Bahasa

Halaman

Hukum

InterChina

Strategy | Corporate Finance

AutoSector Group

www.InterChinaConsulting.comwww.InterChinaPartners.com

Exclusive China Partner of

© InterChinaConfidential

Index

• Sector Dynamics• Our Auto Services & Team• Perspectives On China’s Auto Sector• Consulting Cases• Deal Tombstones

21

345

2

© InterChinaConfidential

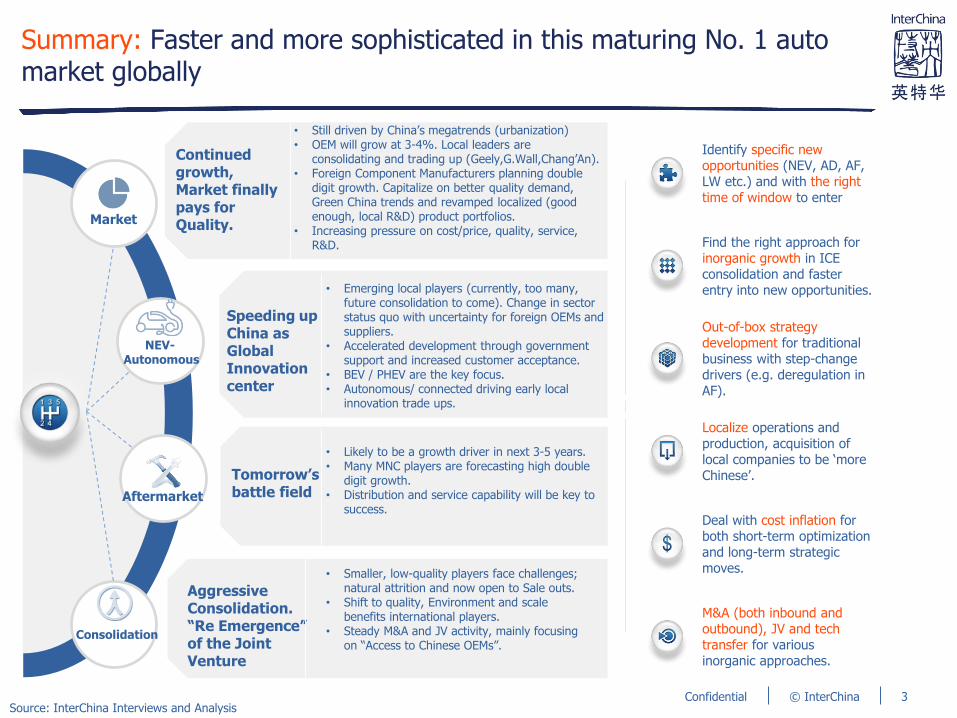

Summary: Faster and more sophisticated in this maturing No. 1 auto market globally

Source: InterChina Interviews and Analysis

M&A (both inbound and outbound), JV and tech transfer for various inorganic approaches.

Find the right approach for inorganic growth in ICE consolidation and faster entry into new opportunities.

Localize operations and production, acquisition of local companies to be ‘more Chinese’.

Out-of-box strategy development for traditional business with step-change drivers (e.g. deregulation in AF).

Deal with cost inflation for both short-term optimization and long-term strategic moves.

Identify specific new opportunities (NEV, AD, AF, LW etc.) and with the right time of window to enter

3

Aggressive Consolidation.“Re Emergence” of the Joint Venture

Continued growth, Market finally pays for Quality.

Tomorrow’s battle field

Speeding upChina as Global Innovationcenter

• Still driven by China’s megatrends (urbanization) • OEM will grow at 3-4%. Local leaders are

consolidating and trading up (Geely,G.Wall,Chang’An).• Foreign Component Manufacturers planning double

digit growth. Capitalize on better quality demand, Green China trends and revamped localized (good enough, local R&D) product portfolios.

• Increasing pressure on cost/price, quality, service, R&D.

• Smaller, low-quality players face challenges; natural attrition and now open to Sale outs.

• Shift to quality, Environment and scale benefits international players.

• Steady M&A and JV activity, mainly focusing on “Access to Chinese OEMs”.

• Likely to be a growth driver in next 3-5 years. • Many MNC players are forecasting high double

digit growth. • Distribution and service capability will be key to

success.

• Emerging local players (currently, too many, future consolidation to come). Change in sector status quo with uncertainty for foreign OEMs and suppliers.

• Accelerated development through government support and increased customer acceptance.

• BEV / PHEV are the key focus. • Autonomous/ connected driving early local

innovation trade ups.

Market

Consolidation

Aftermarket

NEV-Autonomous

© InterChinaConfidential

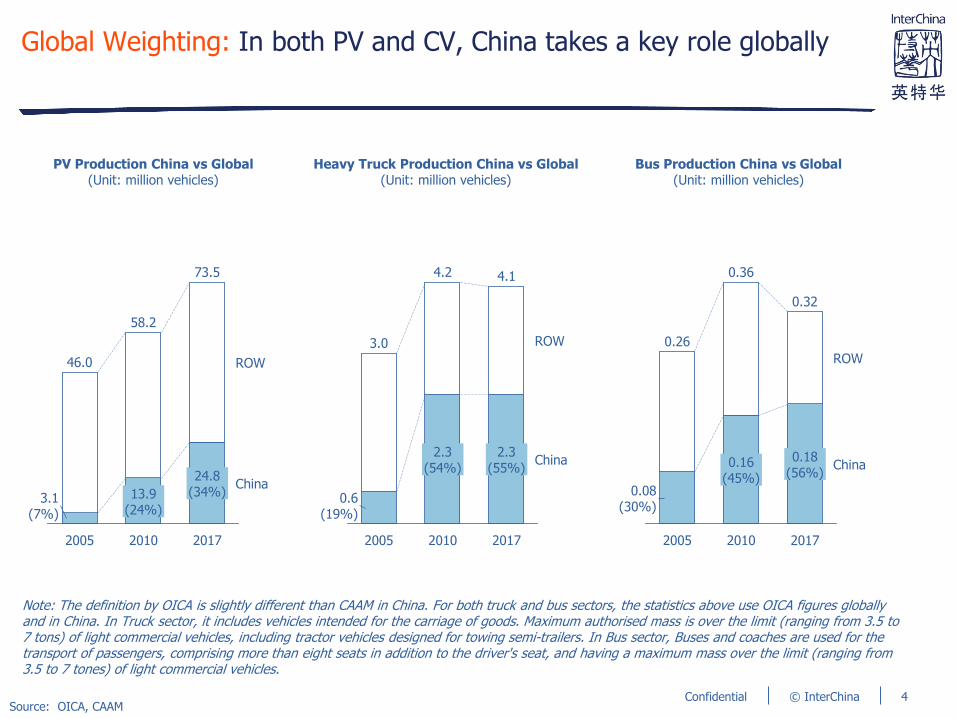

Global Weighting: In both PV and CV, China takes a key role globally

Source: OICA, CAAM

Note: The definition by OICA is slightly different than CAAM in China. For both truck and bus sectors, the statistics above use OICA figures globally and in China. In Truck sector, it includes vehicles intended for the carriage of goods. Maximum authorised mass is over the limit (ranging from 3.5 to 7 tons) of light commercial vehicles, including tractor vehicles designed for towing semi-trailers. In Bus sector, Buses and coaches are used for the transport of passengers, comprising more than eight seats in addition to the driver's seat, and having a maximum mass over the limit (ranging from 3.5 to 7 tones) of light commercial vehicles.

PV Production China vs Global(Unit: million vehicles)

201720102005

46.0

58.2

13.9(24%)

China

ROW

3.1(7%)

73.5

24.8(34%)

3.0

0.6(19%)

ROW

2.3(54%) China

2010

4.2

2005 2017

4.1

2.3(55%)

2005

China0.16(45%)

ROW

2010

0.36

0.08(30%)

0.26

2017

0.18(56%)

0.32

Heavy Truck Production China vs Global(Unit: million vehicles)

Bus Production China vs Global(Unit: million vehicles)

4

© InterChinaConfidential

050

100150200250300350400450500550600650

0 10,000 20,000 30,000 40,000 50,000 60,000

S1 2035

China 2020

Australia

S3 2035

S2 2035

France

Germany

India China 2015

USA

Canada

United Kingdom

Italy

South Korea

Japan

Cars owned per 1,000 people in 2015

GDP per capita measured at purchasing power parity in 2015 (USD)

Global Comparison of Auto Penetration and GDP

China Prospects: Likely further growth in ownership (though well below the levels of developed countries by 2035) will support the long-term development of China’s auto industry

Source: Chinese Yearbook, World Bank, OICA, Trading economics, various other statistics collected by InterChina

S1 2035:5-year disposal scenario

S2 2035: 7-year disposal scenario

S3 2035: 10-year disposal scenario

(Refer to the last slide)

5

© InterChinaConfidential

China PV production will still experience relatively strong growth, with the growth rate fluctuating around the GDP growth rate

Global Gravity: Both the OEM production and the after-market value chains will be the global No 1 with 1/3 of global share

China’s PV Production – History & Forecast

Source: CAAM, InterChina Interviews and Analysis

2035E

33

14

45

2005 2022E2016

4

2010

24

CAGR CAGR 25% 18% 5% 4%29% 10% 5% 3%

Unit: million cars

Ownership in 2035 will provide the next momentum for the market growth

China’s PV Ownership – History & Forecast

Unit: million cars

2035E

350

20162010

58

2022E2005

19

160

220

6

© InterChinaConfidential

Emerging Battlefields: Sector step-changes (e.g. NEV, AD, AF, LW etc.)bringing both opportunities and challenges require tailor-made solutions in China

7

China has a huge market for these emerging tech market, but

not an easy one…

Other challenges (e.g. infrastructure etc.)

Multiple tech routes for cars, but also along the supply chain.

Growing Chinese competition.

