The Role of Budgeting in Enhancing Honesty and Integrity in Financial Administration

31

The Role of Budgeting in Enhancing Honesty and Integrity in Financial Administration Kabir Tahir Hamid, PhD, FCIFC Department of Accounting Bayero University, Kano-Nigeria GSM: 08028376563, 08168743809 Email: [email protected] [email protected] Being a Paper Presented at a Workshop on Financial Impropriety in the Public Sector: Restoring Confidence in Financial Administration in Nigeria, Jointly organized by the Chartered Institute of Finance and Control of 0

Transcript of The Role of Budgeting in Enhancing Honesty and Integrity in Financial Administration

The Role of Budgeting in Enhancing Honesty andIntegrity in Financial Administration

Kabir Tahir Hamid, PhD, FCIFCDepartment of Accounting

Bayero University, Kano-NigeriaGSM: 08028376563, 08168743809Email: [email protected]

Being a Paper Presented at a Workshop on FinancialImpropriety in the Public Sector: Restoring Confidence in Financial

Administration in Nigeria, Jointly organized by theChartered Institute of Finance and Control of

0

Nigeria (CIFCN) and the Office of the SpecialAdviser to the President on Ethics and Values,held from 14th to 16th October, 2014 at Merit

House, Maitama, Abuja, Nigeria

1. INTRODUCTIONEvery government, be it federal, state or local government, is established with a viewto providing social services that would improve the general well being of itscitizenry. For every government therefore, to achieve itsobjectives, it requires to put in place effective budgetingmechanisms with a view to enhancing honesty and integrity infinancial administration. The role of budget in an economycannot, therefore, be overemphasized. A budget is an importantinstrument of national resource mobilization, allocation and economicmanagement. It is an economic instrument for facilitating andrealizing the vision of the government in a given fiscal year.If a national budget is to serve as an effective instrumentfor promoting growth and development of a country, thereshould be proper linkage and management of all the stages ofbudgeting. A budget has to be well-designed, effectively and efficientlyimplemented, adequately monitored and its performance well evaluated with a viewto ensuring the attainment of desired objectives, effectively, economically andefficiently.

According to Akinyele (1996) budgeting in governmentencompasses two phases of the financial management cycle. Thefirst consist of the expression in monetary terms of the shortterm plans of government in terms of policies, programmes,projects and activities and the pre setting of yardsticks foreffecting operation against which numerous activities ofgovernment’s operation one to be measured. The second consistof execution, accounting and internal control.

Budgetary control refers to the process of comparing budgetedstandard with the actual results, with a view to takingnecessary actions to address any deviation (variance), if any,which could affect the achievement of the objectives enshrinedin the budget. Effective budgetary control will, therefore,help to ensure adequate and sustained provision of socialgoods and services, enhanced public performance, provide the

1

necessary social capital to support entrepreneurialdevelopment, provide educational facilities to enhance thequality of education, improves sanitary conditions and healthfacilities, meaningfully engage the restless youths inproductive activities and generally improves the overallwellbeing of the citizenry by bringing about socio-economicgrowth and development.

The objective of this paper, therefore, is to assess the roleof budgeting in enhancing honesty and integrity in financialadministration in public governance in Nigeria. The rest ofthe paper is organized in 3 (three) sections. The nextsection, which is section two, deals with the review of theliterature on the concepts of budgeting/budgetary control,honesty & integrity and financial administration. Sectionthree looks at the relationship between budgeting/budgetarycontrol and honesty and integrity in financial administrationwith particular reference to the Nigerian public sector, aswell as, highlights the role of budgeting on Nigeria’seconomic development. While section four concludes the paperby proffering recommendations that are meant to enhanceeffective budgeting/budgetary control in Nigeria with a viewto improving the general wellbeing of the citizenry, as wellas, bringing about the desired level of socio-economicdevelopment in the country.

2.0 CONCEPTUAL FRAMEWORK AND LITERATURE REVIEW

2. 1 The Concept of Budget The word budget is said to have originated from a from aFrench word bougette which means little bag. In Britain, it wasused to describe the leather bag in which the Chancellor ofthe Exchequer carried the statement of government needs andfinances to parliament. After several thoughts of consensus,the budget became the document contained in the bags whichrepresent plans of government expressed in money and submittedto legislatives for approval.

In the words of Agusto (2005) budgeting, simply put, is theact of preparing or formulating the annual statement of acountry’s income and expenditure. In the Nigerian context,budgeting could, therefore, be defined as the annual statementof income and expenditure at the national, state or localgovernment levels. Budgeting, therefore, remain the mosttactical instrument for both decision-making, as well as,allocation of resources. The annual budgeting procedure can

2

thus perhaps be seen to be, the single most important controlroutine from both the governmental and economic point of view.

There are two aspects of government budget, namely revenue (income) andexpenditure. Revenue refers to money generated by government tocarry out its activities. Money generated by government can bebroadly grouped into, recurrent revenue (i.e. revenue generatedfrom stable sources like taxes, charges paid by consumers ofgoods and services like trade and driving licences and speciallevies by government for specific purposes) and capital revenue(i.e. revenue generated for developmental purposes, includingborrowing, Aids from donor agencies and other countries,dividends which include income from government investments andsales of government assets).

Expenditure on the other hand refers to money spent by governmentto carry out its obligations. This is divided into two, namelyrecurrent expenditure-are regular expenses of running governmentservices namely, salaries and allowances of governmentworkers, maintenance of government equipments, buildings,remuneration for public office holders, travelling,accommodation, electricity, telephone and other expensesincurred by government ministries and departments, governmentsubsidies on agriculture, education and interests on loanobtain by government. While capital expenditure- are expenses ondevelopment projects namely construction of buildings, roads,institutions, drainages, among others, establishment ofindustries and building of hospitals, schools and colleges.Government budget is the aggregate of revenue and expenditureestimates of various government departments for a year.Therefore all government departments participate in the makingof government budget. Considering the sources of revenue andnature of expenditure, it is obvious that government budget isprepared on behalf of the people to serve the interest of thepeople

Government budget has great impact on the people through:taxable measures which may affect people’s income, consumptionand investment; fiscal measures which may affect the prices ofgoods and services; social programmes provided in the budget;and capital projects contained in the budget which may improveproductivity and generate employment. Government budgetdetermines the direction of a country’s economy for aparticular period and this will affect the lives of thepeople. If government overspends or incurs expenses on thingsnot contained in the budget, the economy and the people will

3

suffer for it. Government budget highlights specific projects,which governments plans to carry out for various communitiesin a particular year. Implementation of government budgetdetermines the performance of government.

