UNIT 3 BASICS ACCOUNTING - eGyanKosh

16

UNIT 3 BASICS ACCOUNTING Objectives: After going through this unit, you will understand: What are basic principles in accounting?. a Principle steps in Accounting; The different books of accounts to be maintained by NGOs; L Y The terms Journal, Ledger and Trial Balance; and Preparation of Financial year closing accounts for auditing. @ Structure i 3.1 Introduction 3.2 Legal Requirements 3.3 Need for Maintaining Accounts 3.4 Meaning of Double Entry Book keeping I 3.5 Steps in Accounting Process 3.6 Basic Rules in Accounting 3.7 Journal, Ledger and Trial Balance 3.8 Final Accounts 3.9 . The Capital Fund and Fixed Asset Assessment 3.10 Summary 3.1 1 Self Assessment Questions 3.1 2 Further Readings. 3.1 . INTRODUCTION - - - The need for good financial health of any organization need not be emphasized, more so in the case of NGO' because it is generally managed by non-professionals. It is also important that the founders, members and the general public are aware of the financial standing of the organizations for which they are supportive. The health of the organization needs to be constantly monitored so as to avoid mismanagement, embezzlement and consequent closure. It is also mandatory that the Societies and Trusts are audited wqualified chartered accountants annually. With the above VIEW in view, and to educate the persons involved in the NGOs set up, the Basic Accounting Unit is analyzed and discussed. 3.2 LEGAL REQUIREMENTS The Society's Registration Act and the Indian Trust Act makes it mandatory for NGOs to maintain and submit accounts annually. They require the organizations to have the annual accounts audited by qualified Chartered Accountant before submitting to them. The Income Tax Act also requires the organizations to maintain and submit audited accounts to finalize approval of reliefs under the Act. The accounting year starts from 1 st April to 3 1 March

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of UNIT 3 BASICS ACCOUNTING - eGyanKosh

UNIT 3 BASICS ACCOUNTING

Objectives:

After going through this unit, you will understand:

What are basic principles in accounting?. a

Principle steps in Accounting;

The different books of accounts to be maintained by NGOs; L

Y The terms Journal, Ledger and Trial Balance; and

Preparation of Financial year closing accounts for auditing. @

Structure i 3.1 Introduction

3.2 Legal Requirements 3.3 Need for Maintaining Accounts

3.4 Meaning of Double Entry Book keeping

I 3.5 Steps in Accounting Process 3.6 Basic Rules in Accounting 3.7 Journal, Ledger and Trial Balance 3.8 Final Accounts 3.9 . The Capital Fund and Fixed Asset Assessment 3.10 Summary 3.1 1 Self Assessment Questions 3.1 2 Further Readings.

3.1 . INTRODUCTION - - p p -

The need for good financial health of any organization need not be emphasized, more so in the case of NGO' because it is generally managed by non-professionals. It is also important that the founders, members and the general public are aware of the financial standing of the organizations for which they are supportive. The health of the organization needs to be constantly monitored so as to avoid mismanagement, embezzlement and consequent closure. It is also mandatory that the Societies and Trusts are audited wqualified chartered accountants annually. With the above VIEW in view, and to educate the persons involved in the NGOs set up, the Basic Accounting Unit is analyzed and discussed.

3.2 LEGAL REQUIREMENTS The Society's Registration Act and the Indian Trust Act makes it mandatory for NGOs to maintain and submit accounts annually. They require the organizations to have the annual accounts audited by qualified Chartered Accountant before submitting to them. The Income Tax Act also requires the organizations to maintain and submit audited accounts to finalize approval of reliefs under the Act. The accounting year starts from 1 st April to 3 1 March

I 1

Administration of NGOs of each year. Therefore, the onus is on the NGOs to write up books of 1 accounts, for all the transactions, preferably on daily basis, and have it audited periodically not only for submission to statutory authorities but also to know the financial health of the organization.

3.3 NEED FOR MAINTAINING ACCOUNTS ' The NGOs need to prepare and maintain the accounts on account of the

8

- -

following reasons:

To avoid or to reduce the possibility of misappropriation of h d s by any unscrupulous staff, members and others.

To ascertain whether their incomes for a year would be sufficient to meet their expenses for that year.

