The level of awareness among KENMS and KOED students in IIUM towards ICC and CCC

35

1 Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC The Level of Awareness Among KENMS and KOED Students in IIUM Towards Islamic Credit Card and Conventional Credit Card Muhammad Muzzammil bin Jabarullah Khan (1113657) Muhammad Amirul Syakirin bin Mohd Dzahir (1111607) Kuliyyah of Economics Management and Sciences (KENMS) International Islamic University Malaysia LE 4000: English for Academic Writing (EAW) Section 4

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The level of awareness among KENMS and KOED students in IIUM towards ICC and CCC

1

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

The Level of Awareness Among KENMS and KOED Students in IIUM Towards Islamic Credit

Card and Conventional Credit Card

Muhammad Muzzammil bin Jabarullah Khan (1113657)

Muhammad Amirul Syakirin bin Mohd Dzahir (1111607)

Kuliyyah of Economics Management and Sciences (KENMS)

International Islamic University Malaysia

LE 4000: English for Academic Writing (EAW)

Section 4

2

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Abstract

Interest (riba), uncertainty (gharar), and gambling (maysir) is one of the prohibited elements in

Islamic banking and there is a need for Islamic credit card (ICC) to replace the conventional credit

card (CCC). Hence, it is vital for students to have an awareness regarding the differences between

ICC and CCC. This research aimed to investigate the level of awareness among IIUM students

towards ICC and CCC. The sample consisted of 15 students from Kuliyyah of Economics

Management and Sciences (KENMS) and 15 students from Kuliyyah of Education (KOED) in

International Islamic University Malaysia (IIUM). The material used was questionnaire. The

finding of the survey is that IIUM students from KENMS are more aware towards ICC and CCC.

Furthermore, although the students are aware of the emergence of ICC in Malaysia, they have

constrains in adopting or choosing ICC as they lack of knowledge in terms of the rules and

regulation, operation and payment. Thus, the level of awareness between ICC and CCC is

important in order to ensure the understanding of the product in the market. This paper suggests

that more efforts and facilities need to be built to promote the ICC among students and society.

Keywords: ICC, CCC, Level of awareness

3

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

The Level of Awareness Among KENMS and KOED Students in IIUM Towards Islamic

Credit Card and Conventional Credit Card

Ever-present in society, credit cards have become a fact of life for most students and are a

part of the students’ culture. With the technology expansion such as internet, credit card are more

preferable compare to carrying a bulk of cash. Since credit card is widely accepted around the

world, students find it easy and secure to pay for internet shopping. In this case, conventional credit

card (CCC) has dominated the market in Malaysia since 1970s, until the existence of the first

Islamic credit card (ICC) by Ambank in 1992 (Nazimah Hussin, 2012). The main reason is to

protect Muslims from any prohibited elements in the financial instruments. Therefore, it is

important for students to have an awareness regarding the differences between ICC and CCC.

Although ICC has been in the market for two decade, according to Syahidawati binti Haji

Shahwan and Nuradli Ridzwan Shah Bin Mohd Dali (n.d) and Nazimah Hussin (2012), majority

of respondents do not aware the differences between ICC and CCC. In addition, Nazimah Hussin

(2012) states that 31.9% of the respondents agreed that the terms and conditions in CCC are easier

to understand compared to ICC. This is because the market for ICC is relatively small compared

to CCC plus the lack of understanding and information among the public about Islamic credit card

(Nazimah Hussin, 2012; Umar Mohammed Idris and Muhammad Tahir Jan, 2013). Hence, the

awareness towards ICC and CCC is very important among students nowadays.

According to Niringjuerae (2012), defines ICC as a payment instrument that meet with at

least three criteria of Islamic principles. Firstly, he assert that the card must meets the shariah

requirements on lending, which vary from region to region. In general, it must avoid the three

essential prohibitions in Islamic finance, which are riba, gharar and maysir.

4

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Samsuri Sharif (2010) defines riba (interest) as “addition, growth, expansion or increase”

(p.94). According to the Shariah, riba technically means the premium that must be paid by the

borrower to the lender with the principal amount as a condition for a loan because of the extension

for the repayment (ISRA, 2012). There are also several verses in the Quran which stated the

prohibition of riba like in surah Al-Nisa verse 161 “That they took usury, though they were

forbidden; and they devoured men’s substance wrongfully; we have prepared for those among

them who reject Faith a grievous punishment”. The connotation of the verse is to remind the

Muslims to obey Allah’s command regarding the danger of riba. Another example is in surah Al-

Imran verse 130 “O ye who believe! Devour not usury, doubled and multiplied; but fear Allah;

that ye may (really) prosper”. Therefore, the most important teachings of Islam is to establish

justice and eliminate exploitation in business transaction such as riba (Mohd Nahar bin Mohd

Arshad, 2011). The Prophet also condemned not only those who take riba, but also those who give

riba and those who record the transaction or act as witnesses to it (Bakhshi, 2006). Therefore, in

Islamic banking, the prohibition of riba is the most significance principle

According to Samsuri Sharif (2010), gharar is “unknown consequence either it would

happen or not” (p.103). Basically gharar happens when a person selling something that is not

owned by him and could not deliver the items. Although there is no verse that specially prohibits

gharar in al-Quran there are certain verses that prohibit any transaction that creates injustice to any

parties (ISRA, 2012). In surah al-Nisa, verse 29, the Quran reads: “O you who believe! Eat not

your property among yourself unjustly by falsehood and deception, except it be a trade amongst

you, by mutual consent.” According to ISRA (2012) based on this verse, the jurist has agreed that

gharar (uncertainty) can create injustice in the economic and it should be prohibited.

5

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Meanwhile, maysir or gambling is defined as easily obtaining something without effort

which applies to all activities where a person wins or losses by mere chances (Nor Azizan Che

Embi, 2011). There are several direct verses in the Holy Quran on the prohibition of gambling

which are from surah al- Baqarah verse 219, “They ask thee concerning wine and gambling. Say:

‘In them is great sin and some benefits for people; but the sin is greater than the benefits” and al-

Ma’idah verse 90, “Satan intends to excite enmity and hatred among you with intoxicants and

gabling, and hinder you from remembrance of Allah, and from prayer…” thus, in short, a form of

gambling is a basic prohibitions in Islam (Nor Azizan Che Embi, 2011).

Secondly, according to Niringjuerae (2012) an ICC must have certainty to be accepted

widely. It has to use international payment schemes, such as MasterCard or Visa. Lastly,

Niringjuerae (2012) states that the card should not encourage behavior that is considered haram

(prohibited). To sum up, ICC is a card that adheres with all the shariah principles in terms of

developing, issuing and using the card.

According to Nuradli Ridzwan and Noor Azira (2006), credit card is defined as plastics

money and it has been issued and used. When it deals with conventional credit card there is a

charge on a high management fee and if there is a late payment then there are penalty charge will

be imposed to the customer and the main it solely based on a loan contract (Nuradli Ridzwan and

Noor Azira, 2006).

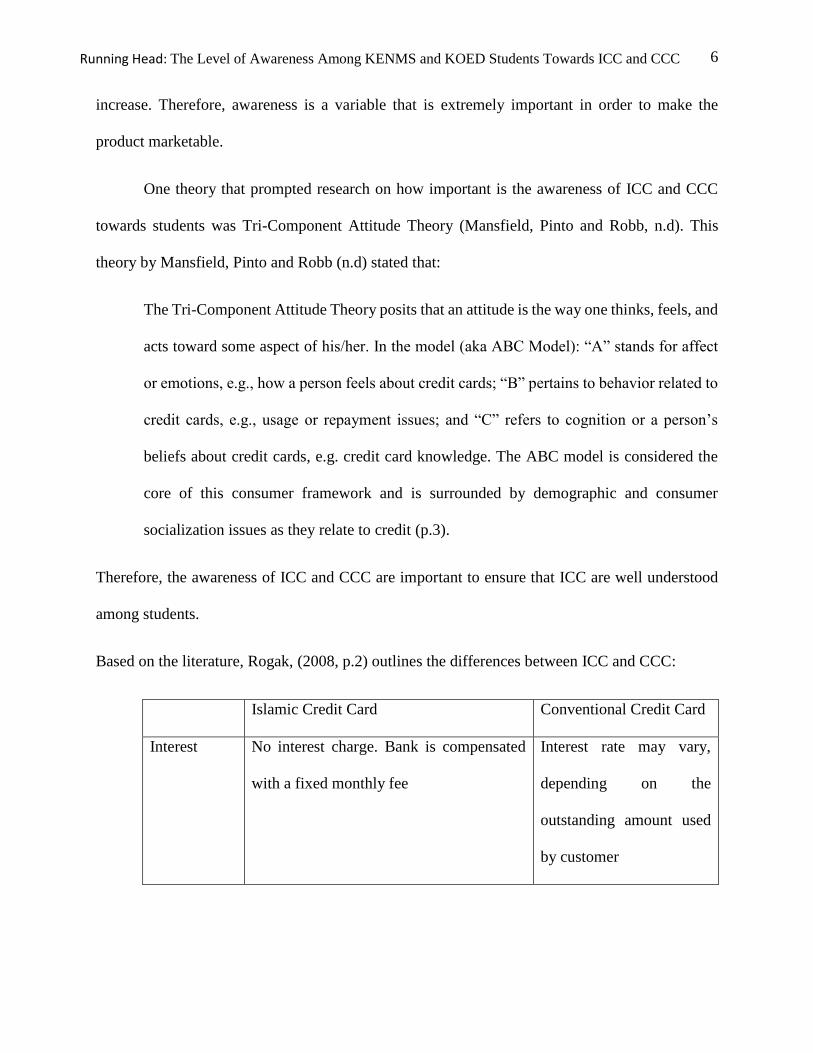

Rohrer (2007) has defined awareness as “perceptive and expressive ability in connection

with the living of the basic rights of existence. We refer to this ability in the following as

awareness.” (p.48). If people do not aware about the product and the service provided they will

not be using that product or service. However, if proper information is delivered to the people the

awareness for that product may be increased and indirectly the usage of the product will also

6

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

increase. Therefore, awareness is a variable that is extremely important in order to make the

product marketable.

