venkateshwara - open university

226

VENKATESHWARA OPEN UNIVERSITY www.vou.ac.in BUSINESS ECONOMICS BBA [BBA-101]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of venkateshwara - open university

BUSINESS ECONOMICS

VENKATESHWARAOPEN UNIVERSITY

www.vou.ac.in

VENKATESHWARAOPEN UNIVERSITY

www.vou.ac.in

BUSINESS ECONOMICS

BUSINESS ECONOMICS

10 MM

BBA[BBA-101]

BUSINESS ECONOMICS

BBA

[BBA-101]

Copyright © D N Dwivedi, 2019

BOARD OF STUDIES

Prof Lalit Kumar SagarVice Chancellor

Dr. S. Raman IyerDirectorDirectorate of Distance Education

SUBJECT EXPERT

Dr. S. Raman IyerDr. Richa AgarwalDr. Anand KumarDr. Babar Ali KhanDr. Adil Hakeem Khan

Programme DirectorAssistant ProfessorAssistant ProfessorProfessor in CommerceProfessor in Management

CO-ORDINATOR

Mr. Tauha KhanRegistrar

All rights reserved. No part of this publication which is material protected by this copyright noticemay be reproduced or transmitted or utilized or stored in any form or by any means now known orhereinafter invented, electronic, digital or mechanical, including photocopying, scanning, recordingor by any information storage or retrieval system, without prior written permission from the Publisher.

Information contained in this book has been published by VIKAS® Publishing House Pvt. Ltd. and hasbeen obtained by its Authors from sources believed to be reliable and are correct to the best of theirknowledge. However, the Publisher and its Authors shall in no event be liable for any errors, omissionsor damages arising out of use of this information and specifically disclaim any implied warranties ormerchantability or fitness for any particular use.

Vikas® is the registered trademark of Vikas® Publishing House Pvt. Ltd.

VIKAS® PUBLISHING HOUSE PVT LTDE-28, Sector-8, Noida - 201301 (UP)Phone: 0120-4078900 Fax: 0120-4078999Regd. Office: A-27, 2nd Floor, Mohan Co-operative Industrial Estate, New Delhi 1100 44Website: www.vikaspublishing.com Email: [email protected]

Concept:Meaning, Nature, Scope and Significance of Business Economic

Utility Approach:Law of Diminishing Marginal Utility, Law of Utility

Demand Analysis and Forecasting:Demand Schedule and Demand Curve, Significance of DemandForecasting and Techniques.

Production Function:Concept, Break Even analysis, Law of Variable Proportion.

Cost… Revenue:Concept, Short Run and Long Run Cost Curves, Concept of Total,Marginal and Average Revenues, Relationships between AverageRevenue, Marginal Revenues and Elasticity of Demand.

Pricing:Objectives of the Firm - Profit Maximization/Sales RevenueMaximization Survival, Pricing under Different Market Structures -Perfect Competition, Monopoly, Discriminating, Product - LinePricing, Joint Product Pricing.

Profit Management:Concept of Profit Management, Profit Planning and Control.

Unit 1: Introduction toBusiness Economics

(Pages: 3-26)

Unit 2: Utility Approach(Pages: 27-61)

Unit 3: Demand Analysis andForecasting

(Pages: 63-96)

Unit 4: Production Function(Pages: 97-128)

Unit 5: Cost and Revenue(Pages: 129-165)

Unit 6: Pricing(Pages: 167-197)

Unit 7: Profit Management(Pages: 199-213)

SYLLABI-BOOK MAPPING TABLEBusiness Economics

Syllabi Mapping in Book

CONTENTSINTRODUCTION 1

UNIT 1 INTRODUCTION TO BUSINESS ECONOMICS 3-261.0 Introduction1.1 Unit Objectives1.2 Understanding Economics and its Scope

1.2.1 Meaning and Nature of Business Economics1.2.2 Scope of Business or Managerial Economics1.2.3 Difference between Business or Managerial Economics and Pure Economics

1.3 Significance of business Decision-Making1.3.1 Managerial Economics: Techniques and Business Decisions1.3.2 Time Perspective in Business Decisions

1.4 Role of a Managerial Economist1.5 Summary1.6 Key Terms1.7 Answers to ‘Check Your Progress’1.8 Questions and Exercises1.9 Further Reading

UNIT 2 UTILITY APPROACH 27-612.0 Introduction2.1 Unit Objectives2.2 Law of Utility2.3 Law of Diminishing Marginal Utility

2.3.1 Analysis of Consumer Behaviour: Cardinal Utility Approach2.3.2 Analysis of Consumer Behaviour: Ordinal Utility Approach2.3.3 Meaning and Nature of Indifference Curve2.3.4 Consumer’s Equilibrium: Ordinal Utility Approach2.3.5 Derivation of Individual Demand Curve2.3.6 Comparison of Cardinal and Ordinal Utility Approaches

2.4 Summary2.5 Key Terms2.6 Answers to ‘Check Your Progress’2.7 Questions and Exercises2.8 Further Reading/Endnotes

UNIT 3 DEMAND ANALYSIS AND FORECASTING 63-963.0 Introduction3.1 Unit Objectives3.2 Demand Schedule and Demand Curve3.3 Significance of Demand Forecasting and Techniques

3.3.1 Steps in Demand Forecasting3.3.2 Techniques of Demand Forecasting

3.4 Some Case Studies of Demand Forecasting3.5 Summary3.6 Key Terms3.7 Answers to ‘Check Your Progress’3.8 Questions and Exercises3.9 Further Reading/Endnotes

UNIT 4 PRODUCTION FUNCTION 97-1284.0 Introduction4.1 Unit Objectives4.2 Production Function: Concept4.3 Break-even Analysis

4.3.1 Contribution Analysis4.3.2 Profit—Volume Ratio4.3.3 Margin of Safety

4.4 Law of Variable Proportion4.4.1 Determining Optimum Employment of Labour4.4.2 Isoquant Curves and their Properties4.4.3 Isoquant Map and Economic Region of Production4.4.4 Elasticity of Factor Substitution4.4.5 Laws of Returns to Scale

4.5 Summary4.6 Key Terms4.7 Answers to ‘Check Your Progress’4.8 Questions and Exercises4.9 Further Reading/Endnotes

UNIT 5 COST AND REVENUE 129-1655.0 Introduction5.1 Unit Objectives5.2 Cost Concepts5.3 Short and Long-Run Cost Curves

5.3.1 Cost Curves and the Law of Diminishing Returns5.4 Total, Marginal and Average Revenues

5.4.1 Price Elasticity of Demand5.4.2 Measuring Price Elasticity from a Demand Function5.4.3 Price Elasticity and Total Revenue5.4.4 Price Elasticity and Marginal Revenue5.4.5 Determinants of Price Elasticity of Demand5.4.6 Cross-Elasticity of Demand5.4.7 Income-Elasticity of Demand5.4.8 Advertisement or Promotional Elasticity of Sales5.4.9 Elasticity of Price Expectations