To know their financial position at the end of each financial year to undertake remedial measures if need be.

I I It acts .as a tool for financial management. 1

I

I I 3.4 DOUBLE ENTRY BOOK KEEPING - Every financial transaction has two aspects. One is 'receiving aspect, and the

I

other is 'giving aspect'. The two terms often used to denote these aspects are called 'DEBIT and CREDIT'. I

!

1 1 Let us understand these two terms, because they form the basis of financial transactions. I

DEBIT: The term 'debit' (Dr) is derived from the Latin word 'debere', which means what is due. So, the term 'debit' means the amount owed by or due from an account or charged to an account for the benefit received by that account. In short, it means the benefit received by an account. I

CREDIT: The term 'credit' (Cr) is derived from the Latin word 'credere', which means trust or belief. Therefore, the term 'credit' means the amount owed to an account for the benefit given by that account in the belief that its value will be returned at a later date. In short it means the amount to be rewarded to an account or the amount of discharge to be given to an account for the benefit given by that account.

1 3.5 STEPS IN ACCOUNTING PR-OCESS

Accounting is the complete sequence of accounting processes or procedures which begin with the recording of financial transactions in the book or books of original entry and end with the preparation of final accounts, and which q e repeated in the same order in each accounting period.

Sequential steps involved in accounting p'rocess are:

First Step: Recording the business transactions in the book or books of originatentry - Each and every financial transaction is entered in the journal or in the subsidiary books, date wise as and when they occur.

i Second Step: Classifying the transactions from the original books to ' B a s h of Accounting

Ledger- Posting or transferring those entries to the appropriate accounts in the ledger periodically. I Third Step: Balancing the various ledger accounts to arrive at the net balance in each account.

Fourth Step: Preparation of trial balance from the balances of various ledger accounts to verify or to check the arithmetical accuracy of ledger accounts.

t Fifth Step: Preparing thefinal accounts orfinancial statemen&: In the case of NGOs it will b&

1 Income and Expenditure account.

1 Receipts and payment account.

( Balance Sheet.

I From the trial balance a d after adjusting the adjustments if any, at the end of the accounting period, the above accounts need to be prepared to know the financial position of the organization. In the case of business organizations, the final accounts will give the profit or loss of the business operations.

BASIC RULES IN ACCOUNTNG

Under the double entry book keeping system, all the financial transactions are classified into three types. They are the following: f

Personal accounts

Real or Asset accounts

Nominal or Fictitious accounts.

I. PERSONAL ACCOUNTS

All financial transactions which relate to individuals, business enterprises or to any organizations are classified as transactions relating to personal accounts. Under the personal account, the person or the entity wholwhich receives the benefit of the transaction should be Debited and the person or the entity who1 which gives the benefit of the transaction should be credited. Therefore the rule is as under:

DEBIT THE RECEIVER AND CREDIT THE GIVER

The rule for debiting and crediting personal accounts can be explained with the help of the following examples:

(a) Received from Shanthi Rs.5000/-

The two accounts which in focus are Cash account and Shanthi's account. The cash account is the receiver and Shanthi is the giver; therefore the entry would be:

DEBIT CASH ACCOUNT Rs.5000/- and CREDIT SHANTHI'S A/C Rs. 5000/-

Administration of NGOS (b) Sold goods to Joseph on credit Rs.6001-

The two accounts which is focus are, goods account and Joseph's accouni Joseph is the receiver of the benefit and goods account is the giver of the benefit.

Therefore the entry would be: I

I

DEBIT JOSEPH ACCOUNT Rs.600/- AND CREDZT GOODS ACCOUNT- Rs. 600/- i 11. REAL OR ASSET ACCOUNT 1 In the case of assets it will either enter the organization or goes out of the organization.

I

Therefore the rule is as under: 1

The debiting of real accounk can be explained with the help of the following example:

1) Bought Office equipments worth Rs.25, QOOI- from M/s.Zenith and Company on credit.

The ofice equipment account and M/s.Zenith and company accounts are in focus.

Therefore the entry would be:

DEB~T OFFICE EQUIPMENTACCOUNT Rs.25000/- and CREDIT M/s.ZENITH AND CQMRANYACCOUNT Rs.25,000/-

111. NOMINAL OR FICTITIOUS ACCOUNT

The items of Expenses or Loss and Income or Gain are considered as Nominal accounts.