Budget is assessed by determining the extent to which thebudget satisfies the economic rights and basic needs of thepeople; the extent to which the budget allocate resourcesequitably across sectors and sections of the economy; theextent to which people participate in the budget process; theextent to which the budget process is open to public scrutinyand access to information; the extent to which specifictargets of the budget are met; the degree of efficiency of thebudget whether or not it achieves value-for-money; and theextent to which the budget performs its stabilisation functionof promoting growth, employment and reducing unemployment andreducing unemployment and inflation. A budget is, therefore, a financial or quantitative statementshowing planned income and expenditure of an organization fora period of time, usually one year. In other words, budgetmay be viewed as means of obtaining accountability and controlover the use of money or overall activities of anorganization. Therefore, a budget could be seen as a“financial map” or “operational guide for an organization”.Simply put a budget is a detailed financial plan thatquantifies future expectations and actions relative toacquiring and using resources.

Budgeting is said to apply in all kinds of organizations,government or private, profit-making or not-for-profit,service or trading, big or small. This is simply because allresources are said to be scarce based on the demand for them.Therefore, the scarce resources of organizations need properutilization, so as to minimize cost, control activities,enhance efficiency and effectiveness, motivate workers,enhance the achievement of desired objectives and avoid cashdisappointments. Although, budgets do not guarantee success,the certainly help to avoid failure.

2.2. Budgeting ProcessThe Official Gazette of Federal Government of (1991), Statesthat the budget cycle is a complete set of events occurring inthe same sequence every year and culminating in the approvedbudget. In most governments where separation of powers existsbetween the Executives and the Legislature, four phases of a

4

budget cycle are discernible, executive preparation andsubmission, legislature consideration and enactment,execution, audit and review.

The first phase begins when the President, the Governor or LocalGovernment Chairman articulating government objectives interms of economics, social and other welfare parameters. Thepriorities and the expected level of achievement are alsoindicated and made known to the Ministry of Budget. Based onthis information and other data available to the Ministry ofBudget, it issues the call circular inviting MDAs to submitadvance proposals. These organizations are expected to submitthese in accordance with, the principles and guidelines set inthe call circular. At the end of this, submission is made tothe government for consideration this includes: review of theeconomy, legislative initiatives for the budget year, expectedrevenues for the budget year, tentative proposals ofMinistries, recommendation on the overall priorities andSuggested budget ceilings.

The second phase involves legislative consideration andenactment, in this phase more political factors are brought tobear on the draft budget. Ideally this phase is expected to beconcluded before the beginning of the budget year. The third phaserefers to the period in which the appropriations are used inincurring expenditures, delivering services and accounting forthe transactions and events relating thereto. The fourth phaserelates to the audit and review.

2.3 Classifications of BudgetThere are various types of budgets; state can preparedepending on the need that arises. Trevor (1986) explains thatbudgets may be classified either based on period or based onactivity as follows:(i) Classification Based on Period (this comprise of

short-term budget, which covers a period of one year or less;medium-term budget, which covers a period of between one tothree years and long term budget, which covers a period ofbetween three to ten years).

(ii) Classification Based on Activity (this comprise ofoperational budget, a budget of revenue and expenditure;cash budget, showing expected cash in-flows and cash out-flows; capital budget, which are directed towardsproposed expenditures capital projects and often require

5

special financing; and administrative overheads budget,covering the administrative expenses of an organization).

International Public Sector Accounting Standards (IPSASs) on itsown part classifies government budget in to six segments, namely: administrative,economic, functional, fund, program and geography. Similarly, the Chartof Accounts (COA) provides a robust mechanism for theclassification of public resources under the budget, as wellas, tracking receipts and payments during budget execution. Inparticular, the new classification system seeks to support oneof the key deliverables of the government’s Economic Reformand Governance Project (ERGP) which is the “adoption of moretransparent and modern economic and financial managementsystems and processes that are less prone to corruption”. Thenew classification system supports all extant reporting anddisclosure requirements under the Nigerian Public FinanceManagement (PFM) legal framework. In addition, it has beendesigned to facilitate compliance with major internationalpublic sector accounting and reporting standards. The COA hasbeen structured to provide a strong foundation for a complete,accurate and detailed classification of all governmentsreceipts and payments in such a manner that will make for easyadoption of all mandatory IPSAS cash basis reporting anddisclosure requirements such as External Assistance, ForeignExchange transactions, consolidation of accounts of controlledentities, full disclosure of cash holdings, among others.Furthermore, the COA is fully compatible with the GovernmentFinance Statistics Manual (GFS) and has adopted in full theUnited Nations Classification of the Functions of Government (COFOG)system.

2.4 Budget Improvement Techniques Every budget starts at a particular stage, hence the use ofnoticeable four improvement techniques in budget preparations.1. Incremental Budgeting (a technique which presumed that

established levels from previous year’s budget are anacceptable baseline, and changes are made based on newinformation, usually leading to incremental increase in thebudgeted amounts).

2. Zero Base Budgeting (a technique which assumes that currentoperations start from zero level, requiring everyexpenditure to be justified for the new budget period,irrespective of whether it is new or continuing ones. Noexpenditure is presumed to be acceptable because it isreflective of the status quo).

6

3. Continuous (Rolling) Budgeting (this budget is formulatedinitially for a period say 1 years, broken down intomonthly or quarterly budget, and as each month or quarterpasses, a budget for the corresponding period of thefollowing period is prepared ensuring that a budget isalways in existence for the immediate future of 1 month orquarter y. For example the 1st 3 months will be planned ingreater detail and the remaining 9 months in lesser detailbecause of the greater uncertainty about longer futureterm).

4. Planning, Programming Budgeting System (a technique whichrequires the analysis of purposes and objectives for whichfunds are requested, the costs of programs for achievingobjectives, the work perform under each program andalternatives courses of action with a view to finding themost effective means of reaching basic program objectives).

