Yuxing InfoTech Holdings Limited ( )* - :: HKEX :: HKEXnews ::

Upload

khangminh22Category

view

0download

0

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

* For identification purposes only

If you are in doubt as to any aspect of the Mexan Offer, you should consult a licensed securities dealer or registeredinstitution in securities, bank manager, solicitor, professional accountant or other professional adviser.

If you have sold or transferred all your shares in MEXAN LIMITED, you should at once hand this Composite OfferDocument and the accompanying Form of Acceptance and Transfer to the purchaser or the transferee, or to the licensedsecurities dealer or registered institution in securities or other agent through whom the sale or the transfer was effected fortransmission to the purchaser or the transferee. This Composite Offer Document should be read in conjunction with theaccompanying Form of Acceptance and Transfer, the provisions of which form part of the terms of the Mexan Offercontained herein.

The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this Composite Offer Document,makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any losshowsoever arising from or in reliance upon the whole or any part of the contents of this Composite Offer Document.

WINLAND WEALTH (BVI) LIMITED M E X A N L I M I T E D(Incorporated in the British Virgin Islands with limited liability) *

(Incorporated in Bermuda with limited liability)(Stock Code: 22)

MANDATORY UNCONDITIONAL CASH OFFER BYBOCI ASIA LIMITED

ON BEHALF OFWINLAND WEALTH (BVI) LIMITED

TO ACQUIRE ALL THE ISSUED SHARES IN MEXAN LIMITED(OTHER THAN THOSE ALREADY OWNED

BY WINLAND WEALTH (BVI) LIMITEDAND PARTIES ACTING IN CONCERT WITH IT)

Financial adviser to Winland Wealth (BVI) Limited

BOCI Asia Limited

Independent financial adviser tothe Independent Board Committee of MEXAN LIMITED

A letter from the Independent Board Committee to the Independent Shareholders in respect of the Mexan Offer is set outon page 17 of this Composite Offer Document. A letter from Hercules containing its advice to the Independent BoardCommittee in the same regard is set out on pages 18 to 34 of this Composite Offer Document.

The procedures for acceptance and settlement of the Mexan Offer are set out on pages 35 to 40 in Appendix I to thisComposite Offer Document and in the accompanying Form of Acceptance and Transfer. Acceptance of the Mexan Offershould be received by the Company’s Hong Kong branch share registrar, Tengis Limited at 26th Floor, Tesbury Centre, 28Queen’s Road East, Wanchai, Hong Kong by no later than 4:00 p.m. on Monday, 7 May 2007.

16 April 2007

CONTENTS

– i –

Page

Expected timetable ....................................................................................................................... ii

Definitions ...................................................................................................................................... 1

Letter from the Board .................................................................................................................. 6

Letter from BOCI ......................................................................................................................... 9

Letter from the Independent Board Committee ...................................................................... 17

Letter from Hercules .................................................................................................................... 18

Appendix I — Further terms and procedures for acceptanceof the Mexan Offer ................................................................................ 35

Appendix II — Financial information on the Group ....................................................... 41

Appendix III — Pro forma financial informationon the Remaining Group ...................................................................... 113

Appendix IV — Property valuation ..................................................................................... 124

Appendix V — General information .................................................................................. 130

EXPECTED TIMETABLE

– ii –

2007

Opening date of the Mexan Offer ...............................................................................Monday, 16 April

Latest time and date for acceptance of the Mexan Offer (Note 1) ......... 4:00 p.m. on Monday, 7 May

Closing Date of the Mexan Offer (Note 2) .................................................................... Monday, 7 May

Announcement of the results of the Mexan Offer postedon the Stock Exchange’s website ................................................... By 7:00 p.m. on Monday, 7 May

Announcement of the results of the Mexan Offerpublished in the newspapers ...................................................................................... Tuesday, 8 May

Latest date for posting of remittances for the amountsdue in respect of valid acceptances receivedunder the Mexan Offer (Note 2) ............................................................................ Thursday, 17 May

Notes:

1. The Mexan Offer, which is unconditional, will be closed at 4:00 p.m. on Monday, 7 May 2007. The Offeror doesnot intend to revise the terms, or extend the period, of the Mexan Offer, and does not reserve the right to do so. Anannouncement in respect of the results of the Mexan Offer will be issued through the Stock Exchange’s website by7:00 p.m. on Monday, 7 May 2007. Such announcement will be published in the newspapers on the next BusinessDay thereafter.

2. Remittances in respect of the cash consideration payable for the Offer Shares tendered under the Mexan Offer willbe posted to the relevant Shareholders by ordinary post at their own risk within 10 days from the date of receipt bythe Registrar of the requisite documents from the relevant Shareholder accepting the Mexan Offer which renderthe relevant acceptances under the Mexan Offer complete and valid.

3. Acceptance of the Mexan Offer shall be irrevocable and not capable of being withdrawn unless the Executiverequires that a right of withdrawal is granted in the event that the requirements of Rule 19 of the Takeovers Codehave not been complied with.

All time references contained in this Composite Offer Document refer to Hong Kong time.

DEFINITIONS

– 1 –

Unless the context requires otherwise, the following expressions shall have the following meanings inthis Composite Offer Document:

“acting in concert” the meaning defined in the Takeovers Code

“associates” the meaning defined in the Listing Rules

“Board” the board of Directors

“BOCI” BOCI Asia Limited, a corporation licensed under the SFO tocarry out Type 1 (dealing in securities) and Type 6 (advising oncorporate finance) regulated activities for the purposes of theSFO, and the financial adviser to the Offeror

“Business Day” a day on which banks are open for business generally in HongKong (excluding a Saturday or a Sunday)

“BVI” British Virgin Islands

“City Promenade” City Promenade Limited, a company incorporated in Hong Kongwith limited liability and a wholly-owned subsidiary of theCompany, which is the registered owner of the Properties andis principally engaged in the Remaining Business

“Circular” the circular of the Company dated 17 March 2007 relating to,among other things, the Proposal

“Company” MEXAN LIMITED, a company incorporated in Bermuda withlimited liability, the Shares of which are listed on the Main Boardof the Stock Exchange

“Completion” completion of the Share Sale Agreement

“Completion Date” 12 April 2007, being the date on which the Completion took place

“Composite Offer Document” this document being a document jointly issued by the Offerorand the Company to the Shareholders in accordance with theTakeovers Code containing, among other things, the terms andconditions of the Mexan Offer, the advice of Hercules to theIndependent Board Committee in respect of the Mexan Offer,and the advice of the Independent Board Committee to theIndependent Shareholders in relation to the Mexan Offer

“Consideration” the cash consideration of HK$102,917,303.93 paid by theOfferor to Mexan Group Limited for the acquisition of the SaleShares pursuant to the Share Sale Agreement

“Directors” the directors of the Company from time to time

DEFINITIONS

– 2 –

“Distributed Businesses” all businesses of the Group, other than the Remaining Business,carried on by the Inventive Group including the Group’s tollroad operation and management as well as investment holding

“Executive” the Executive Director of the Corporate Finance Division ofthe SFC and any delegate of the Executive Director

“Family Member(s)” immediate family member(s)

‘Form of Acceptance and Transfer” the accompanying form(s) of acceptance and transfer in respectof the Mexan Offer

“Group” the Company and its subsidiaries (immediately beforecompletion of the Group Reorganisation)

“Group Reorganisation” the reorganisation of the Group completed on 12 April 2007pursuant to which: (i) the Company continues to be a listedcompany and the Remaining Group carries on the RemainingBusiness; (ii) the Inventive Group carries on the DistributedBusinesses; and (iii) the Shareholders have received by way ofdistribution in specie the Inventive Shares on the basis of oneInventive Share for each Share held on the record date (i.e. 12April 2007)

“Hercules” Hercules Capital Limited, a corporation licensed under the SFOto carry out Type 6 (advising on corporate finance) regulatedactivity for the purposes of the SFO, and the independentfinancial adviser to the Independent Board Committee in respectof the Mexan Offer

“Hotel” Mexan Harbour Hotel located at Hotel 2, Rambler Crest, No. 1Tsing Yi Road, Tsing Yi, New Territories, Hong Kong

“Independent Board Committee” the independent board committee of the Company, comprisingall the three independent non-executive Directors, namely Mr.Chan Wai Dune, Mr. Lau Wai and Mr. Tong Kwai Lai establishedto advise the Independent Shareholders in respect of the MexanOffer

“Independent Shareholders” the Shareholders other than the Offeror and parties acting inconcert with it

“Inventive” INVENTIVE LIMITED, a company incorporated in Bermudawith limited liability

“Inventive Group” Inventive and its subsidiaries

DEFINITIONS

– 3 –

“Inventive Share(s)” ordinary share(s) of HK$0.10 each in the issued share capitalof Inventive

“Inventive Shareholders” holders of the Inventive Shares

“Joint Announcement” the joint announcement dated 16 February 2007 issued by theCompany, Mexan Group Limited, Inventive and the Offeror inrelation to, inter alia, the Mexan Offer

