VIDEO GAMES: CLOUD INVADERS - CitiFirst

162

Citi is one of the world’s largest financial institutions, operating in all major established and emerging markets. Across these world markets, our employees conduct an ongoing multi-disciplinary conversation – accessing information, analyzing data, developing insights, and formulating advice. As our premier thought leadership product, Citi GPS is designed to help our readers navigate the global economy’s most demanding challenges and to anticipate future themes and trends in a fast-changing and interconnected world. Citi GPS accesses the best elements of our global conversation and harvests the thought leadership of a wide range of senior professionals across our firm. This is not a research report and does not constitute advice on investments or a solicitations to buy or sell any financial instruments. For more information on Citi GPS, please visit our website at www.citi.com/citigps. Citi GPS: Global Perspectives & Solutions June 2019 VIDEO GAMES: CLOUD INVADERS Bracing for the Netflix-ization of Gaming

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of VIDEO GAMES: CLOUD INVADERS - CitiFirst

Citi is one of the world’s largest financial institutions, operating in all major established and emerging markets. Across these world markets, our employees conduct an ongoing multi-disciplinary conversation – accessing information, analyzing data, developing insights, and formulating advice. As our premier thought leadership product, Citi GPS is designed to help our readers navigate the global economy’s most demanding challenges and to anticipate future themes and trends in a fast-changing and interconnected world. Citi GPS accesses the best elements of our global conversation and harvests the thought leadership of a wide range of senior professionals across our firm. This is not a research report and does not constitute advice on investments or a solicitations to buy or sell any financial instruments. For more information on Citi GPS, please visit our website at www.citi.com/citigps.

Citi GPS: Global Perspectives & Solutions

June 2019

VIDEO GAMES: CLOUD INVADERSBracing for the Netflix-ization of Gaming

© 2019 Citigroup

Authors

Jason B Bazinet

U.S. Entertainment, Cable & Satellite Analyst

+1-212-816-6395 | [email protected]

Thomas A Singlehurst, CFA

Head of European Media Research Team

+44-20-7986-4051 | [email protected]

Kota Ezawa

Co-Head of Global Technology Research

+81-3-6776-4640 | [email protected]

Mark May

U.S. Internet Analyst

+1-212-816-5564 | [email protected]

Walter H Pritchard, CFA

U.S. Software Analyst

+1-415-951-1770 | [email protected]

Alicia Yap, CFA

Head of Pan-Asia Internet Research

+852-2501-2773 | [email protected]

Expert Commentators

Luke Alvarez

Founding Managing

Partner, Hiro Capital

Ralf Reichart

Co-CEO of ESL

Wil Stephens

CEO, Founder of Fusebox

Games

Global Video Game Team

Hillman Chan, CFA

China Internet & Media Analyst

+852-2501-2777 | [email protected]

Arthur Lai

Greater China Technology Analyst

+852-2501-2758 | [email protected]

Carrie Liu `

Taiwan Technology Hardware Analyst

+886-2-8726-9086 | [email protected]

Atif Malik

U.S. Semiconductor and Semi Equip Analyst

+1-415-951-1892 | [email protected]

Rafal Materka

Poland Investment Research Team

+48-22-690-3288 | [email protected]

Asiya Merchant, CFA

U.S. IT Hardware & Tech Supply Chain Analyst

+1-415-951-1752 | [email protected]

Minami Munakata

Japan Metals & Mining, Media Analyst

+81-3-6776-4632 | [email protected]

Catherine T O'Neill

European Media Analyst

+44-20-7986-8053 | [email protected] +

Ashwin Shirvaikar, CFA

U.S. Payments, Processors & IT Analyst

+1-212-816-0822 | [email protected]

Jim Suva, CPA

IT Hardware & EMS, Telco & Network Equipment Analyst

+1-415-951-1703 | [email protected]

Kyle Twomey

Europe Small Cap Analyst

+44-20-7986-7955 | [email protected]

John Yu

Korea Internet & Media Analyst

+82-2-3705-0721 | [email protected]

© 2019 Citigroup

3

VIDEO GAMES: CLOUD INVADERS Bracing for the Netflix-ization of Gaming What was your first memory of playing video games? Mine was playing Centipede

at the local pizzeria. Armed with quarters and enough money for one slice of pizza,

we would play until we were either broke or our fingers were sore from firing digital

missiles. Eventually my friend got an Atari game system and after months of

begging for the same, my Dad caved in and bought us a gaming system – an

Intellivision game system. He told us over and over that it was a better system to

Atari but it didn’t have all the cool games that my friends played. It was hard

sometimes being the daughter of an engineer who cared about technology

superiority, but at least the hockey game let you punch people.

Game choices moved quickly after that – Tetris on my Macintosh Plus, Donkey

Kong on my Nintendo DS, Brickbreaker on my Blackberry, and now Candy Crush

on my iPhone. The common constraint through the years was that the games I

played continued to be dependent on the device I owned.

When the Internet came about, new firms started disrupting traditional media

businesses such as newspapers, radio, and television by giving consumers what

they wanted, when they wanted, and on the device they wanted. But it didn’t disrupt

the video game industry. Game publishers were able to use the Internet to augment

their revenues. They used the Internet to increase in-game sales and sell software

directly to consumers, and tapped into the smartphone market and the growth of

mobile gaming.

Are video game publishers immune from disruptive threats? The authors of the

report that follows answer with a resounding no. There is a technology on the

horizon that has all the characteristics of a disruptive threat to the video game

ecosystems — the cloud.

The video game ecosystem has been evolving over the last few years — towards

group play vs. single play, to in-game monetization vs. software sales, to renting vs.

buying hardware, to video games being a spectator sport, and to software being

made for all devices vs. software made specifically for hardware. These new trends

in the video game industry could make it much easier for the big cloud players to

come in and start pulling away revenue.

The cloud-based providers will be able to offer low-cost access to cloud-based

gaming and a wide array of gaming content. They will also be able to monetize

gaming in non-traditional ways that play to their strengths — through in-game

monetization, in-game advertising, broadcasting, and digital. For consumers, cloud

will make it easier to play games on different platforms and allow players to be

device agnostic, hitting pause on a PC game and picking it up again on a mobile

device. Game developers will be able to support more devices as compatibility

issues decrease between software and hardware.

eSports, a $1billion business and growing, will have increased opportunities on the

cloud and we believe game publishers will still be able to thrive in the emerging

video game world but will have to adapt their business models to ensure they’re

positioned appropriately..

If the report is right, I may finally be able to play PacMan!

Kathleen Boyle, CFA

Citi GPS Managing Editor

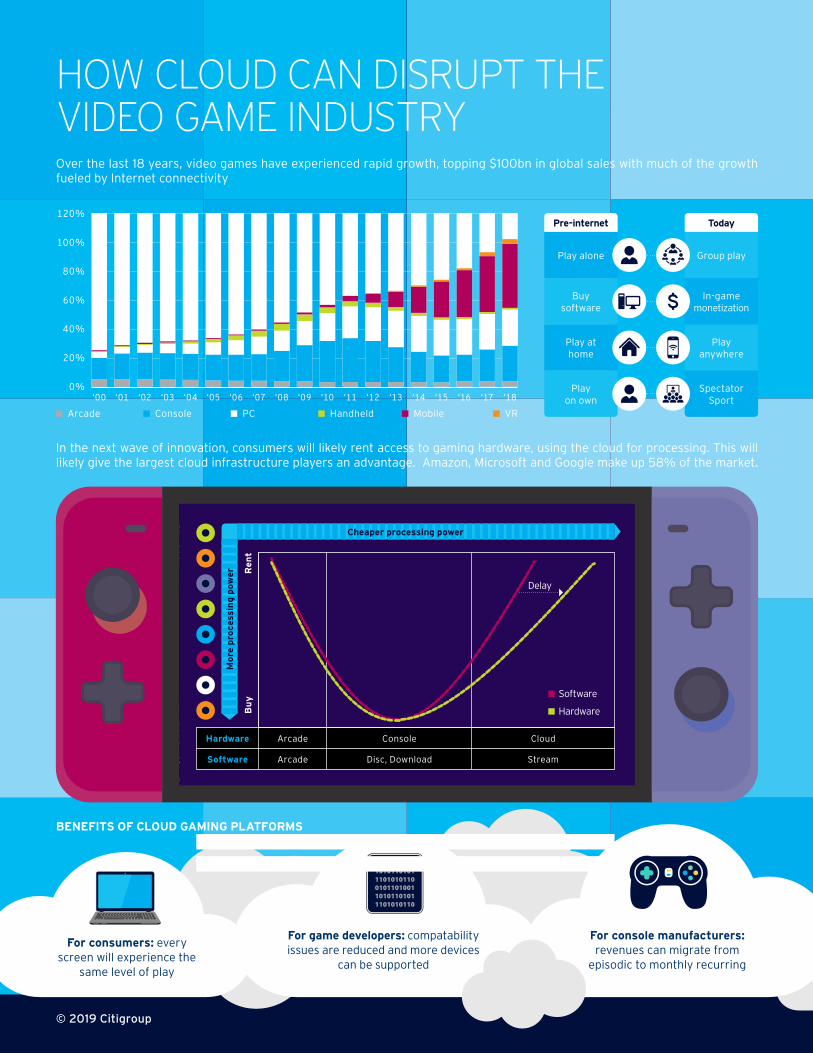

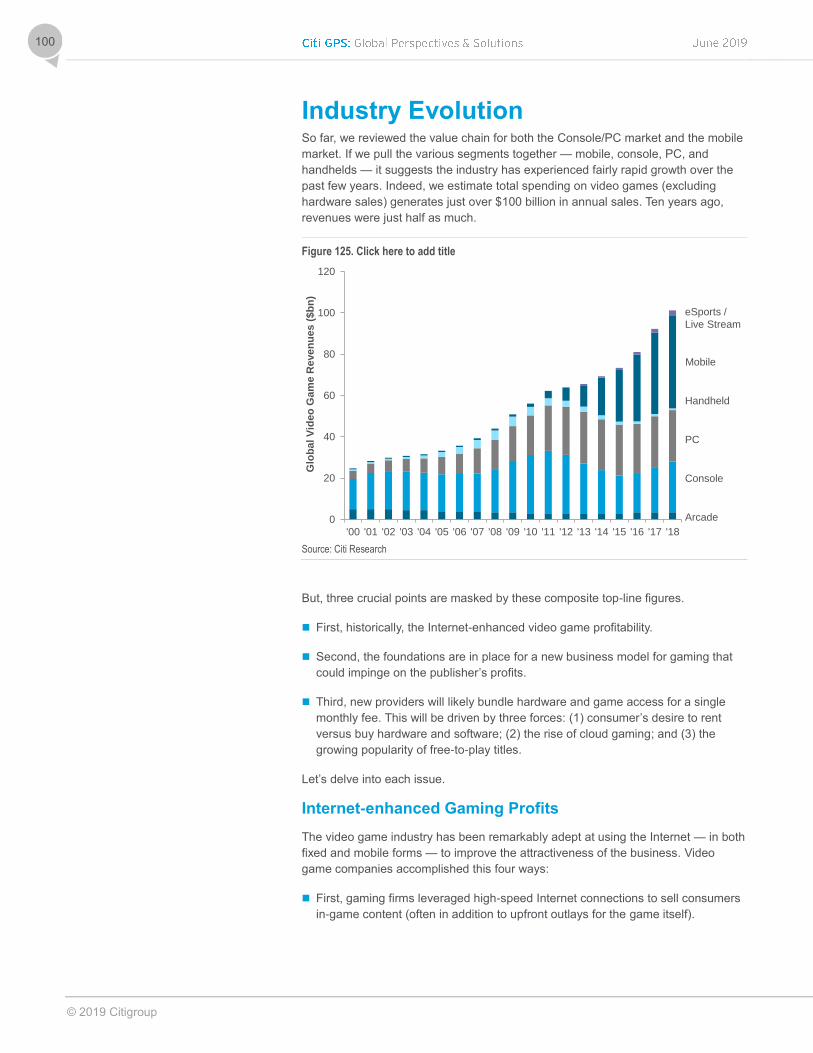

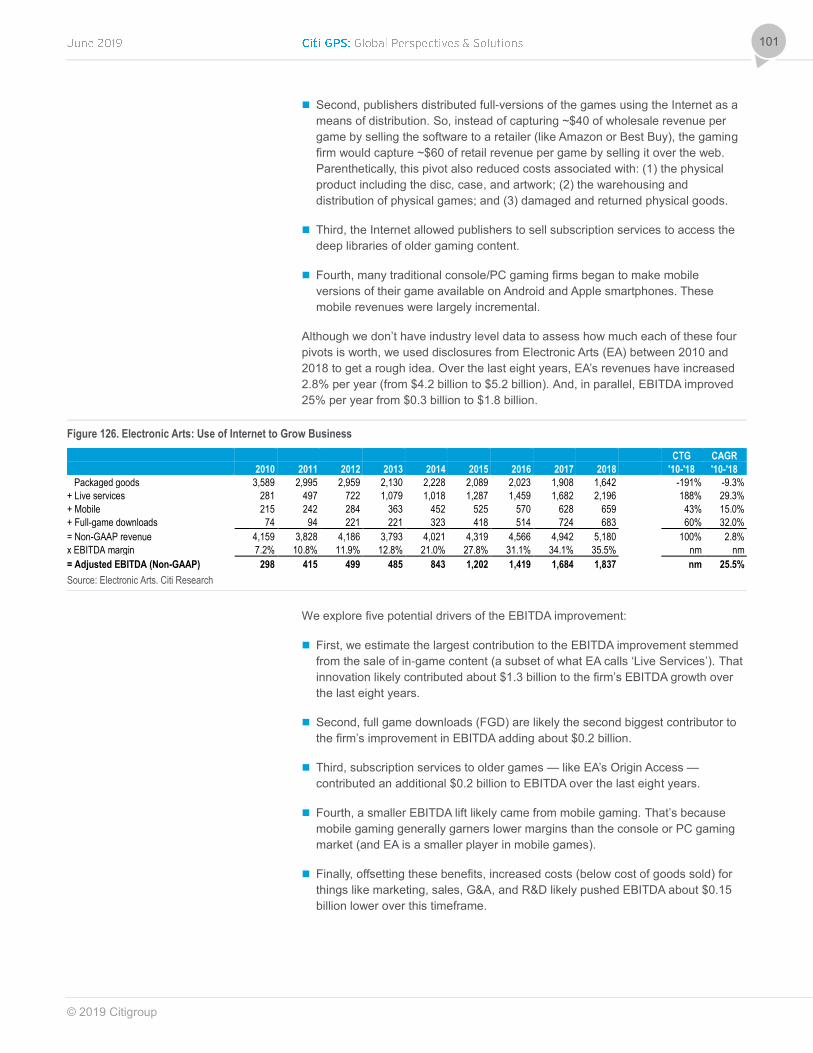

HOW CLOUD CAN DISRUPT THE VIDEO GAME INDUSTRY Over the last 18 years, video games have experienced rapid growth, topping $100bn in global sales with much of the growth fueled by Internet connectivity

In the next wave of innovation, consumers will likely rent access to gaming hardware, using the cloud for processing. This will likely give the largest cloud infrastructure players an advantage. Amazon, Microsoft and Google make up 58% of the market.

Pre-internet Today120%

100%

80%

60%

40%

20%

0%

Arcade Console PC Handheld Mobile VR

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18

© 2019 Citigroup

BENEFITS OF CLOUD GAMING PLATFORMS

For console manufacturers: revenues can migrate from

episodic to monthly recurring

For consumers: every screen will experience the

same level of play

For game developers: compatability issues are reduced and more devices

can be supported

Play alone Group play

Buy software

In-game monetization

Play at home

Play anywhere

Play on own

Spectator Sport

Hardware

Software

Arcade Console Cloud

Arcade Disc, Download Stream

Cheaper processing power

Mor

e pr

oces

sing

pow

er Ren

tB

uy

Software

Hardware

Delay

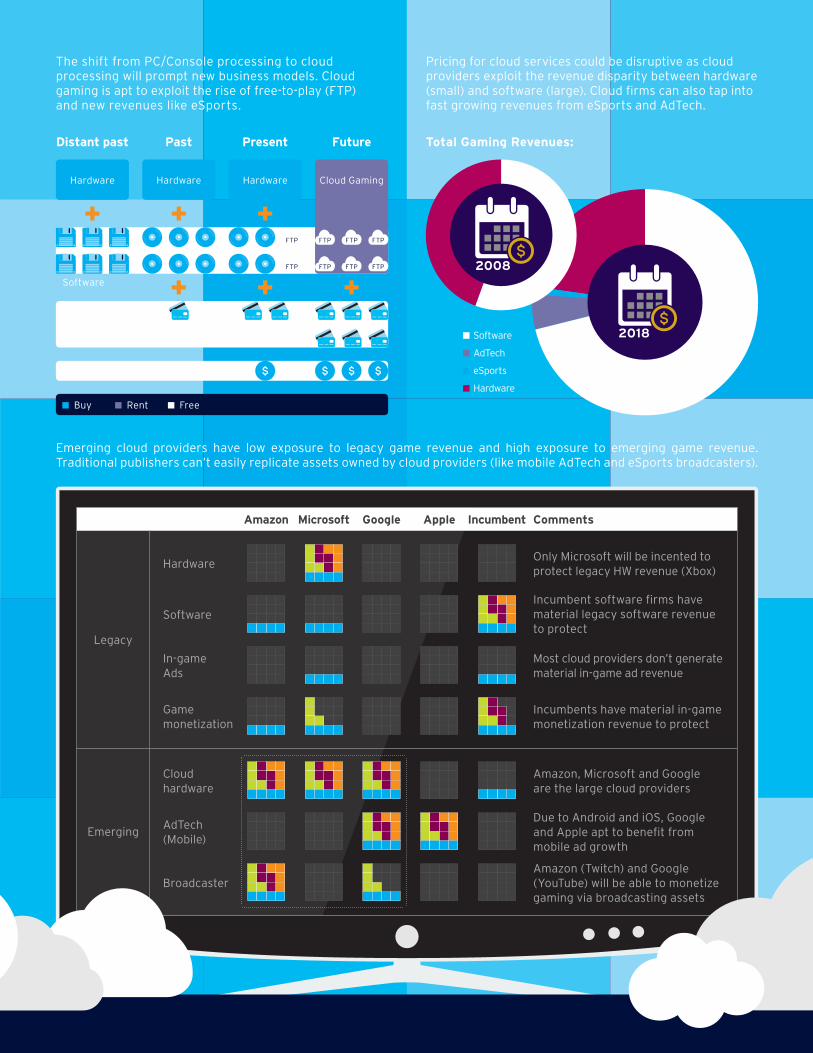

Legacy

In-game Ads

Software

Hardware

Most cloud providers don’t generate material in-game ad revenue

Incumbent software firms have material legacy software revenue to protect

Only Microsoft will be incented to protect legacy HW revenue (Xbox)

Incumbents have material in-game monetization revenue to protect

Amazon, Microsoft and Google are the large cloud providers

Due to Android and iOS, Google and Apple apt to benefit from mobile ad growth

Amazon (Twitch) and Google (YouTube) will be able to monetize gaming via broadcasting assets

Game monetization

Cloud hardware

AdTech (Mobile)

Broadcaster

Emerging

Amazon GoogleMicrosoft Apple Incumbent Comments

Emerging cloud providers have low exposure to legacy game revenue and high exposure to emerging game revenue. Traditional publishers can’t easily replicate assets owned by cloud providers (like mobile AdTech and eSports broadcasters).

Pricing for cloud services could be disruptive as cloud providers exploit the revenue disparity between hardware (small) and software (large). Cloud firms can also tap into fast growing revenues from eSports and AdTech.

Total Gaming Revenues:

Software

AdTech

eSports

Hardware

The shift from PC/Console processing to cloud processing will prompt new business models. Cloud gaming is apt to exploit the rise of free-to-play (FTP) and new revenues like eSports.