Note: NEV = New Energy Vehicle, AD = Autonomous Driving, AF = de-regulated after-market, and LW = Lightweight Tech

Immature but changing pricing mechanism.

Dynamic regulatory environment (new policies, deregulation etc.).

…it asks for FIEs to think globally while acting locally

Global and China Strategy

Parity

In-depth China Market Assessment

Investment Vehicle & Partner

Selection

Government Lobbying

On-going Competitive-

ness

Operational Improve-

ments

Localized solutions required.

© InterChinaConfidential

Inorganic Growth: Cross-border transactions in automotive sectors is still a hot area

8

1417

1515

91010

18

2010 2012 20132011 2014 201720162015

Volume of cross-border automotive deals in China

Value of cross-border automotive deals in China (RMB m)

2,263.0

1,180.0

5,312.0

1,875.81,661.01,229.4

176.5

1,513.0

201420132011 20122010 201720162015

Source: FactSet, Mergermarket, Bloomberg, EMIS Deal Watch, InterChina Analysis

Representative Recent Transactions

The electronic vehiclesmanufacturer NextEVsecured a funding led byUS investment firmSequoia Capital andChinese firm Joy Capital.

Sep. 2015

Asset dealUSD 500 m

Cooper Tire & RubberCo acquired 65% stakein Qingdao Ge Rui DaRubber Co Ltd, amanufacturer of truckand bus radial tire tiresbased in Shandong.

Jan. 2016

65%USD 92 m

Daimler AG announcedthe acquisition of aminority stake in BeijingElectric Vehicle Co. Thedeal has been approvedby NDRC.

Jun. 2017

MinorityUSD 92.61 m

• Nio deal: RMB 3205 m (USD 500 m)

• Others: RMB 2107 m

© InterChinaConfidential

Index

• Sector Dynamics• Our Auto Services & Team• Perspectives On China’s Auto Sector• Consulting Cases• Deal Tombstones

21

345

9

© InterChinaConfidential

Service Needs (1/2): Our strategy and corporate finance teams support our client’s profitable top-line growth along the value chain of auto components and services

• What could be the “realistic” opportunity scale and the “right” time of window to enter(feasibility from all aspects e.g. regulatory, value-chain wise, competition, technicallyetc.)

• How to deal with dynamic and less transparent regulatory environment in decision-making, and in effective communication of China reality back to HQ

• How to shortlist on the “right” tech to go forwards among various competition tech,which is often influenced by the drivers beyond tech advantages

• How to adapt the offerings and positioning to echo the needs in this maturing automarket

• How to develop in-China-for-China capability and capacity to deal with the speed ofmarket development in China

• How to profitably work with Chinese OEMs with more weighting in ICE and NEV butwith rather different client behavior than JV OEMs

• How to capture adjacent product opportunity into emerging battlefields• How to defend the existing portfolio against the threat from new battlefields (e.g. NEV

might make some ICE components redundant)

Consolidate Commercial

Strategy

Capture Component Opportunity

Business Opportunity

Assessment (esp. in emerging

battlefields*)

10Note: The emerging battlefields refer to for example NEV (New Energy Vehicle), AD (Autonomous Driving), AF (de-regulated After-Market), LW (Light Weight tech and materials) and Service etc.

© InterChinaConfidential

Service Needs (2/2): Our strategy and corporate finance teams themes support our client’s profitable top-line growth along the value chain of auto components and services

• How to revamp the business model in China, adapting to the new trends in China (e.g.from multi-step distribution model in aftermarket to one-step model with efficiency andsustainability)

• How to develop out-of-box initiatives to outperform the competition, (e.g. alliance withretail for growth, or distribution platform model in aftermarket, or diversified channelsin auto assistance)

• How to revamp or optimize the route-to-market structure and partners, to respond tothe new differentiation needs

• How to capture the growth opportunity leveraging the sector’s consolidation trend?• How to conduct bolt-on acquisition for further growth• How to develop JV (OEMs, other partners with synergy) to accelerate the growth• How to know and access below-the-radar targets or non-traditional-type targets to

enter into emerging battlefields

• How to develop new sourcing partners to deal with further localization needs• Sourcing best practice benchmarking• How to divest the periphery assets, which is less fit with the core China strategy

Speed-up via Inorganic Approach

Practical Investment

Support

Revamp Service Strategy

11Note: The emerging battlefields refer to for example NEV (New Energy Vehicle), AD (Autonomous Driving), AF (de-regulated After-Market), LW (Light Weight tech and materials) and Service etc.

© InterChinaConfidential

Cases: Deeply engaged with auto clients and projects in China’s front-line in the auto sector

Recent Auto Projects(Selection)

• New Energy Vehicle (NEV) Strategy: We advised a leading European mechatronic players on the design of itsroadmap into NEV. This compromised the assessment of e-mobility in China’s high dynamics regulatory environment, theopportunity product identification, and the investment vehicle strategy.

• Light-weight Component Strategy: We advised the client how to accelerate its development in the light-weightcomponent sector via the localization strategy, via the full assessment of customer voices, the various competingtechnologies, and the likely competition landscaping with the associated key success factors required.

• After-market Strategy: On behalf of a leading US after-market player, we identified the opportunity to deep dive inone-step distribution model in China’s de-regulating auto after-market. In addition, the investment strategy of regionalcluster model via regional alliance and M&A is recommended with the partner screening and evaluation.

• Localization Feasibility: Our client receives mandate to localize in China from one of its global key account OEMs, andour client has three investment options (different models with OEMs in different locations in China). We conducted theassessment of the possible revenues and production cost of the three options and recommended the preferred option.

• Strategy Workshop: For a top international component player, we facilitated a two-day Asia Strategy Workshop withcountry GMs and AP BD VP, and AP President by designing a systematic the strategic planning structure, process andtools, facilitating the efficient discussion on-site and concluding with a set of aligned strategic initiatives.

• Partnership Evaluation: For a leading auto electronics company, we conducted systematic screening and evaluationof the BMS (Battery Management System) related R&D companies in 22 related product sectors (e.g. BMS, DCDC,AutoSAR, ESP, ADAS etc.).

• Auto Service Strategy: Our client is the globally top 3 auto assistance company with the ambition to accelerate itsChina business. With the full-blown customer voices and competition benchmarking, the re-prioritization of the channelsand the re-positioning of the offerings are recommended, with strengthened localization features.

12

© InterChinaConfidential

Client Issues InterChina’s Approach Client Benefits

• What is the size of theaddressable market?

• Regulatory monitoring?• What is the window of

opportunity likely to be?• How to maintain a

competitive advantage inthe long run?

• Whether to enter/expand inChina or not?

• What is the likely downsideif no entry/expansion?

• We use a primary research drivenapproach to piece together a picture fromthe bottom-up

• Given the dynamic and complex evolutionof the auto sector, we use scenarioanalysis to assess the attractiveness ofsectors/segments and the client’s abilityto compete

• In addition, the relevance of China in thecontext of the client’s global strategy iscarefully evaluated

• Our clients are able to take wellinformed ‘go or no go’ decisions onwhether and how to proceed

• Along the way, we encourage theclient to participate in the process,allowing a transfer of understandingto the client, and ultimately the buy-in of the client’s organization intothe strategy

• Moreover, we place ourrecommendations within a strategicframework, so that the client hasreference points for decision-makingnot just for the initial next steps, butalso for expansion thereafter

• Ultimately, our clients benefit from apractical solution in a complex andchallenging environment

The issues above, plus• What is the market

entry/expansion point(target segments, productoffering, value proposition,etc.)?

• What is the route-to-market?• Which investment model?• Expected financial return?• The role of China in the

global strategy?

• Based on the understanding of themarket opportunity, InterChina developsand tests a series of competitive andworkable entry/expansion options for theclient

• In addition, InterChina works with theclient to review the full range of issuesneeded for the client to be ready to startimplementation of the strategy

Approach (1/2): Practical solutions to help our clients to tackle challenges & seek success

Opportunity Assessment

Strategy Development

13

© InterChinaConfidential

Approach (2/2): Practical solutions to help our clients to tackle challenges & seek success

Client Issues InterChina’s Approach Client Benefits

• Which partner to work with?• Which form of alliance?• What trade-off in terms of

what to pay and what togain?

• Implications in terms of thethreat to home markets infuture?

• InterChina develops a comprehensiveand practical framework regardingpotential synergies and risks in thealliance before starting the target searchprocess

• For each shortlisted alliance candidate, atailor-made approach will be developedand tested

• Finally, the implications of the alliance inthe global context will be jointly exploredwith the client (e.g. the alliance partnermight become a threat in future)

• Our clients are able to take wellinformed decisions on whichpartners/ suppliers/ targets topursue, knowing not only theassociated strengths and risks, butalso their relative significance in theChina context

• Our clients have the advantage of usproviding continuity from start tofinish, putting execution within astrategic framework, and therebyincreasing the chances of asuccessful outcome

• Ultimately, our clients benefit fromhaving the right partners/suppliers/targets, a good starting point fortheir relationships, and a robuststructure to work within

• The necessity for sourcing?• What synergies to achieve

through sourcing fromChina?

• What portfolio?• Which partners?• Potential risks and

mitigation plan?

• InterChina conducts a comprehensivestakeholder analysis to explore all therelevant sourcing issues to come up witha realistic action plan

• Then InterChina takes a hands-onapproach to searching for the rightpartners and advising the client on howto best cooperate with these partners

• Acquisition strategy?• Ideal target profile?• Available targets?• Best target?• Deal breaking issues?• How to close in China?

• We conduct systematic target searches,adjusting the ideal target profile duringthe process according the realities wefind, and select the best target usingcomparative analysis

• We also provide technical services (duediligence, valuation) as well astransaction support (negotiation advisory,deal structuring)

Strategic Alliance

Sourcing Strategy

Merger & Acquisition & Alliance

14

© InterChinaConfidential

InterChina’s 20-year experience in China’s consulting sectordifferentiates ourselves from the service by pure strategy firms or bymarket research firms

Abundant sector experience in the varioustraditional and emerging auto sectors.

