Inspect & Service Braking Systems.pdf - Automotive Training ...

Upload

khangminh22Category

view

0download

0

UNIT-I

Introduction

Auditing means to inspect, examine, checking, investigate, scrutinize, company accounts.

Auditing is a systematic examination and verification of firms books of accounts, transactions

records, other relevant documents and physical inspection of inventory by qualified accountants

called auditors.

Origin

The term audit is derived from Latin word ‘audire’ which means to hear. Auditing is as old as

accounting. It was used in all ancient countries such as Greece, Egypt, Rome, U.K, India.

The main objective of auditing is to ascertain the accounts were true and fair and to detect and

prevent errors and frauds.

The International Accounting Standard Committee and the Accounting Standard Board of the

Institute of Chartered Accountants of India have developed standards accounting and auditing

practices to guide the accountants and auditors in the day to day work.

Definition

1. PROF.L.R.Dicksee, “auditing is an examination of accounting records undertaken with a

view to establish whether they correctly and completely reflect the transactions of which

they relate.”

2. R.K.Mautz,” auditing is concerned with the verification of accounting data determining

the accuracy and reliability of accounting statements and reports.”

Functions

1. Study The Accounting System :- It is the basic function of auditing. In order to determine the

nature, timing and extent of the audit procedures auditor should study the accounting system.

2. Internal Control System :- It is a process which determines that management policies are

carried out according the accounting principles. This system is very useful to safeguard the

interest of the enterprise. The auditor determines the effectiveness of this system.

3. Vouching :- This function is essential to determine the accuracy of accounting record.

Through audit those documents can be checked which support and prove the business

transactions. All entries in books of accounts are made on the basis of relevant vouchers.

4. Verification Of Assets :- It is the function of auditing that it should verify the assets of the

business. It is concerned with the determination of value, ownership and possession of business

asset. The auditor can check the existence of asset.

5. Legal Requirement :- It is the function of auditing to verify that statements are prepared

under the legal requirements or not. There are various laws like company and income tax

ordinance which are introduced by the govt.

6. Liabilities Verification :- The liabilities of the business can be verified from the books of

accounts. The auditor can write a letter to the creditors for the verification of liabilities. The

auditor must receive the certificate from the management in this regard.

7. Capital And Revenue :- Auditing should make difference between capital and revenue items.

The capital items are compared to note the financial position of the business. The revenue items

are compared to determine the income. The income and expenses related to many years can be

divided in current and coming year.

8. Valuation Of Liabilities :- Through auditing value of liabilities can be checked from the

books of accounts and other papers. The auditor can also confirm the value from outside sources.

The value of liabilities is given in the balance sheet by the management but it is the function of

auditing which confirms this value.

9. Valuation Of Assets :- The management gives the value of assets and auditor can apply the

accounting principles to assess the value of assets. The auditor critically examines and takes help

from the expert.

10. Reporting :- Auditing important function is reporting. Auditor is an independent person and

it is his duty to submit his report in writing. If he is satisfied he can present clean report

otherwise he can give qualified report.

Objectives

1. Primary Objective

The main objectives of the audit are known as primary objectives of the audit. They are as

follows:

1. Examining the system of internal check.

2. Checking arithmetical accuracy of books of accounts, verifying posting, casting,

balancing etc.

3. Verifying the authenticity and validity of transactions.

4. Checking the proper distinction between capital and revenue nature of transactions.

5. Confirming the existence and value of assets and liabilities.

Verifying whether all the statutory requirements are fulfilled or not. Proving true and fairness of

operating results presented by income statement and financial position presented by the balance

sheet.

2. Subsidiary Objective

These are such objectives which are set up to help in attaining primary objectives. They are as

follows:

(A) Detection and prevention of errors

Errors are those mistakes which are committed due to carelessness or negligence or lack of

knowledge or without having vested interest. Errors may be committed without or with any

vested interest.

So, they are to be checked carefully. Errors are of’ various types. Some of them are:

1.Errors of Accounting principle- When principles of book keeping and accountancy are not

followed in recording of business transactions ,it is known as error of principle.

• Wrong posting of income transaction

• Wrong posting of expenditure

• Wrong allocation of expenditure between capital and revenue. Revenue expenditure may

be treated as capital expenditure and vice-versa.

Such errors are not disclosed in trial balance, debit and credit sides of transactions are same.

Such errors can be detected by thorough checking of each and every transaction.

Error of principle affect the reliability of financial statement. it is an accounting mistake in which

entry is recorded in the incorrect account, the value recorded was the correct but placed

incorrectly.

2. Errors of omission- When a transaction is omitted fully or partly from books of accounts,

such type of errors are known as error of omission. Usually it arises due to mistake of clerk.

• Omission of purchases from purchases book

• Omission of sales from sales book

• Omitting the entry for charging depreciation in the books.

• Rent or interest paid for 11 months, the remaining amount which is unpaid or outstanding

has not been entered in the books.

3. Errors of commission- When the entries made in the books of original entry or ledger are

incorrect wholly or partly, such are called error of commission. Usually these error arise due to

negligence in recording of some business transactions.

➢ Ex:-wrong recording in the books of original entry wholly or partly. Goods purchased for

Rs.10,000 recorded in purchases book as Rs.1000

➢ Rs.500 purchased from m and co, recorded as from n and co.

➢ Wrong totaling of original entry, while totaling sales day book or purchase day book

mistake is made in the total sales. Sales day book is totaled Rs.100 short and posted to

ledger. This error will affect trial balance, the credit side total will be short by Rs.100. it

will lower the profit by Rs.100.

➢ Wrong subsidiary book used for recording a transaction .

For ex:-credit sales to x and co. Were recorded in purchase day book or credit purchases to y and

co. were recorded in sales day book.

4. Compensating errors- When an error offsets the effect of another error, such error is known

as compensating error. These errors don’t affect trial balance.

Sometimes under casting of one account is compensated by over casting of another account, such

as ‘X’ a/c is under totaled by Rs.100 and’ Y’ a/c is over totaled by Rs.100.

5. Errors of Duplication- When a transaction is recorded twice and also posted twice in the

ledger. Such an error will not affect trial balance. It is more difficult to locate such errors. Only

thorough checking and comparing of vouchers with entries in the books. If two entries on the

same side are appearing with the same amount.

(B) Detection and Prevention of frauds

Frauds are those mistakes which are committed knowingly with some vested interest in the

direction of top level management. Management commits frauds to deceive tax, to show the

effectiveness of management, to get more commission, to sell a share in the market or to

maintain the market price of share etc. Detection of fraud is the main job of an auditor. Such

frauds are as follows:

1. Misappropriation of cash- Misappropriation of cash is done by theft of cash receipts, petty

cash, cheques, negotiable instruments, showing fictitious (false, fake) payments to workers,

creditors, purchases etc; misappropriation of cash is very easy. With the increase in size of

business, the opportunities of committing fraud also increase because the owners of the business

have no direct control over receipts and payments of cash.

Examples of misappropriation of cash:-

• Recording fictitious purchases and thereby cash involved there in is

misappropriated.

• Omitting credit note received from the supplier and discount allowed

by them.

• Showing payment of wages to dummy workers in wage sheet.

• Various receipts like bad debts recovered ,sale of scrap or rejected

stock etc;

• Omitting the records of donations receipts or recording lower

amounts.

• The credit sales may not be recorded and money received from

customers pocketed.

2. Misappropriation of goods- The misappropriation of goods is easy in case of a business

which produces or deals in goods of high value and less bulky.