One theory that prompted research on how important is the awareness of ICC and CCC

towards students was Tri-Component Attitude Theory (Mansfield, Pinto and Robb, n.d). This

theory by Mansfield, Pinto and Robb (n.d) stated that:

The Tri-Component Attitude Theory posits that an attitude is the way one thinks, feels, and

acts toward some aspect of his/her. In the model (aka ABC Model): “A” stands for affect

or emotions, e.g., how a person feels about credit cards; “B” pertains to behavior related to

credit cards, e.g., usage or repayment issues; and “C” refers to cognition or a person’s

beliefs about credit cards, e.g. credit card knowledge. The ABC model is considered the

core of this consumer framework and is surrounded by demographic and consumer

socialization issues as they relate to credit (p.3).

Therefore, the awareness of ICC and CCC are important to ensure that ICC are well understood

among students.

Based on the literature, Rogak, (2008, p.2) outlines the differences between ICC and CCC:

Islamic Credit Card Conventional Credit Card

Interest No interest charge. Bank is compensated

with a fixed monthly fee

Interest rate may vary,

depending on the

outstanding amount used

by customer

7

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Collateral Collateral is required in many cases. Most

banks require an undated check or

underlying deposit

No need for collateral

Contract type Lease-based Loan-based

Transaction

restriction

The purchase of prohibited things such as

alcohol, gambling, pork, and sexually-

related items are not allowed

There are no restrictions

on items that can be

purchased

Profit margin

on deposits

Profit is fixed and shared between bank and

customer. The profit also is not

compounded

No deposits

Late payment

fees

Fixed amount + 3% of outstanding balance.

The 3% charge usually donated to charity

Variable & compounded

On the other hand, the literature has revealed that ICC is based on shariah principle, the

profit margin will be fixed, do not include any interest rate for the late payment but it will charge

a low penalty for the late payment and it not based on the loan, instead it is based on the concept

of trading (bay) (ISRA, 2012; Umar Mohammed Idris and Muhammad Tahir Jan, 2013; Rohma

n.d.). In addition, there are certain things that cannot be purchased using the Islamic credit card.

Although ICC has been introduced it still faces some problems in terms of contract and its features.

Ilham Reza Ferdian, Miranti Kartika Dewi and Faried Kurnia Rahman (2008) has

highlighted that there is an issue that ICC is more expensive than CCC. For instance, in Indonesia,

the ICC holder needs to pay 3% administration cost of the total amount of transaction that they

8

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

conducted which is more expensive than the conventional (Ilham Reza Ferdian, Miranti Kartika

Dewi and Faried Kurnia Rahman, 2008). There is another shariah issue that arise in Indonesia

which is the ICC is not different with other CCC and it still include “implicit” riba in its scheme

(Ilham Reza Ferdian, Miranti Kartika Dewi and Faried Kurnia Rahman, 2008).

Ilham Reza Ferdian, Miranti Kartika Dewi and Faried Kurnia Rahman (2008) stated that

the card issuer only changes the interest with the term of ‘administration cost’ and it resembles the

conventional interest rate, some scholar are afraid that this scheme is just a back door to avoid riba

by change the name. Their argument is that why that the customer needs to pay the administration

cost based on the transaction amount because the administration cost needed to be fixed so that it

will be the same for any amount of transaction. If they charge based on the amount of transaction,

then it resembles lending money. They will get an extra amount based on the amount being lend

and it will fall under riba. This is the common problem that ICC face, argued Ilham Reza Ferdian,

Miranti Kartika Dewi and Faried Kurnia Rahman (2008).

However, Edward (2011) argued that ICC is based on a fee and the problem arises when

the fee charges are high compared to CCC that use the mechanism of interest rate. Sometimes

when the consumer make a late payment, they will be charged a penalty in order to encourage user

to pay within the specific period and the amount will be given to charity (Edward, 2011).

Rohma (n.d), pointed out that ICC that is being practiced will imposed two kinds of

compounds and it is called tawidh and it is calculated by multiplying 3% from the balance account

as the late charge fee. In addition, customers must pay a monthly fee, (3.25 – 3.5) % and this fee

is as same as the amount of interest in the CCC (Rohma, n.d). In addition, Rohma (n.d) stated that

in Indonesia, ICC face some problems regarding the problem of high costs and the strategy of

promotions.

9

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Engku Rabiah Adawiyah Engku Ali and Mohd Daud Bakar (2008) mentioned that the bank

charges a fee (ujr) from the customer for providing this credit card service and this is where the

problem starts. This is a very sensitive issues because for what that this fee (ujr) is charge and why

it must be charged based on the transaction amount (Najeeb and Lahsasna, n.d). Furthermore, The

Islamic Fiqh Academy of OIC (1986) has come out with a rule that this service fee (ujr) needs to

be fixed in an exact amount and it must based on the actual cost incurred by the bank when

providing the services such the cost of printing and more (Najeeb and Lahsasna, n.d). According

to Najeeb and Lahsasna (n.d) the service fee (ujr) charge cannot be according to the amount being

used by the ICC holder if it is charged according to the transaction amount that customer used,

then it will leads to riba.

The impact of awareness on usage of credit cards was studied by Delener and Katzenstein

(1994) found that Asian and Hispanic consumers do not prefer credit card so there is a need to

promote credit card services to encourage it use. In addition, Durkin and Price (2000) suggested

by providing all relevant information to the customer will increase the level of awareness regarding

the credit card. Gan, Maysami, and Koh (2008) mentioned that the lack of understanding or

minimal information of industry among the society is one of the biggest dilemmas in the credit

cards market and this indirectly will affects adoption and usage of credit cards. Moreover, the

promotional campaigns play a vital role on the awareness towards ICC in order to avoid the

elements of gharar or uncertainty (Syed Alwi Mohamed Sultan, 2001). Thus, the awareness of

credit card among society is essential.

According to a study done by Syahidawati binti Haji Shahwan and Nuradli Ridzwan Shah

Bin Mohd Dali (n.d), 30% of the academic staff from IIUM do not really aware and do not fully

understand the contracts being implemented in ICC in Malaysia. In addition to that 50.5% of the

10

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

respondents agreed that CCC are widely accepted compared to 14.3 % disagree (Nazimah Hussin,

2012). Although several studies being done regarding the level of awareness of ICC and CCC but

there was little empirical study focuses on university student.

The purpose of this study is to investigate the level of awareness of Kuliyyah of Economics

and Sciences (KENMS) students and Kuliyyah of Education (KOED) students in International

Islamic University Malaysia (IIUM) towards ICC and CCC.

The research questions of this study are:

1. What is the level of awareness among KENMS and KOED students in IIUM towards ICC?

2. What is the level of awareness among KENMS and KOED students in IIUM towards CCC?

11

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Methods

The purpose of this research is to identify the level of awareness among KENMS and

KOED students towards ICC and CCC. A quantitative methodological approach was used in this

research to make it easier to analyse the feedback.

Respondents of the study

The population of this study is International Islamic University Malaysia (IIUM) students

that are pursuing their degree at International Islamic University Malaysia (IIUM), Gombak. The

sample comprised of 15 students from Kuliyyah of Economic and Science Management (KENMS)

and 15 students from Kuliyyah of Education (KOED) who were picked randomly. Since the

respondents are from two different kuliyyah, KENMS students are expected to be more aware

regarding ICC and CCC compared to KOED students.

Materials/Research Instruments

For the purpose of collecting data, a set of questionnaire was used as an instrument in this

study. The questionnaire was divided into three parts and the respondents had to answer all parts.

Part A of the questionnaire is for the collection of personal information which includes the question

regarding their respective kuliyyah, age, level of study and do you use credit card. For section B,

four points Likert Scale questions was used to identify the students awareness on ICC and the

students need to answer eight questions to complete this part. The third part is Part C where

questions were designed to identify the students awareness on CCC and the questions were similar

to section B. The preservation of anonymity ensured that the data collected in this research would

be private and confidential.

12

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Research Procedure

The research process started during the 11th week of the semester 1, 2014/2015. Then, on

25/11/2014 the researcher distributed the questionnaire to 15 students randomly at Kuliyyah of

Economic and Sciences Management (KENMS) cafe, IIUM. Next, after completed the survey at

KENMS cafe then the researcher move to Kuliyyah of Education (KOED) cafe and distribute

another 15 questionnaire to KOED students. It took about five hours to complete the survey

distribution. During the distribution of questionnaires the respondents were briefed on how to

respond to the questions in the questionnaire. They were instructed to read the instruction carefully

before answering the questions. In fact, the researcher managed to collect all 30 questionnaires at

the end of the sessions.

Data analysis

The result of the questionnaire was analyzed using Microsoft Excel. In this questionnaire,

frequencies such as percentages and bar graphs were used in describing the data as it will focus on

the differences such as the highest and lowest amount which will assist in examining the level of

awareness among KENMS and KOED students in IIUM towards ICC and CCC.

13

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Results

The purpose of this study was to investigate the level of awareness among KENMS and

KOED students in IIUM towards ICC and CCC. Therefore, the researcher went out to seek what

is the level of awareness regarding ICC and CCC among KENMS and KOED students in IIUM.

Thirty questionnaires were distributed to 15 KENMS students and 15 KOED students and the

results were acquired from it. The Figure 1 to Figure 8 shown below is the result from the first

research question which is “What is the level of awareness among KENMS and KOED students

in IIUM towards ICC?”