Senior interviewers; conducted hundredssenior-level interviews.

Transparent process towards clients.

Strong access to the different level of themarket.

Strategic thinking, in addition tostructured analysis data process.

Value-added to The Client’s Project

• Reliability

• Credibility

• Depth

• Practicality

• Transparency

Practical thinking and solutions, alignedwith the client’s decision-making.

InterChina’s Service

Offerings

Our Value: Rely on a practical approach to align with the client’s decision-making process

High senior involvement in projects(partners and sector group members).

15

© InterChinaConfidential

Our Value: InterChina Corporate Finance is different from global and big-4 investment banking firms

• 90% buy-side advisory; skill sets more towards strategic considerations

• Has the boutique focus; Cross-border M&A advisory is the main service offering

• Ability and resources to identify the below the radar acquisition targets

• Better access channels and databases than most bulge bracket firms, and commit serious resources on target screening and identification (instead of opportunistic)

• Knows how to understand and motivate the sellerand handle the early stage communication

• 70% sell-side, 30% buy-side; skill sets more towards marketing

• Investment banking is often a supplement to other financing activities which are the core revenue drivers

• Because of overhead structure, cannot commit to smaller deals. Attention is mostly focused on large transactions. POEs

• More analytical/desktop driven.. They lack the focus and skills to develop complicated family owned transactions, where subjective skills are needed.

Global Investment Banking FirmsInterChina

Deal Origination

Transaction Execution

• On the ground resources (sizeable team in China,larger than some regional and global i-banks)

• Commit senior resources to every stage of the transaction. Act as an extension to client’s in-house team. Easy to work with

• Knows how to manage Target’s expectations• Early red flag identification: Knows the intricacy

of dealing with local entrepreneurs, SOEs, and listed companies

• In-depth sector and commercial knowledge

• Fly in senior resources (HK or Singapore regional team)

• Mostly involved in valuation and structure; less hands on day to day aspects. • Ivy league background. Interact with clients

well, but less effective with the Chinese target (perceived as too cold or distant on their approach).

16

© InterChinaConfidential

Customer Base: We provide tailored strategy and M&A advisory for over 100+ auto component and service players in China

17

OEMs & Organization

Auto Component

Player

Auto Service / Materials

17

© InterChinaConfidential

Project Impact: We receive high notes from our clients regarding the impact on their development in China, on both our service quality and their actions upon our recommendations…

Company Sponsor Feedback

A global top 50 auto component player

Asia & Europe BD VP

"Your guys have done a pretty good job. The findings are quite solid in such a fragmented and emerging market…This will be an important part of China strategy going forwards, and we have already recruited a new director for distribution business…"

A leading European player

Global BD Director

"As you can see in our feedback on your performance sheet, we were highly satisfied with your work and the results and would work with you again in the future. We would like to highlight especially the insights from your interviews and market analysis, which clearly is a unique advantage. "

A top int’l glass company

Group Vice President

“I appreciate all the hard work you put in ... You have a hard-working and committed team that is polite, considerate and easy to communicate with ... We have been very comfortable working with InterChina ... Overall you have taken a very professional approach to our project”

A niche auto solution provider

China Senior Advisor

“Your team had done an outstanding job, even from the perspectives of the 'specialists' in our company.”

A leading US player

Global BD Director

“I think the analysis and recommendation is very comprehensive…We are very happy and satisfied with the work done by you"

A auto component group in Nordic

President & CEO "Very good conclusion... Thanks so much…I will send this to the board of the company, and I plan to have a trip in China to further discuss about next steps."

A global top 3 auto assistance company

Asia Director “We are pretty much satisfied with your work, though the project is a difficult one….You are very serious…We worked with KPMG in India for the same type of project, and the solution they recommended just can't be done (e.g. the recommendation to add 45 people for 3 new business lines)."

18

© InterChinaConfidential

… 2/3 of our business is with long-term clients who regard InterChina as a trusted advisor

19

• Nearly 20 year relationship from early 2000s to present, despite leadership succession.

• Supported various JV, WFOE and M&A engagements, with 5+ successful transactions.

Long-Term Client Relationships(Selected Examples)

13Engagements

• Recently established relationship, supporting this globally top 10 component players for their expansion in China.

• Supported in the acquisition in both traditional components and next generation tech fields.

3Engagements

• Example of supporting the client with strategic feasibility study and then moving to M&A actions.

• Engagements spanned (a) opportunity assessment and entry point identification (b) deal origination (c) transaction advisory.

3Engagements

• Worked with this global leading component players cross various BU.

• Projects were focused on both NEV components and after-market in China.

• Were trusted to advise on the fast changing market and competitive environment in China.

4Engagements

• Maintained with a decade relationship with various BU including auto glass and other auto components.

• Supported the expansion in this highly competitive China market.

4Engagements

• Example of starting with inorganic growth support and moving to organic growth support.

• Supported the client with M&A and JV with OEMs for the growth in the traditional ICE sector, and then supported organic growth strategy in NEV.

3Engagements

MAP STP

© InterChinaConfidential

Contribution: Auto contributes between 15% - 20% of InterChina’s Net Revenues

17% 21%

31%

20% 18%19%

13%14%

14%

20% 13%

14%

21%

14%

18%22%

32% 40%29%

25%24%

20%

16% 14% 15% 9%16%

23%

8%8%

23%

2014

Automotive

1%

201520131%

Other1%

2017

Industrials

4%

2016

Chem/Energy

C&R/F&B

2018 YTD

2%

Healthcare

Net Revenues By Sector Group

20

© InterChinaConfidential

SG Team: Our team of consultants and advisors focused on auto-related projects re. strategy issues and M&A projects

InterChina’s standing team of project managers and team members InterChina’s senior advisors

Mr. Simon Zhang, Partner, SH• 20 years of consulting/management experience in

China.• Specialist strategy consultant with focus on

chemicals/materials, auto and industrial sectors.• 7 years with Sinopec in corporate development in

Sinopec.• Manager and Supervisor of ~100 projects.• Auto Sector Group Leader.

Ms. Ling Wu, Senior Advisor• >15 years of corporate development,

capital markets and investment bankingexperience

• Previously leadership role in KPMGAdvisory in China and Amherst Partners inUS

• Extensive experience in the automotiverelated sectors

Mr. Eduardo Morcillo, ManagingPartner, SH

• 20 years China M&A experience in F&B, Machinery,Chemical sectors, also some complex JV projects.

• Expertise in negotiation with Chinese companies.• Fmr Marketing manager of Carlsberg Huizhou• Fmr Head of Project Management Dept., Hong Kong

Singlee Investment Management Co., Ltd

Mr. Jan Borgonjon, President, BJ• Resident in China for over 20 years.• Established InterChina in 1994.• Management of over 50 projects in various industries in

China, including chemicals and auto.• Top level negotiation and lobbying.

Mr. Luo Bo, Principal, SH• >10 years work experience in finance field.• Previously worked with Maersk, Hertz and investment

bank with functions in M&A, JV, partnership and FP&A• Extensive experience in investment structuring,

financial modeling, project management and financialplanning and analysis.

Ms. Jane Zhu, InfoCenter Head, BJ• Specialist in industrial data and info research and

analysis. • 10 year experience in supporting InterChina projects in

auto, chemicals and machinery sector, incl. OEMs, comp, aftermarket, machine tools, construction machinery, home appliances, agriculture equipment, etc.

Mr. Anderson Mo, Analyst, SH• Specializes in market intelligence of consumer goods

and machinery, industrial equipment; working withclients sectors such as automotive components, railway,elevators, and chemicals.

• Fmr Supply Manager of Philips Healthcare• Fmr Process Improvement Analyst of Cleveland Clinic• Six Sigma green belt / LEAN certified.

Mr. Jay Cheng, Senior Advisor• Over 25 years of management and

leadership experiences in top tier globalautomotive component companies

• Currently the president of Halla VisteonClimate Control in China

• Formerly with Eaton, GE Hydro and severalBlack Stone Group portfolio companies

Mr. John Mack, Senior Advisor• Previously president and CEO of CIE

Automotive in China• Previously president and CEO of Fiat Group

in APEC region• Other leading roles in GM, BMW and other

top automotive related companies inEurope and Asia

21

Mr. Sylvia Zang, S. Manager, SH• Over 12 years experience in InterChina.• Extensive consulting experience for M&A, strategic

advisory, target search, negotiation support and DD.• Previous project experience in automotive sectors

including automotive comp. and automotive design.• Advised overseas companies incl. Gentherm,

Cooperstandard, IDIADA, Cikautxo, Metalsa, etc

Ms. Emily Zhang, Analyst, SH• 2 years with InterChina.• Previously working with BDO, UK• Primary research expert involved in automotive &

components, chemicals, manufacturing, F&B,renewable energies, incl. clients such as Emerson,SABIC, Gamesa, Dupont, Schindler, Hella, and Brose.

Mr. Shawn Zhang, Associate, Shanghai• Specialized in target search, negotiation and

coordination among parties• Conducted CDD and investment research for clients,

covering industry, HC and auto sectors.• BA in Arts (Nanjing Normal Univ., China). MA in Finance

and Management (University of Melbourne, Australia).

Mr. Delia Zhang, Manager, SH• Over 8 years of investment banking, financial advisory

and M&A advisory experience.• Extensive project experience in M&A and Private Equity

Financing in various sectors.

Mr. Angie Gao, Manager, SH• Actively involving in M&A deal sourcing, business

development, financial analysis, business DD, workingclosely with overseas companies and domestic investors.

• Deals involved in 1) Israel surgeon room interface for$25millions 2) tourism resort in Korean for sale, 3)China Top 500 corporation looking for overseas targetsto acquire etc. Has been involved in post acquisitionmanagement in China & data analysis and project mngt.