• Issuing false credit note to customers for sales returns and such goods are

misappropriated.

• Goods may be stolen by employees from the godowns.

It is not easy to detect the misappropriation of goods. Only the efficient system of record

keeping, periodical checking, internal check etc; will be helpful to avoid misappropriation of

goods.

3. Manipulation of accounts or falsification of accounts without any misappropriation- This

type of fraud is committed by upper level of management with the different objectives to mislead

certain parties within or outside the business. Whenever such fraud is committed, it usually

involves large amounts and it is intentional. This type of fraud is usually committed by

Managers, Directors, Board of directors etc;

(a) Showing low profits than the actual ones:-

To give wrong impression about success of business to competitors. To reduce or avoid

payment of income tax.

To purchase shares at a lower price in the market.

(b) Showing more profits than what actually are:-

-The manager may get more commission if such commission is calculated on the basis of profits

earned.

-To sell the shares at high prices by declaring higher dividends, this is done when such person

hold shares of the company.

-The services of such person may be retained by showing more profits to the shareholders

thereby the confidence of shareholders is maintained.

-To mislead financial institutions for obtaining further credit, the financial position of the

business is shown better than what actually it is.

-When the company is in the process of issuing shares to the public, to attract more subscribers

for such shares.

Manipulation of accounts may be resorted /use the following devices:-----Purchases/expenses

may be inflated / suppressed.

-Sales or other incomes may be inflated /suppressed.

-Stocks may be over or under valued.

-Omission of adjustment of expenses outstanding or prepaid expenses.

-Depreciation of assets may be over or under charged or omitted altogether.

-Assets or liabilities may be over or under valued.

-Treating capital expenditure as revenue expenditure or vice-versa.

Window dressing

The financial position of the business is shown in such a way that it seems better than what

actually it is window dressing is more of misrepresentation than fraud. it is done in the following

ways:-

(a) Purchases of current year may be shown as next year.

(b) Income of previous year may be shown as current year.

(c) Expenses of current year may be shown as next year.

(d) Showing short-term liabilities as long term liabilities.

(e) Charging revenue expenses as capital expenditure.

(f) Over-valuation of closing stock.

(g) Over-valuation of assets or undervaluation of liabilities.

Merits

Assurance of true and fair accounts: An audit provides an assurance to the investors,

government, lenders, creditors, owners, management etc. That the final account presented shows

the true and fair picture of the profit and losses and financial position of the concern

True and fair balance sheet: The user of final accounts can be sure that the assets and liabilities

disclose true and fair view of financial position of the concern, it’s neither more nor less, and it’s

free from window dressing or secret reserve.

True and fair profit and loss account: The user of final accounts should be sure that the profit

and loss account show true amount of profit or less as it is.

Tally with books of accounts: The audited final accounts should tally with the books of

accounts of the concern. So it can be easy to calculate the taxable income without going through

all the transactions.

As per law: The audited final accounts should be prepared as per the rules and guidelines laid

down by law.

Disclose all material facts: The audited final accounts should disclose all material facts, thus

users can rely on them for making useful decisions of lending, investing etc.

Detection of errors and frauds: It is assumed that the audited final accounts are free from errors

and frauds, the auditor with his expertise knowledge would detect the errors and fraud so as to

show the true figure of final accounts.

Moral check on employees: Auditing techniques such as verification, vouching of cash, assets,

stock etc. act as a moral check on the employees, this forces them to keep the accounts up-to-

date and free from errors and frauds.

Advice to concern: Auditor can also advise the client about internal control, taxation, finance,

accounting system etc.

Demerits

All transactions cannot be checked: It is not possible for an auditor to check each and every

transaction; he has to check them on sample basis

Evidence is not conclusive: Audit evidence is not conclusive in nature the confirmation of

debtors is not conclusive evidence that all amount will be collected, the conclusions are

persuasive rather than conclusive.

Not easy to detect some frauds: It’s not easy for an auditor to detect the deeply laid frauds

which involves acts designed to conceal them such as forgery, false explanation, and not

recording transaction and so on.

Audit cannot assure about profitability or efficiency of management: Even though the

accounts are audited it doesn’t mean that the user can take granted the future profitability or

prospects of concern as audit don’t comment on efficiency of the management.

Rely on experts: The auditor has to rely on experts like lawyers, engineers, valuers etc. for

estimation of contingent liability and valuation of fixed assets.

Accounts and Auditing

• Definition: Accounting is keeping records of the financial transactions and preparing

financial statements; but auditing is critical examination of the financial statements to

give an opinion on their fairness.

• Objective: Objective of accounting is to determine the financial position, profitability

and performance; while objective of auditing is to add credibility to the financial

statements and reports of the company.

• Status: Accounting is usually carried out by an internal employee of the company; but

auditing is carried out by an external person or independent agency. Accounting is

governed by Accounting Standards with some degree of discretion; but auditing is

governed by Standards on Auditing and does not provide much flexibility.

• Appointment: Accountant is appointed by the management of the company; while the

auditor is appointed by the shareholders of the company, or a regulator.

• Qualification: Any specific qualification is not compulsory for an accountant; but some

specific qualification is compulsory for an auditor.

• Scope Determination: The scope of accounting is determined by the management of the

company; while the scope of auditing is determined by the relevant laws or regulations.

• Commencement: Accounting starts usually where book-keeping ends; while auditing

always starts where accounting ends.

• Remuneration :Accounting is carried out by a company employee who gets a salary;

while a specific auditing fee is paid to the auditor. Accountant’s remuneration, i.e., salary

is fixed by the management; while auditor’s fee is fixed by the shareholders.

• Period: Accounting mainly concentrates on the current financial transactions and

activities; while auditing concentrates on the past financial statements. Accounting is

carried out on continuous basis with daily recording of financial transactions; while

auditing is basically a periodic process and carried out after the preparation of final

accounts and financial statements, usually on yearly basis.

• Compulsion: Accounting covers all transactions, records and statements having financial

implications; while auditing mainly covers final financial statements and records.

• Report Submission: Accounts are submitted to the management of the organization;

while audit report is submitted to the shareholders.

• Knowledge :- Accountant must have the knowledge of accountancy whereas an Auditor

must have the knowledge of accounting as well as auditing.

Types Of Audit:

(A) On The Basis Of Scope:-

(1) Management audit

(2) Cost audit

(3) Tax audit

(4) Operational audit

(5) Proprietary or Performance audit

(B) On The Basis Of Forms Of Organization :-

1. Sole trader

2. Partnership accounts

3. Hindu undivided family

4. Audit of Association of persons

5. Audit of non-trading concerns

(C) On The Basis of conduct/Method/Approach:

(1) Independent (external)

(2) Internal

(3) Balance sheet audit

(4) Partial audit

(5) Interim audit

(6)Continuous audit

(7)Periodical/ completed annual audit

(A) On The Basis Of Scope:-

An audit examination can be general or specific. A general audit can be independent. On the

other hand, specific audit concentrates on a particular areas, object or may be period.

(1) Cost audit:- Cost audit was first introduced in 1965 in India, when the central govt.

added clauses (d) to section 209 and 233B to section 233 of Companies Act,1956 . Cost audit is

the effective means of control in the hands of management and it is a check on behalf of the

shareholders of the company , consumers and the govt. The cost audit helps in maintaining and

effective control of cost. The cost accountant helps in maintaining proper cost records and

suggests the means for reducing the cost of production.

