USE THE SAME COLORS FOR 2018 AND 2020 - Deloitte

37

How banks are responding to digital (r)evolution? USE THE SAME COLORS FOR 2018 AND 2020 OCTOBER 2020

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of USE THE SAME COLORS FOR 2018 AND 2020 - Deloitte

How banks are responding to digital (r)evolution?

USE THE SAME COLORS FOR 2018

AND 2020

O C T O B E R 2 0 2 0

2 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

K E Y T A K E A W A Y S

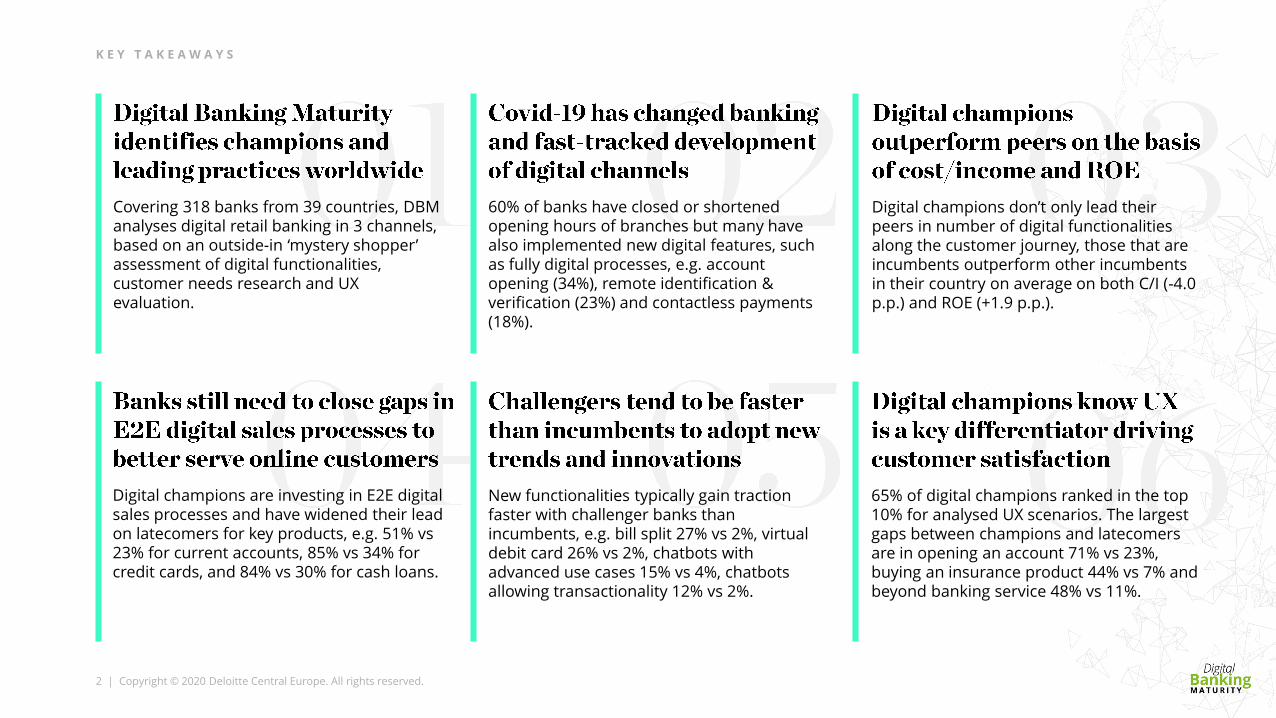

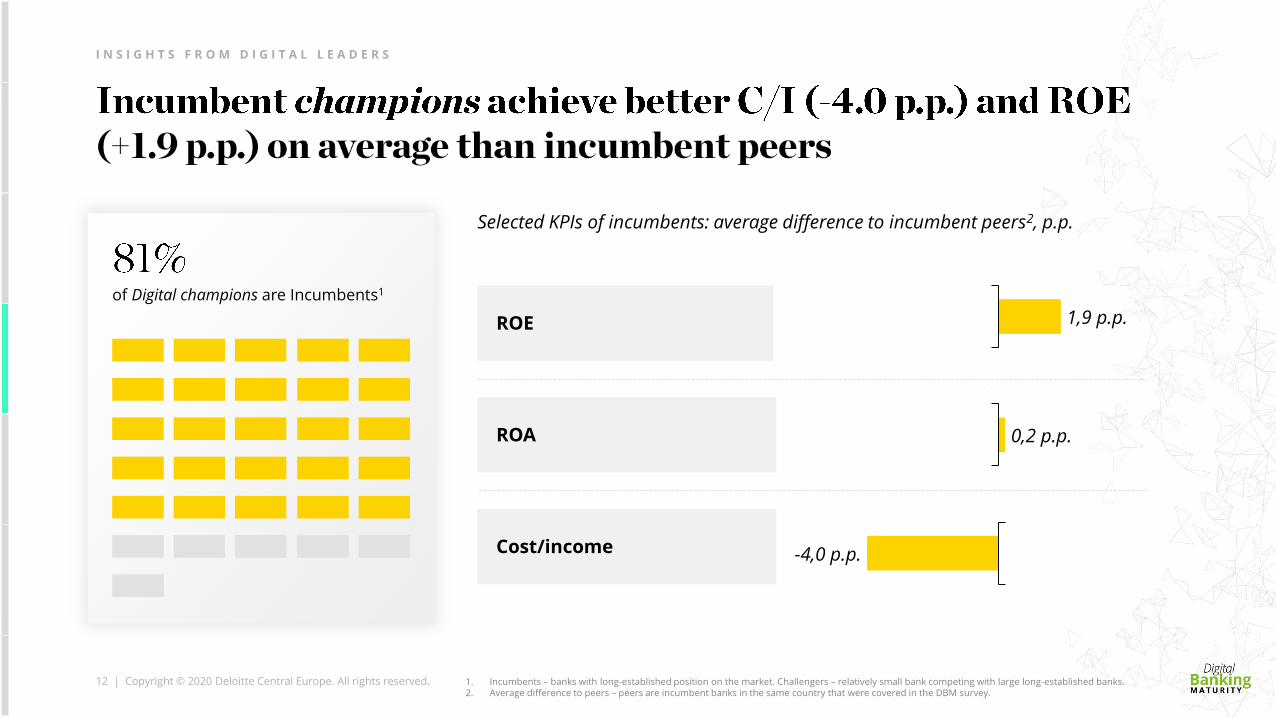

Digital champions don’t only lead their peers in number of digital functionalities along the customer journey, those that are incumbents outperform other incumbents in their country on average on both C/I (-4.0 p.p.) and ROE (+1.9 p.p.).

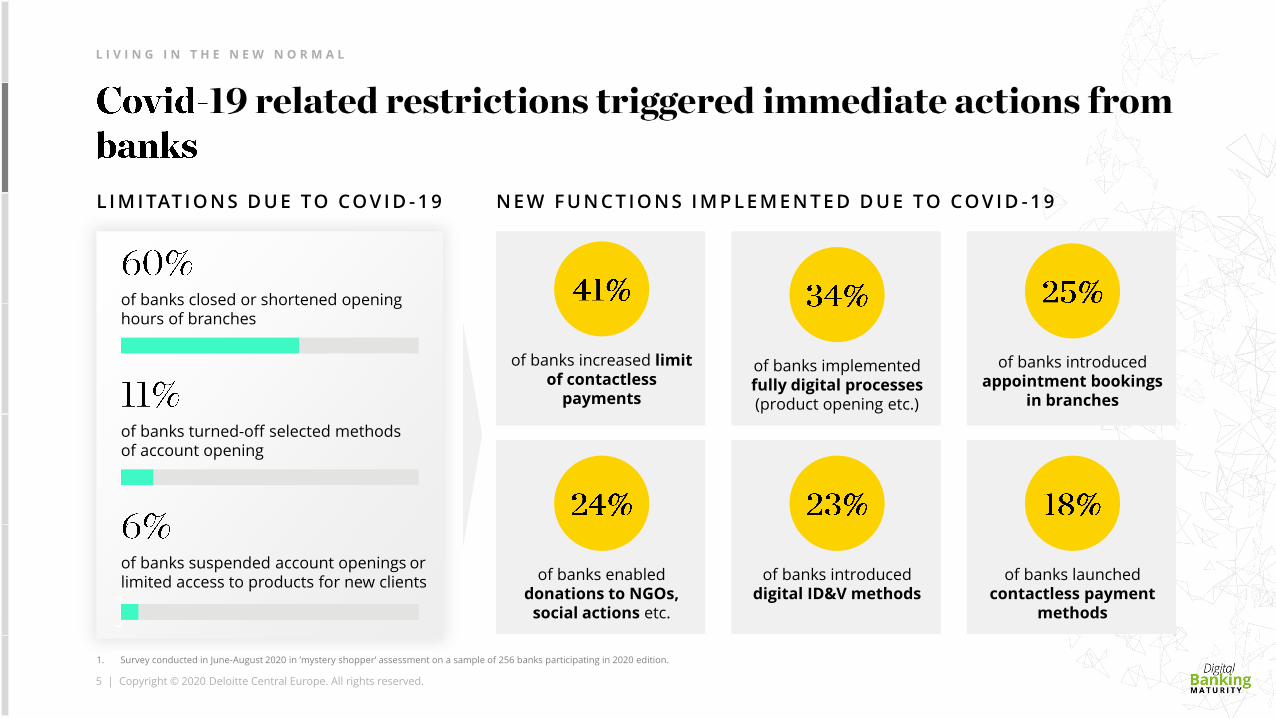

60% of banks have closed or shortened opening hours of branches but many have also implemented new digital features, such as fully digital processes, e.g. account opening (34%), remote identification & verification (23%) and contactless payments (18%).

Digital champions are investing in E2E digital sales processes and have widened their lead on latecomers for key products, e.g. 51% vs 23% for current accounts, 85% vs 34% for credit cards, and 84% vs 30% for cash loans.

65% of digital champions ranked in the top 10% for analysed UX scenarios. The largest gaps between champions and latecomers are in opening an account 71% vs 23%, buying an insurance product 44% vs 7% and beyond banking service 48% vs 11%.

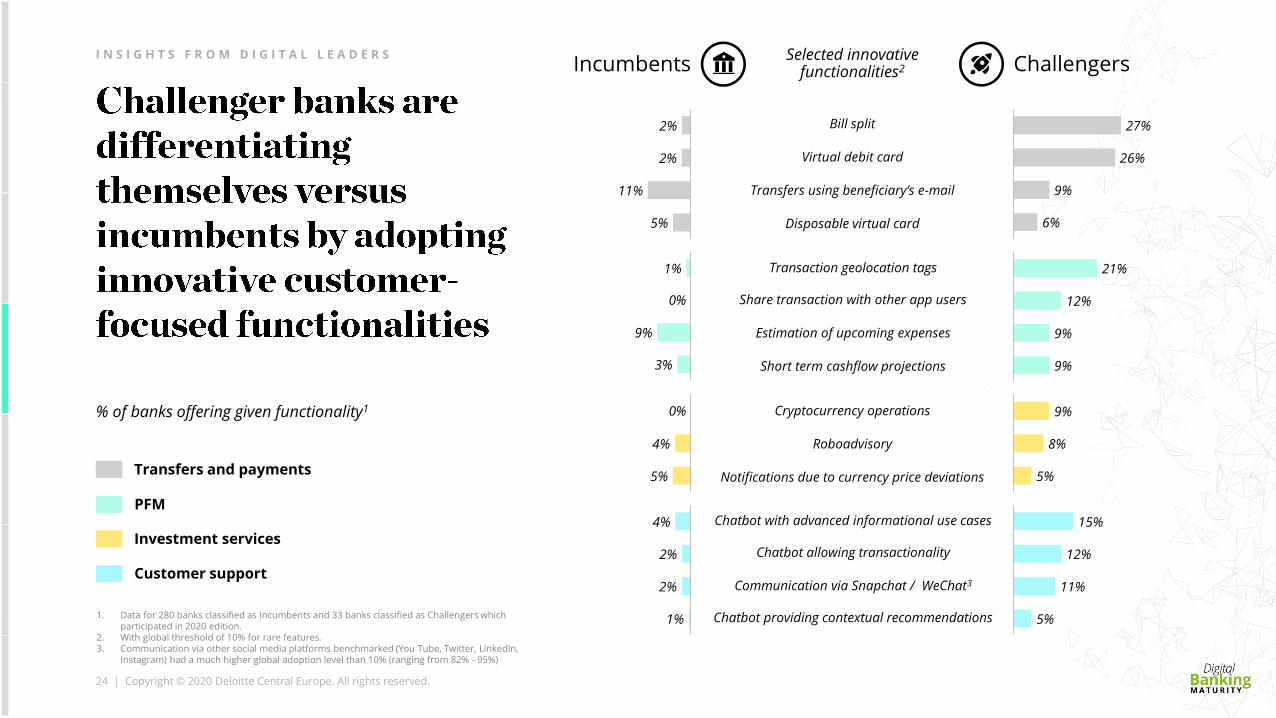

New functionalities typically gain traction faster with challenger banks than incumbents, e.g. bill split 27% vs 2%, virtual debit card 26% vs 2%, chatbots with advanced use cases 15% vs 4%, chatbotsallowing transactionality 12% vs 2%.