2.5 The Uses and Benefits of Budgeting as a Control Mechanismin the Public Sector Budgetary control refers to the control exercised over thegeneration, usage and maintenance of financial resources, witha view to ensuring proper management and accountability offinancial resources generated or used, through the instrumentof the budget. It is thus the establishment of budgetsrelating the responsibilities of principal officers of theorganisation to the requirements of identified policies andthe continuous comparison of actual with budgeted results,either to secure by individual action, the objectives ofpolicies or to provide basis for revision of the policies(Watoseninyi, 1996).Every government, at whatever level prepares a spendingprofile which specifies the expected revenue and expenditureof the government during the fiscal period. According toIbitoye (1995), budgetary control is the process of comparingthe actual results with the planned performance andhighlighting variances, which can then be analyzed by causeand responsibility. Mathematical deviations from actual andexpected results are termed variances. Variance analysis istherefore the logical examination of deviations in an attemptto identify areas for improvement. Oshisami (1992) andDandago (2005) argue that budgetary control can be regarded asencompassing the following functions: (i)Fund Control: This is the management of legislative

appropriations to ensure that they are used for thepurposes for which they are intended, that they are used

7

economically and efficiently, that commitments andexpenditure do not exceed amounts approved or madeavailable and that activities not approved by governmentare not pursued with approved funds. This control isexercised through appropriation monitoring and financialstatements.

(ii) Expenditure Control: This relates primarily tocontrol on amounts being expended. The ultimateresponsibility for this rests with the chief executive ofministries and agencies who are entrusted with theexpenditure of public funds falling within the head ofbudgetary account of their ministries and agencies.

(iii) Revenue Control: This deals with the timelycollections of revenue due to the government, ensuring thatamounts due are actually collected and that what iscollected gets into the coffers of the government.

(iv) Cash control: This concerns all controlsinstituted to ensure safety of cash collections intogovernment coffers.

Watoseninyi (1996), finds that budgeting as a conventional ortraditional financial control technique in the public sectoris used in (i) controlling costs by providing a yardstick bywhich actual costs can be measured; and (ii) control ofperformance. Fakiyesi (1998) explains that budgetary controlis a means of control by which the actual state of affairs iscompared with the budget so that action may be taken withregards to deviations. Okoye (1995) argues that budgeting isone of the three tools used for financial management andcontrol and provides a mechanism for ensuring that adequatecontrols are maintained over expenditure and revenue.

Agusto (2005) on his part discovers that over the years, thevarious governments in the country had tried to utilize theannual budgets to serve as a tool of control of governmentfinances but, unfortunately, this had not been possible.Rather what exists has been unrealistic budgets lacking infiscal discipline. He submits that budgets have merely beendemonstrating short-term outlook of government spendingwithout showing value of money; that there has not beenpredictability in government spending; and above all,budgeting has been characterized by weak monitoring, lowaccountability and lack of transparency. The author concludesthat a new budgetary system is imperative in order to serve asa veritable instrument for sound socio-economic empowermentand development of Nigeria. Arguing on the issue, Watoseninyi

8

(1996) contends that the practice of comparing actual withbudgeted results is not being effectively followed in Nigeriaas performance evaluation is not generally emphasized. Thecomparison of actual with budgeted results becomes difficultbecause of lack of data since expenditure attract attentionmainly at the point of incurrence. Where variances are notproperly calculated, or not calculated at all, implementationof corrective and control actions or modification to existingplans becomes meaningless.

Similarly, Fakiyesi (1998) and Kiabel (2000) in trying tojustify the benefits that accrue to public organizations frombudgetary control opine that budgetary control is generallyregarded as an element of Internal Control System which themanagement uses in achieving the overall control of theenterprise; it ensures expenditure control and the provisionof financial information needed for efficient financialmanagement; assists management in its day-to-day decisionmaking; serving as a means of communication between themanagement and subordinate staff and making seniors moreappreciative of subordinate’s roles and problems.

2.6 Operational Budgeting Technique in the Nigerian PublicSector Akinyele (1980) reported that the traditional system ofbudgeting has been criticized on the grounds that it is short-ranged in view and that, because of its structural design, itemphasizes the principle of control and offers little help inestablishing the remaining two objectives of efficiency andeffectiveness, thus, the adoption of Programme PerformanceBudgeting System (PPBS). The PPBS includes the basic processesof planning, budgeting and evaluation in an integratedfashion. Omolehinwa (1989) examines the attempts made by theNigerian Government to make PPBS part of its budgeting system.He explains that though it was the intention of the governmentto use an adapted PPBS (calling its own version of PPBS‘Programme Performance Budgetary System’ instead of PlanningProgramming Budgeting System) to achieve a ‘coordinated andcomprehensive’ budgetary system that relates cost with outputin order to achieve ‘quick result’ in the implementation ofits program, not much was achieved in Nigeria. He argues thatthe effectiveness of PPBS was circumscribed by a variety ofinstitutional, economic and political factors. Similarly,Jenfa (2005) finds that PPBS has not effectively yielded

9

desired results due to the basic problem of securing adequate,reliable and up-to-date data for planning; complete lack offundamental re-appraisal of purposes, methods and performancelevel of current projects and activities; and poor budgetmonitoring among others. He concludes that unless Nigeriabegins to recreate the system of values that can inspireefficiency, loyalty and dedication in our bureaucracies,restore the moral tone of our public officers, and inducingthem to greater productivity, Nigeria shall sadly remain thegiant with the feet of clay.

2.3 The Concepts of Honesty and IntegrityHonesty is the condition of being sincere, truthful, fair and straightforward inconduct. Honesty also implies doing one's work as sincerely andas perfectly as possible. Honesty also implies carrying outduties as fully as possible whether the person is supervisedor not. Honesty means giving every person his due rightswithout his asking for these rights.

Integrity has been defined as “includ(ing), but not limited toprobity, impartiality, fairness, honesty and truthfulness. Inpublic administration, integrity refers to “honesty” or“trustworthiness” in the discharge of official duties, servingas an antithesis to “corruption” or “the abuse of office.”Integrity entails that decisions must be carried out in thebest interest of all and with utmost honesty, being straightforward and ensuring honesty in all official relationships,developing an unquestionable ability to discharge theirassigned responsibilities, avoiding conflict of interest andcommunicating every relevant information to all stakeholdersand not soliciting nor accepting anything from their fellowcitizens by public officials to perform their duties.

