westfield - Scentre Group

188

WESTFIELD FIFTIETH ANNIVERSARY

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of westfield - Scentre Group

Westfieldfiftieth

AnniversAry

Westfield Holdings Limited.Westfield Fiftieth Anniversary. Edited by Paul McNally and Margaret Malone.

Includes index.ISBN 978098078513 (hbk)ISBN 0780980783506 (pbk)

Westfield Holdings Ltd. – History.Corporations – Australia – History.

333.33870994

This book is copyright. Apart from any fair dealing for the purposes of private study, research and criticism or review, as permitted under the Copyright Act, no part may be reproduced by any process without written permission. Inquiries should be addressed to the publishers, Westfield Holdings Limited.

Every effort has been made by Westfield to ascertain copyright ownership of images contained herein, however in some cases information regarding copyright is absent or insufficient. Information regarding the copyright of these images is welcomed by Westfield.

Designed by Stephen Smedley, Tonto Design.Produced and published on behalf of Westfield by Hardie Grant Magazines, Australia.General Manager Mark PatonPublishing Director Lisa PatonPublisher Caroline LowryPrinted in Australia by Blue Star Print Melbourne.

Contents

Introduction 6

1956–1959WestfieldStirs 10From Productive Partnership to Private Enterprise to Public Company

1960–1969Determination,DriveandDebentures 28Setbacks, New Frontiers and the Getting of Market Wisdom

1970–1979 TheQuantumLeap 54Restructuring in Australia, Expanding into America

1980–1989RaisingtheStakes 72Keeping the Core Business Strong in a Turbulent Decade

1990–1999BuildingonStrength 96Capitalising on Hard-Earned Gains and Becoming a Global Player

2000–2009AGlobalStructureforaGlobalCompany 114The Westfield Group Comes of Age

Westfield Honours 162

Westfield Milestones 172

Picture credits 174

Index 175

Chairman’s Review – Annual Report 2009 178

6 WeSTfIeLD5 0ye ARS

Introduction

The original delicatessen, opened by John Saunders and Frank Lowy in March 1955. Situated opposite Blacktown railway station, the shop would be full for half an hour after each train came in from the city, with commuters buying the continental small goods that were still scarce at the time in Sydney.

Half a century ago, in September, 1960, Westfield began its life as a public company with two shopping centres in Sydney’s then outer suburbs and two residential developments.

In the space of one business generation, Westfield has grown to become one of the world’s largest shopping centre owners and managers, and is a market leader in Australia, New Zealand, the United States and the United Kingdom. Throughout, it has played a major part in changing the way the world shops.

Over those 50 years, shareholders in the entities which today comprise the Westfield Group have contributed equity of $19.9 billion and received back some $15.6 billion in dividends and distributions. With a market capitalisation at 31 December 2009 of around $29 billion, some $25 billion of wealth has been created for Westfield shareholders.

Since 1960 original shareholders in the Westfield Development Corporation have received a total return of 27.63% per annum, compared with 10.91% for the Australian Stock Exchange index over the same period.

It is an extraordinary story of industry, persistence, inspiration, drive, leadership and creativity, of careful planning and bold execution.

It is a story that is 50 years old, but it seems every decade brings a new beginning …

Westfield and its centres invoke in the minds of shoppers and competitors a specific image of quality that no other shopping centre company has achieved.TheInTeRnATIonALCounCILofShoppInGCenTeRS.

Introduction 7

8 WeSTfIeLD5 0ye ARS

Right: Sydney, 1958 – the city that would be home to Westfield. Excavation was underway for the Sydney Opera House at Bennelong Point (bottom left) next to the ferry wharves at Circular Quay. The AMP building at the quay was still under construction and the AWA tower was the city’s highest point.

1956–1959 WestfieldStirs

From Productive Partnership to Private Enterprise to Public Company

12 WeSTfIeLD5 0ye ARS

When the two men who were to found Westfield arrived in Australia after the Second World War, there was not a shopping centre in the entire country.

Serious shopping took place in the cities, where large department stores continued to dominate the retail scene as they had done for more than a century. Women wore hats and gloves and a visit to a multistorey department store, with its sweeping aisles, doormen and stylish windows, was a special occasion.

David Jones, arguably the world’s first department store, had been trading in Australia since 1838. In the wake of its success, other nineteenth-century retail giants such as Anthony Hordern, Farmer’s and Grace Bros opened their doors too.

As the cities buzzed, Australia’s suburbs remained quiet and undisturbed, with little promise of change.

Through their department stores, the so-called ‘dukes

of drapery’ experienced unprecedented growth. By 1896, for example, Anthony Hordern had a showroom 100 metres long, employed 4000 people, conducted six million transactions with customers across its counters and delivered two million parcels in its horse-drawn vans.

By the dawn of the twentieth century, the department store dynasties had become part of Australia’s economic elite, ranking alongside the ‘squattocracy’ of rich wool growers in social prestige. As the century progressed, the dynasties disappeared but many of their names continued.

There is some irony in the fact that today these retail pioneers, whose names are cornerstones of Australia’s economic history, are among the anchor tenants of the regional shopping centres pioneered by two European immigrants whose nous for small business and retailing had its genesis in Czechoslovakia and Hungary.

ThepioneerRetailGiants

Left: Monolithic and eternal – at the turn of the twentieth century it seemed department stores like Anthony Hordern would dominate retailing forever. They provided a world within a world – a place to visit by carriage or by catalogue.

Right: Farmer & Co. in 1912. It was grand, modern, and packed with up-to-date merchandise and imported fashion items. Farmer’s was a place to see and to be seen. How could it not continue to flourish indefinitely?

14 WeSTfIeLD5 0ye ARS

Towards the end of the nineteenth century, the concept of the ‘shopping arcade’ reached Australia and was embraced with much enthusiasm in Melbourne and Sydney.

Arcades or gallerias, originally an Arabian concept and later refined in Italy, had proved fashionable in London, Naples, Milan, Brussels and Moscow.

Australian builders immediately set to work on a series of lofty and ornate glass-roofed atriums built to house hundreds of new city shops.

They gave them names redolent of Australia’s British heritage — The Strand, The Victoria, The Imperial, The Royal, Her Majesty’s, and The Piccadilly.

Crowds flocked to these contemporary and sophisticated centres to marvel at the marble and iron lacework and to promenade under their chandeliers.

These arcades of the 1890s could arguably be seen as early shopping centres, or at least forerunners of the modern centres built in the Australian suburbs by Westfield over half a century later.

First among these nineteenth-century arcades was Sydney’s Queen Victoria Building, a palatial retail centre bigger than any of its European models, and so ambitious that it was doomed to failure.

It began life as a municipal market, offering the convenience of one-stop shopping. However, although it was a triumph of the visual, its commercial viability was weak. Its ratios were unsustainable, with rentable space sacrificed for public or decorative space.

Suffering constant and unsustainable financial losses, it fell into neglect and disrepair for decades until it was eventually restored, almost 100 years later, becoming what French fashion designer and retailer Pierre Cardin considered to be ‘the most beautiful shopping centre in the world’.

Like all other modern suburban shopping centres, the reborn QVB offered parking on site.

Arcades

The first shopping centres

Stylish, ornate and protected from the elements, arcades offered diversity, interest and a fashionable place to promenade. They were like an enclosed ‘ high street’.

16 WeSTfIeLD5 0ye ARS

JohnSaundersAs a child, John Saunders would often spend time in his father’s leather-goods shop in north-eastern Hungary. It was the 1920s and as he watched his father negotiating, he never imagined that in a few years he would find himself behind the same counter.

Following his father’s untimely death from illness, John gave up school and committed himself to the business. He was 13 and, with the entrepreneurial flair that would eventually become his trademark, he doubled the shop’s turnover in a year.

Business flourished until 1943 when the pro-Nazi state police singled Saunders out. At the age of 21, he found himself in a detention centre for Jews.

It wasn’t long, however, before he began to extract privileges, managing on several occasions to visit the family home. Through natural charm and intuition he always found a way to better his lot.

Later he was taken to a concentration camp. Driven by his highly developed instinct for survival, he again organised for himself a relatively comfortable situation with good access to food.

When the war was over, he returned home to resume the leather trade and begin a new woodworking business, which thrived, eventually employing 40 people.

But the new communist regime nationalised his businesses without offering compensation, and in 1949 Saunders decided to flee Hungary.

In mid January 1950 his ship docked in Sydney. In his luggage was an English dictionary in which the word ‘impossible’ had been scratched out.

John Saunders, aged 25, in Hungary before migrating to Australia.

195 6 –1959 Westfield Stirs 17

frankLowyGrowing up in a small rural town in southern Czechoslovakia in the 1930s, Frank Lowy witnessed financial hardship at close quarters. His family was of modest means and during his childhood Lowy would help in his mother’s grocery shop. When the Second World War broke out, his family sold the shop and sought sanctuary in Budapest. The family pitched in to help each other out financially and by the age of 13, Frank was assisting his brother who had a small enterprise, buying and selling metalware.

He also had a minor entrepreneurial venture himself. When his formal education ended with the Nazi invasion of Hungary in March 1944, young Lowy was forced to live by his wits. Living mostly on the streets, he quickly learned the value of vigilance and developed a respect for detail that would serve him for the rest of his life.