5.5 Summary5.6 Key Terms5.7 Answers to ‘Check Your Progress’5.8 Questions and Exercises5.9 Further Reading/Endnotes

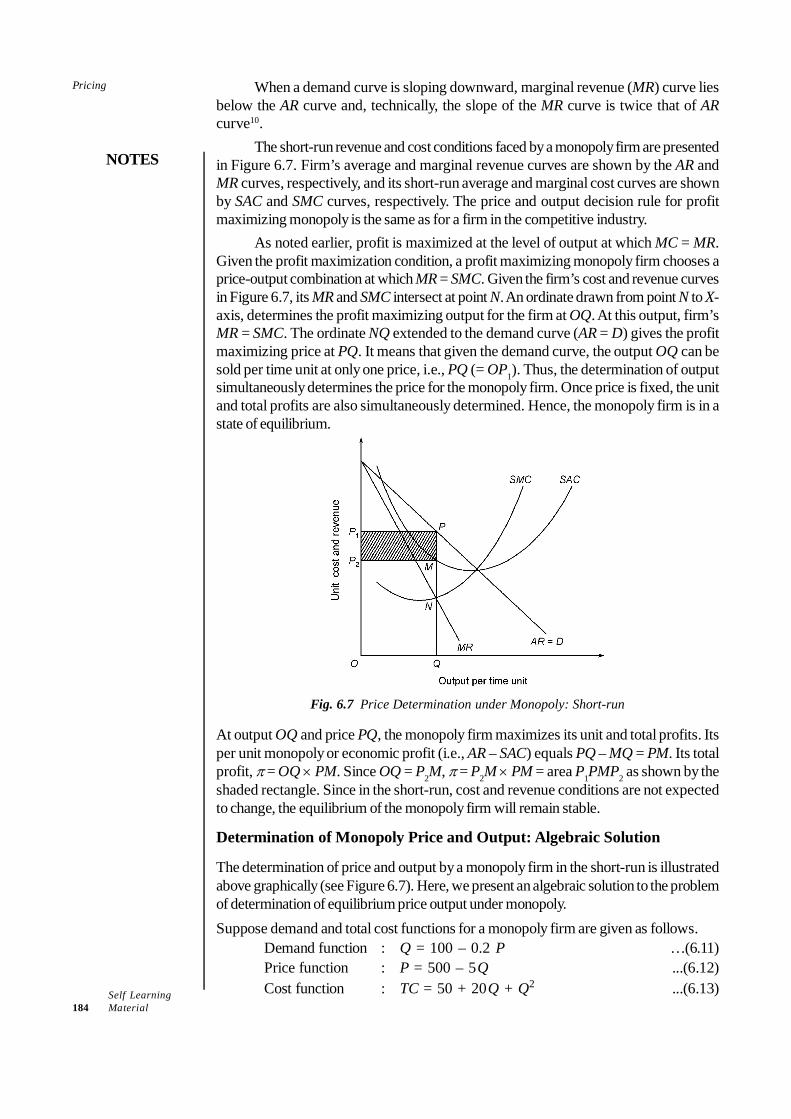

UNIT 6 PRICING 167-1976.0 Introduction6.1 Unit Objectives6.2 Objectives of the Firm

6.2.1 Profit Maximization6.2.2 Sales Revenue Maximization

6.3 Pricing Under Different Market Structures6.3.1 Perfect Competion6.3.2 Monopoly6.3.3 Price Discrimination Under Monopoly6.3.4 Price Discrimination by Degrees

6.4 Product Line Pricing6.4.1 Joint Product Pricing

6.5 Summary6.6 Key Terms6.7 Answers to ‘Check Your Progress’6.8 Questions and Exercises6.9 Further Reading/Endnotes

UNIT 7 PROFIT MANAGEMENT 199-2137.0 Introduction7.1 Unit Objectives7.2 Concept of Profit Management

7.2.1 Monopoly Power as Source of Profit7.2.2 Problems in Profit Measurement7.2.3 Problem in Measuring Depreciation7.2.4 Treatment of Capital Gains and Losses7.2.5 Current vs Historical Costs

7.3 Profit Planning and Control7.3.1 Profit as Control Measure

7.4 Summary7.5 Key Terms7.6 Answers to ‘Check Your Progress’7.7 Questions and Exercises7.8 Further Reading/Endnotes

Self-InstructionalMaterial 1

Introduction

NOTES

INTRODUCTIONThe natural curiosity of a student, who begins to study a subject, is to know its natureand scope. Such as it is, a student of economics would like to know ‘what is economics’and ‘what is its subject matter’. Surprisingly, there is no precise answer to these questions.

Attempts made by economists over the past 300 years to define economics havenot yielded a precise and universally acceptable definition of economics. Economistsright from Adam Smith—the ‘father of economics’—down to modern economists havedefined economics differently, depending on their own perception of the subject matterof economics of their era. Thus, economics is fundamentally the study of choice-makingbehaviour of the people. The choice-making behaviour of the people is studied in asystematic or scientific manner. This gives economics the status of a social science.However, the scope of economics, as it is known today, has expanded vastly in the post-World War II period. Modern economics is now divided into two major branches:Microeconomics and Macroeconomics. Microeconomics is concerned with themicroscopic study of the various elements of the economic system and not with thesystem as a whole.

As economist Abba P. Lerner has put it, ‘Microeconomics consists of looking atthe economy through a microscope, as it were, to see how the millions of cells in bodyeconomic—the individuals or households as consumers and the individuals or firms asproducers—play their part in the working of the whole economic organism.’Macroeconomics is a relatively new branch of economics. Macroeconomics is the studyof the nature, relationship and behaviour of aggregates and averages of economicvariables. Therefore, the technique and process of business decision-making has of latechanged tremendously.

The basic functions of business managers is to take appropriate decisions onbusiness matters, to manage and organize resources, and to make optimum use of availableresources with the objective of achieving the business goals. In today’s world, businessdecision-making has become an extremely complex task due to the ever-growingcomplexity of the business world and the business environment. It is in this context thatmodern economics—howsoever defined—contributes a great deal towards businessdecision-making and performance of managerial duties and responsibilities. Just as biologycontributes to the medical profession and physics to engineering, economics contributesto the managerial profession.

The book has been written in keeping with the self-instructional mode or the SIM(self instructional material) format for distance learning. Each unit begins with anIntroduction to the topic, followed by an outline of the Unit Objectives. The detailedcontent is then presented in a simple and organized manner, interspersed with ‘CheckYour Progress’ questions to test the student’s understanding of the topics covered. ASummary along with a list of Key Terms and a set of Questions and Exercises isprovided at the end of each unit for effective recapitulation.

Self-InstructionalMaterial 3

Introduction to BusinessEconomics

NOTES

UNIT 1 INTRODUCTION TOBUSINESS ECONOMICS

Structure1.0 Introduction1.1 Unit Objectives1.2 Understanding Economics and its Scope

1.2.1 Meaning and Nature of Business Economics1.2.2 Scope of Business or Managerial Economics1.2.3 Difference between Business or Managerial Economics and Pure Economics

1.3 Significance of business Decision-Making1.3.1 Managerial Economics: Techniques and Business Decisions1.3.2 Time Perspective in Business Decisions

1.4 Role of a Managerial Economist1.5 Summary1.6 Key Terms1.7 Answers to ‘Check Your Progress’1.8 Questions and Exercises1.9 Further Reading

1.0 INTRODUCTION

Emergence of business or managerial economics as a separate course of managementstudies can be attributed to at least three factors: (a) growing complexity of the businessdecision-making process due to changing market conditions and business environment,(b) consequent upon, the increasing use of economic logic, concepts, theories andtools of economic analysis in the process of business decision-making, and (c) rapidincrease in demand for professionally trained managerial manpower. Let us have aglance at how these factors have contributed to the creation of ‘managerial economics’as a separate branch of study.

It is a widely accepted fact that the business decision-making process has becomeincreasingly complicated due to ever growing complexities in the business world.There was a time when business units (shops, firms, factories, mills) were set up,owned and managed by individuals or business families. In India, there were 22 topbusiness families like the Tatas, Birlas, Singhanias, Ambanis and Premjis. Big industrieswere few and the scale of business operation was relatively small. The managerialskills acquired through traditional family training and experience were sufficient tomanage small and medium scale businesses. Although a large part of private businessis still run on a small scale and managed in the traditional style of business management,the industrial business world has changed drastically in size, nature and content. Thegrowing complexity of the business world can be attributed to the growth of largescale industries, growth of a large variety of industries, diversification of industrialproducts, expansion and diversification of business activities of corporate firms, growthof multinational corporations, and mergers and takeovers, especially after the SecondWorld War. These factors have contributed a great deal to the recent increase in inter-firm, inter-industry and international rivalry, competition, risk and uncertainty. Business

Self-Instructional4 Material

Introduction to BusinessEconomics

NOTES

decision-making in this kind of business environment is a very complex affair. The familytraining and experience is no longer sufficient to meet the managerial challenges.

