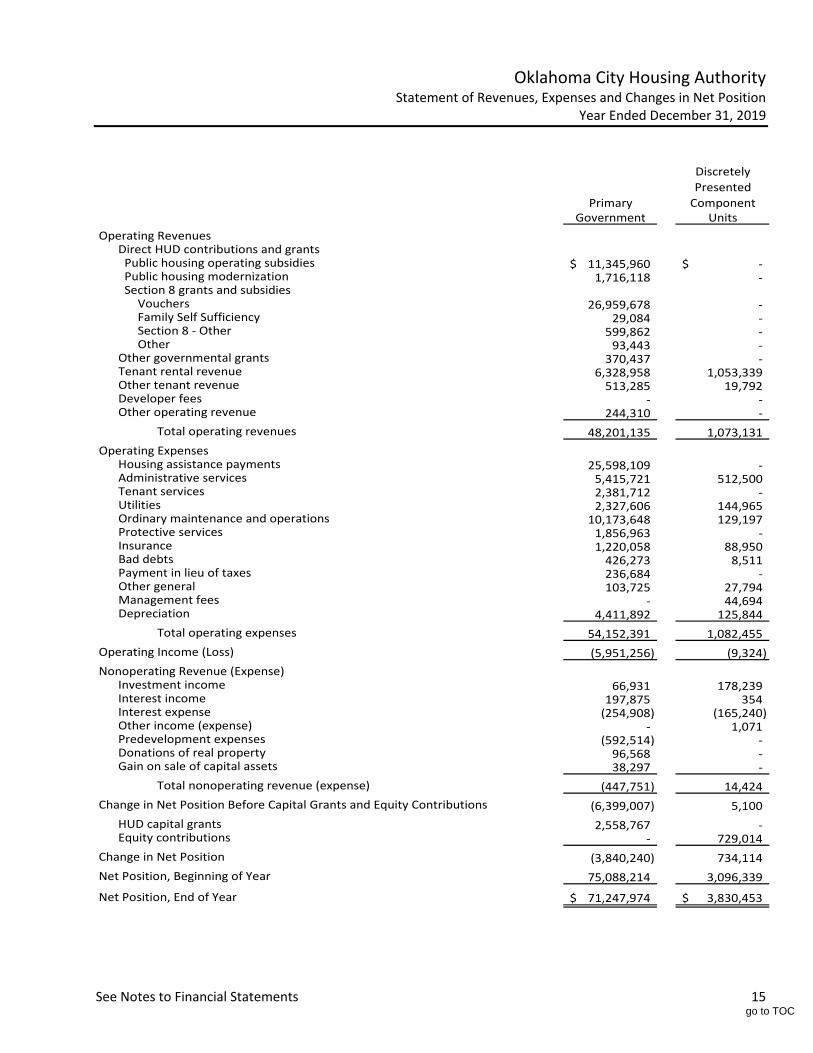

Oklahoma City Housing Authority Statement of Revenues, Expenses and Changes in Net Position

Year Ended December 31, 2019

Discretely

Presented

Primary ComponentGovernment Units

Operating RevenuesDirect HUD contributions and grants Public housing operating subsidies 11,345,960$ ‐$ Public housing modernization 1,716,118 ‐ Section 8 grants and subsidies

Vouchers 26,959,678 ‐ Family Self Sufficiency 29,084 ‐ Section 8 ‐ Other 599,862 ‐ Other 93,443 ‐

Other governmental grants 370,437 ‐ Tenant rental revenue 6,328,958 1,053,339 Other tenant revenue 513,285 19,792 Developer fees ‐ ‐ Other operating revenue 244,310 ‐

Total operating revenues 48,201,135 1,073,131

Operating ExpensesHousing assistance payments 25,598,109 ‐ Administrative services 5,415,721 512,500 Tenant services 2,381,712 ‐ Utilities 2,327,606 144,965 Ordinary maintenance and operations 10,173,648 129,197 Protective services 1,856,963 ‐ Insurance 1,220,058 88,950 Bad debts 426,273 8,511 Payment in lieu of taxes 236,684 ‐ Other general 103,725 27,794 Management fees ‐ 44,694 Depreciation 4,411,892 125,844

Total operating expenses 54,152,391 1,082,455

Operating Income (Loss) (5,951,256) (9,324)

Nonoperating Revenue (Expense)Investment income 66,931 178,239 Interest income 197,875 354 Interest expense (254,908) (165,240) Other income (expense) ‐ 1,071 Predevelopment expenses (592,514) ‐ Donations of real property 96,568 ‐ Gain on sale of capital assets 38,297 ‐

