Topic 5 Capital Budgeting Technique 2

47

Topic 5: Topic 5: Capital Budgeting Capital Budgeting Techniques Techniques BWFF2023 FINANCIAL MANAGEMENT II BWFF2023 FINANCIAL MANAGEMENT II

Transcript of Topic 5 Capital Budgeting Technique 2

Topic 5:Topic 5:Capital Budgeting Capital Budgeting

TechniquesTechniques

BWFF2023 FINANCIAL MANAGEMENT IIBWFF2023 FINANCIAL MANAGEMENT II

Capital BudgetingCapital Budgeting: : The process of planning for The process of planning for purchases of purchases of long-term assetslong-term assets..- Accept or Reject?- Accept or Reject?- Focus on Cash Flow- Focus on Cash Flow

For example: Suppose our firm must decide whether to purchase a new plastic molding machine for $125,000. How do we decide?

Will the machine be profitable?Will our firm earn a high rate of return on the investment?

Decision-making Decision-making Criteria in Capital Criteria in Capital BudgetingBudgeting

How do we decide if a capital

investment project should be accepted or rejected?

Decision-making Decision-making Criteria in Capital Criteria in Capital BudgetingBudgeting

The ideal evaluation method should:a) include all cash flows that occur during the life of the project,

b) consider the time value of money, and

c) incorporate the required rate of return on the project.

Decision-making Decision-making Criteria in Capital Criteria in Capital BudgetingBudgeting

Firms invest in 2 categories of projects:

1)Independent projects – do not compete with each other. A firm may accept none, some, or all from among a group of independent projects.

2)Mutually exclusive projects – compete against each other. The best project from among group of acceptable mutually exclusive projects is selected.

Techniques in Techniques in Capital BudgetingCapital Budgeting

1) Payback period2) Discounted Payback Period3) Net Present Value (NPV)4) Profitability Index (PI)5) Internal Rate of Return

(IRR)

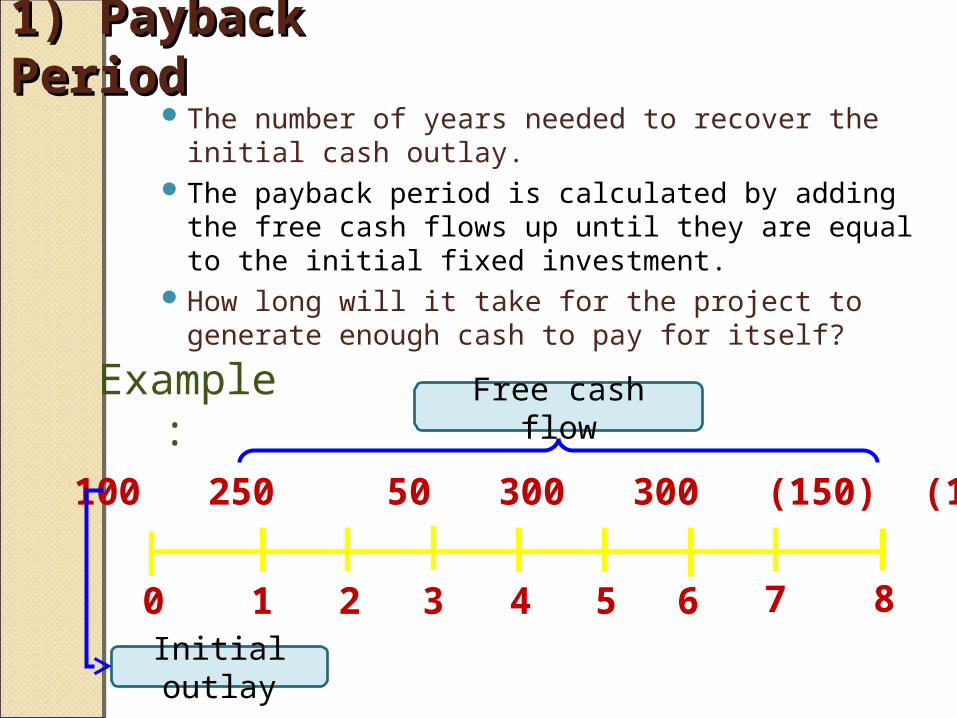

1) Payback 1) Payback PeriodPeriod

The number of years needed to recover the initial cash outlay.

The payback period is calculated by adding the free cash flows up until they are equal to the initial fixed investment.

How long will it take for the project to generate enough cash to pay for itself?

