The Effects of Regulating Mobile Termination Rates for Asymmetric Networks

16

The E ff ects of Regulating Mobile Termination Rates for Asymmetric Networks ∗ Ralf Dewenter † Helmut-Schmidt University Justus Haucap ‡ Ruhr-University of Bochum December 2004 Abstract This paper examines mobile termination fees and their regulation when net- works are asymmetric in size. It is demonstrated that with consumer ignorance about the exact termination rates (a) a mobile network’s termination rate is the higher the smaller the network’s size (as measured through its subscriber base) and (b) asymmetric regulation of only the larger operators in a market will, ce- teris paribus, induce the smaller operators to increase their termination rates. The results are supported by empirical evidence using data on mobile termination rates from 48 European mobile operators from 2001 to 2003. Keywords : mobile termination, telecommunications, consumer ignorance, price regulation To be published in: European Journal of Law and Economics 20, 2005, 185-197. ∗ For most helpful comments and discussions, we thank Michael Bräuninger, Jörn Kruse, Johannes Mönius and seminar participants at the 4th ZEW-Conference on the Economics of Information and Communication Technologies at Mannheim, the International Industrial Organization Conference at Chicago, and the 15th Biennial Conference of the International Telecommunications Society (ITS) at Berlin. Furthermore, we are grateful to Tobias Hartwich for his critical review of the manuscript. Of course, the usual disclaimer applies. † Helmut-Schmidt University, University of the Federal Armed Forces Hamburg, Institute for Eco- nomic Policy, Holstenhofweg 85, D-22043 Hamburg, Germany; e-mail: ralf.dewenter@hsu-hh.de. ‡ Ruhr-University of Bochum, Department of Economics, Universitätsstr. 150, D-44780 Bochum, Germany; e-mail: justus.haucap@rub.de. 1

-

Upload

uni-duesseldorf -

Category

Documents

-

view

0 -

download

0

Transcript of The Effects of Regulating Mobile Termination Rates for Asymmetric Networks

The Effects of Regulating Mobile Termination Rates

for Asymmetric Networks∗

Ralf Dewenter†

Helmut-Schmidt University

Justus Haucap‡

Ruhr-University of Bochum

December 2004

Abstract

This paper examines mobile termination fees and their regulation when net-

works are asymmetric in size. It is demonstrated that with consumer ignorance

about the exact termination rates (a) a mobile network’s termination rate is the

higher the smaller the network’s size (as measured through its subscriber base)

and (b) asymmetric regulation of only the larger operators in a market will, ce-

teris paribus, induce the smaller operators to increase their termination rates. The

results are supported by empirical evidence using data on mobile termination rates

from 48 European mobile operators from 2001 to 2003.

Keywords: mobile termination, telecommunications, consumer ignorance, price

regulation

To be published in: European Journal of Law and Economics 20, 2005, 185-197.

∗For most helpful comments and discussions, we thank Michael Bräuninger, Jörn Kruse, JohannesMönius and seminar participants at the 4th ZEW-Conference on the Economics of Information andCommunication Technologies at Mannheim, the International Industrial Organization Conference atChicago, and the 15th Biennial Conference of the International Telecommunications Society (ITS) atBerlin. Furthermore, we are grateful to Tobias Hartwich for his critical review of the manuscript. Ofcourse, the usual disclaimer applies.

†Helmut-Schmidt University, University of the Federal Armed Forces Hamburg, Institute for Eco-nomic Policy, Holstenhofweg 85, D-22043 Hamburg, Germany; e-mail: [email protected].

‡Ruhr-University of Bochum, Department of Economics, Universitätsstr. 150, D-44780 Bochum,Germany; e-mail: [email protected].

1

1 Introduction

While in many mobile telecommunications markets across the world competition has

long been left without much regulatory intervention, recently some aspects have come

under close scrutiny by regulatory authorities. Apart from mobile number portability

and national and international roaming, one of the key areas under investigation are

mobile termination charges (see, e.g., European Commission, 2004, Ofcom, 2004).

While mobile termination rates are already regulated in some countries (such as

Austria and the UK), they are not regulated in others (such as Germany or Switzerland).

In some other countries again (such as the Netherlands or Spain), only the termination

rates of the larger mobile operators (which are supposed to be dominant or to enjoy

significant market power) are regulated. In the latter case operators are regulated in an

asymmetric fashion, with some termination rates being regulated while others are set

by unregulated firms. In fact, this pattern of asymmetric regulation has been discussed

in most European countries and is currently applied in a number of jurisdictions.

Two policy questions arise, given these different institutional frameworks governing

mobile termination: First, what termination rates do emerge if prices are left unregu-

lated? And secondly, how are these rates affected by regulation?

Gans and King (2000) have addressed exactly these questions. Their finding is that

mobile termination rates will be excessive due to a negative pricing externality, which

results from consumer ignorance regarding prices. Consumer ignorance is a particular

problem of mobile telephony as customers are often not able to identify which specific

network they are calling. This is because consumers may not know which operator is

associated with each particular number. As a consequence, consumers are often ignorant

about the price that they actually have to pay for a mobile call if prices differ between

different networks (see Gans and King, 2000; Wright, 2002). In addition, mobile number

portability is likely to exacerbate this problem as mobile prefixes will no longer identify

networks (see Bühler and Haucap, 2004).1 Hence, as Gans and King (2000) have pointed

out consumers are likely to base their calling decisions on average prices. This will be

the case if either carriers are unable to set different prices for different mobile networks

anyway or if consumers cannot determine ex ante which mobile network they are actually

ringing when placing a call, i.e. if callers suffer from consumer ignorance.