Total nonoperating revenue (expense) (447,751) 14,424

Change in Net Position Before Capital Grants and Equity Contributions (6,399,007) 5,100

HUD capital grants 2,558,767 ‐ Equity contributions ‐ 729,014

Change in Net Position (3,840,240) 734,114

Net Position, Beginning of Year 75,088,214 3,096,339

Net Position, End of Year 71,247,974$ 3,830,453$

go to TOC

See Notes to Financial Statements 16

Oklahoma City Housing Authority Statement of Revenues, Expenses and Changes in Net Position

Year Ended December 31, 2018

Discretely

Presented

Primary ComponentGovernment Units

Operating RevenuesDirect HUD contributions and grants Public housing operating subsidies 11,391,281$ ‐$ Public housing modernization 1,792,681 ‐ Section 8 grants and subsidies

Vouchers 28,498,386 ‐ Family Self Sufficiency 38,243 ‐ Section 8 ‐ Other 802,154 ‐ Other 131,166 ‐

Other governmental grants 50,000 ‐ Tenant rental revenue 6,510,403 163,070 Other tenant revenue 386,145 ‐ Developer fees 625,000 ‐ Other operating revenue 1,947,144 ‐

Total operating revenues 52,172,603 163,070

Operating ExpensesHousing assistance payments 25,557,664 ‐ Administrative services 5,772,448 11,595 Tenant services 2,161,857 ‐ Utilities 2,445,074 10,083 Ordinary maintenance and operations 8,502,771 22,456 Protective services 2,091,040 ‐ Insurance 1,200,368 ‐ Bad debts 353,017 ‐ Payment in lieu of taxes 209,494 ‐ Other general 101,320 581 Management fees ‐ 428 Depreciation 3,822,187 25,229

Total operating expenses 52,217,240 70,372

Operating Loss (44,637) 92,698

Nonoperating Revenue (Expense)Investment income 81,028 ‐ Interest income 41,310 ‐ Interest expense (226,232) (8,502) Gain on disposition of capital assets 3,999,146 ‐

Total nonoperating revenue (expense) 3,895,252 (8,502)

Change in Net Position Before Capital Grants and Equity Contributions 3,850,615 84,196

HUD capital grants 1,908,373 ‐ Transfers ‐ ‐ Equity contributions ‐ 1,629,115

Change in Net Position 5,758,988 1,713,311

Net Position, Beginning of Year 69,329,226 1,383,028

Net Position, End of Year 75,088,214$ 3,096,339$

go to TOC

See Notes to Financial Statements 17

Oklahoma City Housing Authority Statements of Cash Flows

Years Ended December 31, 2019 and 2018

2019 2018

Operating ActivitiesCash received from government grants and subsidies 40,415,589$ 43,163,574$ Cash received from tenants 6,528,312 6,886,046 Cash received from other sources 1,184,495 2,404,734 Cash payments to housing assistance payments (24,875,892) (25,557,664) Cash payments to employees for services (10,716,341) (10,428,412) Cash payments for goods or services (13,364,171) (14,466,942)

Net Cash (used for) from Operating Activities (828,008) 2,001,336

Capital and Related Financing ActivitiesHUD capital grants 2,558,767 1,908,373 Principal payments on long‐term debt (737,663) (695,313) Proceeds from issuance of long‐term debt 492,441 2,490,244 Purchases of capital assets (5,846,509) (11,045,436) Proceeds from the sale of capital assets 38,297 39,856 Interest payments on mortgage notes and bonds payable (293,281) (194,809)

Net Cash used for Capital and Related Financing Activities (3,787,948) (7,497,085)

Investing ActivitiesInvestments in future developments (677,299) (601,027) Payments received on investments in future developments 42,500 788,813 Issuance of notes receivable (2,551,022) ‐ Purchase of investments ‐ (1,470,000) Sales and maturities of investments 1,470,000 4,410,000 Investment income 35,636 79,688

Net Cash (used for) from Investing Activities (1,680,185) 3,207,474

Net Change in Cash and Cash Equivalents (6,296,141) (2,288,275)

Cash and Cash Equivalents, Beginning of Year 12,417,425 14,705,700

Cash and Cash Equivalents, End of Year 6,121,284$ 12,417,425$

Primary Government

go to TOC

See Notes to Financial Statements 18

Oklahoma City Housing Authority Statements of Cash Flows

Years Ended December 31, 2019 and 2018

2019 2018(As Restated)