(2) Management Audit:- Management audit is to evaluate various management functions

and processes. According to Leslie R.Howard “ an investigation of a business from the highest

level downward in order to ascertain whether sound management prevails throughout, thus

facilitating the most effective relationship with outside world and the most efficient organization

and smooth running of internal organizations.”

(3) Performance audit:- It is to determine whether the various activities of the organization

are being carried out efficiently. It is to ensure effective control in the organisation. It examines

the relationship between production and sales to maximize the profits of the organization.

(4) Operational audit: This audit aims at improving the operations of business.

• To make recommendations for the improvement of profitability of the organization.

• To help in achieving other objectives of business such as workers satisfaction,

improvement in company’s image.

(5) Tax audit :-Under Income Tax Act, profits shown by profit and loss a/c have to be

adjusted as per the provisions of the Act. In this way profits for accounting and profits for

taxation are not the same. This profit differ due to various reasons. Profits for accounting

are ascertained as per accounting policies and standards but profits for tax purpose are

computed as per the provisions and rules of Income Tax Act.

(B) On The Basis Of Forms Of Organization or Statutory:-

(a) Audit of sole traders :- In case of proprietary concern, the owner himself takes the

decision to get the accounts audited. The auditing work will depend upon the

agreement of audit. It will be safe for the auditor to get the agreement in writing from

the trader.

(b) Audit of accounts of partnership firms:-To avoid any misunderstandings and

doubts, partnership firms recognize the advantage of audit of financial statements.

Partnership deed on mutual agreement between the partners may provide for audit of

final statements. Auditors are appointed by the mutual consent of all the partners.

Rights, duties and liabilities of the auditors are defined in the mutual agreement and

can be modified by the partners.

(c) Audit of accounts of individuals:-Many of the individuals derive from income from

property, shares, investments and other sources. They may be incurring heavy expenses for

earning such incomes. Like insurance agents earn a commission. Auditor may be appointed to

audit the accounts and to verify the accuracy. He must get clear instructions from his client. His

scope of work will depend upon the agreement with his client.

(d) Audit of companies:-Under Companies Act, audit of accounts of companies in India

is compulsory. Independent Chartered Accountant who is professionally qualified is

required for audit of accounts of companies. Indian Companies, Act 1913 for the first

time made it compulsory for joint stock companies to get their accounts audited by a

qualified accountant. A number of amendments have been made in Companies Act, 1956

regarding appointment, duties, qualifications, power and liabilities of a qualified auditor.

(e) Audit of accounts of trust:-Accounts of trust are maintained as per the conditions and

terms of the trust deed. The income of the trust is distributed to the beneficiaries. There

are more chances of frauds and mis-appropriation of incomes. In the trust deed as well as

in the trust by a qualified auditor. The audited accounts of the trust nsure true and fair

view of accounts of trust.

(f) Audit of accounts of Co-operative Societies:-co-operative societies are established

under the Co-operative Societies Act, 1912. It contains various provisions for regulation

and working of these societies. The auditor of co-operative society should have an expert

knowledge of the particular Act. Companies Act is no applicable for co-operative

societies.

(g) Audit of accounts of other institutions:-other corporate bodies like banks, insurance

companies, electricity companies etc. formed under the Special Acts of the parliament

shall get their accounts audited as per the provisions of the respective Act.

(C) On The Basis Of Conduct/Method/Approach:-

It is classified into external and internal audit. An independent or external audit is conducted

by an independent, professionally qualified person who is not an employee of the organization.

An independent audit enjoys better credibility in the eyes of public. Indian companies Act, and

Chartered Accountants Act contain number of provisions to ensure the independence of the

auditor. On the other hand, i internal audit is conducted by employee of the organization to

enable better exercise of managerial control.

(1) Internal audit implies the audit of accounts by the staff of the business. The staff may or

may not have professional qualification for audit of accounts. The internal audit staff is

permanent in nature and helps the business in detection of errors and frauds. Partial audit:-

When an auditor is asked to audit certain category of transactions or transactions made during a

post of period, it is called as partial audit.

(2) Partial audit:- It is conducted as a special event, normally in those organizations where

routine audits are not taking place. For ex,in a partnership firm when a new partner is to be

admitted or where govt. orders a special audit to investigate in to certain matters.

(3)Interim audit:-When an audit is conducted between two annual audits, such audit is known

as interim audit. It may involve complete checking of accounts for a part of the year. Sometimes

it is conducted to enable the Board of Directors to declare an interim dividend.

(4) Continuous audit: It is a detailed examination when an audit is done at certain levels but

from where it is left . The reasons may be where there are large volumes of transactions or

internal control or check is weak.

(5) Balance sheet audit: It is an in depth examination of all items of balance sheet, profit and

loss account, original entries etc.. Vouchers are examined only to a necessary extent.

Basic Principles Governing an Audit

The Auditing and Assurance Standard 1 (SA 200) on “Basic Principles Governing an Audit”

issued by the Institute of Chartered Accountants of India describes the basic principles which

govern the auditor’s professional responsibilities and which should be complied with whenever

an audit of financial information of an entity is carried out. The basic principles as stated in this

statement are:

(i) Integrity, Objectivity and Independence: The auditor should be straightforward, honest

and sincere in his approach to his professional work. He should maintain an impartial attitude

and both be and appear to be free of any interest which might be regarded, whatever its actual

effect on being incompatible with integrity and objectivity.

(ii) Confidentiality: The auditor should respect the confidentiality of information acquired in

the course of his work and should not disclose any such information to a third party without

specific authority or unless there is a legal or professional duty to disclose.

(iii) Skill and Competence: The audit should be performed and the report prepared with due

professional care by persons who have adequate training, experience and competence in auditing.

(iv) Work Performed by Others: When the auditor delegates work to assistants or uses

work performed by other auditors and experts, he will be entitled to rely on work performed by

others provided he exercises adequate skill and care and is not aware of any reasons to believe

that he should not have so relied. The auditor should carefully direct, supervise and review work

delegated to assistants and obtain reasonable assurance that work performed by other auditors or

experts is adequate for his purpose since he will continue to be responsible for forming and

expressing his opinion on the financial information.

(v) Documentation: The auditor should document matters which are important in providing

evidence that the audit was carried in accordance with the basic principles.

(vi) Planning: Planning enables the auditor to conduct and effective audit in an efficient and

timely manner. Primarily, planning should be based on the knowledge of the client’s business.

Plans should be further developed and revised as necessary during the course of the audit.

(vii) Audit Evidence: The auditor should obtain sufficient appropriate audit evidence through

the performance of compliance and substantive procedures to enable him to draw reasonable

conclusions there from on which to base his opinion on the financing information.

(viii) Accounting System and Internal Control: The auditor should reasonably assure

himself that the accounting system is adequate and that all the accounting information which

should be recorded has in fact been recorded. Internal controls normally contribute to such

assurance. The auditor should gain an understanding of the accounting system and related

internal controls and evaluate the same to determine the nature, timing and extent of other audit

procedures.

(ix) Audit Conclusions and Reporting: The auditor should review and assess the

conclusions drawn from the audit evidence obtained and from his knowledge of business of the

entity as the basis for the expression of his opinion on the financial information. This review and

assessment involves forming an overall conclusion as to whether:

(a) the financial information has been prepared using acceptable accounting policies

which have been consistently applied;

(b) the financial information complies with relevant regulations and statutory

requirements;

(c) there is adequate disclosure of all material matters relevant to the proper

presentation of the financial information, subject to statutory requirements, where applicable.