Distant past Past Present Future

Buy Rent Free

Hardware

Software

In-game spend

New monetization (eSports, Mobile, AdTech)

Hardware Hardware Cloud Gaming

FTPFTP

FTPFTP

FTP

FTP

FTP

FTP

2018

2008

© 2019 Citigroup

6

Contents Summary 7

The Console/PC Value Chain 11

Layer I: Intellectual Property 12 Layer II: Game Developers 14

The Genres 20 AAA Versus Independent Games 21

Layer III: Game Publishers 26 Layer IV: Hardware 29

Arcades: Where the Games Begin 29 Console and Handsets: Where the Market Expands 30 Handheld Market 32 PC Market 38

Layer V: Distribution 40 Cloud Gaming 45

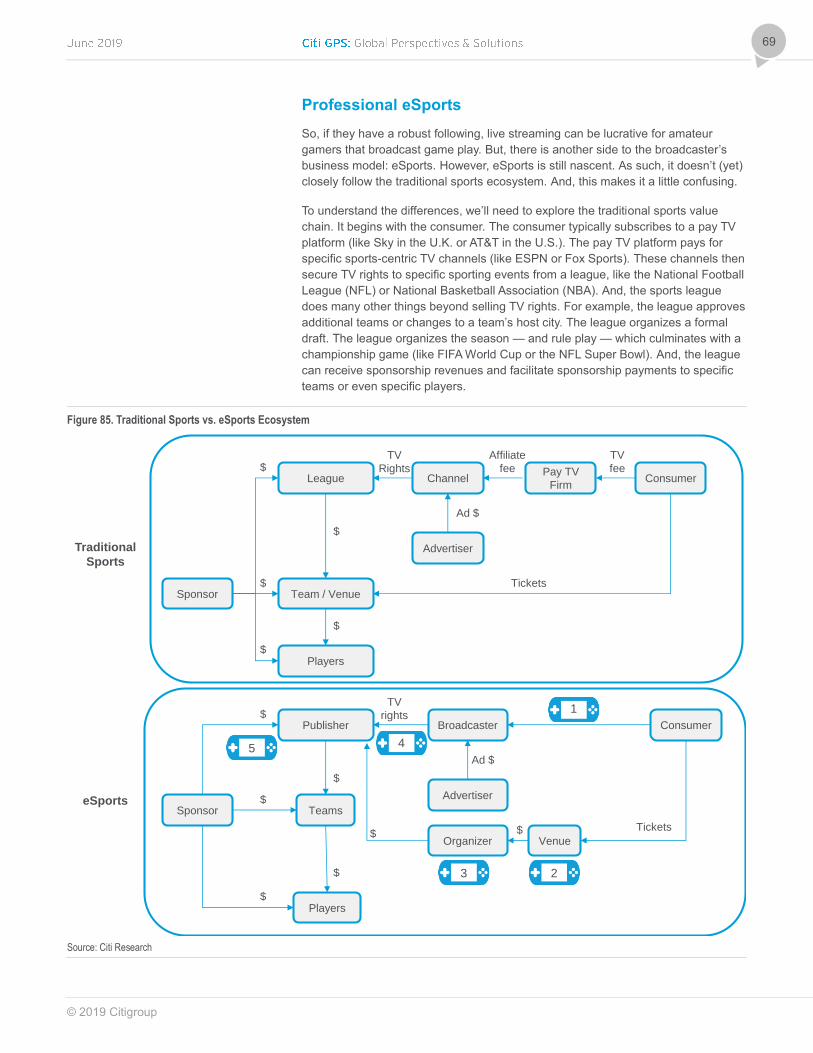

Layer VI: Consumer 53 Layer VII: eSports 55

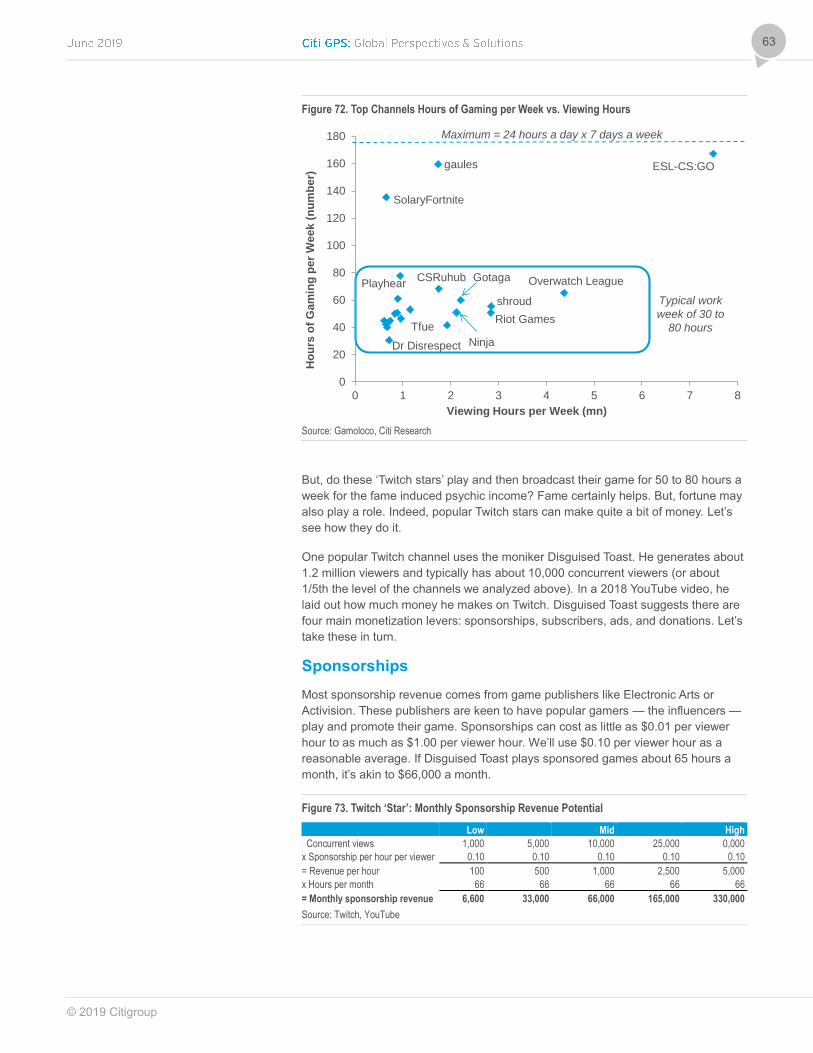

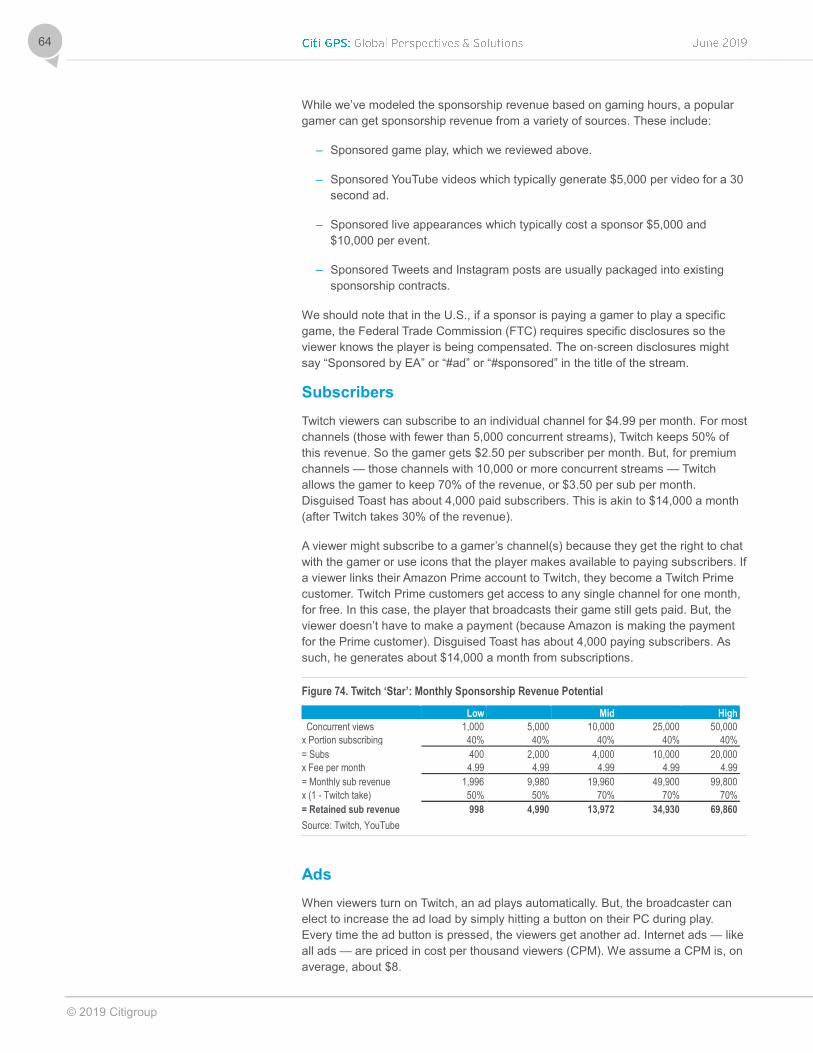

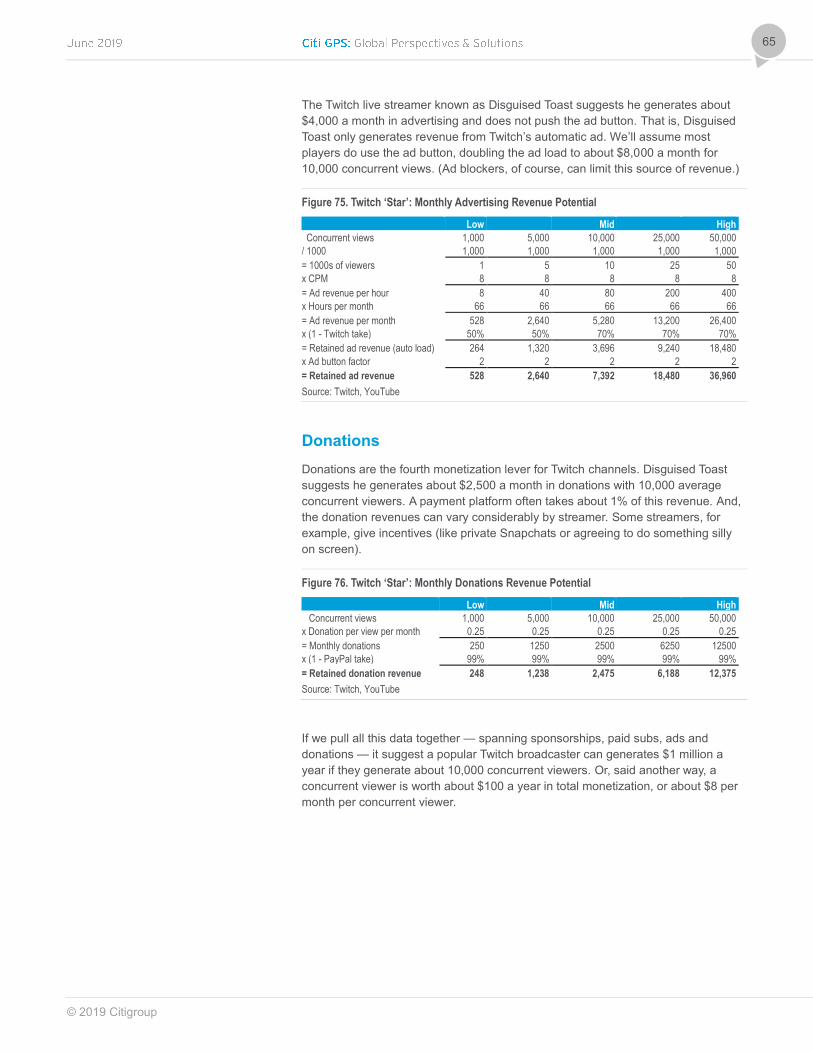

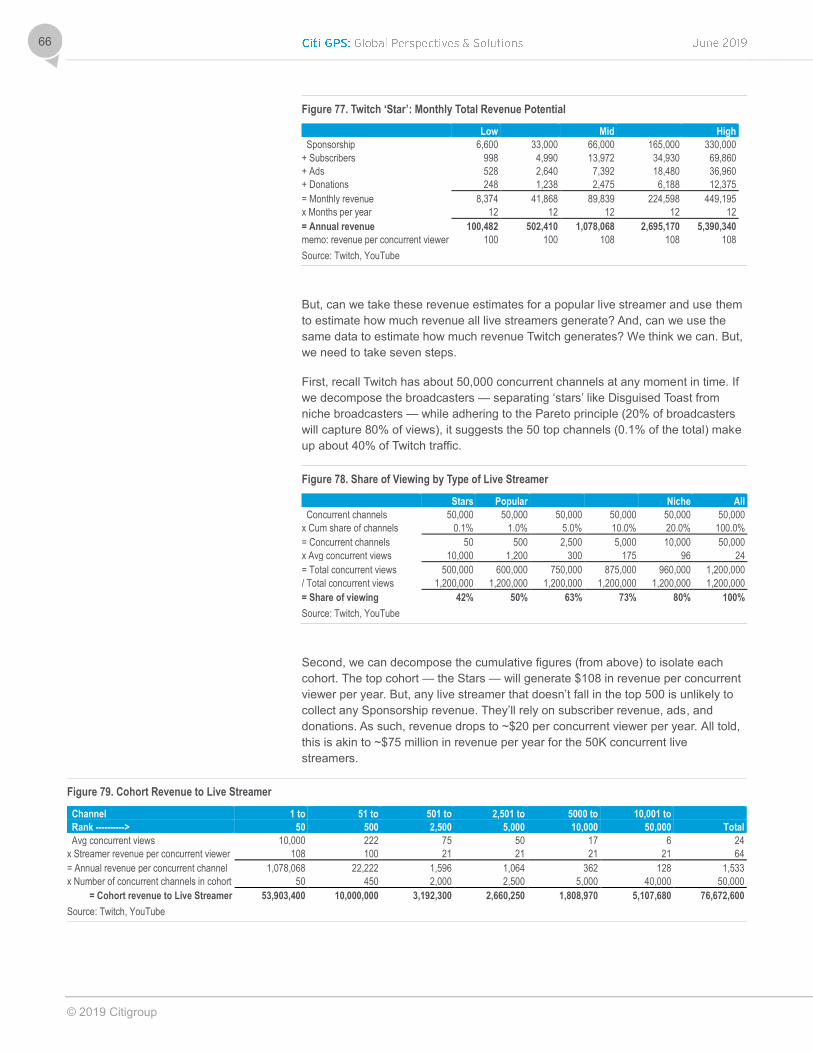

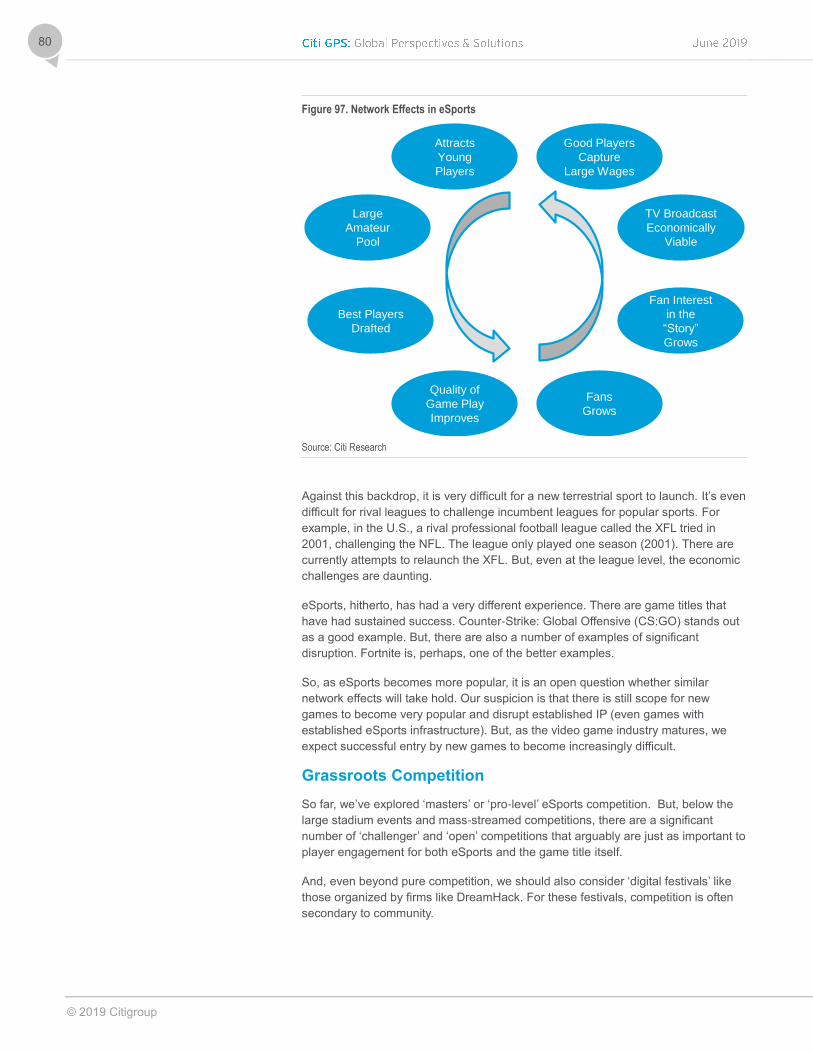

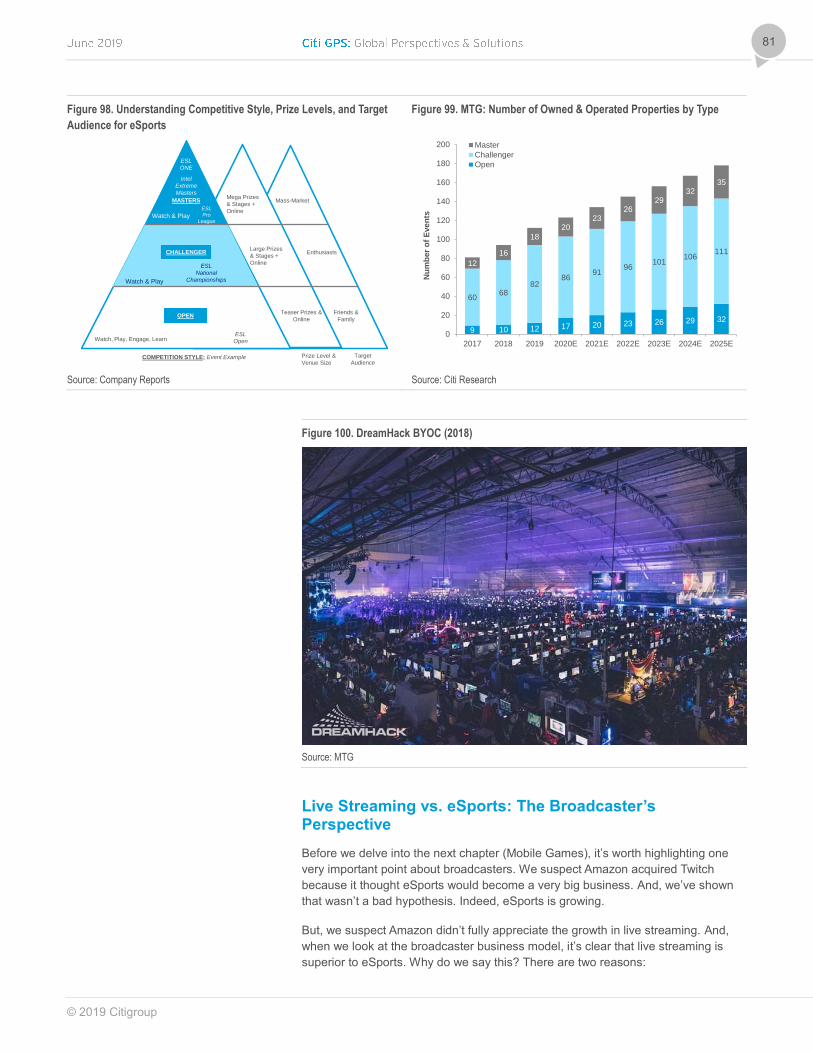

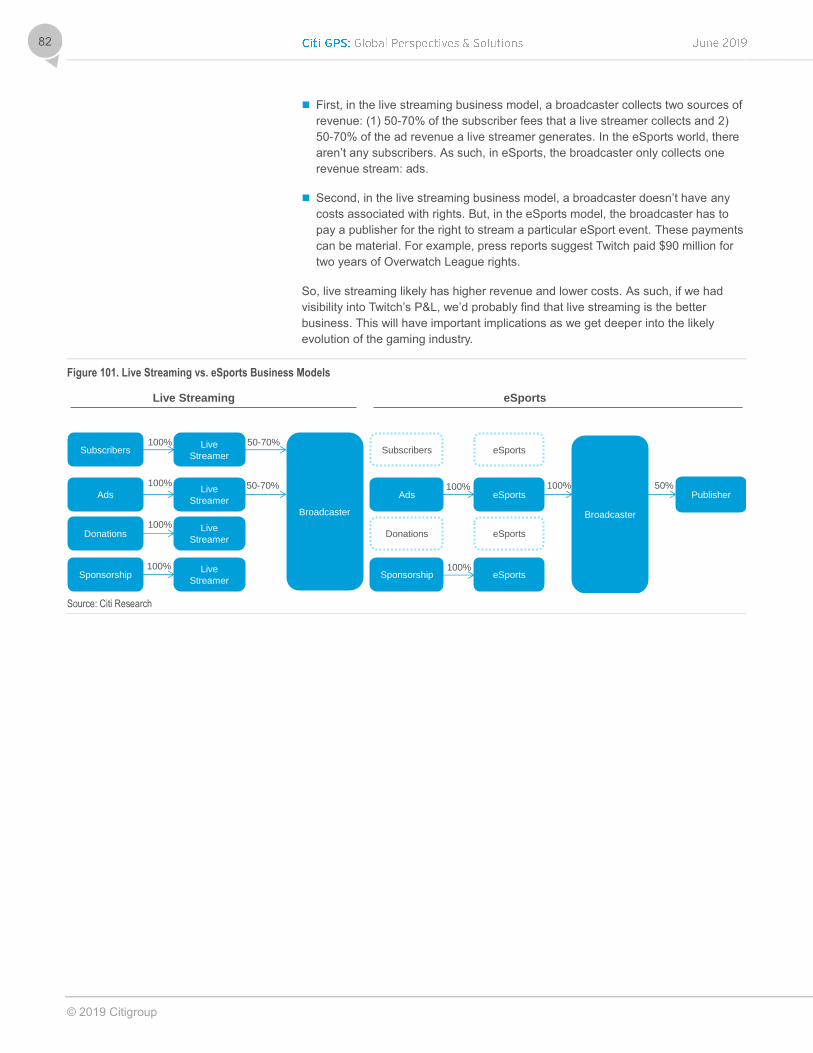

Mode of Distribution 55 Live Streamers 58 Sponsorships 63 Subscribers 64 Ads 64 Donations 65 Professional eSports 69 Turnover of eSports Titles a Key Consideration 79 Grassroots Competition 80 Live Streaming vs. eSports: The Broadcaster’s Perspective 81