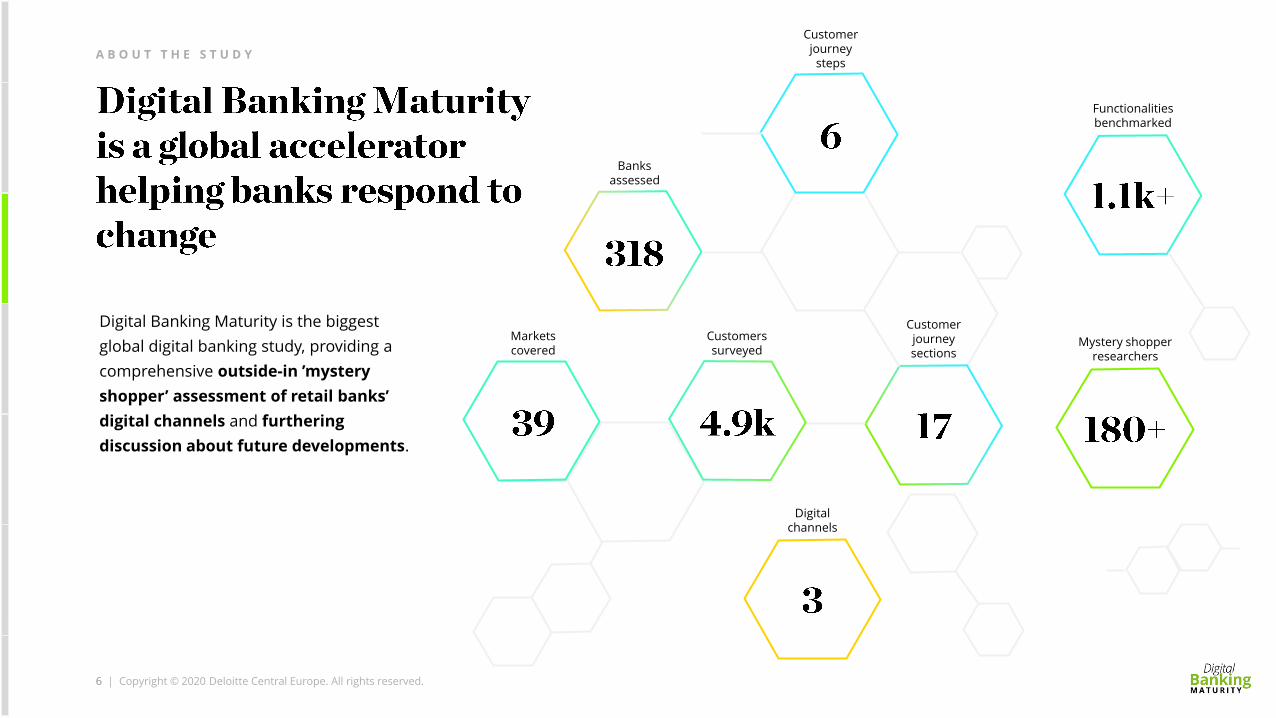

Covering 318 banks from 39 countries, DBM analyses digital retail banking in 3 channels, based on an outside-in ‘mystery shopper’ assessment of digital functionalities, customer needs research and UX evaluation.

3 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

5.

A G E N D A

1.

2.

3.

4.Digital Banking Maturity 2020 is the

4th edition of the largest global

benchmarking of digital retail

banking channels, answering what

leaders are doing to win in the

digitalization race.

L I V I N G I N T H E N E W N O R M A L

A B O U T T H E S T U D Y

I N S I G H T S F R O M D I G I T A L L E A D E R S

S T A T E O F U X

S T R A T E G Y F O R T H E F U T U R E

4 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

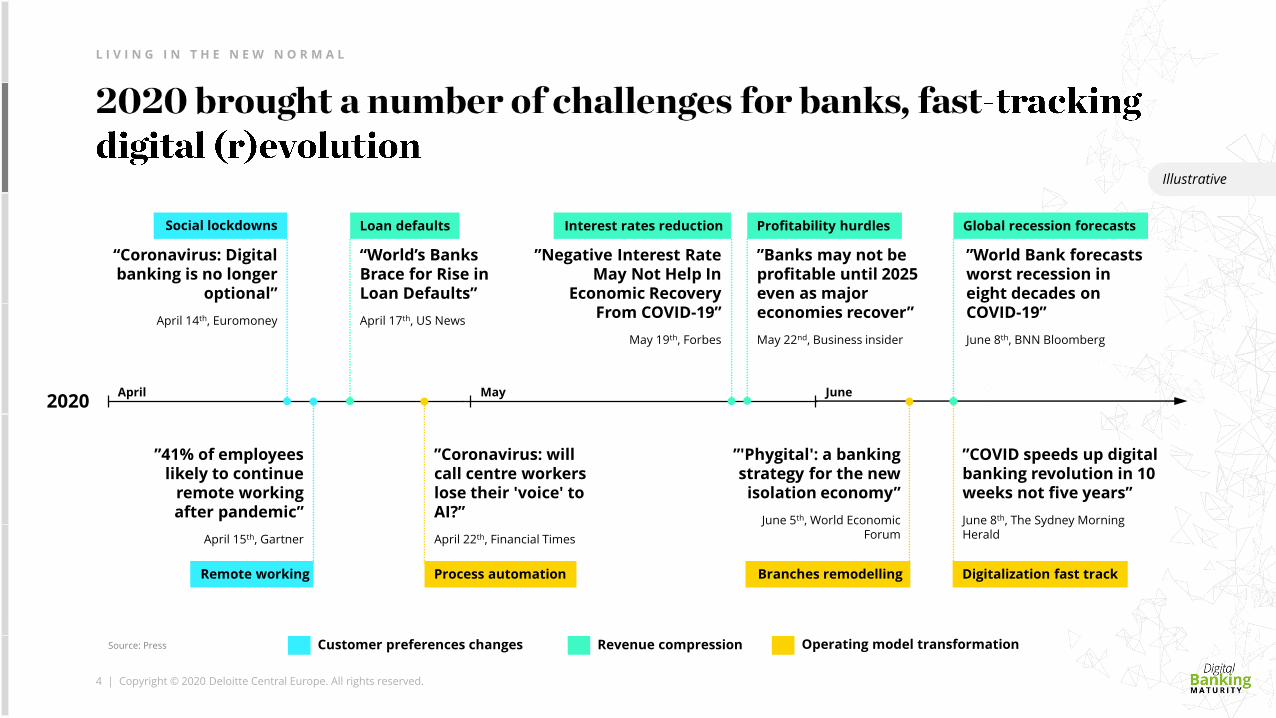

”World Bank forecasts worst recession in eight decades on COVID-19”

June 8th, BNN Bloomberg

Global recession forecasts

2020

Revenue compressionCustomer preferences changes Operating model transformation

Interest rates reduction

Remote working

”COVID speeds up digital banking revolution in 10 weeks not five years”

June 8th, The Sydney Morning Herald

“Coronavirus: Digital banking is no longer

optional”

April 14th, Euromoney

Digitalization fast track

”41% of employees likely to continue

remote working after pandemic”

April 15th, Gartner

”Negative Interest Rate May Not Help In

Economic Recovery From COVID-19”

May 19th, Forbes

Loan defaults

“World’s Banks Brace for Rise in Loan Defaults”

April 17th, US News

Social lockdowns

April May June

”'Phygital': a banking strategy for the new

isolation economy”

June 5th, World Economic Forum

Branches remodelling

”Coronavirus: will call centre workers lose their 'voice' to AI?”

April 22th, Financial Times

Process automation

”Banks may not be profitable until 2025 even as major economies recover”

May 22nd, Business insider

Profitability hurdles

L I V I N G I N T H E N E W N O R M A L

Illustrative

Source: Press

5 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

1. Survey conducted in June-August 2020 in ’mystery shopper’ assessment on a sample of 256 banks participating in 2020 edition.

of banks closed or shortened opening hours of branches

of banks turned-off selected methods of account opening

of banks suspended account openings or limited access to products for new clients

of banks implemented fully digital processes (product opening etc.)

of banks increased limit of contactless

payments

of banks introduced digital ID&V methods

of banks introduced appointment bookings

in branches

of banks launched contactless payment

methods

of banks enabled donations to NGOs,

social actions etc.

L I V I N G I N T H E N E W N O R M A L

L I M I TAT I O N S D U E TO CO V I D - 1 9 N E W F U N C T I O N S I M P L E M E N T E D D U E TO CO V I D - 1 9

Digital Banking Maturity is the biggest

global digital banking study, providing a

comprehensive outside-in ’mystery

shopper’ assessment of retail banks’

digital channels and furthering

discussion about future developments.

Functionalities benchmarked

Mystery shopper researchers

Customer journey sections

Customer journey

steps

Banksassessed

Markets covered

Digital channels

Customers surveyed

A B O U T T H E S T U D Y

66 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

7 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

banks

countries

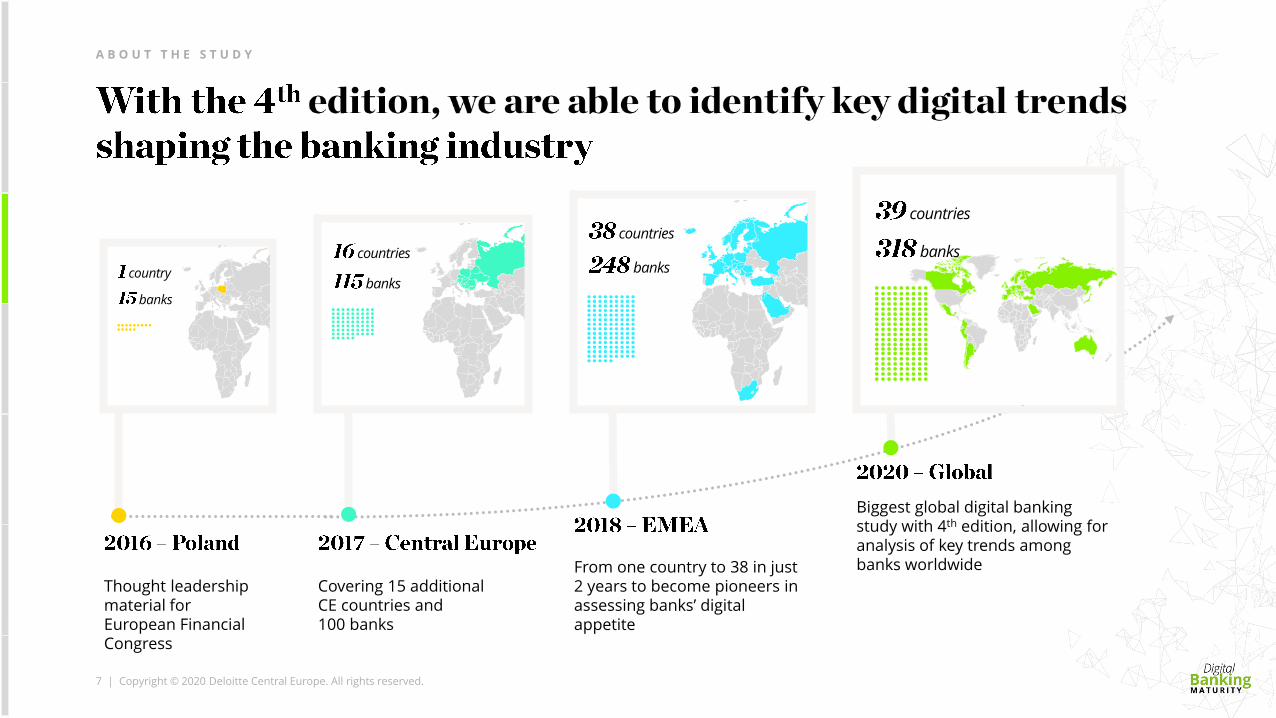

Thought leadership material forEuropean Financial Congress

Covering 15 additional CE countries and 100 banks

From one country to 38 in just 2 years to become pioneers in assessing banks’ digital appetite

banks

country banks

countries

Biggest global digital banking study with 4th edition, allowing for analysis of key trends among banks worldwide