0 1 2 3 4 5 86 7

(500) 100 250 50 300 300 (150) (150) (150)

Example:

Initial outlay

Free cash flow

Project AYear Cash flow1 $1002 $2503 $504 $3005 $3006 ($150)7 ($150)8 ($150)

Initial outlay = $500.00Annual free cash flows:Year 1 : $100, balance left : $400Year 2 : $250, balance left : $150Year 3 : $50, balance left : $100 Year 4 : $300

We know that the payback period is 3 years ++ and the

remaining $100 can be recaptured during year 4, but how to

find the remaining period?

To determine the remaining period: = $ 100 (balance left in year 3) $ 300 (cash flow in year 4) = 0.33 year.

So the payback period for this project is 3.33 years.

Payback PeriodPayback Period

500 - 100400 - 250150 - 50

Payback PeriodPayback Period 3 + ($100/$300) = 3 + 0.33 = 3.33 years Is a 3.33 year payback period good? Is it acceptable? Firms that use this method will compare the payback calculation to some standard set by the firm.

If our senior management had set a cut-off of 5 years for projects like ours, what would be our decision?

Accept the projectDECISION RULE :

ACCEPTACCEPT if payback < maximum acceptable payback period.REJECTREJECT if payback > maximum acceptable payback period.

Advantages of Payback Advantages of Payback PeriodPeriod

Uses free cash flows – measures the true timing of benefit.

Easy to calculate and understand.

May be used as rough screening device.

Drawbacks of Payback Drawbacks of Payback PeriodPeriod

Firm cutoffs are subjective.

Does not consider time value of money.

Does not consider any required rate of return.

Does not consider all of the project’s cash flows.

2) Discounted Payback 2) Discounted Payback PeriodPeriod

The number of years needed to recover initial cash outlay from the discounted free cash flows.

Discounts the cash flows at the firm’s required rate of return.

Payback period is calculated by adding up these discounted net cash flows until they are equal to the initial outlay.

Discounted Payback PeriodDiscounted Payback Period

Year Free Cash DiscountedFlow CF (14%) Balance Left

0 -500 -500.00 1 250 219.30280.70

2 250 192.37 88.33

3 250 168.74

0 1 2 3 4 5

(500) 250 250 250 250 250 Initial outlay = $500.00Discounted free cash flows:Year 1 : $219.30, balance

left : $ 280.70Year 2 : $192.37, balance

left : $88.33Year 3 : $168.74

We know that the payback period is 2

years ++ and the remaining $88.33 can be

recaptured during year 3, but how to find

the remaining period?

To determine the remaining period:

= $ 88.33 (balance left in year 2)

$ 168.74 (discounted cash flow year 3)

= 0.52 year. So the payback period for

this project is 2.52 years.

FCF (1 +

k)n

Discounted Payback Discounted Payback PeriodPeriod

Discounted payback period is 2.52 years.

Is it acceptable?

ACCEPTACCEPT if discounted payback < maximum acceptable discounted payback period.

REJECTREJECT if discounted payback > maximum acceptable discounted payback period.

Discounted Payback Discounted Payback PeriodPeriod

Advantages:Uses free cash flowsEasy to calculate and to understand

Considers time value of money

Disadvantages:Ignores free cash flows occurring after the payback period.

Selection of the maximum acceptable discounted payback period is arbitrary.

Exercise:Exercise:You are considering a project with an initial outlay of $70,000 and expected free cash flows of $20,000 at the end of each year for six years. The required rate of return for this project is 10%.

a.What is the project’s payback period?b.What is the project’s discounted payback period?

Exercise:Exercise:You are considering a project with an initial outlay of $70,000 and expected free cash flows of $20,000 at the end of each year for six years. The required rate of return for this project is 10%.

a.What is the project’s payback period?b.What is the project’s discounted payback period?

Solution:

Payback period Cash Flow Balance leftYear 0 (70,000) -70,000Year 1 20,000 -50,000Year 2 20,000 -30,000Year 3 20,000 -10,000Year 4 20,000

Payback period = 3 + (10,000/20,000) = 3.5 years (balance left in year 3) (cash flow in year 4)

Exercise:Exercise:You are considering a project with an initial outlay of $70,000 and expected free cash flows of $20,000 at the end of each year for six years. The required rate of return for this project is 10%.

a.What is the project’s payback period?b.What is the project’s discounted payback period?