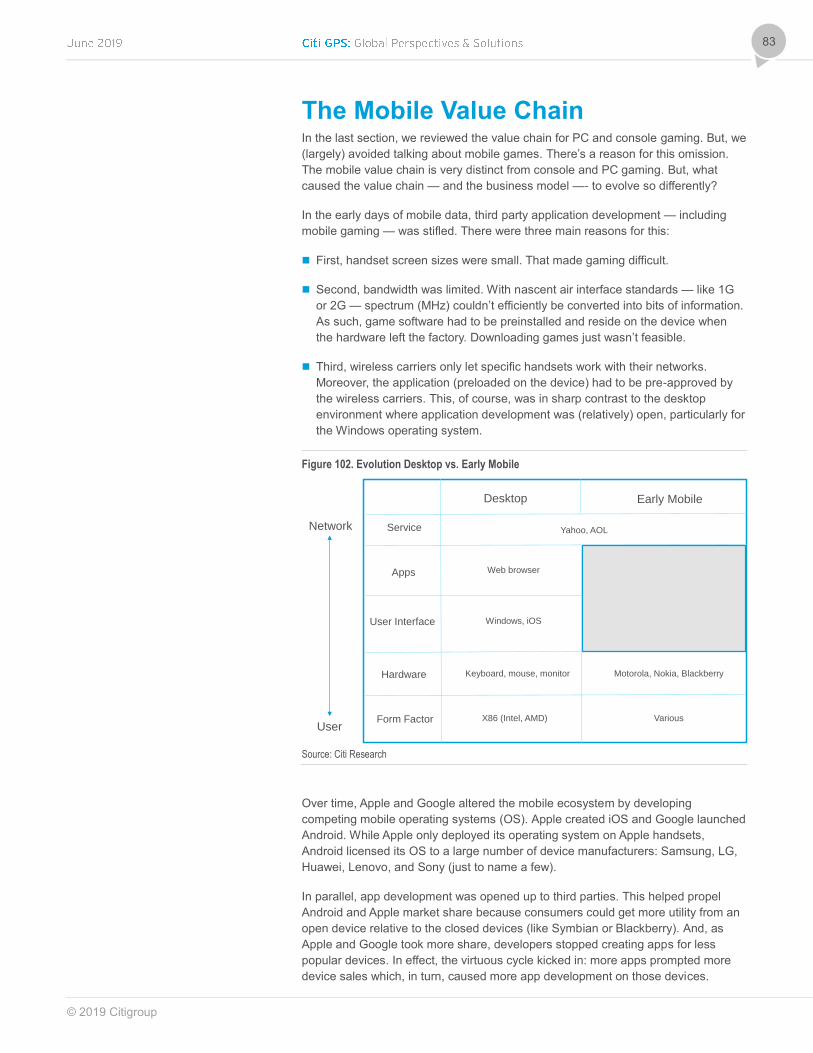

The Mobile Value Chain 83 Layer I: Intellectual Property 86 Layer II: Developers and Publishers 87 Layer III: Installs 89 Layer IV: Mobile OS 92 Layer V: Generate Advertising 93 Layer VI: Advertiser 95 Layer VII: Consumer 96

Mobile Economics 97 Mobile Gaming Revenues 99

Industry Evolution 100 Internet-enhanced Gaming Profits 100 Foundation In Place for a New Model 102 What the New Model Might Look Like 107 Pricing of Cloud Gaming Services 114 Regulations 121

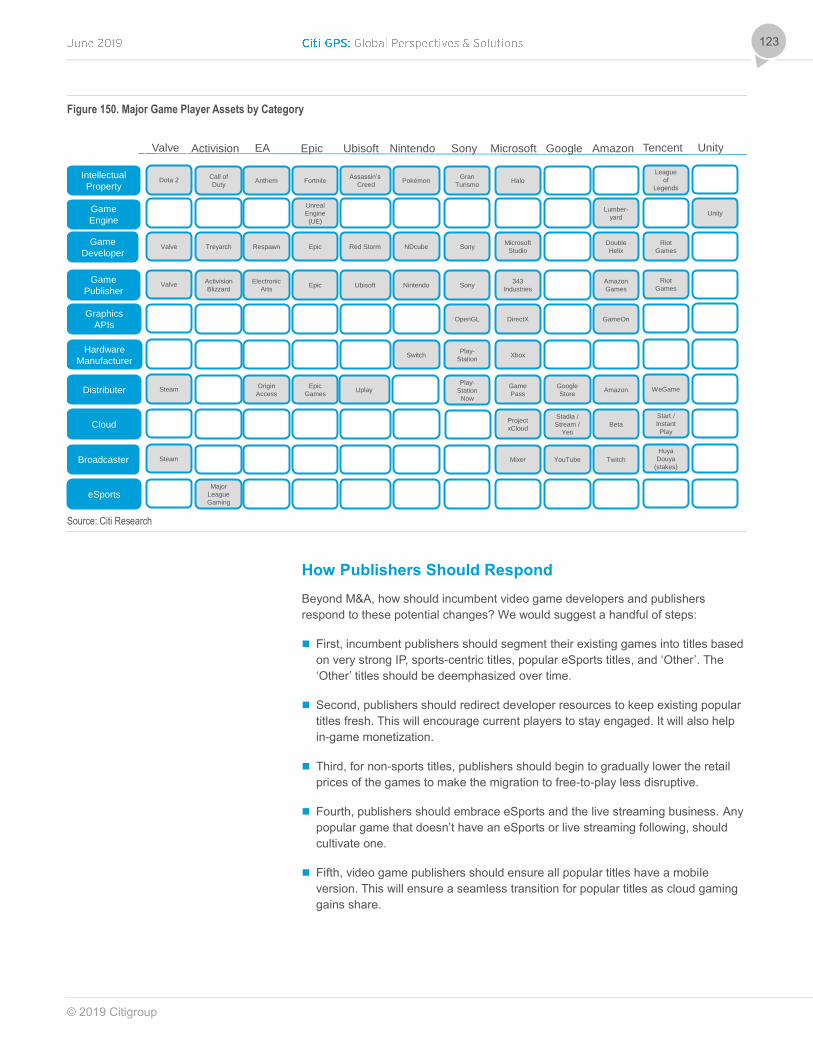

Prudent Strategic Responses 122 Potential M&A 122 How Publishers Should Respond 123

Expert Views 128

Expert Views from the Gaming Industry 129 A Conversation with Luke Alvarez 130 A Conversation with Ralf Reichart 138 A Conversation with Wil Stephens 146

© 2019 Citigroup

7

Summary Eight years ago, Marc Andreesen – of Netscape fame – penned an article in The

Wall Street Journal titled: ‘Why Software is Eating the World’. Mr. Andreesen’s idea,

like all good ideas, was simple: software — riding on top of the Internet — was

changing everything. For the software owners, it was a boon. But, for incumbents, it

represented unrelenting value destruction.

In the wake of this software-induced upheaval, non-software centric firms have

been dented, damaged, upended, or dethroned. The list of victims is long: book

stores (Amazon), brick-based retail (Amazon), travel agencies (Expedia), taxi cabs

(Uber), phone books (Google), photos (Apple), newspapers (Google), magazines

(Facebook), radio stations (Spotify), and cable networks (Netflix).

Indeed, over the last 20 years, five U.S. leviathans have proven particularly adept at

using software to create significant economic value. Wall Street’s shorthand for

these firms is FAANG: Facebook, Apple, Amazon, Netflix, and Google. In Asia, there

are three disruptive firms — Baidu, Alibaba and Tencent — or BAT. Each firm —

and a handful of smaller entities — has used software and the Internet to give

consumers what they want, when they want it, at far lower cost.

After the FAANG or BAT transformation is complete, these giants jockey for position

to ensure they capture the lion’s share of the sector’s remaining, albeit diminished,

profits. In the process, the largest Internet firms get bigger. Incumbent firms stall,

shrink, or sometimes, disappear.

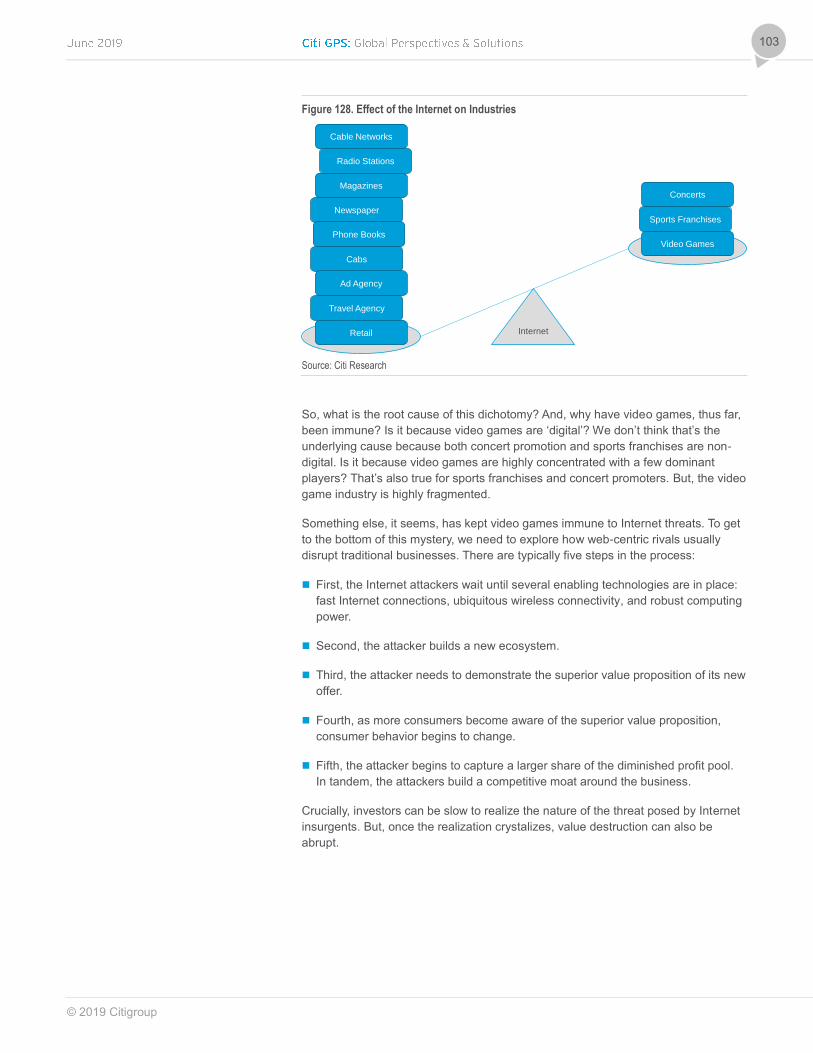

Within the entertainment sector, however, there’s a small collection of rarefied

entities. To date, these few firms have been immune to the software-centric,

Internet-enabled FAANG assault: Sports teams, concert promoters, and video game

publishers. Indeed, each of these businesses has actually used the Internet to

improve results:

Sports teams sold digital content rights on top of traditional TV rights.

Concert promoters — like Live Nation —- benefitted as lucrative CD sales

collapsed. That’s because rock stars toured more often to preserve their

lifestyles.

Video game publishers have deftly used the Internet to: (1) sell copies of their

software directly to consumers, disintermediating retailers; (2) augment game

sales with in-game monetization (like loot boxes); and (3) tap into explosive

smartphone growth to monetize mobile games.

But, will video game publishers remain immune to the FAANG threat? We don’t

think so. A number of large firms — including Google, Amazon, and Microsoft — are

rapidly building cloud scale. And, we suspect a natural way to leverage this

infrastructure is to move into gaming. Moreover, there’s quite a bit of money up for

grabs: $100 billion per year for software and $35 billion a year for hardware.

But, to understand why we’re so focused on Google, Amazon, and Microsoft, we

need to understand five powerful trends that are — or will — rumble across the

video game ecosystem.

© 2019 Citigroup

8

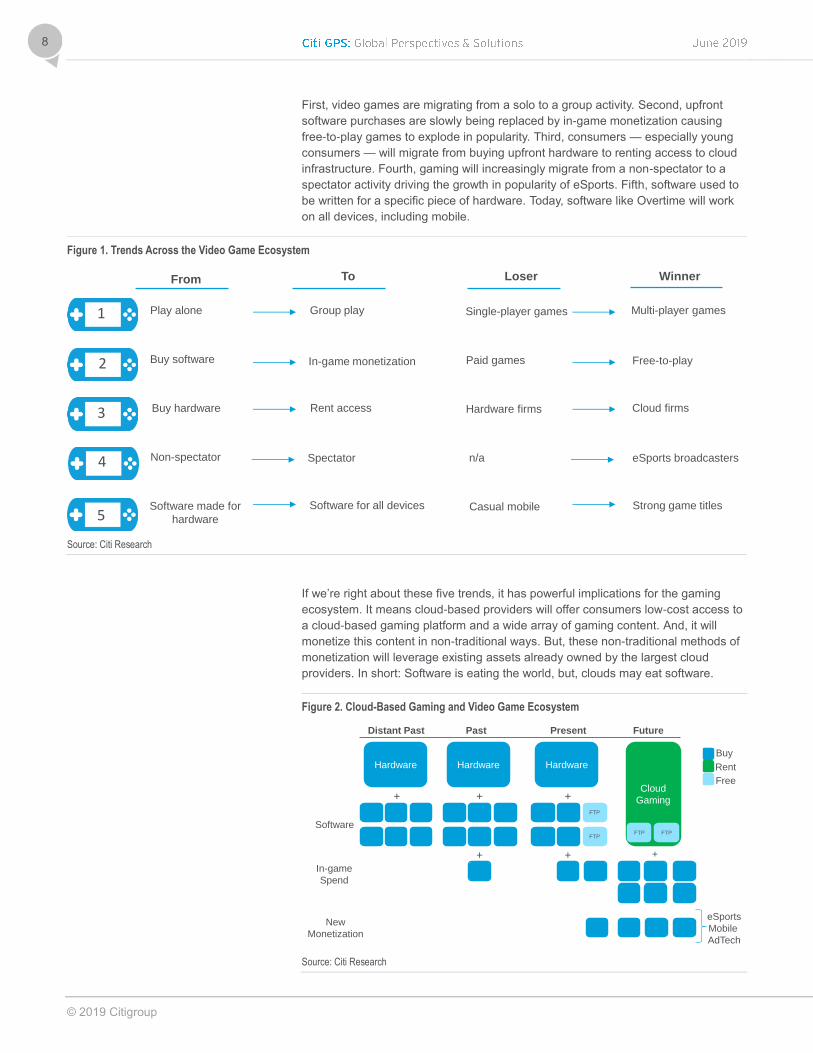

First, video games are migrating from a solo to a group activity. Second, upfront

software purchases are slowly being replaced by in-game monetization causing

free-to-play games to explode in popularity. Third, consumers — especially young

consumers — will migrate from buying upfront hardware to renting access to cloud

infrastructure. Fourth, gaming will increasingly migrate from a non-spectator to a

spectator activity driving the growth in popularity of eSports. Fifth, software used to

be written for a specific piece of hardware. Today, software like Overtime will work

on all devices, including mobile.

Figure 1. Trends Across the Video Game Ecosystem

Source: Citi Research

If we’re right about these five trends, it has powerful implications for the gaming

ecosystem. It means cloud-based providers will offer consumers low-cost access to

a cloud-based gaming platform and a wide array of gaming content. And, it will

monetize this content in non-traditional ways. But, these non-traditional methods of

monetization will leverage existing assets already owned by the largest cloud

providers. In short: Software is eating the world, but, clouds may eat software.

Figure 2. Cloud-Based Gaming and Video Game Ecosystem

Source: Citi Research

From To Loser Winner

Software made for

hardware

Software for all devices Casual mobile Strong game titles5

Non-spectator Spectator n/a eSports broadcasters4

Buy hardware Rent access Hardware firms Cloud firms3

Buy software In-game monetization Paid games Free-to-play2

Play alone Group play Single-player games Multi-player games1

Hardware

+

Software

Hardware

+

In-game

Spend

+

Hardware

FTP

+

+

Cloud

Gaming

+

Present FuturePast

FTP

Distant Past

Buy

New

Monetization

FTPFTP

eSports

Mobile

AdTech

Rent

Free

© 2019 Citigroup

9

What assets will a cloud-based firm leverage? There are quite a few:

First, Google, Amazon, and Microsoft are the largest providers of cloud-based

services (with ~60% share as of the fourth quarter of 2018). This will enable low-

cost cloud gaming services.

Second, the largest game broadcasters are Twitch (owned by Amazon) and

YouTube (owned by Google). This gives two cloud-based firms indirect methods

of monetization that cannot be matched by incumbent game publishers.

Third, a large portion of gaming revenues stem from in-game advertising,

particularly on mobile devices. And, the mobile AdTech ecosystem is controlled

by two firms: Apple and Google.

Fourth, digital distribution — particularly for Amazon — is a core competency. As

such, these cloud-based firms could open (or acquire) gaming distribution

platforms like Valve’s Steam.

Fifth, cloud gaming companies have ample means to cross-sell their offerings.

Cross-selling opportunities span both hardware (FireTV, AppleTV, Alexa) and

software (YouTube Premium, Amazon Prime).

If we’re correct, video game publishers that are over-monetizing their intellectual

property (IP) by selling the game plus in-game content could see long-term top-line

pressures. How can incumbent gaming firms respond? We think there are five key

steps:

First, incumbents should deemphasize titles that aren’t tied to sports, have weak

IP, and don’t have a robust eSports (or live streamer) community. That’s because

sports titles tend to have a very loyal following (and are likely less prone to cloud-

based price competition). And, we expect eSports to play a larger role in the

gaming ecosystem as fewer very popular games (with robust IP) increasingly

dominate the gaming ecosystem.