If consumers are not aware of the correct prices and base their demand on the average

price, a negative pricing externality arises as the price of one firm will not only affect its

own demand, but also that of its rivals. This induces firms to increase their termination

1While some countries (such as Finland) have tried to solve this problem through acoustic signalsthat identify the called network, many consumers have found these mechanisms so annoying that theacoustic signals were abandoned again.

2

rates to inefficiently high levels as they do not account for the effect that their own price

has on the average price perception and, thereby, their rivals’ demand. This externality

problem comes on top of any monopoly and associated double marginalization problems.2

If market shares are endogenous and termination rates are set prior to other prices,

termination rates may even be set so high that they ”choke” off the demand for mobile

termination altogether (see Gans and King, 2000, p. 323). Consequently, demand for

termination services will increase with any downward regulation of termination rates.

We build on this research and extend it into three directions: Firstly, we will introduce

network asymmetry into the model and consider mobile networks of different sizes (in

terms of their subscriber bases). While Gans and King (2000) analyze a symmetric

duopoly, we will provide a model with four asymmetric mobile network operators. Also,

in the model developed by Gans and King all calls originate in a single fixed network,

whereas we will focus on calls between mobile operators. Secondly, we will analyze the

effects of asymmetric regulation in this framework. In reality, asymmetric regulation is a

common feature of many European telecommunications markets, which has been largely

neglected so far. And thirdly, we will provide empirical evidence for our model.

The main results of our paper are, firstly, that smaller mobile operators will charge

higher termination rates than larger operators, as a small operator’s impact on the

weighted average price is relatively small so that smaller operators can increase their

prices significantly without a major reduction in the quantity demanded. In contrast, a

large operator also has a larger impact on the weighted average price so that the firm

is more constrained in its pricing policy. Secondly, asymmetric regulation of the larger

operators will, ceteris paribus, induce the small operators to increase their termination

rates even further. These results are supported by our empirical findings.

The remainder of the paper is organized as follows. In Section 2 we introduce the

model and present the key results of our analysis. In Section 3, we provide empirical

evidence to test the model’s hypotheses. Finally, section 4 discusses policy implications

and concludes.2Note that a grand merger could actually solve this particular problem as has been pointed out

by Salsas and Koboldt (2004) in the context of international roaming. However, while such a mergerwould solve the problem of high termination rates it would also reduce competition in all other mobilemarkets (such as call origination and mobile subscriptions) and, therefore, most likely not be authorizedby competition authorities.

3

2 The Model

There are four mobile networks i = 1, 2, 3, 4, which differ in the size of their subscriber

base. We assume that the four mobile networks’ market shares do not depend on the

respective termination charges, i.e. consumers do not base their subscription decision

on the price for being called. More precisely, we assume that the mobile networks’ mar-

ket shares are already given when termination rates are set so that we can treat them

as exogenous.3 Let us also assume that there are two large and two small mobile net-

works, which is a fairly typical market structure for many European telecommunications

markets. The two large networks {i = 1, 2} have a subscriber base of x1 = x2 = xL cus-

tomers, while the small networks’ subscriber base is denoted by xS with x3 = x4 = xS.

We also assume that each individual subscriber has a linear inverse demand for mobile-

to-mobile telephone calls, which is given by

q = a− bp,

where p denotes the perceived price for mobile-to-mobile calls. We follow Ofcom (2004)

and the European Commision (2003) and regard the market for mobile termination

services as a relevant market in its own. Furthermore, we assume that the marginal cost

of terminating a mobile call is negligible and that prices for mobile-to-mobile calls are

effectively determined through the respective termination charges. That is, we abstract

from any double mark-up problem which may result if operators were competing in linear

tariffs. As is well known from the literature (see, e.g., Laffont and Tirole, 1998, orWright,

2002), the double mark-up problem vanishes if operators set two-part tariffs consisting

of a fixed (monthly) fee and a price per calling minute. Given that mobile operators

usually set multi-part tariffs we abstract from potential double marginalization problems

and assume that the price for a call from, say, mobile network 1 to mobile network 2, is

given by p12 = t2 where t2 is the termination rate set by operator 2.

If consumers have perfect knowledge and are not ignorant about a network’s identity,

the price for a calling unit from mobile network i to mobile network j will simply equal

the monopoly mobile termination rate that network j will set, i.e. pij = tM = a/(2b) for

j = 1, 2, 3, 4 and i 6= j (that means, j denotes the terminating network).

To capture the idea of consumer ignorance, we now follow Gans and King (2000) and

assume that it is the average price which determines consumer demand for calls to other

mobile networks. To focus on the termination market we restrict the analysis to off-net

calls and ignore on-net calls which are calls that originate and terminate within the same3Note that this assumption is also employed by Gans and King (2000) in much of their analysis. In

addition, it has proven extremely difficult to analyze termination rates with endogenous market shares,as the optimization problem is no longer supermodular (see, e.g, Bühler, 2002).