banks

countries

A B O U T T H E S T U D Y

8 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

Italy

Luxemburg

Netherlands

Norway

Poland

Portugal

Romania

Russia

Serbia

Slovakia

Slovenia

Spain

Germany

Greece

Hungary

Ireland

Czech Republic

France

Belgium

Bulgaria

Croatia

E U R O P E

Peru

UruguayCanada

Mexico

N O R T H A M E R I C A

Argentina

Chile

Colombia

S O U T H A M E R I C A

A B O U T T H E S T U D Y

A U S T R A L I A

Kuwait

Qatar

Saudi Arabia

United Arab Emirates

Singapore

Sweden

Switzerland

Turkey

United Kingdom

A S I A

Japan

9 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

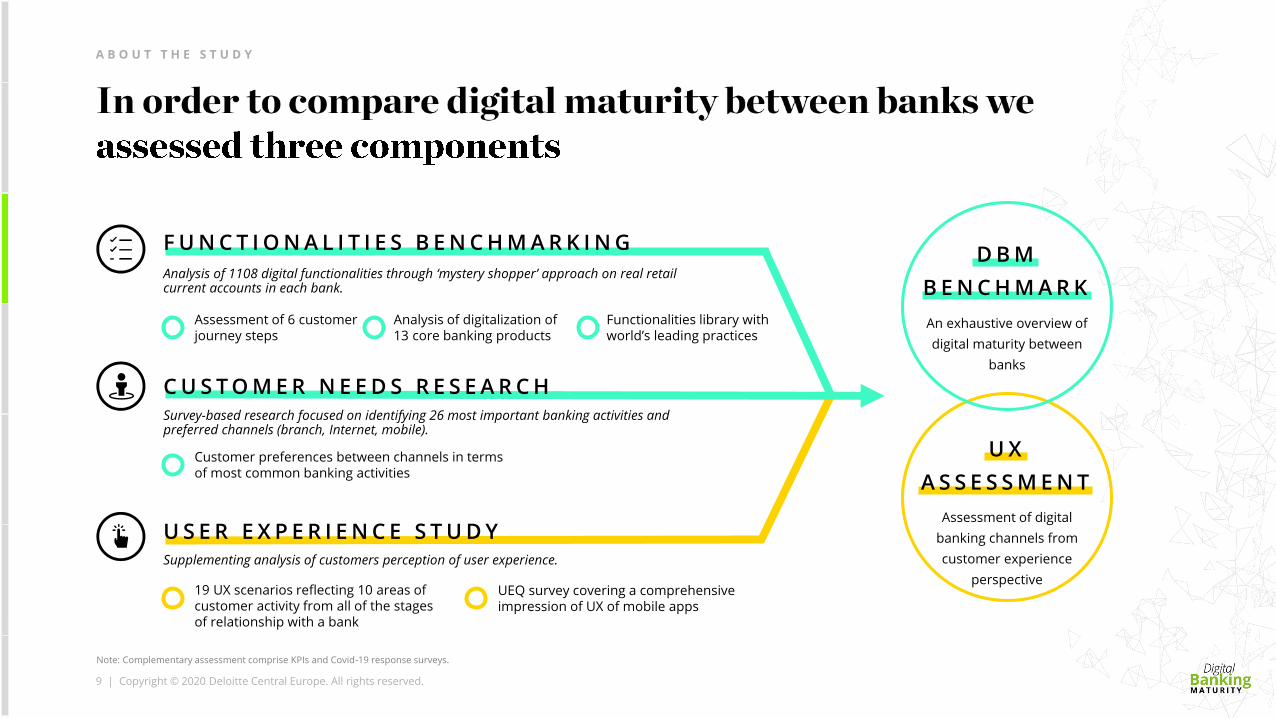

U S E R E X P E R I E N C E S T U D Y

F U N C T I O N A L I T I E S B E N C H M A R K I N G

Assessment of 6 customer journey steps

Analysis of digitalization of 13 core banking products

Customer preferences between channels in terms of most common banking activities

19 UX scenarios reflecting 10 areas of customer activity from all of the stages of relationship with a bank

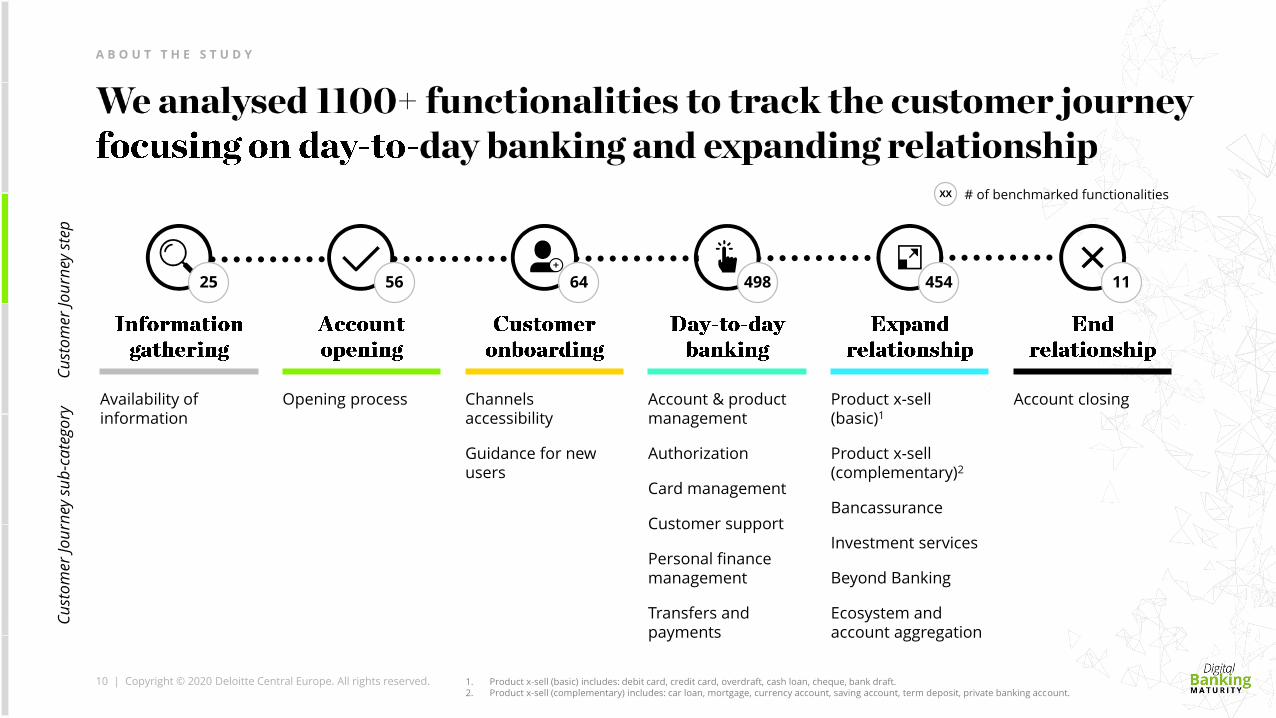

Analysis of 1108 digital functionalities through ‘mystery shopper’ approach on real retail current accounts in each bank.

Survey-based research focused on identifying 26 most important banking activities and preferred channels (branch, Internet, mobile).

Supplementing analysis of customers perception of user experience.

Functionalities library with world’s leading practices

An exhaustive overview of

digital maturity between

banks

C U S T O M E R N E E D S R E S E A R C H

D B M

B E N C H M A R K

Assessment of digital

banking channels from

customer experience

perspective

U X

A S S E S S M E N T

UEQ survey covering a comprehensive impression of UX of mobile apps

A B O U T T H E S T U D Y

Note: Complementary assessment comprise KPIs and Covid-19 response surveys.

10 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

XX # of benchmarked functionalities

Availability of information

Opening process Channels accessibility

Guidance for new users

Account & product management

Authorization

Card management

Customer support

Personal finance management

Transfers and payments

Account closingProduct x-sell (basic)1

Product x-sell (complementary)2

Bancassurance

Investment services

Beyond Banking

Ecosystem and account aggregation

Cu

sto

mer

Jo

urn

ey s

tep

Cu

sto

mer

Jo

urn

ey s

ub

-ca

tego

ry

25 56 64 498 454 11

1. Product x-sell (basic) includes: debit card, credit card, overdraft, cash loan, cheque, bank draft.2. Product x-sell (complementary) includes: car loan, mortgage, currency account, saving account, term deposit, private banking account.

A B O U T T H E S T U D Y

11 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

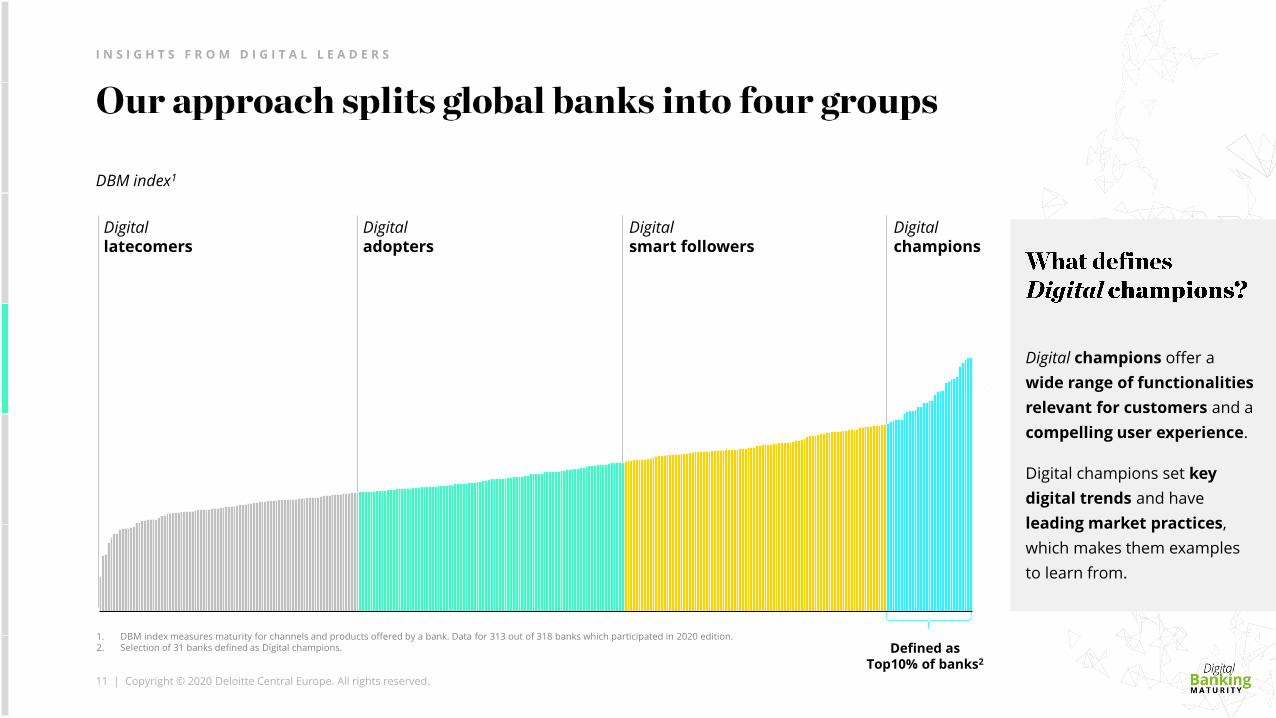

I N S I G H T S F R O M D I G I T A L L E A D E R S

Digitallatecomers

Digitaladopters

Digitalsmart followers

Digitalchampions

Digital champions offer a

wide range of functionalities

relevant for customers and a

compelling user experience.

Digital champions set key

digital trends and have

leading market practices,

which makes them examples

to learn from.

DBM index1

Defined as Top10% of banks2

1. DBM index measures maturity for channels and products offered by a bank. Data for 313 out of 318 banks which participated in 2020 edition.2. Selection of 31 banks defined as Digital champions.

12 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

1,9 p.p.

I N S I G H T S F R O M D I G I T A L L E A D E R S

1. Incumbents – banks with long-established position on the market. Challengers – relatively small bank competing with large long-established banks.2. Average difference to peers – peers are incumbent banks in the same country that were covered in the DBM survey.

of Digital champions are Incumbents1

Selected KPIs of incumbents: average difference to incumbent peers2, p.p.

ROE

ROA

Cost/income

0,2 p.p.

-4,0 p.p.

13 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

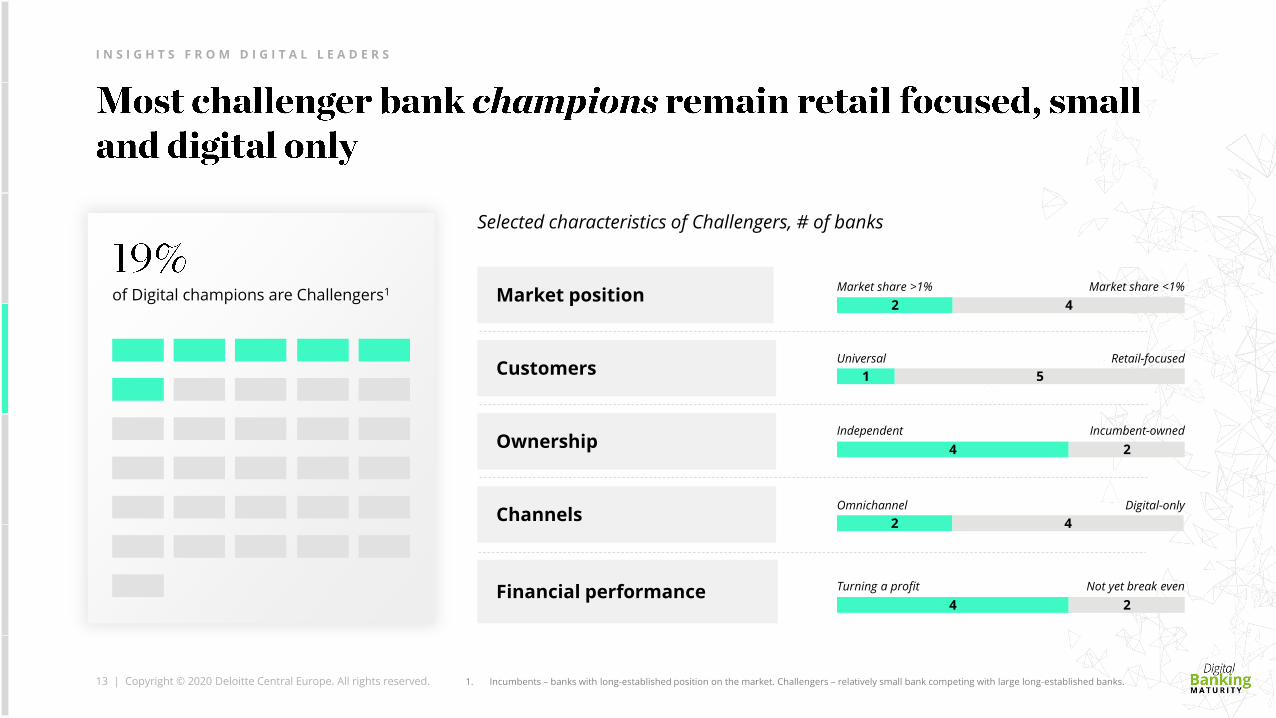

I N S I G H T S F R O M D I G I T A L L E A D E R S

Market position

Customers

Ownership

Channels

Financial performance

42

51

24

42

24

Market share >1%

Universal

Omnichannel

Independent

Turning a profit

Market share <1%

Retail-focused

Digital-only

Incumbent-owned

Not yet break even

of Digital champions are Challengers1

1. Incumbents – banks with long-established position on the market. Challengers – relatively small bank competing with large long-established banks.