Mr. Dow Zhou, Associate, SH• 3 years of equity investment, M&A, and strategic

planning experience.• Formally with the overseas investment team of Fosun.• Industry experience in consumer products, auto,

intelligent manufacturing and TMT.

© InterChinaConfidential

Simon Zhang

Partner In ChargeStrategy PracticeShanghai Office Chinese

Education & Qualifications

• MBA, Cranfield School of Management (U.K.)• Postgraduate Diploma in Marketing, Chartered

Institute of Marketing (U.K.) • BA, English Literature, Southeast University (China)

Sector Competencies

Profession Experience Functional Competencies

Project Experience

• Leader of InterChina’s Chemicals Sector Group• Energy and clean tech (incl. environment)• Automotive• Industrial Equipment

• Partner In Charge, Strategy Practice of InterChina Consulting

• Prior to joining InterChina, Mr. Zhang worked for SINOPEC Shanghai Petrochemical Co. Ltd, formerly as Marketing Manager and latterly as Enterprise Transformation Manager.

• Mr. Zhang is an Associate of the Chartered Institute of Marketing (ACIM) and in the process of qualifying to become a Certified Public Accountant (CPA).

• Opportunity identification.• Go-to-market strategy development.• Investment feasibility study.• Partnership strategy.• Lobbying strategy.• Acquisition strategies, deal origination.• Commercial due diligence.• Business model transformation.• Complexity management.

• Strategy Planning: Supervised and managed over 100 strategy projects in which he has helped to advise both global Fortune 500 and medium sized foreign companies on their organic and inorganic strategic needs in China and globally.

• Recent Clients served: BASF, Bayer, Dupont, Air Products, Honeywell, Johnson Matthey, Clariant, Hella, Federal Mogul, KSPG, Schindler, UTC, Gamesa, Zeiss, Abengoa, Warburg Pincus etc.

22

Tao Lin

Partner Strategy PracticeShanghai Office Chinese American

Education & Qualifications

• MBA, INSEAD (France & Singapore)• Management Programs, University of Chicago Booth

School of Business (USA) • Chemistry & Biology, Illinois State University (USA)

Sector Competencies

Profession Experience Functional Competencies

Project Experience

• Digitalization• Sustainable manufacturing and automation• Industry 4.0 and Made in China 2025• Industrial Internet of Things

• Prior to joining InterChina, Mr. LIN was in leadership, business development and execution positions for boutique European firms such as goetzpartners and Value Partners in China.

• Mr LIN started his consulting career with Deloitte and was with the firm in the USA, UK/Europe and China.

• In 20 years in Strategy & Management consulting, Mr. Lin has gained experience and exceled in research-driven strategy work in market entry, competition, transformation and sustainability.

• Strategy Planning: Managed 100+ strategy and management projects with a variety of companies including MNCs, SOEs, POEs and governments.

• Recent Clients served: John Deere, Cummins, Caterpillar, Swarovski, Schunk, BMW, Schaeffler, Triton, RiverlandCapital, Yunnan Provincial Government, Taian (Shangdong) Government, Shaanxi Mining Corporation, MingRJewelries, etc.

© InterChinaConfidential

Eduardo Morcillo

Managing PartnerShanghai Office Spanish

Education & Qualifications

• BA in Law (Carlos III University, Spain).• MA in International Trade & Investment Law (University of

Newcastle upon Tyne, UK).• Executive MBA (IESE, Spain).

Sector Competencies

Project Experience

• Automotive (components- Stamping, HMI, Power Train, Electrical)

• Chemicals (mid and downstream)• Infrastructure (environment, energy)• Healthcare (pharma, equipment).

• Sinclair Roche & Temperley (United Kingdom).• Credit Suisse (Spain).• InterChina: 1999-2001: Beijing. Director; 2002-2006:

Shanghai. M&A Practice Director; 2006- 2010: Shanghai/ Madrid. EMEA Director; 2010- Current: Shanghai. Managing Partner.

• Other Experience: Board of Director Member (in three China corporations); Member of Executive Board of Directors (three global organizations CWI, IMAP, EUCCC); Associate Professor MBA Schools (IE, Cheung Kong Business School)

• M&A • Strategic Alliances and Investment projects• Corporate restructuring• Corporate lobbying

• M&A: 15 Transaction deals (Auto components, infrastructures, Chemicals, Steel, Foundry and Healthcare). Average Transaction Value: from 20 to 100 million Usd.

• Strategic Alliances: Establishment of 12 Joint ventures (Auto components, chemical/petrochemical, franchise, machine tool, elevator industry, Energy and food business). Average Transaction Value: 50 to 300 million Usd.

• 100% Controlled Investment Projects: 10 WFOEs (Auto components, chemical, petrochemical,). Average Investment volume ranging from 30 to 400 million Usd.

• Corporate Lobbying: Corporate restructuring strategy and negotiation (energy, infrastructure, mining) with government bodies and institutions.

• Recent Clients served: Faurecia, Hella, Grupo Antolin, Grupo Maier, Federal Mogul, Bimbo, Girbau, Maxam Corp, Air Products, Abengoa, etc

Professional ExperienceFunctional Competencies

24

© InterChinaConfidential

PresidentShanghai OfficeBelgian

Education & Qualifications

• MBA (Henley, UK)• Chinese Language Specialization, Nanjing University,

1983-1985• BA Chinese Studies (Leuven University, Belgium)

Sector Competencies

Project Experience

• Chemicals• Automotive (components, Tier 1)• Industrial (Machinery, Machine Tools,

Components)

• 1985-1987:China Europe Institute, KU Leuven, Administrator

• 1988-1994: Adminstrator and later Director China Europe Management Insitute (CEMI), Beijing

• 1994: Acting President CEIBS, Shanghai• 1994-current: President InterChina• Other : Advisor to the Minister of Foreign Trade of

Belgium. Member of the Board of Directors CEIBS, Shanghai 2000-2014. Vice President and Member of the Executive Committee EUCCC (2002-2006). Commander in the Order of Civil Merit of Spain

• Strategic Alliances and Investment projects• Strategic Advise• Corporate lobbying

• Strategic advise: Leadership of over 50 projects related to market entry or business expansion for western companies in China. CEO level advise to large western corporations related to China operations

• Top level negotiation: corporate restructuring strategy and negotiation for several companies in China; alliances with Chinese groups; negotiation of numerous joint ventures and 100% controlled investments mainly in industrial sectors; acquisitions of Chinese companies.

• Government contacts & lobbying: has been in charge of several projects involving government contacts at both national and local level. Obtained approval for automotive distribution company, government relations advise to one of the largest global steel companies, establishment of GR structure for large paper MNC.

Professional Experience Functional Competencies

Jan Borgonjon

25

© InterChinaConfidential

Luo Bo

DirectorShanghai OfficeChinese

Education & Qualifications

• Bachelor of Business Administration, Simon Fraser University (Canada)

• MBA, INSEAD (France and Singapore)• CFA (Chartered Financial Analyst) chart holder

Sector Competencies

Project Experience

• Transportation • Automotive • Chemicals• Industrial/ Mining

• Senior Business Development Manager, Maersk• Associate Director, Somerley Investment Consulting• Senior M&A Manager, Hertz China• CFO, Xingwang Coal Mining Company• Other Experience: the founder of a truck components

trading company; and military experience in Chinese navy

• M&A • JV• Strategic Alliances and Investment projects• Corporate restructurings• Corporate lobbying

• M&A: Actively participated as lead negotiator in several Acquisition and Divestment projects: • Minority acquisition of the largest car rental company in China with the market value of USD 1 billion. • Establishment of Joint Venture via Acquisition between leading multinational and the sixth largest port

worldwide. • Established a partnership via M&A with the largest chauffeur-served car rental company in Japan to

enter into China. • Several M&A investments into coal mining (Jiangxi Province) and iron mine in China. • Participation in Divestment processes in the mining field in China.

• Main Role: Support on identification of targets/ partners/ investors; Coordination of Due diligence, financial modeling and valuations; Key document drafting and coordination of service providers (ie. Lawyers); Negotiations, closure, and integration

Professional Experience Functional Competencies

26

© InterChinaConfidential

MNC Base: Supported top global auto comp. leaders, while serving sector niche leaders as well; maintaining / expanding contact base

InterChina MNC Contacts (Auto)• 700+ active decision-maker contacts at international companies

in the auto sectors.• 40% of these decision-makers are China-based, with the

balance at headquarters in Europe and the US.

InterChina Client Base in Global 100 Chemicals Co.• Out of 80 non-JP/KR top 100, we work with ¼ of those leading

players, while having regular contacts in China and globallyfrom another ¼ of those leading players.