The accounting rule for the nominal accounts is as under:

DEBITALL EXPENSESAND LOSSES AND CREDZT INCOMESAND GAINS

The rule of debiting. ancl crediting nominal accounts may be explaned with ihe help of the following examples:

(a) &id Salary Rs.5001- to Mr. Rajesh

The two accounts that are in focus are salary account and Rajesh's account. The salary account is an expenses account to the organization. Therefore the entry would be:

DEBIT SALARYACCOUNTAND CREDIT RAJESH'S ACCOUNT

(b) Received commission from Bank

The two accounts that are in focus are, commission account and Bank account.

Commission is an income, therefore the entry would be:

DEBIT BANKACCOUNTAND CREDIT COMMISSIONACCOUNT

3.7 JOURNAL, LEDGER AND TRIAL BALANCE Basics of Accounti

1) JOURNAL (a) The term 'journal' is derived fi-om the French work 'jour, which means a

day. Journal, therefore, means a day book or a daily record. It is a book of original entry in which transactions are first recorded chronologically. It is written in the order of occurrence or order of dates fiom the source documents. In the journal, each transaction is analyzed in to debit (i.e., receiving or incoming), and credit (i.e., giving or outgoing) aspects, and both the debit and credit are recorded together in one entry, width a brief explanation for the entry called narration. Therefore, the 'journal' is:

Day book or daily record

chronological record or book date wise

Original entry, as all transactions are entered first in the journal. .

(b) The steps to be taken for each transaction to journalise the entry.

Ascertain the two accounts involved in the transaction.

Ascertain the classes of accounts these two accounts involve, namely whether it is Personal account, Real account or Nominal account.

Apply the relevant rules of debit and credit for each transaction.

ILLUSTRATION 1

Journalise the following transactions in the books of National High School:

2007

1. May 1 Library books purchased worth by cash Rs.5,000.

.2. " 2 Paid in to Bank Rs. 1000.

3. " 5 ~ & h t school fiuniture for Rs.2000 from M/s.Noble Furnitures on credit.

4. " 7 Paid salary by cash to Manager Rs. 1,000.

5. " 10 Fees received h m student Mr. John Rs.2000.

Explanation for the above transactions:

1) In the first transaction, the accounts that are involved are Cash account and Books account. The class of the account is Real or asset account.

2) In the second transaction, the accounts that are involved are Cash account and Bank account. The class of accounts is both Real and Personal.

3) In the third transaction, the accounts that are involved are Furniture account and M/s.Npble Furnitures account. The class of accounts is both Real and Personal.

4) In the fourth transaction, the accounts involved are, Salary account and Cash account. The class of accounts is Real account.

Administration of NGOs 5) In the fifth transdction, we find Fee account and Mr. Jon's account. The class of accounts is both Real and Personal.

I / (cj The journal entries for the above transactions will be: I 1

1

Journal Entries

Date ~ a d i c u ~ a r s LF Dr. Cr. m.1 m.1

2007 ' ,

May 1 Books account 5,000 To Cash account 5,000 (Being books purchased by cash)

i I

,, 2 Bank account 1,000 i i To Cash account 1,000 (Being cash remitted to bank account)

3

i

,, 5 Furniture account 2,000 To Noble Furniture account 2,000

i Being furniture bought on credit)

7 9 7 Salaryaccount To Cash account

,, 10 Fee account 2,000 To John's account 2,000 (Being fees received from John)

LEDGER

The term Ledger is derived from the Dutch work "Legger", which means a book where the various accounts are kept. A ledger is a summary statement of all transactions relating to a particular person, asset, expenses or income

. which have taken place during a given period of time. A ledger contains accounts for all the persons with whom the organization deals namely accounts of all personal accounts, real accounts and nominal accounts. Therefore the main features of a 'Ledger' is:

It is summarized analytical record of all transactions.

It is a secondary record, the primary record being 'Journal'. /

It is called as the principal book or king of books, because it contains information about all financial transactions of the organizations.