Selected characteristics of Challengers, # of banks

14 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

I N S I G H T S F R O M D I G I T A L L E A D E R S

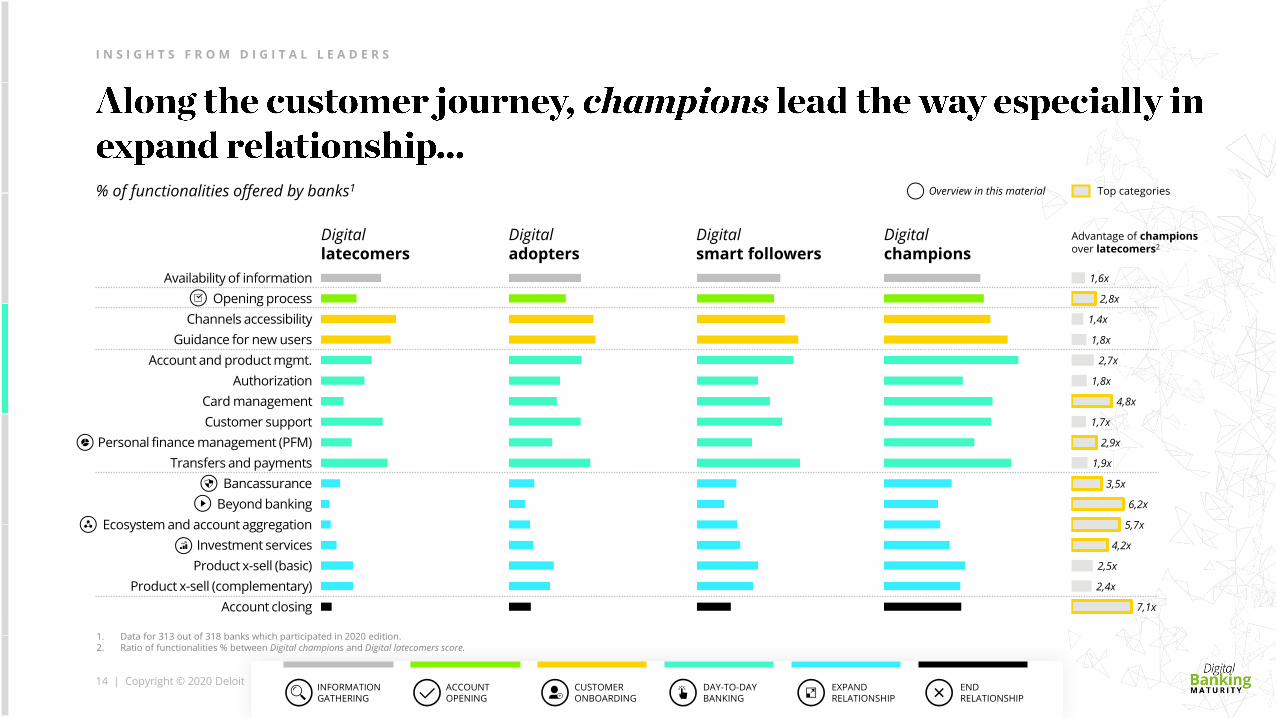

Authorization

Guidance for new users

Account closing

Card management

Availability of information

Account and product mgmt.

Channels accessibility

Opening process

Customer support

Personal finance management (PFM)

Transfers and payments

Beyond banking

Bancassurance

Ecosystem and account aggregation

Investment services

Product x-sell (basic)

Product x-sell (complementary)

Digitallatecomers

Digitaladopters

Digitalsmart followers

Digitalchampions

% of functionalities offered by banks1

INFORMATION GATHERING

ACCOUNT OPENING

CUSTOMER ONBOARDING

END RELATIONSHIP

DAY-TO-DAY BANKING

EXPAND RELATIONSHIP

1,6x

2,8x

1,4x

1,8x

2,7x

1,8x

4,8x

1,7x

2,9x

1,9x

3,5x

6,2x

5,7x

4,2x

2,5x

2,4x

7,1x

Advantage of championsover latecomers2

Top categoriesOverview in this material

1. Data for 313 out of 318 banks which participated in 2020 edition.2. Ratio of functionalities % between Digital champions and Digital latecomers score.

15 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

I N S I G H T S F R O M D I G I T A L L E A D E R S

INFORMATION GATHERING

ACCOUNT OPENING

CUSTOMER ONBOARDING

END RELATIONSHIP

DAY-TO-DAY BANKING

EXPAND RELATIONSHIP

1. Based on the data for 152 banks which participated in 2018 and 2020 edition.

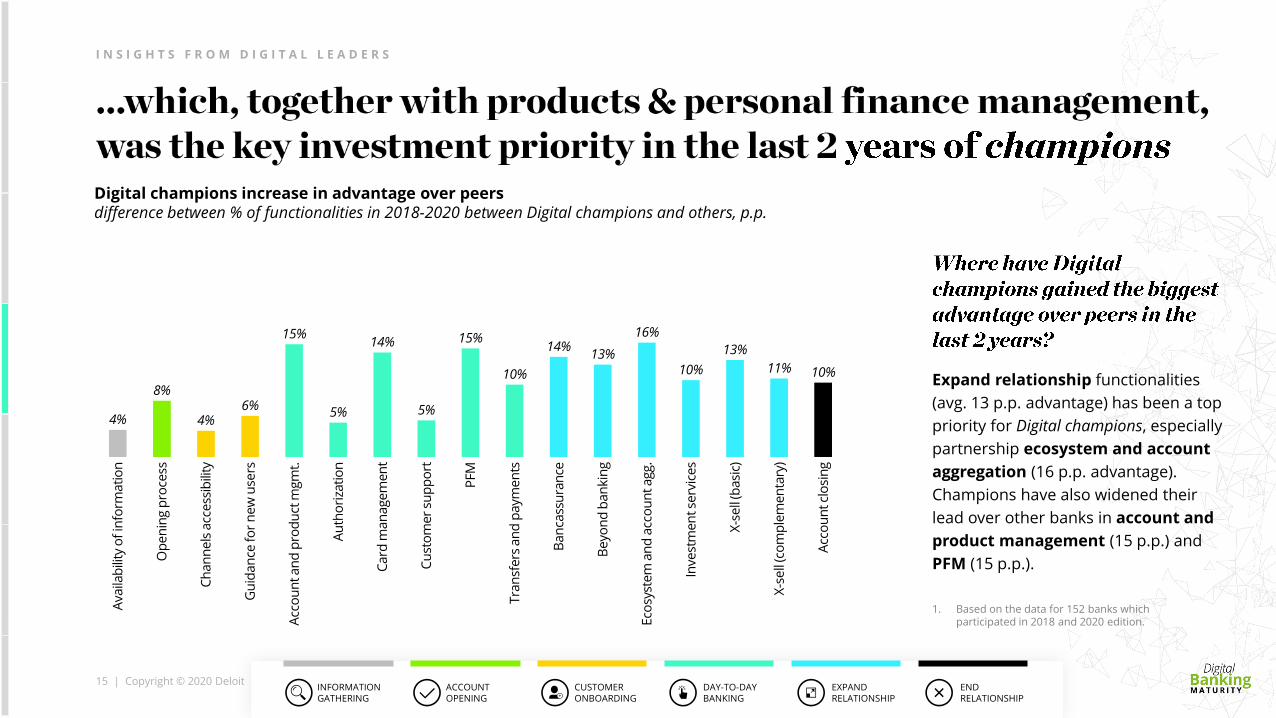

Digital champions increase in advantage over peersdifference between % of functionalities in 2018-2020 between Digital champions and others, p.p.

Expand relationship functionalities

(avg. 13 p.p. advantage) has been a top

priority for Digital champions, especially

partnership ecosystem and account

aggregation (16 p.p. advantage).

Champions have also widened their

lead over other banks in account and

product management (15 p.p.) and

PFM (15 p.p.).Ca

rd m

an

age

me

nt

Au

tho

riza

tio

n

Op

en

ing p

roce

ss

Ch

an

ne

ls a

cce

ssib

ility

Gu

ida

nce

fo

r n

ew

use

rs

13%

Acc

ou

nt a

nd

pro

du

ct m

gm

t.

10%11%

4%C

ust

om

er

sup

po

rt

PFM

Tra

nsf

ers

an

d p

aym

en

ts

Ba

nca

ssu

ran

ce

Be

yon

d b

an

kin

g

14%

Ava

ilab

ility

of

info

rma

tio

n

Inve

stm

en

t se

rvic

es

X-s

ell

(ba

sic)

X-s

ell

(co

mp

lem

en

tary

)

Acc

ou

nt cl

osi

ng

8%

4%6%

15%

5%

14%

5%

15%13%

10%

16%

10%

Eco

syst

em

an

d a

cco

un

t a

gg.

16 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

I N S I G H T S F R O M D I G I T A L L E A D E R S

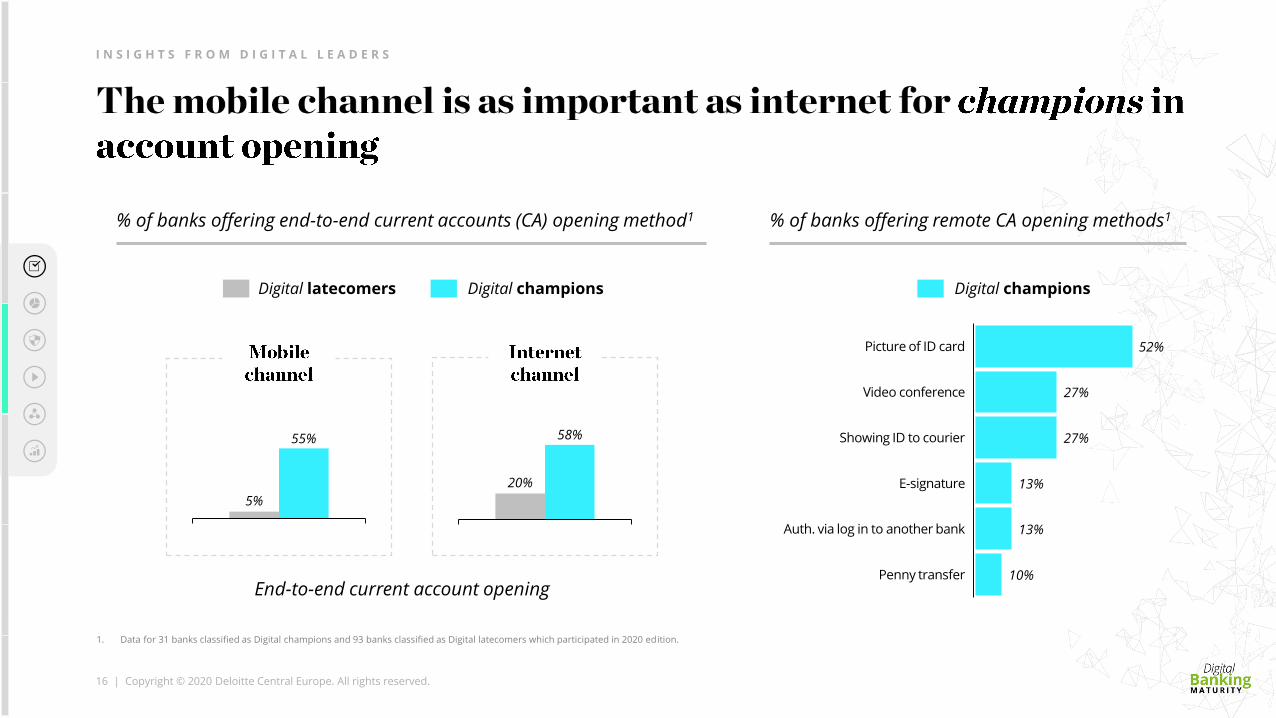

% of banks offering end-to-end current accounts (CA) opening method1

5%

55%

20%

58%

Digital latecomers Digital champions

End-to-end current account opening

% of banks offering remote CA opening methods1

52%

27%

27%

13%

13%

10%Penny transfer

Showing ID to courier

Picture of ID card

E-signature

Video conference

Auth. via log in to another bank

Digital champions

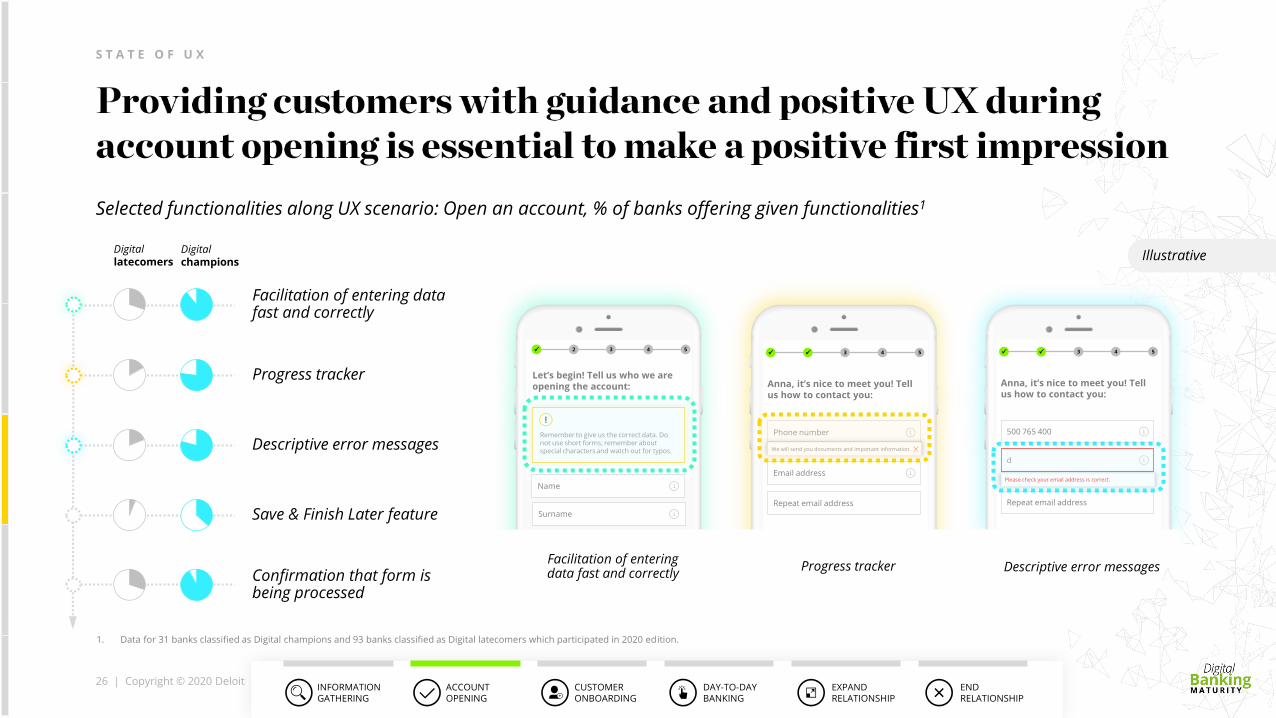

1. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition.