27

ID Company Contact Contact Title Position email Office Office Office Mailing Sector L-1 Sector L-2 Country1152 Shanghai GM Hao Ren 任皓 Mr. Vehicle Line hao ren@s Shanghai Shanghai China 上海浦东金 Industrials Automobile Germany419 Shanghai Udo von Mr Dipl -ing udo klot@c Shanghai Shanghai China 中国上海安 Industrials Automobile Germany

8690 SIEMENS Jeff Zhou 周建峰 Dr. Vice jeff.zhou@ Shanghai Shanghai China 上海闵行区 Industrials Automobile Germany6816 Simoldes Jaime Sa Mr General Jaime sa@ Oliveira de Portugal Portugal Rua Industrials Automobile Spain2075 SKF Chenggui 柳承贵 Mr Project chenggui liu Shanghai Shanghai China 上海北京东 Industrials Automobile7946 SKF Hawking 张晶 Ms. Head of hawking.zh Shanghai Shanghai China 上海半淞园 Industrials Automobile Sweden6681 SKF Michel Ms BD michel zha Shanghai Shanghai China No 377 Industrials Automobile Sweden6794 SKF Rakesh Mr. President rakesh.ma Sweden SE-415 50 Industrials Automobile Sweden6682 SKF (China) Co., Ulrich A. 邬力 Mr. Director, ulrich.selig Shanghai Shanghai China No.377 Industrials Automobile Sweden8054 Sogefi Eric Liu 刘正 Mr Sales KAM eric liu@so Suzhou Zhejiang China No 1028 Industrials Automobile8141 Sogefi Marie- Ms. Head of marie- France Sogefi Industrials Automobile France8052 Sogefi Olivier 欧苙玮 Mr. China olivier.cuzin Suzhou Zhejiang China No.1028 Industrials Automobile8140 Sogefi RAUCY Mr Global cedric rauc France Industrials Automobile France8053 Sogefi Sebastien 博文 Mr. General sebastien.b Suzhou Zhejiang China No.1028 Industrials Automobile731 Somema Fernando Mr. Director somema@ Portugal Rualde Industrials Automobile Portugal

8331 SPJ Espejos y Victor Mr Area Sales victor pont Lleida Spain Poligono Industrials Automobile Spain10157 SRG Jason Plating jyang1@sr Zone, Industrials Automobile Global4259 SRG GLOBAL Dave Mr Business dingram@s Shanghai Shanghai China Room6F1 Z Industrials Automobile US3287 SRG Global Jon Mr Vice jdegaynor US 23751 Industrials Automobile

10564 STABILUS Alex Tian 田学峰 CEO/ xftian@sta Changzhou Jiangsu China No.8 Industrials Automobile Germany10589 STABILUS Thorsten Head of tschell@sta Koblenz Germany Wallershei Industrials Automobile Germany10063 Standard Motor Hap Acee Mr. VP/ hap.acee@ Hong Kong Hong Kong China Unit C, Industrials Automobile US1836 Strattec Thomas Mr. Product thermann WI US Strattec Industrials Automobile US8387 Streparava Carlo Mr Senior c bignardi@ Brescia Brescia Italy 13 Via Industrials Automobile Italy8386 Streparava Enrico Mr. Business E.Deltratti Brescia Brescia Italy 13, Via Industrials Automobile Italy8808 Streparava Francesco Mr. Supplier contact@st Brescia Brescia Italy 13, Via Industrials Automobile Italy6770 Streparava Pier Luigi Mr President contact@st Italy 13 Via Industrials Automobile Italy8809 Streparava Renato Mr. Product contact@st Brescia Brescia Italy 13, Via Industrials Automobile Italy2643 Sunred Joan Orus i Mr. General joanorus@ Barcelona Spain C/ Juan de Industrials Automobile Spain4745 Sunwin Bus Rune General rune lundb Shanghai Shanghai China 上海市闵行 Industrials Automobile9254 SUSPA Jin Shen 沈金鑫 Dr. General jshen@cn. Nanjing Jiangsu China No.2, West Industrials Automobile Germany8897 TE Gary Li 李万祥 Mr Sr Dir Sales gary li@te Shanghai Shanghai China Building 5 Automobile US8898 TE Kate Zhou 周宇君 Ms Manager kate zhou Shanghai Shanghai China Bldg 5 Automobile US8900 TE Peter W. Mr. General peter.cirino Singapore No. 26 Ang Automobile US7895 TE Thomas 刘沈明 Mr Vice thomas sh Shanghai Shanghai China Building 5 Industrials Automobile US286 Tecniacero Francesc Mr. Director francesc.fa Barcelona Spain Ctra. Industrials Automobile Spain994 Teco Barbettin Mr. General teco@teco. Italy Via Pio La Industrials Automobile Italy

2766 Think Global Richard P Mr MD U K & rbl@think n London UK Chenil Industrials Automobile Norway2321 TI Group Enric Jornet Mr. Comercial ejornet@es Barcelona Spain Muntaner Industrials Automobile Spain7143 Tianjin Santroll Guo Zhi Mr. Product yf16@sant Tianjin Tianjin China Industrials Automobile1601 Troqueleria Oscar Mr Director juan tobia Barcelona Spain P L Industrials Automobile Spain5472 TRW Mark Mr. Vice mark.stew Shanghai Shanghai China 6F, Building Industrials Automobile US7324 TRW Automative Eric NI Mr. Aftermarke eric ni@trw Shanghai Shanghai China 5F 62 Industrials Automobile7323 TRW Automative Kitty Zhu Ms Product kitty zhu@t Shanghai Shanghai China 5F 62 Industrials Automobile5471 TRW Automative Laurent Mr. Vice laurent.cro Shanghai Shanghai China 5F, Building Industrials Automobile US7325 TRW Automative Tim Ward Mr Aftermarke tim ward@t Shanghai Shanghai China 5F 62 Industrials Automobile7894 Tungray Shaojian Vice Chair shaojian z Shanghai Shanghai China City Industrials Automobile US8896 Tyco Electronics Carl Smiley Mr. Senior Vice carl.smiley Singapore No. 26 Ang Automobile US6699 UFI Filters Kelvin Mr Asia Pacific kelvin wang Shanghai Shanghai China 上海市青浦 Industrials Automobile

10306 UFI Filters Luca Biagini APAC COO luca.biagini No.9785 Industrials Automobile China6697 UFI Filters Rinaldo Mr. Chief rinaldo.facc Italy 1-37060 Industrials Automobile Italy3488 Ultra Parts Mark Mr Managing mpagliaroni US 33525 Industrials Automobile

10531 Uriel Inversiones Francisco Mr. Director fsoto@urieli Madrid Spain P de La Industrials Automobile Spain4046 Uriel Inversiones Juan Felix Mr. Presidente jfhuarte@u Madrid Spain P de La Industrials Automobile Spain3737 Valeo Ian Wang 王依润 Mr Director yirun wang Shanghai Shanghai China 上海市漕河 Industrials Automobile331 Valeo Michel Mr. Group Asia michel pagl Shanghai Shanghai China Industrials Automobile France

1633 Veritas Jose Ma Mr. Director josemjane Barcelona Spain Av Industrials Automobile Spain904 VOLKSWAGEN Bojun Song Mr Assistant bojun song Germany Volkswagen Industrials Automobile Germany903 Volkswagen Kai Mr. Manager kai.grueber Beijing Beijing China 北京市建国 Industrials Automobile Germany273 Volkswagen Klaus-Uwe Mr k Schaffrat Beijing Beijing China 北京建国门 Industrials Automobile Germany902 Volkswagen Melanie Ms PR officer melanie be Beijing Beijing China 北京市建国 Industrials Automobile Germany675 Volkswagen Zhang Mr. Executive suixin.zhan Beijing Beijing China 北京市建国 Industrials Automobile Germany271 Volkswagen Zhao Mr Senior jiayou zhao Beijing Beijing China 北京市建国 Industrials Automobile Germany

7924 Volkswagen Bahong Su 苏巴鸿 Mr. Director, bahong.su Beijing Beijing China 北京朝阳区 Industrials Automobile Germany7033 VOLVO Dzeki Mr. Vice dzeki.macki Shanghai Shangahi China No.2095, Industrials Automobile5099 VOLVO Harry Li Mr VP harry li@vol Sweden Sweden 上海市嘉定 Industrials Automobile Sweden5100 VOLVO Karin Malm Mr. Purchasing kribarit@vol Sweden China Dept Industrials Automobile Sweden7034 VOLVO KATARINA Mr. Vice katarina.fjo Shanghai Shangahi China No.1180 Industrials Automobile6914 VOLVO Lars Falk Mr Vice lfalk5@volv Goteborg Sweden Dept Industrials Automobile Sweden5102 VOLVO Luc Mr. VP STA lsemeese@ Sweden Sweden Dept. Industrials Automobile Sweden8000 VOLVO Nicolas 赵智国 Mr IT Director nicolas zha Beijing Beijing China 11F Tower Industrials Automobile7032 VOLVO Sylvain Di Director sylvain di- Shanghai Shangahi China No 2095 Industrials Automobile5103 VOLVO Thomas Mr. VP Interior thomas.gro Sweden Dept Industrials Automobile Sweden5106 VOLVO Thomas Mr Director 40 thomas vq Sweden UK 53084 Industrials Automobile Sweden4487 Webasto Christian Mr Strategic christian hai Germany Friedrichsh Industrials Automobile Germany6833 Webasto Fernando Mr. Head of fernando.v San Spain C/Mar Industrials Automobile Spain4260 Webasto Thomas Mr General thomas lue Beijing Beijing China A2103 Tow Industrials Automobile Germany4283 Webasto Wang Mr. Head of xiaoming.w Beijing Beijing China 北京市朝阳 Industrials Automobile Germany2016 Welly Automotive Mitchell Lou Mr. Chairman [email protected] Shanghai Shanghai China No. 60, Industrials Automobile China532 Zadi Bruno Mr Consultani brunopr@t 138 Via C Industrials Automobile Italy

4376 Zanini Antonio Mr. Corporate amolon@z Spain Industrials Automobile Spain3245 Zanini Conrad Mr. Strategic ctorras@m Barcelona Spain Marineta, Industrials Automobile Spain

© InterChinaConfidential

Chinese Contacts (1/2): Maintained strong network with proactive and reactive Chinese investors and institutes

Example Chinese Investor List (Auto) Networking (Examples): Associations, Chinese OEMs, and Chinese component players)

28

No. Buyer Name Type Industry1 Ningbo Joyson Electronic Corp Strategic Auto/Trk Prts&Equip-Orig2 Zhejiang Geely Holding Group Co Ltd Strategic Auto-Cars/Light Trucks3 Wanxiang Group Corp Strategic Auto/Trk Prts&Equip-Orig4 SAIC Motor Corp Ltd Strategic Auto-Cars/Light Trucks5 Jiangsu Olive Sensors High-Tech Co Ltd Strategic Auto/Trk Prts&Equip-Orig6 Zhejiang Vie Science & Technology Co Ltd Strategic Auto/Trk Prts&Equip-Orig7 Ningbo Huaxiang Electronic Co Ltd Strategic Auto/Trk Prts&Equip-Orig8 Sailun Jinyu Group Co Ltd Strategic Rubber-Tires9 ZMFY Automobile Glass Services Ltd Strategic Auto/Trk Prts&Equip-Orig