4

mobile network. Hence, we only consider the demand for calls which originate in one

network and are terminated in another network, i.e. calls from network 1 to networks 2,

3 and 4, from network 2 to networks 1, 3 and 4, and so on. More specifically, we assume

that the probability that an off-net call is made to one particular network depends on

the size of its subscriber base relative to other networks’ subscriber bases. Hence, the

probability that an off-net call from a large network is terminated on the other large

network is given by xL/(xL + 2xS). Similarly, the probability that an off-net call from

a large network is terminated on a particular small network is given by xS/(xL + 2xS).

This assumption should be plausible under consumer ignorance as consumers do not

differentiate between networks. If the probabilities of networks being called depend

on their relative size, then consumers form average prices for off-net calls (possibly by

retrospectively looking at their monthly bills) by weighting prices with these respective

probabilities. Hence, the according demand for off-net calls from network 1 to network

2, 3 and 4 is given by

q1 = xL(xL + 2xS)

µa− b

µxL

xL + 2xSp12 +

xSxL + 2xS

p13 +xS

xL + 2xSp14

¶¶,

where p12 = t2, p13 = t3 and p14 = t4. Hence, the demand for off-net calls from network

1 into other networks depends on the size of its subscriber base (xL), the aggregate size

of the other networks’ subscriber base (xL+2xS) and the weighted average termination

rate charged by the three other networks. Let us also note that the quantity of calls

from network 1 to network 2 is given by q12 = [xL/(xL + 2xS)]q1, while the quantities

of calls from network 1 to networks 3 and 4 are given by q13 = q14 = [xS/(xL + 2xS)]q1

with q1 = q12+ q13+ q14. Similarly, we can express the demand for off-net calls from the

three other networks. Since the two small networks have a subscriber base of size xS,

making off-net calls to a total of (2xL+xS) subscribers on the three other networks, we

can write the demand for off-net calls from network 3 to other networks as

q3 = xS(2xL + xS)

µa− b

µxL

2xL + xSp31 +

xL2xL + xS

p32 +xS

2xL + xSp34

¶¶,

where again p3j = tj for j = 1, 2, 4.

The profit that an operator i generates from termination depends on its termination

rate, ti, and the number of incoming calls from other networks. Assuming balanced

calling patterns, operator 1’s profit is now given by

π1 = t1

µxL

xL + 2xSq2 +

xL2xL + xS

q3 +xL

2xL + xSq4

¶.

Similarly, operator 3’s profit (as a small operator) is given by

π3 = t3

µxS

xL + 2xSq1 +

xSxL + 2xS

q2 +xS

2xL + xSq4

¶.

5

Maximizing with respect to t and taking into account both the symmetry between the

two large networks (1 and 2) and between the two small networks (3 and 4) we obtain

the following best response functions

tL =1

4xL

a

b

2x3L + 9x2LxS + 12xLx

2S + 4x

3S

x2L + 2xLxS + 3x2S

− xSxL

x2L + xLxS + x2Sx2L + 2xLxS + 3x

2S

tS, (1)

tS =1

4xS

a

b

2x3S + 9xLx2S + 12x

2LxS + 4x

3L

x2L + 2xLxS + 3x2S

− xLxS

x2L + xLxS + x2Sx2L + 2xLxS + 3x

2S

tL.

Note that, even though operators do not set quantities but prices, the networks’ prices

are strategic substitutes as ∂tI/∂tJ < 0. This contrasts with price setting under Bertrand

competition and with vertically related markets with double marginalization problems

where prices are strategic complements.

As pointed out above, many European countries have either discussed or actually

introduced asymmetric regulation patterns according to which only the large operators’

termination fees are regulated while smaller operators are left unregulated. In this

context, the following observation should be interesting:

Remark 1. As termination rates under consumer ignorance are strategic substitutes,any downward regulation of the large operators’ termination rates will, ceteris paribus,

lead to an increase in the small operators’ termination rates (as ∂tI/∂tJ < 0).

As can be easily seen by equation (1), if tL were regulated down to zero, tS would

take the maximum value for all tL ≥ 0. While regulation usually takes the form of

cost based price regulation (see European Commission, 2004), Remark 1 implies that

the small mobile operators will increase their termination fees above the unregulated

equilibrium level for any binding regulatory constraint that actually suppresses the large

operators’ termination rates below the unconstrained equilibrium level. If instead mobile

termination rates are left unregulated, the unregulated equilibrium termination rates can

be obtained by solving the best response functions given above:

tL =1

4xL

a

b

2x5S + 9xLx4S + 22x

2Lx

3S + 31x

3Lx

2S + 15x

4LxS + 2x

5L

2x4L + 6x3LxS + 11x

2Lx

2S + 6xLx

3S + 2x

4S

, (2)

tS =1

4xS

a

b

2x5L + 9x4LxS + 22x

3Lx

2S + 31x

2Lx

3S + 15xLx

4S + 2x

5S

2x4L + 6x3LxS + 11x

2Lx

2S + 6xLx

3S + 2x

4S

.

Comparing tL and tS we can state the following result:

Proposition. The small operators’ termination rate, tS, is strictly larger than thelarge operators’ rate, tL, ( tS > tL) if xL > xS.

