Xiao Nan Guo Restaurants Holdings Limited 小南國餐飲控股 ...

391

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and the Securities and Futures Commission take no responsibility for the contents of this Web Proof Information Pack, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Web Proof Information Pack. Web Proof Information Pack of Xiao Nan Guo Restaurants Holdings Limited 小南國餐飲控股有限公司 (Incorporated in the Cayman Islands with limited liability) WARNING This Web Proof Information Pack is being published as required by The Stock Exchange of Hong Kong Limited (‘‘HKEx’’) and the Securities and Futures Commission solely for the purpose of providing information to the public in Hong Kong. This Web Proof Information Pack is in draft form. The information contained in it is incomplete and is subject to change which can be material. By viewing this Web Proof Information Pack, you acknowledge, accept and agree with Xiao Nan Guo Restaurants Holdings Limited (the “Company”), any of its affiliates, the joint sponsors, any of the advisers and/or members of the underwriting syndicates that: (a) this Web Proof Information Pack is only for the purpose of providing information and facilitating equal dissemination of information to investors in Hong Kong and not for any other purposes. No investment decision should be made based on the information contained in this Web Proof Information Pack; (b) the posting of the Web Proof Information Pack or any supplemental, revised or replacement pages thereof on the website of HKEx does not give rise to any obligation of the Company, any of its affiliates, the joint sponsors, the advisers and/or members of the underwriting syndicates to proceed with an offering in Hong Kong or any other jurisdiction. There is no assurance that the Company will proceed with any offering; (c) the contents of the Web Proof Information Pack or any supplemental, revised or replacement pages thereof may or may not be replicated in full or in part in the actual prospectus; (d) this Web Proof Information Pack is in draft form and may be changed, updated or revised by the Company from time to time and the changes, updates and/or revisions could be material, but neither the Company nor any of its affiliates, the joint sponsors, the advisers or members of the underwriting syndicates is under any obligation, legal or otherwise, to update any information contained in this Web Proof Information Pack; (e) this Web Proof Information Pack does not constitute a prospectus as defined in the Companies Ordinance (Chapter 32 of the Laws of Hong Kong) (the ‘‘ Companies Ordinance’’) or a notice, circular, brochure or advertisement or other document offering to sell any securities to the public in any jurisdiction, nor is it an invitation or solicitation to the public to make offers to acquire, subscribe for or purchase any securities, nor is it calculated to invite or solicit offers by the public to acquire, subscribe for or purchase any securities; (f) this Web Proof Information Pack must not be regarded as an inducement to subscribe for or purchase any securities, and no such inducement is intended; (g) neither the Company nor any of its affiliates, the joint sponsors, the advisers or members of the underwriting syndicates is offering, or is soliciting offers to buy, any securities in any jurisdiction through the publication of this Web Proof Information Pack; (h) neither the Web Proof Information Pack nor anything contained herein shall form the basis of or be relied on in connection with any contract or commitment whatsoever; (i) neither the Company nor any of its affiliates, the joint sponsors, the advisers or members of the underwriting syndicates makes any express or implied representation or warranty as to the accuracy or completeness of the information contained in the Web Proof Information Pack; (j) each of the Company and its affiliates, the joint sponsors, the advisers and the members of the underwriting syndicates expressly disclaims any and all liability on the basis of any information contained in or omitted from, or any inaccuracies or errors in, the Web Proof Information Pack; (k) securities may not be offered or sold in the United States absent registration under the United States Securities Act of 1933, as amended (the ‘‘ U.S. Securities Act ’’) and any applicable state securities laws of the United States, or an available exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and any applicable state securities laws of the United States. The securities referred to in this Web Proof Information Pack have not been registered under the U.S. Securities Act or any state securities laws of the United States. The Company does not intend to register the securities under the U.S. Securities Act or any state securities laws of the United States or conduct a public offering in the United States. This Web Proof Information Pack is not an offer of securities for sale in the United States. You confirm that you are accessing this Web Proof Information Pack from outside of the United States; and (l) as there may be legal restrictions on the distribution of this Web Proof Information Pack or dissemination of any information contained in this Web Proof Information Pack, you agree to inform yourself about and observe any such restrictions applicable to you. THIS WEB PROOF INFORMATION PACK IS NOT FOR PUBLICATION OR DISTRIBUTION TO PERSONS IN THE UNITED STATES. ANY SECURITIES REFERRED TO HEREIN HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE U.S. SECURITIES ACT, AND MAY NOT BE OFFERED, SOLD OR DELIVERED IN THE UNITED STATES WITHOUT REGISTRATION THEREUNDER OR PURSUANT TO AN AVAILABLE EXEMPTION THEREFROM. NO PUBLIC OFFERING OF THE SECURITIES WILL BE MADE IN THE UNITED STATES. NEITHER THIS WEB PROOF INFORMATION PACK NOR ANY INFORMATION CONTAINED HEREIN CONSTITUTES OR FORMS A PART OF AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN THE UNITED STATES OR IN ANY OTHER JURISDICTIONS WHERE SUCH AN OFFER OR SALE IS NOT PERMITTED. THIS WEB PROOF INFORMATION PACK IS NOT BEING MADE AND MAY NOT BE DISTRIBUTED OR SENT INTO ANY JURISDICTION WHERE SUCH DISTRIBUTION OR DELIVERY IS NOT PERMITTED. No offer or invitation to the public in Hong Kong will be made until and unless a prospectus of the Company is registered with the Registrar of Companies in Hong Kong in accordance with the Companies Ordinance. If an offer or an invitation is made to the public in Hong Kong in due course, prospective investors are reminded to make their investment decisions solely based on a prospectus of the Company registered with the Registrar of Companies in Hong Kong, copies of which will be distributed to the public during the offer period. No offer or invitation to the public in Hong Kong is made on the basis of this Web Proof Information Pack.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Xiao Nan Guo Restaurants Holdings Limited 小南國餐飲控股 ...

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and the Securities and Futures Commissiontake no responsibility for the contents of this Web Proof Information Pack, make no representation as to its accuracy or completenessand expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of thecontents of this Web Proof Information Pack.

Web Proof Information Pack of

Xiao Nan Guo Restaurants Holdings Limited小 南 國 餐 飲 控 股 有 限 公 司

(Incorporated in the Cayman Islands with limited liability)

WARNING

This Web Proof Information Pack is being published as required by The Stock Exchange of Hong Kong Limited (‘‘HKEx’’) andthe Securities and Futures Commission solely for the purpose of providing information to the public in Hong Kong.

This Web Proof Information Pack is in draft form. The information contained in it is incomplete and is subject to change which can bematerial. By viewing this Web Proof Information Pack, you acknowledge, accept and agree with Xiao Nan Guo Restaurants HoldingsLimited (the “Company”), any of its affiliates, the joint sponsors, any of the advisers and/or members of the underwriting syndicatesthat:

(a) this Web Proof Information Pack is only for the purpose of providing information and facilitating equal dissemination ofinformation to investors in Hong Kong and not for any other purposes. No investment decision should be made based on theinformation contained in this Web Proof Information Pack;

(b) the posting of the Web Proof Information Pack or any supplemental, revised or replacement pages thereof on the website of HKExdoes not give rise to any obligation of the Company, any of its affiliates, the joint sponsors, the advisers and/or members of theunderwriting syndicates to proceed with an offering in Hong Kong or any other jurisdiction. There is no assurance that theCompany will proceed with any offering;

(c) the contents of the Web Proof Information Pack or any supplemental, revised or replacement pages thereof may or may not bereplicated in full or in part in the actual prospectus;

(d) this Web Proof Information Pack is in draft form and may be changed, updated or revised by the Company from time to timeand the changes, updates and/or revisions could be material, but neither the Company nor any of its affiliates, the joint sponsors,the advisers or members of the underwriting syndicates is under any obligation, legal or otherwise, to update any informationcontained in this Web Proof Information Pack;

(e) this Web Proof Information Pack does not constitute a prospectus as defined in the Companies Ordinance (Chapter 32 of the Lawsof Hong Kong) (the ‘‘Companies Ordinance’’) or a notice, circular, brochure or advertisement or other document offering tosell any securities to the public in any jurisdiction, nor is it an invitation or solicitation to the public to make offers to acquire,subscribe for or purchase any securities, nor is it calculated to invite or solicit offers by the public to acquire, subscribe for orpurchase any securities;

(f) this Web Proof Information Pack must not be regarded as an inducement to subscribe for or purchase any securities, and no suchinducement is intended;

(g) neither the Company nor any of its affiliates, the joint sponsors, the advisers or members of the underwriting syndicates isoffering, or is soliciting offers to buy, any securities in any jurisdiction through the publication of this Web Proof InformationPack;

(h) neither the Web Proof Information Pack nor anything contained herein shall form the basis of or be relied on in connection withany contract or commitment whatsoever;

(i) neither the Company nor any of its affiliates, the joint sponsors, the advisers or members of the underwriting syndicates makesany express or implied representation or warranty as to the accuracy or completeness of the information contained in the WebProof Information Pack;

(j) each of the Company and its affiliates, the joint sponsors, the advisers and the members of the underwriting syndicates expresslydisclaims any and all liability on the basis of any information contained in or omitted from, or any inaccuracies or errors in, theWeb Proof Information Pack;

(k) securities may not be offered or sold in the United States absent registration under the United States Securities Act of 1933, asamended (the ‘‘U.S. Securities Act’’) and any applicable state securities laws of the United States, or an available exemptionfrom, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and any applicable state securitieslaws of the United States. The securities referred to in this Web Proof Information Pack have not been registered under the U.S.Securities Act or any state securities laws of the United States. The Company does not intend to register the securities under theU.S. Securities Act or any state securities laws of the United States or conduct a public offering in the United States. This WebProof Information Pack is not an offer of securities for sale in the United States. You confirm that you are accessing this WebProof Information Pack from outside of the United States; and

(l) as there may be legal restrictions on the distribution of this Web Proof Information Pack or dissemination of any informationcontained in this Web Proof Information Pack, you agree to inform yourself about and observe any such restrictions applicableto you.

THIS WEB PROOF INFORMATION PACK IS NOT FOR PUBLICATION OR DISTRIBUTION TO PERSONS IN THE UNITEDSTATES. ANY SECURITIES REFERRED TO HEREIN HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THEU.S. SECURITIES ACT, AND MAY NOT BE OFFERED, SOLD OR DELIVERED IN THE UNITED STATES WITHOUTREGISTRATION THEREUNDER OR PURSUANT TO AN AVAILABLE EXEMPTION THEREFROM. NO PUBLIC OFFERINGOF THE SECURITIES WILL BE MADE IN THE UNITED STATES.

NEITHER THIS WEB PROOF INFORMATION PACK NOR ANY INFORMATION CONTAINED HEREIN CONSTITUTES ORFORMS A PART OF AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITIES IN THE UNITEDSTATES OR IN ANY OTHER JURISDICTIONS WHERE SUCH AN OFFER OR SALE IS NOT PERMITTED. THIS WEBPROOF INFORMATION PACK IS NOT BEING MADE AND MAY NOT BE DISTRIBUTED OR SENT INTO ANYJURISDICTION WHERE SUCH DISTRIBUTION OR DELIVERY IS NOT PERMITTED.

No offer or invitation to the public in Hong Kong will be made until and unless a prospectus of the Company is registered with theRegistrar of Companies in Hong Kong in accordance with the Companies Ordinance. If an offer or an invitation is made to the publicin Hong Kong in due course, prospective investors are reminded to make their investment decisions solely based on a prospectus of theCompany registered with the Registrar of Companies in Hong Kong, copies of which will be distributed to the public during the offerperiod. No offer or invitation to the public in Hong Kong is made on the basis of this Web Proof Information Pack.