Solution: FCF

(1 + k)n

Discounted Payback period Year Free Cash Flow Discounted Cash Flow Balance left 0 (70,000) (70,000) -70,000 1 20,000 18,181.82 -51,818.18 2 20,000 16,528.93 -35,289.25 3 20,000 15,026.30 -20,262.95 4 20,000 13,660.27 -6,602.68 5 20,000 12,418.43 Payback period = 4 + (6,602.68/12,418.43) = 4.53 years (balance left in year 4) (discounted cash flow in year 5)

Exercise:Exercise:You are considering 3 independent projects; project A, project B and project C. The required rate of return is 10% on each. Given the following free cash flow information, calculate the payback period and discounted payback period for each .

YEAR PROJECT A PROJECT B PROJECT C0 - $

1,000 - $ 10, 000

- $5, 000

1 600

5,000

1,000

2 300

3,000

1,000

3 200

3,000

2,000

4 100

3,000

2,000

5 500

3,000

2,000

If you required a three-year payback for both the traditional and discounted payback period methods before an investment can be accepted, which project would be accepted under each method?

Other MethodsOther Methods

3) Net Present Value (NPV)4) Profitability Index (PI)5) Internal Rate of Return (IRR)

Consider each of these decision-making criteria:

All net cash flows.The time value of money.The required rate of return.

3) Net Present Value 3) Net Present Value (NPV)(NPV)

NPV = the total of all PV of the annual net cash flows – the initial outlay

Net Present Value (NPV)Net Present Value (NPV)

Decision rule :

ACCEPTACCEPT if NPV is positive { NPV > 0.0 }

REJECTREJECT if NPV is negative { NPV < 0.0 }

NPV ExampleNPV ExampleSuppose we are considering a capital investment that costs $250,000 and provides annual net cash flows of $100,000 for five years. The firm’s required rate of return is 15%.

(250,000) 100,000 100,000 100,000 100,000 100,000

0 1 2 3 4 5

NPV ExampleNPV ExampleSuppose we are considering a capital investment that costs $250,000 and provides annual net cash flows of $100,000 for five years. The firm’s required rate of return is 15%.

(250,000) 100,000 100,000 100,000 100,000 100,000

0 1 2 3 4 5 (n=1)

(n=2)

(n=3)

(n=4)

(n=5)

1. Find the PV for every cash flows discounted @ the investors required rate of return

2. Sum up the PV of all the cash flow involved

3. Minus the initial outlay from the total of PV of all cash flows

Steps to calculate NPV Steps to calculate NPV

Year Cash flow PVIFk,n PV of cash flows

1 $100,000 (0.870) =$87,000

2 $100,000 (0.756) =$75,600

3 $100,000 (0.658) =$65,800

4 $100,000 (0.572) =$57,200

5 $100,000 (0.497) =$49,700 ∑ PV =$335,300 minus IO = (250,000) NPV = $85,300

Solution:Solution:

Since the NPV is positive ( > 0.0 ) , so we should accept this project.

NPV = 100,000 100,000 100,000 100,000 100,000

(1.15)1 (1.15)2 (1.15)3

(1.15)4 (1.15)5

= 335215.50 – 250,000 = 85,215.50

Solution:Solution:

Since the NPV is positive ( > 0.0 ) , so we should accept this project.

+ + + + - 250,000

n = 5 k = 15% PMT = 100,000PV of cash flows = 100,000 (PVIFA15%,5) = 100,000 (3.352)

= $335,200

NPV = total PV – IO = 335,200 – 250,000

= $85,200

NPV > 0.0 , so ACCEPT

Since the amount of annual cash flow is equal for each period (an annuity), total PV can be determined as follows:

Alternative Solution:Alternative Solution:

Find the NPV of project A if the expected free cash flows are as follows. The firm required rate of return is 10%.

Year Free cash flows 0 (110,000) 1 20,000 2 30,000 3 40,000 4 50,000

Exercise:Exercise:

Find the NPV of project A if the expected free cash flows are as follows. The firm required rate of return is 10%.

Year Free cash flows 0 (110,000) 1 20,000 2 30,000 3 40,000 4 50,000

NPV = 20000 30000 40000 50000 (1.10)1 (1.10)2

(1.10)3 (1.10)4

= 107178.47 – 110,000 = - 2821.53

Exercise:Exercise:

+ + + - 110,000

(REJECT)

Also known as profit and cost ratio, i.e benefit/costs

PI = Present value of future free cash flow Initial outlay

4) Profitability Index 4) Profitability Index (PI)(PI)

Decision rule :ACCEPTACCEPT if PI is greater than or equal

to one { PI > 1.0}REJECTREJECT if PI is less than one { PI <

1.0 }

Profitability IndexProfitability IndexAdvantages:Uses free cash flowsRecognizes the time value of money

Consistent with the firm’s goal of shareholder wealth maximization.