Proof. See Appendix.

The intuition for this result is that the small operators only have a relatively small

impact on the average price, which determines demand. Hence, if a small operator

6

0

0.5

1

1.5

2

2.5

3

3.5

0.09

0.15

0.21

0.27

0.33

0.39

0.45

0.51

0.57

0.63

0.69

0.75

0.81

0.87

0.93

0.99

g

t

ts

tLtM

g*

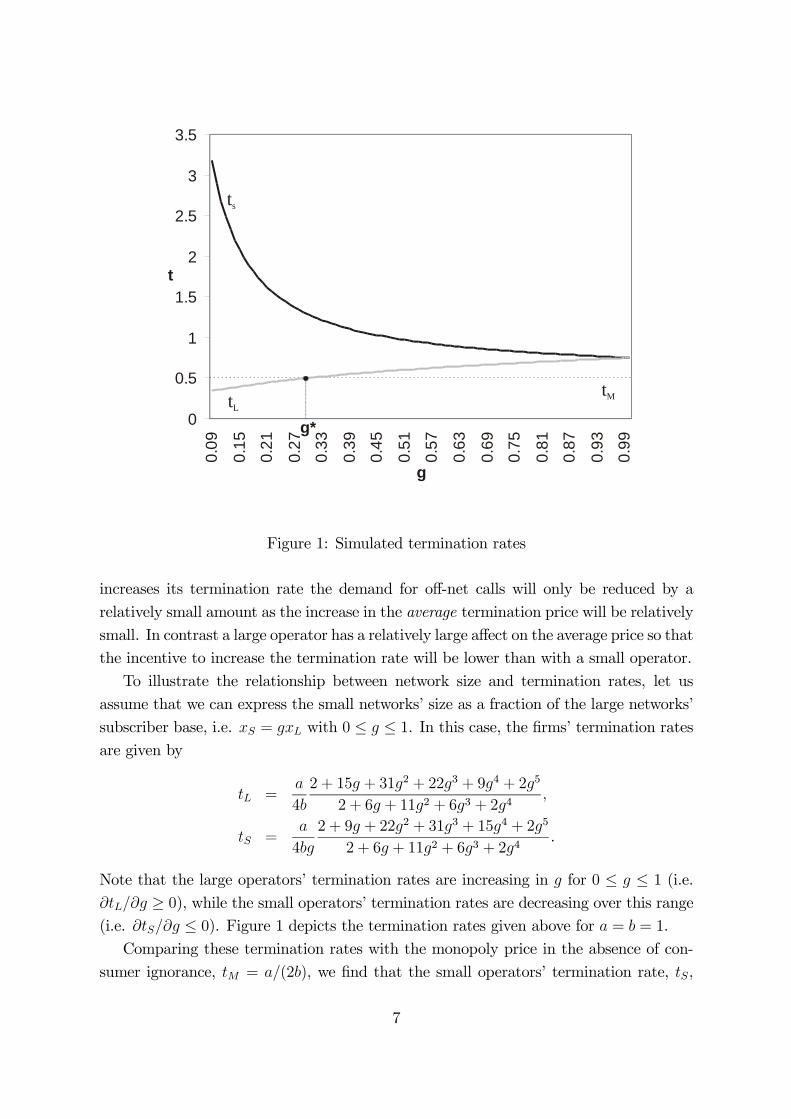

Figure 1: Simulated termination rates

increases its termination rate the demand for off-net calls will only be reduced by a

relatively small amount as the increase in the average termination price will be relatively

small. In contrast a large operator has a relatively large affect on the average price so that

the incentive to increase the termination rate will be lower than with a small operator.

To illustrate the relationship between network size and termination rates, let us

assume that we can express the small networks’ size as a fraction of the large networks’

subscriber base, i.e. xS = gxL with 0 ≤ g ≤ 1. In this case, the firms’ termination ratesare given by

tL =a

4b

2 + 15g + 31g2 + 22g3 + 9g4 + 2g5

2 + 6g + 11g2 + 6g3 + 2g4,

tS =a

4bg

2 + 9g + 22g2 + 31g3 + 15g4 + 2g5

2 + 6g + 11g2 + 6g3 + 2g4.

Note that the large operators’ termination rates are increasing in g for 0 ≤ g ≤ 1 (i.e.∂tL/∂g ≥ 0), while the small operators’ termination rates are decreasing over this range(i.e. ∂tS/∂g ≤ 0). Figure 1 depicts the termination rates given above for a = b = 1.

Comparing these termination rates with the monopoly price in the absence of con-

sumer ignorance, tM = a/(2b), we find that the small operators’ termination rate, tS,

7

will always exceed tM , while the large operators’ rate, tL, will only exceed the monopoly

benchmark for g ≥ g∗ ≈ 0.29783. Otherwise, the negative pricing externality createdby the small operator is so large that the large operators’ price will be constrained even

below the monopoly level.

In summary, as can be seen from the Proposition and Remark 1, our theoretical model

suggests (a) that a network’s termination rate is the higher the smaller the network’s

size (as measured through its subscriber base) and vice versa and (b) that asymmetric

regulation of only the larger operators in a market will, ceteris paribus, induce the

smaller operators to increase their termination rates. In the following section, we will

provide some empirical evidence to test these two hypotheses.