3.0 Budgeting, Honesty and Integrity and Effective FinancialManagement Budget is a major tool for implementing government policiesand programmes as all activities of government and programmeswere design through a budgetary provisions. In general,government budget is the financial plan of a government for agiven period usually for a fiscal year which shows that itsresources are, and how they will be generated and used overthe fiscal period. The Government Budget is a key instrumentfor promoting its socio-economic objectives. It is aconstitutional responsibility that every state governmentshould plan its own activities for proper implementation using

10

budget as mechanism. Healthy Financial administration ingovernment rest on two prerequisite system, accounting andfinancial control and these are the main concern. These twosystems in turn rest squarely on the budgetary process i.e.the continuum of budget preparation, approval, execution,reporting, audit and review. Government use budgets as aguiding tool for planning and control of its resources, be itfinancial or otherwise. The use of budget involves knowing howmuch money you earn and spend over a period, particularly oneyear. When a budget of an establishment, department orministry is created, it means creating a plan for spending andsaving money.

Achievement of objectives of budget need to be effectivelymonitored by the Executive (through regulations, circulars anddirectives issued to accounting officers in governmentministries/ departments on how to keep records; financial lawsprescribing procedures for awarding contracts and institutionsestablished to ensure compliance; Office of Auditor Generalwhich scrutinizes and audits government expenditure; andAppropriate government agencies responsible for monitoringprojects executed by government), the Legislature (through thevarious committees of the legislature overseeing theactivities of ministries and departments to ensure that theyconform with provisions of the budget; and receives andscrutinizes audit report from the office of Auditor General toensure that various ministries and departments account forgovernment revenue and expenditure) and the Citizens ( which arethe generality of the people including civil society groups,labour and professional associations who are required by lawto perform the civic responsibility of monitoring governmentbudget through analysing budget estimates to determine theextent to which they reflect the needs of the people andwhether resources are allocated equitably among varioussectors/ sections of the country; ensuring that they receivebudgeted and allocated resources and services; monitoringcompliance of government’s ministries and departments withbudget estimates and the level of effectiveness of budgetimplementation; and providing the media with information onbudget violation or deviation).

What are being monitored in a budget include actual allocationresources to various sectors of the economy and sections ofthe polity, specific targets of the budget in terms of thebeneficiaries, specific projects to be executed and when theyare to be completed, money released for the execution of the

11

projects, procedures for procurement or award of contracts,who are the contractors that carry out the projects? and whichprojects are executed, when and where? When all these aredone, they help to ensure honesty and integrity in financialadministration. Table 1 shows State Governments’ expenditure(per GDP) 2006-2012.

Table 1: Summary of Federation Accounts Operations & FG Finances, 2008-2012 (Billion in N )

Federation Accounts Operations (Naira Billion)2008 2009 2010 2011 2012/1

Gross revenue7,866.6

64,844.

607,303.

7011,116.

9010,654.

70Percentage Change (%) -

-38.416

50.75961

52.20915

-4.15763

Net oil Revenue3,269.5

02,017.

203,002.

404,015.4

04,182.2

0

Percentage Change (%) -

-38.302

548.839

9833.7396

74.15400

7Net Non-Oil Revenue

1,283.40

1,582.90

1,782.00

2,143.00

2,383.00

Percentage Change (%) -

23.33645

12.57818

20.25814

11.19925

Net Federally Collected Revenue

3,931.10

2,831.70

3,865.90

5,085.40

5,288.30

Percentage Change (%) - -27.96 36.52 31.55

3.989853

Federal Government Finances (Naira in Billion)Fed. Govt. retained revenue

3,193.40

2,643.00

3,089.20

3,553.50

3,629.60

Recurrent expenditure

3,240.80

3,453.00

4,194.60 4,712

4,605.30

Capital Expenditure & Net Lending 960.9

1,152.80 883.9 918.5 874.8

Overall Surplus (+)/Deficit(-) -47.40

-810.00

-1,105.

40

-1,158.5

0 -975.70

Note 1/ProvisionalSource: CBN Annual Report and Accounts 2012, Pp 292-306

Figure I: Federation Accounts Operations 2008-2012 (Nairain Billion)

12

Source: Developed by the Author from Table 1

Table 1 and Figure I show that there was no appreciableincrement in gross revenue accruing to the Federation Accountin the period under review, except in 2011 were gross revenuerose by 52.21 per cent from N7, 303.70 billion in 2010 to N11,116.90 billion in 2011. After which, the gross revenuedecreased by 4.16 per cent from N11,116.90 billion in 2011 toN10,654.70 billion in 2012. In recent times, there had beenpersistent decline in gross federally collected revenueaccruing to the Federation Account. For example, the FederalGovernment had projected a monthly earning of N702.54bn in the2013 budget, but it only surpassed that target once during thefirst seven months of this year, earning N651.26bn in January;N571.7bn in February; and N595.71bn in March. In the months ofApril, May, June and July, the revenue earned by the countrywas N621.07bn, N590.77bn, N863.02bn and N497.98bn,respectively. As a result of the shortfall, The FederalMinistry of Finance said revenues would hence forth be sharedon the basis of the actual amount earned rather than what wasbudgeted. The Federal Government said that in spite of thefavourable oil prices at the international market, the lower-than-projected performance of the net oil revenue in the firstquarter of 2013 was due to the fall in oil lifting figuresduring the period, as a result of incessant crude oil theft,bunkering, pipeline vandalisation, which had been on theincrease in recent times in the Niger Delta region and theforce majeure declared by Agip Oil during the period.Similarly, the trend of both net oil revenue and net non-oilrevenue show that there were only marginal increments in thetwo revenue items between 2008 to 2012.