Disadvantages:Requires detailed long-term forecasts of a project’s free cash flows.

Emerald Corp. is considering an investment with a cost of $250,000 and future benefits of $100,000 every year. If the company’s required rate of return is 15%, based on the profitability index (PI), should the Emerald accept the project?

Example:Example:

Year Cash flow PVIFk,n PV of cash flow

1 $100,000 (0.870) =$87,000 2 $100,000(0.756) =$75,600

3 $100,000 (0.658) =$65,800 4 $100,000 (0.572) =$57,200 5 $100,000 (0.497) =$49,700 ∑ PV=$335,300 PI = $335,300/250,000 = 1.3412 (Accept)

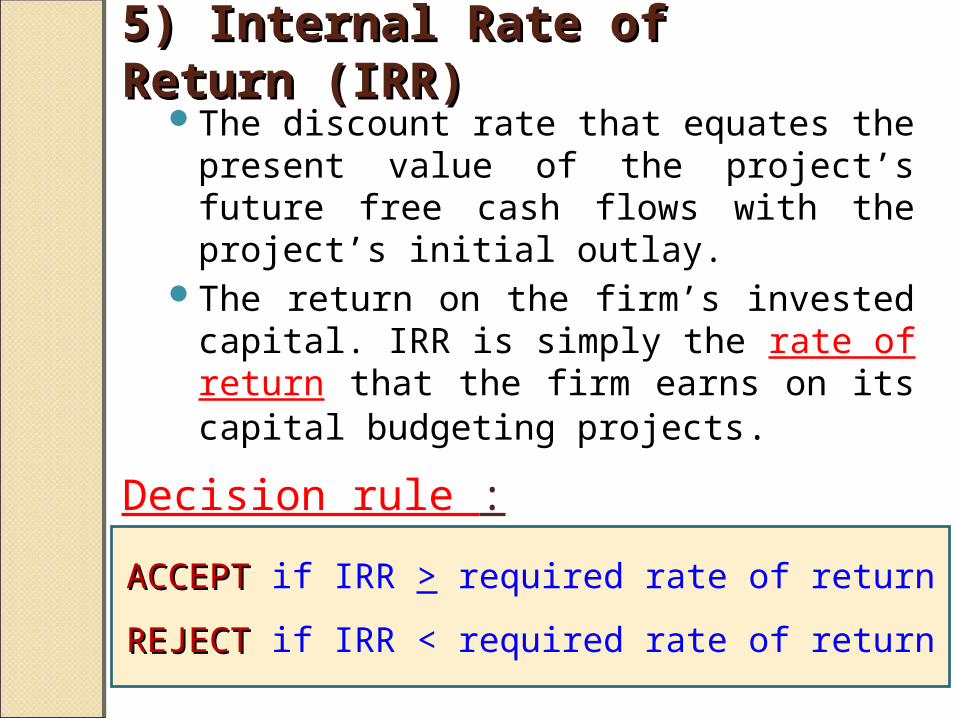

The discount rate that equates the present value of the project’s future free cash flows with the project’s initial outlay.

The return on the firm’s invested capital. IRR is simply the rate of return that the firm earns on its capital budgeting projects.

5) Internal Rate of 5) Internal Rate of Return (IRR)Return (IRR)

ACCEPTACCEPT if IRR > required rate of returnREJECTREJECT if IRR < required rate of return

Decision rule :

IRR is the rate of return that makes the PV of the cash flows equal to the initial outlay.

This looks very similar to our Yield to Maturity formula for bonds. In fact, YTM is the IRR of a bond.

n

t=1IRR:

= IO FCFt(1 + IRR)t

Internal Rate of Return Internal Rate of Return (IRR)(IRR)

InternalInternal Rate of Return Rate of ReturnAdvantages:Uses free cash flowsRecognizes the time value of moneyConsistent with the firm’s goal of shareholder wealth maximization.

Disadvantages:Possibility of multiple IRRsAssumes cash flows over the life of the project are reinvested at the IRR.

Requires detailed long-term forecasts of a project’s free cash flows.

Calculating IRRCalculating IRR•Looking again at our problem:•The IRR is the discount rate that makes the PV of the projected cash flows equal to the initial outlay. – req. rtn 15%

0 1 2 3 4 5

(250,000) 100,000 100,000 100,000 100,000 100,000

Method: trial and error/Interpolation1.Choose any discount rate [(randomly) – TIPs used req. rate as a base].