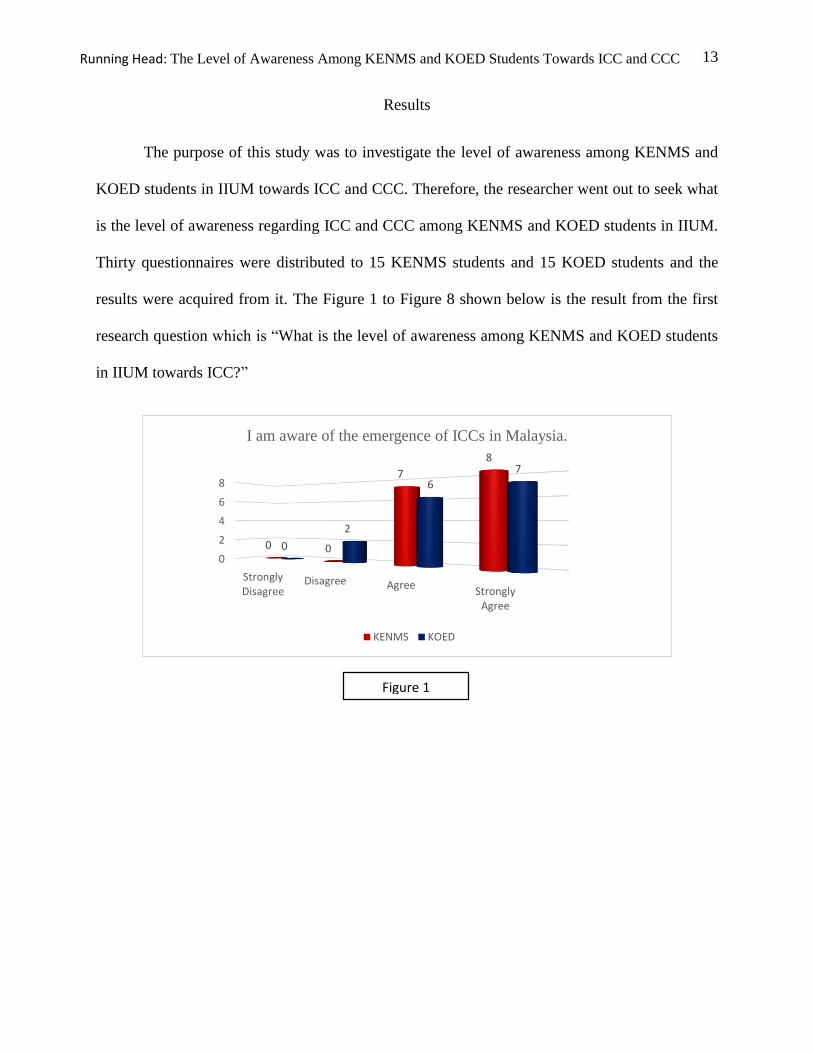

Figure 1

0

2

4

6

8

StronglyDisagree

Disagree AgreeStrongly

Agree

0 0

7

8

0

2

6

7

I am aware of the emergence of ICCs in Malaysia.

KENMS KOED

14

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

From the Figure 1 above, it shows that 100% of the students from KENMS are aware on the

emergence of ICCs in Malaysia. While, 87% of KOED students are aware on the emergence of

ICCs in Malaysia. Thus, it shows that KENMS students are more aware of the emergence of ICCs

in Malaysia compare to KOED students.

Then, in Figure 2, for the question regarding on the Shariah principle of ICCs, all of the

KENMS students agreed that ICCs is free from interest. However, there are more than half of the

students from KOED disagreed that ICCs is an interest-free based.

0

2

4

6

8

10

StronglyDisagree

Disagree AgreeStrongly

Agree

0 0

9

6

0

10

32

I am aware that ICCs is interest-free

KENMS KOED

Figure 2

15

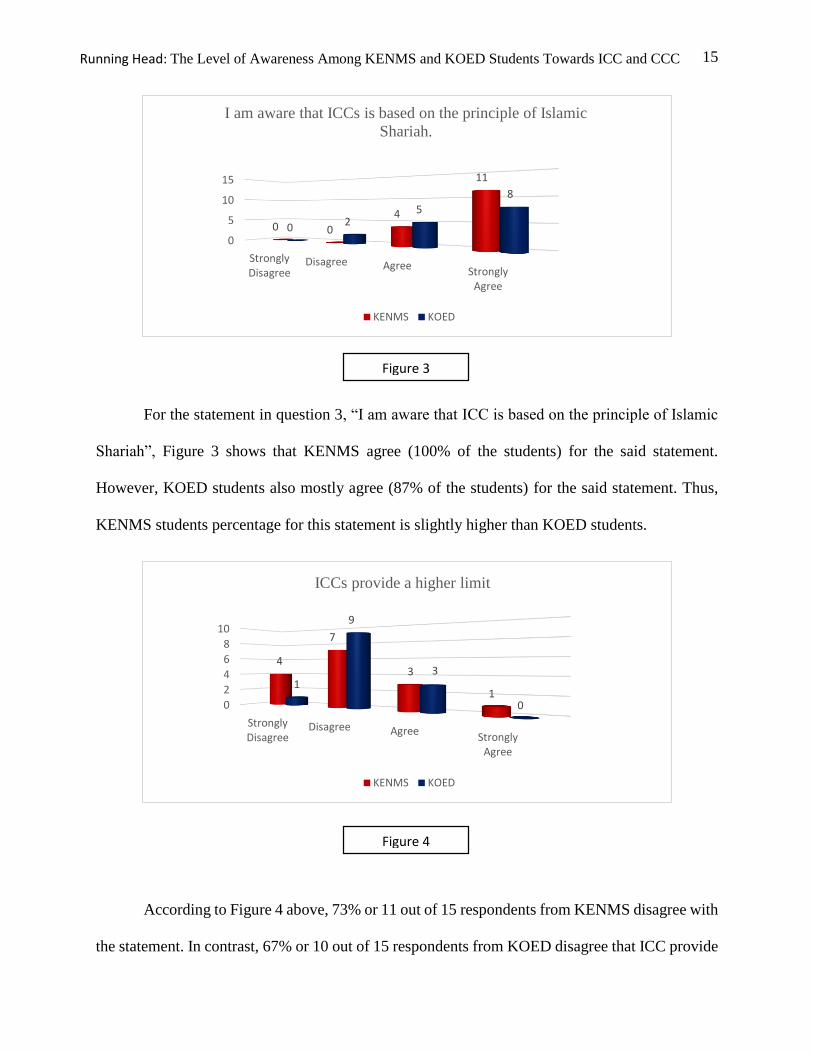

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

For the statement in question 3, “I am aware that ICC is based on the principle of Islamic

Shariah”, Figure 3 shows that KENMS agree (100% of the students) for the said statement.

However, KOED students also mostly agree (87% of the students) for the said statement. Thus,

KENMS students percentage for this statement is slightly higher than KOED students.

According to Figure 4 above, 73% or 11 out of 15 respondents from KENMS disagree with

the statement. In contrast, 67% or 10 out of 15 respondents from KOED disagree that ICC provide

0

5

10

15

StronglyDisagree

Disagree Agree StronglyAgree

0 0

4

11

0 25

8

I am aware that ICCs is based on the principle of Islamic

Shariah.

KENMS KOED

Figure 3

0

2

4

6

8

10

StronglyDisagree

Disagree AgreeStrongly

Agree

4

7

3

11

9

3

0

ICCs provide a higher limit

KENMS KOED

Figure 4

16

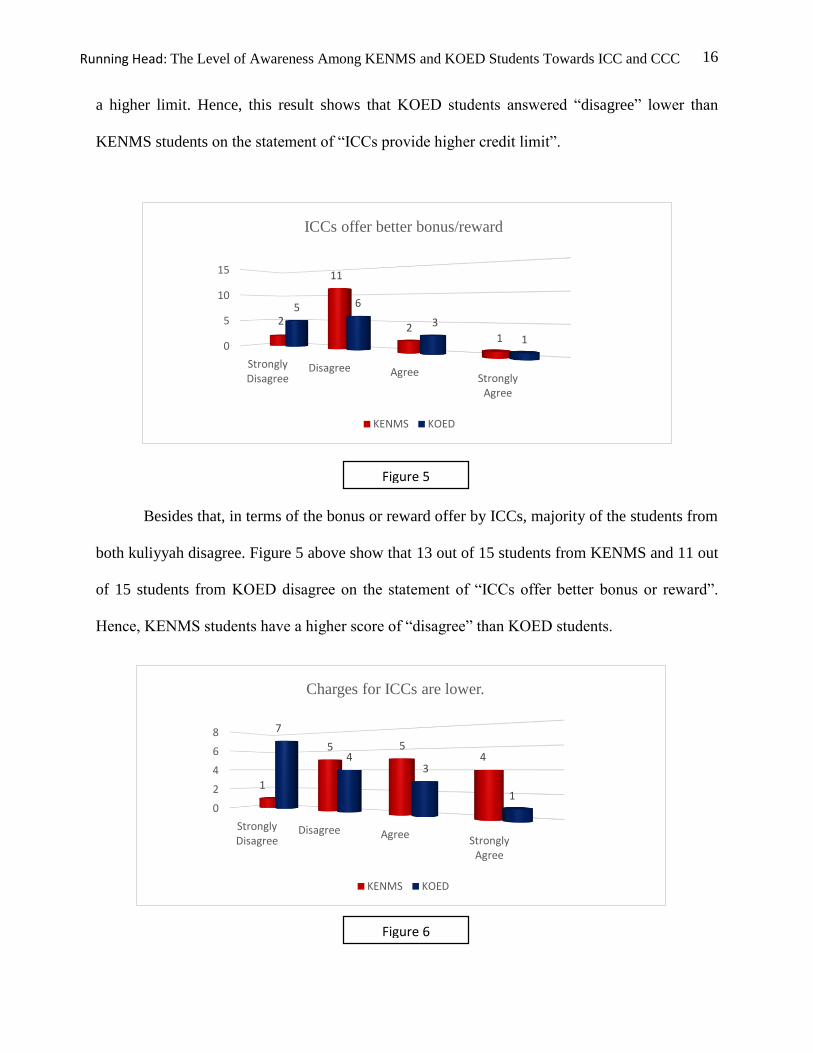

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

a higher limit. Hence, this result shows that KOED students answered “disagree” lower than

KENMS students on the statement of “ICCs provide higher credit limit”.