“Latest Practicable Date” 13 April 2007, being the latest practicable date prior to theprinting of this Composite Offer Document for ascertainingcertain information contained herein

“Last Trading Day” 2 January 2007, being the last day on which the Shares weretraded on the Stock Exchange prior to suspension of trading inthe Shares pending release of the Joint Announcement

“Listing Rules” the Rules Governing the Listing of Securities on the StockExchange

“Management Contract” as defined in the first paragraph under the section “Intention ofthe Offeror regarding the Remaining Group” in the “Letter fromBOCI” contained in the Composite Offer Document

“Mexan Offer” the mandatory unconditional cash offer by BOCI on behalf ofthe Offeror to acquire all the Shares (other than those alreadyowned by the Offeror and parties acting in concert with it) ex-entitlements to the distribution in specie of the Inventive Sharespursuant to the Group Reorganisation and the Special CashDividend

“Mr. Lau” Mr. Lau Kan Shan, the chairman of the Company and anexecutive Director as at the Latest Practicable Date

“Mr. Lun” Mr. Lun Chi Yim

“Offeror” Winland Wealth (BVI) Limited, a company incorporated in theBVI with limited liability and beneficially and indirectly wholly-owned by Mr. Lun

“Offer Shares” the Shares subject to the Mexan Offer

DEFINITIONS

– 4 –

“Overseas Shareholders” Shareholders whose addresses on the register of members ofthe Company are outside Hong Kong

“PRC” People’s Republic of China

“Privateco Offer” the voluntary unconditional cash offer by Somerley Limited onbehalf of Mexan Group Limited to acquire all the InventiveShares other than those already owned by Mexan Group Limitedand parties acting in concert with it

“Properties” (i) the Hotel; and (ii) Commercial Unit No.2 of the commercialaccommodation of Rambler Crest, No.1 Tsing Yi Road, TsingYi, New Territories, Hong Kong

“Proposal” the proposal approved at the SGM in respect of the GroupReorganisation (including the distribution in specie of theInventive Shares), the Special Cash Dividend, the TerminationDeed, the Deed of Novation, and the transactions contemplatedthereunder, taking into account the Privateco Offer and theMexan Offer

“Registrar” Tengis Limited, the Company’s Hong Kong branch shareregistrar, whose address is 26th Floor, Tesbury Centre, 28Queen’s Road East, Wanchai, Hong Kong

“Remaining Business” the Group’s business of hotel investment and operation carryingon by the Remaining Group

“Remaining Group” the Company and its subsidiaries (excluding companiescomprising the Inventive Group)

“Sale Share(s)” 964,548,303 Shares disposed of by Mexan Group Limited tothe Offeror pursuant to the Share Sale Agreement (representingapproximately 73.58% of the issued share capital of theCompany as at the Latest Practicable Date)

“SFC” Securities and Futures Commission of Hong Kong

“SFO” the Securities and Futures Ordinance (Chapter 571 of the Lawsof Hong Kong)

“SGM” the special general meeting of the Company held on 12 April2007 at which the Proposal was approved by the IndependentShareholders

DEFINITIONS

– 5 –

“Share Sale Agreement” the conditional sale and purchase agreement dated 2 January2007 (as amended and supplemented by the supplementalagreements dated 6 February 2007 and 12 April 2007) enteredinto between, among others, the Offeror and Mexan GroupLimited for the disposal of the Sale Shares by Mexan GroupLimited to the Offeror

“Share(s)” ordinary share(s) of HK$0.10 each in the issued share capitalof the Company

“Shareholder(s)” holder(s) of the Share(s)

“Special Cash Dividend” a special cash dividend approved at the SGM and to bedistributed to the Shareholders

“Stock Exchange” The Stock Exchange of Hong Kong Limited

“Takeovers Code” the Hong Kong Code on Takeovers and Mergers

“Winland Enterprises” Winland Enterprises Limited, a company incorporated in HongKong with limited liability and controlled by Mr. Lun and hisFamily Member. Save for Mr. Lun’s interest in the share capitalof and directorship in the Offeror and Winland Enterprises, theydo not have any other relationship

“Winland Finance” Winland Finance Limited, a company incorporated in HongKong with limited liability and controlled by Mr. Lun and hisFamily Member. Save for Mr. Lun’s interest in the share capitalof and directorship in the Offeror and Winland Finance, theydo not have any other relationship

“Termination Deed” as defined in the first paragraph under the section “Intention ofthe Offeror regarding the Remaining Group” in the “Letter fromBOCI” contained in this Composite Offer Document

“HK$” Hong Kong dollars

“sq.ft.” square feet

“sq.m.” square metres

“%” per cent.

LETTER FROM THE BOARD

– 6 –

M E X A N L I M I T E D*

(Incorporated in Bermuda with limited liability)

(Stock Code: 22)

Executive Directors: Registered office:Lau Kan Shan (Chairman) Clarendon HouseTse On Kin (Managing Director) Church StreetChing Yung Hamilton HM 11

BermudaIndependent Non-executive Directors:Chan Wai Dune Principal place of businessLau Wai in Hong Kong:Tong Kwai Lai 7th Floor

Mexan Harbour HotelHotel 2, Rambler CrestNo.1 Tsing Yi RoadTsing Yi, New TerritoriesHong Kong

16 April 2007

To the Shareholders

Dear Sir or Madam,

MANDATORY UNCONDITIONAL CASH OFFERTO ACQUIRE ALL THE ISSUED SHARES IN MEXAN LIMITED(OTHER THAN THOSE ALREADY OWNED BY THE OFFEROR

AND PARTIES ACTING IN CONCERT WITH IT)

INTRODUCTION

Further to the joint announcements of the Company, Mexan Group Limited (the Company’s thencontrolling Shareholder), Inventive and the Offeror dated 16 February 2007, 8 March 2007 and 12April 2007, the announcement of the Company dated 14 March 2007 and the circular of the Companydated 17 March 2007 regarding, inter alia, the Mexan Offer, and following fulfilment of the pre-condition i.e. Completion taking place on 12 April 2007, the Mexan Offer is now made. The MexanOffer is unconditional.

The Composite Offer Document provides you with, inter alia, information on and the procedures foracceptance and settlement of the Mexan Offer, the recommendation of the Independent BoardCommittee and advice of Hercules (i) as to whether the Mexan Offer is, or is not, fair and reasonable;and (ii) as to acceptance.

* For identification purposes only

LETTER FROM THE BOARD

– 7 –

MEXAN OFFER

The SGM was held on 12 April 2007 at which the Proposal (including the Group Reorganisation andthe Special Cash Dividend) was approved. Pursuant to the Share Sale Agreement, the Offeror hasacquired all 964,548,303 Sale Shares from Mexan Group Limited (representing approximately 73.58%of the issued share capital of the Company) for an aggregate consideration of HK$102,917,303.93(equivalent to approximately HK$0.1067 per Sale Share).

Following Completion, BOCI, on behalf of the Offeror and pursuant to the Takeovers Code, is makinga mandatory unconditional cash offer to the Independent Shareholders to acquire all the Shares otherthan those already owned by the Offeror and parties acting in concert with it on the following basis:

For each Offer Share ............................................................................................. HK$0.1067 in cash

The Mexan Offer price of HK$0.1067, being the same as the price per Sale Share, represents:

(i) a discount of approximately 74.6% to the closing price of HK$0.4200 per Share (ex-rights ofthe distribution in specie of the Inventive Shares pursuant to the Group Reorganisation and theSpecial Cash Dividend) as quoted on the Stock Exchange as at the Latest Practicable Date; and

(ii) a discount of approximately 42.0% to the unaudited pro forma consolidated net assets perShare of the Remaining Group of approximately HK$0.1839 set out in Appendix III to theComposite Offer Document.

Further details of the Mexan Offer

Further details of the Mexan Offer including, inter alia, the terms and conditions and the proceduresfor acceptance and settlement are set out in the “Letter from BOCI” and Appendix I to the CompositeOffer Document and the accompanying Form of Acceptance and Transfer.

INTENTIONS OF THE OFFEROR REGARDING THE REMAINING GROUP

Your attention is drawn to the “Letter from BOCI” in the Composite Offer Document for the intentionsof the Offeror regarding the Remaining Group.

RECOMMENDATION

The Independent Board Committee comprising all the three independent non-executive Directors(who have no direct or indirect interest in the Mexan Offer) has been established to make arecommendation (i) as to whether the Mexan Offer is, or is not, fair and reasonable; and (ii) as toacceptance. Hercules has advised the Independent Board Committee in that regard.

Your attention is drawn to the recommendation of the Independent Board Committee on page 17 ofthe Composite Offer Document and the advice of Hercules on pages 18 to 34 of the Composite OfferDocument.

LETTER FROM THE BOARD

– 8 –

ADDITIONAL INFORMATION

Your attention is also drawn to the “Letter from BOCI” set out on pages 9 to 16 of the CompositeOffer Document as well as the additional information contained in Appendices I to V to the CompositeOffer Document and the accompanying Form of Acceptance and Transfer.