After the war he left Europe for Palestine and, at the age of 17, became a commando in the Golani Brigade, which was fighting for Israel’s independence. It was during this period that he discovered the power of trust and teamwork. When the Israeli War of Independence ended, he found a job at a bank and studied accountancy at night.

In the meantime, the surviving members of his family had immigrated to Australia. By 1952, propelled by the desire to be reunited with his family, he left Israel and arrived in Sydney on 26 January, Australia Day. All he possessed was a small suitcase, a little knowledge of English and a debt — his airfare to Sydney.

Frank Lowy, aged 21, photographed before leaving Israel for Australia.

18 WeSTfIeLD5 0ye ARS

In the early 1950s, the recently arrived John Saunders set himself up in business at Sydney’s Town Hall railway station. He had persuaded the authorities to let him have what was no more than ‘a hole in the wall’ from which he could sell sandwiches and smallgoods to commuters who flowed constantly in and out of the station.

It was here that Saunders first came into contact with Frank Lowy, who had a smallgoods delivery run. Lowy, also of similar background, impressed Saunders with his reliability, natural courtesy and accuracy. Saunders never had to weigh the goods Lowy brought because they matched his invoices, neither too much nor too little — right on the mark.

Saunders, who already had several years of business experience in Europe, had a gut feeling that young Lowy, eight years his junior, would make an excellent partner. In him, he saw qualities they shared — energy, drive and a determination to make a success of himself in the new country.

A partnership was duly forged and together they took a step that would set the direction for their commercial future. They both knew the food business and, instead of taking the easier option of opening a new shop in the inner city, they looked to the suburbs for more daring but lucrative opportunities.

The outlying western suburb of Blacktown was on the brink of a boom. The railway had just been electrified and newly arrived immigrants were pouring into the area. Many had come to work in industries associated with the massive Snowy Mountains Hydro-Electric Scheme.

The partners found a vacant shop in Blacktown and telephoned its owner, Jim Simpson, whose reluctance to rent his shop to immigrants eventually gave way as a result of the duo’s persistent badgering.

An hour’s train ride from the city, the shop was situated directly opposite Blacktown railway station, perfectly positioned to catch the tide of daily commuters.

With its barrels of olives and herrings, rounds of cheese, meats and fresh rye bread, it supplied Blacktown’s burgeoning population with continental fare they couldn’t get anywhere else.

As Saunders used to say, ‘In the city delicatessens, Australians buy devon by the slice; in Blacktown, immigrants buy salami by the yard.’

The shop flourished. Just as the suburbs had proved a boon for this first venture, so they would continue to provide the budding partners with undreamed-of opportunities in the future.

GoWest,youngMen!

Right: Robinson’s Street Directory of 1956 showing the route from Sydney to Parramatta and on to Blacktown.

New to Sydney, the pioneering Westfield pair established themselves in an area more than an hour’s drive from the CBD.

20 WeSTfIeLD5 0ye ARS

Above: 1950s Sydney. The bitumen and telegraph poles of Parramatta Road heading west out of Sydney. Together, and often singing, Saunders and Lowy drove down this road six days a week.

Right: Blacktown’s Main Road in the early 1950s. Not yet a thriving metropolis, the town was on the cusp of dramatic economic change. Soon, the railway would be electrified and immigrants would flood in. Saunders and Lowy would buy the GG store, knock it down and build shops on the site.

195 6 –1959Westfield Stirs 21

Below: A celebration to mark the electrification of the railway in 1955. The next big celebration in Blacktown would be the opening of Westfield Plaza some four years later.

22 WeSTfIeLD5 0ye ARS

Each day, over the counter at their shop, Saunders and Lowy heard about people who had come to Blacktown but had nowhere to live. The situation was unusual because there was employment to be found in companies like EPT (Electric Power Transmission), an Italian operation which built electric cables for the Snowy Mountains Hydro-Electric Scheme, but no ready accommodation.

The Snowy scheme, described as one of the world’s great engineering feats and perhaps the most imaginative of all postwar Australian construction projects, needed vast supplies of manpower to build a system of dams and tunnels for the development of hydro-electricity and to irrigate the dry western areas of New South Wales.

Although the scheme drew workers from all over the world, most came from Europe. These Europeans would have found outlying Blacktown provincial, if not plain dull. Sensing this, Saunders and Lowy found another shop a few doors down and opened their next business, a coffee lounge. With its tables and chairs on the footpath, music, genuine espresso and continental atmosphere, it offered people a small taste of the life they had left behind.

But something bigger was exercising the partners’ minds — instead of just providing coffee, why not provide houses too!

Between 1954 and 1961 the population of Blacktown almost tripled. It was the biggest increase the area had ever experienced, and to meet the demand for housing, the local council began to rezone farmland for residential use. Typically, it allowed a ten-acre farm to be subdivided into small plots which could then be sold off for £1000 each. Onto these plots, people could bring inexpensive mobile homes.

The process seemed relatively straightforward so Saunders and Lowy borrowed money and plunged in. They persuaded a local farmer that it was an excellent time to sell. Six months later, they were counting their profits, which were encouraging rather than large.

The coffee shop had become something of a talking point in Blacktown, and when a Greek couple offered a staggering £10 000 to buy it, the partners agreed immediately and put their £8000 profit into their next property venture.

Using the back shelf of the delicatessen as an office, they did all the property development work themselves — negotiating the purchase, employing contractors to put down roads, advertising, and then selling off the plots.

While Saunders would converse easily with customers and acquaintances and, in the process, learn about new opportunities for development, Lowy began to learn about the Australian banking system, the value of leverage and the importance of legal documentation.

A solid relationship with the local bank manager helped the partners through many tight squeezes. One minute Lowy would be behind the counter, in his white coat, weighing sausages, and the next he would be in a suit and tie, sitting across the desk from the bank manager. One transaction might have been worth sixpence, and the other £10 000, but to the partners they were equally important — every detail mattered.

Then one day something happened which would change the course of their remarkable lives once again.

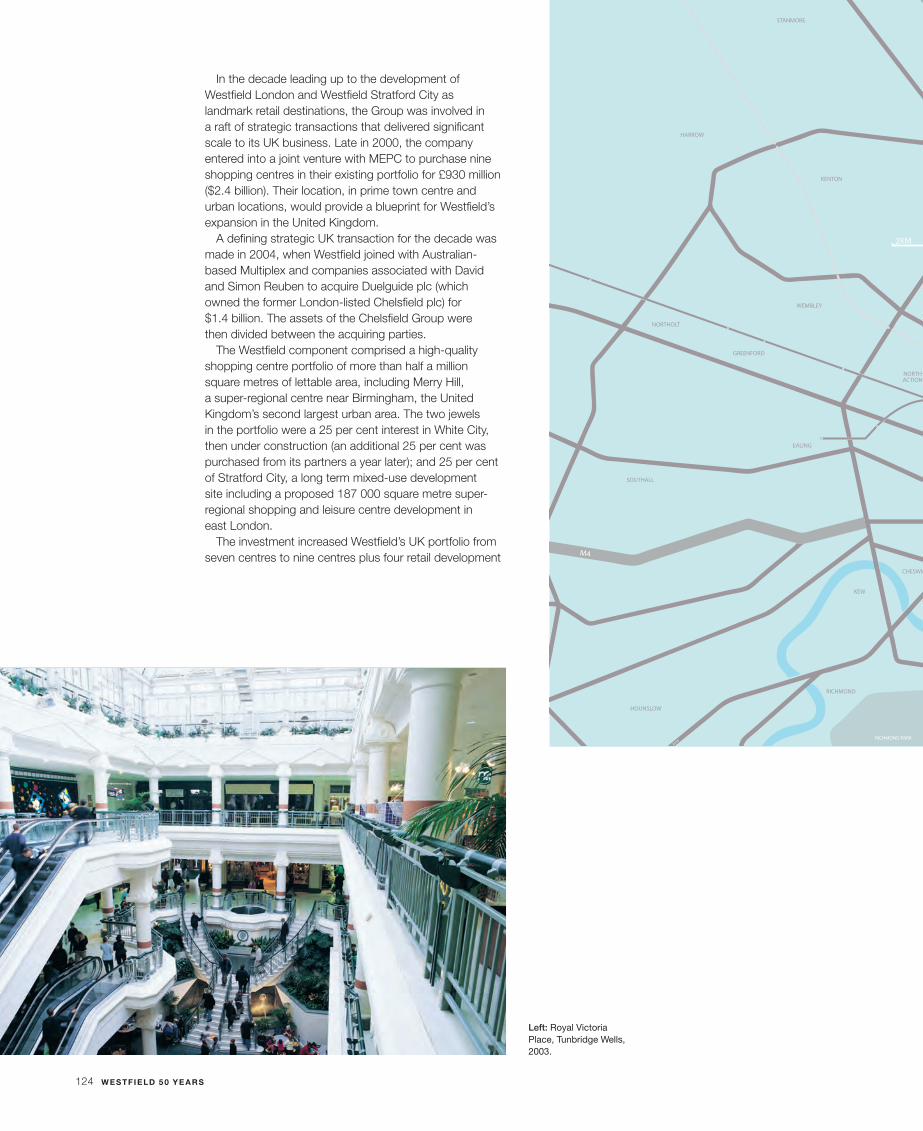

BuyingIntotheBoom

195 6 –1959Westfield Stirs 23

Right and below: Following the Second World War, Australia threw open its doors to immigrants. ‘Populate or Perish’ was the slogan of its nation-building drive. Here, immigrants arrive on the ship Empire Brent in 1948. After lining up and posing for an official photograph, they boarded buses waiting to take them away from Circular Quay.