Second, publishers should redirect developer time to refreshing existing titles to

keep in-game monetization robust and consumer engagement consistent.

Third, for non-sports titles with weaker IP, publishers should begin to gradually

lower the retail prices of the games while simultaneously investing in in-game

monetization. This will make the transition to free-to-play less disruptive.

Fourth, publishers should invest in eSports and develop games that are likely to

have a strong live streaming following.

Fifth, video game firms should ensure that every popular title has a viable mobile

version. This will prepare firms for the inevitability of cloud gaming (when

mobile/personal computer (PC)/console gaming platforms converge).

So, the ‘salad days’ for video game publishers — where the Internet enhanced

profits — probably won’t last. But, there are clearly steps video game publishers can

make today to ensure they still play a viable part in the new cloud-based, platform-

converged, eSports-centric video game ecosystem.

© 2019 Citigroup

10

To explore our thesis, we have divided this report into three main sections. First,

we’ll unpack the video game value chain tackling the console/PC market and the

mobile market separately. Second, we’ll suggest how the video game industry will

likely evolve. Third, we’ll review the strategic implications — and potential next

steps — for the video game incumbents.

Before we dive in, a quick disclaimer. As we did this work, we were struck by both

the level and quality of debate related to cloud computing and its impact on the

video game ecosystem. There are strong arguments on both sides of the debate.

Obviously, we have our view. But, we are conscious not all readers will agree with

us. With this in mind, we hope readers will find the ‘Expert Views’ section at the

back of the report helpful. These experts have decades of experience in the space.

We are also very open to feedback: Please do get in touch if you think we’ve

missed something or have drawn the wrong conclusions. We are keen to engage.

© 2019 Citigroup

11

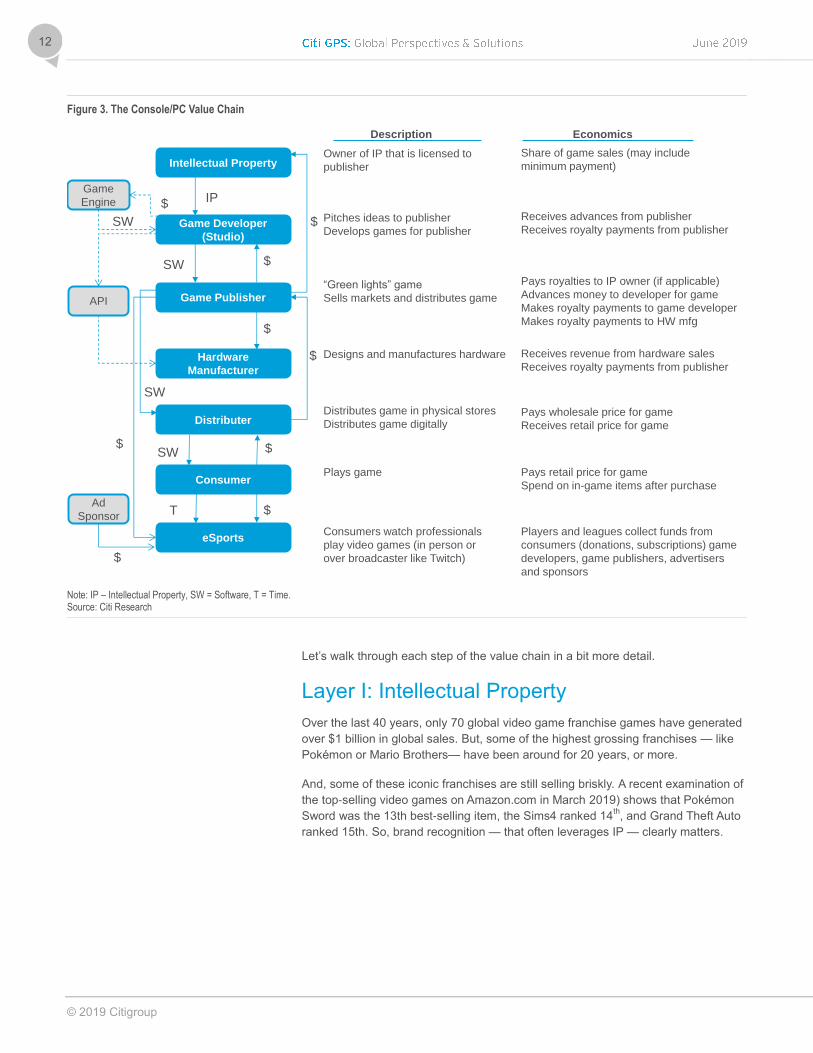

The Console/PC Value Chain The video game industry has a long history. Back in 1958, a physicist, William

Higinbotham, created the first video game: Tennis for Two. It took about 15 years

before the business world took notice. The Magnavox Odyssey debuted in 1972.

Over the next 60 years, a rather complex industry organically evolved. In the PC

and console market, the video game value chain has seven layers:

Intellectual Property (IP): At the top of the stack are owners of intellectual

property. This includes sports leagues (FIFA, NFL), movies (Star Wars), books

(Tom Clancy), and toys (Lego). This IP is often licensed for a royalty payment.

Developers: Video game developers are one layer down the value chain. These

entities write code to create the game. They receive a fee and perhaps a royalty

(if the game is successful) from the game publisher. They may rely on — and pay

for — game engines to accelerate game development. If not, they’ll use specific

application programming interfaces (APIs) that allow the software to work easily

with a variety of hardware platforms.

Publishers: Toward the middle of the stack are game publishers. Publishers sell

and market video games. They make three types of payments: (1) payments to

the owner of the underlying IP (if applicable); (2) payments to the game

developer; and (3) payments to the manufacturer of the console (but not PC

firms). If the game is distributed digitally, they may also make a payment to the

digital storefront.

Hardware: The game developer and game publisher will agree to develop the

game for a specific type of hardware. It could be a console — like PlayStation,

Xbox or Nintendo — or a PC. In the future, this may be a ‘virtual hardware’

presence that is a streaming service across any hardware.

Distributors: Toward the bottom of the stack are the distributors. They sell the

game to the consumer. Delivery could be via a physical disc (GameStop,

Amazon) or a digital file (Steam, Electronic Art’s Origin).

Consumers: Near the bottom of the value chain, you’ll find the consumer. They

spend money to enjoy the underlying game.

eSports: The final layer of the value chain is eSports. eSports can include

professional teams (in tournaments). Or, it may capture consumers watching

amateurs play video games on a broadcast platform (like Twitch). These

amateurs are also called ‘live streamers’.

© 2019 Citigroup

12

Figure 3. The Console/PC Value Chain

Note: IP – Intellectual Property, SW = Software, T = Time. Source: Citi Research

Let’s walk through each step of the value chain in a bit more detail.

Layer I: Intellectual Property

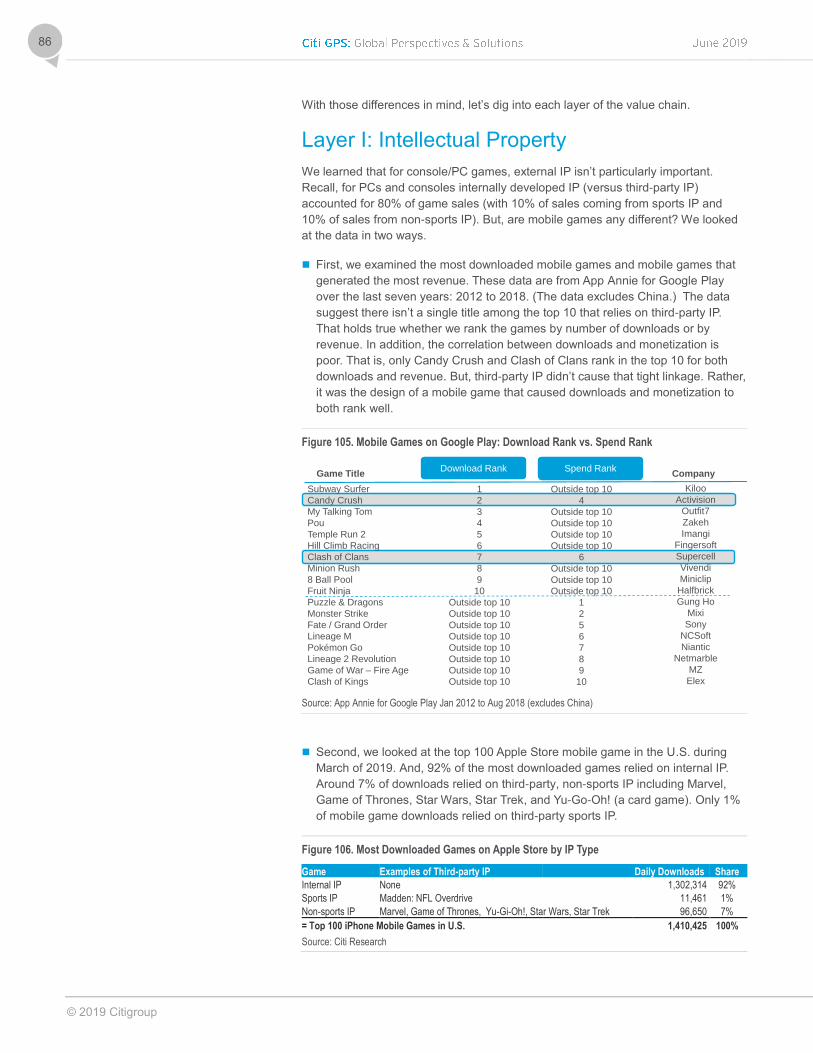

Over the last 40 years, only 70 global video game franchise games have generated

over $1 billion in global sales. But, some of the highest grossing franchises — like

Pokémon or Mario Brothers— have been around for 20 years, or more.

And, some of these iconic franchises are still selling briskly. A recent examination of

the top-selling video games on Amazon.com in March 2019) shows that Pokémon

Sword was the 13th best-selling item, the Sims4 ranked 14th, and Grand Theft Auto

ranked 15th. So, brand recognition — that often leverages IP — clearly matters.

Intellectual Property

Game Developer

(Studio)

Game Publisher

Hardware

Manufacturer

Distributer

Consumer

Description

Owner of IP that is licensed to

publisher

Pitches ideas to publisher

Develops games for publisher

Economics

Share of game sales (may include

minimum payment)

Receives advances from publisher

Receives royalty payments from publisher

“Green lights” game

Sells markets and distributes game

Pays royalties to IP owner (if applicable)

Advances money to developer for game

Makes royalty payments to game developer

Makes royalty payments to HW mfg

Designs and manufactures hardware Receives revenue from hardware sales

Receives royalty payments from publisher

Distributes game in physical stores

Distributes game digitally

Plays game Pays retail price for game

Spend on in-game items after purchase

Pays wholesale price for game

Receives retail price for game

$

$

$

$

$

IP

SW

SW

SW

API

Game

Engine $

SW

eSportsConsumers watch professionals

play video games (in person or

over broadcaster like Twitch)

Players and leagues collect funds from

consumers (donations, subscriptions) game

developers, game publishers, advertisers

and sponsors

$

TAd

Sponsor

$

$

© 2019 Citigroup

13

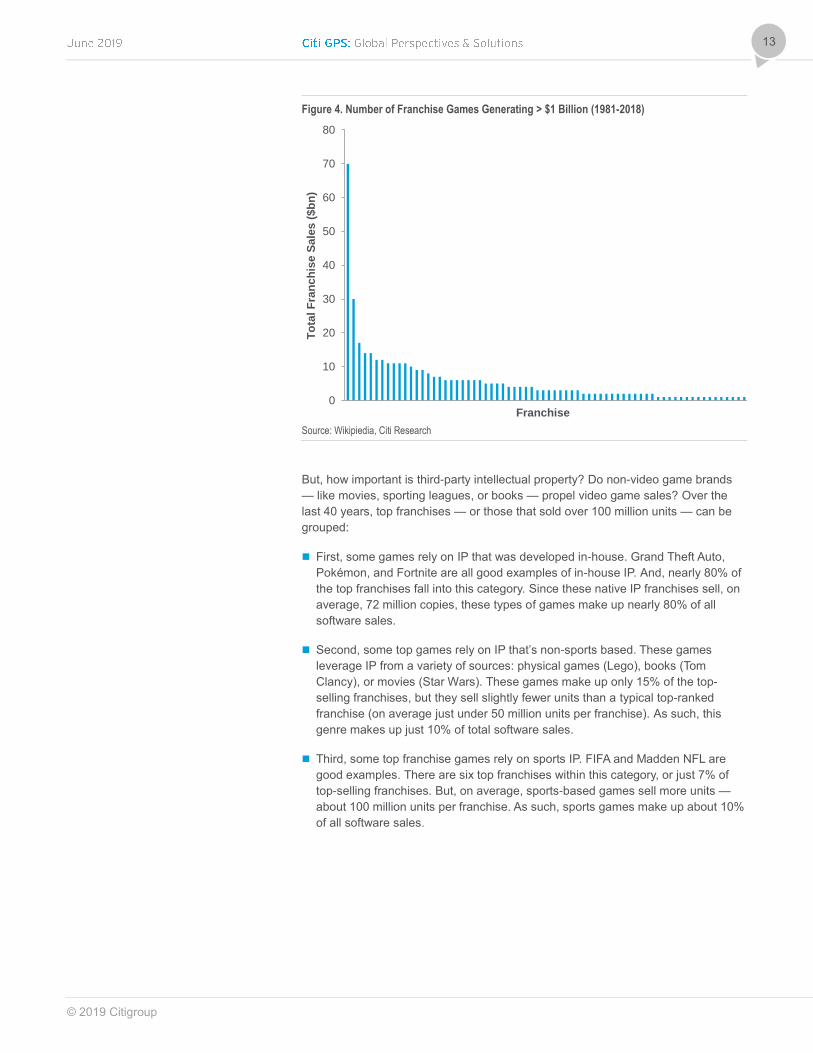

Figure 4. Number of Franchise Games Generating > $1 Billion (1981-2018)

Source: Wikipiedia, Citi Research

But, how important is third-party intellectual property? Do non-video game brands

— like movies, sporting leagues, or books — propel video game sales? Over the

last 40 years, top franchises — or those that sold over 100 million units — can be

grouped:

First, some games rely on IP that was developed in-house. Grand Theft Auto,

Pokémon, and Fortnite are all good examples of in-house IP. And, nearly 80% of

the top franchises fall into this category. Since these native IP franchises sell, on

average, 72 million copies, these types of games make up nearly 80% of all

software sales.

Second, some top games rely on IP that’s non-sports based. These games

leverage IP from a variety of sources: physical games (Lego), books (Tom

Clancy), or movies (Star Wars). These games make up only 15% of the top-

selling franchises, but they sell slightly fewer units than a typical top-ranked

franchise (on average just under 50 million units per franchise). As such, this

genre makes up just 10% of total software sales.

Third, some top franchise games rely on sports IP. FIFA and Madden NFL are

good examples. There are six top franchises within this category, or just 7% of

top-selling franchises. But, on average, sports-based games sell more units —

about 100 million units per franchise. As such, sports games make up about 10%

of all software sales.

0

10

20

30

40

50

60

70

80

To

tal F

ran

ch

ise S

ale

s (

$b

n)

Franchise

© 2019 Citigroup

14

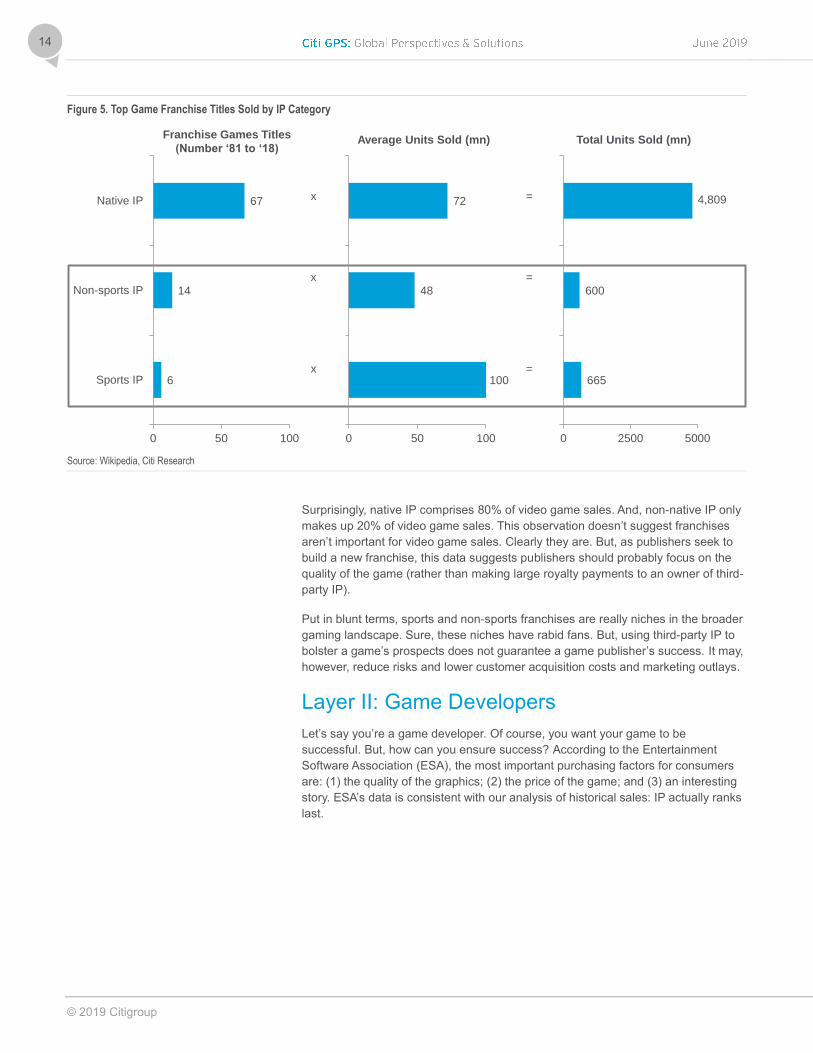

Figure 5. Top Game Franchise Titles Sold by IP Category

Source: Wikipedia, Citi Research

Surprisingly, native IP comprises 80% of video game sales. And, non-native IP only

makes up 20% of video game sales. This observation doesn’t suggest franchises

aren’t important for video game sales. Clearly they are. But, as publishers seek to

build a new franchise, this data suggests publishers should probably focus on the

quality of the game (rather than making large royalty payments to an owner of third-

party IP).

Put in blunt terms, sports and non-sports franchises are really niches in the broader

gaming landscape. Sure, these niches have rabid fans. But, using third-party IP to

bolster a game’s prospects does not guarantee a game publisher’s success. It may,

however, reduce risks and lower customer acquisition costs and marketing outlays.