It is called the permanent storehouse of all the transactions.

d) Points to be noted while preparing ledger accounts:

1) Open separate account in the ledger for each account found in the

2) For all transactions relating to one account, only one account to be

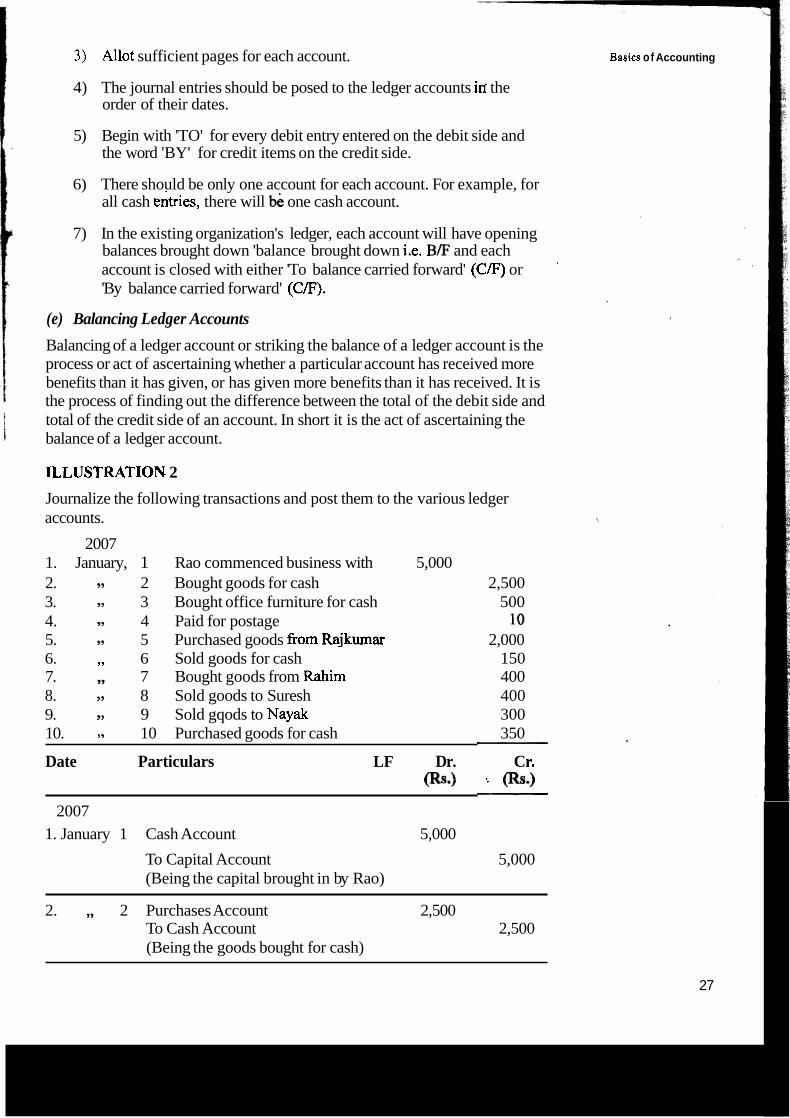

3) Allot sufficient pages for each account. Basies of Accounting

4) The journal entries should be posed to the ledger accounts iri the order of their dates.

5) Begin with 'TO' for every debit entry entered on the debit side and the word 'BY' for credit items on the credit side.

6) There should be only one account for each account. For example, for all cash entries, there will be one cash account.

7) In the existing organization's ledger, each account will have opening balances brought down 'balance brought down i.e. B E and each account is closed with either 'To balance carried forward' (CIF) or 'By balance carried forward' (C/F).

(e) Balancing Ledger Accounts

Balancing of a ledger account or striking the balance of a ledger account is the process or act of ascertaining whether a particular account has received more benefits than it has given, or has given more benefits than it has received. It is the process of finding out the difference between the total of the debit side and total of the credit side of an account. In short it is the act of ascertaining the i balance of a ledger account.