24 WeSTfIeLD5 0ye ARS

From time to time Erwin Graf, a Hungarian-born architect who was putting up houses around Blacktown, would drop into Saunders and Lowy’s delicatessen to buy lunch. He and the partners would chat about prospects in the area.

When Graf’s company bought some land near their shop and, instead of putting up houses, unexpectedly built half a dozen shops, Saunders and Lowy had a bright idea: they could do that too!

By then their property business had brought them £30 000 and, on advice from their solicitor, they transformed their partnership into a private company. But what to call it? One day, while travelling home from Blacktown together, they hit on the name ‘Westfield’. As they were doing business in the western suburbs, the word ‘west’ was a natural choice and, as they were subdividing farmland, ‘field’ seemed appropriate. It felt right and Westfield Investments Pty Ltd was born.

Energised by their new venture, the pair began searching for land suitable for retail development. They didn’t have to look far because, a short while later, a customer told Saunders that a couple of old shops, owned by a local resident, would be coming up for sale. The shops were around the corner from the delicatessen and, as they were located between the Graf shops and the local post office, well positioned for passing trade. The partners took one look and saw potential. The two existing shops could be pulled down and more built on the same site.

Soon four new shops went up on this site. There was a ready market and they were swiftly sold.

Word quickly spread and the partners were approached by the clothing store Sydney Snow Pty Ltd. Snow’s wanted its own large and spacious new shop next door to the line of four and it wanted Westfield to build it as a package deal.

Neither Saunders nor Lowy knew what a package deal was, but they soon found out, agreed to the deal and delivered. This project yielded Westfield a tidy £8000 profit.

Very early in 1958 Saunders and Lowy were ready to take off their aprons and concentrate on the lucrative margins of the property development business.

The delicatessen was sold for £20 000 and they took offices above some shops around the corner.

Interested in the retail scene, they would devour any international magazines and journals about trends and innovations they could get their hands on. The fastgrowing shopping centre phenomenon in the United States captured their imagination. What was stopping them from getting a piece of the action?

Shopping centres were just beginning to emerge in Australia. In 1957 two centres opened, the Chermside Drive-In Shopping Centre in Brisbane, and the Top Ryde Shopping Centre in Sydney.

Westfield bought an acreage abutting the shops below its office from landlord Jim Simpson and began to plan its first shopping centre. While the plans were on the drawing board, Saunders took a trip to the United States to see this mall phenomenon with his own eyes.

hey,WeCanDoThatToo!

195 6 –1959Westfield Stirs 25

Right and below: 1950s merchandise. A child roadtesting the latest tricycle; men’s suits being carefully inspected.

26 WeSTfIeLD5 0ye ARS

The official opening of Westfield Plaza in July 1959 was the biggest event in Blacktown since the celebrations marking the electrification of the railway in 1955.

Newspapers described it as ‘the most modern American-type combined retail centre’. People flocked to see it.

The NSW Minister for Labour and Industry, Mr J. J. Maloney, who officially opened the new centre, predicted it would establish Blacktown as a major shopping venue on the now fast and efficient Western Line.

With its supermarket, two department stores and 12 shops built around a courtyard, Westfield Plaza was a showcase for new trends and technology.

Individual shops, harmoniously decorated in accordance with the centre’s colour scheme, were arranged to allow individual expression by their shopkeepers.

There were large show windows, special sprayed plastic finishes ‘carried out under licence to an American

company’, imported mosaic tiles arranged in candy stripes, and stairs with distinctive imported plastic handrails.

From his visit to the United States, John Saunders had witnessed first-hand the importance of the car in the future of shopping centres, and Westfield Plaza provided for its customers 50 free on-site parking spaces.

The centre cost £250 000 and gave the principals of Westfield Investments Pty Ltd their first tough lesson in adapting to council regulations.

Although there were moments when the project looked wobbly, the principals’ determination to succeed never waned.

Within weeks of the opening, Westfield Investments Pty Ltd found itself in great demand as offers of new partnerships and joint ventures flooded in.

Modern,American,Convenientandnew

Below: Westfield Plaza — the modest first link in a chain of shopping centres that was destined to stretch across continents.

Below right: Newspapers of the time described Westfield Plaza as ‘a most modern centre with its own car park, situated in the heart of Blacktown shopping area, only 50 yards from the railway station’. One paper speculated that ‘it could well be the forerunner of a new deal for the harassed housewife who has had to put up with so much in the postwar period’.

Westfield opens its first shopping centre

195 6 –1959Westfield Stirs 27

Having established a base, a reputation, and some working capital, the Westfield partners felt ready for bigger challenges. Were they to base themselves in the city, rather than on its outskirts, it was likely more opportunities would come their way. There, they could mingle with bigger business and be closer to their other projects. So it was that they made the far-reaching decision of keeping an office in Blacktown, while turning their eyes to the CBD and also, as it turned out, to the Sydney Stock Exchange.

ThenextStep

Above: By Christmas 1959, Westfield Plaza was established as the commercial hub of Blacktown’s 100-odd businesses and services. With the railway line and parking, it attracted shoppers from all over the area. For people in outlying districts, there was also a bus network to bring them to the ‘progressive shopping centre’.

From Blacktown to the city

Setbacks, New Frontiers and the Getting of Market Wisdom

1960–1969 Determination,DriveandDebentures

30 WeSTfIeLD5 0ye ARS

The success of the newly formed Westfield Investments venture in Blacktown caught the attention of developers all over Sydney and within weeks of Westfield Plaza’s opening, Saunders and Lowy found themselves in demand, with offers of joint ventures, partnerships and commissions coming from unexpected quarters. They immediately took up several of these offers. With one partner they bought more land for subdivision in Blacktown; with a consortium they bought land at Turramurra in the northern suburbs of Sydney; and for Snow’s they undertook a large contract to build new stores at Cabramatta and Penrith.

Typically, Saunders and Lowy would contribute 20 per cent of the capital, and the financial partner the remaining 80 per cent. These deals required moving thousands of pounds around and, from time to time, Westfield’s overdraft was fully extended. The local bank manager saw their potential, trusted them implicitly and would give them short periods of grace. One day, however, a supervisor from the bank’s head office discovered they were £15 000 over their limit and was apoplectic. However, such was the bank manager’s trust in Saunders and Lowy that he wrote out a personal cheque to cover this amount.

Although Westfield Investments was the proverbial honey pot of Blacktown, with people and activity buzzing around

it, Saunders and Lowy knew opportunities in the city would be greater. So, after taking the precaution of setting up new contacts, they made the move to Caltex House in the CBD, which was the first modern high-rise office block in the city. Westfield took along a handful of employees including an accountant, a builder and a scout to look for new projects, and leased a modest amount of office space. As before, Saunders and Lowy shared an office.

From their new premises they began to make fresh contacts and were persuaded by a fellow Hungarian immigrant, Paul Kent, then managing director of the publicly listed Astor Consolidated Mills Ltd, that there would be tremendous advantages in taking Westfield public. It would, he argued, raise funds which they could use for bigger, more lucrative developments. After much deliberation, Kent introduced Saunders and Lowy to the principals of stockbroker Clarence Degenhardt and Co. He in turn introduced them to Don Stephens, chairman of the publicly listed transport company FH Stephens, and suggested Stephens be chairman of the new publicly listed Westfield. Stephens had ‘establishment’ contacts and would be able to open doors.

TotheCBD

Saunders and Lowy made the move from Blacktown to Caltex House in the CBD — the first modern high-rise office block in the city.

19 6 0 –19 6 9Determination, Drive and Debentures 31

Above: Caltex House in 1959, the year Westfield moved in.

32 WeSTfIeLD5 0ye ARS

By the time the company went public, Saunders and Lowy had already successfully undertaken many projects including obtaining a site for a motel in Sydney’s North Shore, subdividing for home building sites, and building shopping centres. Although Westfield Development Corporation Ltd, as the public company would be known, would concentrate on real estate and property development in general, the prospectus highlighted the fact that it would retain a special focus on shopping centres. It predicted there would be a rapid expansion of shopping centres in Australia and noted that both Saunders and Lowy had given undertakings that they would not engage in shopping centre developments other than through this company. In what would later prove to be a remarkable understatement, the prospectus also stated that shopping centres ‘would yield satisfactory returns’.

It was decided that four of Westfield’s projects would be put into the public company. These included a recently acquired site at Hornsby, on the northern outskirts of Sydney, a shopping centre under construction at Sutherland, and residential developments at Pennant Hills and St Ives. On the strength of these projects, Westfield Development Corporation Ltd floated in September 1960.

The issue was for 300 000 ordinary shares priced at 5/–, half of which was payable on application, so raising £75 000, with a further £75 000 payable by January 1961. There was also an issue of 300 000 unsecured convertible notes at 5/– each. About 38 per cent of the stock went to the public, 20 per cent went to Kent, with Saunders and Lowy each owning half of the remaining 42 per cent. The board comprised founding chairman Don Stephens, Paul Kent, Saunders and Lowy.