Layer II: Game Developers

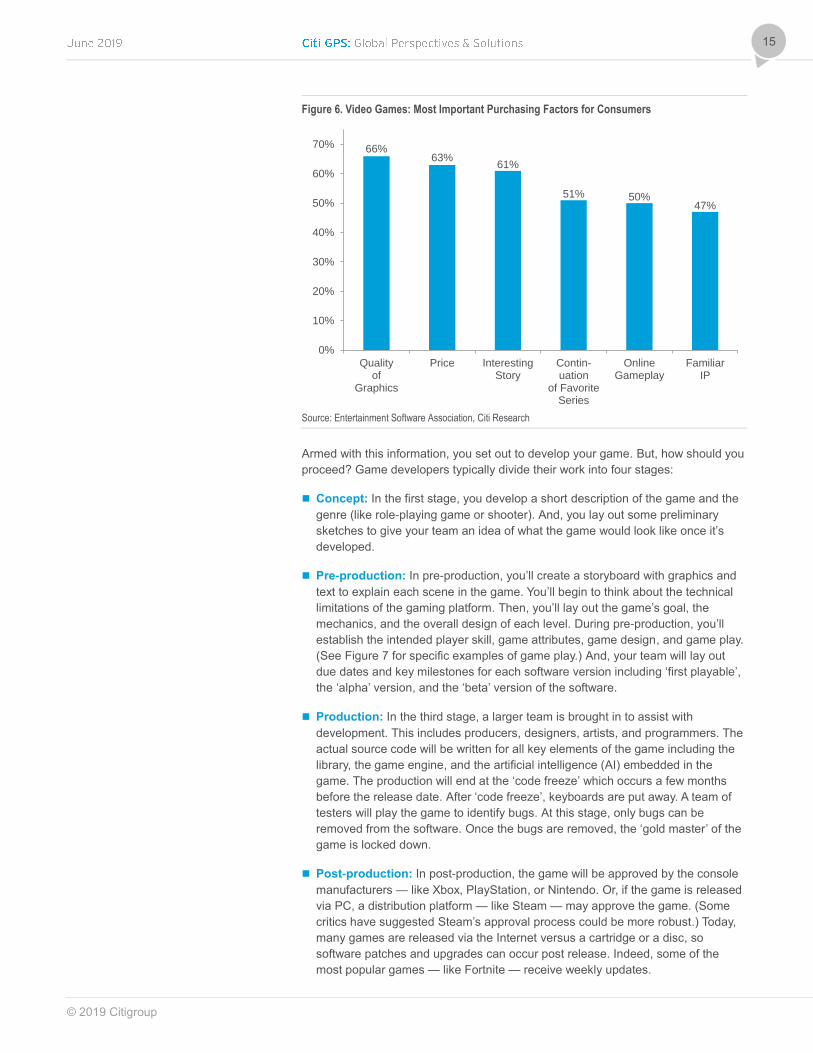

Let’s say you’re a game developer. Of course, you want your game to be

successful. But, how can you ensure success? According to the Entertainment

Software Association (ESA), the most important purchasing factors for consumers

are: (1) the quality of the graphics; (2) the price of the game; and (3) an interesting

story. ESA’s data is consistent with our analysis of historical sales: IP actually ranks

last.

100

48

72

0 50 100

Average Units Sold (mn)

6

14

67

0 50 100

Sports IP

Non-sports IP

Native IP

Franchise Games Titles

(Number ‘81 to ‘18)

665

600

0 2500 5000

4,809

Total Units Sold (mn)

x

x

x

=

=

=

© 2019 Citigroup

15

Figure 6. Video Games: Most Important Purchasing Factors for Consumers

Source: Entertainment Software Association, Citi Research

Armed with this information, you set out to develop your game. But, how should you

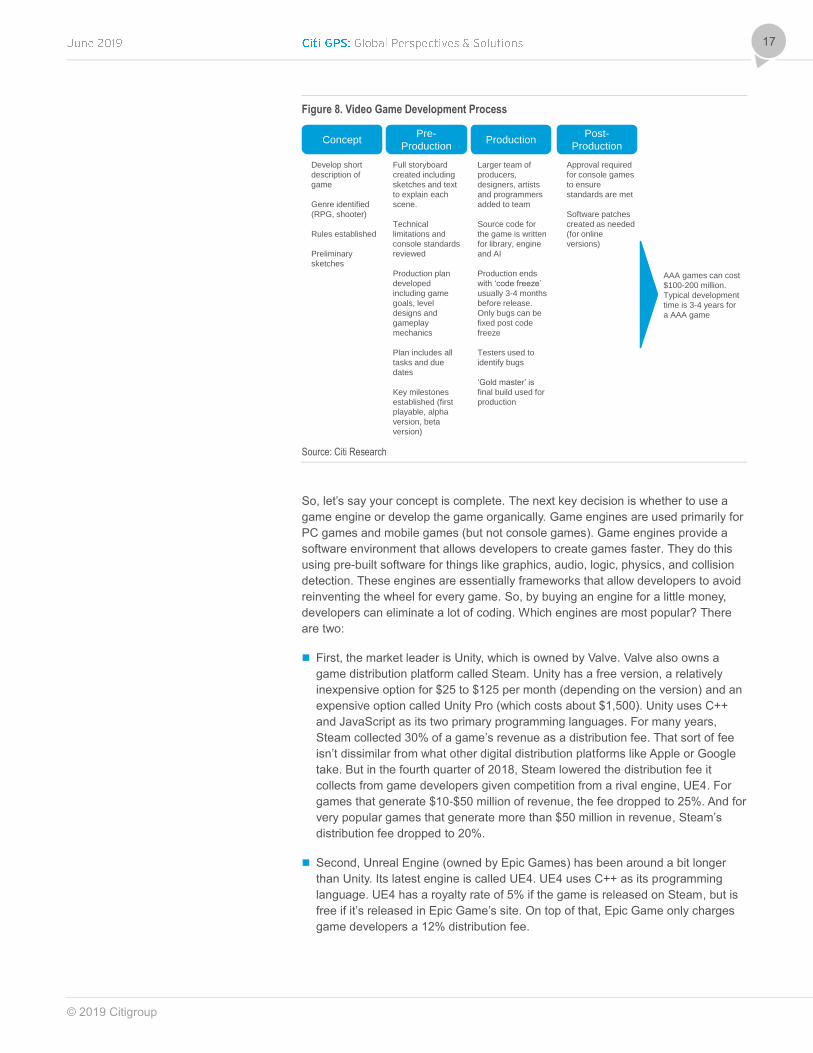

proceed? Game developers typically divide their work into four stages:

Concept: In the first stage, you develop a short description of the game and the

genre (like role-playing game or shooter). And, you lay out some preliminary

sketches to give your team an idea of what the game would look like once it’s

developed.

Pre-production: In pre-production, you’ll create a storyboard with graphics and

text to explain each scene in the game. You’ll begin to think about the technical

limitations of the gaming platform. Then, you’ll lay out the game’s goal, the

mechanics, and the overall design of each level. During pre-production, you’ll

establish the intended player skill, game attributes, game design, and game play.

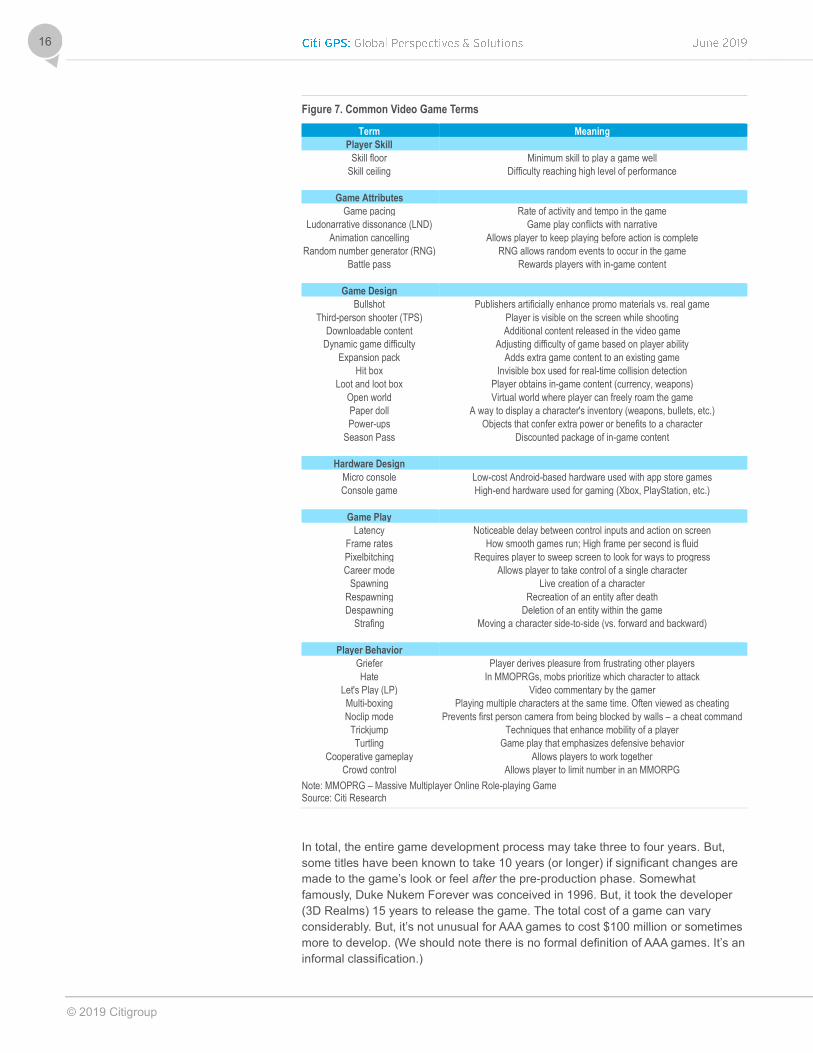

(See Figure 7 for specific examples of game play.) And, your team will lay out

due dates and key milestones for each software version including ‘first playable’,

the ‘alpha’ version, and the ‘beta’ version of the software.

Production: In the third stage, a larger team is brought in to assist with

development. This includes producers, designers, artists, and programmers. The

actual source code will be written for all key elements of the game including the

library, the game engine, and the artificial intelligence (AI) embedded in the

game. The production will end at the ‘code freeze’ which occurs a few months

before the release date. After ‘code freeze’, keyboards are put away. A team of

testers will play the game to identify bugs. At this stage, only bugs can be

removed from the software. Once the bugs are removed, the ‘gold master’ of the

game is locked down.

Post-production: In post-production, the game will be approved by the console

manufacturers — like Xbox, PlayStation, or Nintendo. Or, if the game is released

via PC, a distribution platform — like Steam — may approve the game. (Some

critics have suggested Steam’s approval process could be more robust.) Today,

many games are released via the Internet versus a cartridge or a disc, so

software patches and upgrades can occur post release. Indeed, some of the

most popular games — like Fortnite — receive weekly updates.

66%63%

61%

51% 50%47%

0%

10%

20%

30%

40%

50%

60%

70%

Qualityof

Graphics

Price InterestingStory

Contin-uation

of FavoriteSeries

OnlineGameplay

FamiliarIP

© 2019 Citigroup

16

Figure 7. Common Video Game Terms

Term Meaning

Player Skill

Skill floor Minimum skill to play a game well

Skill ceiling Difficulty reaching high level of performance

Game Attributes

Game pacing Rate of activity and tempo in the game

Ludonarrative dissonance (LND) Game play conflicts with narrative

Animation cancelling Allows player to keep playing before action is complete

Random number generator (RNG) RNG allows random events to occur in the game

Battle pass Rewards players with in-game content

Game Design

Bullshot Publishers artificially enhance promo materials vs. real game

Third-person shooter (TPS) Player is visible on the screen while shooting

Downloadable content Additional content released in the video game

Dynamic game difficulty Adjusting difficulty of game based on player ability

Expansion pack Adds extra game content to an existing game

Hit box Invisible box used for real-time collision detection

Loot and loot box Player obtains in-game content (currency, weapons)

Open world Virtual world where player can freely roam the game

Paper doll A way to display a character's inventory (weapons, bullets, etc.)

Power-ups Objects that confer extra power or benefits to a character

Season Pass Discounted package of in-game content

Hardware Design

Micro console Low-cost Android-based hardware used with app store games

Console game High-end hardware used for gaming (Xbox, PlayStation, etc.)

Game Play

Latency Noticeable delay between control inputs and action on screen

Frame rates How smooth games run; High frame per second is fluid

Pixelbitching Requires player to sweep screen to look for ways to progress

Career mode Allows player to take control of a single character

Spawning Live creation of a character

Respawning Recreation of an entity after death

Despawning Deletion of an entity within the game

Strafing Moving a character side-to-side (vs. forward and backward)

Player Behavior

Griefer Player derives pleasure from frustrating other players

Hate In MMOPRGs, mobs prioritize which character to attack

Let's Play (LP) Video commentary by the gamer

Multi-boxing Playing multiple characters at the same time. Often viewed as cheating

Noclip mode Prevents first person camera from being blocked by walls – a cheat command

Trickjump Techniques that enhance mobility of a player

Turtling Game play that emphasizes defensive behavior

Cooperative gameplay Allows players to work together

Crowd control Allows player to limit number in an MMORPG

Note: MMOPRG – Massive Multiplayer Online Role-playing Game Source: Citi Research

In total, the entire game development process may take three to four years. But,

some titles have been known to take 10 years (or longer) if significant changes are

made to the game’s look or feel after the pre-production phase. Somewhat

famously, Duke Nukem Forever was conceived in 1996. But, it took the developer

(3D Realms) 15 years to release the game. The total cost of a game can vary

considerably. But, it’s not unusual for AAA games to cost $100 million or sometimes

more to develop. (We should note there is no formal definition of AAA games. It’s an

informal classification.)

© 2019 Citigroup

17

Figure 8. Video Game Development Process

Source: Citi Research

So, let’s say your concept is complete. The next key decision is whether to use a

game engine or develop the game organically. Game engines are used primarily for

PC games and mobile games (but not console games). Game engines provide a

software environment that allows developers to create games faster. They do this

using pre-built software for things like graphics, audio, logic, physics, and collision

detection. These engines are essentially frameworks that allow developers to avoid

reinventing the wheel for every game. So, by buying an engine for a little money,

developers can eliminate a lot of coding. Which engines are most popular? There

are two:

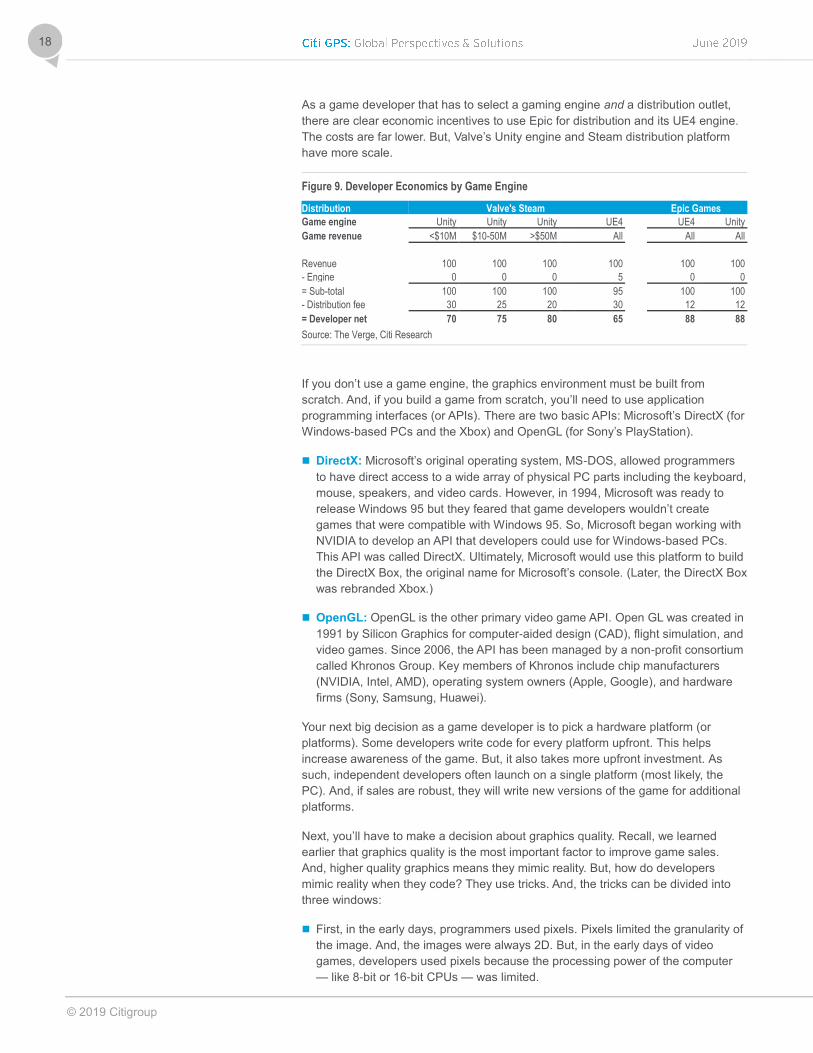

First, the market leader is Unity, which is owned by Valve. Valve also owns a

game distribution platform called Steam. Unity has a free version, a relatively

inexpensive option for $25 to $125 per month (depending on the version) and an

expensive option called Unity Pro (which costs about $1,500). Unity uses C++

and JavaScript as its two primary programming languages. For many years,

Steam collected 30% of a game’s revenue as a distribution fee. That sort of fee

isn’t dissimilar from what other digital distribution platforms like Apple or Google

take. But in the fourth quarter of 2018, Steam lowered the distribution fee it

collects from game developers given competition from a rival engine, UE4. For

games that generate $10-$50 million of revenue, the fee dropped to 25%. And for

very popular games that generate more than $50 million in revenue, Steam’s

distribution fee dropped to 20%.

Second, Unreal Engine (owned by Epic Games) has been around a bit longer

than Unity. Its latest engine is called UE4. UE4 uses C++ as its programming

language. UE4 has a royalty rate of 5% if the game is released on Steam, but is

free if it’s released in Epic Game’s site. On top of that, Epic Game only charges

game developers a 12% distribution fee.

ConceptPre-

ProductionProduction

Post-

Production

Develop short

description of

game

Genre identified

(RPG, shooter)

Rules established

Preliminary

sketches

Approval required

for console games

to ensure

standards are met

Software patches

created as needed

(for online

versions)

Full storyboard

created including

sketches and text

to explain each

scene.

Technical

limitations and

console standards

reviewed

Production plan

developed

including game

goals, level

designs and

gameplay

mechanics

Plan includes all

tasks and due

dates

Key milestones

established (first

playable, alpha

version, beta

version)

Larger team of

producers,

designers, artists

and programmers

added to team

Source code for

the game is written

for library, engine

and AI

Production ends

with ‘code freeze’

usually 3-4 months

before release.

Only bugs can be

fixed post code

freeze

Testers used to

identify bugs

‘Gold master’ is

final build used for

production

AAA games can cost

$100-200 million.

Typical development

time is 3-4 years for

a AAA game

© 2019 Citigroup

18

As a game developer that has to select a gaming engine and a distribution outlet,

there are clear economic incentives to use Epic for distribution and its UE4 engine.

The costs are far lower. But, Valve’s Unity engine and Steam distribution platform

have more scale.

Figure 9. Developer Economics by Game Engine

Distribution Valve's Steam Epic Games

Game engine Unity Unity Unity UE4 UE4 Unity

Game revenue <$10M $10-50M >$50M All All All

Revenue 100 100 100 100 100 100

- Engine 0 0 0 5 0 0

= Sub-total 100 100 100 95 100 100

- Distribution fee 30 25 20 30 12 12

= Developer net 70 75 80 65 88 88

Source: The Verge, Citi Research

If you don’t use a game engine, the graphics environment must be built from

scratch. And, if you build a game from scratch, you’ll need to use application

programming interfaces (or APIs). There are two basic APIs: Microsoft’s DirectX (for

Windows-based PCs and the Xbox) and OpenGL (for Sony’s PlayStation).

DirectX: Microsoft’s original operating system, MS-DOS, allowed programmers

to have direct access to a wide array of physical PC parts including the keyboard,

mouse, speakers, and video cards. However, in 1994, Microsoft was ready to

release Windows 95 but they feared that game developers wouldn’t create

games that were compatible with Windows 95. So, Microsoft began working with

NVIDIA to develop an API that developers could use for Windows-based PCs.

This API was called DirectX. Ultimately, Microsoft would use this platform to build

the DirectX Box, the original name for Microsoft’s console. (Later, the DirectX Box

was rebranded Xbox.)

OpenGL: OpenGL is the other primary video game API. Open GL was created in

1991 by Silicon Graphics for computer-aided design (CAD), flight simulation, and

video games. Since 2006, the API has been managed by a non-profit consortium

called Khronos Group. Key members of Khronos include chip manufacturers

(NVIDIA, Intel, AMD), operating system owners (Apple, Google), and hardware

firms (Sony, Samsung, Huawei).

Your next big decision as a game developer is to pick a hardware platform (or

platforms). Some developers write code for every platform upfront. This helps

increase awareness of the game. But, it also takes more upfront investment. As

such, independent developers often launch on a single platform (most likely, the

PC). And, if sales are robust, they will write new versions of the game for additional

platforms.

Next, you’ll have to make a decision about graphics quality. Recall, we learned

earlier that graphics quality is the most important factor to improve game sales.