This Web Proof Information Pack contains the following information relating to the Company

extracted from the draft document:

Summary

Definitions

Forward-Looking Statements

Risk Factors

Directors

Corporate Information

Regulation

Industry Overview

History and Development

Business

Relationship with Controlling Shareholders

Connected Transactions

Directors and Senior Management

Share Capital

Financial Information

Appendix I - Accountants’ Report

Appendix IV - Summary of the Constitution of the Company and Cayman Islands Company Law

Appendix V - Statutory and General Information

YOU SHOULD READ THE SECTION HEADED “WARNING” ON THE COVER OF THIS WEBPROOF INFORMATION PACK

CONTENTS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

OVERVIEW

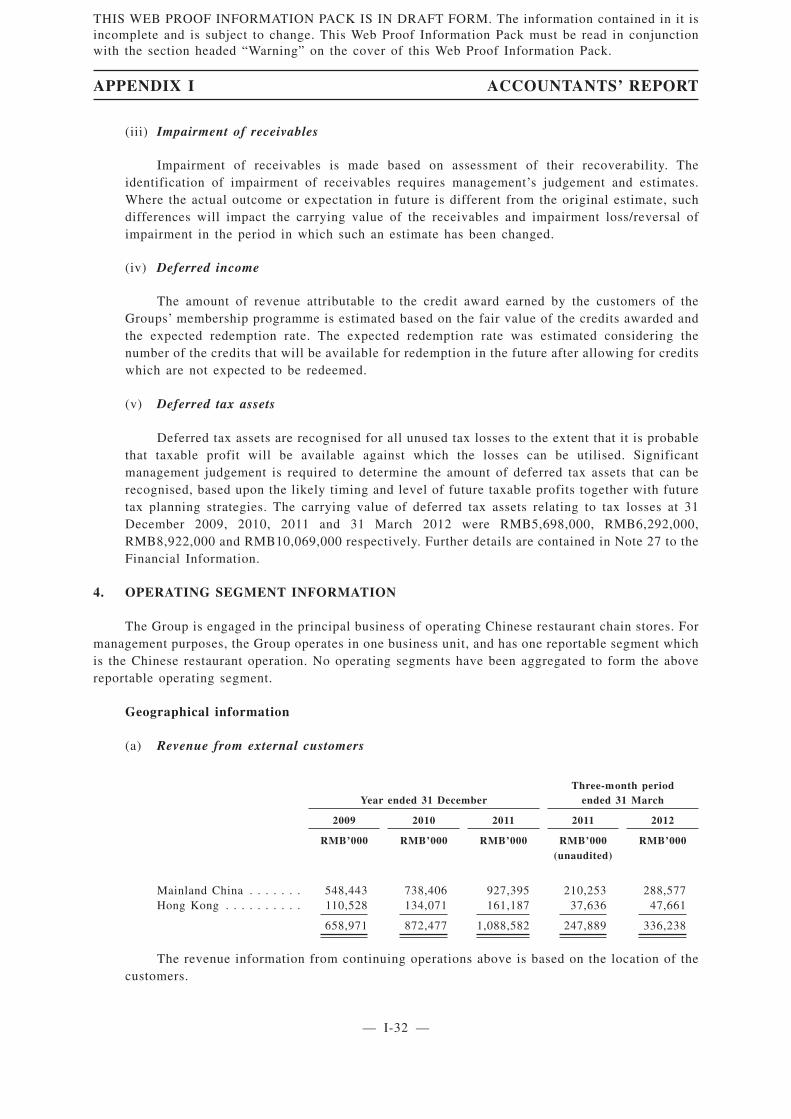

We are the largest self-owned mid-to high-end Chinese cuisine full-service restaurant chainheadquartered in the PRC, based on number of self-owned restaurants in Greater China as ofDecember 31, 2011, according to Euromonitor International, an independent market research firm.(1)

We own and operate restaurants under a portfolio of Chinese cuisine brands spanning diverse marketsegments: “Shanghai Xiao Nan Guo (上海小南國)”— our core brand and a premier mid- to high-endrestaurant chain with 57 restaurants as of the Latest Practicable Date; “Maison De L’Hui (慧公館)” —a recently-developed high-end brand focused on business clientele with three restaurants as of thesame date; and “the dining room (南小館)” — a pilot casual dining brand launched in June 2012 inHong Kong with one restaurant as of the Latest Practicable Date. In recognition of its reputation andmarket awareness, the Xiao Nan Guo brand, with a history since 1987, has been designated as a“Well-known Trademark” by the SAIC, and is, we believe, one of the strongest Chinese cuisine brandsin China.

Restaurant Brands

We ownd and operated restaurants under two brands during the period consisting of the threeyears ended December 31, 2011 and the three months ended March 31, 2012, Shanghai Xiao Nan Guoand Maison De L’Hui. The following table presents our revenue by brands and regions during theperiod consisting of the three years ended December 31, 2011 and the three months ended March 31,2012. For more details, please see the section headed “Business — Restaurant Brands” of thisdocument.

For the year ended December 31,

For the threemonths ended

March 31,

2009 2010 2011 2012

Amount(RMB’000)

% Amount(RMB’000)

% Amount(RMB’000)

% Amount(RMB’000)

%

ChinaShanghai Xiao Nan Guo

Eastern China . . . . . . 430,484 67.6 576,033 68.2 672,520 63.9 216,858 65.6Northern China . . . . . 96,384 15.1 124,590 14.7 171,108 16.3 50,188 15.2Southern China . . . . . — — — — 2,602 0.2 4,818 1.5

Subtotal . . . . . . . . 526,868 82.7 700,623 82.9 846,230 80.4 271,864 82.3Maison De L’Hui . . . . . . — — 11,199 1.3 44,994 4.3 10,936 3.3

Hong KongShanghai Xiao Nan Guo . . 110,528 17.3 134,071 15.8 161,187 15.3 47,661 14.4

Total revenue of restaurantoperations . . . . . . . . . . . . 637,396 100.0 845,893 100.0 1,052,411 100.0 330,461 100.0

(1) According to Euromonitor International, full-service restaurants are traditional sit-down restaurants with full tableservice provided by waiters, where the focus of the guest experience is on food rather than drink; a Chinese full-servicerestaurant chain operates a minimum of ten branded outlets; and the mid- to high-end market segment in China refersto restaurants where the average guest check is in the range of RMB150 to RMB300 or above, and the dishes offeredare generally made of premium food materials or ingredients. For more details, please see the section headed “IndustryOverview”.

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 1 —

The following table sets forth our gross profit by brands and regions during the period consistingof the three years ended December 31, 2011 and the three months ended March 31, 2012. For moredetails, please see the section headed “Business — Restaurant Brands” of this document.

For the year ended December 31,

For the threemonths ended

March 31,

2009 2010 2011 2012

Amount(RMB’000)

% Amount(RMB’000)

% Amount(RMB’000)

% Amount(RMB’000)

%

ChinaShanghai Xiao Nan Guo

Eastern China . . . . . . 272,021 64.9 369,565 65.9 434,094 61.5 143,830 63.8Northern China . . . . . 60,143 14.3 81,574 14.6 117,454 16.6 34,781 15.4Southern China . . . . . — — — — 1,743 0.2 3,594 1.6

Subtotal . . . . . . . . 332,164 79.2 451,139 80.5 553,291 78.3 182,205 80.8Maison De L’Hui . . . . . . — — 6,920 1.2 30,344 4.3 6,668 3.0

Hong KongShanghai Xiao Nan Guo . . 87,035 20.8 102,806 18.3 121,943 17.4 36,418 16.2

Total gross profit ofrestaurant operations. . . . . . 419,199 100.0 560,865 100.0 705,578 100.0 225,291 100.0

Expansion Strategy and Plan

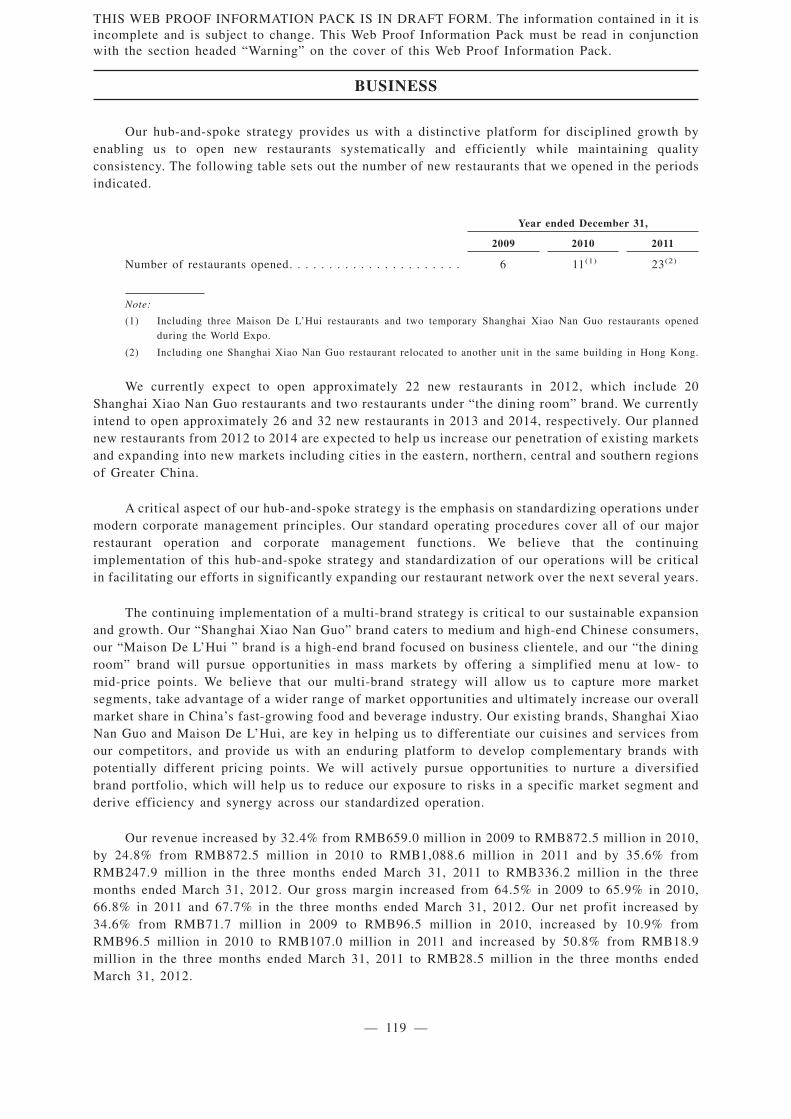

We have expanded our restaurant base in new and existing markets based on a distinctivehub-and-spoke strategy. Under this strategy, within any new regional market, we seek to initiallyestablish a cluster of restaurant locations in key economic centers in the region, or “hubs”, allowingus to derive greater economies of scale and ensure consistent quality of food through centralized foodpreparation, procurement and logistics functions at our central kitchens and central warehouses. Weleverage these centralized functions to support our expansion into neighboring cities, or the “spokes”,which, as they gain critical mass, eventually become new “hubs”. As of the Latest Practicable Date,we operated six central kitchens and five central warehouses, servicing our restaurant network of 57Shanghai Xiao Nan Guo restaurants, three Maison De L’Hui restaurants and one “the dining room”restaurant, which covered some of the most affluent and fastest-growing cities in Greater China,including Shanghai, Beijing, Dalian, Suzhou, Nanjing, Tianjin, Ningbo, Wuxi, Shenzhen and HongKong.

Our hub-and-spoke strategy provides us with a distinctive platform for disciplined growth byenabling us to open new restaurants systematically and efficiently while maintaining qualityconsistency. The following table sets out the number of new restaurants that we opened in the periodsindicated.