The float brought a change in banking relationships for Westfield. The bank that had been so helpful a few years earlier was not willing to support this bold step. Despite the move to the city, the pair had continued their relationship with the bank at Blacktown. However, the size of the loan was beyond the capacity of the local bank manager with whom Saunders and Lowy had enjoyed such a good rapport. When this manager referred the application to his head office, it was rejected. The risk was too big. Paul Kent then decided to introduce Westfield to his banker, the National Bank of Australasia, which later became the National Australia Bank. Fifty years later the relationship between Westfield and National Australia Bank continues.

Thefloat

Left: A call at the Sydney Stock Exchange, 1960.

Right: The Sydney Stock Exchange building, 1960.

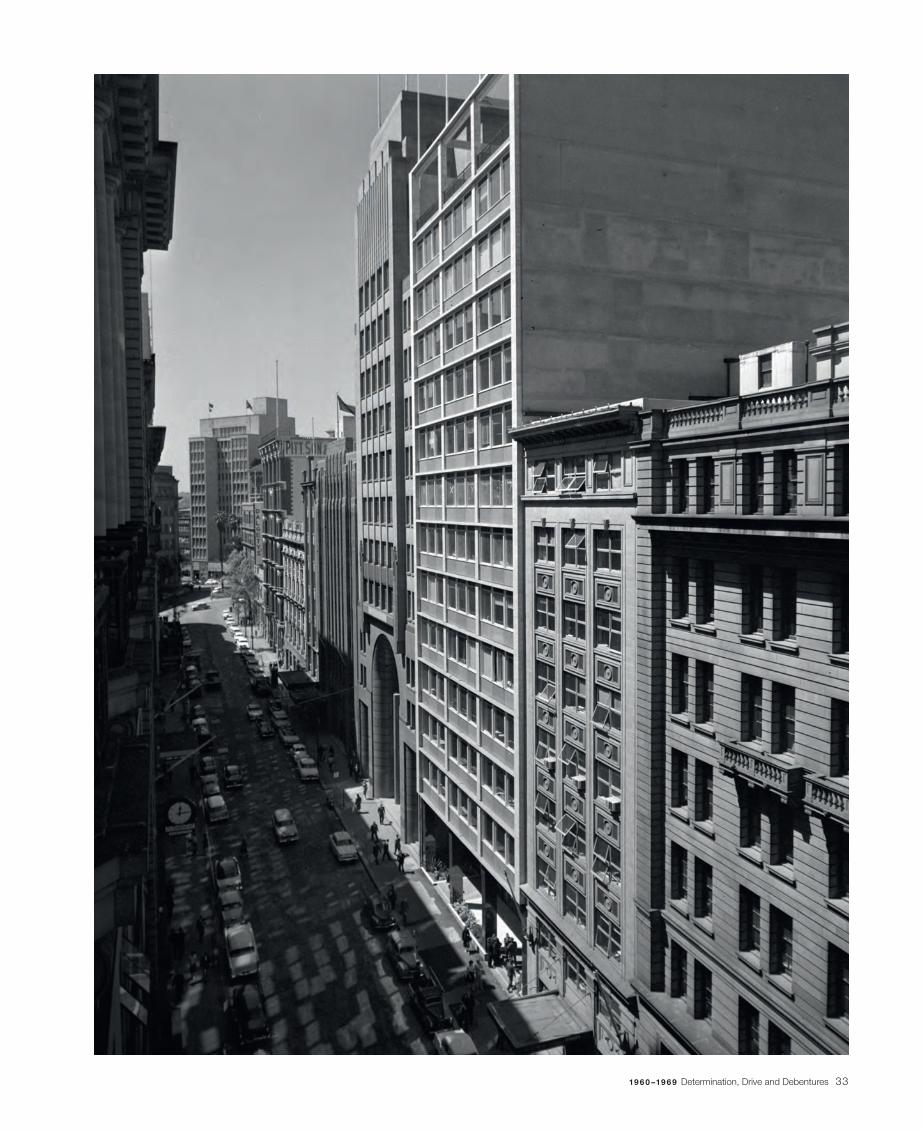

19 6 0 –19 6 9Determination, Drive and Debentures 33

34 WeSTfIeLD5 0ye ARS

Left and below: Anyone who invested £500 in this float in 1960 and kept the shares for 50 years – provided they reinvested all dividends and bonus issues – would have, by the end of 2009, made about $159 million (according to ASX/S&P Index Services). This investment return is unrivalled in Australia.

In 1959, while young Kerry Stephen was serving on HMAS Tobruk in the Far East, most of his fortnightly wages were going directly into his bank account in Sydney.

He was a naval lieutenant with the Royal Australian Navy ships deployed to assist during the Malayan Emergency and had little opportunity to spend money. For ten months, his bank account grew steadily.

When he eventually returned to Sydney in 1960, his father Alex, who was aware of the money he had saved, had some financial advice for him. ‘Buy yourself some Westfield Development Corporation shares,’ he said.

Kerry, then 22 years old, had never owned shares but had faith in his father’s judgment. He withdrew a few hundred pounds — his life savings and accumulated wages — and bought directly into the Westfield float.

It was the best investment he would ever make. In the first few years, before he started a family, he would reinvest all the dividends and bonuses.

‘With five children and a Navy salary it was difficult, if not impossible, to put them all through private schools. However, by owning Westfield shares it was possible. Every time school bills arrived, I would be able to sell some of my Westfield shares,’ Kerry says.

‘I have continuously owned Westfield shares for 40 years and still have a few left. I know that if I’d kept them all, I would have many millions of dollars today, but my children would not have had the start in life that they have been given.’

Kerry Stephen AM left the Navy in 1986 with the rank of Commander and has no doubt that the investment he made 40 years ago changed the course of his and his family’s life.

‘I will always be grateful for my father’s advice and Westfield’s growth,’ Kerry says.

KerryStephen

‘All on my father’s advice … ’

19 6 0 –19 6 9Determination, Drive and Debentures 35

36 WeSTfIeLD5 0ye ARS

Left: Westfield Plaza shopping centre, Hornsby, Sydney, New South Wales, September 1961.

Right: Putting up advertising billboards for the Hornsby centre prior to its construction.

After the buoyant economic activity of the late 1950s, Westfield’s maiden year as a public company in 1960 was marked by a severe credit squeeze, the first of many to befall the fledgling company. This did not augur well for Westfield which urgently needed funds for several crucial projects. At the time, it was impossible to foresee that the 1960s would eventually become one of the most prosperous periods in Australia’s economic history.

The 1960s were all about opportunity. Australia’s population in 1945 was 7 million; by 1963 it was 11 million. Car ownership, a key factor for retailers who offered parking, grew from one vehicle for every nine people in 1945 to one for every three by 1968. Spending was booming too. New suburbs were appearing everywhere. In 1947 some 47 per cent of families did not own their own homes. By 1961, 70 per cent were homeowners or mortgage payers.

It was also the decade which would see the Vietnam War tear at Australia’s heart and in which, in 1966, the new decimal currency came into circulation.

Into all of this came television and its bountiful opportunities for advertising.

Commercial television and retailing seemed made for each other. Television stars began ‘launching’ new supermarkets and soon politicians followed suit.

Even the Prime Minister, Sir Robert Menzies, agreed to speak at the opening of a supermarket in Canberra in 1963. The grandson of a grocer himself, he described the supermarket as ‘the last word in shopping facilities’.

In 1960, Westfield most pressingly needed funds to complete the shopping centre at Hornsby, but there was a building industry recession and banks and finance companies were unsupportive of shopping centres. Westfield was also an unknown quantity and banks didn’t feel comfortable taking the risk. To get out of the squeeze, Kent approached his stockbrokers again, who agreed to underwrite a £150 000 debenture issue.

By the time the prospectus for this issue was published in 1961, Westfield had refined its business focus to acquiring and developing carefully selected projects for retention as income-producing investments; and to acquire real estate for development and re-sale.

Because of rising interest rates, the timing of the debenture issue was poor and it closed three months later raising slightly more than half of the amount sought. The underwriter honoured its agreement and Westfield was saved from serious financial hardship. Westfield also managed to obtain some help from T&G Insurance company (later AXA), which came in as a long-term lender, assuring the future of the Hornsby centre.

AWobblyStarttoaprosperousDecade

Westfield’s maiden year

19 6 0 –19 6 9Determination, Drive and Debentures 37

38 WeSTfIeLD5 0ye ARS

Brisbane was the home of Australia’s first-ever shopping centre. The Chermside Drive-In Shopping Centre, which opened in May 1957, was built by Allen & Stark Ltd and was the first development of its kind outside of the United States. Because of its free off-street parking for 700 cars, it was marketed as ‘an island of retailing in a lake of parking’. It was such a noteworthy development that a crowd of more than 150 000 shoppers gathered to watch the Premier of Queensland, Jack Duggan, turn the key at the main entrance.

Chermside went through numerous redevelopments, survived storms, floods and fires and, just before its

fortieth birthday, was purchased by Westfield and became Westfield Shoppingtown Chermside. A few months later, it was ravaged by yet another hailstorm.

Shortly after Chermside’s debut, in November 1957, the Top Ryde Shopping Centre opened its doors in Sydney. It drew shoppers from far afield who wanted to avail themselves of excellent service and a variety of quality merchandise which could be had all under the one roof.

Westfield Plaza in Blacktown was considerably smaller than Chermside and opened next, in July 1959. The following year, a blockbuster shopping centre opened in Melbourne.

Australia’sfirstShoppingCentres

Below: The opening of the Chermside Drive-In Shopping Centre in Brisbane, 1957.