And, higher quality graphics means they mimic reality. But, how do developers

mimic reality when they code? They use tricks. And, the tricks can be divided into

three windows:

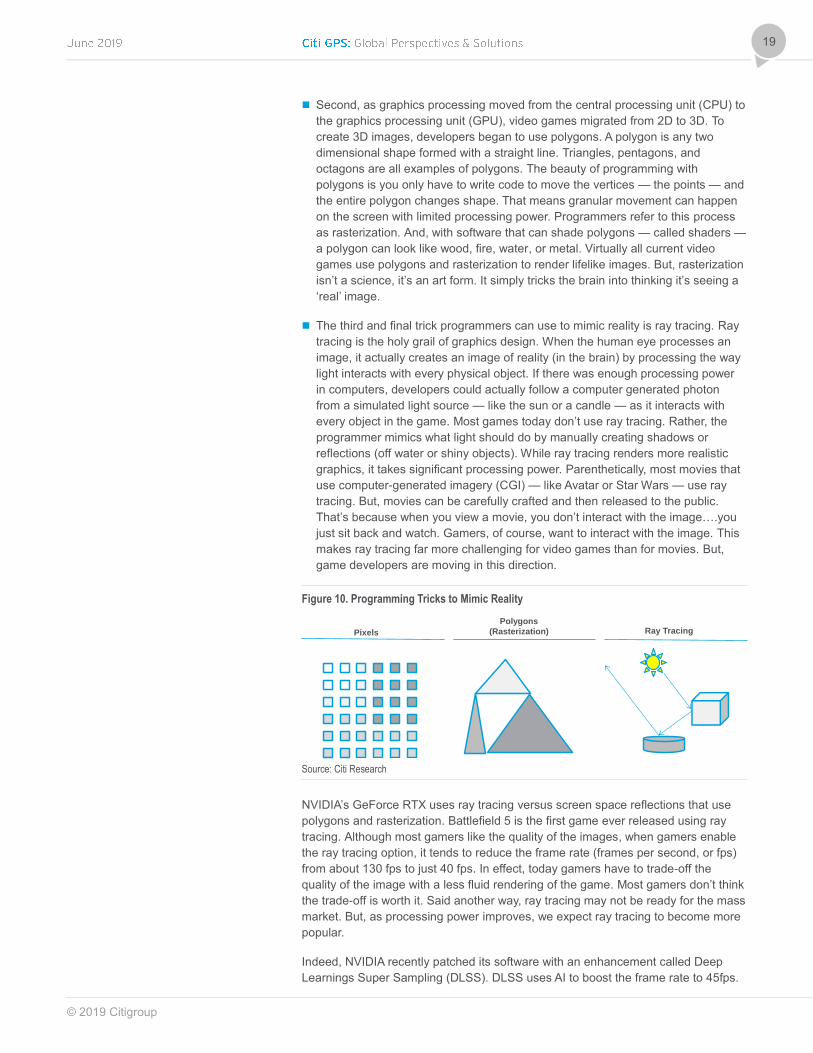

First, in the early days, programmers used pixels. Pixels limited the granularity of

the image. And, the images were always 2D. But, in the early days of video

games, developers used pixels because the processing power of the computer

— like 8-bit or 16-bit CPUs — was limited.

© 2019 Citigroup

19

Second, as graphics processing moved from the central processing unit (CPU) to

the graphics processing unit (GPU), video games migrated from 2D to 3D. To

create 3D images, developers began to use polygons. A polygon is any two

dimensional shape formed with a straight line. Triangles, pentagons, and

octagons are all examples of polygons. The beauty of programming with

polygons is you only have to write code to move the vertices — the points — and

the entire polygon changes shape. That means granular movement can happen

on the screen with limited processing power. Programmers refer to this process

as rasterization. And, with software that can shade polygons — called shaders —

a polygon can look like wood, fire, water, or metal. Virtually all current video

games use polygons and rasterization to render lifelike images. But, rasterization

isn’t a science, it’s an art form. It simply tricks the brain into thinking it’s seeing a

‘real’ image.

The third and final trick programmers can use to mimic reality is ray tracing. Ray

tracing is the holy grail of graphics design. When the human eye processes an

image, it actually creates an image of reality (in the brain) by processing the way

light interacts with every physical object. If there was enough processing power

in computers, developers could actually follow a computer generated photon

from a simulated light source — like the sun or a candle — as it interacts with

every object in the game. Most games today don’t use ray tracing. Rather, the

programmer mimics what light should do by manually creating shadows or

reflections (off water or shiny objects). While ray tracing renders more realistic

graphics, it takes significant processing power. Parenthetically, most movies that

use computer-generated imagery (CGI) — like Avatar or Star Wars — use ray

tracing. But, movies can be carefully crafted and then released to the public.

That’s because when you view a movie, you don’t interact with the image….you

just sit back and watch. Gamers, of course, want to interact with the image. This

makes ray tracing far more challenging for video games than for movies. But,

game developers are moving in this direction.

Figure 10. Programming Tricks to Mimic Reality

Source: Citi Research

NVIDIA’s GeForce RTX uses ray tracing versus screen space reflections that use

polygons and rasterization. Battlefield 5 is the first game ever released using ray

tracing. Although most gamers like the quality of the images, when gamers enable

the ray tracing option, it tends to reduce the frame rate (frames per second, or fps)

from about 130 fps to just 40 fps. In effect, today gamers have to trade-off the

quality of the image with a less fluid rendering of the game. Most gamers don’t think

the trade-off is worth it. Said another way, ray tracing may not be ready for the mass

market. But, as processing power improves, we expect ray tracing to become more

popular.

Indeed, NVIDIA recently patched its software with an enhancement called Deep

Learnings Super Sampling (DLSS). DLSS uses AI to boost the frame rate to 45fps.

Pixels

Polygons

(Rasterization) Ray Tracing

© 2019 Citigroup

20

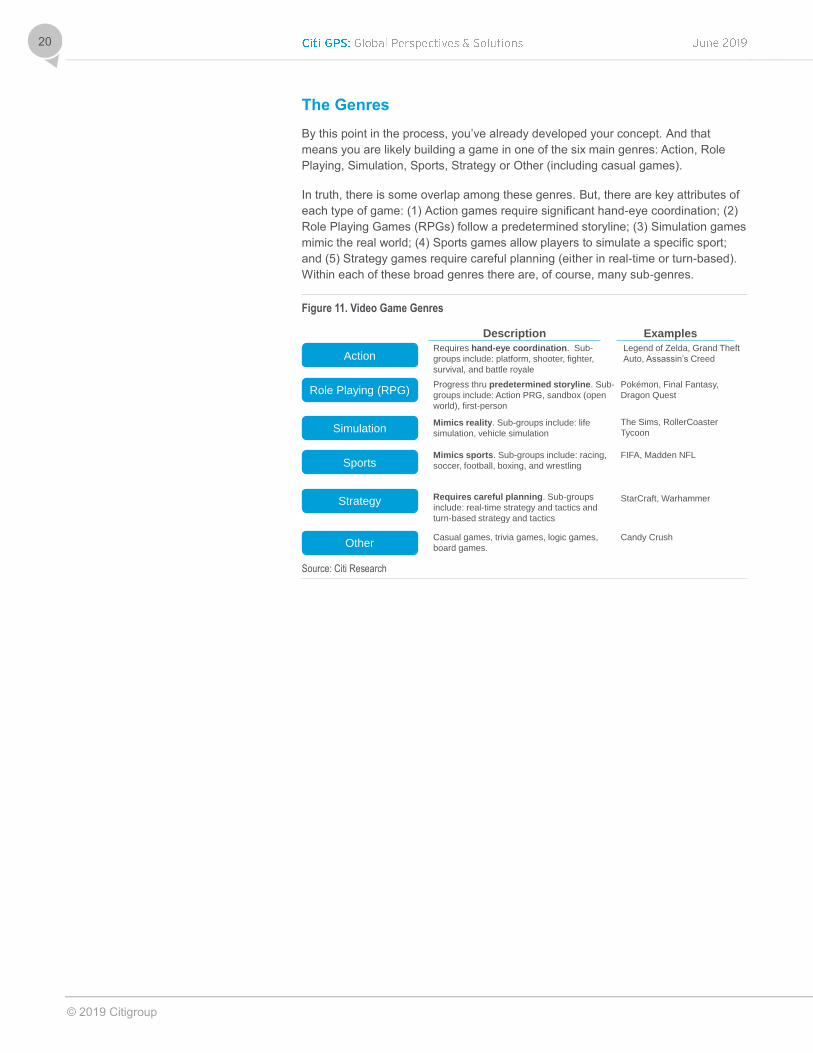

The Genres

By this point in the process, you’ve already developed your concept. And that

means you are likely building a game in one of the six main genres: Action, Role

Playing, Simulation, Sports, Strategy or Other (including casual games).

In truth, there is some overlap among these genres. But, there are key attributes of

each type of game: (1) Action games require significant hand-eye coordination; (2)

Role Playing Games (RPGs) follow a predetermined storyline; (3) Simulation games

mimic the real world; (4) Sports games allow players to simulate a specific sport;

and (5) Strategy games require careful planning (either in real-time or turn-based).

Within each of these broad genres there are, of course, many sub-genres.

Figure 11. Video Game Genres

Source: Citi Research

Action

Role Playing (RPG)

Simulation

Sports

Strategy

Other

Requires hand-eye coordination. Sub-

groups include: platform, shooter, fighter,

survival, and battle royale

Progress thru predetermined storyline. Sub-

groups include: Action PRG, sandbox (open

world), first-person

Mimics reality. Sub-groups include: life

simulation, vehicle simulation

Mimics sports. Sub-groups include: racing,

soccer, football, boxing, and wrestling

Requires careful planning. Sub-groups

include: real-time strategy and tactics and

turn-based strategy and tactics

Casual games, trivia games, logic games,

board games.

Description Examples

Pokémon, Final Fantasy,

Dragon Quest

FIFA, Madden NFL

Candy Crush

Legend of Zelda, Grand Theft

Auto, Assassin’s Creed

The Sims, RollerCoaster

Tycoon

StarCraft, Warhammer

© 2019 Citigroup

21

Figure 12. Types of Video Game by Genre

Group Sub-Group Class Description

Action Requires hand-eye coordination

Platform Game play centers around jumping and climbing

Shooter Lethal weapons used to damage opponents

First player Played from protagonists perspective

Third player Protagonist's body can be seen

Fighter Close range combat

Survival Player in an open-world, hostile environment

Battle Royale Blends survival with last man standing objective

Role-Playing Progress through predetermined storyline

Action RPG Action based role-paying game

MMORPG Massively multiplayer online role-playing game

Sandbox Open world role playing game

First-person RPG where player leads a party

Simulation Mimic a real or fictional reality

Life simulation Control one or more artificial lives

Vehicle simulation Flight or racing simulator

Strategy Requires careful planning to win

4X Four goals: Explore, expand, exploit and exterminate

Artillery Two or three player typically with tanks

Real-time strategy Action in the game in continuous

Real-time tactics Simulates real time warfare

MOBA Multi-player online battle areas; akin to Action Real-time Strategy

Turn-based strategy Allows period of analysis before committing to action

Turn-based tactics Mimics military tactics and operations

Sports Mimic a sport

Racing Auto racing

Sports games Non-auto racing sport games

Non-fighting Football, basketball, hockey, etc.

Fighting Boxing or wrestling

Other

Casual games Designed for short bursts of playing time

Trivia games Player answers questions

Logic games Puzzle games

Party games Designed for many players

Board games Games like chess, checkers and Othello

Card games Solitaire, poker, and games like Go

Source: Citi Research

AAA Versus Independent Games

In broad terms, there are two types of game developers: (1) developers that work

for publishers and (2) independent publishers. Hardcore gamers typically divide the

world into two types of games: AAA games and Independent games. Although there

isn’t a formal definition of AAA games, there are widely agreed upon attributes: (1)

AAA games typically work on both consoles and PCs; (2) AAA games have large

1marketing budgets; and (3) AAA games are often developed and published by the

same firm. Independent games, on the other hand, usually only work on PCs. They

have smaller marketing budgets and, they are often distributed on third party sites,

like Steam.

The conventional view is that AAA games are high quality and Independent games

are lower quality. But, in truth, if you speak with avid gamers, there are exceptions

to this rule. That is, some Independent games are actually high-quality and garner

significant game play while some AAA games flop at the time of release.

© 2019 Citigroup

22

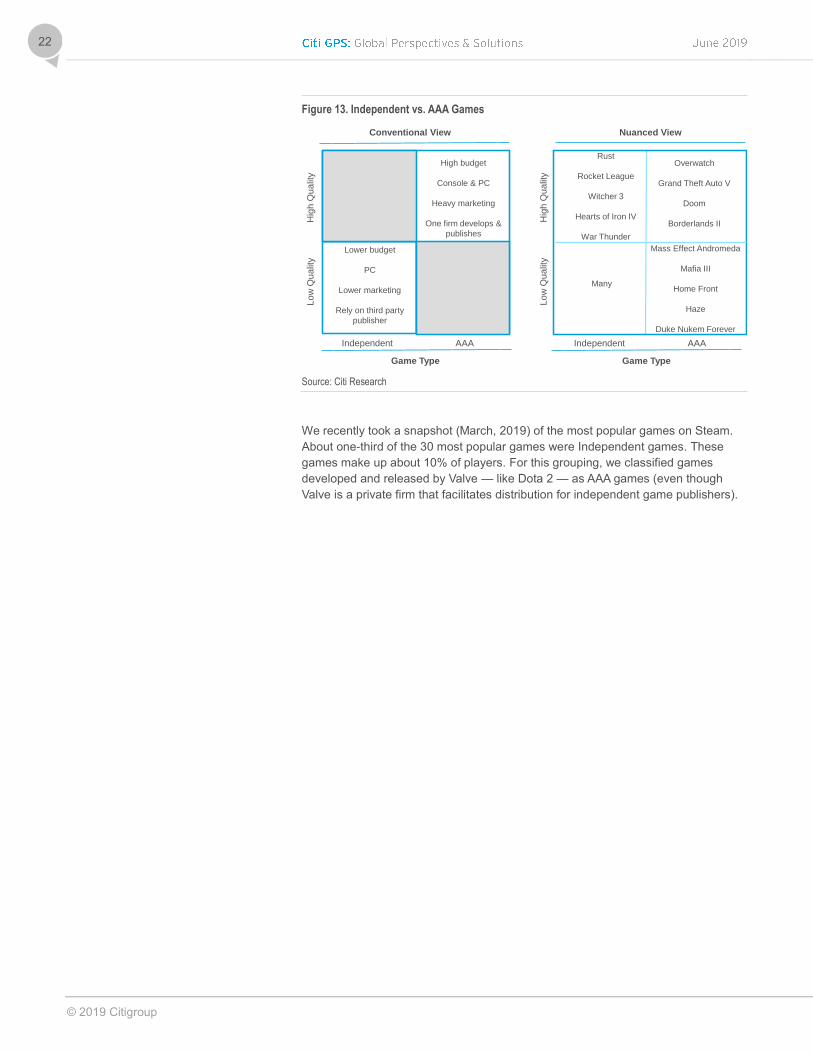

Figure 13. Independent vs. AAA Games

Source: Citi Research

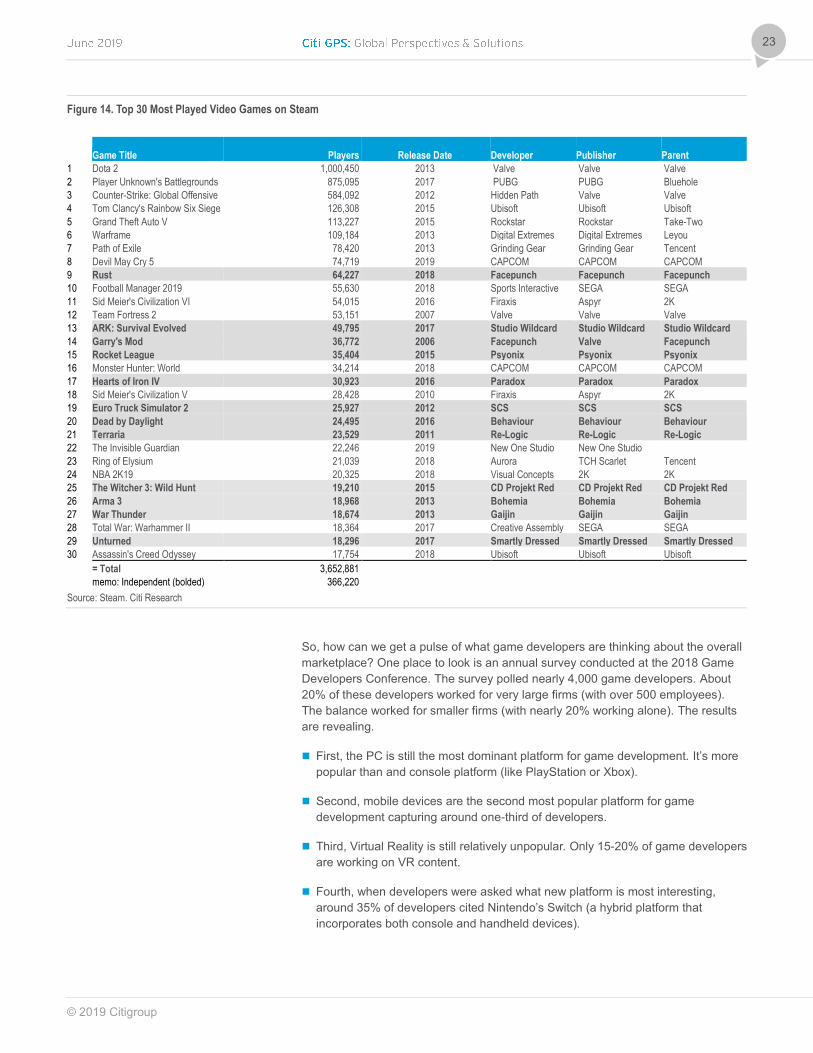

We recently took a snapshot (March, 2019) of the most popular games on Steam.

About one-third of the 30 most popular games were Independent games. These

games make up about 10% of players. For this grouping, we classified games

developed and released by Valve — like Dota 2 — as AAA games (even though

Valve is a private firm that facilitates distribution for independent game publishers).