The auditor should contain a clear written expression of opinion on the financial information and

if the form or content of the report is laid down in or prescribed under any agreement or statute

or regulation, the audit report should comply with such requirements. When a qualified opinion,

adverse opinion or a disclaimer of opinion is to be given or reservation of opinion on any matters

is to be made, the audit report should state the reasons therefore.

Audit Planning

Proper implementation of any plan depends upon a good programme me. While preparing audit

programme me, the auditor must keep in mind size and composition of the organization and

nature and extent of internal control. An auditor prepares a plan after the selection of senior and

junior staffs allocating the jobs to them, mentioning when to start, how to do the work etc; this

plan is known as audit programme.

An auditor should include all the procedures in written form, objectives of each sector and all the

directions which are to be given to the staff, which helps to control their work and helps to

implement such programmes in to action.

Preparation before commencement of audit

It means that when an organization is going to start final audit

before commencement of audit the following instruction must be given by the auditor to his

client.

1. To ascertain nature and scope of his duties.

2. An engagement letter called audit contract should be procured from the client in which it

contains all the terms and conditions between auditor and his client.

3. A list of book in use, list of employees, their duties and internal control should be provided to

the audit staff.

4. Books of original entry, ledgers, trial balance and Final accounts should be provided to the

auditor to know the internal control system.

5. All supporting document should be properly arranged.

6. List and schedule of assets and liabilities should be arranged properly for the examination to

the audit staff managed properly for the examination to the audit staff.

7. The auditor of the newly established company should also carry out the following primary

work before commencing the audit.

8. To understand the nature of transaction of the client the auditor should acquire technical

knowledge.

Audit Programme

Audit programme is a detailed work plan which includes the time of doing work and how to

do the work which includes audit procedures. It also estimates the duration to complete the

audit task. Senior staffs prepares audit programme to junior staff on the basis of nature of

business. Auditor has to keep in mind the size and composition of organisation nature and

extent of internal control for audit program.

Advantages

(1) Audit programme saves time and labour:- All the directions which are to be given to

assistant are clearly stated in the audit programme which helps to complete the task in

time.

(2) Audit programme increases efficiency:- The responsibilities of auditor are divided

among the number of staffs considering their skill and intelligence which helps to

complete the work of audit properly.

(3) Audit programme helps to control:- An auditor can compare the work performed by

the assistants on the basis of audit programme which helps to control their wok.

(4) Audit programme helps to maintain uniformity:- work is divided among the assistant

staffs, so there is no chance of leaving non-audited statements. If the work of audit is

performed every year, uniformity can be maintained in the work of audit which helps to

compare the report of various years.

(5) Audit programme help to make responsible:- work of assistant is clearly defined in the

audit programme and assistant puts signature in the completed work. So, if any work is

left out, assistant can be made liable for such work.

(6) Audit programme helps to maintain continuity:- Audit programme clearly shows the

completed task and procedures of doing work. So, if any staff leaves the job or remains

absent, new staff can easily continue the job of audit.

(7) Audit programme helps to present as proof:- Auditor can present audit programme as

proof. If he/ she done negligence or misfeasance, can get clearance from such accusation.

Audit programme can be presented in court also.

Disadvantages

Even though audit programme has number of advantages it is not free from limitations. Some of

the major disadvantages of audit programme are as follows:-

(1) Audit programme harasses staff:-All the staff should perform task within the limitation

given in audit programme. So, staff can’t use their knowledge and calibre which harasses

to them.

(2) Possibility of being unsuitable:- Nature and size of business differs. So, the programme

which is prepared at the beginning of the year remains unsuitable. Different organisations

may have their own problems.so, similar type of programme may not be applicable to all.

(3) Audit programme increases the chance of fraud:- Staff of the client got information

about the audit programme in advance which increases the chance of committing frauds.

Similarly, it harasses the audit staff, so they perform the work of audit carelessly which

also increases the chance of committing frauds.

(4) Audit programme is unsuitable to small concerns:- Small concerns has less

transactions and work of audit can be completed in short period of time. So, audit

programme is not essential to audit such concern.

(5) Exclusion of problems of new technology:- New techniques and technologies are used

in the work of accounting. Such technology creates the problem in the work of audit.

Audit Note Book:-

Audit note book is a diary or register maintained by audit staff to note errors, doubtful queries

and difficulties. The purpose is to note down various points which need to be either clarified with

the client o the chief auditor. The audit note book is also used for recording important points to

be included in the auditor’s report. It is a complete record of doubts and their clarification.

Contents of Audit Note Book:-

(1) A list of books of accounts maintained.

(2) The names, duties and responsibilities of principal officers.

(3) The particulars of missing receipts and vouchers.

(4) Mistakes and errors detected.

(5) The points calling for clarification and explanations.

(6) The points deserving the attention of the auditor.

(7) Various totals and balances.

(8) Extracts from minutes and contracts.

(9) Points to be part of auditor's report.

(10) Date of commencement and completion of audit.

Audit papers or Audit Working Papers:-

Audit working papers are the documents which record all audit evidence obtained during

financial statements auditing, internal management auditing, information system auditing and

investigations. These papers contain essential facts about accounts which are under audit.They

show the audit was:

• Properly planned;

• Carried out;

• There was adequate supervision;

• That the appropriate review was undertaken; & finally and most importantly;

• That the evidence is sufficient and appropriate to support the audit opinion.

Purpose of Audit Working Papers

1. Working papers represent the volume of work performed by the auditor and his staff. Hence,

they enable the easy drafting and preparation of a detailed audit report.

2. The various minute details and aspects of the audit report can be well substantiated based on

the findings summarized in the report.

3. They become a valuable documentary evidence for the auditor on the occasions when he has

to defend himself against the charges of negligence, etc. leveled against him.

4. They enable auditor to coordinate and organize the work of audit clerks.

5. They enable the auditor to advice his client regarding the improvement of the system of

internal check and efficiency of the accounting system.

6. They serve as a guide to the auditor in subsequent examinations and help the auditor to plan

for the succeeding year.

7. They serve as a means to give training to the audit clerks to summarize the work done by

them.

8. The purpose of audit working papers is to prepare written record as a proof of audit work

done.

9. Audit staff keeps audit working papers so long these are needed for future use such record is

the property of an auditor. He can keep it as long as he thinks necessary.

10. The auditor can be assisted in forming an opinion about financial statements.

Latest Trends in audit

The AC (Audit Committee) plays a critical role in helping organizations navigate today’s

challenging business environment, providing guidance and oversight on a wide range of complex

issues. This means audit committees must focus on ensuring the right skills are at the table and

that all members continue to expand their knowledge in key areas. Encouragingly, more than 70

percent of respondents indicated that their board assesses its skills on an annual basis with an eye

to facing evolving challenges.

1. Talent and human capital: So much data gathering work is being automated now in internal

audit and finance. Talent-wise, that means internal audit will be looking for people who are more

astute on the levels of data and information analysis – people who can use data strategically to

help the organization realize its vision and goals. We’re really seeing the emergence of a

different capability in internal audit, where it’s moving from a ‘doing’ function to a ‘leading/

influencing’ function.

2. Technology and cyber security: Businesses really need to think harder about technology

infrastructure, as it appears to be moving from one model to another model. Organizations are

unsure what their capital investment should look like going forward, as a pay-as-you go

approach is becoming more practical. This is an area that is changing at a tremendous rate and it

just isn’t as well understood as it should be. For those that get it right, it could create significant

innovation differentiation.

3. Disruption to business models: It is clear that the innovation agenda will continue to be a

core focus for organizations, whether to optimize cost, differentiate the customer experience or

grow new products and services. It is critical to move past the buzzwords and for ACs to truly

understand the existing and future risks and opportunities posed through innovation disruption,

which is occurring at an exponential rate.