10 Shandong Yongtai Chemical Group Co Ltd Strategic Rubber-Tires11 Zhejiang Shibao Co Ltd Strategic Auto/Trk Prts&Equip-Orig12 Ford Motor Co Strategic Auto-Cars/Light Trucks13 Dah Chong Hong Holdings Ltd Strategic Auto-Cars/Light Trucks14 Weichai Power Co Ltd Strategic Auto/Trk Prts&Equip-Repl15 Tianjin Motor Dies Co Ltd Strategic Auto/Trk Prts&Equip-Orig16 Mubea Automotive Components Taicang Co Ltd Strategic Auto/Trk Prts&Equip-Orig17 Zhejiang Youngman Passenger Car Group Co Ltd Strategic Auto-Cars/Light Trucks18 Fuyao Glass Industry Group Co Ltd Strategic Auto/Trk Prts&Equip-Orig19 Beijing Automotive Industry Holding Co Ltd Strategic Auto-Cars/Light Trucks20 Guangzhou Automobile Group Co Ltd Strategic Auto-Cars/Light Trucks21 FAW CAR Co Ltd Strategic Auto-Cars/Light Trucks22 Hyundai Motor Co Strategic Auto-Cars/Light Trucks23 Fangda Special Steel Technology Co Ltd Strategic Auto/Trk Prts&Equip-Orig24 Shanghai Fosun Pharmaceutical Group Co Ltd Strategic Medical-Drugs25 Northeast Industries Group Co Ltd Strategic Retail-Automobile26 Chongqing Skyman Industrial Group Co Ltd Strategic Auto/Trk Prts&Equip-Orig27 HNA Group Co Ltd Strategic Airlines28 Tencent Holdings Ltd Strategic Internet Applic Sftwr29 Tianjin THSG Corp Strategic Investment Companies30 PAG Financial Private Equity31 GO Scale Capital Ltd Strategic Finance-Investment Fund32 Daqing State-owned Assets Management Co Ltd Strategic Investment Companies33 Aerospace Hi-Tech Holdings Grp Ltd Strategic Auto/Trk Prts&Equip-Orig34 Transportation Technology Ventures LLC Financial Venture Capital35 Shanghai International Group Co Ltd Strategic Investment Companies36 Reliance Venture Asset Management Pvt Ltd Financial Venture Capital37 Yuan Capital Financial Venture Capital38 Shanghai Jiaerwo Investment Co Ltd Strategic Investment Companies39 Ningbo Jifeng Auto Parts Co Ltd Strategic Auto/Trk Prts&Equip-Orig40 Sichuan Bohong Industry Co Ltd Strategic Auto/Trk Prts&Equip-Orig41 Xiaoju Kuaizhi Inc Strategic Investment Companies42 China Taiping Insurance Holdings Co Ltd Strategic Multi-line Insurance43 Cayman Engley Industrial Co Ltd Strategic Auto-Cars/Light Trucks44 Chongqing Sokon Industry Group Co Ltd Strategic Auto-Cars/Light Trucks45 Anhui Zhongding Holding Group Co Ltd Strategic Auto/Trk Prts&Equip-Orig46 Xiangyang Automobile Bearing Co Ltd Strategic Auto/Trk Prts&Equip-Orig47 Ningbo Joyson Automotive Electronic Holding Co Ltd Strategic Auto/Trk Prts&Equip-Orig48 Qingdao Doublestar Co Ltd Strategic Rubber-Tires49 Baidu Inc Strategic Web Portals/ISP50 GSR Ventures Management Co Ltd Financial Venture Capital

• 80+ deals for top 50 in the past 5 years…• …with deal value totally above USD 130 bil …• …with the median deal value at USD 70 mil.• We have maintained decent relations with 1/2 of

them, plus other potential investors.

© InterChinaConfidential

Index

• Sector Dynamics• Our Auto Services & Team• Perspectives On China’s Auto Sector• Consulting Cases• Deal Tombstones

21

345

29

© InterChinaConfidential

NEVs In China: China will most likely lead the global NEV wave, but needs more balanced efforts from all stakeholders…

China’s Government• Address the challenges of oil dependency.• Address the challenges of emissions

controls.• Leapfrog China’s automotive tech globally.

Consumers In China’s Market• Expectations of NEV’s

performance.• Expectations of NEV’s safety

and reliability. • Price-sensitive.• Occasional personal

image/activism-based decision making.

OEMs & Supply Chain• Investment in technology

development.• Technology route selection. • New car models.• Supply chain development.

Infrastructure• Who will fund and who will benefit?• The power consumption of NEVs is

10% of China’s grid power at maximum.

Source: China’s NEV 12th FYP; MOST

BEV (incl. PHEV)

2012

0.5 million

2020 Planned

Ownership

2015 Planned

Ownership

5 million

* Actual BEV (incl. PHEV) ownership by 2015 isslightly below 0.5 million* HEV: <20k in 2012; without gov. goals in 2015and 2020.

Note: The existing composition of NEV might have commercial vehicles (usually with demonstration projects and corporate purchases) taking the majority of sales; however, in 2015 - 2020, passenger vehicles will take the majority. The report doesn’t include low-speed electric vehicles produced by non-qualified players.

30

© InterChinaConfidential

Future Direction in China: …Heavily influenced by the gov. policies, for both scale and tech routes…

China’s Government

OEMs For China’s Market

Consumers In China

Infrastructure investors

NEV Vision

Subsidy/ Double-credit

System

Chinese OEM

Non-JP Foreign OEM

JP OEM

Major Stakeholders Preference for BEV, including PHEV (i.e. Attitude & Achievements) Now Future

Now 2015 – 2020• Determined government policies on NEV (especially BEV).• Will maintain the policy direction.

• Largely in favor of BEV/PHEV; very little preference for HEV. • Phase-out subsidy scheme with double-credit system taking over.

• Price-sensitiveness + Mileage Anxiety + Perceived Tech Instability > current environmental concern.

• With technology improvements and cost reductions, there will likely be more purchases.

• Concerned with IPR now; might take opportunistic approach at this time.• However, might transfer some BEV/PHEV models to China upon initiation of

the market.

• Significant focus on HEV.

• Large investment in BEV, as well as PHEV (according to industrial insiders).• Many registered models .• Technology gap with the international market might begin to close.

• Follow the market demands.• Various business models (different investor profiles; battery charging vs.

battery swapping).

Largely favorable to BEV now Less favorable to BEV now Favorable development to BEV 2015-2020

Less Favorable development to BEV 2015-2020

31

© InterChinaConfidential

Market Volume: …are we close to the tipping point?...

EV + PHEV Sales Volume

Source: CAAM, MOST

(unit)

Targets in China’s NEV 12th FYP

0.5 million planned ownership in 2015 is narrowly missed

5 million planned ownership in 2020 possible?

(China’s NEV 12th FYP)

?

168

2015

17,799

PV - EV

9,908

2012

2,153

2013 2014

3,785

2009

330,200

PV - PHEV

74,763

2010 2011

CV - PHEV

CV - EV

Actual ownership by 2015: 0.45 million units, close to targeted volume

32

© InterChinaConfidential

Infrastructure: …Implementation has lagged behind the plan, coastal region takes the lead…

Source: MIIT, CSR of State Grid and South Grid, China NEV Yearbook 2012, NDRC, National Energy Administration, InterChina Consulting interviews and analysis.

Notes: This applies to both private cars and vehicles of companies (e.g. taxi, bus).

Lagging behind the plan significantly; land availability, possible low utilization rates and the coordination of various gov. bodies present challenges

But policies with implementation measures are “speeding up” in China, with a positive impact on the market

Charging Stations

Charging Piles

• The number of charging stations in 2015 is 23% of the2020 target; charging piles are only 1% of the target.

• SAIC recently invested RMB 300 m in establishing a newcompany designated for building charging piles, with theaim of completing 50,000 charging piles countrywide by2020.

Time Region MeasuresDec2014

Jiangsu • Provincial gov. gives RMB 800-1200/kwof subsidies for construction ofcharging facilities

• City gov. provides same amount ofsubsidies as the provincial level

Nov 2014

National • Central gov. awards subsidies to localgovernments who reach NEVapplication targets

• Budgeted subsidy amount is estimatedto be RMB 10 bn for 2015

Jun 2014

Shanghai • Municipal gov. provides up to 30% ofinvestment to charging/swap facilityconstruction/operation companies intheir projects of building qualifiedcharging/swap facilities

Jun2014

Wuhan • City gov. gives subsidy to purchasersof charging poles through publicbidding process, with the amount of20% of purchasing price, or max. RMB3 m

Apr 2014

Shenzhen • City gov. gives 30% subsidies basedon equipment investment amount of acharging/swap station, or max. RMB300,000

Oct2015

National • Central gov. awards annual subsidiesto provincial governments reachingNEV application targets during 2016-2020, max. RMB 200 million

12,000

3,60073241837115510012

2020Goal

2015201420132012201120102009

49,00028,00022,25617,932

2014 2020 Goal20132012 2015

4,800,000

33

© InterChinaConfidential

Opportunities Along Value Chain: …new and unique, which may open up new opportunities along the value chain

34

NEV Exclusive Components

For Example:• Battery Pack• Motor System• Control system

ICE Components But Required Tech Modification

For Example:• Brake• Inverter / Converter• Air conditioner

Traditional Components In ICE

For Example:• Engine• Transmission System• Chassis

NEV will require a very different set of components…

…which may present many opportunities along the new value chain…

Battery Pack

Battery pack case

Battery modules (cells

included)BMS and

electronic parts

Battery positive terminal, Battery negative terminal, Service plug, Main fuse, Relays, Current sensors, Voltage sensor

Top cover, Gasket, Insulator, Safety vent, Separator, Water based binder, Electrolyte, Anode negative electrodes, Cathode positive electrodes, Tab, Inner pack, Battery cell carrier