Reconciliation of Operating Loss to Net Cash (Used For) From Operating Activities

Operating loss (5,951,256)$ (44,637)$ Adjustments to reconcile operating loss to

net cash (used for) from operating activities Depreciation 4,411,892 3,822,187 Changes in assets and liabilities

Accounts receivable (380,073) (163,858) Inventory 107,693 (40,406) Prepaid expenses and other assets 43,008 (493,219) Accounts payable ‐ Intergovernmental grants 393,548 98,312 Accounts payable 228,075 (2,340,064) Accrued liabilities (289,811) 929,466 Tenant security deposits payable 9,664 8,896 Unearned revenue 599,252 224,659

Net Cash (used for) from Operating Activities (828,008)$ 2,001,336$

Supplemental Schedule of Noncash Capital and Related Financing ActivitiesIncrease in capital assets from accounts payable ‐ construction 314,573$ 1,905,605$

Increase in notes receivable from the sale of capital assetsIncrease in notes receivable 612,082$ 5,400,000$ Gain on sale of capital assets 1,224,164 4,378,703

Decrease in capital assets (612,082)$ 1,021,297$

Primary Government

go to TOC

19

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Note 1 ‐ Summary of Significant Accounting Policies Nature of the Organization The Oklahoma City Housing Authority (the “Authority”) is a municipal entity organized in 1965 for the development, operation and administration of low‐rent housing programs. The programs are administered through the U.S. Department of Housing and Urban Development (“HUD”) under the U.S. Housing Act of 1937, as amended. The primary purpose of the programs is to provide safe, decent and sanitary housing for low‐income families in Oklahoma City, Oklahoma. The Authority operates its programs primarily with grants and subsidies received from HUD under contractual agreements and with rental proceeds received from tenants. Funds for the acquisition, development or modernization of dwelling units have generally been derived from HUD through the sale of notes and bonds and from HUD grants. Reporting Entity The Authority’s financial statements include the accounts of all Authority operations. The criteria for including organizations as component units within the Authority reporting entity, as set forth in Section 2100 of the Governmental Accounting Standards Board’s (GASB) Codification of Government Accounting and Financial Reporting Standards, include whether:

The organization is legally separated (can sue and be sued in their own name).

The Authority holds the corporate powers of the organization. The Authority appoints a voting majority of the organization’s board.

The Authority is able to impose its will on the organization.

The organization has the potential to impose a financial benefit/burden on the Authority.

There is fiscal dependency by the organization on the Authority. Based on the aforementioned criteria, the Authority is not a component unit within another reporting entity. Blended Component Units Included within the reporting entity is the Community Enhancement Corporation (“CEC”), which is an Oklahoma not‐for‐profit corporation formed June 15, 1984, in an effort to expand into charitable housing programs offered to lower‐income citizens of Oklahoma City. In 1994, CEC acquired from HUD, at a nominal price, several single‐family homes and a multi‐family apartment complex. CEC receives housing assistance payments for these projects pursuant to Section 8 of the U.S. Housing Act of 1937. In addition, CEC receives Federal funds used for the purchase and rehabilitation of Section 8 rental units. There are separate financial statements for CEC, which may be obtained at the Authority’s administrative offices. Included within the reporting entity of the Authority, through CEC, as blended component units are JHJ GP, LLC and Sooner Haven MM, LLC. JHJ GP, LLC and Sooner Haven MM, LLC are wholly owned by CEC. JHJ GP, LLC is the managing general partner of John H Johnson ALF, LP, a discretely presented component unit. Sooner Haven MM, LLC is the managing member of Sooner Haven, LLC, a discretely presented component unit. Separate set of financial statements for JHJ GP, LLC and Sooner Haven MM, LLC are not issued.