4. Evolving regulatory landscape: In our globalized economy, organizations should start

thinking not just about complying with regulations in other countries, but about whether their

operations in those countries are living up to home country standards and regulations. This is

particularly relevant given the rapid rise of social media and its use to highlight what individuals

believe to be inappropriate corporate behaviour. Companies have a social responsibility to think

about these issues, and their brand can be damaged if they are not properly addressed.

5. Political and economic uncertainty: For ACs to address risk issues around uncertainty –

whether political or economic – they need access to, and engagement with, leading insights.

Those insights can come from a variety of places: subject matter experts, experience gleaned

from other boards, or external advisors who can assess the business and understand how the

broad range of uncertainty-based risks applies.

6. Changing reporting expectations: The importance of operational and non-financial metrics

will only continue to increase. As a result, the finance function’s responsibilities will expand

beyond traditional financial reporting and controls. Audit committees should ensure their finance

function is taking the full range of externally reported KPIs(Key Performance Indicators) into

account and leveraging them to give external stakeholders more assurance around the accuracy

of all reports.

7. Environment and climate change: Many of Canada’s leading industry sectors could well

suffer negative consequences from climate change if they don’t take action. The cost of recent

catastrophic weather events and the potential negative impact of climate change on business

models and asset valuations are increasingly driving home this realization. To play an effective

role, ACs have a responsibility to understand and ensure that management has addressed the

potentially material impacts of climate change and related disclosure requirements.

UNIT-2

AUDIT AND AUDIT PROCEDURE

AUDIT EVIDENCE:

Auditing is primarily concerned with the verification and examination of the accounting data. The auditor

should give his opinion on the financial statements and should investigate into the accounts of the company to

establish a basis for his opinion.

During the process of investigation, the auditor should collect and evaluate the evidence to establish the facts

and to draw conclusions and opinions.

The auditor should obtain sufficient and competent evidence before expressing any opinion on the financial

statements.

The term evidence includes all influences on the mind of an auditor which affects his judgment about the

truthfulness of the proportions submitted to him for review.

In simple words an auditor must gather sufficient and appropriate audit evidence and test them to make judgment

of opinion.

Audit evidence is information obtained and recorded by the auditor is arriving at the conclusions on which he

bases his opinion on the financial statements. Main source of audit evidence includes:

1 Accounting system and underlying documentation of the

enterprise.

2 Tangible asset.

3 Management and employees of the organization.

4 Customers, suppliers and other third parties who have dealing with or knowledge of the enterprise or it’s

business.

Thus with the help of the evidence the auditor can form an opinion whether the financial statements show a

true and fair view of the affairs of the company.

CONCEPTOF MATERIALITY:

Materiality determines which information should be presented in the financial statements. There is no definite

criterion for determining the materiality of information. Information is said to be material if its omission or

misstatement would influence the economic decisions taken by the users based on the financial statements.

Thus it can be said that information is material if it is relevant to the decision of the users. Hence, materiality

and relevance have much in common as both defined by the reference to the needs of users in making economic

decisions.

Kohler’s defines Materiality as the characteristic attaching to a statement, fact or item where by its disclosure

or the method giving it expression would likely to influence the judgment of a reasonable person.

According to this concept only those events should be recorded which have a significant bearing and

insignificant things should be ignored. The avoidance of insignificant things will not materially affect the

records of the business. There is no formula in making a distinction between material and immaterial events. It

is a matter of judgment and it is left to the accountant or auditor for taking a decision.

The principle of materiality is and has always been fundament6al to the whole process of accounting. An

auditor has also to be quite concerned with regard to the concept of materiality. In fact, he has analyze and take

decision regarding various items whether they are material or not during the course of an audit. This would

require thorough knowledge, competence and experience on his part. In case, he finds that an item is quite

material in nature, he would have to give careful consideration to its checking & would call for more evidence

in support. In fact, he would have to undertake an ‘audit in depth’ to satisfy himself regarding such material

item.

Accounting standard 1 defines material items as relatively important and relevant items i.e items ‘the

knowledge of which would influence the decisions of the users of the financial statements’.

In companies act 2013, the word material has been used in schedule 3, part 2 of schedule 3 requires the financial

statements and profit and loss account to disclose all material items, features. Similarly schedule 2 of chartered

accounts act 1949 clause 5,6,8 and 9 of part 1 refer to material facts, material misstatement, material exceptions

and material departure. It’s importance is also been in the statement on auditing practices.

It has been stated that “the concept of materiality is fundamental to the process of recognition, aggregation,

classification and presentation of financial information. It is also an important consideration for an auditor who

has constantly to judge whether a particular item of transaction is material or not”.

INTERNAL CONTROL: Internal control means controlling the whole management system financial or non-

financial. It means internal control involves a number of checks and controls exercised in a business to ensure its

efficient and economic working.

SPICER AND PEGLER: Define the internal control as “internal control is best regarded as the whole system

of controls, financial and otherwise, established by the management is the conduct of a business including

internal check, internal audit and other forms of control.

MEANING:

1 The internal control is a system of controls.

2 Controls are established over financial and non-financial areas.

3 The mechanism of control may manifest itself in the forms of internal check or internal audit or other firm.

According to The American Institute of Certified Public Accountants:

“Internal control comprises of the plan of organization and all the co-ordinate methods and measures

adopted within a business to safeguard its assets, check the accuracy and reliability of its accounting data

to promote operational efficiency and to encourage adherence to prescribed managerial policies.

SCOPE OF INTERNAL CONTROL:

1 FINANCIAL CONTROL: It is concerned with an efficient system of accounting, adequate supervision,

recording and duplicating system.

2 CASH CONTROL: It includes controlling of the receipts, payments and balances remaining. Proper steps

should be taken to avoid misappropriation of cash.

3 CONTROL OVER TRADING TRANSACTIONS: This deals with the system of controlling purchases

and sales transaction. Proper procedures should be made for handling, acquiring and accounting of goods

purchased and for recording and handling of goods sold.

4 CONTROL OVER EMPLOYEES REMUNERATION: The preparation and maintenance of records for

remuneration to employees, methods of payments etc have to be properly dealt with. This should be done to

avoid defalcation and misappropriation of cash payments to be made to the employees.

5 CAPITAL EXPENDITURE CONTROL: The expenditure on capital assets must be kept under proper

control. It should be properly used and sanctioned and feedback reports must be prepared and submitted.

6 OTHERS:

a) Stock maintenance

b) Control over investments

c) Maintenance of staff

relationship

OBJECTIVES:

Before depending upon the internal control system, the auditor should ensure that the following objectives have

been achieved by the organization.

1. Assets Protection: The purpose of internal control is to protect assets of the business entity, The assets

are used in the business. These assets are in the custody of responsible officers. So assets are not

destroyed or misused.

2. Accurate Record: The purpose of internal control is to maintain accurate accounting record. The

business transactions are processed under generally accepted accounting principles after authorization of

competent person.

3. Follow Policies: The purpose of internal control is to follow policies management. The policies are broad

guidelines for obtaining business objectives. All employees try their best to follow rules of the game.

4. Prevention of Errors: The purpose of internal control is to prevent errors. There may be an unintentional

mistake due to overwork or carelessness. There is normal workload with every person. The senior person

checks the work of a junior person.

5. Prevention of Frauds: The purpose of internal control is to prevent frauds. It is an intentional

misrepresentation of financial information by one or more individuals among management, employees

or third parties.