Besides that, in terms of the bonus or reward offer by ICCs, majority of the students from

both kuliyyah disagree. Figure 5 above show that 13 out of 15 students from KENMS and 11 out

of 15 students from KOED disagree on the statement of “ICCs offer better bonus or reward”.

Hence, KENMS students have a higher score of “disagree” than KOED students.

0

5

10

15

StronglyDisagree

Disagree AgreeStrongly

Agree

2

11

21

5 6

3

1

ICCs offer better bonus/reward

KENMS KOED

Figure 5

0

2

4

6

8

StronglyDisagree

Disagree AgreeStrongly

Agree

1

5 54

7

43

1

Charges for ICCs are lower.

KENMS KOED

Figure 6

17

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Next, for Figure 6, more than half of the students which is 9 out of 15 from KENMS agreed

that ICCs charges is lower. While, students of KOED disagree on the charges of ICCs is lower

which is 11 out of 15. Therefore, from this result, KENMS students agreed ICCs charges is lower

however, KOED students disagree on the statement.

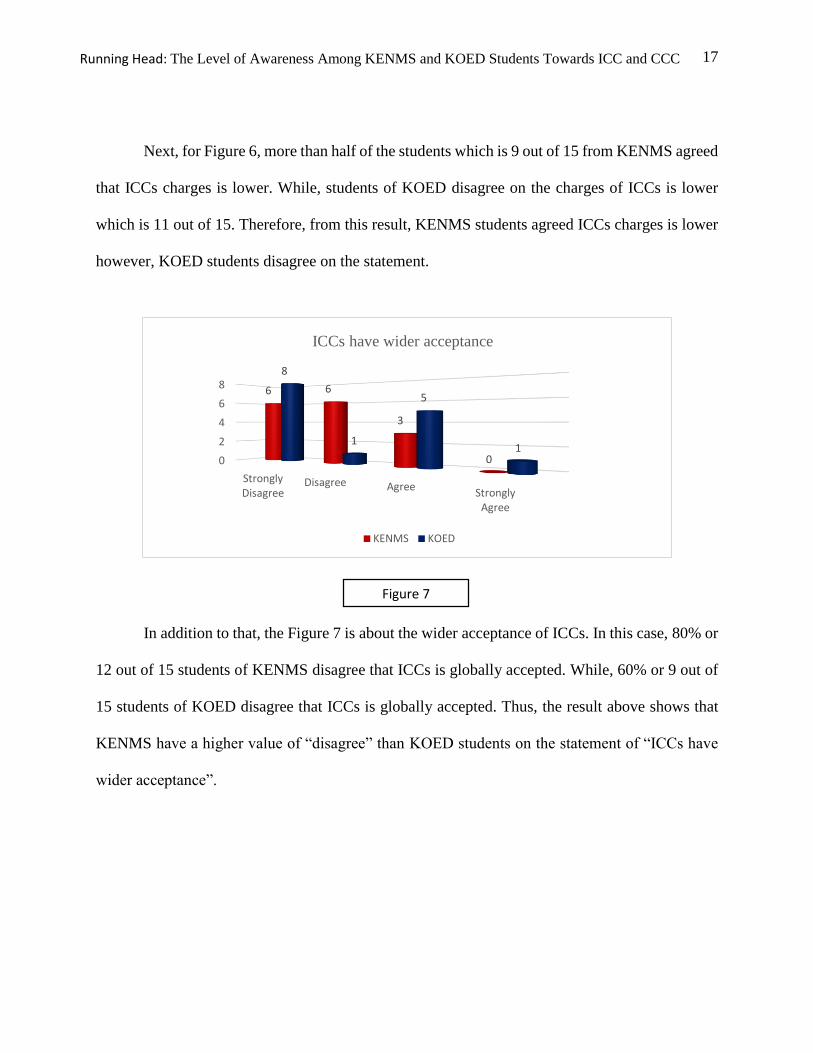

In addition to that, the Figure 7 is about the wider acceptance of ICCs. In this case, 80% or

12 out of 15 students of KENMS disagree that ICCs is globally accepted. While, 60% or 9 out of

15 students of KOED disagree that ICCs is globally accepted. Thus, the result above shows that

KENMS have a higher value of “disagree” than KOED students on the statement of “ICCs have

wider acceptance”.

0

2

4

6

8

StronglyDisagree

Disagree AgreeStrongly

Agree

6 6

3

0

8

1

5

1

ICCs have wider acceptance

KENMS KOED

Figure 7

18

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

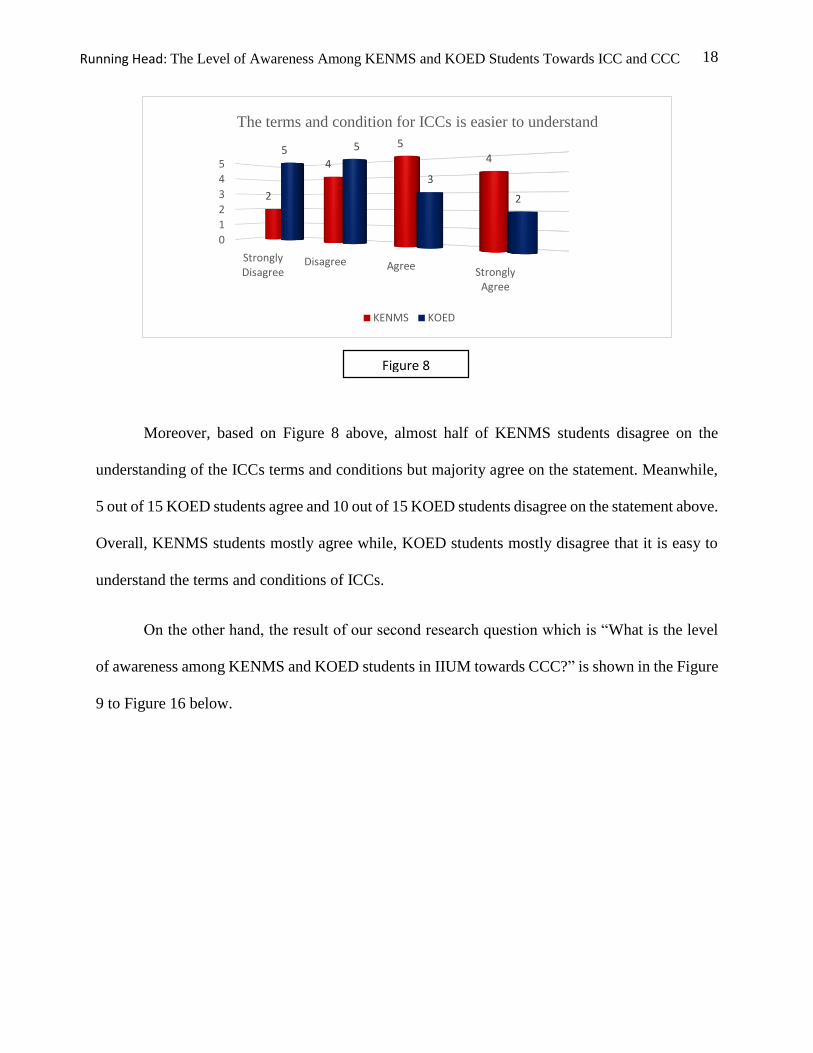

Moreover, based on Figure 8 above, almost half of KENMS students disagree on the

understanding of the ICCs terms and conditions but majority agree on the statement. Meanwhile,

5 out of 15 KOED students agree and 10 out of 15 KOED students disagree on the statement above.

Overall, KENMS students mostly agree while, KOED students mostly disagree that it is easy to

understand the terms and conditions of ICCs.

On the other hand, the result of our second research question which is “What is the level

of awareness among KENMS and KOED students in IIUM towards CCC?” is shown in the Figure

9 to Figure 16 below.

0

1

2

3

4

5

StronglyDisagree

Disagree AgreeStrongly

Agree

2

4

54

5 5

3

2

The terms and condition for ICCs is easier to understand

KENMS KOED

Figure 8

19

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

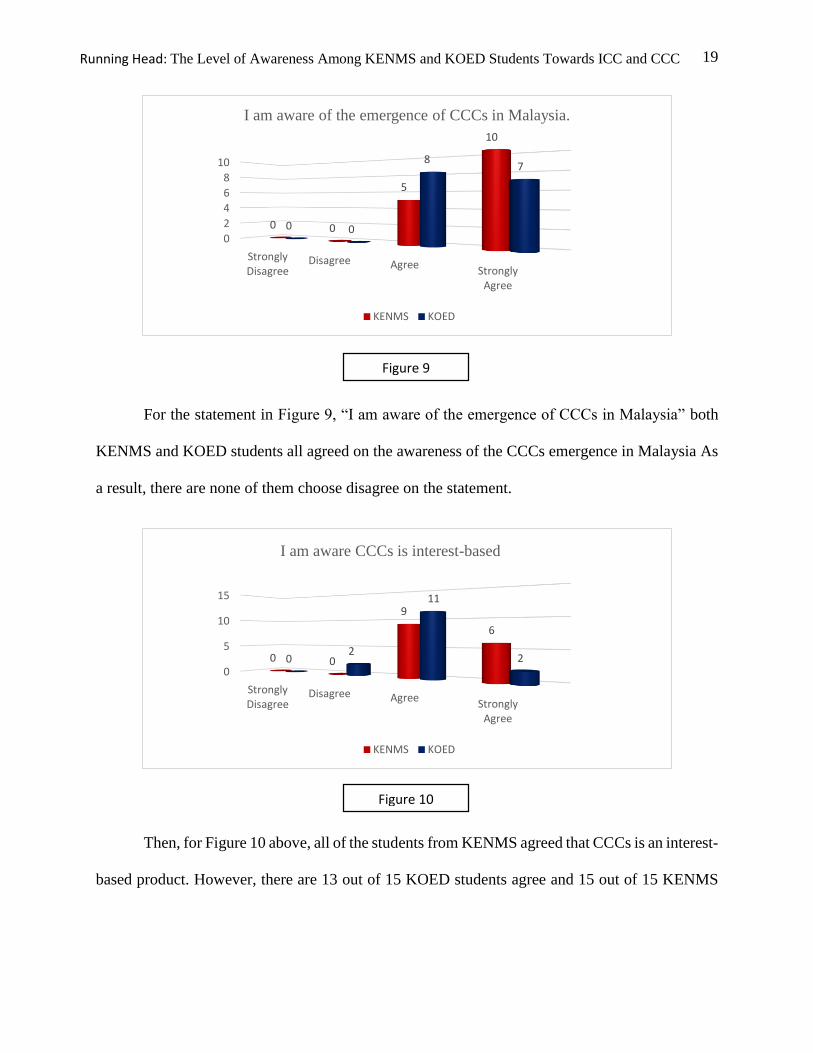

For the statement in Figure 9, “I am aware of the emergence of CCCs in Malaysia” both

KENMS and KOED students all agreed on the awareness of the CCCs emergence in Malaysia As

a result, there are none of them choose disagree on the statement.