Yours faithfully,By Order of the Board

Tse On KinManaging Director

LETTER FROM BOCI

– 9 –

26th Floor,Bank of China Tower,

1 Garden Road,Hong Kong

16 April 2007To the Independent Shareholders

Dear Sir or Madam,

MANDATORY UNCONDITIONAL CASH OFFER BYBOCI ASIA LIMITED

ON BEHALF OFWINLAND WEALTH (BVI) LIMITED

TO ACQUIRE ALL THE ISSUED SHARES IN MEXAN LIMITED(OTHER THAN THOSE ALREADY OWNED

BY WINLAND WEALTH (BVI) LIMITEDAND PARTIES ACTING IN CONCERT WITH IT)

INTRODUCTION

On 16 February 2007, the Offeror, Mexan Group Limited, Inventive and the Company jointlyannounced, among other things, that the Offeror (as purchaser), Winland Enterprises (as purchaser’sguarantor), Mexan Group Limited (as vendor) and Mr. Lau (as vendor’s guarantor) entered into a saleand purchase agreement on 2 January 2007 (as amended and supplemented by a supplementalagreement dated 6 February 2007) pursuant to which the Offeror conditionally agreed to acquire964,548,303 Shares from Mexan Group Limited for an aggregate consideration of HK$102,917,303.93,equivalent to approximately HK$0.1067 per Sale Share. The aforesaid sale and purchase agreementwas further supplemented by a supplemental agreement dated 12 April 2007, details of which are setout in the joint announcement issued by the Company, Mexan Group Limited, the Offeror and Inventiveon the same date.

On 12 April 2007, the Share Sale Agreement was completed and the Offeror and parties acting inconcert with it owned in aggregate 964,548,303 Shares, representing approximately 73.58% of theissued share capital of the Company as at the Completion Date. As a result, the Offeror is requiredunder Rule 26 of the Takeovers Code to make a mandatory unconditional cash offer to acquire all theissued Shares other than those already owned by the Offeror and parties acting in concert with it. TheMexan Offer is unconditional as to acceptance.

This letter, together with Appendix I to the Composite Offer Document and the accompanying Formof Acceptance and Transfer, set out, among other things, the terms of the Mexan Offer, proceduresfor acceptance of the Mexan Offer, information regarding the Offeror and the intention of the Offerorin respect of the Remaining Group. Unless the context otherwise requires, terms used herein have thesame meanings as those defined in the Composite Offer Document of which this letter forms part.

LETTER FROM BOCI

– 10 –

Independent Shareholders are advised to carefully consider the information contained in the “Letterfrom the Board” as set out on pages 6 to 8, the letter from the Independent Board Committee as setout on page 17 and the “Letter from Hercules” as set out on pages 18 to 34 of the Composite OfferDocument.

MANDATORY UNCONDITIONAL CASH OFFER

The Mexan Offer

BOCI, on behalf of the Offeror and pursuant to the Takeovers Code, makes the Mexan Offer to theIndependent Shareholders to acquire all the Shares other than those already owned by the Offeror andparties acting in concert with it on the following basis:

For each Share........................................................................................................ HK$0.1067 in cash

The offer price per Share of HK$0.1067 is the same as the price per Sale Share. The Offeror does notintend to revise the terms, or extend the period, of the Mexan Offer, and does not reserve the rights todo so. The Mexan Offer is required to be open for acceptance for at least 21 days after the depatch ofthe Composite Offer Document. Your attention is drawn to the expected timetable set out in thesection headed “Expected Timetable” of the Composite Offer Document.

Comparison of value

The offer price per Share of HK$0.1067 represents:

(i) a discount of approximately 78.66% to the closing price of HK$0.50 per Share as quoted onthe Stock Exchange on 16 November 2006, being the last Business Day prior to thecommencement date of the Mexan Offer period pursuant to the Takeovers Code;

(ii) a discount of approximately 41.98% to the unaudited pro forma consolidated net asset valueper Share of the Company of approximately HK$0.1839 as at 30 September 2006 which iscalculated based on the unaudited pro forma consolidated net asset value of the RemainingGroup of approximately HK$241.1 million as at 30 September 2006 set out in Appendix III tothe Composite Offer Document and 1,310,925,244 Shares in issue as at 30 September 2006 setout in note 30 to the financial information on the Group in Appendix II to the Composite OfferDocument;

(iii) a discount of approximately 77.05% to the closing price of HK$0.465 per Share as quoted onthe Stock Exchange on 3 April 2007, being the first date of dealings in Shares on an ex-rightsbasis in respect of the distribution in specie of the Inventive Shares and the Special CashDividend; and

(iv) a discount of approximately 74.60% to the closing price of HK$0.420 per Share as quoted onthe Stock Exchange as at the Latest Practicable Date.

LETTER FROM BOCI

– 11 –

Dealings in the Shares and other securities by the Offeror

Save for the entering into the Share Sale Agreement, the Offeror confirms that none of the Offerorand parties acting in concert with it had dealt in or owned any Shares, options, warrants, derivativesand securities convertible into Shares during the period beginning six months prior to the initialannouncement of the Company dated 17 November 2006 (being the commencement date of the MexanOffer period pursuant to the Takeovers Code) up to the Latest Practicable Date.

Highest and lowest closing prices of the Shares

The highest and lowest closing prices of the Shares as quoted on the Stock Exchange during theperiod beginning six months prior to the initial announcement of the Company dated 17 November2006 (being the commencement date of the Mexan Offer period pursuant to the Takeovers Code) upto the Latest Practicable Date were HK$0.680 per Share on 21 February 2007 and HK$0.415 perShare on 27 July 2006, 28 July 2006 and 17 August 2006 respectively.

Total Consideration and Financial Resources

As at the Latest Practicable Date, the Company has 1,310,925,244 Shares in issue of which 346,376,941Shares are subject to the Mexan Offer. Based on the offer price of HK$0.1067 per Share, the totalconsideration payable by the Offeror under the Mexan Offer amounts to approximately HK$37.0million.

BOCI is satisfied that sufficient financial resources are available to the Offeror to meet full acceptanceof the Mexan Offer. The Mexan Offer is financed by the Offeror’s own resources and is not conditionalon any financing.

Effect of accepting the Mexan Offer

By accepting the Mexan Offer, the Shareholders will agree to sell their Shares and all rights attachedthereto to the Offeror free from all liens, charges, claims and encumbrances and any third party rightstogether with all rights attached to them, including the right to receive all dividends and distributionsdeclared, paid or made on or after 2 January 2007. For the avoidance of doubt, the Shares subject tothe Mexan Offer will be acquired ex-entitlements to the distribution in specie of the Inventive Sharespursuant to the Group Reorganisation and the Special Cash Dividend which were declared by theBoard and approved by the Independent Shareholders at the SGM. According to the joint announcementissued by the Offeror, Mexan Group Limited, Inventive and the Company on 12 April 2007, theremittances for the Special Cash Dividend will be posted to the Shareholders on or around 20 April2007 whilst according to the Circular, the Inventive Share certificates will be posted to the InventiveShareholders who do not accept the Privateco Offer on or before 17 May 2007. Shareholders andInventive Shareholders are advised to refer to the aforesaid joint announcement and the Circular fordetails in this regard.

Hong Kong Stamp Duty

Seller’s ad valorem stamp duty payable by the Shareholders who accept the Mexan Offer amounts toHK$1.00 for every HK$1,000 (or part thereof) of the greater of (i) the consideration payable; and (ii)the market value of the relevant Shares under the Mexan Offer, will be deducted by the Offeror fromthe amount payable to the Shareholders on acceptance of the Mexan Offer. The Offeror will then paythe Hong Kong stamp duty on behalf of the Shareholders who have accepted the Mexan Offer.

LETTER FROM BOCI

– 12 –

Compulsory acquisition

The Offeror does not intend to apply any right which may be available to it to acquire compulsorilyany Shares outstanding after the close of the Mexan Offer, but reserves the right to do so.

INFORMATION ON THE OFFEROR

The Offeror, a company incorporated in the BVI on 29 November 2006, was established solely forthe purpose of the acquisition of the Sale Shares. Mr. Lun is the sole director and ultimate soleshareholder of the Offeror. Save for the entering into the Share Sale Agreement, the Offeror has notconducted any other business since its incorporation and has no material assets and liabilities otherthan the amounts required to finance the acquisition of the Sale Shares and the Mexan Offer.

Mr. Lun, aged 73, is an experienced real property investor in Hong Kong since the 1970’s. Mr. Lun isa graduate in the Civil Engineering Department of the South China University of Technology in 1957and has been a Guest Professor of the South China University of Technology since 2001. He is thePermanent Honorary President of the Hong Kong Real Estate Agencies General Association Limitedand an honorary citizen of the city of Lo Din in Guangdong Province of the PRC.

Mr. Lun is the founder of the Winland group of companies established in Hong Kong which areprincipally engaged in the businesses of property investment, money lending (only on security ofimmovable properties or listed company shares) and the provision of hotel and property managementservices. Mr. Lun also engages in various infrastructure investments in the PRC through joint ventures.