19 6 0 –19 6 9Determination, Drive and Debentures 39

Right: The Top Ryde Shopping Centre, Sydney, in 1958 – the second shopping centre in Australia.

Below: The covered bus port and facade of the main building of Chermside, 1957.

40 WeSTfIeLD5 0ye ARS

In October 1960, an important event in Australian retailing took place in Melbourne. The country’s biggest regional shopping centre, Chadstone, opened. It had cost £6 million, housed 83 retailers, had parking for 2500 cars and, in every way, was state of the art. Built by the Myer Emporium, it was described as ‘a town within a town’ and was said to represent a turning point in retailing.

As much as they yearned to be on the guest list, Saunders and Lowy did not receive an invitation to the opening. Undeterred, Saunders flew to Melbourne, took a taxi out to Chadstone, crawled under the fence, being careful to protect his suit, and mingled with the crowd. He had a splendid morning, looking around, admiring the features, noting the innovations and listening carefully to the speeches. He collected as much information as he could, left via the official exit and hailed a taxi for the airport.

Nothing that he had picked up went to waste. In fact, Saunders was an obsessive reader of newspapers, magazines and journals — anything that provided new ideas that could augment the business. One such idea he was extremely keen on was the motel.

In 1959, Saunders and his wife had travelled to an international shopping centre convention in Las Vegas and, along the way, went motel sightseeing between San Francisco and Los Angeles. There were very few motels in Australia and those were shabby and poorly serviced. In contrast, US motels were pristine and

the rooms had televisions, refrigerators and modern bathrooms. Inspired, Saunders returned home with plans to build a high-quality motel in Sydney. A few months later, Lowy would make a similar reconnaissance of motels and shopping centres along the US West Coast, but this time accompanied by an architect, Emery Nemes. Together, they measured and analysed and checked and rechecked and, by the time they returned to Australia, they had the business mapped out.

Westfield found a parcel of land north of the Sydney Harbour Bridge on the Pacific Highway and began the planning for the Shore Motel. One afternoon, while Saunders was checking progress at the site, a man approached him claiming to be a Swiss graduate of one of the famous hotelier schools. Saunders hired him as manager on the spot.

This was typical of Saunders’s instinctive style of business and by 1962 the Shore Motel had exceeded even the company’s high expectations. Years later, it would be expanded, gain an exotic Spanish-style façade, complete with a tower, become a local landmark and be renamed the Shore Inn.

Saunders’s unconventional hiring practices were on display again in the 1980s, when he invited a chef in Hungary to work at the Shore Inn. The chef accepted and the Shore Inn flourished. It has since undergone another transformation, being converted into an apartment building.

ChutzpahandtheGatheringofIntelligence

The Shore Motel

Left: Chadstone shopping centre, Melbourne, in 1960.

19 6 0 –19 6 9Determination, Drive and Debentures 41

Below: The Shore Motel, Pacific Highway, Artarmon, in Sydney’s North Shore, as it was in 1962. This was Saunders’ ‘baby’, a project that he took a great personal interest in and nurtured. When he left Westfield, in the 1980s, he bought it for himself.

42 WeSTfIeLD5 0ye ARS

While the Hornsby centre was going up, one prospective tenant, the grocery chain Matthew Thompson, was taken over by the large Melbourne retailer G. J. Coles. Coles wanted to enter New South Wales and expand beyond its variety range into food.

Lowy approached Coles and managed to persuade the company to take space in the new Hornsby centre. During the negotiations, he and Saunders met Coles’ chairman, Sir Edgar Coles, and mentioned they had a couple of other suburban sites the newly arrived Coles may well find suitable for its expansionary plans.

Sir Edgar, impressed by what he heard, sensed potential in the relationship with Westfield and commissioned it to build more supermarkets.

With Lowy and others, he would drive around Sydney and its environs in a chauffeur-driven car, looking for well positioned sites in densely populated suburbs with poor retail services. Sir Edgar would sit in the front seat and, through the window, point and say, ‘Get me a site here and get me a site there.’

‘And we did,’ remembers Lowy. ‘It was music to our ears.’

Westfield quickly understood exactly what Coles required and deployed scouts to locate sites. In the early 1960s, in a matter of three years, it had built seventeen supermarkets for Coles, and played a major role in getting Coles established in New South Wales.

‘Musictoourears’

Opposite: Three examples of Coles supermarkets built by Westfield in the early 1960s. From top: Baulkham Hills, Liverpool, and Gosford.

Coles expands into New South Wales

A beaming Frank Lowy. Seventeen supermarkets for Coles in three years spelt success for Westfield.

19 6 0 –19 6 9Determination, Drive and Debentures 43

44 WeSTfIeLD5 0ye ARS

When the Hornsby shopping centre began trading in the early 1960s, it initiated a social shift across the shire. Up until then, the area had suffered from a lack of welcoming meeting places in which people could congregate. Unlike, for example, the piazzas in Italy, there were no designated spaces in the built environment where people could gather. There was just bland suburban sprawl.

Although Hornsby had experienced considerable population growth, its retail heart had remained static.

Westfield changed that. With a department store, hardware store, 22 shops, a supermarket and ample parking, it drew in people from all over the district. It

generated new jobs and the suburb buzzed with activity. Although the primary function of retailing has always

been about the exchange of goods and services for money, its secondary function has been to provide an environment for social interaction. Westfield recognised this early on and concentrated on promoting this secondary aspect. While ensuring the commercial fundamentals were sound, it placed great importance on community needs, and on providing a place for people to meet and have an experience so pleasurable they would want to do it over and over again.

TheAussiepiazza

An unexpected development

19 6 0 –19 6 9Determination, Drive and Debentures 45

By its third year as a public company, Westfield had experienced considerable growth in its operations. The economic shakiness of its early months was but a memory and the company was on firm and lucrative ground. Not only had business opportunities increased but Westfield had evolved into a one-stop shopping centre company. It did most things for itself — it built, planned, designed and developed all within its own organisation. This resulted in the construction of highly efficient centres with low capital costs.

By the end of 1962, Westfield had these eight projects either completed, on the drawing board or under way in metropolitan Sydney.

Growth,Growth,Growth…

Left: An architect’s drawing of the proposed Hornsby development.

Right: Westfield’s eight projects in Sydney by the end of 1962.

Westfield’s third year

46 WeSTfIeLD5 0ye ARS

Large stores, such as Mark Foy’s in Sydney, dominated retailing in Australia between the wars. Many such stores had become prosperous enough by the end of the nineteenth century and the beginning of the twentieth to erect impressive, ornate buildings. They had also become household names, trading on customer goodwill and faultless reputation.

After the First World War, these grand retailing houses quickly detected the public’s need to put faith in the country’s institutions. Thus they promoted themselves as bastions of traditional values and patriotism and, when the

Second World War loomed, became involved in the war effort.

The culture of these big retail institutions was largely British. All had well-established London buying offices, UK-trained managers and ran promotions like ‘Empire Week’. Tremendous value was placed on the phrase ‘British Made’. When it was used to describe merchandise, it was synonymous with quality.

The big stores actively exploited the gulf between the city and the suburban shopping experience. The city was cosmopolitan and in the big stores customers were made

howDidThis…BecomeThat?

Right and opposite: The grand and commanding Mark Foy’s department store, set on a full city block, Sydney, 1939 …

Australia’s grand retailers

19 6 0 –19 6 9Determination, Drive and Debentures 47

to feel important. Staff were excessively polite, liveried doormen opened doors and made polite greetings, and customers could choose to be personally guided through the store during their visit. There was an exaggerated emphasis on ‘good service’.

However, by the 1930s chainstores offering cheap merchandise which customers could pick off the shelves themselves were flourishing in the suburbs. These American forerunners of modern self-serve supermarkets began emerging at the beginning of the Depression. The busy atmosphere, the goods on open display, the ability to examine merchandise, the bins and ‘cash only’

transactions gave the impression of bargain shopping. In fact, the first Woolworths was set in a basement and became known to its customers as a ‘bargain basement’. The resurgence in suburban retailing began to affect the city retail houses.

Eventually, only large stores in the very heart of Sydney, such as David Jones and Gowings, remained in place. Those just outside the heartland, such as Mark Foy’s, struggled on futilely. Despite their size, range and priceless street frontage, these stores couldn’t survive. Ironically, what did survive in the Australian idiom was the saying, ‘He’s got more front than Mark Foy’s.’

… and downsized in Westfield’s Eastwood shopping centre, 1964.

48 WeSTfIeLD5 0ye ARS

In 1966, when Burwood Shoppingtown opened six months ahead of schedule, it was hailed as one of the most beautiful and finely detailed air-conditioned indoor shopping centres in the world. Its trade area potential covered more than 150 000 people with a total annual retail expenditure of over $100 million.

For Westfield, the Burwood centre represented many firsts: • It was the first centre to open with a major department

store. In this case it was the leading national

department store chain, Farmer’s, and Burwood marked the beginning of a long and fruitful business relationship between the two companies.

• It was also the first centre to benefit from a major marketing effort. As part of that campaign, it became the first to be branded with the Shoppingtown logo and to use the Westfield ‘family of five’ in its advertisements.

WestfieldComestoTown

Burwood Shoppingtown

Above: A Westfield advertisement in The Sun newspaper, October 1966.

By the second half of the 1960s, shareholders in Westfield would have had good reason to congratulate themselves on their investment. A shareholder who invested $1000 in the company in 1960 had, by 1965, an investment worth $2817, assuming that all dividends and other benefits were invested in additional shares. Over the next five years, this investment would soar to $16 850.