go to TOC

20

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Discretely Presented Component Units The component unit column in the financial statements include the financial data of the Authority’s discretely presented component units as of December 31, 2019 and 2018. The component units are reported in a separate column to emphasize that they are legally separate from the Authority. John H. Johnson ALF, LP (the Partnership or JHJ, LP) was formed for the purpose of owning and operating a 130‐unit low‐income housing project in Oklahoma City, Oklahoma. As previously mentioned, JHJ GP, LLC is the managing general partner of the Partnership, and has on ownership percentage of 0.01% in the Partnership. Sooner Haven, LLC was formed for the purpose of owning and operating an existing 150‐unit low‐income Rental Assistance Demonstration (RAD) project in Oklahoma City, Oklahoma. As mentioned above, Sooner Haven MM, LLC is the managing general partner of Sooner Haven, LLC and has an ownership percentage of 0.01% in Sooner Haven, LLC. The financial statements of the discretely presented component units are presented in CEC’s basic financial statements. Separate financial statements for the Partnership are not issued. Complete financial statements for Sooner Haven, LLC can be obtained from CEC’s administrative offices at 1700 N E 4 St., Oklahoma City, Oklahoma, 73117‐3800. Program Accounting The accounts of the Authority are organized on the basis of programs, each of which is considered a separate accounting entity. The operations of each program are accounted for with a separate set of self‐balancing accounts that comprise its assets, liabilities, net position, revenues, and expenses. The Authority classifies its programs as proprietary. Basis of Accounting and Measurement Focus The Department of Housing and Urban Development Real Estate Assessment Center (REAC) assesses the financial condition of Public Housing Authorities (PHA’s). To uniformly and consistently assess the PHA’s, REAC requires that PHA’s financial statements conform to Generally Accepted Accounting Principles (GAAP). The accounting and financial reporting treatment applied to a fund is determined by its measurement focus. All proprietary funds are accounted for using the economic resources measurement focus. With this measurement focus, all assets and liabilities associated with the operation of these funds are included on the statement of net position. Net position is segregated into invested in capital assets, restricted and unrestricted components. The statement of revenues, expenses and changes in net position presents increases (e.g., revenues) and decreases (e.g., expenses) in total net position. When both restricted and unrestricted net position is available for use, generally, it is the Authority’s policy to use restricted net position first, and then unrestricted net position as it is needed. The statement of cash flow presents the cash flows for operating activities, investing activities, capital and related financing activities and non‐capital financing activities.

go to TOC

21

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Use of Estimates The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Cash and Cash Equivalents The Authority's cash deposits can only be invested in HUD approved investments: direct obligations of the Federal Government backed by the full faith and credit of the United States, obligations of government agencies, securities of government sponsored agencies, demand and savings deposits, time deposits, repurchase agreements, and other securities approved by HUD. For the purpose of the statement of cash flows, the Authority considers cash deposits and highly liquid investments with a maturity of three months or less when purchased to be cash equivalents. Accounts Receivable Revenues are recorded when earned and are reported as accounts receivable until collected. Accounts receivable are expensed as bad debts at the time they are determined to be uncollectible. Management has established an allowance for doubtful accounts for amounts that may not be collectible in the future. Receivables are reported net of the related allowance. Investments Investments, including restricted investments, if any, consist of certificates of deposit as of December 31, 2019 and 2018. The investments are recorded at cost, which approximates market. Restricted investments, if any, generally include amounts restricted for Section 8 Housing Assistance payments and Section 8 Family Self Sufficiency (“FSS”) funds. Section 8 FSS funds are offset by FSS liabilities. Inventory Inventory consists of expendable materials and supplies and is stated at weighted‐average cost. Capital Assets Capital assets are recorded at cost, which is comprised of development and modernization costs funded by capital grants, the fair value of donated assets, and property additions from operations. The Authority uses a capitalization threshold of $5,000 or more and useful life of more than one year. The costs of normal maintenance and repairs that do not add to the value of the asset or materially extend lives are not expensed as incurred. Upon sale or retirement, the costs are removed from the accounts, and the resulting gain or loss is included in revenue or expense.

go to TOC

22

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Depreciation of capital assets is provided using the straight‐line method over the estimated lives of the respective assets as follows: Buildings and improvements 20 ‐ 40 years Furniture and equipment 5 ‐ 10 years Long‐lived assets held and used by an entity are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. No impairment loss has been recognized for the years ended December 31, 2019 and 2018. Land Leases Unearned land lease revenue is being amortized over the terms of the leases using the straight‐line method of amortization (Note 9). Notes and Interest Receivable Notes and interest receivable are carried at amounts advanced, net of reserve for uncollectible accounts, if any. As of December 31, 2019 and 2018, the Authority considered all notes and interest receivables to be fully collectable. Investment in Future Developments Investments in future developments represents costs incurred by the Authority for future developments and are recorded at cost until a project is established. If a potential project is no longer deemed to be feasible, the costs are charged to expense in the year the project is abandoned. Compensated Absences Vested personal leave is recorded as an expense as the benefits accrue to employees. Unearned Revenue Unearned revenue consists primarily of advance rental payments received from tenants. Unearned Land Leases Unearned land lease revenue for the Authority is being amortized over the terms of the leases using the straight‐line method of amortization (Note 9). Income Taxes The Authority, as a governmental entity, is not liable for federal and state income taxes. However, the Authority does make annual payments in lieu of taxes (“PILOT”) to local school districts. CEC is an organization exempt from federal income taxes under Internal Revenue Code Section 501(c)(3).

go to TOC

23

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Components of Net Position Components of net position include the following:

Net Investment in Capital Assets – Consists of capital assets, net of accumulated depreciation and reduced by outstanding balances of debt issued to finance the acquisition, improvement, or construction of those assets.