INTENTION OF THE OFFEROR REGARDING THE REMAINING GROUP

Business

It is the intention of the Offeror to continue the Remaining Business of hotel investment and operationfollowing the close of the Mexan Offer. Immediately before Completion, the Properties are operatedand managed by Winland Hotel Management Limited, a company controlled by Mr. Lun. As it is theintention of the Offeror to appoint new directors to the Board who have relevant experience in hotelinvestment and operation and for the Remaining Group to operate and manage the Properties itselfafter Completion, City Promenade, Winland Hotel Management Limited, Winland Finance and theCompany have entered into the deed of release and termination on 2 January 2007 (the “TerminationDeed”) pursuant to which it was conditionally agreed that the hotel management contract dated 10November 2005 (as supplemented by a supplemental management contract dated 11 November 2005)(together, the “Management Contract”) in respect of the management and operation of the Propertiesbe terminated and the obligations and liabilities of the parties thereto be released. The conditions tothe Termination Deed, being approval of the same by the Independent Shareholders at the SGM andcompletion of the Share Sale Agreement, have been fulfilled and therefore the Termination Deed hasbecame unconditional. Details of the Termination Deed are set out in Appendix I to the Circular.

LETTER FROM BOCI

– 13 –

The Offeror will regularly conduct review of the Remaining Group’s financial position and businessactivities in order to formulate its business and strategic development plans and continue to explorefurther suitable investment opportunities for the Remaining Group. Depending on the results of theabove reviews and provided that suitable investment opportunities arise, the Offeror may considerdiversifying the business of the Remaining Group with an aim to expand its source of income andenhance its financial position. Nevertheless, the Offeror has not identified any such investment orbusiness opportunities as at the Latest Practicable Date. The Offeror considers it commerciallyjustifiable to make investment in the hotel business which will be continued by the Remaining Group.The Offeror has no intention to dispose of or re-deploy the assets of the Remaining Group. Anyfuture acquisition or disposal of assets by the Company after the Completion will be subject to theprovisions of the Listing Rules and in particular, the Stock Exchange may aggregate a series oftransactions of the Company and such transactions may result in the Company being treated as a newapplicant under the Listing Rules.

Board of Directors, management and employees

As at the Latest Practicable Date, the Company has three executive Directors, namely Mr. Lau, Mr.Tse On Kin and Ms. Ching Yung and three independent non-executive Directors, namely, Mr. ChanWai Dune, Mr. Lau Wai and Mr. Tong Kwai Lai. It has been the intention that there will be a changein the composition of the Board and company secretary of the Company and new directors (includingMr. Lun as referred to below) will be appointed to the Board at the earliest time as allowed under theTakeovers Code and any such appointment will be made in compliance with the Takeovers Code andthe Listing Rules. Upon Completion, Ms. Nip Suk Ching was appointed as the new company secretaryof the Company in replacement of Ms. Chan Wai Ming and the Offeror intends to nominate Mr. Lunas an executive Director. Further announcement(s) will be made as and when there is a change in thecomposition of the Board (including new directors to be appointed onto the Board).

Save for the proposed change in the composition of the Board and the change of the company secretaryof the Company, the Offeror has no intention to discontinue the employment of the employees of theRemaining Group.

The Bank Loan and the Winland Loan

Prior to completion of the Share Sale Agreement, City Promenade, a member of the Group and alsothe registered owner of the Properties, had (i) a loan facility obtained from an independent commercialbank in Hong Kong (the “Bank”) with an outstanding principal amount of approximately HK$380.2million (the “Bank Loan”) as at the Latest Practicable Date and (ii) a loan facility obtained fromWinland Finance with an outstanding principal amount of approximately HK$59.4 million (the“Winland Loan”) as at the Latest Practicable Date. The Bank Loan was secured by, among others, afirst mortgage on the Properties and an assignment of earnings of the Properties, corporate guaranteesgiven by the Company and certain other companies controlled by Mr. Lun and his Family Membersand personal guarantee given by Mr. Lun and his Family Member whilst the Winland Loan is securedby a second mortgage on the Properties, a second assignment of earnings of the Properties, a sharecharge on all issued shares of City Promenade and a corporate guarantee given by the Company.Details of the above mortgages, assignments and charges are set out in Appendix I to the Circular.

LETTER FROM BOCI

– 14 –

As detailed in the Circular, the Offeror has made arrangements with the Bank and Winland Financeso that, after the Completion, the Bank Loan will be revised to a maximum principal amount ofHK$455 million which will comprise (i) an instalment loan of up to HK$185 million and a revolvingloan of up to HK$200 million to be made available to City Promenade; and (ii) an instalment loan ofup to HK$70 million to be made available to the holding company of City Promenade, namelyGoodnews Investments Limited (collectively, the “Revised Bank Loan Facility”) on the security ofthe Properties. As part of the aforesaid arrangements with the Bank and Winland Finance, the corporateguarantees given by certain companies controlled by Mr. Lun and his Family Members and the personalguarantee given by Mr. Lun and his Family Member will be discharged and a corporate guaranteewill be executed by the Company in respect of the liabilities of City Promenade and GoodnewsInvestments Limited of no less than HK$455 million under the Revised Bank Loan Facility. Theformal documentation in respect of the Revised Bank Loan Facility is now in progress and once it iscompleted, the Remaining Group will make a drawdown under the Revised Bank Loan Facility torepay the Winland Loan in full. As set out in the Circular, the Winland Loan constitutes a continuingconnected transaction for the Company for the purpose of the Listing Rules upon Completion. Afterthe aforesaid repayment of the Winland Loan to be made by the Remaining Group, this continuingconnected transaction will no longer exist.

The Deed of Novation

On 11 November 2005, the acquisition of the commercial and carpark complex of a property knownas Elizabeth House in Causeway Bay, Hong Kong from the Group by Express Chain Limited (“ExpressChain”), a company ultimately controlled by Mr. Lun and his Family Members, was completed. Onthe same date, at the request of Express Chain as the purchaser of the above property, the Companyexecuted a deed of undertaking and indemnity (the “Deed of Undertaking”) in favour of ExpressChain pursuant to which the Company has undertaken to share with it, among other things, any taxliabilities incurred by the owner of Elizabeth House up to and inclusive of 11 November 2005 in themanner as stipulated therein. At the time of execution of the Deed of Undertaking, the Company wasindirectly controlled by Mr. Lau. Details of the acquisition of the Elizabeth House are set out in theannouncements of the Company dated 15 July 2005, 27 October 2005 and 14 November 2005 and thecircular of the Company dated 15 August 2005.

As explained in Appendix I to the Circular, as the Company ceased to be controlled by Mr. Lau andbecame controlled by Mr. Lun through the Offeror upon Completion, Mr. Lau has agreed that theobligations of the Company under the Deed of Undertaking will be novated to him upon Completion,and hence, it is provided under the Share Sale Agreement that upon Completion, a deed of novationwould be entered into among Express Chain, the Company and Mr. Lau (the “Deed of Novation”)pursuant to which, all the obligations and liabilities imposed or to be imposed on the Company underthe Deed of Undertaking will be transferred to and assumed by Mr. Lau, and the Company will bereleased and discharged from its obligations and liabilities under the Deed of Undertaking with effectfrom Completion.

LETTER FROM BOCI

– 15 –

The entering into of the Deed of Novation by the Company was duly approved by the IndependentShareholders at the SGM. On 12 April 2007, the Company and Mr. Lau have executed the Deed ofNovation.

MAINTAINING THE LISTING STATUS OF THE COMPANY

It is the intention of the Offeror to maintain the listing status of the Company on the Stock Exchange.The director of the Offeror and the new directors to be appointed to the Board will jointly and severallyundertake to the Stock Exchange to take appropriate steps to ensure that sufficient public float existsin the Shares.

The Stock Exchange has stated that if, at the close of the Mexan Offer, less than the minimumprescribed percentage applicable to the Company, being 25% of the Shares, are held by thepublic, or if the Stock Exchange believes that (i) a false market exists or may exist in the tradingof the Shares; or (ii) there are insufficient Shares in public hands to maintain an orderly market,it will consider exercising its discretion to suspend dealings in the Shares.

ACCEPTANCE AND SETTLEMENT

Your attention is drawn to the details in respect of the procedures for acceptance and settlement setout in Appendix I to the Composite Offer Document and the accompanying Form of Acceptance andTransfer.

GENERAL

To ensure equality of treatment of all Shareholders, those registered Shareholders who hold Shares asnominee for more than one beneficial owner should, as far as practicable, treat the holding of eachbeneficial owner separately. In order for the beneficial owners of the Shares whose investments areregistered in nominee names to accept the Mexan Offer, it is essential that they provide instructionsto their nominees of their intentions with regard to the Mexan Offer.

All communications, notices, Forms of Acceptance and Transfer, Share certificates, transfer receipts,other documents of title (and/or any indemnity or indemnities required in respect thereof) andremittances to be delivered by or sent to or from the Shareholders will be delivered by or sent to orfrom them, or their respective agents, through ordinary post at their own risks, and none of the Offeror,BOCI, the Registrar or any of their respective agents, accepts any liability for any loss in postage orany other liabilities that may arise as a result thereof.