Then, for Figure 10 above, all of the students from KENMS agreed that CCCs is an interest-

based product. However, there are 13 out of 15 KOED students agree and 15 out of 15 KENMS

0

2

4

6

8

10

StronglyDisagree

Disagree AgreeStrongly

Agree

0 0

5

10

0 0

87

I am aware of the emergence of CCCs in Malaysia.

KENMS KOED

Figure 9

0

5

10

15

StronglyDisagree

Disagree AgreeStrongly

Agree

0 0

9

6

02

11

2

I am aware CCCs is interest-based

KENMS KOED

Figure 10

20

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

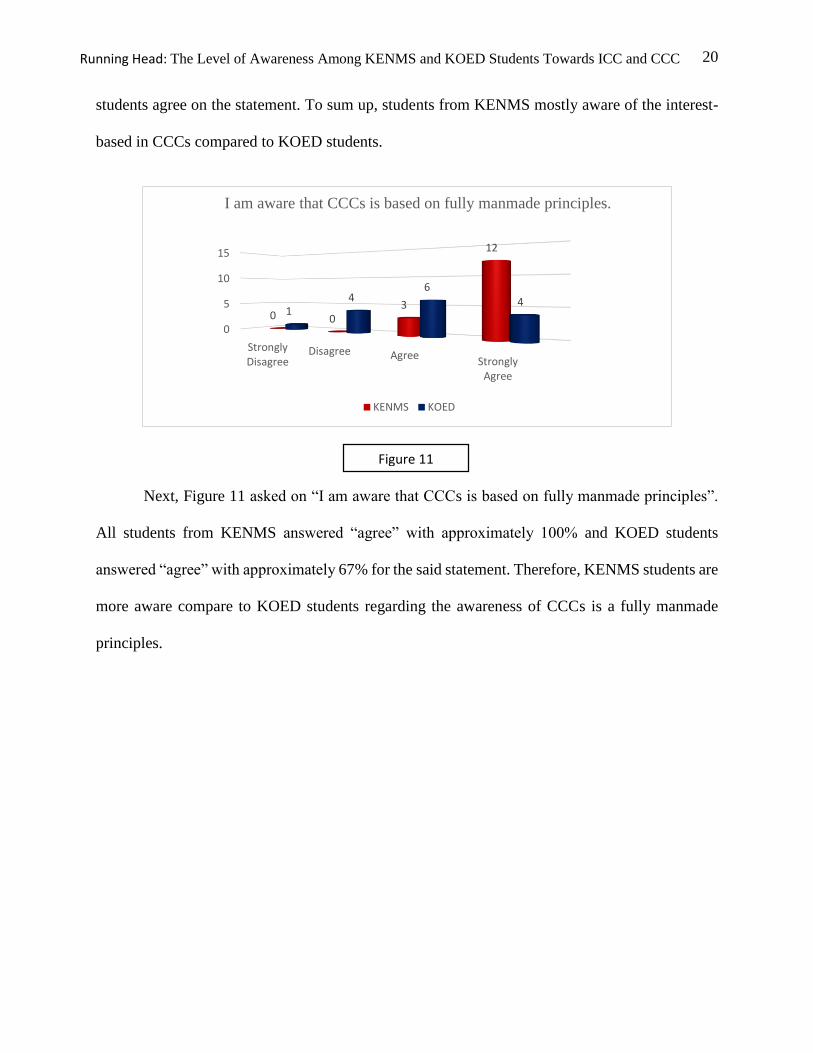

students agree on the statement. To sum up, students from KENMS mostly aware of the interest-

based in CCCs compared to KOED students.

Next, Figure 11 asked on “I am aware that CCCs is based on fully manmade principles”.

All students from KENMS answered “agree” with approximately 100% and KOED students

answered “agree” with approximately 67% for the said statement. Therefore, KENMS students are

more aware compare to KOED students regarding the awareness of CCCs is a fully manmade

principles.

0

5

10

15

StronglyDisagree

Disagree AgreeStrongly

Agree

0 03

12

14

64

I am aware that CCCs is based on fully manmade principles.

KENMS KOED

Figure 11

21

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

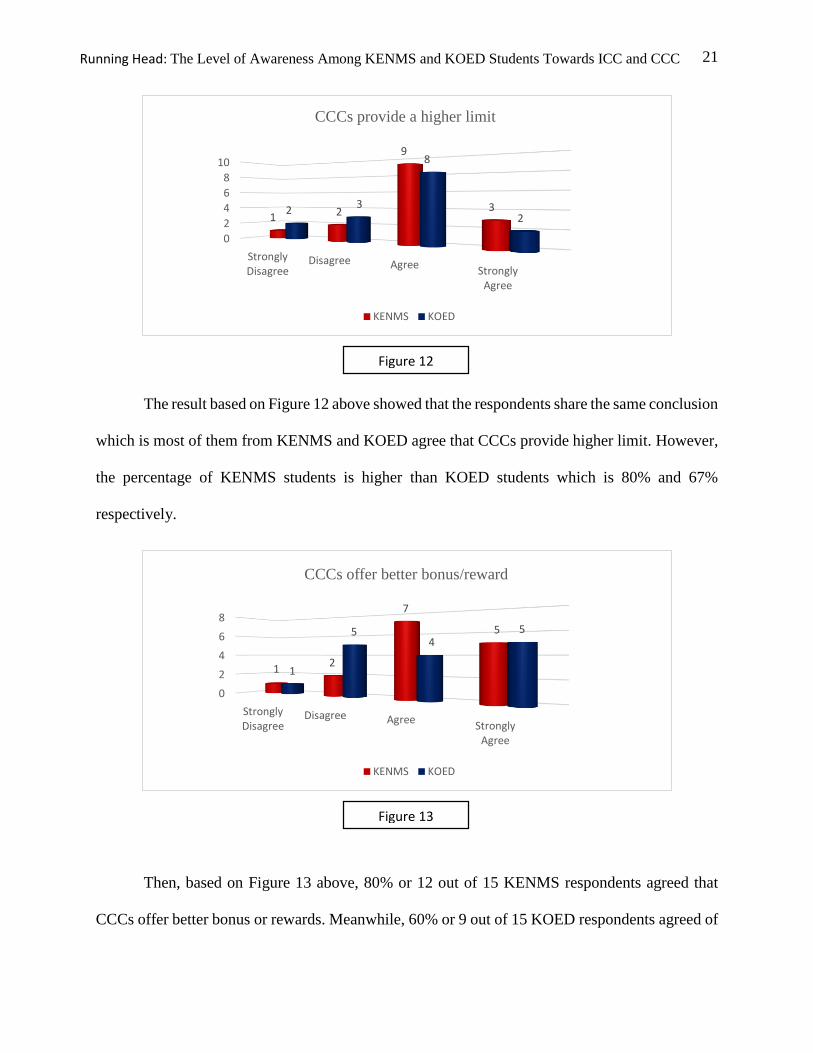

The result based on Figure 12 above showed that the respondents share the same conclusion

which is most of them from KENMS and KOED agree that CCCs provide higher limit. However,

the percentage of KENMS students is higher than KOED students which is 80% and 67%

respectively.

Then, based on Figure 13 above, 80% or 12 out of 15 KENMS respondents agreed that

CCCs offer better bonus or rewards. Meanwhile, 60% or 9 out of 15 KOED respondents agreed of