17 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

I N S I G H T S F R O M D I G I T A L L E A D E R S

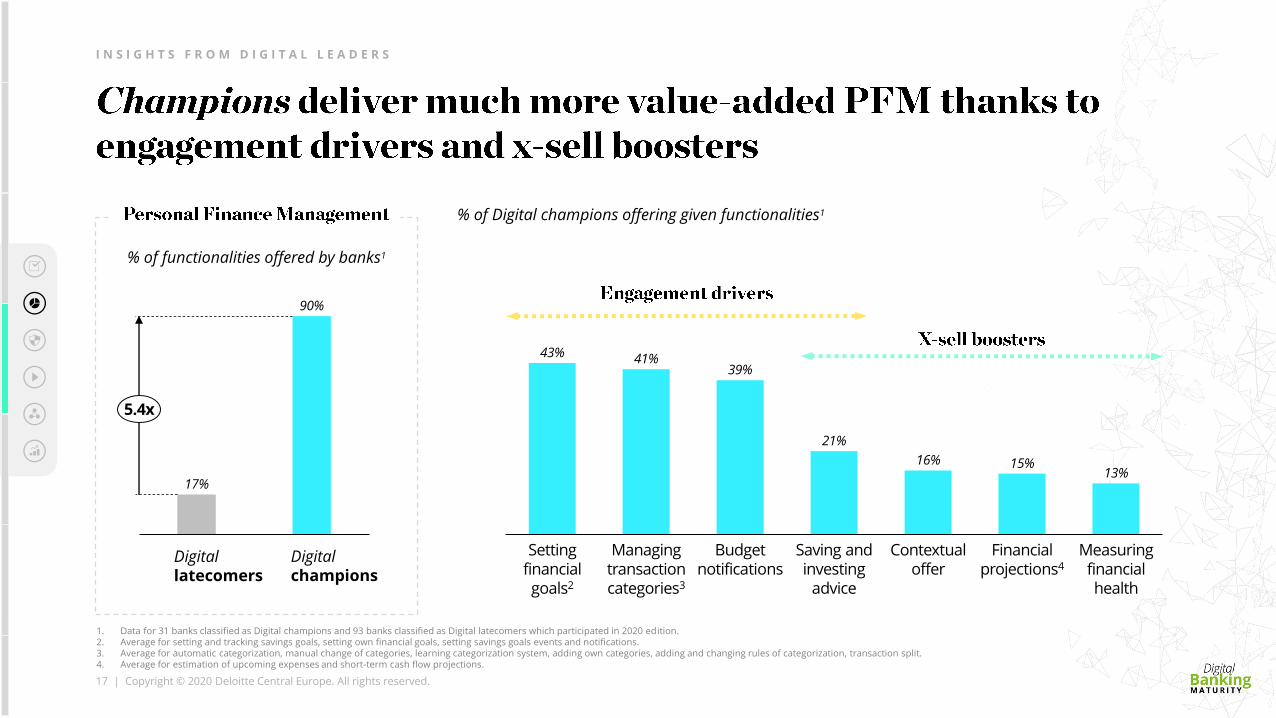

17%

90%

5.4x

Financial projections4

Managing transaction categories3

Setting financial goals2

43%

Budget notifications

Contextual offer

Saving and investing

advice

Measuring financial health

41%39%

21%

16% 15%13%

Digital latecomers

Digital champions

% of Digital champions offering given functionalities1

% of functionalities offered by banks1

1. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition.2. Average for setting and tracking savings goals, setting own financial goals, setting savings goals events and notifications.3. Average for automatic categorization, manual change of categories, learning categorization system, adding own categories, adding and changing rules of categorization, transaction split.4. Average for estimation of upcoming expenses and short-term cash flow projections.

18 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

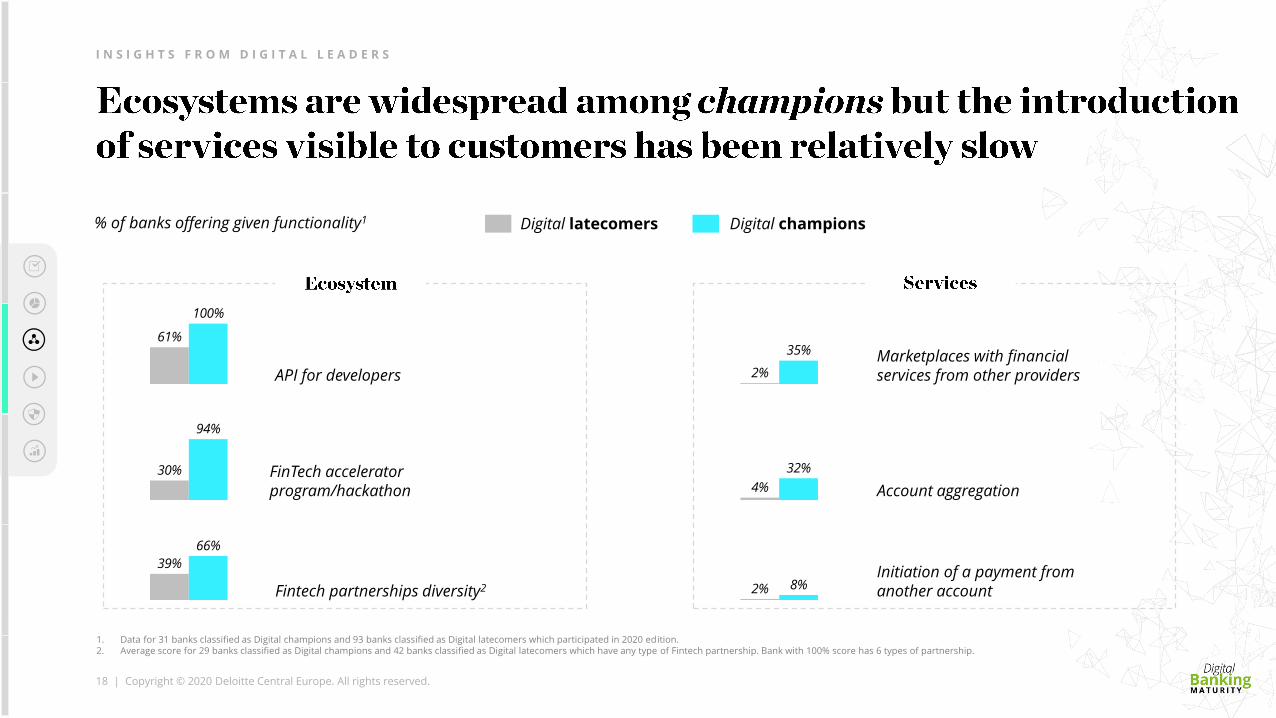

% of banks offering given functionality1

I N S I G H T S F R O M D I G I T A L L E A D E R S

Initiation of a payment from another account

Account aggregation

API for developers

30%

94%

39%

66%

4%

32%

2% 8%

FinTech accelerator program/hackathon

Fintech partnerships diversity2

Marketplaces with financial services from other providers2%

35%

1. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition.2. Average score for 29 banks classified as Digital champions and 42 banks classified as Digital latecomers which have any type of Fintech partnership. Bank with 100% score has 6 types of partnership.