The attention of Overseas Shareholders is drawn to the section headed “Overseas Shareholders” inAppendix I to the Composite Offer Document.

LETTER FROM BOCI

– 16 –

ADDITIONAL INFORMATION

Your attention is drawn to the additional information set out in the Appendices, which form part ofthe Composite Offer Document.

Yours faithfully,For and on behalf ofBOCI Asia Limited

Daniel NG Raymond LEUNGManaging Director Vice President

Head of Corporate Finance

LETTER FROM THE INDEPENDENT BOARD COMMITTEE

– 17 –

The following is the text of a letter from the Independent Board Committee setting out itsrecommendation to the Independent Shareholders in respect of the Mexan Offer:

M E X A N L I M I T E D*

(Incorporated in Bermuda with limited liability)

(Stock Code: 22)

16 April 2007

To the Independent Shareholders

Dear Sirs or Madam,

MANDATORY UNCONDITIONAL CASH OFFERTO ACQUIRE ALL THE ISSUED SHARES IN MEXAN LIMITED

(OTHER THAN THOSE SHARES ALREADY OWNED BY THE OFFERORAND PARTIES ACTING IN CONCERT WITH IT)

We refer to the Composite Offer Document dated 16 April 2007 of which this letter forms part. Asthe Independent Board Committee, we advise you in connection with the Mexan Offer, details ofwhich are set out in the Composite Offer Document. Terms used in this letter have the meaningsgiven to them in the Composite Offer Document unless the context otherwise requires.

Hercules has been appointed to advise us in connection with the Mexan Offer. Details of its adviceand the principal factors and reasons that it has considered are set out in its letter on pages 18 to 34 ofthe Composite Offer Document.

Having considered the terms of the Mexan Offer and the advice of Hercules in relation thereto, weare of the opinion that the Mexan Offer price is not fair and, on this basis, the Mexan Offer is neitherfair nor reasonable so far as you are concerned. We therefore recommend that you consider not toaccept the Mexan Offer.

Yours faithfully,Independent Board Committee

Chan Wai Dune Lau Wai Tong Kwai LaiIndependent non-executive Directors

* For identification purposes only

LETTER FROM HERCULES

– 18 –

The following is the full text of a letter of advice from Hercules to the Independent Board Committee,which has been prepared for the purpose of incorporation into this Composite Offer Document, settingout its advice to the Independent Board Committee in connection with the Mexan Offer:

Hercules Capital Limited

1503 Ruttonjee House11 Duddell StreetCentralHong Kong

16 April 2007

To the Independent Board Committee ofMEXAN LIMITED

Dear Sir or Madam,

MANDATORY UNCONDITIONAL CASH OFFER BYBOCI ASIA LIMITED

ON BEHALF OFWINLAND WEALTH (BVI) LIMITED

TO ACQUIRE ALL THE ISSUED SHARES IN MEXAN LIMITED(OTHER THAN THOSE ALREADY OWNED

BY WINLAND WEALTH (BVI) LIMITEDAND PARTIES ACTING IN CONCERT WITH IT)

INTRODUCTION

We refer to our appointment as the independent financial adviser to advise the Independent BoardCommittee with respect to the terms of the Mexan Offer, details of which are set out in the compositeoffer document dated 16 April 2007 (the “Composite Offer Document”) addressed to theShareholders, of which this letter forms part. Terms used in this letter have the same meanings asdefined elsewhere in the Composite Offer Document unless the context requires otherwise.

As at the Latest Practicable Date, there were a total of three non-executive Directors on the Board,namely Messrs Chan Wai Dune, Lau Wai and Tong Kwai Lai, all of whom are independent non-executive Directors. Pursuant to Rule 2.1 of the Takeovers Code, the Independent Board Committeehas been formed to advise the Independent Shareholders as to whether the Mexan Offer is, or is not,fair and reasonable, and as to acceptance. Hercules has been engaged to advise the IndependentBoard Committee in these regards.

LETTER FROM HERCULES

– 19 –

In formulating our recommendations, we have reviewed, inter alia, the Circular, the Composite OfferDocument and certain related agreements and certain publicly available financial statements andother business and financial information relating to the Remaining Group. We have also reviewedcertain information provided by management of the Company relating to the operations, financialcondition and prospects of the Company. We have also considered the terms of all offers made withinthe twelve full month period prior to the Latest Practicable Date for companies listed on the mainboard of the Stock Exchange, and such other information, financial studies, analyses and investigationsand financial, economic and market criteria which we deemed relevant. The Directors have jointlyand severally accepted full responsibility for the accuracy of the information contained in the CompositeOffer Document (other than those relating to the Offeror, the terms and conditions of the MexanOffer and the Offeror’s intention regarding the Remaining Group) and the sole director of the Offerorhas accepted full responsibility for the accuracy of the information contained in the Composite OfferDocument relating to the Offeror, the terms and conditions of the Mexan Offer and the Offeror’sintention regarding the Remaining Group. The directors of the Company and the Offeror haveconfirmed, having made all reasonable enquiries, that to the best of their knowledge, opinions expressedin the Composite Offer Document (in the case of the Directors, other than those relating to the Offeror,the terms and conditions of the Mexan Offer and the Offeror’s intention regarding the RemainingGroup and, in the case of the sole director of the Offeror, only those relating to the Offeror, the termsand conditions of the Mexan Offer and the Offeror’s intention regarding the Remaining Group), havebeen arrived at after due and careful consideration and there are no other facts not contained in theComposite Offer Document, the omission of which would make any statements in the CompositeOffer Document misleading. We have relied on, and assumed, without independent verification, theaccuracy and completeness of the information reviewed by us for the purpose of this opinion. Wehave not, for the purpose of this exercise, conducted any independent detailed investigation into oraudit of the businesses, financial conditions or affairs or the future prospects of the Remaining Group.Our opinion is necessarily based on financial, economic, market and other conditions in effect, andthe information made available to us, at the Latest Practicable Date.

We have not considered the tax consequences for the Independent Shareholders arising fromacceptances or non-acceptances of the Mexan Offer since these are particular to their individualcircumstances. In particular, the Independent Shareholders who are resident outside of Hong Kong orsubject to overseas taxes, or Hong Kong taxation on securities dealings should consider their taxposition with regard to the Mexan Offer and, if in any doubt, should consult their own professionaladvisers.

In addition, we refer you to the letter from the Board and the letter from BOCI contained in theComposite Offer Document, which give full details of the Mexan Offer, and the appendices to theComposite Offer Document which give further information on the Remaining Group as required bythe Takeovers Code. We advise that the Independent Shareholders read carefully the Composite OfferDocument before they decide what action they should take.

LETTER FROM HERCULES

– 20 –

PRINCIPAL FACTORS AND REASONS CONSIDERED

In formulating our opinion, we have taken into consideration the following principal factors andreasons:

A. Background to the Mexan Offer

On 2 January 2007, Mexan Group Limited entered into the Share Sale Agreement (as amendedand supplemented by the supplemental agreements dated 6 February and 12 April 2007) with,inter alia, the Offeror pursuant to which, and subject to, inter alia, approval by the IndependentShareholders of the Group Reorganisation and the Special Cash Dividend, the Offeror agreedto acquire 964,548,303 Shares from Mexan Group Limited for a total consideration ofHK$102,917,303.93, equivalent to approximately HK$0.1067 per Share.

The Group Reorganisation and the Special Cash Dividend were approved by the IndependentShareholders at the SGM despite our advice to the contrary.

All conditions precedent to the Share Sales Agreement were satisfied on 12 April 2007 andCompletion took place on the same date. Accordingly, the Offeror became owner of 964,548,303Shares, representing approximately 73.58% of the issued share capital of the Company, as atthe Completion Date. The Offeror is therefore obliged under Rule 26 of the Takeovers Code tomake a mandatory unconditional offer to acquire all the issued Shares (other than those alreadyowned by the Offeror and parties acting in concert with it).

BOCI is making the Mexan Offer on behalf of the Offeror on the following basis:

For each Share HK$0.1067 in cash

The Mexan Offer price of HK$0.1067 per Share is the same as the price per Sale Share paid bythe Offeror under the Share Sale Agreement.

Further details of the Mexan Offer including, inter alia, the terms and conditions, and theprocedures for acceptance and settlement are set out in the letter from BOCI, Appendix I to theComposite Offer Document and the accompanying Form of Acceptance and Transfer.