Conventional View Nuanced View

Independent AAA

Hig

h Q

ua

lity

Lo

w Q

ua

lity

High budget

Console & PC

Heavy marketing

One firm develops &

publishes

Lower budget

PC

Lower marketing

Rely on third party

publisher

Independent AAA

Hig

h Q

ua

lity

Lo

w Q

ua

lity

Game Type Game Type

Rust

Rocket League

Witcher 3

Hearts of Iron IV

War Thunder

Mass Effect Andromeda

Mafia III

Home Front

Haze

Duke Nukem Forever

Overwatch

Grand Theft Auto V

Doom

Borderlands II

Many

© 2019 Citigroup

23

Figure 14. Top 30 Most Played Video Games on Steam

Game Title Players

Release Date Developer Publisher Parent

1 Dota 2 1,000,450 2013 Valve Valve Valve

2 Player Unknown's Battlegrounds 875,095 2017 PUBG PUBG Bluehole

3 Counter-Strike: Global Offensive 584,092 2012 Hidden Path Valve Valve

4 Tom Clancy's Rainbow Six Siege 126,308 2015 Ubisoft Ubisoft Ubisoft

5 Grand Theft Auto V 113,227 2015 Rockstar Rockstar Take-Two

6 Warframe 109,184 2013 Digital Extremes Digital Extremes Leyou

7 Path of Exile 78,420 2013 Grinding Gear Grinding Gear Tencent

8 Devil May Cry 5 74,719 2019 CAPCOM CAPCOM CAPCOM

9 Rust 64,227 2018 Facepunch Facepunch Facepunch

10 Football Manager 2019 55,630 2018 Sports Interactive SEGA SEGA

11 Sid Meier's Civilization VI 54,015 2016 Firaxis Aspyr 2K

12 Team Fortress 2 53,151 2007 Valve Valve Valve

13 ARK: Survival Evolved 49,795 2017 Studio Wildcard Studio Wildcard Studio Wildcard

14 Garry's Mod 36,772 2006 Facepunch Valve Facepunch

15 Rocket League 35,404 2015 Psyonix Psyonix Psyonix

16 Monster Hunter: World 34,214 2018 CAPCOM CAPCOM CAPCOM

17 Hearts of Iron IV 30,923 2016 Paradox Paradox Paradox

18 Sid Meier's Civilization V 28,428 2010 Firaxis Aspyr 2K

19 Euro Truck Simulator 2 25,927 2012 SCS SCS SCS

20 Dead by Daylight 24,495 2016 Behaviour Behaviour Behaviour

21 Terraria 23,529 2011 Re-Logic Re-Logic Re-Logic

22 The Invisible Guardian 22,246 2019 New One Studio New One Studio

23 Ring of Elysium 21,039 2018 Aurora TCH Scarlet Tencent

24 NBA 2K19 20,325 2018 Visual Concepts 2K 2K

25 The Witcher 3: Wild Hunt 19,210 2015 CD Projekt Red CD Projekt Red CD Projekt Red

26 Arma 3 18,968 2013 Bohemia Bohemia Bohemia

27 War Thunder 18,674 2013 Gaijin Gaijin Gaijin

28 Total War: Warhammer II 18,364 2017 Creative Assembly SEGA SEGA

29 Unturned 18,296 2017 Smartly Dressed Smartly Dressed Smartly Dressed

30 Assassin's Creed Odyssey 17,754 2018 Ubisoft Ubisoft Ubisoft

= Total 3,652,881

memo: Independent (bolded) 366,220

Source: Steam. Citi Research

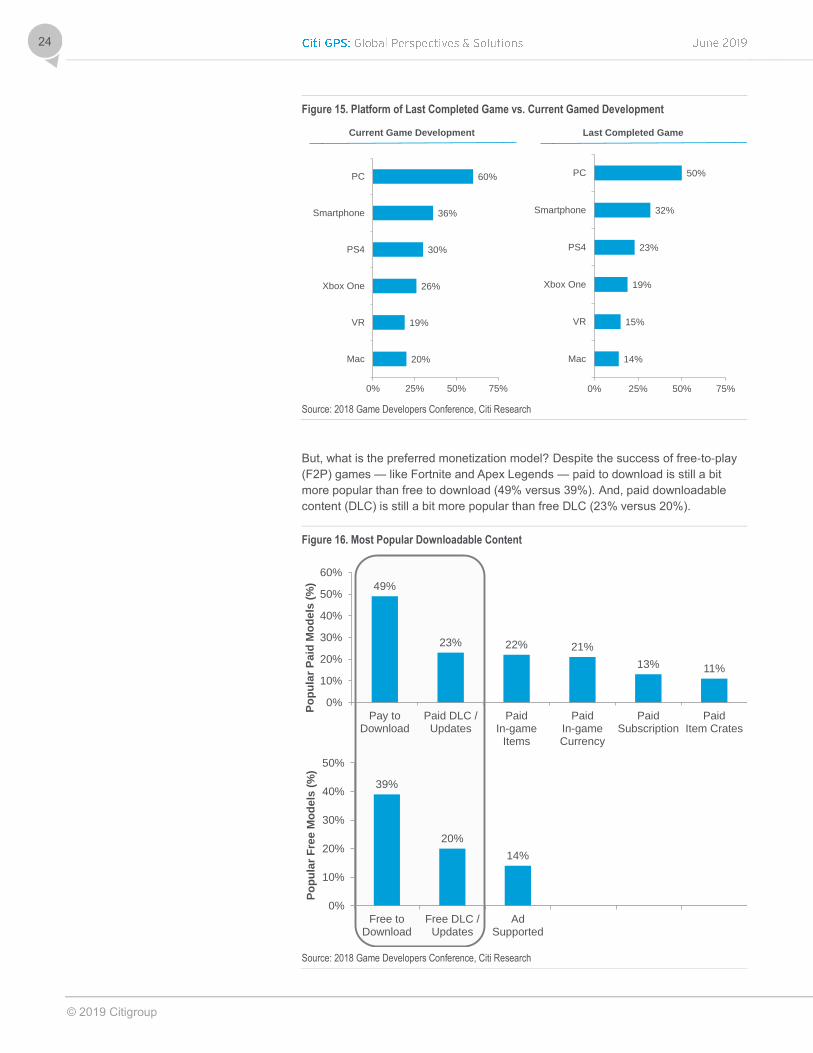

So, how can we get a pulse of what game developers are thinking about the overall

marketplace? One place to look is an annual survey conducted at the 2018 Game

Developers Conference. The survey polled nearly 4,000 game developers. About

20% of these developers worked for very large firms (with over 500 employees).

The balance worked for smaller firms (with nearly 20% working alone). The results

are revealing.

First, the PC is still the most dominant platform for game development. It’s more

popular than and console platform (like PlayStation or Xbox).

Second, mobile devices are the second most popular platform for game

development capturing around one-third of developers.

Third, Virtual Reality is still relatively unpopular. Only 15-20% of game developers

are working on VR content.

Fourth, when developers were asked what new platform is most interesting,

around 35% of developers cited Nintendo’s Switch (a hybrid platform that

incorporates both console and handheld devices).

© 2019 Citigroup

24

Figure 15. Platform of Last Completed Game vs. Current Gamed Development

Source: 2018 Game Developers Conference, Citi Research

But, what is the preferred monetization model? Despite the success of free-to-play

(F2P) games — like Fortnite and Apex Legends — paid to download is still a bit

more popular than free to download (49% versus 39%). And, paid downloadable

content (DLC) is still a bit more popular than free DLC (23% versus 20%).

Figure 16. Most Popular Downloadable Content

Source: 2018 Game Developers Conference, Citi Research

20%

19%

26%

30%

36%

60%

0% 25% 50% 75%

Mac

VR

Xbox One

PS4

Smartphone

PC

14%

15%

19%

23%

32%

50%

0% 25% 50% 75%

Mac

VR

Xbox One

PS4

Smartphone

PC

Current Game Development Last Completed Game

39%

20%

14%

0%

10%

20%

30%

40%

50%

Free toDownload

Free DLC /Updates

AdSupported

Po

pu

lar

Fre

e M

od

els

(%

)

49%

23% 22% 21%

13% 11%

0%

10%

20%

30%

40%

50%

60%

Pay toDownload

Paid DLC /Updates

PaidIn-game

Items

PaidIn-gameCurrency

PaidSubscription

PaidItem Crates

Po

pu

lar

Pa

id M

od

els

(%

)

© 2019 Citigroup

25

Once the game is developed, how are developers marketing their games? There is

remarkably little agreement. While social media (Twitter, Facebook) are certainly

popular, this method of promotion only garnered 20% of the vote. Digital storefronts

(like Valve’s Steam) were almost as popular. Surprisingly, Amazon’s Twitch

garnered less than 10% of developer’s votes as the most effective method of

promotion. Moreover, there was remarkably little difference between preferred

methods to market the last game versus the next game. That is, marketing

preferences don’t seem to be changing.

Figure 17. Most Effective Ways for Developers to Promote, Market New Games

Source: 2018 Game Developers Conference, Citi Research

And, who will take the lead executing the marketing plan? About 40% of developers

plan to handle their own marketing. And, about one-third pay a full-time or part-time

public relations firm. Fewer (less than 25%) work with video game publishers. But,

for those developers that work with publishers, nearly twice as many get paid by the

publisher in advance (17%) versus a pure revenue share model (6%).

Figure 18. How Do Developers Market?

Source: 2018 Game Developers Conference, Citi Research

6%

7%

8%

10%

11%

13%

13%

16%

19%

22%

0% 5% 10% 15% 20% 25%

Discord, Slack

Forums

Live Events

Twitch

Press,Bloggers

Paid Ads

YouTube

Word ofMouth

Digital Store

Twitter,Facebook

5%

7%

7%

8%

11%

12%

12%

17%

19%

22%

0% 5% 10% 15% 20% 25%

Discord, Slack

Forums

Live Events

Twitch

Press,Bloggers

Paid Ads

YouTube

Word of Mouth

Digital Store

Twitter,Facebook

Effective Discovery of Last Game Effective Discovery of Next Game

38%33%

17%

11%

6%

0%

10%

20%

30%

40%

Self Marketing Pay InternalPR Firm

Publisher PaidUs in Advance,Takes Share of

Sales

Pay ExternalPR Firm

Publisher NotPaid in

Advance, TakesShare of Sales

© 2019 Citigroup

26

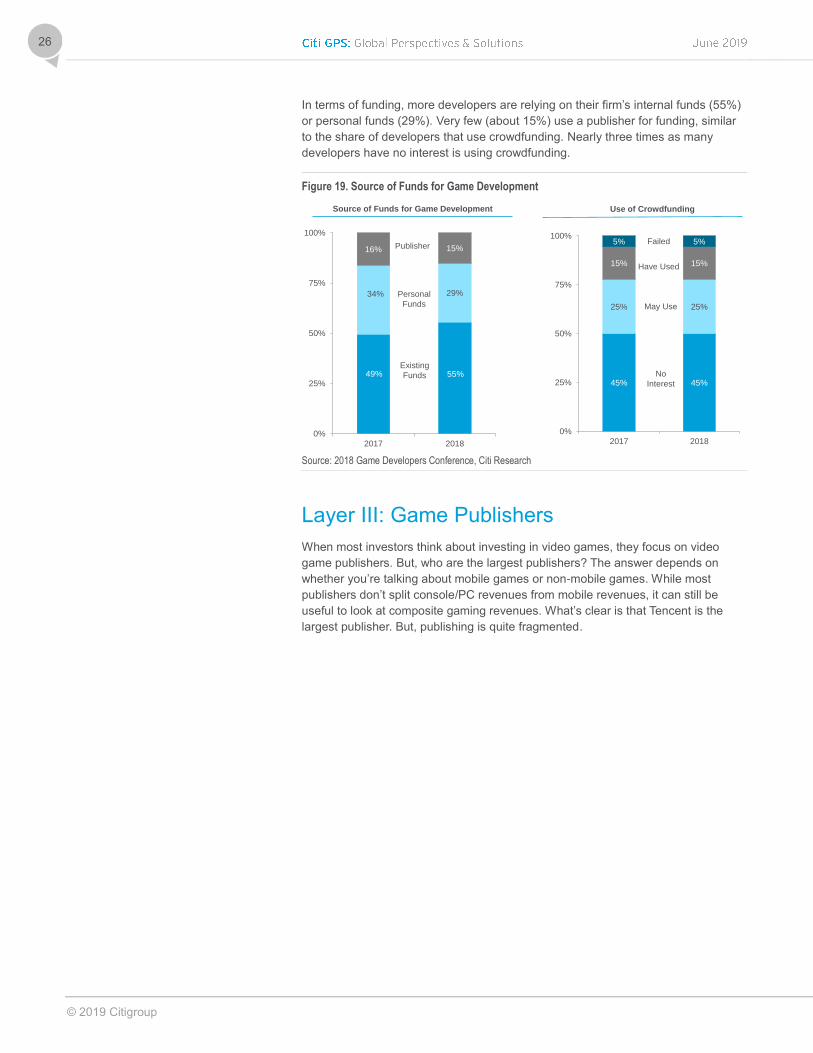

In terms of funding, more developers are relying on their firm’s internal funds (55%)

or personal funds (29%). Very few (about 15%) use a publisher for funding, similar

to the share of developers that use crowdfunding. Nearly three times as many

developers have no interest is using crowdfunding.

Figure 19. Source of Funds for Game Development

Source: 2018 Game Developers Conference, Citi Research

Layer III: Game Publishers

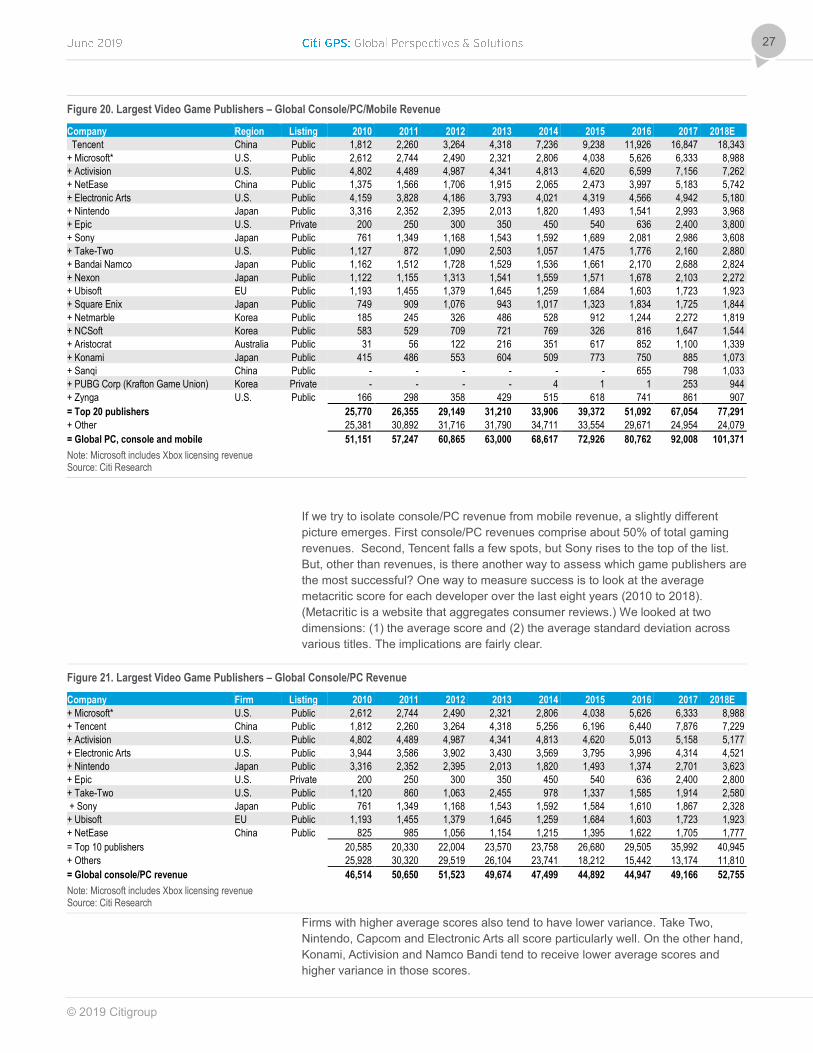

When most investors think about investing in video games, they focus on video

game publishers. But, who are the largest publishers? The answer depends on

whether you’re talking about mobile games or non-mobile games. While most

publishers don’t split console/PC revenues from mobile revenues, it can still be

useful to look at composite gaming revenues. What’s clear is that Tencent is the

largest publisher. But, publishing is quite fragmented.

49% 55%

34% 29%

16% 15%

0%

25%

50%

75%

100%

2017 2018

45% 45%

25% 25%

15% 15%

5% 5%

0%

25%

50%

75%

100%

2017 2018

Existing

Funds

Personal

Funds

Publisher

No

Interest

May Use

Have Used

Failed

Source of Funds for Game Development Use of Crowdfunding

© 2019 Citigroup

27

Figure 20. Largest Video Game Publishers – Global Console/PC/Mobile Revenue

Company Region Listing 2010 2011 2012 2013 2014 2015 2016 2017 2018E

Tencent China Public 1,812 2,260 3,264 4,318 7,236 9,238 11,926 16,847 18,343

+ Microsoft* U.S. Public 2,612 2,744 2,490 2,321 2,806 4,038 5,626 6,333 8,988

+ Activision U.S. Public 4,802 4,489 4,987 4,341 4,813 4,620 6,599 7,156 7,262

+ NetEase China Public 1,375 1,566 1,706 1,915 2,065 2,473 3,997 5,183 5,742

+ Electronic Arts U.S. Public 4,159 3,828 4,186 3,793 4,021 4,319 4,566 4,942 5,180

+ Nintendo Japan Public 3,316 2,352 2,395 2,013 1,820 1,493 1,541 2,993 3,968

+ Epic U.S. Private 200 250 300 350 450 540 636 2,400 3,800

+ Sony Japan Public 761 1,349 1,168 1,543 1,592 1,689 2,081 2,986 3,608

+ Take-Two U.S. Public 1,127 872 1,090 2,503 1,057 1,475 1,776 2,160 2,880

+ Bandai Namco Japan Public 1,162 1,512 1,728 1,529 1,536 1,661 2,170 2,688 2,824

+ Nexon Japan Public 1,122 1,155 1,313 1,541 1,559 1,571 1,678 2,103 2,272

+ Ubisoft EU Public 1,193 1,455 1,379 1,645 1,259 1,684 1,603 1,723 1,923

+ Square Enix Japan Public 749 909 1,076 943 1,017 1,323 1,834 1,725 1,844

+ Netmarble Korea Public 185 245 326 486 528 912 1,244 2,272 1,819

+ NCSoft Korea Public 583 529 709 721 769 326 816 1,647 1,544

+ Aristocrat Australia Public 31 56 122 216 351 617 852 1,100 1,339

+ Konami Japan Public 415 486 553 604 509 773 750 885 1,073

+ Sanqi China Public - - - - - - 655 798 1,033

+ PUBG Corp (Krafton Game Union) Korea Private - - - - 4 1 1 253 944

+ Zynga U.S. Public 166 298 358 429 515 618 741 861 907

= Top 20 publishers 25,770 26,355 29,149 31,210 33,906 39,372 51,092 67,054 77,291

+ Other 25,381 30,892 31,716 31,790 34,711 33,554 29,671 24,954 24,079

= Global PC, console and mobile 51,151 57,247 60,865 63,000 68,617 72,926 80,762 92,008 101,371

Note: Microsoft includes Xbox licensing revenue Source: Citi Research

If we try to isolate console/PC revenue from mobile revenue, a slightly different

picture emerges. First console/PC revenues comprise about 50% of total gaming

revenues. Second, Tencent falls a few spots, but Sony rises to the top of the list.

But, other than revenues, is there another way to assess which game publishers are

the most successful? One way to measure success is to look at the average

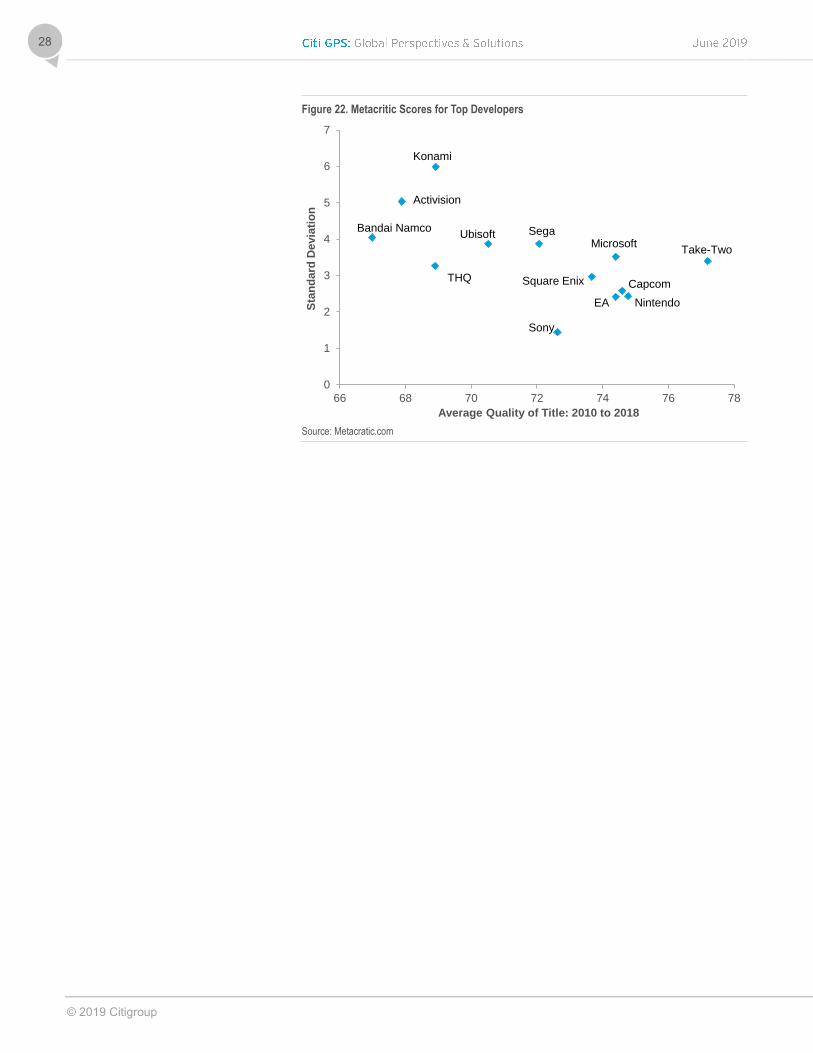

metacritic score for each developer over the last eight years (2010 to 2018).

