Weather Based Crop Insurance Scheme_ By George James

12

EVALUATION OF WEATHER BASED CROP INSURANCE SCHEME OF PADDY Dr. R Sendil Kumar 1 & George James 2 1. Associate Professor, Dept. of Co-operative Management, Kerala Agricultural University, Thrissur, 2. MBA-Agribusiness Management, Kerala Agricultural University, Thrissur Abstract Crop insurance is one protective instrument for farmers to tackle their risks associated with farming. India have been witnessed several experiments on various crop insurance schemes. Weather based crop insurance scheme is the latest among them, getting popularity in India. Weather index insurance has similar advantages to those of area yield insurance. It provides timely compensation made on the basis of weather index. This insurance covers a wide section of people and a variety of crops; its operational costs are also low. Recently this insurance scheme has been introduced in Paddy and several other crops in Kerala. An evaluation study was conducted in Palakkad district of Kerala. Both loanee and non-loanne farmers were interviewed to know their response towards the scheme. Also focus group discussion of other stakeholders like Insurance agents, Bank officials, Agricultural officer, Padashekara Samidi heads were done. The study highlighted the need for improvement in this scheme to make this scheme transparent. Also objective calculation of weather index and quick settlement of claims are essential for making it attractive to farmers. Key words: Crop Insurance, Weather Insurance, Paddy Insurance Introduction Agriculture is inevitable for a country like India to achieve its economical and developmental goals. This major sector is facing challenges from different perspectives. Weather fluctuation is one such challenge on which farmer have least control. The atmospheric variables like temperature, humidity, precipitation etc. have shown a high degree of variability in the recent times. Reports says that the annual mean temperature in India had increased by 0.49% in the last century at the same time the increase in temperature had reduced global farm output by roughly 1.5% in the last decade. These variations have great significance as far as farming is concerned.

-

Upload

keralaagricultural -

Category

Documents

-

view

1 -

download

0

Transcript of Weather Based Crop Insurance Scheme_ By George James

EVALUATION OF WEATHER BASED CROP INSURANCE SCHEME OF PADDY

Dr. R Sendil Kumar 1 & George James2

1. Associate Professor, Dept. of Co-operative Management, Kerala Agricultural University,

Thrissur, 2. MBA-Agribusiness Management, Kerala Agricultural University, Thrissur

Abstract

Crop insurance is one protective instrument for farmers to tackle their risks associated with

farming. India have been witnessed several experiments on various crop insurance schemes.

Weather based crop insurance scheme is the latest among them, getting popularity in India.

Weather index insurance has similar advantages to those of area yield insurance. It provides timely

compensation made on the basis of weather index. This insurance covers a wide section of people

and a variety of crops; its operational costs are also low. Recently this insurance scheme has been

introduced in Paddy and several other crops in Kerala. An evaluation study was conducted in

Palakkad district of Kerala. Both loanee and non-loanne farmers were interviewed to know their

response towards the scheme. Also focus group discussion of other stakeholders like Insurance

agents, Bank officials, Agricultural officer, Padashekara Samidi heads were done. The study

highlighted the need for improvement in this scheme to make this scheme transparent. Also

objective calculation of weather index and quick settlement of claims are essential for making it

attractive to farmers.

Key words: Crop Insurance, Weather Insurance, Paddy Insurance

Introduction

Agriculture is inevitable for a country like India to achieve its economical and

developmental goals. This major sector is facing challenges from different perspectives. Weather

fluctuation is one such challenge on which farmer have least control. The atmospheric variables

like temperature, humidity, precipitation etc. have shown a high degree of variability in the recent

times. Reports says that the annual mean temperature in India had increased by 0.49% in the last

century at the same time the increase in temperature had reduced global farm output by roughly

1.5% in the last decade. These variations have great significance as far as farming is concerned.

Especially for a country like India where farming is entirely depended on monsoon, weather

fluctuation and its impact are always a concern.

In the face of uncertainty and risk faced by the farming community, various schemes have

been evolved over time in India to protect farmers against risks. Crop insurance is one such

protective instrument for farmers to tackle the risks. India have been witnessed several experiments

on various crop insurance schemes. From 1985 onwards Comprehensive Crop Insurance Scheme

(CCIS) was implemented in India which then replaced with National Agricultural Insurance

Scheme (NAIS) in 1999. In crop insurance uncertainty faced by individual farmers is transferred to

the insurer through their participation in large numbers, and the farmers pay a risk premium in

return for the benefit. At present four crop Insurance schemes namely National Agricultural

Insurance Scheme (NAIS), Pilot Modified National Agricultural Insurance Scheme (MNAIS), Pilot

Weather Based Crop Insurance Scheme (WBCIS) and Pilot Coconut Palm Insurance Scheme

(CPIS) is being implemented in the country.