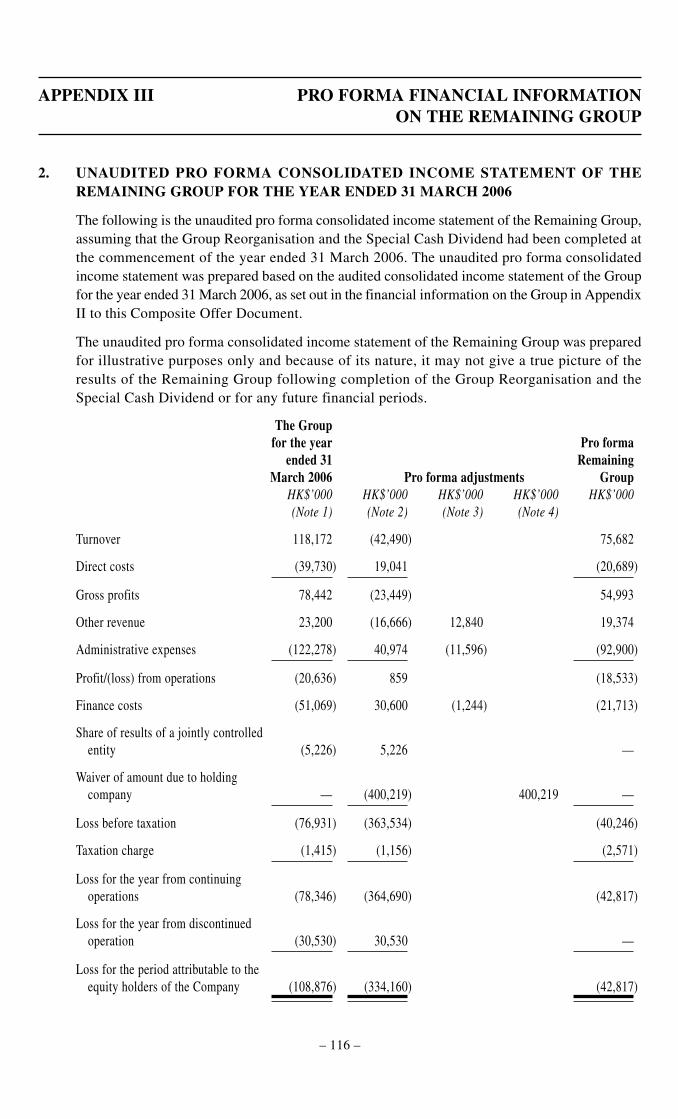

B. Financial information of the Remaining Group

Set out in Table 1 below is a summary of the unaudited pro forma consolidated income statementof the Remaining Group upon completion of the Proposal (but excluding the Mexan Offer andthe Privateco Offer) as set out in Appendix III to the Composite Offer Document.

LETTER FROM HERCULES

– 21 –

Table 1 - Summary unaudited pro forma consolidated income statement of the RemainingGroup

For the year ended31 March 2006

HK$’000

Turnover 75,682

Direct costs (20,689)

Gross profit 54,993Gross profit margin 72.7%

Other revenue 19,374Administrative expenses (92,900)

Loss from operations (18,533)Operating margin —

Finance costs (21,713)

Loss before taxation (40,246)Taxation charge (2,571)

Loss attributable to equity holdersof the Company (42,817)

Net margin —

Following the Group Reorganisation, the remaining principal business of the Remaining Groupis hotel investment and operations. Pro forma turnover for the year ended 31 March 2006 fromhotel operations amounted to HK$75.7 million. For the year ended 31 March 2006, theRemaining Group posted a pro forma net loss of HK$42.8 million due primarily to substantialadministrative expenses and finance costs. As the Remaining Group reported a pro forma lossbefore interest and tax for the year ended 31 March 2006, an interest coverage ratio could notbe produced.

LETTER FROM HERCULES

– 22 –

Summarised in Table 2 below is the Remaining Group’s unaudited pro forma consolidatedbalance sheet as set out in Appendix III to the Composite Offer Document.

Table 2 - Summary unaudited pro forma consolidated balance sheet of the RemainingGroup

As at30 September 2006

HK$’000

Non-current assetsProperty, plant and equipment 657,775Intangible assets 11,764Investments in club debentures 1,350

670,889

Current assetsTrade and other receivables, deposits

and prepayments 24,549Cash at banks and in hand 2,962

27,511

Current liabilitiesOther payables, deposits received

and accrued charges 16,473Dividend payable 1,175Current portion of bank loans 34,732

52,380

Non-current liabilitiesBank loans 362,685Other loans 42,203

404,888

241,132

EquityShare capital 131,092Reserves 110,040

241,132

Current ratio 0.53

Total debt/equity 182.3%

Long term debt/equity 167.9%

LETTER FROM HERCULES

– 23 –

Property, plant and equipment accounted for 94.2% of the Remaining Group’s pro forma totalassets as at 30 September 2006. Cash and cash equivalents accounted for only 0.4% of theRemaining Group’s pro forma total assets.

Bank and other loans accounted for 96.1% of the Remaining Group’s pro forma total liabilitiesas at 30 September 2006. Current portion of bank loans accounted for 7.9% of the RemainingGroup’s total bank and other loans as at 30 September 2006. The Remaining Group was highlygeared as at 30 September 2006, with a long term debt to equity ratio of 167.9% and a totaldebt to equity ratio of 182.3%.

Based on the foregoing, we are of the view that the interest payments may put a strain onprofits and restrict or prevent payment of dividends to Shareholders. In addition, in the eventthat a substantial amount of capital is required for the development of the Remaining Business,the Company may find it hard to obtain further borrowings from banks and other financialinstitutions and may have to raise equity funding, which may lead to dilution to Shareholders.

C. Future prospects and outlook of the Remaining Group

As discussed in the section headed “B.2. Hotel investments and operations” set out on page 28of the Circular, operation of Mexan Harbour Hotel, an 800-room fully furnished hotel in TsingYi, benefiting from its strategic location of close proximity to both the Hong Kong InternationalAirport and the Hong Kong Disneyland, achieved an average occupancy rate of approximately88% for the period from its opening in late December 2004 to 31 March 2006 and 86% for thesix months ended 30 September 2006. The opening of the AsiaWorld-Expo in December 2005has attracted more international business visitors from convention and exhibition markets toHong Kong, and the various new attractions of Hong Kong are expected to stimulate the demandfor hotel rooms and benefit the hotel operations of the Remaining Group.

Nevertheless, the Remaining Group is highly geared with a total debt to equity ratio of 182.3%as at 30 September 2006, and it incurred HK$21.7 million in interest expense for the yearended 31 March 2006. As no plan to reduce the debt had been announced by the Company upto the Latest Practicable Date, we consider the borrowed funds a burden to the Company interms of interest payments and eventual capital repayments, and the Remaining Group’s futureprofitability could be adversely affected by fluctuations in interest rates. As noted in the Group’slatest interim report, the Board anticipated that additional cash outlay would be required for athorough refurbishment of the Hotel in 2007 in order to maintain its competitive edge.

LETTER FROM HERCULES

– 24 –

D. Trading performance of the Shares

Set out in Table 3 are the trading statistics of the Shares for the period from 3 April 2007 (beingthe first day the Shares commenced trading on the Stock Exchange on an ex-rights basis) to theLatest Practicable Date (the “Review Period”).

Table 3: Trading Statistics for the Review Period

Discount Asimplied by a percentage

Closing the Mexan Total trading to free floatprice Offer price volume Shares(1)

HK$ % Shares %

20073 April 0.465 77.1 30,571,686 8.84 April 0.460 76.8 8,194,000 2.410 April 0.445 76.0 2,200,000 0.611 April 0.435 75.5 5,630,299 1.612 April 0.430 75.2 4,524,723 1.3Latest Practicable Date 0.420 74.6 3,640,000 1.1

Highest 0.465 77.1 30,571,686 8.8Lowest 0.420 74.6 2,200,000 0.6Average 0.443 75.9 9,126,785 2.6

Source: the Stock Exchange website

Note:

1. Based on 346,376,941 free float Shares, calculated as 1,310,925,244 Shares in issue less 964,548,303Shares held by the Offeror as at the Latest Practicable Date.

As shown in Table 3, closing prices of the Shares were at a premium over the Mexan Offerprice during the entire Review Period. However, we note that the trading volume of the Sharesduring the Review Period was moderate with average trading volume of approximately 2.6%of the free float Shares. As at the Latest Practicable Date, the aggregate amount of Sharesowned by the Independent Shareholders represented approximately 38.0 times the averagedaily trading volume for the Review Period.

Having regard to the medium level of liquidity in the trading of the Shares during the ReviewPeriod and the possible reduced free float Shares as a result of the Mexan Offer, IndependentShareholders would unlikely be able to sell a significant number of their Shares in the marketwithout depressing the market price of the Shares. The Mexan Offer as such represents analternative exit to the open market for Independent Shareholders to realise their investments.

LETTER FROM HERCULES

– 25 –

E. Indicative valuation benchmarks

(a) Price/book ratio (“P/B”)

Based on the “Pro forma consolidated balance sheet of the Remaining Group as at 30September 2006” as set out in Appendix III to the Composite Offer Document, the proforma net asset value per Share amounted to approximately HK$0.184. The Mexan Offerprice represents a discount of approximately 42.0% to the pro forma net asset value perShare and a P/B of approximately 0.58 times.

(b) Price/earnings multiple

We note from the “Unaudited pro forma consolidated income statement of the RemainingGroup for the year ended 31 March 2006” set out in Appendix III to the Composite OfferDocument that the Remaining Group had a pro forma net loss of approximately HK$42.8million, the use of a price/earnings multiple as reference to assess the Mexan Offer priceis therefore not applicable.