CAN / Chips, PC board, MOS transistors, Isolation chips, CPU, Transformer, relays, CAN / Chips, PC board, MOS transistors, Isolation chips, CPU, Transformer, relays, BMS case, Temperature sensors, Thermal conductive materials, PTC heater, A/C chiller, Fan

© InterChinaConfidential

Aftermarket Potential: Likely to gain much more importance in theautomotive sector in China…

Sources: CAAM, Development Research Center of the State Council, InterChina Interviews and Analysis

The Scale of The Component Industry in China (Unit: bn USD)

80

Non-AF Comp Sales

AF CompSales

2013

437

357

2009

177

154

23

43%

20%

45%

60%12%

20%

100%

Spare parts

After-services

New car sales

North American

China Overall

CAGR (2009-2013)

37%

23%

Sales of AF (Aftermarket) components in China are growing faster than total component sales due to booming new car sales…

…and the industry is shifting to a more balanced situation of OEM and aftermarket sales

The Profit Allocation Structure

35

© InterChinaConfidential

Geo. Focus: …but the future battlefield is around T2 cities (incl. provincial capitals in T3)…

Source: InterChina analysis

68

315

327

9.8

34.2

34.8

28%

27%

22%

8,000

12,500

2,500

25

30

38

PV ownership (2013, million)

PV ownership CAGR

(2008-2013)# of 4S shops

(2013)Average disposable income per capita (2012, RMB 1,000)

Competition of distributors

Urban Population(2012, million)

T1 cities: Have already reached mature growth due to large ownership base and new purchase restriction, plus there is high density of distributor as competitors.T2+T3 provincial capitals: Have the high growth potential because of smaller ownership base and only few big cities have imposed restriction. And the competition is not so strong.The total in all other 600+ cities: Good new car growth rate but very small car ownership based due to low population and disposable income. And there is lack of qualified distributors.

T2 & T3 Provincial Capitals provide a strong growth platform, with decent size now and strong growth potential plus the moderate competition yet

T1 Cities

T2+T3 provincial capitals

Other Cities

36

© InterChinaConfidential

Aftermarket Transformation: …and success in the aftermarket largely depends on quality and concentration of channels & distributors…

Existing automotive after market under OEM monopolized model is mainly authorized with varied quality…

…Future automotive after-market with de-regulate model will largely depend on concentrated co-existed authorized and independent channel with quality

Component maker

OEMs

Authorized Channel

4S, 3S Dealer

Large-Scale Auto Part Market

Large Volume

Wholesaler

Parts Retailer

Non Authorized Channel

Car Owners

Component maker

OEMs

Authorized Channel

4S, 3S Dealer

Distributor of Component

makers

Non Authorized Channel, including more quality chains

Car Owners

mainstream minor stream mainstream minor stream

37

© InterChinaConfidential

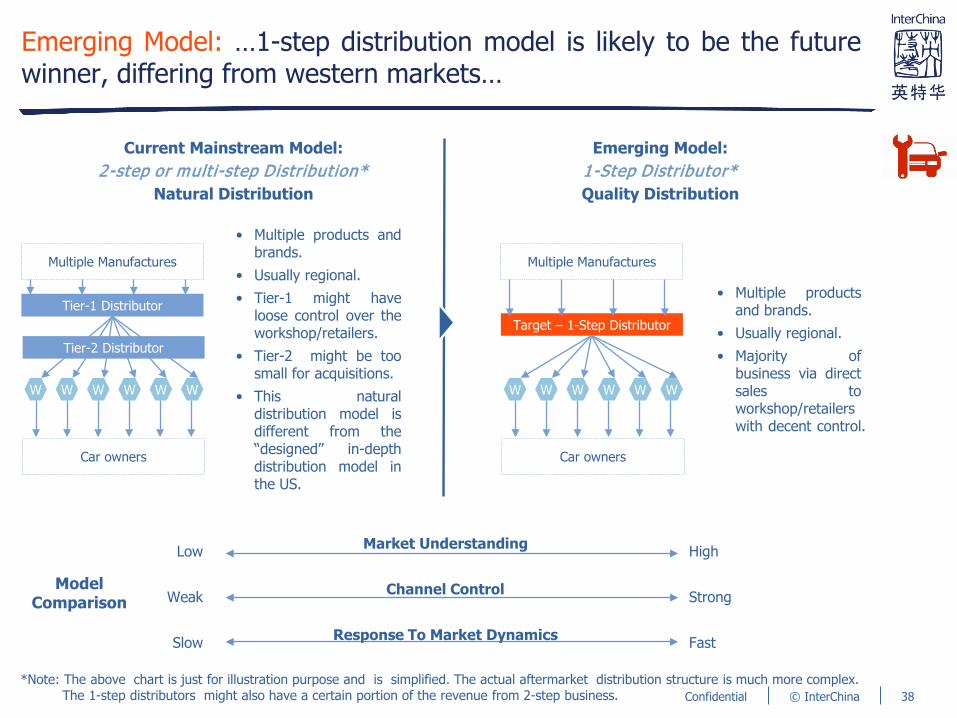

Emerging Model: …1-step distribution model is likely to be the futurewinner, differing from western markets…

Emerging Model: 1-Step Distributor*Quality Distribution

Current Mainstream Model: 2-step or multi-step Distribution*

Natural Distribution

*Note: The above chart is just for illustration purpose and is simplified. The actual aftermarket distribution structure is much more complex. The 1-step distributors might also have a certain portion of the revenue from 2-step business.

Target – 1-Step Distributor

W W W W W W

Car owners

Multiple Manufactures

Tier-1 Distributor

W W W W W W

Car owners

Multiple Manufactures

Tier-2 Distributor

• Multiple productsand brands.

• Usually regional.• Majority of

business via directsales toworkshop/retailerswith decent control.

• Multiple products andbrands.

• Usually regional.• Tier-1 might have

loose control over theworkshop/retailers.

• Tier-2 might be toosmall for acquisitions.

• This naturaldistribution model isdifferent from the“designed” in-depthdistribution model inthe US.

Low

Weak

Slow

High

Strong

Fast

Market Understanding

Channel Control

Response To Market Dynamics

Model Comparison

38

© InterChinaConfidential

Key challenges – and success factors – for foreign investors

Source: InterChina Consulting analysis.

Insufficient market understanding in China’s complex

aftermarket1

Significant differences between China and foreign aftermarket

business models2

Lack of acquirable quality distributors3

How to speed up China know-how building4

• Avoid boiling the ocean.• Dig deep in a focused way.• Avoid investing either too ahead of or too far behind the trend.

• Fit for China: Local design of the distribution model.• Tailor-made communication message to global HQ.

• Avoid waiting for the perfect target profile.• Focus on critical factors, e.g. sustainable channel access and control.• Systematic search and screening.• Warm-up and maintain relations with targets .

• Local team building with HQ trust and support.• Result management, rather than process management. • Best practice learning via benchmarking.

• China way…• …but strictly following the home-country regulations such as FCPA.

How to effectively mitigate possible risks5

39

© InterChinaConfidential

LW Drivers: Lightweight automobiles have become a global must-do in the recent future

Lightweight automobiles will help reduce Greenhouse gas emissions, while China is one generation behind the EU and US

Lightweight automobiles will also enhance the driving performance of the vehicles

Lowering the weight of automobiles has become a global trend in world’s major auto producing countries

Lightweight automobiles will improve fuel consumption, acceleration and braking distance, which influence the overall driving performance of the vehicles.

Source: InterChina Interviews & Analysis

65

2020

100

502030

200

2010

150 140

95

2010 2030

200

50

150

100

2020

200

110

200

50

150

2025

100

20202015

117

161

Euro Regulation2009/443/EC US Regulation China: MIIT

Emissions control targets of key countries (g/km)

Note: The emission control is either taken from the policy directly or calculated based on the capped fuel consumption by the gov. (e.g. 5 litre/km in 2020).

-100 Kg Fuel Consumption -0.4 L/100km

Acceleration +8%~+10%

Brake Distance -2~-7m

Drivability

LowerWeight

Better Performance

Safety

Research from Volkswagen has shown that lightweight automobiles will reduce CO2 emission per km by 8-11 grams

40

© InterChinaConfidential

Toyota Target2010-2015 • Reduce weight by 100kg

for 3 types of carsAfter 2016 • Reduce weight by 200kg

for larger car scope

LW In Action: Various OEMs have set different automobile weight reduction goals

Major OEM targets are clear in their roadmap schedules

Some models from major OEMs have reduced weight despite larger sizes

Mazda Target

2011-2015• Reduce weight by 100kg

via body structure optimization

After 2016 • Reduce weight by 100kg during each redesign

Volkswagen TargetMOQ Platform • Reduce weight by 100kg

on each Golf modelAudi A3 Platform • Reduce 79.8kg on new A3

series

Ford Motor TargetAfter 2020 • Reduce weight around

318kg via new materials

GM TargetAfter 2016 • Reduce weight by 100kg

via material improvement

Length

Polo GTI Mk5 (2014) Mk6 (2018) VAR

Length (mm) 3,972 4,053 +81

Width (mm) 1,682 1,751 +69

Height (mm) 1,453 1,446 -7

Wheel Base (mm) 2,470 2,564 +94

Weight (kg) 1,269 1,199 -70

Source: InterChina Interviews & Analysis , OEM Interview

Width

Height

Skoda Octavia Model 2014 Model 2018 VAR

Length (mm) 4,658 4,675 +7

Width (mm) 1,814 1,814 +0

Height (mm) 1,459 1,460 +1

Wheel Base (mm) 2,684 2,686 +1

Weight (kg) 1,215 1,200 -15Chang’an TargetAfter 2020 • Reduce weight by 40kg-

50kg for each new model

41

© InterChinaConfidential

LW Opportunity: Plastics play a significant role

Plastics play important roles in the evolution of lightweight automobiles…

• Plastics also face the competition from other materials for the lightweight of PV.