13

The sum of N6, 565.2 billion accrued to the Federation Accountin 2012, indicating an increase of 6.6 per cent over the levelin 2011. Of this amount, N681.7 billion, N206.8 billion andN388.4 billion, respectively, were transferred to the VAT PoolAccount, the FG Independent Revenue and ‘Other transfers’,respectively, leaving a net revenue of N5,288.3 billion. Inaddition, N387.7 billion, N167.2 billion, N373.9 billion,N150.0 billion, N560.4 billion and N284.4 billion respectivelywere drawn from the Excess Crude and Excess Non-oil Accountsfor: excess crude revenue sharing, exchange rate gain/NNPCrefunds to state and local governments, recovery ofunderstated revenue, excess non-oil revenue, budgetaugmentation, and Subsidy Reinvestment and EmpowermentProgramme (SURE-P), respectively. These amounts were added tothe federally-collected revenue (net) to boost thedistributable pool to N7, 212.0 billion. Analysis of thedistribution among the three tiers of government3, showed thatthe Federal Government (including Special Funds) received thesum of N3,349.5 billion; state governments,N1,743.8 billion;and local governments, N1,344.4 billion; while the sum ofN774.3 billion was shared among the oil-producing states as13% Derivation Fund.

Figure II: Federal Government Finances 2008-2012 (Naira inBillion)

Source: Developed by the Author from Table 1

Table 1 and figure II show the trend of FG capitalexpenditure and net lending, recurrent expenditure andoverall surplus/deficit from 2008 to 2012. Figure II showsa discouraging scenario for FG expenditure from 2008-2012,where the recurrent expenditure far outweighs the capitalexpenditure with a ratio of about 84:16 in favour ofrecurrent expenditure. This situation is not good foreconomic growth and development of the Country. Similarly,the overall fiscal operations of the Federal Government

14

resulted in a deficit of N975.7 billion, or 2.4 per cent ofGDP, compared with the deficit of N1, 158.5 billion, or 3.1per cent of GDP in 2011. The overall budget deficit wasfinanced from domestic sources.

Table 2: Summary of States/FCT and Local Govt. Finances, 2008-2012 (Billion Naira )

State Governments' and FCT Finances (Naira in Billion)

2008 2009 2010 20112012/1

Total revenue plusgrants

2,934.80

2,590.70

3,162.50

3,410.10

3,572.50

Total Expenditure3,021.66

2,776.90

3,266.20

3,542.00

3,844.90

Recurrent Expenditure

1,505.60

1,426.10

1,648.40 2,056

1,664.30

Capital Expenditure

1,455.70

1,284.20

1,522.40

1,375.20

1,965.30

Extra-Budgetary Expenditure 60.30 66.70 95.40

111.00

215.40

Overall Balance 86.80186.20

103.70

131.90

272.40

Loans: External 38.30 8.00 7.60413.00 10.40

Internal 60.20

162.30 88.10

170.40

223.40

Local Government Finances (Naira in Billion)

2008 2009 2010 20112012/1

Total revenue1,379.00

1,069.40

1,359.20

1,636.20

1,644.30

Recurrent expenditure

819.40

704.60

823.70 1,280

1,342.40

Capital Expenditure & Net Lending 562.6

363.00 533 352.1 304.4

Overall Surplus (+)/Deficit(-) -3.00 1.80 2.50 4.30 -2.40

Outstanding Loans -6.10-46.30 36.20 25.10

-26.90

Note 1/ProvisionalSource: CBN Annual Report and Accounts 2012, Pp 292-306

15

Figure III: States (and FCT) Revenue & Expenditure Comparison 2008-2012 (Naira in Billion)

Source: Developed by the Author from Table 2

Total revenue of the state governments increased by 4.8 percent to N3, 572.5 billion, or 8.8 percent of GDP in 2012,compared with N3, 410.1 billion or 9.1 per cent of GDP in2011. The analysis of the revenue indicated that allocationsfrom the Federation Account (including 13% derivation fund)was N1,857.0 billion, or 52.0 per cent; the VAT Pool Accountwas N347.7 billion, or 9.7 per cent,and Internally Generated Revenue (IGR) was N548.1 billion, or15.3 per cent. Others were the Stabilization Account, N1.3billion, or 0.1 per cent; the Excess Crude Account (includingbudget augmentation, SURE-P, exchange rate gains and refund tothe state governments by the NNPC), N542.4 billion or 15.1 percent; grants, N95.7 billion or 2.7 per cent, while “others”accounted for N180.4 billion or 5.1 per cent of total.Provisional data on state governments’ finances (including theFCT) showed that the overall deficit increased from N131.9billion in 2011 to N272.4 billion in 2012. As a ratio of GDP,at 0.7 per cent, the deficit rose relative to 2011. Thedeficit was financed largely through borrowing from theDeposit Money Banks (DMBs).

On the other hand, estimated total expenditure of the stategovernments increased by 8.6 per cent to N3, 844.9 billion, or9.5 per cent of GDP in 2012. A breakdown showed that, at N1,664.3 billion or 4.1 per cent of GDP, recurrent expenditurewas 19.0 per cent lower than the level in the preceding yearand accounted for 43.3 per cent of the total. Similarly,

16

extra-budgetary expenditure grew by 94.0 per cent andaccounted for 5.6 per cent of the total in 2012. This is not a goodscenario as the expenditure of the States was greater than their revenuesthroughout the period under review, thus compelling the states to compete withinvestors and business entrepreneurs for credit facilities from the DMBs in order tofinance deficit. The situation could be brought under control if extra-budgetaryexpenditure is to be minimized and efficiency, economy and prudence is to beenhanced in the management of the State Government finances.

17

Table 3: State Government's Finances (2002-2012) (Naira in Billion)

2002 2003 2004 2005 2006 2007 20008 2009 2010 201120121/

ATotal Revenue Plus Grants

669.83

855.01

1113.96

1419.66

1543.80

2065.40

2943.80

2590.70

3162.50

3410.10

3572.50

Share of FederationA/c 2/

388.30

535.18

777.21

921.00

1016.10

1109.30

1709.20

978.38

1.353.7

1786.30

1857.00

Share of Excess OilRevenue - - - -

154.70

258.90

354.10

376.80

322.40

167.00

143.90

Share of Augmentation - - - - - - -

272.80

162.90

510.70

208.00

Exchange Gain - - - - - - - 58.90 14.80 18.90190.5

0

Share of VAT52.6

365.8

9 96.20 87.45110.6

0144.4

0198.1

0229.3

0275.6

03180.