3 Empirical Evidence

3.1 Data

To test our model’s hypotheses empirically, we have assembled data on mobile termi-

nation rates and the subscriber base of 48 different mobile operators from 17 European

countries.4 Data on the networks’ subscriber base has been gathered from Mobile Com-

munications, while the termination rates have been obtained from various issues of the

Cullen Report, published by Cullen International. Information on regulatory regimes has

also been obtained from this source and also from various regulatory authorities. Our

earliest observations are from February 2001 and our most recent one from February

2003. Hence, our data set includes regulated and unregulated termination rates. While

we use monthly data in principle, there are missing observations for several months due

to limited data availability.5 Therefore, we cannot conduct a panel data analysis, but

have to confine our analysis to pooled estimations.

The endogenous variable of our analysis is the operators’ termination rate. Since

termination rates differ in their structure across countries and at times even across

firms,6 we have calculated termination rates for a twominute call. We have also restricted

the analysis to peak-time tariffs. As exogenous variables we have used (apart from a

4These are the 15 EU countries plus Norway and Switzerland.5In total, we have data for 13 different months, namely: February 2001, April 2001, June 2001,

September 2001, November 2001, January 2002, March 2002, May 2002, July 2002, September 2002,October 2002, December 2002, and February 2003. Since we cannot observe all operators’ prices forevery observation point (especially in 2001), we have less than 13 observations for some of the 48operators. The total number of observations is 458.

6While most countries use linear tariffs, some countries have two-part tariffs consisting of a callset-up fee and a variable per minute charge.

8

constant) market shares (based on subscriber numbers), the Herfindahl Index (HHI),

market size (based on total subscriber numbers), a dummy variable (GSM1800) for the

mobile network technology employed by an operator and two dummy variables (RC and

RF ) describing the regulatory framework in place.

The dummy variable describing an operator’s technology (GSM1800) is set to one

if an operator excluxively uses GSM1800 MHz technologies, while it is set to zero if an

operator either exclusively uses GSM900 MHz technologies or hybrid networks. This

dummy varibale is introduced in order to account for potential cost differences between

networks, as pure GSM1800 MHz networks are sometimes considered to be somewhat

more costly (see, e.g., Ofcom, 2004). In fact, as virtually all European countries have

sequentially licensed mobile operators, it is usually the smaller operators (which have

entered the markets at a later stage), who have exclusively adopted the GSM1800 MHz

technology. Therefore, we have included an explanatory dummy variable (GSM1800)

to account for any possible cost differences.

Concerning the regulatory framework the variable RC is set to one if any mobile

termination rate in a specific country is regulated, while RC is zero if none of the mobile

operators’ termination rates is regulated. Furthermore, the variable RF is set to one if

a specific firm’s termination rate is regulated, while RF is zero if the firm’s termination

rate is not regulated. Using two dummy variables is necessary because in some countries

all mobile termination rates are regulated, in others only some termination rates (usually

those of large operators) are regulated, and in others again none are regulated. Hence,

RC = RF = 1 if all firms are regulated in a country, RC = RF = 0 if none is regulated,

and RC = 1 and RF ∈ [0, 1] if some firms, but not all are regulated in a country. Wehave also used dummy variables indicating the respective year and country to control

for eventual time trends and country-specific effects.

Before we present our empirical results let us briefly provide some descriptive statis-

tics of our variables to shed some light on price trends and regulatory practice in Europe.

The (unweighted) average termination rate across all 48 operators decreases from 54.2

Eurocents in 2001 to 38.5 Eurocents in 2002 and 37.8 Eurocents in February 2003. While

the maximum rate in 2001 has been 80 Eurocents and the minimum 37 Eurocents, in

2003 the maximum rate has been 54 Eurocents and the minimum 19.7 Eurocents. Over

this period the regulated firms’ average termination rate has been 42.3 Eurocents, while

it has been 45.3 Eurocents for unregulated firms. Looking at the different countries, the

average termination rate in regulated countries has been 44.4 Eurocents, while it has

only been 42.8 Eurocents in unregulated countries. This indicates that termination rates

have been higher on average in regulated countries. In this context, it may be interesting

to note that only 14 operators had been regulated in February 2001 while there have

9

been 26 regulated firms in February 2003.

The observed firms’ average market share has been steadily around 33 percent, rang-

ing from less than 2 per cent for the smallest operator (Italy’s Blu in February 2001)

and more than 75 percent for the largest operator (Norway’s Telenor also in February

2001). Finally, market size obviously varies considerably between countries ranging from

304,000 subscribers in Luxembourg in February 2001 up to more than 57 million sub-

scribers in Germany in February 2003. More detailed descriptive statistics can be found

in Table 1 in the Appendix.