ILLUSTRATION- 2

Journalize the following transactions and post them to the various ledger accounts. 1

2007 1. January, 1 Rao commenced business with 5,000 2. ,, 2 Bought goods for cash 2,500 3. ,, 3 Bought office furniture for cash 500 4. ,, 4 Paid for postage 5. ,9 5 Purchased goods fiom Rajkumar 2,000 6. ,, 6 Sold goods for cash 150 7. ,, 7 Bought goods from Rahim 400 8. ,, 8 Sold goods to Suresh 400 9. ,' 9 Sold gqods to Nayak 300 10. " 10 Purchased goods for cash 350

Date Particulars LF Dr. C r. (&*I - @.I

2007 1. January 1 Cash Account 5,000

To Capital Account 5,000 (Being the capital brought in by Rao)

2. ,, 2 Purchases Account 2,500 To Cash Account 2,500 (Being the goods bought for cash)

27

Administration of NGOs 3. ,, 3 OficeFurniture

Account To Cash Account (Being the ofice furniture bought for cash)

4. ,, 4 Postage Account 10 To Cash Account 10 (Being the cash paid for postage)

5. ,, 5 Purchases Account 2,000 To Raj kurnar 's Account 2,000 (Being the goods bought from Raj kumar on credit)

6. ,, 7 Cash Account 400 To Sales Account 400 (Being the goods sold for cash)

7. ,, 8 Purchases Account 150 To Rahim's Account 150 (Being the goods brought from Rahim on credit)

- 8. ,, 9 Suresh's Account 400

To Sales Account 400 .,

( ~ ' e i n ~ the goods sold to Suresh on credit)

9. ,, 10 Nayak Account 300 To Sales Account 300 (Being the goods sold to Nayak on Credit)

\11 Puchases Account 350 I 10. ,, 1

To Cash Account 350 (Being the goods purchase6 for cash)

LEDGER

,The above journal entries are to be posted to the various ledger accounts in the following manner:

Cr. . . 2007 S . 2007 Rs.

January 3 1 Jh Balance cld. 5.000 January 1 By Cash Alc.5,000 5,000 5,000

Feb. 1 By Balance bld. 5,000

?rrr>:i;eses Account Cr. 3 . 220CL

Jan. L3 2 TO Cash Alc. 2 . - 2 Jan. 3 1 By ~Aanck cld. 4,900 5 ,, X~j~curr.~.:.''. ;/c. 2,C.. -

,, RZ;..;::~'S LA':. 9,

11 [ ,:;: Y Y 9'

Feb. 1 To Ba:r.:.!-,:: ;/r .

Dr. Sales Account Basics of Accounting Cr.

2007 Rs. 2007 Rs. Jan. 31 To Balance cld. 850 Jan. 7 By CashNc. 150

,, 9 " Suresh Alc. 400 ,, 10 " Nayak's Nc. 300

850 850 Feb. 1 By Balance b/d. 850

Dr. Office Furniture Account Cr.

2007 Rs. 2007 Rs. Jan. 3 To CashNc. 500 Jan. 31 By Balance cld. 500

500 500 I

Feb. 1 To Balance bid. 500 I

1 I

Dr. Nayak's Account Cr. 2007 Rs. 2007 Rs. Jan. 10 To Sales Nc. 300 Jan. 13 By Balance cld. 300

300 ,, 31 300 Feb. 1 300

Dr. Postage Account Cr. 2007 Rs. 2007 Rs. Jan. 4 To CashNc. 10 Jan. 31 By Balance cld. 10

10 10 Feb. 1 To Balance bid. 10

Dr. Cash Account Cr. 2007 . Rs. 2007 Rs. Jan. 1 To Capital 5,000 Jan. 2 By purchases 2,500 Jan. 7 To sales 150 Jan. 3 By Ofice 500

furniture Jan. 4 By Postage 10 Jan. 11 By Goods 350 Jan. 31 By Balance 1,790

5,150 5,150

Dr. Suresh Cr. 2007 Rs. 2007 &. Jan. 9 By Sales 400 Jan 31 By Balance cld 400

400 400

Dr. Goods Account Cr. 2007 Rs. 2007 Rs. Jan. 11 To Cash 350 Jan. 31 By Balance cld 350

350 350

TRIAL BALANCE The main objective of accounting is to ascertain the profit or loss and the financial position of the business organization. This can be achieved by preparing the final accounts of the organization. The final accounts have to be prepared on the basis of balances of various accounts in the ledger. Since the ledger accounts are spread over many pages besides there are additional

Administration of NG, ,. Trail balance facilitates in preparation of final accounts as all the balanct., found in the ledger accounts are available in one statement. In the words of J.R.Batliboi: "Trial Balance is a statement, prepared with the debit and credit ki#wp of.