The growing complexity of business decision-making has inevitably increased theapplication of economic concepts, theories and tools of economic analysis in this area.The reason is that making an appropriate business decision requires a clear understandingof market conditions, the nature and degree of competition, market fundamentals andthe business environment. This requires an intensive and extensive analysis of the marketconditions in the product market, input market and financial market. On the other hand,economic theories, logic and tools of analysis have been developed to analyse and predictmarket behaviour. The application of economic concepts, theories, logic and analyticaltools in the assessment and prediction of market conditions and business environmenthas proved to be of great help in business decision-making. The contribution of economicsto business decision-making has come to be widely recognized. Consequently, economictheories and analytical tools, which are widely used in business decision-making havecrystallized into a separate branch of management studies, called managerial economicsor business economics.

1.1 UNIT OBJECTIVES

After going through this unit, you will be able to:• Discuss the concept of economics and its scope• Explain the nature and scope of business economics• Discuss the significance of business decision-making• Discuss the role and responsibility of a managerial economist in a business

enterprise

1.2 UNDERSTANDING ECONOMICS AND ITSSCOPE

Let us begin our study of business or managerial economics by learning• What is economics?• What are business or managerial decision-making problems?• How does economics contribute to business decision-making?

What is Economics?

The natural curiosity of a student who begins to study a subject is to know the natureand scope of the subject of his study. Such as it is, a student of economics would liketo know ‘What is economics’ and ‘What is its subject matter’. Surprisingly, there isno precise answer to these questions. Attempts made by economists over the past 300years to define economics have not yielded a precise and universally acceptabledefinition of economics. Economists right from Adam Smith—the ‘father ofeconomics’—down to modern economists have defined economics differently,depending on their own perception of the subject of their era. For example, AdamSmith (1776) defined economics as ‘an inquiry into the nature and causes of thewealth of the nations’. Nearly one-and-half centuries later, Alfred Marshall, an all-time

Self-InstructionalMaterial 5

Introduction to BusinessEconomics

NOTES

great economist, defined economics differently. According to Alfred Marshall (1922),‘Economics is the study of mankind in the ordinary business of life; it examines that partof individual and social action which is most closely connected with the attainment andwith the use of the material requisites of well being.’ Lionel Robbins (1932) has definedit more precisely: ‘Economics is the science which studies human behaviour as arelationship between ends and scarce means which have alternative uses.’ One can finda number of other definitions in various writings on economics. None of these definitionshowever, capture the entire subject matter of modern economics, although each throwssome light on what economics is about.

The fact is that economics has not yet been defined precisely and appropriately.The reason is, as Zeuthen has observed, ‘Economics is an unfinished science’ and asSchultz has remarked, ‘Economics is still a very young science and many problems init are almost untouched.’ These observations, made half a century ago, still hold true.It seems that after Robbins, no serious attempt was made to define economics. Definingeconomics has been such a fruitless endeavour that some modern authors of economicstexts, including those by reputed economists like Samuelson, Baumol and Stiglitz,avoid the issue of defining economics. For example, William J. Baumol (a Nobellaureate) and Allen S. Blinder write in their own text, ‘Many definitions of economicshave been proposed, but we prefer to avoid any attempt to define the discipline in asingle sentence or paragraph’, and let ‘the subject matter speak for itself.’

However, the study of economic science, or of any science for that matter,must commence with a working definition of it. In this regard, most modern textsfollow Robbins’ definition of economics, even though modern economics goes farbeyond what Robbins thought the subject matter of economics was. Let us begin bylooking at Robbins’ view and then study how far economics goes beyond his view.

Economics is a Social Science

Economics as a social science studies economic behaviour of the people and itsconsequences. What is economic behaviour? Economic behaviour is essentially theprocess of evaluating economic opportunities open to an individual or a society and,given the resources, making a choice of the best of these opportunities. The objectivebehind this is to maximize gains from the available resources and opportunities. Intheir efforts to maximize gains from their resources, people have to make a numberof choices regarding the use of resources and spending their earnings.

The basic function of economics is to observe, explain and predict how people(individuals, households, firms and the government) as decision-makers make choicesabout the use of resources (land, labour, capital, knowledge and skills, technology,time and space, etc.) in order to maximize their income, as well as how they, asconsumers, decide how to spend their income to maximize their total utility. Thus,economics is fundamentally the study of choice-making behaviour of the people.Studying it in a systematic or scientific manner gives economics the status of a socialscience.

For the purpose of economic analysis, people are classified according to theirdecision-making capacity as individuals, households, firms and the society; andaccording to the nature of their economic activity as consumers, producers, factoryowners and economy managers, i.e., the government. As consumers, individuals andhouseholds, with a given income they have to decide ‘what to consume and howmuch to consume’. They have to make these decisions because consumers are, by

Self-Instructional6 Material

Introduction to BusinessEconomics

NOTES

nature, utility maximizers, and consuming any commodity in any quantity does notmaximize their gains or their satisfaction. As producers, firms, farms, factories,shopkeepers, banks, transporters, etc., they have to choose ‘what to produce, how muchto produce and how to produce’, because they too are gain maximizers and producingany commodity in any quantity by any technique will not maximize their gains (profits).As labour, they have to choose between alternative occupations and places of workbecause any occupation at any place will not maximize their earnings. Likewise, thegovernment has to choose how to tax, whom to tax, how much to spend and how tospend, so that social welfare is maximized at a given social cost. Economics as a socialscience studies how people make their choices.

It is this economic behaviour of the individuals, households, firms, governmentand the society as a whole which forms the central theme of economics as a socialscience. Thus, economics is fundamentally the study of how people allocate theirlimited resources to produce and consume goods and services to satisfy their endlesswants, with the objective of maximizing their gains.

Why does the problem of making choices arise?

The need for making choice arises because of some basic facts of economic life. Letus look at the basic facts of human life in some detail and how they create the problemof choice-making.

(i) Human wants, desires and aspirations are limitless: The history of humancivilization bears evidence to the fact that human desire to consume more andmore of better and better goods and services has always been increasing. Forexample, the housing need has risen from a hut to a luxury palace, and if possible,a house in space; the need for means of transportation has gone up from mulesand camels to supersonic jet planes; demand for means of communication hasrisen from messengers and postal services to cell phones with cameras; needfor computational facility from manual calculation to superfast computers, andso on. For an individual, only the end of life brings an end to his/her needs.

Human wants, desires and needs are endless in the sense that they go onincreasing with increase in people’s ability to satisfy them. The endlessness ofhuman wants can be attributed to (i) people’s insatiable desire to raise theirstandard of living, comforts and efficiency, (ii) human tendency to accumulatethings beyond their present need, (iii) increase in knowledge about inventionsand innovations of new goods and services with greater convenience, efficiencyand serviceability, (iv) multiplicative nature of some want (e.g., buying a carcreates want for many other things—petrol, driver, cleaning, parking place,safety locks, spare parts, insurance), (v) biological needs (e.g., food, water)are repetitive, (vi) imitative and competitive nature of needs of human beingsdue to demonstration and bandwagon effects, and (vii) influence ofadvertisements in modern times creating new kinds of wants. For these reasons,human wants continue to increase endlessly.

Apart from being unlimited, another and an equally important feature ofhuman wants is that they are gradable. In simple words, all human wants are notequally urgent and pressing at a point of time, or over a period of time. Whilesome wants have to be satisfied as and when they arise (e.g., food, clothes andshelter), some can be postponed (e.g., purchase of a car). Also, satisfyingsome wants provides greater satisfaction than others. Given their intensity and

Self-InstructionalMaterial 7

Introduction to BusinessEconomics

NOTES

urgency, human wants can be arranged in the order of their priority. The priorityof wants, however, varies from person to person, and from time to time for thesame person. Therefore the question arises as to ‘which want to satisfy first’ and‘which the last’. Thus, consumers have to make a choice between ‘what toconsume’ and ‘how much to consume’. Economics studies how consumers(individuals and household) make choices between their wants and how theyallocate their expenditure between the different kinds of goods and servicesthey choose to consume.