2.Compare ACF in step 1 with IO. If ACF = IO, we successfully find the IRR. If not, try again (step 3).

3.If ACF > IO , you should increased the discount rate.BUT, if ACF < IO, you should reduced the discount rate. Continue until you find the exact IRR (approximately).

4. After we have decide IRR is between the TWO discount rate that we choose, then use the interpolation method.

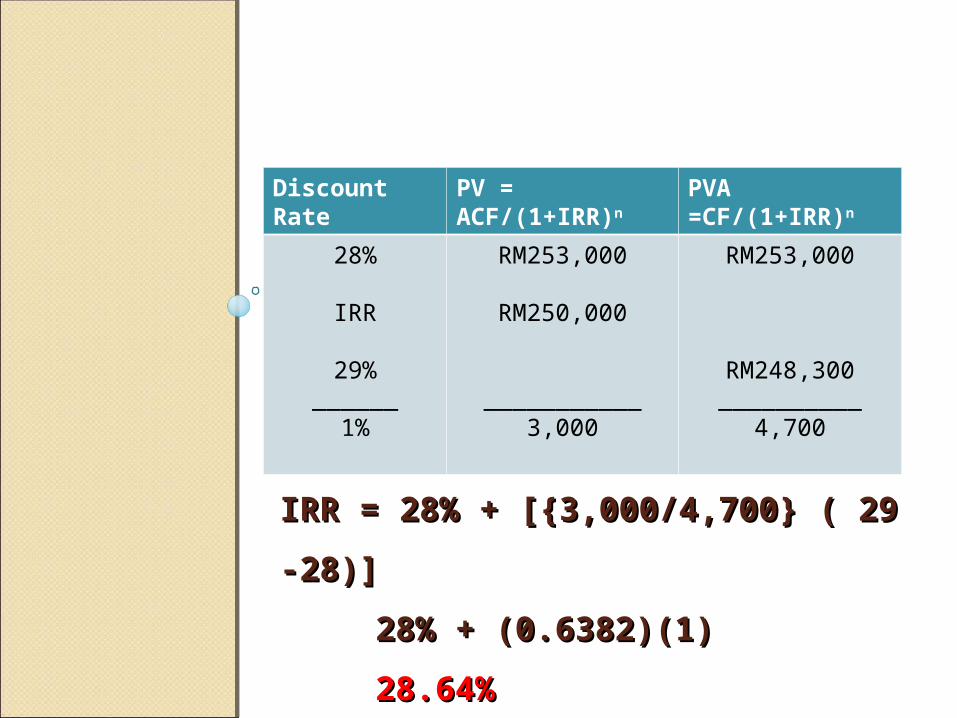

Calculating IRRCalculating IRR

IRR = 28% + [{3,000/4,700} ( 29 IRR = 28% + [{3,000/4,700} ( 29 -28)]-28)]

28% + (0.6382)(1)28% + (0.6382)(1)28.64%28.64%

Discount Rate

PV = ACF/(1+IRR)n

PVA =CF/(1+IRR)n

28%

IRR

29%______

1%

RM253,000

RM250,000

___________3,000

RM253,000

RM248,300__________

4,700

EXAMPLE:

Example:Example:Syarikat ABC is considering one project with an initial investment of RM49,900. This project is expected to produce ACF RM15,146 for the next 5 years. If the cost of capital (discount rate) is 13%, what is Syarikat ABC IRR?

•IRR is a good decision-making tool as long as cash flows are conventional.

•Problem: If there are multiple sign changes in the cash flow stream, we could get multiple IRRs.

0 1 2 3 4 5

(500) 200 100 (200) 400 3001 2 3

Noraziah Che Arshad 45

Summary ProblemSummary Problem

• Enter the cash flows only once.• Find the IRR.• Using a discount rate of 15%, find NPV.

• Add back IO and divide by IO to get PI.

0 1 2 3 4 5

(900) 300 400 400 500 600

Summary ProblemSummary Problem

•IRR = 34.37%.•Using a discount rate of 15%,

•NPV = $510.52.•PI = 1.57.

0 1 2 3 4 5

(900) 300 400 400 500 600

Modified Internal Rate of Modified Internal Rate of Return (MIRR)Return (MIRR)

• IRR assumes that all cash flows are reinvested at the IRR.

• MIRR provides a rate of return measure that assumes cash flows are reinvested at the required rate of return.