0

2

4

6

8

10

StronglyDisagree

Disagree AgreeStrongly

Agree

1 2

9

323

8

2

CCCs provide a higher limit

KENMS KOED

Figure 12

0

2

4

6

8

StronglyDisagree

Disagree AgreeStrongly

Agree

12

7

5

1

54

5

CCCs offer better bonus/reward

KENMS KOED

Figure 13

22

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

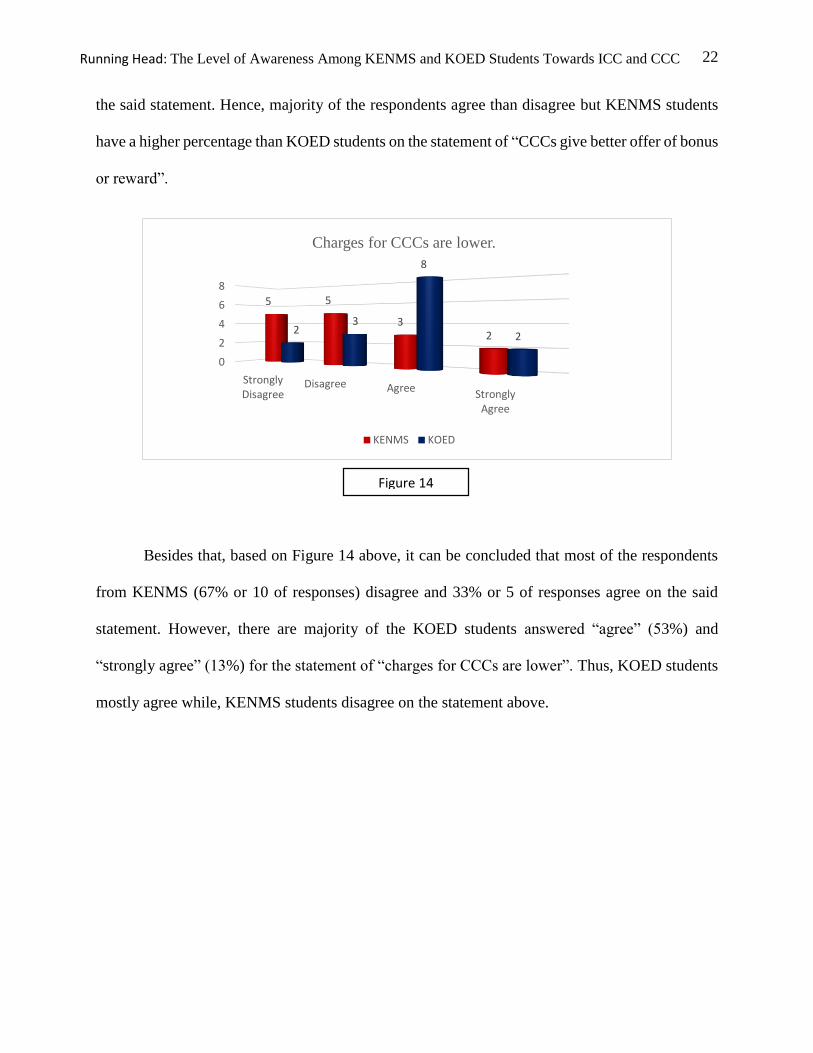

the said statement. Hence, majority of the respondents agree than disagree but KENMS students

have a higher percentage than KOED students on the statement of “CCCs give better offer of bonus

or reward”.

Besides that, based on Figure 14 above, it can be concluded that most of the respondents

from KENMS (67% or 10 of responses) disagree and 33% or 5 of responses agree on the said

statement. However, there are majority of the KOED students answered “agree” (53%) and

“strongly agree” (13%) for the statement of “charges for CCCs are lower”. Thus, KOED students

mostly agree while, KENMS students disagree on the statement above.

0

2

4

6

8

StronglyDisagree

Disagree AgreeStrongly

Agree

5 5

322

3

8

2

Charges for CCCs are lower.

KENMS KOED

Figure 14

23

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

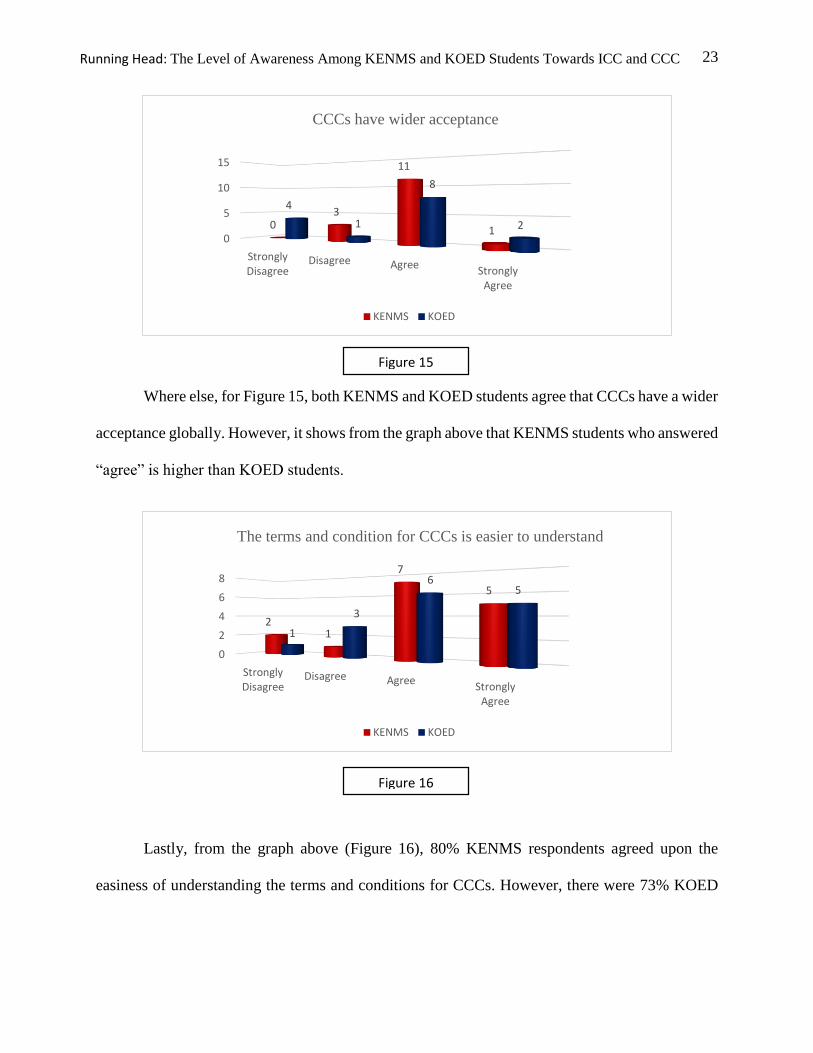

Where else, for Figure 15, both KENMS and KOED students agree that CCCs have a wider

acceptance globally. However, it shows from the graph above that KENMS students who answered

“agree” is higher than KOED students.

Lastly, from the graph above (Figure 16), 80% KENMS respondents agreed upon the

easiness of understanding the terms and conditions for CCCs. However, there were 73% KOED

0

5

10

15

StronglyDisagree

Disagree AgreeStrongly

Agree

03

11

1

4

1

8

2

CCCs have wider acceptance

KENMS KOED

Figure 15

0

2

4

6

8

StronglyDisagree

Disagree AgreeStrongly

Agree

21

7

5

1

3

65

The terms and condition for CCCs is easier to understand

KENMS KOED

Figure 16

24

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

students agreed on the statement. As a result, KENMS have a higher score of answering “agree”

rather than KOED students on the said statement.

Discussion

The aim of this study was to investigate the level of awareness of KENMS and KOED

students in IIUM towards ICC and CCC. Based on the study, KENMS students have higher

awareness towards ICC compared to KOED students. The result from part b of the survey

regarding the awareness of ICC has shown that KENMS students has higher percentage in all

statement compared to KOED students. As an example, the statement of “ICC is based on the

principle of Islamic Shariah” has clearly shows that all KENMS students aware compared to

KOED students. This is in line with our expectations that KENMS students will have better

understanding regarding ICC as they learned Islamic transaction in most of the subjects such as

Bank Management and Marketing for Islamic Financial Institutions. This results correlates with

the research done by Syahidawati binti Haji Shahwan and Nuradli Ridzwan Shah Bin Mohd Dali

(n.d) that assume most of the IIUM staff that have knowledge regarding ICC will have better

awareness towards ICC. Therefore, these findings answered the first research question regarding

the awareness of KENMS and KOED towards ICC.

Regarding second research question which asked about the awareness of KENMS and

KOED students towards CCC, the result show that KENMS students still have higher awareness

compared to KOED students. For the first statement “I am aware of the emergence of CCC in

Malaysia” it clearly shows that all students from both kuliyyah aware that CCC are emergence in

Malaysia. The reason is that the students have heard about CCC either through advertisement or

maybe their parents give the students the credit card as a supplementary user. Next, for questions

2 until 5 most KENMS students has a better level of awareness compared to KOED students. This

25

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

happens because KENMS students learned about CCC and they need to do research about CCC in

some subjects within their course. 67% of KENMS students do not agree with the statement of

“Charges for CCCs are lower” as they realize that the penalty rate for CCC are higher. In contrast

with previous studies by Nazimah Hussin (2012), 22% of the respondents agree that CCC charges

are lower. For questions 7 and 8 based on the result, it clearly shows that KENMS students are

more aware compared to KOED students. This is because KOED students just have a basic

knowledge regarding CCC but they do not learn in details about CCC compare to KENMS

students.

Based on the study, it shows that all respondents aware regarding ICC but they do not

understand the essence of the card especially KOED respondents. KENMS respondents have

higher level or awareness towards ICC and CCC in contrast with KOED respondents. Suppose the

KOED student are not being exposed or teach regarding the operation and terms in ICC perhaps,

in future ICC would not be competitive to CCC. This will affect the Islamic banking sector as

credit card is becoming one of the necessity things needed by a common men. Islamic bank need

to play vital roles to promote their banking products especially ICC using more alternatives ways

so that people can understand well the products. In addition, Islamic bank need to improve their

services and enlarge the market so that more people will attracted to engage with Islamic bank.

In conclusion, this study has investigated the level of awareness among KENMS and

KOED students in IIUM towards ICC and CCC. The data were collected by randomly distributing

questionnaires to 30 IIUM students which consists of 15 students from KENMS and 15 students

from KOED. The research questions in this study are answered whereby KENMS and KOED

students in IIUM have different level of awareness between ICC and CCC. The major finding of

the research is that most students from KENMS have higher awareness toward ICC and CCC

26

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

compared to KOED students because they know the differences between both cards and have

learned about ICC and CCC in certain subjects. Although most of the students are aware that ICC

is emerging in Malaysia, they do not have an adequate knowledge regarding the operation, rules

and regulations and charges.

This study has several implications. The first implications that can be obtained from this

study is to create and highlight about the importance of knowledge of IIUM students toward ICC

and CCC. This study can benefit them especially to be more aware about the importance of having

ICC compare to CCC. This study also helps others to understand the importance of understanding

the knowledge regarding ICC and CCC. Besides, it also helps students to use ICC in future if they

are exposed about the differences of ICC and CCC. In addition, this study will helps Islamic

banking to improve their marketing strategy on ICC and their services in order to stay competitive

with CCC in market. Lastly, probably Islamic banking need to organize a campaign regarding

Islamic banking products especially ICC and CCC among university students.