3.2 Empirical Results

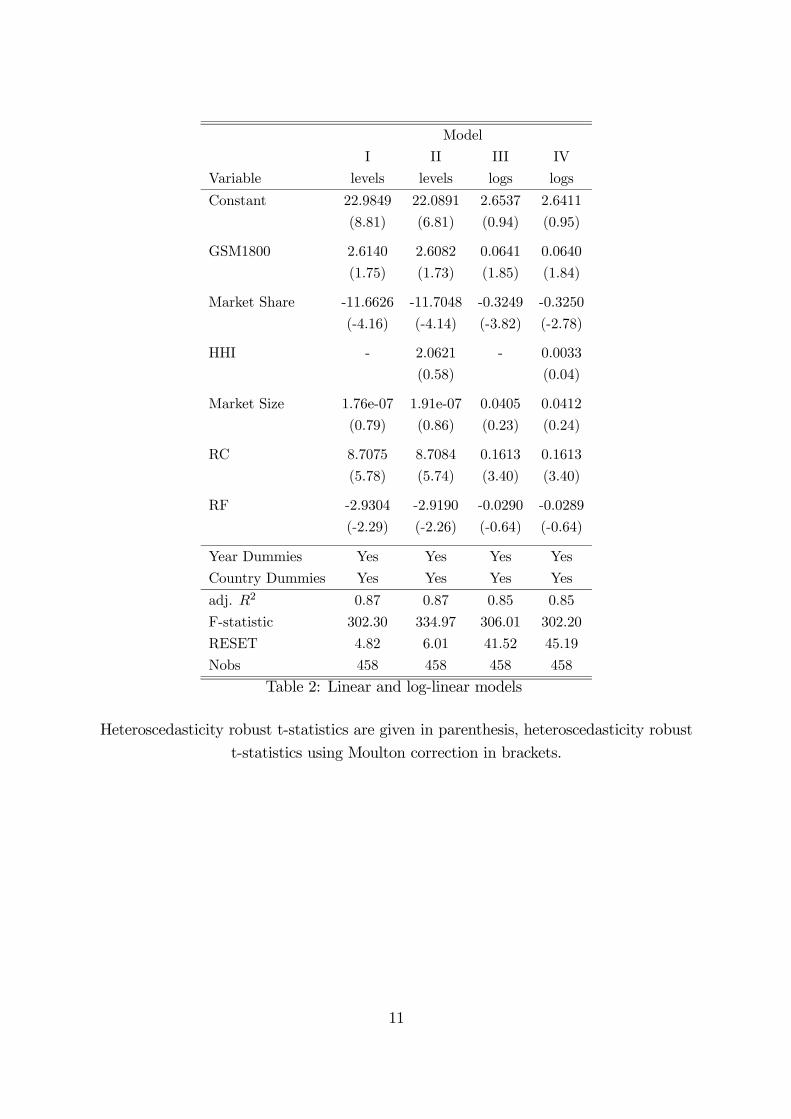

Table 2 reports estimation results of price levels and logarithms of the price (in that

case also using logarithms of the market size). In order to determine an adequate

functional form we have applied Ramsey’s (1969) RESET tests for omitted variables.

As can be observed from Table 2, linear specifications are found to be adequate. In

the regressions we have also calculated Moulton (1990) corrected t-statistics in order to

correct for potential biases that arise if aggregated variables are used to measure effects

on micro units. Since the assumption of independent disturbances is usually violated

with aggregated exogenous variables, using ordinary least squares can lead to standard

errors that are seriously biased downwards. Hence, it is important to bear in mind the

data’s group structure as suggested by Moulton (1990).7

The analysis reveals that technology has a positive and statistically significant impact

on termination rates, at least at the 10% level of significance. Firms using exclusively

the GSM1800 technology tend, therefore, to have higher termination rates by about 2.6

Eurocents on average for a two minute peak-time call.

Operators’ market shares tend to have a statistically significant impact on their

termination rates with the sign as predicted by our model, i.e. smaller operators tend to

have significantly higher mobile termination rates. In light of our hypothesis, this may

indeed indicate that especially the smaller operators can exploit consumers’ ignorance

and set relatively high termination rates as they only have small effects on average prices.

7Furthermore, we have applied Hausman-Wu test to analyze a possible endogeneity of market struc-ture. Even though we have assumed market structure to be exogenous in the theoretical part of thispaper, endogeneity could of course be an empirical problem. In none of the specifications the hypothesesof exogenous market structure could have been rejected.

10

Model

I II III IV

Variable levels levels logs logs

Constant 22.9849 22.0891 2.6537 2.6411

(8.81) (6.81) (0.94) (0.95)

GSM1800 2.6140 2.6082 0.0641 0.0640

(1.75) (1.73) (1.85) (1.84)

Market Share -11.6626 -11.7048 -0.3249 -0.3250

(-4.16) (-4.14) (-3.82) (-2.78)

HHI - 2.0621 - 0.0033

(0.58) (0.04)

Market Size 1.76e-07 1.91e-07 0.0405 0.0412

(0.79) (0.86) (0.23) (0.24)

RC 8.7075 8.7084 0.1613 0.1613

(5.78) (5.74) (3.40) (3.40)

RF -2.9304 -2.9190 -0.0290 -0.0289

(-2.29) (-2.26) (-0.64) (-0.64)

Year Dummies Yes Yes Yes Yes

Country Dummies Yes Yes Yes Yes

adj. R2 0.87 0.87 0.85 0.85

F-statistic 302.30 334.97 306.01 302.20

RESET 4.82 6.01 41.52 45.19

Nobs 458 458 458 458

Table 2: Linear and log-linear models

Heteroscedasticity robust t-statistics are given in parenthesis, heteroscedasticity robust

t-statistics using Moulton correction in brackets.