(ii) Resources are scarce: The need for making a choice between the variousgoods that people want to produce and consume arises mainly because theresources that are available to the people at any point of time for satisfying theirwants are scarce and limited. What are these resources? Conceptually, anythingwhich is available and can be used to satisfy human wants and desires is aresource. In economics, however, the resources that are available to individuals,households, firms, and societies at any point of time are traditionally classifiedas follows:• Natural resources (including cultivable land surface, space, lakes, rivers,

coastal range, minerals, wildlife, forest, climate, rainfall, etc.).• Human resources (including manpower, human energy, talent, professional

skill, innovative ability and organizational skill, jointly called labour).• Man-made resources (including machinery, equipments, tools, technology

and building, called together capital).• Entrepreneurship, i.e., the ability, knowledge and talent to put land, labour

and capital in the process of production, and the ability and willingness toassume risk in business.

To these basic resources, economists add other categories of resources, viz.,time, technology and information. All these resources are scarce. Resourcescarcity is a relative term. It implies that resources are scarce in relation to thedemand for resources. The scarcity of resources is the mother of all economicproblems. If resources were unlimited, like human wants, there would be noeconomic problem and, perhaps, no economics as a subject of study. It is thescarcity of resources in relation to human wants that forces people to makechoices.

Furthermore, the problem of making choices arises also because resourceshave alternative uses and these alternative uses have different returns or earnings.For example, a building can be used to set up a shopping centre, businessoffice, a public school, a hospital or for residential purposes. But the return onthe building varies according to the use of the building. Therefore, a return-maximizing building owner has to make a choice between the alternative uses ofthe building. If the building is put to a particular use, the landlord has to foregothe return expected from its other alternative uses. This is called opportunitycost. Economics as a social science analyses how people (individuals andsociety) make choices between the economic goals they want to achieve, betweenthe goods and services they want to produce, and between the alternative usesof their resources with the objective of maximizing their gains. The gain-maximizers evaluate the costs and benefits of the alternatives while deciding onthe final use of the resources. Economics studies the process of making choicesbetween the alternative uses. According to Robbins, this is what constitutes thesubject matter of economics.

Self-Instructional8 Material

Introduction to BusinessEconomics

NOTES

(iii) People are gain maximizers: Yet another important aspect of human naturethat leads to choice-making behaviour is that most people aim at maximizing theirgains from the use of their limited resources. ‘Why people want to maximize theirgains’ is a no concern in economics. Traditional economics assumes maximizingbehaviour of the people as a part of their rational economic behaviour. Thisassumption is based on observed facts. As consumers, they want to maximizetheir utility or satisfaction; as producers, they want to maximize their output orprofit; and as factor owners, they want to maximize their earnings. People’sdesire to maximize their gains is a very important aspect of economic behaviourof the people giving rise to the need to study economics. If people did not want tomaximize their gains, the problem of choice-making would not arise. Consumerswould not bother as to ‘what to consume’ and ‘how much to consume’; producerswould not bother as to ‘what to produce’, ‘how much to produce’ and ‘how toproduce’; and factor owners would not care as to where and how to use theresources. But, in reality, they do maximize their gains and economics studieshow people maximize their gains.

Economics goes far beyond choice-making behaviour

The foregoing description of economics may give the impression that economics endswith the study of choice-making behaviour of the people but it is not quite so. Economicsgoes far beyond the scope of microeconomics. If economics is confined to the study ofchoice-making behaviour of the individual, many other and more important economicissues that constitute a major part of modern economic science will have to be left out.Look at some of the major national and international, economic issues:

• How is the level of national output and employment determined in a country?• Why are some countries very rich and some countries very poor?• What are the factors that determine the overall economic growth of a country?• What causes fluctuations in the national output, employment and the general price

level?• How do international trade and international capital flows affect the domestic

economy?• What causes inflation and what are its effects on the economy’s growth and

employment?• Why is about 35 per cent of India’s population still ‘below the poverty line’

even after five decades of planned development with emphasis on ‘removal ofpoverty’?

• Why is there large-scale unemployment in India and why have the efforts tosolve the problem of unemployment failed?

• Why has the Government of India been faced with fiscal deficits of a dangerousmagnitude over the past two decades and why has it failed to reduce it to amanageable level?

• Why does the government need to intervene with the market system and adoptmeasures to control and regulate production and consumption, saving andinvestment, export and imports, wages and prices, and so on?One can point out many other issues which do not fall within the purview of

microeconomics. Analysis of and finding answers to such economic problems now

Self-InstructionalMaterial 9

Introduction to BusinessEconomics

NOTES

constitute a major and a more important subject matter of economics than the choice-making aspect of it. The study of the issues mentioned above has created a relativelynew branch of economics, called macroeconomics. As noted above, the field ofeconomics continues to grow and expand in its scope, size and analytical rigour.Boundaries of economic science are not yet precisely marked, though economics isclaimed to be ‘the oldest and best developed of the social sciences’. Let us nowglance at the scope of economics as it is known today, and the major branches andspecialized areas of economics.

Scope of Economics

As noted earlier, the scope of economics is not marked precisely and, as it appears, itcannot be. However, the scope of economics, as it is known today, has expandedvastly in the post-World War II period. Modern economics is now divided into twomajor branches: microeconomics and macroeconomics. A brief description of thesubject matter and approach of microeconomics and macroeconomics is given below.

Microeconomics

Microeconomics is concerned with the microscopic study of the various elements ofthe economic system and not with the system as a whole. As Lerner has put it,‘Microeconomics consists of looking at the economy through a microscope, as itwere, to see how the million of cells in body economic—the individuals or householdsas consumers and the individuals or firms as producers—play their part in the workingof the whole economic organism.’ Thus, microeconomics is the study of the economicbehaviour of the individual consumer and producer and of individual economicvariables, i.e., production and pricing of individual goods and services. Microeconomicsstudies how consumers and producers make their choices; how their decisions andchoices affect the market demand and supply conditions; how consumers and producersinteract to settle-on the prices of goods and services in the market; how prices aredetermined in different market settings; and how total output is distributed amongthose who contribute to production, i.e., between landlords, labour, capital suppliersand the entrepreneurs. Briefly speaking, theories of consumer behaviour, theories ofproduction and cost of production, theories of commodity and factor pricing, efficientallocation of output and factors of production (called welfare economics) constitutethe main themes of microeconomics.

Macroeconomics

Macroeconomics is a relatively new branch of economics. It was only after thepublication of Keynes’s ‘The General Theory of Employment, Interest and Money’in 1936, that macroeconomics crystallized as a separate branch of economics.Macroeconomics studies the working and performance of the economy as a whole. Itanalyses behaviour of the national aggregates including national income, aggregateconsumption, savings, investment, total employment, the general price level and thecountry’s balance of payments. According to Boulding, ‘Macroeconomics is the studyof the nature, relationship and behaviour of aggregates and averages of economicquantities.’ He contrasts macroeconomics with microeconomics in the following words:‘Macroeconomics ... deals not with individual quantities, as such, but aggregates ofthese quantities—not with individual incomes, but with the national income, not withindividual prices but with price levels, not with individual output but with the national

Self-Instructional10 Material

Introduction to BusinessEconomics

NOTES

output.’ More importantly, macroeconomics analyses relationship between nationalaggregate variables and how these aggregate variables interact with one another todetermine each other. It also studies the impact of public revenue and public expenditure,government’s economic activities and policies on the economy. An important aspectof macroeconomics studies is the consequences of international trade and othereconomic relations between nations. The study of these aspects of economic phenomenaconstitutes the major theme of macroeconomics.

Basic Problems of an Economy

Let us now turn to the basic problems of an economy that lie in the background of alleconomic decisions, and also form the basis of economic studies and generalizations.The major economic problems faced by an economy—whether capitalist, socialist ormixed—may be classified into two broad groups:

• Microeconomic problems which are related to the working of the economicsystem

• Macroeconomic problems related to the growth, employment, stability, externalbalance, and macroeconomic policies for the management of the economy as awholeWe will first discuss the microeconomic problems which are immediately relevant

to our simplified economic system. Macroeconomic problems will be taken up in thefollowing sub-section.

1. Microeconomic problems

The basic microeconomic problems are:• What to produce and how much to produce?• How to produce?• For whom to produce or how to distribute the social output?