Crop Insurance Approaches

In the beginning, crop insurance was based on either Area approach or Individual approach. Area

approach is based on defined areas, which could be a district, a taluk, a block/a mandal or any other

smaller contiguous area. The actual average yield / hectare for the defined area is determined on the

basis of Crop Cutting Experiments (CCEs). These CCEs are the same conducted as part of General

Crop Estimation Survey (GCES) in various states. If the actual yield in CCEs of an insured crop for

the defined area falls short of the specified guaranteed yield or threshold yield, all the insured

farmers growing that crop in the area are entitled for claims.

The claims are paid to the credit institutions in the case of loanee farmers and to the individuals

who insured their crops in the other cases. The credit institution would adjust the amount against

the crop loan and pay the residual amount, if any, to the farmer. Area yield insurance is practically

an all-risk insurance. This is very important for developing countries with a large number of small

farms. However, there are delays in compensation payments

In the case of individual approach, assessment of loss is made separately for each insured farmer.

It could be for each plot or for the farm as a whole (consisting of more than one plot at different

locations). Individual farm-based insurance is suitable for high-value crops grown under standard

practices. Liability is limited to cost of cultivation. This type of insurance provides for accurate and

timely compensation. However, it involves high administrative costs.

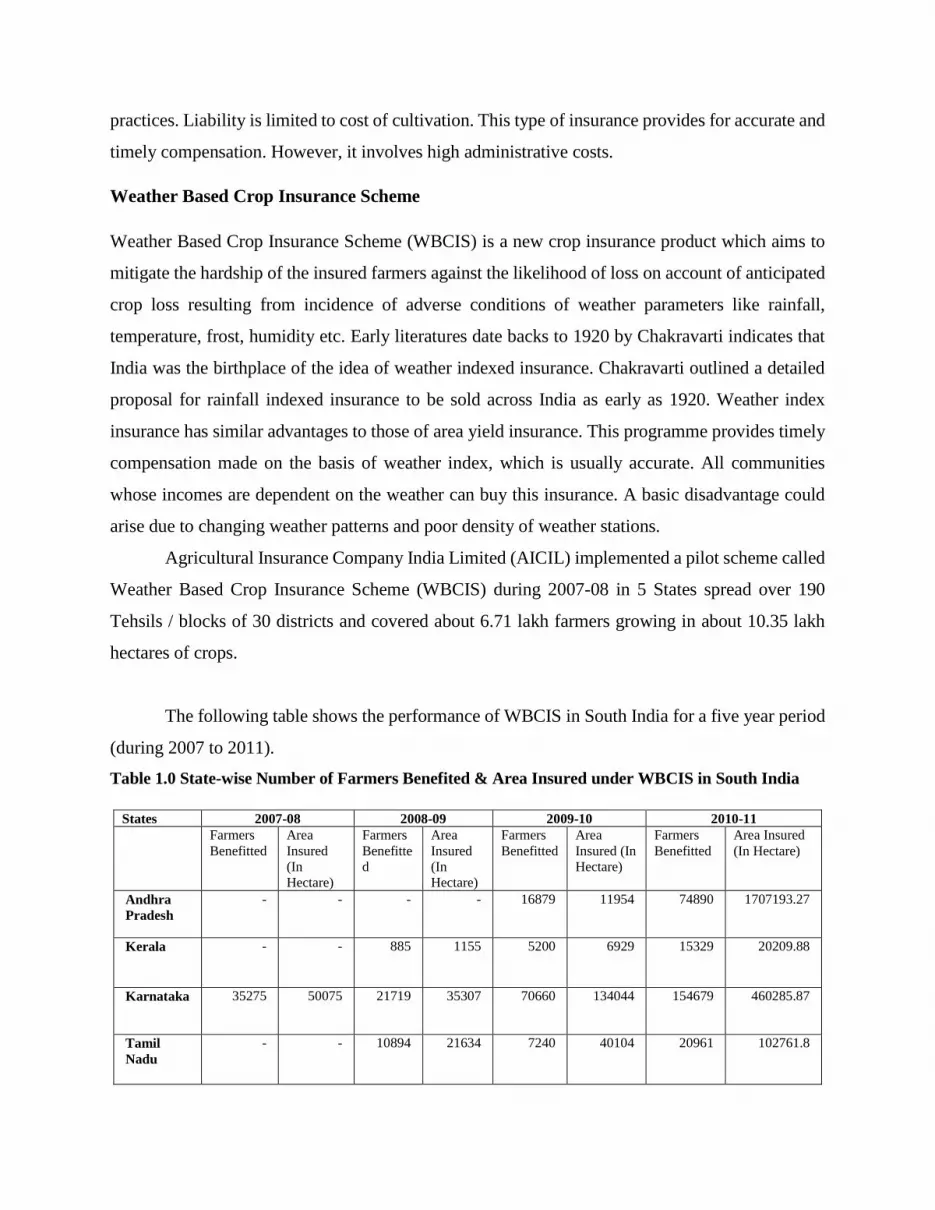

Weather Based Crop Insurance Scheme

Weather Based Crop Insurance Scheme (WBCIS) is a new crop insurance product which aims to

mitigate the hardship of the insured farmers against the likelihood of loss on account of anticipated

crop loss resulting from incidence of adverse conditions of weather parameters like rainfall,

temperature, frost, humidity etc. Early literatures date backs to 1920 by Chakravarti indicates that

India was the birthplace of the idea of weather indexed insurance. Chakravarti outlined a detailed

proposal for rainfall indexed insurance to be sold across India as early as 1920. Weather index

insurance has similar advantages to those of area yield insurance. This programme provides timely

compensation made on the basis of weather index, which is usually accurate. All communities

whose incomes are dependent on the weather can buy this insurance. A basic disadvantage could

arise due to changing weather patterns and poor density of weather stations.