11

In contrast, the Herfindahl Index does not appear to be statistically significant for

explaining termination rates. Hence, market concentration is apparently less of an issue

for the determination of termination rates than an operator’s relative size or, more

precisely, its relative smallness. Admittedly, we would expect that concentration had a

significant impact on termination rates as well, since under consumer ignorance large

asymmetries should lead the small operators to charge higher termination rates as Figure

1 illustrates. However, market shares and concentration are usually highly correlated,

which may reduce the explanatory power of HHI in combination with market shares

due to their collinearity.

While market size is not statistically significant, we find statistically significant ef-

fects for the regulatory framework. On the one hand, and not surprisingly, firm-specific

regulation tends to lower the regulated firm’s termination rate. Regulated firms termi-

nation charges are lower by about 3 Eurocents for a two minute peak—time call. On

the other hand, termination rates in regulated countries tend to be higher overall by

about 8.7 Eurocents for a two minute peak—time call. Remember that while RF is a

dummy variable set equal to one (and otherwise zero) for regulated firms, independent

of the regulation of their competitors, RC always equals one if at least one firm in

the same country is regulated. The estimated coefficient of RF therefore measures the

average difference between regulated firms’ termination rates and average termination

rates overall. The coefficient of RC, in contrast, estimates the difference between aver-

age termination rates in regulated and unregulated countries. The combination of both

variables (RC-RF ) thus calculates the markup in average termination rates for unregu-

lated firms whose competitors are regulated. Hence unregulated firms’ termination rates

in regulated countries are higher by about 8.7-(-2.9)=11.6 Eurocents for a two minute

peak—time call.

Overall, the above results are consistent with our hypothesis formulated in Remark 1,

i.e. that downward regulation of competitors’ termination rates leads, ceteris paribus, to

an increase in the unregulated firms’ termination rate, as termination rates are strategic

substitutes if consumers are ignorant.

3.3 Discussion

In summary, our empirical analysis tends to support the hypotheses derived from our

theoretical model. Firstly, smaller mobile operators tend to have higher termination rates

than their larger competitors. Secondly, downward regulation of the large operators’

rates tends to have a positive effect on the termination rates of unregulated operators.

At this point, some general remarks about the desirability of regulating mobile ter-

mination rates may be adequate. First of all, it is important to emphasize that customer

12

ignorance by itself is not a justification for economic regulation.8 In fact for the con-

sumer ignorance problem remedies other than price regulation (such as an automated

price information) may already solve the problem. This would not require Government

intervention, as market mechanisms may solve these information problems. However,

as long as consumer ignorance plays a role, our paper offers one potential explanation

for the apparently counter-intuitive observation that smaller operators charge higher

prices.9

With respect to the more general question whether mobile termination rates should

be regulated at all, one should note that there are a number of strong arguments against

their regulation: First of all, it is not only necessary, but even efficient that some prices

exceed marginal costs in an industry characterized by significant sunk and common

costs. If mobile termination rates exceed marginal costs because of Ramsey-type pric-

ing patterns, there is little reason for regulatory intervention (see, e.g., Kruse, 2003, or

Koboldt, 2003). And secondly, profits from high termination fees may be used to subsi-

dize mobile handsets, thereby allowing a faster diffusion of mobile telephony in general

and new mobile services (such as UMTS) in particular (see Wright, 2002). While these

arguments have to be weighed against arguments in favor of regulation (such as some

potentially inefficient substitution between fixed-line and mobile telephony), we concur

with Crandall and Sidak (2004) that overall there are convincing arguments against the

regulation of mobile termination fees.

In addition to the general concerns about the regulation of mobile termination rates,

this paper has also demonstrated that there are significant costs associated with an

asymmetric regulation of mobile termination rates, which is sometimes seen as some

”lighter” form of regulation and, therefore, applied in a number of European countries.

As we have shown asymmetric regulation of only the larger operators leads smaller

operators to increase their termination fees even further if consumers are ignorant about

operator-specific termination charges. Hence, we would issue a warning against this

supposedly ”lighter” form of regulation.

8We are grateful to one referee to point this out.9As one referee pointed out Ramsey-like pricing patterns in market characterized by economies of

scale and scope may offer an alternative explanation. As cost differences do not suffice to explain thedifferent pricing behavior of large and small firms, this would require very different elasticities for callsto small and to large networks. While this may, in theory, be possible, there is currently no empiricalevidence to support the view that calls to smaller mobile networks have different elasticities than callsto larger networks.

13

4 Conclusions

In this paper, a simple theoretical model has been developed to show (a) that a mobile

network’s termination rate is the higher the smaller the network’s size (as measured

through its subscriber base) and vice versa and (b) that asymmetric regulation of only

the larger operators in a market will, ceteris paribus, induce the smaller operators to

increase their termination rates. These theoretical results are based on the notion that

consumer ignorance induces pricing externalities. In fact, empirical evidence from 48

European mobile operators supports these hypotheses. In all our regressions market

share has a statistically significant and negative impact on firms’ termination rates, as

predicted by the model. Furthermore, unregulated firms in regulated markets tend to

have higher termination rates than firms in unregulated markets.