> . r i 5

ledger accounts to test the arithmetical accuracy of the booksl!. & the words of Spicer and Pegler: "a trial balance is a list of all the balances sqd ipg fie ledger q ~ p o y t s and

i - . rrl r

cash book of a xncern at any given date". Advantages of Trial Balance:

I The balances of ledger accounts can be l~fated iq one place. i '

I It helps in checking aritkfneticg acC:wqFy. < '

I , ,_-. It helps in locating errors.

It helps in preqvation of fi@ q c ~ w t s . . * . .&

To help to carry out adjustments i f p y .

Noq-Profit Organiqti~ns q Ncq=Fjov%men@\ Organizatiaas fNQ(Si3) dg ~ s t norqqly yqdertake @+ding. But q m p NfSOs undewe trading ip ~ 7 , mall way like selling greetiqp F@S, etc. in ardpr ta be fipwcially sowd, Most: nfthem are involved in so&& senices such qr(g eduation, hospitals, and povpm alleviations. A few ~ f i ~ e m are /nv~]yed in w e q ~ n d @6, sciesw, literature sports etc. At the end of the year the padiqp t l rgwt ions tam interested knowing how much profit (N- loss they h&! made, L the awe d . non-profit organizations this i s not veq jmpo&t fay &w. But nevertheleyss. financial management i s necesgyy fay ~Q#I type sntitieai All s~mlzations need to use the financial resewps wja ~ p t k u r n ef8~ieooy. Tho non-pmht organizations prepare the foll~winq final weclunte (rt the end af the financial Year.

o Receipts and Payment account

Income and Expenditure Account

Balancesheet.

We will now try to understand these accounts in detail.

Receipts and Payments Aceount

A Receipts and Payments Account is a surnsqggy ~f a s h rseia& m(S payments relating to a given p~d of time, y ~ \ y (I It c~n&&a QW receipts and paymeqtg ~ f & g vq imspectiye ~ f t b a naM ePW i(pnu (i.e., whether they are capiM iteqs, feyegue item+ All oph tmmg~tiana which takes place d m 6 tbt pafFfc@q Y P ~ is q c w @ d W p e c t i w of the fact the items may y ~ l a e t~ p y i ~ ~ g QT q~bqgqya year. We Various items of cash receipts and cashhpayrne~tr recorded in the Cash Book are s m ~ m d and classified v d sh~wn iq the Receipts and P a p n t g Iq~gount. Tkg~ Receipts are rsorded en €he debit side a l e are rewrded on credit side. The essential features of a J&qqipts and Payme~ta mcoimt me:

1) It is prepared on the cash system of accounting.

2) it is prepared fiom the cash book.

3) It is prepared at the end of the financial or accounting year. I- 4) It starts with the opening cash and bank balances, and ends with the

closing cash and bank balances.

I 5) The receipts area shown in the debit side and payments are shown on the cpdit side.

r 6) incl@s b~~ capital and Revenue items of the year.

7) As it is suqqw of acQal cash receipts and actual cash payments, it does not include outstanding receipts and payments.

8) f{ dpes not include non cash items like bad debts, depreciation etc.

9) It does nc# t.ev& e e surplus (i.e., profit) or deficit (i.e., loss). It merely shows ~ balance of q& in tqpd p d at bank at the end of the accounting year.

10) ft blps in the fq~epargti~p of $hg jncome and expenditure account and bdwei sheet at b e d af the year or when ever required.

At end of the yaw, & fRMw q d E4pe@ipre ~ ~ c o u n t , reveals whefher tbe organization has ended with surplus or &figit. $ Qe iase of trading c(meems, Profit an4 b.8~ acGavnt i s prep& t~ p~erf@fl gwfit pr 19~s 17t dje end of the par. & income anQ $xpe&i@re fip$punt i s a revenue wg~ul)f aqd @kes into wcount only revenue items. It jq a summary of incomes and expenses for a particular period, ~suztlly a year.

%.".., , .

Receipts and Income and Payments Account Expenditure Account

1. It is a summary of actual cash receipts 1. It is a summary of incomes And cash payments of a given period. and expenses, for a .

particular period

3. It is prepared on the cash system of 2. It is prepared on the acp~@ting. accrual system of

accounting. - 3. It i ~ b & s b ~ t ~ @&?3i;ki3 V&l 3. It includes onlyrevenue

Revenue items. items.