Agricultural Insurance Company India Limited (AICIL) implemented a pilot scheme called

Weather Based Crop Insurance Scheme (WBCIS) during 2007-08 in 5 States spread over 190

Tehsils / blocks of 30 districts and covered about 6.71 lakh farmers growing in about 10.35 lakh

hectares of crops.

The following table shows the performance of WBCIS in South India for a five year period

(during 2007 to 2011).

Table 1.0 State-wise Number of Farmers Benefited & Area Insured under WBCIS in South India

States 2007-08 2008-09 2009-10 2010-11

Farmers

Benefitted

Area

Insured

(In

Hectare)

Farmers

Benefitte

d

Area

Insured

(In

Hectare)

Farmers

Benefitted

Area

Insured (In

Hectare)

Farmers

Benefitted

Area Insured

(In Hectare)

Andhra

Pradesh

- - - - 16879 11954 74890 1707193.27

Kerala - - 885 1155 5200 6929 15329 20209.88

Karnataka 35275 50075 21719 35307 70660 134044 154679 460285.87

Tamil

Nadu

- - 10894 21634 7240 40104 20961 102761.8

Southern

India

35275 50075 33498 58096 99979 193031 265859 2290450.82

India 228002 1068329 229752 487336 1134549 3472629 6159739 27867544.65

Source: Compiled by Datanet India from Ministry of Agriculture, Govt. of India.

Fig. 1.0 State-wise number of farmers benefited under WBCIS in South India

Source: Compiled from secondary data

WBCIS of Paddy in Kerala

In Kerala WBCIS is implemented in different crops like paddy, banana, coconut, turmeric,

pepper, cardamom etc. Paddy crop in 11 districts has been brought under weather-based crop

insurance scheme launched by the Agriculture Insurance Company of India. In Kerala problems of

water logging, lodging of paddy and shedding of grains due to heavy wind and rain is common in

paddy crop which leads to problems in harvest. And in this situation the newly launched WBCIS

have great importance as a risk management mechanism for farmers in the case of adverse weather

conditions. Agricultural department, Central and State government, banks, insurance agencies are

also involved in the implementation of this scheme. During 2013 about 18,000 farmers in Palakkad

had got enrolled in the scheme out of which 15,000 received insurance claims arising out of bad

weather which affected their crop. WBCIS in paddy was extended to Thiruvananthapuram, Kollam,

Idukki, Ernakulam, Thrissur, Malappuram, Kozhikode, Kannur, Wayanad and Kasaragod districts

from 2014 onwards. As the scheme is new in paddy it is important to study its design, effectiveness,

and also the response of farmers towards the scheme. Hence a study was conducted to evaluate the

Weather Based Crop Insurance Scheme of paddy in Palakkad district of Kerala.