Digital latecomers Digital champions

100%

61%

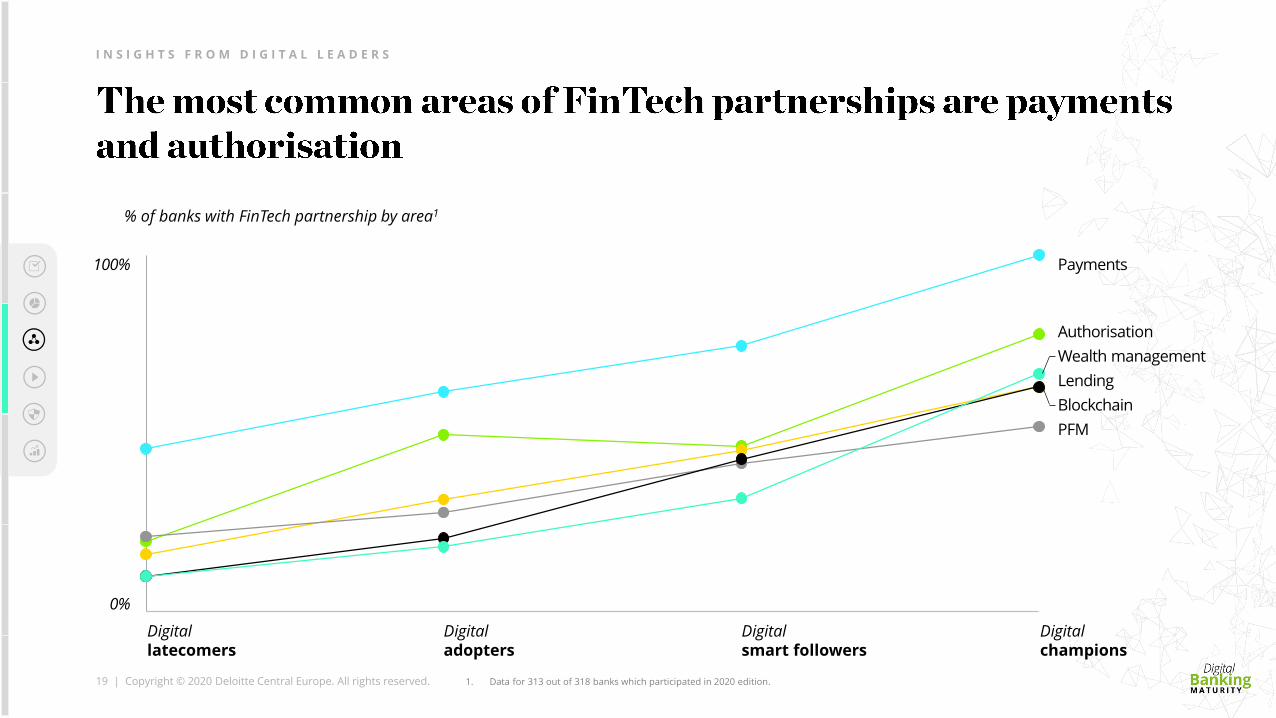

19 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

Authorisation

Payments

Lending

Blockchain

PFM

Wealth management

0%

100%

% of banks with FinTech partnership by area1

I N S I G H T S F R O M D I G I T A L L E A D E R S

Digitallatecomers

Digitaladopters

Digitalsmart followers

Digitalchampions

1. Data for 313 out of 318 banks which participated in 2020 edition.

20 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

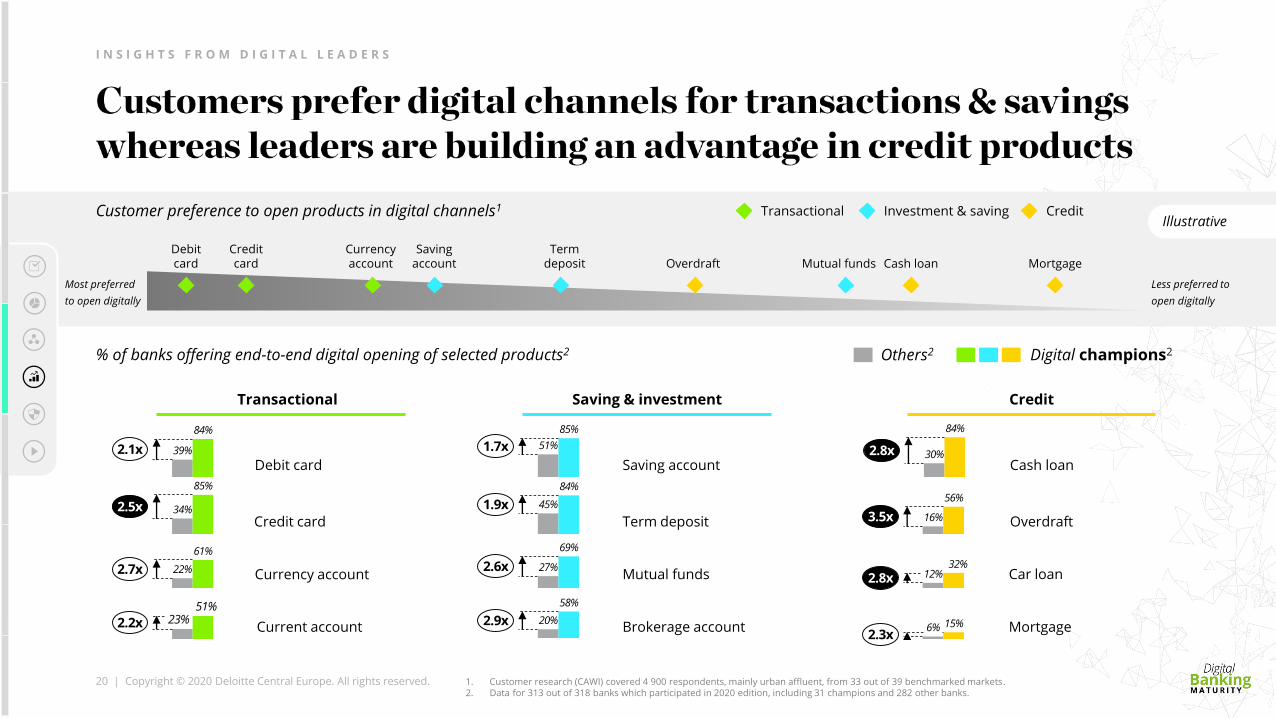

Credit card

Debit card

Currency account

Saving account

Term deposit MortgageOverdraft Mutual funds Cash loan

Customer preference to open products in digital channels1

Most preferred

to open digitally

Less preferred to

open digitally

Transactional Investment & saving Credit

I N S I G H T S F R O M D I G I T A L L E A D E R S

84%

30%2.8x

34%

85%

2.5x16%

56%

3.5x

6% 15%2.3x

23%51%

2.2x

84%

39%2.1x

84%

45%1.9x

61%

22%2.7x 27%

69%

2.6x

51%

85%

1.7x

20%

58%

2.9x

Credit card

Cash loan

Car loan

Mortgage

Term deposit

Debit card

Currency account

Current account

CreditTransactional Saving & investment

Saving account

Brokerage account

Mutual funds

% of banks offering end-to-end digital opening of selected products2

12%32%

2.8x

Overdraft

Others2 Digital champions2

1. Customer research (CAWI) covered 4 900 respondents, mainly urban affluent, from 33 out of 39 benchmarked markets.2. Data for 313 out of 318 banks which participated in 2020 edition, including 31 champions and 282 other banks.

Illustrative

21 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

I N S I G H T S F R O M D I G I T A L L E A D E R S

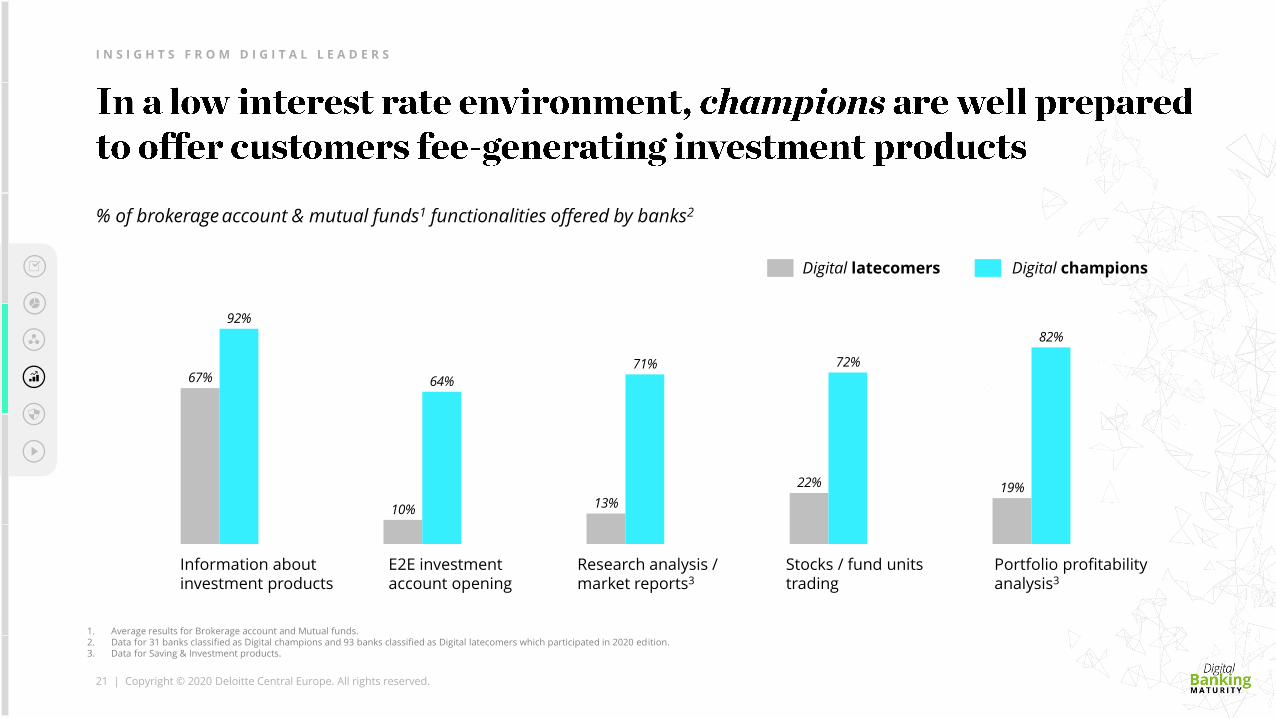

Digital latecomers Digital champions

67%

92%

Information about investment products

22%

72%

Stocks / fund units trading

% of brokerage account & mutual funds1 functionalities offered by banks2

10%

64%

E2E investment account opening

82%

19%

Portfolio profitability analysis3

71%

13%

Research analysis / market reports3

1. Average results for Brokerage account and Mutual funds.2. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition.3. Data for Saving & Investment products.

22 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

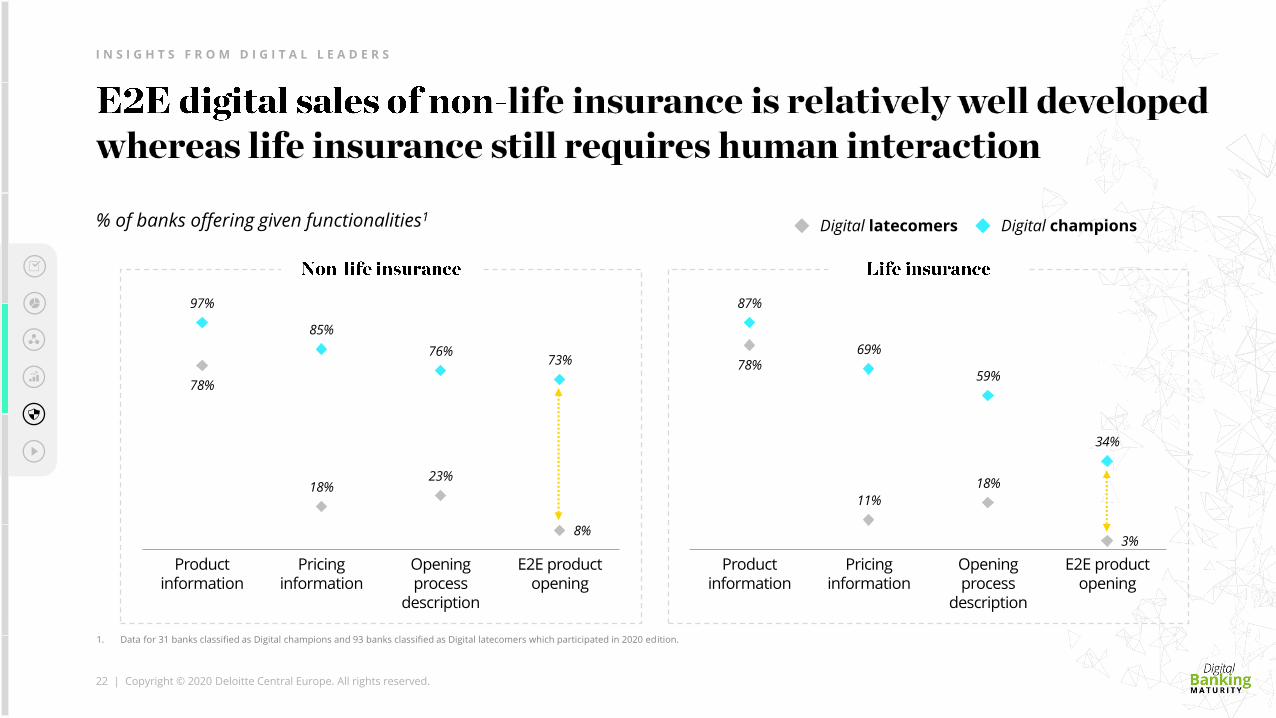

I N S I G H T S F R O M D I G I T A L L E A D E R S

85%

78%

76%

23%

97%

Product information

18%

Pricing information

Opening process

description

8%

73%

E2E product opening

18%

11%

Pricing information

69%

Product information

78%59%

87%

Opening process

description

3%

34%

E2E product opening

% of banks offering given functionalities1Digital latecomers Digital champions

1. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition.

23 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

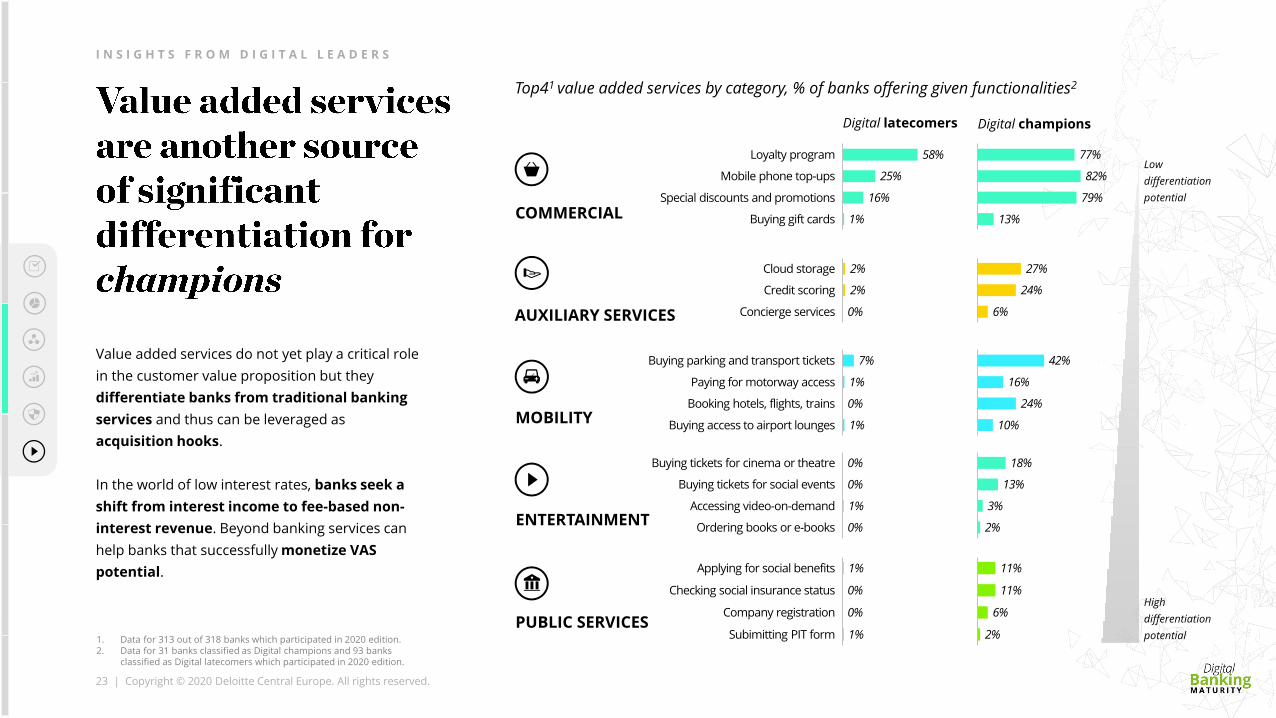

Loyalty program

Mobile phone top-ups

Special discounts and promotions

Buying gift cards

58%

16%

25%

1%

0%

1%

7%

Booking hotels, flights, trains

Buying parking and transport tickets

Buying access to airport lounges

Paying for motorway access 1%

Ordering books or e-books

Buying tickets for social events

1%

Buying tickets for cinema or theatre 0%

Accessing video-on-demand

0%

0%

COMMERCIAL

ENTERTAINMENT

Top41 value added services by category, % of banks offering given functionalities2

MOBILITY

Applying for social benefits

Checking social insurance status

1%

Company registration

0%

Subimitting PIT form

1%

0%

Cloud storage 2%

Concierge services

Credit scoring 2%

0%

PUBLIC SERVICES

AUXILIARY SERVICES

Value added services do not yet play a critical role

in the customer value proposition but they

differentiate banks from traditional banking

services and thus can be leveraged as

acquisition hooks.

In the world of low interest rates, banks seek a

shift from interest income to fee-based non-

interest revenue. Beyond banking services can

help banks that successfully monetize VAS

potential.