These problems assume a macro nature when considered at the larger economiclevel. However, we will first discuss them at the micro level because these problemshave to be resolved at the micro before the macro level.(i) What to produce? The problem of ‘what to produce’ is the problem of choicebetween commodities. This problem arises mainly for two reasons: (i) scarcity ofresources does not permit production of all the goods and services that people wouldlike to consume, and (ii) all the goods and services are not equally valued in terms oftheir utility by the consumers. Some commodities yield higher utility than the others.Since all the goods and services cannot be produced for lack of resources, and all thatis produced may not be bought by the consumers, the problem of choice between thecommodities arises. The problem ‘what to produce’ is essentially the problem ofefficient allocation of scarce resources so that output is maximum and output-mix isoptimum. The objective is to satisfy the maximum needs of the maximum number ofpeople.

The question ‘how much to produce’ is the problem of determining the quantityof each commodity and service to be produced. This problem, too, arises due toscarcity of resources since, surplus production would mean wastage of scarceresources. This problem also determines the allocation of resources between variousgoods and services to be produced.

Self-InstructionalMaterial 11

Introduction to BusinessEconomics

NOTES

The basic economic problem of unlimited wants and limited resources makes itnecessary for an economic system to devise some method of determining ‘what toproduce’ and ‘how much to produce’, and ways and means to allocate the availableresources for the production of goods and services. In a free enterprise economy, thesolution to the problems ‘what to produce’ and ‘how much to produce’ is provided bythe price mechanism.(ii) How to produce? The problem ‘how to produce’ is the problem of choice oftechnique. Here the problem is to determine an optimum combination of inputs—labour and capital—to be used in the production of goods or services. This problemarises mainly because of scarcity of resources. If labour and capital were available inunlimited quantities, any amount of labour and capital could be combined to producea commodity. But since resources are scarce, it becomes imperative to choose atechnology which uses resources most economically.

Another very important factor which gives rise to this problem is that a givenquantity of a commodity can be produced with a number of alternative techniques,i.e., alternative input combinations. For example, it is always technically possible toproduce a given quantity of wheat with more labour and less capital (i.e., with alabour-intensive technology) and with more capital and less labour (i.e., with a capital-intensive technology). The same is true of most commodities. In the case of somecommodities, however, choices are limited. For example, production of woollen carpetsand other handicraft items is by nature labour-intensive, while production of cars, TVsets, computers, aircraft, etc., is capital-intensive.

Moreover, in the case of most commodities, alternative technology may beavailable. But the alternative techniques of production involve varying costs. Therefore,the problem of choice of technology arises.

In a free market economy, the market system itself provides the solution to theproblem of choice of technology through the price mechanism. The market mechanismyields a pricing system which determines the prices of both labour and capital. Factorprices and factor-quantities determine the cost of production for business firms. Profit-maximizing firms find out an input combination which minimizes their cost of production.This becomes inevitable for these firms because their resources are limited and, withgiven resources, they intend to maximize their profits.

The process through which business firms arrive at the optimum inputcombination and make choices between the alternative techniques of production arediscussed later in this book.(iii) For whom to produce or how to distribute social output? In a moderneconomy, all the goods and services are produced by business firms. The total outputgenerated by business firms is known as ‘society’s total product’ or ‘national output’.The total output ultimately flows to the households. Here a question arises: how is thenational output shared among the households or what determines the share of eachhousehold? A possible answer to this question is that, in a free enterprise economy, itis the price-mechanism which determines the distribution pattern of the national output.Price-mechanism determines the price of each factor in the factor market. Once thefactor price is determined, the income of each household is determined by the quantityof the factor(s) which it sells in the factor market. Those who possess a large amountof highly priced resources, are able to earn higher incomes and consume a largerproportion of national output than those who possess a small quantity of low-pricedresources.

Self-Instructional12 Material

Introduction to BusinessEconomics

NOTES

But the problem does not end here. For, other questions then arise: why do somepeople have a command over a larger proportion of resources than others? Why dothose who have more, get more and more? Why do those who have less, get less andless? In other words, why do the rich get richer and the poor poorer? Is this distributionof national production fair? If not, how can disparities in incomes or sources of incomesbe removed, or at least, reduced?

The price mechanism of a free enterprise system has not been able to provide asolution to these questions. These problems have long been debated inconclusively.They remain as alive today as they were during the days of Adam Smith and DavidRicardo.

When questions related to production and distribution are looked into from theefficiency point of view, economists address themselves to other questions like: Howefficient is the society’s production and distribution system? How does it affect thewelfare of the society? How can production and distribution be made more efficientor welfare oriented? Economists’ attempts to answer these questions has led to growthof another branch of economics, i.e., welfare economics.

2. Macroeconomic problems

The economic problems discussed above are of micro nature. These problems togethermake up the subject matter of Microeconomic Theory or ‘Price Theory’. Apart frommicro problems, there are certain macroeconomic problems of prime importanceconfronted by an economy. Following Lipsey, these problems may be specified asfollows:

(i) How to increase the production capacity of the economy: This is essentiallythe problem related to the economic growth of the country. The need forincreasing the production capacity of the economy arises for at least two reasons.First, most economies of the world have realized by experience that theirpopulation has grown at a rate much higher than their productive resources.This leads to poverty, especially in the less developed countries. Poverty initself is a cause of a number of socio-economic problems. Besides, it hasfrequently jeopardized the sovereignty and integrity of nations. Colonization ofpoor nations by the richer and powerful imperialist nations during the pre-20thcentury period is evidence of this fact. Therefore, growth of the economy andsparing resources for defence has become a necessity. Second, over time someeconomies have grown faster than others while some economies have remainedalmost stagnant. The poor nations have been subjected to exploitation andeconomic discrimination. This has impelled the poor nations to make theireconomies grow, to protect themselves from exploitation and to give their peoplea respectable status in the international community.

While various economies have been facing the problem of growth,economists have engaged themselves in finding an answer to such questionsas: What makes an economy grow? Why do some economies grow faster thanthe others? This has led to the growth of theories of Economic Growth.

(ii) How to stabilize the economy: An important feature of the free enterprisesystem has been the economic fluctuation of these economies. Though economicups-and-downs are not unknown in controlled economies, free enterpriseeconomies have experienced it more frequently and more severely. Economicfluctuations cause wastage of resources, e.g., idleness of manpower or involuntary

Self-InstructionalMaterial 13

Introduction to BusinessEconomics

NOTES

unemployment, idle capital stock–particularly during the periods of depression.Economists have devoted a good deal of attention to explain this phenomenon.This problem is studied under trade cycles or business cycles.

(iii) Other problems of macro nature: In addition to the macro problems mentionedabove, there are many other economic problems of this nature, which economistshave studied extensively and intensively. The most important problems of thiscategory are the problems of unemployment and inflation. While widespreadunemployment is the biggest problem confronting developing economies, inflationis a global problem. The abounding literation on these problems has yet to offera solution to these problems. Another set of macro problems is associated withinternational trade. The major questions to which economists have devoted agood deal of their attention are: What is the basis of trade between the nations?How are the gains from trade shared between the nations? Why do deficits andsurpluses arise in trade balances? How is an economy affected by deficits orsurplus in its balance of payment position? New problems continue to emergeas an economy passes through different phases of economic growth.

1.2.1 Meaning and Nature of Business Economics

While economics is the oldest social science, the emergence of business or managerialeconomics as a separate branch of economic study is a recent phenomenon. Theemergence of managerial economics as a separate branch of economic study can beattributed to three factors:

• Growing complexity of business decision-making due to rapid expansion of businessand rapidly changing market conditions and business environment

• Consequent to an increasing use of economic theory, logic, concepts and tools ofeconomic analysis in the process of business decision-making

• Rapid increase in demand for professionally trained managerial manpowerThe growing complexity of business decision-making has inevitably increased the

application of economic theories, concepts and tools of analysis to find an appropriatesolution to business problems, in conformity with the goals of objectives of businessfirms. The reason is that making an appropriate decision, especially under the conditionsof risk and uncertainty, requires a clear understanding of market conditions, nature anddegree of competition, market fundamentals and the business environment. This requiresan intensive and extensive analysis of market conditions regarding the product, input andfinancial markets. On the other hand, the basis function of economics is to offer a logicalanalysis and interpretation of the business world. The application of economic theories,logic and polls of analysis to the assessment and prediction of market conditions hasproved to be a great help in business decision-making. Consequently, economic theoriesand analytical tools that are widely used in business decision-making have crystallized asa separate and specialized branch of study, called ‘business or managerial economics’.