6. Best Use of Resources: The purpose of internal control is the best use of resources. There is a need for

an optimum combination of resources for maximizing profits. Internal control can point out a weakness

that can be removed.

7. Nature of Test Audit: The purpose of internal control is to determine the nature and extent of audit test.

When there is effective internal control there will be few audit tests otherwise there will be a need for

thorough checking.

8. Reliable Record: The purpose of internal control is to maintain reliable accounting record. The equal

distribution of work among the employees provides the complete and reliable record, as it is free from

errors and frauds.

9. Reduce Workload: The purpose of internal controls is reduction of workload. The effective internal

controls can be useful for auditors. They can check few items remaining items will be treated as checked

by the auditor.

10. Location of Errors and Frauds: The purpose of internal controls is to locate frauds and errors. There

are many types of errors and frauds that may be found in the accounting record. The compliance and

substantive tests may be applied to detect the frauds.

INTERNAL CHECK:

It is an arrangement of the duties of members of staff in such a manner that the work performed by one person is

automatically and independently checked by the other.

Spicer and Pegler “Internal check is an arrangement of the duties of the staff members of the accounting

functions in such a way that the work performed by a person is automatically checked by another”.

Ronald A Irish “Internal check refers to the organization of office duties in such a way as to prevent or disclose

both errors or frauds”.

INTERNAL AUDIT:

It is the independent appraisal activity within an organization for the review of accounting, financial and other

business practices.

DEFINITION: Watter B Meigs “Internal auditing consists of a continuous and critical review of financial and

operating activities by a staff of auditors functioning as full time salaried employee”.

DISTINCTION BETWEEN INTERNAL AUDIT AND INTERNAL CHECK

Basis Internal check Internal audit

1.Meaning It is an arrangement ai duties allocated in

such a way that the work of one person is

checked by another.

It is an independent appraisal of the operations

and records of the company.

2.Object Is to prevent on minimize the of errors,

frauds

or irregularities.

It is to detect the errors and frauds which have

already been committed.

3. Separate staff

required

no new appointment is required. It is

arrangement of duties of staff in a

particular

way.

A separate staff of employees is appointed for

this.

4.Nature of work It is a process under which the work goes

on uninterruptedly & the checking is more

or

less automatic.

The internal auditor has to report to the

management about the inefficiencies and

suggest

improvements.

5.Timing of work It is in operations during the course of

transactions.

It starts when the accounting process of different

transactions is finished.

6.Device It is a device for doing the work. It is a device for checking the work.

7.Errors& frauds Errors and frauds are discovered during the

course of work.

Errors and frauds are detected after the

completion

of work.

8.Scope of work Scope is very limited. Scope is broad.

9.Involment A Large number of employees are needed

for implementation.

A Much smaller number is needed

for implementation.

INTERNAL CHECK WITH REGARD TO CASH TRANSACTIONS

The risk of misappropriation of cash and chances of frauds are numerous in cash transactions. Hence the

following points should be taken into consideration while devising a good and proper system of internal check

for cash transactions.

CASH RECEIPTS.

1. The cashier should have no access to the ledgers and other books of original entry except the cash book.

2. The printed receipts books, serially numbered, should be used when cash is collected and should me

countersigned by the responsible manager.

3. All cheques should be marked not negotiable and A|c payee only.

4. All the receipts should be acknowledged by means of a printed receipt.

5. Incoming correspondence and remittances should be opened by the cashier in the presence of responsible

officer.

6. Account collections both cash and cheque should be deposited into the bank daily. The counter –foil of the

pay-in-slip should be filled by the clerk and the portion to be retained by the bank should be filled by the

cashier.

7. Bank reconciliation statement (B.R.S) should be prepared at regular intervals by the cashier to know the

actual position of bank balance.

8. Any spoiled slips should be cancelled but not removed from the receipt book. Overwriting should be

discouraged and fresh writing with proper initials is encouraged.

9. Copies of the receipts previously issued must be marked duplicate.

10. Some responsible person from the firm should verify the balance of cash by carrying out a surprise physical

check.

CASH SALES.

Cash sales in of three types.

1. Sales at counter: The following procedure should be followed for cash sales.

a. The sales man should be properly named and a specific number to each salesman should be allocated.

b. Cash memo should be printed in numerical sequence every salesman should be given a separate book of

bank copies of cash memos.

c. The salesman sells goods to customers and prepares 4 copies of cash memos, 3 to be given to customers and

4th to be retained by the salesman.

d. All those copies are checked by another official.

e. The customers carries the 2 copies to the cashier, who after collecting the amount and after recording the

sale, returns 2 copies marked cash paid.

f. Goods are handed over to the customer by the gate keeper and ‘1’ copy of cash memo is retained by the gate

keeper.

g. At the end of the day, the salesman, cashier and gatekeeper prepare summary of the cash separately.

h. Receipts from cash sales should be deposited in the bank on the same day, if sales are made after banking

hours Kama the same may be deposited the next day.

i. Where cash recording machines are used, the total of cash received has given by the machine, should be

checked with the amount actually banked.

2. Travelling salesman: These salesmen collect debts from the old customers and accept advance from the

new ones. The following measures should be adopted to check the salesman.

a. Travelling salesman should be given pre numbered rough receipts books. Hence they issue a rough receipt

to the customers for cash received and the final receipt is issued by the head office.

b. The customer can directly contact the head office if they do not receive the final receipt within a period of time.

c. No travelling salesman is instructed to deposit all the cash receive to the head office, without making any

deductions from commissions or any expenditure.

d. Head officer regularly statement of accounts to their old customers to appraise them of their debts and balance.

e. Special attention should be given to defaulters.

f. Salesman should be transferred from one area to another to avoid fraud and increase efficiency of the

salesman.

3. postal sales:

a. There should be a separate register to Record sales by post or V.P.P.

b. When cash is received against a V.P.P sale, it should be entered in the separate register.

c. Separate bank pay in slips should be prepared to deposit cash received against postal sales.

d. An officer should be deputed to check the register and special attention should be given to those goods which

have been returned.

CASH PAYMENTS.

a. All the payment should be made by account payee cheque.

b. The person in-charge of making payment should have no connection with the person receiving cash.

c. It should be seen that all the cheques have been signed by the authorized person.

d. All the unused cheques should be kept in proper safe custody.

e. Payment always by reference to appropriate documentary evidence.

f. Payment for Rs.20000/- or more always by A/C payee cheques.

g. Use of revenue stamps for cash payments exceeding Rs.5000/-

h. Continuous serial numbering of all cheques/cash vouchers.

i. Recording all payments in cash book.

j. Vouchers supporting payment should not be presented twice. Such vouchers should be stamped as 'paid'

before the cheques are signed.

k. An official should check the statement received from creditors and verify within the invoice and ledger

account. Only after verification the cheque should be drawn in favor of the creditor. Confirmation of account

should also be made with the credit card through check correspondence.

l. No payments against ‘LOU and On account’ without sanction of an appropriate authority.

m. B.R.S should be prepared to reconcile bank and cash balance from time to time by some authorities other

than the cashier.