Year ended December 31,

2009 2010 2011

Number of restaurants opened. . . . . . . . . . . . . . . . . . . . . . . . . . 6 11(1) 23(2)

Note:

(1) Including three Maison De L’Hui restaurants and two temporary Shanghai Xiao Nan Guo restaurants opened during theWorld Expo.

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 2 —

(2) Including one Shanghai Xiao Nan Guo restaurant relocated to another unit in the same building in Hong Kong.

We currently expect to open approximately 22 new restaurants in 2012, which include 20Shanghai Xiao Nan Guo restaurants and two restaurants under “the dining room” brand. We intend toopen approximately 26 and 32 new restaurants in 2013 and 2014, respectively, with two restaurantsunder “the dining room” brand planned for each year and all other restaurants under our Shanghai XiaoNan Guo brand. Our planned new restaurants from 2012 to 2014 are expected to help us increase ourpenetration of existing markets and expand into new markets including cities in the eastern, northern,central and southern regions of Greater China.

A critical aspect of our hub-and-spoke strategy is the emphasis on standardizing operations undermodern corporate management principles. Our standard operating procedures cover all of our majorrestaurant operation and corporate management functions. We believe that the continuingimplementation of this hub-and-spoke strategy and standardization of our operations will be criticalin facilitating our efforts in significantly expanding our restaurant network over the next several years.

The continuing implementation of a multi-brand strategy is critical to our sustainable expansionand growth. Our “Shanghai Xiao Nan Guo” brand caters to medium and high-end Chinese consumers,our “Maison De L’Hui ” brand is a high-end brand focused on business clientele, and our “the diningroom” brand will pursue opportunities in mass markets by offering a simplified menu at low- tomid-price points. We believe that our multi-brand strategy will allow us to capture more marketsegments, take advantage of a wider range of market opportunities and ultimately increase our overallmarket share in China’s fast-growing food and beverage industry. Our existing brands, Shanghai XiaoNan Guo and Maison De L’Hui, are key in helping us to differentiate our cuisines and services fromour competitors, and provide us with an enduring platform to develop complementary brands withpotentially different pricing points. We will actively pursue opportunities to nurture a diversifiedbrand portfolio, which will help us to reduce our exposure to risks in a specific market segment andderive efficiency and synergy across our standardized operation.

Competition

The restaurant industry is intensely competitive with respect to food quality and consistency,price-value relationships, ambiance, service, location, supply of quality food ingredients andemployees. Many existing restaurants compete with us at each of our locations. Key competitivefactors in the industry include type of cuisine, food choice, food quality and consistency, quality ofservice, price, dining experience, restaurant location and the ambiance of the facilities. According toEuromonitor International, the total sales value of Asian cuisine full-service restaurants in Chinaamounted to approximately RMB1,986 billion in 2011. Euromonitor International expects Asiancuisine full service restaurants in China to continue to experience robust growth at a CAGR of 10.1%in terms of sales value from 2012 to 2016.

According to Euromonitor International, there are only a limited number of nationwide brandedChinese cuisine full-service restaurant chains. See the section headed “Industry Overview” of thisdocument. We believe we are competitively positioned based on the history of more than two decadesof our brand, standardized operation model under modern corporate management principles andtime-tested signature dishes with wide customer appeal. See the section headed “Risk Factors — RisksRelating to Our Industry and Business — Intense competition in the restaurant industry could preventus from increasing or sustaining our revenues and profitability” of this document.

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 3 —

Purchasing

We purchase food and supplies from more than 200 suppliers. Other than those suppliers from

which we only made insignificant purchases, the majority of our suppliers have been our suppliers for

more than three years as of the Latest Practicable Date. We have adopted procurement strategies for

all of our product categories that include contingency plans for key products, ingredients and supplies.

During the period consisting of the three years ended December 31, 2011 and the three months ended

March 31, 2012, we did not experience any interruption of the food ingredients supply, early

termination of supply agreements, or failure to secure sufficient quantities of irreplaceable food

ingredients that had any material adverse impact on our business and results of operations. For more

details about our supplier management, purchase cost control, and purchasing procedures and

management, please see the section headed “Business — Purchasing” of this document.

COMPETITIVE STRENGTHS

We believe the following key strengths of our Company distinguish us from our competitors, and

we expect that they will help us to enter a period of significant growth in the future:

• premier mid- to high-end Chinese cuisine brand in a large and fast-growing market;

• established hub-and-spoke network for rapid expansion;

• standardized operations driving scalability and efficiency;

• high-quality cuisine and innovative product development;

• loyal and diversified customer base generating significant recurring revenue; and

• leadership under an experienced restaurateur complemented by an energetic professional

management team.

BUSINESS STRATEGY

Our objective is to become a world-leading full-service Chinese restaurant chain operator. To this

end, we intend to pursue a business strategy with the following key aspects:

• replicate success by continuing expansion under our hub-and-spoke strategy;

• capture more market segments by pursuing a multi-brand strategy;

• continue to strengthen operational infrastructure to deliver sustainable growth;

• enhance comparable restaurant sales growth and profitability; and

• continue to promote brand image and recognition.

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 4 —

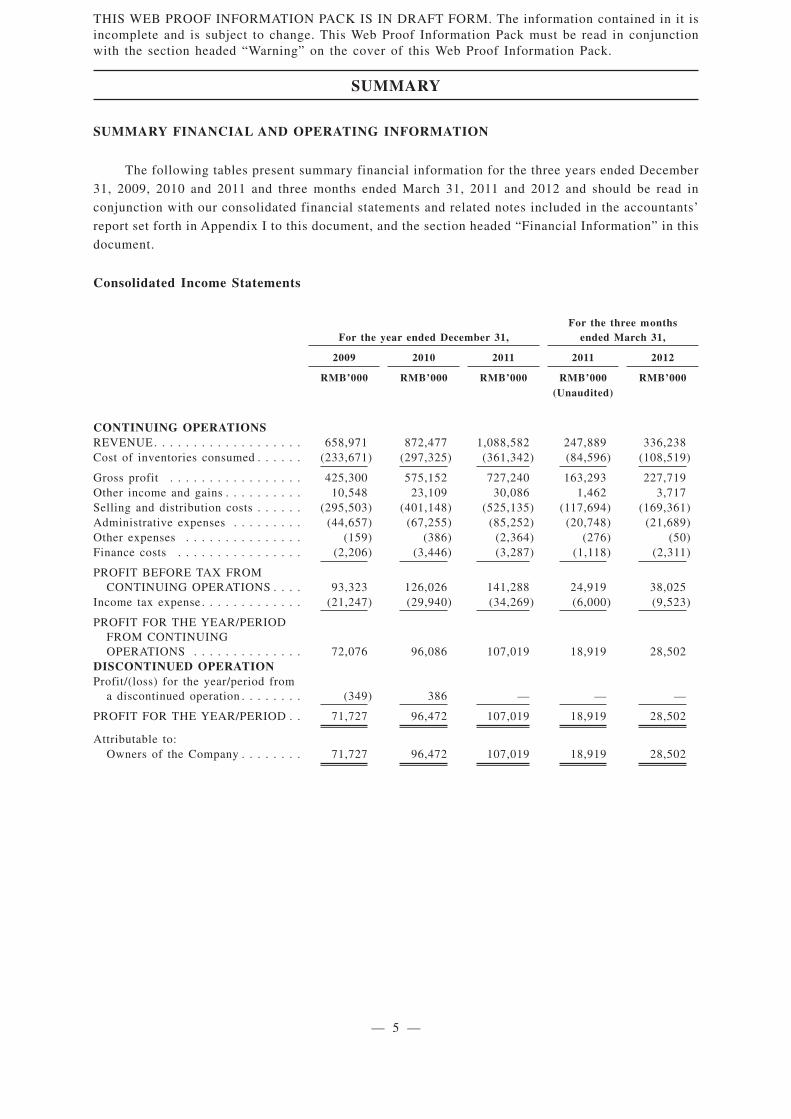

SUMMARY FINANCIAL AND OPERATING INFORMATION

The following tables present summary financial information for the three years ended December

31, 2009, 2010 and 2011 and three months ended March 31, 2011 and 2012 and should be read in

conjunction with our consolidated financial statements and related notes included in the accountants’

report set forth in Appendix I to this document, and the section headed “Financial Information” in this

document.