During this five-year period of unprecedented growth, Westfield completed major projects every year. It was busy expanding beyond not only Sydney, but beyond New South Wales.

In 1965 it completed a supermarket for Coles and opened a shopping centre at Figtree in Wollongong, south of Sydney. The following year it completed another Coles supermarket and then opened the Burwood centre six months ahead of schedule.

Not stopping to draw breath in 1967, it established a conspicuous presence in Queensland with the opening of the Toombul shopping centre.

In the meantime, it had been renovating and enlarging the Hornsby centre to four times its original size and opened this new redevelopment in 1968.

Then, in 1969, it bought the ailing Miranda centre from Farmer’s (now part of Coles Myer) and began to remodel it. This year also saw Westfield make its debut appearance in Victoria with an impressive new centre at Doncaster.

BuildingupaheadofSteam

19 6 0 –19 6 9Determination, Drive and Debentures 49

Right: The Sun newspaper reporting on the development of Burwood Shoppingtown and featuring the Westfield family of five.

Expanding beyond Sydney

50 WeSTfIeLD5 0ye ARS

GrowthRecord($’000s)1961–1970

Right: The Dee Why centre going up on Sydney’s northern beaches.

Monthly Net IncomeIncome Type Amount

Monthly Net Income

Other Monthly Income

$4,500

$2,500

Available Cash $7,000

Monthly ExpensesExpense Costs

Mortgage

Taxes

Car Payment

Car Insurance

Home Owners Insurance

Cable Bill

Gas/Electric

Monthly Prescription

$2,300

$600

$350

$60

$127

$120

$88

$50

Total Monthly Expenses $3,695

Growth Record ($'000s) 1961–1970Income and Expenses 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970

Net Profit (After Tax) $54 $2,226 $2,815 $3,098 $3,210 $5,097 $6,207 $10,448 $14,903 $33,748

Net Profit (After Tax) $54 $119 $147 $164 $182 $216 $231 $333 $520 $703

Additional IncomeDetails Month Amount

Mid Year Bonus

Year End Bonus

June $2,000

December $3,000

January

Total Additional Income $5,000

Planned ExpensesExpenditure Month Amount

November vacation

Home for the holidays

Gifts for family

Family vacation

November $450

December $600

December $300

July $880

January

January

January

January

Total Planned Expenses $2,230

0

200

400

600

800

0

200

400

600

800

1961 1963 1965 1967 1969

1.Enter your income information in the two income tables.

2.Enter your expenses. Use the Monthly Expenses table for recurring expenses.

3.Enter a starting balance in the January column on the Annual Budget table.

Personal Budget

Monthly Net IncomeIncome Type Amount

Monthly Net Income

Other Monthly Income

$4,500

$2,500

Available Cash $7,000

Monthly ExpensesExpense Costs

Mortgage

Taxes

Car Payment

Car Insurance

Home Owners Insurance

Cable Bill

Gas/Electric

Monthly Prescription

$2,300

$600

$350

$60

$127

$120

$88

$50

Total Monthly Expenses $3,695

Growth Record ($'000s) 1961–1970Income and Expenses 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970

Total Assets $1,426 $2,226 $2,815 $3,098 $3,210 $5,097 $6,207 $10,448 $14,903 $33,748

Total assets $1,426 $2,226 $2,815 $3,098 $3,210 $5,097 $6,207 $10,448 $14,903 $33,748

Additional IncomeDetails Month Amount

Mid Year Bonus

Year End Bonus

June $2,000

December $3,000

January

Total Additional Income $5,000

Planned ExpensesExpenditure Month Amount

November vacation

Home for the holidays

Gifts for family

Family vacation

November $450

December $600

December $300

July $880

January

January

January

January

Total Planned Expenses $2,230

0

10 000

20 000

30 000

40 000

0

10 000

20 000

30 000

40 000

1961 1963 1965 1967 1969

1.Enter your income information in the two income tables.

2.Enter your expenses. Use the Monthly Expenses table for recurring expenses.

3.Enter a starting balance in the January column on the Annual Budget table.

Personal Budget

Monthly Net IncomeIncome Type Amount

Monthly Net Income

Other Monthly Income

$4,500

$2,500

Available Cash $7,000

Monthly ExpensesExpense Costs

Mortgage

Taxes

Car Payment

Car Insurance

Home Owners Insurance

Cable Bill

Gas/Electric

Monthly Prescription

$2,300

$600

$350

$60

$127

$120

$88

$50

Total Monthly Expenses $3,695

Growth Record ($'000s) 1961–1970Income and Expenses 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970

Stockholders’ Funds $761 $1,021 $1,236 $1,337 $1,421 $1,644 $1,943 $2,115 $4,665 $9,207

Additional IncomeDetails Month Amount

Mid Year Bonus

Year End Bonus

June $2,000

December $3,000

January

Total Additional Income $5,000

Planned ExpensesExpenditure Month Amount

November vacation

Home for the holidays

Gifts for family

Family vacation

November $450

December $600

December $300

July $880

January

January

January

January

Total Planned Expenses $2,230

0

2500

5000

7500

10 000

0

2500

5000

7500

10 000

1961 1963 1965 1967 1969

1.Enter your income information in the two income tables.

2.Enter your expenses. Use the Monthly Expenses table for recurring expenses.

3.Enter a starting balance in the January column on the Annual Budget table.

Personal Budget

Total Assets Net Profit (After Tax) Stockholders’ Funds

19 6 0 –19 6 9Determination, Drive and Debentures 51

Westfield’seightRulesofShoppingCentreDevelopment

As explained to investors in a pamphlet in 1968

1SiteSelectionA site is selected only after careful assessment of what the future development of the total environment is likely to be.

Surveys are often conducted in liaison with major retailers who then become important merchants — magnets for customers in the completed centre.

2DesignThe design department at Westfield takes in needs and aspirations of the entire potential customer base. The social and economic background of the trading area is considered in the creation of a pleasant, harmonious atmosphere. Special architectural features, shopfront designs, commissions from outside clients and the many merchant and customer facilities are brought together to stimulate the best trading conditions.

3LeasingFor continuous and sound trading, it is essential that the ‘balance’ of shops in a centre be wide and varied — emulating the traditional facilities of a shopping precinct in a normal town. To achieve a good balance of retailers, leasing begins at an early stage of the design.

4ConstructionFor this, a very high degree of organisation is required. The building division of Westfield controls the detail and finish of the project according to the total concept. Using the latest techniques and time-planning control methods, constructions are completed in the shortest possible time.

Westfield builds for itself and other developers.

5financingFinancing of multimillion-dollar centres is managed by a group of specialised executives under central finance control. The capital structuring of each project requires individual attention and a decision has to be made whether, on completion, the project will be: 1. owned straight out 2. jointly owned

3. sold outright 4. sold and leased back

Each requires a different approach to funding and is handled by the company’s own specialist in each field.

6ManagementStaff chosen for management positions will have already experienced the retail field. They have to manage the complex requirements of the retailers, the customers and the facilities.

Further training in such tasks is provided by sending staff to courses and conventions in the United States and other countries. Westfield is a member of the International Council of Shopping Centres, which ensures it is well placed to study all development trends in retailing anywhere in the world. Where applicable, these ideas are implemented.

7promotionPromotion is the active spearhead of the combined efforts of developer, landlord and merchants within a centre. Continuous study of changing fashions is undertaken so that promotions fulfil the entire merchandising needs of communicating to the widest possible audience. A Merchants’ Association is established within the centre. After Westfield has organised this association, it continues to play an active role, with staff and financial assistance, to ensure that merchants obtain the maximum benefit from combining their own promotional efforts.

8CateringtotheCustomerThe shopping centre aims to meet the sophisticated tastes of modern shoppers, stimulate their imaginations, elevate their sense of wellbeing and widen their everyday world, linked as it is, to other forms of mass communication. By providing an atmosphere of excitement through the visual, aural and tactile senses, the centres attempt to generate an ever-increasing trade potential.

All ages are catered for. For children, there are nurseries, playgrounds and entertainment. Music, food and clothing stores encourage teenagers to use the centres as gathering points. For the housewife, shopping becomes a pleasure, with easy access and everything under one airconditioned roof.

52 WeSTfIeLD5 0ye ARS

Queensland

Withexpansionaryeyes,WestfieldGoesInterstate

Right: An aerial view of Toombul Shoppingtown under construction, showing the canal.

Moving beyond New South Wales

In the mid 1960s Westfield turned its attention to Queensland. John Lowy (brother of Frank), together with an engineer who was familiar with Brisbane, found a site at Toombul – shown to them by local real estate agent Donald Petrie – 10 kms from the CBD and superbly located in the middle of a densely populated area. When Saunders and Lowy later saw the site they instantly realised its commercial potential and took an option over it.

But there was a problem. The Chermside centre was nearby and housed a Myer department store, making it

difficult for Westfield to attract another department store as its anchor tenant. After some effort, Westfield finally found a secondary department store and secured a Coles supermarket. However, that wasn’t the end of its worries. As Westfield was an unknown quantity in Brisbane, how was it to fill the 60 untenanted shops? Frank Lowy took on the job with Petrie and walked the streets of the CBD, calling on retailers to attract them to the new centre.