(Metacritic is a website that aggregates consumer reviews.) We looked at two

dimensions: (1) the average score and (2) the average standard deviation across

various titles. The implications are fairly clear.

Figure 21. Largest Video Game Publishers – Global Console/PC Revenue

Company Firm Listing 2010 2011 2012 2013 2014 2015 2016 2017 2018E

+ Microsoft* U.S. Public 2,612 2,744 2,490 2,321 2,806 4,038 5,626 6,333 8,988

+ Tencent China Public 1,812 2,260 3,264 4,318 5,256 6,196 6,440 7,876 7,229

+ Activision U.S. Public 4,802 4,489 4,987 4,341 4,813 4,620 5,013 5,158 5,177

+ Electronic Arts U.S. Public 3,944 3,586 3,902 3,430 3,569 3,795 3,996 4,314 4,521

+ Nintendo Japan Public 3,316 2,352 2,395 2,013 1,820 1,493 1,374 2,701 3,623

+ Epic U.S. Private 200 250 300 350 450 540 636 2,400 2,800

+ Take-Two U.S. Public 1,120 860 1,063 2,455 978 1,337 1,585 1,914 2,580

+ Sony Japan Public 761 1,349 1,168 1,543 1,592 1,584 1,610 1,867 2,328

+ Ubisoft EU Public 1,193 1,455 1,379 1,645 1,259 1,684 1,603 1,723 1,923

+ NetEase China Public 825 985 1,056 1,154 1,215 1,395 1,622 1,705 1,777

= Top 10 publishers 20,585 20,330 22,004 23,570 23,758 26,680 29,505 35,992 40,945

+ Others 25,928 30,320 29,519 26,104 23,741 18,212 15,442 13,174 11,810

= Global console/PC revenue 46,514 50,650 51,523 49,674 47,499 44,892 44,947 49,166 52,755

Note: Microsoft includes Xbox licensing revenue Source: Citi Research

Firms with higher average scores also tend to have lower variance. Take Two,

Nintendo, Capcom and Electronic Arts all score particularly well. On the other hand,

Konami, Activision and Namco Bandi tend to receive lower average scores and

higher variance in those scores.

© 2019 Citigroup

28

Figure 22. Metacritic Scores for Top Developers

Source: Metacratic.com

0

1

2

3

4

5

6

7

66 68 70 72 74 76 78

Sta

nd

ard

De

via

tio

n

Average Quality of Title: 2010 to 2018

Take-Two

Nintendo

Capcom

EA

Microsoft

Square Enix

Sony

SegaUbisoft

THQ

Konami

Activision

Bandai Namco

© 2019 Citigroup

29

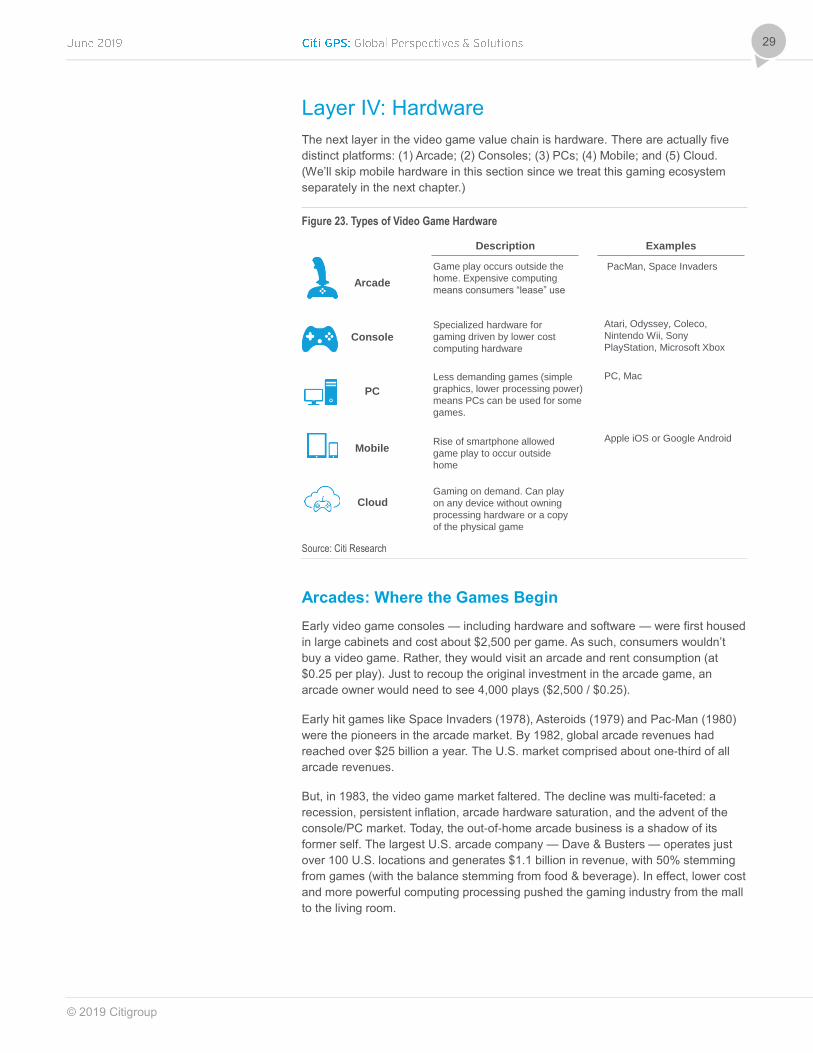

Layer IV: Hardware

The next layer in the video game value chain is hardware. There are actually five

distinct platforms: (1) Arcade; (2) Consoles; (3) PCs; (4) Mobile; and (5) Cloud.

(We’ll skip mobile hardware in this section since we treat this gaming ecosystem

separately in the next chapter.)

Figure 23. Types of Video Game Hardware

Source: Citi Research

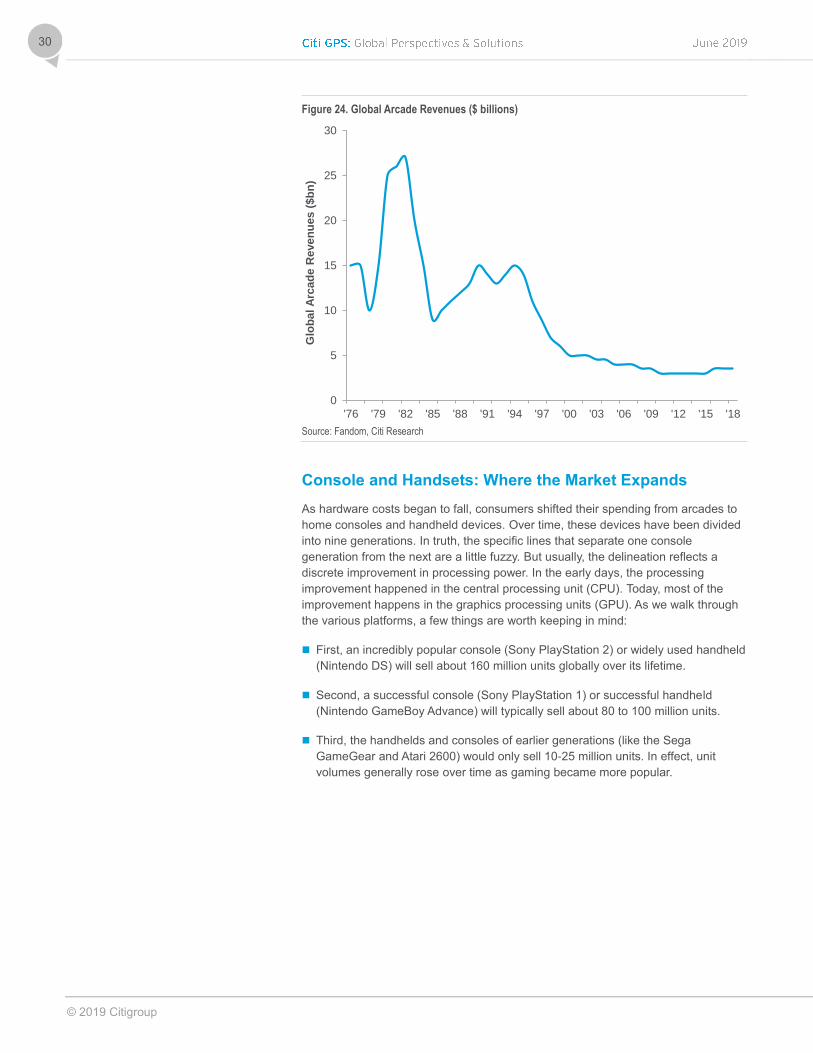

Arcades: Where the Games Begin

Early video game consoles — including hardware and software — were first housed

in large cabinets and cost about $2,500 per game. As such, consumers wouldn’t

buy a video game. Rather, they would visit an arcade and rent consumption (at

$0.25 per play). Just to recoup the original investment in the arcade game, an

arcade owner would need to see 4,000 plays ($2,500 / $0.25).

Early hit games like Space Invaders (1978), Asteroids (1979) and Pac-Man (1980)

were the pioneers in the arcade market. By 1982, global arcade revenues had

reached over $25 billion a year. The U.S. market comprised about one-third of all

arcade revenues.

But, in 1983, the video game market faltered. The decline was multi-faceted: a

recession, persistent inflation, arcade hardware saturation, and the advent of the

console/PC market. Today, the out-of-home arcade business is a shadow of its

former self. The largest U.S. arcade company — Dave & Busters — operates just

over 100 U.S. locations and generates $1.1 billion in revenue, with 50% stemming

from games (with the balance stemming from food & beverage). In effect, lower cost

and more powerful computing processing pushed the gaming industry from the mall

to the living room.

Arcade

Console

Cloud

PC

Mobile

Description Examples

Game play occurs outside the

home. Expensive computing

means consumers “lease” use

PacMan, Space Invaders

Specialized hardware for

gaming driven by lower cost

computing hardware

Atari, Odyssey, Coleco,

Nintendo Wii, Sony

PlayStation, Microsoft Xbox

Less demanding games (simple

graphics, lower processing power)

means PCs can be used for some

games.

PC, Mac

Rise of smartphone allowed

game play to occur outside

home

Gaming on demand. Can play

on any device without owning

processing hardware or a copy

of the physical game

Apple iOS or Google Android

© 2019 Citigroup

30

Figure 24. Global Arcade Revenues ($ billions)

Source: Fandom, Citi Research

Console and Handsets: Where the Market Expands

As hardware costs began to fall, consumers shifted their spending from arcades to

home consoles and handheld devices. Over time, these devices have been divided

into nine generations. In truth, the specific lines that separate one console

generation from the next are a little fuzzy. But usually, the delineation reflects a

discrete improvement in processing power. In the early days, the processing

improvement happened in the central processing unit (CPU). Today, most of the

improvement happens in the graphics processing units (GPU). As we walk through

the various platforms, a few things are worth keeping in mind:

First, an incredibly popular console (Sony PlayStation 2) or widely used handheld

(Nintendo DS) will sell about 160 million units globally over its lifetime.

Second, a successful console (Sony PlayStation 1) or successful handheld

(Nintendo GameBoy Advance) will typically sell about 80 to 100 million units.

Third, the handhelds and consoles of earlier generations (like the Sega

GameGear and Atari 2600) would only sell 10-25 million units. In effect, unit

volumes generally rose over time as gaming became more popular.

0

5

10

15

20

25

30

'76 '79 '82 '85 '88 '91 '94 '97 '00 '03 '06 '09 '12 '15 '18

Glo

ba

l A

rca

de

Re

ve

nu

es

($

bn

)

© 2019 Citigroup

31

Figure 25. Unit Sales of Consoles and Handheld Devices

Source: The Video Game Textbook, Citi Research

If we focus on consoles (but exclude handhelds for a moment), five important trends

are important:

First, in the 1st and 2nd generation, the console manufacturers were comprised

of four main firms: Atari, Magnavox, Mattel and Coleco. Only one of these firms

— Atari — would survive to the 4th generation.

Second, between the 3rd and 6th generation, three firms battled for dominance:

Atari, Nintendo and Sega. But, only one of these firms — Nintendo — would

survive to the 7th generation. Both Atari and Sega dropped out.

Third, during the 5th generation, Sony entered the market. And, two cycles later

(7th generation), Microsoft entered the market. During the 7th and 8th

generation, three firms competed for share: Nintendo (the stalwart), Sony, and

Microsoft.

Fourth, between the 1st and 7th generation, global console sales improved. Only

in the most recent generation — the 8th generation — have console sales

faltered. We suspect this is due, in part, to the rise of mobile gaming (which we’ll

review in more detail a bit later).s

Fifth, as we look at winners and losers within each generation, there isn’t a hard

and fast rule for who takes the most market share. While we ran many

regressions to crack the code for console sales, there doesn’t seem to be a clear

set of variables that drive market share in each generation.

0

20

40

60

80

100

120

140

160

180

Un

its

So

ld (

mn

)

Console

Handheld

© 2019 Citigroup

32

Figure 26. Console Unit Sales Sold by Generation

Source: The Video Game Textbook, Citi Research

Handheld Market

So far, we’ve focused on the console market. But, beginning in 1988 a new market

developed: the handheld gaming market. With the exception of a few short periods

(’90 to ’94) and (’04 to ’07), the console market sold more units than the handheld

market. More recently, we’ve seen the entrance of hybrid devices that serve the

console and handheld market with a single device (the 9th Generation Nintendo

Switch).

Figure 27. Console, Handheld & Hybrid Units Sold

Source: The Video Game Textbook, Citi Research

0

20

40

60

80

100

120

'76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Co

ns

ole

Un

its

So

ld (

mn

)

Atari

Magnavox

Mattel

Coleco

Sega

Nintendo

Sony

Microsoft

Console Generation

In total, nearly 1

billion video game

consoles have

been sold.

Each generation

of improved

graphics with

richer colors,

faster processing

and improved

sound.

2nd 3rd 4th 5th 6th 7th 8th

0

10

20

30

40

50

60

70

'76 '80 '84 '88 '92 '96 '00 '04 '08 '12 '16

Co

nso

le &

Han

dh

eld

Un

its S

old

(m

n)

Console

Hybrid

(Console +

Handheld)

Handheld

© 2019 Citigroup

33

If we look at the various firms that sold handhelds, it’s quite different than the

console market. Since handhelds hit the market long after Atari, Magnavox, Mattel,

and Coleco exited gaming, there are far fewer handheld players. Moreover,

Microsoft has never rolled out a handheld device. As such, today, there is only one

firm that sells handhelds — Nintendo — and, it’s a hybrid device.

Figure 28. Handheld Units Solid by Generation

Source: The Video Game Textbook, Citi Research

If we look at handheld market shares, there are a few important observations. First,

Nintendo is the clear market leader with about 20 million units sold in 2018. Second,

Sega exited the market back in the late 1990s. Third, Sony’s latest entry (the

PlayStation Vita) will cease production in 2019. As such, in 2020, Nintendo will be

the only firm selling handheld devices.

Figure 29. Handheld Units Sold by Manufacturer

Source: The Video Game Textbook, Citi Research

0

10

20

30

40

50

60

'76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Ha

nd

he

ld U

nit

s S

old

(m

n)

Sega

Nintendo

Sony

Handheld Generation

In total, nearly 575

million video game

consoles have

been sold.

Each generation

of improved

graphics with

richer colors,

faster processing

and improved

sound.

2nd 3rd 4th 5th 6th 7th 8th

0

5

10

15

20

25

30

35

40

'76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18

Ha

nd

he

ld U

nit

s S

old

(m

n)

Nintendo

Sony

Sega

In total, nearly

575 million

handheld video

game devices

have been sold.

Nintendo is the

market leader,

followed by Sony.

© 2019 Citigroup

34

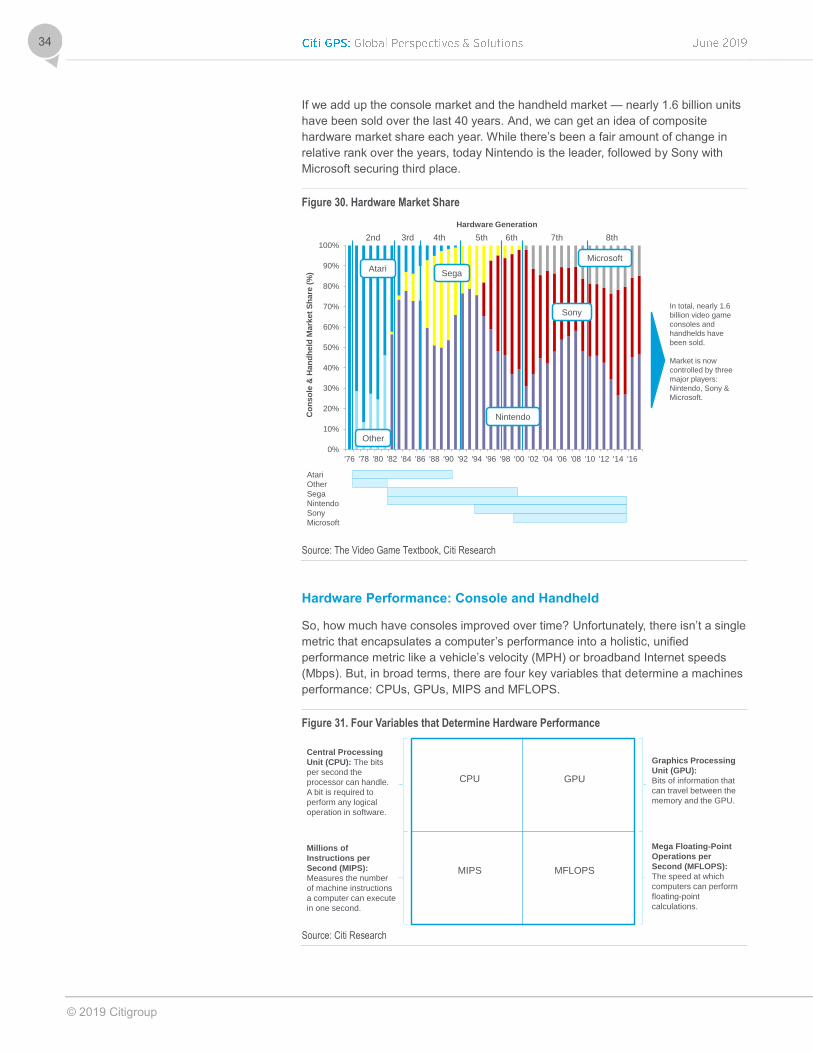

If we add up the console market and the handheld market — nearly 1.6 billion units

have been sold over the last 40 years. And, we can get an idea of composite

hardware market share each year. While there’s been a fair amount of change in

relative rank over the years, today Nintendo is the leader, followed by Sony with

Microsoft securing third place.

Figure 30. Hardware Market Share

Source: The Video Game Textbook, Citi Research

Hardware Performance: Console and Handheld

So, how much have consoles improved over time? Unfortunately, there isn’t a single

metric that encapsulates a computer’s performance into a holistic, unified

performance metric like a vehicle’s velocity (MPH) or broadband Internet speeds

(Mbps). But, in broad terms, there are four key variables that determine a machines

performance: CPUs, GPUs, MIPS and MFLOPS.

Figure 31. Four Variables that Determine Hardware Performance

Source: Citi Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16

Co

nso

le &

Han

dh

eld

Mark

et

Sh

are

(%

)

Hardware Generation

In total, nearly 1.6

billion video game

consoles and

handhelds have

been sold.

Market is now

controlled by three

major players:

Nintendo, Sony &

Microsoft.

2nd 3rd 4th 5th 6th 7th 8th

Atari

Other

Sega

Nintendo

Sony

Microsoft

Nintendo

Sony

Sega

Microsoft

Atari

Other

CPU GPU

MIPS MFLOPS

Central Processing

Unit (CPU): The bits

per second the

processor can handle.

A bit is required to

perform any logical

operation in software.

Millions of

Instructions per

Second (MIPS):

Measures the number

of machine instructions

a computer can execute

in one second.

Graphics Processing

Unit (GPU):

Bits of information that

can travel between the

memory and the GPU.

Mega Floating-Point

Operations per

Second (MFLOPS):

The speed at which

computers can perform

floating-point

calculations.

© 2019 Citigroup