Let us now see how business or managerial economics can be defined.Business or managerial economics is essentially that part of economics which is

applied to business decision-making. As noted above, economic science is a body ofknowledge consisting of economic concepts, logic and reasoning, economic laws andtheories, and tools and techniques for analysing economic phenomena, evaluating economicoptions and for optimizing allocation of resources. The part of economic science that isapplied to business analysis and decision-making constitutes business or managerialeconomics.

Self-Instructional14 Material

Introduction to BusinessEconomics

NOTES

Business or managerial economics can be defined more comprehensively. Businessor managerial economics is the study of economic theories, concepts, logic and tools ofanalysis that are used in analyzing business conditions with the objective of finding anappropriate solution to business problems. As regards its nature, business or managerialeconomics is essentially applied micro economics.

1.2.2 Scope of Business or Managerial Economics

In general, the scope of business managerial economics comprehends all those economicconcepts, theories and tools of analysis which can be used to analyse the businessenvironment and to find solutions to practical business problems. In other words,managerial economics is economics applied to the analysis of business problems anddecision-making. Broadly speaking, it is applied economics.

The areas of business issues to which economic theories can be directly appliedmay be broadly divided into two categories: (a) operational or internal issues, and(b) environment or external issues.

Microeconomics Applied to Operational Issues

Operational problems are of an internal nature. They include all those problems whicharise within the business organization and fall within the purview and control of themanagement. Some of the basic internal issues are: (i) choice of business and thenature of product, i.e. what to produce, (ii) choice of size of the firm, i.e., how muchto produce, (iii) choice of technology, i.e., choosing the factor-combination, (iv) choiceof price, i.e., how to price the commodity, (v) how to promote sales, (vi) how to faceprice competition, (vii) how to decide on new investments, (viii) how to manageprofit and capital, and (ix) how to manage inventory, i.e., stock of both finished goodsand raw materials. These problems may also figure in forward planning.Microeconomics deals with these questions and the like confronted by managers ofthe business enterprises. The microeconomic theories which deal with most of thesequestions are the following:

(i) Theory of demand: Demand theory explains the consumer’s behaviour. Itanswers the questions: How do the consumers decide whether or not to buy acommodity? How do they decide on the quantity of a commodity to bepurchased? When do they stop consuming a commodity? How do the consumersbehave when price of the commodity, their income and tastes and fashions,etc., change? At what level of demand, does changing price becomeinconsequential in terms of total revenue? The knowledge of demand theorycan, therefore, be helpful in the choice of commodities for production.

(ii) Theory of production and production decisions: Production theory, alsocalled ‘theory of firm’, explains the relationship between inputs and output. It alsoexplains under what conditions costs increase or decrease; how total outputincreases when units of one factor (input) are increased keeping other factorsconstant, or when all factors are simultaneously increased; how can output bemaximized from a given quantity of resources; and how can optimum size ofoutput be determined? Production theory, thus, helps in determining the size ofthe firm, size of the total output and the amount of capital and labour to beemployed.

(iii) Analysis of market-structure and pricing theory: Price theory explains howprices are determined under different market conditions; when price discrimination

Self-InstructionalMaterial 15

Introduction to BusinessEconomics

NOTES

is desirable, feasible and profitable; to what extent advertising can be helpful inexpanding sales in a competitive market. Thus, price theory can be helpful indetermining the price policy of the firm. Price and production theories together, infact, help in determining the optimum size of the firm.

(iv) Profit analysis and profit management: Profit making is the most commonobjective of all business undertakings. But, making a satisfactory profit is notalways guaranteed because a firm has to carry out its activities under conditionsof uncertainty with regard to (i) demand for the product, (ii) input prices in thefactor market, (iii) nature and degree of competition in the product market, and(iv) price behaviour under changing conditions in the product market. Therefore,an element of risk is always there even if the most efficient techniques are usedfor predicting future and even if business activities are meticulously planned.The firms are, therefore, supposed to safeguard their interest and avert, as faras possible, the possibilities of risk or try to minimize it. Profit theory guidesfirms in the measurement and management of profit, in making allowances forthe risk premium, in calculating the pure return on capital and pure profit andalso for future profit planning.

(v) Theory of capital and investment decisions: Capital, like all other inputs, is ascarce and expensive factor. Capital is the foundation of business. Its efficientallocation and management is one of the most important tasks of managers anda determinant of the success level of the firm. The major issues related to capitalare (i) choice of investment project, (ii) assessing the efficiency of capital, and(iii) most efficient allocation of capital. Knowledge of capital theory can contributea great deal in investment decision-making, choice of projects, maintaining capitalintact, capital budgeting, etc.

Macroeconomics Applied to Business Environment

Environmental issues pertain to the general business environment in which a businessoperates. They are related to the overall economic, social and political atmosphere ofthe country. The factors which constitute the economic environment of a countryinclude the following:

• The type of economic system of the country• General trends in production, employment, income, prices, saving and investment• Structure of and trends in the working of financial institutions, e.g., banks,

financial corporations and insurance companies• Magnitude of and trends in foreign trade• Trends in labour and capital markets• Government's economic policies, e.g., industrial policy, monetary policy, fiscal

policy and price policy• Social factors like the value system of the society, property rights, customs and

habits• Social organizations like trade unions, consumers’ cooperatives and producers

unions• Political environment comprises such factors as political system—democratic,

authoritarian, socialist, or otherwise,–state’s attitude towards private business,size and working of the public sector and political stability

Self-Instructional16 Material

Introduction to BusinessEconomics

NOTES

• The degree of openness of the economy and the influence of MNCs on thedomestic marketsThe environmental factors have a far-reaching bearing upon the functioning and

performance of firms. Therefore, business decision makers have to take into accountthe changing economic, political and social conditions in the country and give dueconsideration to the environmental factors in the process of decision-making. This isessential because business decisions taken in isolation of environmental factors may notonly prove infructuous, but may also lead to heavy losses. For instance, a decision to setup a new alcohol manufacturing unit or to expand the existing ones ignoring impendingprohibition—a political factor—would be suicidal for the firm; a decision to expand thebusiness beyond the paid-up capital permissible under Monopoly and Restrictive TradePractices Act (MRTP Act) amounts to inviting legal shackles and hammer; a decision toemploy a highly sophisticated, labour-saving technology ignoring the prevalence of massopen unemployment—an economic factor—may prove to be self-defeating; a decisionto expand the business on a large scale, in a society having a low per capita income andhence a low purchasing power stagnated over a long period, may lead to wastage ofresources. The managers of a firm are, therefore, supposed to be fully aware of theeconomic, social and political conditions prevailing in the country while taking decisionson the wider issues of the business. We will however confine ourselves to only themacroeconomic issues pertaining to business decision-making.The major macroeconomic or environmental issues which figure in business decision-making, particularly with regard to forward planning and formulation of the future strategy,may be described under the following three categories.

1. Issues related to macro variables: There are issues that are related to thetrends in macro variables, e.g., the general trend in the economic activities of thecountry, investment climate, trends in output and employment and price trends.These factors not only determine the prospects of private business, but also greatlyinfluence the functioning of individual firms. Therefore, a firm planning to set upa new unit or to expand its existing size would like to ask itself: What is thegeneral trend in the economy? What would be the consumption level and patternof the society? Will it be profitable to expand the business? Answers to thesequestions and the like are sought through macroeconomic studies.

2. Issues related to foreign trade: An economy is also affected by its traderelations with other countries. The sectors and firms dealing in exports and importsare affected directly and more than the rest of the economy. Fluctuations in theinternational market, exchange rate and inflows and outflows of capital in anopen economy have a serious bearing on its economic environment and, thereby,on the functioning of its business undertakings. The managers of a firm would,therefore, be interested in knowing the trends in international trade, prices, exchangerates and prospects in the international market. Answers to such problems areobtained through the study of international trade and the international monetarymechanism.