We believe that these findings may be helpful for regulatory authorities that analyze

mobile termination rates and their regulation. While we hold the view that there are,

quite generally, strong reasons for not regulating mobile termination rates (see, e.g.,

Kruse, 2003; Crandall and Sidak, 2004), we do not want to repeat these general argu-

ments here. Instead our paper complements these arguments, as we have shown that

an asymmetric regulation pattern (where only the larger mobile operators’ termination

rates are regulated) is likely to carry perverse incentives for smaller operators to increase

their termination rates.

One should keep in mind, however, that we have adopted a very simple model of

termination rate setting. In particular, we have abstracted from the challenging issue

of endogenous market shares and ignored the possibility of further entry into mobile

telecommunications markets. Future research into these directions might prove to be

instructive for theorists and practitioners alike.

References

Bühler, S. (2002). “Network Competition and Supermodularity - A Note.” Discussion

Paper 0302, University of Zurich.

Bühler, S. & Haucap, J. (2004). “Mobile Number Portability.” Journal of Industry,

Competition and Trade. 4, 223-238.

Crandall, R.W. & Sidak, G. (2004). “Should Regulators Set Rates to Terminate Calls

on Mobile Networks?” Yale Journal on Regulation. 21, 261-314.

European Commission. (2003). Recommendation on Relevant Product and Service

Markets Within the Electronic Communications Sector, COM(2003) 497. Brussels:

14

February 2003.

European Commission. (2004). Tenth Report from the Commission on the Implemen-

tation of the Telecommunications Regulatory Package, COM(2004) 759. Brussels:

December 2004.

Gans, J.S. & King, S.P. (2000). “Mobile Network Competition, Customer Ignorance

and Fixed-to-Mobile Call Prices.” Information Economics and Policy. 12, 301-

327.

Koboldt, C. (2003). “A Perfect Miss: Cost-Based Regulation of Mobile Termination

Charges.” In J. Kruse & J. Haucap (eds.), Mobilfunk zwischen Wettbewerb und

Regulierung. München: Fischer Verlag, pp. 89-109.

Kruse, J. (2003). “Regulierung der Terminierungsentgelte der deutschen Mobilfunk-

netze?” Wirtschaftsdienst. 83, 203-208.

Laffont, J.J., Rey, P. & Tirole, J. (1998). “Network Competition I: Overview and

Nondiscriminatory Pricing.” RAND Journal of Econmics. 29, 1-37.

Laffont, J.J. & Tirole, J. (2000). Competition in Telecommunications. Cambridge,

MA: MIT Press.

Moulton, B.R. (1990). “An Illustration of a Pitfall in Estimating the Effects of Aggre-

gate Variables on Micro Units.” Review of Economics and Statistics. 72, 334-338.

Ofcom (2004), Wholesale Mobile Voice Call Termination. London: June 2004. Avail-

able at http://www.ofcom.org.uk/consultations/past/wmvct/wmvct.pdf.

Ramsey J.B. (1969). “Tests for Specification Error in Classical Linear Least Squares

Regression Analysis.” Journal of the Royal Statistical Society Series B. 31, 350-

371.

Salsas, R. & Koboldt, C. (2004). “Roaming Free? Roaming Network Selection and

Inter-Operator Tariffs.” Information Economics and Policy. 16, 497-517.

Wright, J. (2002). “Access Pricing Under Competition: An Application to Cellular

Networks.” Journal of Industrial Economics. 50, 289-315.

15

Appendix

Proof of the Proposition.We have to compare tL and tS as given in (2). Obviously, tL < tS iff tL − tS < 0,

which can also be written as

1

2a8x8S + 30x

7SxL + 43x

6Sx

2L + 35x

3Lx

5S − 35x5Lx3S − 43x6Lx2S − 30xSx7L − 8x8L

xLb (16x6S + 105x4Lx

2S + 48x

5SxL + 105x

4Sx

2L + 148x

3Sx

3L + 16x

6L + 48x

5LxS)xS

< 0.

The sign of the left-hand side of the inequality above is determined by the sign of

8(x8S − x8L) + 30(x7SxL − xSx

7L) + 43(x

6Sx

2L − x6Lx

2S) + 35(x

3Lx

5S − x5Lx

3S).

Close inspection reveals that this term is always negative for xS < xL, so that tL < tS

always holds for xS < xL.

Table 1: Summary statistics

Year Price Market Share HHI

2001 Mean 54.15 0.3213 0.3872

Range 43.00 0.6005 0.5555

Min 37.00 0.0239 0.0722

Max 80.00 0.6244 0.6278

S.D. 9.10 0.1580 0.1004

2002 Mean 38.48 0.3194 0.3731

Range 40.48 0.5518 0.5160

Min 19.70 0.0404 0.0555

Max 60.18 0.5923 0.5715

S.D. 9.47 0.1530 0.0915

2003 Mean 37.80 0.3161 0.3801

Range 34.30 0.5110 0.7037

Min 19.70 0.0456 0.0624

Max 54.00 0.5567 0.7661

S.D. 8.97 0.1537 0.1181

Total Mean 43.78 0.3199 0.3791

Range 60.30 0.6005 0.7106

Min 19.70 0.0239 0.0555

Max 80.00 0.6244 0.7661

S.D 11.93 0.1544 0.0972

16