4, It may oon&n &@ items of previous 4. It will contain only items and subsequent year. of current year.

'

5 . It dois pot iiclude non-cash items like 5. It includes items like bad Bad debts and &pteciatiun. 1 debts, and depreciation.

6.Receipt.s ara slwwq ol) &debit si& 'i And paymenu are an the i~redit side debit side and Income on

the credit side

Administration of NGOs

BALANCE SHEET

The Balance Sheet is a significant financial statement of an organization. As the name suggests, the balance sheet provides information about the financial standinglposition of an organization at a particular point of time, say as at March 3 1 .In order to give a complete picture of the state of affairs of a Non- Governmental Organisation, the income and expenditure account should be accompanied by a Balance Sheet.

7. It begins with an opening balance of Cash on hand and cash at Bank.

8. The closing balance represents cash

The balance sheet of a non-trading concern is prepared in the same manner as that of a trading loncern, showing the liabilities on the left-hand side, and the assets on the right-hand side of the Balance Sheet. However, the following main differences between two may be noted.

7. It does not begin with any opening balance.

8. The closing balance of this'

1) The balance sheet of a trading concern is prepared from the trial balance and adjustments, if any. On the other hand, the balance sheet of an NGO is

- prepared from the Receipts and Payments account, and other information

on hand and cash at Bank, normally account may be debit or a debit balance. credit balance.

9. The closing balance of this account is 9. The closing balance of this brought down to the next accounting account is, generally, not year. Brought down to the next

year.

available.

In the case of a trading concern, the capital is contributed by the owners, ar . the same is entered on the liabilities side of the bdance sheet. But in the c;-2 of NGOs, it is generally promoted by its members and promoters. It does not have capital contribution, instead, it has capital fund, general fund or accumulated fund. The capital fund is the accumulated surpluses over a number of years and the capitalized receipts. The capital fund on any date is the excess of assets over liabilities on that date. The capital fund is entered on the liabilities side of its balance sheet.

The contents of the Balance Sheet The assets side of the balance sheet of an NGO is generhuy. consists of:

r - ,+ Current Assets such as Cash on hand, Cash at h n k , d~btors, Stock, * '~b'tgtanding incomes and prepaid expenses, etc.

lavkhents, and Fixed Assets, such as Buildings, Furniture, Vehicles etc.

r"he Ubiliiies side of the balance sheet of an NGO usually consists of: cub& Liabilities like Creditors, outstanding expenses, income received in advance, etc.

Low-term fiabilities like Loans and deposits taken from others.

S~ecial Funds such as building fund, endowment fund, etc., and The closinp capital fund.

3.9 CAPITAL FUND AND FIXED ASSET Basics of Accounilng I

ASSESSMENT I The closing capital fund, or the general fund or accumulated fund of an NGO, which has been in existence for more than a year, can be ascertained by adding the capitalized receipts of the current year like, life membership fees, entrance fees etc., and the surplus ( i.e., the excess of income over expenditure) of the. current year with the opening capital fund. In case of deficit, (excess of expenditure over income) during the current year, it should be deducted fiom the total of the opening capital fund and the capitalized receipts of the current year.

In the case of newly started NGOs the capital fund can be ascertained by totalling up the capitalized receipts such as legacies, life membership fees, donations and the surplus (i.e., excess of income over expenditure of the - - current year. In case of deficit, the same is to be deducted. ,

The Fixed hs t s The closing balance or value of every fixed asset needs to be ascertained and entered on the asset side of the balance sheet. It can be ascertained as under:

Rs. Value of the fixed asset as at the beginning of - the current year - .................................... Add: Value of the fixed asset purchased during

.................................... Less: Book value of the fixed asset sold during the current year - - .................................... 'Less: Depreciation charged on the fixed asset during the current year - - .................................... Value of the fixed asset as at the end of the

- - .................................... . ILLUSTRATION 3

From the following statement of an Education Society, prepare an Income and Expenditure Account for the year ended 3 1 - 12-1 995 and the Balance Sheet as on that date.