For future research, it is recommended that the research will be done in a more

comprehensive procedure in which it can be done to all level of peoples in the university rather

than just focusing on students only. In fact, this will help the researcher to know exactly the level

of awareness of all Malaysian people towards ICC and CCC so that it will give the awareness to

the society in large about the importance of ICC compared to CCC. Future researcher should use

larger sample size such as 150 respondents to get more precise result. In addition, future researcher

may use mixed methods in conducting their research rather than just using single method such as

questionnaire. Instead, they could also use both questionnaire and interview. This is because it will

help the researcher to observe the attitude of the respondents in answering the questions pertaining

to knowledge of ICC and CCC.

27

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

In spite of the results and findings of this survey, there are few limitations that must be

considered. The results of this study might not represent everyone as the sample used as the

population is only students from IIUM. The findings that were conducted among IIUM students

cannot be generalized to other university or public. The researchers have encountered obstacles

while conducting the research where some of the respondents refused to give their cooperation in

answering the questionnaire. This somehow prevents the process of distributing the questionnaires

to the target group from running smoothly. Besides that, due to time and financial resources

constraints, the sample size which only includes of 30 students is relatively small. Therefore, study

related to this issue should be continued on a large sample size which includes more level of the

society.

28

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

References

Al-Quran

Bakhshi, Adil Manzoor. 2006. “Developing of Financial Model for Islamic Credit Card for UK”.

Retrieved on October 12, 2014. < http://www.kantakji.com/fiqh/Files/Finance/223.pdf>

Delener, N., & Katzenstein, H. (1994). Credit card possession and other payment systems.

International Journal of Bank Marketing, 12 (4), 13-24.

Durkin, T.A. and Price, N. (2000), “Credit cards: use and consumer attitudes, 1970-2000”, Federal

Reserve Bulletin, September, pp. 623-34.

Edward, L. (2011, January 31). An Islamic Banking Model in Canada .

dtpr.lib.athabascau.ca/action/download.php?filename=mba-11/open/.... Retrieved

September 28, 2014, from

http://dtpr.lib.athabascau.ca/action/download.php?filename=mba-

11/open/edwardlauraProject.pdf

Engku Rabiah Adawiyah Engku Ali and Mohd Daud Bakar. (2008b). “Issues in Islamic debt

securitization”. In Bakar, M. and Engku Ali, E.R. (Eds.), Essential Readings in Islamic

Finance (pp. 443-491).

Gan, L. L., Mayrami, R. G., & Koh, H. G. (2008). Singapore credit cardholders: ownership, usage

patterns, and perception. Journal of Services Marketing, 22 (4), 267-279.

Ilham Reza Ferdian, Miranti Kartika Dewi and Faried Kurnia Rahman. (2008, August 3). The

Practice of Islamic Credit Cards: A Comparative Look between Bank Danamon

29

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Indonesia’s Dirham Card and Bank Islam Malaysia’s BI Card. Retrieved November 11,

2014, from http://staff.ui.ac.id/system/files/users/miranti

ISRA: Islamic Financial System Principles and Operation. (2012). Kuala Lumpur: International

Shariah Research Academy for Islamic Finance (ISRA).

M. Mansfield, P., Beth Pinto, M., & A. Robb, C. (n.d.). Consumers and credit cards: A Review of

Emphirical Literature. Journal of Management and Marketing Research, 3-3.

Mohd Nahar bin Mohd Arshad. (2011). Foundation of Islamic Economics. International Islamic

University Malaysia.

Najeeb, S. F., & Lahsasna, A. (n.d.). Qard Hasan: Its Rules And Applications In Islamic Finance.

Qard Hasan: Its Rules And Applications In Islamic Finance. Retrieved November 1, 2014,

from http://www.sahulat.org/

Nazimah Hussin. (2012). Perception of Malaysian Credit Cardholders on Conventional Cards in

Comparison to Islamic Cards. International Journal of Advances in Management and

Economics, 1(4), 85-94.

Niringjuerae, M. (2012, March 1). almanawee. : Islamic Credit Card. Retrieved October 20, 2014,

from http://almanawee.blogspot.com/2012/03/islamic-credit-card.html

Nor Azizan Che Embi. (2011). Foundation of Islamic Finance. Kuala Lumpur: International

Islamic University Malausia (IIUM).

Nuradli Ridzwan and Noor Azira. (2006). Factors Influencing Islamic Credit Cards Holders. An

Online Study. | Nuradli Ridzwan Shah Mohd Dali - Academia.edu. Factors Influencing

30

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Islamic Credit Cards Holders. An Online Study. | Nuradli Ridzwan Shah Mohd Dali -

Academia.edu. Retrieved November 15, 2014, from

https://www.academia.edu/2070620/Factors

Rogak, L. (2008, July 29). Shariah-compliant credit cards become more common. CreditCardscom

News. Retrieved October 26, 2014, from http://www.creditcards.com/credit-card-

news/shariah-compliant-credit-cards-1273.php

Rohrer, J. (2007). ABC of Awareness.Personal Development as the Meaning of Life, 1(3), 48-48.

Rohma, S. (n.d.). Islamic Credit Cards: A Comparison Study between Its Application in Malaysia

and Indonesia. Retrieved October 11, 2014, from

http://www.academia.edu/.../Islamic_Credit_Cards_A_Comparison_Study_bet...

Syahidawati binti Haji Shahwan and Nuradli Ridzwan Shah Bin Mohd Dali. (n.d.). Islamic Credit

Card Industry in Malaysia: Customers’ Perceptions and Awareness.. Academia.edu.

Retrieved October 20, 2014, from https://www.academia.edu/2070610/Islamic_Credit

Syed Alwi Mohamed Sultan. (2001). Islamic Credit Card: A Framework of Implementation in

Malaysia. MBA Dissertation, International Islamic University Malaysia.

31

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

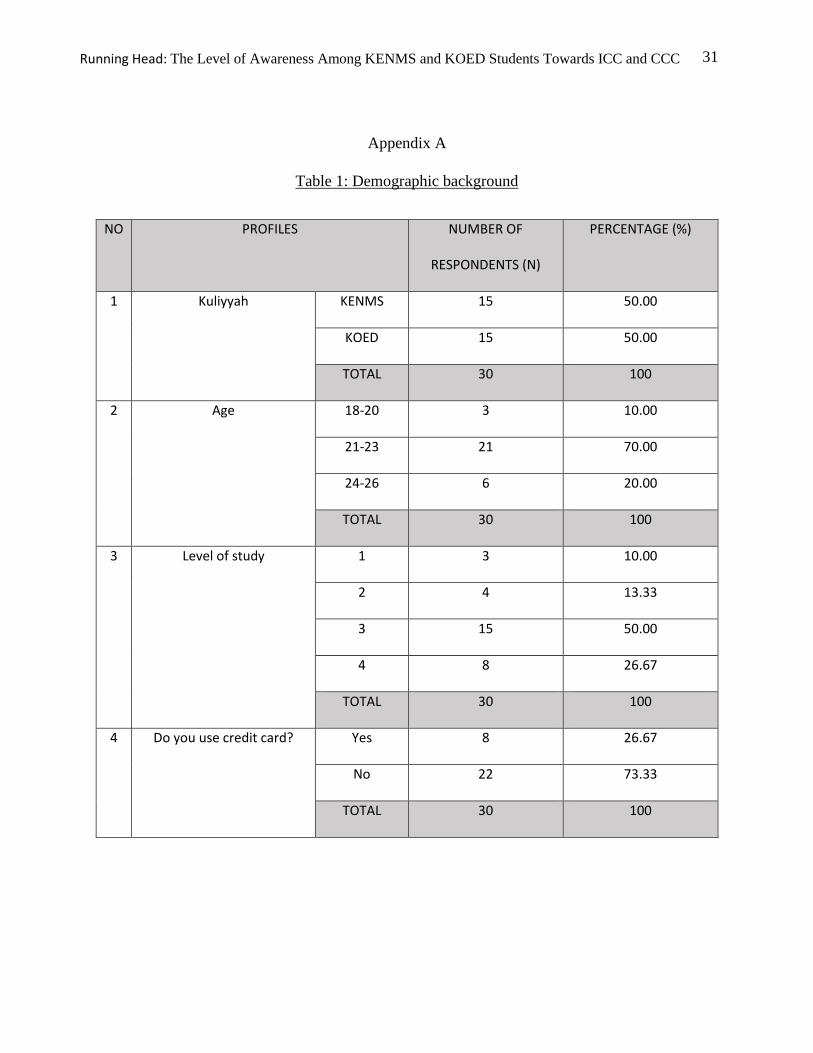

Appendix A

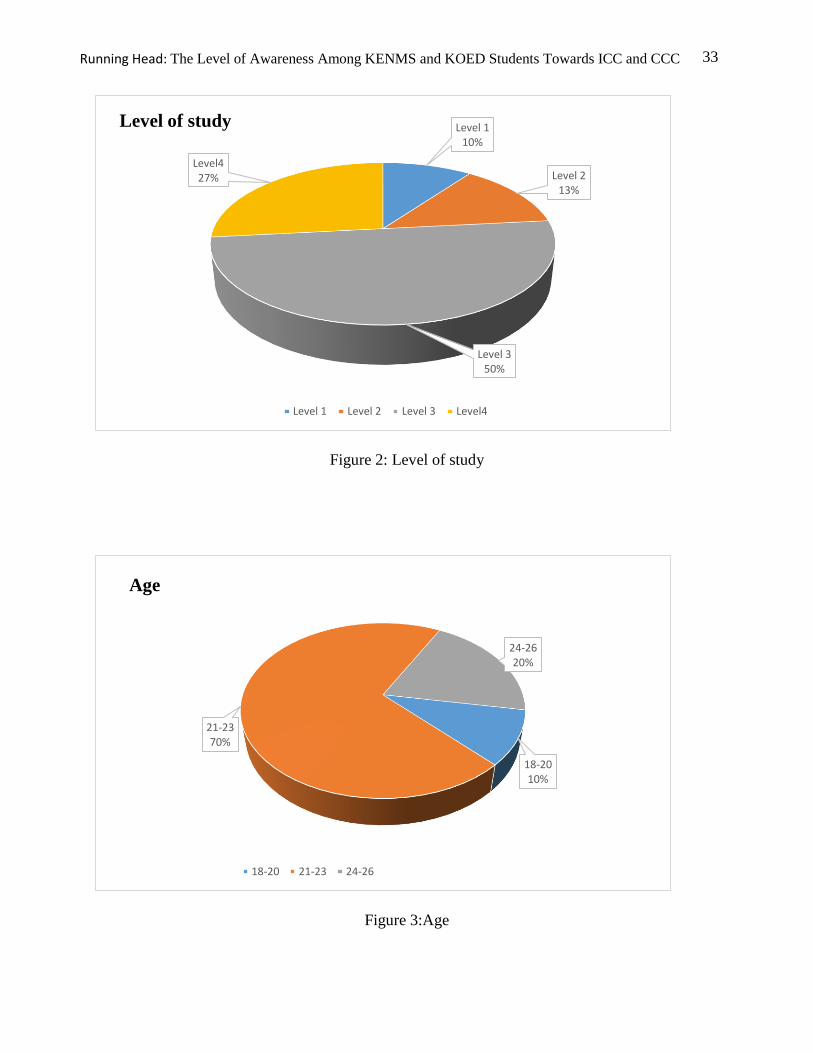

Table 1: Demographic background

NO PROFILES NUMBER OF

RESPONDENTS (N)