Restricted Net Position – Consists of assets and deferred outflows less related liabilities and deferred inflows reported in the basic statement of net position that are subject to restraints on their use by HUD. As of December 31, 2019 and 2018, restricted net position totaled $) and $879,554, respectively. Restricted net position consists of Section 8 Choice Voucher payments received from HUD but not yet paid to eligible individuals.

Unrestricted Net Position – Consists of assets and deferred outflows less related liabilities and deferred inflows reported in the basic statement of net position that are not subject to restraints on their use.

Operating Revenues and Expenses The Authority considers all revenues and expenses (including HUD intergovernmental revenues and expenses) as operating items with the exception of interest expense, interest revenue, and gain/loss on disposal of capital assets which are considered non‐operating for financial reporting purposes. Restricted and Unrestricted Resources The Authority applies restricted resources first when an expense is incurred for purposes for which both restricted and unrestricted resources are available. Fraud Recovery HUD requires the Authority to account for monies recovered from tenants who committed fraud or misrepresentation in the application process for rent calculations and now owe additional rent for prior periods or retroactive rent as fraud recovery. The monies recovered are shared by HUD and the local authority.

go to TOC

24

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Note 2 ‐ Cash and Cash Equivalents Primary Government Deposits It is the Authority’s policy to invest in those securities which are authorized by HUD. Such investments generally consist of obligations of the U.S. government and its agencies and instrumentalities, collateralized or insured certificates of deposit or other bank deposits, and certain other commercial instruments. The primary objectives of the Authority’s investment policy are safety, liquidity, yield, and administrative costs. Custodial Credit Risk Custodial credit risk that, in the event of a bank failure, the Authority’s deposits may not be returned to it. As of December 31, 2019 and 2018, the Authority's deposits were not exposed to custodial credit risk, as all deposits were insured by the Federal Deposit Insurance Commission (FDIC) and collateralized with securities held by a pledging financial institution in accordance with PDPA. At December 31, 2019, the Authority’s carrying amount of deposits was $8,653,919, including cash and cash equivalents and certificates of deposit, and the bank balance was $9,448,113. Of the bank balances, $1,377,208 was covered by Federal Depository Insurance and the remaining balance of $8,096,053 was collateralized with securities held by a pledging financial institution’s agent in the Authority’s or CEC’s name. At December 31, 2018, the Authority’s carrying amount of deposits was $16,387,425, including cash and cash equivalents and certificates of deposit, and the bank balance was $16,568,286. Of the bank balances, $4,658,896 were covered by Federal Depository Insurance and the remaining balance of $11,909,390 was collateralized with securities held by a pledging financial institution’s agent in the Authority’s or CEC’s name. Included in cash and cash equivalents are replacement reserves of approximately $127,000 as of December 31, 2019 and 2018. Discretely Presented Component Units Credit Risk Custodial credit risk is the risk that, in the event of a bank failure, the Partnership’s deposits may not be returned to it. As of December 31, 2019, JHJ, LP’s bank balances were covered by Federal Depository Insurance. As of December 31, 2018, the JHJ, LP had carrying amounts and bank balances in excess of the federally insured limit of $250,000. As of December 31, 2019 and 2018, Sooner Haven, LLC had carrying amounts and bank balances in excess of the federally insured limit of $250,000. Management monitors the financial ratings of such financial institutions and does not believe that the deposits are exposed to a significant level of risk.

go to TOC

25

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

Note 3 ‐ Restricted Cash Primary Government Restricted cash as of December 31, 2019 consists of $526,420 in tenant security deposits, $90,948 in the housing choice voucher program for FSS escrow, and $0 in the housing choice voucher program for unspent vouchers. Restricted cash as of December 31, 2018 consists of $516,756 in tenant security deposits, $59,780 in the housing choice voucher program for FSS escrow, and $879,554 in the housing choice voucher program for unspent vouchers. Discretely Presented Component Units

Restricted cash consists of various bond trust accounts as required by the bond documents (Note 6), tenant security deposits, and various reserves and escrows required by HUD and the partnership/operating agreements. Total restricted cash as of December 31, 2019 and 2018 was $12,968,117 and $16,904,244, respectively.