Balance Sheet as on 31-12-1994 Capital Fund Audit Fees Creditors 200

/-- 3,890

Maps and Charts 3% Govt Bonds Subscription Outstand'mg

Administration of NGOs Receipts and payments Account as on 31-12-1995 To Bhlance b/d

,3 S~bscriptiona ,, Special Donations ,, Interest on Govt Bonda

By Audit Pees ,, Rent ,, Maps and Charts ,, Statione:y and Postage ,, Paid to Cr zditors

,, Salary ,, Functions ,, Balance

- 1) Audit fees Rs. 50 is still outstanding 2) Charge Rs. 25 as depreciation on furniture. 3) ?4 of the special donations is to be capitalized. (Adapted from Karnataka State I1 P.U.C., April, 1984) Solution: Education Society To Audit fees Less: last year's Outsunding (as given in the opening bsl: ace sheet) Add: Current year's Outstanding ,, Rent ;, Stationery and ,, Postage

,, Salary (Expenses on)

,, Functions ,, Depreciation on ,, furniture '' Excess on Income Over Expenditure

By Subscriptions Less: Last year's Outstanding (as given in the opening balance sheet) ,, Special donations (Half of the amount treated as revenue receipts or incomes) ,,Interest on investments received Add : Outstanding Interest Balance Sheet as on 3 1" ~ecember, 1995

RS. 50

(Currefla yeiiPs) outstanding

Audit feee Cfditors 420tb1TS) Closing Capital Fund Opening ~apital f l i ~ d Add: Speci~l donations Capitalized (950 p: '1'2) Add: Exce~d of Incurfie Over ~x~enditure

Aasets Gash trl kwd [ C w n l yeafig) O~tstafldihg Inteteat drl fnve~tmefl€s Itlv38tfie~s

Map8 and cham: Open@ value Add: Additional '

Maps and chans Purchased during The year Furnim Le~s: Depredation note^:

Basics of Accountlrrg

Rs. 160

1) Half of the special donations., viz., Rs. (250 x !A) 125, a e capitalized. The special domition8 capitalized, viz., Rs. 125, should be added to capital fund on the liabilities side of the closing balance sheet.

2) Outstanding interest on government bonds, viz., Rs. 48 has been arrived at as follows:

Amount invested m government bonds is Rs. 3,100. The investments on government bonds has been there throughout the year. The rate of interest on investments is 3% So, the interest on investments for the year should be Rs. (3,100 x 311 00) 93. but the interest on investments received during the year *is only Rs. 45. That means, the remaining interest of Rs. (93-45) 48 should be outstanding.

3) Maps and charts are fixed assets. So, they should appear on the assets side of the closing balance sheet. '

4) The term 'functions' given on the payments side of the Receipts and Payments account should be taken to mean expenses on functions. So, this item should appear on the debit side of Income and Expenditure Account.

5) The amount of creditors shown on the liabilities side of the closing balance sheet, viz., Rs. 25, has been arrived at as follows:

Administration of NGOs Creditors as per opening balance sheet 200

Less: Amount paid to creditors during the year as per the Receipts and Payments Account 175

Balance of creditors to be s!~.om. as a liability in the closing 25 . Balance sheet

3.10 SUMMARY This unit familarizes you with the basics of accounting. It gives an idea as to . how the accounting concepts can be applied to the NGO sector. The various concepts like trial balance and different types of accounts have been discussed.

3.11 SELF-ASSESSMENT OWESTIONS

Q1. Explain the concept of accounting giving examples.

42. Differentiate between journal, ledger and a trial balance.

4 3 . Explain how a balance sheet is prepared giving hypothetical example.

4.12 FURTHER READINGS Raman B.S., 2005. 'Accountancy ', United publisher's Press. Mangalore.

Raman B.S., 1996. 'Text Book ofAccountancy ', United Publishers, Mangalore.

Chandra, Prasanna. 1985. 'Manager h Guide to Finance andAccounting', Tata McGraw-Hill: Delhi.

Shukla, M.C, and Grewal, T.S, Gupta S.C. 2006. "Advanced Accounting", Sultan Chand & Co. Ltd, New Delhi.

Iyengar. S.P, "Accountancy", 2002. Sultan Chand & Co. Ltd, New Delhi.

Nabhi Kurnar Jain, 200 1 . 'Formation & Manqgement of a Trust ', Taj Press, New Delhi.