3. Issues related to government policies: Government policies designed to controland regulate economic activities of the private business firms affect the functioningof private business undertakings. Besides, firms’ activities as producers and theirattempt to maximize their private gains or profits lead to considerable social costs,in terms of environmental pollution, congestion in the cities, creation of slums, etc.Such social costs not only bring a firm’s interests in conflict with those of the

Self-InstructionalMaterial 17

Introduction to BusinessEconomics

NOTES

society, but also impose a social responsibility on the firms. The government’spolicies and its various regulatory measures are designed, by and large, to minimizesuch conflicts. Managers should, therefore, be fully aware of the aspirations ofthe people and give such factors a due consideration in their decisions. The forcedclosure of polluting industrial units set up in the residential areas of Delhi city andthe consequent loss of business worth billion of rupees in 2000, is a recent exampleof the result of ignoring the public laws and the social responsibility of thebusinessmen. The economic concepts and tools of analysis help in determiningsuch costs and benefits.

Economic theories, both micro and macro, have wide applications in the process ofbusiness decision-making. Briefly speaking, microeconomic theories including thetheory of demand, theory of production, theory of price determination, theory of profitand capital budgeting, and macroeconomic theories including theory of national income,theory of economic growth and fluctuations, international trade and monetarymechanism, and the study of state policies and their repercussions on the privatebusiness activities, by and large, constitute the scope of managerial economics. Thishowever, should not mean that only these economic theories form the subject-matterof managerial economics. Nor does the knowledge of these theories fulfill wholly therequirement of economic logic in decision-making. An overall study of economicsand a wider understanding of economic behaviour of the society, individuals, firmsand state would always be desirable and more helpful.

1.2.3 Difference between Business or Managerial Economics andPure Economics

We have studied in detail about economics and business or managerial economics. Letus have a brief discussion on how business or managerial economics is different frompure economics.

Pure economics is a social science. Its basic function is to study how people—individuals, households, firms and nations—maximize their gains from their limitedresources and opportunities. Whereas, managerial economics is the practicalapplication of economic analysis in the management of an enterprise or business.Davis and Chang state that ‘managerial economics applies the principles and methodsof economics to analyze problems faced by management of a business, or other typesof organizations and to help find solutions that advance the best interests of suchorganizations’. One must note that unlike managerial economics, pure economics doesnot cover the application of the knowledge. It is concerned with models, theory andmethods of analysis.Some of the prime differences between business or managerial economics and pureeconomics are as follows:

(i) Managerial economics is micro in character. Pure economics is both micro and macro.

(ii) Managerial economics is concerned with practical application of the principlesand methods of economics to the problem of a firm. Pure economics deals with the study of principles itself.

(iii) Managerial economics deals with the economic problems of a firm.Pure economics deals with economic problems of the firm and individuals as well.

Check Your Progress

1. What is economicbehaviour?

2. What are the twomajor problems ofan economy?

3. Name the twomajor branches ofeconomics.

4. Define businesseconomics.

5. Business economicsis that part ofeconomics that isapplied to:(a) Social science

(b)Microeconomics

(c) Macroeconomics

(d) Businessdecision-making

6. Business economicsdeals with:(a) Theories,

models andmethods ofanalysis

(b) Practicalapplication ofthe principlesand methods ofeconomics tothe problem of afirm

(c) Economicproblems of thefirm andindividuals

(d) Study ofprinciples

Self-Instructional18 Material

Introduction to BusinessEconomics

NOTES

1.3 SIGNIFICANCE OF BUSINESS DECISION-MAKING

Business decision-making is essentially a process of selecting the best out of alternativeopportunities open to the firm. The process of decision-making comprises four mainphases:

(i) Determining and defining the objective to be achieved(ii) Collections and analysis of information regarding economic, social, political and

technological environment and foreseeing the necessity and occasion for decision(iii) Inventing, developing and analysing a possible course of action(iv) Selecting a particular course of action, from the available alternatives

This process of decision-making is, however, not as simple as it appears to be. Steps (ii)and (iii) are crucial in business decision-making. These steps put managers’ analyticalability to test and determine the appropriateness and validity of decisions in the modernbusiness world. Modern business conditions are changing so fast and becoming socompetitive and complex that personal business sense, intuition and experience aloneare not sufficient to make appropriate business decisions. Personal intelligence, experience,intuition and business acumen of the decision-makers need to be supplemented withquantitative analysis of business data on market conditions and business environment. Itis in this area of decision-making that economic theories and tools of economic analysiscontribute a great deal.

Suppose a firm, for instance, plans to launch a new product for which closesubstitutes are available in the market. One method of deciding whether or not tolaunch the product is to obtain the services of business consultants or to seek expertopinion. If the matter has to be decided by the managers of the firm themselves, thetwo areas which they will need to investigate and analyse thoroughly are:

• Production-related issues• Sale prospects and problems

In the field of production, managers will be required to collect and analyse data on thefollowing aspects of production decisions:

• Available techniques of production• Cost of production associated with each production technique• Supply position of inputs required to produce the planned commodity• Price structure of inputs• Cost structure of competitive products• Availability of foreign exchange if inputs are to be imported

In order to assess the sales prospects, managers will be required to collect and analysedata on the following aspects of the market:

• General market trends• Trends in the industry to which the planned product belongs• Major existing and potential competitors and their respective market shares• Prices of the competing products

Self-InstructionalMaterial 19

Introduction to BusinessEconomics

NOTES

• Cross-elasticity of demand with respect to competitive products or brands• Pricing strategy of the prospective competitors• Market structure and degree of competition• Supply position of complementary goods

It is in this kind of input and output market analysis that knowledge of economic theoriesand tools of economic analysis adds to the process of decision-making in a significantway.

Economic theories state the functional relationship between two or more economicvariables, under certain given conditions. Application of relevant economic theories tothe problems of business facilitates decision-making in three ways:

(i) It gives a clear understanding of various economic concepts (i.e., cost, price,demand, etc.) used in business analysis. For example, the concept of ‘cost’includes ‘total’, ‘average’, ‘marginal’, ‘fixed’, ‘variable’, actual costs, andopportunity cost. Economics clarifies which cost concepts are relevant and inwhat context.

(ii) It helps in ascertaining the relevant variables and specifying the relevant data.For example, it helps in deciding what variables need to be considered inestimating the demand for two different sources of energy—e.g., petrol andelectricity.

(iii) Economic theories state the general relationship between two or more economicvariables and events. The application of relevant economic theory providesconsistency to business analysis and helps in arriving at right conclusions. Thus,application of economic theories to the problems of business not only guides,assists and streamlines the process of decision-making but also contributes agood deal to the validity of decisions.

1.3.1 Managerial Economics: Techniques and Business Decisions

It is a well-known fact that with the growing complexity of the business environment,the usefulness of economic theory as a tool of business analysis has increased. Itscontribution to the process of decision-making is a widely recognized fact today. Inmanagerial economics, microeconomic analysis is a common tool for specific businessdecisions. This is why it bridges economic theory and economics in practice. Managerialeconomics makes good use of quantitative techniques like regression analysis andcorrelation techniques and Lagrangian linear calculus. Marginalization and incrementalprinciple are also important techniques of managerial economics. Marginal analysisuses marginal change in the dependent variable resulting from a unit change in itsdeterminant and the independent variable. The incremental principle is applied tobusiness decisions which involve a large increase in total cost and total revenue. Mosteconomic managers strive to optimize business decisions given their firm’s objectivesas well as constraints imposed by scarcity. Operation research and programming proveto be very handy in this.We can use the managerial economics techniques to analyse any business decision.However,these techniques are most frequently applied in case of the following:

(i) Risk analysis: It refers to a technique for identifying and assessing those factorsor elements which have the potential to mar the success of a business enterprise.Through risk analysis, we can determine preventive measures so that these factors

Self-Instructional20 Material

Introduction to BusinessEconomics

NOTES

do not occur. Such an analysis can also help us decide counter measures tosuccessfully deal with such probable obstacles. To determine or assess theriskiness of a business decision,we have the options to use several uncertaintymodels and risk quantification techniques.