Andhra PradeshKerala

Karnataka

Tamil Nadu

Southern India

0

100000

200000

300000

400000

500000

600000

2007-08 2008-09 2009-10 2010-11No

. of

Farm

ers

Ben

efit

ed

State-wise Number of Farmers Benefited under WBCIS in Southern India

Methodology of Study

Both primary and secondary data were used for the study. Primary data were collected from

randomly selected paddy farmers using a structured interview schedule and focus group discussion

with Agricultural Officers, Insurance agents, and Padashekara Samidhi heads. And secondary data

was collected from various publications, earlier studies, research articles, and records and

notifications of Agricultural Insurance Company. The study was focused on paddy farmers of

Alathur block of Palakkad district. The population list was obtained from the authorized insurance

agent of AIC and from that a sample of 60 paddy farmers which consists of 45 loanee farmers and

15 non-loanee farmers were selected. Data were analyzed with the help of appropriate tools such as

percentage and index. For measuring the attitude level of paddy farmers about WBCIS, Satisfaction

Index were developed. For the construction of indices the respondents were asked to rate the

statements regarding features of WBCIS of paddy. The opinion of respondents were assigned to

marks of 7,5,3 and 1 representing the most positive degree of opinion to most negative degree of

opinion.

The scores of all respondents for each variable were summed up to arrive at the total score. The

total score thus obtained by each variable was then divided by the maximum possible score obtained

for that variable to obtain the index of that variable. Index for a statement is calculated using the

formula.

M= Maximum score

N= Number of respondents

S= Number of statements

The indices were then classified into three zones as follows for interpreting the results.

Table 1.3 Satisfaction Index

Results and findings of the study

The major results and finding of the study are discussed in different headings.

A) Seasonal demand for WBCIS of paddy.

Table 1.1 Seasonal demand for WBCIS of paddy n=60

Season

Frequency Percentage

Loanne

farmer

Non-loanne

farmer

Loanne

farmer

Non-loanne

farmer

Virippu 8 2 17.78 13.33

Mundakan 13 5 28.89 33.33

Both Virippu and

Mundakan 24 8 53.33 53.33

Total 45 15 100 100

Source: Compiled from primary data

The table 1.1 shows that half of the loanne and non loanne farmers (53.33 %) cultivate paddy in

Virippu as well as Mundakan seasons. This shows that there is a high demand for the WBCIS in

both Virippu & Mundakan season (May to December). And no farmers cultivate paddy in Punja

or summer season and there is zero demand for the scheme during the period of January to March.

B) Impact of yield in adoption of WBCIS of paddy

Table 1.2 Impact of yield in adoption of WBCIS of paddy n=60

Yield Virippu Mundakan

Loanne Non-loanne Loanne Non-loanne

Average Yield 17.60 18.40 22.47 23.47

Maximum 22.00 20.00 25.00 26.00

Minimum 14.00 16.00 20.00 20.00 Source: Compiled from primary data

From the table 1.2 it is clear that yield of paddy is more in Mundakan season than Virippu. Earlier

interpretation (Table 1.1) explains that the demand for WBCIS in paddy is more in Mundakan

season and hence it could be concluded that as yield increases the risk also increase and more

farmers adopt WBCIS. This shows that the farmers in the study area have adopted ex-ante strategy

to combat the climate risk, because of their rich experience.

C) Factors causing yield reduction in paddy

Table 1.6 Factors causing yield reduction in paddy n=60

Res

po

nd

en

ts

Drought Heavy Rain Unseasonal

Rain Heavy Wind Pest & Diseases

Freque

ncy

% Freque

ncy

% Frequ

ency

% Frequ

ency

% Frequen

cy

%

Loanne 25 55.56 3 6.67 11 24.44 3 6.67 3 6.67

Non-

loanne

13 86.67 0 0 0 0 0 0 2 13.3

3

Total 38 63.33 3 5 11 18.33 3 5 5 8.33

Source: Compiled from primary data

According to the study two third of the respondents (63.33%), said drought was considered as the

major weather factor, which reduce yield in paddy. Other factors causing yield reduction are

unseasonal rain fall (18.33%), pest and disease (8.33%) and heavy rain and heavy wind

contributing to 5% yield loss. Palakkad experienced an intermittent drought and this conditioned

to high acceptance of weather based crop insurances, especially for paddy. In WBCIS weather

fluctuations like reduction in rainfall (drought), unseasonal rain, heavy rain, and heavy wind are

covered. This feature of WBCIS make it more preferable to farmers than other crop insurance

schemes, were the claim is based on yield attributes.