The effort paid off. When the Toombul centre opened 100 per cent leased in 1967, it was Brisbane’s first fully air-conditioned drive-in centre with parking for 1500 cars.

19 6 0 –19 6 9Determination, Drive and Debentures 53

Victoria

Right: An architect’s early sketch of Doncaster Shoppingtown.

While Toombul was opening, so Westfield was busily constructing its biggest centre at Doncaster in Melbourne.

It had been offered this golden opportunity by Coles, which wanted a supermarket in the affluent and fast-developing area of Doncaster but wanted it bundled with a major department store; in particular, a Myer store. Coles had the land but lacked the expertise to put such a project together. Westfield was called in.

Westfield could see the potential. Nearby orchards and farms were being rezoned for residential and commercial uses and new roads were being constructed. It readily

accepted the offer to buy the land and build a shopping centre meeting Coles’ requirements.

Thus, in 1969, with much fanfare, the then Premier of Victoria, Sir Henry Bolte, opened the $12 million, fully air-conditioned Doncaster Shoppingtown. It had 80 shops, five major stores, a tower with professional services and amenities, and parking for 3000 cars.

It had been financed on a sale-and-leaseback arrangement with Temperance and General and was Westfield’s eighth major centre development. Like the original development at Hornsby, it provided extra stimulus to community growth in the surrounding area.

Restructuring in Australia, Expanding into America

1970–1979 TheQuantumLeap

56 WeSTfIeLD5 0ye ARS

Unsettled conditions in the 1970s tested everyone in the Australian property market. Investors who had been burnt in the sharemarket boom–bust of the late 1960s and early 1970s had turned to property, hoping to find stability. Instead, by 1974, world oil prices had quadrupled and economic pain was being felt everywhere.

In Australia, inflation peaked at over 20 per cent and a liquidity squeeze saw interest rates rocket. Bank bills hit 17 per cent and the short-term money market was paying up to 25 per cent for overnight cash.

The tough conditions led to the collapse of five major property companies that year, the biggest of which was Cambridge Credit Corporation. Confidence in property companies and their financiers slumped. Even the Australian Stock Exchange reduced its trading hours.

Liquidity problems forced the closure of the well-known sharebroking firm, Patrick Partners. In early 1979,

Associated Securities Ltd, Australia’s fourth-largest finance company, collapsed, affecting thousands of investors.

While Westfield went through some very tight squeezes, it expanded steadily during this turbulent decade, confirming the theory that the shopping centre business can be counter-cyclical.

In the 1970s, investors in Westfield saw the value of their shares multiply many times over. Apart from the dividend doubling from 10 per cent to 20 per cent, investors were also the recipients of four bonus share issues, culminating in a capital reconstruction which further increased their wealth more than eightfold.

Against the background of economic hardship, Westfield spent the decade improving properties it already owned, building major new centres and expanding offshore into the United States, the home of the shopping centre.

flourishingInToughConditions

Right: Shoppers pick up some bargains in 1974.

1970 –1979 The Quantum Leap 57

Mr J. Saunders Mr D. R. Stephens (Chairman) Mr F. P. Lowy Mr L. L. Winter Mr R. W. Stevens (Secretary)

Above: The board that saw Westfield through the financial turbulence of the 70s, and then into new financial territory, bringing profits that could never have been anticipated. The four members of this board remained in place for 15 years from 1965. It was only in 1980, when Leslie Winter reached the statutory age for retirement, that a change took place. David Lowy, Frank’s eldest son, took Winter’s place.

58 WeSTfIeLD5 0ye ARS

In the early 1970s, Sydney City Council had a grand vision for Sydney. It wanted to transform the eastern entrance to the city from a windy traffic corridor into a sweeping, stylish boulevard. In short, it wanted to turn William Street between Kings Cross and the Town Hall into Sydney’s own version of the Champs-Elysées. Westfield played a key role in implementing this urban ‘renaissance’.

Westfield had acquired some 2.6 acres fronting William Street and intended to develop this in stages over the next few years at a total cost of about $60 million as an office block, a hotel and convention halls all linked by galleries, shops and terraces.

A new division was formed within the company for the purpose of multistorey commercial developments, and for its first project, it took on Stage One of the William Street development. This entailed building the 24-storey office block and, immediately next door,

a 280-suite international-standard hotel and two levels of retail shops. This initial stage of development would take up less than an acre of the vacant land and cost $13 million.

As Westfield Towers and the Boulevard Hotel were going up, the recession of the early 1970s hit, the council’s enthusiasm for the project waned and other developers fell away. Westfield was left with Stage One completed. The rest was scaled down.

Westfield decided to lease the hotel on a long-term basis. Because Westfield Towers was just outside the CBD, it took some years for it to achieve full occupancy. The ‘Champs-Elysées’ idea was revived from time to time but no action ever followed the enthusiasm. When Saunders retired from Westfield some 15 years later, he bought the remaining land and built an office and residential complex on it.

DreamingoftheChamps-elysees

Right: The Westfield Towers complex, the only piece of the ‘Champs-Elysées dream’ to see the light of day.

Below right: An artist’s rendering of how the grand complex should have looked (red dots). Ultimately, only the outlined section would be built (yellow line) by Westfield. Drawn in 1969, the plan includes the proposed Eastern Distributor which only became a reality 30 years later.

Right: A view of William Street in the early 1970s – a short stroll from the buzz of the CBD.

William Street, Sydney

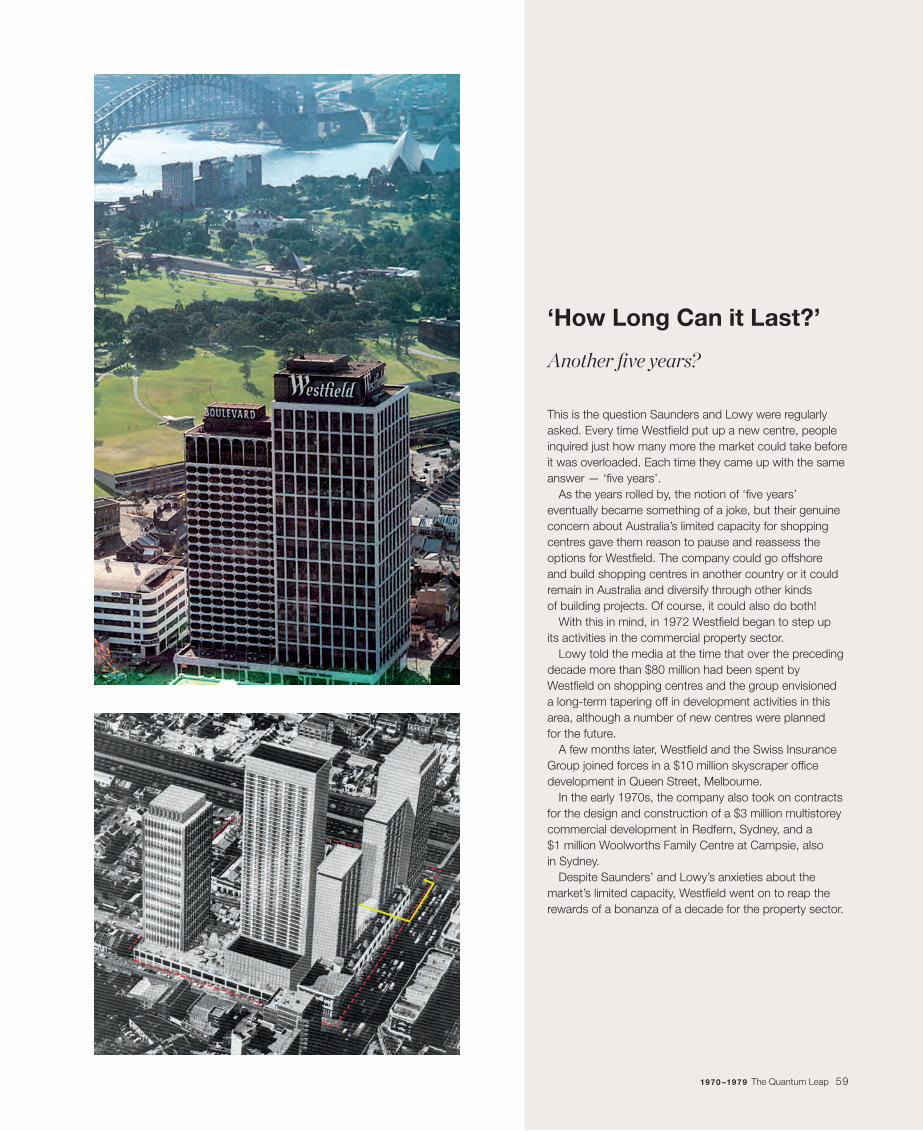

This is the question Saunders and Lowy were regularly asked. Every time Westfield put up a new centre, people inquired just how many more the market could take before it was overloaded. Each time they came up with the same answer — ‘five years’.

As the years rolled by, the notion of ‘five years’ eventually became something of a joke, but their genuine concern about Australia’s limited capacity for shopping centres gave them reason to pause and reassess the options for Westfield. The company could go offshore and build shopping centres in another country or it could remain in Australia and diversify through other kinds of building projects. Of course, it could also do both!

With this in mind, in 1972 Westfield began to step up its activities in the commercial property sector.

Lowy told the media at the time that over the preceding decade more than $80 million had been spent by Westfield on shopping centres and the group envisioned a long-term tapering off in development activities in this area, although a number of new centres were planned for the future.