Note 4 ‐ Accounts Receivable‐Intergovernmental Accounts receivable‐intergovernmental consists of the following as of December 31, 2019 and 2018:

2019 2018

HUD

Capital fund program 337,712$ 108,392$

Community Development Block Grant 34,359 35,485

Resident Opportunity and Supportive Services 14,836 ‐

Total HUD 386,907 143,877

Sober Living 8,333 ‐

Continuum of Care 3,152 26,376

398,392$ 170,253$

go to TOC

26

Oklahoma City Housing Authority Notes to Financial Statements December 31, 2019 and 2018

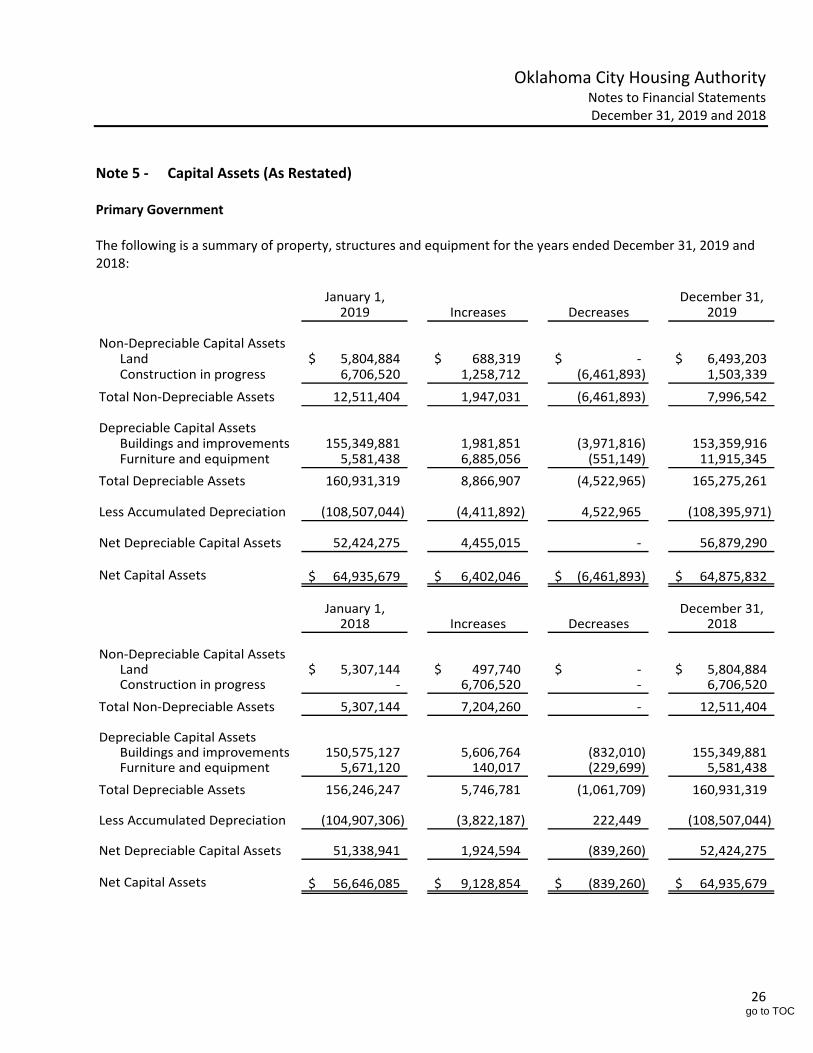

Note 5 ‐ Capital Assets (As Restated) Primary Government The following is a summary of property, structures and equipment for the years ended December 31, 2019 and 2018:

January 1, December 31,2019 Increases Decreases 2019

Non‐Depreciable Capital AssetsLand 5,804,884$ 688,319$ ‐$ 6,493,203$ Construction in progress 6,706,520 1,258,712 (6,461,893) 1,503,339

Total Non‐Depreciable Assets 12,511,404 1,947,031 (6,461,893) 7,996,542

Depreciable Capital AssetsBuildings and improvements 155,349,881 1,981,851 (3,971,816) 153,359,916 Furniture and equipment 5,581,438 6,885,056 (551,149) 11,915,345