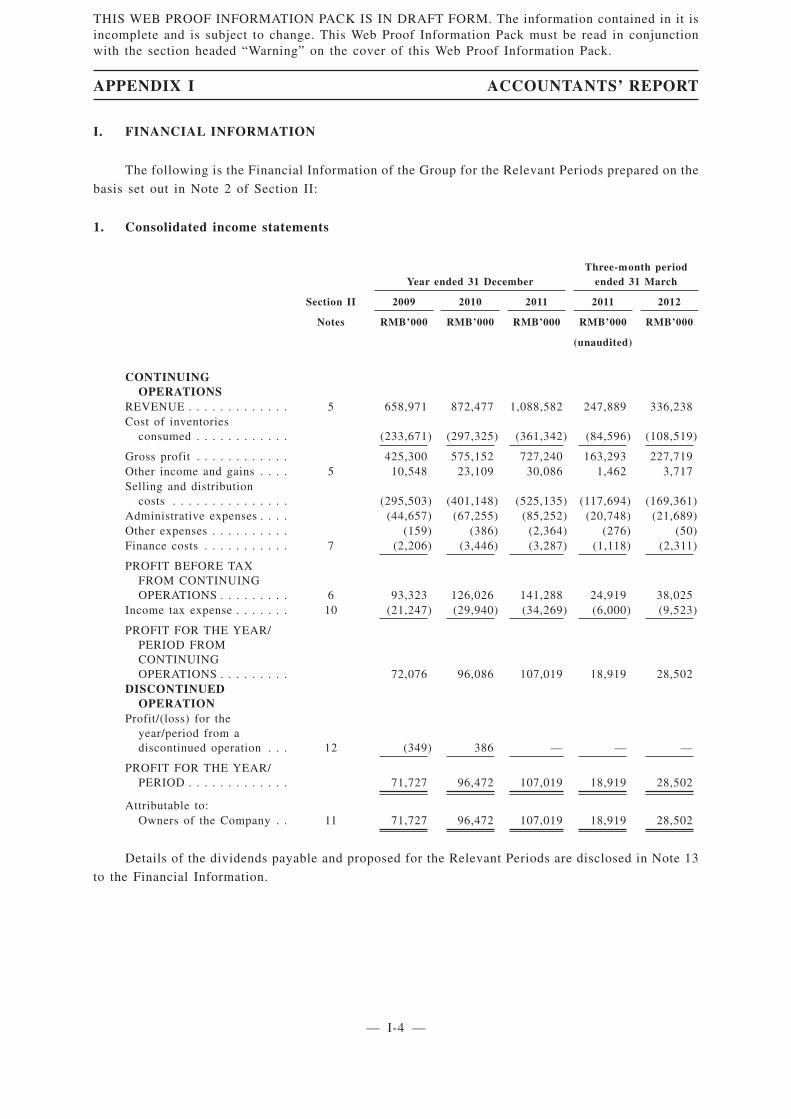

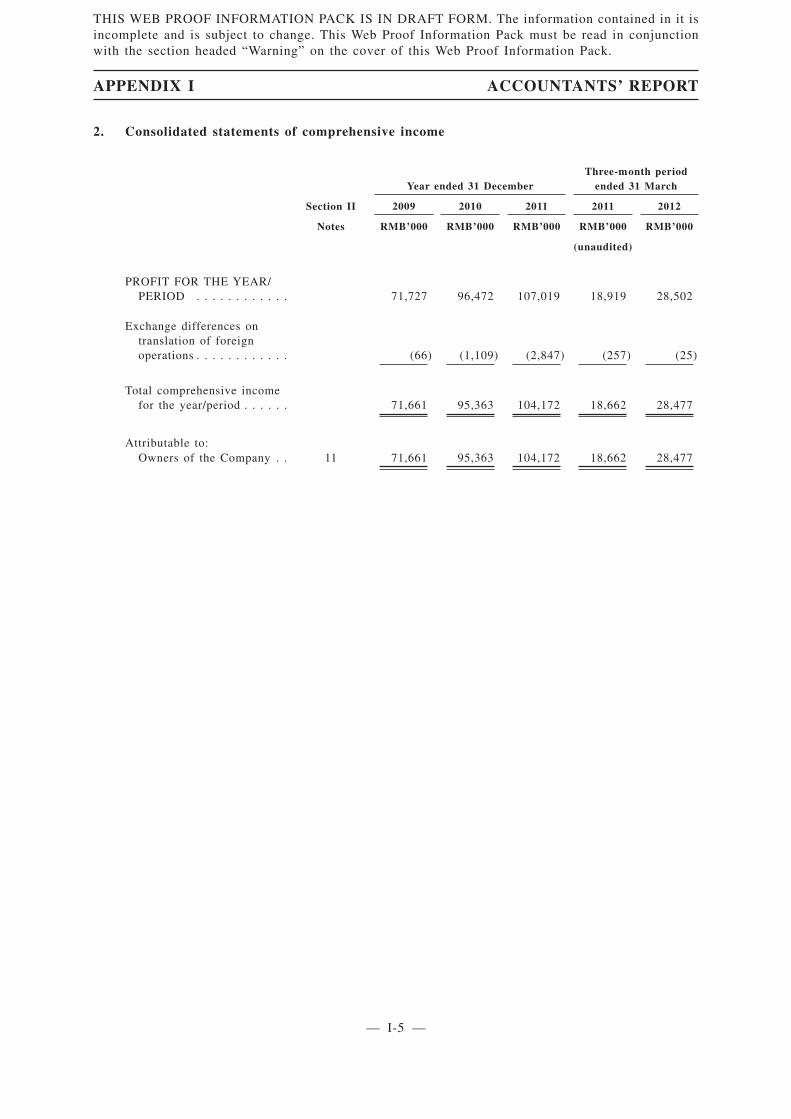

Consolidated Income Statements

For the year ended December 31,For the three months

ended March 31,

2009 2010 2011 2011 2012

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(Unaudited)

CONTINUING OPERATIONSREVENUE. . . . . . . . . . . . . . . . . . . 658,971 872,477 1,088,582 247,889 336,238Cost of inventories consumed . . . . . . (233,671) (297,325) (361,342) (84,596) (108,519)

Gross profit . . . . . . . . . . . . . . . . . 425,300 575,152 727,240 163,293 227,719Other income and gains . . . . . . . . . . 10,548 23,109 30,086 1,462 3,717Selling and distribution costs . . . . . . (295,503) (401,148) (525,135) (117,694) (169,361)Administrative expenses . . . . . . . . . (44,657) (67,255) (85,252) (20,748) (21,689)Other expenses . . . . . . . . . . . . . . . (159) (386) (2,364) (276) (50)Finance costs . . . . . . . . . . . . . . . . (2,206) (3,446) (3,287) (1,118) (2,311)

PROFIT BEFORE TAX FROMCONTINUING OPERATIONS . . . . 93,323 126,026 141,288 24,919 38,025

Income tax expense . . . . . . . . . . . . . (21,247) (29,940) (34,269) (6,000) (9,523)

PROFIT FOR THE YEAR/PERIODFROM CONTINUINGOPERATIONS . . . . . . . . . . . . . . 72,076 96,086 107,019 18,919 28,502

DISCONTINUED OPERATIONProfit/(loss) for the year/period from

a discontinued operation . . . . . . . . (349) 386 — — —

PROFIT FOR THE YEAR/PERIOD . . 71,727 96,472 107,019 18,919 28,502

Attributable to:Owners of the Company . . . . . . . . 71,727 96,472 107,019 18,919 28,502

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 5 —

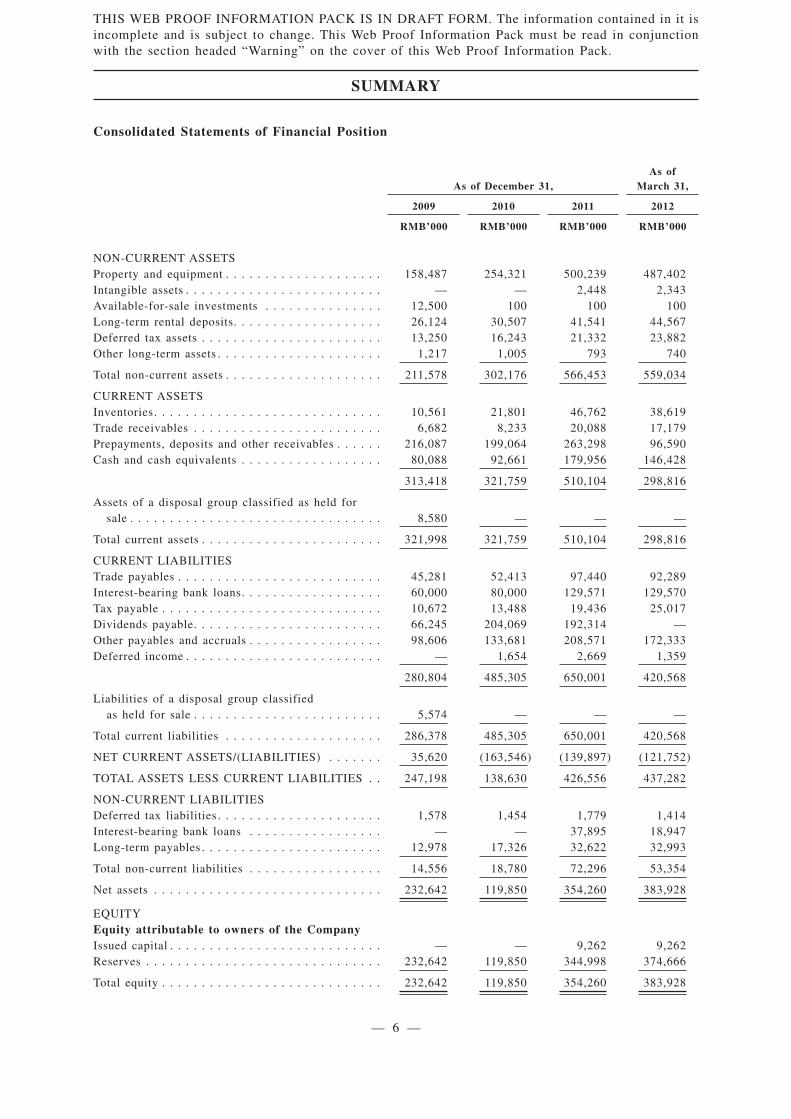

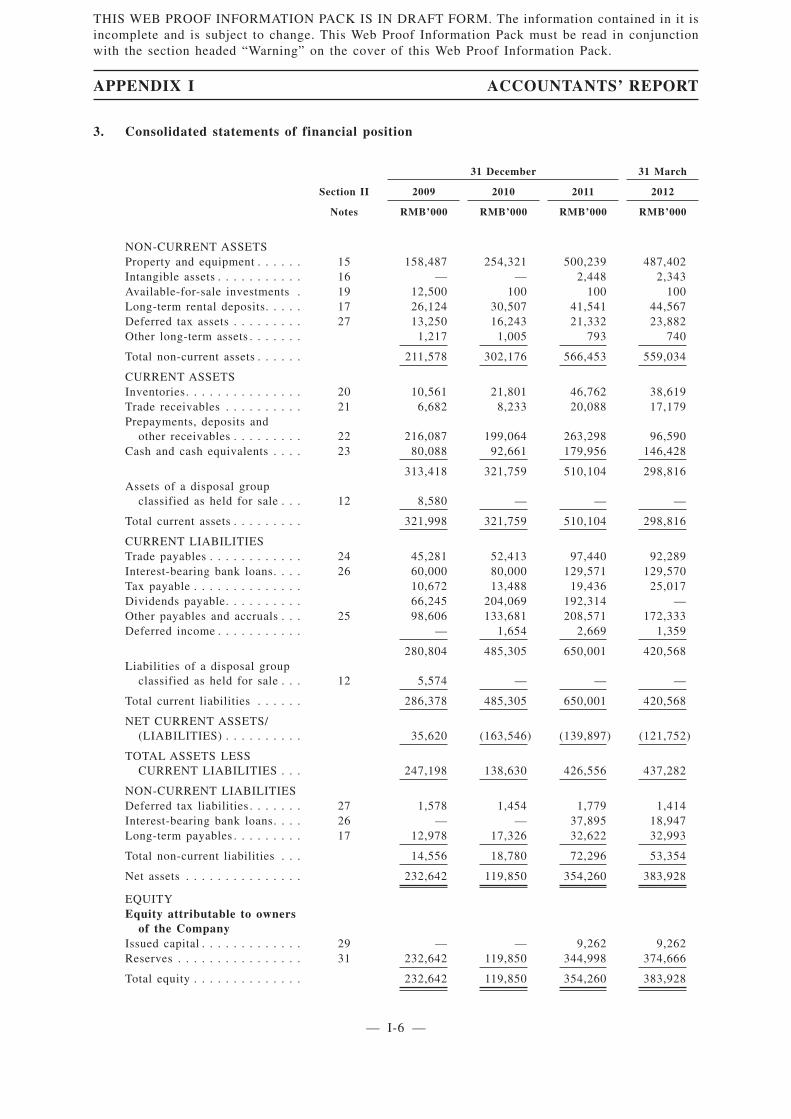

Consolidated Statements of Financial Position

As of December 31,As of

March 31,

2009 2010 2011 2012

RMB’000 RMB’000 RMB’000 RMB’000

NON-CURRENT ASSETSProperty and equipment . . . . . . . . . . . . . . . . . . . . 158,487 254,321 500,239 487,402Intangible assets . . . . . . . . . . . . . . . . . . . . . . . . . — — 2,448 2,343Available-for-sale investments . . . . . . . . . . . . . . . 12,500 100 100 100Long-term rental deposits. . . . . . . . . . . . . . . . . . . 26,124 30,507 41,541 44,567Deferred tax assets . . . . . . . . . . . . . . . . . . . . . . . 13,250 16,243 21,332 23,882Other long-term assets . . . . . . . . . . . . . . . . . . . . . 1,217 1,005 793 740

Total non-current assets . . . . . . . . . . . . . . . . . . . . 211,578 302,176 566,453 559,034

CURRENT ASSETSInventories. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,561 21,801 46,762 38,619Trade receivables . . . . . . . . . . . . . . . . . . . . . . . . 6,682 8,233 20,088 17,179Prepayments, deposits and other receivables . . . . . . 216,087 199,064 263,298 96,590Cash and cash equivalents . . . . . . . . . . . . . . . . . . 80,088 92,661 179,956 146,428

313,418 321,759 510,104 298,816

Assets of a disposal group classified as held forsale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,580 — — —

Total current assets . . . . . . . . . . . . . . . . . . . . . . . 321,998 321,759 510,104 298,816

CURRENT LIABILITIESTrade payables . . . . . . . . . . . . . . . . . . . . . . . . . . 45,281 52,413 97,440 92,289Interest-bearing bank loans. . . . . . . . . . . . . . . . . . 60,000 80,000 129,571 129,570Tax payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,672 13,488 19,436 25,017Dividends payable. . . . . . . . . . . . . . . . . . . . . . . . 66,245 204,069 192,314 —Other payables and accruals . . . . . . . . . . . . . . . . . 98,606 133,681 208,571 172,333Deferred income . . . . . . . . . . . . . . . . . . . . . . . . . — 1,654 2,669 1,359

280,804 485,305 650,001 420,568

Liabilities of a disposal group classifiedas held for sale . . . . . . . . . . . . . . . . . . . . . . . . 5,574 — — —

Total current liabilities . . . . . . . . . . . . . . . . . . . . 286,378 485,305 650,001 420,568

NET CURRENT ASSETS/(LIABILITIES) . . . . . . . 35,620 (163,546) (139,897) (121,752)

TOTAL ASSETS LESS CURRENT LIABILITIES . . 247,198 138,630 426,556 437,282

NON-CURRENT LIABILITIESDeferred tax liabilities . . . . . . . . . . . . . . . . . . . . . 1,578 1,454 1,779 1,414Interest-bearing bank loans . . . . . . . . . . . . . . . . . — — 37,895 18,947Long-term payables . . . . . . . . . . . . . . . . . . . . . . . 12,978 17,326 32,622 32,993

Total non-current liabilities . . . . . . . . . . . . . . . . . 14,556 18,780 72,296 53,354

Net assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 232,642 119,850 354,260 383,928

EQUITYEquity attributable to owners of the CompanyIssued capital . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 9,262 9,262Reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 232,642 119,850 344,998 374,666

Total equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . 232,642 119,850 354,260 383,928

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 6 —

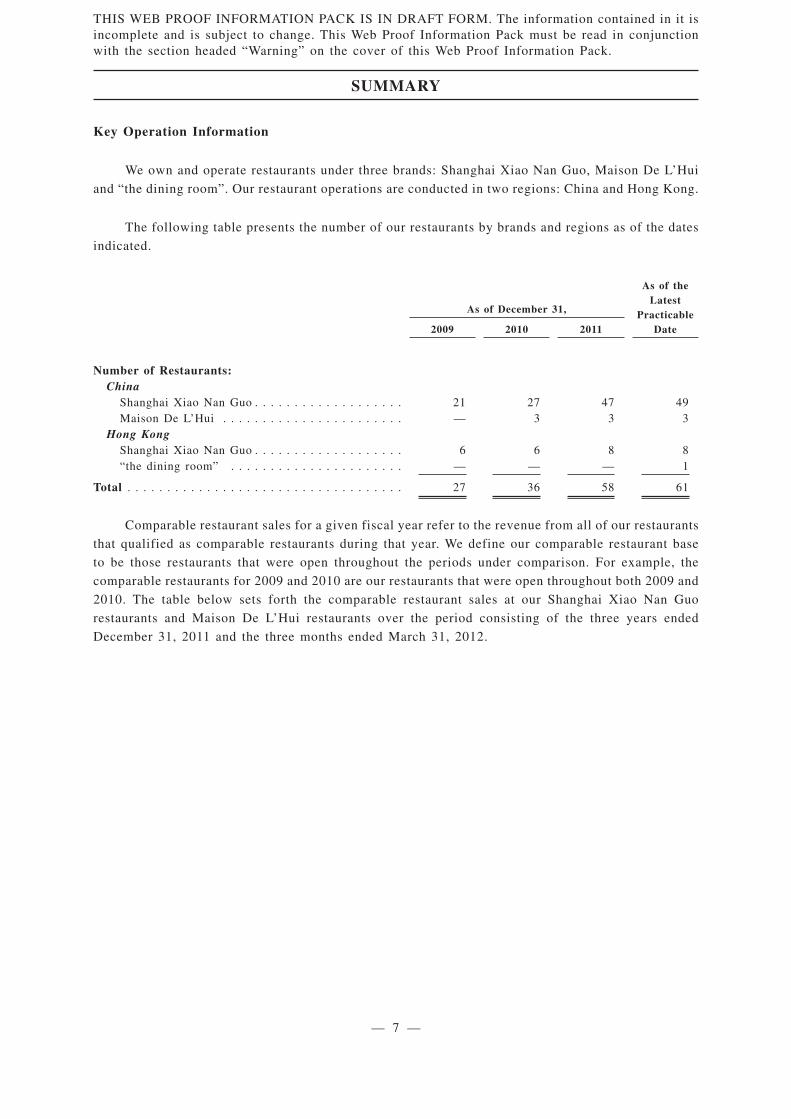

Key Operation Information

We own and operate restaurants under three brands: Shanghai Xiao Nan Guo, Maison De L’Hui

and “the dining room”. Our restaurant operations are conducted in two regions: China and Hong Kong.

The following table presents the number of our restaurants by brands and regions as of the dates

indicated.

As of December 31,

As of theLatest

PracticableDate2009 2010 2011

Number of Restaurants:China

Shanghai Xiao Nan Guo . . . . . . . . . . . . . . . . . . . 21 27 47 49Maison De L’Hui . . . . . . . . . . . . . . . . . . . . . . . — 3 3 3

Hong KongShanghai Xiao Nan Guo . . . . . . . . . . . . . . . . . . . 6 6 8 8“the dining room” . . . . . . . . . . . . . . . . . . . . . . — — — 1

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 36 58 61

Comparable restaurant sales for a given fiscal year refer to the revenue from all of our restaurants

that qualified as comparable restaurants during that year. We define our comparable restaurant base

to be those restaurants that were open throughout the periods under comparison. For example, the

comparable restaurants for 2009 and 2010 are our restaurants that were open throughout both 2009 and

2010. The table below sets forth the comparable restaurant sales at our Shanghai Xiao Nan Guo

restaurants and Maison De L’Hui restaurants over the period consisting of the three years ended

December 31, 2011 and the three months ended March 31, 2012.

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 7 —

For the year endedDecember 31,

For the year endedDecember 31,

For the three monthsended March 31,

2009 2010 2010 2011 2011 2012

Sh

angh

aiX

iao

Nan

Gu

o

Number of comparable restaurantsChina

Shanghai . . . . . . . . . . . . . . . . . 12 12 11 11(1) 15(2) 15(2)

Other cities . . . . . . . . . . . . . . . 4 4 8 8 10(2) 10(2)

Subtotal. . . . . . . . . . . . . . . . . . 16 16 19 19(1) 25(2) 25(2)

Hong Kong . . . . . . . . . . . . . . . . . 5 5 5 5 5 5Total number . . . . . . . . . . . . . . . . 21 21 24 24(1) 30(2) 30(2)

Comparable restaurants salesChina (RMB thousands)

Shanghai . . . . . . . . . . . . . . . . . 386,200 446,428 402,843 391,258 136,686 127,852Other cities . . . . . . . . . . . . . . . 96,805 105,624 166,835 178,574 49,936 53,038Subtotal. . . . . . . . . . . . . . . . . . 483,005 552,052 569,678 569,832 186,622 180,890

Hong KongPresented in HK$ thousands . . . . 122,755 135,120 136,650 155,993 39,268 39,121Presented in RMB thousands . . . 108,172 116,973(3) 118,298 129,599(4) 33,244 31,715(5)

Total sales (RMB thousands) . . . . . 591,177 669,025 687,976 699,431 219,866 212,605Daily average revenue per

comparable restaurantChina (RMB)

Shanghai . . . . . . . . . . . . . . . . . 88,174 101,924 100,334 97,449 101,249 93,664Other cities . . . . . . . . . . . . . . . 66,305 72,345 57,135 61,155 55,484 58,284National . . . . . . . . . . . . . . . . . 82,706 94,529 82,145 82,168 82,943 79,512

Hong KongPresented in HK$ . . . . . . . . . . . 67,263 74,038 74,877 85,476 87,262 85,980Presented in RMB. . . . . . . . . . . 59,272 64,095 64,821 71,013 73,876 69,703

Total daily average revenue (RMB). 77,127 87,283 78,536 79,844 81,432 77,877Increase/(decrease) of comparable

restaurants sales duringcomparable periodsChina

Shanghai . . . . . . . . . . . . . . . . . 15.6% (2.9)% (6.5)%Other cities . . . . . . . . . . . . . . . 9.1% 7.0% 6.2%National . . . . . . . . . . . . . . . . . 14.3% 0.0% (3.1)%

Hong KongPresented in HK$ . . . . . . . . . . . 10.1% 14.2% (0.4)%Presented in RMB. . . . . . . . . . . 8.1% 9.6% (4.6)%

Total increase/(decrease) . . . . . . . . 13.2% 1.7% (3.3)%

Mai

son

De

L’H

ui Number of comparable restaurants(6) . — — — — 2 2

Comparable restaurant sales(RMB thousands) . . . . . . . . . . . . . — — — — 6,482 8,868

Daily average revenue per comparablerestaurants (RMB) . . . . . . . . . . . . — — — — 36,011 48,725

Increase of comparable restaurantsales during comparable periods . . . — — 36.8%

Tot

al

Total comparable restaurant sales(RMB thousands) . . . . . . . . . . . . . 591,177 669,025 687,976 699,431 226,348 221,473

Total increase/(decrease) ofcomparable restaurant sales duringcomparable periods. . . . . . . . . . . . 13.2% 1.7% (2.2)%

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 8 —

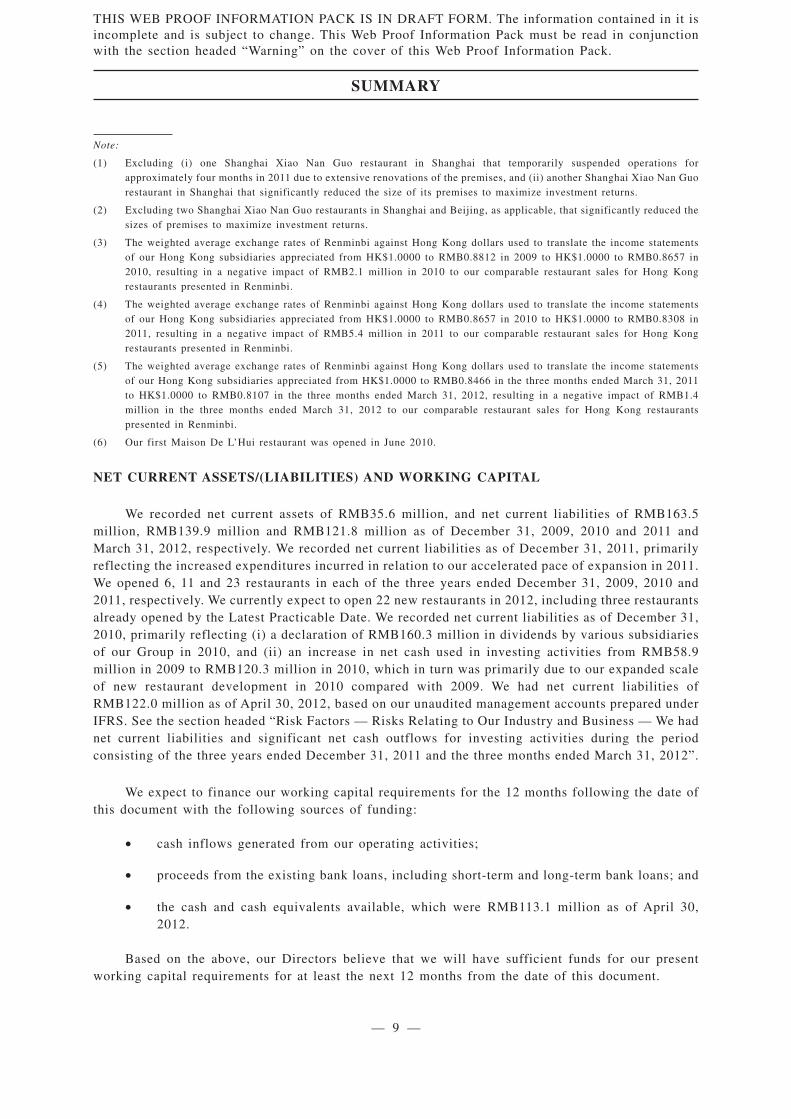

Note:

(1) Excluding (i) one Shanghai Xiao Nan Guo restaurant in Shanghai that temporarily suspended operations forapproximately four months in 2011 due to extensive renovations of the premises, and (ii) another Shanghai Xiao Nan Guorestaurant in Shanghai that significantly reduced the size of its premises to maximize investment returns.

(2) Excluding two Shanghai Xiao Nan Guo restaurants in Shanghai and Beijing, as applicable, that significantly reduced thesizes of premises to maximize investment returns.

(3) The weighted average exchange rates of Renminbi against Hong Kong dollars used to translate the income statementsof our Hong Kong subsidiaries appreciated from HK$1.0000 to RMB0.8812 in 2009 to HK$1.0000 to RMB0.8657 in2010, resulting in a negative impact of RMB2.1 million in 2010 to our comparable restaurant sales for Hong Kongrestaurants presented in Renminbi.

(4) The weighted average exchange rates of Renminbi against Hong Kong dollars used to translate the income statementsof our Hong Kong subsidiaries appreciated from HK$1.0000 to RMB0.8657 in 2010 to HK$1.0000 to RMB0.8308 in2011, resulting in a negative impact of RMB5.4 million in 2011 to our comparable restaurant sales for Hong Kongrestaurants presented in Renminbi.

(5) The weighted average exchange rates of Renminbi against Hong Kong dollars used to translate the income statementsof our Hong Kong subsidiaries appreciated from HK$1.0000 to RMB0.8466 in the three months ended March 31, 2011to HK$1.0000 to RMB0.8107 in the three months ended March 31, 2012, resulting in a negative impact of RMB1.4million in the three months ended March 31, 2012 to our comparable restaurant sales for Hong Kong restaurantspresented in Renminbi.

(6) Our first Maison De L’Hui restaurant was opened in June 2010.

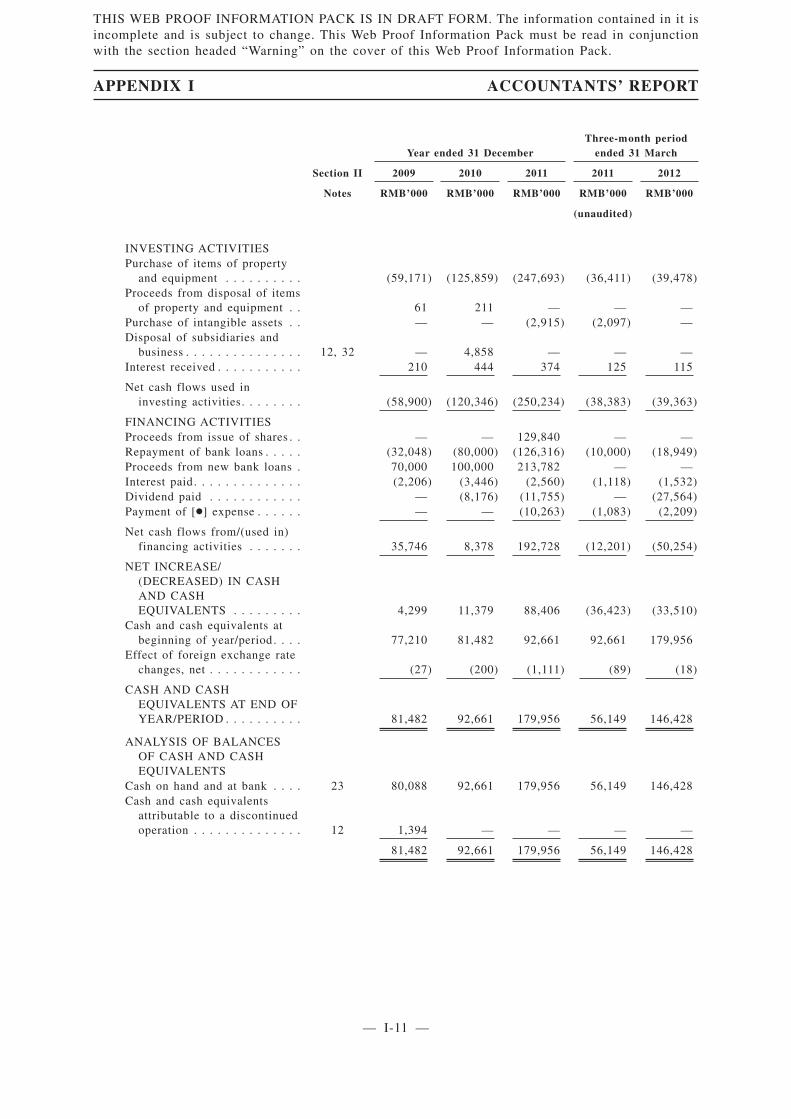

NET CURRENT ASSETS/(LIABILITIES) AND WORKING CAPITAL

We recorded net current assets of RMB35.6 million, and net current liabilities of RMB163.5million, RMB139.9 million and RMB121.8 million as of December 31, 2009, 2010 and 2011 andMarch 31, 2012, respectively. We recorded net current liabilities as of December 31, 2011, primarilyreflecting the increased expenditures incurred in relation to our accelerated pace of expansion in 2011.We opened 6, 11 and 23 restaurants in each of the three years ended December 31, 2009, 2010 and2011, respectively. We currently expect to open 22 new restaurants in 2012, including three restaurantsalready opened by the Latest Practicable Date. We recorded net current liabilities as of December 31,2010, primarily reflecting (i) a declaration of RMB160.3 million in dividends by various subsidiariesof our Group in 2010, and (ii) an increase in net cash used in investing activities from RMB58.9million in 2009 to RMB120.3 million in 2010, which in turn was primarily due to our expanded scaleof new restaurant development in 2010 compared with 2009. We had net current liabilities ofRMB122.0 million as of April 30, 2012, based on our unaudited management accounts prepared underIFRS. See the section headed “Risk Factors — Risks Relating to Our Industry and Business — We hadnet current liabilities and significant net cash outflows for investing activities during the periodconsisting of the three years ended December 31, 2011 and the three months ended March 31, 2012”.

We expect to finance our working capital requirements for the 12 months following the date ofthis document with the following sources of funding:

• cash inflows generated from our operating activities;

• proceeds from the existing bank loans, including short-term and long-term bank loans; and

• the cash and cash equivalents available, which were RMB113.1 million as of April 30,2012.

Based on the above, our Directors believe that we will have sufficient funds for our presentworking capital requirements for at least the next 12 months from the date of this document.

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 9 —

DIVIDEND POLICY

Our Directors currently intend to declare in 2013 a dividend of about 30% of our annual netprofit after tax attributable to owners of our Company in respect of the year ending December 31,2012. Such intention does not amount to any guarantee, representation or indication that the Companymust or will declare and pay dividends in such manner or at all. The amount of dividend to be declaredby our Directors in the future beyond 2013 will depend upon (i) our overall results of operation, (ii)our financial position, (iii) our capital requirements, (iv) our shareholders’ interests, (v) our futureprospect, and (vi) other factors that our Directors deem relevant. See “Risk factors — Risks Relatingto Our Industry and Business — Our historical dividend may not be indicative of our future dividends,and our ability to pay dividends and dispose of assets may be limited by contractual restrictions underour credit facilities” of this document. For more details, please see the section headed “FinancialInformation — Dividends and Dividend Policy” of this document.

Major Market Trends and Recent Development

The mid- to high-end Chinese cuisine FSR chains in China is a rapidly growing segment, withan expanding customer base who are increasingly conscious about food safety and quality, cuisineflavor, ambience and brand image of a restaurant. We believe that as a leader among industry peersin developing and implementing standardized operations under modern corporate managementprinciples, we are well-positioned for significant growth.

We opened 6, 11 and 23 restaurants in 2009, 2010 and 2011, respectively. We currently plan toopen a total of approximately 22 restaurants in 2012, including 20 restaurants under the Shanghai XiaoNan Guo brand and two restaurants under “the dining room” brand. Among the 22 new restaurantsplanned to be opened in 2012, we have already opened two Shanghai Xiao Nan Guo restaurants andone “the dining room” restaurant by the Latest Practicable Date, and have entered into letters of intentor binding leases for the sites of another 11 restaurants. We currently expect our total planned capitalexpenditure for 2012 to be approximately RMB298.0 million. Our capital expenditure for the threemonths ended March 31, 2012 amounted to RMB10.6 million. From March 31, 2012 up to April 30,2012, the capital expenditure we incurred amounted to RMB4.0 million. Our contracted but notprovided for capital commitments were RMB42.1 million as of April 30, 2012, which related to capitalcommitments for five new restaurants planned to be opened in 2012 in Shanghai, Nanjing, Wuxi andHong Kong. Considering the cash inflows generated from our operating activities, proceeds from theexisting bank loans, the cash and cash equivalents available, our Directors believe that the Companywill have sufficient funds for our current expansion plan in 2012.

Our revenue from restaurant operations increased by RMB 85.6 million, or 35.0%, fromRMB244.8 million in the three months ended on March 31, 2011 to RMB 330.4 million in the threemonths ended on March 31, 2012. Our profit increased by RMB 9.6 million, or 50.8%, from RMB 18.9million in the three months ended on March 31, 2011 to RMB 28.5 million in the three months endedon March 31, 2012. Our net profit margin increased from 7.6% in the three months ended on March31, 2011 to 8.5% in the three months ended on March 31, 2012. Our Directors preliminarily estimatethat revenue from our restaurant operations in the month ended on April 30, 2012 is expected to recordan increase from revenue from our restaurant operations in the month ended on April 30, 2011,primarily reflecting our expanded restaurant network. Although our cost of inventories consumed inApril 2012 is expected to increase from that in April 2011, our gross profit margin in April 2012 isalso expected to increase from that in April in 2011. In addition, our profit and net profit margin inApril 2012 are expected to increase from those in April 2011. Our total comparable restaurant salesand daily average revenue per comparable restaurant in the four months ended April 30, 2012

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 10 —

compared with those in the four months ended April 30, 2011 are expected to follow the same trend

of our total comparable restaurant sales and daily average revenue per comparable restaurant in the

three months ended March 31, 2012 compared with those in the three months ended March 31, 2011.

Our actual results may differ materially from these estimates. We cannot assure you that our business,

financial condition, results of operation and prospects will continue to grow or improve for the

remainder of 2012 or beyond. Please see the section headed “Risk Factors — Risks Relating to our

Industry and Business — Our historical financial and operating results may not be indicative of future

performance, and we may not be able to achieve and sustain the historical level of revenue and

profitability” in this document.

Our Directors confirm that except as described in the section headed “Financial Information —

Indebtedness” in this document, there has been no material adverse change in our financial or trading

position or our prospects since March 31, 2012 and up to the date of this document.

RISK FACTORS

We believe that there are certain risks involved in our operations, many of which are beyond our

control. These risks are set forth in the section headed “Risk Factors” section and are summarized

below.

We believe that the following are some of the major risks that may materially and adversely

affect us.

• Any significant liability claims or complaints from our customers or adverse publicity

involving our products or services could adversely affect our business and operations

• We face risks related to instances of food-borne illnesses, health epidemics and other

outbreaks

• Our operations are susceptible to increases in our purchase costs of food ingredients, which

could adversely affect our margins and results of operations

• Labor shortages or increases in labor costs could slow our growth, harm our business and

reduce our profitability

• Our restaurants are subject to risks in relation to occupancy costs, renewal of existing

leases and long-term non-terminable leases

• We had net current liabilities and significant net cash outflows from investing activities

during the period consisting of the three years ended December 31, 2011 and the three

months ended March 31, 2012

SUMMARY

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 11 —

Unless the context otherwise requires, the following expressions have the following meaningsin this document.

“Affluent Harvest” Affluent Harvest Limited, a company incorporated in theBVI on October 26, 2011 and wholly-owned by ourCompany

“Apex Keen” Apex Keen Limited (鼎建有限公司), a companyincorporated in the BVI on December 13, 2011 andwholly-owned by Mr. He Jianxing

“Articles of Association” or “Articles” our articles of association, as adopted on February 2,2010, and as amended from time to time, a summary ofwhich is contained in Appendix IV to this document

“Audit Committee” the audit committee of the Board

“Beijing Shining” Beijing Shining Cuisine Investment Management Co.,Ltd. (北京尚心尚食投資管理有限公司), a companyincorporated in the PRC on October 22, 2009 as aninvestment company and is a fellow subsidiary ofSunshine Property under the common control of ShiningCapital Holdings L.P. in the PRC

“Board of Directors” or “Board” our board of Directors

“Brilliant South” Brilliant South Limited (佳南有限公司), a companyincorporated in the BVI on November 8, 2010 andwholly-owned by Ms. Wu Wen, one of our executiveDirectors

“Business Day” a day (other than a Saturday or a Sunday) on which banksin Hong Kong are generally open for normal bankingbusiness

“BVI” the British Virgin Islands

“CAGR” compound annual growth rate

“China” or “PRC” the People’s Republic of China, which for the purpose ofthis document and for geographical reference only,excludes Hong Kong, Macau and Taiwan

“China Wealth” China Wealth Enterprises Ltd., an exempted companyincorporated in the BVI on May 28, 2008 and aconnected person upon completion of the [●]Reorganization with its shareholding structure before andafter the [●] Reorganization set out under the sectionheaded “History and Development — [●]Reorganization”

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 12 —

“Companies Law” the Companies Law, Cap 22 (Law 3 of 1961, asconsolidated and revised) of the Cayman Islands

“Companies Ordinance” the Companies Ordinance (Chapter 32 of the Laws ofHong Kong), as amended, supplemented or otherwisemodified from time to time

“Company”, or “our Company” Xiao Nan Guo Restaurants Holdings Limited (小南國餐飲控股有限公司), previously known as Xiao Nan Guo(Cayman) Holdings Ltd., an exempted companyincorporated under the laws of the Cayman Islands onFebruary 2, 2010 with limited liability

“Company Law” or “PRC CompanyLaw”

Company Law of the People’s Republic of China(中華人民共和國公司法), as amended at the EighteenthSession of the Standing Committee of the Tenth NPC onOctober 27, 2005, effective from January 1, 2006 (2005Amendment), and as amended, supplemented orotherwise modified from time to time

“connected person(s)” has the meaning ascribed thereto under certain rules andregulations

“Controlling Shareholders” has the meaning ascribed thereto under the [●] and, in thecontext of this document, means the controllingshareholders of our Company, being Ms. Wang, theTrustee, Value Boost, Expert City, Fast Thinker, FastGlow, Full Health and Well Reach, and each a“Controlling Shareholder”. See the section headed“Relationship with Controlling Shareholders”

“Core Strength” Core Strength Limited, a company incorporated in theBVI on February 2, 2010 and wholly-owned by Ms.Wang, one of our executive Directors

“CSI Capital, L.P.” an exempted limited partnership registered under thelaws of Cayman Islands on March 31, 2009 and a privateequity fund focusing on private equity investments inChina with limited partners mainly comprising ofinstitutional investors

“Director(s)” the director(s) of the Company or any one of them

“EFG Atlantis” EFG Atlantis China [●] Master Fund L.P., a companyincorporated in the Cayman Islands on February 21, 2011

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 13 —

“Elite Land” Elite Land Development Limited, a companyincorporated in the BVI on April 28, 1999 and owned asto 50% by Mr. Cheung Yik Man, an Independent ThirdParty and 50% by Ms. Wang Zhongying, an IndependentThird Party

“Employee Trust” an employee trust established by our Company onDecember 30, 2011. See the section headed “FurtherInformation about Directors, Management and Staff —Summary of Terms of the Employee Trust” in AppendixV to this document

“Euromonitor Report” a commissioned report prepared by EuromonitorInternational, a global research organization, for thepurpose of preparing this document

“Ever Project” Ever Project Investments Limited (恒業投資有限公司), acompany incorporated in the BVI on November 26, 2010and wholly-owned by Ms. Wang Huili, one of ournon-executive Directors

“Excluded Businesses” other than our Group, businesses which Ms. Wang hascontrol of or interests in, details of which are set out inthe section headed “Relationship with ControllingShareholders — Excluded Businesses of Ms. Wang”

“Expert City” Expert City International Limited (巧城國際有限公司), acompany incorporated in the BVI on November 26, 2010,which is legally owned by Ms. Wang and beneficiallyowned by Apex Keen

“Fast Glow” Fast Glow Limited (迅暉有限公司), a companyincorporated in the BVI on October 18, 2010, which islegally owned by Ms. Wang and beneficially owned byVictor Merit

“Fast Thinker” Fast Thinker Limited (俊捷有限公司), a companyincorporated in the BVI on May 11, 2012, which islegally owned by Ms. Wang and beneficially owned byEver Project

“Full Health” Full Health Limited (康富有限公司), a companyincorporated in the BVI on October 15, 2010, which islegally owned by Ms. Wang and beneficially owned byWealth Boom

“GDP” gross domestic product

“Greater China” China, including Hong Kong, Macau and Taiwan

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 14 —

“Group”, “our Group”, “we”, “our” or“us”

the Company and its subsidiaries or, where the context sorequires, with respect to the period before which theCompany became the holding company of its currentsubsidiaries, the Company’s current subsidiaries or thebusinesses operated by such subsidiaries or theirpredecessors (as the case may be)

“Hang Lik” Hang Lik International Development Ltd. (恆力國際發展有限公司), a company incorporated in Hong Kong onNovember 12, 2003 and wholly-owned by Ms. Wang’sdaughter

“HIBOR” Hong Kong Interbank Offer Rate

“HK$” or “Hong Kong dollars” Hong Kong dollars and cents, respectively, the lawfulcurrency of Hong Kong

“Hong Kong” the Hong Kong Special Administrative Region of thePRC

“Independent Third Party” a party which is not connected (as defined in certain rulesand regulations) to our Company or our connectedpersons

“Latest Practicable Date” June 12, 2012, being the latest practicable date prior tothe printing of this document for the purpose ofascertaining certain information contained in thisdocument

“Macau” the Macau Special Administrative Region of the PRC

“Memorandum of Association” or“Memorandum”

the memorandum of association of our Company (asamended from time to time), a summary of which is setout in “Appendix IV — Summary of the Constitution ofthe Company and Cayman Islands Company Law” to thisdocument

“Ministry of Commerce” or “MOC” the Ministry of Commerce of the People’s Republic ofChina (中華人民共和國商務部)

“Moon Glory” Moon Glory Enterprises Limited, a companyincorporated in the BVI on March 31, 2010 andwholly-owned by CSI Capital, L.P.

“Ms. Wang” Ms. Wang Huimin, our founder, the chairlady, aControlling Shareholder and an executive Director

“Nan Feng” Nan Feng International Holdings Limited, a companyincorporated in the BVI on July 2, 2003 andwholly-owned by Ms. Wang

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 15 —

“New EIT Law” the Enterprise Income Tax Law promulgated by theNational People’s Congress on March 16, 2007 andbecame effective on January 1, 2008

“PBOC” the People’s Bank of China (中國人民銀行), the centralbank of the PRC

“Preferred Shares” Series A Preferred Shares, Series B Preferred Shares andSeries C Preferred Shares

“[●] Investors” Moon Glory, Sunshine Property and EFG Atlantis, andeach a “[●] Investor”

“[●] Share Option Schemes” and each a“[●] Share Option Scheme”

the [●] share option schemes adopted by the Company onFebruary 10, 2010 and March 15, 2011 (amended onAugust 10, 2011), respectively, the principal terms ofwhich are summarized in the section headed “Statutoryand General Information — Share Option Schemes —Summary of Terms of the [●] Share Option Schemes” inAppendix V to this document

“[●] Reorganization” the reorganization arrangements undertaken by ourGroup in preparation for the [●], which are described inmore detail in the sections headed “History andDevelopment — [●] Reorganization” and “Statutory andGeneral Information — Further Information about OurCompany — Reorganization” in Appendix V to thisdocument

“Province” or “province” each being a province or, where the context requires, aprovincial level autonomous region or a provincial-levelcity under the direct supervision of the centralgovernment of the PRC

“RMB” Renminbi, the lawful currency of the PRC

“SAFE” the State Administration for Foreign Exchange of thePRC (中華人民共和國國家外匯管理局)

“SAIC” the State Administration of Industry and Commerce ofthe PRC (中華人民共和國國家工商行政管理總局)

“Series A Offshore Investment” the investment in our Group made by Sunshine Propertyunder a series of agreements in 2008 and 2009, details ofwhich are set out under the section headed “History andDevelopment — [●] Investments — Series A OffshoreInvestment and Series A Onshore Investment”

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 16 —

“Series A Onshore Investment” the investment in our Group made by Lao NiuDevelopment Investment Co., Ltd. (老牛創業投資發展有限公司) and Beijing Shining under a series of agreementsin 2008 and 2009, details of which are set out under thesection headed “History and Development — [●]Investments — Series A Offshore Investment and SeriesA Onshore Investment”

“Series A Preferred Shares” series A redeemable convertible preferred shares, with apar value of US$0.01 per share, of China Wealth, withthe terms set forth in the Series B Investment Agreementand the amended and restated memorandum and articlesof association of China Wealth

“Series B Investment” the investment in our Group made by the Series B [●]Investors under a series of investment agreements in2010, details of which are set out under the sectionheaded “History and Development — [●] Investments —Series B Investment by the Series B [●] Investors”

“Series B Investment Agreement” the investment agreement dated June 29, 2010, enteredinto among Ms. Wang, Core Strength, China Wealth andthe Series B [●] Investors, details of which are set outunder the section headed “History and Development —[●] Investments — Series B Investment by the Series B[●] Investors”

“Series B Preferred Shares” Series B redeemable convertible preferred shares, parvalue US$0.01 per share, of China Wealth, with the termsset forth in the Series B Investment Agreement and theamended and restated memorandum and articles ofassociation of China Wealth

“Series B [●] Investors” Moon Glory and Sunshine Property under Series BInvestment, and each a “Series B [●] Investor”

“Series B Shareholders’ Agreement” an agreement dated September 3, 2010, entered intoamong the parties to the Series B Investment Agreementrelating to their rights and obligations, details of whichare set out under the section headed “History andDevelopment — [●] Investments — Series B Investmentby the Series B [●] Investors”

“Series B Supplemental Agreement” the supplemental agreement dated August 26, 2011entered into among the parties to the Series B InvestmentAgreement

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 17 —

“Series C Investment” the investment in our Group made by the Series C [●]Investors under the Series C Investment Agreement,details of which are set out under the section headed“History and Development — [●] Investments — SeriesC Investment”

“Series C Investment Agreement” the investment agreement dated November 8, 2011,entered into among Ms. Wang, Value Boost, ChinaWealth, Sunshine Property and EFG Atlantis, details ofwhich are set out under the section headed “History andDevelopment — [●] Investments — Series C Investment”

“Series C Preferred Shares” Series C redeemable convertible preferred shares, parvalue US$0.01 per share, of China Wealth, with the termsset forth in the Series C Investment Agreement and theamended and restated memorandum and articles ofassociation of China Wealth

“Series C [●] Investors” Sunshine Property and EFG Atlantis under Series CInvestment, and each a “Series C [●] Investor”