INTERNAL CHECK WITH REGARD TO PURCHASES

Purchase is of two types. cash purchases and credit purchases. The internal check has regard cash and credit

purchases are given as follows.

a. No purchase should be made without purchase requisition slip issued by store department. The details about

the quantity, quality and the time by which the goods must be supplied be clearly mentioned in the requisition

slip.

b. In order to purchase the required item, the purchase department makes an enquiry about the terms and

conditions of purchase from different suppliers. Tenders one also invited and the one with the lowest prices

accepted.

c. The purchase manager should be given the authority to issue purchase order 1 original and with '3' copies of

the order should be prepared. The original copy sent to the suppliers, one copy sent to the account department,

1 to the store department and 1 is retained by the purchase department for reference.

d. All the goods received should be checked with the purchase order from and with the challenge of the

suppliers. After the goods have been inspected for quality and quantity, a goods receipts register is to be

maintained for recording the same at the store department or centralized warehouse.

All the invoices (bills) received from the supplier’s one to be entered in the purchase day book.

e. The purchase department should properly check the invoices and send the same to the account department for

payment. The accounts department compares its invoice with the purchased order, and also verify the bill

amount. An A/c payee cheque is then to be issued and these cheques should be marked as 'paid'.

INTERNALS CHECK WITH REGARDS TO SALES:

Sales are the important source of revenue in a business. The system of internal check regarding sales should be

extremely efficient otherwise frauds might take place. Hence the whole system of credit sales should be kept

under proper control and supervision.

1. When an order is received, it should be recorded in the other received book. With the details like date of

receiving the order, name of the customer, particulars about goods, date of delivery, mode of transport etc. If

it is a verbal order, a confirmatory written order should be obtained.

2. The copy of the order should be sent to the dispatch department with necessary particulars. It should see

that the order is executed according to specification.

3. The dispatch department should take step to pack the goods as part of the order. Another clerk should

compare the goods so dispatched with the order, to see that the whole order is met and another list in prepared

showing the goods in package and this list is sent to the counting house.

4. A responsible official will mark the rate at which the goods are to be charged, the terms and conditions of

the order so that there is no complaints from the buyer.

5. with the help of the copy of the invoice, entries should be made in the sales day book.

6. On dispatch of the goods records should be made in the goods outward book.

7. Two copies of the invoice are rent to the customer, who will return one of them after signing it. It acts as a

delivery note. Third copy is retained for future reference.

8. Entry should be made inwards book, for goods returned by customers (sales returns). credit note should be

prepared and checked and signed by the responsible official.

9. With the help of credit note, record should be made in the sales returns

book.

INTERNAL CHECK WITH REGARD TO STORES (STOCK)

1. The store room should be located at a convenient place. It should have proper stores facilities so that goods

may not be misplaced, misused or wasted.

2. On receiving the goods, it should be properly recorded by the store keeper on goods received sheets in

triplicate. One copy to be given to account department, one to buying (purchase) department and third to be

retained by the stores.

3. All the items in the stores should bear a reference number and should be stored at their allotted rack and bins.

Bin cards should be used in the stores which should hang outside each bin. Stock- taking should be carried out

at regular intervals it should be done by an independent person who is not involved in any way with purchase,

issues or maintenance of stores.

4. No item from the store should be issued to any person without formal requisition from some authority. Only

authorized person should be allowed to remove articles from the stores according to requisition. For

material or stores returned from the job of department. Material return notes should be written and properly

accounted for. Material transfer note should be issued for transferring material from one department to

another. The gatekeeper should be instructed not to allow any material out of the factory without permit from

the store keeper.

5. After the issue of materials from the stores, the issue requisition should be sent to the stores. Account section

for proper record. The bin cards should be checked and compared from time to time with stores records.

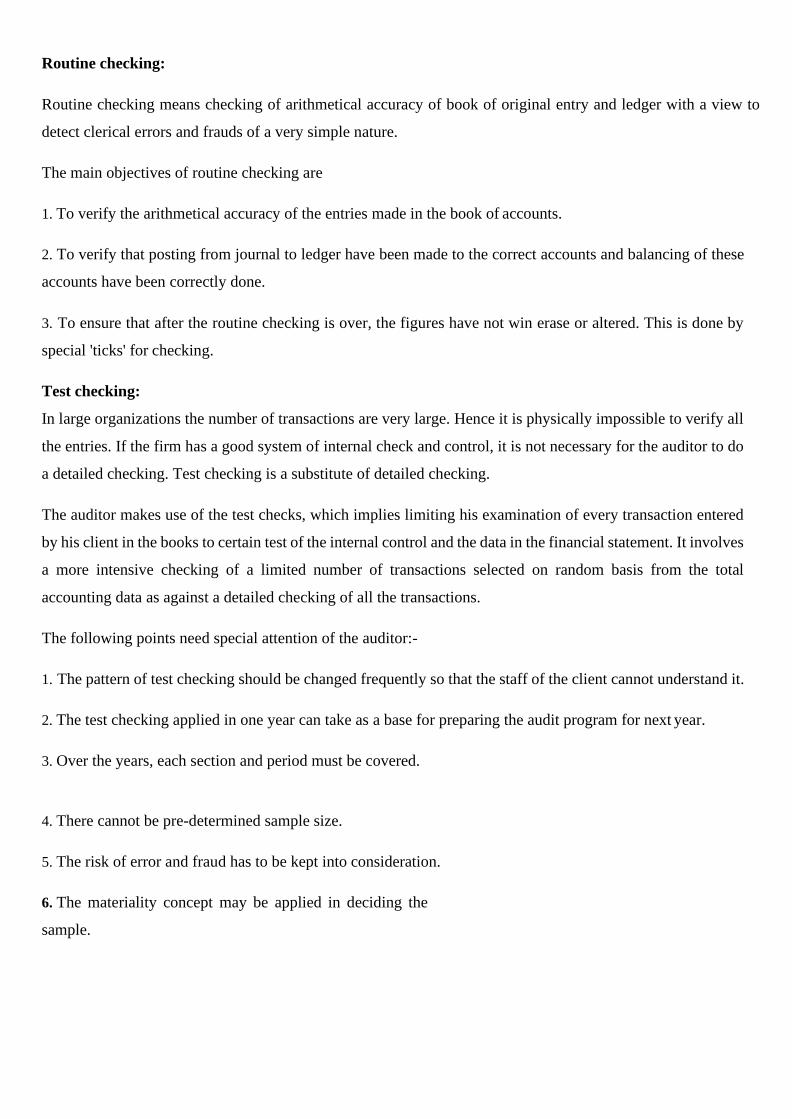

Routine checking:

Routine checking means checking of arithmetical accuracy of book of original entry and ledger with a view to

detect clerical errors and frauds of a very simple nature.

The main objectives of routine checking are

1. To verify the arithmetical accuracy of the entries made in the book of accounts.

2. To verify that posting from journal to ledger have been made to the correct accounts and balancing of these

accounts have been correctly done.

3. To ensure that after the routine checking is over, the figures have not win erase or altered. This is done by

special 'ticks' for checking.

Test checking:

In large organizations the number of transactions are very large. Hence it is physically impossible to verify all

the entries. If the firm has a good system of internal check and control, it is not necessary for the auditor to do

a detailed checking. Test checking is a substitute of detailed checking.

The auditor makes use of the test checks, which implies limiting his examination of every transaction entered

by his client in the books to certain test of the internal control and the data in the financial statement. It involves

a more intensive checking of a limited number of transactions selected on random basis from the total

accounting data as against a detailed checking of all the transactions.

The following points need special attention of the auditor:-

1. The pattern of test checking should be changed frequently so that the staff of the client cannot understand it.

2. The test checking applied in one year can take as a base for preparing the audit program for next year.

3. Over the years, each section and period must be covered.

4. There cannot be pre-determined sample size.

5. The risk of error and fraud has to be kept into consideration.

6. The materiality concept may be applied in deciding the

sample.