00347.7

0Internally Generated Revenue

89.61

118.76

134.20

122.74

125.20

305.70

441.10

461.20

757.90

509.30

548.10

Grants and Others129.72

134.18

104.35

137.45

125.30

209.40

179.00

188.00

224.20 88.70 95.70

Share of Stabilization Fund 9.57 1.00 2.00 10.78 11.90 37.70 53.40 29.70 51.00 11.20 1.30

State Allocation -

-

-

140.24 - - - - -

180.40

B Total Expenditure724.55

921.16

1125.06

1478.60

1586.80

2116.10

3021.60

2776.90

3266.20

3542.00

3844.90

Recurrent Expenditure

424.20

545.31

556.81

789.13

894.30

1217.40

1505.60

1426.10

1648.40

2055.8

1664.30

18

Capital Expenditure283.48

324.02

412.93

514.73

584.00

854.80

1455.70

1284.20

1522.40

1375.20

1965.30

Extra-Budgetary Exp. 3/

16.87

51.83

155.32

174.74

108.50 43.90 60.30 66.70 95.40

111.00

215.40

C Current Balance 4245.60

309.69

557.13

630.51

649.40

848.00

1429.20

1164.60

1514.10

1354.40

1908.20

D Overall Balance 4

-54.7

2

-66.1

5-

11.10-

58.94-

43.00-

50.70-

86.80

-186.2

0

-103.7

0

-131.9

0

-272.4

0

E Financing54.7

466.1

7 11.12 58.96 43.00 50.70 86.80186.2

0103.7

0131.8

0272.4

0

External Loans15.9

014.6

8 -

- - 5.90 38.30 8.00 7.60 41.30 10.40

Internal Loans32.4

571.0

3 4.40 22.56 27.00 25.70 60.20162.3

0 88.10170.4

0223.4

0

Other Funds 1.30

-32.5

5 6.72 3.14 16.10 19.10-

11.70 16.00 8.00 79.90 38.60Note 1/Provisional 2/Gross Statutory Allocation 3/Includes contribution to external debt fund and other deductions at source 4/ Positive (+) sign connotes surplus while (-) sign connotes deficit Sources: State Government Ministries of Finance & Office of Accountant-General of the Federation's Report (2002-2012)

19

Central Bank of Nigeria Annual Report and Statement of Accounts (2002-2012)

20

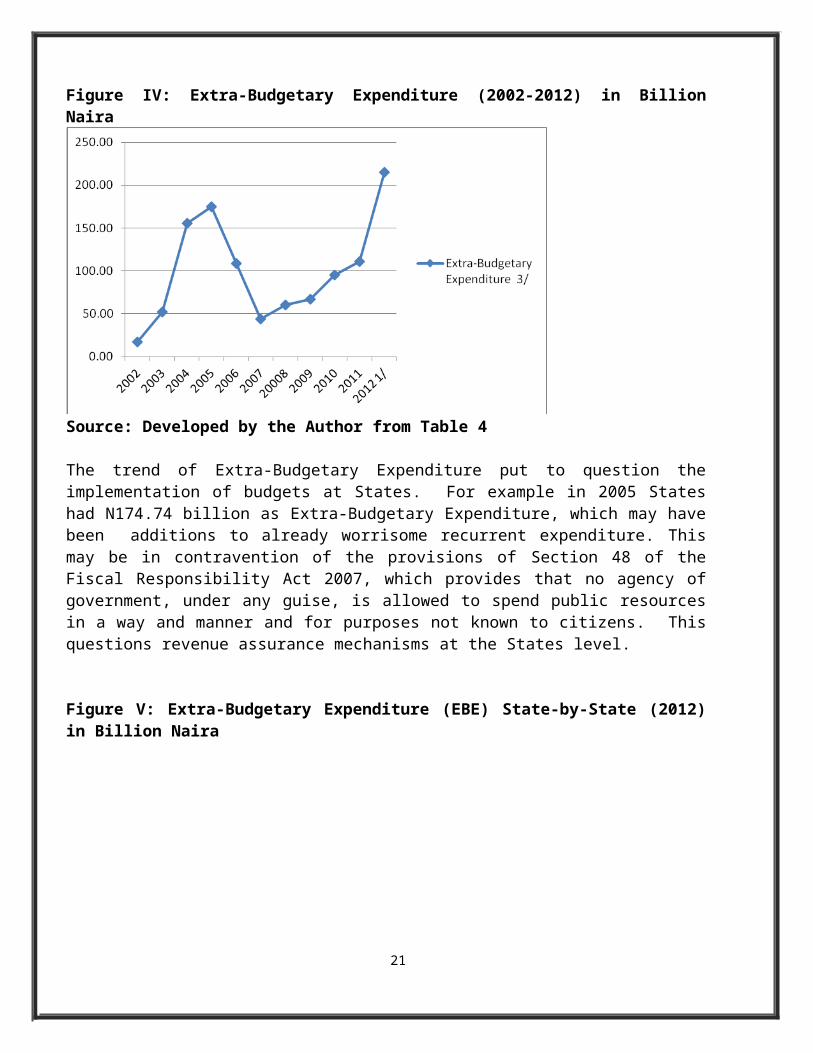

Figure IV: Extra-Budgetary Expenditure (2002-2012) in BillionNaira

Source: Developed by the Author from Table 4

The trend of Extra-Budgetary Expenditure put to question theimplementation of budgets at States. For example in 2005 Stateshad N174.74 billion as Extra-Budgetary Expenditure, which may havebeen additions to already worrisome recurrent expenditure. Thismay be in contravention of the provisions of Section 48 of theFiscal Responsibility Act 2007, which provides that no agency ofgovernment, under any guise, is allowed to spend public resourcesin a way and manner and for purposes not known to citizens. Thisquestions revenue assurance mechanisms at the States level.

Figure V: Extra-Budgetary Expenditure (EBE) State-by-State (2012)in Billion Naira

21

Source: Developed by the Author CBN Annual Report and Accounts,2012

Surprisingly, Figure V reveals that most of the States with higherextra-budgetary expenditure had lower IGR and higher personnel andoverhead expenses. These question the cost minimization strategiesand revenue assurance mechanisms in the States.