(ii) Production analysis: Managerial economics techniques are used to analyseseveral factors relating to production of an enterprise, such as productionefficiency, enterprise’s cost function and optimum factor allocation.

(iii) Pricing analysis: It refers to examination and evaluation of a proposed price.It does not include the evaluation of its separate cost elements and proposedprofit. Managerial economics techniques are very useful in analysing the variouspricing decisions by policy decision-makers and business managers, such astransfer pricing, joint product pricing, price discrimination, price elasticityestimations. These techniques are also helpful in choosing the optimum pricingmethod.

(iv) Capital budgeting: Also called investment proposal, it refers to the planningprocess which is used to assess whether a firm’s long term investments areworth pursuing.These long term investments could range from replacement ofmachinary to R&D projects. Business managers take the help of investment-related theories to determine an enterprise’s capital puchasing decisions. Capitalbudgeting involves the various methods, such as net present value (NPV),internal rate of return (IRR), equivalent annuity, profitability index, and modifiedinternal rate of return (MIRR).

1.3.2 Time Perspective in Business Decisions

All business decisions are taken with a certain time perspective. The time perspectiverefers to the duration of time period extending from the relevant past and foreseeablefuture taken in view while taking a business decision. Relevant past refers to the periodof past experience and trends which are relevant for business decisions with long-runimplications. All business decisions do not have the same time perspective. Somebusiness decisions have short-run repercussions and, therefore, involve short-run timeperspective. A decision to buy explosive materials, for example, for manufacturingcrackers involves short-run demand prospects. Similarly, a decision regarding buildinginventories of finished products involves a short-run time perspective.

There are, however, a large number of business decisions which have long-runrepercussions, e.g., investment in a plant, building, machinery, land; spending on labourwelfare activities; expansion of the scale of production; introduction of a new product;advertisement; bribing a government officer and investment abroad. The decision aboutsuch business issues may not be profitable in the short-run but may prove very profitablein the long-run. The introduction of a new product, for example, may not be profitable inthe short-run but may prove very profitable in the long-run, e.g., the introduction of anew product may not catch up in the market quickly and smoothly. It may be difficult toeven cover the variable costs. But in the long-run it may result in a roaring business.Also, spending on labour welfare may enhance costs in the present scenario and maylead to a decline in profit. But in the long-run, it may increase labour productivity in amuch greater proportion as compared to an increase in cost. Therefore, while taking abusiness decision with long-term implications, it is immensely important to keep a well-worked out time perspective in view.

Self-InstructionalMaterial 21

Introduction to BusinessEconomics

NOTES

The business decision-makers must assess and determine the time perspective ofbusiness propositions well in advance and make decisions accordingly. Determination oftime perspective is of a great significance, especially where projections are involved.The decision makers must decide on an appropriate future period for projecting thevalue of a variable. Otherwise, projections may prove meaningless from the analysispoint of view and decisions based thereon may result in poor pay-offs. In a businessdecision, for example, regarding the establishment of a Management Institute, projectinga short-run demand and taking a short-run time perspective will be unwise, and in buyingexplosive materials for manufacturing crackers for Deepawali, a long-run perspective isunwise.

1.4 ROLE OF A MANAGERIAL ECONOMIST

Economics contributes a great deal towards the performance of managerial duties andresponsibilities. Just as biology contributes to the medical profession and physics toengineering, economics contributes to the managerial profession. All other qualificationsbeing the same, managers with a working knowledge of economics can perform theirfunctions more efficiently than those without it. The basic function of managerialeconomists is to achieve the objective of the firm to the maximum possible extent withthe limited resources placed at their disposal. The emphasis here is on the maximizationof the objective and limitedness of the resources. Had the resources been unlimited,likse sunshine and air, the problem of economizing on resources or resource managementwould have never arisen. But resources, howsoever defined, are limited. Resources atthe disposal of a firm, whether finance, men or material, are by all means limited.Therefore, the basic task of the economist is to help the management optimize the use ofthe resources.

As mentioned erlier, economics, though variously defined, is essentially the studyof logic, tools and techniques of making optimum use of the available resources to achievethe given ends. Economics thus provides analytical tools and techniques that managersneed, to achieve the goals of the organization they manage. Therefore, a workingknowledge of economics, not necessarily a formal degree, is essential for managers.Managers are essentially practising economists.

In performing his functions, a managerial economist has to take a number ofdecisions in conformity with the goals of the firm. Many business decisions are takenunder the condition of uncertainty and risk. Uncertainty and risk arise mainly due touncertain behaviour of the market forces, changing business environment, emergenceof competitors with highly competitive products, government policy, external influenceon the domestic market and social and political changes in the country. The complexityof the modern business world adds complexity to business decision making. However,the degree of uncertainty and risk can be greatly reduced if market conditions are predictedwith a high degree of reliability. The prediction of the future course of the businessenvironment alone is not sufficient. What is equally important is to take appropriatebusiness decisions and to formulate a business strategy in conformity with the goals ofthe firm. This is where a managerial economist’s role is most important.

Taking appropriate business decisions requires a clear understanding of the technicaland environmental conditions under which business decisions are taken. Application ofeconomic theories to explain and analyse the technical conditions and the businessenvironment contributes a good deal to the rational decision-making process. Economic

Self-Instructional22 Material

Introduction to BusinessEconomics

NOTES

theories have, therefore, gained a wide range of application in the analysis of practicalproblems of business. With the growing complexity of the business environment, theusefulness of economic theory as a tool of analysis and its contribution to the process ofdecision-making has been widely recognized.

Baumol has pointed out three main contributions of economic theory to businessecomomics.

First, ‘one of the most important things which the economic (theories) cancontribute to the management science’ is building analytical models which help torecognize the structure of managerial problems, eliminate the minor details whichmight obstruct decision-making, and help to concentrate on the main issue.

Second, economic theory contributes to the business analysis ‘a set of analyticalmethods’ which may not be applied directly to specific business problems, but theydo enhance the analytical capabilities of the business analyst.

Third, economic theories offer clarity to the various concepts used in businessanalysis, which enables the managers to avoid conceptual pitfalls.

1.5 SUMMARY

• According to Alfred Marshall (1922), ‘Economics is the study of mankind inthe ordinary business of life; it examines that part of individual and social actionwhich is most closely connected with the attainment and with the use of thematerial requisites of well being.’

• Lionel Robbins (1932) has defined economics as ‘the science which studieshuman behaviour as a relationship between ends and scarce means which havealternative uses.’

• Economics as a social science studies economic behaviour of the people andits consequences.

• Economic behaviour is essentially the process of evaluating economicopportunities open to an individual or a society and, given the resources, makinga choice of the best of these opportunities.

• The basic function of economics is to observe, explain and predict how peopleas decision-makers make choices about the use of resources in order to maximizetheir income, as well as how they, as consumers, decide how to spend theirincome to maximize their total utility.

• For the purpose of economic analysis, people are classified according to theirdecision-making capacity as individuals, households, firms and the society; andaccording to the nature of their economic activity as consumers, producers, factoryowners and economy managers, i.e., the government.

• It is this economic behaviour of the individuals, households, firms, governmentand the society as a whole which forms the central theme of economics as asocial science. Thus, economics is fundamentally the study of how peopleallocate their limited resources to produce and consume goods and services tosatisfy their endless wants, with the objective of maximizing their gains.

• The scope of economics, as it is known today, has expanded vastly in the post-World War II period. Modern economics is now divided into two majorbranches: microeconomics and macroeconomics.

Check Your Progress

7. What are the fourmain phases ofdecision-makingprocess?

8. List the three maincontributions ofeconomic theory tobusiness economics.

9. The basic functionof managerialeconomists is toachieve:(a) Assess and

determine thetimeperspective ofbusinesspropositionswell in advanceand makedecisionsaccordingly

(b) Objective of thefirm to themaximumpossible extentwith the limitedresources placedat their disposal

(c) Invent, developand analyse apossible courseof action

(d) Understand thetechnical andenvironmentalconditionsunder whichbusinessdecisions aretaken

Self-InstructionalMaterial 23

Introduction to BusinessEconomics

NOTES