UNIT-III

VOUCHING

Meaning

• Vouching is concerned with examining documentary evidence to ascertain the authenticity of entries in

books of entries in books of accounts. It is an inspection by the auditor of an evidence supporting and

substantiating the transaction made in the books. It is a technique used by the auditor to judge the truth of

entries appearing in the books of accounts. All accounting entries must be supported by a document. It is

not only examining the documentary evidence but sometimes auditor has to go behind recorded evidence

to eliminate any possibility of fraud.

DEFINITION

• “Vouching is the examination of the evidence offered in substantiation of entries in the book including in

such examination the proof, so far as possible, that no entries have been omitted from the books” -Taylor

and Perry.

OBJECTIVES OF VOUCHING

• To ensure recording of all transactions.

• To verify that all transactions recorded in the books of accounts are supported by a

documentary evidence.

• To verify the validity of the vouchers which support the entries and to ascertain whether

these are authentic, addressed to the business and properly dated.

• To verify that no fraud or error has been committed while recording the transactions in the

books of accounts.

• To ensure that the vouchers have been processed carefully through various stages of internal check

system.

• To verify whether every transaction recorded has been adequately authenticated by a responsible

person.

• To know that while recording the transaction whether distinction has been made between capital and

revenue items.

• To ensure whether accuracy has been observed while totaling, carrying forward and recording and

amount in the account.

• To verify that all the transactions connected with the business have been recorded in the books of

accounts.

• To check vouchers which support entries are legal, valid, authentic, addressed to the business and

properly dated.

• To have greater precision in reporting the financial information as true and fair.

• To ensure reliability of figures entered in the books of accounts.

• To confirm that no transaction has been recorded in the books of accounts which are not related to

the entity under audit.

POINTS TO BE NOTED WHILE VOUCHING

1. Auditor must verify the authenticity of transactions, accuracy of amount recorded and proper

classification of account.

2. All the vouchers are numbered serially and dated. To avoid wasting of time in locating a voucher,

they have to be arranged serially.

3. The voucher checked by the auditor should be stamped or tick marked with a special sign, to avoid its use

again.

4. The amount in the receipt must be shown in words and figures. If there is a difference, it should be

investigated.

5. The receipt should indicate the period for which the payment has been made. It will show the payments

made in advance.

6. If the voucher is in the personal name of the partners, manager, director or any other person, it should be

properly treated in the books of accounts.

7. The auditor should proceed cautiously and use special ticks for the vouchers which are doubtful.

8. Every voucher should be certified by a responsible officer of the business.

9. All expenses pertaining to the business should be examined by the auditor.

10. A receipt obtained from a party for Rs.20/- or more should bear the revenue stamp.

11. The auditor should see that proper account is debited or credited and proper classification of accounts

has been done.

12. Distinction is made between capital and revenue items while vouching.

13. Alterations in the vouchers must be supported by the concerned officer’s initials.

14. Auditor should use specific ticks for vouching cash payments, receipts, purchases, sales etc.

A) VOUCHING OF TRADING TRANSACTIONS

1. VOUCHING OF PURCHASE BOOKS.

1 . The main aim of vouching of purchases book is to see that all purchases invoices are entered in

purchases book and the goods are entered in the purchases book are actually received by the business.

2. Payment is made for only those goods which are delivered by the supplier.

3. Vouching normally depends on the frequency of purchases, size of the organization and the staff

employed.

4. If the internal control system for purchases is inadequate, the auditor has to exercise a greater care in

vouching the purchase transactions.

Auditor’s Duties While Vouching Credit Purchases

1. a) There should be proper record for all the purchase orders. A duplicate copy of order is kept in the office

for record.

b) A copy of purchase order shall be sent to Accounts Department.

c) All goods received should be recorded on goods received note; a copy of it should be sent to Accounts

Department.

d) Payment of supplier is made only after verification of receipt of goods and the price quoted in purchase order.

2) The auditor should see that only credit purchases of goods are recorded in purchase book.

3) The purchases book can be verified from purchase invoices, copies of orders placed, goods received note,

goods inward book, copies of challans from suppliers.

4) The quantity mentioned in the invoice must be the same as in shown in the Purchase order.

5) The price charged by the supplier must be as per quotation/price list of supplier.

6) The supplier bill must in the name of the business and for the period under audit.

7) The goods purchased must not be for the personal use of Directors or officers.

8) While vouching the purchase vouchers, each voucher should be stamped or initiated after examination, so

that it cannot be produced again.

9) The totaling and casting of purchases book should be verified. It should also be seen that all Taxes,

octroi, and freight are added to the purchases and trade discounts allowed are deducted.

10) In certain cases, statement from the suppliers may be obtained to verify his purchases

records.

11) The auditor should be more careful while vouching the purchases made in the first and the last month of the

accounting period, because sometimes the purchases of the last year may be included in the purchases of

first month of the current year or purchases of the last month of the current year may be recorded in the

next.

12) Duplicate invoices must not be entered in the purchases book if original invoices have already been recorded

2. VOUCHING OF PURCHASE RETURNS

Sometimes the purchased goods are returned back to the supplier for the various reasons. The goods

purchased may not correspond to the quality or the specifications ordered. The auditor should see

that there exists a proper system to record such returns. In such cases, the purchaser sends back the

invoice or alternatively a credit note may be obtained from the supplier. The credit note should

include the amount which was originally included in the invoice. A separate returns book is

maintained to record the returns. If the supplier replaces the goods returned, the information must

be sent to both departments.

AUDITOR’S DUTY

o He should see that a Debit note has been sent to the supplier or Credit note has been received from

the supplier.

o The quantity returned must correspond with the store-keeper’s record, return outward register

and gatekeeper’s outward register.

o The amount shown in Credit note should be verified.

o The auditor should be careful about the recording of purchases return in the current year.

Sometimes the profits of current year may be manipulated by recording current year’s

purchases returns in the subsequent years.

o The purchases return of the first month and last month of the accounting year should be vouched

carefully, to detect any manipulation of amounts.

3. VOUCHING OF CREDIT SALES

In big organizations sales are made on credit basis. The client himself prepares the sales invoices and

records credit sales in the sales book. The auditor can depend on sale invoices, and internal control

system for credit sales in operation.

INTERNAL CONTROL OF CREDIT SALES

• Any order received or booked should be recorded in a separate register, giving full details of the goods

ordered. The details are: a) Name of the customer b) Quantity ordered c) Selling Price d) Reference

number e) Date of delivery f) Mode of delivery g) Particulars regarding sales tax, excise duty and

insurance.

• After receiving the order, a copy of the same is sent to dispatch section, where the clerk will keep the

goods separate for the purpose of dispatch.

• Another clerk will prepare the list of goods and verify the goods dispatched with the customer’s order.

• Three copies of the challan should be prepared giving the full details of goods dispatched. One copy will

be kept by the dispatch Department and other two copies will be sent along with the goods.

• One copy will be received back duly receipted, which serves as the proof of dispatch of goods. The

original copy of invoice is sent the customer, and another copy to Accounts Department.

• If the orders are received through agent, a copy of sales invoice will be sent to the agent for sales

commission and execution of sales order.

• If agent collects the payment from customers, necessary information shall be provided.

• For collection of amount of Sales Invoice either Sales or Accounts Department may make cautious efforts

to collect the amount after expiry of credit period.

• Up-to-date record shall be maintained by Departments.

AUDITOR’S DUTIES

• He should examine the internal control system to assess the efficiency of the system by test checking. If not