Figure VI: Local Government Finances, 2008-2012 (Naira in Billion)

Source: Developed by the Author from Table 3

The total revenue of local governments, at N1, 644.3 billion,represented an increase of 0.5 per cent over the level in2011. The

22

revenue comprised allocations from the Federation Account (N977.4billion), the share of Excess Crude Account (N69.6 billion), NNPCrefunds to LGs (N34.6 billion), budget augmentation (N100.4 billion),exchange rate gain (N13.6 billion), SURE-P (N51.0 billion), VAT(N238.5 billion), IGR (N26.6 billion), grants/others’(N26.7 billion),Stabilization Fund (N3.2 billion), state allocation (N4.7 billion)and “others” (N97.8 billion).At N1,646.8 billion, the totalexpenditure of local governments indicated an increase of 0.9 percent above the level in 2011 and represented 4.1 per cent of GDP. Abreakdown indicated that recurrent outlay stood at N1, 342.4 billion,or 81.5 per cent, while capital expenditure amounted to N304.4billion, or 18.5 per cent of the total.

A disaggregation of recurrent expenditure showed that personnel costwas N954.4 billion, while overheads and the consolidated fundcharges/others amounted to N263.1 billion and N124.9 billion,respectively. Analysis of capital expenditure (functionalclassification) revealed that the share of administration was N51.5billion; economic services (N112.9 billion); social and communityservices (N104.4 billion); and transfers (N35.5 billion). However,the most worrisome issue is that the recurrent expenditure faroutweighs capital expenditure, more especially in 2011 and 2012 whichstrongly questions efficient discharge of services by the LGAs thatare geared towards improving the wellbeing of people at the grossroot level.

Table 4: Corruption Perception Index: Comparative

2012 Rank

2011 2008 Country CPI Score

1

1 4 New Zealand

90

1

2 1 Denmark 90

143 141 Nigeria

23

139 27 64

69 62 Ghana 45

17

UK 74

19

USA 73

20

Chile 72

20

Uruguay 72

22

France 71

69

South Africa

43

1 = Least Corrupt

Source: Soyode, 2013 Pp 1

These appear to be what has been consistently summarized in thepublished and widely disseminated indices of corruption. The 2013Transparency International's Perception Index has rated Nigeria asthe 8th most corrupt nation in the world. (See table 4) Nigeria wasrated 139 (out of 174) in 2012 as the 35th most corrupt nation. In2010, she scored 2.4 out of 10, the same as 2009, and was rated12thposition from the bottom. What do these rankings indicate on thelevel of honesty and integrity in financial administration inNigeria? Have the budgets being able to enhance that over the years?The Transparency International Global Corruption Barometer (GCB)scored Nigeria Legislatures 4.2.; and Public/Civil Servants wererated 4.0 out of 5.0 (extremely corrupt). The GCB measures "personalexperiences of paying bribes for government services and theirperception of the integrity of their country's major publicinstitutions (Soyode, 2013). To what can this be said to haveaffected budget implementation and budgetary performance over theyears?

From the foregoing discussion, it can be seen that budgeting plays animportant role in enhancing honesty and integrity of public financialmanagers in Nigeria. It is one that leads to the other in an endless

24

cyclic manner. The years of poor budgeting and budgetary controlcorresponds with the years of more significant unimpressive economicdevelopment. If budgeting is to improved, the path to economicdevelopment becomes relatively easier.

4. CONCLUSION AND RECOMMENDATIONS

Effective budgeting in Nigeria requires: adequate knowledge of theimpact of the budget on the economy; an effective communication andreporting system which supplies vital information to policy makers;early approval of budget and supplementary budget (where necessary);maintaining budget discipline; good working relationship andunderstanding among the legislature, executives and other interestgroups on issues relating to budgeting; and courage on the part ofelected representatives to do the right thing at the right time.

Honesty & integrity in budgeting are indispensable vehicles forenhancing efficiency, effectiveness and economy in the management ofpublic resources with a view to improving the general well being ofthe citizenry, as well as, bringing about the desired socio-economicdevelopment. They are important devices for making government moreefficient on all fronts, which help to control costs and achieve theoverall objectives of government. The ability of a government toeffectively manage and budget for its revenues and control itsbudgets invariably affects its level of development.No matter the quantum of financial resources in hands of thegovernment, the desired objectives may not be achieved if there is nohonesty and integrity in budgeting and budgetary control. This isnecessary to ensuring effective cost control, minimizations ofexpenses, blockage of revenue leakages, control of fraud, excessesand abuses, reducing financial impropriety and extravaganzas, as wellas, achieving the objectives of governance.The following recommendations are given for the enhancement ofhonesty and integrity in budgeting in Nigerian Public sector with aview to improving the general wellbeing of the citizenry, as well as,bringing about the desired level of socio-economic development in thecountry.

25

(i) Government should put in place effective strategies thatcan be used to counteract financial improprieties in theNigerian public sector with a view to curtailing wastefulexpenditure, increasing the level of productivity and efficiencyand enhancing public confidence in Government financialadministration.

(ii) The Office of the Auditor General at the three tiers ofgovernment, the budget office, the due process office, theexecutive, the legislature and the civil society should ensureeffective budget monitoring and tracking with a view toenhancing honesty and integrity in financial administration forattainment of budget objectives.

(iii) The Organized Private Sector, Civil Society and thePolitical Class should develop effective safe strategies forwhistle blowing to ICPC and EFCC to guard against financialimpropriety in public governance and enhance integrity infinancial administration.

(iv) Public officials in charge of public financialadministration should also ensure compliance with ethics, dueprocess and norms of fund management and public procurement toensure value for money in projects implementation and enhancepublic accountability.

(v) Governments at all levels through the appropriateMinistries, Departments and Agencies (MDAs) should ensuringbudget discipline (adherence to limits) and curtailing extra-budgetary expenditure. This can be done by enhancing budgetarycontrol and variance analysis and limiting some expenditure ofMDAs of government through “expenditure envelopes” from whichthey are to meet all their needs and deliver public goods andservices. The allocation of such envelopes is to be done by theBudget Office in conjunction with all relevant stakeholderstaking into account the size of each MDA’s payroll and prioritylevel accorded to the services to be delivered by each MDAagainst the background of the priorities of the Government asdocumented in NEEDS, SEEDS, the MDGs, Vision 20:2020 andstakeholders’ inputs.