(c) Dividend yield

As discussed in the subsection headed “D.1.(iii) Dividend yield” set out on page 34 ofthe Circular, given that (i) the Group did not maintain a standard dividend payment inthe past; and (ii) save for the distribution in specie of the Inventive Shares pursuant to theGroup Reorganisation and the Special Cash Dividend, the Company has not formulatedany dividend payment policy, we consider the use of dividend yield as reference to assessthe Mexan Offer price is not applicable.

F. Cash offer precedents

For the purpose of assessing the fairness and reasonableness of the Mexan Offer price, we haveattempted to compare it with the cash offers made within a twelve-month period prior to theLatest Practicable Date for companies listed on the main board of the Stock Exchange whichare engaged in businesses similar to the Remaining Business. However, we were unable toidentify any cash offers in the aforesaid period by companies engaged in similar businesses tothe Remaining Group. In the absence of industry comparables, we have identified, to the bestof our knowledge and based on the information from the website of the Stock Exchange, alloffers made for companies that are listed on the main board of the Stock Exchange within atwelve-month period prior to the Latest Practicable Date (the “Comparable Offers”) andreviewed their valuation statistics. Table 6 sets out a summary of the valuation statistics of theComparable Offers.

LETTER FROM HERCULES

– 26 –

Table 4: Comparable Offers

Premium/(discount)represented by

the share offer priceover/(to)

Company Date of Market the closing price Dividend(stock code) Principal activities announcement capitalisation(1) on the last trading day P/E(2) P/B(3) yield(4)

HK$’million % times times %

Chun Wo Holdings Civil engineering, 22-Feb-06 625 18.3 12.0 0.8 3.0Limited (711) electrical and 9-May-06 (12)

mechanical engineering,foundation and buildingconstruction work,property development andproperty investment

Nority International Manufacture 4-Apr-06 126 14.6 n.a. 0.9 n.a.Group Limited and export of athletic,(660) athletic-style leisure footwear

and sports shoes

The Cross-Harbour Investment holdings, 10-Apr-06 1,228 (39.5 ) 7.4 0.6 6.9(Holdings) operation of driverLimited (32) training centres and,

through its associatedcompanies, operation ofthe Western Harbour Tunneland an electronic tollcollection system

First Pacific Telecommunications 28-Apr-06 7,015 (32.3 ) 8.7 2.3 1.4Company Limited and consumer food(142) products operation

CSMC Technologies Operation of 12-May-06 1,124 5.0 n.a. 0.9 n.a.Corporation (597) semi-conductor

foundries in China

Shun Cheong Provision of building 16-May-06 35 (18.9 ) n.a. 0.6 n.a.Holdings Limited related maintenance(650) services

LETTER FROM HERCULES

– 27 –

Premium/(discount)represented by

the share offer priceover/(to)

Company Date of Market the closing price Dividend(stock code) Principal activities announcement capitalisation(1) on the last trading day P/E(2) P/B(3) yield(4)

HK$’million % times times %

China Paradise Operation of household 25-Jul-06 5,219 9.0 13.3 2.4 1.7Electronics Retail appliances retail chainLimited (503)(5) in China

Golden Resorts Holding and operation 25-Jul-06 2,353 (3.0 ) n.a. 1.0 n.a.Group Limited of hotels with(1031) gaming facilities in

Macau

Asia Financial Provision of insurance 9-Aug-06 3,703 (17.5 ) 20.1 1.0 2.9Holdings Limited and investment services(662)

Senyuan Manufacture of vacuum 22-Aug-06 454 4.2 8.3 2.3 3.7International circuit breakers andHoldings Limited other components of(3333) switchgears in the PRC

CASH Retail Operation of department 28-Aug-06 393 (11.1 ) n.a. 1.6 n.a.Management store and provision ofGroup Limited store management(996) services in the PRC

Hanny Holdings Trading of securities, 1-Sep-06 1,997 7.6 96.4 0.5 2.6Limited (275) property investment

and trading, holdingof vessels for sandmining and otherstrategic investments

China Motion Provision of international 8-Sep-06 30 (50.0 ) n.a. 0.6 n.a.Telecom telecommunication services,International mobile communicationsLimited (989) services and distribution

and retail chain

LETTER FROM HERCULES

– 28 –

Premium/(discount)represented by

the share offer priceover/(to)

Company Date of Market the closing price Dividend(stock code) Principal activities announcement capitalisation(1) on the last trading day P/E(2) P/B(3) yield(4)

HK$’million % times times %

Cosmopolitan Investment in properties 4-Oct-06 80(6) (41.9 ) n.a. 0.4 n.a.International and securities andHoldings provision of informationLimited (120) technology services

Quality HealthCare Health administration, 5-Oct-06 652 (16.7 ) 11.6 3.7 1.8Asia Limited medical scheme(593) administration, and

the provision ofhealthcare services

AV Concept Marketing and distribution 9-Oct-06 215 8.2 20.4 0.5 3.8Holdings Limited of semiconductors and(595) electronic components,

and design andmanufacturingof electronic productsand Internet appliances

Asia Commercial Watch trading and luxury 27-Oct-06 227 (25.3 ) 41.9 1.3 n.a.Holdings Limited products retailing(104)

Apex Capital Acquisition and disposal 31-Oct-06 17 (6.1 ) n.a. 1.6 n.a.Limited (905) of investment in listed

and unlisted securities

New World Mobile Technology-related business 22-Nov-06 63(7) 51.2(8) 0.1 n.a. n.a.Holdings Limited and holding of 23.60%(862) interest in the issued share

capital of CSL New WorldMobility Limited

Linmark Group Sourcing of apparel and 12-Dec-06 700 12.9 8.5 1.2 5.3Limited (915) accessories, hardgoods and

electronics consumer goodsas well as other relatedbusinesses

LETTER FROM HERCULES

– 29 –

Premium/(discount)represented by

the share offer priceover/(to)

Company Date of Market the closing price Dividend(stock code) Principal activities announcement capitalisation(1) on the last trading day P/E(2) P/B(3) yield(4)

HK$’million % times times %

Foundation Group Apparel trading, securities 22-Dec-06 1,575(9) (19.0 ) n.a. 1.2 n.a.Limited (1182) trading and strategic

investments

Nority International Manufacture and export of 24-Nov-06 111 (12.3 ) n.a. 1.2 n.a.Group Limited athletic and athletic-style(660) leisure footwear, as well

as the manufacture ofworking shoes, safetyshoes, golf shoes andother functional shoes

Climax International Manufacturing, marketing 6-Jan-07 62(6) (23.1 ) n.a. 0.3 n.a.Company Limited and distribution of paper(439) products, the original

equipment manufacturingbusiness, whereby thegroup buys materials andmanufactures paper productsfor wholesalers and retailchain stores worldwide

Zhongtian Provision of system integration 13-Feb-07 40 (42.9 ) 4.2 0.3 7.5International services, development ofLimited (2379) customised software products,

sale of software and hardwareproducts; and provision ofmaintenance and other services

Pacific Century Individual and group life insurance 1-Mar-07 6,672 58.2 20.6 2.4 0.6Insurance Holdings and asset managementLimited (65)

Maximum 58.2 96.4 3.7 7.5Minimum (50.0 ) 0.1 0.3 0.6Mean discount (24.0 ) 19.5 1.2 3.4

premium 18.9Median (11.1 ) 11.8 1.0 2.9

The Company Remaining Business 16-Feb-07 140 (74.6)(10) n.a. 0.6 n.a.

LETTER FROM HERCULES

– 30 –

Notes:

1. Based on the offer price and outstanding shares as at the date of the respective announcements.

2. Calculated as offer price divided by the latest audited earnings per share set out in the respective offer/response document.

3. Calculated as offer price divided by the latest published net asset value per share set out in the respectiveoffer/response document.

4. Calculated as offer price divided by the dividend paid for the ordinary shares for the latest financial yearset out in the respective offer/response document.

5. The offer price of HK$2.2354 comprised cash consideration of HK$0.1736 and the value of 0.3247 sharesin GOME Electrical Appliances Holding Limited (“GOME Shares”) based on the closing price of eachGOME Share of HK$6.35, as quoted on the Stock Exchange on 17 July 2006, being the last trading day forGOME Shares prior to the date of the announcement.

6. Adjustments made to take into account the effect of an open offer.

7. Adjustments made to take into account the new shares to be issued upon the exercise of certain outstandingoptions.

8. Based on the ex-dividend price.

9. Adjustments made to take into account the effect of a share subscription.

10. Based on the closing price of the Shares as at the Latest Practicable Date.

11. n.a. denotes not applicable as the company recorded net loss or net deficit or declared and paid no dividend.

12. The share offer price was revised upwards.

As indicated in the table above, the share offer prices of the Comparable Offers when comparedto their respective closing prices as at the last trading day range from a premium of approximately58.2% to a discount of approximately 50.0%. The discount represented by the Mexan Offerprice of HK$0.1067 to the closing price of the Shares as at the Latest Practicable Date isdeeper than the mean discount and median of the Comparable Offers.