“Series C Shareholders’ Agreement” an agreement dated November 17, 2011, entered intoamong the parties to the Series C Investment Agreementand Moon Glory relating to their rights and obligations,details of which are set out under the section headed“History and Development — [●]Investments — Series CInvestment”

“Series C Supplemental Agreement” the supplemental agreement dated June 8, 2012 andentered into among the parties to the Series CShareholders’ Agreement

“Shanghai Hongqiao” Shanghai Hongqiao Xiao Nan Guo RestaurantsManagement Co., Ltd. (上海虹橋小南國餐飲管理有限公司), a company incorporated in the PRC on January 7,1999 and owned as to 99% by Ms. Wang and as to 1% byMs. Wang Huili, one of our non-executive Directors

“Shanghai Rongyi” Shanghai Rongyi Commercial Development Ltd.(上海融怡商貿發展有限公司), a company incorporatedin the PRC November 17, 2003 and wholly-owned by Ms.Wang

“Shanghai Xiao Nan Guo Group” Xiao Nan Guo (Group) Company Ltd. (小南國(集團)有限公司), previously known as Shanghai Xiao Nan GuoHotel Management Co., Ltd. (上海小南國酒店管理有限公司), a limited liability company incorporated in thePRC on December 2, 2003 and indirectly wholly-ownedby Ms. Wang

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 18 —

“Shanghai Xiao Nan Guo Restaurant” Shanghai Xiao Nan Guo Restaurant Co., Ltd.,(上海小南國餐飲有限公司), a company incorporated inthe PRC on April 5, 2002 and wholly-owned by Xiao NanGuo WFOE

“Shanghai Xin Di” Shanghai Xin Di Restaurant Co., Ltd. (上海鑫迪餐飲有限公司), a limited liability company incorporated in thePRC on August 27, 2009 and indirectly wholly-owned byMs. Wang for operating a Chinese food take-away anddelivery business, Xiao Nan Guo Da Wei Lai

“Share(s)” ordinary share(s) of HK$0.01 each in the issued sharecapital of our Company

“Share Adjustment Agreement” the agreement dated May 11, 2011 entered into amongthe parties to the Series B Investment Agreement relatingto the share adjustment right disclosed in the sectionheaded “History and Development — [●] Investments —Principal Terms of the Series B [●] Investment —Exercise of the Series B Share Adjustment Right” in thisdocument

“Shareholder(s)” holder(s) of Shares

“Share Option Scheme” the share option scheme conditionally adopted by theCompany June 8 2012, the principal terms of which aresummarized in the section headed “Statutory and GeneralInformation — Share Option Schemes” in Appendix V tothis document

“Shining Capital Holdings L.P.” Shining Capital Holdings L.P., an exempted limitedpartnership registered under the laws of Cayman Islandson December 28, 2007, and a private equity fundfocusing on private equity investments with limitedpartners mainly comprising of international institutionalinvestors

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 19 —

“Spa Business” the businesses of spa services operated by (i) ShanghaiXiao Nan Guo Tang He Yuan SPAs ManagementCo., Ltd. (上海小南國湯河源沐浴管理有限公司), alimited liability company incorporated in the PRC, 55%of its equity interest being held by Ms. Wang and theremaining equity interest being held by IndependentThird Parties (“Tang He Yuan Spa”), (ii) ShanghaiPudong Xiao Nan Guo Casual Dining Management Co.,Ltd. (上海浦東小南國休閑美食管理有限公司), a limitedliability company incorporated in the PRC, 55% of itsequity interest being held by Ms. Wang and the remainingequity interest being held by Independent Third Parties(“Pudong Spa”), (iii) Shanghai Jing’an Hai Zhi YuanCasual Dining Management Co., Ltd. (上海靜安海之源休閑美食管理有限公司), a limited liability companyincorporated in the PRC, 100% of its equity interestbeing indirectly held by Ms. Wang (“Jing’an Spa”), (iv)Shanghai Wanli Hai Zhi Yuan Casual DiningManagement Co., Ltd. (上海萬里海之源休閒美食管理有限公司), a limited company incorporated in the PRC,55% of its equity interest being held by Ms. Wang andthe remaining equity interest being held by anIndependent Third Party (“Wanli Spa”), and

(v) Shanghai Yuan Zhi Yuan Co., Ltd. (上海源之圓美容有限公司), a limited company incorporated in the PRC,55% of its equity interest being indirectly held by Ms.Wang and the remaining equity interest being held by anIndependent Third Party (“Yuan Zhi Yuan Spa”),respectively

“sq.m.” square meter

“Standard Chartered Offshore Facility” a term loan facility entered into between our Companyand Standard Chartered Bank (Hong Kong) Limited, anaffiliate of [●], in May 2011. See “Financial Information— Indebtedness — Bank Borrowings”

“Standard Chartered OnshoreFacilities”

the senior credit facilities entered into between ourCompany and Standard Chartered Bank (China) Limited,in March 2011. See “Financial Information —Indebtedness — Bank Borrowings”

“State”, “state”, “PRC government” or“government”

the government of the PRC including all politicalsubdivisions (including provincial, municipal and otherregional or local government entities) and theirinstrumentalities thereof or, where the context requires,any of them

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 20 —

“Sunshine Property” Sunshine Property I Limited, a company incorporatedunder the laws of the Cayman Islands on December 7,2007 and wholly-owned by Shining Capital HoldingsL.P.

“The Wang Trust” a declaration of trust established by Ms. Wang on August27, 2011, the current beneficiary of which is Ms. Wangand in the event of her decease, her personalrepresentative(s)

“Trustee” Extensive Power Limited, a company incorporated inHong Kong on November 8, 2010, and the current trusteeof The Wang Trust, which is legally and beneficiallywholly-owned by Ms. Wang, and of which Ms. Wang isthe sole director

“United States” or “U.S.” the United States

“US$” or “U.S. dollars” United States dollars, the lawful currency of the UnitedStates

“Value Boost” Value Boost Limited, a company incorporated in the BVIon April 6, 2011 and wholly-owned by the Trustee

“Victor Merit” Victor Merit Limited, a company incorporated in the BVIon November 8, 2010 and wholly-owned by Mr. KangJie, one of our executive Directors

“Wealth Boom” Wealth Boom Enterprises Limited (富旺企業有限公司), acompany incorporated in the BVI on September 16, 2010and wholly-owned by Mr. Wang Hairong, the brother ofMs. Wang

“Well Reach” Well Reach Limited (佳達有限公司), a companyincorporated in the BVI on October 8, 2010, which islegally owned by Ms. Wang and beneficially owned byBrilliant South

“Wisecorp” Wisecorp Worldwide Development Limited (協和環球發展有限公司), a company incorporated in Hong Kong onNovember 24, 2004 and wholly-owned by Xiao Nan GuoHK R

“Xiao Nan Guo Da Wei Lai” the Chinese food take-away and delivery businessoperated by Shanghai Xin Di. See “Relationship withControlling Shareholders — Excluded Businesses of Ms.Wang”

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 21 —

“Xiao Nan Guo HK R” Xiao Nan Guo (Hong Kong) Restaurant GroupLimited (小南國(香港)餐飲集團有限公司), a companyincorporated in the BVI on April 16, 2008 and currentlywholly-owned by the Company

“Xiao Nan Guo Holdings BVI” Xiao Nan Guo Holdings Limited, a companyincorporated in the BVI on July 2, 2003 and currentlywholly-owned by the Company

“Xiao Nan Guo Holdings HK” Xiao Nan Guo Holdings Limited (小南國控股有限公司),a company incorporated in Hong Kong on April 7, 2005and currently wholly-owned by Xiao Nan Guo HoldingsBVI

“Xiao Nan Guo Nutritional” Shanghai Xiao Nan Guo Nutritional Food Co., Ltd. (上海小南國營養餐食品有限公司), a company formerlyknown as Shanghai Kangdian Nutritional Food Co., Ltd.(上海康點營養餐食品有限公司) and incorporated in thePRC on March 9, 2006, which was wholly acquired by uson February 29, 2008 from Independent Third Parties

“Xiao Nan Guo WFOE” Shanghai Xiao Nan Guo Hai Zhi Yuan RestaurantManagement Co., Ltd. (上海小南國海之源餐飲管理有限公司), a company formerly known as Shanghai Xiao NanGuo Hai Zhi Yuan Gym Co., Ltd. (上海小南國海之源健身有限公司), a wholly foreign-owned enterpriseincorporated in Shanghai under the laws of the People’sRepublic of China on September 15, 2004

“%” per cent.

All times refer to Hong Kong time.

Unless otherwise specified, references to years in this document are to calendar years.

If there is any inconsistency between the Chinese name of the PRC laws and regulations or PRC

entities mentioned in this document and their English translation, the Chinese version shall prevail.

Translated English names of Chinese natural persons, legal persons, governmental authorities,

institutions or other entities for which no official English translation exist are unofficial translations

for identification purposes only.

Any discrepancies in any table between totals and sums of amounts listed therein are due to

rounding.

Unless otherwise specified, discussions on and disclosure of financial data under the

consolidated statements of comprehensive income are in relation to continuing operations.

DEFINITIONS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 22 —

This document contains forward-looking statements that are, by their nature, subject tosignificant risks and uncertainties, including the risk factors described in this document.Forward-looking statements can be identified by words such as “may,” “will,” “should,” “would,”“could,” “believe,” “expect,” “anticipate,” “intend,” “plan,” “continue,” “seek,” “estimate” or thenegative of these terms or other comparable terminology. Examples of forward-looking statementsinclude, but are not limited to, statements we make regarding our projections, business strategy anddevelopment activities as well as other capital spending, financing sources, the effects of regulation,expectations concerning future operations, margins, profitability and competition. The foregoing isnot an exclusive list of all forward-looking statements we make.

Forward-looking statements are based on our current expectations and assumptions regarding ourbusiness, the economy and other future conditions. We give no assurance that these expectations andassumptions will prove to have been correct. Because forward-looking statements relate to the future,they are subject to inherent uncertainties, risks and changes in circumstances that are difficult topredict. Our results may differ materially from those contemplated by the forward-looking statements.They are neither statements of historical fact nor guarantees or assurances of future performance. Wecaution you therefore against placing undue reliance on any of these forward-looking statements.Important factors that could cause actual results to differ materially from those in the forward-lookingstatements include, but not limited to, regional, national or global political economic, business,competitive, market and regulatory conditions and the following:

• success of our existing and new restaurants;

• our ability to effectively manage our planned expansion;

• our ability to stay abreast of market trends and maintain commercially reasonablerelationships with our customers and suppliers;

• our ability to retain core team members and recruit qualified and experienced new teammembers;

• our ability to obtain adequate financing on terms acceptable to us;

• our ability to maintain an effective quality control system;

• our ability to maintain our current preferential tax treatment status under Chinese law;

• our levels of indebtedness and interest payment obligations;

• rules and regulations for the restaurant industry imposed by the PRC government;

• future developments, trends and conditions in China’s restaurant industry;

• other prospective financial information; and

• the other factors that are described in the section headed “Risk Factors” in this document.

Any forward-looking statement made by us in this document speaks only as of the date on whichit is made. Factors or events that could cause our actual results to differ may emerge from time to time,and it is not possible for us to predict all of them. Subject to the requirements of applicable laws, rulesand regulations, we undertake no obligation to update any forward-looking statement, whether as aresult of new information, future developments or otherwise. All forward-looking statementscontained in this document are qualified by reference to this cautionary statement.

FORWARD-LOOKING STATEMENTS

THIS WEB PROOF INFORMATION PACK IS IN DRAFT FORM. The information contained in it isincomplete and is subject to change. This Web Proof Information Pack must be read in conjunctionwith the section headed “Warning” on the cover of this Web Proof Information Pack.

— 23 —