PERCENTAGE (%)

1 Kuliyyah KENMS 15 50.00

KOED 15 50.00

TOTAL 30 100

2 Age 18-20 3 10.00

21-23 21 70.00

24-26 6 20.00

TOTAL 30 100

3 Level of study 1 3 10.00

2 4 13.33

3 15 50.00

4 8 26.67

TOTAL 30 100

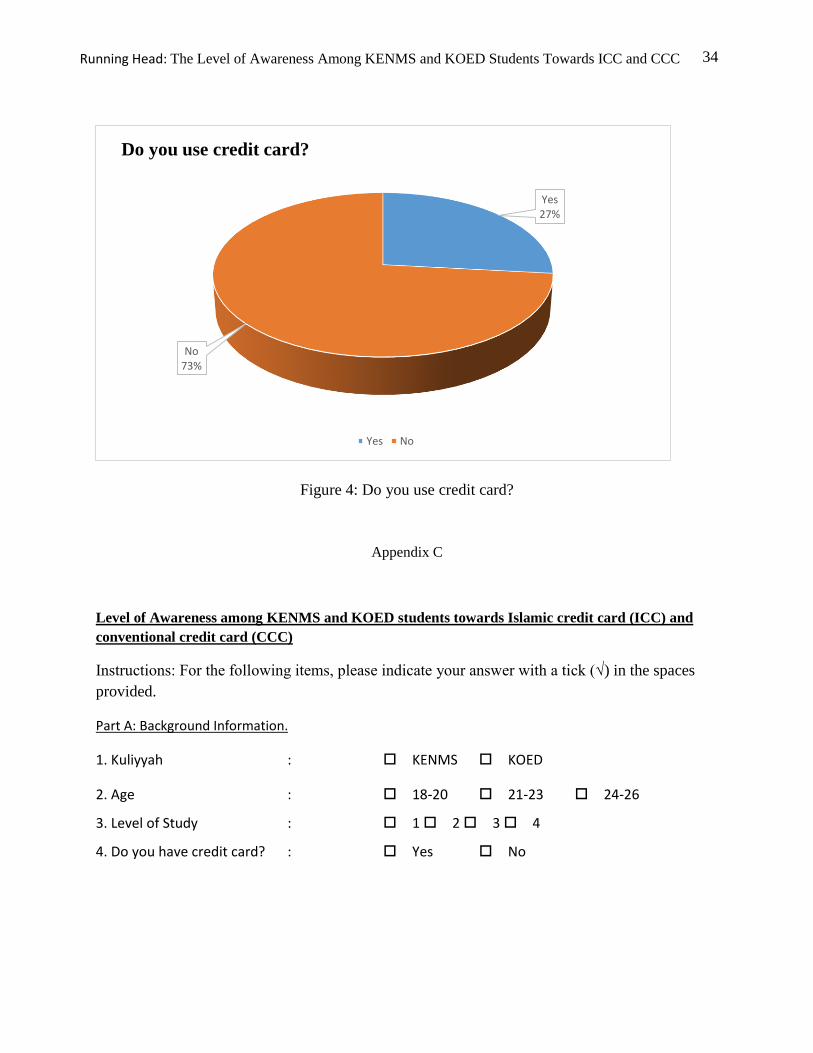

4 Do you use credit card? Yes 8 26.67

No 22 73.33

TOTAL 30 100

32

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Table 1 represents a brief profiling of the respondents. The respondents consists of 15

students from Kuliyyah of Economic and Sciences Management (KENMS) and 15 students from

Kuliyyah of Education (KOED). Majority of the respondents coming from the 21-23 years old

with 70% of respondents. About 20% of the respondents are in the age of 24-26 while the lowest

age group is those between 18-20 years old with 10%. Majority of the respondents were in third

year with 50% of respondents while 26.67 % in fourth year. For level one and level two both

consists of 10% and 13.33 % of the respondents. Most of the respondents did not use credit card

(73.33%) while 26.67% use credit card.

Appendix B

Figure 1: Gender

KENMS, 50%

KOED, 50%

Kuliyyah

KENMS KOED

33

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Figure 2: Level of study

Figure 3:Age

Level 110%

Level 213%

Level 350%

Level427%

Level of study

Level 1 Level 2 Level 3 Level4

18-2010%

21-2370%

24-2620%

Age

18-20 21-23 24-26

34

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Figure 4: Do you use credit card?

Appendix C

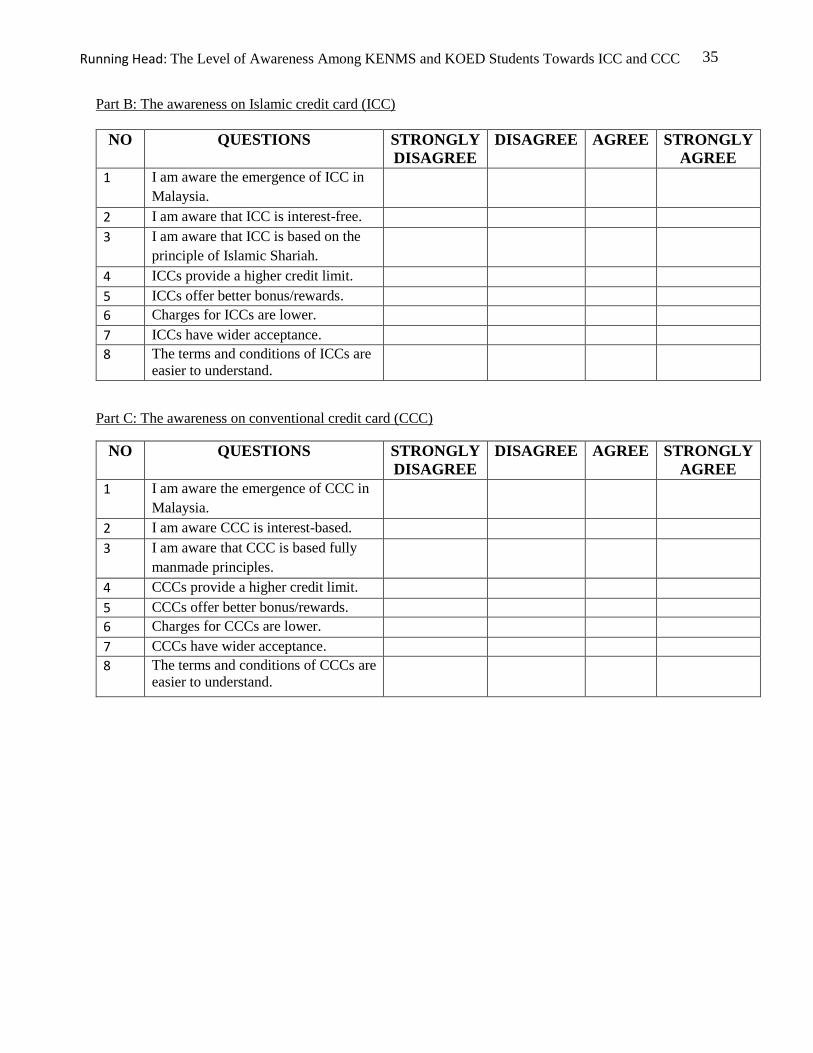

Level of Awareness among KENMS and KOED students towards Islamic credit card (ICC) and

conventional credit card (CCC)

Instructions: For the following items, please indicate your answer with a tick (√) in the spaces

provided.

Part A: Background Information.

1. Kuliyyah : KENMS KOED

2. Age : 18-20 21-23 24-26

3. Level of Study : 1 2 3 4

4. Do you have credit card? : Yes No

Yes27%

No73%

Do you use credit card?

Yes No

35

Running Head: The Level of Awareness Among KENMS and KOED Students Towards ICC and CCC

Part B: The awareness on Islamic credit card (ICC)

Part C: The awareness on conventional credit card (CCC)

NO QUESTIONS STRONGLY

DISAGREE

DISAGREE AGREE STRONGLY

AGREE

1 I am aware the emergence of ICC in

Malaysia.

2 I am aware that ICC is interest-free.

3 I am aware that ICC is based on the

principle of Islamic Shariah.

4 ICCs provide a higher credit limit.

5 ICCs offer better bonus/rewards.

6 Charges for ICCs are lower.

7 ICCs have wider acceptance.

8 The terms and conditions of ICCs are

easier to understand.

NO QUESTIONS STRONGLY

DISAGREE

DISAGREE AGREE STRONGLY

AGREE

1 I am aware the emergence of CCC in

Malaysia.

2 I am aware CCC is interest-based.

3 I am aware that CCC is based fully

manmade principles.

4 CCCs provide a higher credit limit.

5 CCCs offer better bonus/rewards.

6 Charges for CCCs are lower.

7 CCCs have wider acceptance.

8 The terms and conditions of CCCs are

easier to understand.