Total Depreciable Assets 160,931,319 8,866,907 (4,522,965) 165,275,261

Less Accumulated Depreciation (108,507,044) (4,411,892) 4,522,965 (108,395,971)

Net Depreciable Capital Assets 52,424,275 4,455,015 ‐ 56,879,290

Net Capital Assets 64,935,679$ 6,402,046$ (6,461,893)$ 64,875,832$

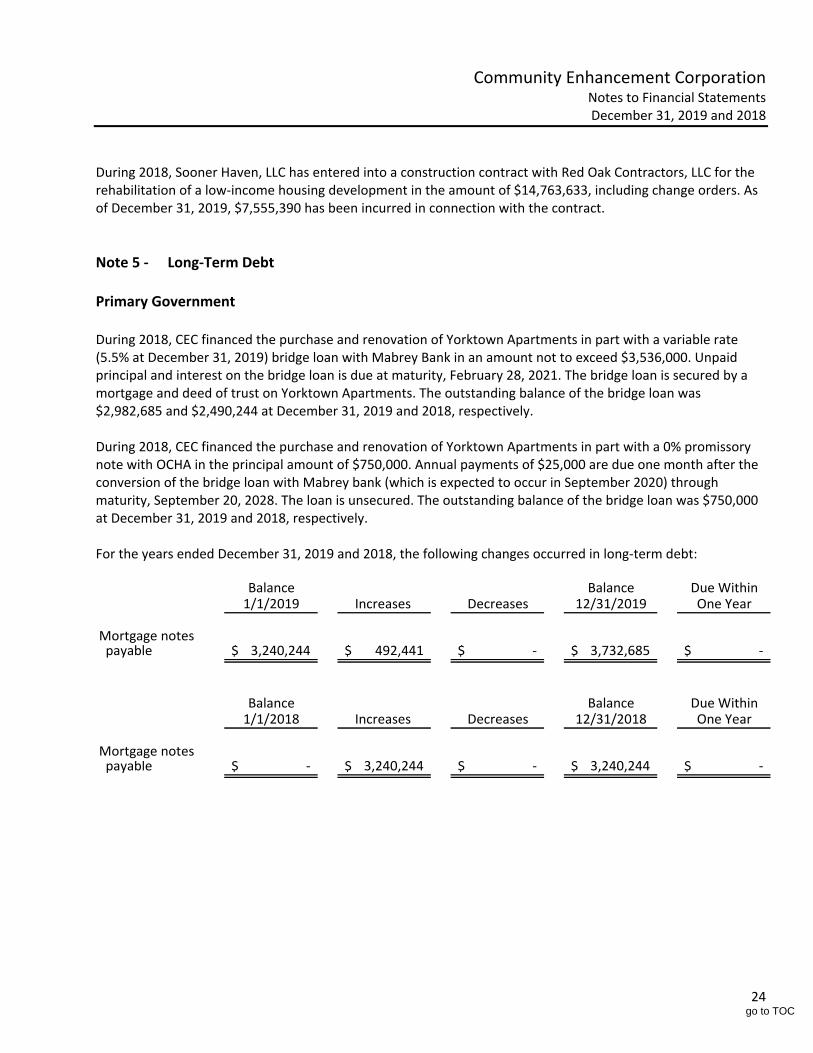

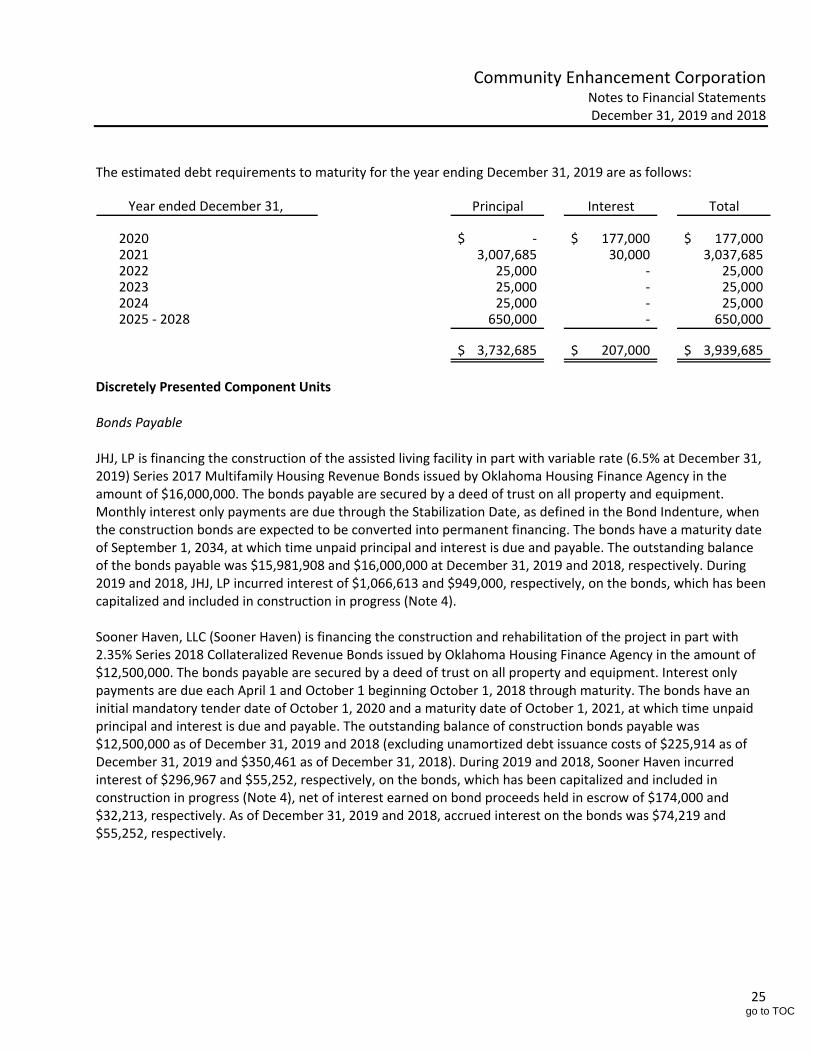

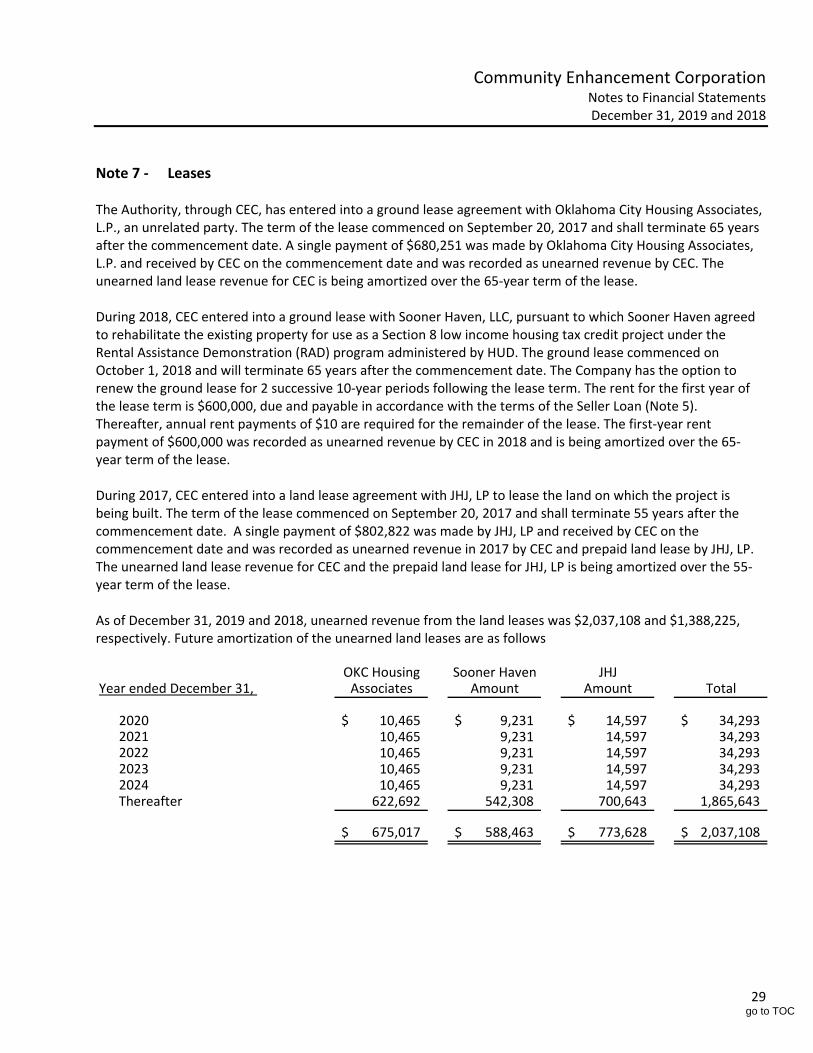

January 1, December 31,2018 Increases Decreases 2018