Carbon Fiber Composite

Nature Hemp

Glass Fiber Composite

… China still lags behind in the utilization of light weight materials for cars, but has potential to grow faster…

Lightweight Technique Weighting

Definition: Penetration rate of China is only for Local OEMs

Source: InterChina Interviews & Analysis & China Plastic Association

Modified PlasticsPP,PE,PVC,ABS,PBT…

50%

~40%

100%

~10%

Metal Alloy

PlasticsComposite

DesignOptimization

• Technological innovation may expedite the penetration of lightweight materials in local OEMs, but penetration will slow down due to plastic replacement application caps.

200156139

90

20202016 20352010

Pure Chinese OEM Plastic Usage per PV (kg)

Global OEM Plastic Usage per PV (kg)

250194178

130

20222016 20352010

450364334

230

2035202220162010

The basis of forecast (kg)Realistic China OEM Plastic Usage per PV (Chinese OEMs use less plastic, and JV OEMs in China might have “lower standards” plastics consumption in China.)

42

© InterChinaConfidential

Market Paradigm: China will catch up with int’l markets for plastic light weight (PLW) adoption … especially driven by Chinese OEMs

Source: “Technology Roadmap For Energy Saving and New Energy Vehicles” by SAE, InterChina Interviews and Analysis

China lags behind in PLW adoption compared with other int’l markets, and will be picking up quickly, driven by Gov. Vision and Chinese OEMs increasing tech know

PLW Adoption geographic markets comparison, 2017

PLW

Tec

hnol

ogy

Know

-how

High

Low

PLW Application Mindset

Low High

*Note: PLW = plastic light weight

Illustrative

365250220

15090

GermanyFrance

x3

US JapanChina

Unit: kg plastics per car in average

• China lags behind for PLW adoption for passenger carscompared with other international market.

• This is because a) the OEMs technology know-how,mindset is weak, b) overall supply chain readiness is low

Chinese OEMs will be catching up with Int’l markets quickly

Other Chinese OEMs

followers

Early Adopters

• Chinese OEMs have been closing the gap in bothPLW mindset and know-how.

• Some Chinese OEMs like Geely, Chery amongothers are more active in adopting PLW.

• They will set up role models for followers,together with improving readiness of supply chainwill boost the overall adoption of PLW.

Chinese Gov. sets up ambitious weight reduction target for PV fleets

70%80%

2020

90%

2015

100%

20302025

-30%

“Aggressively promote the application of high duty steel..., plastics and composite materials application.” ~ SAE

43

© InterChinaConfidential

• Nissan, X-trail• Rear door• From 38kg to 25kg• LFT

Which Customer Base To Alliance?: Among Chinese OEMs’ early PLW adopters are Geely, Chang’an, and Chery… they will become role models for market followers

Chinese OEMs

• VW, Magotan• Front end carrier• 20% weight reduced• LFT

2007 2008

211171

2016 2017

185180

2016 2017

• VW, Sagitar• Front end carrier

3433

20172016

Source: InterChina Interviews and Analysis

• Mercedez, Class E• Dashboard Frame• -3.2kg• LFT

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018E

57113

2016 2017

Though lag behind JV OEMs in PLW adoption, Chinese OEMs have been picking up PLW very recently, with front end carriers as initial focus

• Chang’an, Yidong• Front end carrier• -4kg, 40%• LFT

92156

20172016

• Chang’an, CX30• Front end

carrier• -4kg, 40%• LFT

• Chery, Aizerui7• Front end carrier• LFT

Unit: K units cars soldIn China market

417

2016 2017

• Geely Boyue• Beam• -2kg, 50%

• Geely, Dihao GS• Battery Tray• Front end• -1kg

JVOEMs

44

© InterChinaConfidential

Which Products To Invest in R&D?: PLW will be more adopted by (semi-) structural parts

Source: InterChina Interviews and Analysis

Auto parts applying PLW Key drivers of PLW

0

2

4

6

8

2015 2020 2025 2030

ChinaEU

U.S.

Fuel Consumption Targets for PV

Door

Frame of Instrument Board

Front-end Carrier

Anti-collision beam

• Fuel Saving: Lightweight isone of the most efficient waysto reduce fuel consumption.To comply with Chinese Gov.regulation on CAFC(5L/100km, 4L/100km,3.2L/100Km in 2020, 20252030, OEMs need to applyvarious engine optimizationtechnology incl. PLW.

Unit: L/100 KM

• Efficiency improvement:Unlike metal parts, the moreflexible processing technologymake it possible for plasticparts to integrate dozens ofauto part into one.

• Cost Saving: Reducing theauto parts need means amore efficient process and abetter cost performance.

BackSeat2/3 Seat

1/3 SeatSpare Tire Well

Rear Door1/3 Seat

2/3 Seat

Engine CoverBattery Frame

“LFT is mainly used in semi-structure parts, while IMC can beused in structural parts with higher strength coefficient, sothe substitution target for IMC is both LFT and metal parts.”

---- Ningbo Huaxiang

Front-end Carrier

Rear Door

Not exhaustive

CAFC: Corporate average fuel consumption. 45

© InterChinaConfidential

Automated Driving Policy: China is on parallel with leading countries in the development of automated driving technology…

World

China

1970s 1980s

China started relevant research

1990s 2005 2011

FAW conducted road test for its HQ3 automated driving vehicle

2014 2016

1992: National University of Defense Technology developed China’s first automated driving vehicle

Shanghai JiaotongUniversity developed first urban automated driving vehicle

2014-2016: many partnerships formed between OEMs and internet/tech firms, such as Baidu-BMW, Dongfeng-Huawei, BAIC-LeSee, etc.

2009

Nevada of US become world’s first region to allow automated driving cars on ordinary roads.

2004

• UK: gov. invested GBP 19 m for road testing in 4 cities

• France: Roadmap released, gov. to invest EUR 100 m in three years

• US: Federal Automated Vehicles Policy

• UN: International Road Transportation Treaty that allows automated driving under conditions

• South Korea: issued first driver license to an automated driving car; invest KRW 145.5 bn since 2017 for development of automated driving vehicles

• Japan: Road map; by 2020 allow automated vehicle driving on express ways.

Google started automated driving research

• US: DARPA had achievement

• Italy: AGRO project road test

US, UK and Germany started relevant research

Google released its first automated driving car

Source: Analysys – China Automated Driving Industry Report 2016, public literature

Automated Driving Vehicle Development Milestones

• Apr 2016: Chang’an ran 2,000 km road test for its automated driving vehicle

• Oct 2016: Technology Road Map released

Baidustarted automated driving research

46

© InterChinaConfidential

Emerging Value China: Chinese enterprises from relevant segments have formed a ecosystem for automated driving vehicle development

Chinese Enterprises Involved in the Development of Automated Driving Vehicles

Source: Analysys – China Automated Driving Industry Report 2016

Component Suppliers Vehicle Suppliers

Technology Suppliers

Contents Suppliers

Intelligent Sensing Chips OEMs Internet/Technology Firms

Cloud Car ConnectivityAlgorithm

HMIPlatformControlling & actuating Interaction

Navigation Entertainment, communication, service

47

© InterChinaConfidential

OEM Partnership: Chinese OEMs’ are actively developing the automated driving vehicles in partnership with various technology firms

Domestic OEM Progress and PartnershipsFAW 2011: HQ3 286 km road test Changsha-Wuhan

Targeting on 50% of all its models to be automated driving by 2025Dongfeng 2014: Partnership with Huawei

Chery 2016: Partnership with APG which targets auto driving by 2018

BAIC 2015: Partnership with LeSee

Chang’an 2014: Partnership with Huawei2016: completed 2000-km road test Chongqing-Beijing

ZTE 2016: ZTE acquired 70% share in the Guangdong Granton Bus and established ZTE Smart Auto

SAIC 2016: released Roewe RX5 with YunOS automated control system, jointly developed with Alibaba.

Geely 2017: will start construction of testing ground in H2, targeting on fully automated driving by 2024

BYD 2014: Partnership with Singapore Agency for Science, Technology and Research2016: Partnership with Baidu

Great wall Started research in 2012, targeting on rolling out automated car for expressway by 2020

Chinese OEMs Involved in Automated Driving Vehicle Development

48

© InterChinaConfidential

Supporting Policies: The government attaches high importance to the development of automated driving technology

GovernmentBody

Action Time Highlights

National NaturalScience Foundation of China国家自然科学基金委

Organization of tech competition: Intelligent Vehicle Future Challenge 智能车未来挑战赛

Annuallysince 2009

• A nationwide competition on the automated driving technologies

• Participants: Universities, science and technology research institutions, enterprises

• Top winners: Tsinghua University, National University of Defense Technology, Beijing Institute of Technology

State Council Released Plan of Made in China 2025

2015 • Automated driving vehicles is one of the important directions for the upgrade of China’s auto industry.

Ministry of Industry and Information Technology (MIIT)

Approved National Intelligent Connectivity Vehicles (Shanghai) Pilot Demonstration Area国家智能网联汽车(上海)试点示范区

June 2016 • Function: a closed area for comprehensive testing of automated driving vehicles

• Area: 5 square km (phase 1), will be extended to 100 square km by 2020

Society of Automotive Engineers of China中国汽车工程学会

Released Intelligent ConnectivityVehicle Technology Road Map智能网联汽车技术路线图

October2016

Targeted milestones:• 2020: Driver assisted/partial self-driving vehicles

take 50% market share• 2025: Highly automated driving vehicles take 15%

market share• 2030: entirely automated driving vehicles take 10%

market share

National Technical Committee of Auto Standardization全国汽车标准化技术委员会

Formulation of the Frameworkof Standards for Intelligent Connectivity Vehicle

Drafting started in 2014, now completed and pending approval by MIIT

Framework structure:• Basis: terms and definitions, classification and

codes, identification and symbols• General specification: Grading of intelligent