(vi) Effectiveness of internal audit should be enhanced in allMDAs with a view to improving control over public expenditure

26

management, ensures compliance with government’s policies andlaid down procedures and assist to secure accountability andtransparency in government financial activities. This would helpto ensure that government internal audit function adds value togovernment’s operations, thereby contributing to the success ofthe Economic Reform and Governance Project (ERGP). This alsoentails the need to promote One of the most challengingimperatives in restoring trust in the government is reforming

(vii) There is the need for the re-moulding of the individualsand collective perspectives or paradigms of public officialswith a view to enhancing their moral intelligence (integrity,honesty, compassion, and forgiveness). These personal valueshelp an individual in setting personal goals and daily conductand conforming ethical code both at personal and organizationallevels in any reform effort.

(viii) The Executives should ensure that only civil servants withpersonal integrity and who are not afraid to public scrutinyshould be appointed to head MDAs. Leadership is a crucialmatter in public administration to influence the capacity ofgovernments that accounts the success or failure of thegovernment, Effective leadership is central to effective andsustainable implementation. Thus, it plays a vital role in thesuccess or failure of the government.

(ix) The Government should form a strong monitoring committeewho will ensure that all monies allocated to the Ministries,Departments and Agencies have been judiciously utilized inaccordance with financial rules and regulations. Major stepsshould be taken to arrest the cash management problem so thatfull budgetary provision would be implemented.

(x) Periodic intensive training on the use of budgetary controlsystem should be organized for public officers.

(xi) MDAs should be directed towards maximization of internalgenerated revenue of the governments by improving revenuecollection machinery, reducing wasteful and avoidableexpenditure, judicious spending of available funds and properaccountability.

27

(xii) There should be participation of all and sundry in thebudget process including executive arm of government,legislative arm of government, civil society and internationalinstitutions.

(xiii) Budgeting monitoring by the executive, legislature and thecitizens should be improved with a view to documentingobservation of processes and activities of government gearedtowards implementing the budget over a period. It is a way ofensuring that monies voted for various projects and activitiesin the budget are actually spent and put into good use.

(xiv) A well planned and articulated budget cycle should beevolved such that the debate by the legislature and the signinginto law of the appropriation act are concluded before thecommencement of the new fiscal years. This would help to ensureeffective budgetary performance in the country.

(xv) Independent body is expected to check, monitor, andinvestigate the execution of budget of every tiers of governmentas it is done elsewhere like USA, UK and developed nations ofthe world. Fiscal Responsibility Commission should be given highdegree of independence to oversee the implementation andexecution of the budgets of government at all the three tiers ofgovernment. This can be done by enforcing rule of law of budgetimplementation any unauthorized spending should be reported tothe appropriate authority for disciplinary action.

(xvi) There should be more budget discipline at all the tiers ofgovernment, where money spent must be justified and satisfied byall the established budgetary and budget monitoring organs.

(xvii) There is the need for values that can inspire honesty,integrity efficiency, loyalty and dedication in ourbureaucracies with a view to restoring the moral tone of ourpublic officers, and inducing them to greater productivity.

References

28

Abiola, A.G. (2006). Fiscal Indiscipline, Official Corruption andEconomic Growth in Nigeria: An Examination of Possible Nexus.In: Feridun, M. (2006) edited. Nigerian Economy: Essays onEconomic Development. MPRA Paper No. 1025. http://mpra.ub.uni-muenchen.de/1025/. (Accessed 27/05/2012).

Ajakaiye, O. (1999). “Towards Effective Budgeting under a Democratic system”Bullion 24 (1): 65-68

Akinyele, T. A. (1981). “Budgetary System in Presidential Government: Factors forEffective Reforms”. Paper presented at Public Service Lecture atNigerian Institute of International Affairs Lagos, 4th November.

Bragg, S.M. (2010). Treasury Management: The Practitioner’s, New Jersey, USA:John Wiley & Sons, Inc.

Feridun, M. and Akindele, S. T. (2006). Nigerian Economy: Essays on EconomicDevelopment. Online at http:// mpra.ub.uni-muenchen.de/ 1025/MPRA Paper No. 1025, posted 04. December 2006 /19:37 (Accessed12 May, 2011)

Dandago, K.I. (2001). “Major Winners and Losers of Budget ofTransition” Proceedings of Faculty Seminar Series: Vol.1. pp157-172 BayeroUniversity, Kano, Nigeria.

Hamid, K.T. (2008). Promoting Good Public Governance andTransparency. A Paper Presented at a Two-Day SensitizationWorkshop for the Commemoration of the International DayAgainst Corruption, Organized by the Kano State PublicComplaints and Anti-corruption Directorate, held on Wednesday31st December 2008 (6th Muharram, 1430 A.H.) at the MurtalaMuhammad Library, Ahmed Bello Way, Kano. Available athttp://www.acdemia.edu

Hamid, K.T. (2011). Reducing the Cost of Governance for RevenueAssurance at States Level in Nigeria Being a Paper Presentedat the 7th Northern District Accountants Conference,Organized by the Institute of Chartered Accountants ofNigeria (ICAN), Held at the Royal Tropicana Hotel, Kano, from16th to 19th April, 2012. Available at http://www.acdemia.edu

Hamid, K.T. (2012). Budgetary Control and Debt Management forEconomic Development. Being a Paper Presented at the MCPTP ofthe Chartered Institute of Treasury Management of Nigeria(CITM), Held at the Manpower Development Institute, Dutse,Jigawa State-Nigeria, from 4th to 5th October, 2012.

29

Hamid, K.T. (2014). Revenue Assurance for Enhanced Service DeliveryAt the three-Tiers of Government in Nigeria. Being a PaperPresentated at the Eighteenth Annual Financial Reporting andBusiness Communication Conference organised by the Universityof Bristol and the BAFA FARSIG, to be held at the University ofBristol from 3rd to 4th July 2014.

Oshionebi, B. O. (1999).“Transparency and Accountability inBudgeting” Paper presented at a Workshop on Budgeting andFinancial Management under Democratic Government for BudgetOfficers in the Federal Public Service at NCEMA, Ibadan, 6th -17th

September.Phillips Committee (2000). “Strengthening the Federal Budget System

in 2000 and Beyond” Report on the Budget System Review Committee MainReport Volume 1. March

Soyode, A. (2013). The Impact of Corruption on Sustainable EconomicReforms. *An invited paper presented at the 2013 Annual Conference of theAssociation of National Accountants of Nigeria, Abuja. Available Online.

30