The P/B ratio implied by the Mexan Offer price is close to the bottom end of the range andrepresents significant discounts of 50.0% and 40.0% respectively to the mean and median P/Bratio of the Comparable Offers. The Mexan Offer price is thus inadequate relative to theComparable Offers.

LETTER FROM HERCULES

– 31 –

G. Trading statistics of Industry Comparable

In assessing the fairness and reasonableness of the Mexan Offer price, we have also reviewedthe trading statistics of a company listed on the main board of the Stock Exchange (the “IndustryComparable”) whose businesses to a considerable extent consist of hotel operations andmanagement in Hong Kong and are considered to be broadly comparable to the principal businessof the Remaining Group, and with over 90% of its turnover derived from hotel operationsbased on its latest published annual report prior to the Latest Practicable Date:

Table 5: Trading Statistics of the Industry Comparable

Comparables Number of Market Dividend(stock code) Principal activities hotels owned capitalisation(1) P/E(2) P/B(2) yield(2)

HK$’million x x %

Sino Hotels (Holdings) Hotel, restaurant and club 3(4) 4,636 72.97 1.86 0.91Ltd. (1221) operation; share investment

and investment holdings

The Company 1 140 n.a. 0.58 n.a.

Notes:

1. Market capitalisation of the Industry Comparable as at the Latest Practicable Date was quoted fromBloomberg. Market capitalisation of the Company is calculated based on the Mexan Offer price and1,310,925,244 Shares in issue as at the Latest Practicable Date.

2. Trading multiples for the Industry Comparable as at the Latest Practicable Date were quoted from Bloomberg.Implied P/B for the Company is calculated based on the Mexan Offer price.

3. n.a. denotes not applicable.

4. Including the 25% owned Royal Pacific Hotel & Towers and the 50% owned Conrad Hong Kong.

As illustrated in Table 5 above, the Company’s implied P/B ratio, based on the Mexan Offerprice for the Shares, of 0.58 times is significantly below the Industry Comparable. Nevertheless,we note that the Comparable has greater market capitalisation and is a profit-making company.We are of the view that the above analysis is of limited relevance as there are no listed companiesthat are truly comparable to the Company.

Based on the foregoing and our analysis in the preceding section, we are of the view that theMexan Offer price is neither fair nor reasonable to the Independent Shareholders.

LETTER FROM HERCULES

– 32 –

H. Intention of the Offeror regarding the future of the Company

As noted in the letter from BOCI, it is the intention of the Offeror to continue the RemainingBusiness and regularly review the Remaining Group’s financial position and business activitiesin order to formulate its business and strategic development plans and continue to explorefurther suitable investment opportunities for the Remaining Group. The Offeror has no intentionto discontinue the employment of the existing employees (save for a possible change in thecomposition of the Board and company secretary of the Company) nor to dispose of or re-deploy the assets of the Remaining Group. Due to lack of specific information on the futurebusiness plans of the Offeror, we can not draw the conclusion that there will or will not be anysignificant change in the operation of the Remaining Group in the foreseeable future.

I. Maintaining the listing status of the Company

The letter from BOCI states, inter alia, that the Stock Exchange has stated that if, at the closeof the Mexan Offer, less than the minimum prescribed percentage applicable to the Company,being 25% of the Shares, are held by the public, or if the Stock Exchange believes that a falsemarket exists or may exist in the trading of the Shares or that there are insufficient Shares inpublic hands to maintain an orderly market, it will consider exercising its discretion to suspenddealing in the Shares.

In light of the above statements made by the Stock Exchange, and subject to results ofacceptances by Independent Shareholders of the Mexan Offer, Independent Shareholders shouldnote that, upon completion of the Mexan Offer, there may be insufficient public float for theShares and therefore dealing in the Shares may be suspended until a sufficient level of publicfloat is attained.

LETTER FROM HERCULES

– 33 –

RECOMMENDATION

Having considered the principal factors discussed above, in summary:

1. the business prospects of the Remaining Business are, in general, positive;

2. the Mexan Offer price represents discounts of approximately 74.6% and 75.9% to the closingprice of the Shares as quoted on the Stock Exchange on the Latest Practicable Date and theaverage closing price of the Shares as quoted on the Stock Exchange during the Review Periodrespectively, implying that the realisable amount from the sale of the Shares in the open marketmay exceed that receivable under the Mexan Offer;

3. the offer price implies a P/B ratio which is inadequate relative to the Comparable Offers andthe market valuation of the Industry Comparable discussed in the sections headed “F. Cashoffer precedents” and “G. Trading statistics of Industry Comparable” above, and thus does notreflect the underlying fair value of the Shares;

we are of the view that the Mexan Offer price is not fair and, on this basis, the Mexan Offer is neitherfair nor reasonable so far as the Independent Shareholders are concerned. We therefore recommendthe Independent Board Committee to advise the Independent Shareholders not to accept the MexanOffer.

However, Independent Shareholders should note that the Remaining Group is highly geared and noplan to reduce the debt had been announced by the Company up to the Latest Practicable Date. Theborrowed funds could be a burden to the Company in terms of interest payments and eventual capitalrepayments. The high level of interest payment will put a strain on profits and restrict or preventpayment of dividends. The additional cash outlay for the thorough refurbishment of the hotel in 2007will inevitably put pressure on the cash flow of the Remaining Business. In addition, in the event thata substantial amount of capital is required for the development of the Remaining Business, the Companymay find it hard to obtain further borrowings from banks and other financial institutions and mayhave to raise equity funding, which may lead to dilution to Shareholders. Independent Shareholderswho are not comfortable with the outlook for the Remaining Group due to its high gearing level and/or the ability of the Remaining Group to satisfy its future funding requirements may consider todispose of the Shares in the open market if the net realisable amount from the sale of such Shareswould exceed that receivable under the Mexan Offer.

Independent Shareholders should nevertheless note that the aggregate amount of Shares owned bythe Independent Shareholders as at the Latest Practicable Date represents approximately 38.0 timesthe average daily trading volume for the Review Period. Independent Shareholders, especially thosewith relatively sizeable shareholdings, may find it difficult to dispose of their Shares in the openmarket without adversely affecting the market price of the Shares in the short term. Accordingly,Independent Shareholders who, having regard to their own circumstances, intend to realise part of alltheir investments in the Shares but believe that because of the size of their shareholding they will beunable to sell the Shares in the open market at a price higher than the Mexan Offer price couldconsider the Mexan Offer as an alternative exit for their investments.

LETTER FROM HERCULES

– 34 –

For those Independent Shareholders who, having regard to their own circumstances, wish to realisepart or all of their investments in the Shares, are reminded that they should closely monitor themarket price and the liquidity of the Shares during the offer period and consider selling their Sharesin the open market during the offer period, rather than accepting the Mexan Offer, if the realisableamount from the sale of such Shares in the open market would exceed that receivable under theMexan Offer.

Independent Shareholders who believe the operations of the Remaining Group will benefit from Mr.Lun’s experiences in property investment, money lending (on security of immovable properties orlisted company shares) and the provision of hotel and property management services could also considerto continue to hold the Shares.

Independent Shareholders should read carefully the procedures for accepting the Mexan Offer asdetailed in Appendix I to the Composite Offer Document and are strongly advised that acceptance orrejection of the Mexan Offer is a matter for individual shareholders based on their own views as tofair value and future market conditions, investment objectives, their assessment of the other meritsand issues discussed above, and their risk profile, liquidity preference, tax position and other factors.In particular, taxation consequences will vary widely across Shareholders. Independent Shareholderswill need to consider these consequences and consult their own professional advisers if appropriate.

Yours faithfully,For and on behalf of

Hercules Capital LimitedLouis Koo

Managing Director

APPENDIX I FURTHER TERMS AND PROCEDURESFOR ACCEPTANCE OF THE MEXAN OFFER

– 35 –

PROCEDURES FOR ACCEPTANCE

(a) If the Share certificate(s) and/or transfer receipt(s) and/or any other document(s) of title (and/or any satisfactory indemnity or indemnities required in respect thereof) in respect of yourShares is/are in your name and you wish to accept the Mexan Offer, you must send the dulycompleted Form of Acceptance and Transfer together with the relevant Share certificate(s)and/or transfer receipt(s) and/or any other document(s) of title and/or any satisfactory indemnityor indemnities required in respect thereof, by post or by hand marked “Mexan Limited Offer”on the face of the envelope to the Registrar, located at 26th Floor, Tesbury Centre, 28 Queen’sRoad East, Wanchai, Hong Kong by not later than 4:00 p.m. on Monday, 7 May 2007.

(b) If the Share certificate(s) and/or transfer receipt(s) and/or any other document(s) of title (and/or any satisfactory indemnity or indemnities required in respect thereof) in respect of yourShares is/are in the name of a nominee company or some names other than your own and youwish to accept the Mexan Offer in respect of your Shares, whether in full or in part, you musteither: