Title of the course

160

Title of the course MANAGERIATACCOUNTING AND CONTROL [ABM-504] Class, Year & Sem. MBA, I & II Topic Management Accounting Features of Management Accounting Management Accounting Information and their use Role of Management Accountancy Unit I Faculty i DEEPAK PAL & LAVEENA SHARMA Institute Institute of Agribusiness Management, JNKVV 1 Disclaimer: The information contained in this note is for general guidance & collected from various direct and indirect sources like websites, blogs, books, articles and open study sources. Author(s) make no representation for any legal responsibility or any other aspect of information contained.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Title of the course

Title of the course MANAGERIATACCOUNTING AND CONTROL [ABM-504]

Class, Year & Sem. MBA, I & II

Topic Management Accounting

Features of Management Accounting

Management Accounting Information and their use

Role of Management Accountancy

Unit I

Facultyi DEEPAK PAL & LAVEENA SHARMA

Institute Institute of Agribusiness Management, JNKVV

1 Disclaimer: The information contained in this note is for general guidance & collected from various direct and indirect

sources like websites, blogs, books, articles and open study sources. Author(s) make no representation for any legal

responsibility or any other aspect of information contained.

Management Accounting

Introduction :- The scope of Management Accounting is broader than the scope of cost accounting.

In cost accounting, as we have seen, the primary emphasis is on cost and it deals with collection,

analysis, relevance, interpretation and presentation for various problems of management. Management

Accounting is an accounting system which will help the Management to improve its efficiency. The

main thrust of Management Accounting is towards determining policy and formulating plans to achieve

desired objectives of management. It helps the Management in planning, controlling and analyzing the

performance of the organization in order to follow the path of continuous improvement. Management

Accounting utilizes the principle and practices of financial accounting and cost accounting in addition to

other modern management techniques for effective operation of a company. In fact there is an overlapping

in various areas of cost accounting and management accounting. However, the distinguishing features of

Management Accounting are given below.

Features of Management Accounting

The features of Management Accounting are given below.

1. The Management Accounting data are derived from both, the financial accounting and cost

accounting.

2. The main thrust in management accounting is towards determining policy and formulating plans to

achieve desired objectives of management.

3. Management Accounting makes corporate planning and strategy effective and meaningful.

4. It is concerned with short and long range planning and uses highly sophisticated techniques like

sensitivity analysis, probability techniques, decision tree, ratio analysis etc for planning, control and

evaluation.

5. It is futuristic in approach and predictive in nature.

6. Management Accounting system cannot be installed without proper cost accounting system.

7. Management Accounting systems generate various reports which are extremely useful from the

Management point of view.

Management Accounting Information and their use

In the above paragraphs, we have seen the utility of Management Accounting. One of the distinguishing

factors between the financial accounting and management accounting is that the management accounting

does not have a unified structure. The format in which it is prepared varies widely according to the

circumstances in each case and the purpose for which the information is being summarized. The

management accounting generates information, which is used for three different purposes. I] Measurement

II] Control and III] Decision making [Alternative choice problems] For each of these purposes, management

accounting generates vital information. The uses of information for each of the three purposes of

management accounting is explained below.

I. Measurement: For measurement of full costs, the management accounting system focuses on the

measurement of full costs. Full costs are the total costs required for producing goods or offering

services. These costs are divided into A] Direct costs and B] Indirect costs. Direct costs are identifiable

or traceable to the products or services offered while indirect costs are not traceable to the products or

services. Full cost accounting measures not only the total costs [direct plus indirect costs] required for

producing products or services but also the full costs required to run other activity like conducting a

research project or running a welfare scheme and so on. Thus full cost accounting is not restricted to

solely to measure the cost of manufacturing.

II. Control: An important aspect of the management accounting information is to provide information,

which can be used for ‘Control’. The management accounting system is structured in such a manner

that information is generated for each ‘Responsibility Center’. A responsibility center is an organization

unit headed by a manager who is responsible for its operations and performance. Management

accounting helps to prepare budget for each responsibility center and also facilitates comparison

between the budgeted and actual results. A report is prepared for each responsibility center, which

shows the budgeted and actual performance and also the difference between the two. This enables

the performance analysis of each responsibility center so that proper corrective action can be taken in

this respect.

III. Decision Making: Management accounting generates useful information for decision making.

Management has to take several decisions in the course of business. Some of the major decisions are,

Make or Buy, Accepting or rejecting of an Export Order, Working of second shift, Fixation of selling

price, Capital expenditure decisions, Increasing production capacity, Optimizing of Product Mix and

so on. For all these decisions, providing of information is necessary and the management accounting

generates this information, which enables the management to take such decisions.

Role of Management Accountancy

The role of management accounting and financial accounting is quite different from each other as they

have different goals altogether. Management Accounting measures, analyzes and reports financial and

non financial information that helps managers to take decisions to fulfill the goals of an organization.

Managers use management accounting information to choose, communicate and implement strategy. They

also use management accounting information to coordinate product design, production and marketing

decisions. Management accounting focuses on internal reporting. The following points highlight the role

played by Management Accounting in the business organization.

I. Implementing Strategy: Managers implement strategies by translating them into actions. Creating

value for customers is an important part of planning and implementation of strategies. Strategic

planning and implementation will include decisions regarding the design of products, services or

processes, research and development, production, marketing, distribution and customer services.

Each of this area is important for satisfying customers and keeping them satisfied. Management

accounting will help to track the costs of each of the activity mentioned above. The ultimate target

is to reduce costs in each category and to improve efficiency. Cost information also helps managers

make cost benefit analysis. For example, managers can find out that is it cheaper to buy products from

outside vendors or to do manufacturing in-house? Is it worthwhile to invest more resources in design

and manufacturing if it reduces costs in marketing and customer service?

II. Supply Chain Analysis: Companies can also implement strategy, cut costs and create value by

enhancing their supply chain. The term ‘Supply Chain’ describes the flow of goods, services and

information from the initial sources of materials and services to the delivery of products to customers

regardless of whether those activities occur in the same organization or in other organization.

Customers expect improved performance from companies through the supply chain. They expect

that the companies should perform all these activities in an efficient manner so as to reduce costs and

also maintain quality of the products and the products be available easily for them. This is no doubt a

daunting task and the management accounting plays a vital role in ensuring value for money for the

customers. Tools like standard costing and target costing can be used effectively for cost control and

cost reduction and thus ensure reasonable prices for customers. A system of budgets and budgetary

control will ensure continuous planning and monitoring various functions and thus provide for

introspection. Continuous improvement in these activities will help in creating value for customers.

III. Decision Making: One of the important functions of management is decision making. Management

Accounting helps in this crucial area by providing relevant information to the management.

Techniques like marginal costing helps to generate information, which will be useful for taking

decisions. Decisions include make or buy decisions, adding or dropping a product line, working of

additional shift, shut down or continue operations, capital expenditure decisions and so on. Decisions

based on information are expected to be more rational and objective rather than subjective.

IV. Performance Measurement: Management accounting helps immensely for the measurement of

performance of the organization. The main aspect of performance measurement is comparison

between the targets and actual. There are several tools and techniques like budgets and budgetary

control, standard costing and marginal costing, which are used in measuring the actual performance

against the target performance. This will facilitate introspection and corrective action can be taken for

further improving the performance.

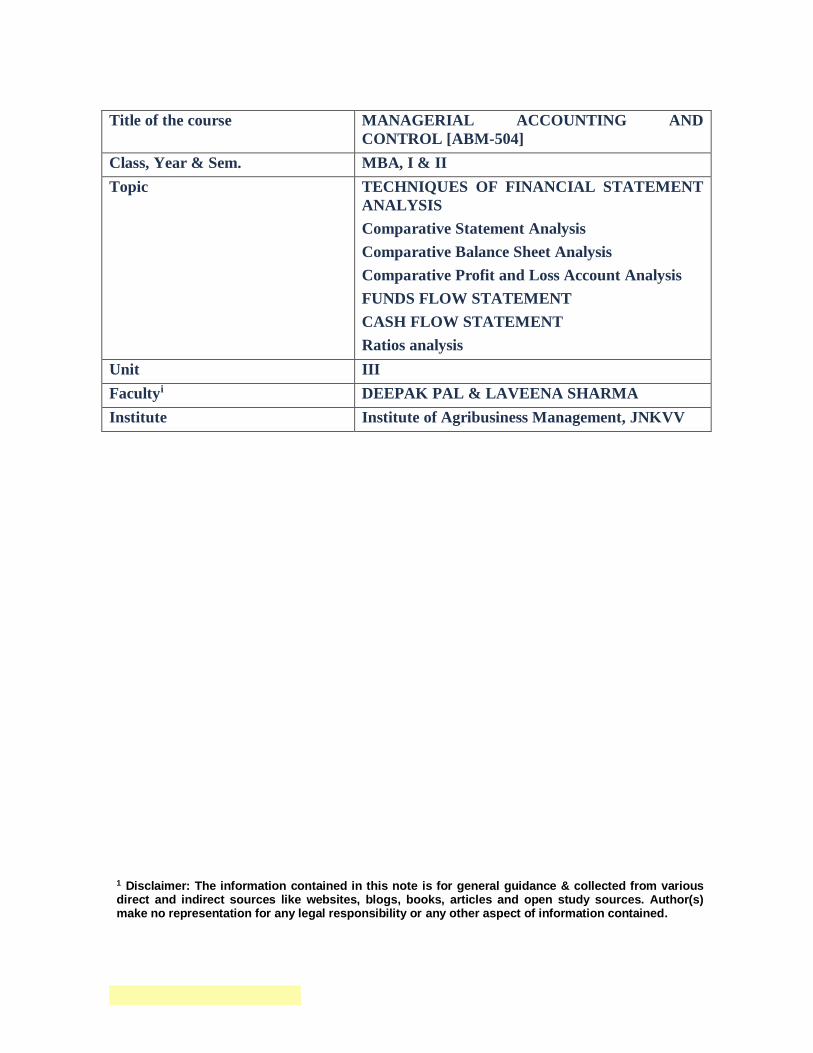

Title of the course MANAGERIAL ACCOUNTING AND

CONTROL [ABM-504]

Class, Year & Sem. MBA, I & II

Topic TECHNIQUES OF FINANCIAL STATEMENT

ANALYSIS

Comparative Statement Analysis

Comparative Balance Sheet Analysis

Comparative Profit and Loss Account Analysis

FUNDS FLOW STATEMENT

CASH FLOW STATEMENT

Ratios analysis

Unit III

Facultyi DEEPAK PAL & LAVEENA SHARMA

Institute Institute of Agribusiness Management, JNKVV

1 Disclaimer: The information contained in this note is for general guidance & collected from various direct and indirect sources like websites, blogs, books, articles and open study sources. Author(s) make no representation for any legal responsibility or any other aspect of information contained.

TECHNIQUES OF FINANCIAL STATEMENT ANALYSIS

Financial statement analysis is interpreted mainly to determine the financial and operational performance of the business concern. A number of methods or techniques are used to analyse the financial statement of the business concern. The following are the common methods or techniques, which are widely used by the business concern.

Fig. 2.3 Techniques of Financial Statement Analysis

1. Comparative Statement Analysis

A. Comparative Income Statement Analysis

B. Comparative Position Statement Analysis

Ratio Analysis

Comparative Statement

Trend Analysis

Common Size

Analysis

Funds Flow Statement

Cash Flow Statement

Techniques

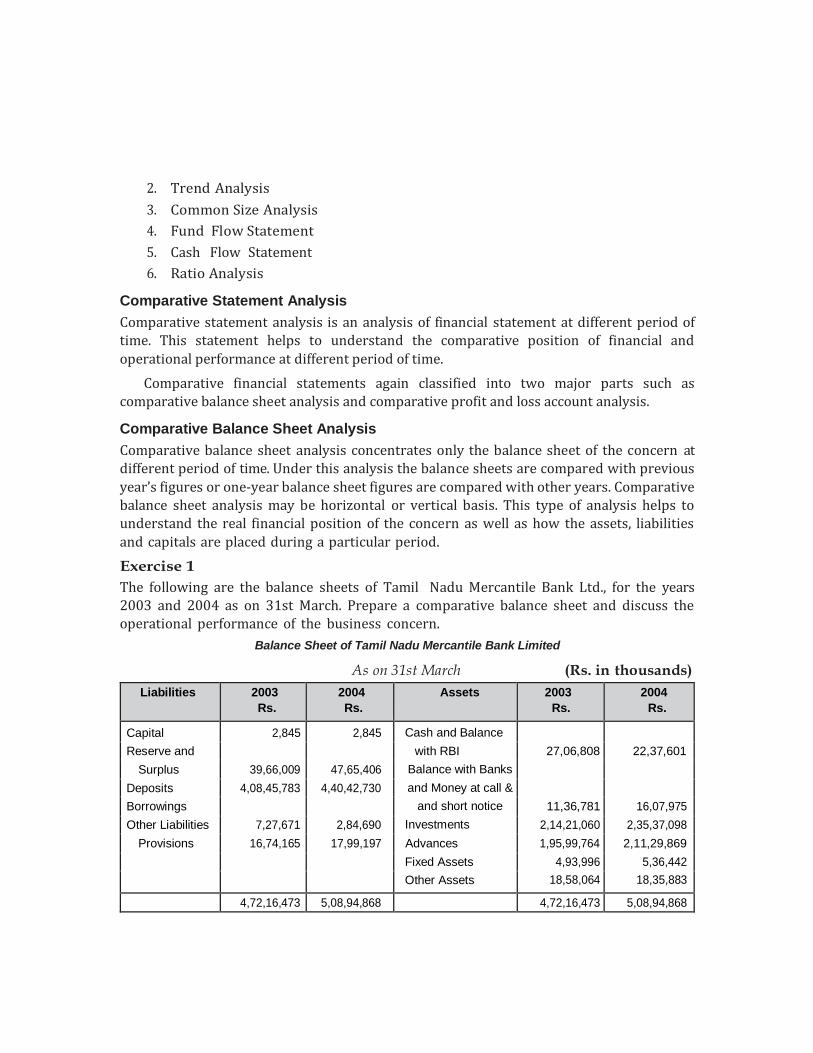

2. Trend Analysis

3. Common Size Analysis

4. Fund Flow Statement

5. Cash Flow Statement

6. Ratio Analysis

Comparative Statement Analysis

Comparative statement analysis is an analysis of financial statement at different period of time. This statement helps to understand the comparative position of financial and

operational performance at different period of time.

Comparative financial statements again classified into two major parts such as comparative balance sheet analysis and comparative profit and loss account analysis.

Comparative Balance Sheet Analysis

Comparative balance sheet analysis concentrates only the balance sheet of the concern at different period of time. Under this analysis the balance sheets are compared with previous

year’s figures or one-year balance sheet figures are compared with other years. Comparative balance sheet analysis may be horizontal or vertical basis. This type of analysis helps to understand the real financial position of the concern as well as how the assets, liabilities

and capitals are placed during a particular period.

Exercise 1

The following are the balance sheets of Tamil Nadu Mercantile Bank Ltd., for the years 2003 and 2004 as on 31st March. Prepare a comparative balance sheet and discuss the operational performance of the business concern.

Balance Sheet of Tamil Nadu Mercantile Bank Limited

As on 31st March (Rs. in thousands)

Liabilities 2003

Rs.

2004

Rs.

Assets 2003

Rs.

2004

Rs.

Capital 2,845 2,845 Cash and Balance

with RBI

Balance with Banks

and Money at call &

and short notice

Investments

Advances

Fixed Assets

Other Assets

Reserve and 27,06,808 22,37,601

Surplus 39,66,009 47,65,406

Deposits 4,08,45,783 4,40,42,730

Borrowings 11,36,781 16,07,975

Other Liabilities 7,27,671 2,84,690 2,14,21,060 2,35,37,098

Provisions 16,74,165 17,99,197 1,95,99,764 2,11,29,869

4,93,996 5,36,442

18,58,064 18,35,883

4,72,16,473 5,08,94,868 4,72,16,473 5,08,94,868

Solution

Comparative Balance Sheet Analysis

Particulars

Year ending 31st March

Increased/

Decreased

(Amount)

Increased/

Decreased

(Percentage)

2003

Rs.

2004

Rs.

Rs.

Rs.

Assets

Current Assets

Cash and Balance with

RBI

Balance with Banks and

money at call and short notice

27,06,808

11,36,781

22,37,601

16,07,975

(+) 4,69,207

(–) 4,71,194

(+) 17.33

(–) 41.45

Total Current Assets 38,43,589 38,45,576 1987 0.052

Fixed Assets

Investments 2,14,21,060 2,35,37,098 (-) 21,16,038 (-) 9.88

Advances 1,95,99,764 2,11,39,869 (-) 15,40,105 (-) 7.86

Fixed Assets 4,93,996 5,36,442 (-) 42,446 (-) 8.59

Other Assets 18,58,064 18,35,883 (+) 22,181 (+) 1.19

Total Fixed Assets 4,33,72,884 4,70,49,292 (+) 36,76,408 8.48

Total Assets 4,72,16,473 5,08,94,868 36,78,395 7.79

Current Liabilities

Borrowings 7,27,671 2,84,690 (+) 4,42,981 60.88

Other Liability and

Provisions 16,74,165 17,99,197 (–) 1,25,032 7.47

Total Current Liability 24,01,836 20,83,887 3,17,949 13.24

Fixed Liability Capital 2,845 2,845 — —

Reserves surplus 39,66,009 47,65,406 (+) 7,99,397 20.16

Deposit 4,08,45,783 4,40,42,730 (+) 31,96,947 7.83

Total Fixed Liability 4,48,14,637 4,88,10,981 (+) 39,96,344 8.92

Total Liability 4,72,16,473 5,08,94,868 36,78,395 7.79

Comparative Profit and Loss Account Analysis

Another comparative financial statement analysis is comparative profit and loss account

analysis. Under this analysis, only profit and loss account is taken to compare with previous

year’s figure or compare within the statement. This analysis helps to understand the

operational performance of the business concern in a given period. It may be analyzed on

horizontal basis or vertical basis.

Trend Analysis

The financial statements may be analysed by computing trends of series of information. It

may be upward or downward directions which involve the percentage relationship of each

and every item of the statement with the common value of 100%. Trend analysis helps to

understand the trend relationship with various items, which appear in the financial

statements. These percentages may also be taken as index number showing relative changes

in the financial information resulting with the various period of time. In this analysis, only

major items are considered for calculating the trend percentage.

Exercise 2

Calculate the Trend Analysis from the following information of Tamilnadu Mercantile

Bank Ltd., taking 1999 as a base year and interpret them (in thousands).

Year Deposits Advances Profit

1999 2,05,59,498 97,14,728 3,50,311

2000 2,66,45,251 1,25,50,440 4,06,287

2001 3,19,80,696 1,58,83,495 5,04,020

2002 3,72,99,877 1,77,26,607 5,53,525

2003 4,08,45,783 1,95,99,764 6,37,634

2004 4,40,42,730 2,11,39,869 8,06,755

Solution

Trend Analysis (Base year 1999=100)

(Rs. in thousands)

Year

Deposits Advances Profits

Amount

Rs.

Trend

Percentage

Amount

Rs.

Trend

Percentage

Amount

Rs.

Trend

Percentage

1999 2,05,59,498 100.0 97,14,728 100.0 3,50,311 100.0

2000 2,66,45,251 129.6 1,25,50,440 129.2 4,06,287 115.9

2001 3,19,80,696 155.5 1,58,83,495 163.5 5,04,020 143.9

2002 3,72,99,877 181.4 1,77,26,607 182.5 5,53,525 150.0

2003 4,08,45,783 198.7 1,95,99,764 201.8 6,37,634 182.0

2004 4,40,42,730 214.2 2,11,39,869 217.6 8,06,755 230.3

Common Size Analysis

Another important financial statement analysis techniques are common size analysis in which figures reported are converted into percentage to some common base. In the balance sheet the total assets figures is assumed to be 100 and all figures are expressed as a percentage of this total. It is one of the simplest methods of financial statement analysis, which reflects the relationship of each and every item with the base value of 100%.

Exercise 3

Common size balance sheet of Tamilnadu Mercantile Bank Ltd., as on 31st March 2003

and 2004.

Particulars 31st March 2003 Amount

Percentage

31st March 2004 Amount

Percentage

Fixed Assets

Investments 2,14,21,060 45.37 2,35,37,098 46.25

Advances 1,95,99,764 41.51 2,11,39,869 41.54

Fixed Assets 4,93,996 1.05 5,36,442 1.05

Other Assets 18,58,064 3.94 18,35,883 3.61

Total Fixed Assets 4,33,72,884 91.86 4,70,49,292 94.44

Current Assets

Cash and Balance with

RBI 27,06,808 5.73 22,37,601 4.40

Balance with banks

and money at call

and short notice 11,36,781 2.41 16,07,975 3.20

Total Current Assets 38,43,589 8.14 38,45,576 7.60

Total Assets 4,72,16,473 100.00 5,08,94,868 100.00

Fixed Liabilities

Capital 2,845 0.01 2,845 0.01 Reserve and Surplus 39,66,009 8.40 47,65,406 9.36

Deposits 4,08,45,783 86.50 4,40,42,730 86.54

Total Fixed Liabilities 4,48,14,637 94.91 4,88,10,981 95.91

Current Liability

Borrowings 7,27,671 1.54 2,84,690 0.56

Other Liabilities

Provisions 16,74,165 3.55 17,99,197 3.53

Total Current Liability 24,01,836 5.09 20,83,887 4.09

Total Liabilities 4,72,16,473 100.00 5,08,94,868 100.00

FUNDS FLOW STATEMENT

Funds flow statement is one of the important tools, which is used in many ways. It helps to understand the changes in the financial position of a business enterprise between the

beginning and ending financial statement dates. It is also called as statement of sources and uses of funds.

Institute of Cost and Works Accounts of India, funds flow statement is defined as “a statement prospective or retrospective, setting out the sources and application of the funds

of an enterprise. The purpose of the statement is to indicate clearly the requirement of funds and how they are proposed to be raised and the efficient utilization and application of the same”.

CASH FLOW STATEMENT

Cash flow statement is a statement which shows the sources of cash inflow and uses of

cash out-flow of the business concern during a particular period of time. It is the statement,

which involves only short-term financial position of the business concern. Cash flow

statement provides a summary of operating, investment and financing cash flows and

reconciles them with changes in its cash and cash equivalents such as marketable securities.

Institute of Chartered Accountants of India issued the Accounting Standard (AS-3) related

to the preparation of cash flow statement in 1998.

Difference Between Funds Flow and Cash Flow Statement

Funds Flow Statement Cash Flow Statement

1. Funds flow statement is the report on the

movement of funds or working capital

2. Funds flow statement explains how working

capital is raised and used during the particular

3. The main objective of fund flow statement is

to show the how the resources have been

balanced mobilized and used.

4. Funds flow statement indicates the results of

current financial management.

5. In a funds flow statement increase or decrease

in working capital is recorded.

6. In funds flow statement there is no opening

and closing balances.

1. Cash flow statement is the report showing

sources and uses of cash.

2. Cash flow statement explains the inflow and

out flow of cash during the particular period.

3. The main objective of the cash flow statement

is to show the causes of changes in cash

between two balance sheet dates.

4. Cash flow statement indicates the factors

contributing to the reduction of cash balance

in spite of increase in profit and vice-versa.

5. In a cash flow statement only cash receipt and

payments are recorded.

6. Cash flow statement starts with opening cash

balance and ends with closing cash balance.

Exercise 4

From the following balance sheet of A Company Ltd. you are required to prepare a schedule

of changes in working capital and statement of flow of funds.

Balance Sheet of A Company Ltd., as on 31st March

Liabilities 2004 2005 Assets 2004 2005

Share Capital 1,00,000 1,10,000 Land and Building 60,000 60,000

Profit and Loss a/c 20,000 23,000 Plant and Machinery 35,000 45,000

Loans — 10,000 Stock 20,000 25,000

Creditors 15,000 18,000 Debtors 18,000 28,000

Bills payable 5,000 4,000 Bills receivable 2,000 1,000

Cash 5,000 6,000

1,40,000 1,65,000 1,40,000 1,65,000

Solution

Schedule of Changes in Working Capital

Particulars 2004

Rs.

2005

Rs.

Incharge

Rs.

Decharge

Rs.

Current Assets

Stock 20,000 25,000 5,000 —

Debtors 18,000 28,000 10,000 —

Bills Receivable 2,000 1,000 — 1,000

Cash 5,000 6,000 1,000

A 45,000 60,000

Less Current Liabilities

Creditors 15,000 18,000 3,000

Bills Payable 5,000 4,000 1,000

B 20,000 22,000 17,000 4,000

A-B 25,000 38,000 — 13,000

Increase in W.C. 38,000 38,000 17,000 17,000

Fund Flow Statement

Sources Rs. Application Rs.

Issued Share Capital 10,000 Purchase of Plant and Machinery 10,000

Loan 10,000 Increase in Working Capital 13,000

Funds From Operations 3,000

23,000 23,000

Exercise 5

From the above example 4 prepare a Cash Flow Statement.

Solution

Cash Flow Statement

Inflow Rs. Outflow Rs.

Balance b/d 5,000 Purchase of plant 10,000

Issued Share Capital 10,000 Increase Current Assets

Loan 10,000 Stock

Cash Opening Profit 3,000 Decrease in Bills Payable 5,000

Decrease in Bills 1,000 Balance c/d 10,000

Receivable 3,000 1,000

Increase in Creditors 6,000

32,000 32,000

RATIO ANALYSIS

Ratio analysis is a commonly used tool of financial statement analysis. Ratio is a mathematical relationship between one number to another number. Ratio is used as an index for evaluating the financial performance of the business concern. An accounting ratio shows

the mathematical relationship between two figures, which have meaningful relation with each other. Ratio can be classified into various types. Classification from the point of view of financial management is as follows:

● Liquidity Ratio

● Activity Ratio

● Solvency Ratio

● Profitability Ratio

Liquidity Ratio

It is also called as short-term ratio. This ratio helps to understand the liquidity in a business which is the potential ability to meet current obligations. This ratio expresses the relationship between current assets and current assets of the business concern during a particular period. The following are the major liquidity ratio:

S. No. Ratio Formula Significant Ratio

1.

Current Ratio

Current Assets

Current Liability

2 : 1

2.

Quick Ratio

Quick Assets

Quick / Current Liability

1 : 1

Activity Ratio

It is also called as turnover ratio. This ratio measures the efficiency of the current assets and liabilities in the business concern during a particular period. This ratio is helpful to understand the performance of the business concern. Some of the activity ratios are given below:

S. No. Ratio Formula

1.

Stock Turnover Ratio

Costof Sales

Average Inventory

2.

Debtors Turnover Ratio

Credit Sales

Average Debtors

3.

Creditors Turnover Ratio

Credit Purchase

AverageCredit

4.

Working Capital Turnover Ratio

Sales

Net WorkingCapital

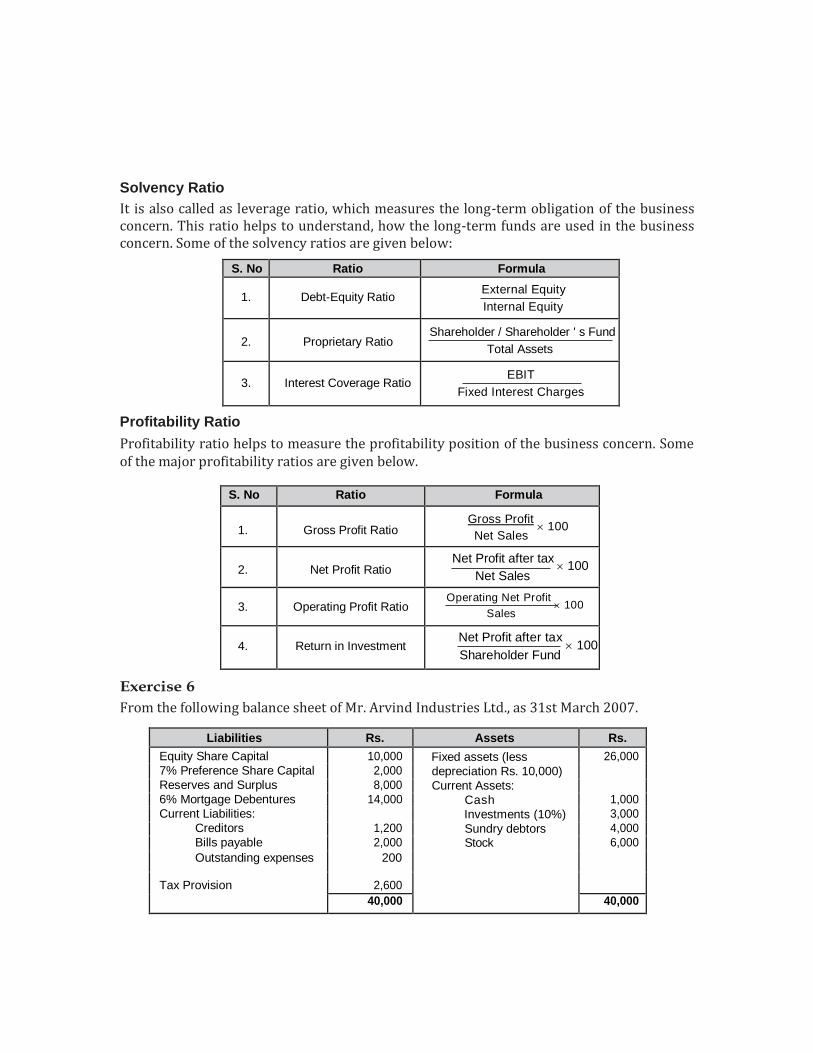

Solvency Ratio

It is also called as leverage ratio, which measures the long-term obligation of the business concern. This ratio helps to understand, how the long-term funds are used in the business concern. Some of the solvency ratios are given below:

S. No Ratio Formula

1.

Debt-Equity Ratio External Equity

Internal Equity

2.

Proprietary Ratio

Shareholder / Shareholder ' s Fund

Total Assets

3.

Interest Coverage Ratio

EBIT

Fixed Interest Charges

Profitability Ratio

Profitability ratio helps to measure the profitability position of the business concern. Some of the major profitability ratios are given below.

S. No Ratio Formula

1.

Gross Profit Ratio

Gross Profit 100

Net Sales

2.

Net Profit Ratio

Net Profit after tax 100

Net Sales

3.

Operating Profit Ratio Operating Net Profit

100 Sales

4.

Return in Investment

Net Profit after tax 100

Shareholder Fund

Exercise 6

From the following balance sheet of Mr. Arvind Industries Ltd., as 31st March 2007.

Liabilities Rs. Assets Rs.

Equity Share Capital 10,000 Fixed assets (less

depreciation Rs. 10,000)

Current Assets:

Cash

Investments (10%)

Sundry debtors Stock

26,000

7% Preference Share Capital 2,000

Reserves and Surplus 8,000

6% Mortgage Debentures 14,000 1,000

Current Liabilities: 3,000

Creditors 1,200 4,000

Bills payable 2,000 6,000

Outstanding expenses 200

Tax Provision 2,600

40,000 40,000

Other information:

1. Net sales Rs. 60,000

2. Cost of goods sold Rs. 51,600

3. Net income before tax Rs. 4,000

4. Net income after tax Rs. 2,000

Calculate appropriate ratios.

Solution

Short-term solvency ratios

Current Ratio = Current Assets

14,000 2.33 : 1

Current Liability 6,000

Liquid Ratio = Liquid Ratio

8,000

1.33 : 1 Current Liability 6,000

Long-term solvency ratios

Proprietary ratio = Proprietors funds

20,000

0.5 : 1

Total Assets 40,000

Proprietor’s fund or Shareholder’s fund=Equity share capital+Preference share

capital+Reserve and surplus

= 10,000+2,000+8,000=20,000

Debt-Equity ratio = External equities

20,000

1:1

Internal equities 20,000

Interest coverage ratio = EBIT

= 4,000+840

=5.7times Fixed interest charges 840

Fixed interest charges = 6% on debentures of Rs.14,000

= Rs. 840

Activity Ratio

Stock Turnover Ratio = Cost of Sales

= 51,600

=8.6 times Average Inventory 6,000

As there is no opening stock, closing stock is taken as average stock.

Debtors Turnover Ratio = Credit Sales

= 60,000

=10 times Average Debtors 6,000

In the absence of credit sales and opening debtors, total sales is considered as credit

sales and closing debtors as average debtors.

Creditors turn over ratio = Credit Purchases

43,200

36 times Average Creditors 1,200

In absence of purchases, cost of goods sold – gross profit treated as credit purchases and in the absence of opening creditors, closing creditors are treated as average creditors.

Working Capital Turnover Ratio = Sales

60,000 7.5times

Profitability Ratios

Gross profit ratio =

Net Working Capital 8,000

Gross Profit

100= 8,400

100=14%

Sales 60,000

Net profit ratio =

Net Profit 100=

2,000 100=3.33%

Sales 60,000

In the absence of non-operating income, operating profit ratio is equal to net profit ratio.

Return of Investment =

Net Profit after Tax 100=

2,000 100=10%

Shareholders Fund 20,000

MODEL QUESTIONS

1. What is financial statement?

2. What is financial statement analysis?

3. Discuss various types of financial statement analysis.

4. Explain various methods of financial statement analysis.

5. What are the differences between fund flow and cash flow?

6. What is ratio analysis? Explain its types.

Title of the course MANAGERIATACCOUNTING AND CONTROL [ABM-504]

Class, Year & Sem. MBA, I & II

Topic COST ACCOUNTING

-ACCOUNTING vs FINANCIAL ACCOUNTING

-Scope of Accounting

-Nature of Accounting

-Objectives of Cost Accounting

-Essentials of a good Costing system

-Important terms

-Cost vs Profit Centre

- Costing type

Unit IV

Faculty DEEPAK PAL & LAVEENA SHARMA

Institution Institute of Agribusiness Management, JNKVV

[i] Disclaimer: The information contained in this note is for general guidance & collected from various direct and indirect sources like websites, blogs, books, articles and open studysources. Author(s) make no representation for any legal responsibility or any other aspect of information contained.

COST ACCOUNTING

ACCOUNTING vs

FINANCIAL ACCOUNTING?

• In traditional accounting, the profit and loss is derived by deducting expensesfrom income whereas in cost accounting the motive is to be cost effective byreducing costs of process, production or project.

• Financial accounting views an organization in entirety whereas cost accountingsegregates the organization into various processes, projects or productionunits.

• Financial accounting is used to present the position of the organization to itsstakeholders whereas cost accounting is used for internal review of costs.

• Financial accounting is uniform across various businesses, however, costaccounting methods vary based on the type of business.

Scope of Accounting:

• Accounting has got a very wide scope and area of application.

• Not confined to the business world alone, but spread over in all the spheres ofthe society and in all professions.

• Now-a-days, in any social institution or professional activity, whether that isprofit earning or not, financial transactions must take place. So there arisesthe need for recording and summarizing these transactions when they occurand the necessity of finding out the net result of the same after the expiry of acertain fixed period.

• Need for interpretation and communication of those information to theappropriate persons.

• Only accounting use can help overcome these problems.

• In the modern world, accounting system is practiced no only in all thebusiness institutions but also in many non-trading institutions like Schools,Colleges, Hospitals, Charitable Trust Clubs, Co-operative Society etc.and alsoGovernment and Local Self-Government in the form of Municipality,Panchayat.

• The professional persons like Medical practitioners, practicing Lawyers,Chartered Accountants etc. also adopt some suitable types of accountingmethods. As a matter of fact, accounting methods are used by all who areinvolved in a series of financial transactions.

• The scope of accounting as it was in earlier days has undergone lots ofchanges in recent times. As accounting is a dynamic subject, its scope andarea of operation have been always increasing keeping pace with thechanges in socio-economic changes. As a result of continuous research inthis field the new areas of application of accounting principles and policiesare emerged.– National accounting, human resources accounting and social Accounting are examples of

the new areas of application of accounting systems.

Nature of Accounting1. Accounting is a process: A process refers to the method of performing any

specific job step by step according to the objectives, or target.– Accounting is identified as a process as it performs the specific task of collecting,

processing and communicating financial information. In doing so, it follows some definitesteps like collection of data recording, classification summarization, finalization andreporting.

2. Accounting is an art: Accounting is an art of recording, classifying,summarizing and finalizing the financial data.

The word ‘art’ refers to the way of performing something. It is abehavioral knowledge involving certain creativity and skill that may help usto attain some specific objectives. Accounting is a systematic methodconsisting of definite techniques and its proper application requires appliedskill and expertise. So, by nature accounting is an art.

3. Accounting is means and not an end: Accounting finds out the financial resultsand position of an entity and the same time,

-it communicates this information to its users. The users then take theirown decisions on the basis of such information. So, it can be said that merekeeping of accounts can be the primary objective of any person or entity.

On the other hand, the main objective may be identified as takingdecisions on the basis of financial information supplied by accounting. Thus,accounting itself is not an objective, it helps attaining a specific objective. So itis said the accounting is ‘a means to an end’ and it is not ‘an end in itself.’

4. Accounting deals with financial information and transactions; Accountingrecords the financial transactions and date after classifying the same andfinalizes their result for a definite period for conveying them to their users. So,from starting to the end, at every stage, accounting deals with financialinformation. Only financial information is its subject matter. It does not dealwith non-monetary information of non-financial aspect.

5. Accounting is an information system: Accounting is recognized andcharacterized as a storehouse of information. As a service function, it collectsprocesses and communicates financial information of any entity. This disciplineof knowledge has been evolved out to meet the need of financial informationrequired by different interested groups.

Objectives of Cost Accounting

• Determination of Cost: To accumulate, allocate and ascertain cost foreach cost object is the primary objective of the cost accounting.

• Basis for fixing selling prices: As the prices of the cost object, i.e. theproduct is determined by the external factors such as– market demand for the product,– competitor’s price, etc.

However, the basis for ascertaining the price is the total cost of productionand the cost accounting techniques helps in determining it. Along with that,it acts as a guide for estimating prices for tender and quotations.

• Cost Control: Another important objective of the cost accountingsystem is to control the costs. It keeps a check on the expenses madeby the company, against the set standards and the deviations arerecorded and reported continuously.

• Cost Reduction: The management works to further reduce the cost toincrease the profitability of the company. Cost reduction implies the actualand permanent reduction in the cost of production without compromisingwith the quality and the suitability of its desired use.

• Determination of Closing Inventory: To ascertain the value of closinginventory at the end of the period for the preparation of financialstatements of the concern.

• Assisting Management: To report to the management about theinefficiencies of the workers and eliminates wastes like material, expenses,equipment, tools and so forth. It also ensures optimum utilization ofresources of the organization by making sure that no machines are left idle,the workers get incentives for their performance, proper utilization of by-products and so forth.

• Economies of Production: To reflect different sources of economies of scale,concerning the process, type of equipment, inputs used, the outputgenerated etc.

ELEMENTS OF COST IN GENERALFor a standard manufacturing unit the various costs involved can be

segregated into the following :MaterialLabourOther expenses

These can be further segregated into the following:DirectIndirect

IllustrationSay a toy manufacturing unit procures plastic as a raw material. The

cost of plastic is direct material cost. The costs incurred in thepacking and transportation of the same is the indirect materialcost. Similarly, the labour cost for the production of toys is thedirect labour cost whereas the salary of the production supervisorwill be indirect labour cost.

Essentials of a good Costing system :-For availing of maximum benefits, a good costing system

should possess the following characteristics.

A. Costing system adopted in any organization should be suitable to its nature and size of the

business and its information needs.

B. A costing system should be such that it is economical and the benefits derived from the same

should be more than the cost of operating of the same.

C. Costing system should be simple to operate and understand. Unnecessary complications should be

avoided.

D. Costing system should ensure proper system of accounting for material, labor and overheads and

there should be proper classifi cation made at the time of recording of the transaction itself.

E. Before designing a costing system, need and objectives of the system should be identified.

F. The costing system should ensure that the final aim of ascertaining of cost as accurately possible

should be achieved.

Important termsA. Cost Center :-

• Cost Center is defined as, ‘a production or service, function, activity or item ofequipment whose costs may be attributed to cost units. A cost center is thesmallest organizational sub unit for which separate cost allocation is attempted’.• To put in simple words, a cost center is nothing but a location, person or itemof equipment for which cost may be ascertained and used for the purpose ofcost control. For example, a production department, stores department, salesdepartment can be cost centers.• Similarly, an item of equipment like a lathe, fork-lift, truck or delivery vehiclecan be cost center, a person like sales manager can be a cost center.• The main object of identifying a cost center is to facilitate collection of costs sothat further accounting will be easy. A cost center can be either personal orimpersonal,• similarly it can be a production cost center or service cost center. A cost centerin which a specific process or a continuous sequence of operations is carried out

is known as Process Cost Center.

B. Profit Center :-

Profit Center is defined as, ‘a segment of the business entity by whichboth revenues are received and expenses are incurred orcontrolled’.

• A profit center is any sub unit of an organization to which bothrevenues and costs are assigned.

• As explained above, cost center is an activity to which only costs areassigned but a profit center is one where costs and revenues areassigned so that profit can be ascertained.

• Such revenues and expenditure are being used to evaluatesegmental performance as well as managerial performance. Adivision of an organization may be called as profit center.

• The performance of profit center is evaluated in terms of the factwhether the center has achieved its budgeted profits.

• Thus the profit center concept is used for evaluation ofperformance.

Cost vs Profit Centre

• Cost centers and profit centers are bothreasons for which a business becomessuccessful.

• A cost center is a sub-unit of a company whichtakes care of the costs of that unit.

• On the other hand, a profit center is a subunitof a company which is responsible forrevenues, profits, and costs.

Costing Systems :-

A. Historical Costing :-

B. Absorption Costing

C. Marginal Costing :-

D. Uniform Costing :-

A. Historical Costing :-

In this system, costs are ascertained only after they areincurred and that is why it is called as historicalcosting system. For example, costs incurred in themonth of April, 2007 may be ascertained andcollected in the month of May. Such type of costingsystem is extremely useful for conducting post-mortem examination of costs, i.e. analysis of the costsincurred in the past.

Historical costing system may not be useful from costcontrol point of view but it certainly indicates a trendin the behavior of costs and is useful for estimation ofcosts in future.

Absorption Costing :-

In this type of costing system, costs are absorbedin the product units irrespective of theirnature.

In other words, all fixed and variable costs areabsorbed in the products. It is based on theprinciple that costs should be charged orabsorbed to whatever is being costed,whether it is a cost unit, cost center.

Marginal Costing :-

In Marginal Costing, only variable costs arecharged to the products and fixed costs arewritten off to the Costing Profit and Loss A/c.

The principle followed in this case is that sincefixed costs are largely period costs, theyshould not enter into the production units.

Naturally, the fixed costs will not enter into theinventories and they will be valued at marginalcosts only.

Uniform Costing :-

This is not a distinct method of costing but is theadoption of identical costing principles andprocedures by several units of the sameindustry or by several undertakings by mutualagreement. Uniform costing facilitates validcomparisons between organizations and helpsin eliminating inefficiencies.

Classification of Cost

A. Classification according to elements :-B. Classification according to nature :-C. Classification according to behaviorD. Classification according to functionsE. Classification according to timeF. Classification of costs for Management decision making

A. Classification according to elements :-

Costs can be classified according to the elements. There are three elements of costing, viz. material, labor and expenses.

Total cost of production/services can be divided into the three elements to find out the contribution of each element in the total costs.

B. Classification according to nature :-

As per this classification, costs can be classified intoDirect and Indirect.

Direct costs are the costs which are identifiable withthe product unit or cost center while indirect costsare not identifiable with the product unit or costcenter and hence they are to be allocated,apportioned and then absorb in the productionunits.

All elements of costs like material, labor and expensescan be classified into direct and indirect.

They are mentioned in next slide

i. Direct and Indirect Material :-

Direct material is the material which is identifiable withthe product. For example, in a cup of tea, quantityof milk consumed can be identified, quantity ofglass in a glass bottle can be identified and so thesewill be direct materials for these products.

Indirect material cannot be identified with the product,for example lubricants, fuel, oil, cotton wastes etccannot be identified with a given unit of productand hence these are the examples of indirectmaterials.

ii. Direct and Indirect Labor :-

Direct labor can be identified with a given unit ofproduct, for example, when wages are paid accordingto the piece rate, wages per unit can be identified.Similarly wages paid to workers who are directlyengaged in the production can also be identified andhence they are direct wages.

On the other hand, wages paid to workers likesweepers, gardeners, maintenance workers etc areindirect wages as they cannot be identified with thegiven unit of production

iii. Direct and Indirect Expenses :-Direct expenses refers to expenses that are specifically

incurred and charged for specific or particular job, process,service, cost center or cost unit. These expenses are alsocalled as chargeable expenses. Examples of these expensesare cost of drawing, design and layout, royalties payable onuse of patents, copyrights etc, consultation fees paid toarchitects, surveyors etc.

Indirect expenses on the other hand cannot be traced tospecific product, job, process, service or cost center or costunit. Several examples of indirect expenses can be givenlike insurance, electricity, rent, salaries, advertising etc.

It should be noted that the total of direct expenses is known as ‘Prime Cost’ while the total of all indirect expenses is known as ‘Overheads’.

• C. Classification according to behavior :-

i. Fixed Costs :- Out of the total costs, some costs remain fixedirrespective of changes in the production volume. Thesecosts are called as fixed costs.

The feature of these costs is that the total costs remain samewhile per unit fixed cost is always variable.

Examples of these costs are salaries, insurance, rent, etc.

ii. Variable Costs :-

These costs are variable in nature, i.e. they change according to the volume ofproduction. Their variability is in the same proportion to the production.

For example, if the production units are 2,000 and the variable cost is Rs. 5per unit, the total variable cost will be Rs. 10,000, if the production unitsare increased to 5,000 units, the total variable costs will be Rs. 25,000, i.e.the increase is exactly in the same proportion of the production.

Another feature of the variable cost is that per unit variable cost remainssame while the total variable costs will vary. In the example given above,the per unit variable cost remains Rs. 2 per unit while total variable costschange.

Examples of variable costs are direct materials, direct labor etc.

iii. Semi-variable Costs :-

Certain costs are partly fixed and partly variable. Inother words, they contain the features of both typesof costs. These costs are neither totally fixed nortotally variable. Maintenance costs, supervisory costsetc are examples of semi-variable costs. These costsare also called as ‘stepped costs’.

D. Classification according to functions :-

i. Production Costs :- All costs incurred for production of goods are known as production costs.

ii. Administrative Costs :- Costs incurred for administration are known as administrative costs.

Examples of these costs are office salaries, printing and stationery, office telephone, office rent, office insurance etc.

iii. Selling and Distribution Costs :- All costs incurred forprocuring an order are called as selling costs while all costsincurred for execution of order are distribution costs.

Market research expenses, advertising, sales staff salary, salespromotion expenses are some of the examples of sellingcosts.

Transportation expenses incurred on sales, warehouse rent etcare examples of distribution costs.

iv. Research and Development Costs :- In the modern days,research and development has become one of the importantfunctions of a business organization. Expenditure incurred forthis function can be classified as Research and DevelopmentCosts.

E. Classification according to time

I. Historical Costs :-

These are the costs which are incurred in the past, i.e. inthe past year, past month or even in the last weekor yesterday. The historical costs are ascertainedafter the period is over.

In other words it becomes a post-mortem analysis ofwhat has happened in the past.

Though historical costs have limited importance, stillthey can be used for estimating the trends of thefuture, i.e. they can be effectively used forpredicting the future costs.

II. Predetermined Cost :-

These costs relating to the product are computed in advance ofproduction, on the basis of a specification of all the factors affectingcost and cost data.

Pre determined costs may be either standard or estimated. StandardCost is a predetermined calculation of how much cost should beunder specific working conditions.

It is based on technical studies regarding material, labor and expenses.The main purpose of standard Financial Accounting, Cost Accounting

and Management Accounting cost is to have some kind ofbenchmark for comparing the actual performance with thestandards.

On the other hand, estimated costs are predetermined costs based onpast performance and adjusted to the anticipated changes. It canbe used in any business situation or decision making which doesnot require accurate cost.

F. Classification of costs for Management decision making

One of the important function of costaccounting is to present information to theManagement for the purpose of decisionmaking.

For decision making certain types of costs arerelevant. Classification of costs based on thecriteria of decision making can be done in thecoming manner………..

I. Marginal Cost :- Marginal cost is the change in theaggregate costs due to change in the volume ofoutput by one unit.

For example, suppose a manufacturing companyproduces 10,000 units and the aggregate costs areRs. 25,000, if 10,001 units are produced theaggregate costs may be Rs. 25,020 which meansthat the marginal cost is Rs. 20.

Marginal cost is also termed as variable cost and henceper unit marginal cost is always same, i.e. per unitmarginal cost is always fixed.

Marginal cost can be effectively used for decisionmaking in various areas.

II. Differential Costs :-

Differential costs are also known as incremental cost.This cost is the difference in total cost that will arisefrom the selection of one alternative to the other.

In other words, it is an added cost of a change in thelevel of activity. This type of analysis is useful fortaking various decisions like change in the level ofactivity, adding or dropping a product, change inproduct mix, make or buy decisions, accepting anexport offer and so on.

III. Opportunity Costs :-

It is the value of benefit sacrificed in favor of analternative course of action. It is the maximumamount that could be obtained at any given point oftime if a resource was sold or put to the mostvaluable alternative use that would be practicable.

Opportunity cost of goods or services is measured interms of revenue which could have been earned byemploying that goods or services in some otheralternative uses.

IV. Relevant Cost :-

The relevant cost is a cost which is relevant in various decisionsof management. Decision making involves consideration ofseveral alternative courses of action. In this process, whatevercosts are relevant are to be taken into consideration.

In other words, costs which are going to be affected matter themost and these costs are called as relevant costs. Relevantcost is a future cost which is different for differentalternatives.

It can also be defined as any cost which is affected by thedecision on hand. Thus in decision making relevant costs playa vital role.

V. Replacement Cost :-

This cost is the cost at which existing items of material or fixedassets can be replaced. Thus this is the cost of replacingexisting assets at present or at a future date.

VI. Abnormal Costs :-

It is an unusual or a typical cost whose occurrence isusually not regular and is unexpected.

This cost arises due to some abnormal situation ofproduction.

Abnormal cost arises due to idle time, may be due tosome unexpected heavy breakdown of machinery.They are not taken into consideration whilecomputing cost of production or for decision making.

VII. Controllable Costs :-

In cost accounting, cost control and cost reduction areextremely important.

In fact, in the competitive environment, cost control andreduction are the key words. Hence it is essential toidentify the controllable and uncontrollable costs.

Controllable costs are those which can be controlled orinfluenced by a conscious management action.

For example, costs like telephone, printing stationery etccan be controlled while costs like salaries etc cannot becontrolled at least in the short run.

Generally, direct costs are controllable whileuncontrollable costs are beyond the control of anindividual in a given period of time.

VIII. Shutdown Cost :-

These costs are the costs which are incurred if theoperations are shut down and they will disappear ifthe operations are continued.

Examples of these costs are costs of sheltering theplant and machinery and construction of sheds forstoring exposed property.

Computation of shutdown costs is extremely importantfor taking a decision of continuing or shutting downoperations

IX. Capacity Cost :-

These costs are normally fixed costs. The cost incurred by acompany for providing production, administration and sellingand distribution capabilities in order to perform variousfunctions.

Capacity costs include the costs of plant, machinery and buildingfor production, warehouses and vehicles for distribution andkey personnel for administration.

These costs are in the nature of long-term costs and are incurredas a result of planning decisions.

X. Urgent Costs :-

These costs are those which must be incurred in order tocontinue operations of the firm.

For example, cost of material and labor must be incurred ifproduction is to take place.

Title of the courseMANAGERIATACCOUNTING AND

CONTROL [ABM-504]

Class, Year & Sem. MBA, I & II

Topic Costing Methods

Unit IV

Faculty DEEPAK PAL & LAVEENA SHARMA

InstitutionInstitute of Agribusiness Management,

JNKVV

[i] Disclaimer: The information contained in this note is for general guidance & collected from various direct and indirect sources like websites, blogs, books, articles and open studysources. Author(s) make no representation for any legal responsibility or any other aspect of information contained.

Costing Methods Introduction• The term ‘costing’ refers to the techniques and processes of determining costs

of a product manufactured or services rendered.

• The first stage in cost accounting is to ascertain the cost of the product offeredor the services provided.

• In order to do the same, it is necessary to follow a particular method ofascertaining the cost.

• The methods of costing are applied in various business units to ascertain thecost of product or service offered.

• Different methods of costing are required to be used in different types ofbusinesses.– For example, costing methods used in a manufacturing business will differ from the

methods used in a business that is offering services. Even in a manufacturing business,some business units may have production in a continuous process, i.e. output of a processis an input of the subsequent process and so on, while in some businesses production isdone according to the requirements of customers and hence each job is different fromthe other one.

• Different methods of costing are used to suit these diverse requirements.

There are two principle methods of costing. These methodsare as follows

I] Job Costing

II] Process Costing

Other methods of costing are the variations of these twoprinciple methods. The variations of these methods ofcosting are as follows.

I]Job Costing: Batch Costing, Contract Costing, Multiple Costing.

II]Process Costing: Unit or Single Output Costing, Operating Costing,

Operation Costing

I] Job Costing: *****

• This method of costing is used in Job Order Industries where theproduction is as per the requirements of the customer.

• In Job Order industries, the production is not on continuous basis,rather it is only when order from customers is received and that tooas per the specifications of the customers.

• Consequently, each job can be different from the other one.• Method used in such type of business organizations is the Job

Costing or Job Order Costing.• The objective of this method of costing is to work out the cost of

each job by preparing the Job Cost Sheet.• A job may be a product, unit, batch, sales order, project, contract,

service, specific program or any other cost objective that isdistinguishable clearly and unique in terms of materials and otherservices used.

• The cost of completed job will be the materials used for the job, thedirect labor employed for the same and the production overheadsand other overheads if any charged to the job.

The following are the features of job costing.****

• It is a specific order costing

• A job is carried out or a product is produced is produced tomeet the specific requirements of the order

• Job costing enables a business to ascertain the cost of a job onthe basis of which quotation for the job may be given.

• While computing the cost, direct costs are charged to the jobdirectly as they are traceable to the job. Indirect expenses i.e.overheads are charged to the job on some suitable basis.

• Each job completed may be different from other jobs andhence it is difficult to have standardization of controls andtherefore more detailed supervision and control is necessary.

• At the end of the accounting period, work in progress may ormay not exist.

Methodology used in Job Costing*****

The objective of job costing is to ascertain the cost of a job that is producedas per the requirements of the customers. Hence it is necessary to identifythe costs associated with the job and present it in the form of job costsheet for showing various types of costs. Various costs are recorded in thefollowing manner:

Direct Material Costs

Direct Labor Cost

Direct Expenses

Overheads:

Work in Progress:

Direct Material Costs: • Material used during the production process of a job and identified with

the job is the direct material. The cost of such material consumed is thedirect material cost.

• Direct material cost is identifiable with the job and is charged directly. Thesource document for ascertaining this cost is the material requisition slipfrom which the quantity of material consumed can be worked out.

• Cost of the same can be worked out according to any method of pricing ofthe issues like first in first out [FIFO], last in first out [LIFO] or averagemethod as per the policy of the organization.

• The actual material cost can be compared with standard cost to find outany variations between the two. However, as each job may be differentfrom the other, standardization is difficult but efforts can be made for thesame.

Direct Labor Cost:

• This cost is also identifiable with a particular job and can beworked out with the help of ‘Job Time Tickets’ which is a recordof time spent by a worker on a particular job.

• The ‘job time ticket’ has the record of starting time andcompletion time of the job and the time required for the jobcan be worked out easily from the same.

• Calculation of wages can be done by multiplying the time spentby the hourly rate. Here also standards can be set for the timeas well as the rate so that comparison between the standardcost and actual cost can be very useful.

Direct Expenses:Direct expenses are chargeable directly to the concerned job. The invoices or

any other document can be marked with the number of job and thus theamount of direct expenses can be ascertained.

Overheads:• This is really a challenging task as the overheads are all indirect expenses

incurred for the job. Because of their nature, overheads cannot beidentified with the job and so they are apportioned to a particular job onsome suitable basis.

• Pre determined rates of absorption of overheads are generally used forcharging the overheads. This is done on the basis of the budgeted data. Ifthe predetermined rates are used, under/over absorption of overheads isinevitable and hence rectification of the same becomes necessary.

Work in Progress:

• On the completion of a job, the total cost is worked out by addingthe overhead expenses in the direct cost.

• In other word, the overheads are added to the prime cost. The costsheet is then marked as ‘completed’ and proper entries are made inthe finished goods ledger. If a job remains incomplete at the end ofan accounting period, the total cost incurred on the same becomesthe cost of work in progress.

The work in progress at the end of the accounting period becomes-The closing work in progress and

-The same becomes the opening work in progress at thebeginning of the next accounting period.

• A separate account for work in progress is maintained.

Advantages of Job Costing• Accurate information is available regarding the cost of the job

completed and the profits generated from the same.• Proper records are maintained regarding the material, labor and

overheads so that a costing system is built up• Useful cost data is generated from the point of view of

management for proper control and analysis.• Performance analysis with other jobs is possible by comparing the

data of various jobs. However it should be remembered that eachjob completed may be different from the other.

• If standard costing system is in use, the actual cost of job can becompared with the standard to find out any deviation between thetwo.

• Some jobs are priced on the basis of cost plus basis. In such cases, aprofit margin is added in the cost of the job. In such situation, acustomer will be willing to pay the price if the cost data is reliable.Job costing helps in maintaining this reliability and the data madeavailable becomes credible.

Limitations of Job Costing

These are as follows.• It is said that it is too time consuming and requires

detailed record keeping. This makes the method moreexpensive.

• Record keeping for different jobs may provecomplicated.

• Inefficiencies of the organization may be charged to ajob though it may not be responsible for the same.

In spite of the above limitations, it can be said that job costing is an extremelyuseful method for computation of the cost of a job. The limitation of timeconsuming can be removed by computerization and this can also reducethe complexity of the record keeping.

II] Batch Costing:• In the job costing, we have seen that the production is as per the orders of the

customers and according to the specifications mentioned by them.

• On the other hand, batch costing is used where units of a product are manufactured in

batches and used in the assembly of the final product.

– Thus components of products like television, radio sets, air conditioners and other consumer goods are

manufactured in batches to maintain uniformity in all respects.

– It is not possible here to manufacture as per the requirements of customers and hence rather than

manufacturing a single unit, several units of the component are manufactured.

– For example, rather than manufacturing a single unit, it will be always beneficial to manufacture say, 75, 000

units of the component as it will reduce the cost of production substantially and also bring standardization

in the quality and other aspects of the product.

• The finished units are held in stock and normal inventory control techniques are used for

controlling the inventory. Batch number is given to each batch manufactured and

accordingly the cost is worked out.

• Costing procedure in batch costing is more or less similar to the job costing in the sense

that cost is worked out for each batch rather than job.

Direct costs like direct materials, direct labor and direct expenses are charged directly to the job as they are traceable to the job. The source documents used for them are material requisitions, labor records and records pertaining to the direct expenses. Indirect costs, i.e. overheads are allocated or apportioned to the batch on some suitable basis. Thus a batch cost sheet is prepared to show the total cost of the batch.

One of the important aspects of batch type production is to decide the batch size.

Actually the determination of appropriate batch size of the production has conflicting views. Ifproduction is produced in large quantities, the impact of the setting up cost will be lower as thesetting up cost is fixed per batch. But on the other hand if the production quantity is large, theinventory carrying cost will be high as more inventory will have to be carried over in the store.The carrying cost of the inventory includes cost of storage, risk of pilferage, spoilage,obsolescence and interest on the investments blocked in the inventories. Therefore the size ofthe batch should not be either too small or too large. On the basis of a trade off between largesize and small size, an appropriate size of the batch should be decided. This batch size is known asEconomic Batch Quantity that is similar to the concept of Economic Order Quantity. This quantityis determined with the help of the following formula.

Economic Batch Quantity = 2AS/C

Where A = Annual requirements of the product

S = Setting up cost per batch

C = Carrying cost per unit of inventory per annum.

III] Contract Costing:Contract Costing is a method used in construction industry to find out the

cost and profit of a particular construction assignment.

The principles of job costing are also applicable in contract costing. In factContract Costing can be termed as an extension of Job Costing as eachcontract is nothing but a job completed.

Contract Costing is used by concerns like construction firms, civil engineeringcontractors, and engineering firms.

One of the important features of contract costing is that most of the expensescan be traced to a particular contract. Those expenses that cannot betraced to a particular contract are apportioned to the contract on somesuitable basis. The cost computation in case of a contract is done on thefollowing basis.

• Material Cost

• Labor Cost

• Expenses:

• Plant and Machinery:

A. Material Cost: • Direct Material required for a particular contract is

debited to the Contract Account.• There may be some quantity of material which is

returned back to the store. In such cases, materialreturned note is prepared and is either credited to theContract Account or deducted from the materialdebited to the Contract Account.

• Similar treatment is given to the material transferredfrom one contract to another one. Material TransferNote is prepared to record these transactions oftransfer.

• Material remaining at the site at the end of a particularaccounting period is shown as closing stock aftervaluation of the same and carried forward to the nextperiod.

B. Labor Cost:

Wages paid to the workers engaged on a particularcontract should be charged to that contractirrespective of the work performed by them. Ifthere are common workers on more than onecontract and/or if the workers are transferredfrom one contract to the other contract, timesheets must be maintained and wages may bedistributed on the basis of time spent on eachcontract. Some of the workers may be working inthe central office or central stores, their wagescan be apportioned to a particular contract onsuitable basis like time spent etc.

C. Expenses:

All expenses incurred for a particular contract should be chargedto that contract. In case of any indirect expenses incurred forthe organization as a whole, they should be charged to thecontract on some suitable basis. Direct expenses can becharged directly to the contract.

D. Plant and Machinery:

Depreciation on the plant and machinery used for the contract is to be chargedto the contract account. The depreciation may be charged on any of thefollowing basis.

• If a plant is specially purchased for a particular contract and is expected tobe used for the contract for long time, thus being exhausted at site, thetotal cost of the plant will be debited to the contract account.– After the completion of the contract, if it is no longer required, it will be

sold at the site itself and the sale proceeds are credited to the contractaccount.

– If it is not sold, the contract is credited with the depreciated [revaluedamount value].

– Thus the amount of depreciation is debited to the contract account. Themain drawback of this method is that the debit side of the contractaccount is unnecessarily inflated with the cost of the plant value andthus the cost of contract is shown very high.

– For removing this drawback, the difference between the original cost atthe commencement of the contract and the depreciated value at theend of the period is worked out and charged to the contract account asdepreciation.

Continue…..

• If a plant is used for a contract for a short period, thereis no need of debiting the cost of the plant to thecontract account. The amount of depreciation isworked out on the basis of per hour and charged to thecontract on that basis. The hourly rate is calculated bydividing the depreciation and other operating expensesof the plant by the total estimated working hours ofthe plant.

• Sometimes plants may be taken on hire for a particularcontract. In such cases the amount of rent paid shouldbe debited to the contract account.

V. Subcontract:

Sometimes due to certain situations, a sub contractor is appointed to carryout certain special work for the main contract. This special work done bythe sub contractor becomes a direct charge to the main contract andaccordingly debited to the contract account. The payments made to thesub contractor are charged to the main contract as direct expenses and nodetailed break up of the same is required. Material supplied to the subcontractor without any charge, is debited to the contract account as directmaterial and machinery, tools etc supplied to him on rent should bedepreciated on appropriate basis and debited to the contract account.Rent received for the use of such tools and machines should be credited tothe contract account or deducted from the final bill of the sub contractor.

Process Costing-

Search in bucket

Title of the course MANAGERIAL ACCOUNTING AND CONTROL

[ABM-504]

Class, Year & Sem. MBA, I & II

Topic What is Cost Volume Profit Analysis ?

Importance of Cost Volume Profit Analysis

Cost Volume Profit Analysis Formula

Benefits of Cost-Volume Analysis (CVP)

Limitations of Cost-Volume Analysis (CVP) Unit IV

Faculty1 LAVEENA SHARMA

Institute Institute of Agribusiness Management, JNKVV

1

1 Disclaimer: The information contained in this note is for general guidance & collected from various direct and indirect sources like websites, blogs, books, articles and open study sources. Author(s) make no representation for any legal responsibility or any other aspect of information contained.

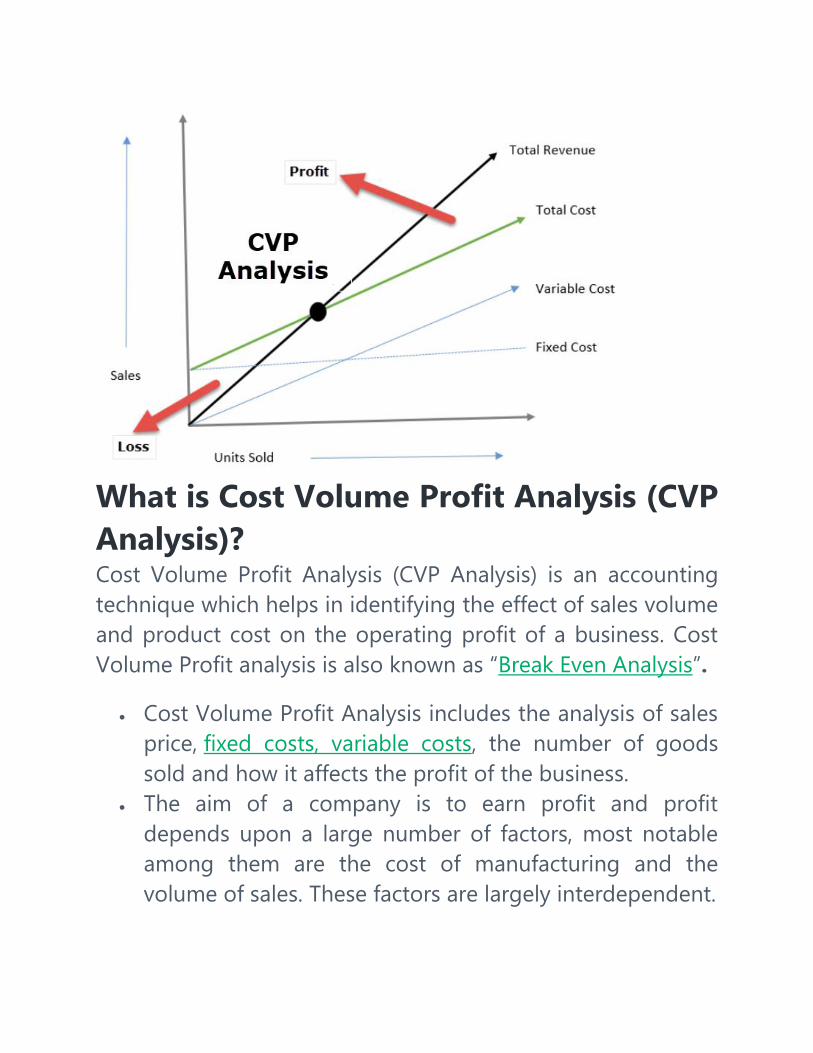

What is Cost Volume Profit Analysis (CVP

Analysis)? Cost Volume Profit Analysis (CVP Analysis) is an accounting

technique which helps in identifying the effect of sales volume

and product cost on the operating profit of a business. Cost

Volume Profit analysis is also known as “Break Even Analysis”.

Cost Volume Profit Analysis includes the analysis of sales

price, fixed costs, variable costs, the number of goods

sold and how it affects the profit of the business.

The aim of a company is to earn profit and profit

depends upon a large number of factors, most notable

among them are the cost of manufacturing and the

volume of sales. These factors are largely interdependent.

The volume of sales is dependent upon production

volume which in turn is related to costs which are

affected by Volume of production, product mix, internal

efficiency of the business, production method used etc.

CVP analysis helps management in finding out the

relationship between cost and revenue to generate profit.

CVP Analysis helps them to determine the break-even

point for different sales volume and cost structures.

With CVP Analysis information, the management can

better understand the overall performance and

determine what units it should sell to break even or to

reach a certain level of profit.

Importance of Cost Volume Profit Analysis CVP analysis helps in determining the level at which all

relevant cost is recovered and there is no profit or loss which

is also called the breakeven point. It is that point at which

volume of sales equal total expenses (both fixed and variable).

Thus CVP analysis helps decision makers understand the

effect of a change in sales volume, price and variable cost on

the profit of an entity while taking fixed cost as unchangeable.

CVP Analysis helps in understanding the relationship between

profits and costs on the one hand and volume on the other.

CVP Analysis useful for setting up flexible budgets which

indicate costs at various levels of activity. CVP Analysis also

helpful when a business is trying to determine the level of

sales to reach a targeted income.

Cost Volume Profit Analysis Formula

The computing of Cost volume profit analysis formula is as

follows:

Examples of Cost Volume Profit Analysis Let’s understand examples of Cost volume profit analysis with

the help of a few examples:

Cost Volume Profit Analysis Examples #1

XYZ wishes to make an annual profit of $100000 from the sale

of appliances. Details of manufacturing and annual capacity

are as follows:

Based on the above information let’s plug the numbers in CVP

equation:

10000*p= (10000*30) +$30000+$100000

10000p = ($300000+$30000+$100000)

10000p=$430000

Price per unit= ($430000/10000) = $43

Thus price per unit comes out to $43 which implies that XYZ

will have to price its product $43 and need to sell 10000 units

to achieve its targeted profit of $100000.Further, we can see

that the fixed cost remain constant ($30000) irrespective of

the level of sales.

Cost Volume Profit Analysis Examples #2

ABC Limited has entered into the business of making Electrical

fans. The management of the company is interested in

knowing the breakeven point at which there will be no

profit/loss. Below are the details pertaining to the cost

incurred:

No. of units sold by ABC limited: ($300000/$300) = 1000 units

Variable cost per unit= ($240000/1000)=$240

Contribution per unit= Selling price per unit-Variable

Cost per unit

= ($300-$240)

= $60 per unit

Break Even Point= (Fixed Cost/Variable Cost per unit)

= ($60000/$60)

=10000 units

Thus ABC limited need to sell 10000 units of electric fans to

break even at the current cost structure.

Benefits of Cost-Volume Analysis (CVP)

1. CVP analysis provides a clear and simple understanding

of the level of sales which are required for a business to

break even (No profit No loss), level of sales required to

achieve targeted Profit.

2. CVP analysis helps management to understand the

different cost at different levels of production/sales

volume. CVP analysis helps decision makers in

forecasting cost and profit on account of change in

volume.

3. CVP Analysis helps business analyze during recessionary

times the comparative effects of shutting down a

business or continuing business at a loss; as it clearly

bifurcates the Direct and Indirect cost.

4. Effects of changes in fixed and variable cost help

management decide the optimum level of production

Limitations of Cost-Volume Analysis (CVP)

1. CVP analysis assumes fixed cost is constant which is not

the case always; beyond certain level fixed cost also

changes.

2. Variable cost is assumed to vary proportionately which

doesn’t happen in reality.

3. Cost volume profit analysis assumes costs are either fixed

or variable; however, in reality, some costs are semi-fixed

in nature. For example, Telephone expenses which

comprise a fixed monthly charge and a variable charge

based on the number of calls made.

Final Thoughts No business can decide with accuracy its expected level of

sales volume. Such decisions are usually based on past

estimates and market research regarding the demand for

products which are offered by the business. CVP Analysis

helps business in determining how much they need to sell to