High

differentiation

potential

Low

differentiation

potential

I N S I G H T S F R O M D I G I T A L L E A D E R S

Digital latecomers Digital champions

13%

82%

77%

79%

42%

24%

16%

10%

3%

13%

18%

2%

11%

11%

6%

2%

6%

27%

24%

1. Data for 313 out of 318 banks which participated in 2020 edition.2. Data for 31 banks classified as Digital champions and 93 banks

classified as Digital latecomers which participated in 2020 edition.

24 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

I N S I G H T S F R O M D I G I T A L L E A D E R S

Transfers and payments

Customer support

PFM

Investment services

% of banks offering given functionality1

27%

26%

9%

6%

15%

12%

11%

5%

9%

8%

5%

21%

12%

9%

9%

2%

2%

11%

5%

4%

2%

2%

1%

4%

5%

0%

1%

9%

3%

0%

Disposable virtual card

Transfers using beneficiary’s e-mail

Bill split

Virtual debit card

Chatbot with advanced informational use cases

Communication via Snapchat / WeChat3

Chatbot allowing transactionality

Chatbot providing contextual recommendations

Notifications due to currency price deviations

Roboadvisory

Cryptocurrency operations

Estimation of upcoming expenses

Transaction geolocation tags

Short term cashflow projections

Share transaction with other app users

Incumbents ChallengersSelected innovative

functionalities2

1. Data for 280 banks classified as Incumbents and 33 banks classified as Challengers which participated in 2020 edition.

2. With global threshold of 10% for rare features.3. Communication via other social media platforms benchmarked (You Tube, Twitter, LinkedIn,

Instagram) had a much higher global adoption level than 10% (ranging from 82% - 95%)

25 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

67%

38%

2. Open an account

71%

61%

44%

1. Gather account

information

23%

22%

6. Buy an insurance

3. Onboarding

30%

38%

65%

4. Report lost card

45%

54%

2%

79%

5. Make a transfer

7%

44%

11%

48%

7. Use beyond banking services

8. Add accounts

from other banks

75%

9. Buy a credit

product

5%

10. Close an account

S T A T E O F U X

INFORMATION GATHERING

ACCOUNT OPENING

CUSTOMER ONBOARDING

END RELATIONSHIP

DAY-TO-DAY BANKING

EXPAND RELATIONSHIP

% of UX-related functionalities offered by banks1 Digital latecomers Digital champions

+48p.p.

+25p.p.

+30p.p.A global assessment of 19

user scenarios reflecting 10

areas of customer activity

provides insight into the

development of UX along the

customer journey

1. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition. UX score based on 209 unique functionalities. 65% of Digital champions have been classified in top10% of banks by UX score.

26 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

S T A T E O F U X

Selected functionalities along UX scenario: Open an account, % of banks offering given functionalities1

Digital latecomers

Digital champions

Facilitation of entering data fast and correctly

Descriptive error messages

Progress tracker

Save & Finish Later feature

INFORMATION GATHERING

ACCOUNT OPENING

CUSTOMER ONBOARDING

END RELATIONSHIP

DAY-TO-DAY BANKING

EXPAND RELATIONSHIP

Confirmation that form is being processed

Illustrative

1. Data for 31 banks classified as Digital champions and 93 banks classified as Digital latecomers which participated in 2020 edition.

Descriptive error messagesProgress tracker

Anna, it’s nice to meet you! Tell us how to contact you:

Phone number

Email address

Repeat email address

We will send you documents and important information.

3 4 5

Facilitation of entering data fast and correctly

Let’s begin! Tell us who we are opening the account:

Remember to give us the correct data. Do not use short forms, remember about special characters and watch out for typos.

2 3 4 5

Name

Surname

Anna, it’s nice to meet you! Tell us how to contact you:

500 765 400

d

Repeat email address

3 4 5

Please check your email address is correct.

27 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

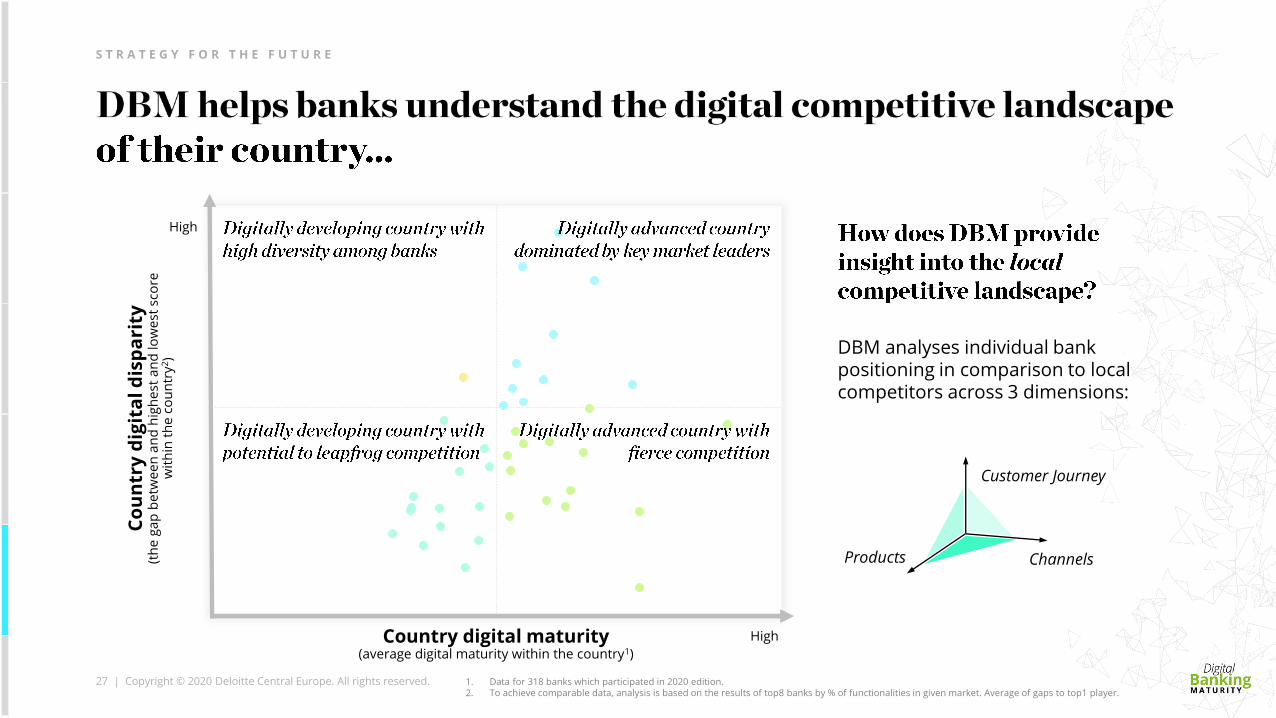

Country digital maturity(average digital maturity within the country1)

High

S T R A T E G Y F O R T H E F U T U R E

DBM analyses individual bank positioning in comparison to local competitors across 3 dimensions:

Co

un

try

dig

ita

l d

isp

ari

ty(t

he

ga

p b

etw

ee

n a

nd

hig

he

st a

nd

lo

we

st s

core

w

ith

in t

he

co

un

try

2)

High

Customer Journey

Products Channels

1. Data for 318 banks which participated in 2020 edition.2. To achieve comparable data, analysis is based on the results of top8 banks by % of functionalities in given market. Average of gaps to top1 player.

28 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

S T R A T E G Y F O R T H E F U T U R E

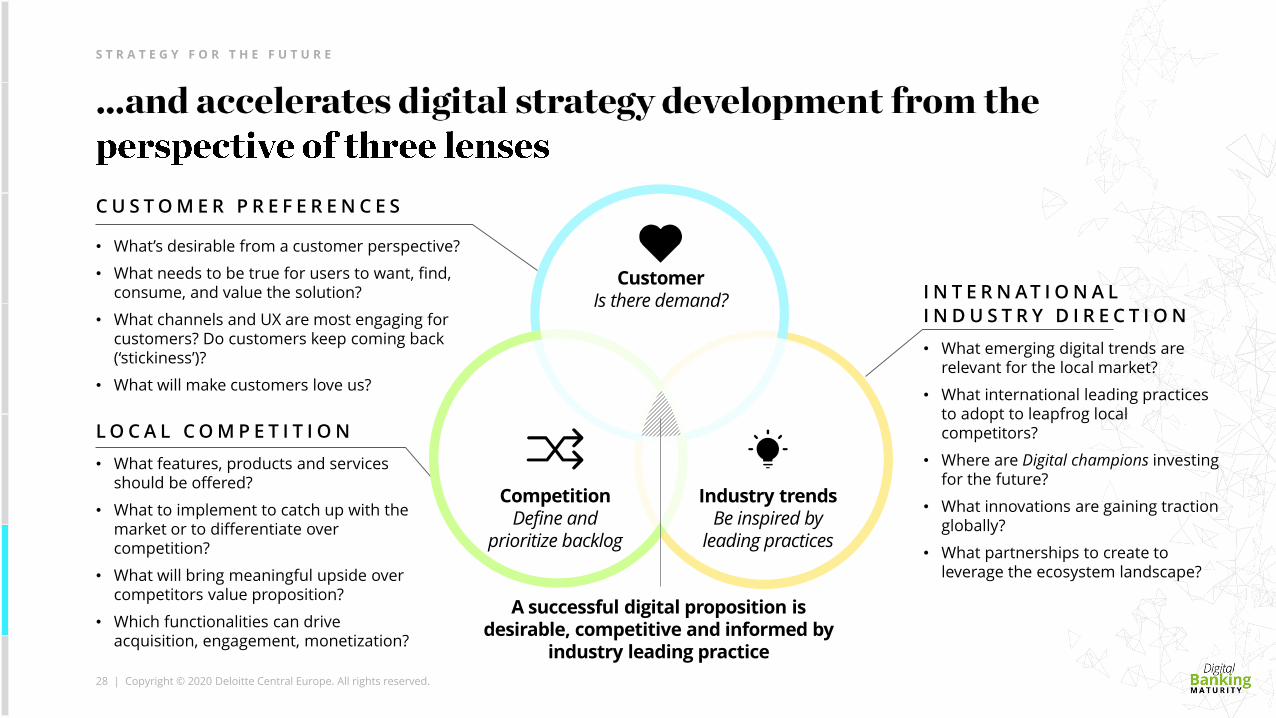

C U S T O M E R P R E F E R E N C E S

• What’s desirable from a customer perspective?

• What needs to be true for users to want, find, consume, and value the solution?

• What channels and UX are most engaging for customers? Do customers keep coming back (‘stickiness’)?

• What will make customers love us?

I N T E R N A T I O N A L

I N D U S T R Y D I R E C T I O N

• What emerging digital trends are relevant for the local market?

• What international leading practices to adopt to leapfrog local competitors?

• Where are Digital champions investing for the future?

• What innovations are gaining traction globally?

• What partnerships to create to leverage the ecosystem landscape?

CustomerIs there demand?

Industry trendsBe inspired by

leading practices

CompetitionDefine and

prioritize backlog

L O C A L C O M P E T I T I O N

• What features, products and services should be offered?

• What to implement to catch up with the market or to differentiate over competition?

• What will bring meaningful upside over competitors value proposition?

• Which functionalities can drive acquisition, engagement, monetization?

A successful digital proposition isdesirable, competitive and informed by

industry leading practice

29 | Copyright © 2020 Deloitte Central Europe. All rights reserved.

S T R A T E G Y F O R T H E F U T U R E

A dedicated workshop that discusses an individual

bank’s digital maturity in retail banking

channels, competitive positioning and which

can help to identify potential digital initiatives,

based on gaps to local and global leaders.

We’ve identified leading market practices worldwide

Learn more about the latest trends and developments in digital retail

banking channels.

Outcome: Introduction to trends, innovations and example use cases with

assessment of relevance for the individual bank.

We understand the importance of UX for customers

Examine how UX features and functionalities are helping improve

customer satisfaction.

Outcome: Overview of leading UX market practices and identification of

key improvement areas from a customer perspective.

We know the digital maturity of retail banking channels

Gain insights into the positioning of an individual bank in comparison

to local and global leaders and key gaps.

Outcome: Identification of opportunities and strategic implications based

on individual bank’s positioning versus peers.