A few months later, Westfield and the Swiss Insurance Group joined forces in a $10 million skyscraper office development in Queen Street, Melbourne.

In the early 1970s, the company also took on contracts for the design and construction of a $3 million multistorey commercial development in Redfern, Sydney, and a $1 million Woolworths Family Centre at Campsie, also in Sydney.

Despite Saunders’ and Lowy’s anxieties about the market’s limited capacity, Westfield went on to reap the rewards of a bonanza of a decade for the property sector.

‘howLongCanitLast?’

Another five years?

1970 –1979The Quantum Leap 59

Many of the big-name stores that dominated Australian retailing in the first half of the twentieth century had all but disappeared by the beginning of the twenty-first.

In their day, they had dominated in size, reputation, name and service. Then, it seemed the likes of Farmer & Co, Foy’s Ltd, Anthony Hordern & Sons, Sydney Snow Ltd, Ways, Winns, Waltons, Western, McDowells, Marcus Clarke, and Nock and Kirby would last forever.

Some became embroiled in complex takeovers, some were sold in sections and some joined forces and continued for a limited period before being subsumed by a third party. A few struggled on until defeated by the modern economy and others just petered out. Those that survived, in one form or another, such as David Jones, Myer and Grace Bros, Coles and Woolworths, continued to trade into the new century.

• In 1960, for example, the grand Farmer & Co, which had played such an integral role in so many Australians lives and had absorbed other retailers, such as Ways, acquired for itself twelve Western Stores in the countryside to meet retail growth in those areas. Later that year, it merged with Myer of Melbourne and then disappeared from the retail scene when its stores were retired and renamed Grace Bros.

• After Foy’s flagship store in Sydney lost clientele because of new transport systems and altered pedestrian traffic flow in the city, it was sold to Grace Bros. Its branch stores were sold separately.

• Income from the Federal Government for the use of its buildings during the Second World War helped to relieve some of Grace Bros’ retailing problems and it went on to open several suburban stores in the 1950s and 1960s. Later it was taken over by Myer which, in turn, was taken over by Coles. Myer traded for some years as a division of Coles before being sold to a private equity group. It was then listed in 2009.

• Horderns suffered badly in the Depression and the valuable city site was ultimately sold to an overseas construction company.

• Following the Depression, the Second World War, book debts and the closure of its mail-order catalogue trade, Marcus Clarke accepted a takeover offer from Waltons in the 1960s. In the 1970s Waltons took over McDowells and then was itself taken over by the Bond Corporation in the 1980s. Soon after, it vanished from the retail landscape.

• For Snow’s and Winns, business dwindled steadily until Snow’s sold out and Winns closed its doors.

Whateverhappenedto…

60 WeSTfIeLD5 0ye ARS

Right: A Waltons department store in the 1970s.

1970 –1979The Quantum Leap 61

Left: Winns department store, Hunter Street, Newcastle 1972.

Below: Anthony Hordern Palace Emporium, George St, Sydney.

62 WeSTfIeLD5 0ye ARS

In its first decade as a public company, Westfield continually fine-tuned its financial strategy. It dropped residential development and began to concentrate on the investment aspect of its business. To free up capital for further development, it entered into sale–leaseback arrangements.

Three years later it improved the way it financed developments by using short to medium term finance for the construction phase.

By 1972, Westfield had passed the $1 million earnings mark, had a joint venture with Credit Suisse, and approximately 65 per cent of its profit before tax was derived from income-producing properties.

Halfway through its second decade, Westfield’s income was coming from a property portfolio consisting of eight freehold shopping centres, with three on long-term leasehold and two jointly owned. There was also an income stream from a freehold office block, hotel and motel.

By 1977 the company had identified a new source of finance — superannuation funds. Since the loosening of restrictions on permissible avenues of investment for superannuation funds, investment in property had become a notable feature of the real estate scene. The cash flowing into superannuation schemes from rising, wage-indexed salaries had underpinned the Australian property market for the preceding two or three years.

In 1977, Westfield embarked on the construction of the Hurstville complex, a sale–leaseback arrangement with the NSW State Superannuation Board. A year later, Westfield had all the hallmarks of a company over-leveraged.

For 17 years it had grown without interruption. A large part of its business had been financed through borrowings and its liabilities had grown to $125 million. Its assets stood at $153 million and it had $28 million in shareholders’ funds. However, its assets had not been revalued since 1971 and their true value was not reflected in the share price.

In mid 1978, Westfield announced it was considering a reappraisal of the value of its properties. Westfield’s share price soared from a low of $2.75 in January 1978 to a high of $7.50 in November of the same year.

In November 1978, on the official announcement of its intention to form a property trust which would increase shareholders’ dividend income eightfold, the shares surged to $8.30.

In July 1979, Westfield Ltd was delisted and in its place Westfield Holdings Limited and the Westfield Property Trust were listed. The sale of Westfield Limited’s wholly owned properties, a result of the establishment of the trust, constituted what was at the time probably the largest-ever property transaction in Australian history.

While most of the transfer was ‘in-house’, two of the largest properties were sold to the Superannuation Fund Investment Trust (SFIT), generating a capital profit of $80 million. This was distributed to shareholders through the issue of eight units in the trust for each ordinary share.

In its grand finale before the 2 July reconstruction, earnings for Westfield Ltd increased 25.8 per cent to $4.4 million in the year to 30 June 1979. This was the company’s 19th consecutive profit.

Following the restructure, the Westfield Property Trust became the equity provider for the capital-hungry Westfield shopping centres and the value of the two entities, the units and the shares, shot up to $12.

The outcome was extraordinary. Westfield’s leverage was eliminated, it had $25 million in the bank and shareholder wealth had grown exponentially.

Westfield Holdings was concentrating on fee-generating management and development activities. It was manager of the Westfield Property Trust and was also manager and service provider to the centres. While Westfield Holdings offered growth, the Westfield Property Trust, with its minimal borrowings, offered secure and steady returns.

Westfield had ended its second decade as a public company in a position of unprecedented strength.

But there was bad news around the corner. A year after the restructure, the Government changed the rules retrospectively, forcing Westfield to re-achieve the same result using other tactics. It succeeded and, in 1982, a new trust was floated.

GainingfinancialSophistication

1970 –1979The Quantum Leap 63

Monthly Net IncomeIncome Type Amount

Monthly Net Income

Other Monthly Income

$4,500

$2,500

Available Cash $7,000

Monthly ExpensesExpense Costs

Mortgage

Taxes

Car Payment

Car Insurance

Home Owners Insurance

Cable Bill

Gas/Electric

Monthly Prescription

$2,300

$600

$350

$60

$127

$120

$88

$50

Total Monthly Expenses $3,695

Growth Record ($'000s) 1961–1970Income and Expenses 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979

Total Assets 16 33 46 71 95 102 116 125 152 155 147

Total assets 16 33 46 71 95 102 116 125 152 155 147

Additional IncomeDetails Month Amount

Mid Year Bonus

Year End Bonus

June $2,000

December $3,000

January

Total Additional Income $5,000

Planned ExpensesExpenditure Month Amount

November vacation

Home for the holidays

Gifts for family

Family vacation

November $450

December $600

December $300

July $880

January

January

January

January

Total Planned Expenses $2,230

0

50

100

150

200

0

50

100

150

200

19691970

19711972

19731974

19751976

197719781979

1.Enter your income information in the two income tables.

2.Enter your expenses. Use the Monthly Expenses table for recurring expenses.

3.Enter a starting balance in the January column on the Annual Budget table.

Personal Budget

Monthly Net IncomeIncome Type Amount

Monthly Net Income

Other Monthly Income

$4,500

$2,500

Available Cash $7,000

Monthly ExpensesExpense Costs

Mortgage

Taxes

Car Payment

Car Insurance

Home Owners Insurance

Cable Bill

Gas/Electric

Monthly Prescription

$2,300

$600

$350

$60

$127

$120

$88

$50

Total Monthly Expenses $3,695

Growth Record ($'000s) 1961–1970Income and Expenses 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979

Total Assets 0.51 0.72 0.92 1.07 1.38 1.56 1.74 2.14 2.66 3.42 4.3

Total assets 0.51 0.72 0.92 1.07 1.38 1.56 1.74 2.14 2.66 3.42 4.3

Additional IncomeDetails Month Amount

Mid Year Bonus

Year End Bonus

June $2,000

December $3,000

January

Total Additional Income $5,000

Planned ExpensesExpenditure Month Amount

November vacation

Home for the holidays

Gifts for family

Family vacation

November $450

December $600

December $300

July $880

January

January

January

January

Total Planned Expenses $2,230

0

1.25

2.50

3.75

5.00

0

1.25

2.50

3.75

5.00

19691970

19711972

19731974

19751976

197719781979

1.Enter your income information in the two income tables.

2.Enter your expenses. Use the Monthly Expenses table for recurring expenses.

3.Enter a starting balance in the January column on the Annual Budget table.

Personal Budget

Monthly Net IncomeIncome Type Amount

Monthly Net Income

Other Monthly Income

$4,500

$2,500

Available Cash $7,000

Monthly ExpensesExpense Costs

Mortgage

Taxes

Car Payment

Car Insurance

Home Owners Insurance

Cable Bill

Gas/Electric

Monthly Prescription

$2,300

$600

$350

$60

$127

$120

$88

$50

Total Monthly Expenses $3,695