D) Source of information about WBCIS

The information dissemination of WBCIS is diffused through various agencies like Padashekara

Samidi, Insurance agents, Banks and Krishibhavan. However ATMA and Media were not a

preferred channel for information dissemination for WBCIS in the study area.

Source: Compiled from primary data

E) Reasons for choosing WBCIS of paddy

According to this study, two-third of the respondents (61.67%) adopted WBCIS of paddy due to

the compulsion from bank authority while taking crop loan. Around one-fifth of the insurers

(21.67%) used this scheme as they realized that there could be a high yield reduction in paddy due

to weather fluctuations like poor rain, unseasonal rain, heavy wind etc. Only 11.67% of farmers

said that the WBCIS offered them short claim settlement period than NAIS which heavily

influenced them in choosing WBCIS of paddy.

F) Satisfaction of farmers towards WBCIS in Paddy n=60

Statement

No. of respondents Max.

obtainable

score

Score

obtained

Index

SA

(7)

A

(5)

D

(3)

SD

(1)

Information about WBCIS is

sufficiently available

9 37 14 0 420 290 69.05

Krishibhavan23%

Padashekara Samidi27%

ATMA0%

Insurance Agents25%

Bank25%

Media0%

Source of Information about WBCIS

Krishibhavan Padashekara Samidi ATMA Insurance Agents Bank Media

Procedure for enrolment is not

convenient

2 21 35 2 420 254 60.48

Actual risk is covered 5 14 26 15 420 198 47.14

Sum insured fixed is not adequate 24 21 14 1 420 164 39.05

Premium rate is affordable 8 40 9 3 420 286 68.1

Method of calculating crop loss is not

proper

17 26 14 3 420 186 44.29

AWS is fixed in a representative area 3 26 28 3 420 238 56.67

Settlement of claim is done in shorter

period

3 29 19 9 420 232 55.24

Response of intermediaries is not

proper

5 25 28 2 420 234 55.71

There is a good grievance redresses

mechanism

3 18 28 11 420 206 49.05

Total 79 257 215 49 4200 2288 544.76

Source: Compiled from primary data

Note: “SA” indicates Strongly Agree, “A” indicates Agree, “D” indicates Disagree and “SD”

indicates Strongly Disagree

Overall index = 54.48%

Regarding information availability of the scheme there is a high level of satisfaction among

farmers (69.05%). This can be inferred by the fact that there are several channels for passing

information about the scheme like Padashekara Samidi, Banks, Insurance agents, Krishi Bhavan

etc. Customers showed a medium (60.48%) level of satisfaction towards convenience in enrolment

into the scheme. As the scheme is now implemented through private agencies like United India

Insurance Company (in the survey area) the reach is more compared to other schemes. The

insurance agents are initiating the enrollment process and farmers only need to give the necessary

details like ID proof, Possession certificate/ Land tax receipt, and bank account details. Regarding

coverage of actual risk the farmers expressed a medium level (47.14%) of satisfaction.

According to the paddy farmers the average cost of cultivation of paddy is around Rs. 25,000/acre,

but the maximum sum insured is Rs. 14,000/acre. Farmers expressed a low level (39.05%) of

satisfaction towards sum insured and they want an increase in the sum insured amount. Farmers

are satisfied with the premium rate of WBCIS fixed by government which is now at Rs. 350/acre

after central government subsidy (75%) and state government subsidy (50 %). Around two third

(68.01%) of the respondents said the premium is affordable to them. At present the premium rate

for paddy under WBCIS is 10 % and the farmer need to pay only 2.5% of premium (as per Kharif

2014 season). There is a low level of satisfaction (44.29%) regarding the method of calculating

crop loss in WBCIS. Now WBCIS adopts ‘area approach’ for the calculation of crop loss. Loss in

each notified Reference Unit Area (RUA) is calculated based on the weather data during the

insurance period as received from the respective notified Reference Weather Station (RWS).

Farmers express a deep concern about the chance of missing their farm and corresponding weather

details while calculating crop loss. Beneficiaries showed a medium (56.67) satisfaction about the

location of Automatic Weather Station (AWS) installed for collecting weather parameters. Many

of the farmers are not confident about the working efficiency and accuracy of AWS installed in a

distant place. Farmers are moderately satisfied with the claim settlement period under WBCIS.