For more details, reach out to your local representative

on the following slides or [email protected]

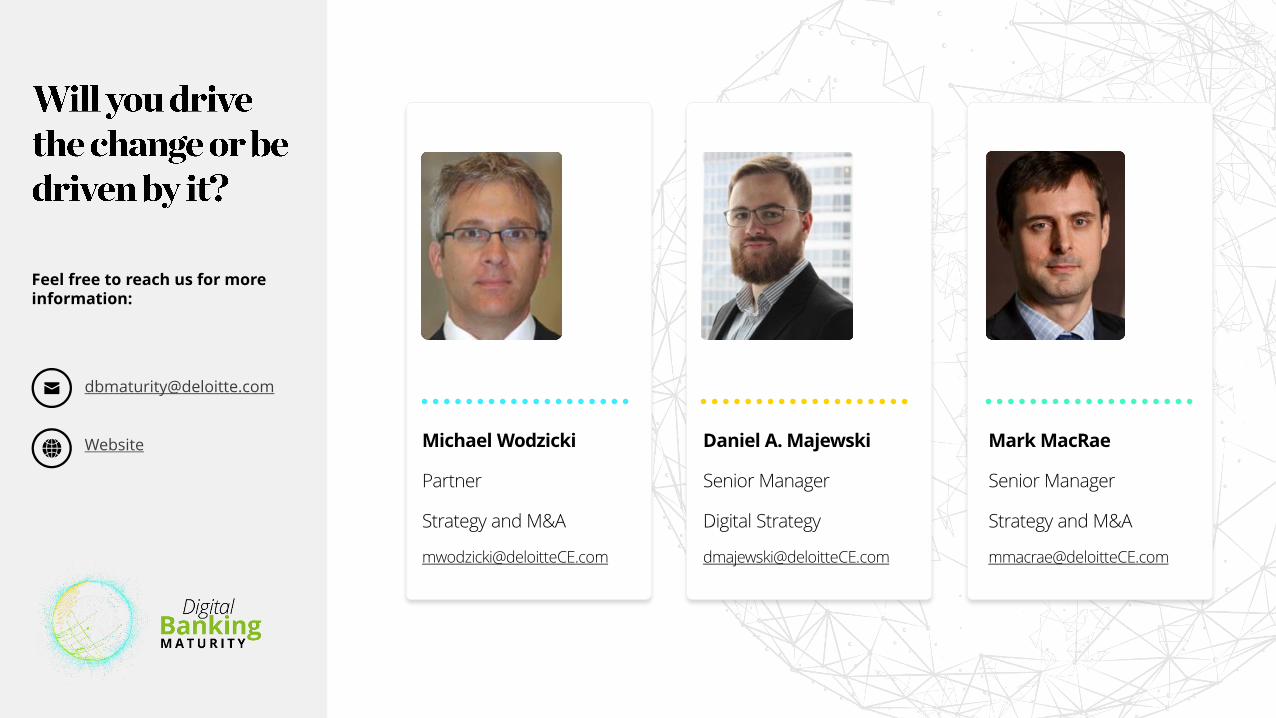

Feel free to reach us for more information:

Daniel A. Majewski

Senior Manager

Digital Strategy

Mark MacRae

Senior Manager

Strategy and M&A

Michael Wodzicki

Partner

Strategy and M&A

Website

31 | Copyright © 2020 Deloitte Development LLC. All rights reserved.

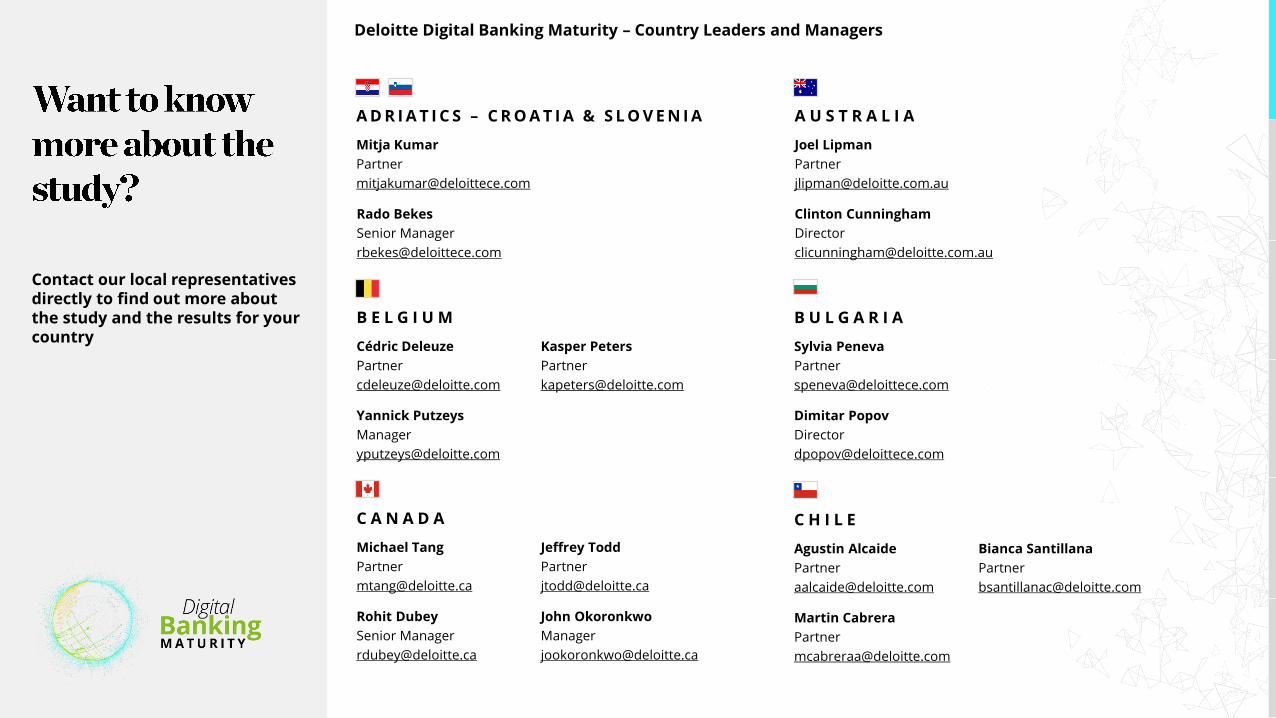

Deloitte Digital Banking Maturity – Country Leaders and Managers

Contact our local representatives directly to find out more about the study and the results for your country

A D R I A T I C S – C R O A T I A & S L O V E N I A

Mitja Kumar

Partner

Rado Bekes

Senior Manager

B U L G A R I A

Sylvia Peneva

Partner

Dimitar Popov

Director

C A N A D A

Rohit Dubey

Senior Manager

Michael Tang

Partner

Jeffrey Todd

Partner

John Okoronkwo

Manager

A U S T R A L I A

Joel Lipman

Partner

Clinton Cunningham

Director

B E L G I U M

Cédric Deleuze

Partner

Kasper Peters

Partner

Yannick Putzeys

Manager

C H I L E

Agustin Alcaide

Partner

Martin Cabrera

Partner

Bianca Santillana

Partner

32 | Copyright © 2020 Deloitte Development LLC. All rights reserved.

Deloitte Digital Banking Maturity – Country Leaders and Managers

C Z E C H R E P U B L I C

Eva Bartůňková

Senior Consultant

Pavel Šiška

Partner

Štěpán Húsek

Partner

G E R M A N Y

Jürgen Lademann

Partner

Julia Ivanova

Senior Consultant

Alice Georget

Senior Manager

F R A N C E

Julien Maldonato

Partner

H U N G A R Y

Tamas Schenk

Partner

Andras Fulop

Partner

Daniel Dracz

Senior Manager

G R E E C E

Katerina Glava

Partner

George Gialitakis

Manager

I R E L A N D

Yvonne Byrne

Partner

Graham Kinsella

Senior Manager

David Dalton

Partner

Adrian Hayes

Director

Contact our local representatives directly to find out more about the study and the results for your country

33 | Copyright © 2020 Deloitte Development LLC. All rights reserved.

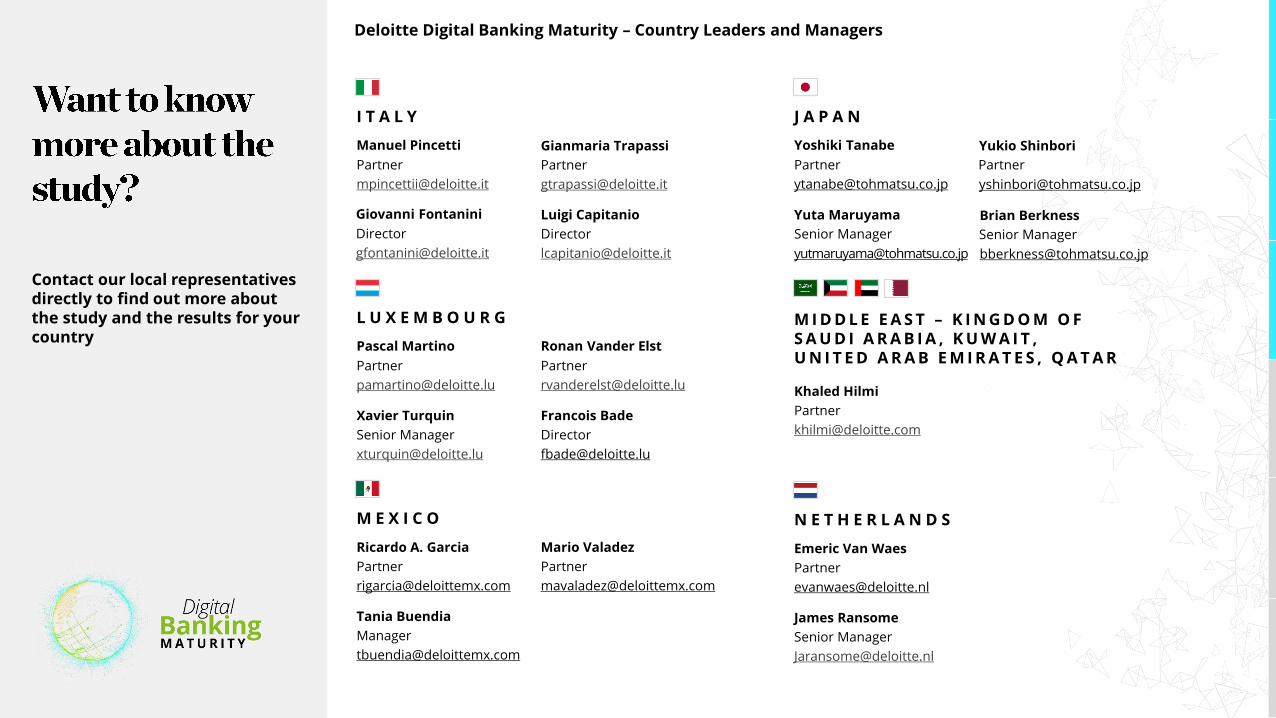

Deloitte Digital Banking Maturity – Country Leaders and Managers

N E T H E R L A N D S

Emeric Van Waes

Partner

James Ransome

Senior Manager

M E X I C O

Ricardo A. Garcia

Partner

Tania Buendia

Manager

Mario Valadez

Partner

M I D D L E E A S T – K I N G D O M O F S A U D I A R A B I A , K U W A I T , U N I T E D A R A B E M I R A T E S , Q A T A R

Khaled Hilmi

Partner

I T A L Y

Manuel Pincetti

Partner

Gianmaria Trapassi

Partner

Luigi Capitanio

Director

L U X E M B O U R G

Pascal Martino

Partner

Xavier Turquin

Senior Manager

Francois Bade

Director

Ronan Vander Elst

Partner

J A P A N

Yoshiki Tanabe

Partner

Yukio Shinbori

Senior Manager

Yuta Maruyama

Partner

Brian Berkness

Senior Manager

Giovanni Fontanini

Director

Contact our local representatives directly to find out more about the study and the results for your country

34 | Copyright © 2020 Deloitte Development LLC. All rights reserved.

Deloitte Digital Banking Maturity – Country Leaders and Managers

R O M A N I A

Vladimir Aninoiu

Director

Claudiu Constantinescu

Senior Manager

Andrei Ionescu

Partner

R U S S I A

Ekaterina Trofimova

Partner

Maxim Nalyutin

Director

P O R T U G A L

Joao Matias Ferreira

Associate Partner

Gustavo Carvalho Romao

Manager

P O L A N D

Michael Wodzicki

Partner

Mark MacRae

Senior Manager

Daniel Majewski

Senior Manager

Kirsti Merethe Tranby

Partner

Partner

Kasper Loke

Senior Consultant

Mårten Sellgren

Aleksandar Petrovic

Senior Consultant

N O R D I C S – N O R W A Y A N D S W E D E N

S E R B I A

Ivan Stefanovic

Manager

Mitja Kumar

Partner

Contact our local representatives directly to find out more about the study and the results for your country

35 | Copyright © 2020 Deloitte Development LLC. All rights reserved.

Deloitte Digital Banking Maturity – Country Leaders and Managers

S P A I N

Gerard Sanz

Partner

Hugo Aldonza

Manager

Marcelo De Castro

Manager

Michal Kopanic

Partner

Milos Cerovsky

Manager

S L O V A K I A

S W I T Z E R L A N D

Marius Virmond

Director

Patrik Spiller

Partner

Cyrill Kiefer

Partner

SP ANISH LATIN AMERIC A - ARGENTINA, C O LOMBIA, P ERU , U RU GU AY

Pablo Peso

Partner

Maximiliano Nardi

Senior Manager

Fernando Oliva

Partner

S I N G A P O R E

Kok Yong Ho

Partner

Alexander Douglas-Jones

Director

Nai Seng Wong

Partner

Eng Hong Lim

Partner

Veronika Hraskova

Senior Manager

Contact our local representatives directly to find out more about the study and the results for your country

36 | Copyright © 2020 Deloitte Development LLC. All rights reserved.

Deloitte Digital Banking Maturity – Country Leaders and Managers

T U R K E Y

Yaman Polat

Partner

Ilkay Cakir

Senior Specialist

Ali Cicekli

Partner

U N I T E D K I N G D O M

Jonathan Gray

Partner

Edward J Matheson

Manager

Gareth Addison

Director

Contact our local representatives directly to find out more about the study and the results for your country

This communication contains general information only, and none of Deloitte Touche

Tohmatsu Limited („DTTL“), its global network of member firms or their related

entities (collectively, the “Deloitte organization”) is, by means of this communication,

rendering professional advice or services. Before making any decision or taking any

action that may affect your finances or your business, you should consult a qualified

professional adviser.

No representations, warranties or undertakings (express or implied) are given as to

the accuracy or completeness of the information in this communication, and none

of DTTL, its member firms, related entities, employees or agents shall be liable or

responsible for any loss or damage whatsoever arising directly or indirectly in

connection with any person relying on this communication. DTTL and each of its

member firms, and their related entities, are legally separate and independent

entities.

Copyright © 2020 Deloitte Central Europe. All rights reserved. Member of Deloitte Touche Tohmatsu Limited.