The satisfaction level is medium (55.24%) and farmers said that they receive the claim on an

average of six months duration which is comparatively better. The satisfaction level of farmers

towards the responsiveness of intermediaries and availability of redressal mechanism are medium

(55.71 %, 49.05% respectively). Farmers are moderately satisfied with the performance of various

intermediaries involved in WBCIS such as Insurance agents, Banks, Krishibhavan etc.

Suggestions for Improvement of WBCIS

Target small farmers: The study reveals that the scheme is more popular among small

farmers who are having less land and financial resources. They are highly exposed to

climate risks and hence they have to be given more importance.

Address seasonal demand: Give more publicity and reach to this insurance product during

Mundakan season compared to Virippu season.

Improve awareness about the scheme.

o Many farmers chose this scheme due to compulsion from bank. By educating about

the functioning of WBCIS more farmers can be added to this scheme voluntarily.

o Farmers should be educated about the crop loss estimation method in this scheme.

Many farmers have doubt and apprehension about this.

o As it is implemented through a private insurance agency the faith of farmers on this

scheme is comparatively less. So this problem should be addressed by using the

service of extension agents like AO, ATMA workers etc.

Advance AWS network: More AWS have to be installed to maximize accuracy of

measurement of weather parameters.

Conclusion:

To conclude the study, Weather Based Crop Insurance Scheme of Paddy is designed well to

compensate the climate risks associated with paddy cultivation. As different players are involved

in the implementation of this scheme the level of awareness is also more. Many farmers expect

frequent weather fluctuation and this is the scope for wider expansion of the scheme. Small farmers

utilize this scheme as an ex-ante strategy to combat climate risks. By improving awareness and

infrastructural facilities like AWS, accuracy in measurement of weather parameters can be

achieved.

BIBILIOGRAPHY

Botts, R.R., J. N. “Boles Use of Normal Curve Theory in Crop Insurance Rate-Making”,

J.Farm Econ. Vol. 40, 1958.

Chandrakanth, M.G., N.S.P. Rebello. “Crop Insurance for Potatoes: A case study”,

Financing Agriculture,Vol. 4, 1980.

Dandekar V. M. “Crop Insurance in India”, Econ. Polit. WeeklyVol. 11, 1976.

Daniel J. Clarke et al.,Weather Based Crop Insurance in India,Policy Research Working

Paper,The World Bank Financial and Private Sector Development Vice Presidency Non-

Banking Financial Institutions Unit,2012.

Hazel, P.P and Valdes, A., 1985, crop insurance for agricultural development. Issues and

experience, Baltimore, Maryland, USA John Hopkins University Press, International Food

Policy Research Institute, Washington, USA.

Knight F.M., 1971, Risk, Uncertainity and Profit, University of Chicago

press,Chicago,60637, p.233-234.

Manojkumar K et al.,Crop Insurance Scheme: A case study of banana farmers in Wayanad

district,Discussion,Kerala Research Programme on Local Level Development Centre for

Development Studies.

Niranjanlal Tiwari R. and Tiwari R., 2000, Farmers Awareness about the crop Insurance.

Rural India, p. 225-229.

Panthak B.S., 1986, Crop Insurance: Retrospects and Prospects, Paper presented at the

National Seminar on Crop Insurance Through Cooperatives,Pune,p.24-26.

Ramaswami B., 1993, Supply response to agricultural insurance- Risk reduction and moral

hazards effects. American Journal of Agricultural Economics, p.914-923.

Ray P.K., 1960, Crop insurance as a measure of Agricultural Support: National and

International action. International journal of Agricultural Economics, 15(3): p.1-14.

Raushan Bokusheva, The Effectiveness of Weather-Based Index Insurance and Area-Yield

Crop Insurance: How Reliable are ex post Predictions for Yield Risk Reduction, Quarterly

Journal of International Agriculture 51 No. 2: 135-156, 2012.

Report on impact evaluation of pilot weather based crop insurance scheme, Agricultural

Finance Corporation Ltd. Head Office, Mumbai,January,2011.

Rustagi, N. K. Crop insurance in India: An analysis, Delhi: B. L. Publishing Co., 1988.

Shobharani S., 1989, An economic analysis of crop insurance for Ragi in Banglore rural

districts. Msc.(Agri) thesis, University of Agricultural Science, Banglore.

Subrahmanian, K. K. Economic Feasibility for Crop Insurance for Coffee,

Unpublishedthesis. UAS, Bangalore, 1984.